Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-09102

iShares, Inc.

(Exact name of Registrant as specified in charter)

c/o: State Street Bank and Trust Company

1 Iron Street, Boston, MA 02210

(Address of principal executive offices) (Zip code)

The Corporation Trust Incorporated

351 West Camden Street, Baltimore, MD 21201

(Name and address of agent for service)

Registrant’s telephone number, including area code: 415-670-2000

Date of fiscal year end: August 31, 2014

Date of reporting period: August 31, 2014

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

AUGUST 31, 2014

2014 ANNUAL REPORT |  |

iShares, Inc.

| Ø | iShares MSCI Austria Capped ETF | EWO | NYSE Arca |

| Ø | iShares MSCI Belgium Capped ETF | EWK | NYSE Arca |

| Ø | iShares MSCI Emerging Markets Eastern Europe ETF | ESR | NYSE Arca |

| Ø | iShares MSCI France ETF | EWQ | NYSE Arca |

| Ø | iShares MSCI Italy Capped ETF | EWI | NYSE Arca |

| Ø | iShares MSCI Netherlands ETF | EWN | NYSE Arca |

| Ø | iShares MSCI Spain Capped ETF | EWP | NYSE Arca |

| Ø | iShares MSCI Sweden ETF | EWD | NYSE Arca |

| Ø | iShares MSCI Switzerland Capped ETF | EWL | NYSE Arca |

| Ø | iShares MSCI United Kingdom ETF | EWU | NYSE Arca |

Table of Contents

| 5 | ||||

| 26 | ||||

| 26 | ||||

| 27 | ||||

| 27 | ||||

| 29 | ||||

| 31 | ||||

| 33 | ||||

| 36 | ||||

| 38 | ||||

| 40 | ||||

| 41 | ||||

| 43 | ||||

| 45 | ||||

| 48 | ||||

| 61 | ||||

| 71 | ||||

| 86 | ||||

| 87 | ||||

| 88 | ||||

| 95 | ||||

| 103 |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES®, INC.

INTERNATIONAL MARKET OVERVIEW

International equities rose during the 12-month period ended August 31, 2014 (the “reporting period”), as modest economic growth and solid corporate profits offset concerns about global growth, the banking system and geopolitical events. Monetary policy continued to be a driving force for international equities, as several countries took steps to stimulate economic growth (as measured by gross domestic product, or “GDP”). The European Central Bank (“ECB”) cut interest rates several times, the Bank of Japan continued its bond purchasing efforts, and the U.S. Federal Reserve Bank (the “Fed”) reduced its unprecedented stimulus program.

Accommodative monetary policy and improving global growth led to a sustained rally in international equities from September to December 2013. However, events in early 2014 dampened the rally, as slow economic growth in the U.S. and China and the conflict in Ukraine raised concerns for international investors. In the final months of the reporting period, stagnant European growth, a Portuguese bank default and military escalation in Ukraine dampened international markets’ performance, particularly in Europe. Despite these challenges, most international markets finished with a solid return for the reporting period.

North American markets delivered strong gains during the reporting period. The U.S. economy strengthened in the latter half of the reporting period, as the combination of accommodative monetary policy, low inflation, steady job growth and rising corporate profits drove economic growth. Canada and Mexico also generated steady economic growth and rising stock prices during the reporting period.

Asian markets advanced during the reporting period, as investors generally embraced the region’s progress toward economic and political reform. Slow global growth presented new challenges for China and India after rapid economic growth in past decades. China, India and Japan, the three largest economies in the region, pursued dramatic changes to improve their competitive edge in the changing global economy.

China, Asia’s largest economy, continued to transition from an economy based on investment and manufacturing toward one based on consumption and services, which led to slowing economic growth. India underwent substantial political and economic change during the reporting period. The Bank of India made significant progress on curbing inflation, while the Indian government pursued growth-oriented political reform. By contrast, Japan attempted to reignite economic growth with monetary stimulus and political reform after twenty years of economic stagnation.

European equities posted solid gains while trailing developed markets in Asia and North America. Europe took steps toward an economic recovery during the reporting period after enduring a financial crisis and an economic recession. Europe’s uneven path to recovery included an improving credit environment and lower interest rates, as well as declining inflation and stagnant demand. France and Germany were mired in sluggish economic growth, while the United Kingdom expanded at a moderate pace during the reporting period. Spain and Italy experienced dramatically improving credit markets and lower interest rates, helping to revive investors’ interest in Spanish and Italian financial markets. European equity markets declined during the final months of the reporting period, as fear of economic stagnation and declining prices spurred the ECB to consider additional monetary support.

At the highest level, economic crosscurrents rippled across markets, while the ebb and flow of geopolitical risks drove market performance during the reporting period. International markets advanced through the uncertainty, as investors welcomed moderate global growth, low inflation and improving credit conditions.

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 5 |

Table of Contents

Management’s Discussion of Fund Performance

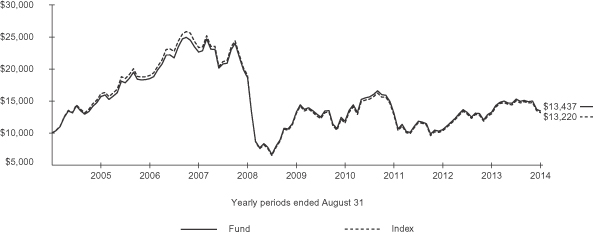

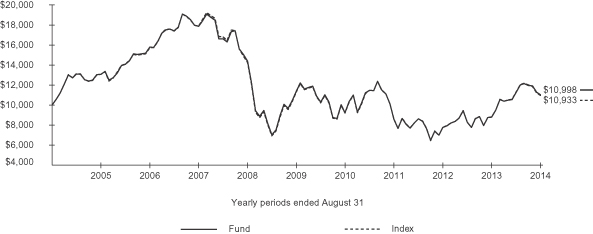

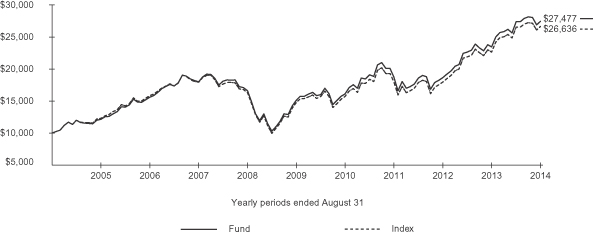

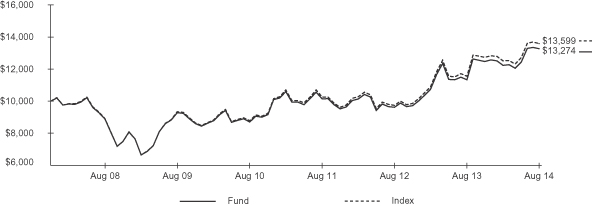

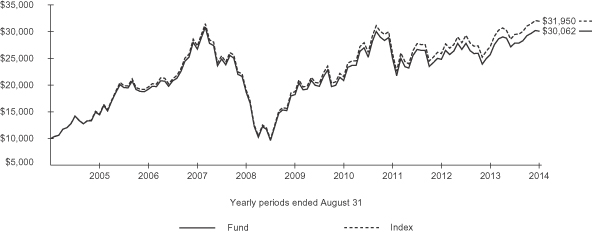

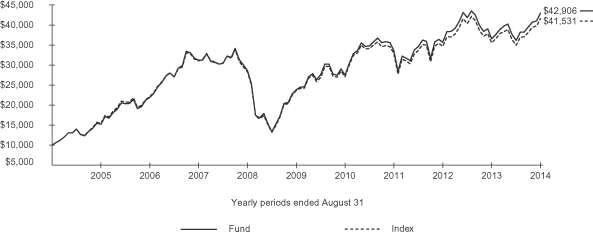

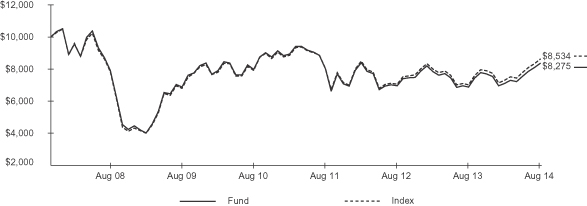

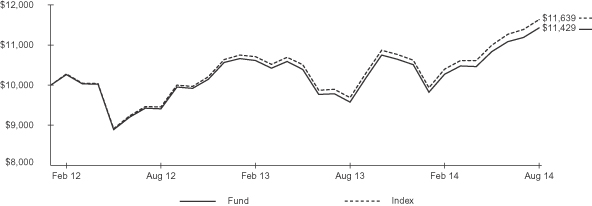

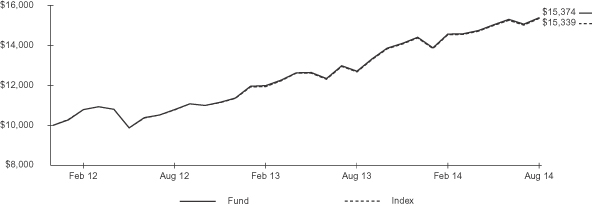

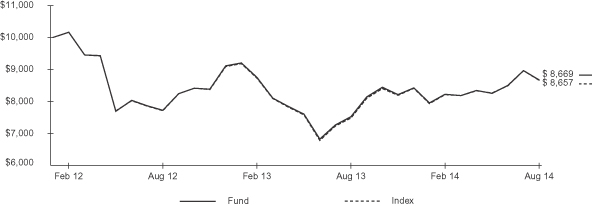

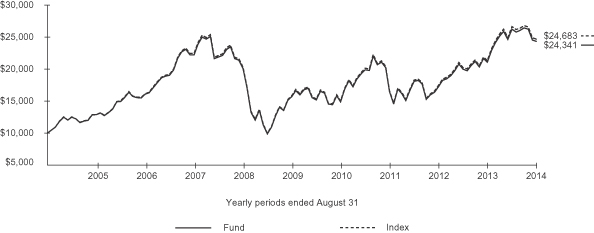

iSHARES® MSCI AUSTRIA CAPPED ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 1.56% | 1.03% | 1.64% | 1.56% | 1.03% | 1.64% | ||||||||||||||||||||

