UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08510

Matthews International Funds

(Exact name of registrant as specified in charter)

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Address of principal executive offices) (Zip code)

G. Paul Matthews, President

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-788-6036

Date of fiscal year end: August 31

Date of reporting period: August 31, 2004

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

| | | |

| | | |

| | | |

| | | |

Matthews Asian Funds Matthews Asian Funds |

|

| | | | |

| | ANNUAL REPORT

| | |

| | AUGUST 31, 2004

| | |

| | | Pacific Tiger Fund

Asian Growth and Income Fund

Korea Fund

China Fund

Japan Fund

Asian Technology Fund

Asia Pacific Fund

| |

| | | | | | | |

Matthews Asian Funds

|

| |  | |  | |  | |

| |

A Decade in Asia

Investing in the future

of Asia since 1994 |

www.matthewsfunds.com

| | | | | |

| | | It is important to keep in mind that the views expressed in this report by the Investment Advisor and its portfolio managers should not be construed as investment advice or promises, and may not be relied upon as an indication of trading intent on the part of any of the Matthews Asian Funds. | |

| | |

| | |

| | |

|

|

| | | CONTENTS |

| |

|

| | |

| |

| Message to Shareholders | 2 | | | |

| Redemption Fee Policy and Investor Disclosure | 5 | | | |

| Morningstar Ratings and Analysis | 6 | | | |

| Manager Comments, Performance and

Schedule of Investments: | | | | |

| Matthews Pacific Tiger Fund | 8 | | | |

| Matthews Asian Growth and Income Fund | 12 | | | |

| Matthews Korea Fund | 18 | | | |

| Matthews China Fund | 24 | | | |

| Matthews Japan Fund | 30 | | | |

| Matthews Asian Technology Fund | 36 | | | |

| Matthews Asia Pacific Fund | 40 | | | |

| Disclosure of Fund Expenses | 46 | | | |

| Statement of Assets and Liabilities | 48 | | | |

| Statement of Operations | 50 | | | |

| Statement of Changes in Net Assets | 52 | | | |

| Financial Highlights | 56 | | | |

| Notes to Financial Statements | 63 | | | |

| Tax Information | 70 | | | |

| Report of Independent Registered Public

Accounting Firm | 71 | | | |

| Trustees and Officers | 72 | | | | |

M E S S A G E T O S H A R E H O L D E R S

FROM THE INVESTMENT ADVISOR

Dear Shareholder,

We are pleased to present the annual report for the Matthews Asian Funds for the fiscal year ended August 31, 2004. During this period, the financial markets of Asia enjoyed strong returns, benefiting from a quick recovery from the SARS crisis of early 2003 and from generally positive economic conditions around the region.

Of the seven funds that comprise the Matthews Asian Funds, the six that were in operation for the full fiscal year enjoyed returns for the period ranging from 9.91% for the Matthews Korea Fund to 35.14% for the Matthews Japan Fund. It should be noted that the majority of the Funds’ returns for the fiscal year ended August 31 occurred in the first half of the year. While we are pleased with these results and excited about the future, as always, we would caution investors that Asian markets have historically exhibited higher volatility than their more mature counterparts elsewhere, and we do not anticipate any near-term change in this respect.

Shortly after the end of the fiscal year, the fund family reached an important milestone—celebrating the ten-year anniversary of the launch of the fund family’s first two funds, the Matthews Pacific Tiger Fund and the Matthews Asian Growth and Income Fund. The past decade in Asia has been a period of remarkable—if tumultuous—development for the economies of Asia, and we remain as excited today about Asia’s long-term future as we were at the launch of the fund family ten years ago.

Since 1994, we have been witness to a number of significant events in Asia. Most memorable, perhaps, was the Asian financial crisis of 1997–98. We have seen China rise from relative economic obscurity to an important part of the global economy, while Japan has struggled to retain its economic leadership in the region. India has emerged as a true contender in a number of global industries, and most economies in the region have become increasingly integrated with each other. Most important, we believe that the primary trends in the region have generally been toward more economic openness and less government intervention. We believe that this trend bodes well for the future as Asians continue to seek ways to bring their average living standards up to levels more comparable to those generally enjoyed in the developed countries of Europe and North America.

2 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4 n

During the past 12 months, China’s economy has risen to greater prominence in the eyes of many economic forecasters and commentators. Following a period of particularly strong economic growth, however, there has been much speculation as to how long this growth can be sustained and whether the authorities can successfully slow the economy while avoiding damaging side effects. Over the years, we have found that forecasting macro events is fraught with challenge and is not conducive to long-term performance; our focus is more on understanding how individual companies are positioned for the long term—where we have great confidence that the trends of the past decade can be continued. In the near term, China faces a number of challenges, the most important of which, in our opinion, remain the restructuring of its banking system and the establishment of a timetable for opening its currency on the capital account.

Our investment portfolios in Asia remain focused in three general sectors: consumer, technology and financials; while we have tended to underweight more cyclical, capital-intensive and heavily regulated areas. In Japan, which remains a substantially more developed and mature economy than much of the rest of Asia, our analysts and portfolio managers are looking for company managements that have acknowledged the growing openness of the rest of the region and are positioning themselves accordingly. We continue to believe that the Japanese economy is making significant progress. Corporate Japan is more flexible and far more focused on the bottom line than in the past. The expanding economic relations between Japan and China bode well for both nations. Our bottom-up focus across the entire region drives a process that is based on seeking growth at a reasonable price, and we adopt an all-capitalization approach that encompasses companies of all sizes.

G. Paul Matthews Chairman and Chief Investment Officer (left)

Mark W. Headley President and Portfolio Manager

800.789.ASIA [2742] www.matthewsfunds.com 3

M E S S A G E T O S H A R E H O L D E R S

In terms of shareholder reporting, the Board of Trustees of the Matthews Asian Funds has recently concluded that it would be more convenient for shareholders if the Funds’ fiscal year were changed from August 31 to December 31, which will make performance and reporting easier to compare and understand. This change will occur in the fiscal year just begun, resulting in a “stub” year for the four months ending December 31, 2004. As a result, the Funds will not issue a quarterly report to shareholders for the three months ending November 30, 2004; however, portfolio holdings will be filed with the SEC on Form N-Q. The next report you receive will cover the four-month period ending December. From that point forward, shareholder reports will be distributed on a quarterly basis consistent with calendar quarter-ends.

In regard to the mutual fund scandal that has dominated headlines in the past year, we at Matthews International Capital Management, LLC, remain committed to the highest ethical standards in our role as Advisor to the Matthews Asian Funds. The Board of Trustees of the Funds has had an independent chairman since 2000. The Funds’ expense ratios are decreasing as asset growth provides economies of scale. We believe that the long-established short-term redemption fee policy has discouraged abuses by fund timers. Constant improvement of the efficiency and the quality of service of the Funds is our goal, and we thank those of you who have helped us improve with your comments and suggestions.

We thank you for your continued confidence in our work.

G. Paul Matthews

Chairman and Chief Investment Officer

Matthews International Capital Management, LLC

Mark W. Headley

President and Portfolio Manager

Matthews International Capital Management, LLC

Free e-mail communications on Asia and the Funds

are available at www.matthewsfunds.com

n Asia Weekly

n Asia Insight (monthly)

n AsiaNow Special Reports

n Occasional Fund Updates

4 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4 n

REDEMPTION FEE POLICY

The Funds assess a redemption fee of 2.00% of the total redemption proceeds if you sell your shares within 90 days after purchasing them. The redemption fee is paid directly to the Funds and is designed to offset transaction costs associated with short-term trading of Fund shares. For more information about this policy, please see the Funds’ prospectus.

INVESTOR DISCLOSURE

Past Performance: All performance quoted in this report is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the returns quoted. Returns are net of the Funds’ management fee and other operating expenses. If certain of the Funds’ fees and expenses had not been waived, returns would have been lower. For the Funds’ most recent month-end performance, please call 800-789-ASIA [2742] or visit www.matthewsfunds.com.

Investment Risk: Mutual fund shares are not deposits or obligations of, or guaranteed by, any depositary institution. Shares are not insured by the FDIC, Federal Reserve Board or any government agency and are subject to investment risks, including possible loss of principal amount invested. Investing in international markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific industry, sector or geographic location.

Fund Holdings: The Fund holdings shown in this report are as of August 31, 2004. Holdings are subject to change at any time, so holdings shown in this report may not reflect current Fund holdings. The Funds file complete schedules of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q, the first of which will be filed for the quarter ending November 30, 2004. The Funds’ Form N-Q will be available on the SEC’s website at www.sec.gov and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. Matthews Asian Funds publishes quarterly reports containing the information filed in the form N-Q, copies of which may be obtained by visiting the Funds’ website at www.matthewsfunds.com or by calling 1-800-789-ASIA [2742].

Proxy Voting Record: The Funds’ Statement of Additional Information (“SAI”) containing a description of the policies and procedures that the Matthews Asian Funds use to determine how to vote proxies relating to portfolio securities, along with each Fund’s proxy voting record relating to portfolio securities held during the 12-month period ended June 30, 2004, is available upon request, at no charge, at the phone number and website below or on the SEC’s website at www.sec.gov.

This report is submitted for the general information of the shareholders of the Matthews Asian Funds. It is authorized for distribution only if preceded or accompanied by a current Matthews Asian Funds prospectus. Additional copies of the prospectus may be obtained by calling 800-789-ASIA [2742] or can be downloaded from the Funds’ website at www.matthewsfunds.com. Please read the prospectus carefully before you invest or send money, as it explains the risks, fees and expenses of investing in the Funds.

