UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-08614

Brandes Investment Trust

(Exact name of registrant as specified in charter)

4275 Executive Square, 5th Floor

La Jolla, CA 92037

(Address of principal executive offices) (Zip code)

Lea Anne Copenhefer

Morgan, Lewis & Bockius LLP

One Federal Street

Boston, MA 02110-1726

(Name and address of agent for service)

(858) 755-0239

Registrant’s telephone number, including area code

Date of fiscal year end: September 30

Date of reporting period: March 31, 2024

Item 1. Reports to Stockholders.

(a) The following is a copy of the reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (the “Act”) (17 CFR 270.30e-1):

1

SEMI-ANNUAL

REPORT

INTERNATIONAL EQUITY FUND

GLOBAL EQUITY FUND

EMERGING MARKETS VALUE FUND

INTERNATIONAL SMALL CAP EQUITY FUND

SMALL CAP VALUE FUND

CORE PLUS FIXED INCOME FUND

For the six months ended March 31, 2024

Table of Contents

1

Brandes International Equity Fund

Dear Fellow Investor,

The net asset value of the Brandes International Equity Fund (Class I Shares) advanced 16.46% in the six months ended March 31, 2024. During the same period, the MSCI EAFE Index gained 16.81%.

The primary drivers of performance were holdings in industrials and materials. Aerospace and defense companies Rolls-Royce and Embraer, as well as construction materials firm Heidelberg Materials, stood out as leading contributors.

Rolls-Royce and Embraer continued to benefit from the ongoing recovery in passenger air travel that has led to solid revenue growth, expanding profit margins, healthier cash-flow generation, and healed balance sheets. These positive fundamental developments helped confirm our long-term thesis around franchise quality, balance sheet durability, and end-market recovery potential for these holdings. Moreover, record backlogs highlighted—in our view—the appealing long-term secular growth outlook for global passenger air travel in an industry that has historically allowed incumbents to generate attractive returns on capital. Consequently, we revised our intrinsic value estimates for these companies upward, and believe they continue to offer an attractive risk/reward tradeoff at current valuation levels.

Select technology holdings also delivered solid performance. Notably, Taiwan Semiconductor Manufacturing Company (TSMC) appreciated as the proliferation of artificial intelligence (AI) applications fueled rising demand for semiconductor content. Besides TSMC, German software firm SAP also contributed positively to returns.

Health care holdings, such as Spain’s Grifols and pharmaceutical companies Sanofi, Takeda Pharmaceutical, and Astellas Pharma, were notable detractors in the period.

Biotechnology firm Grifols grappled with multiple declines in its share price following a short seller’s report that questioned the company’s debt and corporate governance practices. In our opinion, the risks highlighted in the report had been largely known, and we maintained our position in the company despite the volatility.

We continue to believe there is potentially meaningful upside in the stock. Grifols’ plasma business weathered considerable challenges amid the COVID-19 pandemic, including decreased blood donations and higher costs associated with compensating donors. Additionally, we appreciate Grifols’ competitive position in a consolidated industry with appealing potential growth.

Sanofi saw its share price decline after announcing a significant increase in research and development investment in its late-stage drug pipeline, which is expected to impact its near-term financial results. Taking a long-term view, however, we believe the share-price drop was overdone. The shares now trade at a low double-digit multiple of what we believe will likely be trough-level earnings, offering an appealing long-term risk/reward tradeoff, in our opinion.

Past performance is not a guarantee of future results.

Brandes International Equity Fund

Outside of health care, shares of Chinese internet retailer Alibaba fell after the company abandoned plans to spin off its cloud business. While Alibaba’s announcement was disappointing as it removed a potential catalyst for unlocking the significant value that we see in one of its businesses, we continue to believe the company is well positioned. Following the decline, Alibaba now trades at what we consider an attractive valuation of 8x forward earnings.

Select Portfolio Activity

There were several new purchases over the period, including U.K. health care equipment firm Smith & Nephew, consumer goods company Unilever, China-based battery maker Contemporary Amperex Technology Co. (CATL) and Mexico-based telecommunications services provider America Movil.

Smith & Nephew, a global leader in medical devices, specializes in orthopedics (including knee and hip replacements), sports medicine, ENT (ear, nose, and throat), and wound care. Over the past three years, the company’s shares have been under pressure as many elective but crucial medical procedures, such as knee and hip replacement surgeries, were delayed due to the COVID-19 pandemic. More recently, Smith & Nephew has also faced inflation challenges in its supply chain, which will likely impact its near-term margins. Nevertheless, we see the company as an appealing investment opportunity. We believe it is well positioned for a recovery in demand for elective procedures.

One of the world’s largest fast moving consumer goods companies, Unilever derives over half of its sales from emerging markets. Its shares recently slipped on concerns about slowing growth and margin pressures. Following several earnings downgrades, Unilever now trades at a discount to its European consumer staples peers. In our opinion, the share-price decline has offered an appealing opportunity to invest in a well-positioned company at a discounted valuation.

Contemporary Amperex Technology Co. (CATL) is the world’s largest producer of lithium-ion batteries for electric vehicles and energy storage systems, with an estimated global market share of approximately 35% in each segment. Known for its technological and cost leadership, CATL offers products for both premium and mass-market electric vehicles.

CATL stands out as a high-quality player in the global battery supply chain, excelling in technology, cost efficiency, cash-flow generation, and balance-sheet strength. At its current valuations, we believe the stock represents an attractive opportunity to invest in an industry leader amid a weak point in the industry cycle while keeping in mind the long-term trend of increasing levels of vehicle electrification.

Other major portfolio activity included the divestments of Taisho Pharmaceutical, insurers MS&AD Holdings (Japan) and Aegon (Netherlands), as well as Japan-based communication services company Softbank which we sold as they appreciated to our estimate of their intrinsic values.

3

Brandes International Equity Fund

Looking Forward

The portfolio has overweight positions in the United Kingdom, France, and emerging markets, and underweight positions in Australia and Japan. From a sector perspective, it holds key overweights to communication services, health care, and consumer staples, while maintaining meaningful underweights to industrials, technology, and financials.

At quarter end, value stocks continue to trade in the least expensive decile relative to growth (MSCI EAFE Value vs. MSCI EAFE Growth) since the inception of the style indices. This is evident across various valuation measures, including price/earnings, price/cash flow, and enterprise value/sales. Historically, such discount levels often signaled attractive subsequent returns for value stocks. This is encouraging for us as the Fund, guided by our value philosophy and process, has had the tendency to outperform the value index when it outperformed the benchmark.

Looking ahead, we remain optimistic about the prospects of our holdings. As of March 31, 2024, the Brandes International Equity Fund trades at more compelling valuation levels, in our opinion, while offering more attractive long-term growth characteristics relative to the benchmark and the MSCI EAFE Value Index.

For 50 years, Brandes Investment Partners has had the same goal: Seek better-than-market returns to help you pursue your long-term investment goals. We believe steadfast adherence to our value investing approach can help us achieve this aim because it compels us to invest in companies we view as strong yet appealingly priced. We thank you for your confidence and for investing with us.

Sincerely yours,

The Brandes International Large-Cap Investment Committee

Brandes Investment Trust

For term definitions, please refer to https://www.brandes.com/termdefinitions

Past Performance is not a guarantee of future results.

