As filed with the Securities and Exchange Commission on March 9, 2007

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08360 |

|

GUINNESS ATKINSON FUNDS |

(Exact name of registrant as specified in charter) |

|

21550 Oxnard Street, Suite 750, Woodland Hills, CA | | 91367 |

(Address of principal executive offices) | | (Zip code) |

|

James J. Atkinson, Jr. |

21550 Oxnard Street, Suite 750, Woodland Hills, CA 91367 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (800) 915-6566 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2006 | |

| | | | | | | | |

Item 1. Report to Stockholders.

Annual

Report

December 31, 2006

• Alternative Energy Fund

• Asia Focus Fund

• Asia Pacific Dividend Fund

• China & Hong Kong Fund

• Global Energy Fund

• Global Innovators Fund

Guinness Atkinson Funds

Annual Report

December 31, 2006

TABLE OF CONTENTS

| | 3 | | | Letter to Shareholders | |

|

| | 6 | | | Alternative Energy Fund | |

|

| | 14 | | | Asia Focus Fund | |

|

| | 22 | | | Asia Pacific Dividend Fund | |

|

| | 29 | | | China & Hong Kong Fund | |

|

| | 35 | | | Global Energy Fund | |

|

| | 42 | | | Global Innovators Fund | |

|

| | 49 | | | Statements of Assets and Liabilities | |

|

| | 51 | | | Statements of Operations | |

|

| | 54 | | | Statements of Changes in Net Assets | |

|

| | 56 | | | Financial Highlights | |

|

| | 62 | | | Notes to Financial Statements | |

|

| | 77 | | | Guinness Atkinson Funds Information | |

|

2

January 29, 2007

Dear Guinness Atkinson Funds Shareholders,

One year ago in this letter we reminded investors that past performance is not indicative of future results and wished we could continue our 2005 performance through 2006. And yet here we are, one year later, with most – but not all – of the Guinness Atkinson Funds producing total returns in 2006 that topped the returns of 2005. Before we get to the performance details we would be remiss if we didn't mention the launch of the two newest Guinness Atkinson Funds, the Asia Pacific Dividend Fund and the Alternative Energy Fund. We welcome the shareholders of these two Funds as well as to the shareholders that joined us in the more seasoned Guinness Atkinson Funds.

Fund Performance

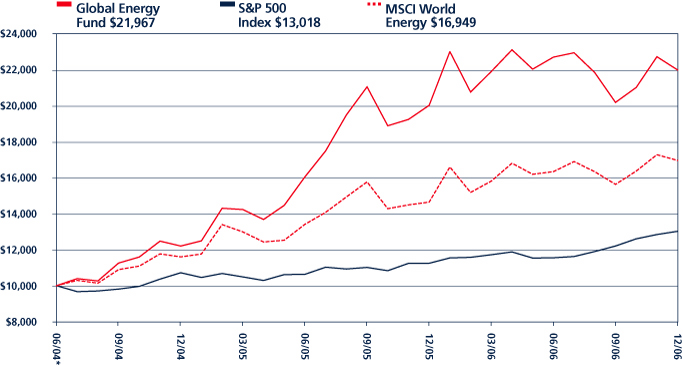

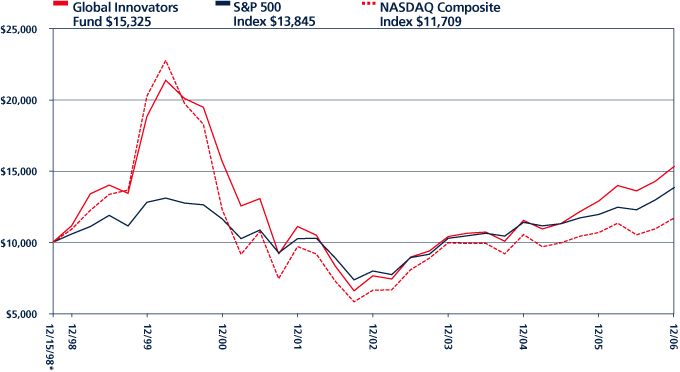

Returns for the periods ending December 31, 2006 are provided in the table below. For the calendar year each of the four funds in existence over the entire period had positive returns. Of these four the laggard for one year performance was the Global Energy Fund which returned 9.80% for the year. The Global Innovators Fund produced a total return of 18.76%; the Asia Focus Fund 36.15% and the China & Hong Kong Fund 39.65%. From their inception on March 31, 2006 the Alternative Energy Fund produced a negative return of 8.24% while the Asia Pacific Dividend Fund produced a positive return of 10.59%.

| Fund (inception date) | | 1-year | | 3-year | | 5-year | | 10-year | | From Inception | |

| Alternative Energy Fund (March 31, 2006) | | | | | | | | | | | | | | | | | -8.24 | % | |

| Asia Focus (April 29, 1996) | | | 36.15 | % | | | 21.86 | % | | | 22.73 | % | | | 2.13 | % | | | 3.17 | % | |

| Asia Pacific Dividend Fund (March 31, 2006) | | | | | | | | | | | | | | | | | 10.59 | % | |

| China & Hong Kong (June 30, 1994) | | | 39.65 | % | | | 18.64 | % | | | 19.19 | % | | | 6.76 | % | | | 8.80 | % | |

| Global Energy Fund (June 30, 2004) | | | 9.85 | % | | | | | | | | | | | | | 36.93 | % | |

| Global Innovators Fund (December 15, 1998) | | | 18.76 | % | | | 13.77 | % | | | 6.64 | % | | | | | 5.45 | % | |

Periods of greater than one year are average annualized returns; one year or less are actual returns. All returns are for the periods ending December 31, 2006.

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Each of the Funds impose a 2% redemption fee on shares held less than 30 days. The performance data does not reflect this redemption fee. Had this fee been included, returns would be lower. Total returns reflect a waiver in effect and in the absence of this waiver, the total returns would be lower.

As usual Tim Guinness and Edmund Harriss provide their views on the past year and look ahead to the current year for each of the six Guinness Atkinson Funds. You will find these comments preceding the financial results for the Funds which follow this letter. Also, we've provided a table showing the year-end Morningstar ratings for the three Guinness Atkinson Funds that have a track record of three years or more. That table appears immediately after this letter.

The Big Picture

Each of the six Guinness Atkinson Funds is inextricably linked to one of the major stories unfolding over the course of the 21st century. It is virtually impossible to pick up a newspaper without seeing extensive coverage concerning energy – including oil and alternative energy; China and Asia; or to read about the dynamic nature of business and innovative change. It is indeed an exciting time to be a shareholder in the Guinness Atkinson Funds. With the launch of each of these Funds we were thinking long term.

3

Just as we believe that each of these major forces will have a dramatic impact on the entire planet, so too do we understand that they will take time to unfold. It is very easy to get caught up in the short term headlines (and subsequent price movements). So, we feel the urge to provide some paternalistic advice, specifically, don't let our short-term results distract you from what we consider the much more important long-term. Clearly 2006 was a good if not great period for most of our Funds. But, as we stated last year, recent past performance is not a sufficient reason to invest. We are hopeful that all of our shareholders share our long term vision of the future.

We appreciate the confidence you have placed in us and our management team and appreciate the opportunity to serve you.

Sincerely,

Timothy Guinness James Atkinson

Morningstar Ratings through 12/31/06

Below is a table listing the Morningstar star ratings for the three Guinness Atkinson Funds that have at least a three year history.

| Fund | | Category | | Overall | | 3-year | | 5-year | | 10-year | |

Asia Focus

| | Pacific/Asia

ex-Japan Stk | | 2**

(86 funds) | | 3***

(86 funds) | | 3***

(78 funds) | | 1*

(37 funds) | |

China & Hong Kong

| | Pacific/Asia

ex-Japan Stk | | 2**

(86 funds) | | 1*

(86 funds) | | 2**

(78 funds) | | 3***

(37 funds) | |

Global Innovators Fund

| | Large Growth

| | 4****

(1,405 funds) | | 5*****

(1,405 funds) | | 4****

(1,109 funds) | | N/A

| |

For each fund with at least a three-year history, Morningstar calculates a Morningstar Rating(TM) based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund's monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in distribution percentages.)

©2007 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The Funds invest in foreign securities which involves greater volatility and political, economic and currency risks and differences in accounting methods.

4

GUINNESS ATKINSON FUNDS

Expense Examples (Unaudited)

As a shareholder of the Funds, you incur two types of costs: (1) redemption fees; and (2) ongoing costs, including advisory fees; and other Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the period shown and held for the entire period from July 1, 2006 to December 31, 2006.

