UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08282

Loomis Sayles Funds I

(Exact name of Registrant as specified in charter)

| | |

| 399 Boylston Street, Boston, Massachusetts 02116 |

| (Address of principal executive offices) (Zip code) |

Coleen Downs Dinneen, Esq.

Natixis Distributors, L.P.

399 Boylston Street

Boston, Massachusetts 02116

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2810

Date of fiscal year end: September 30

Date of reporting period: March 31, 2008

| Item 1. | Reports to Stockholders. |

The Registrant’s semi-annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

Loomis Sayles Mid Cap Growth Fund

Loomis Sayles Small Cap Growth Fund

Loomis Sayles Small Cap Value Fund

Loomis Sayles Tax-Managed Equity Fund

SEMIANNUAL REPORT

MARCH 31, 2008 (Unaudited)

FUND AND MANAGER REVIEW

Loomis Sayles Mid Cap Growth Fund

Phil Fine, CFA

Manager since February 1999

FUND FACTS

Symbol | Institutional: LSAIX;

Retail: LAGRX

Objective | Long-term capital growth from investments in common stocks or similar securities

Strategy | Invests at least 80% of its net assets (plus any borrowings made for investment purposes) in common stocks or other equity securities (which may include securities offered in the secondary markets or in initial public offerings) of companies with market capitalizations that fall within the capitalization range of the Russell Midcap Growth Index, although the Fund may invest in companies of any size

Fund Inception Date | 12/31/96

Commencement of Operations of Class | Institutional: 1/2/97;

Retail: 1/2/97

Total Net Assets | $123.5 million

PORTFOLIO REVIEW

In a difficult period for the securities markets, the Fund held up better than its Benchmark, the Russell Midcap Growth Index, for the six months ended March 31, 2008. The Fund’s outperformance was primarily due to good stock selection in the materials and processing, healthcare, consumer discretionary and technology sectors. Stock selection in the financial services and utilities sectors detracted from relative performance.

The materials and processing and energy sectors were the only sectors posting positive absolute returns for the Fund. Good stock selection in the overweight materials sector had the greatest positive impact on performance, both in absolute and relative terms. Our strongest performers included steel and fertilizer stocks, which benefited from rising commodity prices, supported by structural imbalances between supply and demand. Mosaic, a phosphate and potash producer, was the Fund’s top performer. Prices and cash margins for both nutrients have risen sharply, due to strong demand, low inventories and supply constraints. We were modestly underweight in energy, but our holdings outperformed the Benchmark’s energy stocks. Our top contributors included two exploration and production companies, Range Resources and Southwestern Energy.

The Fund’s weakest sector on an absolute basis was financial services. The technology and consumer discretionary sectors were also weak on an absolute basis, but when viewed on a relative basis, these sectors added value because of good stock selection. In the first quarter of 2008, virtually every company related to the capital markets came under pressure, due to the turmoil in the credit markets. For example, FCStone, a commodities broker and consultant, plunged in value due to its perceived exposure to counterparty credit risk and concerns that trading volumes could suffer if hedge fund clients were forced to deleverage. We sold the stock. In technology, the Fund experienced losses in telecommunication equipment and computer stocks, and our solar stocks were hit by profit-taking. Nevertheless, our position in First Solar, a producer of solar modules, was a top contributor. We believe the company’s proprietary technology gives it a cost advantage relative to competitors, and management has done an exceptional job ramping up new capacity.

NII Holdings, a provider of wireless communication services in Latin America, detracted from the Fund’s performance. The company reported disappointing net subscriber additions in its two largest markets, Mexico and Brazil, and announced price cuts to match competitor promotions. We sold the position.

OUTLOOK

Uncertainty and fear often create attractive buying opportunities, as emotion overcomes fundamentals. We anticipate improving conditions in the equity markets during 2008. We believe pessimism is high, risk appetites are low, and concerns about corporate profit growth may be overstated. In our view, this suggests that valuations are attractive, and the market is well-positioned for a recovery if the fog of uncertainty begins to clear and investors return to looking at normalized earnings and cash-flow growth rates.

1

AVERAGE ANNUAL TOTAL RETURNS

Periods Ended March 31, 2008

| | | | | | | | | | | | | |

| 6 Months | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception | |

| Loomis Sayles Mid Cap Growth: Institutional | |

| -7.74 | % | | 9.82 | % | | 19.85 | % | | 8.76 | % | | 10.28 | % |

| Loomis Sayles Mid Cap Growth: Retail | |

| -7.86 | | | 9.57 | | | 19.54 | | | 8.46 | | | 9.98 | |

| Russell Midcap Growth Index(c) | |

| -12.46 | | | -4.55 | | | 15.20 | | | 5.15 | | | 7.55 | |

| Lipper Mid-Cap Growth Funds Index(c) | |

| -12.81 | | | 1.09 | | | 15.12 | | | 5.12 | | | 6.61 | |

| | | | | | | | |

| Gross expense ratio (before reductions and reimbursements)* |

| Institutional: 1.10% | | Retail: 1.43% | | |

| Net expense ratio (after reductions and reimbursements)* |

| Institutional: 1.00% | | Retail: 1.25% | | |

* As stated in the most recent prospectus

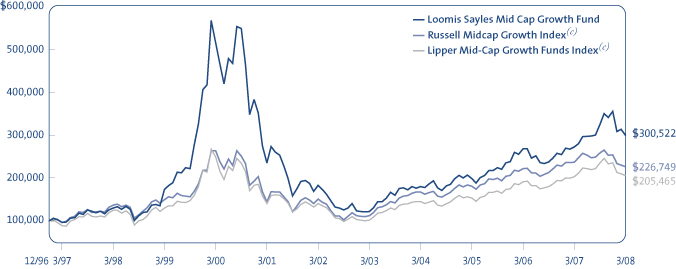

CUMULATIVE PERFORMANCE

Inception to March 31, 2008(a)(b)

Data quoted reflects past performance and cannot guarantee future results. Average annual total returns assume reinvestment of dividends and capital gain distributions. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. For performance current to the most recent month end, please visit the Loomis Sayles website. Current performance may be higher or lower than quoted.

Returns do not reflect the taxes that a shareholder would pay on fund distributions or the redemption of shares. Periods of less than one year are not annualized. Performance data reflects certain fee reductions and reimbursements, if any, without which performance would be lower.

(a) Cumulative performance is shown for the Institutional Class of Shares. Performance of the Retail Class would be lower due to higher fees. (b) The mountain chart is based on the initial investment minimum of $100,000 for the Institutional Class. (c) See page 9 for a description of the Indices.

WHAT YOU SHOULD KNOW

Small- and mid-cap stocks may be more volatile than larger, more established companies. The secondary market for these stocks may be less liquid, which could adversely impact the Fund’s value. Growth funds involve increased risks, in part, because the value of the underlying securities is based on future expectations that may or may not be met.

The Fund can invest a significant percentage of assets in foreign securities and the value of the fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments. In emerging markets these risks can be significant. The Fund is subject to currency risk, which is the risk that fluctuations in exchange rates between the US dollar and foreign currencies may cause the value of a Fund’s investments to decline. Fund shares should be viewed as a long-term investment.

2

FUND AND MANAGER REVIEW

Loomis Sayles Small Cap Growth Fund

Mark F. Burns, CFA

Manager since January 2005

John Slavik, CFA

Manager since April 2005

FUND FACTS

Symbol | Institutional: LSSIX;

Retail: LCGRX

Objective | Long-term capital growth from investments in common stocks or other equity securities

Strategy | Invests at least 80% of its net assets (plus any borrowings made for investment purposes) in equity securities of companies with market capitalizations that fall within the capitalization range of the Russell 2000 Index. Unlike the Index, the Fund may invest in companies of any size

Fund Inception Date | 12/31/96

Commencement of Operations of Class | Institutional: 1/2/97;

Retail: 1/2/97

Total Net Assets | $103.1 million

PORTFOLIO REVIEW

The Fund underperformed its Benchmarks, the Russell 2000 Growth and the Russell 2000 Indices, for the six months ended March 31, 2008. Poor stock selection in the financial services and healthcare sectors accounted for the majority of the performance shortfall versus the Benchmarks.

On an absolute basis, energy was the only sector in the Fund’s portfolio that offered a positive return for the period. The technology, healthcare and consumer discretionary sectors made the largest negative contributions to the Fund’s absolute performance. Within these sectors, Inverness Medical Innovations, a diagnostic testing company; Life Time Fitness, a nationwide owner of health clubs; and Tessera Technologies, a semiconductor company, were among the Fund’s worst performers. Each of these positions was sold.

In light of the recent stock market volatility, we sought to limit the Fund’s risk by reducing exposure to the technology and financial services sectors. In financial services, we cut exposure to companies that were influenced by the ongoing credit crisis. In the technology sector, we reduced exposure to the semiconductor industry, which was experiencing a cyclical slowdown.

We also reduced the Fund’s consumer discretionary exposure aggressively in the fourth quarter of 2007, as it became evident the US consumer was becoming more cautious about the economy, but we started adding back exposure in the first quarter of 2008. To offset these reductions, we increased the Fund’s exposure to the healthcare, producer durables and energy sectors.

OUTLOOK

Although we expected some challenges as the market adjusted to the economic slowdown, the depth of the markets’ sell-off across nearly every sector was larger than we had anticipated. Turmoil in the credit markets led to fears about the financial system’s vulnerability, and this, combined with growing inflationary pressures, fueled the rise in volatility. Economic uncertainty is never pleasant, but the market has a long history of coping with it. The Federal Reserve has been working to support the economy and instill order and confidence in the financial markets.

Uncertainty and fear often create attractive buying opportunities, as emotion overcomes fundamentals. We anticipate improvements in the equity markets during 2008. We believe pessimism is high, risk appetites are low, and concerns about corporate profit growth may be overstated. In our view, this suggests valuations are attractive, and the market is well-positioned for a recovery if the fog of uncertainty begins to clear and investors return to looking at normalized earnings and cash-flow growth rates.

