UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08104

Touchstone Funds Group Trust

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-638-8194

Date of fiscal year end: September 30

Date of reporting period: September 30, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

September 30, 2018

Annual Report

Touchstone Funds Group Trust

Touchstone Active Bond Fund

Touchstone Arbitrage Fund

Touchstone Emerging Markets Small Cap Fund

Touchstone High Yield Fund

Touchstone Impact Bond Fund (formerly known as Touchstone Total Return Bond Fund)

Touchstone Merger Arbitrage Fund

Touchstone Mid Cap Fund

Touchstone Mid Cap Value Fund

Touchstone Premium Yield Equity Fund

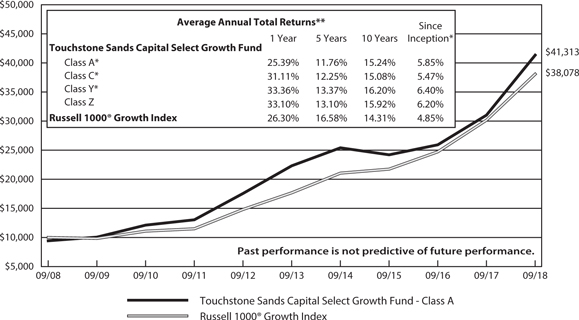

Touchstone Sands Capital Select Growth Fund

Touchstone Small Cap Fund

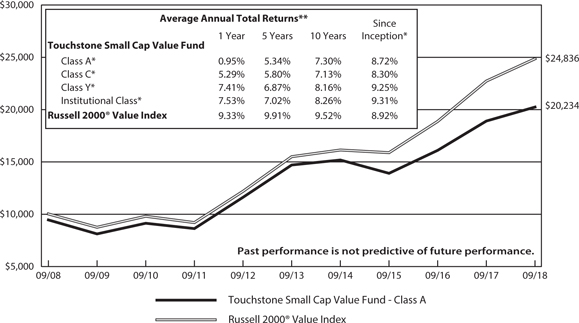

Touchstone Small Cap Value Fund

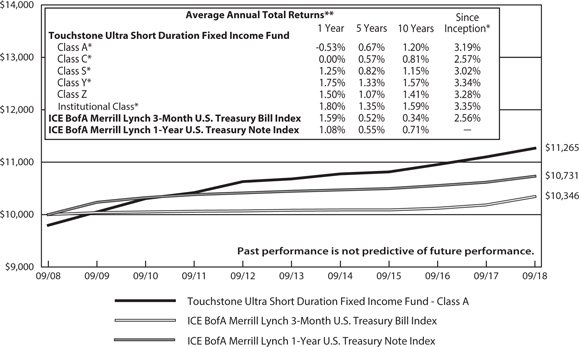

Touchstone Ultra Short Duration Fixed Income Fund

IMPORTANT NOTE: Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Touchstone Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the shareholder reports from Touchstone Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, annual and semi-annual shareholder reports will be available on the Touchstone Funds’ website (TouchstoneInvestments.com/Resources), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

Beginning on January 1, 2019, you may elect to receive all future annual and semi-annual shareholder reports in paper, free of charge. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. To elect to receive paper copies of shareholder reports through the mail or otherwise change your delivery method, contact your financial intermediary or, if you hold your shares directly through Touchstone Funds, visit TouchstoneInvestments.com/Resources/Edelivery or call Touchstone Funds toll-free at 1.800.543.0407. Your election to receive shareholder reports in paper will apply to all Touchstone Funds that you hold through the financial intermediary, or directly with Touchstone.

Table of Contents

This report identifies the Funds' investments on September 30, 2018. These holdings are subject to change. Not all investments in each Fund performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

| 2 |

Dear Shareholder:

We are pleased to provide you with the Touchstone Funds Group Trust Annual Report. It includes key financial information, as well as manager commentaries for the Funds, for the 12 months ended September 30, 2018.

The global economic recovery, now in its 10th year following the 2008 Credit Crisis, gained momentum in 2017 as the U.S., Japan, the European Union (EU) and China all reported solid economic growth through much of the 12 months. Notably, U.S. Gross Domestic Product growth is on track to report its first 3+ percent growth rate in over a decade. Despite the overall solid economic fundamentals, much of the period saw an increase in market volatility as tariffs and trade tensions raised the specter of an escalating global trade war. The “synchronized global expansion” showed signs of unraveling because of these growing trade tensions. Yet, the latter portion of the fiscal year saw some resolution on trade tensions as the U.S. reached preliminary trade deals with Canada, Mexico and South Korea, as well as a tariff truce with the EU. Throughout the period, monetary policies across the major central banks continued their divergent paths as the Bank of Japan and the European Central Bank maintained accommodative stances, while the U.S. Federal Reserve Board (Fed) continued toward its goal of monetary policy normalization by raising rates four times in the fiscal year. Additionally, the Fed began executing on a plan to reduce the size of its balance sheet by selling securities it had acquired during its post-Crisis Quantitative Easing programs.

A strengthening U.S. dollar, diverging economic data and widening trade disputes in the fiscal year’s second half affected performance results overseas. Global equities posted dramatically different results with U.S. equity markets posting double-digit returns compared to low single-digit returns from developed markets. The aforementioned strong U.S. dollar and trade tensions weighed on emerging markets equities as they posted slightly negative returns. Within the U.S. equity markets, growth-oriented stocks outpaced their value-oriented counterparts, while large-capitalization stocks outperformed mid- and small-capitalization stocks.

The Fed’s four rate hikes during the period drove short-term rates higher, while longer-term rates also moved higher but at a slower pace, resulting in a flattening of the yield curve. This increase in rates resulted in negative returns for investment grade bonds. However, non-investment grade bonds generated positive returns because they were less sensitive to interest rate changes and more correlated to economic activity.

With 2019 right around the corner, the post-Crisis bull market is approaching its 10-year anniversary. While it has certainly contained periods of volatility, the length and strength of this market environment only reinforces our view that investing is a long-term endeavor. A disciplined approach and appropriate time horizon can deter short-term thinking and reactive decision making. Your financial advisor can help you by identifying a risk-return profile and developing an investment plan that will help address your long-term financial goals.

We greatly appreciate your continued support. Thank you for including Touchstone as part of your investment plan.

Sincerely,

Jill T. McGruder

President

Touchstone Funds Group Trust

| 3 |

Management's Discussion of Fund Performance (Unaudited)

Touchstone Active Bond Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone Active Bond Fund seeks to provide as high a level of current income as is consistent with the preservation of capital. Capital appreciation is a secondary goal. In deciding what securities to buy and sell for the Fund, the overall investment opportunities and risks in different sectors of the debt securities market are analyzed by focusing on maximizing total return and reducing volatility of the Fund’s portfolio. A disciplined sector allocation process is followed in order to build a broadly diversified portfolio of bonds.

Fund Performance

The Touchstone Active Bond Fund (Class A Shares) underperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the 12-month period ended September 30, 2018. The Fund’s total return was -1.87 percent (calculated excluding the maximum sales charge) while the total return of the benchmark was -1.22 percent.

Market Environment

The return of volatility during the period reflected concerns about inflation and rising interest rates, as well as uncertainty surrounding global trade. As the 12-month period came to an end, markets waited anxiously for a resolution between the U.S. and its global trading partners as tensions continued to mount.

