| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | October 31, 2006 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .19.3 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-7978 |

|

ING Mayflower Trust |

(Exact name of registrant as specified in charter) |

|

7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

(Address of principal executive offices) | | (Zip code) |

|

C T Corporation system, 101 Federal Street, Boston, MA 02110 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-800-992-0180 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | October 31, 2004 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Funds

Annual Report

October 31, 2004

Classes A, B, C and M

International Equity Funds

n ING Emerging Countries Fund

n ING Foreign Fund

n ING International Fund

n ING International SmallCap Growth Fund

n ING International Value Fund

n ING Precious Metals Fund

n ING Russia Fund

Global Equity Funds

n ING Global Equity Dividend Fund

n ING Global Real Estate Fund

n ING Worldwide Growth Fund

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds' investment objectives, risks, charges, expenses and other information. This information should be read carefully.

TABLE OF CONTENTS

| President's Letter | | | 1 | | |

|

| Market Perspective | | | 2 | | |

|

| Portfolio Managers' Reports | | | 4 | | |

|

| Shareholder Expense Examples | | | 24 | | |

|

| Report of Independent Registered Public Accounting Firm | | | 28 | | |

|

| Statements of Assets and Liabilities | | | 29 | | |

|

| Statements of Operations | | | 33 | | |

|

| Statements of Changes in Net Assets | | | 35 | | |

|

| Financial Highlights | | | 40 | | |

|

| Notes to Financial Statements | | | 55 | | |

|

| Portfolios of Investments | | | 70 | | |

|

| Tax Information | | | 96 | | |

|

| Trustee and Officer Information | | | 97 | | |

|

(THIS PAGE INTENTIONALLY LEFT BLANK)

PRESIDENT'S LETTER

Dear Shareholder:

As we complete another six months of serving the needs of investors, we are pleased to see that the conclusion of the recent presidential election appears to have had a positive impact on major U.S. stock markets. With moderately low interest rates being controlled by the Federal Reserve Board, rising corporate earnings, and an increasingly optimistic job outlook, we are hopeful that the economy will continue to prosper through the end of the year.

As always, we continue to look for ways to make investing with our company more pleasant and efficient. When our clients complete a transaction with ING Funds, first and foremost, we want them to have peace of mind.

We are eager to meet these goals and we look forward to continuing to do business with you in the coming year.

Sincerely,

James M. Hennessy

President

ING Funds

December 9, 2004

JAMES M. HENNESSY

1

MARKET PERSPECTIVE: YEAR ENDED OCTOBER 31, 2004

In our semi-annual report, we described economies and markets in a positive context that changed radically on April 2, 2004 with a very bullish U.S. employment report. A few days of euphoria vanished as it became clear that as the job market tightens, inflation picks up and rising interest rates cannot be far away. Stock and bond markets promptly gave back most, if not all of their gains for 2004, and it was in this frame of mind that investors entered the second half of the year. Sentiment would shift again in these six months as economies stumbled, undermined by the price of oil, which resumed its relentless upward march.

Global equities added 4.4%, net of withholding tax on dividends, in the six months ended October 31, 2004, according to the Morgan Stanley Capital International ("MSCI") World Index(1) in dollars, about half due to dollar weakness. For the whole twelve months, global equities returned 13.3%. Among currencies the euro, yen and pound all gained on the dollar, although for much of the time the pendulum swung back and forth. Ultimately the dollar succumbed to record U.S. trade deficits, and in October 2004, to the news that non-U.S. investors were buying fewer U.S. financial assets. Between the end of April and the end of October, the euro appreciated 6.8%, the yen 4.5% and the pound 3.3%.

Investment grade U.S. fixed income classes initially bore the brunt of fears of a new cycle of rising interest rates from multi-decade low levels, as evidence mounted that inflation was on the rise. In the six months ended October 31, 2004, the Federal Reserve ("Fed") would increase the Fed Funds rate three times to 1.75%, even as the economy clearly decelerated again. During this time, the total return of the Lehman Brothers Aggregate Bond Index(2) of investment grade bonds was 4.2%. High yield bonds fared comparatively well, the Lehman Brothers U.S. Corporate High Yield Bond Index(3) returning 6.4% for the six months. The most noteworthy aspect of the last few months of our period was the flattening of the yield curve, where short-term interest rates drifted up in anticipation of continued tightening by the Fed, while bond yields ignored this and fell in the face of uninspiring economic data. For the six months, the yield on 10-year Treasury Notes fell by 47 basis points to 4.0%, but the yield on 13-week Treasury Bills rose 92 basis points to 1.9%.

The U.S. equities market in the form of the Standard & Poor's ("S&P") 500 Index(4), rose 3.0%, including dividends in the six months ended October 31, 2004. At this point, the market was trading at a price to earnings ("P/E") level of around 151/2 times 2005 estimated earnings. As mentioned above, strong monthly employment reports from April 2004 set the tone. After an initial scare about the rise in interest rates that this implied, investors regained their nerve and as the Fed embarked on its tightening cycle at the end of June, the market was challenging its best levels of 2004. And yet in the week before the increase, the wind seemed to shift again with some unexpectedly downbeat economic releases. From July through October, the employment reports were neutral to shockingly weak, while oil prices continued their rise, peaking on Friday, October 22, 2004 at 50% above April 30, 2004 levels. This effective deflationary "tax" on worldwide consumers troubled equity markets, and the S&P 500 I ndex reached its lowest point of 2004 on August 12, 2004. Only in the last few days of October did oil prices fall back significantly, leaving a much relieved stock market to eke out its six-month gain.

Among other major equities markets in the six months ended October 31, 2004, Japan was hardest hit, falling 3.5% in dollars, according to the MSCI Japan Index(5) with net dividends. At that point, stocks were trading at about 161/4 times 2005 estimated earnings. Investors were initially encouraged by surprisingly strong 6.1% first calendar quarter gross domestic product ("GDP") growth. It was well recognized that exports were the source, however. So when, in May 2004, the Chinese government announced its intention to cool its booming economy, which absorbs 32% of Japan's exports, Japanese stocks fell about 5%. The market level of April 30, 2004 would not be seen again until late June and then only briefly as deteriorating economic data and rising oil prices depressed sentiment.

For the six months, European ex UK markets gained 8.2% in dollars, the vast majority due to the weakness of that currency, according to the MSCI Europe ex UK Index(6) with net dividends. Markets in this region were then trading on average at just under 13 times 2005 estimated earnings. Growth in this region appears to be held back by weak domestic demand restrained by high unemployment, nearly 9%, in inflexible labor markets. This region's main attracti on continues to be its relative cheapness, with earnings growth likely to be faster than the U.S. next year. The concern is the fragility of this picture, given its export dependency.

2

MARKET PERSPECTIVE: YEAR ENDED OCTOBER 31, 2004

The UK market rose 7.6% in dollars between April and October 2004, based on the MSCI UK Index(7) with net dividends. The UK market was then trading at 16 times 2005 estimated earnings. The situation in the UK could not have been much more different from that on the Continent. Here, it appears the Bank of England has been trying to cool an economy that strains at full employment, with over-committed, property owning consumers, enriched (at least in their own minds), by a housing price bubble. It was noted with relief that five interest rate increases since November 2003 were at last having an effect, as in the last few days of our reporting period housing prices were reportedly edging down.

(1) The MSCI World Index measures the performance of over 1,400 securities listed on exchanges in the United States, Europe, Canada, Australia, New Zealand and the Far East.

(2) The Lehman Brothers Aggregate Bond Index is composed of securities from the Lehman Brothers Government/Corporate Bond Index, Mortgage-Backed Securities Index, and the Asset-Backed Securities Index. Total return comprises price appreciation/ depreciation and income as a percentage of the original investment.

(3) The Lehman Brothers U.S. Corporate High Yield Bond Index is generally representative of corporate bonds rated below investment-grade.

(4) The Standard & Poor's 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

(5) The MSCI Japan Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan.

(6) The MSCI Europe ex UK Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK.

