united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-08542

The Saratoga Advantage Trust

(Exact name of registrant as specified in charter)

12725 W. Indian School Rd, Suite E-101, Avondale, AZ 85392

(Address of principal executive offices) (Zip code)

Stuart M Strauss, Esq. Dechert LLP

1095 Avenue of the Americas, New York, NY, 10036

(Name and address of agent for service)

Registrant's telephone number, including area code: 623-266-4567

Date of fiscal year end: 8/31

Date of reporting period: 8/31/22

Item 1. Reports to Stockholders.

| ||

| Class A and C Shares | ||

| ANNUAL REPORT | ||

| As Of August 31, 2022 | ||

| THIS REPORT IS AUTHORIZED FOR DISTRIBUTION ONLY TO SHAREHOLDERS | ||

| AND TO OTHERS WHO HAVE RECEIVED A COPY OF THE PROSPECTUS. | ||

TABLE OF CONTENTS

| Chairman’s Letter | Page 1 |

| Investment Review | Page 6 |

| Schedules of Investments | Page 44 |

| Statements of Assets and Liabilities | Page 84 |

| Statements of Operations | Page 88 |

| Statements of Changes in Net Assets | Page 92 |

| Notes to Financials | Page 98 |

| Financial Highlights | Page 119 |

| Report of Independent Registered Public Accounting Firm | Page 137 |

| Supplemental Information | Page 139 |

| Privacy Notice | Page 150 |

| TRUSTEES AND OFFICERS | |

| Bruce E. Ventimiglia | Trustee, Chairman, President & CEO |

| Patrick H. McCollough | Trustee |

| Udo W. Koopmann | Trustee |

| Floyd E. Seal | Trustee |

| Stephen H. Hamrick | Trustee |

| Stephen Ventimiglia | Vice President & Secretary |

| Jonathan W. Ventimiglia | Vice President, Assistant Secretary, |

| Treasurer & Chief Financial Officer | |

| Frederick C. Teufel, Jr | Chief Compliance Officer |

| Timothy J. Burdick | Assistant Secretary |

| Richard S. Gleason | Assistant Treasurer |

| Investment Manager | Distributor |

| Saratoga Capital Management, LLC | Northern Lights Distributors, LLC |

| 12725 W. Indian School Road, Suite E-101 | 4221 N 203rd Street, Suite 100 |

| Avondale, Arizona 85392 | Elkhorn, Nebraska 68022 |

| Transfer & Shareholder Servicing Agent | Custodian |

| Ultimus Fund Solutions, LLC | BNY Mellon Corp. |

| 4221 N 203rd Street, Suite 100 | 225 Liberty Street |

| Elkhorn, Nebraska 68022 | New York, New York 10286 |

| Administrator & Fund Accounting Agent | Custody Administrator |

| Ultimus Fund Solutions, LLC | Ultimus Fund Solutions, LLC |

| 4221 N 203rd Street, Suite 100 | 4221 N 203rd Street, Suite 100 |

| Elkhorn, Nebraska 68022 | Elkhorn, Nebraska 68022 |

THE SARATOGA ADVANTAGE TRUST

Annual Report to Shareholders

October 23, 2022

Dear Shareholder:

We are pleased to provide you with this annual report on the investment strategies and performance of the portfolios in the Saratoga Advantage Trust (the “Trust”). This report covers the twelve months from September 1, 2021, through August 31, 2022.

We believe that successful investing requires discipline and patience. Try to stay focused on your long-term investment goals. Don’t let short-term stock and bond market fluctuations or investment manias change your long-term investment strategy. The Saratoga Advantage Trust’s portfolios are managed by some of the world’s leading institutional investment advisory firms. Combining the strength of the Trust’s performance with a well-designed asset allocation plan can help you to achieve your long-term investment goals.

ECONOMIC OVERVIEW

As measured by Real Gross Domestic Product (GDP), the value of the production of goods and services in the United States regressed by an annualized growth rate of -0.6% (AGR) during the second quarter of 2022, up from the -1.6% AGR during the first quarter of 2022. The steady growth that the US economy enjoyed prior to, and during its recovery from, the pandemic-related recession is being eaten away at by inflation. Thus far, the National Bureau of Economic Research (NBER) has yet to characterize the current economic environment as a recession; our own proprietary economic stage analysis has generally agreed with the NBER’s historical characterizations, and we believe it is important to use a nuanced framework when approaching recession determinations. We would not be surprised to see the economy bounce around near zero growth while inflation remains elevated. And, while our metrics indicate the economy is likely already in, or will shortly enter, recession, we believe it is important to note that investing based on economic stages requires looking well beyond the broad macro environment.

Looking at the main components of GDP during the quarter, Personal Consumption Expenditures (PCE) advanced by 2.0%, while Gross Private Domestic Investment (GPDI) fell sharply, down over 14%, and government spending fell again. Government spending, which accounts for both consumption and gross investment, has now fallen for five straight quarters and seven of the last eight. Non-defense spending by the government continues to fall, as federal, state, and local budgets tighten. Though fiscal tightening has not been extreme, the fall in government spending sheds light on the particular difficulty leaders are facing as they deal with the current economy: in an environment where we might usually see fiscal largesse, inflation is forcing governments to spend less out of fear consumer demand will continue to run amuck.

1

While consumer spending grew during the quarter, the Goods portion of PCE continues to deteriorate. The Services portion of PCE represents consumer spending on services, which accounts for roughly 40% of the entire US economy; it is undeniably positive to see services spending remain resilient, though it is likewise fair to point out that not much else in the current GDP report is inspiring. Though the freefall of investment in Residential and Nonresidential Structures is unsurprising as the cost of debt moves higher, it is nonetheless a heavy burden on the economy.

As we wrote in last quarter’s MIVI, the depth of economic pain we see will likely correlate with how inflation persists. While many may focus on inflation falling back to the Federal Reserve’s (Fed) nominal 2.0% target, we believe inflation around 4.0% should allow the economy and earnings to recover and investors to see some relief.

Monetary Policy: The Federal Reserve continues its tapering program. The Fed balance sheet topped out at roughly $8.96 trillion in April 2022 and has dropped to $8.79 at the end of September 2022.

As of August, the monetary base fell -11.79% y-o-y, down from a cycle high of 57.7%. It is not unprecedented for the Fed to take out the monetary base at this rate, but it is still a significant development. The monetary base dropping will put downward pressure on inflation, however that effect can take considerable time. Within the monetary base, we see the Fed is manipulating policy considerably via currency in circulation (CiC). CiC hit a pandemic-high growth rate of 17% y-o-y in 2020; that figure has now dropped to 4.0% y-o-y, far below its mean historical y-o-y growth rate of roughly 7.0%. M2, one of the most widely used monetary figures for measuring liquidity in the economy, is also down significantly from its cycle high 22% y-o-y growth in February 2021 to 4.1% y-o-y currently, also well below its long-term mean of 7.1% y-o-y.

In the earlier months of Fed tightening, we wrote that while the Fed was pulling back on their accommodation, they were still supporting liquidity via their monetary policy. This is no longer the case. Extraordinarily loose monetary policy has reversed into a somewhat tight policy that should both dampen inflationary pressures and economic growth. Now the question becomes, how quickly and to what degree will these effects become realized? Historically, monetary tightening has had a faster effect than loosening, so we should perhaps be unsurprised that the Fed already seems to be having success in pressuring the economy.

Interest Rates: One-year treasuries continue to move up rapidly; we generally see this treasury issue move up when inflation is high and the market is anticipating the Fed will move their target rates higher. One- and two-year treasuries, which had been mostly rangebound through last summer, have moved up sharply since fall 2021. Three-month treasuries were in a slight downtrend through last summer and their yields remained under 0.10 as recently as the start of 2022; however, year-to-date these short-term issues have put in an extreme uptrend as the market and the Fed finally seemed to accept the economy was running hot on inflation. We previously wrote that interest rate performance suggested the economy might not be as strong as it looked toward the end of 2021, and that seems to have been confirmed by the current negative GDP environment.

Regarding long-term corporate bonds, the quality spread as measured by Moody’s-rated Baa bonds minus Aaa bonds continues moving up. The quality spread has historically been a good predictor of confidence in the corporate bond market and helps us establish a baseline expectation for corporate earnings. The quality spread approached a long-term low of 0.65 during June 2021 but

2

has more recently moved up to 1.10 in September 2022. We mentioned last quarter that spread moves had broken a number of technical barriers to the upside, suggesting corporate earnings might begin to stall. This quarter’s further move up gives us further confidence that weak earnings are likely on the table; we are unsurprised to see earnings estimates continue to be revised to the downside.

Equity Valuations: As of September 30, 2022, the S&P 500 index was at 3,585. Our proprietary valuation work suggests a fair value for the S&P 500 around 3,525. Earnings growth projections are facing slight adjustments downward. We believe PE levels are likely to stay suppressed below their modern historical (1990 to present) mean of roughly 24.9 as inflation and intermediate-to-long-term interest rates are presenting a headwind to valuations. Earnings are generally a leading indicator, peaking slightly before recessions. Earnings have potentially put in a near-term peak; however, it is not a foregone conclusion that they will fall precipitously. It appears earnings estimates are factoring in a touch-and-go recessionary environment, as opposed to a deep recession, and this is a base case we tentatively agree seems likely, though continued hot inflation could change that assumption.

