Exhibit (c)(2)

| John Q. Hammons Hotels, Inc. Presentation to the Special Committee of the Board of Directors June 14, 2005 Confidential Presentation to: |

| Table of Contents Situation Overview Summary of Proposed Transaction Management Financial Projections Summary Valuation Analysis of Consideration to Mr. Hammons |

| Situation Overview |

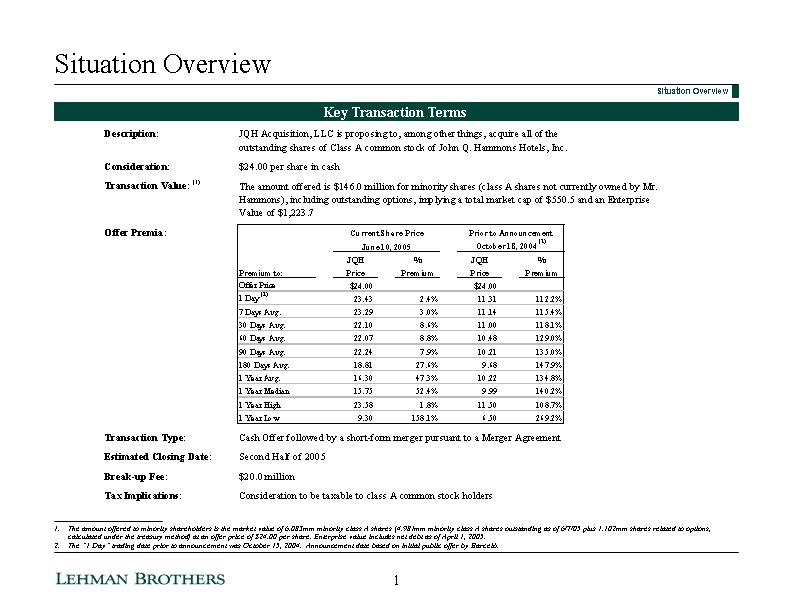

| Situation Overview Key Transaction Terms Situation Overview The amount offered to minority shareholders is the market value of 6.083mm minority class A shares (4.981mm minority class A shares outstanding as of 6/7/05 plus 1.102mm shares related to options, calculated under the treasury method) at an offer price of $24.00 per share. Enterprise value includes net debt as of April 1, 2005. The "1 Day" trading date prior to announcement was October 15, 2004. Announcement date based on initial public offer by Barcelo. 1 |

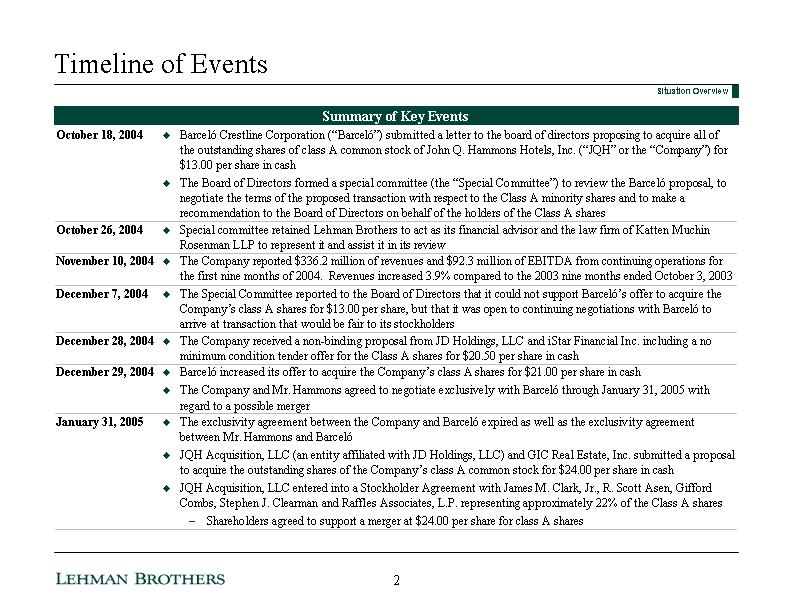

| Timeline of Events Summary of Key Events Situation Overview October 18, 2004 Barcelo Crestline Corporation ("Barcelo") submitted a letter to the board of directors proposing to acquire all of the outstanding shares of class A common stock of John Q. Hammons Hotels, Inc. ("JQH" or the "Company") for $13.00 per share in cash The Board of Directors formed a special committee (the "Special Committee") to review the Barcelo proposal, to negotiate the terms of the proposed transaction with respect to the Class A minority shares and to make a recommendation to the Board of Directors on behalf of the holders of the Class A shares October 26, 2004 Special committee retained Lehman Brothers to act as its financial advisor and the law firm of Katten Muchin Rosenman LLP to represent it and assist it in its review November 10, 2004 The Company reported $336.2 million of revenues and $92.3 million of EBITDA from continuing operations for the first nine months of 2004. Revenues increased 3.9% compared to the 2003 nine months ended October 3, 2003 December 7, 2004 The Special Committee reported to the Board of Directors that it could not support Barcelo's offer to acquire the Company's class A shares for $13.00 per share, but that it was open to continuing negotiations with Barcelo to arrive at transaction that would be fair to its stockholders December 28, 2004 The Company received a non-binding proposal from JD Holdings, LLC and iStar Financial Inc. including a no minimum condition tender offer for the Class A shares for $20.50 per share in cash December 29, 2004 Barcelo increased its offer to acquire the Company's class A shares for $21.00 per share in cash The Company and Mr. Hammons agreed to negotiate exclusively with Barcelo through January 31, 2005 with regard to a possible merger January 31, 2005 The exclusivity agreement between the Company and Barcelo expired as well as the exclusivity agreement between Mr. Hammons and Barcelo JQH Acquisition, LLC (an entity affiliated with JD Holdings, LLC) and GIC Real Estate, Inc. submitted a proposal to acquire the outstanding shares of the Company's class A common stock for $24.00 per share in cash JQH Acquisition, LLC entered into a Stockholder Agreement with James M. Clark, Jr., R. Scott Asen, Gifford Combs, Stephen J. Clearman and Raffles Associates, L.P. representing approximately 22% of the Class A shares Shareholders agreed to support a merger at $24.00 per share for class A shares 2 |

