Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07455

Virtus Opportunities Trust

(Exact name of registrant as specified in charter)

101 Munson Street

Greenfield, MA 01301-9668

(Address of principal executive offices) (Zip code)

Kevin J. Carr, Esq.

Senior Vice President, Chief Legal Officer, Counsel and Secretary for Registrant

100 Pearl Street

Hartford, CT 06103-4506

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 243-1574

Date of fiscal year end: September 30

Date of reporting period: September 30, 2016

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Table of Contents

ANNUAL REPORT

Virtus Bond Fund*

Virtus CA Tax-Exempt Bond Fund

Virtus Essential Resources Fund*

Virtus High Yield Fund*

Virtus Low Duration Income Fund

Virtus Low Volatility Equity Fund*

Virtus Multi-Sector Intermediate Bond Fund

Virtus Senior Floating Rate Fund*

Virtus Tax-Exempt Bond Fund

Virtus Wealth Masters Fund

September 30, 2016 TRUST NAME: VIRTUS OPPORTUNITIES TRUST * Prospectus and Statement of Additional Information supplements applicable to these Funds |

|

Not FDIC Insured

No Bank Guarantee

May Lose Value

Table of Contents

| 1 | ||||||||

| 2 | ||||||||

| 4 | ||||||||

| Fund | Fund Summary | Schedule of Investments | ||||||

| 7 | 31 | |||||||

| 9 | 38 | |||||||

Virtus Essential Resources Fund (“Essential Resources Fund”) | 12 | 41 | ||||||

| 14 | 43 | |||||||

Virtus Low Duration Income Fund (“Low Duration Income Fund”) | 17 | 49 | ||||||

Virtus Low Volatility Equity Fund (“Low Volatility Equity Fund”) | 19 | 58 | ||||||

Virtus Multi-Sector Intermediate Bond Fund (“Multi-Sector Intermediate Bond Fund”) | 21 | 59 | ||||||

Virtus Senior Floating Rate Fund (“Senior Floating Rate Fund”) | 23 | 68 | ||||||

| 26 | 74 | |||||||

| 29 | 79 | |||||||

| 81 | ||||||||

| 84 | ||||||||

| 88 | ||||||||

| 95 | ||||||||

| 101 | ||||||||

| 116 | ||||||||

| 117 | ||||||||

Consideration of Advisory and Subadvisory Agreements by the Board of Trustees | 118 | |||||||

| 120 | ||||||||

| 124 | ||||||||

Proxy Voting Procedures and Voting Record (Form N-PX)

The subadvisers vote proxies relating to portfolio securities in accordance with procedures that have been approved by the Board of Trustees of the Trust (“Trustees,” or the “Board”). You may obtain a description of these procedures, along with information regarding how the Funds voted proxies during the most recent 12-month period ended June 30, free of charge, by calling toll-free 1-800-243-1574. This information is also available through the Securities and Exchange Commission’s (the “SEC”) website at http://www.sec.gov.

Form N-Q Information

The Trust files a complete schedule of portfolio holdings for each Fund with the SEC for the first and third quarters of each fiscal year on Form N-Q. Form N-Q is available on the SEC’s website at http://www.sec.gov. Form N-Q may be reviewed and copied at the SEC’s Public Reference Room. Information on the operation of the SEC’s Public Reference Room can be obtained by calling toll-free 1-800-SEC-0330.

This report is not authorized for distribution to prospective investors in the Funds presented in this book unless preceded or accompanied by an effective prospectus which includes information concerning the sales charge, each Fund’s record and other pertinent information.

Table of Contents

To My Fellow Shareholders of Virtus Mutual Funds:

| I am pleased to present this annual report that reviews the performance of your fund for the 12 months ended September 30, 2016.

During the first half of the fiscal year, global equity markets were challenged by falling oil prices, China’s slowdown, and concerns over the Federal Reserve’s (“the Fed”) first rate hike in nine years, which occurred in December 2015. Equities plummeted in early 2016, but stabilizing oil prices and the Fed’s softened stance on further rate hikes for 2016 sparked a rally in mid-February that lasted until June. The U.K.’s June 23 “Brexit” decision to leave the European Union triggered a selloff that was largely | |

short-lived. Calm was restored by better-than-expected corporate earnings, an improving global economic picture, and reassurance that the world’s central banks would continue to provide monetary stimulus. By the end of September, U.S. equity markets had recovered much of their losses, and the 12-month period was positive for many asset classes.

For the 12 months ended September 30, 2016, U.S. small-cap stocks kept pace with U.S. large-cap stocks, as measured by the 15.47% and 15.43% returns of the Russell 2000® Index and S&P 500® Index, respectively. Within international equities, emerging markets significantly outperformed their developed peers, with the MSCI Emerging Markets Index (net) up 16.78%, while the MSCI EAFE® Index (net) returned 6.52%.

Demand for U.S. Treasuries remained strong, driven by foreign investors seeking safe havens and yield in light of the negative interest rate environment in many international economies. On September 30, 2016, the benchmark 10-year U.S. Treasury yielded 1.60% compared with 2.06% one year earlier. For the 12 months ended September 30, 2016, the broader U.S. fixed income market, as represented by the Bloomberg Barclays U.S. Aggregate Bond Index, which tracks Treasuries and other investment-grade debt securities, gained 5.19%, while non-investment grade bonds rose 12.73%, as measured by the Bloomberg Barclays U.S. Corporate High Yield Bond Index.

The strength of the global economy will likely remain a leading concern for markets in the months ahead, and investors will watch with great interest the actions of the Fed and other major central banks. The U.S. economy’s continued growth, as evidenced by recent strong jobs, housing, and consumer spending data, should give investors reason for optimism, but future market direction will be determined largely by the ability of corporations to continue to produce robust earnings.

Market uncertainty is an ever-present reminder of the importance of portfolio diversification, including exposure to both traditional and alternative asset classes. While diversification cannot guarantee a profit or prevent a loss, owning a variety of asset classes may cushion your portfolio against inevitable market fluctuations. Your financial advisor can help you ensure that your portfolio is adequately diversified across asset classes and investment strategies.

As always, thank you for entrusting Virtus with your assets. Should you have questions about your account or require assistance, please visit our website at Virtus.com, or call our customer service team at 1-800-243-1574. We appreciate your business and remain committed to your long-term financial success.

Sincerely,

George R. Aylward President, Virtus Mutual Funds

October 2016 | ||

Performance data quoted represents past results. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

1

Table of Contents

VIRTUS OPPORTUNITIES TRUST

Disclosure of Fund Expenses (Unaudited)

FOR THE SIX-MONTH PERIOD OF APRIL 1, 2016 TO SEPTEMBER 30, 2016

We believe it is important for you to understand the impact of costs on your investment. All mutual funds have operating expenses. As a shareholder of a Virtus Opportunities Trust Fund (each, a “Fund”) you may incur two types of costs: (1) transaction costs, including sales charges on purchases of Class A shares and contingent deferred sales charges on Class B and Class C shares; and (2) ongoing costs, including investment advisory fees, distribution and service fees, and other expenses. Class I shares and Class R6 shares are sold without sales charges and do not incur distribution and service fees. For further information regarding applicable sales charges, see Note 1 in the Notes to Financial Statements. These examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. These examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period. The following Expense Table illustrates your Fund’s costs in two ways.

