As filed with the Securities and Exchange Commission on June 3, 2016

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-08846

Tributary Funds, Inc.

Tributary Capital Management, LLC

1620 Dodge Street

Omaha, Nebraska 68197

Karen Shaw

Atlantic Fund Services, LLC

Three Canal Plaza, Suite 600

Portland, ME 04101

Registrant's telephone number, including area code: (800) 662-4203

Date of fiscal year end: March 31

Date of reporting period: April 1, 2015 – March 31, 2016

| Table of Contents | ||

Shareholder Letter | 1 | |

Management Discussion and Analysis | 3 | |

Schedules of Portfolio Investments | 15 | |

Statements of Assets and Liabilities | 36 | |

Statements of Operations | 38 | |

Statements of Changes in Net Assets | 40 | |

Financial Highlights | 42 | |

Notes to Financial Statements | 44 | |

Additional Fund Information | 53 | |

Directors and Officers | 55 | |

Investment Advisory Agreement Approval | 57 | |

Dear Shareholder:

As of March 31, 2016, our fiscal year end, Tributary Funds' net assets stood at $902 million, an increase of 12.1%, or just under $100 million year over year. This growth was achieved against a backdrop of challenging equity markets, with the bellwether benchmark S&P 500 Index up a modest 1.77% for the same period. We continued in 2015 to see a positive trend the Funds have seen over the last several years, with net inflows into the complex of over $81 million. We are pushing our distribution opportunities out on a national basis, the most recent wins with UBS and Wells Fargo, two powerful and significant national and international distribution channels. We recently were chosen by Charles Schwab to participate in their "Select List" with our Small Company Fund. This designation is the highest stamp of approval within the Schwab mutual fund system, and has been delivering steady flows to the complex over the last quarter. As of the writing of this letter, of our 5 funds ranked by Morningstar, the Small Company Fund is ranked 5 stars, out of 643 Small Blend funds. The Growth Opportunities, Income and Balanced Funds received 4 stars, out of 640 Mid-Cap Growth, 951 Intermediate-Term Bond and 856 Moderate Allocation Bond funds respectively. Our Short Intermediate Fund received a 3 star rating out of 490 Short-Term Bond funds. (Morningstar proprietary ratings reflect risk-adjusted performance through March 31, 2016.) This reflects commitment of our portfolio managers in each of these strategies to deliver strong risk adjusted returns on behalf of our valued clients. Finally, consistent with our niche oriented boutique funds distribution strategy, we added a new fund at the end of 2015, the Nebraska Tax Free Fund, whose target market will be residents of Nebraska looking for the dual benefit of income free of taxes at both the Federal and State levels.

Our Mutual Fund family began operations as the First Omaha Funds in 1992, whose sole purpose was to support the investment management function of the trust department of the First National Bank of Omaha. With the advent of stronger technology through internet based operational platforms in the mid to late 1990s, it became possible for most investment management organizations to access funds from almost any provider. First National Bank decided to embrace this industry best practice in 1999, which shifted our fund strategy away from one local source of distribution to a more nationally oriented distribution strategy by necessity. However, to compete on a national level, fund offerings needed to be strong in both performance and process. In 2001, the name of the complex was changed from First Omaha to First Focus, to allow us a brand not tied to a specific geography.

Over the ensuing nine year period, the complex battled the necessary exodus from the parent company of assets driven by this new technology driven open architecture concept. At the same time, we struggled to attract assets from the outside. At the end of 2001, the complex stood at $762 million in assets. Nine years later, at the end of 2010, the assets stood at $853 million. Although an increase of 12%, we were suffering negative inflows, simply put a lack of organic growth.

Understanding the necessity of external national distribution for the long-term viability of the complex, the Board of Director's embarked on a new and fresh four-point strategy in 2010.

| · | Rebrand the complex to reflect a brand not tied to any one particular organization |

| · | Rationalize critically each individual offering and close those without a strong value proposition |

| · | Take the best of these funds and work on a national level to secure distribution agreements |

| · | Stabilize the assets from the First National Organization through better product offerings |

I am pleased to report that we have executed on all four points of this plan. The complex was rebranded Tributary in 2010. The name was chosen in part to show recognition that we owe our very existence to our much larger parent, First National Bank. We are a "tributary" if you will of this incredible institution, whose efforts have created many other small bodies of water, or tributaries, over their 150 plus year history. And in part, the name reflects our approach to investing, letting the rough and sometimes rapidly moving rivers of the Wall Street world roar by as we stay in the much calmer and more stable tributary waters.

Secondly, we have closed three funds over the last five years. These funds value propositions were no longer embraced by the marketplace, and the decision was made to focus on the five Funds in which we had been able to demonstrate strong competency and in which we felt offered a strong value proposition for our clients.

As to point three of the plan, we've signed over 50 selling agreements with fund distributors around the country, including industry power houses Wells Fargo, Charles Schwab, Fidelity, Merrill Lynch, UBS and JP Morgan.

And finally, with this more narrowly focused boutique styled approach, we've been able to stabilize and grow the remaining funds within the distribution channel of our parent company, First National Bank.

As we approach the magical $1 billion dollar mark, I look fondly back upon these challenges, as they have made our complex and distribution strategies much more competitive and durable over the long haul. We are currently working on a new strategy, focused on

1 |

maximizing the opportunities that we have with the 50+ selling agreements we have in place, as well as building the Tributary Brand in the market place. More to come.

Recent market performance has been much less exciting than the growth momentum we have seen at Tributary. Expectations around returns for both equities and bonds going forward seem to be stuck somewhere in the low to mid-single digits. The U.S. economic growth picture, although very anemic at 2% - 2.5%, still seems to be the bright spot of the developed world. Financial assets in the U.S. have been reflecting this scenario for some time now, and seems to offer limited upside without a boost to economic output, or put another way, we need to get our economy growing at a 3.5% - 5% rate to really get investors back off the sidelines and excited about owning stocks again. There does appear to be a movement back towards investing in international markets, both developed and emerging, not necessarily based on economic strength in these countries, but rather valuation levels that look attractive vs. the U.S.

The general mood of the investing class seems to be resigned to low returns for an extended period of time. But as we all know, it is more often than not prudent to take a contrarian position to conventional wisdom to make money over time. There are record low interest rates and commodity prices throughout the world. There also is an unprecedented and available level of cash sitting on corporate balance sheets waiting to be deployed. I would like to make the case that if our policy makers could craft a tax policy more conducive to capital investment and loosen the punitive mindset of regulators around business in general, that the ingredients exist for our economy to grow at a much higher level, creating many new jobs and revenue for our government to be able to distribute to help those that truly are in need of help in our country.

Thank you for your continued support of the Tributary Family of Funds.

Best regards,

Stephen R. Frantz

President

sfrantz@tributarycapital.com

© 2016 Morningstar, Inc. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the confidential and proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analysis or opinions or their use.

For each fund with at least a three-year history, Morningstar calculates a Morningstar Rating™ based on a Morningstar Risk- Adjusted Return measure that accounts for variation in a fund's monthly performance (including the effects of sales charges, loads, and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. For the period ended March 31, 2016, the Tributary Balanced Fund received 4, 4 and 4 stars out of 854, 744 and 504 Moderate Allocation funds for the three-, five- and ten-year periods, respectively; The Tributary Small Company Fund received 5, 4 and 5 stars out of 643, 562 and 370 Small Blend funds, respectively; The Tributary Growth Opportunities Fund received 3, 3 and 4 stars out of 640, 574 and 428 Mid-Cap Growth funds, respectively. The Short-Intermediate Bond Fund received 3, 4 and 3 stars out of 490, 404 and 280 Short-Term Bond funds, respectively. The Income Fund received 4, 4 and 3 stars out of 951, 827 and 602 Intermediate-Term Bond funds, respectively.

Morningstar proprietary ratings reflect one-year risk-adjusted performance through 03/31/2016. The ratings are subject to change every month. Morningstar ratings are calculated from the funds' 3, 5 and 10-year returns (as applicable), with fee adjustments in excess of 90-day Treasury bill returns, and a risk factor that reflects fund performance below 90-day T-Bill returns. The top 10% of the funds in a rating universe receive 5-stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars and the bottom 10% receive 1 star.

For performance to the most recent month end, please visit www.tributaryfunds.com or call (800) 662-4203.

Comments are provided as a general market overview and should not be considered investment advice or predictive of any future market performance.

2 |

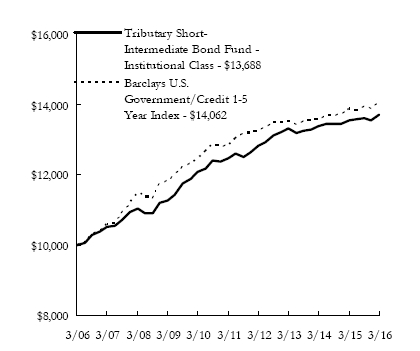

SHORT-INTERMEDIATE BOND FUND (Unaudited)

SHORT-INTERMEDIATE BOND FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2016

| Portfolio Composition as of March 31, 2016 | ||

| Percentage Based on Total Value of Investments | ||

| (Portfolio composition is subject to change) | ||

| Corporate Bonds | 27.8 | % |

| U.S. Treasury Securities | 22.4 | % |

| Non-Agency Residential Mortgage Backed Securities | 15.3 | % |

| Asset Backed Securities | 13.3 | % |

| Non-Agency Commercial Mortgage Backed Securities | 11.7 | % |

| Short-Term Investments | 4.1 | % |

| U.S. Government Mortage Backed Securities | 3.5 | % |

| Municipals | 1.5 | % |

| Preferred Stocks | 0.4 | % |

| 100.0 | % | |

| Portfolio Analysis as of March 31, 2016 | ||||

| (Portfolio composition is subject to change) | ||||

| Weighted Average to Maturity: | 4.9 | years | ||

| Average Annual Total Returns for the Year Ended March 31, 2016* | |||||

| 1 Year | 5 Year | 10 Year | |||

| Tributary Short-Intermediate Bond Fund — Institutional Class | 1.11 | % | 1.89 | % | 3.19 | % | ||

| Barclays U.S. Government/Credit 1-5 Year Index | 1.62 | % | 1.88 | % | 3.47 | % |

Prospectus Expense Ratio (Gross/Net)† | 1.04 | % | 0.78 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 1.11 | % | 0.76 | % |

| 1 Year | Since Inception†† |

| Tributary Short-Intermediate Bond Fund — Institutional Plus Class | 1.32 | % | 2.32 | % |

Prospectus Expense Ratio (Gross/Net)† | 0.80 | % | 0.54 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 0.77 | % | 0.54 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower to higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†) The expense ratios are from the Fund's prospectus dated August 1, 2015. Net expense ratios are net of contractual waivers which are in effect from August 1, 2015 through July 31, 2016.

