UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07685

Frontegra Funds, Inc.

(Exact name of registrant as specified in charter)

400 Skokie Blvd.

Suite 500

Northbrook, Illinois 60062

(Address of principal executive offices) (Zip code)

William D. Forsyth III

400 Skokie Blvd., Suite 500

Northbrook, Illinois 60062

(Name and address of agent for service)

(847) 509-9860

Registrant's telephone number, including area code

Date of fiscal year end: June 30, 2010

Date of reporting period: December 31, 2009

Item 1. Reports to Stockholders.

SEMI-ANNUAL REPORT

Frontegra Columbus Core Plus Fund

Frontegra Columbus Core Fund

Frontegra IronBridge Small Cap Fund

Frontegra IronBridge SMID Fund

Frontegra IronBridge Global Focus Fund

Frontegra Mastholm International Equity Fund

Frontegra Netols Small Cap Value Fund

Frontegra Asset Management, Inc.

________

December 31, 2009

TABLE OF CONTENTS

| Shareholder Letter | 1 |

| Expense Example | 2 |

| Frontegra Columbus Core Plus Fund | |

| Frontegra Columbus Core Fund | |

| Report from Reams Asset Management Company, LLC | 6 |

| Investment Highlights | 9 |

| Schedule of Investments | 10 |

| Statement of Assets and Liabilities | 16 |

| Statement of Operations | 17 |

| Statements of Changes in Net Assets | 18 |

| Financial Highlights | 19 |

| Investment Highlights | 21 |

| Schedule of Investments | 22 |

| Statement of Assets and Liabilities | 27 |

| Statement of Operations | 28 |

| Statements of Changes in Net Assets | 29 |

| Financial Highlights | 30 |

| Frontegra IronBridge Small Cap Fund | |

| Frontegra IronBridge SMID Fund | |

| Report from IronBridge Capital Management, L.P. | 32 |

| Investment Highlights | 34 |

| Schedule of Investments | 35 |

| Statement of Assets and Liabilities | 39 |

| Statement of Operations | 40 |

| Statements of Changes in Net Assets | 41 |

| Financial Highlights | 42 |

| Investment Highlights | 43 |

| Schedule of Investments | 44 |

| Statement of Assets and Liabilities | 48 |

| Statement of Operations | 49 |

| Statements of Changes in Net Assets | 50 |

| Financial Highlights | 51 |

| | |

| Frontegra IronBridge Global Focus Fund | |

| Report from IronBridge Capital Management, L.P. | 53 |

| Investment Highlights | 55 |

| Schedule of Investments | 56 |

| Portfolio Diversification | 58 |

| Statement of Assets and Liabilities | 59 |

| Statement of Operations | 60 |

| Statements of Changes in Net Assets | 61 |

| Financial Highlights | 62 |

| Frontegra Mastholm International Equity Fund | |

| Report from Mastholm Asset Management, LLC | 64 |

| Investment Highlights | 65 |

| Schedule of Investments | 66 |

| Portfolio Diversification | 68 |

| Statement of Assets and Liabilities | 69 |

| Statement of Operations | 70 |

| Statements of Changes in Net Assets | 71 |

| Financial Highlights | 72 |

| Frontegra Netols Small Cap Value Fund | |

| Report from Netols Asset Management, Inc. | 74 |

| Investment Highlights | 75 |

| Schedule of Investments | 76 |

| Statement of Assets and Liabilities | 79 |

| Statement of Operations | 80 |

| Statements of Changes in Net Assets | 81 |

| Financial Highlights | 82 |

| Notes to Financial Statements | 84 |

| Board of Directors’ Approval of Advisory and Subadvisory Agreements | 97 |

| Voting Results of Special Meeting of Shareholders | 106 |

| | |

This report is submitted for the general information of the shareholders of the Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by an effective Prospectus for the applicable Fund. The Prospectus may be obtained by calling 1-888-825-2100. Each Prospectus includes more complete information about management fees and expenses, investment objectives, risks and operating policies of the applicable Fund. Please read the Prospectus carefully.

Frontegra Funds, Inc. are distributed by Frontegra Strategies, LLC, 400 Skokie Blvd., Suite 500, Northbrook, IL 60062. Frontegra Strategies, LLC, member of FINRA and SIPC, is an affiliate of Frontegra Asset Management, Inc., the Funds’ investment adviser.

This page intentionally left blank.

DEAR FELLOW SHAREHOLDERS:

We are pleased to report on the progress of the Frontegra Funds over the past six months ending December 31, 2009. Markets rebounded sharply in the second half of 2009 following a significant downturn. The S&P 500 Index was up over 21% for the period. Small capitalization stocks were up, with the Russell 2000 Index returning 23.90%. International stocks, as measured by the MSCI EAFE Index, returned 22.18% over the same time frame. The U.S. bond market, as measured by the Barclays Capital U.S. Aggregate Bond Index, was up 3.95% for the six-month

period due to the strength of the non-Treasury sectors.

Fund Results

For the six month period ending December 31, 2009, the Funds generated the following net (i.e. after fee) returns:

The Frontegra Columbus Core Plus Fund - Institutional Class, managed by Reams Asset Management Company, returned 11.02% versus the 3.95% return of the Barclays Capital U.S. Aggregate Bond Index; the Frontegra Columbus Core Fund, also managed by Reams Asset Management Company, returned 9.33%.

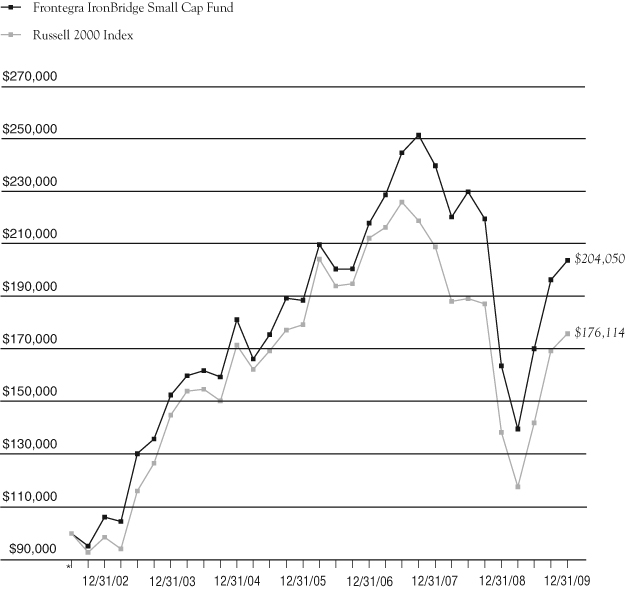

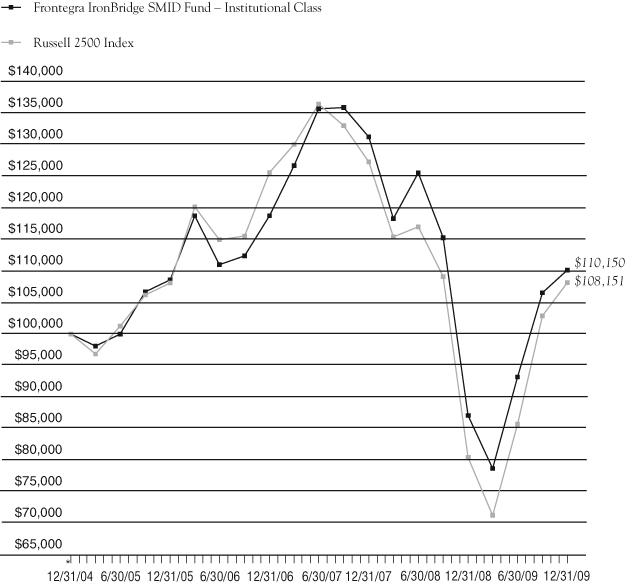

The Frontegra IronBridge Small Cap Fund, managed by IronBridge Capital Management, returned 19.78% versus the 23.90% return for the Russell 2000 Index; the Frontegra IronBridge SMID Fund returned 18.19% versus the Russell 2500 Index return of 26.16%.

The Frontegra Mastholm International Equity Fund, managed by Mastholm Asset Management, returned 17.03% versus the benchmark return of 22.18% for the MSCI EAFE Index.

The Frontegra Netols Small Cap Value Fund – Institutional Class, managed by Netols Asset Management, returned 17.86% versus the Russell 2000 Value Index return of 27.15%.

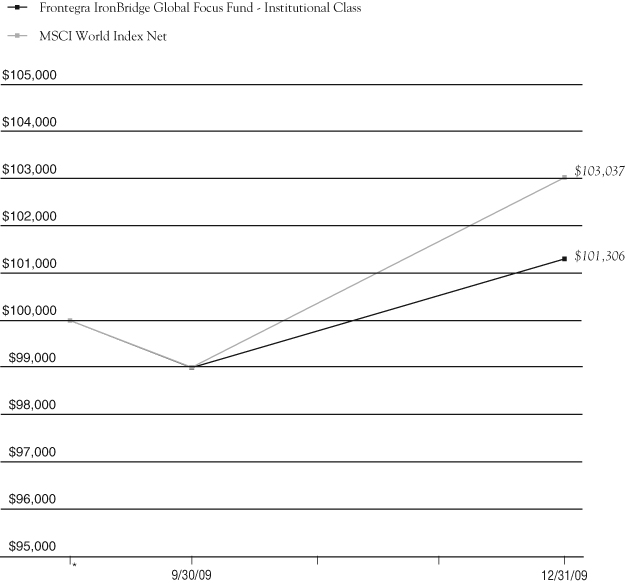

For the period from September 18, 2009 through December 31, 2009, the Frontegra IronBridge Global Focus Fund, also managed by IronBridge Capital Management, returned 1.31% versus the MSCI World Index Net return of 3.04%.

Outlook

The markets continue to be volatile due to concerns with the global economy. We and the subadvisers of the Frontegra Funds will strive to manage skillfully in these turbulent markets.

We will continue to oversee the investment management of the Frontegra Funds with the care and diligence that have served our shareholders well in the past. As always, we appreciate your investment and your continued confidence in the Frontegra Funds.

Best regards,

William D. Forsyth, CFA

President

Frontegra Funds, Inc.

