UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07185 | |||||||

| ||||||||

Morgan Stanley Select Dimensions Investment Series | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

522 Fifth Avenue, New York, New York |

| 10036 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Randy Takian 522 Fifth Avenue, New York, New York 10036 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 212-296-6990 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31, 2008 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2008 |

| ||||||

Item 1 - Report to Shareholders

MORGAN STANLEY

SELECT DIMENSIONS INVESTMENT SERIES

Annual Report

DECEMBER 31, 2008

The Portfolios are intended to be the funding vehicle for variable annuity contracts and variable life insurance policies offered by the separate accounts of certain life insurance companies.

Morgan Stanley Select Dimensions Investment Series

Table of Contents

| Letter to the Shareholders | 1 | ||||||||||

| Expense Example | 20 | ||||||||||

| Portfolio of Investments: | |||||||||||

| Money Market | 25 | ||||||||||

| Flexible Income | 28 | ||||||||||

| Balanced | 50 | ||||||||||

| Global Infrastructure | 66 | ||||||||||

| Dividend Growth | 73 | ||||||||||

| Equally-Weighted S&P 500 | 77 | ||||||||||

| Capital Growth | 89 | ||||||||||

| Focus Growth | 92 | ||||||||||

| Capital Opportunities | 95 | ||||||||||

| Global Equity | 98 | ||||||||||

| Mid Cap Growth | 102 | ||||||||||

| Financial Statements: | |||||||||||

| Statements of Assets and Liabilities | 106 | ||||||||||

| Statements of Operations | 108 | ||||||||||

| Statements of Changes in Net Assets | 110 | ||||||||||

| Notes to Financial Statements | 118 | ||||||||||

| Financial Highlights | 138 | ||||||||||

| Report of Independent Registered Public Accounting Firm | 146 | ||||||||||

| U.S. Privacy Policy Notice | 147 | ||||||||||

| Trustee and Officer Information | 149 | ||||||||||

| Federal Tax Notice | 155 | ||||||||||

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008

Dear Shareholder,

By all accounts, 2008 was one of the worst years in the history of the financial markets. The credit crisis that originated in the U.S. with the collapse of the subprime mortgage market quickly spread across the globe as it became apparent a growing number of financial entities were exposed through their portfolios. Market volatility rose as investors became increasingly concerned about the health of the financial sector. These concerns grew to a full panic by September when the U.S. government took Fannie Mae and Freddie Mac, the two bedrock government-sponsored entities that own or guarantee about half of the nation's outstanding mortgage debt, into receivership, and Lehman Brothers filed for bankruptcy. Risk aversion soared, banks became reluctant to lend and the credit markets seized. As a growing number of large financial institutions in the U.S. and abroad were nationalized, forced to merge, or failed entirely, investor co nfidence plummeted, sparking a dramatic sell off in the markets that accelerated at an alarming pace.

Evidence of slowing economic growth exacerbated the market's deterioration. Concerns about inflation due to rising food and energy costs in the first half of the year were replaced with fears of recession and deflation in the latter months as oil prices fell, the housing market continued to diminish, unemployment rose and consumer spending declined. Although governments and central banks around the world responded with unprecedented monetary and fiscal stimulus measures, their efforts brought little relief to slowing economies and the fear-driven markets. As year end approached, economic indicators continued to weaken and market volatility remained high as investor confidence was further undermined by news that most of the developed world, as well as several emerging economies, had fallen into recession.

Domestic Equity Overview

The credit crisis, the presumed (and eventually confirmed) recession, and the reshuffling of Wall Street led the U.S. equity market to one of its worst years since the Great Depression. The S&P 500® Index, a widely cited gauge of U.S. stock market performance, fell 37.00% in the year ended December 31, 2008. Volatility was widespread across all sectors, market capitalization and style segments, as investors fled equities for relatively safer U.S. Treasuries and cash.

All ten sectors within the S&P 500 Index had double-digit negative returns during the period. The weakest group was not surprisingly financials, given the sector's historic (in magnitude and speed) bankruptcies, rescues, and mergers during the period. The economically sensitive materials and information technology sectors were also among the bottom performing sectors. The top performers were the consumer staples, health care and utilities sectors, which are traditionally viewed as defensive sectors, or those less affected by slowing economic conditions.

1

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

Small-cap stocks (as measured by the Russell 2000® Index) performed slightly better than mid- and large-cap stocks, and value stocks beat growth stocks. However, in this case, outperformance only meant a lesser relative decline.

Fixed Income Overview

Although the bond market fared better than equities during the year, performance in most sectors was disappointing. The volatile and risk-averse environment led to a flight to quality as investors shunned riskier assets in favor of the relative safe haven of government bonds and cash. This fueled a prolonged rally in the U.S. Treasury market and a dramatic decline in yields. As a result, Treasury securities were the top-performers in the U.S. market, outpacing all sectors of the stock and bond markets. Within U.S. investment grade fixed income, corporate bonds turned in the weakest performance. This segment of the market was dragged down by the financial sector, which was at the epicenter of the credit crisis and experienced the greatest stress amid the reshaping of the financial industry. Not surprisingly given the environment, high-yield bonds underperformed investment-grade bonds, with all sectors posting negative returns for the year. Within high yield, real estate investment trusts (REITs) was the worst performing sector while the environmental sector turned in the best performance. Fixed income markets outside the U.S. experienced similar trends with developed government bond markets outpacing those of emerging markets.

International Equity Overview

For the most part, international equities began the year seemingly insulated from the U.S. subprime mortgage crisis. However, the credit crisis quickly spread around the world, sapping liquidity and dampening the global economy. Investor sentiment turned decidedly negative as it became apparent that a global recession would be deeper and possibly longer than initially thought. Risk aversion increased dramatically, prompting a downward spiral in equity prices in markets across the world.

