UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07454

Pacific Capital Funds

(Exact name of registrant as specified in charter)

3435 Stelzer Rd Columbus, OH 43219

(Address of principal executive offices) (Zip code)

Citi Fund Services 3435 Stelzer Road Columbus, OH 43219

(Name and address of agent for service)

Registrant’s telephone number, including area code: 614-470-8000

Date of fiscal year end: 7/31

Date of reporting period: 7/31/08

| Item 1. | Reports to Stockholders. |

Table of Contents

Letter to Shareholders

Page 1

Fund Performance Review

Page 3

Statements of Assets and Liabilities

Page 31

Statements of Operations

Page 34

Statements of Changes in Net Assets

Page 37

Schedules of Portfolio Investments

Page 45

Notes to Financial Statements

Page 77

Financial Highlights

Page 87

Report of Independent Registered Public Accounting Firm

Page 99

Additional Tax Information

Page 100

Trustees and Officers

Page 101

Board Determinations

Page 104

Expense Examples

Page 105

Proxy Voting and Portfolio Holdings Information

Page 108

Letter to Shareholders

Dear Shareholders:

Thank you for investing with Pacific Capital Funds. We value the trust you place in us, and we seek to provide world-class investment management to help you meet your financial goals.

Pacific Capital Funds draw upon the investment expertise of the Asset Management Group of Bank of Hawaii (AMG), which has approximately $5 billion in mutual fund assets under management. AMG has partnered with a select list of sub-advisors to provide Pacific Capital Funds’ shareholders with greater investment opportunities, broader diversification and access to an elite group of institutional money managers:

| | • | | Chicago Equity Partners, LLC, which specializes in domestic equity markets, serves as Sub-Adviser to the Pacific Capital Mid-Cap Fund, Pacific Capital Growth Stock Fund, Pacific Capital Growth and Income Fund and Pacific Capital Value Fund. |

| | • | | First State Investments International, Limited, a specialist in single-country, regional and sector-specific investments, serves as Sub-Adviser to the Pacific Capital New Asia Growth Fund. |

| | • | | Hansberger Global Investors, Inc., a specialist in international equity investments, serves as Sub-Adviser to the Pacific Capital International Stock Fund. |

| | • | | Nicholas-Applegate Capital Management, which specializes in global, international and domestic equity and special strategy management acts as one of three Sub-Advisers to the Pacific Capital Small Cap Fund, managing the U.S. Systematic Small Cap Core portion of the portfolio. |

| | • | | Wellington Management Company, LLP, one of the largest independent investment management firms in the world with more than $550 billion in assets, also serves as a Sub-Adviser to the Pacific Capital Small Cap Fund, managing the Small Cap Growth portion of the portfolio. |

| | • | | Mellon Capital Management Corporation, with more than $200 billion in assets, manages the Small Cap Value portion of the portfolio as the third Sub-Adviser for the Pacific Capital Small Cap Fund. |

Annual Review

The 12 months between August 2007 and July 2008 were difficult for the economy, as a number of headwinds led to a pronounced slowdown in U.S. economic growth. Gross domestic product expanded at a 4.8% rate during the third calendar quarter of 2007, but contracted slightly during 2007’s fourth quarter and remained sluggish in the early months of 2008.

Troubles in the credit markets contributed to economic weakness. Overextended homebuyers increasingly defaulted on mortgages, which in turn led to defaults on mortgage-backed bonds. Many leading financial institutions were forced to write down billions of dollars in investment losses as a result. Investors and policymakers, worried that some financial institutions may not be able to meet their obligations, became concerned about the stability of the financial system. Meanwhile, lenders became highly cautious about extending credit, and a credit and liquidity crunch resulted.

The Federal Reserve acted aggressively to restore liquidity and shore up the financial system. The Fed reduced its target short-term interest rate from 5.25% to 2.00% in order to make cash more readily available. It also extended credit to a wider range of financial institutions than it had in the past, orchestrated a buyout of troubled investment bank Bear Stearns, and acted to solidify investors’ confidence in faltering Government-Sponsored Enterprises Fannie Mae and Freddie Mac.

The housing market remained in a deep slump throughout this period. Falling home values reduced consumers’ purchasing power by diminishing their borrowing capacity and depressed parts of the economy related to housing. Meanwhile, prices on energy, food and other commodities shot higher through early July as demand outstripped supply. Consumers, squeezed by higher prices, lower home values and a weakening job market, cut back their spending, which accounts for two-thirds of U.S. economic activity, and thus weighed heavily on growth.

Not all economic news was negative during the fiscal year. A weakening dollar led to a surge in exports, as U.S. companies’ goods and services became more competitive abroad. Government stimulus checks, which Americans received beginning in May, provided a temporary boost to consumer spending. Those two factors helped propel GDP to 3.3% growth during the second quarter of 2008, according to preliminary figures.

Stocks enter bear territory

Investors’ worries about the economic slowdown and problems in the financial system caused the S&P 500 index to decline 11.09% for this 12-month period. Small-cap stocks as measured by the Russell 2000 fell 6.71%, while the MSCI EAFE Index of 21 developed foreign stock markets lost 14.58%.

During the early part of the period, through early October 2007, stocks climbed. Many investors believed the economy could escape the housing slowdown without serious harm, and were encouraged by strong profits from non-financial corporations. Declining oil prices during this early part of the period also boosted the stock market.

Stocks subsequently fell steadily, however, as the sub-prime mortgage crisis and the resulting credit crunch unfolded, commodity prices skyrocketed, the housing recession deepened and the job market weakened. The S&P 500 lost more than 20% of its value between its peak on October 9 and its low point on July 15, meeting the technical definition for a bear market.

Financial stocks led the decline. The financial sector in aggregate lost nearly a third of its value during the 12-month period, as investors, worried about large write-downs and the credit market’s troubles, fled financial stocks. Telecommunications, industrial and consumer discretionary stocks also performed poorly. Investors favored the defensive nature of consumer staples stocks, helping that sector lead the market for the period. Meanwhile, high commodity prices buoyed energy and materials stocks.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232, or visit the Funds’ website at pacificcapitalfunds.com.

1

Letter to Shareholders (cont.)

With regard to style, growth stocks generally outperformed value stocks. Financial stocks comprise a much larger portion of value indices than growth indices, so their losses dragged down value’s performance. The Russell 3000 Growth Index, which measures the returns of large, medium-sized and small growth-oriented stocks, lost 6.11% for the period, while its value counterpart fell 14.75%.

Small and large stocks traded market leadership multiple times during this period, as investors tried to gauge the effects of swirling market conditions on various types of companies. Large-cap stocks produced superior returns for much of the period, as investors favored shares of firms with exposure overseas and the ability to self-finance growth. Small stocks overtook their larger counterparts late in the fiscal year, however.

Foreign stocks surged early in the period, led by strong returns from emerging markets in Latin America and Asia, and then declined significantly for the rest of the fiscal year. Signs that the U.S. economic slowdown could spread to overseas markets caused investors to flee foreign stocks, as did a general aversion to risk.

Bond investors favor quality over all else

Concerns about the financial system and the economic outlook caused fixed-income investors to pile into the highest-quality bonds. The bond market as a whole, as measured by the Lehman Brothers Aggregate Bond Index, gained 6.15% during the 12 months under review— but that healthy overall return masked the degree of turmoil and volatility in the fixed-income markets.

Treasury bonds rallied throughout the period, as investors sought a safe haven. Treasury Inflation Protected Securities, which provide shelter from both credit risk and inflation risk, performed especially well. Prices on existing Treasury securities rose substantially, while yields, which move in the opposite direction of bond prices, declined considerably.

