UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08846 | |||||||

| ||||||||

Tributary Funds, Inc. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

Tributary Capital Management, LLC 1620 Dodge Street Omaha, Nebraska |

| 68197 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Daniel W. Koors Jackson Fund Services 225 West Wacker Drive, Suite 1200 Chicago, Illinois 60606 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (800) 662-4203 |

| ||||||

| ||||||||

Date of fiscal year end: | March 31 |

| ||||||

| ||||||||

Date of reporting period: | March 31, 2014 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

Item 1. Report to Shareholders.

![]()

Tributary Funds®

Annual Report

March 31, 2014

Tributary Short-Intermediate Bond Fund

Institutional Class: FOSIX

Institutional Plus Class: FOSPX

Tributary Income Fund

Institutional Class: FOINX

Institutional Plus Class: FOIPX

Tributary Balanced Fund

Institutional Class: FOBAX

Institutional Plus Class: FOBPX

Tributary Growth Opportunities Fund

Institutional Class: FOGRX

Institutional Plus Class: FOGPX

Tributary Small Company Fund

Institutional Class: FOSCX

Institutional Plus Class: FOSBX

Notice to Investors

Shares of Tributary Funds:

· ARE NOT FDIC INSURED · MAY LOSE VALUE · HAVE NO BANK GUARANTEE

Investors should carefully consider the investment objectives, risks, charges and expenses of the Tributary Funds. Mutual funds involve risk including loss of principal. This and other important information about the Tributary Funds is contained in the prospectus, which can be obtained by calling 1-800-662-4203 or by visiting www.tributaryfunds.com. The prospectus should be read carefully before investing. The Tributary Funds are distributed by Northern Lights Distributors, LLC member FINRA. Northern Lights and the Tributary Funds’ investment adviser are not affiliated.

Dear Shareholder:

According to DictionaryFocus.com, the term recentism is defined as “a focus on recent events to the exclusion of history”. This phenomenon exists in all walks of life, and in this day and age of the 24 hour news cycle, Twitter, Facebook and other forms of social media, the danger of recentism becomes even greater. It is easy to take a relatively short-term phenomenon and build some type of fancy algorithm to extrapolate these trends far into the future. Sure, it is exciting to make dire predications about the next great stock market crash, what the planet is going to look like in 100 years or the effects that a certain governmental policy will have 50 years from now based on current trends. It sells books. It makes great news bites for Cable TV talk shows. It grabs your attention. I get it. The problem is that these long term projections very rarely turn out to be factual (at least in my experience), and their authors have usually cashed their checks and are long gone by the time we find out if their predictions actually pan out.

I have either been blessed or cursed, depending on your age and viewpoint, to be in my 30th year in this business. I have seen many of these new age products come to the marketplace, embraced by the chatter class as revolutionary and game changing only to fail miserably. In the middle to late 1980’s, computer based algorithms built on relatively short historical data points were used to create program trading and portfolio insurance. One popular explanation for the 1987 crash was indiscriminate selling by program traders. As computer technology became more readily available, the use of program trading grew dramatically. After the great crash of 1987, many blamed program trading strategies for blindly selling stocks as markets fell, exacerbating the decline, which was exactly the opposite of what these programs had been designed to do.

Flash forward about a decade to the late 1990’s. Recent history had proven that if you took all of your money, risky or not, and just invested it in high flying technology and internet stocks, you could become rich almost overnight. And this theory, based on data points from 1995-1999, worked phenomenally well, until it didn’t. The crash in the NASDAQ, an exchange that at the time was dominated by tech stocks, literally wiped out many investors overnight.

After the great bear markets of 2000, 2001 and 2007-2008, people had become fatigued with the volatility of equities and began searching for “alternatives”. According to the pundits, traditional buy and hold investing was dead, and the great marketers of Wall Street needed to concoct new and creative ways to deliver product to the masses based on these recent data points. Hedge funds, real estate funds, esoteric trading funds, commodity funds and a whole host of other products that were sold as alternatives to traditional stocks and bonds proliferated in the first decade of the new millennium. These products were sold as “non-correlated” options to stocks and bonds, which simply stated means they should offer some stability to your portfolio in times when things are difficult in traditional arenas. The first real test of these new products came with the great market upheaval of 2007-2008, and in my analysis they failed miserably. Turns out these products built by the best minds from Academia and Wall Street were much more highly correlated to the economy and traditional stocks and bonds than advertised, and suffered the same fate, falling sharply for their investors during this period, at the same time earning their creators and underwriters considerable fees. And since bottoming in early March 2009, stocks have been on an incredible upswing, with unfortunately very little participation from the average investor, who based their decision to abandon equities after six or seven years of very negative data points—the theory of recentism.

One recent trend that I find quite encouraging coming out of the last ten years of volatility has a couple of names; institutional investors call it Liability Based Investing and individual investors call it Outcome Based Investing. It is a relatively simple concept, but one that is based in discipline and vision, two qualities that when applied effectively almost always have positive results. Simply put, start first by understanding your liabilities, or desired end game or outcome, and then figure out what types of products or tools will be required to help you achieve those goals. There are literally thousands of different tools available today to help you achieve your long-term financial objectives. There are active funds, index funds, exchange traded funds, alternative funds; the list goes on and on. They are all built a little differently, and all will react differently based on the scenario. Without a well thought out vision of your financial goals and aspirations, and some understanding of your personal tolerance for risk along the way, trying to sort out all of these tools available can become an exercise in futility. What the market does over the next 10-20 years is irrelevant to you, what your personal portfolio does versus your desired outcome is what matters in the end.

So how does this all relate to the Tributary Funds? As an investor, it is important for you to understand our value proposition as a set of tools that you will use in creating the type of financial outcome you are striving to achieve. First of all, our strategies are based on principals that have stood the test of time, so as to counter-act the tendencies people have towards recentism. All of the Funds are managed by teams whose leaders have between 10 to 15 years of experience at the helm. We believe the long-run returns will be driven by the ability of underlying securities in each portfolio to deliver strong results to their shareholders and bond holders. This is known as a fundamental approach to investing. Again, if you follow the law of recentism, fundamental investing has been somewhat challenging. As the U.S. Federal Reserve has been attempting to reignite the U.S. economy from the worst recession since the Great Depression, they have been printing money at an unprecedented pace, flooding the financial system with almost free money. In this type of environment, companies with less than stellar management and financial characteristics are “propped up” by the availability of free money, as investors don’t seem to care much about doing the hard work necessary to differentiate between these companies and their more well run competition. However, if you look at history, and take an extended view, stocks clearly follow a pattern of being valued by their ability to deliver results to their shareholders.

As a valued shareholder of Tributary Funds, I would encourage you to look at our long-term demonstrated track record of value creation, and decide for yourself if this indeed aligns with your financial goals.

Wishing you continued health and prosperity….

Best regards,

Stephen R. Frantz

President

sfrantz@tributarycapital.com

Comments are provided as a general market overview and should not be considered investment advice or predictive of any future market performance.

ANNUAL REPORT 2014

SHORT-INTERMEDIATE BOND FUND (Unaudited)

Investment Objective

The Tributary Short-Intermediate Bond Fund seeks to maximize total return in a manner consistent with the generation of current income, preservation of capital and reduced price volatility.

Manager Commentary

For the year ended March 31, 2014, Tributary Short-Intermediate Bond Fund returned 0.40% (Institutional Class at NAV) and 0.77% (Institutional Plus Class at NAV) compared to a 0.42% return for the Barclay's Capital U.S. Government/Credit 1-5 Year Index. The outperformance after expenses of the Institutional Plus class, which has a lower expense ratio than the Institutional Class, was due to lower duration exposure relative to the benchmark, the overweight allocation to non-agency mortgage backed securities ("MBS") and corporate bonds, as well as the Fund's modest down-in-quality bias. U.S. Treasury yields rose dramatically during the year as the U.S. Federal Reserve ("Fed") signaled an end to the era of quantitative easing ("QE"), with the 5-year yield rising by 95 basis points ("bps") and the 30-year yield by 46 bps (for perspective, a 100 bps rise in the 30-year yield is roughly equivalent to an 18% decrease in price). Credit-sensitive sectors performed very well over the trailing 12 months. Relative to similar-maturity U.S. Treasuries for example, corporate bonds generated an excess return of nearly 3.50%. The non-agency MBS and asset backed securities ("ABS") sectors were also strong performers over the past year. The broad private-label securitized space continued to benefit from relatively attractive yield profiles and fundamental improvement in underlying collateral values, whether residential or commercial properties or credit card receivables.

