UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08510

Matthews International Funds

(Exact name of registrant as specified in charter)

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Address of principal executive offices) (Zip code)

William J. Hackett, President

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-788-7553

Date of fiscal year end: December 31

Date of reporting period: December 31, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

| | (a) | The Report to Shareholders is attached herewith. |

Matthews Asia Funds | Annual Report

December 31, 2020 | matthewsasia.com

GLOBAL EMERGING MARKETS STRATEGY

Matthews Emerging Markets Equity Fund

ASIA FIXED INCOME STRATEGIES

Matthews Asia Total Return Bond Fund

Matthews Asia Credit Opportunities Fund

ASIA GROWTH AND INCOME STRATEGIES

Matthews Asian Growth and Income Fund

Matthews Asia Dividend Fund

Matthews China Dividend Fund

ASIA GROWTH STRATEGIES

Matthews Asia Growth Fund

Matthews Pacific Tiger Fund

Matthews Asia ESG Fund

Matthews Emerging Asia Fund

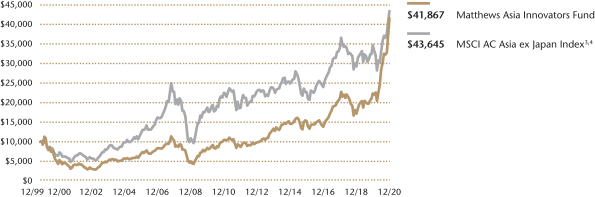

Matthews Asia Innovators Fund

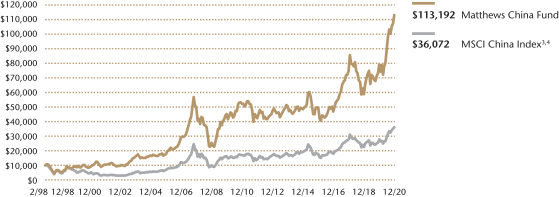

Matthews China Fund

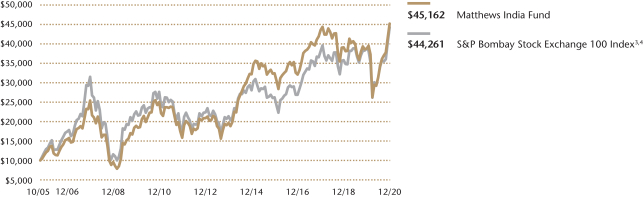

Matthews India Fund

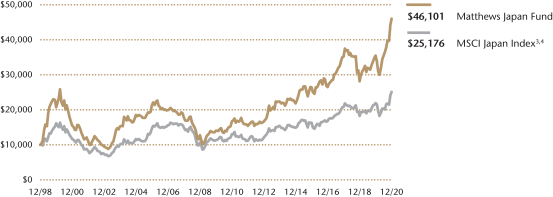

Matthews Japan Fund

Matthews Korea Fund

ASIA SMALL COMPANY STRATEGIES

Matthews Asia Small Companies Fund

Matthews China Small Companies Fund

As of January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports are no longer being sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website matthewsasia.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report. You may elect to receive paper copies of shareholder reports and other communications from the Funds anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling 800.789.ASIA (2742).

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with a Fund, you can call 800.789.ASIA (2742) to let the Fund know you wish to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds held in your account if you invest through your financial intermediary or all Funds held directly with Matthews Asia Funds.

Investor Class Performance and Expense Ratios (December 31, 2020) (unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Average Annual Total Return† | | | | | | 2020

Annual

Operating

Expense

Ratios* | | | 2020

Annual

Operating

Expense

Ratios

after Fee

Waiver

and

Expense

Reim- bursement** | | | Prospectus

Expense

Ratios‡ | | | Prospectus

Expense

Ratios

after Fee

Waiver

and

Expense

Reim- bursement‡ | |

| Investor Class | | 1 year | | | 5 years | | | 10 years | | | Since

Inception | | | Inception

Date | |

GLOBAL EMERGING MARKETS STRATEGY | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Emerging Markets Equity Fund (MEGMX) | | | n.a. | | | | n.a. | | | | n.a. | | | | 61.23% | | | | 4/30/20 | | | | 2.76% | | | | 1.08% | 1 | | | 2.77% | | | | 1.15% | 1 |

ASIA FIXED INCOME STRATEGIES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Asia Total Return Bond Fund (MAINX)§ | | | 5.36% | | | | 6.35% | | | | n.a. | | | | 5.01% | | | | 11/30/11 | | | | 1.15% | | | | 1.12% | 1 | | | 1.08% | | | | 1.07% | 1 |

| | | | | | | | | |

Asia Credit Opportunities Fund (MCRDX) | | | 1.80% | | | | n.a. | | | | n.a. | | | | 5.16% | | | | 4/29/16 | | | | 1.14% | | | | 1.14% | 1 | | | 1.24% | | | | 1.12% | 1 |

ASIA GROWTH AND INCOME STRATEGIES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Asian Growth and Income Fund (MACSX) | | | 16.00% | | | | 8.38% | | | | 5.37% | | | | 9.22% | | | | 9/12/94 | | | | 1.09% | | | | 1.09% | | | | 1.08% | | | | 1.08% | |

| | | | | | | | | |

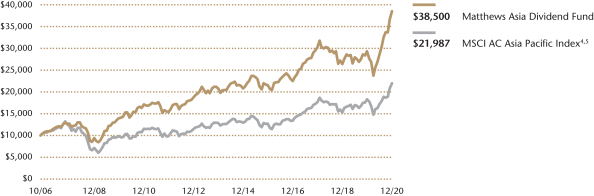

Asia Dividend Fund (MAPIX) | | | 31.25% | | | | 12.30% | | | | 8.46% | | | | 9.98% | | | | 10/31/06 | | | | 1.03% | | | | 1.02% | 2 | | | 1.03% | | | | 1.02% | 2 |

| | | | | | | | | |

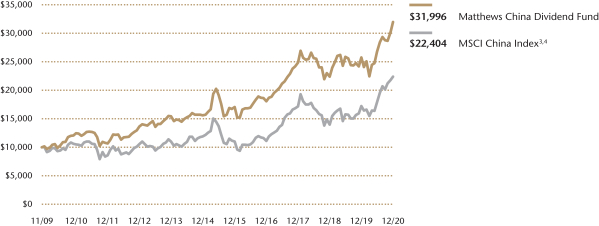

China Dividend Fund (MCDFX) | | | 24.22% | | | | 13.36% | | | | 9.88% | | | | 11.06% | | | | 11/30/09 | | | | 1.15% | | | | 1.15% | | | | 1.15% | | | | 1.15% | |

ASIA GROWTH STRATEGIES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

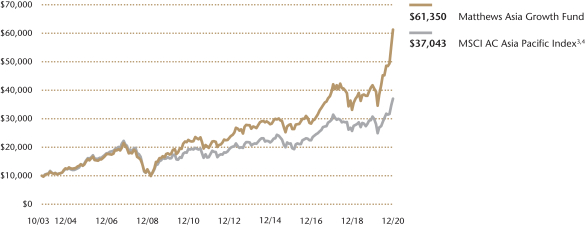

Asia Growth Fund (MPACX) | | | 46.76% | | | | 16.88% | | | | 10.48% | | | | 11.15% | | | | 10/31/03 | | | | 1.08% | | | | 1.08% | | | | 1.09% | | | | 1.09% | |

| | | | | | | | | |

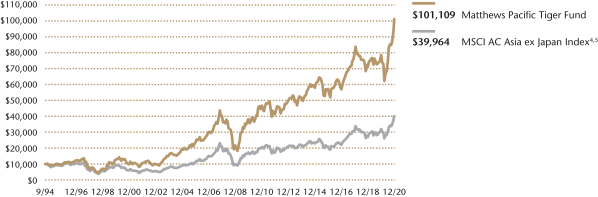

Pacific Tiger Fund (MAPTX) | | | 28.83% | | | | 12.12% | | | | 8.06% | | | | 9.20% | | | | 9/12/94 | | | | 1.08% | | | | 1.06% | 2 | | | 1.08% | | | | 1.05% | 2 |