5 Years | 0.16% | 0.02% | 0.19% | 0.80% | 0.11% | 0.97% | ||||||||||||||||||||

10 Years | 3.00% | 2.86% | 2.83% | 34.37% | 32.64% | 32.20% | ||||||||||||||||||||

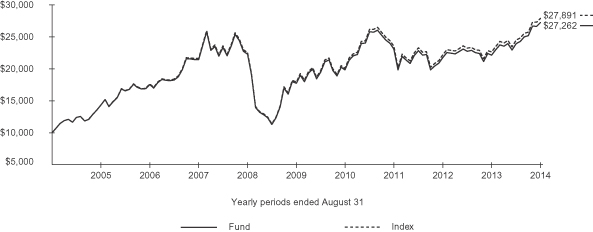

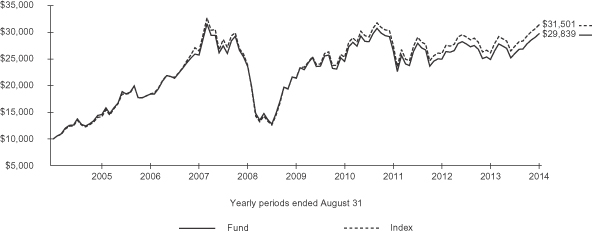

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Index performance through January 31, 2008 reflects the performance of the MSCI Austria Index. Index performance beginning on February 1, 2008 through February 11, 2013 reflects the performance of the MSCI Austria Investable Market Index. Index performance beginning on February 12, 2013 reflects the performance of the MSCI Austria Investable Market Index 25/50.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 879.20 | $ | 2.27 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 6 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI AUSTRIA CAPPED ETF

The iShares MSCI Austria Capped ETF (the “Fund”) seeks to track the investment results of a broad-based index composed of Austrian equities, as represented by the MSCI Austria Investable Market Index 25/50 (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 1.56%, net of fees, while the total return for the Index was 1.64%.

The Index posted a modestly positive return for the reporting period. The Index underperformed on local credit concerns while the broad international developed markets, as measured by the MSCI EAFE Index, advanced on improving credit conditions and generally accommodative monetary policy. During the first half of the reporting period, Austrian stocks benefited from the broad rally in international stocks. However, Austrian stocks declined sharply and trailed international stocks in the second half of the reporting period.

The financials sector, the largest sector representation in the Index, weighed on performance during the reporting period. Austrian banks have struggled to rebuild capital since the financial crisis in 2008. During the reporting period, Austria’s banking issues continued to raise concerns for investors. In particular, loans made to emerging European countries, as well as exposures in Russia and Ukraine, became problematic for several Austrian banks.

The Index declined sharply in the last two months of the reporting period as investors’ scrutiny intensified on the Austrian banking sector after a series of negative headlines. Hungarian legislation that required banks to reimburse borrowers for credit costs weighed on the profits of Austrian banks. The continued weakness in the credit quality of Austrian loans also prompted negative views from a major credit agency. Similarly, the Austrian central bank criticized lending practices, stating that lenders should review their business model.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Financials | 40.53 | % | ||

Industrials | 22.91 | |||

Materials | 16.22 | |||

Energy | 13.75 | |||

Telecommunication Services | 2.45 | |||

Information Technology | 1.95 | |||

Utilities | 1.62 | |||

Consumer Discretionary | 0.57 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

Erste Group Bank AG | 13.88 | % | ||

OMV AG | 10.65 | |||

Voestalpine AG | 8.72 | |||

Andritz AG | 6.86 | |||

Raiffeisen International Bank Holding AG | 4.96 | |||

IMMOFINANZ AG | 4.54 | |||

Vienna Insurance Group AG | 4.48 | |||

Wienerberger AG | 4.34 | |||

Oesterreichische Post AG | 3.96 | |||

CA Immobilien Anlagen AG | 3.92 | |||

|

| |||

TOTAL | 66.31 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 7 |

Table of Contents

Management’s Discussion of Fund Performance

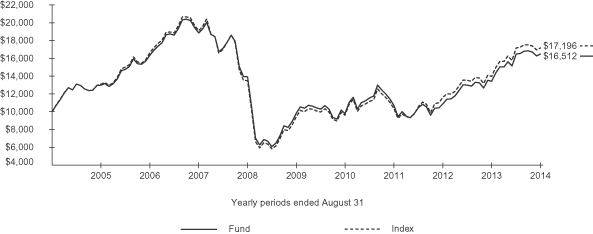

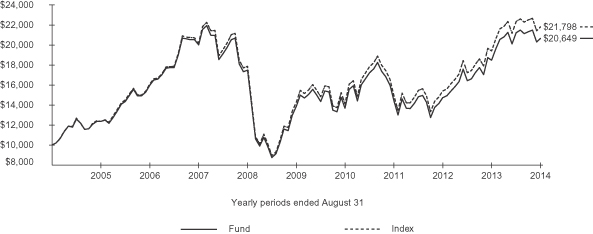

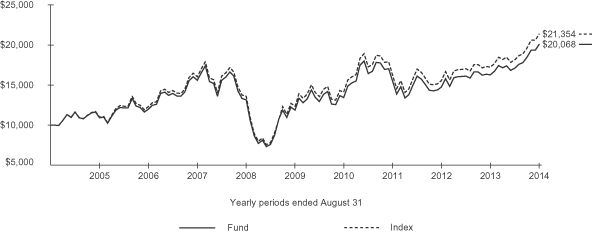

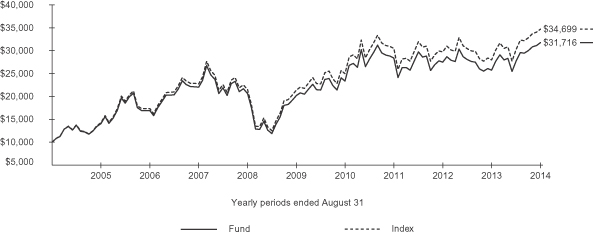

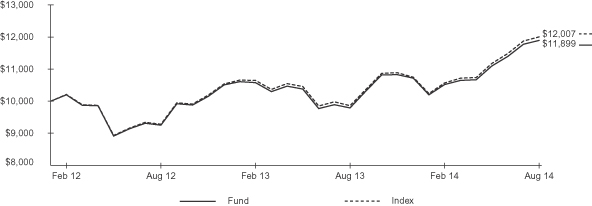

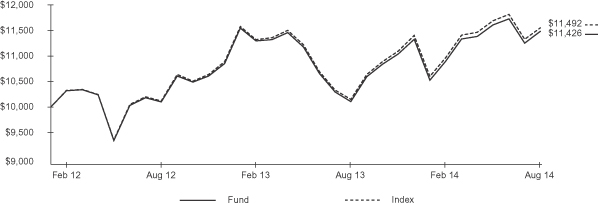

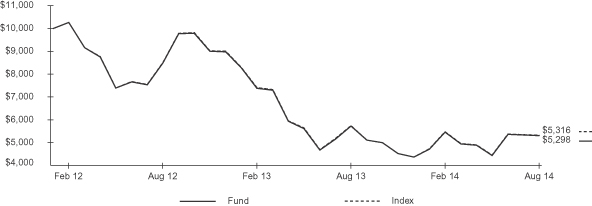

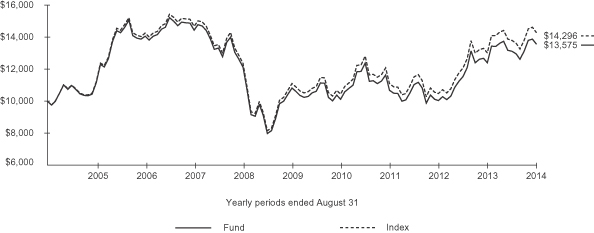

iSHARES® MSCI BELGIUM CAPPED ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 23.05% | 22.79% | 23.12% | 23.05% | 22.79% | 23.12% | ||||||||||||||||||||

5 Years | 10.84% | 10.80% | 12.67% | 67.29% | 66.98% | 81.58% | ||||||||||||||||||||

10 Years | 5.14% | 5.03% | 5.57% | 65.12% | 63.38% | 71.96% | ||||||||||||||||||||

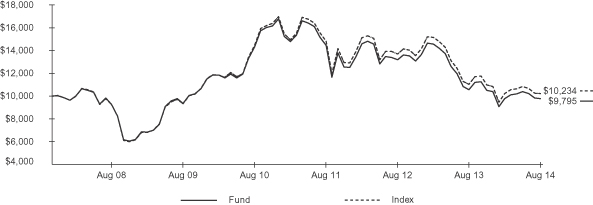

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Index performance through November 30, 2007 reflects the performance of the MSCI Belgium Index. Index performance beginning on December 1, 2007 through November 8, 2012 reflects the performance of the MSCI Belgium Investable Market Index. Index performance beginning on November 9, 2012 reflects the performance of the MSCI Belgium Investable Market Index 25/50.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 1,000.30 | $ | 2.42 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 8 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI BELGIUM CAPPED ETF

The iShares MSCI Belgium Capped ETF (the “Fund”) seeks to track the investment results of a broad-based index composed of Belgian equities, as represented by the MSCI Belgium Investable Market Index 25/50 (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 23.05%, net of fees, while the total return for the Index was 23.12%.

Belgian stocks, as represented by the Index, posted a strong return for the reporting period, outperforming the broad international developed markets, as measured by the MSCI EAFE Index.