(7) The MSCI UK Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Funds' current performance is subject to change since the period's end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of the Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

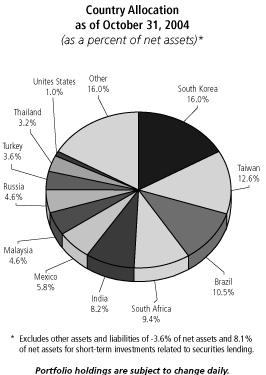

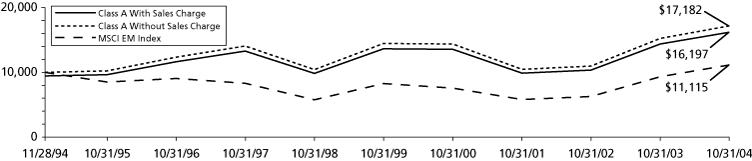

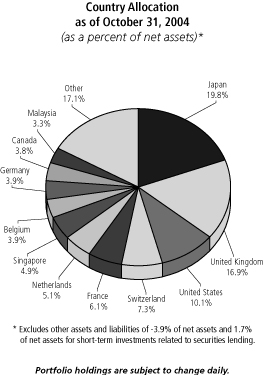

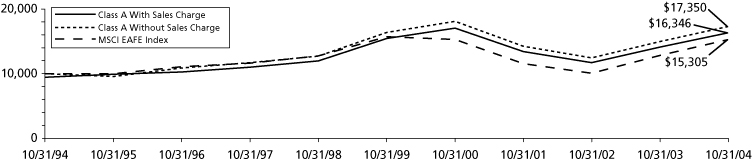

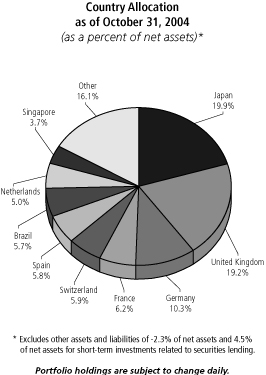

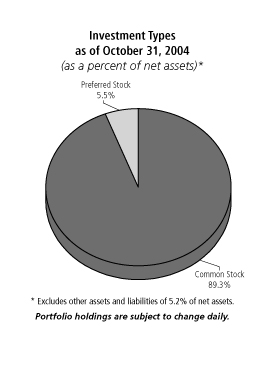

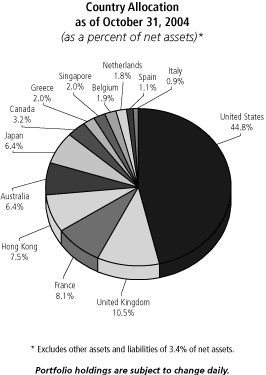

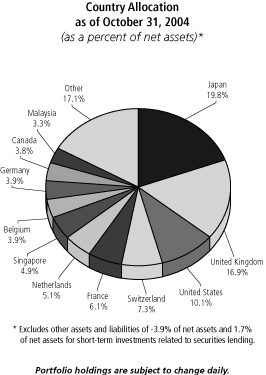

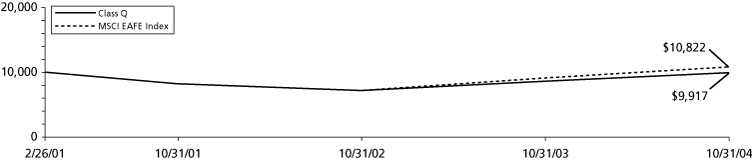

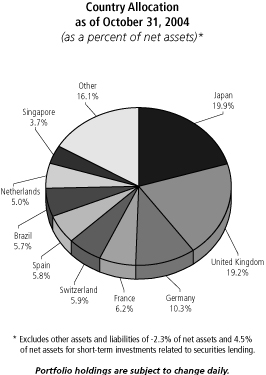

ING EMERGING COUNTRIES FUND

PORTFOLIO MANAGERS' REPORT

The ING Emerging Countries Fund (the "Fund") seeks to maximize long-term capital appreciation. The Fund is managed by Jan-Wim Derks, Director of Global Emerging Markets Equities, and Eric Conrads, Portfolio Manager, ING Investment Management Advisors B.V. - the Sub-Adviser.

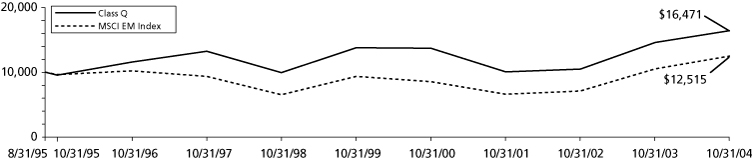

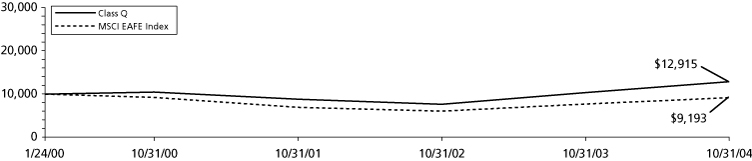

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 12.58% compared to the Morgan Stanley Capital International ("MSCI") Emerging Markets ("EM") Index(5), which returned 19.40% for the same period.

Portfolio Specifics: For the year ended October 31, 2004, the MSCI EM Index outperformed the MSCI World Index(9) by a substantial margin. Emerging Markets continued to perform well on the back of a global increase in risk appetite and a search for higher yielding assets. The year 2003 was one of the best years ever for investors in Emerging Markets equities, and the two final months of 2003 were no exception. Also during the first quarter of 2004, Emerging Markets' performance was strong. However, during the second quarter Emerging Markets suffe red from speculation that the United States Federal Reserve ("Fed") would have to raise interest rates as early as June to slow down the economy. Between mid April and mid May, the markets dropped more then 15%. Once the markets realized that the Fed would only raise rates gradually, they have recovered from the weakness in April/May and are up 10% year-to-date.

Over the reporting period, the Fund has underperformed its MSCI EM benchmark. The Fund's overweight position in Asia has hurt the performance. The Asian region has been lagging the Europe, Middle East, Africa ("EMEA") and Latin American regions for some time. The region is suffering from the current high oil prices and fears of a hard landing of the Chinese economy. In addition, regional stock selection in Korea, Taiwan, South Africa and Brazil was also a major detractor from performance. Our underweight in some commodity producing countries like South Africa and Chile, and our underweight position in the materials sector in general, has also taken its toll. Sector stock selection in energy and materials was also a drag on performance. We missed out on the rally in Hungarian shares due to concerns that the currency was overvalued. In the future, we remain confident that the Asian region will catch up wit h the other regions, and that companies in long-term growth sectors will outperform the ones in highly cyclical sectors.

Current Strategy and Outlook: Including calendar year 2004, Emerging Markets have outperformed developed markets during 5 of the last 6 years. With inflation and interest rates rising across the Global Emerging Markets ("GEMS") universe, it is difficult to anticipate a further strong out performance in the near term. Global economic growth will probably be lower in 2005 than in 2004. As a result, export growth from emerging countries into the United States and China will likely show a slowdown next year. In addition, as a result of higher input prices, corporate margins will be under pressure. However, on the positive side, the fundamentals of Emerging Markets are stronger than during previous periods of globally rising interest rates, and therefore, the vulnerabilities have diminished. Economic growth in emerging countries remains robust with expectations of 5-6% gross domestic product ("GDP") growth on average in 2004/2005. We still believe that the large discount of Emerging Markets vis-à-vis developed markets is unjustified and that Emerging Markets continue to offer good relative value with a 2004/2005 average price to earnings ("P/E") ratio of around 10 times.

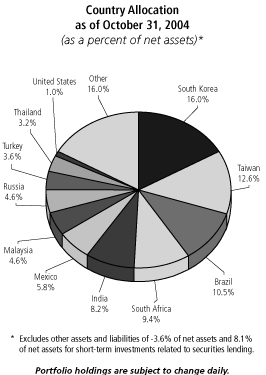

Our investment strategy is to focus on countries where economic growth is robust and on companies with improving cash flows, solid balance sheets in Brazil, Taiwan, India, Thailand and Turkey while shunning South Africa, China, Hungary and Israel.