Without question the primary event of the last year was the change in Fed policy expectations, which led to what many market pundits have labeled the "taper tantrum." When Fed Chairman Bernanke indicated in May 2013 that the Fed could begin reducing (or tapering) its purchases of U.S. Treasuries and Agency MBS, the market quickly re-priced and drove bond yields significantly higher. The government shutdown in October and growing unrest and uncertainty in emerging economies subsequently caused some flight-to-quality in the Treasury market in the Fall of 2013 and into early 2014. However, economic data was generally at or above expectations for most of the year, which further helped to lift bond yields and compress corporate and other credit-sensitive yield spreads.

Over the last year the Fund increased duration exposure to the non-agency MBS and ABS sectors given relatively attractive yield and return profiles. Our corporate bond exposure ended the year lower as we found fewer favorable opportunities, while the agency MBS allocation increased modestly in duration terms. Our allocation to the U.S. Government

sector was essentially unchanged over the year. The Fund continues to maintain a AA- weighted average credit rating.

As the investor optimism on display during late 2013 faded during the most recent quarter, market participants were forced to re-evaluate their forecasts for the remainder of the year. Estimates for first quarter growth were revised lower as the economic statistics disappointed, to varying degrees due to bad weather. The uncertainty created by the tension in the Ukraine and weaker Chinese growth was another shock to confidence, leaving longer-term interest rates below the highs reached during 2013.

For our part, we continue to believe that interest rates could drift higher over the coming year. As the negative economic impact of the harsh winter recedes, growth should return. Furthermore, the Fed is determined to continue tapering its current QE program and will likely be finished by the end of 2014. We are therefore maintaining a shorter duration position in the portfolio, relative to the benchmark. Nonetheless, we do not expect dramatically higher rates as significant headwinds exist in the form of a soft labor market, a lack of meaningful real wage growth, low inflation and tepid real trend growth.

With respect to spread sectors of the bond market, we are becoming increasingly cautious as robust investor confidence has driven spreads significantly narrower. Corporate bonds are for the most part fully valued and we are moving to a more neutral weighting in corporate credit. We remain overweight in the housing-sensitive non-agency MBS sector, the private-label ABS and commercial mortgage backed securities ("CMBS") sectors, and continue to keep a modest exposure to the agency MBS sector. We remain underweight to the traditional U.S. Government bond sector.

As always, we remain committed to seeking prudent, value-enhancing investment opportunities consistent with our disciplined approach of managing for the long-term.

ANNUAL REPORT 2014

SHORT-INTERMEDIATE BOND FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2014

Portfolio Composition as of March 31, 2014

Percentage Based on Total Value of Investments

(Portfolio composition is subject to change)

U.S. Treasury Securities | 35.3 | % | |||||

Mortgage Related | 26.9 | % | |||||

Corporate Bonds | 24.5 | % | |||||

U.S. Government Mortgage-Backed Securities | 5.4 | % | |||||

Municipals | 4.0 | % | |||||

Short Term Investments | 3.5 | % | |||||

Other | 0.4 | % | |||||

100.0 | % | ||||||

Portfolio Analysis as of March 31, 2014

(Portfolio composition is subject to change)

Weighted Average Maturity: | 3.4 years | ||||||

Average Annual Total Returns for the Year Ended March 31, 2014*

1 Year | 5 Year | 10 Year | |||||||||||||

| Tributary Short-Intermediate Bond Fund - Institutional Class | 0.40 | % | 3.48 | % | 3.04 | % | |||||||||

| Barclays Capital U.S. Government/Credit 1-5 Year Index | 0.42 | % | 2.83 | % | 3.27 | % | |||||||||

Prospectus Expense Ratio (Gross/Net)† | 1.05%/0.83% | ||||||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 1.01%/0.79% | ||||||||||||||

1 Year | Since Inception†† | ||||||||||

| Tributary Short-Intermediate Bond Fund - Institutional Plus Class | 0.77 | % | 3.04 | % | |||||||

Prospectus Expense Ratio (Gross/Net)† | 0.80%/0.58% | ||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 0.80%/0.58% | ||||||||||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†)The expense ratios are from the Fund's prospectus dated July 26, 2013. Net expense ratio is net of contractual waivers which are in effect from August 1, 2013 through July 31, 2014.

(††)Commencement date for the Institutional Plus Class was October 14, 2011.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2004. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by each class.

Barclays Capital U.S. Government/Credit 1-5 Year Index is an unmanaged index which measures the performance of U.S. Treasury and agency securities, and corporate bonds with 1-5 year maturities. The index is unmanaged and does not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot invest directly in the index.

ANNUAL REPORT 2014

INCOME FUND (Unaudited)

Investment Objective

The Tributary Income Fund seeks the generation of current income in a manner consistent with preserving capital and maximizing total return.

Manager Commentary

For the year ended March 31, 2014, Tributary Income Fund returned 0.72% (Institutional Class at NAV) and 0.79% (Institutional Plus Class at NAV) compared to a -0.10% return for the Barclay's Capital U.S. Aggregate Bond Index. The outperformance was due to lower duration exposure relative to the benchmark, the overweight allocation to non-agency mortgage backed securities ("MBS") and corporate bonds, as well as the Fund's modest down-in-quality bias. U.S. Treasury yields rose dramatically during the year as the U.S. Federal Reserve ("Fed") signaled an end to the era of quantitative easing ("QE"), with the 5-year yield rising by 95 basis points ("bps") and the 30-year yield by 46 bps (for perspective, a 100 bps rise in the 30-year yield is roughly equivalent to an 18% decrease in price). Credit-sensitive sectors performed very well over the trailing 12 months. Relative to similar-maturity U.S. Treasuries for example, corporate bonds generated an excess return of nearly 3.50%. The non-agency MBS and asset backed securities ("ABS") sectors were also strong performers over the past year. The broad private-label securitized space continued to benefit from relatively attractive yield profiles and fundamental improvement in underlying collateral values, whether residential or commercial properties or credit card receivables.

Without question the primary event of the last year was the change in Fed policy expectations, which led to what many market pundits have labeled the "taper tantrum." When Fed Chairman Bernanke indicated in May 2013 that the Fed could begin reducing (or tapering) its purchases of U.S. Treasuries and agency MBS, the market quickly re-priced and drove bond yields significantly higher. The government shutdown in October and growing unrest and uncertainty in emerging economies subsequently caused some flight-to-quality in the Treasury market in the Fall of 2013 and into early 2014. However, economic data was generally at or above expectations for most of the year, which further helped to lift bond yields and compress corporate and other credit-sensitive yield spreads.

Over the last year the Fund increased duration exposure to the non-agency MBS and ABS sectors given relatively attractive yield and return profiles. We also added to the U.S. Treasury sector, primarily due to significant net inflows into the Fund over the past 3 months. Our corporate bond exposure ended the year slightly lower, while the agency MBS allocation increased modestly in duration terms. The Fund continues to maintain a AA- weighted average credit rating.

As the investor optimism on display during late 2013 faded during the most recent quarter, market participants were

forced to re-evaluate their forecasts for the remainder of the year. Estimates for first quarter growth were revised lower as the economic statistics disappointed, to varying degrees due to bad weather. The uncertainty created by the tension in the Ukraine and weaker Chinese growth was another shock to confidence, leaving longer-term interest rates below the highs reached during 2013.

For our part, we continue to believe that interest rates could drift higher over the coming year. As the negative economic impact of the harsh winter recedes, growth should return. Furthermore, the Fed is determined to continue tapering its current QE program and will likely be finished by the end of 2014. We are therefore maintaining a shorter duration position in the portfolio, relative to the benchmark. Nonetheless, we do not expect dramatically higher rates as significant headwinds exist in the form of a soft labor market, a lack of meaningful real wage growth, low inflation and tepid real trend growth.

With respect to spread sectors of the bond market, we are becoming increasingly cautious as robust investor confidence has driven spreads significantly narrower. Corporate bonds are for the most part fully valued and we are moving to a more neutral weighting in corporate credit. We remain overweight in the housing-sensitive non-agency MBS sector, the private-label ABS and commercial mortgage backed securities ("CMBS") sectors. We continue to maintain an underweight to the richly-valued agency MBS sector as well as the traditional U.S. government bond sector.

As always, we remain committed to seeking prudent, value-enhancing investment opportunities consistent with our disciplined approach of managing for the long-term.

