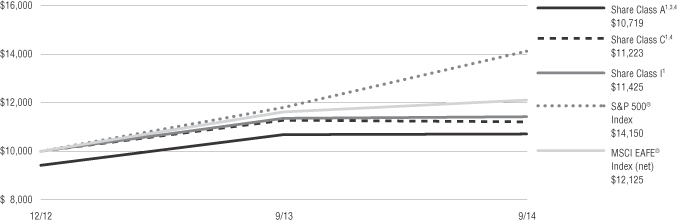

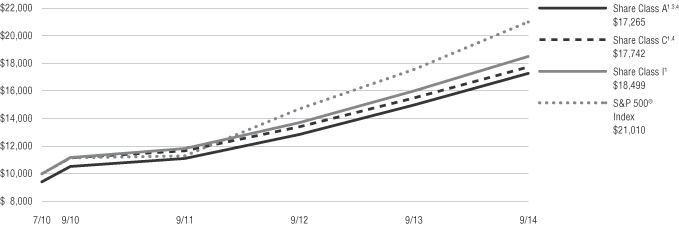

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07455

Virtus Opportunities Trust

(Exact name of registrant as specified in charter)

101 Munson Street

Greenfield, MA 01301-9668

(Address of principal executive offices) (Zip code)

Kevin J. Carr, Esq.

Vice President, Chief Legal Officer, Counsel and Secretary for Registrant

100 Pearl Street

Hartford, CT 06103-4506

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 243-1574

Date of fiscal year end: September 30

Date of reporting period: September 30, 2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Table of Contents

ANNUAL REPORT

Virtus Bond Fund

Virtus CA Tax-Exempt Bond Fund

Virtus High Yield Fund

Virtus Low Volatility Equity Fund

Virtus Multi-Sector Intermediate Bond Fund

Virtus Senior Floating Rate Fund

Virtus Wealth Masters Fund

September 30, 2014 TRUST NAME: VIRTUS OPPORTUNITIES TRUST |

|

Not FDIC Insured

No Bank Guarantee

May Lose Value

Table of Contents

| 1 | ||||||||

| 2 | ||||||||

| 4 | ||||||||

| Fund | Fund Summary | Schedule of Investments | ||||||

| 6 | 21 | |||||||

| 8 | 28 | |||||||

| 11 | 30 | |||||||

Virtus Low Volatility Equity Fund (“Low Volatility Equity Fund”) | 13 | 36 | ||||||

Virtus Multi-Sector Intermediate Bond Fund (“Multi-Sector Intermediate Bond Fund”) | 15 | 37 | ||||||

Virtus Senior Floating Rate Fund (“Senior Floating Rate Fund”) | 17 | 46 | ||||||

| 19 | 53 | |||||||

| 55 | ||||||||

| 57 | ||||||||

| 59 | ||||||||

| 63 | ||||||||

| 68 | ||||||||

| 80 | ||||||||

| 81 | ||||||||

| 82 | ||||||||

Proxy Voting Procedures and Voting Record (Form N-PX)

The subadvisers vote proxies relating to portfolio securities in accordance with procedures that have been approved by the Board of Trustees of the Trust (“Trustees,” or the “Board”). You may obtain a description of these procedures, along with information regarding how the Funds voted proxies during the most recent 12-month period ended June 30, free of charge, by calling toll-free 1-800-243-1574. This information is also available through the Securities and Exchange Commission’s (the “SEC”) website at http://www.sec.gov.

Form N-Q Information

The Trust files a complete schedule of portfolio holdings for each Fund with the SEC for the first and third quarters of each fiscal year on Form N-Q. Form N-Q is available on the SEC’s website at http://www.sec.gov. Form N-Q may be reviewed and copied at the SEC’s Public Reference Room. Information on the operation of the SEC’s Public Reference Room can be obtained by calling toll-free 1-800-SEC-0330.

This report is not authorized for distribution to prospective investors in the Funds presented in this book unless preceded or accompanied by an effective prospectus which includes information concerning the sales charge, each Fund’s record and other pertinent information.

Table of Contents

Dear Fellow Shareholders of Virtus Mutual Funds:

| I am pleased to present this annual report which highlights performance of your fund for the 12 months ended September 30, 2014, including comments from the money manager.

The past 12 months were generally strong for equities, although market volatility increased over the last quarter, driven by geopolitical risks and a slowdown in the global economy. While the economies of Europe, Japan, and China weakened, the U.S. economy accelerated and the U.S. dollar rallied strongly. Broad U.S. equity indexes registered double-digit gains for the 12 months ended September 30, 2014. The S&P 500® Index returned 19.73%, the Dow Jones Industrial Average rose 15.29%, and the NASDAQ | |

Composite Index® was up 20.61%. By comparison, international equity returns were significantly smaller, including for both developed markets and emerging markets.

In mid-September, the Federal Reserve provided much needed assurance to investors by announcing that it intends to keep interest rates low for a “considerable time” after its bond buying program ends in October. Against this backdrop, the bellwether 10-year U.S. Treasury yield ended at 2.52% on September 30, 2014 compared with 2.64% a year earlier. The broader fixed income market, as measured by the Barclays U.S. Aggregate Bond Index, rose 3.96% for the 12 months ended September 30, 2014.

The uncertain state of the global economy is likely to remain a concern for markets in the months ahead. However, the health of the U.S. economy – including improving hiring, manufacturing, and housing data – gives investors reason for optimism. Future market direction will be determined largely by the ability of corporations to continue to produce robust earnings.

Market volatility is an ever-present reminder of the importance of portfolio diversification. While diversification cannot guarantee a profit or prevent loss, owning a variety of asset classes may cushion your portfolio against inevitable market fluctuations. Your financial advisor can help you ensure that your portfolio is adequately diversified across asset classes and investment strategies.

As always, thank you for entrusting Virtus with your assets. Should you have questions or require assistance, our customer service team is here to help at 1-866-270-7788. We appreciate your business and remain committed to your long-term financial success.

Sincerely,

George R. Aylward President, Virtus Mutual Funds

October 2014 | ||

Whenever you have questions about your account, or require additional information, please visit us on the Web at www.virtus.com or call our shareowner service group toll-free at 1-800-243-1574.

Performance data quoted represents past results. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above.

1

Table of Contents

VIRTUS OPPORTUNITIES TRUST

Disclosure of Fund Expenses (Unaudited)

For the six-month period of April 1, 2014 to September 30, 2014

We believe it is important for you to understand the impact of costs on your investment. All mutual funds have operating expenses. As a shareholder of a Virtus Opportunities Trust Fund (each, a “Fund”) you may incur two types of costs: (1) transaction costs, including sales charges on purchases of Class A shares and contingent deferred sales charges on Class B and Class C shares; and (2) ongoing costs, including investment advisory fees, distribution and service fees, and other expenses. Class I shares are sold without sales charges. For further information regarding applicable sales charges, see Note 1 in the Notes to Financial Statements. These examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. These examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period. The following Expense Table illustrates your Fund’s costs in two ways.

Actual Expenses

The first section of the accompanying table provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your Fund under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second section of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not your Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the accompanying table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges or contingent deferred sales charges. Therefore, the second section of the accompanying table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

| Expense Table | ||||||||||||||||

| Beginning Account Value April 1, 2014 | Ending Account Value September 30, 2014 | Annualized Expense Ratio | Expenses Paid During the Period* | |||||||||||||

Bond Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,018.10 | 0.85 | % | $4.30 | |||||||||

Class B | 1,000.00 | 1,013.80 | 1.60 | 8.08 | ||||||||||||

Class C | 1,000.00 | 1,014.70 | 1.60 | 8.08 | ||||||||||||

Class I | 1,000.00 | 1,019.10 | 0.60 | 3.04 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,020.75 | 0.85 | 4.32 | ||||||||||||

Class B | 1,000.00 | 1,016.95 | 1.60 | 8.12 | ||||||||||||

Class C | 1,000.00 | 1,016.95 | 1.60 | 8.12 | ||||||||||||

Class I | 1,000.00 | 1,022.02 | 0.60 | 3.05 | ||||||||||||

CA Tax Exempt Bond Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,049.70 | 0.85 | % | $4.37 | |||||||||

Class I | 1,000.00 | 1,050.20 | 0.60 | 3.08 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,020.75 | 0.85 | 4.32 | ||||||||||||

