UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | for the fiscal year ended December 28, 2008 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 0-32233

PEET’S COFFEE & TEA, INC.

(Exact Name of Registrant as Specified in Its Charter)

| | |

| Washington | | 91-0863396 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

1400 Park Avenue

Emeryville, California 94608-3520

(Address of Principal Executive Offices)(Zip Code)

(510) 594-2100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

Common Stock, no par value | | The Nasdaq National Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark whether the registrant is well-known, seasoned filer (as defined in Rule 405 under the Securities Act). Yes ¨ No x

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ¨ Accelerated Filer x Non-Accelerated Filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ¨ No x

The approximate aggregate market value of the voting stock held by non-affiliates of the registrant based on the closing price and shares of the Common Stock outstanding on June 29, 2008 (the registrant’s most recently completed second quarter), as reported by the Nasdaq National Market, was $284,850,079. Shares of Common Stock held by each officer, director and each person known to the Company to hold 5% or more of the outstanding Common Stock have been excluded as such persons may be deemed to be affiliates of the Company. Such determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 1, 2009, 12,980,673 shares of registrant’s Common Stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement related to the registrant’s 2008 annual meeting of shareholders, which proxy statement will be filed under the Securities Exchange Act of 1934 within 120 days of the end of the registrant’s fiscal year ended December 28, 2008, are incorporated by reference into Part III of this annual report on Form 10-K.

TABLE OF CONTENTS

References to “we”, “us”, “our”, “Peet’s”, and the “Company” in this annual report on Form 10-K refer to Peet’s Coffee & Tea, Inc.

FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K (this “report”) contains forward-looking statements, including in the sections entitled “Business,” “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. Forward-looking statements include statements about:

| | • | | Our expectations regarding the cost and availability of high qualityArabica coffee beans. |

| | • | | Our expectations regarding the uninterrupted operation of our roasting and distribution facility. |

| | • | | Our ability to successfully implement our business strategy including our ability to market our products and increase our brand recognition. |

| | • | | The impact of the current recession or a worsening of the United States and global economy on our business. |

| | • | | The impact of potential litigation or disputes on our business. |

| | • | | Our ability to continue leasing our retail locations and obtain leases for new stores. |

| | • | | Our ability to promote and enhance our brand. |

| | • | | Our ability to hire and retain well-qualified management and other personnel. |

| | • | | Our ability to attract and retain customers. |

| | • | | Our expectations regarding consumers’ tastes and preferences. |

| | • | | Our ability to successfully compete in our markets. |

In some cases, you can identify forward-looking statements by terminology, such as “may,” “should,” “could,” “predict,” “potential,” “continue,” “expect,” “anticipate,” “future,” “intend,” “plan,” “believe,” “estimate,” “forecast” and similar expressions (or the negative of such expressions.) Forward-looking statements reflect our current views with respect to future events, are based on assumptions, and are subject to risks, uncertainties and other important factors. We discuss many of these risks, uncertainties and other important factors in this report in greater detail in the section entitled “Risk Factors” under Part I, Item 1A below. Given these risks, uncertainties and other important factors, you should not place undue reliance on these forward-looking statements. Also, forward-looking statements represent our estimates and assumptions only as of the date of this report. You should read this report and the documents that we incorporate by reference in and have filed as exhibits to this report, completely and with the understanding that our actual future results may be materially different from what we expect.

Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

1

PART I

Peet’s Coffee & Tea is a specialty coffee roaster and marketer of fresh roasted whole bean coffee and tea. We sell our coffee under strict freshness standards through multiple channels of distribution including grocery stores, home delivery, office, restaurant and foodservice accounts and Company-owned and operated stores in six states. We operate our business through two reportable segments: retail and specialty sales. See Note 11, “Segment Information” to the “Notes to Consolidated Financial Statements” included elsewhere in this report.

Since we believe that roasted coffee is a perishable product, we pursue distribution channels that are consistent with our strict freshness standards. For instance, our distribution to grocery stores emphasizes the use of a direct store delivery (“DSD”) system whereby our employees or agents deliver fresh goods to our grocery partners. We roast to order and ship coffee directly from our roasting facility to our home delivery customers. Our goal is to ensure that customers receive coffee within days of roasting.

Our corporate website is located at www.peets.com. Our annual report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, as well as any amendments or exhibits to those reports, are available free of charge through our website at www.peets.com as soon as reasonably practicable after we file them with, or furnish them to, the Securities and Exchange Commission (“SEC”). The content on any website referred to in this report is not incorporated by reference into this report unless expressly noted. The Company was organized as a Washington corporation in 1971.

Company Retail Stores

As of December 28, 2008 we operated 188 retail stores in six states through which we sell whole bean coffee, beverages and pastries, tea, and other related items. Our stores are designed to facilitate the sale of fresh whole bean coffee and to encourage customer trial of our coffee through coffee beverages. Each store has a dedicated staff person at the bean counter to take orders and assist customers with questions on coffee origins and on home brewing. Upon order, beans are scooped and ground to the customer’s specific requirements. At our beverage counter, we rotate and sell freshly-brewed coffees and coffee-based beverages to promote customer familiarity, sampling, and sales of whole-bean coffees. To ensure that our freshness standards are consistently met, it is our policy not to serve brewed coffee that is more than 30 minutes old and every espresso based drink is made to order using freshly pulled shots of espresso and freshly steamed milk. See “Item 2. Properties” for further discussion about our retail stores.

Specialty Sales

Grocery

In addition to sales through our retail stores, we sell our products through a network of grocery stores, including Safeway, Albertson’s, Ralph’s, Kroger, Publix and Whole Foods Market. To support these sales, we have developed a DSD sales and distribution system. Peet’s DSD route sales representatives deliver directly to their stores anywhere between one to three times per week, properly shelve the product, rotate to ensure freshness, sell and erect free-standing displays and forge store-level selling relationships. We currently have 51 company-operated DSD route sales representatives and approximately 160 independent distributors to support our expansion into new grocery accounts and our existing grocery customers.

Home Delivery

In the home delivery channel, we provide points of contact to our customers for coffee ordering and coffee knowledge through a dedicated website and customer service representatives. Our website features an Express

2

Buy function for registered customers for speed and ease, special coffee and tea programs and a coffee and tea selector to assist the customer in choosing a product based upon certain characteristics. Peets.com also features a proprietary tool that allows customers to manage the timing and delivery of their recurring orders. We reward our most loyal home delivery customers who maintain regular, ongoing deliveries of coffee or tea through our Peetnik Loyalty Program. This program has proven to be successful in growing our home delivery business online by encouraging our most loyal customers to establish regular deliveries of fresh roasted coffee or tea. In addition to our website, we have a team of customer service representatives who assist customers in placing customer orders, choosing a gift item, providing product information and resolving customer issues. Customer service representatives are regularly trained on Peet’s product offerings through weekly coffee and tea tastings.

Foodservice and Office

In the foodservice and office business, we have a staff of sales and account managers who make sales calls to potential accounts and conduct quality audits at our existing accounts. Additionally, we have established relationships with foodservice and office distributors to expand our account base in select markets and channels. These distributors have their own sales and account management resources. We have two models for servicing our foodservice accounts and distributing our products: “We Proudly Brew” (“WPB”) accounts and licensing accounts. WPB accounts are foodservice accounts where Peet’s supplies the equipment and product to brew and resell our products. Licensing accounts involve the creation of a full Peet’s beverage store within another location such as an airport, grocery store or college campus. The license partner is responsible for the build-out and management of the unit and we provide training and operations oversight. The office coffee channel is a distributor based business where we sell to specialty distributors who in turn sell our products for brewing to individual offices.

