|

| OMB APPROVAL | ||

|

| OMB Number: | 3235-0570 | |

|

| Expires: | January 31, 2014 | |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .20.6 | ||

| SECURITIES AND EXCHANGE COMMISSION |

| ||

| Washington, D.C. 20549 |

| ||

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-8220 | ||||||||

| |||||||||

ING Variable Products Trust | |||||||||

(Exact name of registrant as specified in charter) | |||||||||

| |||||||||

7337 E. Doubletree Ranch Rd., Scottsdale, AZ |

| 85258 | |||||||

(Address of principal executive offices) |

| (Zip code) | |||||||

| |||||||||

CT Corporation System, 101 Federal Street, Boston, MA 02110 | |||||||||

(Name and address of agent for service) | |||||||||

| |||||||||

Registrant’s telephone number, including area code: | 1-800-992-0180 |

| |||||||

| |||||||||

Date of fiscal year end: | December 31 |

| |||||||

| |||||||||

Date of reporting period: | January 1, 2012 to December 31, 2012 |

| |||||||

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

| n | ING International Value Portfolio | |

| n | ING MidCap Opportunities Portfolio | |

| n | ING SmallCap Opportunities Portfolio |

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. |

| MUTUAL FUNDS |

President’s Letter | 1 | |||||

Market Perspective | 2 | |||||

Portfolio Managers’ Report | 4 | |||||

Shareholder Expense Examples | 10 | |||||

Report of Independent Registered Public Accounting Firm | 11 | |||||

Statements of Assets and Liabilities | 12 | |||||

Statements of Operations | 14 | |||||

Statements of Changes in Net Assets | 15 | |||||

Financial Highlights | 17 | |||||

Notes to Financial Statements | 19 | |||||

Summary Portfolios of Investments | 30 | |||||

Tax Information | 39 | |||||

Trustee and Officer Information | 40 | |||||

Advisory Contract Approval Discussion | 44 |

Looking Forward

President and Chief Executive Officer

ING Funds

January 4, 2013

| Index | Description | |||||

|---|---|---|---|---|---|---|

Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index | An unmanaged index that includes all fixed-income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million, and at least one year to maturity. | |||||

Barclays Capital U.S. Aggregate Bond Index | An unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. | |||||

Barclays Capital U.S. Corporate Investment Grade Bond Index | An unmanaged index consisting of publicly issued, fixed rate, nonconvertible, investment grade debt securities. | |||||

Barclays Capital U.S. Treasury Index | An unmanaged index that includes public obligations of the U.S. Treasury. Treasury bills, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS and STRIPS, are excluded. | |||||

MSCI EAFE® Index | An unmanaged index that measures the performance of securities listed on exchanges in markets in Europe, Australasia and the Far East. It includes the reinvestment of dividends net of withholding taxes, but does not reflect fees, brokerage commissions or other expenses of investing. | |||||

MSCI Europe ex UK® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK. | |||||

MSCI Japan® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan. | |||||

MSCI UK® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK. | |||||

MSCI World IndexSM | An unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. | |||||

Russell 2000® Growth Index | An unmanaged index that measures the performance of securities of smaller U.S. companies with greater than average growth orientation. | |||||

Russell 2000® Index | An unmanaged index that measures the performance of securities of small U.S. companies. | |||||

Russell Midcap® Growth Index | An unmanaged index that measures the performance of those companies included in the Russell Midcap® Index with relatively higher price-to-book ratios and higher forecasted growth values. | |||||

Russell Midcap® Index | An unmanaged index that measures the performance of the 800 smallest companies in the Russell 1000® Index, which represents approximately 26% of the total market capitalization of the Russell 1000® Index. | |||||

S&P 500® Index | An unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets. | |||||

S&P/Case-Shiller 20-City Composite Home Price Index | A composite index of the home price index for the top 20 Metropolitan Statistical Areas in the United States. The index is published monthly by Standard & Poor’s | |||||

| ING INTERNATIONAL VALUE PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| Geographic Diversification as of December 31, 2012 (as a percentage of net assets) | |||||||

United Kingdom | 21.6 | % | |||||

Japan | 20.2 | % | |||||

France | 11.2 | % | |||||

Germany | 9.4 | % | |||||

Netherlands | 7.9 | % | |||||

Switzerland | 5.8 | % | |||||

Italy | 4.8 | % | |||||

Hong Kong | 4.0 | % | |||||

Singapore | 3.1 | % | |||||

United States | 1.8 | % | |||||

Countries between 0.6%–1.4%ˆ | 9.3 | % | |||||

Assets in Excess of Other Liabilities* | 0.9 | % | |||||

Net Assets | 100.0 | % | |||||

| * Includes short-term investments. | |||||||

| ^ Includes 10 countries, which each represents 0.6%–1.4% of net assets. | |||||||

| Portfolio holdings are subject to change daily. | |||||||

| Top Ten Holdings as of December 31, 2012 (as a percentage of net assets) | |||||||

Royal Dutch Shell PLC — Class A | 3.3 | % | |||||

Roche Holding AG — Genusschein | 2.8 | % | |||||

BHP Billiton PLC | 2.5 | % | |||||

Vodafone Group PLC | 2.5 | % | |||||

Siemens AG | 2.4 | % | |||||

Rio Tinto PLC | 2.4 | % | |||||

HSBC Holdings PLC | 2.2 | % | |||||

Sumitomo Mitsui Financial Group, Inc. | 2.0 | % | |||||

Barclays PLC | 1.9 | % | |||||

Sanofi-Aventis SA | 1.8 | % | |||||

| Portfolio holdings are subject to change daily. | |||||||

| PORTFOLIO MANAGERS’ REPORT | ING INTERNATIONAL VALUE PORTFOLIO |

| Average Annual Returns for the Periods Ended December 31, 2012 | ||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 Year | 5 Year | 10 Year | Since Inception of Class ADV December 29, 2006 | Since Inception of Class S2 February 27, 2009 | ||||||||||||||||||||

Class ADV | 18.64 | % | (5.87 | )% | — | (3.01 | )% | — | ||||||||||||||||

Class I | 19.23 | % | (5.43 | )% | 6.37 | % | — | — | ||||||||||||||||

Class S | 18.90 | % | (5.52 | )% | 6.15 | % | — | — | ||||||||||||||||

Class S2 | 18.67 | % | — | — | — | 13.36 | % | |||||||||||||||||

MSCI EAFE® Index | 17.32 | % | (3.69 | )% | 8.21 | % | (1.36 | )%(1) | 16.71% | (2) | ||||||||||||||

(1) | Since inception performance for the index is shown from January 1, 2007. |

(2) | Since inception performance for the index is shown from March 1, 2009. |

| ING MIDCAP OPPORTUNITIES PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| Sector Diversification as of December 31, 2012 (as a percentage of net assets) | |||||||

Consumer Discretionary | 25.6 | % | |||||

Industrials | 16.6 | % | |||||

Information Technology | 15.8 | % | |||||

Health Care | 14.0 | % | |||||

Financials | 8.0 | % | |||||

Energy | 6.3 | % | |||||

Consumer Staples | 6.1 | % | |||||

Materials | 4.6 | % | |||||

Telecommunication Services | 1.7 | % | |||||

Assets in Excess of Other Liabilities* | 1.3 | % | |||||

Net Assets | 100.0 | % | |||||

| * Includes short-term investments. | |||||||

| Portfolio holdings are subject to change daily. | |||||||

| Top Ten Holdings as of December 31, 2012 (as a percentage of net assets) | |||||||

Intuit, Inc. | 2.2 | % | |||||

Delphi Automotive PLC | 2.2 | % | |||||

Discovery Communications, Inc. — Class A | 2.1 | % | |||||

Roper Industries, Inc. | 2.0 | % | |||||

NetApp, Inc. | 2.0 | % | |||||

Coca-Cola Enterprises, Inc. | 2.0 | % | |||||

Cameron International Corp. | 2.0 | % | |||||

Autodesk, Inc. | 1.9 | % | |||||

Whole Foods Market, Inc. | 1.9 | % | |||||

Eastman Chemical Co. | 1.9 | % | |||||

| Portfolio holdings are subject to change daily. | |||||||

| * | Effective April 30, 2012, Mike Pytosh and Kristin Manning were added as portfolio managers to the Portfolio and effective October 1, 2012, James Hasso was removed as a portfolio manager to the Portfolio. |

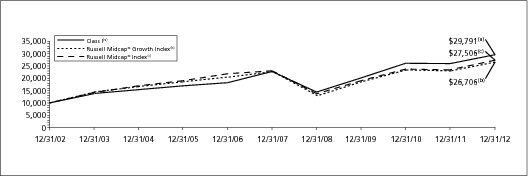

| PORTFOLIO MANAGERS’ REPORT | ING MIDCAP OPPORTUNITIES PORTFOLIO |

| Average Annual Returns for the Periods Ended December 31, 2012 | ||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 Year | 5 Year | 10 Year | Since Inception of Class ADV December 29, 2006 | Since Inception of Class S2 February 27, 2009 | ||||||||||||||||||||

Class ADV | 13.61 | % | 4.89 | % | — | 7.99 | % | — | ||||||||||||||||

Class I | 14.20 | % | 5.50 | % | 11.53 | % | — | — | ||||||||||||||||

Class S | 13.92 | % | 5.23 | % | 11.29 | % | — | — | ||||||||||||||||

Class S2 | 13.79 | % | — | — | — | 24.87 | % | |||||||||||||||||

Russell Midcap® Growth Index | 15.81 | % | 3.23 | % | 10.32 | % | 4.55% | (1) | 25.44% | (2) | ||||||||||||||

Russell Midcap® Index | 17.28 | % | 3.57 | % | 10.65 | % | 3.90% | (1) | 26.17% | (2) | ||||||||||||||

(1) | Since inception performance for the indices is shown from January 1, 2007. |

(2) | Since inception performance for the indices is shown from March 1, 2009. |

| ING SMALLCAP OPPORTUNITIES PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| Sector Diversification as of December 31, 2012 (as a percentage of net assets) | |||||||

