UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-07619

Nuveen Investment Trust

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: June 30

Date of reporting period: June 30, 2007

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

NUVEEN INVESTMENTS VALUED AND BALANCED FUNDS

| | |

| | |

Annual Report dated June 30, 2007 | | For investors seeking long-term growth potential. |

Nuveen Investments

Value and Balanced Funds

Nuveen Large-Cap Value Fund

Nuveen Balanced Municipal and Stock Fund

Nuveen Balanced Stock and Bond Fund

NOW YOU CAN RECEIVE YOUR

NUVEEN INVESTMENTS FUND REPORTS FASTER.

NO MORE WAITING.

SIGN UP TODAY TO RECEIVE NUVEEN INVESTMENTS FUND INFORMATION BY E-MAIL.

It only takes a minute to sign up for E-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Investments Fund information is ready — no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report, and save it on your computer if your wish.

IT’S FAST, EASY & FREE:

www.investordelivery.com

if you get your Nuveen Investments Fund dividends and statements from your financial advisor or brokerage account.

(Be sure to have the address sheet that accompanied this report handy. You’ll need it to complete the enrollment process.)

OR

www.nuveen.com/accountaccess

if you get your Nuveen Investments Fund dividends and statements directly from Nuveen Investments.

| | | | | | |

| Must be preceded by or accompanied by a prospectus. | | NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

“No one knows

what the future

will bring, which

is why we think

a well-balanced

portfolio ... is

an important

component in

achieving your

long-term

financial goals.”

Dear Shareholder,

Detailed information on your Fund’s performance can be found in the Portfolio Managers’ Comments and Fund Spotlight sections of this report. The Funds feature portfolio management by Institutional Capital LLC (ICAP), with Nuveen Asset Management managing the municipal portion of the Nuveen Balanced Municipal and Stock Fund. I urge you to take the time to read the Portfolio Managers’ Comments.

I also wanted to take this opportunity to report some important news about Nuveen Investments. The company has accepted a buyout offer from a private equity investment firm. While this may affect the corporate structure of Nuveen Investments, it will have no impact on the investment objectives of the Funds, their portfolio management strategies or their dividend policies. We will provide you with additional information about this transaction as more details become available.

With the recent volatility in the stock market, many have begun to wonder which way the market is headed, and whether they need to adjust their holdings of investments. No one knows what the future will bring, which is why we think a well-balanced portfolio that is structured and carefully monitored with the help of an investment professional is an important component in achieving your long-term financial goals. A well-diversified portfolio may actually help to reduce your overall investment risk, and we believe that investments like your Nuveen Investments Fund can be important building blocks in a portfolio crafted to perform well through a variety of market conditions.

Since 1898, Nuveen Investments has offered financial products and solutions that incorporate careful research, diversification, and the application of conservative risk-management principles. We are grateful that you have chosen us as a partner as you pursue your financial goals. We look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Timothy R. Schwertfeger

Chairman of the Board

August 15, 2007

Annual Report Page 1

Portfolio Managers’ Comments

The Nuveen Large-Cap Value, Balanced Municipal and Stock, and Balanced Stock and Bond Funds feature equity management by Institutional Capital Corporation (ICAP). The municipal portion of the Balanced Municipal and Stock Fund is managed by Nuveen Asset Management (NAM). We recently asked Jerry Senser, chief executive officer and chief investment officer of ICAP, and Tom Spalding of NAM to discuss the key portfolio management strategies and the performance of these three Funds for the 12-month reporting period ended June 30, 2007.

On July 31, 2007, the Board of Trustees of the Large-Cap Value Fund approved HydePark Investment Strategies, LLC (“HydePark”) and Symphony Asset Management LLC (“Symphony”) as additional sub-advisors for the Fund. If approved by Large-Cap Value Fund shareholders on October 12, 2007, the additional sub-advisory agreements are anticipated to take effect on or about November 1, 2007. In the event shareholders of the Large-Cap Value Fund do not approve an additional sub-advisory agreement, the Fund’s portfolio will continue to be managed solely by its current sub-adviser.

What type of economic and stock market backdrop did the Funds encounter during the past year?

The market enjoyed strong gains, with the Standard & Poor’s 500 Index rising roughly 21 percent during the reporting period. Stock prices benefited from continued increases in corporate profits and stable monetary policy on the part of the U.S. Federal Reserve (Fed).

Nevertheless, the stock price gains came despite a variety of challenges for equity investors. Compared to the robust growth of 2005 and early 2006, the U.S. economy was slowing down, expanding by 2.0 percent in the third quarter of 2006, 2.5 percent in the fourth quarter, and just 0.7 percent in the first three months of the new year – although many economists were anticipating a rebound in 2007’s second quarter. One reason for the slower growth was the weaker housing market, whose fall was worsened by troubles in the subprime segment of the mortgage industry. Rising energy prices during the second half of the reporting period in particular also weighed on the economy. Yet despite higher oil costs, core inflation remained under control, enabling the Fed to maintain its benchmark short-term interest rate at 5.25 percent.

How did the Funds perform during the 12 months ending June 30, 2007?

The table on page three provides performance information for the three Funds (Class A shares at NAV). The table also compares the Funds’ performance to appropriate benchmarks.

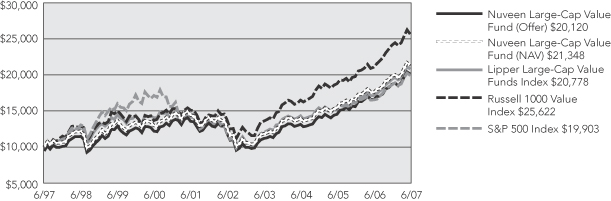

The Nuveen Large-Cap Value Fund (Class A shares at net asset value) outpaced the broad stock market, as measured by the S&P 500 Index, while very modestly trailing the large-cap value Russell 1000 Value Index. It outpaced its peer group, the Lipper Large-Cap Value Funds Index. Compared to the Russell index, the Fund benefited from favorable stock selection in the health care, consumer staples, and information technology sectors. On a sector basis, the Fund benefited from our stock selections and overweighting in basic industry stocks, despite the sector’s underperformance of the overall large-cap value stock market, as well as from an underweighting in the weak-performing financials sector. In contrast, the Fund’s performance was hampered by our stock selection in the energy, retail, and transportation sectors. In all three cases, the stocks chosen for the portfolio failed to go up as much as those in the benchmark. Our overweighting in the transportation sector and our underweighting in telecommunications stocks further detracted from performance.

Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The views expressed herein represent those of the portfolio managers as of the date of this report and are subject to change at any time, based on market conditions and other factors. The Funds disclaim any obligation to advise shareholders of such changes.

Annual Report Page 2

Class A Shares

Average Annual Total Returns as of 6/30/07

| | | | | | |

| | | 1-Year | | 5-Year | | 10-Year |

Nuveen Large-Cap Value Fund | | | | | | |

A Shares at NAV | | 21.71% | | 11.14% | | 7.89% |

A Shares at Offer | | 14.71% | | 9.84% | | 7.26% |

Lipper Large-Cap Value Funds Index1 | | 21.46% | | 11.30% | | 7.59% |

Russell 1000 Value Index2 | | 21.87% | | 13.31% | | 9.87% |

S&P 500 Index3 | | 20.59% | | 10.71% | | 7.13% |

| | | |

Nuveen Balanced Municipal and

Stock Fund | | | | | | |

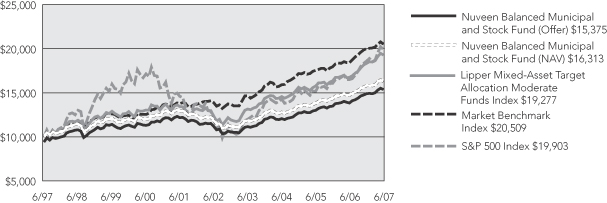

A Shares at NAV | | 10.90% | | 6.59% | | 5.02% |

A Shares at Offer | | 4.51% | | 5.33% | | 4.40% |

Lipper Mixed-Asset Target Allocation Moderate Funds Index4 | | 15.08% | | 9.30% | | 6.78% |

Market Benchmark Index5 | | 11.39% | | 8.10% | | 7.45% |

S&P 500 Index3 | | 20.59% | | 10.71% | | 7.13% |

| | | |

Nuveen Balanced Stock and

Bond Fund | | | | | | |

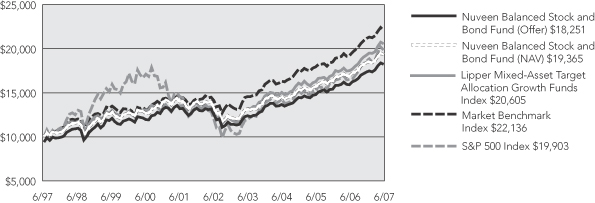

A Shares at NAV | | 14.40% | | 7.82% | | 6.84% |

A Shares at Offer | | 7.82% | | 6.55% | | 6.21% |

Lipper Mixed-Asset Target Allocation Growth Funds Index6 | | 17.52% | | 9.92% | | 7.50% |

Market Benchmark Index7 | | 15.04% | | 9.44% | | 8.27% |

S&P 500 Index3 | | 20.59% | | 10.71% | | 7.13% |

Returns quoted represent past performance, which is no guarantee of future results. Returns at NAV would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Class A shares have a 5.75% maximum sales charge. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance, visit www.nuveen.com or call (800) 257-8787.

