UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file Number: 811-07470

CARILLON SERIES TRUST

(Exact name of Registrant as Specified in Charter)

880 Carillon Parkway

St. Petersburg, FL 33716

(Address of Principal Executive Office) (Zip Code)

Registrant’s Telephone Number, including Area Code: (727) 567-1000

SUSAN L. WALZER, PRINCIPAL EXECUTIVE OFFICER

880 Carillon Parkway

St. Petersburg, FL 33716

(Name and Address of Agent for Service)

Copy to:

KATHY KRESCH INGBER, ESQ.

K&L Gates, LLP

1601 K Street, NW

Washington, D.C. 20006

Date of fiscal year end: October 31

Date of reporting period: October 31, 2018

Item 1. Reports to Shareholders

Annual Report | ||

and Investment Performance Review for the fiscal year ended October 31, 2018 | ||

Equity Funds | ||

Carillon ClariVest Capital Appreciation Fund | ||

Carillon ClariVest International Stock Fund | ||

Carillon Cougar Tactical Allocation Fund | ||

Carillon Eagle Growth & Income Fund | ||

Carillon Eagle Mid Cap Growth Fund | ||

Carillon Eagle Small Cap Growth Fund | ||

Carillon Scout International Fund | ||

Carillon Scout Mid Cap Fund | ||

Carillon Scout Small Cap Fund | ||

Fixed Income Funds | ||

Carillon Reams Core Bond Fund | ||

Carillon Reams Core Plus Bond Fund | ||

Carillon Reams Unconstrained Bond Fund | ||

Visit carillontower.com/eDelivery to receive shareholder communications including prospectuses and fund reports with a service that helps protect the environment:

Environmentally friendly. Go green with eDelivery by reducing the number of trees used to produce paper.

Efficient. Stop waiting on regular mail. Your documents will be sent via email as soon as they are available.

Easy. Download and save files using your home computer with a few clicks of a mouse.

Dear Fellow Shareholders:

I am pleased to present the annual report and investment-performance review of the Carillon Family of Funds for the 12-month period that ended on October 31, 2018.

In the past year, the dedicated women and men at Carillon Tower Advisers, Inc. (“Carillon”) have worked to enhance investment opportunities and control costs for you and your funds. As part of our efforts to bring high quality managers to you, alpha-oriented* equity manager Scout Investments, Inc., and its fixed income specialist division, Reams Asset Management, joined our existing affiliate line up of Eagle Asset Management, Inc., ClariVest Asset Management LLC, and Cougar Global Investments Ltd., resulting in fund options covering an expanded range of asset classes and investment strategies. We are delighted to have this new firm in our family.

Fiscal year 2018 presented different market conditions throughout the reporting period, suggesting increased volatility and long-term opportunities to come. The S&P 500 Index, buoyed in part by the Tax Cuts and Jobs Act of 2017 and strong corporate earnings, presented early gains; yet the period also saw heightened volatility and sharp market declines. A decade’s worth of accommodative monetary policy by the U.S. Federal Reserve (“the Fed”) continues to be withdrawn, and the Fed has indicated rates will continue to rise: our investment teams strive to identify which companies stand to benefit amidst these changes.

With an outlook growing potentially more complex, we continue to believe that our investment teams’ abilities to distinguish among competitive businesses, quality companies and earnings potential can help investors seek their long-term financial goals. Our multi-boutique affiliate model offers an array of actively managed solutions for clients navigating uncertain times.

As with all investments, investing in any mutual fund carries certain risks. The principal risk factors for each fund are described at the end of this annual report. Carefully consider the investment objectives, charges and expenses of any fund before you invest. Contact us at 800.421.4184 or carillontower.com or call your financial advisor for a prospectus, or summary prospectus, which contains this and other important information about the Carillon Family of Funds. Read the prospectus, or summary prospectus, carefully before you invest or send money.

We are grateful for your continued support of the Carillon Family of Funds.

Sincerely,

J. Cooper Abbott, CAIA, CFA

President

December 19, 2018

Performance data represented are historical and do not guarantee future results. Investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please call us at 800.421.4184 or visit our website at carillontower.com.

* Alpha measures performance vs. a benchmark on a risk-adjusted basis. A positive alpha of 1.0 means the portfolio has outperformed its benchmark on a risk adjusted basis. Correspondingly, a similar negative alpha would indicate an underperformance of 1%.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of Morgan Stanley Capital International, Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

| 1 |

Performance Summary and Commentary

| Carillon ClariVest Capital Appreciation Fund |

Portfolio Managers | David J. Pavan, CFA®, C. Frank Feng, Ph.D., Ed Wagner, CFA®, and Stacey R. Nutt, Ph.D., of ClariVest Asset Management LLC (“ClariVest”), are Co-Portfolio Managers of the ClariVest Capital Appreciation Fund (the “Fund”) and have been responsible for the day-to-day management of the Fund’s investment portfolio since June 2013.

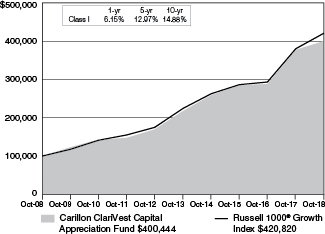

Performance discussion | For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned 6.15%, underperforming its benchmark index, the Russell 1000® Growth Index, which returned 10.71%. The Fund’s performance, relative to the benchmark, was negative, primarily due to stock selection, where selection within the Health Care and Materials sectors was strongest, and was weak within the Consumer Discretionary and Information Technology sectors. Sector selection was also negative, where underweights to the Industrials and Real Estate sectors contributed to performance, while the Fund lost ground from an underweight to the Consumer Staples sector and an overweight to the Energy sector. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore, its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are

calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Underperformers | Facebook, the social media company, was hurt by concerns widely publicized regarding the security of user data. The company missed estimates on revenue for the first time in three years, and it expects the revenue slowdown to continue. The position was trimmed. Owens Corning is in the business of residential and commercial building materials such as composites, insulation, and roofing. A weak outlook for roofing and composites appeared to weigh on the company due to inflationary cost pressures for oil, asphalt, and transportation. The stock was sold from the portfolio. Micron Technology Inc. engages in the provision of innovative memory and storage solutions. The stock struggled as the markets for both DRAM and NAND continued to slide. Meanwhile, supply growth accelerated, leading to oversupply in both markets. The Fund continues to hold this security. Applied Materials, the worldwide semiconductor equipment manufacturer and services company, fell on a weak forward guidance driven by weaker adoption of its organic light-emitting diode (OLED) display in smartphones. Trade disputes also have appeared to negatively impact sentiment for the semiconductor industry. The stock was sold from the portfolio. Lam Research, a semiconductor manufacturing equipment maker, fell after a lower forecast for shipments overshadowed strong results. The stock was sold from the portfolio.