Information Technology | 21.5 | % | |||||

Consumer Discretionary | 18.1 | % | |||||

Health Care | 18.1 | % | |||||

Industrials | 16.6 | % | |||||

Financials | 9.5 | % | |||||

Energy | 6.0 | % | |||||

Materials | 4.1 | % | |||||

Exchange-Traded Funds | 2.1 | % | |||||

Consumer Staples | 2.0 | % | |||||

Assets in Excess of Other Liabilities* | 2.0 | % | |||||

Net Assets | 100.0 | % | |||||

| * Includes short-term investments. | |||||||

| Portfolio holdings are subject to change daily. | |||||||

| Top Ten Holdings as of December 31, 2012* (as a percentage of net assets) | |||||||

iShares Russell 2000 Growth Index Fund | 2.1 | % | |||||

Aspen Technology, Inc. | 1.3 | % | |||||

Acuity Brands, Inc. | 1.2 | % | |||||

Parametric Technology Corp. | 1.1 | % | |||||

Aruba Networks, Inc. | 1.1 | % | |||||

Portfolio Recovery Associates, Inc. | 1.1 | % | |||||

Life Time Fitness, Inc. | 1.0 | % | |||||

Cooper Tire & Rubber Co. | 1.0 | % | |||||

Healthsouth Corp. | 1.0 | % | |||||

Semtech Corp. | 1.0 | % | |||||

| * Excludes short-term investments. | |||||||

| Portfolio holdings are subject to change daily. | |||||||

| * | Effective April 30, 2012, Joseph Basset was added as a portfolio manager to the Portfolio. |

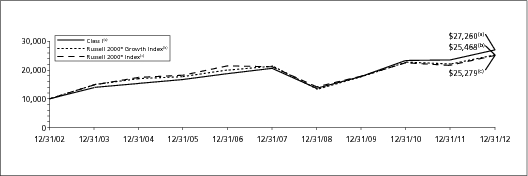

| PORTFOLIO MANAGERS’ REPORT | ING SMALLCAP OPPORTUNITIES PORTFOLIO |

| Average Annual Returns for the Periods Ended December 31, 2012 | ||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 Year | 5 Year | 10 Year | Since Inception of Class ADV November 20, 2008 | Since Inception of Class S2 February 27, 2009 | ||||||||||||||||||||

Class ADV | 14.63 | % | — | — | 24.57 | % | — | |||||||||||||||||

Class I | 15.18 | % | 5.71 | % | 10.55 | % | — | — | ||||||||||||||||

Class S | 14.95 | % | 5.46 | % | 10.30 | % | — | — | ||||||||||||||||

Class S2 | 14.79 | % | — | — | — | 25.84 | % | |||||||||||||||||

Russell 2000® Growth Index | 14.59 | % | 3.49 | % | 9.80 | % | 19.01% | (1) | 24.68% | (2) | ||||||||||||||

Russell 2000® Index | 16.35 | % | 3.56 | % | 9.72 | % | 17.06% | (1) | 24.29% | (2) | ||||||||||||||

(1) | Since inception performance for the indices is shown from December 1, 2008. |

(2) | Since inception performance for the indices is shown from March 1, 2009. |

| Actual Portfolio Return | Hypothetical (5% return before expenses) | ||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Beginning Account Value July 1, 2012 | Ending Account Value December 31, 2012 | Annualized Expense Ratio | Expenses Paid During the Period Ended December 31, 2012* | Beginning Account Value July 1, 2012 | Ending Account Value December 31, 2012 | Annualized Expense Ratio | Expenses Paid During the Period Ended December 31, 2012* | ||||||||||||||||||||||||||||

ING International Value Portfolio | |||||||||||||||||||||||||||||||||||

Class ADV | $ | 1,000.00 | $ | 1,142.70 | 1.50 | % | $ | 8.08 | $ | 1,000.00 | $ | 1,017.60 | 1.50 | % | $ | 7.61 | |||||||||||||||||||

Class I | 1,000.00 | 1,145.60 | 1.00 | 5.39 | 1,000.00 | 1,020.11 | 1.00 | 5.08 | |||||||||||||||||||||||||||

Class S | 1,000.00 | 1,143.90 | 1.20 | 6.47 | 1,000.00 | 1,019.10 | 1.20 | 6.09 | |||||||||||||||||||||||||||

Class S2 | 1,000.00 | 1,142.80 | 1.40 | 7.54 | 1,000.00 | 1,018.10 | 1.40 | 7.10 | |||||||||||||||||||||||||||

ING MidCap Opportunities Portfolio | |||||||||||||||||||||||||||||||||||

Class ADV | $ | 1,000.00 | $ | 1,049.60 | 1.34 | % | $ | 6.90 | $ | 1,000.00 | $ | 1,018.40 | 1.34 | % | $ | 6.80 | |||||||||||||||||||

Class I | 1,000.00 | 1,052.20 | 0.84 | 4.33 | 1,000.00 | 1,020.91 | 0.84 | 4.27 | |||||||||||||||||||||||||||

Class S | 1,000.00 | 1,050.70 | 1.09 | 5.62 | 1,000.00 | 1,019.66 | 1.09 | 5.53 | |||||||||||||||||||||||||||

Class S2 | 1,000.00 | 1,049.90 | 1.24 | 6.39 | 1,000.00 | 1,018.90 | 1.24 | 6.29 | |||||||||||||||||||||||||||

ING SmallCap Opportunities Portfolio | |||||||||||||||||||||||||||||||||||

Class ADV | $ | 1,000.00 | $ | 1,051.90 | 1.41 | % | $ | 7.27 | $ | 1,000.00 | $ | 1,018.05 | 1.41 | % | $ | 7.15 | |||||||||||||||||||

Class I | 1,000.00 | 1,055.00 | 0.91 | 4.70 | 1,000.00 | 1,020.56 | 0.91 | 4.62 | |||||||||||||||||||||||||||

Class S | 1,000.00 | 1,053.70 | 1.16 | 5.99 | 1,000.00 | 1,019.30 | 1.16 | 5.89 | |||||||||||||||||||||||||||

Class S2 | 1,000.00 | 1,052.70 | 1.31 | 6.76 | 1,000.00 | 1,018.55 | 1.31 | 6.65 | |||||||||||||||||||||||||||

| * | Expenses are equal to each Portfolio’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 184/366 to reflect the most recent fiscal half-year. |

ING Variable Products Trust

February 15, 2013

| ING International Value Portfolio | ING MidCap Opportunities Portfolio | ING SmallCap Opportunities Portfolio | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

ASSETS: | ||||||||||||||||||

Investments in securities at fair value+* | $ | 132,343,456 | $ | 1,124,459,113 | $ | 217,926,645 | ||||||||||||

Short-term investments at fair value** | 1,592,618 | 25,701,154 | 11,281,853 | |||||||||||||||

Total Investments at fair value | $ | 133,936,074 | $ | 1,150,160,267 | $ | 229,208,498 | ||||||||||||

Cash | 385 | 280 | 14,659 | |||||||||||||||

Foreign currencies at value*** | 73,003 | — | — | |||||||||||||||

Receivables: | ||||||||||||||||||

Investment securities sold | 2,624,052 | — | 1,091,472 | |||||||||||||||

Fund shares sold | 44,307 | 1,059,482 | 103,758 | |||||||||||||||

Dividends | 160,898 | 484,152 | 65,817 | |||||||||||||||

Foreign tax reclaims | 121,490 | — | — | |||||||||||||||

Prepaid expenses | 1,132 | 9,737 | 1,825 | |||||||||||||||

Total assets | 136,961,341 | 1,151,713,918 | 230,486,029 | |||||||||||||||

LIABILITIES: | ||||||||||||||||||

Payable for investment securities purchased | 2,164,990 | — | 1,238,888 | |||||||||||||||

Payable for fund shares redeemed | 79,063 | 1,429,778 | 111,968 | |||||||||||||||

Payable upon receipt of securities loaned | 984,618 | 10,761,154 | 6,485,853 | |||||||||||||||

Payable for investment management fees | 151,442 | 665,101 | 137,786 | |||||||||||||||

Payable for administrative fees | 11,179 | 96,321 | 18,371 | |||||||||||||||

Payable for distribution and shareholder service fees | 1,759 | 126,858 | 20,737 | |||||||||||||||

Payable for trustee fees | 682 | 5,406 | 1,036 | |||||||||||||||

Other accrued expenses and liabilities | 89,109 | 186,629 | 48,605 | |||||||||||||||

Total liabilities | 3,482,842 | 13,271,247 | 8,063,244 | |||||||||||||||

NET ASSETS | $ | 133,478,499 | $ | 1,138,442,671 | $ | 222,422,785 | ||||||||||||

NET ASSETS WERE COMPRISED OF: | ||||||||||||||||||

Paid-in capital | $ | 317,530,610 | $ | 969,396,331 | $ | 187,571,534 | ||||||||||||

Undistributed (distributions in excess of) net investment income | 612,282 | (11,133 | ) | (3,017 | ) | |||||||||||||

Accumulated net realized gain (loss) | (195,422,202 | ) | 34,269,306 | 14,448,733 | ||||||||||||||

Net unrealized appreciation | 10,757,809 | 134,788,167 | 20,405,535 | |||||||||||||||

NET ASSETS | $ | 133,478,499 | $ | 1,138,442,671 | $ | 222,422,785 | ||||||||||||

____________________ | ||||||||||||||||||

+ Including securities loaned at value | $ | 937,117 | $ | 10,503,678 | $ | 6,324,534 | ||||||||||||

* Cost of investments in securities | $ | 121,585,457 | $ | 989,670,946 | $ | 197,521,110 | ||||||||||||

** Cost of short-term investments | $ | 1,592,618 | $ | 25,701,154 | $ | 11,281,853 | ||||||||||||

*** Cost of foreign currencies | $ | 73,046 | $ | — | $ | — | ||||||||||||

| ING International Value Portfolio | ING MidCap Opportunities Portfolio | ING SmallCap Opportunities Portfolio | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Class ADV | ||||||||||||||||||

Net assets | $ | 1,122,670 | $ | 81,463,056 | $ | 14,235,945 | ||||||||||||

Shares authorized | unlimited | unlimited | unlimited | |||||||||||||||

Par value | $ | 0.01 | $ | 0.01 | $ | 0.01 | ||||||||||||

Shares outstanding | 138,331 | 6,512,407 | 666,143 | |||||||||||||||

Net asset value and redemption price per share | $ | 8.12 | $ | 12.51 | $ | 21.37 | ||||||||||||

Class I | ||||||||||||||||||

Net assets | $ | 124,728,119 | $ | 614,151,445 | $ | 136,299,785 | ||||||||||||

Shares authorized | unlimited | unlimited | unlimited | |||||||||||||||

Par value | $ | 0.01 | $ | 0.01 | $ | 0.01 | ||||||||||||

Shares outstanding | 15,249,358 | 47,696,491 | 6,107,149 | |||||||||||||||

Net asset value and redemption price per share | $ | 8.18 | $ | 12.88 | $ | 22.32 | ||||||||||||