Frontegra Funds

EXPENSE EXAMPLE

December 31, 2009 (Unaudited)

As a shareholder of a mutual fund, you incur two types of costs: (1) transaction costs, including redemption fees, and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees and other fund expenses. Although the Funds charge no sales loads, you will be assessed fees for outgoing wire transfers, returned checks and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Funds’ transfer agent. If you request that a redemption be made by wire transfer, currently the Funds’ transfer agent charges a $15.00 fee. A redemption fee of 2.00% of the then current value of the shares redeemed may be imposed on certain redemptions of shares made within 30 days of purchase for the Frontegra IronBridge Global Focus and Mastholm International Equity Funds.

This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (7/1/09 – 12/31/09).

Actual Expenses

The first line of the table on the following page for each Fund provides information about actual account values and actual expenses. The Example includes management fees, registration fees, fee waivers/reimbursements and other expenses. However, the Example does not include portfolio trading commissions and related expenses and other extraordinary expenses as determined under generally accepted accounting principles. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period’’ to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table for each Fund provides information about hypothetical account values and hypothetical expenses based on each of the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each of the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs could have been higher.

Frontegra Funds

EXPENSE EXAMPLE (continued)

December 31, 2009 (Unaudited)

| | Beginning Account | Ending Account | Annualized | Expenses Paid |

| Frontegra Fund | Value 7/1/2009 | Value 12/31/2009 | Expense Ratio* | During the Period* |

| Columbus Core Plus | | | | |

| Fund – Institutional Class | | | | |

| Actual Fund Return | $1,000.00 | $1,110.20 | 0.35% | $1.86 |

| Hypothetical 5% Return | $1,000.00 | $1,023.44 | 0.35% | $1.79 |

| | | | | |

| Columbus Core Fund | | | | |

| Actual Fund Return | $1,000.00 | $1,093.30 | 0.35% | $1.85 |

| Hypothetical 5% Return | $1,000.00 | $1,023.44 | 0.35% | $1.79 |

| | | | | |

| IronBridge Small Cap Fund | | | | |

| Actual Fund Return | $1,000.00 | $1,197.80 | 1.07% | $6.09 |

| Hypothetical 5% Return | $1,000.00 | $1,019.66 | 1.07% | $5.60 |

| | | | | |

| IronBridge SMID Fund | | | | |

| Actual Fund Return | $1,000.00 | $1,181.90 | 0.95% | $5.22 |

| Hypothetical 5% Return | $1,000.00 | $1,020.42 | 0.95% | $4.84 |

| | | | | |

| Mastholm International Equity Fund | | | | |

| Actual Fund Return | $1,000.00 | $1,170.30 | 0.75% | $4.10 |

| Hypothetical 5% Return | $1,000.00 | $1,021.42 | 0.75% | $3.82 |

| | | | | |

| Netols Small Cap Value | | | | |

| Fund – Institutional Class | | | | |

| Actual Fund Return | $1,000.00 | $1,178.60 | 1.10% | $6.10 |

| Hypothetical 5% Return | $1,000.00 | $1,019.61 | 1.10% | $5.65 |

| | | | | |

| Netols Small Cap | | | | |

| Value Fund – Class Y | | | | |

| Actual Fund Return | $1,000.00 | $1,177.10 | 1.50% | $8.29 |

| Hypothetical 5% Return | $1,000.00 | $1,017.59 | 1.50% | $7.68 |

| * | Expenses are equal to each Fund’s annualized expense ratio indicated above, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

Frontegra Funds

EXPENSE EXAMPLE (continued)

December 31, 2009 (Unaudited)

| | Beginning Account | Ending Account | Annualized | Expenses Paid |

| Frontegra Fund | Value | Value 12/31/2009 | Expense Ratio* | During the Period* |

| | | | | |

| Columbus Core Plus Fund – Y Class | | | | |

| Actual Fund Return* | $1,000.00 | $1,002.30 | 0.75% | $1.01 |

| Hypothetical 5% Return** | $1,000.00 | $1,021.42 | 0.75% | $3.82 |

| * | Actual expenses are equal to the Fund’s annualized expense ratio of 0.75% multiplied by the average account value over the period, multiplied by 49/365 to reflect the most recent fiscal period end since the Class Y Shares commenced operations on November 12, 2009. |

| ** | Hypothetical expenses are equal to the Fund’s annualized expense ratio of 0.75% multiplied by the average account value over the period commencing July 1, 2009, multiplied by 184/365 to reflect information had the Class Y Shares been in operation for the entire fiscal half year. |

| | Beginning Account | Ending Account | Annualized | Expenses Paid |

| Frontegra Fund | Value | Value 12/31/2009 | Expense Ratio* | During the Period* |

| | | | | |

| IronBridge Global Focus Fund | | | | |

| Actual Fund Return* | $1,000.00 | $1,013.10 | 1.00% | $2.81 |

| Hypothetical 5% Return** | $1,000.00 | $1,020.16 | 1.00% | $5.09 |

| * | Actual expenses are equal to the Fund’s annualized expense ratio of 1.00% multiplied by the average account value over the period, multiplied by 104/365 to reflect the most recent fiscal period end since the Class Y Shares commenced operations on September 18, 2009. |

| ** | Hypothetical expenses are equal to the Fund’s annualized expense ratio of 1.00% multiplied by the average account value over the period commencing July 1, 2009, multiplied by 184/365 to reflect information had the IronBridge Global Focus Fund been in operation for the entire fiscal half year. |

FRONTEGRA

COLUMBUS CORE PLUS FUND

FRONTEGRA

COLUMBUS CORE FUND

REPORT FROM REAMS ASSET

MANAGEMENT COMPANY, LLC:

Dear Fellow Shareholders:

The Frontegra Columbus Core Plus Fund strives to achieve a high level of total return consistent with the preservation of capital by investing in a diversified portfolio of fixed income securities of varying maturities. This objective is relative to and measured against the Barclays Capital U.S. Aggregate Bond Index.

The Frontegra Columbus Core Fund strives to achieve a high level of total return consistent with the preservation of capital by investing in a diversified portfolio of investment grade bonds of varying maturities. This objective is relative to and measured against the Barclays Capital U.S. Aggregate Bond Index.

Performance Review

For the six month period ending December 31, 2009, the Frontegra Columbus Core Plus Fund (Institutional Class) had a net return of 11.02% compared to a return of 3.95% for the benchmark, the Barclays Capital U.S. Aggregate Bond Index. Duration strategy added 16 basis points to performance for the period as the portfolio duration was positioned aggressively as the Treasury yield curve fell during the third quarter. Yield curve strategy added 3 basis points as the portfolio was overweighted the long end of the yield curve when the curve flattened slightly during the third quarter. Sector selection added 398 basis points to performance and security selection added 307 basis points. Within these categories, investment grade credit holdings added 323 basis points to performance, high yield holdings added 205 basis points, asset backed securities (“ABS”) added 131 basis points and commercial mortgage backed securities (“CMBS”) added 80 basis points to performance as all four sectors outperformed and were overweighted in the portfolio. Government related holdings subtracted 23 basis points and mortgage backed securities (“MBS”) subtracted 11 basis points as both sectors performed well but were underweighted in the portfolio.

For the six month period ending December 31, 2009, the Frontegra Columbus Core Fund had a net return of 9.33% compared to a return of 3.95% for the benchmark, the Barclays Capital U.S. Aggregate Bond Index. Duration strategy added 29 basis points to performance for the period as the portfolio duration was positioned aggressively as the Treasury yield curve fell during the third quarter. Yield curve strategy added 5 basis points as the portfolio was overweighted the long end of the yield curve when the curve flattened slightly during the third quarter. Sector selection added 312 basis points to performance and security selection added 209 basis points. Within these categories, investment grade credit holdings added 417 basis points to performance, CMBS added 56 basis points and ABS added 40 basis points to performance as all three sectors outperformed and were overweighted in the portfolio. MBS added 30 basis points to performance due to an overweight in certain non-agency MBS holdings. Government related holdings subtracted 22 basis points as the sector performed well but was underweighted in the portfolio.

Fixed Income Outlook

Non government-guaranteed sectors continued to outperform during the fourth quarter. Economic numbers have been stabilizing and beginning to improve, particularly toward the end of the quarter. It remains unclear if the magnitude of improvement in the capital markets will be justified by a solid, long-term recovery in the economy. If the underlying economic recovery does not follow through over the next several quarters, returns in the capital markets could be volatile.

| | • | Fed rate policy remains grounded at the current 0.0% to 0.25% level with overt indications that rates will remain low for an “extended period of time.” Although the economy in general, and the labor market specifically, have been slow to respond to the low rates, the Fed acknowledged the danger that the low rates may be sparking undue financial market speculation. This highlights a broader concern that financial markets, which have shown exceptional returns in the last three quarters of 2009, are perhaps getting a bit too far ahead of the true economic condition of the country. |

| | • | Corporate earnings reports for the third quarter were frequently ahead of analyst estimates although revenue was often short of the estimates. It appears that cost cutting drove the better-than-expected earnings results. Overall, investors were disappointed as they were looking for better revenue numbers which would indicate the beginning of an economic recovery. |

| | • | Moves in the U.S. dollar generated considerable media attention during the quarter. The U.S. Dollar Index, an index that averages the exchange rates between the U.S. dollar and six major world currencies, declined nearly 16% from its early March peak through the end of November. The consistent message from the Fed indicating low interest rates will be around for “an extended period of time” has provided a fertile environment for dollar weakness. When a country’s short-term interest rates are low, it is difficult to attract capital in the short-run, keeping downward pressure on the currency. Expectations that the Fed may have to move off its extremely low interest rate policy sooner sparked a small U.S. dollar rally in December, moving the U.S. Dollar Index up almost 4%. |

| | • | A call for a payment standstill by Dubai World sent a mini-shockwave through world markets during the Thanksgiving holiday. The total size of the affected debt was relatively small, but fears centered on a follow-on or domino effect. These fears proved to be unfounded as this incident appeared to be isolated with few follow-on effects. However, this should serve as a “wake-up call” to other emerging markets that have become increasingly complacent regarding the risk of debts that were made during less prudent times. |

| | • | Several Western European country debt issues were downgraded by rating agencies late in the quarter. This resulted in some weakness in the sovereign debt markets. Greece, Spain, and Portugal were singled out for downgrades and increased scrutiny as the rating agencies highlighted high debt to GDP ratios and the deterioration in these measures due to the global recession. |

| | • | With the excessive stimulus and loose monetary policy currently in place, economic data in the first half of 2010 should be relatively strong. However, the high debt levels in the developed markets will take multiple years to be reduced, dampening growth for years to come. As a result, we anticipate increased volatility in capital markets going forward. |

| | • | In regard to market performance, high yield was the best performing sector during the quarter, with option-adjusted spreads tightening nearly 155 basis points. CMBS tightened 65 basis points as investors were willing to assume additional risk in response to recent positive economic data. The investment grade corporate and ABS sectors both exhibited positive performance as well, tightening 47 and 33 basis points, respectively. An already steep Treasury yield curve steepened further as 30-year Treasury rates moved up about 60 basis points while two-year rates increased only about 20 basis points. Concerns continue to be voiced regarding the extensive new issue supply that is expected from the Treasury, but individual auctions have been well received by the market. |