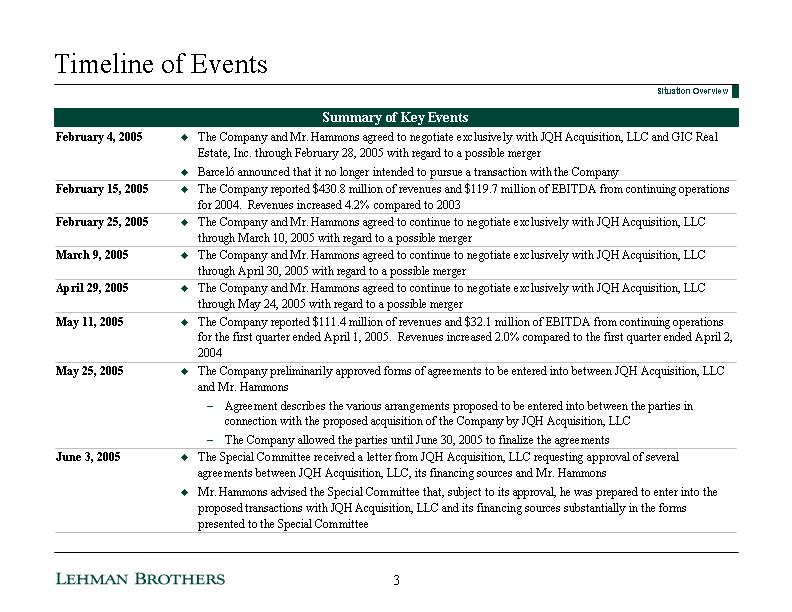

| Timeline of Events Summary of Key Events Situation Overview February 4, 2005 The Company and Mr. Hammons agreed to negotiate exclusively with JQH Acquisition, LLC and GIC Real Estate, Inc. through February 28, 2005 with regard to a possible merger Barcelo announced that it no longer intended to pursue a transaction with the Company February 15, 2005 The Company reported $430.8 million of revenues and $119.7 million of EBITDA from continuing operations for 2004. Revenues increased 4.2% compared to 2003 February 25, 2005 The Company and Mr. Hammons agreed to continue to negotiate exclusively with JQH Acquisition, LLC through March 10, 2005 with regard to a possible merger March 9, 2005 The Company and Mr. Hammons agreed to continue to negotiate exclusively with JQH Acquisition, LLC through April 30, 2005 with regard to a possible merger April 29, 2005 The Company and Mr. Hammons agreed to continue to negotiate exclusively with JQH Acquisition, LLC through May 24, 2005 with regard to a possible merger May 11, 2005 The Company reported $111.4 million of revenues and $32.1 million of EBITDA from continuing operations for the first quarter ended April 1, 2005. Revenues increased 2.0% compared to the first quarter ended April 2, 2004 May 25, 2005 The Company preliminarily approved forms of agreements to be entered into between JQH Acquisition, LLC and Mr. Hammons Agreement describes the various arrangements proposed to be entered into between the parties in connection with the proposed acquisition of the Company by JQH Acquisition, LLC The Company allowed the parties until June 30, 2005 to finalize the agreements June 3, 2005 The Special Committee received a letter from JQH Acquisition, LLC requesting approval of several agreements between JQH Acquisition, LLC, its financing sources and Mr. Hammons Mr. Hammons advised the Special Committee that, subject to its approval, he was prepared to enter into the proposed transactions with JQH Acquisition, LLC and its financing sources substantially in the forms presented to the Special Committee 3 |

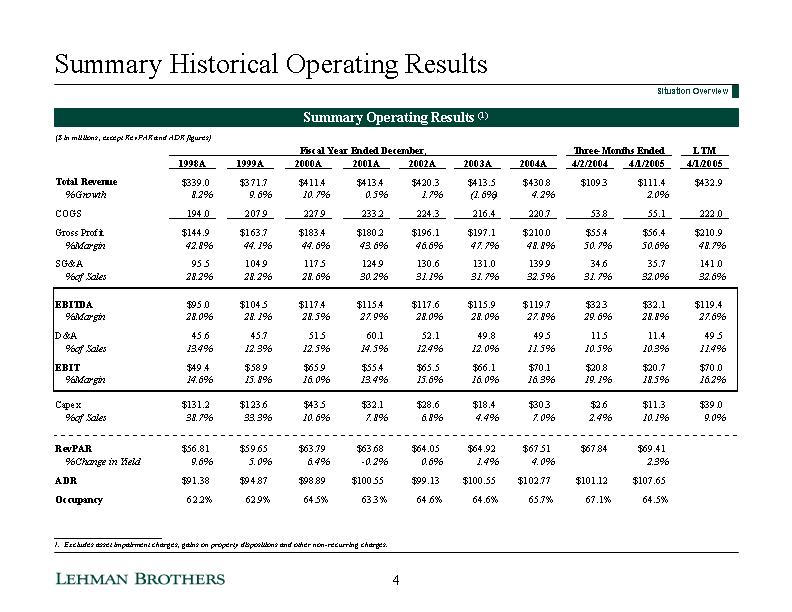

| Summary Historical Operating Results Summary Operating Results (1) ___________________________ 1. Excludes asset impairment charges, gains on property dispositions and other non-recurring charges. Situation Overview 4 |

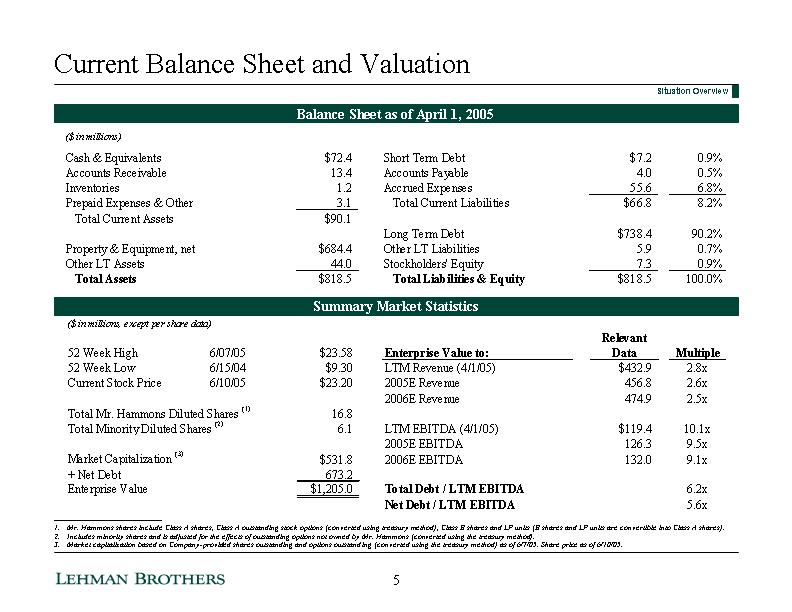

| Current Balance Sheet and Valuation Balance Sheet as of April 1, 2005 Summary Market Statistics ___________________________ Mr. Hammons shares include Class A shares, Class A outstanding stock options (converted using treasury method), Class B shares and LP units (B shares and LP units are convertible into Class A shares). Includes minority shares and is adjusted for the effects of outstanding options not owned by Mr. Hammons (converted using the treasury method). Market capitalization based on Company-provided shares outstanding and options outstanding (converted using the treasury method) as of 6/7/05. Share price as of 6/10/05. Situation Overview 5 |

