UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07454

Pacific Capital Funds

(Exact name of registrant as specified in charter)

| | |

| 3435 Stelzer Rd. Columbus, OH | | 43219 |

|

| (Address of principal executive offices) | | (Zip code) |

BISYS Fund Services 3435 Stelzer Road Columbus, OH 43219

(Name and address of agent for service)

Registrant’s telephone number, including area code: 614-470-8000

Date of fiscal year end: 7/31/05

Date of reporting period: 7/31/05

Item 1. Reports to Stockholders.

PACIFIC CAPITAL FUNDS

Annual Report

As of July 31, 2005

MUTUAL FUNDS: ARE NOT FDIC INSURED HAVE NO BANK GUARANTEE MAY LOSE VALUE

Table of Contents

Letter to Shareholders

Page 1

Fund Performance Review

Page 3

Statements of Assets and Liabilities

Page 29

Statements of Operations

Page 32

Statements of Changes in Net Assets

Page 35

Schedules of Portfolio Investments

Page 39

Notes to Financial Statements

Page 69

Financial Highlights

Page 83

Report of Independent Registered Public Accounting Firm

Page 95

Trustees and Executive Officers

Page 96

Additional Tax Information (unaudited)

Page 99

Expense Examples

Page 100

Letter to Shareholders

Dear Shareholders:

Thank you for investing with Pacific Capital Funds. We value the trust you place in us and we seek to provide world-class investment management to help you meet your financial goals.

Pacific Capital Funds draw on the expertise of the Asset Management Group of Bank of Hawaii (AMG). Founded in 1898, AMG represents the largest, most experienced staff of investment professionals in Hawaii, and oversees $6.4 billion in assets under management. In specialized securities markets, AMG has partnered with a select list of sub-advisors to provide Pacific Capital Funds’ shareholders with greater investment opportunities, broader diversification, and access to an elite group of institutional money managers:

| | • | | Bankoh Investment Partners, LLC, a joint venture between Bank of Hawaii and Chicago Equity Partners (CEP), serves as Sub-Adviser to the Pacific Capital Mid-Cap Fund. CEP specializes in core domestic equity markets and currently oversees $8.6 billion in assets under management. The firm’s investment management team has an average of 17 years experience. |

| | • | | First State Investments (FSI), which specializes in single-country, regional and sector-specific investments, serves as Sub-Adviser to the Pacific Capital New Asia Growth Fund. FSI oversees almost $82 billion in assets under management. |

| | • | | Hansberger Global Investors (HGI), founded in 1995 by former Templeton Worldwide President and CEO Thomas L. Hansberger, serves as Sub-Adviser to the Pacific Capital International Stock Fund. The firm’s 19 investment professionals represent 16 different nationalities and oversee $6.4 billion in assets under management. |

| | • | | Nicholas Applegate Capital Management (NACM), which specializes in global, international and domestic equity and special strategy management, serves as Sub-Adviser to the Pacific Capital Small Cap Fund. NACM employs 58 investment professionals and oversees $14.8 billion in assets under management. |

Annual Review

The U.S. economy posted better-than-expected growth during the 12-month period between August 1, 2004 and July 31, 2005. Despite rising interest rates, historically high energy prices, and a relatively weak U.S. Dollar, business and consumer spending remained strong. In the business sector, corporations with large cash stakes, supported by powerful earnings and cash flows, increased outlays for equipment and personnel. Meanwhile, in the consumer sector, low mortgage rates enabled homeowners to free up cash by refinancing their home loans.

The Federal Reserve Board (the “Fed”) increased short-term interest rates eight times during the period, bringing the benchmark federal funds rate from 1.25% at the beginning of the period to 3.25% as of July 31, 2005. These rate increases had only a modest impact on economic growth, however, as consistently low interest rates on long-term debt allowed businesses and individuals to continue borrowing at low cost.

Energy prices rose considerably during the year and finished the period at historically high levels. However, rising energy prices had only a modestly negative impact on economic growth, as low mortgage rates enabled consumers to offset rising costs by refinancing home loans, while improvements in energy efficiency at U.S. corporations reduced the business sector’s exposure to rising fuel costs.

The U.S. dollar began the period relatively weak against major foreign currencies. That weakness boosted the manufacturing sector of the economy by making U.S. exporters’ products more affordable for foreign consumers. The dollar strengthened during the first half of the period, reducing that competitive advantage, but declined again during early 2005.

Stocks Post Healthy Gains

The Standard & Poor’s 500 Index1 gained 14.04% during the 12-month period ended July 31, 2005. Strong corporate earnings gains helped to propel stock prices higher across most segments of the market with particularly strong gains concentrated in the energy, utilities, basic materials and homebuilding sectors.

| 1 | Standard & Poor’s 500 Index is an unmanaged index of 500 selected common stocks, most of which are listed on the New York Stock Exchange, and is a measure of the U.S. stock market as a whole. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

1

Letter to Shareholders (cont.)

Energy stocks led the market, as surging oil and gas prices led to powerful profit growth within the sector. Utilities stocks also performed well, particularly those with oil and gas properties and/or low cost generating capacity. Basic materials stocks benefited, as robust construction activity and demand from China and India supported high prices for products such as steel, copper and concrete. Meanwhile, continued strength in the residential real estate markets resulted in a banner year for the home builders.

Technology and healthcare were two weaker performing segments of the market. Although technology stocks rebounded near the end of the period, they struggled during much of the year due to concerns about inventories and the sustainability of corporate spending on information technology. Health-care stocks suffered due to troubles at some of the larger pharmaceutical companies, including product related litigation, weak new drug pipelines and patent expirations.

Smaller market capitalization stocks performed better than larger capitalization stocks during the year and those with a value orientation performed better than those with a growth orientation. This multi year pattern reflects superior earnings growth in the stronger segments of the market and investor preference for higher risk/higher return investments.

The Yield Curve Flattens

Yields on short-term bonds rose consistently in response to the Fed’s interest rate hikes. Long-term bond yields declined modestly, helping those bonds post solid returns.

The decline in long-term bond yields surprised most market observers, who expected economic growth and higher short-term rates to push long-term yields higher. However, strong demand for risk-free income, a benign inflationary environment and Treasury bond purchases by foreign central banks helped to push long-term yields down.

Corporate bonds generally outperformed government issues during the period. Corporations’ large cash positions, clean balance sheets and healthy earnings and cash flows encouraged fixed-income investors to move into corporate issues. Lower-quality bonds outperformed higher-quality bonds during much of the period, but that trend reversed itself in the spring.

Looking Forward

We expect the economy to continue to generate healthy growth during the coming months. Stocks currently look more attractive than fixed-income securities given the solid economy, corporations’ strong, high-quality earnings, modest stock valuations and relatively low bond yields.

