Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07874

| JPMorgan Insurance Trust |

(Exact name of registrant as specified in charter)

1111 Polaris Parkway Columbus, Ohio 43240 |

(Address of principal executive offices) (Zip code)

Frank J. Nasta 270 Park Avenue New York, NY 10017 |

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: December 31

Date of reporting period: January 1, 2010 through December 31, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Table of Contents

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Table of Contents

Annual Report

JPMorgan Insurance Trust

December 31, 2010

JPMorgan Insurance Trust Core Bond Portfolio

NOT FDIC INSURED Ÿ NO BANK GUARANTEE Ÿ MAY LOSE VALUE

This material must be preceded or accompanied by a current prospectus. |  |

Table of Contents

Investments in the Portfolio are not bank deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when the Portfolio’s share price is lower than when you invested.

Past performance is no guarantee for future performance. The general market views expressed in this report are opinions based on conditions through the end of the reporting period and are subject to change without notice based on market and other conditions. These views are not intended to predict the future performance of the Portfolio or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of the Portfolio.

This Portfolio is intended to be a funding vehicle for variable annuity contracts and variable life insurance policies (collectively “Policies”) offered by separate accounts of participating insurance companies. Portfolio shares are also offered through qualified pension and retirement plans (“Eligible Plans”). Individuals may not purchase shares directly from the Portfolio.

Prospective investors should refer to the Portfolio’s prospectus for a discussion of the Portfolio’s investment objective, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about the Portfolio including management fees and other expenses. Please read it carefully before investing.

Table of Contents

January 20, 2011 (Unaudited)

Dear Shareholder:

It’s only natural for investors to try to ring in the new year with some degree of optimism. Last year, for example, as we slowly emerged from the global financial crisis, we welcomed some encouraging signs that a modest economic recovery was beginning. Today, although the economy can hardly be described as robust, we continue to see signs of improvement.

|

“Today, although the economy can hardly be described as robust, we continue to see signs of improvement.” |

Despite volatility, equities turn in double-digit performance

Investors kicked off 2010 by reacting positively to two consecutive quarters of positive earnings reports. However, this optimism was tempered by a wave of both discouraging U.S. economic data and sovereign debt issues in Europe, which led to a market correction in the middle of 2010.

After experiencing a period of volatility towards the end of the summer, the markets finished the year strongly and posted a second year of double digit returns. Investors were encouraged by improved economic expectations and job growth, as well as the combination of the Federal Reserve’s (the “Fed”) launch of quantitative easing (QE2) and Congress’ extension of the Bush-era tax cuts. As of the 12-month reporting period ended December 31, 2010, the S&P 500 had reached a level of 1,258, an increase of 15.1% from a year prior.

Small and mid cap stocks lead style categories

Small and mid cap stocks led the style categories over the 12 month period ended December 31, 2010 (the Russell 2000 Index returned 26.9% and the Russell Mid Cap Index returned 25.5% compared to 16.1% as measured by the Russell 1000 Index). Overall, growth stocks fared better than value in the small cap, mid cap and large cap space. The Russell 1000 Growth Index returned 16.7% for the 12-month reporting period, compared to 15.5% for the Russell 1000 Value Index. With regard to mid cap stocks, the Russell Midcap Growth Index returned 26.4%, while the Russell Midcap Value Index returned 24.8%. In the small cap segment, the Russell 2000 Growth Index outpaced the Russell 2000 Value Index, with a return of 29.1%, compared to 24.5%, as of the end of the 12-month period.

Treasuries move higher, pushing yields to historic lows

As investors continued to move into the relative safety of fixed income, yields trended lower, often to historical levels, for most of 2010. Yet, as the year drew to a close, investors began to seek out riskier assets, causing yields to spike sharply. As of the end of the 12-month period ended December 31, 2010, the yields on the benchmark 10-year U.S. Treasury bond declined from 3.9% to 3.3%. Yields on the 30-year U.S. Treasury bond slid from 4.6% to 4.3% as of the end of the period, and the two-year U.S. Treasury note dipped from 1.1% to 0.6%.

In this environment, the Barclays Capital U.S. Aggregate Bond Index returned 6.5%, while the Barclays Capital High Yield Index returned 15.1%, and the Barclays Capital Emerging Markets Index returned 12.8% for the 12-month period ended December 31, 2010.

The pace of recovery

Despite last year’s stock market gains, the economy continues to send mixed signals about the recovery. On the one hand, we are encouraged that gross domestic product (GDP) continues to grow and that corporate earnings continue to exceed estimates. On the other hand, we are discouraged by the fact the economy continues to be restrained by state and local government cutbacks, sluggish job growth, and a hibernating home building industry. Against this backdrop, it makes sense for investors to maintain a balanced approach, as while some aspects of the economy appear to be improving, other aspects continue to struggle, and as of this writing, remain quite unpredictable.

On behalf of everyone at J.P. Morgan Asset Management, thank you for your continued confidence. We look forward to managing your investment needs for years to come. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

George C.W. Gatch

CEO-Investment Management Americas

J.P. Morgan Asset Management

| DECEMBER 31, 2010 | JPMORGAN INSURANCE TRUST | 1 | ||||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

PORTFOLIO COMMENTARY

TWELVE MONTHS ENDED DECEMBER 31, 2010 (Unaudited)

| REPORTING PERIOD RETURN: | ||||

| Portfolio (Class 1 Shares)* | 9.24% | |||

| Barclays Capital U.S. Aggregate Index | 6.54% | |||

| Net Assets as of 12/31/2010. | $ | 245,696,906 | ||

INVESTMENT OBJECTIVE**

The JPMorgan Insurance Trust Core Bond Portfolio (the “Portfolio”) seeks to maximize total return by investing primarily in a diversified portfolio of intermediate- and long-term debt securities.

HOW DID THE MARKET PERFORM?

After a relatively uneventful beginning to 2010, risk aversion returned in April due to concerns about the threat of systemic fallout from Europe’s debt crisis. The risk aversion led many investors to seek haven in U.S. Treasuries, sending their prices higher and yields sharply lower. Investors’ appetite for risk did not recover until the third and fourth quarters of 2010, when strong corporate earnings, better-than-expected economic data, a return of merger and acquisition activity and accommodative policies from the U.S. Federal Reserve lifted investor sentiment. Investors were also encouraged by the U.S. government’s two-year extension of the Bush era tax cuts, emergency unemployment benefits and a payroll tax cut. Accordingly, the yield curve (the yield curve shows the relationship between yields and maturity dates for a set of similar bonds, usually U.S. Treasuries, at a given point in time) steepened significantly during the third and fourth quarters of 2010, with yields rising and Treasury prices declining across the board (generally, bond prices increase/decline when yields decline/increase).

The mortgage-backed securities market saw volatility during the reporting period, driven by concerns that the U.S. government would implement programs that encourage borrowers to refinance their mortgages (mortgage refinancing can hurt bondholders by returning the money they invested more quickly than anticipated). Meanwhile, the supply/demand backdrop continued to be favorable in the non-agency mortgage-backed security market, outweighing concerns about the fundamentals of the housing market. Supply for non-agency mortgage-backed securities declined, while demand was strong due to the sector’s high yield relative to other areas of the fixed income market. This favorable environment helped support the non-agency mortgage market during the reporting period.

WHAT WERE THE MAIN DRIVERS OF THE PORTFOLIO’S PERFORMANCE?

The Portfolio (Class 1 Shares) outperformed the Barclays Capital U.S. Aggregate Index (the “Benchmark”) for the twelve months ended December 31, 2010.

The Portfolio’s overweight in non-U.S. Treasuries and underweight U.S. Treasuries helped the Fund’s relative performance, as non-U.S. Treasuries outperformed U.S. Treasuries during the reporting period. Among the Portfolio’s spread sector holdings, non-agency mortgage-backed securities, which are not represented in the Benchmark, were strong contributors to relative performance as the sector was supported by a favorable supply/demand environment. Meanwhile, the Portfolio’s positioning on

the yield curve contributed to relative performance, benefiting from its overweight position of the 7 to 10 year portion of the yield curve as yields for these U.S. Treasury securities declined and their prices increased during the reporting period.

On the negative side, the Portfolio’s underweight in commercial mortgage-backed securities (CMBS) hurt relative performance, as their spreads narrowed during the reporting period (generally, when spreads of a particular group of securities narrow, their prices rise and their yields fall). In addition, the Fund’s underweight of the credit sector, particularly among issuances from financial companies, hurt the Portfolio’s relative performance versus the Benchmark as credit spreads also narrowed during the reporting period.

HOW WAS THE PORTFOLIO POSITIONED?

The Portfolio’s primary strategy continued to be security selection and relative value, which seeks to exploit pricing discrepancies between individual securities or market sectors. The portfolio managers used bottom-up fundamental research to construct, in their view, a portfolio of undervalued fixed income securities. The Portfolio was overweight the intermediate part of the yield curve (7 to 10 year maturities) as the portfolio managers believed that these U.S. Treasuries had the most attractive risk/reward profile. Meanwhile, although the Fund’s portfolio managers identified what they believed were select pockets of value among commercial mortgage-backed securities, they remained underweight the sector, believing that higher vacancies, continued credit deterioration and increased defaults diminish the outlook for favorable longer-term investments within the sector.

PORTFOLIO COMPOSITION*** | ||||

| Collateralized Mortgage Obligations | 49.2 | % | ||

| U.S. Treasury Obligations | 16.6 | |||

| Corporate Bonds | 14.0 | |||

| U.S. Government Agency Securities | 9.8 | |||

| Mortgage Pass-Through Securities | 6.2 | |||

| Commercial Mortgage-Backed Securities | 1.7 | |||

| Asset-Backed Securities | 1.1 | |||

| Others (each less than 1.0%) | 0.3 | |||

| Short-Term Investment | 1.1 | |||

| * | The return shown is based on net asset value calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset value in accordance with accounting principles generally accepted in the United States of America. |

| ** | The advisor seeks to achieve the Portfolio’s objectives. There can be no guarantee it will be achieved. |

| *** | Percentages indicated are based upon total investments as of December 31, 2010. The Portfolio’s composition is subject to change. |

| 2 | JPMORGAN INSURANCE TRUST | DECEMBER 31, 2010 | ||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

PORTFOLIO COMMENTARY

TWELVE MONTHS ENDED DECEMBER 31, 2010 (Unaudited) (continued)

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2010 | ||||||||||||||||

| INCEPTION DATE OF CLASS | 1 YEAR | 5 YEAR | 10 YEAR | |||||||||||||

CLASS 1 SHARES | 5/1/97 | 9.24 | % | 6.08 | % | 5.94 | % | |||||||||

CLASS 2 SHARES | 8/16/06 | 8.97 | 5.86 | 5.83 | ||||||||||||

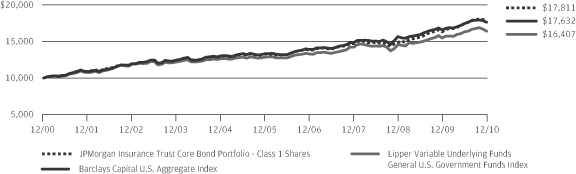

TEN YEAR PERFORMANCE (12/31/00 TO 12/31/10)

Source: Lipper, Inc. The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class 2 Shares prior to their inception date are based on the performance of Class 1 Shares. The actual returns of Class 2 Shares would have been lower than shown because Class 2 Shares have higher expenses than Class 1 Shares.

