UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file Number: 811-07470

EAGLE SERIES TRUST

(Exact name of Registrant as Specified in Charter)

880 Carillon Parkway

St. Petersburg, FL 33716

(Address of Principal Executive Office) (Zip Code)

Registrant’s Telephone Number, including Area Code: (727) 567-8143

SUSAN L. WALZER, PRINCIPAL EXECUTIVE OFFICER

880 Carillon Parkway

St. Petersburg, FL 33716

(Name and Address of Agent for Service)

Copy to:

KATHY KRESCH INGBER, ESQ.

K&L Gates, LLP

1601 K Street, NW

Washington, D.C. 20006

Date of fiscal year end: October 31

Date of reporting period: October 31, 2017

| Item 1. | Reports to Shareholders |

EAGLE MUTUAL FUNDS

(now known as Carillon Mutual Funds)

Annual Report

and Investment Performance Review for the

fiscal year ended October 31, 2017

Eagle Capital Appreciation Fund

Eagle Growth & Income Fund

Eagle International Stock Fund

Eagle Investment Grade Bond Fund

Eagle Mid Cap Growth Fund

Eagle Mid Cap Stock Fund

Eagle Small Cap Growth Fund

Eagle Smaller Company Fund

Eagle Tactical Allocation Fund

| ||||

| Go Paperless with eDelivery | visit carillontower.com/eDelivery | For more information, see inside. | ||

Table of Contents

Visit eagleasset.com/eDelivery to receive shareholder communications including prospectuses and fund reports with a service that helps protect the environment:

Environmentally friendly. Go green with eDelivery by reducing the number of trees used to produce paper.

Efficient. Stop waiting on regular mail. Your documents will be sent via email as soon as they are available.

Easy. Download and save files using your home computer with a few clicks of a mouse.

Dear Fellow Shareholders:

I am pleased to present the annual report and investment-performance review of the Eagle Family of Funds for the 12-month period that ended October 31, 2017.

As we head into the last months of 2017, the broad equity market (as measured by the S&P 500 Index) is at or near nominal highs with unusually low volatility while the U.S. Federal Reserve Board has kept interest rates low. Over the last year, it appears to us that markets alternatively have ridden waves of optimism (a new U.S. president perceived to be pro-business and signs of global economic growth) and worry (disasters, both man-made and natural). It has been almost a decade since the financial crisis but this period has not been “normal” and we believe some historical cyclicality trends may re-emerge.

Against this backdrop, we believe that the fund managers’ ability to identify competitive businesses, quality companies and future earnings potential can provide an opportunity to deliver value and help investors achieve their long-term financial goals. We believe that our strategies can provide opportunities to take advantage of these market dynamics.

Our fund managers believe that there remain pockets of longer-term opportunity as global economies continue to improve. We also believe that macroeconomic developments, political uncertainty and the markets’ dynamism may result in increased volatility that could create an environment in which well-seasoned, research-based investment strategies can demonstrate their advantages for long-term investors.

On November 17, 2017, the Eagle Mutual Funds were reorganized into Carillon Series Trust, a Delaware statutory trust. The fund family is now known as Carillon Mutual Funds and the Funds’ names include “Carillon” to help connect them with the Carillon Family of investment managers and funds.

Additionally, we are pleased to report that, on November 17, 2017, Carillon Tower Advisers, Inc. (“Carillon Tower”) acquired Scout Investments, Inc. (“Scout”) and seven series of the Scout Funds, which were advised by Scout, were reorganized into Carillon Series Trust. This acquisition significantly increases Carillon Tower’s mutual fund assets under management and enhances its portfolio management and research staff. Carillon Tower now serves as the investment adviser and Scout serves as the subadviser to each Fund that previously was advised by Scout. Please refer to the “Subsequent events” section of the Notes to the Financial Statements for more information regarding these and other material events or transactions that occurred after the close of the reporting period.

As with all investments, I would remind you that investing in any mutual fund carries certain risks. The principal risk factors for each fund are described at the end of this annual report. Carefully consider the investment objectives, charges and expenses of any fund before you invest. Contact us at 800.421.4184 or carillontower.com or your financial advisor for a prospectus, or summary prospectus, which contains this and other important information about the Eagle Family of Funds. Read the prospectus, or summary prospectus, carefully before you invest or send money.

I hope you will find the portfolio manager commentaries that follow of interest. In uncertain times, I believe that there is little substitute for active research and experience. We are grateful for your continued support of the Eagle Family of Funds.

Sincerely,

J. Cooper Abbott, CFA

President

November 10, 2017

Performance data represented are historical and do not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of Morgan Stanley Capital International, Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

| 1 |

Performance Summary and Commentary

| Eagle Capital Appreciation Fund | ||

Portfolio Managers | David J. Pavan, CFA®, C. Frank Feng, Ph.D., Ed Wagner, CFA®, and Stacey R. Nutt, Ph.D., of ClariVest Asset Management LLC (“ClariVest”), are Co-Portfolio Managers of the Eagle Capital Appreciation Fund (the “Fund”) and have been responsible for the day-to-day management of the Fund’s investment portfolio since 2013.

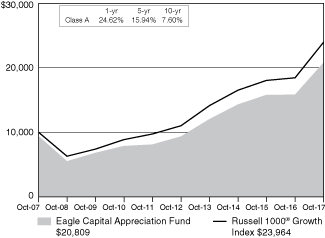

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 30.84% (excluding front-end sales charges of 4.75%), outperforming its benchmark index, the Russell 1000® Growth Index, which returned 29.71%. The Fund’s performance relative to the benchmark was positive, primarily due to stock selection, where selection within the consumer discretionary and information technology sectors was strongest, and was weak within the financials and health care sectors. Sector selection was also positive, where an overweight to information technology and an underweight to real estate contributed to performance, while the Fund lost ground due to an overweight position in the energy and financials sectors. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore, its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 10/31/07 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3, Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/ or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top performers | Apple Inc., designer, manufacturer, and marketer of mobile communication and media devices, personal computing products, and portable digital music players, outperformed other stocks in the information technology sector during the time period leading up to the launch of its new iPhone 8 and iPhone X. Additionally, strong sales of its Mac and Service products drove higher-than-expected earnings. Microsoft Corp. develops and markets software and hardware services. The Fund’s Portfolio Management team (“PM team”) believes that the momentum of the company’s cloud services platform and strong Office 365 sales drove outperformance when compared to other stocks in the information technology sector. Applied Materials, Inc., the worldwide semiconductor equipment manufacturer and services company, appeared to benefit from strong demand for chip equipment and strength in its OLED display segment. NVIDIA Corp., a visual computing company that primarily focuses on 3D graphics, had strong growth in its data center business, core gaming segment, and auto division, which is focused on autonomous car driving technologies. The PM team believes that acceleration of AI (artificial intelligence) technology is driving strong demand for the company’s high-performance processors. Facebook Inc. (Class A), is a social media company. The PM team believes that the company benefitted from continued growth of its active users and was helped by strength in its mobile advertising business. The Fund continues to hold each of the securities noted above as “top performers.”

