UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8056

Praxis Mutual Funds

(Exact name of registrant as specified in charter)

1110 N. Main Street

Goshen, IN 46527

(Address of principal executive offices) (Zip code)

Anthony Zacharski

Dechert LLP

200 Clarendon Street, 27th Floor

Boston, MA 02116

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 977-2947

Date of fiscal year end: December 31

Date of reporting period: December 31, 2014

| Item 1. | Reports To Stockholders. |

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Praxis Mutual Funds

Annual Report

for the 12 months ending Dec. 31, 2014

| Praxis Mutual Funds | Class A | Class I | ||

| Intermediate Income Fund | MIIAX | MIIIX | ||

| International Index Fund | MPLAX | MPLIX | ||

| Value Index Fund | MVIAX | MVIIX | ||

| Growth Index Fund | MGNDX | MMDEX | ||

| Small Cap Fund | MMSCX | MMSIX | ||

| Praxis Genesis Portfolios | Class A | |||

| Conservative Portfolio | MCONX | |||

| Balanced Portfolio | MBAPX | |||

| Growth Portfolio | MGAFX | |||

| Message from the President | Annual report to shareholders |

Dear Praxis shareholder:

In many ways, 2014 was a continuation on the theme we’ve experienced over the past few years. The U.S. economy continued to improve – sometimes with surprising strength – while the rest of the world struggled to regain its prior form. For one thing, the unemployment rate in the U.S. fell throughout the year. Economic growth was slow in the first quarter (in part due to weather), but it regained its strength during the second and third quarters. And, corporate profits continued to be fairly strong.

All of this is good news for the average investor, who is hoping to achieve a positive return. But, increasingly, investors want to accomplish more than just a positive return in their portfolios. More and more people hope to make an impact through their investments – looking for ways to enhance and enrich their local and global communities.

This is exactly what Praxis Mutual Funds is trying to accomplish, through our stewardship investing strategy – a philosophy of financial decision-making that balances social and financial considerations and is motivated and informed by Praxis Mutual Funds’ faith convictions. Our focus is driven by our core values, which include the need to respect the dignity and value of all people, demonstrate a concern for justice in a global society and work toward environmental sustainability.

At Praxis, we apply this approach to all of our mutual funds. Particularly noteworthy is the Praxis Intermediate Income Fund, which holds more than 17 percent of its assets in positive social impact bonds. In 2014, some of the most significant purchases made by the Fund include:

| • | $2.5 million in the first ever Education, Youth and Employment (EYE) Bond through the Inter-American Development Bank, designed to support loans that specifically focus on education, youth and employment programs in the Caribbean and Latin America. |

| • | $1 million in the very first REIT green bond through Regency Centers, and another $1 million in a green bond offering from Vornado Realty, to go toward the acquisition, construction, development or redevelopment of LEED certified buildings. |

| • | Along with Everence, a $3.5 million purchase in the auto industry’s inaugural green bond through Toyota Financial Services. Proceeds of the bond will fund new retail finance and lease contracts for qualified Toyota and Lexus hybrid or alternative fuel powertrain vehicles. |

At Praxis, we are committed to looking at both our financial returns and the impact of our investments on others. This is why we continue to participate in green bonds and other positive impact investments.

On the following pages, you will find portfolio managers’ letters and performance reviews for each of the Praxis Mutual Funds. I encourage you to read these letters for further explanation of our investment strategies and perspectives. In addition, you will find an update on our stewardship investing activities. The work we do on your behalf in company screening, shareholder advocacy and community development are reminders that you are investing in what matters.

Thank you for investing in what matters, with Praxis Mutual Funds. We are doing better together – making a difference in the world, one investment at a time. We appreciate your support.

Sincerely,

David C. Gautsche

President

Praxis Mutual Funds are advised by Everence Capital Management and distributed through FINRA member BHIL Distributors, Inc.

The Fund’s stewardship investing strategy could cause the fund to sell or avoid securities that may subsequently perform well, and the application of social screens may cause the Fund to lag the performance of its index.

The views expressed are those of the Praxis Mutual Funds president as of Dec. 31, 2014, are subject to change, and may differ from the views of portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. All data referenced are from sources deemed to be reliable but cannot be guaranteed. Securities and sectors referenced should not be construed as a solicitation or recommendation or be used as the sole basis for any investment decision.

1

| Message from the Vice President of Stewardship Investing | Annual report to shareholders |

The implementation of a strong, values-driven investment program integrating environmental, social and governance (ESG) considerations can take many forms. Praxis Mutual Funds continually works to expand its efforts in these areas, exploring all opportunities to help ensure our processes reflect our strong commitment to stewardship investing values. Some of the highlights in 2014 include:

| • | Implementation of a new environmental screen designed to integrate forward-looking data related to the impact of climate change. Launched at the end of 2013, we have worked closely with long-time social research partner, MSCI ESG Research, to ensure we are making a difference through our investments, and not just a statement as the world moves toward a low carbon future. This new screen significantly impacted our list of restricted companies, adding all coal and nearly-all major tar sands companies, in addition to others with high climate risk. |

| • | Relatedly, Praxis has continued its commitment to help fund the low-carbon energy transition through the Praxis Intermediate Income Fund, which has become a recognized leader in green bonds and renewable energy investments. In 2014, the Fund invested in at least three-quarters of the new-issue, U.S. labeled green bonds – making it one of the most committed investors in these types of investments in the socially responsible investing mutual fund space. In addition, we continue to invest in other “positive social impact” bonds, which altogether account for over 17 percent of the Fund’s assets. |

| • | Proxy voting remains a critical means of communicating our concerns and priorities as values-driven investors to the management of the corporations in which we invest. In 2014, we supported shareholder measures to encourage positive policy changes and corporate reform. Overall, Praxis voted on more than 10,000 corporate resolutions during 784 company meetings, addressing issues of corporate governance, environmental practices and human rights. |

| • | Shareholder advocacy remains one of our most effective tools in impacting the world through our investments. In 2014, through collaborative shareholder advocacy work, Praxis was pleased to be part of positive corporate changes, including: |

Avon’s announcement to remove triclosan, a suspected endocrine disrupter, from all beauty and personal care products.

Anglo American’s decision to withdraw from the proposed Pebble Mine project in Bristol Bay, Alaska, which threatened endangered habitats and indigenous communities.

ConocoPhillips’s commitment to set an aggressive 3 to 5 percent carbon-reduction target for 2015, following shareholder engagement on concerns about carbon asset risk.

Statoil’s withdrawal, for a minimum of three years, from its tar sands project in Alberta, Canada. This follows productive engagement with shareholders on the topic of carbon asset risk.

Prior to the August United Nations Climate Summit, a joint call with over 350 global investors – including Praxis – representing over $24 trillion in assets, asking government leaders to provide stable, reliable and economically meaningful carbon pricing that helps redirect investment commensurate with the scale of the climate change challenge.

Hershey’s first corporate sustainability report detailing its efforts to address poverty and child slavery in West Africa. This report includes the announcement that Hershey purchased nearly 18 percent of its cocoa beans in 2013 from sources certified for environmental and labor standards, nearly doubling its earlier projections. The company is seeking to purchase 100 percent certified beans by 2020.

Amazon, at the urging of a shareholder coalition including Praxis, removed many semi-automatic weapons accessories from its online catalog.

| • | Praxis Mutual Funds continues to be a leader among SRI/ESG mutual funds in dedicating a full 1 percent in every Fund to community development investing. These investments focus on opening doors of economic opportunity for disadvantaged individuals and communities. Recent investments include: |

Partners for the Common Good, a faith-based community lending organization making loans across the country.

Craft3, a community development financial institution with a mission to strengthen economic, ecological and family resilience in Pacific Northwest.

Opportunity Fund, a California-based microloan and micro-savings institution.

2

| Message from the Vice President of Stewardship Investing (continued) | Annual report to shareholders |

We believe you – and our world – deserve to engage every opportunity to make a difference through the investments you hold. Praxis Mutual Funds is committed to understanding and implementing these opportunities while faithfully and productively managing financial performance.

Mark Regier

Vice President of Stewardship Investing

Everence Financial

Praxis Mutual Funds are advised by Everence Capital Management and distributed through FINRA member BHIL Distributors, Inc.

The views expressed are those of the Praxis Mutual Funds Vice President of Stewardship Investing as of Dec. 31, 2014, are subject to change, and may differ from the views of portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. All data referenced are from sources deemed to be reliable but cannot be guaranteed. Securities and sectors referenced should not be construed as a solicitation or recommendation or be used as the sole basis for any investment decision.

3

Praxis Intermediate Income Fund

Annual report to shareholders

Portfolio Managers’ Commentary

For the year ended Dec. 31, 2014, the Praxis Intermediate Income Fund’s Class I Shares had a return of 5.66 percent, and the Class A Shares (without load) returned 5.21 percent. The Barclays U.S. Aggregate Bond Index, the Fund’s benchmark, returned 5.97 percent.

The Fund and the benchmark both benefitted, on an absolute basis, from the sharp decline in Treasury rates for maturities five years and longer. The five-year Treasury began the year at 1.74 percent and ended it at 1.65 percent. Further out the yield curve, the 10-year Treasury yield fell from 3.03 percent to 2.17 percent, while the 30-year Treasury fell from 3.70 percent to 2.75 percent. When bond prices rise, interest rates generally fall. The longer the maturity, the greater the price increase for a given fall in interest rates. We generally expected interest rates to rise in 2014, and that led us to have a shorter duration than the benchmark. This call on interest rates was the biggest factor for our underperformance versus the benchmark.

For the year, the best performing asset classes were CMBS (Commercial Mortgage Backed Securities), ABS (Asset Backed Securities) and agencies. The Fund was overweight in all three of these asset classes, and this was beneficial to our performance versus the benchmark.

For 2015, we expect a continuation from the second half of 2014 of the solid growth pattern for the U.S. economy. We expect growth to be around 3 percent. We also expect the unemployment rate to fall below 5.5 percent, which should lead the Federal Reserve to begin raising the federal funds rate in 2015.

While we believe that eventually this will push interest rates up across the yield curve, there are some major uncertainties. First, Europe is struggling to generate any economic growth, which is leading the European Central Bank to engage in quantitative easing. This has driven interest rates in Germany to record lows. As a result, capital is flowing to the U.S. bond market to buy bonds at interest rates that are comparatively high.

Further, falling oil prices are driving down inflation, which lessens the Federal Reserve’s urgency to raise interest rates. On top of this, the dollar is strong versus other currencies. So while normally a strong economy in the U.S. and a more restrictive Federal Reserve policy would push up rates, this has only happened for short maturities so far. We do not believe that rates will stay low throughout the year, but these factors may limit how high rates will rise.

One of the more exciting parts of 2014 for the Fund was the growth of the positive impact bond portion of our portfolio. By year-end, 17 percent of the Fund was invested in bonds that benefit the climate and/or the community. This story has been attracting interest from new investors around the country. Putting positive impact bonds in the Fund that have competitive returns at appropriate risk levels has made for a very compelling story.

As we move into 2015, we are positioned for higher rates in the long run, but are looking at a variety of strategies to take advantage of the opportunities we see in corporate bonds and other parts of the bond market.

Benjamin J. Bailey, CFA®

Praxis Intermediate Income Fund Co-Manager

Everence Financial

Delmar King

Praxis Intermediate Income Fund Co-Manager

Everence Financial

The views expressed are those of the portfolio managers as of Dec. 31, 2014, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. All data referenced are from sources deemed to be reliable but cannot be guaranteed. Securities and sectors referenced should not be construed as a solicitation or recommendation or be used as the sole basis for any investment decision.

