UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08282

Loomis Sayles Funds I

(Exact name of Registrant as specified in charter)

| 888 Boylston Street, Suite 800 Boston, Massachusetts | 02199-8197 | |

| (Address of principal executive offices) | (Zip code) |

Susan McWhan Tobin, Esq.

Natixis Distribution, LLC

888 Boylston Street, Suite 800

Boston, Massachusetts 02199-8197

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2139

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Item 1. Reports to Stockholders.

| (a) | The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows: |

Loomis Sayles Bond Fund

Loomis Sayles Investment Grade Fixed Income Fund

Annual Report

December 31, 2022

| TABLE OF CONTENTS | ||||

| Portfolio Review | 1 | |||

| Portfolio of Investments | 9 | |||

| Financial Statements | 39 | |||

| Notes to Financial Statements | 47 | |||

| Managers | Symbols | |||

| Matthew J. Eagan, CFA® | Institutional Class | LSBDX | ||

| Brian P. Kennedy | Retail Class | LSBRX | ||

| Elaine M. Stokes | Admin Class | LBFAX | ||

| Class N | LSBNX | |||

Investment Objective

The Fund’s investment objective is high total investment return through a combination of current income and capital appreciation.

Market Conditions

The global bond market suffered pronounced weakness in 2022. Coming into the year, investors were already on edge as the investment community slowly began to understand that inflation would not be as “transitory” as initially expected. The outlook grew even more challenging after Russia’s invasion of Ukraine caused a jump in commodity prices and additional disruptions in global supply chains. Consumer price inflation (CPI) further increased as a result, with year-over-year gains of more than 8% in each monthly report of the second quarter. Inflation stayed elevated for the rest of the year before showing signs of cooling in the fourth quarter. Still, CPI remained above 6% through the last three quarters of the year, well above the US Federal Reserve’s (Fed’s) 2% target.

These developments prompted the Fed and other major central banks to tighten monetary policy aggressively. The Fed, in addition to ending its stimulative quantitative easing policy, raised interest rates at seven consecutive meetings from March onward. The benchmark fed funds rate, which stood in a range of 0% to 0.25% at the start of 2022, finished the year at 4.25% to 4.50%. This represented the most aggressive increase in short-term rates since the early 1980s.

The backdrop of high inflation and rising rates weighed heavily on US Treasuries. The yield on the two-year note surged from 0.39% to 4.41% over the course of 2022, while the 10-year yield climbed from 1.44% to 3.88%. The Treasury market suffered its second consecutive year of negative returns in 2022 – the first time this has happened since 1958–59. One result of these moves was that the yield curve inverted significantly (meaning that short-term yields traded above those on longer-term debt), an unusual event that typically precedes a recession.

Investment grade corporate bonds posted a double-digit loss and lagged US Treasuries. In addition to suffering from the uptrend in prevailing yields, corporates experienced a large increase in yield spreads relative to government debt. Rising spreads were the result of investors’ declining appetite for risk and concerns about the impact slowing economic growth could have on corporations’ earnings and balance sheets.

High yield bonds, while finishing 2022 in the red, outperformed US Treasuries and other segments of the investment grade market. The category was helped by its higher income, lower interest rate sensitivity, and a relatively large representation of the energy sector. Senior loans, which experienced elevated demand due to their floating rate feature, were the best-performing segment of the fixed income market for the year with a return just below the break-even mark.

Securitized assets – including agency mortgage-backed securities (MBS), asset-backed securities (ABS), and commercial mortgage-backed securities (CMBS) – posted negative total returns but outperformed the broader US bond market due to the category’s shorter duration (lower interest rate sensitivity). ABS, particularly credit card and auto ABS, were the strongest performers among securitized assets due to their higher quality, better liquidity, and shorter duration.

Emerging market bonds underperformed the US due to the combination of growth fears, investors’ increased aversion to risk, the conflict in Ukraine, and negative headlines out of China. US-based investors were also hurt by a meaningful decline in emerging market currencies in relation to the US dollar.

Performance Results

For the 12 months ended December 31, 2022, Institutional Class shares of the Loomis Sayles Bond Fund returned -12.49% at net asset value. The Fund outperformed its benchmark, the Bloomberg U.S. Government/Credit Bond Index, which returned -13.58%.

Explanation of Fund Performance

Despite an extremely challenging year for fixed income markets, the Fund posted positive relative returns versus its benchmark. Yield curve positioning was the primary source of outperformance. The Fund has been targeting an overall duration shorter than that of the benchmark, which has been a positive contributor given the sharp upward movement in interest rates. We utilized Treasury futures to assist with meeting this objective. We have added back duration over the course of the year, but on a relative basis, remain short versus the benchmark. Securitized credit was also beneficial given the sector’s shorter duration profile. Here, holdings in asset-backed securities (ABS) and collateralized loan obligations (CLOs) aided returns. An allocation to equities was also positive for relative returns. For equities, the team has employed a basket approach – seeking a diversified allocation that provides attractive dividend yields and capital appreciation potential versus fixed income. This exposure was reduced during the year as fixed income yields increased. Finally, performance was aided by defensive, reserve-like positions as risk-off sentiment prevailed.

1 |

Exposure to high yield credit was the primary source of underperformance for the Fund. High yield has lagged as aggressive central bank policy and an increasingly slower growth outlook have put pressure on risk assets. In addition, a handful of our higher conviction positions, particularly in the communications sector, have underperformed the broader market. The team’s investment thesis for these higher conviction positions started to play out in the second half of the year, but was not enough to offset the drawdown experienced earlier in the period. An allocation to emerging market credit was also a detractor of relative returns, with holdings in Chinese property developers as the main sources of underperformance. Extended Covid-related lockdowns in China had exacerbated already-declining housing sales and government measures taken thus far to alleviate stresses on this sector had been limited, resulting in further bond price erosion. More recently, however, we have started to see coordinated efforts here as Chinese authorities release rounds of policies to support the property sector. Finally, convertible securities weighed on returns given the tumultuous equity market backdrop. Here, selected communications holdings were performance laggards.

Outlook

Initial inflation data in the beginning of the fourth quarter of 2022 came in above expectations; however, subsequent readings were moderately positive, suggesting we may have passed peak inflation. The positive news appeared to usher in optimism that perhaps the Fed’s aggressive rate hiking cycle is finally working to bring inflation down. As we moved closer to the potential peak in Fed policy, risk assets stabilized and spreads on investment grade and high yield corporates finished the quarter at tighter levels.

In our view, the credit cycle1 is firmly in the late cycle stage and the risk of downturn has become more balanced. We expect growth to continue to trend lower as manufacturing and housing metrics have deteriorated; however, in our view the US consumer appears on solid footing, maintaining strong levels of excess savings and continuing to spend at a healthy rate. Labor markets remain tight. We’ve observed higher wages, cost of living adjustments, an elevated number of job openings and employers who are reluctant to shed workers in industries where they may have trouble getting them back, which could help to support consumer confidence. We believe a healthy consumer combined with positive corporate fundamentals and a strong banking system should help provide a floor to economic activity and support credit fundamentals to some degree.

While inflation has likely peaked and positive real rates should have the effect of slowing growth and rolling inflation down over time, we believe inflation will likely remain sticky and above the Fed’s target throughout 2023, primarily as result of wage pressure. We now believe much of the movement from the Fed has occurred or is currently being priced into the market, which in turn may also put a cap on the Treasury curve. We’re currently expecting an additional 50 bps of tightening in the first quarter of 2023, which would bring the policy rate up to 5.00% after the March meeting. In our view, the market continues to want to compress this cycle and lean towards a Fed pivot, but we believe inflation is structural at this point. We find it difficult for the Fed to begin cutting rates when inflation remains above their target. As a result, we’re anticipating a Fed pause after the March meeting which would likely extend into the latter stage of 2023. Throughout the year, the Fed will likely be driven by the extent to which there is firm evidence of inflation moderating, and at this point, we have not eliminated the possibility that the next Fed move could be a rate hike. We expect the US 10-year bond yield to move only modestly higher from here and we continue to be positioned defensively on rate risk, but to a lesser extent than earlier in 2022.

We believe that value has returned to US fixed income markets. Bond structures (price, yield and spread) appear relatively attractive. While corporate bond spreads in both investment grade and high yield are currently tighter than their long-term averages, we believe overall yields remain favorable post the 2008 Great Financial Crisis (GFC). Dollar prices on bonds are also currently at post-GFC lows. We believe the combination of discount-to-par and attractive yield could be increasing the potential value opportunity in bonds. We remain mindful of the risks to the global economy, such as tighter financial conditions, slowing Chinese growth, the Eastern Europe conflict, disruptions to the global supply chain and the lingering effects of the Covid pandemic. All of the turmoil around the world leaves us with a wide range of potential outcomes for growth, inflation, and central bank policy response. With the likelihood of downturn in 2023 rising, we have been holding larger than average liquid reserves and seeking to maintain an up-in-quality bias. If volatility increases and we see what we view as more attractive yields and spreads, we would consider redeploying reserves. At the same time, short-term yields have risen meaningfully and we are comfortable with how we are being compensated as we wait for opportunities to potentially develop.

| 1 | A credit cycle is a cyclical pattern that follows credit availability and corporate health. |

| 2

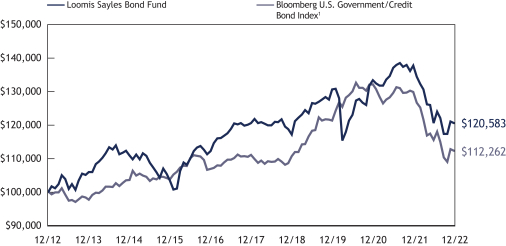

LOOMIS SAYLES BOND FUND

Hypothetical Growth of $100,000 Investment in Institutional Class Shares2

December 31, 2012 through December 31, 2022

Average Annual Total Returns — December 31, 20222

Life of | Expense Ratios3 | |||||||||||||||||||||||

1 Year | 5 Years | 10 Years | Class N | Gross | Net | |||||||||||||||||||

Institutional Class | -12.49 | % | 0.00 | % | 1.89 | % | — | % | 0.68 | % | 0.67 | % | ||||||||||||

Retail Class | -12.78 | -0.26 | 1.63 | — | 0.93 | 0.92 | ||||||||||||||||||

Admin Class | -12.91 | -0.49 | 1.39 | — | 1.16 | 1.15 | ||||||||||||||||||

Class N (Inception 2/1/13) | -12.46 | 0.05 | — | 1.78 | 0.61 | 0.61 | ||||||||||||||||||

Comparative Performance | ||||||||||||||||||||||||

Bloomberg U.S. Government/Credit Bond Index1 | -13.58 | 0.21 | 1.16 | 1.26 | ||||||||||||||||||||

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit loomissayles.com. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Bloomberg U.S. Government/Credit Bond Index is the non-securitized component of the U.S. Aggregate Index. The U.S. Government/Credit Bond Index includes investment grade, U.S. dollar-denominated, fixed rate Treasuries (i.e., public obligations of the U.S. Treasury that have remaining maturities of more than one year), government-related issues (i.e., agency, sovereign, supranational, and local authority debt), and corporate securities. The U.S. Government/Credit Index was launched on January 1, 1979, with index history backfilled to 1973, and is a subset of the U.S. Aggregate Index. |

| 2 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 3 | Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/23. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

3 |

LOOMIS SAYLES INVESTMENT GRADE FIXED INCOME FUND

| Managers | Symbols | |||

| Matthew J. Eagan, CFA® | Institutional Class | LSIGX | ||

| Brian P. Kennedy | ||||

| Elaine M. Stokes | ||||

Investment Objective

The Fund’s investment objective is above-average total investment return through a combination of current income and capital appreciation.