3

We expect the stocks of companies that benefit from corporate spending, non-US earnings streams and strong emerging-market economies to perform better than those tied to the US economy in general and to US consumer spending in particular.

AVERAGE ANNUAL TOTAL RETURNS

Periods Ended March 31, 2008

| | | | | | | | | | | | | |

| 6 Months | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception | |

| Loomis Sayles Small Cap Growth: Institutional | |

| -15.75 | % | | -1.11 | % | | 17.03 | % | | 1.15 | % | | 3.68 | % |

| Loomis Sayles Small Cap Growth: Retail | |

| -15.86 | | | -1.29 | | | 16.76 | | | 0.89 | | | 3.42 | |

| Russell 2000 Growth Index(c) | |

| -14.66 | | | -8.94 | | | 14.24 | | | 1.75 | | | 3.69 | |

| Russell 2000 Index(c) | |

| -14.02 | | | -13.00 | | | 14.90 | | | 4.96 | | | 7.20 | |

| Lipper Small-Cap Growth Funds Index(c) | |

| -16.90 | | | -9.53 | | | 12.68 | | | 3.98 | | | 5.51 | |

| Gross expense ratio (before reductions and reimbursements)* | |

| Institutional: 1.23% | | | Retail: 1.50% | | | | |

| Net expense ratio (after reductions and reimbursements)* | |

| Institutional: 1.00% | | | Retail: 1.25% | | | | |

* As stated in the most recent prospectus

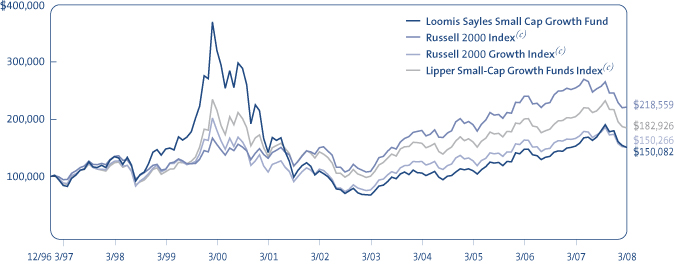

CUMULATIVE PERFORMANCE

Inception to March 31, 2008(a)(b)

Data quoted reflects past performance and cannot guarantee future results. Average annual total returns assume reinvestment of dividends and capital gains distributions. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. For performance current to the most recent month end, please visit the Loomis Sayles website. Current performance may be higher or lower than quoted.

Returns do not reflect the taxes that a shareholder would pay on fund distributions or the redemption of shares. Periods of less than one year are not annualized. Performance data reflects certain fee reductions and reimbursements, if any, without which performance would be lower.

(a) Cumulative performance is shown for the Institutional Class of Shares. Performance of the Retail Class would be lower due to higher fees. (b) The mountain chart is based on the initial investment minimum of $100,000 for the Institutional Class. (c) See page 9 for a description of the Indices.

WHAT YOU SHOULD KNOW

Small- and mid-cap stocks may be more volatile than larger, more established companies. The secondary market for these stocks may be less liquid, which could adversely impact the Fund’s value. Growth funds involve increased risks, in part, because the value of the underlying securities is based on future expectations that may or may not be met.

The Fund can invest a significant percentage of assets in foreign securities and the value of the fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments. In emerging markets these risks can be significant. The Fund is subject to currency risk, which is the risk that fluctuations in exchange rates between the US dollar and foreign currencies may cause the value of a Fund’s investments to decline. Fund shares should be viewed as a long-term investment.

4

FUND AND MANAGER REVIEW

Loomis Sayles Small Cap Value Fund

Manager since January 2000

Manager since April 2000

FUND FACTS

Symbol | Institutional: LSSCX;

Retail: LSCRX; Admin: LSVAX

Objective | Long-term capital growth from investments in common stocks or other equity securities

Strategy | Invests at least 80% of its net assets (plus any borrowings made for investment purposes) in equity securities of companies with market capitalizations that fall within the capitalization range of the Russell 2000 Index. Unlike the Index, the Fund may invest in companies of any size

Fund Inception Date | 5/13/91

Commencement of Operations of Class | Institutional: 5/13/91;

Retail: 1/2/97; Admin: 1/2/98

Total Net Assets | $1,008.8 million

PORTFOLIO REVIEW

The Fund underperformed one of its Benchmarks, the Russell 2000 Value Index, and outperformed its other Benchmark, the Russell 2000 Index, during the six months ended March 31, 2008. The Fund’s underperformance was primarily due to poor stock selection in the financial services and energy sectors. However, stock selection in the autos and transportation and technology sectors aided the Fund’s relative performance.

The Fund’s worst performing sector was financial services. Our cautious stance and underweight positions were positive factors late in 2007, but we were not positioned for the surprising resilience demonstrated by small banks and real estate investment trusts in early 2008. They held up remarkably well, despite significantly negative revisions to earnings estimates, a broadening of the liquidity crisis, and the near collapse of several high-profile financial institutions. In addition, a handful of financial services names suffered, from a fundamental perspective, including National Financial Partners, a distributor of financial services products to businesses and individuals, and Advanta Corp., a provider of credit cards and related products to business. We sold both positions.

The automotive and transportation sector was one of the Fund’s strongest positions. Transportation stocks generally perform well in anticipation of an economic recovery after a recession. Short-line railroad operator Genesee & Wyoming, which has been in the portfolio for a long time, paced the sector with a strongly positive return.

“Broken-deal” stocks are a new theme pursued in the portfolio as opportunities appeared. These are situations where leveraged buyouts collapsed as buyers and banks felt the pressure of the weakening debt and credit markets, causing the deals to fall through. These situations included new positions in Alliance Data Systems, a financial data-services provider, Myers Industries, a rubber and plastics manufacturer, and PHH Corp., a provider of mortgage management services.

OUTLOOK

Although we expected some challenges as the market adjusted to the economic slowdown, the depth of the markets’ sell-off across nearly every sector was larger than we had anticipated. Turmoil in the credit markets led to fears about the financial system’s vulnerability. This, along with growing inflation pressures, fueled the rise in volatility. Economic uncertainty is never pleasant, but the market has a long history of coping with it. The Federal Reserve has been working to support the economy and instill order and confidence in the financial markets.

Uncertainty and fear often create attractive buying opportunities, as emotion overcomes fundamentals. We anticipate improvements in the equity markets during 2008. We believe pessimism is high, risk appetites are low, and concerns over corporate profit growth may be overstated. In our view, this suggests valuations are attractive, and the market is well-positioned for a recovery if the fog of uncertainty begins to clear and investors return to looking at normalized earnings and cash-flow growth rates.

5

AVERAGE ANNUAL TOTAL RETURNS

Periods Ended March 31, 2008

| | | | | | | | | | | | |

| 6 Months | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception(a)(b) |

| Loomis Sayles Small Cap Value: Institutional |

| -13.74 | % | | -10.22 | % | | 15.13 | % | | 7.88 | % | | 13.56% |

| Loomis Sayles Small Cap Value: Retail(a) |

| -13.85 | | | -10.43 | | | 14.83 | | | 7.61 | | | 13.36 |

| Loomis Sayles Small Cap Value: Admin(a) |

| -13.98 | | | -10.68 | | | 14.53 | | | 7.32 | | | 13.01 |

| Russell 2000 Value Index(c) |

| -13.33 | | | -16.88 | | | 15.45 | | | 7.46 | | | 12.81 |

| Russell 2000 Index(c) |

| -14.02 | | | -13.00 | | | 14.90 | | | 4.96 | | | 10.11 |

| Lipper Small-Cap Core Funds Index(b)(c) |

| -13.03 | | | -10.26 | | | 14.76 | | | 6.20 | | | N/A |

| Gross expense ratio (before reductions and reimbursements)* |

| Institutional: 0.89% | | | Retail: 1.24% | | | Admin: 1.57% |

| Net expense ratio (after reductions and reimbursements)* |

| Institutional: 0.89% | | | Retail: 1.16% | | | Admin: 1.41% |

* As stated in the most recent prospectus

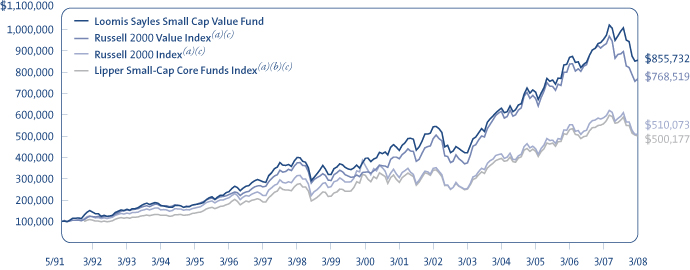

CUMULATIVE PERFORMANCE

Inception to March 31, 2008(d)(e)

Data quoted reflects past performance and cannot guarantee future results. Average annual total returns assume reinvestment of dividends and capital gains distributions. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. For performance current to the most recent month end, please visit the Loomis Sayles website. Current performance may be higher or lower than quoted.

Returns do not reflect the taxes that a shareholder would pay on fund distributions or the redemption of shares. Periods of less than one year are not annualized. Performance data reflects certain fee reductions and reimbursements, if any, without which performance would be lower.

(a) Performance shown for periods prior to the inception date of the Retail Class (12/31/96) and Admin Class (1/02/98) represents the performance of the Institutional Class of shares during the periods shown, adjusted to reflect current levels of 12b-1 fees payable by the respective Classes. Since index performance data is not available coincident with the Fund’s inception date, the beginning value of the index is the value as of the month end closest to the Fund’s inception date. (b) The Lipper Small-Cap Core Funds Index performance data is not available prior to January 1, 1992. (c) See page 9 for a description of the Indices. (d) Cumulative performance is shown for the Institutional Class of Shares. Performance of the Retail and Admin Classes would be lower due to higher fees and expenses. (e) The mountain chart is based on the initial investment minimum of $100,000 for the Institutional Class.

