Exhibit 99(c)(4)

| John Q. Hammons Hotels, Inc. Presentation to the Special Committee of the Board of Directors December 29, 2004 Confidential Presentation to: |

| Table of Contents Summary of Proposals Summary Valuation Analysis of Consideration to Mr. Hammons |

| Summary of Proposals |

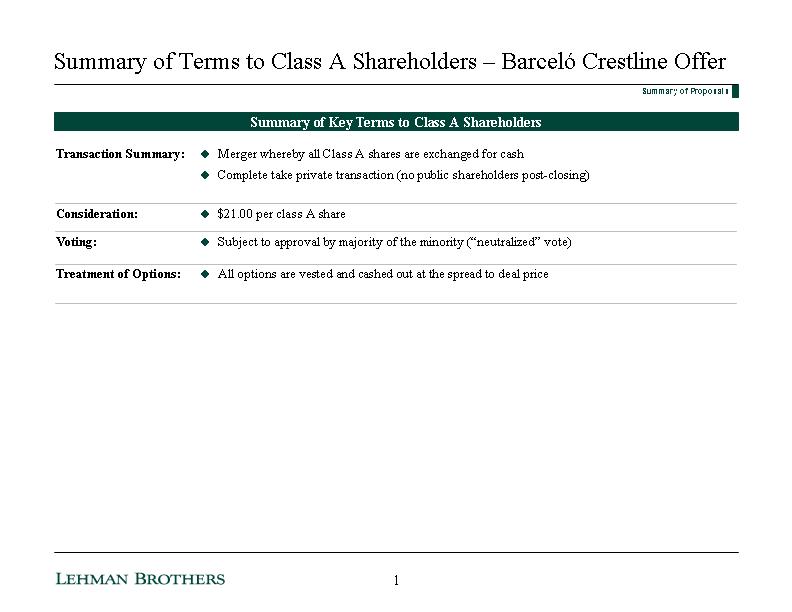

| Summary of Terms to Class A Shareholders - Barcelo Crestline Offer Summary of Key Terms to Class A Shareholders Transaction Summary: Merger whereby all Class A shares are exchanged for cash Complete take private transaction (no public shareholders post-closing) Consideration: $21.00 per class A share Voting: Subject to approval by majority of the minority ("neutralized" vote) Treatment of Options: All options are vested and cashed out at the spread to deal price Summary of Proposals 1 |

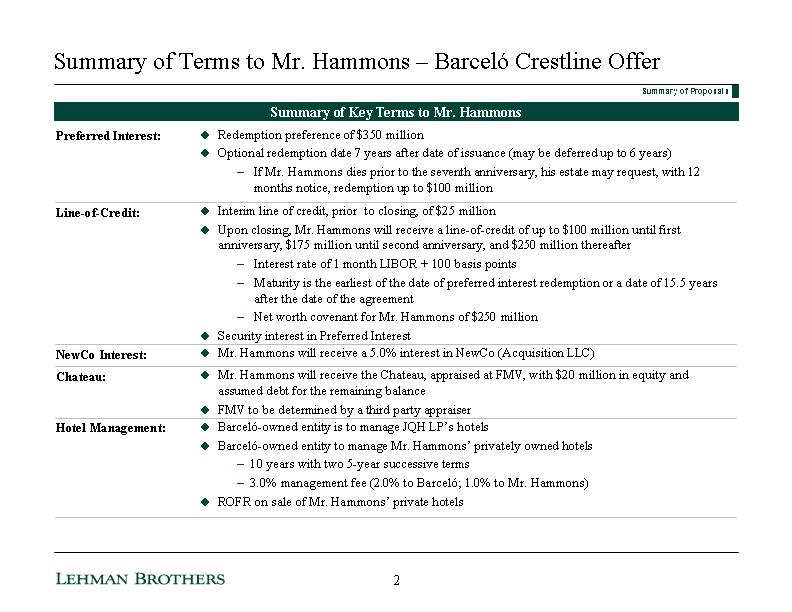

| Summary of Terms to Mr. Hammons - Barcelo Crestline Offer Summary of Key Terms to Mr. Hammons Preferred Interest: Redemption preference of $350 million Optional redemption date 7 years after date of issuance (may be deferred up to 6 years) If Mr. Hammons dies prior to the seventh anniversary, his estate may request, with 12 months notice, redemption up to $100 million Line-of-Credit: Interim line of credit, prior to closing, of $25 million Upon closing, Mr. Hammons will receive a line-of-credit of up to $100 million until first anniversary, $175 million until second anniversary, and $250 million thereafter Interest rate of 1 month LIBOR + 100 basis points Maturity is the earliest of the date of preferred interest redemption or a date of 15.5 years after the date of the agreement Net worth covenant for Mr. Hammons of $250 million Security interest in Preferred Interest NewCo Interest: Mr. Hammons will receive a 5.0% interest in NewCo (Acquisition LLC) Chateau: Mr. Hammons will receive the Chateau, appraised at FMV, with $20 million in equity and assumed debt for the remaining balance FMV to be determined by a third party appraiser Hotel Management: Barcelo-owned entity is to manage JQH LP's hotels Barcelo-owned entity to manage Mr. Hammons' privately owned hotels 10 years with two 5-year successive terms 3.0% management fee (2.0% to Barcelo; 1.0% to Mr. Hammons) ROFR on sale of Mr. Hammons' private hotels Summary of Proposals 2 |

