UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-07470

Carillon Series Trust

(Exact name of registrant as specified in charter)

880 Carillon Parkway

St. Petersburg, FL 33716

(Address of principal executive offices)

Susan L. Walzer, Principal Executive Officer

880 Carillon Parkway

St. Petersburg, FL 33716

(Name and address of agent for service)

Registrant’s telephone number, including area code: (727) 567-8143

Date of fiscal year end: June 30

Date of reporting period: October 31, 2017

Explanatory Note: The information included in this filing relates to Scout Core Bond Fund, Scout Core Plus Bond Fund, Scout International Fund, Scout Low Duration Bond Fund, Scout Mid Cap Fund, Scout Small Cap Fund, and Scout Unconstrained Bond Fund (each a “Target Fund” and collectively, the “Target Funds”), each a series of the Scout Funds. Subsequent to the date of the reporting period, each of the Target Funds was reorganized into a corresponding new series of Carillon Series Trust (the “Acquiring Funds”). Therefore, although this filing is being made by Carillon Series Trust, certain of the information in this filing relates to the Target Funds for the period July 1, 2017 to October 31, 2017, as indicated below.

Item 1. Reports to Stockholders

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

| Financial Report | |

| and Investment Performance Review | |

| for the Fiscal Period Ended October 31, 2017 | |

| International Fund | |

| Scout International Fund (UMBWX) | |

| Domestic Equity Funds | |

| Scout Mid Cap Fund (UMBMX) | |

| Scout Small Cap Fund (UMBHX) | |

| Fixed Income Funds | |

| Scout Low Duration Bond Fund (SCLDX) | |

| Scout Core Bond Fund | |

| Institutional Class (SCCIX) | |

| Class Y (SCCYX) | |

| Scout Core Plus Bond Fund | |

| Institutional Class (SCPZX) | |

| Class Y (SCPYX) | |

| Scout Unconstrained Bond Fund | |

| Institutional Class (SUBFX) | |

| Class Y (SUBYX) |

Table of Contents

| International Fund | 1 |

| Mid Cap Fund | 7 |

| Small Cap Fund | 13 |

| Low Duration Bond Fund | 18 |

| Core Bond Fund | 26 |

| Core Plus Bond Fund | 32 |

| Unconstrained Bond Fund | 39 |

| Statements of Assets and Liabilities | 46 |

| Statements of Operations | 48 |

| Statements of Changes in Net Assets | 50 |

| Financial Highlights | 54 |

| Notes to Financial Statements | 60 |

| Report of Independent Registered Certified Public Accounting Firm | 73 |

| Expense Examples | 74 |

| Results of the Special Meeting of Shareholders | 75 |

| Other Information | 76 |

| Trustees and Officers | 82 |

| Privacy Policy | 84 |

| Glossary of Investment Terms | 86 |

Shares of the Scout Funds are not deposits or obligations of, nor guaranteed by, UMB Bank, n.a. or any other banking institution; nor are they insured by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. These shares involve investment risks, including the possible loss of the principal invested.

SCOUT FUNDS ANNUAL REPORT

Scout International Fund

UMBWX

As a result of a reorganization that was completed after the close of business on November 17, 2017, the Scout International Fund is now the Carillon Scout International Fund. The commentary that follows is for the 12 months ended October 31, 2017.

MARKET REVIEW

International markets, represented by the MSCI EAFE® Index, were strong during the 12-month period ending Oct. 31, 2017, delivering a 23.44 percent return. Investors experienced a whirlwind of political events during the time period. In December, the Italian constitutional referendum was decisively defeated and subsequently Prime Minister Matteo Renzi submitted his resignation. In May, Emmanuel Macron was elected president of France inspiring hopes of a new approach and the possibility of a better integrated Eurozone. The following month, Prime Minister Theresa May failed to consolidate her position after calling a snap election, thus weakening her standing, which could lead to a softer Brexit than had previously been expected. But the biggest impact on global equity markets was the surprise election of Donald Trump as president of the United States in November. Markets initially treated his election with skepticism but this reaction was soon overshadowed by optimism regarding increased spending programs, reduced regulation, and tax reform. Much of the early hype has dwindled amid dramatic reorganizations in the White House. But, in spite of this and a few Federal Reserve interest-rate increases, equity markets have powered ahead.

Against this backdrop, Europe continues to show signs of recovery, with unemployment levels at their lowest since 2009. Some of the highlights included Spain reporting its best economic performance in two years, Portugal obtaining an investment-grade credit rating (after having a junk rating since 2012) and continued progress in Germany with regard to forming a coalition government. Additionally, Mario Draghi, the European Central Bank (ECB) President, implied that the central bank is nearing a formal tightening of its monetary policy. Meanwhile, returns in emerging markets have generally outpaced those of developed markets. That said, concerns around the stability of the Chinese financial sector, a flattening Chinese yield curve and the slowing Chinese economy generated angst among some investors. Nevertheless, overall, equity investor optimism remains high in most developed and emerging markets leaving equity-market volatility near historical lows and the popularity of the momentum trade high.

PORTFOLIO REVIEW

The Scout International Fund (UMBWX) returned 22.98 percent for the 12 months ended October 31, 2017, slightly underperforming the MSCI EAFE® Index’s return of 23.44 percent. At the country level, China, Taiwan, Australia, Sweden and Ireland added the most value, while Netherlands, France, Canada, Denmark and Singapore detracted from relative results.

At the sector level, holdings in information technology, industrials and healthcare were the Fund’s top performers. AAC Technologies Holdings, Inc. and Tokyo Electron Ltd. propelled the information technology sector. AAC Technologies, a manufacturer of mico-components used within smartphones, continues to benefit from market-share gains as stereo sound and waterproof designs gain adoption across a variety of digital devices. Tokyo Electron, a Japanese manufacturer and distributor of semiconductors and flat-panel display equipment, advanced after reporting significantly higher orders. Additionally, management suggested that the semiconductor market may grow by 10 percent year-over-year during 2017, while the flat panel display equipment market is expected to grow by 30 percent. Leading the industrials sector was discount airline Ryanair Holdings PLC, which has reported strong growth. Additionally, stock performance has been buoyed by the improving economic backdrop in Europe, a material decline in fuel prices during the second half of the fiscal year and support from an ongoing stock buyback program.

In contrast, consumer discretionary, energy and consumer staples detracted from relative results. Holdings in the consumer discretionary sector provided mixed results. The detractors were led by Pandora A/S, a hand-crafted jewelry manufacturer that has delivered weaker than expected total retail sales. Within the energy sector, Enbridge, Inc. and Imperial Oil Ltd. suffered during the time period as both crude oil and natural gas prices declined throughout much of the fiscal year. Enbridge, an energy transportation company and distributor, suffered as natural gas retreated from

| OCTOBER 31, 2017 | 1 |

Scout International Fund

UMBWX

highs reached in late December. Imperial Oil, an oil sands producer, suffered as a result of the company’s sensitivity to fluctuations in oil prices. Specifically, oil sands projects are more costly to develop per barrel of oil than a typical onshore project. As such, these projects require higher oil prices to generate free-cash-flow. Consumer staples company Carrefour, a hypermarket and supermarket operator in Europe, struggled as the company’s French hypermarket business showed no signs of improving. In addition, the company continues to lose market share to competitors who moved earlier and more aggressively into online food offerings.

MARKET OUTLOOK

Even with the Federal Reserve having announced that it would begin to pare back its huge balance sheet in October and continue increasing interest rates toward the end of the year, markets continued to march higher on the back of economic strength and hopes for tax reform. Continued economic improvements throughout much of the Eurozone has left European market conditions favorable in the short term at least and while China has allowed monetary conditions to tighten throughout much of 2017, central bank policy remains accommodative. Additionally, the Japanese corporate sector is performing well this year on the back of solid earnings and revenue growth.

Michael D. Stack, CFA

Lead Portfolio Manager

Angel M. Lupercio

Co-Portfolio Manager

| 2 | SCOUT FUNDS ANNUAL REPORT |

| Scout International Fund |

| UMBWX |

OBJECTIVE & STRATEGY (Unaudited)

The Scout International Fund seeks long-term growth of capital and income by investing in a diversified portfolio consisting primarily of equity securities of established companies either located outside the United States or whose primary business is carried on outside the United States.

PORTFOLIO MANAGEMENT TEAM

Michael D. Stack, CFA

Lead Portfolio Manager

Angel M. Lupercio

Co-Portfolio Manager

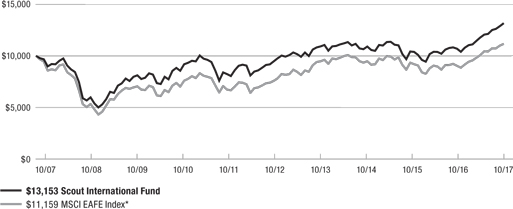

HYPOTHETICAL GROWTH OF $10,000 (Unaudited)

as of October 31, 2017

Performance returns for the Scout International Fund and MSCI EAFE Index assume dividends were reinvested for the entire period.

For illustrative purposes only; may not represent your returns.

| * | Unmanaged index of stocks, bonds or mutual funds. It is not possible to invest directly in an index. The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. |

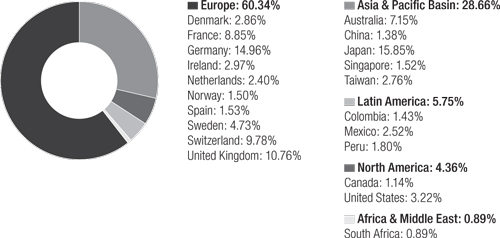

REGION/COUNTRY ALLOCATION (Unaudited)

(as a % of total portfolio equities)

Portfolio composition will change due to ongoing management of the Fund. References to specific securities should not be construed as recommendations by the Fund, its Advisor or Distributor.

Risk considerations: Foreign investments present additional risks due to currency fluctuations, economic and political factors, government regulations, differences in accounting standards, reduced liquidity and other factors. Investments in emerging markets involve even greater risks.

| OCTOBER 31, 2017 | 3 |

Scout International Fund

UMBWX

COMPARATIVE RATES OF RETURN (Unaudited)

as of October 31, 2017

| 1 Year | 3 Years | 5 Years | 10 Years | |||||

| Scout International Fund | 22.98% | 7.30% | 7.45% | 2.78% | ||||

| MSCI EAFE Index* | 23.44% | 6.08% | 8.53% | 1.10% |

Returns for periods greater than one year are compounded average annual rates of return.