The graph illustrates comparative performance for $10,000 invested in Class 1 Shares of the JPMorgan Insurance Trust Core Bond Portfolio, the Barclays Capital U.S. Aggregate Index and the Lipper Variable Underlying Funds General U.S. Government Funds Index from December 31, 2000 to December 31, 2010. The performance of the Portfolio assumes reinvestment of all dividends and capital gains, if any. The performance of the Barclays Capital U.S. Aggregate Index does not reflect the deduction of expenses associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gains of the securities included in the benchmark. The performance of the Lipper Variable Underlying Funds General U.S. Government Funds Index includes expenses

associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses charged by the Portfolio. The Barclays Capital U.S. Aggregate Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, mortgage-backed securities (MBS) (agency fixed-rate and hybrid adjustable rate mortgage (ARM) passthroughs), asset-backed securities (ABS), and commercial mortgage-backed securities (CMBS). The Lipper Variable Underlying Funds General U.S. Government Funds Index is an index based on the total returns of certain mutual funds within the Portfolio’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

The performance does not reflect any charges imposed by the Policies or Eligible Plans. If these charges were included, the returns would be lower than shown. Performance may reflect the waiver of the Portfolio’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements performance would have been lower. The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| DECEMBER 31, 2010 | JPMORGAN INSURANCE TRUST | 3 | ||||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2010

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Asset-Backed Securities — 1.1% | |||||||

| 50,000 | Ally Auto Receivables Trust, Series 2010-1, Class A3, 1.450%, 05/15/14 | 50,309 | ||||||

AmeriCredit Automobile Receivables Trust, | ||||||||

| 192,365 | Series 2006-BG, Class A4, 5.210%, 09/06/13 | 195,401 | ||||||

| 22,228 | Series 2010-1, Class A2, 0.970%, 01/15/13 | 22,237 | ||||||

| 25,000 | Series 2010-1, Class A3, 1.660%, 03/17/14 | 25,141 | ||||||

Bank of America Auto Trust, | ||||||||

| 168,303 | Series 2009-1A, Class A3, 2.670%, 07/15/13 (e) | 170,100 | ||||||

| 100,000 | Series 2010-1A, Class A3, 1.390%, 03/15/14 (e) | 100,560 | ||||||

| 100,000 | Series 2010-1A, Class A4, 2.180%, 02/15/17 (e) | 101,765 | ||||||

| 41,608 | Bear Stearns Asset-Backed Securities Trust, Series 2006-SD1, Class A, VAR, 0.631%, 04/25/36 | 28,453 | ||||||

| 60,000 | CarMax Auto Owner Trust, Series 2010-1, | 60,470 | ||||||

| 200,000 | Centex Home Equity, Series 2004-D, | 197,878 | ||||||

| 450,000 | Citibank Credit Card Issuance Trust, | 473,857 | ||||||

| 125,000 | CNH Equipment Trust, Series 2010-A, Class A3, 1.540%, 07/15/14 | 126,012 | ||||||

Countrywide Asset-Backed Certificates, | ||||||||

| 1,056 | Series 2004-1, Class 3A, VAR, 0.541%, 04/25/34 | 875 | ||||||

| 120,000 | Series 2004-1, Class M1, VAR, 0.761%, 03/25/34 | 97,694 | ||||||

| 100,000 | Series 2004-1, Class M2, VAR, 0.811%, 03/25/34 | 84,709 | ||||||

| 23,313 | Countrywide Home Equity Loan Trust, | 11,245 | ||||||

| 86,177 | Ford Credit Auto Owner Trust, Series 2009-B, Class A3, 2.790%, 08/15/13 | 87,310 | ||||||

| 100,000 | Honda Auto Receivables Owner Trust, | 105,378 | ||||||

Long Beach Mortgage Loan Trust, | ||||||||

| 244,198 | Series 2003-4, Class M1, VAR, 1.281%, 08/25/33 | 201,846 | ||||||

| 190,000 | Series 2004-1, Class M1, VAR, | 163,439 | ||||||

| 125,000 | Series 2004-1, Class M2, VAR, | 111,330 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| 37,065 | Series 2006-WL2, Class 2A3, VAR, | 30,515 | ||||||

| 160,000 | MBNA Credit Card Master Note Trust, | 168,349 | ||||||

| 125,000 | New Century Home Equity Loan Trust, Series 2005-1, Class M1, VAR, | 97,590 | ||||||

| 12,001 | Residential Asset Securities Corp., | 6,141 | ||||||

| 90,000 | World Omni Auto Receivables Trust, | 91,870 | ||||||

Total Asset-Backed Securities | 2,810,474 | |||||||

| Collateralized Mortgage Obligations — 49.1% | |||||||

Agency CMO — 38.0% | ||||||||

| 273,353 | Federal Home Loan Mortgage Corp. – Government National Mortgage Association, Series 8, Class ZA, 7.000%, 03/25/23 | 308,600 | ||||||

Federal Home Loan Mortgage Corp. REMICS, | ||||||||

| 1,463 | Series 1065, Class J, 9.000%, 04/15/21 | 1,664 | ||||||

| 8,701 | Series 11, Class D, 9.500%, 07/15/19 | 9,395 | ||||||

| 180,901 | Series 1113, Class J, 8.500%, 06/15/21 | 209,298 | ||||||

| 9,911 | Series 1250, Class J, 7.000%, 05/15/22 | 11,630 | ||||||

| 17,746 | Series 1316, Class Z, 8.000%, 06/15/22 | 20,454 | ||||||

| 29,282 | Series 1324, Class Z, 7.000%, 07/15/22 | 32,958 | ||||||

| 141,480 | Series 1343, Class LA, 8.000%, 08/15/22 | 163,807 | ||||||

| 29,123 | Series 1343, Class LB, 7.500%, 08/15/22 | 34,566 | ||||||

| 18,954 | Series 1394, Class ID, IF, 9.566%, 10/15/22 | 19,763 | ||||||

| 17,940 | Series 1395, Class G, 6.000%, 10/15/22 | 19,745 | ||||||

| 12,670 | Series 1505, Class Q, 7.000%, 05/15/23 | 14,867 | ||||||

| 24,952 | Series 1518, Class G, IF, 8.753%, 05/15/23 | 28,171 | ||||||

| 25,046 | Series 1541, Class O, VAR, 2.230%, 07/15/23 | 26,240 | ||||||

| 399,959 | Series 1577, Class PV, 6.500%, 09/15/23 | 435,076 | ||||||

| 508,093 | Series 1584, Class L, 6.500%, 09/15/23 | 564,149 | ||||||

| 16,532 | Series 1596, Class D, 6.500%, 10/15/13 | 16,527 | ||||||

| 8,029 | Series 1607, Class SA, IF, 18.799%, 10/15/13 | 9,307 | ||||||

| 19,552 | Series 1609, Class LG, IF, 16.656%, 11/15/23 | 23,498 | ||||||

| 519,233 | Series 1633, Class Z, 6.500%, 12/15/23 | 561,459 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| 4 | JPMORGAN INSURANCE TRUST | DECEMBER 31, 2010 | ||||

Table of Contents

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Agency CMO — Continued | ||||||||

| 500,000 | Series 1638, Class H, 6.500%, 12/15/23 | 574,219 | ||||||

| 2,387 | Series 1671, Class QC, IF, 10.000%, 02/15/24 | 2,703 | ||||||

| 118,832 | Series 1694, Class PK, 6.500%, 03/15/24 | 128,759 | ||||||

| 16,260 | Series 1700, Class GA, PO, 02/15/24 | 14,688 | ||||||

| 64,875 | Series 1798, Class F, 5.000%, 05/15/23 | 69,638 | ||||||

| 141,797 | Series 1863, Class Z, 6.500%, 07/15/26 | 157,742 | ||||||

| 4,027 | Series 1865, Class D, PO, 02/15/24 | 2,920 | ||||||

| 45,397 | Series 1981, Class Z, 6.000%, 05/15/27 | 49,965 | ||||||

| 58,859 | Series 1987, Class PE, 7.500%, 09/15/27 | 68,217 | ||||||

| 222,159 | Series 1999, Class PU, 7.000%, 10/15/27 | 255,850 | ||||||

| 11,814 | Series 2025, Class PE, 6.300%, 01/15/13 | 11,810 | ||||||

| 362,085 | Series 2031, Class PG, 7.000%, 02/15/28 (m) | 408,341 | ||||||

| 14,532 | Series 2033, Class SN, HB, IF, 24.003%, 03/15/24 | 9,007 | ||||||

| 336,236 | Series 2035, Class PC, 6.950%, 03/15/28 | 344,427 | ||||||

| 24,714 | Series 2038, Class PN, IO, 7.000%, 03/15/28 | 4,840 | ||||||

| 71,279 | Series 2054, Class PV, 7.500%, 05/15/28 | 74,927 | ||||||

| 20,863 | Series 2055, Class OE, 6.500%, 05/15/13 | 20,950 | ||||||

| 384,321 | Series 2057, Class PE, 6.750%, 05/15/28 | 450,976 | ||||||

| 118,168 | Series 2064, Class TE, 7.000%, 06/15/28 | 135,751 | ||||||

| 83,699 | Series 2075, Class PH, 6.500%, 08/15/28 | 96,123 | ||||||

| 341,768 | Series 2095, Class PE, 6.000%, 11/15/28 | 376,821 | ||||||

| 35,793 | Series 2102, Class TU, 6.000%, 12/15/13 | 37,653 | ||||||

| 79,689 | Series 2115, Class PE, 6.000%, 01/15/14 | 83,171 | ||||||

| 17,582 | Series 2132, Class SB, HB, IF, 29.434%, 03/15/29 | 26,806 | ||||||

| 34,809 | Series 2134, Class PI, IO, 6.500%, 03/15/19 | 4,627 | ||||||

| 5,123 | Series 2135, Class UK, IO, 6.500%, 03/15/14 | 341 | ||||||

| 125,916 | Series 2178, Class PB, 7.000%, 08/15/29 | 147,754 | ||||||

| 168,171 | Series 2182, Class ZB, 8.000%, 09/15/29 | 195,717 | ||||||

| 6,893 | Series 22, Class C, 9.500%, 04/15/20 | 7,530 | ||||||

| 29,887 | Series 2247, Class Z, 7.500%, 08/15/30 | 34,180 | ||||||

| 336,913 | Series 2259, Class ZC, 7.350%, 10/15/30 | 386,749 | ||||||

| 9,612 | Series 2261, Class ZY, 7.500%, 10/15/30 | 11,081 | ||||||

| 162,819 | Series 2283, Class K, 6.500%, 12/15/23 | 176,163 | ||||||

| 16,674 | Series 2306, Class K, PO, 05/15/24 | 14,452 | ||||||

| 40,018 | Series 2306, Class SE, IF, IO, 7.710%, 05/15/24 | 7,511 | ||||||

| 54,983 | Series 2325, Class PM, 7.000%, 06/15/31 | 61,294 | ||||||

| 284,899 | Series 2344, Class ZD, 6.500%, 08/15/31 | 313,434 | ||||||

| 49,494 | Series 2344, Class ZJ, 6.500%, 08/15/31 | 54,460 | ||||||

| 27,575 | Series 2345, Class NE, 6.500%, 08/15/31 | 29,594 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Agency CMO — Continued | ||||||||