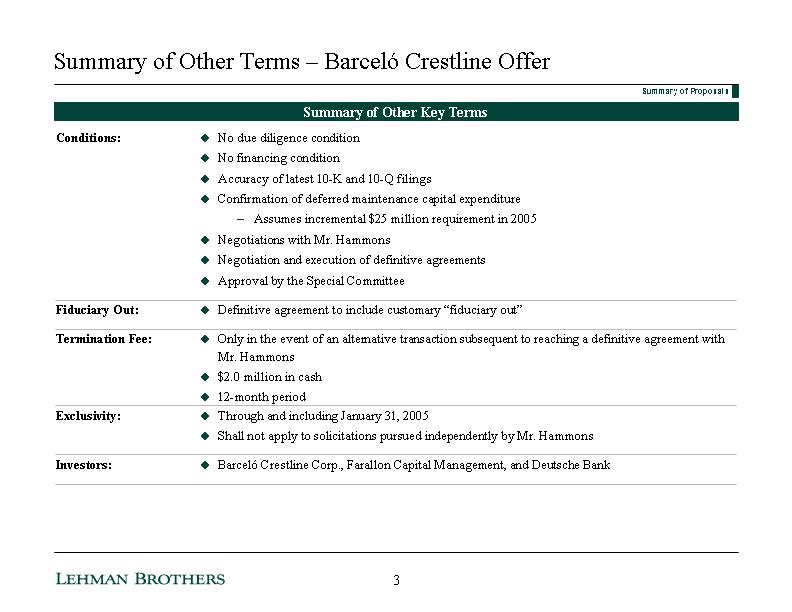

| Summary of Other Terms - Barcelo Crestline Offer Summary of Other Key Terms Conditions: No due diligence condition No financing condition Accuracy of latest 10-K and 10-Q filings Confirmation of deferred maintenance capital expenditure Assumes incremental $25 million requirement in 2005 Negotiations with Mr. Hammons Negotiation and execution of definitive agreements Approval by the Special Committee Fiduciary Out: Definitive agreement to include customary "fiduciary out" Termination Fee: Only in the event of an alternative transaction subsequent to reaching a definitive agreement with Mr. Hammons $2.0 million in cash 12-month period Exclusivity: Through and including January 31, 2005 Shall not apply to solicitations pursued independently by Mr. Hammons Investors: Barcelo Crestline Corp., Farallon Capital Management, and Deutsche Bank Summary of Proposals 3 |

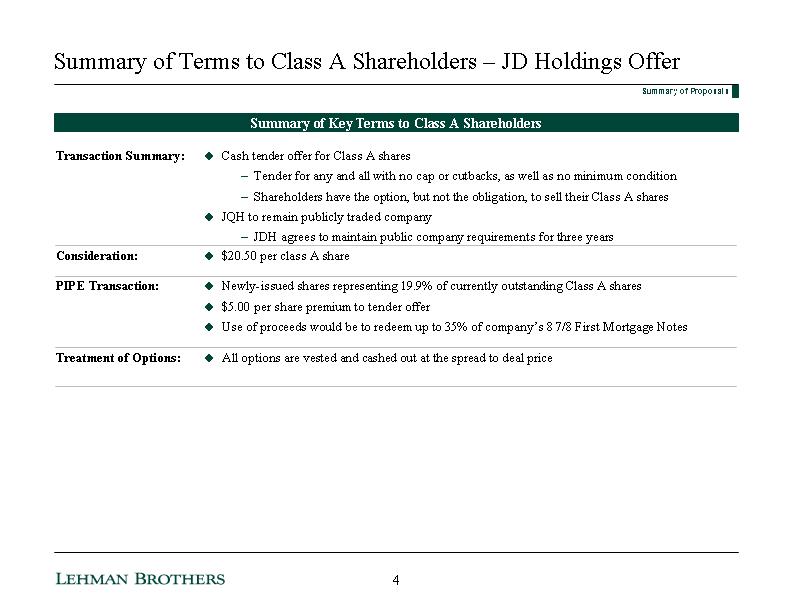

| Summary of Terms to Class A Shareholders - JD Holdings Offer Summary of Key Terms to Class A Shareholders Transaction Summary: Cash tender offer for Class A shares Tender for any and all with no cap or cutbacks, as well as no minimum condition Shareholders have the option, but not the obligation, to sell their Class A shares JQH to remain publicly traded company JDH agrees to maintain public company requirements for three years Consideration: $20.50 per class A share PIPE Transaction: Newly-issued shares representing 19.9% of currently outstanding Class A shares $5.00 per share premium to tender offer Use of proceeds would be to redeem up to 35% of company's 8 7/8 First Mortgage Notes Treatment of Options: All options are vested and cashed out at the spread to deal price Summary of Proposals 4 |