The Belgian economy experienced slightly positive growth during the reporting period, as the eurozone’s economy emerged from recession. Low and falling inflation during the reporting period led to concern that the Belgian economy was at risk of a deflationary cycle. Nevertheless, investors found reasons for optimism, as Belgium was well-positioned to benefit from a broader European economic recovery. Belgium’s export-based economy relies heavily on trade with the rest of Europe. Signs of rising demand in Europe boosted industrial production in Belgium, leading investors to Belgian stocks that would benefit from the European recovery. Stock performance was especially strong in the first half of the reporting period, before stagnating in the second half of the reporting period.

Anheuser-Busch InBev NV, the largest constituent in the Index, comprised approximately 20% of the Index as of the end of the reporting period. The stock rallied during the reporting period, contributing to the strong performance of the Index.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Consumer Staples | 28.91 | % | ||

Financials | 26.29 | |||

Health Care | 12.61 | |||

Materials | 12.35 | |||

Telecommunication Services | 4.38 | |||

Consumer Discretionary | 4.35 | |||

Information Technology | 3.98 | |||

Industrials | 3.48 | |||

Energy | 2.37 | |||

Utilities | 1.28 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

Anheuser-Busch InBev NV | 22.33 | % | ||

KBC Groep NV | 7.72 | |||

UCB SA | 6.67 | |||

Solvay SA | 5.15 | |||

Groupe Bruxelles Lambert SA | 4.43 | |||

Delhaize Brothers and Co. “The Lion” (Delhaize Group) SA | 4.26 | |||

Ageas | 4.17 | |||

Belgacom SA | 3.53 | |||

Umicore SA | 3.31 | |||

Colruyt SA | 2.31 | |||

|

| |||

TOTAL | 63.88 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 9 |

Table of Contents

Management’s Discussion of Fund Performance

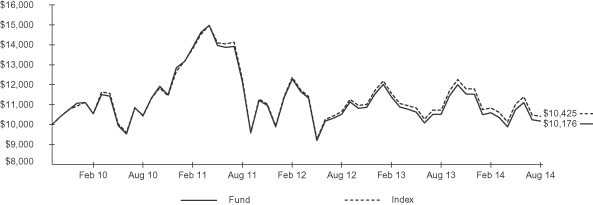

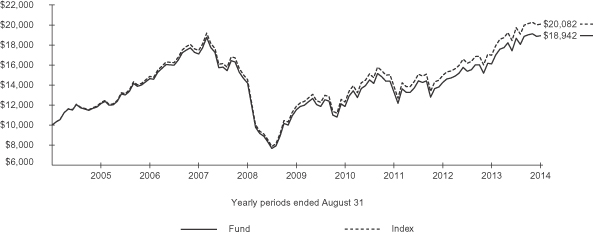

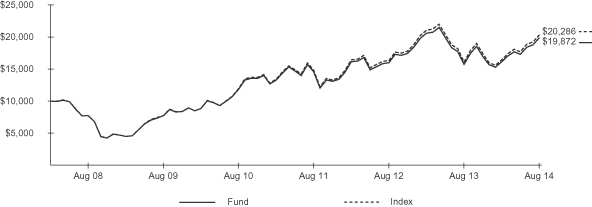

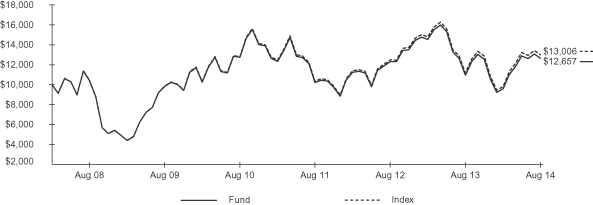

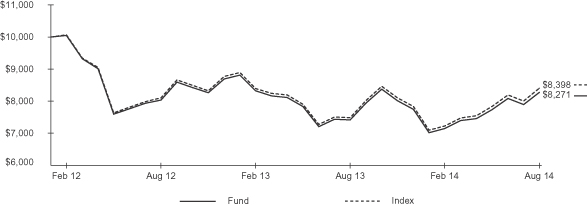

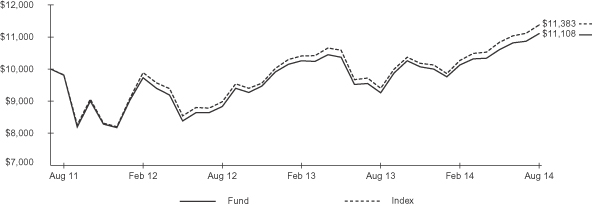

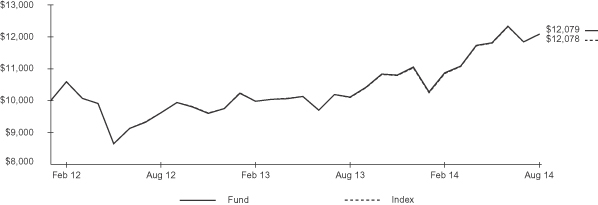

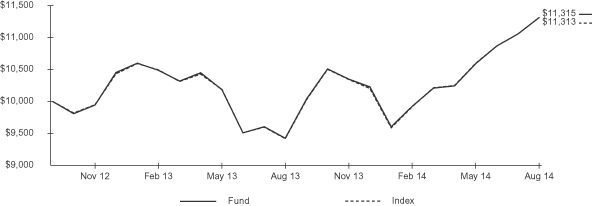

iSHARES® MSCI EMERGING MARKETS EASTERN EUROPE ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | (3.21)% | (2.90)% | (2.83)% | (3.21)% | (2.90)% | (2.83)% | ||||||||||||||||||||

Since Inception | 0.36% | 0.34% | 0.85% | 1.76% | 1.70% | 4.25% | ||||||||||||||||||||

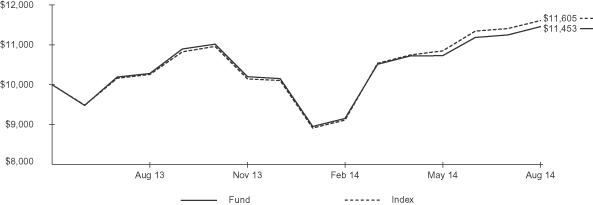

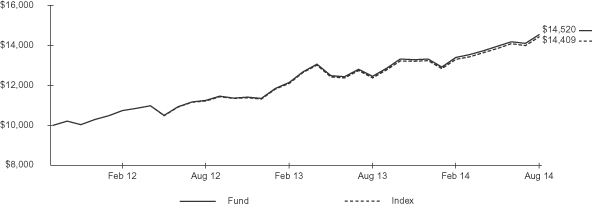

GROWTH OF $10,000 INVESTMENT

(SINCE INCEPTION AT NET ASSET VALUE)

The inception date of the Fund was 9/30/09. The first day of secondary market trading was 10/2/09.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 961.10 | $ | 3.36 | $ | 1,000.00 | $ | 1,021.80 | $ | 3.47 | 0.68% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 10 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI EMERGING MARKETS EASTERN EUROPE ETF

The iShares MSCI Emerging Markets Eastern Europe ETF (the “Fund”) seeks to track the investment results of an index composed of Eastern European emerging market equities, as represented by the MSCI Emerging Markets Eastern Europe Index (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was -3.21%, net of fees, while the total return for the Index was -2.83%.

As represented by the Index, emerging markets stocks in Eastern Europe declined by approximately 3% for the reporting period, underperforming the gain of the broad MSCI Emerging Markets Index.

The key factor behind the overall decline for the Index was a negative return for Russian stocks, which comprised approximately 72% of the Index on average for the reporting period. The Russian constituents of the Index declined by 6% for the reporting period as persistent weakness in the Russian economy and an armed conflict in neighboring Ukraine weighed on the country’s equity market.

Among the other three countries in the Index, Poland and the Czech Republic (together comprising approximately one-quarter of the Index) posted positive returns, gaining 7% and 18%, respectively, for the reporting period. The economies in both countries began to recover after an extended period of weakness. The remaining country within the Index, Hungary, produced a large decline, falling by 17% amid a softening economy and its close proximity to the conflict in the Ukraine.

Currency fluctuations relative to the U.S. dollar also contributed to the decline in the Index for the reporting period. A stronger U.S. dollar reduces international equity returns for U.S. investors. Although the U.S. dollar declined by 1% against the Polish zloty, it appreciated by 5% versus the Hungarian forint, 8% against the Czech koruna, and 11% versus the Russian ruble during the reporting period.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Energy | 42.26 | % | ||

