Erich M. Patten

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| The Cutler Trust | |

CUTLER EQUITY FUND

CUTLER FIXED INCOME FUND

CUTLER EMERGING MARKETS FUND

ANNUAL REPORT

June 30, 2016

THE CUTLER TRUST

TABLE OF CONTENTS

| | Page |

Letter to Shareholders | 2 |

Management Discussion of Fund Performance | 4 |

Performance Information | 10 |

Portfolio Information | 13 |

Schedules of Investments | 16 |

Statements of Assets and Liabilities | 27 |

Statements of Operations | 28 |

Statements of Changes in Net Assets | 29 |

Financial Highlights | 32 |

Notes to Financial Statements | 35 |

Report of Independent Registered Public Accounting Firm | 47 |

About Your Fund’s Expenses | 48 |

Federal Tax Information | 49 |

Trustees and Officers of the Trust | 50 |

Additional Information | 52 |

Approval of Investment Advisory Agreement | 53 |

1

THE CUTLER TRUST

LETTER TO SHAREHOLDERS

To The Cutler Funds Shareholders:

The enclosure represents the annual report to shareholders for the Cutler Trust for the year ended June 30, 2016. This past fiscal year has been quite eventful, yet little seems to have changed. Investors, governments and companies continue searching for answers to the slow growth world in which we find ourselves today. Last year, we stated in this report, “As we see things from here, we do not anticipate dramatically higher rates going forward. Our Funds are positioned to benefit from a “mild” rate environment; we believe dividend stocks should hold relative value versus other income producing investments, and we view the Fixed Income Fund as well-positioned to benefit from a flattening yield curve. This mild-rate environment should allow further stimulus for a rising stock market, but at the onset of the end of ZIRP (Zero Interest Rate Policy), we are proceeding cautiously with our security selection.”

We feel similarly today.

Last year, the predominant investment theme was the strength of the U.S. Dollar. This is still the most frequently cited issue on company earnings calls, but the impact has lessened. A currency headwind makes it very challenging for companies with international exposure to grow earnings, and U.S. exports were increasingly under pricing pressure. The trend remains intact, but the impact is not as profound. Following the dollar, Brexit (the U.K. vote to exit the European Union) has recently been the most common theme that CEO’s have discussed. Brexit may have long-term repercussions on global trade, but the near-term impacts have been limited. In fact, Brexit has been primarily a positive for equities and fixed income thus far, as central banks have remained stimulative in deference to a future unknown impact.

This past year, the Cutler Trust added the Cutler Emerging Markets Fund to the fund family. This fund was established to take advantage of global macro-economic trends that Cutler feels will hold significant investment opportunities going forward. The growth of a global middle-class will create new businesses, entrepreneurs and success stories over the next century. As always, Cutler has approached this asset class with a bias toward income and dividend paying securities. In fact, for the vast majority of the portfolio, we look for a 15-year dividend history, providing further transparency and risk management to the management style.

2

THE CUTLER TRUST

LETTER TO SHAREHOLDERS (Continued)

As always, we welcome your questions or requests for a personal meeting. Thank you for your continued support.

Sincerely,

|

|

Matthew C. Patten | Erich M. Patten |

Chairman | Chief Investment Officer |

The Cutler Trust | Cutler Investment Counsel, LLC |

| | |

| |

Xavier J. Urpi | |

Director of Fixed Income | |

Cutler Investment Counsel, LLC | |

Before investing you should carefully consider the Cutler Funds’ investment objectives, risks, charges and expenses. This and other information is in the prospectus, a copy of which may be obtained by calling 1-800-228-8537. Please read the prospectus carefully before you invest.

The views in this report were those of the Cutler Funds’ investment adviser as of June 30, 2016 and may not reflect its views on the date this report is first published or anytime thereafter. These views are intended to assist shareholders in understanding their investment in the Cutler Funds and do not constitute investment advice.

3

CUTLER EQUITY FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

1) | How did the Equity Fund perform last year? |

The Equity Fund returned 7.40% for the year ended June 30, 2016.

2) | What were the most significant market factors affecting the Fund’s performance during the past year? |

Market factors were similar to 2015, including:

| | 1) | The increase in the U.S. Dollar versus other foreign currencies |

| | 3) | Incrementally positive economic growth |

3) | Why did the Fund outperform relative to the Benchmark? |

The S&P 500 Total Return Index (the “S&P 500”) returned 3.99% for the year ended June 30, 2016. The Equity Fund performance was driven by both macro sector allocations and fundamental stock selection. The Equity Fund’s overweight in utilities stocks produced the greatest contribution to outperformance, while the health care positions had the largest stock specific impact on the total performance. Overall, this past year represented a more amenable investment environment for dividend stocks, as interest rates remained low and value outperformed growth.

4) | What strategies did you use to manage the Fund? |

Cutler’s investment process focuses on dividends as the primary driver of investment returns. The strategy was unchanged in the previous year, and the management of the Equity Fund was consistent with previous years. We look for holdings in the portfolio that maintain a 10-year record of consistent dividend payments and typically have a total market capitalization of at least $10 billion. We seek relative value as compared to other companies in similar industries. The Equity Fund has a value bias, but is benchmarked to the S&P 500. The strategy is further detailed in the Equity Fund’s prospectus.

5) | What were the primary strategic factors that guided your management of the Fund? |

Cutler’s dividend criteria have been the primary strategic factors used in managing the Equity Fund this past year. For example, Cutler looks for companies that have at least a 10-year history of maintaining or increasing dividends. We believe this criterion results in a portfolio of companies with stable earnings and sound business models. In addition, the Equity Fund’s Portfolio Managers continue to focus on companies they believe offer attractive current yields and the potential for total return. A lower risk profile than the market was also a primary strategy, as the Equity Fund maintained a below market “beta,” a measure of systematic risk, throughout the time period.

4

CUTLER EQUITY FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

(Continued)

Turnover of the Fund remained low this past year at just over 10%. We have remained patient with our current holdings in a sustained bull market, believing that we are well-positioned for volatility should the market direction shift.

6) | What were some of the key trends in each of the regions/significant industries in which the Fund invests? |

The Equity Fund’s holdings remain 100% domiciled in the U.S., and the strategies employed do not have any additional regional bias. In certain cases, holdings may have legal registration outside of the U.S., but are considered domestic due to the locality of their operations.

The U.S. markets continued the bull market that was born from the financial crisis, albeit the pace of returns slowed. Earnings growth has been driven substantially by share buybacks, as GDP growth has been below long-term trends for an economic recovery. Due to this lackluster growth, the Federal Reserve has remained accommodative, keeping rates near zero during the past year. The prospect of higher short-term rates has led to a U.S. dollar rally versus most currencies, which remains one of the most important economic trends. Oil has also been a significant trend, as the bear market continued for the first half of the fiscal year and then reversed course as 2016 progressed.

7) | Which securities helped the Fund’s performance against the Benchmark? |

| | a) | Chubb Corporation (The) |

| | b) | Becton, Dickinson & Company |

| | e) | Texas Instruments, Inc. |

8) | Did any securities hurt the Fund’s performance against the Benchmark? |

| | c) | National Fuel Gas Company |

| | d) | Walt Disney Company (The) |

* | Apple was not held in the Equity Fund but represents a large portion of S&P 500, the Equity Fund’s benchmark. The negative 26% return of Apple, contributed +0.72% performance to the Equity Fund versus the S&P 500 during the period. Amazon.com was also not held, but represents a large portion of the benchmark. The 61% return of Amazon.com contributed -0.75% performance to the Equity Fund versus the S&P 500 during the period. |

5

CUTLER FIXED INCOME FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

1) | How did the Fixed Income Fund perform last year? |

The Fixed Income Fund was up 2.91% for the year ended June 30, 2016.

2) | What were the most significant market factors affecting the Fixed Income Fund’s performance during the past year? |

Market factors included:

| | 1) | Global demand for yield |

| | 2) | Continued quantitative easing and rate reductions around the globe by central banks |

| | 3) | Slow to moderate global economic growth |

| | 4) | Fall of oil prices leading to low inflation expectations |

3) | Explain the Fixed Income Fund’s performance relative to the benchmark. |

The Barclays Intermediate U.S. Government/Credit Index (the “Index”) was up 4.33% for the year ended June 30, 2016. The under performance of the Fixed Income Fund during this time period can be attributed to a more conservative stance in the duration of the portfolio versus the Index in a period of time when interest rates continued to decline.

4) | What strategies did you use to manage the Fixed Income Fund? |

The Fixed Income Fund anticipated a flattening of the yield curve and tried to capitalize on this trend, brought about by demand by pension plans, insurance companies and international funds for high quality yields in the long-term sector of the U.S. fixed income market. This demand caused long-term interest rates to decline much more than short-term interest rates thereby causing a flattening term structure of interest rates.

Another strategy employed was investing in interest only stripped mortgage-backed (IO) securities. These securities provide interest should any refinancing occur and with interest rates falling refinancing increased. This niche sector of the market produced cash flows that exceeded Cutler’s expectation to the Fixed Income Fund; however, due to their short-duration, the Fund’s IOs did not perform as well as longer-dated securities.

5) | What were the primary strategic factors that guided your management of the Fixed Income Fund? |

Cutler, as a consequence of global central banks’ posturing on quantitative easing, felt that long-term interest rates would continue to fall not only world-wide, but here in the U.S.. In addition, these lower interest rates would financially motivate real-estate investors to refinance their multi-family homes prematurely in order to ‘lock-in’ lower rates and save costs in the long-term. This was the basis of our strategy to invest in IO securities that are backed by multi-family loans. These securities, in such a scenario, would provide a significant interest payment. We also believe

6

CUTLER FIXED INCOME FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

(Continued)

that the continued chatter by the Federal Reserve regarding increasing short-term rates may have pushed some of those loan holders that were on the fence to refinance. The combination of these two strategies was a positive factor, but the conservative nature of the portfolio detracted from that value versus the Index.

