As filed with the Securities and Exchange Commission on March 3, 2008

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07763

The Masters’ Select Funds Trust

(Exact name of registrant as specified in charter)

4 Orinda Way, Suite 200-D, Orinda, CA 94563

(Address of principal executive offices) (Zip code)

Kenneth E. Gregory

4 Orinda Way, Suite 200-D

Orinda, CA 94563

(Name and address of agent for service)

(925) 254-8999

Registrant's telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: December 31, 2007

Item 1. Report to Stockholders.

The Masters’ Select Funds Trust

Annual Report

The Masters’ Select Equity Fund

The Masters’ Select International Fund

The Masters’ Select Value Fund

The Masters’ Select Smaller Companies Fund

The Masters’ Select Focused Opportunities Fund

December 31, 2007

www.mastersfunds.com

The Masters’ Select Concept

In constructing the Masters’ Select Funds, our goal was to design funds that would isolate the stock-picking skills of a group of highly regarded portfolio managers. To meet this objective, we designed the funds with both risk and return in mind, placing particular emphasis on the following factors:

| 1. | First, only stock pickers we believe to be exceptionally skilled are chosen to manage each fund’s sub-portfolios. |

| 2. | Second, and of equal importance, each stock picker runs a very focused sub-portfolio of not more than 15 of his or her favorite stocks within each Masters’ Select Fund; the exception being the Masters’ Select Focused Opportunities Fund, in which each manager selects no more than 7 of their highest conviction ideas. We believe that most stock pickers have an unusually high level of conviction in only a small number of stocks and that a portfolio limited to these stocks will, on average, outperform (a more diversified portfolio) over a market cycle. |

| 3. | Third, even though each manager’s portfolio is focused, we seek ways to diversify each of our funds. With the Equity, International and Focused Opportunities funds, we have done this by including managers with differing investment styles and market-cap orientations (the Focused Opportunities Fund is classified as non-diversified so that it may invest in a smaller range (15-21) of securities). With the Value Fund, we have selected managers who each take a distinctive approach to assessing companies and defining value. With the Smaller Companies Fund, we have selected managers with varying investment approaches who each focus on the securities of smaller companies. |

| 4. | Finally, we believe that excessive asset growth can result in diminished performance. We have committed to closing each Masters’ Select Fund to new shareholders at levels that we believe will preserve the managers’ ability to effectively implement the “select” concept. |

Portfolio Fit

As with all equity funds, Masters’ Select Funds are appropriate for investors with a long-term time horizon, who are willing to ride out occasional periods when the funds’ net asset values decline. Within that context, we created the Masters’ Select Equity and Masters’ Select International Funds to be used as core equity and international fund holdings. Masters’ Select Smaller Companies Fund has been created to provide a core domestic small-cap investment opportunity. We created Masters’ Select Value Fund for investors who seek additional, dedicated value exposure in their portfolios. Masters’ Select Focused Opportunities Fund has been created to provide a core large-cap holding for long-term investors. Although performance in each specific down market will vary, we purposely set the allocations to each manager with the objective of keeping risk about equal to the funds’ overall benchmarks. In the end, the focus on the highest conviction stocks of a group of very distinguished managers with superior track records is what we believe makes the funds ideal portfolio holdings.

Contents

| Fund’s Performance | 2 |

| Our Commitment to Shareholders | 3 |

| Letter to Shareholders | 4 |

| Long-Term Performance Metrics | 6 |

| Masters’ Select Equity Fund | |

Equity Fund Review | 8 |

Equity Fund Managers | 13 |

Equity Fund Stock Highlights | 14 |

Equity Fund Schedule of Investments | 17 |

| Masters’ Select International Fund | |

International Fund Review | 19 |

International Fund Managers | 23 |

International Fund Stock Highlights | 24 |

International Fund Schedule of Investments | 27 |

| Masters’ Select Value Fund | |

Value Fund Review | 29 |

Value Fund Managers | 33 |

Value Fund Stock Highlights | 34 |

Value Fund Schedule of Investments | 36 |

| Masters’ Select Smaller Companies Fund | |

Smaller Companies Fund Review | 37 |

Smaller Companies Fund Managers | 40 |

Smaller Companies Fund Stock Highlights | 41 |

Smaller Companies Fund Schedule of Investments | 43 |

| Masters’ Select Focused Opportunities Fund | |

Focused Opportunities Fund Review | 45 |

Focused Opportunities Fund Managers | 48 |

Focused Opportunities Fund Stock Highlights | 49 |

Focused Opportunities Fund Schedule of Investments | 50 |

| Expense Examples | 51 |

| Statements of Assets and Liabilities | 52 |

| Statements of Operations | 53 |

| Statements of Changes in Net Assets | |

Equity Fund | 54 |

International Fund | 54 |

Value Fund | 55 |

Smaller Companies Fund | 55 |

Focused Opportunities Fund | 56 |

| Financial Highlights | |

Equity Fund | 57 |

International Fund | 58 |

Value Fund | 59 |

Smaller Companies Fund | 60 |

Focused Opportunities Fund | 61 |

| Notes to Financial Statements | 62 |

| Report of Independent Registered Public Accounting Firm | 69 |

| Other Information | 70 |

| Tax Information | 74 |

| Index Definitions | 76 |

| Industry Terms and Definitions | 77 |

| Trustee and Officer Information | 78 |

This report is intended for shareholders of the funds and may not be used as sales literature unless preceded or accompanied by a current prospectus for the Masters’ Select Funds. Statements and other information in this report are dated and are subject to change.