Within the index, Investment Grade Corporate Bonds, Mortgage-Backed Securities (MBS), Asset-Backed Securities (ABS) and Commercial Mortgage-Backed Securities (CMBS) all outperformed U.S. Treasuries during the period. However, High Yield Bonds also outperformed all fixed income sectors during the period.

During the 12-month period, the yield curve flattened as external forces depressed the long end of the curve while the U.S. Federal Reserve Board (Fed) increased the federal funds rate a total of four times. In general, yields moved rather significantly. In fact, yields on both the 10-year and 2-year U.S. Treasuries ended the period notably higher and tighter. The relationship between the two yields, commonly referenced as a market indicator on investor sentiment, began to concern many investors as it tightened to levels that many felt would invert, which is a strong signal for an impending recession.

Market expectations of additional Fed rate hikes also increased which was a reaction to strong underlying fundamentals. Underlying growth of the U.S. economy remained solidly above trend with third quarter growth projected to be approximately 3 percent. The strength of the economy was broad-based given the tailwinds from strong labor markets and fiscal policy; consensus expectations suggested a continuation of current growth rates. Labor markets consistently added over 150,000 jobs per month and remained tight. Wage growth was also strong and began to show signs of acceleration. Core inflation readings remained in line with the Fed’s 2 percent target.

Broad financial conditions were generally supportive of risk assets and economic growth, yet by the end of the period they were near the long-term average. At these levels, financial conditions no longer provided a tailwind for growth but instead were neutral. Driving financial conditions were the higher federal funds rate and a stronger U.S. dollar. And, while global central bank policy was generally accommodative, it began moving toward a more neutral level, as led by the Fed.

Portfolio Review

An overweight to Investment Grade Corporate Bond exposure was the main detractor of performance over the 12-month period.

| 4 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

The Funds allocation to U.S. dollar-denominated Emerging Markets debt was additive over the period, while security selection was strong within Securitized Assets, particularly within ABS and Non-Agency MBS. The Fund’s allocation to Treasury Inflation-Protected Securities (TIPS) was also positive, particularly at the end of 2017 as the Fund took advantage of sharp increases in inflation expectations on the back of rising commodity prices and strong economic data.

The Fund benefited from a rotation out of High Yield in favor of Securitized Assets in early October 2017 as spreads tightened significantly. Throughout the 12-month period, High Yield spreads continued to grind tighter. We believed Securitized Assets offered a more attractive risk/reward profile, particularly within the ABS and Non-Agency MBS sectors. We like these sectors as they closely relate to the health of the U.S. consumer, which we believe to be strong.

We made a modest allocation to U.S. dollar-denominated Emerging Markets debt. Valuations in this asset class were at attractive levels as spreads relative to domestic Investment Grade Corporates and High Yield reached pre-crisis highs. Combined with global growth conditions and supportive fundamentals, we believe the sector offered good opportunity.

Outlook

Going forward, we believe the greatest potential is the Fund’s risk assets, driven by U.S. economic growth, steady inflation and accommodative central bank policy. While financial conditions are no longer accommodative to growth, we believe they are not a hindrance either. Valuations have adjusted to reflect uncertainty around trade issues and how it will impact growth, and we believe the potential upside for price appreciation is limited. We have been taking advantage of opportunities among securitized assets when possible, where we believe attractive risk/reward profiles can be found in the ABS and Non-Agency MBS sectors. We like these sectors’ close connections to consumer spending, which continues to be healthy.

We believe global central banks need to maintain accommodative policies in order to support expansion abroad. Rate hikes by the Fed will further tighten financial conditions as the year progresses, which may become a headwind for the Fund’s overweight position to risk assets. Further escalation of trade disputes, specifically between the U.S. and China, may also impact risk assets.

We believe interest rates are generally fair, and currently reflect the positive economic outlook. As a result, in the near-term, the Fund is positioned with a long duration and neutral curve relative to the benchmark, and we will look to opportunistically take advantage of dislocations in the market as they arise.

| 5 |

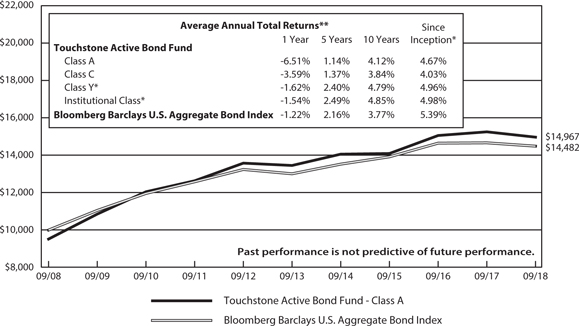

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Active Bond Fund - Class A*and the

Bloomberg Barclays U.S. Aggregate Bond Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was October 3, 1994, October 3, 1994, April 12, 2012, and April 12, 2012, respectively. Class Y shares' and Institutional Class shares' performance was calculated using the historical performance of Class A shares for the periods prior to April 12, 2012. The returns have been restated for sales loads and fees applicable to Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. Effective August 17, 2018, the maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 2.04% of the NAV (or 2.00% of the offering price). Prior to August 17, 2018, the maximum offering price per share of Class A shares was equal to the NAV per share plus a sales load equal to 4.99% of the NAV (or 4.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

| 6 |

Management's Discussion of Fund Performance (Unaudited)

Touchstone Arbitrage Fund

Sub-Advised by Longfellow Investment Management Co., LLC

Investment Philosophy

The Touchstone Arbitrage Fund seeks to achieve positive absolute returns over the long term regardless of market conditions by investing primarily in securities of companies that are involved in publicly announced mergers, takeovers, tender offers, debt restructurings, minority purchases, leveraged buyouts, spin-offs, liquidations and other corporate reorganizations.

Fund Performance

The Touchstone Arbitrage Fund (Class A shares) underperformed its benchmark, the ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index, for the 12-month period ended September 30, 2018. The Fund’s total return was -1.18 percent (calculated excluding the maximum sales charge) while the benchmark’s total return was 1.59 percent.

Market Environment

During the 12-month period ended September 30, 2018, risk assets continued to generate strong returns, however volatility increased. Earnings growth remained strong and U.S. corporations have begun to benefit from the lower corporate tax rate as part of the 2017 corporate tax reform.

The U.S. Federal Reserve Board (Fed) was firmly committed to a schedule for rate increases, with 25 basis point increases in each of the last four quarters. While rates remained low relative to historical averages and access to capital markets to facilitate acquisitions was abundant, there was implied risk that the Fed moved too quickly and disrupted what has been a slow and steady recovery in the economy since the depths of the Financial Crisis ten years ago.

Deal spread levels remained below what was anticipated given the increase in short rates. In terms of deal activity, Information Technology and Health Care were the busiest industries in the Fund’s investable universe. While the market sentiment for deal-making appears to be robust, there seems to be an impact from both geopolitical trade pressures and general uncertainty as it relates to tariffs and the emerging trade war issues between the United States and China.

Portfolio Review

While the Fund’s positioning frequently changed due to companies with new deals being added and completed deals being removed, there were no significant changes to its overall positioning. During the period, the Fund’s holdings had 71 deals close and the Fund invested in 80 new companies with pending transactions.