Actual Expenses

For each Fund, the first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each Fund, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any redemption fees. Therefore, the second line for each Fund of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these redemption fees were included, your costs would have been higher.

| | | Beginning

Account

Value

(07/01/06) | | Ending

Account

Value

(12/31/06) | | Expenses Paid

During Period*

(07/01/06 to

12/31/06) | | Expense Ratio

During Period*

(07/01/06 to

12/31/06) | |

| Guinness Atkinson Alternative Energy Fund Actual^ | | $ | 1,000.00 | | | $ | 1,026.90 | | | $ | 10.12 | | | | 1.98 | %† | |

Guinness Atkinson Alternative Energy Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.22 | | | $ | 10.06 | | | | 1.98 | %† | |

| Guinness Atkinson Asia Focus Fund Actual | | $ | 1,000.00 | | | $ | 1,225.90 | | | $ | 11.33 | | | | 2.02 | % | |

Guinness Atkinson Asia Focus Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.03 | | | $ | 10.25 | | | | 2.02 | % | |

| Guinness Atkinson Asia Pacific Dividend Fund Actual^ | | $ | 1,000.00 | | | $ | 1,194.50 | | | $ | 10.95 | | | | 1.98 | %† | |

Guinness Atkinson Asia Pacific Dividend Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.22 | | | $ | 10.06 | | | | 1.98 | %† | |

| Guinness Atkinson China & Hong Kong Fund Actual | | $ | 1,000.00 | | | $ | 1,247.20 | | | $ | 8.97 | | | | 1.58 | % | |

Guinness Atkinson China & Hong Kong Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.22 | | | $ | 8.05 | | | | 1.58 | % | |

| Guinness Atkinson Global Energy Fund Actual | | $ | 1,000.00 | | | $ | 968.60 | | | $ | 7.19 | | | | 1.45 | %† | |

Guinness Atkinson Global Energy Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.90 | | | $ | 7.37 | | | | 1.45 | %† | |

| Guinness Atkinson Global Innovators Fund Actual | | $ | 1,000.00 | | | $ | 1,125.90 | | | $ | 8.31 | | | | 1.64 | %† | |

Guinness Atkinson Global Innovators Fund Hypothetical

(5% return before expenses) | | $ | 1,000.00 | | | $ | 1,017.39 | | | $ | 7.88 | | | | 1.64 | %† | |

*Expenses are equal to the Funds' annualized expense ratio as indicated, multiplied by the average account value over the period, multiplied by the number of days in most recent fiscal half-year period (184), then divided by the number of days in the fiscal year (365) (to reflect the one-half year period).

†Net of fee waivers and/or expense reimbursements. If those fee waivers and/or expense reimbursements had not been in effect, the Fund's actual expenses would have been higher.

^The Fund commenced operations on March 31, 2006. Actual expenses shown for the Fund are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by 275/365 (to reflect the period from March 31, 2006 to December 31, 2006).

5

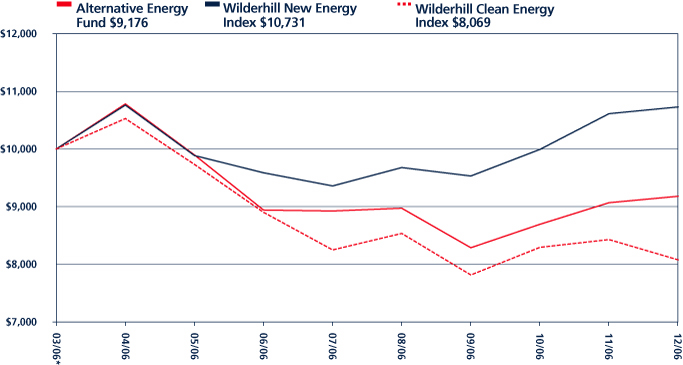

ALTERNATIVE ENERGY FUND for the period ended December 31, 2006

1. Performance

TOTAL RETURNS

| | | Since

Inception

31 March 2006

(actual) | |

| Fund | | | -8.24 | % | |

| Benchmark Index: | |

| Wilderhill Clean Energy Index (ECO) | | | -19.32 | % | |

| Wilderhill New Energy Global Innovation Index (NEX) | | | 7.32 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

The Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data does not reflect the redemption fee. If it had, returns would be lower. Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower.

The Alternative Energy Fund was launched 31 March 2006. It has been a volatile first 9 months for the fund. The fund was up 11.28% on the 5th of May but subsequently fell later in May along with global equity markets in general and was down 10.64% at the end of June. By the end of the year the fund had made some further ground and ended down 8.24%. The fund beat the Wilderhill Clean Energy Index (-19.32%) but not the Wilderhill New Energy Global Innovation Index (7.32%).

2. Activity

Our initial portfolio was made up of 45 stocks with the three most represented sectors being Biofuels, Solar and Fuelcells. By the end of the first quarter we had added 5 further stocks from the Biofuels, Solar, Fuelcells and Emissions Trading sectors. We continued to rebalance the portfolio each time flows necessitated dealing and we kept equal weightings in all positions with the exception of one wind stock where we took a double weighted position.

Over the next six months we reduced our exposure to Fuelcells and increased our exposure to the Solar, Wind and Biofuel sectors. At the end of November we sold all our core holdings in ethanol companies. During this period we moved the portfolio towards a model where we held 30 equally weighted units. These 30 units were split whereby we had 12 full positions, 27 stocks each allocated half a unit and 14 research holdings making up 4.5 units.

The best performing sector since launch was the Wind sector with the majority of the stocks up over 50%. The worst performing sector was the Fuelcell sector. While the wind sector continued to grow on strong demand for turbines technological breakthroughs were few and far between in the Fuelcell sector.

6

3. Portfolio Position

| Country | | % of Assets | |

| | | 30-Jun | | 30-Sep | | 29-Dec | |

| Australia | | | 7.70 | % | | | 7.00 | % | | | 6.66 | % | |

| Austria | | | 0.00 | % | | | 0.00 | % | | | 1.92 | % | |

| Brazil | | | 2.00 | % | | | 2.10 | % | | | 1.96 | % | |

| Canada | | | 17.40 | % | | | 19.20 | % | | | 13.62 | % | |

| China | | | 1.90 | % | | | 2.20 | % | | | 3.74 | % | |

| Denmark | | | 2.10 | % | | | 2.10 | % | | | 2.58 | % | |

| France | | | 2.20 | % | | | 2.00 | % | | | 1.66 | % | |

| Germany | | | 14.60 | % | | | 14.40 | % | | | 22.1 | % | |

| Ireland | | | 1.90 | % | | | 1.80 | % | | | 1.52 | % | |

| Malaysia | | | 4.20 | % | | | 1.90 | % | | | 1.58 | % | |

| Spain | | | 2.40 | % | | | 3.10 | % | | | 5.80 | % | |

| Thailand | | | 1.50 | % | | | 2.50 | % | | | 1.24 | % | |

| UK | | | 13.70 | % | | | 16.90 | % | | | 14.26 | % | |

| USA | | | 26.40 | % | | | 22.90 | % | | | 21.12 | % | |

| | | | 100 | % | | | 100 | % | | | 100 | % | |

| Sector | | % of Assets | |

| | | 30-Jun | | 30-Sep | | 29-Dec | |

| Solar | | | 18.60 | % | | | 18.30 | % | | | 21.10 | % | |

| Biofuels | | | 16.40 | % | | | 19.80 | % | | | 20.70 | % | |

| Fuel cells | | | 15.70 | % | | | 14.50 | % | | | 11.70 | % | |

| Wind | | | 12.10 | % | | | 13.20 | % | | | 15.50 | % | |

| Hybrid | | | 8.40 | % | | | 7.50 | % | | | 6.50 | % | |

| Other | | | 8.00 | % | | | 7.90 | % | | | 7.30 | % | |

| Hydro | | | 6.90 | % | | | 7.00 | % | | | 9.40 | % | |

| Palmoil | | | 4.20 | % | | | 1.90 | % | | | 1.60 | % | |

| Storage | | | 4.00 | % | | | 2.50 | % | | | 1.50 | % | |

| Geothermal | | | 3.60 | % | | | 3.40 | % | | | 2.80 | % | |

| Efficiency | | | 2.00 | % | | | 2.40 | % | | | 1.80 | % | |

| | | | 100 | % | | | 100 | % | | | 100 | % | |

7

ALTERNATIVE ENERGY FUND

| Market Capitalization (in $ millions) | | | |

| >1000 | | | 12 | | |

| 500-1000 | | | 5 | | |

| 250-500 | | | 9 | | |

| 100-250 | | | 14 | | |

| 50-100 | | | 11 | | |

| <50 | | | 4 | | |

| Total | | | 55 | | |

The Geographic, Sector and Market Capitalization weightings of the portfolio (ignoring cash) at the end of each quarter are shown above.

4. Investment Approach

In managing the Alternative Energy Fund we normally only invest in companies with a Market Capitalization of at least $50 million and where 50% of their value is derived from Alternative Energy. We see Solar, Biofuels, Wind and Fuelcells as core sectors/themes each offering different opportunities but attractive in its own way. Efficiency is a further sector/theme we are working on building up over the months ahead.