WHAT YOU SHOULD KNOW

Value stocks may fall out of favor with investors and underperform the overall equity market during any given period. Small- and mid-cap stocks may be more volatile than larger, more established companies. The secondary market for these stocks may be less liquid, which could adversely impact the Fund’s value. Foreign investments involve special risks, including greater economic, political and currency fluctuation risks, which may be even greater in emerging markets. Foreign countries may have different accounting standards than US standards.

The Fund can invest a significant percentage of assets in foreign securities and the value of the fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments. In emerging markets these risks can be significant. The Fund is subject to currency risk, which is the risk that fluctuations in exchange rates between the US dollar and foreign currencies may cause the value of a Fund’s investments to decline. Fund shares should be viewed as a long-term investment.

6

FUND AND MANAGER REVIEW

Loomis Sayles Tax-Managed Equity Fund

Mark Shank, CFA, CIC

Manager since June 2003

David Sowerby, CFA

Manager since August 2005

FUND FACTS

Symbol | LSCGX

Objective | Long-term capital growth

Strategy | Invests at least 80% of net assets (plus any borrowings made for investment purposes) in equity securities and may invest in companies of any size; the Fund uses a tax-managed approach in an effort to minimize the effect of US federal income tax

Fund Inception Date | 10/1/95

Fund Registration Date | 3/7/97

Total Net Assets | $6.5 million

PORTFOLIO REVIEW

The Fund outperformed its Benchmark, the S&P 500 Index, for the six months ended March 31, 2008, primarily due to stock selection and an underweight in the financials sector, which was the worst-performing sector for the period. For example, our positions in Aflac and State Street were both up significantly, while the Benchmark financials fell sharply. In addition, our stock selection in the energy and consumer discretionary sectors helped performance, while our underweights in consumer staples and utilities, which outperformed during the period, modestly detracted from relative results.

On an absolute basis, consumer staples and energy were the only sectors that generated a positive total return for the Fund. In the consumer staples sector, Alberto-Culver and Colgate-Palmolive both appreciated significantly, while the S&P 500 Index’s consumer staples sector only managed a small gain. Alberto-Culver specializes in personal care products and manufactures such brand names as Tresemme and Nexxus. The company’s operating profit margins have improved due to double-digit revenue growth and cost savings from more efficient manufacturing operations. Colgate-Palmolive, which has been a steady wealth creator, was added to the Fund in the fourth quarter at what appeared to be an attractive valuation relative to other consumer staples companies. In the energy sector, Devon Energy and Transocean were among our best performers. Devon Energy explores and produces oil and gas and has recently witnessed a favorable acceleration in earnings. Devon has been a Fund holding for over seven years. The world’s largest offshore drilling contractor, Transocean last year merged with another drilling company, Global Santa Fe.

The information technology, industrials and financials sectors—the Fund’s largest sector weights—had the greatest negative impact on absolute return. Within information technology, Cisco Systems was among the Fund’s worst performers, declining on concerns about worldwide economic growth. The company supplies such data networking products as routers for the internet. While Cisco detracted from performance for the period, the stock has been a positive contributor to investment returns following our increased allocation in early 2006. We believe the stock remains attractive, so we took advantage of low prices to modestly add to our position during the period. Overall, though, we reduced the Fund’s information technology weighting.

In the industrials sector, Boeing experienced delays in delivering its new aircraft, which resulted in a strong stock-price decline. Financial stocks faced a series of ongoing challenges primarily related to asset write-downs resulting from the subprime lending crisis, which led to disappointing performance. We reduced the Fund’s financial holdings by selling positions in Allstate, Citigroup and Zions, and by reducing positions in Goldman Sachs and State Street.

OUTLOOK

Although we expected some challenges as the market adjusted to the economic slowdown, the depth of the sell-off across nearly every sector was larger than we had anticipated. Turmoil in the credit markets led to fears about the financial system’s vulnerability, and this, coupled with growing inflationary pressures, fueled the

7

rise in volatility. Economic and market uncertainty is never pleasant, but the market has a long history of coping with it. The Federal Reserve has been working to support the economy and instill order and confidence in the financial markets.

Uncertainty and fear often create attractive buying opportunities, as emotion overcomes investors’ ability to evaluate fundamentals. We anticipate improvements in the equity markets during 2008. We believe pessimism is high, risk appetites are low, and concerns about corporate profit growth may be overstated. In our view, this suggests that valuations are attractive and the market is well-positioned for a recovery, if the fog of uncertainty begins to clear and investors return to looking at normalized earnings and cash-flow growth rates.

AVERAGE ANNUAL TOTAL RETURNS

Periods Ended March 31, 2008

| | | | | | | | | | | | | | | |

| 6 Months | | 1 Year | | | 5 Years | | | 10 Years | | | Since Registration(a)(b) | | | Since Inception(a)(b) | |

| Loomis Sayles Tax Managed Equity: Institutional | |

| -9.67% | | -1.61 | % | | 10.22 | % | | 7.01 | % | | 8.29 | % | | 9.27 | % |

| Return After Taxes on Distributions(c) | |

| -10.08 | | -2.05 | | | 9.93 | | | 4.28 | | | 5.59 | | | 6.82 | |

| Return After Taxes on Distributions and Sale of Fund Shares(c) | |

| -6.12 | | -0.86 | | | 8.80 | | | 4.51 | | | 5.70 | | | 6.78 | |

| S&P 500 Index(c) | |

| -12.46 | | -5.08 | | | 11.32 | | | 3.50 | | | 6.47 | | | 8.57 | |

| Lipper Large-Cap Core Funds Index(c) | |

| -11.72 | | -4.32 | | | 10.04 | | | 2.87 | | | 5.70 | | | 7.43 | |

| Gross expense ratio (before reductions and reimbursements)* | |

| Institutional: 1.92% | | | | | | | |

| Net expense ratio (after reductions and reimbursements)* | |

| Institutional: 0.65% | | | | | | | |

* As stated in the most recent prospectus

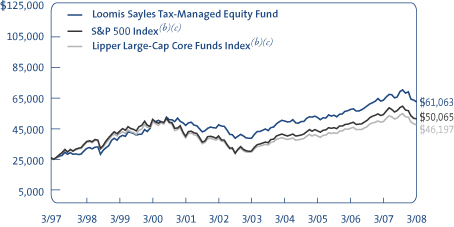

CUMULATIVE PERFORMANCE

Registration to March 31, 2008(d)

Inception to March 31, 2008(d)

Data quoted reflects past performance and cannot guarantee future results. Average annual total returns assume reinvestment of dividends and capital gains distributions. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. For performance current to the most recent month end, please visit the Loomis Sayles website. Current performance may be higher or lower than quoted.

Performance data reflects certain fee reductions and reimbursements, if any, without which performance would be lower. Except as indicated in the table above, returns do not reflect the taxes that a shareholder would pay on fund distributions or the redemption of shares.

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their shares through tax-deferred arrangements, such as 401(k) plans, qualified plans, education savings accounts or individual retirement accounts. Under certain circumstances, the addition of the tax benefits from capital losses resulting from redemptions may cause the Return After Taxes on Distributions and Sale of Fund Shares to be greater than the Return After Taxes on Distributions or even the Return Before Taxes.

(a) Shares of the Fund were registered for offer under the Securities Act of 1933 on March 7, 1997. In accordance with regulations, performance information is provided for the period beginning on March 7, 1997 (“Registration”). Performance from inception is also provided for the convenience of our shareholders. (b) Index performance is not available coincident with the Fund’s inception and registration dates; comparative performance is presented from the month end closest to the Fund’s inception and registration dates. (c) See page 9 for a description of the Indices and disclosure related to after-tax returns. (d) The mountain chart is based on the Fund’s initial minimum investment of $25,000.

WHAT YOU SHOULD KNOW

Growth funds involve increased risks, in part, because the value of the underlying securities is based on future expectations that may or may not be met. The Fund can invest a significant percentage of assets in foreign securities and the value of the Fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments. In emerging markets these risks can be significant. The Fund is subject to currency risk, which is the risk that fluctuations in exchange rates between the US dollar and foreign currencies may cause the value of a Fund’s investments to decline. Fund shares should be viewed as a long-term investment.

8

ADDITIONAL INFORMATION

Index Definitions

Indexes are unmanaged and do not have expenses that affect results, unlike mutual funds. Index returns are adjusted for the reinvestment of capital gain distributions and income dividends. It is not possible to invest directly in an index.

Lipper Mid-Cap Growth Funds Index is an equally weighted index of typically the 30 largest mutual funds within the mid-cap growth funds investment objective.

Lipper Large-Cap Core Funds Index is an equally weighted index of typically the 30 largest mutual funds within the large-cap core funds investment objective.

Lipper Small-Cap Core Funds Index is an equally weighted index of typically the 30 largest mutual funds within the small-cap core funds investment objective.

Lipper Small-Cap Growth Funds Index is an equally weighted index of typically the 30 largest mutual funds within the small-cap growth funds investment objective.

Source: Lipper, Inc.

Russell Midcap Growth Index is a market capitalization weighted index of medium capitalization stocks determined by Russell to be growth stocks as measured by their price-to-book ratios and forecasted growth values. The stocks are also members of the Russell 1000 Growth Index.

Russell 2000 Growth Index is an index comprised of those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 2000 Index is an index comprised of the 2,000 smallest companies in the Russell 3000 Index (a broad market index), representing approximately 8% of the Russell 3000 total market capitalization.

Russell 2000 Value Index is an index comprised of those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

S&P 500 Index consists of 500 stocks chosen for market size, liquidity, and industry group representation. A commonly used benchmark of US equity securities, it is a market-value weighted index (stock price times number of shares outstanding), with each stock’s weight in the index proportionate to its market value.

After-Tax Returns

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their shares through tax-deferred arrangements, such as 401(k) plans, qualified plans, education savings accounts or individual retirement accounts. Under certain circumstances, the addition of the tax benefits from capital losses resulting from redemptions may cause the return after taxes on distributions and sale of fund shares to be greater than the return after taxes on distribution or even the return before taxes.