Class S | ||||||||||||||||||

Net assets | $ | 7,623,216 | $ | 435,585,589 | $ | 68,682,262 | ||||||||||||

Shares authorized | �� | unlimited | unlimited | unlimited | ||||||||||||||

Par value | $ | 0.01 | $ | 0.01 | $ | 0.01 | ||||||||||||

Shares outstanding | 913,650 | 34,653,482 | 3,174,380 | |||||||||||||||

Net asset value and redemption price per share | $ | 8.34 | $ | 12.57 | $ | 21.64 | ||||||||||||

Class S2 | ||||||||||||||||||

Net assets | $ | 4,494 | $ | 7,242,581 | $ | 3,204,793 | ||||||||||||

Shares authorized | unlimited | unlimited | unlimited | |||||||||||||||

Par value | $ | 0.01 | $ | 0.01 | $ | 0.01 | ||||||||||||

Shares outstanding | 552 | 575,782 | 149,301 | |||||||||||||||

Net asset value and redemption price per share | $ | 8.14 | $ | 12.58 | $ | 21.47 | ||||||||||||

| ING International Value Portfolio | ING MidCap Opportunities Portfolio | ING SmallCap Opportunities Portfolio | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

INVESTMENT INCOME: | ||||||||||||||||||

Dividends, net of foreign taxes withheld* | $ | 4,616,935 | $ | 14,977,113 | $ | 1,913,842 | ||||||||||||

Securities lending income, net | 189,530 | 81,936 | 59,120 | |||||||||||||||

Total investment income | 4,806,465 | 15,059,049 | 1,972,962 | |||||||||||||||

EXPENSES: | ||||||||||||||||||

Investment management fees | 1,090,681 | 7,469,155 | 1,553,980 | |||||||||||||||

Distribution and shareholder service fees: | ||||||||||||||||||

Class ADV | 5,573 | 314,783 | 43,180 | |||||||||||||||

Class S | 20,020 | 1,125,670 | 165,005 | |||||||||||||||

Class S2 | 22 | 27,062 | 10,849 | |||||||||||||||

Transfer agent fees | 129 | 2,915 | 1,277 | |||||||||||||||

Administrative service fees | 136,333 | 1,081,135 | 207,194 | |||||||||||||||

Shareholder reporting expense | 24,623 | 108,694 | 25,480 | |||||||||||||||

Professional fees | 10,226 | 166,384 | 40,029 | |||||||||||||||

Custody and accounting expense | 26,207 | 147,523 | 40,175 | |||||||||||||||

Trustee fees | 4,090 | 32,435 | 6,216 | |||||||||||||||

Miscellaneous expense | 9,702 | 75,594 | 20,523 | |||||||||||||||

Interest expense | 1,552 | 1,087 | 35 | |||||||||||||||

Total expenses | 1,329,158 | 10,552,437 | 2,113,943 | |||||||||||||||

Net recouped/waived and reimbursed fees | 58,001 | (5,412 | ) | (2,170 | ) | |||||||||||||

Net expenses | 1,387,159 | 10,547,025 | 2,111,773 | |||||||||||||||

Net investment income (loss) | 3,419,306 | 4,512,024 | (138,811 | ) | ||||||||||||||

REALIZED AND UNREALIZED GAIN (LOSS): | ||||||||||||||||||

Net realized gain (loss) on: | ||||||||||||||||||

Investments | (3,323,496 | ) | 38,292,709 | 17,557,510 | ||||||||||||||

Foreign currency related transactions | (19,301 | ) | — | — | ||||||||||||||

Net realized gain (loss) | (3,342,797 | ) | 38,292,709 | 17,557,510 | ||||||||||||||

Net change in unrealized appreciation (depreciation) on: | ||||||||||||||||||

Investments | 23,582,777 | 83,191,903 | 11,039,728 | |||||||||||||||

Foreign currency related transactions | 2,781 | — | — | |||||||||||||||

Net change in unrealized appreciation (depreciation) | 23,585,558 | 83,191,903 | 11,039,728 | |||||||||||||||

Net realized and unrealized gain | 20,242,761 | 121,484,612 | 28,597,238 | |||||||||||||||

Increase in net assets resulting from operations | $ | 23,662,067 | $ | 125,996,636 | $ | 28,458,427 | ||||||||||||

____________________ | ||||||||||||||||||

* Foreign taxes withheld | $ | 397,486 | $ | — | $ | 1,492 | ||||||||||||

| ING International Value Portfolio | ING MidCap Opportunities Portfolio | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended December 31, 2012 | Year Ended December 31, 2011 | Year Ended December 31, 2012 | Year Ended December 31, 2011 | ||||||||||||||||

FROM OPERATIONS: | |||||||||||||||||||

Net investment income | $ | 3,419,306 | $ | 5,150,987 | $ | 4,512,024 | $ | 749,989 | |||||||||||

Net realized gain (loss) | (3,342,797 | ) | (8,660,848 | ) | 38,292,709 | 107,215,387 | |||||||||||||

Net change in unrealized appreciation (depreciation) | 23,585,558 | (24,435,594 | ) | 83,191,903 | (125,180,937 | ) | |||||||||||||

Increase (decrease) in net assets resulting from operations | 23,662,067 | (27,945,455 | ) | 125,996,636 | (17,215,561 | ) | |||||||||||||

FROM DISTRIBUTIONS TO SHAREHOLDERS: | |||||||||||||||||||

Net investment income: | |||||||||||||||||||

Class ADV | (23,251 | ) | (6,162 | ) | (211,627 | ) | — | ||||||||||||

Class I | (3,266,996 | ) | (4,629,604 | ) | (3,079,188 | ) | — | ||||||||||||

Class S | (188,642 | ) | (216,050 | ) | (1,767,703 | ) | — | ||||||||||||

Class S2 | (90 | ) | (93 | ) | (17,753 | ) | — | ||||||||||||

Net realized gains: | |||||||||||||||||||

Class ADV | — | — | (1,672,340 | ) | — | ||||||||||||||

Class I | — | — | (14,851,704 | ) | — | ||||||||||||||

Class S | — | — | (11,557,737 | ) | — | ||||||||||||||

Class S2 | — | — | (148,840 | ) | — | ||||||||||||||

Return of capital: | |||||||||||||||||||

Class ADV | — | (202 | ) | — | — | ||||||||||||||

Class I | — | (140,121 | ) | — | — | ||||||||||||||

Class S | — | (7,139 | ) | — | — | ||||||||||||||

Class S2 | — | (3 | ) | — | — | ||||||||||||||

Total distributions | (3,478,979 | ) | (4,999,374 | ) | (33,306,892 | ) | — | ||||||||||||

FROM CAPITAL SHARE TRANSACTIONS: | |||||||||||||||||||

Net proceeds from sale of shares | 2,093,271 | 4,373,279 | 329,680,490 | 329,723,536 | |||||||||||||||

Reinvestment of distributions | 3,478,889 | �� | 4,999,277 | 33,306,892 | — | ||||||||||||||

| 5,572,160 | 9,372,556 | 362,987,382 | 329,723,536 | ||||||||||||||||

Cost of shares redeemed | (37,263,739 | ) | (73,380,297 | ) | (210,453,525 | ) | (236,047,779 | ) | |||||||||||

Net increase (decrease) in net assets resulting from capital share transactions | (31,691,579 | ) | (64,007,741 | ) | 152,533,857 | 93,675,757 | |||||||||||||

Net increase (decrease) in net assets | (11,508,491 | ) | (96,952,570 | ) | 245,223,601 | 76,460,196 | |||||||||||||

NET ASSETS: | |||||||||||||||||||

Beginning of year or period | 144,986,990 | 241,939,560 | 893,219,070 | 816,758,874 | |||||||||||||||

End of year or period | $ | 133,478,499 | $ | 144,986,990 | $ | 1,138,442,671 | $ | 893,219,070 | |||||||||||

Undistributed (distributions in excess of) net investment income at end of year or period | $ | 612,282 | $ | (4,728 | ) | $ | (11,133 | ) | $ | 719,633 | |||||||||

| ING SmallCap Opportunities Portfolio | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Year Ended December 31, 2012 | Year Ended December 31, 2011 | ||||||||||

FROM OPERATIONS: | |||||||||||

Net investment (loss) | $ | (138,811 | ) | $ | (549,128 | ) | |||||

Net realized gain | 17,557,510 | 26,968,415 | |||||||||

Net change in unrealized appreciation (depreciation) | 11,039,728 | (25,574,840 | ) | ||||||||

Increase in net assets resulting from operations | 28,458,427 | 844,447 | |||||||||

FROM DISTRIBUTIONS TO SHAREHOLDERS: | |||||||||||

Net realized gains: | |||||||||||

Class ADV | (821,671 | ) | — | ||||||||

Class I | (12,759,239 | ) | — | ||||||||

Class S | (6,522,015 | ) | — | ||||||||

Class S2 | (226,396 | ) | — | ||||||||

Total distributions | (20,329,321 | ) | — | ||||||||

FROM CAPITAL SHARE TRANSACTIONS: | |||||||||||

Net proceeds from sale of shares | 38,981,797 | 53,542,558 | |||||||||

Reinvestment of distributions | 20,329,321 | — | |||||||||

| 59,311,118 | 53,542,558 | ||||||||||

Cost of shares redeemed | (32,862,233 | ) | (54,935,659 | ) | |||||||

Net increase (decrease) in net assets resulting from capital share transactions | 26,448,885 | (1,393,101 | ) | ||||||||

Net increase (decrease) in net assets | 34,577,991 | (548,654 | ) | ||||||||

NET ASSETS: | |||||||||||

Beginning of year or period | 187,844,794 | 188,393,448 | |||||||||

End of year or period | $ | 222,422,785 | $ | 187,844,794 | |||||||

Accumulated net investment loss at end of year or period | $ | (3,017 | ) | $ | (2,339 | ) | |||||

| Income (loss) from investment operations | | Less distributions | | Ratios to average net assets | Supplemental data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Net asset value, beginning of year or period | | Net investment income (loss) | | Net realized and unrealized gain (loss) | | Total from investment operations | | From net investment income | | From net realized gains | | From return of capital | | Total distributions | | Payment by affiliate | | Net asset value, end of year or period | | Total Return (1) | | Expenses before reductions/ additions (2)(3)(4) | | Expenses net of fee waivers and/or recoupments, if any (2)(3)(4) | | Expenses net of all reductions/ additions (2)(3)(4) | | Net investment income (loss) (2)(4) | | Net assets, end of year or period | | Portfolio turnover rate | ||||||||||||||||||||||||||||||||||||||||||

| Year or period ended | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | (%) | | (%) | | (%) | | (%) | | (%) | | ($000’s) | | (%) | ||||||||||||||||||||||||||||||||||||||||