| Summary of Terms to Mr. Hammons - JD Holdings' Offer Summary of Key Terms to Mr. Hammons Preferred Interest: Redemption preference of $375 million (backstop guarantee by iStar Financial) Either member may request redemption after the sooner of 13 years after issuance or Mr. Hammons demise (but not less than 7 years) If Mr. Hammons dies prior to the seventh anniversary, his estate may request, with 12 months notice, redemption up to $100 million Line-of-Credit: Interim line of credit, prior to closing, of $25 million Upon closing, Mr. Hammons will receive a 13 year line-of-credit of up to $100 million until first anniversary, $200 million until second anniversary and $250 million for the duration of the line Interest rate of 1 month LIBOR + 100 basis points Guaranteed by iStar Financial Would not require a pledge of stock or partnership interest NewCo Interest: Mr. Hammons will receive a 5.0% interest in NewCo (Acquisition LLC) Chateau: To be sold to Mr. Hammons (including assumption of existing debt) at FMV, as determined by third party appraisal Hotel Management: JQH LP will distribute ownership and control over the hotel management company back to Mr. Hammons (along with its employees, systems and trade name) Mr. Hammons will become Chairman and CEO 2.5% annual management fee (10-year term) Not to exceed $10 million of fair market value; otherwise adjust redemption preference amount ROFR on sale of Mr. Hammons private hotels Summary of Proposals 5 |

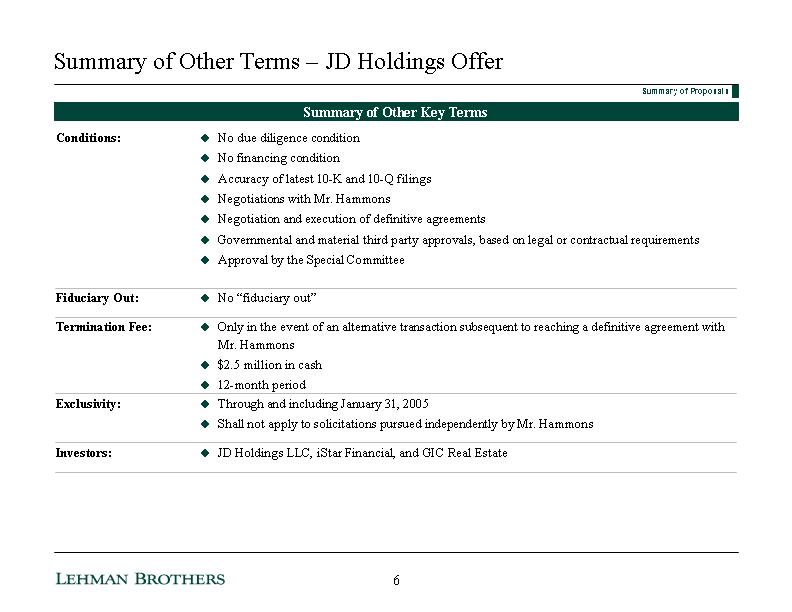

| Summary of Other Terms - JD Holdings Offer Summary of Other Key Terms Conditions: No due diligence condition No financing condition Accuracy of latest 10-K and 10-Q filings Negotiations with Mr. Hammons Negotiation and execution of definitive agreements Governmental and material third party approvals, based on legal or contractual requirements Approval by the Special Committee Fiduciary Out: No "fiduciary out" Termination Fee: Only in the event of an alternative transaction subsequent to reaching a definitive agreement with Mr. Hammons $2.5 million in cash 12-month period Exclusivity: Through and including January 31, 2005 Shall not apply to solicitations pursued independently by Mr. Hammons Investors: JD Holdings LLC, iStar Financial, and GIC Real Estate Summary of Proposals 6 |