Please see each Fund’s Spotlight Page later in this report for more complete performance data and expense ratios.

The Nuveen Balanced Municipal and Stock Fund (Class A shares at NAV) trailed its peer group, the Lipper Mixed-Asset Target Allocation Moderate Funds Index, as well as its blended benchmark, the 40% Russell 1000 Value Index/60% Lehman Brothers 10-Year Municipal Bond Index. The Nuveen Balanced Stock and Bond Fund (Class A shares at NAV) also trailed its peer group, the Lipper Mixed-Asset Target Allocation Growth Funds Index, and its blended benchmark, the 60% Russell 1000 Value Index/40% Lehman Brothers Intermediate Treasury Index.

What was your strategy in managing the equity portion of the Funds?

As the period began, the portfolios were positioned to benefit from what we believed was an imbalance between supply and demand in both the energy and transportation sectors. Because we believed this supply/demand imbalance could boost a number of stocks in these two areas of the market, we added to our oil-company investments as well as to railroad stocks, which we thought were well positioned to benefit from favorable macroeconomic trends. By the third quarter of 2006, however, we came to believe that these investment themes had largely run their course, leading us to reduce our relative allocation to the transportation sector. By period end, we were

| 1 | The Lipper Large-Cap Value Funds Index is a managed index that represents the average annualized total return of the 30 largest funds in the Lipper Large-Cap Value Funds category. The returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 2 | The Russell 1000 Value Index is a market capitalization-weighted index of those firms in the Russell 1000 Index with lower price-to-book ratios and lower forecasted growth value. The index returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 3 | The S&P 500 Index is an unmanaged index generally considered to be representative of the U.S. stock market. The index returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 4 | The Lipper Mixed Asset Target Allocation Moderate Funds Index is a managed index that represents the average annualized total returns of the 10 largest funds in the Lipper Mixed Asset Target Allocation Moderate Fund category. The returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 5 | The Market Benchmark Index is comprised of a 40% weighting in the Russell 1000 Value Index and 60% in the Lehman Brothers 10-Year Municipal Bond Index. The Russell 1000 Value Index is a market capitalization-weighted index of those firms in the Russell 1000 Index with lower price-to-book ratios and lower forecasted growth value. The Lehman Brothers 10-Year Municipal Bond Index is an unmanaged index comprised of a broad range of investment-grade municipal bonds with maturities ranging from 8 to 12 years. The index returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 6 | The Lipper Mixed Asset Target Allocation Growth Funds Index is a managed index that represents the average annualized total returns of the 10 largest funds in the Lipper Mixed Asset Target Allocation Growth Fund category. The returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 7 | The Market Benchmark Index is comprised of a 60% weighting in the Russell 1000 Value Index and 40% in the Lehman Brothers Intermediate Treasury Index. The Russell 1000 Value Index is a market capitalization-weighted index of those firms in the Russell 1000 Index with lower price-to-book ratios and lower forecasted growth value. The Lehman Brothers Intermediate Treasury Index is an unmanaged index comprised of treasury securities with maturities ranging from 1-10 years. The returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

Annual Report Page 3

essentially neutrally weighted compared to the benchmark in the energy sector. We maintained only a modest overweighting in transportation, still favoring railroad companies, whose fundamentals remained favorable, in our view.

Overall, we continued to choose stocks for the portfolio based on company-specific reasons. For example, we identified catalysts, such as an expected restructuring, improved pricing power, or a new management team, that we believed could lead to a rising stock price and stronger future performance. As a result of this “bottom-up” security selection approach, we maintained overweightings in the technology, retail, basic industries, and consumer durables sectors; four areas of the market in which we found a number of individual opportunities that we believed offered good values and future investment potential for our shareholders.

What were some of the Funds’ best-performing stocks of the period?

Our strongest contributor to performance over the past 12 months was restaurant company McDonald’s, which benefited from continued growth in international markets, improved financial performance in the United States, and the successful introduction of new menu items. We sold our position in McDonald’s after the stock reached our target price and appeared to provide more limited appreciation potential. Another positive contributor was energy giant Exxon Mobil, which continued to generate record profits in line with historically high oil prices. Conglomerate Honeywell saw its shares rise on higher revenues and profits, while Australian metal and mining company Rio Tinto gained on increased raw material sales, particularly to emerging market countries. In the telecommunications sector, BellSouth contributed nicely to returns, as the company was acquired for a generous premium by rival AT&T.

Which stocks were recent disappointments?

Energy contractor Halliburton was our largest detractor. The company underperformed as the market became concerned about pricing power in its important U.S. pressure pumping business. We sold our shares of Halliburton in early 2007 because we believed they provided too much risk relative to their reward potential. Another underperformer was communications equipment company Motorola, whose flagship mobile telephone business weighed on the company’s stock. Consumer finance stock Capital One, which we sold from the portfolio early in the period, underperformed as the company spent more money than expected to integrate businesses it had previously acquired. Of final note, office supply retailer Office Depot fell on weaker-than-expected same-store sales.

How did you manage the municipal portion of the Balanced Municipal and Stock Fund?

Although municipal yields ended the 12-month period not far from where they began it, we actually saw two very different market environments during the past year. During most of the first half of the period, bonds rallied, causing their yields to fall and their prices to rise (bond yields and prices move in opposite directions). During most of the period’s second half, however, bond yields reversed course and began to rise, as the likelihood of an interest rate cut from the Fed appeared to wane.

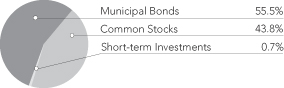

Throughout the past year, we kept the Fund’s duration, meaning its sensitivity to interest rates, relatively close to our internal target and made relatively few changes to the portfolio. As new assets requiring reinvestment came into the Fund, generally as the result of call activity, we established a variety of new positions that we believed offered good future performance potential. For example, we purchased some lower-rated holdings, including some tobacco revenue bonds, while balancing these securities with higher-rated debt that provided the portfolio with additional defensiveness. Many of our new additions focused on bonds with 15-year maturities, the part of the yield curve we believed offered investors the best relative values. At period end, 56 percent of the portfolio was invested in

Annual Report Page 4

municipal bond securities, compared with 44 percent invested in equities.

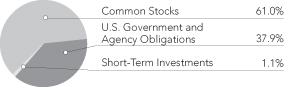

How did you manage the Treasury portion of the Balanced Stock and Bond Fund?

The Fund’s fixed-income portfolio, which consists entirely of U.S. Treasury securities of varying maturities, was managed conservatively during the past year. In July 2006 and again in June 2007, when yields on the 10-year Treasury note were above 5 percent, we lengthened the portfolio’s average maturity to take advantage of price weakness in the bond market.

Dividend Information

The Nuveen Balanced Municipal and Stock Fund seeks to pay dividends at a rate that reflects the past and projected performance of the Fund. To permit the Fund to maintain a more stable dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net investment income actually earned by the Fund during the period. If the Fund has cumulatively earned more than it has paid in dividends, it will hold the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s net asset value. Conversely, if the Fund has cumulatively paid out dividends more than it has earned, the excess will constitute a negative UNII, which will likewise be reflected in the Fund’s net asset value. The Fund will, over time, pay all its net investment income as dividends to shareholders. As of June 30, 2007, the Nuveen Balanced Municipal and Stock Fund had a positive UNII balance for both financial statement and income tax purposes.

Annual Report Page 5

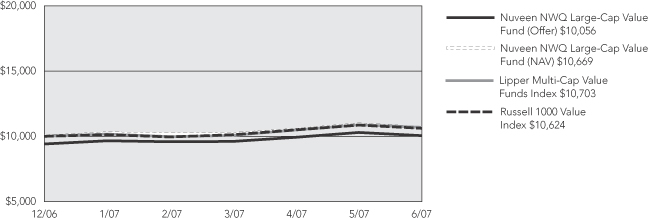

Nuveen Large-Cap Value Fund

Growth of an Assumed $10,000 Investment

Nuveen Balanced Municipal and Stock Fund

Growth of an Assumed $10,000 Investment

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of shares.