To create a range of equity market outcomes, we use a valuation tool which we refer to as our Proper PE Valuation™ tool. Among other things, this analysis provides us with a set of ranges above and below which we consider the S&P 500 overvalued or undervalued, respectively. Our proprietary valuation work currently sets an appropriate S&P 500 PE from 18.5 to 19.5. This produces a fair value range of 3,525 to 3,715 over the next 6 months. Earnings growth is stalling, and our valuation work has reduced PE projections from our last report. The current levels and trends of the underlying data we analyze, including our technical work, indicates that we are likely to stay in or near fair- value range for the near-term, however there is likely more risk to that target on the downside than the upside.

Inflation: The Saratoga Economic Strength Monitor™ (ESM) has typically trended with, or in advance of, the Consumer Price Index and Fed activity. In March of 2021, ESM signaled that the Fed was being confronted with a “hot” economy, and that it would potentially make sense to begin removing accommodation from the economy; it took the Fed nearly a year to react. Now, we’re looking at nearly the opposite scenario. In May of this year, ESM dropped precipitously, and continues to hover near levels at which it would likely be appropriate for the Fed to “wait and see” just how much damage they’ve done while adopting a more neutral stance. Nevertheless, the Fed seems intent to continue on its dizzyingly quick path of large interest rate hikes.

Wages have historically played a large roll in our inflation research. In particular, we focus on average weekly earnings of Production and Non-Supervisory employees, specifically for Goods-producing workers (Goods Wages), as a reliable leading indicator for inflation. It is useful to think about the growth of these types of wages in comparison to the growth of inflation. As of December 2020, Goods Wages had risen 7.8% y-o-y, while CPI was at just 1.3%. However, that story has changed. Over the past year, Goods Wages are up just 4.8% while CPI remains over 8%; it is unlikely wages can continue to push inflation while their growth runs so far behind CPI.

On the supply side of the economy, certain commodities show signs of a slowdown. Copper and cotton, two important economic inputs, have fallen by over 20% this year, while lumber is down over 50%; however, of course, consumers are still facing painful energy inflation.

3

COMPARING THE PORTFOLIOS’ PERFORMANCE TO BENCHMARKS

When reviewing the performance of the portfolios against their benchmarks, it is important to note that the Trust is designed to help investors to implement an asset allocation strategy to meet their individual needs as well as select individual investments within each asset category among the myriad of choices available. Each Saratoga portfolio was formed to represent an asset class, and each portfolio’s institutional money manager was selected based on their ability to manage money within that class.

Therefore, the Saratoga portfolios may help investors to properly implement their asset allocation decisions and keep their investments within the risk parameters that they establish with their investment consultants. Without the intended asset class consistency of the Saratoga portfolios, even the most carefully crafted allocation strategy could be negated. Furthermore, the benchmarks do not necessarily provide precise standards against which to measure the portfolios, in that the characteristics of the benchmarks can vary widely at different points in time from the Saratoga portfolios (e.g., characteristics such as: average market capitalizations, price-to-earnings and price-to-book ratios, bond quality ratings and maturities, etc.). In addition, the benchmarks can potentially have a survivor bias built into them (i.e., the performance of only funds that are still in existence may remain part of the benchmark’s performance while funds that do not exist anymore may be removed from the benchmark’s performance).

ELECTRONIC DELIVERY AVAILABLE

This report can be delivered to you electronically. Electronic delivery can help simplify your record keeping. With electronic delivery, you’ll receive an email with a link to your Saratoga Advantage Trust quarterly statement, daily confirmations and/or semi-annual and annual reports each time one is available. You have the ability to choose which items you want delivered electronically. Choose one item or all items. It’s up to you. Please call our Customer Service Department toll-free at 1-888-672-4839 for instructions on how to establish electronic delivery.

4

AUTOMATED ACCOUNT UPDATES

I am pleased to inform you that you can get automated updates on your investments in the Saratoga Advantage Trust 24 hours a day, every day, by calling toll-free 1-888-672-4839. For additional information about the Trust, please call your financial advisor, visit our website at www.saratogacap.com or call 1-800-807-FUND.

Finally, following you will find specific information on the investment strategy and performance of each of the Trust’s portfolios. Please speak with your financial advisor if you have any questions about your investment in the Saratoga Advantage Trust or your allocation of assets among the Trust’s portfolios.

We remain dedicated to serving your investment needs.

Thank you for investing with us.

Best wishes,

Bruce E. Ventimiglia

Chairman, President and

Chief Executive Officer

Investors should consider the investment objectives, risks, charges, and expenses of the Saratoga Funds carefully. This and other information about the Saratoga Funds is contained in your prospectus, which should be read carefully. To obtain an additional copy of the prospectus, please call (800) 807-FUND. Past performance is not indicative of future results. Investments in stocks, bonds and mutual funds are not guaranteed and the principal value and investment return can fluctuate. Consequently, investors may receive back less than invested.

The S&P 500 is an unmanaged, capitalization-weighted index. It is not possible to invest directly in the S&P 500.

The security holdings discussed may not be representative of the Funds’ current or future investments. Portfolio holdings are subject to change and should not be considered to be investment advice. Any statements not of a factual nature constitute opinions which are subject to change without notice. Information contained herein was obtained from recognized statistical services and other sources believed to be reliable and we therefore cannot make any representation as to its completeness or accuracy. The Funds of the Saratoga Advantage Trust are distributed by Northern Lights Distributors, LLC, member FINRA/SIPC; the Saratoga Advantage Trust and Northern Lights Distributors, LLC are not affiliated entities. 5937-NLD-10262022

5

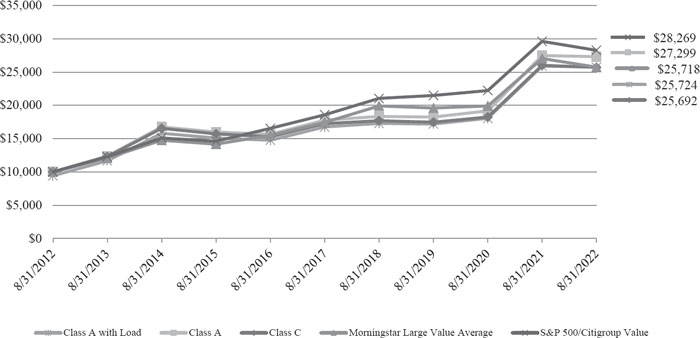

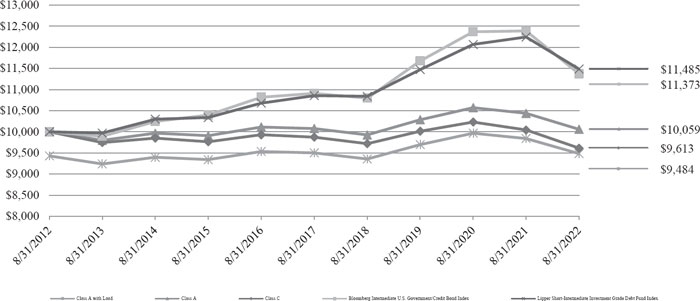

| INVESTMENT REVIEW |

LARGE CAPITALIZATION VALUE PORTFOLIO

Advised by: M.D. Sass Investors Services, Inc., New York, New York

Objective: The Portfolio seeks total return consisting of capital appreciation and dividend income.

| Total Aggregate Return for the Periods Ended August 31, 2022 | |||||

| One Year: | Five Year: | Ten Year: | Inception: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 1/4/99 – 8/31/22* | 2/14/06 – 8/31/22* | |

| Class A | |||||

| With Sales Charge | (6.33)% | 7.68% | 9.91% | NA | 4.54% |

| Without Sales Charge | (0.62)% | 8.96% | 10.56% | NA | 4.92% |

| Class C | |||||

| With Sales Charge | (2.22)% | 8.30% | 9.90% | 3.50% | NA |

| Without Sales Charge | (1.22)% | 8.30% | 9.90% | 3.50% | NA |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 1.72% and 2.31% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

In determining which securities to buy, hold or sell, the Portfolio’s Adviser focuses its investment selection on finding high quality companies with compelling valuations, measurable catalysts to unlock value and above-average long -term earnings growth potential. In general, the Adviser looks for companies that have value-added product lines to help preserve pricing power, a strong history of free cash flow generation, strong balance sheets, competent management with no record of misleading shareholders, and financially sound customers. Independent research is used to produce estimates for future earnings, which are inputs into the Adviser’s proprietary valuation model. The Adviser focuses its investments where it has a differentiated view and there exists, in its view, significant price appreciation potential to its estimate of the stocks’ intrinsic value.