| | | | | | | | | |

Asia ESG Fund (MASGX) | | | 42.87% | | | | 13.87% | | | | n.a. | | | | 10.65% | | | | 4/30/15 | | | | 1.42% | | | | 1.38% | 3 | | | 1.54% | | | | 1.38% | 3 |

| | | | | | | | | |

Emerging Asia Fund (MEASX) | | | -2.16% | | | | 2.43% | | | | n.a. | | | | 3.29% | | | | 4/30/13 | | | | 1.75% | | | | 1.40% | 3 | | | 1.65% | | | | 1.42% | 3 |

| | | | | | | | | |

Asia Innovators Fund (MATFX) | | | 86.72% | | | | 22.31% | | | | 14.87% | | | | 7.05% | | | | 12/27/99 | | | | 1.10% | | | | 1.10% | | | | 1.19% | | | | 1.19% | |

| | | | | | | | | |

China Fund (MCHFX) | | | 43.05% | | | | 17.98% | | | | 8.05% | | | | 11.20% | | | | 2/19/98 | | | | 1.09% | | | | 1.09% | | | | 1.09% | | | | 1.09% | |

| | | | | | | | | |

India Fund (MINDX) | | | 16.45% | | | | 6.84% | | | | 6.10% | | | | 10.45% | | | | 10/31/05 | | | | 1.15% | | | | 1.15% | | | | 1.11% | | | | 1.11% | |

| | | | | | | | | |

Japan Fund (MJFOX) | | | 29.82% | | | | 11.80% | | | | 10.66% | | | | 7.19% | | | | 12/31/98 | | | | 0.95% | | | | 0.95% | | | | 0.93% | | | | 0.93% | |

| | | | | | | | | |

Korea Fund (MAKOX) | | | 40.77% | | | | 8.88% | | | | 8.38% | | | | 6.79% | | | | 1/3/95 | | | | 1.19% | | | | 1.19% | | | | 1.15% | | | | 1.15% | |

ASIA SMALL COMPANY STRATEGIES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Asia Small Companies Fund (MSMLX) | | | 43.68% | | | | 12.21% | | | | 6.66% | | | | 12.25% | | | | 9/15/08 | | | | 1.57% | | | | 1.39% | 3 | | | 1.60% | | | | 1.41% | 3 |

| | | | | | | | | |

China Small Companies Fund (MCSMX) | | | 82.52% | | | | 25.05% | | | | n.a. | | | | 12.48% | | | | 5/31/11 | | | | 1.52% | | | | 1.43% | 3 | | | 1.62% | | | | 1.38% | 3 |

| † | Annualized performance for periods of at least one year, otherwise cumulative. |

| * | Before fee waivers and expense reimbursement. |

| ** | Expense ratio represents the actual expense ratio a shareholder would have paid if they had been invested the entire year. |

| ‡ | These figures are from the Funds’ prospectus dated as of April 29, 2020, and may differ from the actual expense ratios for fiscal year 2020, as shown in the financial highlights section of this report. |

| § | The Fund’s name changed from Matthews Asia Strategic Income Fund to Matthews Asia Total Return Bond Fund on January 31, 2020. |

| 1 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. Pursuant to this agreement, any amount waived for prior fiscal years with respect to the Matthews Asia Total Return Bond Fund and the Matthews Asia Credit Opportunities Fund is not subject to recoupment. For the Matthews Emerging Markets Equity Fund, if the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 2 | Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund’s average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2022 and may be terminated (i) at any time by the Board of Trustees upon 60 days’ prior written notice to Matthews; or (ii) by Matthews at the annual expiration date of the agreement upon 60 days’ prior written notice to the Trust, in each case without payment of any penalty. |

| 3 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.20% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 1.20% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. Beginning on December 1, 2020 for the Matthews Emerging Asia Fund, Matthews voluntarily reduced this expense limitation to 1.10% for the Institutional Class and waived a corresponding amount (in annual percentage terms) for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 1.20%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

Institutional Class Performance and Expense Ratios (December 31, 2020) (unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | |

Average Annual Total Return† | | | | | | 2020

Annual

Operating

Expense

Ratios* | | | 2020

Annual

Operating

Expense

Ratios

after Fee

Waiver

and

Expense

Reim- bursement** | | | Prospectus

Expense

Ratios‡ | | | Prospectus

Expense

Ratios

after Fee

Waiver

and

Expense

Reim- bursement‡ | |

| Institutional Class | | 1 year | | | 5 years | | | 10 years | | | Since

Inception | | | Inception

Date | |

GLOBAL EMERGING MARKETS STRATEGY | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Emerging Markets Equity Fund (MIEFX) | | | n.a. | | | | n.a. | | | | n.a. | | | | 61.55% | | | | 4/30/20 | | | | 2.65% | | | | 0.90% | 1 | | | 2.57% | | | | 0.90% | 1 |

ASIA FIXED INCOME STRATEGIES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Asia Total Return Bond Fund (MINCX)§ | | | 5.60% | | | | 6.58% | | | | n.a. | | | | 5.23% | | | | 11/30/11 | | | | 1.00% | | | | 0.90% | 1 | | | 0.97% | | | | 0.90% | 1 |

| | | | | | | | | |

Asia Credit Opportunities Fund (MICPX) | | | 2.05% | | | | n.a. | | | | n.a. | | | | 5.41% | | | | 4/29/16 | | | | 0.98% | | | | 0.90% | 1 | | | 1.07% | | | | 0.90% | 1 |

ASIA GROWTH AND INCOME STRATEGIES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Asian Growth and Income Fund (MICSX) | | | 16.18% | | | | 8.53% | | | | 5.52% | | | | 5.68% | | | | 10/29/10 | | | | 0.96% | | | | 0.96% | | | | 0.94% | | | | 0.94% | |

| | | | | | | | | |

Asia Dividend Fund (MIPIX) | | | 31.29% | | | | 12.42% | | | | 8.57% | | | | 8.73% | | | | 10/29/10 | | | | 0.93% | | | | 0.93% | 2 | | | 0.93% | | | | 0.92% | 2 |

| | | | | | | | | |

China Dividend Fund (MICDX) | | | 24.37% | | | | 13.53% | | | | 10.07% | | | | 10.31% | | | | 10/29/10 | | | | 1.02% | | | | 1.02% | | | | 1.01% | | | | 1.01% | |

ASIA GROWTH STRATEGIES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Asia Growth Fund (MIAPX) | | | 47.01% | | | | 17.07% | | | | 10.67% | | | | 10.78% | | | | 10/29/10 | | | | 0.95% | | | | 0.95% | | | | 0.94% | | | | 0.94% | |

| | | | | | | | | |

Pacific Tiger Fund (MIPTX) | | | 28.98% | | | | 12.30% | | | | 8.24% | | | | 8.17% | | | | 10/29/10 | | | | 0.94% | | | | 0.92% | 2 | | | 0.93% | | | | 0.91% | 2 |

| | | | | | | | | |

Asia ESG Fund (MISFX) | | | 43.13% | | | | 14.12% | | | | n.a. | | | | 10.89% | | | | 4/30/15 | | | | 1.29% | | | | 1.20% | 3 | | | 1.41% | | | | 1.20% | 3 |

| | | | | | | | | |

Emerging Asia Fund (MIASX) | | | -1.94% | | | | 2.65% | | | | n.a. | | | | 3.51% | | | | 4/30/13 | | | | 1.62% | | | | 1.19% | 3 | | | 1.51% | | | | 1.20% | 3 |

| | | | | | | | | |

Asia Innovators Fund (MITEX) | | | 87.01% | | | | 22.53% | | | | n.a. | | | | 19.63% | | | | 4/30/13 | | | | 0.95% | | | | 0.95% | | | | 1.05% | | | | 1.05% | |

| | | | | | | | | |

China Fund (MICFX) | | | 43.23% | | | | 18.18% | | | | 8.23% | | | | 7.91% | | | | 10/29/10 | | | | 0.93% | | | | 0.93% | | | | 0.91% | | | | 0.91% | |

| | | | | | | | | |

India Fund (MIDNX) | | | 16.65% | | | | 7.03% | | | | 6.29% | | | | 5.97% | | | | 10/29/10 | | | | 1.03% | | | | 1.03% | | | | 0.94% | | | | 0.94% | |

| | | | | | | | | |

Japan Fund (MIJFX) | | | 29.85% | | | | 11.87% | | | | 10.76% | | | | 11.73% | | | | 10/29/10 | | | | 0.91% | | | | 0.91% | | | | 0.88% | | | | 0.88% | |

| | | | | | | | | |

Korea Fund (MIKOX) | | | 40.76% | | | | 9.00% | | | | 8.52% | | | | 9.24% | | | | 10/29/10 | | | | 1.05% | | | | 1.05% | | | | 1.05% | | | | 1.05% | |