Litman/Gregory Fund Advisors, LLC has ultimate responsibility for the funds’ performance due to its responsibility to oversee its investment managers and recommend their hiring, termination and replacement.

v2008-02

Table of Contents | 1 |

Masters’ Select Funds’ Performance

Average Annual Total Returns | |||||

Performance as of 12/31/2007 | One-Year | Three- Year | Five-Year | Ten-Year | Since Inception |

Masters’ Select Equity Fund 12/31/1996 | 4.57% | 6.27% | 12.44% | 7.83% | 9.61% |

| Custom Equity Index | 4.69% | 9.16% | 14.48% | 6.63% | 8.41% |

| Russell 3000 Index | 5.14% | 8.89% | 13.63% | 6.22% | 8.32% |

| Lipper Multi Cap Core Index | 5.98% | 9.39% | 14.07% | 6.46% | 8.12% |

| Gross Expense Ratio: 1.19% | |||||

Masters’ Select International Fund 12/1/1997 | 20.75% | 22.70% | 24.00% | 14.37% | 14.10% |

| S&P Citigroup PMI Global (ex US) Index | 17.95% | 20.59% | 24.39% | 10.28% | 10.34% |

| Lipper International Fund Index | 14.24% | 18.49% | 21.83% | 9.46% | 9.46% |

| Gross Expense Ratio: 1.21% Net Expense Ratio as of 12/31/07: 1.03% | |||||

Masters’ Select Value Fund 6/30/2000 | -2.34% | 5.90% | 12.50% | n/a | 7.94% |

| Russell 3000 Value Index | -1.01% | 8.97% | 14.69% | n/a | 8.18% |

| Lipper Multi-Cap Value Index | -1.04% | 7.20% | 13.45% | n/a | 7.61% |

| Gross Expense Ratio: 1.24% Net Expense Ratio as of 12/31/07: 1.21% | |||||

Masters’ Select Smaller Companies Fund 6/30/2003 | 1.64% | 5.49% | n/a | n/a | 12.41% |

| Russell 2000 Index | -1.57% | 6.80% | n/a | n/a | 13.96% |

| Lipper Small Cap Core Index | 1.92% | 7.62% | n/a | n/a | 14.21% |

| Gross Expense Ratio: 1.32% Net Expense Ratio as of 12/31/07: 1.31% | |||||

Masters’ Select Focused Opportunities Fund 6/30/2006 | 7.73% | n/a | n/a | n/a | 12.12% |

| S&P 500 Index | 5.49% | n/a | n/a | n/a | 12.25% |

| Gross Expense Ratio: 1.63% Net Expense Ratio as of 12/31/07: 1.26% | |||||

Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. To obtain the performance of the funds as of the most recently completed calendar month, please visit our website at www.mastersfunds.com or call 1-800-960-0188. The Fund imposes a 2% redemption fee on shares held less than 180 days. Performance does not reflect the redemption fee. If reflected, performance would be lower.

The performance quoted does not include a deduction for taxes that a shareholder would pay on distributions or the redemption of fund shares. Indexes are unmanaged, do not incur expenses, taxes or fees and cannot be invested in directly. See page 76 for the index definitions.

Each of the funds may invest in foreign securities. Investing in foreign securities exposes investors to economic, political and market risks and fluctuations in foreign currencies. Each of the funds may invest in the securities of small companies. Small-company investing subjects investors to additional risks, including security price volatility and less liquidity than investing in larger companies. Masters’ Select Value and Masters’ Select Focused Opportunities are non-diversified funds, which means that each respective fund may concentrate more of its assets in fewer individual holdings than a diversified fund. Though primarily equity funds, the Value and Focused Opportunities funds may invest portions of assets in securities of distressed companies. Debt obligations of distressed companies typically are unrated, lower rated, in default or close to default and may become worthless.

Gross expense ratios are per the Prospectus dated April 30, 2007. Through December 31, 2008, Litman/Gregory has contractually agreed to waive a portion of its advisory fees effectively reducing total advisory fees to approximately 0.97% of the average daily net assets of the International Fund and 1.08% of the average daily net assets of the Value Fund. Litman/Gregory may voluntarily waive a portion of its advisory fee in addition to those fees that are contractually waived. Litman/Gregory has agreed not to seek recoupment of advisory fees waived. Through 12/31/08, Litman/Gregory has voluntarily agreed to waive a portion of its management fee to pass through any costs benefits resulting from changes in the sub-advisory fee schedules or allocations within the Equity Fund and Smaller Companies Fund. Through December 31, 2007, the Advisor had agreed to reimburse the Focused Opportunities Fund for any ordinary operating expenses above 1.50% of the Fund’s average daily net assets. The Advisor reserves the right to be repaid by the Fund within three fiscal years, provided the Fund remains within the applicable expense limitation for the relevant fiscal year. The Advisor may not request or receive reimbursement of such amounts before payment of the Fund’s operating expenses for the current fiscal year.

| 2 | The Masters’ Select Funds Trust |

Litman/Gregory Fund Advisors’

Commitment to Shareholders

We are deeply committed to making each Masters’ Select Fund a highly satisfying long-term investment for shareholders. In following through on this commitment we are guided by our core values, which influence four specific areas of service:

First, we are committed to the Masters’ Select concept.

| • | We will only hire managers who we strongly believe will deliver exceptional long-term returns relative to their benchmarks. We base this belief on extremely thorough due diligence research. This not only requires us to assess their stock-picking skills, but also to evaluate their ability to add incremental performance by investing in a concentrated portfolio of their highest conviction ideas. |

| • | We will monitor each of the managers so that we can maintain our confidence in their ability to deliver the long-term performance we expect. In addition, our monitoring will seek to assess whether they are staying true to their Masters’ Select mandate. Consistent with this mandate we focus on long-term performance evaluation so that the Masters’ Select stock pickers will not be distracted by short-term performance pressure. |

Second, we will do all we can to ensure that the framework within which our stock pickers do their work further increases the odds of success.

| • | New investments in each Fund are expected to be limited when that Fund reaches certain asset levels. By limiting Fund size in this manner, we believe each manager’s Masters’ Select asset base will remain small enough so that a high level of flexibility to add value through individual stock picking will be retained. |

| • | The framework also includes the diversified multi-manager structure that makes it possible for each manager to invest in a concentrated manner knowing that the potential volatility within his or her portfolio will be diluted at the fund level by the performance of the other managers. The multi-manager structure seeks to provide the diversification necessary to temper the volatility of each manager’s sub-portfolio. |

| • | We will work hard to discourage short-term speculators so that cash flows into the Funds are not volatile. Lower volatility helps prevent our managers from being forced to sell stocks at inopportune times or to hold excessive cash for non-investment purposes. This is why years ago the Funds implemented a 2% redemption fee for the first 180 days of a shareholder’s investment in any Fund, which is paid to each Fund for the benefit of shareholders. |

