Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08510

Matthews International Funds

(Exact name of registrant as specified in charter)

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Address of principal executive offices) (Zip code)

William J. Hackett, President

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-788-7553

Date of fiscal year end: December 31

Date of reporting period:December 31, 2018

FormN-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule30e-1 under the Investment Company Act of 1940 (17 CFR270.30e-1). The Commission may use the information provided on FormN-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by FormN-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained inForm N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Table of Contents

Matthews Asia Funds | Annual Report

December 31, 2018 | matthewsasia.com

ASIA FIXED INCOME STRATEGIES

Matthews Asia Strategic Income Fund

Matthews Asia Credit Opportunities Fund

ASIA GROWTH AND INCOME STRATEGIES

Matthews Asian Growth and Income Fund

Matthews Asia Dividend Fund

Matthews China Dividend Fund

ASIA VALUE STRATEGY

Matthews Asia Value Fund

ASIA GROWTH STRATEGIES

Matthews Asia Focus Fund

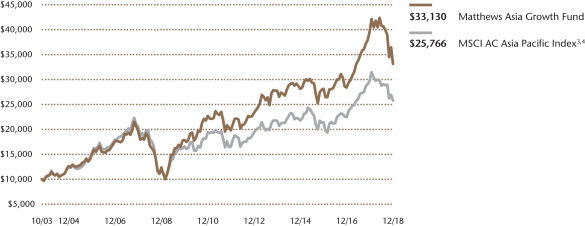

Matthews Asia Growth Fund

Matthews Pacific Tiger Fund

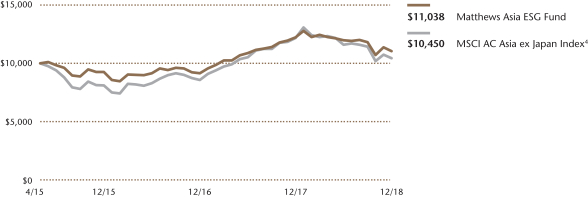

Matthews Asia ESG Fund

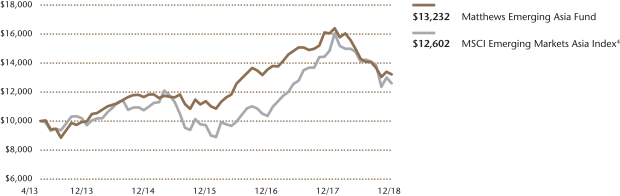

Matthews Emerging Asia Fund

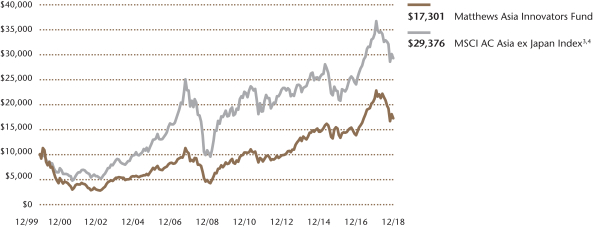

Matthews Asia Innovators Fund

Matthews China Fund

Matthews India Fund

Matthews Japan Fund

Matthews Korea Fund

ASIA SMALL COMPANY STRATEGIES

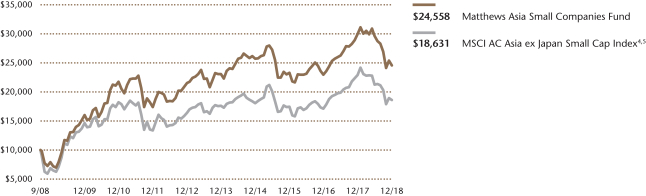

Matthews Asia Small Companies Fund

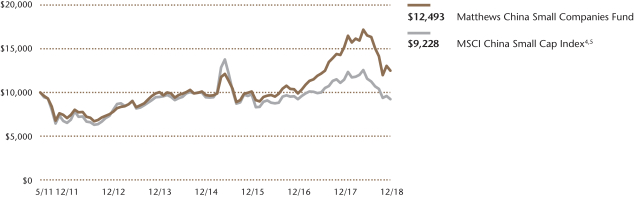

Matthews China Small Companies Fund

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual andsemi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website matthewsasia.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling 800.789.ASIA (2742).

Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with a Fund, you can call 800.789.ASIA (2742) to let the Fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds held in your account if you invest through your financial intermediary or all Funds held directly with Matthews Asia Funds.

Table of Contents

Investor Class Performance and Expenses(December 31, 2018)

|

| Average Annual Total Return† | Inception Date | 2018 Annual Operating Expenses* | 2018 Annual Operating Expenses after Fee Waiver and Expense Reimbursement** | Prospectus Annual Operating Expense Ratios‡ | Prospectus Annual Operating Expense Ratios after Fee Waiver and Expense Reimbursement‡ | ||||||||||||||||||||||||||||||

| Investor Class | 1 year | 5 years | 10 years | Since Inception | ||||||||||||||||||||||||||||||||

ASIA FIXED INCOME STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Strategic Income Fund (MAINX) | -4.05% | 3.10% | n.a. | 3.89% | 11/30/11 | 1.23% | 1.15% | 2 | 1.19% | 1 | 1.15% | 2 | ||||||||||||||||||||||||

Asia Credit Opportunities Fund (MCRDX) | -2.88% | n.a. | n.a. | 3.50% | 4/29/16 | 1.44% | 1.15% | 2 | 1.76% | 1 | 1.15% | 2 | ||||||||||||||||||||||||

ASIA GROWTH AND INCOME STRATEGIES |

| |||||||||||||||||||||||||||||||||||

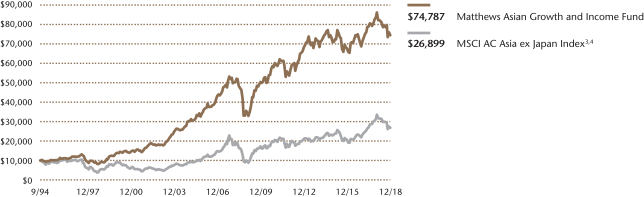

Asian Growth and Income Fund (MACSX) | -10.96% | 0.85% | 7.65% | 8.63% | 9/12/94 | 1.08% | 1.08% | 1.07% | 1.07% | |||||||||||||||||||||||||||

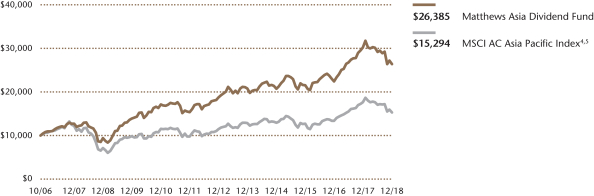

Asia Dividend Fund (MAPIX) | -12.72% | 4.85% | 10.84% | 8.30% | 10/31/06 | 1.02% | 1.01% | 3 | 1.03% | 1.02% | 3 | |||||||||||||||||||||||||

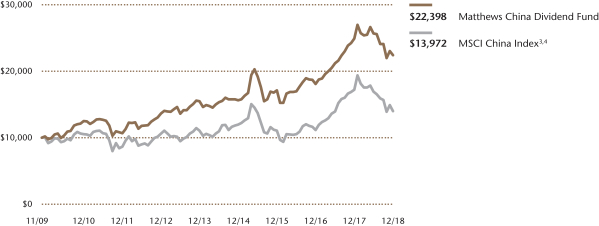

China Dividend Fund (MCDFX) | -9.98% | 7.70% | n.a. | 9.28% | 11/30/09 | 1.15% | 1.15% | 1.19% | 1.19% | |||||||||||||||||||||||||||

ASIA VALUE STRATEGY | ||||||||||||||||||||||||||||||||||||

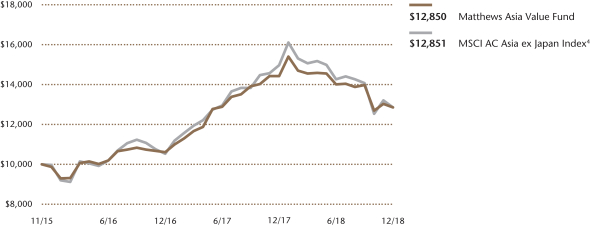

Asia Value Fund (MAVRX) | -10.93% | n.a. | n.a. | 8.47% | 11/30/15 | 1.77% | 1.50% | 4 | 2.32% | 1.50% | 4 | |||||||||||||||||||||||||

ASIA GROWTH STRATEGIES | ||||||||||||||||||||||||||||||||||||

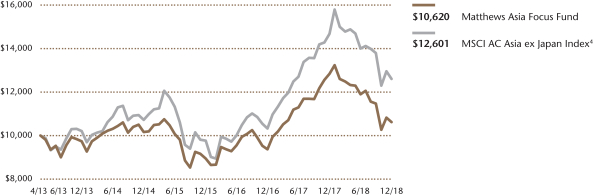

Asia Focus Fund (MAFSX) | -17.24% | 1.75% | n.a. | 1.07% | 4/30/13 | 3.18% | 1.50% | 4 | 2.45% | 1.50% | 4 | |||||||||||||||||||||||||