The Matthews Asian Funds are distributed by PFPC Distributors, Inc., 760 Moore Road, King of Prussia, PA 19406.

800.789.ASIA [2742] www.matthewsfunds.com 5

MORNINGSTAR RATINGS

Derived from a weighted average of a fund’s three-, five- and ten-year (if applicable) risk-adjusted returns.

Matthews Pacific Tiger Fund

Overall Morningstar rating as of 8/31/04 out of 68 Pacific/Asia ex-Japan Funds

Matthews Asian Growth and Income Fund

(Closed to most new investors)

Overall Morningstar rating as of 8/31/04 out of 68 Pacific/Asia ex-Japan Funds

Matthews Korea Fund

Overall Morningstar rating as of 8/31/04 out of 68 Pacific/Asia ex-Japan Funds

Matthews China Fund

Overall Morningstar rating as of 8/31/04 out of 68 Pacific/Asia ex-Japan Funds

Matthews Japan Fund

Overall Morningstar rating as of 8/31/04 out of 41 Japan Funds

Matthews Asian Technology Fund

Overall Morningstar rating as of 8/31/04 out of 264 Specialty-Technology Funds

Investing in foreign securities may involve certain additional risks including exchange rate fluctuations, reduced liquidity, greater volatility, and less regulation. Past performance does not guarantee future results. Investment return and principal value of mutual funds will vary with market conditions, so that shares, when redeemed, may be worth more or less than their original cost. As of 6/30/04, the 1-year total return for the Matthews Pacific Tiger Fund was 37.88%, the 5-year average annual total return was 6.83% and since inception (9/12/94) the average annual total return was 4.64%. As of August 31, 2004, the Matthews Pacific Tiger Fund received an Overall Morningstar RatingTM of 4 stars out of 68 funds in the Pacific/Asia ex-Japan stock category, 4 stars out of 68 funds for the 3-year period, and 4 stars out of 58 funds for the five-year period. As of 6/30/04, the 1-year total return for the Matthews Asian Growth and Income Fund was 30.79%, the 5-year average annual total return was 16.71% and since inception (9/12/94) the average annual total return was 10.22%. As of August 31, 2004, the Matthews Asian Growth and Income Fund received an Overall Morningstar RatingTM of 5 stars out of 68 funds in the Pacific/Asia ex-Japan stock category, 5 stars out of 68 funds for the 3-year period, and 5 stars out of 58 funds for the 5-year period. As of 6/30/04, the 1-year total return for the Matthews Korea Fund was 24.10%, the 5-year average annual total return was 6.01% and since inception (1/3/95) the average annual total return was 0.23%. As of August 31, 2004, the Matthews Korea Fund received an Overall Morningstar RatingTM of 4 stars out of 68 funds in the Pacific/Asia ex-Japan stock category, 5 stars out of 68 funds for the 3-year period, and 3 stars out of 58 funds for the 5-year period. As of 6/30/04, the 1-year total return for the Matthews China Fund was 37.94%, the 5-year average annual total return was 9.46% and since inception (2/19/98) the average annual total return was 6.69%. As of August 31, 2004, the Matthews China Fund received an Overall Morningstar RatingTM

(continued on page 7)

6 MATTHEWS ASIAN FUNDS

MORNINGSTAR ANALYST REPORT

Matthews Pacific Tiger Fund

Strong up-market returns aren’t the only attraction here.

Matthews Pacific Tiger prospers when emerging Asia’s markets surge. It soared 60% in 2003, landing in its category’s top quartile, as Advanced Information Services and other picks in Thailand, Hong Kong, and Korea zoomed. It performed even better, especially in absolute terms, in 1999’s global rally, and it distinguished itself in 1998’s more-moderate upswing, thanks to excellent stock selection from Paul Matthews and Mark Headley.

Moreover, though this growth fan has struggled in some of its region’s slumps–and has suffered significant volatility over time–it has also held up fairly well in other sell-offs. It suffered much less than most of its rivals, for example, as China and other developing Asia markets have declined sharply the past two months. Overall, the fund has outgained 15 of its 16 Pacific/Asia peers since opening in late 1994.

The fund also has better diversification than most of its rivals. Matthews and Headley readily consider smaller-market opportunities, as the fund’s 4.5% position in Indonesia attests. The two managers also pay a lot of attention to smaller caps as they pursue firms with strong long-term earnings prospects and reasonable prices, so the fund’s average market cap is well below the group norm.

Meanwhile, the fund’s annualized expense ratio declined to a relatively fetching 1.48% for the six months ending Feb. 29. And the fund has a talented and growing investment team. Matthews and Headley are two of the savviest Asia hands around, and their firm just hired two analysts and plans to hire two more, which would bring the overall investment team to nine.

All this makes the fund one of its group’s best. It’s a great option for those who can handle the volatility that comes with investing in emerging Asia.

—William Samuel Rocco

Senior Fund Analyst, Morningstar

May 6, 2004

of 4 stars out of 68 funds in the Pacific/Asia ex-Japan stock category, 3 stars out of 68 funds for the 3-year period, and 4 stars out of 58 funds for the 5-year period. As of 6/30/04, the 1-year total return for the Matthews Japan Fund was 75.31%, the 5-year average annual total return was -0.89% and since inception (12/31/98) the average annual total return was 11.46%. As of August 31, 2004, the Matthews Japan Fund received an Overall Morningstar RatingTM of 3 stars out of 41 funds in the Japan stock category, 4 stars out of 41 funds for the 3-year period, and 3 stars out of 28 funds for the 5-year period. As of 6/30/04, the 1-year total return for the Matthews Asian Technology Fund was 47.92%, and since inception (12/27/99) the average annual total return was -12.82%. As of August 31, 2004, the Matthews Asian Technology Fund received an Overall Morningstar RatingTM of 5 stars out of 264 funds in the Specialty-Technology category and 5 stars out of 264 funds for the 3-year period. For each fund with at least a three-year history, Morningstar calculates a Morningstar RatingTM based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star. (Each share class is counted as a fraction of one fund within this scale and rated separately, which may cause slight variations in the distribution percentages.) The Overall Morningstar Rating for a fund is derived from a weighted-average of the performance figures associated with its three-, five- and ten-year (if applicable) Morningstar Rating metrics. A fund’s rating may change at any time based on new data. Ratings are historical and do not represent future performance. Past performance is no guarantee of future results. Reprinted by permission of Morningstar.

800.789.ASIA [2742] www.matthewsfunds.com 7

M A T T H E W S P A C I F I C T I G E R F U N D

| CO-PORTFOLIO MANAGERS | SYMBOL: MAPTX |

Mark W. Headley and G. Paul Matthews

The Matthews Pacific Tiger Fund invests at least 80% of its assets in the common and preferred stocks of companies located in the Pacific Tiger countries of China, Hong Kong, India, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand.

PORTFOLIO MANAGER COMMENTARY

For the fiscal year ended August 31, 2004, the Matthews Pacific Tiger Fund gained 18.45%. This return compared favorably to the 14.53% gain for the Fund’s benchmark MSCI All Country Far East Free ex-Japan Index and the 13.93% gain of the Lipper Pacific ex-Japan Funds category average, but slightly lagged the 19.13% gain of the benchmark MSCI All Country Asia Pacific Free ex-Japan Index. We are very pleased that the Fund has also significantly exceeded all three of these measures for the three-year and five-year periods and since the Fund’s inception in September 1994. Over the past decade, the Fund has participated in a period of tremendous turbulence and dramatic changes in Asia ex-Japan. The region is rapidly evolving into a more open and integrated environment that should allow well-positioned and well-managed corporations significant growth opportunities.

Positive performance for the Fund over the fiscal year was dominated by consumer-related companies and financials—two of

(continued on page 10)

GROWTH OF A $10,000 INVESTMENT

The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions or redemption of fund shares.

8 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

| FUND HIGHLIGHTS | Fund Inception: 9/12/94 |

- ---------------------------------------------------------------------------------------------------------

AVERAGE ANNUAL RETURNS AS OF AUGUST 31, 2004*

- ---------------------------------------------------------------------------------------------------------

SINCE

3 MTHS 1 YR 3 YRS 5 YRS INCEPTION

- ---------------------------------------------------------------------------------------------------------

Matthews Pacific Tiger Fund 0.76% 18.45% 18.99% 8.19% 4.67%

MSCI All Country Far East Free ex-Japan Index(1) 1.50% 14.53% 13.53% -1.22% -2.72%+

MSCI All Asia Pacific Free ex-Japan Index(2) 2.18% 19.13% 15.36% 1.97% -0.19%+

Lipper Pacific ex-Japan Funds Category Average(3) 0.37% 13.93% 13.17% 1.93% -0.37%+

- ---------------------------------------------------------------------------------------------------------

+Calculated from 8/31/94

- ---------------------------------------------------------------------------------------------------------

MATTHEWS PACIFIC TIGER FUND AVERAGE ANNUAL RETURNS AS OF*:

- ---------------------------------------------------------------------------------------------------------

SINCE

1 YR 3 YRS 5 YRS 10 YRS INCEPTION

- ---------------------------------------------------------------------------------------------------------

June 30, 2004 37.88% 14.68% 6.83% -- 4.64%

September 30, 2004 21.73% 27.09% 11.40% 5.22% 5.20%

- ---------------------------------------------------------------------------------------------------------

*Assumes reinvestment of all dividends. Past performance is not indicative of future results.