Diversification does not assure a profit or protect against a loss.

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and

4

Brandes International Equity Fund

may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Value stocks typically are less volatile than growth stocks; however, issues of value stocks typically have a lower expected growth rate in earnings and sales than issues of growth stocks.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI EAFE Index with net dividends captures large and mid cap representation of developed market countries excluding the U.S. and Canada.

The MSCI EAFE Value Index with gross dividends captures large and mid cap securities across developed market countries, excluding the United States and Canada, exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

The MSCI EAFE Growth Index with gross dividends captures large and mid cap securities across developed market countries, excluding the United States and Canada, exhibiting growth style characteristics, defined using long-term forward earnings per share (EPS) growth rate, short-term forward EPS growth rate, current internal growth rate, long-term historical EPS growth trend, and long-term historical sales per share growth trend.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes International Equity Fund is distributed by ALPS Distributors, Inc.

5

Brandes International Equity Fund

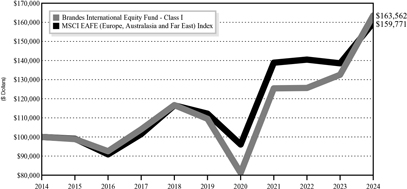

The following chart compares the value of a hypothetical $100,000 investment in the Brandes International Equity Fund – Class I from March 31, 2014 to March 31, 2024 with the value of such an investment in the MSCI EAFE (Europe, Australasia and Far East) Index for the same period.

Value of $100,000 Investment vs MSCI

EAFE (Europe, Australasia and Far East) Index (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Total Return | |

| | | Periods Ended March 31, 2024 | |

| | | One | | | Three | | | Five | | | Ten | | | Since | |

| | | Year | | | Years | | | Years | | | Years | | | Inception(1) | |

Brandes International Equity Fund | | | | | | | | | | | | | | | | | | | | |

Class A(2) | | | 23.09 | % | | | 8.96 | % | | | 8.06 | % | | | 4.80 | % | | | 7.46% | |

Class A (2) (with maximum sales charge) | | | 15.99 | % | | | 6.82 | % | | | 6.79 | % | | | 4.19 | % | | | 7.22% | |

Class C(3) | | | 22.10 | % | | | 8.23 | % | | | 7.31 | % | | | 4.20 | % | | | N/A | |

Class C (3) (with maximum sales charge) | | | 21.10 | % | | | 8.23 | % | | | 7.31 | % | | | 4.20 | % | | | N/A | |

Class I | | | 23.39 | % | | | 9.24 | % | | | 8.36 | % | | | 5.04 | % | | | 7.70% | |

Class R6(4) | | | 23.54 | % | | | 9.36 | % | | | 8.46 | % | | | 5.16 | % | | | 7.78% | |

MSCI EAFE (Europe, Australasia and Far East) Index | | | 15.32 | % | | | 4.78 | % | | | 7.33 | % | | | 4.80 | % | | | 5.08% | |

| (1) | The inception date is January 2, 1997. |

| (2) | Performance shown prior to January 31, 2011 for Class A shares reflects the performance of Class I shares adjusted to reflect Class A expenses. |

| (3) | Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. The Class C shares’ average annual total return for the 10-year period assumes that Class C shares automatically converted to Class A shares 8 years after the start of the |

6

Brandes International Equity Fund

| | period. The Class C shares’ average annual total return for the since inception period cannot be calculated as the Class A shares did not yet exist 8 years after the Fund’s inception date. |

| (4) | Performance shown prior to February 1, 2016 for Class R6 shares reflects the performance of Class I shares adjusted to reflect Class R6 expenses. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Brandes Investment Partners, L.P., the Advisor, has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

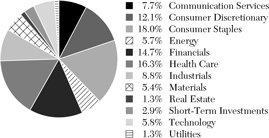

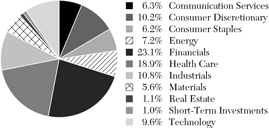

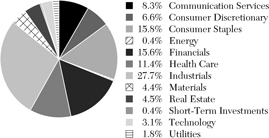

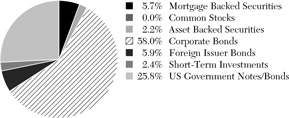

Sector Allocation as a Percentage of Total Investments as of

March 31, 2024 (Unaudited)

The sector classifications represented in the graph above are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC.

7

Brandes Global Equity Fund

Dear Fellow Investor,

The net asset value of the Brandes Global Equity Fund (Class I Shares) increased 22.28% in the six months ended March 31, 2024. During the same period, the MSCI World Index rose 21.31%.

From an industry perspective, Fund holdings in the Aerospace & Defense and Banking industries were meaningful contributors to performance.

Both Rolls-Royce and Embraer continued to benefit from recoveries in their commercial aerospace end-markets, resulting in improved cash-flow generation and stronger balance sheets. This positive development has mitigated the downside risks associated with the investments, while amplifying their upside potential. Consequently, we revised our intrinsic value estimates for these companies upward and believe they continue to offer attractive margins of safety at current valuation levels. The margin of safety for any security is the discount of market price to our estimate of intrinsic value.

U.S. money center banks Citigroup and Wells Fargo sustained their recent positive momentum continuing to contribute to the Fund’s outperformance.

And our technology holdings, particularly semiconductor-related firms such as Taiwan Semiconductor and U.S.-based Micron Technology, also delivered solid performance. This was fueled by the improving semiconductor market and rising demand for semiconductor content, driven at least partially by the proliferation of artificial intelligence (AI) applications. German software company SAP also experienced a rise in its share price.

Performance detractors during the period included holdings in the Biotechnology and Pharmaceuticals industires.

Biotechnology firm Grifols grappled with multiple declines in its share price following a short seller’s report that questioned the company’s accounting and corporate governance practices. In our opinion, the risks highlighted in the report had been largely known, and we maintained our modest-sized position in the company despite the volatility—albeit now at a lower weighting due to the share-price decline. While we have long been concerned with the company’s balance sheet, there is a potential near-term catalyst for its improvement as Grifols is expected to complete the sale of its ownership stake in Shanghai RAAS in the first half of this year and use the proceeds to pay down a significant portion of its debt.

We continue to believe there is potentially meaningful upside in the stock. Grifols’ plasma business weathered considerable challenges amid the COVID-19 pandemic, including decreased blood donations and higher costs associated with compensating donors. The company had also made substantial investments to expand capacity for future growth, which further weighed on its profitability. While the recovery has been slower than anticipated, assuming the Shanghai RAAS transaction concludes as expected, Grifols appears attractively valued to us, trading at a single-digit multiple of

Past performance is not a guarantee of future results.

8

Brandes Global Equity Fund

pre-COVID earnings. Additionally, we appreciate Grifols’ competitive position in a consolidated industry with appealing long-term potential growth.

Pfizer’s stock price dropped as the market continued to express concern over the decrease in its COVID-related revenue and near-term growth prospects. Nevertheless, we believe the company represents an appealing long-term risk/reward tradeoff given its broad product portfolio and significant investments in research and development (R&D). We took advantage of the share-price reduction to increase our allocation.