Our Coffee

Coffee Beans

Coffee is an agricultural crop that undergoes quality changes and price fluctuation depending on weather, economic and political conditions in coffee producing countries. We purchase onlyarabica coffee beans, which are considered superior to beans traded in the commodity market. Thearabicabeans purchased by us tend to trade on a negotiated basis at a substantial premium above commodity coffee prices, depending upon the supply and demand at the time of purchase. Our access to high qualityarabicabeans depends on our relationships with coffee brokers, exporters and growers, with whom we have built long-term relationships to ensure a steady supply of coffee beans. We believe that, as a result of our reputation that has been built over 40 years, we have access to some of the highest quality coffee beans from the finest estates and growing regions around the world and we are occasionally presented with opportunities to purchase unique and special coffees.

Unlike roasted coffee beans, green coffee beans are not highly perishable. We generally turn our inventory of green coffee beans two to three times per year. We typically carry approximately $14 million to $20 million of green coffee beans in our inventory. We currently use fixed-price purchase commitments, but in the past have used and may potentially in the future use coffee futures and coffee futures options to manage coffee supply and price risk.

Our Roasting Method

Our roasting method was first developed by Alfred Peet and further honed by our talented and skilled roasting personnel. We roast by hand in small batches, and we rely on the skills and training of each roaster to maximize the flavor and potential in our beans. Our roasters undergo an extensive apprenticeship program to learn our roasting method and to gain the skills necessary to roast coffee at Peet’s and make a long-term commitment to our artisan craft.

3

Coffee Types and Blends

Beyond sourcing and roasting, we have developed a reputation for expert coffee blending. Our blends, such as Major Dickason’s Blend®, are well regarded by our customers for their uniqueness, consistency and special flavor characteristics. We sell approximately 25 types of coffee as regular menu items, including approximately 14 blends and 11 single origin coffees such as Colombia, Guatemala, Sumatra and Kenya. We also offer a line of high-end reserve coffees including JR Reserve Blend® and Kona, and we have also featured seasonal reserve coffees such as Jamaica Blue Mountain and Panama Esmeralda. We are active in seeking, roasting and selling unique special lot and one-time coffees. On average, we offer four to six such coffees every year, including our Anniversary Blend and Holiday Blend.

Tea, Food and Merchandise

Peet’s offers a line of hand selected whole leaf and bagged tea. Our quality standards for tea are very high. We purchase tea directly from importers and brokers and store and pack the tea at our facility in Emeryville, California. We offer a limited line of specialty food items, such as jellies, jams and candies. These products are carefully selected for quality and uniqueness.

Our merchandise program consists of items such as brewing equipment for coffee and tea, paper filters and brewing accessories and branded and non-branded cups, saucers, travel mugs and serveware. We do not emphasize these items, but we carry them in retail stores and offer them through home delivery as a means to reinforce our commitment to premium home-brewed coffee and tea.

Competitive Positioning

The specialty coffee category is competitive, but it is dominated by Starbucks Corporation, which is larger than all the competitors combined. The specialty coffee market generates most of its sales from coffeehouses that currently number over 20,000 in the United States. In addition, coffee is sold by coffee roasters like Peet’s to foodservice operators, grocery stores, direct to consumers through websites and mail order, offices and other places where coffee is consumed or purchased for home consumption.

In the coffeehouse business, Starbucks is our primary competition, but we also compete with small single unit mom and pop coffee houses and local chains such as, Coffee Bean & Tea Leaf, Tully’s and Caribou Coffee. In addition, the consumer has a choice to purchase their prepared coffee beverages at countless locations such as convenience stores, bakeries and restaurants.

Outside of the coffeehouse business (our Specialty segment), Starbucks is also our primary competitor but we also compete with Green Mountain Coffee, Illy Caffé, Millstone (Smucker’s), Seattle’s Best (Starbucks), Tully’s and Dunkin’ Donuts as well as numerous smaller, regional brands. To a lesser extent, we may also compete with more mainstream coffee such as Maxwell House and Folger’s, but we believe that this overlap is negligible.

We believe that our customers choose among specialty coffee brands based the total value proposition that includes quality, variety, convenience, and price. We believe that our market share in the specialty category in all channels is driven by the quality of our product, which is based on a differentiated position built on our bean selectivity, freshness standards and artisan-roasting style. Because of the fragmented nature of the specialty coffee market, we cannot accurately estimate our market share across the whole category.

Our roasted coffee that is sold to the end consumer is priced in tiers. Our regular menu coffees are currently priced in our retail locations within a range of $10.95 to $19.95 per pound. Our line of high-end reserve coffees is priced between $49.90 and $79.90 per pound. In the grocery channel, we sell our coffee in 12 ounce packages at prices established by the grocery store. Most grocery stores sell our product at a price between $8.99 and $11.99 for a 12 ounce bag.

4

Intellectual Property

We regard intellectual property and other proprietary rights as important to our success. We place high value on our Peet’s trade name, and we own several trademarks and service marks that have been registered with the United States Patent and Trademark Office, including Peet’s®, Peet’s Coffee & Tea®, peets.com®, Blend 101®, eCup®, Espresso Forte®, Fresh Fridays®, Gaia Organic Blend®, Garuda Blend®, JR Reserve Blend®, Major Dickason’s Blend®, Peetniks®, Pride of the Port®, Pumphrey’s Blend®, Summer House®, and Snow Leopard®. We also have registered trademarks on our stylized logo and our P-mug design. In addition, we have applications pending with the United States Patent and Trademark Office for a number of additional marks including Freddo™, and Blended Freddo™. We own registered trademarks for our name and logo in Argentina, Australia, Brazil, Canada, Chile, China, the European Union, Hong Kong, Japan, Paraguay, Singapore, South Korea, Taiwan and Thailand. We have filed additional applications for trademark protection in Indonesia and the Philippines. In addition to peets.com and coffee.com, we own several other domain names relating to coffee, Peet’s and our roasting process.

In addition to registered and pending trademarks, we consider the packaging for our coffee beans (consisting of dark brown coloring with African-style motif and lettering with a white band running around the lower quarter of the bag) and the design of the interior of our stores (consisting of dark wood fixtures, classic lighting, granite countertops and understated color) to be strong identifiers of our brand. Although we consider our packaging and store design to be essential to our brand identity, we have not applied to register these trademarks and trade dress, and thus cannot rely on the legal protections afforded by trademark registration.

Our ability to differentiate our brand from those of our competitors depends, in part, on the strength and enforcement of our trademarks. We must constantly protect against any infringement by competitors. If a competitor infringes on our trademark rights, we may have to litigate to protect our rights, in which case, we may incur significant expenses and divert significant attention from our business operations.

Information Systems

The information systems installed at Peet’s are used to manage our operations and increase the productivity of our workforce. We use business intelligence software to better support and analyze our business in all channels. We have a retail point-of-sale system that we believe increases store productivity, provides a higher level of service to our customers and maintains timely information for performance evaluation. Our registers have touch screen components and full point-of-sale capability. We have an integrated labor and scheduling system in our retail stores that enhances productivity and customer service. In 2007, we tested a new inventory management system in our retail stores, which we implemented in all our stores in 2008. In 2008, we also completed the design and development of an enhanced grocery route management system with increased capacity and upgraded our DSD handheld software. We began design and development of a new $6 million enterprise resource planning system that we plan to implement in 2009.

Our websites, peets.com and peetscoffee.com offer several customer-centered functions. We offer full-functioning e-commerce at peets.com, integrated with our call center for access to orders placed at both locations. Online delivery confirmation is provided by United Parcel Service and the United States Postal Service. Manage Deliveries is an application which enables consumers to schedule recurring deliveries including choosing specific coffees and teas to be delivered at the frequency of their choice. Other important customer functions include a coffee and tea selector, Express Buy and multiple “ship-to” capability on a single bill, and store locators. Additionally, customers with Peet’s cards can check their balance as well as reload their card online. We have dedicated information technology employees and marketing staffers for website maintenance, improvement, development and performance.