Asia Growth Fund (MPACX) | -16.25% | 3.62% | 10.39% | 8.22% | 10/31/03 | 1.10% | 1.10% | 1.12% | 1.12% | |||||||||||||||||||||||||||

Pacific Tiger Fund (MAPTX) | -11.11% | 6.50% | 12.56% | 8.39% | 9/12/94 | 1.07% | 1.04% | 3 | 1.08% | 1.06% | 3 | |||||||||||||||||||||||||

Asia ESG Fund (MASGX) | -9.73% | n.a. | n.a. | 2.73% | 4/30/15 | 2.20% | 1.50% | 4 | 2.65% | 1.50% | 4 | |||||||||||||||||||||||||

Emerging Asia Fund (MEASX) | -17.58% | 5.89% | n.a. | 5.06% | 4/30/13 | 1.66% | 1.48% | 4 | 1.70% | 1.48% | 4 | |||||||||||||||||||||||||

Asia Innovators Fund (MATFX) | -18.62% | 5.24% | 13.27% | 2.93% | 12/27/99 | 1.19% | 1.19% | 1.24% | 1.24% | |||||||||||||||||||||||||||

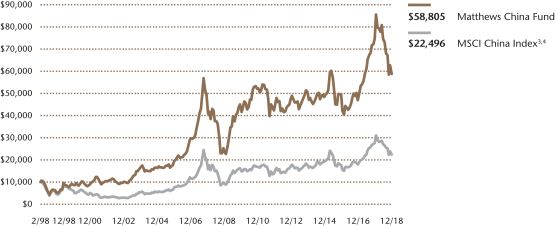

China Fund (MCHFX) | -21.42% | 3.06% | 8.81% | 8.86% | 2/19/98 | 1.10% | 1.10% | 1.09% | 1.09% | |||||||||||||||||||||||||||

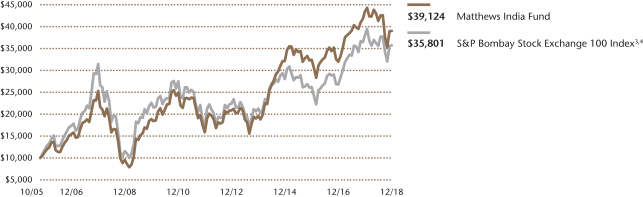

India Fund (MINDX) | -10.09% | 14.78% | 15.14% | 10.92% | 10/31/05 | 1.09% | 1.09% | 1.09% | 1.09% | |||||||||||||||||||||||||||

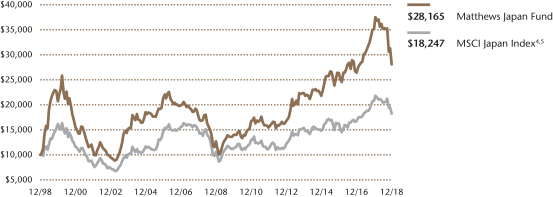

Japan Fund (MJFOX) | -20.18% | 4.66% | 8.27% | 5.31% | 12/31/98 | 0.91% | 0.91% | 3 | 0.95% | 0.94% | 3 | |||||||||||||||||||||||||

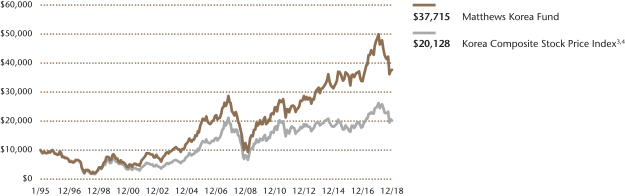

Korea Fund (MAKOX) | -22.21% | 3.67% | 11.75% | 5.69% | 1/3/95 | 1.14% | 1.14% | 1.15% | 1.15% | |||||||||||||||||||||||||||

ASIA SMALL COMPANY STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Small Companies Fund (MSMLX) | -18.05% | 1.25% | 12.01% | 9.12% | 9/15/08 | 1.51% | 1.46% | 4 | 1.49% | 1.46% | 4 | |||||||||||||||||||||||||

China Small Companies Fund (MCSMX) | -17.68% | 4.47% | n.a. | 2.98% | 5/31/11 | 1.97% | 1.50% | 4 | 2.34% | 1.50% | 4 | |||||||||||||||||||||||||

| * | Before fee waivers and expense reimbursement. |

| ** | Expense ratio represents the actual expense ratio a shareholder would have paid if they had been invested the entire year. |

| † | Annualized performance for periods of at least one year, otherwise cumulative. |

| ‡ | These figures are from the Funds’ prospectus dated as of April 30, 2018, and may differ from the actual expense ratios for fiscal year 2018, as shown in the financial highlights section of this report. |

| 1 | Effective October 1, 2018. |

| 2 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of the (i) expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2019 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 3 | Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund’s average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2019 and may be terminated (i) at any time by the Board of Trustees upon 60 days’ prior written notice to Matthews; or (ii) by Matthews at the annual expiration date of the agreement upon 60 days’ prior written notice to the Trust, in each case without payment of any penalty. |

| 4 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.25% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 1.25% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 1.25%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2019 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 1 | MATTHEWS ASIA FUNDS |

Table of Contents

Institutional Class Performance and Expenses(December 31, 2018)

|

| Average Annual Total Return† | Inception Date | 2018 Annual Operating Expenses* | 2018 Annual Operating Expenses after Fee Waiver and Expense Reimbursement** | Prospectus Annual Operating Expense Ratios‡ | Prospectus Annual Operating Expense Ratios after Fee Waiver and Expense Reimbursement‡ | ||||||||||||||||||||||||||||||

| Institutional Class | 1 year | 5 years | 10 years | Since Inception | ||||||||||||||||||||||||||||||||

ASIA FIXED INCOME STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Strategic Income Fund (MINCX) | -3.78% | 3.32% | n.a. | 4.11% | 11/30/11 | 1.04% | 0.90% | 2 | 0.98% | 1 | 0.90% | 2 | ||||||||||||||||||||||||

Asia Credit Opportunities Fund (MICPX) | -2.75% | n.a. | n.a. | 3.71% | 4/29/16 | 1.25% | 0.90% | 2 | 1.52% | 1 | 0.90% | 2 | ||||||||||||||||||||||||

ASIA GROWTH AND INCOME STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asian Growth and Income Fund (MICSX) | -10.84% | 0.99% | n.a. | 3.13% | 10/29/10 | 0.93% | 0.93% | 0.93% | 0.93% | |||||||||||||||||||||||||||

Asia Dividend Fund (MIPIX) | -12.64% | 4.97% | n.a. | 5.94% | 10/29/10 | 0.91% | 0.90% | 3 | 0.92% | 0.91% | 3 | |||||||||||||||||||||||||

China Dividend Fund (MICDX) | -9.83% | 7.87% | n.a. | 8.12% | 10/29/10 | 1.01% | 1.01% | 1.04% | 1.04% | |||||||||||||||||||||||||||

ASIA VALUE STRATEGY | ||||||||||||||||||||||||||||||||||||

Asia Value Fund (MAVAX) | -10.65% | n.a. | n.a. | 8.75% | 11/30/15 | 1.54% | 1.25% | 4 | 2.08% | 1.25% | 4 | |||||||||||||||||||||||||

ASIA GROWTH STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Focus Fund (MIFSX) | -17.04% | 2.00% | n.a. | 1.31% | 4/30/13 | 2.98% | 1.25% | 4 | 2.27% | 1.25% | 4 | |||||||||||||||||||||||||

Asia Growth Fund (MIAPX) | -16.10% | 3.82% | n.a. | 5.30% | 10/29/10 | 0.93% | 0.93% | 0.93% | 0.93% | |||||||||||||||||||||||||||

Pacific Tiger Fund (MIPTX) | -10.94% | 6.70% | n.a. | 5.54% | 10/29/10 | 0.90% | 0.88% | 3 | 0.91% | 0.89% | 3 | |||||||||||||||||||||||||

Asia ESG Fund (MISFX) | -9.52% | n.a. | n.a. | 2.98% | 4/30/15 | 2.01% | 1.25% | 4 | 2.46% | 1.25% | 4 | |||||||||||||||||||||||||

Emerging Asia Fund (MIASX) | -17.41% | 6.15% | n.a. | 5.30% | 4/30/13 | 1.50% | 1.25% | 4 | 1.52% | 1.25% | 4 | |||||||||||||||||||||||||

Asia Innovators Fund (MITEX) | -18.40% | 5.46% | n.a. | 9.01% | 4/30/13 | 1.02% | 1.02% | 1.05% | 1.05% | |||||||||||||||||||||||||||

