2006 Second Quarter Results

July 19, 2006

Safe Harbor

“Safe Harbor” Statement under the U.S. Private Securities

Litigation Reform Act of 1995: the matters discussed in this

document may include forward-looking statements that are

subject to risks and uncertainties including, but not limited to:

economic conditions, product demand and semiconductor

equipment industry capacity, worldwide demand and

manufacturing capacity utilization for semiconductors (the

principal product of our customer base), competitive products

and pricing, manufacturing efficiencies, new product

development, ability to enforce patents, the outcome of

intellectual property litigation, availability of raw materials and

critical manufacturing equipment, trade environment, the

prevailing market price for ASML shares, and other risks

indicated in the risk factors included in ASML’s Annual

Report on Form 20-F and other filings with the U.S.

Securities and Exchange Commission.

/ Slide 2

Agenda

Q2 2006: Solid execution

Q2 2006: Technology accomplishments

Q2 2006: Shipment and bookings review

Financial summary

Q3 2006: Outlook

Share buyback program

Company focus for remainder 2006

ASML’s drivers for growth

/ Slide 3

Q2 2006: Solid execution

Growth

Sales of € 942 million, an increase of 50% compared with Q1

2006, strongest quarterly sales in history of the company

Increased market share by winning new 300mm fab

opportunities and with continued success in Japan

Profitability

Posted highest quarterly operating margin of 25.2% and highest

net profit of 17.7% (as a percentage of sales)

Gross margin increased to 40.4% from 40.0% in Q1 2006

Cash generation

Strong cash generation from operations of € 330 million

Bought back 19.9 million shares (4.11% of outstanding shares)

for an aggregate amount of € 314 million of which € 253 million

paid in Q2 2006

/ Slide 4

Q2 2006: Technology accomplishments

Important quarter for our leading immersion products

Brought to market eight TWINSCAN XT:1700i, 45nm volume

production tools, totaling 21 ASML immersion tools worldwide

Shipped one XT:1700i to Japan

As of Q2 2006, three immersion tools are installed in Japan

Customers report stable, low defect performance of XT:1700i

Recent announcement of XT:1900i introduction. Preparations

underway for ramp to volume production by H1 2007

EUV milestones

Two full field 0.25NA tools to be shipped in Q3 2006 – IMEC

and ANT – for use in worldwide customer evaluations and

infrastructure development

/ Slide 5

ASML earns top customer satisfaction ratings

four years in a row

/ Slide 6

Source: VLSI Research, June 2006

Top 10 Large Suppliers of

Chip Making Equipment

2006

Rank

Company

1

Varian Semiconductor

2

ASML

3

Hitachi Kokusai Electric Inc.

4

Tokyo Electron Limited

5

Dainippon Screen Mfg. Co., Ltd.

6

Hitachi High

-

Technologies Corp.

7

ASM International N.V.

8

Applied Materials, Inc.

9

Novellus Systems, Inc.

10

ULVAC, Inc.

Q2 2006: Shipment and bookings review

Excellent shipment quarter with record quarterly revenue

Shipped 72 systems with ASP of € 11.7 million from € 10.8 million

in Q1 2006 due to higher percentage of new systems in the mix

including the new XT:1700i tool

Shipped 58 new systems with ASP of € 13.7 million, an increase

from € 13.5 million in Q1 2006

Mix of products contains significant i-line, KrF in addition to ArF

and ArFi to support customer production capacity

Achieved target for unit booking guidance

50% above Q1 2006 at 93 units (78 new)