6) | What were some of the key trends in each of the regions/significant industries in which the Fixed Income Fund invests? |

The Fixed Income Fund is heavily weighted in the U.S. Government agency commercial mortgage-backed securities sector. This sector has had excellent performance over the last few years as the combination of lower interest rates and higher real estate values has elevated the value of the securities. However, the key this past year was not only those elements, but the securities which we focused on were mostly U.S. Government-backed thereby reducing the credit risk. This past year, with the drop in oil prices causing stress in not only the energy sector of the fixed income markets, U.S. Government-backed bonds performed very well compared to the credit sector.

The credit sector, after the debacle in the second half of 2015, in which oil prices tumbled causing a large price decline in bonds backed by oil and commodities, came roaring back in the first six months of 2016. Our strategy did not incorporate a tactical strategy to take advantage of the snap-back, as we position the Fund more conservatively than the Index.

The Fund also invests in U.S. Government agency securities in order to provide safety and liquidity. This sector performed well over the last fiscal year; however, it struggles to provide much yield due to its high quality and short-term structure. Additionally, this sector typically lags most other riskier credits during bull markets where interest rates decline along with yield spreads narrowing.

7) | Which securities helped the Fixed Income Fund’s performance? |

| | 1. | Wachovia Bank Commercial Mortgage Trust, IO, Series 2005-C21, 0.078%, 10/01/44 |

| | 2. | U.S. Treasury Bonds, Stripped Principal Payment, 2.500%, 11/15/44 |

| | 3. | FANNIEMAE-ACES, IO, Series 2015-M3, 4.524%, 06/25/18 |

8) | Did any securities hurt the Fixed Income Fund’s performance? |

| | 1. | FANNIEMAE-ACES, IO, Series 2011-M9, 0.094%, 01/25/21 |

| | 2. | Merrill Lynch Mortgage Trust, IO, Series 2008-C1, 144A, 0.477% Due 02/12/51 |

7

CUTLER EMERGING MARKETS FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

1) | How did the Emerging Markets Fund perform last year? |

From July 2, 2015 to June 30, 2016 the return of the Emerging Markets Fund was -15.43%. This negative performance was primarily in the first two months after inception, as the Emerging Markets Fund returned -6.80% and -9.44% in July and August, 2015, respectively.

2) | What were the most significant market factors affecting the Emerging Markets Fund’s performance during the past year? |

In August 2015, China devalued their currency, which roiled global markets. The Emerging Markets Fund was also impacted by global currency fluctuations and the supporting rally of commodity based economies.

3) | Explain the Emerging Markets Fund’s performance relative to the benchmark. |

The MSCI Emerging Markets Total Return Index had a return of -12.04% during the period. The largest impact was the performance of securities domiciled in Brazil, as that stock market had a significant rally during the period.

4) | What strategies did you use to manage the Emerging Markets Fund? |

Cutler utilizes a universe which we refer to as “The 15DU.” The 15DU consists of companies in the emerging markets index that have paid dividends for at least 14 of the last 15 years. The bulk of the portfolio is comprised of these securities. Additionally, Cutler will use ETFs to gain exposure to markets with less liquidity or as a way to provide trading liquidity for shareholder transactions.

5) | What were the primary strategic factors that guided your management of the Emerging Markets Fund? |

In combination with our economic outlook, Cutler considers geo-political risk when assessing our country weightings. In general, Cutler is biased against less stable political environments. Instead, we prefer to invest into faster growing economies with favorable demographic trends. Cutler believes that emerging markets investing should primarily be focused on consumer based investment themes, not commodities. When possible, we will look for 15DU securities that are exposed to a growing middle-class in countries and regions.

6) | What were some of the key trends in each of the regions/significant industries in which the Emerging Markets Fund invests? |

Emerging markets are diverse, yet global correlations exist that impact total portfolio performance. The most significant trend of the past year occurred in the second half of the fiscal year, which was a broad-based commodity rally off of February lows. This provided strength in many global

8

CUTLER EMERGING MARKETS FUND

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

(Continued)

currencies, which was a tailwind for the Emerging Markets Fund. It also led to a strong rally in many commodity stocks, in which the Emerging Markets Fund has a general underweight position. Additional trends include a slow devaluation of the Chinese Yuan, broadly lower interest rates, mild global inflation, and buoyant real estate valuations.

7) | Which securities helped the Emerging Markets Fund’s performance? |

| | a. | Samsung Electronics Company Ltd. |

| | b. | Telekomunikasi Indonesia Persero Tbk PT - ADR |

| | c. | Sinopec Shanghai Petrochemical Company Ltd. - ADR |

| | d. | China Resources Beer Holdings Company Ltd. |

| | e. | President Chain Store Corporation |

8) | Did any securities hurt the Emerging Markets Fund’s performance? |

| | a. | iShares MSCI Taiwan ETF |

| | b. | iShares MSCI South Korea Capped ETF |

| | c. | iShares China Large-Cap ETF |

| | d. | Huaneng Power International, Inc. - ADR |

| | e. | America Movil S.A.B. de C.V. – Series L - ADR |

9

CUTLER EQUITY FUND

PERFORMANCE INFORMATION

June 30, 2016 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in

Cutler Equity Fund and S&P 500 Total Return Index

Average Annual Total Returns(a)

(for periods ended June 30, 2016) |

| | 1 Year | 5 Years | 10 Years | |

Cutler Equity Fund | 7.40% | 10.21% | 7.52% | |

S&P 500 Total Return Index(b) | 3.99% | 12.10% | 7.42% | |

| | | | | | |

(a) | Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. | |

(b) | The S&P 500 Total Return Index is a market capitalization weighted index that is widely used as a barometer of U.S. stock market performance. The index is unmanaged and shown for illustration purposes only. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. | |

10

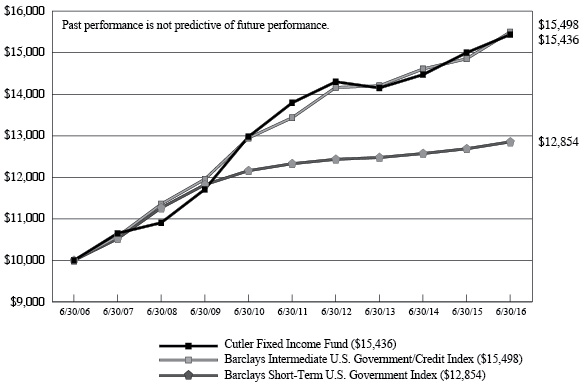

CUTLER FIXED INCOME FUND

PERFORMANCE INFORMATION

June 30, 2016 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in

Cutler Fixed Income Fund, Barclays Intermediate U.S. Government/Credit Index and

Barclays Short-Term U.S. Government Index

Average Annual Total Returns(a)

(for periods ended June 30, 2016) |

| | 1 Year | 5 Years | 10 Years | |

Cutler Fixed Income Fund | 2.91% | 2.28% | 4.44% | |

Barclays Intermediate U.S. Government/Credit Index(b) | 4.33% | 2.90% | 4.48% | |

Barclays Short-Term U.S. Government Index(b) | 1.31% | 0.84% | 2.54% | |

| | | | | | |

(a) | Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. | |

(b) | The Barclays Intermediate U.S. Government/Credit Index and the Barclays Short-Term U.S. Government Index cover intermediate and short-term, respectively, fixed income securities of the U.S government and publicly issued U.S. corporate and foreign debentures and secured notes that meet specified maturity, liquidity, and quality requirements. The indices are unmanaged and shown for illustration purposes only. An investor cannot invest in an index and its returns are not indicative of the performance or any specific investment. | |

11

CUTLER EMERGING MARKETS FUND

PERFORMANCE INFORMATION

June 30, 2016 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in

Cutler Emerging Markets Fund and MSCI Emerging Markets Index

Total Returns(a)

(for the period ended June 30, 2016) |

| | | | Since

Inception(b) | |

Cutler Emerging Markets Fund | | | (15.43%) | |

MSCI Emerging Markets Index(c) | | | (12.04%) | |

| | | | | | |

(a) | Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. | |

(b) | The Fund commenced operations on July 2, 2015. | |

(c) | The MSCI Emerging Markets Index captures large and mid cap representation across 23 emerging markets: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Russia, Qatar, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates. The index is unmanaged and shown for illustration purposes only. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. | |

12

CUTLER EQUITY FUND

PORTFOLIO INFORMATION

June 30, 2016 (Unaudited)

Sector Allocation (% of Net Assets)

13

CUTLER FIXED INCOME FUND

PORTFOLIO INFORMATION

June 30, 2016 (Unaudited)

Asset Allocation (% of Net Assets)

14

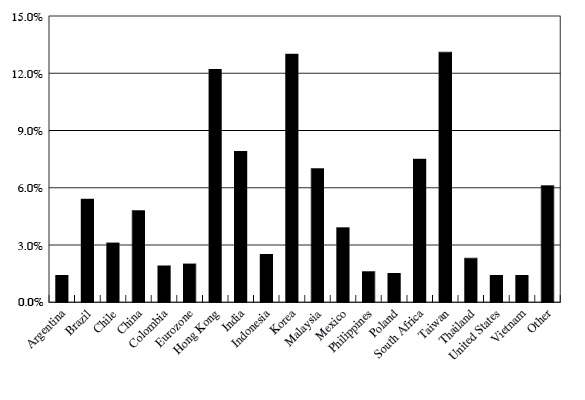

CUTLER EMERGING MARKETS FUND

PORTFOLIO INFORMATION

June 30, 2016 (Unaudited)

