UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08932

Artisan Funds, Inc.

(Exact name of registrant as specified in charter)

875 East Wisconsin Avenue, Suite 800

Milwaukee, WI 53202

(Address of principal executive offices) (Zip Code)

| | |

| Janet D. Olsen | | Bruce A. Rosenblum |

| Artisan Funds, Inc. | | Bell, Boyd & Lloyd LLP |

| 875 East Wisconsin Avenue, #800 | | 1615 L Street, N.W., Suite 1200 |

| Milwaukee, Wisconsin 53202 | | Washington, D.C. 20036 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (414) 390-6100

Date of fiscal year end: 09/30/08

Date of reporting period: 03/31/08

| Item 1. | Reports to Shareholders. |

SEMIANNUAL

R E P O R T

MARCH 31, 2008

ARTISAN GLOBAL VALUE FUND

ARTISAN INTERNATIONAL FUND

ARTISAN INTERNATIONAL SMALL CAP FUND

ARTISAN INTERNATIONAL VALUE FUND

ARTISAN MID CAP FUND

ARTISAN MID CAP VALUE FUND

ARTISAN OPPORTUNISTIC VALUE FUND

ARTISAN SMALL CAP FUND

ARTISAN SMALL CAP VALUE FUND

ARTISAN FUNDS, INC.

INVESTOR SHARES

ARTISAN FUNDS

P.O. BOX 8412

BOSTON, MA 02266-8412

This report and the unaudited financial statements contained herein are provided for the general information of the shareholders of Artisan Funds. Before investing, investors should consider carefully each Fund’s investment objective, risks and charges and expenses. For a prospectus, which contains that information and more information about each Fund, please call 800.344.1770 or visit our website at www.artisanfunds.com. Read it carefully before you invest or send money.

Company discussions are for illustration only and are not intended as recommendations of individual stocks. The discussions present information about the companies believed to be accurate, and the views of the portfolio managers, as of March 31, 2008. That information and those views may change, and the Funds disclaim any obligation to advise shareholders of any such changes. Artisan Emerging Markets Fund, Artisan International Fund, Artisan International Value Fund and Artisan Mid Cap Fund offer institutional classes of shares for institutional investors meeting certain minimum investment requirements. A report on each institutional class is available under separate cover.

Artisan Funds offered through Artisan Distributors LLC, member FINRA.

TABLE OF CONTENTS

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | | | | | | | | | | | | |

| | | Inception

Date | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan Global Value Fund | | 12/10/07 | | NA | | | NA | | | NA | | | NA | | | -10.20 | % |

Artisan International Fund | | 12/28/95 | | 1.36 | % | | 15.93 | % | | 22.37 | % | | 11.10 | % | | 13.63 | |

Artisan International Small Cap Fund | | 12/21/01 | | 6.89 | | | 21.89 | | | 31.80 | | | NA | | | 23.73 | |

Artisan International Value Fund | | 9/23/02 | | -7.96 | | | 11.22 | | | 24.53 | | | NA | | | 22.45 | |

Artisan Mid Cap Fund | | 6/27/97 | | 2.36 | | | 9.19 | | | 14.52 | | | 12.58 | | | 15.72 | |

Artisan Mid Cap Value Fund | | 3/28/01 | | -5.95 | | | 7.32 | | | 18.00 | | | NA | | | 12.68 | |

Artisan Opportunistic Value Fund | | 3/27/06 | | -6.64 | | | NA | | | NA | | | NA | | | 4.87 | |

Artisan Small Cap Fund | | 3/28/95 | | -12.04 | | | 1.93 | | | 12.73 | | | 2.99 | | | 7.71 | |

Artisan Small Cap Value Fund | | 9/29/97 | | -10.18 | | | 6.37 | | | 16.88 | | | 10.77 | | | 11.45 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in a Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The performance information shown for Artisan Global Value Fund, Artisan International Fund, Artisan International Small Cap Fund and Artisan International Value Fund does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. Artisan International Small Cap Fund’s investments in initial public offerings (IPOs) made a material contribution to the Fund’s performance. IPO investments are not an integral component of the Fund’s investment process and may not be available in the future. The performance shown for Artisan Global Value Fund is not annualized and may vary greatly over short periods, and current performance may be materially lower or higher than the performance data quoted. The performance information shown for Artisan Opportunistic Value Fund and Artisan Global Value Fund reflects Artisan Partners’ voluntary undertaking to limit each Fund’s expenses when they exceed 1.50%, which may be terminated at any time, has been in effect since each Fund’s inception and has had a material impact on each Fund’s performance. Absent that expense waiver, each Fund’s performance would have been lower.

Artisan Global Value, Artisan International, Artisan International Small Cap, Artisan International Value & Artisan Opportunistic Value: International investments involve special risks, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems and higher transaction costs. These risks are typically greater in emerging markets.

Artisan International, Artisan International Small Cap, Artisan Mid Cap & Artisan Small Cap: Growth stocks may underperform other asset types during a given period.

Artisan Global Value, Artisan International Value, Artisan Opportunistic Value, Artisan Mid Cap Value & Artisan Small Cap Value: Value stocks may underperform other asset types during a given period.

Artisan International Small Cap, Artisan International Value, Artisan Small Cap & Artisan Small Cap Value: Stocks of smaller companies tend to be more volatile and less liquid than those of large companies, have underperformed the stocks of larger companies during some periods and tend to have a shorter history of operations than larger companies.

Artisan International Value, Artisan Mid Cap, and Artisan Mid Cap Value & Artisan Opportunistic Value: Stocks of medium-sized companies tend to be more volatile than those of large companies, and have underperformed the stocks of small and large companies during some periods.

ARTISAN GLOBAL VALUE FUND (ARTGX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Global Value Fund uses a bottom-up investment process to construct a diversified portfolio of securities of undervalued U.S. and non-U.S. companies. The Fund’s investment process is focused on identifying what the investment team considers to be high quality, undervalued businesses that offer the potential for superior risk/reward outcomes. The team’s in-depth research process focuses on four key investment characteristics:

Undervaluation. Determining the intrinsic value of the business is the heart of the team’s research process. The team believes that intrinsic value represents the amount that a buyer would pay to own a company’s future cash flows. The team seeks to invest at a significant discount to the team’s estimate of the intrinsic value of a business.

Business quality. The team seeks to invest in companies with histories of generating strong free cash flow, improving returns on capital and strong competitive positions in their industries.

Financial strength. The team believes that investing in companies with strong balance sheets helps to reduce the potential for capital risk and provides company management the ability to build value when attractive opportunities are available.

Shareholder-oriented management. The team’s research process attempts to identify management teams with a history of building value for shareholders.

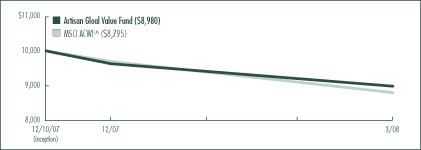

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (12/10/2007 to 3/31/2008)(1)

TOTAL RETURNS (as of 3/31/2008)

| | | |

| Fund / Index | | Since(1)

Inception | |

Artisan Global Value Fund | | -10.20 | % |

MSCI ACWI (All Country World Index) IndexSM | | -12.05 | |

(1) | For the period from commencement of operations (December 10, 2007) through March 31, 2008; not annualized |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. The Fund’s return may vary greatly over short periods, and current performance may be materially lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. The Fund’s performance information reflects Artisan Partners’ voluntary undertaking to limit the Fund’s expenses when they exceed 1.50%, which may be terminated at any time, has been in effect since the Fund’s inception and has had a material impact on the Fund’s performance, which would have been lower in its absence. In addition, the outside directors of Artisan Funds have waived that portion of their fees allocable to the Fund until September 30, 2008. Absent that expense waiver, the Fund’s performance would have been lower. See page 87 for a description of each index.

2

INVESTING ENVIRONMENT

The financial markets around the world were extremely volatile from the inception of Artisan Global Value Fund through March 31, 2008 as concerns over the housing and credit markets weighed on the overall global economy. Most sectors and countries recorded losses. In addition, we saw a continuation of the long-term trend of the devaluation of the U.S. dollar and dollar-based assets in favor of international currencies and international assets during the period.