Short-term government securities experienced the greatest yield declines, pushed down by reductions in the Fed Funds target rate as well as investors’ desire for liquidity. Indeed, investor concerns about safety and liquidity caused demand for Treasury bills to reach a fever pitch at times.

In other sectors of the bond market, higher-quality sectors outperformed lower-quality sectors across the board. Agency issues outperformed high-quality corporate bonds, and high-quality corporates outperformed high-yield bonds.

Our perspective

We view the current environment with a great deal of caution, as we are concerned about both inflation and economic growth. We have focused on maintaining appropriate asset allocations for a slower economy, while emphasizing high quality in both equities and fixed-income securities.

We would like to take this opportunity to remind investors of the importance of diversification. Proper diversification for your financial goals can help you manage difficult periods in the markets, without sacrificing the growth potential you need to reach long-term objectives.

Thank you for your confidence in Pacific Capital Funds. If you have any questions or would like a Fund prospectus, we encourage you to contact your registered investment professional, call Pacific Capital Funds at (800) 258-9232 or visit our website at www.pacificcapitalfunds.com.

|

| Sincerely, |

|

|

| Tobias M. Martyn |

| Senior Executive Vice President & Chief Investment Officer |

| Asset Management Group of Bank of Hawaii |

The foregoing information and opinions and following management discussions and analysis are for general information only. The Asset Management Group of Bank of Hawaii does not guarantee the accuracy or completeness, nor assume liability for any loss, which may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice, are for general information only and are not intended as an offer or solicitation with respect to the purchase or sale of any security or offering of individual or personalized investment advice.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232, or visit the Funds’ website at pacificcapitalfunds.com.

| * | For additional information regarding Fund performance, please refer to the Funds’ commentary section. |

NOTICE ABOUT DUPLICATE MAILINGS

In order to reduce expenses incurred in connection with the mailing of prospectuses, prospectus supplements, semi-annual reports and annual reports to multiple shareholders at the same address, Pacific Capital Funds may in the future deliver one copy of a prospectus, prospectus supplement, semi-annual report or annual report to a single investor sharing a street address or post office box with other investors, provided that all such investors have the same last name or are believed to be members of the same family. This process, called “householding,” will continue indefinitely unless you instruct us otherwise. If you share an address with another investor and wish to receive your own prospectus, prospectus supplements, semi-annual reports and annual reports, please call the Trust toll-free at 1-800-258-9232.

2

Pacific Capital New Asia Growth Fund

Investment Style

Regional, multi-cap, growth

Investment Objective

Long-term capital appreciation by investing in a broadly diversified portfolio of companies located in Asia’s developing regions, excluding Japan. Investments are not limited to any particular size or sector.

Investment Considerations

An investment in this Fund entails the special risks of international investing, including currency exchange fluctuation, government regulations, and the potential for political and economic instability. The Fund’s share price is expected to be more volatile than that of a U.S.-only fund. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| | • | | Follow active bottom-up investment approach |

| | • | | Invest for absolute versus relative return |

| | • | | Look outside benchmark representation for fresh opportunities |

| | • | | Identify sensibly priced, high-quality companies that exhibit long-term growth potential |

Investment Management

Advised by Asset Management Group of Bank of Hawaii

Sub-Advised by First State Investments International Limited (since June 29, 2006)

| | • | | First State Investments is part of Colonial First State Global Asset Management (CFS GAM), the consolidated asset management business of the Commonwealth Bank of Australia (CBA) |

| | • | | CFS GAM’S combined investment businesses manage approximately US$148 billion globally |

| | • | | CFS GAM has offices in London, Edinburgh, Sydney, Hong Kong, Singapore and Jakarta |

| | • | | Specialist in single country, regional, global and sector specific investments |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2008, the Fund returned -5.38% (Class A Shares without sales charge), outperforming its benchmark, the MSCI® AC Far East Free Index1 (excluding Japan), which returned -12.45%.

What were the major factors in the market that influenced the Fund’s performance?

The MSCI® AC Far East Free Index (excluding Japan) underperformed global indices for the year ended July 31, 2008. The MSCI World Index returned -10.38% and the MSCI Emerging Markets Index returned - -4.09% in U.S. dollar terms.

Asian markets were weak on concerns about rising inflationary pressures, driven by the oil price which hit new highs above $140 per barrel. Inflation data in the region was higher than expected and concerns emerged about the prospect of stagflation.

At a sector level Energy, Consumer Staples, Telecom Services and Utilities outperformed the MSCI Far East ex-Japan Index. Energy continued to rise in line with the price of oil while the other sectors benefited as investors moved into more defensive stocks. The cyclical Industrials sector underperformed and Information Technology lagged on poor demand and a weak outlook.

What helped the Fund’s performance?

Positions in Taiwan outperformed the MSCI Far East ex-Japan Index, in particular Uni-President Enterprises (Consumer Staples) and Chunghwa Telecom (Telecom Services) as investors anticipated that a presidential election victory by the KMT would be positive for relations with Mainland China and thus economic growth in Taiwan.†

Several positions in China also performed strongly during the period including Energy company CNOOC, which rallied as the price of oil reached record highs. China Telecom also outperformed as it benefited from the restructuring of the Chinese telecom industry and was expected to gain market share from China Mobile.†

What hurt the Fund’s performance?

On the negative side Lihir Gold (Australia: Materials) declined as the price of gold fell on profit taking and China Resources Enterprise (China: Consumer Discretionary) underperfomed the MSCI Far East ex-Japan Index on concerns over slowing beer consumption in China and loss of market share for its livestock distribution business in Hong Kong. Shinsegae (South Korea: Consumer Staples) lagged on worries about a slow down in the South Korean economy.†

In the Information Technology sector Delta Electronics (Taiwan) and Samsung Electronics (South Korea) both underperformed as demand continued to disappoint.†

What major changes have occurred in the portfolio during the period covered by this report?

Over the year we continued to increase our exposure to companies in the Telecom Services sector, purchasing Chunghwa Telecom (Taiwan), a strong stable integrated telecoms franchise with a growing dividend yield, and Singapore Telecom, which is growing earnings from its investments in emerging market telecom companies and has strong cash generation from Australia and Singapore.†

Elsewhere we purchased Lihir Gold (Australia: Materials) which we believe should benefit from the potential long-term rise in the price of gold, Yuhan Corporation (South Korea: Health Care), a leading pharmaceutical company conservatively run with a strong track record, and Taiwanese Information Technology company Mediatek which was attractively valued due to poor sentiment towards

Past performance does not guarantee future results.

1 | The Morgan Stanley Capital International (MSCI®) All Country (AC) Far East Free Index (excluding Japan) is a free float-adjusted market capitalization index that is designed to measure equity market performance in the Far East, excluding Japan. Investors cannot invest directly in an index. |

† | The composition of the Fund’s portfolio is subject to change. |

3

Pacific Capital New Asia Growth Fund (cont.)

technology stocks. We also bought Hong Kong utilities group CLP which we believe offers relatively predictable earnings in a difficult environment and President Chain Store (Taiwan: Consumer Staples) because of its attractive growth profile and the positive outlook following its recent award of Shanghai’s 7-11 franchise.†

We sold Sembcorp Industries (Singapore: Industrials) due to worries on whether the company can execute its growth strategy successfully. We also sold financial stocks Shinhan Financial (South Korea), Standard Chartered (UK) and Cathay Financial (Taiwan) as part of our strategy to reduce exposure to the sector.†

We took profits in China Shenhua (China: Energy) and Kingboard Chemicals (Hong Kong: Information Technology), and sold Hon Hai Precision (Taiwan: Information Technology) on valuation concerns.†

What is your outlook for the Fund?