Sanofi saw its share price decline after announcing a significant R&D investment increase in its late-stage drug pipeline, which we expect to affect its near-term financial results. However, taking a long-term view, we believe that the discount has been overly punitive. Sanofi’s shares now trade at a low double-digit multiple of what appears to us as trough-level earnings, thus offering an attractive opportunity over a longer time horizon.

From a country perspective, Fund holdings in the United States, the United Kingdom and Brazil contributed to performance, while results were hampered by holdings in China, Spain and Thailand.

Select Portfolio Activity

The investment committee initiated new positions in Switzerland-based luxury goods business Compagnie Financiere Richemont and Canadian aerospace and defense company CAE, while divesting our holdings in semiconductor equipment firm Applied Materials and multinational financial institution JPMorgan Chase.

CAE supplies simulation equipment and integrated pilot training services to both civil aviation and military customers. Competing in a market dominated by two key players (the other being Flight Safety), CAE boasts the world’s largest installed base of full-flight simulators. Over the past 20 years, CAE has diversified into the less cyclical pilot training business, offering training services through a global network of over 250 civil aviation and military training locations across 40 countries. The company derives 40% of its revenues from simulation products and 60% from training and services.

Our coverage of CAE began in 2011, and since then, our assessment of the company’s core franchise quality remains unchanged. It is notable that during the COVID-19 pandemic, CAE took significant steps to strengthen its competitive position and improve industry structure. Firstly, the company leveraged its financial strength to complete a series of opportunistic acquisitions, purchasing nine companies at what we deemed attractive prices. This has helped CAE consolidate end-markets and expand its capabilities. Secondly, it restructured its cost base, closing nine plants and removing $70 million in annualized costs that resulted in a 1.5% margin benefit on sales. Lastly, CAE expanded its relationship with mainline airlines, which chose to outsource an increasing share of their internal training needs. To satisfy this new demand, CAE embarked on a heavy capital expenditure cycle over the course of the pandemic that we believe will benefit shareholders in the years ahead.

9

Brandes Global Equity Fund

The opportunity to initiate a position in CAE came as investors have been concerned about recent margin weakness within the company’s defense segment. However, we view these challenges as temporary. Inflation and supply chain pressures have started to ease, Many of CAE’s under-earning, fixed-price contracts are set to expire by 2025. We expect that CAE is positioned to improve its profitability as legacy fixed priced contracts roll over and as new high-margin defense contracts begin to ramp up. The company has given guidance for mid-double-digit margins on new contracts versus mid-single digit on legacy fixed-price contracts that were impacted by pandemic-related cost pressures.

CAE’s investment case is supported by its dominant position within flight simulation and pilot training services that offer moat-like characteristics, strong free cash flow and high tangible returns on capital with favorable medium-term growth characteristics. The company also has access to attractive financing in the form of perpetual, zero-cost loans from the Canadian government for research and development initiatives.

We initially bought Applied Materials, the world’s largest supplier of wafer fabrication equipment for semiconductor production, when its shares declined in 2022 due to concerns about industry-wide semiconductor capital expenditures (capex). Although near-term earnings expectations were undermined by the cyclical downturn, we believed Applied Materials was well-positioned to capitalize on increased silicon intensity over the medium-term. Driven by rising need for DRAM and NAND memory, as well as the expanding use case for semiconductors across a variety of end-markets, we foresaw a potential uptick in demand for production equipment from companies like Applied Materials. Looking beyond short-term fluctuations, we anticipated that greater long-term semiconductor capex spending would be necessary to drive bit growth if the underlying requirement for memory chips and other semiconductors remained robust. With Applied Materials’ stock price dipping below its historical trading multiples, we saw an attractive long-term risk/reward tradeoff.

The market has increasingly favored semiconductor-related companies because of rising demand driven primarily by AI. We opted to sell our position in Applied Materials after the shares rose over the past 18 months and they reached our estimate of their intrinsic value.

Looking Forward

At the end of March, the Brandes Global Equity Fund continues to hold its key positions in the economically sensitive financials sector and the more defensive health care sector. Our largest sector underweight remains to technology, which rose above a 20% allocation in the MSCI World Index due to its price appreciation this past year. Our allocation is under half the benchmark weighting.

Geographically, we continue to hold overweight positions in the United Kingdom, France, and emerging markets, while maintaining underweights to the United States and Japan.

10

Brandes Global Equity Fund

Within the benchmark, a wide dispersion of sector performance has continued, with companies in the technology and communication services sectors materially outperforming the broad index. Meanwhile, more defensive groupings—such as consumer staples, utilities, and health care—have underperformed. We have begun to notice more attractively valued companies in these sectors and have modestly increased our allocation over the past year.

We believe that the current fundamentals of the Fund’s holdings bode well for the long term. As of March 31, 2024, the Brandes Global Equity Fund trades at more compelling valuation levels than the benchmark, in our opinion, and the Fund’s holdings in aggregate have stronger balance sheets than the companies that comprise the MSCI World and MSCI World Value indices, as highlighted by leverage metrics such as net debt to EBITDA (earnings before interest, taxes, depreciation and amortization).

With the valuation gap between value and growth stocks widening in the past year, we are increasingly optimistic about the return potential for value stocks. Following the performance of the growth index, fueled largely by a few U.S. tech-related companies, value stocks are trading at the largest discount relative to growth stocks (MSCI World Value vs. MSCI World Growth) since the inception of the style indices. This valuation disparity is evident across various metrics, such as price/earnings, price/cash flow and enterprise value/sales. Historically, such valuation differentials have often signaled attractive future returns for value stocks over longer term horizons.

Notably, the Fund, guided by our value philosophy and process, has tended to outperform the benchmark when value stocks have outperformed the MSCI World Index. We believe the Fund is an excellent complement and diversifier to passive and growth-oriented strategies. Going forward, we remain optimistic about the long-term prospects of the Fund’s holdings.

Brandes Investment Partners has had the same goal since we started 50 years ago: Realize above-market gains to help you pursue your long-term investment objectives. We aim to do so by staying true to our value approach, which seeks fundamentally sound but potentially undervalued companies for your portfolio. Thank you for investing with us.

Sincerely yours,

The Brandes Global Large-Cap Investment Committee

Brandes Investment Trust

For term definitions, please refer to https://www.brandes.com/termdefinitions

Past Performance is not a guarantee of future results.

Diversification does not assure a profit or protect against a loss.

11

Brandes Global Equity Fund

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Value stocks typically are less volatile than growth stocks; however, issues of value stocks typically have a lower expected growth rate in earnings and sales than issues of growth stocks.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI World Index with net dividends captures large and mid cap representation of developed markets.

The MSCI World Value Index with net dividends captures large and mid cap securities across developed market countries exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

The MSCI World Growth Index with gross dividends captures large and mid cap securities across developed market countries exhibiting growth style characteristics, defined using long-term forward earnings per share (EPS) growth rate, short-term forward EPS growth rate, current internal growth rate, long-term historical EPS growth trend, and long-term historical sales per share growth trend.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

12

Brandes Global Equity Fund

The Brandes Global Equity Fund is distributed by ALPS Distributors, Inc.

