| OMB APPROVAL | |

| OMB Number: | 3235-0570 |

| Expires: | January 31, 2017 |

| Estimated average burden hours per response. . . . . . . . . . .20.6 | |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-8220

Voya Variable Products Trust

(Exact name of registrant as specified in charter)

7337 E. Doubletree Ranch Rd., Scottsdale, AZ 85258

(Address of principal executive offices) (Zip code)

CT Corporation System, 101 Federal Street, Boston, MA 02110

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: December 31

Date of reporting period: January 1, 2014 to December 31, 2014

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Annual Report

December 31, 2014

Classes ADV, I, S and S2

Voya Variable Products Trust

| ■ | Voya International Value Portfolio |

| ■ | Voya MidCap Opportunities Portfolio |

| ■ | Voya SmallCap Opportunities Portfolio |

| This report is submitted for general information to shareholders of the Voya mutual funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. |

TABLE OF CONTENTS

PROXY VOTING INFORMATION

A description of the policies and procedures that the Portfolios use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the Portfolios’ website at www.voyainvestments.com; and (3) on the U.S. Securities and Exchange Commission’s (“SEC’s”) website at www.sec.gov. Information regarding how the Portfolios voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the Portfolios’ website at www.voyainvestments.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Portfolios file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. This report contains a summary portfolio of investments for the Portfolios. The Portfolios’ Forms N-Q are available on the SEC’s website at www.sec.gov. The Portfolios’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. The Portfolios’ Forms N-Q, as well as a complete portfolio of investments, are available without charge upon request from the Portfolios by calling Shareholder Services toll-free at (800) 992-0180.

New Year, Hopeful View

Dear Shareholder,

As 2014 came to a close, U.S. economic growth accelerated, Japan and Europe were struggling and volatility re-emerged in markets around the world. Though periods of volatility may challenge investor resolve over the course of the year, we believe resilience will prevail thanks to continued improvements in global consumer and business spending and ample global liquidity.

Resilience has been a defining characteristic of markets for some time now, as we have seen them shake off such potentially destabilizing events as Europe’s chronic economic malaise, China’s growth slowdown and Japan’s sharp and surprising return to recession. And that’s not to mention the various geopolitical hotspots — Ukraine, the Middle East and elsewhere — that have flared up from time to time. Along the way markets have been fortified by all-time high U.S. corporate earnings; renewed monetary stimulus from central banks in Japan, Europe and China; and plummeting oil prices that have provided a positive supply shock to consumers and businesses. This confluence of events has bolstered markets worldwide and has raised investor confidence that such trends can be sustained into 2015.

Despite our optimism, we — as always — advocate a well-balanced, globally diversified portfolio. We believe such an approach is the best way to potentially benefit from whatever opportunities may arise, while limiting the potential for over-exposure to as-yet-unidentified risks. Also as always, be sure to review your investment strategy and portfolio with your financial advisor to ensure they continue to reflect your goals and needs. Thoroughly discuss any potential portfolio changes with your advisor before taking action.

We appreciate your continued confidence in us, and we look forward to serving your investment needs in the future.

Sincerely,

Shaun Mathews

Executive Vice President

Voya Family of Funds

January 28, 2015

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and the Voya mutual funds disclaim any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for a Voya mutual fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any Voya mutual fund. Reference to specific company securities should not be construed as recommendations or investment advice.

International investing poses special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic.

| 1 |

Market Perspective: Year Ended December 31, 2014

Global equities, in the form of the MSCI World IndexSM (the “Index”) measured in local currencies, including net reinvested dividends ended 2013 at a record high. Investor sentiment had evidently reconciled itself to the tapering of the U.S. Federal Reserve Board’s (“Fed’s”) $85 billion of monthly Treasury and mortgage-backed securities purchases. The Fed’s December 18 announcement of a reduction in purchases to $75 billion per month with more to come was taken in stride. There was still plenty to worry about however and the Index endured an early slump and wide swings late in 2014 before ending up 9.81% for the year. (The Index returned 4.94% for the one year ended December 31, 2014, measured in U.S. dollars.)

It did not take long for worries about a flagging U.S. economy to resurface. A disappointingly weak employment report on January 10 showed only 74,000 jobs created in December, the lowest in nearly three years. A cold and snowy winter was thought to be depressing hiring and other key statistics like durable goods orders and home sales.

The Index reached its low point on February 3, down almost exactly 5% in 2014. Yet it took only 18 days to erase the loss despite new political turmoil that flared in Eastern Europe as Russia annexed Crimea after the president of Ukraine was deposed.

With the improvement in the season came a pick-up in U.S. economic data. Employment reports were looking better and the unemployment rate fell below 6%. The December bulletin marked the eighth consecutive month in which more than 200,000 jobs were created. National purchasing managers’ activity indices signaled healthy expansion. While the housing market was cooling, the annualized rate of existing home sales exceeded 5 million for five straight months. Consumer confidence touched seven-year high levels. Growth in gross domestic product (“GDP”) was -2.1% (annualized) in the first quarter but bounced back to 5.0% in the third.

Yet concerns remained about the sustainability of the recovery in the U.S. and worldwide. The improving U.S. employment situation was accompanied by labor force participation rates at or near the lowest since 1978. Wage growth was sluggish near 2% annually. The Fed’s monthly Treasury and mortgage-backed securities purchases ended in October.

Outside of the U.S., growth in China was decelerating, which also weighed on global commodity supplying countries. Japan re-entered recession in the third quarter after an April rise in consumption tax. But it was the euro zone that was the most problematic. Growth almost ground to a halt in the second and third quarters. Unemployment seemed stuck at 11.5%, while deflation was perilously close. Markets became increasingly skeptical that the European Central Bank (“ECB”) could attempt U.S., UK and Japan-style quantitative easing with Germany unequivocally opposed. Oil prices had been steadily falling since late June and would halve by year-end. Increased shale oil production notwithstanding, was this also a signal that global economic activity was weaker than anyone had imagined?

Securities prices mirrored investors’ mood swings in the last few months. The Index actually reached a new peak on September 19, but by October 16 fell 8.2%. From there the Index rebounded 12% to December 5, fell 5% to December 16 then rose 4% to end the year 1.3% below its all-time high.

In U.S. fixed income markets, the Barclays Long-Term U.S. Treasury sub-index returned a remarkable 25.07% in 2014; the

Barclays Short-Term U.S. Treasury sub-index just 0.09% as the Treasury yield curve flattened. The Barclays U.S. Aggregate Bond Index (“Barclays Aggregate”) added 5.97%, while the Barclays U.S. Corporate Investment Grade Bond sub-index gained 7.46%. Both outperformed the Barclays High Yield Bond — 2% Issuer Constrained Composite Index (not a part of the Barclays Aggregate), which gained only 2.46%, perhaps reflecting growing disillusionment with the risk/reward profile of high yield bonds after strong returns in recent years.

U.S. equities, represented by the S&P 500® Index including dividends, returned 13.69% in the fiscal year, about 1.5% below its all-time high. The utilities sector was the top performer, returning 28.98%; not surprisingly, the only loser was energy, which dropped 7.78% as oil prices sagged. Record operating earnings per share for S&P 500® companies in the second and third quarters were supported by low interest rates, slow wage growth and historically high share buy-back volumes. Operating margins breached 10% for the first time.

In currencies, the dollar advanced against most other currencies over the year. The dollar surged 13.60% against the euro, on the U.S.’s much better growth and interest rate increase prospects, and 13.74% against the yen, on the likelihood of further monetary easing in Japan and an announced partial re-allocation into non-yen securities for the giant Government Pension Investment Fund (“GPIF”). The dollar gained less, 6.29%, on the pound. The UK had a better growth story than the euro zone, which however is the destination for about 40% of the UK’s exports.

In international markets, the MSCI Japan® Index rose 9.48% in 2014, boosted in the case of Japan’s large exporters by the falling yen and in general by the GPIF’s announcement described above. The MSCI Europe ex UK® Index added 6.63%. The poor economic data referred to above and the lingering conflict in Ukraine dampened markets, which were spasmodically supported by the possibility of quantitative easing. The strong health care sector contributed about one third of the total. Despite superior economic results, the MSCI UK® Index was much weaker, edging up 0.50%. UK stock indices are not particularly representative of the UK economy: the largest 14 names account for half of the index and comprise mostly global banking, energy, pharmaceuticals and materials companies. As a group, they held back returns by about 1.80%.