Backlog value rises by 14.7% over Q1 2006. Current backlog is

127 units and € 1,830 million

The backlog is shipping to about 50 different fabs

Current immersion backlog is 19 units

/ Slide 7

Financial summary

/ Slide 8

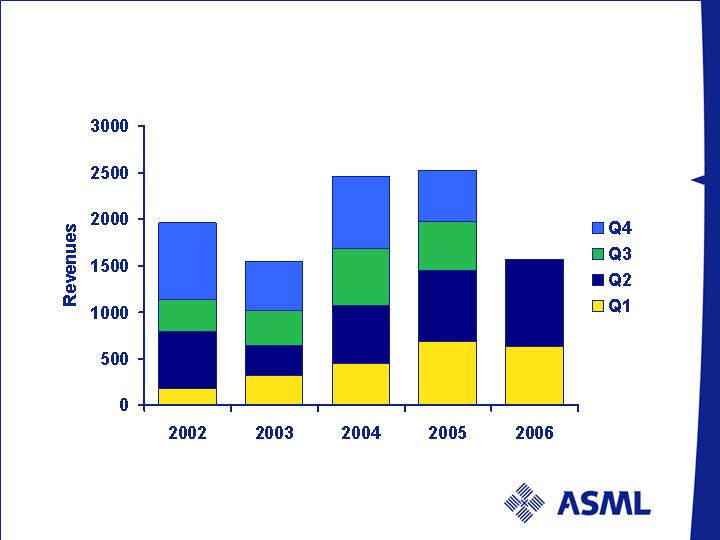

Total revenues M€

179

609

351

820

526

370

329

318

785

611

616

453

548

533

763

685

629

1959

1543

2465

2529

942

/ Slide 9

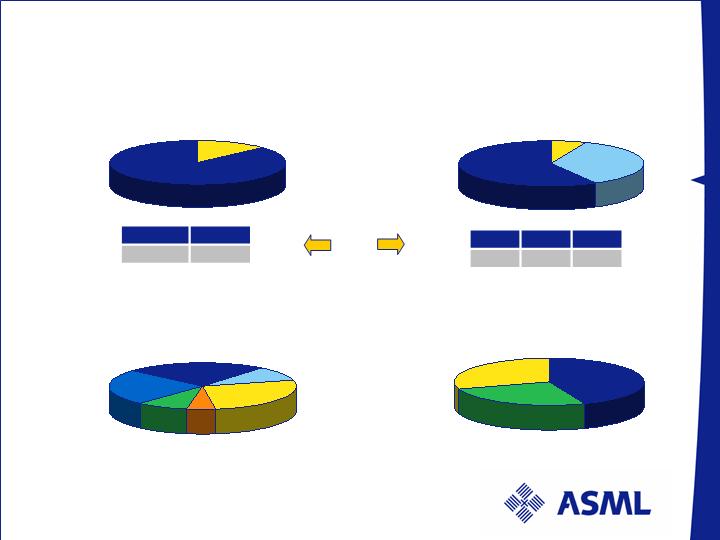

Revenue breakdown: Q2 2006

Value per type

Value per technology

TWINSCAN

87%

Others

13%

Value per region

Value per end-use

Foundry

26%

Memory

44%

IDM

30%

KrF

36%

ArF

58%

i-line

6%

U.S.