China Fund (MICFX) | -21.32% | 3.21% | n.a. | 1.43% | 10/29/10 | 0.91% | 0.91% | 0.93% | 0.93% | |||||||||||||||||||||||||||

India Fund (MIDNX) | -9.92% | 14.98% | n.a. | 5.57% | 10/29/10 | 0.90% | 0.90% | 0.89% | 0.89% | |||||||||||||||||||||||||||

Japan Fund (MIJFX) | -20.08% | 4.77% | n.a. | 8.08% | 10/29/10 | 0.85% | 0.84% | 3 | 0.87% | 0.86% | 3 | |||||||||||||||||||||||||

Korea Fund (MIKOX) | -22.15% | 3.83% | n.a. | 6.54% | 10/29/10 | 1.02% | 1.02% | 1.01% | 1.01% | |||||||||||||||||||||||||||

ASIA SMALL COMPANY STRATEGIES | ||||||||||||||||||||||||||||||||||||

Asia Small Companies Fund (MISMX) | -17.86% | 1.47% | n.a. | 1.32% | 4/30/13 | 1.37% | 1.25% | 4 | 1.35% | 1.25% | 4 | |||||||||||||||||||||||||

China Small Companies Fund (MICHX) | -17.48% | 4.53% | n.a. | 3.01% | 11/30/17 | 1.79% | 1.25% | 4 | 2.09% | 1.25% | 4 | |||||||||||||||||||||||||

| * | Before fee waivers and expense reimbursement. |

| ** | Expense ratio represents the actual expense ratio a shareholder would have paid if they had been invested the entire year. |

| † | Annualized performance for periods of at least one year, otherwise cumulative. |

| ‡ | These figures are from the Funds’ prospectus dated as of April 30, 2018, and may differ from the actual expense ratios for fiscal year 2018, as shown in the financial highlights section of this report. |

| 1 | Effective October 1, 2018. |

| 2 | Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2019 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 3 | Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund’s average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2019 and may be terminated (i) at any time by the Board of Trustees upon 60 days’ prior written notice to Matthews; or (ii) by Matthews at the annual expiration date of the agreement upon 60 days’ prior written notice to the Trust, in each case without payment of any penalty. |

| 4 | Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.25%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2019 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

Past Performance: All performance quoted in this report is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the returns quoted. If certain of the Funds’ fees and expenses had not been waived, returns would have been lower. For the Funds’ most recent month-end performance, please call 800.789.ASIA (2742) or visit matthewsasia.com.

| matthewsasia.com | 800.789.ASIA | 2 |

Table of Contents

Table of Contents

Cover photo: Chinese New Year lantern and gold coin decorations along the Hong Kong harbor.

This report has been prepared for Matthews International Funds (d/b/a Matthews Asia Funds) shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Matthews Asia Funds prospectus, which contains more complete information about the Funds’ investment objectives, risks and expenses. Additional copies of the prospectus or summary prospectus may be obtained at matthewsasia.com. Please read the prospectus carefully before you invest or send money.

The views and opinions in this report were current as of December 31, 2018. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Fund’s future investment intent. Current and future portfolio holdings are subject to risk.

Statements of fact are from sources considered reliable, but neither the Funds nor the Investment Advisor makes any representation or guarantee as to their completeness or accuracy.

Investment Risk: Mutual fund shares are not deposits or obligations of, or guaranteed by, any depositary institution. Shares are not insured by the FDIC, Federal Reserve Board or any government agency and are subject to investment risks, including possible loss of principal amount invested. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Fixed income investments are subject to additional risks, including, but not limited to, interest rate, credit and inflation risks. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of a concentration in a specific industry, sector or geographic location. Investing in small and mid-size companies is more risky than investing in large companies as they may be more volatile and less liquid than larger companies. Please see the Funds’ Prospectuses and Statement of Additional Information for more risk disclosure.

Table of Contents

Message to Shareholders from the

President of the Matthews Asia Funds

Dear Valued Shareholder,

Asia’s markets endured a challenging year in 2018. Investor sentiment was negatively affected by macro headwinds including U.S.–China trade tensions, a string of interest rate increases by the U.S. Federal Reserve, as well as the end of global quantitative easing policies by central banks (as discussed in the year-end shareholder letter from our chief investment officer). Against this backdrop of generally weak markets across Asia in 2018—which appears to have been driven largely by a short-term shift in sentiment, rather than a deterioration of fundamentals—the performance across the Matthews Asia Funds was mixed overall. However, I am proud that many of our regional strategies outperformed their benchmarks amid this difficult environment.

At Matthews Asia, we have experienced this type of volatility and swings in sentiment in the past, and Asia’s markets are bound to face—and surmount—similar struggles in the future. Such turbulence is a byproduct of the significant changes taking place as the region continues its rapid pace of growth. The long-term investment case for Asia remains solid, particularly with the continued rise of its emerging and frontier economies, and the ongoing reform and liberalization of China’s economy. We firmly believe that patience, resilience and focus will help us to deliver the most favorable results for our valued and growing shareholder base.

China as an Investment

Over the past few years, China has been making significant efforts to further open its capital markets, including its domestic A-share market. In recognition of this, index provider MSCI over the past year began including China’s select domestic A-shares into its Emerging Markets Index. We believe China’s A-share market has simply been too big to be overlooked by global investors—and indeed our Funds have been accessing A-share listed companies via the Qualified Foreign Institutional Investor program and more recently through the “Stock Connect” programs, which link the Shanghai and Shenzhen Stock Exchanges to the Hong Kong Stock Exchange. But we are increasingly seeing investors paying more attention to China as a dedicated investment in their portfolios.

We believe our role is to help them understand the risk and opportunities and how best to access them. Our view is that identifying quality companies as part of an active strategy remains an essential part of investing in the country. A theme we are seeing not only in China but across Asia is that a more innovation-led economy can lead to new investment opportunities. Yes, China’s market can be volatile as it remains a developing market, but we believe this is all the more reason to take an active approach rather than passively following market indices.

2019 and Beyond

Despite the volatility of the past year, we continue to be optimistic about the prospects for Asia securities. We are hopeful that the U.S.–China trade talks will bring a positive outcome and that there will be a marked improvement in relations between the two nations in the coming year. Chinese business sentiment is improving and the markets have reflected that in early 2019. The attention paid to trade issues may fade as the year progresses and other important events such as elections in India come into focus.

As the global investment management industry continues to evolve, we remain prepared to not only keep pace but to lead the way through innovation—continuously evaluating client needs, industry issues and the competitive landscape while enhancing our investment capabilities. Active managers must deliver superior investment performance and this will remain our primary focus in the coming year and well beyond. Matthews Asia continues to offer a singular and distinctive approach to investing in Asia. The region represents the world’s growth engine, and arguably the single most important part of the world when it comes to future growth and investment opportunities. There may be some near-term market uncertainty on the horizon in the coming year, but along with that comes opportunities for active investors. Our investment team will continue to do its utmost in identifying well-managed, sustainable businesses, trading at reasonable valuations, on behalf of our clients. Thank you for being a valued shareholder.

William J. Hackett

President of Matthews Asia Funds

| 4 | MATTHEWS ASIA FUNDS |

Table of Contents

Message to Shareholders from the Investment Advisor

Dear Valued Investors,

2018 was a bad year for Asia’s stock markets, but Asia’s markets are not the same as their economies, which for the most part remained unscathed. Not just unscathed but in fact remarkably resilient given the tightening monetary policy in the U.S. and China and the fractious political relationship between the two countries over trade. And although it is true that we are investing in the markets, not the economies, having a stable economic background is important as it underpins both Asia’s currencies and the profits of the firms whose bonds and equities we hold.

So, why have the markets been so weak? Well, as I have mentioned, tighter money has been a big part of this. The tight money in the U.S. may well continue and there is an increasing risk that the U.S. Federal Reserve may tighten too far. Its job is complicated by low unemployment levels and corporate profits that are likely to struggle to maintain the growth rates of recent years. That is a headwind for all markets but it is surely going to have its biggest impact in the U.S. (Indeed, as I write this, Asia’s markets have fallen just 6% in December as the Nasdaq has tumbled 14%.) Currencies such as Indonesia’s rupiah seem to have stabilized. The Asian markets seem further along through this market downturn—and they are already showing good value for patient investors. Indeed, the dividend yield on a broad universe of Asia equities is higher than it has been for 90% of the past 15 years.

So, why is Asia further through this downturn and why does it seem so reasonably priced? Because the main reason for Asia’s weakness was probably not the Fed, but the People’s Bank of China. Tighter money in China has depressed nominal demand and also had a knock-on effect to other countries in the region, from Vietnam to Japan to Australia. Tighter money in China has not been a deliberate policy choice, but rather a side effect of trying to make the debt issues in local government finance vehicles both more transparent and easier to resolve. This is an important step for China and the fact that the government decided to tackle it while the global economy was still strong will likely be seen as wise in hindsight. The global economy may not be as strong in 2019, and the Chinese have taken the opportunity to deal with the issue while they could.