The Wind industry is the most mature of the four. Wind power generating costs are now competitive and capacity globally has gone through 50GW. It is now over 1% of global electricity capacity and has the opportunity to grow its share to 5-10%. It offers manufacturing companies in it 10-20 years of good growth and utility companies that build/acquire generating capacity a prospect of growing returns if energy prices trend higher over time.

Biofuels offering potentially carbon neutral and more secure supplies of transportation fuels have received much publicity since the fund was launched. We are concerned about the recent increase in price of corn squeezing ethanol refiners' margins.

The Solar and Fuelcell industries are at earlier stages of development and are riskier but the upside may be commensurately greater. The fund has exposure to the rapid expansion of photovoltaic cell manufacturing. In the Fuelcell area we have targeted small scale fuel cells (for eg consumer and military applications rather than the transportation sector). When considering stocks for purchase we use a traditional growth at reasonable value approach supported by a four factor screening method in a similar way as for our other funds. We also study sector specific issues and how well placed companies are against their peers.

Other areas in which we are invested are Hydro, Wave Power, Energy Storage and Hybrid vehicles, each of which provides interesting opportunities with differing economics and market dynamics.

We continue to believe that Alternative Energy will be the solution to how we meet rising demand for energy in the face of increasing depletion of fossil fuel reserves and the case for curbing carbon emissions. This means that companies active in this space should enjoy high rates of growth over quite a number of years. We would however warn investors that investing in Alternative Energy should be seen as a long-term investment as there are still limited (albeit growing) pure play public company opportunities in the space and investor interest is considerable meaning valuations are rarely cheap and valuation levels can fluctuate with changing sentiment and changes in eg the long run oil price. The right way to look at an investment in this fund is to think of it as investing in a group of companies which can potentially grow 6x (20% pa) per decade (ie 36X over 20 years) (this is supported if Alternate Energy sources of energy ex Hydro grows from 1% of total energy used to eg 36%). It may be the time scale will be longer than this and/or the amount of penetration achieved less but the direction and order of magnitude seem not implausible. High initial valuations and high volatility are probably an inevitable price to pay for such an opportunity. We see our task being to navigate as best we can the changes in sentiment, new opportunities thrown up by technological breakthroughs, and changing governmental policies and to combine this with trying to pick the winners in the space at moments when they are reasonably valued yet at the same time keeping a well diversified portfolio so we maintain exposure to a good spread of sub sectors.

Tim Guinness 31 January 2007

8

Short-term performance, in particular, is not a good indication of the Fund's future performance and an investment should not be made based solely on returns.

The Fund invests in foreign securities which will involve greater volatility, political, economic and currency risks and differences in accounting methods.

The Wilderhill New Energy Global Innovation Index (NEX) is a modified dollar weighted index of publicly traded companies, which are active in renewable and low-carbon energy, and which stand to benefit from responses to climate change and energy security concern. The Wilderhill Clean Energy Index (ECO) is a modified equal dollar weighted index comprised of publicly traded companies whose businesses stand to benefit substantially from societal transition toward the use of cleaner energy and conservation.

Please refer to the Schedule of Investments for details on fund holdings. Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

The information provided herein represents the opinion of Guinness Atkinson Management and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

9

ALTERNATIVE ENERGY FUND

Growth of $10,000

Total Return

Periods Ended December 31, 2006

Since Inception

(03/31/06) | |

| | -8.24 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The Wilderhill New Energy Global Innovations Index (NEX) is a modified dollar weighted index of publicly traded companies, which are active in renewable and low-carbon energy, and which stand to benefit from responses to climate change and energy security concern. The Wilderhill Clean Energy Index (ECO) is a modified equal dollar weighted index comprised of publicly traded companies whose businesses stand to benefit substantially from societal transition toward the use of cleaner energy and conservation.

10

FUND HIGHLIGHTS at December 31, 2006

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

| # of Holdings in Portfolio: | | | 55 | | |

| Portfolio Turnover: | | | 31.4 | % | |

| % of Stocks in Top 10: | | | 30.3 | % | |

| Fund Managers: | |

| Timothy W.N. Guinness; | |

| Edmund Harriss | | | | | |

| Top 10 Holdings (% of net assets) | | | | Breakdown (% of Investments) | | | |

| Q-Cells AG | | | 4.0 | % | | Biofuel | | | 24.3 | % | |

| Nordex AG | | | 3.9 | % | | Solar | | | 21.1 | % | |

| Biopetrol Industries AG | | | 3.7 | % | | Wind | | | 15.4 | % | |

| Iberdrola SA | | | 3.7 | % | | Fuelcell | | | 10.0 | % | |

| Environmental Power Corp | | | 3.1 | % | | Hydro | | | 9.0 | % | |

| Vestas Wind Systems A/S | | | 2.5 | % | | Hybrid | | | 6.6 | % | |

| Clipper Windpower PLC | | | 2.5 | % | | Other | | | 5.8 | % | |

| Repower Systems AG | | | 2.5 | % | | Geothermal | | | 2.8 | % | |

| Climate Exchange PLC | | | 2.2 | % | | Efficiency | | | 1.8 | % | |

| Fuel Systems Solutions Inc. | | | 2.2 | % | | Palmoil | | | 1.7 | % | |

| | | | | | | Storage | | | 1.5 | % | |

11

SCHEDULE OF INVESTMENTS IN SECURITIES

at December 31, 2006

GUINNESS ATKINSON ALTERNATIVE ENERGY FUND

| Shares | | COMMON STOCKS: 97.5% | | Value | |

| Biofuel: 20.2% | | | |

| | 843,987 | | | Alkane Energy PLC* | | $ | 322,366 | | |

| | 734,040 | | | Australian Ethanol, Ltd.* | | | 224,995 | | |

| | 147,834 | | | Babcock & Brown Environmental Investments, Ltd.* | | | 174,561 | | |

| | 48,000 | | | Biopetrol Industries AG* | | | 577,995 | | |

| | 54,882 | | | Environmental Power Corporation* | | | 485,706 | | |

| | 25,000 | | | Futurefuel Corporation* | | | 216,500 | | |

| | 25,000 | | | Futurefuel Corporation Warrant* | | | 80,000 | | |

| | 2,354 | | | Green Plains Renewable Energy, Inc.* | | | 58,262 | | |

| | 29,998 | | | GTL Resources PLC* | | | 117,517 | | |

| | 226,667 | | | Natural Fuel, Ltd.* | | | 206,390 | | |

| | 216,147 | | | Novera Energy, Ltd.* | | | 249,793 | | |

| | 197,142 | | | Renewable Power & Light PLC* | | | 299,268 | | |

| | 41,095 | | | Renova Energy, PLC | | | 155,857 | | |

| | | | 3,169,210 | | |

| Efficiency: 1.7% | | | |

| | 34,408 | | | Echelon Corporation* | | | 275,264 | | |

| Fuelcell: 11.3% | | | |

| | 42,088 | | | Ballard Power Systems, Inc.* | | | 239,481 | | |

| | 57,146 | | | Ceres Power Holdings PLC* | | | 245,101 | | |

| | 90,756 | | | CMR Fuel Cells PLC* | | | 287,435 | | |

| | 28,548 | | | FuelCell Energy, Inc.* | | | 184,420 | | |

| | 150,820 | | | Hydrogenics Corporation* | | | 191,608 | | |

| | 111,519 | | | Mechanical Technology, Inc.* | | | 210,771 | | |

| | 140,964 | | | Polyfuel, Inc.* | | | 133,915 | | |

| | 176,142 | | | Quantum Fuel Systems Technologies Worldwide, Inc.* | | | 281,827 | | |

| | | | 1,774,558 | | |

| Geothermal: 2.8% | | | |

| | 234,246 | | | Geodynamics, Ltd.* | | | 161,603 | | |

| | 7,419 | | | Ormat Technologies, Inc. | | | 273,168 | | |

| | | | 434,771 | | |

| Hybrid: 6.4% | | | |

| | 344,865 | | | Azure Dynamics Corporation* | | | 233,867 | | |

| | 15,749 | | | Fuel Systems Solutions, Inc.* | | | 347,738 | | |

| | 107,765 | | | Railpower Technologies Corporation* | | | 139,684 | | |

| | 268,136 | | | Westport Innovations, Inc.* | | | 278,504 | | |

| | | | 999,793 | | |

| Hydro: 9.2% | | | |

| | 30,037 | | | Boralex, Inc.* | | | 268,153 | | |

| | 6,224 | | | Cia Energetica de Minas Gerais – ADR | | | 299,997 | | |

| | 13,189 | | | Iberdrola SA | | | 574,903 | | |

| | 5,490 | | | Oesterreichische Elektrizitaetswirtschafts AG | | | 292,024 | | |

| | | | 1,435,077 | | |

The accompanying notes are an integral part of these financial statements.