Employees

As of March 1, 2009, we employed a workforce of 3,750 people, approximately 748 of whom work approximately 40 hours per week and are considered full-time employees. We consider our relationship with our

5

employees to be good. Since 1979, we have provided full benefits to all employees who work at least 21 hours per week and have worked at least 500 total hours for the Company. We believe we offer competitive benefits packages to attract and retain valuable employees.

Government Regulation

Our coffee roasting operations and our retail stores are subject to various governmental laws, regulations, and licenses relating to customs, health and safety, building and land use, and environmental protection. Our roasting facility is subject to state and local air-quality and emissions regulations. If we encounter difficulties in obtaining any necessary licenses or complying with these laws and regulations, then:

| | • | | The opening of new retail locations could be delayed; |

| | • | | The operation of existing retail locations or our coffee roasting operations could be interrupted; or |

| | • | | Our product offerings could be limited. |

We believe that we are in compliance in all material respects with all such laws and regulations and that we have obtained all material licenses that are required for the operation of our business. We are not aware of any environmental regulations that have or that we believe will have a material adverse effect on our operations.

Executive Officers of the Registrant

Set forth below is information with respect to the names, ages, positions and offices of our executive officers as of March 1, 2009.

| | | | |

Name | | Age | | Position |

Patrick J. O’Dea | | 47 | | Chief Executive Officer, President and Director |

Thomas P. Cawley | | 48 | | Chief Financial Officer, Vice President and Secretary |

P. Christine Lansing | | 45 | | Vice President, General Manager Consumer Business |

Kay L. Bogeajis | | 54 | | Vice President, Retail Operations |

Patrick J. O’Deahas served as Chief Executive Officer, President and as a director since May 2002. From April 1997 to March 2001, he was CEO of Archway/Mother’s Cookies and Mother’s Cake & Cookie Company. From 1995 to 1997, Mr. O’Dea was the Vice President and General Manager of the Specialty Cheese Division of Stella Foods. From 1984 to 1995, he was with Procter & Gamble, where he marketed several of the company’s snack and beverage brands.

Thomas P. Cawley has served as Chief Financial Officer since July 2003. From August 2000 to June 2003, he was at Gap, Inc. serving as Chief Financial Officer, Gap Brand. From 1986 to August 2000, Mr. Cawley was at PepsiCo/Yum Brands (formerly Tricon Global Restaurants), holding various positions such as Director of Finance, Vice President—Controller, and Chief Financial Officer of Pizza Hut. Previous to 1986, Mr. Cawley was with The Quaker Oats Company and General Foods.

P. Christine Lansingjoined the Company as Vice President, Chief Marketing Officer in October 2005. She assumed additional responsibility for the management of the grocery channel in October 2007 and in November 2008 became the Vice President, General Manager Consumer Business (grocery and home delivery), leading the strategic planning and implementation of Peet’s grocery expansion and innovation efforts. From May 2002 to October 2005, Ms. Lansing served as Vice President of Marketing, Flagship Brands for The Hershey Company. From August 1989 to April 2002, she held a breadth of marketing positions with Procter & Gamble in the United States and Western Europe.

Kay L. Bogeajishas served as Vice President, Retail Operations since she joined the Company in October 2007. From January 2003 to October 2007, Ms. Bogeajis served as Vice President, Western Operations for Taco

6

Bell Corporation, a Yum Brand company, where she was responsible for more than 1,400 stores and approximately $1.4 billion in system-wide sales. From October 2001 to January 2003, she was Vice President Systemwide Operations for Taco Bell. Previously, she held prominent retail operations and sales positions with Taco Bell, Frito-Lay, Inc., a PepsiCo company, and Burger King Corporation.

We may not be successful in the implementation of our business strategy or our business strategy may not be successful, either of which will impede our growth and operating results.

Our business strategy emphasizes expansion through multiple channels of distribution. Our ability to implement this business strategy is dependent on our ability to:

| | • | | Market our products on a national scale and over the internet; |

| | • | | Enter into distribution and other strategic arrangements with third party retailers and other potential distributors of our coffee; |

| | • | | Increase our brand recognition on a national scale; |

| | • | | Identify and lease strategic locations suitable for new stores; and |

| | • | | Manage growth in administrative overhead and distribution costs likely to result from the planned expansion of our retail and non-retail distribution channels. |

We do not know whether we will be able to successfully implement our business strategy or whether our business strategy will be successful. Our revenue may be adversely affected if we fail to implement our business strategy or if we divert resources to a business strategy that ultimately proves unsuccessful.

Because our business is highly dependent on a single product, specialty coffee, if the demand for specialty coffee decreases, our business could suffer.

Sales of specialty coffee constituted approximately 83% of our 2008, 2007 and 2006 net revenue. Demand for specialty coffee is affected by many factors, including:

| | • | | Consumer tastes and preferences; |

| | • | | National, regional and local economic conditions; |

| | • | | Demographic trends; and |

| | • | | Perceived or actual health benefits or risks. |

Because we are highly dependent on consumer demand for specialty coffee, a shift in consumer preferences away from specialty coffee would harm our business more than if we had more diversified product offerings. If customer demand for specialty coffee decreases, our sales would decrease accordingly.

If we fail to continue to develop and maintain our brand, our business could suffer.

We believe that maintaining and developing our brand is critical to our success and that the importance of brand recognition may increase as a result of competitors offering products similar to ours. Because the majority of our retail stores are located on the West Coast, primarily in California, our brand recognition remains largely regional. Our brand building initiative involves increasing the availability of our products and opening new stores to increase awareness of our brand and create and maintain brand loyalty. If our brand building initiative is unsuccessful, we may never recover the expenses incurred in connection with these efforts and we may be unable to increase our future revenue or implement our business strategy.

7

Our success in promoting and enhancing the Peet’s brand will also depend on our ability to provide customers with high quality products and customer service. Although we take measures to ensure that we sell only fresh roasted whole bean coffee and that our retail employees properly prepare our coffee beverages, we have no control over our whole bean coffee products once purchased by customers. Accordingly, customers may prepare coffee from our whole bean coffee inconsistent with our standards, store our whole bean coffee for long periods of time or resell our whole bean coffee without our consent, which in each case, potentially affects the quality of the coffee prepared from our products. If customers do not perceive our products and service to be of high quality, then the value of our brand may be diminished and, consequently, our ability to implement our business strategy may be adversely affected.

Increases in the cost and decreases in availability of high quality Arabica coffee beans could impact our profitability and growth of our business.

Green coffee is our largest single cost of sales. We do not purchase coffee on the commodity markets, but price movements in the trading of coffee do impact the price we pay. Coffee is a trade commodity and, in general, its price can fluctuate depending on:

| | • | | Weather patterns in coffee-producing countries; |

| | • | | Economic and political conditions affecting coffee-producing countries; |

| | • | | Foreign currency fluctuations; |

| | • | | The ability of coffee-producing countries to agree to export quotas; and |

| | • | | General economic conditions that make commodities more or less attractive investment options. |

Coffee commodity costs began to decline in July 2008 after over four years of increases above the prior three to four year range. We expect the commodity market to continue to be volatile as worldwide demand, the strength of the dollar, and weather will continue to cause uncertainty in the market. If coffee costs increase and we are unable to pass along increased coffee costs, our margin will decrease and our profitability will suffer accordingly. If we are not able to purchase sufficient quantities of high quality Arabica beans due to any of the above factors, we many not be able to fulfill the demand for our coffee, our revenue may decrease and our ability to expand our business may also suffer.

The current recession or a worsening of the United States and global economy could materially adversely affect our business.