So, my best guess is that 2019 will be a year of moderate stimulus for the Asian region. I do not anticipate that China will try to loosen aggressively, not while the U.S. may still be tightening. But having dealt with the lion’s share of the local government debt issue, it need no longer face the unintended consequences of that policy. Core inflation is likely to rise somewhat on the back of better monetary policy and that is likely to be good for profits.

Profit growth has certainly been disappointing in Asia over the last few years—slower than Europe, Latin America, and the U.S. (although Japan has done well). Why is this? Well, a Western-centric view of the world would likely put it down to superior standards of governance and regulation—that somehow Western economic systems just work better than the ones in Asia. There is some truth to this. But the West is not as superior as it may think. For how superior can a system be that has allowed profits to grow so quickly on the back of squeezing wages and pumping up profits with one last, one-sided tax bill as we recently saw in the U.S.? Asia underwent a similar cycle in the 2000s but attitudes have changed since the global financial crisis of 2008. The first decade of the century was about “growth” and growth at almost any price—be it the environment or social cohesion. But then the Chinese emphasized not growth but “stability” as they sought to redistribute the gains from economic growth to labor and beyond their own borders to people in the rest of Asia. And now, they emphasize “quality” of economic growth in order to share the growth equally between capital and labor and to achieve better standards of life, including environmental, social, and governance. The West, therefore, is not entirely superior to Asia in many of these respects. And it does seem to be the case that the leadership in the world may be pivoting from West to East.

How to take account of this in our investments and in our portfolios? First is to maintain our focus on domestic demand. This is not just about consumer stocks but all aspects of domestic demand—health care, capital goods and finance. And that will increasingly mean taking advantage of the profitable opportunities offered by the demands of citizens for “quality.” Now is certainly not the time to get pessimistic about Asia’s long-term prospects. That may seem the sensible thing to do and there are many trading the Asian equity and fixed income markets who, having shorter time horizons than we try to maintain, are focused on the potentially difficult weeks and months ahead. But, no, the opportunities that Asia offers are too varied and enticing in the long term and can be bought at relatively inexpensive prices, such that now is the time for portfolios to maintain their focus on growth—growth of the leading entrepreneurs and businesses in industries that we believe will prosper in Asia over the next few decades.

That remains our task as researchers and investors in the region and it is one that we tackle with great passion. We are, as always, privileged to be your Asia investment advisor.

Robert Horrocks, PhD

Chief Investment Officer

Matthews International Capital Management, LLC

| matthewsasia.com | 800.789.ASIA | 5 |

Table of Contents

| PORTFOLIO MANAGERS | ||||

| Teresa Kong, CFA | ||||

Lead Manager | ||||

| Satya Patel | Wei Zhang | |||

Co-Manager | Co-Manager | |||

| FUND FACTS | ||||

| Investor | Institutional | |||

Ticker | MAINX | MINCX | ||

CUSIP | 577125503 | 577125602 | ||

Inception | 11/30/11 | 11/30/11 | ||

NAV | $10.25 | $10.25 | ||

Initial Investment | $2,500 | $100,000 | ||

Gross Expense Ratio1 | 1.23% | 1.04% | ||

After Fee Waiver and Reimbursement2 | 1.15% | 0.90% | ||

Portfolio Statistics | ||||

Total # of Positions | 35 | |||

Net Assets | $100.7 million | |||

Modified Duration3 | 3.09 | |||

Portfolio Turnover4 | 82.32% | |||

Benchmark | ||||

Markit iBoxx Asian Local Bond Index* | ||||

OBJECTIVE

Total return over the long term with an emphasis on income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its net assets, which include borrowings for investment purposes, in income-producing securities including, but not limited to, dividend paying equity securities, and debt and debt-related instruments issued by governments, quasi-governmental entities, supra-national institutions, and companies in Asia. Asia consists of all countries and markets in Asia, such as China and India, and includes developed, emerging, and frontier countries and markets in the Asian region. Investments may be denominated in any currency, and may represent any part of a company’s capital structure from debt to equity or with features of both.

Matthews Asia Strategic Income Fund

Portfolio Manager Commentary (unaudited)

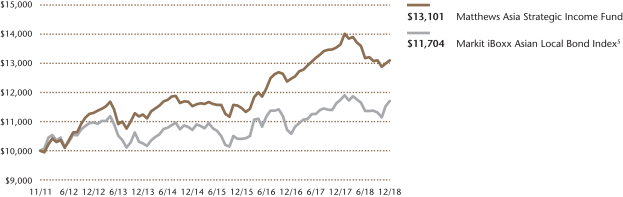

For the year ending December 31, 2018, the Matthews Asia Strategic Income Fund returned –4.05% (Investor Class) and –3.78% (Institutional Class) while its benchmark, the Markit iBoxx Asian Local Bond Index, returned –0.44%. For the fourth quarter, the Fund was flat at 0.0% (Investor and Institutional Classes) versus 3.51% for the Index.

Market Environment:

Asia’s fixed income markets faced challenges in 2018. Starting in the second quarter, volatility was persistent across Asian credit, currencies and interest rates. This was driven by factors such as trade, stress in emerging markets, policy normalization from the U.S. Federal Reserve and an environment that transitioned from synchronized global growth to one in which U.S. growth remained robust while other regions slowed.

The yield on the 10-year U.S. Treasury peaked in early November at 3.24%, up 83 basis points (0.83%) in the year. Late in 2018, as the threat of a disruptive trade war waned and commentary from the Fed became more dovish, U.S. rates moved lower. The shift led to a supportive environment for Asia’s currencies, which outperformed the U.S. dollar into year end.

As we move into 2019, some big risks facing Asian economies have begun to fade. In the second half of 2018, consensus views of the U.S.–China trade dispute shifted toward an escalated and protracted conflict encompassing trade, investment, technology transfer and national security. A turning point was the G-20 meetings in Buenos Aires in November as market volatility motivated both sides to talk. This paradigm shift was reflected in currency markets across the region, which depreciated versus the dollar in the first 10 months of the year, before rebounding as trade tensions dissipated. For instance, in the first 10 months of the year, high beta currencies such as the Indian rupee (–13.6%) and the Indonesian rupiah (–10.8%) depreciated significantly against the U.S. dollar. As trade tensions dissipated late in the year, both the rupee and the rupiah rebounded, with the rupee gaining 6.0% and the rupiah gaining 5.7%.

Returns in Asia credit were negative for the first time in five years, with spreads across investment grade and high yield issuers widening on the year amid the challenging macro environment. In general, performance was a function of credit quality, with issuers from the more highly rated economies of South Korea and Taiwan outperforming while issuers from Sri Lanka and Indonesia underperformed.

Stress in emerging market countries, such as Argentina and Turkey, also weighed on investor sentiment. While market sell-offs in Argentina and Turkey did not directly spread to Asia, high beta markets such as India and Indonesia, nevertheless, struggled in the third quarter. We believe this is unlikely to be repeated in 2019.

Performance Contributors and Detractors:

For the full year, among the biggest contributors to portfolio returns were bonds denominated in Thai baht, Malaysian ringgit and Chinese renminbi (RMB). Our Thai baht performance was driven by the convertible bonds of Bangkok Dusit Medical Services, a Thai hospital company, which performed well on the strength of the underlying equity. Our Malaysian ringgit bonds were driven by government bonds,

(continued)

| * | The Index performance reflects the returns of the discontinued predecessor HSBC Asian Local Bond Index up to December 31, 2012 and the returns of the successor Markit iBoxx Asian Local Bond Index thereafter. |

| 1 | Actual 2018 expense ratios. |

| 2 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2019 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 3 | Modified duration measures the percent change in value of the fixed income portion of the portfolio in response to a 1% change in interest rates. In a multi-currency denominated portfolio with sensitivities to different interest rate regimes, modified duration will not accurately reflect the change in value of the overall portfolio from a change in any one interest rate regime. |

| 4 | The lesser of fiscal year 2018 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| 6 | MATTHEWS ASIA FUNDS |

Table of Contents

| PERFORMANCE AS OF DECEMBER 31, 2018 | ||||||||||||||||||||||||

|

|

| Average Annual Total Returns

|

| |||||||||||||||||||||

| 3 Months | 1 Year | 3 Years | 5 Years | Since Inception | Inception Date | |||||||||||||||||||

| Investor Class (MAINX) | 0.00% | -4.05% | 4.54% | 3.10% | 3.89% | 11/30/11 | ||||||||||||||||||

| Institutional Class (MINCX) | 0.00% | -3.78% | 4.78% | 3.32% | 4.11% | 11/30/11 | ||||||||||||||||||

| Markit iBoxx Asian Local Bond Index5 | 3.51% | -0.44% | 3.99% | 2.67% | 2.25% | |||||||||||||||||||