12

| Shares | | COMMON STOCKS: 97.5% Continued | | Value | |

| Other: 7.2% | | | |

| | 75,318 | | | AgCert International* | | $ | 235,454 | | |

| | 34,368 | | | Climate Exchange PLC* | | | 348,372 | | |

| | 146,638 | | | Ocean Power Technologies, Inc.* | | | 242,707 | | |

| | 113,420 | | | Trading Emissions PLC* | | | 294,065 | | |

| | | | 1,120,598 | | |

| Palmoil: 1.7% | | | |

| | 1,005,100 | | | Carotech Bhd | | | 258,677 | | |

| Solar: 20.5% | | | |

| | 96,107 | | | Carmanah Technologies Corporation* | | | 243,372 | | |

| | 20,658 | | | Evergreen Solar, Inc.* | | | 156,381 | | |

| | 7,140 | | | MEMC Electronic Materials, Inc.* | | | 279,460 | | |

| | 14,000 | | | Q-Cells AG* | | | 626,731 | | |

| | 86,483 | | | SAG Solarstrom AG* | | | 323,211 | | |

| | 13,340 | | | Solar Millenium AG* | | | 315,905 | | |

| | 18,908 | | | Solar-Fabrik AG* | | | 243,977 | | |

| | 1,537,380 | | | Solartron PLC | | | 185,421 | | |

| | 4,410 | | | Solarworld AG | | | 274,805 | | |

| | 9,411 | | | Suntech Power Holdings Co., Ltd. - ADR* | | | 320,068 | | |

| | 35,399 | | | Xantrex Technology, Inc.* | | | 252,817 | | |

| | | | 3,222,148 | | |

| Storage: 1.5% | | | |

| | 488,561 | | | VRB Power Systems, Inc.* | | | 234,855 | | |

| Wind: 15.0% | | | |

| | 33,737 | | | Clipper Windpower PLC* | | | 392,199 | | |

| | 11,220 | | | Gamesa Corporation Tecnologica SA | | | 307,807 | | |

| | 34,220 | | | Nordex AG* | | | 615,527 | | |

| | 3,773 | | | Repower Systems AG* | | | 388,279 | | |

| | 15,661 | | | Theolia SA* | | | 253,762 | | |

| | 9,335 | | | Vestas Wind Systems A/S* | | | 392,839 | | |

| | | | 2,350,413 | | |

| | | | | Total Common Stocks

(cost $16,804,423) | | | 15,275,364 | | |

| | | | | Total Investments in Securities

(cost $16,804,423): 97.5% | | | 15,275,364 | | |

| | | | | Other Assets less Liabilities: 2.5% | | | 388,368 | | |

| | | | | Net Assets: 100.0% | | $ | 15,663,732 | | |

* Non-income producing security.

ADR American Depository Receipt

The accompanying notes are an integral part of these financial statements

13

ASIA FOCUS FUND for the period ended December 31, 2006

1. Performance

AVERAGE ANNUALIZED TOTAL RETURNS

| | | 1 Year

(actual) | | 3 Years | | 5 Years | | 10 Years | |

| Fund | | | 36.15 | % | | | 21.86 | % | | | 22.73 | % | | | 2.13 | % | |

| Benchmark Index: | |

| MSCI AC Far East Free Ex Japan | | | 31.86 | % | | | 23.18 | % | | | 20.41 | % | | | 2.86 | % | |

| S&P 500 | | | 15.78 | % | | | 10.44 | % | | | 6.19 | % | | | 8.42 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

The Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect the redemption fee. If it had, returns would be lower.

Asian markets have had a good 2006 with the regional benchmark index rising 31.86% following on from a rise of 21.13% in 2005. In 2006 the best performing shares were Chinese companies followed by the smaller markets of Indonesia and Philippines.

Most notable has been the increase in Chinese stock valuations where these have been substantially re-rated over the year. Investors now seem to have greater confidence in China's ability to sustain high rates of growth without it leading to a bust. Certainly, China's growth has been impressive. Economic growth is believed to have exceeded 10% again this year and the government has had its work cut out trying to restrain excessive investment. The Chinese have also made significant moves toward financial reform. Three out of the four main banks in China have been listed in Hong Kong. Reforms to the operations of the domestic stock markets in Shanghai and Shenzhen have breathed new life into share prices which had been in the doldrums for years.

Korea and Taiwan had a more difficult year as both countries struggled with weak domestic economies. The problem for them is that while the export companies are no longer the growth driver they once were. Economic growth in Taiwan in 2006 is estimated to have been 4.3% but all of this growth was generated by exports. The difference now is that this exports growth is not driving the domestic economy in the way it once did and in large part this is due to the same "hollowing out" process seen elsewhere in the world. Taiwanese companies are looking for cheaper places to manufacture and for the most part this means China – politics notwithstanding.

The Korean stock market did not perform well in 2006 with earnings believed to have contracted 6% compared to 2005 and perception that prospects for growth were limited. There were bright points however. The shipbuilding sector has continued to grow as the global cycle entered its fourth year. Most of the growth has come from demand for Liquid Natural Gas (LNG) carriers and offshore plant for the oil industry which has taken over from the replacement cycle for container and bulk cargo carriers. As in Taiwan, the weakness has been most glaring in the domestic economy. Consumers remain subdued and after a consumer borrowing binge here (as in Taiwan) there has been little appetite for gearing up.

In South-East Asia, the markets of Indonesia, Malaysia, Singapore and Thailand have had varying fortunes. Both Malaysia and Singapore have had a good year. Malaysia has been an unloved market since the events of 1998 when the previous Prime Minister imposed capital controls to protect the country from the effects of the Asia crisis. While the country was indeed well insulated it also meant there was no impetus to carry out much needed reform. These days Malaysia is moving forward once again with a number of companies restructuring and, more importantly, construction projects which have been on hold for the past three years are now being restarted. The palm oil sector has also been flourishing as crude palm oil prices rise on the back of demand both for foodstuff and also for bio-diesel.

Singapore had another strong year of economic growth with real GDP estimated to have grown 7.7% compared to 6.4% in 2005. Liquidity was plentiful with broad money growth and Foreign Direct Investment reaching record highs. Net immigration is also rising, up 10% in 2006 as the construction boom continues. Singapore is in the process of reconfiguring its economy by boosting its tourism and leisure industry thereby reducing its previous reliance on the highly cyclical electronics industry. The impact is

14

already being felt as although cyclical trade-related activities have slowed materially in recent months (enough in the past to have triggered a recession), growth prospects still look good with 5.1% projected for 2007.

In the weaker economies of Indonesia and Thailand, Indonesia has performed well this year. Interest rates have come down from 12.75% at the start of 2006 to 9.75% by December as inflation fell back from 17% to 6%. The reason for the spike was the government's decision to remove fuel subsidies, which it could no longer afford, and now due to the high base effect we can see that core inflation remained modest. In 2006 we also saw a broader recovery led by net exports. The hope is that this, combined with lower inflation and increased infrastructure spending will lead to a more full-blooded expansion in domestic demand.

Thailand had an extraordinary year in which politics dominated. What started with disapproval of Prime Minister Thaksin gained momentum with his tax-free disposal of his family business to an investment entity owned by the government of Singapore. A snap election was boycotted by most of the opposition parties and was subsequently declared invalid. This was followed by a period of stalemate ending in bloodless coup in September. Finally, the year ended with imposition of wide ranging capital restrictions, which were partially reversed the following day, designed to cope with an appreciating currency (see December 2006 Asia Brief for more detailed discussion). Against this backdrop it was hard for the stock market to make much progress. However, the real economy is not in bad shape with growth of around 4%, inflation at 3.5% and interest rates of 5.25%. Lower interest rates, a resumption of government spending and hopefully an election are wh at the market has to look forward to in 2007.

2. Portfolio Position

Geographically, the portfolio has an overweight position in China, Hong Kong, Malaysia and Thailand relative to the benchmark and is underweight compared to the benchmark in Korea and Singapore. From a sector perspective the Fund's main exposures are to Energy, Technology, Materials and Telecommunication Services. The main underweight exposure at the end of the year was to Banks, Real estate and Utilities.

3. Outlook

It seems hard to believe after all this time, but Asia is only now beginning to emerge from the massive cyclical downturn in 1998, known as the Asia crisis. Over the past eight years Asian countries have been forced to deal with weak domestic demand, excess capacity, depressed asset and property prices and low inflation. It is a core tenet of development economics that emerging nations grow faster than developed nations and that because of the high rate of capital creation through investment, their wealth should grow even faster. This has evidently not been the case for Asia ex Japan over the past ten years, with the notable exceptions of China and India.

The only real functioning driver of growth has been exports and over the last few years we have seen trade balances and foreign exchange reserves move sharply into surplus. And in the past year as the surpluses have grown so large we have seen regional currencies start to appreciate against the Dollar. The rising trade surpluses it should be noted were not due to a massive rise in exports as Asia became super-competitive but instead was the result of an import collapse in 1998/9 and stagnation since led by a drop not in consumption, but in investment.