4

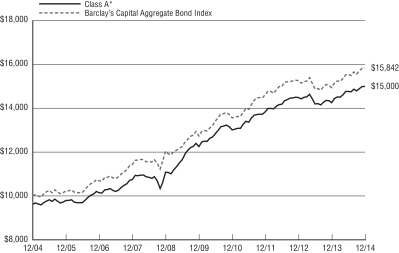

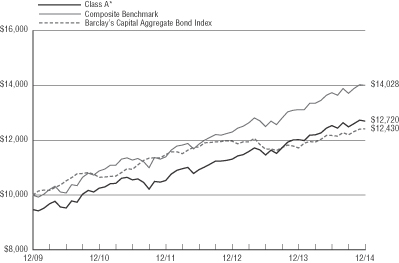

Praxis Intermediate Income Fund

Growth of $10,000 investment from 12/31/04 to 12/31/14

This chart represents historical performance of a hypothetical investment of $10,000 in Class A Shares (adjusted for the maximum sales charge of 3.75%) of the Fund and the Barclay’s Capital Aggregate Bond Index from 12/31/04 to 12/31/14, and includes the reinvestment of dividends and capital gains.

| Annualized | |||||||||||||||||||||||||||||||||||

Inception Date | One Year Ended | Three Year Ended | Five Year Ended | Ten Year Ended | Expense Ratio** Gross / Net | ||||||||||||||||||||||||||||||

| Intermediate Income Fund | |||||||||||||||||||||||||||||||||||

| Class A (Without Load) | 5.21% | 2.68% | 4.13% | 4.54% | 1.00% | 0.95% | |||||||||||||||||||||||||||||

| Class A * | 1.26% | 1.40% | 3.34% | 4.14% | |||||||||||||||||||||||||||||||

| Class I ** | 5/1/06 | 5.66% | 3.08% | 4.55% | 4.83% | 0.55% | 0.55% | ||||||||||||||||||||||||||||

| Barclays Capital Aggregate Bond Index1 | 5.97% | 2.66% | 4.45% | 4.71% | |||||||||||||||||||||||||||||||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. These performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance information current to the most recent month end, please visit www.praxismutualfunds.com.

The total returns shown reflect any expenses that were contractually or voluntarily reduced, reimbursed or paid by any party during the periods presented. In such instances, and without this activity, the total returns would have been lower.

* The total return figures shown reflect the maximum sales charge applicable to Class A Shares. Class A Shares have a maximum sales charge on purchases of 3.75%.

** Class I Share of this Fund was not in existence prior to 5/1/06. Class I Share performance calculated for any period prior to 5/1/06 is based on the performance of Class B Share since inception of 1/4/94 and has been adjusted to reflect differences in sales charges and expenses between the classes. The Class B Shares were exchanged into Class A Shares on August 17, 2009.

*** Reflects the expense ratios as reported in the Prospectus dated April 30, 2014. Contractual fee waivers are in effect from May 1, 2014 through April 30, 2015 for Class A.

1 Barclay’s Capital Aggregate Bond Index is an unmanaged index composed of the Barclay’s Capital Government/Credit Index and the Barclay’s Capital Mortgage-Backed Securities Index and includes Treasury issues, agency issues, corporate bond issues and mortgage-backed securities, and is intended to be generally representative of the bond market as a whole.

The above index is for illustrative purposes only and does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of these services. An investor cannot invest directly in an index, although they can invest in its underlying securities.

5

Schedule of Portfolio Investments

| Praxis Intermediate Income Fund | ||

| December 31, 2014 |

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

ASSET BACKED SECURITIES—3.5% | ||||||||

Ally Auto Receivables Trust, 0.74%, 4/15/16 | $ | 269,905 | $ | 269,972 | ||||

Ally Auto Receivables Trust, 1.61%, 5/16/16 | 182,340 | 182,536 | ||||||

Ally Auto Receivables Trust, 1.75%, 3/15/16 | 93,709 | 93,751 | ||||||

Beacon Container Finance LLC, 3.72%, 9/20/27(a) | 388,059 | 392,892 | ||||||

Cabela’s Credit Card Master Note Trust, 0.76%, 6/17/19+(a) | 1,000,000 | 1,003,090 | ||||||

CLI Funding LLC, 2.83%, 3/18/28(a) | 825,000 | 807,046 | ||||||

Cronos Containers Program I Ltd., 3.27%, 11/18/29(a) | 990,741 | 990,023 | ||||||

Domino’s Pizza Master Issuer LLC, 5.22%, 1/25/42(a) | 966,250 | 1,012,971 | ||||||

Fairway Outdoor Funding LLC, 4.21%, 10/15/42(a) | 469,880 | 471,303 | ||||||

Ford Credit Auto Owner Trust, 0.51%, 4/15/17 | 902,646 | 902,555 | ||||||

Global SC Finance II SRL, 2.98%, 4/17/28(a) | 958,333 | 948,815 | ||||||

GTP Acquisition Partners I LLC, 4.35%, 6/15/16(a) | 800,000 | 814,812 | ||||||

Honda Auto Receivables Owner Trust, 0.74%, 10/15/18 | 985,000 | 985,263 | ||||||

Hyundai Auto Receivables Trust, 1.30%, 2/15/18 | 744,992 | 748,664 | ||||||

Hyundai Auto Receivables Trust, 1.65%, 2/15/17 | 127,540 | 127,646 | ||||||

SBA Tower Trust, 2.90%, 10/15/19(a) | 525,000 | 526,377 | ||||||

Solarcity LMC Series I LLC, 4.80%, 11/20/38(a) | 842,123 | 881,398 | ||||||

Textainer Marine Containers III Ltd., 3.27%, 10/20/39(a) | 491,667 | 491,031 | ||||||

Toyota Auto Receivables Owner Trust, 0.67%, 12/15/17 | 1,900,000 | 1,897,918 | ||||||

Trip Rail Master Funding LLC, 2.66%, 7/15/41+(a) | 589,048 | 603,590 | ||||||

|

| |||||||

| TOTAL ASSET BACKED SECURITIES | 14,151,653 | |||||||

|

| |||||||

COMMERCIAL MORTGAGE BACKED SECURITIES—4.5% |

| |||||||

Bear Stearns Commercial Mortgage Securities, 4.67%, 6/11/41 | 758,853 | 762,340 | ||||||

Bear Stearns Commercial Mortgage Securities, 5.12%, 2/11/41+ | 369,420 | 369,427 | ||||||

Bear Stearns Commercial Mortgage Securities, 5.54%, 9/11/41 | 1,898,446 | 1,996,455 | ||||||

Bear Stearns Commercial Mortgage Securities, 5.74%, 9/11/42+ | 1,000,000 | 1,093,654 | ||||||

Commercial Mortgage Pass Through Certificates, 2.85%, 10/15/45 | 1,000,000 | 1,000,885 | ||||||

Commercial Mortgage Pass Through Certificates, 3.39%, 5/15/45 | 1,000,000 | 1,040,106 | ||||||

CSMC, 5.38%, 2/15/40(a) | 738,944 | 769,150 | ||||||

CSMC, 5.47%, 9/16/39+(a) | 761,520 | 793,116 | ||||||

DBUBS Mortgage Trust, 3.74%, 11/10/46(a) | 820,921 | 841,009 | ||||||

FHLMC Multifamily Structured Pass Through Certificates, 5.09%, 3/25/19 | 1,140,000 | 1,279,814 | ||||||

JPMorgan Chase Commercial Mortgage Securities Corp., 4.92%, 10/15/42+ | 872,547 | 884,306 | ||||||

JPMorgan Chase Commercial Mortgage Securities Corp., 5.40%, 5/15/45 | 1,847,682 | 1,944,146 | ||||||

ML-CFC Commercial Mortgage Trust, 5.42%, 8/12/48 | 250,000 | 262,465 | ||||||

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

COMMERCIAL MORTGAGE BACKED SECURITIES—4.5%, continued |

| |||||||

Morgan Stanley Capital I, Inc., 3.88%, 9/15/47(a) | $ | 1,000,000 | $ | 1,019,722 | ||||

Morgan Stanley Capital I, Inc., 5.81%, 8/12/41+ | 1,000,000 | 1,049,165 | ||||||

OBP Depositor LLC Trust, 4.65%, 7/15/45(a) | 1,040,000 | 1,152,115 | ||||||

RBSCF Trust, 5.94%, 2/16/51+(a) | 1,044,347 | 1,088,097 | ||||||

RBSCF Trust, 6.04%, 12/16/49+(a) | 908,465 | 960,530 | ||||||

|

| |||||||

| TOTAL COMMERCIAL MORTGAGE BACKED SECURITIES | 18,306,502 | |||||||

|

| |||||||

FOREIGN BONDS—2.2% |

| |||||||

Arab Republic of Egypt, 4.45%, 9/15/15 | 2,000,000 | 2,057,434 | ||||||

Export Development Canada, 0.88%, 1/30/17 | 1,500,000 | 1,500,232 | ||||||

Hashemite Kingdom of Jordan, 2.50%, 10/30/20 | 5,000,000 | 5,083,305 | ||||||

|

| |||||||

| TOTAL FOREIGN BONDS | 8,640,971 | |||||||

|

| |||||||

MUNICIPAL BONDS—3.2% |

| |||||||

Bridgeport Connecticut Housing Authority, 1.85%, 12/15/18 | 275,000 | 276,042 | ||||||

Cincinnati Ohio Water System Rev., 6.46%, 12/01/34 | 600,000 | 692,580 | ||||||

City of Lancaster PA, 5.59%, 11/15/34 | 1,000,000 | 1,028,100 | ||||||

Columbus Multi-High School Building Corp. Rev., 6.45%, 1/15/30 | 1,000,000 | 1,095,040 | ||||||

Findlay City School District, 6.25%, 12/01/37 | 270,000 | 275,781 | ||||||

Florida Housing Finance Corp. Multifamily Housing Rev. Garden Vista Apartments, 0.55%, 3/01/16(a) | 1,000,000 | 1,000,190 | ||||||

Florida Housing Finance Corp. Multifamily Housing Rev. Ridge Club Apartments, 0.40%, 12/01/15 | 1,000,000 | 999,580 | ||||||

Fort Wayne International Airport Air Trade Center Building Corp., 4.25%, 7/15/16 | 500,000 | 516,780 | ||||||

Houston Independent School District, 6.17%, 2/15/34 | 1,000,000 | 1,141,040 | ||||||

Indianapolis Public School Multi-School Building, 5.73%, 7/15/29 | 1,500,000 | 1,662,375 | ||||||

LL&P Wind Energy, Inc., 5.73%, 12/01/17(a) | 650,000 | 657,481 | ||||||

New Jersey St Housing and Mortgage Finance, 2.60%, 7/01/23 | 455,000 | 470,452 | ||||||

Osceola County Housing Finance Authority Rev., 3.35%, 7/01/23 | 315,000 | 332,149 | ||||||

State of Hawaii, Department of Business Economic Development & Tourism, 1.47%, 7/01/22 | 1,000,000 | 1,000,850 | ||||||

Warm Springs Reservation Confederated Tribe, 8.25%, 11/01/19 | 895,000 | 992,967 | ||||||

Wisconsin Department of Transportation, 5.84%, 7/01/30 | 800,000 | 893,264 | ||||||

|

| |||||||

| TOTAL MUNICIPAL BONDS | 13,034,671 | |||||||

|

| |||||||

CORPORATE BONDS—37.3% | ||||||||

| AUTO COMPONENTS—0.6% | ||||||||

BorgWarner, Inc., 5.75%, 11/01/16 | 1,000,000 | 1,075,209 | ||||||

Delphi Corp., 5.00%, 2/15/23 | 492,000 | 525,200 | ||||||

Delphi Corp., 6.13%, 5/15/21 | 150,000 | 163,500 | ||||||

TRW Automotive, Inc., 4.50%, 3/01/21(a) | 500,000 | 502,500 | ||||||

|

| |||||||

| 2,266,409 | ||||||||

|

| |||||||

See accompanying notes to financial statements.