(††) Commencement date for the Institutional Plus Class was October 14, 2011.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2006. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by each class.

Barclays U.S. Government/Credit 1-5 Year Index is an unmanaged index which measures the performance of U.S. Treasury and agency securities, and corporate bonds with 1-5 year maturities. The index is unmanaged and does not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot directly invest in the index.

4 |

INCOME FUND (Unaudited)

Investment Objective

The Tributary Income Fund seeks the generation of current income in a manner consistent with preserving capital and maximizing total return.

Manager Commentary

The Tributary Income Fund returned 1.81% (net, Institutional Plus) for the year ended March 31, 2016 compared to a 1.96% return for the Barclay's U.S. Aggregate Bond Index. The U.S. Treasury yield curve shifted somewhat oddly over the trailing 12 months, as the U.S. Federal Reserve ("Fed") finally raised its target for the overnight funds rate. Short-term yields were higher as expected, while intermediate term yields fell 15-20 basis points (bps) and the 30-year yield actually rose slightly. The steepening in the yield curve from the 5-30 year segment was the primary driver of the Fund's underperformance for the trailing 12-month period, as our lower duration exposure in the belly of the curve hurt relative performance. The Fund's underweight in government sectors versus the benchmark also hindered performance as credit spreads on non-government securities widened significantly over the year. Lower-quality corporate bonds were the worst performing asset class in fixed income (the Barclays High Yield index posted a -3.69% return), driven by the precipitous decline in crude oil and other commodities which severely pressured the credit profiles of many issuers. Investment grade corporates fared better, but still underperformed with a -1.77% excess return vs. similar maturity Treasuries. Commercial mortgage backed securities ("MBS") and asset backed securities ("ABS") performed in-line with Treasuries, while agency MBS slightly outperformed given their carry and liquidity advantages.

Not unlike prior years, global concerns and Federal Reserve policy dictated the performance of the bond market over the past year. The weakening Chinese economy and volatile behavior from the government with respect to currency policy drove investors away from emerging markets and intensified the decline in commodity prices for much of the year. Domestically, the market was focused intently on the Federal Reserve's approach to policy normalization. After hinting in the early summer that policy change was coming, the Fed reversed course in the fall due to the global uncertainty emanating from China. From a fundamental standpoint the Fed had evidence to remove accommodation, as economic reports from the labor and consumer markets were mostly positive and core inflation appeared to be moving higher, but "international developments" ruled the day. The Fed eventually did raise its overnight target Fed Funds rate by 0.25% in December after seven years at the zero-lower bound, presumably due to the improved outlook and stability in Chinese and emerging economy financial markets. The final few months of the fiscal year were just as choppy, as the New Year began with Chinese equity markets once again in a tailspin and crude oil plummeting to new lows, which caused a sharp risk-off trade in credit markets. Global monetary authorities reacted swiftly and strongly to prop up the markets and counter the tightening financial conditions, as the PBOC, BoJ and ECB enacted new stimulus programs and the Fed took a decidedly dovish stance in its communications. The bond market ended the period with an upbeat tone, with credit spreads tighter and absolute yields still low.

During the year the Fund's overall sector allocation shifted slightly toward government securities and away from the non-agency structured product space. Specifically, we increased exposure mostly to U.S. Treasuries but also to industrial corporate bonds as spreads widened during the year. We also performed bond swaps by extending maturities in a few names to capture value in what we found to be a steep credit curve. Our agency MBS allocation was essentially unchanged during the year, while our exposure to non-agency product declined due to legacy paydowns and continued lack of new-issue supply. In terms of credit quality there was no significant change during the year, as the Fund maintained a AA- weighted average credit rating.

At the risk of sounding stale, we remain agnostic on the direction of interest rates. While the Fed has officially embarked on a tightening cycle, they have recently acknowledged that global headwinds are a great concern, and as a result, any further rate hikes will be (more) moderate and (more) gradual. We would agree that the global economy is a restraining factor for domestic growth and inflation, and will thus act as a governor on rising interest rates. Nonetheless, as we look at the extremely dovish expectations currently priced into the market, we view the downside risks of higher rates as being greater than the potential upside rewards of further declines in U.S. interest rates. We are therefore maintaining a slightly short duration position relative to our benchmark. As for the Fund's sector allocation, we remain underweight the traditional U.S. government sectors, in addition to an underweight in the agency MBS market given our opinion that the margin of safety in the asset class is low relative to other sectors in the structured securities space. We therefore remain overweight in the non-agency residential mortgage backed securities ("RMBS") and commercial mortgage backed securities ("CMBS") sectors, as well as the traditional ABS space. In the corporate market, spreads have tightened in such swift fashion that we strongly believe individual security selection will be the primary driver of future performance, leading us to a roughly neutral position versus our benchmark.

As always, we remain committed to seeking prudent, value-enhancing investment opportunities consistent with our disciplined approach of managing for the long-term.

INCOME FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2016

NEBRASKA TAX-FREE FUND (Unaudited)

Investment Objective

The Tributary Nebraska Tax-Free Fund seeks as high a level of current income exempt from both federal and Nebraska income tax as is consistent with the preservation of capital.

Manager Commentary

The Fund returned 1.35% (net, Institutional Plus) for the quarter compared to a gross return of 1.46% for the Barclay's 1-15 Year Municipal Blend Index and 1.67% for the Barclay's Municipal Index.

The first quarter of 2016 was a tale of two halves, as the New Year began with volatility and a large downdraft in asset prices, but closed at levels that were essentially unchanged from year-end. Investors initially focused on global concerns, primarily the Chinese equity market's dramatic freefall which caused a halt in trading on two separate occasions within the first week of the year. At the same time, Europe remained mired in a low-growth, low-inflation environment and emerging markets struggled as the dollar remained strong. A negative feedback loop developed, as dollar strength contributed to further declines in the commodities complex, and the U.S. equity market, reacting to weaker energy prices and softer domestic economic data, sold off as well. The risk-off sentiment was broad based among asset classes, with fixed income yield spreads widening in unison with falling equities. Global monetary authorities reacted strongly to prop up the markets and counter tightening financial conditions. The People's Bank of China, the Bank of Japan, and the European Central Bank all took various steps to ease lending conditions and/or increase asset purchases. For its part, the Federal Reserve moderated its somewhat hawkish tone, indicating that due to global developments, it would likely raise the fed funds rate at an even slower pace than it had previously indicated. This global monetary response, combined with stronger domestic employment and economic data in the final weeks of the quarter, led to a swift reemergence of the risk-on trade. During the last half of the quarter, the U.S. equity market largely recovered its earlier losses, while the fixed income market similarly recouped any lost performance. Given the positive impact of central bank policies, U.S Treasuries posted strong returns during the quarter (+3.2%) as yields fell roughly 40-50 basis points across the curve. Municipal bond yields largely followed suit, leading to positive returns in the tax-exempt market as well.

The Nebraska economy continued to perform well for the 12-months ended March 31, 2016. Unemployment rates remain well below the national average (2.9% vs. 5%, respectively), even as state GDP grew modestly less than the national figures (1.1% vs. 2.1%, respectively) for the most updated 4-quarter period ended in September 2015. The state continues to receive solid credit ratings and has largely avoided the pension and post-retirement obligation problems of many peer states and municipalities. One potential area of concern is the impact from the weakening ag sector, given the sharp decline in commodity prices over the past few years and the subsequent drop in land values. Nonetheless, debt levels for most municipalities are very manageable which has provided a cushion against valuation pressures.

On a net basis the Fund underperformed its benchmark for the quarter. The primary detractor from relative performance this quarter was our lower duration exposure versus the benchmark, which led to less price appreciation as interest rates fell.

As indicated in prior communications, we are currently agnostic on the direction of interest rates. While the Fed has officially embarked on a tightening cycle, they have recently acknowledged that global headwinds are a great concern, and as a result, any further rate hikes will be (more) moderate and (more) gradual. We would agree that the global economy is a restraining factor for domestic growth and inflation, and will thus act as a governor on rising interest rates. Nonetheless, as we look at the extremely dovish expectations currently priced into the market, we view the downside risks of higher rates as being greater than the potential upside rewards of further declines in U.S. interest rates. We are therefore maintaining a slightly short duration position relative to our benchmark.

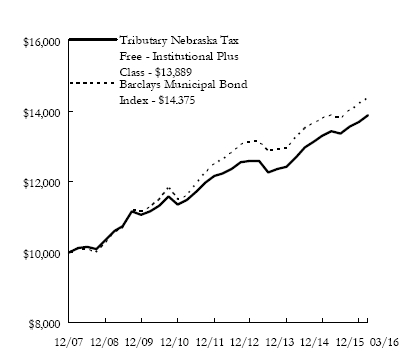

NEBRASKA TAX-FREE FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2016

| Portfolio Composition as of March 31, 2016 | ||

| Percentage Based on Total Value of Investments | ||

| (Portfolio composition is subject to change) | ||

| Municipals | 96.1 | % |

| Short-Term Investments | 3.9 | % |

| 100.0 | % | |

| Average Annual Total Returns for the Year Ended March 31, 2016* | |||||

| 1 Year | 5 Year | Since Inception | |||

Tributary Nebraska Tax-Free Fund — Institutional Plus Class † | 3.39 | % | 3.86 | % | 4.06 | % | ||

| Barclays Municipal Bond Index | 3.98 | % | 5.59 | % | 4.93 | % |

Prospectus Expense Ratio (Gross/Net)†† | 0.78 | % | 0.45 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 0.85 | % | 0.45 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower to higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†) The Fund's Institutional Plus Class performance for periods prior to the commencement of operations (1/1/16) is that of a common trust fund managed by First National Bank of Omaha. The common trust fund commenced operations on December 31, 2007.