Financials | 26.29 | |||

Materials | 10.05 | |||

Telecommunication Services | 7.64 | |||

Utilities | 5.91 | |||

Consumer Staples | 5.72 | |||

Consumer Discretionary | 1.33 | |||

Health Care | 0.80 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

COUNTRY ALLOCATIONS

As of 8/31/14

| Country | Percentage of Total Investments* |

Russia | 69.50 | % | ||

Poland | 24.26 | |||

Czech Republic | 3.32 | |||

Hungary | 2.92 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 11 |

Table of Contents

Management’s Discussion of Fund Performance

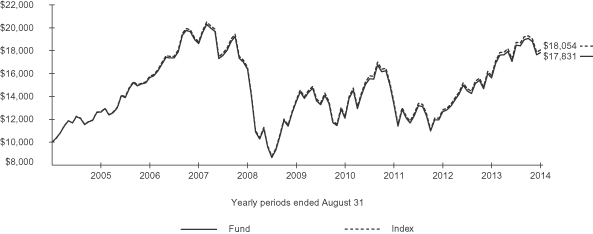

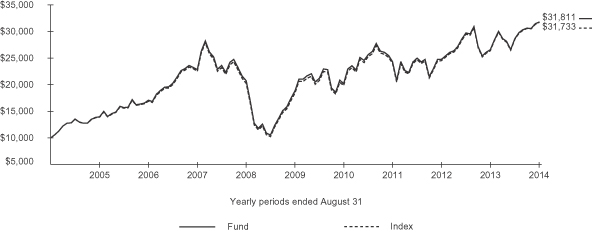

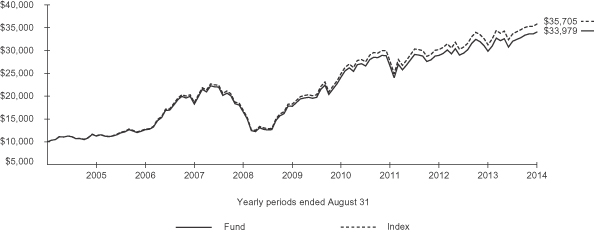

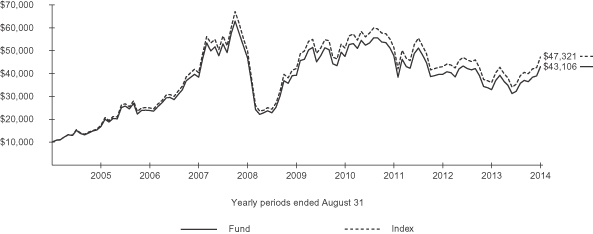

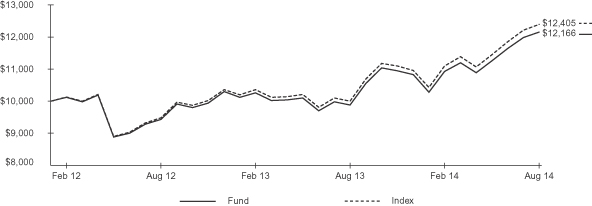

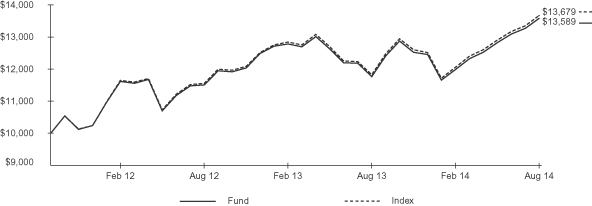

iSHARES® MSCI FRANCE ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 14.07% | 13.45% | 14.11% | 14.07% | 13.45% | 14.11% | ||||||||||||||||||||

5 Years | 5.60% | 5.48% | 5.64% | 31.33% | 30.60% | 31.58% | ||||||||||||||||||||

10 Years | 5.95% | 5.87% | 6.09% | 78.31% | 76.82% | 80.54% | ||||||||||||||||||||

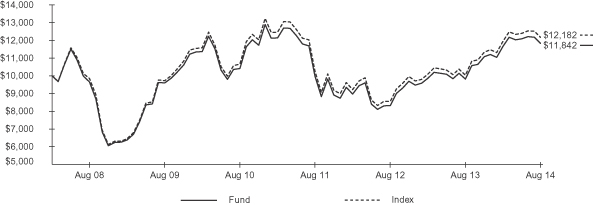

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 965.40 | $ | 2.38 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 12 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI FRANCE ETF

The iShares MSCI France ETF (the “Fund”) seeks to track the investment results of an index composed of French equities, as represented by the MSCI France Index (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 14.07%, net of fees, while the total return for the Index was 14.11%.

French stocks, as represented by the Index, generated solid performance during the reporting period, but underperformed the broad international developed markets, as measured by the MSCI EAFE Index. A sharp correction in the French stock market during the final months of the reporting period limited Index performance, as geopolitical tension, lingering concerns about the banking system and weak economic output discouraged investors.

France, the second largest economy in Europe, experienced stagnant growth for most of the reporting period. Nevertheless, investors found reasons for optimism. Every economic sector in the Index posted a positive return during the reporting period. Financials and industrials stocks, the two largest sectors in the Index, delivered solid gains. Financials stocks rallied on renewed optimism for a sustained European economic recovery, improving credit markets and generally accommodative monetary policy. Industrials stocks advanced despite relatively weak industrial production, as investors anticipated an economic recovery in Europe. The energy sector also generated a solid contribution to the Index return despite declining oil and volatile natural gas prices. The telecommunication services and health care sectors also rallied during the reporting period.

High unemployment, inconsistent consumer spending and relatively lower consumer confidence weighed on consumer-based stocks, which accounted for approximately 24% of the Index during the reporting period. Information technology stocks also lagged the other sectors in the Index.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Industrials | 17.53 | % | ||

Financials | 17.45 | |||

Consumer Discretionary | 13.45 | |||

Health Care | 11.49 | |||

Energy | 11.40 | |||

Consumer Staples | 10.40 | |||

Materials | 6.05 | |||

Telecommunication Services | 4.95 | |||

Utilities | 4.27 | |||

Information Technology | 3.01 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

Total SA | 10.69 | % | ||

Sanofi | 9.85 | |||

BNP Paribas SA | 5.41 | |||

LVMH Moet Hennessy Louis Vuitton SA | 3.67 | |||

AXA SA | 3.41 | |||

Schneider Electric SE | 3.34 | |||

L’Air Liquide SA | 3.33 | |||

L’Oreal SA | 3.15 | |||

Danone SA | 3.06 | |||

Societe Generale | 2.76 | |||

|

| |||

TOTAL | 48.67 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 13 |

Table of Contents

Management’s Discussion of Fund Performance

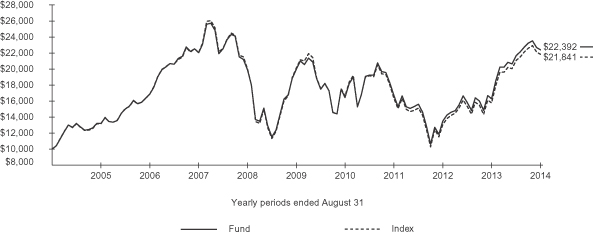

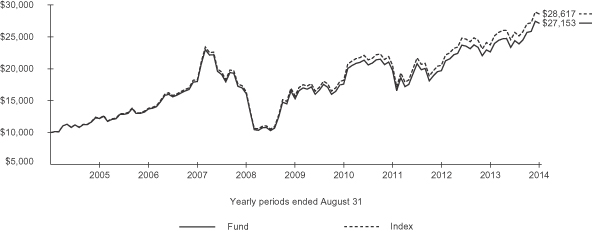

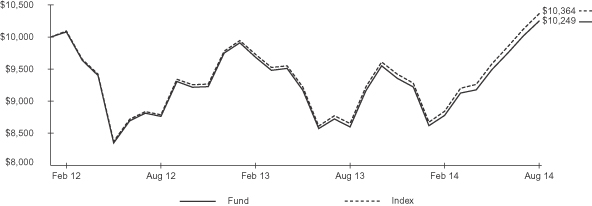

iSHARES® MSCI ITALY CAPPED ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 25.20% | 24.88% | 24.30% | 25.20% | 24.88% | 24.30% | ||||||||||||||||||||

5 Years | (0.71)% | (0.78)% | (0.69)% | (3.48)% | (3.85)% | (3.39)% | ||||||||||||||||||||

10 Years | 0.96% | 0.86% | 0.90% | 9.98% | 8.94% | 9.33% | ||||||||||||||||||||

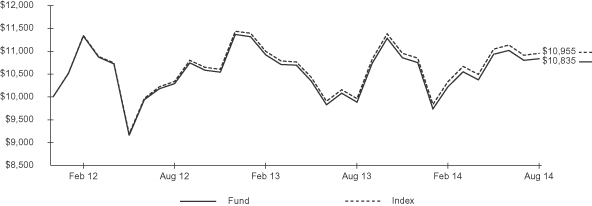

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Index performance through February 11, 2013 reflects the performance of the MSCI Italy Index. Index performance beginning on February 12, 2013 reflects the performance of the MSCI Italy 25/50 Index.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 976.30 | $ | 2.39 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 14 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI ITALY CAPPED ETF

The iShares MSCI Italy Capped ETF (the “Fund”) seeks to track the investment results of an index composed of Italian equities, as represented by the MSCI Italy 25/50 Index (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 25.20%, net of fees, while the total return for the Index was 24.30%.

The Index posted strong performance during the reporting period and outperformed the broad international developed markets, as measured by the MSCI EAFE Index.

The Italian stock market rapidly advanced for most of the reporting period on renewed optimism for Europe’s most beleaguered economies. In the last two months of the reporting period, however, the market declined, as investors shifted their focus to geopolitical tensions in Ukraine and stagnant European growth.

The Italian economy remained mired in a multi-year recession during the reporting period. In addition, Italy’s economy fell into deflation, an extended period of declining prices, for the first time in more than 50 years as the reporting period came to a close. The unemployment rate remained above 12% for the entire reporting period. As a result, consumer spending fell during the first half of the reporting period, before stabilizing during the second half of the reporting period. A bright spot for the Italian economy was declining government bond yields, as the European Union’s lending program, reduced government spending and declining inflation drove bond yields lower.

In that environment, the Index posted a strong gain despite economic weakness, as investors anticipated a recovery in the European economy and better growth prospects for the beleaguered Italian economy. Many of the Index’s individual stocks and several economic sectors advanced during the reporting period.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Financials | 36.11 | % | ||

Energy | 21.98 | |||

Utilities | 17.00 | |||

Industrials | 11.23 | |||

Consumer Discretionary | 9.01 | |||

Telecommunication Services | 4.67 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

Eni SpA | 17.18 | % | ||

Enel SpA | 8.55 | |||

Intesa Sanpaolo SpA | 8.49 | |||

UniCredit SpA | 8.34 | |||

Snam SpA | 4.46 | |||

Assicurazioni Generali SpA | 4.46 | |||

Tenaris SA | 4.05 | |||

Atlantia SpA | 3.93 | |||

Luxottica Group SpA | 3.58 | |||

Fiat SpA | 3.43 | |||

|

| |||

TOTAL | 66.47 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 15 |

Table of Contents

Management’s Discussion of Fund Performance

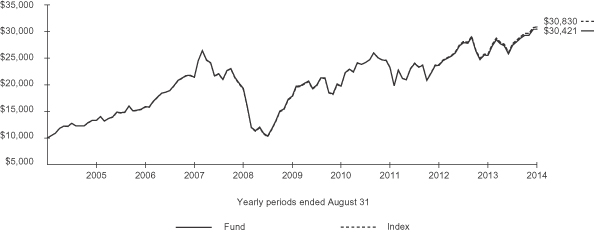

iSHARES® MSCI NETHERLANDS ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 11.80% | 11.48% | 12.30% | 11.80% | 11.48% | 12.30% | ||||||||||||||||||||

5 Years | 8.27% | 8.17% | 8.80% | 48.76% | 48.13% | 52.47% | ||||||||||||||||||||

10 Years | 7.52% | 7.48% | 8.10% | 106.49% | 105.64% | 117.98% | ||||||||||||||||||||

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Index performance through January 31, 2008 reflects the performance of the MSCI Netherlands Index. Index performance beginning on February 1, 2008 reflects the performance of the MSCI Netherlands Investable Market Index.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 973.00 | $ | 2.39 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 16 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI NETHERLANDS ETF

The iShares MSCI Netherlands ETF (the “Fund”) seeks to track the investment results of a broad-based index composed of Dutch equities, as represented by the MSCI Netherlands Investable Market Index (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 11.80%, net of fees, while the total return for the Index was 12.30%.