Top Ten Industries

as of October 31, 2004

(as a percent of net assets)

| Banks | | | 16.4 | % | |

|

| Telecommunications | | | 13.8 | % | |

|

| Oil and Gas | | | 10.9 | % | |

|

| Electrical Components and Equipment | | | 7.4 | % | |

|

| Mining | | | 6.5 | % | |

|

| Chemicals | | | 4.9 | % | |

|

| Engineering and Construction | | | 3.5 | % | |

|

| Semiconductors | | | 2.8 | % | |

|

| Iron/Steel | | | 2.7 | % | |

|

| Electric | | | 2.6 | % | |

|

Portfolio holdings are subject to change daily.

4

ING EMERGING COUNTRIES FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended October 31, 2004 | |

| | | 1 Year | | 5 Year | | Since Inception

of Class A and C

November 28, 1994 | | Since Inception

of Class B

May 31, 1995 | | Since Inception

of Class M

August 5, 2002 | |

| Including Sales Charge: | | | |

|

| Class A(1) | | | 6.10 | % | | | 2.28 | % | | | 4.97 | % | | | - | | | | - | | |

|

| Class B(2) | | | 6.78 | % | | | 2.55 | % | | | - | | | | 5.34 | % | | | - | | |

|

| Class C(3) | | | 10.76 | % | | | 2.65 | % | | | 4.70 | % | | | - | | | | - | | |

|

| Class M(4) | | | 8.15 | % | | | - | | | | - | | | | - | | | | 19.63 | % | |

|

| Excluding Sales Charge: | | | |

|

| Class A | | | 12.58 | % | | | 3.49 | % | | | 5.60 | % | | | - | | | | - | | |

|

| Class B | | | 11.78 | % | | | 2.91 | % | | | - | | | | 5.34 | % | | | - | | |

|

| Class C | | | 11.76 | % | | | 2.65 | % | | | 4.70 | % | | | - | | | | - | | |

|

| Class M | | | 12.07 | % | | | - | | | | - | | | | - | | | | 21.55 | % | |

|

| MSCI EM Index(5) | | | 19.40 | % | | | 6.10 | % | | | 1.07 | %(6) | | | 2.43 | %(7) | | | 27.03 | %(8) | |

|

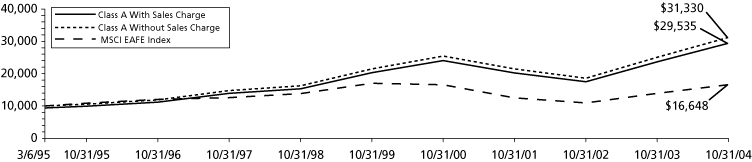

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Emerging Countries Fund against the MSCI EM Index. The Index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reßect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

Total returns reßect the fact that the Investment Manager has waived certain fees and expenses otherwise payable by the Fund. Total returns would have been lower had there been no waiver to the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 5.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 2%, respectively, for the 1 year and 5 year returns.

(3) Reßects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) Reßects deduction of the maximum Class M sales charge of 3.50%.

(5) The MSCI EM Index is an unmanaged index that measures the performance of securities listed on exchanges in developing nations throughout the world.

(6) Since inception performance for index is shown from December 1, 1994.

(7) Since inception performance for index is shown from June 1, 1995.

(8) Since inception performance for index is shown from August 1, 2002.

(9) The MSCI World Index is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East.

5

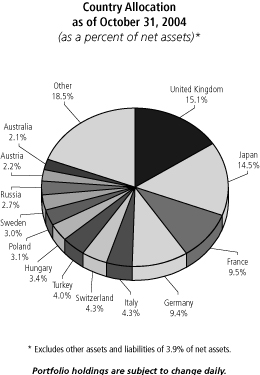

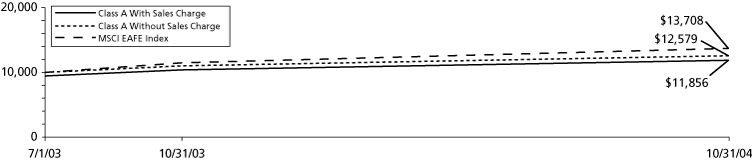

ING FOREIGN FUND

PORTFOLIO MANAGERS' REPORT

The ING Foreign Fund (the "Fund") seeks long-term growth of capital. The Fund is managed by Rudolph-Riad Younes, CFA, Senior Vice President and Head of International Equity and Richard Pell, Senior Vice President and Chief Investment Officer, Julius Baer Investment Management LLC - the Sub-Adviser.

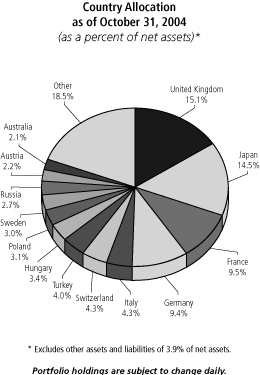

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 14.25% compared to the Morgan Stanley Capital International Europe, Australasia and Far East ("MSCI EAFE") Index(4), which returned 19.27% for the same period.

Portfolio Specifics: During the year ended October 31, 2004, there were several factors, which detracted from our relative results. The allocation to cash equivalents was a detractor to performance during a period where equities exhibited positive results. Our underweight within the United Kingdom and Australia, as well as stock selection detracted from our performance. Finally, stock selection within both the consumer discretionary and consumer staples sectors, as well as stock selection within Switzerland negatively impacted results. Positively contributing to performance were positions held within Eastern Europe and Austria. Many of the top relative performing equities for this period were banking positions in Hungary, Austria, the Czech Republic, Poland and Turkey. Our investments wit hin the emerging markets of Europe have been largely focused on the financial services sector, which we believe will continue to benefit from the growth of the middle class and their demand for financial products and services. Stock selection within the industrial sector, as well as our underweighted position within information technology also positively impacted our relative results.

Much of the relative underperformance within the Fund occurred during the second quarter of 2004. During this period, sentiment shifted toward an environment of risk aversion amid several headline concerns. Specifically, the increase in United States interest rates, rising oil prices and concerns over China's attempts to cool down their fast growing economy elicited a strong response by investors including the hedge fund industry in unwinding speculative positions in emerging markets (equities and debt), Japanese financials, commodities, mining, and various foreign exchange positions. Given our investment within several emerging markets, namely Turkey and Russia, as well as Brazil and India, our relative results were negatively affected during the second quarter of 2004. As the Index against which we are measured does not contain these investments, we underperformed. However, since the end of the second q uarter, many of these markets have rebounded, resulting in our ability to reduce the degree of underperformance relative to the index.

Current Strategy and Outlook: We remain underweight within Japan. With the rise in oil prices, Japan's growth picture appears to be challenged. At the time of this writing, crude oil futures for December delivery prices are still over $48. Concerns that high energy prices may crimp growth and negatively impact corporate earnings have led Japanese stocks lower since the end of the second quarter.

With regard to China, Chinese growth will likely be a force for decades to come. However, recent levels of investment in China are very high, fueled by a credit binge. We believe this investment boom is not sustainable. Investing in basic materials we believe would put us at risk of a short-term slowdown in China, with influential hedge funds dumping both commodities and commodity stocks. Investing in the infrastructure needed to sustain the medium and long term growth of China probably has a better expected return relative to the risk involved.

Within the developed markets of Europe, we continue to have a more defensive bias from a sector perspective. We believe that over the next 6 – 12 months, we may reach peak earnings levels and that the consumer sector may weaken. We remain underweight the United Kingdom as a result of our bottom-up approach to stock selection. The majority of our underweight is attributable to the banking sector, which we view as expensive. We have also commented in previous commentaries on the level of the real estate market, which we find to be unsustainably high.

Our favored area within the international equity strategy remains Eastern Europe. We believe that the region remains the growth engine for the rest of Europe. We find valuations more compelling than in the developed markets and continue to see the development of the middle class as a positive catalyst supporting our investments.