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund’s fees and expenses had not been waived. For the Fund’s most recent month-end performance visit matthewsasia.com.

| INCOME DISTRIBUTION HISTORY | ||||||||||||||||||||||||||||||||||||||||||||

| 2018

| 2017

| |||||||||||||||||||||||||||||||||||||||||||

| Q1 | Q2 | Q3 | Q4 | Total | Q1 | Q2 | Q3 | Q4 | Total | |||||||||||||||||||||||||||||||||||

| Investor (MAINX) | $ | 0.12 | $ | 0.10 | $ | 0.07 | $ | 0.00 | $ | 0.29 | $ | 0.07 | $ | 0.08 | $ | 0.13 | $ | 0.14 | $ | 0.42 | ||||||||||||||||||||||||

| Inst’l (MINCX) | $ | 0.13 | $ | 0.11 | $ | 0.08 | $ | 0.00 | $ | 0.31 | $ | 0.08 | $ | 0.08 | $ | 0.14 | $ | 0.15 | $ | 0.45 | ||||||||||||||||||||||||

Note: This table does not include capital gains distributions. Totals may differ by $0.02 due to rounding. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

Investor Class: 5.29% (5.19% excluding waivers) Institutional Class: 5.54% (5.32% excluding waivers)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 12/31/18, expressed as an annual percentage rate based on the Fund’s share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund’s rate of investment income, and it may not equal the Fund’s actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc. | YIELD TO WORST: 7.46%

Yield to worst is the lowest yield that can be received on a bond assuming that the issuer does not default. It is calculated by utilizing the worst case assumptions for a bond with respect to certain income-reducing factors, including prepayment, call or sinking fund provisions. It does not represent the yield that an investor should expect to receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems | |||

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

| 5 | It is not possible to invest directly in an index. Source: Index data from HSBC, Markit iBoxx and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 91 for index definitions. The Index performance reflects the returns of the discontinued predecessor HSBC Asian Local Bond Index up to December 31, 2012 and the returns of the successor Markit iBoxx Asian Local Bond Index thereafter. |

| TOP TEN HOLDINGS | ||||||||

| Sector | Currency | % of Net Assets | ||||||

| Ctrip.com International, Ltd., Cnv., 1.250%, 09/15/2022 | Consumer Discretionary | U.S. Dollar | 5.3% | |||||

| Debt and Asset Trading Corp., 1.000%, 10/10/2025 | Financials | U.S. Dollar | 4.8% | |||||

| Wanda Properties International Co., Ltd., 7.250%, 01/29/2024 | Real Estate | U.S. Dollar | 4.7% | |||||

| Zhongsheng Group Holdings, Ltd., Cnv., 0.000%, 05/23/2023 | Consumer Discretionary | Hong Kong Dollar | 4.4% | |||||

| Standard Chartered PLC, 6.500%, 12/29/2049 | Financials | U.S. Dollar | 4.2% | |||||

| SoftBank Group Corp., 6.000%, 07/19/2049 | Communication Services | U.S. Dollar | 4.0% | |||||

| KWG Group Holdings, Ltd., 6.000%, 09/15/2022 | Real Estate | U.S. Dollar | 4.0% | |||||

| Chinalco Capital Holdings, Ltd., 4.000%, 08/25/2021 | Materials | U.S. Dollar | 3.9% | |||||

| Indonesia Government Bond, 8.250%, 05/15/2029 | Foreign Government Bonds | Indonesian Rupiah | 3.8% | |||||

| ICTSI Treasury BV, 4.625%, 01/16/2023 | Industrials | U.S. Dollar | 3.4% | |||||

| % OF ASSETS IN TOP TEN | 42.5% | |||||||

| matthewsasia.com | 800.789.ASIA | 7 |

Table of Contents

| CURRENCY ALLOCATION (%)6,7 | ||||

| US Dollar | 73.6 | |||

| Indonesian Rupiah | 6.4 | |||

| Indian Rupee | 5.7 | |||

| Hong Kong Dollar | 4.4 | |||

| Vietnam Dong | 1.9 | |||

| China Renminbi | 1.0 | |||

| Philippine Peso | 0.7 | |||

| South Korean Won | 0.4 | |||

| Cash and Other Assets, Less Liabilities | 5.9 | |||

| COUNTRY ALLOCATION (%)6,7,8 | ||||

| China/Hong Kong | 44.3 | |||

| Indonesia | 13.6 | |||

| India | 7.6 | |||

| Vietnam | 6.6 | |||

| Thailand | 6.3 | |||

| Philippines | 4.2 | |||

| Japan | 4.0 | |||

| Singapore | 3.4 | |||

| Sri Lanka | 1.9 | |||

| United States | 1.8 | |||

| South Korea | 0.4 | |||

| Cash and Other Assets, Less Liabilities | 5.9 | |||

| SECTOR ALLOCATION (%)6,7 | ||||

| Financials | 22.4 | |||

| Real Estate | 16.3 | |||

| Consumer Discretionary | 12.6 | |||

| Foreign Government Bonds | 9.4 | |||

| Materials | 8.5 | |||

| Consumer Staples | 7.8 | |||

| Communication Services | 7.7 | |||

| Industrials | 5.6 | |||

| Utilities | 3.8 | |||

| Cash and Other Assets, Less Liabilities | 5.9 | |||

Please note: Foreign Government Bonds category includes Supranationals.

| ASSET TYPE BREAKDOWN (%)6,7 | ||||

| Non-Convertible Corporate Bonds | 63.8 | |||

| Government Bonds | 14.1 | |||

| Convertible Corporate Bonds | 16.2 | |||

| Cash and Other Assets, Less Liabilities | 5.9 | |||

| 6 | Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent, so the values may not sum to 100% due to rounding. Percentage values may be derived from different data sources and may not be consistent with other Fund literature. |

| 7 | Cash and other assets may include forward currency exchange contracts and certain derivative instruments that have been marked-to-market. |

| 8 | Not all countries where the Fund may invest are included in the benchmark index. |

Matthews Asia Strategic Income Fund

Portfolio Manager Commentary (unaudited) (continued)

which provided attractive carry with minimal impact from currency depreciation. Our gains in Chinese RMB-denominated bonds were driven by a combination of RMB-denominated convertible bonds of China Railway Construction, and our allocation for much of the year to the high-quality onshore bonds of Chinese issuers.

Among the largest detractors to Fund performance in 2018 were our holdings in U.S. dollar-denominated credits, as well as Indian rupee (INR)- and Indonesian rupiah (IDR)-denominated bonds. Asian credit spreads widened throughout the year, with issuers across the region coming under pressure. The Fund’s holdings in companies such as Lippo Karawaci and Modernland in Indonesia, and Ctrip and Tsinghua Unigroup in China, detracted from performance. Our holdings in INR-denominated corporate bonds and IDR-denominated government bonds also performed poorly on a combination of currency depreciation and rising local interest rates.

Notable Portfolio Changes:

In the fourth quarter, we made a number of portfolio changes aimed at increasing our allocation to local currencies. We increased our currency exposure to countries across the region, including South Korea, Singapore, Thailand and Indonesia. South Korea, Singapore and Thailand are low-yielding countries, with interest rates lower than those in many developed countries. With little short-term upside to rates, we increased our exposure through currency forwards. In Indonesia, interest rates were significantly higher in 2018 as the central bank raised rates to defend the currency, and foreigners sold bonds and exited the market. We see room for interest rates to fall in Indonesia, and chose to add duration as well as currency exposure in the country.

In the fourth quarter, we exited a handful of positions as we reshaped the portfolio. We sold the U.S. dollar-denominated high yield bonds of Lippo Karawaci, as well as the convertible bonds of Vipshop and China Overseas Land & Investment. We also significantly decreased our exposure to the RMB. We sold our holdings of onshore bonds issued by state-linked entities after rates and credit spreads came down. We also sold the dim sum bond of China Jinmao (Franshion Brilliant), a high-quality property developer.

Outlook:

After significant repricing in 2018, we see the elements for strong performance across Asian credit, currencies and interest rates.

Since the Fed hiked rates four times in 2018 and stayed the course on balance sheet reduction, we expect no more rate hikes by the Fed in 2019. This would give Asia’s policymakers the ability to slow their pace of rate hikes as well, and given that inflation remains low across the region, we see a broader drop in Asian interest rates.

Our outlook for Asian currencies is also positive. With U.S. growth still positive but decelerating and the Fed appearing to be on hold, we expect Asia’s currencies to outperform. The significant drop in oil prices in the fourth quarter of 2018 also helped shore up oil-importing countries across Asia, providing a boost to foreign exchange reserves, current accounts and fiscal balances.