Class I | 1,000.00 | 1,022.02 | 0.60 | 3.05 | ||||||||||||

High Yield Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,005.70 | 1.15 | % | $5.78 | |||||||||

Class B | 1,000.00 | 1,002.10 | 1.90 | 9.54 | ||||||||||||

Class C | 1,000.00 | 1,002.00 | 1.90 | 9.54 | ||||||||||||

Class I | 1,000.00 | 1,009.30 | 0.90 | 4.53 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,019.23 | 1.15 | 5.84 | ||||||||||||

Class B | 1,000.00 | 1,015.42 | 1.90 | 9.65 | ||||||||||||

Class C | 1,000.00 | 1,015.42 | 1.90 | 9.65 | ||||||||||||

Class I | 1,000.00 | 1,020.50 | 0.90 | 4.57 | ||||||||||||

Low Volatility Equity Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,045.50 | | 1.55 | % | | $7.95 | | ||||||

Class C | 1,000.00 | 1,042.10 | 2.30 | 11.77 | ||||||||||||

Class I | 1,000.00 | 1,046.40 | 1.30 | 6.67 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,017.20 | 1.55 | 7.87 | ||||||||||||

Class C | 1,000.00 | 1,013.39 | 2.30 | 11.68 | ||||||||||||

Class I | 1,000.00 | 1,018.47 | 1.30 | 6.60 | ||||||||||||

Multi-Sector Intermediate Bond Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,013.50 | 1.11 | % | $5.60 | |||||||||

Class B | 1,000.00 | 1,008.80 | 1.86 | 9.37 | ||||||||||||

Class C | 1,000.00 | 1,009.60 | 1.86 | 9.37 | ||||||||||||

Class I | 1,000.00 | 1,014.80 | 0.86 | 4.34 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,019.43 | 1.11 | 5.63 | ||||||||||||

Class B | 1,000.00 | 1,015.63 | 1.86 | 9.44 | ||||||||||||

Class C | 1,000.00 | 1,015.63 | 1.86 | 9.44 | ||||||||||||

Class I | 1,000.00 | 1,020.70 | 0.86 | 4.37 | ||||||||||||

2

Table of Contents

VIRTUS OPPORTUNITIES TRUST

Disclosure of Fund Expenses (Unaudited) (Continued)

For the six-month period of April 1, 2014 to September 30, 2014

| Expense Table | ||||||||||||||||

| Beginning Account Value April 1, 2014 | Ending Account Value September 30, 2014 | Annualized Expense Ratio | Expenses Paid During the Period* | |||||||||||||

Senior Floating Rate Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,002.30 | 1.19 | % | $5.97 | |||||||||

Class C | 1,000.00 | 998.50 | 1.94 | 9.72 | ||||||||||||

Class I | 1,000.00 | 1,003.60 | 0.94 | 4.72 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,019.03 | 1.19 | 6.04 | ||||||||||||

Class C | 1,000.00 | 1,015.22 | 1.94 | 9.85 | ||||||||||||

Class I | 1,000.00 | 1,020.30 | 0.94 | 4.77 | ||||||||||||

Wealth Masters Fund |

| |||||||||||||||

Actual | ||||||||||||||||

Class A | $ | 1,000.00 | $ | 1,005.50 | 1.45 | % | $7.29 | |||||||||

Class C | 1,000.00 | 1,002.10 | 2.20 | 11.04 | ||||||||||||

Class I | 1,000.00 | 1,006.90 | 1.20 | 6.04 | ||||||||||||

Hypothetical (5% return before expenses) |

| |||||||||||||||

Class A | 1,000.00 | 1,017.71 | 1.45 | 7.36 | ||||||||||||

Class C | 1,000.00 | 1,013.90 | 2.20 | 11.17 | ||||||||||||

Class I | 1,000.00 | 1,018.98 | 1.20 | 6.09 | ||||||||||||

| * | Expenses are equal to the relevant Funds’ annualized expense ratio, which is net of waived fees and reimbursed expenses, if applicable, multiplied by the average account value over the period, multiplied by the number of days (183) expenses were accrued in the most recent fiscal half-year, then divided by 365 to reflect the one-half year period. |

For Funds which may invest in other funds, the annualized expense ratios noted above do not reflect fees and expenses associated with the underlying funds. If such fees and expenses had been included, the expenses would have been higher.

You can find more information about the Funds’ expenses in the Financial Statements section that follows. For additional information on operating expenses and other shareholder costs, refer to the prospectus.

3

Table of Contents

American Depositary Receipt (ADR)

Represents shares of foreign companies traded in U.S. dollars on U.S. exchanges that are held by a U.S. bank or a trust. Foreign companies use ADRs in order to make it easier for Americans to buy their shares.

Barclays California Municipal Bond Index

The Barclays California Municipal Bond Index measures long term investment grade, tax-exempt and fixed rate bonds issued in California. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges, and it is not available for direct investment.

Barclays High Yield 2% Issuer Capped Bond Index

The Barclays High-Yield 2% Issuer Capped Bond Index is a market capitalization-weighted index that measures fixed rate non-investment grade debt securities of U.S. and non-U.S. corporations. No single issuer accounts for more than 2% of market cap. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges, and it is not available for direct investment.

Barclays U.S. Aggregate Bond Index

The Barclays U.S. Aggregate Bond Index measures the U.S. investment grade fixed rate bond market. The index is calculated on a total return basis. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges, and it is not available for direct investment.

Dow Jones Industrial Average

A price weighted average of 30 blue chip stocks. The index is calculated on total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges, and it is not available for direct investment.

Exchange-Traded Funds (ETF)

Portfolios of stocks or bonds that track a specific market index.

Federal Reserve (the “Fed”)

The Central Bank of the United States, responsible for controlling the money supply, interest rates and credit with the goal of keeping the U.S. economy and currency stable. Governed by a seven-member board, the system includes 12 regional Federal Reserve Banks, 25 branches and all national and state banks that are part of the system.

Horizon Kinetics ISE Wealth Index (RCH)

Is a public index published by International Securities Exchange, LLC. The index is composed of companies with wealthy individuals in positions of influence or control who have a substantial amount of their personal wealth invested in the business. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges, and it is not available for direct investment.

iShares®

Represents shares of an open-end exchange-traded fund.

NASDAQ Composite Index®

A market-capitalization weighted index of the more than 3,000 common equities listed on the Nasdaq stock exchange. Unlike other market indexes, the NASDAQ composite is not limited to companies that have U.S. headquarters. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges and it is not available for direct investment.

Payment-in-Kind Security (PIK)

A bond which pays interest in the form of additional bonds, or preferred stock which pays dividends in the form of additional preferred stock.

Real Estate Investment Trust (REIT)

A publicly traded company that owns, develops and operates income-producing real estate such as apartments, office buildings, hotels, shopping centers and other commercial properties.

4

Table of Contents

KEY INVESTMENT TERMS (Continued)

Russell 2000® Index

The Russell 2000® Index is a market capitalization-weighted index that measures the performance of the smallest 2,000 companies in the Russell Universe which comprises the 3,000 largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges and it is not available for direct investment.

S&P 100® Index

The S&P 100 Index, a sub-set of the S&P 500®, measures the performance of large-cap U.S. companies, and comprises 100 major, blue chip companies across multiple industry groups.

S&P 500® Index

The S&P 500® Index is a free-float market capitalization-weighted index of 500 of the largest U.S. companies. The index is calculated on a total return basis with dividends reinvested. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges, and it is not available for direct investment.

S&P/LSTA Leveraged Loan Index

The S&P/LSTA Leveraged Loan Index is a daily total return index that uses LSTA/LPC Mark-to-Market Pricing (third-party research data on the price movements of senior secured floating rate loans in the secondary loan market) to calculate market value change. On a real-time basis, the Index tracks the current outstanding balance and spread over LIBOR for fully funded term loans. The facilities included in the Index represent a broad cross section of leveraged loans syndicated in the United States, including dollar-denominated loans to overseas issuers. The index is unmanaged, its returns do not reflect any fees, expenses or sales charges and it is not available for direct investment.

Sponsored ADR (American Depositary Receipt)

An ADR which is issued with the cooperation of the company whose stock will underlie the ADR. Sponsored ADRs generally carry the same rights normally given to stock holders, such as voting rights. ADRs must be sponsored to be able to trade on a major U.S. exchange such as the New York Stock Exchange (NYSE).