The Fund benefited from the outcome of the Broadcom Ltd./Brocade Communications Systems, Inc. deal. Broadcom and Brocade announced a definitive agreement for Broadcom to acquire Brocade for $12.75 per share in cash. The deal closing was subject to regulatory approvals in various jurisdictions, customary closing conditions, as well as the approval of Brocade’s stockholders. One of the regulatory requirements needed was from the Committee on Foreign Investment in the United States (CFIUS). The companies ran into issues getting this approval. Only after an agreement from Broadcom to move its headquarters back to the United States was the deal allowed to close.

Another deal that contributed to Fund performance was the Discovery Communications Inc./Scripps Networks Interactive Inc. deal. Discovery and Scripps announced a definitive agreement for Discovery to acquire Scripps. Shareholders received $90.00 per share under the terms of the agreement, comprised of $63.00 per share in cash and $27.00 per share in Class C common shares of Discovery stock. The deal had been stalled in an

| 7 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

extended regulatory review in which the Department of Justice (DOJ) had asked the companies for more information. The companies supplied the DOJ with what was requested and were then given the approval needed to close the merger.

The Fund’s performance was hurt by its exposure to Akorn Inc., Tribune Media Company and NXP Semiconductors N.V. The Fund continues to hold these companies because of our belief in their future prospects and/or the stock’s valuation dislocations.

Fresenius SE & Co. KGaA announced a definitive agreement to acquire Akorn Inc. for $34.00 a share. The agreement and transaction have been approved by the boards of both companies and recommended by Akorn’s board to its shareholders. Akorn dropped materially following the announcement that their acquirer, Fresenius, terminated the merger agreement on the back of an investigation into Akorn’s data integrity requirements. Akorn filed suit in Delaware court in order to enforce the merger agreement. A Delaware judge ruled that Fresenius had the right to terminate the merger agreement. This ruling is the first in a Delaware court in which a material adverse event had been proven to have occurred during a merger.

Qualcomm Inc. and NXP Semiconductors N.V. announced a definitive agreement for Qualcomm to acquire NXP for $110.00 per share in cash through a tender offer. NXP was trading with a significant discount to the new Qualcomm offer due to the ongoing trade war between China and the United States. The lone remaining regulatory approval by the Ministry of Commerce, People’s Republic of China (MOFCOM) was elusive due to the ongoing trade war. The deal was terminated.

Sinclair Broadcast Group, Inc. and Tribune Media Company announced a definitive agreement under which Sinclair would acquire Tribune for $35.00 in cash and 0.23 shares of Sinclair Class A common stock for each share of Tribune Class A common stock and Class B common stock. The transaction was subject to approval by Tribune’s stockholders, as well as customary closing conditions, including approval by the Federal Communications Commission (FCC) and antitrust clearance. The deal was terminated by Tribune when the FCC stated that it was against the divestiture package put forth by Sinclair.

Outlook

The main entity driving the environment remains CFIUS. With potential new measures being adopted by the U.S. to broaden the purview of CFIUS, we remain highly selective and disciplined in our analysis of any cross-border transaction. Our investment process includes a strong emphasis on buyer due diligence and focus on cross-border buyers that could run afoul of U.S. regulatory bodies. We believe prevailing deal spreads will increase but lag the past four interest rate hikes.

The market continues to differentiate between the riskier and the more straightforward deals. Deals with a greater amount of perceived risk are being assigned a significantly wider spread than transactions with fewer hurdles. This is in contrast to much of recent history when spreads were not necessarily compensating investors appropriately for the amount of risk taken.

We think access to capital, slow global growth, and strong corporate balance sheets will drive incremental strategic Mergers & Acquisitions. We also think that historically low funding costs should provide a tailwind for financial buyers. On balance, we see a backdrop that remains supportive for continued deal activity.

We believe the Fund is well positioned with a strong focus on liquidity management and mitigating downside risk. We are optimistic at the tailwinds for deal activity and potential for wider spreads based on our outlook.

| 8 |

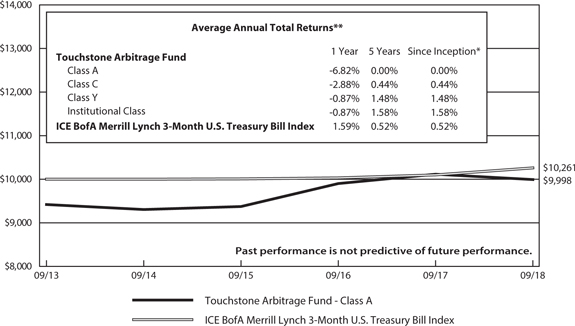

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Arbitrage Fund - Class A* and the

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of the Fund was September 30, 2013. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. Effective August 17, 2018, the maximum offering price per share of Class A shares is equal to the net assets value (“NAV”) per share plus a sales load equal to 5.26% of the NAV (or 5.00% of the offering price). Prior to August 17, 2018, the maximum offering price per share of Class A shares was equal to the NAV per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note To Chart

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged index of Treasury securities maturing in 90 days that assumes reinvestment of all income.

| 9 |

Management's Discussion of Fund Performance (Unaudited)

Touchstone Emerging Markets Small Cap Fund

Sub-Advised by Copper Rock Capital Partners LLC

Investment Philosophy

The Touchstone Emerging Markets Small Cap Fund seeks capital appreciation by primarily investing in equity securities of emerging markets small-cap companies diversified across sectors and industries. The Fund’s investment process seeks to add value through bottom-up stock selection and in-depth fundamental research.

Fund Performance

The Touchstone Emerging Markets Small Cap Fund (Class A shares) underperformed its benchmark, the MSCI Emerging Markets Small Cap Index for the 12-month period ended September 30, 2018. The Fund’s total return was -11.66 percent (calculated excluding the maximum sales charge) while the total return of the benchmark was -4.20 percent.

Market Environment

During the final quarter of 2017, the asset class comprising small market capitalization equities in emerging markets climbed higher, driven by outperforming stocks in the Health Care and Information Technology sectors, a strong consumer and a broad rally in commodities. Market volatility crept higher during the remainder of the 12-month period as investors’ concerns surfaced over slowing global growth and hawkish commentary from the U.S. Federal Reserve Board (Fed). Specifically, from the second quarter of 2018 to the end of the period, stocks of small capitalization companies in emerging markets were broadly pressured and moved into negative territory. In general, the asset class as a whole was negatively impacted by a stronger U.S. dollar, tensions surrounding trade disputes and tariffs and higher U.S. interest rates.

From a sector perspective within the small capitalization emerging markets asset class, only the Health Care and Consumer Staple sectors produced positive returns while the Communications Services, Utilities and Industrials sectors were the largest decliners. In terms of style, growth stocks underperformed their value counterparts.

Portfolio Review

Over the 12-month period, the Fund faced significant headwinds due to market volatility and the impending impact over a protracted trade war. In particular, the Fund’s holdings in most sectors of the Chinese market detracted from performance, as did a lack of exposure to Korean pharmaceutical and biotechnology stocks, which rallied during the period. Stock selection in India also detracted from relative returns. Stock selection in Thailand, combined with an overweight allocation to the country, was additive. Thailand benefited from being one of the most progressive countries in reforming its balance sheet, and from being more insulated than others from concerns over rising U.S. interest rates.

