UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08932

Artisan Funds, Inc.

(Exact name of registrant as specified in charter)

875 East Wisconsin Avenue, Suite 800

Milwaukee, WI 53202

(Address of principal executive offices)

| | |

| Janet D. Olsen | | Kevin J. McCarthy |

| Artisan Funds, Inc. | | Bell, Boyd & Lloyd LLC |

| 875 East Wisconsin Avenue, #800 | | Three First National Plaza, #3100 |

| Milwaukee, Wisconsin 53202 | | Chicago, IL 60602 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (414) 390-6100

Date of fiscal year end: 09/30/06

Date of reporting period: 03/31/06

Item 1. Reports to Shareholders.

SEMIANNUAL

R E P O R T

MARCH 31, 2006

ARTISAN INTERNATIONAL FUND

ARTISAN INTERNATIONAL SMALL CAP FUND

ARTISAN INTERNATIONAL VALUE FUND

ARTISAN MID CAP FUND

ARTISAN MID CAP VALUE FUND

ARTISAN OPPORTUNISTIC VALUE FUND

ARTISAN SMALL CAP FUND

ARTISAN SMALL CAP VALUE FUND

ARTISAN FUNDS, INC.

INVESTOR SHARES

ARTISAN FUNDS

P.O. BOX 8412

BOSTON, MA 02266-8412

This report and the unaudited financial statements contained herein are provided for the general information of the shareholders of Artisan Funds. Before investing, investors should consider carefully each Fund’s investment objective, risks and charges and expenses. For a prospectus, which contains that information and more information about each Fund, please call 800.344.1770 or visit our website at www.artisanfunds.com. Read it carefully before you invest or send money.

Company discussions are for illustration only and are not intended as recommendations of individual stocks. The discussions present information about the companies believed to be accurate, and the views of the portfolio managers, as of March 31, 2006. That information and those views may change, and the Funds disclaim any obligation to advise shareholders of any such changes. Artisan International Fund and Artisan Mid Cap Fund offer institutional classes of shares for institutional investors meeting certain minimum investment requirements. A report on each institutional class is available under separate cover.

Artisan Funds offered through Artisan Distributors LLC, member NASD.

TABLE OF CONTENTS

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/06)

| | | | | | | | | | | | | | | |

| | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan International Fund (inception 12/28/95) | | 29.32 | % | | 31.58 | % | | 8.90 | % | | 13.81 | % | | 14.40 | % |

Artisan International Small Cap Fund (inception 12/21/01) | | 40.92 | | | 45.72 | | | NA | | | NA | | | 28.90 | |

Artisan International Value Fund (inception 9/23/02) | | 23.69 | | | 39.11 | | | NA | | | NA | | | 33.30 | |

Artisan Mid Cap Fund (inception 6/27/97) | | 20.91 | | | 22.31 | | | 8.01 | | | NA | | | 18.64 | |

Artisan Mid Cap Value Fund (inception 3/28/01) | | 15.84 | | | 28.95 | | | 16.52 | | | NA | | | 16.66 | |

Artisan Small Cap Fund (inception 3/28/95) | | 26.39 | | | 29.52 | | | 12.05 | | | 8.35 | | | 10.94 | |

Artisan Small Cap Value Fund (inception 9/29/97) | | 19.11 | | | 29.24 | | | 17.49 | | | NA | | | 14.18 | |

Artisan Opportunistic Value Fund performance is not included above because it commenced operations on 3/27/06.

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in a Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The performance information shown for Artisan International Fund, Artisan International Small Cap Fund and Artisan International Value Fund does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. Artisan International Small Cap Fund’s investments in initial public offerings (IPOs) made a material contribution to the Fund’s performance. IPO investments are not an integral component of the Fund’s investment process and may not be available in the future.

Artisan International Fund, International Small Cap Fund & International Value Fund: International investments involve special risks, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems and higher transaction costs. These risks typically are greater in emerging markets. Artisan International Fund and International Small Cap Fund invest in growth stocks, which may underperform other asset types during a given period. Artisan International Small Cap Fund invests in the stocks of smaller companies, which tend to be more volatile and less liquid than those of larger companies, have underperformed the stocks of larger companies during some periods and tend to have a shorter history of operations than larger companies. Artisan International Value Fund invests in value stocks, which may underperform other asset types during a given period. In addition, the Fund may invest a significant portion of its assets in small and medium-sized companies, which tend to be more volatile and less liquid than those of large companies, have underperformed the stocks of larger companies during some periods and tend to have a shorter history of operations than larger companies.

Artisan Mid Cap Fund, Mid Cap Value Fund & Opportunistic Value Fund: Stocks of medium-sized companies tend to be more volatile than those of larger companies and have underperformed the stocks of small and large companies during some periods. Artisan Mid Cap Fund invests primarily in growth stocks, which may underperform other asset types during a given period. Artisan Mid Cap Value Fund and Artisan Opportunistic Value Fund invest primarily in value stocks, which may underperform other asset types during a given period.

Artisan Small Cap Fund & Small Cap Value Fund: Stocks of smaller companies tend to be more volatile and less liquid than those of larger companies, have underperformed the stocks of larger companies during some periods and tend to have a shorter history of operations than larger companies. Artisan Small Cap Fund invests primarily in growth stocks, which may underperform other asset types during a given period. Artisan Small Cap Value Fund invests primarily in value stocks, which may underperform other asset types during a given period.

ARTISAN INTERNATIONAL FUND (ARTIX)

| | |

| INVESTMENT PROCESS HIGHLIGHTS | | |

Artisan International Fund uses a fundamental stock selection process focused on identifying long-term growth opportunities. Themes. The investment team’s thematic approach identifies catalysts for change and develops investment themes with the objective of capitalizing on them globally. Changing demographics, developing technology, privatization of economic resources and outsourcing are among the long-term catalysts for change that currently form the basis for the team’s investment themes. The team incorporates these catalysts along with sector and regional fundamentals into a long-term global framework for investment analysis and decision-making. Sustainable Growth. The team applies a fundamental approach to identifying the long- term, sustainable growth characteristics of potential investments. The team seeks high quality companies that are well managed, have a dominant or improving market position and competitive advantages compared to industry and regional peers. Valuation. The team assesses the relationship between its estimate of a company’s sustainable growth prospects and its stock price. The team uses multiple valuation metrics to establish price targets. The Fund primarily invests in non-U.S. growth companies of all market capitalizations in developed and emerging markets. |

| | | |

| PERFORMANCE HISTORY | | |

| |

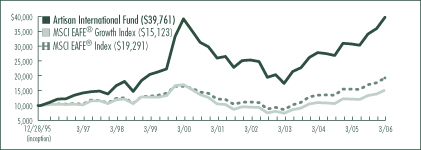

GROWTH OF AN ASSUMED $10,000 INVESTMENT (12/28/95 to 3/31/06)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/06)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan International Fund | | 29.32 | % | | 31.58 | % | | 8.90 | % | | 13.81 | % | | 14.40 | % |

MSCI EAFE® Growth Index | | 24.59 | | | 27.17 | | | 7.53 | | | 3.93 | | | 4.11 | |

MSCI EAFE® Index | | 24.41 | | | 31.13 | | | 9.63 | | | 6.49 | | | 6.62 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. See page 86 for a description of each index.

2

TWO

INVESTING ENVIRONMENT

The backdrop for international equities during the six months ended March 31, 2006 was quite favorable. In general, the growth of the global economy was strong and inflation remained subdued.

The U.S. dollar moved slightly higher versus a number of currencies during the period. The return of the MSCI EAFE® Index for dollar-based investors was 13.86% compared to the 15.88% local return.

Stocks in the financials, industrials, technology and materials sectors gained more than 20%. The price of oil flirted with $70 per barrel, but energy stocks ended the period slightly behind where they started. Telecommunications stocks also lost ground.

PERFORMANCE DISCUSSION

The Fund’s performance was hurt slightly by the increase in the U.S. dollar, but still gained 16.71% during the period, which compared well to the MSCI EAFE® Index. Good security selection was the primary source of the Fund’s relative advantage. Stock selection was particularly strong within our global financials and energy themes. The performance of the stocks in our consumer and media themes and our lack of investment in materials stocks hurt our return compared to the Index.