The index comparisons show the change in value of a $10,000 investment in the Class A shares of the Nuveen Funds compared with the corresponding indexes. The Lipper Large-Cap Value Funds Index is a managed index that represents the average annualized total returns of the 30 largest funds in the Lipper Large-Cap Value Funds category. The Russell 1000 Value Index is a market capitalization-weighted index of those firms in the Russell 1000 Index with lower price-to-book ratios and lower forecasted growth value. The S&P 500 Index is an unmanaged index generally considered to be representative of the U.S. stock market. The Lipper Mixed-Asset Target Allocation Moderate Funds Index is a managed index that represents the average annualized total returns of the 10 largest funds in the Lipper Mixed-Asset Target Allocation Moderate Funds category. The Market Benchmark Index is comprised of a 40% weighting in the Russell 1000 Value Index and 60% in the Lehman Brothers 10-Year Municipal Bond Index. The Lehman Brothers 10-Year Municipal Bond Index is an unmanaged index comprised of a broad range of investment-grade municipal bonds with maturities ranging from 8 to 12 years. The index returns assume reinvestment of dividends and do not reflect any initial or ongoing expenses. You cannot invest directly in an index. The Nuveen Funds’ total returns include reinvestment of all dividends and distributions, and the Funds’ total returns at the offer price depicted in the chart reflects the initial maximum sales charge applicable to A shares (5.75%) and all ongoing Fund expenses. The performance data quoted represents past performance, which is not indicative of future results. Current performance may be lower or higher than the performance shown.

Annual Report Page 6

Nuveen Balanced Stock and Bond Fund

Growth of an Assumed $10,000 Investment

The graph does not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of shares.

The index comparisons show the change in value of a $10,000 investment in the Class A shares of the Nuveen Fund compared with the corresponding indexes. The Lipper Mixed-Asset Target Allocation Growth Funds Index is a managed index that represents the average annualized total returns of the 10 largest funds in the Lipper Mixed-Asset Target Allocation Growth Funds category. The Market Benchmark Index is comprised of a 60% weighting in the Russell 1000 Value Index and 40% in the Lehman Brothers Intermediate Treasury Index. The Russell 1000 Value Index is a market capitalization-weighted index of those firms in the Russell 1000 Index with lower price-to-book ratios and lower forecasted growth value. The Lehman Brothers Intermediate Treasury Index is an unmanaged index comprised of treasury securities with maturities ranging from 1-10 years. The S&P 500 Index is an unmanaged index generally considered to be representative of the U.S. stock market. The index returns assume reinvestment of dividends and do not reflect any initial or ongoing expenses. You cannot invest directly in an index. The Nuveen Fund’s total returns include reinvestment of all dividends and distributions, and the Fund’s total return at the offer price depicted in the chart reflects the initial maximum sales charge applicable to A shares (5.75%) and all ongoing Fund expenses. The performance data quoted represents past performance, which is not indicative of future results. Current performance may be lower or higher than the performance shown.

Annual Report Page 7

Fund Spotlight as of 6/30/07 Nuveen Large-Cap Value Fund

| | | | | | | | |

| Quick Facts | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R Shares |

NAV | | $30.05 | | $29.32 | | $29.27 | | $30.18 |

Latest Capital Gain Distribution1 | | $1.8356 | | $1.8356 | | $1.8356 | | $1.8356 |

Latest Ordinary Income Distribution2 | | $1.0218 | | $0.8117 | | $0.8117 | | $1.0927 |

Inception Date | | 8/07/96 | | 8/07/96 | | 8/07/96 | | 8/07/96 |

Returns quoted represent past performance which is no guarantee of future performance. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Fund returns assume reinvestment of dividends and capital gains. Class A shares have a 5.75% maximum sales charge. Class B shares have a contingent deferred sales charge (CDSC), also known as a back-end sales charge, that for redemptions begins at 5% and declines periodically until after 6 years when the charge becomes 0%. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns may reflect a voluntary expense limitation by the Fund’s investment adviser which may be modified or discontinued at any time without notice.

| | | | |

| Average Annual Total Returns as of 6/30/07 |

| | |

| A Shares | | NAV | | Offer |

1-Year | | 21.71% | | 14.71% |

5-Year | | 11.14% | | 9.84% |

10-Year | | 7.89% | | 7.26% |

| | |

| B Shares | | w/o CDSC | | w/CDSC |

1-Year | | 20.77% | | 16.77% |

5-Year | | 10.31% | | 10.18% |

10-Year | | 7.25% | | 7.25% |

| | |

| C Shares | | NAV | | |

1-Year | | 20.80% | | |

5-Year | | 10.32% | | |

10-Year | | 7.09% | | |

| | |

| R Shares | | NAV | | |

1-Year | | 22.03% | | |

5-Year | | 11.43% | | |

10-Year | | 8.18% | | |

| | |

| Top Five Common Stock Holdings3 |

Citigroup Inc. | | 4.5% |

AT&T Inc. | | 4.0% |

Bank of America Corporation | | 3.6% |

JPMorgan Chase & Co. | | 3.4% |

General Electric Company | | 3.3% |

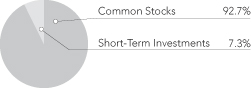

Portfolio Allocation3

| | |

| Portfolio Statistics |

Net Assets ($000) | | $573,077 |

Average Market Capitalization (Common Stocks) | | $122 billion |

Number of Stocks | | 44 |

| | | | | | |

| Expense Ratios | | | | | | |

| | | |

| Share Class | | Gross

Expense

Ratio | | Net

Expense

Ratio | | As of

Date |

Class A | | 1.28% | | 1.28% | | 6/30/06 |

Class B | | 2.03% | | 2.03% | | 6/30/06 |

Class C | | 2.03% | | 2.03% | | 6/30/06 |

Class R | | 1.03% | | 1.03% | | 6/30/06 |

The expense ratios shown factor in Total Annual Fund Operating Expenses including management fees and other fees and expenses.

| 2 | Ordinary income distribution consists of short-term capital gains paid on December 18, 2006 and ordinary income paid on December 29, 2006, if any. |

| 3 | As a percentage of total investments as of June 30, 2007. Holdings are subject to change. |

Annual Report Page 8

Fund Spotlight as of 6/30/07 Nuveen Large-Cap Value Fund

| | |

| Industries1 | | |

Oil, Gas & Consumable Fuels | | 11.6% |

Pharmaceuticals | | 8.2% |

Capital Markets | | 7.6% |

Commercial Banks | | 7.6% |

Communications Equipment | | 5.7% |

Beverages | | 5.5% |

Industrial Conglomerates | | 4.9% |

Diversified Financial Services | | 4.5% |

Diversified Telecommunication Services | | 4.0% |

Insurance | | 3.3% |

Chemicals | | 3.1% |

Household Products | | 2.9% |

Multi-Utilities | | 2.6% |

Metals & Mining | | 2.5% |

Semiconductors & Equipment | | 2.4% |

Aerospace & Defense | | 2.4% |

Computers & Peripherals | | 2.2% |

Food & Staples Retailing | | 2.1% |

Building Products | | 2.0% |

Short Term Investments | | 1.1% |

Other | | 13.8% |

| 1 | As a percentage of total investments as of June 30, 2007. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | Hypothetical Performance

|

| | | Actual Performance | | | | (5% return before expenses) |

| | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R Shares | | | | A Shares | | B Shares | | C Shares | | R Shares |

Beginning Account Value (1/01/07) | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 |

Ending Account Value (6/30/07) | | $ | 1,077.40 | | $ | 1,073.20 | | $ | 1,073.70 | | $ | 1,078.60 | | | | $ | 1,018.55 | | $ | 1,014.78 | | $ | 1,014.83 | | $ | 1,019.79 |

Expenses Incurred During Period | | $ | 6.49 | | $ | 10.38 | | $ | 10.33 | | $ | 5.21 | | | | $ | 6.31 | | $ | 10.09 | | $ | 10.04 | | $ | 5.06 |

For each class of the Fund, expenses are equal to the Fund’s annualized expense ratio of 1.26%, 2.02%, 2.01% and 1.01% for Classes A, B, C and R, respectively, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Annual Report Page 9

Fund Spotlight as of 6/30/07 Nuveen Balanced Municipal and Stock Fund

| | | | | | | | |

| Quick Facts | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R Shares |

NAV | | $25.76 | | $27.36 | | $27.32 | | $25.15 |

Latest Dividend1 | | $0.0405 | | $0.0305 | | $0.0305 | | $0.0435 |

Inception Date | | 8/07/96 | | 8/07/96 | | 8/07/96 | | 8/07/96 |

Returns quoted represent past performance which is no guarantee of future performance. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Fund returns assume reinvestment of dividends and capital gains. Class A shares have a 5.75% maximum sales charge. Class B shares have a contingent deferred sales charge (CDSC), also known as a back-end sales charge, that for redemptions begins at 5% and declines periodically until after 6 years when the charge becomes 0%. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns may reflect a voluntary expense limitation by the Fund’s investment adviser which may be modified or discontinued at any time without notice.