| 233,432 | Series 2345, Class PQ, 6.500%, 08/15/16 | 249,603 | ||||||

| 83,066 | Series 2355, Class BP, 6.000%, 09/15/16 | 89,378 | ||||||

| 214,808 | Series 2359, Class ZB, 8.500%, 06/15/31 | 246,709 | ||||||

| 395,887 | Series 2367, Class ME, 6.500%, 10/15/31 | 434,744 | ||||||

| 47,265 | Series 2390, Class DO, PO, 12/15/31 | 41,021 | ||||||

| 134,197 | Series 2391, Class QR, 5.500%, 12/15/16 | 145,580 | ||||||

| 116,635 | Series 2394, Class MC, 6.000%, 12/15/16 | 126,095 | ||||||

| 65,404 | Series 2410, Class OE, 6.375%, 02/15/32 | 71,684 | ||||||

| 83,394 | Series 2410, Class QS, IF, 18.823%, 02/15/32 | 106,634 | ||||||

| 64,269 | Series 2410, Class QX, IF, IO, 8.390%, 02/15/32 | 15,380 | ||||||

| 73,562 | Series 2412, Class SP, IF, 15.579%, 02/15/32 | 88,187 | ||||||

| 125,831 | Series 2423, Class MC, 7.000%, 03/15/32 | 140,054 | ||||||

| 212,990 | Series 2423, Class MT, 7.000%, 03/15/32 | 237,060 | ||||||

| 227,841 | Series 2435, Class CJ, 6.500%, 04/15/32 | 257,793 | ||||||

| 378,229 | Series 2435, Class VH, 6.000%, 07/15/19 | 387,019 | ||||||

| 90,409 | Series 2444, Class ES, IF, IO, 7.690%, 03/15/32 | 17,598 | ||||||

| 60,272 | Series 2450, Class SW, IF, IO, 7.740%, 03/15/32 | 12,012 | ||||||

| 231,558 | Series 2455, Class GK, 6.500%, 05/15/32 | 254,944 | ||||||

| 21,580 | Series 2460, Class VZ, 6.000%, 11/15/29 | 21,606 | ||||||

| 150,787 | Series 2484, Class LZ, 6.500%, 07/15/32 | 173,170 | ||||||

| 790,000 | Series 2500, Class MC, 6.000%, 09/15/32 | 868,921 | ||||||

| 62,306 | Series 2503, Class BH, 5.500%, 09/15/17 | 67,979 | ||||||

| 137,613 | Series 2515, Class DE, 4.000%, 03/15/32 | 143,354 | ||||||

| 589,561 | Series 2527, Class BP, 5.000%, 11/15/17 | 629,208 | ||||||

| 261,089 | Series 2535, Class BK, 5.500%, 12/15/22 | 287,229 | ||||||

| 5,300,000 | Series 2543, Class YX, 6.000%, 12/15/32 (m) | 5,823,079 | ||||||

| 500,000 | Series 2544, Class HC, 6.000%, 12/15/32 | 550,034 | ||||||

| 22,706 | Series 2565, Class MB, 6.000%, 05/15/30 | 22,916 | ||||||

| 500,000 | Series 2575, Class ME, 6.000%, 02/15/33 | 553,313 | ||||||

| 3,230,000 | Series 2578, Class PG, 5.000%, 02/15/18 | 3,484,840 | ||||||

| 69,705 | Series 2586, Class WI, IO, 6.500%, 03/15/33 | 14,192 | ||||||

| 219,211 | Series 2594, Class VQ, 6.000%, 08/15/20 | 225,681 | ||||||

| 26,317 | Series 2597, Class DS, IF, IO, 7.290%, 02/15/33 | 1,674 | ||||||

| 59,607 | Series 2599, Class DS, IF, IO, 6.740%, 02/15/33 | 1,968 | ||||||

| 147,774 | Series 2610, Class DS, IF, IO, 6.840%, 03/15/33 | 7,715 | ||||||

| 182,873 | Series 2611, Class SH, IF, IO, 7.390%, 10/15/21 | 7,977 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2010 | JPMORGAN INSURANCE TRUST | 5 | ||||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2010 (continued)

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Agency CMO — Continued | ||||||||

| 281,363 | Series 2626, Class KA, 3.000%, 03/15/30 | 284,007 | ||||||

| 460,094 | Series 2626, Class NS, IF, IO, 6.290%, 06/15/23 | 46,928 | ||||||

| 468,292 | Series 2636, Class Z, 4.500%, 06/15/18 | 498,175 | ||||||

| 199,277 | Series 2638, Class DS, IF, 8.340%, 07/15/23 | 200,542 | ||||||

| 4,339 | Series 2643, Class HI, IO, 4.500%, 12/15/16 | 45 | ||||||

| 308,205 | Series 2647, Class A, 3.250%, 04/15/32 | 316,782 | ||||||

| 2,359,229 | Series 2651, Class VZ, 4.500%, 07/15/18 | 2,509,250 | ||||||

| 2,438,000 | Series 2656, Class BG, 5.000%, 10/15/32 | 2,618,670 | ||||||

| 208,147 | Series 2668, Class SB, IF, 6.968%, 10/15/15 | 212,337 | ||||||

| 410,000 | Series 2682, Class LC, 4.500%, 07/15/32 | 435,929 | ||||||

| 159,839 | Series 2682, Class YS, IF, 8.614%, 10/15/33 | 152,082 | ||||||

| 2,500,000 | Series 2684, Class PD, 5.000%, 03/15/29 | 2,553,054 | ||||||

| 131,847 | Series 2684, Class TO, PO, 10/15/33 | 123,877 | ||||||

| 105,775 | Series 2691, Class WS, IF, 8.610%, 10/15/33 | 100,956 | ||||||

| 83,804 | Series 2705, Class SC, IF, 8.610%, 11/15/33 | 80,117 | ||||||

| 127,927 | Series 2705, Class SD, IF, 8.665%, 11/15/33 | 119,418 | ||||||

| 750,000 | Series 2727, Class BS, IF, 8.685%, 01/15/34 | 713,576 | ||||||

| 104,870 | Series 2744, Class FE, VAR, 0.000%, 02/15/34 | 101,871 | ||||||

| 1,144,043 | Series 2749, Class TD, 5.000%, 06/15/21 | 1,179,322 | ||||||

| 2,660 | Series 2753, Class S, IF, 11.479%, 02/15/34 | 2,671 | ||||||

| 98,705 | Series 2755, Class SA, IF, 13.679%, 05/15/30 | 109,210 | ||||||

| 33,263 | Series 2766, Class SX, IF, 15.728%, 03/15/34 | 33,777 | ||||||

| 144,327 | Series 2776, Class SK, IF, 8.685%, 04/15/34 | 140,888 | ||||||

| 126,953 | Series 2780, Class JG, 4.500%, 04/15/19 | 133,786 | ||||||

| 625,000 | Series 2827, Class DG, 4.500%, 07/15/19 | 669,413 | ||||||

| 63,778 | Series 2827, Class SQ, IF, 7.500%, 01/15/19 | 65,590 | ||||||

| 701,402 | Series 2929, Class PC, 5.000%, 01/15/28 | 711,501 | ||||||

| 73,732 | Series 2989, Class PO, PO, 06/15/23 | 69,772 | ||||||

| 300,000 | Series 3047, Class OD, 5.500%, 10/15/35 | 328,546 | ||||||

| 503,675 | Series 3085, Class VS, HB, IF, 27.679%, 12/15/35 | 774,580 | ||||||

| 147,532 | Series 3117, Class EO, PO, 02/15/36 | 128,101 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Agency CMO — Continued | ||||||||

| 172,114 | Series 3260, Class CS, IF, IO, 5.880%, 01/15/37 | 17,459 | ||||||

| 791,486 | Series 3385, Class SN, IF, IO, 5.740%, 11/15/37 | 84,049 | ||||||

| 466,596 | Series 3387, Class SA, IF, IO, 6.160%, 11/15/37 | 69,266 | ||||||

| 832,939 | Series 3430, Class AI, IO, 1.417%, 09/15/12 | 13,269 | ||||||

| 751,569 | Series 3451, Class SA, IF, IO, 5.790%, 05/15/38 | 80,121 | ||||||

| 1,094,954 | Series 3455, Class SE, IF, IO, 5.940%, 06/15/38 | 127,682 | ||||||

| 948,569 | Series 3688, Class NI, IO, 5.000%, 04/15/32 | 130,002 | ||||||

| 299,138 | Series 3759, Class HI, IO, 4.000%, 08/15/37 | 50,219 | ||||||

| 1,300 | Series 47, Class F, 10.000%, 06/15/20 | 1,517 | ||||||

| 1,122 | Series 99, Class Z, 9.500%, 01/15/21 | 1,248 | ||||||

Federal Home Loan Mortgage Corp. STRIPS, | ||||||||

| 479,441 | Series 233, Class 11, IO, 5.000%, 09/15/35 | 97,374 | ||||||

| 951,725 | Series 239, Class S30, IF, IO, 7.440%, 08/15/36 | 149,950 | ||||||

Federal Home Loan Mortgage Corp. Structured Pass-Through Securities, | ||||||||

| 22,551 | Series T-41, Class 3A, VAR, 7.500%, 07/25/32 | 26,224 | ||||||

| 155,237 | Series T-54, Class 2A, 6.500%, 02/25/43 | 178,281 | ||||||

| 70,703 | Series T-54, Class 3A, 7.000%, 02/25/43 | 80,319 | ||||||

| 278,739 | Series T-56, Class APO, PO, | 195,154 | ||||||

| 42,400 | Series T-58, Class APO, PO, 09/25/43 | 30,274 | ||||||

Federal National Mortgage Association REMICS, | ||||||||

| 14,825 | Series 1988-16, Class B, 9.500%, 06/25/18 | 17,000 | ||||||

| 6,870 | Series 1989-83, Class H, 8.500%, 11/25/19 | 8,264 | ||||||

| 1,646 | Series 1990-1, Class D, 8.800%, 01/25/20 | 1,891 | ||||||

| 8,844 | Series 1990-10, Class L, 8.500%, 02/25/20 | 10,633 | ||||||

| 1,262 | Series 1990-93, Class G, 5.500%, 08/25/20 | 1,362 | ||||||

| 31 | Series 1990-140, Class K, HB, 652.145%, 12/25/20 | 411 | ||||||

| 3,008 | Series 1990-143, Class J, 8.750%, 12/25/20 | 3,636 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| 6 | JPMORGAN INSURANCE TRUST | DECEMBER 31, 2010 | ||||

