Table of Contents

OMB APPROVAL | ||

OMB Number: | 3235-0570 | |

Expires: | January 31, 2014 | |

Estimated average burden | ||

hours per response: | 20.6 | |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8934

ING Strategic Allocation Portfolios, Inc.

(Exact name of registrant as specified in charter)

| 7337 E. Doubletree Ranch Rd., Scottsdale, AZ | 85258 | |

| (Address of principal executive offices) | (Zip code) |

The Corporation Trust Incorporated, 300 E. Lombard Street, Baltimore, MD 21201

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: December 31

Date of reporting period: January 1, 2012 to December 31, 2012

Table of Contents

| Item 1. | Reports to Stockholders. |

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Table of Contents

Annual Report

December 31, 2012

Classes I and S

Strategic Allocation Funds-of-Funds

| n | ING Strategic Allocation Conservative Portfolio |

| n | ING Strategic Allocation Growth Portfolio |

| n | ING Strategic Allocation Moderate Portfolio |

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully.

MUTUAL FUNDS |

|

Table of Contents

| 1 | ||||

| 2 | ||||

| 4 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 15 | ||||

| 17 | ||||

| 24 | ||||

| 27 | ||||

| 28 | ||||

| 32 | ||||

PROXY VOTING INFORMATION

A description of the policies and procedures that the Portfolios use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the ING Funds’ website at www.inginvestment.com; and (3) on the U.S. Securities and Exchange Commission’s (“SEC’s”) website at www.sec.gov. Information regarding how the Portfolios voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the ING Funds’ website at www.inginvestment.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Portfolios file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Portfolios’ Forms N-Q are available on the SEC’s website at www.sec.gov. The Portfolios’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. The Portfolios’ Forms N-Q, as well as a complete portfolio of investments, are available without charge upon request from the Portfolios by calling Shareholder Services toll-free at (800) 992-0180.

Table of Contents

Looking Forward

Dear Shareholder,

Normally I end my letters by exhorting clients to keep their portfolios focused on long-term goals and well diversified in terms of assets and geography, and to discuss thoroughly any proposed investment changes with their financial advisors before taking action. This month, the reminders are up front to emphasize their importance as we conclude an eventful year and take a look forward.

A central theme over the past few years has been the impact government and central bank policymaking has had on economic and market outcomes. Private-sector forces, which tend to restore equilibrium in normal times, have not done enough to allow policymakers to scale back their involvement. An important reason for this is that the framework within which private-sector decisions are made requires substantial

overhaul; economic and monetary ties in the euro zone need to be strengthened, the U.S. must make some difficult fiscal decisions and the success of a number of economies depends on the introduction of structural reforms.

Since the world economy is still sluggish, supportive public policies will remain critical in 2013 and beyond. However, what might we anticipate over the long term? For insight into this question, I turned to a recent report published by the National Intelligence Council — a U.S. government agency that serves as a bridge between the U.S. intelligence and policy communities — entitled “Global Trends 2030: Alternative Worlds.” The report identifies four “megatrends” that the Council considers likely to emerge over the next 20 years or so. Among these are two that potentially carry implications for future investment themes. Individual empowerment will accelerate owing to growth of the global middle class, says the Council, potentially leading to a virtuous cycle of global economic expansion and creating dynamic markets for new products and technologies. Meanwhile, emerging nations will wield greater regional influence, and the health of the global economy increasingly will be linked to how well the developing world fares. This suggests that a portfolio of securities that provide exposure to developed and emerging market economies — such as ING Funds seeks to provide — may offer attractive potential for some time to come.

It’s important to remember that these are projections and subject to change, but they point to the value of keeping one’s portfolio well diversified to meet the challenges and take advantage of the opportunities that lie ahead.

All of us at ING Funds extend our best wishes for a happy and prosperous new year. We appreciate your continued confidence in us, and we look forward to serving your investment needs in the future.

Sincerely,

Shaun Mathews

President and Chief Executive Officer

ING Funds

January 4, 2013

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaims any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

International investing poses special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic.

1

Table of Contents

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2012

In the early part of our fiscal year, global equities in the form of the MSCI World IndexSM measured in local currencies including net reinvested dividends, enjoyed the best first quarter rally since 1998. But in the two months from early April the MSCI World IndexSM slumped 11% as, for the third consecutive year, the basis of earlier optimism was undermined by events. The recovery from there was dramatic and the MSCI World IndexSM ended up 15.71% for the whole year, despite slow, patchy improvement in economic data, and investors’ frustration at the futile efforts of global leaders to resolve key problems. It came because central banks, by their actions, made risky assets much more attractive. (The MSCI World IndexSM returned 15.83% for the one year ended December 31, 2012, measured in U.S. dollars.)

Much of the early upbeat sentiment rested on a sharp improvement in the employment situation, probably the most important driver of economic activity. But the improvement faded fast: the three-month average of 245,000 new jobs reported in March slumped to only 94,000 in September, before rebounding less than one third of the way to 139,000 by December. The unemployment rate was still uncomfortably high at 7.7%.

By December, other economic data, from average hourly earnings growth to consumer confidence to retail sales were mostly inconclusive. Final third quarter gross domestic product (“GDP”) growth was revised up to 3.1%, but it didn’t feel like it and the next few quarters were expected to show growth at about half of this level.

The housing market however, seemed clearly to be on the mend. The final S&P/Case-Shiller 20-City Composite Home Price Index showed a 4.3% year-over-year gain, while new home sales in November were the highest since April 2010.

Also in the relative doldrums was China, responsible for much of global GDP growth in recent years. GDP increased by 7.4% in the third quarter of 2012 over the same quarter in 2011, the lowest rise in three years.

And yet despite the shortage of good news, the MSCI World IndexSM ended December 16% above the low point in early June. How could this be? One reason was a growing sense that the euro zone’s enduring sovereign debt crisis might at last be approaching the end-game. Another was a third round of quantitative easing launched by the Federal Reserve.

In the euro zone, amid ongoing protests against fiscal austerity, a €100 billion recapitalization bailout for Spain’s shaky banks was tortuously agreed upon in June. Attention returned to Greece in July where the continuation of the country’s bailout rested on the outcome of an examination by creditors of its parlous fiscal state. With prospects for the euro looking increasingly tenuous, European Central Bank (“ECB”) President Draghi came out on July 26 with a statement unprecedented in its explicitness, that the ECB was “ready to do whatever it takes to preserve the euro.” Under certain conditions, the ECB would buy without limitation the 1-3 year bonds of a country in difficulties.

In September, Federal Reserve Chairman Bernanke announced a third round of quantitative easing: an additional $40 billion of agency mortgage-backed securities would be purchased monthly. Then in December, “Operation Twist” was replaced by $45 billion in monthly Treasury purchases. Exceptionally low policy interest rates would remain at least until the unemployment rate fell to 6.5%.

So the year ended with central bankers sounding increasingly determined to underpin the euro and the prices of risky

assets. This was enough to drive those prices higher despite dark political clouds. In Europe, inter-governmental squabbling dangerously held back agreement on Greece’s next bailout tranche until November 27. In the U.S., the newly-elected Congress looked rather like the old one, and an ominous year-end cocktail of deflationary tax increases and spending cuts was forestalled by an eleventh-hour agreement on tax increases alone which postponed an even bigger conflict on spending and the debt ceiling until March.

In U.S. fixed income markets the Barclays Capital U.S. Aggregate Bond Index (“BCAB”) of investment grade bonds rose 4.22% in 2012. The Barclays Capital U.S. Treasury Index, a sub-index of the BCAB, returned only 1.99% as risk appetite recovered. By contrast the Barclays Capital U.S. Corporate Investment Grade Bond Index, also a sub-index of the BCAB, rose 9.82%, while the Barclays Capital High-Yield Bond — 2% Issuer Constrained Composite Index (not part of the BCAB index) gained 15.78%.