When-issued and Forward Commitments (Delayed Delivery)

Securities purchased on a when-issued or forward commitment basis are also known as delayed delivery transactions. Delayed delivery transactions involve a commitment by a Fund to purchase or sell a security at a future date, ordinarily up to 90 days later. When-issued or forward commitments enable a Fund to lock in what is believed to be an attractive price or yield on a particular security for a period of time, regardless of future changes in interest rates.

5

Table of Contents

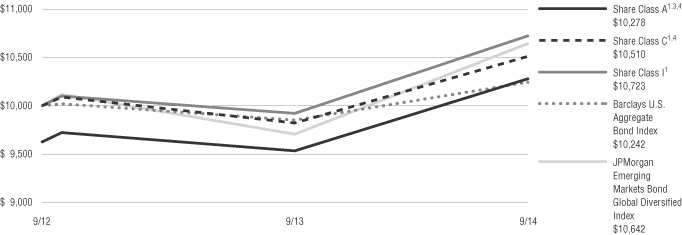

Bond Fund

Fund Summary | Ticker Symbols: Class A: SAVAX Class B: SAVBX Class C: SAVCX Class I: SAVYX |

| ¢ | The Fund is diversified and has an investment objective of high total return from both current income and capital appreciation. |

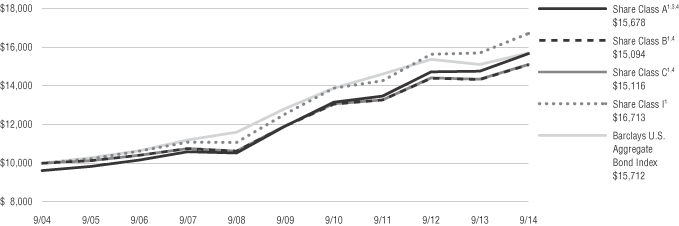

| ¢ | For the fiscal year ended September 30, 2014, the Fund’s Class A shares at NAV returned 6.18%, Class B shares returned 5.27%, Class C shares returned 5.34%, and Class I shares returned 6.35%. For the same period, the Barclays U.S. Aggregate Bond Index, which serves as the broad-based and style-specific benchmark index appropriate for comparison, returned 3.96%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s fiscal year?

| ¢ | Most spread sectors outperformed U.S. Treasuries during the fiscal year. Economic growth in the U.S. improved, but the level of growth remains moderate, which is supportive of fixed income spread sectors. The economy continues to be tempered by a lack of wage growth. This, when combined with slow global growth, concern over a stronger U.S. dollar, and a lack of inflation across the globe, will likely keep the Fed from raising short-term interest rates in the immediate future. Over the fiscal year, spread sectors were supported by an overall improvement in the U.S. macroeconomic environment, positive credit fundamentals, and continued demand for spread product. |

| ¢ | Globally, concerns over slowing growth in China and Europe, as well as increased geopolitical risks stemming from tensions between Ukraine and Russia and the escalation of issues in the Middle East have weighed on the fixed income markets. The global markets were also unsettled over the likelihood that the Fed would raise short-term interest rates sooner than anticipated due to stronger U.S. growth. |

| ¢ | The Fed continued to taper its monthly bond purchases with the expectation that it would be ending its stimulus program during the fourth quarter of 2014. However, the Central Bank has also |

acknowledged that signs of weakness remain in the U.S. economy, and has indicated that short-term rates will remain low in the near term and any future decision on rates will be driven by economic data. |

| ¢ | Over the last 12 months, yields increased at the short maturity end of the U.S. Treasury curve and decreased on the long maturity end, and overall the yield curve flattened. |

What factors affected the Fund’s performance during its fiscal year?

| ¢ | The outperformance of fixed income spread sectors relative to U.S. Treasuries was the key driver of the Fund’s strong performance for the fiscal year. |

| ¢ | The Fund’s allocation to the corporate high yield and corporate high quality sectors made positive contributions to performance for the fiscal year. |

| ¢ | During the fiscal year, the Fund’s allocation to the non-U.S. dollar sector and non-agency commercial mortgage- backed securities detracted from performance. |

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities. Changes in interest rates can cause both extension and prepayment risks for asset and mortgage-backed securities. These securities are also subject to risks associated with the repayment of underlying collateral. Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk. There is a greater level of credit risk and price volatility involved with high-yield securities than investment grade securities.

| Asset Allocation | ||||||||

The following table presents asset allocations within certain sectors and as a percentage of total investments as of September 30, 2014.

|

| |||||||

Corporate Bonds and Notes | 54 | % | ||||||

Financials | 22 | % | ||||||

Energy | 7 | |||||||

Consumer Discretionary | 6 | |||||||

All other Corporate Bonds and Notes | 19 | |||||||

Mortgage-Backed Securities | 21 | |||||||

Loan Agreements | 8 | |||||||

Asset-Backed Securities | 5 | |||||||

Foreign Government Securities | 5 | |||||||

Preferred Stocks | 3 | |||||||

Other (includes short-term investments) | 4 | |||||||

|

| |||||||

Total | 100 | % | ||||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

6

Table of Contents

Bond Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/14 | ||||||||||||

| 1 year | 5 years | 10 years | ||||||||||

| Class A Shares at NAV2 | 6.18 | % | 5.63 | % | 5.00 | % | ||||||

| Class A Shares at POP3 | 2.20 | 4.82 | 4.60 | |||||||||

| Class B Shares at NAV2 | 5.27 | 4.82 | 4.20 | |||||||||

| Class B Shares with CDSC4 | 1.27 | 4.82 | 4.20 | |||||||||

| Class C Shares at NAV2 and with CDSC4 | 5.34 | 4.84 | 4.22 | |||||||||

| Class I Shares at NAV | 6.35 | 5.89 | 5.27 | |||||||||

| Barclays U.S. Aggregate Bond Index | 3.96 | 4.12 | 4.62 | |||||||||

Fund Expense Ratios5: A Shares: Gross 1.06%, Net 0.85%; B Shares: Gross 1.81%, Net 1.60%; C Shares: Gross 1.81%, Net 1.60%; I Shares: Gross 0.81%, Net 0.60%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 3.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for B shares decline from 5% to 0% over a five-year period. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter. |

| 5 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2014, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by voluntary fee waiver which may be discontinued at any time. Gross Expense: Does not reflect the effect of the fee waiver. |

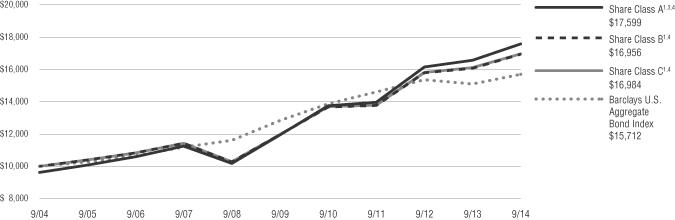

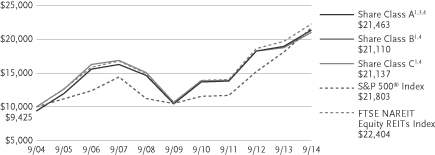

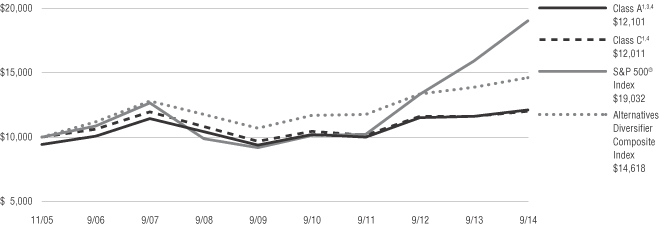

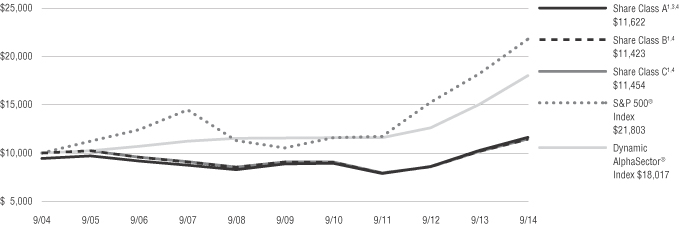

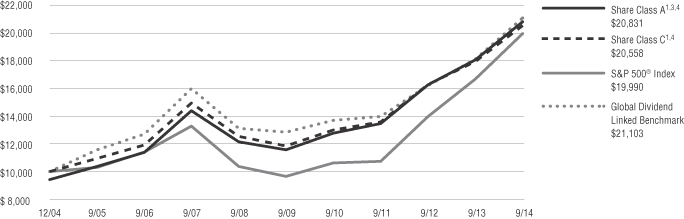

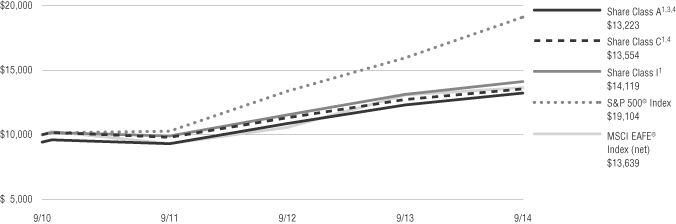

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on September 30, 2004, for Class A, Class B, Class C, and Class I shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