ANNUAL REPORT 2014

INCOME FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2014

Portfolio Composition as of March 31, 2014

Percentage Based on Total Value of Investments

(Portfolio composition is subject to change)

U.S. Treasury Securities | 26.2 | % | |||||

Mortgage Related | 26.0 | % | |||||

Corporate Bonds | 21.8 | % | |||||

U.S. Government Mortgage-Backed Securities | 18.9 | % | |||||

Short Term Investments | 3.1 | % | |||||

Municipals | 1.9 | % | |||||

Investment Companies | 1.2 | % | |||||

Exchange Traded Funds | 0.5 | % | |||||

Other | 0.4 | % | |||||

100.0 | % | ||||||

Portfolio Analysis as of March 31, 2014

(Portfolio composition is subject to change)

Weighted Average Maturity: | 7.4 years | ||||||

Average Annual Total Returns for the Year Ended March 31, 2014*

1 Year | 5 Year | 10 Year | |||||||||||||

| Tributary Income Fund - Institutional Class | 0.72 | % | 5.75 | % | 4.13 | % | |||||||||

| Barclays Capital U.S. Aggregate Bond Index | -0.10 | % | 4.80 | % | 4.46 | % | |||||||||

Prospectus Expense Ratio (Gross/Net)† | 1.17%/0.90% | ||||||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 1.08%/0.81% | ||||||||||||||

1 Year | Since Inception†† | ||||||||||

| Tributary Income Fund - Institutional Plus Class | 0.79 | % | 3.68 | % | |||||||

Prospectus Expense Ratio (Gross/Net)† | 0.92%/0.65% | ||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 0.91%/0.64% | ||||||||||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†)The expense ratios are from the Fund's prospectus dated July 26, 2013. Net expense ratio is net of contractual waivers which are in effect from August 1, 2013 through July 31, 2014.

(††)Commencement date for the Institutional Plus Class was October 28, 2011.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2004. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by each class.

Barclays Capital U.S. Aggregate Bond Index is an unmanaged index and covers the USD-denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, Government Related, Corporate, MBS (agency fixed-rate and hybrid ARM passthroughs), ABS and CMBS sectors. The index is unmanaged and does not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot invest directly in the index.

ANNUAL REPORT 2014

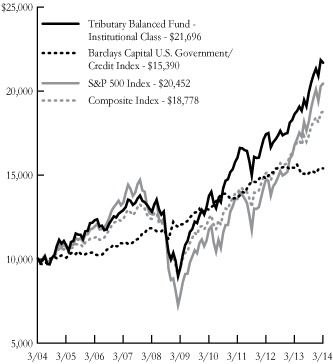

BALANCED FUND (Unaudited)

Investment Objective

The Tributary Balanced Fund seeks capital appreciation and current income.

Manager Commentary

For the year ended March 31, 2014, Tributary Balanced fund returned 16.46% (Institutional Class at NAV) and 16.65% (Institutional Plus Class at NAV) compared to 21.86% for the S&P 500 Index, -0.26% for the Barclay's Capital U.S. Government/Credit Index and 12.65% for the Composite Index which consists of 60% S&P 500 Index and 40% Barclay's Capital U.S. Government/Credit Index.

In the latest fiscal year U.S. stock prices advanced strongly, while bond prices declined moderately as interest rates rose. The advance in stock prices was supported by moderate economic growth and corporate earnings, and an expansion in price to earnings multiples. As the economic recovery matured into an economic expansion, and the U.S. Federal Reserve ("Fed") began to contemplate the end of their efforts to keep interest rates artificially low, interest rates inched higher over the course of the year.

We underweighted the bond segment of the Fund throughout the year and overweighted the allocation to stocks. The bond segment of the Fund matched the return of the Barclay's Capital Intermediate Bond Index for the year, down by about one quarter percent. In addition to reducing the allocation to bonds, we also shortened the average maturity to reduce the risk of losses if interest rates should continue to rise.

The stock segment of the Fund provided the juice for the better relative returns, rising by 27.9% compared to the 21.9% return of the S&P 500 Index. Within the equity segment healthcare stocks were the biggest contributor to excess returns, with our healthcare stocks rising by 42% compared to the 29% return of healthcare stocks in the S&P 500 Index. Medidata Solutions Inc. (up 127%), Biogen Idec Inc. (up 79%), Valeant Pharmaceuticals International Inc. (up 76%) and Thermo Fisher Scientific Inc.(up 59%) all contributed to the very strong returns in this sector.

Consumer discretionary stocks also contributed to excess returns, with a sector return of 34% compared to 24% for this sector in the S&P 500 Index. Priceline Group Inc. (up 69%), Wynn Resorts Ltd. (up 85%) and BorgWarner Inc. (up 60%) were the big contributors in the consumer discretionary sector.

Energy stocks held by the Fund also performed well, returning 25% versus a 15% return for energy stocks in the S&P 500 Index. EOG Resources Inc. (up 43%), Occidental Petroleum Corp. (up 25%) and Schlumberger Ltd. (up 29%) were the big contributors in this sector.

Other individual stocks held by the Fund that did well included Google Inc. (up 47%), IAC/Interactive Corp. (up 63%) and MasterCard Inc. (up 53%) helping the information technology sector of the Fund deliver a strong 33% return compared to 25% for information technology stocks in the S&P 500 Index.

We believe U.S. economic growth should accelerate as we progress through 2014, which should support valuations of U.S. focused companies, as sales and earnings begin another leg higher. Interest rates are likely to trend higher as the Fed removes some of the support they have provided to keep interest rates artificially low. We have positioned the Fund to take advantage of these two trends by underweighting bonds and overweighting stocks.

ANNUAL REPORT 2014

BALANCED FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2014

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

Portfolio Composition as of March 31, 2014

Percentage Based on Total Value of Investments

(Portfolio composition is subject to change)

Industrials | 14.3 | % | |||||

Financials | 13.1 | % | |||||

Health Care | 11.7 | % | |||||

Consumer Discretionary | 10.8 | % | |||||

Government Securities | 10.3 | % | |||||

Information Technology | 9.4 | % | |||||

Short Term Investments | 8.5 | % | |||||

Energy | 7.3 | % | |||||

Consumer Staples | 5.8 | % | |||||

Materials | 5.4 | % | |||||

Utilities | 2.1 | % | |||||

Telecommunication Services | 1.0 | % | |||||

U.S. Government Mortgage-Backed Securities | 0.3 | % | |||||

100.0 | % | ||||||

Average Annual Total Returns for the Year Ended March 31, 2014*

1 Year | 5 Year | 10 Year | |||||||||||||

| Tributary Balanced Fund - Institutional Class | 16.46 | % | 18.05 | % | 8.05 | % | |||||||||

| Barclays Capital U.S. Government/Credit Index | -0.26 | % | 5.07 | % | 4.41 | % | |||||||||

S&P 500 Index | 21.86 | % | 21.16 | % | 7.42 | % | |||||||||

Composite Index | 12.65 | % | 14.78 | % | 6.50 | % | |||||||||

Prospectus Expense Ratio (Gross/Net)† | 1.36%/1.23% | ||||||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 1.29%/1.16% | ||||||||||||||

1 Year | Since Inception†† | ||||||||||

| Tributary Balanced Fund - Institutional Plus Class | 16.65 | % | 14.28 | % | |||||||

Prospectus Expense Ratio (Gross/Net)† | 1.11%/0.98% | ||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 1.08%/0.95% | ||||||||||

(†)The expense ratios are from the Fund's prospectus dated July 26, 2013. Net expense ratio is net of contractual waivers which are in effect from August 1, 2013 through July 31, 2014.

(††)Commencement date for the Institutional Plus Class was October 14, 2011.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2004. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by each class.

The S&P 500 Index is a broad based index of 500 selected common stocks, most of which are listed on the New York Stock Exchange, that measures the U.S. stock market as a whole. The index is heavily weighted toward stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks. Barclays Capital U.S. Government/Credit Index is an unmanaged non-securitized component of the Barclays U.S. Aggregate Index. The U.S. Government/Credit Index includes Treasuries (i.e., public obligations of the U.S. Treasury that have remaining maturities of more than one year), Government-Related issues (i.e., agency, sovereign, supranational and local authority debt) and USD Corporates. The Composite Index is intended to provide a single benchmark that more accurately reflects the composition of securities held by the Tributary Balanced Fund. Sixty percent of the Composite Index is comprised of the S&P 500 Index and forty percent of the Composite index is comprised of the Barclays Capital U.S. Government/Credit Index. The indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot invest directly in the indices.

ANNUAL REPORT 2014

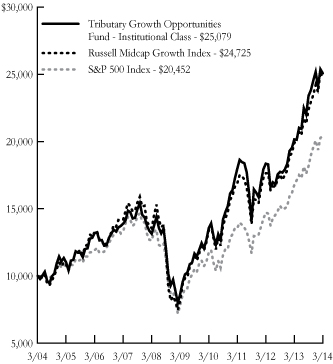

GROWTH OPPORTUNITIES FUND (Unaudited)

Investment Objective

The Tributary Growth Opportunities Fund seeks long-term capital appreciation.

Manager Commentary

For the year ended March 31, 2014, Tributary Growth Opportunities Fund returned 24.36% (Institutional Class at NAV) and 24.65% (Institutional Class Plus at NAV) compared to 24.22% for the Russell Midcap Growth Index and 21.86% for the S&P 500 Index.

Market conditions were, quite obviously, very good for U.S. stocks, and the Fund participated in the advance. The advance in stock prices was supported by moderate economic growth and corporate earnings, and an expansion in price to earnings multiples.