We would like to take this opportunity to remind investors of the importance of constructing diversified portfolios that provide the proper balance of risk and reward for your goals. Pacific Capital Funds are designed to offer shareholders all the elements necessary to construct such portfolios, including funds that invest in a wide range of stocks and bonds.

Thank you for your confidence in Pacific Capital Funds. If you have any questions or would like a Fund prospectus, please contact your registered investment professional or call Pacific Capital Funds at (800) 258-9232 or visit our website at www.pacificcapitalfunds.com.

Sincerely,

Peter Ho

Vice Chairman

Asset Management Group of Bank of Hawaii

The foregoing information and opinions are for general information only. Bank of Hawaii Asset Management Group does not guarantee the accuracy or completeness, nor assume liability for any loss, which may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice, are for general information only and are not intended as an offer or solicitation with respect to the purchase or sale of any security or offering of individual or personalized investment advice.

NOTICE ABOUT DUPLICATE MAILINGS

In order to reduce expenses of the Pacific Capital Funds incurred in connection with the mailing of prospectuses, prospectus supplements, semi-annual reports and annual reports to multiple shareholders at the same address, Pacific Capital Funds may in the future deliver one copy of a prospectus, prospectus supplement, semi-annual report or annual report to a single investor sharing a street address or post office box with other investors, provided that all such investors have the same last name or are believed to be members of the same family. This process, called “householding,” will continue indefinitely unless you instruct us otherwise. If you share an address with another investor and wish to receive your own prospectus, prospectus supplements, semi-annual reports and annual reports, please call the Trust toll-free at (800) 258-9232.

2

Pacific Capital New Asia Growth Fund

Investment Style

Regional, multi-cap, growth.

Investment Objective

Long-term capital appreciation by investing in a broadly diversified portfolio of companies located in Asia’s developing regions, excluding Japan. Investments are not limited to any size or sector.

Investment Considerations

An investment in this Fund entails the special risks of international investing, including currency exchange fluctuation, government regulations, and the potential for political and economic instability. The Fund’s share price is expected to be more volatile than that of a U.S.-only fund. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| • | | Follow active bottom-up investment approach |

| • | | Invest for absolute versus relative return |

| • | | Look outside benchmark representation for fresh opportunities |

| • | | Identify sensibly priced, high-quality companies that exhibit long-term growth potential |

Investment Management

Advised by Asset Management Group of Bank of Hawaii

Sub-Advised by First State (Hong Kong) LLC

| • | | Founded in 1988, with offices in Sydney, London, Edinburgh, Hong Kong, Singapore and Indonesia |

| • | | Specializes in single country, regional and sector specific investments |

| • | | Oversees almost $82 billion in assets |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2005, the Fund gained 36.68% (Class A Shares without sales charge), compared to its benchmark, the MSCI® AC Far East Free Index1 (excluding Japan), which returned 37.53%.

What were the major factors in the market that influenced the Fund’s performance?

Within Asia, all markets delivered positive returns with Korea being one of the strongest in the largest markets. Korea benefited from increased confidence in the domestic economic outlook. Indonesia, Hong Kong and Taiwan also featured on the upside. Malaysia underperformed due to its defensive characteristics, and Thailand disappointed due to a weaker than expected economic performance. Other developments in the region included both China and Malaysia announcing changes to their currency regimes by removing their pegs to the U.S. dollar. The Chinese renminbi and the Malaysian ringgit will now be linked to a basket of currencies.

Across the Asia Pacific region, the Health Care and Energy sectors delivered the strongest returns. Oil prices rallied above US$60 per barrel due to a series of supply disruptions and continued demand growth from China and the U.S. The Utilities sector underperformed the Index.

Stock selection in the Financials sector, particularly overweight positions in non-Index HDFC Bank (India) and Samsung Fire & Marine (Korea), aided Fund returns. The former continued to deliver solid results, while the latter benefited from signs of improving underwriting quality and a gradual recovery in Korean domestic consumption. Hong Kong Land and Swire Pacific (Hong Kong) were other notable performers from the Financials sector. Keppel Corp. (Singapore) a new holding in the Industrial sector of our portfolio also helped performance.†

Holding Samsung Electronics was positive in absolute terms, but being underweight the stock, which makes up 5% of the benchmark, hurt relative performance. Some concerns about corporate governance and our overall avoidance of highly cyclical businesses make it difficult to justify a benchmark weight in the stock. Having no exposure to Hyundai Motors (Korea: Consumer Discretionary) and PetroChina (Energy) also detracted from performance.†

What major changes have occurred in the portfolio during the period covered by the report?

We continue to be heavily overweight in the Consumer sectors where high quality businesses with steady growth are attractively valued.

What is your outlook for the Fund?

We believe the appetite for emerging market assets could surpass the high levels seen in January leaving room for a possible sharp decline in the prices of some stocks. Asian consumption growth could remain strong irrespective of what happens to U.S. demand. It is becoming increasingly difficult to identify value in many quality companies in the region and we continue to expect an extended period of market consolidation at around current levels.†

Past performance does not guarantee future results.

| 1 | The Morgan Stanley Capital International (MSCI) All Country (AC) Far East Free Index (excluding Japan) is generally representative of the 48 developed and emerging markets around the world that collectively comprise virtually all of the foreign equity stock markets. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| † | The composition of the Fund’s portfolio is subject to change. |

3

Pacific Capital New Asia Growth Fund (cont.)

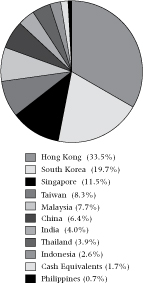

Country Weightings as of July 31, 2005

(as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

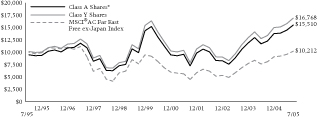

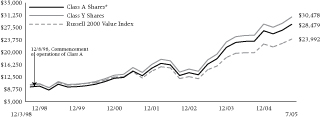

Growth of a $10,000 Investment

The chart above represents a comparison of a hypothetical $10,000 investment in the indicated share class versus a similar investment in the Fund’s benchmark. The chart above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2005

| | | | | | | | | |

| | | 1 Year

| | | 5 Year

| | | 10 Year

| |

Class A Shares* | | 29.56 | % | | 3.64 | % | | 4.49 | % |

Class B Shares** | | 31.66 | % | | 3.91 | % | | 4.53 | % |

Class C Shares** | | 35.73 | % | | 4.09 | % | | 4.54 | % |

Class Y Shares | | 37.07 | % | | 5.02 | % | | 5.31 | % |

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The Pacific Capital Funds are distributed by BISYS Fund Services. The Asset Management Group of Bank of Hawaii provides investment advisory services to the Fund and receives a fee for its services. First State (Hong Kong) LLC is sub-advisor to the Fund and is paid a fee for its services.