We remain defensively positioned and are maintaining a strong focus on sustainable cash flows as well as long-term growth prospects.

We are beginning to see some evidence of a slowdown in growth in the region. Although earnings reports remain in line with expectations we anticipate some negative surprises as the year progresses.

Although the current economic outlook remains unclear, we believe the current problems in the credit markets may have a significant impact on the underlying global economy. We remain cautious in the short-term, as we are concerned about the potential for stagflation. However, we believe that careful stock selection in the region could provide positive long-term returns.

Past performance does not guarantee future results.

† | The composition of the Fund’s portfolio is subject to change. |

4

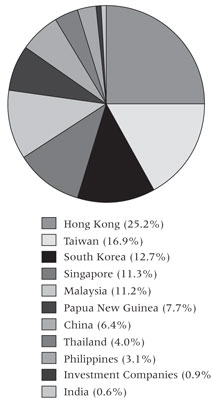

Pacific Capital New Asia Growth Fund (cont.)

Country Weightings as of July 31, 2008 (as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

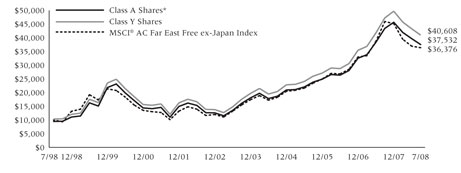

Growth of a $10,000 Investment

The hypothetical $10,000 investment graph above represents a comparison of the performance of the indicated share class versus a similar investment in the Fund’s benchmark. The graph does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2008

| | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

Class A Shares* | | -10.34 | % | | 14.62 | % | | 19.41 | % | | 14.14 | % |

Class B Shares** | | -9.28 | % | | 15.03 | % | | 19.70 | % | | 14.12 | % |

Class C Shares** | | -6.87 | % | | 15.80 | % | | 19.82 | % | | 13.96 | % |

Class Y Shares | | -5.14 | % | | 16.97 | % | | 20.99 | % | | 15.04 | % |

MSCI® AC Far East Free Index (excluding Japan) | | -12.45 | % | | 16.39 | % | | 20.42 | % | | 13.78 | % |

| | | | |

Expense Ratios | | Class A | | | Class B | | | Class C | | | Class Y | |

Gross | | 1.77 | % | | 2.37 | % | | 2.37 | % | | 1.37 | % |

With Contractual Waivers | | 1.62 | % | | 2.37 | % | | 2.37 | % | | 1.37 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The above expense ratios are from the Funds’ prospectus dated November 28, 2007. Additional information pertaining to the Funds’ expense ratios for the year ended July 31, 2008 can be found in the financial highlights.

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The above performance table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Total returns reflect the waiver of various operational fees. Had these waivers not been in effect, performance quoted would have been lower.

The Class C Shares of the Fund commenced operations on April 30, 2004. Performance information for Class C Shares prior to April 30, 2004 is based on the performance of Class B Shares.

The performance of the Pacific Capital New Asia Growth Fund is measured against the MSCI® AC Far East Free ex Japan Index, which is an unmanaged free float-adjusted market capitalization index that is designed to measure equity market performance in the Far East, excluding Japan. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index.

The Pacific Capital Funds are distributed by Foreside Distribution Services, L.P. The Asset Management Group of Bank of Hawaii is investment adviser to the Fund and receives a fee for its services. First State Investments International Limited is sub-adviser to the Fund and is paid a fee for its services.

5

Pacific Capital International Stock Fund

Investment Style

International, multi-cap, blend

Investment Objective

Long-term capital appreciation by investing in a broadly diversified portfolio of companies domiciled outside the United States. Investments are not limited to any particular type or size of company or to any region of the world, including emerging markets countries.

Investment Considerations

An investment in this Fund entails the special risks of international investing, including currency exchange fluctuation, government regulations, and the potential for political and economic instability. The Fund’s share price is expected to be more volatile than that of a U.S.-only fund. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| | • | | Style neutral growth and value discipline |

| | • | | Disciplined bottom-up stock selection |

Investment Management

Advised by Asset Management Group of Bank of Hawaii

Sub-Advised by Hansberger Global Investors, Inc. (since June 1, 2004)

| | • | | Headquartered in Ft. Lauderdale, Florida, with satellite offices in Hong Kong, Moscow, Toronto and Mumbai |

| | • | | 22 investment professionals, 14 nationalities |

| | • | | $8 billion in assets under management, includes $1.5 billion in Advised Managed Accounts of other firms based on HGI models |

| | • | | HGI is an affiliated investment manager of Natixis Global Asset Management (“Natixis”). Natixis has an ownership position of 86%; HGI management and employees own the remaining 14% (both on a fully-diluted basis). |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2008, the Fund outperformed its benchmark, the MSCI® ACWI ex US Index1. The Fund (Class A shares without sales charge) returned -9.03%, while the MSCI® ACWI ex US Index returned -9.30%.

What were the major factors in the market that influenced the Fund’s performance?

Japanese holdings were down 13.4% while the MSCI Japan Index was down 14.8%. Positions in Sumitomo Trust (down 22.3%) and Nitto Denko (down 30.2%) had the largest negative impact on performance.†

European holdings performed better than the MSCI Europe Index, -7.2% to -11.5%.†

Swiss holdings were down 1.6% while the MSCI Switzerland Index was down 6.1%. The Fund benefitted from an average 3.2% overweighting to this market. The Fund’s investment in Roche Holdings had the largest positive impact with an 11.8% return.†

German stocks held by the Fund declined less than the MSCI Germany Index, -2.7% to -2.96%. The Fund’s position in SAP had the largest positive impact with a 16.9% return during the period.†

Holding a different basket of currencies than the MSCI ACWI ex US Index had a positive net effect on the relative return. A 2.2% average overweighting to the Brazilian Real had the largest impact on relative return.†

Cash Reserves, averaging 1.0% of assets, had a small positive net impact.

What major changes have occurred in the portfolio during the period covered by this report?

Change in absolute weights: On an absolute basis, the largest change in the regional weights was a 0.9% decrease to Europe.†

From a sector perspective, the Fund’s largest absolute weighting change was a 1.1% increase to Health Care.†

Change in benchmark-relative weights: Relative to the benchmark, the Fund’s Japanese weight decreased by 1.4% while the Emerging Markets weight increased by 1.0%.†

From a sector perspective, the Materials weight decreased by 1.4% while Industrials increased by 1.1%.†

What is your outlook for the Fund?

As expectations for global economic growth were revised downward for 2008, there may be some negative earnings revisions in the coming quarters. We believe, however, that these expectations may already be reflected in current stock prices. We anticipate that the fallout of the credit crisis, rising inflation, and slower economic growth in some regions may create challenges for equity investors.

Our investment process focuses on stock selection. In keeping with our long time horizon, we put a great deal of effort into researching individual companies: learning as much as possible about each company’s management, policies, challenges, markets, and competition. We believe our diligence leads us to invest in companies which create their own opportunities or that could enjoy improving fundamentals even during this volatile economic period. We believe this process may reward our investors over time.

Past performance does not guarantee future results.

1 | The Morgan Stanley Capital International (MSCI®) All Country World (ACWI) ex US Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets outside the U.S. Investors cannot invest directly in an index. |

† | The composition of the Fund’s portfolio is subject to change. |

6

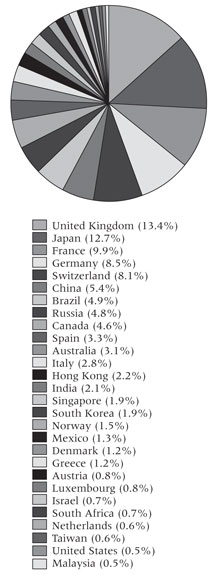

Pacific Capital International Stock Fund (cont.)