Finally, Asia high yield spreads offer attractive values for the long-term investor. With 12-month trailing default rates at 1.03% and spreads hovering around 6% at the end of 2018, the market has priced in substantially higher expected future defaults than the current run rate. We believe the major risks to the region, including a further slowdown in global growth, any escalation in trade shocks or further outflows stemming from policy normalization in the U.S., are priced in at these levels. Furthermore, based on our solvency and liquidity analysis, we do not expect any of the securities in the portfolio to default. As such, the relatively attractive yields in Asia offer a strong base for positive returns.

In sum, we see value in U.S. dollar-denominated debt of corporations in Asia because the valuation can be grounded in intrinsic value. As long as we maintain a long-term investment horizon of greater than three years and experience no defaults, the total return potential for Asia credit offers a compelling investment opportunity at current levels.

| 8 | MATTHEWS ASIA FUNDS |

Table of Contents

Matthews Asia Strategic Income Fund

December 31, 2018

Schedule of Investmentsa

NON-CONVERTIBLE CORPORATE BONDS: 63.7%

| Face Amount* | Value | |||||||

| CHINA/HONG KONG: 30.9% | ||||||||

Wanda Properties International Co., Ltd. | 5,000,000 | $4,754,080 | ||||||

Standard Chartered PLC | 4,350,000 | 4,257,562 | ||||||

KWG Group Holdings, Ltd. | 4,500,000 | 4,009,091 | ||||||

Chinalco Capital Holdings, Ltd. | 4,100,000 | 3,941,285 | ||||||

CIFI Holdings Group Co., Ltd. | 3,200,000 | 3,129,936 | ||||||

Huaneng Hong Kong Capital, Ltd. | 3,300,000 | 2,975,937 | ||||||

West China Cement, Ltd. | 2,800,000 | 2,807,437 | ||||||

HSBC Holdings PLC | 2,500,000 | 2,400,000 | ||||||

China Minmetals Corp. | 2,000,000 | 1,806,592 | ||||||

Franshion Brilliant, Ltd. | CNY 7,000,000 | 1,015,352 | ||||||

|

| |||||||

Total China/Hong Kong | 31,097,272 | |||||||

|

| |||||||

| INDIA: 7.7% | ||||||||

Housing Development Finance Corp., SeriesU-5 |

| |||||||

9.000%, 11/29/28 | INR 200,000,000 | 2,894,347 | ||||||

LIC Housing Finance, Ltd., Series 372 | INR 200,000,000 | 2,860,385 | ||||||

Bharti Airtel, Ltd. | 2,138,000 | 1,944,992 | ||||||

|

| |||||||

Total India | 7,699,724 | |||||||

|

| |||||||

| INDONESIA: 7.2% | ||||||||

PB International BV | 3,000,000 | 2,899,704 | ||||||

Modernland Overseas Pte, Ltd. | 1,900,000 | 1,561,819 | ||||||

Alam Synergy Pte, Ltd. | 1,500,000 | 1,427,700 | ||||||

Listrindo Capital BV | 1,000,000 | 886,500 | ||||||

Alam Synergy Pte, Ltd. | 500,000 | 475,900 | ||||||

|

| |||||||

Total Indonesia | 7,251,623 | |||||||

|

| |||||||

| JAPAN: 4.0% | ||||||||

SoftBank Group Corp. | 4,850,000 | 4,023,075 | ||||||

|

| |||||||

Total Japan | 4,023,075 | |||||||

|

| |||||||

| PHILIPPINES: 3.4% | ||||||||

ICTSI Treasury BV | 3,500,000 | 3,449,600 | ||||||

|

| |||||||

Total Philippines | 3,449,600 | |||||||

|

| |||||||

| SINGAPORE: 3.4% | ||||||||

Olam International, Ltd. | 3,500,000 | 3,441,928 | ||||||

|

| |||||||

Total Singapore | 3,441,928 | |||||||

|

| |||||||

Face Amount* | Value | |||||||

| THAILAND: 3.4% | ||||||||

Krung Thai Bank Public Co., Ltd. | 3,400,000 | $3,429,005 | ||||||

|

| |||||||

Total Thailand | 3,429,005 | |||||||

|

| |||||||

| SRI LANKA: 1.9% | ||||||||

National Savings Bank | 2,000,000 | 1,950,820 | ||||||

|

| |||||||

Total Sri Lanka | 1,950,820 | |||||||

|

| |||||||

| UNITED STATES: 1.8% | ||||||||

Sprint Communications, Inc. | 1,863,000 | 1,828,218 | ||||||

|

| |||||||

Total United States | 1,828,218 | |||||||

|

| |||||||

| TOTALNON-CONVERTIBLE CORPORATE BONDS |

| 64,171,265 | ||||||

|

| |||||||

(Cost $65,448,802) | ||||||||

CONVERTIBLE CORPORATE BONDS: 16.2% |

| |||||||

| CHINA/HONG KONG: 13.4% | ||||||||

Ctrip.com International, Ltd., Cnv. | 5,500,000 | 5,317,928 | ||||||

Zhongsheng Group Holdings, Ltd., Cnv. | ||||||||

0.000%, 05/23/23b | HKD 38,000,000 | 4,463,885 | ||||||

Johnson Electric Holdings, Ltd., Cnv. | 2,000,000 | 2,154,550 | ||||||

China Mengniu Dairy Co., Ltd., Series 2319, Cnv. |

| |||||||

0.000%, 06/05/22b | 1,600,000 | 1,521,266 | ||||||

|

| |||||||

Total China/Hong Kong | 13,457,629 | |||||||

|

| |||||||

| THAILAND: 2.8% | ||||||||

CP Foods Holdings, Ltd., Cnv. | 2,800,000 | 2,876,524 | ||||||

|

| |||||||

Total Thailand | 2,876,524 | |||||||

|

| |||||||

| TOTAL CONVERTIBLE CORPORATE BONDS |

| 16,334,153 | ||||||

|

| |||||||

(Cost $17,090,154) | ||||||||

FOREIGN GOVERNMENT OBLIGATIONS: 14.2% |

| |||||||

| VIETNAM: 6.7% | ||||||||

Debt and Asset Trading Corp. | 6,969,000 | 4,791,187 | ||||||

Socialist Republic of Vietnam | VND 43,000,000,000 | 1,901,505 | ||||||

|

| |||||||

Total Vietnam | 6,692,692 | |||||||

|

| |||||||

| INDONESIA: 6.4% | ||||||||

Indonesia Government Bond | IDR 53,550,000,000 | 3,805,890 | ||||||

Indonesia Government Bond | IDR 38,000,000,000 | 2,638,883 | ||||||

|

| |||||||

Total Indonesia | 6,444,773 | |||||||

|

| |||||||

| matthewsasia.com | 800.789.ASIA | 9 |

Table of Contents

Matthews Asia Strategic Income Fund

December 31, 2018

Schedule of Investmentsa(continued)

FOREIGN GOVERNMENT OBLIGATIONS(continued)

Face Amount* | Value | |||||||

| PHILIPPINES: 0.7% | ||||||||

Republic of Philippines | PHP 40,000,000 | $745,779 | ||||||

|

| |||||||

Total Philippines | 745,779 | |||||||

|

| |||||||

| SOUTH KOREA: 0.4% | ||||||||

Korea Treasury Bond | KRW 400,000,000 | 385,606 | ||||||

|

| |||||||

Total South Korea | 385,606 | |||||||

|

| |||||||

| TOTAL FOREIGN GOVERNMENT OBLIGATIONS |

| 14,268,850 | ||||||

|

| |||||||

(Cost $14,640,649) | ||||||||

| TOTAL INVESTMENTS: 94.1% | 94,774,268 | |||||||

(Cost $97,179,605) | ||||||||

| CASH AND OTHER ASSETS, LESS LIABILITIES: 5.9% | 5,940,915 | |||||||

|

| |||||||

NET ASSETS: 100.0% | $100,715,183 | |||||||

|

| |||||||

| a | Certain securities were fair valued under the valuation policies approved by the Board of Trustees (Note2-A). |

| b | The securities may be resold to qualified foreign investors and foreign institutional buyers under Regulation S of the Securities Act of 1933. |

| c | Security is a fix-to-float security, which carries a fixed coupon until a certain date, upon which it switches to a floating rate. Reference rate and spread are provided if the rate is currently floating. |

| d | Perpetual security with no stated maturity date. First call date is disclosed. |

| e | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. The security may be resold in transactions exempt from registration normally to qualified institutional buyers. The security has been determined to be liquid in accordance with procedures adopted by the Funds’ Board of Trustees. At December 31, 2018, the aggregate value is $1,427,700, which is 1.42% of net assets. |

| * | All Values in USD unless otherwise specified |

| Cnv. | Convertible |

| CNY | Chinese Renminbi (Yuan) |

| HKD | Hong Kong Dollar |

| IDR | Indonesian Rupiah |

| INR | Indian Rupee |

| KRW | Korean Won |

| PHP | Philippine Peso |

| SGD | Singapore Dollar |

| THB | Thai Baht |

| USD | U.S. Dollar |

| VND | Vietnamese Dong |

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS

Currency | Currency Sold | Counterparty | Settlement Date | Unrealized Appreciation (Depreciation) | ||||||||||