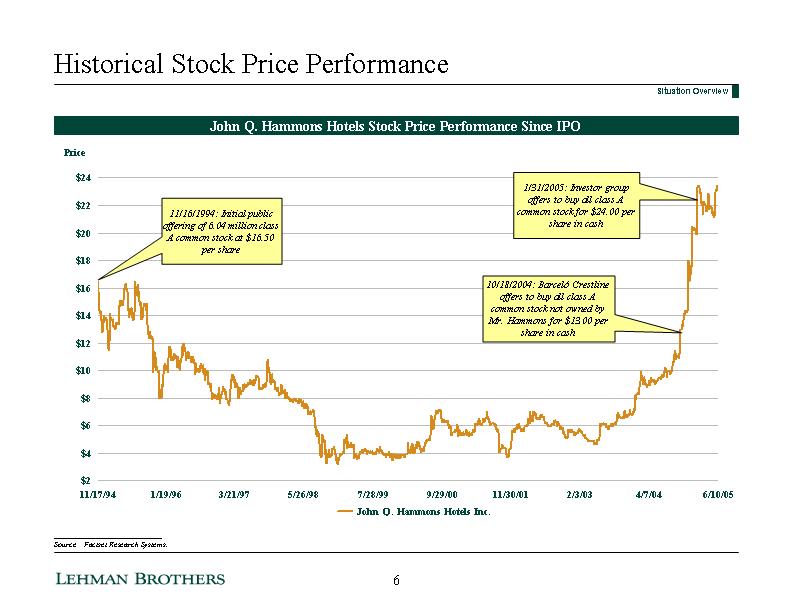

| Historical Stock Price Performance John Q. Hammons Hotels Stock Price Performance Since IPO ___________________________ Source: Factset Research Systems. 10/18/2004: Barcelo Crestline offers to buy all class A common stock not owned by Mr. Hammons for $13.00 per share in cash 11/16/1994: Initial public offering of 6.04 million class A common stock at $16.50 per share Situation Overview 1/31/2005: Investor group offers to buy all class A common stock for $24.00 per share in cash 6 |

| JQH Comparative Stock Price Performance Comparative Stock Price Performance - Trailing Twelve Months 6/10/2005 +144.2% +32.2% +29.3% +35.9% +7.3% ___________________________ Note: Lodging Mid-Cap C-Corps Composite consists of HOT, MAR, HLT, IHG, FHR, FS; Lodging Small-Cap C-Corps Composite consists of WBR, CHH, LQI, OEH, JQH, LGN, WEH, IHR; Lodging REITs Composite consists of HMT, HPT, FCH, MHX, LHO, ENN, KPA, HIH, AHT, WXH, BOY, HT. Situation Overview 7 |

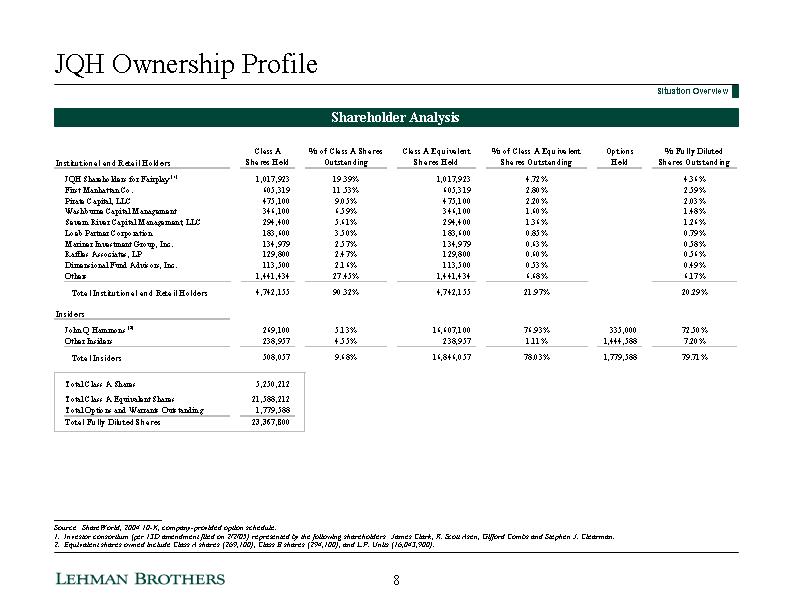

| JQH Ownership Profile Shareholder Analysis ___________________________ Source: ShareWorld, 2004 10-K, company-provided option schedule. 1. Investor consortium (per 13D amendment filed on 2/2/05) represented by the following shareholders: James Clark, R. Scott Asen, Gifford Combs and Stephen J. Clearman. 2. Equivalent shares owned include Class A shares (269,100), Class B shares (294,100), and L.P. Units (16,043,900). Situation Overview 8 |

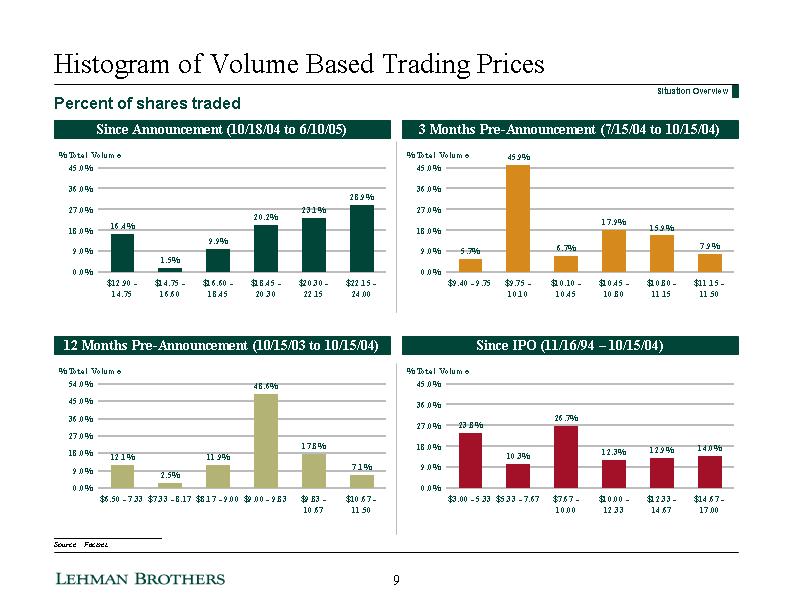

| Histogram of Volume Based Trading Prices Since Announcement (10/18/04 to 6/10/05) 3 Months Pre-Announcement (7/15/04 to 10/15/04) 12 Months Pre-Announcement (10/15/03 to 10/15/04) Since IPO (11/16/94 - 10/15/04) Situation Overview ___________________________ Source: Factset. Percent of shares traded Volume $9.40 - 9.75 0.05692803 $9.75 - 10.10 0.4599892 $10.10 - 10.45 0.06686359 $10.45 - 10.80 0.1785714 $10.80 - 11.15 0.15896885 $11.15 - 11.50 0.07867884 Volume $6.50 - 7.33 0.12107045 $7.33 - 8.17 0.02531033 $8.17 - 9.00 0.11873287 $9.00 - 9.83 0.4856521 $9.83 - 10.67 0.1778978 $10.67 - 11.50 0.07133645 Volume $3.00 - 5.33 0.2377782 $5.33 - 7.67 0.10333604 $7.67 - 10.00 0.2674439 $10.00 - 12.33 0.12310878 $12.33 - 14.67 0.12865079 $14.67 - 17.00 0.13968231 45.9% Volume $12.90 - 14.75 0.1641748 $14.75 - 16.60 0.01478453 $16.60 - 18.45 0.099237 $18.45 - 20.30 0.201873 $20.30 - 22.15 0.2313945 $22.15 - 24.00 0.2885361 9 |