Market Conditions

The global bond market suffered pronounced weakness in 2022. Coming into the year, investors were already on edge as the investment community slowly began to understand that inflation would not be as “transitory” as initially expected. The outlook grew even more challenging after Russia’s invasion of Ukraine caused a jump in commodity prices and additional disruptions in global supply chains. Consumer price inflation (CPI) further increased as a result, with year-over-year gains of more than 8% in each monthly report of the second quarter. Inflation stayed elevated for the rest of the year before showing signs of cooling in the fourth quarter. Still, CPI remained above 6% through the last three quarters of the year, well above the US Federal Reserve’s (Fed’s) 2% target.

These developments prompted the Fed and other major central banks to tighten monetary policy aggressively. The Fed, in addition to ending its stimulative quantitative easing policy, raised interest rates at seven consecutive meetings from March onward. The benchmark fed funds rate, which stood in a range of 0% to 0.25% at the start of 2022, finished the year at 4.25% to 4.50%. This represented the most aggressive increase in short-term rates since the early 1980s.

The backdrop of high inflation and rising rates weighed heavily on US Treasuries. The yield on the two-year note surged from 0.39% to 4.41% over the course of 2022, while the 10-year yield climbed from 1.44% to 3.88%. The Treasury market suffered its second consecutive year of negative returns in 2022 – the first time this has happened since 1958–59. One result of these moves was that the yield curve inverted significantly (meaning that short-term yields traded above those on longer-term debt), an unusual event that typically precedes a recession.

Investment grade corporate bonds posted a double-digit loss and lagged US Treasuries. In addition to suffering from the uptrend in prevailing yields, corporates experienced a large increase in yield spreads relative to government debt. Rising spreads were the result of investors’ declining appetite for risk and concerns about the impact slowing economic growth could have on corporations’ earnings and balance sheets.

High yield bonds, while finishing 2022 in the red, outperformed US Treasuries and other segments of the investment grade market. The category was helped by its higher income, lower interest rate sensitivity, and a relatively large representation of the energy sector. Senior loans, which experienced elevated demand due to their floating rate feature, were the best-performing segment of the fixed income market for the year with a return just below the break-even mark.

Securitized assets – including agency mortgage-backed securities (MBS), asset-backed securities (ABS), and commercial mortgage-backed securities (CMBS) – posted negative total returns but outperformed the broader US bond market due to the category’s shorter duration (lower interest rate sensitivity). ABS, particularly credit card and auto ABS, were the strongest performers among securitized assets due to their higher quality, better liquidity, and shorter duration.

Emerging market bonds underperformed the US due to the combination of growth fears, investors’ increased aversion to risk, the conflict in Ukraine, and negative headlines out of China. US-based investors were also hurt by a meaningful decline in emerging market currencies in relation to the US dollar.

Performance Results

For the 12 months ended December 31, 2022, Institutional Class shares of the Loomis Sayles Investment Grade Fixed Income Fund returned -11.98% at net asset value. The Fund outperformed its benchmark, the Bloomberg U.S. Government/Credit Bond Index, which returned -13.58%.

Explanation of Fund Performance

Despite an extremely challenging year for fixed income markets, the Fund posted positive relative returns versus its benchmark. Yield curve positioning was the primary source of outperformance. The Fund has been targeting an overall duration shorter than that of the benchmark, which has been a positive contributor given the sharp upward movement in interest rates. We utilized Treasury futures to assist with meeting this objective. We have added back duration over the course of the year, but on a relative basis remain moderately short versus the benchmark. Securitized credit was a larger contributor given the sector’s shorter duration profile. Here, holdings in asset-backed securities (ABS) and collateralized loan obligations (CLOs) aided returns. An allocation to equities was also positive for relative returns. For equities, the team has employed a basket approach – seeking a diversified allocation that provides attractive dividend yields and capital appreciation potential versus

| 4

LOOMIS SAYLES INVESTMENT GRADE FIXED INCOME FUND

fixed income. This exposure was reduced during the year as fixed income yields increased. Finally, performance was aided by defensive, reserve-like positions as risk-off sentiment prevailed.

An allocation to emerging market credit was a detractor of relative returns, with holdings in Chinese property developers as the main sources of underperformance. Extended Covid-related lockdowns in China had exacerbated already-declining housing sales and government measures taken thus far to alleviate stresses on this sector had been limited, resulting in further bond price erosion. More recently, however, we have started to see coordinated efforts here as Chinese authorities release rounds of policies to support the property sector. Exposure to high yield was also a source of underperformance for the Fund. High yield has lagged as aggressive central bank policy and an increasingly slower growth outlook has put pressure on risk assets. In addition, a handful of our higher conviction positions, particularly in the communications sector, have underperformed the broader market. The team’s investment thesis for these higher conviction positions started to play out in the second half of the year but was not enough to offset the drawdown experienced earlier in the period.

Outlook

Initial inflation data in the beginning of the fourth quarter of 2022 came in above expectations; however, subsequent readings were moderately positive, suggesting we may have passed peak inflation. The positive news appeared to usher in optimism that perhaps the Fed’s aggressive rate hiking cycle is finally working to bring inflation down. As we moved closer to the potential peak in Fed policy, risk assets stabilized and spreads on investment grade and high yield corporates finished the quarter at tighter levels.

In our view, the credit cycle1 is firmly in the late cycle stage and the risk of downturn has become more balanced. We expect growth to continue to trend lower as manufacturing and housing metrics have deteriorated; however, in our view the US consumer appears on solid footing, maintaining strong levels of excess savings and continuing to spend at a healthy rate. Labor markets remain tight. We’ve observed higher wages, cost of living adjustments, an elevated number of job openings and employers who are reluctant to shed workers in industries where they may have trouble getting them back, which could help to support consumer confidence. We believe a healthy consumer combined with positive corporate fundamentals and a strong banking system should help provide a floor to economic activity and support credit fundamentals to some degree. While inflation has likely peaked and positive real rates should have the effect of slowing growth and rolling inflation down over time, we believe inflation will likely remain sticky and above the Fed’s target throughout 2023, primarily as result of wage pressure. We now believe much of the movement from the Fed has occurred or is currently being priced into the market, which in turn may also put a cap on the Treasury curve. We’re currently expecting an additional 50 bps of tightening in the first quarter of 2023, which would bring the policy rate up to 5.00% after the March meeting. In our view, the market continues to want to compress this cycle and lean towards a Fed pivot, but we believe inflation is structural at this point. We find it difficult for the Fed to begin cutting rates when inflation remains above their target. As a result, we’re anticipating a Fed pause after the March meeting which would likely extend into the latter stage of 2023. Throughout the year, the Fed will likely be driven by the extent to which there is firm evidence of inflation moderating, and at this point, we have not eliminated the possibility that the next Fed move could be a rate hike. We expect the US 10-year bond yield to move only modestly higher from here and we continue to be positioned defensively on rate risk, but to a lesser extent than earlier in 2022.

We believe that value has returned to US fixed income markets. Bond structures (price, yield and spread) appear relatively attractive. While corporate bond spreads in both investment grade and high yield are currently tighter than their long-term averages, we believe overall yields remain favorable post the 2008 Great Financial Crisis (GFC). Dollar prices on bonds are also currently at post-GFC lows. We believe the combination of discount-to-par and attractive yield could be increasing the potential value opportunity in bonds. We remain mindful of the risks to the global economy, such as tighter financial conditions, slowing Chinese growth, the Eastern Europe conflict, disruptions to the global supply chain and the lingering effects of the Covid pandemic. All of the turmoil around the world leaves us with a wide range of potential outcomes for growth, inflation, and central bank policy response. With the likelihood of downturn in 2023 rising, we have been holding larger than average liquid reserves and seeking to maintain an up-in-quality bias. If volatility increases and we see what we view as more attractive yields and spreads, we would consider redeploying reserves. At the same time, short-term yields have risen meaningfully and we are comfortable with how we are being compensated as we wait for opportunities to potentially develop.

| 1 | A credit cycle is a cyclical pattern that follows credit availability and corporate health. |

5 |

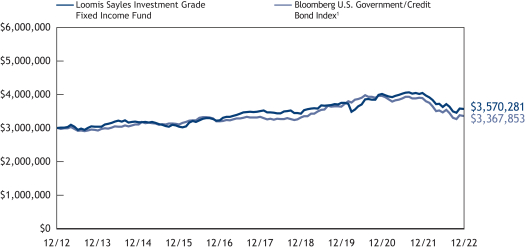

Hypothetical Growth of $3,000,000 Investment in Institutional Class Shares2

December 31, 2012 through December 31, 2022

Average Annual Total Returns — December 31, 20222

| Expense Ratios3 | ||||||||||||||||||||

1 Year | 5 Years | 10 Years | Gross | Net | ||||||||||||||||

Institutional Class | -11.98 | % | 0.36 | % | 1.75 | % | 0.52 | % | 0.52 | % | ||||||||||

Comparative Performance | ||||||||||||||||||||

Bloomberg U.S. Government/Credit Bond Index1 | -13.58 | 0.21 | 1.16 | |||||||||||||||||

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit loomissayles.com. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Bloomberg U.S. Government/Credit Bond Index is the non-securitized component of the U.S. Aggregate Index. The U.S. Government/Credit Bond Index includes investment grade, U.S. dollar-denominated, fixed-rate Treasuries (i.e., public obligations of the U.S. Treasury that have remaining maturities of more than one year), government-related issues (i.e., agency, sovereign, supranational, and local authority debt), and corporate securities. The U.S. Government/Credit Index was launched on January 1, 1979, with index history backfilled to 1973, and is a subset of the Bloomberg U.S. Aggregate Index. |

| 2 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 3 | Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 4/30/23. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| 6

ADDITIONAL INFORMATION

The views expressed in this report reflect those of the portfolio managers as of the dates indicated. The managers’ views are subject to change at any time without notice based on changes in market or other conditions. References to specific securities or industries should not be regarded as investment advice. Because the Fund is actively managed, there is no assurance that they will continue to invest in the securities or industries mentioned.