At last this situation is changing. Asia is now moving from depression economics to normal economics. Construction and investment have ceased their trend declines and have turned positive in the last eighteen months. Domestic oversupply is easing and pushing up property prices across the region and inflation which has averaged around 1-2% is now likely to move back to its normal range of 5-6%. Higher inflation is not only a symptom of renewed activity but can also act as a stimulus for the return of investment.

We believe that Asia is now entering a period of buoyant wealth creation that has been largely absent for ten years. Domestic sectors including banking, construction, and consumer discretionary are all likely to benefit from resurgent domestic growth. Over the next twelve to eighteen months however, Asia still has to contend with the possibility of a global slow down led by the developed markets. Asian market valuations are not stretched either compared to their own history or compared to global peers. Earnings' growth is going to be a key driver from here for most of the region with aggregate growth estimated at 10.74% for 2007 and 12.17% for 2008.

Edmund Harriss February 19, 2007

15

ASIA FOCUS FUND

The Fund invests in foreign securities which involves greater volatility and political, economic and currency risks and differences in accounting methods.

The MSCI AC Far East Free Ex Japan Index is a market-capitalization weighted index of over 450 stocks traded in eight Asian markets, excluding Japan. The Standard & Poor's 500 Index is a market-capitalization weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged, not available for investment and do not incur expenses.

Please refer to the Schedule of Investments for details on fund holdings. Fund holdings and sector allocations are subject to change at any time are not recommendations to buy or sell any security.

The information provided herein represents the opinion of Guinness Atkinson Management and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

16

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2006

| One Year | | Five Years | | Ten Years | |

| | 36.15 | % | | | 22.73 | % | | | 2.13 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The MSCI AC Far East Free Ex Japan Index is a market capitalization weighted index of over 450 stocks traded in eight Asian markets, excluding Japan. The index referenced in this chart is not available for investment and does not incur expenses.

17

FUND HIGHLIGHTS at December 31, 2006

GUINNESS ATKINSON ASIA FOCUS FUND

| # of Holdings in Portfolio: | | | 48 | | |

| Portfolio Turnover: | | | 95.7 | % | |

| % of Stocks in Top 10: | | | 35.1 | % | |

| Fund Managers: | |

| Edmund Harriss; | |

| Timothy W.N. Guinness | | | | | |

| Top 10 Holdings (% of net assets) | |

| China Mobile Ltd. | | | 4.3 | % | | Telekomunikasi Indonesia Tbk PT | | | 3.3 | % | |

| Angang Steel Co., Ltd. | | | 4.2 | % | | Hon Hai Precision Industry | | | 3.3 | % | |

| Samsung Electronics | | | 3.8 | % | | China Shipping Development Co., Ltd. | | | 3.1 | % | |

| POSCO | | | 3.7 | % | | PetroChina Co., Ltd. | | | 3.1 | % | |

| Wistron Corp. | | | 3.5 | % | | Taiwan Semiconductor Manufacturing Co., Ltd. | | | 2.8 | % | |

| Country Breakdown (% of net assets) | |

| China | | | 24 | % | | Thailand | | | 5 | % | |

| Hong Kong | | | 22 | % | | Indonesia | | | 3 | % | |

| Taiwan | | | 20 | % | | Singapore | | | 3 | % | |

| Korea | | | 16 | % | | Philippines | | | 0 | % | |

| Malaysia | | | 7 | % | | Cash | | | 0 | % | |

| Sector Breakdown (% of Investments) | |

| Steel-Producers | | | 12.5 | % | | Agricultural Operations | | | 2.4 | % | |

| Telecommunication Services | | | 8.3 | % | | Non-Ferrous Metals | | | 2.3 | % | |

| Computers | | | 7.2 | % | | Auto-Cars/Light Trucks | | | 2.1 | % | |

| Oil Exploration & Production | | | 6.2 | % | | Entertainment | | | 2.1 | % | |

| Semiconductors | | | 6.0 | % | | Tobacco | | | 2.0 | % | |

| Oil/Integrated | | | 5.7 | % | | Circuit Boards | | | 1.9 | % | |

| Electronic Components | | | 5.4 | % | | Coal | | | 1.9 | % | |

| Transportation | | | 4.9 | % | | Commercial Banks Non-US | | | 1.7 | % | |

| Real Estate Operation/Development | | | 4.4 | % | | Auto/Truck Parts & Equipment | | | 1.4 | % | |

| Cellular Telecom | | | 4.3 | % | | Chemicals-Other | | | 1.3 | % | |

| Electric Products-Misc | | | 3.8 | % | | Electric-Generation | | | 1.1 | % | |

| Metal Processors & Fabrication | | | 3.7 | % | | Textile-Products | | | 1.0 | % | |

| Distribution/Wholesale | | | 2.8 | % | | Machinery - General Industry | | | 0.8 | % | |

| Power Conv/Supply Equip | | | 2.8 | % | | | | | | | |

18

SCHEDULE OF INVESTMENTS IN SECURITIES

at December 31, 2006

GUINNESS ATKINSON ASIA FOCUS FUND

| Shares | | COMMON STOCKS: 99.9% | | Value | |

| China: 24.6% | | | |

| | 1,428,000 | | | Angang Steel Co., Ltd. | | $ | 2,079,549 | | |

| | 29,000 | | | China Coal Energy Co.* | | | 19,064 | | |

| | 1,374,000 | | | China Petroleum & Chemical Corporation | | | 1,272,664 | | |

| | 1,014,000 | | | China Shipping Development Co., Ltd. | | | 1,552,314 | | |

| | 510,000 | | | Dongfang Electrical Machinery Co., Ltd.^ | | | 1,364,671 | | |

| | 510,000 | | | Guangzhou R&F Properties Co., Ltd. | | | 1,106,171 | | |

| | 207,000 | | | Haitian International Holdings Ltd.* | | | 93,204 | | |

| | 1,306,000 | | | Jiangxi Copper Co., Ltd. | | | 1,323,927 | | |

| | 1,088,000 | | | PetroChina Co., Ltd. | | | 1,550,827 | | |

| | 1,450,000 | | | Shenzhen Expressway Co., Ltd. | | | 871,123 | | |

| | 1,122,800 | | | Yanzhou Coal Mining Co., Ltd. | | | 905,659 | | |

| | | | 12,139,173 | | |

| Hong Kong: 21.7% | | | |

| | 470,000 | | | Chen Hsong Holdings | | | 290,829 | | |

| | 244,000 | | | China Mobile, Ltd. | | | 2,121,930 | | |

| | 1,342,000 | | | CNOOC, Ltd. | | | 1,298,270 | | |

| | 1,752,000 | | | CNPC Hong Kong, Ltd. | | | 962,402 | | |

| | 2,524,000 | | | Denway Motors, Ltd. | | | 1,016,315 | | |

| | 124,840 | | | Esprit Holdings, Ltd. | | | 1,384,381 | | |

| | 1,860,000 | | | Fittec International Group, Ltd. | | | 275,173 | | |

| | 45,892 | | | HSBC Holdings Plc | | | 840,111 | | |

| | 165,000 | | | Kingboard Chemical Holdings, Ltd. | | | 641,040 | | |

| | 7,500 | | | Kingboard Laminates Holdings, Ltd.* | | | 8,095 | | |

| | 468,000 | | | Sino Land Co. | | | 1,081,301 | | |

| | 1,832,000 | | | Solomon Systech International, Ltd. | | | 282,814 | | |

| | 1,307,000 | | | Victory City International Holdings | | | 472,472 | | |

| | | | 10,675,133 | | |

| Indonesia: 3.3% | | | |

| | 1,460,000 | | | Telekomunikasi Indonesia Tbk PT | | | 1,643,448 | | |

| Malaysia: 6.9% | | | |

| | 274,700 | | | Digi.Com Bhd | | | 1,213,456 | | |

| | 223,000 | | | IOI Corp. Bhd | | | 1,161,886 | | |

| | 246,000 | | | Resorts World Bhd | | | 1,010,052 | | |

| | | | 3,385,394 | | |

| Singapore: 3.0% | | | |

| | 323,600 | | | Jurong Technologies Industrial Corporation, Ltd. | | | 227,932 | | |

| | 595,650 | | | Singapore Telecommunications, Ltd. | | | 1,258,662 | | |

| | | | 1,486,594 | | |

The accompanying notes are an integral part of these financial statements.