6

Schedule of Portfolio Investments, continued

| Praxis Intermediate Income Fund | ||

| December 31, 2014 |

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

CORPORATE BONDS—37.3%, continued |

| |||||||

| BANKS—1.7% | ||||||||

Bank of America Corp., 1.35%, 11/21/16 | $ | 1,000,000 | $ | 997,157 | ||||

Bank of America Corp., 5.65%, 5/01/18 | 1,250,000 | 1,388,716 | ||||||

Citigroup, Inc., 4.45%, 1/10/17 | 500,000 | 528,542 | ||||||

Citigroup, Inc., 6.13%, 11/21/17 | 1,000,000 | 1,115,084 | ||||||

JPMorgan Chase & Co., 4.63%, 5/10/21 | 500,000 | 550,298 | ||||||

JPMorgan Chase Bank NA, 5.88%, 6/13/16 | 700,000 | 746,185 | ||||||

Manufacturers & Traders Trust Co., 6.63%, 12/04/17 | 600,000 | 678,796 | ||||||

Wells Fargo & Co., 3.50%, 3/08/22 | 887,000 | 925,963 | ||||||

|

| |||||||

| 6,930,741 | ||||||||

|

| |||||||

| BEVERAGES—0.3% | ||||||||

Bottling Group LLC, 5.13%, 1/15/19 | 1,000,000 | 1,117,964 | ||||||

|

| |||||||

| BIOTECHNOLOGY—0.3% | ||||||||

Amgen, Inc., 5.70%, 2/01/19 | 1,000,000 | 1,124,878 | ||||||

|

| |||||||

| BUILDING PRODUCTS—0.3% | ||||||||

Masco Corp., 6.13%, 10/03/16 | 500,000 | 530,250 | ||||||

Owens Corning, 4.20%, 12/01/24 | 750,000 | 740,150 | ||||||

|

| |||||||

| 1,270,400 | ||||||||

|

| |||||||

| CAPITAL MARKETS—1.7% | ||||||||

Goldman Sachs Group, Inc., 6.00%, 6/15/20 | 1,200,000 | 1,387,234 | ||||||

Jefferies Group LLC, 8.50%, 7/15/19 | 900,000 | 1,078,470 | ||||||

Morgan Stanley, 5.63%, 9/23/19 | 1,500,000 | 1,693,191 | ||||||

Raymond James Financial, Inc., 8.60%, 8/15/19 | 1,000,000 | 1,241,569 | ||||||

State Street Corp., 7.35%, 6/15/26 | 1,000,000 | 1,335,455 | ||||||

|

| |||||||

| 6,735,919 | ||||||||

|

| |||||||

| CHEMICALS—0.6% | ||||||||

Methanex Corp., 6.00%, 8/15/15 | 1,000,000 | 1,030,255 | ||||||

NOVA Chemicals Corp., 5.25%, 8/01/23(a) | 500,000 | 505,000 | ||||||

Potash Corp of Saskatchewan, Inc., 5.88%, 12/01/36 | 840,000 | 1,036,642 | ||||||

|

| |||||||

| 2,571,897 | ||||||||

|

| |||||||

| COMMERCIAL SERVICES & SUPPLIES—0.2% | ||||||||

Steelcase, Inc., 6.38%, 2/15/21 | 750,000 | 865,738 | ||||||

|

| |||||||

| CONSTRUCTION MATERIALS—0.3% | ||||||||

Martin Marietta Materials, Inc., 6.60%, 4/15/18 | 1,000,000 | 1,133,639 | ||||||

|

| |||||||

| CONSUMER FINANCE—0.6% | ||||||||

Ally Financial, Inc., 3.25%, 9/29/17 | 500,000 | 500,000 | ||||||

Ford Motor Credit Co. LLC, 4.25%, 2/03/17 | 500,000 | 525,034 | ||||||

Ford Motor Credit Co. LLC, 7.00%, 4/15/15 | 1,000,000 | 1,017,207 | ||||||

Harley-Davidson Financial Services, Inc., 2.70%, 3/15/17(a) | 500,000 | 512,328 | ||||||

|

| |||||||

| 2,554,569 | ||||||||

|

| |||||||

| CONTAINERS & PACKAGING—0.1% | ||||||||

Sonoco Products Co., 5.75%, 11/01/40 | 500,000 | 597,367 | ||||||

|

| |||||||

| DIVERSIFIED CONSUMER SERVICES—0.2% | ||||||||

Washington Post Co., 7.25%, 2/01/19 | 575,000 | 647,871 | ||||||

|

| |||||||

| DIVERSIFIED FINANCIAL SERVICES—0.9% | ||||||||

General Electric Capital Corp., 6.15%, 8/07/37 | 1,000,000 | 1,304,327 | ||||||

Moody’s Corp., 5.50%, 9/01/20 | 1,000,000 | 1,135,454 | ||||||

National Rural Utilities Cooperative Finance Corp., 10.38%, 11/01/18 | 780,000 | 1,016,129 | ||||||

|

| |||||||

| 3,455,910 | ||||||||

|

| |||||||

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

CORPORATE BONDS—37.3%, continued |

| |||||||

| DIVERSIFIED TELECOMMUNICATION SERVICES—0.6% | ||||||||

Frontier Communications Corp., 7.13%, 3/15/19 | $ | 750,000 | $ | 821,250 | ||||

Verizon Communications, Inc., 2.55%, 6/17/19 | 485,000 | 488,845 | ||||||

Verizon Communications, Inc., 6.00%, 4/01/41 | 500,000 | 589,315 | ||||||

Verizon Communications, Inc., 6.55%, 9/15/43 | 500,000 | 640,575 | ||||||

|

| |||||||

| 2,539,985 | ||||||||

|

| |||||||

| EDUCATION—0.3% | ||||||||

Massachusetts Institute of Technology, 3.96%, 7/01/38 | 1,000,000 | 1,060,529 | ||||||

|

| |||||||

| ELECTRIC UTILITIES—2.2% | ||||||||

Florida Power & Light Co., 4.05%, 10/01/44 | 500,000 | 524,360 | ||||||

ITC Holdings Corp., 5.50%, 1/15/20(a) | 500,000 | 538,756 | ||||||

MidAmerican Energy Co., 6.75%, 12/30/31 | 1,500,000 | 2,086,231 | ||||||

NextEra Energy Capital Holdings, Inc., 2.70%, 9/15/19 | 500,000 | 505,144 | ||||||

Oncor Electric Delivery Co. LLC, 6.80%, 9/01/18 | 750,000 | 874,217 | ||||||

Pennsylvania Electric Co., 5.20%, 4/01/20 | 500,000 | 551,251 | ||||||

Portland General Electric Co., 6.10%, 4/15/19 | 1,100,000 | 1,274,460 | ||||||

Potomac Edison Co., 5.13%, 8/15/15 | 1,000,000 | 1,026,135 | ||||||

Potomac Electric Power Co., 6.50%, 11/15/37 | 1,000,000 | 1,391,721 | ||||||

|

| |||||||

| 8,772,275 | ||||||||

|

| |||||||

| ELECTRICAL EQUIPMENT—0.1% | ||||||||

Thomas & Betts Corp., 5.63%, 11/15/21 | 500,000 | 587,381 | ||||||

|

| |||||||

| ELECTRONIC EQUIPMENT, INSTRUMENTS & COMPONENTS—0.2% | ||||||||

Arrow Electronics, Inc., 3.00%, 3/01/18 | 165,000 | 169,197 | ||||||

Arrow Electronics, Inc., 3.38%, 11/01/15 | 500,000 | 509,014 | ||||||

|

| |||||||

| 678,211 | ||||||||

|

| |||||||

| FOOD & STAPLES RETAILING—0.8% | ||||||||

Koninklijke Ahold NV, 7.82%, 1/02/20 | 489,168 | 544,200 | ||||||

Smith’s Food & Drug Centers, Inc. Pass Through Trust, 9.20%, 7/02/18 | 1,051,053 | 1,194,215 | ||||||

Wal-Mart Stores, Inc., 7.55%, 2/15/30 | 1,000,000 | 1,472,705 | ||||||

|

| |||||||

| 3,211,120 | ||||||||

|

| |||||||

| FOOD PRODUCTS—0.8% | ||||||||

Bunge Ltd. Finance Corp., 3.20%, 6/15/17 | 1,000,000 | 1,028,243 | ||||||

Cargill, Inc., 7.50%, 9/01/26(a) | 1,250,000 | 1,705,696 | ||||||

ConAgra Foods, Inc., 4.95%, 8/15/20 | 500,000 | 549,186 | ||||||

|

| |||||||

| 3,283,125 | ||||||||

|

| |||||||

| FOREIGN AGENCY—0.4% | ||||||||

KFW, 1.75%, 10/15/19 | 1,500,000 | 1,502,325 | ||||||

|

| |||||||

| GAS UTILITIES—0.3% | ||||||||

Indiana Gas Co., Inc., 6.55%, 6/30/28 | 250,000 | 296,009 | ||||||

Laclede Group, Inc., 2.55%, 8/15/19 | 285,000 | 282,712 | ||||||

National Fuel Gas Co., 6.50%, 4/15/18 | 500,000 | 569,718 | ||||||

|

| |||||||

| 1,148,439 | ||||||||

|

| |||||||

| HEALTH CARE EQUIPMENT & SUPPLIES—0.6% | ||||||||

DENTSPLY International, Inc., 2.75%, 8/15/16 | 570,000 | 582,452 | ||||||

Mallinckrodt International Finance SA, 3.50%, 4/15/18 | 500,000 | 483,125 | ||||||

See accompanying notes to financial statements.