All investing involves risk, including the risk of loss. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

Additional Index Information

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis Affiliates”) and does not sponsor, endorse or participate in the provision of any Natixis Affiliates services, funds or other financial products.

The index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

Proxy Voting Information

A description of the Fund’s proxy voting policies and procedures is available without charge upon request, by calling Loomis Sayles Funds at 800-633-3330; on the Fund’s website at www.loomissayles.com, and on the Securities and Exchange Commission’s (“SEC’s”) website at www.sec.gov. Information about how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available from the Fund’s website and the SEC’s website.

Quarterly Portfolio Schedules

The Loomis Sayles Funds file a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Funds’ Form N-PORT reports are available on the SEC’s website at www.sec.gov. First and third quarter schedules of portfolio holdings are also available at loomissayles.com. A hard copy may be requested from the Fund at no charge by calling 800-633-3330.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

UNDERSTANDING YOUR FUND’S EXPENSES

As a mutual fund shareholder you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees, distribution and/or service fees (12b-1 fees), and other fund expenses. Certain exemptions may apply. These costs are described in more detail in the Fund’s prospectus. The following examples are intended to help you understand the ongoing costs of investing in the Fund and help you compare these with the ongoing costs of investing in other mutual funds.

The first line in the table for each class of Fund shares shows the actual amount of Fund expenses you would have paid on a $1,000 investment in the Fund from July 1, 2022 through December 31, 2022. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example $8,600 account value divided by $1,000 = 8.6) and multiply the result by the number in the Expenses Paid During Period column as shown below for your class.

The second line in the table for each class of Fund shares provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid on your investment for the period. You may use this information to compare the ongoing costs of investing in the Fund to other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

7 |

Please note that the expenses shown reflect ongoing costs only, and do not include any transaction costs. Therefore, the second line in the table is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. If transaction costs were included, total costs would be higher.

Loomis Sayles Bond Fund

Institutional Class | Beginning Account Value 7/1/2022 | Ending Account Value 12/31/2022 | Expenses Paid During Period* 7/1/2022 – 12/31/2022 | |||||||||

Actual | $1,000.00 | $1,000.20 | $3.38 | |||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,021.83 | $3.41 | |||||||||

Retail Class | ||||||||||||

Actual | $1,000.00 | $998.90 | $4.64 | |||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,020.57 | $4.69 | |||||||||

Admin Class | ||||||||||||

Actual | $1,000.00 | $998.50 | $5.89 | |||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,019.31 | $5.96 | |||||||||

Class N | ||||||||||||

Actual | $1,000.00 | $1,000.50 | $3.18 | |||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,022.03 | $3.21 | |||||||||

* Expenses are equal to the Fund’s annualized expense ratio (after waiver/reimbursement): 0.67%, 0.92%, 1.17% and 0.63% for Institutional Class, Retail Class, Admin Class and Class N, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), divided by 365 (to reflect the half-year period). |

| |||||||||||

Loomis Sayles Investment Grade Fixed Income Fund

Institutional Class | Beginning Account Value 7/1/2022 | Ending Account Value 12/31/2022 | Expenses Paid During Period* 7/1/2022 – 12/31/2022 | |||||||||

Actual | $1,000.00 | $983.70 | $2.70 | |||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,022.48 | $2.75 | |||||||||

* Expenses are equal to the Fund’s annualized expense ratio of 0.54%, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), divided by 365 (to reflect the half-year period). |

| |||||||||||

| 8

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – 91.0% of Net Assets | ||||||||

| Non-Convertible Bonds – 83.8% | ||||||||

| ABS Car Loan – 4.2% | ||||||||

| $ | 12,980,000 | American Credit Acceptance Receivables Trust, Series 2021-4, Class D, 1.820%, 2/14/2028, 144A | $ | 11,882,048 | ||||

| 3,685,000 | American Credit Acceptance Receivables Trust, Series 2022-1, Class D, 2.460%, 3/13/2028, 144A | 3,315,558 | ||||||

| 1,470,000 | American Credit Acceptance Receivables Trust, Series 2022-4, Class C, 7.860%, 2/15/2029, 144A | 1,488,599 | ||||||

| 13,000,000 | Avis Budget Rental Car Funding AESOP LLC, 3.040%, 3/20/2025, 144A | 12,164,594 | ||||||

| 1,680,000 | Avis Budget Rental Car Funding AESOP LLC, Series 2019-2A, Class C, 4.240%, 9/22/2025, 144A | 1,602,771 | ||||||

| 6,300,000 | Avis Budget Rental Car Funding AESOP LLC, Series 2019-3A, Class C, 3.150%, 3/20/2026, 144A | 5,776,735 | ||||||

| 3,880,000 | Avis Budget Rental Car Funding AESOP LLC, Series 2020-2A, Class C, 4.250%, 2/20/2027, 144A | 3,463,979 | ||||||

| 1,745,000 | Avis Budget Rental Car Funding AESOP LLC, Series 2021-1A, Class C, 2.130%, 8/20/2027, 144A | 1,450,524 | ||||||

| 3,470,000 | Avis Budget Rental Car Funding AESOP LLC, Series 2021-2A, Class C, 2.350%, 2/20/2028, 144A | 2,869,490 | ||||||

| 1,255,000 | CarMax Auto Owner Trust, Series 2022-1, Class D, 2.470%, 7/17/2028 | 1,092,192 | ||||||

| 6,243,116 | Carvana Auto Receivables Trust, Series 2021-N3, Class C, 1.020%, 6/12/2028 | 6,034,336 | ||||||

| 2,825,000 | Carvana Auto Receivables Trust, Series 2021-N4, Class C, 1.720%, 9/11/2028 | 2,696,611 | ||||||

| 6,410,000 | Carvana Auto Receivables Trust, Series 2021-N4, Class D, 2.300%, 9/11/2028 | 5,820,010 | ||||||

| 6,400,000 | Carvana Auto Receivables Trust, Series 2021-P3, Class C, 1.930%, 10/12/2027 | 5,095,489 | ||||||

| 3,032,000 | Carvana Auto Receivables Trust, 2.330%, 2/10/2028 | 2,492,395 | ||||||

| 4,020,000 | Credit Acceptance Auto Loan Trust, 1.630%, 9/16/2030, 144A | 3,624,334 | ||||||

| ABS Car Loan – continued | ||||||||

| $ | 8,080,000 | Credit Acceptance Auto Loan Trust, Series 2021-4, Class C, 1.940%, 2/18/2031, 144A | $ | 7,278,908 | ||||

| 3,680,000 | DT Auto Owner Trust, Series 2020-3A, Class C, 1.470%, 6/15/2026, 144A | 3,560,323 | ||||||

| 7,980,000 | DT Auto Owner Trust, Series 2021-4A, Class D, 1.990%, 9/15/2027, 144A | 7,014,524 | ||||||

| 11,340,000 | Exeter Automobile Receivables Trust, Series 2021-2A, Class D, 1.400%, 4/15/2027 | 10,360,902 | ||||||

| 15,295,000 | Exeter Automobile Receivables Trust, Series 2021-3A, Class D, 1.550%, 6/15/2027 | 13,880,347 | ||||||

| 2,010,000 | Exeter Automobile Receivables Trust, Series 2022-6A, Class C, 6.320%, 5/15/2028 | 2,010,915 | ||||||

| 2,820,000 | First Investors Auto Owner Trust, Series 2022-2A, Class D, 8.710%, 10/16/2028, 144A | 2,915,970 | ||||||

| 5,245,000 | Flagship Credit Auto Trust, Series 2021-2, Class D, 1.590%, 6/15/2027, 144A | 4,671,388 | ||||||

| 6,565,000 | Flagship Credit Auto Trust, Series 2021-3, Class D, 1.650%, 9/15/2027, 144A | 5,692,995 | ||||||

| 5,951,000 | Flagship Credit Auto Trust, Series 2021-4, Class C, 1.960%, 12/15/2027, 144A | 5,440,603 | ||||||

| 5,260,000 | Foursight Capital Automobile Receivables Trust, Series 2021-2, Class D, 1.920%, 9/15/2027, 144A | 4,763,089 | ||||||

| 8,425,000 | GLS Auto Receivables Issuer Trust, Series 2021-2A, Class D, 1.420%, 4/15/2027, 144A | 7,643,306 | ||||||

| 10,265,000 | GLS Auto Receivables Issuer Trust, Series 2021-3A, Class D, 1.480%, 7/15/2027, 144A | 9,179,605 | ||||||

| 16,820,000 | GLS Auto Receivables Issuer Trust, Series 2021-4A, Class D, 2.480%, 10/15/2027, 144A | 14,859,076 | ||||||

| 11,029,000 | Hertz Vehicle Financing III LLC, Series 2022-1A, 4.850%, 6/25/2026, 144A | 9,701,715 | ||||||

| 8,512,000 | Hertz Vehicle Financing III LLC, Series 2022-3A, 6.310%, 3/25/2025, 144A | 8,115,749 | ||||||

| 6,205,000 | Hertz Vehicle Financing LLC, Class D, Series 2022-4A, 6.560%, 9/25/2026, 144A | 5,719,515 | ||||||

| 1,814,743 | JPMorgan Chase Bank NA, Series 2021-3, Class D, 1.009%, 2/26/2029, 144A | 1,690,467 | ||||||

| 8,375,000 | Prestige Auto Receivables Trust, Series 2022-1A, Class D, 8.080%, 8/15/2028, 144A | 8,342,423 | ||||||

| 2,305,615 | Santander Bank NA, Series 2021-1A, Class B, 1.833%, 12/15/2031, 144A | 2,217,617 | ||||||

See accompanying notes to financial statements.