19

| Shares | | COMMON STOCKS: 99.9% Continued | | Value | |

| South Korea: 15.5% | | | |

| | 7,750 | | | Hyundai Mobis* | | $ | 711,970 | | |

| | 32,100 | | | Hyundai Steel Co.* | | | 1,162,827 | | |

| | 10,820 | | | Korea Zinc Co., Ltd. | | | 1,147,093 | | |

| | 15,920 | | | KT&G Corporation | | | 967,183 | | |

| | 5,450 | | | POSCO | | | 1,801,662 | | |

| | 2,840 | | | Samsung Electronics Co., Ltd. | | | 1,863,064 | | |

| | | | 7,653,799 | | |

| Taiwan: 20.4% | | | |

| | 1,080,328 | | | China Steel Corporation | | | 1,139,055 | | |

| | 519,031 | | | Compal Electronics, Inc. | | | 461,216 | | |

| | 632,082 | | | Coretronic Corp. | | | 821,654 | | |

| | 68,640 | | | High Tech Computer Corporation | | | 1,356,830 | | |

| | 227,115 | | | HON HAI Precision Industry Co., Ltd. | | | 1,624,291 | | |

| | 225,959 | | | Novatek Microelectronics Corporation Ltd. | | | 1,023,020 | | |

| | 77,000 | | | Shin Zu Shing Co., Ltd. | | | 511,695 | | |

| | 675,178 | | | Taiwan Semiconductor Manufacturing Co., Ltd. | | | 1,388,530 | | |

| | 1,160,791 | | | Wistron Corporation | | | 1,726,275 | | |

| | | | 10,052,566 | | |

| Thailand: 4.5% | | | |

| | 199,500 | | | Electricity Generating Pcl | | | 526,824 | | |

| | 1,220,000 | | | Hana Microelectronics Pcl | | | 932,592 | | |

| | 289,000 | | | PTT Exploration & Production Pcl | | | 775,219 | | |

| | | | 2,234,635 | | |

| | | | | Total Common Stocks

(cost $39,821,319) | | | 49,270,742 | | |

| | | | | Total Investments in Securities

(cost $39,821,319): 99.9% | | | 49,270,742 | | |

| | | | | Other Assets less Liabilities: 0.1% | | | 9,196 | | |

| | | | | Net Assets: 100.0% | | $ | 49,279,938 | | |

* Non-income producing security.

^ Fair valued under direction of the Board of Trustees.

The accompanying notes are an integral part of these financial statements.

20

SCHEDULE OF INVESTMENTS BY INDUSTRY

at December 31, 2006

GUINNESS ATKINSON ASIA FOCUS FUND

| Industry | | % of Net Assets | |

| Steel-Producers | | | 12.5 | % | |

| Telecommunication Services | | | 8.4 | | |

| Computers | | | 7.2 | | |

| Oil Exploration & Production | | | 6.2 | | |

| Semiconductors | | | 6.0 | | |

| Oil/Integrated | | | 5.7 | | |

| Electronic Components | | | 5.4 | | |

| Transportation | | | 4.9 | | |

| Real Estate Operation/Development | | | 4.4 | | |

| Cellular Telecom | | | 4.3 | | |

| Electric Products-Misc | | | 3.8 | | |

| Metal Processors & Fabrication | | | 3.7 | | |

| Distribution/Wholesale | | | 2.8 | | |

| Power Conv/Supply Equip | | | 2.8 | | |

| Agricultural Operations | | | 2.4 | | |

| Non-Ferrous Metals | | | 2.3 | | |

| Auto-Cars/Light Trucks | | | 2.1 | | |

| Entertainment | | | 2.0 | | |

| Tobacco | | | 2.0 | | |

| Circuit Boards | | | 1.9 | | |

| Coal | | | 1.9 | | |

| Commercial Banks Non-US | | | 1.7 | | |

| Auto/Truck Parts & Equipment | | | 1.4 | | |

| Chemicals-Other | | | 1.3 | | |

| Electric-Generation | | | 1.1 | | |

| Textile-Products | | | 1.0 | | |

| Machinery-General Industry | | | 0.8 | % | |

| Total Investments in Securities | | | 100.0 | | |

| Other Assets less Liabilities | | | 0.0 | | |

| Net Assets | | | 100.00 | % | |

The accompanying notes are an integral part of these financial statements.

21

ASIA PACIFIC DIVIDEND FUND for the period ended December 31, 2006

1. Performance

TOTAL RETURNS

| | | 6 Months

(actual) | | Since

Inception

31 March 2006

(actual) | |

| Fund | | | 19.36 | % | | | 10.59 | % | |

| Benchmark Index: | |

| MSCI AC Pacific Ex Japan | | | 22.35 | % | | | 23.48 | % | |

| S&P 500 | | | 12.73 | % | | | 11.11 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

The Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect the redemption fee. If it had, returns would be lower. Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower.

The Fund had a difficult first three months when markets suffered a significant setback in May as investors took fright at signs of increasing inflation concerns coming from the Federal Reserve. The effect was to negate all market gains made in the first half of the year. The second half of the year saw confidence return and the Fund performed very well in the midst of strongly rising markets.

Individual market performances are discussed in greater detail in the Asia Focus Fund report but from this Fund's perspective, holdings in China and Hong Kong performed well as Chinese-related companies made significant gains on greater confidence about growth prospects.

There were also good performances from the Fund's holdings in Malaysia, Indonesia and Singapore. The holdings in Taiwan have been moderate performers which is a reflection of the weak domestic economy. On a sector basis the Fund saw good performance from Materials, especially the steel companies which are held in China, Korea and Taiwan, and from telecom companies held in Indonesia and Malaysia.

The Fund has a significant exposure to Thailand and the extraordinary events there (described in the report for the Asia Focus Fund) including a coup in September and the imposition, followed by a rapid readjustment, of a foreign exchange levy hurt performance at the end of year.

Dividend payouts have been on a rising trend and we have also been seeing more capital restructuring involving the return of cash to shareholders as well as some share buybacks.

2. Portfolio Position

Geographically, the portfolio has an overweight position in Hong Kong, New Zealand, Taiwan and Thailand relative to the benchmark. It is neutrally weighted in China, Indonesia and Malaysia and is underweight compared to the benchmark in Australia, Korea and Singapore. From a sector perspective the Fund has an overweight position in technology, particularly the consumer electronics sector, and is overweight in resources, industrial materials and manufacturing. It has a neutral weight in the consumer sector. The Fund is underweight in telecom and utilities as well as in banks and real estate.

3. Outlook

The following is reproduced from the Asia Focus Fund report:

It seems hard to believe after all this time, but Asia is only now beginning to emerge from the massive cyclical downturn in 1998, known as the Asia crisis. Over the past eight years Asian countries have been forced to deal with weak domestic demand, excess

22

capacity, depressed asset and property prices and low inflation. It is a core tenet of development economics that emerging nations grow faster than developed nations and that because of the high rate of capital creation through investment, their wealth should grow even faster. This has evidently not been the case for Asia ex Japan over the past ten years, with the notable exceptions of China and India.

The only real functioning driver of growth has been exports and over the last few years we have seen trade balances and foreign exchange reserves move sharply into surplus. And in the past year as the surpluses have grown so large we have seen regional currencies start to appreciate against the Dollar. The rising trade surpluses it should be noted were not due to a massive rise in exports as Asia became super-competitive but instead was the result of an import collapse in 1998/9 and stagnation since led by a drop not in consumption, but in investment.

At last this situation is changing. Asia is now moving from depression economics to normal economics. Construction and investment have ceased their trend declines and have turned positive in the last eighteen months. Domestic oversupply is easing and pushing up property prices across the region and inflation which has averaged around 1-2% is now likely to move back to its normal range of 5-6%. Higher inflation is not only a symptom of renewed activity but can also act as a stimulus for the return of investment.

We believe that Asia is now entering a period of buoyant wealth creation that has been largely absent for ten years. Domestic sectors including banking, construction, and consumer discretionary are all likely to benefit from resurgent domestic growth. Over the next twelve to eighteen months however, Asia still has to contend with the possibility of a global slow down led by the developed markets. Asian market valuations are not stretched either compared to their own history or compared to global peers. Earnings' growth is going to be a key driver from here for most of the region with aggregate growth estimated at 10.74% for 2007 and 12.17% for 2008.

From the specific perspective of this fund, we believe that investors should look forward with confidence for the next ten years at least. Asia looks well balanced financially and is on the verge of a domestic led recovery which is now starting to become apparent. Companies have improved and moved on from the previous approach of garnering market share at any cost. There has been a steady increase in dividend payout ratios and a general expectation that companies ought to pay dividends as a sign of awareness of their obligations to shareholders.

Edmund Harriss February 19, 2007

Short-term performance, in particular, is not a good indication of the Fund's future performance and an investment should not be made based solely on returns.

The Fund invests in foreign securities which involves greater volatility and political, economic and currency risks and differences in accounting methods.

The MSCI AC Far East Free Ex Japan Index is a market-capitalization weighted index of over 450 stocks traded in eight Asian markets, excluding Japan. The Standard & Poor's 500 Index is a market-capitalization weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged, not available for investment and do not incur expenses.

Please refer to the Schedule of Investments for details on fund holdings. Fund holdings and sector allocations are subject to change at any time are not recommendations to buy or sell any security.

The information provided herein represents the opinion of Guinness Atkinson Management and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

23

ASIA PACIFIC DIVIDEND FUND

Growth of $10,000

Total Return

Periods Ended December 31, 2006

Since Inception

(03/31/06) | |

| | 10.67 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The MSCI AC Far East Free Ex Japan Index is a market capitalization weighted index of over 450 stocks traded in eight Asian markets, excluding Japan. The index referenced in this chart is not available for investment and does not incur expenses.