Top Ten Industries

as of October 31, 2004

(as a percent of net assets)

| Banks | | | 20.3 | % | |

|

| Oil and Gas | | | 10.6 | % | |

|

| Telecommunications | | | 7.8 | % | |

|

| Pharmaceuticals | | | 5.8 | % | |

|

| Electric | | | 4.1 | % | |

|

| Food | | | 3.8 | % | |

|

| Investment Companies | | | 3.5 | % | |

|

| Media | | | 3.5 | % | |

|

| Diversified Financial Services | | | 3.5 | % | |

|

| Engineering and Construction | | | 3.2 | % | |

|

Portfolio holdings are subject to change daily.

6

ING FOREIGN FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended October 31, 2004 | |

| | | 1 Year | | Since Inception

of Class A

July 1, 2003 | | Since Inception

of Class B

July 8, 2003 | | Since Inception

of Class C

July 7, 2003 | |

| Including Sales Charge: | |

|

| Class A(1) | | | 7.69 | % | | | 13.58 | % | | | - | | | | - | | |

|

| Class B(2) | | | 8.32 | % | | | - | | | | 12.67 | % | | | - | | |

|

| Class C(3) | | | 12.28 | % | | | - | | | | - | | | | 18.05 | % | |

|

| Excluding Sales Charge: | |

|

| Class A | | | 14.25 | % | | | 18.73 | % | | | - | | | | - | | |

|

| Class B | | | 13.32 | % | | | - | | | | 15.58 | % | | | - | | |

|

| Class C | | | 13.28 | % | | | - | | | | - | | | | 18.05 | % | |

|

| MSCI EAFE Index(4) | | | 19.27 | % | | | 26.68 | %(5) | | | 26.68 | %(5) | | | 26.68 | %(5) | |

|

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Foreign Fund against the MSCI EAFE Index. The Index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reßect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

Total returns reßect the fact that the Investment Manager has waived certain fees and expenses otherwise payable by the Fund. Total returns would have been lower had there been no waiver to the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 5.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 4%, respectively, for the 1 year and since inception returns.

(3) Reßects deduction of the Class C deferred sales charge of 1% for the since inception return.

(4) The MSCI EAFE Index is an unmanaged index that measures the performance of securities listed on exchanges in Europe, Australasia and the Far East.

(5) Since inception performance for index is shown from July 1, 2003.

7

ING INTERNATIONAL FUND

PORTFOLIO MANAGERS' REPORT

The ING International Fund (the "Fund") seeks long-term growth of capital through investment in equity securities and equity equivalents of companies outside the United States. The Fund is managed by a team of investment professionals led by Richard T. Saler and Philip A. Schwartz, CFA, each a Senior Vice President and Director of International Investment Strategy, ING Investment Management Co. (formerly, Aeltus Investment Management, Inc.) - the Sub-Adviser.

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 15.49% compared to the Morgan Stanley Capital International Europe, Australasia and Far East ("MSCI EAFE") Index(4), which returned 19.27% for the same period.

Portfolio Specifics: In the first half of the fiscal year ended October 31, 2004, the Fund was repositioned to a more defensive stance to reflect the expected maturing of the global economic recovery. This strategy proved premature, but was rewarded in the second half of the fiscal year as investors turned more cautious. For the year, the underperformance was primarily attributable to regional allocation as the inclusion of emerging markets stocks and an underweighting in Europe detracted from results. Strong performance from exposure to selected Canadian securities reduced this shortfall somewhat. Within the regions, stock selection proved strong in Developed Asia, but was disappointing in Japan. The opportunity cost of holding residual cash in a strong market also detracted from perform ance.

Sector allocation added value, especially by overweighting the strongly performing energy sector and underweighting the weak technology sector. Stock selection within the financials, industrials and information technology sectors negatively impacted performance This was partly offset by positive contributions in the utilities, consumer discretionary and consumer staples sectors.

At the security level, the largest detractor from performance was previously held Gold Fields Ltd., which was unexpectedly impacted by a surging South African currency. In a weak technology sector, the position in Dutch semiconductor equipment manufacturer ASML Holding NV proved detrimental. Japanese broker Nomura Holdings, Inc. cost performance as the stock corrected sharply after a strong 2003 performance. Accounting issues at the Swiss-based temporary workers' agency Adecco SA, which was held during the period, negatively impacted results. The largest positive contribution was generated in the consumer discretionary sector through our position in OPAP SA, a Greek betting and lottery operator. Italian electric utility Enel S.p.A. and British water utility Severn Trent PLC proved to be good choices in a strong utility sector. Canadian gas and oil producer EnCana Corp. and French oil major Total SA were a lso noteworthy positive contributors.

Current Strategy and Outlook: Global economic growth is expected to decelerate in the coming year. U.S. consumption growth, stimulated in recent years by a convergence of low interest rates and tax cuts, should be less robust going forward. This, combined with a global tax in the form of sustained high energy prices, makes the global demand outlook likely to be weaker than in 2003 and 2004. We believe earnings and cash flow growth in this environment may be relatively modest, with the potential for earnings disappointments rising as 2005 progresses. Adding to the uncertainties is the unresolved war in Iraq. Earnings and cash flow sustainability and visibility, and an increasing focus on quality and financial strength, are therefore characteristics likely to be rewarded. We have positioned the Fund accordingly. At the sector level, we are underweight in the consumer discretionary, industrial and information technology sectors, and overweight in the energy, utilities and financial sectors. Despite the risks described above, we continue to see selective opportunities in the emerging markets, albeit fewer than was the case in 2003 and early 2004.

Top Ten Industries

as of October 31, 2004

(as a percent of net assets)

| Banks | | | 17.9 | % | |

|

| Oil and Gas | | | 10.0 | % | |

|

| Pharmaceuticals | | | 8.1 | % | |

|

| Telecommunications | | | 6.9 | % | |

|

| Electric | | | 5.2 | % | |

|

| Diversified Financial Services | | | 5.0 | % | |

|

| Mining | | | 3.7 | % | |

|

| Agriculture | | | 3.5 | % | |

|

| Semiconductors | | | 3.1 | % | |

|

| Insurance | | | 2.8 | % | |

|

Portfolio holdings are subject to change daily.

8

ING INTERNATIONAL FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended October 31, 2004 | |

| | | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class B

August 22, 2000 | | Since Inception

of Class C

September 15, 2000 | |

| Including Sales Charge: | |

|

| Class A(1) | | | 8.85 | % | | | (0.10 | )% | | | 5.03 | % | | | - | | | | - | | |

|

| Class B(2) | | | 9.72 | % | | | - | | | | - | | | | (4.56 | )% | | | - | | |

|

| Class C(3) | | | 13.60 | % | | | - | | | | - | | | | - | | | | (3.04 | )% | |

|

| Excluding Sales Charge: | |

|

| Class A | | | 15.49 | % | | | 1.09 | % | | | 5.65 | % | | | - | | | | - | | |

|

| Class B | | | 14.72 | % | | | - | | | | - | | | | (4.14 | )% | | | - | | |

|

| Class C | | | 14.60 | % | | | - | | | | - | | | | - | | | | (3.04 | )% | |

|

| MSCI EAFE Index(4) | | | 19.27 | % | | | (0.58 | )% | | | 4.35 | % | | | (1.80 | )%(5) | | | (1.80 | )%(5) | |

|

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING International Fund against the MSCI EAFE Index. The Index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reßect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

Total returns reßect the fact that the Investment Manager has waived certain fees and expenses otherwise payable by the Fund. Total returns would have been lower had there been no waiver to the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 5.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 2%, respectively, for the 1 year and since inception returns.

(3) Reßects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) The MSCI EAFE Index is an unmanaged index that measures the performance of securities listed on exchanges in markets in Europe, Australasia and the Far East.

(5) Since inception performance for the index is shown from September 1, 2000.

Effective November 1, 2001, Class A shares liquidated within 30 days of purchase are subject to a 2% redemption fee.