Third, is our commitment to do all we can from an operational standpoint to maximize shareholder returns.

| • | We will remain attentive to Fund overhead, and whenever we achieve savings we will pass them through to shareholders. For example, we have had several manager changes that resulted in lower sub-advisory fees to our Funds. In every case we have passed through the full savings to shareholders in the form of fee waivers. |

| • | There will be no loads, 12b-1 charges or any distribution charges. |

| • | We also will work closely with our sub-advisors to make sure they are aware of tax-loss selling opportunities (only to be taken if there are equally attractive stocks to swap into). We account for partial sales on a specific tax lot basis so that shareholders will benefit from the most favorable tax treatment. The goal is not to favor taxable shareholders over tax-exempt shareholders but to make sure that the Masters’ Select stock pickers are taking advantage of tax savings opportunities when doing so is not expected to reduce pre-tax returns. |

Fourth, is our commitment to communicate honestly about all relevant developments and expectations.

| • | We will continue to do this by providing thorough and educational shareholder reports. |

| • | We will continue to provide what we believe are realistic assessments of the investment environment. |

Our commitment to Masters’ Select is also evidenced by our own investment. Our employees have, collectively, substantial investments in the Funds, as does our company retirement plan. In addition, we use the Funds extensively in the client accounts of our investment advisor practice (through our affiliate Litman/Gregory Asset Management, LLC). We have no financial incentive to do so because the fees we receive from Masters’ Select held in client accounts are fully offset against the advisory fees paid by our clients. In fact, we have a disincentive to use the Funds in our client accounts because each Masters’ Select Fund is capacity constrained (they will be closed at the pre-determined asset levels as mentioned above), and by using them in client accounts we are using up capacity for which we are not paid. But we believe these Funds offer value that we can’t get elsewhere and this is why we enthusiastically invest in them ourselves and on behalf of clients.

While we believe highly in the ability of the Funds’ sub-advisors, our commitments are not intended as guarantees of future results.

This information is authorized for use when preceded or accompanied by a prospectus for the Masters’ Select Funds. Mutual fund investing involves risk; principal loss is possible. While the Funds are no-load, there are management fees and operating expenses that do apply. The prospectus contains more information regarding the Funds’ investment objectives, risks, fees and expenses. Read the prospectus carefully before you invest in the Funds.

Commitment to Shareholders | 3 |

Dear Fellow Shareholder,

The Masters’ Select funds experienced another milestone in 2007 as Masters’ Select International celebrated its 10th anniversary in December. Because our primary goal is excellent performance over the long run, we are particularly pleased to report that as of the end of 2007, the fund’s 10-year return was 4.09 percentage points (409 basis points) ahead of its benchmark, the S&P Citigroup PMI Global (ex U.S.) Index, which placed it in the top 2% of its Morningstar Foreign Large Blend peer group1. As of December 31 2007, Morningstar ranked the Masters’ Select International Fund in the 7th, 4th, 8th, and 2nd percentile among 743, 557, 462, and 227 Foreign Large Blend Funds for the one-, three-, five-, and ten-year periods, respectively, based on total return. At this point, the only other Masters’ Select Fund with a ten-year record is Masters’ Select Equity, which also has a strong record, having beaten the best-performing of its benchmarks, the Custom Equity Index, by 1.2% for the ten-year period ending December 31, 2007. We are quite proud of the long-term performance record delivered by the two oldest Masters’ Select funds.

While we are proud of these long-term records, we are not satisfied with the performance of some of the Masters’ Select funds over the past three years. Masters’ Select Equity and Masters’ Select Value both trail their benchmarks (the Russell 3000 Index and the Russell 3000 Value Index, respectively) over these three years ending December 31, 2007. For both funds, the three-year performance is the result of two mediocre years (slightly trailing their benchmarks) sandwiched around a year of more significant underperformance. Masters’ Select Smaller Companies also trails over three years ending December 31 2007, because of a very poor 2006. The fund actually outperformed its benchmark last year and also in 2005 and 2004. 2

How is it that a concept that we believe is so compelling, and that has delivered over ten years for the two oldest Masters’ Select funds, can fail to deliver over a period as long as three years? For each fund there were specific reasons that are discussed in the individual fund section of this report. However, that the funds underperformed over a three-year period is not altogether surprising. In fact it is consistent with the findings in our study we wrote about in the September 2006 shareholder letter. As we reported back then, we looked at funds in different style categories that outperformed their benchmarks by 1% or more per year over the ten years ending 12/31/2005. We found that almost all the outperforming funds had at least one three-year period in which they underperformed by at least two percentage points per year (depending on the style category the likelihood of this having happened ranged from 88% to 100%). Surprisingly, between 50% and 72% (depending on the style category) of the ten-year outperformers had at least one three-year period in which the fund trailed its benchmark by an even larger amount of at least five percentage points per year (for a three-year period). Even bigger underperformance was less common, but not rare. (Go to www.mastersfunds.com to see the study in our September 2006 shareholder report.)

So experiencing a period of underperformance over three years is more the norm than the exception—even for most funds that have soundly beaten their benchmarks over the long run. In fact, Masters’ Select International, now coming off a very strong year and with an exceptionally high ten-year peer group ranking by Morningstar as noted above, posted the single worst three-year relative return run of all the Masters’ funds! At the end of February 2005, Masters’ Select International trailed its S&P Citigroup PMI Global (ex U.S.) Index benchmark by an annualized 4.16 percentage points. Since that time the fund has rebounded strongly.

But why does underperformance happen to skilled stock pickers? Based on our observations, we’d say it is a confluence of factors that usually includes costly analytical mistakes by the stock picker (they do make mistakes occasionally), unforeseen events that impact some of the holdings, not participating in particularly strong sectors or stocks that are in the benchmark (e.g. energy, recently) and sometimes, a stock picker’s style being temporarily out of sync with the benchmark. Recently, some of the Masters’ funds have suffered through a period where several of our managers have struggled at the same time—something we considered unlikely.