U.S. equities, represented by the S&P 500® Index including dividends, advanced 16.00% in the fiscal year. By sector, financials led the way with a return of 28.82%, followed by consumer discretionary with a return of 23.92%. No sector incurred a loss, but defensive utilities’ slim 1.29% gain reflected improved risk appetite. Operating earnings per share for S&P 500® companies set a new record in the second quarter of 2012, and barely slipped in the third.

In currency markets, the dollar fell 1.76% against the euro, which rebounded after Draghi’s July pronouncements, and 4.38% against the pound, which moved in sympathy with the euro, reflecting close trade ties. But the dollar gained 12.79% over the yen in 2012, as Japan’s parliamentary opposition won a landslide in December elections and promised unlimited monetary easing.

In international markets, the MSCI Japan® Index soared 21.57%, due mainly to the monetary stimulus referred to above. This was despite the effect on Japan’s export focused economy of the euro zone crisis, the slowdown in China and a return to recession. The MSCI Europe ex UK® Index rose 18.78% due to central bank initiatives, in the face of economic news that was unremittingly bad, also including a return to recession and record unemployment at 11.7%. The MSCI UK® Index added 10.19%, boosted by financials but held back by large, lagging energy and materials. The U.K. GDP grew 1% in the third quarter, but this was largely due to one-time statistical anomalies.

Parentheses denote a negative number.

All indices are unmanaged and investors cannot invest directly in an index. Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Portfolios’ performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.inginvestment.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING’s Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

2

Table of Contents

BENCHMARK DESCRIPTIONS

| Index | Description | |

| Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index | An unmanaged index that includes all fixed-income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million, and at least one year to maturity. | |

| Barclays Capital U.S. Aggregate Bond Index | An unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. | |

| Barclays Capital U.S. Corporate Investment Grade Bond Index | An unmanaged index consisting of publicly issued, fixed rate, nonconvertible, investment grade debt securities. | |

| Barclays Capital U.S. Treasury Index | An unmanaged index that includes public obligations of the U.S. Treasury. Treasury bills, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS and STRIPS, are excluded. | |

| MSCI Europe ex UK® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK. | |

| MSCI Japan® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan. | |

| MSCI UK® Index | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK. | |

| MSCI World IndexSM | An unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. | |

| Russell 3000® Index | An unmanaged index that measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market. | |

| S&P 500® Index | An unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets. | |

| S&P/Case-Shiller 20-City Composite Home Price Index | A composite index of the home price index for the top 20 Metropolitan Statistical Areas in the United States. The index is published monthly by Standard & Poor’s. |

3

Table of Contents

| ING STRATEGIC ALLOCATION PORTFOLIOS | PORTFOLIO MANAGERS’ REPORT |

ING Strategic Allocation Conservative Portfolio seeks to provide total return (i.e., income and capital growth, both realized and unrealized) consistent with preservation of capital. ING Strategic Allocation Growth Portfolio seeks to provide capital appreciation. ING Strategic Allocation Moderate Portfolio seeks to provide total return (i.e., income and capital appreciation, both realized and unrealized). ING Strategic Allocation Conservative Portfolio, ING Strategic Allocation Growth Portfolio and ING Strategic Allocation Moderate Portfolio (each a “Portfolio” and collectively, the “Portfolios”) are managed by Paul Zemsky, CFA, and Heather Hackett, CFA, Portfolio Managers of ING Investment Management Co. LLC — the Sub-Adviser.

Performance: For the year ended December 31, 2012, ING Strategic Allocation Conservative Portfolio’s Class I shares provided a total return of 12.31% compared to the Barclays Capital U.S. Aggregate Bond which returned 4.21% for the same period. For the year ended December 31, 2012, ING Strategic Allocation Growth Portfolio’s Class I shares provided a total return of 14.99% compared to the Russell 3000® Index, which returned 16.42% for the same period. For the year ended December 31, 2012, ING Strategic Allocation Moderate Portfolio’s Class I shares provided a total return of 13.60% compared to the Russell 3000® Index, which returned 16.42% for the same period.

Portfolio Specifics: Performance of our tactical asset allocation strategies was additive in 2012. At the

beginning of the year, with investors’ search for yield in full force as the European sovereign debt crisis quieted down and spreads narrowed, we held onto our underweight to U.S. bonds, with a corresponding overweight to high yield. This position was additive and we held it through the end of May. At that time, we eliminated the tactical allocation and implemented a high yield overweight on a strategic allocation basis. Within the ING Strategic Allocation Moderate Portfolio and ING Strategic Allocation Growth Portfolio, we held an overweight to large-cap core, with a corresponding underweight to emerging markets initiated in May and removed in September. This also contributed to relative results as domestic equity outperformed international equity.

Finally, toward the end of the year we initiated a large-cap value overweight with a large-cap growth underweight, which was slightly beneficial. Certain valuation metrics supported this position. Growth stocks outperformed for four years in a period of slow growth and deleveraging in the United States. We believe private sector deleveraging to be complete and anticipate a continued U.S. cyclical recovery, which would aid value stocks. We also believe value’s overweight to financials to be supported by continued quantitative easing from the U.S. Federal Reserve, strength in recovering U.S. housing and expectations of gradual improvement in European financial stocks. We believe the continued negative earnings momentum in technology, overweighted in growth, may reward our underweight growth position.

Target Allocations* | Conservative | Moderate | Growth | |||||||||||||||

US Large Cap Stocks | 28 | % | 34 | % | 40 | % | ||||||||||||

US Mid Cap Stocks | 6 | % | 9 | % | 16 | % | ||||||||||||

US Small Cap Stocks | 0 | % | 4 | % | 4 | % | ||||||||||||

Non US Intl Stocks | 8 | % | 11 | % | 17 | % | ||||||||||||

Emerging Markets Equity | 0 | % | 5 | % | 6 | % | ||||||||||||

Global REITs | 3 | % | 2 | % | 2 | % | ||||||||||||

Core Fixed Income | 42 | % | 30 | % | 10 | % | ||||||||||||

High Yield Bonds | 9 | % | 5 | % | 5 | % | ||||||||||||

Short Term Bonds | 4 | % | 0 | % | 0 | % | ||||||||||||

| 100 | % | 100 | % | 100 | % | |||||||||||||

| * | Portfolio’s current approximate target investment allocations (expressed as a percentage of its net assets) as of December 31, 2012. As these are target allocations, the actual allocations of each Portfolio’s assets may deviate from the percentages shown. Although the Portfolios expect to be fully invested at all times, they may maintain liquidity reserves to meet redemption requests. |

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

4

Table of Contents

| PORTFOLIO MANAGERS’ REPORT | ING STRATEGIC ALLOCATION PORTFOLIOS |

At the beginning of December we initiated an overweight to non-U.S. equity, anticipating that fiscal support would be stronger in non-U.S. countries than in the U.S., where fiscal cliff austerity measures were just beginning. The overweight included MSCI EAFE® and emerging market equities, with a corresponding underweight to large-cap core domestic equities. We increased this position slightly toward the end of the year. We also initiated a modest high yield overweight, with a corresponding U.S. core fixed income underweight toward the end of 2012. The search for yield, plus the factors of further quantitative easing, continued low rates and diminished economic fears provided strong support, in our view, for an overweight to high yield bonds relative to core bonds.

The Strategic Allocation Portfolios use a proprietary asset allocation strategy to determine the percentage of each Portfolio’s net assets to invest in each of the Underlying Funds (the “Target Allocations”) which comprises each Portfolio’s respective strategic allocation benchmark (each a “Composite Benchmark” and collectively, the “Composite Benchmarks”) which returned 10.23%, 12.32% and 14.77% for the ING Strategic Allocation Conservative Portfolio Composite Benchmark, ING Strategic Allocation Moderate Portfolio Composite Benchmark and ING Strategic Allocation Growth Portfolio Composite Benchmark, respectively, for the one year ended December 31, 2012.