7

Table of Contents

Fund Summary | Ticker Symbols: Class A: CTESX Class I: CTXEX |

| ¢ | The Fund is diversified and has an investment objective of obtaining a high level of current income exempt from California state and local income taxes, as well as federal income tax, consistent with the preservation of capital. |

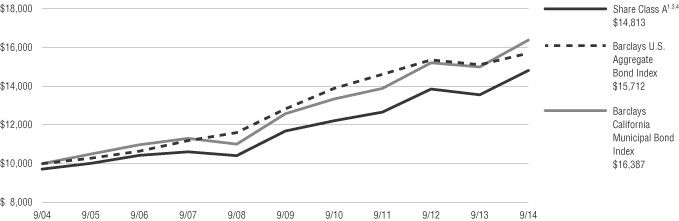

| ¢ | For the fiscal year ended September 30, 2014, the Fund’s Class A shares at NAV returned 9.16% and Class I shares returned 9.36%. For the same period, the Barclays U.S. Aggregate Bond Index, a broad-based fixed income index, returned 3.96%, and the Barclays California Municipal Bond Index, the Fund’s style-specific benchmark appropriate for comparison, returned 9.20%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s fiscal year?

The municipal bond market experienced strong performance over the past 12 months, as AAA-rated tax-free interest rates declined by 37 basis points on 10-year maturities, and by over 100 basis points on 30-year maturities, according to Municipal Market Data. The result of this decline in tax-free interest rates was an increase in the principal value of tax-free municipal bonds, including the bonds in the Virtus California Tax-Exempt Bond Fund. Several factors contributed to the decline in rates over the past year:

| ¢ | Declining U.S. Treasury bond yields driven by economic uncertainty and global tensions |

| ¢ | Reversal of flows into open-end municipal bond mutual funds after record outflows in 2013 |

| ¢ | Substantial decline in the issuance of municipal bonds |

Aided by these strong technical conditions, the municipal market produced a solid 9.20% return over the 12-month period as measured by the Barclays California Municipal Bond Index.

According to the Investment Company Institute (ICI), open-end municipal bond mutual funds have experienced over $15 billion of net inflows through the first nine months of 2014, following $58 billion of

outflows in 2013. Riskier high yield municipal funds have been the beneficiary of much of this year’s inflows, as investor appetite for higher yields, in a declining interest rate environment, is quite strong. In addition to buyers of mutual funds, the market is experiencing strong demand for municipal bonds from other buyers such as retail investors buying individual bonds, separately managed accounts, and banks and insurance companies.

Issuance of new municipal bonds was lower by 10% through September 30, 2014, compared to the same time period in 2013. This lower issuance has been driven by, among other things, fiscal austerity on the part of municipalities, lower levels of refunding deals (after experiencing elevated levels of refundings in 2011- 2013), and a higher percentage of issuers borrowing directly from banks (thus bypassing the public debt markets). In fact, direct lending to municipalities exceeded $40 billion in 2013, which was close to 15% of the market’s municipal bond issuance for the year. This meaningful reduction in the issuance of municipal bonds, combined with a reversal in fund flows, has improved the balance of supply and demand, thereby helping bond prices to rise.

Credit fundamentals for municipal bond issuers have generally moderated across the country, although some states are faring much better than others. Revenues have been slowing at both state and local levels, mostly as a result of lower personal income tax collections. Instead of spending to address aging infrastructure, many municipalities are choosing to implement austerity measures to bring their expenses in line with revenues. While infrastructure is a growing concern among voters, there appears to be little support to meaningfully increase the funding for it. With 36 states casting ballots for new governors in the upcoming midterm elections, it is unlikely the market will see any large-scale changes in municipality spending and increased bond issuance. An issue of particular focus for credit rating agencies is pension funding levels and the ability for states to maintain sustainable budgets. Despite positive assessments for some municipalities, this has not been consistent across the board. Downgrades exceed upgrades, as pensions and other increased fixed costs continue to strain local government budgets. This is one example of why credit selection is a critical component to investing in the municipal bond market.

What factors affected the Fund’s performance during its fiscal year?

Relative portfolio performance was impacted by the exposure to short- to intermediate-term holdings, bonds with shorter call options, and higher quality issues.

Relative portfolio performance benefited from exposure to long maturity bonds, healthcare issues, lower quality issues, and zero coupon securities.

Over the past 12 months, the market’s best performers have been longer duration, lower coupon, and lower credit quality bonds as interest rates have declined and risk premiums have narrowed. While still producing positive performance, bonds will shorter maturities, lower duration, and higher coupons and credit quality have performed relatively weaker.

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities. A fund that focuses its investments in a particular geographic location will be highly sensitive to financial, economic, political, and other developments affecting the fiscal stability of that location. Events negatively impacting a municipal security, or the municipal bond market in general, may cause the fund to decrease in value. A portion of income may be subject to some state and/or local taxes and, for certain investors, a portion may be subject to the federal alternative minimum tax.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

8

Table of Contents

| CA Tax-Exempt Bond Fund (Continued) |

| Asset Allocation | ||||||||

The following table presents asset allocations within certain sectors and as a percentage of total investments as of September 30, 2014.

|

| |||||||

Tax-Exempt Municipal Bonds | 100 | % | ||||||

General Revenue | 27 | % | ||||||

General Obligation | 20 | |||||||

Pre-Refunded | 13 | |||||||

Water & Sewer Revenue | 7 | |||||||

Development Revenue | 6 | |||||||

Medical Revenue | 6 | |||||||

Transportation Revenue | 6 | |||||||

Other | 15 | |||||||

|

| |||||||

Total | 100 | % | ||||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

9

Table of Contents

CA Tax-Exempt Bond Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/14 | ||||||||||||||||||||

| 1 year | 5 years | 10 years | Since Inception | Inception Date | ||||||||||||||||

| Class A Shares at NAV2 | 9.16 | % | 4.84 | % | 4.30 | % | — | — | ||||||||||||

| Class A Shares at POP3,4 | 6.16 | 4.25 | 4.01 | — | — | |||||||||||||||

| Class I Shares at NAV | 9.36 | 5.09 | — | 4.73 | % | 9/29/06 | ||||||||||||||

| Barclays U.S. Aggregate Bond Index | 3.96 | 4.12 | 4.62 | 4.97 | 5 | — | ||||||||||||||

| Barclays California Municipal Bond Index | 9.20 | 5.41 | 5.06 | 5.12 | 5 | — | ||||||||||||||

Fund Expense Ratios6: A Shares: Gross 1.03%, Net 0.85%; I Shares: Gross 0.78%, Net 0.60%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 2.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid are 1% and 0% thereafter. |

| 5 | The since inception index returns are from the inception date of Class I. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2014, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by voluntary fee waiver which may be discontinued at any time. Gross Expense: Does not reflect the effect of the fee waiver. |