| Summary Valuation |

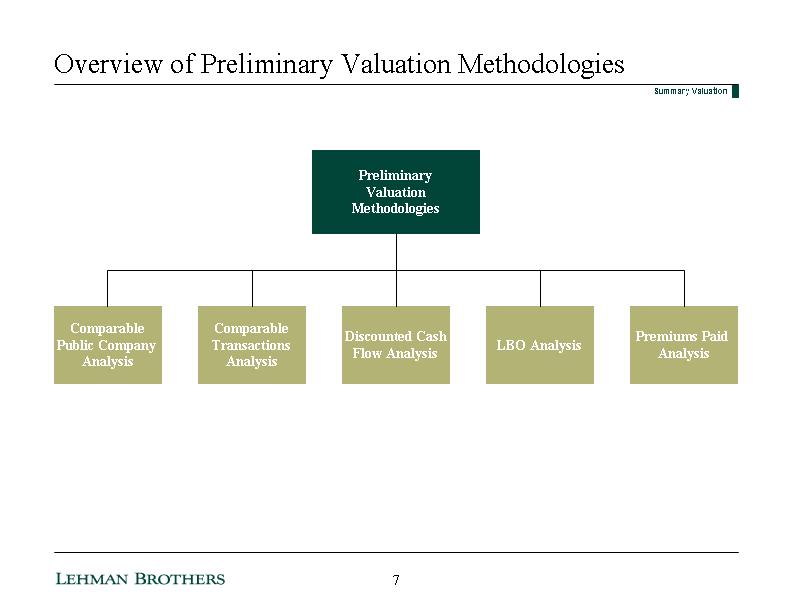

| Overview of Preliminary Valuation Methodologies Preliminary Valuation Methodologies Comparable Transactions Analysis Comparable Public Company Analysis Discounted Cash Flow Analysis LBO Analysis Premiums Paid Analysis Summary Valuation 7 |

| JQH Purchase Price Ratio Analysis Summary Valuation John Q. Hammons Hotels Purchase Price Ratio Analysis ___________________________ Share price at announcement as of 10/15/2004. Diluted shares based on treasury method for accounting of options. Share price current as of 12/27/2004. EBITDA estimates excludes asset impairment charges, debt extinguishment costs, gain on sales, and other one-time items. 8 |

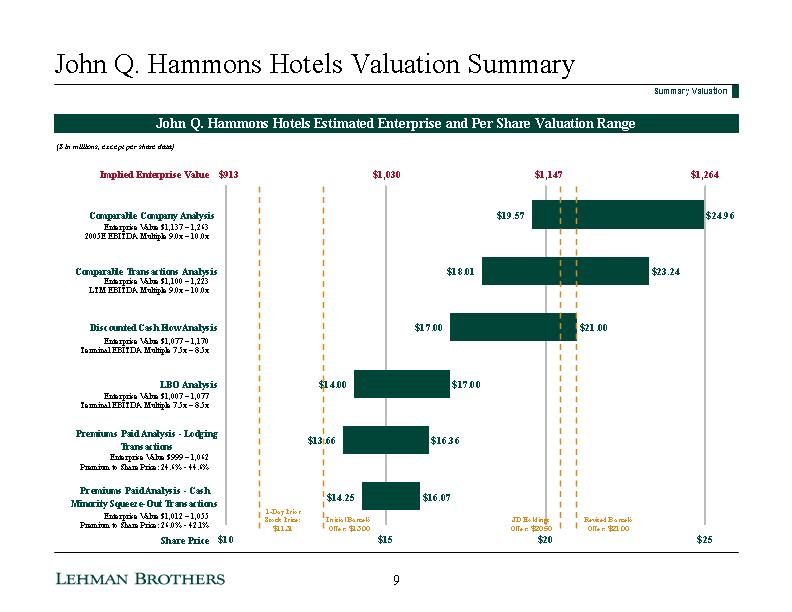

| Low Spread High Premiums Paid Analysis - Cash Minority Squeeze-Out Transactions 14.2503 1.82050735644739 16.0708 Premiums Paid Analysis - Lodging Transactions 13.6581892166836 2.6992487998453 16.3574380165289 LBO Analysis 14 3 17 Discounted Cash Flow Analysis 17 4 21 Comparable Transactions Analysis 18.0099263770773 5.22572528740422 23.2356516644815 Comparable Company Analysis 19.5656842403514 5.39858727221245 24.9642715125638 Revised Barcelo Offer: $21.00 John Q. Hammons Hotels Valuation Summary John Q. Hammons Hotels Estimated Enterprise and Per Share Valuation Range Summary Valuation Implied Enterprise Value Share Price $913 $1,030 $1,147 $1,264 Enterprise Value $1,137 - 1,263 2005E EBITDA Multiple 9.0x - 10.0x Enterprise Value $1,100 - 1,223 LTM EBITDA Multiple 9.0x - 10.0x Enterprise Value $1,077 - 1,170 Terminal EBITDA Multiple 7.5x - 8.5x Enterprise Value $1,007 - 1,077 Terminal EBITDA Multiple 7.5x - 8.5x Enterprise Value $999 - 1,062 Premium to Share Price: 24.6% - 44.6% Enterprise Value $1,012 - 1,055 Premium to Share Price: 26.0% - 42.1% ($ in millions, except per share data) JD Holdings Offer: $20.50 Initial Barcelo Offer: $13.00 1-Day Prior Stock Price: $11.31 9 |