In our global financials theme, we experienced strong gains in many of our holdings. Three of the leading contributors were Japanese real estate and leasing company ORIX Corporation, Korean bank Kookmin Bank and German bank Commerzbank AG. Their stock prices increased roughly 72%, 46% and 46%, respectively.

In Japan, bank lending started to pick up, employment and wages were in a rising trend and the country seemed poised to end its bout with deflation. All of those factors helped support Japanese stocks in general. During the period, ORIX announced a nearly 50% increase in its full-year profit forecast and its leasing and lending businesses expanded while costs declined. Japanese financial companies Mizuho Financial Group, Inc. and Credit Saison Co., Ltd., also performed well.

Late in the period, Kookmin Bank announced that it was the preferred bidder for Korea Exchange Bank (KEB). The combined company is expected to have a large share of the total loan market in Korea, and should produce long-term cost and revenue synergies. Since the deal is expected to be additive to earnings, the news was well-received by the market. Prior to that announcement, Kookmin and our other Korean banks, Shinhan Financial Group Co., Ltd. and Hana Financial Group Inc. (formerly Hana Bank), were supported by asset quality improvements and reduced levels of non-performing loans.

TOP 10 HOLDINGS

| | | | | |

| Company Name | | Country | | 3/31/06 | |

Credit Saison Co., Ltd. | | Japan | | 3.6 | % |

UBS AG | | Switzerland | | 3.5 | |

ORIX Corp. | | Japan | | 2.7 | |

Fortis | | Netherlands | | 2.7 | |

LUKOIL | | Russia | | 2.7 | |

Sega Sammy Holdings, Inc. | | Japan | | 2.6 | |

Mizuho Financial Group, Inc. | | Japan | | 2.5 | |

Kookmin Bank | | South Korea | | 2.3 | |

Saipem S.p.A. | | Italy | | 2.2 | |

China Mobile (Hong Kong) Limited | | China | | 2.1 | |

Total | | | | 26.9 | % |

As a percentage of total net assets. Top 10 Holdings are determined by issuer.

Two drivers of Commerzbank’s share price performance were optimism about Germany’s economic environment and the company’s announced acquisition of Eurohypo AG. The Eurohypo acquisition was expected to add to earnings, due in part to cost savings. Other winners among our European financials included Swiss global investment services firm UBS AG and Dutch financial services companies Fortis and ING Groep N.V.

During the period, our energy stocks generally performed very well. Within the group, Russian oil producer LUKOIL was the largest contributor to our performance, gaining over 44%. We believe that its above average production rates and proven oil reserves were the reasons it did so well in a tough period for energy stocks. We realized some profits during the period by selling shares into strength, but LUKOIL remained a top ten position as of the end of the period.

3

THREE

Expectations for a surge in capital spending in the energy industry due to tight industry capacity, an aging fleet of rigs and a shortage of offshore rigs contributed to very positive sentiment for energy infrastructure companies. Those factors benefited our positions in Italy-based Saipem S.p.A. and Norwegian driller Acergy S.A. (formerly Stolt Offshore S.A.).

Canadian natural gas provider EnCana Corp. fell roughly 20% during the period, after announcing a drop in profits due to hedging contracts that did not allow the company to participate as much as it could have in the rise of natural gas prices.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/05 | | | 3/31/06 | |

Consumer Discretionary | | 23.6 | % | | 15.5 | % |

Consumer Staples | | 9.8 | | | 8.7 | |

Energy | | 8.7 | | | 9.3 | |

Financials | | 30.4 | | | 36.5 | |

Healthcare | | 4.1 | | | 4.6 | |

Industrials | | 8.0 | | | 11.1 | |

Information Technology | | 6.8 | | | 5.1 | |

Telecommunication Services | | 6.1 | | | 3.0 | |

Utilities | | 1.2 | | | 5.0 | |

Other assets less liabilities | | 1.3 | | | 1.2 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

Two other stocks that positively contributed to the Fund’s return were Siemens AG, a Germany-based conglomerate that manufactures a wide range of industrial and consumer products, and Singapore Airlines Ltd. During the period, Siemens announced the divestment of part of its technology services division, which had been a large drag on earnings. Singapore Airlines benefited from the strength of economic growth in the Far East and its relatively low exposure to competition from discount airlines.

The holdings in our consumer and media themes performed reasonably well, but their returns did not keep pace with similar holdings in the MSCI EAFE® Index. U.K. cruise operator Carnival PLC and Japanese cable and Internet service provider Jupiter Telecommunications Co., Ltd. were two stocks that underperformed. Carnival was hurt by concerns about slower bookings and a reduced earnings forecast. Jupiter Telecom fell in part due to concerns about competition from satellite providers and the potential for higher costs and a decline in profitability.

FUND CHANGES

We sold several securities in our consumer, media and communications themes during the period, while we made a number of new purchases in our energy and financials themes.

We pared back our communications theme because we became more concerned about competition due to the convergence of the various communications platforms. Among the stocks we sold were Telefonaktiebolaget LM Ericsson, Nortel Networks Corporation, Chunghwa Telecom Co., Ltd. and Singapore Telecommunications Limited.

Three of the largest sales in our consumer and media themes were U.K. companies Tesco PLC, a food retailer; British Sky Broadcasting Group PLC, a pay television provider; and ITV PLC, a television broadcaster.

In our energy theme, we added Norwegian driller SeaDrill Ltd. We also extended our energy theme and increased our exposure to the utilities sector. Our attraction to utilities in the medium-term was our belief that those companies could increase revenues at a faster pace than costs. This resulted in larger positions in German power producers RWE AG and E.ON AG and initial investments in Finland-based Fortum Oyj and Russia-based RAO Unified Energy System.

A few of the largest additions in our global financials theme were UniCredito Italiano S.p.A, an Italian bank; Mitsubishi UFJ Financial Group, Inc., a Japanese bank; Barclays PLC, a U.K. bank; Millea Holdings, Inc., a Japanese insurance company; and Wiener Staedtische Allgemeine Versicherung AG, an Austrian insurance company.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/05 | | | 3/31/06 | |

Europe | | 55.0 | % | | 54.5 | % |

Pacific Basin | | 25.2 | | | 28.6 | |

Emerging Markets | | 15.3 | | | 13.7 | |

Americas | | 3.2 | | | 2.0 | |

As a percentage of total net assets.

4

FOUR

ARTISAN INTERNATIONAL SMALL CAP FUND (ARTJX)

| | |

| INVESTMENT PROCESS HIGHLIGHTS | | |

Artisan International Small Cap Fund uses a fundamental stock selection process focused on identifying long-term growth opportunities among small non-U.S. companies. Themes. The investment team’s thematic approach identifies catalysts for change and develops investment themes with the objective of capitalizing on them globally. Changing demographics, developing technology, privatization of economic resources and outsourcing are among the long-term catalysts for change that currently form the basis for the team’s investment themes. The team incorporates these catalysts along with sector and regional fundamentals into a long-term global framework for investment analysis and decision-making. Sustainable Growth. The team applies a fundamental approach to identifying the long-term, sustainable growth characteristics of potential investments. The team seeks high quality companies that are well managed, have a dominant or improving market position and competitive advantages compared to industry and regional peers. Valuation. The team assesses the relationship between its estimate of a company’s sustainable growth prospects and its stock price. The team uses multiple valuation metrics to establish price targets. The Fund primarily invests in non-U.S. small-cap growth companies in developed and emerging markets with market capitalizations less than $3 billion at the time of investment. |

| | | |

| PERFORMANCE HISTORY | | |

| |

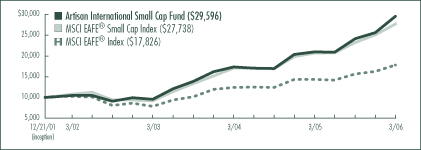

GROWTH OF AN ASSUMED $10,000 INVESTMENT (12/21/01 to 3/31/06)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/06)

| | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | Since

Inception | |

Artisan International Small Cap Fund | | 40.92 | % | | 45.72 | % | | 28.90 | % |

MSCI EAFE® Small Cap Index | | 33.79 | | | 44.73 | | | 26.96 | |

MSCI EAFE® Index | | 24.41 | | | 31.13 | | | 14.48 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. The Fund’s investments in initial public offerings (IPOs) made a material contribution to the Fund’s performance. IPO investments are not an integral component of the Fund’s investment process and may not be available in the future. See page 86 for a description of each index.