The Class B and Class C shares of the Fund commenced operations on March 2, 1998 and April 30, 2004, respectively. Performance information for Class C shares is based upon the performance of Class B shares from inception. Performance calculated for any period up to and through March 2, 1998 is based upon the performance of Class A shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

The performance of the Pacific Capital New Asia Growth Fund is measured against the MSCI® AC Far East Free Index ex-Japan, which is unmanaged and is generally representative of the 48 developed and emerging markets around the world that collectively comprise virtually all of the foreign equity stock markets. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

4

Pacific Capital International Stock Fund

Investment Style

International, multi-cap, blend

Investment Objective

Long-term capital appreciation by investing in a broadly diversified portfolio of companies domiciled outside the United States. Investments are not limited to any particular country or market capitalization.

Investment Considerations

An investment in this Fund entails the special risks of international investing, including currency exchange fluctuation, government regulations, and the potential for political and economic instability. The Fund’s share price is expected to be more volatile than that of a U.S.-only fund. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| • | | Style neutral growth and value discipline |

| • | | 50% managed by growth team—50% managed by value team |

| • | | Disciplined bottom-up stock selection |

| • | | Disciplined risk management framework to control industry and regional weightings |

Investment Management

Advised by Asset Management Group of Bank of Hawaii

Sub-Advised by Hansberger Global Investors, Inc.

| • | | Founded in 1994 by Thomas L. Hansberger, former President and CEO of Templeton Worldwide |

| • | | Headquartered in Ft. Lauderdale, Florida, with satellite offices in Hong Kong, Moscow and Toronto |

| • | | 19 investment professionals, 16 nationalities |

| • | | $6.4 billion in assets under management |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2005, the Fund underperformed its benchmark, the MSCI® ACWI ex US Index1. The Fund (Class A shares without sales charge) was up 21.17% while the MSCI® ACWI ex US Index1 was up 24.90%.

What were the major factors in the market that influenced the Fund’s performance?

The largest factors influencing the Fund’s performance relative to the benchmark were:

The Fund’s average 3.2% cash level had a negative effect on relative return during this period of strong performance.†

The underweighting of 1.7% in the Australian sector, and disappointing results of the Fund’s Australian securities lowered the Fund’s relative return. The Fund’s Australian securities were up 22.1% while the MSCI Australia Index was up 42.2%. Underexposure to the Australian dollar also hurt as that currency strengthened over the past year.†

The Fund had a 1.3% overweighting in the Emerging Markets. The Fund’s Emerging Markets stocks were up 55.3% while the benchmark was up 47.0%. Overweightings to Brazil and Korea were helpful as those currencies strengthened over the year.†

What major changes have occurred in the portfolio during the period covered by the report?

The Fund’s commitment to Europe excluding the United Kingdom increased, with 41.9% of its assets in the Europe ex United Kingdom sector for the period ended July 31, 2005. The Fund’s relative weighting in the Emerging Markets declined by 1.7%, which was about even with the MSCI Index weight in that region. Other large regional weighting differences are an underweighting of 3.1% to Canada and an underweighting of 3.1% to the United Kingdom.†

Financial stocks are the Fund’s largest commitment. The Fund increased the weighting in this sector by 1.9% relative to the benchmark weighting. The Fund’s largest relative weightings were Information Technology, overweighted by 3.3%, Health Care, overweighted by 2.7%, Materials, underweighted by 2.7%, and Energy underweighted by 2.6%.†

What is your outlook for the Fund

Our analysts feel that the combination of commodity price inflation, high oil prices, rising U.S. interest rates, and difficult consumer conditions in the United Kingdom, Japan, Germany, and France could provide a good relative environment for companies that have demonstrated their ability to create their own opportunities for growth in difficult market conditions. We believe that the Fund is structured to excel in that type of environment. Large, well-diversified companies with wide geographic reach and strong market share could be able to provide a better foundation for above average performance over the remainder of 2005. The valuations for these types of companies also remain very attractive versus history and current bond yields in our opinion.†

Past performance does not guarantee future results.

| 1 | The Morgan Stanley Capital International (MSCI) All Country World (ACWI) ex US is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets outside the U.S. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| † | The composition of the Fund’s portfolio is subject to change. |

5

Pacific Capital International Stock Fund (cont.)

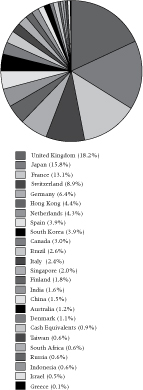

Country Weightings as of July 31, 2005

(as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

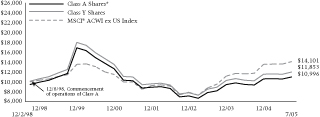

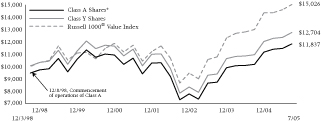

Growth of a $10,000 Investment

The chart above represents a comparison of a hypothetical $10,000 investment in the indicated share class versus a similar investment in the Fund’s benchmark. The chart above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2005

| | | | | | | | | |

| | | 1 Year

| | | 5 Year

| | | Since

Inception

(12/2/98)

| |

Class A Shares* | | 14.82 | % | | -6.06 | % | | 1.43 | % |

Class B Shares** | | 16.43 | % | | -5.78 | % | | 1.59 | % |

Class C Shares** | | 20.30 | % | | -5.65 | % | | 1.57 | % |

Class Y Shares | | 21.61 | % | | -4.68 | % | | 2.58 | % |

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The Pacific Capital Funds are distributed by BISYS Fund Services. The Asset Management Group of Bank of Hawaii provides investment advisory services to the Fund and receives a fee for its services. Hansberger Global Investors, Inc. is sub-advisor to the Fund and is paid a fee for its services.

The Pacific Capital International Stock Fund’s inception date was December 2, 1998. Class A Shares were not in existence prior to December 8, 1998. Performance calculated for any period up to and through December 8, 1998, is based upon the performance of Class Y Shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

Class B and Class C shares were not in existence prior to December 20, 1998 and April 30, 2004, respectively. Performance information for Class C shares is based upon the performance of Class B shares from inception. Performance calculated for any period up to and through such inception dates is based upon the performance of Class Y shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

The performance of the Pacific Capital International Stock Fund is measured against the MSCI® ACWI ex US Index, which is designed to measure equity market performance in the global developed and emerging markets outside the U.S. The index is unmanaged and does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

6

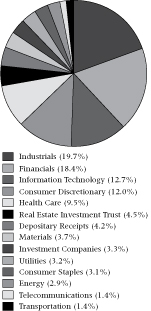

Pacific Capital Small Cap Fund

Investment Style

Domestic, small-cap, value

Investment Objective

Long-term capital appreciation by investing in a diversified portfolio of small-capitalization companies —with a current average market cap of $16 million to $2.7 billion—believed to be undervalued, fundamentally strong and undergoing positive change.