| Summary of Proposed Transaction |

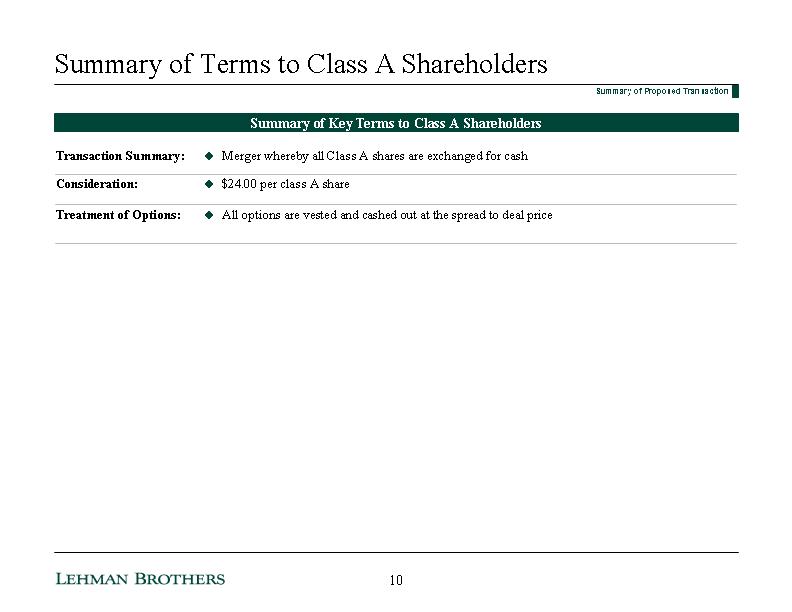

| Summary of Terms to Class A Shareholders Summary of Key Terms to Class A Shareholders Transaction Summary: Merger whereby all Class A shares are exchanged for cash Consideration: $24.00 per class A share Treatment of Options: All options are vested and cashed out at the spread to deal price Summary of Proposed Transaction 10 |

| Summary of Terms to Mr. Hammons Summary of Key Terms to Mr. Hammons Preferred Interest: Redemption preference of $335 million Either member may request redemption after the sooner of 13 years after issuance or Mr. Hammons demise (Mr. Hammons is 86 years old) 18 months to begin liquidation and one year thereafter to complete Earliest obligation, however, would not be until 10 years and 1 month after closing Early Liquidation Preference of $50 million Reduces Redemption Preference Only upon demise of Mr. Hammons (but not earlier than 12 months after closing) 24 months notice Various valuation protective covenants, including net worth covenant (for distributions), maintenance capex requirements, asset sale restrictions, maximum leverage, and others Line-of-Credit: Interim line of credit, prior to closing, of $25 million Upon closing, Mr. Hammons will receive a 13 year line-of-credit of up to $75 million until first anniversary, $175 million until second anniversary, $225 million until third anniversary, $250 million until fourth anniversary and $275 million for the duration of the line Interest rate of 1 month LIBOR + 100 basis points Guaranteed by iStar Financial Mr. Hammons, during his lifetime, may continue to draw on line-of-credit for up to seven years Line-of-credit matures upon redemption of Preferred Interest Except for Early Liquidation Preference, any proceeds from redemption of Preferred Interest must be used to repay the line-of-credit Summary of Proposed Transaction 11 |

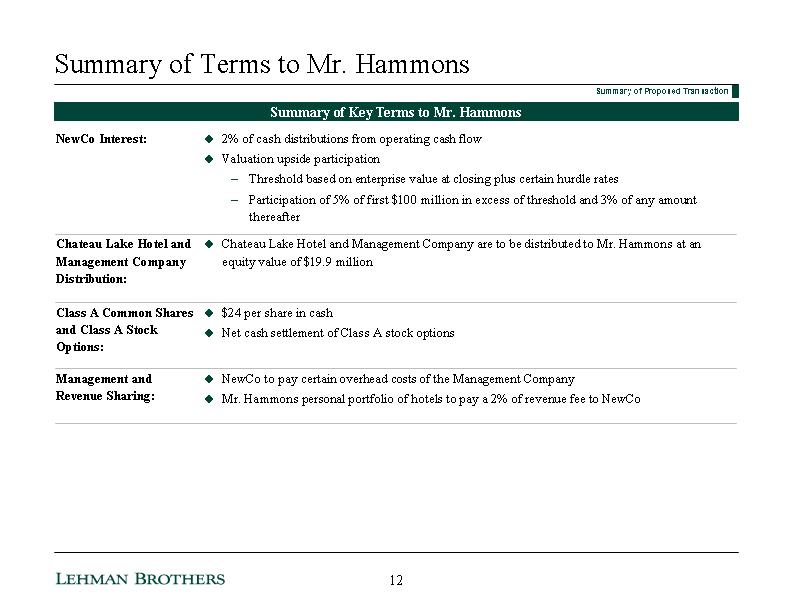

| Summary of Terms to Mr. Hammons Summary of Key Terms to Mr. Hammons NewCo Interest: 2% of cash distributions from operating cash flow Valuation upside participation Threshold based on enterprise value at closing plus certain hurdle rates Participation of 5% of first $100 million in excess of threshold and 3% of any amount thereafter Chateau Lake Hotel and Management Company Distribution: Chateau Lake Hotel and Management Company are to be distributed to Mr. Hammons at an equity value of $19.9 million Class A Common Shares and Class A Stock Options: $24 per share in cash Net cash settlement of Class A stock options Management and Revenue Sharing: NewCo to pay certain overhead costs of the Management Company Mr. Hammons personal portfolio of hotels to pay a 2% of revenue fee to NewCo Summary of Proposed Transaction 12 |

| Summary of Other Terms of Merger Agreement Summary of Other Terms of Merger Agreement Voting Requirement: Subject to majority of minority shareholders Special Committee may waive such requirement Termination Fee: Maximum termination fee of $20 million (inclusive of expense reimbursement) Announcement of alternative transaction within 18 months, payable upon closing Cap on expense reimbursement of $8 million Lower termination fee of $4 million plus expense reimbursement (payable earlier) Mr. Hammons demise and termination of Hammons Transactions In the event of a majority of minority vote, minority shareholders reject the transaction (even in absence of an alternative transaction) Termination fee capped at $3 million until Parent provides financing commitment letter Financing Commitment: Parent must deliver commitment letter or replacement commitment letter by later of 60 days from signing or 7 business days subsequent to receiving notice of completion of Proxy statement Escrow Deposit: $3 million escrow deposit by Parent Summary of Proposed Transaction 13 |