ASIA SMALL COMPANY STRATEGIES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Asia Small Companies Fund (MISMX) | | | 43.90% | | | | 12.44% | | | | n.a. | | | | 8.15% | | | | 4/30/13 | | | | 1.47% | | | | 1.20% | 3 | | | 1.46% | | | | 1.20% | 3 |

| | | | | | | | | |

China Small Companies Fund (MICHX) | | | 82.89% | | | | n.a. | | | | n.a. | | | | 28.63% | | | | 11/30/17 | | | | 1.37% | | | | 1.20% | 3 | | | 1.51% | | | | 1.20% | 3 |

| † | Annualized performance for periods of at least one year, otherwise cumulative. |

| * | Before fee waivers and expense reimbursement. |

| ** | Expense ratio represents the actual expense ratio a shareholder would have paid if they had been invested the entire year. |

| ‡ | These figures are from the Funds’ prospectus dated as of April 29, 2020, and may differ from the actual expense ratios for fiscal year 2020, as shown in the financial highlights section of this report. |

| § | The Fund’s name changed from Matthews Asia Strategic Income Fund to Matthews Asia Total Return Bond Fund on January 31, 2020. |

| 1 | Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90%. Pursuant to this agreement, any amount waived for prior fiscal years with respect to the Matthews Asia Total Return Bond Fund and the Matthews Asia Credit Opportunities Fund is not subject to recoupment. For the Matthews Emerging Markets Equity Fund, if the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 2 | Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund’s average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2022 and may be terminated (i) at any time by the Board of Trustees upon 60 days’ prior written notice to Matthews; or (ii) by Matthews at the annual expiration date of the agreement upon 60 days’ prior written notice to the Trust, in each case without payment of any penalty. |

| 3 | Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.20%. Beginning on December 1, 2020 for the Matthews Emerging Asia Fund, Matthews voluntarily reduced this expense limitation to 1.10% for the Institutional Class. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

Past Performance: All performance quoted in this report is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the returns quoted. If certain of the Funds’ fees and expenses had not been waived, returns would have been lower. For the Funds’ most recent month-end performance, please call 800.789.ASIA (2742) or visit matthewsasia.com.

| | | | |

| matthewsasia.com | 800.789.ASIA | | | 3 | |

Cover photo: Terraced fields at Yunnan, China

This report has been prepared for Matthews International Funds (d/b/a Matthews Asia Funds) shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Matthews Asia Funds prospectus, which contains more complete information about the Funds’ investment objectives, risks and expenses. Additional copies of the prospectus or summary prospectus may be obtained at matthewsasia.com. Please read the prospectus carefully before you invest or send money.

The views and opinions in this report were current as of December 31, 2020. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Fund’s future investment intent. Current and future portfolio holdings are subject to risk.

Statements of fact are from sources considered reliable, but neither the Funds nor the Investment Advisor makes any representation or guarantee as to their completeness or accuracy.

Contents

*The Fund’s name changed from Matthews Asia Strategic Income Fund to Matthews Asia Total Return Bond Fund on January 31, 2020.

Investment Risk: Mutual fund shares are not deposits or obligations of, or guaranteed by, any depositary institution. Shares are not insured by the FDIC, Federal Reserve Board or any government agency and are subject to investment risks, including possible loss of principal amount invested. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Fixed income investments are subject to additional risks, including, but not limited to, interest rate, credit and inflation risks. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of a concentration in a specific industry, sector or geographic location. Investing in small and mid-size companies is more risky than investing in large companies as they may be more volatile and less liquid than larger companies. Please see the Funds’ Prospectuses and Statement of Additional Information for more risk disclosure.

| | | | |

| matthewsasia.com | 800.789.ASIA | | | 5 | |

Message to Shareholders from the President of Matthews Asia Funds

Dear Valued Shareholder,

For most of us, 2020 will be remembered for being an unprecedented year, with the depth and duration of COVID-19 affecting global economic activity and markets across the world. Of course, as we look back, what is most important is not the economic impact but the human one. With that, our thoughts are with all those that have been impacted by the virus, either directly or indirectly, and we extend our gratitude to all health care professionals, scientists and service providers who have diligently worked to help and provide care to those in need around the world.

Notably, we at Matthews Asia are no strangers to operating through health crises, with the infectious diseases SARS, MERS and swine flu all occurring this century. Their ability to cause disruption was fortunately temporary and we hope that the same will be said of the pandemic we currently face. During outbreaks such as COVID-19, our primary objective is the health and well-being of our employees and their families, consideration for our shareholders and our service providers and the continuity of business operations to ensure our portfolios can be managed without interruption. In this regard, I am particularly proud of how our firm has responded despite the significant disruption to daily life that has occurred.

Performance

Against a backdrop of a pandemic, we witnessed an initial collapse in economic activity and plunges in stock markets around the world. Remarkably, however, 2020 may also be remembered for the surprising strength of markets as investors began to reappraise their outlook. This is particularly true of Asia, where control over the pandemic enabled a return to normality and economic output for many of its countries long before those in the West. Following the tumult of the first quarter, equity markets across much of the globe reversed course in the second half of the year. We then saw an uptick in sentiment in the fourth quarter, largely driven by the development and rollout of the coronavirus vaccines as well as prospects for improving China—U.S. relations with the election of a new U.S. president.

We are accustomed to these kinds of swings in markets, given our long history of focusing on Asia. This strengthens our resolve to remain focused on our core investment principles with a bottom-up approach and long-range view. While the lockdowns have limited the amount of travel that our analysts and portfolio managers can do to visit companies, our investment team was still able to conduct 15-20 virtual meetings each a day on average across the team, starting early in the morning and continuing late into the night, to catch the working day in Asia on behalf of our shareholders. Amid the volatile environment, I am proud of the positive relative and absolute performance delivered across most of the Matthews Asia Funds.

Emerging Markets

Despite a challenging year, we successfully launched the Matthews Emerging Markets Equity Fund—an important milestone for Matthews Asia as it is our first strategy to invest in broad emerging markets. For almost 30 years, we have focused our research and investment capabilities within a region that now dominates the emerging markets. Asia’s representation within the MSCI Emerging Market Index has risen to over 75%, with the increasing inclusion of China’s domestically listed A-shares driving recent changes in benchmark weightings. As an Asia investment specialist, we have significant experience investing in the complex and diverse range of countries and economies that comprise the largest segment of emerging markets. We believe we can leverage this expertise in other emerging markets and apply the same established fundamental investment process in order to evaluate a company, its management team and corporate governance.

ESG

We recognize that a growing number of investors are looking for strategies that have ESG integration, particularly given events over the past 12 months. A deep appreciation of corporate governance is built into our DNA and our investment approach has always been committed to assessing corporate governance. We believe governance influences social and environmental factors, providing a starting point for analysis. At Matthews Asia, we remain committed to incorporating ESG considerations within the very fabric of our investment process. We continue to look at integrating ESG practices into our portfolios and further enhancing our ESG capabilities. While strong corporate governance, as well as good ESG practices, may show little direct link to short-term stock performance, we believe they are critical to delivering long-term, risk-adjusted shareholder value.