Going beyond the question of why it can happen, the key factor for investors to consider about underperformance is whether it is likely to continue. If the stock picker is truly skilled and continues to be motivated and focused, we believe he or she is likely to outperform again—as was the case with the group of sub-advisors responsible for Masters’ Select International. This underscores the importance we place on continually assessing our confidence in the stock-picking skills and focus of our sub-advisors. Litman/Gregory’s ongoing evaluation of the quality of each sub-advisor’s investment process, team, research and decision-making usually results in a reaffirmation of our confident view. Occasionally it doesn’t. In these instances we have made changes. And it is important for us to communicate that, having made one manager change in 2007 (and also a manager addition) and one in 2006, we are happy with all of our sub-advisors across all five Masters’ Select funds, despite the poor performance some of them have generated recently. Based on the confidence we have in our sub-advisors, we expect Equity, Value and Smaller Companies to do well going forward. Obviously, this expectation is not a guarantee, and we don’t know when a relative performance rebound might start. But based on the study mentioned above (and our own experience over more than 20 years) we do know that, it is not uncommon for stock pickers who build index-beating long-term records to struggle through surprisingly lengthy periods of underperformance along the way, after which they rebound and perform well again.

Interesting Research

Over the past 20-plus years, Litman/Gregory has researched hundreds of stock pickers and fund managers. Over that time we’ve formed strong opinions about what traits skilled stock pickers have in common. Given our interest in the evaluation of stock pickers, a study published early last year on the concept of “Active Share” caught our eye.

| 1 | Morningstar, Inc., is an independent mutual fund research and rating service. Each Morningstar category represents a universe of funds with similar investment objectives. Rankings for the period shown are based on fund total returns with dividends and distributions reinvested and do not reflect sales charges. The highest percentile rank is 1 and the lowest is 100. The information contained herein: (1) is proprietary to Morningstar; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. |

| 2 | The annual returns for the Masters’ Select Smaller Companies Fund for the years ended 12/31/04, 12/31/05 and 12/31/06 were 21.01%, 5.29% and 9.67%, respectively. The annual returns for the Russell 2000 Index for the years ended 12/31/04, 12/31/05 and 12/31/06 were 18.33%, 4.55% and 18.37%, respectively. |

| 4 | The Masters’ Select Funds Trust |

The study was conducted by two Yale professors, Martijn Cremers and Antti Petajisto. The concept of Active Share has to do with the degree of difference in a fund’s portfolio holdings compared to its benchmark’s holdings. For example, if 70% of a fund’s positions were different than its benchmark, then it would have an “active” weight of 70% (this measure factors in both the different holdings, and the differences in the allocation to common holdings).

There are a number of interesting points in the paper but the most interesting is how Active Share relates to fund performance. Cremers and Petajisto analyzed the period from 1990 through 2003 and found that funds with the highest Active Share (at least 80%) outperformed their benchmarks by 1.39% to 1.49% (they did the study in two different ways so there are two different performance measures) on average (per year), while funds in the bottom quintile of Active Share lagged their benchmarks by 1.41% to 1.79%. Among Cremers and Pentajisto’s conclusions: “The best performers are concentrated stock pickers (high Active Share, high tracking error)… and even after fees and transaction costs the most active of them beat their benchmarks.” They later write that “Funds with the highest Active Share significantly outperform their benchmarks both before and after expenses…”

This is only one study, and the conclusions do not apply to every fund. The evidence of a high correlation between Active Share and outperformance is compelling, but correlation is not the same thing as causation. With regards to the performance conclusions of the study, they are talking about the overall category of high Active Share funds—and some of the funds in that category surely underperform. So even if Cremers’ and Petajisto’s conclusions are good, Active Share would not by itself be a reliable predictor of future performance and we would certainly not be confident in using it as a means of selecting stock pickers or picking funds. That the data is so compelling is somewhat surprising to us. But the conclusions are not surprising to us and are consistent with what we look for in stock pickers: individuals and teams who have the confidence, based on their process and depth of research, to invest in their most compelling ideas and are not afraid to stray from the benchmarks (as opposed to closet indexers).

Recently we measured the Active Share of the Masters’ Select funds using Cremers’ and Petajisto’s methodology. They identified the group of high Active Share managers as those with at least an 80% measure (80% of the portfolio was different than the benchmark). Using September 30, 2007 numbers we found each of the Masters’ funds to have an extremely high level of active management (as we would expect):

Fund | Active Share %* | Benchmark |

| Masters’ Select Equity | 90% | Russell 3000 Index |

| Masters’ Select Focused Opportunities | 91% | S&P 500 Index |

| Masters’ Select Value | 90% | Russell 3000 Value Index |

| Masters’ Select Smaller Companies | 98% | Russell 2000 Index |

| Masters’ Select International | 93% | S&P Citigroup PMI Global ex-US Index |

* Represents the portion of the portfolio that is different from the benchmark portfolio

For a fund to outperform its benchmark by a material margin over the long run requires a portfolio that is consistently different than the benchmark. While this creates the opportunity for outperformance, it also creates opportunity for underperformance, which will also happen at times. If the stock picker is skilled, we believe the likelihood is that over the long run there will be more periods of strong performance than periods of bad performance. If we are right, we expect this would lead to benchmark-beating, long-term returns.

In Closing

As always, we believe it is important to communicate to you the strong financial commitment to the Masters’ Select funds on the part of Litman/Gregory employees and the independent trustees. As of December 31, 2007 employees and trustees held $17.7 million worth of Masters’ Select shares.

We continue to feel fortunate that as of the end of the year, out of the five Masters’ Select funds, the Equity, International, and Smaller Companies funds were included in the small group of actively managed funds named as Fund Analyst picks in their fund categories (Large Blend, Foreign Large Blend, and Small Growth, respectively) by Morningstar.