Investment Considerations

Small-capitalization stocks typically carry additional risk, since smaller companies generally have a higher risk of failure and their stocks have experienced a greater degree of volatility. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| • | | Follow active bottom-up investment approach |

| • | | Assess attractive valuations through price-to-book, price-to-earnings and dividend yield ratios |

| • | | Identify potential improvement based on free cash flow, balance sheet liquidity, inventory sales ratio, insider buying and management change |

Investment Management

Advised by Asset Management Group of Bank of Hawaii

Sub-Advised by Nicholas Applegate Capital Management

| • | | Founded in 1984, NACM employs 58 investment professionals |

| • | | Specializes in global and international equity, domestic equity and special strategy management |

| • | | $14.8 billion in assets under management |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2005, the Fund returned 27.98% (Class A Shares without sales charge), outperforming the Russell 2000® Value Index1 return of 26.72%.

For the same period, the Fund ranked in the 18th percentile among 594 funds in the Lipper Small-Cap Core Funds universe.2

What were the major factors in the market that influenced the Fund’s performance?

The Fund’s outperformance relative to the benchmark was largely a result of strong stock selection in the Information Technology, Utilities, and Consumer Discretionary sectors.†

The Fund posted positive stock selection in seven of the 10 sectors of the Russell Index. That outperformance occurred in an environment in which the U.S. equity markets delivered strong returns. Small cap stocks outpaced large cap stocks during the 12 months ended July 31, 2005, a trend, which has persisted since 1999. The Dow Jones Industrial Average3 gained 4.94% and the NASDAQ Composite Index4 was up 16.49% for the one-year period, while the cyclically heavy Russell Index gained 26.7%.

The broad-based economic recovery that began in the second half of 2003 continued through the first half of 2005. Corporate profits remained healthy, but concerns that record-high oil prices and rising short-term rates would dampen economic and corporate profit growth weighed on investor sentiment. The Fed increased the fed funds target rate beginning in June 2004, and has tightened 2.25% in nine 0.25% increments in its effort to preempt inflation.

Our private placement Real Estate Investment Trust investments contributed nicely to the portfolio. KKR Financial and Diamond Rock Hospitality both priced initial public offerings in 2005 and Ventas acquired Provident Senior Living Trust at a premium.†

Within Information Technology for the period, Comtech Telecommunications Corp. rose 165%, ROFIN-SINAR Technologies gained over 69%, and MTS Systems also contributed to the portfolio, returning 85.3%.†

In Utilities, stock selection was strong relative to the benchmark. The UGI Corp. rose 86.4%, Aquila Inc., rose 48%, and Energen Corp. rose 50.2%, each positively impacting performance during the period.†

The Consumer Discretionary sector added value compared to the benchmark. Hibbett Sporting Goods, Inc. gained over 74% and the Neiman-Marcus Group, Inc. rose 82%, for the period.†

Stock selection in the Financials sector and our underweight in the Energy sector detracted from relative performance.†

Past performance does not guarantee future results.

| 1 | The Russell 2000® Value Index (“Russell Index”) is an unmanaged index which measures the performance of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| 2 | The Lipper Small-Cap Core Funds universe is comprised of mutual of funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) less than 250% of the dollar-weighted median of the smallest 500 of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Small-cap core funds have more latitude in the companies in which they invest. These funds typically have an average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value, compared to the S&P SmallCap 600 Index. For the one-, three- and five-year periods ended July 31, 2005 the Pacific Capital Small Cap Fund ranked 105, 40 and 5 out of 594, 475 and 334 funds in the Lipper Small-Cap Core Funds category, respectively. The Lipper Rankings are based on total returns and do not reflect a sales charge. Funds with multiple share classes have a common portfolio. |

| † | The composition of the Fund’s portfolio is subject to change. |

7

Pacific Capital Small Cap Fund (cont.)

In Financials, Quanta Capital Holdings Ltd. declined 33% over the period. Knight Capital Group, Inc. (formerly Knight Trading) declined 10.7%.†

What major changes have occurred in the portfolio during the period covered by the report?

The Fund’s holdings remain diversified across sectors and industries. Because of the Russell reconstitution on June 30, we are less underweight in Energy and Utilities, less overweight in Technology and more overweight in Producers/ Manufacturers. We are underweight in the banking sector due to a lack of liquidity.

What is your outlook for the Fund?

We believe the outlook for U.S. equities remains mixed. Slowing corporate earnings growth and a spate of new layoff announcements create a headwind for the U.S. economy. Overall, however, corporate balance sheets are in good shape and could provide companies with flexibility to better withstand any economic weakness. Nicholas-Applegate believes that it will be able to successfully invest in companies that can take advantage of the current environment.†

| 3 | The Dow Jones Industrial Average is a price-weighted average based on the price-only performance of 30 blue chip stocks (the average is computed by adding the prices of the 30 stocks and dividing by a denominator, which has been adjusted over the years for stocks splits, stock dividends and substitutions of stocks). |

| 4 | The NASDAQ Composite Index is a market price only index that tracks the performance of U.S. domestic common stocks traded on the regular Nasdaq market as well as National Market System traded foreign common stocks and American Depository Receipts. |

Investors cannot invest directly in an index, although they can invest in its underlying securities.

| † | The composition of the Fund’s portfolio is subject to change. |

8

Pacific Capital Small Cap Fund (cont.)

Sector Weightings as of July 31, 2005

(as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

Growth of a $10,000 Investment

The chart above represents a comparison of a hypothetical $10,000 investment in the indicated share class versus a similar investment in the Fund’s benchmark. The chart above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2005

| | | | | | | | | |

| | | 1 Year

| | | 5 Year

| | | Since

Inception

(12/3/98)

| |

Class A Shares* | | 21.23 | % | | 21.33 | % | | 17.01 | % |

Class B Shares** | | 23.02 | % | | 21.59 | % | | 17.06 | % |

Class C Shares** | | 27.00 | % | | 21.70 | % | | 17.06 | % |

Class Y Shares | | 28.30 | % | | 22.90 | % | | 18.21 | % |

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The Pacific Capital Funds are distributed by BISYS Fund Services. The Asset Management Group of Bank of Hawaii provides investment advisory services to the Fund and receives a fee for its services. Nicholas-Applegate Capital Management is sub-advisor to the Fund and is paid a fee for its services.