(††) The expense ratios are from the Fund's prospectus dated December 31, 2015. Net expense ratios are net of contractual waivers which are in effect from January 1, 2016 through December 31, 2016.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on December 31, 2007. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The Barclays Municipal Bond Index is a broad-based benchmark that measures the investment grade, US dollar-denominated, fixed tax exempt bond market. The index includes state and local general obligation, revenue, insured, and pre-refunded bonds. The Barclays Municipal Index was incepted in January 1980. The index does not reflect the fees and expenses associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot invest directly in the index.

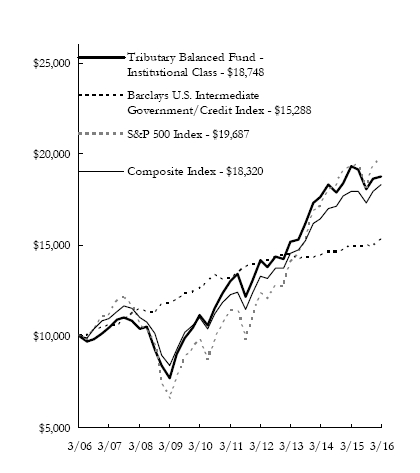

BALANCED FUND (Unaudited)

BALANCED FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2016

| Portfolio Composition as of March 31, 2016 | ||

| Percentage Based on Total Value of Investments | ||

| (Portfolio composition is subject to change) | ||

| Government Securities | 18.5 | % |

| Information Technology | 16.3 | % |

| Financials | 12.3 | % |

| Consumer Discretionary | 10.7 | % |

| Industrials | 8.6 | % |

| Health Care | 8.5 | % |

| Consumer Staples | 6.9 | % |

| Energy | 4.1 | % |

| Short-Term Investments | 2.7 | % |

| Non-Agency Commercial Mortgage Backed Securities | 2.6 | % |

| Asset Backed Securities | 1.9 | % |

| Telecommunication Services | 1.8 | % |

| Non-Agency Residential Mortgage Backed Securities | 1.7 | % |

| Utilities | 1.6 | % |

| Materials | 1.2 | % |

| U.S. Government Mortage Backed Securities | 0.6 | % |

| 100.0 | % | |

| Average Annual Total Returns for the Year Ended March 31, 2016* | |||||

| 1 Year | 5 Year | 10 Year | |||

| Tributary Balanced Fund — Institutional Class | -2.93 | % | 7.54 | % | 6.49 | % | ||

| Barclays U.S. Intermediate Government/Credit Index | 2.06 | % | 3.01 | % | 4.34 | % | ||

| S&P 500 Index | 1.78 | % | 11.58 | % | 7.01 | % | ||

| Composite Index | 2.14 | % | 8.27 | % | 6.24 | % |

Prospectus Expense Ratio (Gross/Net)† | 1.28 | % | 1.21 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 1.26 | % | 1.19 | % |

| 1 Year | Since Inception†† |

| Tributary Balanced Fund — Institutional Plus Class | -2.78 | % | 9.20 | % |

Prospectus Expense Ratio (Gross/Net)† | 1.08 | % | 1.01 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 1.01 | % | 0.99 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower to higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†) The expense ratios are from the Fund's prospectus dated August 1, 2015. Net expense ratios are net of contractual waivers which are in effect from August 1, 2015 through July 31, 2016.

(††) Commencement date for the Institutional Plus Class was October 14, 2011.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2006. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by each class.

The S&P 500 Index is a broad based index of 500 selected common stocks, most of which are listed on the New York Stock Exchange, that measures the U.S. stock market as a whole. The index is heavily weighted towards stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks. The Barclays U.S. Intermediate Government/Credit Index is a market value weighted performance benchmark for government and corporate fixed-rate debt issues (rated Baa/BBB or higher) with maturities between one and ten years. The Composite Index is intended to provide a single benchmark that more accurately reflects the composition of securities held by the Tributary Balanced Fund. Sixty percent of the Composite Index is comprised of the S&P 500 Index and forty percent of the Composite Index is comprised of the Barclays U.S. Intermediate Government/Credit Index. The indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot directly invest in the indices.

GROWTH OPPORTUNITIES FUND (Unaudited)

GROWTH OPPORTUNITIES FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2016

| Portfolio Composition as of March 31, 2016 | ||

| Percentage Based on Total Value of Investments | ||

| (Portfolio composition is subject to change) | ||

| Consumer Discretionary | 23.2 | % |

| Information Technology | 18.9 | % |

| Health Care | 17.3 | % |

| Financials | 12.2 | % |

| Industrials | 11.9 | % |

| Consumer Staples | 11.1 | % |

| Materials | 1.6 | % |

| Utilities | 1.2 | % |

| Energy | 0.4 | % |

| Short-Term Investments | 2.2 | % |

| 100.0 | % | |

| Average Annual Total Returns for the Year Ended March 31, 2016* | |||||

| 1 Year | 5 Year | 10 Year | |||

Tributary Growth Opportunities Fund — Institutional Class | -9.78 | % | 7.29 | % | 6.83 | % | ||

| Russell Midcap Growth Index | -4.74 | % | 9.99 | % | 7.43 | % | ||

| S&P 500 Index | 1.78 | % | 11.58 | % | 7.01 | % |

Prospectus Expense Ratio (Gross/Net)† | 1.23 | % | 1.16 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 1.27 | % | 1.16 | % |

| 1 Year | Since Inception†† |

| Tributary Growth Opportunities Fund — Institutional Plus Class | -9.63 | % | 11.68 | % |

Prospectus Expense Ratio (Gross/Net)† | 1.01 | % | 0.94 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 0.99 | % | 0.94 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower to higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†) The expense ratios are from the Fund's prospectus dated August 1, 2015. Net expense ratios are net of contractual waivers which are in effect from August 1, 2015 through July 31, 2016.

(††) Commencement date for the Institutional Plus Class was October 14, 2011.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2006. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by each class.

The Russell Midcap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values. The Fund's primary index is the Russell Midcap Growth Index, however to provide a broader market comparative, the S&P 500 Index is a secondary benchmark. The S&P 500 Index is a broad based index of 500 selected common stocks, most of which are listed on the New York Stock Exchange, that measures the U.S. stock market as a whole. The index is heavily weighted towards stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks. The indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot directly invest in the indices.

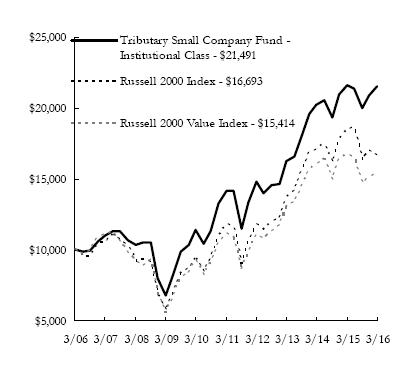

SMALL COMPANY FUND (Unaudited)

The best performing sectors in the small cap market over the last 12 months were Utilities (+9%), Telecommunications Services (+6%) and Consumer Staples (0%). The relative safety of the Utilities sector in a down market, combined with investors' appetite for higher yielding securities, helped propel this sector to a nice positive return over the last 12 months. The Telecommunications Services sector represents less than 1% of the Russell 2000 Index and therefore does not typically have a significant impact on overall Russell 2000 Index performance. However, several stocks posted very good returns, which drove overall sector performance in the last 12 months. Consumer Staples stocks managed a flat return in the past year as that sector tends to hold up well in less robust macroeconomic environments. The weakest performing sectors in the small cap market over the last 12 months were Energy (-44%), Healthcare (-20%) and Materials (-19%). For the second consecutive year, the Energy sector lost more than 40% over the trailing 12 months due to lower oil prices. WTI Crude began the year at just under $48/barrel, moved up to just over $61/barrel in mid-June 2015 before falling to just over $26/barrel in February 2016. Prices did manage to rally back near $37/barrel by March, 31, 2016. In a significant reversal from last year's report ending in March of 2015, the Healthcare sector was negatively impacted by biotech and pharmaceutical stocks that were down nearly 34% and 29% respectively over the last year. In the Materials sector, concerns regarding slow global economic growth helped to push stocks lower.

The Tributary Small Company Fund's strongest relative performance came from the Healthcare and Energy economic sectors. In the Healthcare sector, the Fund's one year return was approximately +3% over the last year compared to a return for the Russell 2000 Healthcare sector of approximately -20%. As mentioned previously, stocks within the biotech and pharmaceutical industries were significant underperformers. The Fund's underweight position in those two industries within Healthcare was a large part of the success we had in that sector over the past year. Additionally, several of our Healthcare holdings generated strong returns due to company specific results. For example, AMN Healthcare Services returned nearly +46% in the last year as the company experienced robust demand for their nursing and physician staffing services and their expectations were for orders to continue to strengthen. In the Energy sector, the Fund managed to generate a small, positive return of just under +1% in the prior 12 months versus a return for energy stocks within the Russell 2000 of nearly -44%. Weak and volatile energy prices were wreaking havoc on earnings, cash flows and balance sheets for companies in the Energy industry. Changes made to the Fund's holdings within this sector dating back to December 2013 proved beneficial as we emphasized owning companies that were well positioned strategically and financially to weather the volatility in energy prices.