Top performers | Apple, the tech giant, released better-than-expected second and third quarter earnings. iPhone revenue grew, with iPhone X as the best-selling iPhone model for every week of the fiscal second quarter. The Fund continues to hold this security. Microsoft develops and markets software and hardware services. The company’s focus on cloud computing and its Azure cloud platform contributed to strong growth and margins. The stock rose following its announcement to acquire GitHub, a leading software development platform. Microsoft also announced a quarterly dividend increase of about 9.5%. The Fund continues to hold this security. Amazon, the world’s largest online retailer, appeared to benefit from strong retail sales in North America; accelerating revenue across its advertising, cloud computing, and third-party marketplace services; improving fulfillment efficiency; and stronger margin guidance. The Fund continues to hold this security. UnitedHealth Group, the largest U.S. health insurer, appeared to benefit from the growth of enrollment in its Medicare Advantage plans. The company also appeared to reduce its risk by withdrawing from the Affordable Care Act (ACA) individual marketplace, while maintaining strong momentum and performance. The Fund continues to hold this security. Boeing Corp., the world’s largest aerospace company, rose on a stronger outlook for commercial aircraft production and margins, in addition to a federal budget deal that increased defense spending. The Fund continues to hold this security.

| 2 |

Performance Summary and Commentary

| Carillon ClariVest International Stock Fund |

Portfolio Managers | David Vaughn, CFA®, Stacey R. Nutt, Ph.D., Alex Turner, CFA®, and Priyanshu Mutreja, CFA®, are Co-Portfolio Managers of the ClariVest International Stock Fund (the “Fund”). Mr. Vaughn and Dr. Nutt have been responsible for the day-to-day management of the Fund’s investment portfolio since 2013. Mr. Turner has been a Co-Portfolio Manager of the Fund since March 2015 and previously served as Assistant Portfolio Manager of the Fund since its inception in 2013. Mr. Mutreja has been a Co-Portfolio Manager since March 2017 and previously served as Assistant Portfolio Manager of the Fund since March 2015.

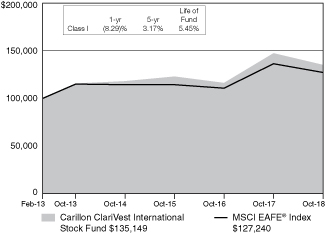

Performance discussion | For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned (8.29)%,underperforming its benchmark index, the MSCI-EAFE Index, which returned (6.85)%. The Fund’s performance, relative to the benchmark, was negative primarily due to stock selection within countries, where selection was strong within Switzerland and Japan, and weak within France and Germany. An overweight to Switzerland and an underweight to Hong Kong contributed to performance, while underweights to Australia and Finland hurt. Stock selection within sectors was strong within the financials and industrials sectors and weak within the information technology and materials sectors. An overweight to the energy sector and an underweight to the consumer discretionary sector helped performance, while underweights to the health care and consumer staples sectors tempered returns. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore, its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 2/28/13 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered

Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Underperformers | Covestro, based in Germany, manufactures polymers and high-performance plastics. The share price fell in concert with other European stocks apparently on tariff concerns, despite announcing fourth quarter earnings that beat expectations. Hitachi Ltd, based in Japan, manufactures electrical equipment. Despite reporting record profits early in the year, the share price fell alongside industry peers apparently due to renewed trade war concerns. NXP Semiconductors NV is a semiconductor company based in Netherlands. The company revised its guidance lower, fueling concerns of a peaking industry. Investors were also disappointed by the ultimate collapse of its proposed acquisition by Qualcomm, as trade relations between the US and China continued to sour. The position was trimmed. Enel SpA, based in Italy, is a holding company which engages in the distribution of electricity and gas. The company struggled apparently due to macroeconomic factors including falling margins in domestic retail activities and the adverse evolution of Latin American exchange rates. BASF SE is a German-based chemical company. The company reported profit that missed analysts’ expectations as it appeared to experience the effects of an automotive slowdown and higher raw-material prices.

Top performers | Xinyi Glass is one of China’s largest glass producers. Strong demand for float glass appeared to help drive price increases which in turn led to higher margins. Marubeni Corporation, a Japanese trading company, posted strong results apparently helped by the rally in commodity prices, the announcement of a higher-than-expected dividend and improved sentiment with regards to global trade. The Fund continues to hold this security. Cosmo Energy, a Japanese holding company involved in the oil business, released strong quarterly results apparently driven by rising Japanese refining margins and an improving balance sheet. Sony Corporation is a Japanese consumer electronics and media company. Apparently contributing to better-than-expected earnings were robust sales of the PlayStation console due to the popularity of new game launches, and strength in the company’s image sensing division. The Fund continues to hold this security. Lonza Group AG is a Switzerland-based chemicals producer. It appeared that strong end-market demand coupled with fast progress in integrating a recent acquisition led to better-than-expected results and improved confidence in its earnings outlook. The Fund continues to hold this security.

| 3 |

Performance Summary and Commentary

| Carillon Cougar Tactical Allocation Fund |

Portfolio Managers | Abdullah Sheikh, FSA, MAAA, of Cougar Global Investments Ltd. (“Cougar”), is the Portfolio Manager of the Cougar Tactical Allocation Fund (the “Fund”) and has been responsible for the day-to-day management of the Fund’s investment portfolio since April 2018. From the Fund’s inception, through September 30, 2018, James Breech, Ph.D. also served as a Portfolio Manager of the Fund.

Performance discussion | During the fiscal period, Cougar’s 12-month forward looking outlook and Macro Economic Scenario analysis (MES) for the U.S. economy remained positive, boosted by the stimulative effects of the Trump administration’s tax cuts, as well as the continued positive performance of the U.S. consumer. The probability assigned to the most optimistic scenario, Growth, rose from 29% to peak at 71% in April, before falling back to 35%. Overall, the outlook remained positive given the continued strength of the labor market and modest inflation. Recession risks remained at 0%. The probability assigned to Inflation hovered at 1 to 3% as transitory effects faded and higher energy prices fed through, but remains at modest levels. Wage inflation has accelerated somewhat in line with expectations. The chance that a high impact, low probability event, Chaos, would occur was stable. It decreased in May to 7% from 8% around a de-escalation of geopolitical risks, in particular North and South Korea holding a historic summit committing to a nuclear-free peninsula and ending the Korean War. The ex-U.S. growth trends showed signs of slowing, albeit from solid levels. Risks stemmed primarily from rising interest rates in the U.S., as well as effects of trade wars initiated by the Trump administration. The firm’s Portfolio Management team (“PM team”) further increased overall equity exposure with an emphasis on diversified exposure in large, mid and small-caps in the U.S. market, which benefitted the Fund’s performance. International holdings were sold given the combination of a rising USD, fallout from tariffs and trade, and geopolitical risks. The improvement in U.S. growth, robust corporate earnings, and modest pace in removal of monetary policy appeared to fuel a continuation of the equity market rally. After new highs in September, October saw what appeared to be a correction take hold as the U.S. succumbed to fears of slowing growth and earnings ahead. Fixed income suffered modest losses as the Fed continued on its tightening path and rates normalized. With the rest of the world’s major central banks largely still in easing mode, the USD strengthened.