Underperformers | Dick’s Sporting Goods, Inc. is a sporting goods retailer that operates stores across the United States. The sporting goods retail industry is under duress due to online competition, and the company forecast weaker margins due to a continuing highly competitive environment. The stock was sold from the portfolio. CVS Health Corporation, is an integrated pharmacy health care provider. The PM Team believes the company was hurt by increasing competition and related rumors that Amazon.com will enter the pharmacy business. Prospects that CVS will acquire the health insurer Aetna, also appeared to weigh on the share price. The position is still held by the Fund; however, it was trimmed. EOG Resources, Inc. explores, develops, produces, and markets natural gas and crude oil. The share price declined with falling crude oil prices. The stock was sold from the portfolio. Foot Locker, Inc., the athletic shoe and sportswear retailer, appeared to be hurt by a decline in same store sales as online traffic increased and mall traffic thinned. The company also cited the challenge to capitalize on new trends as consumers are more quickly moving from one trend to another. The stock was sold from the portfolio. FleetCor Technologies, Inc., is a provider of gas cards. The PM team believes performance was hurt by weakness in Brazil and Russia as well as lower gas prices and a weaker U.K. pound. The stock was sold from the portfolio.

| 2 |

Performance Summary and Commentary

| Eagle Growth & Income Fund | ||

Portfolio Managers | Edmund Cowart, CFA®, David Blount, CFA®, CPA, and Harald Hvideberg, CFA®, are Co-Portfolio Managers of the Eagle Growth & Income Fund (the “Fund”). Messrs. Cowart and Blount have been responsible for the day-to-day management of the Fund’s investment portfolio since 2011 and Mr. Hvideberg since 2014.

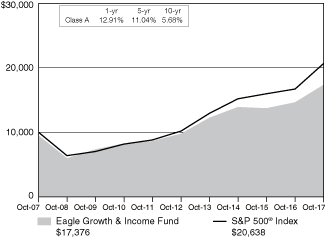

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 18.56% (excluding front-end sales charges of 4.75%), underperforming its benchmark index, the S&P 500® Index, which returned 23.63%. The Fund’s Portfolio Management team (“PM team”) was satisfied with performance compared to the benchmark given the market environment. The underperformance was due, in part, to a dividend-yield headwind. During the fiscal year, dividend paying stocks returned 22.6%, while non-dividend paying stocks returned 29.0%. Furthermore, returns on stocks with above median yields underperformed their below median yield counterparts by 10.76%. This represents a headwind for the strategy. Investments in the consumer discretionary, industrials, and energy sectors contributed positively to performance relative to the benchmark. Meanwhile, investments in the health care sector, as well as an underweight position in information technology and an overweight position in consumer staples, all were detractors from performance. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 10/31/07 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3, Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an

investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Underperformers | Regal Entertainment Group (Class A), an operator of multi-screen theaters, traded lower due to what the PM team believed was fears of technology-based businesses that could disrupt the market. Premium movie-on-demand releases or subscription-based models could disrupt the movie-theater business, but the PM team believes that these fears are unwarranted and the Fund continues to hold the stock. Oil and gas exploration and production company, Occidental Petroleum Corp., experienced weakness after the price of crude oil experienced greater volatility surrounding the Organization of the Petroleum Exporting Countries (OPEC) meeting in November 2016. The company has affirmed its commitment to the dividend and continues to take a long-term approach to developing its rich, unconventional resource base in a measured, efficient manner. The PM team believes the company is in a great position to develop its resources while continuing to drive revenues higher. The Fund continues to hold this position. General Mills Inc., a consumer food manufacturer, traded lower after the company’s management lowered guidance for the year. The company has struggled with falling organic food sales as the PM team believes consumers are switching to smaller, local brands. While the company is working on a cost-savings initiative, weaker margins are still in focus. The PM team believes a new promotion cycle during the upcoming key seasons could boost sales. The Fund continues to hold this position. Nielsen Holdings PLC, a consumer research and consulting services company, continued to experience weakening growth trends in its Buy segment, which is 49% of total company revenue. The PM team believes that growth in developed markets decelerated with sales trends in the broader consumer staples market under pressure and companies reducing/changing their procurement spending patterns. The PM team did not believe that this trend would reverse so the Fund exited its position. Simon Property Group, Inc. an owner of premium retail space, traded lower as online sales continue to gain market share. The PM team believes that these fears are unwarranted and demand for premium retail space will increase as more outdated malls are losing disproportionately greater market share. The Fund continues to hold this position.

Top performers | Apple Inc., designer, manufacturer, and marketer of mobile communication and media devices, personal computing products, and portable digital music players, traded higher as the company prepared for the launch of its next generation of iPhones. The PM team believes that built-up demand will lead to a successful launch and increase unit sales growth. The Fund continues to hold this position. Microsoft Corp., developer and marketer of software and hardware services, appreciated as the company continues to gain market share in its cloud business. Azure, Microsoft’s cloud based business, continued to see higher utilization levels with additional margin expansion. The PM team believes this growth will continue and remains invested in the company. Global investment bank, JPMorgan Chase & Co. traded higher after the outcome of the U.S. presidential election. The PM team believed that the new administration would ease regulatory burdens. The Fed also began raising interest rates, which also enables banks to earn higher fees on loans. The PM team believes these trends will continue and the Fund remains invested in the stock. The PNC Financial Services Group, Inc., another large financial institution, stock also appreciated on many of the same trends. The PM team believes that increased economic-growth expectations will lead to higher loan-growth. The Fund continues to hold this position. Bookings at Carnival Corp., a luxury cruise ship operator, has been at a higher trend than historical levels. Management also increased the company’s dividend by 14.3 percent and authorized an additional $1 billion repurchase program. The PM team believes the company will continue to be competitive and continues to own the stock.

| 3 |

Performance Summary and Commentary

| Eagle International Stock Fund | ||

Portfolio Managers | David V. Vaughn, CFA®, Stacey R. Nutt, Ph.D., Alex Turner, CFA®, and Priyanshu Mutreja, CFA®, are Co-Portfolio Managers of the Eagle International Stock Fund (the “Fund”). Mr. Vaughn and Dr. Nutt have been responsible for the day-to-day management of the Fund’s investment portfolio since 2013. Mr. Turner has been a Co-Portfolio Manager of the Fund since 2015 and previously served as Assistant Portfolio Manager of the Fund since its inception. Mr. Mutreja has been a Co-Portfolio Manager since March 2017 and previously served as Assistant Portfolio Manager of the Fund since 2015.