25%

Taiwan

24%

Korea

27%

China

9%

Europe

10%

ROW

5%

Numbers have been rounded for readers’ convenience

units

Units

23

49

Others

TWINSCAN

16

31

25

i-line

KrF

ArF

/ Slide 10

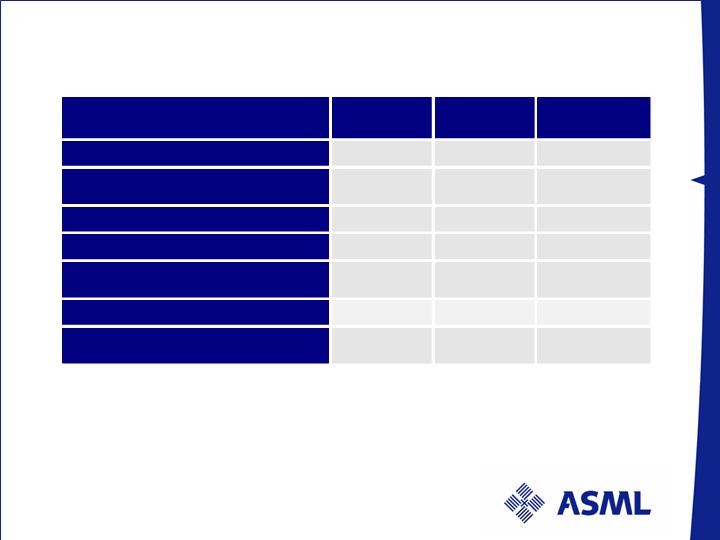

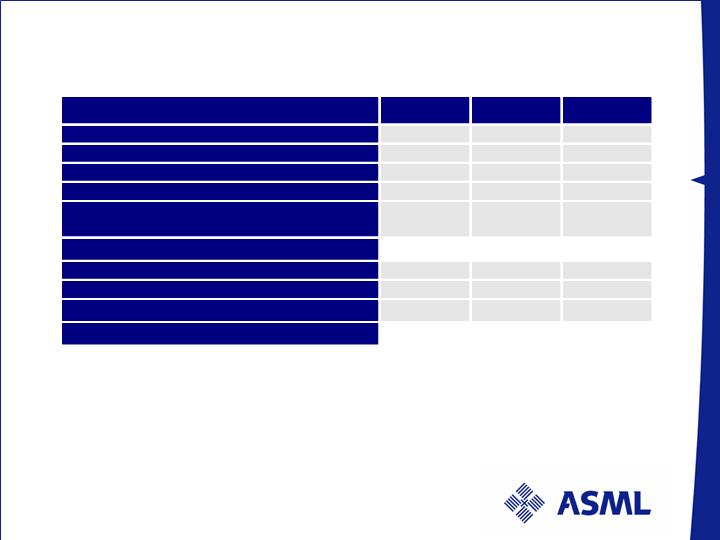

Profit & Loss statement M€

/ Slide 11

Numbers have been rounded for readers’ convenience

Q1 06

Q2 06

YTD

Net sales

629

94

2

157

1

Gross

profit

Gross margin %

252

40.0%

381

40

.

4

%

633

40

.3

%

R&D costs

87

92

179

SG&A costs

50

51

101

Operating income

Operating income %

114

18.2%

238

25

.

2

%

352

22.

4

.

%

Net income

Net income %

80

12.7%

167

1

7

.

7

%

247

15.7.

%

Key financial trends 2005 - 2006

/ Slide 12

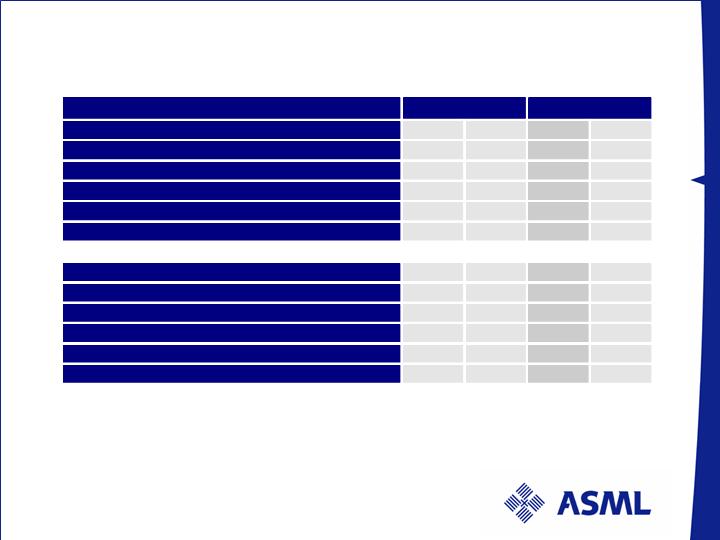

Numbers have been rounded for readers’ convenience

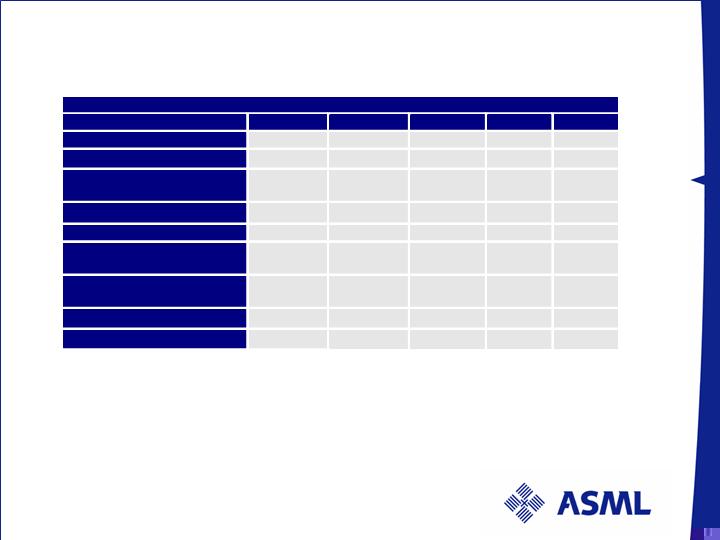

Profit & Loss Statement

M€

Q2 05

Q3 05

Q4 05

Q1 06

Q2 06

Units

51

39

47

51

72

Sales

763

533

548

629

94

2

Gross

profit

Gross margin %

299

39.1

%

197

37.0

%

204

37.3

%

251

40.0

%

381

40

.