Core Plus Portfolio Strategy

| | • | Maintaining a lower risk profile in the portfolio was an increasing focus during the fourth quarter. Our weighting in Treasury securities rose as a result of this risk reduction focus, but also as a result of our positioning to take advantage of a historically steep yield curve. If the yield curve flattens as we expect it to, the portfolio should outperform. We anticipate maintaining an overweight position in Treasury securities until better investment opportunities become available in other sectors of the fixed income markets. |

| | • | The portfolio’s MBS holdings are currently underweight. This is due, in part, to make room for our curve positioning, but also as a result of our view that mortgage pass-through securities may underperform as the government winds down its purchases in this sector and current tight spreads do not adequately compensate the investor for the risks in this sector. |

| | • | We remain overweight in the ABS sector. We continue to find value in the auto finance portion of this sector. |

| | • | We have become increasingly cautious of the corporate sector in general and as a result we have reduced our holdings in the sector. Our positions are focused on specific themes that we expect to outperform. If the corporate market experiences a pullback, an event that we feel is likely, we will be poised to return to an overweight position. |

Core Portfolio Strategy

| | • | Maintaining a lower risk profile in the portfolio was an increasing focus during the fourth quarter. Our weighting in Treasury securities rose as a result of this risk reduction focus, but also as a result of our positioning to take advantage of a historically steep yield curve. If the yield curve flattens as we expect it to, the portfolio should outperform. We anticipate maintaining an overweight position in Treasury securities until better investment opportunities become available in other sectors of the fixed income markets. |

| | • | The portfolio’s MBS holdings are currently underweight. This is due, in part, to make room for our curve positioning, but also as a result of our view that mortgage pass-through securities may underperform as the government winds down its purchases in this sector and current tight spreads do not adequately compensate the investor for the risks in this sector. |

| | • | We remain overweight in the ABS sector. We continue to find value in the auto finance portion of this sector. |

| | • | We have become increasingly cautious of the corporate sector in general and as a result we have reduced our holdings in the sector. Our positions are focused on specific themes that we expect to outperform. If the corporate market experiences a pullback, an event that we feel is likely, we will be poised to return to an overweight position. |

We appreciate your continued support as fellow shareholders in the Funds.

Regards,

|  |

| Mark M. Egan, CFA, CPA | Thomas M. Fink, CFA |

| Reams Asset Management Company, LLC | Reams Asset Management Company, LLC |

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

| | Portfolio Total Return* | | | |

| | FOR PERIODS ENDED 12/31/09 | FUND | INDEX | |

| | | | | |

| | SIX MONTHS | 11.02% | 3.95% | |

| | | | | |

| | ONE YEAR | 35.19% | 5.93% | |

| | | | | |

| | FIVE YEAR | | | |

| | AVERAGE ANNUAL | 7.69% | 4.97% | |

| | | | | |

| | TEN YEAR | | | |

| | AVERAGE ANNUAL | 7.91% | 6.33% | |

This chart assumes an initial gross investment of $100,000 made on 12/31/99. Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of existing fee waivers, total return would be reduced. The recent growth rate in the fixed income market has helped to produce short-term returns for some asset classes that are not typical and may not continue in the future. Because of ongoing market volatility, Fund performance may be subject to substantial short-term changes. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The Barclays Capital U.S. Aggregate Bond Index (formerly the Lehman Brothers Aggregate Bond Index) is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset backed and mortgage backed securities, with maturities of at least one year. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in fixed income securities. A direct investment in the index is not possible.

| * | The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

The above graph relates to Institutional Class shares of the Fund. Performance for Class Y shares will vary from the performance of the Institutional Class shares shown above due to differences in expenses.

Frontegra Columbus Core Plus Fund

SCHEDULE OF INVESTMENTS

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

| ASSET BACKED SECURITIES 10.9% | | | |

| | | American Express Credit | | | |

| $ | 1,710,000 | | 2008-3, Class A, | | | |

| | | | 1.183%, 08/15/2012 | | $ | 1,710,393 | |

| | | | Americredit Automobile | | | | |

| | | | Receivables Trust | | | | |

| | 1,630,000 | | 2008-AF, Class A4, | | | | |

| | | | 6.960%, 10/14/2014 | | | 1,714,432 | |

| | | | Capital One Prime Auto | | | | |

| | 2,060,812 | | 2006-1, Class A-4, | | | | |

| | | | 5.010%, 11/15/2011 | | | 2,064,274 | |

| | | | Chase Issuance Trust | | | | |

| | 3,115,000 | | 2009-A7, Class A7, | | | | |

| | | | 0.683%, 09/15/2012 | | | 3,118,719 | |

| | 1,745,000 | | 2005-8A, Class A, | | | | |

| | | | 0.273%, 10/15/2012 | | | 1,742,672 | |

| | | | Chrysler Financial Auto | | | | |

| | | | Securitization Trust | | | | |

| | 1,800,000 | | 2009-B, Class A-2, | | | | |

| | | | 1.150%, 11/08/2011 | | | 1,799,684 | |

| | | | Chrysler Financial Automobile TALF | | | | |

| | 1,010,000 | | 2009-AF, Class A3, | | | | |

| | | | 2.820%, 01/15/2016 | | | 1,025,187 | |

| | | | Citibank Credit Card Issuance Trust | | | | |

| | 3,995,000 | | 2006-A6, Class A6, | | | | |

| | | | 0.242%, 05/24/2012 | | | 3,989,832 | |

| | | | Countrywide | | | | |

| | | | Asset-Backed Certificates | | | | |

| | 346,220 | | 2006-S3, Class A1, | | | | |

| | | | 5.460%, 06/25/2021 (b) | | | 283,197 | |

| | 482,772 | | 2006-S2, Class A2, | | | | |

| | | | 5.627%, 07/25/2027 | | | 380,743 | |

| | 4,061,254 | | 2006-S2, Class A3, | | | | |

| | | | 5.841%, 07/25/2027 | | | 1,297,431 | |

| | 1,743,085 | | 2006-S2, Class A4, | | | | |

| | | | 6.091%, 07/25/2027 | | | 456,037 | |

| | 1,002,603 | | 2006-S5, Class A3, | | | | |

| | | | 5.762%, 06/25/2035 | | | 253,317 | |

| | 1,615,621 | | 2007-S2, Class A6, | | | | |

| | | | 5.779%, 05/25/2037 | | | 766,698 | |

| | | | Credit Suisse Mortgage | | | | |

| | | | Capital Certificates | | | | |

| | 2,061,000 | | 2009-12R, Class 41A1, | | | | |

| | | | 5.250%, 03/27/2037 | | | 2,061,000 | |

| | | | Discover Card Master Trust I | | | | |

| | 930,000 | | 2003-3, Class A, | | | | |

| | | | 0.445%, 09/15/2012 | | | 929,619 | |

| | | | Ford Credit Auto Owner Trust | | | | |

| | 2,355,000 | | Series 2009-D, Class A3, | | | | |

| | | | 2.170%, 10/15/2013 | | | 2,378,299 | |

| | 444,492 | | 2008-C, Class A2A, | | | | |

| | | | 3.720%, 01/15/2011 | | | 445,696 | |

| | | | GE Capital Credit Card | | | | |

| | | | Master Note Trust | | | | |

| | 2,450,000 | | Series 2009-3, Class A, | | | | |

| | | | 2.540%, 09/15/2014 | | | 2,451,959 | |

| | | | GMAC Mortgage | | | | |

| | | | Corporation Loan Trust | | | | |

| | 1,628,782 | | 2006-HE2, Class A3, | | | | |

| | | | 6.320%, 05/25/2036 | | | 735,092 | |

| | 2,218,201 | | 2006-HE3, Class A3, | | | | |

| | | | 5.805%, 10/25/2036 | | | 1,059,264 | |

| | | | GSAA Home Equity Trust | | | | |

| | 1,303,854 | | 2006-S1, Class 1A1, | | | | |

| | | | 2.621%, 01/25/2037 | | | 203,375 | |

| | | | Hertz Vehicle Financing LLC | | | | |

| | 715,000 | | 2005-1A, Class A4, | | | | |

| | | | 2.711%, 11/25/2011 | | | | |

| | | | (Acquired 08/21/2008 and | | | | |

| | | | 12/10/2008, Cost $670,984) (a)(b) | | | 705,051 | |

| | 880,000 | | 2005-2A, Class A5, | | | | |

| | | | 2.711%, 11/25/2011 | | | | |

| | | | (Acquired 08/01/2008 and | | | | |

| | | | 12/10/2008, Cost $836,302) (a)(b) | | | 867,756 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