5

FIVE

INVESTING ENVIRONMENT

During the semiannual reporting period ended March 31, 2006, international small-cap stocks benefited from what we believe were three major global trends: an extremely favorable economic environment, a lack of inflationary pressure and increasing corporate restructuring leading to a strong wave of merger and acquisition activity.

All sectors in the MSCI EAFE® Small Cap Index advanced during the period. The leading areas were the materials, energy, financial and industrial sectors, all of which increased more than 20%. The U.S. dollar made a small gain over the six-month period ended March 31, 2006. As a result, the MSCI EAFE® Small Cap Index had a local return of 21.82%, while its dollar-based return was 19.23%.

PERFORMANCE DISCUSSION

The Fund returned 22.27% for the six-month period ended March 31, 2006. Outperformance relative to the MSCI EAFE® Small Cap Index was primarily the result of solid stock selection in the industrial and consumer discretionary sectors. Our overweight position and selection in our energy theme also contributed positively to performance. Our results compared to the Index were hindered by weakness in our healthcare and technology holdings.

Two of our leading contributors in the industrial sector were Metso Oyj and Schindler Holding, which posted share price gains of 52% and 37%, respectively. Metso, based in Finland, is the world’s largest manufacturer of rock-crushers and papermaking machinery. During the period, the company announced plans to acquire Aker Kvaerner ASA, a leader in the pulping and chemical recovery businesses. Metso also reported strong orders in both its paper and minerals divisions.

Schindler Holding AG, based in Switzerland, is the world’s leading manufacturer of escalators and the number two manufacturer of lifts. Schindler experienced strength in Europe, as demand for modernization propelled sales within the region.

Solid selection in our consumer theme was driven in part by the strong returns of real-estate developers Cyrela Brazil Realty S.A. Empreendimentos e Participacoes (Brazil), JM AB (Sweden) and Kaufman & Broad S. A. (France), which posted stock price gains of roughly 116%, 59% and 50%, respectively, generating a sizeable performance contribution. Cyrela Brazil reported a 66% increase in revenue partly due to the launch of several new projects and strong unit sales. JM AB benefited from strong demand in the Scandinavian residential market and increased housing prices. Likewise, Kaufman & Broad reported robust sales for both apartments and single-family homes.

In our energy theme, expectations for capital spending were high due to tight industry capacity, an aging fleet of rigs and a shortage of offshore rigs, all of which contributed to ongoing pricing power. We believe this greatly benefited our infrastructure providers during the period, such as Petroleum Geo-Services ASA and SeaDrill Ltd.

TOP 10 HOLDINGS

| | | | | |

| Company Name | | Country | | 3/31/06 | |

Buhrmann NV | | Netherlands | | 3.6 | % |

Petroleum Geo-Services ASA | | Norway | | 2.8 | |

Sulzer AG | | Switzerland | | 2.8 | |

Creed Corporation | | Japan | | 2.7 | |

Elekta AB | | Sweden | | 2.5 | |

Fraser & Neave Limited | | Singapore | | 2.4 | |

Japan Petroleum Exploration Company, Ltd. | | Japan | | 2.4 | |

Sibir Energy PLC | | United Kingdom | | 2.4 | |

Banco Latinoamericano de Exportaciones, S.A. | | Panama | | 2.2 | |

Commercial International Bank | | Egypt | | 2.0 | |

Total | | | | 25.8 | % |

As a percentage of total net assets. Top 10 Holdings are determined by issuer.

Petroleum Geo-Services is one of the world’s largest providers of oilfield-mapping services. The company pioneered the development of multi-streamer seismic acquisition, which produces efficient, high-quality 3D seismic data for the oil industry. In addition to good market conditions, the company announced plans to spin off its oil-production unit. We slightly trimmed our position into strength.

6

SIX

Drilling services provider SeaDrill completed its acquisition of Smedvig ASA (a holding we sold in January), another Norwegian driller.

Japanese real estate firms Creed Corporation and NTT Urban Development Corporation were two additional standout performers. Creed’s assets under management have increased substantially due in part to an increase in real estate acquisitions. NTT Urban Development’s success was partly due to near full occupancy of its buildings in Tokyo and strong profit growth in the company’s condominium business.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/05 | | | 3/31/06 | |

Consumer Discretionary | | 12.8 | % | | 8.6 | % |

Consumer Staples | | 4.4 | | | 3.8 | |

Energy | | 10.7 | | | 13.8 | |

Financials | | 24.6 | | | 30.9 | |

Healthcare | | 6.4 | | | 4.0 | |

Industrials | | 22.6 | | | 27.7 | |

Information Technology | | 5.4 | | | 1.9 | |

Materials | | 2.8 | | | 3.4 | |

Telecommunication Services | | 3.1 | | | 2.4 | |

Utilities | | 2.0 | | | 2.1 | |

Other assets less liabilities | | 5.2 | | | 1.4 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

In the healthcare and technology sectors, weakness in Straumann Holding AG, Q-Free ASA and Sammy NetWorks Co., Ltd. hindered the Fund’s relative performance. Swiss dental implant manufacturer Straumann experienced disappointing sales, partly due to weakness in Europe. Norway-based Q-Free, which is a leading supplier of electronic toll collection systems, experienced downward pressure on earnings, which was partly driven by higher costs, despite an increase in revenue. We sold our position. In the first three months of 2006, our Japanese stocks such as Japanese Internet game and entertainment content provider Sammy NetWorks were generally weaker due in part to the impact of allegations of accounting fraud and market manipulation against livedoor, a Japanese Internet services company.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/05 | | | 3/31/06 | |

Europe | | 49.2 | % | | 50.0 | % |

Pacific Basin | | 22.4 | | | 25.9 | |

Emerging Markets | | 22.0 | | | 21.1 | |

Americas | | 1.2 | | | 1.6 | |

As a percentage of total net assets.

FUND CHANGES

During the period, we increased our financial and industrial weights and reduced our consumer holdings.

Most of the change in our consumer allocation stemmed from the sales of certain media positions. Among those sold were Gruppo Editoriale L’Espresso S.p.A., Ipsos, JC Decaux S.A., John Fairfax Holdings Limited and NRJ Group. Other sales in the consumer sectors included French property developer Nexity, Spanish residential developer Fadesa Inmobiliaria, S.A. and Brazilian beauty products company Natura Cosmeticos S.A.

In the financial sector, our purchases included real estate firms (FJ Next Co., Ltd., Patrizia Immobilien AG, Pirelli & C. Real Estate S.p.A., Tian An China Investments Company Limited and Tokyu Community Corp.), insurance companies (SCOR and Toro Assicurazioni S.p.A. (De Agostini Group)) and capital market firms (Azimut Holding S.p.A., D. Carnegie & Co. AB, DAB Bank AG, Indiabulls Financial Services Ltd. and Korea Investment Holdings Co., Ltd.).

The increase to our industrial weighting resulted from the purchases of Japanese employment and staffing solutions firm Pasona Inc., Japanese construction companies Raito Kogyo Co., Ltd. and Sho-Bond Corporation, European machinery companies IMI PLC and Vossloh AG, the operating company of Austria’s Vienna International Airport, Flughafen Wien AG and French holding company Financiere Marc de Lacharriere SA (Fimalac), which is the parent company of Fitch Group Inc., the world’s third largest rating agency.