4

%

R&D

82

80

82

87

92

SG&A

55

48

47

50

51

Operating

income

Operatin

g income %

162

21.2

%

69

12.9

%

75

13.6

%

114

18.2

%

238

25

.

2

%

Net income

Net income %

112

14.6

%

48

9.0

%

52

9.4

%

80

12.7

%

167

17.7

%

ASP New Systems

14.8

15.0

12.5

13.5

13.

7

Booking Units

24

46

55

62

9

3

Cash flow M€

/ Slide 13

Including payment of Euro 253 million for share buyback

2

Including payment of Euro 79 million for prior year taxes

1

Numbers have been rounded for readers’ convenience

Q1 06

Q2 06

YTD

Net income

80

1

67

247

Depreciation and amortization

22

21

43

Changes in tax assets and liabilities

(5

3

)

1

65

12

Effects of changes in inventories

(16

5

)

12

(153

)

Effects of changes in other assets and

liabilities

(102

)

6

5

(3

7

)

Cash fl

ow from operations

(219)

330

111

Cash flow from investing activities

(16)

(13)

(29)

Cash flow from financing activities

7

(246)

²

(239)

²

Effect of changes in exchange rates on cash

(6)

(10)

(16)

Net cash flow

(23

3

)

60

(173)

Current liabilities include USD 575 million principal amount of ASML’s 5.75 percent Convertible Subordinated

Notes due October 15, 2006.