Volatility plagued all markets, with both developed markets and emerging markets posting substantial declines in 2008. Developed markets outperformed emerging markets, but only in the sense that the developed world's relative declines were less severe. The U.S. and Japan were among the better relative performers, while emerging Eastern Europe was among the worst.

By the end of the period, most of the developed world had entered into recession, and outlooks remained gloomy. The U.S. and Europe grappled with a wave of negative economic data, while Japan continued to suffer from weak domestic demand and falling exports. The Asia Pacific region excluding Japan dealt with the impact of languishing growth both in the developed world and in China, which until then had served as the region's economic engine.

2

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

Balanced Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Balanced Portfolio Class X shares produced a total return of -22.51%, outperforming the Russell 1000® Value Index ("the Russell Index"), which returned -36.85%, and underperforming the Barclays Capital (formerly Lehman Brothers) U.S. Government/Credit Index ("the Barclays Index"), which returned 5.70%. For the same period, the Portfolio's Class Y shares returned -22.64%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

All sectors in the Russell Index had negative absolute returns for the period. Although the same was true for the Portfolio, on a relative basis the Portfolio lost less value than the Index. Specifically, stock selection in the financial services sector was a positive contributor to relative performance. The Portfolio had better relative performance in diversified financial services, due to a holding that was more resilient than many of its peers because of its lower subprime mortgage exposure, and in property and casualty insurance. An overweight position in the consumer staples sector was another positive relative contributor, due to a food and staples retailer that benefited from prudent inventory management and scaling down its growth strategy. Stock selection in the materials sector

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (22.51 | )% | 1.71 | % | 2.55 | % | 6.49 | % | |||||||||||

| Class Y | (22.64 | )% | 1.46 | % | — | 2.83 | % | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® Index companies with lower price-to-book ratios and lower expected growth values. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

(3) The Barclays Capital (formerly Lehman Brothers) U.S. Government/Credit Index tracks the performance of government and corporate obligations, including U.S. government agency and Treasury securities and corporate and Yankee bonds. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

3

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

helped the Portfolio sidestep some of the sector's volatility. The Portfolio avoided exposure to the heavily commodity-oriented companies that declined strongly when commodity prices began to fall and instead held a position in a gold mining company which held up better than other metals and mining companies in the difficult environment.

In contrast, the Portfolio's underweight positions in the energy and utilities sectors were relative detractors. Although the sectors had negative returns for the period, they were among the better performing sectors in the Russell Index. Stock selection in the consumer discretionary sector was an area of weakness, as retail holdings were hurt by falling consumer spending and media holdings saw declining advertising revenues.

In the fixed income portfolio, the primary detractor relative performance was an allocation to non-agency mortgage securities, which are not represented in the Barclays Index. Forced selling, coupled with rising mortgage delinquencies and falling home prices, pressured this segment of the market, causing valuations to decline. By year end, the Portfolio's exposure to non-agency mortgages was eliminated.

The Portfolio's yield curve positioning also detracted from relative performance. Our yield curve strategy involved the use of Treasury futures and zero-coupon swap contracts. In the fourth quarter of the year, the performance of the swap contracts waned, hindering the performance of the overall position.

The Portfolio maintained an underweight corporate credit position for most of the reporting period, which boosted performance as credit spreads widened significantly, causing prices to decline. Additionally, an underweight to commercial mortgage-backed securities (CMBS) was extremely helpful as CMBS spreads rose by a staggering amount in the fourth quarter. An underweight allocation to agency debentures further enhanced performance as spreads in the sector continued to widen.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

4

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

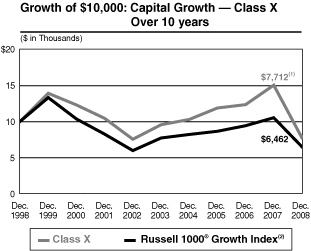

Capital Growth (formerly Growth) Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Capital Growth Portfolio Class X shares produced a total return of -48.70%, underperforming the Russell 1000® Growth Index ("the Index"), which returned -38.44%. For the same period, the Portfolio's Class Y shares returned -48.81%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

Relative performance was largely hampered by stock selection in the consumer discretionary sector, despite the benefit of an overweight there. Within the sector, commercial services and hotel/motel holdings were the leading detractors. Both stock selection and an overweight in the financial services sector had a negative impact on relative performance, led by diversified financial services holdings. Finally, stock selection in the technology sector was an area of weakness, solely due to communications technology holdings.

In contrast, stock selection in the other energy sector was the largest positive contributor to relative performance, although an overweight in the sector slightly offset some of the relative gain. Here, natural gas producers drove performance. Both stock selection and an overweight in autos and transportation added relative value, mainly due to

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (48.70 | )% | (4.16 | )% | (2.57 | )% | 2.98 | % | |||||||||||

| Class Y | (48.81 | )% | (4.39 | )% | — | (7.90 | )% | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® Index companies with higher price-to-book ratios and higher forecasted growth values. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

5

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

miscellaneous transportation (logistics) holdings. Finally, the Portfolio benefited from stock selection in the materials and processing sector, especially in steel companies.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

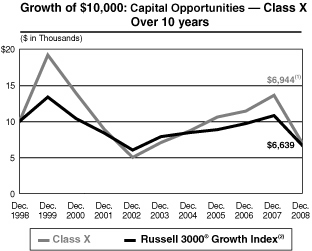

Capital Opportunities Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Capital Opportunities Portfolio Class X shares produced a total return of -49.04%, underperforming the Russell 3000® Growth Index ("the Index"), which returned -38.44%. For the same period, the Portfolio's Class Y shares returned -49.15%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

Relative performance was hampered by stock selection in the consumer discretionary sector, despite the benefit of an overweight there. Within the sector, commercial services and consumer electronics holdings were the leading detractors. Stock selection in the technology sector was an area of weakness, chiefly in communications technology holdings. Finally, stock selection in the financial services sector had a negative impact on relative performance, primarily due to diversified financial services holdings.