24

FUND HIGHLIGHTS at December 31, 2006

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

| # of Holdings in Portfolio: | | | 37 | | |

| Portfolio Turnover: | | | 49.3 | % | |

| % of Stocks in Top 10: | | | 36.7 | % | |

| Fund Managers: | |

| Edmund Harriss; | |

| Timothy W.N. Guinness | | | | | |

| Top 10 Holdings (% of net assets) | |

| Vtech Holdings Ltd | | | 4.4 | % | | High Tech Computer Corp | | | 3.5 | % | |

| Angang Steel Co Ltd | | | 4.4 | % | | China Steel Corp | | | 3.4 | % | |

| Incitec Pivot Ltd | | | 3.9 | % | | United Overseas Bank Ltd | | | 3.3 | % | |

| Telekomunikasi Tbk PT | | | 3.8 | % | | China Shipping Development Co Ltd | | | 3.2 | % | |

| Digi.Com Bhd | | | 3.6 | % | | HSBC Holdings PLC | | | 3.2 | % | |

| Country Breakdown (% of net assets) | |

| Hong Kong | | | 19 | % | | New Zealand | | | 5 | % | |

| Taiwan | | | 18 | % | | Korea | | | 4 | % | |

| China | | | 13 | % | | Indonesia | | | 4 | % | |

| Thailand | | | 13 | % | | Malaysia | | | 4 | % | |

| Australia | | | 11 | % | | Singapore | | | 3 | % | |

| Cash | | | 6 | % | | | | | | | |

| Sector Breakdown (% of Investments) | |

| Commer Banks Non-US | | | 15.7 | % | | Electronic Components | | | 2.6 | % | |

| Steel-Producers | | | 14.4 | % | | Forestry | | | 2.5 | % | |

| Telecommunication | | | 12.6 | % | | Oil Refining & Marketing | | | 2.4 | % | |

| Semiconductors | | | 8.1 | % | | Auto/Truck Parts & Equipment Replacement | | | 2.2 | % | |

| Transportation | | | 6.2 | % | | Finance-Commercial | | | 2.1 | % | |

| Computers | | | 5.8 | % | | Electric-Integrated | | | 1.4 | % | |

| Building & Construction Production | | | 5.7 | % | | Metal Processors & Fabrications | | | 1.2 | % | |

| Agricultural Chemicals | | | 4.2 | % | | Tobacco | | | 1.0 | % | |

| Oil/Integrated | | | 3.2 | % | | Machinery-General Industry | | | 0.2 | % | |

| Distribution/Wholesale | | | 3.1 | % | | Food-Meat Products | | | 0.1 | % | |

| Circuit Boards | | | 2.6 | % | | Coal | | | 0.1 | % | |

| Chemicals-Plastics | | | 2.6 | % | | | | | | | |

25

SCHEDULE OF INVESTMENTS IN SECURITIES

at December 31, 2006

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

| Shares | | COMMON STOCKS: 94.2% | | Value | |

| Australia: 11.2% | | | |

| | 9,150 | | | CSR, Ltd. | | $ | 27,151 | | |

| | 12,100 | | | Great Southern Plantations | | | 27,001 | | |

| | 1,600 | | | Incitec Pivot, Ltd. | | | 44,642 | | |

| | 7,800 | | | Onesteel, Ltd. | | | 28,886 | | |

| | | | 127,680 | | |

| China: 13.6% | | | |

| | 34,000 | | | Angang Steel Co., Ltd. | | | 49,513 | | |

| | 1,000 | | | China Coal Energy Co.* | | | 657 | | |

| | 24,000 | | | China Shipping Development Co., Ltd. | | | 36,741 | | |

| | 5,000 | | | Haitian International Holdings, Ltd.* | | | 2,251 | | |

| | 1,000 | | | People's Food Holdings, Ltd. | | | 809 | | |

| | 24,000 | | | PetroChina Co., Ltd. | | | 34,209 | | |

| | 50,000 | | | Shenzhen Expressway Co., Ltd. | | | 30,039 | | |

| | | | 154,219 | | |

| Hong Kong: 19.1% | | | |

| | 5,600 | | | Bank of East Asia, Ltd. | | | 30,762 | | |

| | 2,000 | | | CLP Holdings, Ltd. | | | 14,730 | | |

| | 3,000 | | | Esprit Holdings, Ltd. | | | 33,268 | | |

| | 400 | | | HSBC Holdings Plc - ADR | | | 36,613 | | |

| | 16,000 | | | Industrial and Commercial Bank of China Asia, Ltd. | | | 30,710 | | |

| | 144,000 | | | Solomon Systech International, Ltd. | | | 22,230 | | |

| | 8,000 | | | Vtech Holdings, Ltd. | | | 49,760 | | |

| | | | 218,073 | | |

| Indonesia: 3.8% | | | |

| | 38,500 | | | Telekomunikasi Indonesia Tbk PT | | | 43,338 | | |

| Malaysia: 3.7% | | | |

| | 9,400 | | | Digi.Com Bhd | | | 41,523 | | |

| New Zealand: 5.3% | | | |

| | 4,400 | | | Fletcher Building, Ltd. | | | 34,321 | | |

| | 5,600 | | | New Zealand Refining Co., Ltd. | | | 25,695 | | |

| | | | 60,016 | | |

| Singapore: 3.3% | | | |

| | 3,000 | | | United Overseas Bank, Ltd | | | 37,762 | | |

| South Korea: 4.2% | | | |

| | 180 | | | KT&G Corporation | | | 10,935 | | |

| | 110 | | | POSCO | | | 36,364 | | |

| | | | 47,299 | | |

The accompanying notes are an integral part of these financial statements.

26

| Shares | | COMMON STOCKS: 94.2% Continued | | Value | |

| Taiwan: 17.8% | | | |

| | 36,910 | | | China Steel Corporation | | $ | 38,916 | | |

| | 25,734 | | | Compal Electronics, Inc. | | | 22,867 | | |

| | 8,400 | | | Depo Auto Parts Ind Co., Ltd. | | | 23,695 | | |

| | 23,096 | | | Greatek Electronics, Inc. | | | 30,590 | | |

| | 2,000 | | | High Tech Computer Corporation | | | 39,535 | | |

| | 7,549 | | | Novatek Microelectronics Corporation, Ltd. | | | 34,178 | | |

| | 2,000 | | | Shin Zu Shing Co., Ltd. | | | 13,291 | | |

| | | | 203,072 | | |

| Thailand: 12.2% | | | |

| | 58,200 | | | Delta Electronics Thai | | | 27,664 | | |

| | 36,800 | | | Hana Microelectronics Pcl | | | 28,131 | | |

| | 98,000 | | | Krung Thai Bank Pcl | | | 32,145 | | |

| | 58,600 | | | Thai Plastic & Chemical Pcl | | | 27,854 | | |

| | 59,300 | | | Thanachart Captial Pcl | | | 22,747 | | |

| | | | 138,541 | | |

| | | | | Total Common Stocks

(cost $991,114) | | | 1,071,523 | | |

| | | | | Total Investments in Securities

(cost $991,114): 94.2% | | | 1,071,523 | | |

| | | | | Other Assets less Liabilities: 5.8% | | | 66,415 | | |

| | | | | Net Assets: 100.0% | | $ | 1,137,938 | | |

* Non-income producing security.

ADR American Depository Receipt

The accompanying notes are an integral part of these financial statements.

27

SCHEDULE OF INVESTMENTS BY INDUSTRY

at December 31, 2006

GUINNESS ATKINSON ASIA PACIFIC DIVIDEND FUND

| Industry | | % of Net Assets | |

| Commer Banks Non-US | | | 14.8 | % | |

| Steel-Producers | | | 13.5 | | |

| Telecommunication Services | | | 11.8 | | |

| Semiconductors | | | 7.6 | | |

| Transportation | | | 5.9 | | |

| Computers | | | 5.5 | | |

| Building & Construction Production | | | 5.4 | | |

| Agricultural Chemicals | | | 3.9 | | |

| Oil/Integrated | | | 3.0 | | |

| Distribution/Wholesale | | | 2.9 | | |

| Circuit Boards | | | 2.5 | | |

| Chemicals-Plastics | | | 2.4 | | |

| Electronic Components | | | 2.4 | | |

| Forestry | | | 2.4 | | |

| Oil Refining & Marketing | | | 2.2 | | |

| Auto/Truck Parts & Equipment Replacement | | | 2.1 | | |

| Finance-Commercial | | | 2.0 | | |

| Electric-Integrated | | | 1.3 | | |

| Metal Processors & Fabrications | | | 1.2 | | |

| Tobacco | | | 1.0 | | |

| Machinery-General Industry | | | 0.2 | | |

| Food-Meat Products | | | 0.1 | | |

| Coal | | | 0.1 | | |

| Total Investments in Securities | | | 94.2 | | |

| Other Assets less Liabilities | | | 5.8 | | |

| Net Assets | | | 100.00 | % | |

The accompanying notes are an integral part of these financial statements.