Proxy Voting Information

A description of the Funds’ proxy voting policies and procedures is available without charge, upon request, (i) by calling Loomis Sayles at 800-633-3330; (ii) on the Funds’ website, www.loomissayles.com, and (iii) on the SEC’s website, www.sec.gov. Information about how the Funds voted proxies relating to portfolio securities during the 12 months ended June 30, 2007 is available on (i) the Funds’ website and (ii) the SEC’s website.

Quarterly Portfolio Schedules

The Funds file a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330.

UNDERSTANDING YOUR FUND’S EXPENSES

As a mutual fund shareholder you incur two types of costs: (1) transaction costs, including redemption fees and certain exchange fees; and (2) ongoing costs, including management fees, distribution and/or service fees (12b-1 fees), and other Fund expenses. These costs are described in more detail in the Funds’ prospectus. The examples below are intended to help you understand the ongoing costs of investing in the Funds and help you compare these with the ongoing costs of investing in other mutual funds.

The first line in the table of each Fund shows the actual amount of Fund expenses you would have paid on a $1,000 investment in the Fund from October 1, 2007 through March 31, 2008. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual fund returns and expenses. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example $8,600 account value divided by $1,000 = 8.6) and multiply the result by the number in the Expenses Paid During the Period column as shown below for your class.

The second line in the table of each Fund provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid on your investment for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

9

Please note that the expenses shown reflect ongoing costs only, and do not include any transaction costs. Therefore, the second line in the table is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. If transaction costs were included, total costs would be higher.

Loomis Sayles Mid Cap Growth Fund

| | | | | | |

Institutional Class | | Beginning

Account Value

10/1/07 | | Ending

Account Value

3/31/08 | | Expenses Paid

During Period*

10/1/07 – 3/31/08 |

Actual | | $1,000.00 | | $ 922.60 | | $4.81 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,020.00 | | $5.05 |

| | | |

Retail Class | | | | | | |

Actual | | $1,000.00 | | $ 921.40 | | $6.00 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,018.75 | | $6.31 |

* Expenses are equal to the Fund’s annualized expense ratio (after fee reduction/reimbursement): 1.00% and 1.25% for the Institutional and Retail Class, respectively, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the half-year period). |

Loomis Sayles Small Cap Growth Fund

| | | | | | |

Institutional Class | | Beginning

Account Value

10/1/07 | | Ending

Account Value

3/31/08 | | Expenses Paid

During Period*

10/1/07 – 3/31/08 |

Actual | | $1,000.00 | | $ 842.50 | | $4.61 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,020.00 | | $5.05 |

| | | |

Retail Class | | | | | | |

Actual | | $1,000.00 | | $ 841.40 | | $5.75 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,018.75 | | $6.31 |

* Expenses are equal to the Fund’s annualized expense ratio (after fee reduction/reimbursement): 1.00% and 1.25% for Institutional and Retail Class, respectively, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the half-year period). |

Loomis Sayles Small Cap Value Fund

| | | | | | |

Institutional Class | | Beginning

Account Value

10/1/07 | | Ending

Account Value

3/31/08 | | Expenses Paid

During Period*

10/1/07 – 3/31/08 |

Actual | | $1,000.00 | | $ 862.60 | | $4.10 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,020.60 | | $4.45 |

| | | |

Retail Class | | | | | | |

Actual | | $1,000.00 | | $ 861.50 | | $5.35 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,019.25 | | $5.81 |

| | | |

Administrative Class | | | | | | |

Actual | | $1,000.00 | | $860.20 | | $6.51 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,018.00 | | $7.06 |

* Expenses are equal to the Fund’s annualized expense ratio (after fee reduction/reimbursement) of 0.88%, 1.15% and 1.40% for the Institutional Class, Retail and Admin Class, respectively, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the half-year period). |

Loomis Sayles Taxed-Managed Equity Fund

| | | | | | |

Institutional Class | | Beginning

Account Value

10/1/07 | | Ending

Account Value

3/31/08 | | Expenses Paid

During Period*

10/1/07 – 3/31/08 |

Actual | | $1,000.00 | | $ 903.30 | | $3.09 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,021.75 | | $3.29 |

* Expenses are equal to the Fund’s annualized expense ratio (after fee reduction/reimbursement) of 0.65%, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the half-year period). |

10

PORTFOLIO OF INVESTMENTS – as of March 31, 2008 (Unaudited)

Loomis Sayles Mid Cap Growth Fund

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – 93.6% of Net Assets | | | | | | | |