Our revenues and performance depend significantly on consumer confidence and spending, which have recently deteriorated due to the recession and may remain depressed for the foreseeable future. Some of the factors that could influence the levels of consumer confidence and spending include, without limitation, continuing conditions in the residential real estate and mortgage markets, access to credit, labor and healthcare costs, increases in fuel and other energy costs, consumer confidence and other macroeconomic factors affecting consumer spending behavior. These and other economic factors could have a material adverse effect on demand for our products and on our financial condition and operating results.

Because our business is based primarily in California, a worsening of economic conditions, a decrease in consumer spending or a change in the competitive conditions in this market may substantially decrease our revenue and may adversely impact our ability to implement our business strategy.

Our California retail stores generated approximately 60% of our 2008, 2007 and 2006 net revenue and a substantial portion of the revenue from our other distribution channels is generated in California. We expect that our California operations will continue to generate a substantial portion of our revenue. In addition, our California retail stores provide us with means for increasing brand awareness, building customer loyalty and

8

creating a premium specialty coffee brand. As a result, if the current economic downturn and decrease in consumer spending in California continues or worsens, it may not only lead to a substantial decrease in revenue, but may also adversely impact our ability to market our brand, build customer loyalty, or otherwise implement our business strategy.

Complaints or claims by current, former or prospective employees or governmental agencies could adversely affect us.

We are subject to a variety of laws and regulations which govern such matters as minimum wages, overtime and other working conditions, various family leave mandates and a variety of other laws enacted, or rules and regulations promulgated, by federal, state and local governmental authorities that govern these and other employment matters. We have been, and in the future may be, the subject of complaints or litigation from current, former or prospective employees or governmental agencies. In addition, successful complaints against our competitors may spur similar lawsuits against us. For instance, in 2003, two lawsuits (which have since been settled) were filed against the Company alleging misclassification of employment position and sought damages, restitution, reclassification and attorneys’ fees and costs. In addition, on July 14, 2008, a complaint was filed alleging that store managers based in California were not paid overtime wages, were not provided meal or rest periods, were not provided accurate wage statements and were not reimbursed for business expenses. These types of claims could divert our management’s time and attention from our business operations and might potentially result in substantial costs of defense, settlement or other disposition, which could have a material adverse effect on our results of operations in one or more fiscal periods.

Potential claims and litigation could have a material adverse effect on us.

In addition to employment related claims, we may be subject to various claims and litigation. For example, in 2007 we were involved as defendants in lawsuits relating to our stock option granting practices. Although these actions have been dismissed, we could in the future become subject to other claims and litigation, which could involve, for example, securities law claims, commercial disputes, and disputes relating to intellectual property. Potential lawsuits could divert management time and attention from day-to-day operations, result in significant legal expenses, and result in an outcome that could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Labor conditions in the grocery business could negatively impact our grocery business.

There have been grocery strikes in the past that have negatively impacted our grocery business and it is possible that future grocery strikes in places where we have large distribution may adversely impact our grocery business.

Government mandatory healthcare requirements could adversely affect our profits.

The Company offers healthcare benefits to all employees who work at least 21 hours a week and meet service eligibility requirements. In the past, some states, including California, have unsuccessfully proposed legislation mandating that employers pay healthcare premiums into a state run fund for all employees immediately upon hiring. If legislation similar to this were to be enacted in the states we do business, it could have an adverse affect on the Company’s results of operations.

If we are unable to continue leasing our retail locations or obtain leases for new stores, our existing operations and our ability to expand may be adversely affected.

All of our 188 retail locations as of year-end are on leased premises. If we are unable to renew these leases, our revenue and profits could suffer. In addition, we intend to lease other premises in connection with the planned expansion of our retail operations. Because we compete with other retailers and restaurants for store sites

9

and some landlords may grant exclusive locations to our competitors, we may not be able to obtain new leases or renew existing leases on acceptable terms. This could adversely impact our revenue growth and brand building initiatives.

Because we rely heavily on common carriers to ship our coffee on a daily basis, any disruption in their services or increase in shipping costs could adversely affect our business.

We rely on a number of common carriers to deliver coffee to our customers and retail stores. We consider roasted coffee a perishable product and we rely on these common carriers to deliver fresh roasted coffee on a daily basis. We have no control over these common carriers and the services provided by them may be interrupted as a result of labor shortages, contract disputes or other factors. If we experience an interruption in these services, we may be unable to ship our coffee in a timely manner. A delay in shipping could:

| | • | | Have an adverse impact on the quality of the coffee shipped, and thereby adversely affect our brand and reputation; |

| | • | | Result in the disposal of an amount of coffee that could not be shipped in a timely manner; and |

| | • | | Require us to contract with alternative, and possibly more expensive, common carriers. |

Any significant increase in shipping costs could lower our profit margins or force us to raise prices, which could cause our revenue and profits to suffer.

We depend on the expertise of key personnel. If these individuals leave or change their role within our Company without effective replacements, our operations may suffer.

The success of our business is dependent to a large degree on our management and our coffee roasters and purchasers. If members of our management leave without effective replacements, our ability to implement our business strategy could be impaired. If we lost the services of our coffee roasters and purchasers, our ability to source and purchase a sufficient supply of high quality coffee beans and roast coffee beans consistent with our quality standards could suffer. In either case, our business and operations could be adversely affected.

We may not be able to hire or retain additional management and other personnel and our recruiting and training costs may increase as a result of turnover, both of which may increase our costs and reduce our profits and may adversely impact our ability to implement our business strategy.

The success of our business depends upon our ability to attract and retain highly motivated, well-qualified management and other personnel, including technical personnel and retail employees. We face significant competition in the recruitment of qualified employees. Our ability to execute our business strategy may suffer if:

| | • | | We are unable to recruit or retain a sufficient number of qualified employees; |

| | • | | The costs of employee compensation or benefits increase substantially; or |

| | • | | The costs of outsourcing certain tasks to third party providers increase substantially. |

Because we have only one roasting facility, a significant interruption in the operation of our roasting and distribution facilities could potentially disrupt our operations.

We have only one roasting and distribution facility. A significant interruption in the operation of this facility, whether as a result of a natural disaster or other causes, could significantly impair our ability to operate our business. Since we only roast our coffee to order, we do not carry inventory of roasted coffee in our roasting plant. Therefore, a disruption in service in our roasting facility would impact our sales in our retail and specialty channels almost immediately. Moreover, our roasting and distribution facilities and most of our stores are located near several major earthquake faults. The impact of a major earthquake on our facilities, infrastructure and overall operations is difficult to predict and an earthquake could seriously disrupt our entire business.

10

Our earthquake insurance covers net income, continuing normal operating expenses and extra expenses incurred during the period of restoration once the large deductible has been exceeded. However, in the event of a catastrophic earthquake, our coverage is limited and would not cover all of our expenses and losses caused by an earthquake.

We have a high deductible workers’ compensation insurance program and more claims and higher costs from these claims may adversely affect our profits.

For the policy years beginning March 2002 through February 2008 our workers’ compensation insurance program was a modified self-insured program with a high deductible with an overall program ceiling to limit exposure. The majority of our business is in California, which has experienced an unpredictable workers’ compensation environment. Therefore, we are highly exposed to this environment. Additionally, we have had to estimate our liability for existing claims whose outcome is uncertain. While we believe our reserve methodology on these claims is appropriate, should a greater amount of claims occur or the settlement costs increase beyond what was anticipated, our expenses could increase and our profitability may decrease. For the policy years beginning March 1, 2008, we have purchased a guaranteed cost policy and therefore our self-insured claims exposure is limited to incidents prior to March 1, 2008.

Our roasting methods are not proprietary, so competitors may be able to duplicate them, which could harm our competitive position.