ING Strategic Allocation Conservative Portfolio’s Composite Benchmark outperformed the Barclays Capital U.S. Aggregate Bond Index because it contained asset classes that outperformed those in the index. ING Strategic Allocation Growth Portfolio’s Composite Benchmark and ING Strategic Allocation Moderate Portfolio’s Composite Benchmark underperformed the Russell 3000® Index because the Composite Benchmarks contained asset classes that underperformed those in the index. The ING Strategic Allocation Growth Portfolio slightly outperformed its Composite Benchmark, both before and after the deduction of

expenses, whereas the ING Strategic Allocation Conservative and ING Strategic Allocation Moderate Portfolios comfortably outperformed their Composite Benchmarks due to the outperformance of the ING Intermediate Bond Fund over the period.

Underlying managers contributed to performance in 2012. The highest relative returns came from ING Intermediate Bond Fund, ING International Index Portfolio and ING High Yield Bond Fund. The lowest relative returns came from ING Large Value Portfolio and ING Mid Cap Opportunities Portfolio.

Current Strategy and Outlook: Despite the thirteenth-hour compromise on the fiscal cliff, risks remain for 2013, but we continue to be optimistic. Global financial markets are currently indicating low levels of stress and turbulence. In addition, we anticipate that monetary and fiscal policies will be more expansionary outside the U.S. than within going forward. With many central banks expected to keep stimulating their economies, we could see further equity gains in 2013. Both European and Japanese valuations are more attractive than those in the U.S., but there are still questions about 2013-14 economic growth in both regions. Chinese economic developments continue to support a recovery in the equity market, and China should be expected to continue to be a catalyst for emerging markets. Looking ahead, we also believe that large-cap value has relatively attractive valuations. It has a concentration in financials, which stand to benefit from improvements in U.S. housing and a continuation of open-ended quantitative easing from the Federal Reserve. The Portfolios’ current positioning reflects these views, with an overweight to value over growth, an overweight to non-U.S. equity, as well as an overweight to high yield bonds. Fundamentals in the high yield asset class are currently attractive, with low defaults rates. We believe returns for high yield bonds may come from the higher coupon rather than broad price movement going forward.

5

Table of Contents

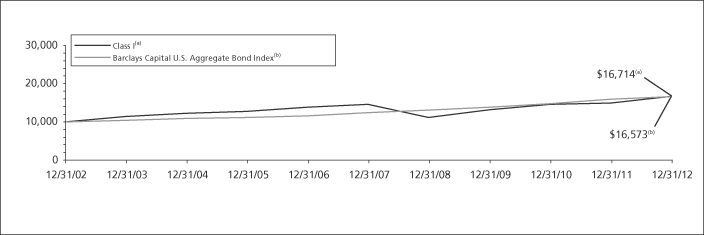

| ING STRATEGIC ALLOCATION CONSERVATIVE PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Average Annual Total Returns for the Periods Ended December 31, 2012 |

| |||||||||||||||||||

1 Year | 5 Year | 10 Year | Since | |||||||||||||||||

Class I | 12.31 | % | 2.73 | % | 5.27 | % | — | |||||||||||||

Class S | 12.02 | % | 2.48 | % | — | 3.70 | % | |||||||||||||

Barclays U.S. Aggregate Bond Index | 4.21 | % | 5.95 | % | 5.18 | % | 5.64 | %(1) | ||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Strategic Allocation Conservative Portfolio against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment

returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.inginvestment.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

| (1) | Since inception performance for the index is shown from August 1, 2005. |

Effective March 1, 2002, ING Investments, LLC began serving as investment adviser and ING Investment Management Co. LLC, the former investment adviser, began serving as sub-adviser to the Portfolio. Effective April 7, 2008, the Portfolio was converted from a mutual fund, which invested directly in securities, to a fund-of-funds, which invests in other mutual funds.

6

Table of Contents

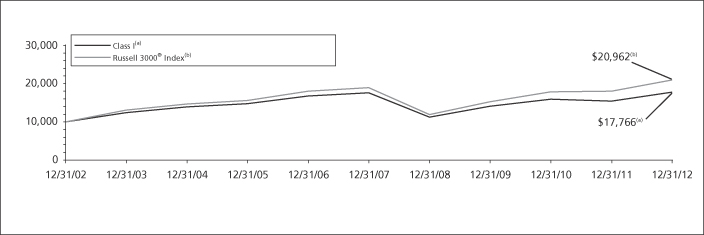

| PORTFOLIO MANAGERS’ REPORT | ING STRATEGIC ALLOCATION GROWTH PORTFOLIO |

Average Annual Total Returns for the Periods Ended December 31, 2012 |

| |||||||||||||||||||

1 Year | 5 Year | 10 Year | Since | |||||||||||||||||

Class I | 14.99 | % | 0.21 | % | 5.92 | % | — | |||||||||||||

Class S | 14.71 | % | (0.03 | )% | — | 2.71 | % | |||||||||||||

Russell 3000® Index | 16.42 | % | 2.04 | % | 7.68 | % | 4.36 | %(1) | ||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Strategic Allocation Growth Portfolio against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment

returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.inginvestment.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

| (1) | Since inception performance for the index is shown from August 1, 2005. |

Effective March 1, 2002, ING Investments, LLC began serving as investment adviser and ING Investment Management Co. LLC, the former investment adviser, began serving as sub-adviser to the Portfolio. Effective April 7, 2008, the Portfolio was converted from a mutual fund, which invested directly in securities, to a fund-of-funds, which invests in other mutual funds.

7

Table of Contents

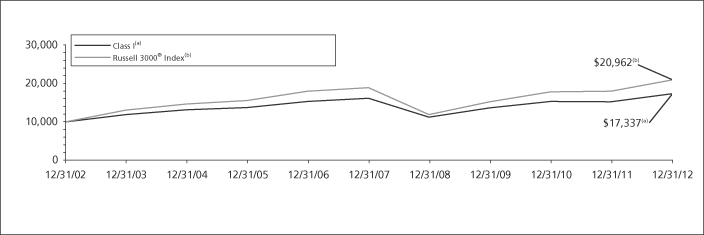

| ING STRATEGIC ALLOCATION MODERATE PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Average Annual Total Returns for the Periods Ended December 31, 2012 |

| |||||||||||||||||||

1 Year | 5 Year | 10 Year | Since | |||||||||||||||||

Class I | 13.60 | % | 1.40 | % | 5.64 | % | — | |||||||||||||

Class S | 13.45 | % | 1.15 | % | — | 3.34 | % | |||||||||||||

Russell 3000® Index | 16.42 | % | 2.04 | % | 7.68 | % | 4.91 | %(1) | ||||||||||||

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Strategic Allocation Moderate Portfolio against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment

returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.inginvestment.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

| (1) | Since inception performance for the index is shown from June 1, 2005. |

Effective March 1, 2002, ING Investments, LLC began serving as investment adviser and ING Investment Management Co. LLC, the former investment adviser, began serving as sub-adviser to the Portfolio. Effective April 7, 2008, the Portfolio was converted from a mutual fund, which invested directly in securities, to a fund-of-funds, which invests in other mutual funds.

8

Table of Contents

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED)

As a shareholder of a Portfolio, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees, and exchange fees; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Portfolio expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2012 to December 31, 2012. The Portfolios’ expenses are shown without the imposition of any sales charges or fees. Expenses would have been higher if such charges were included.