Unusually high returns may not be sustainable. The performance of foreign indices may be based on

different exchange rates than those used by the Fund and, unlike the Fund’s NAV, is not adjusted

to reflect fair value at 4PM Eastern Time.

- -------------------------------------------------------

OPERATING EXPENSES(4)

- -------------------------------------------------------

For Fiscal Year 2004 (ended 8/31/04) 1.48%

- -------------------------------------------------------

- -------------------------------------------------------

PORTFOLIO TURNOVER(5)

- -------------------------------------------------------

For Fiscal Year 2004 (ended 8/31/04) 15.16%

- -------------------------------------------------------

- ------------------------------------------------

COUNTRY ALLOCATION

- ------------------------------------------------

China/Hong Kong 36.1%

South Korea 26.1%

Singapore 13.3%

Thailand 8.7%

India(1) 6.5%

Taiwan 4.5%

Indonesia 4.1%

Philippines 0.1%

Cash and other 0.6%

- ------------------------------------------------

- ------------------------------------------------

SECTOR ALLOCATION

- ------------------------------------------------

Financials 28.6%

Consumer Discretionary 17.9%

Information Technology 16.6%

Consumer Staples 14.4%

Telecommunication Services 8.8%

Industrials 6.7%

Health Care 5.2%

Utilities 1.2%

Cash and other 0.6%

- ------------------------------------------------

- ------------------------------------------------

MARKET CAP EXPOSURE

- ------------------------------------------------

Large cap (over $5 billion) 26.4%

Mid cap ($1-$5 billion) 51.5%

Small cap (under $1 billion) 21.5%

Cash and other 0.6%

- ------------------------------------------------

- ------------------------------------------------------------------

NAV ASSETS REDEMPTION FEE 12b-1 FEES

- ------------------------------------------------------------------

$13.22 $587.1 million 2.00% within 90 days None

- ------------------------------------------------------------------

All data is as of August 31, 2004, unless otherwise noted.

|

| 1 | The MSCI All Country Far East Free ex-Japan Index is an unmanaged capitalization-weighted index of the stock markets of Hong Kong, Taiwan, Singapore, Korea, Indonesia, Malaysia, Philippines, Thailand and China that excludes securities not available to foreign investors. As of August 31, 2004, 6.5% of the assets in the Matthews Pacific Tiger Fund were invested in India, which is not included in the MSCI All Country Far East Free ex-Japan Index. Source: Bloomberg. |

| 2 | The MSCI All Country Asia Pacific Free ex-Japan Index is an unmanaged capitalization-weighted index of the stock markets of Hong Kong, Taiwan, Singapore, Korea, Indonesia, Malaysia, Philippines, Thailand, China, India, Pakistan, Australia, and New Zealand that excludes securities not available to foreign investors. This benchmark has been added for comparison to the Fund due to this index’s inclusion of India. Source: Bloomberg. |

| 3 | As of 8/31/04, the Lipper Pacific ex-Japan Funds Category Average consisted of 61 funds for the three-month period, 59 funds for the one-year period, 50 funds for the three-year period, 41 funds for the five-year period, and 13 funds since 8/31/94. Lipper, Inc. fund performance does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods. |

| 4 | Includes management fee, shareholder services fees and other expenses. Matthews Asian Funds do not charge 12b-1 fees. |

| 5 | The lesser of fiscal year-to-date purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

800.789.ASIA [2742] www.matthewsfunds.com 9

M A T T H E W S P A C I F I C T I G E R F U N D

Portfolio manager commentary,

continued from page 8

the primary areas of the Fund’s long-term focus. While the telecommunications sector was able to contribute positively, information technology was the one notable area of weakness. From a country perspective, Hong Kong and Korea were the two dominant contributors to positive returns. Thailand, Singapore, India and Indonesia all contributed positively as well. Only China and Taiwan delivered negative returns.

The Fund continues to be very focused on domestically and regionally driven companies in Asia, rather than the typical export company. While the Fund does have export-related exposure, exposure to consumer-related companies is roughly double that of its benchmark indices. We continue to believe that the growing consumer power of Asia is one of the primary reasons to focus on Asian equities. Combined with its exposure to Asian financials, the Matthews Pacific Tiger Fund remains very Asia-centric.

The markets in Asia ex-Japan corrected sharply in April and May after almost a year of steady appreciation. That correction brought markets back to much more comfortable valuation levels. We believe that corporate profitability can continue to support the markets, with much of the inevitable uncertainty about future profits stemming not from Asia but from the Middle East and the U.S. economy.

SCHEDULE OF INVESTMENTS

EQUITIES: 99.38%*

SHARES VALUE

=====================================================================

CHINA/HONG KONG: 36.10%

Dah Sing Financial Group 3,653,600 $26,231,143

Giordano International, Ltd. 39,929,000 22,396,217

Swire Pacific, Ltd. A Shares 2,836,000 20,088,462

Lenovo Group, Ltd. 50,510,000 15,865,422

Travelsky Technology,

Ltd. H Shares 18,217,000 12,962,179

PICC Property and Casualty

Co., Ltd. H Shares ** 35,408,000 11,462,279

Shangri-La Asia, Ltd. 12,244,000 11,380,714

Cosco Pacific, Ltd. 7,484,000 11,226,072

Hang Lung Group, Ltd. 7,114,000 10,944,686

BYD Co., Ltd. H Shares 3,407,500 9,239,627

Sa Sa International

Holdings, Ltd. 22,582,000 9,119,712

Television Broadcasts, Ltd. 2,114,700 8,757,083

China Mobile HK, Ltd. 2,533,217 7,388,597

Huaneng Power International,

Inc. ADR 229,000 6,835,650

Moulin International

Holdings, Ltd. 11,174,000 6,088,436

China Pharmaceutical

Group, Ltd. 24,935,000 6,073,949

Asia Satellite Telecommunications

Holdings, Ltd. 3,097,600 5,539,974

Vitasoy International

Holdings, Ltd. 20,782,750 5,302,300

China Mobile HK, Ltd. ADR 346,350 5,063,637

-----------

Total China/Hong Kong 211,966,139

=====================================================================

10 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

SHARES VALUE

=====================================================================

SOUTH KOREA: 26.07%

Hana Bank 1,027,777 $23,065,534

AmorePacific Corp. 113,910 21,657,586

Internet Auction Co., Ltd. ** 196,686 17,553,779

Samsung Electronics Co., Ltd. 33,563 13,141,393

Hite Brewery Co., Ltd. 171,957 11,793,726

Nong Shim Co., Ltd. 56,148 11,747,769

Kookmin Bank ** 279,080 8,916,217

Pulmuone Co., Ltd. 236,540 8,573,638

Samsung Securities Co., Ltd. 472,640 8,124,558

S1 Corp. 294,320 7,576,150

LG Home Shopping, Inc. 186,470 7,511,575

SK Telecom Co., Ltd. 42,705 6,432,537

SK Telecom Co., Ltd. ADR 263,000 4,970,700

Kookmin Bank ADR ** 62,000 1,980,899

-----------

Total South Korea 153,046,061

=====================================================================

SINGAPORE: 13.31%

DBS Group Holdings, Ltd. 2,279,750 20,767,964

Fraser and Neave, Ltd. 2,292,550 18,742,562

Venture Corp., Ltd. 1,881,800 18,681,188

Hyflux, Ltd. 12,418,125 10,732,474

Parkway Holdings, Ltd. 12,339,000 9,222,996

-----------

Total Singapore 78,147,184

=====================================================================

THAILAND: 8.68%

Advanced Info Service Public

Co., Ltd. 9,937,500 22,547,269

Bangkok Bank Public Co., Ltd. ** 9,188,900 21,841,563

Serm Suk Public Co., Ltd. 11,370,300 6,551,913

-----------

Total Thailand 50,940,745

=====================================================================

SHARES VALUE

=====================================================================

INDIA: 6.47%

Infosys Technologies, Ltd. 312,974 $10,635,511

Hero Honda Motors, Ltd. 1,019,800 9,737,005

Cipla, Ltd. 1,759,625 9,038,272

HDFC Bank, Ltd. 1,085,883 8,608,338

-----------

Total India 38,019,126

=====================================================================

TAIWAN: 4.48%

Hon Hai Precision Industry

Co., Ltd. 6,496,687 21,280,276

Taiwan Semiconductor

Manufacturing Co., Ltd. 3,619,045 4,996,919

----------

Total Taiwan 26,277,195

=====================================================================

INDONESIA: 4.15%

PT Astra International, Inc. 14,291,730 9,680,265

PT Ramayana Lestari Sentosa 20,845,600 8,727,358

PT Bank Central Asia 31,131,000 5,977,152

----------

Total Indonesia 24,384,775

=====================================================================

PHILIPPINES: 0.12%

SM Prime Holdings, Inc. 7,030,000 713,324

-----------

Total Philippines 713,324

=====================================================================

TOTAL INVESTMENTS: 99.38% 583,494,549

(Cost $511,247,800***)

CASH AND OTHER ASSETS,

LESS LIABILITIES: 0.62% 3,638,128

------------

NET ASSETS: 100.00% $587,132,677

=====================================================================

| * | | As a percentage of net assets as of August 31, 2004 |

| ** | | Non–income producing security |

| *** | | Cost for Federal tax purposes is $511,773,330 and net unrealized appreciation consists of: |

Gross unrealized appreciation..............$95,952,089

Gross unrealized depreciation..............(24,230,870)

-----------

Net unrealized appreciation................$71,721,219

===========

| ADR | | American Depositary Receipt |

See accompanying notes to financial statements.