Financial stocks held by the Fund were the biggest positive contributor to returns relative to the averages. Our financial stocks returned 43% during the year compared to the 14% return for financials in the Russell Midcap Growth Index, adding 234 basis points ("bps") of excess relative return. Among the financials, Home Bancshares Inc. led the charge (up 85%), followed by Portfolio Recovery Associates Inc. (up 37%), Stifel Financial Corp. (up 44%) and Signature Bank (up 59%).

Our energy stock holdings also did well, returning 33% compared to the 13% return for the energy sector in the Russell Midcap Growth Index. Kodiak Oil & Gas Corp. (up 34%), Lufkin Industries (up 23%) and Concho Resources Inc. (up 26%) all contributed to the sector's strong performance.

Our industrial related holdings did not keep up with the benchmark, returning "only" 18% compared to the 24% return for industrial stocks in the Russell Midcap Growth Index. Consumer discretionary stocks were another weak area for us, with our stocks up "only" 24% compared to a 29% advance for consumer discretionary stocks in the Russell Midcap Growth Index. The underperformance of these two sectors cost the Fund 117 bps of relative performance. Conversant Inc. (-31%), NueStar Inc. (-30%) and Tetra Tech Inc. (-23%) were the worst individual performers last year.

We believe valuations in the domestic mid-cap growth sector remain reasonable based on the fundamental trends in business and the current level of interest rates in spite of the rather large rise in prices and multiples during the past year. U.S. economic growth should accelerate as we progress through 2014, which should benefit in particular medium sized U.S. focused companies.

ANNUAL REPORT 2014

GROWTH OPPORTUNITIES FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2014

Portfolio Composition as of March 31, 2014

Percentage Based on Total Value of Investments

(Portfolio composition is subject to change)

Industrials | 18.1 | % | |||||

Information Technology | 17.8 | % | |||||

Consumer Discretionary | 16.4 | % | |||||

Health Care | 13.6 | % | |||||

Financials | 9.6 | % | |||||

Materials | 8.3 | % | |||||

Energy | 7.6 | % | |||||

Consumer Staples | 5.6 | % | |||||

Short Term Investments | 3.0 | % | |||||

100.0 | % | ||||||

Average Annual Total Returns for the Year Ended March 31, 2014*

| �� | 1 Year | 5 Year | 10 Year | ||||||||||||

| Tributary Growth Opportunities Fund - Institutional Class | 24.36 | % | 23.64 | % | 9.63 | % | |||||||||

Russell Midcap Growth Index | 24.22 | % | 24.73 | % | 9.47 | % | |||||||||

S&P 500 Index | 21.86 | % | 21.16 | % | 7.42 | % | |||||||||

Prospectus Expense Ratio (Gross/Net)† | 1.28%/1.16% | ||||||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 1.20%/1.08% | ||||||||||||||

1 Year | Since Inception†† | ||||||||||

| Tributary Growth Opportunities Fund - Institutional Plus Class | 24.65 | % | 21.04 | % | |||||||

Prospectus Expense Ratio (Gross/Net)† | 1.03%/0.91% | ||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 1.01%/0.89% | ||||||||||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†)The expense ratios are from the Fund's prospectus dated July 26, 2013. Net expense ratio is net of contractual waivers which are in effect from August 1, 2013 through July 31, 2014.

(††)Commencement date for the Institutional Plus Class was October 14, 2011.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2004. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by each class.

The Russell Midcap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values. The Fund's primary index is the Russell Midcap Growth Index, however to provide a boarder market comparative, the S&P 500 Index is a secondary benchmark. The S&P 500 Index is a broad based index of 500 selected common stocks, most of which are listed on the New York Stock Exchange, that measures the U.S. stock market as a whole. The index is heavily weighted toward stocks with large market capitalizations and represents approximately two-thirds of the total market value of all domestic common stocks. The indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot invest directly in the indices.

ANNUAL REPORT 2014

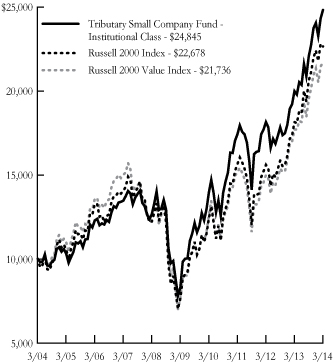

SMALL COMPANY FUND (Unaudited)

Investment Objective

The Tributary Small Company Fund seeks long-term capital appreciation.

Manager Commentary

For the year ended March 31, 2014, Tributary Small Company Fund returned 24.26% (Institutional Class at NAV) and 24.53% (Institutional Plus Class at NAV) compared to 24.90% for the Russell 2000 Index and 22.65% for the Russell 2000 Value Index.

Small cap stocks continued to be in rally mode over the trailing 12 months ending March 31, 2014 as represented by the Fund's benchmark returns. Style-wise, "growth" outperformed "value" with the Russell 2000 Growth Index returning 27.19%. U.S. Federal Reserve ("Fed") policies continue to have a significant influence on the stock market. A consistently low Fed Funds rate and the bond repurchase program instituted by the Fed have helped to drive equity prices upward. However, when Fed Chairman Bernanke mentioned the word "taper" in May of 2013, the market cringed. The mere mention of tapering bond purchases at some point in the future ignited a negative reaction in the stock market. The Fed immediately began to backpedal. They made it clear that tapering would not happen until the economy was strong enough to support it and that short term rates would remain low. The market appears to be addicted to easy money, but this cannot last. The Fed has begun to taper bond purchases and it is expected to be out of the bond buying business by the end of 2014. Theoretically, the Fed is doing this because they see evidence that the economy is improved and does not need the excess liquidity — liquidity that has helped inflate financial assets. In particular, lower quality stocks (negative earnings, higher levered, low/no dividend) seemingly have been a significant beneficiary of these actions. When bond purchases end, we believe the focus will switch to business fundamentals, favoring higher quality companies.

The Fund's weakest relative performance came from portfolio holdings in the industrials and healthcare economic sectors. In industrials, Tetra Tech Inc. ("Tetra Tech") had two negative announcements in 2013 regarding its Eastern Canadian business unit that was experiencing reduced activity from government customers. Ultimately, the company decided to right-size these operations and incurred severance and related charges. In addition, Tetra Tech's mining end markets experienced weakness for part of 2013. Werner Enterprises Inc. was impacted by soft demand over the 12 month period and battled poor winter weather conditions.

In healthcare, biotechnology stocks were up over 40% and pharmaceutical stocks returned over 56% in the 12 month period. Typically, we have few holdings in the biotech and pharmaceutical areas due to the propensity of those companies to be low- or non-earners, exposed to unknown results of developmental pharmaceuticals, or overly dependent on

one or two products. In short, these businesses are typically less predictable and have limited visibility. The combination of strong returns and our underweight position in those industries led to the performance drag within healthcare over the last year.

Lastly, the Fund's average cash position of approximately 2.0% over the 12 month period negatively impacted performance. In strong markets, any amount of cash will be detrimental to relative performance, and while it is our desire to be fully invested in the market, that small amount of cash still was a hindrance.

On the positive side, there were some notable successes within the portfolio in the 12 month period. In the financial sector, Stifel Financial Corp. ("Stifel") and GAMCO Investors Inc. ("GAMCO") had strong years. The Global Wealth Management and Institutional segments at Stifel have been performing well and the company has made several acquisitions that should boost growth in revenues and earnings longer-term. GAMCO results have been buoyed by strong asset inflows and market appreciation, combining to drive assets under management and revenue expectations higher. Additionally, the Real Estate Investment Trusts ("REITs") industry as a whole was a poor relative performer within the financial sector. REITs continue to be richly valued in our opinion and we remain underweight this area. This underweight position contributed to positive relative performance.

In the consumer discretionary sector, Jack In the Box Inc.'s trailing year total return of 70% was a result of improvement in same-store-sales, better margins from its refranchising efforts of the Jack in the Box stores, a restructuring of Qdoba and significant share repurchases. ANN Inc.'s ("ANN") stock reacted positively to its most recent earnings results followed by an announcement that Golden Gate Capital had taken a 9.5% ownership stake in ANN with the intention of helping the company create value for shareholders.

As of March 31, 2014, the portfolio held 63 companies diversified across the major sectors of the market. Twelve new companies were purchased into the Fund in the 12 month period, 7 positions were eliminated and 1 company was acquired.