We consider our roasting methods essential to the flavor and richness of our roasted whole bean coffee and, therefore, essential to our brand. Because we do not hold any patents for our roasting methods, it may be difficult for us to prevent competitors from copying our roasting methods. If our competitors copy our roasting methods, the value of our brand may be diminished, and we may lose customers to our competitors. In addition, competitors may be able to develop roasting methods that are more advanced than our roasting methods, which may also harm our competitive position.

Competition in the specialty coffee market is intense and could affect our profits.

The specialty coffee category is competitive, dominated by Starbucks Corporation, which is larger than all the competitors combined. In addition to Starbucks, our competitors include Green Mountain Coffee, Illy Caffé, Millstone (Smucker’s), Seattle’s Best (Starbucks), Dunkin’ Donuts and Coffee Bean & Tea Leaf,. There are also numerous smaller, regional brands that compete in this category with either coffeehouses of their own or a presence in wholesale, or both. In addition, we indirectly compete with more mainstream brands as Maxwell House (Kraft) and Folgers (Smucker’s). In the grocery channel, Kraft and Smucker’s are the largest players since Kraft distributes its own brands as well as Starbucks and Seattle’s Best while Smucker’s licenses and distributes the Dunkin’ Donut brand in addition to its Folgers and Millstone brands.

In every channel, Peet’s competes against at least one competitor who is much larger and has more financial resources than we do. There is always a risk that one of these competitors could undertake a strategy that involves very high spending or discounting that would negatively impact our operating results.

Adverse public or medical opinion about caffeine may harm our business.

Our specialty coffee contains significant amounts of caffeine and other active compounds, the health effects of some of which are not fully understood. A number of research studies conclude or suggest that excessive consumption of caffeine may lead to increased heart rate, nausea and vomiting, restlessness and anxiety, depression, headaches, tremors, sleeplessness and other adverse health effects. An unfavorable report on the health effects of caffeine or other compounds present in coffee could significantly reduce the demand for coffee, which could harm our business and reduce our sales and profits.

11

Adverse publicity regarding customer complaints may harm our business.

We may be the subject of complaints or litigation from customers alleging beverage and food-related illnesses, injuries suffered on the premises or other quality, health or operational concerns. Adverse publicity resulting from such allegations may materially adversely affect us, regardless of whether such allegations are true or whether we are ultimately held liable.

| Item 1B. | Unresolved Staff Comments |

Not Applicable.

Peet’s headquarters are located in Emeryville, California. The lease for our main office space devoted to general corporate and business channel overhead and a call center for the home delivery business is approximately 60,000 square feet and extends to October 2015 with two five year extension options. In 2008, we completed our renovation of this facility from our roasting plant into office space. In addition, we have a lease for a second office and warehouse space totaling approximately 8,000 square feet through April 30, 2013.

In December 2006, we purchased approximately 460,000 square feet of land and a 138,000 square foot building with related site improvements in Alameda, California for the purpose of operating a new roasting and distribution facility. The final purchase price of the facility and the land was $18.6 million. We transitioned our operations to this facility and were effectively at full production capability by May 2007.

In 2008, we opened 23 new stores. Our retail locations are all company-owned and operated in leased facilities. Our stores are typically located in urban neighborhoods, suburban shopping centers (usually consisting of grocery, specialty and service stores) and on high-traffic streets.

The following table lists the number of retail locations as of December 28, 2008:

| | |

Location | | Number |

Northern California | | 122 |

Southern California | | 40 |

Illinois | | 2 |

Oregon | | 8 |

Massachusetts | | 6 |

Washington | | 7 |

Colorado | | 3 |

| | |

Total | | 188 |

| | |

On July 14, 2008, a complaint was filed against Peet’s Coffee & Tea, Inc. in California Superior Court, Alameda County, by three former employees on behalf of themselves and all other California store managers. The complaint alleges that store managers based in California were not paid overtime wages, were not provided meal or rest periods, were not provided accurate wage statements and were not reimbursed for business expenses. The plaintiffs seek injunctive relief, monetary damages, penalties, costs and attorneys’ fees, and prejudgment interest. On October 8, 2008, the Company filed an answer denying the allegations set forth in the complaint and asserting a number of affirmative defenses thereto. On November 12, 2008, the plaintiffs filed an amended complaint asserting an additional claim for penalties. On November 26, 2008, the Company filed an answer thereto denying the allegations in the first amended complaint and asserting a number of affirmative defenses thereto. At this time, it is not feasible to predict the outcome of or a range of loss, should a loss occur, from this proceeding. The Company intends to vigorously defend against the litigation.

12

We may from time to time become involved in certain legal proceedings in the ordinary course of business. The Company is not a party to any other legal proceedings that management believes would have a material adverse effect on the financial position or results of operations of the Company.

| Item 4. | Submission of Matters to a Vote of Security Holders |

No matters were submitted to a vote of our shareholders during the quarter ended December 28, 2008.

13

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market for the Registrant’s Stock

The Company’s common stock is traded on the Nasdaq National Market under the symbol “PEET”. The following table sets forth, for the periods indicated, the high and low closing prices for our common stock as reported on the Nasdaq National Market for each quarter during the last two fiscal years.

| | | | | | |

| | | High | | Low |

Fiscal Year Ended December 28, 2008 | | | | | | |

Fourth Quarter | | $ | 27.92 | | $ | 19.05 |

Third Quarter | | | 28.88 | | | 18.79 |

Second Quarter | | | 24.92 | | | 20.86 |

First Quarter | | | 29.07 | | | 19.89 |

Fiscal Year Ended December 30, 2007 | | | | | | |

Fourth Quarter | | $ | 30.06 | | $ | 26.02 |

Third Quarter | | | 28.01 | | | 23.35 |

Second Quarter | | | 28.89 | | | 24.63 |

First Quarter | | | 28.20 | | | 24.94 |

As of March 1, 2009, there were approximately 365 registered holders of record of the Company’s common stock. On March 1, 2009, the last sale price reported on the Nasdaq National Market for the common stock was $21.55 per share.

Dividend Policy

We have not declared or paid any dividends on our capital stock since 1990. We expect to retain any future earnings to fund the development and expansion of our business. Therefore, we do not anticipate paying cash dividends on our common stock in the foreseeable future.

Issuer Purchases of Equity Securities

On September 6, 2006, the Company’s Board of Directors authorized the Company to purchase up to one million shares of Peet’s common stock, with no expiration, and the Company announced its plan on September 12, 2006 on Form 8-K. As of December 28, 2008, 941,241 shares had been purchased under this program at an average price of $21.91. On October 27, 2008, the Board of Directors approved a stock purchase program providing for the additional purchase of up to one million shares of the Company’s common stock, with no deadline for completion and the Company announced its plan on October 28, 2008 on Form 8-K. As of December 28, 2008, no shares had been purchased under this program. Purchases under the program would be made from time to time on the open market at prevailing market prices or in negotiated transactions off the market.