Country Weightings as of July 31, 2008 (as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

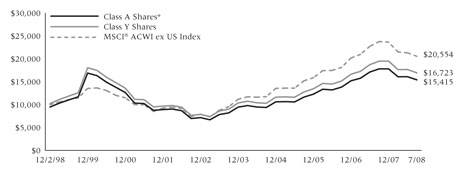

Growth of a $10,000 Investment

The hypothetical $10,000 investment graph above represents a comparison of the performance of the indicated share class versus a similar investment in the Fund’s benchmark. The graph does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2008

| | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | Since Inception

(12/2/98) | |

Class A Shares* | | -13.79 | % | | 9.91 | % | | 13.04 | % | | 4.58 | % |

Class B Shares** | | -13.12 | % | | 10.21 | % | | 13.28 | % | | 4.56 | % |

Class C Shares** | | -10.50 | % | | 11.05 | % | | 13.39 | % | | 4.43 | % |

Class Y Shares | | -8.80 | % | | 12.16 | % | | 14.54 | % | | 5.47 | % |

MSCI® ACWI ex US Index | | -9.30 | % | | 13.38 | % | | 17.93 | % | | 7.74 | %*** |

| | | | |

Expense Ratios | | Class A | | | Class B | | | Class C | | | Class Y | |

Gross | | 1.60 | % | | 2.20 | % | | 2.20 | % | | 1.20 | % |

With Contractual Waivers | | 1.45 | % | | 2.20 | % | | 2.20 | % | | 1.20 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The above expense ratios are from the Funds’ prospectus dated November 28, 2007. Additional information pertaining to the Funds’ expense ratios for the year ended July 31, 2008 can be found in the financial highlights.

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

| *** | Return for the period 11/30/98 to 7/31/08. |

The above performance table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Total returns reflect the waiver of various operational fees. Had these waivers not been in effect, performance quoted would have been lower.

The Pacific Capital International Stock Fund’s inception date was December 2, 1998. The Class A, Class B and Class C Shares were not in existence prior to December 8, 1998, December 20, 1998 and April 30, 2004, respectively. Performance information for Class C Shares prior to April 30, 2004 is based on the performance of Class B Shares. Performance for Class A and Class B Shares for any period prior to the inception date of the share class is based on the performance of the Class Y Shares, which does not reflect the higher 12b-1 fees charged by the Class A and Class B Shares. Had the higher 12b-1 fees been reflected, total return figures may have been adversely affected.

The performance of the Pacific Capital International Stock Fund is measured against the MSCI® ACWI ex US Index, an unmanaged index which is designed to measure equity market performance in the global developed and emerging markets outside the U.S. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index.

The Pacific Capital Funds are distributed by Foreside Distribution Services, L.P. The Asset Management Group of Bank of Hawaii is investment adviser to the Fund and receives a fee for its services. Hansberger Global Investors, Inc. is sub-adviser to the Fund and is paid a fee for its services.

7

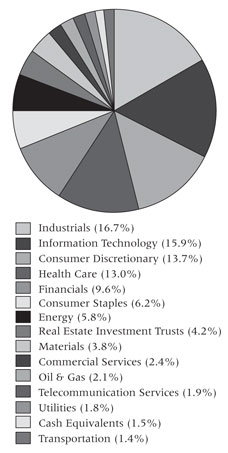

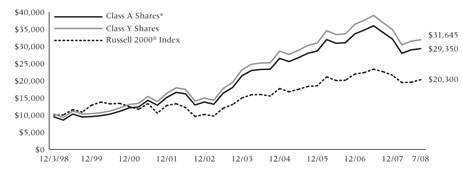

Pacific Capital Small Cap Fund

Investment Style

Domestic, small-cap, blend

Investment Objective

Long-term capital appreciation by investing in a diversified portfolio of small-capitalization companies.

Investment Considerations

Small-capitalization stocks typically carry additional risk, since smaller companies generally have a higher risk of failure and experience a greater degree of volatility than larger companies. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

Nicholas-Applegate Capital Management

| | • | | Systematic small cap strategy: Emphasizes a quantitative stock-selection approach to identify companies with sustainable growth characteristics and timely market recognition |

Wellington Management Company, LLP

| | • | | Small cap growth intersection strategy: Combines fundamental research with quantitative valuation techniques in a disciplined framework to assess investment attractiveness |

Mellon Capital Management Corporation

| | • | | Small cap value strategy: Utilizes a disciplined process that combines computer modeling techniques, fundamental analysis, and risk management to select stocks which Mellon Capital Management Corporation believes are undervalued |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2008, the Fund returned -11.86% (Class A Shares without sales charge), underperforming the Fund’s benchmark, the Russell 2000® Index1, which returned -6.71%.

What were the major factors in the market that influenced the Fund’s performance?

During the fiscal year, large caps (represented by the S&P 500) returned -11.09%, underperforming small caps (represented by the Russell 2000®) which returned -6.71%. Within the small cap universe, growth outperformed value (the Russell 2000® Value Index2 returned -9.95% versus a -3.76% return for the Russell 2000® Growth Index3). Within the Russell 2000® Growth Index, Energy and Utilities were the strongest performers, while Telecommunication Services, Consumer Discretionary, and Information Technology lagged.

During the past twelve months, volatility has persisted as significant consumer headwinds, continued pressure on corporate profits, lingering credit market distress, and investor perception that the central banks of the world must now combat inflation at the expense of growth, weighed on global markets. Momentum trends generally continued within the equity markets, as the Energy sector maintained its strong leadership on the further run-up in commodity prices. Within the United States, tax rebate checks will probably boost domestic spending temporarily, but have not provided significant relief to the consumer from higher energy, food, and debt costs, and eroding home values.

The Fund’s underperformance was primarily due to weak stock selection within the Financials, Industrials, and Health Care sectors of the market. To a limited extent, these weak sectors were counteracted by relative strength in Materials, Telecomm Services, Consumer Staples, and Consumer Discretionary.†

What major changes have occurred in the portfolio during the period covered by the report?

Since June 2006, the Fund has employed a “multi-manager” approach whereby portions of the Fund’s assets are allocated among three different investment sub-advisers: small cap value strategy managed by Mellon Capital Management (“MCM”), systematic small cap core strategy managed by Nicholas-Applegate Capital Management (“NACM”), and small cap growth strategy managed by Wellington Management Company (“WMC”). Each sub-adviser utilizes distinct investment styles intended to complement one another, applying its own methodology for selecting investments.

MCM - Small Cap Value

There have been no major changes in this portion of the portfolio during the period. The portfolio remains diversified across many industry groups. Given the continued volatility in the financial markets, a strategy emphasizing strong fundamentals and sector diversification has served clients well over the long run.†

NACM - Systematic Small Cap

All buys and sells in this portion of the portfolio are driven by NACM’s quantitative stock selection model based on each position’s relative attractiveness and contribution to risk in relation to existing portfolio holdings. During the period, there were minor changes in sector weights in this sleeve of the portfolio relative to the benchmark

Past performance does not guarantee future results.

1 | The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index, which represents approximately 10% of the total market capitalization of the Russell 3000® Index. Investors cannot invest directly in an index. |

2 | The Russell 2000® Value Index is comprised of the securities in the Russell 2000® Index with a less-than-average growth orientation. Companies in this index generally have low price-to-book and price-to-earnings ratios. Investors cannot invest directly in an index. |

3 | The Russell 2000® Growth Index measures the performance of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. |

† | The composition of the Fund’s portfolio is subject to change. |

8

Pacific Capital Small Cap Fund (cont.)