Actual Expenses

The first section of the accompanying table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your Fund under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second section of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not your Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the accompanying table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges or contingent deferred sales charges. Therefore, the second section of the accompanying table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

| Expense Table | ||||||||||||||||

| Beginning Account Value April 1, 2016 | Ending Account Value September 30, 2016 | Annualized Expense Ratio | Expenses Paid During Period* | |||||||||||||

Bond Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,048.70 | 0.87 | % | $ | 4.46 | ||||||||

Class B | 1,000.00 | 1,043.30 | 1.63 | 8.33 | ||||||||||||

Class C | 1,000.00 | 1,044.00 | 1.62 | 8.28 | ||||||||||||

Class I | 1,000.00 | 1,050.20 | 0.62 | 3.18 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,020.65 | 0.87 | 4.39 | ||||||||||||

Class B | 1,000.00 | 1,016.85 | 1.63 | 8.22 | ||||||||||||

Class C | 1,000.00 | 1,016.90 | 1.62 | 8.17 | ||||||||||||

Class I | 1,000.00 | 1,021.90 | 0.62 | 3.13 | ||||||||||||

CA Tax Exempt Bond Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,024.00 | 0.87 | % | $ | 4.41 | ||||||||

Class I | 1,000.00 | 1,026.20 | 0.62 | 3.15 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,020.71 | 0.87 | 4.41 | ||||||||||||

Class I | 1,000.00 | 1,021.96 | 0.62 | 3.14 | ||||||||||||

Essential Resources Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,052.40 | 1.68 | % | $ | 8.64 | ||||||||

Class C | 1,000.00 | 1,049.10 | 2.42 | 12.43 | ||||||||||||

Class I | 1,000.00 | 1,054.80 | 1.42 | 7.31 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,016.60 | 1.68 | 8.47 | ||||||||||||

Class C | 1,000.00 | 1,012.90 | 2.42 | 12.18 | ||||||||||||

Class I | 1,000.00 | 1,017.90 | 1.42 | 7.16 | ||||||||||||

High Yield Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,093.70 | 1.15 | % | $ | 6.02 | ||||||||

Class B | 1,000.00 | 1,089.70 | 1.89 | 9.87 | ||||||||||||

Class C | 1,000.00 | 1,091.30 | 1.90 | 9.93 | ||||||||||||

Class I | 1,000.00 | 1,095.10 | 0.90 | 4.71 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,019.25 | 1.15 | 5.81 | ||||||||||||

Class B | 1,000.00 | 1,015.55 | 1.89 | 9.52 | ||||||||||||

Class C | 1,000.00 | 1,015.50 | 1.90 | 9.57 | ||||||||||||

Class I | 1,000.00 | 1,020.50 | 0.90 | 4.55 | ||||||||||||

Low Duration Income Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,022.20 | 0.77 | % | $ | 3.89 | ||||||||

Class C | 1,000.00 | 1,017.40 | 1.52 | 7.67 | ||||||||||||

Class I | 1,000.00 | 1,023.50 | 0.52 | 2.63 | ||||||||||||

Hypothetical |

| |||||||||||||||

Class A | 1,000.00 | 1,021.15 | 0.77 | 3.89 | ||||||||||||

Class C | 1,000.00 | 1,017.40 | 1.52 | 7.67 | ||||||||||||

Class I | 1,000.00 | 1,022.40 | 0.52 | 2.63 | ||||||||||||

2

Table of Contents

VIRTUS OPPORTUNITIES TRUST

Disclosure of Fund Expenses (Unaudited) (Continued)

FOR THE SIX-MONTH PERIOD OF APRIL 1, 2016 TO SEPTEMBER 30, 2016

| Expense Table | ||||||||||||||||

| Beginning Account Value April 1, 2016 | Ending Account Value September 30, 2016 | Annualized Expense Ratio | Expenses Paid During Period* | |||||||||||||

Low Volatility Equity Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,044.20 | 1.58 | % | $ | 8.07 | ||||||||

Class C | 1,000.00 | 1,041.10 | 2.34 | 11.94 | ||||||||||||

Class I | 1,000.00 | 1,046.80 | 1.33 | 6.81 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,017.10 | 1.58 | 7.97 | ||||||||||||

Class C | 1,000.00 | 1,013.30 | 2.34 | 11.78 | ||||||||||||

Class I | 1,000.00 | 1,018.35 | 1.33 | 6.71 | ||||||||||||

Multi-Sector Intermediate Bond Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,085.90 | 1.15 | % | $ | 6.00 | ||||||||

Class B | 1,000.00 | 1,082.10 | 1.89 | 9.84 | ||||||||||||

Class C | 1,000.00 | 1,082.00 | 1.89 | 9.84 | ||||||||||||

Class I | 1,000.00 | 1,087.20 | 0.89 | 4.64 | ||||||||||||

Class R6 | 1,000.00 | 1,088.70 | 0.83 | 4.33 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,019.25 | 1.15 | 5.81 | ||||||||||||

Class B | 1,000.00 | 1,015.55 | 1.89 | 9.52 | ||||||||||||

Class C | 1,000.00 | 1,015.55 | 1.89 | 9.52 | ||||||||||||

Class I | 1,000.00 | 1,020.55 | 0.89 | 4.50 | ||||||||||||

Class R6 | 1,000.00 | 1,020.85 | 0.83 | 4.19 | ||||||||||||

Senior Floating Rate Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,047.07 | 1.25 | % | $ | 6.40 | ||||||||

Class C | 1,000.00 | 1,043.08 | 2.00 | 10.22 | ||||||||||||

Class I | 1,000.00 | 1,048.44 | 1.00 | 5.12 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,018.75 | 1.25 | 6.31 | ||||||||||||

Class C | 1,000.00 | 1,015.00 | 2.00 | 10.08 | ||||||||||||

Class I | 1,000.00 | 1,020.00 | 1.00 | 5.05 | ||||||||||||

Tax-Exempt Bond Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,015.50 | 0.87 | % | $ | 4.38 | ||||||||

Class C | 1,000.00 | 1,011.60 | 1.62 | 8.15 | ||||||||||||

Class I | 1,000.00 | 1,016.80 | 0.63 | 3.18 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,020.65 | 0.87 | 4.39 | ||||||||||||

Class C | 1,000.00 | 1,016.90 | 1.62 | 8.17 | ||||||||||||

Class I | 1,000.00 | 1,021.85 | 0.63 | 3.18 | ||||||||||||

Wealth Masters Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,090.40 | 1.48 | % | $ | 7.73 | ||||||||

Class C | 1,000.00 | 1,086.10 | 2.23 | 11.63 | ||||||||||||

Class I | 1,000.00 | 1,091.60 | 1.23 | 6.43 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,017.60 | 1.48 | 7.47 | ||||||||||||

Class C | 1,000.00 | 1,013.85 | 2.23 | 11.23 | ||||||||||||

Class I | 1,000.00 | 1,018.85 | 1.23 | 6.21 | ||||||||||||

| * | Expenses are equal to the relevant Funds’ annualized expense ratio, which is net of waived fees and reimbursed expenses, if applicable, multiplied by the average account value over the period, multiplied by the number of days (183) expenses were accrued in the most recent fiscal half-year, then divided by 366 to reflect the one-half year period. |

For Funds which may invest in other funds, the annualized expense ratios noted above do not reflect fees and expenses associated with the underlying funds. If such fees and expenses had been included, the expenses would have been higher.

You can find more information about the Funds’ expenses in the Financial Statements section that follows. For additional information on operating expenses and other shareholder costs, refer to the prospectus.

3

Table of Contents

VIRTUS OPPORTUNITIES TRUST

SEPTEMBER 30, 2016 (Unaudited)

American Depositary Receipt (ADR)

Represents shares of foreign companies traded in U.S. dollars on U.S. exchanges that are held by a U.S. bank or a trust. Foreign companies use ADRs in order to make it easier for Americans to buy their shares.

Bank of Japan (“BOJ”)

The Bank of Japan is the Japanese central bank.