ING International Value Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Class ADV | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 6.99 | 0.15 | 1.14 | 1.29 | 0.16 | — | — | 0.16 | — | 8.12 | 18.64 | 1.46 | 1.50 | 1.50 | 1.99 | 1,123 | 56 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 8.44 | (0.01 | )• | (1.26 | ) | (1.27 | ) | 0.17 | — | 0.01 | 0.18 | — | 6.99 | (15.40 | ) | 1.57 | 1.52 | 1.52 | (0.09 | ) | 1,145 | 69 | ||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 8.41 | 0.11 | 0.05 | 0.16 | 0.13 | — | — | 0.13 | — | 8.44 | 2.02 | 1.56 | 1.50 | † | 1.50 | † | 1.28 | † | 31 | 155 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 6.74 | 0.09 | 1.70 | 1.79 | 0.12 | — | — | 0.12 | — | 8.41 | 26.88 | 1.55 | 1.51 | † | 1.51 | † | 1.10 | † | 21 | 214 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 14.21 | 0.22 | (5.67 | ) | (5.45 | ) | 0.25 | 1.78 | — | 2.03 | 0.01 | 6.74 | (43.11 | )(a) | 1.56 | 1.50 | † | 1.50 | † | 2.06 | † | 0 | 207 | |||||||||||||||||||||||||||||||||||||||||||||||||||

Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 7.04 | 0.19 | 1.14 | 1.33 | 0.19 | — | — | 0.19 | — | 8.18 | 19.23 | 0.96 | 1.00 | 1.00 | 2.52 | 124,728 | 56 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 8.49 | 0.21 | (1.45 | ) | (1.24 | ) | 0.20 | — | 0.01 | 0.21 | — | 7.04 | (14.96 | ) | 1.07 | 1.02 | 1.02 | 2.56 | 135,682 | 69 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 8.46 | 0.16 | • | 0.04 | 0.20 | 0.17 | — | — | 0.17 | — | 8.49 | 2.50 | 1.06 | 1.00 | † | 1.00 | † | 1.96 | † | 230,836 | 155 | |||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 6.77 | 0.13 | 1.68 | 1.81 | 0.12 | — | — | 0.12 | — | 8.46 | 27.18 | 1.05 | 1.01 | † | 1.01 | † | 1.70 | † | 399,689 | 214 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 14.24 | 0.27 | (5.67 | ) | (5.40 | ) | 0.30 | 1.78 | — | 2.08 | 0.01 | 6.77 | (42.76 | )(a) | 1.06 | 1.00 | † | 1.00 | † | 2.59 | † | 340,022 | 207 | |||||||||||||||||||||||||||||||||||||||||||||||||||

Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 7.18 | 0.18 | 1.16 | 1.34 | 0.18 | — | — | 0.18 | — | 8.34 | 18.90 | 1.21 | 1.20 | 1.20 | 2.33 | 7,623 | 56 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 8.64 | 0.19 | (1.46 | ) | (1.27 | ) | 0.18 | — | 0.01 | 0.19 | — | 7.18 | (14.99 | ) | 1.32 | 1.22 | 1.22 | 2.27 | 8,156 | 69 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 8.60 | 0.13 | 0.06 | 0.19 | 0.15 | — | — | 0.15 | — | 8.64 | 2.36 | 1.31 | 1.20 | † | 1.20 | † | 1.61 | † | 11,068 | 155 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 6.93 | 0.11 | 1.68 | 1.79 | 0.12 | — | — | 0.12 | — | 8.60 | 26.13 | 1.30 | 1.21 | † | 1.21 | † | 1.44 | † | 12,076 | 214 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 14.39 | 0.25 | (5.66 | ) | (5.41 | ) | 0.28 | 1.78 | — | 2.06 | 0.01 | 6.93 | (42.31 | )(a) | 1.31 | 1.20 | † | 1.20 | † | 2.35 | † | 9,782 | 207 | |||||||||||||||||||||||||||||||||||||||||||||||||||

Class S2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 7.01 | 0.15 | 1.14 | 1.29 | 0.16 | — | — | 0.16 | — | 8.14 | 18.67 | 1.46 | 1.40 | 1.40 | 2.05 | 4 | 56 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 8.45 | 0.17 | (1.43 | ) | (1.26 | ) | 0.17 | — | 0.01 | 0.18 | — | 7.01 | (15.27 | ) | 1.57 | 1.42 | 1.42 | 2.12 | 4 | 69 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 8.42 | 0.12 | 0.04 | 0.16 | 0.13 | — | — | 0.13 | — | 8.45 | 2.09 | 1.56 | 1.40 | † | 1.40 | † | 1.47 | † | 5 | 155 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

02-27-09(5)–12-31-09 | 5.43 | 0.09 | 3.01 | 3.10 | 0.11 | — | — | 0.11 | — | 8.42 | 57.63 | 1.55 | 1.41 | † | 1.41 | † | 1.39 | † | 5 | 214 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

ING MidCap Opportunities Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Class ADV | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 11.34 | 0.01 | 1.52 | 1.53 | 0.04 | 0.32 | — | 0.36 | — | 12.51 | 13.61 | 1.34 | 1.34 | 1.34 | 0.09 | 81,463 | 89 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 11.46 | (0.02 | ) | (0.10 | ) | (0.12 | ) | — | — | — | — | — | 11.34 | (1.05 | ) | 1.34 | 1.34 | 1.34 | (0.23 | ) | 40,497 | 90 | ||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 8.88 | 0.08 | • | 2.54 | 2.62 | 0.04 | — | — | 0.04 | — | 11.46 | 29.57 | 1.36 | 1.29 | 1.29 | 0.75 | 15,119 | 96 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 6.32 | 0.03 | • | 2.54 | 2.57 | 0.01 | — | — | 0.01 | — | 8.88 | 40.65 | 1.40 | 1.14 | † | 1.14 | † | 0.36 | † | 957 | 169 | |||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 10.20 | (0.03 | )• | (3.85 | ) | (3.88 | ) | — | — | — | — | 0.00 | * | 6.32 | (38.04 | )(b) | 1.38 | 1.20 | † | 1.20 | † | (0.40 | )† | 1 | 191 | |||||||||||||||||||||||||||||||||||||||||||||||||

Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 11.63 | 0.07 | 1.57 | 1.64 | 0.07 | 0.32 | — | 0.39 | — | 12.88 | 14.20 | 0.84 | 0.84 | 0.84 | 0.56 | 614,151 | 89 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 11.69 | 0.03 | (0.09 | ) | (0.06 | ) | — | — | — | — | — | 11.63 | (0.51 | ) | 0.84 | 0.84 | 0.84 | 0.24 | 435,027 | 90 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 9.03 | 0.06 | 2.67 | 2.73 | 0.07 | — | — | 0.07 | — | 11.69 | 30.36 | 0.86 | 0.79 | 0.79 | 0.62 | 350,626 | 96 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 6.40 | 0.04 | 2.61 | 2.65 | 0.02 | — | — | 0.02 | — | 9.03 | 41.44 | 0.90 | 0.64 | † | 0.64 | † | 0.46 | † | 238,426 | 169 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 10.26 | 0.01 | (3.87 | ) | (3.86 | ) | — | — | — | — | 0.00 | * | 6.40 | (37.62 | )(b) | 0.88 | 0.70 | † | 0.70 | † | 0.11 | † | 195,295 | 191 | ||||||||||||||||||||||||||||||||||||||||||||||||||

Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 11.37 | 0.04 | 1.53 | 1.57 | 0.05 | 0.32 | — | 0.37 | — | 12.57 | 13.92 | 1.09 | 1.09 | 1.09 | 0.29 | 435,586 | 89 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 11.46 | (0.00 | )* | (0.09 | ) | (0.09 | ) | — | — | — | — | — | 11.37 | (0.79 | ) | 1.09 | 1.09 | 1.09 | (0.04 | ) | 414,381 | 90 | ||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 8.86 | 0.03 | • | 2.62 | 2.65 | 0.05 | — | — | 0.05 | — | 11.46 | 29.96 | 1.11 | 1.04 | 1.04 | 0.35 | 450,115 | 96 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 6.29 | 0.02 | 2.56 | 2.58 | 0.01 | — | — | 0.01 | — | 8.86 | 41.04 | 1.15 | 0.89 | † | 0.89 | † | 0.25 | † | 333,376 | 169 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 10.10 | (0.00 | )*• | (3.81 | ) | (3.81 | ) | — | — | — | — | 0.00 | * | 6.29 | (37.72 | )(b) | 1.13 | 0.90 | † | 0.90 | † | (0.02 | )† | 249,953 | 191 | |||||||||||||||||||||||||||||||||||||||||||||||||

Class S2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 11.38 | 0.02 | 1.54 | 1.56 | 0.04 | 0.32 | — | 0.36 | — | 12.58 | 13.79 | 1.34 | 1.24 | 1.24 | 0.18 | 7,243 | 89 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 11.49 | (0.01 | ) | (0.10 | ) | (0.11 | ) | — | — | — | — | — | 11.38 | (0.96 | ) | 1.34 | 1.24 | 1.24 | (0.13 | ) | 3,314 | 90 | ||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 8.89 | 0.08 | • | 2.56 | 2.64 | 0.04 | — | — | 0.04 | — | 11.49 | 29.67 | 1.36 | 1.19 | 1.19 | 0.71 | 900 | 96 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