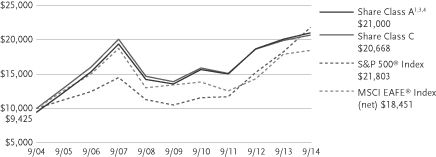

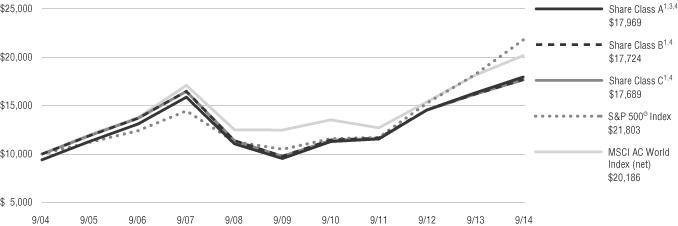

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on September 30, 2004 for Class A shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

10

Table of Contents

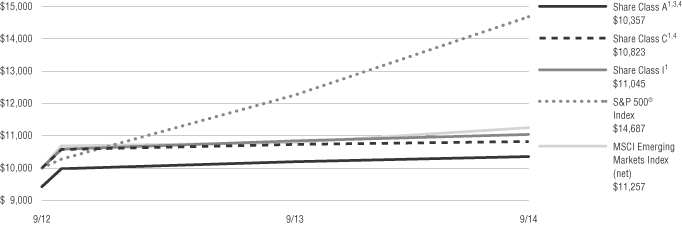

Fund Summary | Ticker Symbols: Class A: PHCHX Class B: PHCCX Class C: PGHCX Class I: PHCIX |

| ¢ | The Fund is diversified and has a primary investment objective of high current income and a secondary objective of capital growth. |

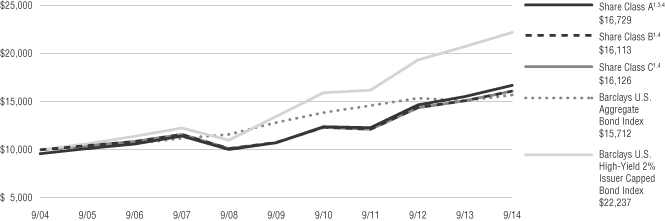

| ¢ | For the fiscal year ended September 30, 2014, the Fund’s Class A shares at NAV returned 7.53%, Class B shares returned 6.68%, and Class C shares returned 6.60%. Class I shares returned 7.80%. For the same period, the Barclays U.S. Aggregate Bond Index, a broad-based fixed income index, returned 3.96%, and the Barclays U.S. High-Yield 2% Issuer Capped Bond Index, the Fund‘s style-specific index appropriate for comparison, returned 7.19%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the market perform during the Fund’s fiscal year?

| ¢ | The U.S. high yield market, as measured by the Barclays High Yield 2% Issuer Capped Bond Index, delivered a 7.19% return for the fiscal year ended September 30, 2014. The streak of consecutive months of positive returns was broken at nine months as volatility increased heading into July. The last three months of the fiscal year saw rather large swings in returns as they turned decidedly negative in July, flipping back to positive in August and finally back to negative in September. The decrease in interest rates over the year helped BB-rated bonds, which tend to have a longer duration, outperform B and CCC-rated bonds. Only a handful of industries actually posted negative returns over the year compared to others such as paper, brokerages, environmental services, wirelines, tobacco, electric utility, insurance, and pipelines which posted double-digit returns. |

| ¢ | In the past, high yield investors have been rewarded during similar stages within a given credit cycle by taking on credit risk. Even though fundamentals have remained solid and defaults remain low relative to historical averages, a blind beta grab of buying any and all CCC bonds has not led to significant outperformance. This fiscal year has been dominated by the unexpected decline in |

interest rates, which has actually helped BBs take the crown as the high yield market’s best performing credit tier. |

| ¢ | Fundamentals remained strong as high yield issuers maintained leverage ratios below those seen right before the last increase in the default rate which happened to be a precursor for the 2008 financial crisis. On the technical side, flows were volatile over the fiscal year, starting out positive for most of the first three quarters and then turned decidedly negative during the fourth quarter. New issuance continued to be robust over the year as companies continued to take advantage of historically low interest rates. Companies have been wise to term out the debt within their capital structures with interest cost savings driving the interest coverage ratio to historical highs for the high yield universe. |

What factors affected the Fund’s performance during its fiscal year?

| ¢ | The strong performance of the high yield sector significantly contributed to the Fund’s positive return for the year. |

| ¢ | The positive contributors to the Fund’s performance during the year were the issue selection within high yield, along with some of our conscientious overweights/underweights within certain industries. The Fund benefited from strong issue selection within health care and technology, which were two of the three most overweight industries within the Fund. The Fund also made a conscious bet to be significantly underweight the metals & mining industry, which added alpha to the portfolio as it continued to underperform with weak economic data flowing out of China. |

| ¢ | The detractors from Fund performance were poor issue selection within the portfolio’s retailer exposure, as well as not having enough exposure within the pipelines industry which was a significant outperformer during the year. |

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objectives.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities. There is a greater level of credit risk and price volatility involved with high-yield securities than investment grade securities. Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk. A fund that focuses its investments in a particular industry or sector will be more sensitive to conditions that affect that industry or sector than a non-concentrated fund.

| Asset Allocation | ||||||||

The following table presents asset allocations within certain sectors as a percentage of total investments as of September 30, 2014.

|

| |||||||

Corporate Bonds and Notes | 79 | % | ||||||

Consumer Discretionary | 18 | % | ||||||

Energy | 11 | |||||||

Financials | 10 | |||||||

Health Care | 9 | |||||||

Materials | 8 | |||||||

Telecommunication Services | 7 | |||||||

Industrials | 6 | |||||||

All other Corporate Bonds and Notes | 10 | |||||||

Loan Agreements | 16 | |||||||

Other (includes short-term investments) | 5 | |||||||

|

| |||||||

Total | 100 | % | ||||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

11

Table of Contents

High Yield Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/14 | ||||||||||||||||||||

| 1 year | 5 years | 10 years | Since Inception | Inception Date | ||||||||||||||||

| Class A Shares at NAV2 | 7.53 | % | 9.23 | % | 5.68 | % | — | — | ||||||||||||

| Class A Shares at POP3,4 | 3.50 | 8.40 | 5.28 | — | — | |||||||||||||||

| Class B Shares at NAV2 | 6.68 | 8.40 | 4.89 | — | — | |||||||||||||||

| Class B Shares with CDSC4 | 2.61 | 8.40 | 4.89 | — | — | |||||||||||||||

| Class C Shares at NAV2 and with CDSC4 | 6.60 | 8.38 | 4.89 | — | — | |||||||||||||||

| Class I Shares at NAV2 | 7.80 | — | — | 7.70 | % | 8/8/12 | ||||||||||||||

| Barclays U.S. Aggregate Bond Index | 3.96 | 4.12 | 4.62 | 1.34 | 5 | — | ||||||||||||||

| Barclays U.S. High-Yield 2% Issuer Capped Bond Index | 7.19 | 10.52 | 8.32 | 7.60 | 5 | — | ||||||||||||||

Fund Expense Ratios6: A Shares: Gross 1.30%, Net 1.15% B Shares: Gross 2.05%, Net 1.90% C Shares: Gross 2.05%, Net 1.90% Class I: Gross 1.05% Net 0.90%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 3.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for B shares decline from 5% to 0% over a five-year period. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter. |

| 5 | The since inception index returns are from the inception date of Class I. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2014, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by voluntary fee waiver which may be discontinued at any time. Gross Expense: Does not reflect the effect of the fee waiver. |

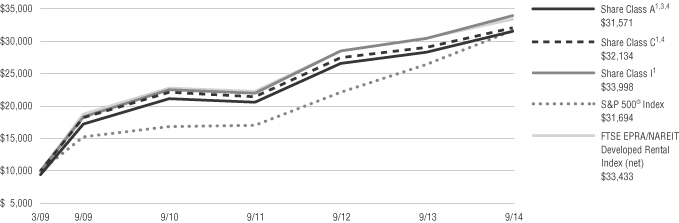

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on September 30, 2004, for Class A, Class B, and Class C shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

12

Table of Contents

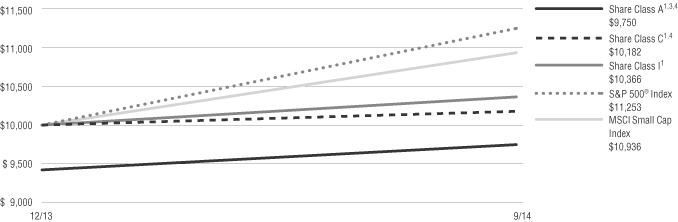

Fund Summary | Ticker Symbols: Class A: VLVAX Class C: VLVIX Class I: VLVCX |

| ¢ | The Fund is diversified and has an investment objective of capital appreciation with lower volatility than U.S. equity markets over a full market cycle. |