The New Matthewsasia.com Website

In December, we launched the newly designed matthewsasia.com website. With a visually engaging design, our new website provides a faster, easier navigation experience—whether on your mobile, tablet or desktop—for quicker access to information and content, including

new scrollable Funds section with fewer tabs and fewer clicks. The site includes a new Insights section that makes finding and accessing content easier with curated articles, whitepapers, webcasts, podcasts and videos that bring Asia to you with rich imagery for a more immersive web experience. We hope you enjoy exploring the new website with its enhanced search function that allows you to explore our extensive resources on Asia and to more easily find the information on your investments and thought leadership from the investment team.

Looking Ahead to 2021

While uncertainty remains as we head into the New Year, we look forward to a successful rollout of vaccinations and the return to normal daily patterns prior to the pandemic. We will continue to maintain a thoughtful but opportunistic approach to identify the most attractive long-term investment opportunities, and we remain steadfast in our investment approach on developing deep insights through fundamental research on behalf of our clients. We take seriously the stewardship of your assets and thank you for being a valued shareholder during what has been a particularly tumultuous and challenging year.

William J. Hackett

President of Matthews Asia Funds

| | | | |

| matthewsasia.com | 800.789.ASIA | | | 7 | |

Message to Shareholders from the

Investment Advisor

Dear Valued Shareholders,

I don’t know if I have ever experienced such a strange year. Perhaps that is a common sentiment. However, I refer less to the lockdown. Nor do I refer about work so much. We were able to keep in touch with each other through technology and socially distanced face-to-face meetings. Through the same use of video conference calls, we were able to maintain contact with companies, both familiar and new. We were able to adapt—we were given lemons and we made lemonade. In many respects, performance of the portfolios has been excellent; so it is hard to see how the environment disadvantaged our investors. Nevertheless, our investment team are all to be congratulated by the way they responded to the environment and continued to make decisions on behalf of clients.

No, none of that has been too strange. But the markets themselves? There, I do pause for thought. Given the set of circumstances we have faced—political, economic and emotional—I would not have expected markets to do so well. So, why have they?

Perhaps we need to go back to the beginning. At least from a market perspective, our initial reaction was sanguine. After all, China had faced things like this before and had dealt with them. In the past, such episodes had little long-term effect on the markets. This turned out, in hindsight, to be more or less true for the current virus, but only for China, which reacted in a way largely consistent with previous outbreaks. For the rest of the world, however, it didn’t start out that way. The economic effects of the lockdown hit hard on expectations of current sales and profits. Only in the virtual world were businesses somewhat protected from the worst, as people could transact with total physical distance.

The virus spread far wider than previous outbreaks and the economic effects were deeper and longer-lasting than we ever suspected. And yet, the idea that this was a temporary disruption to the general trend of economic and human progress has never really gone away. Markets were able to see through the near term and still believe in a “normal” future. So, when the dampening effects of weak current economic activity and raised household savings caused bond yields to fall across much of the world outside of China, valuations soared. After all, if you are able to discount a normal future at abnormally low interest rates, then price-to-earnings ratios (valuation ratio of a company’s current share price compared to its per-share earnings) should be much higher. So, the equity market saw a positive future while bond yields were suppressed by low demand for goods and the persistent lack of demand for new investment that has been a commonplace of recent years.

And so it has been a topsy-turvy world in many ways. Perhaps white is the new black—“watch out when things get better, they may get worse!” In any other year, I might feel self-conscious writing such phrases; but not this year. For I can see it is entirely possible that, in the face of a vaccine and a recovery in economic activity, bond yields may rise again and those valuations that seemed justified may suddenly become unrealistic. Now, how much of a concern is this?

It’s undeniable that some of these valuation effects have helped performance in your portfolios this past year. However, these effects are mitigated by several factors. First, of course, we are aware of these effects and always strive to own securities whose valuations are justifiable in the face of their long-term business prospects. Second, we have been trying to take advantage of those businesses which have suffered most from the direct effects of the lockdown. These are not poor businesses but businesses that many investors have overlooked simply because they have been fascinated by the momentum elsewhere. And finally, when we look at the strange interaction between weak activity, collapsing bond yields and high valuations on weak profits that has been the heady, if startling, recipe of

2020, it is perhaps least in evidence in China—economic activity has bounced back earlier and stronger than elsewhere and bond yields are, for want of a better word, “normal.”

As I look into 2021, the dislocations in the markets that may happen from a return to normality may be more keenly felt in those markets where normal conditions have been suspended the longest. It’s not hard to imagine a vaccine-inspired end of lockdowns in the U.S. and the West leading to a burst of inflationary pressures as demand returns more swiftly than supply, people pay down precautionary savings and enjoy a return to normal spending patterns. My expectation in such a case would be for bond yields to rise and valuations in the most extended parts of all markets, particularly the U.S. and Europe, to revert to something more normal. However, my relative optimism for Asia and the emerging markets extends beyond these short-term effects. In the U.S. we have already seen the first suggestions of a return to more friendly policy internationally, a more pro-labor stance and an administration likely to be supportive of fiscal and monetary expansion. All of this brings the U.S. belatedly in line with some policies that have already been prevalent in Asia for the past decade, to the detriment of Asia’s relative market performance but the benefit of the internal stability of their societies.

The common perception among asset allocators, both in the U.S. and abroad, appears to be that a period of a slightly weaker dollar is the most likely outcome in the currency markets. There is a renewed willingness to look at international markets in general and emerging and Asian markets in particular. I wish the fortunes of these markets were not so tightly tied in the short-run to the direction of the U.S. dollar, but that seems to be one constant of the world. I believe it is a relationship that will gradually weaken along with the continuing development of China’s own capital markets and the likelihood that it will continue to be an international investor. Nevertheless, a weaker dollar, if that is indeed to happen, is an important tailwind for our markets.

And if a weaker dollar should focus investors’ attention a little more on the long-term trends we seek, so much the better. We still believe that one can prosper over the long term by finding businesses that are the leaders of the development of a world class health care industry, indigenous innovation in technology hardware and online business models, the growth and domination of local brand leaders in more traditional business, and the modernization and development of capital markets to support efficient and sustainable growth for more than half the world’s population. So, even in a topsy-turvy 2020, and maybe a turvy-topsy 2021, that is what we will continue to try and do.

Robert Horrocks, PhD

Chief Investment Officer

Matthews International Capital Management, LLC

| | | | |

| matthewsasia.com | 800.789.ASIA | | | 9 | |

| | | | |

| PORTFOLIO MANAGERS |

| |

| John Paul Lech | | |

Lead Manager | | |

|

| FUND FACTS |

| | |

| | | Investor | | Institutional |

Ticker | | MEGMX | | MIEFX |

CUSIP | | 577130651 | | 577130644 |

Inception | | 4/30/20 | | 4/30/20 |

NAV | | $15.76 | | $15.77 |

Initial Investment | | $2,500 | | $100,000 |

Gross Expense Ratio1 | | 2.76% | | 2.65% |

After fee waiver and Reimbursement2 | | 1.08% | | 0.90% |

Portfolio Statistics |

Total # of Positions | | | | 58 |

Net Assets | | | | $44.8 million |

Weighted Average Market Cap | | $154.2 billion |

Portfolio Turnover3 | | | | 62.3% |

Benchmark | | |

MSCI Emerging Markets Index |

OBJECTIVE

Long-term capital appreciation.

STRATEGY

Under normal circumstances, the Matthews Emerging Markets Equity Fund seeks to achieve its investment objective by investing at least 80% of its net assets, which include borrowings for investment purposes, in the common and preferred stocks of companies located in emerging market countries. Emerging market countries generally include every country in the world except the United States, Australia, Canada, Hong Kong, Israel, Japan, New Zealand, Singapore and most of the countries in Western Europe. Certain emerging market countries may also be classified as “frontier” market countries, which are a subset of emerging market countries with newer or even less developed economies and markets, such as Sri Lanka and Vietnam. The list of emerging market countries and frontier market countries may change from time to time. The Fund may also invest in companies located in developed countries; however, the Fund may not invest in any company located in a developed country if, at the time of purchase, more than 20% of the Fund’s assets are invested in developed market companies.