From a sector perspective, the Fund benefited from positive stock selection in the Consumer Staples, Materials, Energy and Financials sectors, while selection in the Health Care, Consumer Discretionary and Real Estate sectors detracted the most.

Among the individual stocks that contributed to Fund performance were KrungThai Card Public Co. Ltd. (Financials sector), TCI Co. Ltd. (Consumer Staples sector), Douzone Bizon Co. Ltd. (Information Technology sector), China Resources Cement Holdings Ltd. (Materials sector) and Muangthai Capital Public Co. Ltd. (Financials sector).

KrungThai is a credit card issuer in Thailand offering both VISA and Mastercard branded cards. The company’s smaller and more nimble size in the market has allowed it to manage the Bank of Thailand’s push to curb countrywide household debt much better than its competitors. The company also reported higher net profits

| 10 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

during the period versus both its competitors and street expectations. While credit card usage has slowed in Thailand, KrungThai’s growth still outpaced the broad industry.

TCI Co. is a Taiwan-based innovative health foods company that develops and produces supplements and nutritional products. The company also makes facial masks which are sold to global consumer retailers like Sephora & Co., among other clients. During the first quarter of 2018, the company announced earnings that beat market expectations, and management guided for strong growth driven by new product innovation over the next five years. Rising wages in China, along with an aging demographic that was more inclined and able to spend on beauty and health care products, were also important growth catalysts for TCI. In addition, the company has production facilities in Taiwan which Chinese customers perceive to be higher quality. Going forward, we expect the company’s sales will benefit from greater demand for health products and nutritional supplements in China and across Asia. We also believe the market is just beginning to appreciate TCI’s strong growth profile and overseas opportunities.

Douzone Bizon is a South Korea-based provider of enterprise risk platforms and accounting software for small to mid-sized enterprises (SME). Similar to other software companies, Douzone Bizon has begun to migrate desktop users to the cloud which results in both higher fees and lower maintenance costs. In 2018, the company started to experience strong SME customer growth through its web-based accounting platform, as well as growth from its new web-based modules. Importantly, the company also won new business from a large conglomerate in Korea.

China Resources Cement is a producer of cement in southeastern China. The company recently benefited from the closure of highly polluting cement plants across China and from price coordination among larger cement companies. In addition, the Greater Bay Area initiative in China – a plan to link nine cities in Guangdong province plus Hong Kong and Macau to form an integrated business hub – has led to government-led infrastructure growth and cement demand. During the quarter, the stock outperformed due to strong first quarter results and continued price increases. As a result of this outperformance, and the company’s increased market cap, we exited the position.

Muangthai Capital is a commercial lending company based in Thailand that provides individual and SME loans targeted to car titles and agricultural vehicle and land titles. Investor concerns over regulatory tightening in the commercial lending space eased during the period and, as final regulations were released, Muangthai was within the guidelines across all categories. This news positively impacted the stock as did reports of strong company fundamentals that were announced in the firm’s latest quarterly update.

Among the individual stocks that detracted from Fund performance were Qualicorp Consultoria e Corretora de Seguros SA (Health Care sector), Sansiri Public Co. Ltd. (Real Estate sector), China Yongda Automobiles Services Holdings Ltd. (Consumer Discretionary sector), L&T Finance Holdings (Financials sector) and AirTAC International Group (Industrials sector).

Qualicorp is a private health insurance distributor in Brazil which offers direct sales to affinity groups and individual customers. While Qualicorp was a long-term contributor to Fund performance, the company recently came under pressure despite delivering strong cash flow and maintaining a favorable balance sheet. Weakness was primarily driven by continued price increases in Brazil’s overall medical costs. Though company management executed a plan to protect its operational key performance indicators, the increased costs began to impact membership in the affinity plans supported by Qualicorp. As a result, we exited the Fund’s position.

Sansiri is a developer of higher end residential properties in Thailand. The company’s third quarter 2017 results showed weaker performance compared to the prior quarter, which raised concerns that the company would not meet its 2017 guidance. In addition, the company guided for slower growth in 2018. While the company

| 11 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

reported solid pre-sales in November 2017, which led to a mild recovery through December, the company did not recover from its previous highs. We exited the Fund’s position as a result.

China Yongda Automobile Services is a retailer of premium international automobile brands in China including BMW, Audi and Porsche. A major portion of our growth thesis for Yongda was the fact that BMW has five new model rollouts through 2019. Unfortunately, several of the model rollouts were significantly delayed in 2018. At the same time, broad auto sales in China have been under significant pressure driven by the USA/China trade dispute. As the fundamental support for the company has also eroded, we decide to liquidate the Fund’s position.

L&T Finance is a non-banking financial company (NBFC) in India with focus on rural, housing and wholesale lending, plus an asset management and wealth management business. All NBFCs in India have been under pressure recently – including L&T Finance – due to pressure on the currency that has resulted in a squeeze on short term liquidity. India’s central bank is addressing some of the liquidity issues for NBFCs and we believe this is having a positive impact. Furthermore, we see a strong growth path ahead for L&T Finance and continue to see it as high quality and buffered from direct impact of the liquidity squeeze. We continue to hold the stock as we believe there is potential opportunity.

AirTAC International Group manufactures pneumatic components and is a key component supplier into the factory automation supply chain. AirTAC has a high quality, focused management team that has shown strict adherence to product development and pricing that drives profitability. A key thesis for our investment in AirTAC was that we expect the growth in factory automation to continue – especially within China – for the next several years. Unfortunately, capital expenditure decisions – especially on spending on factory automation – have broadly been put on hold due to concerns surrounding the USA/China trade dispute. As such, we have decided to exit the Fund’s investment in AirTAC.

At the end of the quarter, the Fund was overweight to the Financials, Consumer Discretionary, Information Technology, Energy and Health Care sectors. It was underweight to the Consumer Staples, Materials, Communication Services, Real Estate, Utilities and Industrials sectors. On a country basis, the Fund was overweight to China, Thailand, India, Korea, Hungary, Greece and Brazil, while the largest underweight allocations were to Chile, Taiwan and Indonesia.

Outlook

Many market strategists are now setting the trade war between the U.S. and China as their base case assumption going forward. This has clearly had a notable impact on investor sentiment for emerging markets equities over the past two quarters, and also extends a broader impact in the emerging markets space beyond just China. Also, India – which seemed to have a longer-term focus driving its broad growth – began to experience some negative impact on its currency and short-term liquidity.

Nonetheless, there were positive factors during the most recent quarter of the 12-month period that were encouraging. Thailand has cleaned up its public balance sheet over the past decade and now stands out economically from the crowd in terms of stability and defensiveness within emerging markets. Mexico has moved past a major election and, after re-establishing the trade agreement with the U.S. and Canada, has shown opportunities for improving growth and company fundamentals. Brazil will be finished with its elections soon which we believe has started to create a stabilizing effect on that market, thereby strengthening the impact of positive fundamentals.