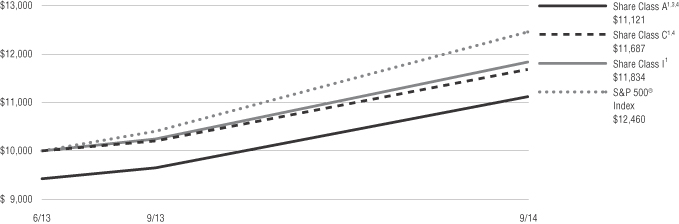

| ¢ | For the fiscal year ended September 30, 2014, the Fund’s Class A shares at NAV returned 15.23%, Class C shares returned 14.47%, and Class I shares returned 15.45%. For the same period, the S&P 500® Index, a broad-based fixed equity index, and the Fund’s style-specific benchmark appropriate for comparison returned 19.73%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s fiscal year?

| ¢ | In the fourth quarter of 2013, capital markets continued to experience strong performance as they had seen throughout the year. Concerns over a government shutdown eased around a federal debt deal, and the S&P 500® Index was up 10.49% during the period. The S&P 500® Index remained strong during the first nine months of 2014, briefly pulling back in January and again over the final two weeks of September. During the Fund’s fiscal year ended September 30, 2014, the S&P 500® Index was up 19.73%. |

| ¢ | Geopolitical risk was a concern throughout the year from the Russian-Ukraine tensions, concerns over the crises in Middle East (ISIS and Hamas-Israel), to the most recent protests in Hong Kong. These risks have increased the level of fear in the market and raised the concern on how they could affect corporate profits going forward. |

| ¢ | Strong U.S. economic numbers raised fears that the Fed might allow rates to rise earlier than anticipated. But, with growing concern over the eurozone’s and China’s economic growth potential, Central Banks have universally remained accommodative. |

What factors affected the Fund’s performance during its fiscal year?

| ¢ | The Fund benefited from its allocation to the larger-capitalization stocks in the S&P 500® Index. The equity portion was invested in the S&P 100® Index, which returned 20.47% over the fiscal year period ended September 30, 2014, while the S&P 500® Index returned 19.73%. |

| ¢ | One of the strategies the Fund utilizes is the selling of S&P 500® Index calls to generate income. This income is then used to purchase a negatively correlated investment, which can rise in value when the S&P 500® Index falls. This defensive investment is a call option on the futures contract of the Chicago Board of Options Exchange Volatility Index (“VIX”). |

| ¢ | The VIX index, a proxy for the 30-day implied volatility of the S&P 500® Index, averaged 13.72 during the fiscal year. Historically, the average level of the VIX, dating back to December 31, 2002, is 19.90. Although we view current levels for the VIX low on a historic basis, we also understand that these periods of low implied volatility can last for extended periods. With implied volatility at the low levels we have seen recently, the defensive allocation to VIX calls will likely continue to be a drag on performance, since the premium generated by writing S&P 500® Index calls has not fully offset this cost. |

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results and there is no guarantee market forecasts will be realized.

There is no guarantee that the Fund will meet its objectives.

The market price of equity securities may be affected by financial market, industry, or issuer-specific events. Focus on a particular style or on small or medium-sized companies may enhance that risk. The value of an ETF may be more volatile than the underlying portfolio of securities the ETF is designed to track. The costs of owning the ETF may exceed the cost of investing directly in the underlying securities. Securities in the fund may go up or down in response to the prospects of individual companies

and general economic conditions. Price changes may be short or long term. Selling call options may limit a fund’s opportunity to profit from the increase in price of its underlying portfolio. Buying call options risks the loss of the premium paid for those options.

| Asset Allocation | ||||

The following table presents asset allocations within certain sectors and as a percentage of total investments as of September 30, 2014.

|

| |||

Exchange Traded Funds | 99 | % | ||

Other (includes short-term investments) | 1 | |||

|

| |||

Total | 100 | % | ||

|

| |||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

13

Table of Contents

Low Volatility Equity Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/14 | ||||||||||||

| 1 year | Since Inception | Inception Date | ||||||||||

| Class A Shares at NAV2 | 15.23 | % | 13.53 | % | 6/11/13 | |||||||

| Class A Shares at POP3,4 | 8.61 | 8.49 | 6/11/13 | |||||||||

| Class C Shares at NAV2 and with CDSC4 | 14.47 | 12.70 | 6/11/13 | |||||||||

| Class I Shares at NAV2 | 15.45 | 13.78 | 6/11/13 | |||||||||

| S&P 500® Index | 19.73 | 18.37 | 5 | — | ||||||||

Fund Expense Ratios6: A Shares: Gross 2.10%, Net 1.55%; C Shares: Gross 2.85%, Net 2.30%; I Shares: Gross 1.85%, Net 1.30%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 5.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter. |

| 5 | The since inception index returns are from the Fund’s inception date. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2014, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by a contractual fee waiver in effect through January 31, 2015. Gross Expense: Does not reflect the effect of the fee waiver. |

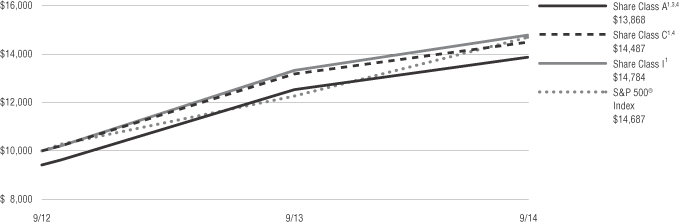

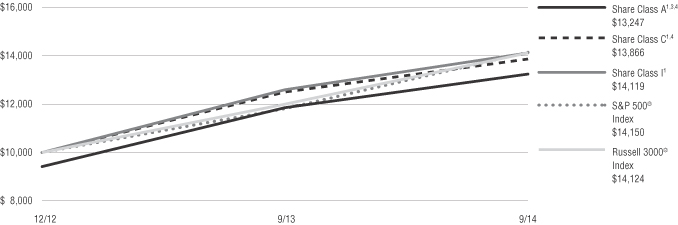

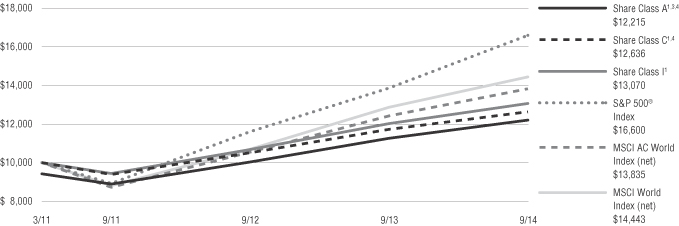

Growth of $10,000 For periods ended 9/30

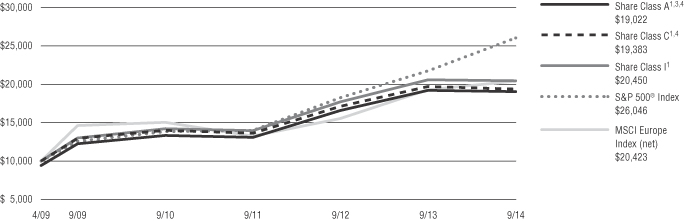

This chart assumes an initial investment of $10,000 made on June 11, 2013 (inception date of the Fund) for Class A, Class C, and Class I shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

14

Table of Contents

Multi-Sector Intermediate Bond Fund

Fund Summary | Ticker Symbols: Class A: NAMFX Class B: NBMFX Class C: NCMFX Class I: VMFIX |

| ¢ | The Fund is diversified and has an investment objective of maximizing current income while preserving capital. |

| ¢ | For the fiscal year ended September 30, 2014, the Fund’s Class A shares at NAV returned 6.18%, Class B shares returned 5.40%, Class C shares returned 5.33%, and Class I shares returned 6.54%. For the same period, the Barclays U.S. Aggregate Bond Index, which is both the Fund’s broad-based and style-specific fixed income index, returned 3.96%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the market perform during the Fund’s fiscal year?