| | | | |

| Average Annual Total Returns as of 6/30/07 |

| A Shares | | NAV | | Offer |

1-Year | | 10.90% | | 4.51% |

5-Year | | 6.59% | | 5.33% |

10-Year | | 5.02% | | 4.40% |

| B Shares | | w/o CDSC | | w/CDSC |

1-Year | | 10.09% | | 6.09% |

5-Year | | 5.79% | | 5.63% |

10-Year | | 4.40% | | 4.40% |

| C Shares | | NAV | | |

1-Year | | 10.10% | | |

5-Year | | 5.79% | | |

10-Year | | 4.24% | | |

| R Shares | | NAV | | |

1-Year | | 11.17% | | |

5-Year | | 6.86% | | |

10-Year | | 5.29% | | |

| Bond Credit Quality2 | | | | |

AAA/U.S. Guaranteed | | | | 64.5% |

AA | | | | 15.9% |

A | | | | 2.9% |

BBB | | | | 14.7% |

BB or Lower | | | | 1.3% |

N/R | | | | 0.7% |

| | | | | | |

| Expense Ratios | | | | | | |

| | | |

| Share Class | | Gross

Expense

Ratio | | Net

Expense

Ratio | | As of

Date |

Class A | |

1.26% | |

1.22% | |

6/30/06 |

Class B | |

2.00% | |

1.97% | |

6/30/06 |

Class C | |

2.01% | |

1.97% | |

6/30/06 |

Class R | |

1.01% | |

0.96% | |

6/30/06 |

The net expense ratio reflects a contractual commitment by the Fund’s investment adviser to waive fees and reimburse expenses through July 31, 2007. The net ratio also reflects a custodian fee credit from the custodian bank whereby certain fees and expenses are reduced by credits earned on the Fund’s cash on deposit with the bank. There is no guarantee that the Fund will earn such credits in the future. Absent the waiver, reimbursement and credit, expenses would be higher and total returns would be less.

| | | | |

| Yields4 |

| A Shares | | NAV | | Offer |

SEC 30-Day Yield | | 2.62% | | 2.47% |

Distribution Rate | | 1.89% | | 1.78% |

| B Shares | | NAV | | |

SEC 30-Day Yield | | 1.85% | | |

Distribution Rate | | 1.34% | | |

| C Shares | | NAV | | |

SEC 30-Day Yield | | 1.88% | | |

Distribution Rate | | 1.34% | | |

| R Shares | | NAV | | |

SEC 30-Day Yield | | 2.88% | | |

Distribution Rate | | 2.08% | | |

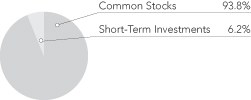

Portfolio Allocation3

| | |

| Portfolio Statistics |

Net Assets ($000) | | $78,381 |

Average Market Capitalization (Common Stocks) | | $122 billion |

Number of Common Stocks | | 44 |

Average Duration (Municipal Bonds) | | 4.82 |

| | |

| Top Five Common Stock Holdings3 | | |

Citigroup Inc. | | 2.0% |

AT&T Inc. | | 1.7% |

Bank of America Corporation | | 1.6% |

JPMorgan Chase & Co. | | 1.5% |

Wells Fargo & Company | | 1.5% |

| 1 | Paid July 2, 2007. This is the latest monthly tax-exempt dividend declared during the period ended June 30, 2007. Income is generally exempt from regular federal income taxes. Income may be subject to state and local taxes and to the federal alternative minimum tax. Capital gains, if any, are subject to tax. |

| 2 | As a percentage of total municipal bond holdings as of June 30, 2007. Holdings are subject to change. |

| 3 | As a percentage of total investments as of June 30, 2007. Holdings are subject to change. |

| 4 | Distribution Rate Yields may differ from SEC 30-Day Yields due to, among other factors, amortization of post-purchase bond premiums and differences between portfolio earnings and distribution rates. |

Annual Report Page 10

Fund Spotlight as of 6/30/07 Nuveen Balanced Municipal and Stock Fund

| | |

Industries1

Common Stocks: | | |

Oil, Gas & Consumable Fuels | | 5.1% |

Pharmaceuticals | | 3.6% |

Commercial Banks | | 3.5% |

Capital Markets | | 3.4% |

Communications Equipment | | 2.6% |

Beverages | | 2.4% |

Industrial Conglomerates | | 2.1% |

Diversified Financial Services | | 2.0% |

Diversified Telecommunication Services | | 1.8% |

Insurance | | 1.4% |

Chemicals | | 1.4% |

Other | | 14.5% |

| | |

Municipal Bonds: | | |

Tax Obligation/Limited | | 11.0% |

U.S. Guaranteed | | 10.7% |

Health Care | | 9.1% |

Utilities | | 5.2% |

Transportation | | 4.8% |

Tax Obligation/General | | 4.0% |

Education and Civic Organizations | | 3.6% |

Consumer Staples | | 3.3% |

Long-Term Care | | 3.1% |

Water and Sewer | | 0.7% |

Housing/Single Family | | 0.7% |

| 1 | As a percentage of total investments as of June 30, 2007. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Hypothetical Performance

|

| | | Actual Performance | | | | (5% return before expenses) |

| | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R Shares | | | | A Shares | | B Shares | | C Shares | | R Shares |

Beginning Account Value (1/01/07) | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 |

Ending Account Value (6/30/07) | | $ | 1,032.80 | | $ | 1,029.00 | | $ | 1,029.40 | | $ | 1,034.00 | | | | $ | 1,018.89 | | $ | 1,015.08 | | $ | 1,015.12 | | $ | 1,020.13 |

Expenses Incurred During Period | | $ | 6.00 | | $ | 9.86 | | $ | 9.81 | | $ | 4.74 | | | | $ | 5.96 | | $ | 9.79 | | $ | 9.74 | | $ | 4.71 |

For each class of the Fund, expenses are equal to the Fund’s annualized expense ratio of 1.19%,1.96%, 1.95% and .94% for Classes A, B, C and R, respectively, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Annual Report Page 11

Fund Spotlight as of 6/30/07 Nuveen Balanced Stock and Bond Fund

| | | | | | | | |

| Quick Facts | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R Shares |

NAV | | $26.73 | | $26.73 | | $26.75 | | $26.73 |

Latest Capital Gain Distribution1 | | $1.1433 | | $1.1433 | | $1.1433 | | $1.1433 |

Latest Ordinary Income Distribution2 | | $0.6188 | | $0.5684 | | $0.5684 | | $0.6356 |

Inception Date | | 8/07/96 | | 8/07/96 | | 8/07/96 | | 8/07/96 |

Returns quoted represent past performance which is no guarantee of future performance. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Fund returns assume reinvestment of dividends and capital gains. Class A shares have a 5.75% maximum sales charge. Class B shares have a contingent deferred sales charge (CDSC), also known as a back-end sales charge, that for redemptions begins at 5% and declines periodically until after 6 years when the charge becomes 0%. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns may reflect a voluntary expense limitation by the Fund’s investment adviser which may be modified or discontinued at any time without notice.

| | | | |

| Average Annual Total Returns as of 6/30/07 |

| | |

| A Shares | | NAV | | Offer |

1-Year | | 14.40% | | 7.82% |

5-Year | | 7.82% | | 6.55% |

10-Year | | 6.84% | | 6.21% |

| | |

| B Shares | | w/o CDSC | | w/CDSC |

1-Year | | 13.55% | | 9.55% |

5-Year | | 7.02% | | 6.87% |

10-Year | | 6.21% | | 6.21% |

| | |

| C Shares | | NAV | | |

1-Year | | 13.54% | | |

5-Year | | 7.03% | | |

10-Year | | 6.06% | | |

| | |

| R Shares | | NAV | | |

1-Year | | 14.68% | | |

5-Year | | 8.10% | | |

10-Year | | 7.11% | | |

| | |

| Top Five Common Stock Holdings3 |

Citigroup Inc. | |

2.8% |

AT&T Inc. | |

2.4% |

Bank of America Corporation | |

2.2% |

JPMorgan Chase & Co. | |

2.1% |

Wells Fargo & Co. | |

2.0% |

| | | | | | |

| Expense Ratios | | | | | | |

| | | |

| Share Class | | Gross

Expense

Ratio | | Net

Expense

Ratio | | As of

Date |

Class A | | 1.31% | | 1.24% | |

6/30/06 |

Class B | | 2.06% | | 1.99% | |

6/30/06 |

Class C | | 2.06% | | 1.99% | |

6/30/06 |

Class R | | 1.06% | | 0.99% | |

6/30/06 |

The net expense ratio reflects a contractual commitment by the Fund’s investment adviser to waive fees and reimburse expenses through July 31, 2007. The net ratio also reflects a custodian fee credit from the custodian bank whereby certain fees and expenses are reduced by credits earned on the Fund’s cash on deposit with the bank. There is no guarantee that the fund will earn such credits in the future. Absent the waiver, reimbursement and credit, expenses would be higher and total returns would be less.