Given this background, we continue to approach the investment opportunities within the emerging markets small cap space by focusing on stocks with strong, well-explained and visible earnings growth supported by valuation levels and management teams that deliver the key drivers of sustainable earnings growth. We do this

| 12 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

within a framework and awareness that recognizes the headwinds and tailwinds associated with the country dynamics that are present today in emerging markets.

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Emerging Markets Small Cap Fund - Class A* and the

MSCI Emerging Markets Small Cap Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of the Fund was September 30, 2009. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. Effective August 17, 2018, the maximum offering price per share of Class A shares is equal to the net assets value (“NAV”) per share plus a sales load equal to 5.26% of the NAV (or 5.00% of the offering price). Prior to August 17, 2018, the maximum offering price per share of Class A shares was equal to the NAV per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

MSCI Emerging Markets Small Cap Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of small companies from emerging markets.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This report is not approved or produced by MSCI.

| 13 |

Management's Discussion of Fund Performance (Unaudited)

Touchstone High Yield Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Touchstone High Yield Fund seeks a high level of income. Capital appreciation is a secondary consideration. The Fund primarily invests in non-investment-grade securities.

Fund Performance

The Touchstone High Yield Fund (Class A shares) underperformed its benchmark, ICE BofA Merrill Lynch High Yield Cash Pay Index, for the 12-month period ended September 30, 2018. The Fund’s total return was 1.24 percent (calculated excluding the maximum sales charge) while the benchmark’s total return was 2.89 percent.

Market Environment

Over the 12-month period, the High Yield market was driven by a handful of larger economic movements that significantly affected the asset class and returns. In part, news was dominated by economic volatility surrounding political rhetoric, tax policy, sanctions and trade tariffs out of Washington, D.C. When taken as a whole, the combination of tax stimulus and fiscal stimulus positively impacted the economy. In particular, it resulted in a rally in risk assets, along with a notable change in interest rates, due to an increase in growth expectations while inflation expectations remained subdued. The market also saw increased volatility from trade rhetoric and the resulting subsequent implementation.

Yields on 2-year and 10-year U.S. Treasuries rose meaningfully and was a significant headwind for fixed income assets. Investment grade corporate securities with long durations and low spreads were affected the most. Below-investment grade securities were able to absorb the headwinds more effectively. Their typically shorter duration were less prone to the intermediate-to-longer-term U.S. Treasury yield increases and outperformed.

During the 12-month period, the top performing sectors were Supermarkets, Pharmaceuticals, Energy and Aerospace/Defense. The common theme among these sectors was that returns were all dominated by low-rated, predominately CCC-rated bonds, which was a headwind to the Fund’s higher quality portfolio and detracted from performance. For example, crude oil prices steadily increased during the period, thus providing a backdrop for high-yielding, lower-quality Energy bonds to continue their recovery from the lows seen in 2015 and 2016. As a result, Independent Energy and Oil Field Services were two of the strongest returning segments in the benchmark. The weakest performing sectors were Auto Parts, Housewares and Apparel.

Portfolio Review

Overall, sector allocation detracted from Fund performance for the 12-month period. The Fund’s overweight positions to Supermarkets and Wirelines contributed to Fund returns, as did underweight positions to Packaging and Wireless. The Fund’s overweight position to Food & Beverage detracted from performance but credit selection within the sector more than offset this allocation effect. The Fund’s underweight to Pharmaceuticals, which was dominated by the returns of CCC-rated Valeant Pharmaceuticals International Inc. and Endo International PLC, negatively impacted performance. These two bonds were a headwind which was difficult to offset. As previously noted, credit quality and duration were the two most significant macroeconomic factors affecting performance for the period.

Security selection detracted from performance and was driven by two main factors: underweight positions in CCC-rated bonds and overweight positions in Diebold Nixdorf Inc. and Ultra Petroleum Corp. Diebold Nixdorf is a financial and retail technology company that specializes in the production of ATMs. The holding was the largest detractor as the company struggled to integrate a large acquisition. Ultra Petroleum, an exploration and

| 14 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

production company, also detracted as the company struggled with commodity pricing, the implementation of a new strategy, and speculation surrounding the management of its balance sheet. GenOn Energy, an energy company and bankruptcy entity rebounded and positively affected performance. Additionally, overweight positions to a Telecommunications company, Frontier Communications Corp. and a Midstream company, NGL Energy Partners LP, also contributed to returns.

The largest overweight sectors within the Fund were Food & Beverage, Consumer Products and Midstream, while the largest underweights were Information Technology, Independent Energy and Wireless Communications.

Fund duration was slightly longer than that of the benchmark as the portfolio is underweight the shortest-to-maturity segment of the market and overweight mid-durations bonds. In general, the Fund does not seek to take an explicit position on duration, preferring instead to let security selection decisions drive relative performance.

Outlook

We believe the greatest opportunities may be a continuation of the current environment of low growth mixed with relatively easy monetary policy, or a meaningful sell-off in the High Yield market. The combination of solid Gross Domestic Product growth, strong employment gains, positive financial conditions and a resetting of interest rates provides an environment in which we believe the High Yield market has potential. This scenario presumes that the ongoing trade talks do not evolve into a market-altering event and that economic activity, which has accelerated domestically, maintains its current pace of expansion.

In light of High Yield’s relatively low spread and yield levels, the Fund is positioned toward the lower portion of its risk range. Yield is below that of the benchmark due to a significant underweight to CCC-rated bonds. We believe that the BB- and B-rated segments of the market are fairly valued. As the business cycle has recovered from the slowdown in 2015 and 2016, and because of the risk asset sell-off, we have reduced the Fund’s CCC-rated exposure. More recently, purchase activity has been tilted towards BB-rated issuers. We believe the Fund’s defensive stance positions it well in a market in which CCC-rated bonds are priced with little room for error and economic activity is currently high.

The Fund’s positioning emphasizes security selection over sector allocation as we believe there are a limited number of sector allocation opportunities in the current environment. Where there are sector opportunities, we express our views through quality (BB versus B) and not necessarily through a large underweight or overweight to a sector.

| 15 |

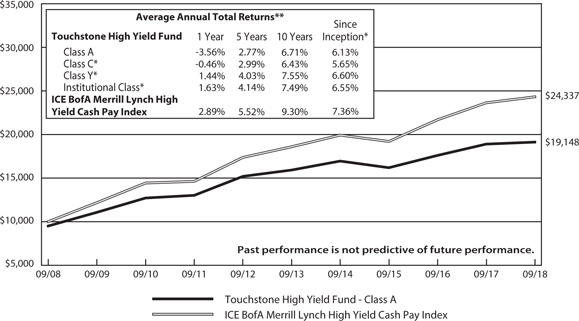

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone High Yield Fund - Class A*and the ICE BofA Merrill Lynch High Yield Cash Pay

Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was May 1, 2000, May 23, 2000, February 1, 2007, and January 27, 2012, respectively. Class C shares', Class Y shares' and Institutional Class shares' performance was calculated using the historical performance of Class A shares for the periods prior to May 23, 2000, February 1, 2007 and January 27, 2012, respectively. The returns have been restated for sales loads and fees applicable to Class C, Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. Effective August 17, 2018, the maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 2.04% of the NAV (or 2.00% of the offering price). Prior to August 17, 2018, the maximum offering price per share of Class A shares was equal to the NAV per share plus a sales load equal to 4.99% of the NAV (or 4.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

ICE BofA Merrill Lynch High Yield Cash Pay Index is an unmanaged index used as a general measure of market performance consisting of fixed-rate, coupon-bearing bonds with an outstanding par which is greater than or equal to $50 million, a maturity range greater than or equal to one year and must be less than BBB/Baa3 rated but not in default.

| 16 |

Management's Discussion of Fund Performance (Unaudited)

Touchstone Impact Bond Fund*

Sub-Advised by EARNEST Partners LLC

Investment Philosophy

The Touchstone Impact Bond Fund seeks current income. Capital appreciation is a secondary goal. The Fund invests primarily in fixed income securities or sectors that are considered undervalued for their risk characteristics.