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (49.04 | )% | (0.28 | )% | (3.58 | )% | (1.35 | )% | |||||||||||

| Class Y | (49.15 | )% | (0.52 | )% | — | (12.99 | )% | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Russell 3000® Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000® Index companies with higher price-to-book ratios and higher forecasted growth values. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of January 21, 1997 for Class X and July 24, 2000 for Class Y.

6

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

In contrast, other positions were favorable to relative performance. Although an overweight to the other energy sector hurt relative performance, stock selection there more than offset the negative influence. Within the sector, holdings in natural gas producers boosted relative performance. Stock selection and an overweight in the autos and transportation sector were also additive to relative performance, led by miscellaneous transportation (logistics) holdings. Finally, an avoidance of the producer durables sector also benefited relative results.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

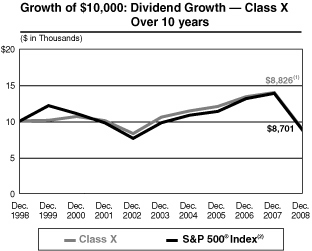

Dividend Growth Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Dividend Growth Portfolio Class X shares produced a total return of -36.60%, modestly outperforming the S&P 500® Index ("the Index"), which returned -37.00%. For the same period, the Portfolio's Class Y shares returned -36.76%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

The main contributors to relative performance were stocks in the financials, industrials, and technology

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (36.60 | )% | (3.41 | )% | (1.24 | )% | 6.14 | % | |||||||||||

| Class Y | (36.76 | )% | (3.66 | )% | — | (0.94 | )% | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Standard & Poor's 500® Index (S&P 500®) measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest dire ctly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

7

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

sectors. In addition, overweight positions in the health care and technology sectors further added value to the Portfolio's relative performance.

The main detractors from relative performance were stocks in the health care and energy sector. The Portfolio was also negatively affected by an underweight in the telecommunication services sector.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

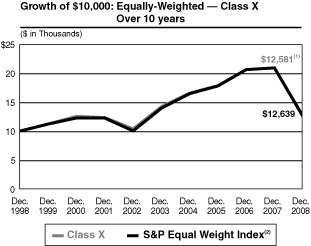

Equally-Weighted S&P 500 Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Equally-Weighted S&P 500 Portfolio Class X shares produced a total return of -40.02%, underperforming the Standard & Poor's Equal Weight Index ("the Index"), which returned -39.72%. For the same period, the Portfolio's Class Y shares returned -40.19%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

The year 2008 was one of the worst years in the history of the financial markets. Over the course of the year, what started as a housing crisis transformed through mortgage-backed securities into a financial crisis, which eventually spilled over into the real

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the eff ect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (40.02 | )% | (2.40 | )% | 2.32 | % | 7.12 | % | |||||||||||

| Class Y | (40.19 | )% | (2.66 | )% | — | 0.98 | % | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Standard & Poor's Equal Weight Index (S&P EWI) is the equally-weighted version of the widely regarded S&P 500® Index, which measures 500 leading companies in leading U.S. industries. The S&P EWI has the same constituents as the capitalization-weighted S&P 500® Index, but each company in the S&P EWI is allocated a fixed weight, rebalancing quarterly. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

8

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

economy. Credit tightening along with the collapse or essential takeover of some financial institutions caused massive dislocations in financial markets and incredibly high volatility.

Within the Index and therefore the Portfolio, all ten sectors had negative absolute performance during the 12-month period, with double-digit negative returns. The worst performing sectors were financials, energy, information technology, materials and consumer discretionary. Not surprisingly, credit market turmoil and other developments in the capital markets most severely impacted financial companies, resulting in a huge negative return. Collapsing commodity prices in 2008 led to the underperformance of the materials and energy sectors as well. At the same time, global recession, higher unemployment and declining consumer confidence led to the negative performance of consumer-oriented stocks.

The underperformance was pervasive, affecting all styles and market capitalization segments as investors tried to move out of equities into relatively safe assets. On an individual stock basis, the worst detractors in the overall portfolio were dominated by financial stocks.

Since the Index and the Portfolio are equally-weighted, the overall contribution of each sector reflects its absolute performance. As such, utilities and consumer staples were the best performing sectors, while financials and information technology were the largest detractors.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

9

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

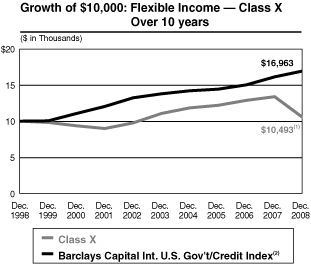

Flexible Income Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Flexible Income Portfolio Class X shares produced a total return of -21.62%, underperforming the Barclays Capital (formerly Lehman Brothers) Intermediate U.S. Government/Credit Index ("the Index"), which returned 5.08%. For the same period, the Portfolio's Class Y shares returned -21.89%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

The overwhelming detractor from the Portfolio's relative performance was an allocation to non-agency mortgage securities, which are not included in the Index. Forced selling, coupled with rising mortgage delinquencies and falling home prices, pressured the non-agency mortgage sector, causing valuations to decline. Over the course of the period, we reduced the Portfolio's allocation to the sector, eliminating it entirely by year end.