PORTFOLIO ADVISER COMMENTARY

The Saratoga Advantage Trust Large Cap Value Portfolio posted negative absolute performance for the period but outperformed on a relative basis. Relative outperformance was driven primarily by stock selection in the Financial, Industrial and Healthcare sectors.

The portfolio’s top contributor during the fiscal year was Quanta Services (0.00%). We believe Quanta is a uniquely positioned leading infrastructure contractor at the epicenter of secular growth markets in electric transmission and distribution (our favored engineering and construction market), renewable generation, and underground utility and infrastructure sectors. The company looks poised to benefit from recent US infrastructure bills. Vertex Pharmaceuticals (0.00%) was the portfolio’s second-best performing stock during this period. This biopharmaceutical company develops small molecule drugs for patients with serious diseases. Vertex stock benefits from strong earnings and its growing pipeline of drug growth and discovery. The company has also benefited from a lack of data coming from AbbVie for a competing cystic fibrosis drug. We have sold, taking profits in both of these positions during the year.

The portfolio’s main detractors were Qorvo Inc. (0.00%), and Alphabet Inc. (4.47%). Qorvo underperformed largely due to investor concerns about a cyclical peak in semiconductor demand for smartphones. Qorvo benefited in 2021 from increased shipments of smartphones with higher content per phone but they extrapolated this demand into 2022 while their specific end markets were slowing materially leading to downward earnings revisions. Alphabet Inc. underperformed due in part to investor concerns about digital ad spending (which is sensitive to the macro economy) and slowing growth at YouTube. However, we believe YouTube should do well over the medium- and longer-term as its video ad impressions could benefit from the shift to ad-supported video on demand and connected TV; additionally, we see Google Search’s deep moat as the best positioned mobile ad product and search advertising remains the most effective ad medium. We sold Qorvo during the year, and still hold Alphabet.

A recent addition to the portfolio was Match Group Inc. (2.43%). Our value-oriented, relatively concentrated approach to stock selection has benefited portfolio performance during the past fiscal year. We believe the challenging, choppy market environment we’ve seen this year is likely to continue, which could continue to favor superior stock selection, in-depth research, and a concentrated value approach.

Within the discussion above, the percentages shown next to specific securities are the percentages of the Portfolio represented by the security on 8/31/22. The securities held in the Portfolio are subject to change and any discussion of those securities should not be considered investment advice.

6

| INVESTMENT REVIEW |

LARGE CAPITALIZATION VALUE PORTFOLIO

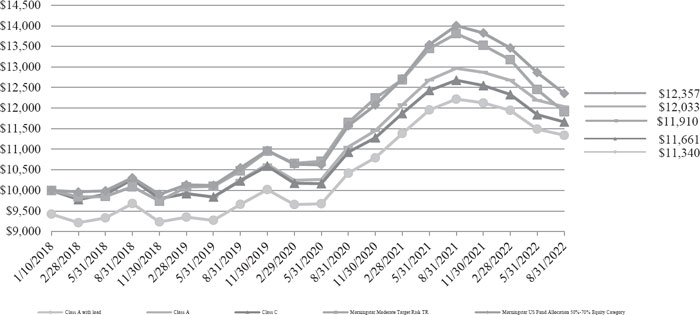

A HYPOTHETICAL COMPARISON OF THE GROWTH OF $10,000 INVESTED IN THE

LARGE CAPITALIZATION VALUE PORTFOLIO VS. BENCHMARK

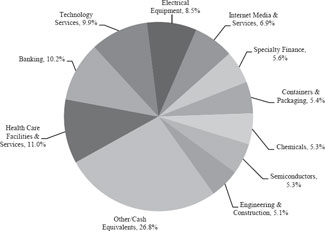

SIGNIFICANT AREAS OF INVESTMENT

AS A PERCENTAGE OF NET ASSETS

| Top 10 Portfolio Holdings* | |

| % of | |

| Company | Net Assets |

| CACI International, Inc., Class A | 7.1% |

| Walker & Dunlop, Inc. | 5.6% |

| East West Bancorp, Inc. | 5.4% |

| Crown Holdings, Inc. | 5.4% |

| ON Semiconductor Corporation | 5.3% |

| Corteva, Inc. | 5.3% |

| MasTec, Inc. | 5.1% |

| Liberty Media Corporation-Liberty Formula One, Class C | 5.0% |

| First Republic Bank | 4.8% |

| Raytheon Technologies Corporation | 4.8% |

| * | Based on total net assets as of August 31, 2022. |

Excludes short-term investments.

Portfolio Composition*

The Morningstar Large Value Average (“Large Value Average”), as of August 31, 2022, consisted of 1,241 mutual funds comprised of large market capitalization value stocks. The Large Value Average is not managed and it is not possible to invest directly in the Large Value Average.

The S&P 500/Citigroup Value Index, is broad, unmanaged-capitalization weighted index which is the successor to the S&P 500/BARRA Value Index, uses a multifactor methodology to score constituents, which are weighted according to market cap and classified as growth, value, or a mix of growth and value. The S&P 500/Citigroup Value Index does not include fees and expenses, and investor may not invest directly in an index.

Past performance is not predictive of future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of the fund shares.

Large Capitalization Value Portfolio is not sponsored, endorsed, sold or promoted by Morningstar, Inc. or any of its affiliates (all such entities, collectively, “Morningstar Entities”). The Morningstar Entities make no representation or warranty, express or implied, to the owners of the Large Capitalization Value Portfolio or any member of the public regarding the advisability of investing in mutual funds comprised of large market capitalization value stocks generally or in the Large Capitalization Value Portfolio in particular or the ability of the Morningstar Large Value Average to track general large market capitalization value stocks market performance.

THE MORNINGSTAR ENTITIES DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE MORNINGSTAR LARGE VALUE AVERAGE CATEGORY OR ANY DATA INCLUDED THEREIN AND MORNINGSTAR ENTITIES SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN.

7

| INVESTMENT REVIEW |

LARGE CAPITALIZATION GROWTH PORTFOLIO

Advised by: Smith Group Asset Management, Dallas, Texas

Objective: The Portfolio seeks capital appreciation.

| Total Aggregate Return for the Periods Ended August 31, 2022 | |||||

| One Year: | Five Year: | Ten Year: | Inception: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 1/4/99 – 8/31/22* | 2/14/06 – 8/31/22* | |

| Class A | |||||

| With Sales Charge | (21.57)% | 11.56% | 13.45% | NA | 9.38% |

| Without Sales Charge | (16.80)% | 12.89% | 14.12% | NA | 9.77% |

| Class C | |||||

| With Sales Charge | (18.28)% | 12.20% | 13.44% | 5.03% | NA |

| Without Sales Charge | (17.28)% | 12.20% | 13.44% | 5.03% | NA |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 1.76% and 2.37% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

The Portfolio’s Adviser employs quantitative and qualitative analysis that seeks to identify high quality companies that it believes have the ability to accelerate earnings growth and exceed investor expectations. The Adviser’s selection process consists of three steps. First, the Adviser reviews a series of screens utilizing the Adviser’s investment models, which are based on fundamental characteristics, designed to eliminate companies that the Adviser’s research shows have a high probability of underperformance. Factors considered when reviewing the screens include a multi-factor valuation framework, earnings quality, capital structure and financial quality. Next, securities that pass the initial screens are then evaluated to try to identify stocks with the highest probability of producing an earnings growth rate that exceeds investor expectations. This process incorporates changes in earnings expectations and earnings quality analysis. Finally, these steps produce a list of eligible companies which are subjected to analysis by the Adviser to further understand each company’s business prospects and earnings potential. The Adviser uses the results of this analysis to construct the Portfolio’s security positions.

PORTFOLIO ADVISOR COMMENTARY

A year ago, financial markets were beginning to become concerned with a rising inflationary and interest rate environment, yet inflation expectations were still firmly anchored at 2.5%, up from 1.8% one-year prior, and the yield on the 10- year Treasury sat at 1.49%. A short nine months later the year-over-year change in the US Consumer Price Index hit 9.0% before modestly retreating to 8.3% over the coming months, the 10-year Treasury yield has more than doubled, and equity markets have entered bear market territory. There is no debate that inflation is back with a vengeance; the debate is now moving to how quickly inflation fades, to what level it fades, and what are the second-order effects on economic growth, corporate earnings, and other factors?

The US economy has seen two consecutive quarters of negative growth and further downturns are possible. The global economy looks to be headed for a period of below trend growth as tight monetary policy potentially constrains economic activity. This below-trend growth will almost assuredly lead to at least a modest adjustment in the outlook for corporate earnings, but that comes off much lower market multiples than have been seen for quite some time.

For the 12-months ended August 31, 2022, the Saratoga Advantage Trust Large Capitalization Growth Portfolio posted strong relative performance, though absolute returns in both the portfolio and asset class were considerably negative. The top performing sector in the portfolio was Communication Services led by television broadcasting and digital media company Nexstar Media (0.52%). Auto parts retailer AutoZone (2.09%) and beauty supply company Ulta Beauty (2.26%) were top performers in the Consumer Discretionary sector. A small over-weight to Moderna, Inc. (0.0%), a biotechnology company most associated with COVID-19 vaccines, hurt performance during the final quarter of 2021 after reporting lower than expected earnings and reducing guidance for vaccine doses and sales.