02-27-09(5)–12-31-09 | 5.55 | 0.01 | 3.34 | 3.35 | 0.01 | — | — | 0.01 | — | 8.89 | 60.41 | 1.40 | 1.04 | † | 1.04 | † | 0.14 | † | 5 | 169 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Income (loss) from investment operations | | Less distributions | | Ratios to average net assets | Supplemental data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Net asset value, beginning of year or period | | Net investment income (loss) | | Net realized and unrealized gain (loss) | | Total from investment operations | | From net investment income | | From net realized gains | | From return of capital | | Total distributions | | Payment by affiliate | | Net asset value, end of year or period | | Total Return (1) | | Expenses before reductions/ additions (2)(3)(4) | | Expenses net of fee waivers and/or recoupments, if any (2)(3)(4) | | Expenses net of all reductions/ additions (2)(3)(4) | | Net investment income (loss) (2)(4) | | Net assets, end of year or period | | Portfolio turnover rate | ||||||||||||||||||||||||||||||||||||

| Year or period ended | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) | | (%) | | (%) | | (%) | | (%) | | (%) | | ($000’s) | | (%) | |||||||||||||||||||||||||||||||||||

ING SmallCap Opportunities Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Class ADV | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 20.73 | (0.07 | )• | 3.00 | 2.93 | — | 2.29 | — | 2.29 | — | 21.37 | 14.63 | 1.41 | 1.41 | 1.41 | (0.34 | ) | 14,236 | 57 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 20.67 | (0.14 | )• | 0.20 | 0.06 | — | — | — | — | — | 20.73 | 0.29 | 1.40 | 1.40 | 1.40 | (0.67 | ) | 4,819 | 72 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 15.69 | (0.10 | )• | 5.08 | 4.98 | — | — | — | — | — | 20.67 | 31.74 | 1.40 | 1.40 | 1.40 | (0.57 | ) | 2,120 | 97 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 12.04 | (0.08 | ) | 3.73 | 3.65 | — | — | — | — | — | 15.69 | 30.32 | 1.46 | 1.43 | 1.43 | (0.61 | ) | 88 | 139 | |||||||||||||||||||||||||||||||||||||||||||||||||

11-20-08(5)–12-31-08 | 9.63 | (0.01 | )• | 2.41 | 2.40 | — | — | — | — | 0.01 | 12.04 | 25.03 | (c) | 1.43 | 1.40 | † | 1.40 | † | (0.93 | )† | 4 | 148 | ||||||||||||||||||||||||||||||||||||||||||||||

Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 21.46 | 0.01 | 3.14 | 3.15 | — | 2.29 | — | 2.29 | — | 22.32 | 15.18 | 0.91 | 0.91 | 0.91 | 0.03 | 136,300 | 57 | |||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 21.28 | (0.04 | ) | 0.22 | 0.18 | — | — | — | — | — | 21.46 | 0.85 | 0.90 | 0.90 | 0.90 | (0.17 | ) | 117,965 | 72 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 16.08 | (0.02 | ) | 5.22 | 5.20 | — | — | — | — | — | 21.28 | 32.34 | 0.90 | 0.90 | 0.90 | (0.14 | ) | 113,938 | 97 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 12.27 | (0.02 | ) | 3.83 | 3.81 | — | — | — | — | — | 16.08 | 31.05 | 0.96 | 0.93 | 0.93 | (0.12 | ) | 79,291 | 139 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 21.98 | (0.01 | ) | (6.61 | ) | (6.62 | ) | — | 3.10 | — | 3.10 | 0.01 | 12.27 | (34.48 | )(c) | 0.93 | 0.90 | † | 0.90 | † | (0.04 | )† | 56,476 | 148 | ||||||||||||||||||||||||||||||||||||||||||||

Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 20.91 | (0.05 | ) | 3.07 | 3.02 | — | 2.29 | — | 2.29 | — | 21.64 | 14.95 | 1.16 | 1.16 | 1.16 | (0.22 | ) | 68,682 | 57 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 20.80 | (0.10 | ) | 0.21 | �� | 0.11 | — | — | — | — | — | 20.91 | 0.53 | 1.15 | 1.15 | 1.15 | (0.47 | ) | 63,588 | 72 | ||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 15.75 | (0.07 | ) | 5.12 | 5.05 | — | — | — | — | — | 20.80 | 32.06 | 1.15 | 1.15 | 1.15 | (0.39 | ) | 71,992 | 97 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 12.05 | (0.05 | ) | 3.75 | 3.70 | — | — | — | — | — | 15.75 | 30.71 | 1.21 | 1.17 | 1.17 | (0.36 | ) | 62,253 | 139 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 21.68 | (0.05 | ) | (6.49 | ) | (6.54 | ) | — | 3.10 | — | 3.10 | 0.01 | 12.05 | (34.59 | )(c) | 1.18 | 1.10 | † | 1.10 | † | (0.26 | )† | 54,163 | 148 | ||||||||||||||||||||||||||||||||||||||||||||

Class S2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 20.79 | (0.06 | )• | 3.03 | 2.97 | — | 2.29 | — | 2.29 | — | 21.47 | 14.79 | 1.41 | 1.31 | 1.31 | (0.27 | ) | 3,205 | 57 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 20.71 | (0.11 | )• | 0.19 | 0.08 | — | — | — | — | — | 20.79 | 0.39 | 1.40 | 1.30 | 1.30 | (0.56 | ) | 1,472 | 72 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 15.71 | (0.09 | )• | 5.09 | 5.00 | — | — | — | — | — | 20.71 | 31.83 | 1.40 | 1.30 | 1.30 | (0.50 | ) | 344 | 97 | |||||||||||||||||||||||||||||||||||||||||||||||||

02-27-09(5)–12-31-09 | 9.88 | (0.06 | ) | 5.89 | 5.83 | — | — | — | — | — | 15.71 | 59.01 | 1.46 | 1.33 | 1.33 | (0.54 | ) | 5 | 139 | |||||||||||||||||||||||||||||||||||||||||||||||||

(1) | Total return is calculated assuming reinvestment of all dividends, capital gain distributions and return of capital distributions, if any, at net asset value and does not reflect the effect of insurance contract charges. Total return for periods less than one year is not annualized. | |

(2) | Annualized for periods less than one year. | |

(3) | Expense ratios do not include fees and expenses charged under the variable annuity contract or variable life insurance policy. | |

(4) | Expense ratios reflect operating expenses of a Portfolio. Expenses before reductions/additions do not reflect amounts reimbursed by an Investment Adviser and/or Distributor or reductions from brokerage service arrangements or other expense offset arrangements and do not represent the amount paid by a Portfolio during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by an Investment Adviser and/or Distributor but prior to reductions from brokerage service arrangements or other expense offset arrangements. Expenses net of all reductions/additions represent the net expenses paid by a Portfolio. Net investment income (loss) is net of all such additions or reductions. | |

(5) | Commencement of operations. | |

(a) | Excluding a $729,720 payment by affiliate in 2008, International Value total return would have been (43.18)%, (42.86)% and (42.43)% on Classes ADV, I and S, respectively. | |

(b) | There was no impact on total return due to payment by affiliate in 2008. | |

(c) | Excluding a $110,798 payment by affiliate in 2008, SmallCap Opportunities total return would have been 24.72%, (34.52)% and (34.64)% for Classes ADV, I and S, respectively. | |

• | Calculated using average number of shares outstanding throughout the period. | |

| * | Amount is less than $0.005 or 0.005% or more than $(0.005) or (0.005)%. | |

| † | Impact of waiving the advisory fee for the ING Institutional Prime Money Market Fund holding has less than 0.005% impact on the expense ratio and net investment income or loss ratio. |

valuation, the potential expiration of restrictions on the security, the existence of any registration rights, the costs to the Portfolios related to registration of the security, as well as factors relevant to the issuer itself. Consideration may also be given to the price and extent of any public trading in similar securities of the issuer or comparable companies’ securities. The value of a foreign security traded on an exchange outside the United States is generally based on its price on the principal foreign exchange where it trades as of the time a Portfolio determines its NAV or if the foreign exchange closes prior to the time a Portfolio determines its NAV, the most recent closing price of the foreign security on its principal exchange. Trading in certain non-U.S. securities may not take place on all days on which the New York Stock Exchange (“NYSE”) is open. Further, trading takes place in various foreign markets on days on which the NYSE is not open. Consequently, the calculation of a Portfolio’s NAV may not take place contemporaneously with the determination of the prices of securities held by a Portfolio in foreign securities markets. Further, the value of a Portfolio’s assets may be significantly affected by foreign trading on days when a shareholder cannot purchase or redeem shares of a Portfolio. In calculating a Portfolio’s NAV, foreign securities denominated in foreign currency are converted to U.S. dollar equivalents. If an event occurs after the time at which the market for foreign securities held by a Portfolio closes but before the time that a Portfolio’s NAV is calculated, such event may cause the closing price on the foreign exchange to not represent a readily available reliable market value quotation for such securities at the time a Portfolio determines its NAV. In such a case, a Portfolio will use the fair value of such securities as determined under a Portfolio’s valuation procedures. Events after the close of trading on a foreign market that could require a Portfolio to fair value some or all of its foreign securities include, among others, securities trading in the U.S. and other markets, corporate announcements, natural and other disasters, and political and other events. Among other elements of analysis in the determination of a security’s fair value, the Board has authorized the use of one or more independent research services to assist with such determinations. An independent research service may use statistical analyses and quantitative models to help determine fair value as of the time a Portfolio calculates its NAV. There can be no assurance that such models accurately reflect the behavior of the applicable markets or the effect of the behavior of such markets on the fair value of securities, or that such markets will continue to behave in a fashion that is consistent with such models. Unlike the closing price of a security on an exchange, fair value determinations employ elements of judgment. Consequently, the fair value assigned to a security may not represent the actual value that a Portfolio could obtain if it were to sell the security at the time of the close of the NYSE. Pursuant to procedures adopted by the Board, a Portfolio is not obligated to use the fair valuations suggested by any research service, and valuation recommendations provided by such research services may be overridden if other events have occurred or if other fair valuations are determined in good faith to be more accurate. Unless an event is such that it causes a Portfolio to determine that the closing prices for one or more securities do not represent readily available reliable market value quotations at the time a Portfolio determines its NAV, events that occur between the time of the close of the foreign market on which they are traded and the close of regular trading on the NYSE will not be reflected in a Portfolio’s NAV.

when determining the fair value of the security. In the event that a security or asset cannot be valued pursuant to one of the valuation methods established by the Board, the fair value of the security or asset will be determined in good faith by the Pricing Committee. When a Portfolio uses these fair valuation methods that use significant unobservable inputs to determine its NAV, securities will be priced by a method that the Pricing Committee believes accurately reflects fair value and are categorized as Level 3 of the fair value hierarchy. The methodologies used for valuing securities are not necessarily an indication of the risks of investing in those securities valued in good faith at fair value nor can it be assured a Portfolio can obtain the fair value assigned to a security if they were to sell the security.