To a lesser extent, the Portfolio's yield curve positioning also detracted from relative performance. Our yield curve strategy involved the use of Treasury futures and zero-coupon swap contracts. In the fourth quarter of the year the swap contracts lost value, hindering the performance of the overall position.

Within the corporate sector, the Portfolio held an underweight relative to the Index in

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (21.62 | )% | (1.06 | )% | 0.48 | % | 2.40 | % | |||||||||||

| Class Y | (21.89 | )% | (1.31 | )% | — | 0.56 | % | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Barclays Capital (formerly Lehman Brothers) Intermediate U.S. Government/Credit Index tracks the performance of U.S. government and corporate obligations, including U.S. government agency and Treasury securities, and corporate and Yankee bonds with maturities of 1 to 10 years. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

10

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

investment-grade credits for much of the period. This positioning benefited relative performance as credit spreads widened significantly. In the third quarter of the year, the position was brought to neutral. However, the Portfolio also had a small allocation to high yield corporate credits, which are not included in the Index.

This allocation detracted slightly from relative performance. Lastly, an underweight allocation to agency debentures relative to the Index enhanced performance as spreads in the sector continued to widen.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

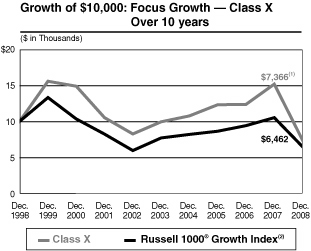

Focus Growth Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Focus Growth Portfolio Class X shares produced a total return of -51.43%, underperforming the Russell 1000® Growth Index ("the Index"), which returned -38.44%. For the same period, the Portfolio's Class Y shares returned -51.57%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

Relative performance was hampered by stock selection in the consumer discretionary sector, despite the benefit of an overweight there. Within the sector, commercial services and consumer electronics holdings were the leading detractors.

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (51.43 | )% | (5.81 | )% | (3.01 | )% | 5.05 | % | |||||||||||

| Class Y | (51.57 | )% | (6.05 | )% | — | (8.73 | )% | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® Index companies with higher price-to-book ratios and higher forecasted growth values. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

11

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

Stock selection and an overweight in the financial services sector had a negative impact on relative performance, primarily in diversified financial services holdings. Finally, stock selection in the technology sector was an area of weakness, solely due to communications technology holdings.

However, stock selection and an overweight in the autos and transportation sector were additive to relative performance, led by miscellaneous transportation (logistics) holdings. An avoidance of the producer durables sector also benefited relative results. An overweight in the utilities sector was the third largest contributor to relative performance, offsetting the negative influence of stock selection there.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

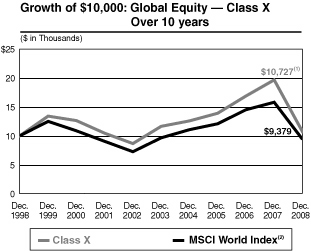

Global Equity Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Global Equity Portfolio Class X shares produced a total return of -45.56%, underperforming the MSCI World Index ("the Index"), which returned -40.71%. For the same period, the Portfolio's Class Y shares returned -45.73%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (45.56 | )% | (1.60 | )% | 0.70 | % | 3.80 | % | |||||||||||

| Class Y | (45.73 | )% | (1.86 | )% | — | (3.17 | )% | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Morgan Stanley Capital International (MSCI) World Index is a free float-adjusted market capitalization weighted index that is designed to measure the global equity market performance of developed markets. The term "free float" represents the portion of shares outstanding that are deemed to be available for purchase in the public equity markets by investors. The MSCI World Index currently consists of 23 developed market country indices. The performance of the Index is listed in U.S. dollars and assumes reinvestment of net dividends. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

12

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

The management team seeks to invest on a bottom-up basis, building a portfolio of securities that we believe are likely to generate consistent long-term earnings growth. While the team does not engage in top-down portfolio construction, the Portfolio's country and sector weights will have an impact on performance relative to the benchmark.

In 2008, the Portfolio's country and sector weights were substantial contributors to relative performance. An overweight allocation to Israel and underweights in Canada and Australia were particularly helpful, while the Portfolio was hurt by underweights in the U.S. and Japan, which were among the best performing markets in 2008. From a sector perspective, the Portfolio benefited from an overweight in health care (the best performing sector in the Index) and underweights in financials and materials (the worst performing sectors in the Index).

However, the positive influence of country and sector allocations was offset by poor stock selection. Particularly detrimental were stock selections in the U.S., Canada and the consumer staples sector. Stock selections in Japan, France, and the telecommunication services sector were slightly additive to relative returns.

Other factors which contributed to relative underperformance included the outperformance of developed markets relative to emerging markets. Although the team can invest up to 15% in emerging market securities to provide added diversification benefits, emerging market securities are not included in the Index. As such, the Portfolio was adversely affected by its exposure to weak performance from emerging markets positions while the Index was not. Additionally, relative performance was hampered by the outperformance of value stocks over growth stocks during the period. Because the team seeks to invest in companies that can generate long-term earnings growth, the Portfolio tends to have a growth bias to its investment style. This growth bias acted as a relative detractor from the Portfolio's performance in this reporting period.

There is no guarantee that any countries or sectors mentioned will continue to perform as discussed above or that securities in such countries or sectors will be held by the Portfolio in the future.