9

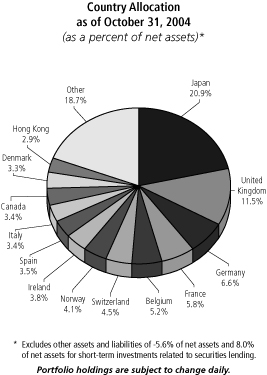

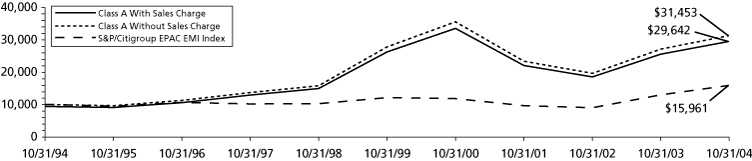

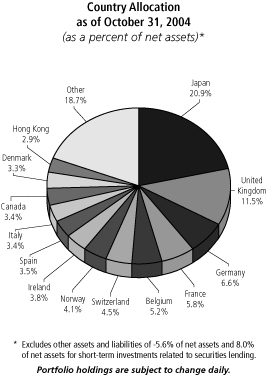

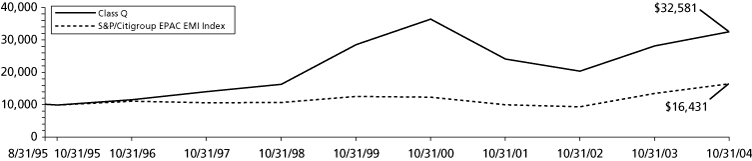

ING INTERNATIONAL SMALLCAP GROWTH FUND

PORTFOLIO MANAGERS' REPORT

The ING International SmallCap Growth Fund (the "Fund") seeks maximum long-term capital appreciation. The Fund is managed by Christopher A. Herrera, Portfolio Manager, Nicholas-Applegate Capital Management - the Sub-Adviser.

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 15.39% compared to the Standard & Poor's/Citigroup Europe, Pacific, Asia Composite/Extended Market Index ("S&P/Citigroup EPAC/EMI")(4), which returned 22.44% for the same period.

Portfolio Specifics: The Fund posted a strong gain in the year ended October 31, 2004; a year which was characterized by a generally favorable global economic and earnings environment, a broad-based decline in the U.S. dollar and rising commodity prices. Holdings in most countries of investment registered solid increases, with notable strength in Norway and Austria, where positions rose by more than 109% and 63%, respectively. Holdings in all sectors advanced except for information technology, as evidence of weakening demand and building inventories amon g technology companies prompted a sell-off in the group. Driven by rising oil prices, the Fund's energy holdings gained more than 50%, making energy one of the best-performing sectors.

While generating an impressive return, the Fund did not keep pace with its Citigroup EPAC/EMI benchmark in the rapidly rising market. One reason the Fund trailed was the fact that international small-cap value stocks outperformed their growth counterparts during the period. This was unfavorable because, consistent with its investment philosophy, the Fund's holdings are concentrated in growth stocks while its style-neutral benchmark includes both growth and value names. Stock selection in the United Kingdom and Germany, as well as the healthcare sector also hurt performance versus the index. Stock selection was positive for the consumer cyclicals and industrial goods and services sectors, but the underweighting versus the benchmark and the currency effect negatively impacted relative returns. On the plus side, stock selection in Norway and the energy and information technology sectors added value relative to the benchmark. An overweight in energy and in information technology was also positive.

Turning to individual stocks, the Fund's best-performing holdings included Frontline Ltd., Precision Drilling Corp. and Marubeni Corp. Frontline Ltd., an oil tanker company based in Bermuda, benefited from favorable industry dynamics, as demand for ships is outpacing vessel capacity. Shares of Precision Drilling Corp., an oil services firm headquartered in Canada, advanced sharply as rising oil prices boosted demand for its drilling rigs. Marubeni Corp., a trading company based in Japan, reported robust earnings driven by increasing prices for many of the commodities it brokers, such as oil, metals and wood pulp.

Current Strategy and Outlook: Nicholas-Applegate's outlook for international small-cap stocks continues to be positive. While economic growth in Continental Europe has been weak, we expect the European Central Bank to maintain interest rates at their present low levels for some time. The Japanese economy continues to gradually expand, and a key measure of Japanese business confidence recently rose to its highest level in more than a decade. We are especially positive about the return prospects of international small-cap growth stocks, as valuations are at attractive levels compared to historical averages.

As a result of our stock-by-stock investment decisions, we are seeing a move in the portfolio toward higher-quality and later-cycle growth companies in the media, healthcare and capital goods industries. This is at the expense of lower-quality, early-cycle companies, which are predominately in the materials, transportation and industrials sectors. At the end of the period, the Fund's largest overweights versus the benchmark were in Norway and the energy sector. The largest underweights were in the United Kingdom and the industrials sector.

Top Ten Industries

as of October 31, 2004

(as a percent of net assets)

| Banks | | | 13.4 | % | |

|

| Retail | | | 9.0 | % | |

|

| Media | | | 5.5 | % | |

|

| Telecommunications | | | 5.2 | % | |

|

| Building Materials | | | 4.9 | % | |

|

| Commercial Services | | | 3.9 | % | |

|

| Pharmaceuticals | | | 3.5 | % | |

|

| Diversified Financial Services | | | 3.3 | % | |

|

| Oil and Gas Services | | | 3.3 | % | |

|

| Miscellaneous Manufacturing | | | 3.2 | % | |

|

Portfolio holdings are subject to change daily.

10

ING INTERNATIONAL SMALLCAP GROWTH FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended October 31, 2004 | |

| | | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class B

May 31, 1995 | |

| Including Sales Charge: | |

|

| Class A(1) | | | 8.76 | % | | | 1.15 | % | | | 11.48 | % | | | - | | |

|

| Class B(2) | | | 9.64 | % | | | 1.41 | % | | | - | | | | 12.83 | % | |

|

| Class C(3) | | | 13.61 | % | | | 1.74 | % | | | 11.23 | % | | | - | | |

|

| Excluding Sales Charge: | |

|

| Class A | | | 15.39 | % | | | 2.36 | % | | | 12.14 | % | | | - | | |

|

| Class B | | | 14.64 | % | | | 1.76 | % | | | - | | | | 12.83 | % | |

|

| Class C | | | 14.61 | % | | | 1.74 | % | | | 11.23 | % | | | - | | |

|

| S&P/Citigroup EPAC/EMI(4) | | | 22.44 | % | | | 5.63 | % | | | 4.79 | % | | | 5.62 | %(5) | |

|

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING International SmallCap Growth Fund against the S&P/Citigroup EPAC/EMI. The Index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reßect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

Total returns reßect the fact that the Investment Manager has waived certain fees and expenses otherwise payable by the Fund. Total returns would have been lower had there been no waiver to the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 5.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 2%, respectively, for the 1 year and 5 year returns.

(3) Reßects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) The S&P/Citigroup EPAC/EMI is an unmanaged index that measures the performance of securities of smaller-capitalization companies in 22 countries excluding the U.S. and Canada.

(5) Since inception performance for index is shown from June 1, 1995.

11

ING INTERNATIONAL VALUE FUND

PORTFOLIO MANAGERS' REPORT

The ING International Value Fund (the "Fund") seeks long-term capital appreciation. The Fund is managed by Brandes Investment Partners, L.P., the Sub-Adviser. Brandes' Large Cap Investment Committee is responsible for making the day-to-day investment decisions for the Fund.

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 24.03% compared to the Morgan Stanley Capital International Europe, Australasia and Far East ("MSCI EAFE") Index(4), which returned 19.27% for the same period.

Portfolio Specifics: Advances for positions in a wide range of industries and countries helped drive the Fund's performance for the year ended October 31, 2004.

From an industry perspective, gains for holdings in diversified telecom services and in commercial banking made the most substantial contribution to performance. Strong performers in these industries included Telefonica SA (Spain), Portugal Telecom SGPA SA (Portugal), and Banco Bilbao Vizcaya Argentaria SA (Spain). Positions in industries such as oil and gas and electric utilities also tended to post gains, while holdings in industries such as food products and food and staples retailing tended to decline.

On a country basis, advances for positions in the United Kingdom and in Japan - including Reuters Group (United Kingdom), which was held during the period, BAE Systems PLC (United Kingdom), and Mitsubishi Tokyo Financial Group, Inc. (Japan) - helped drive returns. Gains for holdings in countries such as Spain and Germany also contributed to results, while modest declines for select positions in the Netherlands and in Canada weighed on performance.