9 |

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund – continued

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – continued | ||||||||

| ABS Car Loan – continued | ||||||||

| $ | 10,510,000 | Westlake Automobile Receivables Trust, Series 2021-3A, Class D, 2.120%, 1/15/2027, 144A | $ | 9,329,033 | ||||

|

| |||||||

| 215,258,135 | ||||||||

|

| |||||||

| ABS Credit Card – 0.1% | ||||||||

| 1,445,000 | Brex Commercial Charge Card Master Trust, Series 2021-1, Class A, 2.090%, 7/15/2024, 144A | 1,429,322 | ||||||

| 5,000,000 | Mercury Financial Credit Card Master Trust, Series 2021-1A, Class C, 4.210%, 3/20/2026, 144A | 4,573,401 | ||||||

| 1,245,000 | Mission Lane Credit Card Master Trust, Series 2021-A, Class B, 2.240%, 9/15/2026, 144A | 1,205,548 | ||||||

|

| |||||||

| 7,208,271 | ||||||||

|

| |||||||

| ABS Home Equity – 4.5% | ||||||||

| 10,690,423 | 510 Asset Backed Trust, Series 2021-NPL1, Class A1, 2.240%, 6/25/2061, 144A(a) | 9,752,542 | ||||||

| 12,850,000 | CAFL Issuer LLC, Series 2021-RTL1, Class A1, 2.239%, 3/28/2029, 144A(a) | 11,685,086 | ||||||

| 2,715,000 | CoreVest American Finance Trust, Series 2021-1, Class C, 2.800%, 4/15/2053, 144A | 2,088,553 | ||||||

| 4,647,000 | CoreVest American Finance Trust, Series 2021-2, Class C, 2.478%, 7/15/2054, 144A | 3,397,365 | ||||||

| 2,280,000 | CoreVest American Finance Trust, Series 2021-3, Class D, 3.469%, 10/15/2054, 144A | 1,723,985 | ||||||

| 16,825,792 | Credit Suisse Mortgage Trust, Series 2021-RPL4, Class A1, 1.796%, 12/27/2060, 144A(a) | 14,974,887 | ||||||

| 3,716,673 | Credit Suisse Mortgage Trust, Series 2021-RPL6, Class M2, 3.125%, 10/25/2060, 144A | 2,812,488 | ||||||

| 7,995,000 | FirstKey Homes Trust, Series 2021-SFR1, Class E1, 2.389%, 8/17/2038, 144A | 6,666,243 | ||||||

| 5,272,000 | FirstKey Homes Trust, Series 2021-SFR2, Class E1, 2.258%, 9/17/2038, 144A | 4,368,388 | ||||||

| 3,120,000 | FirstKey Homes Trust, Series 2021-SFR2, Class E2, 2.358%, 9/17/2038, 144A | 2,563,513 | ||||||

| 2,210,000 | FRTKL, Series 2021-SFR1, Class E1, 2.372%, 9/17/2038, 144A | 1,837,982 | ||||||

| 1,930,000 | FRTKL, Series 2021-SFR1, Class E2, 2.522%, 9/17/2038, 144A | 1,600,671 | ||||||

| 1,284,185 | Home Partners of America Trust, Series 2021-1, Class E, 2.577%, 9/17/2041, 144A | 980,525 | ||||||

| 12,687,594 | Home Partners of America Trust, Series 2021-2, Class E1, 2.852%, 12/17/2026, 144A | 10,354,585 | ||||||

| ABS Home Equity – continued | ||||||||

| $ | 6,348,658 | Home Partners of America Trust, Series 2021-2, Class E2, 2.952%, 12/17/2026, 144A | $ | 5,180,209 | ||||

| 1,783,620 | Legacy Mortgage Asset Trust, Series 2020-GS5, Class A1, 3.250%, 6/25/2060, 144A(a) | 1,754,606 | ||||||

| 7,921,840 | Legacy Mortgage Asset Trust, Series 2021-GS2, Class A1, 1.750%, 4/25/2061, 144A(a) | 7,160,480 | ||||||

| 2,595,718 | Legacy Mortgage Asset Trust, Series 2021-GS4, Class A1, 1.650%, 11/25/2060, 144A(a) | 2,320,291 | ||||||

| 1,720,000 | Mill City Mortgage Loan Trust, Series 2019-GS1, Class M2, 3.250%, 7/25/2059, 144A(a) | 1,384,448 | ||||||

| 1,635,000 | Progress Residential Trust, Series 2021-SFR4, Class E1, 2.409%, 5/17/2038, 144A | 1,365,190 | ||||||

| 1,145,000 | Progress Residential Trust, Series 2021-SFR4, Class E2, 2.559%, 5/17/2038, 144A | 955,105 | ||||||

| 3,535,000 | Progress Residential Trust, Series 2021-SFR5, Class E1, 2.209%, 7/17/2038, 144A | 2,943,620 | ||||||

| 925,000 | Progress Residential Trust, Series 2021-SFR5, Class E2, 2.359%, 7/17/2038, 144A | 765,948 | ||||||

| 4,495,000 | Progress Residential Trust, Series 2021-SFR6, Class E1, 2.425%, 7/17/2038, 144A | 3,726,254 | ||||||

| 2,300,000 | Progress Residential Trust, Series 2021-SFR6, Class E2, 2.525%, 7/17/2038, 144A | 1,882,826 | ||||||

| 5,280,000 | Progress Residential Trust, Series 2021-SFR7, Class E1, 2.591%, 8/17/2040, 144A | 4,063,876 | ||||||

| 1,445,000 | Progress Residential Trust, Series 2021-SFR7, Class E2, 2.640%, 8/17/2040, 144A | 1,106,531 | ||||||

| 1,705,000 | Progress Residential Trust, Series 2021-SFR9, Class E1, 2.811%, 11/17/2040, 144A | 1,323,971 | ||||||

| 1,175,000 | Progress Residential Trust, Series 2021-SFR9, Class E2, 3.010%, 11/17/2040, 144A | 916,329 | ||||||

| 6,952,591 | PRPM LLC, Series 2021-10, Class A1, 2.487%, 10/25/2026, 144A(a) | 6,303,045 | ||||||

| 11,574,090 | PRPM LLC, Series 2021-3, Class A1, 1.867%, 4/25/2026, 144A(a) | 10,318,430 | ||||||

| 11,634,360 | PRPM LLC, Series 2021-4, Class A1, 1.867%, 4/25/2026, 144A(a) | 10,417,815 | ||||||

| 10,422,699 | PRPM LLC, Series 2021-5, Class A1, 1.793%, 6/25/2026, 144A(a) | 9,428,895 | ||||||

| 7,279,208 | PRPM LLC, Series 2021-8, Class A1, 1.743%, 9/25/2026, 144A(a) | 6,521,739 | ||||||

See accompanying notes to financial statements.

| 10

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund – continued

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – continued | ||||||||

| ABS Home Equity – continued | ||||||||

| $ | 7,867,146 | PRPM LLC, Series 2021-9, Class A1, 2.363%, 10/25/2026, 144A(a) | $ | 7,082,094 | ||||

| 9,753,207 | PRPM LLC, Series 2022-5, Class A1, 6.900%, 9/27/2027, 144A(a) | 9,679,362 | ||||||

| 12,050,000 | Toorak Mortgage Corp., Series 2021-1, Class A1, 2.240%, 6/25/2024, 144A(a) | 11,395,608 | ||||||

| 170,000 | Towd Point Mortgage Trust, Series 2015-4, Class M2, 3.750%, 4/25/2055, 144A(a) | 164,795 | ||||||

| 3,660,000 | Towd Point Mortgage Trust, Series 2016-3, Class M2, 4.000%, 4/25/2056, 144A(a) | 3,529,941 | ||||||

| 430,000 | Towd Point Mortgage Trust, Series 2017-3, Class A2, 3.000%, 7/25/2057, 144A(a) | 402,555 | ||||||

| 1,690,000 | Towd Point Mortgage Trust, Series 2017-4, Class M2, 3.250%, 6/25/2057, 144A(a) | 1,368,144 | ||||||

| 1,960,000 | Towd Point Mortgage Trust, Series 2018-5, Class M1, 3.250%, 7/25/2058, 144A(a) | 1,566,975 | ||||||

| 1,195,000 | Towd Point Mortgage Trust, Series 2019-4, Class M1, 3.500%, 10/25/2059, 144A(a) | 969,646 | ||||||

| 905,000 | Towd Point Mortgage Trust, Series 2020-1, Class A2B, 3.250%, 1/25/2060, 144A(a) | 735,085 | ||||||

| 495,000 | Towd Point Mortgage Trust, Series 2020-2, Class A2B, 3.000%, 4/25/2060, 144A(a) | 387,795 | ||||||

| 2,015,000 | Tricon Residential Trust, Series 2021-SFR1, Class E1, 2.794%, 7/17/2038, 144A | 1,692,118 | ||||||

| 5,360,000 | Tricon Residential Trust, Series 2021-SFR1, Class E2, 2.894%, 7/17/2038, 144A | 4,468,936 | ||||||

| 250,853 | VCAT LLC, Series 2021-NPL1, Class A1, 2.289%, 12/26/2050, 144A(a) | 236,795 | ||||||

| 9,676,683 | VCAT LLC, Series 2021-NPL5, Class A1, 1.868%, 8/25/2051, 144A(a) | 8,525,635 | ||||||

| 15,479,206 | VCAT LLC, Series 2021-NPL6, Class A1, 1.917%, 9/25/2051, 144A(a) | 13,475,675 | ||||||

| 8,812,314 | VOLT XCIV LLC, Series 2021-NPL3, Class A1, 2.240%, 2/27/2051, 144A(a) | 7,966,445 | ||||||

|

| |||||||

| 228,294,025 | ||||||||

|

| |||||||

| ABS Other – 3.0% | ||||||||

| 1,290,000 | Affirm Asset Securitization Trust, Series 2021-B, Class C, 1.400%, 8/17/2026, 144A | 1,172,526 | ||||||

| 6,993,753 | Apollo Aviation Securitization Equity Trust, Series 2021-1A, Class A, 2.950%, 11/16/2041, 144A | 5,586,126 | ||||||

| ABS Other – continued | ||||||||

| $ | 2,410,000 | Aqua Finance Trust, Series 2021-A, Class B, 2.400%, 7/17/2046, 144A | $ | 2,028,672 | ||||

| 13,505,000 | BHG Securitization Trust, Series 2022-A, Class B, 2.700%, 2/20/2035, 144A | 11,738,164 | ||||||