13

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

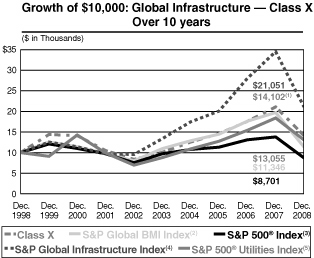

Global Infrastructure (formerly Utilities) Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Global Infrastructure Portfolio Class X shares produced a total return of -33.02%, outperforming the S&P Global BMI Index, which returned -42.42%, the S&P Global Infrastructure Index, which returned -38.98%, and the S&P 500® Index, which returned -37.00%, and underperforming the S&P 500® Utilities Index, which returned -28.98% . For the same period, the Portfolio's Class Y shares returned -33.19%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

All segments of the utilities sector, in which the Portfolio primarily invested through November 5, 2008, declined significantly during the period, with the independent power producers and energy traders segment and the gas utilities segment experiencing the greatest declines. Conversely, multi-utilities was the best-performing segment, followed by electric utilities. Overall, volatility levels in the utilities sector soared from approximately 15% early in the year to 70% in December. Nonetheless, in keeping with historical trends in highly volatile markets, utilities still outperformed the broad equity market (as measured by S&P 500® Utilities Index and S&P 500® Index, respectively).

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (33.02 | )% | 6.96 | % | 3.50 | % | 8.20 | % | |||||||||||

| Class Y | (33.19 | )% | 6.70 | % | — | (1.12 | )% | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Standard & Poor's Global BMI Index (S&P Global BMI Index) is a broad market index designed to capture exposure to equities in all countries in the world that meet minimum size and liquidity requirements. As of the date of this Report, there are approximately 11,000 index members representing 27 developed and 26 emerging market countries. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index. The Portfolio primary benchmark was changed in November 2008 from the S&P 500® Index to the S&P Global BMI Index to more accurately reflect the Portfolio investible universe.

(3) The Standard & Poor's 500® Index (S&P 500®) measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

(4) The Standard & Poor's Global Infrastructure Index (S&P Global Infrastructure Index) is designed to track performance of the stocks of 75 of the largest publicly listed infrastructure companies around the world including both developed and emerging markets. The Index includes companies involved in utilities, energy and transportation infrastructure; airport services; highways and rail tracks; marine ports and services; and electric, gas and water utilities. The Index was launched on November 16, 2001. Returns including periods prior to November 16, 2001 are calculated using the return data of the S&P Global BMI Index through November 16, 2001 and the return data of the S&P Global Infrastructure Index since November 16, 2001. The In dex is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index. The Portfolio's secondary benchmark was changed in November 2008 from the S&P 500® Utilities Index to the S&P® Global Infrastructure Index to more accurately reflect the Portfolio's investible universe.

(5) The Standard & Poor's 500® Utilities Index (S&P 500® Utilities Index) is an unmanaged, market capitalization weighted index consisting of utilities companies in the S&P 500® Index and is designed to measure the performance of the utilities sector. It includes reinvested dividends. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

14

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

For the period from January 1, 2008 through November 5, 2008, the primary contributor to performance relative to the S&P 500® Utilities Index was a significant underweight to electric utilities. Electric utilities lost considerable value and therefore the Portfolio's comparatively lower exposure was beneficial. Security selection in the multi-utilities segment was also additive to performance.

Other positions, however, were disadvantageous. The largest detractor from relative performance was the Portfolio's allocation to the telecommunications sector, which is not represented in the S&P 500® Utilities Index. The telecommunications sector was dragged down by poor results at several wireless companies and generally negative investor sentiment. Our positions in gas utilities and energy transportation also hindered relative performance.

Effective November 6, 2008, the Portfolio's investment focus transitioned from utilities to global infrastructure securities. The infrastructure sector also declined precipitously during the year in tandem with the broad equity markets, but for the period from November 6 through year end the infrastructure sector lost just slightly more than 4.5%. Of the three major components of the S&P 500® Global Infrastructure Index, utilities was the top-performer, followed by transportation and energy. The primary contributors to the Portfolio's performance relative to the S&P Global Infrastructure Index included strong security selection in the transportation segment. A relative underweight in energy was also beneficial as falling commodity prices later in the year hindered the segment's performance. Conversely, sector allocation in the telecommunications, multi-utilities and gas utilities segments detracted from re lative performance.

The Portfolio is managed by the Quantitative and Structured Solutions (QSS) team. The QSS equity management process blends best-in-class, sell-side fundamental research with an established quantitative portfolio construction process. The investment team's systematic approach strives to add excess return while targeting volatility and tracking error to help control risk.

As of year end, the Portfolio's transition to global infrastructure was complete. Given the transitioning, we believe portfolio performance in the latter months of the year is not necessarily indicative of the new strategy's long-term potential. That said, we look forward to the opportunities the new, broader investment focus affords us.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

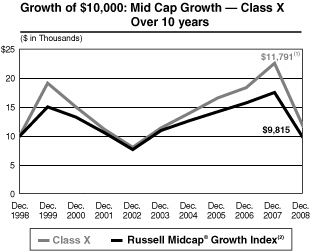

Mid Cap Growth (formerly Developing Growth) Portfolio

For the 12-month period ended December 31, 2008, Select Dimensions — Mid Cap Growth Portfolio Class X shares produced a total return of -48.06%, underperforming the Russell Midcap® Growth Index

15

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

("the Index"), which returned -44.32%. For the same period, the Portfolio's Class Y shares returned -48.20%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

Stock selection in the consumer discretionary sector had by far the largest negative impact on relative performance, despite the positive influence of an overweight there. The main detractors within the sector were holdings in commercial services and hotel/motel stocks. Stock selection in financial services was another relative detractor, which more than offset the benefit of an overweight in the sector. Here, diversified financial services stocks were the primary area of weakness. The third largest area of relative underperformance came from stock selection in the technology sector, where holdings in computer services software and systems lagged.