| Comparable Company Analysis Comparable Company Analysis ___________________________ Source: Company filings and equity research. Summary Valuation EBITDA multiples for the comparable companies are near historical highs as a result of anticipated above average growth in EBITDA JQH's stable portfolio of assets will result in lower EBITDA growth, leading to a lower comparable EBITDA multiple today Additionally, a lower multiple reflects the location of assets (mainly in secondary and tertiary markets) 10 |

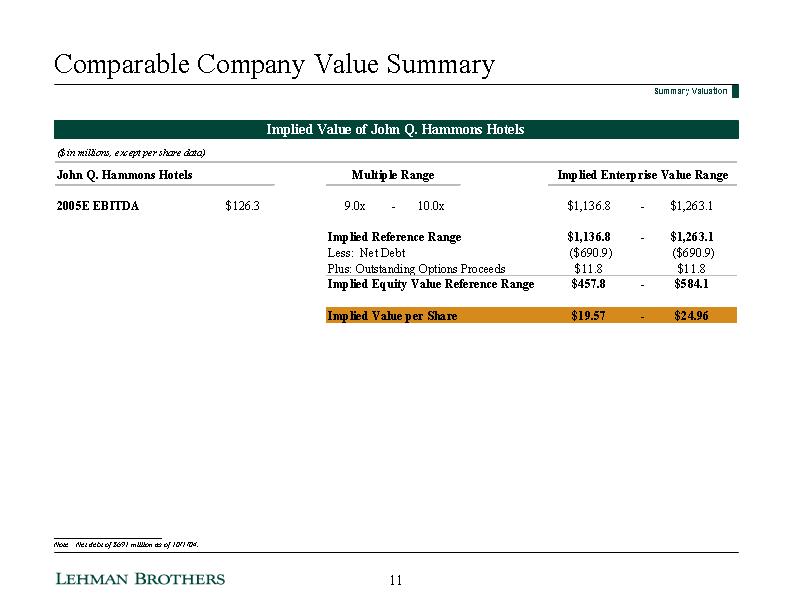

| Comparable Company Value Summary Implied Value of John Q. Hammons Hotels ___________________________ Note: Net debt of $691 million as of 10/1/04. Summary Valuation 11 |

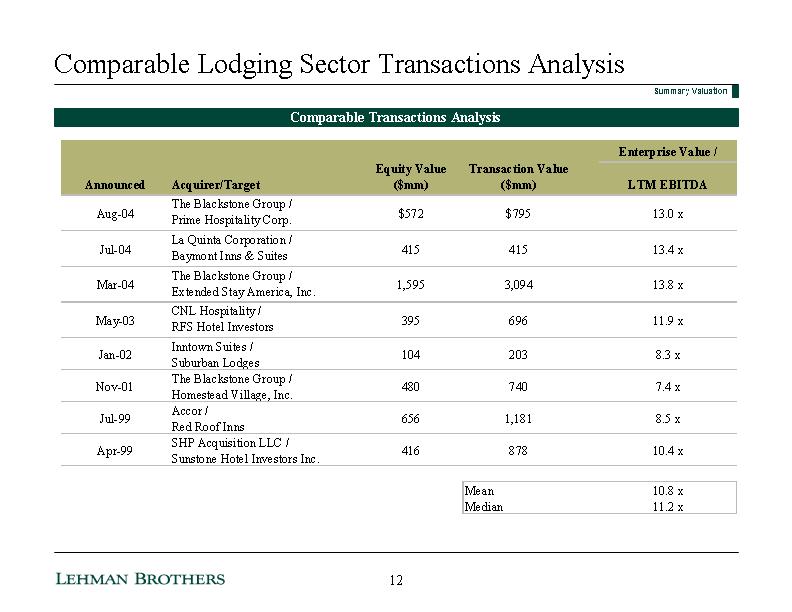

| Comparable Lodging Sector Transactions Analysis Comparable Transactions Analysis Summary Valuation 12 |