14

The following table sets forth all purchases made by us or any “affiliated purchaser” as defined in Rule 10b-18(a)(3) of the Exchange Act of the Company’s common stock during the fourth fiscal quarter of 2008.

| | | | | | | | | |

Period | | Total Number of

Shares Purchased | | Average Price Paid

per Share | | Total Number of

Shares Purchased

as Part of Publicly

Announced Plans

or Programs | | Maximum Number

of Shares that May

Yet Be Purchased

Under the Plans or

Programs |

September 29, 2008 – November 2, 2008 | | 99,442 | | $ | 20.45 | | 99,442 | | 1,460,710 |

November 3, 2008 – November 30, 2008 | | 359,265 | | | 21.41 | | 359,265 | | 1,101,445 |

December 1, 2008 – December 28, 2008 | | 42,686 | | | 20.70 | | 42,686 | | 1,058,759 |

| | | | | | | | | |

Total | | 501,393 | | $ | 21.16 | | 501,393 | | 1,058,759 |

| | | | | | | | | |

15

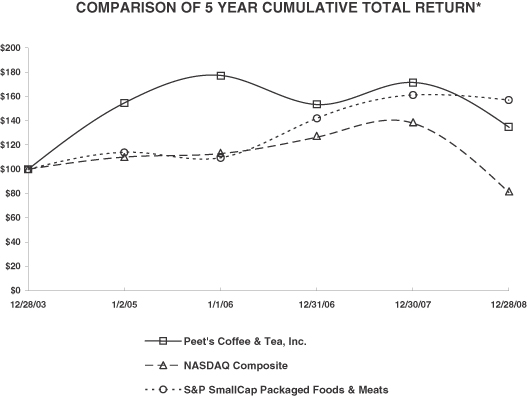

Performance Graph*

The following graph depicts the Company’s total return to shareholders from December 28, 2003 through December 28, 2008, relative to the performance of the NASDAQ Composite Index, and the Standard & Poor’s Smallcap 600 Consumer Goods Sector, Processed and Packaged Foods Industry. All indices shown in the graph have been reset to a base of 100 as of December 28, 2003, assume an investment of $100 on that date and the reinvestment of dividends paid since that date, calculated on a monthly basis. The Company has never paid cash dividends on its common stock. The points represent index levels based on the last trading day of the Company’s fiscal year. The chart set forth below was prepared by Research Data Group, Inc., which holds a license to provide the indices used herein. The stock price performance shown in the graph is not necessarily indicative of future price performance.

| * | This section is not “soliciting material”, is not deemed “filed” with the SEC and is not to be incorporated by reference in any of our filings under the Securities Act or the Securities Exchange Act made before or after the date hereof and irrespective of any general incorporation language in any such filing. |

| Item 6. | Selected Consolidated Financial Data |

The table below shows selected consolidated financial data for our last five fiscal years. Our fiscal year is based on a 52 or 53 week year and ends on the Sunday closest to the last day in December.

The following selected consolidated financial data should be read in conjunction with our consolidated financial statements and related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this report.

16

Selected Consolidated Financial Data

(in thousands, except per share data)

| | | | | | | | | | | | | | | |

| | | Year |

| | | 2008

(52 weeks) | | 2007

(52 weeks) | | 2006

(52 weeks) | | 2005

(52 weeks) | | 2004

(53 weeks) |

Statement of Income Data: | | | | | | | | | | | | | | | |

Net revenue | | $ | 284,822 | | $ | 249,389 | | $ | 210,493 | | $ | 175,198 | | $ | 145,683 |

Cost of sales and related occupancy expenses | | | 133,537 | | | 118,389 | | | 98,928 | | | 80,837 | | | 67,806 |

Operating expenses | | | 98,844 | | | 85,800 | | | 72,272 | | | 57,879 | | | 47,645 |

General and administrative expenses | | | 22,519 | | | 22,682 | | | 20,634 | | | 13,341 | | | 11,439 |

Depreciation and amortization expenses | | | 12,921 | | | 10,912 | | | 8,609 | | | 7,293 | | | 5,787 |

| | | | | | | | | | | | | | | |

Income from operations | | | 17,001 | | | 11,606 | | | 10,050 | | | 15,848 | | | 13,006 |

Interest income | | | 726 | | | 1,446 | | | 2,456 | | | 1,769 | | | 922 |

| | | | | | | | | | | | | | | |

Income before income taxes | | | 17,727 | | | 13,052 | | | 12,506 | | | 17,617 | | | 13,928 |

Income tax provision | | | 6,562 | | | 4,675 | | | 4,690 | | | 6,842 | | | 5,218 |

| | | | | | | | | | | | | | | |

Net income | | $ | 11,165 | | $ | 8,377 | | $ | 7,816 | | $ | 10,775 | | $ | 8,710 |

| | | | | | | | | | | | | | | |

Net income per share: | | | | | | | | | | | | | | | |

Basic | | $ | 0.81 | | $ | 0.61 | | $ | 0.57 | | $ | 0.78 | | $ | 0.65 |

Diluted | | $ | 0.80 | | $ | 0.59 | | $ | 0.55 | | $ | 0.74 | | $ | 0.62 |

Shares used in calculation of net income per share: | | | | | | | | | | | | | | | |

Basic | | | 13,723 | | | 13,724 | | | 13,733 | | | 13,801 | | | 13,308 |

Diluted | | | 13,997 | | | 14,120 | | | 14,202 | | | 14,469 | | | 13,949 |

| | | | | |

Balance Sheet Data: | | | | | | | | | | | | | | | |

Cash and cash equivalents | | $ | 4,719 | | $ | 15,312 | | $ | 7,692 | | $ | 20,623 | | $ | 11,356 |

Working capital | | | 36,422 | | | 38,380 | | | 37,254 | | | 62,584 | | | 16,726 |

Total assets | | | 176,352 | | | 177,547 | | | 153,005 | | | 148,752 | | | 128,944 |

Total shareholders’ equity | | | 143,907 | | | 147,253 | | | 127,439 | | | 126,878 | | | 109,905 |

17

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

You should read the following discussion and analysis in conjunction with our consolidated financial statements and related notes included elsewhere in this report. Except for historical information, the discussion below contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. The fiscal years ended December 28, 2008 (fiscal 2008), December 30, 2007 (fiscal 2007) and December 31, 2006 (fiscal 2006) all included 52 weeks.

Company Overview and Industry Outlook

Peet’s is a specialty coffee roaster and marketer of fresh, deep-roasted whole bean coffee and tea sold through multiple channels of distribution for home and away-from-home enjoyment. Founded in Berkeley, California in 1966, Peet’s has established a loyal customer base with strong brand awareness in California. Our growth strategy is based on the sale of whole bean coffee, tea and high-quality beverages in multiple channels of distribution including our own retail stores, grocery, home delivery, and office and restaurant accounts throughout the United States.

As we grow, we expect our operations to continue to be vertically integrated, allowing us to control the quality of our product at all stages. We purchase high quality Arabica coffee beans from countries around the world, and we use our artisan-roasting technique to bring out the distinctive flavor of our coffees. Because roasted coffee is perishable, we are committed to delivering our coffee under the strictest freshness standards. As a result, we do not stock or inventory roasted coffee. We roast to order and ship fresh coffee daily to our stores and customers. Control of purchasing, roasting, packaging and distribution of our coffee allows us to maintain our commitment to freshness, is cost effective, and enhances our margins and profit potential.

We expect the specialty coffee industry to continue to grow. We believe that this growth will be fueled by continued consumer interest in high quality coffee and related products. We believe that by offering high-quality products to consumers throughout the country, we will attract the same loyal customer base that we have attracted in California. We believe the growth in specialty coffee is particularly strong in grocery where specialty coffee dollars spent in the last year grew an estimated 12%.

We believe growth opportunities exist in all of our distribution channels. We believe that our specialty sales can expand to geographies where we do not have a retail presence. Our first priority has been to develop primarily in the western U.S. markets where we already have a presence and have higher customer awareness. In the long-term, we expect to continue to open new retail stores in strategic west coast locations that meet our demographic profile and partner with distributors and companies who share our passion for quality and freshness and are willing and able to execute accordingly in the foodservice and office environment. In grocery, we expect to continue to expand into new markets although the full extent of our penetration will depend upon the development of specialty coffee as a category in many markets.

Coffee commodity costs began to decline in July 2008 after over four years of increases above the prior three to four year range. We have fixed the price on 95% of our coffee costs in 2009 at a two to three percent increase over 2008. We expect the commodity market to continue to be volatile as worldwide demand, the strength of the dollar, and weather will continue to cause uncertainty in the market.