In contrast, stock selection in the other energy sector was the largest positive contributor to relative performance, although an underweight in the sector slightly offset some of the relative gain. Good relative performance was primarily due to natural gas producers. Both stock selection and an overweight in autos and transportation added relative value, driven by miscellaneous transportation (logistics) holdings. Finally, the Portfolio benefited from both stock selection and an

Performance data quoted represents past performance and is not predictive of future returns. Current performance may be lower or higher than the performance shown. Investment return and principal value will fluctuate. When you sell Portfolio shares, they may be worth less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance for Class Y shares will vary from the performance of Class X shares due to differences in expenses. Performance assumes reinvestment of all distributions for the underlying portfolio based on net asset value (NAV). It does not reflect the deduction of insurance expenses, an annual contract maintenance fee, or surrender charges. If performance information included the effect of these additional charges, the total returns would be lower.

| Average Annual Total Returns as of December 31, 2008 | |||||||||||||||||||

| 1 Year | 5 Years | 10 Years | Since Inception* | ||||||||||||||||

| Class X | (48.06 | )% | 0.52 | % | 1.66 | % | 6.81 | % | |||||||||||

| Class Y | (48.20 | )% | 0.26 | % | — | (4.71 | )% | ||||||||||||

(1) Ending value on December 31, 2008 for the underlying portfolio. This figure does not reflect the deduction of any account fees or sales charges.

(2) The Russell Midcap® Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with higher price-to-book ratios and higher forecasted growth values. The Index is unmanaged and its returns do not include any sales charges or fees. Such costs would lower performance. It is not possible to invest directly in an index.

* Inception dates of November 9, 1994 for Class X and July 24, 2000 for Class Y.

16

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

underweight in the producer durables sector. Within the sector, telecommunications equipment stocks were the strongest contributors.

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

Money Market Portfolio

An investment in a money market fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although money market funds seek to preserve the value of an investment at $1.00 per share, it is possible to lose money by investing in such funds.

As of December 31, 2008, Select Dimensions Money Market Portfolio had net assets of approximately $216 million with an average portfolio maturity of 27 days. For the seven-day period ended December 31, 2008, the Portfolio's Class X shares provided an effective annualized yield of 0.30% and a current yield of 0.30%, while its 30-day moving average yield for December was 0.48%. Yield quotations more closely reflect the current earnings of the Portfolio. For the 12-month period ended December 31, 2008, the Portfolio's Class X shares returned 2.38%. Past performance is no guarantee of future results.

For the seven-day period ended December 31, 2008, the Portfolio's Class Y shares provided an effective annualized yield of 0.06% and a current yield of 0.06%, while its 30-day moving average yield for December was 0.23%. Yield quotations more closely reflect the current earnings of the Portfolio. For the 12-month period ended December 31, 2008, the Portfolio's Class Y shares returned 2.13%. Past performance is no guarantee of future results.

The performance of the Portfolio's two share classes varies because each has different expenses. The Portfolio's total returns assume the reinvestment of all distributions but do not reflect the deduction of any charges by your insurance company. Such costs would lower performance.

Our strategy in managing the Portfolio remained consistent with its long-term focus on maintaining preservation of capital and liquidity. Although the aggressive reductions by the Fed drastically lowered short-term yields, the turmoil and uncertainty in the markets remained in force and indeed worsened over the course of the period. As a result, we concentrated the Portfolio on assets with shorter maturities. We also closely reviewed all of the eligible securities on our purchase list to eliminate unacceptable risks that had come to light, a process which resulted in a significant reduction in the number of approved securities. The Portfolio did not contain any derivative securities during the reporting period. We will continue to focus closely on this strategy in an effort to maximize liquidity for the Portfolio and its shareholders.

17

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

There is no guarantee that any sectors mentioned will continue to perform as discussed above or that securities in such sectors will be held by the Portfolio in the future.

We appreciate your ongoing support of Morgan Stanley Select Dimensions Investment Series and look forward to continuing to serve your investment needs.

Very truly yours,

Randy Takian

President and Principal Executive Officer

18

Morgan Stanley Select Dimensions Investment Series

Letter to the Shareholders n December 31, 2008 continued

Proxy Voting Policy and Procedures and Proxy Voting Record

You may obtain a copy of the Portfolios' Proxy Voting Policy and Procedures without charge, upon request, by calling toll free (800) 869-NEWS or by visiting the Mutual Fund Center on our Web site at www.morganstanley.com. It is also available on the Securities and Exchange Commission's Web site at http://www.sec.gov.

You may obtain information regarding how the Portfolios voted proxies relating to portfolio securities during the most recent twelve-month period ended June 30 without charge by visiting the Mutual Fund Center on our Web site at www.morganstanley.com. This information is also available on the Securities and Exchange Commission's Web site at http://www.sec.gov.

For More Information About Portfolio Holdings

Each Morgan Stanley fund provides a complete schedule of portfolio holdings in its semiannual and annual reports within 60 days of the end of the fund's second and fourth fiscal quarters. The semiannual reports and the annual reports are filed electronically with the Securities and Exchange Commission (SEC) on Form N-CSRS and Form N-CSR, respectively. Morgan Stanley also delivers the semiannual and annual reports to fund shareholders and makes these reports available on its public web site, www.morganstanley.com. Each Morgan Stanley fund also files a complete schedule of portfolio holdings with the SEC for the fund's first and third fiscal quarters on Form N-Q. Morgan Stanley does not deliver the reports for the first and third fiscal quarters to shareholders, nor are the reports posted to the Morgan Stanley public web site. You may, however, obtain the Form N-Q filings (as well as the Form N-CSR and N-CSRS filings) by accessing the SEC's web site, http://www.sec.gov. You may also review and copy them at the SEC's public reference room in Washington, DC. Information on the operation of the SEC's public reference room may be obtained by calling the SEC at (800) SEC-0330. You can also request copies of these materials, upon payment of a duplicating fee, by electronic request at the SEC's e-mail address (publicinfo@sec.gov) or by writing the public reference section of the SEC, Washington, DC 20549-0102.