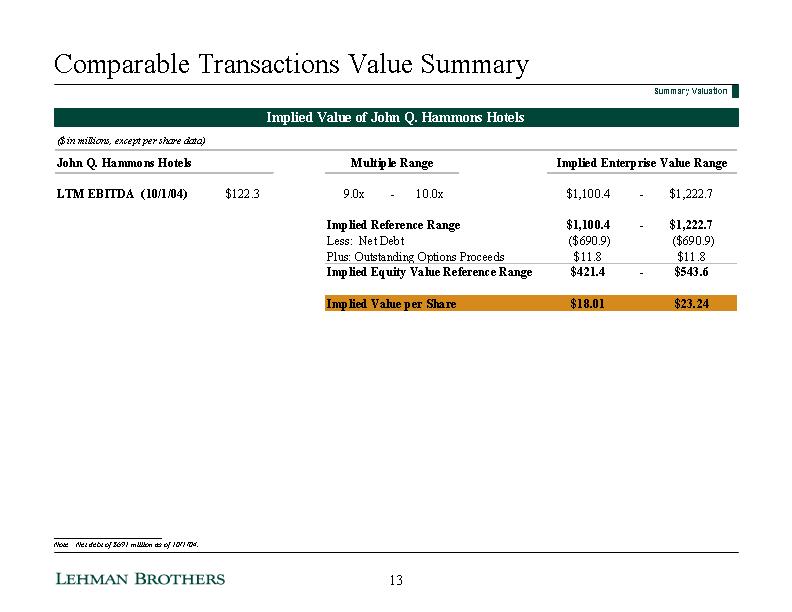

| Comparable Transactions Value Summary Implied Value of John Q. Hammons Hotels ___________________________ Note: Net debt of $691 million as of 10/1/04. Summary Valuation 13 |

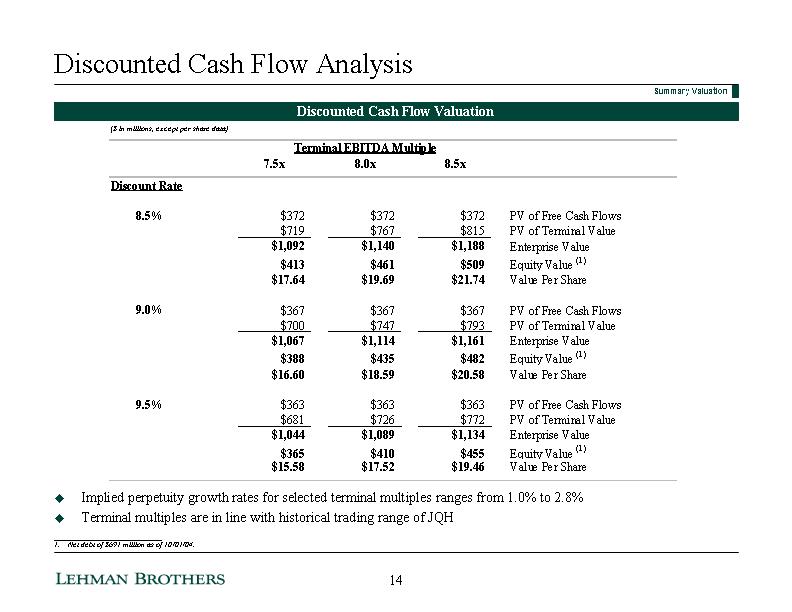

| Discounted Cash Flow Analysis Discounted Cash Flow Valuation ___________________________ 1. Net debt of $691 million as of 10/01/04. ($ in millions, except per share data) Summary Valuation Implied perpetuity growth rates for selected terminal multiples ranges from 1.0% to 2.8% Terminal multiples are in line with historical trading range of JQH 14 |

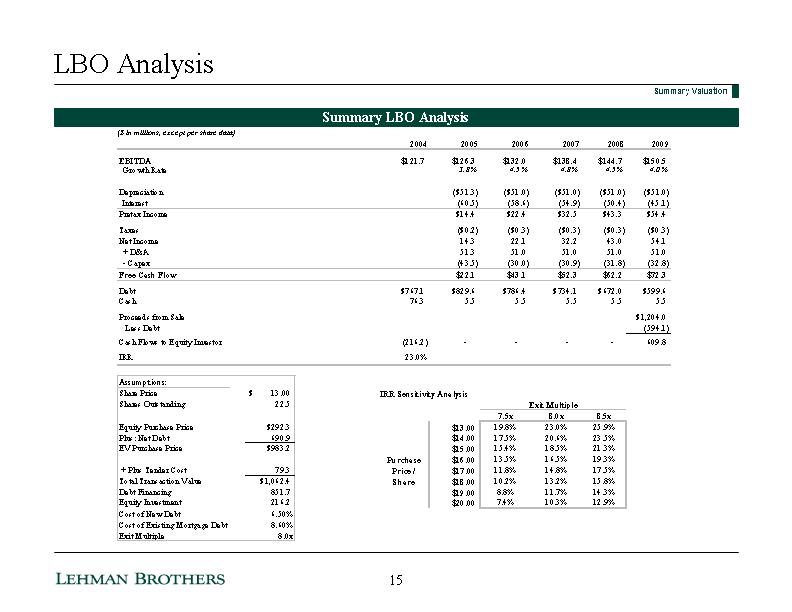

| LBO Analysis ($ in millions, except per share data) Summary LBO Analysis Summary Valuation 15 |