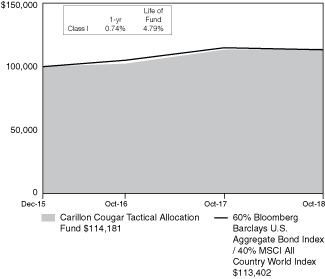

For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned 0.74%, outperforming the Bloomberg Barclays U.S. Aggregate Bond Index and the MSCI ACWI® Index, which performed (2.05)% and (0.52)%, respectively. The Fund also outperformed a custom blended index, which is a combination of the Bloomberg Barclays U.S. Aggregate Bond Index (60%) and the MSCI ACWI® Index (40%), which returned (1.29)% for the same period. The Fund, relative to the blended benchmark, outperformed due to a higher weight to equities than the benchmark for most of the year. At the start of the fiscal year, the Fund’s investments in exchange-traded funds (ETFs) that invest in primarily equity securities represented 67% of its portfolio. This equity allocation was gradually increased to 85%, where it peaked at the end of Q2, before falling back to 80% where it ended the fiscal year. Within equities, international equities peaked at 17% in April and were sold in June, avoiding most of the losses that occurred particularly in Emerging Markets. Within fixed income, the duration of the holdings of the Fund’s investments in ETFs that invested in fixed income was in line with the index exposure. Gold was not held in the fiscal period. The PM team believes that the next 12-month period could be a good year for U.S. large, mid and small cap stocks if economic growth holds up or accelerates. However, the PM team believes that a cautious stance on Emerging Markets is still warranted as the U.S.-China trade war is likely to continue.

Growth of a $100,000 investment from 12/31/15 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top performers | The largest contributors to performance were the ETFs that held large cap U.S. equities. The two S&P 500 ETFs, SPY and IVV represented an average 50% weight over the year and as such the largest asset class exposure.

Underperformers | U.S. small and mid-cap ETFs (IJR, MDY, IJH) at an average 10% and 12% holding respectively were mild detractors due to underperformance later in the fiscal year. The Fund moved to increasing mid- and small-cap equity ETFs as it favored more domestically oriented companies. The largest detractors were Emerging Markets ETFs (IEMG) which entered a bear market apparently due to trade risks and a strong USD, followed by fixed income ETFs (AGG) which was impacted by higher yields. Japan (IJH) and Europe (EWJ) ETFs were very mild detractors.

| 4 |

Performance Summary and Commentary

| Carillon Eagle Growth & Income Fund |

Portfolio Managers | Edmund Cowart, CFA®, David Blount, CFA®, CPA, and Harald Hvideberg, CFA®, are Co-Portfolio Managers of the Eagle Growth & Income Fund (the “Fund”). Messrs. Cowart and Blount have been responsible for the day-to-day management of the Fund’s investment portfolio since June 2011 and Mr. Hvideberg since August 2014.

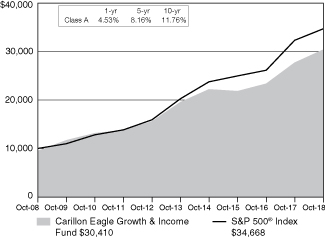

Performance discussion | For the fiscal year ended October 31, 2018, the Fund’s Class A shares returned 9.76% (excluding front-end sales charges of 4.75%), outperforming its benchmark index, the S&P 500® Index, which returned 7.35%. The Fund’s Portfolio Management team (“PM team”) was satisfied with performance compared to the benchmark given the market environment. Positive stock selection in the health care, information technology and industrials sectors contributed positively to the Fund’s outperformance relative to the benchmark. Meanwhile, investments in the materials and consumer discretionary sectors, as well as a small cash position, all were detractors from performance. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class C, Class I, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an

investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top performers | Microsoft Corp., developer and marketer of software and hardware services, appreciated as the company continued to gain market share in its cloud business. Azure, Microsoft’s cloud based business, continued to see higher utilization levels with additional margin expansion. The PM team believes this growth will continue and remains invested in the company. Apple Inc., designer, manufacturer, and marketer of mobile communication and media devices, personal computing products, and portable digital music players, traded higher as the company launched its next generation of iPhones. The PM team believes that built-up demand will lead to a successful launch and increase unit sales growth. The Fund continues to hold this position. Regal Entertainment Group (Class A), an operator of multi-screen theaters, traded higher after the announcement that it was being acquired by a competitor, Cineworld. The acquisition appeared to be a commanding premium so the Fund sold the position prior to the deal closing in early 2018. Cisco Systems, a manufacturer of networking products and services, returned to revenue growth after facing headwinds during its transition to a recurring-revenue model. The company also announced it would bring back all foreign cash and return it to shareholders, thus increasing its dividend and announcing a share buyback. The PM team likes the growth outlook for the company and continues to own the stock. Management at Pfizer, a pharmaceutical products manufacturer, provided bullish commentary around the company’s long term growth prospects, and expressed comfort with the Trump Administration’s efforts to reshape the country’s drug pricing and reimbursement landscape. The PM team believes the stock also benefited from a sector rotation into health care, with favorable Fund flows into the pharmaceutical industry in particular. The Fund continues to hold the position.