Table of Contents

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Agency CMO — Continued | ||||||||

| 43,917 | Series 1992-101, Class J, 7.500%, 06/25/22 | 46,441 | ||||||

| 21,861 | Series 1992-143, Class MA, 5.500%, 09/25/22 | 24,077 | ||||||

| 64,113 | Series 1993-146, Class E, PO, 05/25/23 | 55,155 | ||||||

| 161,811 | Series 1993-155, Class PJ, 7.000%, 09/25/23 | 181,564 | ||||||

| 4,896 | Series 1993-165, Class SD, IF, 11.347%, 09/25/23 | 5,867 | ||||||

| 24,413 | Series 1993-165, Class SK, IF, 12.500%, 09/25/23 | 31,319 | ||||||

| 12,485 | Series 1993-167, Class GA, 7.000%, 09/25/23 | 12,805 | ||||||

| 223,423 | Series 1993-203, Class PL, 6.500%, 10/25/23 | 246,832 | ||||||

| 21,309 | Series 1993-205, Class H, PO, 09/25/23 | 18,946 | ||||||

| 1,523,453 | Series 1993-223, Class PZ, 6.500%, 12/25/23 | 1,694,031 | ||||||

| 194,583 | Series 1993-225, Class UB, 6.500%, 12/25/23 | 209,562 | ||||||

| 5,285 | Series 1993-230, Class FA, VAR, 0.881%, 12/25/23 | 5,336 | ||||||

| 452,629 | Series 1993-250, Class Z, 7.000%, 12/25/23 | 484,858 | ||||||

| 39,952 | Series 1993-257, Class C, PO, 06/25/23 | 37,498 | ||||||

| 523,872 | Series 1994-37, Class L, 6.500%, 03/25/24 | 595,432 | ||||||

| 4,697,780 | Series 1994-72, Class K, 6.000%, 04/25/24 | 5,166,386 | ||||||

| 38,208 | Series 1995-2, Class Z, 8.500%, 01/25/25 | 44,222 | ||||||

| 83,206 | Series 1995-19, Class Z, 6.500%, 11/25/23 | 94,882 | ||||||

| 9,745 | Series 1996-59, Class J, 6.500%, 08/25/22 | 10,863 | ||||||

| 44,691 | Series 1996-59, Class K, 6.500%, 07/25/23 | 46,130 | ||||||

| 310,618 | Series 1997-20, Class IB, IO, VAR, 1.840%, 03/25/27 | 13,481 | ||||||

| 32,175 | Series 1997-39, Class PD, 7.500%, 05/20/27 | 36,552 | ||||||

| 71,048 | Series 1997-46, Class PL, 6.000%, 07/18/27 | 78,171 | ||||||

| 175,173 | Series 1997-61, Class ZC, 7.000%, 02/25/23 | 197,917 | ||||||

| 64,874 | Series 1998-36, Class ZB, 6.000%, 07/18/28 | 71,611 | ||||||

| 75,184 | Series 1998-43, Class SA, IF, IO, 17.260%, 04/25/23 | 26,740 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Agency CMO — Continued | ||||||||

| 104,178 | Series 1998-46, Class GZ, 6.500%, 08/18/28 | 116,149 | ||||||

| 236,467 | Series 1998-58, Class PC, 6.500%, 10/25/28 | 260,223 | ||||||

| 472,783 | Series 1999-39, Class JH, IO, 6.500%, 08/25/29 | 95,821 | ||||||

| 12,492 | Series 2000-52, Class IO, IO, 8.500%, 01/25/31 | 2,662 | ||||||

| 196,023 | Series 2001-4, Class PC, 7.000%, 03/25/21 | 213,976 | ||||||

| 159,588 | Series 2001-30, Class PM, 7.000%, 07/25/31 | 179,997 | ||||||

| 795,749 | Series 2001-33, Class ID, IO, 6.000%, 07/25/31 | 170,416 | ||||||

| 224,328 | Series 2001-36, Class DE, 7.000%, 08/25/31 | 252,845 | ||||||

| 30,897 | Series 2001-44, Class PD, 7.000%, 09/25/31 | 34,832 | ||||||

| 124,284 | Series 2001-52, Class XN, 6.500%, 11/25/15 | 133,918 | ||||||

| 400,728 | Series 2001-61, Class Z, 7.000%, 11/25/31 | 451,999 | ||||||

| 144,593 | Series 2001-69, Class PG, 6.000%, 12/25/16 | 155,970 | ||||||

| 102,985 | Series 2001-71, Class QE, 6.000%, 12/25/16 | 111,097 | ||||||

| 28,788 | Series 2001-80, Class PE, 6.000%, 07/25/29 | 29,592 | ||||||

| 67,514 | Series 2002-1, Class HC, 6.500%, 02/25/22 | 71,689 | ||||||

| 18,597 | Series 2002-1, Class SA, HB, IF, 24.340%, 02/25/32 | 26,075 | ||||||

| 154,088 | Series 2002-2, Class UC, 6.000%, 02/25/17 | 165,689 | ||||||

| 171,652 | Series 2002-3, Class OG, 6.000%, 02/25/17 | 185,215 | ||||||

| 437,180 | Series 2002-13, Class SJ, IF, IO, 1.600%, 03/25/32 | 21,890 | ||||||

| 199,688 | Series 2002-28, Class PK, 6.500%, 05/25/32 | 222,607 | ||||||

| 782,699 | Series 2002-62, Class ZE, 5.500%, 11/25/17 | 849,229 | ||||||

| 527,908 | Series 2002-68, Class SH, IF, IO, 7.739%, 10/18/32 | 94,437 | ||||||

| 67,380 | Series 2002-77, Class S, IF, 14.006%, 12/25/32 | 77,686 | ||||||

| 10,641 | Series 2002-91, Class UH, IO, 5.500%, 06/25/22 | 607 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2010 | JPMORGAN INSURANCE TRUST | 7 | ||||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2010 (continued)

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Agency CMO — Continued | ||||||||

| 500,000 | Series 2002-94, Class BK, 5.500%, 01/25/18 | 548,781 | ||||||

| 363,371 | Series 2003-7, Class A1, 6.500%, 12/25/42 | 417,422 | ||||||

| 293,000 | Series 2003-22, Class UD, 4.000%, 04/25/33 | 296,512 | ||||||

| 1,211,226 | Series 2003-35, Class MD, 5.000%, 11/25/16 | 1,231,463 | ||||||

| 250,000 | Series 2003-41, Class PE, 5.500%, 05/25/23 | 278,110 | ||||||

| 161,311 | Series 2003-44, Class IU, IO, 7.000%, 06/25/33 | 31,151 | ||||||

| 100,000 | Series 2003-47, Class PE, 5.750%, 06/25/33 | 108,538 | ||||||

| 68,048 | Series 2003-64, Class SX, IF, 13.106%, 07/25/33 | 72,352 | ||||||

| 103,635 | Series 2003-66, Class PA, 3.500%, 02/25/33 | 107,547 | ||||||

| 647,059 | Series 2003-68, Class LC, 3.000%, 07/25/22 | 659,356 | ||||||

| 196,551 | Series 2003-68, Class QP, 3.000%, 07/25/22 | 200,206 | ||||||

| 135,509 | Series 2003-71, Class DS, IF, 7.123%, 08/25/33 | 130,440 | ||||||

| 404,746 | Series 2003-71, Class IM, IO, 5.500%, 12/25/31 | 49,555 | ||||||

| 411,539 | Series 2003-80, Class SY, IF, IO, 7.389%, 06/25/23 | 44,927 | ||||||

| 3,600,000 | Series 2003-81, Class MC, 5.000%, 12/25/32 | 3,858,669 | ||||||

| 600,000 | Series 2003-82, Class VB, 5.500%, 08/25/33 | 657,209 | ||||||

| 70,416 | Series 2003-91, Class SD, IF, 12.066%, 09/25/33 | 78,204 | ||||||

| 201,758 | Series 2003-106, Class US, IF, 8.684%, 11/25/23 | 199,221 | ||||||

| 481,747 | Series 2003-116, Class SB, IF, IO, 7.339%, 11/25/33 | 84,081 | ||||||

| 2,901,667 | Series 2003-128, Class DY, 4.500%, 01/25/24 | 3,067,984 | ||||||

| 69,708 | Series 2003-130, Class SX, IF, 11.129%, 01/25/34 | 78,342 | ||||||

| 102,038 | Series 2003-132, Class OA, PO, 08/25/33 | 91,074 | ||||||

| 1,850,000 | Series 2004-2, Class OE, 5.000%, 05/25/23 | 1,986,769 | ||||||

| 210,675 | Series 2004-4, Class QM, IF, 13.679%, 06/25/33 | 243,068 | ||||||

| 131,251 | Series 2004-10, Class SC, HB, IF, 27.557%, 02/25/34 | 193,316 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Agency CMO — Continued | ||||||||

| 106,859 | Series 2004-14, Class SD, IF, 8.684%, 03/25/34 | 102,222 | ||||||

| 140,663 | Series 2004-21, Class CO, PO, 04/25/34 | 104,209 | ||||||

| 102,368 | Series 2004-22, Class A, 4.000%, 04/25/19 | 105,715 | ||||||

| 272,858 | Series 2004-36, Class SA, IF, 18.808%, 05/25/34 | 346,317 | ||||||

| 204,429 | Series 2004-46, Class SK, IF, 15.783%, 05/25/34 | 237,495 | ||||||

| 43,720 | Series 2004-51, Class SY, IF, 13.719%, 07/25/34 | 50,257 | ||||||

| 150,029 | Series 2004-61, Class SK, IF, 8.500%, 11/25/32 | 158,797 | ||||||

| 1,163,494 | Series 2004-75, Class VK, 4.500%, 09/25/22 | 1,226,794 | ||||||

| 200,000 | Series 2004-76, Class CL, 4.000%, 10/25/19 | 211,317 | ||||||

| 59,227 | Series 2004-92, Class JO, PO, 12/25/34 | 58,538 | ||||||

| 207,636 | Series 2005-28, Class JA, 5.000%, 04/25/35 | 208,761 | ||||||

| 398,074 | Series 2005-45, Class DC, HB, IF, 23.354%, 06/25/35 | 608,031 | ||||||

| 59,437 | Series 2005-47, Class AN, 5.000%, 12/25/16 | 59,947 | ||||||

| 193,786 | Series 2005-52, Class PA, 6.500%, 06/25/35 | 210,540 | ||||||

| 853,000 | Series 2005-68, Class BC, 5.250%, 06/25/35 | 927,624 | ||||||

| 584,533 | Series 2005-84, Class XM, 5.750%, 10/25/35 | 639,800 | ||||||

| 700,000 | Series 2005-110, Class MN, 5.500%, 06/25/35 | 771,403 | ||||||

| 146,623 | Series 2006-22, Class AO, PO, 04/25/36 | 129,110 | ||||||

| 104,981 | Series 2006-46, Class SW, HB, IF, 23.244%, 06/25/36 | 145,015 | ||||||

| 328,716 | Series 2006-59, Class QO, PO, 01/25/33 | 305,578 | ||||||

| 375,526 | Series 2006-110, Class PO, PO, 11/25/36 | 328,615 | ||||||

| 749,240 | Series 2006-117, Class GS, IF, IO, 6.389%, 12/25/36 | 97,473 | ||||||

| 444,795 | Series 2007-7, Class SG, IF, IO, 6.239%, 08/25/36 | 64,759 | ||||||

| 1,155,569 | Series 2007-53, Class SH, IF, IO, 5.839%, 06/25/37 | 159,289 | ||||||

| 474,870 | Series 2007-88, Class VI, IF, IO, 6.279%, 09/25/37 | 68,583 | ||||||

| 758,072 | Series 2007-100, Class SM, IF, IO, 6.189%, 10/25/37 | 89,006 | ||||||

| 790,399 | Series 2008-1, Class BI, IF, IO, 5.649%, 02/25/38 | 100,541 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| 8 | JPMORGAN INSURANCE TRUST | DECEMBER 31, 2010 | ||||