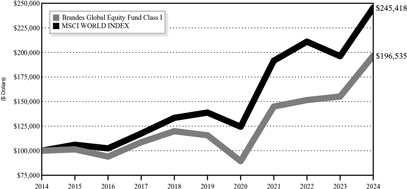

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Global Equity Fund – Class I from March 31, 2014 to March 31, 2024 with the value of such an investment in the MSCI World Index for the same period.

Value of $100,000 Investment vs MSCI

World Index (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Total Return | |

| | | Periods Ended March 31, 2024 | |

| | | One | | | Three | | | Five | | | Ten | | | Since | |

| | | Year | | | Years | | | Years | | | Years | | | Inception(1) | |

Brandes Global Equity Fund | | | | | | | | | | | | | | | | | | | | |

Class A(2) | | | 26.38 | % | | | 10.41 | % | | | 10.91 | % | | | 6.72 | % | | | 7.77% | |

Class A (2) (with maximum sales charge) | | | 19.10 | % | | | 8.25 | % | | | 9.61 | % | | | 6.09 | % | | | 7.36% | |

Class C(3) | | | 25.44 | % | | | 9.60 | % | | | 10.08 | % | | | 6.08 | % | | | 7.34% | |

Class C (3) (with maximum sales charge) | | | 24.44 | % | | | 9.60 | % | | | 10.08 | % | | | 6.08 | % | | | 7.34% | |

Class I | | | 26.69 | % | | | 10.69 | % | | | 11.18 | % | | | 6.99 | % | | | 8.02% | |

MSCI World Index | | | 25.11 | % | | | 8.60 | % | | | 12.07 | % | | | 9.39 | % | | | 9.90% | |

| (1) | The inception date is October 6, 2008. |

| (2) | Performance shown prior to January 31, 2011 for Class A shares reflects the performance of Class I shares adjusted to reflect Class A expenses. |

| (3) | Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. The Class C shares’ average annual total return for the 10-year and since inception periods assumes that Class C shares automatically converted to Class A shares 8 years after the start of the period. |

13

Brandes Global Equity Fund

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Brandes Investment Partners, L.P., the Advisor, has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

Sector Allocation as a Percentage of Total Investments as of

March 31, 2024 (Unaudited)

The sector classifications represented in the graph above are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC.

14

Brandes Emerging Markets Value Fund

Dear Fellow Investor,

The net asset value of the Brandes Emerging Markets Value Fund (Class I Shares) increased 11.35% in the six months ended March 31, 2024. During the same period, the MSCI Emerging Markets Index gained 10.42%.

Notable performers included holdings in Taiwan, South Korea, and Brazil. Specifically, semiconductor firms Taiwan Semiconductor Manufacturing Company (TSMC) and SK Hynix aided returns, as did regional jet manufacturer Embraer.

Embraer continued to benefit from a recovery in its commercial aerospace end-market, resulting in improved cash-flow generation and a stronger balance sheet. Meanwhile, TSMC and SK Hynix appreciated as the proliferation of artificial intelligence (AI) applications fueled rising demand for semiconductor chips and servers.

Several holdings in China detracted from performance, notably TravelSky Technology, Chinasoft International, LONGi Green Energy Technology, and Alibaba.

TravelSky issued a profit warning in January, attributing it to cost inflation mainly driven by increased expenditures in salary compensation, technical support and maintenance, research and development, and system security. Chinasoft declined on weaker-than-anticipated revenue and earnings from the second half of 2023. Meanwhile, LONGi continued to grapple with an industry oversupply issue that has pressured pricing within its wafer segment. We believe LONGi will likely be able to maintain healthy profitability throughout the downcycle, in contrast to its less profitable, second-tier peers.

In addition to these company-specific challenges, many of our Chinese holdings faced subdued investor sentiment stemming from the country’s weaker-than-expected post-COVID economic rebound and consumption, and the persistent downturn in its property sector. While we did not add any new China-based companies to the portfolio during the quarter, we selectively increased our existing positions amid the share-price weakness.

Select Portfolio Activity

During the period, the emerging markets investment committee initiated positions in China-based battery producer Contemporary Amperex Technology Co. and Mexico-based telecom America Movil.

Contemporary Amperex Technology Co. (CATL) is the world’s largest producer of lithium-ion batteries for electric vehicles and energy storage systems, with an estimated global market share of approximately 35% in each segment. Known for its technological and cost leadership, CATL offers products for both premium and mass-market electric vehicles.

CATL stands out as a high-quality player in the global battery supply chain, excelling in technology, cost efficiency, cash-flow generation, and balance-sheet strength. At its

Past performance is not a guarantee of future results.

15

Brandes Emerging Markets Value Fund

current valuations, we believe the stock represents an attractive opportunity to invest in an industry leader amid a weak point in the industry cycle while keeping in mind the long-term trend of increasing levels of vehicle electrification. Boasting market leadership in Latin America, America Movil (AMX) is one of the world’s largest network operators in terms of subscribers. The company’s operations span 22 countries, with a primary focus in Latin America and a presence in Austria and Eastern Europe. Recently, several factors have pressured AMX’s share price. These included a year-over-year contraction in reported service revenue driven by a strong Mexican peso, some negative views on lower-than-expected returns to shareholders, and uncertainty around potential regulatory changes in Mexico, as well as fiscal loosening in the country as the 2024 presidential election approaches.

AMX’s share-price weakness provided a good opportunity to invest in what we consider a fundamentally sound company. AMX has a long history of prudent capital allocation, with a focus on long-term returns on capital and free-cash-flow generation.

Other major portfolio activity included the divestment of Indonesian telecom XL Axiata and electric utility Enel Chile, which we sold as they appreciated to our estimate of their intrinsic values.

Looking Forward

Our portfolio positioning is a result of our bottom-up approach focused on uncovering value potential across all emerging markets. As such, our overweights tend to reflect areas where we have found many compelling opportunities, while our underweights represent those where we have not observed as much value. We believe maintaining the discipline to avoid overpriced businesses and those that are statistically cheap for a reason is just as important as the diligence to identify potentially undervalued companies through rigorous fundamental analysis.

At the end of March, the Fund’s largest country weights were in China and Brazil, and the Fund’s largest industry weights were in Banks and Semiconductors & Semiconductor Equipment.

We continue to hold underweights to companies in India and Taiwan, while maintaining an overweight to Latin America through our diversified positions in telecommunications, utilities, energy, and real estate. In our view, these holdings, including our recent purchase America Movil, have the potential to gain from deflationary input costs and the increasing trend of nearshoring in Mexico and nearby regions.

While value leadership (MSCI EM Value vs. MSCI EM) provided a tailwind for the Fund over the last six months, it was our stock selection across sectors and countries that primarily drove our outperformance. Going forward, we remain optimistic about the portfolio’s holdings composition and the risk/reward tradeoff it offers.

16

Brandes Emerging Markets Value Fund

For 50 years, Brandes Investment Partners has had the same goal: Seek better-than-market returns to help you pursue your long-term investment goals. We believe steadfast adherence to our value investing approach can help us achieve this aim because it compels us to invest in companies we view as strong yet appealingly priced. We thank you for your confidence and for investing with us.