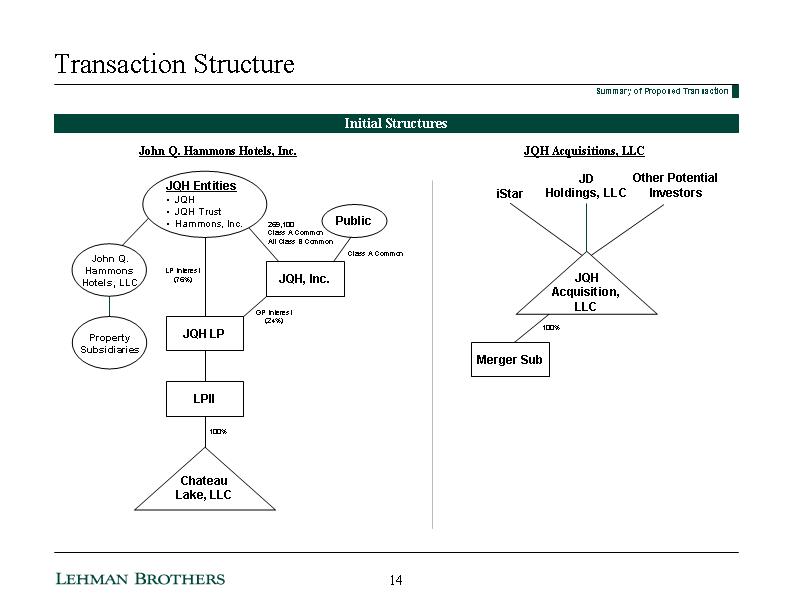

| Transaction Structure Initial Structures Summary of Proposed Transaction Chateau Lake, LLC JQH, Inc. Public JQH LP LPII 100% 269,100 Class A Common All Class B Common Class A Common GP Interest (24%) LP Interest (76%) Property Subsidiaries John Q. Hammons Hotels, LLC JQH Entities • JQH • JQH Trust • Hammons, Inc. John Q. Hammons Hotels, Inc. JQH Acquisitions, LLC iStar JD Holdings, LLC JQH Acquisition, LLC Merger Sub 100% Other Potential Investors 14 |

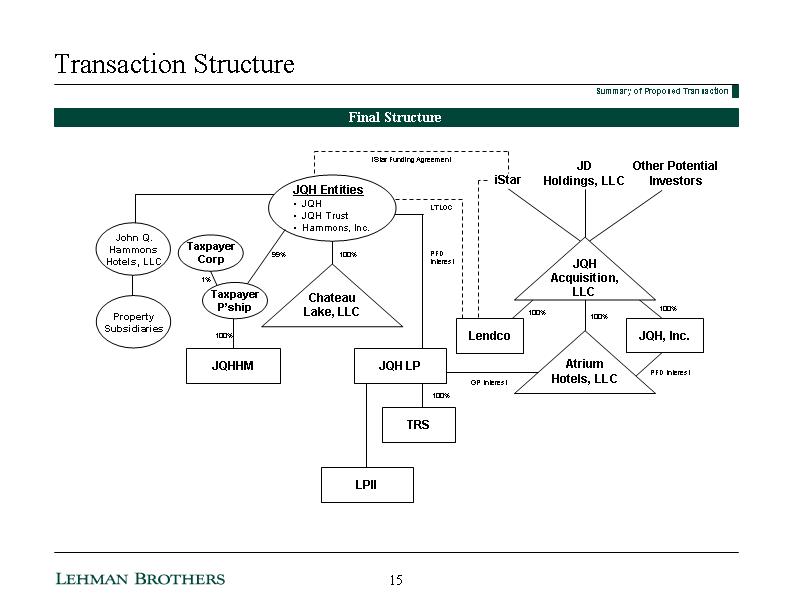

| Transaction Structure Final Structure Summary of Proposed Transaction iStar JD Holdings, LLC Lendco 100% PFD Interest JQH, Inc. TRS 100% 100% 100% PFD Interest Chateau Lake, LLC 100% LPII LTLOC iStar Funding Agreement JQH Acquisition, LLC Atrium Hotels, LLC 99% Taxpayer Corp 100% Property Subsidiaries John Q. Hammons Hotels, LLC 1% JQH Entities • JQH • JQH Trust • Hammons, Inc. JQH LP JQHHM GP Interest Taxpayer P'ship Other Potential Investors 15 |

| Management Financial Projections |

| Historical & Projected JQH & Lodging Industry RevPAR US Lodging Industry John Q Hammons 1997 0.055 0.053 1998 0.026 0.0959 1999 0.029 0.0499 2000 0.068 0.064 2001 -0.07 -0.002 2002 -0.027 0.006 2003 0.004 0.014 2004 0.078 0.04 2005 0.078 0.023 2006 0.06 0.046 Historical and Projected JQH and Lodging Industry RevPAR Growth ___________________________ Source: Company filings, Company projections and PwC research (for U.S. lodging industry). Management Financial Projections 16 |

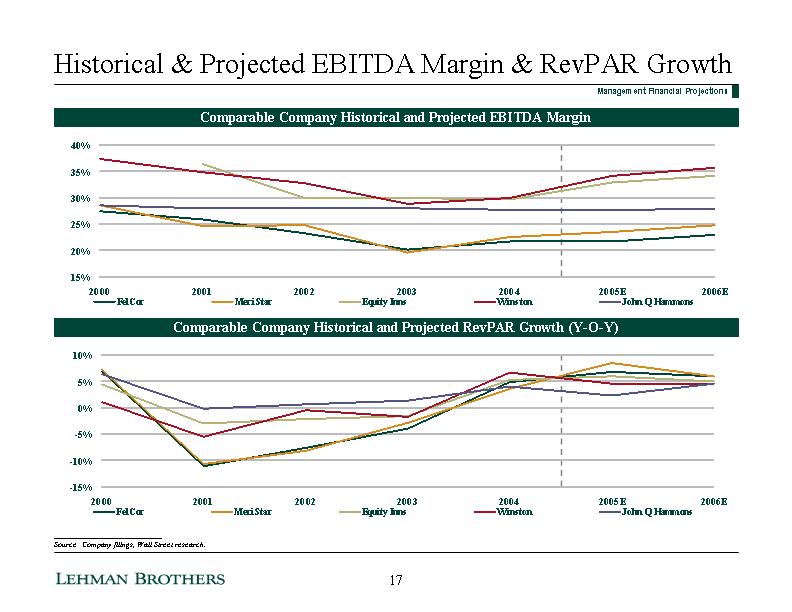

| Historical & Projected EBITDA Margin & RevPAR Growth Comparable Company Historical and Projected EBITDA Margin Comparable Company Historical and Projected RevPAR Growth (Y-O-Y) ___________________________ Source: Company filings, Wall Street research. Management Financial Projections Company FelCor MeriStar Equity Inns Winston John Q Hammons 2000 0.274290907 0.284936626 0.372806398 0.285463548870937 2001 0.258574999 0.246960055 0.364062638 0.348953457 0.279209218845999 2002 0.232596765 0.247731009 0.299812583 0.327702729 0.279750476421592 2003 0.201491673 0.195751771 0.29896737 0.288556406 0.280212830279944 2004 0.217263743051266 0.226056323283207 0.295964719025024 0.29992343364008 0.277751984771809 2005E 0.217697664891438 0.23549364021805 0.328343313373253 0.341935483870968 0.276489323278646 2006E 0.22960399846213 0.247380195455081 0.340909090909091 0.35672514619883 0.278048010107391 Company FelCor MeriStar Equity Inns Winston John Q Hammons 2000 0.0691 0.0727 0.0447 0.0101 0.064 2001 -0.111262242 -0.107322095 -0.0294 -0.0544 -0.002 2002 -0.076 -0.0819 -0.0209 -0.00509 0.006 2003 -0.04 -0.029 -0.016 -0.018 0.014 2004 0.049 0.036 5.27488855869243E-02 0.067 3.98952556993224E-02 2005E 6.82468919030141E-02 0.084 0.06 0.045 2.34039401570139E-02 2006E 0.06 0.0595 0.05 0.045 4.58821826602982E-02 17 |