Of most importance, we are as committed as ever to doing all we can to deliver strong long-term returns relative to each fund’s benchmarks. In this regard we want to recognize our analyst team, who has made important contributions to our initial and ongoing due diligence efforts.

Sincerely,

Ken Gregory and Jeremy DeGroot

Litman/Gregory Fund Advisors, LLC

Advisor to the Masters’ Select Funds

Some of the comments are based on current management expectations and are considered “forward-looking statements”. Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as “estimate”, “may”, “expect”, “should”, “could”, “believe”, “plan” and similar terms. We cannot promise future returns and our opinions are a reflection of our best judgment at the time this report is compiled.

Shareholder Letter | 5 |

Masters’ Select Long-Term Performance Metrics

As we always point out, long-term performance is what we care about, and over long periods of time the Masters’ Select fund family is, we believe, building an encouraging record despite the fact that the last three years have been difficult for several of our funds. There are three metrics we track and present in these reports that serve as a helpful report card on the Masters’ Select long-term performance and ultimately, the success of the Masters’ Select concept. These metrics are updated below:

1st Metric: Each Fund’s Overall Fund Performance Since Inception

The two oldest Masters’ Select Funds have out-returned their passive benchmarks by a clear margin since their inception. Masters’ Select Value, the third oldest Masters’ Select Fund trails its benchmark, the Russell 3000 Value Index, but by a very small margin. Masters’ Select Smaller Companies, which is four and one half years old, also trails its benchmark, the Russell 2000 Index, thus far. At one-and-a-half years old, Masters’ Select Focused Opportunities is not yet old enough to measure long-term performance and therefore is not included in the chart below. As is well documented by others, we believe that beating a benchmark over the long-term is a demanding standard. Nevertheless it is our objective to meet this standard over long time periods for each of our funds.

MASTERS’ SELECT PERFORMANCE VS. BENCHMARKS SINCE INCEPTION | ||||

Fund | Length of Operation as of 12/31/07 | Index Benchmark | Average Annual Out-performance Over Benchmark | |

Masters’ Select Equity | 11 years | Russell 3000 | 1.29% (129 basis points) | |

Masters’ Select International | 10 years and 1 month | S&P CGI PMI Global ex. US Index | 3.76% (376 basis points) | |

Masters’ Select Value | 7 years and 6 months | Russell 3000 Value | -0.24% (-24 basis points) | |

Masters’ Select Smaller Companies | 4 years and 6 months | Russell 2000 | -1.56% (-156 basis points) | |

2nd Metric: Frequency of Long-Term Out-Performance

Because beating a passive index over the long run is a rare feat for active managers there are many investment professionals and academics who believe active management is folly, especially given the alternative of low cost index funds. Given the difficulty in beating a passive benchmark, investors considering an actively managed fund should have some reason to believe it is likely to do better. Though past performance is no guarantee of future performance, an interesting performance measure is the percentage of times that each fund beat its benchmark over longer time periods. The table below shows the aggregate performance of the Masters’ Select Funds over rolling three-year and five-year time periods. Generally we believe five years is a better time frame to measure—especially for funds focused on long-term returns (ten years is even better but we will have to wait another year before we have enough ten-year periods to warrant reporting). While we would like each Masters’ Select Fund to outperform its index benchmark in every three-year period, this is an unrealistic standard given each fund’s extreme lack of benchmark sensitivity, and since one bad year can have a huge impact on any three-year period. What we do seek is for the Masters’ Select Funds to outperform their benchmarks in the majority of the intermediate time period of three years, and a higher percentage of the time over five-year periods. See the report on each fund for more detail.

MASTERS’ SELECT FUNDS: PERFORMANCE VERSUS BENCHMARKS OVER INTERMEDIATE-TERM (THREE YEARS) AND LONG-TERM (FIVE-YEARS) PERIODS* | ||

Three Years | Five Years | |

Percentage of Times Masters’ Select Outperformed | 55% | 67% |

Total Number of Rolling Return Periods** | 238 | 166 |

| * | Masters’ Select Equity is benchmarked against the Russell 3000 Index. Masters’ Select International is benchmarked against the S&P Citigroup PMI Global (ex-US) Index. Masters’ Select Value is benchmarked against the Russell 3000 Value Index. Masters’ Select Smaller Companies is benchmarked against the Russell 2000 Index. |

| ** | The first rolling three-year period is reached 36 months after each fund’s inception (based on month-end dates). The starting and ending periods then “roll” forward one month at a time to comprise a new 36-month period. The first rolling five-year period is reached 60 months after each fund’s inception (based on month-end dates). The starting and ending periods then “roll” forward one month at a time to comprise a new 60-month period. |

We believe the strong out-performance across five-year time periods in particular suggests that Masters’ Select has performed well for reasons that are unlikely to be due to mere chance.

3rd Metric: Performance of the Underlying Sub-advisors

A third measure for assessing performance is the performance of the underlying sub-advisors. If a fund’s success was the result of spectacular performance by one or two sub-advisors, one could perhaps make the argument that there was luck involved and thereby question the likelihood that the out-performance may be repeated. In our opinion, the more managers who outperform their benchmarks over the long run, the more likely it is that the group is truly skilled and that the Masters’ Select structure enhances the ability of managers to succeed. With respect to this test, the evidence seems compelling. Of the 21 sub-advisors who have run a

| 6 | The Masters’ Select Funds Trust |

Masters’ Select portfolio for at least three years (including those no longer part of Masters’ Select) 15 (71%) outperformed his or her benchmark after taking into account all fees for their full tenure with the funds. This includes four managers who are no longer part of Masters’ and four others who are included twice because they are part of two Masters’ Select Funds. We believe the odds of this outperformance happening by chance are quite low.

We continue to believe that together, the above metrics offer strong evidence that the Masters’ Select concept is being well executed.

Performance quoted represents past performance and does not guarantee future results. Please refer to page 2 to view the performance of the funds and their respective benchmarks

See page 76 for index definitions

Indices are unmanaged and do not incur fees, expenses or taxes.