ANNUAL REPORT 2014

SMALL COMPANY FUND (Unaudited)

Return of a $10,000 Investment as of March 31, 2014

Portfolio Composition as of March 31, 2014

Percentage Based on Total Value of Investments

(Portfolio composition is subject to change)

Financials | 21.0 | % | |||||

Information Technology | 19.3 | % | |||||

Industrials | 15.7 | % | |||||

Consumer Discretionary | 13.3 | % | |||||

Health Care | 9.4 | % | |||||

Energy | 6.6 | % | |||||

Materials | 4.6 | % | |||||

Utilities | 3.7 | % | |||||

Short Term Investments | 3.2 | % | |||||

Consumer Staples | 3.2 | % | |||||

100.0 | % | ||||||

Average Annual Total Returns for the Year Ended March 31, 2014*

1 Year | 5 Year | 10 Year | |||||||||||||

| Tributary Small Company Fund - Institutional Class | 24.26 | % | 24.51 | % | 9.53 | % | |||||||||

Russell 2000 Index | 24.90 | % | 24.31 | % | 8.53 | % | |||||||||

Russell 2000 Value Index | 22.65 | % | 23.33 | % | 8.07 | % | |||||||||

Prospectus Expense Ratio (Gross/Net)† | 1.36%/1.23% | ||||||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 1.32%/1.19% | ||||||||||||||

1 Year | Since Inception†† | ||||||||||

| Tributary Small Company Fund - Institutional Plus Class | 24.53 | % | 14.04 | % | |||||||

Prospectus Expense Ratio (Gross/Net)† | 1.11%/0.98% | ||||||||||

| Expense Ratio for the Year Ended March 31, 2014 (Gross/Net) | 1.09%/0.96% | ||||||||||

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. Total returns include change in share price, reinvestment of dividends and capital gains. The investment return and principal value will fluctuate so that an investor's shares, when redeemed may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit our website at www.tributaryfunds.com.

(†)The expense ratios are from the Fund's prospectus dated July 26, 2013. Net expense ratios are net of contractual waivers which are in effect from August 1, 2013 through July 31, 2014.

(††) Commencement date for the Institutional Plus Class was December 17, 2010.

(*) Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects contractual fee waivers in effect for certain periods. Without these fee waivers, the performance would have been lower.

The line chart assumes an initial investment of $10,000 made on March 31, 2004. Total return is based on net change in net asset value ("NAV") assuming reinvestment of all dividends and other distributions.

The performance of Institutional Plus Class will be different than Institutional Class based on differences in fees borne by the different classes.

The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 Value Index measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. The indices are unmanaged and do not reflect the deduction of fees or taxes associated with a mutual fund, such as investment management, administration and other operational fees. Investors cannot invest directly in the indices.

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2014

SHORT-INTERMEDIATE BOND FUND

Principal |

| Security |

| Value |

| ||

Non-U.S. Government Agency Asset-Backed Securities - 26.8% |

|

|

| ||||

$ | 190,977 |

| Bayview Financial Acquisition Trust REMIC, 6.21%, 05/28/37 (a) |

| $ | 203,499 |

|

23,744 |

| Bear Stearns Asset Backed Securities I Trust REMIC, 0.55%, 10/25/34 (a) |

| 23,706 |

| ||

11,916 |

| Bear Stearns Asset Backed Securities I Trust REMIC, 0.37%, 12/25/35 (a) |

| 11,899 |

| ||

47,455 |

| Bear Stearns Asset Backed Securities I Trust REMIC, 0.37%, 02/25/36 (a) |

| 47,409 |

| ||

128,828 |

| Bear Stearns Commercial Mortgage Securities Trust REMIC, 5.53%, 09/11/41 |

| 128,748 |

| ||

975,000 |

| Cabela’s Master Credit Card Trust, 2.17%, 08/16/21 (b) |

| 977,995 |

| ||

27,967 |

| Chase Funding Trust REMIC, 4.40%, 02/25/30 |

| 27,912 |

| ||

965,000 |

| Chase Issuance Trust, 1.15%, 01/15/19 |

| 965,177 |

| ||

109,643 |

| Chase Mortgage Finance Trust REMIC, 5.50%, 05/25/35 |

| 112,810 |

| ||

814,000 |

| Citibank Credit Card Issuance Trust, 5.65%, 09/20/19 |

| 927,771 |

| ||

779,929 |

| Citigroup Mortgage Loan Trust Inc. REMIC, 0.30%, 08/25/36 (a) |

| 758,156 |

| ||

183,758 |

| Citigroup Mortgage Loan Trust Inc. REMIC, 0.30%, 10/25/36 (a) |

| 182,527 |

| ||

135,108 |

| Citimortgage Alternative Loan Trust REMIC, 5.25%, 03/25/21 |

| 137,116 |

| ||

271,807 |

| CNL Commercial Mortgage Loan Trust (insured by AMBAC Assurance Corp.) REMIC, 0.59%, 10/25/30 (a) (b) |

| 232,376 |

| ||

416,328 |

| Countrywide Asset-Backed Certificates REMIC, 4.46%, 10/25/35 (a) |

| 417,243 |

| ||

398,694 |

| Countrywide Asset-Backed Certificates REMIC, 0.33%, 07/25/36 (a) |

| 387,742 |

| ||

76,702 |

| Credit Suisse First Boston Mortgage Securities Corp. REMIC, 5.00%, 08/25/20 |

| 76,675 |

| ||

210,420 |

| Credit Suisse First Boston Mortgage Securities Corp. REMIC, 3.35%, 02/25/33 (a) |

| 210,459 |

| ||

282,136 |

| Credit-Based Asset Servicing and Securitization LLC REMIC, 1.28%, 02/25/33 (a) |

| 260,562 |

| ||

950,000 |

| Credit-Based Asset Servicing and Securitization LLC REMIC, 6.02%, 12/25/37 (a) |

| 1,010,573 |

| ||

915,000 |

| Ford Credit Floorplan Master Owner Trust, 3.50%, 01/15/19 |

| 962,209 |

| ||

654,354 |

| Fremont Home Loan Trust REMIC, 1.02%, 11/25/34 (a) |

| 608,716 |

| ||

650,000 |

| Goldman Sachs Alternative Mortgage Products Trust REMIC, 0.80%, 03/25/34 (a) |

| 647,061 |

| ||

850,000 |

| GS Mortgage Securities Trust REMIC, 3.65%, 03/10/44 (b) |

| 890,259 |

| ||

335,250 |

| GSAMP Trust REMIC, 0.36%, 01/25/36 (a) |

| 325,427 |

| ||

311,804 |

| Irwin Whole Loan Home Equity Trust REMIC, 1.25%, 11/25/28 (a) |

| 310,666 |

| ||

409,290 |

| Irwin Whole Loan Home Equity Trust REMIC, 0.62%, 12/25/29 (a) |

| 392,446 |

| ||

760,000 |

| JPMorgan Chase Commercial Mortgage Securities Trust REMIC, 2.67%, 01/15/46 |

| 775,632 |

| ||

840,000 |

| JPMorgan Mortgage Acquisition Trust REMIC, 0.38%, 07/25/36 (a) |

| 738,920 |

| ||

895,000 |

| Long Beach Mortgage Loan Trust REMIC, 1.05%, 10/25/34 (a) |

| 841,735 |

| ||

562,647 |

| Long Beach Mortgage Loan Trust REMIC, 0.89%, 04/25/35 (a) |

| 561,060 |

| ||

11,652 |

| MASTR Asset Securitization Trust REMIC, 5.25%, 11/25/35 |

| 11,662 |

| ||

494,198 |

| Morgan Stanley Capital I Trust REMIC, 3.22%, 07/15/49 |

| 515,714 |

| ||

450,896 |

| Morgan Stanley Home Equity Loan Trust REMIC, 0.86%, 12/25/34 (a) |

| 449,372 |

| ||

932,000 |

| Newcastle Investment Trust, 6.00%, 07/10/35 |

| 960,511 |

| ||

339,110 |

| Nomura Asset Acceptance Corp. Alternative Loan Trust REMIC, 0.83%, 06/25/35 (a) |

| 332,608 |

| ||

222,448 |

| Nomura Asset Acceptance Corp. Alternative Loan Trust REMIC, 6.00%, 03/25/47 (a) |

| 168,712 |

| ||

385,960 |

| Option One Mortgage Loan Trust Asset-Backed Certificates REMIC, 0.36%, 12/25/35 (a) |

| 380,002 |

| ||

346,503 |

| Origen Manufactured Housing Contract Trust, 5.22%, 05/15/32 |

| 346,957 |

| ||

34,650 |

| Origen Manufactured Housing Contract Trust, 7.17%, 05/15/32 |

| 34,879 |

| ||

407,360 |

| Origen Manufactured Housing Contract Trust, 5.91%, 01/15/35 |

| 432,335 |

| ||

660,000 |

| Park Place Securities Inc. Asset-Backed Pass-Through Certificates REMIC, 1.13%, 10/25/34 (a) |

| 632,540 |

| ||

308,856 |

| Popular ABS Mortgage Pass-Through Trust REMIC, 4.61%, 05/25/35 (a) |

| 311,169 |

| ||

2,101 |

| Popular ABS Mortgage Pass-Through Trust REMIC, 4.62%, 05/25/35 (a) |

| 2,101 |

| ||

746,316 |

| Preferred Term Securities XII Ltd., 0.93%, 12/24/33 (a) (b) |

| 617,577 |

| ||

See accompanying Notes to Financial Statements.