ASSET BACKED SECURITIES 10.9% (continued) | | | |

| $ | 1,825,000 | | 2009-2A, Class A1, | | | |

| | | | 4.260%, 03/25/2014 | | | |

| | | | (Acquired 10/16/2009, | | | |

| | | | Cost $1,824,891) (a)(b) | | $ | 1,818,692 | |

| | | | Home Equity Mortgage Trust | | | | |

| | 1,440,000 | | 2005-5, Class A1F2, | | | | |

| | | | 5.150%, 04/25/2036 | | | 242,604 | |

| | 4,478,097 | | 2006-5, Class A1, | | | | |

| | | | 5.500%, 01/25/2037 | | | 447,577 | |

| | | | Hyundai Auto Receivables Trust | | | | |

| | 4,140,000 | | Series 2009-A, Class A3, | | | | |

| | | | 2.030%, 08/15/2013 | | | 4,167,156 | |

| | | | Keystone Owner Trust | | | | |

| | 6,224 | | 1998-P1, Class M1, | | | | |

| | | | 7.530%, 05/25/2025 (Acquired | | | | |

| | | | 12/10/2008, Cost $5,512) (a) | | | 5,971 | |

| | | | Mid-State Trust | | | | |

| | 930,954 | | 11, Class A1, 4.864%, 07/15/2038 | | | 832,166 | |

| | | | MSCC Heloc Trust | | | | |

| | 1,555,716 | | Series 2007-1, Class A, | | | | |

| | | | 0.385%, 12/25/2031 | | | 664,225 | |

| | | | Residential Funding | | | | |

| | | | Mortgage Securities | | | | |

| | 202,846 | | 2005-HS1, Class AI2, | | | | |

| | | | 4.660%, 07/25/2020 | | | 182,576 | |

| | 568,764 | | 2003-HS1, Class AI6, | | | | |

| | | | 3.830%, 02/25/2033 | | | 440,706 | |

| | 630,000 | | 2005-HS1, Class AI4, | | | | |

| | | | 5.110%, 09/25/2035 | | | 139,435 | |

| | 1,777,206 | | 2006-HSA1, Class A3, | | | | |

| | | | 5.230%, 02/25/2036 | | | 622,017 | |

| | 1,441,511 | | 2006-HSA1, Class A4, | | | | |

| | | | 5.490%, 02/25/2036 | | | 147,602 | |

| | 2,035,526 | | 2006-HSA1, Class A5, | | | | |

| | | | 5.310%, 02/25/2036 | | | 736,348 | |

| | 877,940 | | 2006-HSA2, Class AI2, | | | | |

| | | | 5.494%, 03/25/2036 | | | 781,698 | |

| | 1,160,000 | | 2006-HSA2, Class AI3, | | | | |

| | | | 5.550%, 03/25/2036 | | | 442,720 | |

| | 820,000 | | 2006-HSA2, Class AI4, | | | | |

| | | | 5.810%, 03/25/2036 | | | 74,630 | |

| | | | Saco I Trust | | | | |

| | 1,106,293 | | 2006-9, Class A1, | | | | |

| | | | 5.480%, 08/25/2036 | | | 183,582 | |

| | | | Total Asset Backed Securities | | | | |

| | | | (Cost $47,312,017) | | | 44,369,432 | |

| CORPORATE BONDS 15.3% | | | | |

| | | | Airlines 2.6% | | | | |

| | | | Delta Air Lines, Inc. | | | | |

| | 3,238,112 | | Series 2002-1, 6.718%, 07/02/2024 | | | 2,817,157 | |

| | | | Northwest Airlines, Inc. | | | | |

| | 4,303,892 | | 7.027%, 05/01/2021 | | | 3,808,944 | |

| | | | United Airlines | | | | |

| | 4,489,534 | | Series 071A, 6.636%, 01/02/2022 | | | 3,816,104 | |

| | | | | | | 10,442,205 | |

| | | | Commercial Banks 2.5% | | | | |

| | | | Manufacturers & Traders Trust Co. | | | | |

| | 2,610,000 | | 3.850%, 04/01/2013 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $2,380,600) (a)(b) | | | 2,399,548 | |

| | 1,685,000 | | 5.629%, 12/01/2021 | | | 1,448,499 | |

| | | | Marshall & Ilsley Bank | | | | |

| | 5,935,000 | | 5.413%, 12/04/2012 | | | 4,774,292 | |

| | | | Regions Bank | | | | |

| | 1,745,000 | | 7.500%, 05/15/2018 | | | 1,595,167 | |

| | | | | | | 10,217,506 | |

| | | | Consumer Finance 0.8% | | | | |

| | | | Ford Motor Credit Co. | | | | |

| | 1,540,000 | | 8.000%, 12/15/2016 | | | 1,542,047 | |

| | | | GMAC LLC | | | | |

| | 1,767,000 | | 6.750%, 12/01/2014 | | | | |

| | | | (Acquired 02/05/2009, | | | | |

| | | | Cost $1,232,588) (a) | | | 1,678,650 | |

| | | | | | | 3,220,697 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

CORPORATE BONDS 15.3% (continued) | | | |

| | | Diversified Financial Services 1.6% | | | |

| | | American General Finance | | | |

| $ | 3,075,000 | | 6.900%, 12/15/2017 | | $ | 2,135,138 | |

| | | | International Lease Finance Corp. | | | | |

| | 3,455,000 | | 5.625%, 09/20/2013 | | | 2,710,140 | |

| | | | Lehman Brothers Holdings | | | | |

| | 7,000,000 | | 6.875%, 05/02/2018 | | | | |

| | | | (Acquired 09/16/2008, | | | | |

| | | | Cost $2,313,205) (d) | | | 1,452,500 | |

| | | | | | | 6,297,778 | |

| | | | Diversified Telecommunication | | | | |

| | | | Services 0.5% | | | | |

| | | | Qwest Corp. | | | | |

| | 2,430,000 | | 7.125%, 11/15/2043 | | | 1,992,600 | |

| | | | | | | | |

| | | | Electric Utilities 1.6% | | | | |

| | | | AES Eastern Energy | | | | |

| | 878,785 | | 9.000%, 01/02/2017 | | | 882,081 | |

| | 1,570,000 | | 9.670%, 01/02/2029 | | | 1,652,425 | |

| | | | Indianapolis Power & Light Co. | | | | |

| | 1,100,000 | | 6.050%, 10/01/2036 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $1,061,143) (a) | | | 1,086,809 | |

| | | | Mackinaw Power LLC | | | | |

| | 1,147,297 | | 6.296%, 10/31/2023 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $1,107,221) (a) | | | 1,125,223 | |

| | | | Tenaska Gateway Partners Ltd. | | | | |

| | 553,331 | | 6.052%, 12/30/2023 | | | | |

| | | | (Acquired 05/31/2007 and | | | | |

| | | | 08/03/2007, Cost $553,331) (a) | | | 524,176 | |

| | | | Windsor Financing LLC | | | | |

| | 1,770,075 | | 5.881%, 07/15/2017 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $1,599,428) (a) | | | 1,399,315 | |

| | | | | | | 6,670,029 | |

| | | | Industrial Consumer Services 0.2% | | | | |

| | | | ERAC USA Finance Company | | | | |

| | 980,000 | | 6.375%, 10/15/2017 | | | | |

| | | | (Acquired 10/23/2008 and | | | | |

| | | | 12/10/2008, Cost $738,423) (a) | | | 989,866 | |

| | | | Insurance 3.0% | | | | |

| | | | AIG, Inc. | | | | |

| | 2,020,000 | | 4.250%, 05/15/2013 | | | 1,865,888 | |

| | | | AIG Sunamerica | | | | |

| | 280,000 | | 0.431%, 07/26/2010 | | | 270,900 | |

| | | | AIG Sunamerica Global Financial | | | | |

| | 3,760,000 | | 6.300%, 05/10/2011 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $3,575,876) (a) | | | 3,740,023 | |

| | | | ASIF Global Financing XIX | | | | |

| | 535,000 | | 4.900%, 01/17/2013 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $438,782) (a) | | | 492,335 | |

| | | | Genworth Global Funding | | | | |

| | 430,000 | | 5.250%, 05/15/2012 | | | 434,119 | |

| | | | Jackson National Life Global Funding | | | | |

| | 830,000 | | 5.375%, 05/08/2013 | | | | |

| | | | (Acquired 05/01/2008 and | | | | |

| | | | 12/10/2008, Cost $824,750) (a) | | | 842,882 | |

| | | | Lincoln National Corp. | | | | |

| | 1,270,000 | | 6.250%, 02/15/2020 | | | 1,251,560 | |

| | | | Monumental Global Funding | | | | |

| | 1,605,000 | | 5.500%, 04/22/2013 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $1,603,410) (a) | | | 1,651,389 | |

| | 885,000 | | 5.250%, 01/15/2014 | | | | |

| | | | (Acquired 05/06/2009 and | | | | |

| | | | 06/10/2009, Cost $829,054) (a) | | | 902,935 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