Underperformers | DowDuPont, a global chemicals company, traded lower due to what the PM team believed were continued questions surrounding upcoming corporate actions. The company is expected to split into three units next year. The PM team views the split as positive and believes the market has yet to price the change into the stock. The Fund continues to hold the stock. Management at Carnival Corp., a cruise ship operator, issued forward looking guidance that disappointed many investors. Last year’s hurricane season appears to have softened demand, especially in the affected Eastern Caribbean. The PM team believes the weakness is temporary and continues to own the stock. Management at 3M, a global manufacturer, reduced its growth guidance as well as earnings expectations. The company appears to have signaled a deceleration in organic growth tied to auto aftermarket, oral care and slowing in electronics markets. The company had been growing faster than peers but the deceleration puts it in a weaker position relative to peers. The PM team believes this trend is likely to reverse and the Fund continues to hold the stock. PNC Financial Services Group, Inc, a large financial institution, underperformed apparently as a result of bearish sentiment surrounding financials given the recent trade war fears. Moreover, the bank noted it has become slightly more conservative in its underwriting, which will in turn modestly impact loan growth. The PM team believes the conservative guidance is appropriate in the current economic environment and the Fund continues to own the stock. AT&T, a telecommunications and digital entertainment services provider, reported weakness in its traditional video segment. Cord-cutting accelerated as customers continue to drop or switch to lower margin products. The stock also traded lower following the turbulence surrounding the proposed acquisition of Time Warner. The PM team believes the valuation remains attractive and the Fund continues to own the stock.

| 5 |

Performance Summary and Commentary

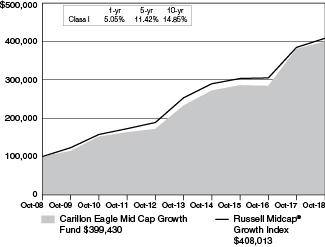

| Carillon Eagle Mid Cap Growth Fund |

Portfolio Managers | Bert L. Boksen, CFA®, and Eric Mintz, CFA®, are Co-Portfolio Managers of the Eagle Mid Cap Growth Fund (the “Fund”). Mr. Boksen has been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in 1998. Mr. Mintz has been a Co-Portfolio Manager of the Fund since March 2011, and had previously served as Assistant Portfolio Manager since 2008. Christopher Sassouni, D.M.D., has served as Assistant Portfolio Manager of the Fund since January 2006.

Performance discussion | For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned 5.05%, underperforming its benchmark index, the Russell Midcap® Growth Index, which returned 6.14%. The Fund’s underperformance relative to the benchmark was driven by weak relative returns within the consumer staples and discretionary sectors which lagged their benchmark counterparts during the reporting period. The Fund did generate solid absolute as well as relative returns within the health care and information technology sectors, offsetting a substantial portion of the Fund’s broader underperformance during the reporting period. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore, its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder

transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Underperformers | Coherent makes laser systems primarily used for industrial applications. Following success in 2017 driven by a new laser integral to producing organic light-emitting diode (OLED) display, shares fell after an underwhelming initial launch, relative to expectations, of Apple’s iPhone X early in the period. Despite the near-term setback, the Portfolio Management team (“PM team”) believes the OLED market will rebound in 2020 and Coherent is oversold at current levels. Veoneer develops and produces automotive safety components. While the firm’s investments in process enhancements are expected to improve longer-term capabilities, the PM team believes that the combination of the near-term costs with softening auto production volumes has weighed on margins and subsequently the stock during the reporting period. Microchip Technology is a microcontroller semiconductor company. The firm encountered what appeared to be acquisition-related growing pains during the period, which have proven challenging in the context of a potential slowdown in the semiconductor industry. The PM team believes the firm possesses a solid track record of effectively integrating and leveraging strategic acquisitions and is keeping a close eye on signs of deterioration within the semiconductor end markets. Fortune Brands Home & Security is a home and security consumer products company. Shares waned as signs of growth moderation in the housing end market, coupled with some weather-related headwinds, appeared to weigh on results within the firm’s building products segment during the period. The PM team maintains a cautiously optimistic view of management’s ability to navigate the firm’s near-term difficulties, through repositioning of some of its existing business segments while continuing to pursue strategic acquisitions to enhance growth prospects going forward. Ameriprise Financial saw what appeared to be the combination of significant market volatility, coupled with outflows from its asset management arm Columbia Threadneedle subsequently lead shares lower during the period. Near-term difficulties aside, the PM team expects Ameriprise’s wealth-management segment to perform well and believes the firm also appears poised to benefit from a rising-interest-rate environment. The Fund continues to hold each of the securities noted above as “under performers.”

Top Performers | Clothing retailer Burlington Stores saw shares climb over the course of the period, benefitting from solid positioning within the strong off-price retail channel. Advanced Micro Devices saw increased adoption in datacenter markets through the application of its graphics-processing units used in artificial intelligence, machine learning and other heavy-duty computing. Square, a mobile-payment service, is experiencing rapid growth due to its easy-to-use hardware and strong capabilities in software. ABIOMED, which sells cardiac medical devices, generated strong results during the period, while possessing a strong pipeline of new technologies in addition to implementing enhancements to its existing platforms. Shares of Illumina, which manufactures genetic sequencing equipment and systems, posted strong results during the period in addition to raising guidance. Demand for its high-end sequencers appears to have continued to remain robust. The Fund continues to hold each of the securities noted above as “top performers.”

| 6 |

Performance Summary and Commentary

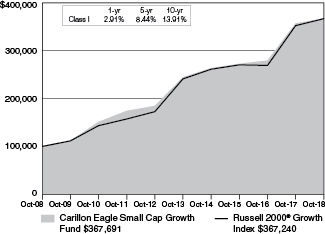

| Carillon Eagle Small Cap Growth Fund |

Portfolio Managers | Bert L. Boksen, CFA®, and Eric Mintz, CFA®, are Co-Portfolio Managers of the Eagle Small Cap Growth Fund (the “Fund”). Mr. Boksen has been responsible for the day-to-day management of the Fund’s investment portfolio since August 1995 and Mr. Mintz since March 2011. Christopher Sassouni, D.M.D., has served as Assistant Portfolio Manager of the Fund since March 2015.