| | | | |

| Yields4 |

| | |

| A Shares | | NAV | | Offer |

SEC 30-Day Yield | | 1.85% | | 1.74% |

Distribution Rate | |

2.59% | |

2.44% |

| | |

| B Shares | | NAV | | |

SEC 30-Day Yield | | 1.10% | | |

Distribution Rate | |

1.84% | | |

| | |

| C Shares | | NAV | | |

SEC 30-Day Yield | | 1.07% | | |

Distribution Rate | |

1.84% | | |

| | |

| R Shares | | NAV | | |

SEC 30-Day Yield | | 2.11% | | |

Distribution Rate | |

2.84% | | |

Portfolio Allocation3

| | |

| Portfolio Statistics |

Net Assets ($000) | | $58,280 |

Average Market Capitalization (Common Stocks) | |

$122 billion |

Number of Common Stocks | | 44 |

Average Duration (Bonds) | | 4.47 |

| 2 | Ordinary income distribution consists of short-term capital gains paid on December 18, 2006, and ordinary income paid on December 29, 2006, if any. |

| 3 | As a percentage of total investments as of June 30, 2007. Holdings are subject to change. |

| 4 | Distribution Rate Yields may differ from SEC 30-Day Yields due to, among other factors, amortization of post-purchase bond premiums and differences between portfolio earnings and distribution rates. |

Annual Report Page 12

Fund Spotlight as of 6/30/07 Nuveen Balanced Stock and Bond Fund

| | |

| Industries1 | | |

U.S. Treasury Notes | | 19.8% |

U.S. Treasury Bonds | | 13.0% |

Oil, Gas & Consumable Fuels | | 7.2% |

U.S. Treasury Obligations | | 5.1% |

Pharmaceuticals | | 5.0% |

Capital Markets | | 4.7% |

Commercial Banks | | 4.7% |

Communications Equipment | | 3.5% |

Beverages | | 3.4% |

Industrial Conglomerates | | 3.0% |

Diversified Financial Services | | 2.8% |

Diversified Telecommunication Services | | 2.4% |

Insurance | | 2.0% |

Chemicals | | 1.9% |

Household Products | | 1.8% |

Multi-Utilities | | 1.6% |

Metals & Mining | | 1.5% |

Semiconductors & Equipment | | 1.4% |

Aerospace & Defense | | 1.4% |

Short Term Investments | | 1.1% |

Other | | 12.7% |

| 1 | As a percentage of total investments as of June 30, 2007. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| | | Actual Performance | | | | Hypothetical Performance

(5% return before expenses) |

| | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R Shares | | | | A Shares | | B Shares | | C Shares | | R Shares |

Beginning Account Value (1/01/07) | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 |

Ending Account Value (6/30/07) | | $ | 1,048.40 | | $ | 1,044.50 | | $ | 1,044.50 | | $ | 1,049.70 | | | | $ | 1,018.50 | | $ | 1,014.73 | | $ | 1,014.73 | | $ | 1,019.74 |

Expenses Incurred During Period | | $ | 6.45 | | $ | 10.29 | | $ | 10.29 | | $ | 5.18 | | | | $ | 6.36 | | $ | 10.14 | | $ | 10.14 | | $ | 5.11 |

For each class of the Fund, expenses are equal to the Fund’s annualized expense ratio of 1.27%, 2.03%, 2.03% and 1.02% for Classes A, B, C and R, respectively, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Annual Report Page 13

Portfolio of Investments

Nuveen Large-Cap Value Fund

June 30, 2007

| | | | | |

| Shares | | Description | | Value |

| | | | | |

| | COMMON STOCKS – 99.0% | | | |

| | |

| | Aerospace & Defense – 2.4% | | | |

| | |

| 240,550 | | Honeywell International Inc. | | $ | 13,538,154 |

| | Automobiles – 0.8% | | | |

| | |

| 75,500 | | Harley-Davidson, Inc. | | | 4,500,555 |

| | Beverages – 5.5% | | | |

| | |

| 279,800 | | Coca-Cola Company | | | 14,636,338 |

| | |

| 259,250 | | PepsiCo, Inc. | | | 16,812,363 |

| | Total Beverages | | | 31,448,701 |

| | |

| | Building Products – 2.0% | | | |

| | |

| 399,600 | | Masco Corporation | | | 11,376,612 |

| | Capital Markets – 7.6% | | | |

| | |

| 277,450 | | Bank of New York Company, Inc. | | | 11,497,528 |

| | |

| 401,250 | | JPMorgan Chase & Co. | | | 19,440,562 |

| | |

| 153,352 | | Morgan Stanley | | | 12,863,166 |

| | Total Capital Markets | | | 43,801,256 |

| | |

| | Chemicals – 3.1% | | | |

| | |

| 345,150 | | E.I. Du Pont de Nemours and Company | | | 17,547,426 |

| | Commercial Banks – 7.6% | | | |

| | |

| 422,850 | | Bank of America Corporation | | | 20,673,136 |

| | |

| 80,750 | | Wachovia Corporation | | | 4,138,438 |

| | |

| 537,400 | | Wells Fargo & Company | | | 18,900,358 |

| | Total Commercial Banks | | | 43,711,932 |

| | |

| | Communications Equipment – 5.7% | | | |

| | |

| 551,000 | | Cisco Systems, Inc., (1) | | | 15,345,350 |

| | |

| 258,400 | | Corning Incorporated, (1) | | | 6,602,120 |

| | |

| 610,750 | | Motorola, Inc. | | | 10,810,275 |

| | Total Communications Equipment | | | 32,757,745 |

| | |

| | Computers & Peripherals – 2.2% | | | |

| | |

| 283,450 | | Hewlett-Packard Company | | | 12,647,539 |

| | Containers & Packaging – 1.4% | | | |

| | |

| 133,950 | | Temple-Inland Inc. | | | 8,241,944 |

| | Diversified Financial Services – 4.5% | | | |

| | |

| 506,061 | | Citigroup Inc. | | | 25,955,868 |

| | Diversified Telecommunication Services – 4.0% | | | |

| | |

| 547,838 | | AT&T Inc. | | | 22,735,276 |

| | Energy Equipment & Services – 1.0% | | | |

| | |

| 65,200 | | Schlumberger Limited | | | 5,538,088 |

| | Food & Staples Retailing – 2.1% | | | |

| | |

| 336,650 | | CVS Caremark Corporation | | | 12,270,893 |

| | Health Care Equipment & Supplies – 1.0% | | | |

| | |

| 140,050 | | Hospira Inc., (1) | | | 5,467,552 |

| | Hotels, Restaurants & Leisure – 0.8% | | | |

| | |

| 195,847 | | Intercontinental Hotels Group PLC, ADR | | | 4,853,089 |

14

| | | | | |

| Shares | | Description | | Value |

| | | | | |

| | Household Products – 2.9% | | | |

| | |

| 274,300 | | Procter & Gamble Company | | $ | 16,784,417 |

| | Industrial Conglomerates – 4.9% | | | |

| | |

| 500,750 | | General Electric Company | | | 19,168,709 |

| | |

| 78,700 | | Textron Inc. | | | 8,665,657 |

| | Total Industrial Conglomerates | | | 27,834,366 |

| | |

| | Insurance – 3.3% | | | |

| | |

| 268,000 | | American International Group, Inc. | | | 18,768,040 |

| | Media – 1.7% | | | |

| | |

| 238,350 | | Viacom Inc., Class B, (1) | | | 9,922,511 |

| | Metals & Mining – 2.5% | | | |

| | |

| 47,475 | | Rio Tinto PLC, Sponsored ADR | | | 14,533,047 |

| | Multiline Retail – 1.8% | | | |

| | |

| 158,650 | | Target Corporation | | | 10,090,140 |

| | Multi-Utilities – 2.6% | | | |

| | |

| 171,050 | | Dominion Resources, Inc. | | | 14,763,326 |

| | Oil, Gas & Consumable Fuels – 11.6% | | | |

| | |

| 168,750 | | Exxon Mobil Corporation | | | 14,154,750 |

| | |

| 160,650 | | Hess Corporation | | | 9,471,924 |

| | |

| 247,050 | | Occidental Petroleum Corporation | | | 14,299,254 |

| | |

| 185,300 | | Total SA, Sponsored ADR | | | 15,005,594 |

| | |

| 224,650 | | XTO Energy, Inc. | | | 13,501,465 |

| | Total Oil, Gas & Consumable Fuels | | | 66,432,987 |

| | |

| | Paper & Forest Products – 1.7% | | | |

| | |

| 247,900 | | International Paper Company | | | 9,680,495 |

| | Pharmaceuticals – 8.2% | | | |

| | |

| 480,250 | | Bristol-Myers Squibb Company | | | 15,156,690 |

| | |

| 285,750 | | Merck & Co. Inc. | | | 14,230,350 |

| | |

| 310,000 | | Norvatis AG, ADR | | | 17,381,700 |

| | Total Pharmaceuticals | | | 46,768,740 |

| | |

| | Real Estate – 0.9% | | | |

| | |

| 229,950 | | Host Hotels & Resorts Inc. | | | 5,316,444 |

| | Road & Rail – 1.7% | | | |

| | |

| 190,600 | | Norfolk Southern Corporation | | | 10,019,842 |

| | Semiconductors & Equipment – 2.4% | | | |

| | |

| 360,650 | | Texas Instruments Incorporated | | | 13,571,260 |

| | Specialty Retail – 1.1% | | | |

| | |

| 205,750 | | Office Depot, Inc., (1) | | | 6,234,225 |

| | Total Common Stocks (cost $449,101,259) | | | 567,112,470 |

| | |

15

Portfolio of Investments

Nuveen Large-Cap Value Fund (continued)