7

SEVEN

ARTISAN INTERNATIONAL VALUE FUND (ARTKX)

| | |

| INVESTMENT PROCESS HIGHLIGHTS | | |

Artisan International Value Fund uses a bottom-up investment process focused on identifying what the investment team believes are high quality, undervalued businesses that offer the potential for superior risk/reward outcomes. Undervaluation. Determining the intrinsic value of the business is the heart of the team’s research process. As long-term investors, it is the team’s core belief that valuation is the most crucial determinant of stock market return over the long-term. Business quality. The team seeks to invest in companies with a history of generating strong free cash flow, improving returns on capital and strong competitive positions in their industries. This criteria helps rule out businesses that are statistically cheap, but whose values are deteriorating over time. Financial strength. The team believes that investing in companies with strong balance sheets helps to reduce the potential for capital risk and provides company management the ability to build value when attractive opportunities are available. Shareholder-oriented management. The team’s research process attempts to identify management teams with a history of building value for shareholders. The Fund primarily invests in undervalued, non-U.S. companies of all market capitalizations in developed and emerging markets. |

| | | |

| PERFORMANCE HISTORY | | |

| |

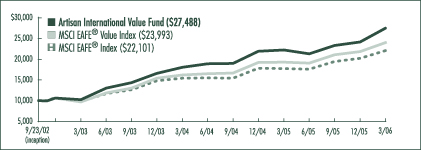

GROWTH OF AN ASSUMED $10,000 INVESTMENT (9/23/02 to 3/31/06)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/06)

| | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | Since

Inception | |

Artisan International Value Fund | | 23.69 | % | | 39.11 | % | | 33.30 | % |

MSCI EAFE® Value Index | | 24.25 | | | 35.08 | | | 28.25 | |

MSCI EAFE® Index | | 24.41 | | | 31.13 | | | 25.29 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. See page 86 for a description of each index.

8

EIGHT

INVESTING ENVIRONMENT

During the six-month period ended March 31, 2006, stock markets in virtually every country outside the U.S. increased. Among developed markets, Japanese equities led the rally with an advance of 24% in local currency terms. Germany, Switzerland and Sweden were also standouts as each returned at least 16% in local currency terms. Developed market currencies were generally weak compared to the U.S. dollar. As a result, U.S. dollar-based returns were slightly lower than local returns, but strong nonetheless.

PERFORMANCE DISCUSSION

Artisan International Value Fund increased 17.77% in the six months ended March 31, 2006, which compared favorably with the MSCI EAFE® Index, which increased 13.86%.

Four equities that made large positive contributions to the Fund’s performance were Euronext N.V., Pfeiffer Vacuum Technology AG, Heidelberger Druckmaschinen AG and Cementir S.p.A.

Euronext, which operates several European stock exchanges and the London International Financial Futures Exchange, performed well. Its stock price advanced more than 87%. During the period, there were many merger discussions surrounding Euronext and other listed European exchanges. Euronext looks to have played its cards very well and increased significantly. We have significantly reduced our position.

Pfeiffer Vacuum’s share price increased by over 34%. Pfeiffer is a German company that designs, manufactures and services a range of vacuum pumps used in a wide variety of applications including optical glass coating, semiconductor manufacturing, and scientific research. During the period, the company reported a record level of operating profits for its fiscal year ended December 31, 2005. In addition, the company announced a significant increase in its dividend.

Heidelberger Druckmaschinen, the world’s leading manufacturer of sheet-fed printing presses, outperformed, and its share price advanced nearly 29%. It rose in part due to strong earnings results, which were driven by demand from China. In addition, the company announced a significant share repurchase program.

Cementir, an Italian cement company, saw its share price increase roughly 46%. During the period, Cementir won the auction of a significant collection of cement assets in Turkey. The company also announced that its Italian cement operations are starting to recover. This resulted in higher earnings estimates, driving the share price to an all-time high.

Two of the worst performing equities in the portfolio during the period were Vodafone Group PLC and Premiere AG.

Vodafone, the world’s largest mobile telecommunications company, underperformed. Its share price declined by more than -19% during the period. On the positive side, operating results were solid and the company increased its share repurchase objective and dividend. The market, however, focused more on expected profitability declines due to increased competition and costs associated with the launch of third generation mobile services. The market took this information and some concerns over the Japanese division poorly, driving the stock back down to levels close to where we initially began purchasing shares. We took the opportunity to buy more shares.

TOP 10 HOLDINGS

| | | | | |

| Company Name | | Country | | 3/31/06 | |

Diageo PLC | | United Kingdom | | 4.9 | % |

Countrywide PLC | | United Kingdom | | 4.4 | |

Pfeiffer Vacuum Technology AG | | Germany | | 4.4 | |

Givaudan S.A. | | Switzerland | | 3.9 | |

Vodafone Group PLC | | United Kingdom | | 3.8 | |

Meitec Corporation | | Japan | | 3.5 | |

Uni-Charm Corporation | | Japan | | 3.3 | |

Tyco International Ltd. | | United States | | 3.3 | |

MFI Furniture Group PLC | | United Kingdom | | 3.0 | |

Benfield Group PLC | | United Kingdom | | 2.9 | |

Total | | | | 37.4 | % |

As a percentage of total net assets. Top 10 Holdings are determined by issuer.

During the period, we became small shareholders of Premiere. Premiere is the leading provider of pay television in Germany and Austria. At the time of initial purchase, the company dominated the ownership of

9

NINE

premium content, such as movies and sporting events, which is a key competitive advantage in this business. Unfortunately, during a recent auction, management made what looked to be a miscalculation and lost a bid for arguably its most important content, the German Bundesliga soccer matches. As a result, the share price suffered a sizeable decline. We sold our shares at a loss.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/05 | | | 3/31/06 | |

Consumer Discretionary | | 21.1 | % | | 23.7 | % |

Consumer Staples | | 14.4 | | | 16.7 | |

Financials | | 24.3 | | | 19.6 | |

Healthcare | | 2.6 | | | — | |

Industrials | | 12.5 | | | 14.8 | |

Information Technology | | 1.6 | | | 3.5 | |

Materials | | 10.8 | | | 8.6 | |

Telecommunication Services | | 4.7 | | | 4.7 | |

Utilities | | 1.6 | | | — | |

Other assets less liabilities | | 6.4 | | | 8.4 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

FUND CHANGES

We exited nine companies since our last report on September 30, 2005. The list of those sold included Olympus Corporation, Zinifex Ltd., Samchully Co., Ltd., Zehnder Group AG, Admiral Group PLC, Rotork PLC, Hunter Douglas N.V. and RADVision Ltd. Each stock reached or exceeded our estimate of fair value.

Proceeds from our sales were used in part to purchase shares in 11 companies. Tyco International Ltd., GUS PLC, Grupo Modelo, S.A. de C.V. and Amdocs Limited were among our largest additions. As of March 31, 2006, those companies represented 3.3%, 1.9%, 1.8% and 1.7% of the portfolio, respectively.

Tyco is a Bermuda-based conglomerate that was a stock market darling in the late 1990s. The stock collapsed in 2002, however, when an investigation began into the company’s accounting practices. Under the current CEO Edward Breene, the company has reduced debt, simplified the organization and consolidated businesses that former management had hastily acquired. We believed the shares were significantly undervalued.

GUS PLC is a U.K.-based conglomerate operating in retail (Argos) and credit information services (Experian) and, before its spinoff of Burberry, luxury goods. The company has committed to splitting up its unrelated retail and credit operations. At purchase, we were particularly enthusiastic about the credit information business, Experian. We believe it is a high growth business operating in an industry with significant barriers to entry and it has had very attractive operating profit margins.

Grupo Modelo is a Mexico-based brewing company. It has held a more than 50% share of the Mexican beer market and has been the largest exporter of beer, with its popular Corona® brand, to the United States. In recent years, Modelo has restructured its distribution operations, consolidating centers and routes, allowing the company to update equipment and machinery, thus creating efficiencies in product distribution. We purchased the shares at what we believed was an attractive valuation that not only discounted the company’s cash flow stream, but also failed to recognize the considerable value in the company’s balance sheet, which had more than $1.5 billion in net cash.