Fund Performance

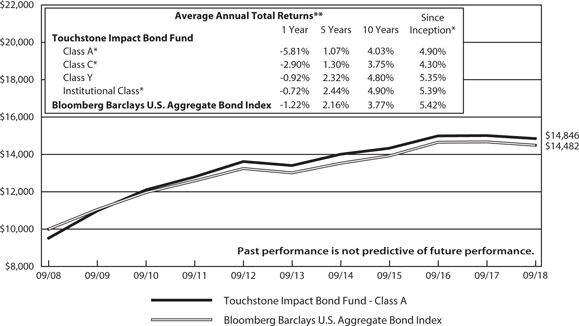

The Touchstone Impact Bond Fund (Class A shares) outperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index for the 12-month period ended September 30, 2018. The Fund’s total return was -1.07 percent (calculated excluding the maximum sales charge) while the benchmark’s total return was -1.22 percent.

Market Environment

U.S. economic data was positive for the 12-month period ended September 30, 2018 in a relatively stable and consistent pattern. Gross domestic product (GDP) reported real gains during all four quarters of the period. The unemployment rate also improved in a somewhat steady fashion and ended the period with the lowest unemployment rate in decades. Meanwhile, labor force participation was steady and wage growth improved as the number of job openings was on par with the number of job seekers. Many companies reported that their single largest challenge was finding employees to fill job openings. While the employment picture improved, inflation remained reasonably stable and well anchored. This was due in part to the U.S. Federal Reserve Board’s (Fed) monetary policy. The Fed raised interest rates once each quarter for the 12-month period, which was done in large part to stem increasing inflation as the economy continued to build momentum.

During the 12-month period, the Bloomberg Barclays U.S. Aggregate Bond Index outperformed relative to similar duration U.S. Treasuries. Lower quality bonds were in particularly high demand during the period as BBB-rated securities delivered the strongest levels of outperformance, whereas high-quality AAA-rated securities were the weakest performers.

Interest rates rose notably during the period, and these increases occurred across the yield curve with the largest moves taking place in the shorter parts of the curve. This was due to a confluence of factors including but not limited to: 1) an increase in U.S. Treasury Bill supply to fund the fiscal deficit, 2) increases in the federal funds rate, 3) reduced demand for U.S. Treasuries from international investors and 4) low inflation expectations by market participants. The rising interest rate environment was especially difficult for U.S. Treasuries, as these securities are inherently exposed to interest rate risk without any of the additional yield spread that bonds can generate. As a result, U.S. Treasuries declined during the period.

During the 12-month period, the stock market’s outperformance and the bond market’s higher yields helped attract assets from U.S. pensions into fixed income assets as funding gaps were narrowed. With these drivers, nearly all spread sectors within the U.S. fixed income market delivered positive relative returns during the quarter. U.S. Credit led the way, with U.S. Corporate Bonds driving much of the performance due to increased earning potential which buoyed optimism for the sector. This sentiment particularly favored issuers from the Industrials sector, as that sector significantly outperformed U.S. Treasuries with similar durations.

Credit-sensitive securities such as Asset-Backed Securities (ABS) and Commercial Mortgage-Backed Securities (CMBS) also posted strong relative returns during the period. Agency Single-Family Mortgage-Backed Securities (MBS) performed well, but to a lesser degree, due to spurts of market volatility. Agency Multi-Family MBS,

| 17 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

which are structured in a way that leaves them less prone to changes in volatility, also outperformed. U.S. Agency bonds also produced positive relative returns for the fiscal year.

Portfolio Review

The Fund’s overweight position in Agency Multi-Family MBS provided a tailwind as the sector outperformed its sister, Agency Single-Family MBS, during the period. The Fund’s overweight to U.S. Agencies provided another tailwind. The Fund’s underweight to CMBS was a headwind as the sector also performed well. This was largely offset by the market’s preference for more cyclical and sensitive portions of the U.S. Corporate Bond sector. More consistent industries such as Utilities generated modest relative returns compared to that of more cyclical industries within the Industrials sector.

Individual issues created a mixture of tailwinds and headwinds during the period. Security selection within U.S. Agencies contributed to performance. Security selection within ABS, in particular the Fund’s rate reduction bonds, outperformed their broader sector. Conversely, positions within U.S. Corporate Bonds detracted. General Electric Co. surprised the majority of the investment community with previously undisclosed impairments and losses. The company is now in the midst of a fundamental transition. We have completely sold the Fund’s position in the company. Alternatively, we have retained the Fund’s investment in South Carolina Electric and Gas Co. despite the headwinds faced by the company and its recent drag on performance. The debt held is secured in nature and we believe, regardless of the pressures faced by the company, the assets backing this mortgage are critical and essential in nature to the local economy it supports.

The Fund does not make any active interest rate bets and, accordingly, the Fund’s effective duration was approximately matched to that of the benchmark at the end of the quarter. By approximately matching the benchmark’s duration, the Fund’s interest rate risk is effectively equal to that of the benchmark over time. Furthermore, while changes in interest rates can impact total return, the Fund attempts to remain relatively neutral. With this approach, we believe changes in interest rates should not have much impact on the relative performance of the Fund.

Outlook

Looking ahead, we believe there are many events and developments taking place that could provide opportunities. As we have previously described, the Fed’s normalization of its balance sheet could provide a tailwind for the Fund as the portfolio is underweight in both U.S. Treasuries and Single-Family MBS. If the Fed, the single largest buyer of these securities, begins to step away from the purchasing table, these sectors could experience relative underperformance. Thus far, the pace of the Fed’s balance sheet tapering has been modest at approximately $150 billion in aggregate, and the run rate is scheduled to reach upwards of $50 billion a month by the end of the year. The divergent monetary policies that have been pursued by the Fed versus the rest of the world has increased currency hedging costs. This, along with trade disputes, has reduced demand for U.S. Treasuries from foreign buyers. Going forward, as these two large sources of demand pull back from the U.S. Treasury market, supply is expected to increase due to budget deficits and expansionary fiscal policy. As a result, the underweight positions to U.S. Treasuries and Single-Family MBS have the potential to benefit the Fund.

Furthermore, unexpected volatility within the financial markets could be fueled by increased levels of leverage, tense trade rhetoric with China, concerns surrounding emerging markets, and potential liquidity implications resulting from central bank actions. However, we believe the Fund’s emphasis on less economically sensitive sectors and higher quality could act to mitigate these impacts. As such, we believe the Fund is positioned well and maintains a discipline that balances risk and return objectives.