During the period, we sold positions such as Reuters Group PLC (United Kingdom), SABMiller PLC (South Africa), and Komatsu Ltd. (Japan) as appreciation pushed their market prices toward our estimates of their long-term values. We also sold portions of other holdings to reduce their Fund weightings and to pursue other investment opportunities.

New purchases for the year included Volkswagen AG (Germany), GlaxoSmithKline PLC (United Kingdom), and Mitsui Sumitomo Insurance Co., Ltd. (Japan), among others. We also added to select existing holdings at prices that we consider attractive.

Current Strategy and Outlook: During the year ended October 31, 2004, the Fund's country and industry exposures shifted slightly due to stock-specific buying and selling as well as changes in the prices of holdings. For example, exposure to the Netherlands increased, while exposure to the oil and gas industry tended to decline. (Keep in mind that the Fund's weightings for industries and countries are not the product of "top-down" forecasts or opinions, but merely stem from our company-by-company search for compelling investment opportunities in markets around the world.)

Overall, while we offer no predictions regarding the short-term direction of international equity markets, we believe the Fund remains well positioned to deliver favorable long-term results. We acknowledge that many of the Fund's current holdings recently have posted significant gains. However, we believe that all holdings remain undervalued, and we expect to realize significant profit as the market recognizes their true worth.

Top Ten Industries

as of October 31, 2004

(as a percent of net assets)

| Telecommunications | | | 22.2 | % | |

|

| Banks | | | 15.6 | % | |

|

| Food | | | 9.0 | % | |

|

| Pharmaceuticals | | | 7.4 | % | |

|

| Insurance | | | 6.0 | % | |

|

| Electric | | | 4.7 | % | |

|

| Agriculture | | | 4.1 | % | |

|

| Oil and Gas | | | 3.8 | % | |

|

| Chemicals | | | 3.6 | % | |

|

| Miscellaneous Manufacturing | | | 2.8 | % | |

|

Portfolio holdings are subject to change daily.

12

ING INTERNATIONAL VALUE FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended October 31, 2004 | |

| | | 1 Year | | 5 Year | | Since Inception

of Class A and C

March 6, 1995 | | Since Inception

of Class B

April 18, 1997 | |

| Including Sales Charge: | | | |

|

| Class A(1) | | | 16.90 | % | | | 6.42 | % | | | 11.85 | % | | | - | | |

|

| Class B(2) | | | 18.27 | % | | | 6.63 | % | | | - | | | | 10.90 | % | |

|

| Class C(3) | | | 22.25 | % | | | 6.95 | % | | | 11.79 | % | | | - | | |

|

| Excluding Sales Charge: | | | |

|

| Class A | | | 24.03 | % | | | 7.69 | % | | | 12.54 | % | | | - | | |

|

| Class B | | | 23.27 | % | | | 6.94 | % | | | - | | | | 10.90 | % | |

|

| Class C | | | 23.25 | % | | | 6.95 | % | | | 11.79 | % | | | - | | |

|

| MSCI EAFE Index(4) | | | 19.27 | % | | | (0.58 | )% | | | 5.41 | %(5) | | | 4.17 | %(6) | |

|

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING International Value Fund against the MSCI EAFE Index. The Index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reßect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

Total returns reßect the fact that the Investment Manager has waived certain fees and expenses otherwise payable by the Fund. Total returns would have been lower had there been no waiver to the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 5.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 2%, respectively, for the 1 year and 5 year returns.

(3) Reßects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) The MSCI EAFE Index is an unmanaged index that measures the performance of securities listed on exchanges in markets in Europe, Australasia and the Far East.

(5) Since inception performance for index is shown from March 1, 1995.

(6) Since inception performance for index is shown from May 1, 1997.

13

ING PRECIOUS METALS FUND

PORTFOLIO MANAGERS' REPORT

The ING Precious Metals Fund (the "Fund") seeks to attain capital appreciation and hedge against the loss of buying power of the U.S. dollar as may be obtained through investment in gold and securities of companies engaged in mining or processing gold throughout the world. The Fund is managed by James A. Vail, CFA, Senior Vice President and Portfolio Manager, ING Investment Management Co. (formerly, Aeltus Investment Management, Inc.) - the Sub-Adviser.

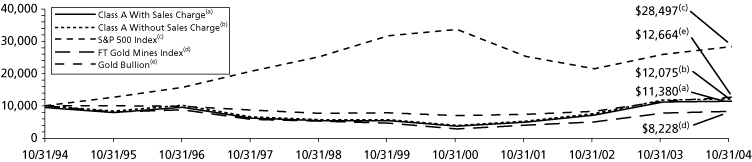

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 2.16% compared to the Standard & Poor's ("S&P") 500 Index(2) and the Financial Times ("FT") Gold Mines Index(3), which returned 9.41% and 7.53%, respectively, for the same period. Gold Bul lion(4) returned 10.88% for the period.

Portfolio Specifics: During the year ended October 31, 2004, Gold Bullion demonstrated a high degree of volatility, opening the period at $384 per ounce, climbing to $426, before retreating to $372 and ending the year at $429 per ounce. Global tensions, a volatile U.S. dollar and global economic growth concerns all contributed to the bullions trading patterns.

During the last twelve months, the gold sector witnessed the emergence of many junior companies possessing attractive exploration potential along with others in early stages of new mine developments. This new investment supply was aggressively received and these shares outperformed the overall sector early in the period. More recently, however, liquidity has dried up and much of the performance has been given back.

Going forward, despite the recent efforts to grow new mine capacity, overall production capacity is expected to decline gradually through 2006/2007, then this decline is expected to accelerate. In this environment, we expect bullion prices to stay high, but with continued volatility.

Based on the universe of precious metals and mining companies, performance benefited from good stock selection, but this was more than offset by under allocating to the gold miners in favor of other metals, mining companies and by holding a cash position averaging nearly 7%. During periods of bullion and stock price volatility, we believe a higher than normal level of cash is warranted, but continue to search for attractive companies capable of growing production in an overall flat industry scenario.

Current Strategy and Outlook: The outlook for lower mine output, and continued currency volatility, bode well for the sustainable higher gold prices over the intermediate term. As global economies strengthen, jewelry demand is expected to rise adding incremental demand to an already tight supply picture. Also, the dollar's performance should continue to influence the price of gold bullion. The growing U.S. current account deficit is expected to put downward pressure on the dollar supporting higher gold prices.

Within this environment, the Fund will continue to seek commitments to companies that can grow production at competitive costs and provide attractive returns to shareholders over the long term.

Industry Allocation

as of October 31, 2004

(as a percent of net assets)

| Gold Mining | | | 63.9 | % | |

|

| Diversified Metals | | | 6.7 | % | |

|

| Metal - Diversified | | | 5.9 | % | |

|

| Silver Mining | | | 5.5 | % | |

|

| Precious Metals | | | 3.3 | % | |

|

| Platinum | | | 3.2 | % | |

|

| Diamonds/Precious Stones | | | 0.4 | % | |

|

Portfolio holdings are subject to change daily.

14

ING PRECIOUS METALS FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Years Ended October 31, 2004 | |

| | | 1 Year | | 5 Year | | 10 Year | |

| Including Sales Charge: | | | |

|

| Class A(1) | | | (3.71 | )% | | | 15.02 | % | | | 1.24 | % | |

|

| Excluding Sales Charge: | | | |

|

| Class A | | | 2.16 | % | | | 16.39 | % | | | 1.84 | % | |

|

| S&P 500 Index(2) | | | 9.41 | % | | | (2.22 | )% | | | 11.04 | % | |

|

| FT Gold Mines Index(3) | | | 7.53 | % | | | 12.59 | % | | | (1.93 | )% | |

|

| Gold Bullion(4) | | | 11.53 | % | | | 7.44 | % | | | 1.09 | % | |

|

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Precious Metals Fund against the S&P 500 Index, the FT Gold Mines Index and the commodity Gold Bullion. The Indices are unmanaged and have no cash in their portfolios, impose no sales charges and incur no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reßect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

Total returns reßect the fact that the Investment Manager has waived certain fees and expenses otherwise payable by the Fund. Total returns would have been lower had there been no waiver to the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 5.75%.