Performance discussion | For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned 2.91%, underperforming its benchmark index, the Russell 2000® Growth Index, which returned 4.13%. The Fund’s underperformance relative to the benchmark was driven by weak relative returns within the information technology and, to a lesser extent, financials sectors which trailed their benchmark counterparts during the reporting period. A bright spot for the Fund was the health care sector which generated very strong absolute and relative returns, offsetting a substantial portion of the Fund’s broader underperformance during the reporting period. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the

performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Under performers | Coherent makes laser systems primarily used for industrial applications. Following success in 2017 driven by a new laser integral to producing organic light-emitting diode (OLED) displays, shares fell after an underwhelming initial launch, relative to expectations, of Apple’s iPhone X early in the period. Despite the near-term setback, the Portfolio Management team (“PM team”) believes the OLED market will rebound in 2020 and that Coherent is oversold at current levels. Universal Electronics, a manufacturer of voice-activated remote controls, provided weak guidance during the period which reflected a significant cutback in orders from Comcast (a 20 percent customer), as well as continued delays in the start-up of multiple new programs for advanced remote controls. Long-delayed programs are now starting to ramp and the PM team believes that 2018 is shaping up as a strong revenue year with margins improving sequentially. Construction materials provider Summit Materials saw shares wane as the firm missed consensus estimates and reduced guidance towards the end of the period. The decline appeared to be attributed in part to a weaker-than-expected pricing environment within its cement segment as well as weather-related delays in projects which tempered cement volumes. The PM team remains constructive on the name at current levels given the reset in investor expectations, and they believe that going forward Summit is also poised to benefit from the easing “year-over-year comparisons. Camping World Holdings, Inc. is a leading retailer of recreational vehicles (RVs) and outdoor lifestyle products across the U.S. Investor concerns arose as moderating growth in the firm’s core RV segment, coupled with Camping World’s recent acquisition of Gander Mountain appear to have pressured the stock during the period. While disappointing in the near-term, the PM team maintains a cautiously optimistic view on the name given Camping World’s favorable alignment with consumers’ increasing preference for experiential-related purchases. Cognex sells “machine vision” systems used to optimize manufacturing processes, which the PM team believes to be a secular growth story. After a very strong run in 2017, Cognex stock performed poorly in 2018 due to what the PM team believes is the cyclicality of a large customer in the consumer electronics segment, as well as geopolitical concerns (tariffs) affecting end demand in China. The PM team continues to like the company’s technology and competitive position and believe that the consumer electronics segment may rebound in 2019. The Fund continues to hold each of the securities noted above as “underperformers.”

Top performers | Sarepta Therapeutics develops therapies used to treat rare neuromuscular diseases. Preliminary results from one of the firm’s clinical trials assessing a Duchenne Muscular Dystrophy (DMD) drug candidate exceeded expectations, which sent shares of Sarepta higher. Planet Fitness operates fitness centers across the United States. The PM team believes that firm’s strong value proposition via clean and well maintained fitness centers providing members with “judgment-free zones” at an affordable price has generated strong membership growth, which has helped drive shares of Planet Fitness higher during the period. Teladoc Health is a telemedicine provider that offers remote physician access to patients. The PM team believes that Teladoc is benefitting from an increasing awareness of its compelling value proposition, while leveraging strategic acquisitions to expand its customer base and further drive growth. Off-price retailer Ollie’s Bargain Outlet Holdings performed well as the PM team believes that its business model demonstrated resiliency to online competition, while management has continued to successfully execute the firm’s prudent growth strategy during the period. SAGE Therapeutics, which develops therapies used to treat rare central-nervous system disorders, saw shares rise during the period after announcing positive trial results for drugs aimed at treating postpartum depression and major depressive disorder. The Fund continues to hold each of the securities noted above as “top performers.”

| 7 |

Performance Summary and Commentary

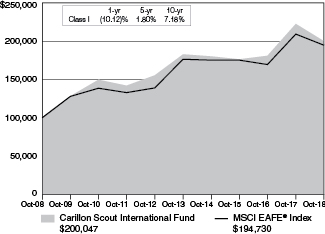

| Carillon Scout International Fund |

Portfolio Managers | Michael D. Stack, CFA®, is Lead Portfolio Manager, and Angel M. Lupercio is Co-Portfolio Manager of the Scout International Fund (the “Fund”). Messrs. Stack and Lupercio have been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in 2017. Mr. Stack was Assistant Portfolio Manager of the Fund’s predecessor from February 2006 through December 2007; Co-Portfolio Manager of the Fund’s predecessor from April 2012 through March 30, 2014; Co-Lead Portfolio Manager of the Fund’s predecessor from March 31, 2014 through December 2014; and Lead Portfolio Manager of the Fund’s predecessor from 2015 to 2017. Mr. Lupercio served as Co-Portfolio Manager of the Fund’s predecessor from 2015 to 2017.

Performance discussion | For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned (10.12)%, underperforming its benchmark index, the MSCI-EAFE Index, which returned (6.85)%. The Fund’s performance, relative to the benchmark, was negative primarily due to stock selection. Stock selection within the financials sector was strong, but stock selection within the industrials and information technology sectors was weak. Country stock selection was strongest in Australia and the Netherlands, while stock selection in Japan and the United Kingdom detracted from performance. An overweight in the energy and consumer staples sectors as well as an underweight in the consumer discretionary sector slightly mitigated the underperformance of those sectors. Exposure to Mexico and Peru positively contributed to performance, while exposure to China and Taiwan detracted from performance. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore, its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are

calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Underperformers | AAC Holdings, Inc., a Chinese miniaturized technologies manufacturer company which is a key supplier of acoustic and haptic components used in Apple products, underperformed due to lower projected demand for the iPhone. Over the long run, the Portfolio Management team (“PM team”) believes that AAC is likely to benefit from an increasing dollar content in smartphones as phone makers migrate to acoustic, radio frequency and haptic components with higher capability. The Fund continues to hold this security. Banco Bilbao Vizcaya Argentaria, S.A. (BBVA), is the largest financial institution in Spain and Mexico with substantial business across the Americas and Turkey. BBVA slumped as the European economic outlook became less certain and the value of the Turkish lira and Argentine peso fell. The PM team believes that market concerns surrounding the Turkish financial system appear to be overblown and BBVA’s diversification across regions will offset risks in individual emerging markets. The Fund continues to hold this security. Adecco Group AG, a generalist human resource and employment services company, underperformed as new staffing technology appeared to create headwinds and the company faced negative outlooks in the European staffing markets. The Fund continues to hold this stock as the company is trading on a FCF yield of 10% and at a discount to the median of global service providers. The PM team believes that BNP Paribas S.A., a global financial service company based in France, underperformed under an uncertain European economic outlook and concerns surrounding the company’s exposure to political and financial stresses in Italy and Turkey. The PM team maintains that the global diversification and growth prospects of BNP’s services remain positive. The Fund continues to hold the stock. Continental AG, a German automobile parts and service provider, underperformed after the company lowered full-year guidance for the second time this year. The PM team believes that several company-specific issues continued to plague the parts supplier and that announced changes following a structural review were less than anticipated. The Fund still holds this stock.