The Tributary Small Company Fund's weakest relative performance came from the Telecommunications Services and Financials economic sectors. Relatively speaking, the underperformance in these two sectors was very small. The Fund does not hold any companies within the Telecommunications Services sector which was up 6% in the Russell 2000 in the last 12 months, resulting in the relative underperformance. In the Financial sector, the Fund's trailing 12-month return of approximately -1.7% was just slightly behind the Russell 2000 Financial sector return of -1.6%.

The Fund's average cash position of approximately 3.9% over the last 12 months had a small, positive impact on performance. In a year when the market return was down nearly 10%, any level of cash will be additive.

It is likely that equity market returns will continue to be influenced by interest rate policymakers from around the globe. The increase in interest rates by the U.S. Federal Reserve ("Fed") back in December of 2015 was thought to be the first of several increases to come as the economy strengthens. However, recent comments out of the Fed appear to remain cautious about the improvement in economic activity. Estimates for real gross domestic product ("GDP") growth are being ratcheted back. In 2016, the U.S. economy is expected to grow 2.1% according to economists surveyed by Bloomberg as of April 4, 2016. This is down from the 2.5% estimate from just three months ago. Declines in GDP growth expectations are being seen in other parts of the world as well. China, in particular, has been a focus for investors. Small cap, U.S.-based companies should be more insulated from some of the macroeconomic pressures. However, they are not immune. Supply and demand fundamentals, as well as political posturing by energy producing nations, will likely result in volatile energy markets. Even with having less foreign revenue exposure than larger companies, small caps can still feel the negative impact that a strong U.S. Dollar can have on their ability to compete on the world stage and on translating overseas revenues back to the United States. While small cap valuations are above longer-term averages, they are not at extreme levels. In addition, small cap valuations continue to look more attractive than large cap valuation. Over the last year, the valuation gap between small cap and large cap stocks has actually widened a bit, resulting in a potentially more favorable outlook for stronger relative performance in smaller companies over the next year.

SMALL COMPANY FUND (Unaudited)

| Portfolio Composition as of March 31, 2016 | ||

| Percentage Based on Total Value of Investments | ||

| (Portfolio composition is subject to change) | ||

| Information Technology | 19.6 | % |

| Financials | 19.5 | % |

| Health Care | 14.8 | % |

| Industrials | 13.9 | % |

| Consumer Discretionary | 12.1 | % |

| Materials | 5.7 | % |

| Energy | 4.2 | % |

| Consumer Staples | 3.7 | % |

| Utilities | 3.4 | % |

| Short-Term Investments | 3.1 | % |

| 100.0 | % | |

| Average Annual Total Returns for the Year Ended March 31, 2016* | ||||||

| 1 Year | 5 Year | 10 Year | ||||

| Tributary Small Company Fund — Institutional Class | -0.65 | % | 8.68 | % | 7.95 | % | ||

| Russell 2000 Index | -9.76 | % | 7.20 | % | 5.26 | % | ||

| Russell 2000 Value Index | -7.72 | % | 6.67 | % | 4.42 | % |

Prospectus Expense Ratio (Gross/Net)† | 1.32 | % | 1.22 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 1.34 | % | 1.18 | % |

| 1 Year | Since Inception†† |

| Tributary Small Company Fund — Institutional Plus Class | -0.48 | % | 9.84 | % |

Prospectus Expense Ratio (Gross/Net)† | 1.10 | % | 1.00 | % | ||

Expense Ratio for the Year Ended March 31, 2016 (Gross/Net) | 1.07 | % | 0.99 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower to higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†) The expense ratios are from the Fund's prospectus dated August 1, 2015. Net expense ratios are net of contractual waivers which are in effect from August 1, 2015 through July 31, 2016.

(††) Commencement date for the Institutional Plus Class was December 17, 2010.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2006. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by each class.

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000®Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 Value Index measures the performance of small-cap value segment of the U.S. equities universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot directly invest in the indices.

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2016

SHORT-INTERMEDIATE BOND FUND

| Principal Amount | Security Description | Value |

| Non-U.S. Government Agency Asset-Backed Securities - 40.0% | ||||||

| Asset Backed Securities - 13.2% | ||||||

| $ | 725,000 | Ally Auto Receivables Trust, 1.53%, 04/15/19 | $ | 727,108 | ||

| 865,000 | American Express Credit Account Master Trust, 0.81%, 12/15/21 (a) | 863,379 | ||||

| 1,035,000 | Ascentium Equipment Receivables, LLC, 1.61%, 10/13/20 (b) | 1,031,916 | ||||

| 1,185,000 | BA Credit Card Trust, 1.36%, 09/15/20 | 1,189,029 | ||||

| 720,000 | Cabela's Credit Card Master Note Trust, 1.45%, 06/15/20 (b) | 721,060 | ||||

| 975,000 | Cabela's Credit Card Master Note Trust, 2.17%, 08/16/21 (b) | 991,938 | ||||

| 510,000 | Capital One Multi-Asset Execution Trust, 1.48%, 07/15/20 | 512,734 | ||||

| 580,000 | Capital One Multi-Asset Execution Trust, 1.60%, 05/17/21 | 584,088 | ||||

| 965,000 | Chase Issuance Trust, 1.15%, 01/15/19 | 966,653 | ||||

| 1,124,000 | Citibank Credit Card Issuance Trust, 5.65%, 09/20/19 | 1,195,730 | ||||

| 168,045 | CNL Commercial Mortgage Loan Trust REMIC, 0.87%, 10/25/30 (a)(b) | 145,685 | ||||

| 1,105,000 | Crown Castle Towers, LLC, 4.17%, 08/15/17 (b) | 1,133,837 | ||||

| 585,000 | Eaton Vance CLO, Ltd., 2.07%, 07/15/26 (a)(b) | 578,419 | ||||

| 1,165,000 | Ford Credit Auto Owner Trust, 1.27%, 12/15/17 | 1,164,751 | ||||

| 1,095,000 | Ford Credit Floorplan Master Owner Trust, 3.50%, 01/15/19 | 1,109,181 | ||||

| 700,000 | Honda Auto Receivables Owner Trust, 1.18%, 05/18/20 | 700,198 | ||||

| 600,000 | Magnetite IX CLO, Ltd., 2.04%, 07/25/26 (a)(b) | 595,525 | ||||

| 190,000 | OneMain Financial Issuance Trust, 2.43%, 06/18/24 (b) | 189,523 | ||||

| 686,629 | Preferred Term Securities XII, Ltd./Preferred Term Securities XII, Inc., 1.34%, 12/24/33 (a)(b) | 563,035 | ||||

| 657,564 | Preferred Term Securities XIV, Ltd. / Preferred Term Securities XIV, Inc., 1.12%, 06/24/34 (a)(b) | 496,461 | ||||

| 658,051 | Preferred Term Securities XXIV, Ltd./Preferred Term Securities XXIV, Inc., 0.93%, 03/22/37 (a)(b) | 445,830 | ||||

| 585,000 | Voya CLO, Ltd., 2.07%, 01/18/26 (a)(b) | 579,273 | ||||

| 16,485,353 | ||||||

| Principal Amount | Security Description | Value | |||

| Non-Agency Commercial Mortgage Backed Securities - 11.6% | ||||||

| $ | 286,069 | 7 WTC Depositor LLC Trust REMIC, 4.08%, 03/13/31 (b) | $ | 289,479 | ||

| 335,000 | Banc of America Large Loan Trust REMIC, 8.70%, 01/25/42 (a)(b) | 343,673 | ||||

| 789,412 | Bayview Commercial Asset Trust REMIC, 1.30%, 12/25/33 (a)(b) | 757,183 | ||||

| 1,152,198 | Bear Stearns Commercial Mortgage Securities Trust, 5.69%, 06/11/50 (a) | 1,195,918 | ||||

| 2,634,350 | Citigroup Commercial Mortgage Trust REMIC, 2.16%, 09/10/45 (a)(b) | 201,511 | ||||

| 1,122,046 | Citigroup Commercial Mortgage Trust REMIC, 5.74%, 06/14/50 (a)(b) | 1,136,519 | ||||

| 1,836,924 | COMM Mortgage Trust Interest Only REMIC, 1.49%, 03/10/46 (a) | 88,164 | ||||

| 148,251 | DBUBS Mortgage Trust Interest Only REMIC, 1.30%, 08/10/44 (a)(b) | 968 | ||||

| 540,000 | FREMF Mortgage Trust REMIC, 4.16%, 09/25/44 (a)(b) | 555,664 | ||||

| 735,000 | FREMF Mortgage Trust REMIC, 2.64%, 03/25/45 (a)(b) | 736,278 | ||||

| 6,713,237 | GS Mortgage Securities Trust REMIC, 1.62%, 08/10/44 (a)(b) | 269,069 | ||||

| 1,135,000 | JP Morgan Chase Commercial Mortgage Securities Trust REMIC, 1.69%, 01/15/32 (a)(b) | 1,117,899 | ||||

| 980,000 | JP Morgan Chase Commercial Mortgage Securities Trust REMIC, 2.67%, 01/15/46 | 1,001,295 | ||||

| 560,000 | JP Morgan Chase Commercial Mortgage Securities Trust REMIC, 4.11%, 07/15/46 (b) | 584,701 | ||||

| 1,060,000 | JPMBB Commercial Mortgage Securities Trust REMIC, 2.42%, 07/15/45 | 1,076,193 | ||||

| 471,723 | JPMBB Commercial Mortgage Securities Trust REMIC, 1.25%, 02/15/47 | 469,077 | ||||

| 1,415,536 | Morgan Stanley Bank of America Merrill Lynch Trust Interest Only REMIC, 1.27%, 12/15/48 (a) | 77,108 | ||||

| 659,095 | Morgan Stanley Capital I Trust REMIC, 3.22%, 07/15/49 | 660,812 | ||||

| 467,000 | Wells Fargo Commercial Mortgage Trust REMIC, 2.53%, 10/15/45 | 477,147 | ||||

| 1,010,000 | Wells Fargo Commercial Mortgage Trust REMIC, 2.97%, 12/15/47 | 1,049,239 | ||||

| 162,579 | Wells Fargo-RBS Commercial Mortgage Trust Interest Only REMIC, 0.81%, 02/15/44 (a)(b) | 5,188 | ||||