Actual Expenses

The left section of the table shown below, “Actual Fund Return,” provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The right section of the table shown below, “Hypothetical (5% return before expenses),” provides information about hypothetical account values and hypothetical expenses based on a Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not a Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Actual Portfolio Return | Hypothetical (5% return before expenses) | |||||||||||||||||||||||||||||||

Beginning | Ending | Annualized | Expenses Paid | Beginning | Ending | Annualized | Expenses Paid | |||||||||||||||||||||||||

ING Strategic Allocation Conservative Portfolio |

| |||||||||||||||||||||||||||||||

Class I | $ | 1,000.00 | $ | 1,065.00 | 0.09 | % | $ | 0.47 | $ | 1,000.00 | $ | 1,024.68 | 0.09 | % | $ | 0.46 | ||||||||||||||||

Class S | 1,000.00 | 1,064.50 | 0.34 | 1.76 | 1,000.00 | 1,023.43 | 0.34 | 1.73 | ||||||||||||||||||||||||

ING Strategic Allocation Growth Portfolio |

| |||||||||||||||||||||||||||||||

Class I | $ | 1,000.00 | $ | 1,082.80 | 0.06 | % | $ | 0.31 | $ | 1,000.00 | $ | 1,024.83 | 0.06 | % | $ | 0.31 | ||||||||||||||||

Class S | 1,000.00 | 1,081.20 | 0.31 | 1.62 | 1,000.00 | 1,023.58 | 0.31 | 1.58 | ||||||||||||||||||||||||

ING Strategic Allocation Moderate Portfolio |

| |||||||||||||||||||||||||||||||

Class I | $ | 1,000.00 | $ | 1,074.90 | 0.09 | % | $ | 0.47 | $ | 1,000.00 | $ | 1,024.68 | 0.09 | % | $ | 0.46 | ||||||||||||||||

Class S | 1,000.00 | 1,073.20 | 0.34 | 1.77 | 1,000.00 | 1,023.43 | 0.34 | 1.73 | ||||||||||||||||||||||||

| * | Expense ratios do not include expenses of the underlying funds. |

| ** | Expenses are equal to each Portfolio’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 184/366 to reflect the most recent fiscal half-year. |

9

Table of Contents

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Shareholders and Board of Directors

ING Strategic Allocation Portfolios, Inc.

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of ING Strategic Allocation Conservative Portfolio, ING Strategic Allocation Growth Portfolio, and ING Strategic Allocation Moderate Portfolio, each a series of ING Strategic Allocation Portfolios, Inc., as of December 31, 2012, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2012, by correspondence with the custodian and transfer agent of the underlying funds. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of ING Strategic Allocation Conservative Portfolio, ING Strategic Allocation Growth Portfolio, and ING Strategic Allocation Moderate Portfolio as of December 31, 2012, and the results of their operations for the year then ended, the changes in their net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

February 25, 2013

10

Table of Contents

STATEMENTS OF ASSETS AND LIABILITIESASOF DECEMBER 31, 2012

ING | ING | ING | ||||||||||

ASSETS: | ||||||||||||

Investments in securities at fair value* | $ | 1,701,266 | $ | 2,940,716 | $ | 2,944,618 | ||||||

Investments in affiliated underlying funds** | 81,304,030 | 139,618,640 | 140,508,590 | |||||||||

|

|

|

|

|

| |||||||

Total Investments at fair value | $ | 83,005,296 | $ | 142,559,356 | $ | 143,453,208 | ||||||

|

|

|

|

|

| |||||||

Cash | 69,269 | 8,741 | 8,769 | |||||||||

Foreign currencies at value*** | — | 2,067 | 985 | |||||||||

Receivables: | ||||||||||||

Investment in affiliated underlying funds sold | — | 1,144,302 | — | |||||||||

Fund shares sold | 94,283 | 2,760 | 32,647 | |||||||||

Dividends | 136,980 | 79,554 | 158,748 | |||||||||

Foreign tax reclaims | — | — | 348 | |||||||||

Prepaid expenses | 1,474 | 2,287 | 2,495 | |||||||||

Reimbursement due from manager | 1,263 | 16,789 | 12,370 | |||||||||

|

|

|

|

|

| |||||||

Total assets | 83,308,565 | 143,815,856 | 143,669,570 | |||||||||

|

|

|

|

|

| |||||||

LIABILITIES: | ||||||||||||

Payable for investments in affiliated underlying funds purchased | 233,015 | 79,656 | 190,335 | |||||||||

Payable for fund shares redeemed | 23 | 1,147,061 | 3,024 | |||||||||

Payable for investment management fees | 5,595 | 9,659 | 9,678 | |||||||||

Payable for administrative fees | 3,846 | 6,640 | 6,654 | |||||||||

Payable for distribution and shareholder service fees | 351 | 136 | 255 | |||||||||

Payable for directors fees | 420 | 720 | 721 | |||||||||

Other accrued expenses and liabilities | 41,499 | 31,636 | 35,852 | |||||||||

|

|

|

|

|

| |||||||

Total liabilities | 284,749 | 1,275,508 | 246,519 | |||||||||

|

|

|

|

|

| |||||||

NET ASSETS | $ | 83,023,816 | $ | 142,540,348 | $ | 143,423,051 | ||||||

|

|

|

|

|

| |||||||

NET ASSETS WERE COMPRISED OF: | ||||||||||||

Paid-in capital | $ | 89,688,025 | $ | 171,630,179 | $ | 166,686,031 | ||||||

Undistributed net investment income | 2,212,734 | 2,543,949 | 3,136,936 | |||||||||

Accumulated net realized loss | (15,285,849 | ) | (51,910,837 | ) | (44,102,854 | ) | ||||||

Net unrealized appreciation | 6,408,906 | 20,277,057 | 17,702,938 | |||||||||

|

|

|

|

|

| |||||||

NET ASSETS | $ | 83,023,816 | $ | 142,540,348 | $ | 143,423,051 | ||||||

|

|

|

|

|

| |||||||

| ||||||||||||

* Cost of investments in securities | $ | 1,658,197 | $ | 2,866,558 | $ | 2,870,261 | ||||||

** Cost of investments in affiliated underlying funds | $ | 74,938,193 | $ | 119,415,794 | $ | 122,880,064 | ||||||

*** Cost of foreign currencies | $ | — | $ | 2,014 | $ | 959 | ||||||

Class I | ||||||||||||

Net assets | $ | 81,359,610 | $ | 141,892,148 | $ | 142,200,187 | ||||||

Shares authorized | 100,000,000 | 100,000,000 | 100,000,000 | |||||||||

Par value | $ | 0.001 | $ | 0.001 | $ | 0.001 | ||||||

Shares outstanding | 7,303,259 | 12,907,247 | 12,869,179 | |||||||||

Net asset value and redemption price per share | $ | 11.14 | $ | 10.99 | $ | 11.05 | ||||||

Class S | ||||||||||||

Net assets | $ | 1,664,206 | $ | 648,200 | $ | 1,222,864 | ||||||

Shares authorized | 100,000,000 | 100,000,000 | 100,000,000 | |||||||||

Par value | $ | 0.001 | $ | 0.001 | $ | 0.001 | ||||||

Shares outstanding | 150,474 | 59,360 | 111,219 | |||||||||

Net asset value and redemption price per share | $ | 11.06 | $ | 10.92 | $ | 11.00 | ||||||

See Accompanying Notes to Financial Statements

11

Table of Contents

STATEMENTS OF OPERATIONSFORTHE YEAR ENDED DECEMBER 31, 2012

ING | ING | ING | ||||||||||

INVESTMENT INCOME: | ||||||||||||

Dividends from affiliated underlying funds | $ | 2,294,150 | $ | 2,627,933 | $ | 3,269,019 | ||||||