Performance Metrics | 7 |

Masters’ Select Equity Fund Review

Falling housing prices, rising sub-prime mortgage defaults, tightening credit and fears of a broad economic slowdown, if not outright recession, weighed on the U.S. stock market in the second half of 2007. The financial sector was the hardest hit, dropping 20%, while consumer discretionary stocks dropped 17%. Energy was the top performer, gaining 12%.

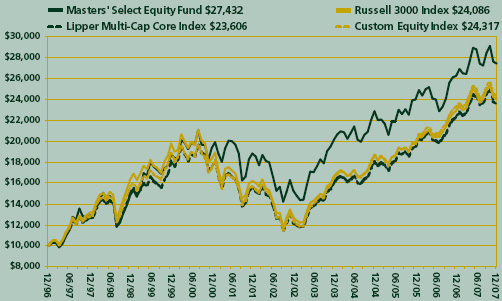

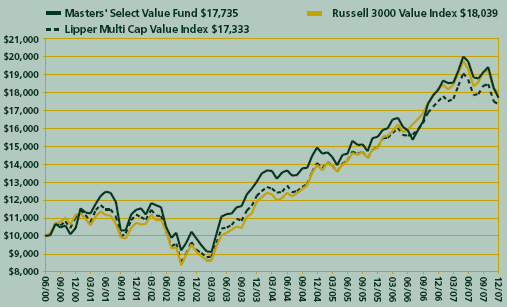

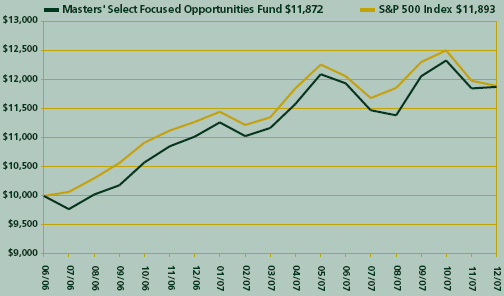

The value of a hypothetical $10,000 investment in the Masters’ Select Equity Fund from inception (12/31/96) to present compared with the Russell 3000 Index and the Lipper Multi-Cap Core Index.

The hypothetical $10,000 investment at fund inception includes changes due to share price and reinvestment of dividends and capital gains. The chart does not imply future performance. Indices are unmanaged, do not incur fees, expenses or taxes and cannot be invested in directly.

Performance as of December 31, 2007

Average Annual Total Returns | ||||

One-Year | Five-Year | Ten-Year | Since Inception | |

Masters’ Select Equity Fund (12/31/96) | 4.57% | 12.44% | 7.83% | 9.61% |

Performance data quoted represents past performance and does not guarantee future results. The funds impose a 2% redemption fee on shares held less than 180 days. Performance data does not reflect the redemption fee. If reflected, total returns would be reduced. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

After a strong first half of 2007, Masters’ Select Equity ended the year trailing its benchmarks by a small margin. In the fourth quarter, the Equity fund declined 3.54%, versus a loss of 3.34% for the Russell 3000 Index. For the year, the Equity fund gained 4.57%, compared to a 5.14% gain for the index. Since inception, the fund has outperformed its benchmarks, gaining 9.61% on an annualized basis, versus 8.32% for the Russell 3000 Index.

As we wrote in the shareholder letter earlier in this report, though we are pleased with Masters’ Select Equity’s long-term performance compared to its benchmarks, we are not satisfied with the fund’s trailing three-year return. (We strongly urge you to read the introductory letter, which provides important perspective to the last three years.) After beating its benchmarks for six consecutive years (1999 through 2004), the fund’s return trails the Russell 3000 Index over the last three years. Over this period, relative performance was driven mostly by a very poor year in 2006, but also lagging performance in 2005 and now to a minor extent 2007.

At a manager level, over the three year time period ended 12/31/07, three of the fund’s managers trailed their benchmarks, two of them by wide margins. Though it is discouraging, performance slumps by managers who outperform over the long run are not rare. (Based on the findings of the study we referenced in the shareholder letter earlier in this report, the majority of managers experience three-year periods of material underperformance—more details of this study were included in the September 2006 shareholder report.) When underperformance happens, it is important to assess whether the factors that supported our confidence in the stock picker are still present. These factors include the investment process, team quality, execution, focus and the ability to successfully implement a concentrated portfolio. In the case of the fund’s underperforming managers, though some stock-picking mistakes were made, we continue to be very confident in their skills, and because of that we believe we will see them eventually begin outperforming again (in fact, one did turn around and put in a strong performance in 2007).

It is worth mentioning that we have been through this before. Masters’ Select International experienced an even more severe period of relative underperformance that ended in early 2005. Since that time the fund has experienced very strong relative and absolute performance and over the last ten years the fund ranks in the top 2% of its Morningstar peer group. As of December 31 2007, Morningstar ranked the Masters’ Select International Fund in the 7th, 4th, 8th, and 2nd percentile among 743, 557, 462, and 227 Foreign Large Blend Funds for the one-, three-, five-, and ten-year periods, respectively, based on total return. While there are obvious differences between the Equity and International Funds, this pattern of ups and downs in relative performance over shorter time periods is not surprising in the context of what the data tell us about funds that have outperformed over the long run.