Table of Contents

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Agency CMO — Continued | ||||||||

| 313,389 | Series 2008-16, Class IS, IF, IO, 5.939%, 03/25/38 | 35,728 | ||||||

| 396,804 | Series 2008-46, Class HI, IO, VAR, 6.675%, 06/25/38 | 32,578 | ||||||

| 281,182 | Series 2008-53, Class CI, IF, IO, 6.939%, 07/25/38 | 41,202 | ||||||

| 862,241 | Series 2009-112, Class ST, IF, IO, 5.989%, 01/25/40 | 99,963 | ||||||

| 496,167 | Series 2010-35, Class SB, IF, IO, 6.159%, 04/25/40 | 62,139 | ||||||

| 7,049 | Series G92-15, Class Z, 7.000%, 01/25/22 | 7,125 | ||||||

| 4,249 | Series G92-42, Class Z, 7.000%, 07/25/22 | 4,783 | ||||||

| 110,895 | Series G92-44, Class ZQ, 8.000%, 07/25/22 | 134,044 | ||||||

| 50,611 | Series G92-54, Class ZQ, 7.500%, 09/25/22 | 57,456 | ||||||

| 3,154 | Series G92-59, Class F, VAR, 2.354%, 10/25/22 | 3,244 | ||||||

| 8,541 | Series G92-61, Class Z, 7.000%, 10/25/22 | 9,544 | ||||||

| 18,954 | Series G92-66, Class KA, 6.000%, 12/25/22 | 21,051 | ||||||

| 89,645 | Series G92-66, Class KB, 7.000%, 12/25/22 | 101,212 | ||||||

| 24,987 | Series G93-1, Class KA, 7.900%, 01/25/23 | 28,874 | ||||||

| 25,931 | Series G93-17, Class SI, IF, 6.000%, 04/25/23 | 25,398 | ||||||

Federal National Mortgage Association STRIPS, | ||||||||

| 53,742 | Series 329, Class 1, PO, 01/01/33 | 47,185 | ||||||

| 223,823 | Series 365, Class 8, IO, 5.500%, 05/01/36 | 37,024 | ||||||

Federal National Mortgage Association Whole Loan, | ||||||||

| 89,596 | Series 1999-W1, Class PO, PO, 02/25/29 | 81,141 | ||||||

| 467,028 | Series 1999-W4, Class A9, 6.250%, 02/25/29 | 498,556 | ||||||

| 803,510 | Series 2002-W7, Class A4, 6.000%, 06/25/29 | 885,368 | ||||||

| 537,725 | Series 2003-W1, Class 1A1, 6.500%, 12/25/42 | 617,712 | ||||||

| 68,403 | Series 2003-W1, Class 2A, VAR, 7.500%, 12/25/42 | 78,228 | ||||||

| 91,983 | Series 2004-W2, Class 2A2, 7.000%, 02/25/44 | 108,425 | ||||||

Government National Mortgage Association, | ||||||||

| 75,070 | Series 1994-3, Class PQ, 7.488%, 07/16/24 | 81,290 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Agency CMO — Continued | ||||||||

| 328,878 | Series 1994-7, Class PQ, 6.500%, 10/16/24 | 380,368 | ||||||

| 78,700 | Series 1996-16, Class E, 7.500%, 08/16/26 | 90,440 | ||||||

| 73,732 | Series 1997-8, Class PN, 7.500%, 05/16/27 | 84,566 | ||||||

| 181,840 | Series 1998-22, Class PD, 6.500%, 09/20/28 | 193,827 | ||||||

| 86,314 | Series 1998-26, Class K, 7.500%, 09/17/25 | 100,509 | ||||||

| 57,876 | Series 1999-17, Class L, 6.000%, 05/20/29 | 62,213 | ||||||

| 69,151 | Series 1999-41, Class Z, 8.000%, 11/16/29 | 80,877 | ||||||

| 45,170 | Series 1999-44, Class PC, 7.500%, 12/20/29 | 52,289 | ||||||

| 58,168 | Series 1999-44, Class ZG, 8.000%, 12/20/29 | 68,054 | ||||||

| 39,179 | Series 2000-6, Class Z, 7.500%, 02/20/30 | 44,590 | ||||||

| 67,774 | Series 2000-14, Class PD, 7.000%, 02/16/30 | 74,170 | ||||||

| 259,346 | Series 2000-21, Class Z, 9.000%, 03/16/30 | 314,700 | ||||||

| 31,083 | Series 2000-26, Class Z, 7.750%, 09/20/30 | 37,281 | ||||||

| 4,705 | Series 2000-36, Class IK, IO, 9.000%, 11/16/30 | 1,078 | ||||||

| 800,000 | Series 2000-36, Class PB, 7.500%, 11/16/30 | 928,684 | ||||||

| 57,960 | Series 2000-37, Class B, 8.000%, 12/20/30 | 68,216 | ||||||

| 15,039 | Series 2000-38, Class AH, 7.150%, 12/20/30 | 17,460 | ||||||

| 42,292 | Series 2001-4, Class SJ, IF, IO, 7.889%, 01/19/30 | 7,012 | ||||||

| 2,230,271 | Series 2001-10, Class PE, 6.500%, 03/16/31 (m) | 2,430,582 | ||||||

| 318,482 | Series 2001-22, Class PS, HB, IF, 20.330%, 03/17/31 | 455,649 | ||||||

| 115,232 | Series 2001-36, Class S, IF, IO, 7.789%, 08/16/31 | 22,494 | ||||||

| 299,787 | Series 2001-53, Class SR, IF, IO, 7.889%, 10/20/31 | 35,910 | ||||||

| 154,481 | Series 2001-64, Class MQ, 6.500%, 12/20/31 | 164,262 | ||||||

| 1,000,000 | Series 2001-64, Class PB, 6.500%, 12/20/31 | 1,095,337 | ||||||

| 20,723 | Series 2002-24, Class SB, IF, 11.534%, 04/16/32 | 24,353 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2010 | JPMORGAN INSURANCE TRUST | 9 | ||||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2010 (continued)

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Agency CMO — Continued | ||||||||

| 98,286 | Series 2002-54, Class GB, 6.500%, 08/20/32 | 108,059 | ||||||

| 73,164 | Series 2003-4, Class NI, IO, 5.500%, 01/20/32 | 5,165 | ||||||

| 12,583 | Series 2003-24, Class PO, PO, 03/16/33 | 11,058 | ||||||

| 4,044,598 | Series 2003-59, Class XA, IO, VAR, 1.788%, 06/16/34 | 200,329 | ||||||

| 1,943,139 | Series 2003-75, Class BE, 6.000%, 04/16/28 | 1,976,580 | ||||||

| 200,867 | Series 2003-76, Class LS, IF, IO, 6.939%, 09/20/31 | 17,946 | ||||||

| 684,740 | Series 2004-11, Class SW, IF, IO, 5.239%, 02/20/34 | 80,449 | ||||||

| 57,847 | Series 2004-28, Class S, IF, 18.946%, 04/16/34 | 71,211 | ||||||

| 981,906 | Series 2004-62, Class VA, 5.500%, 07/20/15 | 1,048,433 | ||||||

| 602,494 | Series 2007-45, Class QA, IF, IO, 6.379%, 07/20/37 | 83,305 | ||||||

| 532,245 | Series 2007-76, Class SA, IF, IO, 6.269%, 11/20/37 | 62,782 | ||||||

| 492,987 | Series 2008-2, Class MS, IF, IO, 6.899%, 01/16/38 | 78,728 | ||||||

| 377,497 | Series 2008-55, Class SA, IF, IO, 5.939%, 06/20/38 | 38,799 | ||||||

| 294,688 | Series 2009-6, Class SA, IF, IO, 5.839%, 02/16/39 | 29,972 | ||||||

| 868,253 | Series 2009-6, Class SH, IF, IO, 5.779%, 02/20/39 | 93,547 | ||||||

| 528,278 | Series 2009-14, Class KI, IO, 6.500%, 03/20/39 | 80,277 | ||||||

| 352,923 | Series 2009-14, Class NI, IO, 6.500%, 03/20/39 | 54,306 | ||||||

| 1,152,969 | Series 2009-22, Class SA, IF, IO, 6.009%, 04/20/39 | 117,212 | ||||||

| 1,169,559 | Series 2009-31, Class ST, IF, IO, 6.089%, 03/20/39 | 132,885 | ||||||

| 1,169,559 | Series 2009-31, Class TS, IF, IO, 6.039%, 03/20/39 | 126,547 | ||||||

| 1,371,037 | Series 2009-64, Class SN, IF, IO, 5.839%, 07/16/39 | 148,653 | ||||||

| 321,501 | Series 2009-79, Class OK, PO, 11/16/37 | 289,997 | ||||||

| 693,662 | Series 2009-102, Class SM, IF, IO, 6.139%, 06/16/39 | 76,462 | ||||||

| 1,454,635 | Series 2009-106, Class ST, VAR, 5.739%, 02/20/38 | 173,181 | ||||||

| 480,585 | Series 2010-130, Class CP, 7.000%, 10/16/40 | 540,412 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Agency CMO — Continued | ||||||||

| 935,365 | NCUA Guaranteed Notes, Series 2010-C1, Class APT, 2.650%, 10/29/20 | 910,786 | ||||||

Vendee Mortgage Trust, | ||||||||

| 97,732 | Series 1994-1, Class 1, VAR, 5.627%, 02/15/24 | 105,072 | ||||||

| 225,265 | Series 1996-1, Class 1Z, 6.750%, 02/15/26 | 253,521 | ||||||

| 123,349 | Series 1996-2, Class 1Z, 6.750%, 06/15/26 | 143,200 | ||||||

| 443,400 | Series 1997-1, Class 2Z, 7.500%, 02/15/27 | 524,459 | ||||||

| 123,551 | Series 1998-1, Class 2E, 7.000%, 03/15/28 | 142,508 | ||||||

| 93,210,458 | ||||||||

Non-Agency CMO — 11.1% |

| |||||||

| 7,835 | Adjustable Rate Mortgage Trust, | 7,630 | ||||||

| 200,000 | American General Mortgage Loan Trust, Series 2009-1, Class A7, VAR, 5.750%, 09/25/48 (e) | 201,905 | ||||||

| 500,000 | American Home Mortgage Investment Trust, Series 2005-3, Class 2A4, VAR, 2.159%, 09/25/35 | 221,007 | ||||||

Banc of America Alternative Loan Trust, | ||||||||

| 206,654 | Series 2003-9, Class 1CB2, 5.500%, 11/25/33 | 209,273 | ||||||

| 314,167 | Series 2004-5, Class 3A3, PO, 06/25/34 | 159,547 | ||||||

| 94,079 | Series 2004-6, Class 15PO, PO, 07/25/19 | 69,088 | ||||||

Banc of America Funding Corp., | ||||||||

| 126,652 | Series 2003-1, Class APO, PO, 05/20/33 | 96,996 | ||||||

| 53,304 | Series 2003-3, Class 1A33, 5.500%, 10/25/33 | 53,829 | ||||||

| 96,956 | Series 2004-1, Class PO, PO, 03/25/34 | 77,565 | ||||||

| 753,954 | Series 2005-6, Class 2A7, 5.500%, 10/25/35 | 707,188 | ||||||

| 142,269 | Series 2005-7, Class 30PO, PO, 11/25/35 | 77,164 | ||||||

| 378,980 | Series 2005-E, Class 4A1, VAR, 2.845%, 03/20/35 | 361,588 | ||||||

Banc of America Mortgage Securities, Inc., | ||||||||

| 39,495 | Series 2003-8, Class APO, PO, 11/25/33 | 27,814 | ||||||

| 200,000 | Series 2004-3, Class 1A26, 5.500%, 04/25/34 | 203,969 | ||||||

| 36,082 | Series 2004-4, Class APO, PO, 05/25/34 | 26,607 | ||||||

| 574,052 | Series 2004-5, Class 2A2, 5.500%, 06/25/34 | 561,879 | ||||||

| 250,000 | Series 2004-6, Class 2A5, PO, 07/25/34 | 185,481 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| 10 | JPMORGAN INSURANCE TRUST | DECEMBER 31, 2010 | ||||

Table of Contents

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Non-Agency CMO — Continued |

| |||||||

| 138,961 | Series 2004-6, Class APO, PO, 07/25/34 | 100,059 | ||||||

| 263,352 | Series 2004-7, Class 1A19, PO, 08/25/34 | 201,641 | ||||||

| 275,045 | Series 2004-J, Class 3A1, VAR, 5.095%, 11/25/34 | 254,132 | ||||||

| 1,236,969 | Series 2005-5, Class 1A26, IO, 5.500%, 06/25/35 | 64,530 | ||||||

Bear Stearns Adjustable Rate Mortgage Trust, | ||||||||

| 129,701 | Series 2003-7, Class 3A, VAR, 2.818%, 10/25/33 | 125,564 | ||||||

| 234,911 | Series 2005-5, Class A1, VAR, 2.330%, 08/25/35 | 224,454 | ||||||

| 608,959 | Series 2006-1, Class A1, VAR, 4.625%, 02/25/36 | 540,819 | ||||||

| 295,544 | Citicorp Mortgage Securities, Inc., Series 2004-5, Class 2A5, 4.500%, 08/25/34 | 299,861 | ||||||