Sincerely yours,

The Brandes Emerging Markets Investment Committee

Brandes Investment Trust

For term definitions, please refer to https://www.brandes.com/termdefinitions

Past Performance is not a guarantee of future results.

Diversification does not assure a profit or protect against a loss.

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Investments in small and medium capitalization companies tend to have limited liquidity and greater price volatility than investments in larger capitalization companies. Value stocks typically are less volatile than growth stocks; however, issues of value stocks typically have a lower expected growth rate in earnings and sales than issues of growth stocks.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

17

Brandes Emerging Markets Value Fund

The MSCI Emerging Markets Index with net dividends captures large and mid cap representation of emerging market countries.

The MSCI Emerging Markets Value Index with net dividends captures large and mid cap securities across emerging markets countries, exhibiting value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes Emerging Markets Value Fund is distributed by ALPS Distributors, Inc.

18

Brandes Emerging Markets Value Fund

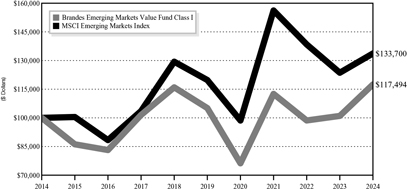

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Emerging Markets Value Fund – Class I from March 31, 2014 to March 31, 2024 with the value of such an investment in the MSCI Emerging Markets Index for the same period.

Value of $100,000 Investment vs MSCI

Emerging Markets Index (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Total Return | |

| | | Periods Ended March 31, 2024(1) | |

| | | One | | | Three | | | Five | | | Ten | | | Since | |

| | | Year | | | Years | | | Years | | | Years | | | Inception(2) | |

Brandes Emerging Markets Value Fund | | | | | | | | | | | | | | | | | | | | |

Class A | | | 16.02 | % | | | 1.23 | % | | | 2.04 | % | | | 1.37 | % | | | 6.09% | |

Class A (with maximum sales charge) | | | 9.35 | % | | | -0.75 | % | | | 0.84 | % | | | 0.77 | % | | | 5.87% | |

Class C(3) | | | 15.17 | % | | | 0.63 | % | | | 1.37 | % | | | 0.81 | % | | | N/A | |

Class C (3) (with maximum sales charge) | | | 14.17 | % | | | 0.63 | % | | | 1.37 | % | | | 0.81 | % | | | N/A | |

Class I | | | 16.31 | % | | | 1.45 | % | | | 2.25 | % | | | 1.63 | % | | | 6.33% | |

Class R6(4) | | | 16.37 | % | | | 1.54 | % | | | 2.39 | % | | | 1.74 | % | | | 6.41% | |

MSCI Emerging Markets Index | | | 8.15 | % | | | -5.05 | % | | | 2.22 | % | | | 2.95 | % | | | N/A | |

| (1) | Prior to January 31, 2011, the Advisor managed a private investment fund with an investment objective, investment policies and strategies that were, in all material respects, equivalent to those of the Brandes Emerging Markets Value Fund. The performance information shown for the Class I shares for periods before January 31, 2011 is that of the private investment fund and reflects the net expenses of the private investment fund. The performance of the private investment fund prior to January 31, 2011 is based on a calculation method that is different from the standardized calculation method prescribed by the SEC. The performance information shown for the Class A shares has been adjusted to reflect the differences in |

19

Brandes Emerging Markets Value Fund

| | the net expense ratios between the Class I and A shares. The private investment fund was not registered under the Investment Company Act of 1940 (“1940 Act”) and was not subject to certain investment limitations, diversification requirements, and other restrictions imposed by the 1940 Act and the Internal Revenue Code of 1986, which, if applicable, may have adversely affected its performance. |

| (2) | The inception date is August 20, 1996. |

| (3) | Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. The Class C shares’ average annual total return for the 10-year period assumes that Class C shares automatically converted to Class A shares 8 years after the start of the period. The Class C shares’ average annual total return for the since inception period cannot be calculated as the Class A shares did not yet exist 8 years after the Fund’s inception date. |

| (4) | Performance shown prior to July 11, 2016 for Class R6 shares reflects the performance of Class I shares adjusted to reflect Class R6 expenses. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Brandes Investment Partners, L.P., the Advisor, has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

Sector Allocation as a Percentage of Total Investments as of

March 31, 2024 (Unaudited)

The sector classifications represented in the graph above are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC.

20

Brandes International Small Cap Equity Fund

Dear Fellow Investor,

The net asset value of the Brandes International Small Cap Equity Fund (Class I Shares) advanced 23.23% in the six months ended March 31, 2024. During the same period, the MSCI ACWI ex USA Small Cap Index rose 12.44%.

Top contributors included holdings in the aerospace and defense industry, led by Rolls-Royce, Embraer, and Montana Aerospace. All three companies continued to see a resurgence in the markets in which they operate.

Our aerospace and defense holdings continued to benefit from the ongoing recovery in passenger air travel that has led to solid revenue growth, expanding profit margins, healthier cash-flow generation, and healed balance sheets. These positive fundamental developments helped confirm our long-term thesis around franchise quality, balance sheet durability, and end-market recovery potential for these holdings. Moreover, record backlogs highlighted—in our view—the appealing long-term secular growth outlook for global passenger air travel in an industry that has historically allowed incumbents to generate attractive returns on capital. Consequently, we revised our intrinsic value estimates for several of our aerospace and defense holdings upward, and believe they continue to offer an attractive risk/reward tradeoff at current valuation levels.

Notable detractors include several health care holdings such as Spain’s Grifols and France-based active pharmaceutical ingredient company Euroapi.

Biotechnology firm Grifols grappled with multiple declines in its share price following a short seller’s report that questioned the company’s debt and corporate governance practices. In our opinion, the risks highlighted in the report had been largely known, and we maintained our position in the company despite the volatility—albeit now at a lower weighting due to the share-price decline. While we have long been concerned with the company’s elevated financial leverage, we recognize that Grifols has several options at its disposal that can help derisk, including the partial sale of its stake in Shanghai RAAS that is scheduled to close in the first half of this year.

Furthermore, we appreciate Grifols’ competitive position in a consolidated industry with high barriers to entry and long-term secular growth, as well as its business model that should allow it to generate steady free cash flow if the industry returns to equilibrium. Trading at a single-digit multiple of pre-COVID earnings, Grifols appears attractively valued to us.

Euroapi issued another profit warning in October, revising down its EBITDA (earnings before interest, taxes, depreciation, and amortization) and sales growth guidance for the 2023 fiscal year, while also suspending its medium-term targets to 2026. Euroapi was carved out of global pharmaceutical firm Sanofi in May 2022, and it was expected that the company could face initial operational challenges as a standalone entity.

Past performance is not a guarantee of future results.

21

Brandes International Small Cap Equity Fund

Despite these short-term issues, we maintain a positive long-term outlook for Euroapi and have taken advantage of the share-price decline to add to our position.

Select Portfolio Activity

The small-cap investment committee initiated positions in Canada-based CAE and Switzerland’s Montana Aerospace.