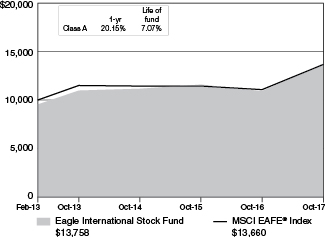

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 26.15% (excluding front-end sales charges of 4.75%), outperforming its benchmark index, the MSCI EAFE® Index which returned 23.44%. The Fund’s performance, relative to the benchmark, was positive primarily due to stock selection, where selection within the information technology and financials sectors was strong, and weak within the health care and consumer discretionary sectors. Stock selection within countries was strongest within Japan and Australia, while investments in the U.K. and Italy detracted from performance. An underweight position in the consumer staples sector and an overweight position in the information technology sector helped performance. Conversely, overweight positions in the telecommunication services and materials sectors tempered returns. An overweight position in Italy and an underweight position in Australia contributed to performance, while overweight positions in Japan and Israel detracted from performance. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore, its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 2/28/13 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3,

Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top performers | Tokyo Electron Ltd. is a Japanese semiconductor equipment manufacturer. The Fund’s Portfolio Management team (“PM team”) believes that rising semiconductor demand driven by the push for artificial intelligence (AI) and cloud computing technologies drove growth. Additionally, increased investment by semiconductor manufacturers, particularly in China, appeared to drive strong earnings. The Fund continues to hold this position. The PM team believes that Mitsubishi UFJ Financial Group, Inc., Japan’s largest financial group, benefitted from the changing macro environment following the U.S. election and the subsequent optimism for eased financial regulations and tax cuts. The Fund still holds this stock. BlueScope Steel Ltd., an Australia-based global steel company, appeared to benefit from strong steel prices and demand primarily driven by China and the U.S. The Fund no longer holds this security. NN Group N.V. is a Netherlands-based insurance company. The PM team believes that the company benefited from underappreciated synergies from its recent acquisition of Delta Lloyd. The Fund still holds this position. The PM team believes that ITOCHU Corp., a Japanese trading firm, saw strong contribution from its metals and minerals segment on the back of higher resource prices. The PM team also believes that improved cash flow and the prospect of additional returns to shareholders helped investor sentiment. The Fund still holds this stock.

Underperformers | Teva Pharmaceutical Industries Ltd., a drug manufacturing company based in Israel, underperformed amid what the PM team believed were concerns about a U.S. investigation into generic drug price collusion. The company’s revenues also fell short of expectations due to pricing pressures. The Fund no longer holds this security. Medipal Holdings Corp., a Japanese pharmaceutical company, appeared to be hurt by a slump in the prescription pharmaceuticals market and lower-than-expected margins. The Fund no longer holds this security. The PM team believed that Toyo Tire & Rubber Co., Ltd., the rubber and chemical goods company based in Japan, underperformed due to pricing competition and higher raw materials costs. The Fund no longer holds this position. Shire PLC, a biotechnology group based in the U.K., was weighed down by drug pricing concerns and weaker sales of one of its key drugs. The Fund continues to hold this stock. Daito Trust Construction Co. Ltd., a construction company in Japan, fell as a slump in orders led investors to believe that tighter rules on apartment loans would impact future earnings. The Fund no longer holds this security.

| 4 |

Performance Summary and Commentary

| Eagle Investment Grade Bond Fund | ||

Portfolio Managers | James C. Camp, CFA®, and Joseph Jackson, CFA®, are Co-Portfolio Managers of the Eagle Investment Grade Bond Fund (the “Fund”) and have been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in 2010.

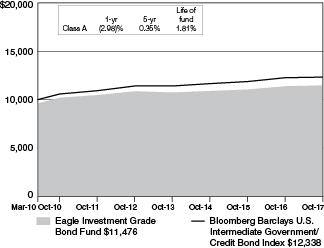

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 0.82% (excluding front-end sales charges of 3.75%), outperforming its benchmark index, the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index, which returned 0.63%. The beginning of the fiscal year was marked by an unprecedented spike in interest rates following the U.S. presidential election. The new administration’s proposed “reflation” policies, including an fiscal stimulus plan and tax reform, added fuel to already rising inflation expectations along with economic data that lead to an unexpected spike in the market. However, following the spike, longer-term interest rates generally stayed range bound for the rest of the period as persistent inflation never materialized nor did any legislative accomplishments. Short-term rates continued to trend higher due to the Federal Reserve Board’s continued efforts to normalize monetary policy through rate hikes and balance sheet tapering. Meanwhile, a strong recovery in corporate earnings along with steady improvement in economic growth in the U.S. and abroad led corporate-credit spreads to tighten during the fiscal year—reaching post-crisis lows in October. The main detractors from the Fund’s performance, relative to the benchmark, were the shorter duration corporate bonds that were held by the Fund. Security selection in agency bonds also hurt the Fund’s performance. The Fund earned positive relative performance largely due to an overweight position to longer duration corporate bonds, which outperformed duration-matched U.S. Treasuries. The Fund’s allocation to asset-backed securities and mortgage-backed securities also added to performance, relative to the benchmark. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 3/1/10 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 3.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3, Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes,

including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carilontower.com.

Top performers | The corporate bond issued by Andeavor, 4.750%, 12/15/23, formerly known as Tesoro Corp., a company which operates refineries and a network of retail and refueling stations, and the corporate bond issued by Valero Energy Partners LP, 4.375%, 12/15/26, a midstream oil and gas master limited partnership that owns, operates, develops, and acquires crude oil and refined petroleum-related assets, contributed to performance due to the recovery in oil prices. The Fund continues to hold these positions as the Fund’s Portfolio Management team (“PM team”) continues to prefer the midstream/downstream segment of the energy sector. The corporate bond issued by BankUnited, Inc., 4.875%, 11/17/25, a bank holding company that, through its subsidiaries, provides a range of financial products and services, including personal, commercial, and business banking, outperformed other holdings during the period. This security appeared to benefit from a general tightening in the financial sector. The Fund continues to hold this position as the PM team believes the credit risk is attractive relative to the rating. The corporate bond issued by Avnet, Inc., 3.750%, 12/01/21, a technology distributor that markets and distributes computer products and semiconductors and provides supply-chain integration, engineering design, and technical services, was a top performer during the period due to what the PM team believes was attractive pricing in the primary market. The PM team continues to feel comfortable owning this security due to the company’s sale of its technology business solutions unit to help fund an acquisition of a components distribution business, which the PM team believes indicates management’s willingness to defend the company’s credit rating. The corporate bond issued by Apollo Management Holding LP, 144A, 4.400%, 05/27/26, a financial services holding company that, through its subsidiaries, invests in private equity, credit, and real estate, as well as manages pension and endowment funds, was a top performer during a period of record fundraising for alternative asset managers. The Fund continues to own this security.