Citigroup Mortgage Loan Trust, Inc., | ||||||||

| 32,660 | Series 2003-UP3, Class A3, 7.000%, 09/25/33 | 32,531 | ||||||

| 109,251 | Series 2003-UST1, Class A1, 5.500%, 12/25/18 | 112,131 | ||||||

| 46,442 | Series 2003-UST1, Class PO1, PO, 12/25/18 | 38,099 | ||||||

| 25,228 | Series 2003-UST1, Class PO3, PO, 12/25/18 | 21,506 | ||||||

| 143,708 | Series 2005-1, Class 2A1A, VAR, 2.895%, 04/25/35 | 85,010 | ||||||

Countrywide Alternative Loan Trust, | ||||||||

| 133,284 | Series 2002-8, Class A4, 6.500%, 07/25/32 | 130,836 | ||||||

| 53,507 | Series 2003-J1, Class PO, PO, 10/25/33 | 42,250 | ||||||

| 1,635,687 | Series 2004-2CB, Class 1A9, 5.750%, 03/25/34 | 1,635,687 | ||||||

| 186,735 | Series 2004-18CB, Class 2A4, 5.700%, 09/25/34 | 186,549 | ||||||

| 162,087 | Series 2005-5R, Class A1, 5.250%, 12/25/18 | 166,493 | ||||||

| 904,915 | Series 2005-20CB, Class 3A8, IF, IO, 4.489%, 07/25/35 | 99,167 | ||||||

| 60,553 | Series 2005-26CB, Class A10, IF, 12.578%, 07/25/35 | 60,379 | ||||||

| 1,163,798 | Series 2005-28CB, Class 1A4, 5.500%, 08/25/35 | 992,334 | ||||||

| 600,000 | Series 2005-54CB, Class 1A11, 5.500%, 11/25/35 | 503,693 | ||||||

| 1,579,791 | Series 2005-22T1, Class A2, IF, IO, 4.809%, 06/25/35 | 152,164 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Non-Agency CMO — Continued |

| |||||||

| 1,534,431 | Series 2005-J1, Class 1A4, IF, IO, 4.839%, 02/25/35 | 170,307 | ||||||

| 200,000 | Series 2007-21CB, Class 1A5, 6.000%, 09/25/37 (f) (i) | 47,898 | ||||||

Countrywide Home Loan Mortgage Pass-Through Trust, | ||||||||

| 362,880 | Series 2003-26, Class 1A6, 3.500%, 08/25/33 | 344,039 | ||||||

| 74,470 | Series 2003-34, Class A11, 5.250%, 09/25/33 | 74,835 | ||||||

| 140,523 | Series 2003-44, Class A6, PO, 10/25/33 | 122,342 | ||||||

| 88,469 | Series 2003-J7, Class 4A3, IF, 9.436%, 08/25/18 | 87,199 | ||||||

| 124,101 | Series 2004-7, Class 2A1, VAR, 2.426%, 06/25/34 | 114,407 | ||||||

| 77,578 | Series 2004-HYB1, Class 2A, VAR, 3.072%, 05/20/34 | 66,435 | ||||||

| 100,933 | Series 2004-HYB3, Class 2A, VAR, 2.663%, 06/20/34 | 85,964 | ||||||

| 304,599 | Series 2004-J8, Class 1A2, 4.750%, 11/25/19 | 311,887 | ||||||

| 71,029 | Series 2004-J8, Class POA, PO, 11/25/19 | 58,280 | ||||||

| 500,000 | Series 2005-16, Class A23, 5.500%, 09/25/35 | 452,368 | ||||||

| 510,307 | Series 2005-22, Class 2A1, VAR, 3.100%, 11/25/35 | 393,254 | ||||||

| 50,789 | Credit Suisse First Boston Mortgage Securities Corp., Series 2004-5, Class 5P, PO, 08/25/19 | 42,450 | ||||||

| 340,139 | First Horizon Alternative Mortgage Securities, Series 2005-FA8, Class 1A19, 5.500%, 11/25/35 | 277,183 | ||||||

First Horizon Asset Securities, Inc., | ||||||||

| 78,969 | Series 2003-3, Class 1A4, 3.900%, 05/25/33 | 78,736 | ||||||

| 138,259 | Series 2004-AR7, Class 2A1, VAR, 2.811%, 02/25/35 | 135,923 | ||||||

| 300,000 | Series 2004-AR7, Class 2A2, VAR, 2.811%, 02/25/35 | 273,961 | ||||||

| 277,723 | Series 2005-AR1, Class 2A2, VAR, 2.875%, 04/25/35 | 266,674 | ||||||

GMAC Mortgage Corp. Loan Trust, | ||||||||

| 281,635 | Series 2003-AR1, Class A4, VAR, 3.407%, 10/19/33 | 279,653 | ||||||

| 301,582 | Series 2004-J5, Class A7, 6.500%, 01/25/35 | 308,713 | ||||||

| 650,000 | Series 2005-AR3, Class 3A4, VAR, 3.222%, 06/19/35 | 517,507 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2010 | JPMORGAN INSURANCE TRUST | 11 | ||||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2010 (continued)

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Non-Agency CMO — Continued |

| |||||||

GSR Mortgage Loan Trust, | ||||||||

| 527,761 | Series 2004-6F, Class 1A2, 5.000%, 05/25/34 | 394,202 | ||||||

| 831,825 | Series 2004-6F, Class 3A4, 6.500%, 05/25/34 | 844,245 | ||||||

| 166,246 | Series 2004-10F, Class 2A1, 5.000%, 08/25/19 | 170,991 | ||||||

| 69,858 | Series 2004-13F, Class 3A3, 6.000%, 11/25/34 | 48,501 | ||||||

| 2,212,667 | Indymac Index Mortgage Loan Trust, Series 2005-AR11, Class A7, IO, VAR, 0.325%, 08/25/35 | 19,361 | ||||||

MASTR Adjustable Rate Mortgages Trust, | ||||||||

| 183,389 | Series 2004-13, Class 2A1, VAR, 2.830%, 04/21/34 | 176,799 | ||||||

| 750,921 | Series 2004-13, Class 3A6, VAR, 2.899%, 11/21/34 | 752,150 | ||||||

MASTR Alternative Loans Trust, | ||||||||

| 223,605 | Series 2003-9, Class 8A1, 6.000%, 01/25/34 | 218,652 | ||||||

| 564,473 | Series 2004-4, Class 10A1, 5.000%, 05/25/24 | 577,234 | ||||||

| 355,487 | Series 2004-6, Class 7A1, 6.000%, 07/25/34 | 361,854 | ||||||

| 48,882 | Series 2004-7, Class 30PO, PO, 08/25/34 | 31,724 | ||||||

| 306,403 | Series 2004-8, Class 6A1, 5.500%, 09/25/19 | 309,996 | ||||||

| 352,165 | Series 2004-10, Class 1A1, 4.500%, 09/25/19 | 356,011 | ||||||

MASTR Asset Securitization Trust, | ||||||||

| 98,418 | Series 2003-12, Class 15, PO, 12/25/18 | 82,592 | ||||||

| 152,540 | Series 2004-6, Class 15PO, PO, 05/25/19 | 125,008 | ||||||

| 130,436 | Series 2004-8, Class PO, PO, 08/25/19 | 105,354 | ||||||

| 271,980 | Series 2004-10, Class 15, PO, 10/25/19 | 223,273 | ||||||

| 494,485 | MASTR Resecuritization Trust, Series 2005-PO, Class 3PO, PO, 05/28/35 (e) | 336,250 | ||||||

| 90,416 | MortgageIT Trust, Series 2005-1, Class 1A1, VAR, 0.581%, 02/25/35 | 67,437 | ||||||

| 81,224 | Nomura Asset Acceptance Corp., Series 2004-R2, Class A1, VAR, 6.500%, 10/25/34 (e) | 83,012 | ||||||

| 667,438 | PHH Alternative Mortgage Trust, Series 2007-2, Class 2X, IO, 6.000%, 05/25/37 | 121,644 | ||||||

Residential Accredit Loans, Inc., | ||||||||

| 159,703 | Series 2002-QS8, Class A5, 6.250%, 06/25/17 | 161,660 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Non-Agency CMO — Continued |

| |||||||

| 900,769 | Series 2003-QR19, Class CB4, 5.750%, 10/25/33 | 803,917 | ||||||

| 39,390 | Series 2003-QS3, Class A2, IF, 15.927%, 02/25/18 | 42,954 | ||||||

| 123,246 | Series 2003-QS3, Class A8, IF, IO, 7.339%, 02/25/18 | 14,188 | ||||||

| 292,529 | Series 2003-QS9, Class A3, IF, IO, 7.289%, 05/25/18 | 41,311 | ||||||

| 374,957 | Series 2003-QS14, Class A1, 5.000%, 07/25/18 | 379,664 | ||||||

| 112,455 | Series 2003-QS18, Class A1, 5.000%, 09/25/18 | 115,276 | ||||||

| 42,933 | Residential Asset Securitization Trust, Series 2003-A14, Class A1, 4.750%, 02/25/19 | 44,180 | ||||||

Residential Funding Mortgage Securities I, | ||||||||

| 10,248 | Series 2003-S7, Class A17, 4.000%, 05/25/33 | 10,230 | ||||||

| 10,291 | Series 2003-S12, Class 4A5, 4.500%, 12/25/32 | 10,340 | ||||||

| 220,633 | Series 2005-SA4, Class 1A1, VAR, 3.247%, 09/25/35 | 172,018 | ||||||

| 10,034 | SACO I, Inc. (Bear Stearns), Series 1997-2, Class 1A5, 7.000%, 08/25/36 (e) | 10,462 | ||||||

Salomon Brothers Mortgage Securities VII, Inc., | ||||||||

| 184,331 | Series 2003-HYB1, Class A, VAR, 3.200%, 09/25/33 | 183,054 | ||||||

| 13,726 | Series 2003-UP2, Class PO1, PO, 12/25/18 | 10,442 | ||||||

| 400,000 | Structured Adjustable Rate Mortgage Loan Trust, Series 2004-6, Class 5A4, VAR, 4.934%, 06/25/34 | 386,056 | ||||||

Structured Asset Securities Corp., | ||||||||

| 207,956 | Series 2003-8, Class 1A2, 5.000%, 04/25/18 | 212,953 | ||||||

| 234,849 | Series 2003-33H, Class 1A1, 5.500%, 10/25/33 | 233,357 | ||||||

| 138,320 | Series 2004-20, Class 1A3, 5.250%, 11/25/34 | 141,528 | ||||||

| 8,369 | Series 2005-6, Class 5A8, IF, 13.379%, 05/25/35 | 8,240 | ||||||

WaMu Mortgage Pass-Through Certificates, | ||||||||

| 40,336 | Series 2003-AR8, Class A, VAR, 2.717%, 08/25/33 | 40,640 | ||||||

| 206,399 | Series 2003-AR9, Class 1A6, VAR, 2.711%, 09/25/33 | 198,724 | ||||||

| 140,982 | Series 2003-S4, Class 3A, 5.500%, 06/25/33 | 148,631 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| 12 | JPMORGAN INSURANCE TRUST | DECEMBER 31, 2010 | ||||