Bloomberg Barclays California Municipal Bond Index

The Bloomberg Barclays California Municipal Bond Index measures long term investment grade, tax-exempt and fixed rate bonds issued in California. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Bloomberg Barclays Municipal Bond Index

The Bloomberg Barclays Municipal Bond Index is a market capitalization-weighted index that measures the long-term tax-exempt bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

Bloomberg Barclays U.S. Aggregate Bond Index

The Bloomberg Barclays U.S. Aggregate Bond Index measures the U.S. investment grade fixed rate bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Bloomberg Barclays U.S. Corporate High Yield Bond Index

The Bloomberg Barclays U.S. Corporate High Yield Bond Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index

The Bloomberg Barclays High-Yield 2% Issuer Capped Bond Index is a market capitalization-weighted index that measures fixed rate non-investment grade debt securities of U.S. and non-U.S. corporations. No single issuer accounts for more than 2% of market cap. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index

The Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index measures U.S. investment grade government and corporate debt securities with an average maturity of 4 to 5 years. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

BofA Merrill Lynch U.S. Municipal Securities Index

The BofA Merrill Lynch U.S. Municipal Securities Index tracks the performance of U.S. dollar denominated investment grade tax-exempt debt publicly issued by U.S. states and territories, and their political subdivisions, in the U.S. domestic market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

BofA Merrill Lynch 1–22 Year U.S. Municipal Securities Index

The BofA Merrill Lynch 1–22 Year U.S. Municipal Securities Index is a a subset of the BofA Merrill Lynch U.S. Municipal Securities Index including all securities with a remaining term to final maturity less than 22 years, calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

Chicago Board Options Exchange (CBOE) Volatility Index

The Chicago Board Options Exchange (CBOE) Volatility Index (“VIX®”) shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500® Index options. This volatility is meant to be forward looking and is calculated from both calls and puts. The VIX® is a widely used measure of market risk and is often referred to as the “investor fear gauge.” The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

4

Table of Contents

VIRTUS OPPORTUNITIES TRUST

KEY INVESTMENT TERMS (Continued)

SEPTEMBER 30, 2016 (Unaudited)

CBOE S&P 500 Buywrite Index

The CBOE S&P 500 Buywrite Index is a passive total return index based on buying an S&P 500® stock index portfolio and “writing” (or selling) the nearterm S&P 500® Index (SPXSM) “covered” call option. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

Collateralized Loan Obligation (“CLO”)

A collateralized loan obligation is a type of security backed by a pool of debt, typically low-rated corporate loans, structured so that there are several classes of bondholders with varying maturities, called tranches.

European Central Bank (“ECB”)

The European Central Bank (ECB) is responsible for conducting monetary policy for the eurozone. The ECB was established as the core of the Eurosystem and the European System of Central Banks (ESCB). The ESCB comprises the ECB and the national central banks (NCBs) of all 17 European Union Member States whether they have adopted the Euro or not.

European Union (“EU”)

The European Union (“EU”) is a unique economic and political union of 28 European countries. The EU was created in the aftermath of the Second World War that has become a single market for goods and services and it created the single currency the euro.

Exchange-Traded Funds (ETF)

A Fund that is traded on a stock exchange. Most ETFs have a portfolio of stocks or bonds that track a specific market index.

Federal Reserve (the “Fed”)

The Central Bank of the United States, responsible for controlling the money supply, interest rates and credit with the goal of keeping the U.S. economy and currency stable. Governed by a seven-member board, the system includes 12 regional Federal Reserve Banks, 25 branches and all national and state banks that are part of the system.

Gross Domestic Product (“GDP”)

The market value of all officially recognized final goods and services produced within a country in a given period.

iShares®

Represents shares of an open-end exchange-traded fund.

London Interbank Offered Rate (LIBOR)

A benchmark rate that some of the world’s leading banks charge each other for short-term loans and that serves as the first step to calculating interest rates on various loans throughout the world.

Mergers and Acquisitions (M&A) Bond

An M&A bond is a type of corporate bond that is used to raise money for financing activities such as mergers and acquisitions.

MSCI EAFE® Index (net)

The MSCI EAFE® Index (net) is a free float-adjusted market capitalization-weighted index that measures developed foreign market equity performance, excluding the U.S. and Canada. The index is calculated on a total return basis with net dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

MSCI Emerging Markets Index (net)

The MSCI Emerging Markets Index (net) is a free float-adjusted market capitalization-weighted index designed to measure equity market performance in the global emerging markets. The index is calculated on a total return basis with net dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

MSCI World Index (net)

The MSCI World Index (net) is a free float-adjusted market capitalization-weighted index that measures developed global market equity performance. The index is calculated on a total return basis with net dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

5

Table of Contents

VIRTUS OPPORTUNITIES TRUST

KEY INVESTMENT TERMS (Continued)

SEPTEMBER 30, 2016 (Unaudited)

Organization of the Petroleum Exporting Countries (OPEC)

The Organization of the Petroleum Exporting Countries was originally organized in September 1960 with 5 member countries and there are currently 12 member countries. The organization’s objective is to co-ordinate and unify petroleum policies among member countries, in order to secure fair and stable prices for petroleum producers; an efficient, economic and regular supply of petroleum to consuming nations; and a fair return on capital to those investing in the industry.

Payment-in-Kind Security (PIK)

A bond which pays interest in the form of additional bonds, or preferred stock which pays dividends in the form of additional preferred stock.

Real Estate Investment Trust (REIT)

A publicly traded company that owns, develops and operates income-producing real estate such as apartments, office buildings, hotels, shopping centers and other commercial properties.

Russell 2000® Index

The Russell 2000® Index is a market capitalization-weighted index of the 2,000 smallest companies in the Russell Universe, which comprises the 3,000 largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment.

S&P 100® Index

The S&P 100® Index, a sub-set of the S&P 500®, measures the performance of large-cap U.S. companies, and comprises 100 major, blue chip companies across multiple industry groups.

S&P 500® Index

The S&P 500® Index is a free-float market capitalization-weighted index of 500 of the largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

S&P Global Natural Resources Index (net)

The S&P Global Natural Resources Index (net) is a free-float market capitalization index calculated on a total return basis with net dividends reinvested. The index consists of 90 of the largest publicly traded companies in natural resources and commodities businesses that meet specific investability requirements, offering investors diversified and investable equity exposure across three primary commodity-related sectors: agribusiness, energy, and metals and mining. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and it is not available for direct investment.

S&P/LSTA Leveraged Loan Index

The S&P/LSTA Leveraged Loan Index is a daily total return index that uses LSTA/LPC Mark-to-Market Pricing (third-party research data on the price movements of senior secured floating rate loans in the secondary loan market) to calculate market value change. On a real-time basis, the Index tracks the current outstanding balance and spread over LIBOR for fully funded term loans. The facilities included in the Index represent a broad cross section of leveraged loans syndicated in the United States, including dollar-denominated loans to overseas issuers. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges and it is not available for direct investment.

Tax-Exempt Bond Linked Benchmark

The Tax-Exempt Bond Linked Benchmark consists of the BofA Merrill Lynch 1-22 Year US Municipal Securities Index, a subset of the BofA Merrill Lynch US Municipal Securities Index including all securities with a remaining term to final maturity less than 22 years, calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses, or sales charges, and is not available for direct investment. Performance of the Tax- Exempt Bond Linked Benchmark prior to 6/30/2012 is that of the Barclays Municipal Bond Index.

When-issued and Forward Commitments (Delayed Delivery)

Securities purchased on a when-issued or forward commitment basis are also known as delayed delivery transactions. Delayed delivery transactions involve a commitment by a Fund to purchase or sell a security at a future date, ordinarily up to 90 days later. When-issued or forward commitments enable a Fund to lock in what is believed to be an attractive price or yield on a particular security for a period of time, regardless of future changes in interest rates.