Amdocs is a leading provider of customer care and billing software to the telecommunications industry. We owned shares in this company several years ago and sold them in 2003 when they hit our fair value estimate. When the stock price fell to a meaningful discount to our fair value estimate, we once again became shareholders.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/05 | | | 3/31/06 | |

Europe | | 64.4 | % | | 61.0 | % |

Pacific Basin | | 17.4 | | | 13.5 | |

Americas | | 5.7 | | | 10.5 | |

Emerging Markets | | 6.1 | | | 6.6 | |

As a percentage of total net assets.

10

TEN

ARTISAN MID CAP FUND (ARTMX)

| | |

| INVESTMENT PROCESS HIGHLIGHTS | | |

Artisan Mid Cap Fund uses a bottom-up investment process to construct a diversified portfolio of U.S. mid-cap growth companies. Security Selection. The team’s investment process begins by identifying companies that possess franchise characteristics (strong competitive positions), selling at attractive valuations and benefiting from an accelerating trend. The investment team looks for companies that are well positioned for long-term growth, driven by demand for their products and services, at an early enough stage in their profit cycle to benefit from the increased cash flows produced by the profit cycle. Capital Allocation. Based on the investment team’s fundamental analysis of a company’s profit cycle, portfolio holdings develop through three stages. GardenSM investments are small positions in the early part of their profit cycle that will warrant a more sizeable allocation once their profit cycle accelerates. CropSM investments are positions that are being increased to a full weight because they are moving through the strongest part of their profit cycle. HarvestSM investments are positions that are being reduced as they near the team’s estimate of full valuation or their profit cycle begins to decelerate. Broad Diversification. The team looks for investment opportunities across the entire economy so that it can find sustainable growth regardless of the sector or industry. The Fund primarily invests in medium-sized U.S. growth companies. The Fund generally maintains median and weighted average market capitalizations of less than $10 billion. |

| | | |

| PERFORMANCE HISTORY | | |

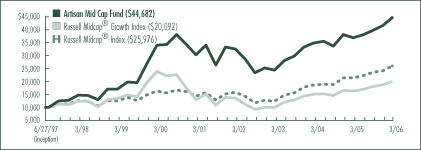

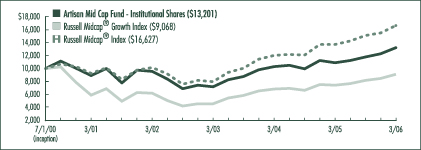

GROWTH OF AN ASSUMED $10,000 INVESTMENT (6/27/97 to 3/31/06)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/06)

| | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | Since

Inception | |

Artisan Mid Cap Fund | | 20.91 | % | | 22.31 | % | | 8.01 | % | | 18.64 | % |

Russell Midcap® Growth Index | | 22.68 | | | 25.75 | | | 8.99 | | | 8.29 | |

Russell Midcap® Index | | 21.54 | | | 27.87 | | | 12.52 | | | 11.51 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 86 for a description of each index.

11

ELEVEN

INVESTING ENVIRONMENT

During the six months ended March 31, 2006, returns generally increased the further you went down the market cap spectrum. The large-cap Russell Top 200® Index gained 5.32%, the Russell Midcap® Index increased 10.14% and the small-cap Russell 2000® Index moved 15.23% higher.

During the period, the Federal Reserve remained on its path to higher interest rates, but the country’s economic performance was generally solid, which was seen in the encouraging sales and profit growth reported by most parts of the economy.

In the Russell Midcap® Index, the best performing sectors were materials, transportation and technology. The energy and utilities sectors were the only groups to post losses, and they were small, at less than 2% each.

PERFORMANCE DISCUSSION

The Fund gained 12.29% during the period, outperforming the Russell Midcap® and Russell Midcap® Growth indices which returned 10.14% and 11.32%, respectively. The main source of our advantage compared to both benchmarks was good security selection. Three areas of particular strength were our healthcare, financial and energy-related stocks, though our performance gains were fairly broad and we had a number of winners in other groups. Relative to the benchmarks, we did not keep pace in the consumer discretionary and technology sectors.

The leading contributor among our healthcare holdings was radiation therapy systems supplier Varian Medical Systems, Inc., the stock price of which increased more than 42%. It reported strong financial results highlighted by impressive growth in orders for the company’s next generation systems in the U.S. and its legacy systems overseas. Drug wholesaler AmerisourceBergen Corporation (ABC) and specialty pharmaceutical company Allergan, Inc. also posted good returns. ABC has been transitioning to a fee-for-services model for drug distribution that has increased cash on hand for share buybacks and debt refinancing. That transition and the strength of its specialty pharmaceutical business supported a strong improvement in earnings. Allergan benefited from the strength of its Botox® brand and expectations for a solid pipeline of new opportunities.

Two of our best performers in the financial sector were student loan outsourcer The First Marblehead Corporation (FMD) and online bill pay software company CheckFree Corporation. FMD extended its relationship with its largest client and announced a sizeable increase in earnings on strong growth in service revenues. CheckFree illustrated the strength of its profit cycle by raising its expectations for future earnings as revenues per transaction increased and e-bill volumes grew.

TOP 10 HOLDINGS

| | | |

| Company Name | | 3/31/06 | |

Smith International, Inc. | | 2.7 | % |

Precision Castparts Corp. | | 2.1 | |

Varian Medical Systems, Inc. | | 2.0 | |

Fisher Scientific International Inc. | | 1.9 | |

Ecolab Inc. | | 1.9 | |

Juniper Networks, Inc. | | 1.8 | |

Electronic Arts Inc. | | 1.8 | |

McDermott International, Inc. | | 1.7 | |

Aon Corporation | | 1.7 | |

Freescale Semiconductor, Inc. | | 1.7 | |

Total | | 19.3 | % |

As a percentage of total net assets. Top 10 Holdings are determined by issuer

Our energy related investments have generally been centered around those companies that we believed were poised to benefit from a lengthy cycle of renewed global spending on energy development and infrastructure. This positioning helped the portfolio in two ways. First, it kept our allocation to crude producers low and crude producers generally declined during the period. Second, it led us to a number of energy infrastructure providers that outperformed. Smith International, Inc., our largest holding as of March 31, 2006, was one of those stocks. Smith International is a worldwide supplier of products and services to the oil and gas exploration and production industry and is a dominant market player in both drill bits and drilling fluids. It benefited from strong earnings growth, positive expectations for increased spending on exploration due to faster depletion rates of existing wells and longer contract terms.

12

TWELVE

Other energy related holdings that performed well included Cooper Cameron Corporation, a leading manufacturer of pressure control systems, equipment and services for oil and gas drilling and production, and worldwide energy services company McDermott International, Inc. Cooper Cameron reported solid earnings supported by an increase in backlog and strong order flow. McDermott International’s marine construction business was expected to benefit from resurgence in offshore drilling activity, and its power generation business from the potential for tighter emissions standards.

Mining equipment provider Joy Global Inc. and logistics company Expeditors International of Washington, Inc. (EXPD) were part of a list of holdings in other sectors that generated solid returns. As a result of the commodities boom, Joy Global has seen aftermarket orders increase at double-digit rates for almost three years. During the period, it reported strong revenues and earnings while further increasing forward estimates. EXPD also reported earnings ahead of expectations on significantly higher revenues and better profit margins.

Our results in the consumer discretionary sector were negatively impacted by weakness in leading Internet media company Yahoo! Inc. and stock photography company Getty Images, Inc. Our investment in Yahoo! has been based on our belief that the company was positioned well over the long-term to benefit from the transition of advertising dollars from offline media to the Internet. However, competition in its Internet search business put pressure on revenues creating some short-term concerns. Getty has a dominant position in the visual content industry, but it was hurt by a revenue report that disappointed the market. We added to our position in Getty on weakness.

In the technology sector, we had a number of strong performers including Network Appliance, Inc., Jabil Circuit, Inc. and Corning Incorporated. However, our results compared to the benchmarks were negatively impacted by disappointments in stocks such as Juniper Networks, Inc. and Intermec, Inc. Juniper Networks, which makes equipment that directs Internet traffic, was hurt by a revenue forecast that disappointed the market. We purchased additional shares on weakness. Intermec, a leading manufacturer of automatic data capture technologies such as bar code and RFID (radio frequency identification) solutions, was hurt in part by higher operating expenses stemming from RFID marketing. We increased the size of our position.