All indices are unmanaged and investors cannot invest directly in an index. Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Portfolios’ performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.voyainvestments.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of Voya Investment Management’s Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

| 2 |

Benchmark Descriptions

| Index | Description | |||||||

| Barclays High Yield Bond — 2% Issuer Constrained Composite Index | An unmanaged index that includes all fixed-income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million, and at least one year to maturity. | |||||||

| Barclays Long-Term U.S. Treasury Index | The Index includes all publicly issued, U.S. Treasury securities that have a remaining maturity of 10 or more years, are rated investment grade, and have $250 million or more of outstanding face value. | |||||||

| Barclays Short-Term U.S. Treasury Index | A market capitalization-weighted index that is composed of fixed-rate, non-convertible U.S. Treasury securities that have a remaining maturity of between one and 12 months and have $250 million or more of outstanding face value. | |||||||

| Barclays U.S. Aggregate Bond Index | An unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. | |||||||

| Barclays U.S. Corporate Investment Grade Bond Index | An unmanaged index consisting of publicly issued, fixed rate, nonconvertible, investment grade debt securities. | |||||||

| MSCI EAFE® Index | An unmanaged index that measures the performance of securities listed on exchanges in markets in Europe, Australasia and the Far East. It includes the reinvestment of dividends net of withholding taxes, but does not reflect fees, brokerage commissions or other expenses of investing. | |||||||

| MSCI Europe ex UK® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK. | |||||||

| MSCI Japan® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan. | |||||||

| MSCI UK® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK. | |||||||

| MSCI World IndexSM | An unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. | |||||||

| Russell 2000® Growth Index | An unmanaged index that measures the performance of securities of smaller U.S. companies with greater than average growth orientation. | |||||||

| Russell 2000® Index | An unmanaged index that measures the performance of securities of small U.S. companies. | |||||||

| Russell Midcap® Growth Index | An unmanaged index that measures the performance of those companies included in the Russell Midcap® Index with relatively higher price-to-book ratios and higher forecasted growth values. | |||||||

| Russell Midcap® Index | An unmanaged index that measures the performance of the 800 smallest companies in the Russell 1000T Index, which represents approximately 26% of the total market capitalization of the Russell 1000® Index. | |||||||

| S&P 500® Index | An unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets. |

| 3 |

| Voya International Value Portfolio | Portfolio Managers’ Report |

Geographic Diversification | |||||

| Japan | 20.6% | ||||

| France | 14.1% | ||||

| United Kingdom | 14.1% | ||||

| Germany | 11.0% | ||||

| Switzerland | 10.6% | ||||

| Netherlands | 8.7% | ||||

| Italy | 3.2% | ||||

| Australia | 3.2% | ||||

| China | 2.4% | ||||

| Sweden | 2.3% | ||||

| Countries between 0.7%-2.2%^ | 8.4% | ||||

| Assets in Excess of Other Liabilities* | 1.4% | ||||

| Net Assets | 100.0% | ||||

| * | Includes short-term investments. | |

| ^ | Includes 7 countries, which each represents 0.7%-2.2% of net assets. | |

| Portfolio holdings are subject to change daily. |

Voya International Value Portfolio (the “Portfolio”) seeks long-term capital appreciation. The Portfolio is managed by Martin Jansen, Senior Portfolio Manager, Joseph Vultaggio, Portfolio Manager, and David Rabinowitz, Portfolio Manager of Voya Investment Management Co. LLC (“Voya IM”) — the Sub-Adviser.*

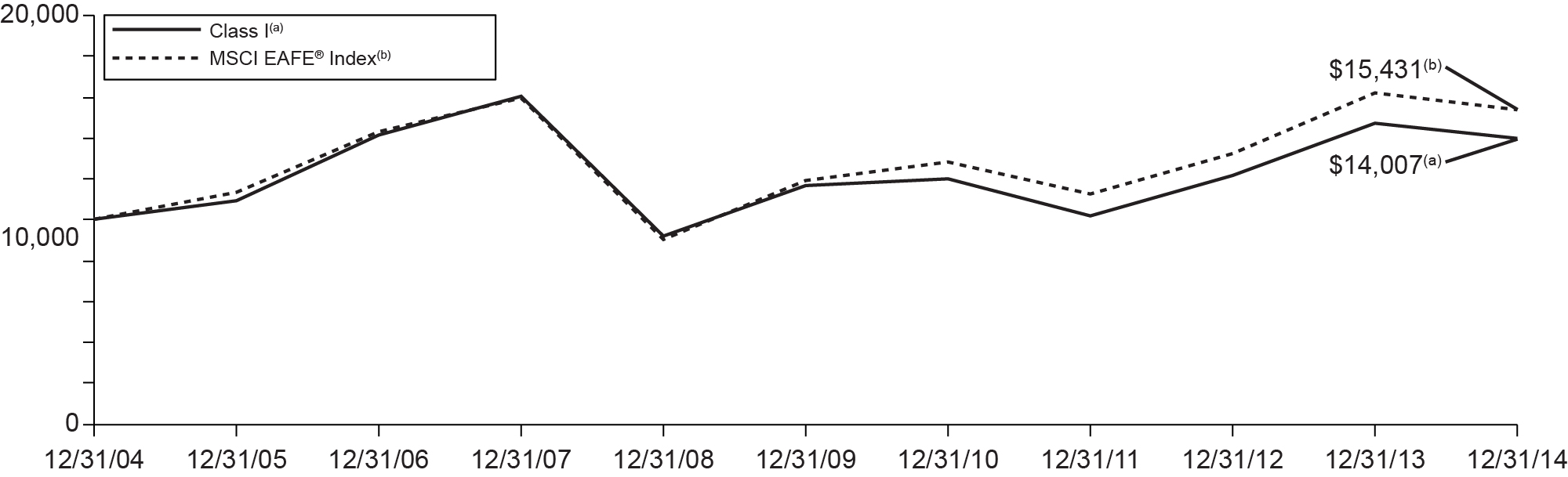

Performance: For the year ended December 31, 2014, the Portfolio’s Class I shares provided a total return of -4.94% compared to the MSCI EAFE® Index, which returned -4.90% for the same period.

Portfolio Specifics: The Portfolio outperformed its benchmark before the deduction of fees and operating expenses, but lagged net of those costs. Performance for the period was due to security selection, particularly in the telecommunications services, energy and health care sectors. Security selection in materials, industrials and financials detracted from relative results. From a regional perspective, stock selection in Europe and allocation to emerging markets contributed the most to performance. In contrast, sector allocation in North America and security selection in Asia Pacific ex-Japan detracted from results.

Among the leading individual contributors to performance were Ajinomoto Co., Inc. (“Ajinomoto”), Orange SA (“Orange”) and Statoil ASA (“Statoil”). Japanese food producer Ajinomoto benefited from the acquisition of Windsor Quality Holdings, a U.S. frozen food maker, which may boost sales, along with cost synergies to create a high margin portfolio. The company may also benefit from announced price increases in frozen foods in February 2015. Telecommunications services supplier Orange released third quarter results slightly better than expected. With improvements in the French market and cost cutting measures coming in ahead of schedule, we believe the company’s fundamentals appear more stable. Statoil, an integrated oil company, benefited from management announcing definitive return and growth targets that tied together the benefits of the company’s exploration success with an improving operational outlook.

Top Ten Holdings | |||||

| Royal Dutch Shell PLC - Class A | 3.5% | ||||

| Novartis AG | 3.2% | ||||

| Roche Holding AG - Genusschein | 2.9% | ||||

| Total S.A. | 2.3% | ||||

| Toyota Motor Corp. | 2.2% | ||||

| Nestle S.A. | 2.1% | ||||

| BHP Billiton Ltd. | 1.9% | ||||

| Bayer AG | 1.9% | ||||

| Barclays PLC | 1.7% | ||||

| Hitachi Ltd. | 1.7% | ||||

| Portfolio holdings are subject to change daily. | |||||

Among the leading detractors from performance were Noble Corporation PLC (“Noble Corp.”), BHP Billiton PLC (“BHP Billiton”) and Fortescue Metals Group Ltd. (“Fortescue Metals”), which were all impacted by the severe contraction in commodity prices during the year. Energy service provider Noble Corp. underperformed after investors reacted badly to management comments early in 2014 about the industry experiencing a short pause in its business cycle, even while reporting earnings that were mostly in line with analysts’ expectations. Falling prices hurt iron-ore producer Fortescue Metals, particularly because of its low quality product. International resources company BHP Billiton, the world’s largest mining group, fell sharply in tandem with the overall underperformance of the energy and metals sectors.