The Pacific Capital Small Cap Fund’s inception date was December 3, 1998. Class A, Class B and Class C shares were not in existence prior to December 8, 1998, December 20, 1998 and April 30, 2004, respectively. Performance information for Class C shares is based upon the performance of Class B shares from inception. Performance calculated for any period up to and through such inception dates is based upon the performance of Class Y shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

The performance of the Pacific Capital Small Cap Fund is measured against the Russell 2000® Value Index, is an unmanaged index which measures the performance of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

9

Pacific Capital Mid-Cap Fund

Investment Style

Domestic, mid-cap, blend

Investment Objective

Long-term capital appreciation by investing in a diversified portfolio of mid-capitalization companies–currently average market cap of $410 million to $11.3 billion–that are reasonably priced, fundamentally strong and exhibit better growth expectations relative to peers.

Investment Considerations

Mid-capitalization stocks typically carry additional risk, since smaller companies generally have a higher risk of failure and have experienced a greater degree of volatility. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| • | | Quantitative research analysis with fundamental research overlay |

| • | | Quantitative analysts use proprietary screen to evaluate expectations, valuation and quality of 3,000 stocks |

| • | | Fundamental analysts identify factors not included in the screen to determine most attractive stocks |

| • | | Portfolio construction emphasizes stock selection and seeks to neutralize risk elements that are not consistently rewarded |

Investment Management

Advised by Asset Management Group of Bank of Hawaii

Sub-Advised by Bankoh Investment Partners, LLC (BIP), a joint venture between Bank of Hawaii and Chicago Equity Partners (CEP)

| • | | Founded in 1989, CEP specializes in core domestic equity markets |

| • | | CEP investment management team averages 17 years experience |

| • | | CEP currently oversees $8.6 billion in assets |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2005, the Fund underperformed its benchmark, the S&P 400 MidCap Index1. The Fund produced a total return of 23.69% (Class A Shares without sales charge) compared to the Index which was up 25.89% for the same period.

What were the major factors in the market that influenced the Fund’s performance?

The equity markets returned to positive territory during the quarter even with powerful headwinds—runaway oil prices, bad trade numbers, the downgrading of GM’s credit ratings, and mostly uninspiring job gains. These factors were countered by the strength of corporate profits, the rise of the U.S. dollar and the decline of long term interest rates.

For the period, momentum factors had positive returns, while value and quality factors were not as strong in the last quarter as they have been in the last twelve months. Over the last 12 months, we have seen positive returns from all three factors (Value, Quality, Momentum), but we have not seen as much discrimination between stocks that have strength in all three factor groups and those that do not. We construct the portfolio with companies that have the broadest exposure to these groups. Because we have not seen the discrimination over the last few months, it has been difficult to produce the expected performance.†

What major changes have occurred in the portfolio during the period covered by the report?

No major changes have occurred in the portfolio other than the typical re-balancing.

What is your outlook for the Fund?

We expect our model to add value and assist in our portfolio construction process as investors focus on companies that exhibit favorable long term fundamentals. As the economy and earnings growth wains, we believe there will be a divergence between companies’ fundamentals and related returns. After mid-cycle slowdowns, the market tends to reward those companies which are more suited to endure a range of market conditions. These are companies that exhibit stronger longer term fundamentals, such as favorable valuations, increasing earnings outlooks and stronger balance sheets. Our model focuses on these factors and we tend to buy companies that have positive exposure to all of these factor groups.†

Past performance does not guarantee future results.

| 1 | The S&P 400 MidCap Index is a market capitalization-weighted index of 400 medium capitalization stocks. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| † | The composition of the Fund’s portfolio is subject to change. |

10

Pacific Capital Mid-Cap Fund (cont.)

Sector Weightings as of July 31, 2005

(as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

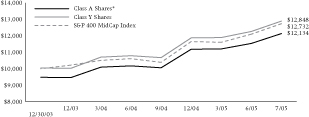

Growth of a $10,000 Investment

The chart above represents a comparison of a hypothetical $10,000 investment in the indicated share class versus a similar investment in the Fund’s benchmark. The chart above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2005

| | | | | | |

| | | 1 Year

| | | Since

Inception

(12/30/03)

| |

Class A Shares* | | 17.22 | % | | 12.97 | % |

Class C Shares** | | 22.87 | % | | 16.23 | % |

Class Y Shares | | 23.92 | % | | 17.12 | % |

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 1.00% (applicable only to redemptions within one year of purchase). |

The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The Pacific Capital Funds are distributed by BISYS Fund Services. The Asset Management Group of Bank of Hawaii provides investment advisory services to the Fund and receives a fee for its services. Bankoh Investment Partners, LLC is sub-advisor to the Fund and is paid a fee for its services.

The Pacific Capital Mid-Cap Fund’s inception date was December 30, 2003. The Class C shares were not in existence prior to April 30, 2004. Performance calculated for any period up to and through April 30, 2004, is based upon the performance of Class A shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

The performance of the Pacific Capital Mid-Cap Fund is measured against the S&P 400 MidCap Index, an unmanaged market capitalization-weighted index of 400 medium capitalization stocks. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

11

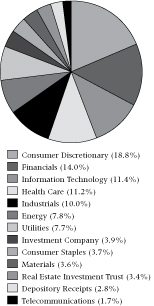

Pacific Capital Growth Stock Fund

Investment Style

Domestic, large-cap, growth

Investment Objective

Long-term capital appreciation with a secondary emphasis on dividend income, by investing in a diversified portfolio of large-capitalization companies – currently greater than $1 billion – whose earnings are expected to grow faster than the average for the U.S. market.

Investment Considerations

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| • | | Top-down macroeconomic analysis of sector trends |

| • | | Bottom-up fundamental research to identify attractive stocks |

| • | | Rigorous quantitative risk analysis |

Investment Management

Advised by Asset Management Group of Bank of Hawaii (AMG)

| • | | Founded in 1898, AMG represents the largest, most experienced staff of investment professionals in Hawaii |

| • | | $6.4 billion in assets under management |

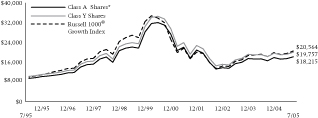

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2005, the Fund (Class A Shares without sales charge) gained 10.29%. The Fund’s benchmark, the Russell 1000® Growth Index1, gained 13.04% during this same period.

What were the major factors in the market that influenced the Fund’s performance?

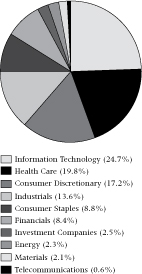

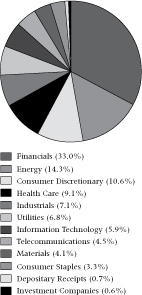

The stock market advanced sharply during the 12 months ended July 31, 2005, reflecting continued expansion of the economy and solid corporate earnings gains. Smaller market capitalization securities were particularly strong as investors showed a preference for riskier issues. In addition, value stocks continued to outperform growth stocks during the period. Leading sectors included Energy, Utilities, and Consumer Discretionary. Lagging sectors included Financials, Consumer Staples, and Industrials.