Within the discussion above, the percentages shown next to specific securities are the percentages of the Portfolio represented by the security on 8/31/22. The securities held in the Portfolio are subject to change and any discussion of those securities should not be considered investment advice.

8

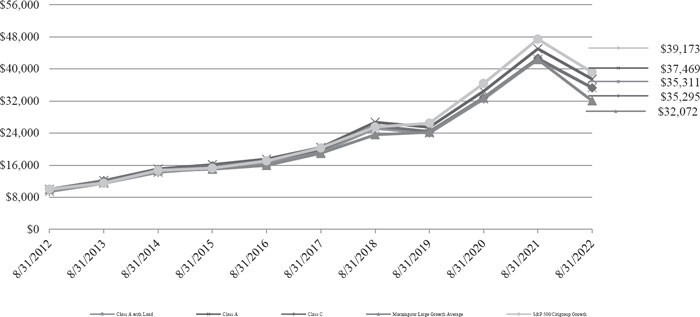

| INVESTMENT REVIEW |

LARGE CAPITALIZATION GROWTH PORTFOLIO

A HYPOTHETICAL COMPARISON OF THE GROWTH OF $10,000 INVESTED IN THE

LARGE CAPITALIZATION GROWTH PORTFOLIO VS. BENCHMARK

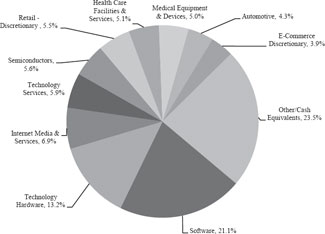

SIGNIFICANT AREAS OF INVESTMENT

AS A PERCENTAGE OF NET ASSETS

| Top 10 Portfolio Holdings* | |

| % of | |

| Company | Net Assets |

| Apple, Inc. | 10.8% |

| Microsoft Corporation | 8.4% |

| Tesla, Inc. | 4.3% |

| Amazon.com, Inc. | 4.0% |

| Costco Wholesale Corporation | 3.3% |

| Waste Management, Inc. | 2.5% |

| Synopsys, Inc. | 2.4% |

| Gartner, Inc. | 2.3% |

| Ulta Beauty, Inc. | 2.3% |

| Paychex, Inc. | 2.2% |

| * | Based on total net assets as of August 31, 2022. |

Excludes short-term investments.

Portfolio Composition*

The Morningstar Large Growth Average (“Large Growth Average”), as of August 31, 2022, consisted of 1,272 mutual funds comprised of large market capitalization growth stocks. The Large Growth Average is not managed and it is not possible to invest directly in the Large Growth Average.

The S&P 500/Citigroup Growth Index, is broad, unmanaged-capitalization weighted index which is the successor to the S&P 500/BARRA Growth Index, uses a multifactor methodology to score constituents, which are weighted according to market cap and classified as growth, value, or a mix of growth and value. The S&P 500/Citigroup Value Index does not include fees and expenses, and investor may not invest directly in an index.

Past performance is not predictive of future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of the fund shares.

Large Capitalization Growth Portfolio is not sponsored, endorsed, sold or promoted by Morningstar, Inc. or any of its affiliates (all such entities, collectively, “Morningstar Entities”). The Morningstar Entities make no representation or warranty, express or implied, to the owners of the Large Capitalization Growth Portfolio or any member of the public regarding the advisability of investing in mutual funds comprised of large market capitalization growth stocks generally or in the Large Capitalization Growth Portfolio in particular or the ability of the Morningstar Large Growth Average to track general large market capitalization growth stocks market performance.

THE MORNINGSTAR ENTITIES DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE MORNINGSTAR LARGE GROWTH AVERAGE CATEGORY OR ANY DATA INCLUDED THEREIN AND MORNINGSTAR ENTITIES SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN.

9

| INVESTMENT REVIEW |

MID CAPITALIZATION PORTFOLIO

Advised by: Vaughn Nelson Investment Management, L.P., Houston, Texas

Objective: The Portfolio seeks long-term capital appreciation.

| Total Aggregate Return for the Year Ended August 31, 2022 | ||||

| One Year: | Five Year: | Ten Year: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 6/28/02 – 8/31/22* | |

| Class A | ||||

| With Sales Charge | (15.42)% | 5.04% | 8.28% | 7.05% |

| Without Sales Charge | (10.28)% | 6.29% | 8.93% | 7.36% |

| Class C | ||||

| With Sales Charge | (11.84)% | 5.65% | 8.29% | 6.73% |

| Without Sales Charge | (10.84)% | 5.65% | 8.29% | 6.73% |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 2.06% and 2.64% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

The Portfolio invests in securities of companies that are believed by the Adviser to be undervalued, thereby offering above-average potential for capital appreciation. The Portfolio may also invest in equity securities of foreign companies. The Adviser invests in medium capitalization companies with a focus on total return using a bottom-up value oriented investment process. The Adviser seeks companies with the following characteristics, although not all of the companies it selects will have these attributes: (i) companies earning a positive economic margin with stable-to-improving returns; (ii) companies valued at a discount to their asset value; and (iii) companies with an attractive dividend yield and minimal basis risk. In selecting investments, the Adviser generally employs the following strategy: (i) value-driven investment philosophy that selects stocks selling at attractive values based upon business fundamentals, economic margin analysis, discounted cash flow models and historical valuation multiples. The Adviser reviews companies that it believes are out-of-favor or misunderstood; (ii) use of value-driven screens to create a research universe of companies with market capitalizations of at least $1 billion; and (iii) use of fundamental and risk analysis to construct a portfolio of securities that the Adviser believes has an attractive return potential.

PORTFOLIO ADVISOR COMMENTARY

During the fourth quarter of 2021, with rising inflationary pressures becoming a political issue, the US Federal Reserve began reducing their Quantitative Easing purchases and provided forward guidance that interest rate increases were on the horizon. US equity markets declined modestly in the next quarter. Capital market performance during the quarter was dominated by Russia’s invasion of Ukraine and NATO’s sharp response. These events further supported inflationary pressures and are an additional weight to future economic growth. Even with the added cost pressures from the invasion of Ukraine, inflation remained elevated relative to recent history. The Federal Reserve raised the Fed Funds rate by twenty-five basis points during the quarter, kicking off the first Fed hiking cycle since 2018.

US equity markets continued their decline throughout the second quarter of 2022, and international markets followed suit. Risk assets continued to be pressured by accelerating inflation, decelerating economic growth, and tightening financial conditions. Inflation in the US moved from goods to services and housing. While interest rates shifted materially higher, the yield curve flattened with money supply decelerating materially. The rapid slowdown in economic growth and tightening financial conditions created a recessionary environment in the US, Europe, and most export led economies.

US and international equity markets remained volatile during the third quarter of 2022. Helping to drive equity markets down was exceptional US dollar strength as the Federal Reserve dramatically tightened financial conditions by increasing interest rates and aggressively shrinking their balance sheet. The strong US dollar accelerated the exportation of US inflation to the rest of the world, forcing nearly all global central banks to follow the US Federal Reserve in raising interest rates.

For the twelve-month period ending 8/31/21, the Saratoga Advantage Trust Mid Capitalization Portfolio posted negative absolute and positive relative performance. Security selection within Communication Services and Information Technology were the largest contributors to relative outperformance. The largest detractor was stock selection within Health Care and Consumer Staples.

Over the short- to medium-term, we believe markets will continue to be heavily influenced by the ongoing energy and capital shortages dominating realpolitik. Given the nature of the challenges, there appear to be no short-term solutions, but only tradeoffs driven by the political calendar and responses to crises as they flare up. As these twin crises confront a developing global recession with all major central banks continuing to tighten financial conditions, equity investors’ underlying premise for optimism must be that countries do not choose bankruptcy via austerity. We have witnessed pivots by the Bank of England, the European Union Bank, the Bank of Japan, and the Bank of Korea supporting this premise as they have reimplemented forms of liquidity support.