Principal |

| Security |

| Value |

| ||

$ | 760,467 |

| Preferred Term Securities XIV Ltd., 0.71%, 06/24/34 (a) (b) |

| $ | 612,176 |

|

505,995 |

| Preferred Term Securities XXIV Ltd., 0.53%, 03/22/37 (a) (b) |

| 394,676 |

| ||

872,799 |

| Renaissance Home Equity Loan Trust REMIC, 4.50%, 08/25/35 |

| 879,622 |

| ||

158,146 |

| Residential Accredit Loans Inc. Trust REMIC, 5.50%, 01/25/34 |

| 161,543 |

| ||

83,178 |

| Residential Accredit Loans Inc. Trust REMIC, 6.00%, 10/25/34 |

| 86,942 |

| ||

199,610 |

| Residential Accredit Loans Inc. Trust REMIC, 5.50%, 02/25/35 |

| 197,951 |

| ||

850,000 |

| Residential Asset Mortgage Products Inc. Trust REMIC, 0.66%, 06/25/35 (a) |

| 783,504 |

| ||

112,357 |

| Residential Asset Mortgage Products Inc. Trust (insured by AMBAC Assurance Corp.) REMIC, 4.02%, 03/25/33 |

| 112,614 |

| ||

307,754 |

| Residential Asset Securities Corp. Trust REMIC, 5.96%, 09/25/31 |

| 314,796 |

| ||

214,194 |

| Residential Asset Securities Corp. Trust REMIC, 3.77%, 01/25/32 (a) |

| 214,956 |

| ||

271,228 |

| Residential Asset Securities Corp. Trust REMIC, 4.47%, 03/25/32 |

| 276,746 |

| ||

473,089 |

| Residential Asset Securities Corp. Trust REMIC, 3.87%, 05/25/33 |

| 482,803 |

| ||

139,168 |

| Residential Asset Securities Corp. Trust REMIC, 4.54%, 12/25/33 |

| 143,442 |

| ||

49,331 |

| Residential Asset Securities Corp. Trust REMIC, 0.34%, 03/25/36 (a) |

| 49,219 |

| ||

177,638 |

| SACO I Trust REMIC, 0.71%, 11/25/35 (a) |

| 176,397 |

| ||

255,059 |

| Springleaf Mortgage Loan Trust REMIC, 4.05%, 01/25/58 (a) (b) |

| 266,949 |

| ||

451,969 |

| Terwin Mortgage Trust REMIC, 3.08%, 11/25/35 (a) |

| 450,461 |

| ||

351,863 |

| Vanderbilt Acquisition Loan Trust REMIC, 7.33%, 05/07/32 |

| 381,612 |

| ||

454,988 |

| Vanderbilt Mortgage Finance REMIC, 6.57%, 08/07/24 |

| 463,699 |

| ||

560,504 |

| Vanderbilt Mortgage Finance, 5.84%, 02/07/26 |

| 570,871 |

| ||

905,000 |

| Vanderbilt Mortgage Finance, 6.96%, 09/07/31 |

| 931,839 |

| ||

698,700 |

| Wachovia Bank Commercial Mortgage Trust REMIC, 5.08%, 03/15/42 (a) |

| 715,888 |

| ||

402,000 |

| Wells Fargo Commercial Mortgage Trust REMIC, 2.53%, 10/15/45 |

| 395,609 |

| ||

205,743 |

| Wells Fargo Home Equity Asset-Backed Securities Trust REMIC, 0.53%, 12/25/35 (a) |

| 202,440 |

| ||

153,945 |

| Wells Fargo Home Equity Asset-Backed Securities Trust REMIC, 0.29%, 07/25/36 (a) |

| 152,489 |

| ||

|

|

|

|

|

| ||

Total Non-U.S. Government Agency Asset-Backed Securities (cost $28,260,336) |

| 28,769,869 |

| ||||

|

|

|

|

|

| ||

Corporate Bonds - 24.4% |

|

|

| ||||

Consumer Discretionary - 3.2% |

|

|

| ||||

880,000 |

| DIRECTV Holdings LLC, 2.40%, 03/15/17 |

| 899,346 |

| ||

360,000 |

| Goodyear Tire & Rubber Co., 6.50%, 03/01/21 |

| 392,400 |

| ||

285,000 |

| Hanesbrands Inc., 6.38%, 12/15/20 |

| 311,362 |

| ||

520,000 |

| Maytag Corp., 5.00%, 05/15/15 |

| 541,395 |

| ||

375,000 |

| Mohawk Industries Inc., 6.13%, 01/15/16 (c) |

| 405,000 |

| ||

860,000 |

| Newell Rubbermaid Inc., 2.05%, 12/01/17 |

| 862,607 |

| ||

|

|

|

| 3,412,110 |

| ||

Consumer Staples - 1.9% |

|

|

| ||||

825,000 |

| Cargill Inc., 1.90%, 03/01/17 (b) |

| 835,459 |

| ||

835,000 |

| Church & Dwight Co. Inc., 3.35%, 12/15/15 |

| 867,610 |

| ||

395,000 |

| Land O’Lakes Capital Trust I, 7.45%, 03/15/28 (b) |

| 385,125 |

| ||

|

|

|

| 2,088,194 |

| ||

Energy - 1.1% |

|

|

| ||||

615,000 |

| ConocoPhillips, 4.60%, 01/15/15 |

| 634,901 |

| ||

500,000 |

| Occidental Petroleum Corp., 1.75%, 02/15/17 |

| 506,683 |

| ||

|

|

|

| 1,141,584 |

| ||

Financials - 14.6% |

|

|

| ||||

735,000 |

| ACE INA Holdings Inc., 5.60%, 05/15/15 |

| 775,612 |

| ||

910,000 |

| American Express Bank FSB, 0.46%, 06/12/17 (a) |

| 903,691 |

| ||

900,000 |

| American Honda Finance Corp., 1.60%, 02/16/18 (b) |

| 890,799 |

| ||

860,000 |

| Bank of America Corp., 5.65%, 05/01/18 |

| 972,408 |

| ||

650,000 |

| Berkshire Hathaway Inc., 1.90%, 01/31/17 |

| 665,272 |

| ||

565,000 |

| Caterpillar Financial Services Corp., 1.63%, 06/01/17 |

| 569,728 |

| ||

905,000 |

| Citigroup Inc., 4.45%, 01/10/17 |

| 977,563 |

| ||

935,000 |

| CME Group Index Services LLC, 4.40%, 03/15/18 (b) |

| 1,012,591 |

| ||

290,000 |

| General Electric Capital Corp., 0.51%, 08/07/18 (a) |

| 286,597 |

| ||

340,000 |

| General Electric Capital Corp., 6.38%, 11/15/67 (a) |

| 374,000 |

| ||

See accompanying Notes to Financial Statements.