June 30, 2007

| | | | | | | | | | |

Principal

Amount (000) | | Description | | Coupon | | Maturity | | Value |

| | | | | | | | | | |

| | | SHORT-TERM INVESTMENTS – 1.0% | | | | | | | |

| | | | |

| $ | 6,139 | | Repurchase Agreement with Fixed Income Clearing Corporation, dated 6/29/07, repurchase price $6,141,508, collateralized by $5,105,000 U.S. Treasury Bonds, 7.25%, due 8/15/22, value $6,266,388 | | 4.000% | | 7/02/07 | | $ | 6,139,462 |

| | | | | | | | | | | |

| | | Total Short-Term Investments (cost $6,139,462) | | | | | | | 6,139,462 |

| | | |

| | | Total Investments (cost $455,240,721) – 100.0% | | | | | | | 573,251,932 |

| | | |

| | | Other Assets Less Liabilities – (0.0)% | | | | | | | (175,164) |

| | | |

| | | Net Assets – 100% | | | | | | $ | 573,076,768 |

| | | |

| | ADR | American Depositary Receipt. |

See accompanying notes to financial statements.

16

Portfolio of Investments

Nuveen Balanced Municipal and Stock Fund

June 30, 2007

| | | | | |

| Shares | | Description | | Value |

| | | | | |

| | COMMON STOCKS – 42.8% | | | |

| | |

| | Aerospace & Defense – 1.0% | | | |

| | |

| 14,250 | | Honeywell International Inc. | | $ | 801,990 |

| | Automobiles – 0.2% | | | |

| | |

| 4,450 | | Harley-Davidson, Inc. | | | 265,265 |

| | Beverages – 2.4% | | | |

| | |

| 16,600 | | Coca-Cola Company | | | 868,346 |

| | |

| 15,350 | | PepsiCo, Inc. | | | 995,448 |

| | Total Beverages | | | 1,863,794 |

| | |

| | Building Products – 0.9% | | | |

| | |

| 23,700 | | Masco Corporation | | | 674,739 |

| | Capital Markets – 3.3% | | | |

| | |

| 16,450 | | Bank of New York Company, Inc. | | | 681,688 |

| | |

| 23,850 | | JPMorgan Chase & Co. | | | 1,155,533 |

| | |

| 9,105 | | Morgan Stanley | | | 763,727 |

| | Total Capital Markets | | | 2,600,948 |

| | |

| | Chemicals – 1.3% | | | |

| | |

| 20,400 | | E.I. Du Pont de Nemours and Company | | | 1,037,136 |

| | Commercial Banks – 3.4% | | | |

| | |

| 24,950 | | Bank of America Corporation | | | 1,219,806 |

| | |

| 6,250 | | Wachovia Corporation | | | 320,313 |

| | |

| 31,800 | | Wells Fargo & Company | | | 1,118,406 |

| | Total Commercial Banks | | | 2,658,525 |

| | |

| | Communications Equipment – 2.5% | | | |

| | |

| 32,650 | | Cisco Systems, Inc., (1) | | | 909,303 |

| | |

| 15,300 | | Corning Incorporated, (1) | | | 390,915 |

| | |

| 36,200 | | Motorola, Inc. | | | 640,740 |

| | Total Communications Equipment | | | 1,940,958 |

| | |

| | Computers & Peripherals – 1.0% | | | |

| | |

| 16,700 | | Hewlett-Packard Company | | | 745,154 |

| | Containers & Packaging – 0.6% | | | |

| | |

| 7,600 | | Temple-Inland Inc. | | | 467,628 |

| | Diversified Financial Services – 2.0% | | | |

| | |

| 29,910 | | Citigroup Inc. | | | 1,534,083 |

| | Diversified Telecommunication Services – 1.7% | | | |

| | |

| 32,312 | | AT&T Inc. | | | 1,340,947 |

| | Energy Equipment & Services – 0.4% | | | |

| | |

| 3,900 | | Schlumberger Limited | | | 331,266 |

| | Food & Staples Retailing – 0.9% | | | |

| | |

| 19,900 | | CVS Caremark Corporation | | | 725,355 |

| | Health Care Equipment & Supplies – 0.4% | | | |

| | |

| 8,100 | | Hospira Inc., (1) | | | 316,224 |

17

Portfolio of Investments

Nuveen Balanced Municipal and Stock Fund (continued)

June 30, 2007

| | | | | |

| Shares | | Description | | Value |

| | | | | |

| | Hotels, Restaurants & Leisure – 0.4% | | | |

| | |

| 11,582 | | Intercontinental Hotels Group PLC, ADR | | $ | 287,002 |

| | Household Products – 1.3% | | | |

| | |

| 16,200 | | Procter & Gamble Company | | | 991,278 |

| | Industrial Conglomerates – 2.1% | | | |

| | |

| 29,000 | | General Electric Company | | | 1,110,120 |

| | |

| 4,650 | | Textron Inc. | | | 512,012 |

| | Total Industrial Conglomerates | | | 1,622,132 |

| | |

| | Insurance – 1.4% | | | |

| | |

| 15,800 | | American International Group, Inc. | | | 1,106,474 |

| | Media – 0.7% | | | |

| | |

| 14,050 | | Viacom Inc., Class B, (1) | | | 584,902 |

| | Metals & Mining – 1.1% | | | |

| | |

| 2,825 | | Rio Tinto PLC, Sponsored ADR | | | 864,789 |

| | Multiline Retail – 0.8% | | | |

| | |

| 9,400 | | Target Corporation | | | 597,840 |

| | Multi-Utilities – 1.1% | | | |

| | |

| 10,150 | | Dominion Resources, Inc. | | | 876,047 |

| | Oil, Gas & Consumable Fuels – 5.0% | | | |

| | |

| 10,000 | | Exxon Mobil Corporation | | | 838,800 |

| | |

| 9,500 | | Hess Corporation | | | 560,120 |

| | |

| 14,650 | | Occidental Petroleum Corporation | | | 847,942 |

| | |

| 10,900 | | Total SA, Sponsored ADR | | | 882,682 |

| | |

| 13,300 | | XTO Energy, Inc. | | | 799,330 |

| | Total Oil, Gas & Consumable Fuels | | | 3,928,874 |

| | |

| | Paper & Forest Products – 0.7% | | | |

| | |

| 14,600 | | International Paper Company | | | 570,130 |

| | Pharmaceuticals – 3.5% | | | |

| | |

| 28,450 | | Bristol-Myers Squibb Company | | | 897,882 |

| | |

| 16,800 | | Merck & Co. Inc. | | | 836,640 |

| | |

| 18,350 | | Norvatis AG, ADR | | | 1,028,885 |

| | Total Pharmaceuticals | | | 2,763,407 |

| | |

| | Real Estate – 0.4% | | | |

| | |

| 13,550 | | Host Hotels & Resorts Inc. | | | 313,276 |

| | Road & Rail – 0.8% | | | |

| | |

| 11,250 | | Norfolk Southern Corporation | | | 591,413 |

| | Semiconductors & Equipment – 1.0% | | | |

| | |

| 21,300 | | Texas Instruments Incorporated | | | 801,519 |

| | Specialty Retail – 0.5% | | | |

| | |

| 12,150 | | Office Depot, Inc., (1) | | | 368,145 |

| | Total Common Stocks (cost $26,472,705) | | | 33,571,240 |

| | |

18

| | | | | | | | | | | |

| | | | |

Principal

Amount (000) | | Description | | Optional Call

Provisions (2) | | Ratings (3) | | | Value |

| | | | | | | | | | | |

| | | MUNICIPAL BONDS – 54.3% | | | | | | | | |

| | | | |

| | | California – 7.1% | | | | | | | | |

| | | | |

| $ | 1,000 | | Alameda Corridor Transportation Authority, California, Subordinate Lien Revenue Bonds, Series 2004A, 0.000%, 10/01/25 – AMBAC Insured | | 10/17 at 100.00 | | AAA | | | $ | 814,130 |

| | | | |

| | 500 | | Calleguas-Las Virgenes Public Finance Authority, California, Water Revenue Bonds, Calleguas Municipal Water District, Series 2003B, 5.250%, 7/01/19 – MBIA Insured | | 7/13 at 100.00 | | AAA | | | | 529,105 |

| | | | |

| | 445 | | Golden State Tobacco Securitization Corporation, California, Enhanced Tobacco Settlement Asset-Backed Bonds, Series 2007A-1, 4.500%, 6/01/27 | | 6/17 at 100.00 | | BBB | | | | 429,923 |

| | | | |

| | 735 | | Northern California Power Agency, Revenue Bonds, Geothermal Project 3, Series 1993,