7

Schedule of Portfolio Investments, continued

| Praxis Intermediate Income Fund | ||

| December 31, 2014 |

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

CORPORATE BONDS—37.3%, continued |

| |||||||

| HEALTH CARE EQUIPMENT & SUPPLIES—0.6%, continued | ||||||||

Medtronic, Inc., 2.50%, 3/15/20(a) | $ | 625,000 | $ | 626,639 | ||||

Zimmer Holdings, Inc., 4.63%, 11/30/19 | 500,000 | 546,183 | ||||||

|

| |||||||

| 2,238,399 | ||||||||

|

| |||||||

| HEALTH CARE PROVIDERS & SERVICES—0.7% | ||||||||

Howard Hughes Medical Institute, 3.50%, 9/01/23 | 1,500,000 | 1,568,532 | ||||||

Laboratory Corp of America Holdings, 3.13%, 5/15/16 | 500,000 | 513,130 | ||||||

McKesson Corp., 6.00%, 3/01/41 | 474,000 | 586,375 | ||||||

|

| |||||||

| 2,668,037 | ||||||||

|

| |||||||

| HOME BUILDERS—0.2% | ||||||||

DR Horton, Inc., 3.63%, 2/15/18 | 750,000 | 759,375 | ||||||

|

| |||||||

| HOTELS, RESTAURANTS & LEISURE—0.4% | ||||||||

Brinker International, Inc., 2.60%, 5/15/18 | 500,000 | 499,044 | ||||||

Darden Restaurants, Inc., 3.35%, 11/01/22 | 145,000 | 134,250 | ||||||

Hyatt Hotels Corp., 3.38%, 7/15/23 | 1,000,000 | 980,546 | ||||||

|

| |||||||

| 1,613,840 | ||||||||

|

| |||||||

| HOUSEHOLD PRODUCTS—0.1% | ||||||||

Church & Dwight Co., Inc., 3.35%, 12/15/15 | 500,000 | 510,907 | ||||||

|

| |||||||

| INDEPENDENT POWER AND RENEWABLE ELECTRICITY PRODUCERS—2.1% | ||||||||

FPL Energy American Wind LLC, 6.64%, 6/20/23(a) | 713,525 | 713,525 | ||||||

FPL Energy National Wind LLC, 5.61%, 3/10/24(a) | 387,283 | 387,283 | ||||||

Harper Lake Solar Funding Corp., 7.65%, 12/31/18(a) | 660,412 | 680,225 | ||||||

LS Power Funding Corp., 8.08%, 12/30/16 | 642,165 | 684,708 | ||||||

Midland Cogeneration Venture LP, 5.25%, 3/15/25(a) | 246,773 | 254,201 | ||||||

Midland Cogeneration Venture LP, 6.00%, 3/15/25(a) | 605,058 | 647,512 | ||||||

NRG Yield Operating LLC, 5.38%, 8/15/24(a) | 500,000 | 507,500 | ||||||

Salton Sea Funding Corp., 7.48%, 11/30/18 | 557,880 | 577,577 | ||||||

Solar Star Funding LLC, 5.38%, 6/30/35(a) | 500,000 | 528,586 | ||||||

SteelRiver Transmission Co. LLC, 4.71%, 6/30/17(a) | 947,542 | 986,601 | ||||||

Tenaska Virginia Partners LP, 6.12%, 3/30/24(a) | 414,960 | 460,636 | ||||||

Topaz Solar Farms LLC, 5.75%, 9/30/39(a) | 800,000 | 902,547 | ||||||

TransAlta Corp., 4.75%, 1/15/15 | 500,000 | 500,448 | ||||||

TransAlta Corp., 6.65%, 5/15/18 | 500,000 | 561,042 | ||||||

Utility Contract Funding LLC, 7.94%, 10/01/16(a) | 294,627 | 311,981 | ||||||

|

| |||||||

| 8,704,372 | ||||||||

|

| |||||||

| INDUSTRIAL CONGLOMERATES—0.1% | ||||||||

Ingersoll-Rand Global Holding Co. Ltd., 2.88%, 1/15/19 | 500,000 | 507,887 | ||||||

|

| |||||||

| INSURANCE—2.5% | ||||||||

Fidelity National Financial, Inc., 5.50%, 9/01/22 | 725,000 | 789,868 | ||||||

Horace Mann Educators Corp., 6.85%, 4/15/16 | 750,000 | 802,183 | ||||||

Kemper Corp., 6.00%, 11/30/15 | 800,000 | 833,955 | ||||||

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

CORPORATE BONDS—37.3%, continued |

| |||||||

| INSURANCE—2.5%, continued | ||||||||

Liberty Mutual Group, Inc., 4.95%, 5/01/22(a) | $ | 1,050,000 | $ | 1,135,962 | ||||

Markel Corp., 3.63%, 3/30/23 | 400,000 | 402,285 | ||||||

Marsh & McLennan Cos., Inc., 2.35%, 9/10/19 | 250,000 | 250,366 | ||||||

Montpelier Re Holdings Ltd., 4.70%, 10/15/22 | 250,000 | 257,554 | ||||||

OneBeacon US Holdings Inc, 4.60%, 11/09/22 | 1,000,000 | 1,040,076 | ||||||

Progressive Corp., 6.70%, 6/15/37+ | 500,000 | 540,875 | ||||||

Provident Cos., Inc., 7.00%, 7/15/18 | 340,000 | 388,601 | ||||||

Prudential Financial, Inc., 5.87%, 9/15/42+ | 500,000 | 527,500 | ||||||

RLI Corp., 4.88%, 9/15/23 | 1,000,000 | 1,053,598 | ||||||

TIAA Asset Management Finance Co. LLC, 2.95%, 11/01/19(a) | 1,000,000 | 1,001,935 | ||||||

W.R. Berkley Corp., 4.63%, 3/15/22 | 250,000 | 268,081 | ||||||

W.R. Berkley Corp., 6.15%, 8/15/19 | 710,000 | 801,346 | ||||||

|

| |||||||

| 10,094,185 | ||||||||

|

| |||||||

| IT SERVICES—0.3% | ||||||||

Broadridge Financial Solutions, Inc., 3.95%, 9/01/20 | 500,000 | 519,713 | ||||||

Xerox Corp., 2.75%, 3/15/19 | 500,000 | 501,248 | ||||||

|

| |||||||

| 1,020,961 | ||||||||

|

| |||||||

| MACHINERY—0.8% | ||||||||

Harsco Corp., 5.75%, 5/15/18 | 750,000 | 789,375 | ||||||

Kennametal, Inc., 2.65%, 11/01/19 | 955,000 | 944,895 | ||||||

Pall Corp., 5.00%, 6/15/20 | 500,000 | 544,768 | ||||||

Snap-On, Inc., 4.25%, 1/15/18 | 500,000 | 529,980 | ||||||

Valmont Industries, Inc., 6.63%, 4/20/20 | 334,000 | 391,993 | ||||||

|

| |||||||

| 3,201,011 | ||||||||

|

| |||||||

| MEDIA—0.8% | ||||||||

Comcast Corp., 4.75%, 3/01/44 | 500,000 | 557,196 | ||||||

Comcast Corp., 5.15%, 3/01/20 | 1,000,000 | 1,132,520 | ||||||

Omnicom Group, Inc., 6.25%, 7/15/19 | 1,000,000 | 1,159,210 | ||||||

Time Warner Cable, Inc., 4.50%, 9/15/42 | 500,000 | 513,972 | ||||||

|

| |||||||

| 3,362,898 | ||||||||

|

| |||||||

| METALS & MINING—0.4% | ||||||||

Newcrest Finance Pty Ltd., 4.45%, 11/15/21(a) | 1,000,000 | 950,278 | ||||||

Reliance Steel & Aluminum Co., 4.50%, 4/15/23 | 705,000 | 690,939 | ||||||

|

| |||||||

| 1,641,217 | ||||||||

|

| |||||||

| MULTILINE RETAIL—0.3% | ||||||||

Dollar General Corp., 4.13%, 7/15/17 | 700,000 | 721,921 | ||||||

Macy’s Retail Holdings, Inc., 9.50%, 4/15/21 | 585,000 | 687,358 | ||||||

|

| |||||||

| 1,409,279 | ||||||||

|

| |||||||

| MULTI-UTILITIES—0.7% | ||||||||

Consumers Energy Co., 6.70%, 9/15/19 | 750,000 | 894,134 | ||||||

Puget Energy, Inc., 5.63%, 7/15/22 | 750,000 | 867,846 | ||||||

Puget Sound Energy, Inc., 6.74%, 6/15/18 | 1,000,000 | 1,155,580 | ||||||

|

| |||||||

| 2,917,560 | ||||||||

|

| |||||||

| OIL, GAS & CONSUMABLE FUELS—2.3% | ||||||||

ConocoPhillips Holding Co., 6.95%, 4/15/29 | 1,000,000 | 1,332,184 | ||||||

Continental Resources, Inc., 4.50%, 4/15/23 | 200,000 | 190,230 | ||||||

Denbury Resources, Inc., 4.63%, 7/15/23 | 600,000 | 520,500 | ||||||

See accompanying notes to financial statements.

8

Schedule of Portfolio Investments, continued

| Praxis Intermediate Income Fund | ||

| December 31, 2014 |

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

CORPORATE BONDS—37.3%, continued |

| |||||||

| OIL, GAS & CONSUMABLE FUELS—2.3%, continued | ||||||||

Enbridge Energy Partners LP, 5.20%, 3/15/20 | $ | 500,000 | $ | 544,811 | ||||

Florida Gas Transmission Co. LLC, 4.00%, 7/15/15(a) | 1,000,000 | 1,013,805 | ||||||

Golden State Petroleum Transport Corp., 8.04%, 2/01/19 | 288,400 | 260,781 | ||||||

Kern River Funding Corp., 6.68%, 7/31/16(a) | 491,177 | 521,975 | ||||||

Merey Sweeny LP, 8.85%, 12/18/19(a) | 512,289 | 591,500 | ||||||

Northern Natural Gas Co., 4.10%, 9/15/42(a) | 1,000,000 | 1,035,919 | ||||||

Pioneer Natural Resources Co., 5.88%, 7/15/16 | 500,000 | 531,040 | ||||||

Ras Laffan Liquefied Natural Gas Co. Ltd. II, 5.30%, 9/30/20(a) | 619,400 | 664,307 | ||||||

Ras Laffan Liquefied Natural Gas Co. Ltd. III, 5.83%, 9/30/16(a) | 379,000 | 394,634 | ||||||

Spectra Energy Capital LLC, 6.75%, 7/15/18 | 800,000 | 903,917 | ||||||

Texas Gas Transmission LLC, 4.60%, 6/01/15 | 1,000,000 | 1,012,843 | ||||||

|

| |||||||

| 9,518,446 | ||||||||

|

| |||||||

| PAPER & FOREST PRODUCTS—0.4% | ||||||||

Domtar Corp., 9.50%, 8/01/16 | 702,000 | 774,957 | ||||||

PH Glatfelter Co., 5.38%, 10/15/20 | 750,000 | 763,125 | ||||||

|

| |||||||

| 1,538,082 | ||||||||

|

| |||||||

| PHARMACEUTICALS—0.1% | ||||||||

AbbVie, Inc., 2.00%, 11/06/18 | 500,000 | 498,322 | ||||||

|

| |||||||

| PROFESSIONAL SERVICES—0.6% | ||||||||

Dun & Bradstreet Corp., 2.88%, 11/15/15 | 250,000 | 251,814 | ||||||

Dun & Bradstreet Corp., 4.38%, 12/01/22 | 1,000,000 | 1,022,939 | ||||||

Verisk Analytics, Inc., 5.80%, 5/01/21 | 960,000 | 1,081,614 | ||||||

|

| |||||||

| 2,356,367 | ||||||||

|

| |||||||

| REAL ESTATE INVESTMENT TRUSTS (REITS)—1.1% | ||||||||

ERP Operating LP, 7.13%, 10/15/17 | 1,104,000 | 1,259,362 | ||||||

Health Care REIT, Inc., 4.70%, 9/15/17 | 1,018,000 | 1,093,789 | ||||||

National Retail Properties, Inc., 3.80%, 10/15/22 | 250,000 | 256,608 | ||||||

Regency Centers LP, 3.75%, 6/15/24 | 1,000,000 | 1,017,639 | ||||||

Vornado Realty LP, 2.50%, 6/30/19 | 1,000,000 | 991,337 | ||||||

|

| |||||||

| 4,618,735 | ||||||||

|

| |||||||

| ROAD & RAIL—1.9% | ||||||||

Burlington Northern Santa Fe LLC, 5.75%, 5/01/40 | 1,000,000 | 1,233,761 | ||||||