6

Table of Contents

Fund Summary | Ticker Symbols: Class A: SAVAX Class B: SAVBX Class C: SAVCX Class I: SAVYX |

Portfolio Manager Commentary by Newfleet Asset Management, LLC

| ¢ | The Fund is diversified and has an investment objective of high total return from both current income and capital appreciation. |

| ¢ | For the fiscal year ended September 30, 2016, the Fund’s Class A shares at NAV returned 6.38%, Class B shares returned 5.47%, Class C shares returned 5.54%, and Class I shares returned 6.63%. For the same period, the Bloomberg Barclays U.S. Aggregate Bond Index, which serves as the broad-based and style-specific benchmark index appropriate for comparison, returned 5.19%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the market perform during the Fund’s fiscal year?

| ¢ | Most fixed income spread sectors outperformed U.S. Treasuries during the fiscal year. The U.S. Federal Reserve’s (“the Fed”) dovish stance in mid-February sparked a rally that turned around a volatile time period that began with fresh concerns over China, plummeting oil prices, and fears that the Fed had raised interest rates too soon. |

| ¢ | Late in June volatility returned briefly with fallout from the U.K.’s unexpected decision to leave the European Union (“Brexit”). Bond yields in the U.S., Japan, and across Europe fell to historic lows in early July as investors fled to the safety of bonds on global growth concerns fueled by the June 23 Brexit vote. Markets recovered rather quickly however from the initial shock. Easing by major central banks and a weaker U.S. dollar helped to improve global risk sentiment and stabilize markets. |

| ¢ | September brought heightened concerns over the ability and willingness of global central banks to fight chronic low inflation and weak growth as the decision by the European Central Bank (“ECB”) to leave interest rates and its stimulus program unchanged was a precipitating factor in a widespread market sell-off, reinforced by fears that |

the Bank of Japan (“BOJ”) had run out of quantitative easing tools. Hawkish signals from the Fed added to the volatility. The BOJ subsequently decided not to reduce interest rates further but to shift its focus to stabilizing rates for longer maturity government bonds. This bolstered market sentiment, as did the Fed’s eventual decision to stand pat at its September monetary policy meeting. |

| ¢ | Over the last 12 months, U.S. Treasury yields increased for shorter maturity bonds while yields decreased for intermediate to longer term bonds. |

What factors affected the Fund’s performance during its fiscal year?

| ¢ | The underperformance of U.S. Treasuries relative to most fixed income spread sectors was the key driver of the Fund’s outperformance for the fiscal year. |

| ¢ | The Fund’s allocation to the corporate high yield sector and issue selection within corporate high quality bonds were the largest positive contributors to performance during the fiscal year. |

| ¢ | During the fiscal year, the Fund’s allocation to asset-backed securities detracted from performance. |

The preceding information is the opinion of portfolio management only through the end of the period stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Credit & Interest: Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a debt security may fail to make interest and/or principal payments. Values of debt securities may rise or fall in response to changes in interest rates, and this risk may be enhanced with longer-term maturities.

Foreign & Emerging Markets: Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.

ABS/MBS: Changes in interest rates can cause both extension and prepayment risks for asset- and mortgage-backed securities. These securities are also subject to risks associated with the repayment of underlying collateral.

High Yield-High Risk Fixed Income Securities: There is a greater level of credit risk and price volatility involved with high yield securities than investment grade securities.

Prospectus: For additional information on risks, please see the fund’s prospectus.

| Asset Allocation | ||||||||

| The following table presents asset allocations within certain sectors and as a percentage of total investments as of September 30, 2016. | ||||||||

Corporate Bonds and Notes | 47 | % | ||||||

Financials | 17 | % | ||||||

Consumer Discretionary | 6 | |||||||

Real Estate | 4 | |||||||

All other Corporate Bonds and Notes | 20 | |||||||

Mortgage-Backed Securities | 27 | |||||||

U.S. Government Securities | 7 | |||||||

Asset-Backed Securities | 5 | |||||||

Loan Agreements | 4 | |||||||

Preferred Stocks | 3 | |||||||

Other Investments | 7 | |||||||

|

| |||||||

Total | 100 | % | ||||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

7

Table of Contents

Bond Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/16 | ||||||||||||

| 1 year | 5 years | 10 years | ||||||||||

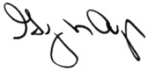

| Class A Shares at NAV2 | 6.38 | % | 4.29 | % | 5.04 | % | ||||||

| Class A Shares at POP3 | 2.39 | 3.50 | 4.64 | |||||||||

| Class B Shares at NAV2 | 5.47 | 3.50 | 4.24 | |||||||||

| Class B Shares with CDSC4 | 1.47 | 3.50 | 4.24 | |||||||||

| Class C Shares at NAV2 | 5.54 | 3.52 | 4.25 | |||||||||

| Class I Shares at NAV | 6.63 | 4.57 | 5.31 | |||||||||

| Bloomberg Barclays U.S. Aggregate Bond Index | 5.19 | 3.08 | 4.79 | |||||||||

Fund Expense Ratios5: A Shares: Gross 1.13%, Net 0.86%; B Shares: Gross 1.88%, Net 1.61%; C Shares: Gross 1.88%, Net 1.61%; I Shares: Gross 0.88%, Net 0.61%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 3.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for B shares decline from 5% to 0% over a five-year period. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter. |

| 5 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2016, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by contractual fee waiver in effect through January 31, 2017. Gross Expense: Does not reflect the effect of the fee waiver. Expense ratios include fees and expenses associated with underlying funds. |