SECTOR DIVERSIFICATION

| | | |

| Sector | | 3/31/2008 | |

Consumer Discretionary | | 30.1 | % |

Consumer Staples | | 13.1 | |

Financials | | 14.7 | |

Healthcare | | 13.4 | |

Industrials | | 10.2 | |

Information Technology | | 9.0 | |

Materials | | 2.6 | |

Telecommunication Services | | 2.7 | |

Other assets less liabilities | | 4.2 | |

Total | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan Global Value Fund declined - -10.20% since its December 10, 2007 inception, compared to its primary benchmark, the MSCI ACWI (All Country World Index)SM, which decreased -12.05% over the same period.

The key guiding point to our investment philosophy is that we are value investors. When we invest in equities, we buy shares in companies where we see a significant discount between the stock prices and what we estimate to be the intrinsic values of those businesses.

The share prices of the following companies had a positive impact on the portfolio during the period: SANKYO CO., LTD., a Japanese pachinko machine manufacturer; Wal-Mart Stores, Inc., a discount retailer; Givaudan SA, a Swiss producer of flavors and fragrances; Neopost SA, a France-based manufacturer of mailing and shipping equipment; and Covidien Ltd., one of the spin-offs of Tyco International Ltd. Most of our stocks declined during this same timeframe. Our worst performers included: Motorola, Inc., a U.S. handset and equipment maker; SK Telecom Co., Ltd., an operator in the South Korean wireless market; Home Retail Group plc, a U.K. home and general merchandise retailer; Wolters Kluwer NV, a Dutch-based professional publishing company; and Guoco Group Limited, a Hong-Kong listed holding company with financial interests throughout Asia.

REGION ALLOCATION

| | | |

| Region | | 3/31/2008 | |

Americas | | 40.9 | % |

Europe | | 37.7 | |

Pacific Basin | | 9.4 | |

Emerging Markets | | 7.8 | |

As a percentage of total net assets.

FUND CHANGES

Due to the volatility, investors sold down many stocks to depressed valuations relative to our estimates of their long-term value. As a result, we found a number of companies that fit our criteria. We added previously mentioned Neopost SA; Cintas Corporation, a U.S. corporate uniform manufacturer; Dell Inc., a U.S. computer manufacturer; Cadbury Schweppes plc, a U.K.-based confectionary and beverage conglomerate; The Sherwin-Williams Company, a U.S. manufacturer of paint; and Panalpina Welttransport Holding AG, a Swiss contract logistics/freight forwarder.

From the Fund’s inception through March 31, 2008, we exited our positions in Heidelberger Druckmaschinen AG, UNI-CHARM CORPORATION and Vodafone Group PLC.

3

ARTISAN INTERNATIONAL FUND (ARTIX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan International Fund uses a fundamental stock selection process focused on identifying long term growth opportunities.

Themes. The investment team’s thematic approach identifies catalysts for change and develops investment themes with the objective of capitalizing on them globally. Changing demographics, developing technology, privatization of economic resources and outsourcing are among the long-term catalysts for change that currently form the basis for the team’s investment themes. The team incorporates these catalysts along with sector and regional fundamentals into a long-term global framework for investment analysis and decision-making.

Sustainable Growth. The team applies a fundamental approach to identifying the long-term, sustainable growth characteristics of potential investments. The team seeks high quality companies that are well managed, have a dominant or improving market position and competitive advantages compared to industry and regional peers.

Valuation. The team assesses the relationship between its estimate of a company’s sustainable growth prospects and the company’s stock price. The team uses multiple valuation metrics to establish price targets.

The Fund primarily invests in non-U.S. growth companies of all market capitalizations in developed and emerging markets.

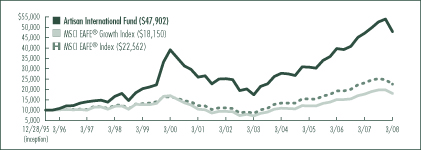

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (12/28/1995 to 3/31/2008)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan International Fund | | 1.36 | % | | 15.93 | % | | 22.37 | % | | 11.10 | % | | 13.63 | % |

MSCI EAFE® Growth Index | | 1.91 | | | 14.35 | | | 19.81 | | | 4.28 | | | 4.98 | |

MSCI EAFE® Index | | -2.70 | | | 13.32 | | | 21.40 | | | 6.18 | | | 6.86 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. See page 87 for a description of each index.

4

INVESTING ENVIRONMENT

International securities retreated during the semiannual reporting period ended March 31, 2008. U.S. economic uncertainties and rising inflation concerns made for an extremely volatile investing environment. The MSCI EAFE® Index returned -17.47% and -10.50% in local currency and U.S. dollar terms, respectively. U.S. dollar-based investors benefited from the rally of many foreign currencies. Weaknesses were evident around the globe, although, on average, emerging markets fared better than developed markets. Japan was among the worst performing countries in the MSCI EAFE® Index in U.S. dollar terms, while China and Turkey were among the weakest performers in emerging markets. While every sector in the Index was under pressure, consumer staples and utilities stocks held up best.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/2007 | | | 3/31/2008 | |

Consumer Discretionary | | 8.4 | % | | 10.6 | % |

Consumer Staples | | 9.1 | | | 8.7 | |

Energy | | 6.4 | | | 9.7 | |

Financials | | 23.4 | | | 14.5 | |

Healthcare | | 2.5 | | | 3.6 | |

Industrials | | 16.1 | | | 18.7 | |

Information Technology | | 3.8 | | | 4.7 | |

Materials | | 7.6 | | | 10.2 | |

Telecommunication Services | | 10.7 | | | 9.1 | |

Utilities | | 8.8 | | | 8.7 | |

Other assets less liabilities | | 3.2 | | | 1.5 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

The Fund outperformed the MSCI EAFE® Index during the six-month period with a return of -8.82%. Our demographics and infrastructure themes were sources of security selection strength in the consumer discretionary, energy, industrials and telecommunication services sectors. Top performers in those themes included Norwegian drilling company SeaDrill Ltd., Hong Kong-based industrial conglomerate NWS Holdings Limited., Chinese wireless

provider China Unicom Limited and Japanese media provider Jupiter Telecommunications Co., Ltd. Finnish utility company Fortum Oyj and German chemicals company Linde AG also performed well.

The Fund’s underperformers were not concentrated in any one area. Norwegian conglomerate Orkla ASA, Japanese heavy machinery manufacturer Mitsubishi Heavy Industries, Ltd., French construction and telecommunications company Bouygues SA, Dutch semiconductor equipment producer ASML Holding N.V. and South Korean bank Kookmin Bank were among our largest detractors.

FUND CHANGES

Our fundamental stock selection process emphasizes companies that we believe are reasonably valued, growing at a sustainable rate, with exposure to the secular themes we have identified.

Given the increased market volatility worldwide, there was a high amount of buy and sell activity this period. We added capital to many of our current positions including Russian natural gas company Gazprom, Orkla ASA, ASML Holding N.V. and Roche Holding AG. Our largest new purchases included Japanese car and motorcycle producer SUZUKI MOTOR CORPORATION and Japanese general trading company MITSUI & CO., LTD.

In order to fund these new purchases we sold a number of our financial holdings, including Swiss Re, Standard Chartered plc, ORIX Corporation, Hana Financial Group Inc. and Urban Corporation. We also sold Siemens AG and China Mobile Limited and a partial position in Mitsubishi Heavy Industries, Ltd. .

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/2007 | | | 3/31/2008 | |

Europe | | 58.9 | % | | 60.7 | % |

Emerging Markets | | 19.1 | | | 19.1 | |

Pacific Basin | | 17.6 | | | 17.1 | |

Americas | | 1.2 | | | 1.6 | |

As a percentage of total net assets.

5

ARTISAN INTERNATIONAL SMALL CAP FUND (ARTJX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan International Small Cap Fund uses a fundamental stock selection process focused on identifying long-term growth opportunities among small non-U.S. companies.

Themes. The investment team’s thematic approach identifies catalysts for change and develops investment themes with the objective of capitalizing on them globally. Changing demographics, developing technology, privatization of economic resources and outsourcing are among the long-term catalysts for change that currently form the basis for the team’s investment themes. The team incorporates these catalysts along with sector and regional fundamentals into a long-term global framework for investment analysis and decision-making.

Sustainable Growth. The team applies a fundamental approach to identifying the long-term, sustainable growth characteristics of potential investments. The team seeks high quality companies that are well managed, have a dominant or improving market position and competitive advantages compared to industry and regional peers.

Valuation. The team assesses the relationship between its estimate of a company’s sustainable growth prospects and the company’s stock price. The team uses multiple valuation metrics to establish price targets.

The Fund primarily invests in non-U.S. small-cap growth companies in developed and emerging markets with market capitalizations less than $3 billion at the time of investment.