5.650%, 7/01/07 | | No Opt. Call | | A2 | | | | 735,059 |

| | | | |

| | 250 | | Orange County, California, Refunding Recovery Bonds, Series 1995A, 6.000%, 6/01/10 – MBIA Insured (ETM) | | No Opt. Call | | AAA | | | | 265,033 |

| | | | |

| | 1,495 | | Palmdale Civic Authority, California, Revenue Refinancing Bonds, Civic Center Project, Series 1997A, 5.375%, 7/01/12 – MBIA Insured | | 7/07 at 102.00 | | AAA | | | | 1,526,648 |

| | | | |

| | 1,000 | | San Diego County, California, Certificates of Participation, Burnham Institute, Series 1999,

5.700%, 9/01/11 (Pre-refunded 9/01/09) | | 9/09 at 101.00 | | Baa3 | (4) | | | 1,038,320 |

| | | | |

| | 250 | | San Diego County, California, Certificates of Participation, Burnham Institute, Series 2006,

5.000%, 9/01/34 | | 9/15 at 102.00 | | Baa3 | | | | 249,245 |

| | 5,675 | | Total California | | | | | | | | 5,587,463 |

| | | Colorado – 5.5% | | | | | | | | |

| | | | |

| | 750 | | Colorado Health Facilities Authority, Revenue Bonds, Longmont United Hospital, Series 2006B, 5.000%, 12/01/23 – RAAI Insured | | 12/16 at 100.00 | | AA | | | | 770,678 |

| | | | |

| | 250 | | Colorado Health Facilities Authority, Revenue Bonds, Vail Valley Medical Center, Series 2004,

5.000%, 1/15/17 | | 1/15 at 100.00 | | BBB+ | | | | 255,668 |

| | | | |

| | 1,000 | | Denver City and County, Colorado, Airport Special Facilities Revenue Bonds, Rental Car Projects, Series 1999A, 6.000%, 1/01/13 – MBIA Insured (Alternative Minimum Tax) | | 1/09 at 101.00 | | AAA | | | | 1,034,790 |

| | | | |

| | | E-470 Public Highway Authority, Colorado, Toll Revenue Bonds, Series 2004B: | | | | | | | | |

| | 370 | | 0.000%, 9/01/28 – MBIA Insured | | 9/20 at 63.98 | | AAA | | | | 124,483 |

| | 2,000 | | 0.000%, 3/01/36 – MBIA Insured | | 9/20 at 41.72 | | AAA | | | | 434,260 |

| | | | |

| | 2,000 | | Metropolitan Football Stadium District, Colorado, Sales Tax Revenue Bonds, Series 1999A,

0.000%, 1/01/12 – MBIA Insured | | No Opt. Call | | AAA | | | | 1,665,759 |

| | | | |

| | 160 | | Northwest Parkway Public Highway Authority, Colorado, Senior Lien Revenue Bonds, Series 2001B,

0.000%, 6/15/27 – AMBAC Insured | | 6/11 at 38.04 | | AAA | | | | 50,755 |

| | 6,530 | | Total Colorado | | | | | | | | 4,336,393 |

| | | Connecticut – 0.7% | | | | | | | | |

| | | | |

| | 400 | | Connecticut Development Authority, First Mortgage Gross Revenue Refunding Healthcare Bonds, Elim Park Baptist Home Inc., Series 1998A, 4.875%, 12/01/07 | | 9/07 at 103.00 | | BBB+ | | | | 401,196 |

| | | | |

| | 185 | | Connecticut Health and Educational Facilities Authority, Revenue Bonds, Hospital for Special Care, Series 1997B, 5.125%, 7/01/07 (ETM) | | No Opt. Call | | BBB–(4) | | | | 185,011 |

| | 585 | | Total Connecticut | | | | | | | | 586,207 |

| | | District Of Columbia – 0.5% | | | | | | | | |

| | | | |

| | 255 | | District of Columbia, General Obligation Refunding Bonds, Series 1994A-1, 6.500%, 6/01/10 – MBIA Insured | | No Opt. Call | | AAA | | | | 272,661 |

| | | | |

| | 130 | | Washington Convention Center Authority, District of Columbia, Senior Lien Dedicated Tax Revenue Bonds, Series 1998, 5.000%, 10/01/21 (Pre-refunded 10/01/08) – AMBAC Insured | | 10/08 at 101.00 | | AAA | | | | 133,136 |

| | 385 | | Total District Of Columbia | | | | | | | | 405,797 |

19

Portfolio of Investments

Nuveen Balanced Municipal and Stock Fund (continued)

June 30, 2007

| | | | | | | | | | | |

| | | | |

Principal

Amount (000) | | Description | | Optional Call

Provisions (2) | | Ratings (3) | | | Value |

| | | | | | | | | | | |

| | | Florida – 0.5% | | | | | | | | |

| | | | |

| $ | 350 | | Jacksonville Economic Development Commission, Florida, Healthcare Facilities Revenue Bonds, Mayo Clinic, Series 2001A, 5.500%, 11/15/36 | | 11/11 at 101.00 | | AA | | | $ | 368,382 |

| | | Idaho – 0.1% | | | | | | | | |

| | | | |

| | 90 | | Idaho Housing and Finance Association, Single Family Mortgage Bonds, Series 1997D, 5.950%, 7/01/09 (Alternative Minimum Tax) | | 7/07 at 102.00 | | Aa3 | | | | 91,370 |

| | | Illinois – 5.1% | | | | | | | | |

| | | | |

| | 870 | | Bolingbrook, Will and DuPage Counties, Illinois, Residential Mortgage Revenue Bonds, Series 1979, 7.500%, 8/01/10 – FGIC Insured (ETM) | | No Opt. Call | | AAA | | | | 917,763 |

| | | | |

| | | Chicago Board of Education, Illinois, Unlimited Tax General Obligation Bonds, Dedicated Tax Revenues, Series 1998B-1: | | | | | | | | |

| | 2,205 | | 0.000%, 12/01/24 – FGIC Insured | | No Opt. Call | | AAA | | | | 979,858 |

| | 2,205 | | 0.000%, 12/01/29 – FGIC Insured | | No Opt. Call | | AAA | | | | 766,238 |

| | | | |

| | | Illinois Development Finance Authority, Economic Development Revenue Bonds, Latin School of Chicago, Series 1998: | | | | | | | | |

| | 270 | | 5.200%, 8/01/11 (Pre-refunded 8/01/08) | | 8/08 at 100.00 | | Baa2 | (4) | | | 273,731 |

| | 200 | | 5.250%, 8/01/12 (Pre-refunded 8/01/08) | | 8/08 at 100.00 | | Baa2 | (4) | | | 202,870 |

| | 580 | | 5.300%, 8/01/13 (Pre-refunded 8/01/08) | | 8/08 at 100.00 | | Baa2 | (4) | | | 588,630 |

| | | | |

| | 250 | | Illinois Health Facilities Authority, Revenue Bonds, Lake Forest Hospital, Series 2002A, 6.000%, 7/01/17 | | 7/12 at 100.00 | | A– | | | | 267,043 |

| | 6,580 | | Total Illinois | | | | | | | | 3,996,133 |

| | | Indiana – 1.5% | | | | | | | | |

| | | | |

| | 300 | | Anderson, Indiana, Economic Development Revenue Bonds, Anderson University, Series 2007, 5.000%, 10/01/24 | | 4/14 at 100.00 | | N/R | | | | 298,776 |

| | | | |

| | 860 | | St. Joseph County Hospital Authority, Indiana, Revenue Bonds, Memorial Health System, Series 1998A, 4.625%, 8/15/28 – MBIA Insured | | 2/08 at 101.00 | | AAA | | | | 846,283 |

| | 1,160 | | Total Indiana | | | | | | | | 1,145,059 |

| | | Iowa – 1.2% | | | | | | | | |

| | | | |

| | 970 | | Iowa Finance Authority, Health Facility Revenue Bonds, Care Initiatives Project, Series 2006A, 5.000%, 7/01/19 | | 7/16 at 100.00 | | BBB– | | | | 964,374 |

| | | Louisiana – 0.6% | | | | | | | | |

| | | | |

| | 340 | | Louisiana Public Facilities Authority, Revenue Bonds, Baton Rouge General Hospital, Series 2004, 5.250%, 7/01/24 – MBIA Insured | | 7/14 at 100.00 | | AAA | | | | 355,905 |

| | | Maine – 0.4% | | | | | | | | |

| | | | |

| | 255 | | Winslow, Maine, General Obligation Tax Increment Financing Bonds, Crowe Rope Industries, Series 1997A, 6.000%, 3/01/11 – MBIA Insured (Alternative Minimum Tax) | | 9/07 at 102.00 | | AAA | | | | 260,457 |

| | | Massachusetts – 1.9% | | | | | | | | |

| | | | |

| | 885 | | Massachusetts Development Finance Agency, Resource Recovery Revenue Bonds, Ogden Haverhill Associates, Series 1998B, 5.200%, 12/01/13 (Alternative Minimum Tax) | | 12/08 at 102.00 | | BBB | | | | 904,691 |

| | | | |

| | 545 | | Massachusetts Turnpike Authority, Western Turnpike Revenue Bonds, Series 1997A,