Dividends | 5,635 | 8,725 | 8,762 | |||||||||

|

|

|

|

|

| |||||||

Total investment income | 2,299,785 | 2,636,658 | 3,277,781 | |||||||||

|

|

|

|

|

| |||||||

EXPENSES: | ||||||||||||

Investment management fees | 67,274 | 115,236 | 115,460 | |||||||||

Distribution and shareholder service fees: | ||||||||||||

Class S | 3,791 | 1,596 | 2,935 | |||||||||

Transfer agent fees | 203 | 267 | 224 | |||||||||

Administrative service fees | 46,249 | 79,223 | 79,377 | |||||||||

Shareholder reporting expense | 17,778 | 30,644 | 31,049 | |||||||||

Registration fees | 241 | — | 112 | |||||||||

Professional fees | 28,890 | 41,873 | 42,090 | |||||||||

Custody and accounting expense | 6,720 | 12,766 | 11,865 | |||||||||

Directors fees | 2,523 | 4,321 | 4,330 | |||||||||

Miscellaneous expense | 14,973 | 7,259 | 10,460 | |||||||||

Interest expense | 5 | 13 | 11 | |||||||||

|

|

|

|

|

| |||||||

Total expenses | 188,647 | 293,198 | 297,913 | |||||||||

Net waived and reimbursed fees | (108,785 | ) | (204,516 | ) | (164,428 | ) | ||||||

|

|

|

|

|

| |||||||

Net expenses | 79,862 | 88,682 | 133,485 | |||||||||

|

|

|

|

|

| |||||||

Net investment income | 2,219,923 | 2,547,976 | 3,144,296 | |||||||||

|

|

|

|

|

| |||||||

REALIZED AND UNREALIZED GAIN (LOSS): | ||||||||||||

Net realized gain (loss) on: | ||||||||||||

Investments | 6,323,430 | 9,212,379 | 7,462,838 | |||||||||

Capital gain distributions from affiliated underlying funds | 186,926 | 938,908 | 660,661 | |||||||||

Foreign currency related transactions | — | 163 | — | |||||||||

|

|

|

|

|

| |||||||

Net realized gain | 6,510,356 | 10,151,450 | 8,123,499 | |||||||||

|

|

|

|

|

| |||||||

Net change in unrealized appreciation (depreciation) on: | ||||||||||||

Affiliated underlying funds | 997,407 | 7,214,611 | 6,992,083 | |||||||||

Foreign currency related transactions | — | 3 | 32 | |||||||||

|

|

|

|

|

| |||||||

Net change in unrealized appreciation (depreciation) | 997,407 | 7,214,614 | 6,992,115 | |||||||||

|

|

|

|

|

| |||||||

Net realized and unrealized gain | 7,507,763 | 17,366,064 | 15,115,614 | |||||||||

|

|

|

|

|

| |||||||

Increase in net assets resulting from operations | $ | 9,727,686 | $ | 19,914,040 | $ | 18,259,910 | ||||||

|

|

|

|

|

| |||||||

* Foreign taxes withheld | $ | — | $ | 2,297 | $ | 959 | ||||||

See Accompanying Notes to Financial Statements

12

Table of Contents

STATEMENTS OF CHANGES IN NET ASSETS

ING Strategic Allocation | ING Strategic Allocation | |||||||||||||||

Year Ended December 31, 2012 | Year Ended December 31, 2011 | Year Ended December 31, 2012 | Year Ended December 31, 2011 | |||||||||||||

FROM OPERATIONS: | ||||||||||||||||

Net investment income | $ | 2,219,923 | $ | 2,255,975 | $ | 2,547,976 | $ | 2,194,582 | ||||||||

Net realized gain (loss) | 6,510,356 | 1,660,213 | 10,151,450 | (4,489,769 | ) | |||||||||||

Net change in unrealized appreciation (depreciation) | 997,407 | (2,237,346 | ) | 7,214,614 | (1,296,236 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Increase (decrease) in net assets resulting from operations | 9,727,686 | 1,678,842 | 19,914,040 | (3,591,423 | ) | |||||||||||

|

|

|

|

|

|

|

| |||||||||

FROM DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||||||

Net investment income: | ||||||||||||||||

Class I | (2,230,977 | ) | (3,394,780 | ) | (2,207,961 | ) | (4,132,232 | ) | ||||||||

Class S | (37,094 | ) | (60,314 | ) | (6,963 | ) | (41,575 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total distributions | (2,268,071 | ) | (3,455,094 | ) | (2,214,924 | ) | (4,173,807 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

FROM CAPITAL SHARE TRANSACTIONS: | ||||||||||||||||

Net proceeds from sale of shares | 8,291,546 | 9,470,306 | 4,520,129 | 4,766,752 | ||||||||||||

Reinvestment of distributions | 2,268,071 | 3,455,094 | 2,214,924 | 4,173,807 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| 10,559,617 | 12,925,400 | 6,735,053 | 8,940,559 | |||||||||||||

Cost of shares redeemed | (17,198,331 | ) | (20,783,769 | ) | (21,156,507 | ) | (34,760,322 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net decrease in net assets resulting from capital share transactions | (6,638,714 | ) | (7,858,369 | ) | (14,421,454 | ) | (25,819,763 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net increase (decrease) in net assets | 820,901 | (9,634,621 | ) | 3,277,662 | (33,584,993 | ) | ||||||||||

|

|

|

|

|

|

|

| |||||||||

NET ASSETS: | ||||||||||||||||

Beginning of year or period | 82,202,915 | 91,837,536 | 139,262,686 | 172,847,679 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

End of year or period | $ | 83,023,816 | $ | 82,202,915 | $ | 142,540,348 | $ | 139,262,686 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Undistributed net investment income at end of year or period | $ | 2,212,734 | $ | 2,254,605 | $ | 2,543,949 | $ | 2,193,907 | ||||||||

|

|

|

|

|

|

|

| |||||||||

See Accompanying Notes to Financial Statements

13

Table of Contents

STATEMENTS OF CHANGES IN NET ASSETS

ING Strategic Allocation | ||||||||

Year Ended December 31, 2012 | Year Ended December 31, 2011 | |||||||

FROM OPERATIONS: | ||||||||

Net investment income | $ | 3,144,296 | $ | 3,021,127 | ||||

Net realized gain | 8,123,499 | 172,986 | ||||||

Net change in unrealized appreciation (depreciation) | 6,992,115 | (3,578,899 | ) | |||||

|

|

|

| |||||

Increase (decrease) in net assets resulting from operations | 18,259,910 | (384,786 | ) | |||||

|

|

|

| |||||

FROM DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||

Net investment income: | ||||||||

Class I | (3,020,695 | ) | (5,188,279 | ) | ||||

Class S | (19,810 | ) | (86,901 | ) | ||||

|

|

|

| |||||

Total distributions | (3,040,505 | ) | (5,275,180 | ) | ||||

|

|

|

| |||||

FROM CAPITAL SHARE TRANSACTIONS: | ||||||||

Net proceeds from sale of shares | 5,332,861 | 6,083,963 | ||||||

Reinvestment of distributions | 3,040,505 | 5,275,180 | ||||||

|

|

|

| |||||

| 8,373,366 | 11,359,143 | |||||||

Cost of shares redeemed | (20,357,242 | ) | (32,797,859 | ) | ||||

|

|

|

| |||||

Net decrease in net assets resulting from capital share transactions | (11,983,876 | ) | (21,438,716 | ) | ||||

|

|

|

| |||||

Net increase (decrease) in net assets | 3,235,529 | (27,098,682 | ) | |||||

|

|

|

| |||||

NET ASSETS: | ||||||||

Beginning of year or period | 140,187,522 | 167,286,204 | ||||||

|

|

|

| |||||

End of year or period | $ | 143,423,051 | $ | 140,187,522 | ||||

|

|

|

| |||||

Undistributed net investment income at end of year or period | $ | 3,136,936 | $ | 3,019,537 | ||||

|

|

|

| |||||

See Accompanying Notes to Financial Statements

14

Table of Contents

Selected data for a share of beneficial interest outstanding throughout each year or period.