CNY 25,000,000 | USD 3,586,029 | Merrill Lynch & Co., Inc. | 01/17/19 | $54,010 | ||||||||||

CNY 26,436,797 | USD 3,796,481 | Merrill Lynch & Co., Inc. | 01/17/19 | 52,758 | ||||||||||

IDR 105,630,000,000 | USD 7,000,000 | Merrill Lynch & Co., Inc. | 02/11/19 | 293,270 | ||||||||||

INR 545,084,000 | USD 7,400,000 | Merrill Lynch & Co., Inc. | 02/11/19 | 404,514 | ||||||||||

KRW 10,054,752,500 | USD 9,025,000 | Merrill Lynch & Co., Inc. | 03/04/19 | 23,343 | ||||||||||

SGD 9,387,888 | USD 6,865,000 | Merrill Lynch & Co., Inc. | 03/04/19 | 32,808 | ||||||||||

THB 148,114,575 | USD 4,515,000 | Merrill Lynch & Co., Inc. | 03/04/19 | 72,082 | ||||||||||

|

| |||||||||||||

| 932,785 | ||||||||||||||

|

| |||||||||||||

USD 7,393,000 | CNY 51,436,797 | Merrill Lynch & Co., Inc. | 01/17/19 | (96,278 | ) | |||||||||

USD 4,912,999 | IDR 72,000,000,000 | Merrill Lynch & Co., Inc. | 02/11/19 | (58,273 | ) | |||||||||

USD 6,215,567 | INR 440,000,000 | Merrill Lynch & Co., Inc. | 02/11/19 | (84,354 | ) | |||||||||

|

| |||||||||||||

| (238,905 | ) | |||||||||||||

|

| |||||||||||||

Net Unrealized Appreciation | $693,880 | |||||||||||||

|

| |||||||||||||

See accompanying notes to financial statements.

| 10 | MATTHEWS ASIA FUNDS |

Table of Contents

| PORTFOLIO MANAGERS | ||||

| Teresa Kong, CFA | Satya Patel | |||

Lead Manager | Lead Manager | |||

| FUND FACTS | ||||

| Investor | Institutional | |||

Ticker | MCRDX | MICPX | ||

CUSIP | 577130677 | 577130669 | ||

Inception | 4/29/16 | 4/29/16 | ||

NAV | $9.76 | $9.75 | ||

Initial Investment | $2,500 | $100,000 | ||

Gross Expense Ratio1 | 1.44% | 1.25% | ||

After Fee Waiver and Reimbursement2 | 1.15% | 0.90% | ||

Portfolio Statistics | ||||

Total # of Positions | 33 | |||

Net Assets | $39.8 million | |||

Modified Duration3 | 2.91 | |||

Portfolio Turnover4 | 49.06% | |||

Benchmark | ||||

J.P. Morgan Asia Credit Index | ||||

OBJECTIVE

Total return over the long term.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its net assets, which include borrowings for investment purposes, in debt and debt-related instruments issued by companies as well as governments, quasi-governmental entities, and supra-national institutions in Asia. Debt and debt-related instruments typically include bonds, debentures, bills, securitized instruments (which are vehicles backed by pools of assets such as loans or other receivables), notes, certificates of deposit and other bank obligations, bank loans, senior secured bank debt, convertible debt securities, exchangeable bonds, credit-linked notes, inflation-linked instruments, repurchase agreements, payment-in-kind securities and derivative instruments with fixed income characteristics. Asia consists of all countries and markets in Asia, such as China and Indonesia, in addition to the developed, emerging, and frontier countries and markets in the Asian region.

Matthews Asia Credit Opportunities Fund

Portfolio Manager Commentary (unaudited)

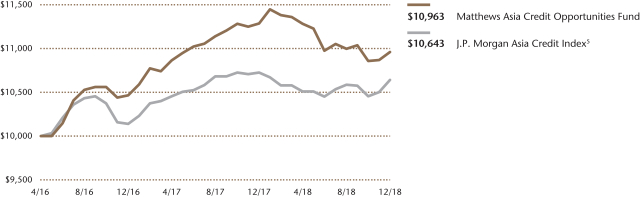

For the year ending December 31, 2018, the Matthews Asia Credit Opportunities Fund returned –2.88% (Investor Class) and –2.75% (Institutional Class), while its benchmark, the J.P. Morgan Asia Credit Index, returned –0.77% over the same period. For the fourth quarter, the Fund returned –0.68% (Investor Class) and –0.72% (Institutional Class), while its benchmark returned 0.65% over the same period.

Market Environment:

2018 was notable as the impact of strong growth in the U.S. and macroeconomic headwinds in China led to tighter financial conditions and wider credit spreads across Asia. The U.S. economy decoupled from the rest of the world as U.S. growth strengthened despite softness in other regions. The U.S. Federal Reserve raised interest rates four times and continued the balance sheet reduction it started in 2017. With a divergence in growth and tighter policy in the U.S., volatility in emerging market asset classes around the world was higher in 2018.

Asia’s credit markets were not immune to tighter financial conditions and higher volatility in 2018. High yield spreads in Asia widened 169 basis points (1.69%) in 2018 from 437 basis points (4.37%) to 606 basis points (6.06%) above U.S. Treasuries. Trade tensions between the U.S. and China, as well as the Chinese government’s deleveraging campaign, led to weaker sentiment. Amid this backdrop, the new issue market was noticeably quieter, with many high yield deals done with a one- to three-year maturity, rather than the more typical three to five years. The most challenged Asian markets included Indonesia, where weakness in the rupiah led to a repricing of U.S. dollar-denominated corporate bonds, and Sri Lanka, where political turmoil led to uncertainty.

Performance Contributors and Detractors:

In 2018, among the biggest contributors to portfolio returns were our holdings in the bonds of Bangkok Dusit Medical Services, Socialist Republic of Vietnam and Pan Brothers International (PB International). Bangkok Dusit Medical is a hospital operator in Thailand. With Bangkok Dusit Medical’s improving results and guidance, its convertible bonds performed well as the underlying equity rallied. We exited the holding in June as we reached our price target. Socialist Republic of Vietnam bonds are Brady bonds issued in 1998. With part of the principal secured by U.S. Treasuries and the ongoing amortization of principal, the bonds earn an attractive coupon with minimal price volatility. Pan Brothers International is a high-quality Indonesian garment manufacturer.

Among the largest detractors to Fund performance in 2018 were our holdings in Lippo Karawaci (Theta Capital Pte.), Modernland and Softbank. Lippo Karawaci and Modernland are property developers in Indonesia. Lippo Karawaci bonds were downgraded by ratings agencies based on the company’s limited liquidity without executing asset sales. Modernland bonds fell on weakness in the Indonesian rupiah and continued softness in Jakarta’s property market. Softbank bonds weakened as investor skepticism of its portfolio of high tech investments rose with the rising volatility of the Nasdaq.

(continued)

| 1 | Actual 2018 expense ratios. |

| 2 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2019 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 3 | Modified duration measures the percent change in value of the fixed income portion of the portfolio in response to a 1% change in interest rates. In a multi-currency denominated portfolio with sensitivities to different interest rate regimes, modified duration will not accurately reflect the change in value of the overall portfolio from a change in any one interest rate regime. |

| 4 | The lesser of fiscal year 2018 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| matthewsasia.com | 800.789.ASIA | 11 |

Table of Contents

| PERFORMANCE AS OF DECEMBER 31, 2018 | ||||||||||||||||

|

|

| Average Annual Total Returns

| ||||||||||||||

| 3 Months | 1 Year | Since Inception | Inception Date | |||||||||||||

| Investor Class (MCRDX) | -0.68% | -2.88% | 3.50% | 4/29/2016 | ||||||||||||

| Institutional Class (MICPX) | -0.72% | -2.75% | 3.71% | 4/29/2016 | ||||||||||||

| J.P. Morgan Asia Credit Index5 | 0.65% | -0.77% | 2.36% | |||||||||||||

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results.Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth moreor less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund’s fees and expenses had not been waived. For the Fund’s most recent month-endperformance, visit matthewsasia.com.

| INCOME DISTRIBUTION HISTORY | ||||||||||||||||||||||||||||||||||||||||||||

| 2018

| 2017

| |||||||||||||||||||||||||||||||||||||||||||

| Q1 | Q2 | Q3 | Q4 | Total | Q1 | Q2 | Q3 | Q4 | Total | |||||||||||||||||||||||||||||||||||

| Investor (MCRDX) | $ | 0.09 | $ | 0.09 | $ | 0.06 | $ | 0.10 | $ | 0.33 | $ | 0.12 | $ | 0.08 | $ | 0.14 | $ | 0.10 | $ | 0.43 | ||||||||||||||||||||||||

| Inst’l (MICPX) | $ | 0.09 | $ | 0.09 | $ | 0.06 | $ | 0.11 | $ | 0.36 | $ | 0.12 | $ | 0.08 | $ | 0.15 | $ | 0.10 | $ | 0.46 | ||||||||||||||||||||||||