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2016

SHORT-INTERMEDIATE BOND FUND

| Principal Amount | Security Description | Value | |||

| $ | 725,000 | Wells Fargo-RBS Commercial Mortgage Trust REMIC, 4.00%, 03/15/44 (b) | $ | 758,355 | ||

| 735,000 | Wells Fargo-RBS Commercial Mortgage Trust REMIC, 4.39%, 06/15/44 (b) | 775,015 | ||||

| 825,000 | Wells Fargo-RBS Commercial Mortgage Trust REMIC, 2.19%, 04/15/45 | 826,997 | ||||

| 14,453,452 | ||||||

| Non-Agency Residential Mortgage Backed Securities - 15.2% | ||||||

| 128,037 | Bayview Financial Acquisition Trust REMIC, 6.21%, 05/28/37 (c) | 133,750 | ||||

| 181,068 | Citicorp Residential Mortgage Trust REMIC, 5.63%, 07/25/36 (c) | 186,186 | ||||

| 681,679 | Citicorp Residential Mortgage Trust REMIC, 5.63%, 07/25/36 (c) | 699,041 | ||||

| 796,219 | Citicorp Residential Mortgage Trust REMIC, 5.78%, 09/25/36 (c) | 823,091 | ||||

| 264,651 | Citigroup Global Markets Mortgage Securities VII, Inc. REMIC, 6.93%, 08/25/28 | 269,791 | ||||

| 381,755 | Citigroup Mortgage Loan Trust REMIC, 4.00%, 01/25/35 (a)(b) | 391,629 | ||||

| 484,597 | Citigroup Mortgage Loan Trust REMIC, 0.58%, 08/25/36 (a) | 462,526 | ||||

| 66,733 | CitiMortgage Alternative Loan Trust REMIC, 5.25%, 03/25/21 | 67,207 | ||||

| 525,459 | Conseco Financial Corp., 7.30%, 09/15/26 (a) | 546,060 | ||||

| 265,653 | Countrywide Asset-Backed Certificates REMIC, 0.80%, 11/25/35 (a)(b) | 262,566 | ||||

| 219,365 | Countrywide Asset-Backed Certificates REMIC, 0.61%, 07/25/36 (a) | 215,184 | ||||

| 31,580 | Credit Suisse First Boston Mortgage Securities Corp. REMIC, 5.00%, 08/25/20 | 31,289 | ||||

| 211,564 | Credit-Based Asset Servicing and Securitization, LLC REMIC, 1.56%, 02/25/33 (a) | 195,900 | ||||

| 733,552 | Credit-Based Asset Servicing and Securitization, LLC REMIC, 6.02%, 12/25/37 (b)(c) | 764,751 | ||||

| 630,559 | First NLC Trust REMIC, 0.70%, 02/25/36 (a) | 619,850 | ||||

| 654,354 | Fremont Home Loan Trust REMIC, 1.30%, 11/25/34 (a) | 550,562 | ||||

| 322,454 | Goldman Sachs Alternative Mortgage Products Trust REMIC, 1.08%, 03/25/34 (a) | 322,454 | ||||

| 79,005 | Goldman Sachs Alternative Mortgage Products Trust REMIC, 0.64%, 01/25/36 (a) | 78,443 | ||||

| Principal Amount | Security Description | Value |

| $ | 1,200,000 | Goldman Sachs Alternative Mortgage Products Trust REMIC, 0.93%, 05/25/36 (a)(b) | $ | 1,116,453 | ||

| 1,126,276 | HSBC Home Equity Loan Trust USA, 1.93%, 11/20/36 (a) | 1,126,906 | ||||

| 155,549 | Irwin Home Equity Loan Trust, 1.78%, 02/25/29 (a) | 150,255 | ||||

| 167,524 | Irwin Whole Loan Home Equity Trust REMIC, 1.53%, 11/25/28 (a) | 163,499 | ||||

| 228,202 | Irwin Whole Loan Home Equity Trust REMIC, 0.90%, 12/25/29 (a) | 222,675 | ||||

| 1,046,446 | Irwin Whole Loan Home Equity Trust REMIC, 1.78%, 06/25/34 (a) | 992,882 | ||||

| 840,000 | JP Morgan Mortgage Acquisition Trust REMIC, 0.66%, 07/25/36 (a) | 795,260 | ||||

| 321,197 | Lehman ABS Manufactured Housing Contract Trust REMIC, 4.35%, 04/15/40 | 325,778 | ||||

| 895,000 | Long Beach Mortgage Loan Trust REMIC, 1.33%, 10/25/34 (a) | 800,748 | ||||

| 86,271 | Morgan Stanley Home Equity Loan Trust REMIC, 1.14%, 12/25/34 (a) | 86,239 | ||||

| 340,627 | New Residential Mortgage Loan Trust REMIC, 3.75%, 05/28/52 (a)(b) | 352,114 | ||||

| 159,583 | New Residential Mortgage Loan Trust REMIC, 3.75%, 11/25/54 (a)(b) | 164,635 | ||||

| 436,636 | New Residential Mortgage Loan Trust REMIC, 3.75%, 08/25/55 (a) | 450,913 | ||||

| 173,693 | Nomura Asset Acceptance Corp. Alternative Loan Trust REMIC, 6.00%, 03/25/47 (c) | 124,148 | ||||

| 210,000 | NovaStar Mortgage Funding Trust REMIC, 2.16%, 03/25/35 (a) | 202,554 | ||||

| 837,470 | Oakwood Mortgage Investors, Inc. REMIC, 0.38%, 03/15/18 (a)(b) | 797,370 | ||||

| 535,242 | Park Place Securities, Inc. Asset-Backed Pass-Through Certificates REMIC, 1.41%, 10/25/34 (a) | 528,599 | ||||

| 193,939 | Popular ABS Mortgage Pass-Through Trust REMIC, 4.42%, 11/25/35 (c) | 193,419 | ||||

| 158,463 | Renaissance Home Equity Loan Trust REMIC, 4.88%, 02/25/35 (c) | 159,227 | ||||

| 391,390 | Renaissance Home Equity Loan Trust REMIC, 4.50%, 08/25/35 (c) | 391,371 | ||||

| 265,427 | Residential Accredit Loans, Inc. Trust REMIC, 13.96%, 03/25/18 (a) | 277,956 | ||||

| 58,012 | Residential Accredit Loans, Inc. Trust REMIC, 6.00%, 10/25/34 | 59,975 | ||||

| 124,477 | Residential Accredit Loans, Inc. Trust REMIC, 5.50%, 02/25/35 | 123,045 | ||||

| 36,636 | Residential Asset Mortgage Products, Inc. Trust REMIC, 4.02%, 03/25/33 (a) | 36,710 |

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2016

SHORT-INTERMEDIATE BOND FUND

| Principal Amount | Security Description | Value | |||

| $ | 850,000 | Residential Asset Mortgage Products, Inc. Trust REMIC, 0.94%, 06/25/35 (a) | $ | 830,992 | ||

| 135,439 | Residential Asset Securities Corp. Trust REMIC, 5.96%, 09/25/31 (a) | 138,281 | ||||

| 63,541 | Residential Asset Securities Corp. Trust REMIC, 4.47%, 03/25/32 (a) | 63,603 | ||||

| 121,651 | Residential Asset Securities Corp. Trust REMIC, 3.87%, 05/25/33 (a) | 123,635 | ||||

| 118,960 | Residential Asset Securities Corp. Trust REMIC, 4.54%, 12/25/33 (a) | 121,947 | ||||

| 117,165 | Residential Asset Securitization Trust REMIC, 3.75%, 10/25/18 | 117,006 | ||||

| 211,474 | Structured Asset Securities Corp. Mortgage Loan Trust REMIC, 5.73%, 06/25/35 (c) | 213,166 | ||||

| 123,828 | Structured Asset Securities Corp. Mortgage Pass-Through Certificates REMIC, 2.08%, 11/25/34 (a) | 120,644 | ||||

| 586,000 | Towd Point Mortgage Trust REMIC, 3.50%, 02/25/55 (a)(b) | 596,530 | ||||

| 244,101 | Vanderbilt Acquisition Loan Trust REMIC, 7.33%, 05/07/32 (a) | 260,309 | ||||

| 40,866 | Wells Fargo Home Equity Asset-Backed Securities Trust REMIC, 0.81%, 12/25/35 (a) | 40,697 | ||||

| 6,147 | Wells Fargo Home Equity Asset-Backed Securities Trust REMIC, 0.57%, 07/25/36 (a) | 6,145 | ||||

| 18,895,966 | ||||||

| Total Non-U.S. Government Agency Asset-Backed Securities (Cost $49,967,881) | 49,834,771 |

| Corporate Bonds - 27.6% | ||||||

| Consumer Discretionary - 3.9% | ||||||

| 440,000 | AMC Networks, Inc., 4.75%, 12/15/22 | 441,100 | ||||

| 405,000 | Hanesbrands, Inc., 6.38%, 12/15/20 | 419,175 | ||||

| 320,000 | Hilton Worldwide Finance, LLC / Hilton Worldwide Finance Corp., 5.63%, 10/15/21 | 331,584 | ||||