The performance data quoted represents past performance and past performance is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call 800-996-2862. For the fiscal year ended June 30, 2017, the gross/net expense ratio for the Fund was 1.06% (as disclosed in the most recent Prospectus) compared to the October 31, 2017, gross/net expense ratio of 1.08%.

The performance shown in the above table and in the graph on the preceding page does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

PORTFOLIO CHARACTERISTICS (Unaudited)

| Scout | ||||

| International | MSCI EAFE* | |||

| Number of Holdings | 67 | 927 | ||

| Weighted Average Market Cap | $56.88B | $63.85B | ||

| Weighted Median Market Cap | $31.61B | $41.16B | ||

| Price/Earnings Ratio (Trailing 1 Year) | 17.69 | 17.86 | ||

| Price/Book Ratio | 2.34 | 1.72 | ||

| EPS Growth (Hist. 5 Yr.) | 8.24% | 7.46% | ||

| Return on Equity | 21.14% | 14.88% | ||

| Standard Deviation (Trailing 3 Years) | 11.39% | 12.23% | ||

| Sharpe Ratio (Trailing 3 Years) | 0.61 | 0.46 | ||

| Beta† | 0.89 | 1.00 | ||

| Alpha† | 1.74% | — | ||

| R-squared† | 0.91 | 1.00 | ||

| Upside Capture† | 90% | 100% | ||

| Downside Capture† | 78% | 100% | ||

| Turnover Ratio (Trailing 1 Year) | 21% | — | ||

| % in Emerging Markets | 10.78% | 0.00% | ||

| Total Net Assets (in Millions) | $1,160.88 | — | ||

| Inception Date | 9/14/1993 | — |

† Measured against the MSCI EAFE Index over the trailing three year time period.

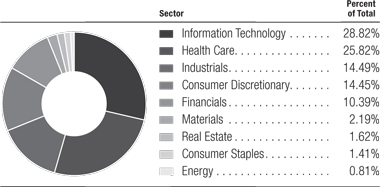

FUND DIVERSIFICATION (Unaudited)

Based on total investments as of October 31, 2017. Subject to change.

TOP 10 EQUITY HOLDINGS (Unaudited)

| Percent of Total | |

| Volkswagen A.G. | 2.26% |

| Subaru Corp. | 1.91% |

| SKF A.B. | 1.85% |

| Tokyo Electron Ltd. | 1.85% |

| Prudential PLC | 1.80% |

| ORIX Corp. | 1.79% |

| AXA S.A. | 1.78% |

| Continental A.G. | 1.77% |

| Credicorp Ltd. | 1.77% |

| Adecco Group A.G. | 1.74% |

| Top 10 Holdings Total | 18.52% |

Based on total investments as of October 31, 2017. Subject to change.

HISTORICAL PER-SHARE RECORD (Unaudited)

| Income & | Cumulative(c) | |||||||||||||||

| Net Asset | Short-Term(b) Gains | Long-Term(b) Gains | Value Per Share | |||||||||||||

| Value | Distribution | Distribution | Plus Distributions | |||||||||||||

| 12/31/12 | $ | 33.35 | $ | 0.53 | $ | — | $ | 43.45 | ||||||||

| 12/31/13 | 37.26 | 0.44 | — | 47.80 | ||||||||||||

| 12/31/14 | 32.59 | 0.52 | 2.57 | 46.22 | ||||||||||||

| 12/31/15 | 23.19 | 0.74 | 7.15 | 44.71 | ||||||||||||

| 12/31/16 | 20.83 | 0.55 | 3.34 | 46.24 | ||||||||||||

| 10/31/17(a) | 25.18 | 0.20 | — | 50.79 | ||||||||||||

| (a) | Ten months only. Distributions typically occur in June and/or December. |

| (b) | Represents distributions for the respective calendar year-to-date period ended. |

| (c) | Does not assume any compounding of reinvested distributions. |

Table shows calendar-year distributions and net asset values; may differ from fiscal-year annual reports.

| * | Unmanaged index of stocks, bonds or mutual funds. It is not possible to invest directly in an index. |

Portfolio composition will change due to ongoing management of the Fund. References to specific securities or sectors should not be construed as a recommendation by the Fund, its Advisor or Distributor. See the accompanying Schedule of Investments for the percentage of the Fund’s portfolio represented by the securities or sectors mentioned above.

| 4 | SCOUT FUNDS ANNUAL REPORT |

SCHEDULE OF INVESTMENTS

October 31, 2017

INTERNATIONAL FUND

| Shares | Value | |||||||

| COMMON STOCKS — 98.1% | ||||||||

| AUSTRALIA — 7.0% | ||||||||

| BHP Billiton Ltd.(a) | 385,986 | $ | 15,817,706 | |||||

| Caltex Australia Ltd. | 644,476 | 16,898,629 | ||||||

| CSL Ltd. | 154,751 | 16,454,582 | ||||||

| Macquarie Group Ltd. | 231,122 | 17,396,945 | ||||||

| Woodside Petroleum Ltd. | 630,711 | 14,833,728 | ||||||

| 81,401,590 | ||||||||

| CANADA — 1.1% | ||||||||

| Enbridge, Inc.(b) | 337,910 | 12,996,019 | ||||||

| CHINA — 1.4% | ||||||||

| AAC Technologies Holdings, Inc. | 861,963 | 15,777,721 | ||||||

| COLOMBIA — 1.4% | ||||||||

| Bancolombia S.A.(a) | 430,457 | 16,249,752 | ||||||

| DENMARK — 2.8% | ||||||||

| Novo Nordisk A/S(a) | 342,920 | 17,073,987 | ||||||

| Pandora A/S | 163,817 | 15,462,901 | ||||||

| 32,536,888 | ||||||||

| FRANCE — 8.7% | ||||||||

| Air Liquide S.A. | 135,987 | 17,313,196 | ||||||

| AXA S.A. | 683,075 | 20,631,491 | ||||||

| BNP Paribas S.A. | 242,718 | 18,953,774 | ||||||

| Dassault Systemes S.E. | 100,159 | 10,636,571 | ||||||

| L’Oreal S.A. | 65,912 | 14,668,011 | ||||||

| TOTAL S.A. | 334,761 | 18,666,289 | ||||||

| 100,869,332 | ||||||||

| GERMANY — 14.7% | ||||||||

| Allianz S.E.(a) | 839,031 | 19,633,661 | ||||||

| BASF S.E. | 182,168 | 19,920,225 | ||||||

| Continental A.G. | 80,508 | 20,488,334 | ||||||

| Fresenius S.E. & Co. KGaA | 170,412 | 14,265,916 | ||||||

| Henkel A.G. & Co. KGaA(a) | 117,220 | 16,557,911 | ||||||

| Muenchener Rueckversicherungs-Gesellschaft A.G. | 83,029 | 18,639,764 | ||||||

| SAP S.E.(a) | 127,762 | 14,590,420 | ||||||

| Siemens A.G. | 139,973 | 20,104,231 | ||||||

| Volkswagen A.G. | 143,018 | 26,186,438 | ||||||

| 170,386,900 | ||||||||

| IRELAND — 2.9% | ||||||||

| Kerry Group PLC — Class A | 153,765 | 15,483,965 | ||||||

| Ryanair Holdings PLC*(a) | 164,023 | 18,388,619 | ||||||

| 33,872,584 | ||||||||

| JAPAN — 15.5% | ||||||||

| Astellas Pharma, Inc. | 1,520,216 | 20,168,381 | ||||||

| FANUC Corp. | 50,502 | 11,712,218 | ||||||

| JGC Corp. | 949,639 | 15,776,510 | ||||||

| Komatsu Ltd. | 509,030 | 16,550,582 | ||||||

| Kubota Corp. | 953,587 | 17,791,960 | ||||||

| Nitto Denko Corp. | 175,459 | 16,210,341 | ||||||

| ORIX Corp. | 1,216,483 | 20,739,214 | ||||||

| Subaru Corp. | 648,558 | 22,176,628 | ||||||

| Sysmex Corp. | 263,978 | 17,946,000 | ||||||

| Tokyo Electron Ltd. | 123,466 | 21,450,867 | ||||||

| 180,522,701 | ||||||||

| MEXICO — 2.5% | ||||||||

| Grupo Financiero Banorte S.A.B. de C.V. — Class O | 2,350,248 | 13,948,154 | ||||||

| Wal-Mart de Mexico S.A.B. de C.V.(a) | 660,819 | 14,785,825 | ||||||

| 28,733,979 | ||||||||

| NETHERLANDS — 2.4% | ||||||||

| Gemalto N.V. | 282,594 | 11,185,258 | ||||||

| Royal Dutch Shell PLC — Class B(a) | 247,662 | 16,187,188 | ||||||

| 27,372,446 | ||||||||

| NORWAY — 1.5% | ||||||||

| DNB A.S.A. | 886,528 | 17,094,535 | ||||||

| PERU — 1.8% | ||||||||

| Credicorp Ltd. | 97,774 | 20,477,787 | ||||||

| SINGAPORE — 1.5% | ||||||||

| Singapore Telecommunications Ltd. | 6,299,987 | 17,331,781 | ||||||

| SOUTH AFRICA — 0.9% | ||||||||

| MTN Group Ltd. | 1,171,615 | 10,173,365 | ||||||

| SPAIN — 1.5% | ||||||||

| Banco Bilbao Vizcaya Argentaria S.A. | 1,997,953 | 17,484,707 | ||||||

| SWEDEN — 4.6% | ||||||||

| Essity A.B. — Class B* | 484,509 | 14,486,019 | ||||||

| Sandvik A.B. | 979,757 | 17,894,196 | ||||||

| SKF A.B.(a) | 924,430 | 21,465,265 | ||||||

| 53,845,480 | ||||||||

| SWITZERLAND — 9.6% | ||||||||

| ABB Ltd. | 685,535 | 17,919,969 | ||||||

| Adecco Group A.G. | 254,946 | 20,225,495 | ||||||

| Coca-Cola HBC A.G.* | 400,516 | 13,538,494 | ||||||

| Givaudan S.A. | 7,612 | 16,998,633 | ||||||

| Nestle S.A.(a) | 169,557 | 14,281,786 | ||||||

| Novartis A.G.(a) | 149,119 | 12,314,247 | ||||||

| Roche Holding A.G. | 69,684 | 16,099,190 | ||||||

| 111,377,814 | ||||||||

(Continued on next page)