Long-Term Performance Analysis

Though occasional periods of lagging performance can be frustrating, investors who have stuck with the fund over its 11-year life have been rewarded. Evidence of the fund’s long-term success and other performance observations are outlined below (all performance numbers are net of all fund fees and expenses including advisory fees, fund operating overhead and trading costs).

| • | The fund has outperformed the Custom Equity Index (a blend of the S&P 500, Russell 2000 and the MSCI EAFE Index), the best-performing of its benchmarks, by 1.19 percentage points (119 basis points) since its inception, as measured by average annual total return. In dollar terms, $10,000 invested in the fund 11 years ago would be worth $27,432 vs. $24,317 for the index. Thus, the fund has generated $17,432 of return vs. $14,317 for the index, or 22% excess total return. |

| • | Over its full life the fund has outperformed the S&P 500 by an average annualized margin of 1.45% (145 basis points). We don't view this index as a primary benchmark because it is more large-cap oriented than Masters' Select Equity. However, it is the most widely followed U.S. equity |

| 8 | The Masters’ Select Funds Trust |

benchmark. The S&P 500 Index’s performance over the past one, five and ten years, and since the fund’s inception date (12/31/96) has been 5.49%, 12.83% 5.91% and 8.16% respectively.

| • | The fund outperformed each of its benchmarks in a variety of environments including strong growth years (1999) and several strong value years (2000, 2001 and 2004). We feel this is a testament to the diversified style exposure in the fund, the flexibility of the managers to pursue the most compelling opportunities without artificial style-box constraints, and of course, the skill of the managers. |

| • | The fund has outperformed, on a total-return basis, all of its benchmarks in down years for the stock market (2000, 2001 and 2002). Its performance has varied in the up years. It outperformed in the very strong return year of 1999. In the very strong return years of 1997 and 2003 it outperformed two of its three benchmarks. However, in 1998 and 2006, also strong years for stocks, the fund underperformed. In the more moderate return year of 2004 it outperformed all three benchmarks but in 2005 and 2007 it trailed its benchmarks. |

| • | We believe consistency over five-year time periods is also an important metric. There have been 73 rolling five-year time periods during the fund’s life (the first starting at the fund's inception, and then in each subsequent period commencing at the beginning of the next month). Masters' Select Equity has out-returned its Russell 3000 benchmark in 60 of these periods as measured by average annual total return. This amounts to outperformance in 82% of the defined five-year periods. We believe this consistency is noteworthy. |

| • | As depicted in the table, the fund’s worst return experiences over one, three and five years have been significantly better than its Russell 3000 benchmark and the fund has experienced fewer negative return periods. |

Performance | MSEFX | Russell 3000 | Number of Periods |

Best Rolling 12-Mo. Period 1 | 47.7% | 47.7% | 121 |

| Worst Rolling 12-Mo. Period | -22.8% | -27.9% | 121 |

| Best Rolling 36-Mo. Period | 104.0% | 105.0% | 97 |

| Worst Rolling 36-Mo. Period | -28.3% | -40.4% | 97 |

| Best Rolling 60-Mo. Period | 99.5% | 111.8% | 73 |

| Worst Rolling 60-Mo. Period | 0.1% | -17.3% | 73 |

| Percent Negative 12-Mo. Rolling | 20.7% | 24.8% | 121 |

| Percent Negative 36-Mo. Rolling | 17.5% | 29.9% | 97 |

| Percent Negative 60-Mo. Rolling | 0.0% | 38.4% | 73 |

| Percent Beat Benchmark 12-Mo. | 61.2% | n/a | 121 |

| Percent Beat Benchmark 36-Mo. | 66.0% | n/a | 97 |

| Percent Beat Benchmark 60-Mo. | 82.2% | n/a | 73 |

| 1 | The best performing 12 and 36 month rolling periods for the Fund commenced in May 1997; the best rolling 60 month period commenced in October 2002. The worst 12, 36 and 60 month rolling periods for the Fund commenced in April 2002, April 2000 and April 1999, respectively. |

| • | Four of the fund’s six long-tenured managers have outperformed their benchmarks during their time with the fund. In addition, Sig Segalas, who was replaced in October 2003, also outperformed his benchmark during his almost seven-year tenure. Two other managers who had been replaced in earlier years did not outperform their benchmarks (one replaced the other and was then replaced by Bill Miller—neither was part of the fund for three years). The following table shows the outperformance of each long-tenured manager (without identifying the managers), relative to his benchmark: |

CURRENT MASTERS’ SELECT MANAGERS’ PERFORMANCE Margin versus BENCHMARKS Manager Return Less Benchmark Return Over Full Tenure Through December 31, 2007* | |

Masters’ Select Equity | Annualized Performance Margin (Net of Allocated Expenses) |

Manager 1 | 11.20% |

Manager 2 | 5.71% |

Manager 3 | 2.68% |

Manager 4 | 2.59% |

Manager 5 | -1.50% |

Manager 6 | -2.55% |

| * | This table does not include the two managers that preceded Bill Miller prior to March 2000. Both of those managers underperformed their benchmarks. It also does not include Sig Segalas who for his almost seven-year tenure outperformed his benchmark. Listed alphabetically are the managers and their respective benchmarks. |

Manager | Tenure | Benchmark |

Craig Blum & Steve Burlingame | 10/31/03 | Russell 1000 Growth Index |

| Bill D’Alonzo | 12/31/96 | Russell 2500 Growth Index |

| Chris Davis | 12/31/96 | S&P 500 Index |

| Mason Hawkins | 12/31/96 | Russell 3000 Value Index |

| Bill Miller | 03/24/00 | S&P 500 Index |

| Dick Weiss | 12/31/96 | Russell 2000 Index |

| • | Masters’ Select Equity’s after-tax returns since inception have also been strong. The fund's average annual return over its life assuming all shares were liquidated on December 31, 2007, and taxes were paid on distributions in each year at the highest tax rate in place at the time of each distribution, was 7.80%. If we assume the Russell 3000 Index compounded without any taxes paid over the same eleven-year period, then was liquidated on December 31, 2007 and paid taxes on accumulated gains at the current capital gains rate of 15%, its theoretical after-tax return would be lower, at 7.42%. (This hypothetical tax calculation on the index unrealistically favors the index because it assumes no taxes on returns from dividends until the liquidation date, and no annual expenses.) Masters’ Select Equity Fund’s average annual total return after taxes on distributions for the one-year, five-year, ten-year and since inception (12/31/96) periods ended December 31, 2007 are 3.38%, 11.80%, 6.63% and 8.17%, respectively. The average annual total return after taxes on distributions and the |

Fund Summary | 9 |

sale of fund shares for the one-year, five-year, ten-year and since inception (12/31/96) periods ended December 31, 2007 are 4.60%, 10.85%, 6.36% and 7.80%, respectively.

Portfolio Commentary

A number of factors contributed to the fund’s performance during 2007. The highlights follow.