Country Allocation (% of Net Assets)

15

CUTLER EQUITY FUND

SCHEDULE OF INVESTMENTS

June 30, 2016 | |

COMMON STOCKS — 95.6% | | Shares | | | Value | |

Consumer Discretionary — 14.2% | | | | | | |

Hotels, Restaurants & Leisure — 3.6% | | | | | | |

McDonald's Corporation | | | 39,655 | | | $ | 4,772,083 | |

| | | | | | | | | |

Media — 3.6% | | | | | | | | |

Walt Disney Company (The) | | | 48,992 | | | | 4,792,397 | |

| | | | | | | | | |

Multi-line Retail — 3.1% | | | | | | | | |

Target Corporation | | | 57,650 | | | | 4,025,123 | |

| | | | | | | | | |

Specialty Retail — 3.9% | | | | | | | | |

Home Depot, Inc. (The) | | | 40,700 | | | | 5,196,983 | |

| | | | | | | | | |

Consumer Staples — 11.2% | | | | | | | | |

Beverages — 3.0% | | | | | | | | |

PepsiCo, Inc. | | | 37,995 | | | | 4,025,190 | |

| | | | | | | | | |

Food & Staples Retailing — 5.3% | | | | | | | | |

Sysco Corporation | | | 60,595 | | | | 3,074,590 | |

Wal-Mart Stores, Inc. | | | 53,677 | | | | 3,919,495 | |

| | | | | | | | 6,994,085 | |

Household Products — 2.9% | | | | | | | | |

Procter & Gamble Company (The) | | | 45,130 | | | | 3,821,157 | |

| | | | | | | | | |

Energy — 8.6% | | | | | | | | |

Energy Equipment & Services — 1.6% | | | | | | | | |

Schlumberger Ltd. | | | 27,000 | | | | 2,135,160 | |

| | | | | | | | | |

Oil, Gas & Consumable Fuels — 7.0% | | | | | | | | |

Chevron Corporation | | | 43,820 | | | | 4,593,650 | |

Exxon Mobil Corporation | | | 49,563 | | | | 4,646,036 | |

| | | | | | | | 9,239,686 | |

Financials — 9.6% | | | | | | | | |

Banks — 2.5% | | | | | | | | |

M&T Bank Corporation | | | 28,340 | | | | 3,350,638 | |

| | | | | | | | | |

Capital Markets — 4.9% | | | | | | | | |

BlackRock, Inc. | | | 11,484 | | | | 3,933,615 | |

Northern Trust Corporation | | | 39,000 | | | | 2,584,140 | |

| | | | | | | | 6,517,755 | |

16

CUTLER EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 95.6% (Continued) | | Shares | | | Value | |

Financials — 9.6% (Continued) | | | | | | |

Consumer Finance — 2.2% | | | | | | |

American Express Company | | | 47,395 | | | $ | 2,879,720 | |

| | | | | | | | | |

Health Care — 13.7% | | | | | | | | |

Health Care Equipment & Supplies — 3.6% | | | | | | | | |

Becton, Dickinson & Company | | | 27,525 | | | | 4,667,965 | |

| | | | | | | | | |

Pharmaceuticals — 10.1% | | | | | | | | |

Bristol-Myers Squibb Company | | | 71,490 | | | | 5,258,089 | |

Johnson & Johnson | | | 37,170 | | | | 4,508,721 | |

Merck & Company, Inc. | | | 62,790 | | | | 3,617,332 | |

| | | | | | | | 13,384,142 | |

Industrials — 11.1% | | | | | | | | |

Aerospace & Defense — 2.7% | | | | | | | | |

United Technologies Corporation | | | 34,510 | | | | 3,539,000 | |

| | | | | | | | | |

Air Freight & Logistics — 3.1% | | | | | | | | |

United Parcel Service, Inc. - Class B | | | 37,950 | | | | 4,087,974 | |

| | | | | | | | | |

Machinery — 5.3% | | | | | | | | |

Caterpillar, Inc. | | | 44,280 | | | | 3,356,867 | |

Deere & Company | | | 45,944 | | | | 3,723,302 | |

| | | | | | | | 7,080,169 | |

Information Technology — 11.9% | | | | | | | | |

Semiconductors & Semiconductor Equipment — 8.7% | | | | | | | | |

Intel Corporation | | | 107,465 | | | | 3,524,852 | |

QUALCOMM, Inc. | | | 56,924 | | | | 3,049,419 | |

Texas Instruments, Inc. | | | 78,900 | | | | 4,943,085 | |

| | | | | | | | 11,517,356 | |

Software — 3.2% | | | | | | | | |

Microsoft Corporation | | | 81,425 | | | | 4,166,517 | |

| | | | | | | | | |

Materials — 2.9% | | | | | | | | |

Chemicals — 2.9% | | | | | | | | |

E.I. du Pont de Nemours and Company | | | 58,405 | | | | 3,784,644 | |

| | | | | | | | | |

Telecommunication Services — 7.0% | | | | | | | | |

Diversified Telecommunication Services — 7.0% | | | | | | | | |

AT&T, Inc. | | | 109,403 | | | | 4,727,304 | |

Verizon Communications, Inc. | | | 80,786 | | | | 4,511,090 | |

| | | | | | | | 9,238,394 | |

17

CUTLER EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 95.6% (Continued) | | Shares | | | Value | |

Utilities — 5.4% | | | | | | |

Gas Utilities — 2.3% | | | | | | |

National Fuel Gas Company | | | 52,145 | | | $ | 2,966,008 | |

| | | | | | | | | |

Multi-utilities — 3.1% | | | | | | | | |

Dominion Resources, Inc. | | | 53,243 | | | | 4,149,227 | |

| | | | | | | | | |

Total Common Stocks (Cost $91,094,427) | | | | | | $ | 126,331,373 | |

| | |

MONEY MARKET FUNDS — 4.3% | | Shares | | | Value | |

Invesco STIT-STIC Prime Portfolio (The) - Institutional Class, 0.34% (a) (Cost $5,725,038) | | | 5,725,038 | | | $ | 5,725,038 | |

| | | | | | | | | |

Total Investments at Value — 99.9% (Cost $96,819,465) | | | | | | $ | 132,056,411 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.1% | | | | | | | 79,349 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 132,135,760 | |

(a) | The rate shown is the 7-day effective yield as of June 30, 2016. |

See accompanying notes to financial statements. |

18

CUTLER FIXED INCOME FUND

SCHEDULE OF INVESTMENTS

June 30, 2016 | |

U.S. TREASURY OBLIGATIONS — 7.2% | | Coupon | | Maturity | | Par Value | | | Value | |

U.S. Treasury Notes | | 2.125% | | 05/15/25 | | $ | 200,000 | | | $ | 211,258 | |

U.S. Treasury Notes | | 1.625% | | 02/15/26 | | | 800,000 | | | | 809,000 | |

U.S. Treasury Bonds, Stripped Principal Payment | | 2.500%(a) | | 11/15/44 | | | 600,000 | | | | 300,446 | |

Total U.S. Treasury Obligations (Cost $1,262,656) | | | $ | 1,320,704 | |

| | |

U.S. GOVERNMENT AGENCY OBLIGATIONS — 10.7% | | Coupon | | Maturity | | Par Value | | | Value | |

Federal Farm Credit Bank — 5.2% | | | | | | | | | | |

Federal Farm Credit Bank | | 2.750% | | 06/26/23 | | $ | 500,000 | | | $ | 540,082 | |

Federal Farm Credit Bank | | 2.370% | | 05/01/25 | | | 400,000 | | | | 417,008 | |

| | | | | | | | | | | | 957,090 | |

Federal Home Loan Bank — 2.0% | | | | | | | | | | | | |

Federal Home Loan Bank | | 2.125% | | 03/10/23 | | | 350,000 | | | | 364,200 | |

| | | | | | | | | | | | | |

Federal National Mortgage Association — 0.4% | | | | | | | | | | | | |

Federal National Mortgage Association | | 2.200% | | 10/25/22 | | | 64,000 | | | | 64,003 | |

| | | | | | | | | | | | | |

Private Export Funding Corporation — 2.2% | | | | | | | | | | | | |

Private Export Funding Corporation | | 4.300% | | 12/15/21 | | | 350,000 | | | | 400,153 | |

| | | | | | | | | | | | | |

U.S. Department of Housing and Urban Development — 0.9% | | | | | | | | | | | | |

U.S. Department of Housing and Urban Development | | 4.130% | | 08/01/25 | | | 150,000 | | | | 167,741 | |

| | | | | | |

Total U.S. Government Agency Obligations (Cost $1,843,006) | | | $ | 1,953,187 | |

| |

MORTGAGE-BACKED SECURITIES — 71.4% | | Coupon | | Maturity | | Par Value | | | Value | |

Commercial — 15.0% | | | | | | | | | | |

Banc of America Commercial Mortgage Trust, IO, Series 2004-4 | | 0.086%(b) | | 07/01/42 | | $ | 2,122,673 | | | $ | 1,303 | |

Bear Stearns Commercial Mortgage Securities Trust, Series 2005-T20 | | 5.296%(b) | | 10/12/42 | | | 200,000 | | | | 197,100 | |

19

CUTLER FIXED INCOME FUND

SCHEDULE OF INVESTMENTS (Continued) | |

MORTGAGE-BACKED

SECURITIES — 71.4% (Continued) | | Coupon | | Maturity | | Par Value | | | Value | |

Commercial — 15.0% (Continued) | | | | | | | | | | |

Credit Suisse First Boston Mortgage Securities Corporation, IO, Series 2004-C1, 144A | | 0.952%(b) | | 01/15/37 | | $ | 8,572,045 | | | $ | 147,665 | |