Top performers | CSL Limited is an Australian biotechnology company specializing in pharmaceuticals and diagnostic products derived from human plasma. The PM team believes that CSL benefited from strong sales of the company’s flu vaccines during the past year’s flu season. The company’s core immunoglobulin and hemophilia franchises appear to be showing stable growth due to new drug launches along with greater usage of chronic therapies and earlier diagnosis. The Fund continues to hold this position. Gemalto N.V. is a Dutch software and services company. News of an expected tender offer from Thales S.A. drove Gemalto’s stock price upward. The PM team capitalized and sold the holding. The PM team believes that Astellas Pharma Inc., one of the largest Japanese prescription drug companies, has benefited from the company’s main drug Xtandi’s approval as treatment for non-metastatic prostate cancer. The Fund continues to hold this position. BHP Billiton Limited, a metals and mining industry company, outperformed as it continued to divest oil holdings and iron ore prices surged in October. The Fund continues to hold this security. Credicorp, Ltd., a financials service holding company operating in Peru, outperformed as political uncertainty declined after Peru’s President Pedro Pablo Kuczynski resigned. The PM team believes that positive Peruvian economic outlook will continue to drive the stock. The Fund still holds this stock.

| 8 |

Performance Summary and Commentary

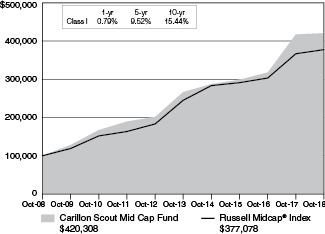

| Carillon Scout Mid Cap Fund |

Portfolio Managers | G. Patrick Dunkerley, CFA® is the Lead Portfolio Manager, and Derek M. Smashey, CFA®, John A. Indellicate II, CFA® and Jason J. Vortruba, CFA®, are Co-Portfolio Managers of the Scout Mid Cap Fund (the “Fund”). Messrs. Dunkerley, Smashey, Indelliate and Vortruba have been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in 2017. Mr. Dunkerley served as Lead Portfolio Manager of the Fund’s predecessor and Mr. Smashey served as Co-Portfolio Manager of the Fund’s predecessor from its inception in 2006 to 2017. Messrs. Indellicate and Votruba served as Co-Portfolio Managers of the Fund’s predecessor from 2011 and 2013, respectively, to 2017.

Performance discussion | For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned 0.79%, underperforming its benchmark index, the Russell Midcap® Index, which returned 2.79%. The Fund’s performance, relative to the benchmark, underperformed due to both sector allocation and stock selection. Positive stock selection in the health care sector, specifically the health care equipment and supplies industry, partially offset negative selection in the information technology, financials, consumer discretionary, and energy sectors. Underweight in the real estate sector benefited the Fund. The Fund’s positioning in the financials and information technology sectors were a slight drag on performance. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder

transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Under performers | Nektar Therapeutics, a biopharmaceutical company focused on cancer, autoimmune diseases and chronic pain, suffered upon disappointing preliminary clinical trial data on an experimental cancer drug. The Portfolio Management team (“PM team”) has historically believed that the expected FDA approval and release of a non-addictive opioid back pain reliever remains a potential growth driver for this company. The Fund continues to hold the security but the PM team is monitoring the FDA approval process closely. The PM team believes that Newfield Exploration Company, an oil and gas exploration and development company, failed to rally with oil prices in the third quarter due to ongoing concern about their pace of oil production growth versus natural gas. The PM team believes these concerns are short-sighted. The Fund continues to hold this stock. Thor Industries, Inc. produces and sells recreational vehicles. The PM team believes that the company underperformed as fears regarding excess recreational vehicle inventory and rising interest rates mount. The Fund still holds this security but the PM team is monitoring inventory levels as well as the Federal Reserve’s interest rate policy which could hinder Thor’s business. SVB Financial Group runs Silicon Valley Bank, focused on serving niche technology and life science industry growth companies. This holding underperformed late in the fiscal year after missing third quarter net interest income estimates. The PM team believes that SVB Financial Group’s dominant position in niche markets (tech and life sciences) offers unique growth opportunities. The Fund still holds this security. Albemarle Corporation, a specialty chemical production company that includes the production of low-cost lithium, underperformed apparently under expectations that the company will lose market share and lithium will be oversupplied after a lithium production competitor resolved a four-year mining dispute allowing them to increase production. The PM team expects ALB to benefit as the transportation industry moves toward battery electric vehicles/plug-in hybrid electric vehicles (BEV/PHEVs) and grid-tied stationary energy storage. The Fund still holds this security.

Top performers | ABIOMED, Inc., a medical device company specializing in cardiovascular pumps, outperformed as it maintained a near monopoly market position in small cardiovascular pumps. The Fund continues to hold this security. Advanced Micro Devices, Inc. (AMD) designs and markets semiconductor products including central processing units (CPUs) and graphics processing units (GPUs). AMD partnered with Taiwan Semiconductor Manufacturing to produce advanced semiconductors that are expected to compete effectively with market leader Intel for the first time in many years. The Fund sold AMD after a strong run in the name pushed valuations higher. Andeavor refines and markets petroleum products. During the second quarter of 2018, Andeavor benefited from a merger offered at a significant premium from Marathon Petroleum Corp. The Fund continues to hold the Marathon Petroleum shares received from this acquisition. Molina Healthcare provides government funded healthcare insurance through Medicaid, Medicare, and state insurance marketplaces. The PM team believes that Molina benefited from a strong cost-cutting initiative instituted by its new management team. The Fund continues to hold this security. The PM team believes that American Eagle Outfitters, Inc., a mall-based clothing retailer, outperformed due, in part, to the growth in market share gained by Aerie, the company’s lingerie brand. The Fund still holds this security.

| 9 |

Performance Summary and Commentary

| Carillon Scout Small Cap Fund |

Portfolio Managers | James R. McBride, CFA®, is Lead Portfolio Manager, and Timothy L. Miller, CFA® is Co-Portfolio Manager of the Scout Small Cap Fund (the “Fund”). Messrs. McBride and Miller have been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in 2017. Mr. McBride was Co-Portfolio Manager of the Fund’s predecessor from 2010 through 2015 and served as Lead Portfolio Manager of the Fund’s predecessor from 2015 to 2017. Mr. Miller served as Co-Portfolio Manager of the Fund’s predecessor from 2013 to 2017.