Current Strategy and Outlook: In our opinion, international developed stocks have modest upside potential from current levels. While we believe the banking crisis in Europe has been substantially resolved, we also believe that economic recovery is proving more elusive than market participants had hoped. Renewed and substantial quantitative easing measures by the European Central Bank are expected to result in a modest recovery in 2015. On balance, we believe the substantial fall in energy and commodity prices should stimulate global consumption and industrial production as 2015 progresses. We believe that the structural growth issues facing the developed world are expected to improve gradually, albeit with some periodic setbacks. We believe the Portfolio is well diversified across both geographic regions and economic sectors; we continue to favor well-capitalized stocks with what we believe to be unrecognized value.

| * | On September 12, 2014, the Board of Trustees approved a proposal, subject to shareholder approval, to reorganize the Portfolio with and into the Voya Global Value Advantage Portfolio. |

| Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. |

| 4 |

Voya International Value Portfolio |

| Average Annual Returns for the Periods Ended December 31, 2014 | ||||||||||||||||||

| 1 Year | 5 Year | 10 Year | Since Inception of Class ADV December 29, 2006 | |||||||||||||||

| Class ADV | -5.44% | 3.14% | — | -0.65% | ||||||||||||||

| Class I | -4.94% | 3.67% | 3.43% | — | ||||||||||||||

| Class S | -5.18% | 3.50% | 3.22% | — | ||||||||||||||

| MSCI EAFE® Index | -4.90% | 5.33% | 4.43% | 0.92% | ||||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Voya International Value Portfolio against the index indicated. The index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

| 5 |

| Voya MidCap Opportunities Portfolio | Portfolio Managers’ Report |

Sector Diversification | |||||

| Consumer Discretionary | 24.9% | ||||

| Information Technology | 17.5% | ||||

| Industrials | 17.1% | ||||

| Health Care | 12.5% | ||||

| Financials | 9.4% | ||||

| Consumer Staples | 8.8% | ||||

| Energy | 4.9% | ||||

| Materials | 4.3% | ||||

| Assets in Excess of Other Liabilities* | 0.6% | ||||

| Net Assets | 100.0% | ||||

| * Includes short-term investments. | |||||

| Portfolio holdings are subject to change daily. | |||||

Voya MidCap Opportunities Portfolio (the “Portfolio”) seeks long-term capital appreciation. The Portfolio is managed by Jeffrey Bianchi and Michael Pytosh, Portfolio Managers of Voya Investment Management Co. LLC (“Voya IM”) — the Sub-Adviser.

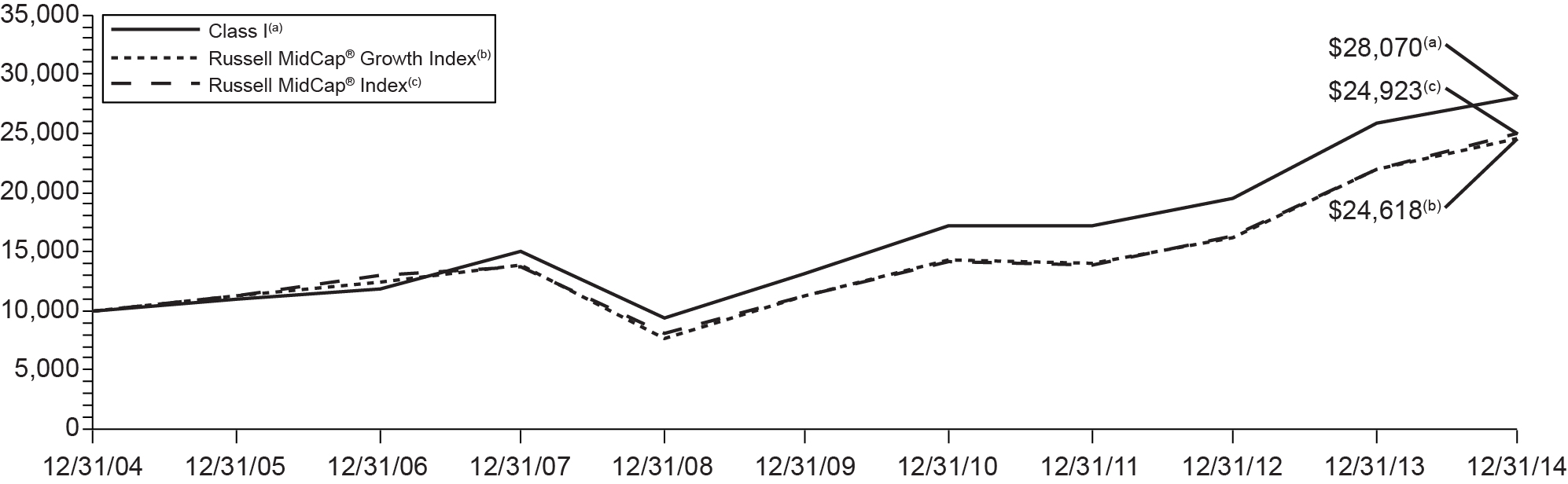

Performance: For the year ended December 31, 2014, the Portfolio’s Class I shares provided a total return of 8.85% compared to the Russell Midcap® Growth Index and the Russell Midcap® Index, which returned 11.90% and 13.22%, respectively, for the same period.

Portfolio Specifics: The Portfolio underperformed its benchmarks during the reporting period, driven primarily by stock selection. In particular, stock selection within the energy and health care sectors detracted the most from performance, while stock selection within the information technology and consumer staples sectors contributed the most to performance.

Best Buy Co., Inc. (“Best Buy”), Informatica Corp. (“Informatica”) and Cabot Oil & Gas Corp. (“Cabot Oil & Gas”) were among the most significant detractors for the reporting period. Our overweight in Best Buy was negative for performance. The stock fell after the company reported disappointing results early in the year, due to the competitive environment in consumer electronics. Stiff competition led to a highly promotional holiday season in 2013 and negatively impacted Best Buy’s revenues and margins. Our overweight in Informatica was a negative for returns. The company reported strong fourth quarter results, but concerns over the company’s competitive position weighed on its share price. The market questioned Informatica’s ability to remain relevant in the era of cloud computing, as a variety of open source software platforms have begun offering alternatives to some of Informatica’s core offerings. Our overweight in Cabot Oil & Gas detracted from performance. The stock fell on concerns of weaker than expected price realization due to an infrastructure bottleneck that limited the company’s ability to transport gas to more attractive markets.

Top Ten Holdings | |||||

| Southwest Airlines Co. | 3.0% | ||||

| Intuit, Inc. | 2.3% | ||||

| VF Corp. | 2.2% | ||||

| Chipotle Mexican Grill, Inc. | 2.0% | ||||

| Jarden Corp. | 2.0% | ||||

| Aon PLC | 1.9% | ||||

| Ametek, Inc. | 1.9% | ||||

| Monster Beverage Corp. | 1.9% | ||||

| Roper Industries, Inc. | 1.9% | ||||

| Mylan Laboratories | 1.8% | ||||

| Portfolio holdings are subject to change daily. | |||||

Southwest Airlines Co. (“Southwest Airlines”), Hillshire Brands Co. (“Hillshire Brands”) and Palo Alto Networks, Inc. (“Palo Alto Networks”) were the largest contributors to performance during the reporting period. Our overweight in the domestic airline Southwest Airlines was beneficial for performance. A strong pricing environment in North America, coupled with solid company cost control, has led to a sizable increase in consensus expectations. An overweight in packaged meat company Hillshire Brands contributed to performance. The stock rose after Pilgrim’s Pride and Tyson Foods entered into a bidding war to acquire the company. In June, Tyson Foods announced a bid to acquire all outstanding shares of Hillshire Brands for $63 per share, up from its previous bid of $50 per share and trumping Pilgrim’s Pride’s offer of $55 per share. An overweight position in Palo Alto Networks was positive for performance. The company reported strong fiscal third quarter results, driven by better than expected billings growth, deferred revenue growth and recurring subscription revenues. In addition, the paid subscriber base for WildFire, one of the company’s key products, continued to experience strong growth. Importantly, the company announced that it reached a settlement with Juniper Networks over a patent infringement case. As part of the settlement, the two companies agreed not to sue each other over patent infringement for eight years.

Current Strategy and Outlook: We believe that the U.S. economy has moved into a phase of self-sustaining, if slow, economic recovery. As we see continued modestly improving economic conditions, consensus expectations are that the U.S. Federal Reserve Board (the “Fed”) may begin to raise the federal funds rate as early as June 2015. The Fed may consider labor market conditions and inflation in its decision to move toward a normalized interest rate environment. We believe the strength of U.S. corporations remains intact, as evidenced by significant amounts of free cash flow and record high incremental margins. U.S. corporations are also actively returning capital to shareholders via dividend increases and share buybacks.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

| 6 |

Portfolio Managers’ Report | Voya MidCap Opportunities Portfolio |

| Average Annual Returns for the Periods Ended December 31, 2014 | ||||||||||||||||||||||

| 1 Year | 5 Year | 10 Year | Since Inception of Class ADV December 29, 2006 | Since Inception of Class S2 February 27, 2009 | ||||||||||||||||||

| Class ADV | 8.29% | 15.68% | — | 10.70% | — | |||||||||||||||||

| Class I | 8.85% | 16.30% | 10.87% | — | — | |||||||||||||||||

| Class S | 8.56% | 15.99% | 10.62% | — | — | |||||||||||||||||

| Class S2 | 8.39% | 15.81% | — | — | 22.96% | |||||||||||||||||

| Russell Midcap® Growth Index | 11.90% | 16.94% | 9.43% | 8.94% | 24.71% | |||||||||||||||||

| Russell Midcap® Index | 13.22% | 17.19% | 9.56% | 8.49% | 25.28% | |||||||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Voya MidCap Opportunities Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable

contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

| 7 |

| Voya SmallCap Opportunities Portfolio | Portfolio Managers’ Report |

| Sector Diversification as of December 31, 2014 (as a percentage of net assets) | |||||

| Information Technology | 23.3% | ||||

| Health Care | 21.4% | ||||

| Consumer Discretionary | 18.2% | ||||

| Industrials | 14.3% | ||||

| Financials | 10.6% | ||||

| Materials | 4.8% | ||||

| Energy | 2.9% | ||||

| Exchange-Traded Funds | 1.7% | ||||

| Consumer Staples | 1.7% | ||||

| Assets in Excess of Other Liabilities* | 1.1% | ||||

| Net Assets | 100.0% | ||||

| * Includes short-term investments. | |||||

| Portfolio holdings are subject to change daily. | |||||

Voya SmallCap Opportunities Portfolio (the “Portfolio”) seeks long-term capital appreciation. The Portfolio is managed by Steve Salopek*, James Hasso and Joseph Basset, CFA, Portfolio Managers of Voya Investment Management Co. LLC (“Voya IM”) — the Sub-Adviser.