The Fund’s underperformance relative to its Russell benchmark was primarily due to the conservative nature of the Fund’s holdings that left it under exposed to some of the more aggressive and mostly smaller segments of the growth stock universe. Sector selection had a relatively minor negative impact on the Fund’s performance as the benefit from an overweight in the Consumer Discretionary sector was offset by unfavorable weightings in most of the other sectors.†

The Fund’s difficult comparisons against its benchmark emerged most noticeably in the fiscal second and fourth quarters in which the stock market underwent a rally which propelled smaller, more volatile stocks sharply higher.

What major changes have occurred in the portfolio during the period covered by the report?

The structure of the portfolio was not changed significantly during the fiscal year although numerous trades were completed to maintain the Fund’s exposure and to comply with its individual security sell discipline. The Fund continues to emphasize securities that possess favorable momentum, value and quality characteristics.†

What is your outlook for the Fund?

The stock market appears to be in the process of regaining its upward momentum after stumbling earlier in the year on worries about high oil prices and its impact on economic growth. The outlook for corporate earnings and domestic economic growth is improving and stock prices are responding positively. Technology stocks, laggards earlier in the year, have sprung back to life and are showing renewed strength, particularly semiconductor stocks. Economically sensitive stocks in the Materials and Industrial sectors are also showing renewed strength after selling off sharply earlier in the year. Therefore, in recent weeks we have taken steps to position the portfolio somewhat more aggressively with a focus on stocks offering the potential to rebound as economic and earnings worries ease. Such purchases include Nucor, Phelps Dodge, Micrel, International Rectifier, Polaris Industries and Grainger.†

Past performance does not guarantee future results.

| 1 | The Russell 1000® Growth Index measures the performance of 1,000 securities found in the Russell universe with higher price-to-book ratios and higher forecasted growth values. Investors cannot invest directly in an index, although they can invest in the underlying securities. |

| † | The composition of the Fund’s portfolio is subject to change. |

12

Pacific Capital Growth Stock Fund (cont.)

Sector Weightings as of July 31, 2005

(as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

Growth of a $10,000 Investment

The chart above represents a comparison of a hypothetical $10,000 investment in the indicated share class versus a similar investment in the Fund’s benchmark. The chart above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2005

| | | | | | | | | |

| | | 1 Year

| | | 5 Year

| | | 10 Year

| |

Class A Shares* | | 4.45 | % | | -10.91 | % | | 6.18 | % |

Class B Shares** | | 5.56 | % | | -10.71 | % | | 6.20 | % |

Class C Shares** | | 9.59 | % | | -10.57 | % | | 6.21 | % |

Class Y Shares | | 10.50 | % | | -9.69 | % | | 7.05 | % |

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The Pacific Capital Funds are distributed by BISYS Fund Services. The Asset Management Group of Bank of Hawaii provides investment advisory services to the Fund and receives a fee for its services.

Class B and Class C shares of the Fund commenced operations on March 2, 1998 and April 30, 2004, respectively. Performance information for Class C shares is based upon the performance of Class B shares from inception. Performance calculated for any period up to and through March 2, 1998 is based upon the performance of Class A shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

The performance of the Pacific Capital Growth Stock Fund is measured against the Russell 1000® Growth Index which measures the performance of 1,000 securities found in the Russell universe with higher price-to-book ratios and higher forecasted growth values. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in the underlying securities.

13

Pacific Capital Growth and Income Fund

Investment Style

Domestic, large-cap, blend

Investment Objective

Long-term capital appreciation with a secondary emphasis on dividend income, by investing in a diversified portfolio of large-capitalization dividend-paying companies – currently greater than $1 billion – whose earnings are expected to grow at above-average rates in relation to industry peers.

Investment Considerations

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| • | | Top-down macroeconomic analysis of sector trends |

| • | | Bottom-up fundamental research to identify attractive stocks |

| • | | Rigorous quantitative risk analysis |

Investment Management

Advised by Asset Management Group of Bank of Hawaii (AMG)

| • | | Founded in 1898, AMG represents the largest, most experienced staff of investment professionals in Hawaii |

| • | | $6.4 billion in assets under management |

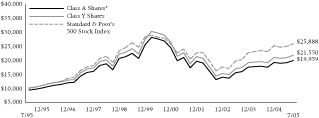

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2005, the Fund (Class A Shares without sales charge) gained 14.83%. The Fund’s benchmark, the S&P 5001, gained 14.04% during this same period.

For the same period, the Fund ranked in the 27th percentile among 882 funds in the Lipper Large-Cap Core universe2.

What were the major factors in the market that influenced the Fund’s performance?

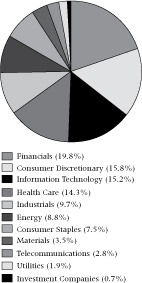

The stock market advanced sharply during the 12 months ended July 31, 2005, reflecting continued expansion of the economy and solid corporate earnings gains. Smaller market capitalization securities were particularly strong as investors showed a preference for riskier issues. In addition, value stocks continued to outperform growth stocks during the period. Leading sectors included Energy, Utilities, and Consumer Discretionary. Lagging sectors included Financials, Consumer Staples, and Industrials.

During the fiscal year, the Fund’s performance outpaced its S&P 500 benchmark primarily due to successful security selection, particularly in the Consumer Cyclical and Technology sectors. Standout performers included the Fund’s holdings in Autodesk, Amphenol Corp., Coach and American Eagle Outfitters. To a lesser extent, sector selection helped the Fund, particularly with over-weighted positions in the Consumer Discretionary and Basic Materials sectors.†

The performance of the Fund compared favorably against its peer group because of its positive relative performance against the S&P 500 and its true core positioning. A fair number of funds within the peer group have a large growth orientation which caused them to substantially under perform the S&P 500.†

What major changes have occurred in the portfolio during the period covered by the report?

The structure of the portfolio was not changed significantly during the fiscal year although numerous trades were completed to maintain the Fund’s exposure and to comply with its individual security sell discipline. The Fund continues to emphasize securities that possess favorable momentum, value and quality characteristics.†

What is your outlook for the Fund?