Underperformers | The U.S. Treasury note, 2.250%, 11/15/25, contributed to Fund underperformance relative to the benchmark as it was a longer-dated Treasury held during the unprecedented spike in interest rates following the U.S. presidential election. This security was sold to manage the Fund’s duration and sector characteristics. The following four securities were underperformers due to the timing of their respective holding periods. The corporate bond issued by Home Depot, 2.125%, 09/15/26, a home improvement retailer, and the corporate bond issued by Illinois Tool Works, Inc., 2.650%, 11/15/26, a designer and manufacturer of fasteners, components, equipment, consumable systems, and a variety of specialty products and equipment, were sold because the PM team felt the spreads were fully priced and that there were better relative-value opportunities. The corporate bond issued by Dr. Snapple Group, Inc., 2.550%, 09/15/26, an integrated brand owner, manufacturer, and distributor of non-alcoholic beverages in the U.S., Canada, and Mexico, and the corporate bond issued by Mondelez International, Inc., 144A, 2.000%, 10/28/21, a food and beverage company that manufactures and markets packaged food products, were sold over concerns for the potential of leveraging M&A activity in the mature global consumer sector. The Fund sold out of these four positions toward the beginning of the fiscal year.

| 5 |

Performance Summary and Commentary

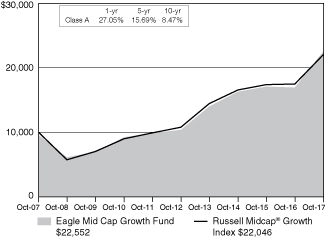

| Eagle Mid Cap Growth Fund | ||

Portfolio Managers | Bert L. Boksen, CFA®, and Eric Mintz, CFA®, are Co-Portfolio Managers of the Eagle Mid Cap Growth Fund (the “Fund”). Mr. Boksen has been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in 1998. Mr. Mintz has been a Co-Portfolio Manager of the Fund since 2011, and had previously served as Assistant Portfolio Manager since 2008. Christopher Sassouni, D.M.D., has served as Assistant Portfolio Manager of the Fund since 2006.

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 33.39% (excluding front-end sales charges of 4.75%), outperforming its benchmark index, the Russell Midcap® Growth Index, which returned 26.25%. The Fund’s outperformance relative to the benchmark was broad-based across multiple sectors, the most notable of which were the consumer discretionary, information technology, and health care sectors, which all generated strong absolute and relative returns during the reporting period. A minimal amount of underperformance was experienced within the real estate and financials sectors which, despite solid absolute returns, were slightly outpaced by those of the benchmark. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore, its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 10/31/07 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3, Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/ or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an

investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top Performers | NVIDIA Corp. manufactures graphics processors used in traditional computers as well as tablets, smartphones and gaming devices. NVIDIA appears to be establishing a favorable position in the fast-developing virtual reality (VR) market while also leveraging its technology in the automotive “infotainment” market. The Fund’s Portfolio Management team (‘PM team”) believes the company remains poised to see increased adoption in datacenter markets through the application of its graphics-processing units used in heavy-duty computing. Align Technology Inc. sells clear “dental-aligner systems” (what used to be called braces). The firm has continued to report solid results: The PM team believes that Align continued to see solid growth in volumes due in part to tailwinds associated with improved products, increased penetration of existing accounts, direct-to-consumer advertising and geographic expansion. Coherent Inc. makes laser-based equipment used in such applications as smartphone and tablet displays. The PM team believes that the firm continues to benefit from strong orders for its product which is used in the fabrication of organic light-emitting diode (OLED) displays that are increasingly used in next-generation smartphones. Further, the PM team believes that the potential for alternative applications of Coherent’s equipment (e.g., in tablets, autos and television) may provide additional upside over the longer term. Micron Technology, Inc. is a key supplier of semiconductor technology products. The firm is benefitting from robust demand for its memory products that, in turn, has kept supply levels in check and translated into strong pricing power. Royal Caribbean Cruises Ltd. has benefited from a healthy pricing and bookings-growth environment while prudently maintaining cost controls to drive earnings growth. The Fund continues to hold each of the securities noted above as “top performers.”

Underperformers | Freeport-McMoRan Inc., a global metals and mining operator, arrived at an unexpected impasse in contract negotiations with the Indonesian government—relating to one of its key copper mines there—which led to production cuts and ultimately pressured the stock. The Fund no longer holds a position in the stock. International Game Technology PLC makes electronic gaming equipment, software and network systems. The PM team believes that results disappointed largely due to poor results in the unpredictable international lottery business. The Fund no longer holds a position in the stock as the PM team believes there are better opportunities in gaming. Brixmor Property Group Inc. owns and operates grocery store-anchored U.S. shopping centers. The PM team believes that the ongoing proliferation of online shopping and retailing has created headwinds for more traditional brick-and-mortar retailers in the current environment, which—in turn—drove an increased occurrence of bankruptcies among Brixmor’s retail-property tenants. The Fund no longer holds a position in the stock. Acuity Brands, Inc., which makes LED lighting fixtures, declined as the firm’s results failed to meet investor expectations due in part to softer-than-expected demand. The PM team continues to believe Acuity is well-aligned with positive trends in non-residential construction as well as from what is expected to be a multibillion-dollar upgrade cycle in general lighting to LED fixtures. The Fund continues to hold this position. Sally Beauty Holdings, Inc. is a retailer of cosmetics, hair- and skin-care goods. Despite ongoing efforts to adjust its strategy through e-commerce enhancements and loyalty programs, Sally Beauty has endured sustained operational and competitive difficulties in recent periods. The Fund no longer holds a position in the stock.

| 6 |

Performance Summary and Commentary

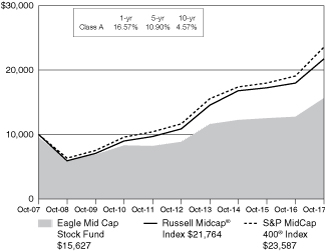

| Eagle Mid Cap Stock Fund | ||

Portfolio Managers | Charles Schwartz, CFA®, Betsy Pecor, CFA®, and Matthew McGeary, CFA®, are Co-Portfolio Managers of the Eagle Mid Cap Stock Fund (the “Fund”) and have been responsible for the day-to-day management of the Fund’s investment portfolio since 2012.

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 22.40% (excluding front-end sales charges of 4.75%), outperforming its primary benchmark index, the Russell Midcap® Index and, underperforming its secondary index, the S&P MidCap 400® Index, which returned 21.09% and 23.48%, respectively. The Fund’s performance, relative to the benchmarks, benefited from strong stock selection in the consumer discretionary and health care sectors. This was partially offset by poor stock selection in the energy, information technology and financial sectors. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 10/31/07 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3, Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top performers | Cognex Corp. is a leader in machine vision systems for manufacturing, inspection, distribution, and logistical automation. The demands for more accurate, faster, and more cost effective work flows (especially in manufacturing and distribution) appears to be a powerful secular driver for the company’s industry leading solutions. Management reported favorable financial results in the quarter and a better than expected outlook. The Fund’s Portfolio Management team (“PM team”) believes that the combination of these solid results and favorable press on the industrial automation space drove the shares higher in the period. The Fund continues to hold this stock. AMETEK Inc., which makes and sells electronic instruments and electromechanical devices used in a variety of markets, reported better-than-expected quarterly results on solid growth following an uncharacteristically soft 2016. The Fund continues to hold this security. Microchip Technology Inc. is a leading provider of microcontrollers, analog, and memory semiconductor solutions to a broad market. The stock performed well as the company reported favorable financial results and outlook in the quarter. Investors also appeared to be pleased that the operating metrics continue to exceed expectations since the Atmel acquisition. In addition, the company is receiving favorable press as its products are at the forefront in addressing industrial, consumer and automotive Iot applications. The Fund continues to hold this position. Panera Bread Company, a fast-casual restaurant and bakery, appreciated apparently as a result of an announcement it was being acquired. The Fund sold its position ahead of the acquisition. Arthur J Gallagher & Co. is one of the world’s largest insurance brokers and the largest third-party property and casualty claims administrator. The stock performed well as the company reported solid financial results and management suggested that the near-term outlook for organic revenue growth is positive. The PM team believes Gallagher is well positioned to benefit from increased insurance pricing driven by property insurance with catastrophe exposed lines as well as continued acquisition activity. The Fund continues to hold this position.