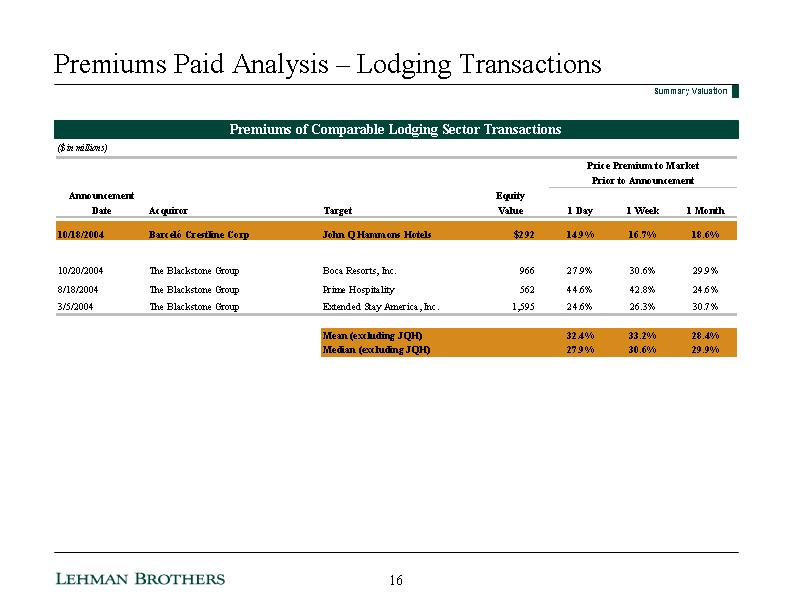

| Premiums Paid Analysis - Lodging Transactions Premiums of Comparable Lodging Sector Transactions Summary Valuation 16 |

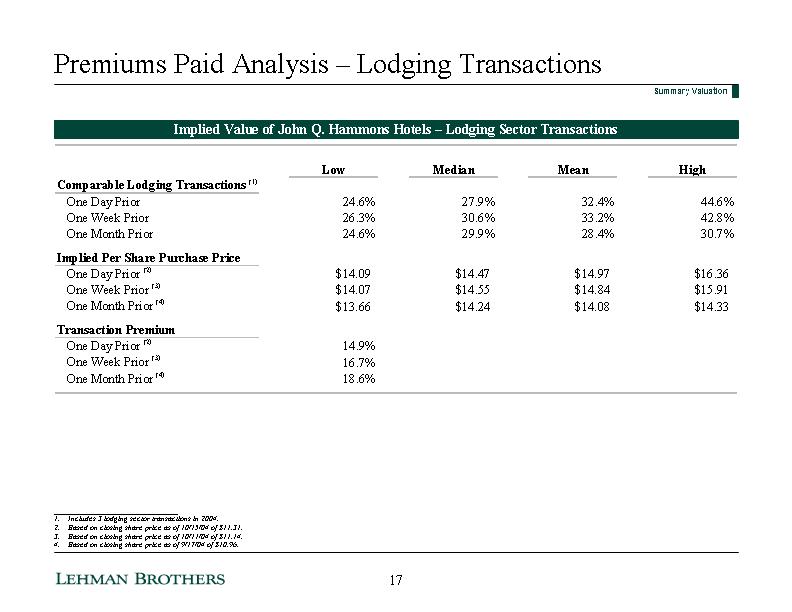

| Premiums Paid Analysis - Lodging Transactions Implied Value of John Q. Hammons Hotels - Lodging Sector Transactions _______________________________ 1. Includes 3 lodging sector transactions in 2004. 2. Based on closing share price as of 10/15/04 of $11.31. 3. Based on closing share price as of 10/11/04 of $11.14. 4. Based on closing share price as of 9/17/04 of $10.96. Summary Valuation 17 |

| Minority Squeeze-Out Premiums Paid Analysis Summary Valuation ___________________________ Includes completed or pending transactions since 1998 where acquiror owned >50% of target before transaction. Acquired equity value of >$100 million. Final premiums are based on final bid per share compared with last published closing price per share prior to the initial deal announcement. Final bump represents % increase between initial bid per share at announcement and final bid per share at closing. Cash Transactions Selected Cash Acquisitions of Minority Interests (1) 18 |

| Minority Squeeze-Out Premiums Paid Analysis Summary Valuation ___________________________ Includes completed or pending transactions since 1998 where acquiror owned >50% of target before transaction. Acquired equity value of >$100 million. Final premiums are based on final bid per share compared with last published closing price per share prior to the initial deal announcement. Final bump represents % increase between initial bid per share at announcement and final bid per share at closing. Includes transactions with stock and cash consideration (stock component representing majority of consideration). Stock Transactions Selected Stock Acquisitions of Minority Interests (1) 19 |