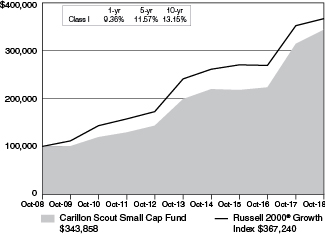

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class I shares returned 9.36%, outperforming its benchmark index, the Russell 2000® Growth Index, which returned 4.13%. The Fund outperformed largely due to positive stock selection, especially the health care and industrials sectors. Within the health care sector, the health care providers and services industry stock selection, which was also positioned largely overweight, was a major contributor to the sector’s relative success. Stock selection within the consumer discretionary and information technology sectors tempered returns. The underweight positioning in the materials sector worked well for the portfolio, while the underweighting in communication services and consumer staples was a drag on performance. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell

shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top performers | Insperity, Inc. provides an array of human resources and business solutions designed to help improve business performance. The Fund’s Portfolio Management team (“PM team”) believes that the holding outperformed as healthy client retention and new sales positioned the company to increase guidance. The PM team believes that good worksite employee (“WSE”) growth as well as gross profit per WSE/month also drove the stock price upward. The Fund continues to hold this security. BioTelemetry, Inc., a medical monitoring and management company, saw strong second quarter results, increased guidance, and well-executed integration synergies from the LifeWatch acquisition that lifted the stock. The Fund continues to hold this security. The Trade Desk, Inc., a global technology company, announced better-than-expected earnings and raised guidance during the third quarter. In addition, Trade Desk has started to experience success in the growth of digital TV ad budgets as well as expectations for new product rollouts. The Fund still holds the security. Molina Healthcare, Inc. provides government-funded healthcare insurance through Medicaid, Medicare, and state insurance marketplaces. The company reported a strong third quarter and increased guidance. The new management team has continued to focus on improved efficiencies and margin performance. The Fund still holds this security. HealthEquity, Inc. provides health savings accounts (HSA) and related services. The holding’s price rose steadily throughout the year, which the PM team believes was driven by growth in custodial assets and higher interest rates. The Fund still holds this security.

Underperformers | The PM team believes that Thor Industries, Inc., a leading manufacturer of motorhomes and towable recreational vehicles (RVs), weakened over concerns about slowing unit growth in the RV industry, heavier dealer inventories, and bad weather that slowed dealer foot traffic during the spring selling season. PM team believes these inventory issues will prove temporary and remains positive on Thor’s future growth prospects. The Fund still holds this security. Installed Building Products, Inc. installs residential insulation. The PM team believes that the company saw stock prices fall due to increased fuel costs, worker compensation, and medical expenses resulting in weaker margins. It also faced headwinds from slower housing starts as rising interest rates impacted housing demand. However revenue results have been positive and the company has continued to diversify its revenue stream by acquiring firms engaged in the installation of other home related items. The Fund still owns this security. Camping World Holdings, Inc. runs RV dealerships. During the first quarter, the stock lagged as the company was unable to file a timely 10-K due to financial reporting issues which have since been corrected. Additionally, the company trailed estimates furthering concerns regarding higher inventory and slowing unit growth within the recreational vehicle industry. Despite the relative underperformance, the PM team believes secular trends point to growth in the RV industry and should benefit the stock. The Fund still holds this security. WageWorks, Inc. is a leading provider and administrator of consumer directed health and commuter benefit programs including Health Savings (HSA) and Flexible Spending (FSA) accounts. The PM team believes that the stock price dropped sharply during the first quarter due to delays in reporting fourth quarter 2017 earnings and filing the company’s 10-K due to an internal financial reporting issue. Looking ahead, the PM team believes WageWorks is positioned to benefit from an increase in the amount of consumer directed plans. The Fund continues to hold this security. Cutera, Inc. develops and manufactures aesthetic laser systems. The PM team believes that the stock underperformed, missing average gross margin estimates, as company management awaited operational and infrastructure improvements to take effect. On the positive side, it appears that Cutera has seen favorable adoption trends with their TruSculpt ID product which, the PM team believes, could provide a strong tailwind for organic growth. The Fund continues to hold this security.

| 10 |

Performance Summary and Commentary

| Carillon Reams Core Bond Fund |

Portfolio Managers | Mark M. Egan, CFA®, is Lead Portfolio Manager, and Thomas M. Fink, CFA®, Todd C. Thompson, CFA®, Stephen T. Vincent, CFA®, Clark W. Holland, CFA® and Jason Hoyer, CFA® are Co-Portfolio Managers of the Reams Core Bond Fund (the “Fund”). Messrs. Egan, Fink, Thompson, Vincent and Holland have been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in 2017. Mr. Hoyer has been responsible for the day-to-day management of the Fund’s investment portfolio since April 2018. Mr. Egan served as the Lead Portfolio Manager of the Fund’s predecessor and Messrs. Fink and Thompson served as Co-Portfolio Managers of the Fund’s predecessor from its inception in 2001 to 2017. Messrs. Vincent and Holland served as Co-Portfolio Managers of the Fund’s predecessor from 2009 and 2014, respectively, to 2017.

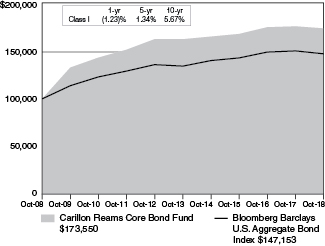

Performance discussion | For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned (1.23)%, outperforming its benchmark index, the Bloomberg Barclays U.S. Aggregate Bond Index, which returned (2.05)%. The primary contributor to the Fund’s performance, relative to the benchmark, was the Fund’s lower-than-benchmark duration positioning. Security selection within the investment-grade corporate sector also contributed to relative performance due to the Fund’s overweight to shorter-maturity corporate bonds. The main detractor from relative performance was security selection within the mortgage-backed securities sector. The Fund’s lack of exposure to the Government-Related sector, which outperformed duration-matched U.S. Treasuries, also detracted from relative performance. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense

reimbursements or recoupments, which affect performance, is included in the Fund’s Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top performers | Early in the fiscal year, the portfolio maintained overall interest rate exposure below that of the benchmark. This appeared to benefit the Fund on a relative basis as interest rates rose. As of the date hereof the Fund’s interest rate exposure is similar to that of the benchmark. Two corporate bonds backed by aircraft leases of Delta Airlines, an air transportation provider, contributed to performance due to their higher ratings and shorter maturities as these more defensive positions outperformed the broadly underperforming corporate sector. The Fund continues to hold these positions as the Fund’s Portfolio Management team (“PM team”) continues to prefer a defensive posture in the investment grade corporate sector. Various corporate bonds issued by AT&T, Inc., a company that, through its subsidiaries provides wireline and wireless phone and data communications, internet, and other telecommunications services, outperformed other holdings during the period. The shorter maturity holdings appeared to benefit the Fund due to their defensive characteristics. The Fund continues to hold these positions. The Fund also benefited from several positions in JP Morgan, a provider of global financial services and retail banking. The Fund continues to hold positions in short-maturity bonds issued by JP Morgan. The Commercial Mortgage Backed Security, MSBAM 2015-C26 A3, is a conduit, or trust, of commercial loans originated by Bank of America and Morgan Stanley in 2015. This CMBS contributed to performance as this sector broadly outperformed. The Fund continues to hold this security as the PM team believes that the credit protection and relative spread remains attractive.