| | | |

| Beverages – 1.6% | | | | | | | |

Central European Distribution Corp.(b)(c) | | | | 34,080 | | $ | 1,983,115 |

| | | | | | | |

| Biotechnology – 2.5% | | | | | | | |

BioMarin Pharmaceutical, Inc.(b)(c) | | | | 36,708 | | | 1,298,362 |

Genzyme Corp.(b)(c) | | | | 24,136 | | | 1,799,097 |

| | | | | | | |

| | | | | | | 3,097,459 |

| | | | | | | |

| Capital Markets – 4.3% | | | | | | | |

BlackRock, Inc.(b) | | | | 14,547 | | | 2,970,207 |

Waddell & Reed Financial, Inc.(b) | | | | 70,878 | | | 2,277,310 |

| | | | | | | |

| | | | | | | 5,247,517 |

| | | | | | | |

| Chemicals – 4.1% | | | | | | | |

CF Industries Holdings, Inc.(b) | | | | 19,448 | | | 2,015,202 |

Mosaic Co. (The)(c) | | | | 29,871 | | | 3,064,764 |

| | | | | | | |

| | | | | | | 5,079,966 |

| | | | | | | |

| Commercial Services & Supplies – 5.9% | | | | | | | |

Corrections Corp. of America(b)(c) | | | | 87,478 | | | 2,407,395 |

FTI Consulting, Inc.(b)(c) | | | | 26,533 | | | 1,884,904 |

Stericycle, Inc.(b)(c) | | | | 59,036 | | | 3,040,354 |

| | | | | | | |

| | | | | | | 7,332,653 |

| | | | | | | |

| Containers & Packaging – 1.6% | | | | | | | |

Crown Holdings, Inc.(c) | | | | 77,669 | | | 1,954,152 |

| | | | | | | |

| Distributors – 2.0% | | | | | | | |

LKQ Corp.(b)(c) | | | | 112,158 | | | 2,520,190 |

| | | | | | | |

| Diversified Financial Services – 3.8% | | | | | | | |

IntercontinentalExchange, Inc.(b)(c) | | | | 19,769 | | | 2,579,855 |

Nasdaq Stock Market, Inc.(b)(c) | | | | 54,309 | | | 2,099,586 |

| | | | | | | |

| | | | | | | 4,679,441 |

| | | | | | | |

| Electrical Equipment – 2.1% | | | | | | | |

First Solar, Inc.(b)(c) | | | | 11,246 | | | 2,599,401 |

| | | | | | | |

| Electronic Equipment & Instruments – 2.0% | | | | | | | |

Mettler-Toledo International, Inc.(c) | | | | 24,851 | | | 2,413,529 |

| | | | | | | |

| Energy Equipment & Services – 3.6% | | | | | | | |

Cameron International Corp.(b)(c) | | | | 46,104 | | | 1,919,770 |

Nabors Industries Ltd.(b)(c) | | | | 75,205 | | | 2,539,673 |

| | | | | | | |

| | | | | | | 4,459,443 |

| | | | | | | |

| Health Care Equipment & Supplies – 4.9% | | | | | | | |

Idexx Laboratories, Inc.(b)(c) | | | | 43,437 | | | 2,139,707 |

Intuitive Surgical, Inc.(b)(c) | | | | 12,066 | | | 3,913,607 |

| | | | | | | |

| | | | | | | 6,053,314 |

| | | | | | | |

| Hotels, Restaurants & Leisure – 3.9% | | | | | | | |

Ctrip.com International Ltd., ADR(b) | | | | 42,567 | | | 2,256,902 |

Yum! Brands, Inc.(b) | | | | 70,286 | | | 2,615,342 |

| | | | | | | |

| | | | | | | 4,872,244 |

| | | | | | | |

| Insurance – 1.4% | | | | | | | |

Fairfax Financial Holdings Ltd.(b) | | | | 5,923 | | | 1,700,493 |

| | | | | | | |

11

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – continued | | | | | | | |

| | | |

| Internet & Catalog Retail – 3.1% | | | | | | | |

Priceline.com, Inc.(b)(c) | | | | 31,476 | | $ | 3,804,189 |

| | | | | | | |

| IT Services – 2.7% | | | | | | | |

MasterCard, Inc., Class A(b) | | | | 15,122 | | | 3,372,055 |

| | | | | | | |

| Life Sciences Tools & Services – 6.6% | | | | | | | |

Covance, Inc.(c) | | | | 27,667 | | | 2,295,531 |

Illumina, Inc.(b)(c) | | | | 46,561 | | | 3,533,980 |

Pharmaceutical Product Development, Inc. | | | | 56,683 | | | 2,375,018 |

| | | | | | | |

| | | | | | | 8,204,529 |

| | | | | | | |

| Machinery – 4.4% | | | | | | | |

AGCO Corp.(b)(c) | | | | 42,257 | | | 2,530,349 |

Flowserve Corp.(b) | | | | 27,306 | | | 2,850,201 |

| | | | | | | |

| | | | | | | 5,380,550 |

| | | | | | | |

| Marine – 1.6% | | | | | | | |

Genco Shipping & Trading Ltd.(b) | | | | 34,554 | | | 1,949,882 |

| | | | | | | |

| Metals & Mining – 5.6% | | | | | | | |

Agnico-Eagle Mines Ltd. | | | | 15,698 | | | 1,062,912 |

Kinross Gold Corp. | | | | 114,921 | | | 2,540,903 |

Steel Dynamics, Inc.(b) | | | | 101,274 | | | 3,346,093 |

| | | | | | | |

| | | | | | | 6,949,908 |

| | | | | | | |

| Oil, Gas & Consumable Fuels – 10.4% | | | | | | | |

Arena Resources, Inc.(b)(c) | | | | 50,568 | | | 1,957,487 |

Denbury Resources, Inc.(c) | | | | 94,020 | | | 2,684,271 |

Petrohawk Energy Corp.(c) | | | | 62,432 | | | 1,259,253 |

Range Resources Corp.(b) | | | | 55,995 | | | 3,552,883 |

Southwestern Energy Co.(b)(c) | | | | 98,830 | | | 3,329,583 |

| | | | | | | |

| | | | | | | 12,783,477 |

| | | | | | | |

| Semiconductors & Semiconductor Equipment – 3.0% | | | | | | | |

Intersil Corp., Class A(b) | | | | 73,972 | | | 1,898,861 |

MEMC Electronic Materials, Inc.(c) | | | | 25,199 | | | 1,786,609 |

| | | | | | | |

| | | | | | | 3,685,470 |

| | | | | | | |

| Software – 4.4% | | | | | | | |

Concur Technologies, Inc.(c) | | | | 36,683 | | | 1,139,007 |

Micros Systems, Inc.(b)(c) | | | | 68,330 | | | 2,299,988 |

Salesforce.com, Inc.(b)(c) | | | | 34,522 | | | 1,997,788 |

| | | | | | | |

| | | | | | | 5,436,783 |

| | | | | | | |

| Specialty Retail – 4.2% | | | | | | | |

TJX Cos., Inc.(b) | | | | 70,689 | | | 2,337,685 |

Urban Outfitters, Inc.(b)(c) | | | | 91,514 | | | 2,868,964 |

| | | | | | | |

| | | | | | | 5,206,649 |

| | | | | | | |

| Wireless Telecommunication Services – 3.9% | | | | | | | |

Millicom International Cellular SA(b)(c) | | | | 18,601 | | | 1,758,725 |

Turkcell Iletisim Hizmet AS, ADR | | | | 58,282 | | | 1,217,511 |

Vimpel-Communications, ADR | | | | 61,272 | | | 1,831,420 |

| | | | | | | |

| | | | | | | 4,807,656 |

| | | | | | | |

| | | |

| TOTAL COMMON STOCKS | | | | | | | |

(Identified Cost $109,720,584) | | | | | | | 115,574,065 |

| | | | | | | |

12

PORTFOLIO OF INVESTMENTS – as of March 31, 2008 (Unaudited)

Loomis Sayles Mid Cap Growth Fund – continued

| | | | | | | | |

| | | | | Shares/

Principal Amount | | Value (†) |

| | | | | | | | |

| | | |

| SHORT-TERM INVESTMENTS – 46.3% | | | | | | | | |

| State Street Navigator Securities Lending Prime Portfolio(d) | | | | | 49,772,699 | | $ | 49,772,699 |

| Tri-Party Repurchase Agreement with Fixed Income Clearing Corporation, dated 3/31/2008 at 1.250% to be repurchased at $7,369,256 on 4/01/2008 collateralized by $7,265,000 Federal National Mortgage Association, 5.020% due 11/21/2012 valued at $7,519,275, including accrued interest (Note 2g of Notes to Financial Statements) | | | | $ | 7,369,000 | | | 7,369,000 |

| | | | | | | | |

| | | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | | | | |

(Identified Cost $57,141,699) | | | | | | | | 57,141,699 |

| | | | | | | | |

| | | |

| TOTAL INVESTMENTS – 139.9% | | | | | | | | |

(Identified Cost $166,862,283)(a) | | | | | | | $ | 172,715,764 |

Other assets less liabilities—(39.9)% | | | | | | | | (49,213,624) |

| | | | | | | | |

| | | |

| NET ASSETS – 100.0% | | | | | | | $ | 123,502,140 |

| | | | | | | | |

| |

(†) See Note 2a of Notes to Financial Statements. | | | |

(a) Federal Tax Information (Amounts exclude certain adjustments made at the end of the Fund’s fiscal year for tax purposes. Such adjustments are primarily due to wash sales.): | | | |

At March 31, 2008, the net unrealized appreciation on investments based on a cost of $166,862,283 for federal income tax purposes was as follows: | | | |

Aggregate gross unrealized appreciation for all investments in which there is an excess of value over tax cost | | $ | 8,919,935 |

Aggregate gross unrealized depreciation for all investments in which there is an excess of tax cost over value | | | (3,066,454) |

| | | | | | | | |

Net unrealized appreciation | | $ | 5,853,481 |

| | | | | | | | |

| (b) | All or a portion of this security was on loan to brokers at March 31, 2008. |

| (c) | Non-income producing security. |

| (d) | Represents investment of securities lending collateral. |

| ADR | An American Depositary Receipt is a certificate issued by a custodian bank representing the right to receive securities of the foreign issuer described. The values of ADRs are significantly influenced by trading on exchanges not located in the United States. |

HOLDINGS AT MARCH 31, 2008 AS A PERCENTAGE OF NET ASSETS (Unaudited)

| | | |

Oil, Gas & Consumable Fuels | | 10.4 | % |

Life Sciences Tools & Services | | 6.6 | |

Commercial Services & Supplies | | 5.9 | |

Metals & Mining | | 5.6 | |

Health Care Equipment & Supplies | | 4.9 | |

Software | | 4.4 | |

Machinery | | 4.4 | |

Capital Markets | | 4.3 | |

Specialty Retail | | 4.2 | |

Chemicals | | 4.1 | |

Hotels, Restaurants & Leisure | | 3.9 | |

Wireless Telecommunication Services | | 3.9 | |

Diversified Financial Services | | 3.8 | |

Energy Equipment & Services | | 3.6 | |

Internet & Catalog Retail | | 3.1 | |

Semiconductors & Semiconductor Equipment | | 3.0 | |

IT Services | | 2.7 | |

Biotechnology | | 2.5 | |

Electrical Equipment | | 2.1 | |

Distributors | | 2.0 | |

Electronic Equipment & Instruments | | 2.0 | |

Other, less than 2% each | | 6.2 | |

See accompanying notes to financial statements.

13

PORTFOLIO OF INVESTMENTS – as of March 31, 2008 (Unaudited)

Loomis Sayles Small Cap Growth Fund

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – 97.4% of Net Assets | | | | | | | |

| | | |

| Aerospace & Defense – 3.1% | | | | | | | |

American Science & Engineering, Inc.(b) | | | | 18,201 | | $ | 993,229 |

Moog, Inc., Class A(b)(c) | | | | 35,487 | | | 1,497,906 |

Taser International, Inc.(b)(c) | | | | 78,806 | | | 740,776 |

| | | | | | | |

| | | | | | | 3,231,911 |

| | | | | | | |

| Biotechnology – 2.8% | | | | | | | |

BioMarin Pharmaceutical, Inc.(b)(c) | | | | 21,655 | | | 765,937 |

Indevus Pharmaceuticals, Inc.(b)(c) | | | | 130,240 | | | 621,245 |

Myriad Genetics, Inc.(b)(c) | | | | 16,305 | | | 656,928 |

United Therapeutics Corp.(c) | | | | 10,034 | | | 869,948 |

| | | | | | | |

| | | | | | | 2,914,058 |

| | | | | | | |

| Chemicals – 0.9% | | | | | | | |

Penford Corp.(b) | | | | 40,706 | | | 884,541 |

| | | | | | | |

| Commercial Banks – 1.3% | | | | | | | |

PrivateBankcorp, Inc.(b) | | | | 26,454 | | | 832,507 |

Westamerica Bancorporation | | | | 10,025 | | | 527,315 |

| | | | | | | |

| | | | | | | 1,359,822 |

| | | | | | | |

| Commercial Services & Supplies – 11.3% | | | | | | | |

Advisory Board Co.(b)(c) | | | | 25,870 | | | 1,421,298 |

FTI Consulting, Inc.(b)(c) | | | | 26,396 | | | 1,875,172 |

Geo Group, Inc. (The)(b)(c) | | | | 47,833 | | | 1,360,371 |

ICF International, Inc.(b)(c) | | | | 45,226 | | | 906,781 |

IHS, Inc., Class A(b)(c) | | | | 20,640 | | | 1,327,358 |

Innerworkings, Inc.(b)(c) | | | | 87,091 | | | 1,221,887 |

Interface, Inc., Class A(b) | | | | 55,208 | | | 775,672 |

Team, Inc.(b)(c) | | | | 40,037 | | | 1,093,010 |

Waste Connections, Inc.(b)(c) | | | | 52,923 | | | 1,626,853 |

| | | | | | | |

| | | | | | | 11,608,402 |

| | | | | | | |

| Communications Equipment – 1.3% | | | | | | | |

Foundry Networks, Inc.(b)(c) | | | | 75,449 | | | 873,699 |

Sonus Networks, Inc.(b)(c) | | | | 147,770 | | | 508,329 |

| | | | | | | |

| | | | | | | 1,382,028 |

| | | | | | | |

| Computers & Peripherals – 1.0% | | | | | | | |

Brocade Communications Systems, Inc.(b)(c) | | | | 137,585 | | | 1,004,371 |

| | | | | | | |

| Construction & Engineering – 1.7% | | | | | | | |

Northwest Pipe Co.(b)(c) | | | | 40,542 | | | 1,722,630 |

| | | | | | | |

| Distributors – 1.6% | | | | | | | |

LKQ Corp.(c) | | | | 73,535 | | | 1,652,331 |

| | | | | | | |

| Diversified Consumer Services – 4.8% | | | | | | | |

American Public Education, Inc.(c) | | | | 26,755 | | | 812,549 |

Bright Horizons Family Solutions, Inc.(b)(c) | | | | 22,076 | | | 950,151 |

Capella Education Co.(b)(c) | | | | 19,739 | | | 1,077,750 |

DeVry, Inc.(b) | | | | 23,457 | | | 981,441 |

INVESTools, Inc.(b)(c) | | | | 105,221 | | | 1,156,379 |

| | | | | | | |

| | | | | | | 4,978,270 |

| | | | | | | |

| Diversified Telecommunication Services – 2.0% | | | | | | | |

Cogent Communications Group, Inc.(b)(c) | | | | 50,663 | | | 927,640 |

NTELOS Holdings Corp. | | | | 48,632 | | | 1,176,894 |

| | | | | | | |

| | | | | | | 2,104,534 |

| | | | | | | |

14

PORTFOLIO OF INVESTMENTS – as of March 31, 2008 (Unaudited)