800.789.ASIA [2742] www.matthewsfunds.com 11

M A T T H E W S A S I A N G R O W T H A N D I N C O M E F U N D

| PORTFOLIO MANAGER | SYMBOL: MACSX |

G. Paul Matthews

The Matthews Asian Growth and Income Fund invests at least 80% of its assets in the dividend-paying equity securities and convertible bonds of companies located in Asia, which includes China, Hong Kong, India, Indonesia, Japan, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand.

Note: This fund is closed to most new investors.

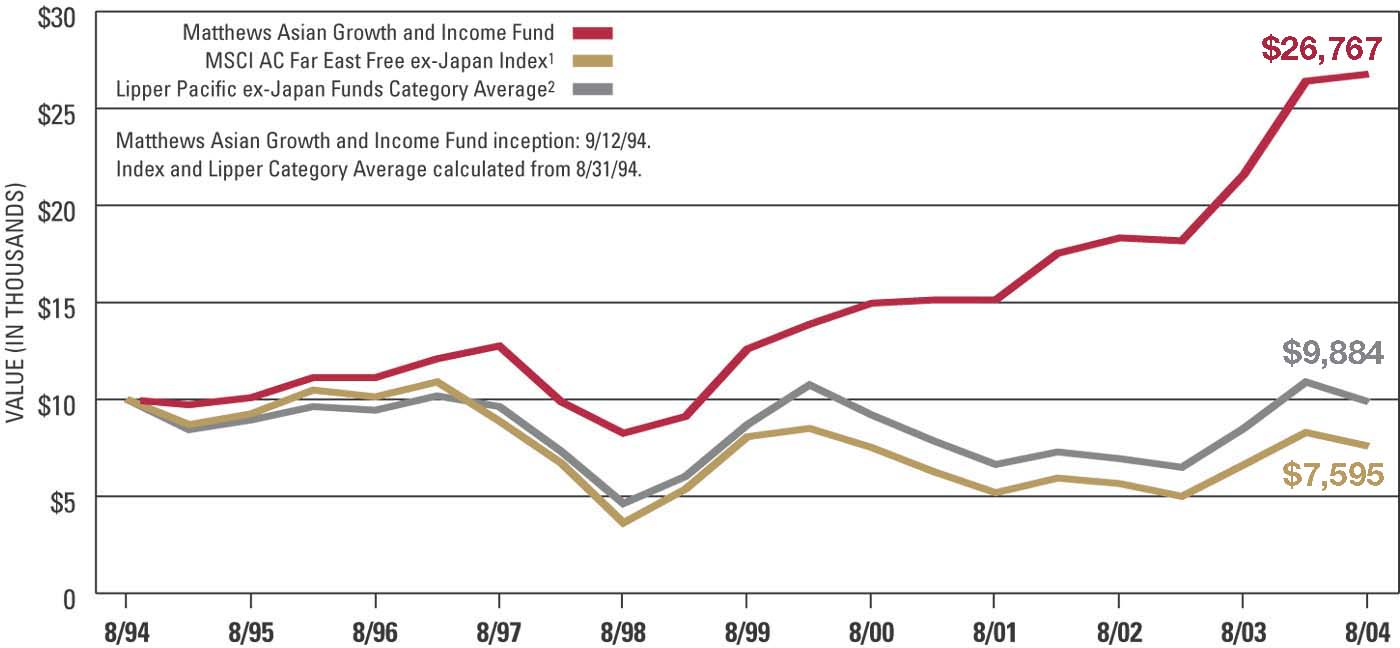

PORTFOLIO MANAGER COMMENTARY

The Matthews Asian Growth and Income Fund gained 23.99% in the fiscal year ended August 31, 2004, outperforming its benchmark indices and peer group average. This outperformance was primarily due to particularly strong returns from higher-yielding equities in Hong Kong, Singapore and Korea. Many of the companies that have historically paid higher-than-average dividends are in businesses and sectors geared toward domestic consumption, which saw a particularly strong recovery from the economic impact of the SARS episode of the prior year.

While the performance of the Fund and its underlying markets was positive for the overall 12-month period under review, the markets during the period were

(continued on page 14)

GROWTH OF A $10,000 INVESTMENT

The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions or redemption of fund shares.

12 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

| FUND HIGHLIGHTS | Fund Inception: 9/12/94 |

- ---------------------------------------------------------------------------------------------------------

AVERAGE ANNUAL RETURNS AS OF AUGUST 31, 2004*

- ---------------------------------------------------------------------------------------------------------

SINCE

3 MTHS 1 YR 3 YRS 5 YRS INCEPTION

- ---------------------------------------------------------------------------------------------------------

Matthews Asian Growth and Income Fund 4.31% 23.99% 20.94% 16.26% 10.38%

MSCI All Country Far East Free ex-Japan Index(1) 1.50% 14.53% 13.53% -1.22% -2.72%+

Lipper Pacific ex-Japan Funds Category Average(2) 0.37% 13.93% 13.17% 1.93% -0.37%+

- ---------------------------------------------------------------------------------------------------------

+Calculated from 8/31/94

- ---------------------------------------------------------------------------------------------------------

MATTHEWS ASIAN GROWTH AND INCOME FUND AVERAGE ANNUAL RETURNS AS OF*:

- ---------------------------------------------------------------------------------------------------------

SINCE

1 YR 3 YRS 5 YRS 10 YRS INCEPTION

- ---------------------------------------------------------------------------------------------------------

June 30, 2004 30.79% 18.28% 16.71% -- 10.22%

September 30, 2004 22.73% 24.29% 17.38% 10.64% 10.60%

- ---------------------------------------------------------------------------------------------------------

*Assumes reinvestment of all dividends. Past performance is not indicative of future results.

Unusually high returns may not be sustainable. The performance of foreign indices may be

based on different exchange rates than those used by the Fund and, unlike the Fund's

NAV, is not adjusted to reflect fair value at 4PM Eastern Time.

- -------------------------------------------------------

OPERATING EXPENSES(3)

- -------------------------------------------------------

For Fiscal Year 2004 (ended 8/31/04) 1.44%

- -------------------------------------------------------

- -------------------------------------------------------

PORTFOLIO TURNOVER(4)

- -------------------------------------------------------

For Fiscal Year 2004 (ended 8/31/04) 17.46%

- -------------------------------------------------------

- ------------------------------------------------

COUNTRY ALLOCATION

- ------------------------------------------------

China/Hong Kong 42.2%

South Korea 20.1%

Singapore 12.6%

Thailand 6.3%

Taiwan 5.7%

Japan(1) 4.2%

United Kingdom(1) 2.5%

Indonesia 2.3%

Australia(1) 1.8%

India(1) 0.8%

Cash and other 1.5%

- ------------------------------------------------

- ------------------------------------------------

SECTOR ALLOCATION

- ------------------------------------------------

Financials 30.8%

Telecommunication Services 21.8%

Consumer Discretionary 15.2%

Utilities 13.0%

Industrials 6.2%

Consumer Staples 5.1%

Energy 3.4%

Materials 1.6%

Health Care 1.4%

Cash and other 1.5%

- ------------------------------------------------

- ------------------------------------------------

BREAKDOWN BY SECURITY TYPE

- ------------------------------------------------

Equities 74.5%

Internationa(1) Dollar Bonds 20.1%

Preferred Equities 3.9%

Cash and other 1.5%

- ------------------------------------------------

- ------------------------------------------------

MARKET CAP EXPOSURE

- ------------------------------------------------

Large cap (over $5 billion) 49.5%

Mid cap ($1-$5 billion) 34.9%

Small cap (under $1 billion) 14.1%

Cash and other 1.5%

- ------------------------------------------------

- ----------------------------------------------------------------

NAV ASSETS REDEMPTION FEE 12b-1 FEES

- ----------------------------------------------------------------

$14.65 $1.01 billion 2.00% within 90 days None

- ----------------------------------------------------------------

All data is as of August, 2004, unless otherwise noted.

|

| 1 | The MSCI All Country Far East Free ex-Japan Index is an unmanaged capitalization-weighted index of the stock markets of Hong Kong, Taiwan, Singapore, Korea, Indonesia, Malaysia, Philippines, Thailand and China that excludes securities not available to foreign investors. As of August 31, 2004, 0.8% of the assets in the Matthews Asian Growth and Income Fund were invested in India, 4.2% of the Fund’s assets were invested in Japan, 1.8% of the Fund’s assets were invested in Australia, and 2.5% of the Fund’s assets were invested in the United Kingdom, which are not included in the MSCI All Country Far East Free ex-Japan Index. Source: Bloomberg. |

| 2 | As of 8/31/04, the Lipper Pacific ex-Japan Funds Category Average consisted of 61 funds for the three-month period, 59 funds for the one-year period, 50 funds for the three-year period, 41 funds for the five-year period, and 13 funds since 8/31/94. Lipper, Inc. fund performance does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods. |

| 3 | Includes management fee, shareholder services fees and other expenses. Matthews Asian Funds do not charge 12b-1 fees. |

| 4 | The lesser of fiscal year-to-date purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

800.789.ASIA [2742] www.matthewsfunds.com 13

M A T T H E W S A S I A N G R O W T H A N D I N C O M E F U N D

Portfolio manager commentary,

continued from page 12

nevertheless quite uneven. Generally speaking, the markets performed well in the final months of calendar 2003 and the early part of 2004, but saw periods of profit-taking and market weakness in the summer months of 2004. Among the reasons cited were the efforts by the authorities in mainland China to slow the pace of economic growth to head off potential imbalances and combat possible inflation. It is probably too early to know if these efforts will be successful, and this has caused some uncertainty in the markets. Whatever the short-term outlook for the economies of the region, we remain confident that over the long term, living standards in the region should continue to improve; and we believe that this should benefit companies exposed to regional consumption, which remains a major concentration for the portfolio.