Underperformers | Several bonds issued by American Express, a global payments and travel company, underperformed as the PM team believes that a flattening yield curve hurt the outlook for the company’s profitability in the future. The Fund continues to hold these bonds as the PM team believes the stability of the business and cash flow potential will not be impacted in the short term by the flat yield curve. The PM team believes that the bonds issued by Wells Fargo, a diversified financial services company, underperformed as the firm underwent scrutiny regarding its client treatment while also facing profitability concerns with a flat yield curve. The PM team maintains its holdings in these positions as the team is comfortable with asset protections for the short maturity holdings. Fannie Mae Conventional 30 year 3.0% coupon Mortgages underperformed relative to the benchmark as rates rose leading to the duration extension of the underlying mortgage loans. This security remains a holding in the Fund although the Fund is underweight to Agency MBS versus the benchmark. A bond issued by AIG, an international insurance organization, AIG 6.4 12/15/20 underperformed modestly. The Fund continues to hold this position. The PM team believes that a bond issued by Bank of America, a provider of banking, investing, asset management, and other financial services, BAC 3.5 4/19/26 underperformed due to the flat yield curve. The Fund continues to hold this position as the PM team believes the stability of the business and cash flow potential will not be impacted in the short term by the flat yield curve.

| 11 |

Performance Summary and Commentary

| Carillon Reams Core Plus Bond Fund |

Portfolio Managers | Mark M. Egan, CFA®, is Lead Portfolio Manager, and Thomas M. Fink, CFA®, Todd C. Thompson, CFA®, Stephen T. Vincent, CFA®, Clark W. Holland, CFA® and Jason Hoyer, CFA® are Co- Portfolio Managers of the Reams Core Plus Bond Fund (the “Fund”). Messrs. Egan, Fink, Thompson, Vincent and Holland have been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in 2017. Mr. Hoyer has been responsible for the day-to-day management of the Fund’s investment portfolio since April 2018. Mr. Egan served as the Lead Portfolio Manager of the Fund’s predecessor from its inception in 1996 or from 2000, 2001, 2009 and 2014, respectively, to 2017.

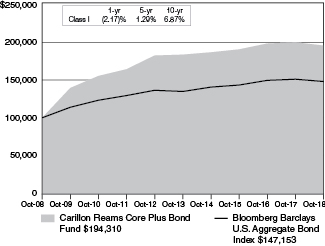

Performance Discussion | For the fiscal year ended October 31, 2018, the Fund’s Class I shares returned (2.17)%, underperforming its benchmark index, the Bloomberg Barclays U.S. Aggregate Bond Index, which returned (2.05)%. The main detractor from the Fund’s performance, relative to the benchmark, was security selection within the mortgage-backed securities sector. The Fund’s lack of exposure to the Government-Related sector, which outperformed duration-matched U.S. Treasuries, also detracted from relative performance. Security selection within the investment-grade corporate sector contributed to relative performance due to the Fund’s overweight to shorter-maturity corporate bonds. Exposure to high yield corporate bonds also contributed to relative performance, as this sector outperformed duration-matched U.S. Treasuries. The Fund’s lower-than-benchmark duration positioning also contributed to relative performance. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $100,000 investment from 10/31/08 to 10/31/18 (a)

(a) The Fund’s values and returns reflect fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2018, the Fund also offered Class A, Class C, Class R-3, Class R-5, Class R-6, and Class Y shares. The value of an investment in other share classes will differ due to each class’s respective sales charges (as applicable) and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s

Prospectus dated March 1, 2018, and elsewhere in this report. Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Underperformers | Several bonds issued by American Express, a global payments and travel company, underperformed as the Fund’s Portfolio Management team (“PM team”) believes that a flattening yield curve hurt the outlook for the company’s profitability in the future. The Fund continues to hold these bonds as the PM team believes the stability of the business and cash flow potential will not be impacted in the short term by the flat yield curve. The PM team believes that bonds issued by Wells Fargo, a diversified financial services company, underperformed as the firm underwent scrutiny regarding its client treatment while also facing profitability concerns with a flat yield curve. The PM team maintains its holdings in these positions as the team is comfortable with asset protections for the short maturity holdings. A bond issued by AIG, an international insurance organization, AIG 6.4 12/15/20 underperformed modestly. The Fund continues to hold this position. The PM team believes that a bond issued by Bank of America, a provider of banking, investing, asset management, and other financial services, BAC 3.5 4/19/26 underperformed due to the flat yield curve. The Fund continues to hold this position as the PM team believes the stability of the business and cash flow potential will not be impacted in the short term by the flat yield curve. Fannie Mae Conventional 30 year 3.0% coupon Mortgages underperformed relative to the benchmark as rates rose leading to the duration extension of the underlying mortgage loans. This security remains a holding in the Fund although the Fund is underweight to Agency MBS versus the benchmark.

Top performers | Early in the fiscal year, the portfolio maintained overall interest rate exposure below that of the benchmark. This appeared to benefit the Fund on a relative basis as interest rates rose. As of the date hereof the Fund’s interest rate exposure is similar to that of the benchmark. Two corporate bonds backed by aircraft leases of Delta Airlines, an air transportation provider, contributed to performance due to their higher ratings and shorter maturities as these more defensive positions outperformed the broadly underperforming corporate sector. The Fund continues to hold these positions as the PM team continues to prefer a defensive posture in the investment grade corporate sector. Various corporate bonds issued by AT&T, Inc., a company that, through its subsidiaries provides wireline and wireless phone and data communications, internet, and other telecommunications services, outperformed other holdings during the period. The shorter maturity holdings appeared to benefit the Fund due to their defensive characteristics. The Fund continues to hold these positions. The Fund also benefited from several positions in JP Morgan, a provider of global financial services and retail banking. The Fund continues to hold positions in short-maturity bonds issued by JP Morgan. The Commercial Mortgage Backed Security, MSBAM 2015-C26 A3, is a conduit, or trust, of commercial loans originated by Bank of America and Morgan Stanley in 2015. This CMBS contributed to performance as this sector broadly outperformed. The Fund continues to hold this security as the PM team believes that the credit protection and relative spread remains attractive. The holding of high yield CDX positively impacted the Fund’s performance during the fiscal year as high yield was the strongest performing sector in the fixed income universe during the fiscal year. The Fund continues to hold positions in high yield CDX.

| 12 |