The stock market appears to be in the process of regaining its upward momentum after stumbling earlier in the year on worries about high oil prices and their impact on economic growth. The outlook for corporate earnings and domestic economic growth is improving and stock prices are responding positively. Technology stocks, laggards earlier in the year, have sprung back to life and are showing renewed strength, particularly semiconductor stocks. Economically sensitive stocks in the Materials and Industrial sectors are also showing renewed strength after selling off sharply earlier in the year. Therefore, in recent weeks we have taken steps to position the portfolio somewhat more aggressively with a focus on stocks offering the potential to rebound as economic and earnings worries ease. Such purchases include Nucor, Phelps Dodge, Sandisk, Polaris Industries and Williams Companies.†

Past performance does not guarantee future results.

| 1 | The Standard & Poor’s 500 Stock Index (“S&P 500”) is a capitalization weighted index that measures the performance of 500 large-capitalization stocks representing all major industries. It is not possible to invest directly in any index. |

| 2 | The Lipper Large-Cap Core universe is comprised of mutual funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) greater than 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Large-cap core funds have more latitude in the companies in which they invest. These funds typically have an average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value, compared to the S&P 500 Index. For the one-, five- and ten-year periods ended July 31, 2005 the Pacific Capital Growth and Income Fund ranked 234, 519 and 13 out of 882, 606 and 221 funds in the Lipper Large-Cap Core Funds category, respectively. The Lipper Rankings are based on total returns and do not reflect a sales charge. Funds with multiple share classes have a common portfolio. |

| † | The composition of the Fund’s portfolio is subject to change. |

14

Pacific Capital Growth and Income Fund (cont.)

Sector Weightings as of July 31, 2005

(as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

Growth of a $10,000 Investment

The chart above represents a comparison of a hypothetical $10,000 investment in the indicated share class versus a similar investment in the Fund’s benchmark. The chart above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2005

| | | | | | | | | |

| | | 1 Year

| | | 5 Year

| | | 10 Year

| |

Class A Shares* | | 8.76 | % | | -7.09 | % | | 7.16 | % |

Class B Shares** | | 9.93 | % | | -6.95 | % | | 7.12 | % |

Class C Shares** | | 14.00 | % | | -6.78 | % | | 7.13 | % |

Class Y Shares | | 15.12 | % | | -5.85 | % | | 7.98 | % |

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The Pacific Capital Funds are distributed by BISYS Fund Services. The Asset Management Group of Bank of Hawaii provides investment advisory services to the Fund and receives a fee for its services.

The Class B and Class C shares of the Fund commenced operations on March 2, 1998 and April 30, 2004, respectively. Performance information for Class C shares is based upon the performance of Class B shares from inception. Performance calculated for any period up to and through March 2, 1998 is based upon the performance of Class A shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

The performance of the Pacific Capital Growth and Income Fund is measured against the Standard & Poor’s 500 Stock Index, an unmanaged index generally representative of the broad domestic stock universe. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

15

Pacific Capital Value Fund

Investment Style

Domestic, large-cap, value

Investment Objective

Long-term capital appreciation with a secondary emphasis on dividend income, by investing in a diversified portfolio of large-capitalization companies – currently greater than $1 billion – believed to be undervalued, fundamentally strong and undergoing positive change.

Investment Considerations

Value-based investments are subject to the risk that the broad market may not recognize their intrinsic value. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| • | | Top-down macroeconomic analysis of sector trends |

| • | | Bottom-up fundamental research to identify attractive stocks |

| • | | Rigorous quantitative risk analysis |

Investment Management

Advised by Asset Management Group of Bank of Hawaii (AMG)

| • | | Founded in 1898, AMG represents the largest, most experienced staff of investment professionals in Hawaii |

| • | | $6.4 billion in assets under management |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2005, the Fund (Class A Shares without sales charge) rose 18.75%. The Fund’s benchmark, the Russell 1000® Value Index1, rose 19.04% during this same period.

The Fund was ranked in the 14th percentile among 442 funds within the Lipper Large Cap Value universe2.

What were the major factors in the market that influenced the Fund’s performance?

The stock market advanced sharply during the 12 months ended July 31, 2005, reflecting continued expansion of the economy and solid corporate earnings gains. Smaller market capitalization securities were particularly strong as investors showed a preference for more volatile issues. In addition, value stocks continued to outperform growth stocks during the period. Leading sectors included Energy, Utilities, and Consumer Discretionary. Lagging sectors included Financials, Consumer Staples, and Industrials.†

For the period ended July 31, 2005 the Fund underperformed its benchmark index, the Russell 1000® Value Index because of Fund expenses which are not included in the index return. Securities negatively impacting performance included Advanced Micro Devices, Rent-A-Center and Smithfield Foods, while stocks such as United Defense Industries, Hibernia and CVS had a positive impact.†

The performance of the Fund compared favorably against its peer group because of its true to style positioning within the value space in a year during which value oriented stocks substantially outperformed growth oriented stocks. A fair number of funds within the peer group have large core orientations which caused them to substantially under perform the Russell Index.

What major changes have occurred in the portfolio during the period covered by the report?

The structure of the portfolio was not changed significantly during the fiscal year although numerous trades were completed to maintain the Fund’s exposure and to comply with its individual security sell discipline. The Fund continues to emphasize securities that possess favorable momentum, value and quality characteristics.†

What is your outlook for the Fund?

The stock market appears to be in the process of regaining its upward momentum after stumbling earlier in the year on worries about high oil prices and their impact on economic growth. The outlook for corporate earnings and domestic economic growth is improving and stock prices are responding positively. Technology stocks, laggards earlier in the year, have sprung back to life and are showing renewed strength, particularly semiconductor stocks. Economically sensitive stocks in the Materials and Industrial sectors are also showing renewed strength after selling off sharply earlier in the year. In recent weeks we have taken steps to position the portfolio somewhat more aggressively with a focus on stocks offering the potential to rebound as economic and earnings worries ease. Such purchases include U.S. Steel, Phelps Dodge, National Semiconductor, Williams Companies, and Polaris Industries.†

Past performance does not guarantee future results.

| 1 | The Russell 1000® Value Index (“Russell Index”) measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values. It is not possible to invest directly in any index. |

| 2 | The Lipper Large-Cap Value universe is comprised of mutual funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) greater than 300% of the dollar-weighted median market capitalization of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Large-cap value funds typically have a below-average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value, compared to the S&P 500 Index. For the one- and five-year periods ended July 31, 2005, the Pacific Capital Value Fund ranked 60 and 196 out of 442 and 239 funds in the Lipper Large-Cap Value Funds category, respectively. The Lipper Rankings are based on total returns and do not reflect a sales charge. Funds with multiple share classes have a common portfolio. |

| † | The composition of the Fund’s portfolio is subject to change. |

16

Pacific Capital Value Fund (cont.)