| OCTOBER 31, 2017 | 5 |

| SCHEDULE OF INVESTMENTS |

| October 31, 2017 |

| INTERNATIONAL FUND (Continued) |

| Shares | Value | |||||||

| TAIWAN — 2.7% | ||||||||

| Largan Precision Co., Ltd. | 81,500 | $ | 15,443,641 | |||||

| MediaTek, Inc. | 1,407,930 | 15,988,860 | ||||||

| 31,432,501 | ||||||||

| UNITED KINGDOM — 10.5% | ||||||||

| British American Tobacco PLC | 278,347 | 18,008,079 | ||||||

| Compass Group PLC | 797,984 | 17,519,824 | ||||||

| Diageo PLC(a) | 122,787 | 16,823,047 | ||||||

| Next PLC | 279,315 | 18,256,197 | ||||||

| Prudential PLC(a) | 424,977 | 20,836,622 | ||||||

| Reckitt Benckiser Group PLC | 175,233 | 15,675,312 | ||||||

| WPP PLC | 869,316 | 15,402,677 | ||||||

| 122,521,758 | ||||||||

| UNITED STATES — 3.1% | ||||||||

| Aflac, Inc. | 219,413 | 18,406,556 | ||||||

| Mettler-Toledo International, Inc.* | 26,717 | 18,237,826 | ||||||

| 36,644,382 | ||||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $755,775,461) — 98.1% | 1,139,104,022 | |||||||

| SHORT-TERM INVESTMENTS — 1.7% | ||||||||

| MONEY MARKET FUNDS | ||||||||

| Fidelity Investments Money Market Funds — | ||||||||

| Treasury Portfolio — Class I, 0.915% | 20,000,000 | 20,000,000 | ||||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $20,000,000) — 1.7% | 20,000,000 | |||||||

| TOTAL INVESTMENTS | ||||||||

| (Cost $775,775,461) — 99.8% | 1,159,104,022 | |||||||

| Other assets less liabilities — 0.2% | 1,773,233 | |||||||

| TOTAL NET ASSETS — 100.0% | ||||||||

| (equivalent to $25.18 per share; | ||||||||

| unlimited shares of $1.00 par value | ||||||||

| capital shares authorized; | ||||||||

| 46,099,545 shares outstanding) | $ | 1,160,877,255 | ||||||

| PLC — Public Limited Company |

| * | Non-income producing security. |

| (a) | ADR — American Depositary Receipt. |

| (b) | Canadian security traded on U.S. stock exchange |

See accompanying Notes to Financial Statements.

| 6 | SCOUT FUNDS ANNUAL REPORT |

Scout Mid Cap Fund

UMBMX

As a result of a reorganization that was completed after the close of business on November 17, 2017, the Scout Mid Cap Fund is now the Carillon Scout Mid Cap Fund. The commentary that follows is for the 12 months ended October 31, 2017.

MARKET REVIEW

The Russell Midcap® Index, a measure of domestic mid-capitalization stocks, gained 21.09 percent during the 12 months ending Oct. 31, 2017. Strong gains during the fiscal year followed the November U.S. elections as investors anticipated tax and regulatory reform. Investor optimism was also bolstered by steadily growing U.S. and foreign economies, which may have improved due to quantitative easing in the European Union and Japan as well as stimulus in China. The Federal Reserve was able to successfully increase short-term interest rates three times this fiscal year given the tighter labor markets and improvement in the U.S. economy. There are some developing credit concerns in subprime auto loans and credit cards but, with unemployment continuing to fall and wages still rising, the yield curve remains upwardly sloped in tandem with positive economic growth.

While showing positive signs, the global economies continue to face significant hurdles to longer-term economic growth, such as poor demographics and high debt levels. To date, this reality has helped constrain long-term U.S. interest rates, as well as in many developed markets overseas. Continued low interest rates may support higher equity prices for now, despite below-average global growth.

PORTFOLIO REVIEW

The Scout Mid Cap Fund (UMBMX) returned 31.32 percent for the 12 months ended October 31, 2017, significantly outperforming the Russell Midcap Index return of 21.09 percent. Stock selection was positive, while sector allocation also provided a favorable impact on relative performance.

At the sector level, we added the most value in information technology, consumer discretionary and industrials. Within technology, global IT provider DXC Technology (formerly known as Computer Sciences Corp.) soared after announcing a lucrative merger with Hewlett-Packard Enterprise - Enterprises Services that promises significant potential for earnings accretion. In addition, NVIDIA Corp. reported better-than-expected earnings driven by growth potential for graphics processing chips for the gaming, artificial intelligence and automotive markets. Within consumer discretionary, Thor Industries, Inc., continued to benefit from the acquisition of a key competitor, Jayco, which provided higher earnings, further industry consolidation and a leading position in the entry-level RV market. Meanwhile, consumer demand for recreational vehicles continued to grow in the United States due to the general popularity of camping. Finally, industrials holding Orbital ATK Inc., soared post a takeover bid from larger defense contractor Northrop Grumman Corp.

In contrast, energy was the weakest sector on a relative basis. A slight underweight position and disappointing performance from Pioneer Natural Resources Co., Parsley Energy Inc. and US Silica Holdings, Inc. resulted in the largest drag on relative performance. Pioneer produces oil and natural gas primarily from the Permian Basin in West Texas, and the Eagleford formation, also in Texas, with additional operations in Colorado. The stock suffered due to temporary weakness in the oil price and as the company announced additional well-completion expenses due to water handling in the Permian field. Parsley Energy, a natural gas and oil company, engages in exploration, production and sale of crude oil and natural gas, primarily in West Texas and Southeast New Mexico. Lower oil prices weighed temporarily on Parsley’s financial results, and investor sentiment for Permian oil producers dropped due to fears others would face similar water-handling issues as Pioneer. U.S. Silica mines and distributes sand products for the fracking of oil and natural gas wells in the United States, and silica for industrial and specialty applications. The stock suffered due to temporary weakness in the oil price and from investor concerns of sand overcapacity. Finally, the portfolio’s underweight in utilities and cash exposure resulted in a drag on relative performance.

OUTLOOK & POSITIONING

Our outlook for U.S. equities remains positive. Within the United States, expected legislation regarding deregulation, tax reform and infrastructure may result in faster economic growth. Risks of protectionism around the globe remain, although growth in major global economies is steady and the near-term risk of deflation in the major economic zones has receded due to aggressive monetary policy actions by foreign central banks. The risk of recession appears remote based on our indicators, so the portfolio is positioned to potentially benefit from continued global economic growth.

| OCTOBER 31, 2017 | 7 |

Scout Mid Cap Fund

UMBMX

We are currently exposed to cyclical sectors that benefit from stronger economic growth, especially technology, and basic materials. We are also slightly overweight in healthcare due to strong company-specific fundamentals and demographics-driven growth in demand. The overall macro environment appears reasonable but we continue to focus on attractive themes and stock-specific ideas. In the financials sector, we favor banks that are realizing higher margins, steady loan growth and low loan losses. We are witnessing exciting innovations within healthcare. One example is ABIOMED, which is improving the treatment of cardiovascular diseases. The defense industry is favored under the current administration; so, we believe that sales in aerospace and defense should grow. We are tuned into the changes in consumer behavior, which is more focused on experiences including travel and entertainment and less likely to shop frequently at physical retail locations. And to benefit from the potential growth in zero- and low-emission vehicles, we retain an investment in Albemarle Corp., the leading producer and processor of lithium used for electric vehicle batteries.

We remain steadfast in our approach to allocate toward equities that adhere to the quality investment process that has benefited our investors in the past, using what we believe are timeless investment principles to select stocks with sound fundamentals and reasonable valuations while steering the portfolio away from perceived problems.

G. Patrick Dunkerley, CFA

Lead Portfolio Manager

Derek M. Smashey, CFA

Co-Portfolio Manager

John A. Indellicate II, CFA

Co-Portfolio Manager

Jason J. Votruba, CFA

Co-Portfolio Manager

| 8 | SCOUT FUNDS ANNUAL REPORT |

Scout Mid Cap Fund

UMBMX

OBJECTIVE & STRATEGY (Unaudited)

The Scout Mid Cap Fund seeks long-term growth of capital by investing in common stocks of mid cap companies.

PORTFOLIO MANAGEMENT TEAM

G. Patrick Dunkerley, CFA

Lead Portfolio Manager

Derek M. Smashey, CFA

Co-Portfolio Manager

John A. Indellicate II, CFA

Co-Portfolio Manager

Jason J. Votruba, CFA

Co-Portfolio Manager

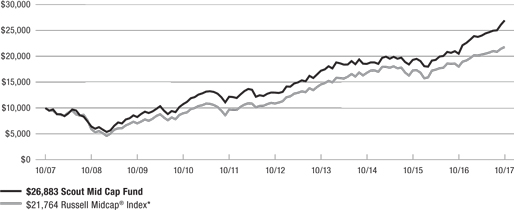

HYPOTHETICAL GROWTH OF $10,000 (Unaudited)

as of October 31, 2017

| Performance returns for the Scout Mid Cap Fund and Russell Midcap® Index assume dividends were reinvested for the entire period. |

| For illustrative purposes only; may not represent your returns. |

| * | Unmanaged index of stocks, bonds or mutual funds. It is not possible to invest directly in an index. The Russell Midcap® Index is a subset of the Russell 1000® Index and measures the performance of approximately 800 of the smallest companies in the Russell 1000® Index. |

Portfolio composition will change due to ongoing management of the Fund. References to specific securities should not be construed as recommendations by the Fund, its Advisor or Distributor.