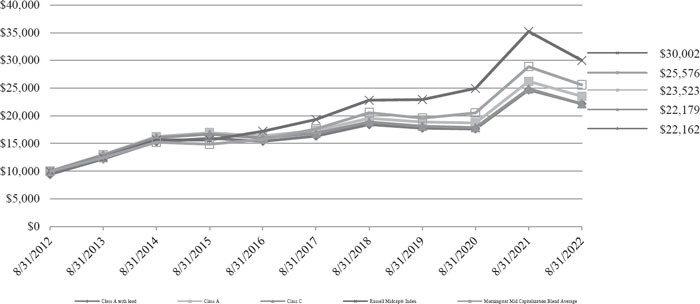

10

| INVESTMENT REVIEW |

MID CAPITALIZATION PORTFOLIO

A HYPOTHETICAL COMPARISON OF THE GROWTH OF $10,000 INVESTED IN THE

MID CAPITALIZATION PORTFOLIO VS. BENCHMARK

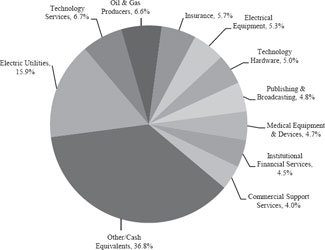

SIGNIFICANT AREAS OF INVESTMENT

AS A PERCENTAGE OF NET ASSETS

| Top 10 Portfolio Holdings* | |

| % of | |

| Company | Net Assets |

| Motorola Solutions, Inc. | 5.0% |

| Nexstar Media Group, Inc. | 4.8% |

| Vistra Corporation | 3.6% |

| Evergy, Inc. | 3.1% |

| Alliant Energy Corporation | 3.1% |

| Ameren Corporation | 3.1% |

| Republic Services, Inc. | 3.0% |

| CMS Energy Corporation | 3.0% |

| WillScot Mobile Mini Holdings Corporation | 2.7% |

| Nasdaq, Inc. | 2.5% |

| * | Based on total net assets as of August 31, 2022. |

Excludes short-term investments.

Portfolio Composition*

The Russell Midcap® Index measures the performance of the mid-cap segment of the US equity universe. The Russell Midcap Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Russell Midcap® Index represents approximately 27% of the total market capitalization of the Russell 1000® companies, as of the most recent reconstitution. The Russell Midcap Index is constructed to provide a comprehensive and unbiased barometer for the mid-cap segment. The index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true midcap opportunity set. Investors may not invest in the Index directly; unlike the Portfolio’s return, the Index does not reflect any fees or expenses.

The Morningstar Mid Capitalization Blend Average (“Mid Cap Blend Average”), as of August 31, 2022, consisted of 417 mutual funds comprised of mid market capitalization stocks. The Mid Cap Blend Average is not managed and it is not possible to invest directly in the Mid Cap Blend Average.

Past performance is not predictive of future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of the fund shares.

Mid Capitalization Portfolio is not sponsored, endorsed, sold or promoted by Morningstar, Inc. or any of its affiliates (all such entities, collectively, “Morningstar Entities”). The Morningstar Entities make no representation or warranty, express or implied, to the owners of the Mid Capitalization Portfolio or any member of the public regarding the advisability of investing in mutual funds comprised of mid market capitalization stocks generally or in the Mid Capitalization Portfolio in particular or the ability of the Morningstar Mid Cap Blend Average to track general mid market capitalization stocks market performance.

THE MORNINGSTAR ENTITIES DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE MORNINGSTAR MID CAP BLEND AVERAGE OR ANY DATA INCLUDED THEREIN AND MORNINGSTAR ENTITIES SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN.

11

| INVESTMENT REVIEW |

SMALL CAPITALIZATION PORTFOLIO

Advised by: Zacks Investment Management, Inc., Chicago, Illinois

Objective: The Portfolio seeks maximum capital appreciation.

| Total Aggregate Return for the Year Ended August 31, 2022 | |||||

| One Year: | Five Year: | Ten Year: | Inception: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 1/4/99 – 8/31/22* | 2/14/06 – 8/31/22* | |

| Class A | |||||

| With Sales Charge | (13.83)% | 6.99% | 7.75% | NA | 5.88% |

| Without Sales Charge | (8.58)% | 8.28% | 8.39% | NA | 6.26% |

| Class C | |||||

| With Sales Charge | (9.75)% | 7.77% | 7.75% | 7.58% | NA |

| Without Sales Charge | (8.75)% | 7.77% | 7.75% | 7.58% | NA |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 2.11% and 2.84% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

In selecting securities for the Portfolio, the Adviser begins with a screening process that seeks to identify growing companies whose stocks sell at discounted price-to-earnings and price-to-cash flow multiples. The Adviser also attempts to discern situations where intrinsic asset values are not widely recognized. The Adviser favors such higher-quality companies that generate strong cash flow, provide above-average free cash flow yields and maintain sound balance sheets. Rigorous fundamental analysis, from both a quantitative and qualitative standpoint, is applied to all investment candidates. While the Adviser employs a disciplined “bottom -up” approach that attempts to identify undervalued stocks, it nonetheless is sensitive to emerging secular trends. The Adviser does not, however, rely on macroeconomic forecasts in its stock selection efforts and prefers to remain fully invested.

PORTFOLIO ADVISOR COMMENTARY

During the first three quarters of the annual period ended August 31, 2022, small-cap stocks as an asset class underperformed mid-cap and large-cap stocks. The period was notable for persistently high levels of inflation, the Federal Reserve’s acceptance that inflation has become more than transitory, and their willingness to start tackling the inflation problem by removing monetary stimulus programs. Coupled with interest rate increases, investors seemed to prefer less growth-sensitive larger stocks.

During the most recent quarter, small-cap stocks outperformed mid-cap and-large cap stocks, as employment growth and the US economy as a whole stayed relatively solid. Russia’s war in Ukraine continued to strain the global energy supply, while China maintained its zero-COVID policy further applying pressure to global supply chains. All of these factors contributed to broad and high inflation. In order to bring inflation down, the Federal Reserve continued the tightening of financial conditions by raising interest rates fast, while winding down its balance sheet. The markets began to anticipate a slowdown in economic growth that may lead to a global recession. In this environment, small-cap companies with a domestic focus outperformed.

The Saratoga Advantage Trust Small Capitalization Portfolio was down for the period, though it outperformed meaningfully on a relative basis. Both Energy and Health Care sector picks in the portfolio outperformed. Stock selection in the Technology and Consumer Discretionary sectors underperformed. The strategy’s overweight exposure to Energy and underweight exposure to Consumer Staples, Utilities, and Technology sectors helped relative performance while an underweight exposure to Health Care and overweight exposure to the Materials detracted.

12

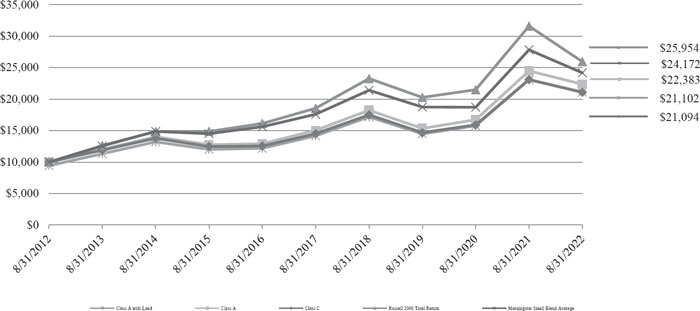

| INVESTMENT REVIEW |

SMALL CAPITALIZATION PORTFOLIO

A HYPOTHETICAL COMPARISON OF THE GROWTH OF $10,000 INVESTED IN THE

SMALL CAPITALIZATION PORTFOLIO VS. BENCHMARK

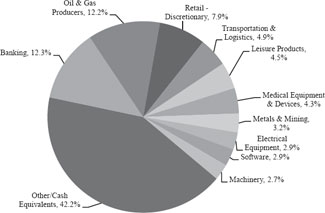

SIGNIFICANT AREAS OF INVESTMENT

AS A PERCENTAGE OF NET ASSETS

| Top 10 Portfolio Holdings* | |

| % of | |

| Company | Net Assets |

| Matador Resources Company | 2.3% |

| WESCO International, Inc. | 2.2% |

| Chord Energy Corporation | 2.0% |

| Chesapeake Energy Corporation | 2.0% |

| Magnolia Oil & Gas Corporation | 1.9% |

| Academy Sports & Outdoors, Inc. | 1.7% |

| Builders FirstSource, Inc. | 1.7% |

| Shockwave Medical, Inc. | 1.7% |

| Molina Healthcare, Inc. | 1.7% |

| Ovintiv, Inc. | 1.6% |

| * | Based on total net assets as of August 31, 2022. |

Excludes short-term investments.

Portfolio Composition*

The Russell 2000 Index is comprised of the 2,000 smallest U.S domicile publicly traded common stock which are included in the Russell 3000 Index. The common stock included in the Russell 2000 Index represent approximately 10% of the U.S equity market as measured by market capitalization. The Russell 3000 Index is an unmanaged index of the 3,000 largest U.S domicile publicity traded common stocks by market capitalization representing approximately 98% of the U.S publicity traded equity market. The Russell 2000 Index is an unmanaged index which does not include fees and expenses, and whose performance reflects reinvested dividends. Investors may not invest in the Index directly.

The Morningstar Small Blend Average (“Small Blend Average”), as of August 31, 2022, consisted of 624 mutual funds comprised of small market capitalization stocks. The Small Blend Average is not managed and it is not possible to invest directly in the Small Blend Average.

Past performance is not predictive of future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of the fund shares.