FUND CHANGES

The healthcare sector fell the most as a percentage of portfolio assets due to sales. Our three largest sales in the area were Aetna Inc., healthcare insurance; Caremark Rx, Inc., pharmacy benefit management; and MedImmune, Inc., a biotechnology company with a focus on respiratory diseases. Other significant sales during the period included payroll processor Paychex, Inc. and cruise operator Royal Caribbean Cruises Ltd.

Five of our largest purchases were Advanced Micro Devices, Inc., one of the largest suppliers of computing processors; Investors Financial Services Corp., which provides an array of complex processing services for mutual funds, investment advisors and banks; Alliance Data Systems Corporation, a transaction processing, credit and marketing services provider; Cooper Industries, Ltd., a global manufacturer of tools and electrical products; and Trimble Navigation Limited, a leading innovator of Global Positioning System technology.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/05 | | | 3/31/06 | |

Auto & Transportation | | 0.9 | % | | 2.4 | % |

Consumer Discretionary | | 17.8 | | | 19.2 | |

Consumer Staples | | 2.8 | | | 1.3 | |

Financial Services | | 11.3 | | | 12.4 | |

Healthcare | | 19.6 | | | 17.7 | |

Materials & Processing | | 7.0 | | | 7.3 | |

Other | | 3.8 | | | 2.6 | |

Other Energy | | 6.8 | | | 5.8 | |

Producer Durables | | 6.7 | | | 4.9 | |

Technology | | 19.0 | | | 21.9 | |

Utilities | | 1.7 | | | 2.6 | |

Other assets less liabilities | | 2.6 | | | 1.9 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

13

THIRTEEN

ARTISAN MID CAP VALUE FUND (ARTQX)

| | |

| INVESTMENT PROCESS HIGHLIGHTS | | |

Artisan Mid Cap Value Fund uses a bottom-up investment process to construct a diversified portfolio of U.S. mid-cap value companies that the investment team believes are undervalued, in sound financial condition and have attractive business economics. Attractive valuation. The team values a business using what it believes are reasonable expectations for the long-term earnings power and capitalization rates of that business. This results in a range of values for the company that the team believes would be reasonable. The team generally will purchase a security if the stock price falls below or toward the lower end of that range. Sound financial condition. The team favors companies with an acceptable level of debt and positive cash flow. At a minimum, the team tries to avoid companies that have so much debt that management may be unable to make decisions that would be in the best interests of the companies’ shareholders. Attractive business economics. The team favors cash-producing businesses that it believes are capable of earning acceptable returns on capital over the company’s business cycle. The team believes companies with these characteristics are less likely to experience eroding values over the long-term. The Fund primarily invests in U.S. securities with market capitalizations between $1.5 billion and $10 billion at the time of purchase. |

| | | |

| PERFORMANCE HISTORY | | |

GROWTH OF AN ASSUMED $10,000 INVESTMENT (3/28/01 to 3/31/06)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/06)

| | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | Since

Inception | |

Artisan Mid Cap Value Fund | | 15.84 | % | | 28.95 | % | | 16.52 | % | | 16.66 | % |

Russell Midcap® Value Index | | 20.30 | | | 29.23 | | | 14.69 | | | 15.01 | |

Russell Midcap® Index | | 21.54 | | | 27.87 | | | 12.52 | | | 12.72 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 86 for a description of each index.

14

FOURTEEN

INVESTING ENVIRONMENT

The six-months ended March 31, 2006 was a strong period for mid-cap stocks as the Russell Midcap® Value and Russell Midcap® indices increased 9.06% and 10.14%, respectively. During the period, market participants priced most sectors in the Russell Midcap® Value Index higher, but the Index was held back by weakness in energy and utility stocks.

PERFORMANCE DISCUSSION

The Fund increased 5.44% during the semiannual period ended March 31, 2006. It was generally supported by the returns of our consumer discretionary and technology stocks during the period. Conversely, our outsized position and selection in energy stocks and selection in the financial sector dragged down returns relative to the Russell Midcap® Value Index.

Claire’s Stores, Inc., Furniture Brands International, Inc., Rent-A-Center, Inc., BEA Systems, Inc. and Ryder System, Inc. were stocks that had a significant positive impact on the portfolio over the six-month period ended March 31, 2006.

Teenage fashion accessory retailer Claire’s Stores increased roughly 50% during the period, contributing positively to our performance. Claire’s Stores benefited from strong sales, particularly in its jewelry category, and announced a share repurchase program. We cut back our position as it entered our target selling range.

Furniture Brands International is one of the largest U.S.-based furniture manufacturers and markets products under brand names such as Broyhill®, Lane®, Thomasville® and Drexel Heritage®. Furniture Brands’ stock struggled in the quarters leading up to September 30, 2005, but reversed course as sentiment improved. During the period, Furniture Brands saw improving sales of its high-end Thomasville® brand, and the company used its strong cash flow to repurchase shares.

Rent-A-Center is the largest rent-to-own operator in the United States with a market share of approximately 38%. Its strong cash flow generation, share repurchase program and relatively low valuation made it an attractive investment. Rent-A-Center reported solid financial results during the period partly due to improving sales trends, which were helped by increased store traffic and promotional offers. Over the past year, the rent-to-own retailer began to benefit from its roll out of larger sized flat panel televisions, such as 42-inch plasma TVs, which grew in popularity among consumers.

Infrastructure software company BEA Systems advanced over 45% during the period, contributing positively to the Fund’s performance. The company benefited from strong sales of its AquaLogicTM platform and double-digit gains in license revenue. We trimmed our position as the stock entered our target selling range.

TOP 10 HOLDINGS

| | | |

| Company Name | | 3/31/06 | |

The Student Loan Corporation | | 4.3 | % |

Nuveen Investments, Inc. | | 3.5 | |

Alleghany Corporation | | 3.1 | |

Pioneer Natural Resources Company | | 3.1 | |

Ryder System, Inc. | | 2.9 | |

White Mountains Insurance Group, Ltd. | | 2.8 | |

Zale Corporation | | 2.7 | |

Avnet, Inc. | | 2.6 | |

Rent-A-Center, Inc. | | 2.6 | |

Liz Claiborne Inc. | | 2.5 | |

Total | | 30.1 | % |

As a percentage of total net assets. Top 10 Holdings are determined by issuer.

Ryder System tacked on an approximate 30% gain during the period. It operates three divisions: Fleet Management Solutions, Supply Chain Solutions and Dedicated Contract Carriage. Ryder has been in a turnaround phase and investments made by the company have weighed on cash flows. During the period, Ryder’s share price surged due in part to a pick up in truck leasing revenues and a strong improvement in margins.

Our outsized investment in energy names worked against us over the past six months, but much of our underperformance came from one name, Pioneer Natural Resources Company. The stock declined in early February after Pioneer reported a significant decline in production. The stock recovered some of its losses later in the period due to takeover speculation.

15

FIFTEEN

Within the financials sector, our underperformance could be partly attributed to our minimal investment in REITs and to weakness in check printing company Deluxe Corporation and tax preparation company H&R Block, Inc. In the Russell Midcap® Value Index, REITs gained over 17% during the period. We continued to believe that the REIT industry had a relatively poor risk/reward tradeoff and kept our investment to a minimum.

Deluxe continued to face pricing pressure and lower demand during the period. A lawsuit filed against H&R Block for fraudulent marketing created headline risk that caused the stock to decline sharply during the period. On the positive side, the company reported better than expected results for the tax season. We added to our position on weakness.

Elsewhere in the portfolio, weakness in computer printer manufacturer Lexmark International, Inc. and auto components manufacturer Lear Corporation hindered the Fund’s relative performance. Lexmark was impacted by acceleration in the competitive landscape of the printer industry. In response, management initiated price cuts to attempt to slow a decline in sales, announced job cuts and became focused on the profitability of the printers the company sells. We decreased our position in the stock and decided to re-evaluate our original thesis as the economics of the company may have changed materially. Lear was partly hurt by higher raw material costs, a weak production environment and the loss of a significant contract.