FREMF Mortgage Trust, IO, Series 2011-K15 (c) | | 0.100%(b) | | 08/01/44 | | | 115,980,806 | | | | 437,712 | |

GMAC Commercial Mortgage Securities, Inc., IO, Series 1997-C1 | | 1.670%(b) | | 07/15/29 | | | 8,908,676 | | | | 247,638 | |

JP Morgan Chase Commercial Mortgage Securities Trust, Series 2005-LDP2 | | 4.842%(b) | | 07/01/42 | | | 13,540 | | | | 13,534 | |

JP Morgan Chase Commercial Mortgage Securties Trust, Series 2006-LDP8 | | 5.549%(b) | | 05/15/45 | | | 500,000 | | | | 480,397 | |

LB Commercial Conduit Mortgage Trust, IO, Series 1999-C2 | | 1.303%(b) | | 10/15/32 | | | 2,177,171 | | | | 72 | |

Merrill Lynch Mortgage Trust, IO, Series 2008-C1, 144A (c) | | 0.477%(b) | | 02/12/51 | | | 118,390,217 | | | | 503,869 | |

Morgan Stanley Capital I Trust, IO, Series 1998-HF2 | | 1.022%(b) | | 11/01/30 | | | 1,192,850 | | | | 16,827 | |

Wachovia Bank Commercial Mortgage Trust, IO, Series 2005-C21 (c) | | 0.078%(b) | | 10/01/44 | | | 390,743,985 | | | | 702,558 | |

| | | | | | | | | | | | 2,748,675 | |

Federal Home Loan Mortgage Corporation — 2.9% | | | | | | | | | | | | |

FHLMC, IO, Series K717 | | 0.636%(b) | | 09/01/21 | | | 19,858,780 | | | | 461,832 | |

FHLMC, Pool #J13584 | | 3.500% | | 11/01/25 | | | 41,289 | | | | 44,105 | |

FHLMC, Series 1963 | | 7.500% | | 01/01/27 | | | 21,324 | | | | 24,607 | |

| | | | | | | | | | | | 530,544 | |

Federal National Mortgage Association — 44.9% | | | | | | | | | | | | |

FANNIEMAE-ACES, IO,

Series 2013-M1 | | 4.572%(b) | | 11/25/16 | | | 5,584,277 | | | | 22,701 | |

FANNIEMAE-ACES, IO,

Series 2012-M14 (c) | | 4.192%(b) | | 02/25/17 | | | 9,676,963 | | | | 141,177 | |

FANNIEMAE-ACES, IO,

Series 2013-M4 (c) | | 3.912%(b) | | 02/25/18 | | | 8,719,757 | | | | 384,602 | |

FANNIEMAE-ACES, IO,

Series 2013-M13 | | 0.000%(b) | | 05/01/18 | | | 151,155,296 | | | | 115,135 | |

FANNIEMAE-ACES, IO,

Series 2014-M8 | | 4.611%(b) | | 05/25/18 | | | 8,769,259 | | | | 251,027 | |

FANNIEMAE-ACES, IO,

Series 2015-M3 (c) | | 4.524%(b) | | 06/25/18 | | | 8,962,464 | | | | 426,784 | |

FANNIEMAE-ACES,

Series 2006-M1 | | 5.385%(b) | | 06/01/19 | | | 48,788 | | | | 49,833 | |

FANNIEMAE-ACES, IO,

Series 2009-M1 | | 0.623%(b) | | 07/25/19 | | | 18,093,645 | | | | 384,660 | |

20

CUTLER FIXED INCOME FUND

SCHEDULE OF INVESTMENTS (Continued) | |

MORTGAGE-BACKED

SECURITIES — 71.4% (Continued) | | Coupon | | Maturity | | Par Value | | | Value | |

Federal National Mortgage Association — 44.9% (Continued) | | | | | | | | | | |

FANNIEMAE-ACES, IO,

Series 2010-M1 | | 0.401%(b) | | 09/25/19 | | $ | 11,422,758 | | | $ | 171,804 | |

FANNIEMAE-ACES, IO,

Series 2010-M3 (c) | | 0.317%(b) | | 03/25/20 | | | 22,942,953 | | | | 455,831 | |

FANNIEMAE-ACES, IO,

Series 2010-M4 | | 0.735%(b) | | 06/25/20 | | | 15,359,234 | | | | 424,706 | |

FANNIEMAE-ACES, IO,

Series 2010-M5 (c) | | 0.894%(b) | | 07/25/20 | | | 12,436,808 | | | | 416,123 | |

FANNIEMAE-ACES, IO,

Series 2011-M9 (c) | | 0.094%(b) | | 01/25/21 | | | 40,537,924 | | | | 243,106 | |

FANNIEMAE-ACES, IO,

Series 2011-M2 (c) | | 0.065%(b) | | 04/25/21 | | | 30,084,734 | | | | 494,653 | |

FANNIEMAE-ACES, IO,

Series 2011-M1 (c) | | 0.021%(b) | | 06/25/21 | | | 42,489,968 | | | | 530,190 | |

FANNIEMAE-ACES, IO,

Series 2012-M1 (c) | | 0.070%(b) | | 10/25/21 | | | 88,212,656 | | | | 705,172 | |

FANNIEMAE-ACES, IO,

Series 2013-M5 | | 2.301%(b) | | 01/01/22 | | | 6,449,653 | | | | 564,644 | |

FANNIEMAE-ACES, IO,

Series 2012-M4 | | 0.630%(b) | | 04/25/22 | | | 13,146,355 | | | | 365,448 | |

FANNIEMAE-ACES, IO,

Series 2015-M4 (c) | | 0.572%(b) | | 07/25/22 | | | 15,166,640 | | | | 420,980 | |

FANNIEMAE-ACES, IO,

Series 2012-M14 | | 0.502%(b) | | 09/25/22 | | | 3,510,090 | | | | 86,177 | |

FANNIEMAE-ACES, IO,

Series 2014-M3 (c) | | 0.105%(b) | | 01/25/24 | | | 37,555,639 | | | | 339,465 | |

FANNIEMAE-ACES, IO,

Series 2015-M1 | | 0.555%(b) | | 09/25/24 | | | 30,154,506 | | | | 1,159,685 | |

FNMA, Series 2003-3 | | 5.000% | | 02/01/18 | | | 5,832 | | | | 5,937 | |

FNMA, Pool #899237 | | 5.000% | | 03/01/22 | | | 8,051 | | | | 8,389 | |

FNMA, Series 2002-93 | | 6.500% | | 03/01/32 | | | 42,908 | | | | 49,609 | |

| | | | | | | | | | | | 8,217,838 | |

Government National Mortgage Association — 8.6% | | | | | | | | | | | | |

GNMA, Pool #577742 | | 5.500% | | 09/01/17 | | | 1,212 | | | | 1,343 | |

GNMA, IO, Series 2011-121 | | 5.658%(b) | | 03/16/43 | | | 1,471,943 | | | | 290,280 | |

GNMA, IO, Series 2010-100 | | 0.185%(b) | | 07/16/50 | | | 11,140,550 | | | | 238,724 | |

GNMA, IO, Series 2012-4 | | 0.778%(b) | | 05/16/52 | | | 3,684,996 | | | | 120,158 | |

GNMA, IO, Series 2012-114 | | 0.901%(b) | | 01/16/53 | | | 3,959,111 | | | | 264,228 | |

GNMA, IO, Series 2012-125 (c) | | 0.502%(b) | | 02/16/53 | | | 15,845,949 | | | | 651,170 | |

| | | | | | | | | | | | 1,565,903 | |

| | | | | | |

Total Mortgage-Backed Securities (Cost $14,624,591) | | | $ | 13,062,960 | |

21

CUTLER FIXED INCOME FUND

SCHEDULE OF INVESTMENTS (Continued) | |

CORPORATE BONDS — 2.2% | | Coupon | | Maturity | | Par Value | | | Value | |

Financials — 1.6% | | | | | | | | | | |

Finial Holdings, Inc. | | 7.125% | | 10/15/23 | | $ | 250,000 | | | $ | 299,722 | |

| | | | | | | | | | | | | |

Industrials — 0.6% | | | | | | | | | | | | |

Kinross Gold Corporation | | 5.125% | | 09/01/21 | | | 100,000 | | | | 99,250 | |

| | | | | | |

Total Corporate Bonds (Cost $388,185) | | | $ | 398,972 | |

| | |

MONEY MARKET FUNDS — 6.3% | | Shares | | | Value | |

Invesco STIT-STIC Prime Portfolio (The) - Institutional Class, 0.34% (d) (Cost $1,147,202) | | | 1,147,202 | | | $ | 1,147,202 | |

| | | | | | | | | |

Total Investments at Value — 97.8% (Cost $19,265,640) | | | | | | $ | 17,883,025 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 2.2% | | | | | | | 405,825 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 18,288,850 | |

IO - Interest only strip. Par value shown is the notional value, not a true par value (Note 6). 144A - This is a restricted security that was sold in a transaction exempt under Rule 144A of the Securities Act of 1933. This security may be sold in transactions exempt from registration, normally to qualified institutional buyers. The total value of such securities is $651,534 at June 30, 2016. |

(a) | Rate shown is the annualized yield at the time of purchase, not a coupon rate. |

(b) | Variable rate security. The rate shown is the effective interest rate as of June 30, 2016. |

(c) | Fair value priced (Note 2). Fair valued securities totaled $6,853,392 at June 30, 2016, representing 37.5% of net assets. |