Note: This table does not include capital gains distributions. Totals may differ by $0.02 due to rounding. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

Investor Class: 5.40% (4.70% excluding waivers) Institutional Class: 5.58% (4.94% excluding waivers)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 12/31/18, expressed as an annual percentage rate based on the Fund’s share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund’s rate of investment income, and it may not equal the Fund’s actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc. | YIELD TO WORST: 7.17%

Yield to worst is the lowest yield that can be received on a bond assuming that the issuer does not default. It is calculated by utilizing the worst case assumptions for a bond with respect to certain income-reducing factors, including prepayment, call or sinking fund provisions. It does not represent the yield that an investor should expect to receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems | |||

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions, or redemption of Fund shares. Values are in US$.

| 5 | It is not possible to invest directly in an index. Source: Index data from J.P. Morgan and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 91 for index definition. |

| TOP TEN HOLDINGS | ||||||||

| Sector | Currency | % of Net Assets | ||||||

| Zhongsheng Group Holdings, Ltd., Cnv., 0.000%, 05/23/2023 | Consumer Discretionary | Hong Kong Dollar | 5.0% | |||||

| Debt and Asset Trading Corp., 1.000%, 10/10/2025 | Financials | U.S. Dollar | 4.7% | |||||

| Standard Chartered PLC, 6.500%, 12/29/2049 | Financials | U.S. Dollar | 4.6% | |||||

| Ctrip.com International, Ltd., Cnv., 1.250%, 09/15/2022 | Consumer Discretionary | U.S. Dollar | 4.5% | |||||

| SoftBank Group Corp., 6.000%, 07/19/2049 | Communication Services | U.S. Dollar | 4.2% | |||||

| China Overseas Finance Investment Cayman V, Ltd., Cnv., 0.000%, 01/05/2023 | Real Estate | U.S. Dollar | 3.7% | |||||

| Chinalco Capital Holdings, Ltd., 4.000%, 08/25/2021 | Materials | U.S. Dollar | 3.7% | |||||

| Olam International, Ltd., 4.500%, 04/12/2021 | Consumer Staples | U.S. Dollar | 3.7% | |||||

| Wanda Properties International Co., Ltd., 7.250%, 01/29/2024 | Real Estate | U.S. Dollar | 3.7% | |||||

| West China Cement, Ltd., 6.500%, 09/11/2019 | Materials | U.S. Dollar | 3.6% | |||||

| % OF ASSETS IN TOP TEN | 41.4% | |||||||

| 12 | MATTHEWS ASIA FUNDS |

Table of Contents

Matthews Asia Credit Opportunities Fund

Portfolio Manager Commentary (unaudited) (continued)

Notable Portfolio Changes:

We made a number of changes to the portfolio in the fourth quarter, adding high quality credits across the region while exiting two credits in Indonesia and China. We added a handful of U.S. dollar-denominated bonds that we believe have attractive yields relative to the risk we are taking. For instance, we initiated a position in China Minmetals, a state-owned enterprise with minimal default risk and attractive upside from our expectation that the company will call the bonds at a higher price. We also added the bonds of Pan Brothers International. Its expertise in performance fabrics along with its strong financials and solid management team are an attractive combination. We also added the bonds of Bharti Airtel, an Indian telecom operator. The bonds are pricing in a downgrade from investment grade to high yield, but we believe many of Bharti’s challenges are behind it.

We sold the bonds of Lippo Karawaci and the convertible bonds of China Railway Construction. In 2018, Lippo Karawaci announced asset sales to help recapitalize its balance sheet, but we believe it will take several years for the company to complete its targeted divestments and normalize operations. We also exited the convertible bonds of China Railway Construction. As the underlying equity rallied, our bonds performed well and reached our price target.

Outlook:

In our view, Asian high yield bonds offer attractive value for the long-term investor. Asian high yield credit spreads are 150 basis points (1.5%) above their historic averages, and this is the first time in several years that Asian spreads have reached a level one standard deviation above their historic averages. In contrast, spreads for U.S. high yield spreads are 20 basis points (0.2%) below average and European high yield spreads are 80 basis points (0.8%) below average. In simple terms, Asian high yield bonds are compensating investors for taking credit risk even with continued volatility.

To be sure, there continue to be risks on the horizon. If a further slowdown in global growth materializes, we expect investor appetite for emerging markets to diminish. Any escalation in trade shocks or further outflows stemming from policy normalization in the U.S. could also put pressure on Asian fixed income markets. If the Chinese economy deteriorates, corporate defaults will likely rise, and Asian credit could come under pressure. Indeed, we see much of this scenario already factored into current valuations as trailing 12-month default rates are hovering at only 1% per annum. Based on our solvency and liquidity analysis, we do not expect any of the securities in the portfolio to default. As such, the relatively attractive yields in Asia offer a strong base for positive returns in 2019.

| CURRENCY ALLOCATION (%)6,7 | ||||

| US Dollar | 92.1 | |||

| Hong Kong Dollar | 5.0 | |||

| Cash and Other Assets, Less Liabilities | 2.9 | |||

| COUNTRY ALLOCATION (%)6,7,8 | ||||

| China/Hong Kong | 50.7 | |||

| Indonesia | 13.6 | |||

| Vietnam | 9.3 | |||

| Thailand | 5.4 | |||

| Philippines | 5.3 | |||

| Japan | 4.2 | |||

| Singapore | 3.7 | |||

| Sri Lanka | 2.0 | |||

| India | 1.9 | |||

| United States | 1.0 | |||

| Cash and Other Assets, Less Liabilities | 2.9 | |||

| SECTOR ALLOCATION (%)6,7 | ||||

| Real Estate | 22.2 | |||

| Financials | 15.2 | |||

| Consumer Discretionary | 12.4 | |||

| Communication Services | 10.6 | |||

| Materials | 9.2 | |||

| Consumer Staples | 8.2 | |||

| Industrials | 7.3 | |||

| Foreign Government Bonds | 6.6 | |||

| Utilities | 5.4 | |||

| Cash and Other Assets, Less Liabilities | 2.9 | |||

| ASSET TYPE BREAKDOWN (%)6,7 | ||||

| Non-Convertible Corporate Bonds | 66.1 | |||

| Convertible Corporate Bonds | 19.8 | |||

| Government Bonds | 11.3 | |||

| Cash and Other Assets, Less Liabilities | 2.9 | |||

| 6 | Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent, so the values may not sum to 100% due to rounding. Percentage values may be derived from different data sources and may not be consistent with other Fund literature. |

| 7 | Cash and other assets may include forward currency exchange contracts and certain derivative instruments that have been marked-to-market. |

| 8 | Not all countries where the Fund may invest are included in the benchmark index. |

| matthewsasia.com | 800.789.ASIA | 13 |

Table of Contents

Matthews Asia Credit Opportunities Fund

December 31, 2018

Schedule of Investmentsa

NON-CONVERTIBLE CORPORATE BONDS: 66.1%

| Face Amount* | Value | |||||||

| CHINA/HONG KONG: 33.0% | ||||||||

Standard Chartered PLC | 1,850,000 | $1,810,687 | ||||||

Chinalco Capital Holdings, Ltd. | 1,543,000 | 1,483,269 | ||||||

Wanda Properties International Co., Ltd. | 1,550,000 | 1,473,765 | ||||||

West China Cement, Ltd. | 1,440,000 | 1,443,825 | ||||||

KWG Group Holdings, Ltd. | 1,500,000 | 1,336,364 | ||||||

Huaneng Hong Kong Capital, Ltd. | 1,400,000 | 1,262,519 | ||||||

HSBC Holdings PLC | 1,100,000 | 1,056,000 | ||||||

CIFI Holdings Group Co., Ltd. | 1,000,000 | 978,105 | ||||||

KWG Group Holdings, Ltd. | 800,000 | 801,622 | ||||||

Shimao Property Holdings, Ltd. | 800,000 | 752,578 | ||||||

China Minmetals Corp. | 800,000 | 722,637 | ||||||

|

| |||||||

Total China/Hong Kong | 13,121,371 | |||||||

|

| |||||||

| INDONESIA: 13.6% | ||||||||

TBG Global Pte, Ltd. | 1,400,000 | 1,369,712 | ||||||

PB International BV | 1,200,000 | 1,159,882 | ||||||

Modernland Overseas Pte, Ltd. | 1,400,000 | 1,150,814 | ||||||

Listrindo Capital BV | 1,000,000 | 886,500 | ||||||