*Formerly Touchstone Total Return Bond Fund.

| 18 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Impact Bond Fund - Class A* and the

Bloomberg Barclays U.S. Aggregate Bond Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was August 16, 2010, August 1, 2011, November 15, 1991 and August 1, 2011, respectively. Class A shares', Class C shares' and Institutional Class shares' performance was calculated using the historical performance of Class Y shares for the periods prior to August 16, 2010, August 1, 2011 and August 1, 2011, respectively. The returns have been restated for sales loads and fees applicable to Class A, Class C and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. Effective August 17, 2018, the maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 2.04% of the NAV (or 2.00% of the offering price). Prior to August 17, 2018, the maximum offering price per share of Class A shares was equal to the NAV per share plus a sales load equal to 4.99% of the NAV (or 4.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

| 19 |

Management's Discussion of Fund Performance (Unaudited)

Touchstone Merger Arbitrage Fund

Sub-Advised by Longfellow Investment Management Co., LLC

Investment Philosophy

The Touchstone Merger Arbitrage Fund seeks to achieve positive absolute returns regardless of market conditions over the long term by investing primarily in securities of companies that are involved in publicly announced mergers and other corporate reorganizations. Merger arbitrage is an investment strategy that seeks to capture the “arbitrage spread” represented by the difference between the market price of the securities of the company being purchased and the value that is offered for these securities by the acquiring company. The Fund selects securities based on proposed financing terms, the size of the transaction, anti-trust concerns, regulatory approvals and shareholder voting requirements.

Fund Performance

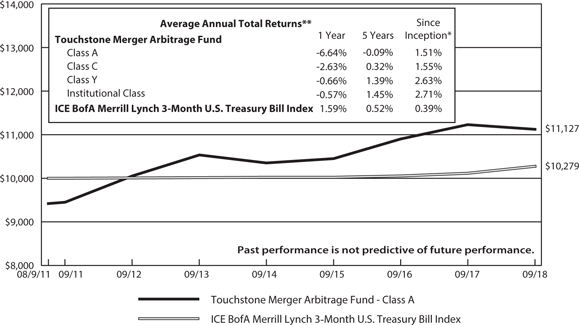

The Touchstone Merger Arbitrage Fund (Class A shares) underperformed its benchmark, the ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index, for the 12-month period ended September 30, 2018. The Fund’s total return was -0.96 percent (calculated excluding the maximum sales charge) while the benchmark’s total return was 1.59 percent.

Market Environment

During the 12-month period ended September 30, 2018, risk assets continued to generate strong returns, however volatility increased. Earnings growth remained strong and U.S. corporations have begun to benefit from the lower corporate tax rate as part of the 2017 corporate tax reform.

The U.S. Federal Reserve Board (Fed) was firmly committed to a schedule for rate increases, with 25 basis point increases in each of the last four quarters. While rates remained low relative to historical averages and access to capital markets to facilitate acquisitions was abundant, there was implied risk that the Fed moved too quickly and disrupted what has been a slow and steady recovery in the economy since the depths of the Financial Crisis ten years ago.

Deal spread levels remained below what was anticipated given the increase in short-term interest rates. In terms of deal activity, Information Technology and Health Care were the busiest industries in the Fund’s investable universe. While the market sentiment for deal-making appears to be robust, there seems to be an impact from both geopolitical trade pressures and general uncertainty as it relates to tariffs and the emerging trade war issues between the United States and China.

Portfolio Review

While the Fund’s positioning frequently changed due to companies with new deals being added and completed deals being removed, there were no significant changes to its overall positioning. During the period, the Fund’s holdings had 73 deals close and the Fund invested in 83 new transactions.

The Fund benefited from the outcome of the Broadcom Ltd./Brocade Communications Systems Inc. deal. Broadcom and Brocade announced a definitive agreement for Broadcom to acquire Brocade for $12.75 per share in cash. The deal closing was subject to regulatory approvals in various jurisdictions, customary closing conditions, as well as the approval of Brocade’s stockholders. One of the regulatory requirements needed was from the Committee on Foreign Investment in the United States (CFIUS). The companies ran into issues getting this approval. Only after an agreement from Broadcom to move its headquarters back to the United States was the deal allowed to close.

| 20 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

Another deal that contributed to Fund performance was the Discovery Communications Inc./Scripps Networks Interactive Inc. deal. Discovery and Scripps announced a definitive agreement for Discovery to acquire Scripps. Shareholders received $90.00 per share under the terms of the agreement, comprised of $63.00 per share in cash and $27.00 per share in Class C common shares of Discovery stock. The deal had been stalled in an extended regulatory review in which the Department of Justice (DOJ) had asked the companies for more information. The companies supplied the DOJ with what was requested and were then given the approval needed to close the merger.

The Fund’s performance was hurt by its exposure to Akorn Inc., Tribune Media Company, NXP Semiconductors N.V. and Sparton Corp. The Fund continues to hold these companies because of our belief in their future prospects and/or the stock’s valuation dislocations.

Fresenius SE & Co. KGaA announced a definitive agreement to acquire Akorn Inc. for $34.00 a share. The agreement and transaction have been approved by the boards of both companies and recommended by Akorn’s board to its shareholders. Akorn dropped materially following the announcement that their acquirer, Fresenius, terminated the merger agreement on the back of an investigation into Akorn’s data integrity requirements. Akorn filed suit in Delaware court in order to enforce the merger agreement. A Delaware judge ruled that Fresenius had the right to terminate the merger agreement. This ruling is the first in a Delaware court in which a material adverse event had been proven to have occurred during a merger.

Qualcomm Inc. and NXP Semiconductors N.V. announced a definitive agreement for Qualcomm to acquire NXP for $110.00 per share in cash through a tender offer. NXP was trading with a significant discount to the new Qualcomm offer due to the ongoing trade war between China and the United States. The lone remaining regulatory approval by the Ministry of Commerce, People’s Republic of China (MOFCOM) was elusive due to the ongoing trade war. The deal was terminated.

Sinclair Broadcast Group Inc. and Tribune Media Company announced a definitive agreement under which Sinclair would acquire Tribune for $35.00 in cash and 0.23 shares of Sinclair Class A common stock for each share of Tribune Class A common stock and Class B common stock. The transaction was subject to approval by Tribune’s stockholders, as well as customary closing conditions, including approval by the Federal Communications Commission (FCC) and antitrust clearance. The deal was terminated by Tribune when the FCC stated that it was against the divestiture package put forth by Sinclair.

Sparton Corporation’s planned merger with Ultra Electronics Holdings PLC was blocked by the U.S. Department of Defense. Sparton immediately announced that it was restarting its sales process as prior to this announced deal several other parties expressed interested in acquiring either the entire company, its Manufacturing & Design Services segment or its Defense & Security Systems segment.

Outlook

The main entity driving the environment remains CFIUS. With potential new measures being adopted by the U.S. to broaden the purview of CFIUS, we remain highly selective and disciplined in our analysis of any cross-border transaction. Our investment process includes a strong emphasis on buyer due diligence and focus on cross-border buyers that could run afoul of U.S. regulatory bodies. We believe prevailing deal spreads will increase but lag the past four interest rate hikes.