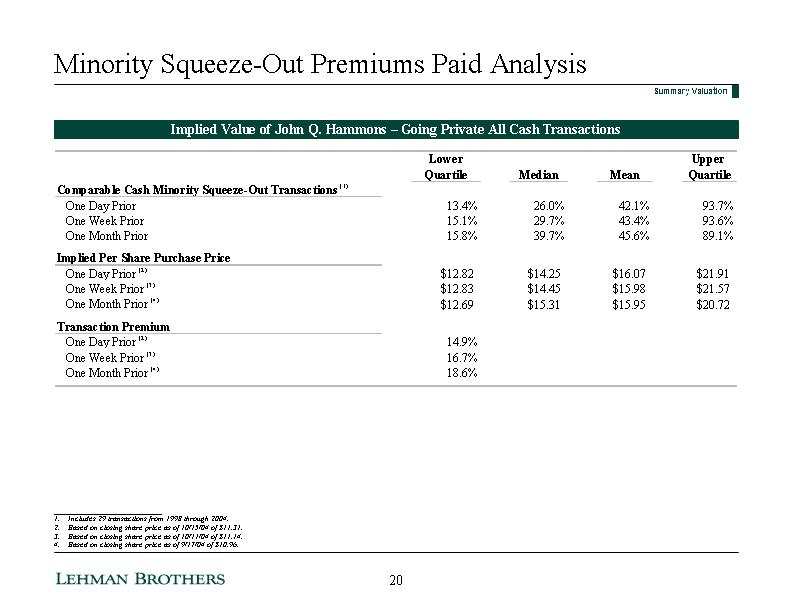

| Minority Squeeze-Out Premiums Paid Analysis Implied Value of John Q. Hammons - Going Private All Cash Transactions ___________________________ 1. Includes 29 transactions from 1998 through 2004. 2. Based on closing share price as of 10/15/04 of $11.31. 3. Based on closing share price as of 10/11/04 of $11.14. 4. Based on closing share price as of 9/17/04 of $10.96. Summary Valuation 20 |

| Analysis of Consideration to Mr. Hammons |

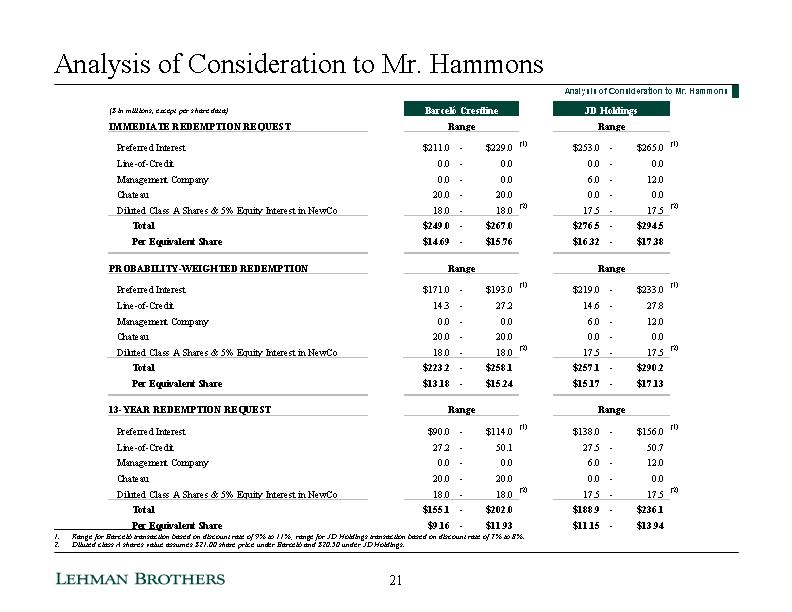

| Analysis of Consideration to Mr. Hammons Analysis of Consideration to Mr. Hammons ___________________________ Range for Barcelo transaction based on discount rate of 9% to 11%; range for JD Holdings transaction based on discount rate of 7% to 8%. Diluted class A shares value assumes $21.00 share price under Barcelo and $20.50 under JD Holdings. 21 |

| Allocation of Value Between Minority Shareholders & Mr. Hammons Analysis of Consideration to Mr. Hammons Summary of Current Economic and Voting Interest Summary of Transaction Value to Shareholders ___________________________ Includes full conversion of class A stock options into class A shares. Excludes consideration to be paid for exercise of stock options. Mr. Hammons owns 269,100 class A shares; 335,000 class A options; 294,000 class B shares; and 16,043,900 L.P. units. Mr. Hammons has voting interests in 604,100 fully converted class A shares and 294,000 class B shares (50:1 voting ratio to class A shares). 22 |