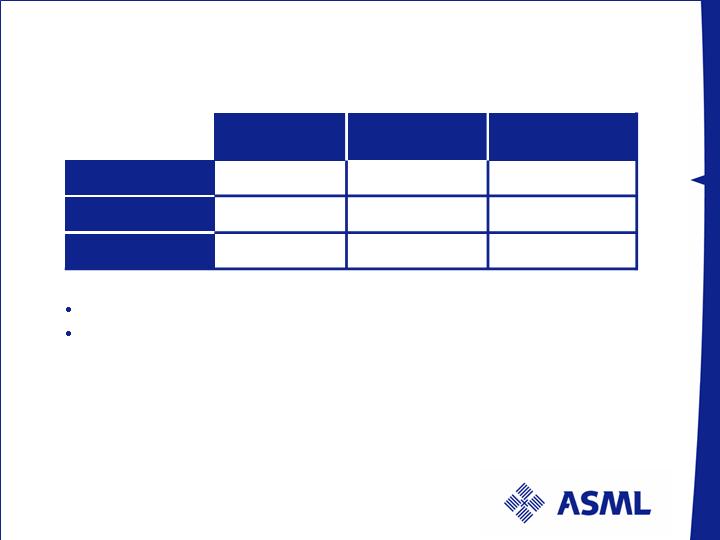

Balance sheet as of July 2, 2006 M€

/ Slide 14

1

Numbers have been rounded for readers’ convenience

ASSETS

March 2006

June

200

6

Cash and cash equivalents

1671

44 %

1731

44

%

Accounts receivable, net

447

12 %

540

14

%

Inventories, net

940

25 %

916

23

%

Other assets

153

4 %

16

7

4

%

Tax assets

297

7 %

273

7

%

Fixed assets

301

8 %

308

8

%

TOTAL ASSE

TS

3809

100%

3935

1

00%

LIABILITIES and SHAREHOLDERS’ EQUITY

Current liabilities

1

1385

36 %

1656

42

%

Convertible subordinated bonds

380

10 %

380

10

%

Long term debts and deferred liabilities

243

7 %

242

6

%

Shareholders’ equity

1801

47 %

165

7

42

%

TOTAL LIABILITIES & SHAREHOLDERS’ EQUITY

3809

100%

3935

1

00%

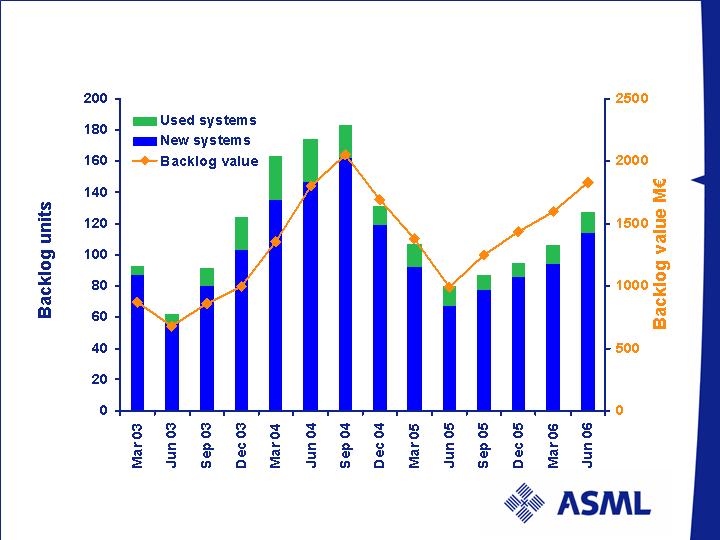

Backlog as of July 2, 2006

88 % of unit backlog carry Q3 + Q4 2006 shipment dates

Q2 net bookings of 93 systems with a value € 1.083 million

including 78 new tools with an ASP of € 13.2 million

Note: Due to possible customer changes in delivery schedules and to cancellation of orders, our backlog at any

particular date is not necessarily indicative of actual sales for any succeeding period

Numbers have been rounded for readers’ convenience

New Systems

Used Systems

Total Backlog

M€ 1.785

M€ 45

M€ 1.830

M€ 15.7

M€ 3.5

M€ 14.4

Backlog

Backlog

114

13

127

Units

Value

ASP

/ Slide 15

Backlog: litho units and value

/ Slide 16

Backlog lithography per July 2, 2006

Total value € 1,830 million

Value per type

Value per technology

TWINSCAN

95%

Others

5%

I-line

5%

ArF dry

42 %

Value per region

Value per end-use

U.S.

20%

Foundry

24%

Memory

49%

Taiwan

14%

IDM

27%

Korea

34%

KrF

26%

ROW

7%

Europe

9%

ArF immersion

27 %

Numbers have been rounded for readers’ convenience

China

7%

Japan

9%

/ Slide 17

Q3 2006: Outlook

Shipment of 62 systems expected in Q3

ASP for new system shipments expected to be € 14.5 million and

€ 12.5 million for new + refurbished systems

Bookings expected above 62 systems in Q3

Gross margin expected at 39% – 41%

R&D and SG&A are expected to be € 100 million net of credit and

€ 51 million respectively

Build-up of semi’s production capacity based on Billings and

Bookings outlook in line with 10% semi’s value growth and 15%

semi’s unit growth

Strong Flash / DRAM bookings, average IDM bookings and mixed

Foundry bookings

Planning to ship two EUV Alpha Demo Tools in Q3 2006

Reiterating shipment forecast of 20-25 immersion systems in 2006

/ Slide 18

Share buyback program

ASML has completed its announced share buyback

of € 400 million as announced on April 19, 2006. This

represents 25,450,296 million shares or 5.25% of

outstanding shares

ASML has a convertible bond of principal amount

USD 575 million due October 15, 2006. In case these

notes were to convert, resulting funds could be used

for additional share buyback

Purpose of share buyback programs is to return

excess cash to shareholders through reduction of the

number of issued shares

/ Slide 19

Company focus for remainder 2006

Continue execution on key points

Execute on volume production ramp of the TWINSCAN

XT:1700i, hyper NA tool for 45 nm node

Execute on cost of goods reduction

Execute on lead time reduction

Increase the technology leadership gap

Ship 2 EUV Alpha demo tools

Prepare for volume manufacturing and shipment of XT:1900i

starting H1 2007

Develop alternative architectures for cost effective

lithography at 32 nm resolution and beyond

/ Slide 20

ASML’s drivers for growth

Lithography enables customers to shrink devices for lower cost

and/or added functionality

ASML continues to grow its worldwide market share

Technology leadership fueled by R&D strength and scale

Five industry segments work together resulting in milder industry

cycles

Each segment represents different growth drivers, all together

contributing to steady, long term industry growth

ASML’s customers are fully represented in all industry segments

and pervasive in all technologies

ASML has long term ASP growth opportunity

/ Slide 21

Commitment