| ¢ | Most spread sectors outperformed U.S. Treasuries during the fiscal year. Economic growth in the U.S. improved, but the level of growth remains moderate, which is supportive of fixed income spread sectors. The economy continues to be tempered by a lack of wage growth. This, when combined with slow global growth, concern over a stronger U.S. dollar, and a lack of inflation across the globe, will likely keep the Fed from raising short-term interest rates in the immediate future. Over the fiscal year, spread sectors were supported by an overall improvement in the U.S. macroeconomic environment, positive credit fundamentals, and continued demand for spread product. |

| ¢ | Globally, concerns over slowing growth in China and Europe, as well as increased geopolitical risks stemming from tensions between Ukraine and Russia and the escalation of issues in the Middle East have weighed on the fixed income markets. The global markets were also unsettled over the likelihood that the Fed would raise short-term interest rates sooner than anticipated due to stronger U.S. growth. |

| ¢ | The Fed continued to taper its monthly bond purchases with the expectation that it would be ending its stimulus program during the fourth quarter of 2014. However, the Central Bank has also |

acknowledged that signs of weakness remain in the U.S. economy, and has indicated that short-term rates will remain low in the near term and any future decision on rates will be driven by economic data. |

| ¢ | Over the last 12 months, yields increased at the short maturity end of the U.S. Treasury curve and decreased on the long maturity end, and overall the yield curve flattened. |

What factors affected the Fund’s performance during its fiscal year?

| ¢ | The outperformance of fixed income spread sectors relative to U.S. Treasuries was the key driver of the Fund’s strong performance for the fiscal year. |

| ¢ | Among fixed income sectors, the Fund’s allocation to corporate high yield, corporate high quality, and Yankee high quality securities were all positive contributors to performance for the fiscal year. |

| ¢ | During the fiscal year, the Fund’s allocation to the non-U.S. dollar sector detracted from performance. |

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities. There is a greater level of credit risk and price volatility involved with high-yield securities than investment grade securities. Changes in interest rates can cause both extension and prepayment risks for asset-backed securities and mortgage-backed securities. These securities are also subject to risks associated with the repayment of underlying collateral. There may be no ready market for loan participation

interests. The fund may have to sell the interests at a substantial discount. Such interests are subject to the credit risk of the underlying corporate borrower. Investing internationally, especially in emerging markets, involves additional risks such as currency, political, accounting, economic, and market risk.

| Asset Allocation | ||||||||

The following table presents asset allocations within certain sectors and as a percentage of total investments as of September 30, 2014.

|

| |||||||

Corporate Bonds and Notes | 59 | % | ||||||

Financials | 20 | % | ||||||

Energy | 11 | |||||||

Consumer Discretionary | 7 | |||||||

Industrials | 6 | |||||||

All other Corporate Bonds and Notes | 15 | |||||||

Loan Agreements | 14 | |||||||

Foreign Government Securities | 10 | |||||||

Mortgage-Backed Securities | 9 | |||||||

Other (includes short-term investments) | 8 | |||||||

|

| |||||||

Total | 100 | % | ||||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

15

Table of Contents

Multi-Sector Intermediate Bond Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/14 | ||||||||||||||||||||

| 1 year | 5 years | 10 years | Since Inception | Inception Date | ||||||||||||||||

| Class A Shares at NAV2 | 6.18 | % | 8.03 | % | 6.22 | % | — | — | ||||||||||||

| Class A Shares at POP3,4 | 2.19 | 7.21 | 5.82 | — | — | |||||||||||||||

| Class B Shares at NAV2 | 5.40 | 7.20 | 5.42 | — | — | |||||||||||||||

| Class B Shares with CDSC4 | 1.43 | 7.20 | 5.42 | — | — | |||||||||||||||

| Class C Shares at NAV2 and with CDSC4 | 5.33 | 7.23 | 5.44 | — | — | |||||||||||||||

| Class I Shares at NAV | 6.54 | — | — | 8.34 | % | 10/1/09 | ||||||||||||||

| Barclays U.S. Aggregate Bond Index | 3.96 | 4.12 | 4.62 | 4.04 | 5 | — | ||||||||||||||

Fund Expense Ratios6: A Shares: 1.09%, B Shares: 1.84%, C Shares: 1.84%, I Shares: 0.84%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 3.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for B shares decline from 5% to 0% over a five-year period. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter. |

| 5 | The since inception index returns are from the inception date of Class I Shares. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2014, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. |

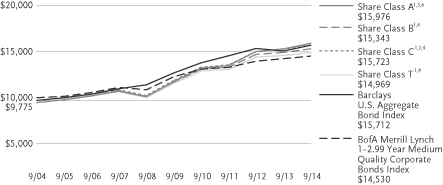

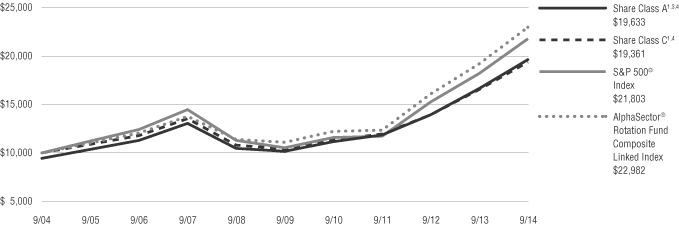

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on September 30, 2004, for Class A, Class B, and Class C shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The index is unmanaged and not available for direct investment; therefore, its performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

16

Table of Contents

Fund Summary | Ticker Symbols: Class A: PSFRX Class C: PFSRX Class I: PSFIX |

| ¢ | The Fund is diversified and has an investment objective of high total return from both current income and capital appreciation. |

| ¢ | For the fiscal year ended September 30, 2014, the Fund’s Class A shares at NAV returned 3.08%, Class C shares returned 2.20%, and Class I shares returned 3.23%. For the same period, the Barclays U.S. Aggregate Bond Index, a fixed income index, returned 3.96%, and the S&P/LSTA Leveraged Loan Index, the Fund’s style-specific benchmark, returned 3.85%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the market perform during the Fund’s fiscal year?

| ¢ | The U.S. leveraged loan market, represented by the S&P/LSTA Leveraged Loan Index, returned 3.85% for the fiscal year ended September 30, 2014. Returns were positive through the first three quarters of the fiscal year but turned negative in the fourth quarter due to weakening technical factors as a result of retail fund outflows and rising net supply due to increased mergers and acquisitions (M&A) issuance. After 21 consecutive monthly inflows, retail fund flows turned negative in April and have experienced six consecutive months of outflows as investor concern over rising interest rates receded as a primary focus with the unexpected rally in U.S. Treasury rates during the first nine months of 2014. |

| ¢ | Bank loans have performed well on a relative basis over the past year despite retail fund outflows, as institutional demand has picked up and mostly replaced the decline in retail demand. In fact, collateralized loan obligation (CLO) issuance has reached a new annual record in calendar year 2014. Fundamentals in the bank loan market remain strong as defaults, by number of issuers, declined to 0.64% as of the end of September, a two-and-a-half year low and well below the 1.78% level from one year ago and the long-term average of 3.0%. |

| ¢ | Within the bank loan market, the lower quality credit rating tiers outperformed over the past year due to very liquid capital markets, strong fundamentals, and strong demand from CLOs. Specifically, distressed, CCC/split-CCC, not rated, and single-B loans outperformed the index while BB loans underperformed the index. |

What factors affected the Fund’s performance during its fiscal year?

| ¢ | The positive return of the U.S. leveraged loan market contributed to the Fund’s positive return during the year. |

| ¢ | Overall, positive issue selection and industry allocation in the Fund relative to the index benefited performance. Specifically, issue selection within the service, retail, and food and tobacco industries helped the Fund’s performance. Issue selection within the utility, diversified media, and energy industries detracted from performance. Remaining nearly fully invested, as well as the Fund’s out-of-index sector allocation to high yield, which is part of its liquidity strategy, also made a positive contribution to performance. |

| ¢ | Overall, a modest overweight to higher quality tiers with an underweight to the lower quality distressed credit tier detracted from Fund performance relative to the index. Issue selection in the split BB and CCC credit tiers contributed positively to performance relative to the index while selection in the single-B and not rated credit tiers detracted from Fund performance relative to the index. |

The preceding information is the opinion of portfolio management. Any such opinions are subject to change at any time based upon market or other conditions and should not be relied upon as investment advice. Past performance is no guarantee of future results, and there is no guarantee that market forecasts will be realized.