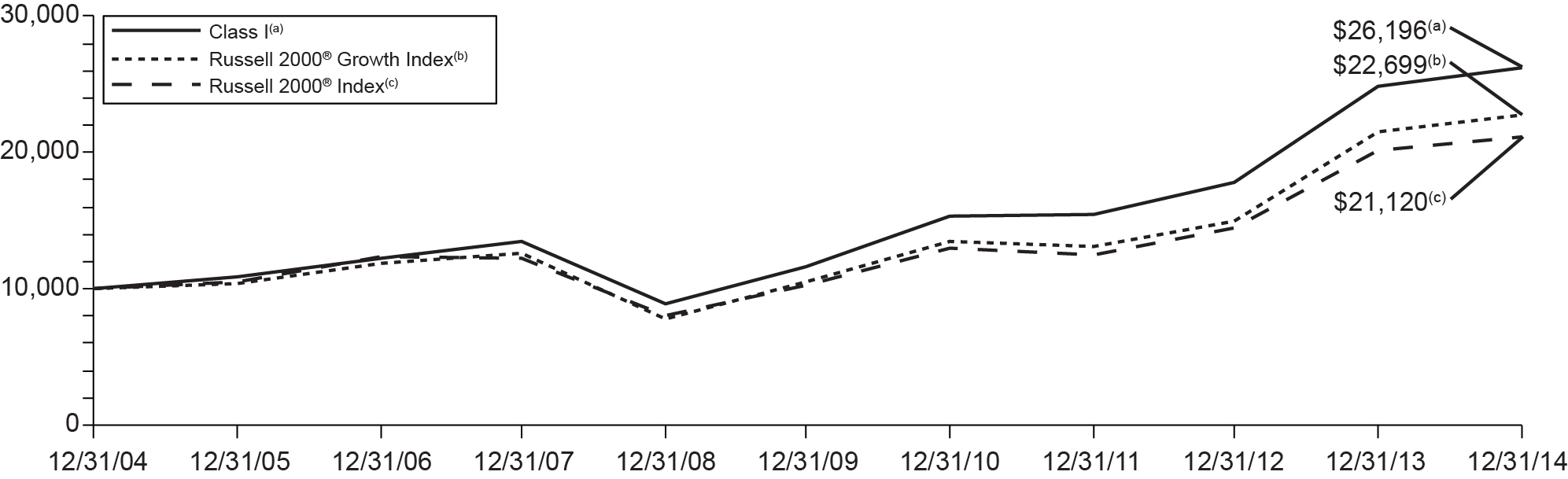

Performance: For the year ended December 31, 2014, the Portfolio’s Class I shares provided a total return of 5.62%, compared to the Russell 2000® Growth Index and the Russell 2000® Index, which returned 5.60% and 4.89%, respectively, for the same period.

Portfolio Specifics: Outperformance for the period was due to favorable stock selection. Security selection within the capital goods and software and services sectors contributed the most to relative performance for the period. By contrast, our underweight to the pharmaceuticals and biotechnology sector detracted the most from returns. Our underweight allocation during the first half of 2014 and subsequent overweight allocation during the second half of 2014 to the energy sector helped performance, but this gain was more than offset by the negative impact of security selection in that sector.

The main individual contributors to performance were Knight Transportation, Inc. (“Knight Transportation”) and InterMune, Inc. (“InterMune”).

Our overweight position in Knight Transportation, a provider of truckload transportation services, contributed to performance due to a steady improvement in overall sentiment in the truckload industry. Over the course of 2013, we had built up our position in Knight Transportation, as we thought that the stock became decoupled from what were increasingly strong truckload fundamentals. The Portfolio’s large overweight position paid off as a strong spring freight market in 2014 and tight truckload capacity resulted in higher spot rates in 2014 and, consequently, higher negotiated contractual rate increases. We believe Knight Transportation is a greater beneficiary of a tight truck market because of its decentralized business model and its policy of committing fewer trucks to contracts.

| Top Ten Holdings as of December 31, 2014* (as a percentage of net assets) | |||||

| iShares Russell 2000 Growth Index Fund | 1.7% | ||||

| Qlik Technologies, Inc. | 1.3% | ||||

| Vail Resorts, Inc. | 1.2% | ||||

| WEX, Inc. | 1.2% | ||||

| j2 Global, Inc. | 1.2% | ||||

| Ultimate Software Group, Inc. | 1.2% | ||||

| Team Health Holdings, Inc. | 1.2% | ||||

| Healthsouth Corp. | 1.1% | ||||

| PRA Group, Inc. | 1.1% | ||||

| Cardtronics, Inc. | 1.1% | ||||

| * | Excludes short-term investments. | ||

| Portfolio holdings are subject to change daily. |

Shares of InterMune, a biotechnology company focused on the research, development and commercializing of innovative therapies in pulmonology and orphan fibrotic diseases, outperformed for the period. During the first quarter, the company reported positive Phase 3 data involving a compound to treat a lung disease called idiopathic pulmonary fibrosis. Investors believed InterMune’s strong trial results would set the company up for Food and Drug Administration approval later this year. Furthermore, in August 2014, the company announced a definitive merger agreement under which Roche will acquire InterMune for $74 per share in an all-cash transaction.

Key detractors from performance were Energy XXI Ltd. and Bill Barrett Corp.

Within the energy sector, our overweight positions in Energy XXI Ltd. and Bill Barrett Corp. detracted the most due to the overall weakness in the sector and declining oil prices.

Current Strategy and Outlook: We continue to monitor changes occurring globally, actions at central banks and overall economic data. Our portfolio positioning has not changed significantly. We seek to remain nimble and continue to focus on quality companies, such as those that, in our opinion, have strong managements, solid balance sheets and good cash flow generation capabilities. Going forward, we believe the portfolio is well positioned, as we think that investors will continue to focus on companies’ fundamentals due to ongoing economic uncertainty.

| * | Steve Salopek has decided to retire from Voya Investment Management Co. LLC effective June 30, 2015. |

| Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. |

| 8 |

Portfolio Managers’ Report | Voya SmallCap Opportunities Portfolio |

| Average Annual Returns for the Periods Ended December 31, 2014 | ||||||||||||||||||||||

| 1 Year | 5 Year | 10 Year | Since Inception of Class ADV November 20, 2008 | Since Inception of Class S2 February 27, 2009 | ||||||||||||||||||

| Class ADV | 5.07% | 17.10% | — | 23.25% | — | |||||||||||||||||

| Class I | 5.62% | 17.69% | 10.11% | — | — | |||||||||||||||||

| Class S | 5.35% | 17.40% | 9.86% | — | — | |||||||||||||||||

| Class S2 | 5.19% | 17.22% | — | — | 24.06% | |||||||||||||||||

| Russell 2000® Growth Index | 5.60% | 16.80% | 8.54% | 24.19% | 24.13% | |||||||||||||||||

| Russell 2000® Index | 4.89% | 15.55% | 7.77% | 22.20% | 23.06% | |||||||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Voya SmallCap Opportunities Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract or life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract and/or a variable universal life policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

| 9 |

SHAREHOLDER EXPENSE EXAMPLES (Unaudited)

As a shareholder of a Portfolio, you incur two types of costs: (1) transaction costs, including redemption fees and exchange fees; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Portfolio expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2014 to December 31, 2014. The Portfolios’ expenses are shown without the imposition of any charges which are, or may be, imposed under your variable annuity contract, variable life insurance policy, qualified pension, or retirement plan. Expenses would have been higher if such charges were included.