Our net revenues depend significantly on consumer confidence and spending, which have recently deteriorated due to the recession and may remain depressed for the foreseeable future. We believe that the current recession negatively impacted our net revenues in 2008. Despite revenue growth that was less than our plan, we were able to meet our targeted net earnings per share by leveraging our infrastructure investments and diligently managing our costs. In addition to achieving this target, we achieved the growth milestones as described below established at the beginning of year.

18

In 2008, the Company continued to pursue its strategy to expand its multiple distribution channels in the United States. The results of the efforts in 2008 include:

| | • | | opening 23 new retail locations, 22 of which were in California; |

| | • | | expanding our grocery network by entering 2,400 new stores, primarily outside of our core western markets. This helped drive 23% revenue growth in our grocery business; |

| | • | | expanding the availability of office coffee through a national partnership with Vistar, the largest office coffee distributor in the United States; and |

| | • | | growing our foodservice business by establishing license kiosks in numerous locations including airports and grocery stores. |

The current recession or a worsening of the United States and global economy could materially adversely affect our business as our revenues depend significantly on consumer confidence and spending. In 2009, while we will continue to grow our business, our primary focus will be on strengthening our core existing businesses with even more emphasis on operational efficiency. As a result, we will only open approximately 10 new stores in 2009, versus 23 in 2008, and expect to gain distribution in approximately 1,000 new grocery stores, versus the 2,400 we added in 2008. We believe this is the right strategic focus for us at this time, as we believe there are growth opportunities in these existing businesses and it will strengthen the Company long term. In 2008, we completed the implementation of a new inventory management system in our retail stores that enabled us to significantly reduce waste in the second half of the year and we will continue to focus on reducing waste and improving operations in 2009. In our specialty segment, we will also focus on leveraging the investments we have made in people and system infrastructure in 2009.

Business Segments

Our coffee and related items are sold through multiple channels of distribution that provide broad market exposure to potential purchasers of fresh roasted whole bean coffee. We are indifferent as to where consumers purchase our coffees and teas, and believe that our specialty and retail segments are synergistic. However, we also recognize that the economics of our retail stores and other distribution channels are different enough that we have chosen to report them as separate segments under SFAS No. 131, “Disclosures about Segments of an Enterprise and Related Information”. Therefore, we currently have two reportable segments, consisting of:

| | • | | Specialty sales, which consist of sales to grocery stores, foodservice and office accounts, and sales to home delivery customers. |

Business Categories

In addition to our reportable segments, we measure our business by monitoring the volume and revenue growth of two distinct business categories:

| | • | | Whole bean coffee and related products, consisting of products for home brewing, tea and packaged foods; and |

| | • | | Beverages and pastries. |

We believe these business categories are useful in understanding our results of operations for the periods presented because we operate our stores and record revenue through these two categories. Our stores are primarily designed to facilitate the sale of fresh whole bean coffee and hand-crafted coffee beverages. The format of our stores replicates that of a specialty grocer. Beans are freshly scooped from bins under the counter, weighed on counter top scales and hand packed into branded bags. In addition, our stores are also designed to encourage customer trial of our coffee through coffee beverages. Each store has a beverage bar that is dedicated to the sale of prepared beverages and artisan baked pastries.

19

Results of Operations

The following discussion on results of operations should be read in conjunction with “Item 6. Selected Consolidated Financial Data,” the consolidated financial statements and accompanying notes and the other financial data included elsewhere in this report.

Our fiscal year is based on a 52 or 53 week year. The fiscal year ends on the Sunday closest to the last day of December. 2008, 2007 and 2006 were all 52 week years.

| | | | | | | | | |

| | | 2008 | | | 2007 | | | 2006 | |

Statement of income as a percent of net revenue: | | | | | | | | | |

Net revenue | | 100.0 | % | | 100.0 | % | | 100.0 | % |

Cost of sales and related occupancy expenses | | 46.9 | | | 47.5 | | | 47.0 | |

Operating expenses | | 34.7 | | | 34.4 | | | 34.3 | |

General and administrative expenses | | 7.9 | | | 9.1 | | | 9.8 | |

Depreciation and amortization expenses | | 4.5 | | | 4.4 | | | 4.1 | |

| | | | | | | | | |

Income from operations | | 6.0 | | | 4.6 | | | 4.8 | |

Interest income | | 0.3 | | | 0.6 | | | 1.2 | |

| | | | | | | | | |

Income before income taxes | | 6.3 | | | 5.2 | | | 6.0 | |

Income tax provision | | 2.3 | | | 1.9 | | | 2.2 | |

| | | | | | | | | |

Net income | | 4.0 | % | | 3.3 | % | | 3.8 | % |

| | | | | | | | | |

Percent of net revenue by business segment: | | | | | | | | | |

Retail stores | | 65.9 | % | | 67.5 | % | | 67.2 | % |

Specialty sales | | 34.1 | | | 32.5 | | | 32.8 | |

Percent of net revenue by business category: | | | | | | | | | |

Whole bean coffee and related products | | 53.0 | % | | 53.8 | % | | 55.8 | % |

Beverages and pastries | | 47.0 | | | 46.2 | | | 44.2 | |

Cost of sales and related occupancy expenses as a percent of segment revenue: | | | | | | | | | |

Retail stores | | 45.5 | % | | 46.6 | % | | 46.2 | % |

Specialty sales | | 49.6 | | | 49.4 | | | 48.6 | |

Operating expenses as a percent of segment revenue: | | | | | | | | | |

Retail stores | | 42.4 | % | | 42.6 | % | | 42.6 | % |

Specialty sales | | 19.8 | | | 17.4 | | | 17.5 | |

Percent increase (decrease) from prior year: | | | | | | | | | |

Net revenue | | 14.2 | % | | 18.5 | % | | 20.1 | % |

Retail stores | | 11.5 | | | 19.1 | | | 19.8 | |

Specialty sales | | 19.9 | | | 17.2 | | | 20.9 | |

Cost of sales and related occupancy expenses | | 12.8 | | | 19.7 | | | 22.4 | |

Operating expenses | | 15.2 | | | 18.7 | | | 24.9 | |

General and administrative expenses | | (0.7 | ) | | 9.9 | | | 54.7 | |

Depreciation and amortization expenses | | 18.4 | | | 26.8 | | | 18.0 | |

| | | |

Selected operating data: | | | | | | | | | |

Number of retail stores in operation: | | | | | | | | | |

Beginning of the year | | 166 | | | 136 | | | 111 | |

Store openings | | 23 | | | 30 | | | 25 | |

Store closures | | (1 | ) | | — | | | — | |

| | | | | | | | | |

End of the year | | 188 | | | 166 | | | 136 | |

| | | | | | | | | |

20

2008 (52 weeks) Compared with 2007 (52 weeks)

Net revenue

Net revenue for 2008 increased 14.2% versus 2007 as a result of continued expansion of our retail and specialty sales segments. Sales of whole bean and related products increased 12.7% to $151.1 million. Sales from beverages and pastries increased 16.0% to $133.8 million.

In the retail segment, net revenue increased 11.5% compared to 2007 as a result of increased sales from new stores and the sales they generated in their first 12 months. Stores operating for at least one year contributed only a nominal amount of sales growth for the Company. We opened 23 new stores in 2008 and 30 new stores in 2007. Sales of whole bean coffee and related products in the retail segment increased by 3.8% to $55.1 million, while sales of beverages and pastries increased by 15.0% to $132.6 million. The increase in beverage and pastry sales was primarily related to sales at the stores we opened in 2007 and 2008 and increased traffic in our existing stores. The slower growth in whole bean and related products was primarily due to continuing cannibalization of bean sales in retail stores as we increased the availability of Peet’s coffee in grocery stores and our own retail stores.