(d) | The rate shown is the 7-day effective yield as of June 30, 2016. |

See accompanying notes to financial statements. |

22

CUTLER EMERGING MARKETS FUND

SCHEDULE OF INVESTMENTS

June 30, 2016 | |

COMMON STOCKS — 82.3% | | Shares | | | Value | |

Brazil — 5.4% | | | | | | |

Ambev S.A. - ADR | | | 27,800 | | | $ | 164,298 | |

Embraer S.A. - ADR | | | 4,895 | | | | 106,319 | |

Itau Unibanco Holding S.A. - ADR | | | 17,519 | | | | 165,379 | |

| | | | | | | | 435,996 | |

Chile — 3.0% | | | | | | | | |

Empresa Nacional de Telecomunicaciones S.A. (a) | | | 13,080 | | | | 118,569 | |

Viña Concha y Toro S.A. | | | 79,500 | | | | 125,516 | |

| | | | | | | | 244,085 | |

China — 4.8% | | | | | | | | |

Huaneng Power International, Inc. - ADR | | | 3,931 | | | | 98,157 | |

PetroChina Company Ltd. - ADR | | | 1,776 | | | | 120,626 | |

Sinopec Shanghi Petrochemical Company Ltd. - ADR | | | 3,704 | | | | 169,902 | |

| | | | | | | | 388,685 | |

Colombia — 1.9% | | | | | | | | |

Grupo de Inversiones Suramericana | | | 12,000 | | | | 157,807 | |

| | | | | | | | | |

Hong Kong — 12.2% | | | | | | | | |

China Overseas Land & Investment Ltd. (b) | | | 49,000 | | | | 156,201 | |

China Overseas Property Holdings Ltd. (b) | | | 15,666 | | | | 2,331 | |

China Resources Beer Holdings Company Ltd. (b) | | | 70,000 | | | | 152,998 | |

China Resources Land Ltd. (b) | | | 64,000 | | | | 150,809 | |

CITIC Ltd. (b) | | | 107,000 | | | | 156,411 | |

COSCO Pacific Ltd. (b) | | | 12,000 | | | | 11,981 | |

Lenovo Group Ltd. - ADR | | | 8,206 | | | | 99,129 | |

Shanghi Industrial Holdings Ltd. (b) | | | 69,000 | | | | 156,861 | |

Tingyi (Cayman Islands) Holding Corporation (b) | | | 110,000 | | | | 104,449 | |

| | | | | | | | 991,170 | |

India — 5.5% | | | | | | | | |

Dr. Reddy's Laboratories Ltd. - ADR | | | 2,651 | | | | 135,811 | |

ICICI Bank Ltd. - ADR | | | 21,160 | | | | 151,929 | |

Infosys Ltd. - ADR | | | 9,128 | | | | 162,935 | |

| | | | | | | | 450,675 | |

Indonesia — 2.5% | | | | | | | | |

Telekomunikasi Indonesia Persero Tbk PT - ADR | | | 3,257 | | | | 200,175 | |

| | | | | | | | | |

Korea (Republic of) — 13.0% | | | | | | | | |

AMOREPACIFIC Group (b) | | | 710 | | | | 104,165 | |

Dongbu Insurance Company Ltd. (b) | | | 1,803 | | | | 108,500 | |

Korea Gas Corporation (b) | | | 3,880 | | | | 134,868 | |

KT Corporation - ADR | | | 11,956 | | | | 170,493 | |

LG Corporation (b) | | | 2,510 | | | | 139,556 | |

POSCO - ADR | | | 1,751 | | | | 77,920 | |

23

CUTLER EMERGING MARKETS FUND

SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 82.3% (Continued) | | Shares | | | Value | |

Korea (Republic of) — 13.0% (Continued) | | | | | | |

Samsung Electronics Company Ltd. (b) | | | 188 | | | $ | 234,075 | |

Samsung Fire & Marine Insurance Company Ltd. (b) | | | 370 | | | | 84,963 | |

| | | | | | | | 1,054,540 | |

Malaysia — 5.7% | | | | | | | | |

CIMB Group Holdings Berhad (b) | | | 139,623 | | | | 153,468 | |

Genting Berhad (b) | | | 76,200 | | | | 156,846 | |

Malayan Banking Berhad (b) | | | 76,633 | | | | 156,649 | |

| | | | | | | | 466,963 | |

Mexico — 3.9% | | | | | | | | |

América Móvil S.A.B. de C.V. - Series L - ADR | | | 13,023 | | | | 159,662 | |

Coca-Cola Femsa S.A.B. de C.V. - Series L | | | 18,800 | | | | 155,652 | |

| | | | | | | | 315,314 | |

Philippines — 1.6% | | | | | | | | |

Universal Robina Corporation (b) | | | 30,070 | | | | 133,346 | |

| | | | | | | | | |

South Africa — 7.5% | | | | | | | | |

Liberty Holdings Ltd. (b) | | | 16,865 | | | | 137,560 | |

Naspers Ltd. - ADR | | | 10,670 | | | | 163,678 | |

Sasol Ltd. - ADR | | | 3,802 | | | | 103,110 | |

Shoprite Holdings Ltd. (b) | | | 9,250 | | | | 104,701 | |

Shoprite Holdings Ltd. - ADR | | | 8,803 | | | | 99,175 | |

| | | | | | | | 608,224 | |

Taiwan Province of China — 11.6% | | | | | | | | |

Cheng Shin Rubber Industry Company Ltd. (b) | | | 54,000 | | | | 113,887 | |

Compal Electronics, Inc. (b) | | | 178,000 | | | | 112,635 | |

CTCI Corporation (b) | | | 132,000 | | | | 193,181 | |

Delta Electronics, Inc. (a) (b) | | | 39,100 | | | | 190,835 | |

Giant Manufacturing Company Ltd. (b) | | | 17,000 | | | | 106,077 | |

President Chain Store Corporation (b) | | | 29,000 | | | | 226,650 | |

| | | | | | | | 943,265 | |

Thailand — 2.3% | | | | | | | | |

Charoen Pokphand Foods plc (b) | | | 229,500 | | | | 188,217 | |

| | | | | | | | | |

United States — 1.4% | | | | | | | | |

Southern Copper Corporation | | | 4,290 | | | | 115,744 | |

| | | | | | | | | |

Total Common Stocks (Cost $6,674,851) | | | | | | $ | 6,694,206 | |

24

CUTLER EMERGING MARKETS FUND

SCHEDULE OF INVESTMENTS (Continued) | |

EXCHANGE-TRADED FUNDS — 9.1% | | Shares | | | Value | |

Global X MSCI Argentina ETF | | | 5,200 | | | $ | 115,960 | |

iShares Currency Hedged MSCI Eurozone ETF | | | 6,738 | | | | 162,184 | |

iShares MSCI Malaysia ETF | | | 12,902 | | | | 106,958 | |

iShares MSCI Taiwan ETF | | | 8,858 | | | | 124,455 | |

VanEck Vectors Poland ETF | | | 9,326 | | | | 120,678 | |

VanEck Vectors Vietnam ETF | | | 7,700 | | | | 112,497 | |

Total Exchange-Traded Funds (Cost $772,048) | | | | | | $ | 742,732 | |

| |

EXCHANGE-TRADED NOTES — 2.4% | | Shares | | | Value | |

iPath MSCI India Index ETN (a) (Cost $199,934) | | | 3,035 | | | $ | 197,427 | |

| | |

RIGHTS — 0.1% | | Shares | | | Value | |

Empresa Nacional de Telecommunicaciones S.A. (a)(b) (Cost $2,846) | | | 3,584 | | | $ | 3,249 | |

| | |

MONEY MARKET FUNDS — 6.0% | | Shares | | | Value | |

Invesco STIT-STIC Prime Portfolio (The) - Institutional Class, 0.34% (c) (Cost $483,769) | | | 483,769 | | | $ | 483,769 | |

| | | | | | | | | |

Total Investments at Value — 99.9% (Cost $8,133,448) | | | | | | $ | 8,121,383 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.1% | | | | | | | 7,064 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 8,128,447 | |

ADR - American Depositary Receipt. |

(a) | Non-income producing security. |

(b) | Fair value priced (Note 2). Fair valued securities totaled $3,675,469 at June 30, 2016, representing 45.2% of net assets. |

(c) | The rate shown is the 7-day effective yield as of June 30, 2016. |

See accompanying notes to financial statements. |

25

CUTLER EMERGING MARKETS FUND

SUMMARY OF COMMON STOCKS

BY SECTOR AND INDUSTRY

June 30, 2016 | |

Sector/Industry | | % of Net Assets | |

Consumer Discretionary — 6.6% | | | |

Auto Components | | | 1.4 | % |

Hotels, Restaurants & Leisure | | | 1.9 | % |

Leisure Products | | | 1.3 | % |

Media | | | 2.0 | % |

Consumer Staples — 19.2% | | | | |

Beverages | | | 5.5 | % |

Food & Staples Retailing | | | 7.2 | % |

Food Products | | | 5.2 | % |

Personal Products | | | 1.3 | % |

Energy — 2.7% | | | | |

Oil, Gas & Consumable Fuels | | | 2.7 | % |

Financials – 17.5% | | | | |

Banks | | | 9.6 | % |

Diversified Financial Services | | | 1.9 | % |

Insurance | | | 4.1 | % |

Real Estate Management & Development | | | 1.9 | % |

Health Care — 1.7% | | | | |

Pharmaceuticals | | | 1.7 | % |

Industrials — 9.4% | | | | |

Aerospace & Defense | | | 1.3 | % |

Construction & Engineering | | | 2.4 | % |

Industrial Conglomerates | | | 5.6 | % |

Transportation Infrastructure | | | 0.1 | % |

Information Technology — 9.8% | | | | |

Electronic Equipment, Instruments & Components | | | 2.3 | % |

IT Services | | | 2.0 | % |

Technology Hardware, Storage & Peripherals | | | 5.5 | % |

Materials — 4.5% | | | | |

Chemicals | | | 2.1 | % |

Metals & Mining | | | 2.4 | % |

Telecommunication Services — 8.0% | | | | |

Diversified Telecommunication Services | | | 4.6 | % |

Wireless Telecommunication Services | | | 3.4 | % |

Utilities — 2.9% | | | | |

Gas Utilities | | | 1.7 | % |

Independent Power and Renewable Electricity Producers | | | 1.2 | % |

| | | | 82.3 | % |

See accompanying notes to financial statements. |

26

THE CUTLER TRUST

STATEMENTS OF ASSETS AND LIABILITIES

June 30, 2016 | |

| | Cutler

Equity Fund | | | Cutler Fixed

Income Fund | | | Cutler Emerging Markets Fund | |

ASSETS | | | | | | | | | |

Investments in securities: | | | | | | | | | |

At acquisition cost | | $ | 96,819,465 | | | $ | 19,265,640 | | | $ | 8,133,448 | |