Investment Management

Advised by Asset Management Group of Bank of Hawaii

Sub-Advised by Nicholas-Applegate Capital Management (since January 31, 2001)

| | • | | Founded in 1984, Nicholas-Applegate is a diversified global investment firm with more than twenty years of experience delivering value to clients |

| | • | | Nicholas-Applegate offers a broad array of investment solutions built on a consistent investment philosophy |

| | • | | Traditional Global, U.S. and non-U.S. |

| | • | | $13.2 billion in assets under management |

Sub-Advised by Wellington Management Company, LLP (since June 14, 2006)

| | • | | Tracing its roots to 1928, Wellington Management is one of the largest independent investment management firms in the world |

| | • | | Serves as investment manager for clients in over 40 countries |

| | • | | $550 billion in assets under management |

Sub-Advised by Mellon Capital Management Corporation (since January 1, 2008)

| | • | | Founded in 1983, Mellon Capital is headquartered in San Francisco with offices in Pittsburgh, Philadelphia, Boston and Jersey City. |

| | • | | Specializes in domestic and global asset allocation strategies, active and passive equity and fixed income strategies, alternative investments, currency strategies, and overlay strategies |

| | • | | Over $204.2 billion in assets under management (including $25.9 billion in overlay assets) driven by stock selection model. Sector weightings in Industrials and Materials were increased, while the weighting in Consumer Staples was reduced.† |

| | • | | Mellon Equity Associates, L.L.P. has managed a small cap portfolio on behalf of the Pacific Capital Small Cap Fund since June 26, 2007. As of January 1, 2008, Mellon Equity merged with its sister subsidiary Mellon Capital Management. |

WMC- Small Cap Growth Intersection

Changes in this portion of the portfolio are driven by bottom-up fundamental and quantitative research rather than sector-level, top-down views. During the 12-month period, the largest new purchases in this portion of the portfolio included Owens & Minor, a distributor of medical and surgical supplies to the acute-care market, WMS Industries, a global provider of gaming products to the legalized gaming industry, and Frontier Oil, a crude oil refiner and wholesale marketer of refined petroleum products. Our largest eliminations included Golden Telecom, a Russia-based telecommunication and internet provider which was acquired during the period, and apparel manufacturer, J. Crew Group.†

What is your outlook for the Fund?

Looking forward, the global economy is expected to slow materially in coming quarters. As surging oil and agricultural prices are boosting inflation rates globally, central banks have become increasingly determined to fight inflation at the expense of economic growth. These negative shocks have come on top of existing concerns about the state of the U.S. economy and the health of the global financial system. In the U.S., the Federal Reserve Bank can find solace in the fact that, thus far, longer-run inflationary expectations are still well anchored. As such, we believe inflation in the U.S. is likely to peak in coming months and should be held back in 2009 by the expected cyclical weakness.

Longer-term, company fundamentals drive stock prices, and we are maintaining our discipline and focus on fundamentals. The sub-advisers will continue to employ a combination of fundamental and quantitative research to identify the most attractive stocks, while maintaining appropriate risk controls relative to the benchmark. Over the long-run, security selection will drive the Fund’s results, and we believe the Fund is well positioned to capitalize on the changing market environment.†

† | The composition of the Fund’s portfolio is subject to change. |

9

Pacific Capital Small Cap Fund (cont.)

Sector Weightings as of July 31, 2008 (as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

Growth of a $10,000 Investment

The hypothetical $10,000 investment graph above represents a comparison of the performance of the indicated share class versus a similar investment in the Fund’s benchmark. The graph does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2008

| | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | Since Inception

(12/3/98) | |

Class A Shares* | | -16.48 | % | | -0.79 | % | | 9.78 | % | | 11.79 | % |

Class B Shares** | | -15.36 | % | | -0.46 | % | | 10.00 | % | | 11.70 | % |

Class C Shares** | | -13.26 | % | | 0.25 | % | | 10.12 | % | | 11.56 | % |

Class Y Shares | | -11.64 | % | | 1.26 | % | | 11.23 | % | | 12.66 | % |

Russell 2000® Index | | -6.71 | % | | 2.92 | % | | 9.75 | % | | 7.68 | % |

| | | | |

Expense Ratios | | Class A | | | Class B | | | Class C | | | Class Y | |

Gross | | 1.83 | % | | 2.43 | % | | 2.43 | % | | 1.43 | % |

With Contractual Waivers | | 1.68 | % | | 2.43 | % | | 2.43 | % | | 1.43 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The above expense ratios are from the Funds’ prospectus dated November 28, 2007. Additional information pertaining to the Funds’ expense ratios for the year ended July 31, 2008 can be found in the financial highlights.

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The above performance table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Total returns reflect the waiver of various operational fees. Had these waivers not been in effect, performance quoted would have been lower.

The Pacific Capital Small Cap Fund’s inception date was December 3, 1998. The Class A, Class B and Class C Shares were not in existence prior to December 8, 1998, December 20, 1998 and April 30, 2004, respectively. Performance information for Class C Shares prior to April 30, 2004 is based on the performance of Class B Shares. Performance for Class A and Class B Shares for any period prior to the inception date of the share class is based on the performance of the Class Y Shares, which does not reflect the higher 12b-1 fees charged by Class A and Class B Shares. Had the higher 12b-1 fees been reflected, total return figures may have been adversely affected.

The performance of the Pacific Capital Small Cap Fund is measured against the Russell 2000® Index, an unmanaged index comprised of the 2,000 smallest companies in the Russell 3000® Index, which represents approximately 10% of the total market capitalization of the Russell 3000® Index (The Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization). The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index.

The Pacific Capital Funds are distributed by Foreside Distribution Services, L.P. The Asset Management Group of Bank of Hawaii is investment adviser to the Fund and receives a fee for its services. Nicholas-Applegate Capital Management,Wellington Management Company, LLP and Mellon Capital Management Corporation are each sub-advisers for a portion of the Fund’s assets and are paid a fee for their services.

10

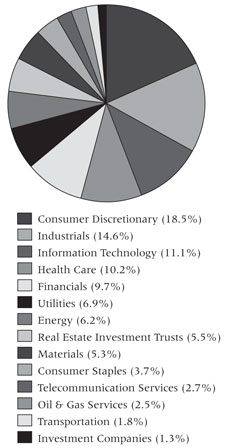

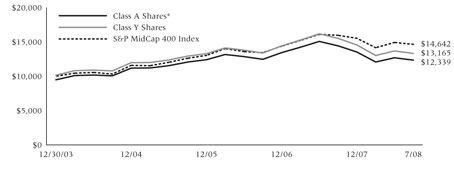

Pacific Capital Mid-Cap Fund

Investment Style

Domestic, mid-cap, blend

Investment Objective

Long-term capital appreciation by investing in a diversified portfolio of mid-capitalization companies the sub-adviser believes are reasonably priced, fundamentally strong and exhibit better growth expectations relative to peers.