CAE supplies simulation equipment and integrated pilot training services to both civil aviation and military customers. Competing in a market dominated by two key players (the other being Flight Safety), CAE boasts the world’s largest installed base of full-flight simulators. Over the past 20 years, CAE has diversified into the less cyclical pilot training business, offering training services through a global network of over 250 civil aviation and military training locations across 40 countries. The company derives 40% of its revenues from simulation products and 60% from training and services. It is notable that during the COVID-19 pandemic, CAE took significant steps to strengthen its competitive position and improve industry structure.

The opportunity to initiate a position in CAE came as investors have been concerned about recent margin weakness within the defense segment. However, we view these challenges as temporary. At its current valuation levels, CAE represents an appealing risk/reward tradeoff, in our opinion.

Montana Aerospace (AERO) is a vertically integrated manufacturer of metallic systems and components (aluminum, titanium) for the commercial aerospace, electric vehicle, and renewable energy end-markets. AERO, which went public in 2021 following its spin-off from parent company Montana Tech Components (MTC), has a relatively short operating history as a publicly traded company. However, its legacy assets date back to the 1990s when the business served as a U.S.-based casting company for Boeing.

AERO boasts a vertically integrated industrial base, expanding manufacturing scale, and low-cost industrial footprint that is intelligently located near customers. These capabilities position AERO as a cost-effective, one-stop-shop solution for aircraft OEMs (original equipment manufacturers) and Tier 1 suppliers (i.e., those that work the most closely with OEMs) looking to rationalize their highly complex and inefficient supply chains. To provide perspective, a typical commercial aircraft is made up of five million parts, and if one part is missing, the OEM can’t finish assembling the plane.

As air traffic has resumed, aircraft production has been ramping up, capital expenditures have been declining, and new factories have become operational. We believe it is an opportune time to invest in a company with an attractive long-term risk/reward tradeoff.

Other major portfolio activity included the full sale of a number of Japanese holdings including Fuji Media, medical device company Fukuda Denshi and Taisho Pharmaceutical.

22

Brandes International Small Cap Equity Fund

Taisho Pharmaceutical appreciated following a management buyout announcement. The offer reflected a 50% premium to Taisho’s six-month average trading price, and we divested our position as the share price surpassed the management buyout offer price.

Looking Forward

Allocations from a country and sector standpoint were largely unchanged during this period. The Fund maintains large allocations to industrials, consumer staples, and healthcare, while holding underweights in technology, materials, and consumer discretionary.

Geographically, the Fund continues to have significant exposure to companies in Japan (although underweight relative to the benchmark), the U.K., Ireland, and Hong Kong. It remains underweight Australia and Sweden relative to the benchmark. We believe the differences between the Fund’s portfolio and the MSCI ACWI ex USA Small Cap Index make it an appealing complement to index-tracking or passively managed strategies.

While value leadership (MSCI ACWI ex USA Small Cap Value vs. MSCI ACWI ex USA Small Cap) did provide a slight tailwind for the Fund over the last six months, it was our stock selection across sectors and countries that primarily drove outperformance. Going forward, we remain optimistic about the portfolio’s holdings composition and the risk/reward tradeoff it offers.

Brandes Investment Partners has had the same goal since we started 50 years ago: Realize above-market gains to help you pursue your long-term investment objectives. We aim to do so by staying true to our value approach, which seeks fundamentally sound but potentially undervalued companies for the Fund. Thank you for investing with us.

Sincerely yours,

The Brandes Small-Cap Investment Committee

Brandes Investment Trust

For term definitions, please refer to https://www.brandes.com/termdefinitions

Past Performance is not a guarantee of future results.

Diversification does not assure a profit or protect against a loss.

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. In addition, the performance of foreign securities depends on the political and economic environments and other overall economic conditions in the countries where the Fund invests. Emerging country markets involve greater risk and volatility than more developed markets. Some

23

Brandes International Small Cap Equity Fund

emerging markets countries may have fixed or managed currencies that are not free-floating against the U.S. dollar. Certain of these currencies have experienced, and may experience in the future, substantial fluctuations or a steady devaluation relative to the U.S. dollar. Investments in small and medium capitalization companies tend to have limited liquidity and greater price volatility than investments in larger capitalization companies. Value stocks typically are less volatile than growth stocks; however, issues of value stocks typically have a lower expected growth rate in earnings and sales than issues of growth stocks.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The MSCI ACWI ex USA Small Cap Index with net dividends captures small-cap representation across developed and emerging markets excluding the United States.

The MSCI ACWI ex USA Small Cap Value Index captures small-cap securities across developed and emerging markets excluding the United States, exhibiting overall value style characteristics, defined using book value to price, 12-month forward earnings to price, and dividend yield.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

One cannot invest directly in an index.

The Brandes International Equity Small Cap Equity Fund is distributed by ALPS Distributors, Inc.

24

Brandes International Small Cap Equity Fund

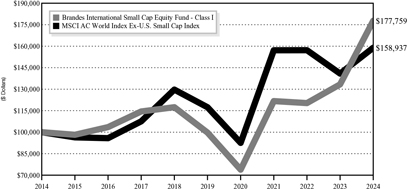

The following chart compares the value of a hypothetical $100,000 investment in the Brandes International Small Cap Fund – Class I from March 31, 2014 to March 31, 2024 with the value of such an investment in the MSCI AC World Index Ex-U.S. Small Cap Index for the same period.

Value of $100,000 Investment vs MSCI AC World Index

Ex-U.S. Small Cap Index (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Total Return | |

| | | Periods Ended March 31, 2024(1) | |

| | | One | | | Three | | | Five | | | Ten | | | Since | |

| | | Year | | | Years | | | Years | | | Years | | | Inception(2) | |

Brandes International Small Cap Equity Fund | | | | | | | | | | | | | | | | | | | | |

Class A | | | 33.07 | % | | | 13.22 | % | | | 12.02 | % | | | 5.70 | % | | | 9.08% | |

Class A (with maximum sales charge) | | | 25.42 | % | | | 11.01 | % | | | 10.70 | % | | | 5.08 | % | | | 8.85% | |

Class C(3) | | | 32.09 | % | | | 12.61 | % | | | 11.33 | % | | | 5.13 | % | | | N/A | |

Class C (3) (with maximum sales charge) | | | 31.09 | % | | | 12.61 | % | | | 11.33 | % | | | 5.13 | % | | | N/A | |

Class I | | | 33.28 | % | | | 13.46 | % | | | 12.25 | % | | | 5.92 | % | | | 9.34% | |

Class R6(4) | | | 33.47 | % | | | 13.61 | % | | | 12.39 | % | | | 6.03 | % | | | 9.41% | |

MSCI AC World Index | | | | | | | | | | | | | | | | | | | | |

Ex-U.S. Small Cap Index | | | 12.80 | % | | | 0.38 | % | | | 6.24 | % | | | 4.74 | % | | | 5.94% | |

| (1) | Prior to February 1, 2012, the Advisor managed a private investment fund with an investment objective, investment policies and strategies that were, in all material respects, equivalent to those of the Brandes International Small Cap Fund. The performance information shown for the Class I shares for periods before February 1, 2012 is that of the private investment fund and reflects the net expenses of the private investment fund. The performance of the private investment fund prior to February 1, 2012 is based on a calculation method that is different from the standardized calculation method prescribed by the SEC. |