Loomis Sayles Small Cap Growth Fund – continued

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – continued | | | | | | | |

| | | |

| Electric Utilities – 1.1% | | | | | | | |

ITC Holdings Corp.(b) | | | | 22,511 | | $ | 1,171,923 |

| | | | | | | |

| Electronic Equipment & Instruments – 0.9% | | | | | | | |

IPG Photonics Corp.(b)(c) | | | | 58,877 | | | 923,780 |

| | | | | | | |

| Energy Equipment & Services – 4.5% | | | | | | | |

Exterran Holdings, Inc.(b)(c) | | | | 16,744 | | | 1,080,658 |

Mitcham Industries, Inc.(b)(c) | | | | 53,292 | | | 949,664 |

T-3 Energy Services, Inc.(b)(c) | | | | 25,290 | | | 1,076,342 |

Tesco Corp.(b)(c) | | | | 29,858 | | | 715,099 |

Trico Marine Services, Inc.(b)(c) | | | | 20,775 | | | 809,602 |

| | | | | | | |

| | | | | | | 4,631,365 |

| | | | | | | |

| Health Care Equipment & Supplies – 7.2% | | | | | | | |

Conceptus, Inc.(b)(c) | | | | 52,110 | | | 967,162 |

Masimo Corp.(b)(c) | | | | 38,963 | | | 1,013,038 |

Meridian Bioscience, Inc.(b) | | | | 27,034 | | | 903,747 |

Natus Medical, Inc.(b)(c) | | | | 62,843 | | | 1,140,600 |

NuVasive, Inc.(b)(c) | | | | 31,566 | | | 1,089,343 |

Orthofix International NV(b)(c) | | | | 19,242 | | | 765,254 |

Quidel Corp.(b)(c) | | | | 47,639 | | | 765,082 |

SonoSite, Inc.(b)(c) | | | | 28,865 | | | 820,632 |

| | | | | | | |

| | | | | | | 7,464,858 |

| | | | | | | |

| Health Care Providers & Services – 7.4% | | | | | | | |

athenahealth, Inc.(c) | | | | 28,425 | | | 672,820 |

CardioNet, Inc.(c) | | | | 41,636 | | | 749,032 |

HealthExtras, Inc.(b)(c) | | | | 50,128 | | | 1,245,179 |

MWI Veterinary Supply, Inc.(b)(c) | | | | 26,305 | | | 927,514 |

Psychiatric Solutions, Inc.(b)(c) | | | | 43,699 | | | 1,482,270 |

RadNet, Inc.(b)(c) | | | | 143,266 | | | 1,008,593 |

Sun Healthcare Group, Inc.(b)(c) | | | | 117,603 | | | 1,545,303 |

| | | | | | | |

| | | | | | | 7,630,711 |

| | | | | | | |

| Health Care Technology – 1.7% | | | | | | | |

Phase Forward, Inc.(b)(c) | | | | 59,931 | | | 1,023,621 |

Trizetto Group(b)(c) | | | | 46,840 | | | 781,760 |

| | | | | | | |

| | | | | | | 1,805,381 |

| | | | | | | |

| Household Durables – 0.7% | | | | | | | |

Jarden Corp.(b)(c) | | | | 32,425 | | | 704,920 |

| | | | | | | |

| Insurance – 3.5% | | | | | | | |

AmTrust Financial Services, Inc. | | | | 25,367 | | | 411,199 |

Arch Capital Group Ltd.(c) | | | | 18,238 | | | 1,252,403 |

eHealth, Inc.(b)(c) | | | | 43,183 | | | 953,049 |

Navigators Group, Inc.(c) | | | | 9,597 | | | 522,077 |

ProAssurance Corp.(b)(c) | | | | 9,206 | | | 495,559 |

| | | | | | | |

| | | | | | | 3,634,287 |

| | | | | | | |

| Internet Software & Services – 3.7% | | | | | | | |

Ariba, Inc.(b)(c) | | | | 128,049 | | | 1,236,953 |

VistaPrint Ltd.(b)(c) | | | | 40,941 | | | 1,430,888 |

Vocus, Inc.(b)(c) | | | | 43,022 | | | 1,135,781 |

| | | | | | | |

| | | | | | | 3,803,622 |

| | | | | | | |

15

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – continued | | | | | | | |

| | | |

| IT Services – 1.4% | | | | | | | |

Information Services Group, Inc.(b)(c) | | | | 95,105 | | $ | 490,742 |

Syntel, Inc.(b) | | | | 35,021 | | | 933,309 |

| | | | | | | |

| | | | | | | 1,424,051 |

| | | | | | | |

| Life Sciences Tools & Services – 3.6% | | | | | | | |

Exelixis, Inc.(b)(c) | | | | 85,166 | | | 591,904 |

Icon PLC, Sponsored ADR(b)(c) | | | | 17,285 | | | 1,121,624 |

Parexel International Corp.(b)(c) | | | | 44,799 | | | 1,169,254 |

Third Wave Technologies(b)(c) | | | | 90,038 | | | 830,150 |

| | | | | | | |

| | | | | | | 3,712,932 |

| | | | | | | |

| Machinery – 3.2% | | | | | | | |

Kadant, Inc.(c) | | | | 49,238 | | | 1,446,612 |

Middleby Corp.(b)(c) | | | | 12,076 | | | 753,422 |

RBC Bearings, Inc.(b)(c) | | | | 29,870 | | | 1,109,073 |

| | | | | | | |

| | | | | | | 3,309,107 |

| | | | | | | |

| Media – 3.1% | | | | | | | |

DG FastChannel, Inc.(b)(c) | | | | 53,746 | | | 1,030,849 |

Knology, Inc.(b)(c) | | | | 80,677 | | | 1,044,767 |

Morningstar, Inc.(b)(c) | | | | 17,875 | | | 1,096,631 |

| | | | | | | |

| | | | | | | 3,172,247 |

| | | | | | | |

| Oil, Gas & Consumable Fuels – 4.3% | | | | | | | |

Arena Resources, Inc.(c) | | | | 22,682 | | | 878,020 |

Carrizo Oil & Gas, Inc.(b)(c) | | | | 15,666 | | | 928,524 |

Petrohawk Energy Corp.(b)(c) | | | | 44,526 | | | 898,089 |

Petroleum Development Corp.(b)(c) | | | | 13,965 | | | 967,356 |

TXCO Resources, Inc.(b)(c) | | | | 60,383 | | | 747,542 |

| | | | | | | |

| | | | | | | 4,419,531 |

| | | | | | | |

| Personal Products – 0.9% | | | | | | | |

Bare Escentuals, Inc.(b)(c) | | | | 38,096 | | | 892,208 |

| | | | | | | |

| Pharmaceuticals – 0.8% | | | | | | | |

K-V Pharmaceutical Co.(b)(c) | | | | 31,351 | | | 782,521 |

| | | | | | | |

| Semiconductors & Semiconductor Equipment – 3.4% | | | | | | | |

ATMI, Inc.(b)(c) | | | | 39,189 | | | 1,090,630 |

Cavium Network, Inc.(b)(c) | | | | 53,397 | | | 875,711 |

Netlogic Microsystems, Inc.(b)(c) | | | | 40,258 | | | 971,828 |

Varian Semiconductor Equipment Associates, Inc.(c) | | | | 18,666 | | | 525,448 |

| | | | | | | |

| | | | | | | 3,463,617 |

| | | | | | | |

| Software – 8.8% | | | | | | | |

Blackbaud, Inc.(b) | | | | 50,104 | | | 1,216,525 |

Blackboard, Inc.(c) | | | | 37,830 | | | 1,260,874 |

BladeLogic, Inc.(b)(c) | | | | 34,677 | | | 972,690 |

Informatica Corp.(b)(c) | | | | 83,128 | | | 1,418,164 |

Solera Holdings, Inc.(c) | | | | 33,588 | | | 818,204 |

Taleo Corp., Class A(b)(c) | | | | 35,163 | | | 682,162 |

Tyler Technologies, Inc.(b)(c) | | | | 103,180 | | | 1,442,456 |

Ultimate Software Group, Inc.(b)(c) | | | | 40,538 | | | 1,218,572 |

| | | | | | | |

| | | | | | | 9,029,647 |

| | | | | | | |

16

PORTFOLIO OF INVESTMENTS – as of March 31, 2008 (Unaudited)