| Projected Operating Results Projected Operating Results (1) ___________________________ 1. Excludes asset impairment charges, gains on property dispositions and other non-recurring charges. Management Financial Projections 18 |

| Summary Valuation |

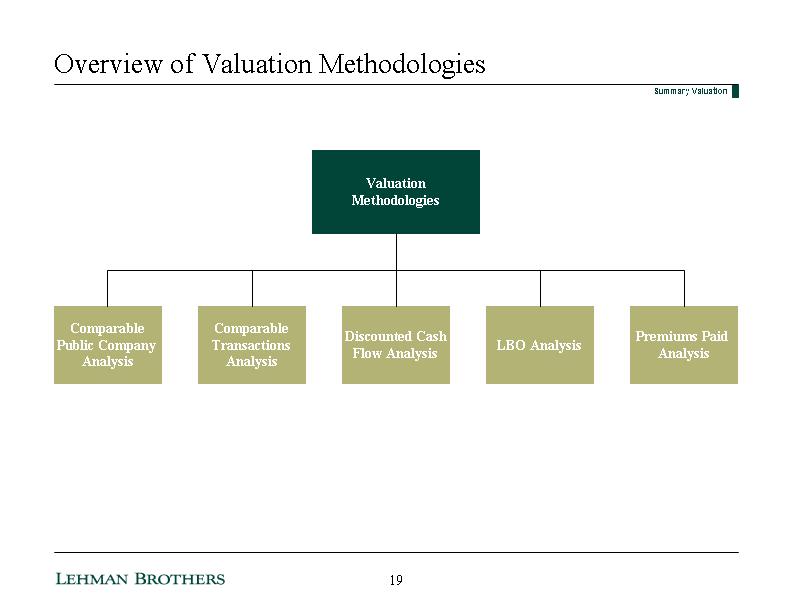

| Overview of Valuation Methodologies Valuation Methodologies Comparable Transactions Analysis Comparable Public Company Analysis Discounted Cash Flow Analysis LBO Analysis Premiums Paid Analysis Summary Valuation 19 |

| JQH Purchase Price Ratio Analysis Summary Valuation John Q. Hammons Hotels Purchase Price Ratio Analysis ___________________________ Share price at announcement as of 10/15/2004. Diluted shares based on treasury method for accounting of options. Share price current as of 6/10/2005. EBITDA estimates excludes asset impairment charges, debt extinguishment costs, gain on sales, and other one-time items. 20 |

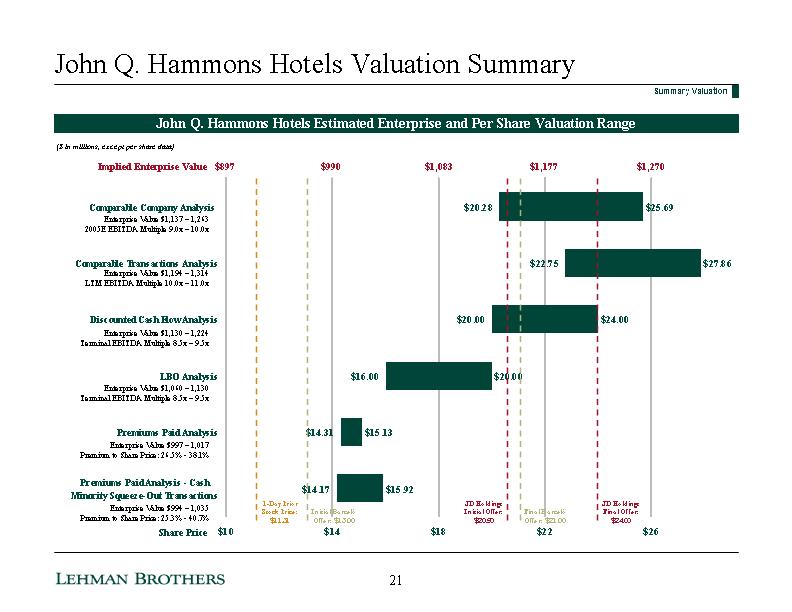

| Low Spread High Premiums Paid Analysis - Cash Minority Squeeze-Out Transactions 14.1671 1.74929807529751 15.9164 Premiums Paid Analysis 14.3058142014793 0.827864637452475 15.1336788389318 LBO Analysis 16 4 20 Discounted Cash Flow Analysis 20 4 24 Comparable Transactions Analysis 22.7468174368148 5.1113926000736 27.8582100368884 Comparable Company Analysis 20.2807677393213 5.40531958924917 25.6860873285705 John Q. Hammons Hotels Valuation Summary John Q. Hammons Hotels Estimated Enterprise and Per Share Valuation Range Summary Valuation Implied Enterprise Value Share Price $897 $1,177 $1,270 Enterprise Value $1,137 - 1,263 2005E EBITDA Multiple 9.0x - 10.0x Enterprise Value $1,194 - 1,314 LTM EBITDA Multiple 10.0x - 11.0x Enterprise Value $1,130 - 1,224 Terminal EBITDA Multiple 8.5x - 9.5x Enterprise Value $1,060 - 1,130 Terminal EBITDA Multiple 8.5x - 9.5x Enterprise Value $997 - 1,017 Premium to Share Price: 26.5% - 38.1% Enterprise Value $994 - 1,035 Premium to Share Price: 25.3% - 40.7% ($ in millions, except per share data) $990 $1,083 JD Holdings Initial Offer: $20.50 1-Day Prior Stock Price: $11.31 JD Holdings Final Offer: $24.00 Final Barcelo Offer: $21.00 Initial Barcelo Offer: $13.00 21 |

| Comparable Company Analysis Comparable Company Analysis ___________________________ Source: Company filings and equity research. (1) Year-over-year growth. (2) Market value, net debt and enterprise value pro forma for six Renaissance hotels portfolio acquisition in April 2005. (3) Represents 2001A EBITDA margin. Comparable 2000A EBITDA margin not available. Summary Valuation Lehman Brothers evaluated a universe of six lodging companies in its comparable company public trading multiples analysis No company used in this analysis is directly comparable to JQH in terms of a number of important factors such as asset type, business model, size, corporate structure, dividend yield and tax situation Lehman Brothers believes the appropriate valuation multiple for JQH is lower than the public valuation multiples for the comparable companies analyzed Current EBITDA multiples for the comparable companies analyzed are at historically high levels due to strong anticipated growth from RevPAR increases and margin improvements JQH's current financial performance is not expected to improve as rapidly as that of the comparable companies analyzed JQH's Q1 2005 RevPAR growth was significantly lower than the Q1 2005 RevPAR growth of comparable companies analyzed JQH's 2005E EBITDA margin is near its 2000A EBITDA margin level while the EBITDA margins of comparable companies remain significantly below historical levels 22 |

| Comparable Company Value Summary Implied Value of John Q. Hammons Hotels Summary Valuation ___________________________ 1. Net debt of $673.2 million as of 4/1/05. 23 |