Small Capitalization Portfolio is not sponsored, endorsed, sold or promoted by Morningstar, Inc. or any of its affiliates (all such entities, collectively, “Morningstar Entities”). The Morningstar Entities make no representation or warranty, express or implied, to the owners of the Small Capitalization Portfolio or any member of the public regarding the advisability of investing in mutual funds comprised of small market capitalization stocks generally or in the Small Capitalization Portfolio in particular or the ability of the Morningstar Small Blend Average to track general small market capitalization stocks market performance.

THE MORNINGSTAR ENTITIES DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE MORNINGSTAR SMALL CAP BLEND AVERAGE OR ANY DATA INCLUDED THEREIN AND MORNINGSTAR ENTITIES SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN.

13

| INVESTMENT REVIEW |

INTERNATIONAL EQUITY PORTFOLIO

Advised by: Smith Group Asset Management, Dallas, Texas

Objective: The Portfolio seeks long-term capital appreciation.

| Total Aggregate Return for the Year Ended August 31, 2022 | |||||

| One Year: | Five Year: | Ten Year: | Inception: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 1/4/99 – 8/31/22* | 2/14/06 – 8/31/22* | |

| Class A | |||||

| With Sales Charge | (29.33)% | (3.49)% | (0.06)% | NA | (1.37)% |

| Without Sales Charge | (25.02)% | (2.35)% | 0.53% | NA | (1.01)% |

| Class C | |||||

| With Sales Charge | (26.55)% | (2.94)% | (0.11)% | (1.03)% | NA |

| Without Sales Charge | (25.55)% | (2.94)% | (0.11)% | (1.03)% | NA |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 2.78% and 3.96% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

The Adviser seeks to purchase reasonably valued stocks it believes have the ability to accelerate earnings growth and exceed investor expectations. The Adviser utilizes a three step process in stock selection. First, the Adviser reviews a series of screens utilizing the Adviser’s investment models, which are based on fundamental characteristics, designed to eliminate companies that the Adviser’s research shows have a high probability of underperformance. Factors considered when reviewing the screens include a multi-factor valuation framework, earnings quality, capital structure and financial quality. Next, securities that pass the initial screens are then evaluated to try to identify stocks with the highest probability of producing an earnings growth rate that exceeds investor expectations. This process incorporates changes in earnings expectations and earnings quality analysis. Finally, these steps produce a list of eligible companies which are subjected to analysis by the Adviser to further understand each company’s business prospects and earnings potential. A stock is sold when it no longer meets the Adviser’s criteria.

PORTFOLIO ADVISOR COMMENTARY

Sentiment has changed dramatically over the last year from one of cautious optimism about the continuation of the recovery to deep concern about high inflation, rising interest rates, and the potential for a global recession. Add to that Russia’s war on Ukraine and the picture is markedly negative. Central banks in most of the developed world (with Japan as a notable exception) are mirroring the actions of the US Federal Reserve by aggressively raising interest rates to combat inflation. Europe faces a greater challenge than its peers due to the war, which, beyond the immeasurable human toll, has meant shortages and skyrocketing energy prices for countries that depend on Russia for a sizable portion of their energy needs.

China’s second quarter GDP came in at just 0.4%, well below expectations, which dashed hopes of the country reaching its full year growth target of 5.2%. China’s anemic growth is due to several factors including a collapse in the real estate market, strict adherence to a zero-Covid policy, and a historic heat wave and drought. Elsewhere in emerging markets, the stronger US dollar has been an additional headwind on top of already rising prices for countries that import a substantial proportion of dollar-denominated goods.

In the Saratoga Advantage Trust International Equity Portfolio, Emerging Asia flipped from best to worst performer between the prior fiscal year and this one. Chinese and Taiwanese names generally fared the worst. Developed Asia was the best relative performer with two Japanese holdings, shipping company Nippon Yusen (2.41%) and healthcare equipment provider Olympus Corporation (2.54%), leading the region. From a sector standpoint, about two thirds of portfolio’s underperformance came from the Financials sector, although this was mostly due to stocks not held. Information Technology was the top contributor for the period, also largely due to stocks avoided.

The World Bank recently warned that if central banks are too aggressive in raising rates to curb inflation the global economy is more likely to tip into recession. Of particular concern is the impact a more severe economic slowdown would have on developing countries, which are more dramatically impacted by rising energy and food prices. The good news is inflation is showing signs of peaking or at least slowing down. And while periods of high inflation have significant follow-on effects for the economy and corporate earnings, analysts are predicting a wider than normal range of outcomes, which suggests a high degree of uncertainty. Stock market returns for 2022 year-to-date reveal the great extent to which many investors are already pricing in potential negative outcomes.

Within the discussion above, the percentages shown next to specific securities are the percentages of the Portfolio represented by the security on 8/31/22. The securities held in the Portfolio are subject to change and any discussion of those securities should not be considered investment advice.

14

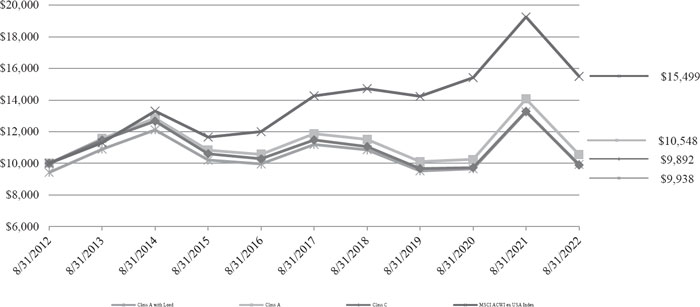

| INVESTMENT REVIEW |

INTERNATIONAL EQUITY PORTFOLIO

A HYPOTHETICAL COMPARISON OF THE GROWTH OF $10,000 INVESTED IN THE

INTERNATIONAL EQUITY PORTFOLIO VS. BENCHMARK

SIGNIFICANT AREAS OF INVESTMENT

AS A PERCENTAGE OF NET ASSETS

| Top 10 Portfolio Holdings* | |

| % of | |

| Company | Net Assets |

| Bumrungrad Hospital PCL | 2.9% |

| Sony Group Corporation | 2.8% |

| Eni SpA | 2.7% |

| Nokia OYJ | 2.7% |

| Woodside Energy Group Ltd. | 2.6% |

| Wal-Mart de Mexico S.A.B. de C.V. | 2.6% |

| Macquarie Group Ltd. | 2.6% |

| Novo Nordisk A/S | 2.5% |

| Olympus Corporation | 2.5% |

| Korean Air Lines Company Ltd. | 2.5% |

| * | Based on total net assets as of August 31, 2022. |

Excludes short-term investments.

Portfolio Compositions*

MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 Developed Markets countries (excluding the US) and 21 Emerging Markets countries. With 1,824 constituents, the index covers approximately 85% of the global equity opportunity set outside the US.

Past performance is not predictive of future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of the fund shares.

15

| INVESTMENT REVIEW |

HEALTH & BIOTECHNOLOGY PORTFOLIO

Advised by: Oak Associates, Ltd., Akron, Ohio

Objective: The Portfolio seeks long-term capital growth.

| Total Aggregate Return for the Year Ended August 31, 2022 | |||||

| One Year: | Five Year: | Ten Year: | Inception: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 7/15/99 – 8/31/22* | 1/18/00 – 8/31/22* | |

| Class A | |||||

| With Sales Charge | (12.60)% | 3.34% | 8.69% | 6.96% | N/A |

| Without Sales Charge | (7.28)% | 4.57% | 9.34% | 7.23% | N/A |

| Class C | |||||

| With Sales Charge | (8.85)% | 3.96% | 8.69% | N/A | 4.46% |

| Without Sales Charge | (7.85)% | 3.96% | 8.69% | N/A | 4.46% |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 2.54% and 3.13% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

The Adviser utilizes a top -down investment approach focused on long-term economic trends. The Adviser begins with the overall outlook for the economy, then seeks to identify specific industries with attractive characteristics and long-term growth potential. Ultimately, the Adviser seeks to identify high-quality companies within the selected industries and to acquire them at attractive prices. The Adviser’s stock selection process is based on an analysis of individual companies’ fundamental values, such as earnings growth potential and the quality of corporate management.

PORTFOLIO ADVISOR COMMENTARY

The Saratoga Advantage Trust Health & Biotechnology Portfolio was down during the annual period but avoided much of the market mayhem that struck other sectors and outperformed handily on a relative basis.

After several years of rising equity prices, US markets retreated during the fiscal year ended August 31st, 2022, as inflation infiltrated both domestic and global economies. The Fed began raising interest rates in March to curb demand, which initially calmed investors. However, as rising prices intensified, the Fed was forced to step up its pace. The fear has now shifted from feeling the Fed was too far behind the curve to get inflation under control to the risk of oversteering and causing a bigger recession than intended or necessary.

The Healthcare sector was down during the period on an absolute basis but solidly outperformed the overall S&P 500 as investors continued to favor more defensive sectors. Within the industry, the Healthcare Distributors substantially outperformed, a result of strong financial performance as well as attractive valuations. The Life Sciences Tools and Services sector was a relative underperformer largely due to peaking Covid-related sales. The passage of the Inflation Reduction Act in August, which included efforts to control high-cost drugs, will also bear monitoring for the Healthcare sector. However, due to the elongated timeframe of its implementation and limited number of initial medications, the ultimate impact will not be known for quite some time.