The market continues to differentiate between the riskier and the more straightforward deals. Deals with a greater amount of perceived risk are being assigned a significantly wider spread than transactions with fewer hurdles. This is in contrast to much of recent history when spreads were not necessarily compensating investors appropriately for the amount of risk taken.

| 21 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

We think access to capital, slow global growth, and strong corporate balance sheets will drive incremental strategic Mergers & Acquisitions. We also think that historically low funding costs should provide a tailwind for financial buyers. On balance, we see a backdrop that remains supportive for continued deal activity.

We believe the Fund is well positioned with a strong focus on liquidity management and mitigating downside risk. We are optimistic at the tailwinds for deal activity and potential for wider spreads based on our outlook.

| 22 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Merger Arbitrage Fund - Class A* and the

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in sales loads and fees paid by shareholders in the different classes. The inception date of the Fund was August 9, 2011. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum sales loads and fees, if applicable. Effective August 17, 2018, the maximum offering price per share of Class A shares is equal to the net assets value (“NAV”) per share plus a sales load equal to 5.26% of the NAV (or 5.00% of the offering price). Prior to August 17, 2018, the maximum offering price per share of Class A shares was equal to the NAV per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed, if redeemed within a one-year period from the date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged index of Treasury securities maturing in 90 days that assumes reinvestment of all income.

| 23 |

Management's Discussion of Fund Performance (Unaudited)

Touchstone Mid Cap Fund

Sub-Advised by The London Company

Investment Philosophy

The Touchstone Mid Cap Fund seeks long-term capital growth by investing primarily in common stocks of mid-cap U.S.-listed companies. The Fund utilizes a bottom-up security selection process that screens potential investments against a proprietary quantitative model for return on capital, earnings-to-enterprise value ratio, and free cash flow yield. Its goal is to purchase financially stable companies that are believed to consistently generate high returns on unleveraged operating capital, are run by shareholder-oriented managements and are trading at a discount to their respective intrinsic values.

Fund Performance

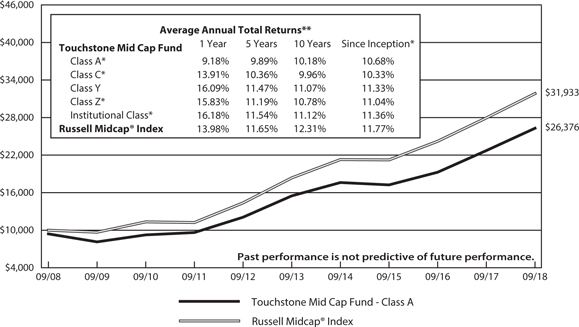

The Touchstone Mid Cap Fund (Class A shares) outperformed its benchmark, the Russell Midcap® Index, for the 12-month period ended September 30, 2018. The Fund’s total return was 15.83 percent (calculated excluding the maximum sales charge) while the benchmark’s total return was 13.98 percent.

Market Environment

U.S. stocks posted positive results driven by strong economic news, solid corporate earnings, and the benefit of individual and corporate tax reductions that took effect at the beginning of 2018. The markets experienced greater volatility and the pace of inflation picked up, but there were few signs of significant pricing pressures. The U.S. Federal Reserve Board (Fed) increased the federal funds rate by 25 basis points four times during the period. Expectations for firming inflation and higher growth, along with balance sheet normalization from the Fed, contributed to higher longer-term rates.

While economic data was mostly positive, there were areas of potential concern, including housing and the impact of tariffs. Housing construction was limited by both supply and demand constraints. While housing starts and existing home sales were relatively stable, growth was limited. The lack of housing supply and rising input costs had a negative impact on the supply side while higher interest rates caused limited demand.

Portfolio Review

During the 12-month period, the Fund benefited from strong stock selection but sector allocation was a headwind for performance. The Information Technology and Health Care sectors were the best performing, however, the Fund’s underweight to both sectors detracted. Stock selection in the Information Technology sector was also a drag on performance. On the other hand, stock selection within the Industrials and Financials sectors was strong enough to offset the underperformance of those sectors and contributed to returns. Overall, the more traditional growth sectors outperformed the more defensive sectors during the period.

Among the individual stocks that contributed to Fund performance were Cintas Corp., Old Dominion Freight Line Inc., Copart Inc. (all three from the Industrials sector), Progressive Corp. (Financials sector) and Deckers Outdoor Corp. (Consumer Discretionary sector). Cintas, a provider of specialized services to businesses, moved higher due to a favorable environment of low unemployment and strong business confidence. The company’s acquisition of G&K Services Inc. exceeded expectations as Cintas has de-levered quickly to its pre-acquisition leverage targets. Old Dominion Freight Line, a national less-than-truckload motor carrier, continued to benefit from tight capacity throughout the industry and strong economic growth, as both volume and pricing improved across the industry. Further, the implementation of electronic logging devices and driver shortages have limited capacity growth, which we believe should be a positive for pricing in the future. Copart, a provider of online vehicle auction services, ended the period significantly higher despite a downward slide earlier in the year. Overall, its business was on solid footing and its operations in Europe showed good potential. We believe the drivers

| 24 |

Management's Discussion of Fund Performance (Unaudited) (Continued)

of Copart’s success remain intact and its operating leverage has improved with greater volume. Progressive, an insurance provider, outperformed as the company continued to post premium growth along with profitable underwriting results, and its combined expense ratio came in lower than expected. The company also posted improved top-line growth in both its auto and home insurance policies, and both of its digital and agency platforms increased market share. Deckers Outdoor, a footwear designer and distributor, increased meaningfully due to improving sales from its UGG brand and progress on margin initiatives. The improved sentiment has reversed the company’s low valuation and low expectations seen earlier in the year.

Among the individual stocks that detracted from performance were Whirlpool Corp. (Consumer Discretionary sector), Edgewell Personal Care Co. (Consumer Staples sector), NewMarket Corp. (Materials sector), Symantec Corp. (Information Technology sector) and CarMax Inc. (Consumer Discretionary sector). Whirlpool, an appliance manufacturer, posted a string of disappointing quarters due to a variety of factors, including rising raw material costs and continued difficulties in its EMEA (Europe, the Middle East and Africa) segment. Further, the company lowered its full-year guidance in July in conjunction with second-quarter earnings. In our view, the negative sentiment was somewhat overdone, as Whirlpool has strong cash flow, leading market share and exposure to the ongoing recovery in the U.S. housing market. Edgewell Personal Care, a consumer products company, moved notably lower as greater competition in the wet shave business negatively impacted sales and pricing. Earlier in the year, the company announced a system-wide restructuring effort to help better position the company for the future. We were skeptical of the plan and elected to exit the position. NewMarket, a petroleum additives company, fell during the period as higher raw material costs and lower pricing were headwinds to performance. We remain attracted to the company’s stable revenue outlook in the fuel additives and lubricants market, pricing power in a consolidated industry, and excellent history of capital allocation. Symantec, a cybersecurity company, declined dramatically during the summer amid accounting concerns. The company’s uncertainty around the issue raised doubts, and we exited the stock on the news. CarMax, a used-car retailer, moved lower as higher interest rates, negative auto sentiment due to trade tariffs, and new competition weighed on the stock. We remain attracted to the company’s business model and the market share opportunities that we believe lie ahead.