(2) The S&P 500 Index is an unmanaged index that measures the performance of securities of approximately 500 large-capitalization U.S. companies whose securities are traded on major U.S. stock markets.

(3) The FT Gold Mines Index® is an unmanaged cap weighted index that is designed to reflect the performance of the worldwide market in the shares of companies whose principal activity is the mining of gold.

(4) GOLD BULLION IS NOT AN INDEX. It is a commodity.

15

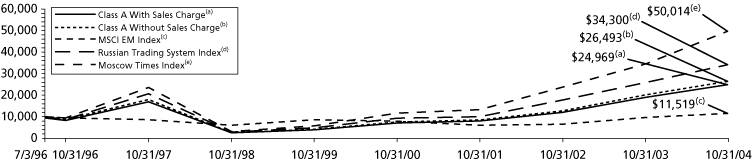

ING RUSSIA FUND

PORTFOLIO MANAGERS' REPORT

The ING Russia Fund (the "Fund") seeks long-term capital appreciation through investment primarily in equity securities of Russian companies. The Fund is managed by Samuel Oubadia, Senior Portfolio Manager, Michiel Bootsma, Investment Manager, Emerging Market Equities, Jan Wim Derks, Director of Global Emerging Markets Equities, and Fritz Moolhuizen, Head of Equity Investments, ING Investment Management Advisors B.V. - the Sub-Adviser.*

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 30.88% compared to the Morgan Stanley Capital International Emerging Markets ("MSCI EM") Index(2) and the Russian Trading System ("RTS") Index(4), which returned 19.40% and 31.84%, respectively, for the same period.

Portfolio Specifics: The Fund performed well for the year ended October 31, 2004; nevertheless, it was a very volatile year for the Russian equity market as the "YUKOS Oil Co. affair" reached its height earlier in 2004. The affair has now continued for over 15 months, and has at times had harsh effects on the entire Russian market.

The overall good performance of the Russian market was underpinned by strong oil prices. As oil stocks still comprise the bulk of the universe of Russian equities, it is perhaps not so surprising that the market continued to perform well. One of the better performing oil stocks was LUKOIL ADR, which gained 54.0% over the year. Recently, the oil giant ConocoPhilips purchased a 7.6% stake in Lukoil from the Russian government for a price of $2.0 billion. The transaction can be viewed as a landmark deal that reinforces the case for FDI in Russia. LUKOIL is the Fund's largest holding. In spite of this, LUKOIL was a source of underperformance, as it comprised about 30.0% of the RTS Index. The Fund was also underweight in the oil company Surgutneftegaz, as the company has a very poor record in its treatment of minority shareholders. As Surgutneftegaz is a large component of the RTS Index, and also a very strong performer, the underweight hurt performance.

The YUKOS Oil Co. ("YUKOS") affair was arguably the most publicized business story of the year making the headlines on a daily basis for a stretch. The affair may have reached its peak in the summer with the news that the government planned to sell YUKOS' main asset as a means of collecting tax claims that date as far back as the year 2000. Clearly, the news had a negative effect on the Fund; however, the underweight of YUKOS until the middle of 2004 was a benefit to the Fund. During the period under review, YUKOS share price plummeted more than 62.0%.

Moving away for the oil and gas sector, another segment of the Russian economy that has performed very well over the past year has been that of mobile telecommunications. Russia's cellular operators have experienced tremendous growth in subscribers with mobile penetration now at 87.0% in Moscow and 34.0% in Russia's other regions. This compares to 67.0% and 17.0%, respectively , at the start of the year. Subsequently, Russia's publicly traded cellular operators Mobile Telesystems OJSC ("MTS") and Vimpel-Communications have seen their share price surge. Over the past year, MTS has jumped 87.3%, while Vimpel-Communications has gained 75.1%. The Fund holds substantial positions in both stocks.

Finally, the Fund's cash holdings ranged between 5.0 and 6.0% during the period under review. This also held back the Fund's performance given that, in spite of the strong volatility, the overall trend of the market was positive over the past year.

Current Strategy and Outlook: Throughout the past year, the Fund has intentionally sought to keep a ceiling on its exposure to the Russian oil sector. Given that the universe of Russian equities is dominated by the oil sector, the Fund makes a point of trying to gain exposure to other segments of the Russian economy. As the oil sector has performed very well in recent months, and because we believe that the oil price is likely to decline from its current levels, we intend to maintain our upper limit on oil stocks.

Even with the assumption that oil prices will fall from the current levels, Russia's economic outlook remains positive. This is based on an expected (year-end 2004) surplus in both the federal budget and the current account. Furthermore, foreign exchange reserves have recently reached an all-time high of over $100 billion.

The issue that draws the most concern among investors is that of economic reform. The negative side of the high commodity prices is that huge tax revenues give the Russian authorities less incentive to push through the reform agenda. The areas where we hope to see more progress are the electricity sector, the banking sector and administrative reform.

*Effective January 1, 2005, Fritz Moolhuizen will no longer be a member of the Portfolio Management team to the Fund.

Top Ten Industries

as of October 31, 2004

(as a percent of net assets)

| Oil and Gas | | | 40.5 | % | |

|

| Telecommunications | | | 17.5 | % | |

|

| Mining | | | 9.0 | % | |

|

| Electric | | | 5.8 | % | |

|

| Investment Companies | | | 5.5 | % | |

|

| Banks | | | 5.2 | % | |

|

| Iron/Steel | | | 5.0 | % | |

|

| Pipelines | | | 2.6 | % | |

|

| Metal Fabricate/Hardware | | | 1.4 | % | |

|

| Internet | | | 1.0 | % | |

|

Portfolio holdings are subject to change daily.

16

ING RUSSIA FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended October 31, 2004 | |

| | | 1 Year | | 5 Year | | Since Inception

July 3, 1996 | |

| Including Sales Charge: | | | |

|

| Class A(1) | | | 23.36 | % | | | 43.49 | % | | | 11.60 | % | |

|

| Excluding Sales Charge: | | | |

|

| Class A | | | 30.88 | % | | | 45.19 | % | | | 12.40 | % | |

|

| MSCI EM Index(2) | | | 19.40 | % | | | 6.10 | % | | | 1.71 | %(3) | |

|

| Russian Trading System Index(4) | | | 31.84 | % | | | 46.60 | % | | | 15.18 | %(3) | |

|

| Moscow Times Index(5) | | | 43.60 | % | | | 54.20 | % | | | 20.57 | %(3) | |

|

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Russia Fund against the MSCI EM Index, the Moscow Times Index and the Russian Trading System Index. The Indices are unmanaged and have no cash in their portfolios, impose no sales charges and incur no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reßect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

Total returns reßect the fact that the Investment Manager has waived certain fees and expenses otherwise payable by the Fund. Total returns would have been lower had there been no waiver to the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 5.75%.

(2) The MSCI EM Index is an unmanaged index that measures the performance of securities listed on exchanges in developing nations throughout the world.

(3) Since inception performance for index is shown from July 1, 1996.

(4) The Russian Trading System Index is a capitalization-weighted index that is calculated in U.S. dollars. The index tracks the performance of Russia's 106 most active stocks traded on the Russian Trading System. The index is operated by the National Association of Participants in the Securities Markets, a non-profit body.

(5) The Moscow Times Index is an unmanaged index that measures the performance of 50 Russian stocks considered to represent the most liquid and most highly capitalized Russian stocks.

Redemptions on shares held less than 365 days are subject to a redemption fee of 2% of the redemption proceeds.