25

Brandes International Small Cap Equity Fund

| | The performance information shown for the Class A shares has been adjusted to reflect the differences in the net expense ratios between the Class I and A shares. The private investment fund was not registered under the Investment Company Act of 1940 (“1940 Act”) and was not subject to certain investment limitations, diversification requirements, and other restrictions imposed by the 1940 Act and the Internal Revenue Code of 1986, which, if applicable, may have adversely affected its performance. |

| (2) | The inception date is August 19, 1996. |

| (3) | Performance shown prior to January 31, 2013 for Class C shares reflects the performance of Class I shares adjusted to reflect Class C expenses. The Class C shares’ average annual total return for the 10-year period assumes that Class C shares automatically converted to Class A shares 8 years after the start of the period. The Class C shares’ average annual total return for the since inception period cannot be calculated as the Class A shares did not yet exist 8 years after the Fund’s inception date. |

| (4) | Performance shown prior to June 27, 2016 for Class R6 shares reflects the performance of Class I shares adjusted to reflect Class R6 expenses. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Brandes Investment Partners, L.P., the Advisor, has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

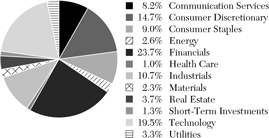

Sector Allocation as a Percentage of Total Investments as of

March 31, 2024 (Unaudited)

The sector classifications represented in the graph above are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC.

26

Brandes Small Cap Value Fund

Dear Fellow Investor,

The net asset value of the Brandes Small Cap Value Fund (Class I Shares) rose 21.23% in the six months ended March 31, 2024. During the same period, the Russell 2000 Index increased 19.94%.

From an industry perspective, the Fund’s aerospace and defense holdings such as Moog and Embraer continued to benefit from the ongoing recovery in passenger air travel that has led to solid revenue growth, expanding profit margins, healthier cash-flow generation, and healed balance sheets. These positive fundamental developments helped confirm our long-term thesis around franchise quality, balance sheet durability, and end-market recovery potential for these holdings. Moreover, record backlogs highlighted—in our view—the appealing long-term secular growth outlook for global passenger air travel in an industry that has historically allowed incumbents to generate attractive returns on capital. Consequently, we revised our intrinsic value estimates for several of the Fund’s aerospace and defense holdings upward, and believe they continue to offer an attractive risk/reward tradeoff at current valuation levels.

Other standout performers included Machinery businesses Graham Corporation and L.B. Foster Company, as well as Pharmaceuticals such as Elanco Animal Health, Prestige Consumer Healthcare, and Avadel Pharmaceuticals.

While the Fund’s Pharmaceutical industry holdings contributed in aggregate, Eagle Pharmaceuticals and Pediatrix Medical Group declined.

Eagle Pharmaceuticals declined after the company’s founding chief executive abruptly resigned and Nasdaq issued a non-compliance notice related to its late quarterly earnings filing. The company had previously noted a delay in releasing its third-quarter results due to potential adjustments for reporting Pemfexy (a cancer treatment) sales.

Other detractors were energy company Dril-Quip and outdoor sports company American Outdoor Brands

Select Portfolio Activity

The small-cap investment committee initiated positions in gas utility companies Spire and Northwest Natural Holding, as well as aerospace and defense business Spirit AeroSystems.

Spire Inc., formerly The Laclede Group, was formed in 2000 as the holding company for the Laclede Gas Company based in Missouri. Laclede Gas was founded in 1857 and was listed in 1889. Between 2013 and 2016, the company spent $2.6 billion acquiring three regulated natural gas utilities in Alabama, Missouri, and Mississippi. The company has three reportable business segments: gas utility, gas marketing and midstream. The gas utility segment includes the regulated operations of Spire Missouri, Spire Alabama, Spire Gulf and Spire Mississippi, which serve 1.7 million customers.

Past performance is not a guarantee of future results.

27

Brandes Small Cap Value Fund

Other gas-related businesses include unregulated natural gas marketing services and highly contracted midstream activities (pipelines and storage).

Spire earns an above-average (tangible) return on equity and has an earnings per share (EPS) growth profile similar to its peers. The company targets around 6% EPS growth over the medium term underpinned by a robust 10-year capex plan that implies 7%-8% annual rate base growth with good visibility on timely cost recovery. The shares trade at a discount of approximately 10% relative to their peers. This discount may reflect lingering negative perceptions of the regulatory climate in Missouri (68% of rate base) following a cost recovery dispute (since resolved). Other considerations include execution and capital allocation issues outside the regulated utilities and uncertainty about the timing (but not the outcome) for the recovery of its deferred gas purchases. These are based on a volumetric formula and thus tied to customer demand in winter. We believe Spire’s utilities have an average or above-average regulatory profile: Alabama and Mississippi are two of the most investor-friendly states in the country, and recent developments in Missouri have significantly improved its regulatory environment. With respect to capital allocation, 97% of Spire’s 10-year capex plan is allocated to the regulated utilities, providing good visibility of its earnings growth and returns.

Northwest Natural Holding Company (NW Holdings) is headquartered in Portland, OR. Its primary business is the distribution of natural gas to 800,000 customers in the state, including the Portland metropolitan area, as well as in southwest Washington. The company also engages in other business activities, including a gas storage facility, water utilities and in unregulated, renewable natural gas.

NW Holdings targets about 5% EPS growth for the 2022-27 period and is dependent on continuous rate case filings to sustain a return on equity of around 8%. Like Spire, it trades at a discount relative to its peers. Some of the discount seems justified, given the company’s below-average return on equity and low EPS growth potential, but we believe current levels are not too significant. As for shareholder returns, NW Holdings has grown its dividends for 68 years, making it one of only three companies listed on the NYSE with this legacy.

Looking Forward

At the end of March, the Fund maintains its largest weights in industrials, health care and information technology (although an underweight relative to the benchmark). The Fund’s most notable underweights are in consumer discretionary, financials, and real estate.

Compared with the Russell 2000 Value Index, we have significantly less exposure to financials and real estate. In our opinion, the differences between the Brandes Small Cap Value Fund and the broader U.S. small-cap market continue to make it an attractive complement to other small-cap offerings. The Fund exhibits lower valuations than the Russell 2000 Index, while offering exposure to companies with what we

28

Brandes Small Cap Value Fund

consider are strong balance sheets, compelling growth prospects, and a history of durable free cash flow generation. We are optimistic about the potential of value stocks in general and believe the Brandes Small Cap Value Fund remains well positioned from a long-term risk/reward perspective.

After a half-century of professional investing, Brandes Investment Partners remains fixed on its original goal. We pursue above-market returns to help you fulfill your long-term investment objectives. Our approach remains deeply rooted in the value philosophy and seeks to identify worthy but potentially underpriced companies. Thank you for your confidence in our approach.

Sincerely yours,

The Brandes Small-Cap Investment Committee

Brandes Investment Trust

For term definitions, please refer to https://www.brandes.com/termdefinitions.

Past Performance is not a guarantee of future results.

Diversification does not assure a profit or protect against a loss.