Table of Contents

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Collateralized Mortgage Obligations — Continued | |||||||

Non-Agency CMO — Continued |

| |||||||

| 263,047 | Series 2003-S8, Class A4, 4.500%, 09/25/18 | 268,489 | ||||||

| 515,775 | Series 2003-S10, Class A5, 5.000%, 10/25/18 | 523,326 | ||||||

| 39,675 | Series 2003-S10, Class A6, PO, 10/25/18 | 39,500 | ||||||

| 108,255 | Series 2003-S11, Class 2A5, IF, 16.333%, 11/25/33 | 119,217 | ||||||

| 74,148 | Series 2004-AR3, Class A2, VAR, 2.707%, 06/25/34 | 71,673 | ||||||

Washington Mutual Alternative Mortgage Pass-Through Certificates, | ||||||||

| 2,232,723 | Series 2005-2, Class 1A4, IF, IO, 4.789%, 04/25/35 | 312,433 | ||||||

| 775,872 | Series 2005-2, Class 2A3, IF, IO, 4.739%, 04/25/35 | 102,429 | ||||||

| 593,194 | Series 2005-3, Class CX, IO, 5.500%, 05/25/35 | 102,725 | ||||||

| 775,634 | Series 2005-4, Class CB7, 5.500%, 06/25/35 | 661,302 | ||||||

| 60,307 | Series 2005-4, Class DP, PO, 06/25/20 | 40,763 | ||||||

| 220,212 | Series 2005-6, Class 2A4, 5.500%, 08/25/35 | 191,311 | ||||||

| 21,733 | Washington Mutual MSC Mortgage Pass-Through Certificates, Series 2002-MS12, Class A, 6.500%, 05/25/32 | 22,545 | ||||||

Wells Fargo Mortgage-Backed Securities Trust, | ||||||||

| 107,384 | Series 2003-8, Class A9, 4.500%, 08/25/18 | 111,579 | ||||||

| 567,086 | Series 2003-11, Class 1A4, 4.750%, 10/25/18 | 571,173 | ||||||

| 38,221 | Series 2003-11, Class 1APO, PO, 10/25/18 | 32,403 | ||||||

| 138,781 | Series 2003-15, Class 1A1, 4.750%, 12/25/18 | 141,851 | ||||||

| 118,063 | Series 2003-K, Class 1A1, VAR, 4.468%, 11/25/33 | 118,838 | ||||||

| 236,126 | Series 2003-K, Class 1A2, VAR, 4.468%, 11/25/33 | 243,151 | ||||||

| 145,163 | Series 2004-7, Class 2A2, 5.000%, 07/25/19 | 150,976 | ||||||

| 148,021 | Series 2004-EE, Class 3A1, VAR, 2.966%, 12/25/34 | 145,415 | ||||||

| 386,935 | Series 2004-P, Class 2A1, VAR, 2.911%, 09/25/34 | 383,549 | ||||||

| 212,692 | Series 2005-AR8, Class 2A1, VAR, 2.879%, 06/25/35 | 205,839 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Non-Agency CMO — Continued |

| |||||||

| 140,040 | Series 2005-AR16, Class 2A1, VAR, 2.847%, 10/25/35 | 132,368 | ||||||

| 27,297,404 | ||||||||

Total Collateralized Mortgage Obligations | 120,507,862 | |||||||

| Commercial Mortgage-Backed Securities — 1.7% |

| ||||||

Banc of America Commercial Mortgage, Inc., | ||||||||

| 125,000 | Series 2005-3, Class A4, 4.668%, 07/10/43 | 131,299 | ||||||

| 125,000 | Series 2005-3, Class AM, 4.727%, 07/10/43 | 122,758 | ||||||

| 549,925 | Series 2005-6, Class ASB, VAR, 5.195%, 09/10/47 | 583,087 | ||||||

| 250,000 | Series 2006-4, Class A4, 5.634%, 07/10/46 | 268,237 | ||||||

Bear Stearns Commercial Mortgage Securities, | ||||||||

| 250,000 | Series 2005-PWR8, Class A4, 4.674%, 06/11/41 | 262,281 | ||||||

| 233,253 | Series 2005-PWR9, Class AAB, 4.804%, 09/11/42 | 243,085 | ||||||

| 360,000 | Series 2006-PW11, Class A4, VAR, 5.456%, 03/11/39 | 389,228 | ||||||

| 100,871 | Series 2006-PW14, Class A1, 5.044%, 12/11/38 | 102,351 | ||||||

Citigroup Commercial Mortgage Trust, | ||||||||

| 100,000 | Series 2005-C3, Class AM, VAR, 4.830%, 05/15/43 | 102,436 | ||||||

| 43,324 | Series 2006-C4, Class A1, VAR, 5.728%, 03/15/49 | 43,585 | ||||||

| 565,000 | Credit Suisse Mortgage Capital Certificates, Series 2006-C1, Class A4, VAR, 5.539%, 02/15/39 | 607,975 | ||||||

| 100,000 | GMAC Commercial Mortgage Securities, Inc., Series 2006-C1, Class A4, VAR, 5.238%, 11/10/45 | 106,116 | ||||||

| 75,000 | LB-UBS Commercial Mortgage Trust, Series 2005-C1, Class A4, 4.742%, 02/15/30 | 78,557 | ||||||

| 295,381 | Merrill Lynch Mortgage Trust, Series 2005-MCP1, Class ASB, VAR, 4.674%, 06/12/43 | 309,088 | ||||||

| 11,114 | Morgan Stanley Capital I, Series 2006-T23, Class A1, 5.682%, 08/12/41 | 11,181 | ||||||

| 400,000 | TIAA Seasoned Commercial Mortgage Trust, Series 2007-C4, Class A3, VAR, 6.049%, 08/15/39 | 439,695 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2010 | JPMORGAN INSURANCE TRUST | 13 | ||||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2010 (continued)

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Commercial Mortgage-Backed Securities — Continued |

| ||||||

| 346,843 | Wachovia Bank Commercial Mortgage Trust, Series 2004-C15, Class A2, 4.039%, 10/15/41 | 348,613 | ||||||

Total Commercial Mortgage-Backed Securities | 4,149,572 | |||||||

| Corporate Bonds — 13.9% |

| ||||||

Consumer Discretionary — 1.0% |

| |||||||

Automobiles — 0.0% (g) |

| |||||||

| 60,000 | Daimler Finance North America LLC, 7.300%, 01/15/12 | 63,749 | ||||||

Household Durables — 0.0% (g) |

| |||||||

| 50,000 | Newell Rubbermaid, Inc., 4.700%, 08/15/20 | 49,598 | ||||||

Media — 0.9% |

| |||||||

CBS Corp., | ||||||||

| 21,000 | 5.750%, 04/15/20 | 22,316 | ||||||

| 50,000 | 7.875%, 07/30/30 | 59,034 | ||||||

| 125,000 | Comcast Cable Communications LLC, 7.125%, 06/15/13 | 140,255 | ||||||

Comcast Cable Holdings LLC, | ||||||||

| 335,000 | 9.800%, 02/01/12 | 364,625 | ||||||

| 75,000 | 10.125%, 04/15/22 | 101,711 | ||||||

Comcast Corp., | ||||||||

| 100,000 | 5.500%, 03/15/11 | 100,976 | ||||||

| 50,000 | 5.900%, 03/15/16 | 55,977 | ||||||

| 30,000 | 6.500%, 01/15/17 | 34,583 | ||||||

| 35,000 | 6.500%, 11/15/35 | 37,617 | ||||||

| 30,000 | Cox Communications, Inc., 5.450%, 12/15/14 | 33,026 | ||||||

DIRECTV Holdings LLC/DIRECTV Financing Co., Inc., | ||||||||

| 125,000 | 4.600%, 02/15/21 | 123,374 | ||||||

| 125,000 | 6.000%, 08/15/40 | 125,491 | ||||||

| 100,000 | Historic TW, Inc., 9.150%, 02/01/23 | 131,226 | ||||||

| 75,000 | NBC Universal, Inc., 5.950%, 04/01/41 (e) | 74,992 | ||||||

News America, Inc., | ||||||||

| 50,000 | 7.250%, 05/18/18 | 60,326 | ||||||

| 150,000 | 7.300%, 04/30/28 | 169,178 | ||||||

Time Warner Cable, Inc., | ||||||||

| 50,000 | 6.750%, 07/01/18 | 58,284 | ||||||

| 50,000 | 7.300%, 07/01/38 | 58,466 | ||||||

| 70,000 | 8.250%, 02/14/14 | 81,253 | ||||||

Time Warner Entertainment Co. LP, | ||||||||

| 50,000 | 8.375%, 03/15/23 | 62,781 | ||||||

| 25,000 | 8.375%, 07/15/33 | 31,549 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Media — Continued |

| |||||||

| 150,000 | 10.150%, 05/01/12 | 166,563 | ||||||

| 75,000 | Time Warner, Inc., 6.200%, 03/15/40 | 79,729 | ||||||

| 50,000 | Viacom, Inc., 6.250%, 04/30/16 | 56,901 | ||||||

| 2,230,233 | ||||||||

Specialty Retail — 0.1% |

| |||||||

| 70,000 | Home Depot, Inc., 5.400%, 03/01/16 | 78,442 | ||||||

| 75,000 | Lowe’s Cos., Inc., 7.110%, 05/15/37 | 90,220 | ||||||

| 35,000 | Staples, Inc., 9.750%, 01/15/14 | 42,415 | ||||||

| 211,077 | ||||||||

Total Consumer Discretionary | 2,554,657 | |||||||

Consumer Staples — 0.5% |

| |||||||

Beverages — 0.2% |

| |||||||

Anheuser-Busch InBev Worldwide, Inc., | ||||||||

| 50,000 | 7.200%, 01/15/14 (e) | 57,180 | ||||||

| 125,000 | 7.750%, 01/15/19 (e) | 155,543 | ||||||

| 50,000 | Coca-Cola Enterprises, Inc., 8.500%, 02/01/12 | 54,111 | ||||||

| 95,000 | Diageo Capital plc, (United Kingdom), 5.750%, 10/23/17 | 107,750 | ||||||

| 20,000 | Diageo Finance B.V., (Netherlands), 5.300%, 10/28/15 | 22,253 | ||||||

| 15,000 | FBG Finance Ltd., (Australia), 5.125%, 06/15/15 (e) | 15,918 | ||||||

| 412,755 | ||||||||

Food & Staples Retailing — 0.1% |

| |||||||

| 30,000 | CVS Caremark Corp., 6.125%, 09/15/39 | 32,054 | ||||||

Kroger Co. (The), | ||||||||

| 18,000 | 5.400%, 07/15/40 | 17,061 | ||||||

| 25,000 | 7.500%, 04/01/31 | 30,223 | ||||||

| 70,000 | Wal-Mart Stores, Inc., 6.500%, 08/15/37 | 82,239 | ||||||

| 161,577 | ||||||||

Food Products — 0.2% |

| |||||||

| 50,000 | Bunge Ltd. Finance Corp., 5.875%, 05/15/13 | 53,529 | ||||||

| 27,000 | Bunge N.A. Finance LP, 5.900%, 04/01/17 | 27,787 | ||||||

| 50,000 | Kellogg Co., 4.250%, 03/06/13 | 53,070 | ||||||

Kraft Foods, Inc., | ||||||||

| 127,000 | 5.375%, 02/10/20 | 136,686 | ||||||

| 165,000 | 6.125%, 02/01/18 | 188,479 | ||||||

| 100,000 | 6.875%, 02/01/38 | 116,106 | ||||||

| 575,657 | ||||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| 14 | JPMORGAN INSURANCE TRUST | DECEMBER 31, 2010 | ||||