Matthews Emerging Markets Equity Fund

Portfolio Manager Commentary (unaudited)

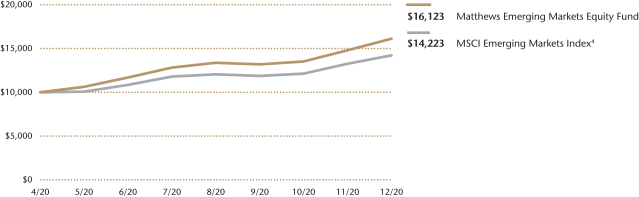

The Matthews Emerging Markets Equity Fund launched on April 30, 2020. From inception to December 31, 2020, the Fund returned 61.23% (Investor Class) and 61.55% (Institutional Class), while its benchmark, the MSCI Emerging Markets Index, returned 42.23%. For the quarter ending December 31, 2020, the Fund returned 22.15% (Investor Class) and 22.30% (Institutional Class) versus 19.77% for the index.

Market Environment:

Global equities were volatile in the year, but ultimately generated attractive returns, and this was particularly pronounced in Asian and emerging markets more broadly. Global markets fell in the first quarter, as worries surrounding the spread of COVID-19 moved beyond China. Fears of a global growth slowdown turned into reality as governments worldwide began to implement different versions of ‘shelter in place’ to contain the movement of the virus. Markets recovered in part due to the extraordinary fiscal and monetary measures put in place by many countries. Early in the year, cyclically sensitive sectors like energy, materials, industrials and financials suffered most while companies related to communication services and technology performed better. In the second quarter, most global financial markets, including Asia’s, began to rise as major economies began to relax prior pandemic-related restrictions. The gradual reopening of businesses—especially those focused on services and consumption—helped bolster sentiment and bring a floor to stock prices globally.

In the third quarter, economic recovery and improved sentiment began to take hold as major economies continued to relax COVID-19 lockdown restrictions even further. China’s V-shaped recovery in manufacturing along with a steady recovery in domestic consumption brought some normalcy to daily life. Emerging market currencies rallied slightly against the US dollar in the third quarter, acting as a slight tailwind for EM equities. Growth stocks outpaced value and small caps outperformed large caps in the third quarter. The fourth quarter saw further economic strengthening. Cyclical stocks in beaten up or export driven markets such as Indonesia and Korea rallied most in the fourth quarter, while markets that experienced early recovery like China, Japan and India lagged slightly. Market strength gained momentum following the U.S. Presidential elections in November as markets hoped for less confrontational U.S.—China relations, combined with an announcement of several approved COVID-19 vaccines that were due for distribution early in 2021.

Performance Contributors and Detractors:

For the fourth quarter, stock selection in China and Hong Kong was a notable contributor to performance from a regional perspective. On the other hand, stock selection in South Korea was a detractor. From a sector perspective, stock selection in communication services and financials was a contributor. Meanwhile, stock selection in energy and an overweight in real estate were slight detractors.

Samsung Electronics was a major contributor to portfolio returns in the fourth quarter as expectations regarding the company’s semiconductor business, which is the majority of the firm’s profitability, remain positive. The semiconductor

(continued)

| 1 | Actual 2020 expense ratios. |

| 2 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 3 | The lesser of fiscal year 2020 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| | | | | | | | | | | | |

| | | |

| PERFORMANCE AS OF DECEMBER 31, 2020 | | | | | | |

| | | | | | Actual Return,

Not Annualized | |

| | | 3 Months | | | Since

Inception | | | Inception

date | |

| Investor Class (MEGMX) | | | 22.15% | | | | 61.23% | | | | 04/30/20 | |

| Institutional Class (MIEFX) | | | 22.30% | | | | 61.55% | | | | 04/30/20 | |

| MSCI Emerging Markets Index4 | | | 19.77% | | | | 42.23% | | | | | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund’s fees and expenses had not been waived. For the Fund’s most recent month-end performance visit matthewsasia.com.

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

| | 4 | It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 93 for index definition. |

| | | | | | | | |

| | | | |

| TOP TEN HOLDINGS5 | | | | | | | |

| | | Sector | | Country | | % of Net Assets | |

| Samsung Electronics Co., Ltd., Pfd. | | Information Technology | | South Korea | | | 5.8% | |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | Information Technology | | Taiwan | | | 5.8% | |

| Alibaba Group Holding, Ltd. | | Consumer Discretionary | | China/Hong Kong | | | 3.9% | |

| Tencent Holdings, Ltd. | | Communication Services | | China/Hong Kong | | | 3.2% | |

| AIA Group, Ltd. | | Financials | | China/Hong Kong | | | 3.0% | |

| LVMH Moet Hennessy Louis Vuitton SE | | Consumer Discretionary | | France | | | 2.6% | |

| LUKOIL PJSC | | Energy | | Russia | | | 2.1% | |

| CapitaLand, Ltd. | | Real Estate | | Singapore | | | 2.0% | |

| Heineken N.V. | | Consumer Staples | | Netherlands | | | 2.0% | |

| Kotak Mahindra Bank, Ltd. | | Financials | | India | | | 2.0% | |

| % OF ASSETS IN TOP 10 | | | | | | | 32.4% | |

| | 5 | Holdings may combine more than one security from same issuer and related depositary receipts. |

| | | | |

| matthewsasia.com | 800.789.ASIA | | | 11 | |

Matthews Emerging Markets Equity Fund

Portfolio Manager Commentary (unaudited) (continued)

business can be divided between memory and logic, both of which are becoming more consolidated. We believe Samsung Electronics’ governance, balance sheet and competitive position are all attractive attributes.

On the other hand, Anhui Conch Cement was a slight detractor. The company is considered a leader in its industry with some of the lowest costs and a good history of capital allocation. We remain positive on the company’s prospects as its core product is an essential component of any increase in construction or infrastructure spending.

Notable Portfolio Changes:

The year’s market volatility required an active approach to portfolio construction and we initiated positions over the fourth quarter. We added Allegro, an e-commerce company in Poland that does more than 10 times the gross merchandise value (GMV) of its next largest competitor. In China, we augmented our holdings in the consumer discretionary by adding JD.com which has a growing business in grocery delivery—an underpenetrated segment of online retail. We also added a position in Grupo Aeroportuario del Sureste, which operates several airports across Mexico and could be a beneficiary of increased travel once vaccinations against COVID-19 become more widely implemented.

Outlook:

Looking back at an extraordinary year, North Asia handled the pandemic significantly better than other parts of the world, and this was largely reflected in the outperformance of the MSCI Emerging Markets Asia Index from the March lows versus the rest of emerging markets. When considering this outperformance, it is important to remember that equities are fundamentally an anticipatory asset class: What has happened is less important than what is likely to happen and how fast potential changes may happen.

In the year ahead, we will continue to look for good investment opportunities across a broad swath of geographies including Southeast Asia, Russia and Brazil. In all markets, we believe fundamental research is the name of the game. We find that China in particular is a market where looking beyond the leading companies could prove fruitful to active investors. The incoming Biden administration in the U.S. may decrease the vitriol and unpredictability that has existed between the U.S. and China. A more predictable relationship is a positive development for markets globally. Risks in 2021 include the potential for an uneven global economic recovery, but we are also focused on political and ESG risks. In terms of currency moves, the consensus view is for a weakening U.S. dollar versus many emerging market currencies.