| 11,522,588 | CLI Funding VIII LLC, Series 2021-1A, Class A, 1.640%, 2/18/2046, 144A | 9,825,010 | ||||||

| 10,751,400 | DB Master Finance LLC, Series 2021-1A, Class A2II, 2.493%, 11/20/2051, 144A | 8,836,866 | ||||||

| 759,600 | Elara HGV Timeshare Issuer LLC, Series 2021-A, Class C, 2.090%, 8/27/2035, 144A | 673,466 | ||||||

| 3,565,000 | FREED ABS Trust, Series 2022-1FP, Class D, 3.350%, 3/19/2029, 144A | 3,259,651 | ||||||

| 1,630,000 | Freedom Financial Trust, Series 2021-2, Class C, 1.940%, 6/19/2028, 144A | 1,582,841 | ||||||

| 3,495,000 | Freedom Financial Trust, Series 2021-3FP, Class D, 2.370%, 11/20/2028, 144A | 3,179,774 | ||||||

| 68,231 | HIN Timeshare Trust, Series 2020-A, Class C, 3.420%, 10/09/2039, 144A | 62,541 | ||||||

| 3,980,000 | HPEFS Equipment Trust, Series 2021-1A, Class D, 1.030%, 3/20/2031, 144A | 3,754,083 | ||||||

| 3,645,000 | HPEFS Equipment Trust, Series 2022-1A, Class D, 2.400%, 11/20/2029, 144A | 3,302,035 | ||||||

| 10,066,726 | Lunar Structured Aircraft Portfolio Notes, Series 2021-1, Class A, 2.636%, 10/15/2046, 144A | 8,227,515 | ||||||

| 18,189,677 | MAPS Trust, Series 2021-1A, Class A, 2.521%, 6/15/2046, 144A | 14,739,586 | ||||||

| 1,733,000 | Marlette Funding Trust, Series 2021-2A, Class C, 1.500%, 9/15/2031, 144A | 1,601,714 | ||||||

| 3,210,000 | Marlette Funding Trust, Series 2021-3A, Class C, 1.810%, 12/15/2031, 144A | 2,874,252 | ||||||

| 12,050,722 | MVW LLC, Series 2021-2A, Class C, 2.230%, 5/20/2039, 144A | 10,859,279 | ||||||

| 15,350,996 | Navigator Aircraft ABS Ltd., Series 2021-1, Class A, 2.771%, 11/15/2046, 144A(a) | 12,894,096 | ||||||

| 3,250,000 | Nelnet Student Loan Trust, Series 2021-A, Class B2, 2.850%, 4/20/2062, 144A | 2,582,823 | ||||||

| 1,145,000 | OneMain Financial Issuance Trust, Series 2018-2A, Class A, 3.570%, 3/14/2033, 144A | 1,122,491 | ||||||

| 1,835,000 | OneMain Financial Issuance Trust, Series 2020-2A, Class A, 1.750%, 9/14/2035, 144A | 1,603,002 | ||||||

| 5,485,000 | OneMain Financial Issuance Trust, Series 2021-1A, Class D, 2.470%, 6/16/2036, 144A | 4,201,606 | ||||||

See accompanying notes to financial statements.

11 |

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund – continued

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – continued | ||||||||

| ABS Other – continued | ||||||||

| $ | 800,000 | Republic Finance Issuance Trust, Series 2021-A, Class C, 3.530%, 12/22/2031, 144A | $ | 694,966 | ||||

| 1,128,492 | S-Jets Ltd., Series 2017-1, Class A, 3.967%, 8/15/2042, 144A | 874,592 | ||||||

| 725,000 | SCF Equipment Leasing LLC, Series 2021-1A, Class D, 1.930%, 9/20/2030, 144A | 632,387 | ||||||

| 4,060,000 | SCF Equipment Leasing LLC, Series 2022-2A, Class C, 6.500%, 8/20/2032, 144A | 3,959,436 | ||||||

| 899,626 | Shenton Aircraft Investment I Ltd., Series 2015-1A, Class A, 4.750%, 10/15/2042, 144A | 688,223 | ||||||

| 14,961,362 | SLAM Ltd., Series 2021-1A, Class A, 2.434%, 6/15/2046, 144A | 12,378,133 | ||||||

| 1,440,000 | SoFi Consumer Loan Program Trust, Series 2021-1, Class D, 2.040%, 9/25/2030, 144A | 1,304,882 | ||||||

| 3,500,000 | Towd Point Mortgage Trust, Series 2017-1, Class M1, 3.750%, 10/25/2056, 144A(a) | 3,262,654 | ||||||

| 2,746,206 | Wave Trust, Series 2017-1A, Class A, 3.844%, 11/15/2042, 144A | 2,073,413 | ||||||

| 12,327,772 | Willis Engine Structured Trust VI, Series 2021-A, Class A, 3.104%, 5/15/2046, 144A | 9,022,561 | ||||||

|

| |||||||

| 150,599,366 | ||||||||

|

| |||||||

| ABS Student Loan – 0.5% | ||||||||

| 2,760,000 | College Ave Student Loans LLC, Series 2021-A, Class C, 2.920%, 7/25/2051, 144A | 2,476,177 | ||||||

| 2,157,000 | College Ave Student Loans LLC, Series 2021-C, Class D, 4.110%, 7/26/2055, 144A | 1,679,771 | ||||||

| 763,709 | ELFI Graduate Loan Program LLC, Series 2021-A, Class B, 2.090%, 12/26/2046, 144A(a) | 652,841 | ||||||

| 2,565,000 | Navient Private Education Refi Loan Trust, Series 2021-EA, Class B, 2.030%, 12/16/2069, 144A | 1,634,218 | ||||||

| 5,895,000 | Navient Private Education Refi Loan Trust, Series 2021-FA, Class B, 2.120%, 2/18/2070, 144A | 3,798,442 | ||||||

| 2,120,000 | Nelnet Student Loan Trust, Series 2021-DA, Class C, 3.500%, 4/20/2062, 144A | 1,714,234 | ||||||

| 863,000 | Nelnet Student Loan Trust, Series 2021-DA, Class D, 4.380%, 4/20/2062, 144A | 702,445 | ||||||

| 5,735,000 | SMB Private Education Loan Trust, Series 2021-B, Class B, 2.650%, 7/17/2051, 144A | 4,566,955 | ||||||

| 7,070,000 | SMB Private Education Loan Trust, Series 2021-E, Class B, 2.490%, 2/15/2051, 144A | 5,426,134 | ||||||

| 630,000 | SoFi Professional Loan Program LLC, Series 2017-A, Class C, 4.430%, 3/26/2040, 144A(a) | 578,168 | ||||||

|

| |||||||

| 23,229,385 | ||||||||

|

| |||||||

| ABS Whole Business – 0.4% | ||||||||

| 1,673,775 | DB Master Finance LLC, Series 2019-1A, Class A23, 4.352%, 5/20/2049, 144A | 1,526,121 | ||||||

| 7,229,900 | Domino’s Pizza Master Issuer LLC, Series 2021-1A, Class A2I, 2.662%, 4/25/2051, 144A | 6,082,088 | ||||||

| 3,422,875 | Hardee’s Funding LLC, Series 2021-1A, Class A2, 2.865%, 6/20/2051, 144A | 2,728,589 | ||||||

| 1,144,600 | Planet Fitness Master Issuer LLC, Series 2019-1A, Class A2, 3.858%, 12/05/2049, 144A | 950,805 | ||||||

| 203,463 | Planet Fitness Master Issuer LLC, Series 2022-1A, Class A2I, 3.251%, 12/05/2051, 144A | 178,404 | ||||||

| 11,081,250 | Wendy’s Funding LLC, Series 2021-1A, Class A2I, 2.370%, 6/15/2051, 144A | 8,946,159 | ||||||

|

| |||||||

| 20,412,166 | ||||||||

|

| |||||||

| Aerospace & Defense – 1.0% | ||||||||

| 22,105,000 | Boeing Co. (The), 3.625%, 2/01/2031 | 19,367,671 | ||||||

| 2,995,000 | Boeing Co. (The), 3.625%, 3/01/2048 | 1,959,524 | ||||||

| 3,525,000 | Boeing Co. (The), 3.750%, 2/01/2050 | 2,429,783 | ||||||

| 6,180,000 | Boeing Co. (The), 3.825%, 3/01/2059 | 3,950,872 | ||||||

| 1,200,000 | Boeing Co. (The), 3.850%, 11/01/2048 | 823,676 | ||||||

| 8,855,000 | Boeing Co. (The), 3.900%, 5/01/2049 | 6,217,671 | ||||||

| 4,830,000 | Boeing Co. (The), 5.150%, 5/01/2030 | 4,712,338 | ||||||

| 4,055,000 | Embraer Netherlands Finance BV, 5.400%, 2/01/2027 | 3,882,662 | ||||||

| 5,995,000 | TransDigm, Inc., 6.250%, 3/15/2026, 144A | 5,912,209 | ||||||

|

| |||||||

| 49,256,406 | ||||||||

|

| |||||||

| Airlines – 1.9% | ||||||||

| 21,828,987 | Air Canada Pass Through Trust, Series 2020-2A, 5.250%, 10/01/2030, 144A | 20,477,336 | ||||||

| 2,910,400 | American Airlines Pass Through Trust, Series 2016-3, Class B, 3.750%, 4/15/2027 | 2,585,366 | ||||||

| 2,673,333 | American Airlines Pass Through Trust, Series 2017-2, Class B, 3.700%, 4/15/2027 | 2,402,142 | ||||||

| 37,797,936 | Mileage Plus Holdings LLC/Mileage Plus Intellectual Property Assets Ltd., 6.500%, 6/20/2027, 144A | 37,578,778 | ||||||

| 4,070,441 | United Airlines Pass Through Trust, Series 2014-1, Class A, 4.000%, 10/11/2027 | 3,781,729 | ||||||

| 25,478,007 | United Airlines Pass Through Trust, Series 2020-1, Class A, 5.875%, 4/15/2029 | 25,096,601 | ||||||

See accompanying notes to financial statements.