There is no guarantee that the Fund will meet its objective.

Debt securities are subject to various risks, the most prominent of which are credit and interest rate risk. The issuer of a security may fail to make payments in a timely manner. Values of debt securities may rise and fall in response to changes in interest rates. This risk may be enhanced with longer-term maturities.

There may be no ready market for loan participation interests. The fund may have to sell the interests at a substantial discount. Such interests are subject to the credit risk of the underlying corporate borrower. There is a greater level of credit risk and price volatility involved with high-yield securities than investment grade securities. When a fund leverages its portfolio, the value of its shares may be more volatile and all other risks may be compounded. Certain securities may be difficult to sell at a time and price beneficial to the fund.

| Asset Allocation | ||||||||

The following table presents asset allocations within certain sectors and as a percentage of total investments as of September 30, 2014.

|

| |||||||

Loan Agreements | 92 | % | ||||||

Consumer Discretionary | 28 | % | ||||||

Health Care | 14 | |||||||

Information Technology | 12 | |||||||

Industrials | 11 | |||||||

Materials | 6 | |||||||

All other Loan Agreements | 21 | |||||||

Corporate Bonds and Notes | 7 | |||||||

Other | 1 | |||||||

|

| |||||||

Total | 100 | % | ||||||

|

| |||||||

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

17

Table of Contents

Senior Floating Rate Fund (Continued)

| Average Annual Total Returns1 for periods ended 9/30/14 | ||||||||||||||||

| 1 year | 5 years | Since Inception | Inception Date | |||||||||||||

| Class A Shares at NAV2 | 3.08 | % | 5.62 | % | 5.59 | % | 1/31/08 | |||||||||

| Class A Shares at POP3,4 | 0.24 | 5.03 | 5.15 | 1/31/08 | ||||||||||||

| Class C Shares at NAV2 and with CDSC4 | �� | 2.20 | 4.84 | 4.82 | 1/31/08 | |||||||||||

| Class I Shares at NAV | 3.23 | 5.89 | 5.85 | 1/31/08 | ||||||||||||

| Barclays U.S. Aggregate Bond Index | 3.96 | 4.12 | 4.48 | 5 | — | |||||||||||

| S&P/LSTA Leveraged Loan Index | 3.85 | 6.47 | 5.89 | 5 | — | |||||||||||

Fund Expense Ratios6: A Shares: Gross 1.22%, Net 1.20%; C Shares: Gross 1.97%, Net 1.95%; I Shares: Gross 0.97%, Net 0.95%.

All returns represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The above table and graph below do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of shares. Please visit Virtus.com for performance data current to the most recent month-end.

| 1 | Total returns are historical and include changes in share price and the reinvestment of both dividends and capital gains distributions. |

| 2 | “NAV” (Net Asset Value) total returns do not include the effect of any sales charge. |

| 3 | “POP” (Public Offering Price) total returns include the effect of the maximum front-end 2.75% sales charge. |

| 4 | “CDSC” (Contingent Deferred Sales Charge) is applied to redemptions of certain classes of shares that do not have a sales charge applied at the time of purchase. CDSC charges for certain redemptions of Class A shares made within 18 months of purchase in which a finder’s fee was paid and all redemptions of Class C shares within the first year are 1% and 0% thereafter. |

| 5 | The since inception index returns are from the Fund’s inception date. |

| 6 | The expense ratios of the Fund are set forth according to the prospectus for the Fund effective January 28, 2014, as supplemented and revised, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. See the Financial Highlights for more current expense ratios. Net Expense: Expenses reduced by voluntary fee waiver which may be discontinued at any time. Gross Expense: Includes leverage expenses and does not reflect the effect of the fee waiver. |

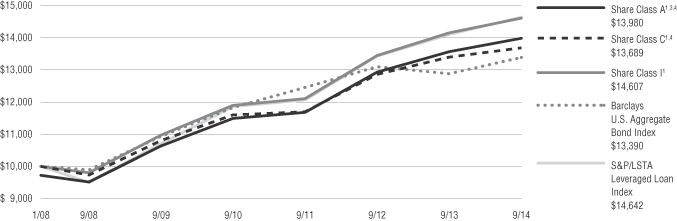

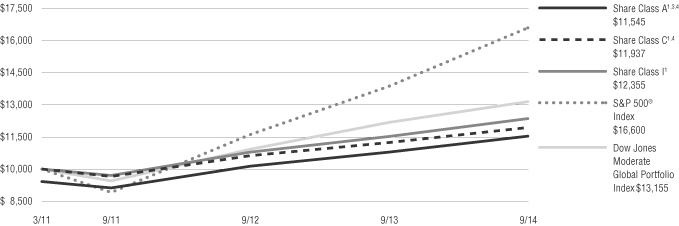

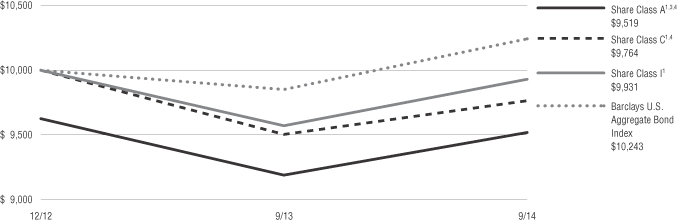

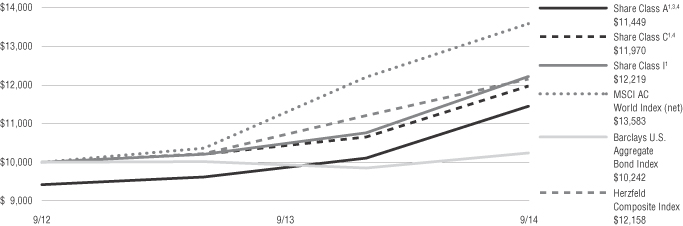

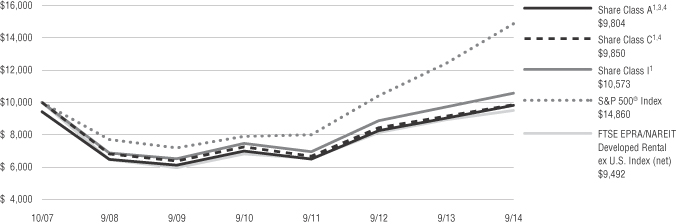

Growth of $10,000 For periods ended 9/30

This chart assumes an initial investment of $10,000 made on January 31, 2008 (inception date of the Fund), for Class A, Class C and Class I shares including any applicable sales charges or fees. Performance assumes reinvestment of dividends and capital gain distributions.

The indexes are unmanaged and not available for direct investment; therefore, their performance does not reflect the expenses associated with active management of an actual portfolio.

For information regarding the indexes and certain investment terms, see the Key Investment Terms starting on page 4.

18

Table of Contents

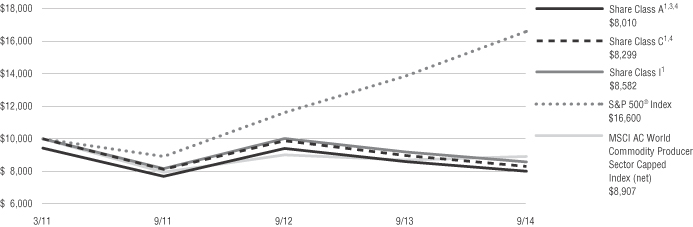

Fund Summary | Ticker Symbols: Class A: VWMAX Class C: VWMCX Class I: VWMIX |

| ¢ | The Fund is diversified and has an investment objective of capital appreciation. |

| ¢ | For the fiscal year ended September 30, 2014, the Fund’s Class A shares at NAV returned 10.67%, Class C shares returned 9.90%, and Class I shares returned 10.96%. For the same period, the S&P 500® Index, a broad-based equity index, and the Fund’s style-specific benchmark, returned 19.73%. |

All performance figures assume reinvestment of distributions and exclude the effect of sales charges. Past performance is no guarantee of future results, and current performance may be higher or lower than the performance shown above.

How did the markets perform during the Fund’s fiscal year?

During the 12-month fiscal period, the broader equity markets appreciated considerably, with the S&P 500® Index returning 19.73%. However, while valuations expanded, the operating results of S&P 500 constituents did not necessarily improve.