CORPORATE BONDS 15.3% (continued) | | | |

| | | Insurance 3.0% (continued) | | | |

| | | Nationwide Life Global Fund | | | |

| $ | 795,000 | | 5.450%, 10/02/2012 | | | |

| | | | (Acquired 09/25/2007 and | | | |

| | | | 12/10/2008, Cost $793,054) (a) | | $ | 785,296 | |

| | | | | | | 12,237,327 | |

| | | | Metals & Mining 0.9% | | | | |

| | | | Alcoa Inc. | | | | |

| | 1,175,000 | | 5.950%, 02/01/2037 | | | 1,008,411 | |

| | | | Arcelormittal SA Luxembourg | | | | |

| | 1,070,000 | | 6.125%, 06/01/2018 | | | 1,104,064 | |

| | | | U.S. Steel Corp. | | | | |

| | 1,410,000 | | 5.650%, 06/01/2013 | | | 1,402,961 | |

| | | | | | | 3,515,436 | |

| | | | Multi-Utilities & | | | | |

| | | | Unregulated Power 1.4% | | | | |

| | | | Borger Energy Funding | | | | |

| | 2,483,572 | | 7.260%, 12/31/2022 | | | | |

| | | | (Acquired 08/14/2008 and | | | | |

| | | | 12/10/2008, Cost $2,392,160) (a) | | | 2,309,722 | |

| | | | Homer City Funding LLC | | | | |

| | 3,015,272 | | 8.734%, 10/01/2026 | | | 2,909,737 | |

| | | | Kiowa Power Partners LLC | | | | |

| | 620,339 | | 4.811%, 12/30/2013 | | | | |

| | | | (Acquired multiple dates, | | | | |

| | | | Cost $618,166) (a)(b) | | | 626,325 | |

| | | | | | | 5,845,784 | |

| | | | Oil, Gas & Consumable Fuels 0.2% | | | | |

| | | | USX Marathon Group | | | | |

| | 665,000 | | 8.125%, 07/15/2023 | | | 746,466 | |

| | | | Total Corporate Bonds | | | | |

| | | | (Cost $58,262,295) | | | 62,175,694 | |

| | | | | | | | |

| MORTGAGE BACKED SECURITIES 24.7% | | | | |

| | | | Bank of America | | | | |

| | | | Commercial Mortgage, Inc. | | | | |

| | 4,825,000 | | Series 2006-3, Class A4, | | | | |

| | | | 5.889%, 07/10/2044 | | | 4,390,524 | |

| | 4,440,000 | | Series 2009-UB1, Class A4, | | | | |

| | | | 5.620%, 06/24/2050 | | | | |

| | | | (Acquired 06/18/2009 and | | | | |

| | | | 07/07/2009, Cost $3,641,699) (a) | | | 4,031,883 | |

| | | | CitiMortgage Alternative Loan Trust | | | | |

| | 2,037,106 | | Series 2007-A4, Class 2A1, | | | | |

| | | | 5.500%, 04/25/2022 | | | 1,644,963 | |

| | | | Credit Suisse First Boston | | | | |

| | | | Mortgage Securities Corp. | | | | |

| | 337,985 | | Pool # 2005-10, 5.000%, 09/25/2015 | | | 332,915 | |

| | 72,604 | | Pool # 2003-1, 7.000%, 02/25/2033 | | | 71,446 | |

| | | | Credit Suisse Mortgage | | | | |

| | 2,625,000 | | Pool #2009-RR1, | | | | |

| | | | 5.383%, 11/15/2016 | | | | |

| | | | (Acquired 07/09/2009 and | | | | |

| | | | 12/29/2009, Cost $2,133,170) (a) | | | 2,337,741 | |

| | | | FHLMC REMIC (e) | | | | |

| | 2,045,000 | | Series 3563, 4.000%, 08/15/2024 | | | 1,935,075 | |

| | 5,595,000 | | Series 3577, 4.000%, 09/15/2024 | | | 5,315,336 | |

| | 9,810,000 | | Series 3609, 4.000%, 12/15/2024 | | | 10,121,546 | |

| | 501,923 | | Series 2750, 4.000%, 05/15/2026 | | | 508,988 | |

| | | | FNMA (e) | | | | |

| | 4,913,245 | | Pool #931711, 4.000%, 08/01/2019 | | | 5,025,863 | |

| | 2,539,872 | | Pool #MA0174, 4.000%, 09/25/2019 | | | 2,598,089 | |

| | 10,395,516 | | Pool #932108, 4.000%, 11/25/2019 | | | 10,633,795 | |

| | 15,965,000 | | Pool #MA0298, 4.000%, 01/01/2020 | | | 16,346,663 | |

| | | | FNMA REMIC (e) | | | | |

| | 70,068 | | Series 1994-3, Class PL, | | | | |

| | | | 5.500%, 01/25/2024 | | | 74,570 | |

| | | | FNMA TBA (e) | | | | |

| | 12,975,000 | | Pool #000TBA, 6.500%, 02/01/2038 | | | 13,854,861 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

| MORTGAGE BACKED | | | |

SECURITIES 24.7% (continued) | | | |

| | | GS Mortgage Securities Corp. II | | | |

| $ | 3,225,119 | | Series 2007-EOP, Class A1, | | | |

| | | | 5.410%, 03/06/2020 | | | |

| | | | (Acquired Multiple Dates, | | | |

| | | | Cost $3,167,669) (a)(b) | | $ | 3,067,677 | |

| | | | LB-UBS Commercial Mortgage Trust | | | | |

| | 2,610,000 | | Series 2007-C1, Class A4, | | | | |

| | | | 5.424%, 02/15/2040 | | | 2,161,419 | |

| | 4,410,000 | | Series 2007-C2, Class A3, | | | | |

| | | | 5.430%, 02/15/2040 | | | 3,809,311 | |

| | 787,500 | | Series 2007-C3, Class A4, | | | | |

| | | | 6.136%, 07/15/2044 (b) | | | 650,884 | |

| | | | Master Asset Securitization Trust | | | | |

| | 280,415 | | Pool # 2004-3, 4.750%, 01/25/2014 | | | 269,198 | |

| | | | Morgan Stanley Mortgage Loan Trust | | | | |

| | 878,047 | | Series 2006-7, 5.000%, 06/25/2021 | | | 769,251 | |

| | | | Residential Accredit Loans, Inc. | | | | |

| | 1,078,559 | | Series 2005-QS3, Class A1, | | | | |

| | | | 5.000%, 03/25/2020 | | | 962,617 | |

| | 1,233,875 | | Series 2004-QS4, Class A1, | | | | |

| | | | 4.350%, 03/25/2034 | | | 1,125,261 | |

| | | | Wachovia Bank Commercial | | | | |

| | | | Mortgage Trust | | | | |

| | 2,478,474 | | Series 2003-C7, Class A1, 4.241%, | | | | |

| | | | 10/15/2035 (Acquired 12/04/2009 | | | | |

| | | | and 12/29/2009, Cost $2,497,167) (a) | | | 2,494,491 | |

| | 2,650,000 | | Series 2006-C23, Class A4, | | | | |

| | | | 5.418%, 01/15/2045 | | | 2,538,399 | |

| | | | Wells Fargo Alternative Loan Trust | | | | |

| | 1,789,120 | | Series 2007-PA3, Class 6A1, | | | | |

| | | | 5.500%, 07/25/2037 | | | 1,444,714 | |

| | | | Wells Fargo Mortgage | | | | |

| | | | Backed Securities Trust | | | | |

| | 1,993,370 | | Pool # 2006-3, 5.500%, 03/25/2036 | | | 1,826,740 | |

| | | | Total Mortgage Backed Securities | | | | |

| | | | (Cost $100,173,056) | | | 100,344,220 | |

| INSTITUTIONAL TERM LOANS 0.0% | | | | |

| | | | Chrysler LLC | | | | |

| | 7,153,130 | | 6.467%, 11/29/2013 | | | | |

| | | | (Acquired 08/13/2008 and | | | | |

| | | | 08/15/2008, Cost $3,433,612) (d) | | | 125,180 | |

| | | | Total Institutional Term Loans | | | | |

| | | | (Cost $3,433,612) | | | 125,180 | |

| | | | | | | | |

| Number of Shares | | | | | | |

| PREFERRED STOCKS 0.1% | | | | |

| | | | Thrifts & Mortgage Finance 0.1% | | | | |

| | 169,732 | | Fannie Mae | | | | |

| | | | 8.250%, 12/31/2010 (b)(e) | | | 186,705 | |

| | 141,065 | | Freddie Mac | | | | |

| | | | 8.375%, 12/31/2012 (b)(e) | | | 148,118 | |

| | | | Total Preferred Stocks | | | | |

| | | | (Cost $4,155,967) | | | 334,823 | |

| | | | | | | | |

| Principal Amount | | | | | | |

| U.S. TREASURY OBLIGATIONS 49.4% | | | | |

| | | | United States Treasury Bonds 4.9% | | | | |

| $ | 20,435,000 | | 4.500%, 08/15/2039 | | | 19,972,025 | |

| | | | | | | | |

| | | | United States Treasury Notes 40.7% | | | | |

| | 56,825,000 | | 0.875%, 05/31/2011 | | | 56,893,815 | |

| | 6,815,000 | | 1.125%, 06/30/2011 | | | 6,842,682 | |

| | 25,410,000 | | 1.125%, 01/15/2012 | | | 25,386,166 | |

| | 29,530,000 | | 2.125%, 11/30/2014 | | | 28,831,025 | |

| | 7,605,000 | | 3.125%, 10/31/2016 | | | 7,509,344 | |

| | 18,165,000 | | 2.750%, 11/30/2016 | | | 17,488,063 | |

| | 23,215,000 | | 3.375%, 11/15/2019 | | | 22,330,044 | |

| | | | | | | 165,281,139 | |

| | | | United States Treasury Strip 3.8% | | | | |

| | 64,255,000 | | Principal only, 11/15/2039 | | | 15,461,359 | |

| | | | Total U.S. Treasury Obligations | | | | |

| | | | (Cost $203,382,936) | | | 200,714,523 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

| SHORT TERM INVESTMENTS 9.7% | | | |

| | | Commercial Paper 9.4% | | | |

| $ | 38,090,000 | | U.S. Bank, N.A., | | | |

| | | | 0.040%, 01/04/2010 | | $ | 38,090,000 | |

| | | | | | | | |

| | | | Variable Rate Demand Notes 0.3% (c) | | | | |

| | 1,408,627 | | American Family Financial | | | | |

| | | | Services, Inc., 0.100% | | | 1,408,627 | |

| | 19,951 | | U.S. Bank, N.A., 0.000% | | | 19,951 | |

| | | | | | | 1,428,578 | |

| | | | Total Short-Term Investments | | | | |

| | | | (Cost $39,518,366) | | | 39,518,578 | |

| | | | | | | | |

| | | | Total Investments 110.1% | | | | |

| | | | (Cost $456,238,249) | | | 447,582,450 | |

| | | | | | | | |

| | | | Liabilities in Excess of | | | | |

| | | | Other Assets (10.1)% | | | (41,144,331 | ) |

| | | | | | | | |

| | | | TOTAL NET ASSETS 100.0% | | $ | 406,438,119 | |

| (a) | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration normally to qualified institutional buyers. The total value of these securities amounted to $35,883,756 (8.8% of net assets) at December 31, 2009. |

| (c) | Variable rate demand notes are considered short-term obligations and are payable upon demand. Interest rates change periodically on specified dates. The rates listed are as of December 31, 2009. |

| (d) | Security is in default. |

| (e) | Entity under conservatorship of the federal government |

ALLOCATION OF PORTFOLIO HOLDINGS

At December 31, 2009, the allocation of portfolio holdings as a percentage of the Fund’s total net assets were:

| Asset-Backed Securities | | | 10.9 | % | Preferred Stocks | | | 0.1 | |

| Corporate Bonds | | | 15.3 | | U.S. Treasury Obligations | | | 49.4 | |

| Mortgage-Backed Securities | | | 24.7 | | Short-Term Investments | | | 9.7 | |

| Institutional Term Loans | | | 0.0 | | Liabilities in Excess of Other Assets | | | (10.1 | ) |

| | | | | | | | | 100.0 | % |

| | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2009 (Unaudited)

| Assets: | | | |

| Investments at value (cost $456,238,249) | | $ | 447,582,450 | |

| Cash | | | 40,199 | |

| Interest receivable | | | 2,122,153 | |

| Receivable for Fund shares sold | | | 1,259,059 | |

| Receivable for investments sold | | | 163,133,553 | |

| Prepaid expenses and other assets | | | 52,695 | |

| Unrealized appreciation on foreign currency contracts | | | 77,705 | |

| Total assets | | | 614,267,814 | |

| | | | | |

| Liabilities: | | | | |

| Payable for investments purchased | | | 207,426,087 | |

| Payable for Fund shares purchased | | | 178,325 | |

| Accrued investment advisory fee | | | 85,792 | |

| Accrued distribution and shareholder servicing fees | | | 248 | |

| Accrued expenses | | | 56,435 | |

| Unrealized depreciation on foreign currency contracts | | | 82,808 | |

| Total liabilities | | | 207,829,695 | |

| Net Assets | | $ | 406,438,119 | |

| | | | | |

| Net Assets Consist of: | | | | |

| Paid in capital | | $ | 412,669,863 | |

| Undistributed net investment income | | | 375,033 | |

| Accumulated net realized gain on investments sold, swap contracts and foreign currency | | | 2,054,125 | |

| Net unrealized appreciation (depreciation) on: | | | | |

| Investments | | | (8,655,799 | ) |

| Foreign currency | | | (5,103 | ) |

| Net Assets | | $ | 406,438,119 | |

| | | | | |

| Capital Stock, $0.01 Par Value | | | | |

| Institutional Class Shares Authorized | | | 100,000,000 | |

| Class Y Shares Authorized | | | 50,000,000 | |

| | | | | |

| Institutional Class: | | | | |

| Net Assets | | $ | 404,794,456 | |

| Issued and Outstanding | | | 12,992,929 | |

| Net Asset Value, Redemption Price and Offering Price Per Share | | $ | 31.15 | |

| | | | | |

| Class Y: | | | | |

| Net Assets | | $ | 1,643,663 | |

| Issued and outstanding | | | 52,759 | |

| Net Asset Value, Redemption Price and Offering Price Per Share | | $ | 31.15 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