Loomis Sayles Small Cap Growth Fund – continued

| | | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | | |

| | | |

| COMMON STOCKS – continued | | | | | | | | |

| | | |

| Specialty Retail – 2.6% | | | | | | | | |

Aeropostale, Inc.(b)(c) | | | | | 29,940 | | $ | 811,673 |

Dick’s Sporting Goods, Inc.(b)(c) | | | | | 39,722 | | | 1,063,755 |

Gymboree Corp.(b)(c) | | | | | 20,593 | | | 821,249 |

| | | | | | | | |

| | | | | | | | 2,696,677 |

| | | | | | | | |

| Textiles, Apparel & Luxury Goods – 0.4% | | | | | | | | |

Movado Group, Inc.(b) | | | | | 22,245 | | | 433,555 |

| | | | | | | | |

| Trading Companies & Distributors – 1.0% | | | | | | | | |

Kaman Corp.(b) | | | | | 35,355 | | | 1,000,193 |

| | | | | | | | |

| Wireless Telecommunication Services – 1.4% | | | | | | | | |

SBA Communications Corp., Class A(b)(c) | | | | | 47,798 | | | 1,425,814 |

| | | | | | | | |

| | | |

| TOTAL COMMON STOCKS | | | | | | | | |

(Identified Cost $102,936,522) | | | | | | | | 100,375,845 |

| | | | | | | | |

| | | |

| | | | | Shares/

Principal Amount | | |

| | | |

| SHORT-TERM INVESTMENTS – 50.7% | | | | | | | | |

| State Street Navigator Securities Lending Prime Portfolio(d) | | | | | 50,220,457 | | | 50,220,457 |

| Tri-Party Repurchase Agreement with Fixed Income Clearing Corporation, dated 3/31/08 at 1.250% to be repurchased at $2,096,073 on 4/01/08 collateralized by $2,130,000 Federal Home Loan Mortgage Corp., 5.510% due 1/23/23 valued at $2,141,161 including accrued interest (Note 2g of Notes to Financial Statements) | | | | $ | 2,096,000 | | | 2,096,000 |

| | | | | | | | |

| | | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | | | | |

(Identified Cost $52,316,457) | | | | | | | | 52,316,457 |

| | | | | | | | |

| | | |

| TOTAL INVESTMENTS – 148.1% | | | | | | | | |

(Identified Cost $155,252,979)(a) | | | | | | | | 152,692,302 |

Other assets less liabilities—(48.1)% | | | | | | | | (49,581,723) |

| | | | | | | | |

| | | |

| NET ASSETS – 100.0% | | | | | | | $ | 103,110,579 |

| | | | | | | | |

| |

(†) See Note 2a of Notes to Financial Statements. | | | |

(a) Federal Tax Information (Amounts exclude certain adjustments made at the end of the Fund’s fiscal year for tax purposes. Such adjustments are primarily due to wash sales.): | | | |

At March 31, 2008, the net unrealized depreciation on investments based on a cost of $155,252,979 for federal income tax purposes was as follows: | | | |

Aggregate gross unrealized appreciation for all investments in which there is an excess of value over tax cost | | $ | 3,002,601 |

Aggregate gross unrealized depreciation for all investments in which there is an excess of tax cost over value | | | (5,563,278) |

| | | | | | | | |

Net unrealized depreciation | | | | | $ | (2,560,677) |

| | | | | | | | |

| (b) | All or a portion of this security was on loan to brokers at March 31, 2008. |

| (c) | Non-income producing security. |

| (d) | Represents investment of securities lending collateral. |

ADR An American Depositary Receipt is a certificate issued by a custodian bank representing the right to receive securities of the foreign issuer described. The values of ADRs are significantly influenced by trading on exchanges not located in the United States.

17

HOLDINGS AT MARCH 31, 2008 AS A PERCENTAGE OF NET ASSETS (Unaudited)

| | | |

Commercial Services & Supplies | | 11.3 | % |

Software | | 8.8 | |

Health Care Providers & Services | | 7.4 | |

Health Care Equipment & Supplies | | 7.2 | |

Diversified Consumer Services | | 4.8 | |

Energy Equipment & Services | | 4.5 | |

Oil, Gas & Consumable Fuels | | 4.3 | |

Internet Software & Services | | 3.7 | |

Life Sciences Tools & Services | | 3.6 | |

Insurance | | 3.5 | |

Semiconductors & Semiconductor Equipment | | 3.4 | |

Machinery | | 3.2 | |

Aerospace & Defense | | 3.1 | |

Media | | 3.1 | |

Biotechnology | | 2.8 | |

Specialty Retail | | 2.6 | |

Diversified Telecommunication Services | | 2.0 | |

Other, less than 2% each | | 18.1 | |

See accompanying notes to financial statements.

18

PORTFOLIO OF INVESTMENTS – as of March 31, 2008 (Unaudited)

Loomis Sayles Small Cap Value Fund

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – 93.2% of Net Assets | | | | | | | |