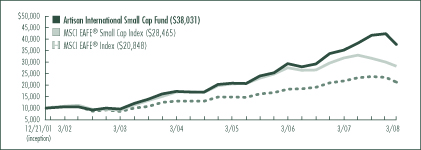

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (12/21/2001 to 3/31/2008)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | Since

Inception | |

Artisan International Small Cap Fund | | 6.89 | % | | 21.89 | % | | 31.80 | % | | 23.73 | % |

MSCI EAFE® Small Cap Index | | -11.19 | | | 11.14 | | | 25.48 | | | 18.14 | |

MSCI EAFE® Index | | -2.70 | | | 13.32 | | | 21.40 | | | 12.42 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. The Fund’s investments in initial public offerings (IPOs) made a material contribution to the Fund’s performance. IPO investments are not an integral component of the Fund’s investment process and may not be available in the future. See page 87 for a description of each index.

6

INVESTING ENVIRONMENT

International securities retreated during the semiannual reporting period ended March 31, 2008. The MSCI EAFE® Small Cap Index returned -17.82% and -10.78% in local currency and U.S. dollar terms, respectively. U.S. dollar based investors benefited from the rally of many foreign currencies. Weaknesses were evident around the globe, although, on average, emerging markets fared better than developed markets. A wide range of countries in the MSCI EAFE® Small Cap Index reported a negative U.S. dollar based return of more than -20%, including Germany, France, Italy, Japan and Hong Kong. China was among the worst performing emerging markets. Every sector in the MSCI EAFE® Small Cap Index was under pressure. The consumer staples and energy sectors held up best.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/2007 | | | 3/31/2008 | |

Consumer Discretionary | | 10.7 | % | | 10.2 | % |

Consumer Staples | | 7.6 | | | 12.0 | |

Energy | | 7.7 | | | 8.6 | |

Financials | | 30.0 | | | 24.7 | |

Healthcare | | 0.7 | | | 0.8 | |

Industrials | | 27.0 | | | 21.7 | |

Information Technology | | 2.0 | | | 6.9 | |

Materials | | 2.5 | | | 3.6 | |

Telecommunication Services | | 1.2 | | | 1.0 | |

Utilities | | 1.9 | | | 1.7 | |

Other assets less liabilities | | 8.7 | | | 8.8 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

The Fund outperformed the MSCI EAFE® Small Cap Index with a six-month return of -9.73%. Our consumer discretionary and information technology holdings, a number of which were found in Europe, were key sources of security selection strength during the period. Dutch digital road maps producer Tele Atlas NV, German DIY construction supplies store operator Praktiker Bau- und Heimwerkermaerkte Holding AG, which we purchased during the period, and Japanese theme park operator USJ Co. Ltd. were among our top contributing consumer discretionary holdings. We sold our position in Tele Atlas. German internet payment and processing services company Wirecard AG and German semiconductor machinery manufacturer Aixtron AG were two of our top performing information technology stocks.

Our holdings in Hong Kong and China were areas of weakness during the semiannual reporting period. Beijing Airport operator Beijing Capital International Airport Company Limited, financial conglomerate China Everbright Limited, securities and derivatives exchange operator Hong Kong Exchanges & Clearing Limited., and real estate developers Tian An China Investments Company Limited and Allied Properties (H.K.) Limited, were among our holdings in those countries that underperformed. Japanese personnel services company en-japan inc. and Finnish industrial machinery supplier Metso Corporation were also notable detractors.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/2007 | | | 3/31/2008 | |

Europe | | 42.0 | % | | 49.0 | % |

Emerging Markets | | 25.9 | | | 22.2 | |

Pacific Basin | | 21.9 | | | 18.4 | |

Americas | | 1.5 | | | 1.6 | |

As a percentage of total net assets.

FUND CHANGES

We continued to add positions to the Fund when we were able to find companies that exhibited the sustainable growth characteristics that we look for in potential investments. Most recently we have purchased Malaysian exchange operator Bursa Malaysia Bhd, United Kingdom-based personnel services provider Robert Walters plc and Greece’s securities market operator Hellenic Exchanges S.A.

The funding of these purchases came in part from the liquidation of other positions. Our largest sales included Tele Atlas NV, Beijing Capital International Airport Co. Ltd., Azimut Holding SpA, Indiabulls Financial Services Ltd., VastNed Retail NV, Metso Corporation and Indiabulls Real Estate Limited.

7

ARTISAN INTERNATIONAL VALUE FUND (ARTKX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan International Value Fund uses a bottom-up investment process focused on identifying what the investment team believes are high quality, undervalued businesses that offer the potential for superior risk/reward outcomes.

The team’s in-depth research process focuses on four key investment characteristics:

Undervaluation. Determining the intrinsic value of the business is the heart of the team’s research process. The team believes that intrinsic value represents the amount that a buyer would pay to own a company’s future cash flows. The team seeks to invest at a significant discount to its estimate of the intrinsic value of a business.

Business quality. The team seeks to invest in companies with histories of generating strong free cash flow, improving returns on capital and strong competitive positions in their industries.

Financial strength. The team believes that investing in companies with strong balance sheets helps to reduce the potential for capital risk and provides company management the ability to build value when attractive opportunities are available.

Shareholder-oriented management. The team’s research process attempts to identify management teams with a history of building value for shareholders.

The Fund primarily invests in common stocks and other equity securities of non-U.S. companies of all market capitalizations in developed and emerging markets.

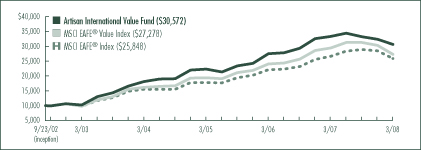

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (9/23/2002 to 3/31/2008)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | Since

Inception | |

Artisan International Value Fund | | -7.96 | % | | 11.22 | % | | 24.53 | % | | 22.45 | % |

MSCI EAFE® Value Index | | -7.25 | | | 12.20 | | | 22.88 | | | 19.95 | |

MSCI EAFE® Index | | -2.70 | | | 13.32 | | | 21.40 | | | 18.78 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. The performance shown does not reflect the deduction of a 2% redemption fee on shares held by an investor for 90 days or less and, if reflected, the fee would reduce the performance quoted. See page 87 for a description of each index.

8

INVESTING ENVIRONMENT

During the semiannual reporting period ended March 31, 2008, international stocks suffered as housing and credit market concerns caused tremendous volatility in financial markets across the world and weighed on overall global economic activity. Most sectors and countries recorded losses. In addition, we saw a continuation of the long-term trend of the devaluation of the U.S. dollar and dollar-based assets in favor of international currencies and international assets during the period.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/2007 | | | 3/31/2008 | |

Consumer Discretionary | | 23.5 | % | | 23.4 | % |

Consumer Staples | | 14.5 | | | 14.6 | |

Financials | | 16.1 | | | 16.5 | |

Healthcare | | 8.7 | | | 11.0 | |

Industrials | | 14.5 | | | 15.7 | |

Information Technology | | 5.9 | | | 11.0 | |

Materials | | 2.8 | | | 2.2 | |

Telecommunication Services | | 7.9 | | | 1.7 | |

Other assets less liabilities | | 6.1 | | | 3.9 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan International Value Fund declined -7.77% during the period, holding up better than the MSCI EAFE® Index, which decreased -10.50% over the same period.

We are value investors. We buy shares in companies where we see a significant discount between the stock prices and what we estimate to be the intrinsic value of the business.

The performance of the following companies had a meaningful positive impact on the portfolio during the semiannual period: SANKYO CO., LTD., a Japanese pachinko machine manufacturer; Covidien Ltd., one of the spin-offs of Tyco International Ltd.; UNICHARM CORPORATION, a Japanese manufacturer of diapers and feminine products; and new purchases Samsung Electronics Co., Ltd., a Korean company with a diverse portfolio of electronics-related businesses and Neopost SA, a France-based manufacturer of mailing and shipping equipment. Most of our stocks declined during the semiannual period. Our worst performers included: CanWest Global Communications Corp., a holding company that owns one of Canada’s television networks; Heidelberger Druckmaschinen AG, a German manufacturer of sheetfed printing presses; Signet Group plc, a U.K.-based jewelry retailer; and Galiform Plc, a U.K. kitchen business.