| Income (loss) from investment operations | Less distributions | Ratios to average net assets | Supplemental data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net asset value, beginning of year or period | Net investment income (loss) | Net realized and unrealized gain (loss) | Total from investment operations | From net investment income | From net realized gains | From return of capital | Total distributions | Payment by affiliate | Net asset value, end of year or period | Total Return(1) | Expenses before reductions/ additions(2)(3)(4) | Expenses net of fee waivers and/ or recoupments if any(2)(3)(4) | Expense net of all reductions/ additions(2)(3)(4) | Net investment income (loss)(2)(4) | Net assets, end of year or period | Portfolio turnover rate | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Year or period ended | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | (%) | (%) | (%) | (%) | (%) | ($000’s) | (%) | |||||||||||||||||||||||||||||||||||||||||||||||||||

ING Strategic Allocation Conservative Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 10.19 | 0.28 | • | 0.96 | 1.24 | 0.29 | — | — | 0.29 | — | 11.14 | 12.31 | 0.22 | 0.09 | 0.09 | 2.64 | 81,360 | 107 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 10.41 | 0.27 | • | (0.07 | ) | 0.20 | 0.42 | — | — | 0.42 | — | 10.19 | 1.79 | 0.22 | 0.06 | 0.06 | 2.63 | 80,825 | 59 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 9.80 | 0.36 | • | 0.70 | 1.06 | 0.45 | — | — | 0.45 | — | 10.41 | 11.07 | 0.20 | 0.09 | 0.09 | 3.66 | 90,086 | 88 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 9.13 | 0.45 | • | 1.03 | 1.48 | 0.81 | — | — | 0.81 | — | 9.80 | 18.00 | 0.20 | 0.10 | 0.10 | 5.04 | 93,792 | 56 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 13.51 | 0.51 | (3.39 | ) | (2.88 | ) | 0.51 | 0.99 | — | 1.50 | — | 9.13 | (23.65 | ) | 0.39 | 0.27 | † | 0.27 | † | 3.99 | † | 86,257 | 277 | |||||||||||||||||||||||||||||||||||||||||||||

Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 10.12 | 0.24 | 0.96 | 1.20 | 0.26 | — | — | 0.26 | — | 11.06 | 12.02 | 0.47 | 0.34 | 0.34 | 2.51 | 1,664 | 107 | |||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 10.34 | 0.24 | • | (0.07 | ) | 0.17 | 0.39 | — | — | 0.39 | — | 10.12 | 1.53 | 0.47 | 0.31 | 0.31 | 2.29 | 1,378 | 59 | |||||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 9.73 | 0.34 | 0.70 | 1.04 | 0.43 | — | — | 0.43 | — | 10.34 | 10.91 | 0.45 | 0.34 | 0.34 | 3.53 | 1,752 | 88 | |||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 9.06 | 0.43 | • | 1.02 | 1.45 | 0.78 | — | — | 0.78 | — | 9.73 | 17.79 | 0.45 | 0.35 | 0.35 | 4.89 | 1,631 | 56 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 13.44 | 0.39 | (3.29 | ) | (2.90 | ) | 0.49 | 0.99 | — | 1.48 | — | 9.06 | (23.92 | ) | 0.64 | 0.52 | † | 0.52 | † | 3.89 | † | 1,368 | 277 | |||||||||||||||||||||||||||||||||||||||||||||

ING Strategic Allocation Growth Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 9.70 | 0.18 | • | 1.27 | 1.45 | 0.16 | — | — | 0.16 | — | 10.99 | 14.99 | 0.20 | 0.06 | 0.06 | 1.77 | 141,892 | 74 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 10.24 | 0.14 | • | (0.41 | ) | (0.27 | ) | 0.27 | — | — | 0.27 | — | 9.70 | (2.92 | ) | 0.20 | 0.05 | 0.05 | 1.42 | 138,642 | 53 | |||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 9.39 | 0.23 | • | 0.97 | 1.20 | 0.35 | — | — | 0.35 | — | 10.24 | 13.06 | 0.19 | 0.09 | 0.09 | 2.47 | 171,094 | 36 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 9.04 | 0.37 | 1.48 | 1.85 | 0.97 | 0.53 | — | 1.50 | — | 9.39 | 25.37 | 0.20 | 0.13 | 0.13 | 4.12 | 168,071 | 75 | |||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 16.57 | 0.38 | (5.65 | ) | (5.27 | ) | 0.33 | 1.93 | — | 2.26 | — | 9.04 | (36.13 | ) | 0.39 | 0.33 | † | 0.33 | † | 2.83 | † | 146,862 | 235 | |||||||||||||||||||||||||||||||||||||||||||||

Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 9.62 | 0.16 | • | 1.25 | 1.41 | 0.11 | — | — | 0.11 | — | 10.92 | 14.71 | 0.45 | 0.31 | 0.31 | 1.51 | 648 | 74 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 10.16 | 0.12 | • | (0.42 | ) | (0.30 | ) | 0.24 | — | — | 0.24 | — | 9.62 | (3.16 | ) | 0.45 | 0.30 | 0.30 | 1.14 | 620 | 53 | |||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 9.32 | 0.21 | • | 0.96 | 1.17 | 0.33 | — | — | 0.33 | — | 10.16 | 12.81 | 0.44 | 0.34 | 0.34 | 2.22 | 1,753 | 36 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 8.99 | 0.32 | • | 1.49 | 1.81 | 0.95 | 0.53 | — | 1.48 | — | 9.32 | 24.90 | 0.45 | 0.38 | 0.38 | 3.88 | 1,715 | 75 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 16.49 | 0.32 | • | (5.57 | ) | (5.25 | ) | 0.32 | 1.93 | — | 2.25 | — | 8.99 | (36.19 | ) | 0.64 | 0.58 | † | 0.58 | † | 2.72 | † | 1,322 | 235 | ||||||||||||||||||||||||||||||||||||||||||||

ING Strategic Allocation Moderate Portfolio | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Class I | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 9.93 | 0.23 | • | 1.11 | 1.34 | 0.22 | — | — | 0.22 | — | 11.05 | 13.60 | 0.20 | 0.09 | 0.09 | 2.18 | 142,200 | 84 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 10.31 | 0.20 | • | (0.24 | ) | (0.04 | ) | 0.34 | — | — | 0.34 | — | 9.93 | (0.57 | ) | 0.21 | 0.07 | 0.07 | 1.97 | 139,057 | 57 | |||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 9.58 | 0.30 | • | 0.83 | 1.13 | 0.40 | — | — | 0.40 | — | 10.31 | 12.03 | 0.19 | 0.10 | 0.10 | 3.15 | 164,412 | 60 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 9.10 | 0.39 | • | 1.30 | 1.69 | 0.91 | 0.30 | — | 1.21 | — | 9.58 | 21.84 | 0.21 | 0.13 | 0.13 | 4.47 | 166,449 | 62 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 15.16 | 0.44 | (4.54 | ) | (4.10 | ) | 0.40 | 1.56 | — | 1.96 | — | 9.10 | (30.48 | ) | 0.38 | 0.31 | † | 0.31 | † | 3.35 | † | 152,965 | 255 | |||||||||||||||||||||||||||||||||||||||||||||

See Accompanying Notes to Financial Statements

15

Table of Contents

FINANCIAL HIGHLIGHTS (CONTINUED)

| Income (loss) from investment operations | Less distributions | Ratios to average net assets | Supplemental data | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net asset value, beginning of year or period | Net investment income (loss) | Net realized and unrealized gain (loss) | Total from investment operations | From net investment income | From net realized gains | From return of capital | Total distributions | Payment by affiliate | Net asset value, end of year or period | Total Return(1) | Expenses before reductions/ additions(2)(3)(4) | Expenses net of fee waivers and/ or recoupments if any(2)(3)(4) | Expense net of all reductions/ additions(2)(3)(4) | Net investment income (loss)(2)(4) | Net assets, end of year or period | Portfolio turnover rate | ||||||||||||||||||||||||||||||||||||||||||||||||||||