Under performers | Range Resources Corp. is an oil and gas exploration and production company. While the company has a history of solid execution, the PM team believes that investors remain concerned about the large acquisition the company made for assets in northern Louisiana. The Fund sold the shares as the PM team saw better opportunities elsewhere. Spectrum Brands Holdings, Inc. is a consumer products company that operates through five segments: Global Batteries and Appliances, Global Pet Supplies, Home and Garden, Hardware & Home Improvement, and Global Auto Care. The company’s shares underperformed expectations following a second straight quarter of year-over-year declines in sales that the PM team believes were driven by category weakness, retailer inventory management, unfavorable weather, the exit of unprofitable businesses, a voluntary recall, increased competitor promotions, and supply chain disruption from production facility consolidation. While it could take a few quarters for sales to normalize, the PM team continues to like the company’s proven acquisition track record, white space opportunities into new categories and strong margin profile and free cash flow generation. Therefore, the Fund continues to maintain a position in the company. The PM team believes that Hanesbrands, Inc., a leading marketer of basic apparel, underperformed expectations due to volatility in sales, a levered balance sheet, complex acquisition accounting, exposure to mass/department stores, the potential for a higher foreign tax rate and the potential for supply-chain disruption in the event of increased tariffs/import taxes. The Fund exited its position. For many years MEDNAX, Inc. was solely an outsourcing company for neonatal and pediatric care for hospitals with an excellent track record. The company later became involved in anesthesia, a few years ago, to re-accelerate its growth and, most recently, announced its introduction into telemedicine for radiology. Over the past two years, execution has been inconsistent and this quarter proved more of the same with core trends in neonatal deteriorating due to lower volumes. Although the PM team has had a long-term relationship with the management, they decided to exit the Fund’s position. Noble Energy, Inc., an oil and gas exploration-and-production firm, traded down along with its sector peers on lower oil prices. The PM team continues to believe that the company’s long-term fundamentals remain intact and, therefore, the Fund continues to hold this stock.

| 7 |

Performance Summary and Commentary

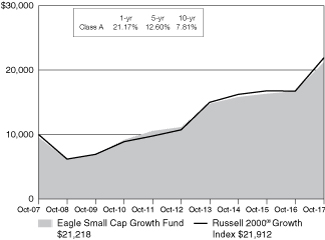

| Eagle Small Cap Growth Fund | ||

Portfolio Managers | Bert L. Boksen, CFA®, and Eric Mintz, CFA®, are Co-Portfolio Managers of the Eagle Small Cap Growth Fund (the “Fund”). Mr. Boksen has been responsible for the day-to-day management of the Fund’s investment portfolio since August 1995 and Mr. Mintz since March 2011. Christopher Sassouni, D.M.D., has served as Assistant Portfolio Manager of the Fund since March 2015.

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 27.22% (excluding front-end sales charges of 4.75%), underperforming its benchmark index, the Russell 2000® Growth Index, which returned 31.00%. The Fund’s underperformance relative to the benchmark was driven by weak relative returns within the health care and consumer discretionary sectors which, despite solid absolute returns, failed to keep up with strong benchmark returns during the reporting period. A bright spot for the Fund was the information technology sector which generated very strong absolute and relative returns, offsetting some of the Fund’s broader underperformance during the reporting period. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 10/31/07 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3, Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/ or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Under performers | Shares of long-term holding Genesco Inc.—a footwear, apparel and accessories retailer—have faced ongoing pressure in what the Fund’s Portfolio Management team (‘PM team”) believes remains a difficult environment for mall-based retailers as Amazon continues to redevelop the landscape. Genesco continues to drive improved results within its e-commerce channel, which—when coupled with sharp rent reductions—the PM team believes should help offset some of the headwinds affecting the traditional brick-and-mortar channel. The Fund continues to hold a position in the stock. Specialty retailer Vitamin Shoppe, Inc. lagged as ever-evolving competitive pressures appear to have plagued the firm in recent periods. The PM team believes that expanded product offerings from conventional retailers and online vendors continue to encroach on Vitamin Shoppe’s market share. The Fund no longer holds a position in the stock. Universal Electronics Inc., a manufacturer of remote controls for television sets, has encountered some weakness during the period that the PM team believes is the result of pushouts of anticipated orders for its next-generation remote control. The delays appear to have been primarily a function of its end-market cable-service providers taking longer than expected to get rid of old remotes. The PM team expects order growth of the company’s advanced remote to accelerate as its customers work through their remaining inventory, which should help position the stock for renewed strength. The Fund continues to hold a position in the stock. Adeptus Health, Inc. (Class A) operates a network of independent, freestanding emergency rooms across the United States. The PM team believes that the confluence of the ongoing deterioration of inpatient volumes, in tandem with the firm’s sizeable capital expenditures (used to build new facilities to expand its network), combined to weigh heavily on Adeptus’ results and, in the PM team’s view, have compromised earnings visibility. The Fund no longer holds a position in the stock. Ambarella Inc. is a provider of video chips that enable high definition video capture, sharing and display. Shares encountered some downward pressure resulting in part from product release delays as well as softer-than-expected demand for its products within its drone segment during the reporting period. The Fund no longer holds a position in the stock.

Top performers | Coherent, Inc. makes laser-based equipment used in such applications as smartphone and tablet displays. The PM team believes that the firm continues to benefit from strong orders for its product which is used in the fabrication of organic light-emitting diode (OLED) displays that are increasingly used in next-generation smartphones. Further, the PM team believes that the potential for alternative applications of Coherent’s equipment (e.g., in tablets, autos and television) may provide additional upside over the longer term. Cognex Corp. manufactures machine “vision” systems used to monitor various aspects of manufacturing and distribution processes. The stock has performed very well as the PM team believes that the company continues to enhance its positioning as a key player within the growing factory- and industrial-automation and logistics markets. IPG Photonics Corp. makes lasers used in research markets, such as communications and medical applications. The firm has benefitted from the solid competitive positioning of its high-power lasers as well as via cost advantages generated through efficient vertical integration. The PM team believes that solid-waste company, Waste Connections, Inc. has continued to benefit from strong pricing power while leveraging a measured approach of organic growth and strategic acquisitions. The PM team believes that the firm is also indirectly benefitting from gradual improvements in consumer sentiment via increased consumption. Exact Sciences Corp. designs and develops molecular diagnostic tests used in cancer screening. Shares continued their upward trend as the firm appears to have benefitted from substantially increased insurance coverage (e.g., United Healthcare and Aetna) for its Cologuard exam product. In addition, increased physician adoption and an effective direct-to-consumer campaign are combining to help drive sales growth. The Fund continues to hold each of the securities noted above as “top performers.”

| 8 |

Performance Summary and Commentary

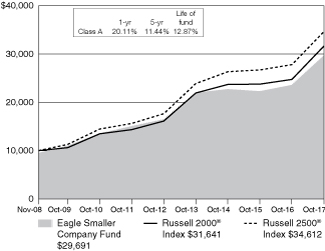

| Eagle Smaller Company Fund | ||

Portfolio Managers | Charles Schwartz, CFA®, Betsy Pecor, CFA®, and Matthew McGeary, CFA®, are Co-Portfolio Managers of the Eagle Smaller Company Fund (the “Fund”) and have been responsible for the day-to-day management of the Fund’s investment portfolio since October 2014.