FUND CHANGES

During the period, stock prices were very volatile and generally declined, which created disconnect between the stock price and our estimate of long-term business value. As a result, our research lists expanded and we added several new investments to the portfolio including previously mentioned Samsung Electronics Co., Ltd and Neopost SA; Cadbury Schweppes plc, a confectionary and beverage conglomerate; Société Télévision Française 1, a French television broadcast network; and Panalpina Welttransport Holding AG, a Swiss contract logistics/freight forwarder.

We exited a number of positions during the period, including Vodafone Group PLC, Tyco International Ltd., Vivendi, and SurfControl plc. Pacific Century Premium Developments Limited received a take-over offer and we also sold all of our shares of Central Japan Railway Company.

REGION ALLOCATION

| | | | | | |

| Region | | 9/30/2007 | | | 3/31/2008 | |

Europe | | 55.5 | % | | 58.3 | % |

Pacific Basin | | 19.4 | | | 16.9 | |

Emerging Markets | | 8.7 | | | 11.2 | |

Americas | | 10.3 | | | 9.7 | |

As a percentage of total net assets.

9

ARTISAN MID CAP FUND (ARTMX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Mid Cap Fund uses a bottom-up investment process to construct a diversified portfolio of U.S. mid-cap growth companies.

Security Selection. The team’s investment process begins by identifying companies that possess franchise characteristics (strong competitive positions), selling at attractive valuations and benefiting from an accelerating trend. The investment team looks for companies that are well positioned for long-term growth, driven by demand for their products and services, at an early enough stage in their profit cycle to benefit from the increased cash flows produced by the profit cycle.

Capital Allocation. Based on the investment team’s fundamental analysis of a company’s profit cycle, portfolio holdings develop through three stages. GardenSM investments are small positions in the early part of their profit cycle that will warrant a more sizeable allocation once their profit cycle accelerates. CropSM investments are positions that are being increased to a full weight because they are moving through the strongest part of their profit cycle. HarvestSM investments are positions that are being reduced as they near the team’s estimate of full valuation or their profit cycle begins to decelerate.

Broad Diversification. The team looks for investment opportunities across the entire economy so that it can find sustainable growth regardless of the sector or industry.

The Fund primarily invests in medium-sized U.S. growth companies. The Fund generally maintains a weighted average market capitalization of not more than 1.5 times the weighted average market capitalization of companies included in the Russell Midcap® Index.

PERFORMANCE HISTORY

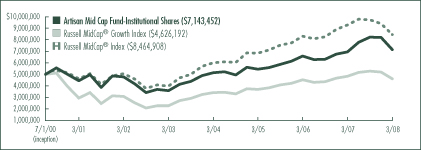

GROWTH OF AN ASSUMED $10,000 INVESTMENT (6/27/1997 to 3/31/2008)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception |

Artisan Mid Cap Fund | | 2.36 | % | | 9.19 | % | | 14.52 | % | | 12.58 | % | | 15.72% |

Russell MidCap® Growth Index | | -4.55 | | | 7.77 | | | 15.20 | | | 5.15 | | | 6.90 |

Russell MidCap® Index | | -8.92 | | | 7.36 | | | 16.31 | | | 7.65 | | | 9.46 |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 87 for a description of each index.

10

INVESTING ENVIRONMENT

The semiannual reporting period ended March 31, 2008 was a rough time for equities as markets were shaken by weakening economic conditions, rising energy prices and ongoing turmoil in the financials sector and housing market. The Russell Midcap® Growth Index returned -12.46%, holding a slight edge relative to its Value counterpart. Within the growth index, only the energy sector managed to post a gain on the heels of a strong increase in the price of oil. All other sectors declined, with telecommunication services, consumer discretionary and information technology stocks struggling the most.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/2007 | | | 3/31/2008 | |

Consumer Discretionary | | 9.9 | % | | 10.7 | % |

Consumer Staples | | 4.9 | | | 5.7 | |

Energy | | 3.7 | | | 4.1 | |

Financials | | 6.5 | | | 7.4 | |

Healthcare | | 22.7 | | | 23.8 | |

Industrials | | 13.1 | | | 15.4 | |

Information Technology | | 31.1 | | | 27.8 | |

Materials | | 1.3 | | �� | 1.3 | |

Telecommunication Services | | 1.7 | | | 0.7 | |

Utilities | | — | | | 0.4 | |

Other assets less liabilities | | 5.1 | | | 2.7 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

The Fund underperformed the Russell Midcap® Growth Index as the Fund fell -13.32% for the six months ended March 31, 2008. Relative to the benchmark, our security selection strength was most evident in the healthcare, materials and financials sectors. Top performers within the healthcare sector included robotic surgery systems manufacturer Intuitive Surgical, Inc., biopharmaceutical company Celgene Corporation, radiation therapy systems provider Varian Medical Systems, Inc. and medical device company C.R. Bard, Inc. Our success in the materials and financials sectors was largely due to fertilizer producer The Mosaic Company and Florida real estate developer The St. Joe Company, respectively.

The key sources of weakness compared to the benchmark were our relatively low weight in energy stocks and select technology and consumer staples holdings. Semiconductor provider Broadcom Corporation, programmable graphics technology provider NVIDIA Corporation, network infrastructure company Juniper Networks, Inc., and virtualization solutions provider VMware, Inc. were among our worst performing information technology holdings. Our underperformance in the consumer staples sector was driven mostly by a decline in alternative beverage producer Hansen Natural Corporation.

FUND CHANGES

Our security selection process is focused on identifying companies with franchise characteristics and an attractive valuation that are benefiting from an accelerating trend. Our transaction activity was not concentrated in any one sector. Our largest new positions included Celgene Corp., construction and engineering company Fluor Corporation and beauty product marketer Avon Products, Inc. We also added capital to many existing positions, most notably to Broadcom Corporation and healthcare technology and services provider Cerner Corporation.

We funded our new purchases with sales from a broad range of sectors. Patterson Cos. Inc., McDermott International Inc., Linear Technology Corp. and SUPERVALU Inc. were all top 30 positions as of the beginning of the reporting period that were subsequently liquidated. Ventana Medical Systems Inc. was the subject of a takeover offer by Swiss pharmaceutical and diagnostics company Roche Holding AG. The transaction was completed during the period.

11

ARTISAN MID CAP VALUE FUND (ARTQX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Mid Cap Value Fund uses a bottom-up investment process to construct a diversified portfolio of stocks of medium-sized U.S. companies that the investment team believes are undervalued, in solid financial condition and have attractive business economics. The team believes companies with these characteristics are less likely to experience eroding values over the long term.

Attractive valuation. The team values a business using what it believes are reasonable expectations for the long-term earnings power and capitalization rates of that business. This results in a range of values for the company that the team believes would be reasonable. The team generally will purchase a security if the stock price falls below or toward the lower end of that range.

Sound financial condition. The team favors companies with an acceptable level of debt and positive cash flow. At a minimum, the team tries to avoid companies that have so much debt that management may be unable to make decisions that would be in the best interests of the companies’ shareholders.

Attractive business economics. The team favors cash-producing businesses that it believes are capable of earning acceptable returns on capital over the company’s business cycle.

The Fund will generally not initiate a position in a company unless it has a market capitalization between $2 billion and $15 billion.

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (3/28/2001 to 3/31/2008)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | Since

Inception | |

Artisan Mid Cap Value Fund | | -5.95 | % | | 7.32 | % | | 18.00 | % | | 12.68 | % |

Russell Midcap® Value Index | | -14.12 | | | 6.57 | | | 16.77 | | | 10.60 | |

Russell Midcap® Index | | -8.92 | | | 7.36 | | | 16.31 | | | 9.21 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 87 for a description of each index.