| 1,045,000 | Newell Rubbermaid, Inc., 2.05%, 12/01/17 | 1,048,251 | ||||

| 720,000 | Newell Rubbermaid, Inc., 3.15%, 04/01/21 | 739,928 | ||||

| 445,000 | PVH Corp., 4.50%, 12/15/22 | 456,125 | ||||

| 405,000 | The Goodyear Tire & Rubber Co., 6.50%, 03/01/21 | 426,263 | ||||

| 970,000 | Whirlpool Corp., 1.65%, 11/01/17 | 972,193 | ||||

| 4,834,619 | ||||||

| Consumer Staples - 2.8% | ||||||

| 562,000 | Bottling Group, LLC, 5.13%, 01/15/19 | 621,446 | ||||

| 975,000 | Cargill, Inc., 1.90%, 03/01/17 (b) | 983,036 | ||||

| 550,000 | Church & Dwight Co., Inc., 2.45%, 12/15/19 | 556,721 | ||||

| Principal Amount | Security Description | Value |

| $ | 346,000 | Church & Dwight Co., Inc., 2.88%, 10/01/22 | $ | 350,136 | ||

| 119,000 | Kraft Heinz Foods Co., 4.88%, 02/15/25 (b) | 131,145 | ||||

| 395,000 | Land O'Lakes Capital Trust I, 7.45%, 03/15/28 (b) | 414,750 | ||||

| 475,000 | PepsiCo., Inc., 1.50%, 02/22/19 | 480,982 | ||||

| 3,538,216 | ||||||

| Energy - 1.2% | ||||||

| 900,000 | Anadarko Petroleum Corp., 6.38%, 09/15/17 | 942,497 | ||||

| 500,000 | Occidental Petroleum Corp., 1.75%, 02/15/17 | 501,027 | ||||

| 1,443,524 | ||||||

| Financials - 12.5% | ||||||

| 910,000 | American Express Bank FSB, 0.74%, 06/12/17 (a) | 904,540 | ||||

| 1,280,000 | American Honda Finance Corp., 1.60%, 02/16/18 (b) | 1,287,877 | ||||

| 1,060,000 | Bank of America Corp., MTN, 5.65%, 05/01/18 | 1,138,018 | ||||

| 1,090,000 | Chubb INA Holdings, Inc., 2.30%, 11/03/20 | 1,108,615 | ||||

| 1,150,000 | Citigroup, Inc., 2.55%, 04/08/19 | 1,167,411 | ||||

| 510,000 | Genworth Holdings, Inc., 4.80%, 02/15/24 | 373,575 | ||||

| 1,135,000 | JPMorgan Chase & Co., 7.90% (callable at 100 beginning 04/30/18) (a)(d) | 1,135,000 | ||||

| 1,020,000 | KeyCorp, MTN, 2.90%, 09/15/20 | 1,037,142 | ||||

| 1,140,000 | Metropolitan Life Global Funding I, 2.30%, 04/10/19 (b) | 1,159,994 | ||||

| 1,100,000 | Morgan Stanley, 4.75%, 03/22/17 | 1,136,153 | ||||

| 1,086,000 | Murray Street Investment Trust I, 4.65%, 03/09/17 (c) | 1,116,568 | ||||

| 670,000 | Pricoa Global Funding I, MTN, 0.84%, 06/24/16 (a)(b) | 670,082 | ||||

| 1,030,000 | Regions Financial Corp., 2.00%, 05/15/18 | 1,023,589 | ||||

| 1,060,000 | The Hartford Financial Services Group, Inc., 5.50%, 03/30/20 | 1,176,719 | ||||

| 1,130,000 | Wells Fargo & Co., Series K, 7.98% (callable at 100 beginning 03/15/18) (a)(d) | 1,169,437 | ||||

| 15,604,720 | ||||||

| Industrials - 2.4% | ||||||

| 1,077,000 | Burlington Northern Santa Fe, LLC, 5.75%, 03/15/18 | 1,171,365 | ||||

| 290,000 | General Electric Capital Corp., MTN, 0.89%, 08/07/18 (a) | 285,750 | ||||

| 310,000 | Huntington Ingalls Industries, Inc., 5.00%, 11/15/25 (b) | 324,725 | ||||

| 1,185,000 | Textron, Inc., 3.65%, 03/01/21 | 1,221,532 | ||||

| 3,003,372 | ||||||

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2016

SHORT-INTERMEDIATE BOND FUND

| Principal Amount | Security Description | Value | |||

| Information Technology - 2.1% | ||||||

| $ | 250,000 | Apple, Inc., 1.70%, 02/22/19 | $ | 253,861 | ||

| 1,050,000 | Oracle Corp., 2.25%, 10/08/19 | 1,083,604 | ||||

| 1,197,000 | QUALCOMM, Inc., 2.25%, 05/20/20 | 1,227,523 | ||||

| 2,564,988 | ||||||

| Telecommunication Services - 2.0% | ||||||

| 449,000 | AT&T, Inc., 2.40%, 03/15/17 | 454,261 | ||||

| 715,000 | AT&T, Inc., 3.80%, 03/15/22 | 753,853 | ||||

| 1,194,000 | Verizon Communications, Inc., 2.63%, 02/21/20 | 1,228,656 | ||||

| 2,436,770 | ||||||

| Utilities - 0.7% | ||||||

| 850,000 | PacifiCorp, 5.50%, 01/15/19 | 936,597 | ||||

| Total Corporate Bonds (Cost $34,279,626) | 34,362,806 |

| Government & Agency Obligations - 27.1% | |||||||

| GOVERNMENT SECURITIES - 23.7% | |||||||

| Municipals - 1.5% | |||||||

| 380,000 | City of Omaha, NE Sewer Revenue, Nebraska RB, 2.40%, 12/01/16 | 384,074 | |||||

| 250,000 | Lincoln Airport Authority, Nebraska RB, 1.33%, 07/01/16 | 250,077 | |||||

| 585,000 | Montana Board of Housing, Montana RB, 1.60%, 06/01/16 | 585,322 | |||||

| 245,000 | North Carolina Housing Finance Agency, North Carolina RB, 2.34%, 01/01/19 | 249,018 | |||||

| 325,000 | State of Mississippi, GO Bond, 2.63%, 11/01/16 | 328,500 | |||||

| 1,796,991 | |||||||

| U.S. Treasury Securities - 22.2% | |||||||

| 4,200,000 | U.S. Treasury Note, 0.63%, 09/30/17 | 4,194,750 | |||||

| 20,760,000 | U.S. Treasury Note, 1.25%, 01/31/19 | 20,995,169 | |||||

| 2,400,000 | U.S. Treasury Note, 2.00%, 02/28/21 | 2,488,032 | |||||

| 27,677,951 | |||||||

| U.S. GOVERNMENT MORTAGE BACKED-SECURITIES - 3.4% | |||||||

| Federal Home Loan Mortgage Corp. - 0.1% | |||||||

| 3,033,652 | Federal Home Loan Mortgage Corp. Multifamily Structured Pass Through Certificates Interest Only REMIC, 1.55%, 08/25/16 (a) | 6,347 | |||||

| 177,889 | Federal Home Loan Mortgage Corp. REMIC, 4.00%, 03/15/20 | 184,122 | |||||

| 190,469 | |||||||

| Federal National Mortgage Association - 2.2% | ||||||

| 883,244 | Federal National Mortgage Association Pool #AJ4087, 3.00%, 10/01/26 | 924,742 | ||||

| 85,250 | Federal National Mortgage Association REMIC, 4.00%, 07/25/21 | 88,442 | ||||

| 214,636 | Federal National Mortgage Association REMIC, 4.00%, 02/25/26 | 227,424 | ||||

| 316,435 | Federal National Mortgage Association REMIC, 3.00%, 04/25/37 | 323,655 | ||||

| Shares or Principal Amount | Security Description | Value |

| $ | 112,018 | Federal National Mortgage Association REMIC, 5.00%, 03/25/39 | $ | 3,187 | |||

| 530,071 | Federal National Mortgage Association REMIC, 2.50%, 09/25/39 | 541,271 | |||||

| 630,369 | Federal National Mortgage Association REMIC, 3.50%, 05/25/41 | 669,994 | |||||

| 2,778,715 | |||||||

| Government National Mortgage Association - 1.1% | |||||||

| 369,646 | Government National Mortgage Association II Pool #751404, 4.72%, 06/20/61 | 387,021 | |||||

| 937,998 | Government National Mortgage Association REMIC, 2.67%, 02/16/44 | 954,168 | |||||

| 1,341,189 | |||||||

Total Government & Agency Obligations (Cost $33,454,482) | 33,785,315 |

| Preferred Stocks - 0.4% | |||||||

| Financials - 0.4% | |||||||

| 550 | U.S. Bancorp., Series A, 3.50% (callable at 1,000 beginning on 05/02/16) (a)(d) | 438,075 | |||||

| Total Preferred Stocks (Cost $564,327) | 438,075 |

| Short-Term Investments - 4.1% | |||||||

| Investment Company - 4.1% | |||||||

| 5,123,220 | BlackRock Liquidity Funds T-Fund Portfolio, 0.18% (e) | 5,123,220 | |||||

| Total Short-Term Investments (Cost $5,123,220) | 5,123,220 |

| Total Investments - 99.2% (Cost $123,389,536) | 123,544,187 |

| Other assets in excess of liabilities – 0.8% | 965,753 | ||

| NET ASSETS – 100.0% | $ | 124,509,940 |

| (a) | Variable rate security. Rate presented is as of March 31, 2016. |

| (b) | The Sub-Adviser has deemed this security which is exempt from registration under the Securities Act of 1933 to be liquid based on procedures approved by Tributary Funds' Board of Directors. As of March 31, 2016, the aggregate value of these liquid securities was $24,421,661 which represented 19.6% of net assets. |

| (c) | Debt obligation initially issued at one coupon rate which converts to higher coupon rate at a specified date. Rate presented is as of March 31, 2016. |

| (d) | Perpetual maturity security. |

| (e) | Dividend yield changes to reflect current market conditions. Rate was the quoted yield as of March 31, 2016. |