Risk considerations: Mid-cap stocks may temporarily fall out of favor or perform poorly relative to other types of investments. While stocks of mid-cap companies may be slightly less volatile than those of small-cap companies, they still involve substantial risk. Real Estate Investment Trusts (REITS) may be affected by economic conditions including credit risk, interest rate risk and other factors that affect property values, rents or occupancies of real estate. Foreign investments present additional risks due to currency fluctuations, economic and political factors, government regulations, differences in accounting standards and other factors. Investments in emerging markets involve even greater risks. Groups of stocks, such as value and growth, go in and out of favor which may cause certain funds to underperform other equity funds.

The Fund may, at times, experience higher-than-average portfolio turnover which may generate significant taxable gains and increased trading expenses which in turn may lower the Fund’s return.

| OCTOBER 31, 2017 | 9 |

Scout Mid Cap Fund

UMBMX

COMPARATIVE RATES OF RETURN (Unaudited)

as of October 31, 2017

| 1 Year | 3 Years | 5 Years | 10 Years | |||||

| Scout Mid Cap Fund | 31.32% | 13.25% | 15.69% | 10.39% | ||||

| Russell Midcap® Index* | 21.09% | 9.04% | 14.87% | 8.09% |

Returns for periods greater than one year are compounded average annual rates of return.

The performance data quoted represents past performance and past performance is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call 800-996-2862. For the fiscal year ended June 30, 2017, the gross/net expense ratio for the Fund was 1.03% (as disclosed in the most recent Prospectus) compared to the October 31, 2017, gross/net expense ratio of 1.01%.

The “10 Years” performance return for the Fund reflects a fee waiver that was in effect. In absence of such waiver, the return would be reduced.

The Fund may, at times, experience higher-than-average portfolio turnover which may generate significant taxable gains and increased trading expenses which in turn may lower the Fund’s return.

The performance shown in the above table and in the graph on the preceding page does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

PORTFOLIO CHARACTERISTICS (Unaudited)

| Scout | Russell | |||

| Mid Cap | Midcap®* | |||

| Number of Holdings | 145 | 781 | ||

| Weighted Average Market Cap | $14.01B | $14.46B | ||

| Weighted Median Market Cap | $10.96B | $12.80B | ||

| Price to Earnings Ratio (Trailing 1 Year) | 23.47 | 21.41 | ||

| Price/Book Ratio | 3.02 | 2.66 | ||

| EPS Growth (Hist. 5 Yr.) | 13.52% | 8.22% | ||

| Return on Equity | 18.82% | 15.02% | ||

| Standard Deviation (Trailing 3 Years) | 10.07% | 10.46% | ||

| Sharpe Ratio (Trailing 3 Years) | 1.27 | 0.82 | ||

| Beta† | 0.91 | 1.00 | ||

| Alpha† | 4.58% | — | ||

| R-squared† | 0.89 | 1.00 | ||

| Upside Capture† | 114% | 100% | ||

| Downside Capture† | 85% | 100% | ||

| Turnover Ratio (Trailing 1 Year) | 75% | — | ||

| Total Net Assets (in Millions) | $1,675.21 | — | ||

| Inception Date | 10/31/2006 | — |

† Measured against the Russell Midcap® Index over the trailing three year time period.

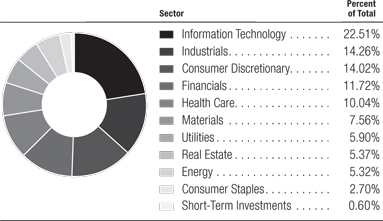

FUND DIVERSIFICATION (Unaudited)

Based on total investments as of October 31, 2017. Subject to change.

TOP 10 EQUITY HOLDINGS (Unaudited)

| Percent | ||

| of Total | ||

| DXC Technology Co. | 3.61% | |

| ABIOMED, Inc. | 3.43% | |

| Atmos Energy Corp. | 1.88% | |

| Thor Industries, Inc. | 1.73% | |

| Citizens Financial Group, Inc. | 1.53% | |

| Xcel Energy, Inc. | 1.52% | |

| IPG Photonics Corp. | 1.40% | |

| SunTrust Banks, Inc. | 1.17% | |

| Arista Networks, Inc. | 1.17% | |

| Comerica, Inc. | 1.15% | |

| Top 10 Holdings Total | 18.59% |

Based on total investments as of October 31, 2017. Subject to change.

HISTORICAL PER-SHARE RECORD (Unaudited)

| Income & | Cumulative(c) | |||||||||||||||

| Net Asset | Short-Term(b) Gains | Long-Term(b) Gains | Value Per Share | |||||||||||||

| Value | Distribution | Distribution | Plus Distributions | |||||||||||||

| 12/31/12 | $ | 13.67 | $ | 0.24 | $ | 0.06 | $ | 16.22 | ||||||||

| 12/31/13 | 17.81 | 0.44 | 0.55 | 21.35 | ||||||||||||

| 12/31/14 | 15.44 | 0.61 | 2.48 | 22.07 | ||||||||||||

| 12/31/15 | 14.38 | 0.13 | 1.13 | 22.27 | ||||||||||||

| 12/31/16 | 16.61 | 0.11 | 0.29 | 24.90 | ||||||||||||

| 10/31/17(a) | 19.77 | 0.03 | — | 28.09 | ||||||||||||

| (a) | Ten months only. Distributions typically occur in June and/or December. |

| (b) | Represents distributions for the respective calendar year-to-date period ended. |

| (c) | Does not assume any compounding of reinvested distributions. |

Table shows calendar-year distributions and asset values; may differ from fiscal-year annual reports.

| * | Unmanaged index of stocks, bonds or mutual funds. It is not possible to invest directly in an index. |

Portfolio composition will change due to ongoing management of the Fund. References to specific securities or sectors should not be construed as a recommendation by the Fund, its Advisor or Distributor. See the accompanying Schedule of Investments for the percentage of the Fund’s portfolio represented by the securities or sectors mentioned above.