Investment Considerations

Mid-capitalization stocks typically carry additional risk, since smaller companies generally have a higher risk of failure and a greater degree of volatility than larger companies. Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| | • | | Quantitative research analysis with fundamental research overlay |

| | • | | Quantitative analysts use proprietary screen to evaluate expectations, valuation and quality of 3,000 stocks |

| | • | | Fundamental analysts identify factors not included in the screen to determine most attractive stocks |

| | • | | Portfolio construction emphasizes stock selection and seeks to neutralize risk elements that are not consistently rewarded |

Investment Management

Advised by Asset Management Group of Bank of Hawaii

Sub-Advised by Chicago Equity Partners, LLC (“CEP”) (since October 10, 2006)

| | • | | Founded in 1989, CEP specializes in core domestic equity markets |

| | • | | CEP investment management team averages 19 years experience |

| | • | | $9.3 billion in assets under management |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2008, the Fund underperformed its benchmark, the S&P MidCap 400 Index1. The Fund produced a total return of -13.60% (Class A Shares without sales charge), compared to the S&P MidCap 400 Index which returned -4.96% for the same period.

What were the major factors in the market that influenced the Fund’s performance?

The day-to-day turbulence experienced in the latter half of 2007 and the first quarter of 2008 subsided during the second quarter, while recession and inflation fears took hold of the worldwide economy. Gross Domestic Product2 (GDP) growth for the first quarter of 2008 was finalized at 0.9%, up from the fourth quarter 2007 reading of -0.2%. With the advent of stimulus checks in late April, retail sales spiked in May. This is expected to be a temporary elevation and is unlikely to stop another quarter of below-trend growth. The Index of Leading Economic Indicators, an amalgamation of 10 individual financial and economic variables, continued to fall and has not recorded a positive monthly reading since July 2007. Unemployment spiked to 5.5% in May, where it remained in June. This is the highest level since mid-2004, and is expected to continue to rise over the remainder of the year. Consumer confidence plunged to a five-year low, which is nearly half its July 2006 level. Rising food and energy costs continued to hit consumers hard, eroding the value of wage increases. Oil closed the second quarter at $140 per barrel, up approximately 50% in 2008 and the national average for a gallon of gasoline topped $4. The U.S. housing market continued to sag with year-over-year price depreciation of over 8.5% on existing homes, according to the S&P/Case-Schiller Home Price index.3 Housing starts hit their lowest levels since the recession of 1991.

Over the long term, our proprietary quantitative model shows strong discrimination between the lowest and highest rated stocks. The stocks in the highest deciles have an “intersection” of the following qualities:

| | • | | They are trading at a reasonable price versus peer companies; |

| | • | | They are growing at a faster rate; |

| | • | | They have strong balance sheets and have a higher quality aspect to them; and |

| | • | | They are responsible with their capital. |

An intersection of these factor groups was heavily punished during the second half of 2007 and the beginning of 2008. Stocks that had a combination of lower valuations, sustainable earnings growth and higher quality financials underperformed the S&P MidCap 400 Index in this market environment. The Fund held a majority of its weight in these types of stocks. The best performing combination of factors were stocks with high growth expectations, expensive valuations, and lower quality balance sheets. The Mid-Cap Fund holds none of its weight in these stocks. We believe that over the long term, portfolios with these characteristics do not outperform the market. We continue to stick with our discipline of buying companies with improving expectations, high quality balance sheets and reasonable valuations. Over the last several months, we have seen an improvement in our model’s discrimination between the highest ranked stocks and lowest ranked stocks, and have experienced a significant improvement in performance.†

What major changes have occurred in the portfolio during the period covered by the report?

Other than typical re-balancing, no major changes occurred during the period. We are maintaining our disciplined process that has delivered competitive returns. We have analyzed the current underperformance and firmly expect a reversion to characteristics that have worked in the past. In past periods of underperformance, we have “bounced back” as the cycle returned to reward our investment style.

11

Pacific Capital Mid-Cap Fund (cont.)

What is your outlook for the Fund?

We believe dislocations in the markets tend to create opportunity for our alpha4 model to outperform. We believe patient investors could be rewarded as these dislocations revert. Our stock selection model is dynamic and we have adjusted the portfolio to have greater exposures to quality and momentum, while maintaining the value factor exposure. In recessionary environments, we believe the following trends occur:

| | • | | momentum tends to do well as a leading indicator for future performance; |

| | • | | quality also does well as investors believe companies with strong balance sheets will outperform their weaker peers; |

| | • | | value tends to underperform as investors prefer to own companies with the most favorable outlooks. |

Our portfolio is positioned to have a broad exposure to the various factor groups with a tilt toward momentum and quality, while maintaining a value exposure. We believe the cheaper stocks in the universe should begin to see more positive returns when the market believes the economy has hit an inflection point. Going forward, we anticipate that reasonably priced stocks should not detract from performance like they did in the second half of 2007. We believe the portfolio is positioned to do well as our strongest performance tends to follow periods of underperformance.†

Past performance does not guarantee future results.

1 | The S&P MidCap 400 Index is a market capitalization-weighted index of 400 medium capitalization stocks. Investors cannot invest directly in an index. |

2 | The Gross Domestic Product (GDP) is the measure of the market value of the goods and services produced by labor and property in the United States. |

3 | The S&P/Case-Shiller Home Price Index measures the residential housing market, tracking changes in the value of the residential real estate market in 20 metropolitan regions across the United States. |

4 | Alpha is a measure of risk, used for a mutual fund with regards to its relation to the market. A positive alpha is the extra return awarded to the investor for taking a risk instead of accepting the market return. |

† | The composition of the Fund’s portfolio is subject to change. |

12

Pacific Capital Mid-Cap Fund (cont.)

Sector Weightings as of July 31, 2008 (as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

Growth of a $10,000 Investment

The hypothetical $10,000 investment graph above represents a comparison of the performance of the indicated share class versus a similar investment in the Fund’s benchmark. The graph does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2008

| | | | | | | | | |

| | | 1 Year | | | 3 Year | | | Since Inception

(12/30/03) | |

Class A Shares* | | -18.11 | % | | -1.24 | % | | 4.69 | % |

Class C Shares** | | -14.99 | % | | -0.18 | % | | 5.22 | % |

Class Y Shares | | -13.36 | % | | 0.81 | % | | 6.18 | % |

S&P MidCap 400 Index | | -4.96 | % | | 4.98 | % | | 8.67 | % |

| | | |

Expense Ratios | | Class A | | | Class C | | | Class Y | |

Gross | | 1.60 | % | | 2.20 | % | | 1.20 | % |

With Contractual Waivers | | 1.45 | % | | 2.20 | % | | 1.20 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The above expense ratios are from the Funds’ prospectus dated November 28, 2007. Additional information pertaining to the Funds’ expense ratios for the year ended July 31, 2008 can be found in the financial highlights.

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 1.00% (applicable only to redemptions within one year of purchase). |

The above performance table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Total returns reflect the waiver of various operational fees. Had these waivers not been in effect, performance quoted would have been lower.

The Pacific Capital Mid-Cap Fund’s inception date was December 30, 2003. The Class C Shares were not in existence prior to April 30, 2004. Performance information for the Class C Shares prior to April 30, 2004 is based on the performance of Class A Shares, which does not reflect the higher 12b-1 fees charged to Class C Shares. Had the higher 12b-1 fees been reflected, total return figures may have been adversely affected.

The performance of the Pacific Capital Mid-Cap Fund is measured against the S&P MidCap 400 Index, an unmanaged market capitalization-weighted index of 400 medium capitalization stocks. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index.

The Pacific Capital Funds are distributed by Foreside Distribution Services, L.P. The Asset Management Group of Bank of Hawaii is investment adviser to the Fund and receives a fee for its services. Chicago Equity Partners, LLC, is sub-adviser to the Fund and is paid a fee for its services.

13

Pacific Capital Growth Stock Fund

Investment Style

Domestic, large-cap, growth

Investment Objective

Long-term capital appreciation and dividend income by investing in a diversified portfolio of large-capitalization companies whose earnings are expected to grow faster than the average of other companies in their industries.