Actual Expenses

The left section of the table shown below, “Actual Portfolio Return,” provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The right section of the table shown below, “Hypothetical (5% return before expenses),” provides information about hypothetical account values and hypothetical expenses based on a Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not a Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Portfolio and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different mutual funds. In addition, if these transactional costs were included, your costs would have been higher.

| Actual Portfolio Return | Hypothetical (5% return before expenses) | |||||||||||||||||||||||||||||||

| Beginning Account Value July 1, 2014 | Ending Account Value December 31, 2014 | Annualized Expense Ratio | Expenses Paid During the Period Ended December 31, 2014* | Beginning Account Value July 1, 2014 | Ending Account Value December 31, 2014 | Annualized Expense Ratio | Expenses Paid During the Period Ended December 31, 2014* | |||||||||||||||||||||||||

| Voya International Value Portfolio | ||||||||||||||||||||||||||||||||

| Class ADV | $ | 1,000.00 | $ | 897.90 | 1.45 | % | $ | 6.94 | $ | 1,000.00 | $ | 1,017.90 | 1.45 | % | $ | 7.37 | ||||||||||||||||

| Class I | 1,000.00 | 900.20 | 0.95 | 4.55 | 1,000.00 | 1,020.42 | 0.95 | 4.84 | ||||||||||||||||||||||||

| Class S | 1,000.00 | 899.20 | 1.15 | 5.51 | 1,000.00 | 1,019.41 | 1.15 | 5.85 | ||||||||||||||||||||||||

| Voya MidCap Opportunities Portfolio | ||||||||||||||||||||||||||||||||

| Class ADV | $ | 1,000.00 | $ | 1,062.90 | 1.30 | % | $ | 6.76 | $ | 1,000.00 | $ | 1,018.65 | 1.30 | % | $ | 6.61 | ||||||||||||||||

| Class I | 1,000.00 | 1,065.20 | 0.80 | 4.16 | 1,000.00 | 1,021.17 | 0.80 | 4.08 | ||||||||||||||||||||||||

| Class S | 1,000.00 | 1,063.70 | 1.05 | 5.46 | 1,000.00 | 1,019.91 | 1.05 | 5.35 | ||||||||||||||||||||||||

| Class S2 | 1,000.00 | 1,063.00 | 1.20 | 6.24 | 1,000.00 | 1,019.16 | 1.20 | 6.11 | ||||||||||||||||||||||||

| Voya SmallCap Opportunities Portfolio | ||||||||||||||||||||||||||||||||

| Class ADV | $ | 1,000.00 | $ | 1,028.10 | 1.38 | % | $ | 7.05 | $ | 1,000.00 | $ | 1,018.25 | 1.38 | % | $ | 7.02 | ||||||||||||||||

| Class I | 1,000.00 | 1,030.70 | 0.88 | 4.50 | 1,000.00 | 1,020.77 | 0.88 | 4.48 | ||||||||||||||||||||||||

| Class S | 1,000.00 | 1,029.40 | 1.13 | 5.78 | 1,000.00 | 1,019.51 | 1.13 | 5.75 | ||||||||||||||||||||||||

| Class S2 | 1,000.00 | 1,028.60 | 1.28 | 6.54 | 1,000.00 | 1,018.75 | 1.28 | 6.51 | ||||||||||||||||||||||||

| * | Expenses are equal to each Portfolio’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 184/365 to reflect the most recent fiscal half-year. |

| 10 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Shareholders and Board of Trustees

Voya Variable Products Trust

We have audited the accompanying statements of assets and liabilities, including the summary portfolios of investments, of Voya International Value Portfolio, Voya MidCap Opportunities Portfolio, and Voya SmallCap Opportunities Portfolio, each a series of Voya Variable Products Trust, as of December 31, 2014, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2014, by correspondence with custodian, transfer agent, and brokers, or by other appropriate auditing procedures when replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the aforementioned funds of Voya Variable Products Trust as of December 31, 2014, the results of their operations for the year then ended, the changes in their net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

February 16, 2015

| 11 |

Statements of Assets and Liabilities as of December 31, 2014

| Voya International Value Portfolio | Voya MidCap Opportunities Portfolio | Voya SmallCap Opportunities Portfolio | ||||||||||

| ASSETS: | ||||||||||||

| Investments in securities at fair value+* | $ | 109,265,944 | $ | 1,486,968,309 | $ | 323,140,539 | ||||||

| Short-term investments at fair value** | 1,552,927 | 23,057,672 | 10,651,655 | |||||||||

| Total investments at fair value | $ | 110,818,871 | $ | 1,510,025,981 | $ | 333,792,194 | ||||||

| Cash | 437 | 889 | 329 | |||||||||

| Foreign currencies at value*** | 65,702 | — | — | |||||||||

| Receivables: | ||||||||||||

| Investment securities sold | 1,123,523 | — | 1,201,481 | |||||||||

| Fund shares sold | 229,064 | 219,604 | 128,948 | |||||||||

| Dividends | 41,315 | 807,179 | 273,804 | |||||||||

| Foreign tax reclaims | 202,468 | 26,288 | — | |||||||||

| Unrealized appreciation on forward foreign currency contracts | 1,359 | — | — | |||||||||

| Prepaid expenses | 939 | 11,384 | 2,446 | |||||||||

| Reimbursement due from manager | 56,161 | — | — | |||||||||

| Other assets | 5,042 | 18,048 | 4,195 | |||||||||

| Total assets | 112,544,881 | 1,511,109,373 | 335,403,397 | |||||||||

| LIABILITIES: | ||||||||||||

| Payable for investment securities purchased | 308 | — | 1,274,916 | |||||||||

| Payable for fund shares redeemed | 40,789 | 5,372,378 | 537,814 | |||||||||

| Payable upon receipt of securities loaned | 1,447,927 | 7,637,672 | 6,707,524 | |||||||||

| Payable for investment management fees | 77,739 | 845,265 | 203,571 | |||||||||

| Payable for administrative fees | 9,717 | 126,721 | 27,564 | |||||||||

| Payable for distribution and shareholder service fees | 1,698 | 194,581 | 38,571 | |||||||||

| Payable for directors fees | 633 | 7,571 | 1,609 | |||||||||

| Payable to directors under the deferred compensation plan (Note 6) | 5,042 | 18,048 | 4,195 | |||||||||

| Payable for proxy and solicitation costs (Note 6) | 82,159 | — | — | |||||||||

| Other accrued expenses and liabilities | 28,240 | 187,321 | 48,896 | |||||||||

| Total liabilities | 1,694,252 | 14,389,557 | 8,844,660 | |||||||||

| NET ASSETS | $ | 110,850,629 | $ | 1,496,719,816 | $ | 326,558,737 | ||||||

| NET ASSETS WERE COMPRISED OF: | ||||||||||||

| Paid-in capital | $ | 282,794,801 | $ | 1,080,691,569 | $ | 230,244,711 | ||||||

| Undistributed (distributions in excess of) net investment income | 220,428 | (18,415 | ) | (4,478 | ) | |||||||

| Accumulated net realized gain (loss) | (174,242,776 | ) | 186,666,648 | 35,175,830 | ||||||||

| Net unrealized appreciation | 2,078,176 | 229,380,014 | 61,142,674 | |||||||||

| NET ASSETS | $ | 110,850,629 | $ | 1,496,719,816 | $ | 326,558,737 | ||||||

| | ||||||||||||

| + Including securities loaned at value | $ | 1,388,982 | $ | 7,475,595 | $ | 6,553,854 | ||||||

| * Cost of investments in securities | $ | 107,169,211 | $ | 1,257,586,468 | $ | 261,997,865 | ||||||

| ** Cost of short-term investments | $ | 1,552,927 | $ | 23,057,672 | $ | 10,651,655 | ||||||

| *** Cost of foreign currencies | $ | 66,198 | $ | — | $ | — | ||||||

See Accompanying Notes to Financial Statements

| 12 |

Statements of Assets and Liabilities as of December 31, 2014 (continued)

| Voya MidCap | Voya SmallCap | |||||||||||

| Voya International | Opportunities | Opportunities | ||||||||||

| Value Portfolio | Portfolio | Portfolio | ||||||||||

| Class ADV | ||||||||||||

| Net assets | $ | 1,264,337 | $ | 143,532,447 | $ | 48,982,093 | ||||||

| Shares authorized | unlimited | unlimited | unlimited | |||||||||

| Par value | $ | 0.010 | $ | 0.010 | $ | 0.010 | ||||||

| Shares outstanding | 143,691 | 9,899,597 | 1,865,186 | |||||||||

| Net asset value and redemption price per share | $ | 8.80 | $ | 14.50 | $ | 26.26 | ||||||

| Class I | ||||||||||||

| Net assets | $ | 102,751,524 | $ | 733,894,218 | $ | 195,608,407 | ||||||

| Shares authorized | unlimited | unlimited | unlimited | |||||||||

| Par value | $ | 0.010 | $ | 0.010 | $ | 0.010 | ||||||

| Shares outstanding | 11,564,202 | 48,376,466 | 6,999,439 | |||||||||

| Net asset value and redemption price per share | $ | 8.89 | $ | 15.17 | $ | 27.95 | ||||||

| Class S | ||||||||||||

| Net assets | $ | 6,834,768 | $ | 605,241,236 | $ | 77,319,179 | ||||||

| Shares authorized | unlimited | unlimited | unlimited | |||||||||

| Par value | $ | 0.010 | $ | 0.010 | $ | 0.010 | ||||||

| Shares outstanding | 753,581 | 41,281,863 | 2,885,531 | |||||||||

| Net asset value and redemption price per share | $ | 9.07 | $ | 14.66 | $ | 26.80 | ||||||

| Class S2 | ||||||||||||

| Net assets | n/a | $ | 14,051,915 | $ | 4,649,058 | |||||||

| Shares authorized | n/a | unlimited | unlimited | |||||||||

| Par value | n/a | $ | 0.010 | $ | 0.010 | |||||||

| Shares outstanding | n/a | 960,513 | 175,725 | |||||||||

| Net asset value and redemption price per share | n/a | $ | 14.63 | $ | 26.46 | |||||||