12

INVESTING ENVIRONMENT

For the six-month period ended March 31, 2008, the Russell Midcap® Value and Russell Midcap® indices returned -14.09% and -13.17%, respectively. The past six months were challenging as investors grappled with a slowing economy and continued stress in the capital markets. In the Russell Midcap® Value Index, most sectors declined during the period. The information technology and telecommunication services sectors were among the worst performing groups with declines of more than -24%. The energy sector was the exception with strong positive returns on the heels of rising oil and gas prices.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/2007 | | | 3/31/2008 | |

Consumer Discretionary | | 14.5 | % | | 14.5 | % |

Consumer Staples | | 2.6 | | | 2.2 | |

Energy | | 18.6 | | | 15.3 | |

Financials | | 23.6 | | | 15.4 | |

Healthcare | | — | | | 2.0 | |

Industrials | | 12.2 | | | 21.5 | |

Information Technology | | 18.7 | | | 18.9 | |

Utilities | | 2.8 | | | 1.6 | |

Other assets less liabilities | | 7.0 | | | 8.6 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

The Fund returned -8.29% during the six-month period ended March 31, 2008. Strong stock selection in the information technology, industrials and consumer discretionary sectors added significant value to the Fund’s relative performance. We also benefited from strength among our energy holdings during the period. Detracting from performance were our holdings in the financials sector and a few select holdings in other areas. Oil and gas exploration and production companies Cimarex Energy Co., Mariner Energy, Inc. and Forest Oil Corporation, transportation services provider Ryder System, Inc., real estate investment trust Annaly Capital Management, Inc. and hard disk drive manufacturer Western Digital Corporation were our leading contributors during the period. In the financials sector, our weakest performers included financial guarantor MBIA Inc., student loan originator The Student Loan Corporation, hybrid thrift/mortgage bank IndyMac Bancorp, Inc., banking and financial services provider Zions Bancorporation and insurance provider Brown & Brown, Inc. Other stocks that underperformed included specialty women’s apparel retailer Chico’s FAS, Inc., electric utility company PNM Resources, Inc. and technology products and services distributor Ingram Micro Inc.

FUND CHANGES

The biggest changes to the portfolio over the past six months were a decrease in our weight in the financials sector and an increase in our weight in the industrials sector. Our reduced exposure to the financials sector resulted from our sale of Annaly Capital Management, Inc., which we sold as its share price reached our target selling range, and from our sales of Zions Bancorporation, MBIA Inc. and IndyMac Bancorp, Inc., which were sold due to deteriorating fundamentals. Our exposure to the energy sector also decreased during the period, mostly due to our sales of Apache Corporation and Forest Oil Corporation, which had reached our target selling ranges. We found a few attractive investment opportunities in the industrials sector — corporate uniform manufacturer Cintas Corporation, lighting manufacturer Acuity Brands, Inc. and electrical components manufacturer Thomas & Betts Corporation. We also re-established a position in former holding Manpower Inc., an employment services provider. We were attracted to all of our new positions based on the key characteristics of our investment process.

13

ARTISAN OPPORTUNISTIC VALUE FUND (ARTLX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Opportunistic Value Fund uses a bottom-up investment process to construct a diversified portfolio of stocks that the team believes are undervalued, in solid financial condition with attractive business economics and that offer the potential for superior risk/reward outcomes. The team believes companies with these characteristics are less likely to experience eroding values over the long term.

Attractive valuation. The team values a business using what it believes are reasonable expectations for the long-term earnings power and capitalization rates of that business. This results in a range of values for the company that the team believes would be reasonable. The team generally will purchase a security if the stock price falls below or toward the lower end of that range.

Sound financial condition. The team favors companies with an acceptable level of debt and positive cash flow. At a minimum, the team tries to avoid companies that have so much debt that management may be unable to make decisions that would be in the best interest of the companies’ shareholders.

Attractive business economics. The team favors cash-producing businesses that it believes are capable of earning acceptable returns on capital over the company’s business cycle.

The Fund will invest in U.S. companies with market capitalizations of at least $2 billion at the time of initial purchase, and may invest up to 25% of its net assets at market value at the time of purchase in non-U.S. securities.

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (3/27/2006 to 3/31/2008)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | |

| Fund / Index | | 1-Year | | | Since

Inception | |

Artisan Opportunistic Value Fund | | -6.64 | % | | 4.87 | % |

Russell 1000® Value Index | | -9.99 | | | 2.23 | |

Russell 1000® Index | | -5.40 | | | 2.69 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 87 for a description of each index.

14

INVESTING ENVIRONMENT

Stocks of all sizes suffered losses during the six-month period ended March 31, 2008. It was a challenging period as a slowing economy and continued stress in the capital markets weighed on the minds of investors. The Russell 1000® and Russell 1000® Value indices returned -12.41% and - -14.01%, respectively, during the period. Weakness in the market was broad across sectors. Financials, telecommunication services and consumer discretionary stocks were among the weakest performers. In contrast, the consumer staples, energy and materials sectors held up the best in the weak market.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/2007 | | | 3/31/2008 | |

Consumer Discretionary | | 9.2 | % | | 10.5 | % |

Consumer Staples | | 5.8 | | | 4.9 | |

Energy | | 11.2 | | | 8.7 | |

Financials | | 47.9 | | | 26.4 | |

Healthcare | | 4.3 | | | 5.5 | |

Industrials | | 3.5 | | | 3.5 | |

Information Technology | | 13.9 | | | 26.7 | |

Other assets less liabilities | | 4.2 | | | 13.8 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

Artisan Opportunistic Value Fund is constructed from the bottom up without concern for the characteristics of a benchmark, so the success of our security selection is the primary driver of portfolio returns. For the six-month period ended March 31, 2008, the Fund returned -10.92%. Our strongest positive contributors to performance were oil and natural gas producer Apache Corporation, discount retailer Wal-Mart Stores, Inc., holding company Berkshire Hathaway Inc., real estate investment trust Annaly Capital Management, Inc. and land drilling contractor Nabors Industries Ltd. The Fund’s largest decliners were insurance provider American International Group, Inc., hybrid thrift/mortgage bank IndyMac Bancorp, Inc. and banking and financial services providers Wachovia Corporation, Royal Bank of Scotland Group plc and Citigroup Inc.

FUND CHANGES

Two of the most notable changes in the portfolio over the past six months were in the financials and technology sectors. At the end of the period, we still had a number of holdings in the financials sector, but our overall weight fell from nearly 48% six months ago to approximately 27% as of March 31, 2008. We trimmed a number of holdings and completely sold out of a few others. Our sales in this area included Annaly Capital Management, Inc., Royal Bank of Scotland Group plc, Citigroup Inc. and IndyMac Bancorp, Inc.

As consistent with our process, we often find opportunities in the downtrodden, unloved areas of the market. From time to time, these opportunities will cluster, and they did so in the information technology sector over the past six months. We ended the period with a nearly 27% weight in the technology sector, up from approximately 14% six months ago. The increase in our exposure was due to a combination of increasing some of our existing positions and adding a few new ones to the mix. The new additions were ethernet and IP network solutions provider Cisco Systems, Inc. and computing, imaging solutions and services provider Hewlett-Packard Company. During the period we also re-initiated positions in computer maker Dell Inc. and consulting services firm Accenture Ltd.

15

ARTISAN SMALL CAP FUND (ARTSX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Small Cap Fund uses a bottom-up investment process to construct a diversified portfolio of U.S. small-cap growth companies.

Competitive advantages. A sustainable competitive advantage is critical to producing above-average growth and profitability. Identifying the source of a company’s competitive advantage lends confidence to the team’s assessment of intrinsic value.

Return on invested capital. The team believes that, over time, a company with improving returns on its invested capital will be rewarded with a higher valuation. The team determines how much capital investment is needed to achieve a company’s continued growth and analyzes management’s ability to use that capital in the most effective way to support that growth.

Intrinsic value. The team estimates a company’s intrinsic value—the value it thinks a buyer would pay to buy the entire company. The team bases its buy and sell targets for a company’s stock on its intrinsic value estimates.

The Fund will not initiate a position in a company unless it has a market capitalization between $300 million and $2.5 billion and meets the team’s standards for earnings growth and sustainable growth prospects.

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (3/28/1995 to 3/31/2008)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan Small Cap Fund | | -12.04 | % | | 1.93 | % | | 12.73 | % | | 2.99 | % | | 7.71 | % |

Russell 2000® Growth Index | | -8.94 | | | 5.74 | | | 14.24 | | | 1.75 | | | 5.75 | |

Russell 2000® Index | | -13.00 | | | 5.06 | | | 14.90 | | | 4.96 | | | 9.18 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 87 for a description of each index.