By country, the greatest contribution to Fund performance came from its positions in Hong Kong, followed by Singapore and Korea. During the fiscal-year period, all of the underlying countries to which the Fund had exposure produced positive returns—which is unusual. However, the Fund’s positions in convertible bonds did not perform as well as its holdings in dividend-paying equities.

SCHEDULE OF INVESTMENTS

EQUITIES: 78.36%*

SHARES VALUE

==================================================================

CHINA/HONG KONG: 31.04%

Hongkong Land Holdings, Ltd. 15,727,700 $29,725,353

Hongkong Electric Holdings, Ltd. 5,914,500 26,387,938

CLP Holdings, Ltd. 4,518,200 26,124,632

Hong Kong & China Gas

Co., Ltd. 13,382,000 24,104,911

Sun Hung Kai Properties, Ltd. 1,878,000 17,455,881

Caf, de Coral Holdings, Ltd. 15,091,100 17,219,442

Television Broadcasts, Ltd. 3,806,000 15,760,845

Hang Seng Bank, Ltd. 1,128,800 15,050,763

Wharf Holdings, Ltd. 4,553,000 15,030,834

MTR Corp., Ltd. 9,636,800 14,764,166

Shangri-La Asia, Ltd. 15,641,400 14,538,574

Giordano International, Ltd. 24,585,000 13,789,752

PCCW, Ltd. ** 19,206,000 12,804,082

Citic Pacific, Ltd. 4,842,000 12,353,387

Cheung Kong Infrastructure

Holdings, Ltd. 4,475,500 11,102,754

Hengan International Group

Co., Ltd. 18,148,000 10,760,902

PetroChina Co., Ltd. ADR 202,250 10,185,310

Hang Lung Group, Ltd. 5,693,000 8,758,518

PetroChina Co., Ltd. H Shares 15,666,000 7,883,262

Vitasoy International

Holdings, Ltd. 26,825,000 6,843,858

Lerado Group Holding Co., Ltd. 6,396,000 1,107,007

China Hong Kong Photo Products

Holdings, Ltd. 14,998,003 922,960

-----------

Total China/Hong Kong 312,675,131

==================================================================

14 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

SHARES VALUE

==================================================================

SOUTH KOREA: 14.64%

Shinhan Financial Group Co., Ltd. 1,127,590 $19,089,296

Korea Gas Corp. 658,590 18,525,256

Hyundai Motor Co., Ltd., Pfd. 721,890 15,887,409

Hyundai Motor Co., Ltd., 2nd Pfd. 510,230 12,159,407

KT Corp. ADR 631,800 11,069,136

Samsung Fire & Marine Insurance

Co., Ltd. 171,260 10,214,491

Korean Reinsurance Co. 2,186,690 7,270,932

SK Telecom Co., Ltd. ADR 368,300 6,960,870

Korea Electric Power Corp. ADR 620,950 6,234,338

LG Ad, Inc. 340,870 5,933,449

Samsung Securities Co., Ltd. 341,260 5,866,170

Sindo Ricoh Co., Ltd. 121,490 5,801,059

LG Chem Ltd., Pfd. 200,380 4,523,054

Korea Electric Power Corp. 238,500 4,192,929

Samsung Fire & Marine Insurance

Co., Ltd., Pfd. 142,820 3,998,737

Daehan City Gas Co., Ltd. 280,300 3,820,558

Samchully Co., Ltd. 66,410 3,217,153

LG Household & Health Care,

Ltd., Pfd. 177,830 2,701,762

-----------

Total South Korea 147,466,006

==================================================================

SINGAPORE: 12.62%

Singapore Post, Ltd. 56,996,000 26,127,396

Fraser and Neave, Ltd. 2,754,820 22,521,814

Singapore Telecommunications,

Ltd. 15,769,000 21,087,337

Singapore Press Holdings, Ltd. 7,725,500 19,489,130

CapitalMall Trust REIT 16,663,900 16,348,128

Singapore Exchange, Ltd. 13,787,000 14,330,848

Parkway Holdings, Ltd. 6,749,000 5,044,655

Singapore Technologies

Engineering, Ltd. 1,742,000 2,136,238

-----------

Total Singapore 127,085,546

==================================================================

SHARES VALUE

==================================================================

THAILAND: 6.29%

Advanced Info Service Public

Co., Ltd. 7,370,000 $16,721,849

PTT Public Co., Ltd. 4,554,700 6,403,481

BEC World Public Co., Ltd. 28,857,300 12,748,483

Bangkok Bank Public Co., Ltd. ** 4,196,300 9,974,399

Charoen Pokphand Foods

Public Co., Ltd. 52,037,000 4,747,673

Thai Reinsurance Public

Co., Ltd. 25,672,800 2,675,149

Charoen Pokphand Foods Public

Co., Ltd. Warrants,

Expires 7/21/05 ** 638,000 35,232

----------

Total Thailand 63,306,266

==================================================================

JAPAN: 4.24%

Japan Real Estate Investment

Corp. REIT 1,998 15,329,318

Japan Retail Fund Investment

Corp. REIT 1,980 14,271,083

Nippon Building Fund, Inc. REIT 1,748 13,060,823

----------

Total Japan 42,661,224

==================================================================

UNITED KINGDOM: 2.46%

HSBC Holdings PLC ADR 278,700 21,705,156

HSBC Holdings PLC 196,800 3,052,943

----------

Total United Kingdom 24,758,099

==================================================================

See footnotes on page 17.

800.789.ASIA [2742] www.matthewsfunds.com 15

M A T T H E W S A S I A N G R O W T H A N D I N C O M E F U N D

SCHEDULE OF INVESTMENTS (continued)

EQUITIES (continued)

SHARES VALUE

==================================================================

INDONESIA: 2.30%

PT Telekomunikasi Indonesia

ADR 745,500 $12,121,830

PT Tempo Scan Pacific 12,357,000 8,765,232

PT Ramayana Lestari Sentosa 5,424,500 2,271,057

-----------

Total Indonesia 23,158,119

==================================================================

TAIWAN: 2.22%

Chunghwa Telecom Co.,

Ltd. ADR 1,252,200 21,362,532

Chunghwa Telecom Co., Ltd. 648,000 1,027,967

----------

Total Taiwan 22,390,499

==================================================================

AUSTRALIA: 1.78%

AXA Asia Pacific Holdings, Ltd. 6,585,658 17,950,759

----------

Total Australia 17,950,759

==================================================================

INDIA: 0.77%

Hero Honda Motors, Ltd. 812,300 7,755,804

---------

Total India 7,755,804

==================================================================

TOTAL EQUITIES

(Cost $627,302,151) 789,207,453

==================================================================

INTERNATIONAL DOLLAR BONDS: 20.11%*

FACE AMOUNT VALUE

==================================================================

CHINA/HONG KONG: 11.20%

China Mobile Hong Kong, Ltd., Cnv.

2.25%, 11/03/05 $47,650,000 $47,530,875

PCCW Capital II, Ltd., Cnv.

1.00%, 01/29/07 26,050,000 29,273,688

Shangri-La Finance, Ltd., Cnv.

0.00%, 03/15/09 14,722,000 14,722,000

Hang Lung Properties, Ltd., Cnv.

5.50%, 12/29/49 11,550,000 13,744,500

Tingyi (C.I.) Holding Corp., Cnv.

3.50%, 06/04/05 3,500,000 3,911,250

PCCW Capital, Ltd., Cnv.

3.50%, 12/05/05 3,000,000 3,605,940

-----------

Total China/Hong Kong 112,788,253

==================================================================

SOUTH KOREA: 5.42%

KT Corp., Cnv.

0.25%, 01/04/07 35,825,000 35,778,089

Korea Deposit Insurance Corp., Cnv.

2.25%, 10/11/05 14,820,000 18,450,900

KT Corp., Cnv.***

0.25%, 01/04/07 375,000 378,471

----------

Total South Korea 54,607,460

==================================================================

16 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

FACE AMOUNT VALUE

==================================================================

TAIWAN: 3.49%

Cathay Financial Holding Co., Cnv.

0.00%, 05/20/07 $22,042,000 $26,395,295

Sinopac Holdings Co., Cnv.

0.00%, 07/12/07 7,177,000 8,791,825

-----------

Total Taiwan 35,187,120

==================================================================

TOTAL INTERNATIONAL

DOLLAR BONDS 202,582,833

(Cost $198,423,318)

- ------------------------------------------------------------------

TOTAL INVESTMENTS: 98.47%* 991,790,286

(Cost $825,725,469****)

CASH AND OTHER ASSETS,

LESS LIABILITIES: 1.53% 15,396,230

--------------

NET ASSETS: 100.00% $1,007,186,516

==================================================================

| * | As a percentage of net assets as of August 31, 2004

|

| ** | Non–income producing security.

|

| *** | Security exempt from registration under rule 144A of the Securities Act of 1933. This security may be resold in transactions exempt from registration, normally to qualified, institutional buyers. At August 31, 2004, the value of this security amounted to $378,471 or 0.04% of net assets.

|

| **** | Cost for Federal tax purposes is $839,645,410 and net unrealized appreciation consists of: |

Gross unrealized appreciation.............$161,217,772

Gross unrealized depreciation............. (9,072,896)

------------

Net unrealized appreciation...............$152,144,876

============

| ADR | American Depositary Receipt

|

| Cnv. | Convertible

|

| Pfd. | Preferred

|

| REIT | Real Estate Investment Trust

|

See accompanying notes to financial statements.