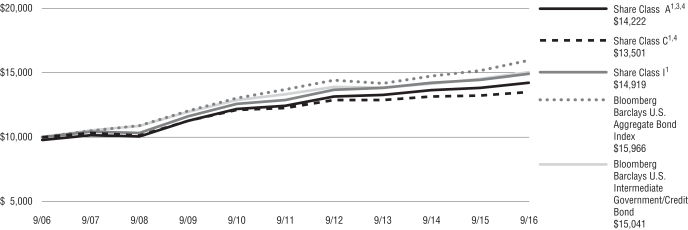

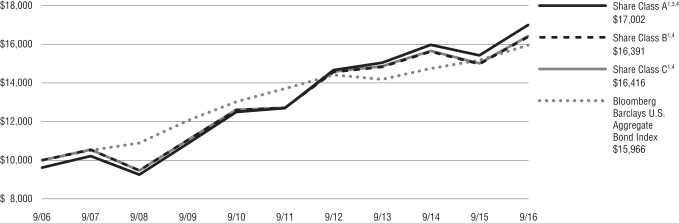

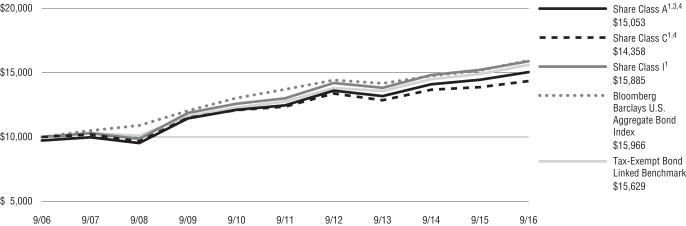

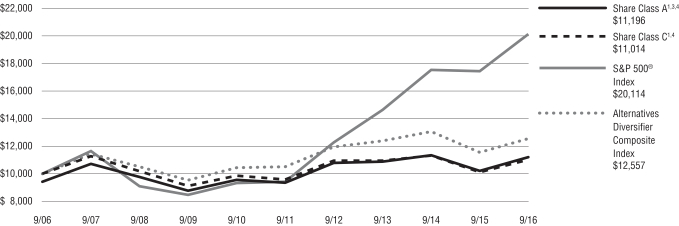

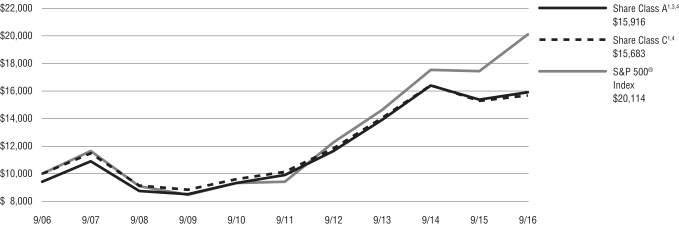

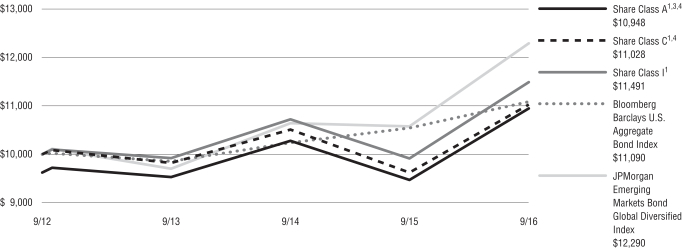

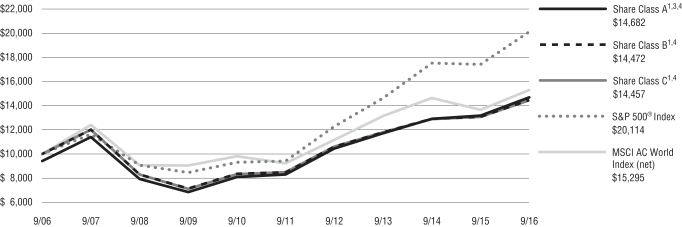

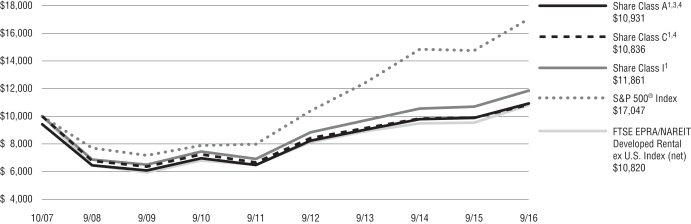

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on September 30, 2006, for Class A, Class B, Class C, and Class I shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

8

Table of Contents

Fund Summary | Ticker Symbols: Class A: CTESX Class I: CTXEX |

Portfolio Manager Commentary by Newfleet Asset Management, LLC

| ¢ | The Fund is diversified and has an investment objective of obtaining a high level of current income exempt from California state and local income taxes, as well as federal income tax, consistent with the preservation of capital. |

| ¢ | For the fiscal year ended September 30, 2016, the Fund’s Class A shares at NAV returned 5.56% and Class I shares returned 5.83%. For the same period, the Bloomberg Barclays U.S. Aggregate Bond Index, a broad-based fixed income index, returned 5.19%, and the Bloomberg Barclays California Municipal Bond Index, the Fund’s style-specific benchmark appropriate for comparison, returned 5.45%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s fiscal year?

The municipal bond market experienced solid performance over the 12 months ended September 30, 2016, as tax-free interest rates declined and credit risk spreads narrowed. The market’s technical conditions (supply and demand) remained strong for much of the period, with investors continuing to pour money into open-end municipal bond mutual funds and new issuance of municipal bonds mostly manageable despite interest rates hovering near generational low levels. However, the technical support weakened somewhat as the end of September approached. U.S. Treasury yields began to rise and tax-free interest rates followed, as the market priced in a higher probability of a rate hike by the Federal Reserve (“the Fed”). At the same time, municipal bond supply increased as municipalities issued bonds to get ahead of potential Fed rate hikes and perhaps to catch up on issuance delayed as a result of disruptions related to the U.K.’s “Brexit” vote in late June. The markets also were receptive to lower-rated credits as investors reached for yield across all areas of the fixed income market. As a result of the rise in yields and surge in supply, municipal bond performance turned negative for the first time in over a year.

The municipal market was otherwise resilient in the face of a number of market events and conditions, including repercussions from the U.K.’s surprising Brexit vote outcome; Puerto Rico’s default on its general obligation bonds and select public corporations; oil price volatility; the increasing and decreasing probabilities of a Fed rate hike; the U.S. presidential election; and the problems surrounding underfunded pension plans across the country. Aside from Puerto Rico, defaults have been very low in the municipal bond sector.

Demand for municipal bonds continued unabated, with 52 consecutive weeks of inflows into municipal bond mutual funds totaling over $50 billion. While long-term funds represented the bulk of the assets in terms of flows, the highest percentage increase of assets under management occurred among high yield funds. Though interrupted by the recent increase in supply, strong technicals have been the driving factor in the municipal market’s strength.

The economy continued to expand during the period, but the slow pace of growth continued to have an adverse effect on state budgets. State and local sales tax growth remained positive, but showed signs of slowing. Personal tax collections in the second quarter of 2016 grew by only 1.8% year-over-year, according to the Rockefeller Institute. Local property taxes, however, continued to benefit from an improving housing market and home prices.

By far, the largest challenge to the municipal credit remained the extent of underfunded pension obligations. Pension funds across the country have been struggling to meet assumed rates of return in the current low interest rate/stagnant stock market environment. As an example of a particularly serious situation, the California Public Employees’ Retirement System (“CALPERS”) reported a 0.6% return in its last fiscal year, far short of an assumed rate of return of 7.5%. The impact of lower-than-expected returns on pension funding levels has increased the stress on municipal budgets to increase annual contributions and divert funds from other spending.

What factors affected the Fund’s performance during its fiscal year?

Over the past 12 months, the market’s best performers were longer duration, lower coupon, and lower credit quality bonds as interest rates declined beyond five years and risk premiums narrowed.

While they still produced positive performance, bonds with shorter maturities, lower duration, and higher credit quality displayed relatively weaker performance for most of the year.

The Fund’s performance relative to the benchmark benefited from exposure to bonds with long maturities, lower-rated securities (including below-investment grade-rated bonds), and lower coupon securities. The Fund’s relative performance was negatively impacted by exposure to short-term maturities, higher coupons, better quality, and pre-refunded bonds.

The preceding information is the opinion of portfolio management only through the end of the period stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Credit & Interest: Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a debt security may fail to make interest and/or principal payments. Values of debt securities may rise or fall in response to changes in interest rates, and this risk may be enhanced with longer-term maturities.

Geographic Concentration: A fund that focuses its investments in a particular geographic location will be highly sensitive to financial, economic, political, and other developments affecting the fiscal stability of that location.

Municipal Market: Events negatively impacting a municipal security, or the municipal bond market in general, may cause the fund to decrease in value.

State & AMT Tax: A portion of income may be subject to some state and/or local taxes and, for certain investors, a portion may be subject to the federal alternative minimum tax.

High Yield-High Risk Fixed Income Securities: There is a greater level of credit risk and price volatility involved with high yield securities than investment grade securities.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

9

Table of Contents

| CA Tax-Exempt Bond Fund (Continued) |

Prospectus: For additional information on risks, please see the fund’s prospectus.

| Asset Allocation | ||||||||

The following table presents asset allocations within certain sectors and as a percentage of total investments as of September 30, 2016.

|

| |||||||

Tax-Exempt Municipal Bonds | 100 | % | ||||||

Pre-Refunded | 15 | % | ||||||

General Obligation | 13 | |||||||

Development Revenue | 13 | |||||||

Water & Sewer Revenue | 11 | |||||||

Lease Revenue | 10 | |||||||

General Revenue | 9 | |||||||

Medical Revenue | 8 | |||||||

Other | 21 | |||||||

|

| |||||||

Total | 100 | % | ||||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

10

Table of Contents

CA Tax-Exempt Bond Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/16 | ||||||||||||

| 1 year | 5 years | 10 years | ||||||||||

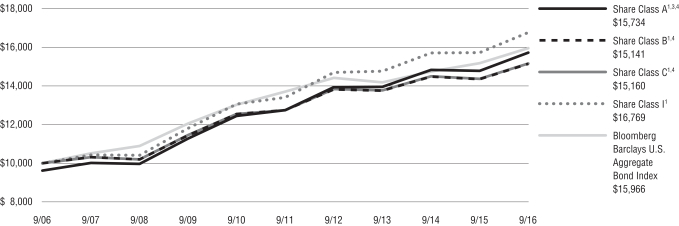

| Class A Shares at NAV2 | 5.56 | % | 5.00 | % | 4.48 | % | ||||||

| Class A Shares at POP3,4 | 2.66 | 4.42 | 4.19 | |||||||||

| Class I Shares at NAV | 5.83 | 5.25 | 4.74 | |||||||||

| Bloomberg Barclays U.S. Aggregate Bond Index | 5.19 | 3.08 | 4.79 | |||||||||

| Bloomberg Barclays California Municipal Bond Index | 5.45 | 5.17 | 4.98 | |||||||||