Burlington Northern Santa Fe LLC, 7.16%, 1/02/20 | 660,223 | 738,015 | ||||||

ERAC USA Finance LLC, 5.90%, 11/15/15(a) | 1,000,000 | 1,043,364 | ||||||

JB Hunt Transport Services, Inc., 3.38%, 9/15/15 | 1,000,000 | 1,017,159 | ||||||

Kansas City Southern de Mexico SA de CV, 2.35%, 5/15/20 | 500,000 | 479,786 | ||||||

Norfolk Southern Corp., 4.84%, 10/01/41 | 1,000,000 | 1,109,319 | ||||||

Penske Truck Leasing Co. LP/PTL Finance Corp., 3.75%, 5/11/17(a) | 1,000,000 | 1,045,108 | ||||||

TTX Co., 4.90%, 3/01/15(a) | 1,000,000 | 1,006,572 | ||||||

|

| |||||||

| 7,673,084 | ||||||||

|

| |||||||

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

CORPORATE BONDS—37.3%, continued |

| |||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—0.5% | ||||||||

Applied Materials, Inc., 7.13%, 10/15/17 | $ | 500,000 | $ | 566,915 | ||||

KLA-Tencor Corp., 3.38%, 11/01/19 | 600,000 | 611,298 | ||||||

Maxim Integrated Products, Inc., 3.38%, 3/15/23 | 500,000 | 492,676 | ||||||

Xilinx, Inc., 2.13%, 3/15/19 | 500,000 | 496,788 | ||||||

|

| |||||||

| 2,167,677 | ||||||||

|

| |||||||

| SOFTWARE—0.1% | ||||||||

Symantec Corp., 2.75%, 6/15/17 | 500,000 | 507,373 | ||||||

|

| |||||||

| SPECIALTY RETAIL—0.6% | ||||||||

Advance Auto Parts, Inc., 4.50%, 1/15/22 | 402,000 | 426,725 | ||||||

Ethan Allen Global, Inc., 5.38%, 10/01/15 | 500,000 | 506,250 | ||||||

O’Reilly Automotive, Inc., 3.80%, 9/01/22 | 1,000,000 | 1,033,009 | ||||||

Staples, Inc., 2.75%, 1/12/18 | 580,000 | 579,394 | ||||||

|

| |||||||

| 2,545,378 | ||||||||

|

| |||||||

| SUPRANATIONAL—5.6% | ||||||||

African Development Bank, 0.75%, 10/18/16 | 1,000,000 | 1,000,151 | ||||||

European Bank for Reconstruction & Development, 1.63%, 4/10/18 | 500,000 | 503,006 | ||||||

European Investment Bank, 2.50%, 10/15/24 | 1,000,000 | 1,014,369 | ||||||

Inter-American Development Bank, 1.50%, 9/25/18 | 2,500,000 | 2,502,128 | ||||||

Inter-American Development Bank, 2.13%, 11/09/20 | 3,000,000 | 3,027,183 | ||||||

Inter-American Development Bank, 4.38%, 1/24/44 | 3,000,000 | 3,699,519 | ||||||

International Bank for Reconstruction & Development, 0.17%, 7/22/15+ | 500,000 | 499,830 | ||||||

International Bank for Reconstruction & Development, 0.38%, 8/24/15 | 1,000,000 | 1,000,279 | ||||||

International Finance Corp., 0.50%, 5/16/16 | 3,250,000 | 3,243,945 | ||||||

International Finance Corp., 0.63%, 11/15/16 | 2,000,000 | 1,992,602 | ||||||

International Finance Facility for Immunisation, 0.42%, 7/05/16+(a) | 2,000,000 | 2,000,298 | ||||||

Nordic Investment Bank, 2.25%, 9/30/21 | 1,000,000 | 1,011,087 | ||||||

North American Development Bank, 2.30%, 10/10/18 | 1,000,000 | 1,012,679 | ||||||

|

| |||||||

| 22,507,076 | ||||||||

|

| |||||||

| TECHNOLOGY HARDWARE, STORAGE & PERIPHERALS—0.2% | ||||||||

Hewlett-Packard Co., 3.30%, 12/09/16 | 500,000 | 516,362 | ||||||

Seagate HDD Cayman, 3.75%, 11/15/18(a) | 450,000 | 461,813 | ||||||

|

| |||||||

| 978,175 | ||||||||

|

| |||||||

| TEXTILES, APPAREL & LUXURY GOODS—0.4% | ||||||||

Hanesbrands, Inc., 6.38%, 12/15/20 | 745,000 | 789,700 | ||||||

Levi Strauss & Co., 6.88%, 5/01/22 | 750,000 | 806,250 | ||||||

|

| |||||||

| 1,595,950 | ||||||||

|

| |||||||

| TOTAL CORPORATE BONDS | 151,211,285 | |||||||

|

| |||||||

CORPORATE NOTES—0.9% | ||||||||

| COMMUNITY DEVELOPMENT—0.9% | ||||||||

Calvert Social Investment Foundation, Inc., 1.00%, 12/15/17 | 1,200,000 | 1,200,000 | ||||||

Everence Community Investment, Inc., 1.00%, 12/15/15+(b) | 1,340,000 | 1,337,795 | ||||||

See accompanying notes to financial statements.

9

Schedule of Portfolio Investments, continued

| Praxis Intermediate Income Fund | ||

| December 31, 2014 |

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

CORPORATE NOTES—0.9%, continued | ||||||||

| COMMUNITY DEVELOPMENT—0.9%, continued | ||||||||

Everence Community Investment, Inc., 1.50%, 12/15/16+(b) | $ | 1,307,500 | $ | 1,311,744 | ||||