STATEMENT OF OPERATIONS

| | | Six Months Ended | |

| | | December 31, 2009 | |

| | | (Unaudited) | |

| Investment Income: | | | |

| Interest income | | $ | 14,161,031 | |

| Total Investment Income | | | 14,161,031 | |

| | | | | |

| Expenses: | | | | |

| Investment advisory fees (Note 3) | | | 816,050 | |

| Fund administration and accounting fees | | | 59,926 | |

| Custody fees | | | 21,177 | |

| Federal and state registration fees | | | 18,205 | |

| Audit fees | | | 18,121 | |

| Shareholder servicing fees | | | 17,288 | |

| Legal fees | | | 16,766 | |

| Reports to shareholders | | | 6,649 | |

| Directors’ fees and related expenses | | | 4,232 | |

| Compliance related expenses | | | 816 | |

| Distribution and shareholder servicing fees - Class Y (Note 8) | | | 662 | |

| Other | | | 9,612 | |

| Total expenses before waiver and reimbursement | | | 989,504 | |

| Waiver and reimbursement of expenses by Adviser (Note 3) | | | (274,798 | ) |

| Net expenses | | | 714,706 | |

| Net Investment Income | | | 13,446,325 | |

| | | | | |

| Realized and Unrealized Gain (Loss) on Investments: | | | | |

| Net realized gain on : | | | | |

| Investments | | | 29,074,741 | |

| Swap contracts | | | 331,205 | |

| Futures | | | 69,372 | |

| Change in net unrealized appreciation (depreciation) on: | | | | |

| Investments | | | (149,995 | ) |

| Swap contracts | | | (422,098 | ) |

| Foreign currency contracts | | | (5,103 | ) |

| Net Realized and Unrealized Gain on Investments | | | 28,898,122 | |

| Net Increase in Net Assets Resulting from Operations | | $ | 42,344,447 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

STATEMENTS OF CHANGES IN NET ASSETS

| | | For the Six | | | | |

| | | Months Ended | | | For the | |

| | | December 31, 2009 | | | Year Ended | |

| | | (Unaudited) | | | June 30, 2009 | |

| Operations: | | | | | | |

| Net investment income | | $ | 13,446,325 | | | $ | 35,153,932 | |

| Net realized gain (loss) on: | | | | | | | | |

| Investments | | | 29,074,741 | | | | (8,895,311 | ) |

| Swap contracts | | | 331,205 | | | | 2,197,511 | |

| Foreign currency translation | | | — | | | | 831,878 | |

| Futures | | | 69,372 | | | | — | |

| Change in net unrealized appreciation (depreciation) on: | | | | | | | | |

| Investments | | | (149,995 | ) | | | 354,573 | |

| Swap contracts | | | (422,098 | ) | | | 1,390,660 | |

| Foreign currency contracts | | | (5,103 | ) | | | — | |

| Net increase in net assets resulting from operations | | | 42,344,447 | | | | 31,033,243 | |

| Distributions Paid to Institutional Class Shareholders From: | | | | | | | | |

| Net investment income | | | (14,315,502 | ) | | | (33,077,660 | ) |

| Net realized gain | | | (16,735,772 | ) | | | (9,661,730 | ) |

| Net decrease in net assets resulting from distributions paid | | | (31,051,274 | ) | | | (42,739,390 | ) |

| Distributions Paid to Class Y Shareholders From: | | | | | | | | |

| Net investment income | | | (29,063 | ) | | | — | |

| Net realized gain | | | (71,341 | ) | | | — | |

| Net decrease in net assets resulting from distributions paid | | | (100,404 | ) | | | — | |

| Capital Share Transactions: | | | | | | | | |

| Shares sold - Institutional Class | | | 79,536,986 | | | | 110,670,953 | |

| Shares sold - Class Y | | | 1,650,150 | | | | — | |

| Shares issued to holders in reinvestment of distributions - Institutional Class | | | 26,700,859 | | | | 33,980,127 | |

| Shares issued to holders in reinvestment of distributions - Class Y | | | 100,403 | | | | — | |

| Shares redeemed - Institutional Class | | | (109,454,123 | ) | | | (170,148,652 | ) |

| Shares redeemed - Class Y | | | (50 | ) | | | — | |

| Net decrease in net assets resulting from capital share transactions | | | (1,465,775 | ) | | | (25,497,572 | ) |

| Total Increase (Decrease) in Net Assets | | | 9,726,994 | | | | (37,203,719 | ) |

| Net Assets: | | | | | | | | |

| Beginning of Period | | | 396,711,125 | | | | 433,914,844 | |

| End of Period (includes undistributed net investment income of $375,033 and $1,273,273 respectively) | | $ | 406,438,119 | | | $ | 396,711,125 | |

| Transactions In Shares – Institutional Class: | | | | | | | | |

| Shares sold | | | 2,456,141 | | | | 4,019,040 | |

| Shares issued to holders in reinvestment of distributions | | | 841,965 | | | | 1,277,512 | |

| Shares redeemed | | | (3,353,063 | ) | | | (6,367,246 | ) |

| Net decrease in shares outstanding | | | (54,957 | ) | | | (1,070,694 | ) |

| Transactions In Shares – Class Y: | | | | | | | | |

| Shares sold | | | 49,568 | | | | n/a | |

| Shares issued to holders in reinvestment of distributions | | | 3,193 | | | | n/a | |

| Shares redeemed | | | (2 | ) | | | n/a | |

| Net increase in shares outstanding | | | 52,759 | | | | n/a | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

FINANCIAL HIGHLIGHTS

| | | Institutional Class | |

| | | Six Months | | | | | | | | | | | | | | | | |

| | | Ended | | | Year | | | Year | | | Year | | | Year | | | Year | |

| | | December 31, | | | Ended | | | Ended | | | Ended | | | Ended | | | Ended | |

| | | 2009 | | | June 30, | | | June 30, | | | June 30, | | | June 30, | | | June 30, | |

| | | (Unaudited) | | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| Net Asset Value, Beginning of Period | | $ | 30.40 | | | $ | 30.73 | | | $ | 30.40 | | | $ | 29.72 | | | $ | 31.50 | | | $ | 30.51 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Income (Loss) from | | | | | | | | | | | | | | | | | | | | | | | | |

| Investment Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 1.13 | | | | 2.50 | | | | 1.48 | | | | 1.54 | | | | 1.41 | | | | 1.13 | |

| Net realized and unrealized gain (loss) on investments | | | 2.26 | | | | 0.16 | | | | 0.61 | | | | 0.68 | | | | (1.30 | ) | | | 0.98 | |

| Total Income from Investment Operations | | | 3.39 | | | | 2.66 | | | | 2.09 | | | | 2.22 | | | | 0.11 | | | | 2.11 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Less Distributions: | | | | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (1.20 | ) | | | (2.33 | ) | | | (1.49 | ) | | | (1.54 | ) | | | (1.45 | ) | | | (1.12 | ) |

| From net realized gain on investments | | | (1.44 | ) | | | (0.66 | ) | | | (0.27 | ) | | | — | | | | (0.44 | ) | | | — | |

| Total Distributions | | | (2.64 | ) | | | (2.99 | ) | | | (1.76 | ) | | | (1.54 | ) | | | (1.89 | ) | | | (1.12 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net Asset Value, End of Period | | $ | 31.15 | | | $ | 30.40 | | | $ | 30.73 | | | $ | 30.40 | | | $ | 29.72 | | | $ | 31.50 | |

| Total Return | | | 11.02 | %(1) | | | 10.52 | % | | | 6.92 | % | | | 7.52 | % | | | 0.36 | % | | | 7.00 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Supplemental Data and Ratios: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (in thousands) | | $ | 404,794 | | | $ | 396,711 | | | $ | 433,915 | | | $ | 276,830 | | | $ | 313,880 | | | $ | 316,474 | |

| Ratio of expenses to average net assets | | | | | | | | | | | | | | | | | | | | | | | | |

| Before waivers and reimbursements | | | 0.48 | %(2) | | | 0.49 | % | | | 0.49 | % | | | 0.50 | % | | | 0.50 | % | | | 0.50 | % |

| Net of waivers and reimbursements | | | 0.35 | %(2) | | | 0.35 | % | | | 0.30 | % | | | 0.20 | % | | | 0.20 | % | | | 0.41 | % |

| Ratio of net investment income to average net assets | | | | | | | | | | | | | | | | | | | | | | | | |

| Before waivers and reimbursements | | | 6.59 | %(2) | | | 8.68 | % | | | 4.68 | % | | | 4.65 | % | | | 4.29 | % | | | 3.21 | % |

| Net of waivers and reimbursements | | | 6.46 | %(2) | | | 8.82 | % | | | 4.87 | % | | | 4.95 | % | | | 4.59 | % | | | 3.30 | % |

| Portfolio turnover rate | | | 450 | %(1) | | | 424 | % | | | 1,093 | % | | | 978 | % | | | 1,247 | % | | | 1,222 | % |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Plus Fund

FINANCIAL HIGHLIGHTS

| | | Class Y | |

| | | Six Months | |

| | | Ended | |

| | | December 31, | |

| | | 2009(1) | |

| | | (Unaudited) | |

| Net Asset Value, Beginning of Period | | $ | 33.08 | |

| | | | | |

| Income (Loss) from | | | | |

| Investment Operations: | | | | |

| Net investment income | | | 0.18 | |

| Net realized and unrealized loss on investments | | | (0.08 | ) |

| Total Income from Investment Operations | | | 0.10 | |

| | | | | |

| Less Distributions: | | | | |

| From net investment income | | | (0.59 | ) |

| From net realized gain on investments | | | (1.44 | ) |

| Total Distributions | | | (2.03 | ) |

| | | | | |

| Net Asset Value, End of Period | | $ | 31.15 | |

| Total Return | | | 0.23 | %(2) |

| | | | | |

| Supplemental Data and Ratios: | | | | |

| Net assets, end of period (in thousands) | | $ | 1,644 | |

| Ratio of expenses to average net assets | | | | |

| Before waivers and reimbursements | | | 0.81 | %(3) |

| Net of waivers and reimbursements | | | 0.75 | %(3) |

| Ratio of net investment income to average net assets | | | | |

| Before waivers and reimbursements | | | 4.71 | %(3) |

| Net of waivers and reimbursements | | | 4.65 | %(3) |

| Portfolio turnover rate | | | 450 | %(2) |

| (1) | Commenced operations on November 12, 2009. |

The accompanying notes are an integral part of these financial statements.