Fund Expense Ratios5: A Shares: Gross 1.18%, Net 0.85%; I Shares: Gross 0.93%, Net 0.60%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 2.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid are 1% and 0% thereafter. |

| 5 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2016, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by contractual fee waiver in effect through January 31, 2017. Gross Expense: Does not reflect the effect of the fee waiver. |

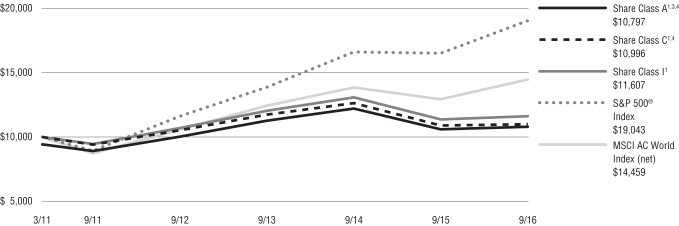

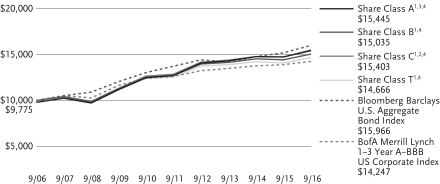

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on September 30, 2006 for Class A and Class I shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

11

Table of Contents

Fund Summary | Ticker Symbols: Class A: VERAX Class C: VERCX Class I: VERIX |

Portfolio Manager Commentary by KBI Global Investors (North America) Ltd.

| ¢ | The Fund is diversified and has an investment objective of capital appreciation. |

| ¢ | For the fiscal year ended September 30, 2016, the Fund’s Class A shares at NAV returned 12.93%, Class C shares returned 12.07%, and Class I shares returned 13.27%. For the same period, the S&P 500® Index, a broad-based fixed equity index, returned 15.43% and the S&P Global Natural Resources Index (net) the Fund’s style-specific benchmark appropriate for comparison returned 23.89%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s fiscal year?

During the Fund’s fiscal year, global stock markets made strong gains, bond yields continued to trend lower, and commodity prices were generally higher. The S&P Global Natural Resources Index returned a stellar 23.89% (net), in U.S. dollars (USD), outperforming the MSCI World Index (net) (+11.4% net, in USD) by a significant margin.

The extraordinary easy monetary policy being pursued by central banks globally since 2008 continued throughout the period. More recently, this journey has resulted in increasingly negative interest rates and bond yields around the globe. Indeed, the decision of the U.S. Federal Reserve to raise interest rates last December, even if repeated in coming months, is looking more and more like an anomaly in this overall context. Low rates and yields have become the new normal. Emerging markets have proven to be particular beneficiaries. A generally better tone for commodity prices and better-than-feared data from China also helped emerging market equities to outperform during the period.

The announcement in late September from oil cartel OPEC that it would scale back production later this year helped oil prices rally towards $50 a barrel. Latin America benefited in particular from strong gains in

Brazil. Growing expectations of improved earnings and economic growth continued to support the recovery there.

What factors affected the Fund’s performance during its fiscal year?

The Fund underperformed the S&P Global Natural Resources Index during the fiscal year ended September 30, 2016. Sector allocation was important as there is a high degree of difference between the composition of the Fund and the Index, both at the sector and stock levels. The Index had a high exposure to energy stocks (roughly 29%), which benefited from a very strong run due to rising oil prices, while the Fund had only 2% in energy stocks and zero exposure to oil stocks. The Index also had a large weighting in the materials sector (about 65%), which benefited from a rebound in mining and gold names. These stocks of extractive industries which the Fund did not hold. In terms of positive contributors, the Fund had positive stock selection in the consumer staples sector, and a larger exposure to this sector than the Index.

Water was the best performing sector for the Fund, both on a relative and absolute basis, followed by energy solutions. The agribusiness sector was the poorest performer. The Fund remained broadly equally weighted to the water, energy solutions, and agribusiness sectors, allowing for market movements.

Cyclical stocks came back into favor in 2016 as relatively cheap valuations saw value-oriented names outperform the growth stocks that had previously seen a lot of momentum. Company earnings over the period were also more in line with expectations and this provided support for many of our water-related stocks, particularly in instances where there was less certainty in the lead-up to results. The utility segment was a strong performer in the period due to its defensive nature as significant political and macro uncertainty provided momentum. The infrastructure segment also saw strong performance, particularly in the second half of the period, as our most cyclical segment benefited from the outperformance of stocks with more cyclical end markets.

The preceding information is the opinion of portfolio management only through the end of the period stated on the cover. Any such opinions are subject to

change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results and there is no guarantee market forecasts will be realized.

There is no guarantee that the Fund will meet its objectives.

Equity Securities: The market price of equity securities may be adversely affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk.

Foreign & Emerging Markets: Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

Prospectus: For additional information on risks, please see the fund’s prospectus.

| Asset Allocation | ||||

The following table presents asset allocations within certain sectors and as a percentage of total investments as of September 30, 2016.

|

| |||

Industrials | 27 | % | ||

Consumer Staples | 16 | |||

Utilities | 16 | |||

Materials | 14 | |||

Information Technology | 8 | |||

Consumer Discretionary | 7 | |||

Financials | 4 | |||

Other | 8 | |||

|

| |||

Total | 100 | % | ||

|

| |||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

12

Table of Contents

Essential Resources Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/16 | ||||||||||||

| 1 year | Since Inception | Inception Date | ||||||||||

| Class A Shares at NAV2 | 12.93 | % | -6.14 | % | 3/24/15 | |||||||

| Class A Shares at POP3,4 | 6.44 | -9.72 | 3/24/15 | |||||||||

| Class C Shares at NAV2 and with CDSC4 | 12.07 | -6.84 | 3/24/15 | |||||||||

| Class I Shares at NAV2 | 13.27 | -5.88 | 3/24/15 | |||||||||

| S&P 500® Index | 15.43 | 4.62 | 5 | — | ||||||||

| S&P Global Natural Resources Index (net) | 23.89 | -4.13 | 5 | — | ||||||||

Fund Expense Ratios6: A Shares: Gross 6.27%, Net 1.66%; C Shares: Gross 7.02%, Net 2.41%; I Shares: Gross 6.02%, Net 1.41%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 5.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter. |

| 5 | The since inception index returns are from the Fund’s inception date. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2016, as supplemented and revised and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by a contractual fee waiver in effect through January 31, 2017. Gross Expense: Does not reflect the effect of the fee waiver. Expense ratios include fees and expenses associated with underlying funds. |