17

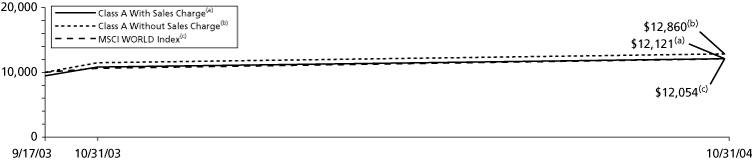

ING GLOBAL EQUITY DIVIDEND FUND

PORTFOLIO MANAGERS' REPORT

The ING Global Equity Dividend Fund (the "Fund") seeks growth of capital with dividend income as a secondary consideration. The Fund is managed by Jorik van den Bos, Director, Global Equities, Joris Franssen, Portfolio Manager and Joost de Graaf, CFA, Senior Investment Manager, ING Investment Management Advisors B.V. - the Sub-Adviser.

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 22.59% compared to the Morgan Stanley Capital International ("MSCI") World Index(4), which returned 13.76% for the same period.

Portfolio Specifics: During the year ended October 31, 2004, the Fund had a very strong performance. Defensive sectors like energy, utilities and real estate performed very well across the board. The Fund's strategy (the "strategy") has large positions in all these sectors. The strategy also benefited from its underweight position in information technology and healthcare. Within financials, the strategy benefited from an overweight position in regional banks, while insurance and diversified financials were underweight. Within consumer staples, a large position in tobacco producers helped the strategy although litigation issues continue to result in higher volatility.

Regionally, the Fund profited from its large position in Emerging Markets and Australia. Both regions still offer many investment opportunities with very attractive dividend yields, sound fundamentals and above average growth prospects.

In general, stock picking clearly had a positive contribution. The best performing stock during the reporting period was Frontline Ltd. (over 300% total return since inclusion in the Fund), one of the world's largest oil-tanker owner by capacity. Quarter after quarter, the company reported record profits as rising demand for crude oil in the U.S. and Asia boosted shipping rates. The company paid several special dividends. The worst performing stock was Merck & Co., Inc. The shares collapsed after the pharmaceutical had to withdraw its Vioxx painkiller. Although near term litigation fears may dominate headlines, the dividend appears to be safe. Also without Vioxx, Merck will continue to generate more than enough operating cash flow to maintain its dividend. Of course, we follow the developments very closely.

During the reporting period, exposure to defensive sectors like real estate, utilities and energy was reduced. A very strong performance in these sectors has resulted in less compelling valuations. The proceeds were invested in more cyclical sectors like materials and industrials. Exposure to healthcare was also increased after a very poor performance in this sector. Regionally, exposure to the United Kingdom was reduced after a very strong performance at the start of the year. The weighting in Euro-zone and Emerging Markets was increased slightly.

Current Strategy and Outlook: The outlook for the Fund remains positive. Investments in defensive sectors like utilities, real estate and consumer staples give the strategy downside protection. These sectors are relatively cheap, less dependent on the economic environment and offer stable, high dividend yields. This will likely result in outperformance versus global equities if they fall significantly.

If the equity markets move sideways, stock selection and the consistent, disciplined strategy will likely add value. In this scenario, dividends will make up for an important part of the total return. This may result in positive absolute returns and outperformance of global equities.

Only in the case of a strong rally it may be difficult to outperform global equities. If the rally is broadly driven, investments in financials and more cyclical sectors like industrials, consumer cyclicals and basic materials are also expected to show a strong performance. A rally driven by growth stocks (especially information technology and healthcare) may be the most difficult environment for the strategy. Although we do not expect that absolute returns will be positive in that scenario.

Top Ten Industries

as of October 31, 2004

(as a percent of net assets)

| Banks | | | 18.6 | % | |

|

| Electric | | | 9.2 | % | |

|

| Telecommunications | | | 8.7 | % | |

|

| Real Estate Investment Trusts | | | 7.0 | % | |

|

| Oil and Gas | | | 7.3 | % | |

|

| Agriculture | | | 4.6 | % | |

|

| Commercial Services | | | 2.8 | % | |

|

| Pharmaceuticals | | | 2.8 | % | |

|

| Diversified Financial Services | | | 2.6 | % | |

|

| Chemicals | | | 2.1 | % | |

|

Portfolio holdings are subject to change daily.

18

ING GLOBAL EQUITY DIVIDEND FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended October 31, 2004 | |

| | | 1 Year | | Since Inception

of Class A

September 17, 2003 | | Since Inception

of Class B

October 24, 2003 | | Since Inception

of Class C

October 29, 2003 | |

| Including Sales Charge: | | | |

|

| Class A(1) | | | 15.54 | % | | | 18.67 | % | | | - | | | | - | | |

|

| Class B(2) | | | 16.92 | % | | | - | | | | 19.57 | % | | | - | | |

|

| Class C(3) | | | 20.99 | % | | | - | | | | - | | | | 22.26 | % | |

|

| Excluding Sales Charge: | | | |

|

| Class A | | | 22.59 | % | | | 25.10 | % | | | - | | | | - | | |

|

| Class B | | | 21.92 | % | | | - | | | | 23.47 | % | | | - | | |

|

| Class C | | | 21.99 | % | | | - | | | | - | | | | 22.26 | % | |

|

| MSCI World Index(4) | | | 13.76 | % | | | 18.82 | %(5) | | | 13.76 | %(6) | | | 13.76 | %(6) | |

|

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Global Equity Dividend Fund against the FTSE World Index and the MSCI World Index. The Indices are unmanaged and have no cash in their portfolios, impose no sales charges and incur no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance graph and table do not reßect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

Total returns reßect the fact that the Investment Manager has waived certain fees and expenses otherwise payable by the Fund. Total returns would have been lower had there been no waiver to the Fund.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's current performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

It is important to note that the Fund has a limited operating history. Performance over a longer period of time may be more meaningful than short-term performance.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 5.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 4%, respectively, for the 1 year and since inception returns.

(3) Reßects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) The MSCI World Index is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East.

(5) Since inception performance for the index is shown from October 1, 2003.

(6) Since inception performance for the index is shown from November 1, 2003.

19

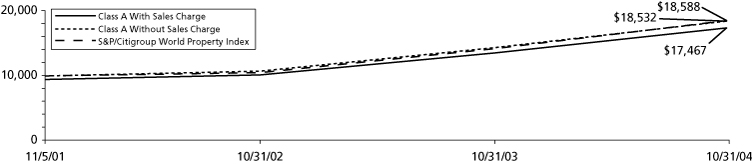

ING GLOBAL REAL ESTATE FUND

PORTFOLIO MANAGERS' REPORT

The ING Global Real Estate Fund (the "Fund") seeks to provide investors with high total return. The Fund is managed by T. Ritson Ferguson, Chief Investment Officer, Kenneth D. Campbell, Managing Director and Steven D. Burton, Director and Portfolio Manager, ING Clarion Real Estate Securities L.P. - the Sub-Adviser.

Performance: For the year ended October 31, 2004, the Fund's Class A shares, excluding sales charges, provided a total return of 28.90% compared to the Standard & Poor's ("S&P")/Citigroup World Property Index(4), which returned 30.79% for the same period.

Portfolio Specifics: The Fund recorded total return of 28.9% for the year ended October 31, 2004, versus 30.8% for the S&P/Citigroup World Property Index with less volatility than that of the benchmark (13.9% standard deviation of monthly total returns for the Fund versus 14.6% benchmark). Relative underperformance of the Fund was caused by stock selection, most notably the drag caused by an average 2.6% cash position, which if invested with the rest of the Fund would have increased the return by 75 basis points given the 28.9% return, and being on the short end of some mergers and acquisitions (for example, General Growth Properties, Inc.'s acquisition of Rouse Company announced in August, causing 40 basis points relative underperformance).

The Fund was generally well positioned geographically, as underweights in North America and the Asia-Pacific region plus an overweight in Europe all were the right calls based on relative total return. Europe, where the Fund was overweighted, recorded total return of 46.3%, as both continental Europe (44.7%) and the UK (47.5%) were strong. The Fund's underweight in the Asia-Pacific region also proved to be the correct relative decision as the highly volatile Hong Kong and Japan markets underperformed - Hong Kong was 15.5% and Japan 23.4%; Australia was the only bright light among major countries in this region 31.4%. Total return for the Asia-Pacific region over the past year was 23.7%. Total return for North America was just shy of the global index total return for the year at 29.6% versus 30.8% for the global index, with much of this return achieved over the past six months.