|

| |||||||

| TOTAL CORPORATE NOTES | 3,849,539 | |||||||

|

| |||||||

U.S. GOVERNMENT AGENCIES—44.7% |

| |||||||

| FEDERAL FARM CREDIT BANK—0.5% | ||||||||

4.88%, 12/16/15 | 2,000,000 | 2,086,960 | ||||||

|

| |||||||

| FEDERAL HOME LOAN BANK—4.0% | ||||||||

3.38%, 6/12/20 | 1,000,000 | 1,075,758 | ||||||

5.00%, 11/17/17 | 5,500,000 | 6,113,189 | ||||||

5.50%, 7/15/36 | 6,570,000 | 9,010,269 | ||||||

|

| |||||||

| 16,199,216 | ||||||||

|

| |||||||

| FEDERAL HOME LOAN MORTGAGE CORP.—19.2% | ||||||||

1.25%, 10/02/19 | 2,710,000 | 2,651,385 | ||||||

1.38%, 5/01/20 | 4,000,000 | 3,900,664 | ||||||

2.36%, 5/01/34+ | 200,103 | 212,487 | ||||||

2.36%, 5/01/34+ | 111,429 | 119,118 | ||||||

2.38%, 1/13/22 | 5,960,000 | 6,021,352 | ||||||

2.50%, 10/01/27 | 1,516,038 | 1,546,112 | ||||||

3.00%, 11/01/32 | 2,530,707 | 2,613,444 | ||||||

3.00%, 11/01/32 | 1,687,762 | 1,742,934 | ||||||

3.00%, 1/01/43 | 1,875,655 | 1,898,670 | ||||||

3.00%, 5/01/43 | 2,752,574 | 2,785,108 | ||||||

3.50%, 10/01/41 | 1,373,824 | 1,431,519 | ||||||

3.50%, 2/01/42 | 2,023,135 | 2,107,856 | ||||||

3.50%, 6/01/42 | 2,228,647 | 2,321,020 | ||||||

3.50%, 6/01/42 | 2,204,270 | 2,295,570 | ||||||

3.50%, 8/01/42 | 2,441,309 | 2,542,275 | ||||||

3.50%, 11/01/44 | 2,990,847 | 3,113,123 | ||||||

3.75%, 3/27/19 | 3,020,000 | 3,286,829 | ||||||

4.00%, 11/01/24 | 1,071,220 | 1,140,252 | ||||||

4.00%, 10/01/25 | 458,814 | 489,968 | ||||||

4.00%, 10/01/41 | 1,334,001 | 1,423,700 | ||||||

4.00%, 2/01/42 | 776,803 | 829,036 | ||||||

4.50%, 6/01/18 | 145,027 | 152,299 | ||||||

4.50%, 10/01/35 | 537,623 | 585,698 | ||||||

4.50%, 6/01/39 | 843,261 | 914,024 | ||||||

4.50%, 7/01/39 | 968,548 | 1,049,660 | ||||||

4.50%, 11/01/39 | 937,672 | 1,016,511 | ||||||

4.50%, 9/01/40 | 1,316,426 | 1,428,577 | ||||||

4.50%, 5/01/41 | 2,541,189 | 2,757,923 | ||||||

4.50%, 7/01/41 | 2,687,365 | 2,912,051 | ||||||

4.88%, 6/13/18 | 6,200,000 | 6,930,825 | ||||||

5.00%, 4/01/19 | 106,758 | 113,181 | ||||||

5.00%, 12/01/21 | 215,997 | 231,892 | ||||||

5.00%, 7/01/35 | 238,024 | 263,293 | ||||||

5.00%, 3/01/38 | 871,373 | 961,126 | ||||||

5.00%, 6/01/39 | 1,354,400 | 1,495,509 | ||||||

5.00%, 9/01/41 | 1,294,854 | 1,433,345 | ||||||

5.50%, 7/18/16 | 3,500,000 | 3,766,840 | ||||||

5.50%, 4/01/22 | 139,318 | 151,744 | ||||||

5.50%, 11/01/33 | 98,968 | 111,388 | ||||||

5.50%, 3/01/36 | 127,804 | 143,215 | ||||||

5.50%, 6/01/36 | 208,686 | 233,915 | ||||||

5.50%, 12/01/36 | 184,660 | 206,655 | ||||||

6.00%, 9/01/17 | 87,521 | 91,632 | ||||||

6.00%, 4/01/27 | 313,398 | 354,794 | ||||||

| PRINCIPAL AMOUNT | FAIR VALUE | |||||||

U.S. GOVERNMENT AGENCIES—44.7%, continued |

| |||||||

| FEDERAL HOME LOAN MORTGAGE CORP.—19.2%, continued | ||||||||

6.00%, 6/01/36 | $ | 198,262 | $ | 226,802 | ||||

6.00%, 8/01/37 | 102,339 | 115,596 | ||||||

6.25%, 7/15/32 | 3,500,000 | 5,115,719 | ||||||

7.00%, 2/01/30 | 147,604 | 165,113 | ||||||

7.00%, 3/01/31 | 97,284 | 111,329 | ||||||

7.50%, 7/01/30 | 243,693 | 287,427 | ||||||

|

| |||||||

| 77,800,505 | ||||||||

|

| |||||||

| FEDERAL NATIONAL MORTGAGE ASSOCIATION—19.6% | ||||||||

1.13%, 4/27/17 | 2,000,000 | 2,011,156 | ||||||

1.63%, 10/26/15 | 3,600,000 | 3,640,968 | ||||||

1.82%, 2/01/34+ | 167,811 | 172,729 | ||||||

2.15%, 6/01/33+ | 76,709 | 80,160 | ||||||

2.19%, 1/01/23 | 2,000,000 | 1,955,798 | ||||||

2.27%, 5/01/37+ | 245,030 | 264,559 | ||||||

2.32%, 5/01/34+ | 151,835 | 162,500 | ||||||

2.50%, 9/01/27 | 1,893,374 | 1,932,902 | ||||||

2.50%, 11/01/27 | 2,693,387 | 2,747,990 | ||||||

2.50%, 1/01/28 | 1,787,465 | 1,823,692 | ||||||

2.63%, 9/06/24 | 3,250,000 | 3,291,343 | ||||||

3.00%, 12/01/32 | 2,538,769 | 2,625,292 | ||||||

3.00%, 6/01/42 | 2,712,902 | 2,749,871 | ||||||

3.00%, 8/01/42 | 2,464,565 | 2,498,251 | ||||||

3.00%, 8/01/42 | 2,437,332 | 2,470,615 | ||||||

3.00%, 6/01/43 | 2,324,783 | 2,355,066 | ||||||

3.50%, 7/01/20 | 566,539 | 599,115 | ||||||

3.50%, 10/01/25 | 444,349 | 470,033 | ||||||

3.50%, 2/01/41 | 1,617,688 | 1,689,230 | ||||||

3.50%, 5/01/42 | 1,950,519 | 2,036,640 | ||||||

3.50%, 12/01/42 | 2,913,033 | 3,047,778 | ||||||

4.00%, 3/01/26 | 1,462,851 | 1,566,858 | ||||||

4.00%, 12/01/40 | 1,721,179 | 1,840,208 | ||||||

4.00%, 1/01/41 | 1,242,852 | 1,328,006 | ||||||

4.00%, 10/01/41 | 1,142,816 | 1,221,117 | ||||||

4.00%, 11/01/41 | 1,042,171 | 1,113,575 | ||||||

4.00%, 12/01/41 | 2,673,695 | 2,856,883 | ||||||

4.00%, 12/01/41 | 1,436,036 | 1,534,426 | ||||||

4.00%, 1/01/42 | 2,771,773 | 2,978,504 | ||||||

4.38%, 10/15/15 | 4,700,000 | 4,852,219 | ||||||

4.50%, 9/01/40 | 852,569 | 926,371 | ||||||

4.50%, 10/01/40 | 841,538 | 914,570 | ||||||

5.00%, 4/15/15 | 5,500,000 | 5,576,203 | ||||||

5.00%, 2/13/17 | 1,800,000 | 1,956,973 | ||||||

5.00%, 7/01/18 | 107,793 | 113,638 | ||||||

5.00%, 9/01/18 | 134,745 | 142,046 | ||||||

5.00%, 4/01/25 | 246,129 | 271,734 | ||||||

5.00%, 7/01/25 | 189,451 | 209,160 | ||||||

5.00%, 10/01/25 | 240,757 | 265,803 | ||||||

5.00%, 10/01/35 | 335,821 | 371,762 | ||||||

5.50%, 6/01/22 | 206,364 | 226,844 | ||||||

5.50%, 11/01/25 | 76 | 85 | ||||||

5.50%, 2/01/34 | 135,542 | 152,611 | ||||||

5.50%, 1/01/35 | 249,458 | 279,982 | ||||||

5.50%, 10/01/35 | 366,728 | 411,031 | ||||||

5.50%, 6/01/36 | 87,005 | 97,222 | ||||||

5.50%, 11/01/36 | 163,135 | 182,291 | ||||||

5.63%, 7/15/37 | 6,000,000 | 8,445,234 | ||||||

6.00%, 10/01/33 | 96,970 | 110,719 | ||||||

See accompanying notes to financial statements.

10

Schedule of Portfolio Investments, continued

| Praxis Intermediate Income Fund | ||

| December 31, 2014 |

PRINCIPAL SHARES | FAIR VALUE | |||||||

U.S. GOVERNMENT AGENCIES—44.7%, continued |

| |||||||

| FEDERAL NATIONAL MORTGAGE ASSOCIATION—19.6%, continued | ||||||||

6.00%, 11/01/34 | $ | 300,751 | $ | 343,471 | ||||

6.00%, 10/01/35 | 178,298 | 203,629 | ||||||

6.00%, 6/01/36 | 112,880 | 128,188 | ||||||

6.63%, 11/15/30 | 250,000 | 371,214 | ||||||

7.00%, 7/01/15 | 348 | 349 | ||||||

7.00%, 11/01/19 | 19,271 | 20,713 | ||||||

7.00%, 11/01/19 | 13,801 | 14,710 | ||||||

8.50%, 9/01/26 | 63,801 | 72,090 | ||||||

|

| |||||||

| 79,726,127 | ||||||||

|

| |||||||

| GOVERNMENT NATIONAL MORTGAGE ASSOCIATION—0.5% | ||||||||

1.63%, 1/20/34+ | 92,706 | 96,515 | ||||||

2.25%, 4/16/42 | 1,482,575 | 1,511,442 | ||||||

5.50%, 10/20/38 | 74,228 | 79,346 | ||||||

6.50%, 11/20/38 | 29,905 | 32,934 | ||||||

6.75%, 4/15/16 | 5,459 | 5,500 | ||||||

7.00%, 12/20/30 | 36,886 | 43,898 | ||||||

7.00%, 10/20/31 | 26,927 | 32,106 | ||||||

7.00%, 3/20/32 | 90,441 | 108,114 | ||||||

|

| |||||||

| 1,909,855 | ||||||||

|

| |||||||

| OVERSEAS PRIVATE INVESTMENT CORP.—0.8% | ||||||||

3.28%, 9/15/29 | 1,100,000 | 1,143,979 | ||||||

3.54%, 6/15/30 | 911,768 | 965,390 | ||||||

3.82%, 6/01/33 | 1,000,000 | 1,068,233 | ||||||

|

| |||||||

| 3,177,602 | ||||||||

|

| |||||||

| SMALL BUSINESS ADMINISTRATION—0.1% | ||||||||

0.60%, 2/25/32+ | 424,400 | 422,815 | ||||||

|

| |||||||

| TOTAL U.S. GOVERNMENT AGENCIES | 181,323,080 | |||||||

|

| |||||||

INVESTMENT COMPANY—0.9% | ||||||||

| MUTUAL FUND—0.9% | ||||||||

Pax World High Yield Bond Fund, Individual Investor Class | 530,984 | 3,722,196 | ||||||

|

| |||||||

| TOTAL INVESTMENTS (Cost* 380,073,366—Unrealized gain/loss $14,166,531)—97.2% | $ | 394,239,897 | ||||||

Other assets in excess of liabilities—2.8% |

| 11,452,734 | ||||||

|

| |||||||

| NET ASSETS—100% | $ | 405,692,631 | ||||||

|

| |||||||

| + | Variable rate security. Rates presented are the rates in effect at December 31, 2014. |

| (a) | 144a security is restricted as to resale to institutional investors. These securities were deemed liquid under guidelines established by the Board of Trustees. At December 31, 2014, these securities were valued at $40,863,744 or 10.1% of net assets. |

| (b) | Represents affiliated restricted security as to resale to shareholders and is not registered under the Securities Act of 1933. These securities have been fair valued by the Pricing Committee and have been deemed illiquid under guidelines established by the Board of Trustees: |

| Security | Yield | Maturity Date | Principal Amount | Cost | Acquisition Date | |||||||||||||||

Everence Community Investment, Inc. |

| |||||||||||||||||||

| 1.00 | % | 12/15/2015 | $ | 1,340,000 | $ | 1,340,000 | 12/13/2012 | |||||||||||||

| 1.50 | 12/15/2016 | 1,307,500 | 1,307,500 | 12/13/2013 | ||||||||||||||||

At December 31, 2014, these securities had an aggregate market value of $2,649,539, representing 0.6% of net assets.

| * | Represents cost for financial reporting purposes. |

Rev. | — | Revenue | ||

REIT | — | Real Estate Investment Trust |

See accompanying notes to financial statements.

11

Praxis International Index Fund

Annual report to shareholders

Portfolio Managers’ Commentary

Foreign equity markets went through a turbulent period in 2014. The MSCI All Country World ex-U.S. Index posted a return of -3.87 percent for the year. The Praxis International Index Fund Class A Shares (without load) closely tracked the index and posted a return of -5.70 percent.

The Praxis International Index Fund seeks to generate performance that reflects the performance of both foreign developed and emerging equity markets, as measured by the MSCI All Country World ex-U.S. Index. The Fund holdings are constructed using optimization techniques to have characteristics similar to the benchmark index. Limitations due to the screens and the lower number of holdings versus the benchmark are expected to cause the Fund’s performance to deviate from the benchmark over short periods of time, but the goal over long periods of time is for the Fund to perform in line with the benchmark before fees.

During the period, these factors, including a difference in timing between the pricing of the securities and the benchmark, had a small positive contribution to the Fund’s returns. However, the results were consistent with our forecasted tracking error – a measure of variability of relative returns – for a fund subject to the constraints we discussed above.

Ran Leshem

Praxis International Index Fund Portfolio Manager

Aperio Group LLC

Patrick Geddes

Praxis International Index Fund Portfolio Manager

Aperio Group LLC

The views expressed are those of the portfolio managers as of Dec. 31, 2014, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. All data referenced are from sources deemed to be reliable but cannot be guaranteed. Securities and sectors referenced should not be construed as a solicitation or recommendation or be used as the sole basis for any investment decision.

12

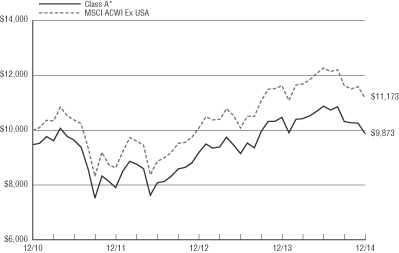

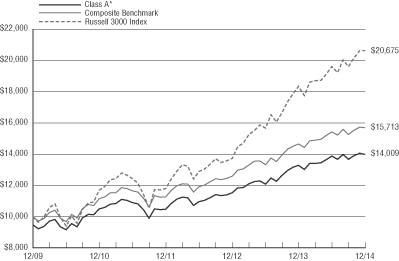

Praxis International Index Fund

Growth of $10,000 investment from 12/31/10 to 12/31/14

This chart represents historical performance of a hypothetical investment of $10,000 in Class A Shares (adjusted for the maximum sales charge of 5.25%) of the Fund and the MSCI All Country World Index ex-US from 12/31/10 to 12/31/14, and includes the reinvestment of dividends and capital gains.

| Annualized | ||||||||||||||||||||||||||||||

| Inception Date | One Year Ended | Three Year Ended | Since Inception | Expense Ratio** Gross / Net | ||||||||||||||||||||||||||

| International Index Fund | ||||||||||||||||||||||||||||||

| Class A (Without Load) | 12/31/10 | -5.70% | 7.66% | 1.02% | 1.43% | 1.43% | ||||||||||||||||||||||||

| Class A * | 12/31/10 | -10.66% | 5.73% | -0.32% | ||||||||||||||||||||||||||

| Class I | 12/31/10 | -5.36% | 8.37% | 1.67% | 0.80% | 0.80% | ||||||||||||||||||||||||

| MSCI All Country World Index ex-US1 | -3.87% | 8.99% | 2.81% | |||||||||||||||||||||||||||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. These performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. To obtain performance information current to the most recent month end, please visit www.praxismutualfunds.com.

The total returns shown reflect any expenses that were contractually or voluntarily reduced, reimbursed or paid by any party during the periods presented. In such instances, and without this activity, the total returns would have been lower.

* The total return figures shown reflect the maximum sales charge applicable to Class A Shares. Class A Shares have a maximum sales charge on purchases of 5.25%.