| 12

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund – continued

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – continued | ||||||||

| Airlines – continued | ||||||||

| $ | 3,665,220 | United Airlines Pass Through Trust, Series 2020-1, Class B, 4.875%, 7/15/2027 | $ | 3,450,365 | ||||

|

| |||||||

| 95,372,317 | ||||||||

|

| |||||||

| Automotive – 1.2% | ||||||||

| 2,355,000 | Ford Motor Co., 3.250%, 2/12/2032 | 1,766,113 | ||||||

| 14,465,000 | Ford Motor Co., 4.750%, 1/15/2043 | 10,382,874 | ||||||

| 1,560,000 | Ford Motor Co., 6.625%, 2/15/2028 | 1,567,005 | ||||||

| 1,580,000 | Ford Motor Co., 7.500%, 8/01/2026 | 1,644,701 | ||||||

| 3,505,000 | General Motors Co., 5.200%, 4/01/2045 | 2,848,760 | ||||||

| 1,750,000 | General Motors Co., 6.250%, 10/02/2043 | 1,617,925 | ||||||

| 44,900,000 | General Motors Financial Co., Inc., 3.600%, 6/21/2030 | 37,786,155 | ||||||

| 815,000 | General Motors Financial Co., Inc., Series A, (fixed rate to 9/30/2027, variable rate thereafter), 5.750%(b) | 686,146 | ||||||

| 1,305,000 | General Motors Financial Co., Inc., Series C, (fixed rate to 9/30/2030, variable rate thereafter), 5.700%(b) | 1,104,519 | ||||||

|

| |||||||

| 59,404,198 | ||||||||

|

| |||||||

| Banking – 4.1% | ||||||||

| 20,700,000 | Ally Financial, Inc., Series B, (fixed rate to 5/15/2026, variable rate thereafter), 4.700%(b) | 13,843,125 | ||||||

| 15,605,000 | Ally Financial, Inc., Series C, (fixed rate to 5/15/2028, variable rate thereafter), 4.700%(b) | 9,772,631 | ||||||

| 17,805,000 | Barclays PLC, (fixed rate to 3/15/2028, variable rate thereafter), 4.375%(b) | 13,576,312 | ||||||

| 47,298,000 | Barclays PLC, (fixed rate to 9/23/2030, variable rate thereafter), 3.564%, 9/23/2035 | 35,991,159 | ||||||

| 14,253,000 | BNP Paribas S.A., (fixed rate to 8/12/2030, variable rate thereafter), 2.588%, 8/12/2035, 144A | 10,451,155 | ||||||

| 8,140,000 | Credit Agricole S.A., (fixed rate to 1/10/2028, variable rate thereafter), EMTN, 4.000%, 1/10/2033 | 7,092,219 | ||||||

| 605,000 | Credit Suisse Group AG, (fixed rate to 1/12/2028, variable rate thereafter), 3.869%, 1/12/2029, 144A | 484,937 | ||||||

| 5,470,000 | Credit Suisse Group AG, (fixed rate to 11/15/2032, variable rate thereafter), 9.016%, 11/15/2033, 144A | 5,600,553 | ||||||

| 510,000 | Credit Suisse Group AG, (fixed rate to 5/14/2031, variable rate thereafter), 3.091%, 5/14/2032, 144A | 352,383 | ||||||

| 8,165,000 | Credit Suisse Group AG, (fixed rate to 6/05/2025, variable rate thereafter), 2.193%, 6/05/2026, 144A | 6,973,659 | ||||||

| Banking – continued | ||||||||

| 11,755,000 | Credit Suisse Group AG, (fixed rate to 7/15/2025, variable rate thereafter), 6.373%, 7/15/2026, 144A | 11,036,172 | ||||||

| 11,645,000 | Credit Suisse Group AG, (fixed rate to 8/11/2027, variable rate thereafter), 6.442%, 8/11/2028, 144A | 10,606,965 | ||||||

| 5,690,000 | Credit Suisse Group AG, (fixed rate to 8/12/2032, variable rate thereafter), 6.537%, 8/12/2033, 144A | 4,998,551 | ||||||

| 4,195,000 | Deutsche Bank AG, (fixed rate to 10/07/2031, variable rate thereafter), 3.742%, 1/07/2033 | 2,979,187 | ||||||

| 25,209,000 | Deutsche Bank AG, (fixed rate to 10/14/2030, variable rate thereafter), 3.729%, 1/14/2032 | 18,483,586 | ||||||

| 2,275,000 | Deutsche Bank AG, (fixed rate to 12/01/2027, variable rate thereafter), 4.875%, 12/01/2032 | 1,901,487 | ||||||

| 3,380,000 | Intesa Sanpaolo SpA, (fixed rate to 6/01/2031, variable rate thereafter), 4.198%, 6/01/2032, 144A | 2,491,297 | ||||||

| 22,550,000 | NatWest Group PLC, (fixed rate to 8/28/2030, variable rate thereafter), 3.032%, 11/28/2035 | 16,635,811 | ||||||

| 2,900,000 | NatWest Group PLC, (fixed rate to 9/30/2027, variable rate thereafter), 5.516%, 9/30/2028 | 2,864,277 | ||||||

| 4,370,000 | Synchrony Bank, 5.400%, 8/22/2025 | 4,311,005 | ||||||

| 8,885,000 | Synchrony Bank, 5.625%, 8/23/2027 | 8,675,758 | ||||||

| 22,400,000 | UniCredit SpA, (fixed rate to 6/30/2030, variable rate thereafter), 5.459%, 6/30/2035, 144A | 18,198,837 | ||||||

|

| |||||||

| 207,321,066 | ||||||||

|

| |||||||

| Brokerage – 0.1% | ||||||||

| 5,731,000 | Jefferies Financial Group, Inc., 6.250%, 1/15/2036 | 5,779,778 | ||||||

|

| |||||||

| Building Materials – 1.5% | ||||||||

| 57,099,000 | Cemex SAB de CV, 3.875%, 7/11/2031, 144A | 48,193,549 | ||||||

| 3,605,000 | Cemex SAB de CV, 5.200%, 9/17/2030, 144A | 3,363,058 | ||||||

| 9,035,000 | Cemex SAB de CV, (fixed rate to 6/08/2026, variable rate thereafter), 5.125%, 144A(b) | 8,348,430 | ||||||

| 4,057,000 | Masco Corp., 6.500%, 8/15/2032 | 4,153,024 | ||||||

| 4,534,000 | Masco Corp., 7.750%, 8/01/2029 | 4,955,757 | ||||||

| 6,344,000 | Owens Corning, 7.000%, 12/01/2036 | 6,713,760 | ||||||

|

| |||||||

| 75,727,578 | ||||||||

|

| |||||||

| Cable Satellite – 4.1% | ||||||||

| 36,985,000 | CCO Holdings LLC/CCO Holdings Capital Corp., 4.250%, 1/15/2034, 144A | 27,296,594 | ||||||

| 11,015,000 | Charter Communications Operating LLC/Charter Communications Operating Capital, 2.300%, 2/01/2032 | 8,113,081 | ||||||

See accompanying notes to financial statements.

13 |

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund – continued

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – continued | ||||||||

| Cable Satellite – continued | ||||||||

| $ | 35,342,000 | Charter Communications Operating LLC/Charter Communications Operating Capital, 2.800%, 4/01/2031 | $ | 27,514,021 | ||||

| 24,940,000 | Charter Communications Operating LLC/Charter Communications Operating Capital, 3.700%, 4/01/2051 | 15,165,210 | ||||||

| 1,438,000 | Charter Communications Operating LLC/Charter Communications Operating Capital, 3.850%, 4/01/2061 | 831,682 | ||||||

| 46,770,000 | Charter Communications Operating LLC/Charter Communications Operating Capital, 3.950%, 6/30/2062 | 27,589,626 | ||||||

| 6,805,000 | Charter Communications Operating LLC/Charter Communications Operating Capital, 4.400%, 4/01/2033 | 5,822,761 | ||||||

| 5,935,000 | Charter Communications Operating LLC/Charter Communications Operating Capital, 5.125%, 7/01/2049 | 4,487,821 | ||||||

| 45,882,000 | CSC Holdings LLC, 4.625%, 12/01/2030, 144A | 25,355,956 | ||||||

| 1,875,000 | CSC Holdings LLC, 5.000%, 11/15/2031, 144A | 1,047,563 | ||||||

| 22,585,000 | CSC Holdings LLC, 5.375%, 2/01/2028, 144A | 18,209,156 | ||||||

| 1,390,000 | CSC Holdings LLC, 5.750%, 1/15/2030, 144A | 783,946 | ||||||

| 9,430,000 | DISH DBS Corp., 5.125%, 6/01/2029 | 6,083,387 | ||||||

| 26,600,000 | DISH DBS Corp., 5.250%, 12/01/2026, 144A | 22,406,111 | ||||||

| 14,719,000 | DISH DBS Corp., 7.750%, 7/01/2026 | 11,869,255 | ||||||

| 6,190,000 | Time Warner Cable LLC, 4.500%, 9/15/2042 | 4,531,727 | ||||||

| 535,000 | Time Warner Cable LLC, 5.875%, 11/15/2040 | 466,106 | ||||||

|

| |||||||

| 207,574,003 | ||||||||

|

| |||||||

| Chemicals – 0.4% | ||||||||

| 5,450,000 | Alpek SAB de CV, 3.250%, 2/25/2031, 144A | 4,541,220 | ||||||

| 1,995,000 | Braskem Netherlands Finance BV, 4.500%, 1/31/2030, 144A | 1,696,665 | ||||||

| 10,170,000 | Braskem Netherlands Finance BV, 5.875%, 1/31/2050, 144A | 7,878,357 | ||||||

| 4,310,000 | Celanese U.S. Holdings LLC, 6.330%, 7/15/2029 | 4,187,775 | ||||||

| 3,175,000 | Celanese U.S. Holdings LLC, 6.379%, 7/15/2032 | 3,019,260 | ||||||

| 1,360,000 | INEOS Quattro Finance 2 PLC, 3.375%, 1/15/2026, 144A | 1,249,500 | ||||||

|

| |||||||

| 22,572,777 | ||||||||

|

| |||||||

| Construction Machinery – 0.6% | ||||||||

| 2,300,000 | Ashtead Capital, Inc., 5.500%, 8/11/2032, 144A | 2,199,879 | ||||||

| 27,030,000 | Toro Co. (The), 6.625%, 5/01/2037 | 27,621,023 | ||||||

|

| |||||||

| 29,820,902 | ||||||||

|

| |||||||

| Consumer Cyclical Services – 2.2% |

| |||||||

| 2,700,000 | Expedia Group, Inc., 2.950%, 3/15/2031 | 2,171,154 | ||||||

| 2,255,000 | Expedia Group, Inc., 3.250%, 2/15/2030 | 1,912,906 | ||||||

| 14,700,000 | TriNet Group, Inc., 3.500%, 3/01/2029, 144A | 12,086,340 | ||||||

| 33,255,000 | Uber Technologies, Inc., 4.500%, 8/15/2029, 144A | 28,973,585 | ||||||