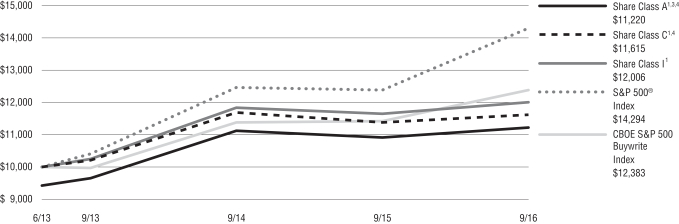

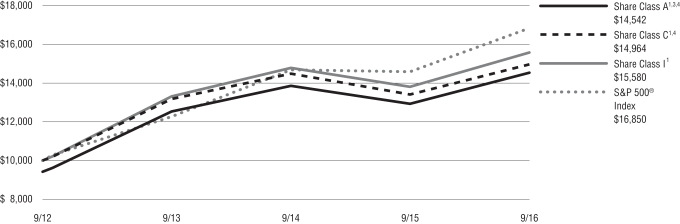

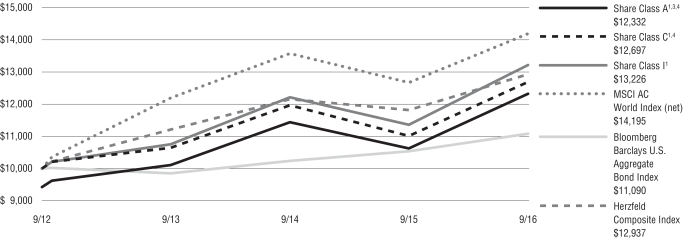

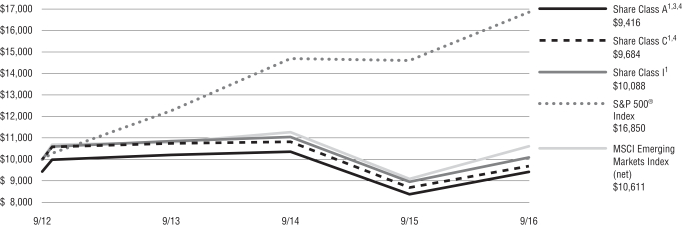

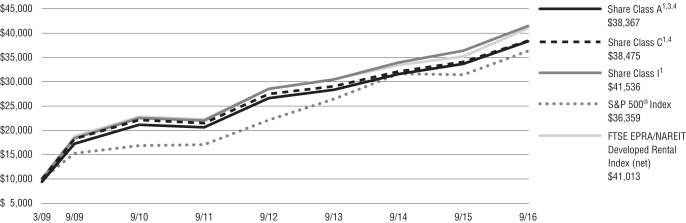

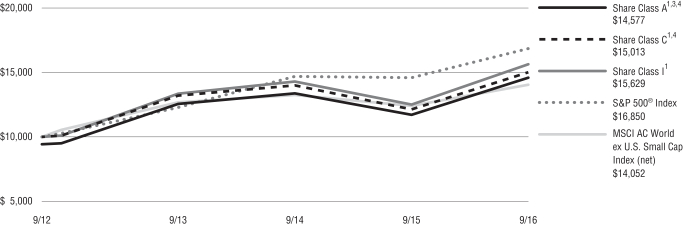

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on March 24, 2015 (inception date of the Fund) for Class A, Class C, and Class I shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

13

Table of Contents

Fund Summary | Ticker Symbols: Class A: PHCHX Class B: PHCCX Class C: PGHCX Class I: PHCIX |

Portfolio Manager Commentary by Newfleet Asset Management, LLC

| ¢ | The Fund is diversified and has a primary investment objective of high current income and a secondary objective of capital growth. |

| ¢ | For the fiscal year ended September 30, 2016, the Fund’s Class A shares at NAV returned 10.59%, Class B shares returned 9.52%, and Class C shares returned 9.68%. Class I shares returned 10.86%. For the same period, the Bloomberg Barclays U.S. Aggregate Bond Index, a broad-based fixed income index, returned 5.19%, and the Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index, the Fund‘s style-specific index appropriate for comparison, returned 12.74%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the market perform during the Fund’s fiscal year?

The U.S. high yield market, as measured by the Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index, posted a 12.74% return for the fiscal year ended September 30, 2016. There was a sharp contrast in performance between the first quarter and the rest of the fiscal year. Heightened concerns over China’s slowdown and its adverse impact on commodity prices and currencies weighed heavily on the high yield sector from October to December 2015, producing a negative result. The energy and metals & mining industries led the sector down with double-digit negative returns, but other favorably-viewed industries followed them into negative territory. The turbulence continued into January and early February. The Federal Reserve’s dovish tone in mid-February, however, sparked a rally and a demand for risk assets that continued almost unabated for the rest of the year. As of September 30, the high yield sector had posted eight consecutive months of positive returns.

The steep recovery of the energy and metals & mining industry groups within the high yield benchmark index best accounts for the strength in the high yield market over the fiscal year. For the first

nine months of 2016, metals & mining gained 41.1%; for the last 12 months, which includes the negative performance from October to December 2015, the gain was 27.7%. The nine- and 12-month returns for energy were 29.81% and 13.09%, respectively, but the strong performance of the high yield sector really began February 11 with the Index returning 21.37%, while the underlying metals & mining and energy industries returned 48.51%, and 60.40%, respectively, from that point until the end of the fiscal year.

The returns across the rating spectrum demonstrated the effect of easy global monetary policy and the lack of viable income alternatives. As investors reached for yield, the lower credit tiers outperformed, as measured by the high yield benchmark index, with CCCs, Bs, and BBs returning 25.55%, 13.52%, and 12.29% over the last nine months, and 16.12%, 11.29%, and 12.13% for the full fiscal year, respectively.

Fundamentals have weakened, particularly in the energy and metals & mining industries. As is consistent with the later stages of the credit cycle, leverage has crept up, cash as a percentage of debt has decreased, and the default rate has continued to climb. The default rate rose to 5.4% as of the end of the Fund’s fiscal year.

From a technical perspective, the high yield sector experienced considerable outflows during October to December 2015. A dramatic reversal occurred in mid-February and flows were mostly positive after that watershed event. Similarly, initially anemic issuance turned robust over the last three quarters of the fiscal year.

What factors affected the Fund’s performance during its fiscal year?

The positive performance of the U.S. high yield market contributed to the Fund’s positive return during the year.

The top contributors to the Fund’s performance during the year were issue selection, as well as some of our conscious overweights and underweights within certain industries. In particular, the portfolio benefited from issue selection within the cable-satellite, wireline, and supermarket industries, and our allocations to gaming and banking. Our allocation

and issue selection to electric utilities was also additive to performance.

A primary detractor from performance was higher quality bias. Our underweight to the energy and metals & mining industries helped performance early in the year. However, our relatively lower risk positioning held the Fund back after the mid-February rally. We added some risk to the portfolio and brought up our energy and metals & mining weightings, but we did not chase yields in the most downtrodden areas of the high yield sector where the bulk of performance occurred.

The preceding information is the opinion of portfolio management only through the end of the period stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objectives.

Credit & Interest: Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a debt security may fail to make interest and/or principal payments. Values of debt securities may rise or fall in response to changes in interest rates, and this risk may be enhanced with longer-term maturities.

High Yield-High Risk Fixed Income Securities: There is a greater level of credit risk and price volatility involved with high yield securities than investment grade securities.

Foreign Investing: Investing internationally involves additional risks such as currency, political, accounting, economic, and market risk.