** Reflects the expense ratios as reported in the Prospectus dated April 30, 2014. Contractual fee waivers are in effect from May 1, 2014 through April 30, 2015 for Class A.

1 The MSCI All Country World Index ex-US is a market-capitalization-weighted index designed to provide a broad measure of stock performance throughout the world, with the exception of U.S. based companies. The index includes both developed and emerging markets.

The above index is for illustrative purposes only and does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of these services. An investor cannot invest directly in an index, although they can invest in its underlying securities.

13

Schedule of Portfolio Investments

| Praxis International Index Fund | ||

| December 31, 2014 |

| SHARES | FAIR VALUE | |||||||

COMMON STOCKS—98.0% |

| |||||||

AUSTRALIA—5.9% | ||||||||

| BANKS—2.1% | ||||||||

Australia & New Zealand Banking Group Ltd. | 6,107 | $ | 158,904 | |||||

Australia & New Zealand Banking Group Ltd.- ADR | 36,061 | 937,586 | ||||||

Commonwealth Bank of Australia | 3,955 | 274,789 | ||||||

Commonwealth Bank of Australia- ADR | 613 | 42,732 | ||||||

National Australia Bank Ltd. | 4,644 | 126,643 | ||||||

National Australia Bank Ltd.- ADR | 57,186 | 780,017 | ||||||

Westpac Banking Corp. | 4,051 | 108,955 | ||||||

Westpac Banking Corp.- ADR | 43,855 | 1,179,699 | ||||||

|

| |||||||

| 3,609,325 | ||||||||

|

| |||||||

| BIOTECHNOLOGY—0.2% | ||||||||

CSL Ltd. | 2,979 | 209,262 | ||||||

CSL Ltd.- ADR | 6,332 | 223,836 | ||||||

|

| |||||||

| 433,098 | ||||||||

|

| |||||||

| CAPITAL MARKETS—0.2% | ||||||||

Macquarie Group Ltd. | 3,958 | 186,647 | ||||||

Macquarie Group Ltd.- ADR | 2,747 | 130,345 | ||||||

|

| |||||||

| 316,992 | ||||||||

|

| |||||||

| CHEMICALS—0.2% | ||||||||

Orica Ltd. | 19,480 | 298,504 | ||||||

|

| |||||||

| CONTAINERS & PACKAGING—0.2% | ||||||||

Amcor Ltd. | 15,893 | 174,860 | ||||||

Amcor Ltd.- ADR | 3,500 | 154,665 | ||||||

|

| |||||||

| 329,525 | ||||||||

|

| |||||||

| DIVERSIFIED TELECOMMUNICATION SERVICES—0.2% | ||||||||

Telstra Corp. Ltd. | 17,682 | 85,843 | ||||||

Telstra Corp. Ltd.- ADR | 10,910 | 265,277 | ||||||

|

| |||||||

| 351,120 | ||||||||

|

| |||||||

| FOOD & STAPLES RETAILING—0.3% | ||||||||

Wesfarmers Ltd. | 16,433 | 556,383 | ||||||

|

| |||||||

| INSURANCE—0.3% | ||||||||

Suncorp Group Ltd. | 46,152 | 527,231 | ||||||

|

| |||||||

| METALS & MINING—1.6% | ||||||||

Alumina Ltd.- ADR(a) | 41,858 | 243,195 | ||||||

BHP Billiton Ltd.- ADR | 35,787 | 1,693,441 | ||||||

BHP Billiton plc | 30,582 | 655,413 | ||||||

Newcrest Mining Ltd.- ADR(a) | 9,928 | 88,518 | ||||||

|

| |||||||

| 2,680,567 | ||||||||

|

| |||||||

| OIL, GAS & CONSUMABLE FUELS—0.5% | ||||||||

Origin Energy Ltd. | 43,674 | 413,219 | ||||||

Woodside Petroleum Ltd. | 10,861 | 335,902 | ||||||

Woodside Petroleum Ltd.- ADR | 5,235 | 161,866 | ||||||

|

| |||||||

| 910,987 | ||||||||

|

| |||||||

| REAL ESTATE INVESTMENT TRUSTS (REITS)—0.1% | ||||||||

Scentre Group REIT(a) | 25,459 | 72,130 | ||||||

Shopping Centres Australasia Property Group REIT | 1 | 2 | ||||||

Westfield Corp. REIT | 20,433 | 149,781 | ||||||

|

| |||||||

| 221,913 | ||||||||

|

| |||||||

| SHARES | FAIR VALUE | |||||||

COMMON STOCKS—98.0%, continued |

| |||||||

AUSTRALIA—5.9%, continued |

| |||||||

| TRANSPORTATION INFRASTRUCTURE—0.0%** | ||||||||

Sydney Airport | 463 | $ | 1,772 | |||||

|

| |||||||

| 10,237,417 | ||||||||

|

| |||||||

AUSTRIA—0.1% | ||||||||

| BANKS—0.1% | ||||||||

Erste Group Bank AG | 757 | 17,607 | ||||||

Erste Group Bank AG- ADR | 12,078 | 138,293 | ||||||

|

| |||||||

| 155,900 | ||||||||

|

| |||||||

BELGIUM—0.4% | ||||||||

| FOOD & STAPLES RETAILING—0.4% | ||||||||

Colruyt SA | 2,958 | 137,516 | ||||||

Delhaize Group SA | 1,156 | 84,186 | ||||||

Delhaize Group SA- ADR | 22,300 | 404,076 | ||||||

|

| |||||||

| 625,778 | ||||||||

|

| |||||||

BRAZIL—1.9% | ||||||||

| BANKS—0.3% | ||||||||

Banco Bradesco SA- ADR | 36,665 | 490,211 | ||||||

|

| |||||||

| CHEMICALS—0.1% | ||||||||

Braskem SA- ADR | 17,283 | 223,124 | ||||||

|

| |||||||

| ELECTRIC UTILITIES—0.2% | ||||||||

Cia Energetica de Minas Gerais- ADR | 52,928 | 263,052 | ||||||

|

| |||||||

| FOOD PRODUCTS—0.3% | ||||||||

BRF SA- ADR | 21,929 | 512,042 | ||||||

|

| |||||||

| METALS & MINING—0.4% | ||||||||

Cia Siderurgica Nacional SA- ADR | 57,569 | 119,744 | ||||||

Gerdau SA- ADR | 59,830 | 212,396 | ||||||

Vale SA- ADR | 51,251 | 419,233 | ||||||

|

| |||||||

| 751,373 | ||||||||

|

| |||||||

| OIL, GAS & CONSUMABLE FUELS—0.5% | ||||||||

Petroleo Brasileiro SA- ADR | 53,888 | 393,382 | ||||||

Ultrapar Participacoes SA- ADR | 21,797 | 415,669 | ||||||

|

| |||||||

| 809,051 | ||||||||

|

| |||||||

| WATER UTILITIES—0.1% | ||||||||

Cia de Saneamento Basico do Estado de Sao Paulo- ADR | 26,970 | 169,642 | ||||||

|

| |||||||

| 3,218,495 | ||||||||

|

| |||||||

CANADA—7.6% | ||||||||

| AUTO COMPONENTS—0.3% | ||||||||

Magna International, Inc. | 5,715 | 621,164 | ||||||

|

| |||||||

| BANKS—2.4% | ||||||||

Bank of Montreal | 9,619 | 680,352 | ||||||

Bank of Nova Scotia | 15,522 | 885,996 | ||||||

Canadian Imperial Bank of Commerce | 3,074 | 264,210 | ||||||

Royal Bank of Canada | 17,247 | 1,191,250 | ||||||

Toronto-Dominion Bank | 22,495 | 1,074,811 | ||||||

|

| |||||||

| 4,096,619 | ||||||||

|

| |||||||

| CHEMICALS—0.6% | ||||||||

Agrium, Inc. | 3,522 | 333,604 | ||||||

Methanex Corp. | 7,953 | 364,486 | ||||||

See accompanying notes to financial statements.