16

INVESTING ENVIRONMENT

Domestic equities struggled during the semiannual reporting period ended March 31, 2008. Weakening economic conditions and the stress in the financials sector contributed to investor anxiety. The Russell 2000® Growth Index declined -14.66%. Within the Russell 2000® Growth Index, energy was the only sector to post a gain as the price of oil shot past $100 per barrel. Utilities and consumer staples stocks held up relatively well. The benchmark’s principal sources of weakness were the telecommunication services, information technology and consumer discretionary sectors, as each fell more than 20%.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/2007 | | | 3/31/2008 | |

Consumer Discretionary | | 16.1 | % | | 12.2 | % |

Consumer Staples | | 2.1 | | | 1.3 | |

Energy | | 5.3 | | | 7.2 | |

Financials | | 10.0 | | | 4.3 | |

Healthcare | | 17.4 | | | 20.2 | |

Industrials | | 19.7 | | | 29.5 | |

Information Technology | | 23.0 | | | 19.2 | |

Telecommunication Services | | 0.7 | | | — | |

Utilities | | 1.6 | | | 2.0 | |

Other assets less liabilities | | 4.1 | | | 4.1 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

PERFORMANCE DISCUSSION

The Fund returned -19.16% this period, underperforming the Russell 2000® Growth Index. Our overall return was hindered by the negative contributions of select holdings in the information technology, healthcare and financials sectors. Our list of underperformers in the information technology sector included enterprise wireless systems provider Aruba Networks Inc., GPS technology supplier SiRF Technology Holdings, Inc., anti-piracy and content protection software producer Macrovision Corporation and Global Cash Access Holdings, Inc., a provider of cash access products to the gaming industry. In the healthcare and financials sectors, returns were hindered by weakness in medical device manufacturers NxStage Medical Inc. and ArthoCare Corporation, newly purchased Obagi Medical Products, Inc., which serves the therapeutic skin care market, and National Financial Partners Corp., an independent distributor of financial services products.

This period’s top performers came from various sectors. Bright Horizons Family Solutions, Inc. and Performance Food Group were the beneficiaries of premium takeout offers. Other winners included trucking company Old Dominion Freight Line, Inc., contract research organization ICON PLC, automotive aftermarket parts provider LKQ Corporation (which purchased another of our holdings, Keystone Automotive Industries), and online options broker optionsXpress Holdings, Inc.

FUND CHANGES

The high volatility of the period created many new purchase opportunities. We invested in a number of positions that met our security selection criteria: a competitive advantage, a high return on invested capital, and an attractive price relative to our intrinsic value estimate. Our largest purchases were Psychiatric Solutions, Inc., a behavioral healthcare services provider, Life Time Fitness, Inc., an operator of athletic and health facilities around the country, and Ladish Co., Inc., which produces metal components for the aerospace industry.

We funded our purchases in part with the sales of previously mentioned SiRF Technology Holdings, Inc. and optionsXpress Holdings, Inc. ACI Worldwide, Inc., Brightpoint, Inc., Wind River Systems, Inc., Thoratec Corporation, Alabama National BanCorporation and ICU Medical, Inc. were also sold during the period.

17

ARTISAN SMALL CAP VALUE FUND (ARTVX)

INVESTMENT PROCESS HIGHLIGHTS

Artisan Small Cap Value Fund uses a bottom-up investment process to construct a diversified portfolio of small-cap U.S. companies that the team believes are undervalued, in solid financial condition and have attractive business economics. The team believes companies with these characteristics are less likely to experience eroding values over the long term.

Attractive valuation. The team values a business using what it believes are reasonable expectations for the long-term earnings power and capitalization rates of that business. This results in a range of values for the company that the team believes would be reasonable. The team generally will purchase a security if the stock price falls below or toward the lower end of that range.

Sound financial condition. The team favors companies with an acceptable level of debt and positive cash flow. At a minimum, the team tries to avoid companies that have so much debt that management may be unable to make decisions that would be in the best interest of the companies’ shareholders.

Attractive business economics. The team favors cash-producing businesses that it believes are capable of earning acceptable returns on capital over the company’s business cycle.

The Fund will not initiate a position in a company unless it has a market capitalization below $2 billion.

PERFORMANCE HISTORY

GROWTH OF AN ASSUMED $10,000 INVESTMENT (9/29/1997 to 3/31/2008)

AVERAGE ANNUAL TOTAL RETURNS (as of 3/31/2008)

| | | | | | | | | | | | | | | |

| Fund / Index | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | | | Since

Inception | |

Artisan Small Cap Value Fund | | -10.18 | % | | 6.37 | % | | 16.88 | % | | 10.77 | % | | 11.45 | % |

Russell 2000® Value Index | | -16.88 | | | 4.33 | | | 15.45 | | | 7.46 | | | 8.14 | |

Russell 2000® Index | | -13.00 | | | 5.06 | | | 14.90 | | | 4.96 | | | 5.40 | |

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate, so that an investor’s shares in the Fund, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For current to most recent month-end performance information, visit www.artisanfunds.com or call 800.344.1770. The graph and table above do not reflect the deduction of taxes that a shareholder would pay on distributions or sale of Fund shares. See page 87 for a description of each index.

18

INVESTING ENVIRONMENT

For the six-month period ended March 31, 2008, the Russell 2000® Value and Russell 2000® indices returned -13.33% and -14.02%, respectively. The period was challenging for equity markets as investors grappled with a slowing economy and continued stress in the capital markets. During the period, nearly every sector in the Russell 2000® Value Index declined. The biggest losers were the consumer discretionary, information technology and telecommunication services sectors. The one exception was the energy sector which closed out the period with a positive return as rising oil and gas prices supported the shares of many energy stocks.

SECTOR DIVERSIFICATION

| | | | | | |

| Sector | | 9/30/2007 | | | 3/31/2008 | |

Consumer Discretionary | | 15.2 | % | | 11.3 | % |

Consumer Staples | | 1.5 | | | 1.9 | |

Energy | | 17.4 | | | 14.7 | |

Financials | | 11.0 | | | 8.6 | |

Healthcare | | 7.7 | | | 6.5 | |

Industrials | | 11.2 | | | 13.4 | |

Information Technology | | 24.7 | | | 28.6 | |

Materials | | 3.0 | | | 3.7 | |

Telecommunication Services | | 0.4 | | | 0.0 | (1) |

Utilities | | 5.1 | | | 3.9 | |

Other assets less liabilities | | 2.8 | | | 7.4 | |

Total | | 100.0 | % | | 100.0 | % |

As a percentage of total net assets.

(1) | Represents less than 0.1% of total net assets. |

PERFORMANCE DISCUSSION

The Fund returned -7.26% for the six-month period ended March 31, 2008. Strong stock selection was the primary reason for our outperformance relative to the Russell 2000® Value Index. The Fund benefited from its holdings in the consumer discretionary, energy, information technology and industrials sectors. There was no identifiable trend among our weakest performers. Our leading gainers during the period included oil and gas exploration and production companies Cimarex Energy Co., Mariner Energy, Inc., St. Mary Land & Exploration Company and Comstock Resources, Inc., lighting fixtures manufacturer The Genlyte Group Incorporated, metal products manufacturer Quanex Corporation and less-than-truckload carrier Con-way Inc. On the downside, stocks that hindered our results during the period included insurance broker Hilb Rogal & Hobbs Company, healthcare staffing services provider Cross Country Healthcare, Inc., federal government information technology solutions provider SI International Inc., title insurer Stewart Information Services Corporation and Benchmark Electronics, Inc., a provider of contract electronics manufacturing and design services.

FUND CHANGES

We found several opportunities during the period to purchase new names and sold several others. We were attracted to our new positions based on the key characteristics of our investment process: attractive valuation, sound financial condition and attractive business economics.

We reestablished positions in a few former holdings, including Manhattan Associates, Inc., EMCOR Group, Inc. and Acuity Brands, Inc. We also purchased less-than-truckload carrier Con-way Inc., excimer laser illumination source supplier Cymer, Inc., facility services contractor ABM Industries Incorporated and contract drilling services provider Parker Drilling Company during the period.

We had a handful of holdings in the portfolio that were acquired and, at the close of the transactions, we received cash for our shares. These companies were RARE Hospitality International, Inc., Kellwood Company, SEMCO Energy, Inc. and The Genlyte Group Incorporated. Our sales during the period included Forest Oil Corporation, Stone Energy Corporation, Walter Industries, Inc., Annaly Capital Management, Inc. and Albany International Corp.