Performance discussion | For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 26.11% (excluding front-end sales charges of 4.75%), outperforming its primary benchmark index, the Russell 2500® Index and underperforming its secondary index, the Russell 2000® Index, which returned 24.68% and 27.85%, respectively. The Fund’s performance benefited from strong stock selection in the real estate sector, primarily within real estate investment trusts, as well as an overall underweight position relative to the benchmark. In addition, the Fund also outperformed in the financial sector, where stock selection in the thrifts and mortgage finance industry benefited the Fund. In contrast, the Fund’s holdings in the energy sector led to underperformance versus the benchmark. Furthermore, the Fund’s relative performance suffered due to stock selection within the information technology sector. As you review this summary and the table below, please keep in mind that an index is not available for direct investment; therefore its performance does not reflect the expenses associated with the management of an actual portfolio.

Growth of a $10,000 investment from 11/3/08 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3, Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

Top performers | Cognex Corporation is a leader in machine “vision” systems for manufacturing and other automation uses. The demand for more accurate, faster and

cost-effective work flows is a powerful driver for the company. Cognex reported favorable financial results and a better-than-expected outlook. The Fund continues to hold this stock. LendingTree Inc., an online marketplace connecting prospective borrowers with lenders, continued its upward momentum when it reported another strong quarter. The Fund’s Portfolio Management team (“PM team”) believes that this financial performance helped demonstrate the company’s ability to continue to grow its mortgage business and, more importantly, diversify its growth among home-equity loans, credit cards and personal loans. The company continues to launch new products and make small acquisitions that may allow it to enter new channels, such as small-business loans, insurance and deposits. After a period of significant outperformance by the company, as compared to their peers in the financials sector, the price exceeded the price target set by the PM team and pushed the valuation beyond what was supported by their discipline and the Fund exited its position. HEICO Corporation drove the Fund’s strong results in the aerospace industry. HEICO has continued to exceed consensus expectations and raised its outlook due to solid execution in its core businesses and completing beneficial acquisitions. The Fund continues to hold this stock. Catalent, Inc. is a global leader in the drug delivery outsourcing market. The PM team continues to believe in the company because there are a lot of secular trends in its favor including low penetration rates for outsourcing and growing demand for complex dose forms for a growing biopharmaceutical market. Catalent reported a strong quarter with revenue growth of 19% and over 25% growth in profitability. The company continues to guide conservatively, and the PM team believes that the company has plenty of levers to exceed expectations. The Fund continues to maintain a position in this health care company. Graco Inc. is a manufacturer of precision dispensing equipment used in numerous industrial applications. The stock performed well as the company posted its third consecutive quarter of double-digit organic sales growth and management raised its 2017 outlook to high single digit growth across every geography. The PM team continues to believe in the company’s consistent sales growth (which appears to be driven by new product and program launches as well as emerging market expansion), operating margin expansion opportunities, under-levered balance sheet, and optionality to deploy capital and best-in-class returns. The Fund continues to hold this stock.

Underperformers | Carrizo Oil & Gas Inc. is an oil and gas exploration and development company operating in several basins throughout North America. The company’s shares performed poorly due primarily to overall weakness in the sector resulting from lower oil prices and poor investor sentiment. Investors also appeared to be concerned about Carrizo making a large acquisition in the Permian basin. Late in the quarter, the company did purchase acreage in the Permian basin, however the company’s assets appear attractive and the price is reasonable. The PM team will be watching for non-core asset sales to help finance this deal. The Fund continues to hold this position. Gulfport Energy Corp. is an oil and gas exploration and production company with assets focused in the Utica Shale region. The company’s shares contributed to the Fund’s underperformance for two primary reasons. First, the entire energy sector traded off on commodity-price concerns and the company’s shares appeared to be caught in that downdraft. Second, Gulfport announced an acquisition of assets outside its core area of operation. Although, the PM team believes the deal makes sense because it offers geographic and geologic diversification to the business model, the Fund no longer holds this position. MDC Partners, Inc. (Class A), a global marketing consultancy, contributed to Fund underperformance as it posted weak 4Q16 results and lowered its earnings guidance. The company also hired LionTree Advisors to explore “financial and capital structure” strategies and suspended its dividend to improve its balance sheet and reinvest in the business. The Fund sold its position. Ellie Mae, Inc. is a leading provider of software solutions for the mortgage-origination business. The company reported underwhelming results and guidance. Refinancing volumes in particular were lower than expected as were purchase volumes due to tight supply issues. The Fund continues to hold this stock. IMAX Corp. offers a unique end-to-end cinematic solution combining its proprietary software, theater architecture and equipment to create a high-quality, immersive motion picture experience. The stock price decreased due to concerns over weaker second quarter box office results, declining global per screen averages/moviegoer frequency and competition from premium video on demand (due to the possibility of a shortened movie release window). The Fund no longer holds this stock.

| 9 |

Performance Summary and Commentary

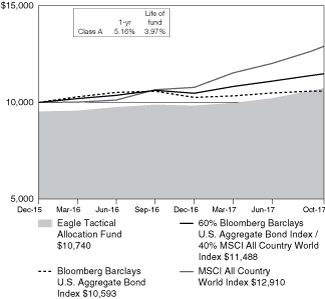

| Eagle Tactical Allocation Fund | ||

Portfolio Managers | James Breech, Ph.D., of Cougar Global Investments Ltd. (“Cougar”), is the Portfolio Manager of the Eagle Tactical Allocation Fund (the “Fund”) and has been responsible for the day-to-day management of the Fund’s investment portfolio since its inception in December 2015.