At value (Note 2) | | $ | 132,056,411 | | | $ | 17,883,025 | | | $ | 8,121,383 | |

Cash denominated in foreign currency (Cost $8,769) | | | — | | | | — | | | | 8,776 | |

Dividends and interest receivable | | | 166,335 | | | | 460,663 | | | | 24,810 | |

Receivable for capital shares sold | | | 206,435 | | | | 754 | | | | 71 | |

Receivable from Adviser (Note 3) | | | — | | | | — | | | | 3,855 | |

Other assets | | | 5,639 | | | | 3,786 | | | | 3,584 | |

Total assets | | | 132,434,820 | | | | 18,348,228 | | | | 8,162,479 | |

| | | | | | | | | | | | | |

LIABILITIES | | | | | | | | | | | | |

Distributions payable | | | 7,139 | | | | 10,518 | | | | — | |

Payable for capital shares redeemed | | | 149,418 | | | | 15,460 | | | | 4,102 | |

Payable to Adviser (Note 3) | | | 90,558 | | | | 7,360 | | | | — | |

Payable to administrator (Note 3) | | | 16,000 | | | | 6,000 | | | | 6,500 | |

Other accrued expenses | | | 35,945 | | | | 20,040 | | | | 23,430 | |

Total liabilities | | | 299,060 | | | | 59,378 | | | | 34,032 | |

| | | | | | | | | | | | | |

NET ASSETS | | $ | 132,135,760 | | | $ | 18,288,850 | | | $ | 8,128,447 | |

| | | | | | | | | | | | | |

NET ASSETS CONSIST OF: | | | | | | | | | | | | |

Paid-in capital | | $ | 97,544,480 | | | $ | 19,013,719 | | | $ | 8,198,001 | |

Undistributed net investment income | | | 81,678 | | | | 726,754 | | | | 15,308 | |

Accumulated net realized losses from security transactions | | | (727,344 | ) | | | (69,008 | ) | | | (72,833 | ) |

Net unrealized appreciation (depreciation) on investments | | | 35,236,946 | | | | (1,382,615 | ) | | | (12,065 | ) |

Net unrealized appreciation on translation of assets and liabilities in foreign currencies | | | — | | | | — | | | | 36 | |

NET ASSETS | | $ | 132,135,760 | | | $ | 18,288,850 | | | $ | 8,128,447 | |

| | | | | | | | | | | | | |

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | | | 7,704,758 | | | | 1,886,761 | | | | 969,795 | |

| | | | | | | | | | | | | |

Net asset value, offering price and redemption price per share (Note 2) | | $ | 17.15 | | | $ | 9.69 | | | $ | 8.38 | |

See accompanying notes to financial statements. |

27

THE CUTLER TRUST

STATEMENTS OF OPERATIONS

For the Year Ended June 30, 2016 (a) | |

| | Cutler

Equity Fund | | | Cutler Fixed

Income Fund | | | Cutler Emerging Markets Fund | |

INVESTMENT INCOME | | | | | | | | | |

Dividend income | | $ | 3,538,206 | | | $ | 1,246 | | | $ | 175,131 | |

Interest income | | | — | | | | 1,685,944 | (b) | | | — | |

Foreign withholding taxes on dividends | | | — | | | | — | | | | (9,375 | ) |

Total investment income | | | 3,538,206 | | | | 1,687,190 | | | | 165,756 | |

| | | | | | | | | | | | | |

EXPENSES | | | | | | | | | | | | |

Investment advisory fees (Note 3) | | | 903,484 | | | | 86,289 | | | | 45,243 | |

Administration fees (Note 3) | | | 181,033 | | | | 72,000 | | | | 78,000 | |

Shareholder servicing fees (Note 3) | | | 136,941 | | | | — | | | | — | |

Professional fees | | | 52,674 | | | | 22,727 | | | | 21,354 | |

Custody and bank service fees | | | 14,611 | | | | 6,197 | | | | 25,673 | |

Registration and filing fees | | | 22,861 | | | | 14,117 | | | | 8,941 | |

Trustees’ fees and expenses (Note 3) | | | 32,790 | | | | 5,613 | | | | 2,290 | |

Pricing costs | | | 626 | | | | 11,235 | | | | 10,232 | |

Insurance expense | | | 16,252 | | | | 2,676 | | | | 664 | |

Printing of shareholder reports | | | 8,641 | | | | 4,392 | | | | 3,881 | |

Postage and supplies | | | 8,978 | | | | 3,656 | | | | 3,030 | |

Other expenses | | | 8,040 | | | | 6,217 | | | | 6,160 | |

Total expenses | | | 1,386,931 | | | | 235,119 | | | | 205,468 | |

Less fee reductions and expense reimbursements by the Adviser (Note 3) | | | (4,100 | ) | | | — | | | | (122,966 | ) |

Net expenses | | | 1,382,831 | | | | 235,119 | | | | 82,502 | |

| | | | | | | | | | | | | |

NET INVESTMENT INCOME | | | 2,155,375 | | | | 1,452,071 | | | | 83,254 | |

| | | | | | | | | | | | | |

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS AND FOREIGN CURRENCY TRANSLATION | | | | | | | | | | | | |

Net realized gains (losses) from: | | | | | | | | | | | | |

Investment transactions | | | 3,709,722 | | | | 222,816 | | | | (77,414 | ) |

Capital gain distributions from regulated investment companies | | | — | | | | — | | | | 4,581 | |

Foreign currency transactions | | | — | | | | — | | | | (14,522 | ) |

Net change in unrealized appreciation (depreciation) on: | | | | | | | | | | | | |

Investments | | | 3,239,050 | | | | (1,156,745 | ) | | | (12,065 | ) |

Foreign currency translation | | | — | | | | — | | | | 36 | |

NET REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS AND FOREIGN CURRENCY TRANSLATION | | | 6,948,772 | | | | (933,929 | ) | | | (99,384 | ) |

| | | | | | | | | | | | | |

NET INCREASE (DECREASE) IN NET ASSETS FROM OPERATIONS | | $ | 9,104,147 | | | $ | 518,142 | | | $ | (16,130 | ) |

(a) | Except for Cutler Emerging Markets Fund, which represents the period from the commencement of operations (July 2, 2015) through June 30, 2016. |

(b) | Includes income received from prepayment penalties for IO securities (Note 6.) |

See accompanying notes to financial statements. |

28

CUTLER EQUITY FUND

STATEMENTS OF CHANGES IN NET ASSETS | |

| | Year

Ended

June 30,

2016 | | | Year

Ended

June 30,

2015 | |

FROM OPERATIONS | | | | | | |

Net investment income | | $ | 2,155,375 | | | $ | 1,765,921 | |

Net realized gains from investment transactions | | | 3,709,722 | | | | 6,862,815 | |

Net change in unrealized appreciation (depreciation) on investments | | | 3,239,050 | | | | (6,933,714 | ) |

Net increase in net assets from operations | | | 9,104,147 | | | | 1,695,022 | |

| | | | | | | | | |

DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

From net investment income | | | (2,076,985 | ) | | | (1,763,636 | ) |

From net realized gains | | | (5,633,681 | ) | | | (2,012,254 | ) |

Decrease in net assets from distributions to shareholders | | | (7,710,666 | ) | | | (3,775,890 | ) |

| | | | | | | | | |

CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 16,579,609 | | | | 15,931,481 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 7,635,321 | | | | 3,718,498 | |

Payments for shares redeemed | | | (16,212,052 | ) | | | (17,059,447 | ) |

Net increase from capital share transactions | | | 8,002,878 | | | | 2,590,532 | |

| | | | | | | | | |

TOTAL INCREASE IN NET ASSETS | | | 9,396,359 | | | | 509,664 | |

| | | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of year | | | 122,739,401 | | | | 122,229,737 | |

End of year | | $ | 132,135,760 | | | $ | 122,739,401 | |

| | | | | | | | | |

UNDISTRIBUTED NET INVESTMENT INCOME | | $ | 81,678 | | | $ | 3,288 | |

| | | | | | | | | |

CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 1,015,316 | | | | 910,186 | |

Shares reinvested | | | 472,948 | | | | 212,456 | |

Shares redeemed | | | (978,883 | ) | | | (979,513 | ) |

Net increase in shares outstanding | | | 509,381 | | | | 143,129 | |

Shares outstanding at beginning of year | | | 7,195,377 | | | | 7,052,248 | |

Shares outstanding at end of year | | | 7,704,758 | | | | 7,195,377 | |

See accompanying notes to financial statements. |

29

CUTLER FIXED INCOME FUND

STATEMENTS OF CHANGES IN NET ASSETS | |

| | Year

Ended

June 30,

2016 | | | Year

Ended

June 30,

2015 | |

FROM OPERATIONS | | | | | | |

Net investment income | | $ | 1,452,071 | | | $ | 799,969 | |

Net realized gains from investment transactions | | | 222,816 | | | | 82,692 | |

Net change in unrealized appreciation (depreciation) on investments | | | (1,156,745 | ) | | | (315,043 | ) |