| 10 | SCOUT FUNDS ANNUAL REPORT |

SCHEDULE OF INVESTMENTS

October 31, 2017

MID CAP FUND

| Shares | Value | |||||||

| COMMON STOCKS — 99.4% | ||||||||

| CONSUMER DISCRETIONARY — 14.0% | ||||||||

| American Eagle Outfitters, Inc. | 596,525 | $ | 7,766,756 | |||||

| Brunswick Corp. | 152,025 | 7,700,066 | ||||||

| Chipotle Mexican Grill, Inc.* | 30,179 | 8,205,670 | ||||||

| Darden Restaurants, Inc. | 94,150 | 7,745,721 | ||||||

| DISH Network Corp. — Class A* | 117,950 | 5,725,293 | ||||||

| DR Horton, Inc. | 191,600 | 8,470,636 | ||||||

| Expedia, Inc. | 87,500 | 10,907,750 | ||||||

| Garmin Ltd.(a) | 102,500 | 5,802,525 | ||||||

| Hilton Grand Vacations, Inc.* | 322,950 | 13,228,032 | ||||||

| Lear Corp. | 53,500 | 9,394,065 | ||||||

| Live Nation Entertainment, Inc.* | 321,275 | 14,065,419 | ||||||

| Mohawk Industries, Inc.* | 42,425 | 11,105,168 | ||||||

| NVR, Inc.* | 1,359 | 4,459,382 | ||||||

| Polaris Industries, Inc. | 73,675 | 8,725,330 | ||||||

| PulteGroup, Inc. | 212,625 | 6,427,654 | ||||||

| PVH Corp. | 49,550 | 6,283,436 | ||||||

| Ross Stores, Inc. | 158,600 | 10,069,514 | ||||||

| Royal Caribbean Cruises Ltd.(a) | 121,000 | 14,976,170 | ||||||

| Six Flags Entertainment Corp. | 139,025 | 8,729,380 | ||||||

| Skechers U.S.A., Inc. — Class A* | 341,675 | 10,906,266 | ||||||

| Tenneco, Inc. | 94,625 | 5,498,659 | ||||||

| Texas Roadhouse, Inc. | 120,644 | 6,033,406 | ||||||

| Thor Industries, Inc. | 212,024 | 28,881,909 | ||||||

| Ulta Beauty, Inc.* | 17,875 | 3,606,996 | ||||||

| Vail Resorts, Inc. | 44,825 | 10,265,821 | ||||||

| 234,981,024 | ||||||||

| CONSUMER STAPLES — 2.7% | ||||||||

| Clorox Co. | 55,325 | 7,000,272 | ||||||

| Conagra Brands, Inc. | 152,450 | 5,207,692 | ||||||

| Hormel Foods Corp. | 227,300 | 7,082,668 | ||||||

| Monster Beverage Corp.* | 169,095 | 9,795,674 | ||||||

| Tyson Foods, Inc. — Class A | 222,175 | 16,198,779 | ||||||

| 45,285,085 | ||||||||

| ENERGY — 5.3% | ||||||||

| Andeavor | 63,325 | 6,727,648 | ||||||

| Devon Energy Corp. | 496,075 | 18,305,167 | ||||||

| Energen Corp.* | 220,375 | 11,393,388 | ||||||

| Marathon Petroleum Corp. | 271,825 | 16,238,825 | ||||||

| Newfield Exploration Co.* | 306,150 | 9,426,359 | ||||||

| Oceaneering International, Inc. | 305,541 | 6,178,039 | ||||||

| Patterson-UTI Energy, Inc. | 335,300 | 6,632,234 | ||||||

| RPC, Inc. | 333,050 | 8,096,446 | ||||||

| TechnipFMC PLC*(a) | 227,775 | 6,238,757 | ||||||

| 89,236,863 | ||||||||

| FINANCIALS — 11.7% | ||||||||

| Affiliated Managers Group, Inc. | 29,128 | 5,432,372 | ||||||

| Arch Capital Group Ltd.*(a) | 76,875 | 7,659,825 | ||||||

| Axis Capital Holdings Ltd.(a) | 47,903 | 2,605,444 | ||||||

| Cboe Global Markets, Inc. | 91,971 | 10,398,241 | ||||||

| Citizens Financial Group, Inc. | 671,942 | 25,540,515 | ||||||

| Comerica, Inc. | 245,350 | 19,277,149 | ||||||

| KeyCorp. | 947,900 | 17,299,175 | ||||||

| LendingTree, Inc.* | 52,850 | 14,166,443 | ||||||

| Lincoln National Corp. | 114,525 | 8,678,705 | ||||||

| MarketAxess Holdings, Inc. | 39,875 | 6,938,250 | ||||||

| S&P Global, Inc. | 72,000 | 11,265,840 | ||||||

| SunTrust Banks, Inc. | 324,875 | 19,560,724 | ||||||

| T. Rowe Price Group, Inc. | 61,996 | 5,759,428 | ||||||

| Umpqua Holdings Corp. | 511,475 | 10,464,779 | ||||||

| Unum Group | 123,850 | 6,445,154 | ||||||

| Voya Financial, Inc. | 442,275 | 17,761,764 | ||||||

| White Mountains Insurance Group Ltd.(a) | 7,950 | 7,068,743 | ||||||

| 196,322,551 | ||||||||

| HEALTH CARE — 10.0% | ||||||||

| ABIOMED, Inc.* | 297,250 | 57,345,470 | ||||||

| Align Technology, Inc.* | 31,125 | 7,438,252 | ||||||

| BioMarin Pharmaceutical, Inc.* | 84,125 | 6,905,821 | ||||||

| Edwards Lifesciences Corp.* | 149,175 | 15,250,160 | ||||||

| Hologic, Inc.* | 164,975 | 6,244,304 | ||||||

| Humana, Inc. | 30,548 | 7,800,432 | ||||||

| Illumina, Inc.* | 41,225 | 8,458,958 | ||||||

| Incyte Corp.* | 50,475 | 5,716,294 | ||||||

| Ionis Pharmaceuticals, Inc.* | 83,275 | 4,755,835 | ||||||

| Molina Healthcare, Inc.* | 184,497 | 12,514,432 | ||||||

| NuVasive, Inc.* | 147,150 | 8,347,819 | ||||||

| Supernus Pharmaceuticals, Inc.* | 229,625 | 9,552,400 | ||||||

| Teleflex, Inc. | 39,175 | 9,283,691 | ||||||

| Universal Health Services, Inc. — Class B | 11,775 | 1,209,293 | ||||||

| Veeva Systems, Inc. — Class A* | 121,600 | 7,410,304 | ||||||

| 168,233,465 | ||||||||

(Continued on next page)

| OCTOBER 31, 2017 | 11 |

SCHEDULE OF INVESTMENTS

October 31, 2017

MID CAP FUND (Continued)

| Shares | Value | |||||||

| INDUSTRIALS — 14.3% | ||||||||

| Aerojet Rocketdyne Holdings, Inc.* | 407,325 | $ | 12,863,323 | |||||

| AGCO Corp. | 114,900 | 7,878,693 | ||||||

| Alaska Air Group, Inc. | 123,175 | 8,133,245 | ||||||

| Allison Transmission Holdings, Inc. | 196,425 | 8,346,098 | ||||||

| AMERCO | 18,225 | 7,155,864 | ||||||

| BWX Technologies, Inc. | 286,575 | 17,171,574 | ||||||

| Dycom Industries, Inc.* | 128,750 | 11,308,112 | ||||||

| Hexcel Corp. | 169,975 | 10,315,783 | ||||||

| Huntington Ingalls Industries, Inc. | 61,925 | 14,417,998 | ||||||

| ManpowerGroup, Inc. | 132,025 | 16,276,042 | ||||||

| Masco Corp. | 220,575 | 8,783,297 | ||||||

| Norfolk Southern Corp. | 89,400 | 11,748,948 | ||||||

| Old Dominion Freight Line, Inc. | 71,475 | 8,657,767 | ||||||

| Owens Corning | 148,800 | 12,304,272 | ||||||

| Parker-Hannifin Corp. | 63,150 | 11,531,821 | ||||||

| Robert Half International, Inc. | 167,800 | 8,687,006 | ||||||

| Rockwell Automation, Inc. | 50,725 | 10,186,595 | ||||||

| Textron, Inc. | 256,584 | 13,532,240 | ||||||

| Timken Co. | 210,125 | 9,907,394 | ||||||

| United Rentals, Inc.* | 94,875 | 13,422,915 | ||||||

| Xylem, Inc. | 246,375 | 16,391,329 | ||||||

| 239,020,316 | ||||||||

| INFORMATION TECHNOLOGY — 22.5% | ||||||||

| Analog Devices, Inc. | 93,000 | 8,490,900 | ||||||

| Arista Networks, Inc.* | 97,850 | 19,559,236 | ||||||

| Aspen Technology, Inc.* | 52,400 | 3,380,848 | ||||||

| Coherent, Inc.* | 35,975 | 9,450,992 | ||||||

| CSRA, Inc. | 409,155 | 13,088,868 | ||||||

| DXC Technology Co. | 662,675 | 60,648,016 | ||||||

| eBay, Inc.* | 164,325 | 6,185,193 | ||||||

| Ellie Mae, Inc.* | 64,550 | 5,806,273 | ||||||

| Fiserv, Inc.* | 85,350 | 11,046,851 | ||||||

| Harris Corp. | 116,850 | 16,279,542 | ||||||

| IAC/InterActiveCorp* | 85,625 | 11,049,906 | ||||||

| IPG Photonics Corp.* | 109,875 | 23,393,486 | ||||||

| Jack Henry & Associates, Inc. | 112,725 | 12,414,404 | ||||||

| Keysight Technologies, Inc.* | 408,150 | 18,232,060 | ||||||

| KLA-Tencor Corp. | 46,300 | 5,041,607 | ||||||

| Lam Research Corp. | 76,700 | 15,997,319 | ||||||

| Match Group, Inc.* | 489,925 | 13,100,595 | ||||||

| Micron Technology, Inc.* | 261,550 | 11,589,281 | ||||||

| ON Semiconductor Corp.* | 469,800 | 10,016,136 | ||||||

| Palo Alto Networks, Inc.* | 30,525 | 4,493,280 | ||||||

| Proofpoint, Inc.* | 81,000 | 7,485,210 | ||||||

| Red Hat, Inc.* | 86,475 | 10,448,774 | ||||||

| Science Applications International Corp. | 174,008 | 12,761,747 | ||||||

| ServiceNow, Inc.* | 77,500 | 9,793,675 | ||||||

| Skyworks Solutions, Inc. | 136,178 | 15,505,227 | ||||||

| Take-Two Interactive Software, Inc.* | 74,300 | 8,221,295 | ||||||

| Universal Display Corp. | 56,000 | 8,204,000 | ||||||

| Western Digital Corp. | 105,950 | 9,458,157 | ||||||

| Workday, Inc. — Class A* | 71,775 | 7,966,307 | ||||||

| Xilinx, Inc. | 109,075 | 8,037,737 | ||||||

| 377,146,922 | ||||||||

| MATERIALS — 7.6% | ||||||||

| Albemarle Corp. | 114,250 | 16,096,682 | ||||||

| Celanese Corp. | 102,275 | 10,668,305 | ||||||

| CF Industries Holdings, Inc. | 406,255 | 15,429,565 | ||||||

| Chemours Co. | 279,425 | 15,818,249 | ||||||

| Martin Marietta Materials, Inc. | 56,873 | 12,332,910 | ||||||

| Newmont Mining Corp. | 432,475 | 15,638,296 | ||||||

| Steel Dynamics, Inc. | 342,825 | 12,756,518 | ||||||

| Vulcan Materials Co. | 81,025 | 9,864,794 | ||||||

| Westlake Chemical Corp. | 192,200 | 16,319,702 | ||||||

| Wheaton Precious Metals Corp.(a) | 82,875 | 1,718,828 | ||||||

| 126,643,849 | ||||||||

| REAL ESTATE — 5.4% | ||||||||

| Cousins Properties, Inc. REIT | 1,476,225 | 13,315,550 | ||||||

| EPR Properties REIT | 194,375 | 13,446,862 | ||||||

| Host Hotels & Resorts, Inc. REIT | 857,875 | 16,780,035 | ||||||

| Lamar Advertising Co. — Class A REIT | 238,730 | 16,816,141 | ||||||

| Omega Healthcare Investors, Inc. REIT | 223,623 | 6,453,760 | ||||||

| Outfront Media, Inc. REIT | 600,614 | 14,084,398 | ||||||

| Senior Housing Properties Trust REIT | 491,719 | 9,047,630 | ||||||

| 89,944,376 | ||||||||

| UTILITIES — 5.9% | ||||||||

| American Water Works Co., Inc. | 113,100 | 9,925,656 | ||||||

| Atmos Energy Corp. | 360,399 | 31,441,209 | ||||||

| CMS Energy Corp. | 179,425 | 8,678,787 | ||||||

| ONE Gas, Inc. | 164,231 | 12,642,502 | ||||||

| PG&E Corp. | 183,700 | 10,612,349 | ||||||

| Xcel Energy, Inc. | 514,925 | 25,499,086 | ||||||

| 98,799,589 | ||||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $1,323,490,686) — 99.4% | 1,665,614,040 | |||||||

| SHORT-TERM INVESTMENTS — 0.6% | ||||||||

| MONEY MARKET FUNDS | ||||||||

| Fidelity Investments Money Market Funds — | ||||||||

| Treasury Portfolio — Class I, 0.915% | 10,000,000 | 10,000,000 | ||||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $10,000,000) — 0.6% | 10,000,000 | |||||||

| TOTAL INVESTMENTS | ||||||||

| (Cost $1,333,490,686) — 100.0% | 1,675,614,040 | |||||||

| Liabilities less other assets — 0.0% | (399,842 | ) | ||||||

| TOTAL NET ASSETS — 100.0% | ||||||||

| (equivalent to $19.77 per share; | ||||||||

| unlimited shares of $1.00 par value | ||||||||

| capital shares authorized; | ||||||||

| 84,714,099 shares outstanding) | $ | 1,675,214,198 | ||||||

PLC — Public Limited Company

REIT — Real Estate Investment Trust

| * | Non-income producing security. |

| (a) | Foreign security denominated in U.S. dollars. |

See accompanying Notes to Financial Statements.

| 12 | SCOUT FUNDS ANNUAL REPORT |

Scout Small Cap Fund

UMBHX

As a result of a reorganization that was completed after the close of business on November 17, 2017, the Scout Small Cap Fund is now the Carillon Scout Small Cap Fund. The commentary that follows is for the 12 months ended October 31, 2017.