Thematically, we are thinking in terms of a re-opening and the “next normal.” The key is to separate companies that artificially benefit from the pandemic from companies where long-term fundamentals have been catalytically charged by it. We are encouraged by the rapid scientific progress related to the vaccines. In the third quarter of 2020, many analysts were hoping for a vaccine with perhaps 50% effectiveness. So, distribution challenges aside, the announcement of multiple vaccines with 80%+ effectiveness during the fourth quarter should be seen as positive news. Strong local currencies and a re-opening of the world economy bode well for emerging markets to potentially offer attractive equity gains in 2021.

| | | | |

| |

| COUNTRY ALLOCATION (%)6,7 | |

| China/Hong Kong | | | 30.0 | |

| South Korea | | | 11.9 | |

| India | | | 11.2 | |

| Brazil | | | 6.3 | |

| Taiwan | | | 5.8 | |

| Russia | | | 5.4 | |

| Singapore | | | 3.3 | |

| Mexico | | | 3.2 | |

| Poland | | | 3.1 | |

| France | | | 2.6 | |

| Netherlands | | | 2.0 | |

| United Kingdom | | | 1.8 | |

| Indonesia | | | 1.7 | |

| Canada | | | 1.6 | |

| Philippines | | | 1.3 | |

| Peru | | | 1.3 | |

| Argentina | | | 1.3 | |

| South Africa | | | 1.1 | |

| Vietnam | | | 0.7 | |

| Cyprus | | | 0.4 | |

| Cash and Other Assets, Less Liabilities | | | 4.0 | |

| | | | |

| |

| SECTOR ALLOCATION (%)7 | |

| Information Technology | | | 19.3 | |

| Consumer Discretionary | | | 18.6 | |

| Financials | | | 17.7 | |

| Communication Services | | | 9.0 | |

| Materials | | | 6.7 | |

| Health Care | | | 6.6 | |

| Energy | | | 5.2 | |

| Consumer Staples | | | 5.0 | |

| Industrials | | | 4.0 | |

| Real Estate | | | 3.9 | |

| Cash and Other Assets, Less Liabilities | | | 4.0 | |

| | | | |

| |

| MARKET CAP EXPOSURE (%)7 | |

| Mega Cap (over $25B) | | | 57.4 | |

| Large Cap ($10B–$25B) | | | 18.6 | |

| Mid Cap ($3B–10B) | | | 12.1 | |

| Small Cap (under $3B) | | | 7.8 | |

| Cash and Other Assets, Less Liabilities | | | 4.0 | |

| 6 | Not all countries where the Fund may invest are included in the benchmark index. |

| 7 | Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent, so the values may not sum to 100% due to rounding. Country allocations and percentage values may be derived from different data sources and may not be consistent with other Fund literature. |

Matthews Emerging Markets Equity Fund

December 31, 2020

Schedule of Investmentsa

COMMON EQUITIES: 90.2%

| | | | | | | | |

| | | Shares | | | Value | |

| | |

| CHINA/HONG KONG: 30.0% | | | | | | | | |

Tencent Holdings, Ltd. | | | 20,200 | | | | $1,453,467 | |

| | |

AIA Group, Ltd. | | | 108,600 | | | | 1,323,413 | |

| | |

Alibaba Group Holding, Ltd.b | | | 37,700 | | | | 1,096,487 | |

| | |

Ping An Insurance Group Co. of China, Ltd. A Shares | | | 67,100 | | | | 897,912 | |

| | |

Midea Group Co., Ltd. A Shares | | | 56,400 | | | | 849,407 | |

| | |

Bilibili, Inc. ADRb | | | 9,800 | | | | 840,056 | |

| | |

Yum China Holdings, Inc. | | | 13,900 | | | | 793,551 | |

| | |

Wuxi Biologics Cayman, Inc.b,c,d | | | 59,000 | | | | 782,419 | |

| | |

Techtronic Industries Co., Ltd. | | | 50,000 | | | | 714,671 | |

| | |

Alibaba Group Holding, Ltd. ADRb | | | 2,800 | | | | 651,644 | |

| | |

Anhui Conch Cement Co., Ltd. A Shares | | | 81,400 | | | | 647,105 | |

| | |

Lepu Medical Technology Beijing Co., Ltd. A Shares | | | 154,242 | | | | 644,763 | |

| | |

JD.com, Inc. ADRb | | | 6,600 | | | | 580,140 | |

| | |

JD Health International, Inc.b,c,d | | | 29,400 | | | | 568,853 | |

| | |

China International Capital Corp., Ltd. H Sharesb,c,d | | | 206,000 | | | | 558,517 | |

| | |

Estun Automation Co., Ltd. A Sharesb | | | 117,000 | | | | 537,070 | |

| | |

Jiumaojiu International Holdings, Ltd.b,c,d | | | 161,000 | | | | 490,584 | |

| | | | | | | | |

Total China/Hong Kong | | | | | | | 13,430,059 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| INDIA: 11.2% | | | | | | | | |

Kotak Mahindra Bank, Ltd.b | | | 33,183 | | | | 906,914 | |

| | |

Infosys, Ltd. ADR | | | 43,100 | | | | 730,545 | |

| | |

HDFC Bank, Ltd. ADRb | | | 9,700 | | | | 700,922 | |

| | |

Reliance Industries, Ltd. | | | 22,763 | | | | 619,357 | |

| | |

Colgate-Palmolive India, Ltd. | | | 25,684 | | | | 550,933 | |

| | |

Aditya Birla Capital, Ltd.b | | | 436,712 | | | | 508,062 | |

| | |

PI Industries, Ltd. | | | 16,884 | | | | 507,694 | |

| | |

Dr. Reddy’s Laboratories, Ltd. ADR | | | 6,800 | | | | 484,772 | |

| | | | | | | | |

Total India | | | | | | | 5,009,199 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| BRAZIL: 6.3% | | | | | | | | |

Banco BTG Pactual SA | | | 38,400 | | | | 694,035 | |

| | |

Vale SA ADR | | | 39,100 | | | | 655,316 | |

| | |

Pagseguro Digital, Ltd. Class Ab | | | 10,300 | | | | 585,864 | |

| | |

Hapvida Participacoes e Investimentos SAc,d | | | 158,500 | | | | 467,615 | |

| | |

Magazine Luiza SA | | | 91,200 | | | | 437,319 | |

| | | | | | | | |

Total Brazil | | | | | | | 2,840,149 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| SOUTH KOREA: 6.1% | | | | | | | | |

LG Household & Health Care, Ltd. | | | 510 | | | | 761,188 | |

| | |

Hugel, Inc.b | | | 3,372 | | | | 583,375 | |

| | |

Macquarie Korea Infrastructure Fund | | | 50,756 | | | | 497,990 | |

| | |

Kia Motors Corp. | | | 7,876 | | | | 453,790 | |

| | |

NAVER Corp. | | | 1,614 | | | | 435,085 | |

| | | | | | | | |

Total South Korea | | | | | | | 2,731,428 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| TAIWAN: 5.8% | | | | | | | | |

Taiwan Semiconductor Manufacturing Co., Ltd. | | | 138,000 | | | | 2,610,611 | |

| | | | | | | | |

Total Taiwan | | | | | | | 2,610,611 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| RUSSIA: 5.8% | | | | | | | | |

LUKOIL PJSC ADR | | | 14,063 | | | | 956,467 | |

| | |

Novatek PJSC GDRd | | | 4,556 | | | | 741,934 | |

| | |

Yandex N.V. Class Ab | | | 10,500 | | | | 730,590 | |

| | |

Polymetal International PLC | | | 7,700 | | | | 177,256 | |

| | | | | | | | |

Total Russia | | | | | | | 2,606,247 | |

| | | | | | | | |

| | | | | | | | |

| | | Shares | | | Value | |

| | |

| MEXICO: 3.8% | | | | | | | | |

Prologis Property Mexico SA de CV, REIT | | | 380,638 | | | | $853,875 | |

| | |

Grupo Aeroportuario del Sureste S.A.B. de CV. ADRb | | | 3,400 | | | | 560,762 | |

| | |

Fresnillo PLC | | | 18,347 | | | | 283,380 | |

| | | | | | | | |

Total Mexico | | | | | | | 1,698,017 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| SINGAPORE: 3.3% | | | | | | | | |

CapitaLand, Ltd. | | | 366,000 | | | | 908,145 | |

| | |

Sea, Ltd. ADRb | | | 2,800 | | | | 557,340 | |

| | | | | | | | |

Total Singapore | | | | | | | 1,465,485 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| POLAND: 3.1% | | | | | | | | |

Allegro.eu SAb,c,d | | | 30,763 | | | | 697,493 | |

| | |

LiveChat Software SA | | | 24,646 | | | | 692,730 | |

| | | | | | | | |

Total Poland | | | | | | | 1,390,223 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| FRANCE: 2.6% | | | | | | | | |