19

ARTISAN GLOBAL VALUE FUND

Schedule of Investments – March 31, 2008 (Unaudited)

| | | | | |

| | | Shares

Held | | Value |

| | | | | |

| COMMON STOCKS - 95.8% | | | | | |

| | | | | |

| FRANCE - 2.2% | | | | | |

Neopost SA | | 1,002 | | $ | 112,458 |

Sanofi-Aventis | | 1,216 | | | 91,227 |

| | | | | |

| | | | | 203,685 |

| HONG KONG - 2.1% | | | | | |

Guoco Group Limited | | 20,450 | | | 200,226 |

| | | | | |

| JAPAN - 7.3% | | | | | |

Credit Saison Co., Ltd. | | 9,100 | | | 253,792 |

SANKYO CO., LTD. | | 3,983 | | | 236,550 |

Sekisui House, Ltd. | | 21,150 | | | 195,629 |

| | | | | |

| | | | | 685,971 |

| MEXICO - 2.6% | | | | | |

Grupo Modelo, S.A. de C.V., Series C | | 55,500 | | | 243,063 |

| | | | | |

| NETHERLANDS - 4.3% | | | | | |

Wolters Kluwer NV | | 15,055 | | | 398,590 |

| | | | | |

| SOUTH KOREA - 5.2% | | | | | |

Samsung Electronics Co., Ltd. | | 226 | | | 142,170 |

Samsung Electronics Co., Ltd. (DR) | | 300 | | | 93,675 |

SK Telecom Co., Ltd. (DR) | | 11,685 | | | 252,513 |

| | | | | |

| | | | | 488,358 |

| SWITZERLAND - 16.2% | | | | | |

Adecco SA | | 4,932 | | | 284,815 |

Givaudan SA | | 242 | | | 239,417 |

Novartis AG | | 10,783 | | | 552,668 |

Panalpina Welttransport Holding AG | | 1,151 | | | 140,818 |

Pargesa Holding SA | | 2,665 | | | 297,065 |

| | | | | |

| | | | | 1,514,783 |

| UNITED KINGDOM - 15.0% | | | | | |

Cadbury Schweppes plc | | 10,122 | | | 111,191 |

Cadbury Schweppes plc (DR) | | 1,525 | | | 67,435 |

Diageo plc | | 9,389 | | | 189,320 |

Experian Group Ltd. | | 34,970 | | | 254,710 |

Home Retail Group plc | | 45,954 | | | 238,267 |

Signet Group plc | | 290,198 | | | 355,644 |

Unilever plc (DR) | | 5,540 | | | 186,809 |

| | | | | |

| | | | | 1,403,376 |

| UNITED STATES - 40.9% | | | | | |

American Express Company | | 1,750 | | | 76,510 |

Cintas Corporation | | 9,685 | | | 276,410 |

| | | | | | | |

| | | Shares

Held | | Value | |

| | | | | | | |

| UNITED STATES (CONTINUED) | | | | | | | |

Covidien Ltd. | | | 4,835 | | $ | 213,949 | |

Dell Inc.(1) | | | 12,600 | | | 250,992 | |

The Home Depot, Inc. | | | 6,130 | | | 171,456 | |

International Speedway Corporation, Class A | | | 6,500 | | | 267,800 | |

Johnson & Johnson | | | 6,125 | | | 397,329 | |

Legg Mason, Inc. | | | 1,300 | | | 72,774 | |

Marsh & McLennan Companies, Inc. | | | 19,425 | | | 472,999 | |

Mattel, Inc. | | | 10,085 | | | 200,691 | |

Mohawk Industries, Inc.(1) | | | 6,595 | | | 472,268 | |

Motorola, Inc. | | | 26,150 | | | 243,195 | |

The Sherwin-Williams Company | | | 3,050 | | | 155,672 | |

Wal-Mart Stores, Inc. | | | 8,120 | | | 427,762 | |

The Washington Post Company, Class B | | | 196 | | | 129,654 | |

| | | | | | | |

| | | | | | 3,829,461 | |

| | | | | | | |

Total common stocks

(Cost $9,570,114) | | | | | | 8,967,513 | |

| | | Par

Amount | | | |

SHORT-TERM INVESTMENTS

(CASH EQUIVALENTS) - 7.0% | | | | | | | |

Repurchase agreement with Fixed Income Clearing Corporation, 1.10%, dated 3/31/08, due 4/1/08, maturity value $660,020(2)

(Cost $660,000) | | $ | 660,000 | | | 660,000 | |

| | | | | | | |

| | | | | | | |

Total investments - 102.8% (Cost $10,230,114) | | | | | | 9,627,513 | |

| | | | | | | |

Other assets less liabilities - (2.8%) | | | | | | (266,181 | ) |

| | | | | | | |

| | | | | | | |

Total net assets - 100.0%(3) | | | | | $ | 9,361,332 | |

| | | | | | | |

(1) | Non-income producing security. |

| | | | | | | |

Issuer | | Rate | | | Maturity | | Value |

U.S. Treasury Bond | | 8.75 | % | | 8/15/20 | | $678,500 |

(3) | Percentages for the various classifications relate to total net assets. |

Company names are as reported by a data service provider and in some cases are translations; a company’s legal name may be different.

(DR) Depository Receipt, voting rights may vary.

20

| | | | | | | |

PORTFOLIO DIVERSIFICATION - March 31, 2008 (Unaudited) | |

| | | Value | | | Percentage

of Total

Net Assets | |

Consumer Discretionary | | $ | 2,822,221 | | | 30.1 | % |

Consumer Staples | | | 1,225,580 | | | 13.1 | |

Financials | | | 1,373,366 | | | 14.7 | |

Healthcare | | | 1,255,173 | | | 13.4 | |

Industrials | | | 956,753 | | | 10.2 | |

Information Technology | | | 842,490 | | | 9.0 | |

Materials | | | 239,417 | | | 2.6 | |

Telecommunication Services | | | 252,513 | | | 2.7 | |

| | | | | | | |

Total common stocks | | | 8,967,513 | | | 95.8 | |

Short-term investments | | | 660,000 | | | 7.0 | |

| | | | | | | |

Total investments | | | 9,627,513 | | | 102.8 | |

Other assets less liabilities | | | (266,181 | ) | | (2.8 | ) |

| | | | | | | |

Total net assets | | $ | 9,361,332 | | | 100.0 | % |

| | | | | | | |

| | | | | | |

CURRENCY EXPOSURE - March 31, 2008 (Unaudited) | |

| | | Value | | Percentage

of Total

Investments | |

British pound | | $ | 1,149,132 | | 11.9 | % |

Euro | | | 602,275 | | 6.3 | |

Hong Kong dollar | | | 200,226 | | 2.1 | |

Japanese yen | | | 685,971 | | 7.1 | |

Mexican peso | | | 243,063 | | 2.5 | |

South Korean won | | | 142,170 | | 1.5 | |

Swiss franc | | | 1,514,783 | | 15.7 | |

US dollar | | | 5,089,893 | | 52.9 | |

| | | | | | |

Total investments | | $ | 9,627,513 | | 100.0 | % |

| | | | | | |

| | | | | |

TOP TEN HOLDINGS - March 31, 2008 (Unaudited) | |

Company Name | | Country | | Percentage

of Total

Net Assets | |

Novartis AG | | Switzerland | | 5.9 | % |

Marsh & McLennan Companies, Inc. | | United States | | 5.1 | |

Mohawk Industries, Inc. | | United States | | 5.0 | |

Wal-Mart Stores, Inc. | | United States | | 4.6 | |

Wolters Kluwer NV | | Netherlands | | 4.3 | |

Johnson & Johnson | | United States | | 4.2 | |

Signet Group plc | | United Kingdom | | 3.8 | |

Pargesa Holding SA | | Switzerland | | 3.2 | |

Adecco SA | | Switzerland | | 3.0 | |

Cintas Corporation | | United States | | 3.0 | |

| | | | | |

Total | | | | 42.1 | % |

| | | | | |

For the purpose of determining the Fund’s top ten holdings, securities of the same issuer are aggregated to determine the weight in the Fund.

The accompanying notes are an integral part of the financial statements.