800.789.ASIA [2742] www.matthewsfunds.com 17

M A T T H E W S K O R E A F U N D

| CO-PORTFOLIO MANAGERS | SYMBOL: MAKOX |

G. Paul Matthews and Mark W. Headley

The Matthews Korea Fund invests at least 80% of its assets in the common and preferred stocks of companies located in South Korea.

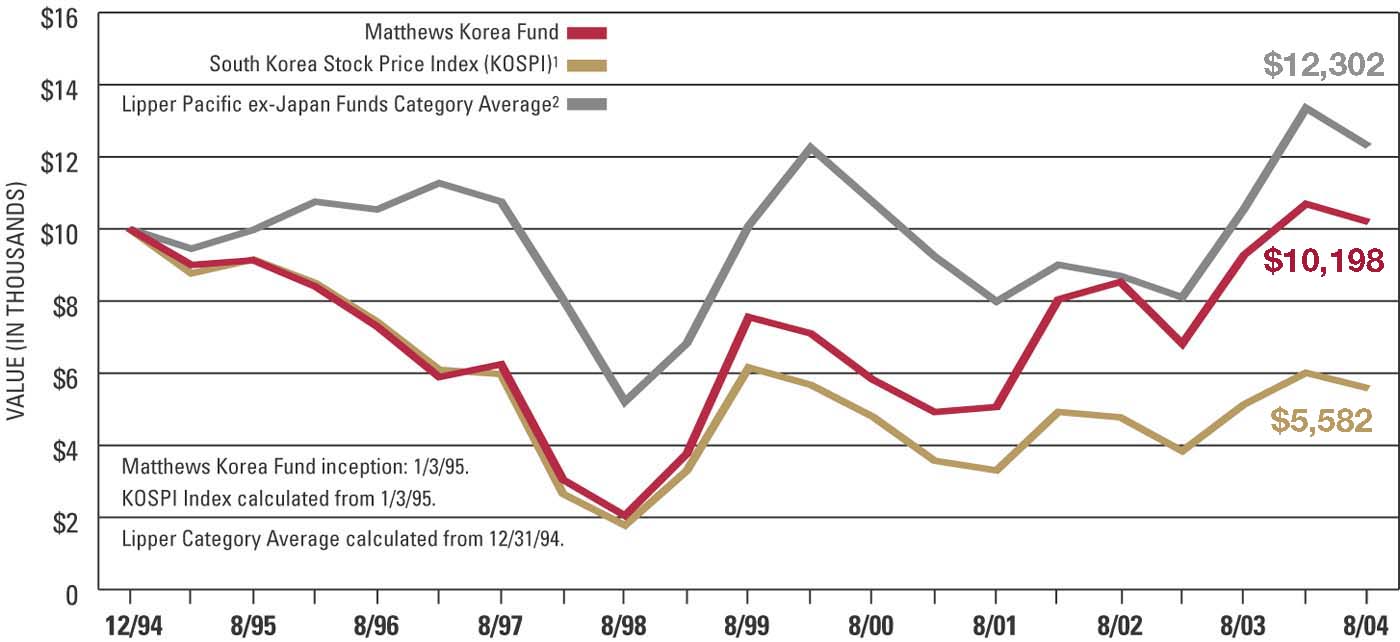

PORTFOLIO MANAGER COMMENTARY

Despite a challenging domestic economy and tough political environment, Korean equities managed a positive return during the fiscal year ended August 31, 2004. The Matthews Korea Fund gained 9.91%, while its benchmark KOSPI Index returned 8.73%. The Fund has historically underweighted capital-intensive industries, which performed well during the first half of the year. However, the Fund’s overweight positions in the consumer and financial sectors—which outperformed the market during the second half of the year—helped the Fund outperform the benchmark. The telecommunications sector hurt the performance of the Fund during the fiscal year.

The domestic economy remained weak during the fiscal year, and the consumer-debt problem, which began in late 2002, continued to hurt domestic sentiment in South Korea. To help revive the domestic

(continued on page 20)

GROWTH OF A $10,000 INVESTMENT

The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions or redemption of fund shares.

18 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

| FUND HIGHLIGHTS | Fund Inception: 1/3/95 |

- ---------------------------------------------------------------------------------------------------------

AVERAGE ANNUAL RETURNS AS OF AUGUST 31, 2004*

- ---------------------------------------------------------------------------------------------------------

SINCE

3 MTHS 1 YR 3 YRS 5 YRS INCEPTION

- ---------------------------------------------------------------------------------------------------------

Matthews Korea Fund 0.25% 9.91% 26.30% 6.18% 0.20%

KOSPI Index(1) 0.70% 8.73% 18.95% -1.95% -5.85%

Lipper Pacific ex-Japan Funds Category Average(2) 0.37% 13.93% 13.17% 1.93% 1.63%+

- ---------------------------------------------------------------------------------------------------------

+Calculated from 12/31/94

- ---------------------------------------------------------------------------------------------------------

MATTHEWS KOREA FUND AVERAGE ANNUAL RETURNS AS OF*:

- ---------------------------------------------------------------------------------------------------------

SINCE

1 YR 3 YRS 5 YRS INCEPTION

- ---------------------------------------------------------------------------------------------------------

June 30, 2004 24.10% 24.87% 6.01% 0.23%

September 30, 2004 19.84% 31.80% 10.23% 0.51%

- ---------------------------------------------------------------------------------------------------------

*Assumes reinvestment of all dividends. Past performance is not indicative of future results.

Unusually high returns may not be sustainable. The performance of foreign indices may be based

on different exchange rates than those used by the Fund and, unlike the Fund's NAV, is not

adjusted to reflect fair value at 4PM Eastern Time.

- -------------------------------------------------------

OPERATING EXPENSES(3)

- -------------------------------------------------------

For Fiscal Year 2004 (ended 8/31/04) 1.50%

- -------------------------------------------------------

- -------------------------------------------------------

PORTFOLIO TURNOVER(4)

- -------------------------------------------------------

For Fiscal Year 2004 (ended 8/31/04) 18.40%

- -------------------------------------------------------

- ------------------------------------------------

COUNTRY ALLOCATION

- ------------------------------------------------

South Korea 99.2%

Cash and other 0.8%

- ------------------------------------------------

- ------------------------------------------------

SECTOR ALLOCATION

- ------------------------------------------------

Financials 21.6%

Information Technology 21.3%

Consumer Discretionary 20.8%

Consumer Staples 11.7%

Telecommunication Services 8.0%

Industrials 7.4%

Health Care 6.1%

Utilities 1.5%

Materials 0.8%

Cash and other 0.8%

- ------------------------------------------------

- ------------------------------------------------

MARKET CAP EXPOSURE

- ------------------------------------------------

Large cap (over $5 billion) 35.2%

Mid cap ($1-$5 billion) 30.3%

Small cap (under $1 billion) 33.7%

Cash and other 0.8%

- ------------------------------------------------

- ---------------------------------------------------------------

NAV ASSETS REDEMPTION FEE 12b-1 FEES

- ---------------------------------------------------------------

$3.94 $110.2 million 2.00% within 90 days None

- ---------------------------------------------------------------

All data is as of August, 2004, unless otherwise noted.

|

| 1 | The South Korea Stock Price Index (KOSPI) is a capitalization-weighted index of all common stocks listed on the Korea Stock Exchange. Source: Bloomberg. |

| 2 | As of 8/31/04, the Lipper Pacific ex-Japan Funds Category Average consisted of 61 funds for the three-month period, 59 funds for the one-year period, 50 funds for the three-year period, 41 funds for the five-year period, and 16 funds since 12/31/94. Lipper, Inc. fund performance does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods. |

| 3 | Includes management fee, shareholder services fees and other expenses. Matthews Asian Funds do not charge 12b-1 fees. |

| 4 | The lesser of fiscal year-to-date purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

800.789.ASIA [2742] www.matthewsfunds.com 19

M A T T H E W S K O R E A F U N D

Portfolio manager commentary,

continued from page 18

economy, the government implemented various measures: The central bank lowered interest rates despite rising interest rates in the U.S., and the government cut taxes on various consumer products. Political parties remained deeply divided on issues such as moving the nation’s capital from Seoul to another location approximately 100 miles away. No major improvements between North and South Korea relations were made during the year, and North Korea remains one of the key risks for the South Korean economy.

During the fiscal year, exports fared well despite persisting concerns over China’s slowdown. Korean-made automobiles and IT products continued to fare well in North America and also showed strong growth in the European market. South Korean firms maintained their strong positions in memory chips and flat-panel monitors.

The Fund remains focused on the consumer, financial and technology sectors, which we believe will benefit most from the development of the South Korean economy and the increasing wealth of its population.