In the specialty sales segment, net revenue increased 19.9% compared to 2007 as summarized by business channel below. The growth in net revenue in grocery was due to the 2,400 new stores we added during the year, bringing the number of grocery stores selling Peet’s coffee to approximately 8,200, as well as growth in our existing accounts in the western United States. Foodservice and office net revenue increased 34.7% over the prior year primarily due to 38 new licensed partner locations opened during the year and 150 additional “We Proudly Brew” accounts that serve Peet’s coffee in their own branded locations. Net revenue in the home delivery channel declined primarily due to cannibalization from our grocery business expanding in the eastern U.S. and lower gift sales during the 2008 holiday season.

| | | | | | | | | | | | | |

| (dollars in thousands) | | 2008 | | 2007 | | Increase/(Decrease) | |

Grocery | | $ | 51,490 | | $ | 41,879 | | $ | 9,611 | | | 22.9 | % |

Foodservice and office | | | 27,516 | | | 20,430 | | | 7,087 | | | 34.7 | % |

Home delivery | | | 18,096 | | | 18,688 | | | (592 | ) | | -3.2 | % |

| | | | | | | | | | | | | |

Total specialty | | $ | 97,103 | | $ | 80,997 | | $ | 16,106 | | | 19.9 | % |

| | | | | | | | | | | | | |

Cost of sales and related occupancy expenses

Cost of sales and related occupancy expenses consist of product costs, including manufacturing costs, rent and other occupancy costs. As a percent of net revenue, cost of sales decreased from 47.5% in 2007 to 46.9% in 2008. The decrease from last year was primarily due to procurement savings (-0.7%), leverage of costs related to the roasting facility that opened last year (-0.4%), and increased prices in retail and grocery (-0.3%), partially offset by higher green coffee costs (0.8%).

We expect cost of sales and related occupancy expenses as a percent of net revenue to continue to decrease in 2009 due to leverage of our new roasting facility, improved waste management in retail, and neutral commodity costs in aggregate.

Operating expenses

Operating expenses consist of both retail store and specialty operating costs, such as employee labor and benefits, repairs and maintenance, supplies, training, travel and banking and card processing fees. Operating expenses as a percent of net revenue for 2008 increased 0.3% to 34.7%. The increase was primarily due to higher costs associated with expanding the grocery business (0.7%), opening 53 new retail stores in the last two years (0.2%), partially offset by favorable workers’ compensation insurance expense (-0.3%) and other cost savings. The favorable workers’ compensation expense resulted primarily from a decrease in our self-insurance reserve for prior policy years due to favorable claims experience and settlement history.

21

General and administrative expenses

General and administrative expenses in 2008 were $22.5 million, or 7.9% of net revenue, compared to $22.7 million, or 9.1% in 2007. The decrease in expenses as a percent of net revenue is primarily due to higher net revenue (1.1%) and lower professional fees associated with our stock option review and related litigation (0.5%), partially offset by increases in headcount (0.2%) and various professional services. Professional fees associated with our stock option review and related litigation were $1.4 million in 2007 and $16,000 in 2008. The related lawsuits were dismissed in March 2008.

Depreciation and amortization expenses

Depreciation and amortization expenses increased in 2008 primarily due to the 53 stores we opened during 2008 and 2007.

Interest income

We currently invest in U.S. government, agency, municipal and guaranteed student loan obligations. Interest income includes interest income and gains or losses from the sale of these instruments. We earned $726,000 in interest income in 2008, compared to $1.4 million in 2007, due to our lower average cash and investment balances and lower interest rates. The Company does not have exposure in its investment portfolio for subprime mortgages or auction rate securities.

Income tax provision

The effective income tax rate for 2008 was 37.0% compared to 35.8% in 2007. Our effective rate increased 1.2% primarily due to a lower impact from the domestic production deduction and decreased tax-exempt interest income.

2007 (52 weeks) Compared with 2006 (52 weeks)

Net revenue

Net revenue for 2007 increased 18.5% versus 2006 as a result of continued expansion of our retail and specialty sales segments. Sales of whole bean and related products increased 14.0% to $134.1 million. Sales from beverages and pastries increased 24.1% to $115.3 million.

In the retail segment, net revenue increased 19.1% in 2007 compared to 2006 primarily as a result of increased sales from new stores we opened in 2006 and 2007 and growth in the existing stores. We opened 30 new stores in 2007 and 25 stores in 2006. Sales of whole bean coffee and related products in the retail segment increased by 8.1% to $53.1 million, while sales of beverages and pastries increased by 24.9% to $115.3 million. The increase in beverage and pastry sales was primarily related to sales at the stores we opened in 2006 and 2007 and increased traffic in our existing stores. The slower growth in whole bean and related products was primarily due to continuing cannibalization of bean sales in retail stores as we increased the availability of Peet’s coffee in grocery stores and our own retail stores.

22

In the specialty sales segment, net revenue increased 17.2% in 2007 compared to 2006 as summarized by business channel below. Grocery had the highest growth rate in the segment with a 21.6% increase compared to 2006, primarily due to continued strong growth in our existing accounts and secondarily due to new accounts we added in 2007. We added 1,400 new stores during 2007, bringing the number of grocery stores selling Peet’s coffee to approximately 5,800 at the end of 2007. Foodservice and office coffee net revenue increased 18.7% primarily due to our effort to expand distributorships and licensed partners. Net revenue in the home delivery channel grew 7.0% compared to 2006 due primarily to special offerings to our existing customers.

| | | | | | | | | | | | |

| (dollars in thousands) | | 2007 | | 2006 | | Increase | |

Grocery | | $ | 41,879 | | $ | 34,440 | | $ | 7,439 | | 21.6 | % |

Foodservice and office | | | 20,430 | | | 17,211 | | | 3,219 | | 18.7 | % |

Home delivery | | | 18,688 | | | 17,465 | | | 1,223 | | 7.0 | % |

| | | | | | | | | | | | |

Total specialty | | $ | 80,997 | | $ | 69,116 | | $ | 11,881 | | 17.2 | % |

| | | | | | | | | | | | |

Cost of sales and related occupancy expenses

Cost of sales and related occupancy expenses consist of product costs, including manufacturing costs, rent and other occupancy costs. As a percent of net revenue, cost of sales increased from 47.0% in 2006 to 47.5% in 2007. This increase was driven by an increase of occupancy as a percent of net revenue. Occupancy increased approximately 0.5% compared to 2006 due primarily to the impact of opening new stores, which had lower sales levels. Product cost was about equal in 2007 and 2006 as the retail price increase we took in November 2006 combined with procurement and waste savings offset inflation in milk and coffee and the cost of the new roasting plant in 2007.

Operating expenses

Operating expenses consist of both retail store and specialty operating costs, such as employee labor and benefits, repairs and maintenance, supplies, training, travel and banking and card processing fees. Operating expenses as a percent of net revenue for 2007 increased 0.1% to 34.4% from 2006. The increase was primarily due to a 1.2% increase from opening 55 new stores in the last two years, largely offset by the November 2006 retail price increase (0.5%) and leverage of retail overhead (0.6%).

General and administrative expenses

General and administrative expenses in 2007 were $22.7 million, or 9.1% of net revenue, compared to $20.6 million, or 9.8% for 2006. The decrease in expenses as a percent of net revenue is primarily due to higher net revenue (1.5%) and partially due to lower professional fees associated with our stock option review and related litigation (0.3%), partially offset by increases in headcount (0.9%). Professional fees associated with our stock option review and related litigation were $1.4 million in 2007 and $1.8 million in 2006.

Depreciation and amortization expenses

Depreciation and amortization expenses increased in 2007 primarily due to the 55 stores we opened during 2007 and 2006.

Interest income