5.550%, 1/01/17 – MBIA Insured | | 7/07 at 100.00 | | AAA | | | | 562,516 |

| | 1,430 | | Total Massachusetts | | | | | | | | 1,467,207 |

| | | Michigan – 0.7% | | | | | | | | |

| | | | |

| | 540 | | Michigan State Hospital Finance Authority, Hospital Revenue Bonds, Detroit Medical Center Obligated Group, Series 1998A, 5.000%, 8/15/13 | | 8/08 at 101.00 | | BB– | | | | 540,022 |

| | | Minnesota – 0.6% | | | | | | | | |

| | | | |

| | 500 | | Minnesota, General Obligation Bonds, Series 1998, 5.000%, 11/01/17 (Pre-refunded 11/01/08) | | 11/08 at 100.00 | | AAA | | | | 508,050 |

20

| | | | | | | | | | | |

| | | | |

Principal

Amount (000) | | Description | | Optional Call

Provisions (2) | | Ratings (3) | | | Value |

| | | | | | | | | | | |

| | | Mississippi – 1.3% | | | | | | | | |

| | | | |

| $ | 500 | | Jones County, Mississippi, Hospital Revenue Bonds, South Central Regional Medical Center, Series 1997, 5.400%, 12/01/11 (Pre-refunded 12/01/07) | | 12/07 at 100.00 | | N/R | (4) | | $ | 503,155 |

| | | | |

| | 500 | | Mississippi Development Bank, Revenue Bonds, Mississippi Municipal Energy Agency, Mississippi Power, Series 2006A, 5.000%, 3/01/21 – XLCA Insured | | 3/16 at 100.00 | | AAA | | | | 520,490 |

| | 1,000 | | Total Mississippi | | | | | | | | 1,023,645 |

| | | Missouri – 1.2% | | | | | | | | |

| | | | |

| | 1,000 | | Kansas City Municipal Assistance Corporation, Missouri, Leasehold Revenue Bonds, Series 2004B-1, 0.000%, 4/15/27 – AMBAC Insured | | No Opt. Call | | AAA | | | | 394,090 |

| | | | |

| | 500 | | Missouri Joint Municipal Electric Utility Commission, Plum Point Project, Revenue Bonds, Series 2006, 5.000%, 1/01/21 – MBIA Insured | | 1/16 at 100.00 | | AAA | | | | 523,080 |

| | 1,500 | | Total Missouri | | | | | | | | 917,170 |

| | | Nevada – 0.7% | | | | | | | | |

| | | | |

| | 480 | | Clark County, Nevada, Motor Vehicle Fuel Tax Highway Improvement Revenue Bonds, Series 2003, 5.125%, 7/01/17 – AMBAC Insured | | 7/13 at 100.00 | | AAA | | | | 506,477 |

| | | | |

| | 15 | | Nevada Housing Division, Single Family Mortgage Bonds, Mezzanine Series 1997B-1, 6.000%, 4/01/15 (Alternative Minimum Tax) | | 10/07 at 102.00 | | Aa3 | | | | 15,114 |

| | 495 | | Total Nevada | | | | | | | | 521,591 |

| | | New Jersey – 1.0% | | | | | | | | |

| | | | |

| | 500 | | New Jersey Transportation Trust Fund Authority, Transportation System Bonds, Series 2006A, 5.250%, 12/15/22 – FSA Insured | | No Opt. Call | | AAA | | | | 548,185 |

| | | | |

| | 245 | | Tobacco Settlement Financing Corporation, New Jersey, Tobacco Settlement Asset-Backed Bonds, Series 2002, 5.750%, 6/01/32 (Pre-refunded 6/01/12) | | 6/12 at 100.00 | | AAA | | | | 260,768 |

| | 745 | | Total New Jersey | | | | | | | | 808,953 |

| | | New York – 4.1% | | | | | | | | |

| | | | |

| | 500 | | Dormitory Authority of the State of New York, FHA-Insured Mortgage Revenue Bonds, Montefiore Hospital, Series 2004, 5.000%, 2/01/19 – FGIC Insured | | 2/15 at 100.00 | | AAA | | | | 523,230 |

| | | | |

| | 125 | | New York City, New York, General Obligation Bonds, Fiscal Series 1997D, 5.875%, 11/01/11 | | 11/08 at 100.00 | | AA | | | | 127,061 |

| | | | |

| | 700 | | New York City, New York, General Obligation Bonds, Fiscal Series 1998D, 5.500%, 8/01/10 | | 8/07 at 101.00 | | AA | | | | 707,896 |

| | | | |

| | 300 | | New York City, New York, General Obligation Bonds, Fiscal Series 1998D, 5.500%, 8/01/10 (Pre-refunded 8/01/07) | | 8/07 at 101.00 | | AA | (4) | | | 303,438 |

| | | | |

| | | New York State Tobacco Settlement Financing Corporation, Tobacco Settlement Asset-Backed and State Contingency Contract-Backed Bonds, Series 2003B-1C: | | | | | | | | |

| | 1,000 | | 5.500%, 6/01/15 | | 6/10 at 100.00 | | AA– | | | | 1,039,970 |

| | 500 | | 5.500%, 6/01/16 | | 6/11 at 100.00 | | AA– | | | | 525,755 |

| | 3,125 | | Total New York | | | | | | | | 3,227,350 |

| | | North Carolina – 1.8% | | | | | | | | |

| | | | |

| | 515 | | North Carolina Eastern Municipal Power Agency, Power System Revenue Refunding Bonds, Series 1997A, 5.375%, 1/01/24 – MBIA Insured | | 1/08 at 101.00 | | AAA | | | | 523,477 |

| | | | |

| | 835 | | North Carolina Municipal Power Agency 1, Catawba Electric Revenue Bonds, Series 1980,

10.500%, 1/01/10 (ETM) | | No Opt. Call | | AAA | | | | 912,997 |

| | 1,350 | | Total North Carolina | | | | | | | | 1,436,474 |

21

Portfolio of Investments

Nuveen Balanced Municipal and Stock Fund (continued)

June 30, 2007

| | | | | | | | | | | |

| | | | |

Principal

Amount (000) | | Description | | Optional Call

Provisions (2) | | Ratings (3) | | | Value |

| | | | | | | | | | | |

| | | Ohio – 1.6% | | | | | | | | |

| | | | |

| $ | 250 | | Cuyahoga County, Ohio, Revenue Refunding Bonds, Cleveland Clinic Health System, Series 2003A, 5.750%, 1/01/22 | | 7/13 at 100.00 | | AA– | | | $ | 268,528 |

| | | | |

| | 1,000 | | Lorain County, Ohio, Healthcare Facilities Revenue Refunding Bonds, Kendal at Oberlin, Series 1998A, 5.375%, 2/01/12 | | 2/08 at 101.00 | | BBB | | | | 1,008,420 |

| | 1,250 | | Total Ohio | | | | | | | | 1,276,948 |

| | | Oklahoma – 1.9% | | | | | | | | |

| | | | |

| | 470 | | Edmond Public Works Authority, Oklahoma, Utility System Revenue Refunding Bonds, Series 1999, 5.600%, 7/01/19 (Pre-refunded 7/01/09) – AMBAC Insured | | 7/09 at 100.00 | | AAA | | | | 485,867 |

| | | | |

| | 1,000 | | Oklahoma State Industries Authority, Health System Revenue Refunding Bonds, Baptist Medical Center, Series 1995D, 6.000%, 8/15/07 – AMBAC Insured | | No Opt. Call | | AAA | | | | 1,002,760 |

| | 1,470 | | Total Oklahoma | | | | | | | | 1,488,627 |

| | | Oregon – 0.5% | | | | | | | | |

| | | | |