28

CHINA & HONG KONG FUND for the period ended December 31, 2006

1. Performance

AVERAGE ANNUALIZED TOTAL RETURNS

| | | 1 Year

(actual) | |

3 Years | |

5 Years | |

10 Years | |

| Fund | | | 39.65 | % | | | 18.64 | % | | | 19.19 | % | | | 6.76 | % | |

| Benchmark Index: | |

| Hang Seng Composite | | | 47.87 | % | | | 23.84 | % | | | 19.93 | % | | | N/A | | |

| Hang Seng | | | 38.51 | % | | | 20.79 | % | | | 16.09 | % | | | 7.49 | % | |

| S&P 500 | | | 15.78 | % | | | 10.44 | % | | | 6.19 | % | | | 8.42 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

The Fund imposes a 2% redemption fee on shares held less than 30 days. Performance data quoted does not reflect the redemption fee. If it had, returns would be lower.

Shares in China and Hong Kong had a strong year overall in 2006 although in truth most of the gains were made in the second half of the year. The year opened with strong equity markets but in May investors took fright concerned that inflation pressures in the US and elsewhere would precipitate more severe monetary tightening. Most markets gave up whatever gains they had made and retreated to levels at which they began the year. When these fears subsided then investors' enthusiasm returned in earnest.

Chinese shares including H shares, Red Chips and other China-related companies were substantially re-rated. This was fuelled by a belief that China's economic growth is now sufficiently robust to withstand periodic overheating of some sectors and that policymakers have sufficient control over the economy to make the necessary adjustment without precipitating a sharp overall downturn.

Another driving factor is the clear decision to allow the currency to appreciate against the US Dollar. The trade surplus and the accumulation of foreign exchange reserves have now reached levels that pose economic concerns as well as political and trade tensions. It seems very likely that this ballooning surplus is a temporary phenomenon and has more to do with policymakers' efforts to slow hot domestic investment, resulting in a substantial fall in imports in 2005 and 2006, rather than a structural issue. Investment will definitely pick up again but the challenge will be to ensure this is directed productively rather than to yet another steel mill or aluminium smelter. In the meantime, a trend of appreciation in the currency is expected to continue.

Two sectors that performed especially well in the year were Chinese financial companies, including banks and insurance, and real estate companies. China has now listed three of the big four commercial banks, the most recent being the $21 billion offering of the Industrial and Commercial Bank of China (ICBC). There has also been a series of smaller regional banks coming to the market.

It is worth pointing out that the Fund has not been invested in this area, other than to take a small initial position in ICBC at the offering. The financial sector is one of the last remaining areas in China where pricing is regulated. Banks cannot price deposits above a certain level and cannot offer loans below a certain level. In the same way life assurance products cannot offer guaranteed returns above a level broadly equivalent to deposit rates. This means that profitability is ensured by regulated pricing. What we also know is that China is moving, with plenty of encouragement from the US, toward restructuring its financial markets, weaning banks away from interest income toward fee-based products such as bank assurance and introducing flexibility to the currency. This will mean de-regulation and opening intense competition between banks and insurers which is presently officially contained.

Hong Kong also performed well in 2006. For a number of years since the downturn in 1998 the market has been hobbling along, either held back or overshadowed by China and trying to come to terms with collapse in property prices and the subsequent overhang of excess real estate supply. Construction activity has been weak and inflation has been slow to turn positive after a long period of falling prices. However, this year things have come good. Property prices have moved higher and stayed higher as the supply overhang looks ready to clear. Wage growth has picked up and is expected to accelerate into 2007; and as inflation picks up from around 1% to 2% in 2006 to 3% on average in 2007 real interest rates will come down. The government too is feeling more confident as a rising corporate tax take improves the budget and has encouraged it to increase spending.

29

CHINA & HONG KONG FUND

2. Portfolio Position

At the end of the year 72% of the portfolio was invested in H Shares, red Chips and China Plays and 26% was invested in Hong Kong companies. On a sector basis the key exposures were to consumer stocks, industrial companies including steel, metals and manufacturers and to resources, namely coal and oil. The Fund also had an overweight position in the transport sector and had a significant position on mobile telephony. The Fund had an underweight position in the financials sector both in Hong Kong and China.

3. Outlook

The strong performance we have seen in Chinese companies is welcome inasmuch as it reflects what we believe to be the case, namely that China's economy has moved on in the last five years to become a broader and more balanced economy and one that no long depends on Central Government pump-priming. The success that China has had in slowing certain sectors while allowing others to continue to flourish, without it all grinding to a halt as in the recent past is testimony to how far it has come.

However, just as we have seen certain economic sectors overheat so too we have seen certain market sectors become heavily over-valued, in our opinion. It is unfortunate that the sectors where this is most apparent are also those that are most opaque and the least free in the scope of their operations and the most vulnerable to regulatory changes. These sectors are also in the firing line for the most challenging stage of China's journey to a true market-based economy. Secretary Paulson has made the point that financial reform is crucial not only to address global imbalances but also to address China's own domestic imbalances. In that respect the efficient allocation of capital is of key importance.

We do not believe that investors should be put off by the foregoing but that it is important to understand what needs to happen in China and how best to benefit from it. Investment growth in China is still substantial with major power, resources and infrastructure projects (especially rail projects) planned or underway. China's manufacturing base is becoming more sophisticated and lower end labour intensive businesses are already moving away to countries like Vietnam and Bangladesh. At the same time there are still 200 million rural labourers yet to be absorbed into the manufacturing economy. This story has a long way to run.

In the meantime we would like to thank investors for choosing this Fund and to assure investors that we are firm believers in the China story. At the same time we will continue to serve what we believe to be investors' best interests by focusing on those companies that offer value, whose businesses are more predictable and that we believe will be the prime beneficiaries of this extraordinary social, cultural and economic transformation.

Edmund Harriss February 19, 2007

The Hang Seng Composite Index is a market-capitalization weighted index that comprises the top 200 companies listed on the Hong Kong Stock Exchange, based on the average market-capitalization for the past twelve months. The Hang Seng Composite Index commenced on January3, 2000 and therefore does not have five-year returns or returns since the Fund's inception. The Hang Seng Index is a barometer of the Hong Kong Stock Market which comprises 33 constituent stocks, whose aggregate market-capitalization accounts for about 70% of the total market-capitalization of the Stock Exchange of Hong Kong Limited. The Standard & Poor's 500 Index is a market-capitalization weighted index composed of 500 widely held common stocks of U.S. companies. These indices are unmanaged, not available for investment and do not incur expenses.

The Fund invests in foreign securities which involves greater volatility and political, economic and currency risks and differences in accounting methods.

Please refer to the Schedule of Investments for details on fund holdings. Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

The information provided herein represents the opinion of Guinness Atkinson Management and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

30

Growth of $10,000

Average Annual Total Return

Periods Ended December 31, 2006

| One Year | | Five Years | | Ten Years | |

| | 39.65 | % | | | 19.19 | % | | | 6.76 | % | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting www.gafunds.com.

Total returns reflect a fee waiver in effect and in the absence of this waiver, the total returns would be lower. The Fund imposes a 2% redemption fee on shares held less than 30 days.

The Hang Seng Composite Index is a market-capitalization weighted index that comprises the top 200 companies listed on the Hong Kong Stock Exchange, based on the average market capitalization for the past twelve months. The Fund changed its benchmark from the Hang Seng to the Hang Seng Composite Index to more accurately reflect the market sectors in which the Fund invests. The Hang Seng Composite Index commenced on 01/31/00. The index referenced in this chart is not available for investment and does not incur expenses.

31

FUND HIGHLIGHTS at December 31, 2006

Guinness Atkinson China & Hong Kong Fund

| # of Holdings in Portfolio: | | | 42 | | |

| Portfolio Turnover: | | | 64.8 | % | |

| % of Stocks in Top 10: | | | 53.7 | % | |

| Fund Managers: | |

| Edmund Harriss; | |

| Timothy W.N. Guinness | |

| Top 10 Holdings (% of net assets) | |

| PetroChina Co Ltd. | | | 8.2 | % | | HSBC Holdings PLC | | | 4.6 | % | |

| China Mobile Ltd. | | | 8.1 | % | | Esprit Holdings Ltd. | | | 4.0 | % | |

| CNOOC Ltd. | | | 7.4 | % | | Dongfang Electrical Machinery Co., Ltd. | | | 4.0 | % | |

| Angang Steel Co., Ltd. | | | 5.5 | % | | China Petroleum & Chemical Corp. | | | 3.6 | % | |

| China Shipping Development Co., Ltd. | | | 4.8 | % | | Guangzhou R&F Properties Co., Ltd. | | | 3.5 | % | |