19

Morgan Stanley Select Dimensions Investment Series

Expense Example n December 31, 2008

As a shareholder of the Portfolio, you incur two types of costs: (1) insurance company charges; and (2) ongoing costs, including advisory fees; distribution and service (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period 07/01/08 – 12/31/08.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your accoun t during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical expenses based on the Portfolio's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing cost of investing in the Portfolio and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any insurance company charges. Therefore, the second line of the table is useful in comparing ongoing costs, and will not help you determine the relative total cost of owning different funds. In addition, if these insurance company charges were included, your costs would have been higher.

20

Morgan Stanley Select Dimensions Investment Series

Expense Example n December 31, 2008 continued

Money Market

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (0.83% return) | $ | 1,000.00 | $ | 1,008.30 | $ | 2.93 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,022.22 | $ | 2.95 | |||||||||

| Class Y | |||||||||||||||

| Actual (0.70% return) | $ | 1,000.00 | $ | 1,007.00 | $ | 4.19 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,020.96 | $ | 4.22 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 0.58% and 0.83% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Flexible Income

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-14.80% return) | $ | 1,000.00 | $ | 852.00 | $ | 3.26 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,021.62 | $ | 3.56 | |||||||||

| Class Y | |||||||||||||||

| Actual (-14.87% return) | $ | 1,000.00 | $ | 851.30 | $ | 4.42 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,020.36 | $ | 4.82 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 0.70% and 0.95% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Balanced

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-14.67% return) | $ | 1,000.00 | $ | 853.30 | $ | 4.66 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,020.11 | $ | 5.08 | |||||||||

| Class Y | |||||||||||||||

| Actual (-14.73% return) | $ | 1,000.00 | $ | 852.70 | $ | 5.82 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,018.85 | $ | 6.34 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 1.00% and 1.25% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). If the Portfolio had borne all of its expenses, the annualized expense ratios would have been 1.01% and 1.26% for Class X and Class Y shares, respectively.

21

Morgan Stanley Select Dimensions Investment Series

Expense Example n December 31, 2008 continued

Global Infrastructure

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-29.95% return) | $ | 1,000.00 | $ | 700.50 | $ | 5.00 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,019.25 | $ | 5.94 | |||||||||

| Class Y | |||||||||||||||

| Actual (-30.03% return) | $ | 1,000.00 | $ | 699.70 | $ | 6.07 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,018.00 | $ | 7.20 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 1.17% and 1.42% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Dividend Growth

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-28.41% return) | $ | 1,000.00 | $ | 715.90 | $ | 3.11 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,021.52 | $ | 3.66 | |||||||||

| Class Y | |||||||||||||||

| Actual (-28.52% return) | $ | 1,000.00 | $ | 714.80 | $ | 4.18 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,020.26 | $ | 4.93 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 0.72% and 0.97% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Equally-Weighted S&P 500

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-32.54% return) | $ | 1,000.00 | $ | 674.60 | $ | 1.43 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,023.43 | $ | 1.73 | |||||||||

| Class Y | |||||||||||||||

| Actual (-32.65% return) | $ | 1,000.00 | $ | 673.50 | $ | 2.48 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,022.17 | $ | 3.00 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 0.34% and 0.59% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

22

Morgan Stanley Select Dimensions Investment Series

Expense Example n December 31, 2008 continued

Capital Growth

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-43.02% return) | $ | 1,000.00 | $ | 569.80 | $ | 3.63 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,020.51 | $ | 4.67 | |||||||||

| Class Y | |||||||||||||||

| Actual (-43.08% return) | $ | 1,000.00 | $ | 569.20 | $ | 4.61 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,019.25 | $ | 5.94 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 0.92% and 1.17% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period). If the Portfolio had borne all of its expenses, the annualized expense ratios would have been 0.93% and 1.18% for Class X and Class Y shares, respectively.

Focus Growth

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-47.27% return) | $ | 1,000.00 | $ | 527.30 | $ | 2.61 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,021.72 | $ | 3.46 | |||||||||

| Class Y | |||||||||||||||

| Actual (-47.35% return) | $ | 1,000.00 | $ | 526.50 | $ | 3.57 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,020.46 | $ | 4.72 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 0.68% and 0.93% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Capital Opportunities

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-45.88% return) | $ | 1,000.00 | $ | 541.20 | $ | 4.49 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,019.30 | $ | 5.89 | |||||||||

| Class Y | |||||||||||||||

| Actual (-45.94% return) | $ | 1,000.00 | $ | 540.60 | $ | 5.46 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,018.05 | $ | 7.15 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 1.16% and 1.41% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

23

Morgan Stanley Select Dimensions Investment Series

Expense Example n December 31, 2008 continued

Global Equity

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-33.98% return) | $ | 1,000.00 | $ | 660.20 | $ | 4.67 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,019.51 | $ | 5.69 | |||||||||

| Class Y | |||||||||||||||

| Actual (-34.11% return) | $ | 1,000.00 | $ | 658.90 | $ | 5.71 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,018.25 | $ | 6.95 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 1.12% and 1.37% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

Mid Cap Growth

| Beginning Account Value | Ending Account Value | Expenses Paid During Period@ | |||||||||||||

| 07/01/08 | 12/31/08 | 07/01/08 – 12/31/08 | |||||||||||||

| Class X | |||||||||||||||

| Actual (-42.47% return) | $ | 1,000.00 | $ | 575.30 | $ | 3.21 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,021.06 | $ | 4.12 | |||||||||

| Class Y | |||||||||||||||

| Actual (-42.55% return) | $ | 1,000.00 | $ | 574.50 | $ | 4.20 | |||||||||

| Hypothetical (5% annual return before expenses) | $ | 1,000.00 | $ | 1,019.81 | $ | 5.38 | |||||||||

@ Expenses are equal to the Portfolio's annualized expense ratios of 0.81% and 1.06% for Class X and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half year period).