INVESTMENT HIGHLIGHTS

Growth of a $100,000 Investment (Unaudited)

* 2/23/01 commencement of operations.

| | Portfolio Total Return** | | | |

| | FOR PERIODS ENDED 12/31/09 | FUND | INDEX | |

| | | | | |

| | SIX MONTHS | 9.33% | 3.95% | |

| | | | | |

| | ONE YEAR | 28.36% | 5.93% | |

| | | | | |

| | FIVE YEAR | | | |

| | AVERAGE ANNUAL | 6.76% | 4.97% | |

| | | | | |

| | SINCE COMMENCEMENT | | | |

| | AVERAGE ANNUAL | 6.40% | 5.66% | |

This chart assumes an initial gross investment of $100,000 made on 2/23/01 (commencement of operations). Returns shown include the reinvestment of all distributions. Past performance is not predictive of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. In the absence of existing fee waivers, total return would be reduced. The recent growth rate in the fixed income market has helped to produce short-term returns for some asset classes that are not typical and may not continue in the future. Because of ongoing market volatility, Fund performance may be subject to substantial short-term changes. To receive current to the most recent month-end performance, please call 1-888-825-2100.

The Barclays Capital U.S. Aggregate Bond Index (formerly the Lehman Brothers Aggregate Bond Index) is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset backed and mortgage backed securities, with maturities of at least one year. The Index does not reflect investment management fees, brokerage commissions and other expenses associated with investing in fixed income securities. A direct investment in the index is not possible.

| ** | The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

Frontegra Columbus Core Fund

SCHEDULE OF INVESTMENTS

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

| ASSET BACKED SECURITIES 8.2% | | | |

| | | American Express Credit | | | |

| $ | 260,000 | | 2008-3, Class A, | | | |

| | | | 1.183%, 08/15/2012 | | $ | 260,060 | |

| | | | Americredit Automobile | | | | |

| | | | Receivables Trust | | | | |

| | 355,000 | | 2008-AF, Class A4, | | | | |

| | | | 6.960%, 10/14/2014 | | | 373,389 | |

| | | | Capital One Prime Auto | | | | |

| | 356,885 | | 2006-1, Class A4, | | | | |

| | | | 5.010%, 11/15/2011 | | | 357,485 | |

| | | | Chase Issuance Trust | | | | |

| | 525,000 | | 2009-A7, Class A7, | | | | |

| | | | 0.695%, 09/17/2012 | | | 525,627 | |

| | 280,000 | | 2005-8A, Class A8, | | | | |

| | | | 0.273%, 10/15/2012 | | | 279,626 | |

| | | | Chrysler Financial | | | | |

| | | | Auto Securitization Trust | | | | |

| | 290,000 | | 2009-B, Class A2, | | | | |

| | | | 1.150%, 11/08/2011 | | | 289,949 | |

| | | | Chrysler Financial Automobile TALF | | | | |

| | 150,000 | | 2009-AF, Class A3, | | | | |

| | | | 2.820%, 01/15/2016 | | | 152,255 | |

| | | | Citibank Credit Card Issuance Trust | | | | |

| | 635,000 | | 2006-A6, Class A6, | | | | |

| | | | 0.242%, 05/24/2012 | | | 634,179 | |

| | | | Credit Suisse Mortgage | | | | |

| | | | Capital Certificates | | | | |

| | 316,133 | | 2009-12R, 41A1, | | | | |

| | | | 5.250%, 03/27/2037 | | | 316,133 | |

| | | | Discover Card Master Trust I | | | | |

| | 145,000 | | 2003-3, Class A, 0.445%, 09/15/2012 | | | 144,941 | |

| | | | Ford Credit Auto Owner Trust | | | | |

| | 375,000 | | Series 2009-D, Class A3, | | | | |

| | | | 2.170%, 10/15/2013 | | | 378,710 | |

| | 69,592 | | Series 2008-C, Class A2A, | | | | |

| | | | 3.720%, 01/15/2011 | | | 69,781 | |

| | | | GE Capital Credit Card | | | | |

| | | | Master Note Trust | | | | |

| | 385,000 | | Series 2009-3, Class A, | | | | |

| | | | 2.540%, 09/15/2014 | | | 385,308 | |

| | | | Hertz Vehicle Financing LLC | | | | |

| | 160,000 | | 2005-1A, Class A4, | | | | |

| | | | 2.711%, 11/25/2011 | | | | |

| | | | (Acquired 08/21/2008, | | | | |

| | | | Cost $152,092) (a)(b) | | | 157,774 | |

| | 200,000 | | 2005-2A, Class A5, | | | | |

| | | | 2.711%, 11/25/2011 | | | | |

| | | | (Acquired 08/01/2008, | | | | |

| | | | Cost $192,363) (a)(b) | | | 197,217 | |

| | 280,000 | | 2009-2A, Class A1, | | | | |

| | | | 4.260%, 03/25/2014 | | | | |

| | | | (Acquired 10/16/2009, | | | | |

| | | | Cost $279,983) (a)(b) | | | 279,032 | |

| | | | Hyundai Auto Receivables Trust | | | | |

| | 640,000 | | Series 2009-A, Class A3, | | | | |

| | | | 2.030%, 08/15/2013 | | | 644,198 | |

| | | | Keystone Owner Trust | | | | |

| | 28,009 | | 1998-P1, Class M1, | | | | |

| | | | 7.530%, 05/25/2025 | | | | |

| | | | (Acquired 04/22/2003, | | | | |

| | | | Cost $28,740) (a) | | | 26,870 | |

| | | | Mid-State Trust | | | | |

| | 247,917 | | 11, Class A1, 4.864%, 07/15/2038 | | | 221,609 | |

| | | | Total Asset Backed Securities | | | | |

| | | | (Cost $5,684,001) | | | 5,694,143 | |

| | | | | | | | |

| CORPORATE BONDS 13.0% | | | | |

| | | | Airlines 1.0% | | | | |

| | | | Northwest Airlines, Inc. | | | | |

| | 785,203 | | 7.027%, 11/01/2019 | | | 694,904 | |

| | | | | | | | |

| | | | Commercial Banks 1.4% | | | | |

| | | | Manufacturers & Traders Trust Co. | | | | |

| | 335,000 | | 5.629%, 12/01/2021 | | | 287,981 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

CORPORATE BONDS 13.0% (continued) | | | |

| | | Commercial Banks 1.4% (continued) | | | |

| | | Marshall & Ilsley Bank | | | |

| $ | 880,000 | | 5.413%, 12/04/2012 | | $ | 707,898 | |

| | | | | | | 995,879 | |

| | | | Construction Materials 0.1% | | | | |

| | | | Lafarge Coppee SA | | | | |

| | 70,000 | | 6.500%, 07/15/2016 | | | 74,214 | |

| | | | Diversified Financial Services 0.9% | | | | |

| | | | General Electric Company | | | | |

| | 285,000 | | 6.000%, 08/07/2019 | | | 295,836 | |

| | | | International Lease Finance Corp. | | | | |

| | 455,000 | | 5.625%, 09/20/2013 | | | 356,907 | |

| | | | | | | 652,743 | |

| | | | Electric Utilities 1.3% | | | | |

| | | | Entergy Arkansas Inc. | | | | |

| | 175,000 | | 5.000%, 07/01/2018 | | | 168,402 | |

| | | | Indianapolis Power & Light Co. | | | | |

| | 350,000 | | 6.050%, 10/01/2036 (Acquired | | | | |

| | | | Multiple Dates, Cost $337,293) (a) | | | 345,803 | |

| | | | Mackinaw Power LLC | | | | |

| | 309,733 | | 6.296%, 10/31/2023 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $300,162) (a) | | | 303,774 | |

| | | | Ohio Power Co. | | | | |

| | 60,000 | | 6.000%, 06/01/2016 | | | 63,610 | |

| | | | | | | 881,589 | |

| | | | Gas Utilities 0.5% | | | | |

| | | | EQT Corp. | | | | |

| | 270,000 | | 8.125%, 06/01/2019 | | | 311,951 | |

| | | | Industrial Consumer Services 0.5% | | | | |

| | | | ERAC USA Finance Company | | | | |

| | 305,000 | | 6.375%, 10/15/2017 | | | | |

| | | | (Acquired 10/21/2008 and | | | | |

| | | | 10/23/2008, Cost $231,598) (a) | | | 308,070 | |

| | | | Insurance 5.2% | | | | |

| | | | AIG Sunamerica Global Financial | | | | |

| | 500,000 | | 6.300%, 05/10/2011 | | | | |

| | | | (Acquired 09/30/2009, | | | | |

| | | | Cost $494,039) (a) | | | 497,344 | |

| | | | Farmers Insurance Exchange | | | | |

| | 230,000 | | 6.000%, 08/01/2014 | | | | |

| | | | (Acquired 07/15/2009, | | | | |

| | | | Cost $195,814) (a) | | | 216,991 | |

| | | | Genworth Global Funding | | | | |

| | 965,000 | | 5.875%, 05/03/2013 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $761,765) (a) | | | 956,014 | |

| | | | Jackson National Life Global Funding | | | | |

| | 235,000 | | 5.375%, 05/08/2013 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $235,494) (a) | | | 238,647 | |

| | | | Lincoln National Corp. | | | | |

| | 210,000 | | 6.250%, 02/15/2020 | | | 206,951 | |

| | | | Monumental Global Funding | | | | |

| | 390,000 | | 5.500%, 04/22/2013 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $393,523) (a) | | | 401,272 | |