The Index delivered a solid return for the reporting period. The Dutch stock market rallied sharply in the first few months of the reporting period, but ultimately lagged the MSCI EAFE Index, a broad gauge of international developed market stocks, for the duration of the reporting period.

Consumer-based stocks, which comprised approximately 37% of the Index on average during the reporting period, rallied as consumer spending increased during the second half of the reporting period, aided by rising home prices. As a result, consumer-based stocks posted a solid contribution to the Index’s return. The financials sector was a source of strong performance, as financials stocks rallied on improving credit conditions and lower interest rates in many European countries. The telecommunication services sector also outperformed the overall Index, contributing to the Index’s performance.

The energy sector declined amid volatile oil and natural gas prices, and detracted from the Index’s performance during the reporting period. Other sectors with exposure to the economic cycle, including the industrials and materials sectors, lagged the overall Index, as industrial production declined sharply during the winter of 2013. Information technology stocks also delivered modest results during the reporting period.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Consumer Staples | 29.35 | % | ||

Financials | 21.37 | |||

Industrials | 15.00 | |||

Information Technology | 11.56 | |||

Consumer Discretionary | 8.07 | |||

Materials | 7.65 | |||

Telecommunication Services | 4.62 | |||

Energy | 2.38 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

Unilever NV CVA | 17.63 | % | ||

ING Groep NV CVA | 13.81 | |||

ASML Holding NV | 8.91 | |||

Koninklijke Philips NV | 7.70 | |||

Heineken NV | 4.57 | |||

Akzo Nobel NV | 4.42 | |||

Reed Elsevier NV | 4.15 | |||

Koninklijke Ahold NV | 4.14 | |||

AEGON NV | 3.73 | |||

Koninklijke DSM NV | 3.00 | |||

|

| |||

TOTAL | 72.06 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 17 |

Table of Contents

Management’s Discussion of Fund Performance

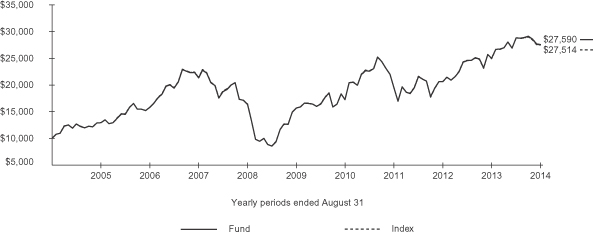

iSHARES® MSCI SPAIN CAPPED ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 37.39% | 36.88% | 38.55% | 37.39% | 36.88% | 38.55% | ||||||||||||||||||||

5 Years | 2.27% | 2.20% | 1.63% | 11.90% | 11.51% | 8.40% | ||||||||||||||||||||

10 Years | 8.40% | 8.29% | 8.13% | 123.92% | 121.84% | 118.41% | ||||||||||||||||||||

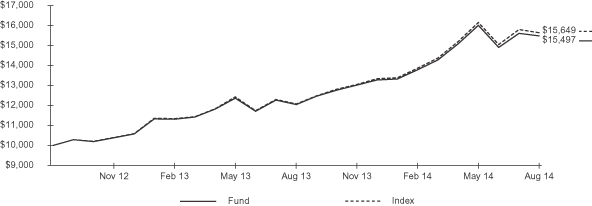

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Index performance through February 11, 2013 reflects the performance of the MSCI Spain Index. Index performance beginning on February 12, 2013 reflects the performance of the MSCI Spain 25/50 Index.

Certain sectors and markets performed exceptionally well based on market conditions during the one-year period. Achieving such exceptional returns involves the risk of volatility and investors should not expect that such exceptional returns will be repeated.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 1,031.70 | $ | 2.46 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 18 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI SPAIN CAPPED ETF

The iShares MSCI Spain Capped ETF (the “Fund”) seeks to track the investment results of an index composed of Spanish equities, as represented by the MSCI Spain 25/50 Index (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 37.39%, net of fees, while the total return for the Index was 38.55%.

The Index posted strong performance during the reporting period, significantly outperforming the broad international developed markets, as measured by the MSCI EAFE Index.

The Spanish stock market rapidly advanced for most of the reporting period on renewed optimism for Europe’s most beleaguered economies. In the last two months of the reporting period, however, the market declined, as investors shifted their focus to geopolitical tensions in Ukraine and stagnant European growth.

Spain’s economy began to recover during the reporting period, exiting its second recession since the financial crisis in 2008. The unemployment rate remained stubbornly high, exceeding 25% for most of the reporting period. Nevertheless, consumer spending logged consistent growth during the second half of the reporting period, while manufacturing expanded at a steady pace. Spain, similar to many countries throughout the world, experienced strong economic growth in pre-recession years due in part to a housing boom. Sharply declining home prices and high government debt levels have weighed on the economy since 2008. Housing prices declined at a much slower rate during the reporting period, which led to speculation that housing prices could be stabilizing. Similarly, financial reforms also helped drive lending rates on Spanish government debt dramatically lower.

The broad-based equity market rally meant many companies contributed to positive performance during the reporting period. Banco Santander SA, the Index’s largest weighting at approximately 22% as of the end of the reporting period, experienced strong performance on Spain’s improving financial and economic conditions.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Financials | 48.42 | % | ||

Utilities | 11.68 | |||

Industrials | 11.50 | |||

Telecommunication Services | 10.98 | |||

Consumer Discretionary | 4.70 | |||

Energy | 4.61 | |||

Information Technology | 3.81 | |||

Health Care | 2.32 | |||

Consumer Staples | 1.98 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

Banco Santander SA | 22.45 | % | ||

Banco Bilbao Vizcaya Argentaria SA | 12.16 | |||

Telefonica SA | 10.98 | |||

Iberdrola SA | 4.86 | |||

Inditex SA | 4.70 | |||

Repsol SA | 4.61 | |||

Amadeus IT Holding SA Class A | 3.80 | |||

Gas Natural SDG SA | 3.47 | |||

Banco Popular Espanol SA | 3.25 | |||

CaixaBank SA | 3.14 | |||

|

| |||

TOTAL | 73.42 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 19 |

Table of Contents

Management’s Discussion of Fund Performance

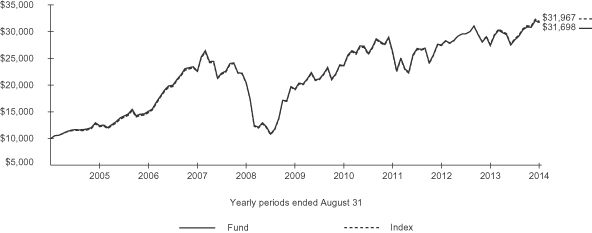

iSHARES® MSCI SWEDEN ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 10.49% | 10.31% | 10.41% | 10.49% | 10.31% | 10.41% | ||||||||||||||||||||

5 Years | 11.92% | 11.84% | 11.87% | 75.59% | 75.02% | 75.20% | ||||||||||||||||||||

10 Years | 10.68% | 10.60% | 10.65% | 175.90% | 173.85% | 175.14% | ||||||||||||||||||||

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 957.00 | $ | 2.37 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 20 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI SWEDEN ETF

The iShares MSCI Sweden ETF (the “Fund”) seeks to track the investment results of an index composed of Swedish equities, as represented by the MSCI Sweden Index (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 10.49%, net of fees, while the total return for the Index was 10.41%.

Swedish stocks, as represented by the Index, posted a modest return during the reporting period, underperforming the broad international developed markets, as measured by the MSCI EAFE Index.

Sector performance varied widely during the reporting period, as some economic sectors posted double-digit positive returns, while other sectors delivered negative returns. The financials sector was the largest contributor to Index performance, as financials stocks rallied on improving credit conditions and lower interest rates in many European countries. Financials stocks represented approximately one-third of the Index’s weight on average, and contributed more than half of the Index’s total return. The consumer discretionary sector was another large contributor, as consumer spending increased steadily during the reporting period. The information technology sector also delivered a solid contribution to Index return, as Swedish technology stocks performed in line with the broader Index.