| ABS | Asset Backed Security |

| CLO | Collateralized Loan Obligation |

| GO | General Obligation |

| LLC | Limited Liability Company |

| MTN | Medium Term Note |

| RB | Revenue Bond |

| REMIC | Real Estate Mortgage Investment Conduit |

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2016

INCOME FUND

| Principal Amount | Security Description | Value |

| Non-U.S. Government Agency Asset-Backed Securities - 31.9% | ||||||

| Asset Backed Securities - 8.9% | ||||||

| $ | 800,000 | Ally Auto Receivables Trust, 1.53%, 04/15/19 | $ | 802,327 | ||

| 735,000 | Ascentium Equipment Receivables, LLC, 1.57%, 12/11/17 (a) | 736,135 | ||||

| 1,220,000 | Ascentium Equipment Receivables, LLC, 1.61%, 10/13/20 (a) | 1,216,364 | ||||

| 1,000,000 | BA Credit Card Trust, 1.36%, 09/15/20 | 1,003,400 | ||||

| 855,000 | Cabela's Credit Card Master Note Trust, 1.63%, 02/18/20 (a) | 856,749 | ||||

| 1,085,000 | Cabela's Credit Card Master Note Trust, 2.71%, 02/17/26 (a) | 1,103,625 | ||||

| 1,000,000 | Capital One Multi-Asset Execution Trust, 1.48%, 07/15/20 | 1,005,361 | ||||

| 785,000 | Chase Issuance Trust, 1.15%, 01/15/19 | 786,345 | ||||

| 1,440,000 | Citibank Credit Card Issuance Trust, 5.65%, 09/20/19 | 1,531,896 | ||||

| 152,671 | CNL Commercial Mortgage Loan Trust (insured by AMBAC Assurance Corp.) REMIC, 0.87%, 10/25/30 (a)(b) | 132,356 | ||||

| 630,000 | Eaton Vance CLO, Ltd., 2.07%, 07/15/26 (a)(b) | 622,912 | ||||

| 1,226,000 | Ford Credit Auto Owner Trust, 1.27%, 12/15/17 | 1,225,738 | ||||

| 925,000 | Ford Credit Floorplan Master Owner Trust, 3.50%, 01/15/19 | 936,980 | ||||

| 1,040,000 | Magnetite IX CLO, Ltd., 2.04%, 07/25/26 (a)(b) | 1,032,244 | ||||

| 990,000 | OneMain Financial Issuance Trust, 2.43%, 06/18/24 (a) | 987,513 | ||||

| 1,605,029 | Preferred Term Securities XII, Ltd. / Preferred Term Securities XII, Inc., 1.34%, 12/24/33 (a)(b) | 1,316,124 | ||||

| 657,564 | Preferred Term Securities XIV, Ltd. / Preferred Term Securities XIV, Inc., 1.12%, 06/24/34 (a)(b) | 496,461 | ||||

| 896,396 | Preferred Term Securities XXI, Ltd. / Preferred Term Securities XXI, Inc., 1.28%, 03/22/38 (a)(b) | 416,824 | ||||

| 707,160 | Preferred Term Securities XXIV, Ltd. / Preferred Term Securities XXIV, Inc., 0.93%, 03/22/37 (a)(b) | 479,101 | ||||

| 650,000 | Voya CLO, Ltd., 2.07%, 01/18/26 (a)(b) | 643,637 | ||||

| 17,332,092 | ||||||

| Non-Agency Commercial Mortgage Backed Securities - 9.5% | ||||||

| 597,111 | 7 WTC Depositor, LLC Trust, 4.08%, 03/13/31 (a) | 604,229 | ||||

| 1,200,000 | American Tower Trust I, 3.07%, 03/15/23 (a) | 1,200,021 | ||||

| Principal Amount | Security Description | Value | |||

| $ | 934,369 | Bayview Commercial Asset Trust REMIC, 1.30%, 12/25/33 (a)(b) | $ | 896,222 | ||

| 787,335 | Bear Stearns Commercial Mortgage Securities Trust REMIC, 5.69%, 06/11/50 (b) | 817,211 | ||||

| 3,998,905 | Citigroup Commercial Mortgage Trust REMIC, 2.16%, 09/10/45 (a)(b) | 305,891 | ||||

| 1,683,069 | Citigroup Commercial Mortgage Trust REMIC, 5.74%, 06/14/50 (a)(b) | 1,704,778 | ||||

| 1,836,924 | COMM Mortgage Trust Interest Only REMIC, 1.49%, 03/10/46 (b) | 88,164 | ||||

| 900,000 | Credit Suisse First Boston Mortgage Securities Corp. REMIC, 5.74%, 05/15/36 (a)(b) | 944,748 | ||||

| 148,251 | DBUBS Mortgage Trust Interest Only REMIC, 1.30%, 08/10/44 (a)(b) | 968 | ||||

| 735,000 | FREMF Mortgage Trust REMIC, 4.16%, 09/25/44 (a)(b) | 756,321 | ||||

| 1,030,000 | FREMF Mortgage Trust REMIC, 2.64%, 03/25/45 (a)(b) | 1,031,791 | ||||

| 1,623,714 | FRESB Mortgage Trust REMIC, 3.22%, 08/25/35 (b) | 1,658,462 | ||||

| 10,168,387 | GS Mortgage Securities Trust REMIC, 1.62%, 08/10/44 (a)(b) | 407,553 | ||||

| 840,000 | JP Morgan Chase Commercial Mortgage Securities Trust REMIC, 1.69%, 01/15/32 (a)(b) | 827,343 | ||||

| 1,055,000 | JP Morgan Chase Commercial Mortgage Securities Trust REMIC, 2.67%, 01/15/46 | 1,077,924 | ||||

| 800,000 | JP Morgan Chase Commercial Mortgage Securities Trust REMIC, 4.11%, 07/15/46 (a) | 835,288 | ||||

| 1,200,000 | JPMBB Commercial Mortgage Securities Trust REMIC, 2.42%, 07/15/45 | 1,218,332 | ||||

| 899,326 | Morgan Stanley Capital I Trust REMIC, 3.22%, 07/15/49 | 901,668 | ||||

| 1,131,711 | Wells Fargo Commercial Mortgage Trust Interest Only REMIC, 2.05%, 10/15/45 (a)(b) | 95,312 | ||||

| 890,000 | Wells Fargo Commercial Mortgage Trust REMIC, 2.53%, 10/15/45 | 909,338 | ||||

| 995,000 | Wells Fargo-RBS Commercial Mortgage Trust REMIC, 2.63%, 03/15/45 | 1,017,083 | ||||

| 1,045,000 | Wells Fargo-RBS Commercial Mortgage Trust REMIC, 2.19%, 04/15/45 | 1,047,529 | ||||

| 695,019 | Wells Fargo-RBS Commercial Mortgage Trust REMIC, 2.16%, 11/15/45 (a)(b) | 60,549 | ||||

| 18,406,725 | ||||||

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2016

INCOME FUND

| Principal Amount | Security Description | Value |

| Non-Agency Residential Mortgage Backed Securities - 13.5% | ||||||

| $ | 215,291 | Bayview Financial Mortgage Pass-Through Trust REMIC, 5.70%, 02/28/41 (c) | $ | 244,393 | ||

| 217,002 | Citicorp Residential Mortgage Trust REMIC, 5.63%, 07/25/36 (c) | 223,135 | ||||

| 739,871 | Citicorp Residential Mortgage Trust REMIC, 5.63%, 07/25/36 (c) | 758,716 | ||||

| 1,064,824 | Citicorp Residential Mortgage Trust REMIC, 5.78%, 09/25/36 (c) | 1,100,760 | ||||

| 891,238 | Citigroup Global Markets Mortgage Securities VII, Inc. REMIC, 6.93%, 08/25/28 | 908,549 | ||||

| 1,149,920 | Citigroup Mortgage Loan Trust REMIC, 4.00%, 01/25/35 (a)(b) | 1,179,662 | ||||

| 510,102 | Citigroup Mortgage Loan Trust REMIC, 0.58%, 08/25/36 (b) | 486,869 | ||||

| 366,103 | Citigroup Mortgage Loan Trust, Inc. REMIC, 6.50%, 07/25/34 | 380,752 | ||||

| 98,510 | CitiMortgage Alternative Loan Trust REMIC, 5.25%, 03/25/21 | 99,210 | ||||

| 822,457 | Conseco Financial Corp., 7.30%, 09/15/26 (b) | 854,703 | ||||

| 277,532 | Countrywide Asset-Backed Certificates REMIC, 0.80%, 11/25/35 (a)(b) | 274,306 | ||||

| 137,568 | Countrywide Asset-Backed Certificates REMIC, 0.61%, 07/25/36 (b) | 134,946 | ||||

| 31,580 | Credit Suisse First Boston Mortgage Securities Corp. REMIC, 5.00%, 08/25/20 | 31,289 | ||||

| 62,686 | Credit Suisse First Boston Mortgage Securities Corp. REMIC, 5.75%, 04/25/33 | 64,419 | ||||

| 211,564 | Credit-Based Asset Servicing and Securitization, LLC REMIC, 1.56%, 02/25/33 (b) | 195,900 | ||||

| 656,336 | Credit-Based Asset Servicing and Securitization, LLC REMIC, 6.02%, 12/25/37 (a)(c) | 684,251 | ||||

| 809,864 | First NLC Trust REMIC, 0.70%, 02/25/36 (b) | 796,111 | ||||

| 463,501 | Fremont Home Loan Trust, 1.30%, 11/25/34 (b) | 389,982 | ||||

| 223,237 | Goldman Sachs Alternative Mortgage Products Trust REMIC, 1.08%, 03/25/34 (b) | 223,237 | ||||

| 72,928 | Goldman Sachs Alternative Mortgage Products Trust REMIC, 0.64%, 01/25/36 (b) | 72,409 | ||||

| 865,000 | Goldman Sachs Alternative Mortgage Products Trust REMIC, 0.93%, 05/25/36 (a)(b) | 804,777 | ||||