| | | |

| Aerospace & Defense – 3.6% | | | | | | | |

AAR Corp.(b)(c) | | | | 132,450 | | $ | 3,611,912 |

BE Aerospace, Inc.(c) | | | | 163,519 | | | 5,714,989 |

Ducommun, Inc.(c) | | | | 181,638 | | | 5,025,923 |

Moog, Inc., Class A(c) | | | | 255,144 | | | 10,769,628 |

Teledyne Technologies, Inc.(c) | | | | 243,109 | | | 11,426,123 |

| | | | | | | |

| | | | | | | 36,548,575 |

| | | | | | | |

| Air Freight & Logistics – 0.8% | | | | | | | |

Hub Group, Inc., Class A(c) | | | | 229,667 | | | 7,553,748 |

| | | | | | | |

| Auto Components – 0.6% | | | | | | | |

Drew Industries, Inc.(b)(c) | | | | 46,020 | | | 1,125,649 |

Gentex Corp.(b) | | | | 298,422 | | | 5,117,938 |

| | | | | | | |

| | | | | | | 6,243,587 |

| | | | | | | |

| Automobiles – 0.2% | | | | | | | |

Winnebago Industries, Inc.(b) | | | | 119,847 | | | 2,025,414 |

| | | | | | | |

| Building Products – 0.7% | | | | | | | |

Armstrong World Industries, Inc. | | | | 205,788 | | | 7,338,400 |

| | | | | | | |

| Capital Markets – 1.8% | | | | | | | |

Investment Technology Group, Inc.(c) | | | | 166,685 | | | 7,697,513 |

JMP Group, Inc.(b) | | | | 356,233 | | | 2,493,631 |

Stifel Financial Corp.(b)(c) | | | | 166,015 | | | 7,454,074 |

| | | | | | | |

| | | | | | | 17,645,218 |

| | | | | | | |

| Chemicals – 2.7% | | | | | | | |

Cytec Industries, Inc. | | | | 99,270 | | | 5,345,689 |

FMC Corp. | | | | 143,416 | | | 7,958,154 |

Minerals Technologies, Inc.(b) | | | | 96,191 | | | 6,040,795 |

Scotts Miracle-Gro Co., Class A | | | | 142,935 | | | 4,633,953 |

Zep, Inc.(b) | | | | 167,579 | | | 2,718,131 |

| | | | | | | |

| | | | | | | 26,696,722 |

| | | | | | | |

| Commercial Banks – 6.0% | | | | | | | |

Bank of the Ozarks, Inc.(b) | | | | 195,451 | | | 4,671,279 |

CVB Financial Corp.(b) | | | | 452,459 | | | 4,710,098 |

East West Bancorp, Inc.(b) | | | | 355,616 | | | 6,312,184 |

First State Bancorporation(b) | | | | 310,157 | | | 4,153,002 |

Hancock Holding Co.(b) | | | | 199,734 | | | 8,392,823 |

IBERIABANK Corp.(b) | | | | 110,759 | | | 4,901,086 |

Old National Bancorp.(b) | | | | 196,430 | | | 3,535,740 |

Pennsylvania Commerce Bancorp, Inc.(b)(c) | | | | 105,394 | | | 2,766,592 |

Prosperity Bancshares, Inc.(b) | | | | 245,189 | | | 7,027,117 |

Signature Bank(b)(c) | | | | 145,458 | | | 3,709,179 |

Sterling Bancshares, Inc.(b) | | | | 722,735 | | | 7,183,986 |

United Community Banks, Inc.(b) | | | | 205,643 | | | 3,491,818 |

| | | | | | | |

| | | | | | | 60,854,904 |

| | | | | | | |

| Commercial Services & Supplies – 6.4% | | | | | | | |

ABM Industries, Inc. | | | | 345,259 | | | 7,747,612 |

American Ecology Corp. | | | | 215,698 | | | 5,463,630 |

Geo Group, Inc. (The)(b)(c) | | | | 259,868 | | | 7,390,646 |

McGrath Rentcorp(b) | | | | 302,894 | | | 7,302,774 |

PHH Corp.(c) | | | | 170,632 | | | 2,974,116 |

Rollins, Inc. | | | | 823,475 | | | 14,567,273 |

19

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – continued | | | | | | | |

| | | |

| Commercial Services & Supplies – continued | | | | | | | |

Standard Parking Corp.(b)(c) | | | | 481,547 | | $ | 10,093,225 |

Waste Connections, Inc.(c) | | | | 302,690 | | | 9,304,691 |

| | | | | | | |

| | | | | | | 64,843,967 |

| | | | | | | |

| Communications Equipment – 2.5% | | | | | | | |

ADTRAN, Inc. | | | | 350,473 | | | 6,483,750 |

Anaren, Inc.(b)(c) | | | | 316,301 | | | 4,004,371 |

Black Box Corp. | | | | 112,911 | | | 3,483,304 |

CommScope, Inc.(b)(c) | | | | 74,336 | | | 2,589,123 |

Harris Stratex Networks, Inc., Class A(b)(c) | | | | 223,458 | | | 2,241,284 |

Tekelec(b)(c) | | | | 527,089 | | | 6,562,258 |

| | | | | | | |

| | | | | | | 25,364,090 |

| | | | | | | |

| Computers & Peripherals – 0.5% | | | | | | | |

Emulex Corp.(c) | | | | 315,984 | | | 5,131,580 |

| | | | | | | |

| Construction & Engineering – 0.4% | | | | | | | |

Granite Construction, Inc.(b) | | | | 83,247 | | | 2,723,009 |

Michael Baker Corp.(c) | | | | 69,561 | | | 1,562,340 |

| | | | | | | |

| | | | | | | 4,285,349 |

| | | | | | | |

| Construction Materials – 0.6% | | | | | | | |

Texas Industries, Inc.(b) | | | | 101,723 | | | 6,114,570 |

| | | | | | | |

| Consumer Finance – 1.0% | | | | | | | |

Dollar Financial Corp.(b)(c) | | | | 307,638 | | | 7,075,674 |

First Cash Financial Services, Inc.(b)(c) | | | | 285,707 | | | 2,951,353 |

| | | | | | | |

| | | | | | | 10,027,027 |

| | | | | | | |

| Containers & Packaging – 1.4% | | | | | | | |

Greif, Inc. | | | | 66,346 | | | 4,506,884 |

Myers Industries, Inc.(b) | | | | 261,593 | | | 3,434,716 |

Rock-Tenn Co., Class A | | | | 205,117 | | | 6,147,356 |

| | | | | | | |

| | | | | | | 14,088,956 |

| | | | | | | |

| Distributors – 0.2% | | | | | | | |

Core-Mark Holding Co., Inc.(b)(c) | | | | 57,420 | | | 1,650,251 |

| | | | | | | |

| Diversified Consumer Services – 0.6% | | | | | | | |

INVESTools, Inc.(b)(c) | | | | 408,757 | | | 4,492,240 |

Jackson Hewitt Tax Service, Inc.(b) | | | | 122,022 | | | 1,399,592 |

| | | | | | | |

| | | | | | | 5,891,832 |

| | | | | | | |

| Electric Utilities – 1.8% | | | | | | | |

ALLETE, Inc.(b) | | | | 169,935 | | | 6,562,889 |

ITC Holdings Corp.(b) | | | | 122,562 | | | 6,380,578 |

Portland General Electric Co. | | | | 230,716 | | | 5,202,646 |

| | | | | | | |

| | | | | | | 18,146,113 |

| | | | | | | |

| Electrical Equipment – 3.0% | | | | | | | |

Acuity Brands, Inc.(b) | | | | 137,851 | | | 5,920,700 |

Belden, Inc.(b) | | | | 69,862 | | | 2,467,526 |

General Cable Corp.(b)(c) | | | | 133,851 | | | 7,906,579 |

II-VI, Inc.(b)(c) | | | | 228,348 | | | 8,672,657 |

Polypore International, Inc.(b)(c) | | | | 242,680 | | | 5,021,049 |

| | | | | | | |

| | | | | | | 29,988,511 |

| | | | | | | |

20

PORTFOLIO OF INVESTMENTS – as of March 31, 2008 (Unaudited)

Loomis Sayles Small Cap Value Fund – continued

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – continued | | | | | | | |

| | | |

| Electronic Equipment & Instruments – 3.9% | | | | | | | |

Agilysys, Inc.(b) | | | | 246,591 | | $ | 2,860,456 |

Anixter International, Inc.(b)(c) | | | | 72,597 | | | 4,649,112 |

Excel Technology, Inc.(c) | | | | 161,670 | | | 4,358,623 |

Littelfuse, Inc.(c) | | | | 330,808 | | | 11,568,356 |

Plexus Corp.(c) | | | | 154,220 | | | 4,325,871 |

Rofin-Sinar Technologies, Inc.(c) | | | | 118,661 | | | 5,327,879 |

Vishay Intertechnology, Inc.(c) | | | | 514,017 | | | 4,656,994 |

X-Rite, Inc.(b)(c) | | | | 244,088 | | | 1,457,205 |

| | | | | | | |

| | | | | | | 39,204,496 |

| | | | | | | |

| Energy Equipment & Services – 2.6% | | | | | | | |

Dresser-Rand Group, Inc.(c) | | | | 207,410 | | | 6,377,858 |

Exterran Holdings, Inc.(b)(c) | | | | 77,026 | | | 4,971,258 |

Helix Energy Solutions Group, Inc.(c) | | | | 130,358 | | | 4,106,277 |

Oceaneering International, Inc.(c) | | | | 117,421 | | | 7,397,523 |

TETRA Technologies, Inc.(b)(c) | | | | 185,237 | | | 2,934,154 |

| | | | | | | |

| | | | | | | 25,787,070 |

| | | | | | | |

| Food & Staples Retailing – 1.3% | | | | | | | |

Casey’s General Stores, Inc.(b) | | | | 231,251 | | | 5,226,273 |

Spartan Stores, Inc.(b) | | | | 388,250 | | | 8,095,012 |

| | | | | | | |

| | | | | | | 13,321,285 |

| | | | | | | |

| Food Products – 1.2% | | | | | | | |

J & J Snack Foods Corp. | | | | 142,510 | | | 3,914,750 |

Ralcorp Holdings, Inc.(b)(c) | | | | 141,367 | | | 8,220,491 |

| | | | | | | |

| | | | | | | 12,135,241 |

| | | | | | | |

| Gas Utilities – 1.4% | | | | | | | |

UGI Corp. | | | | 552,790 | | | 13,775,527 |

| | | | | | | |

| Health Care Equipment & Supplies – 1.3% | | | | | | | |

Orthofix International NV(c) | | | | 121,813 | | | 4,844,503 |

West Pharmaceutical Services, Inc.(b) | | | | 194,888 | | | 8,619,896 |

| | | | | | | |

| | | | | | | 13,464,399 |

| | | | | | | |

| Health Care Providers & Services – 3.2% | | | | | | | |

Amedisys, Inc.(b)(c) | | | | 153,931 | | | 6,055,645 |

CorVel Corp.(c) | | | | 208,162 | | | 6,367,676 |

Healthspring, Inc.(c) | | | | 182,675 | | | 2,572,064 |

inVentiv Health, Inc.(c) | | | | 263,574 | | | 7,593,567 |

MWI Veterinary Supply, Inc.(b)(c) | | | | 120,394 | | | 4,245,092 |

Skilled Healthcare Group, Inc., Class A(b)(c) | | | | 476,366 | | | 5,230,499 |

| | | | | | | |

| | | | | | | 32,064,543 |

| | | | | | | |

| Hotels, Restaurants & Leisure – 1.7% | | | | | | | |

Bob Evans Farms, Inc.(b) | | | | 213,375 | | | 5,887,016 |

CEC Entertainment, Inc.(c) | | | | 259,820 | | | 7,503,602 |

Cosi, Inc.(b)(c) | | | | 1,391,575 | | | 3,993,820 |

| | | | | | | |

| | | | | | | 17,384,438 |

| | | | | | | |

| Industrial Conglomerates – 0.9% | | | | | | | |

Teleflex, Inc. | | | | 128,379 | | | 6,124,962 |

Walter Industries, Inc. | | | | 43,550 | | | 2,727,537 |

| | | | | | | |

| | | | | | | 8,852,499 |

| | | | | | | |

21

| | | | | | | |

| | | | | Shares | | Value (†) |

| | | | | | | |

| | | |

| COMMON STOCKS – continued | | | | | | | |

| | | |

| Insurance – 4.8% | | | | | | | |

American Equity Investment Life Holding Co.(b) | | | | 555,085 | | $ | 5,151,189 |

American Physicians Capital, Inc. | | | | 96,826 | | | 4,488,853 |

Delphi Financial Group, Inc. | | | | 210,969 | | | 6,166,624 |

Employers Holdings, Inc. | | | | 336,817 | | | 6,244,587 |

First Mercury Financial Corp.(c) | | | | 94,334 | | | 1,642,355 |

Midland Co. (The)(b) | | | | 124,506 | | | 8,084,175 |

Navigators Group, Inc.(c) | | | | 103,178 | | | 5,612,883 |

ProAssurance Corp.(b)(c) | | | | 96,672 | | | 5,203,854 |

RLI Corp.(b) | | | | 120,788 | | | 5,987,461 |

| | | | | | | |

| | | | | | | 48,581,981 |

| | | | | | | |

| Internet Software & Services – 0.4% | | | | | | | |

United Online, Inc.(b) | | | | 418,576 | | | 4,420,163 |

| | | | | | | |

| IT Services – 3.7% | | | | | | | |

Alliance Data Systems Corp.(c) | | | | 209,706 | | | 9,963,132 |

Broadridge Financial Solutions, Inc. | | | | 512,615 | | | 9,022,024 |

Perot Systems Corp., Class A(c) | | | | 410,651 | | | 6,176,191 |

Wright Express Corp.(c) | | | | 408,653 | | | 12,557,907 |

| | | | | | | |

| | | | | | | 37,719,254 |

| | | | | | | |

| Leisure Equipment & Products – 0.5% | | | | | | | |

Steinway Musical Instruments, Inc.(b)(c) | | | | 158,470 | | | 4,519,564 |

| | | | | | | |

| Life Sciences Tools & Services – 0.7% | | | | | | | |

PerkinElmer, Inc. | | | | 280,637 | | | 6,805,447 |

| | | | | | | |

| Machinery – 4.7% | | | | | | | |

Actuant Corp., Class A(b) | | | | 332,237 | | | 10,036,880 |

CLARCOR, Inc.(b) | | | | 145,721 | | | 5,180,382 |

Commercial Vehicle Group, Inc.(b)(c) | | | | 210,155 | | | 2,082,636 |

ESCO Technologies, Inc.(b)(c) | | | | 121,429 | | | 4,823,160 |

Harsco Corp. | | | | 135,666 | | | 7,513,183 |

Nordson Corp.(b) | | | | 59,559 | | | 3,207,252 |

RBC Bearings, Inc.(c) | | | | 195,392 | | | 7,254,905 |

Wabtec Corp. | | | | 179,423 | | | 6,757,070 |

| | | | | | | |

| | | | | | | 46,855,468 |

| | | | | | | |

| Media – 3.0% | | | | | | | |

A H Belo Corp., Class A(b) | | | | 323,897 | | | 3,702,143 |

Alloy, Inc.(c) | | | | 231,904 | | | 1,704,494 |

Belo Corp., Class A | | | | 298,257 | | | 3,152,576 |

Interactive Data Corp. | | | | 342,107 | | | 9,739,786 |

John Wiley & Sons, Inc., Class A | | | | 296,265 | | | 11,761,721 |

| | | | | | | |

| | | | | | | 30,060,720 |

| | | | | | | |

| Metals & Mining – 1.2% | | | | | | | |

Haynes International, Inc.(b)(c) | | | | 54,118 | | | 2,969,996 |

Reliance Steel & Aluminum Co.(b) | | | | 159,568 | | | 9,551,740 |

| | | | | | | |

| | | | | | | 12,521,736 |

| | | | | | | |

| Multi-Utilities & Unregulated Power – 0.4% | | | | | | | |