MARKET REVIEW

Small-cap stocks, broadly represented by the Russell 2000® Index, provided solid returns during the fiscal year ended Oct. 31, 2017, with the index gaining 27.85 percent. A vast majority of the gains during the fiscal year followed the U.S. presidential election as investors anticipated tax and regulatory reform.

The Federal Reserve (the Fed) was able to successfully hike interest rates three times this fiscal year given the tighter labor markets and improvement in the U.S. economy. There are some developing credit concerns in subprime auto loans and credit cards but, with unemployment continuing to fall and wages still rising, the yield curve remains upwardly sloped and economic growth is still positive.

The price of oil, a key component in the overall economy, closed the fiscal year relatively unchanged. We believe Saudi Arabia would like to conduct an initial public offering of its national oil company, Aramco, sometime in 2018; so, we expect they will be supportive of orderly oil markets to set the stage for the offering and shore up their government’s budget.

PORTFOLIO REVIEW

The Scout Small Cap Fund (UMBHX) returned 40.69 percent for the 12 months ended October 31, 2017, outperforming the Russell 2000 Growth Index return of 31.00 percent. Positive stock selection in information technology, consumer discretionary and financials accounted for the majority of the relative outperformance. An overweight in healthcare along with an underweight in the consumer staples and the real estate sectors also added to relative performance. In contrast, disappointing stock selection in the energy sector offset the positive effect of the Fund’s underweight position. An underweight position and disappointing stock selection in the materials sector also provided a negative impact on relative performance.

Stocks providing the most positive contribution to performance included LendingTree, Inc.; ePlus, Inc.; Cognex Corp.; Supernus Pharmaceuticals, Inc.; and Thor Industries, Inc. The financials sector benefited from LendingTree, Inc., an online loan marketplace for consumers seeking loans, which reported strong earnings and provided encouraging guidance for fiscal year 2017. In addition, the company has executed well and continues to diversify revenue streams away from mortgage-related products. ePLUS provides IT solutions for data center, cloud computing and security via hardware, software and services. Better-than-expected results driven by a large networking infrastructure contract for Apple drove the stock higher. The company continues to expect above industry growth, as well as continued mergers and acquisition activity. Cognex produces machine vision systems and software used in industrial automation and barcode ID reading. Very strong demand across the company’s end markets and geographies has driven earnings results and guidance well above expectations. Supernus Pharmaceuticals is focused on developing and commercializing products for the treatment of central nervous system diseases. The company recently received approval for an expanded label for Trokendi and Oxtellar XR, which has increased revenues. Thor is the leading manufacturer of motorhomes and towable RVs. The company reported significantly better-than-expected earnings results that were driven by strong results in both “towables” and motorhomes from its core business and recently acquired Jayco Company.

Some of the Fund’s main detractors on an individual stock basis were Electronics for Imaging; Adeptus Health, Inc.; Cambrex Corp.; Gulfport Energy Corp.; and Monro, Inc. Electronics for Imaging is a leading provider of industrial inkjet printers, inks and software. The stock has been weak following a pair of disappointing earnings results and guidance. Adeptus Health operates an independent network of free-standing emergency rooms. The company announced a significant miss and reset of expectations along with multiple management changes, which negatively impacted the stock. Cambrex is a company that produces small-molecule Active Pharmaceutical Ingredients. The company’s largest customer, Gilead, has struggled with slower Hepatitis C sales. Continued outsourcing of small-molecule production should be beneficial to Cambrex. Gulfport Energy is engaged in the exploration and production of oil and natural gas, primarily in the Northeast and Midwestern United States. The stock has been weak following a large acquisition that broadened the company’s exposure to a second major oil and gas basin.

| OCTOBER 31, 2017 | 13 |

Scout Small Cap Fund

UMBHX

Monro Muffler Brake operates a chain of automotive repair and service stores throughout the United States. The stock has been weak due to continued sluggishness in same-store sales across all categories of the business. Additionally, in late June the company announced the retirement of both its longtime CEO and the chairman of its board of directors.

MARKET OUTLOOK

Markets continue to climb on optimism for faster economic growth within the United States due in part to the promise of deregulation, tax reform and infrastructure investments. However, investor concerns have emerged as the potential for a trade war due to tough rhetoric from the administration, the unknown reaction to the Fed’s balance sheet reduction and the uncertainty of passing tax reform could place a damper on the markets. Overall the growth in the world economy appears strong.

PORTFOLIO STRATEGY

The Scout Small Cap Fund invests in a diversified portfolio of equity securities that are selected based on their above-average potential for long-term growth of capital. Today, we are finding many of those opportunities in the financials, information technology and healthcare sectors. While sector allocations are a by-product of the investment process (with each portfolio candidate assessed on its own merit) these sectors represent the Fund’s largest overweight positions relative to the benchmark. In contrast, the Fund’s largest underweight position is in industrials, reflecting fewer growth investment opportunities in this area.

James R. McBride, CFA

Lead Portfolio Manager

Timothy L. Miller, CFA

Co-Portfolio Manager

| 14 | SCOUT FUNDS ANNUAL REPORT |

Scout Small Cap Fund

UMBHX

OBJECTIVE & STRATEGY (Unaudited)

The Scout Small Cap Fund seeks long-term growth of capital by investing in a diversified portfolio of equity securities of small cap companies located anywhere in the United States.

PORTFOLIO MANAGEMENT TEAM

James R. McBride, CFA

Lead Portfolio Manager

Timothy L. Miller, CFA

Co-Portfolio Manager

HYPOTHETICAL GROWTH OF $10,000 (Unaudited)

as of October 31, 2017

Performance returns for the Scout Small Cap Fund and Russell 2000® Growth Index assume dividends were reinvested for the entire period.

For illustrative purposes only; may not represent your returns.

| * | Unmanaged index of stocks, bonds or mutual funds. It is not possible to invest directly in an index. The Russell 2000® Growth Index measures the performance of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Index is a small-cap stock market index that measures the performance of the 1001st through 3000th largest companies in the US as measured by float-adjusted market capitalization. |

Portfolio composition will change due to ongoing management of the Fund. References to specific securities should not be construed as recommendations by the Fund, its Advisor or Distributor.

Risk considerations: Due to the limited focus, the Fund is more susceptible to market volatility because smaller companies may not have the management experience, financial resources, product diversification and competitive strengths of larger companies. Additionally, smaller company stocks tend to be sold less often and in smaller amounts than larger company stocks. Real Estate Investment Trusts (REITS) may be affected by economic conditions including credit risk, interest rate risk and other factors that affect property values, rents or occupancies of real estate. Foreign investments present additional risks due to currency fluctuations, economic and political factors, government regulations, differences in accounting standards and other factors. Investments in emerging markets involve even greater risks. Groups of stocks, such as value and growth, go in and out of favor which may cause certain funds to underperform other equity funds.

| OCTOBER 31, 2017 | 15 |

Scout Small Cap Fund

UMBHX

COMPARATIVE RATES OF RETURN (Unaudited)

as of October 31, 2017

| 1 Year | 3 Years | 5 Years | 10 Years | |||||

| Scout Small Cap Fund | 40.69% | 12.65% | 16.99% | 7.02% | ||||

| Russell 2000® Growth Index* | 31.00% | 10.51% | 15.36% | 8.16% |

Returns for periods greater than one year are compounded average annual rates of return.

The performance data quoted represents past performance and past performance is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call 800-996-2862. For the fiscal year ended June 30, 2017, the gross/net expense ratio for the Fund was 1.04% (as disclosed in the most recent Prospectus) compared to the October 31, 2017, gross/net expense ratio of 1.03%.

The performance shown in the above table and in the graph on the preceding page does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

PORTFOLIO CHARACTERISTICS (Unaudited)

| Scout | Russell 2000® | |||

| Small Cap | Growth* | |||

| Number of Holdings | 72 | 1,163 | ||

| Weighted Average Market Cap | $2.87B | $2.52B | ||

| Weighted Median Market Cap | $2.26B | $2.38B | ||

| Price to Earnings Ratio (Trailing 1 Year) | 28.96 | 26.17 | ||

| Price/Book Ratio | 3.52 | 4.29 | ||

| EPS Growth (Hist. 5 Yr.) | 7.29% | 8.12% | ||

| Return on Equity | 14.37% | 8.29% | ||

| Standard Deviation (Trailing 3 Years) | 13.64% | 14.80% | ||

| Sharpe Ratio (Trailing 3 Years) | 0.90 | 0.68 | ||

| Beta† | 0.87 | 1.00 | ||

| Alpha† | 3.18% | — | ||

| R-squared† | 0.89 | 1.00 | ||

| Upside Capture† | 96% | 100% | ||

| Downside Capture† | 82% | 100% | ||

| Turnover Ratio (Trailing 1 Year) | 28% | — | ||

| Total Net Assets (in Millions) | $270.53 | — | ||

| Inception Date | 12/18/1986 | — |

† Measured against the Russell 2000® Growth Index over the trailing three year time period.

FUND DIVERSIFICATION (Unaudited)

Based on total investments as of October 31, 2017. Subject to change.

TOP 10 EQUITY HOLDINGS (Unaudited)

| Percent of Total | ||

| ICU Medical, Inc. | 2.88% | |

| Thor Industries, Inc. | 2.85% | |

| BroadSoft, Inc. | 2.83% | |

| II-VI, Inc. | 2.71% | |

| ePlus, Inc. | 2.69% | |

| Omnicell, Inc. | 2.68% | |

| LendingTree, Inc. | 2.67% | |

| Teledyne Technologies, Inc. | 2.38% | |

| Supernus Pharmaceuticals, Inc. | 2.34% | |

| Cracker Barrel Old Country Store, Inc. | 2.18% | |

| Top 10 Holdings Total | 26.21% |

Based on total investments as of October 31, 2017. Subject to change.