Going forward, all eyes will be on the Federal Reserve until we have more evidence of slowing economic growth and reduced inflationary pressures. We expect to see further evidence in the coming quarters as the accumulated efforts of monetary policy both through rate hikes and quantitative tightening work their way through the economy. With the S&P 500 retreating to June lows, valuations have contracted and investor sentiment, a contrarian indicator, now sits near its trough which is a stronger foundation from which to build. As we have seen, strong rallies can occur as the market works to find a bottom.

16

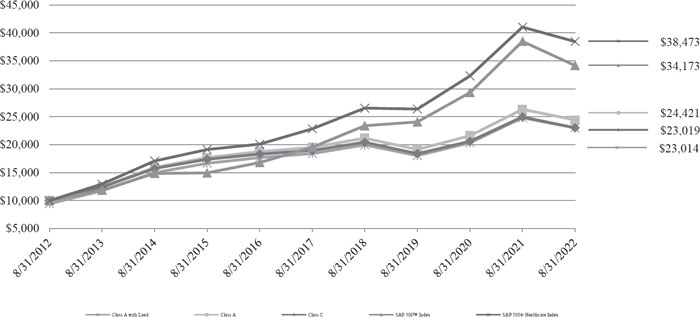

| INVESTMENT REVIEW |

HEALTH & BIOTECHNOLOGY PORTFOLIO

A HYPOTHETICAL COMPARISON OF THE GROWTH OF $10,000 INVESTED IN THE

HEALTH & BIOTECHNOLOGY PORTFOLIO VS. BENCHMARK

SIGNIFICANT AREAS OF INVESTMENT

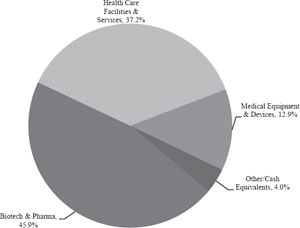

AS A PERCENTAGE OF NET ASSETS

| Top 10 Portfolio Holdings* | |

| % of | |

| Company | Net Assets |

| UnitedHealth Group, Inc. | 6.1% |

| Elevance Health, Inc. | 5.8% |

| United Therapeutics Corporation | 5.7% |

| McKesson Corporation | 5.4% |

| Amgen, Inc. | 5.3% |

| Cardinal Health, Inc. | 3.7% |

| Jazz Pharmaceuticals plc | 3.5% |

| Merck & Company, Inc. | 3.4% |

| Regeneron Pharmaceuticals, Inc. | 3.4% |

| Gilead Sciences, Inc. | 3.3% |

| * | Based on total net assets as of August 31, 2022. |

Excludes short-term investments.

Portfolio Composition*

The S&P 500™ Index is an unmanaged index. Index returns assume reinvestment of dividends. Investors may not invest in the Index directly; unlike the Portfolio’s returns, the Index does not reflect any fees or expenses.

The S&P 500® Healthcare Index is a widely-recognized, unmanaged, equally-weighted Index, adjusted for capital gains distribution and income dividends, of securities of companies engaged in the healthcare/biotechnology and medical industries. Index returns assume reinvestment of dividends; unlike the Portfolio’s returns, however, Index returns do not reflect any fees or expenses. Such costs would lower performance. It is not possible to invest directly in an Index.

Past performance is not predictive of future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of the fund shares.

17

| INVESTMENT REVIEW |

TECHNOLOGY & COMMUNICATIONS PORTFOLIO

Advised by: Oak Associates, Ltd., Akron, Ohio

Objective: The Portfolio seeks long-term growth of capital.

| Total Aggregate Return for the Year Ended August 31, 2022 | |||||

| One Year: | Five Year: | Ten Year: | Inception: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 10/22/97 – 8/31/22* | 1/14/00 – 8/31/22* | |

| Class A | |||||

| With Sales Charge | (30.59)% | 8.53% | 11.98% | 6.69% | NA |

| Without Sales Charge | (26.36)% | 9.83% | 12.65% | 6.94% | NA |

| Class C | |||||

| With Sales Charge | (27.74)% | 9.18% | 11.97% | NA | 0.77% |

| Without Sales Charge | (26.74)% | 9.18% | 11.97% | NA | 0.77% |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 2.39% and 2.97% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

In buying and selling securities for the Portfolio, the Adviser relies on fundamental analysis of each issuer and its potential for success in light of its current financial condition, its industry position and economic and market conditions. Factors considered include growth potential, earnings, valuation, competitive advantages and management.

PORTFOLIO ADVISOR COMMENTARY

The Saratoga Advantage Trust Technology & Communications Portfolio was down for the annual period, though relative performance was positive.

Inflationary pressures both domestically and abroad helped cause US markets to fall considerably during the period. Consumers and investors alike have enjoyed easy money policies both monetarily and fiscally for much of the past decade largely without inflation rearing its head. However, the substantial accommodative measures employed to overcome the pandemic created abundant demand that overwhelmed depleted inventories and disrupted supply chains. Further compounding the global supply shock has been the war in Ukraine as well as continued lockdowns in China.

During the period, the Technology sector underperformed the broader market as slowing growth pushed investors to more defensive segments of the economy. Within the industry, outperformance came from those companies with an enterprise focus. As employees return to the office in bigger numbers, corporations are once again spending on hardware, software, and services to support them. Alternatively, as expectations for economic growth slowed, consumer-oriented companies such as those in the Media and Marketing space lagged.

Despite its underperformance over the past year, we remain constructive on the broader Technology industry and believe its secular trends continue to make it one of the most profitable and fastest growing sectors within the market. With the S&P 500 retreating to June lows, valuations have contracted and investor sentiment, a contrarian indicator, now sits near its trough which is a stronger foundation from which to build. We see several segments of the industry as particularly attractive on a relative valuation basis including Software, Semiconductors, and Semiconductor Capital Equipment for long-term investors.

18

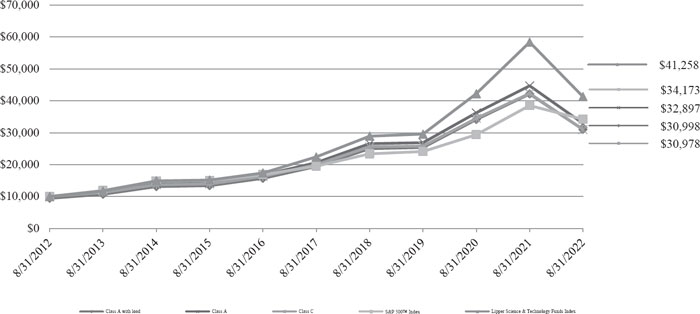

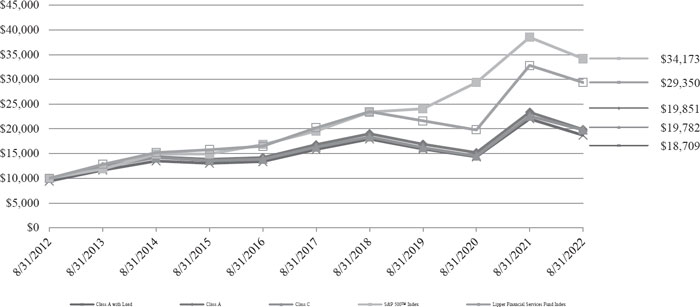

| INVESTMENT REVIEW |

TECHNOLOGY & COMMUNICATIONS PORTFOLIO

A HYPOTHETICAL COMPARISON OF THE GROWTH OF $10,000 INVESTED IN THE

TECHNOLOGY & COMMUNICATIONS PORTFOLIO VS. BENCHMARK

SIGNIFICANT AREAS OF INVESTMENT

AS A PERCENTAGE OF NET ASSETS

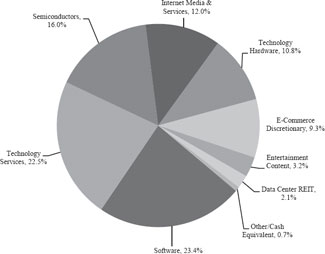

| Top 10 Portfolio Holdings* | |

| % of | |

| Company | Net Assets |

| Alphabet, Inc. | 8.2% |

| Amazon.com, Inc. | 6.5% |

| Apple, Inc. | 5.7% |

| Microsoft Corporation | 5.2% |

| KLA Corporation | 5.2% |

| Oracle Corporation | 5.2% |

| Cisco Systems, Inc. | 5.2% |

| QUALCOMM, Inc. | 4.7% |

| Visa, Inc. | 4.7% |

| Synopsys, Inc. | 3.9% |

| * | Based on total net assets as of August 31, 2022. |

Excludes short-term investments.

Portfolio Composition*

The S&P 500™ Index is an unmanaged index. Index returns assume reinvestment of dividends. Investors may not invest in the Index directly; unlike the Portfolio’s returns, the Index does not reflect any fees or expenses.