Net increase in net assets from operations | | | 518,142 | | | | 567,618 | |

| | | | | | | | | |

DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

From net investment income | | | (1,372,984 | ) | | | (316,510 | ) |

| | | | | | | | | |

CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 2,761,155 | | | | 4,231,423 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 1,353,754 | | | | 312,258 | |

Payments for shares redeemed | | | (2,402,222 | ) | | | (2,304,712 | ) |

Net increase from capital share transactions | | | 1,712,687 | | | | 2,238,969 | |

| | | | | | | | | |

TOTAL INCREASE IN NET ASSETS | | | 857,845 | | | | 2,490,077 | |

| | | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of year | | | 17,431,005 | | | | 14,940,928 | |

End of year | | $ | 18,288,850 | | | $ | 17,431,005 | |

| | | | | | | | | |

UNDISTRIBUTED NET INVESTMENT INCOME | | $ | 726,754 | | | $ | 458,277 | |

| | | | | | | | | |

CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 278,143 | | | | 417,628 | |

Shares reinvested | | | 138,586 | | | | 30,536 | |

Shares redeemed | | | (242,801 | ) | | | (227,592 | ) |

Net increase in shares outstanding | | | 173,928 | | | | 220,572 | |

Shares outstanding at beginning of year | | | 1,712,833 | | | | 1,492,261 | |

Shares outstanding at end of year | | | 1,886,761 | | | | 1,712,833 | |

See accompanying notes to financial statements. |

30

CUTLER EMERGING MARKETS FUND

STATEMENT OF CHANGES IN NET ASSETS | |

| | Period

Ended

June 30,

2016 (a) | |

FROM OPERATIONS | | | |

Net investment income | | $ | 83,254 | |

Net realized losses from: | | | | |

Investment transactions | | | (77,414 | ) |

Capital gain distributions from regulated investment companies | | | 4,581 | |

Foreign currency transactions | | | (14,522 | ) |

Net change in unrealized appreciation (depreciation) on: | | | | |

Investments | | | (12,065 | ) |

Foreign currency translation | | | 36 | |

Net decrease in net assets from operations | | | (16,130 | ) |

| | | | | |

DISTRIBUTIONS TO SHAREHOLDERS | | | | |

From net investment income | | | (53,424 | ) |

| | | | | |

CAPITAL SHARE TRANSACTIONS | | | | |

Proceeds from shares sold | | | 8,462,679 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 53,424 | |

Payments for shares redeemed | | | (318,102 | ) |

Net increase from capital share transactions | | | 8,198,001 | |

| | | | | |

TOTAL INCREASE IN NET ASSETS | | | 8,128,447 | |

| | | | | |

NET ASSETS | | | | |

Beginning of period | | | — | |

End of period | | $ | 8,128,447 | |

| | | | | |

UNDISTRIBUTED NET INVESTMENT INCOME | | $ | 15,308 | |

| | | | | |

CAPITAL SHARE ACTIVITY | | | | |

Shares sold | | | 1,003,439 | |

Shares reinvested | | | 6,612 | |

Shares redeemed | | | (40,256 | ) |

Net increase in shares outstanding | | | 969,795 | |

Shares outstanding at beginning of period | | | — | |

Shares outstanding at end of period | | | 969,795 | |

(a) | Represents the period from commencement of operations (July 2, 2015) through June 30, 2016. |

See accompanying notes to financial statements. |

31

CUTLER EQUITY FUND

FINANCIAL HIGHLIGHTS | |

Per Share Data for a Share Outstanding Throughout Each Year | |

| | Years Ended June 30, | |

| | 2016 | | | 2015 | | | 2014 | | | 2013 | | | 2012 | |

Net asset value at beginning of year | | $ | 17.06 | | | $ | 17.33 | | | $ | 14.94 | | | $ | 12.70 | | | $ | 12.18 | |

| | | | | | | | | | | | | | | | | | | | | |

Income from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.30 | | | | 0.25 | | | | 0.22 | | | | 0.19 | | | | 0.19 | |

Net realized and unrealized gains on investments | | | 0.88 | | | | 0.02 | (a) | | | 2.47 | | | | 2.24 | | | | 0.52 | |

Total from investment operations | | | 1.18 | | | | 0.27 | | | | 2.69 | | | | 2.43 | | | | 0.71 | |

| | | | | | | | | | | | | | | | | | | | | |

Less distributions from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.28 | ) | | | (0.25 | ) | | | (0.22 | ) | | | (0.19 | ) | | | (0.19 | ) |

Net realized gains | | | (0.81 | ) | | | (0.29 | ) | | | (0.08 | ) | | | — | | | | — | |

Total distributions | | | (1.09 | ) | | | (0.54 | ) | | | (0.30 | ) | | | (0.19 | ) | | | (0.19 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Net asset value at end of year | | $ | 17.15 | | | $ | 17.06 | | | $ | 17.33 | | | $ | 14.94 | | | $ | 12.70 | |

| | | | | | | | | | | | | | | | | | | | | |

Total return (b) | | | 7.40 | % | | | 1.49 | % | | | 18.13 | % | | | 19.26 | % | | | 5.90 | % |

| | | | | | | | | | | | | | | | | | | | | |

Net assets at end of year (000’s) | | $ | 132,136 | | | $ | 122,739 | | | $ | 122,230 | | | $ | 101,184 | | | $ | 49,416 | |

| | | | | | | | | | | | | | | | | | | | | |

Ratios/supplementary data: | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Ratio of net expenses to average net assets | | | 1.15 | %(c) | | | 1.15 | % | | | 1.15 | % | | | 1.15 | % | | | 1.27 | % |

| | | | | | | | | | | | | | | | | | | | | |

Ratio of net investment income

to average net assets | | | 1.79 | % | | | 1.42 | % | | | 1.37 | % | | | 1.53 | % | | | 1.57 | % |

| | | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 11 | % | | | 14 | % | | | 8 | % | | | 8 | %(d) | | | 9 | % |

(a) | The amount of net gains on investments (both realized and unrealized) does not accord with the amounts reported in the Statement of Changes due to the timing of purchases and redemptions of Fund shares during the period. |

(b) | Total return is a measure of the change in value of an investment in the Fund over the period covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(c) | Absent investment advisory fee reductions by the Adviser, the ratio of expenses to average net assets would have been 1.15% for the year ended June 30, 2016 (Note 3). |

(d) | Excludes the value of securities sold to realign the Fund’s portfolio following the merger with The Elite Growth & Income Fund (Note 1). |

See accompanying notes to financial statements. |

32

CUTLER FIXED INCOME FUND

FINANCIAL HIGHLIGHTS | |

Per Share Data for a Share Outstanding Throughout Each Period | |

| | | Year

Ended

June 30, 2016 | | | Year

Ended

June 30, 2015 | | | Year

Ended

June 30, 2014 | | | Nine

Months

Ended

June 30,

2013(a) | | |

Years Ended

September 30,

| |

| | | 2012 | | | | 2011 | |

Net asset value at beginning of period | | $ | 10.18 | | | $ | 10.01 | | | $ | 9.98 | | | $ | 10.40 | | | $ | 10.27 | | | $ | 10.79 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.79 | | | | 0.49 | | | | 0.05 | | | | 0.05 | | | | 0.21 | | | | 0.28 | |

Net realized and unrealized gains (losses) on investments | | | (0.50 | ) | | | (0.12 | ) | | | 0.17 | | | | (0.27 | ) | | | 0.31 | | | | (0.09 | ) |

Total from investment operations | | | 0.29 | | | | 0.37 | | | | 0.22 | | | | (0.22 | ) | | | 0.52 | | | | 0.19 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Less distributions from: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.78 | ) | | | (0.20 | ) | | | (0.14 | ) | | | (0.20 | ) | | | (0.39 | ) | | | (0.46 | ) |

Net realized gains | | | — | | | | — | | | | (0.05 | ) | | | — | | | | — | | | | (0.25 | ) |

Total distributions | | | (0.78 | ) | | | (0.20 | ) | | | (0.19 | ) | | | (0.20 | ) | | | (0.39 | ) | | | (0.71 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value at end of period | | $ | 9.69 | | | $ | 10.18 | | | $ | 10.01 | | | $ | 9.98 | | | $ | 10.40 | | | $ | 10.27 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Total return (b) | | | 2.91 | % | | | 3.65 | % | | | 2.26 | % | | | (2.16% | )(c) | | | 5.07 | % | | | 1.87 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets at end of period (000’s) | | $ | 18,289 | | | $ | 17,431 | | | $ | 14,941 | | | $ | 16,262 | | | $ | 19,693 | | | $ | 21,242 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Ratios/supplementary data: | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Ratio of expenses to average net assets | | | 1.36 | % | | | 1.41 | % | | | 1.52 | % | | | 1.54 | %(d) | | | 1.52 | % | | | 1.28 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Ratio of net investment income to average net assets | | | 8.42 | %(e) | | | 4.95 | %(e) | | | 0.61 | % | | | 0.95 | %(d) | | | 2.03 | % | | | 2.51 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 71 | % | | | 85 | % | | | 55 | % | | | 34 | %(c) | | | 53 | % | | | 83 | % |

(a) | Fund changed its fiscal year end to June 30. |

(b) | Total return is a measure of the change in value of an investment in the Fund over the period covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(e) | Ratio includes income from prepayment penalties received for IO securities of 6.90% and 4.57% of average net assets for the years ended June 30, 2016 and 2015, respectively (Note 6). |