Principal |

| Security |

| Value |

| ||

$ | 440,000 |

| Genworth Financial Inc., 7.63%, 09/24/21 |

| $ | 542,089 |

|

725,000 |

| Hartford Financial Services Group Inc., 5.50%, 03/30/20 |

| 821,387 |

| ||

785,000 |

| JPMorgan Chase & Co., 7.90% (callable at 100 beginning 04/30/18) (d) |

| 887,050 |

| ||

510,000 |

| KeyBank NA, 4.95%, 09/15/15 |

| 538,346 |

| ||

680,000 |

| Metropolitan Life Global Funding I, 1.70%, 06/29/15 (b) |

| 688,996 |

| ||

800,000 |

| Morgan Stanley, 4.75%, 03/22/17 |

| 873,194 |

| ||

900,000 |

| Murray Street Investment Trust I, 4.65%, 03/09/17 |

| 972,264 |

| ||

670,000 |

| Pricoa Global Funding I, 0.44%, 06/24/16 (a) (b) |

| 665,794 |

| ||

140,000 |

| Regions Financial Corp., 7.75%, 11/10/14 |

| 145,891 |

| ||

585,000 |

| Regions Financial Corp., 2.00%, 05/15/18 |

| 573,507 |

| ||

650,000 |

| State Street Bank & Trust Co., 0.44%, 12/08/15 (a) |

| 649,319 |

| ||

780,000 |

| Wells Fargo & Co., 7.98% (callable at 100 beginning 03/15/18) (d) |

| 886,275 |

| ||

|

|

|

| 15,672,373 |

| ||

Industrials - 1.3% |

|

|

| ||||

745,000 |

| Textron Inc., 6.20%, 03/15/15 |

| 782,072 |

| ||

495,000 |

| Union Pacific Corp., 5.70%, 08/15/18 |

| 566,854 |

| ||

|

|

|

| 1,348,926 |

| ||

Information Technology - 0.6% |

|

|

| ||||

625,000 |

| CA Inc., 6.13%, 12/01/14 |

| 646,994 |

| ||

|

|

|

|

|

| ||

Materials - 0.4% |

|

|

| ||||

475,000 |

| Rio Tinto Finance USA Ltd., 8.95%, 05/01/14 (c) |

| 478,181 |

| ||

|

|

|

|

|

| ||

Telecommunication Services - 0.8% |

|

|

| ||||

350,000 |

| Crown Castle International Corp., 7.13%, 11/01/19 |

| 372,313 |

| ||

410,000 |

| Verizon Communications Inc., 3.65%, 09/14/18 |

| 436,576 |

| ||

|

|

|

| 808,889 |

| ||

Utilities - 0.5% |

|

|

| ||||

565,000 |

| Georgia Power Co., 3.00%, 04/15/16 |

| 589,947 |

| ||

|

|

|

|

|

| ||

Total Corporate Bonds (cost $25,742,609) |

| 26,187,198 |

| ||||

|

|

|

| ||||

Government and Agency Obligations - 44.5% |

|

|

| ||||

GOVERNMENT SECURITIES - 39.1% |

|

|

| ||||

Municipals - 4.0% |

|

|

| ||||

455,000 |

| City of Indianapolis, Indiana, 0.63%, 07/01/14 |

| 455,096 |

| ||

165,000 |

| City of Lincoln, Nebraska, 4.25%, 11/01/14 |

| 167,409 |

| ||

380,000 |

| City of Omaha, Nebraska, RB, 2.40%, 12/01/16 |

| 389,515 |

| ||

250,000 |

| Lincoln Airport Authority, 1.33%, 07/01/16 |

| 249,508 |

| ||

730,000 |

| Montana Board of Housing, 1.60%, 06/01/16 |

| 735,584 |

| ||

530,000 |

| Nebraska Investment Finance Authority, 0.90%, 03/01/15 |

| 532,602 |

| ||

600,000 |

| New York City Transitional Finance Authority, 3.02%, 02/01/16 |

| 624,702 |

| ||

325,000 |

| State of Mississippi, 2.63%, 11/01/16 |

| 339,635 |

| ||

760,000 |

| Tennessee Housing Development Agency, 0.50%, 07/01/14 |

| 760,479 |

| ||

|

|

|

| 4,254,530 |

| ||

Treasury Inflation Index Securities - 0.7% |

|

|

| ||||

715,325 |

| U.S. Treasury Inflation Indexed Note, 0.13%, 04/15/16 (e) |

| 734,716 |

| ||

|

|

|

|

|

| ||

U.S. Treasury Securities - 34.4% |

|

|

| ||||

14,525,000 |

| U.S. Treasury Note, 0.25%, 12/15/15 |

| 14,510,242 |

| ||

6,835,000 |

| U.S. Treasury Note, 1.75%, 05/31/16 |

| 7,017,091 |

| ||

13,560,000 |

| U.S. Treasury Note, 0.63%, 09/30/17 |

| 13,309,981 |

| ||

2,160,000 |

| U.S. Treasury Note, 1.25%, 01/31/19 |

| 2,116,800 |

| ||

|

|

|

| 36,954,114 |

| ||

U.S. GOVERNMENT MORTGAGE-BACKED SECURITIES - 5.4% |

|

|

| ||||

Federal Home Loan Mortgage Corp. - 0.8% |

|

|

| ||||

366,576 |

| Federal Home Loan Mortgage Corp. REMIC, 4.00%, 03/15/20 |

| 386,665 |

| ||

450,000 |

| Federal Home Loan Mortgage Corp. REMIC, 4.00%, 02/15/27 |

| 462,090 |

| ||

|

|

|

| 848,755 |

| ||

Federal National Mortgage Association - 4.6% |

|

|

| ||||

192,185 |

| Federal National Mortgage Association REMIC, 4.00%, 07/25/21 |

| 203,331 |

| ||

602,909 |

| Federal National Mortgage Association REMIC, 4.50%, 08/25/21 |

| 620,180 |

| ||

118,082 |

| Federal National Mortgage Association REMIC, 4.50%, 11/25/23 |

| 121,346 |

| ||

390,095 |

| Federal National Mortgage Association REMIC, 4.00%, 02/25/26 |

| 413,519 |

| ||

1,321,428 |

| Federal National Mortgage Association, 3.00%, 10/01/26 |

| 1,358,288 |

| ||

567,714 |

| Federal National Mortgage Association REMIC, 3.00%, 04/25/37 |

| 583,293 |

| ||

660,000 |

| Federal National Mortgage Association REMIC, 2.50%, 09/25/39 |

| 664,941 |

| ||

See accompanying Notes to Financial Statements.

Shares or |

| Security |

| Value |

| ||

$ | 869,412 |

| Federal National Mortgage Association REMIC, 3.50%, 05/25/41 |

| $ | 905,058 |

|

320,832 |

| Federal National Mortgage Association, Interest Only REMIC, 5.00%, 03/25/39 |

| 26,785 |

| ||

|

|

|

| 4,896,741 |

| ||

Total Government and Agency Obligations (cost $47,755,858) |

| 47,688,856 |

| ||||

|

|

|

| ||||

Preferred Stocks - 0.4% |

|

|

| ||||

550 |

| U.S. Bancorp, Series A, 3.50% (callable at 1,000 beginning on 05/05/14) (d) |

| 445,357 |

| ||

|

|

|

|

|

| ||

Total Preferred Stocks (cost $564,328) |

| 445,357 |

| ||||

|

|

|

| ||||

Short Term Investments - 3.5% |

|

|

| ||||

Investment Company - 3.5% |

|

|

| ||||

3,714,552 |

| Goldman Sachs Financial Square Funds, Treasury Obligations Fund, 0.01% (f) |

| 3,714,552 |

| ||

|

|

|

|

|

| ||

Total Short Term Investments (cost $3,714,552) |

| 3,714,552 |

| ||||

|

|

|

|

|

| ||

Total Investments - 99.6% (cost $106,037,683) |

| 106,805,832 |

| ||||

Other assets in excess of liabilities - 0.4% |

| 465,785 |

| ||||

NET ASSETS - 100% |

| $ | 107,271,617 |

| |||

(a) | Variable rate security. The rate reflected is the rate in effect at March 31, 2014. |

(b) | Rule 144A, Section 4(2) of the Securities Act of 1933 or other security which is restricted to resale to institutional investors. The Fund’s investment adviser has deemed these securities to be liquid based on procedures approved by Tributary Funds’ Board of Directors. |

(c) | The interest rate for this security is inversely affected by upgrades or downgrades to the credit rating of the issuer. |

(d) | Perpetual maturity security. |

(e) | U.S. Treasury inflation indexed note, par amount is adjusted for inflation. |

(f) | Dividend yield changes daily to reflect current market conditions. Rate was the quoted yield as of March 31, 2014. |

|

|

ABS | Asset Backed Security |

AMBAC | AMBAC Indemnity Corp. |

RB | Revenue Bond |

REMIC | Real Estate Mortgage Investment Conduit |

See accompanying Notes to Financial Statements.

SCHEDULES OF PORTFOLIO INVESTMENTS

March 31, 2014

INCOME FUND

Principal |

| Security |

| Value |

| ||

Non-U.S. Government Agency Asset-Backed Securities - 26.2% |

|

|

| ||||

$ | 1,348,000 |

| Banc of America Commercial Mortgage Inc. REMIC, 5.18%, 09/10/47 (a) |

| $ | 1,422,819 |

|

1,030,130 |

| Bayview Financial Mortgage Pass-Through Trust REMIC, 5.70%, 02/28/41 (a) |

| 1,061,068 |

| ||

144,751 |

| Bear Stearns Commercial Mortgage Securities Trust REMIC, 5.53%, 09/11/41 |

| 144,660 |

| ||

685,000 |

| Cabela’s Master Credit Card Trust, 2.71%, 02/17/26 (b) |

| 652,100 |

| ||

740,000 |

| Chase Issuance Trust, 1.15%, 01/15/19 |

| 740,135 |

| ||

124,262 |

| Chase Mortgage Finance Trust REMIC, 5.50%, 05/25/35 |

| 127,851 |

| ||

320,000 |

| Citibank Credit Card Issuance Trust, 5.65%, 09/20/19 |

| 364,726 |

| ||

539,564 |

| Citigroup Mortgage Loan Trust Inc. REMIC, 6.50%, 07/25/34 |

| 578,536 |

| ||

990,436 |

| Citigroup Mortgage Loan Trust Inc. REMIC, 4.00%, 01/25/35 (a) |

| 1,028,773 |

| ||

820,978 |

| Citigroup Mortgage Loan Trust Inc. REMIC, 0.30%, 08/25/36 (a) |

| 798,059 |

| ||

146,064 |

| Citigroup Mortgage Loan Trust Inc. REMIC, 0.30%, 10/25/36 (a) |

| 145,085 |

| ||

135,108 |

| Citimortgage Alternative Loan Trust REMIC, 5.25%, 03/25/21 |

| 137,116 |

| ||

225,542 |

| CNL Commercial Mortgage Loan Trust (insured by AMBAC Assurance Corp.) REMIC, 0.59%, 10/25/30 (a) (b) |