| 20,723,000 | Uber Technologies, Inc., 6.250%, 1/15/2028, 144A | 19,894,077 | ||||||

| 44,403,000 | Uber Technologies, Inc., 7.500%, 9/15/2027, 144A | 44,434,082 | ||||||

| 1,720,000 | Uber Technologies, Inc., 8.000%, 11/01/2026, 144A | 1,725,920 | ||||||

|

| |||||||

| 111,198,064 | ||||||||

|

| |||||||

| Consumer Products – 0.4% | ||||||||

| 12,778,000 | Avon Products, Inc., 8.450%, 3/15/2043 | 12,233,657 | ||||||

| 9,385,000 | Natura Cosmeticos S.A., 4.125%, 5/03/2028, 144A | 7,658,254 | ||||||

|

| |||||||

| 19,891,911 | ||||||||

|

| |||||||

| Diversified Manufacturing – 0.0% |

| |||||||

| 2,080,000 | General Electric Co., Series D, 3-month LIBOR + 3.330%, 8.099%(b)(c) | 2,043,480 | ||||||

|

| |||||||

| Electric – 1.0% | ||||||||

| 27,504,380 | Alta Wind Holdings LLC, 7.000%, 6/30/2035, 144A | 27,182,351 | ||||||

| 8,663,000 | Enel Generacion Chile S.A., 7.875%, 2/01/2027 | 9,139,465 | ||||||

| 9,495,000 | Pacific Gas & Electric Co., 4.300%, 3/15/2045 | 6,731,841 | ||||||

| 6,825,000 | Pacific Gas & Electric Co., 4.750%, 2/15/2044 | 5,221,699 | ||||||

| 3,790,000 | Pacific Gas & Electric Co., 5.450%, 6/15/2027 | 3,737,352 | ||||||

|

| |||||||

| 52,012,708 | ||||||||

|

| |||||||

| Finance Companies – 5.0% | ||||||||

| 12,050,000 | AerCap Ireland Capital DAC/AerCap Global Aviation Trust, 3.300%, 1/30/2032 | 9,420,217 | ||||||

| 3,100,000 | AGFC Capital Trust I, 3-month LIBOR + 1.750%, 5.829%, 1/15/2067, 144A(c) | 1,668,265 | ||||||

| 6,606,000 | Air Lease Corp., 4.625%, 10/01/2028 | 6,178,860 | ||||||

| 17,166,000 | Air Lease Corp., Series B, (fixed rate to 6/15/2026, variable rate thereafter), 4.650%(b) | 14,345,968 | ||||||

| 5,325,000 | Aircastle Ltd., Series A (fixed rate to 6/15/2026, variable rate thereafter), 5.250%, 144A(b) | 4,100,250 | ||||||

See accompanying notes to financial statements.

| 14

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund – continued

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – continued | ||||||||

| Finance Companies – continued | ||||||||

| $ | 12,465,000 | Ares Capital Corp., 2.875%, 6/15/2028 | $ | 9,994,799 | ||||

| 17,495,000 | Ares Capital Corp., 3.200%, 11/15/2031 | 12,838,706 | ||||||

| 3,260,000 | Aviation Capital Group LLC, 1.950%, 1/30/2026, 144A | 2,838,085 | ||||||

| 9,790,000 | Barings BDC, Inc., 3.300%, 11/23/2026 | 8,297,791 | ||||||

| 22,260,000 | Blackstone Secured Lending Fund, 2.125%, 2/15/2027 | 18,431,636 | ||||||

| 11,475,000 | FS KKR Capital Corp., 3.125%, 10/12/2028 | 9,250,796 | ||||||

| 8,178,000 | FS KKR Capital Corp., 3.400%, 1/15/2026 | 7,251,868 | ||||||

| 445,000 | Navient Corp., 5.000%, 3/15/2027 | 389,559 | ||||||

| 9,706,000 | Navient Corp., 6.750%, 6/15/2026 | 9,199,217 | ||||||

| 5,750,000 | Navient Corp., Series A, 5.625%, 8/01/2033 | 4,096,216 | ||||||

| 10,145,000 | OneMain Finance Corp., 7.125%, 3/15/2026 | 9,646,678 | ||||||

| 7,975,000 | Owl Rock Capital Corp., 2.875%, 6/11/2028 | 6,261,765 | ||||||

| 14,750,000 | Owl Rock Capital Corp., 4.250%, 1/15/2026 | 13,540,772 | ||||||

| 13,420,000 | Owl Rock Technology Finance Corp., 4.750%, 12/15/2025, 144A | 12,151,540 | ||||||

| 30,029,000 | Rocket Mortgage LLC/Rocket Mortgage Co-Issuer, Inc., 2.875%, 10/15/2026, 144A | 25,739,729 | ||||||

| 19,614,000 | Rocket Mortgage LLC/Rocket Mortgage Co-Issuer, Inc., 3.625%, 3/01/2029, 144A | 15,542,880 | ||||||

| 53,876,000 | Rocket Mortgage LLC/Rocket Mortgage Co-Issuer, Inc., 3.875%, 3/01/2031, 144A | 41,122,227 | ||||||

| 15,738,000 | Rocket Mortgage LLC/Rocket Mortgage Co-Issuer, Inc., 4.000%, 10/15/2033, 144A | 11,754,083 | ||||||

|

| |||||||

| 254,061,907 | ||||||||

|

| |||||||

| Financial Other – 1.5% | ||||||||

| 9,560,000 | Agile Group Holdings Ltd., 6.050%, 10/13/2025 | 4,423,221 | ||||||

| 2,700,000 | Central China Real Estate Ltd., 7.250%, 4/24/2023 | 1,163,766 | ||||||

| 3,680,000 | Central China Real Estate Ltd., 7.250%, 7/16/2024 | 1,043,758 | ||||||

| 1,455,000 | Central China Real Estate Ltd., 7.250%, 8/13/2024 | 407,124 | ||||||

| 3,675,000 | Central China Real Estate Ltd., 7.500%, 7/14/2025 | 1,010,089 | ||||||

| 945,000 | Central China Real Estate Ltd., 7.650%, 8/27/2023 | 337,951 | ||||||

| 730,000 | Central China Real Estate Ltd., 7.750%, 5/24/2024 | 225,490 | ||||||

| 2,815,000 | CIFI Holdings Group Co. Ltd., 6.000%, 7/16/2025 | 725,678 | ||||||

| 990,000 | CIFI Holdings Group Co. Ltd., 6.450%, 11/07/2024 | 259,875 | ||||||

| 7,770,000 | Country Garden Holdings Co. Ltd., 3.300%, 1/12/2031 | 4,110,874 | ||||||

| Financial Other – continued | ||||||||

| 36,625,000 | Icahn Enterprises LP/Icahn Enterprises Finance Corp., 4.375%, 2/01/2029 | 30,971,931 | ||||||

| 19,485,000 | Kaisa Group Holdings Ltd., 9.375%, 6/30/2024(d) | 2,652,103 | ||||||

| 1,845,000 | Kaisa Group Holdings Ltd., 9.950%, 7/23/2025(d) | 249,795 | ||||||

| 2,400,000 | Kaisa Group Holdings Ltd., 10.500%, 1/15/2025(d) | 325,128 | ||||||

| 24,005,000 | Kaisa Group Holdings Ltd., 11.250%, 4/16/2025(d) | 3,249,797 | ||||||

| 1,305,000 | Kaisa Group Holdings Ltd., 11.650%, 6/01/2026(d) | 176,449 | ||||||

| 1,735,000 | Kaisa Group Holdings Ltd., 11.700%, 11/11/2025(d) | 235,318 | ||||||

| 5,965,000 | Logan Group Co. Ltd., 4.250%, 7/12/2025(e) | 1,331,507 | ||||||

| 5,148,000 | Logan Group Co. Ltd., 4.850%, 12/14/2026(e) | 1,159,227 | ||||||

| 14,125,000 | Nationstar Mortgage Holdings, Inc., 5.500%, 8/15/2028, 144A | 11,517,685 | ||||||

| 6,195,000 | Shimao Group Holdings Ltd., 3.450%, 1/11/2031(d) | 1,108,905 | ||||||

| 400,000 | Shimao Group Holdings Ltd., 4.600%, 7/13/2030(d) | 73,624 | ||||||

| 1,515,000 | Shimao Group Holdings Ltd., 5.200%, 1/16/2027(d) | 272,700 | ||||||

| 4,675,000 | Shimao Group Holdings Ltd., 5.600%, 7/15/2026(d) | 865,997 | ||||||

| 1,465,000 | Shimao Group Holdings Ltd., 6.125%, 2/21/2024(d) | 273,486 | ||||||

| 575,000 | Sunac China Holdings Ltd., 5.950%, 4/26/2024(d) | 123,527 | ||||||

| 6,810,000 | Sunac China Holdings Ltd., 6.500%, 1/10/2025(d) | 1,455,978 | ||||||

| 3,575,000 | Sunac China Holdings Ltd., 6.500%, 1/26/2026(d) | 761,511 | ||||||

| 460,000 | Sunac China Holdings Ltd., 6.650%, 8/03/2024(d) | 98,592 | ||||||

| 5,930,000 | Sunac China Holdings Ltd., 7.000%, 7/09/2025(d) | 1,267,715 | ||||||

| 1,120,000 | Times China Holdings Ltd., 5.750%, 1/14/2027 | 182,011 | ||||||

| 7,485,000 | Times China Holdings Ltd., 6.200%, 3/22/2026 | 1,213,393 | ||||||

| 440,000 | Times China Holdings Ltd., 6.750%, 7/08/2025 | 72,745 | ||||||

| 3,175,000 | Yuzhou Group Holdings Co. Ltd., 6.350%, 1/13/2027(d) | 293,243 | ||||||

| 6,250,000 | Yuzhou Group Holdings Co. Ltd., 7.700%, 2/20/2025(d) | 579,000 | ||||||

| 1,585,000 | Yuzhou Group Holdings Co. Ltd., 7.850%, 8/12/2026(d) | 146,660 | ||||||

| 4,025,000 | Yuzhou Group Holdings Co. Ltd., 8.300%, 5/27/2025(d) | 372,876 | ||||||

|

| |||||||

| 74,738,729 | ||||||||

|

| |||||||

| Food & Beverage – 0.4% | ||||||||

| 965,000 | Darling Ingredients, Inc., 6.000%, 6/15/2030, 144A | 943,288 | ||||||

| 5,695,000 | JBS USA LUX S.A./JBS USA Food Co./JBS USA Finance, Inc., 3.000%, 2/02/2029, 144A | 4,713,436 | ||||||

See accompanying notes to financial statements.