| 1. | Market value of investment securities, other assets and liabilities — at the exchange rates prevailing at the end of the day. |

| 2. | Purchases and sales of investment securities, income and expenses — at the rates of exchange prevailing on the respective dates of such transactions. |

brokers, dealers or other financial institutions in exchange for a negotiated lender’s fee. The borrower is required to fully collateralize the loans with cash or U.S. government securities. Generally, in the event of counterparty default, a Portfolio has the right to use collateral to offset losses incurred. There would be potential loss to a Portfolio in the event a Portfolio is delayed or prevented from exercising its right to dispose of the collateral. Each Portfolio bears the risk of loss with respect to the investment of collateral with the following exception: The Bank of New York Mellon (“BNY”) provides each Portfolio indemnification from loss with respect to the investment of collateral provided that the cash collateral is invested solely in overnight repurchase agreements. Engaging in securities lending could have a leveraging effect, which may intensify the credit, market and other risks associated with investing in a Portfolio.

| Purchases | Sales | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

International Value | $ | 76,268,448 | $ | 108,104,180 | ||||||

MidCap Opportunities | 1,050,801,009 | 937,737,497 | ||||||||

SmallCap Opportunities | 120,344,229 | 116,109,529 | ||||||||

| Affiliated Investment Company/Subsidiary | Portfolios | Percentage | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

ING Life Insurance and Annuity Company | International Value | 81.86 | % | |||||||

MidCap Opportunities | 20.58 | |||||||||

SmallCap Opportunities | 37.65 | |||||||||

ING National Trust | MidCap Opportunities | 8.64 | ||||||||

SmallCap Opportunities | 16.74 | |||||||||

ING Solution 2025 Portfolio | MidCap Opportunities | 6.52 | ||||||||

ING Solution 2035 Portfolio | MidCap Opportunities | 5.61 | ||||||||

ING USA Annuity and Life Insurance Company | International Value | 5.12 | ||||||||

MidCap Opportunities | 33.16 | |||||||||

SmallCap Opportunities | 26.69 | |||||||||

ReliaStar Life Insurance Company | International Value | 12.52 | ||||||||

SmallCap Opportunities | 15.48 | |||||||||

| Portfolio | Class ADV | Class I | Class S | Class S2 | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

International Value | 1.50 | % | 1.00 | % | 1.20 | % | 1.40% | |||||||||||

MidCap Opportunities(1) | 1.40 | % | 0.90 | % | 1.10 | % | 1.30% | |||||||||||

SmallCap Opportunities | 1.42 | % | 0.92 | % | 1.17 | % | 1.32% | |||||||||||

(1) | Pursuant to a side agreement, ING Investments has further lowered the expense limits for MidCap Opportunities. The expense limits for MidCap Opportunities are 1.35%, 0.85%, 1.10%, and 1.25% for Class ADV, Class I, Class S and Class S2, respectively. |

| December 31, | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2013 | 2014 | 2015 | Total | ||||||||||||||||

International Value | $ | 104,977 | $ | 114,048 | $ | — | $ | 219,025 | |||||||||||

MidCap Opportunities | 456,511 | — | — | 456,511 | |||||||||||||||

| Portfolio | Days Utilized | Approximate Average Daily Balance For Days Utilized | Approximate Weighted Average Interest Rate For Days Utilized | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

International Value | 24 | $ | 734,792 | 1.17 | % | |||||||||

MidCap Opportunities | 7 | 4,527,857 | 1.19 | |||||||||||

| Shares sold | Shares issued in merger | Reinvestment of distributions | Shares redeemed | Net increase (decrease) in shares outstanding | Shares sold | Proceeds from shares issued in merger | Reinvestment of distributions | Shares redeemed | Net increase (decrease) | |||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year or period ended | # | # | # | # | # | ($) | ($) | ($) | ($) | ($) | ||||||||||||||||||||||||||||||||||

International Value | ||||||||||||||||||||||||||||||||||||||||||||

Class ADV | ||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 21,917 | — | 3,140 | (50,540 | ) | (25,483 | ) | 163,899 | — | 23,251 | (379,216 | ) | (192,066 | ) | ||||||||||||||||||||||||||||||

12-31-11 | 172,355 | — | 909 | (13,100 | ) | 160,164 | 1,189,691 | — | 6,364 | (91,115 | ) | 1,104,940 | ||||||||||||||||||||||||||||||||

Class I | ||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 191,682 | — | 434,722 | (4,644,704 | ) | (4,018,300 | ) | 1,584,454 | — | 3,266,996 | (34,633,292 | ) | (29,781,842 | ) | ||||||||||||||||||||||||||||||

12-31-11 | 265,232 | — | 577,484 | (8,763,651 | ) | (7,920,935 | ) | 2,267,084 | — | 4,769,724 | (70,879,215 | ) | (63,842,407 | ) | ||||||||||||||||||||||||||||||

| Shares sold | Shares issued in merger | Reinvestment of distributions | Shares redeemed | Net increase (decrease) in shares outstanding | Shares sold | Proceeds from shares issued in merger | Reinvestment of distributions | Shares redeemed | Net increase (decrease) | ||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year or period ended | # | # | # | # | # | ($) | ($) | ($) | ($) | ($) | |||||||||||||||||||||||||||||||||||

International Value (continued) | |||||||||||||||||||||||||||||||||||||||||||||

Class S | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 45,298 | — | 24,675 | (292,320 | ) | (222,347 | ) | 344,918 | — | 188,642 | (2,251,231 | ) | (1,717,671 | ) | |||||||||||||||||||||||||||||||

12-31-11 | 119,083 | — | 26,684 | (291,227 | ) | (145,460 | ) | 916,504 | — | 223,189 | (2,409,967 | ) | (1,270,274 | ) | |||||||||||||||||||||||||||||||

Class S2 | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||

12-31-11 | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||

MidCap Opportunities | |||||||||||||||||||||||||||||||||||||||||||||

Class ADV | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 3,262,730 | — | 156,062 | (478,994 | ) | 2,939,798 | 40,501,115 | — | 1,883,967 | (5,869,659 | ) | 36,515,423 | |||||||||||||||||||||||||||||||||

12-31-11 | 2,696,115 | — | — | (443,229 | ) | 2,252,886 | 31,468,035 | — | — | (5,070,573 | ) | 26,397,462 | |||||||||||||||||||||||||||||||||

Class I | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 17,744,681 | — | 1,445,316 | (8,913,964 | ) | 10,276,033 | 229,130,303 | — | 17,930,893 | (113,212,077 | ) | 133,849,119 | |||||||||||||||||||||||||||||||||

12-31-11 | 14,841,264 | — | — | (7,414,500 | ) | 7,426,764 | 182,175,215 | — | — | (89,401,686 | ) | 92,773,529 | |||||||||||||||||||||||||||||||||

Class S | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 4,459,935 | — | 1,099,327 | (7,354,907 | ) | (1,795,645 | ) | 55,627,523 | — | 13,325,440 | (90,292,802 | ) | (21,339,839 | ) | |||||||||||||||||||||||||||||||

12-31-11 | 9,540,260 | — | — | (12,365,666 | ) | (2,825,406 | ) | 112,747,662 | — | — | (140,813,080 | ) | (28,065,418 | ) | |||||||||||||||||||||||||||||||

Class S2 | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 357,431 | — | 13,756 | (86,559 | ) | 284,628 | 4,421,549 | — | 166,592 | (1,078,987 | ) | 3,509,154 | |||||||||||||||||||||||||||||||||

12-31-11 | 279,661 | — | — | (66,807 | ) | 212,854 | 3,332,624 | — | — | (762,440 | ) | 2,570,184 | |||||||||||||||||||||||||||||||||

SmallCap Opportunities | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 432,701 | — | 40,219 | (39,220 | ) | 433,700 | 9,230,774 | — | 821,671 | (831,937 | ) | 9,220,508 | |||||||||||||||||||||||||||||||||

12-31-11 | 216,528 | — | — | (86,661 | ) | 129,867 | 4,539,946 | — | — | (1,801,342 | ) | 2,738,604 | |||||||||||||||||||||||||||||||||

Class I | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 958,527 | — | 599,307 | (948,582 | ) | 609,252 | 21,692,600 | — | 12,759,240 | (21,299,008 | ) | 13,152,832 | |||||||||||||||||||||||||||||||||

12-31-11 | 2,071,993 | — | — | (1,927,340 | ) | 144,653 | 45,472,333 | — | — | (41,994,897 | ) | 3,477,436 | |||||||||||||||||||||||||||||||||

Class S | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 297,152 | — | 315,683 | (478,822 | ) | 134,013 | 6,321,495 | — | 6,522,014 | (10,423,979 | ) | 2,419,530 | |||||||||||||||||||||||||||||||||

12-31-11 | 104,380 | — | — | (525,451 | ) | (421,071 | ) | 2,181,461 | — | — | (10,942,390 | ) | (8,760,929 | ) | |||||||||||||||||||||||||||||||

Class S2 | |||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 81,518 | — | 11,038 | (14,063 | ) | 78,493 | 1,736,928 | — | 226,396 | (307,309 | ) | 1,656,015 | |||||||||||||||||||||||||||||||||

12-31-11 | 63,506 | — | — | (9,287 | ) | 54,219 | 1,348,818 | — | — | (197,030 | ) | 1,151,788 | |||||||||||||||||||||||||||||||||

| Portfolio | Value of Securities Loaned | Cash Collateral Received | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

International Value | $ | 937,117 | $ | 984,618 | ||||||

MidCap Opportunities | 10,503,678 | 10,761,154 | ||||||||

SmallCap Opportunities | 6,324,534 | 6,485,853 | ||||||||

| Paid-in Capital | Undistributed Net Investment Income | Accumulated Net Realized Gains/(Losses) | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

International Value | $ | — | $ | 676,683 | $ | (676,683 | ) | |||||||

MidCap Opportunities | (88,974 | ) | (166,519 | ) | 255,493 | |||||||||

SmallCap Opportunities | — | 138,133 | (138,133 | ) | ||||||||||

| Year Ended December 31, 2012 | Year Ended December 31, 2011 | ||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Ordinary Income | Long-term Capital Gains | Ordinary Income | Return of Capital | ||||||||||||||||||||

International Value | $ | 3,478,979 | $ | — | $ | 4,851,909 | $ | 147,465 | |||||||||||||||