Investment Considerations

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| | • | | Quantitative research analysis with fundamental research overlay |

| | • | | Quantitative analysts use proprietary screen to evaluate expectations, valuation and quality of 3,000 stocks |

| | • | | Fundamental analysts identify factors not included in the screen to determine most attractive stocks |

| | • | | Portfolio construction emphasizes stock selection and seeks to neutralize risk elements that are not consistently rewarded |

Investment Management

Advised by Asset Management Group of Bank of Hawaii (AMG)

Sub-Advised by Chicago Equity Partners, LLC (“CEP”) (since June 29, 2007)

| | • | | Founded in 1989, CEP specializes in core domestic equity markets |

| | • | | CEP investment management team averages 19 years experience |

| | • | | $9.3 billion in assets under management |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2008, the Fund produced a -7.20% total return (Class A Shares without sales charge), underperforming its benchmark, the S&P 500/Citigroup Growth Index1 which returned -6.29%.

What were the major factors in the market that influenced the Fund’s performance?

The day-to-day turbulence experienced in the latter half of 2007 and the first quarter of 2008 subsided during the second quarter, while recession and inflation fears took hold of the worldwide economy. Gross Domestic Product2 growth for the first quarter of 2008 was finalized at 0.9%, up from the fourth quarter 2007 reading of -0.2%. With the advent of stimulus checks in late April, retail sales spiked in May. This is expected to be a temporary elevation and is unlikely to stop another quarter of below-trend growth. The Index of Leading Economic Indicators, an amalgamation of 10 individual financial and economic variables, continued to fall and has not recorded a positive monthly reading since July 2007. Unemployment spiked to 5.5% in May, where it remained in June. This is the highest level since mid-2004, and is expected to continue to rise over the remainder of the year. Consumer confidence plunged to a five-year low, which is nearly half its July 2006 level. Rising food and energy costs continued to hit consumers hard, eroding the value of wage increases. Oil closed the second quarter at $140 per barrel, up approximately 50% in 2008 and the national average for a gallon of gasoline topped $4. The U.S. housing market continued to sag with year-over-year price depreciation of over 8.5% on existing homes, according to the S&P/Case-Schiller Home Price Index.3 Housing starts hit their lowest levels since the recession of 1991.

During the trailing end of 2007 and the beginning of 2008, stocks that had a combination of lower valuations, sustainable earnings growth and higher quality financials underperformed the S&P 500/Citigroup Growth Index in this market environment. The Fund held a majority of its weight in these types of stocks, which was the primary factor that influenced the Fund’s performance. However, as concerns continued to mount regarding the growth of the economy, investors began to focus on companies that exhibited strong long-term investment fundamentals. Our long standing approach of selecting companies with favorable earnings outlooks, reasonable valuations, high quality financials and strong growth characteristics performed well during this time. The model’s performance was strong during the first quarter of 2008 led by our momentum factor. This factor favors stocks with good prospects for future earnings and strong price performance. The quality factor continued to add value as we expected in this difficult economy. This factor favors companies with good capital discipline and balance sheet quality. Value factors continued to lag as cheap companies have written down book value and cut earnings projections. The strength in the combination of factors in our model led to good discrimination between the highest rated names and the lowest rated stocks. Over 70% of the weight of the portfolio is in the top two ranked quintiles. Our overall relative performance benefited both from the stocks that we owned, as well as avoiding many lower quality names.†

What major changes have occurred in the portfolio during the period covered by the report?

Other than typical re-balancing, no major changes occurred during the period. We are maintaining our disciplined process that has historically helped the Fund to deliver competitive returns.

What is your outlook for the Fund?

The economy continues to slow and market volatility is up as uncertainty has risen. During periods of high uncertainty, we believe our portfolio should outperform the S&P 500/Citigroup Growth Index. Going forward, we believe that reasonably priced stocks should not detract from performance like they did in the second half of 2007. Dislocations in the markets tend to create opportunity for our alpha4 model to outperform. We believe patient investors will be rewarded as these dislocations revert.

Past performance does not guarantee future results.

1 | The S&P 500/Citigroup Growth Index measures the performance of all stocks in the S&P 500 Index (the 500 largest U.S. companies based on total market capitalization) that are classified as growth stocks. Investors cannot invest directly in an index. |

2 | The Gross Domestic Product is the measure of the market value of the goods and services produced by labor and property in the United States. |

3 | The S&P/Case-Shiller Home Price Index measures the residential housing market, tracking changes in the value of the residential real estate market in 20 metropolitan regions across the United States. |

4 | Alpha is a measure of risk, used for a mutual fund with regards to its relation to the market. A positive alpha is the extra return awarded to the investor for taking a risk instead of accepting the market return. |

† | The composition of the Fund’s portfolio is subject to change. |

14

Pacific Capital Growth Stock Fund (cont.)

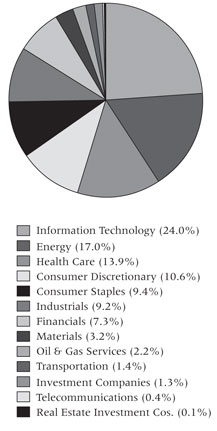

Sector Weightings as of July 31, 2008 (as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

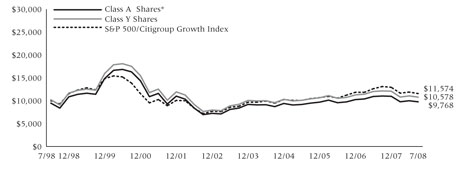

Growth of a $10,000 Investment

The hypothetical $10,000 investment graph above represents a comparison of the performance of the indicated share class versus a similar investment in the Fund’s benchmarks. The graph does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2008

| | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

Class A Shares* | | -12.09 | % | | -1.12 | % | | 2.00 | % | | -0.23 | % |

Class B Shares** | | -11.62 | % | | -1.12 | % | | 2.15 | % | | -0.28 | % |

Class C Shares** | | -8.87 | % | | -0.12 | % | | 2.33 | % | | -0.43 | % |

Class Y Shares | | -6.98 | % | | 0.91 | % | | 3.35 | % | | 0.56 | % |

S&P 500/Citigroup Growth Index | | -6.29 | % | | 3.21 | % | | 5.92 | % | | 1.47 | % |

| | | | |

Expense Ratios | | Class A | | | Class B | | | Class C | | | Class Y | |

Gross | | 1.51 | % | | 2.11 | % | | 2.11 | % | | 1.11 | % |

With Contractual Waivers | | 1.36 | % | | 2.11 | % | | 2.11 | % | | 1.11 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The above expense ratios are from the Funds’ prospectus dated November 28, 2007 and excludes the impact of underlying fund fees and expenses. Additional information pertaining to the Funds’ expense ratios for the year ended July 31, 2008 can be found in the financial highlights.

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The above performance table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Total returns reflect the waiver of various operational fees. Had these waivers not been in effect, performance quoted would have been lower.

The Class C Shares of the Fund commenced operations on April 30, 2004. Performance information for Class C Shares prior to April 30, 2004 is based on the performance of Class B Shares.

The performance of the Pacific Capital Growth Stock Fund is measured against the S&P 500/Citigroup Growth Index, which measures the performance of all stocks in the S&P 500 Index (the 500 largest U.S. companies based on total market capitalization) that are classified as growth stocks. The index is unmanaged and does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index.

The Pacific Capital Funds are distributed by Foreside Distribution Services, L.P. The Asset Management Group of Bank of Hawaii is investment adviser to the Fund and receives a fee for its services. Chicago Equity Partners, LLC, is sub-adviser to the Fund and is paid a fee for its services.