15 |

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund – continued

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – continued | ||||||||

| Food & Beverage – continued | ||||||||

| $ | 17,905,000 | Pilgrim’s Pride Corp., 3.500%, 3/01/2032, 144A | $ | 13,995,622 | ||||

| 995,000 | Pilgrim’s Pride Corp., 4.250%, 4/15/2031, 144A | 846,302 | ||||||

|

| |||||||

| 20,498,648 | ||||||||

|

| |||||||

| Gaming – 1.0% | ||||||||

| 19,755,000 | Genm Capital Labuan Ltd., 3.882%, 4/19/2031, 144A | 14,708,527 | ||||||

| 5,810,000 | GLP Capital LP/GLP Financing II, Inc., 3.250%, 1/15/2032 | 4,644,426 | ||||||

| 415,000 | Scientific Games International, Inc., 7.250%, 11/15/2029, 144A | 398,400 | ||||||

| 10,488,000 | VICI Properties LP/VICI Note Co., Inc., 4.250%, 12/01/2026, 144A | 9,784,504 | ||||||

| 8,621,000 | VICI Properties LP/VICI Note Co., Inc., 4.500%, 9/01/2026, 144A | 8,113,029 | ||||||

| 7,500,000 | VICI Properties LP/VICI Note Co., Inc., 4.625%, 6/15/2025, 144A | 7,190,625 | ||||||

| 6,163,000 | VICI Properties LP/VICI Note Co., Inc., 5.625%, 5/01/2024, 144A | 6,102,972 | ||||||

|

| |||||||

| 50,942,483 | ||||||||

|

| |||||||

| Government Owned – No Guarantee – 1.3% |

| |||||||

| 27,210,000 | Antares Holdings LP, 8.500%, 5/18/2025, 144A | 27,778,430 | ||||||

| 6,170,000 | EcoPetrol S.A., 4.625%, 11/02/2031 | 4,712,892 | ||||||

| 8,465,000 | Pertamina Persero PT, 6.450%, 5/30/2044, 144A | 8,435,684 | ||||||

| 28,145,000 | Petroleos Mexicanos, 5.950%, 1/28/2031 | 21,301,487 | ||||||

| 2,735,000 | Sino-Ocean Land Treasure IV Ltd., 4.750%, 8/05/2029 | 1,482,917 | ||||||

| 5,250,000 | Sino-Ocean Land Treasure IV Ltd., 4.750%, 1/14/2030 | 2,674,875 | ||||||

|

| |||||||

| 66,386,285 | ||||||||

|

| |||||||

| Health Insurance – 0.7% | ||||||||

| 23,625,000 | Centene Corp., 2.500%, 3/01/2031 | 18,485,927 | ||||||

| 8,940,000 | Centene Corp., 2.625%, 8/01/2031 | 7,025,052 | ||||||

| 6,921,000 | Centene Corp., 3.000%, 10/15/2030 | 5,673,484 | ||||||

| 6,470,000 | Molina Healthcare, Inc., 3.875%, 5/15/2032, 144A | 5,372,943 | ||||||

|

| |||||||

| 36,557,406 | ||||||||

|

| |||||||

| Healthcare – 0.2% | ||||||||

| 9,725,000 | HCA, Inc., 4.125%, 6/15/2029 | 8,877,866 | ||||||

|

| |||||||

| Home Construction – 0.9% | ||||||||

| 50,680,000 | PulteGroup, Inc., 6.000%, 2/15/2035 | 48,458,269 | ||||||

|

| |||||||

| Independent Energy – 4.2% | ||||||||

| 17,555,000 | Aker BP ASA, 4.000%, 1/15/2031, 144A | 15,385,148 | ||||||

| 12,960,000 | Continental Resources, Inc., 2.875%, 4/01/2032, 144A | 9,599,319 | ||||||

| 56,135,000 | Continental Resources, Inc., 5.750%, 1/15/2031, 144A | 52,253,844 | ||||||

| 3,985,000 | Devon Energy Corp., 4.500%, 1/15/2030 | 3,710,009 | ||||||

| Independent Energy – continued | ||||||||

| 9,555,000 | Energean Israel Finance Ltd., 5.375%, 3/30/2028, 144A | 8,551,725 | ||||||

| 12,510,000 | Energean Israel Finance Ltd., 5.875%, 3/30/2031, 144A | 10,899,338 | ||||||

| 2,690,000 | EQT Corp., 3.125%, 5/15/2026, 144A | 2,472,204 | ||||||

| 11,721,000 | EQT Corp., 3.625%, 5/15/2031, 144A | 9,932,799 | ||||||

| 11,753,000 | EQT Corp., 3.900%, 10/01/2027 | 10,849,961 | ||||||

| 2,329,000 | EQT Corp., 5.000%, 1/15/2029 | 2,186,368 | ||||||

| 2,215,000 | EQT Corp., 5.700%, 4/01/2028 | 2,203,098 | ||||||

| 620,000 | Occidental Petroleum Corp., 6.125%, 1/01/2031 | 625,698 | ||||||

| 37,985,000 | Occidental Petroleum Corp., 6.625%, 9/01/2030 | 39,252,939 | ||||||

| 985,000 | Occidental Petroleum Corp., 7.875%, 9/15/2031 | 1,087,440 | ||||||

| 980,000 | Occidental Petroleum Corp., 8.875%, 7/15/2030 | 1,106,424 | ||||||

| 15,296,000 | Ovintiv, Inc., 6.500%, 8/15/2034 | 15,391,559 | ||||||

| 828,000 | Ovintiv, Inc., 6.500%, 2/01/2038 | 820,336 | ||||||

| 4,156,000 | Ovintiv, Inc., 6.625%, 8/15/2037 | 4,179,882 | ||||||

| 553,000 | Ovintiv, Inc., 7.200%, 11/01/2031 | 580,431 | ||||||

| 1,815,000 | Ovintiv, Inc., 7.375%, 11/01/2031 | 1,931,862 | ||||||

| 2,285,000 | Ovintiv, Inc., 8.125%, 9/15/2030 | 2,507,461 | ||||||

| 190,000 | Range Resources Corp., 4.875%, 5/15/2025 | 180,482 | ||||||

| 27,050,000 | Sanchez Energy Corp., 6.125%, 1/15/2023(d) | 371,938 | ||||||

| 12,420,000 | Sanchez Energy Corp., 7.750%, 6/15/2021(d) | 170,775 | ||||||

| 2,150,000 | Southwestern Energy Co., 4.750%, 2/01/2032 | 1,837,369 | ||||||

| 4,695,000 | Var Energi ASA, 7.500%, 1/15/2028, 144A | 4,782,335 | ||||||

| 10,345,000 | Var Energi ASA, 8.000%, 11/15/2032, 144A | 10,683,466 | ||||||

|

| |||||||

| 213,554,210 | ||||||||

|

| �� | ||||||

| Industrial Other – 0.1% |

| |||||||

| 5,995,000 | TopBuild Corp., 4.125%, 2/15/2032, 144A | 4,871,597 | ||||||

|

| |||||||

| Leisure – 0.9% |

| |||||||

| 13,160,000 | Carnival Corp., 5.750%, 3/01/2027, 144A | 9,396,767 | ||||||

| 3,415,000 | Carnival Corp., 6.000%, 5/01/2029, 144A | 2,275,694 | ||||||

| 10,030,000 | NCL Corp. Ltd., 5.875%, 3/15/2026, 144A | 7,878,264 | ||||||

| 7,630,000 | NCL Corp. Ltd., 5.875%, 2/15/2027, 144A | 6,604,223 | ||||||

| 3,695,000 | NCL Finance Ltd., 6.125%, 3/15/2028, 144A | 2,727,728 | ||||||

| 18,780,000 | Royal Caribbean Cruises Ltd., 5.500%, 4/01/2028, 144A | 14,987,285 | ||||||

|

| |||||||

| 43,869,961 | ||||||||

|

| |||||||

| Life Insurance – 3.3% |

| |||||||

| 5,935,000 | Athene Global Funding, 1.716%, 1/07/2025, 144A | 5,475,698 | ||||||

| 6,099,000 | Brighthouse Financial, Inc., 4.700%, 6/22/2047 | 4,461,459 | ||||||

See accompanying notes to financial statements.

| 16

Portfolio of Investments – as of December 31, 2022

Loomis Sayles Bond Fund – continued

Principal Amount | Description | Value (†) | ||||||

| Bonds and Notes – continued | ||||||||

| Life Insurance – continued |

| |||||||

| $ | 20,335,000 | Brighthouse Financial, Inc., 5.625%, 5/15/2030 | $ | 19,340,130 | ||||

| 2,030,000 | MetLife, Inc., 9.250%, 4/08/2068, 144A | 2,364,825 | ||||||

| 10,175,000 | MetLife, Inc., 10.750%, 8/01/2069 | 13,499,071 | ||||||

| 57,985,000 | Mutual of Omaha Insurance Co., 6.800%, 6/15/2036, 144A | 60,335,097 | ||||||

| 38,476,000 | National Life Insurance Co., 10.500%, 9/15/2039, 144A | 50,217,721 | ||||||

| 12,950,000 | NLV Financial Corp., 7.500%, 8/15/2033, 144A | 14,220,654 | ||||||

|

| |||||||

| 169,914,655 | ||||||||

|

| |||||||

| Lodging – 1.0% |

| |||||||

| 11,490,000 | Hilton Domestic Operating Co., Inc., 3.625%, 2/15/2032, 144A | 9,201,192 | ||||||

| 2,475,000 | Hilton Grand Vacations Borrower Escrow LLC/Hilton Grand Vacations Borrower Escrow, 4.875%, 7/01/2031, 144A | 2,019,979 | ||||||

| 8,090,000 | Hilton Grand Vacations Borrower Escrow LLC/Hilton Grand Vacations Borrower Escrow, 5.000%, 6/01/2029, 144A | 6,957,400 | ||||||

| 11,290,000 | Marriott International, Inc., Series HH, 2.850%, 4/15/2031 | 9,142,446 | ||||||