| 192,823 |

| ||

319,973 |

| Countrywide Asset-Backed Certificates REMIC, 4.46%, 10/25/35 (a) |

| 320,676 |

| ||

250,029 |

| Countrywide Asset-Backed Certificates REMIC, 0.33%, 07/25/36 (a) |

| 243,160 |

| ||

76,703 |

| Credit Suisse First Boston Mortgage Securities Corp. REMIC, 5.00%, 08/25/20 |

| 76,675 |

| ||

107,655 |

| Credit Suisse First Boston Mortgage Securities Corp. REMIC, 5.75%, 04/25/33 |

| 114,994 |

| ||

282,136 |

| Credit-Based Asset Servicing and Securitization LLC REMIC, 1.28%, 02/25/33 (a) |

| 260,562 |

| ||

231,252 |

| Credit-Based Asset Servicing and Securitization LLC REMIC, 5.75%, 12/25/37 (a) |

| 231,298 |

| ||

850,000 |

| Credit-Based Asset Servicing and Securitization LLC REMIC, 6.02%, 12/25/37 (a) |

| 904,197 |

| ||

455,000 |

| Ford Credit Floorplan Master Owner Trust, 3.50%, 01/15/19 |

| 478,475 |

| ||

500,000 |

| Goldman Sachs Alternative Mortgage Products Trust REMIC, 0.80%, 03/25/34 (a) |

| 497,740 |

| ||

575,000 |

| GS Mortgage Securities Trust REMIC, 3.65%, 03/10/44 (b) |

| 602,234 |

| ||

309,461 |

| GSAMP Trust REMIC, 0.36%, 01/25/36 (a) |

| 300,394 |

| ||

324,531 |

| Irwin Whole Loan Home Equity Trust REMIC, 1.25%, 11/25/28 (a) |

| 323,347 |

| ||

798,614 |

| Irwin Whole Loan Home Equity Trust REMIC, 0.62%, 12/25/29 (a) |

| 765,749 |

| ||

480,000 |

| JPMorgan Chase Commercial Mortgage Securities Trust REMIC, 2.67%, 01/15/46 |

| 489,873 |

| ||

860,000 |

| JPMorgan Mortgage Acquisition Trust REMIC, 0.38%, 07/25/36 (a) |

| 756,514 |

| ||

10,756 |

| MASTR Asset Securitization Trust REMIC, 5.25%, 11/25/35 |

| 10,765 |

| ||

784,064 |

| Morgan Stanley Capital I Trust REMIC, 3.22%, 07/15/49 |

| 818,200 |

| ||

339,162 |

| Nomura Asset Acceptance Corp. Alternative Loan Trust REMIC, 0.83%, 06/25/35 (a) |

| 332,659 |

| ||

240,986 |

| Nomura Asset Acceptance Corp. Alternative Loan Trust REMIC, 6.00%, 03/25/47 (a) |

| 182,772 |

| ||

300,000 |

| NovaStar Mortgage Funding Trust REMIC, 1.80%, 03/25/35 (a) |

| 295,215 |

| ||

421,047 |

| Option One Mortgage Loan Trust Asset-Backed Certificates REMIC, 0.36%, 12/25/35 (a) |

| 414,548 |

| ||

497,885 |

| Origen Manufactured Housing Contract Trust, 5.91%, 01/15/35 |

| 528,410 |

| ||

86,098 |

| Park Place Securities Inc. Asset-Backed Pass-Through Certificates REMIC, 1.08%, 10/25/34 (a) |

| 86,078 |

| ||

793,164 |

| Preferred Term Securities XII Ltd., 0.93%, 12/24/33 (a) (b) |

| 656,343 |

| ||

760,467 |

| Preferred Term Securities XIV Ltd., 0.71%, 06/24/34 (a) (b) |

| 612,176 |

| ||

973,929 |

| Preferred Term Securities XXI Ltd., 0.88%, 03/22/38 (a) (b) (c) |

| 465,051 |

| ||

494,667 |

| Preferred Term Securities XXIV Ltd., 0.53%, 03/22/37 (a) (b) |

| 385,840 |

| ||

647,279 |

| Renaissance Home Equity Loan Trust REMIC, 4.50%, 08/25/35 |

| 652,339 |

| ||

165,498 |

| Residential Accredit Loans Inc. Trust REMIC, 5.50%, 01/25/34 |

| 169,053 |

| ||

410,756 |

| Residential Accredit Loans Inc. Trust REMIC, 6.00%, 10/25/34 |

| 429,342 |

| ||

134,465 |

| Residential Accredit Loans Inc. Trust REMIC, 5.50%, 02/25/35 |

| 133,348 |

| ||

See accompanying Notes to Financial Statements.

Principal |

| Security |

| Value |

| ||

$ | 467,602 |

| Residential Asset Mortgage Products Inc. Trust REMIC, 5.63%, 01/25/34 |

| $ | 497,163 |

|

870,000 |

| Residential Asset Mortgage Products Inc. Trust REMIC, 0.66%, 06/25/35 (a) |

| 801,939 |

| ||

163,858 |

| Residential Asset Mortgage Products Inc. Trust (insured by AMBAC Assurance Corp.) REMIC, 4.02%, 03/25/33 |

| 164,233 |

| ||

258,514 |

| Residential Asset Securities Corp. Trust REMIC, 5.96%, 09/25/31 |

| 264,429 |

| ||

252,305 |

| Residential Asset Securities Corp. Trust REMIC, 4.47%, 03/25/32 |

| 257,438 |

| ||

139,168 |

| Residential Asset Securities Corp. Trust REMIC, 4.54%, 12/25/33 |

| 143,442 |

| ||

203,955 |

| SACO I Trust REMIC, 0.71%, 11/25/35 (a) |

| 202,530 |

| ||

304,324 |

| Structured Asset Securities Corp. REMIC, 1.20%, 11/25/34 (a) |

| 284,932 |

| ||

56,319 |

| Structured Asset Securities Corp. (insured by MBIA Assurance Corp.) REMIC, 5.80%, 09/25/33 (a) |

| 57,895 |

| ||

940,396 |

| Vanderbilt Acquisition Loan Trust REMIC, 7.33%, 05/07/32 |

| 1,019,904 |

| ||

256,048 |

| Vanderbilt Mortgage Finance, 5.84%, 02/07/26 |

| 260,784 |

| ||

675,000 |

| Vanderbilt Mortgage Finance, 6.96%, 09/07/31 |

| 695,018 |

| ||

795,000 |

| Wells Fargo Commercial Mortgage Trust REMIC, 2.53%, 10/15/45 |

| 782,361 |

| ||

388,154 |

| Wells Fargo Home Equity Asset-Backed Securities Trust REMIC, 0.53%, 12/25/35 (a) |

| 381,923 |

| ||

92,310 |

| Wells Fargo Home Equity Asset-Backed Securities Trust REMIC, 0.29%, 07/25/36 (a) |

| 91,437 |

| ||

174,666 |

| Wells Fargo Mortgage Backed Securities Trust REMIC, 5.00%, 11/25/36 |

| 180,408 |

| ||

625,000 |

| Wells Fargo-RBS Commercial Mortgage Trust REMIC, 2.63%, 03/15/45 |

| 612,906 |

| ||

485,000 |

| Wells Fargo-RBS Commercial Mortgage Trust REMIC, 2.19%, 04/15/45 |

| 495,919 |

| ||

Total Non-U.S. Government Agency Asset-Backed Securities (cost $27,066,828) |

| 27,126,439 |

| ||||

Corporate Bonds - 22.0% |

|

|

| ||||

Consumer Discretionary - 2.3% |

|

|

| ||||

525,000 |

| DIRECTV Holdings LLC, 3.80%, 03/15/22 |

| 519,572 |

| ||

300,000 |

| Goodyear Tire & Rubber Co., 6.50%, 03/01/21 |

| 327,000 |

| ||

290,000 |

| Hanesbrands Inc., 6.38%, 12/15/20 |

| 316,825 |

| ||

325,000 |

| Mohawk Industries Inc., 6.13%, 01/15/16 (d) |

| 351,000 |

| ||

375,000 |

| Newell Rubbermaid Inc., 4.70%, 08/15/20 |