The industrials sector, which represented approximately 26% of the Index on average during the reporting period, posted a modest return, but trailed the broader Index by a wide margin as Swedish industrial production contracted during the reporting period. Several of the Index’s smaller sectors, including health care, energy and consumer staples, detracted from Index performance. The negative impact of these sectors on Index performance was limited, as each sector accounted for approximately 5% or less of the Index on average during the reporting period.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Financials | 33.47 | % | ||

Industrials | 26.34 | |||

Consumer Discretionary | 12.31 | |||

Information Technology | 11.49 | |||

Telecommunication Services | 6.78 | |||

Consumer Staples | 5.18 | |||

Health Care | 2.34 | |||

Materials | 1.08 | |||

Energy | 1.01 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

Hennes & Mauritz AB Class B | 10.03 | % | ||

Nordea Bank AB | 9.84 | |||

Telefonaktiebolaget LM Ericsson Class B | 9.42 | |||

Svenska Handelsbanken AB Class A | 5.82 | |||

Swedbank AB Class A | 5.73 | |||

Skandinaviska Enskilda Banken AB Class A | 4.86 | |||

Atlas Copco AB Class A | 4.85 | |||

Volvo AB Class B | 4.54 | |||

TeliaSonera AB | 4.32 | |||

Investor AB Class B | 4.20 | |||

|

| |||

TOTAL | 63.61 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 21 |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES® MSCI SWITZERLAND CAPPED ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 17.21% | 17.14% | 17.49% | 17.21% | 17.14% | 17.49% | ||||||||||||||||||||

5 Years | 12.64% | 12.59% | 12.46% | 81.29% | 80.89% | 79.86% | ||||||||||||||||||||

10 Years | 10.64% | 10.63% | 10.29% | 174.77% | 174.66% | 166.36% | ||||||||||||||||||||

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Index performance through February 11, 2013 reflects the performance of the MSCI Switzerland Index. Index performance beginning on February 12, 2013 reflects the performance of the MSCI Switzerland 25/50 Index.

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 1,003.00 | $ | 2.42 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 22 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI SWITZERLAND CAPPED ETF

The iShares MSCI Switzerland Capped ETF (the “Fund”) seeks to track the investment results of an index composed of Swiss equities, as represented by the MSCI Switzerland 25/50 Index (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 17.21%, net of fees, while the total return for the Index was 17.49%.

Swiss stocks, as represented by the Index, posted solid performance during the reporting period. The Swiss stock market reflected the contours of the broader European equity market, while slightly outpacing the broad international developed markets, as measured by the MSCI EAFE Index.

Switzerland’s economy grew at a modest pace during the reporting period, as the eurozone began to recover from its economic recession. Weak consumer spending was a source of weakness for the Swiss economy. The Swiss franc, which is considered a high-quality currency known for its stability, weakened relative to the U.S. dollar and strengthened relative to the euro in the final months of the reporting period. The stronger U.S. dollar also decreased international equity returns for U.S. investors.

The European food giant Nestle SA and the pharmaceutical company Novartis AG accounted for a combined Index weighting of approximately 28% as of the end of the reporting period. Both stocks performed relatively well, helping propel the broader Swiss stock market to solid gains. Health care company Roche Holding AG, which represented approximately 14% of the Index as of August 31, 2014, posted a modest gain, limiting Index performance.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Health Care | 31.10 | % | ||

Consumer Staples | 20.71 | |||

Financials | 19.70 | |||

Industrials | 11.12 | |||

Materials | 7.96 | |||

Consumer Discretionary | 6.59 | |||

Telecommunication Services | 1.44 | |||

Energy | 1.38 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

Nestle SA Registered | 17.48 | % | ||

Novartis AG Registered | 13.87 | |||

Roche Holding AG Genusschein | 13.77 | |||

UBS AG Registered | 4.52 | |||

ABB Ltd. Registered | 4.34 | |||

Compagnie Financiere Richemont SA Class A Bearer | 4.33 | |||

Zurich Insurance Group AG | 4.00 | |||

Credit Suisse Group AG Registered | 3.79 | |||

Syngenta AG Registered | 3.00 | |||

Swiss Re AG | 2.64 | |||

|

| |||

TOTAL | 71.74 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 23 |

Table of Contents

Management’s Discussion of Fund Performance

iSHARES® MSCI UNITED KINGDOM ETF

Performance as of August 31, 2014

| Average Annual Total Returns | Cumulative Total Returns | |||||||||||||||||||||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||||||||||||||||||||

1 Year | 17.56% | 16.91% | 18.19% | 17.56% | 16.91% | 18.19% | ||||||||||||||||||||

5 Years | 10.43% | 10.44% | 11.05% | 64.26% | 64.31% | 68.90% | ||||||||||||||||||||

10 Years | 6.60% | 6.44% | 7.22% | 89.42% | 86.60% | 100.82% | ||||||||||||||||||||

GROWTH OF $10,000 INVESTMENT

(AT NET ASSET VALUE)

Past performance is no guarantee of future results. Performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. See “About Fund Performance” on page 26 for more information.

| Shareholder Expenses | ||||||||||||||||||||||||||

| Actual | Hypothetical 5% Return | |||||||||||||||||||||||||

| Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Beginning Account Value (3/1/14) | Ending Account Value (8/31/14) | Expenses Paid During Period a | Annualized Expense Ratio | ||||||||||||||||||||

| $ | 1,000.00 | $ | 1,015.00 | $ | 2.44 | $ | 1,000.00 | $ | 1,022.80 | $ | 2.45 | 0.48% | ||||||||||||||

| a | Expenses are calculated using the Fund’s annualized expense ratio (as disclosed in the table), multiplied by the average account value for the period, multiplied by the number of days in the period (184 days) and divided by the number of days in the year (365 days). See “Shareholder Expenses” on page 26 for more information. |

| 24 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Management’s Discussion of Fund Performance (Continued)

iSHARES® MSCI UNITED KINGDOM ETF

The iShares MSCI United Kingdom ETF (the “Fund”) seeks to track the investment results of an index composed of U.K. equities, as represented by the MSCI United Kingdom Index (the “Index”). The Fund invests in a representative sample of securities included in the Index that collectively has an investment profile similar to the Index. Due to the use of representative sampling, the Fund may or may not hold all of the securities that are included in the Index. For the 12-month reporting period ended August 31, 2014, the total return for the Fund was 17.56%, net of fees, while the total return for the Index was 18.19%.

United Kingdom stocks, as represented by the Index, posted a solid return for the reporting period, outpacing the broad international developed markets, as measured by the MSCI EAFE Index.

The United Kingdom experienced healthy economic growth during the period. The country’s GDP growth improved throughout the reporting period, expanding by 0.9% during the second quarter of 2014, and nominal GDP surpassed its pre-crisis peak from 2008 on the strength of its services and production sectors. On an annual basis, GDP growth for the second quarter of 2014 was 3.2% versus the second quarter of 2013. In addition, the unemployment rate continued to fall, finishing the reporting period at its lowest rate since late 2008.

Every economic sector in the Index delivered a double-digit positive return, as the United Kingdom experienced a broad-based rally during the reporting period. The energy sector generated the largest contribution to the Index’s return, as England’s global, diversified petroleum companies posted solid returns despite volatile oil and gas prices. The health care sector was the third largest contributor to the Index’s performance during the reporting period, reflecting the strong performance of large pharmaceuticals companies. The materials and consumer discretionary sectors performed in line with the Index, which increased the Index’s total return.

The financials sector, the largest sector in the Index with a 22% weighting on average, lagged several other sectors in the Index while generating the second largest contribution to the Index’s return. Similarly, the telecommunication services and consumer staples sectors posted solid returns while trailing the overall Index during the reporting period.

PORTFOLIO ALLOCATION

As of 8/31/14

| Sector | Percentage of Total Investments* |

Financials | 22.54 | % | ||

Energy | 17.23 | |||

Consumer Staples | 15.97 | |||

Health Care | 9.60 | |||

Materials | 9.38 | |||

Consumer Discretionary | 8.10 | |||

Industrials | 6.79 | |||

Telecommunication Services | 5.06 | |||

Utilities | 4.30 | |||

Information Technology | 1.03 | |||

|

| |||

TOTAL | 100.00 | % | ||

|

|

TEN LARGEST FUND HOLDINGS

As of 8/31/14

| Security | Percentage of Total Investments* |

HSBC Holdings PLC | 7.12 | % | ||

Royal Dutch Shell PLC Class A | 5.49 | |||

BP PLC | 5.09 | |||

GlaxoSmithKline PLC | 4.10 | |||

British American Tobacco PLC | 3.81 | |||

Royal Dutch Shell PLC Class B | 3.56 | |||

AstraZeneca PLC | 3.30 | |||

Vodafone Group PLC | 3.13 | |||

Diageo PLC | 2.56 | |||

Lloyds Banking Group PLC | 2.50 | |||

|

| |||

TOTAL | 40.66 | % | ||

|

|

| * | Excludes money market funds. |

MANAGEMENT’S DISCUSSIONSOF FUND PERFORMANCE | 25 |

Table of Contents

Past performance is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Performance data current to the most recent month-end is available at www.iShares.com. Performance results assume reinvestment of all dividends and capital gain distributions and do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption or sale of fund shares. The investment return and principal value of shares will vary with changes in market conditions. Shares may be worth more or less than their original cost when they are redeemed or sold in the market. Performance for certain funds may reflect a waiver of a portion of investment management fees. Without such waiver, performance would have been lower.

Net asset value or “NAV” is the value of one share of a fund as calculated in accordance with the standard formula for valuing mutual fund shares. The price used to calculate market return (“Market Price”) is determined by using the midpoint between the highest bid and the lowest offer on the primary stock exchange on which shares of a fund are listed for trading, as of the time that such fund’s NAV is calculated. Since shares of a fund may not have traded in the secondary market until after the fund’s inception, for the period from inception to the first day of secondary trading, the NAV of the fund is used as a proxy for the Market Price to calculate market returns. Market and NAV returns assume that dividends and capital gain distributions have been reinvested at Market Price and NAV, respectively.

An index is a statistical composite that tracks a specified financial market or sector. Unlike a fund, an index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by a fund. These expenses negatively impact fund performance. Also, market returns do not include brokerage commissions that may be payable on secondary market transactions. If brokerage commissions were included, market returns would be lower.

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including brokerage commissions on purchases and sales of fund shares and (2) ongoing costs, including management fees and other fund expenses. The expense example, which is based on an investment of $1,000 invested on March 1, 2014 and held through August 31, 2014, is intended to help you understand your ongoing costs (in dollars and cents) of investing in a Fund and to compare these costs with the ongoing costs of investing in other funds.

Actual Expenses — The table provides information about actual account values and actual expenses. Annualized expense ratios reflect contractual and voluntary fee waivers, if any. To estimate the expenses that you paid on your account over the period, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number for your Fund under the heading entitled “Expenses Paid During Period.”