See Accompanying Notes to Financial Statements

| 13 |

STATEMENTS OF OPERATIONS For the Year ended December 31, 2014

| Voya International Value Portfolio | Voya MidCap Opportunities Portfolio | Voya SmallCap Opportunities Portfolio | ||||||||||

| INVESTMENT INCOME: | ||||||||||||

| Dividends, net of foreign taxes withheld* | $ | 5,172,700 | $ | 19,536,253 | $ | 2,552,913 | ||||||

| Securities lending income, net | 111,257 | 41,802 | 176,151 | |||||||||

| Total investment income | 5,283,957 | 19,578,055 | 2,729,064 | |||||||||

| EXPENSES: | ||||||||||||

| Investment management fees | 1,012,219 | 10,084,888 | 2,378,252 | |||||||||

| Distribution and shareholder service fees: | ||||||||||||

| Class ADV | 6,739 | 699,094 | 222,094 | |||||||||

| Class S | 18,607 | 1,579,804 | 204,596 | |||||||||

| Class S2 | — | 71,171 | 22,072 | |||||||||

| Transfer agent fees | 260 | 4,246 | 485 | |||||||||

| Administrative service fees | 126,526 | 1,514,133 | 321,890 | |||||||||

| Shareholder reporting expense | 17,647 | 187,955 | 33,850 | |||||||||

| Registration fees | — | 3,600 | — | |||||||||

| Professional fees | 17,007 | 135,044 | 33,465 | |||||||||

| Custody and accounting expense | 62,689 | 161,997 | 43,247 | |||||||||

| Directors fees | 3,796 | 45,424 | 9,657 | |||||||||

| Proxy and solicitation costs (Note 6) | 92,000 | — | — | |||||||||

| Miscellaneous expense | 6,962 | 42,232 | 12,021 | |||||||||

| Interest expense | 734 | 112 | — | |||||||||

| Total expenses | 1,365,186 | 14,529,700 | 3,281,629 | |||||||||

| Net waived and reimbursed fees | (140,276 | ) | (14,234 | ) | (4,415 | ) | ||||||

| Net expenses | 1,224,910 | 14,515,466 | 3,277,214 | |||||||||

| Net investment income (loss) | 4,059,047 | 5,062,589 | (548,150 | ) | ||||||||

| REALIZED AND UNREALIZED GAIN (LOSS): | ||||||||||||

| Net realized gain (loss) on: | ||||||||||||

| Investments | 9,881,098 | 192,717,522 | 37,876,510 | |||||||||

| Foreign currency related transactions | (62,118 | ) | 3,012 | — | ||||||||

| Net realized gain | 9,818,980 | 192,720,534 | 37,876,510 | |||||||||

| Net change in unrealized appreciation (depreciation) on: | ||||||||||||

| Investments | (19,635,698 | ) | (78,266,986 | ) | (20,492,687 | ) | ||||||

| Foreign currency related transactions | (26,501 | ) | (3,010 | ) | — | |||||||

| Net change in unrealized appreciation (depreciation) | (19,662,199 | ) | (78,269,996 | ) | (20,492,687 | ) | ||||||

| Net realized and unrealized gain (loss) | (9,843,219 | ) | 114,450,538 | 17,383,823 | ||||||||

| Increase (decrease) in net assets resulting from operations | $ | (5,784,172 | ) | $ | 119,513,127 | $ | 16,835,673 | |||||

| | ||||||||||||

| * Foreign taxes withheld | $ | 392,942 | $ | 25,290 | $ | 524 | ||||||

See Accompanying Notes to Financial Statements

| 14 |

STATEMENTS OF CHANGES IN NET ASSETS

| Voya International Value Portfolio | Voya MidCap Opportunities Portfolio | |||||||||||||||

| Year Ended December 31, 2014 | Year Ended December 31, 2013 | Year Ended December 31, 2014 | Year Ended December 31, 2013 | |||||||||||||

| FROM OPERATIONS: | ||||||||||||||||

| Net investment income | $ | 4,059,047 | $ | 2,860,612 | $ | 5,062,589 | $ | 162,017 | ||||||||

| Net realized gain | 9,818,980 | 11,593,490 | 192,720,534 | 224,720,220 | ||||||||||||

| Net change in unrealized appreciation (depreciation) | (19,662,199 | ) | 10,982,566 | (78,269,996 | ) | 172,203,045 | ||||||||||

| Increase (decrease) in net assets resulting from operations | (5,784,172 | ) | 25,436,668 | 119,513,127 | 397,085,282 | |||||||||||

| FROM DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||||||

| Net investment income: | ||||||||||||||||

| Class ADV | (38,981 | ) | (24,731 | ) | (372,599 | ) | — | |||||||||

| Class I | (3,829,633 | ) | (3,244,667 | ) | (2,906,345 | ) | (240,392 | ) | ||||||||

| Class S | (224,859 | ) | (181,650 | ) | (2,115,878 | ) | — | |||||||||

| Class S2(1) | — | (36 | ) | (41,187 | ) | — | ||||||||||

| Net realized gains: | ||||||||||||||||

| Class ADV | — | — | (21,781,737 | ) | (3,104,778 | ) | ||||||||||

| Class I | — | — | (107,183,194 | ) | (18,427,132 | ) | ||||||||||

| Class S | — | — | (94,686,748 | ) | (16,070,181 | ) | ||||||||||

| Class S2 | — | — | (2,148,091 | ) | (268,315 | ) | ||||||||||

| Total distributions | (4,093,473 | ) | (3,451,084 | ) | (231,235,779 | ) | (38,110,798 | ) | ||||||||

| FROM CAPITAL SHARE TRANSACTIONS: | ||||||||||||||||

| Net proceeds from sale of shares | 3,613,888 | 3,398,016 | 135,276,944 | 151,192,057 | ||||||||||||

| Proceeds from shares issued in merger (Note 11) | — | — | — | 303,156,146 | ||||||||||||

| Reinvestment of distributions | 4,093,473 | 3,451,047 | 231,235,779 | 38,110,798 | ||||||||||||

| 7,707,361 | 6,849,063 | 366,512,723 | 492,459,001 | |||||||||||||

| Cost of shares redeemed | (21,637,594 | ) | (27,654,639 | ) | (401,000,843 | ) | (346,945,568 | ) | ||||||||

| Net increase (decrease) in net assets resulting from capital share transactions | (13,930,233 | ) | (20,805,576 | ) | (34,488,120 | ) | 145,513,433 | |||||||||

| Net increase (decrease) in net assets | (23,807,878 | ) | 1,180,008 | (146,210,772 | ) | 504,487,917 | ||||||||||

| NET ASSETS: | ||||||||||||||||

| Beginning of year or period | 134,658,507 | 133,478,499 | 1,642,930,588 | 1,138,442,671 | ||||||||||||

| End of year or period | $ | 110,850,629 | $ | 134,658,507 | $ | 1,496,719,816 | $ | 1,642,930,588 | ||||||||

| Undistributed (distributions in excess of) net investment income at end of year or period | $ | 220,428 | $ | 95,861 | $ | (18,415 | ) | $ | (15,669 | ) | ||||||

| (1) | Class S2 of Voya International Value Portfolio liquidated on April 30, 2013. |

See Accompanying Notes to Financial Statements

| 15 |

STATEMENTS OF CHANGES IN NET ASSETS

| Voya SmallCap Opportunities Portfolio | ||||||||

| Year Ended December 31, 2014 | Year Ended December 31, 2013 | |||||||

| FROM OPERATIONS: | ||||||||

| Net investment (loss) | $ | (548,150 | ) | $ | (802,356 | ) | ||

| Net realized gain | 37,876,510 | 29,411,052 | ||||||

| Net change in unrealized appreciation (depreciation) | (20,492,687 | ) | 61,229,826 | |||||

| Increase in net assets resulting from operations | 16,835,673 | 89,838,522 | ||||||

| FROM DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||

| Net realized gains: | ||||||||

| Class ADV | (4,289,810 | ) | (1,712,645 | ) | ||||

| Class I | (16,435,008 | ) | (9,938,817 | ) | ||||

| Class S | (7,206,064 | ) | (4,998,362 | ) | ||||

| Class S2 | (404,768 | ) | (225,946 | ) | ||||

| Total distributions | (28,335,650 | ) | (16,875,770 | ) | ||||

| FROM CAPITAL SHARE TRANSACTIONS: | ||||||||

| Net proceeds from sale of shares | 34,764,289 | 60,766,106 | ||||||

| Reinvestment of distributions | 28,335,650 | 16,875,770 | ||||||

| 63,099,939 | 77,641,876 | |||||||

| Cost of shares redeemed | (57,691,615 | ) | (40,377,023 | ) | ||||

| Net increase in net assets resulting from capital share transactions | 5,408,324 | 37,264,853 | ||||||

| Net increase (decrease) in net assets | (6,091,653 | ) | 110,227,605 | |||||

| NET ASSETS: | ||||||||

| Beginning of year or period | 332,650,390 | 222,422,785 | ||||||

| End of year or period | $ | 326,558,737 | $ | 332,650,390 | ||||

| Distributions in excess of net investment income at end of year or period | $ | (4,478 | ) | $ | (3,889 | ) | ||