FUND CHANGES

Two of our larger purchases during the period were Pilgrim’s Pride Corporation and Con-way Inc. (formerly named CNF Inc.). Pilgrim’s Pride is the second-largest chicken producer in the U.S. and Mexico. Concerns about Avian flu outbreaks drove poultry exports down and caused chicken prices to decline to levels not seen in nearly twenty years. This put downward pressure on the shares of chicken producers, including Pilgrim’s Pride, creating an appealing investment opportunity. We were also attracted to the company’s leading market position, solid balance sheet and low P/E valuation.

Con-way is a global provider of transportation and supply chain management services. We believed that Con-way’s valuation understated its potential to improve earnings given the strength of its market position, pricing discipline and superior return on capital.

Our purchases were funded in part by the sales of Siebel Systems, Inc., CNA Financial Corporation, BMC Software, Inc., Jacobs Engineering Group Inc. and Darden Restaurants, Inc. Shares of eBusiness application provider Siebel Systems surged last September when the company accepted an acquisition offer from Oracle Corporation. We sold our shares prior to the completion of the transaction. We were concerned over BMC’s future revenue and use of cash flow. Nonetheless, we were able to sell our position at a profit. Jacobs Engineering Group, a diverse provider of technical services to industrial, government and commercial clients, was sold as its share price moved up to our target selling range due in part to a strong order backlog and higher revenues in most of its markets. The ongoing strength of Darden Restaurants’ Olive Garden® brand and the improved sales growth at its Red Lobster® brand helped push this casual dining company up to our target selling range.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/05 | | | 3/31/06 | |

Auto & Transportation | | 2.9 | % | | 3.9 | % |

Consumer Discretionary | | 28.7 | | | 31.9 | |

Consumer Staples | | — | | | 2.9 | |

Financial Services | | 27.1 | | | 29.4 | |

Materials & Processing | | 7.0 | | | 5.5 | |

Other Energy | | 14.8 | | | 14.1 | |

Producer Durables | | 3.6 | | | 2.4 | |

Technology | | 7.9 | | | 6.0 | |

Utilities | | 1.0 | | | 0.9 | |

Other assets less liabilities | | 7.0 | | | 3.0 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

16

SIXTEEN

ARTISAN OPPORTUNISTIC VALUE FUND (ARTLX)

|

| On March 27, 2006, Artisan Funds introduced its eighth fund—Artisan Opportunistic Value Fund. This semiannual report has been designed to provide an overview of the Fund. We will review the investment process, the investment team and one of our initial holdings to illustrate our process. Because the Fund only had a few days of performance prior to March 31, 2006, we have not reviewed Fund performance here, but will provide a review of performance since the inception of the Fund in the September 2006 Annual Report. |

| | |

| INVESTMENT APPROACH | | |

| Artisan Opportunistic Value Fund pursues long-term capital growth by investing primarily in undervalued U.S. companies across a broad capitalization range. The Fund also has the flexibility to invest a portion of its assets in non-U.S. securities and to take larger positions in a portion of the portfolio. The Fund’s performance is typically benchmarked against the Russell 1000® and Russell 1000® Value indices over a full market cycle. |

| | | |

| INVESTMENT TEAM |

| The co-managers of Artisan Opportunistic Value Fund are George Sertl, CFA, James Kieffer, CFA and Scott Satterwhite, CFA. Mr. Sertl, Mr. Kieffer and Mr. Satterwhite are also co-managers of Artisan Mid Cap Value Fund and Artisan Small Cap Value Fund. |

INVESTMENT PROCESS HIGHLIGHTS

Artisan Opportunistic Value Fund uses a bottom-up investment process to construct a flexible portfolio of value-oriented companies that the team believes are undervalued, in solid financial condition and have attractive business economics.

Attractive valuation. The team values a business using what it believes are reasonable expectations for the long-term earnings power and capitalization rates of that business. This results in a range of values for the company that the team believes would be reasonable. The team generally will purchase a security if the stock price falls below or toward the lower end of that range.

Sound financial condition. The team favors companies with an acceptable level of debt and positive cash flow. At a minimum, the team tries to avoid companies that have so much debt that management may be unable to make decisions that would be in the best interests of the companies’ shareholders.

Attractive business economics. The team favors cash-producing businesses that it believes are capable of earning acceptable returns on capital over the company’s business cycle. The team believes companies with these characteristics are less likely to experience eroding values over the long-term.

The team often finds investment opportunities in companies that have one or more of the following characteristics:

Turnarounds. At times, the team invests in companies that have had poor results due to company-specific and/or industry-wide conditions that it believes will not continue indefinitely.

Companies in transition. A company’s stock price may not always reflect positive change in the business, such as new management, new products or a cyclical uptrend in an industry. The team tries to identify investments for the Fund ahead of broad recognition of changes that may be expected to cause the stock’s price to rise.

Earnings shortfalls. The team may invest in a company in a group or industry that is out of favor, or whose earnings have disappointed, causing its stock price to drop below the team’s estimate of the value of the business, creating the potential for patient investors to benefit when those earnings improve.

17

SEVENTEEN

TOP 10 HOLDINGS

| | | |

| Company Name | | 3/31/06 | |

Apache Corporation | | 4.7 | % |

Wal-Mart Stores, Inc. | | 4.7 | |

The Student Loan Corporation(1) | | 3.9 | |

Berkshire Hathaway Inc. | | 3.9 | |

American International Group, Inc. | | 3.8 | |

NIKE, Inc. | | 3.8 | |

Citigroup Inc.(1) | | 3.8 | |

Microsoft Corporation | | 3.8 | |

Johnson & Johnson | | 3.7 | |

Avnet, Inc. | | 2.8 | |

Total | | 38.9 | % |

As a percentage of total net assets. Top 10 Holdings are determined by issuer.

(1) Citibank, N.A., an indirect wholly-owned subsidiary of Citigroup Inc., is the primary shareholder of The Student Loan Corporation, with an ownership of 80% of The Student Loan Corporation’s outstanding common stock.

EXAMPLE HOLDING

NIKE, Inc. is a holding that we purchased at inception. NIKE creates athletic footwear, apparel, equipment, and accessories for sports and fitness enthusiasts. The company, through its subsidiaries, designs and sells a line of men’s and women’s dress and casual shoes and accessories. NIKE also markets licensed headwear, and designs, markets, and sells hockey equipment.

We purchased NIKE because we believed it was attractively valued, in sound financial condition, with attractive business economics. Our thoughts about each point are summarized below.

VALUATION

| • | | At our initial purchase, we thought that the historically undemanding, low teens P/E at which NIKE was trading understated the company’s normalized earnings power and cash flow generating ability. |

FINANCIAL CONDITION

| • | | NIKE had a combination of net cash on the balance sheet of nearly $5 per share and strong free cash flow that the company could use to pay dividends, engage in share repurchases or pursue other value creating initiatives. |

BUSINESS ECONOMICS

| • | | NIKE outsources its manufacturing needs, and thus has low capital requirements, and has a strong brand franchise. Those two traits have been among the reasons that NIKE has been able to generate a return on equity (a measure of corporate profitability) that has averaged 19% over the last 10 years. |

FLEXIBLE PORTFOLIO CONSTRUCTION

Artisan Opportunistic Value Fund is structured to provide the investment team with broad flexibility to build a high value-added, bottom-up investment portfolio.

| • | | The team can invest in securities with market capitalizations greater than $1.5 billion at the time of purchase. |

| • | | The team can invest up to 25% of the Fund’s assets in non-U.S. securities. |

| • | | The Fund tries to maintain a cash position of no more than 15% of its net assets, although cash flows from shareholder investments and redemptions and purchases and sales of portfolio securities may cause the Fund’s cash position to be larger or smaller. |

| • | | The Fund’s maximum position size is 5% of assets at the time of purchase in 75% of the portfolio, but in the remaining 25% of the portfolio the team can invest up to 10% of Fund assets at the time of purchase in a single position. |

SECTOR DIVERSIFICATION

| | | |

| Sector | | 3/31/06 | |

Consumer Discretionary | | 25.4 | % |

Consumer Staples | | 2.3 | |

Financial Services | | 27.2 | |

Healthcare | | 6.5 | |

Integrated Oils | | 2.3 | |

Materials & Processing | | 2.8 | |

Other | | 5.7 | |

Other Energy | | 4.7 | |

Technology | | 10.3 | |

Utilities | | 1.8 | |

Other assets less liabilities | | 11.0 | |

Total | | 100.0 | % |

As a percentage of total net assets.