| | 135,000 | | 5.250%, 01/15/2014 | | | | |

| | | | (Acquired 06/10/2009 and | | | | |

| | | | 09/30/2009, Cost $129,727) (a) | | | 137,736 | |

| | | | Nationwide Life Global Fund | | | | |

| | 965,000 | | 5.450%, 10/02/2012 | | | | |

| | | | (Acquired 09/25/2007 and | | | | |

| | | | 09/30/2009, Cost $962,774) (a) | | | 953,221 | |

| | | | | | | 3,608,176 | |

| | | | Machinery Manufacturing 0.3% | | | | |

| | | | Weatherford International Ltd. | | | | |

| | 215,000 | | 6.500%, 08/01/2036 | | | 205,331 | |

| | | | Media 0.3% | | | | |

| | | | Time Warner Entertainment Co. LP | | | | |

| | 190,000 | | 8.375%, 07/15/2033 | | | 227,134 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2009 (Unaudited)

| Principal Amount | | | | Value | |

CORPORATE BONDS 13.0% (continued) | | | |

| | | Metals & Mining 0.7% | | | |

| | | Alcoa Inc. | | | |

| $ | 275,000 | | 5.900%, 02/01/2027 | | $ | 247,903 | |

| | 235,000 | | 5.950%, 02/01/2037 | | | 201,682 | |

| | | | | | | 449,585 | |

| | | | Multi-Utilities & | | | | |

| | | | Unregulated Power 0.3% | | | | |

| | | | Kiowa Power Partners LLC | | | | |

| | 173,902 | | 4.811%, 12/30/2013 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $173,720) (a)(b) | | | 175,580 | |

| | | | Oil, Gas & Consumable Fuels 0.5% | | | | |

| | | | Talisman Energy, Inc. | | | | |

| | 280,000 | | 7.750%, 06/01/2019 | | | 328,834 | |

| | | | Total Corporate Bonds | | | | |

| | | | (Cost $8,168,125) | | | 8,913,990 | |

| | | | | | | | |

| MORTGAGE BACKED SECURITIES 27.3% | | | | |

| | | | Bank of America | | | | |

| | | | Commercial Mortgage Inc. | | | | |

| | 385,000 | | Series 2006-3, Class A4, | | | | |

| | | | 5.889%, 07/10/2044 | | | 350,332 | |

| | 720,000 | | Series 2009-UB1, Class A4, | | | | |

| | | | 5.620%, 06/24/2050 | | | | |

| | | | (Acquired Multiple Dates, | | | | |

| | | | Cost $602,220) (a) | | | 653,819 | |

| | | | CitiMortgage Alternative Loan Trust | | �� | | |

| | 1,237,688 | | Series 2007-A7, Class 3A1, | | | | |

| | | | 5.750%, 07/25/2022 | | | 1,010,843 | |

| | | | Credit Suisse First Boston | | | | |

| | | | Mortgage Securities Corp. | | | | |

| | 89,467 | | Pool # 2005-10, 5.000%, 09/25/2015 | | | 88,125 | |

| | 20,704 | | Pool # 2003-1, 7.000%, 02/25/2033 | | | 20,373 | |

| | | | FHLMC Pools (d) | | | | |

| | 88,129 | | Pool #G1-8105, 5.000%, 03/01/2021 | | | 92,464 | |

| | 32,574 | | Pool #G1-1989, 5.500%, 04/01/2021 | | | 34,675 | |

| | 52,185 | | Pool #G1-2522, 5.000%, 02/01/2022 | | | 54,751 | |

| | 107,139 | | Pool #G1-8229, 5.000%, 01/01/2023 | | | 112,174 | |

| | 122,898 | | Pool #G0-2123, 5.500%, 03/01/2036 | | | 129,210 | |

| | 38,663 | | Pool #G0-8131, 7.000%, 03/01/2036 | | | 42,180 | |

| | 59,410 | | Pool #G0-2184, 5.000%, 04/01/2036 | | | 61,038 | |

| | 31,618 | | Pool #G0-2196, 6.500%, 05/01/2036 | | | 33,880 | |

| | 21,949 | | Pool #A5-2716, 6.500%, 10/01/2036 | | | 23,520 | |

| | 202,282 | | Pool #A6-1562, 5.500%, 10/01/2036 | | | 212,291 | |

| | 37,594 | | Pool #G0-4260, 5.500%, 05/01/2038 | | | 39,423 | |

| | 250,227 | | Pool #G0-5092, 5.000%, 11/01/2038 | | | 257,395 | |

| | | | FHLMC REMIC (d) | | | | |

| | 315,000 | | Series 3563, 4.000%, 08/15/2024 | | | 298,068 | |

| | 860,000 | | Series 3577, 4.000%, 09/15/2024 | | | 817,013 | |

| | 1,610,000 | | Series 3609, 4.000%, 12/15/2024 | | | 1,661,130 | |

| | 75,872 | | Series 2750, 4.000%, 05/15/2026 | | | 76,940 | |

| | | | FNMA (d) | | | | |

| | 789,125 | | Pool #931711, 4.000%, 08/01/2019 | | | 807,213 | |

| | 388,903 | | Pool #MA0174, 4.000%, 09/25/2019 | | | 397,817 | |

| | 868,286 | | Pool #MA0235, 4.000%, 11/01/2019 | | | 888,188 | |

| | 777,184 | | Pool #932108, 4.000%, 11/25/2019 | | | 794,998 | |

| | 2,870,000 | | Pool #MA0298, 4.000%, 01/01/2020 | | | 2,938,611 | |

| | 12,548 | | Pool #254711, 4.000%, 03/01/2010 | | | 12,662 | |

| | 24,727 | | Pool #255666, 5.000%, 04/01/2020 | | | 25,990 | |

| | 55,070 | | Pool #735407, 5.000%, 04/01/2020 | | | 57,951 | |

| | 108,308 | | Pool #813929, 4.500%, 11/01/2020 | | | 112,415 | |

| | 89,851 | | Pool #963138, 5.000%, 05/01/2023 | | | 93,999 | |

| | 36,039 | | Pool #256272, 5.500%, 06/01/2026 | | | 38,052 | |

| | 46,079 | | Pool #256751, 5.500%, 06/01/2027 | | | 48,631 | |

| | 59,011 | | Pool #255813, 5.000%, 08/01/2035 | | | 60,674 | |

| | 191,549 | | Pool #255898, 5.000%, 10/01/2035 | | | 196,946 | |

| | 87,896 | | Pool #891475, 6.500%, 04/01/2036 | | | 94,323 | |

| | 95,627 | | Pool #745516, 5.500%, 05/01/2036 | | | 100,448 | |

| | 32,417 | | Pool #256283, 7.000%, 06/01/2036 | | | 35,568 | |

| | 137,847 | | Pool #745875, 6.500%, 09/01/2036 | | | 147,927 | |

| | 175,548 | | Pool #745932, 6.500%, 11/01/2036 | | | 188,385 | |

| | 143,784 | | Pool #256513, 5.500%, 12/01/2036 | | | 150,786 | |

| | 122,888 | | Pool #888129, 5.500%, 02/01/2037 | | | 128,872 | |

| | 134,971 | | Pool #917810, 5.500%, 05/01/2037 | | | 141,439 | |

The accompanying notes are an integral part of these financial statements.

Frontegra Columbus Core Fund

SCHEDULE OF INVESTMENTS (continued)

December 31, 2009 (Unaudited)

��

| Principal Amount | | | | Value | |

| MORTGAGE BACKED | | | |

SECURITIES 27.3% (continued) | | | |

| $ | 239,049 | | Pool #995022, 5.500%, 08/01/2037 | | $ | 251,101 | |

| | 90,205 | | Pool #257161, 5.500%, 04/01/2038 | | | 94,527 | |

| | 122,807 | | Pool #962874, 5.000%, 05/01/2038 | | | 126,165 | |

| | | | FNMA TBA (d) | | | | |

| | 2,235,000 | | Pool #000TBA, 6.500%, 02/01/2038 | | | 2,386,560 | |

| | | | GS Mortgage Securities Corp. II | | | | |

| | 529,906 | | Series 2007-EOP, Class A1, | | | | |

| | | | 5.410%, 03/06/2020 | | | | |

| | | | (Acquired 09/17/2007 and | | | | |

| | | | 04/22/2008, Cost $521,749) (a)(b) | | | 504,038 | |

| | | | LB-UBS Commercial Mortgage Trust | | | | |

| | 580,000 | | Series 2007-C1, Class A4, | | | | |

| | | | 5.424%, 02/15/2040 | | | 480,315 | |

| | 360,000 | | Series 2007-C2, Class A3, | | | | |

| | | | 5.430%, 02/15/2040 | | | 310,964 | |

| | 113,000 | | Series 2007-C3, Class A4, | | | | |

| | | | 6.136%, 07/15/2044 (b) | | | 93,397 | |

| | | | Master Asset Securitization Trust | | | | |

| | 74,090 | | Pool # 2004-3, 4.750%, 01/25/2014 | | | 71,126 | |

| | | | Residential Accredit Loans, Inc. | | | | |

| | 258,681 | | Series 2004-QS4, Class A1, | | | | |

| | | | 4.350%, 03/25/2034 | | | 235,910 | |

| | | | Residential Asset Securitization Trust | | | | |

| | 164,371 | | Series 2003-A6, Class A1, | | | | |

| | | | 4.500%, 07/25/2033 | | | 158,090 | |

| | | | Wachovia Bank | | | | |

| | | | Commercial Mortgage Trust | | | | |

| | 298,611 | | Series 2003-C7, Class A1, | | | | |

| | | | 4.241%, 10/15/2035 | | | | |

| | | | (Acquired 12/04/2009, | | | | |

| | | | Cost $300,940) (a) | | | 300,541 | |

| | 325,000 | | Series 2006-C23, Class A4, | | | | |

| | | | 5.418%, 01/15/2045 | | | 311,313 | |

| | | | Total Mortgage Backed Securities | | | | |

| | | | (Cost $19,026,439) | | | 18,855,586 | |

| | | | | | | | |

| U.S. GOVERNMENT AGENCY ISSUES 0.1% | | | | |

| | | | GNMA | | | | |

| | 30,637 | | Pool #3840, 5.000%, 04/20/2036 | | | 31,561 | |

| | 51,454 | | Pool #3841, 5.500%, 04/20/2036 | | | 54,051 | |

| | | | | | | 85,612 | |

| | | | Total U.S. Government | | | | |