SCHEDULE OF INVESTMENTS

EQUITIES: SOUTH KOREA: 99.21%*

SHARES VALUE

===============================================================

FINANCIALS: 21.56%

Commercial Banks: 15.25%

Hana Bank 271,544 $6,094,033

Kookmin Bank ** 166,992 5,335,161

Shinhan Financial Group Co., Ltd. 231,612 3,921,026

Kookmin Bank ADR ** 45,439 1,451,776

----------

16,801,996

----------

Insurance: 4.07%

Samsung Fire & Marine

Insurance Co., Ltd. 52,523 3,132,639

Samsung Fire & Marine

Insurance Co., Ltd., Pfd. 48,440 1,356,244

----------

4,488,883

----------

Capital Markets: 2.24%

Samsung Securities Co., Ltd. 143,555 2,467,673

----------

Total Financials 23,758,552

===============================================================

INFORMATION TECHNOLOGY: 21.29%

Semiconductors & Semiconductor Equipment:

10.22%

Samsung Electronics Co., Ltd. 24,701 9,671,529

Samsung Electronics Co., Ltd., Pfd. 6,180 1,593,489

----------

11,265,018

----------

Electronic Equipment & Instruments: 4.78%

Kumho Electric Inc. 59,130 1,943,023

Power Logics Co., Ltd. ** 113,725 1,194,663

Daeduck GDS Co., Ltd. 134,520 1,122,314

Amotech Co., Ltd. 72,976 1,007,352

----------

5,267,352

----------

Internet Software & Services: 2.72%

NHN Corp. 35,064 2,998,484

----------

Software: 2.49%

NCsoft Corp. ** 37,926 2,739,457

----------

Computers & Peripherals: 1.08%

LG.Philips LCD Co., Ltd. ADR** 80,000 1,190,400

----------

Total Information Technology 23,460,711

===============================================================

20 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

SHARES VALUE

===============================================================

CONSUMER DISCRETIONARY: 20.80%

Media: 6.09%

CJ Entertainment, Inc. 203,508 $3,074,219

Cheil Communications, Inc. 18,840 2,461,623

LG Ad, Inc. 67,430 1,173,739

----------

6,709,581

----------

Automobiles: 5.76%

Hyundai Motor Co. 90,691 3,928,880

Hyundai Motor Co., Pfd. 109,890 2,418,467

----------

6,347,347

----------

Internet & Catalog Retail: 3.97%

Internet Auction Co., Ltd. ** 30,824 2,750,972

LG Home Shopping, Inc. 40,430 1,628,643

----------

4,379,615

----------

Multiline Retail: 3.50%

Hyundai Department Store

Co., Ltd. 96,300 2,871,819

Taegu Department Store Co., Ltd. 133,110 986,900

----------

3,858,719

----------

Auto Components: 0.93%

Korea Electric Terminal Co., Ltd. 62,460 1,024,868

----------

Textiles, Apparel & Luxury Goods: 0.55%

Handsome Co., Ltd. 75,869 600,049

----------

Total Consumer Discretionary 22,920,179

===============================================================

SHARES VALUE

===============================================================

CONSUMER STAPLES: 11.70%

Food Products: 5.54%

Nong Shim Co., Ltd. 16,390 $3,429,257

Pulmuone Co., Ltd. 43,510 1,577,065

ORION Corp. 15,760 1,101,428

----------

6,107,750

----------

Personal Products: 3.52%

AmorePacific Corp. 20,390 3,876,730

----------

Beverages: 2.64%

Hite Brewery Co., Ltd. 42,481 2,913,573

----------

Total Consumer Staples 12,898,053

===============================================================

TELECOMMUNICATION SERVICES: 7.95%

Wireless Telecommunication Services: 4.87%

SK Telecom Co., Ltd. 19,845 2,989,198

SK Telecom Co., Ltd. ADR 86,900 1,642,410

KT Freetel Co., Ltd. 46,671 737,433

----------

5,369,041

----------

Diversified Telecommunication Services: 3.08%

KT Corp. 59,720 1,889,824

KT Corp. ADR 85,600 1,499,712

----------

3,389,536

----------

Total Telecommunication Services 8,758,577

===============================================================

See footnotes on page 23.

800.789.ASIA [2742] www.matthewsfunds.com 21

M A T T H E W S K O R E A F U N D

SCHEDULE OF INVESTMENTS (continued)

EQUITIES: SOUTH KOREA (continued)

SHARES VALUE

===============================================================

INDUSTRIALS: 7.40%

Commercial Services & Supplies: 5.45%

S1 Corp. 126,665 $3,260,509

Sindo Ricoh Co., Ltd. 34,526 1,648,591

Shinsegae Food Systems Co., Ltd. 36,059 1,095,685

----------

6,004,785

----------

Construction & Engineering: 1.95%

Tae Young Corp. 69,020 2,145,172

----------

Total Industrials 8,149,957

===============================================================

HEALTH CARE: 6.11%

Pharmaceuticals: 6.11%

Yuhan Corp. 36,505 2,164,597

Hanmi Pharm Co., Ltd. 59,880 1,858,497

LG Life Sciences, Ltd. ** 57,640 1,651,361

Daewoong Pharmaceutical

Co., Ltd. 68,210 1,059,998

----------

Total Health Care 6,734,453

===============================================================

SHARES VALUE

===============================================================

UTILITIES: 1.56%

Electric Utilities: 1.09%

Korea Electric Power Corp. 68,510 $1,204,434

----------

Gas Utilities: 0.47%

Samchully Co., Ltd. 10,570 512,051

----------

Total Utilities 1,716,485

===============================================================

MATERIALS: 0.84%

Chemicals: 0.84%

LG Chem, Ltd. 24,420 928,590

----------

Total Materials 928,590

===============================================================

22 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

VALUE

===============================================================

TOTAL INVESTMENTS: 99.21% $109,325,557

(Cost $79,010,320***)

CASH AND OTHER ASSETS,

LESS LIABILITIES: 0.79% 873,618

------------

NET ASSETS: 100.00% $110,199,175

===============================================================

| * | As a percentage of net assets as of August 31, 2004

|

| ** | Non–income producing security.

|

| *** | Cost for Federal tax purposes is $80,410,374 and net unrealized appreciation consists of: |

Gross unrealized appreciation..................$35,211,134

Gross unrealized depreciation.................. (6,295,951)

-----------

Net unrealized appreciation....................$28,915,183

===========

| ADR | American Depositary Receipt

|

| GDS | Global Depositary Shares

|

| Pfd. | Preferred |

See accompanying notes to financial statements.

800.789.ASIA [2742] www.matthewsfunds.com 23

M A T T H E W S C H I N A F U N D

| CO-PORTFOLIO MANAGERS | SYMBOL: MCHFX |

Richard H. Gao, Mark W. Headley and G. Paul Matthews

The Matthews China Fund invests at least 80% of its assets in the common and preferred stocks of companies located in China. China includes Taiwan and Hong Kong.

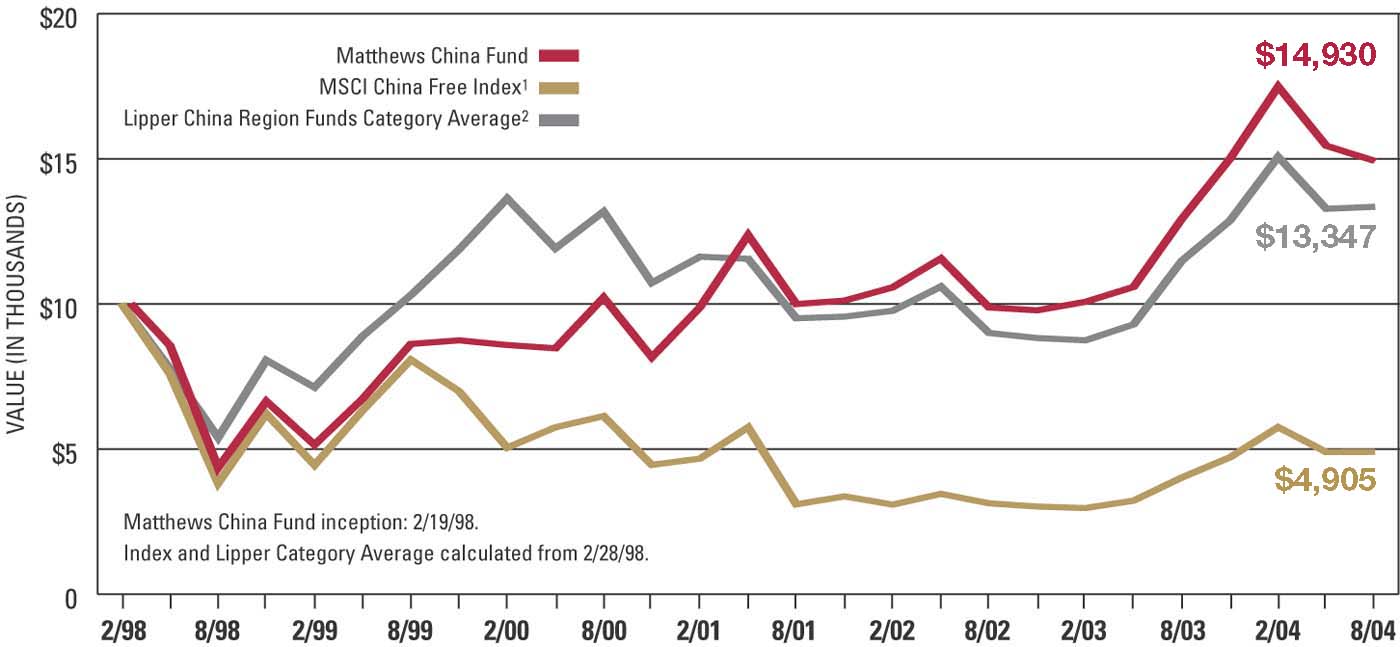

PORTFOLIO MANAGER COMMENTARY

For the fiscal year ended August 31, 2004, the Matthews China Fund gained 15.48%, underperforming its benchmark, the MSCI China Free Index, which gained 21.91% over the same period. However, the Fund outperformed its peer group as measured by the Lipper China Region Funds category average, which gained 14.92% on average.