Because the values of the Fund’s investments will fluctuate with market conditions, so will the value of your investment in the Fund. You could lose money on your investment in the Fund, or the Fund could underperform other investments. The values of the Fund’s investments fluctuate in response to the activities of individual companies and general stock market and economic conditions. Investments in small and medium capitalization companies tend to have limited liquidity and greater price volatility than investments in larger capitalization companies. Value stocks typically are less volatile than growth stocks; however, issues of value stocks typically have a lower expected growth rate in earnings and sales than issues of growth stocks.

Please refer to the Schedule of Investments in the report for complete holdings information. Fund holdings, geographic allocations and/or sector allocations are subject to change at any time and are not considered a recommendation to buy or sell any security.

The foregoing reflects the thoughts and opinions of Brandes Investment Partners® exclusively and is subject to change without notice.

Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada.

Must be preceded or accompanied by a prospectus.

Index Guide

The Russell 2000 Index with gross dividends measures the performance of the small cap segment of the U.S. equity universe.

29

Brandes Small Cap Value Fund

The Russell 2000 Value Index with gross dividends measures performance of the small cap value segment of the U.S. equity universe. Securities are categorized as growth or value based on their relative book-to-price ratios, historical sales growth, and expected earnings growth.

One cannot invest directly in an index.

The Brandes Small Cap Value Fund is distributed by ALPS Distributors, Inc.

30

Brandes Small Cap Value Fund

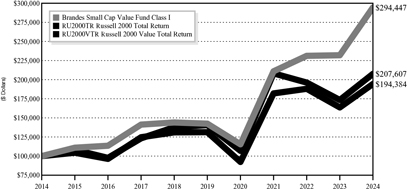

The following chart compares the value of a hypothetical $100,000 investment in the Brandes Small Cap Value Fund – Class I from March 31, 2014 to March 31, 2024 with the value of such an investment in the Russell 2000 Total Return Index and Russell 2000 Value Total Return Index for the same period.

Value of $100,000 Investment vs Russell 2000 Total

Return Index & Russell 2000 Value Total

Return Index (Unaudited)

| | | | | | | | | | | | | | | | | | | | |

| | | Average Annual Total Return | |

| | | Periods Ended March 31, 2024(2) | |

| | | One | | | Three | | | Five | | | Ten | | | Since | |

| | | Year | | | Years | | | Years | | | Years | | | Inception(1) | |

Brandes Small Cap Value Fund | | | | | | | | | | | | | | | | | | | | |

Class A | | | 26.63 | % | | | 11.47 | % | | | 15.31 | % | | | 11.11 | % | | | 8.07% | |

Class A (with maximum sales charge) | | | 19.32 | % | | | 9.28 | % | | | 13.95 | % | | | 10.45 | % | | | 7.83% | |

Class I | | | 26.93 | % | | | 11.75 | % | | | 15.64 | % | | | 11.40 | % | | | 8.35% | |

Class R6(3) | | | 27.14 | % | | | 12.06 | % | | | 14.25 | % | | | 10.80 | % | | | 8.12% | |

Russell 2000 Total Return Index | | | 19.71 | % | | | -0.10 | % | | | 8.10 | % | | | 7.58 | % | | | 7.41% | |

Russell 2000 Value Total Return Index | | | 18.75 | % | | | 2.22 | % | | | 8.17 | % | | | 6.87 | % | | | 7.99% | |

| (1) | The inception date is September 30, 1997. |

| (2) | Prior to January 2, 2018, the Advisor managed a private investment fund with an investment objective, investment policies and strategies that were, in all material respects, equivalent to those of the Brandes Small Cap Value Fund. The performance information shown for the Class I shares for periods before January 2, 2018 is that of the private investment fund and reflects the net expenses of the private investment fund. The performance of the private investment fund prior to January 2, 2018 is based on a calculation method that is different from the standardized calculation method prescribed by the SEC. |

31

Brandes Small Cap Value Fund

| | The performance information shown for the Class A shares has been adjusted to reflect the differences in the net expense ratios between the Class I and A shares. |

| (3) | Performance shown prior to January 2, 2018 for Class R6 shares reflects the performance of Class I shares. The private investment fund was not registered under the Investment Company Act of 1940 (“1940 Act”) and was not subject to certain investment limitations, diversification requirements, and other restrictions imposed by the 1940 Act and the Internal Revenue Code of 1986, which, if applicable, may have adversely affected its performance. |

Performance data quoted represents past performance; past performance does not indicate future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800-331-2979.

The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Brandes Investment Partners, L.P., the Advisor, has a fee waiver arrangement in place to limit the Fund’s annual operating expenses.

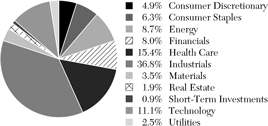

Sector Allocation as a Percentage of Total Investments as of

March 31, 2024 (Unaudited)

The sector classifications represented in the graph above are in accordance with Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC.

32

Brandes Core Plus Fixed Income Fund

Dear Fellow Investor,

In the six months ended March 31, 2024, the Brandes Core Plus Fixed Income Fund (Class I Shares) increased 6.77%, while its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, increased 5.99%.

Bond prices rallied in the fourth quarter of 2023 as the Fed (Federal Reserve) appeared to indicate that not only are further fed funds rate increases off the table, but the next move is likely a cut in rates. Taxable fixed income (as measured by the Bloomberg U.S. Aggregate Bond Index) delivered positive returns not only for the quarter but also the year.

In the credit markets, both investment grade and high yield bonds (as measured by Bloomberg’s U.S. Credit and U.S. Corporate High Yield Bond Indices respectively) posted strong absolute returns as well as positive returns relative to U.S. Treasury securities. Even after a sharp move downward during the quarter, yields on corporate bonds remain near the highest we have seen in close to 15 years, which has led to considerable market optimism about the opportunities in the asset class.

By the standards of the past few years, the start of 2024 was relatively benign – no global pandemic (2020 & 2021), no beginning of a significant rate hike cycle (2022), and no banking chaos (2023). During the first quarter, equity markets moved higher, credit spreads moved tighter, and interest rates moved upwards as the continued resilience in the U.S. economy forced investors to rethink the timing and number of rate cuts for the coming year.

The first three months of 2024 have seen an acceleration in upside surprises in economic data as demonstrated by the US Citigroup Economic Surprise Index, which has ultimately led the market to price in rate cuts starting later in the year and fewer overall – leading to a rise in U.S Treasury rates during the quarter.

We believe that the primary reason that the Fed and investors are eager to see rate cuts as soon as possible is that it seems they assume that the current fed funds rate is indeed restrictive. We would question this. The Bloomberg U.S. Financial Conditions Index shows that financial conditions are easier now than when the Fed began its rate hikes. If so, why do many investors still think the current fed funds rate is restrictive and thus keep planning for imminent rate cuts? In an ideal world, there should be little distinction between what a central bank like the Fed should do and what it will do. The Fed seems intent on easing policy despite stubborn inflation data and a clear easing of financial conditions over the past several months. Let’s hope market pressure for lower rates does not push the Fed into policy errors like those made in the 1970s.

Select Portfolio Activity

Fund activity was modest during the six months ending March 31, 2024.

In mid-October 2023 we added approximately 3% in agency mortgage-backed securities (“MBS”) to the Fund but remain underweight the sector relative to the

Past performance is not a guarantee of future results.

33

Brandes Core Plus Fixed Income Fund