24

Money Market

Portfolio of Investments n December 31, 2008

| PRINCIPAL AMOUNT IN THOUSANDS | ANNUALIZED YIELD ON DATE OF PURCHASE | MATURITY DATE | VALUE | ||||||||||||||||

| Commercial Paper (58.6%) | |||||||||||||||||||

| Asset-Backed - Consumer Credit (9.3%) | |||||||||||||||||||

| $ | 10,000 | Old Line Funding, LLC (a) | 0.75 | % | 03/19/09 - 03/20/09 | $ | 9,983,854 | ||||||||||||

| 10,000 | Ranger Funding Co., LLC (a) | 1.15 - 1.40 | 01/22/09 - 03/20/09 | 9,979,658 | |||||||||||||||

| 19,963,512 | |||||||||||||||||||

| Asset-Backed - Consumer Diversified (11.1%) | |||||||||||||||||||

| 2,500 | Amsterdam Funding Corp. (a) | 1.56 | 02/18/09 | 2,494,833 | |||||||||||||||

| 1,483 | Enterprise Funding Co., LLC (a) | 1.40 | 01/08/09 | 1,482,596 | |||||||||||||||

| 10,000 | Sheffield Receivables Corp. (a) | 0.75 - 1.45 | 01/23/09 - 03/12/09 | 9,985,719 | |||||||||||||||

| 10,000 | Windmill Funding Corp. (a) | 1.15 - 1.40 | 01/27/09 - 03/19/09 | 9,982,646 | |||||||||||||||

| 23,945,794 | |||||||||||||||||||

| Asset-Backed - Consumer Loans (7.0%) | |||||||||||||||||||

| 5,000 | Barton Capital, LLC (a) | 1.47 - 1.50 | 01/22/09 - 01/23/09 | 4,995,476 | |||||||||||||||

| 5,000 | Jupiter Securitization (a) | 1.40 | 01/22/09 | 4,995,917 | |||||||||||||||

| 5,000 | Yorktown Capital, LLC (a) | 1.40 - 1.45 | 01/21/09 - 01/23/09 | 4,995,872 | |||||||||||||||

| 14,987,265 | |||||||||||||||||||

| Asset-Backed - Corporate (4.6%) | |||||||||||||||||||

| 10,000 | Atlantis One Funding (a) | 0.50 - 0.70 | 03/17/09 - 04/22/09 | 9,984,000 | |||||||||||||||

| Asset-Backed - Diversified (4.6%) | |||||||||||||||||||

| 10,000 | Falcon Asset Securitization Co., LLC (a) | 0.50 - 1.40 | 01/20/09 - 03/20/09 | 9,990,994 | |||||||||||||||

| Asset-Backed - Government (0.9%) | |||||||||||||||||||

| 2,000 | Govco, LLC (a) | 0.75 | 03/23/09 | 1,996,625 | |||||||||||||||

| Banking (5.6%) | |||||||||||||||||||

| 4,000 | Bank of America Corp. | 0.01 | 01/02/09 | 3,999,999 | |||||||||||||||

| 8,000 | HSBC USA Inc. | 0.30 - 0.32 | 01/13/09 - 01/14/09 | 7,999,153 | |||||||||||||||

| 11,999,152 | |||||||||||||||||||

| International Banks (15.5%) | |||||||||||||||||||

| 3,000 | Abbey National N.A., LLC | 0.25 | 01/12/09 | 2,999,771 | |||||||||||||||

| 5,000 | BNP Paribas Finance Inc. | 0.22 | 01/07/09 | 4,999,817 | |||||||||||||||

| 2,000 | ING (U.S.) Funding, LLC | 0.30 | 01/16/09 | 1,999,750 | |||||||||||||||

| 5,000 | Rabobank (U.S.) Finance Corp. | 0.01 | 01/02/09 | 4,999,999 | |||||||||||||||

| 500 | Royal Bank of Scotland PLC | 3.10 | 03/16/09 | 496,855 | |||||||||||||||

| 8,000 | Societe Generale N.A., Inc. | 0.37 - 0.45 | 01/16/09 | 7,998,600 | |||||||||||||||

| 10,000 | UBS Finance (Delaware) LLC | 0.70 | 01/15/09 | 9,997,278 | |||||||||||||||

| 33,492,070 | |||||||||||||||||||

| Total Commercial Paper (Cost $126,359,412) | 126,359,412 | ||||||||||||||||||

See Notes to Financial Statements

25

Money Market

Portfolio of Investments n December 31, 2008 continued

| PRINCIPAL AMOUNT IN THOUSANDS | ANNUALIZED YIELD ON DATE OF PURCHASE | MATURITY DATE | VALUE | ||||||||||||||||

| Repurchase Agreements (17.6%) | |||||||||||||||||||

| $ | 7,945 | Barclays Capital LLC (dated 12/31/08; proceeds $7,945,026); fully collateralized by Federal National Mortgage Assoc., 3.28%-8.50%, due 02/01/15-10/01/44; Federal Home Loan Mortgage Corp., 4.33%-6.95%, due 04/01/09-07/01/37; Government National Mortgage Assoc., 4.00%, due 02/20/35, valued at $8,183,351 | 0.06 | % | 01/02/09 | $ | 7,945,000 | ||||||||||||