HISTORICAL PER-SHARE RECORD (Unaudited)

| Income & | Cumulative(c) | |||||||||||||||

| Net Asset | Short-Term(b) Gains | Long-Term(b) Gains | Value Per Share | |||||||||||||

| Value | Distribution | Distribution | Plus Distributions | |||||||||||||

| 12/31/12 | $ | 17.45 | $ | 0.06 | $ | — | $ | 31.61 | ||||||||

| 12/31/13 | 23.91 | — | — | 38.07 | ||||||||||||

| 12/31/14 | 25.03 | — | 0.18 | 39.37 | ||||||||||||

| 12/31/15 | 21.60 | — | 3.54 | 39.48 | ||||||||||||

| 12/31/16 | 23.24 | 0.01 | 1.05 | 42.18 | ||||||||||||

| 10/31/17(a) | 29.33 | — | — | 48.27 | ||||||||||||

| (a) | Ten months only. Distributions typically occur in June and/or December. |

| (b) | Represents distributions for the respective calendar year-to-date period ended. |

| (c) | Does not assume any compounding of reinvested distributions. |

Table shows calendar-year distributions and net asset values; may differ from fiscal-year annual reports.

| * | Unmanaged index of stocks, bonds or mutual funds. It is not possible to invest directly in an index. |

Portfolio composition will change due to ongoing management of the Fund. References to specific securities or sectors should not be construed as a recommendation by the Fund, its Advisor or Distributor. See the accompanying Schedule of Investments for the percentage of the Fund’s portfolio represented by the securities or sectors mentioned above.

| 16 | SCOUT FUNDS ANNUAL REPORT |

SCHEDULE OF INVESTMENTS

October 31, 2017

SMALL CAP FUND

| Shares | Value | |||||||

| COMMON STOCKS — 99.3% | ||||||||

| CONSUMER DISCRETIONARY — 14.4% | ||||||||

| Camping World Holdings, Inc. — Class A | 67,500 | $ | 2,836,350 | |||||

| Cheesecake Factory, Inc. | 58,800 | 2,630,712 | ||||||

| Cracker Barrel Old Country Store, Inc. | 37,900 | 5,917,327 | ||||||

| G-III Apparel Group Ltd.* | 68,100 | 1,725,654 | ||||||

| Installed Building Products, Inc.* | 66,500 | 4,635,050 | ||||||

| iRobot Corp.* | 60,900 | 4,091,871 | ||||||

| LGI Homes, Inc.* | 49,800 | 3,004,434 | ||||||

| Lindblad Expeditions Holdings, Inc.* | 155,200 | 1,663,744 | ||||||

| Monro, Inc. | 92,700 | 4,574,745 | ||||||

| Thor Industries, Inc. | 56,631 | 7,714,275 | ||||||

| 38,794,162 | ||||||||

| CONSUMER STAPLES — 1.4% | ||||||||

| Performance Food Group Co.* | 134,200 | 3,797,860 | ||||||

| ENERGY — 0.8% | ||||||||

| Geospace Technologies Corp.* | 61,060 | 917,121 | ||||||

| Gulfport Energy Corp.* | 92,800 | 1,271,360 | ||||||

| 2,188,481 | ||||||||

| FINANCIALS — 10.3% | ||||||||

| BofI Holding, Inc.* | 112,500 | 3,026,250 | ||||||

| CNO Financial Group, Inc. | 202,400 | 4,851,528 | ||||||

| Cohen & Steers, Inc. | 104,826 | 4,558,883 | ||||||

| Financial Engines, Inc. | 89,200 | 3,220,120 | ||||||

| Hilltop Holdings, Inc. | 119,900 | 2,824,844 | ||||||

| LendingTree, Inc.* | 27,000 | 7,237,350 | ||||||

| PRA Group, Inc.* | 77,910 | 2,173,689 | ||||||

| 27,892,664 | ||||||||

| HEALTH CARE — 25.6% | ||||||||

| Acorda Therapeutics, Inc.* | 43,800 | 1,163,985 | ||||||

| Almost Family, Inc.* | 57,800 | 2,557,650 | ||||||

| AMN Healthcare Services, Inc.* | 95,600 | 4,196,840 | ||||||

| BioTelemetry, Inc.* | 118,600 | 3,445,330 | ||||||

| Bruker Corp. | 163,200 | 5,124,480 | ||||||

| Cambrex Corp.* | 77,900 | 3,369,175 | ||||||

| Cutera, Inc.* | 54,290 | 2,133,597 | ||||||

| Exactech, Inc.* | 20,500 | 857,925 | ||||||

| Genomic Health, Inc.* | 70,700 | 2,318,253 | ||||||

| HealthEquity, Inc.* | 79,600 | 3,997,512 | ||||||

| HMS Holdings Corp.* | 140,600 | 2,705,144 | ||||||

| ICU Medical, Inc.* | 40,845 | 7,805,479 | ||||||

| Impax Laboratories, Inc.* | 92,300 | 1,675,245 | ||||||

| Molina Healthcare, Inc.* | 57,100 | 3,873,093 | ||||||

| Omnicell, Inc.* | 145,600 | 7,250,880 | ||||||

| PRA Health Sciences, Inc.* | 67,400 | 5,488,382 | ||||||

| Supernus Pharmaceuticals, Inc.* | 152,100 | 6,327,360 | ||||||

| U.S. Physical Therapy, Inc. | 74,550 | 5,065,673 | ||||||

| 69,356,003 | ||||||||

| INDUSTRIALS — 14.4% | ||||||||

| Albany International Corp. — Class A | 57,000 | 3,439,950 | ||||||

| Astronics Corp.* | 89,900 | 3,092,560 | ||||||

| Chart Industries, Inc.* | 45,500 | 1,979,250 | ||||||

| Dycom Industries, Inc.* | 64,400 | 5,656,252 | ||||||

| Healthcare Services Group, Inc. | 66,800 | 3,533,052 | ||||||

| InnerWorkings, Inc.* | 194,558 | 2,116,791 | ||||||

| Insperity, Inc. | 35,100 | 3,330,990 | ||||||

| Proto Labs, Inc.* | 55,300 | 4,824,925 | ||||||

| Radiant Logistics, Inc.* | 263,800 | 1,287,344 | ||||||

| Teledyne Technologies, Inc.* | 37,900 | 6,441,484 | ||||||

| WageWorks, Inc.* | 50,200 | 3,200,250 | ||||||

| 38,902,848 | ||||||||

| INFORMATION TECHNOLOGY — 28.6% | ||||||||

| Acxiom Corp.* | 44,400 | 1,117,104 | ||||||

| Ambarella, Inc.*(a) | 63,500 | 3,583,940 | ||||||

| Barracuda Networks, Inc.* | 132,800 | 3,095,568 | ||||||

| BroadSoft, Inc.* | 139,600 | 7,657,060 | ||||||

| Cognex Corp. | 33,600 | 4,137,840 | ||||||

| Descartes Systems Group, Inc.*(a) | 112,900 | 3,279,745 | ||||||

| Electronics For Imaging, Inc.* | 80,100 | 2,471,886 | ||||||

| Entegris, Inc. | 101,100 | 3,311,025 | ||||||

| Envestnet, Inc.* | 83,400 | 4,453,560 | ||||||

| ePlus, Inc.* | 76,300 | 7,294,280 | ||||||

| II-VI, Inc.* | 162,200 | 7,331,440 | ||||||

| Impinj, Inc.* | 45,900 | 1,567,026 | ||||||

| Inphi Corp.* | 42,800 | 1,753,944 | ||||||

| j2 Global, Inc. | 71,000 | 5,263,940 | ||||||

| Jack Henry & Associates, Inc. | 49,400 | 5,440,422 | ||||||

| Pegasystems, Inc. | 92,000 | 5,363,600 | ||||||

| Semtech Corp.* | 139,300 | 5,718,265 | ||||||

| Veeco Instruments, Inc.* | 125,800 | 2,270,690 | ||||||

| Virtusa Corp.* | 59,800 | 2,281,968 | ||||||

| 77,393,303 | ||||||||

| MATERIALS — 2.2% | ||||||||

| Balchem Corp. | 50,600 | 4,265,074 | ||||||

| Carpenter Technology Corp. | 32,500 | 1,618,175 | ||||||

| 5,883,249 | ||||||||

| REAL ESTATE — 1.6% | ||||||||

| CareTrust REIT, Inc. | 113,100 | 2,137,590 | ||||||

| QTS Realty Trust, Inc. — Class A REIT | 38,300 | 2,215,655 | ||||||

| 4,353,245 | ||||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $170,041,724) — 99.3% | 268,561,815 | |||||||

| TOTAL INVESTMENTS | ||||||||

| (Cost $170,041,724) — 99.3% | 268,561,815 | |||||||

| Other assets less liabilities — 0.7% | 1,969,221 | |||||||

| TOTAL NET ASSETS — 100.0% | ||||||||

| (equivalent to $29.33 per share; | ||||||||

| unlimited shares of $1.00 par value | ||||||||

| capital shares authorized; | ||||||||

| 9,223,646 shares outstanding) | $ | 270,531,036 | ||||||

REIT — Real Estate Investment Trust

| * | Non-income producing security. |

| (a) | Foreign security denominated in U.S. dollars. |

See accompanying Notes to Financial Statements.

| OCTOBER 31, 2017 | 17 |

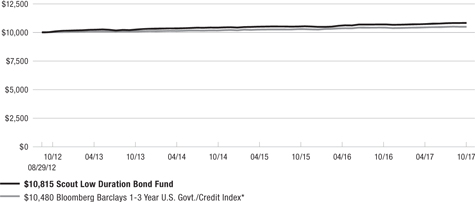

Scout Low Duration Bond Fund

SCLDX

As a result of a reorganization that was completed after the close of business on November 17, 2017, the Scout Low Duration Bond Fund is now the Carillon Reams Low Duration Bond Fund. The commentary that follows is for the 12 months ended October 31, 2017.