LVMH Moet Hennessy Louis Vuitton SE | | | 1,836 | | | | 1,149,339 | |

| | | | | | | | |

Total France | | | | | | | 1,149,339 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| NETHERLANDS: 2.0% | | | | | | | | |

Heineken N.V. | | | 8,147 | | | | 907,893 | |

| | | | | | | | |

Total Netherlands | | | | | | | 907,893 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| INDONESIA: 1.7% | | | | | | | | |

PT Bank Rakyat Indonesia Persero | | | 2,488,300 | | | | 739,780 | |

| | | | | | | | |

Total Indonesia | | | | | | | 739,780 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| ZAMBIA: 1.6% | | | | | | | | |

First Quantum Minerals, Ltd. | | | 40,300 | | | | 723,431 | |

| | | | | | | | |

Total Zambia | | | | | | | 723,431 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| PERU: 1.3% | | | | | | | | |

Credicorp, Ltd. | | | 3,600 | | | | 590,472 | |

| | | | | | | | |

Total Peru | | | | | | | 590,472 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| ARGENTINA: 1.3% | | | | | | | | |

Globant SAb | | | 2,700 | | | | 587,547 | |

| | | | | | | | |

Total Argentina | | | | | | | 587,547 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| PHILIPPINES: 1.3% | | | | | | | | |

Wilcon Depot, Inc. | | | 1,602,300 | | | | 565,079 | |

| | | | | | | | |

Total Philippines | | | | | | | 565,079 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| UNITED KINGDOM: 1.2% | | | | | | | | |

Avast PLCc,d | | | 73,218 | | | | 537,623 | |

| | | | | | | | |

Total United Kingdom | | | | | | | 537,623 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| SOUTH AFRICA: 1.1% | | | | | | | | |

Discovery, Ltd. | | | 46,887 | | | | 490,169 | |

| | | | | | | | |

Total South Africa | | | | | | | 490,169 | |

| | | | | | | | |

| | | | | | | | |

| | | |

| VIETNAM: 0.7% | | | | | | | | |

FPT Corp. | | | 120,914 | | | | 309,358 | |

| | | | | | | | |

Total Vietnam | | | | | | | 309,358 | |

| | | | | | | | |

| | | | | | | | |

| | |

| TOTAL COMMON EQUITIES | | | | 40,382,109 | |

| | | | | | | | |

(Cost $34,381,230) | | | | | | | | |

| | | | |

| matthewsasia.com | 800.789.ASIA | | | 13 | |

Matthews Emerging Markets Equity Fund

December 31, 2020

Schedule of Investmentsa (continued)

PREFERRED EQUITIES: 5.8%

| | | | | | | | |

| | | Shares | | | Value | |

|

| SOUTH KOREA: 5.8% | |

Samsung Electronics Co., Ltd., Pfd. | | | 38,490 | | | | $2,611,045 | |

| | | | | | | | |

Total South Korea | | | | | | | 2,611,045 | |

| | | | | | | | |

| | | | | | | | |

| | |

| TOTAL PREFERRED EQUITIES | | | | 2,611,045 | |

| | | | | | | | |

(Cost $1,638,350) | | | | | | | | |

| | | | | | | | |

| | |

| TOTAL INVESTMENTS: 96.0% | | | | 42,993,154 | |

(Cost $36,019,580) | | | | | | | | |

| | | | | | | | |

| | |

CASH AND OTHER ASSETS,

LESS LIABILITIES: 4.0% | | | | | | | 1,798,943 | |

| | | | | | | | |

| | |

NET ASSETS: 100.0% | | | | | | | $44,792,097 | |

| | | | | | | | |

| a | Certain securities were fair valued under the valuation policies approved by the Board of Trustees (Note 2-A). |

| b | Non-income producing security. |

| c | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. The security may be resold in transactions exempt from registration normally to qualified institutional buyers. The security has been determined to be liquid in accordance with procedures adopted by the Funds’ Board of Trustees. At December 31, 2020, the aggregate value is $4,103,104, which is 9.16% of net assets. |

| d | The securities may be resold to qualified foreign investors and foreign institutional buyers under Regulation S of the Securities Act of 1933. |

| ADR | American Depositary Receipt |

| GDR | Global Depositary Receipt |

| REIT | Real Estate Investment Trust |

See accompanying notes to financial statements.

| | | | |

| PORTFOLIO MANAGERS |

| |

| Teresa Kong, CFA | | |

Lead Manager | | |

| |

| Satya Patel | | Wei Zhang |

Co-Manager | | Co-Manager |

|

| FUND FACTS |

| | |

| | | Investor | | Institutional |

Ticker | | MAINX | | MINCX |

CUSIP | | 577125503 | | 577125602 |

Inception | | 11/30/11 | | 11/30/11 |

NAV | | $11.25 | | $11.25 |

Initial Investment | | $2,500 | | $100,000 |

Gross Expense Ratio1 | | 1.15% | | 1.00% |

After Fee Waiver and Reimbursement2 | | 1.12% | | 0.90% |

Portfolio Statistics | | | | |

Total # of Positions | | 42 | | |

Net Assets | |

$114.8 million | |

|

Modified Duration3 | | 4.3 | | |

Portfolio Turnover4 | | 39.7% | | |

Benchmark | | |

| 50% Markit iBoxx Asian Local Bond Index, 50% J.P. Morgan Asia Credit Index* |

OBJECTIVE

Total return over the long term with an emphasis on income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its net assets, which include borrowings for investment purposes, in debt and debt-related instruments issued by governments, quasi-governmental entities, supra-national institutions, and companies in Asia. Asia consists of all countries and markets in Asia, such as China and India, and includes developed, emerging, and frontier countries and markets in the Asian region. The Fund’s investments in debt securities may be denominated in any currency, may be of any quality or may be unrated, and may have no stated maturity or duration target.

Matthews Asia Total Return Bond Fund†

Portfolio Manager Commentary (unaudited)

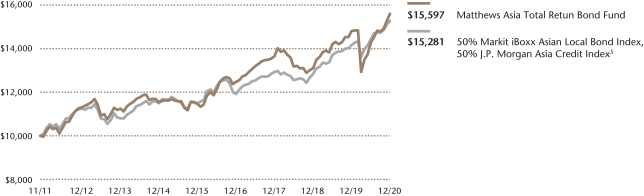

For the year ending December 31, 2020, the Matthews Asia Total Return Fund returned 5.36% (Investor Class) and 5.60% (Institutional Class), while its benchmark, the 50% Markit iBoxx Asian Local Bond/50% J.P. Morgan Asia Credit Index returned 7.95%. For the fourth quarter of the year, the Fund returned 5.41% (Investor Class) and 5.48% (Institutional Class) versus 3.70% for the Index.

Market Discussion:

Just as the COVID-19 pandemic re-shaped our daily lives, it also reshaped markets. Sectors that were traditionally considered risky, such as IT, became darlings as work-from-home became “safe” while traditionally “safe” sectors like gaming and real estate investment trusts (REITs—REITs are income-generating vehicles designed to pay out maximum amounts of their underlying cash flow as dividends to their unit holders) became “risky” as all sectors faced a new paradigm of virtual over bricks and mortar. The theme of safety, and safety over risky, dominated all asset classes. Investment grade outperformed high yield (A high-yield bond has a credit rating of below investment grade. Credit ratings are issued by three major credit rating agencies: S&P, Moody’s and Fitch. If the bond is rated AAA to BBB-, then it is considered investment grade. If it is BBB- to C-, it is considered to be high yield. If it’s below C-, it’s a defaulted bond. Issuers with lower bond ratings and higher default risks need to offer higher yields to compensate for the higher risk.), developed markets (DM) rates outperformed emerging markets (EM) rates, gold outperformed copper and oil. Within Asia high yield, companies with little liquidity risks outperformed those with more murky stories. The equity market was no different, favoring safe themes such as companies that benefited from stay-at-home or tech names that benefited from secular growth trends. Growth vastly outperformed value, with the S&P 500 Growth Index returning 20% for the first three quarters of 2020 compared to the S&P 500 Value Index which returned -14%, a gap of 34%. Growth represented safety while value represented risk as cyclical companies were the most affected by the pandemic.