Table of Contents

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Corporate Bonds — Continued |

| ||||||

Household Products — 0.0% (g) | ||||||||

| 83,131 | Procter & Gamble - ESOP, 9.360%, 01/01/21 | 104,374 | ||||||

Total Consumer Staples | 1,254,363 | |||||||

Energy — 0.4% |

| |||||||

Energy Equipment & Services — 0.0% (g) |

| |||||||

| 75,000 | Transocean, Inc., (Cayman Islands), 6.500%, 11/15/20 | 79,629 | ||||||

Oil, Gas & Consumable Fuels — 0.4% |

| |||||||

| 100,000 | Canadian Natural Resources Ltd., (Canada), 5.900%, 02/01/18 | 113,890 | ||||||

ConocoPhillips, | ||||||||

| 25,000 | 5.750%, 02/01/19 | 28,490 | ||||||

| 120,000 | 6.000%, 01/15/20 | 139,711 | ||||||

| 150,000 | Marathon Oil Corp., 6.000%, 10/01/17 | 170,364 | ||||||

| 60,000 | Petro-Canada, (Canada), 6.800%, 05/15/38 | 68,346 | ||||||

| 60,000 | Shell International Finance B.V., (Netherlands), 6.375%, 12/15/38 | 71,114 | ||||||

| 50,000 | Statoil ASA, (Norway), 3.125%, 08/17/17 | 49,512 | ||||||

| 45,000 | Suncor Energy, Inc., (Canada), 6.850%, 06/01/39 | 51,739 | ||||||

| 150,000 | Total Capital S.A., (France), 2.300%, 03/15/16 | 146,530 | ||||||

| 95,000 | XTO Energy, Inc., 5.750%, 12/15/13 | 107,043 | ||||||

| 946,739 | ||||||||

Total Energy | 1,026,368 | |||||||

Financials — 8.3% |

| |||||||

Capital Markets — 2.1% |

| |||||||

Bank of New York Mellon Corp. (The), | ||||||||

| 75,000 | 2.950%, 06/18/15 | 75,962 | ||||||

| 55,000 | 4.600%, 01/15/20 | 57,710 | ||||||

BlackRock, Inc., | ||||||||

| 80,000 | 3.500%, 12/10/14 | 82,961 | ||||||

| 130,000 | 5.000%, 12/10/19 | 135,749 | ||||||

| 65,000 | 6.250%, 09/15/17 | 73,170 | ||||||

| 100,000 | Blackstone Holdings Finance Co. LLC, 5.875%, 03/15/21 (e) | 95,671 | ||||||

Credit Suisse USA, Inc., | ||||||||

| 50,000 | 4.875%, 01/15/15 | 53,907 | ||||||

| 400,000 | 6.125%, 11/15/11 | 419,106 | ||||||

Goldman Sachs Group, Inc. (The), | ||||||||

| 40,000 | 3.700%, 08/01/15 | 40,756 | ||||||

| 375,000 | 4.750%, 07/15/13 | 399,478 | ||||||

| 55,000 | 5.150%, 01/15/14 | 59,238 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Capital Markets — Continued |

| |||||||

| 150,000 | 5.250%, 10/15/13 | 162,333 | ||||||

| 156,000 | 5.375%, 03/15/20 | 161,204 | ||||||

| 100,000 | 5.500%, 11/15/14 | 108,145 | ||||||

| 150,000 | 5.950%, 01/18/18 | 162,733 | ||||||

| 75,000 | 5.950%, 01/15/27 | 71,936 | ||||||

| 100,000 | 6.250%, 09/01/17 | 110,355 | ||||||

| 80,000 | 6.750%, 10/01/37 | 81,792 | ||||||

| 200,000 | 6.875%, 01/15/11 | 200,506 | ||||||

| 125,000 | 7.500%, 02/15/19 | 145,749 | ||||||

Jefferies Group, Inc., | ||||||||

| 55,000 | 3.875%, 11/09/15 | 54,060 | ||||||

| 110,000 | 6.450%, 06/08/27 | 105,173 | ||||||

| 100,000 | 8.500%, 07/15/19 | 114,338 | ||||||

Lehman Brothers Holdings, Inc., | ||||||||

| 315,000 | 0.000%, 11/10/09 (d) | 72,056 | ||||||

| 200,000 | 4.800%, 03/13/14 (d) | 46,250 | ||||||

| 100,000 | 5.750%, 05/17/13 (d) | 23,125 | ||||||

| 175,000 | 6.625%, 01/18/12 (d) | 40,469 | ||||||

| 50,000 | Macquarie Group Ltd., (Australia), 7.300%, 08/01/14 (e) | 54,603 | ||||||

Merrill Lynch & Co., Inc., | ||||||||

| 120,000 | 5.450%, 07/15/14 | 126,160 | ||||||

| 274,000 | 6.150%, 04/25/13 | 294,004 | ||||||

| 135,000 | 6.400%, 08/28/17 | 142,732 | ||||||

| 90,000 | 6.875%, 04/25/18 | 98,492 | ||||||

Morgan Stanley, | ||||||||

| 100,000 | 4.200%, 11/20/14 | 102,164 | ||||||

| 400,000 | 4.750%, 04/01/14 | 409,611 | ||||||

| 300,000 | 5.300%, 03/01/13 | 319,685 | ||||||

| 100,000 | 5.625%, 09/23/19 | 101,968 | ||||||

| 130,000 | 6.250%, 08/28/17 | 140,032 | ||||||

| 100,000 | 6.750%, 04/15/11 | 101,668 | ||||||

| 136,000 | Nomura Holdings, Inc., (Japan), 6.700%, 03/04/20 | 145,560 | ||||||

| 5,190,611 | ||||||||

Commercial Banks — 2.0% |

| |||||||

| 82,000 | Bank of Nova Scotia, (Canada), 3.400%, 01/22/15 | 85,109 | ||||||

Barclays Bank plc, (United Kingdom), | ||||||||

| 110,000 | 2.500%, 01/23/13 | 111,786 | ||||||

| 106,000 | 3.900%, 04/07/15 | 109,303 | ||||||

| 100,000 | 5.200%, 07/10/14 | 108,008 | ||||||

| 150,000 | 6.050%, 12/04/17 (e) | 153,870 | ||||||

BB&T Corp., | ||||||||

| 50,000 | 3.375%, 09/25/13 | 52,362 | ||||||

SEE NOTES TO FINANCIAL STATEMENTS.

| DECEMBER 31, 2010 | JPMORGAN INSURANCE TRUST | 15 | ||||||

Table of Contents

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2010 (continued)

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

| Corporate Bonds — Continued |

| ||||||

Commercial Banks — Continued |

| |||||||

| 110,000 | 3.850%, 07/27/12 | 114,432 | ||||||

| 100,000 | 3.950%, 04/29/16 | 103,214 | ||||||

| 50,000 | 4.900%, 06/30/17 | 52,001 | ||||||

| 75,000 | Branch Banking & Trust Co., 4.875%, 01/15/13 | 79,649 | ||||||

| 150,000 | Credit Suisse, (Switzerland), 5.000%, 05/15/13 | 161,442 | ||||||

| 350,000 | Glitnir Banki HF, (Iceland)10/15/08 (d) (e) (f) (i) | 104,125 | ||||||

HSBC Bank plc, (United Kingdom), | ||||||||

| 100,000 | 3.500%, 06/28/15 (e) | 102,511 | ||||||

| 111,000 | 4.125%, 08/12/20 (e) | 106,684 | ||||||

| 35,000 | KeyCorp, 6.500%, 05/14/13 | 38,000 | ||||||

| 75,000 | Marshall & Ilsley Corp., 5.350%, 04/01/11 | 75,604 | ||||||

National Australia Bank Ltd., (Australia), | ||||||||

| 200,000 | 2.500%, 01/08/13 (e) | 203,802 | ||||||

| 200,000 | 2.750%, 09/28/15 (e) | 196,928 | ||||||

| 100,000 | 3.750%, 03/02/15 (e) | 103,420 | ||||||

| 100,000 | Nordea Bank AB, (Sweden), 1.750%, 10/04/13 (e) | 99,506 | ||||||

PNC Funding Corp., | ||||||||

| 150,000 | 5.125%, 02/08/20 | 156,344 | ||||||

| 25,000 | 5.250%, 11/15/15 | 26,755 | ||||||

| 25,000 | 5.625%, 02/01/17 | 26,723 | ||||||

| 25,000 | 6.700%, 06/10/19 | 28,783 | ||||||

| 200,000 | Rabobank Nederland N.V., (Netherlands), 3.200%, 03/11/15 (e) | 203,600 | ||||||

| 250,000 | SunTrust Banks, Inc., 6.375%, 04/01/11 | 253,151 | ||||||

U.S. Bancorp, | ||||||||

| 90,000 | 2.000%, 06/14/13 | 91,342 | ||||||

| 100,000 | 7.500%, 06/01/26 | 112,337 | ||||||

UBS AG, (Switzerland), | ||||||||

| 250,000 | 3.875%, 01/15/15 | 257,656 | ||||||

| 100,000 | 5.750%, 04/25/18 | 108,673 | ||||||

Wachovia Bank N.A., | ||||||||

| 250,000 | 6.000%, 11/15/17 | 277,366 | ||||||

| 250,000 | 6.600%, 01/15/38 | 275,268 | ||||||

| 250,000 | VAR, 0.632%, 03/15/16 | 234,209 | ||||||

Wachovia Corp., | ||||||||

| 250,000 | 5.500%, 05/01/13 | 272,049 | ||||||

| 50,000 | 5.750%, 02/01/18 | 55,515 | ||||||

| 200,000 | Wells Fargo & Co., 3.750%, 10/01/14 | 208,777 | ||||||

Westpac Banking Corp., (Australia), | ||||||||

| 65,000 | 4.200%, 02/27/15 | 68,221 | ||||||

| PRINCIPAL AMOUNT($) | SECURITY DESCRIPTION | VALUE($) | ||||||

Commercial Banks — Continued |

| |||||||

| 121,000 | 4.875%, 11/19/19 | 127,147 | ||||||

| 4,945,672 | ||||||||

Consumer Finance — 0.5% |

| |||||||

| 50,000 | American Express Credit Corp., 7.300%, 08/20/13 | 56,343 | ||||||

Capital One Financial Corp., | ||||||||

| 65,000 | 5.700%, 09/15/11 | 67,100 | ||||||

| 185,000 | 6.250%, 11/15/13 | 203,050 | ||||||

| 50,000 | 6.750%, 09/15/17 | 57,618 | ||||||

HSBC Finance Corp., | ||||||||

| 13,000 | 4.750%, 07/15/13 | 13,711 | ||||||

| 150,000 | 5.000%, 06/30/15 | 159,330 | ||||||

| 150,000 | 5.250%, 01/15/14 | 161,011 | ||||||

| 50,000 | 7.350%, 11/27/32 | 50,375 | ||||||

| 100,000 | VAR, 0.539%, 01/15/14 | 95,956 | ||||||

| 20,000 | John Deere Capital Corp., 4.500%, 04/03/13 | 21,392 | ||||||

| 100,000 | SLM Corp., 5.375%, 01/15/13 | 101,997 | ||||||

| 87,000 | Toyota Motor Credit Corp., 3.200%, 06/17/15 | 89,866 | ||||||

| 100,000 | Washington Mutual Finance Corp., 6.875%, 05/15/11 | 102,088 | ||||||

| 1,179,837 | ||||||||

Diversified Financial Services — 2.1% |

| |||||||