See accompanying notes to financial statements. |

33

CUTLER EMERGING MARKETS FUND

FINANCIAL HIGHLIGHTS | |

Per Share Data for a Share Outstanding Throughout The Period | |

| | | Period Ended

June 30, 2016 (a) | |

|

Net asset value at beginning of period | | $ | 10.00 | |

| | | | | |

Income (loss) from investment operations: | | | | |

Net investment income | | | 0.10 | |

Net realized and unrealized losses on investments | | | (1.65 | ) |

Total from investment operations | | | (1.55 | ) |

| | | | | |

Less distributions from: | | | | |

Net investment income | | | (0.07 | ) |

| | | | | |

Net asset value at end of period | | $ | 8.38 | |

| | | | | |

Total return (b) | | | (15.43% | )(c) |

| | | | | |

Net assets at end of period (000’s) | | $ | 8,128 | |

| | | | | |

Ratios/supplementary data: | | | | |

| | | | | |

Ratio of net expenses to average net assets (d) | | | 1.55 | %(e) |

| | | | | |

Ratio of net investment income to average net assets | | | 1.56 | %(e) |

| | | | | |

Portfolio turnover rate | | | 10 | %(c) |

(a) | Represents the period from the commencement of operations (July 2, 2015) through June 30, 2016. |

(b) | Total return is a measure of the change in value of an investment in the Fund over the period covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. The return shown does not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(d) | Absent investment advisory fee reductions and expense reimbursements by the Adviser, the ratio of expenses to average net assets would have been 3.85%(e) for the period ended June 30, 2016 (Note 3). |

See accompanying notes to financial statements. |

34

THE CUTLER TRUST

NOTES TO FINANCIAL STATEMENTS

June 30, 2016

1. Organization

Cutler Equity Fund, Cutler Fixed Income Fund and Cutler Emerging Markets Fund (individually, a “Fund” and collectively, the “Funds”) are each a diversified series of The Cutler Trust (the “Trust”). The Trust is a Delaware statutory trust that is registered as an open-end management investment company under the Investment Company Act of 1940 (the “1940 Act”). Under its Trust Instrument, the Trust is authorized to issue an unlimited number of Fund shares of beneficial interest without par value.

Cutler Equity Fund commenced operations on October 2, 1992. On September 28, 2012, Cutler Equity Fund consummated a tax-free merger with The Elite Growth & Income Fund, previously a series of The Elite Group of Mutual Funds. Pursuant to the terms of the agreement governing the merger, each share of The Elite Growth & Income Fund was converted into an equivalent dollar amount of shares of Cutler Equity Fund, based on the net asset value of Cutler Equity Fund and The Elite Growth & Income Fund as of September 27, 2012. The basis of the assets transferred from The Elite Growth & Income Fund reflected the historical basis of the assets as of the date of the tax-free merger. Cutler Equity Fund seeks current income and long-term capital appreciation.

The Elite Income Fund (the “Predecessor Fund”), a series of The Elite Group of Mutual Funds, was reorganized into Cutler Fixed Income Fund (the “Reorganization”) effective September 28, 2012, pursuant to an Agreement and Plan of Reorganization. The Reorganization was approved by the shareholders of the Predecessor Fund at a meeting held on September 27, 2012. The Predecessor Fund transferred all its assets to Cutler Fixed Income Fund in exchange for shares of Cutler Fixed Income Fund and the assumption by Cutler Fixed Income Fund of all the known liabilities of the Predecessor Fund. Cutler Fixed Income Fund did not have any significant assets or liabilities immediately prior to the consummation of the Reorganization. The Reorganization was treated as a tax-free reorganization for federal income tax purposes and, accordingly, the basis of the assets transferred reflected the historical basis of the assets as of the date of the Reorganization. Cutler Fixed Income Fund seeks to achieve high income over the long-term.

Cutler Emerging Markets Fund commenced operations on July 2, 2015. Cutler Emerging Markets Fund seeks current income and long-term capital appreciation.

2. Significant Accounting Policies

The following summarizes the significant accounting policies of the Funds. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). As an investment company, as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Update 2013-08, the Funds follow accounting and reporting guidance under FASB Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.”

35

THE CUTLER TRUST

NOTES TO FINANCIAL STATEMENTS (Continued)

Securities Valuation — Portfolio securities are valued as of the close of regular trading on the New York Stock Exchange (“NYSE”) (normally, 4:00 p.m., Eastern time) on each day the NYSE is open. Exchange traded securities are valued using the last reported sales price on the exchanges on which they are primarily traded. In the absence of a sale, such securities are valued at the mean of the last bid and asked price. Securities which are quoted by NASDAQ are valued at the NASDAQ Official Closing Price. Securities principally traded in non-U.S. markets that may close at different times than U.S. markets are typically fair valued by an independent pricing service and translated from the local currency into U.S. dollars using currency exchange rates supplied by an independent pricing service. Non-exchange traded securities for which over-the-counter quotations are available are generally valued at the closing bid price. Fixed income securities are generally valued using prices provided by an independent pricing service. The independent pricing service uses information with respect to transactions in bonds, quotations from bond dealers, market transactions in comparable securities, and various relationships between securities in determining the prices. Investments in shares of other open-end investment companies are valued at their net asset value as reported by such companies.

The Funds value securities at fair value pursuant to procedures adopted by the Trust’s Board of Trustees (the “Board”) if (1) market quotations are insufficient or not readily available or (2) the Funds’ investment adviser believes that the prices or values available are unreliable due to, among other things, the occurrence of events after the close of the securities markets on which the Funds’ securities primarily trade but before the time as of which the Funds calculate their net asset values. In instances where the investment adviser believes that the prices received from the independent pricing service are unreliable, proprietary valuation models may be used that consider benchmark yield curves, estimated default rates, coupon rates, anticipated timing of principal repayments and other unique security features to estimate the relevant cash flows, which are discounted to calculate the fair values. Fair valued securities will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used.

The Board approves the independent pricing services used by the Funds.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires disclosures about fair value measurements.

Various inputs are used in determining the value of each Fund’s investments. These inputs are summarized in the three broad levels listed below:

| | ● | Level 1 – quoted unadjusted prices for identical instruments in active markets to which the Fund has access at the date of measurement. |

| | ● | Level 2 – quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model derived valuations in which all significant inputs and significant value drivers are observable. Level 2 inputs are those |

36

THE CUTLER TRUST

NOTES TO FINANCIAL STATEMENTS (Continued)

in markets for which there are few transactions, the prices are not current, little public information exists or instances where prices vary substantially over time or among brokered market makers.

| | ● | Level 3 – model derived valuations in which one or more significant inputs or significant value drivers are unobservable. Unobservable inputs are those inputs that reflect the Fund’s own assumptions that market participants would use to price the asset or liability based on the best available information. |

Fixed income securities other than certain interest-only mortgage-backed securities held by Cutler Fixed Income Fund are classified as Level 2 since the values for the fixed income securities are based on prices that utilize various “other significant observable inputs” including bid and ask quotations, prices of similar securities and interest rates, among other factors. Certain interest-only mortgage-backed securities held by Cutler Fixed Income Fund are classified as Level 3 since the values for these securities are based on prices derived from models that utilize one or more significant inputs that are unobservable, including an assumed constant prepayment rate, among other factors.

Securities of Cutler Emerging Markets Fund traded in foreign markets may be classified as Level 2 despite the availability of closing prices because such securities are typically fair valued by an independent pricing service approved by the Board. These foreign securities may be priced at their fair value because the value of the securities may be materially affected by events occurring before the Fund’s pricing time but after the close of the primary markets or exchanges on which such foreign securities are traded. These intervening events might be country-specific (e.g., natural disaster, economic or political developments, interest rate change); issuer-specific (e.g., earnings report, merger announcement); or U.S. markets-specific (such as a significant movement in the U.S. markets that is deemed to affect the value of foreign securities). The pricing service uses an automated system incorporating a model based on multiple parameters, including a security’s local closing price, relevant general and sector indices, currency fluctuations, trading in depositary receipts and futures, if applicable, and/or research valuations by its staff, in determining what it believes is the fair value of the securities.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

37

THE CUTLER TRUST

NOTES TO FINANCIAL STATEMENTS (Continued)

The following is a summary of the inputs used to value each Fund’s investments as of June 30, 2016 by security type:

Cutler Equity Fund | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Common Stocks | | $ | 126,331,373 | | | $ | — | | | $ | — | | | $ | 126,331,373 | |

Money Market Funds | | | 5,725,038 | | | | — | | | | — | | | | 5,725,038 | |

Total | | $ | 132,056,411 | | | $ | — | | | $ | — | | | $ | 132,056,411 | |

Cutler Fixed Income Fund | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

U.S. Treasury Obligations | | $ | — | | | $ | 1,320,704 | | | $ | — | | | $ | 1,320,704 | |

U.S. Government Agency Obligations | | | — | | | | 1,953,187 | | | | — | | | | 1,953,187 | |

Mortgage-Backed Securities | | | — | | | | 6,209,568 | | | | 6,853,392 | | | | 13,062,960 | |

Corporate Bonds | | | — | | | | 398,972 | | | | — | | | | 398,972 | |

Money Market Funds | | | 1,147,202 | | | | — | | | | — | | | | 1,147,202 | |

Total | | $ | 1,147,202 | | | $ | 9,882,431 | | | $ | 6,853,392 | | | $ | 17,883,025 | |

Cutler Emerging Markets Fund | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Common Stocks | | $ | 3,021,986 | | | $ | 3,672,220 | | | $ | — | | | $ | 6,694,206 | |

Exchange-Traded Funds | | | 742,732 | | | | — | | | | — | | | | 742,732 | |