Industry/Sector Concentration: A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

Prospectus: For additional information on risks, please see the fund’s prospectus.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

14

Table of Contents

| High Yield Fund (Continued) |

| Asset Allocation | ||||||||

The following table presents asset allocations within certain sectors as a percentage of total investments as of September 30, 2016.

|

| |||||||

Corporate Bonds and Notes | 82 | % | ||||||

Consumer Discretionary | 22 | % | ||||||

Energy | 13 | |||||||

Health Care | 11 | |||||||

Materials | 9 | |||||||

Telecommunication Services | 7 | |||||||

Financials | 6 | |||||||

Industrials | 6 | |||||||

All other Corporate Bonds and Notes | 8 | |||||||

Loan Agreements | 10 | |||||||

Other (includes short-term investments) | 8 | |||||||

|

| |||||||

Total | 100 | % | ||||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

15

Table of Contents

High Yield Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/16 | ||||||||||||||||||||

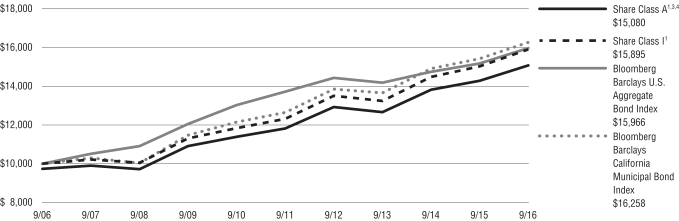

| 1 year | 5 years | 10 years | Since Inception | Inception Date | ||||||||||||||||

| Class A Shares at NAV2 | 10.59 | % | 7.73 | % | 5.33 | % | — | — | ||||||||||||

| Class A Shares at POP3,4 | 6.44 | 6.91 | 4.93 | — | — | |||||||||||||||

| Class B Shares at NAV2 | 9.52 | 6.91 | 4.54 | — | — | |||||||||||||||

| Class B Shares with CDSC4 | 5.52 | 6.91 | 4.54 | — | — | |||||||||||||||

| Class C Shares at NAV2 and with CDSC4 | 9.68 | 6.94 | 4.57 | — | — | |||||||||||||||

| Class I Shares at NAV2 | 10.86 | — | — | 5.71 | % | 8/8/12 | ||||||||||||||

| Bloomberg Barclays U.S. Aggregate Bond Index | 5.19 | 3.08 | 4.79 | 2.64 | 5 | — | ||||||||||||||

| Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index | 12.74 | 8.34 | 7.80 | 6.02 | 5 | — | ||||||||||||||

Fund Expense Ratios6: A Shares: Gross 1.33%, Net 1.16% B Shares: Gross 2.08%, Net 1.91% C Shares: Gross 2.08%, Net 1.91% Class I: Gross 1.08% Net 0.91%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 3.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for B shares decline from 5% to 0% over a five-year period. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter. |

| 5 | The since inception index returns are from the inception date of Class I. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2016, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by contractual fee waiver in effect through January 31, 2017. Gross Expense: Does not reflect the effect of the fee waiver. Expense ratios include fees and expenses associated with underlying funds. |

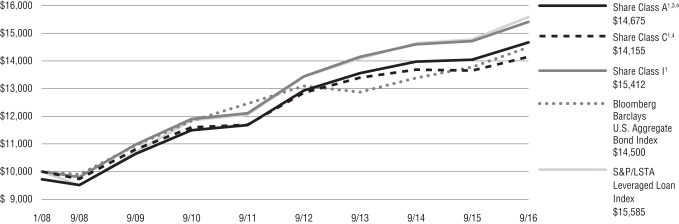

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on September 30, 2006, for Class A, Class B, and Class C shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

16

Table of Contents

Fund Summary | Ticker Symbols: A Share: HIMZX C Share: PCMZX I Share: HIBIX |

Portfolio Manager Commentary by Newfleet Asset Management, LLC

| ¢ | The Fund is diversified and has an investment objective to provide a high level of total return, including a competitive level of current income, while limiting fluctuations in net asset value due to changes in interest rates. |

| Effective September 23, 2016, the Virtus Low Duration Fund was reorganized as a series of Virtus Opportunities Trust and its fiscal year end changed from December 31 to September 30. As a result, the commentary addresses nine months of performance through September 30. |

| ¢ | For the fiscal period January 1, 2016, through September 30, 2016, the Fund’s Class A shares at NAV returned 3.25%*, Class C shares at NAV returned 2.67%* and Class I shares at NAV returned 3.44%*. For the same period, the Bloomberg Barclays U.S. Aggregate Bond Index, a broad-based fixed income index, returned 5.80%* and the Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index, which is the Fund’s style-specific benchmark appropriate for comparison, returned 4.23%*. |

| * | Returns less than 1 year are not annualized. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the market perform during the Fund’s nine- month fiscal period?

| ¢ | Most fixed income spread sectors outperformed U.S. Treasuries during the nine months ended September 30, 2016. The U.S. Federal Reserve’s (“the Fed”) dovish stance in mid-February sparked a rally that turned around a volatile time period that began with fresh concerns over China, plummeting oil prices, and fears that the Fed had raised interest rates too soon. |

| ¢ | Late in June volatility returned briefly with fallout from the U.K.’s unexpected decision to leave the European Union (“Brexit”). Bond yields in the U.S., Japan, and across Europe fell to historic lows in early July as investors fled to the safety of bonds |

on global growth concerns fueled by the June 23 Brexit vote. Markets recovered rather quickly, however, from the initial shock. Easing by major central banks and a weaker U.S. dollar helped to improve global risk sentiment and stabilize markets. |

| ¢ | September brought heightened concerns over the ability and willingness of global central banks to fight chronic low inflation and weak growth as the decision by the European Central Bank (“ECB”) to leave interest rates and its stimulus program unchanged was a precipitating factor in a widespread market sell-off, reinforced by fears that the Bank of Japan (“BOJ”) had run out of quantitative easing tools. Hawkish signals from the Fed added to the volatility. The BOJ subsequently decided not to reduce interest rates further but to shift its focus to stabilizing rates for longer maturity government bonds. This bolstered market sentiment, as did the Fed’s eventual decision to stand pat at its September monetary policy meeting. |

| ¢ | Over the last nine months, yields largely decreased for both shorter maturity and longer term U.S. Treasury bonds. |

What factors affected the Fund’s performance during the Fund’s nine-month fiscal period?

| ¢ | The underperformance of U.S. Treasuries relative to most fixed income spread sectors was the key driver of the Fund’s positive performance for the nine months ended September 30, 2016. |

| ¢ | The Fund’s allocation to corporate high yield securities was the largest positive contributor to performance during the nine month period. |

| ¢ | During the nine month period, the Fund’s allocation to asset-backed securities detracted from performance. |

The preceding information is the opinion of portfolio management only through the end of the period of the report as stated on the cover. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice.

There is no guarantee that the Fund will meet its objective.

ABS/MBS: Changes in interest rates can cause both extension and prepayment risks for asset- and mortgage-backed securities. These securities are also subject to risks associated with the repayment of underlying collateral.

Credit & Interest: Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a debt security may fail to make interest and/or principal payments. Values of debt securities may rise or fall in response to changes in interest rates, and this risk may be enhanced with longer-term maturities.

Foreign & Emerging Markets: Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.

High Yield-High Risk Fixed Income Securities: There is a greater level of credit risk and price volatility involved with high yield securities than investment grade securities.

Prospectus: For additional information on risks, please see the fund’s prospectus.

| Asset Allocation | ||||||||

The following table presents asset allocations within certain sectors as a percentage of total investments at September 30, 2016.

|

| |||||||

Mortgage-Backed Securities | 41 | % | ||||||

Asset-Backed Securities | 24 | |||||||

Corporate Bonds and Notes | 18 | |||||||

Financials | 7 | % | ||||||

Industrials | 2 | |||||||

Health Care | 2 | |||||||

Total of all others | 7 | |||||||

U.S. Government Securities | 10 | |||||||

Loan Agreements | 4 | |||||||

Other | 3 | |||||||

|

| |||||||

Total |

| 100 | % | |||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

17

Table of Contents

Low Duration Income Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/16 | ||||||||||||

| 1 year | 5 years | 10 years | ||||||||||

| Class A Shares at NAV2 | 2.78 | % | 2.71 | % | 3.82 | % | ||||||

| Class A Shares at POP3,4 | 0.47 | 2.24 | 3.58 | |||||||||

| Class C Shares at NAV2 and CDSC4 | 2.01 | 1.94 | 3.05 | |||||||||

| Class I Shares at NAV2 | 3.14 | 2.97 | 4.08 | |||||||||

| Bloomberg Barclays U.S. Aggregate Bond Index | 5.19 | 3.08 | 4.79 | |||||||||