See Accompanying Notes to Financial Statements

| 16 |

Selected data for a share of beneficial interest outstanding throughout each year or period.

| Income (loss) from investment operations | Less Distributions | Ratios to average net assets | Supplemental Data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net asset value, beginning of year or period | Net investment income (loss) | Net realized and unrealized gain (loss) | Total from investment operations | From net investment income | From net realized gains | From return of capital | Total distributions | Payment by affiliate | Net asset value, end of year or period | Total Return(1) | Expenses before reductions/ additions(2)(3)(4) | Expenses net of fee waivers and/or recoupments if any | Expense net of all reductions/ additions(2)(3)(4) | Net investment income (loss)(2)(3) | Net assets, end of year or period | Portfolio turnover rate | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Year or | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| period ended | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | (%) | (%) | (%) | (%) | (%) | ($000’s) | (%) | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Voya International Value Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Class ADV | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 9.57 | 0.25 | (0.75 | ) | (0.50 | ) | 0.27 | — | — | 0.27 | — | 8.80 | (5.44 | ) | 1.56 | 1.45 | 1.45 | 2.66 | 1,264 | 55 | ||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 8.12 | 0.14 | 1.50 | 1.64 | 0.19 | — | — | 0.19 | — | 9.57 | 20.54 | 1.46 | 1.50 | 1.50 | 1.61 | 1,315 | 62 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 6.99 | 0.15 | 1.14 | 1.29 | 0.16 | — | — | 0.16 | — | 8.12 | 18.64 | 1.46 | 1.50 | 1.50 | 1.99 | 1,123 | 56 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 8.44 | (0.01 | )* | (1.26 | ) | (1.27 | ) | 0.17 | — | 0.01 | 0.18 | — | 6.99 | (15.40 | ) | 1.57 | 1.52 | 1.52 | (0.09 | ) | 1,145 | 69 | ||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 8.41 | 0.11 | 0.05 | 0.16 | 0.13 | — | — | 0.13 | — | 8.44 | 2.02 | 1.56 | 1.50 | † | 1.50 | † | 1.28 | † | 31 | 155 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 9.65 | 0.31 | (0.76 | ) | (0.45 | ) | 0.31 | — | — | 0.31 | — | 8.89 | (4.94 | ) | 1.06 | 0.95 | 0.95 | 3.23 | 102,752 | 55 | ||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 8.18 | 0.19 | 1.51 | 1.70 | 0.23 | — | — | 0.23 | — | 9.65 | 21.21 | 0.96 | 1.00 | 1.00 | 2.18 | 125,423 | 62 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 7.04 | 0.19 | 1.14 | 1.33 | 0.19 | — | — | 0.19 | — | 8.18 | 19.23 | 0.96 | 1.00 | 1.00 | 2.52 | 124,728 | 56 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 8.49 | 0.21 | (1.45 | ) | (1.24 | ) | 0.20 | — | 0.01 | 0.21 | — | 7.04 | (14.96 | ) | 1.07 | 1.02 | 1.02 | 2.56 | 135,682 | 69 | ||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 8.46 | 0.16• | 0.04 | 0.20 | 0.17 | — | — | 0.17 | — | 8.49 | 2.50 | 1.06 | 1.00 | † | 1.00 | † | 1.96 | † | 230,836 | 155 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 9.85 | 0.30 | (0.79 | ) | (0.49 | ) | 0.29 | — | — | 0.29 | — | 9.07 | (5.18 | ) | 1.31 | 1.15 | 1.15 | 3.02 | 6,835 | 55 | ||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 8.34 | 0.18 | 1.54 | 1.72 | 0.21 | — | — | 0.21 | — | 9.85 | 21.05 | 1.21 | 1.20 | 1.20 | 1.95 | 7,920 | 62 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 7.18 | 0.18 | 1.16 | 1.34 | 0.18 | — | — | 0.18 | — | 8.34 | 18.90 | 1.21 | 1.20 | 1.20 | 2.33 | 7,623 | 56 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 8.64 | 0.19 | (1.46 | ) | (1.27 | ) | 0.18 | — | 0.01 | 0.19 | — | 7.18 | (14.99 | ) | 1.32 | 1.22 | 1.22 | 2.27 | 8,156 | 69 | ||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 8.60 | 0.13 | 0.06 | 0.19 | 0.15 | — | — | 0.15 | — | 8.64 | 2.36 | 1.31 | 1.20 | † | 1.20 | † | 1.61 | † | 11,068 | 155 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Voya MidCap Opportunities Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Class ADV | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 16.02 | (0.00 | )*• | 1.11 | 1.11 | 0.04 | 2.59 | — | 2.63 | — | 14.50 | 8.29 | 1.30 | 1.30 | 1.30 | (0.03 | ) | 143,532 | 98 | |||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 12.51 | (0.05 | ) | 3.92 | 3.87 | — | 0.36 | — | 0.36 | — | 16.02 | 31.34 | 1.30 | 1.30 | 1.30 | (0.34 | ) | 143,300 | 81 | |||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 11.34 | 0.01 | 1.52 | 1.53 | 0.04 | 0.32 | — | 0.36 | — | 12.51 | 13.61 | 1.34 | 1.34 | 1.34 | 0.09 | 81,463 | 89 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 11.46 | (0.02 | ) | (0.10 | ) | (0.12 | ) | — | — | — | — | — | 11.34 | (1.05 | ) | 1.34 | 1.34 | 1.34 | (0.23 | ) | 40,497 | 90 | ||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 8.88 | 0.08• | 2.54 | 2.62 | 0.04 | — | — | 0.04 | — | 11.46 | 29.57 | 1.36 | 1.29 | † | 1.29 | † | 0.75 | † | 15,119 | 96 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 16.58 | 0.08 | 1.16 | 1.24 | 0.06 | 2.59 | — | 2.65 | — | 15.17 | 8.85 | 0.80 | 0.80 | 0.80 | 0.49 | 733,894 | 98 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 12.88 | 0.02 | 4.05 | 4.07 | 0.01 | 0.36 | — | 0.37 | — | 16.58 | 31.97 | 0.80 | 0.80 | 0.80 | 0.16 | 796,010 | 81 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 11.63 | 0.07 | 1.57 | 1.64 | 0.07 | 0.32 | — | 0.39 | — | 12.88 | 14.20 | 0.84 | 0.84 | 0.84 | 0.56 | 614,151 | 89 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 11.69 | 0.03 | (0.09 | ) | (0.06 | ) | — | — | — | — | — | 11.63 | (0.51 | ) | 0.84 | 0.84 | 0.84 | 0.24 | 435,027 | 90 | ||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 9.03 | 0.06 | 2.67 | 2.73 | 0.07 | — | — | 0.07 | — | 11.69 | 30.36 | 0.86 | 0.79 | † | 0.79 | † | 0.62 | † | 350,626 | 96 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 16.14 | 0.04 | 1.12 | 1.16 | 0.05 | 2.59 | — | 2.64 | — | 14.66 | 8.56 | 1.05 | 1.05 | 1.05 | 0.24 | 605,241 | 98 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 12.57 | (0.01 | ) | 3.94 | 3.93 | — | 0.36 | — | 0.36 | — | 16.14 | 31.68 | 1.05 | 1.05 | 1.05 | (0.09 | ) | 689,091 | 81 | |||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 11.37 | 0.04 | 1.53 | 1.57 | 0.05 | 0.32 | — | 0.37 | — | 12.57 | 13.92 | 1.09 | 1.09 | 1.09 | 0.29 | 435,586 | 89 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 11.46 | (0.00 | )* | (0.09 | ) | (0.09 | ) | — | — | — | — | — | 11.37 | (0.79 | ) | 1.09 | 1.09 | 1.09 | (0.04 | ) | 414,381 | 90 | ||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 8.86 | 0.03• | 2.62 | 2.65 | 0.05 | — | — | 0.05 | — | 11.46 | 29.96 | 1.11 | 1.04 | † | 1.04 | † | 0.35 | † | 450,115 | 96 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Class S2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 16.13 | 0.01 | 1.13 | 1.14 | 0.05 | 2.59 | — | 2.64 | — | 14.63 | 8.39 | 1.30 | 1.20 | 1.20 | 0.06 | 14,052 | 98 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 12.58 | (0.03 | ) | 3.94 | 3.91 | — | 0.36 | — | 0.36 | — | 16.13 | 31.49 | 1.30 | 1.20 | 1.20 | (0.24 | ) | 14,530 | 81 | |||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 11.38 | 0.02 | 1.54 | 1.56 | 0.04 | 0.32 | — | 0.36 | — | 12.58 | 13.79 | 1.34 | 1.24 | 1.24 | 0.18 | 7,243 | 89 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 11.49 | (0.01 | ) | (0.10 | ) | (0.11 | ) | — | — | — | — | — | 11.38 | (0.96 | ) | 1.34 | 1.24 | 1.24 | (0.13 | ) | 3,314 | 90 | ||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 8.89 | 0.08• | 2.56 | 2.64 | 0.04 | — | — | 0.04 | — | 11.49 | 29.67 | 1.36 | 1.19 | † | 1.19 | † | 0.71 | † | 900 | 96 | ||||||||||||||||||||||||||||||||||||||||||||||||