Performance discussion | For the fiscal year ended October 31 2017, Cougar’s 12-month forward looking outlook improved to incorporate a more robust assessment of the macro economic environment. This improvement was largely attributed to the global economy, where essentially every major developed and emerging market economy is growing simultaneously for the first time since the Global Financial Crisis. The probability assigned to the most optimistic scenario, Growth, rose from 0% over the course of the year and stood at a high of 45% in August. The increase came primarily from the sluggish growth scenario, Stagnation. The U.S. economy once again emerged from a weak start to the year, with employment gains fueling consumption as the growth driver. The probability assigned to Inflation decreased from 8% to 1% as energy prices remained range-bound, wage inflation muted, and some dampening potentially transitory factors. The chance that a high impact, low probability event, Chaos, would occur was increased in September from 6% to 8% to account for heightened geopolitical risks primarily stemming from tensions around North Korea and the immense progress of its nuclear program. Given the improved outlook, the Fund’s Portfolio Management team (“PM team”) increased equity exposure, and added international exposure. The improvement in global growth, corporate earnings recovery, and continuation of accommodative monetary policy appeared to fuel a continuation of the equity market rally. Fixed income also performed well, given that the Federal Reserve Board (“Fed”) refrained again from raising interest rates as much as had been originally expected. This led to a weakening of the U.S. dollar, benefitting commodities and non-U.S. exposures, in particular the Emerging Markets, which the Fund held. Meanwhile, the economic recovery and improved political climate in Europe boosted both equities and the Euro, which the Fund also held. The PM team believes that, while the Fed is inching away from ultra-loose monetary policy and unwinding its balance sheet, other major central banks are still likely to pursue accommodative policies, resulting in modest rises to bond yields globally.

For the fiscal year ended October 31, 2017, the Fund’s Class A shares returned 10.42% (excluding front-end sales charges of 4.75%), outperforming the Bloomberg Barclays U.S. Aggregate Bond Index and underperforming the MSCI ACWI® Index, which performed 0.90% and 23.20%, respectively. The Fund also outperformed a custom blended index, which is a combination of the Bloomberg Barclays U.S. Aggregate Bond Index (60%) and the MSCI ACWI® Index (40%), which returned 9.35% for the same period. The Fund, relative to the blended benchmark, outperformed due to a higher weight to equities than the benchmark for most of the year. At the start of the fiscal year, the Fund’s investments in exchange-traded funds (ETFs) that invest in primarily equity securities represented 34% of its portfolio. This equity allocation was gradually increased to over 50% at the end of Q1, peaking at 78% during Q2, before falling back to 67% in Q3. Within equities, the increase in international exposures to 17% also contributed to outperformance. Within fixed income, the duration of the aggregate holdings of the Fund’s investments in ETFs that invested in fixed income was broadly in line with the index exposure. Gold was sold early in the fiscal period as its relative attractiveness as a safe haven declined.

Top performers | The largest contributors to performance were U.S. equities. Both the SPDR S&P 500 ETF Trust (SPY) and the iShares Core S&P 500 ETF (IVV) represented an average 36% weight over the year and, as such, the largest asset class exposure. U.S. mid-caps, SPDR S&P Midcap 400 ETF Trust (MDY), at an average 12% holding also contributed to performance, as did a smaller average 7% weight in U.S. small-caps. International results were also positive. This includes the following European holdings, both currency hedged and then unhedged, iShares Currency Hedged MSCI Eurozone ETF (HEZU) and iShares MSCI Eurozone ETF (EZU), Japan, iShares MSCI Japan ETF (EWJ), and Emerging Markets holdings, iShares Core MSCI Emerging Markets ETF (IEMG). The Fund reduced equities and sold most of the international exposure as a softening in the outlook

and increase in Chaos required additional fixed income exposure to meet its risk constraint. The Fund however remains overweight equities, and favors e-globally oriented U.S. large cap equities.

Underperformers | Currency hedged Japan, iShares Currency Hedged MSCI Japan ETF (HEWJ), was the only outright detractor from performance, albeit only mildly. It was held early in the period on a currency hedged basis. The PM team believes that the yen strengthened as it benefitted from its safe haven status as the North Korea tensions escalated, resulting in a period of underperformance of North Korea’s stock market. The ETF was sold so the Fund could purchase into iShares MSCI Japan ETF (EWJ) to diversify currency exposure within the portfolio. U.S. small and mid-caps were relative underperformers. This holding was sold during Q1 so the Fund could purchase into U.S. large cap given uncertainty over tax reform and a better outlook for large-caps given the global environment and more stable dollar.

Growth of a $10,000 investment from 12/31/15 to 10/31/17 (a)

(a) The Fund’s values and returns reflect the maximum front-end sales charge of 4.75%, fund expenses and the reinvestment of dividends; however, they do not reflect the deduction of taxes that you would pay on fund distributions or redemption of fund shares. As of October 31, 2017, the Fund also offered Class C, Class I, Class R-3, Class R-5 and Class R-6 shares. The value of an investment in other share classes will differ due to each class’s respective sales charges and expenses. Additional information regarding the performance and the expenses of the Fund’s share classes, including fee waivers and/or expense reimbursements or recoupments, which affect performance, is included in the Fund’s prospectus dated November 20, 2017, and elsewhere in this report.

Performance data represented is historical and does not guarantee future results. The investment return and principal value of an investment will fluctuate, and you may have a gain or loss when you sell shares. Current performance may be higher or lower than the performance data quoted. To obtain more current performance data as of the most recent month-end, please visit our website at carillontower.com.

| 10 |

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

The Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index includes U.S. government and investment grade credit securities that have a greater than or equal to one year and less than ten years remaining to maturity and have $250,000,000 or more of outstanding face value. The returns of the index do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The MSCI All Country World Index is a market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. The index is maintained by Morgan Stanley Capital International, and is comprised of stocks from both developed and emerging markets.

The MSCI EAFE® Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The index consists of 21 developed market country indices. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The Russell 2500® Index measures the performance of the small to mid-cap segment of the U.S. equity universe, commonly referred to as “smid” cap. The Russell 2500® Index is a subset of the Russell 3000® Index. It includes approximately 2,500 of the smallest securities based on a combination of their market cap and current index membership. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000® Index companies with higher price-to-value ratios and higher forecasted growth values. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The Russell Midcap® Index measures the performance of the mid-cap segment of the U.S. equity universe. The index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The Russell Midcap® Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with higher price-to-book ratios and higher forecasted growth values. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The S&P 500® Index is an unmanaged index of 500 U.S. stocks and gives a broad look at how stock prices have performed. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

The S&P MidCap 400® Index is an unmanaged index that measures the performance of the mid-sized company segment of the U.S. market. Its returns do not include the effect of any sales charges. That means that actual returns would be lower if they included the effect of sales charges.

Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and / or Russell ratings or underlying data and no party may rely on any Russell Indexes and / or Russell ratings and / or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication.

| 11 |

Investment Portfolios

| 10.31.2017 |

| COMMON STOCKS—99.2% | Shares | Value | ||||||||||

| Household durables—2.0% | ||||||||||||

D.R. Horton, Inc. | 123,800 | $5,473,198 | ||||||||||

Mohawk Industries, Inc.* | 9,300 | 2,434,368 | ||||||||||

| Insurance—0.5% | ||||||||||||

The Progressive Corp. | 38,400 | 1,868,160 | ||||||||||

| Internet & direct marketing retail—3.5% | ||||||||||||

Amazon.com, Inc.* | 12,500 | 13,816,000 | ||||||||||

| Internet software & services—11.4% | ||||||||||||

Alphabet, Inc., Class A* | 11,014 | 11,377,902 | ||||||||||

Alphabet, Inc., Class C* | 11,012 | 11,195,240 | ||||||||||

eBay, Inc.* | 102,500 | 3,858,100 | ||||||||||

Facebook, Inc., Class A* | 100,100 | 18,024,006 | ||||||||||

| IT services—6.4% | ||||||||||||

Amdocs Ltd. | 18,900 | 1,230,390 | ||||||||||

Fiserv, Inc.* | 33,000 | 4,271,190 | ||||||||||

Global Payments, Inc. | 19,800 | 2,058,210 | ||||||||||

MasterCard, Inc., Class A | 44,730 | 6,654,482 | ||||||||||

Vantiv, Inc., Class A* | 67,504 | 4,725,280 | ||||||||||

Visa, Inc., Class A | 56,700 | 6,235,866 | ||||||||||

| Life sciences tools & services—1.5% | ||||||||||||

Thermo Fisher Scientific, Inc. | 31,200 | 6,047,496 | ||||||||||

| Machinery—3.5% | ||||||||||||

Caterpillar, Inc. | 34,800 | 4,725,840 | ||||||||||

Ingersoll-Rand PLC | 42,600 | 3,774,360 | ||||||||||

Oshkosh Corp. | 32,100 | 2,939,076 | ||||||||||

Parker-Hannifin Corp. | 12,500 | 2,282,625 | ||||||||||

| Media—1.2% | ||||||||||||

Comcast Corp., Class A | 125,900 | 4,536,177 | ||||||||||

| Metals & mining—1.0% | ||||||||||||

Steel Dynamics, Inc. | 107,300 | 3,992,633 | ||||||||||

| Semiconductors & semiconductor equipment—6.9% | ||||||||||||

Applied Materials, Inc. | 165,900 | 9,361,737 | ||||||||||

KLA-Tencor Corp. | 17,900 | 1,949,131 | ||||||||||

Lam Research Corp. | 33,400 | 6,966,238 | ||||||||||

Microchip Technology, Inc. | 32,500 | 3,081,000 | ||||||||||

NVIDIA Corp. | 26,700 | 5,521,827 | ||||||||||

| Software—11.2% | ||||||||||||

Activision Blizzard, Inc. | 68,100 | 4,459,869 | ||||||||||

Adobe Systems, Inc.* | 24,300 | 4,256,388 | ||||||||||

Electronic Arts, Inc.* | 45,100 | 5,393,960 | ||||||||||

Microsoft Corp. | 258,300 | 21,485,394 | ||||||||||

Oracle Corp. | 64,000 | 3,257,600 | ||||||||||

Synopsys, Inc.* | 56,400 | 4,879,728 | ||||||||||

| Specialty retail—2.8% | ||||||||||||

Ross Stores, Inc. | 33,300 | 2,114,217 | ||||||||||

The Home Depot, Inc. | 54,000 | 8,952,120 | ||||||||||

| Technology hardware, storage & peripherals—6.4% | ||||||||||||

Apple, Inc. | 132,366 | 22,375,149 | ||||||||||

NetApp, Inc. | 59,300 | 2,634,106 | ||||||||||

| Textiles, apparel & luxury goods—1.1% | ||||||||||||

PVH Corp. | 34,100 | 4,324,221 | ||||||||||

| 12 | The accompanying notes are an integral part of the financial statements. |

Investment Portfolios

| 10.31.2017 |

| EAGLE CAPITAL APPRECIATION FUND (cont’d) | ||||||||||||

| COMMON STOCKS—99.2% | Shares | Value | ||||||||||

| Trading companies & distributors—0.7% | ||||||||||||

United Rentals, Inc.* | 18,400 | $2,603,232 | ||||||||||

| Total common stocks (cost $225,358,650) | 387,861,670 | |||||||||||

| Total investment portfolio (cost $225,358,650)—99.2% | 387,861,670 | |||||||||||

Other assets in excess of liabilities—0.8% |

| 3,033,357 | ||||||||||

| Total net assets—100.0% | $390,895,027 | |||||||||||

* Non-income producing security

| Sector allocation (unaudited) | ||||

| Sector | Percent of net assets | |||

| Information technology | 42.3% | |||

| Consumer discretionary | 17.0% | |||

| Health care | 14.5% | |||

| Industrials | 11.6% | |||

| Consumer staples | 7.2% | |||

| Financials | 3.0% | |||

| Materials | 2.7% | |||

| Real estate | 0.9% | |||

| COMMON STOCKS—96.5% | Shares | Value | ||||||||||

| Food products—1.7% | ||||||||||||

General Mills, Inc. | 193,875 | $10,065,990 | ||||||||||

| Health care equipment & supplies—3.9% | ||||||||||||

Abbott Laboratories | 242,099 | 13,129,029 | ||||||||||

Medtronic PLC | 128,275 | 10,328,703 | ||||||||||

| Hotels, restaurants & leisure—5.9% | ||||||||||||

Carnival Corp. | 334,608 | 22,214,625 | ||||||||||

McDonald’s Corp. | 81,079 | 13,532,896 | ||||||||||

| Household products—2.3% | ||||||||||||

The Procter & Gamble Co. | 158,140 | 13,653,808 | ||||||||||

| Industrial conglomerates—6.2% | ||||||||||||

3M Co. | 66,586 | 15,327,431 | ||||||||||

Honeywell International, Inc. | 154,193 | 22,228,463 | ||||||||||

| Media—2.6% | ||||||||||||

Regal Entertainment Group, Class A | 966,060 | 15,795,081 | ||||||||||

| Multi-utilities—2.0% | ||||||||||||

Sempra Energy | 102,793 | 12,078,177 | ||||||||||

| Oil, gas & consumable fuels—8.2% | ||||||||||||

Chevron Corp. | 153,728 | 17,815,538 | ||||||||||

Occidental Petroleum Corp. | 227,379 | 14,681,862 | ||||||||||

TOTAL S.A., Sponsored ADR | 304,174 | 16,948,575 | ||||||||||

| Pharmaceuticals—9.5% | ||||||||||||

Johnson & Johnson | 163,277 | 22,762,447 | ||||||||||

Merck & Co., Inc. | 245,981 | 13,551,093 | ||||||||||

Pfizer, Inc. | 596,524 | 20,914,131 | ||||||||||

| Road & rail—2.5% | ||||||||||||

Union Pacific Corp. | 133,501 | 15,458,081 | ||||||||||

| Software—4.5% | ||||||||||||

Microsoft Corp. | 326,064 | 27,122,004 | ||||||||||

| Specialty retail—3.2% | ||||||||||||

The Home Depot, Inc. | 118,307 | 19,612,934 | ||||||||||

| Technology hardware, storage & peripherals—4.8% | ||||||||||||

Apple, Inc. | 170,906 | 28,889,950 | ||||||||||

| Tobacco—2.5% | ||||||||||||

Altria Group, Inc. | 236,030 | 15,157,847 | ||||||||||

| Total common stocks (cost $388,758,208) | 582,973,249 | |||||||||||

| Total investment portfolio (cost $388,758,208)—96.5% | 582,973,249 | |||||||||||