MidCap Opportunities | 4,876,122 | 28,430,770 | — | — | |||||||||||||||||||

SmallCap Opportunities | 3,546,008 | 16,783,313 | — | — | |||||||||||||||||||

| Capital Loss Carryforwards | |||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Undistributed Ordinary Income | Undistributed Long-term Capital Gains | Unrealized Appreciation/ (Depreciation) | Amount | Character | Expiration | ||||||||||||||||||||||

International Value | $ | 590,204 | $ | — | $ | 9,698,492 | $ | (76,969,718 | ) | Short-term | 2016 | ||||||||||||||||

| (104,716,147 | ) | Short-term | 2017 | ||||||||||||||||||||||||

| (8,802,519 | ) | Short-term | None | ||||||||||||||||||||||||

| (3,846,488 | ) | Long-term | None | ||||||||||||||||||||||||

| $ | (194,334,872 | ) | |||||||||||||||||||||||||

MidCap Opportunities | — | 37,865,152 | 132,170,308 | (61,883 | ) | Short-term | 2015 | ||||||||||||||||||||

| (820,634 | ) | Short-term | 2016 | ||||||||||||||||||||||||

| (95,470 | ) | Short-term | 2017 | ||||||||||||||||||||||||

| $ | (977,987 | )* | |||||||||||||||||||||||||

SmallCap Opportunities | 4,939,752 | 11,929,506 | 17,985,010 | — | — | — | |||||||||||||||||||||

| * | Utilization of these capital losses is subject to annual limitations under Section 382 of the Internal Revenue Code. |

Completion of the Restructuring Plan is expected to result in the Investment Adviser’s loss of access to the resources of ING Groep, which could adversely affect its business. Currently, the Investment Adviser does not anticipate that the Restructuring Plan will have an adverse impact on its operations or the operations of the Portfolios.

| ING INTERNATIONAL VALUE PORTFOLIO | SUMMARY PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2012 |

| Shares | | | | Value | | Percentage of Net Assets | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

COMMON STOCK: 99.1% | |||||||||||||||||||

Australia: 1.2% | |||||||||||||||||||

63,454 | Australia & New Zealand Banking Group Ltd. | $ | 1,671,163 | 1.2 | |||||||||||||||

Belgium: 1.4% | |||||||||||||||||||

54,585 | KBC Groep NV | 1,902,420 | 1.4 | ||||||||||||||||

Canada: 0.6% | |||||||||||||||||||

23,500 | Other Securities | 822,735 | 0.6 | ||||||||||||||||

China: 0.9% | |||||||||||||||||||

400,000 | Other Securities | 1,216,172 | 0.9 | ||||||||||||||||

Denmark: 1.2% | |||||||||||||||||||

92,552 | @ | Danske Bank A/S | 1,571,919 | 1.2 | |||||||||||||||

France: 11.2% | |||||||||||||||||||

123,367 | AXA S.A. | 2,215,163 | 1.7 | ||||||||||||||||

38,467 | BNP Paribas | 2,189,940 | 1.7 | ||||||||||||||||

7,800 | PPR | 1,464,932 | 1.1 | ||||||||||||||||

29,437 | Renault S.A. | 1,598,674 | 1.2 | ||||||||||||||||

25,843 | Sanofi-Aventis SA | 2,450,702 | 1.8 | ||||||||||||||||

46,957 | @ | Societe Generale | 1,785,430 | 1.3 | |||||||||||||||

30,853 | Total S.A. | 1,605,380 | 1.2 | ||||||||||||||||

13,262 | Other Securities | 1,605,649 | 1.2 | ||||||||||||||||

| 14,915,870 | 11.2 | ||||||||||||||||||

Germany: 9.4% | |||||||||||||||||||

15,280 | BASF AG | 1,444,883 | 1.1 | ||||||||||||||||

21,450 | Bayer AG | 2,045,522 | 1.5 | ||||||||||||||||

17,143 | Bayerische Motoren Werke AG | 1,668,212 | 1.3 | ||||||||||||||||

92,843 | Deutsche Post AG | 2,044,925 | 1.5 | ||||||||||||||||

29,756 | Siemens AG | 3,253,854 | 2.4 | ||||||||||||||||

144,704 | Other Securities | 2,115,401 | 1.6 | ||||||||||||||||

| 12,572,797 | 9.4 | ||||||||||||||||||

Hong Kong: 4.0% | |||||||||||||||||||

151,500 | Power Assets Holdings Ltd. | 1,299,804 | 1.0 | ||||||||||||||||

214,000 | Wharf Holdings Ltd. | 1,705,521 | 1.3 | ||||||||||||||||

785,700 | Other Securities | 2,281,300 | 1.7 | ||||||||||||||||

| 5,286,625 | 4.0 | ||||||||||||||||||

Italy: 4.8% | |||||||||||||||||||

348,450 | Enel S.p.A. | 1,449,379 | 1.1 | ||||||||||||||||

86,161 | ENI S.p.A. | 2,110,742 | 1.6 | ||||||||||||||||

135,149 | Fiat Industrial SpA | 1,480,643 | 1.1 | ||||||||||||||||

1,498,335 | Telecom Italia S.p.A. | 1,359,096 | 1.0 | ||||||||||||||||

| 6,399,860 | 4.8 | ||||||||||||||||||

Japan: 20.2% | |||||||||||||||||||

389,112 | Hitachi Ltd. | 2,289,733 | 1.7 | ||||||||||||||||

38,000 | Honda Motor Co., Ltd. | 1,407,316 | 1.1 | ||||||||||||||||

70,800 | Hoya Corp. | 1,395,039 | 1.0 | ||||||||||||||||

67,800 | Japan Tobacco, Inc. | $ | 1,915,308 | 1.4 | |||||||||||||||

46,000 | JGC Corp. | 1,433,428 | 1.1 | ||||||||||||||||

53,200 | Komatsu Ltd. | 1,365,133 | 1.0 | ||||||||||||||||

55,000 | Mitsubishi Estate Co., Ltd. | 1,316,739 | 1.0 | ||||||||||||||||

87,500 | Omron Corp. | 2,100,293 | 1.6 | ||||||||||||||||

14,220 | ORIX Corp. | 1,606,270 | 1.2 | ||||||||||||||||

75,000 | Sumitomo Mitsui Financial Group, Inc. | 2,725,636 | 2.0 | ||||||||||||||||

74,300 | Tokio Marine Holdings, Inc. | 2,069,944 | 1.6 | ||||||||||||||||

33,100 | Tokyo Electron Ltd. | 1,526,614 | 1.1 | ||||||||||||||||

515,750 | Other Securities(a) | 5,832,538 | 4.4 | ||||||||||||||||

| 26,983,991 | 20.2 | ||||||||||||||||||

Netherlands: 7.9% | |||||||||||||||||||

32,839 | European Aeronautic Defence and Space Co. NV | 1,294,561 | 1.0 | ||||||||||||||||

74,771 | Koninklijke Philips Electronics NV | 1,979,962 | 1.5 | ||||||||||||||||

128,392 | Royal Dutch Shell PLC — Class A | 4,456,533 | 3.3 | ||||||||||||||||

49,642 | Unilever NV | 1,899,492 | 1.4 | ||||||||||||||||

15,298 | Other Securities | 932,352 | 0.7 | ||||||||||||||||

| 10,562,900 | 7.9 | ||||||||||||||||||

New Zealand: 0.9% | |||||||||||||||||||

648,468 | Other Securities | 1,227,426 | 0.9 | ||||||||||||||||

Norway: 1.2% | |||||||||||||||||||

61,236 | Statoil ASA | 1,543,430 | 1.2 | ||||||||||||||||

Singapore: 3.1% | |||||||||||||||||||

517,000 | Singapore Telecommunications Ltd. | 1,406,772 | 1.1 | ||||||||||||||||

89,100 | United Overseas Bank Ltd. | 1,461,600 | 1.1 | ||||||||||||||||

154,000 | Other Securities | 1,240,930 | 0.9 | ||||||||||||||||

| �� | 4,109,302 | 3.1 | |||||||||||||||||

Spain: 0.9% | |||||||||||||||||||

69,684 | Other Securities | 1,256,224 | 0.9 | ||||||||||||||||

Sweden: 1.0% | |||||||||||||||||||

130,151 | Telefonaktiebolaget LM Ericsson | 1,314,688 | 1.0 | ||||||||||||||||

Switzerland: 5.8% | |||||||||||||||||||

29,515 | Nestle S.A. | 1,925,661 | 1.4 | ||||||||||||||||

33,147 | Novartis AG | 2,094,005 | 1.6 | ||||||||||||||||

18,626 | Roche Holding AG —Genusschein | 3,765,827 | 2.8 | ||||||||||||||||

| 7,785,493 | 5.8 | ||||||||||||||||||

| ING INTERNATIONAL VALUE PORTFOLIO | SUMMARY PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2012 (CONTINUED) |

| Shares | | | | Value | | Percentage of Net Assets | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

COMMON STOCK: (continued) | |||||||||||||||||||

United Kingdom: 21.6% | |||||||||||||||||||

576,579 | Barclays PLC | $ | 2,504,660 | 1.9 | |||||||||||||||

96,076 | BHP Billiton PLC | 3,388,952 | 2.5 | ||||||||||||||||

99,869 | GlaxoSmithKline PLC | 2,174,389 | 1.6 | ||||||||||||||||

276,751 | HSBC Holdings PLC | 2,932,682 | 2.2 | ||||||||||||||||

657,481 | Legal & General Group PLC | 1,576,561 | 1.2 | ||||||||||||||||

2,686,551 | @ | Lloyds TSB Group PLC | 2,140,909 | 1.6 | |||||||||||||||

54,951 | Rio Tinto PLC | 3,205,069 | 2.4 | ||||||||||||||||

354,444 | Tesco PLC | 1,952,492 | 1.5 | ||||||||||||||||

1,346,232 | Vodafone Group PLC | 3,388,840 | 2.5 | ||||||||||||||||

270,687 | Other Securities | 5,529,010 | 4.2 | ||||||||||||||||

| 28,793,564 | 21.6 | ||||||||||||||||||

United States: 1.8% | |||||||||||||||||||

45,600 | Coca-Cola Enterprises, Inc. | 1,446,888 | 1.1 | ||||||||||||||||

30,700 | Other Securities | 959,989 | 0.7 | ||||||||||||||||

| 2,406,877 | 1.8 | ||||||||||||||||||

Total Common Stock | |||||||||||||||||||

(Cost $121,585,457) | 132,343,456 | 99.1 | |||||||||||||||||

| Principal Amount† | | | | Value | | Percentage of Net Assets | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