21

ARTISAN INTERNATIONAL FUND

Schedule of Investments – March 31, 2008 (Unaudited)

| | | | | |

| | | Shares

Held | | Value |

| | | | | |

| COMMON AND PREFERRED STOCKS - 98.5% | | | | | |

| | | | | |

| ARGENTINA - 0.2% | | | | | |

Tenaris S.A. | | 1,067,782 | | $ | 26,584,428 |

| | | | | |

| AUSTRALIA - 0.1% | | | | | |

Babcock & Brown Infrastructure Group (Units) | | 10,250,819 | | | 11,007,659 |

| | | | | |

| BELGIUM - 0.8% | | | | | |

Delhaize Group | | 903,146 | | | 71,063,898 |

Umicore | | 962,030 | | | 50,059,770 |

| | | | | |

| | | | | 121,123,668 |

| BRAZIL - 0.6% | | | | | |

Redecard SA | | 768,400 | | | 12,782,582 |

Vivo Participacoes S.A., Preferred (DR)(1) | | 13,449,768 | | | 80,160,617 |

| | | | | |

| | | | | 92,943,199 |

| CANADA - 1.6% | | | | | |

Canadian Pacific Railway Limited | | 3,903,727 | | | 250,970,609 |

| | | | | |

| CHINA - 6.9% | | | | | |

China Construction Bank, H Shares | | 222,901,200 | | | 165,257,326 |

China Life Insurance Co., Limited, H Shares | | 17,544,900 | | | 60,304,148 |

China Merchants Holdings International Company Limited | | 21,764,900 | | | 103,473,920 |

China Netcom Group Corporation (Hong Kong) Limited | | 33,608,000 | | | 96,298,613 |

China Petroleum and Chemical Corporation, H Shares | | 129,688,900 | | | 110,814,592 |

China Resources Land Limited | | 89,337,600 | | | 154,967,473 |

China Unicom Limited | | 123,073,243 | | | 259,029,986 |

PICC Property and Casualty Company Limited, H Shares | | 64,895,600 | | | 58,703,016 |

Shanghai Electric Group Company Limited, H Shares(2) | | 150,931,921 | | | 90,954,972 |

| | | | | |

| | | | | 1,099,804,046 |

| FINLAND - 2.6% | | | | | |

Fortum Oyj(1) | | 10,393,326 | | | 423,502,113 |

| | | | | |

| FRANCE - 13.2% | | | | | |

Alstom | | 1,212,137 | | | 262,783,764 |

Bouygues SA | | 4,098,979 | | | 260,403,425 |

Carrefour SA | | 2,526,126 | | | 194,899,343 |

Electricite de France | | 3,554,045 | | | 309,219,135 |

| | | | | |

| | | Shares

Held | | Value |

| | | | | |

| FRANCE (CONTINUED) | | | | | |

France Telecom SA | | 3,930,966 | | $ | 132,187,965 |

LVMH Moet Hennessy Louis Vuitton SA | | 2,884,752 | | | 321,078,058 |

Technip SA | | 2,854,266 | | | 222,289,315 |

Vinci SA | | 5,712,190 | | | 412,939,394 |

| | | | | |

| | | | | 2,115,800,399 |

| GERMANY - 15.0% | | | | | |

Allianz SE | | 1,197,159 | | | 237,158,870 |

Bayer AG | | 5,546,124 | | | 444,451,336 |

Daimler AG | | 4,034,936 | | | 344,943,638 |

Deutsche Telekom AG | | 9,995,280 | | | 166,479,381 |

Fraport AG | | 2,700,531 | | | 194,925,392 |

IVG Immobilien AG | | 1,234,066 | | | 34,523,525 |

Linde AG | | 2,388,590 | | | 337,465,317 |

RWE AG | | 1,241,824 | | | 152,646,720 |

United Internet AG | | 2,909,638 | | | 62,610,597 |

Wacker Chemie AG | | 2,106,268 | | | 431,553,285 |

| | | | | |

| | | | | 2,406,758,061 |

| HONG KONG - 6.5% | | | | | |

The Bank of East Asia, Ltd. | | 36,555,400 | | | 184,123,875 |

Hutchison Whampoa Limited | | 38,661,324 | | | 365,120,790 |

New World Development Company Limited | | 8,818,400 | | | 21,369,973 |

NWS Holdings Limited | | 40,157,746 | | | 136,221,530 |

Sun Hung Kai Properties Limited | | 12,954,000 | | | 200,568,829 |

Swire Pacific Limited, Class A | | 12,439,389 | | | 140,335,021 |

| | | | | |

| | | | | 1,047,740,018 |

| INDIA - 0.3% | | | | | |

Housing Development Finance Corporation Ltd. | | 942,615 | | | 55,798,015 |

| | | | | |

| ITALY - 0.8% | | | | | |

Intesa Sanpaolo | | 17,162,974 | | | 120,983,748 |

| | | | | |

| JAPAN - 10.5% | | | | | |

CANON INC. | | 1,133,500 | | | 52,194,673 |

Credit Saison Co., Ltd. | | 6,562,750 | | | 183,030,146 |

DENSO CORPORATION | | 2,846,700 | | | 91,958,006 |

HONDA MOTOR CO., LTD. | | 3,216,500 | | | 91,803,195 |

JAPAN TOBACCO INC. | | 64,853 | | | 324,655,367 |

Jupiter Telecommunications Co., Ltd.(1) | | 212,121 | | | 198,331,433 |

Mitsubishi Estate Company Ltd. | | 4,531,400 | | | 110,011,918 |

Mitsubishi Heavy Industries, Ltd. | | 43,559,800 | | | 186,160,461 |

MITSUI & CO., LTD. | | 6,897,100 | | | 139,768,680 |

Mitsui Fudosan Co., Ltd. | | 5,327,525 | | | 105,770,184 |

SUZUKI MOTOR CORPORATION | | 5,859,800 | | | 147,847,081 |

22

| | | | | |

| | | Shares

Held | | Value |

| | | | | |

| JAPAN (CONTINUED) | | | | | |

TOKYU LAND CORPORATION | | 9,432,850 | | $ | 59,144,575 |

| | | | | |

| | | | | 1,690,675,719 |

| LUXEMBOURG - 0.6% | | | | | |

RTL Group | | 767,688 | | | 96,971,039 |

| | | | | |

| MEXICO - 0.3% | | | | | |

Grupo Televisa S.A. (DR) | | 2,333,970 | | | 56,575,433 |

| | | | | |

| NETHERLANDS - 2.4% | | | | | |

ASML Holding N.V.(1) | | 15,487,048 | | | 380,933,463 |

| | | | | |

| NORWAY - 5.5% | | | | | |

Acergy SA | | 1,774,025 | | | 38,233,673 |

Orkla ASA | | 28,506,515 | | | 361,065,170 |

Renewable Energy Corp AS(1) | | 2,359,200 | | | 65,786,209 |

SeaDrill Ltd. | | 15,552,805 | | | 416,891,589 |

| | | | | |

| | | | | 881,976,641 |

| QATAR - 0.4% | | | | | |

Industries Qatar | | 1,406,183 | | | 50,241,525 |

Industries Qatar, Equity-Linked Security(3)(4) | | 210,776 | | | 7,531,026 |

| | | | | |

| | | | | 57,772,551 |

| RUSSIA - 6.7% | | | | | |

Gazprom (DR) | | 7,560,478 | | | 385,584,378 |

LUKOIL (DR) | | 3,956,872 | | | 339,499,618 |

Mining and Metallurgical Company Norilsk Nickel (DR) | | 3,232,440 | | | 90,993,186 |

Novorossiysk Sea Trade Port (DR)(1)(3) | | 198,700 | | | 2,980,500 |

OAO TMK (DR)(3) | | 650,022 | | | 21,125,715 |

RAO Unified Energy System (DR)(1) | | 2,065,483 | | | 214,293,861 |

Uralkali (DR)(1)(3) | | 369,750 | | | 14,327,812 |

| | | | | |

| | | | | 1,068,805,070 |

| SOUTH AFRICA - 0.6% | | | | | |

Naspers Limited | | 5,713,602 | | | 99,336,360 |

| | | | | |

| SOUTH KOREA - 3.1% | | | | | |

Kookmin Bank | | 3,600,944 | | | 201,436,157 |

KT Corporation | | 1,210,422 | | | 57,383,059 |

NHN Corp.(1) | | 1,042,935 | | | 243,370,807 |

| | | | | |

| | | | | 502,190,023 |

| SPAIN - 4.9% | | | | | |

Gamesa Corporacion Tecnologica, S.A. | | 4,899,299 | | | 223,534,631 |

Industria de Diseno Textil, S.A. | | 2,832,865 | | | 157,383,128 |

Telefonica S.A. | | 14,319,729 | | | 411,452,035 |

| | | | | |

| | | | | 792,369,794 |

| SWEDEN - 0.1% | | | | | |

Assa Abloy AB, Class B | | 760,600 | | | 13,792,783 |

| | | | | |

| SWITZERLAND - 9.9% | | | | | |

Adecco SA | | 2,112,469 | | | 121,991,841 |

Compagnie Financiere Richemont SA (‘A’ Units) | | 1,576,855 | | | 88,441,067 |

| | | | | | | |

| | | Shares

Held | | Value | |

| | | | | | | |

| SWITZERLAND (CONTINUED) | | | | |

Holcim Ltd. | | | 2,516,008 | | $ | 264,242,911 | |