Chinese equities had a volatile trading period during the fiscal year. China shares staged a huge rally in the first half, driven by a strong economic recovery after the SARS epidemic. The market later encountered a substantial correction in March and April, after signs of overheating appeared in the economy and tightening measures were carried out by the central bank. Toward the end of the fiscal year, China shares stabilized as investors became less worried about a hard-landing scenario in the economy.

(continued on page 26)

GROWTH OF A $10,000 INVESTMENT

The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gain distributions or redemption of fund shares.

24 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

| FUND HIGHLIGHTS | Fund Inception: 2/19/98 |

- ---------------------------------------------------------------------------------------------------------

AVERAGE ANNUAL RETURNS AS OF AUGUST 31, 2004*

- ---------------------------------------------------------------------------------------------------------

SINCE

3 MTHS 1 YR 3 YRS 5 YRS INCEPTION

- ---------------------------------------------------------------------------------------------------------

Matthews China Fund -3.35% 15.48% 14.31% 11.60% 6.33%

MSCI China Free Index(1) 0.17% 21.91% 16.50% -9.36% -10.33%+

Lipper China Region Funds Category Average(2) -0.27% 14.92% 12.50% 6.57% 4.35%+

- ---------------------------------------------------------------------------------------------------------

+Calculated from 2/28/98

- ---------------------------------------------------------------------------------------------------------

MATTHEWS CHINA FUND AVERAGE ANNUAL RETURNS AS OF*:

- ---------------------------------------------------------------------------------------------------------

SINCE

1 YR 3 YRS 5 YRS INCEPTION

- ---------------------------------------------------------------------------------------------------------

June 30, 2004 37.94% 6.99% 9.46% 6.69%

September 30, 2004 19.44% 20.78% 14.36% 7.20%

- ---------------------------------------------------------------------------------------------------------

*Assumes reinvestment of all dividends. Past performance is not indicative of future results.

Unusually high returns may not be sustainable. The performance of foreign indices may be based

on different exchange rates than those used by the Fund and, unlike the Fund's NAV, is not

adjusted to reflect fair value at 4PM Eastern Time.

- -------------------------------------------------------

OPERATING EXPENSES(3)

- -------------------------------------------------------

For Fiscal Year 2004 (ended 8/31/04) 1.50%

- -------------------------------------------------------

- -------------------------------------------------------

PORTFOLIO TURNOVER(4)

- -------------------------------------------------------

For Fiscal Year 2004 (ended 8/31/04) 28.99%

- -------------------------------------------------------

- ------------------------------------------------

CHINA EXPOSURE(5)

- ------------------------------------------------

China Play 34.0%

Red Chip 30.3%

H Share 28.4%

B Share 6.3%

Cash and other 1.0%

- ------------------------------------------------

- ------------------------------------------------

SECTOR ALLOCATION

- ------------------------------------------------

Consumer Discretionary 23.0%

Industrials 16.8%

Financials 13.7%

Utilities 10.5%

Information Technology 8.9%

Energy 7.3%

Telecommunications Services 7.3%

Materials 4.1%

Health Care 4.0%

Consumer Staples 3.4%

Cash and other 1.0%

- ------------------------------------------------

- ------------------------------------------------

MARKET CAP EXPOSURE

- ------------------------------------------------

Large cap (over $5 billion) 29.7%

Mid cap ($1-$5 billion) 46.2%

Small cap (under $1 billion) 23.1%

Cash and other 1.0%

- ------------------------------------------------

- ---------------------------------------------------------------

NAV ASSETS REDEMPTION FEE 12b-1 FEES

- ---------------------------------------------------------------

$13.26 $340.3 million 2.00% within 90 days None

- ---------------------------------------------------------------

All data is as of August, 2004, unless otherwise noted.

|

| 1 | The MSCI China Free Index is an unmanaged capitalization-weighted index of Chinese equities that includes Red Chips and H shares listed on the Hong Kong exchange, and B shares listed on the Shanghai and Shenzhen exchanges. Source: Bloomberg. |

| 2 | As of 8/31/04, the Lipper China Region Funds Category Average consisted of 22 funds for the three-month, one-year and three-year periods; 20 funds for the five-year period; and 16 funds since 2/28/98. Lipper, Inc. fund performance does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods. |

| 3 | Includes management fee, shareholder services fees and other expenses. Matthews Asian Funds do not charge 12b-1 fees. |

| 4 | The lesser of fiscal year-to-date purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| 5 | China Plays are Hong Kong companies that conduct the majority of their business in mainland China. Red Chips are Mainland Chinese companies listed on the Hong Kong stock exchange and incorporated in Hong Kong. H shares are Mainland Chinese companies listed on the Hong Kong stock exchange; companies are incorporated in Mainland China and approved by the China Securities Regulatory Commission for a listing in Hong Kong. B Shares are Mainland Chinese stocks listed on the Shanghai and Shenzhen stock exchanges, available to Chinese and foreign investors. |

800.789.ASIA [2742] www.matthewsfunds.com 25

M A T T H E W S C H I N A F U N D

Portfolio manager commentary,

continued from page 24

Over the year, the Matthews China Fund benefited most from its positions in the industrials, consumer discretionary and energy sectors, while the information technology sector produced negative returns. The Fund’s relative underweighting in the commodity-related energy and basic materials sectors, which accounted for almost 30% of the benchmark index, was the primary reason why the Fund’s performance lagged that of its benchmark. Although commodity-related stocks declined sharply in the second half of the year, they were still the largest contributors to the benchmark index due to their huge gains in the first half.

The Fund has been shifting its positions out of some H-share companies into China plays that we believe will benefit from business developments not only in China but also in Hong Kong, whose economy is undergoing a recovery. We also added some new positions, mainly in the consumer, technology and financial sectors. China’s economic tightening measures are underway, which the Chinese authorities hope will lead to an economic soft landing. We continue with our bottom-up stock picking approach, building a portfolio with companies that we believe will be long-term beneficiaries of China’s economic development.

SCHEDULE OF INVESTMENTS

EQUITIES: CHINA/HONG KONG: 99.00%*

SHARES VALUE

==================================================================

CONSUMER DISCRETIONARY: 22.97%

Hotels, Restaurants & Leisure: 4.89%

Shangri-La Asia, Ltd. 8,465,600 $7,868,717

Cafe de Coral Holdings, Ltd. 4,152,100 4,737,683

China Travel International

Investment Hong Kong, Ltd. 19,264,000 3,951,615

China Travel International Investment

Hong Kong, Ltd. Warrants,

Expires 5/31/06 ** 2,942,400 94,308

----------

16,652,323

----------

Media: 4.41%

Television Broadcasts, Ltd. 2,542,000 10,526,554

Clear Media, Ltd. ** 6,079,000 4,481,343

----------

15,007,897

----------

Household Durables: 3.84%

TCL International Holdings, Ltd. 24,764,000 8,889,698

Lerado Group Holding Co., Ltd. 24,089,000 4,169,277

----------

13,058,975

----------

Textiles, Apparel & Luxury Goods: 3.01%

Weiqiao Textile Co., Ltd.

H Shares 3,870,000 6,177,155

Texwinca Holdings, Ltd. 4,742,000 4,073,283

----------

10,250,438

----------

Automobiles: 2.99%

Denway Motors, Ltd. 25,805,200 10,173,269

----------

Distributors: 2.15%

Li & Fung, Ltd. 5,704,000 7,312,867

----------

Specialty Retail: 1.68%

Giordano International, Ltd. 10,188,000 5,714,460

----------

Total Consumer Discretionary 78,170,229

==================================================================

26 MATTHEWS ASIAN FUNDS

A U G U S T 3 1, 2 0 0 4

SHARES VALUE

==================================================================

INDUSTRIALS: 16.78%

Transportation Infrastructure: 8.92%

Cosco Pacific Ltd. 5,604,000 $8,406,054

Zhejiang Expressway Co.,

Ltd. H Shares 9,656,000 6,561,170

Beijing Capital International

Airport Co., Ltd. H Shares 11,944,000 4,172,770

China Merchants Holdings

International Co., Ltd. 5,205,000 7,907,647

GZI Transport, Ltd. 12,384,000 3,294,483

----------

30,342,124

----------

Electrical Equipment: 2.73%

BYD Co., Ltd. H Shares 3,429,500 9,299,281

----------

Machinery: 1.93%

Shanghai Zhenhua Port Machinery

Co., Ltd. B Shares 8,729,682 6,582,180

----------

Industrial Conglomerates: 1.21%

Shanghai Industrial

Holdings, Ltd. 2,239,000 4,119,212

----------

Airlines: 1.01%

China Southern Airlines Co.,

Ltd. H Shares ** 9,958,000 3,447,022

----------

Air Freight & Logistics: 0.98%

Sinotrans, Ltd. H Shares 10,566,000 3,318,829

----------

Total Industrials 57,108,648

==================================================================

SHARES VALUE

==================================================================

FINANCIALS: 13.71%

Real Estate: 7.30%

Swire Pacific, Ltd. A Shares 2,103,500 $14,899,887

China Vanke Co., Ltd. B Shares 20,396,858 9,936,995

-----------

24,836,882