| Principal Amount | Security Description | Value | |||

| $ | 540,615 | Greenpoint Manufactured Housing, 7.27%, 06/15/29 | $ | 532,540 | ||

| 993,366 | HSBC Home Equity Loan Trust USA, 1.93%, 11/20/36 (b) | 993,923 | ||||

| 155,549 | Irwin Home Equity Loan Trust, 1.78%, 02/25/29 (b) | 150,254 | ||||

| 174,362 | Irwin Whole Loan Home Equity Trust REMIC, 1.53%, 11/25/28 (b) | 170,172 | ||||

| 385,694 | Irwin Whole Loan Home Equity Trust REMIC, 0.90%, 12/25/29 (b) | 376,351 | ||||

| 1,232,508 | Irwin Whole Loan Home Equity Trust REMIC, 1.78%, 06/25/34 (b) | 1,169,420 | ||||

| 860,000 | JP Morgan Mortgage Acquisition Trust REMIC, 0.66%, 07/25/36 (b) | 814,195 | ||||

| 469,982 | Lehman ABS Manufactured Housing Contract Trust REMIC, 4.35%, 04/15/40 | 476,686 | ||||

| 867,050 | New Residential Mortgage Loan Trust REMIC, 3.75%, 05/28/52 (a)(b) | 896,291 | ||||

| 880,186 | New Residential Mortgage Loan Trust REMIC, 3.75%, 11/25/54 (a)(b) | 908,047 | ||||

| 1,556,096 | New Residential Mortgage Loan Trust REMIC, 3.75%, 08/25/55 (b) | 1,606,978 | ||||

| 188,167 | Nomura Asset Acceptance Corp. Alternative Loan Trust REMIC, 6.00%, 03/25/47 (c) | 134,494 | ||||

| 249,000 | NovaStar Mortgage Funding Trust REMIC, 2.16%, 03/25/35 (b) | 240,171 | ||||

| 363,812 | NovaStar Mortgage Funding Trust REMIC, 2.08%, 03/25/35 (b) | 359,418 | ||||

| 264,105 | Renaissance Home Equity Loan Trust REMIC, 4.88%, 02/25/35 (c) | 265,378 | ||||

| 620,741 | Renaissance Home Equity Loan Trust REMIC, 4.50%, 08/25/35 (c) | 620,711 | ||||

| 311,623 | Residential Accredit Loans, Inc. Trust REMIC, 13.96%, 03/25/18 (b) | 326,332 | ||||

| 286,476 | Residential Accredit Loans, Inc. Trust REMIC, 6.00%, 10/25/34 | 296,171 | ||||

| �� | 83,853 | Residential Accredit Loans, Inc. Trust REMIC, 5.50%, 02/25/35 | 82,888 | |||

| 53,429 | Residential Asset Mortgage Products, Inc. Trust (insured by AMBAC Assurance Corp.) REMIC, 4.02%, 03/25/33 (b) | 53,537 | ||||

| 870,000 | Residential Asset Mortgage Products, Inc. Trust REMIC, 0.94%, 06/25/35 (b) | 850,545 | ||||

| 113,769 | Residential Asset Securities Corp. Trust REMIC, 5.96%, 09/25/31 (b) | 116,156 | ||||

| 40,344 | Residential Asset Securities Corp. Trust REMIC, 4.47%, 03/25/32 (b) | 40,383 | ||||

| 150,631 | Residential Asset Securities Corp. Trust REMIC, 4.54%, 12/25/33 (b) | 154,413 | ||||

| 1,574,949 | Sequoia Mortgage Trust REMIC, 3.00%, 11/25/30 (a)(b) | 1,603,898 |

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2016

INCOME FUND

| Principal Amount | Security Description | Value | |||

| $ | 211,474 | Structured Asset Securities Corp. Mortgage Loan Trust REMIC, 5.73%, 06/25/35 (c) | $ | 213,166 | ||

| 17,309 | Structured Asset Securities Corp. Mortgage Pass-Through Certificates REMIC, 5.80%, 09/25/33 (c) | 17,446 | ||||

| 134,147 | Structured Asset Securities Corp. Mortgage Pass-Through Certificates REMIC, 2.08%, 11/25/34 (b) | 130,698 | ||||

| 181,812 | Structured Asset Securities Corp. Mortgage Pass-Through Certificates REMIC, 1.48%, 11/25/34 (b) | 173,861 | ||||

| 1,825,000 | Towd Point Mortgage Trust REMIC, 3.50%, 02/25/55 (a)(b) | 1,857,793 | ||||

| 652,390 | Vanderbilt Acquisition Loan Trust REMIC, 7.33%, 05/07/32 (b) | 695,707 | ||||

| 77,098 | Wells Fargo Home Equity Asset-Backed Securities Trust REMIC, 0.81%, 12/25/35 (b) | 76,779 | ||||

| 3,686 | Wells Fargo Home Equity Asset-Backed Securities Trust REMIC, 0.57%, 07/25/36 (b) | 3,685 | ||||

| 26,316,863 | ||||||

| Total Non-U.S. Government Agency Asset-Backed Securities (Cost $62,544,273) | 62,055,680 |

| Corporate Bonds - 23.9% | ||||||

| Consumer Discretionary - 3.3% | ||||||

| 729,000 | AMC Networks, Inc., 4.75%, 12/15/22 | 730,822 | ||||

| 959,000 | Dollar General Corp., 3.25%, 04/15/23 | 968,218 | ||||

| 460,000 | Hanesbrands, Inc., 6.38%, 12/15/20 | 476,100 | ||||

| 490,000 | Hilton Worldwide Finance, LLC / Hilton Worldwide Finance Corp., 5.63%, 10/15/21 | 507,738 | ||||

| 615,000 | Newell Rubbermaid, Inc., 4.00%, 06/15/22 | 633,695 | ||||

| 320,000 | Newell Rubbermaid, Inc., 4.00%, 12/01/24 | 326,764 | ||||

| 300,000 | Newell Rubbermaid, Inc., 4.20%, 04/01/26 | 313,770 | ||||

| 760,000 | PVH Corp., 4.50%, 12/15/22 | 779,000 | ||||

| 665,000 | The Goodyear Tire & Rubber Co., 6.50%, 03/01/21 | 699,912 | ||||

| 925,000 | Whirlpool Corp., 4.70%, 06/01/22 | 1,017,047 | ||||

| 6,453,066 | ||||||

| Consumer Staples - 2.5% | ||||||

| 534,000 | Cargill, Inc., 4.10%, 11/01/42 (a) | 512,640 | ||||

| 1,165,000 | Church & Dwight Co., Inc. 2.88%, 11/01/22 | 1,178,926 | ||||

| 165,000 | Kraft Heinz Foods Co., 4.88%, 02/15/25 (a) | 181,840 | ||||

| 455,000 | Land O'Lakes Capital Trust I, 7.45%, 03/15/28 (a) | 477,750 | ||||

| 1,012,000 | PepsiCo, Inc., 4.88%, 11/01/40 | 1,139,352 | ||||

| 155,000 | PepsiCo., Inc., 2.85%, 02/24/26 | 159,184 | ||||

| Principal Amount | Security Description | Value | |||

| $ | 895,000 | Wal-Mart Stores, Inc., 5.63%, 04/15/41 | $ | 1,157,613 | ||

| 4,807,305 | ||||||

| Energy - 1.1% | ||||||

| 905,000 | Anadarko Petroleum Corp., 3.45%, 07/15/24 | 806,245 | ||||

| 515,000 | EOG Resources, Inc., 4.15%, 01/15/26 | 534,021 | ||||

| 645,000 | Tosco Corp., 8.13%, 02/15/30 | 794,646 | ||||

| 2,134,912 | ||||||

| Financials - 9.8% | ||||||

| 485,153 | Altitude Investments 16, LLC, 2.49%, 03/14/26 | 498,691 | ||||

| 1,120,000 | American Honda Finance Corp., 1.60%, 02/16/18 (a) | 1,126,892 | ||||

| 1,139,000 | Bank of America Corp., MTN, 4.13%, 01/22/24 | 1,206,983 | ||||

| 550,000 | Berkshire Hathaway, Inc., 2.20%, 03/15/21 | 561,440 | ||||

| 355,000 | Chubb INA Holdings, Inc., 5.90%, 06/15/19 | 399,949 | ||||

| 1,125,000 | Citigroup, Inc., 2.55%, 04/08/19 | 1,142,033 | ||||

| 1,140,000 | CME Group, Inc./IL, 3.00%, 03/15/25 | 1,155,845 | ||||

| 494,000 | Crown Castle International Corp., 4.88%, 04/15/22 | 528,679 | ||||

| 880,000 | Genworth Holdings, Inc., 4.80%, 02/15/24 | 644,600 | ||||

| 1,150,000 | JPMorgan Chase & Co., Series 1, 7.90% (callable at 100 beginning 04/30/18) (b)(d) | 1,150,000 | ||||

| 1,050,000 | KeyCorp, MTN, 2.90%, 09/15/20 | 1,067,646 | ||||

| 1,071,000 | Metropolitan Life Global Funding I, 2.30%, 04/10/19 (a) | 1,089,784 | ||||

| 1,155,000 | Morgan Stanley, 3.75%, 02/25/23 | 1,203,820 | ||||

| 865,000 | Prudential Financial, Inc., MTN, 7.38%, 06/15/19 | 1,004,005 | ||||

| 1,020,000 | Regions Financial Corp., 2.00%, 05/15/18 | 1,013,652 | ||||

| 520,000 | The Bank of New York Mellon Corp., MTN, 2.30%, 09/11/19 | 533,061 | ||||

| 707,000 | The Chubb Corp., 6.80%, 11/15/31 | 948,235 | ||||

| 974,000 | The Goldman Sachs Group, Inc., 6.45%, 05/01/36 | 1,129,565 | ||||

| 939,000 | The Hartford Financial Services Group, Inc., 5.50%, 03/30/20 | 1,042,395 | ||||