See Accompanying Notes to Financial Statements

| 17 |

Financial Highlights (continued)

| Income (loss) from investment operations | Less Distributions | Ratios to average net assets | Supplemental Data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net asset value, beginning of year or period | Net investment income (loss) | Net realized and unrealized gain (loss) | Total from investment operations | From net investment income | From net realized gains | From return of capital | Total distributions | Payment by affiliate | Net asset value, end of year or period | Total Return(1) | Expenses before reductions/ additions(2)(3)(4) | Expenses net of fee waivers and/or recoupments if any(2)(3)(4) | Expense net of all reductions/ additions(2)(3)(4) | Net investment income (loss)(2)(3) | Net assets, end of year or period | Portfolio turnover rate | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Year or period ended | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | (%) | (%) | (%) | (%) | (%) | ($000’s) | (%) | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Voya SmallCap Opportunities Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Class ADV | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 27.68 | (0.14 | )• | 1.29 | 1.15 | — | 2.57 | — | 2.57 | — | 26.26 | 5.07 | 1.38 | 1.38 | 1.38 | (0.53) | 48,982 | 33 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 21.37 | (0.16 | )• | 8.07 | 7.91 | — | 1.60 | — | 1.60 | — | 27.68 | 38.39 | 1.38 | 1.38 | 1.38 | (0.63) | 42,105 | 40 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 20.73 | (0.07 | )• | 3.00 | 2.93 | — | 2.29 | — | 2.29 | — | 21.37 | 14.63 | 1.41 | 1.41 | 1.41 | (0.34) | 14,236 | 57 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 20.67 | (0.14 | )• | 0.20 | 0.06 | — | — | — | — | — | 20.73 | 0.29 | 1.40 | 1.40 | 1.40 | (0.67) | 4,819 | 72 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 15.69 | (0.10 | )• | 5.08 | 4.98 | — | — | — | — | — | 20.67 | 31.74 | 1.40 | 1.40 | † | 1.40 | † | (0.57) | † | 2,120 | 97 | |||||||||||||||||||||||||||||||||||||||||||||||

| Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 29.14 | (0.01 | ) | 1.39 | 1.38 | — | 2.57 | — | 2.57 | — | 27.95 | 5.62 | 0.88 | 0.88 | 0.88 | (0.03) | 195,608 | 33 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 22.32 | (0.04 | ) | 8.46 | 8.42 | — | 1.60 | — | 1.60 | — | 29.14 | 39.06 | 0.88 | 0.88 | 0.88 | (0.16) | 196,665 | 40 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 21.46 | 0.01 | 3.14 | 3.15 | — | 2.29 | — | 2.29 | — | 22.32 | 15.18 | 0.91 | 0.91 | 0.91 | 0.03 | 136,300 | 57 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 21.28 | (0.04 | ) | 0.22 | 0.18 | — | — | — | — | — | 21.46 | 0.85 | 0.90 | 0.90 | 0.90 | (0.17) | 117,965 | 72 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 16.08 | (0.02 | ) | 5.22 | 5.20 | — | — | — | — | — | 21.28 | 32.34 | 0.90 | 0.90 | † | 0.90 | † | (0.14) | † | 113,938 | 97 | |||||||||||||||||||||||||||||||||||||||||||||||

| Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 28.12 | (0.08 | ) | 1.33 | 1.25 | — | 2.57 | — | 2.57 | — | 26.80 | 5.35 | 1.13 | 1.13 | 1.13 | (0.29) | 77,319 | 33 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 21.64 | (0.11 | )• | 8.19 | 8.08 | — | 1.60 | — | 1.60 | — | 28.12 | 38.71 | 1.13 | 1.13 | 1.13 | (0.42) | 89,527 | 40 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 20.91 | (0.05 | ) | 3.07 | 3.02 | — | 2.29 | — | 2.29 | — | 21.64 | 14.95 | 1.16 | 1.16 | 1.16 | (0.22) | 68,682 | 57 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 20.80 | (0.10 | ) | 0.21 | 0.11 | — | — | — | — | — | 20.91 | 0.53 | 1.15 | 1.15 | 1.15 | (0.47) | 63,588 | 72 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 15.75 | (0.07 | ) | 5.12 | 5.05 | — | — | — | — | — | 20.80 | 32.06 | 1.15 | 1.15 | † | 1.15 | † | (0.39) | † | 71,992 | 97 | |||||||||||||||||||||||||||||||||||||||||||||||

| Class S2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-14 | 27.84 | (0.11 | ) | 1.30 | 1.19 | — | 2.57 | — | 2.57 | — | 26.46 | 5.19 | 1.38 | 1.28 | 1.28 | (0.43) | 4,649 | 33 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-13 | 21.47 | (0.13 | ) | 8.10 | 7.97 | — | 1.60 | — | 1.60 | — | 27.84 | 38.50 | 1.38 | 1.28 | 1.28 | (0.57) | 4,354 | 40 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-12 | 20.79 | (0.06 | )• | 3.03 | 2.97 | — | 2.29 | — | 2.29 | — | 21.47 | 14.79 | 1.41 | 1.31 | 1.31 | (0.27) | 3,205 | 57 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-11 | 20.71 | (0.11 | )• | 0.19 | 0.08 | — | — | — | — | — | 20.79 | 0.39 | 1.40 | 1.30 | 1.30 | (0.56) | 1,472 | 72 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12-31-10 | 15.71 | (0.09 | )• | 5.09 | 5.00 | — | — | — | — | — | 20.71 | 31.83 | 1.40 | 1.30 | † | 1.30 | † | (0.50) | † | 344 | 97 | |||||||||||||||||||||||||||||||||||||||||||||||

| (1) | Total return is calculated assuming reinvestment of all dividends, capital gain distributions and return of capital distributions, if any, at net asset value and does not reflect the effect of insurance contract charges. Total return for periods less than one year is not annualized. |

| (2) | Annualized for periods less than one year. |

| (3) | Ratios reflect operating expenses of a Portfolio. Expenses before reductions/additions do not reflect amounts reimbursed by an Investment Adviser and/or Distributor or reductions from brokerage service arrangements or other expense offset arrangements and do not represent the amount paid by a Portfolio during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by an Investment Adviser and/or Distributor but prior to reductions from brokerage service arrangements or other expense offset arrangements. Expenses net of all reductions/additions represent the net expenses paid by a Portfolio. Net investment income (loss) is net of all such additions or reductions. |

| (4) | Ratios do not include fees and expenses charged under the variable annuity contract or variable life insurance policy. |

| • | Calculated using average number of shares outstanding throughout the period. |

| * | Amount is less than $0.005 or 0.005% or more than $(0.005) or (0.005)%. |

| † | Impact of waiving the advisory fee for the ING Institutional Prime Money Market Fund holding has less than 0.005% impact on the expense ratio and net investment income or loss ratio. |

See Accompanying Notes to Financial Statements

| 18 |

NOTES TO FINANCIAL STATEMENTS as of December 31, 2014

NOTE 1 — ORGANIZATION

Voya Variable Products Trust (the “Trust”) is a business trust organized under the laws of the Commonwealth of Massachusetts on December 17, 1993 and registered under the Investment Company Act of 1940, as amended (“1940 Act”), as a diversified, open-end management investment company. There are three active separate investment series (each a “Portfolio” and collectively the “Portfolios”) that comprise the Trust: Voya International Value Portfolio (“International Value”), Voya MidCap Opportunities Portfolio (“MidCap Opportunities”) and Voya SmallCap Opportunities Portfolio (“SmallCap Opportunities”), each a diversified series of the Trust. The investment objective of the Portfolios is described in the Portfolios’ Prospectus.

Each Portfolio offers at least three of the following classes of shares: Adviser Class (“Class ADV”), Class I, Class S, and Service 2 Class (“Class S2”). Each class has equal rights as to voting privileges. The classes differ principally in the applicable distribution and shareholder service fees. Generally, shareholders of each class also bear certain expenses that pertain to that particular class. All shareholders bear the common expenses of a portfolio and earn income and realized gains/losses from a portfolio pro rata based on the daily ending net assets of each class, without distinction between share classes. Expenses that are specific to a portfolio or a class are charged directly to that portfolio or class. Other operating expenses shared by several portfolios are generally allocated among those portfolios based on average net assets. Distributions are determined separately for each class based on income and expenses allocated to each class. Realized gain distributions are allocated to each class pro rata based on the shares outstanding of each class on the date of distribution. Differences in per share dividend rates generally result from differences in separate class expenses, including distribution and shareholder service fees, if applicable.