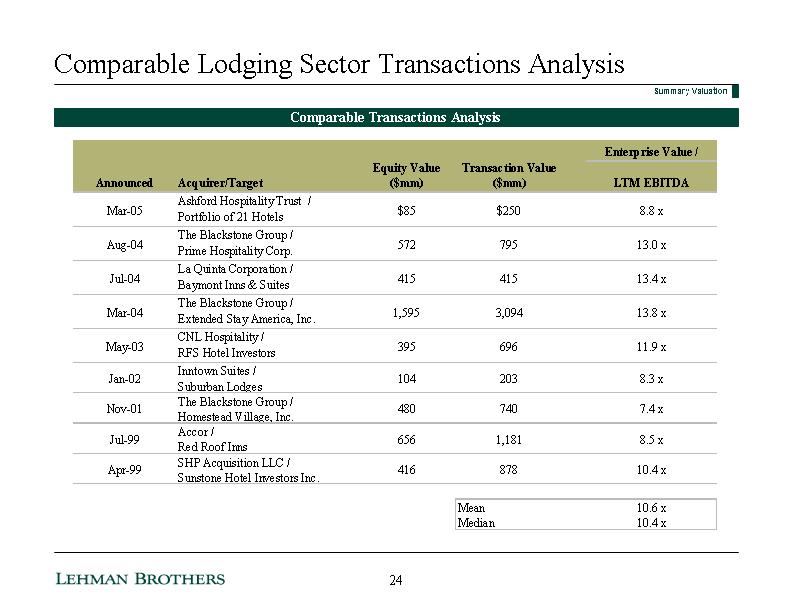

| Comparable Lodging Sector Transactions Analysis Comparable Transactions Analysis Summary Valuation 24 |

| Comparable Transactions Value Summary Implied Value of John Q. Hammons Hotels Summary Valuation ___________________________ 1. Net debt of $673.2 million as of 4/1/05. 25 |

| Discounted Cash Flow Analysis Discounted Cash Flow Valuation Summary Valuation Implied perpetuity growth rates for selected terminal multiples ranges from 1.8% to 3.5% Terminal multiples are in line with historical trading range of JQH ___________________________ 1. Net debt of $673.2 million as of 4/1/05. 26 |

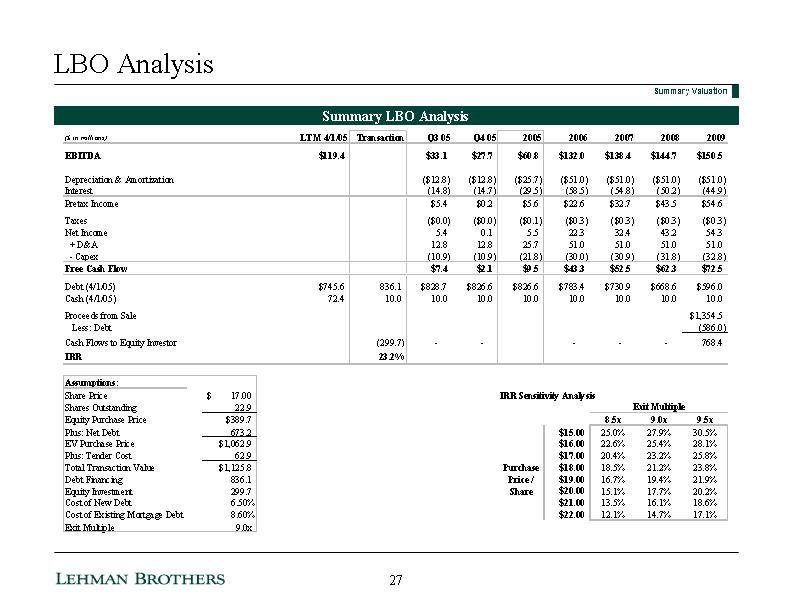

| LBO Analysis Summary LBO Analysis Summary Valuation 27 |

| Premiums Paid Analysis Premiums of Transactions From $1.0 billion to $1.5 billion Over Last Twelve Months Summary Valuation ___________________________ Source: SDC. 28 |

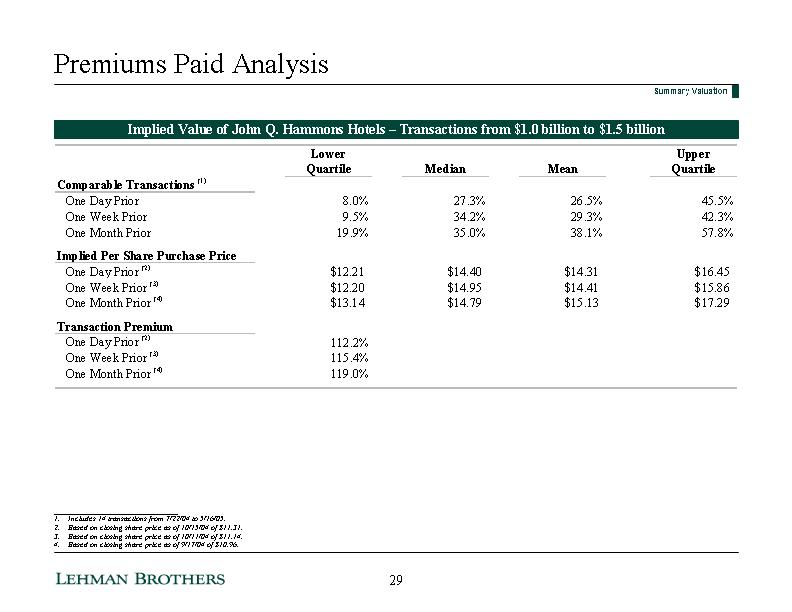

| Premiums Paid Analysis Implied Value of John Q. Hammons Hotels - Transactions from $1.0 billion to $1.5 billion _______________________________ 1. Includes 14 transactions from 7/22/04 to 5/16/05. 2. Based on closing share price as of 10/15/04 of $11.31. 3. Based on closing share price as of 10/11/04 of $11.14. 4. Based on closing share price as of 9/17/04 of $10.96. Summary Valuation 29 |

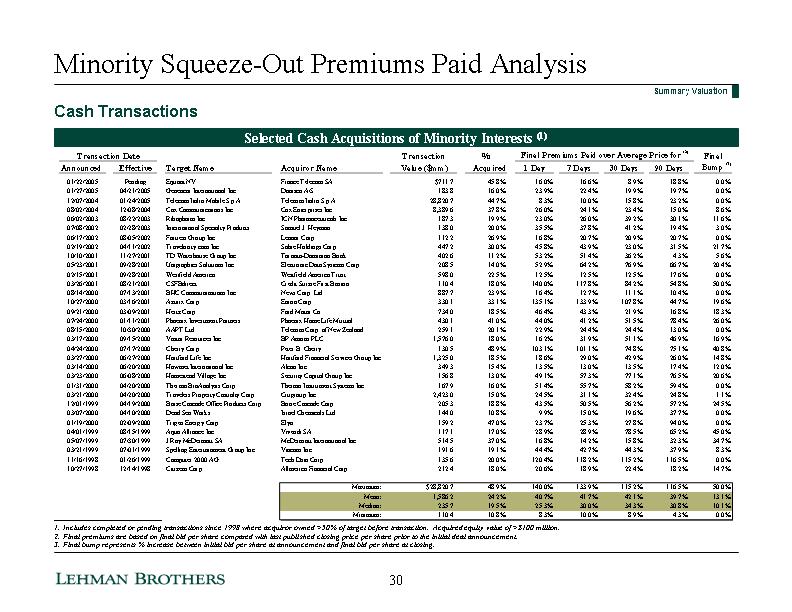

| Minority Squeeze-Out Premiums Paid Analysis Summary Valuation ___________________________ Includes completed or pending transactions since 1998 where acquiror owned >50% of target before transaction. Acquired equity value of >$100 million. Final premiums are based on final bid per share compared with last published closing price per share prior to the initial deal announcement. Final bump represents % increase between initial bid per share at announcement and final bid per share at closing. Cash Transactions Selected Cash Acquisitions of Minority Interests (1) 30 |