Year or period ended | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | ($) | (%) | (%) | (%) | (%) | (%) | ($000’s) | (%) | |||||||||||||||||||||||||||||||||||||||||||||||||||

ING Strategic Allocation Moderate Portfolio (Continued) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Class S | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-12 | 9.86 | 0.21 | • | 1.11 | 1.32 | 0.18 | — | — | 0.18 | — | 11.00 | 13.45 | 0.45 | 0.34 | 0.34 | 1.96 | 1,223 | 84 | ||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-11 | 10.25 | 0.15 | • | (0.22 | ) | (0.07 | ) | 0.32 | — | — | 0.32 | — | 9.86 | (0.91 | ) | 0.46 | 0.32 | 0.32 | 1.44 | 1,131 | 57 | |||||||||||||||||||||||||||||||||||||||||||||||

12-31-10 | 9.53 | 0.27 | 0.83 | 1.10 | 0.38 | — | — | 0.38 | — | 10.25 | 11.77 | 0.44 | 0.35 | 0.35 | 2.92 | 2,874 | 60 | |||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-09 | 9.05 | 0.38 | 1.28 | 1.66 | 0.88 | 0.30 | — | 1.18 | — | 9.53 | 21.60 | 0.46 | 0.38 | 0.38 | 4.34 | 2,703 | 62 | |||||||||||||||||||||||||||||||||||||||||||||||||||

12-31-08 | 15.10 | 0.37 | • | (4.48 | ) | (4.11 | ) | 0.38 | 1.56 | — | 1.94 | — | 9.05 | (30.68 | ) | 0.63 | 0.56 | † | 0.56 | † | 3.30 | † | 2,192 | 255 | ||||||||||||||||||||||||||||||||||||||||||||

| (1) | Total return is calculated assuming reinvestment of all dividends, capital gain distributions and return of capital distributions, if any, at net asset value and does not reflect the effect of insurance contract charges. Total return for periods less than one year is not annualized. |

| (2) | Annualized for periods less than one year. |

| (3) | Expense ratios do not include expenses of underlying funds and do not include fees and expenses charged under the variable annuity contract or variable life insurance policy. |

| (4) | Expense ratios reflect operating expenses of a Portfolio. Expenses before reductions/additions do not reflect amounts reimbursed by an Investment Adviser and/or Distributor or reductions from brokerage service arrangements or other expense offset arrangements and do not represent the amount paid by a Portfolio during periods when reimbursements or reductions occur. Expenses net of fee waivers reflect expenses after reimbursement by an Investment Adviser and/or Distributor but prior to reductions from brokerage service arrangements or other expense offset arrangements. Expenses net of all reductions/additions represent the net expenses paid by a Portfolio. Net investment income (loss) is net of all such additions or reductions. |

| • | Calculated using average number of shares outstanding throughout the period. |

| † | Impact of waiving the advisory fee for the ING Institutional Prime Money Market Fund holding has less than 0.005% impact on the expense ratio and net investment income or loss ratio. |

See Accompanying Notes to Financial Statements

16

Table of Contents

NOTES TO FINANCIAL STATEMENTSASOF DECEMBER 31, 2012

NOTE 1 — ORGANIZATION

ING Strategic Allocation Portfolios, Inc. (the “Company”) is registered under the Investment Company Act of 1940, as amended (“1940 Act”), as an open-end management investment company.

The Company was incorporated under the laws of Maryland on October 14, 1994. There are three separate investment series (each a “Portfolio”, collectively the “Portfolios”) that comprise the Company: ING Strategic Allocation Conservative Portfolio (“Strategic Allocation Conservative”), ING Strategic Allocation Growth Portfolio (“Strategic Allocation Growth”), and ING Strategic Allocation Moderate Portfolio (“Strategic Allocation Moderate”). Each Portfolio currently seeks to achieve its investment objective by investing in other ING Funds (“Underlying Funds”) and each uses asset allocation strategies to determine how to invest in the Underlying Funds. The Underlying Funds, in turn, invest in equity and fixed-income securities and money market instruments.

Each Portfolio offers Class I and Class S shares. Each class has equal rights as to class and voting privileges. The two classes differ principally in the applicable distribution and service fees. Shareholders of each class also bear certain expenses that pertain to that particular class. All shareholders bear the common expenses of the Portfolios and earn income and realized gains/losses from a Portfolio pro rata based on the average daily net assets of each class, without distinction between share classes. Expenses that are specific to a Portfolio or a class are charged directly to that Portfolio or class. Other operating expenses shared by several Portfolios are generally allocated among those Portfolios based on average net assets. Distributions are determined separately for each class based on income and expenses allocable to each class. Realized gain distributions are allocated to each class pro rata based on the shares outstanding of each class on the date of distribution. Differences in per share dividend rates generally result from differences in separate class expenses, including distribution and shareholder service fees, if applicable.

ING Investments, LLC serves as the investment adviser (“ING Investments” or the “Investment Adviser”) to the Portfolios. ING Investment Management Co. LLC serves as the Sub-Adviser (“ING IIM” or the “Sub-Adviser”) to the Portfolios. ING Funds Services, LLC serves as the administrator (“IFS” or the “Administrator”) for the Portfolios. ING Investments Distributor, LLC (“IID” or the “Distributor”) serves as the principal underwriter to the Portfolios.

NOTE 2 — SIGNIFICANT ACCOUNTING POLICIES

The following significant accounting policies are consistently followed by the Portfolios in the preparation of their financial statements. Such policies are in conformity with U.S. generally accepted accounting principles (“GAAP”) for investment companies.

A. Security Valuation. All investments in Underlying Funds are recorded at their estimated fair value, as described below. The valuations of the Portfolios’ investments in Underlying Funds are based on the net asset value of the Underlying Funds each business day.

Fair value is defined as the price that a Portfolio would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. Each investment asset or liability of a Portfolio is assigned a level at measurement date based on the significance and source of the inputs to its valuation. Quoted prices in active markets for identical securities are classified as “Level 1,” inputs other than quoted prices for an asset or liability that are observable are classified as “Level 2” and unobservable inputs, including the sub-adviser’s judgment about the assumptions that a market participant would use in pricing an asset or liability are classified as “Level 3.” The inputs used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. Short-term securities of sufficient credit quality which are valued at amortized cost, which approximates fair value, are generally considered to be Level 2 securities under applicable accounting rules. A table summarizing each Portfolio’s investments under these levels of classification is included following the Portfolio of Investments.

The Board has adopted methods for valuing securities and other assets in circumstances where market quotes are not readily available, and has delegated the responsibility for applying the valuation methods to the “Pricing Committee” as established by the fund’s Administrator. The Pricing Committee considers all facts they deem relevant that are reasonably available, through either public information or information available to the Investment Adviser or sub-adviser, when determining the fair value of the security. In the event that a security or asset cannot be valued pursuant to one of the valuation methods established by the Board, the fair value of the security or asset will be determined in good faith by the Pricing Committee. When a Portfolio uses these fair valuation methods that use significant unobservable inputs to determine its NAV, securities will be priced by a method that the

17

Table of Contents

NOTES TO FINANCIAL STATEMENTSASOF DECEMBER 31, 2012 (CONTINUED)

NOTE 2 — SIGNIFICANT ACCOUNTING POLICIES (continued)

Pricing Committee believes accurately reflects fair value and are categorized as Level 3 of the fair value hierarchy. The methodologies used for valuing securities are not necessarily an indication of the risks of investing in those securities valued in good faith at fair value nor can it be assured a Portfolio can obtain the fair value assigned to a security if they were to sell the security.