In the fourth quarter, as people grew weary of continued lock-downs, the market charted a new direction. With the announcement of successful vaccine trials, the mood turned decidedly risk-on. High yield outperformed investment grade, EM (including Asia) outperformed U.S. equities, local currencies rose versus the U.S. dollar, and U.S. treasury yields rose. Up until then, these fourth quarter outperformers had been among the biggest losers of the year.

Within Asian local bonds, the Philippines was the top performer in 2020, followed by Taiwan, Malaysia, and China. However, in the fourth quarter, the top performers were Indonesia and Thailand which were hit hard by the pandemic due to their reliance on tourism, as well as commodities exports in the case of Indonesia. China bonds benefited from the country’s relative success in virus containment, greater government measures to open up the local bond market to foreign investment, as well as greater foreign investment interest due to the decline in rates across the DM world.

Performance Contributors and Detractors:

The Fund’s top contribution to performance came from our overweight to U.S. dollar-denominated high yield credit and allocation to local-currency Chinese credit. However, an underweight to local rates, such as Hong Kong, Singapore and India, as well as an underweight to U.S. dollar-denominated investment grade credit detracted from performance. By currency, our overweights in Chinese renminbi, Singaporean dollar and South Korean won contributed positively, while exposures in Indian rupee and Indonesian rupiah detracted from performance.

The top contributors to Fund performance during the fourth quarter came from U.S. dollar-denominated high yield credit. In terms of country allocation, exposures to South Korea currency and Indonesian local bonds contributed. The top detractors came from China and India, where we have a slight underweight in terms of rates. Currency contributed positively to performance in the quarter, led by our overweights in Chinese

(continued)

| † | The Fund’s name changed from Matthews Asia Strategic Income Fund to Matthews Asia Total Return Bond Fund on January 31, 2020. |

| * | Effective January 31, 2020, the Fund changed its benchmark to a blended benchmark comprised of 50% Markit iBoxx Asian Local Bond Index and 50% J.P. Morgan Asia Credit Index. Prior to January 31, 2020, the Fund’s benchmark was the Markit iBoxx Asian Local Bond Index. Matthews believes that the blended benchmark is more appropriate in light of the Fund’s current investment strategy. The Markit iBoxx Local Bond Index performance reflects the returns of the discontinued predecessor HSBC Asia Local Bond Index up to December 31, 2012 and the returns of the successor Markit iBoxx Local Bond Index thereafter. |

| 1 | Actual 2020 expense ratios. |

| 2 | Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (i.e., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g. custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. Pursuant to this agreement, any amount waived for prior fiscal years with respect to the Fund is not subject to recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

| 3 | Modified duration measures the percent change in value of the fixed income portion of the portfolio in response to a 1% change in interest rates. In a multi-currency denominated portfolio with sensitivities to different interest rate regimes, modified duration will not accurately reflect the change in value of the overall portfolio from a change in any one interest rate regime. |

| 4 | The lesser of fiscal year 2020 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities. |

| | | | |

| matthewsasia.com | 800.789.ASIA | | | 15 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

PERFORMANCE AS OF DECEMBER 31, 2020 | | | | | | | | | | | | | | | | | | |

| | | | | | | | | Average Annual Total Returns | | | | |

| | | 3 Months | | | 1 Year | | | 3 Years | | | 5 Years | | | Since

Inception | | | Inception

Date | |

| Investor Class (MAINX) | | | 5.41% | | | | 5.36% | | | | 4.54% | | | | 6.35% | | | | 5.01% | | | | 11/30/11 | |

| Institutional Class (MINCX) | | | 5.48% | | | | 5.60% | | | | 4.77% | | | | 6.58% | | | | 5.23% | | | | 11/30/11 | |

| 50% Markit iBoxx Asian Local Bond Index, 50% J.P. Morgan Asia Credit Index5 | | | 3.70% | | | | 7.95% | | | | 5.74% | | | | 5.87% | | | | 4.78% | | | | | |

| Markit iBoxx Asian Local Bond Index5 | | | 5.61% | | | | 9.55% | | | | 5.93% | | | | 6.07% | | | | 3.75% | | | | | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund’s fees and expenses had not been waived. For the Fund’s most recent month-end performance visit matthewsasia.com.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| INCOME DISTRIBUTION HISTORY | |

| | | 2020 | | | | | | 2019 | |

| | Jan. | | | Feb. | | | Mar. | | | Apr. | | | May | | | June | | | July | | | Aug. | | | Sept. | | | Oct. | | | Nov. | | | Dec. | | | Total | | | | | | Q1 | | | Q2 | | | Q3 | | | Q4 | | | Total | |

| Investor (MAINX) | | | n.a. | | | $ | 0.06 | | | $ | 0.04 | | | $ | 0.00 | | | $ | 0.03 | | | $ | 0.04 | | | $ | 0.03 | | | $ | 0.04 | | | $ | 0.04 | | | $ | 0.04 | | | $ | 0.03 | | | $ | 0.08 | | | $ | 0.44 | | | | | | | $ | 0.08 | | | $ | 0.10 | | | $ | 0.14 | | | $ | 0.12 | | | $ | 0.44 | |

| Inst’l (MINCX) | | | n.a. | | | $ | 0.07 | | | $ | 0.04 | | | $ | 0.01 | | | $ | 0.03 | | | $ | 0.04 | | | $ | 0.04 | | | $ | 0.04 | | | $ | 0.04 | | | $ | 0.04 | | | $ | 0.04 | | | $ | 0.09 | | | $ | 0.46 | | | | | | | $ | 0.09 | | | $ | 0.11 | | | $ | 0.14 | | | $ | 0.12 | | | $ | 0.46 | |

Note: This table does not include capital gains distributions. Totals may differ by $0.02 due to rounding. For income distribution history, visit matthewsasia.com.

| | | | |

| | | |

30-DAY YIELD: Investor Class: 4.80% (4.68% excluding waivers) Institutional Class: 5.04% (4.82% excluding waivers) The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 12/31/20, expressed as an annual percentage rate based on the Fund’s share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund’s rate of investment income, and it may not equal the Fund’s actual income distribution rate. Source: BNY Mellon Investment Servicing (US) Inc. | | | | YIELD TO WORST: 6.27% Yield to worst is the lowest yield that can be received on a bond assuming that the issuer does not default. It is calculated by utilizing the worst case assumptions for a bond with respect to certain income-reducing factors, including prepayment, call or sinking fund provisions. It does not represent the yield that an investor should expect to receive. Past yields are no guarantee of future yields. Source: FactSet Research Systems |

GROWTH OF A HYPOTHETICAL $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

| | 5 | It is not possible to invest directly in an index. Source: Index data from HSBC, Markit iBoxx and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 93 for index definitions. Effective January 31, 2020, the Fund changed its benchmark to a blended benchmark comprised of 50% Markit iBoxx Asian Local Bond Index and 50% J.P. Morgan Asia Credit Index. Prior to January 31, 2020, the Fund’s benchmark was the Markit iBoxx Asian Local Bond Index. Matthews believes that the blended benchmark is more appropriate in light of the Fund’s current investment strategy. The Markit iBoxx Asian Local Bond Index performance reflects the returns of the discontinued predecessor HSBC Asian Local Bond Index up to December 31, 2012 and the returns of the successor Markit iBoxx Asian Local Bond Index thereafter. |

| | | | | | | | |

| | | | |

| TOP TEN HOLDINGS | | | | | | | |

| | | Sector | | Currency | | % of Net Assets | |

| Network i2i, Ltd., 5.650%, 04/15/2068 | | Communication Services | | U.S. Dollar | | | 5.7% | |

| Wanda Properties International Co., Ltd., 7.250%, 01/29/2024 | | Real Estate | | U.S. Dollar | | | 4.7% | |

| Viet Nam Debt & Asset Trading Corp., 1.000%, 10/10/2025 | | Financials | | U.S. Dollar | | | 4.7% | |