SHORT-TERM INVESTMENTS: 1.2% | |||||||||||||||||||

Securities Lending Collateralcc(1): 0.7% | |||||||||||||||||||

974,058 | BNP Paribas Bank, Repurchase Agreement dated 12/31/12, 0.20%, due 01/02/13 (Repurchase Amount $974,069, collateralized by various U.S. Government Agency Obligations, 3.000%–3.500%, Market Value plus accrued interest $993,539, due 09/15/42–11/15/42) | $ | 974,058 | 0.7 | |||||||||||||||

10,560 | Merrill Lynch & Co., Inc., Repurchase Agreement dated 12/31/12, 0.14%, due 01/02/13 (Repurchase Amount $10,560, collateralized by various U.S. Government Agency Obligations, 0.500%–6.000%, Market Value plus accrued interest $10,771, due 08/09/13–04/18/36) | 10,560 | 0.0 | ||||||||||||||||

| 984,618 | 0.7 | ||||||||||||||||||

| Shares | | | | Value | | Percentage of Net Assets | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

SHORT-TERM INVESTMENTS: (continued) | |||||||||||||||||||

Mutual Funds: 0.5% | |||||||||||||||||||

608,000 | BlackRock Liquidity Funds, TempFund, Institutional Class | ||||||||||||||||||

(Cost $608,000) | $ | 608,000 | 0.5 | ||||||||||||||||

Total Short-Term Investments | |||||||||||||||||||

(Cost $1,592,618) | 1,592,618 | 1.2 | |||||||||||||||||

Total Investments in Securities (Cost $123,178,075) | $ | 133,936,074 | 100.3 | ||||||||||||||||

Liabilities in Excess of Other Assets | (457,575 | ) | (0.3 | ) | |||||||||||||||

Net Assets | $ | 133,478,499 | 100.0 | ||||||||||||||||

| † | Unless otherwise indicated, principal amount is shown in USD. | |

| @ | Non-income producing security | |

| cc | Securities purchased with cash collateral for securities loaned. | |

| (1) | Collateral received from brokers for securities lending was invested into these short-term investments. | |

| (a) | This grouping contains securities on loan. | |

| Cost for federal income tax purposes is $124,265,405. |

Net unrealized appreciation consists of: | ||||||

Gross Unrealized Appreciation | $ | 13,489,760 | ||||

Gross Unrealized Depreciation | (3,819,091 | ) | ||||

Net Unrealized Appreciation | $ | 9,670,669 |

| Sector Diversification | Percentage of Net Assets | |||||

|---|---|---|---|---|---|---|

Financials | 26.9 | % | ||||

Energy | 11.0 | |||||

Industrials | 9.6 | |||||

Health Care | 9.3 | |||||

Materials | 8.5 | |||||

Consumer Staples | 8.5 | |||||

Consumer Discretionary | 8.1 | |||||

Information Technology | 7.1 | |||||

Telecommunication Services | 6.2 | |||||

Utilities | 3.9 | |||||

Short-Term Investments | 1.2 | |||||

Liabilities in Excess of Other Assets | (0.3 | ) | ||||

Net Assets | 100.0 | % | ||||

| ING INTERNATIONAL VALUE PORTFOLIO | SUMMARY PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2012 (CONTINUED) |

| Quoted Prices in Active Markets for Identical Investments (Level 1) | Significant Other Observable Inputs # (Level 2) | Significant Unobservable Inputs (Level 3) | Fair Value at 12/31/2012 | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Asset Table | ||||||||||||||||||

Investments, at fair value | ||||||||||||||||||

Common Stock | ||||||||||||||||||

Australia | $ | — | $ | 1,671,163 | $ | — | $ | 1,671,163 | ||||||||||

Belgium | — | 1,902,420 | — | 1,902,420 | ||||||||||||||

Canada | 822,735 | — | — | 822,735 | ||||||||||||||

China | — | 1,216,172 | — | 1,216,172 | ||||||||||||||

Denmark | — | 1,571,919 | — | 1,571,919 | ||||||||||||||

France | — | 14,915,870 | — | 14,915,870 | ||||||||||||||

Germany | — | 12,572,797 | — | 12,572,797 | ||||||||||||||

Hong Kong | — | 5,286,625 | — | 5,286,625 | ||||||||||||||

Italy | — | 6,399,860 | — | 6,399,860 | ||||||||||||||

Japan | 371,185 | 26,612,806 | — | 26,983,991 | ||||||||||||||

Netherlands | — | 10,562,900 | — | 10,562,900 | ||||||||||||||

New Zealand | — | 1,227,426 | — | 1,227,426 | ||||||||||||||

Norway | — | 1,543,430 | — | 1,543,430 | ||||||||||||||

Singapore | — | 4,109,302 | — | 4,109,302 | ||||||||||||||

Spain | — | 1,256,224 | — | 1,256,224 | ||||||||||||||

Sweden | — | 1,314,688 | — | 1,314,688 | ||||||||||||||

Switzerland | — | 7,785,493 | — | 7,785,493 | ||||||||||||||

United Kingdom | 2,377,776 | 26,415,788 | — | 28,793,564 | ||||||||||||||

United States | 2,406,877 | — | — | 2,406,877 | ||||||||||||||

Total Common Stock | 5,978,573 | 126,364,883 | — | 132,343,456 | ||||||||||||||

Short-Term Investments | 608,000 | 984,618 | — | 1,592,618 | ||||||||||||||

Total Investments, at fair value | $ | 6,586,573 | $ | 127,349,501 | $ | — | $ | 133,936,074 | ||||||||||

| ˆ | See Note 2, “Significant Accounting Policies” in the Notes to Financial Statements for additional information. |

| # | The earlier close of the foreign markets gives rise to the possibility that significant events, including broad market moves, may have occurred in the interim and may materially affect the value of those securities. To account for this, the Portfolio may frequently value many of its foreign equity securities using fair value prices based on third party vendor modeling tools to the extent available. Accordingly, a portion of the Portfolio’s investments are categorized as Level 2 investments. |

| ING MIDCAP OPPORTUNITIES PORTFOLIO | SUMMARY PORTFOLIO OF INVESTMENTS AS OF DECEMBER 31, 2012 |

| Shares | | | | Value | | Percentage of Net Assets | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

COMMON STOCK: 98.7% | |||||||||||||||||||

Consumer Discretionary: 25.6% | |||||||||||||||||||

473,651 | Brinker International, Inc. | $ | 14,678,445 | 1.3 | |||||||||||||||

640,380 | @ | Delphi Automotive PLC | 24,494,535 | 2.2 | |||||||||||||||

383,640 | @ | Discovery Communications, Inc.—Class A | 24,353,467 | 2.1 | |||||||||||||||

515,350 | Foot Locker, Inc. | 16,553,042 | 1.5 | ||||||||||||||||

621,730 | Gap, Inc. | 19,298,499 | 1.7 | ||||||||||||||||

336,360 | Harley-Davidson, Inc. | 16,427,822 | 1.4 | ||||||||||||||||

102,109 | @ | Liberty Media Corp.—Liberty Capital | 11,845,665 | 1.1 | |||||||||||||||

669,810 | @, L | Lions Gate Entertainment Corp. | 10,984,884 | 1.0 | |||||||||||||||

462,134 | Macy’s, Inc. | 18,032,469 | 1.6 | ||||||||||||||||

319,140 | @ | Michael Kors Holdings Ltd. | 16,285,714 | 1.4 | |||||||||||||||

787,680 | Newell Rubbermaid, Inc. | 17,541,634 | 1.5 | ||||||||||||||||

231,160 | @ | Penn National Gaming, Inc. | 11,352,268 | 1.0 | |||||||||||||||

265,680 | Petsmart, Inc. | 18,156,571 | 1.6 | ||||||||||||||||

193,440 | Scripps Networks Interactive — Class A | 11,204,045 | 1.0 | ||||||||||||||||

187,770 | Six Flags Entertainment Corp. | 11,491,524 | 1.0 | ||||||||||||||||

150,340 | @ | Ulta Salon Cosmetics & Fragrance, Inc. | 14,772,408 | 1.3 | |||||||||||||||

296,014 | Wyndham Worldwide Corp. | 15,750,905 | 1.4 | ||||||||||||||||

363,090 | Other Securities | 17,806,085 | 1.5 | ||||||||||||||||

| 291,029,982 | 25.6 | ||||||||||||||||||

Consumer Staples: 6.1% | |||||||||||||||||||

713,260 | Coca-Cola Enterprises, Inc. | 22,631,740 | 2.0 | ||||||||||||||||

167,290 | JM Smucker Co. | 14,427,090 | 1.3 | ||||||||||||||||

237,340 | Whole Foods Market, Inc. | 21,676,262 | 1.9 | ||||||||||||||||

175,278 | Other Securities | 10,707,733 | 0.9 | ||||||||||||||||

| 69,442,825 | 6.1 | ||||||||||||||||||

Energy: 6.3% | |||||||||||||||||||

395,470 | @ | Cameron International Corp. | 22,328,236 | 2.0 | |||||||||||||||

898,940 | @ | Denbury Resources, Inc. | 14,562,828 | 1.3 | |||||||||||||||

398,040 | @ | Oasis Petroleum, Inc. | 12,657,672 | 1.1 | |||||||||||||||

296,460 | Range Resources Corp. | 18,626,582 | 1.6 | ||||||||||||||||

121,850 | Other Securities | 4,071,009 | 0.3 | ||||||||||||||||

| 72,246,327 | 6.3 | ||||||||||||||||||

Financials: 8.0% | |||||||||||||||||||

101,890 | @ | Affiliated Managers Group, Inc. | 13,260,984 | 1.1 | |||||||||||||||

182,650 | Ameriprise Financial, Inc. | 11,439,370 | 1.0 | ||||||||||||||||

802,430 | Fifth Third Bancorp. | 12,188,912 | 1.1 | ||||||||||||||||

498,442 | Nasdaq Stock Market, Inc. | 12,466,034 | 1.1 | ||||||||||||||||

243,780 | T. Rowe Price Group, Inc. | $ | 15,877,391 | 1.4 | |||||||||||||||

334,290 | Tanger Factory Outlet Centers, Inc. | 11,432,718 | 1.0 | ||||||||||||||||

541,530 | Other Securities | 14,776,020 | 1.3 | ||||||||||||||||