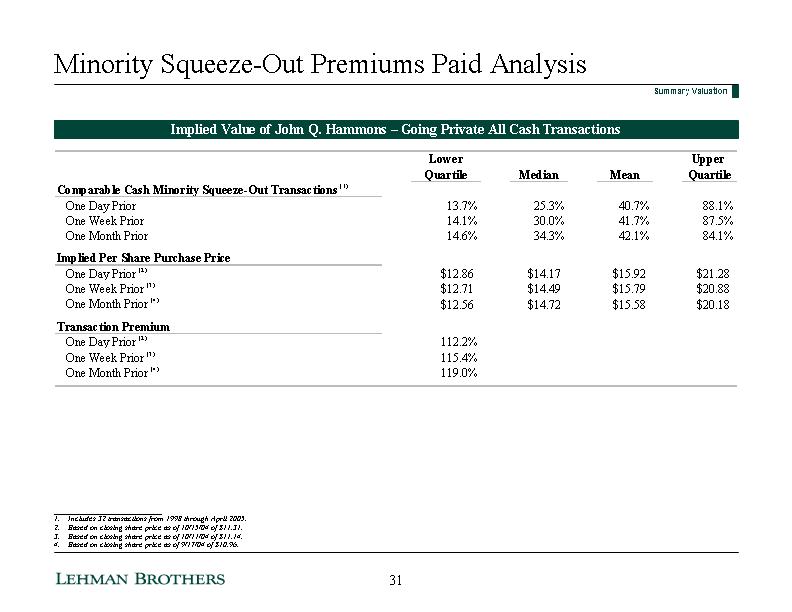

| Minority Squeeze-Out Premiums Paid Analysis Implied Value of John Q. Hammons - Going Private All Cash Transactions ___________________________ 1. Includes 32 transactions from 1998 through April 2005. 2. Based on closing share price as of 10/15/04 of $11.31. 3. Based on closing share price as of 10/11/04 of $11.14. 4. Based on closing share price as of 9/17/04 of $10.96. Summary Valuation 31 |

| Analysis of Consideration to Mr. Hammons |

| Analysis of Consideration to Mr. Hammons In analyzing the financial consideration provided to Mr. Hammons and his affiliates, Lehman Brothers reviewed the terms and conditions of the transactions set forth in the Amended and Restated Transaction Agreement, dated June 14, 2005, by and among John Q. Hammons, Revocable Trust of John Q. Hammons, Hammons, Inc., JD Holdings, LLC and JQH Acquisition and the exhibits and schedules thereto Based on representations and warranties in the merger agreement and other assurances provided to us, we understand (and have assumed) that these agreements are all of the agreements, commitments and understandings between Mr. Hammons and his affiliates, on the one hand, and JQH Acquisition and its affiliates, on the other hand, and that there have been and will be no material modifications to these documents and no "side" agreements or arrangements In deriving the financial value provided to Mr. Hammons and his affiliates, Lehman Brothers examined the value under three scenarios: A scenario assuming the immediate demise of Mr. Hammons upon closing A scenario assuming Mr. Hammons lives beyond the term of the agreements which contain provisions whose value is dependent on Mr. Hammons' survival, and A probability weighted scenario, based on mortality rates provided by the U.S. Social Security Administration's period life table (updated November 2004) With respect to the preferred interest and line-of-credit provided to Mr. Hammons, Lehman Brothers compared the terms provided to Mr. Hammons with other comparable market securities in order to determine the appropriate value, discount rates and cost savings to Mr. Hammons Discount rate for valuation of preferred interest was derived from examining, among other things, JQH cost of equity, JQH cost of debt and market rates for pay-in-kind securities Interest cost savings on Mr. Hammons' line-of-credit was determined based on a theoretical "arms-length" line-of-credit cost to Mr. Hammons A number of the terms in these agreements may either add to or subtract from the net value realized by Mr. Hammons and his affiliates in the transactions, but presently do not have a quantifiable valuation from a financial point of view Lehman Brothers considered and made inquiries regarding these terms and have no information that leads us to believe the net effect of these terms would be material to our valuation of the consideration to Mr. Hammons and his affiliates as of the date of this presentation or to our assessment of the reasonableness of that consideration relative to the consideration being paid for the minority shares Analysis of Consideration to Mr. Hammons 32 |

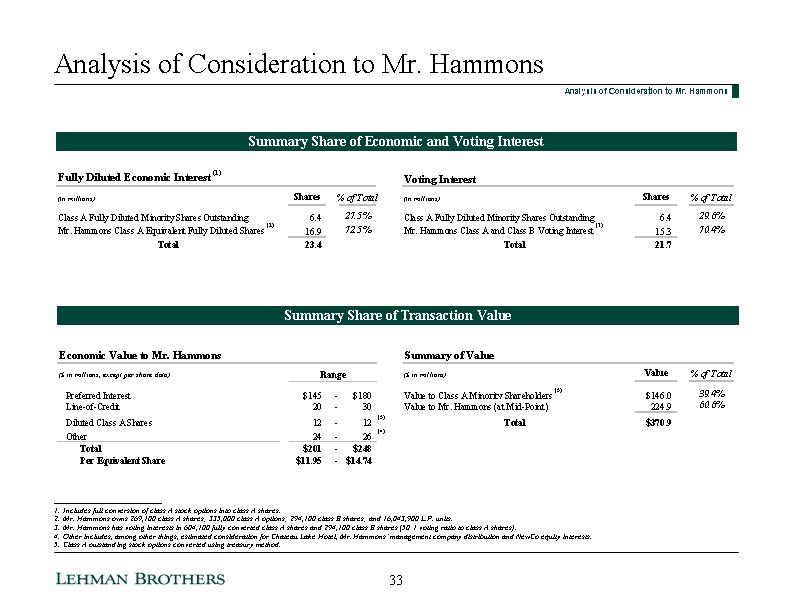

| Analysis of Consideration to Mr. Hammons Analysis of Consideration to Mr. Hammons Summary Share of Economic and Voting Interest ___________________________ Includes full conversion of class A stock options into class A shares. Mr. Hammons owns 269,100 class A shares; 335,000 class A options; 294,100 class B shares; and 16,043,900 L.P. units. Mr. Hammons has voting interests in 604,100 fully converted class A shares and 294,100 class B shares (50:1 voting ratio to class A shares). Other includes, among other things, estimated consideration for Chateau Lake Hotel, Mr. Hammons' management company distribution and NewCo equity interests. Class A outstanding stock options converted using treasury method. Summary Share of Transaction Value 33 |