Sector Weightings as of July 31, 2005

(as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

Growth of a $10,000 Investment

The chart above represents a comparison of a hypothetical $10,000 investment in the indicated share class versus a similar investment in the Fund’s benchmark. The chart above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2005

| | | | | | | | | |

| | | 1 Year

| | | 5 Year

| | | Since

Inception

(12/3/98)

| |

Class A Shares* | | 12.57 | % | | 0.76 | % | | 2.56 | % |

Class B Shares** | | 14.00 | % | | 0.93 | % | | 2.63 | % |

Class C Shares** | | 18.00 | % | | 1.13 | % | | 2.65 | % |

Class Y Shares | | 19.12 | % | | 2.11 | % | | 3.66 | % |

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The Pacific Capital Funds are distributed by BISYS Fund Services. The Asset Management Group of Bank of Hawaii provides investment advisory services to the Fund and receives a fee for its services.

The Pacific Capital Value Fund’s inception date was December 3, 1998. The Class A, Class B and Class C shares were not in existence prior to December 8, 1998, December 13, 1998 and April 30, 2004, respectively. Performance information for Class C shares is based upon the performance of Class B shares from inception. Performance calculated for any period up to and through such inception dates is based upon the performance of Class Y shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

The performance of the Pacific Capital Value Fund is measured against the Russell 1000® Value Index, an unmanaged index comprised of the securities in the Russell universe that tend to exhibit low price-to-book and price-to-earnings ratios. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

17

Pacific Capital Diversified Fixed Income Fund

Investment Style

High-quality, intermediate-term, taxable

Investment Objective

High current income consistent with capital preservation by investing at least 80% in fixed income securities, with most of its assets in debt securities issued or guaranteed by the U.S. Government and corporate debt securities rated “A” or better by Standard & Poor’s.

Investment Considerations

Bonds offer a relatively stable level of income, although bond prices will fluctuate with interest rate changes providing the potential for principal gain or loss. Generally, bond prices fall when interest rates rise, and vice versa. Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return.

Investment Process

| • | | Top-down macroeconomic analysis of interest rate trends |

| • | | Bottom-up credit research to identify high quality bonds |

| • | | Rigorous quantitative risk analysis |

Investment Management

Advised by Asset Management Group of Bank of Hawaii (AMG)

| • | | Founded in 1898, AMG represents the largest, most experienced staff of investment professionals in Hawaii |

| • | | $6.4 billion in assets under management |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2005, the Fund underperformed its benchmark. The return for the Fund was 3.67% (Class A Shares without sales charge), versus the Merrill Lynch Government/Corporate Master Index1 return of 4.99%.

What were the major factors in the market that influenced the Fund’s performance?

The most significant negative impact on portfolio performance was the higher quality of our corporate bonds. Spreads on lower quality bonds tightened significantly through the end of March, resulting in better performance. Investors moved further out on the credit curve, taking on more risk to achieve higher income in the persistent low-rate environment. Subsequently through the end of June, 2005, lower quality bond spreads widened markedly as investors shunned risk and higher quality bonds prevailed.

What major changes have occurred in the portfolio during the period covered by the report?

Although the rate on the 10-year Treasury was little changed year-over-year, there was some volatility during the period that gave us opportunities to adjust the average maturity of the portfolio to address market conditions. During the calendar quarter ended September 30, 2004, the 10-year rate fell to 4%, below our trading range forecast. We shortened the average maturity of the portfolio in anticipation of higher rates, and extended back to benchmark maturity in late March when the 10-year Treasury rose to our “re-entry” level.†

Although corporate bond spreads remain at fairly narrow levels, issuance (supply) has declined and demand, especially from foreign entities, has been strong. We don’t anticipate that this situation will change dramatically and thus will likely maintain our overweight position in higher quality corporate bonds.†

We increased our positions in floating rate notes, which has worked out well as a defense in an environment of rising short term rates. These securities maintain a more stable market value, while providing an increasing income stream as their coupon rates adjust to higher rates.†

What is your outlook for the Fund?

We anticipate the Fed may increase short term rates at least one, possibly two more times through year-end. We expect that longer rates may remain in a trading range of approximately 4-4.5% given our current inflation and economic outlook. In this environment, we believe the next fiscal year to be very similar in performance to this reporting period, with income being the major contributor to performance.†

Past performance does not guarantee future results.

| 1 | The Merrill Lynch Government/ Corporate Master Index is generally representative of the performance of corporate and U.S. Government bonds. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| † | The composition of the Fund’s portfolio is subject to change. |

18

Pacific Capital Diversified Fixed Income Fund (cont.)

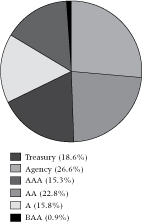

Credit Quality as of July 31, 2005

(as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

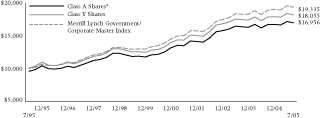

Growth of a $10,000 Investment

The chart above represents a comparison of a hypothetical $10,000 investment in the indicated share class versus a similar investment in the Fund’s benchmark. The chart above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2005

| | | | | | | | | |

| | | 1 Year

| | | 5 Year

| | | 10 Year

| |

Class A Shares* | | -0.48 | % | | 5.77 | % | | 5.42 | % |

Class B Shares** | | -1.09 | % | | 5.70 | % | | 5.30 | % |

Class C Shares** | | 3.00 | % | | 5.86 | % | | 5.30 | % |

Class Y Shares | | 3.90 | % | | 6.92 | % | | 6.09 | % |

| * | Reflects 4.00% Maximum Front-End Sales Charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The Pacific Capital Funds are distributed by BISYS Fund Services. The Asset Management Group of Bank of Hawaii provides investment advisory services to the Fund and receives a fee for its services.

The Class B and Class C shares of the Fund commenced operations on March 2, 1998 and April 30, 2004, respectively. Performance information for Class C shares is based upon the performance of Class B shares from inception. Performance calculated for any period up to and through March 2, 1998 is based upon the performance of Class A shares, which does not reflect the higher 12b-1 fees. Had the higher 12b-1 fees been incorporated, total return figures may have been adversely affected.

The performance of the Pacific Capital Diversified Fixed Income Fund is measured against the Merrill Lynch Government/Corporate Master Index, an unmanaged index generally representative of the performance of corporate and U.S. Government bonds. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

19

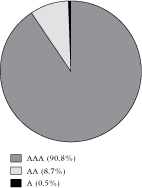

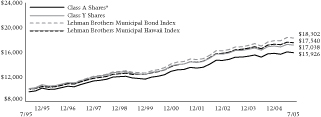

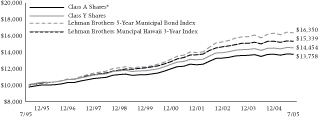

Pacific Capital Tax Free Securities Fund

Investment Style

High-quality, intermediate-term, tax-exempt

Investment Objective

High level of tax-exempt income by investing at least 80% in debt securities exempt from federal and alternative minimum tax, with 50% to 60% in Hawaii municipal obligations exempt from Hawaii state tax.

Investment Considerations