MARKET REVIEW

The Bloomberg Barclays U.S. Aggregate Index® returned 0.90 percent for the 12 months ending Oct. 31, 2017.1 Interest-rates increased sharply following President Donald Trump’s election as investors anticipated significant fiscal stimulus. The yield on the bellwether 10-Year Treasury Bond also improved, increasing from 1.83 percent on Nov. 1, 2016, to 2.38 percent by Oct. 31, 2017. Risk-asset valuations rose and spreads continued to tighten throughout 2017.

Volatility, as measured by the Chicago Board Options Exchange (CBOE) Volatility Index® (“VIX”), hit a record low and asset prices crept steadily higher. Even the typically volatile months of September and October passed quietly. The Fed surprised the market a bit as it formally began to reduce its balance sheet in October. This action joins other central banks around the globe in a fledgling effort to scale back the emergency monetary stimulus that has been in place for many years. The combination of increasing short-term rates and lowered inflation expectations has caused classic, Fed-induced yield-curve flattening. Historically, a flat yield curve is negative for spread sectors but credit spreads remained very tight in the current environment of risk apathy.

The European Central Bank (ECB) was late in arriving to the global quantitative easing (QE) party, but it has now indicated that a tapering of its program is near. ECB tightening might in fact have occurred earlier were it not for the headwind of a sharply higher euro. Now, as the ECB prepares to halt its QE program, the downward pressure on their currency has begun to relent. Fallout from disappointing U.S. fiscal stimulus has exacerbated the euro’s move higher vs. the dollar, providing an example of how “beggar thy neighbor” QE polices frequently provide only temporary help in currency depreciation.

Given the number of threats to fixed-income security prices — from rising interest rates and geopolitical uncertainty to the choppy transition from monetary to fiscal stimulus — we view rising yields and tighter spreads as further evidence that bond investors have become desensitized to risk.

PORTFOLIO REVIEW

The Scout Low Duration Bond Fund (SCLDX) returned 1.19 percent for the 12 months ended October 31, 2017, outperforming the Bloomberg Barclays 1-3 Year U.S. Government/Credit Index® return of 0.67 percent. Macroeconomic factors were positive over the time period. The Fund benefited from a shorter duration position as short-term interest rates rose. Yield curve modestly added to performance.

Performance was overwhelmingly positive at the sector level. Investment-grade credit, high-yield credit, asset-backed securities (ABS) and commercial mortgage-backed securities (CMBS) all added to performance due to the Fund’s overweight positions in these outperforming sectors. Mortgage-backed securities (MBS) further bolstered returns due to gains in the Fund’s multi-family agency holdings. In contrast, government-related securities detracted from relative results due to the Fund’s underweight position.

MARKET OUTLOOK

For much of 2017, volatility has been anchored near the low end of its historic range. This is inconsistent with the increasingly risky geopolitical climate as well as the anticipated trend away from global monetary stimulus, which has been dampening volatility since central banks opened the spigot in the wake of 2008’s financial crisis. At the same time, general corporate spreads remain near historic tights and anecdotal evidence suggests that we are in the late stages of the credit cycle. For these reasons, we expect to see an increase in volatility as global central banks pull back their monetary stimulus.

Recent Fed communication points to three rate increases in 2018. This is aggressive, and we believe that the consensus view of one or two rate increases is more realistic, albeit still optimistic. Inflation, apart from asset-price inflation, has remained stubbornly low and below the Fed’s target levels. Short of significant fiscal stimulus hitting the market, we do not expect inflation to be a problem. If the capital markets falter, the Fed may quickly back away from the rate-hike action, as it seems more

| 1 | https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yieldYear&year=2017 |

| 18 | SCOUT FUNDS ANNUAL REPORT |

| Scout Low Duration Bond Fund |

| SCLDX |

focused on enabling capital markets instead of holding to a constant rate-setting rationale. A flat yield curve indicates concern that the Fed may raise rates too far and choke off growth.

Meanwhile, Treasury rates remain at modest levels as President Trump’s fiscal stimulus agenda continues to experience setbacks. A bold tax-reform plan has been proposed by the administration but the combination of delays, distraction from failed healthcare reform and lack of concentrated support in Congress leaves its fate in question, although its prospects improved late in 2017. We expect that some tax cut will be passed eventually but how much it adds in stimulus is difficult to ascertain at this point. This confirms our initial skepticism regarding the ease of the handoff from monetary to fiscal stimulus that was anticipated with Trump’s election.

PORTFOLIO STRATEGY

The factors above reinforce our belief that current bond market valuations do not reflect its risks. While we continue to be cautious on valuations broadly in the fixed-income markets, we do view the low-duration investment-grade credit and mortgage-backed securities sectors as attractive. If the Fed continues down the path of raising the front end of the yield curve, the danger of a flat or inverted curve increases. Both scenarios are almost always negative for spread sector performance, with an inverted yield curve being particularly problematic. For these reasons, we are continuing to position our portfolios defensively and avoiding the intermediate and longer-term portions of the spread sectors. We expect that this will enable us to protect our clients from the price declines that may be on the horizon as well as to take advantage of the opportunities for future outperformance that those declines may create.

Mark M. Egan, CFA

Lead Portfolio Manager

Thomas M. Fink, CFA

Co-Portfolio Manager

Todd C. Thompson, CFA

Co-Portfolio Manager

Stephen T. Vincent, CFA

Co-Portfolio Manager

Clark W. Holland, CFA

Co-Portfolio Manager

| OCTOBER 31, 2017 | 19 |

| Scout Low Duration Bond Fund |

| SCLDX |

| OBJECTIVE & STRATEGY (Unaudited) |

The Scout Low Duration Bond Fund seeks a high level of total return consistent with the preservation of capital by investing in fixed income instruments and targeting an estimated average portfolio duration of one to four years.

| PORTFOLIO MANAGEMENT TEAM |

Mark M. Egan, CFA

Lead Portfolio Manager

Thomas M. Fink, CFA

Co-Portfolio Manager

Todd C. Thompson, CFA

Co-Portfolio Manager

Stephen T. Vincent, CFA

Co-Portfolio Manager

Clark W. Holland, CFA

Co-Portfolio Manager

| HYPOTHETICAL GROWTH OF $10,000 (Unaudited) |

as of October 31, 2017

Performance returns for the Scout Low Duration Bond Fund and Bloomberg Barclays 1-3 Year U.S. Government/Credit Index assume dividends were reinvested for the entire period.

For Illustrative purposes only; may not represent your returns.

| * | Unmanaged index of stocks, bonds or mutual funds. It is not possible to invest directly in an index. The Bloomberg Barclays 1-3 Year U.S. Government/Credit Index measures the performance of Treasuries, government-related issues and corporate bonds with maturities from one to three years. |

Portfolio composition will change due to ongoing management of the Fund. References to specific securities should not be construed as recommendations by the Fund, its Advisor or Distributor.

Risk considerations: The return of principal in a fixed income fund is not guaranteed. Fixed income funds have the same issuer, interest rate, inflation, maturity and credit risks that are associated with underlying fixed income securities owned by the Fund. High yield securities involve greater risk than investment grade securities. Mortgage- and Asset-Backed Securities are subject to prepayment risk and the risk of default on the underlying mortgages or other assets. Foreign investments present additional risks due to currency fluctuations, economic and political factors, government regulations, differences in accounting standards and other factors.

Derivatives such as options, futures contracts, currency forwards or swap agreements may involve greater risks than if the Fund invested in the referenced obligation directly. Derivatives are subject to risks such as market risk, liquidity risk, interest rate risk, credit risk, and management risk. Derivative investments could lose more than the principal amount invested. The Fund may use derivatives for hedging purposes or as part of its investment strategy. The use of leverage and derivatives investments could accelerate losses to the Fund. These losses could exceed the amount originally invested.

The Fund may, at times, experience higher-than-average portfolio turnover which may generate significant taxable gains and increased trading expenses which in turn may lower the Fund’s return.

| 20 | SCOUT FUNDS ANNUAL REPORT |

| Scout Low Duration Bond Fund |

| SCLDX |

| COMPARATIVE RATES OF RETURN (Unaudited) |

as of October 31, 2017

| Since | ||||||||

| 1 Year | 3 Years | 5 Years | Inception† | |||||

| Scout Low Duration Bond Fund | 1.19% | 1.21% | 1.32% | 1.53% | ||||

| Bloomberg Barclays 1-3 Year U.S. Government/Credit Index* | 0.67% | 0.95% | 0.90% | 0.91% |

| † | Inception – August 29, 2012. |

Returns for periods greater than one year are compounded average annual rates of return.

The performance data quoted represents past performance and past performance is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call 800-996-2862. For the fiscal year ended June 30, 2017, the gross expense ratio for the Fund was 0.76% (as disclosed in the most recent Prospectus) compared to the October 31, 2017, gross expense ratio of 0.75%.

The performance returns for the Fund reflect a fee waiver in effect. In absence of such waiver, the returns would be reduced. The Advisor has contractually agreed to waive fees and assume certain fund expenses through October 30, 2018, and may recoup previously waived fees and expenses that it assumed during the previous three fiscal years.

The Fund may, at times, experience higher-than-average portfolio turnover which may generate significant taxable gains and increased trading expenses which in turn may lower the Fund’s return.

The performance shown in the above table and in the graph on the preceding page does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| FUND DIVERSIFICATION (Unaudited) |

Based on total investments as of October 31, 2017. Subject to change.

| HISTORICAL PER-SHARE RECORD (Unaudited) |

| Income & | Cumulative(c) | |||||||||||||||

| Net Asset | Short-Term(b) Gains | Long-Term(b) Gains | Value Per Share | |||||||||||||

| Value | Distribution | Distribution | Plus Distributions | |||||||||||||

| 12/31/12 | $ | 10.10 | $ | 0.07 | $ | — | $ | 10.17 | ||||||||

| 12/31/13 | 10.09 | 0.15 | — | 10.31 | ||||||||||||

| 12/31/14 | 10.04 | 0.13 | 0.02 | 10.41 | ||||||||||||

| 12/31/15 | 9.98 | 0.12 | — | 10.47 | ||||||||||||

| 12/31/16 | 10.03 | 0.13 | — | 10.65 | ||||||||||||

| 10/31/17(a) | 10.05 | 0.12 | — | 10.79 | ||||||||||||