To assess the continuing appropriateness of security valuations, the Pricing Committee may compare prior day prices, prices on comparable securities, and traded prices to the prior or current day prices and the Pricing Committee challenges those prices exceeding certain tolerance levels with the third party pricing service or broker source. For those securities valued in good faith at fair value, the Pricing Committee reviews and affirms the reasonableness of the valuation on a regular basis after considering all relevant information that is reasonably available.

For fair valuations using significant unobservable inputs, U.S. GAAP requires a reconciliation of the beginning to ending balances for reported fair values that presents changes attributable to total realized and unrealized gains or losses, purchases and sales, and transfers in or out of the Level 3 category during the period. The end of period timing recognition is used for the transfers between Levels of a Portfolio’s assets and liabilities. A reconciliation of Level 3 investments is presented when a Portfolio has a significant amount of Level 3 investments.

For the year ended December 31, 2012, there have been no significant changes to the fair valuation methodologies.

The Portfolios classify each of their investments in the Underlying Funds as Level 1, without consideration as to the classification level of the specific investments held by the Underlying Funds.

B. Security Transactions and Revenue Recognition. Security transactions are accounted for on trade date. Dividend income received from the affiliated funds is recognized on the ex-dividend date and is recorded as income distributions in the Statement of Operations. Capital gain distributions received from the affiliated funds are recognized on ex-dividend date and are

recorded on the Statement of Operations as such. Costs used in determining realized gains and losses on the sales of investment securities are on the basis of specific identification.

C. Distributions to Shareholders. The Portfolios record distributions to their shareholders on the ex-dividend date. Dividends from net investment income and capital gains, if any, are declared and paid annually by the Portfolios. The Portfolios may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code. The characteristics of income and gains to be distributed are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles for investment companies.

D. Federal Income Taxes. It is the policy of each Portfolio to comply with subchapter M of the Internal Revenue Code and related excise tax provisions applicable to regulated investment companies and to distribute substantially all of its net investment income and any net realized capital gains to their shareholders. Management has considered the sustainability of the Portfolios’ tax positions taken on federal income tax returns for all open tax years in making this determination. Therefore, no federal income tax provision is required. No capital gain distributions shall be made until any capital loss carryforwards have been fully utilized or expired.

E. Use of Estimates. The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

F. Indemnifications. In the normal course of business, the Company may enter into contracts that provide certain indemnifications. The Company’s maximum exposure under these arrangements is dependent on future claims that may be made against the Portfolios and, therefore, cannot be estimated; however, based on experience, management considers the risk of loss from such claims remote.

18

Table of Contents

NOTES TO FINANCIAL STATEMENTSASOF DECEMBER 31, 2012 (CONTINUED)

NOTE 3 — INVESTMENT TRANSACTIONS

For the year ended December 31, 2012, the cost of purchases and the proceeds from the sales of the Underlying Funds, were as follows:

Purchases | Sales | |||||||

Strategic Allocation Conservative | $ | 89,767,477 | $ | 96,636,651 | ||||

Strategic Allocation Growth | 106,752,431 | 120,932,200 | ||||||

Strategic Allocation Moderate | 121,671,656 | 133,711,145 | ||||||

NOTE 4 — INVESTMENT MANAGEMENT AND ADMINISTRATIVE FEES

The Portfolios entered into an investment management agreement (“Investment Management Agreement”) with the Investment Adviser.

The Investment Management Agreement compensates the Investment Adviser with a fee of 0.08% of each Portfolio’s average daily net assets invested in Underlying Funds and a fee of 0.60% of each Portfolio’s average daily net assets invested in direct investments.

The Investment Adviser entered into a sub-advisory agreement with ING IM with respect to each Portfolio. Subject to such policies as the board of directors (“Board”) or the Investment Adviser may determine, ING IM manages the Portfolios’ assets in accordance with the Portfolios’ investment objectives, policies, and limitations.

Pursuant to the Administration Agreement, IFS acts as administrator and provides certain administrative and shareholder services necessary for Portfolio operations and is responsible for the supervision of other service providers. IFS is entitled to receive from each Portfolio a fee at an annual rate of 0.055% on the first $5 billion of daily net assets and 0.030% thereafter.

NOTE 5 — DISTRIBUTION AND SERVICE FEES

Class S shares of the Portfolios have adopted a Distribution Plan pursuant to Rule 12b-1 under the 1940 Act (the “12b-1 Plan”), whereby the Distributor is compensated by each Portfolio for expenses incurred in the distribution of each Portfolio’s Class S shares. Pursuant to the 12b-1 Plan, the Distributor is entitled to a payment each month to compensate for expenses incurred in the distribution and promotion of each Portfolio’s S shares, including expenses incurred in printing prospectuses and reports used for sales purposes, expenses incurred in preparing and printing sales literature and other such distribution related expenses, including any distribution or shareholder servicing fees paid to securities dealers who have executed a distribution agreement with the Distributor.

Under the 12b-1 Plan, Class S shares of the Portfolios pay the Distributor a fee calculated at an annual rate of 0.25% of average daily net assets.

NOTE 6 — OTHER TRANSACTIONS WITH AFFILIATED AND RELATED PARTIES

At December 31, 2012, the following indirect, wholly-owned subsidiaries of ING U.S., Inc. owned more than 5% of the following Portfolios:

Subsidiary | Portfolios | Percentage | ||||

ING Life Insurance and Annuity Company | Strategic Allocation Conservative | 91.24 | % | |||

| Strategic Allocation Growth | 92.46 | |||||

| Strategic Allocation Moderate | 89.32 | |||||

ReliaStar Life Insurance Company | Strategic Allocation Conservative | 5.63 | ||||

| Strategic Allocation Growth | 5.10 | |||||

| Strategic Allocation Moderate | 8.11 | |||||

Control is defined by the 1940 Act as the beneficial ownership, either directly or through one or more controlled companies, of more than 25% of the voting securities of a company. The 1940 Act defines affiliates as companies that are under common control. Therefore, because the Portfolios have a common owner that owns over 25% of the outstanding securities of the Portfolios, they are deemed to be affiliates of each other. Investment activities of these shareholders could have a material impact on the Portfolios.

The Company has adopted a Deferred Compensation Plan (“Policy”), which allows eligible non-affiliated directors as described in the Policy to defer the receipt of all or a portion of the directors’ fees payable. Amounts deferred are treated as though invested in various “notional” funds advised by ING Investments until distribution in accordance with the Policy.

NOTE 7 — EXPENSE LIMITATION AGREEMENTS

ING Investments entered into written expense limitation agreements (“Expense Limitation Agreements”) with each of the Portfolios whereby the Investment Adviser has agreed to limit expenses, excluding interest, taxes, brokerage commissions and extraordinary expenses to the levels listed below:

Portfolio(1) | Class I | Class S | ||||||

Strategic Allocation Conservative | 0.65 | % | 0.90 | % | ||||

Strategic Allocation Growth(2) | 0.75 | % | 1.00 | % | ||||

Strategic Allocation Moderate | 0.70 | % | 0.95 | % | ||||

| (1) | These operating expense limits take into account operating expenses incurred at the underlying fund level. The amount of fees and expenses of an Underlying Fund borne by each Portfolio will vary based on each Portfolio’s allocation of assets to, and the net expenses of, a particular Underlying Fund. |

| (2) | The Adviser has further agreed to limit expenses for the Portfolio to 0.71% and 0.96% for Classes I and S, respectively. |

19

Table of Contents

NOTES TO FINANCIAL STATEMENTSASOF DECEMBER 31, 2012 (CONTINUED)

NOTE 7 — EXPENSE LIMITATION AGREEMENTS

(continued)