14

Schedule of Portfolio Investments, continued

| Praxis International Index Fund | ||

| December 31, 2014 |

| SHARES | FAIR VALUE | |||||||

COMMON STOCKS—98.0%, continued |

| |||||||

CANADA—7.6%, continued | ||||||||

| CHEMICALS—0.6%, continued | ||||||||

Potash Corp of Saskatchewan, Inc. | 10,495 | $ | 370,683 | |||||

|

| |||||||

| 1,068,773 | ||||||||

|

| |||||||

| INDEPENDENT POWER AND RENEWABLE ELECTRICITY PRODUCERS—0.1% | ||||||||

TransAlta Corp. | 14,668 | 132,892 | ||||||

|

| |||||||

| INSURANCE—0.4% | ||||||||

Manulife Financial Corp. | 22,525 | 430,002 | ||||||

Sun Life Financial, Inc. | 10,301 | 371,454 | ||||||

|

| |||||||

| 801,456 | ||||||||

|

| |||||||

| MEDIA—0.1% | ||||||||

Shaw Communications, Inc., Class B | 4,888 | 131,927 | ||||||

|

| |||||||

| METALS & MINING—0.4% | ||||||||

Barrick Gold Corp. | 18,692 | 200,939 | ||||||

Goldcorp, Inc. | 14,567 | 269,781 | ||||||

Teck Resources Ltd., Class B | 16,007 | 218,335 | ||||||

|

| |||||||

| 689,055 | ||||||||

|

| |||||||

| OIL, GAS & CONSUMABLE FUELS—1.8% | ||||||||

Advantage Oil & Gas Ltd.(a) | 18,950 | 90,771 | ||||||

Canadian Natural Resources Ltd. | 15,131 | 467,245 | ||||||

Cenovus Energy, Inc. | 19,412 | 400,275 | ||||||

Enbridge, Inc. | 18,096 | 930,315 | ||||||

Encana Corp. | 12,672 | 175,761 | ||||||

Suncor Energy, Inc. | 22,801 | 724,616 | ||||||

Talisman Energy, Inc. | 35,278 | 276,227 | ||||||

|

| |||||||

| 3,065,210 | ||||||||

|

| |||||||

| REAL ESTATE MANAGEMENT & DEVELOPMENT—0.4% | ||||||||

Brookfield Asset Management, Inc., Class A | 13,674 | 685,478 | ||||||

|

| |||||||

| ROAD & RAIL—1.1% | ||||||||

Canadian National Railway Co. | 12,210 | 841,391 | ||||||

Canadian Pacific Railway Ltd. | 5,165 | 995,244 | ||||||

|

| |||||||

| 1,836,635 | ||||||||

|

| |||||||

| 13,129,209 | ||||||||

|

| |||||||

CHILE—0.4% | ||||||||

| AIRLINES—0.2% | ||||||||

Latam Airlines Group SA- ADR(a) | 21,752 | 260,589 | ||||||

|

| |||||||

| BEVERAGES—0.1% | ||||||||

Embotelladora Andina SA, Class B- ADR | 6,720 | 114,240 | ||||||

|

| |||||||

| CHEMICALS—0.1% | ||||||||

Sociedad Quimica y Minera de Chile SA- ADR | 10,318 | 246,394 | ||||||

|

| |||||||

| 621,223 | ||||||||

|

| |||||||

CHINA—3.3% | ||||||||

| AIRLINES—0.1% | ||||||||

China Southern Airlines Co. Ltd.- ADR | 5,546 | 132,549 | ||||||

|

| |||||||

| BANKS—0.5% | ||||||||

China Construction Bank Corp.- ADR | 52,971 | 871,373 | ||||||

|

| |||||||

| CHEMICALS—0.1% | ||||||||

Sinopec Shanghai Petrochemical Co. Ltd.- ADR | 7,041 | 206,512 | ||||||

|

| |||||||

| DIVERSIFIED TELECOMMUNICATION SERVICES—0.2% | ||||||||

China Telecom Corp. Ltd.- ADR | 6,115 | 359,012 | ||||||

|

| |||||||

| INSURANCE—1.0% | ||||||||

China Life Insurance Co. Ltd.- ADR | 22,204 | 1,303,597 | ||||||

| SHARES | FAIR VALUE | |||||||

COMMON STOCKS—98.0%, continued |

| |||||||

CHINA—3.3%, continued | ||||||||

| INSURANCE—1.0%, continued | ||||||||

Ping An Insurance Group Co. of China Ltd.- ADR | 15,855 | $ | 323,283 | |||||

|

| |||||||

| 1,626,880 | ||||||||

|

| |||||||

| INTERNET SOFTWARE & SERVICES—1.0% | ||||||||

Tencent Holdings Ltd.- ADR | 119,811 | 1,738,458 | ||||||

|

| |||||||

| ROAD & RAIL—0.1% | ||||||||

Guangshen Railway Co. Ltd.- ADR | 8,797 | 212,272 | ||||||

|

| |||||||

| TECHNOLOGY HARDWARE, STORAGE & PERIPHERALS—0.3% | ||||||||

Lenovo Group Ltd.- ADR | 18,577 | 487,089 | ||||||

|

| |||||||

| 5,634,145 | ||||||||

|

| |||||||

COLOMBIA—0.6% | ||||||||

| BANKS—0.3% | ||||||||

BanColombia SA- ADR | 9,278 | 444,231 | ||||||

|

| |||||||

| OIL, GAS & CONSUMABLE FUELS—0.3% | ||||||||

Ecopetrol SA- ADR | 34,095 | 583,706 | ||||||

|

| |||||||

| 1,027,937 | ||||||||

|

| |||||||

DENMARK—0.9% | ||||||||

| BANKS—0.2% | ||||||||

Danske Bank A/S | 7,264 | 196,389 | ||||||

Danske Bank A/S- ADR | 6,614 | 88,991 | ||||||

|

| |||||||

| 285,380 | ||||||||

|

| |||||||

| PHARMACEUTICALS—0.7% | ||||||||

Novo Nordisk A/S- ADR | 28,510 | 1,206,543 | ||||||

|

| |||||||

| 1,491,923 | ||||||||

|

| |||||||

FINLAND—0.5% | ||||||||

| COMMUNICATIONS EQUIPMENT—0.2% | ||||||||

Nokia OYJ- ADR | 46,570 | 366,040 | ||||||

|

| |||||||

| MACHINERY—0.1% | ||||||||

Kone OYJ, Class B | 6,179 | 281,316 | ||||||

|

| |||||||

| PAPER & FOREST PRODUCTS—0.2% | ||||||||

Stora Enso OYJ- ADR | 32,308 | 286,249 | ||||||

|

| |||||||

| 933,605 | ||||||||

|

| |||||||

FRANCE—6.4% | ||||||||

| AUTO COMPONENTS—0.5% | ||||||||

Cie Generale des Etablissements Michelin- ADR | 25,215 | 454,879 | ||||||

Cie Generale des Etablissements Michelin, Class B | 1,074 | 96,947 | ||||||

Valeo SA | 338 | 42,057 | ||||||

Valeo SA- ADR | 4,352 | 269,519 | ||||||

|

| |||||||

| 863,402 | ||||||||

|

| |||||||

| AUTOMOBILES—0.2% | ||||||||

Renault SA | 5,464 | 397,978 | ||||||

|

| |||||||

| BANKS—0.8% | ||||||||

BNP Paribas SA- ADR | 28,958 | 850,786 | ||||||

Credit Agricole SA | 11,014 | 142,174 | ||||||

Credit Agricole SA- ADR | 14,211 | 90,666 | ||||||

Societe Generale SA | 1,991 | 83,324 | ||||||

Societe Generale SA- ADR | 36,300 | 302,016 | ||||||

|

| |||||||

| 1,468,966 | ||||||||

|

| |||||||

See accompanying notes to financial statements.

15

Schedule of Portfolio Investments, continued

| Praxis International Index Fund | ||

| December 31, 2014 |

| SHARES | FAIR VALUE | |||||||

COMMON STOCKS—98.0%, continued |

| |||||||

FRANCE—6.4%, continued | ||||||||

| BUILDING PRODUCTS—0.3% | ||||||||

Cie de Saint-Gobain | 11,742 | $ | 497,401 | |||||

|

| |||||||

| CONSTRUCTION & ENGINEERING—0.3% | ||||||||

Bouygues SA | 956 | 34,520 | ||||||

Vinci SA- ADR | 30,694 | 415,750 | ||||||

|

| |||||||

| 450,270 | ||||||||

|

| |||||||

| CONSTRUCTION MATERIALS—0.1% | ||||||||

Lafarge SA | 430 | 30,186 | ||||||

Lafarge SA- ADR | 6,876 | 119,917 | ||||||

|

| |||||||

| 150,103 | ||||||||

|

| |||||||

| DIVERSIFIED TELECOMMUNICATION SERVICES—0.3% | ||||||||

Orange SA- ADR | 20,175 | 341,361 | ||||||

Vivendi SA(a) | 9,270 | 230,735 | ||||||

|

| |||||||

| 572,096 | ||||||||

|

| |||||||

| ELECTRICAL EQUIPMENT—0.5% | ||||||||

Legrand SA | 17,254 | 905,113 | ||||||

|

| |||||||

| ENERGY EQUIPMENT & SERVICES—0.2% | ||||||||

CGG SA(a) | 670 | 3,948 | ||||||

CGG SA- ADR(a) | 7,732 | 45,619 | ||||||

Technip SA- ADR | 21,292 | 315,015 | ||||||

|

| |||||||

| 364,582 | ||||||||

|

| |||||||

| FOOD & STAPLES RETAILING—0.2% | ||||||||

Carrefour SA | 1,523 | 46,347 | ||||||

Carrefour SA- ADR | 49,035 | 295,191 | ||||||

|

| |||||||

| 341,538 | ||||||||

|

| |||||||

| FOOD PRODUCTS—0.7% | ||||||||

Danone SA- ADR | 86,450 | 1,125,320 | ||||||

|

| |||||||

| HEALTH CARE EQUIPMENT & SUPPLIES—0.3% | ||||||||

Essilor International SA | 4,503 | 502,171 | ||||||

Essilor International SA- ADR | 952 | 52,965 | ||||||

|

| |||||||

| 555,136 | ||||||||

|

| |||||||

| INSURANCE—0.5% | ||||||||

AXA SA- ADR | 34,977 | 800,624 | ||||||

|

| |||||||

| MEDIA—0.3% | ||||||||

Publicis Groupe SA- ADR | 26,260 | 468,478 | ||||||

|

| |||||||

| MULTI-UTILITIES—0.5% | ||||||||

GDF Suez | 2,524 | 58,857 | ||||||

GDF Suez- ADR | 17,681 | 411,923 | ||||||

Veolia Environnement SA | 11,656 | 206,461 | ||||||

Veolia Environnement SA- ADR | 8,771 | 154,194 | ||||||

|

| |||||||

| 831,435 | ||||||||

|

| |||||||

| PERSONAL PRODUCTS—0.5% | ||||||||

L’Oreal SA | 382 | 63,936 | ||||||

L’Oreal SA- ADR | 25,935 | 864,414 | ||||||

|

| |||||||

| 928,350 | ||||||||

|

| |||||||

| SOFTWARE—0.2% | ||||||||

Dassault Systemes- ADR | 6,224 | 379,664 | ||||||

|

| |||||||

| 11,100,456 | ||||||||

|

| |||||||

| SHARES | FAIR VALUE | |||||||

COMMON STOCKS—98.0%, continued |

| |||||||

GERMANY—6.2% | ||||||||

| AIR FREIGHT & LOGISTICS—0.5% | ||||||||

Deutsche Post AG | 10,161 | $ | 329,846 | |||||

Deutsche Post AG- ADR | 14,832 | 481,298 | ||||||

|

| |||||||

| 811,144 | ||||||||

|

| |||||||

| AIRLINES—0.1% | ||||||||

Deutsche Lufthansa AG- ADR | 10,201 | 169,898 | ||||||

|

| |||||||

| AUTOMOBILES—0.6% | ||||||||

Bayerische Motoren Werke AG- ADR | 27,692 | 986,389 | ||||||

|

| |||||||

| CAPITAL MARKETS—0.3% | ||||||||

Deutsche Bank AG | 18,882 | 566,838 | ||||||

|

| |||||||

| CHEMICALS—0.6% | ||||||||

BASF SE- ADR | 13,580 | 1,132,436 | ||||||

|

| |||||||

| DIVERSIFIED FINANCIAL SERVICES—0.2% | ||||||||

Deutsche Boerse AG | 2,890 | 205,369 | ||||||

Deutsche Boerse AG- ADR | 15,060 | 106,625 | ||||||

|

| |||||||

| 311,994 | ||||||||

|

| |||||||

| DIVERSIFIED TELECOMMUNICATION SERVICES—0.3% | ||||||||

Deutsche Telekom AG- ADR | 32,617 | 518,284 | ||||||

|

| |||||||

| HEALTH CARE PROVIDERS & SERVICES—0.6% | ||||||||

Fresenius Medical Care AG & Co. KGaA- ADR | 19,354 | 718,808 | ||||||

Fresenius SE & Co. KGaA | 5,130 | 266,729 | ||||||

|

| |||||||

| 985,537 | ||||||||

|

| |||||||

| INSURANCE—1.1% | ||||||||

Allianz SE- ADR | 76,050 | 1,260,148 | ||||||

Muenchener Rueckversicherungs-Gesellschaft AG | 1,682 | 334,949 | ||||||

Muenchener Rueckversicherungs-Gesellschaft AG- ADR | 18,890 | 374,778 | ||||||

|

| |||||||

| 1,969,875 | ||||||||

|

| |||||||

| MULTI-UTILITIES—0.1% | ||||||||

RWE AG | 2,125 | 65,587 | ||||||

RWE AG- ADR | 5,585 | 172,856 | ||||||

|

| |||||||

| 238,443 | ||||||||

|

| |||||||

| PHARMACEUTICALS—0.8% | ||||||||

Bayer AG- ADR | 9,846 | 1,347,327 | ||||||

|

| |||||||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—0.1% | ||||||||

Infineon Technologies AG- ADR | 12,109 | 128,961 | ||||||

|

| |||||||

| SOFTWARE—0.5% | ||||||||

SAP SE- ADR | 12,252 | 853,352 | ||||||

|

| |||||||

| TEXTILES, APPAREL & LUXURY GOODS—0.3% | ||||||||

adidas AG | 1,323 | 91,876 | ||||||

adidas AG- ADR | 9,964 | 343,808 | ||||||

Puma SE | 285 | 59,175 | ||||||

|

| |||||||

| 494,859 | ||||||||

|

| |||||||

| TRADING COMPANIES & DISTRIBUTORS—0.1% | ||||||||

Brenntag AG | 3,519 | 196,747 | ||||||

|

| |||||||

| 10,712,084 | ||||||||

|

| |||||||

See accompanying notes to financial statements.

16