Hypothetical Example for Comparison Purposes — The table also provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as brokerage commissions paid on purchases and sales of fund shares. Therefore, the hypothetical examples are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| 26 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

iSHARES® MSCI AUSTRIA CAPPED ETF

August 31, 2014

| Security | Shares | Value | ||||||

COMMON STOCKS — 98.44% |

| |||||||

AIR FREIGHT & LOGISTICS — 3.90% |

| |||||||

Oesterreichische Post AG | 52,488 | $ | 2,463,359 | |||||

|

| |||||||

| 2,463,359 | ||||||||

BUILDING PRODUCTS — 4.27% |

| |||||||

Wienerberger AG | 179,964 | 2,697,613 | ||||||

|

| |||||||

| 2,697,613 | ||||||||

CHEMICALS — 1.59% |

| |||||||

Lenzing AGa | 16,488 | 1,004,675 | ||||||

|

| |||||||

| 1,004,675 | ||||||||

COMMERCIAL BANKS — 18.55% |

| |||||||

Erste Group Bank AG | 335,484 | 8,630,300 | ||||||

Raiffeisen International Bank Holding AG | 120,132 | 3,085,639 | ||||||

|

| |||||||

| 11,715,939 | ||||||||

CONSTRUCTION MATERIALS — 1.94% |

| |||||||

RHI AG | 40,788 | 1,225,489 | ||||||

|

| |||||||

| 1,225,489 | ||||||||

CONTAINERS & PACKAGING — 2.78% |

| |||||||

Mayr-Melnhof Karton AG | 15,048 | 1,759,332 | ||||||

|

| |||||||

| 1,759,332 | ||||||||

DIVERSIFIED TELECOMMUNICATION SERVICES — 2.41% |

| |||||||

Telekom Austria AG | 162,504 | 1,524,038 | ||||||

|

| |||||||

| 1,524,038 | ||||||||

ELECTRIC UTILITIES — 1.59% |

| |||||||

EVN AG | 74,160 | 1,006,141 | ||||||

|

| |||||||

| 1,006,141 | ||||||||

ELECTRICAL EQUIPMENT — 1.81% | ||||||||

Zumtobel AG | 54,576 | 1,140,855 | ||||||

|

| |||||||

| 1,140,855 | ||||||||

ELECTRONIC EQUIPMENT, INSTRUMENTS & |

| |||||||

Austria Technologie & Systemtechnik AG | 65,988 | 763,152 | ||||||

Kapsch TrafficCom AG | 15,336 | 447,443 | ||||||

|

| |||||||

| 1,210,595 | ||||||||

ENERGY EQUIPMENT & SERVICES — 3.06% |

| |||||||

Schoeller-Bleckmann Oilfield Equipment AG | 18,324 | 1,930,910 | ||||||

|

| |||||||

| 1,930,910 | ||||||||

| Security | Shares | Value | ||||||

HOTELS, RESTAURANTS & LEISURE — 0.56% |

| |||||||

DO & Co. AG | 5,184 | $ | 352,958 | |||||

|

| |||||||

| 352,958 | ||||||||

INSURANCE — 7.47% |

| |||||||

UNIQA Insurance Group AG | 161,100 | 1,937,395 | ||||||

Vienna Insurance Group AG | 57,276 | 2,782,750 | ||||||

|

| |||||||

| 4,720,145 | ||||||||

MACHINERY — 10.00% |

| |||||||

Andritz AG | 79,560 | 4,267,311 | ||||||

Palfinger AG | 28,260 | 903,056 | ||||||

Semperit AG Holding | 20,232 | 1,148,598 | ||||||

|

| |||||||

| 6,318,965 | ||||||||

METALS & MINING — 9.65% |

| |||||||

AMAG Austria Metall AGb | 19,224 | 672,295 | ||||||

Voestalpine AG | 126,108 | 5,423,475 | ||||||

|

| |||||||

| 6,095,770 | ||||||||

OIL, GAS & CONSUMABLE FUELS — 10.48% |

| |||||||

OMV AG | 171,000 | 6,622,093 | ||||||

|

| |||||||

| 6,622,093 | ||||||||

REAL ESTATE MANAGEMENT & DEVELOPMENT — 13.88% |

| |||||||

BUWOG AGc | 64,008 | 1,252,024 | ||||||

CA Immobilien Anlagen AGc | 117,792 | 2,440,598 | ||||||

conwert Immobilien Invest SE | 107,892 | 1,348,391 | ||||||

IMMOEAST AG Escrowc,d | 998,769 | 13 | ||||||

IMMOFINANZ AGc | 898,380 | 2,822,281 | ||||||

IMMOFINANZ AG Escrowc,d | 897,599 | 12 | ||||||

S IMMO AG | 117,252 | 904,272 | ||||||

|

| |||||||

| 8,767,591 | ||||||||

TRANSPORTATION INFRASTRUCTURE — 2.58% |

| |||||||

Flughafen Wien AG | 18,108 | 1,626,936 | ||||||

|

| |||||||

| 1,626,936 | ||||||||

|

| |||||||

TOTAL COMMON STOCKS |

| |||||||

(Cost: $83,626,133) |

| 62,183,404 | ||||||

SHORT-TERM INVESTMENTS — 0.51% |

| |||||||

MONEY MARKET FUNDS — 0.51% |

| |||||||

BlackRock Cash Funds: Institutional, |

| |||||||

0.14%e,f,g | 297,991 | 297,991 | ||||||

BlackRock Cash Funds: Prime, |

| |||||||

0.11%e,f,g | 18,759 | 18,759 | ||||||

SCHEDULESOF INVESTMENTS | 27 |

Table of Contents

Schedule of Investments (Continued)

iSHARES® MSCI AUSTRIA CAPPED ETF

August 31, 2014

| Security | Shares | Value | ||||||

BlackRock Cash Funds: Treasury, |

| |||||||

0.00%e,f | 5,110 | $ | 5,110 | |||||

|

| |||||||

| 321,860 | ||||||||

|

| |||||||

TOTAL SHORT-TERM INVESTMENTS |

| |||||||

(Cost: $321,860) |

| 321,860 | ||||||

|

| |||||||

TOTAL INVESTMENTS |

| |||||||

(Cost: $83,947,993) | 62,505,264 | |||||||

Other Assets, Less Liabilities — 1.05% |

| 664,907 | ||||||

|

| |||||||

NET ASSETS — 100.00% |

| $ | 63,170,171 | |||||

|

| |||||||

| a | All or a portion of this security represents a security on loan. See Note 1. |

| b | This security may be resold to qualified institutional buyers under Rule 144A of the Securities Act of 1933. |

| c | Non-income earning security. |

| d | Security valued using Level 3 inputs in accordance with management’s fair valuation policy. See Note 1. |

| e | Affiliated issuer. See Note 2. |

| f | The rate quoted is the annualized seven-day yield of the fund at period end. |

| g | All or a portion of this security represents an investment of securities lending collateral. See Note 1. |

See notes to financial statements.

| 28 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Schedule of Investments

iSHARES® MSCI BELGIUM CAPPED ETF

August 31, 2014

| Security | Shares | Value | ||||||

COMMON STOCKS — 99.90% |

| |||||||

AIR FREIGHT & LOGISTICS — 1.33% |

| |||||||

bpost SA | 88,693 | $ | 2,189,913 | |||||

|

| |||||||

| 2,189,913 | ||||||||

BEVERAGES — 22.31% |

| |||||||

Anheuser-Busch InBev NV | 330,088 | 36,761,664 | ||||||

|

| |||||||

| 36,761,664 | ||||||||

BIOTECHNOLOGY — 1.58% |

| |||||||

Ablynx NVa | 164,205 | 1,860,102 | ||||||

ThromboGenics NVa,b | 67,881 | 743,915 | ||||||

|

| |||||||

| 2,604,017 | ||||||||

CAPITAL MARKETS — 1.77% |

| |||||||

GIMV NV | 33,759 | 1,653,964 | ||||||

RHJ International SAa | 248,413 | 1,269,573 | ||||||

|

| |||||||

| 2,923,537 | ||||||||

CHEMICALS — 9.37% |

| |||||||

Solvay SA | 53,724 | 8,474,140 | ||||||

Tessenderlo Chemie NVa | 50,578 | 1,518,634 | ||||||

Umicore SA | 112,167 | 5,439,284 | ||||||

|

| |||||||

| 15,432,058 | ||||||||

COMMERCIAL BANKS — 7.72% |

| |||||||

KBC Groep NVa | 222,519 | 12,713,303 | ||||||

|

| |||||||

| 12,713,303 | ||||||||

COMMUNICATIONS EQUIPMENT — 0.74% |

| |||||||

EVS Broadcast Equipment SAb | 28,314 | 1,225,520 | ||||||

|

| |||||||

| 1,225,520 | ||||||||

CONSTRUCTION & ENGINEERING — 1.38% |

| |||||||

Compagnie d’Entreprises CFE SA | 21,417 | 2,280,817 | ||||||

|

| |||||||

| 2,280,817 | ||||||||

DISTRIBUTORS — 1.03% |

| |||||||

SA D’Ieteren NV | 40,686 | 1,693,227 | ||||||

|

| |||||||

| 1,693,227 | ||||||||

DIVERSIFIED FINANCIAL SERVICES — 7.73% |

| |||||||

Ackermans & van Haaren NV | 28,834 | 3,497,592 | ||||||

Groupe Bruxelles Lambert SA | 73,931 | 7,286,116 | ||||||

KBC Ancora SCAa | 59,290 | 1,948,516 | ||||||

|

| |||||||

| 12,732,224 | ||||||||

DIVERSIFIED TELECOMMUNICATION SERVICES — 3.52% |

| |||||||

Belgacom SA | 162,382 | 5,803,895 | ||||||

|

| |||||||

| 5,803,895 | ||||||||

ELECTRIC UTILITIES — 1.28% |

| |||||||

Elia System Operator SA | 43,197 | 2,112,664 | ||||||

|

| |||||||

| 2,112,664 | ||||||||

| Security | Shares | Value | ||||||

ELECTRONIC EQUIPMENT, INSTRUMENTS & |

| |||||||

Barco NV | 21,103 | $ | 1,499,363 | |||||

|

| |||||||

| 1,499,363 | ||||||||

FOOD & STAPLES RETAILING — 6.57% |

| |||||||

Colruyt SA | 79,618 | 3,806,884 | ||||||

Delhaize Brothers and Co. “The Lion” (Delhaize Group) SA | 100,430 | 7,017,795 | ||||||