18

EIGHTEEN

ARTISAN SMALL CAP FUND (ARTSX)

| | |

| INVESTMENT PROCESS HIGHLIGHTS | | |

Artisan Small Cap Fund uses a bottom-up investment process to construct a diversified portfolio of U.S. small-cap growth companies. Competitive advantages. A sustainable competitive advantage is critical to producing above average growth and profitability. Identifying the source of a company’s competitive advantage lends confidence to the team’s assessment of intrinsic value. Return on invested capital. The team believes that, over time, a company with improving returns on its invested capital will be rewarded with a higher valuation. The team determines how much capital investment is needed to achieve a company’s continued growth and analyzes management’s ability to use that capital in the most effective way to support that growth. Intrinsic value. The team estimates a company’s intrinsic value—the value it thinks a buyer would pay to buy the entire company. The team bases its buy and sell targets for a company’s stock on its intrinsic value estimates. The Fund primarily invests in companies with market capitalizations between $200 million and $1.5 billion that meet its standards for earnings growth and sustainable growth prospects. |

| | | |

| PERFORMANCE HISTORY | | |

GROWTH OF AN ASSUMED $10,000 INVESTMENT (3/28/95 to 3/31/06)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/06)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan Small Cap Fund | | 26.39 | % | | 29.52 | % | | 12.05 | % | | 8.35 | % | | 10.94 | % |

Russell 2000® Growth Index | | 27.84 | | | 28.14 | | | 8.59 | | | 5.51 | | | 7.59 | |

Russell 2000® Index | | 25.85 | | | 29.53 | | | 12.59 | | | 10.15 | | | 11.76 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 86 for a description of each index.

19

NINETEEN

INVESTING ENVIRONMENT

The six months ended March 31, 2006 was a very good period for small-cap stocks, with the last three months accounting for the lion’s share of performance. There were a number of factors that contributed to the market’s optimism. Earnings growth remained robust, corporate spending continued to pick up, the price of natural gas fell rather significantly and inflation stayed relatively contained.

There were, however, factors that raised caution in the market. The Federal Reserve continued its series of interest rate hikes, which reached 15 in a row as of March 31, 2006. There was also concern because low quality, high valuation and low-priced stocks were among the leading performers in the indices late in the period.

In the Russell 2000® and Russell 2000® Growth indices, the technology, producer durables and materials sectors were among the leading performers as each group gained more than 20%. Most other sectors posted double-digit returns, although energy and utility stocks managed only single-digit gains.

PERFORMANCE DISCUSSION

The Fund gained 12.59% for the six-month period, which compared to the 15.23% and 16.20% returns for the Russell 2000® and Russell 2000® Growth indices, respectively. The financial, consumer discretionary and transportation sectors were areas of strength for the portfolio relative to the benchmarks. The Fund lagged in the technology, healthcare and producer durables sectors.

In the financial sector, three of our leading contributors were The First Marblehead Corporation, HealthExtras, Inc. and optionsXpress Holdings, Inc. The stock price of First Marblehead, a private student loan outsourcer, increased more than 70%. We invested in First Marblehead because we believed that its share price had experienced an unwarranted decline due to market concerns about management changes and the company’s ability to extend its contract with its largest partner. During the period, First Marblehead reported increases in total service revenue and loan volume and extended its contract with arguably its most important strategic partner. Pharmacy benefit manager HealthExtras won a large contract to provide services to 1.3 million BlueCross® BlueShield® members in Iowa and South Dakota. optionsXpress, a leading online brokerage firm specializing in options trading, reported increased trading activity, solid asset growth and good traction in new accounts. We sold our position as it reached our target price.

Children’s clothing retailer The Children’s Place Retail Stores, Inc., sporting goods store operator Hibbett Sporting Goods, Inc. and restaurant owner RARE Hospitality International, Inc. were among our strongest contributors in the consumer discretionary sector. Their stock prices increased roughly 62%, 48% and 35%, respectively. Children’s Place has worked on the repositioning of its merchandise, announced a meaningful improvement in operating margins and continued to take market share in the specialty retail channel. Hibbett reported double-digit growth in sales for its 2006 fiscal year. RARE Hospitality was supported by continued same-store sales improvement at its LongHorn SteakhousesSM and upscale Capital GrilleSM restaurants.

The leading performer among our transportation holdings was aftermarket car parts distributor Keystone Automotive Industries, Inc., the stock price of which gained more than 46%. We invested in Keystone because we believe it has a strong competitive position in a business that is not dependent on the cyclicality of the economy — its business

TOP 10 HOLDINGS

| | | |

| Company Name | | 3/31/06 | |

Bright Horizons Family Solutions, Inc. | | 1.7 | % |

Strayer Education, Inc. | | 1.7 | |

Hornbeck Offshore Services, Inc. | | 1.7 | |

DSP Group, Inc. | | 1.6 | |

California Pizza Kitchen, Inc. | | 1.6 | |

Interline Brands, Inc. | | 1.6 | |

Tekelec | | 1.6 | |

ESCO Technologies Inc. | | 1.6 | |

Avocent Corporation | | 1.6 | |

Waste Connections, Inc. | | 1.6 | |

Total | | 16.3 | % |

As a percentage of total net assets. Top 10 Holdings are determined by issuer.

20

TWENTY

is driven by accident frequency. In addition, the insurance industry’s adoption of generic and aftermarket parts created a solid long-term growth backdrop given the very low current utilization rate. During the period, Keystone benefited from solid sales and earnings and positive expectations for operating improvements. Low-fare airline AirTran Holdings, Inc., aftermarket aircraft parts provider Aviall, Inc. and third-party logistics provider Pacer International, Inc. also performed well. We sold AirTran as it had reached our target price.

Our technology holdings collectively turned in a nice gain for the period, but they fell short of the stellar advance of those in the benchmarks. Two of our most disappointing performers in the sector were network systems manufacturer Tekelec and Dendrite International, Inc., a leading supplier of sales force software and support services to the pharmaceutical industry. Tekelec generally reported good results, but the resignation of the CEO and financial reporting issues pressured the company’s shares. We sold our position in Dendrite because the combination of a restructuring and management change left the company unable to generate the type of earnings growth we like to see.

The main cause of our underperformance in the healthcare sector was pharmaceutical research firm SFBC International, Inc. Its shares came under pressure in November, as the company became the target of negative press reports alleging deficiencies in the U.S. drug-testing industry. We sold our shares, realizing a loss. Symmetry Medical Inc., a manufacturer of medical devices for the orthopedics industry, and PRA International, a contract research organization, also hurt results.

In the producer durables sector, luxury Florida homebuilder WCI Communities was a source of weakness, negatively impacted by an increase in inventory in its markets, causing order growth to slow. We sold our position because of a lack of earnings momentum.

FUND CHANGES

The number of securities we held fell from 84 as of 9/30/05 to 79 as of 3/31/06. The two primary reasons for our sales during the period were stocks reaching our price targets and takeovers or announced takeovers.

Stocks that reached our target prices, other than those already mentioned, included Unit Corporation, Gardner Denver, Inc., Coldwater Creek Inc., TODCO and SiRF Technology Holdings, Inc. Takeovers or announced takeovers resulted in the sales of IDX Systems Corporation (General Electric Company), Anteon International Corporation (General Dynamics Corporation), La Quinta Corporation (private investment firm), Serena Software Inc. (private equity firm), Hughes Supply, Inc. (The Home Depot, Inc.) and Main Street Banks, Inc. (BB&T Corporation). We also sold Axcelis Technologies, Inc. because we were concerned about management’s strategy and the company’s competitive position.