The Lipper Science & Technology Funds Index is an equal-weighted performance Index, adjusted for capital gain distribution and income dividends, of the largest qualifying funds within the Science and Technology fund classification, as defined by Lipper. Indexes are not managed and it is not possible directly in an Index.

Past performance is not predictive of future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of the fund shares.

19

| INVESTMENT REVIEW |

ENERGY & BASIC MATERIALS PORTFOLIO

Advised by: Smith Group Asset Management, Dallas, Texas

Objective: The Portfolio seeks long-term growth of capital.

| Total Aggregate Return for the Year Ended August 31, 2022 | |||||

| One Year: | Five Year: | Ten Year: | Inception: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 10/23/97 - 8/31/22* | 1/7/03 - 8/31/22* | |

| Class A | |||||

| With Sales Charge | 9.79% | (0.53)% | (1.65)% | 3.33% | NA |

| Without Sales Charge | 16.54% | 0.66% | (1.07)% | 3.58% | NA |

| Class C | |||||

| With Sales Charge | 14.66% | 0.35% | (1.51)% | NA | 3.44% |

| Without Sales Charge | 15.66% | 0.35% | (1.51)% | NA | 3.44% |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 4.43% and 5.06% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

The Adviser employs quantitative and qualitative analysis that seeks to identify reasonably valued, high quality companies within the energy and basic materials sectors. The Adviser’s selection process incorporates a multi-factor valuation framework, capital structure, and financial quality analysis. The valuation framework includes, but is not limited to, analysis of price to earnings, price to sales, price to book, and price to operating cash flow. Valuation methodology is industry-specific within the energy and basic materials sectors. This process produces a list of eligible companies which are then subjected to analysis by the Adviser to further understand each company’s business prospects and earnings potential. The Adviser uses the results of this analysis to construct the Portfolio’s security positions.

PORTFOLIO ADVISOR COMMENTARY

A year ago, financial markets were beginning to become concerned with a rising inflationary and interest rate environment, yet inflation expectations were still firmly anchored at 2.5%, up from 1.8% one-year prior, and the yield on the 10-year Treasury sat at 1.49%. A short nine months later the year-over-year change in the US Consumer Price Index hit 9.0% before modestly retreating to 8.3% over the coming months, the 10-year Treasury yield has more than doubled, and equity markets have entered bear market territory. There is no debate that inflation is back with a vengeance; the debate is now moving to how quickly inflation fades, to what level it fades, and what are the second-order effects on economic growth, corporate earnings, and other factors?

The US economy has seen two consecutive quarters of negative growth and further downturns are possible. The global economy looks to be headed for a period of below trend growth as tight monetary policy potentially constrains economic activity. This below-trend growth will almost assuredly lead to at least a modest adjustment in the outlook for corporate earnings, but that comes off much lower market multiples than have been seen for quite some time.

The price of West Texas Intermediate (WTI) rose from $68 per barrel on August 31, 2021, to $92 per barrel on August 31, 2022. Prices spiked above $120 per barrel in February on Russia’s invasion and again in June largely due to constrained supplies. However, prices have been trending down since then as global demand weakens.

The Saratoga Advantage Trust Energy & Basic Materials Portfolio’s holdings in the Energy sector (roughly 56% of portfolio weight on average during the period) were positive for the year. Exploration and Production names almost doubled in value and an overweight to this industry aided returns, making it the best absolute and relative performer. Equipment & Services was the worst absolute performer and Storage & Transportation was the worst on a relative basis. The portfolio’s Basic Materials holdings (42% of portfolio weight on average) produced a negative return for the year. Fertilizers & Agricultural Chemicals had the best absolute returns, while Specialty Chemicals had the worst. An overweight to Commodity Chemicals detracted from performance while an underweight to Industrial Gases and Construction Materials helped.

20

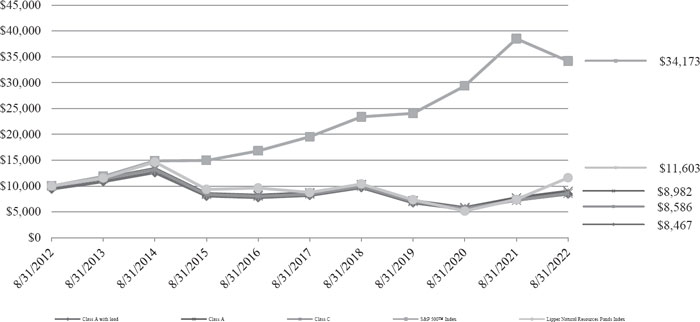

| INVESTMENT REVIEW |

ENERGY & BASIC MATERIALS PORTFOLIO

A HYPOTHETICAL COMPARISON OF THE GROWTH OF $10,000 INVESTED IN THE

ENERGY & BASIC MATERIALS PORTFOLIO VS. BENCHMARK

SIGNIFICANT AREAS OF INVESTMENT

AS A PERCENTAGE OF NET ASSETS

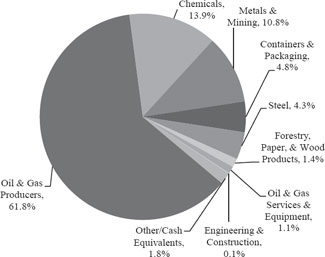

| Top 10 Portfolio Holdings* | |

| % of | |

| Company | Net Assets |

| Exxon Mobil Corporation | 9.9% |

| Chevron Corporation | 7.2% |

| PetroChina Company Ltd. | 4.0% |

| Valero Energy Corporation | 3.6% |

| EOG Resources, Inc. | 3.5% |

| BP plc | 3.4% |

| China Petroleum & Chemical Corporation | 3.3% |

| Canadian Natural Resources Ltd. | 3.1% |

| Shell plc | 2.9% |

| Chesapeake Energy Corporation | 2.7% |

| * | Based on total net assets as of August 31, 2022. |

Excludes short-term investments.

Portfolio Composition*

The S&P 500™ Index is an unmanaged index. Index returns assume reinvestment of dividends. Investors may not invest in the Index directly; unlike the Portfolio’s returns, the Index does not reflect any fees or expenses.

The Lipper Natural Resources Funds Index is an equal-weighted performance Index, adjusted for capital gain distributions and income dividends, of the largest qualifying funds within the Natural Resources fund classification, as defined by Lipper. Indexes are not managed and it is not possible to invest directly in an Index.

Past performance is not predictive of future performance. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of the fund shares.

21

| INVESTMENT REVIEW |

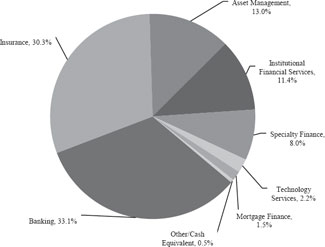

FINANCIAL SERVICES PORTFOLIO

Advised by: Smith Group Asset Management, Dallas, Texas

Objective: The Portfolio seeks long-term growth of capital.

| Total Aggregate Return for the Year Ended August 31, 2022 | ||||

| One Year: | Five Year: | Ten Year: | Inception: | |

| 9/1/21 – 8/31/22 | 9/1/17 – 8/31/22* | 9/1/12 – 8/31/22* | 8/1/00 – 2/28/22* | |

| Class A | ||||

| With Sales Charge | (19.92)% | 2.19% | 6.46% | 2.23% |

| Without Sales Charge | (15.00)% | 3.40% | 7.10% | 2.50% |

| Class C | ||||

| With Sales Charge | (13.37)% | 3.96% | 7.06% | 2.15% |

| Without Sales Charge | (12.37)% | 3.96% | 7.06% | 2.15% |

| * | Annualized performance for periods greater than one year. |

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (800) 807-FUND. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemptions of fund shares. The total operating expense ratios as stated in the fee table to the Portfolio’s prospectus dated December 28, 2021, are 3.81% and 4.41% for the A and C Classes, respectively.

PORTFOLIO INVESTMENT STRATEGIES AND TECHNIQUES

The Adviser employs quantitative and qualitative analysis that seeks to identify reasonably valued, high quality financial services companies that it believes have the ability to accelerate earnings growth and exceed investor expectations. The Adviser’s selection process consists of three steps. First, the Adviser reviews a series of screens utilizing the Adviser’s investment models, which are based on fundamental characteristics designed to eliminate companies that the Adviser’s research shows have a high probability of underperformance. Factors considered when reviewing the screens include a multi-factor valuation framework, earnings quality, and capital structure. The valuation framework includes, but is not limited to, analysis of price to earnings, price to sales, price to book, cash held to price and various cash flow ratios. Valuation methodology is industry-specific within the financial services sector. Next, securities that pass the initial screens are then evaluated to try to identify stocks with the highest probability of producing an earnings growth rate that exceeds investor expectations. This process incorporates changes in earnings expectations and earnings quality analysis. Finally, these steps produce a list of eligible companies which are subjected to analysis by the Adviser to further understand each company’s business prospects and earnings potential. The Adviser uses the results of this analysis to construct the Portfolio’s security positions.

PORTFOLIO ADVISOR COMMENTARY