|

| |||||||

| 10,824,679 | ||||||||

HEALTH CARE EQUIPMENT & SUPPLIES — 1.15% |

| |||||||

Ion Beam Applications SAa | 124,509 | 1,897,518 | ||||||

|

| |||||||

| 1,897,518 | ||||||||

HEALTH CARE PROVIDERS & SERVICES — 1.51% |

| |||||||

Arseus NV | 45,617 | 2,489,693 | ||||||

|

| |||||||

| 2,489,693 | ||||||||

HEALTH CARE TECHNOLOGY — 1.03% |

| |||||||

Agfa-Gevaert NVa | 591,690 | 1,706,050 | ||||||

|

| |||||||

| 1,706,050 | ||||||||

INSURANCE — 4.17% |

| |||||||

Ageas | 204,127 | 6,868,441 | ||||||

|

| |||||||

| 6,868,441 | ||||||||

IT SERVICES — 0.89% |

| |||||||

Econocom Group SA | 161,777 | 1,461,177 | ||||||

|

| |||||||

| 1,461,177 | ||||||||

MARINE — 0.76% |

| |||||||

Compagnie Maritime Belge SA | 52,151 | 1,251,249 | ||||||

|

| |||||||

| 1,251,249 | ||||||||

MEDIA — 3.32% |

| |||||||

Kinepolis Group | 50,959 | 1,928,114 | ||||||

Telenet Group Holding NVa | 60,379 | 3,536,754 | ||||||

|

| |||||||

| 5,464,868 | ||||||||

METALS & MINING — 2.97% |

| |||||||

Bekaert NV | 61,710 | 2,298,724 | ||||||

Nyrstar NVa,b | 397,969 | 1,544,832 | ||||||

Viohalco SAa,b | 191,664 | 1,047,708 | ||||||

|

| |||||||

| 4,891,264 | ||||||||

OIL, GAS & CONSUMABLE FUELS — 2.37% |

| |||||||

Euronav SAa | 198,440 | 2,424,086 | ||||||

Exmar NV | 94,864 | 1,474,468 | ||||||

|

| |||||||

| 3,898,554 | ||||||||

PHARMACEUTICALS — 7.31% |

| |||||||

Galapagos NVa,b | 65,340 | 1,082,708 | ||||||

UCB SA | 113,014 | 10,971,135 | ||||||

|

| |||||||

| 12,053,843 | ||||||||

SCHEDULESOF INVESTMENTS | 29 |

Table of Contents

Schedule of Investments (Continued)

iSHARES® MSCI BELGIUM CAPPED ETF

August 31, 2014

| Security | Shares | Value | ||||||

REAL ESTATE INVESTMENT TRUSTS (REITS) — 4.88% |

| |||||||

Befimmo SA | 29,403 | $ | 2,381,485 | |||||

Cofinimmo SA | 22,264 | 2,754,312 | ||||||

Intervest Offices & Warehouses NV | 38,841 | 1,196,664 | ||||||

Warehouses De Pauw SCA | 22,627 | 1,706,296 | ||||||

|

| |||||||

| 8,038,757 | ||||||||

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT — 1.44% |

| |||||||

Melexis NV | 51,546 | 2,369,584 | ||||||

|

| |||||||

| 2,369,584 | ||||||||

WIRELESS TELECOMMUNICATION SERVICES — 0.86% |

| |||||||

Mobistar SAa | 71,269 | 1,412,358 | ||||||

|

| |||||||

| 1,412,358 | ||||||||

|

| |||||||

TOTAL COMMON STOCKS |

| |||||||

(Cost: $156,766,118) |

| 164,600,237 | ||||||

SHORT-TERM INVESTMENTS — 2.47% |

| |||||||

MONEY MARKET FUNDS — 2.47% |

| |||||||

BlackRock Cash Funds: Institutional, |

| |||||||

0.14%c,d,e | 3,733,359 | 3,733,359 | ||||||

BlackRock Cash Funds: Prime, |

| |||||||

0.11%c,d,e | 235,025 | 235,025 | ||||||

BlackRock Cash Funds: Treasury, |

| |||||||

0.00%c,d | 108,461 | 108,461 | ||||||

|

| |||||||

| 4,076,845 | ||||||||

|

| |||||||

TOTAL SHORT-TERM INVESTMENTS |

| |||||||

(Cost: $4,076,845) |

| 4,076,845 | ||||||

|

| |||||||

TOTAL INVESTMENTS |

| |||||||

(Cost: $160,842,963) | 168,677,082 | |||||||

Other Assets, Less Liabilities — (2.37)% |

| (3,912,026 | ) | |||||

|

| |||||||

NET ASSETS — 100.00% |

| $ | 164,765,056 | |||||

|

| |||||||

| a | Non-income earning security. |

| b | All or a portion of this security represents a security on loan. See Note 1. |

| c | Affiliated issuer. See Note 2. |

| d | The rate quoted is the annualized seven-day yield of the fund at period end. |

| e | All or a portion of this security represents an investment of securities lending collateral. See Note 1. |

See notes to financial statements.

| 30 | 2014 iSHARES ANNUAL REPORTTO SHAREHOLDERS |

Table of Contents

Schedule of Investments

iSHARES® MSCI EMERGING MARKETS EASTERN EUROPE ETF

August 31, 2014

| Security | Shares | Value | ||||||

COMMON STOCKS — 96.21% |

| |||||||

CZECH REPUBLIC — 3.32% |

| |||||||

CEZ AS | 86,424 | $ | 2,512,409 | |||||

Komercni Banka AS | 8,141 | 1,893,319 | ||||||

O2 Czech Republic AS | 42,118 | 591,710 | ||||||

|

| |||||||

| 4,997,438 | ||||||||

HUNGARY — 2.91% |

| |||||||

MOL Hungarian Oil and Gas PLC | 22,392 | 1,103,289 | ||||||

OTP Bank PLC | 119,951 | 2,073,569 | ||||||

Richter Gedeon Nyrt | 74,863 | 1,204,740 | ||||||

|

| |||||||

| 4,381,598 | ||||||||

POLAND — 24.20% |

| |||||||

Alior Bank SAa | 24,358 | 580,582 | ||||||

Bank Handlowy w Warszawie SA | 17,500 | 626,691 | ||||||

Bank Millennium SA | 227,496 | 571,346 | ||||||

Bank Pekao SA | 70,268 | 3,958,049 | ||||||

Bank Zachodni WBK SA | 15,919 | 1,844,649 | ||||||

Cyfrowy Polsat SA | 102,431 | 819,807 | ||||||

ENEA SA | 118,263 | 554,817 | ||||||

Energa SA | 108,504 | 707,557 | ||||||

Eurocash SA | 44,545 | 480,649 | ||||||

Getin Noble Bank SAa | 639,019 | 519,633 | ||||||

Grupa Azoty SA | 26,489 | 619,279 | ||||||

Grupa Lotos SAa | 34,452 | 324,764 | ||||||

Jastrzebska Spolka Weglowa SAa | 28,329 | 296,638 | ||||||

KGHM Polska Miedz SA | 74,963 | 3,090,097 | ||||||

LPP SA | 445 | 1,183,011 | ||||||

mBank SA | 7,905 | 1,145,939 | ||||||

Orange Polska SA | 351,442 | 1,180,505 | ||||||

Polska Grupa Energetyczna SA | 450,148 | 3,070,583 | ||||||

Polski Koncern Naftowy Orlen SA | 171,776 | 2,118,357 | ||||||

Polskie Gornictwo Naftowe i Gazownictwo SA | 947,915 | 1,446,768 | ||||||

Powszechna Kasa Oszczednosci Bank Polski SA | 468,491 | 5,604,573 | ||||||

Powszechny Zaklad Ubezpieczen SA | 30,053 | 4,408,293 | ||||||

Synthos SA | 281,674 | 405,242 | ||||||

Tauron Polska Energia SA | 565,356 | 882,333 | ||||||

|

| |||||||

| 36,440,162 | ||||||||

| Security | Shares | Value | ||||||

RUSSIA — 65.78% |

| |||||||

Alrosa AO | 986,100 | $ | 1,155,669 | |||||

Gazprom OAO | 6,337,232 | 22,581,624 | ||||||

LUKOIL OAO | 273,231 | 15,210,050 | ||||||

Magnit OJSC SP GDR | 139,229 | 8,103,128 | ||||||

MegaFon OAO SP GDR | 49,806 | 1,409,510 | ||||||

MMC Norilsk Nickel OJSC | 29,654 | 5,835,382 | ||||||

Mobile TeleSystems OJSC SP ADR | 276,601 | 5,103,288 | ||||||

Moscow Exchange MICEX-RTS OJSC | 730,690 | 1,226,493 | ||||||

NovaTek OAO SP GDR | 48,744 | 4,903,646 | ||||||

Rosneft Oil Co. OJSC | 623,804 | 3,848,264 | ||||||

Rostelecom OJSC | 428,880 | 1,140,774 | ||||||

RusHydro OJSC | 62,061,000 | 1,150,977 | ||||||

Sberbank of Russia | 5,782,285 | 11,378,514 | ||||||

Severstal OAO | 112,169 | 1,079,602 | ||||||

Sistema JSFC SP GDR | 90,428 | 2,057,237 | ||||||