15

Pacific Capital Growth and Income Fund

Investment Style

Domestic, large-cap, blend

Investment Objective

Long-term capital appreciation and current income by investing in a diversified portfolio of large-capitalization dividend-paying companies whose earnings are expected to grow at above-average rates in relation to other companies in their industries.

Investment Considerations

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, such as investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes.

Investment Process

| | • | | Quantitative research analysis with fundamental research overlay |

| | • | | Quantitative analysts use proprietary screen to evaluate expectations, valuation and quality of 3,000 stocks |

| | • | | Fundamental analysts identify factors not included in the screen to determine most attractive stocks |

| | • | | Portfolio construction emphasizes stock selection and seeks to neutralize risk elements that are not consistently rewarded |

Investment Management

Advised by Asset Management Group of Bank of Hawaii (AMG)

Sub-Advised by Chicago Equity Partners, LLC (“CEP”) (since June 29, 2007)

| | • | | Founded in 1989, CEP specializes in core domestic equity markets |

| | • | | CEP investment management team averages 19 years experience |

| | • | | $9.3 billion in assets under management |

How did the Fund perform compared to its benchmark?

For the 12-month period ended July 31, 2008, the Fund returned -10.65% (Class A Shares without sales charge), outperforming its benchmark, the S&P 500 Index1, which returned -11.09%.

What were the major factors in the market that influenced the Fund’s performance?

The day-to-day turbulence experienced in the latter half of 2007 and the first quarter of 2008 subsided during the second quarter, while recession and inflation fears took hold of the worldwide economy. Gross Domestic Product2 (GDP) growth for the first quarter of 2008 was finalized at 0.9%, up from the fourth quarter 2007 reading of -0.2%. With the advent of stimulus checks in late April, retail sales spiked in May. This is expected to be a temporary elevation and is unlikely to stop another quarter of below-trend growth. The Index of Leading Economic Indicators, an amalgamation of 10 individual financial and economic variables, continued to fall and has not recorded a positive monthly reading since July 2007. Unemployment spiked to 5.5% in May, where it remained in June. This is the highest level since mid-2004, and is expected to continue to rise over the remainder of the year. Consumer confidence plunged to a five-year low, which is nearly half its July 2006 level. Rising food and energy costs continued to hit consumers hard, eroding the value of wage increases. Oil closed the second quarter at $140 per barrel, up approximately 50% in 2008 and the national average for a gallon of gasoline topped $4. The U.S. housing market continued to sag with year-over-year price depreciation of over 8.5% on existing homes, according to the S&P/Case-Schiller Home Price Index.3 Housing starts hit their lowest levels since the recession of 1991.

As concerns continued to mount regarding the growth of the economy, investors began to focus on companies that exhibited strong long-term investment fundamentals. Our long standing approach of selecting companies with favorable earnings outlooks, reasonable valuations, high quality financials and strong growth characteristics performed well during this period of uncertainty. The model’s performance was strong during the first quarter of 2008 led by our momentum factor. This factor favors stocks with good prospects for future earnings and strong price performance. The quality factor continued to add value as we expected in this difficult economy. This factor favors companies with good capital discipline and balance sheet quality. Value factors continued to lag as cheap companies have written down book value and cut earnings projections. The strength in the combination of factors in our model led to good discrimination between the highest rated names and the lowest rated stocks. Over 70% of the weight of the portfolio is in the top two ranked quintiles. Our overall relative performance benefited both from the stocks that we owned, as well as avoiding many lower quality names.†

What major changes have occurred in the portfolio during the period covered by the report?

Other than typical re-balancing, no major changes occurred during the period. We are maintaining our disciplined process that has historically helped the Fund to deliver competitive returns.

What is your outlook for the Fund?

The economy continues to slow and market volatility is up as uncertainty has risen. During periods of high uncertainty, we believe our portfolio should continue to outperform the S&P 500 Index. The cheaper stocks in the universe should begin to see more positive returns when the market believes the economy has hit an inflection point. Going forward, we believe that reasonably priced stocks should not detract from performance like they did in the second half of 2007.

Past performance does not guarantee future results.

1 | The Standard & Poor’s 500 Index (“S&P 500 Index”) is an index of 500 selected common stocks, most of which are listed on the New York Stock Exchange, and is a measure of the U.S. stock market as a whole. Investors cannot invest directly in an index. |

2 | The Gross Domestic Product (GDP) is the measure of the market value of the goods and services produced by labor and property in the United States. |

3 | The S&P/Case-Shiller Home Price Index measures the residential housing market, tracking changes in the value of the residential real estate market in 20 metropolitan regions across the United States. |

† | The composition of the Fund’s portfolio is subject to change. |

16

Pacific Capital Growth and Income Fund (cont.)

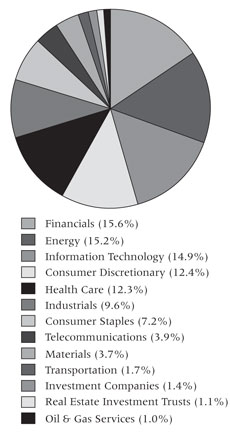

Sector Weightings as of July 31, 2008 (as a percentage of total investments)

The composition of the Fund’s portfolio is subject to change.

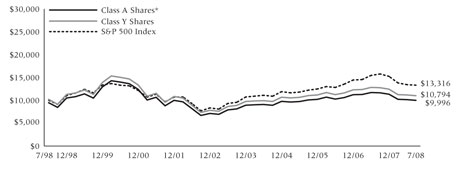

Growth of a $10,000 Investment

The hypothetical $10,000 investment graph above represents a comparison of the performance of the indicated share class versus a similar investment in the Fund’s benchmark. The graph does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

Average Annual Total Returns as of July 31, 2008

| | | | | | | | | | | | |

| | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | |

Class A Shares* | | -15.36 | % | | -2.24 | % | | 3.20 | % | | 0.00 | % |

Class B Shares** | | -14.72 | % | | -2.17 | % | | 3.35 | % | | -0.08 | % |

Class C Shares** | | -12.21 | % | | -1.23 | % | | 3.54 | % | | -0.23 | % |

Class Y Shares | | -10.48 | % | | -0.22 | % | | 4.58 | % | | 0.77 | % |

S&P 500 Index | | -11.09 | % | | 2.85 | % | | 7.03 | % | | 2.91 | % |

| | | | |

Expense Ratios | | Class A | | | Class B | | | Class C | | | Class Y | |

Gross | | 1.48 | % | | 2.08 | % | | 2.08 | % | | 1.08 | % |

With Contractual Waivers | | 1.33 | % | | 2.08 | % | | 2.08 | % | | 1.08 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please call 1-800-258-9232 or visit the Funds’ website at pacificcapitalfunds.com.

The above expense ratios are from the Funds’ prospectus dated November 28, 2007 and excludes the impact of underlying fund fees and expenses. Additional information pertaining to the Funds’ expense ratios for the year ended July 31, 2008 can be found in the financial highlights.

| * | Reflects 5.25% maximum front-end sales charge. |

| ** | Reflects maximum contingent deferred sales charge (CDSC) of up to 5.00% for the Class B Shares and a maximum CDSC of 1.00% for the Class C Shares (applicable only to redemptions within one year of purchase). |

The above performance table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Total returns reflect the waiver of various operational fees. Had these waivers not been in effect, performance quoted would have been lower.

The Class C Shares of the Fund commenced operations on April 30, 2004. Performance information for Class C Shares prior to April 30, 2004 is based on the performance of Class B Shares.