Performance of managers: In 2007, four of the six Masters’ Select Equity stock pickers outperformed their respective benchmarks; the other two managers underperformed their respective benchmarks. For the year, the individual sub-advisors’ returns ranged from a loss of 5.9% to a gain of 14.8%.

Over shorter time periods, it is typical for some, but not all, managers to beat their benchmarks. However, we are focused primarily on long-term performance and we aim to select sub-advisors who will beat their benchmarks over longer time periods. Through 2007, four of the six sub-advisors have achieved that goal by a significant margin since their respective inception dates. While the other two managers trail their benchmarks, we believe that they will ultimately outperform, as well.

Sector and stock-picking impact: Though all the Masters’ Select funds are driven by bottom-up stock picking, the sector exposure that results from this may provide some insight into the fund’s relative performance. Based on our attribution analysis, the fund’s overall sector exposure detracted from performance relative to the Russell 3000 benchmark. The fund’s overweighting to the top-performing materials sector was a positive, but this was more than offset by the fund’s over-allocation to the hard-hit consumer discretionary sector. In contrast, stock selection was a positive contributor to relative performance. The fund’s financial and consumer-discretionary stocks, in particular, added value relative to the benchmark’s returns for those sectors. This includes the 106% return for Amazon.com, the fund’s top holding. On the negative side, the fund’s telecom services and materials stocks hurt performance relative to the benchmark’s returns for those sectors.

Leaders and laggards: During 2007, four of the fund’s six sub-advisors had at least two stocks that were among the fund’s ten largest percentage gainers; those same sub-advisors also had at least two stocks that were among the fund’s largest percentage losers. Chris Davis/Ken Feinberg and Mason Hawkins were not on either list. Bill D’Alonzo claimed the portfolio’s biggest percentage winner for the year: Aquantive, which was a digital marketing company that was acquired by Microsoft in the second quarter. Interestingly, Amazon.com—the fund’s largest position and owned by both Bill Miller and Craig Blum/ Stephen Burlingame—was one of the best-performing stocks in the portfolio for 2007 after being one of the fund’s worst performers the year before. Other big winners by percentage include Taser (up 99%), Arcelor Mittal (up 81%), VMWare (up 77%), and FMC Technologies (up 76%). The two largest percentage losers for the year were housing-related stocks Countrywide Financial (down 56%) and Pulte Homes (down 51%). Seven of the fund’s ten largest winners and seven of the ten largest losers remained in the portfolio at the end of the year.

See the table on page 12 for a list of the leaders and laggards over the past six and 12 months. The table includes dollar gains and losses as well as percentage gains and losses. It is important to understand that the fact a stock has lost (or made) money for Masters’ Select Equity for the 12-month period ended December 31, 2007 tells us nothing about how successful the holding has been during the entire period it was held, or how successful it may become. The fund will hold many stocks for significantly longer periods of time and the success of these holdings won’t be known until they are ultimately sold. So in that respect, while it is interesting to know how specific stocks performed during the period, this information is of limited value in assessing the ultimate success of these stock holdings.

Portfolio mix: There were some notable changes to the fund’s sector exposure during the year. The fund’s allocation to the technology sector ended the year at 20.7%, up 4.3% from year-end 2006—making it the portfolio’s second-largest sector exposure behind financials, which were down slightly from the prior year to 22.6%. Energy accounted for 12.6% of the fund at year-end (compared to 7.6% the year before), making it the third-largest sector allocation. The consumer discretionary and materials sectors—the fund’s fourth- and fifth-largest sector allocations—accounted for 18.0% (down 4.8% from the year before) and 9.5% (up 3.0% from the prior year), respectively. Relative to the Russell 3000 benchmark, at year-end the fund was significantly overweighted to the consumer discretionary, materials, financial, and technology sectors while being heavily underweighted to health care, consumer staples, industrials, and utilities.

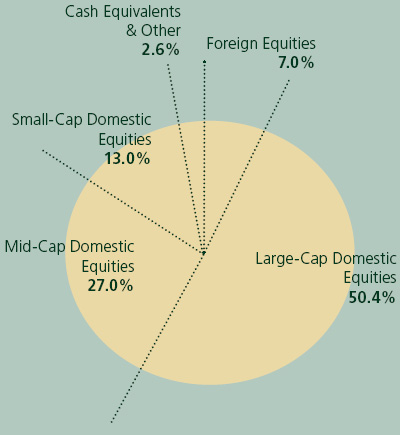

The fund’s exposure to large-cap stocks (with market caps greater than $18.3 billion) and small-cap stocks (with market caps less than $2.5 billion) rose in the fourth quarter, ending the year at 50.4% and 13.0%, respectively. This came at the expense of mid-caps, which were down to 27.0% at year-end. (Note that we updated our market-cap definitions after the 6/30/07 shareholder report.) The rest of the portfolio was comprised of foreign stocks (up slightly from the year before, to 7.0%) and cash (2.6%).

Please see page 13 for a breakout of the fund’s sector and market-cap exposures.

Miscellaneous

Taxes: Masters’ Select Equity distributed $1.27 in capital gains in December. Approximately 98% of the gains were long-term. We will continue to work with the fund’s sub-advisors to manage the fund in a tax-aware manner. This will include taking short-term losses when there is an alternative investment that is equally attractive, and using other tax-management techniques. However, the managers will not sacrifice pre-tax performance in pursuit of after-tax performance since the fund has both tax-exempt and taxable shareholders.

Accolades: Masters’ Select Equity continues to be included as a Fund Analyst Pick in the Large Blend Category by Morningstar, the fund rating firm. Morningstar updated their opinion of the fund in December in a report titled: “Masters’ Select Equity can be streaky, but it’s one of our favorite large-blend funds.”

| 10 | The Masters’ Select Funds Trust |

In Closing

As we write this, recession fears are rising and the stock market is coming off of a negative quarter and has declined more in the first couple of weeks in 2008. However, negative headlines don’t necessarily foreshadow rough performance periods—though they can. Often headlines can be a contrarian indicator as the stock market tends to be forward looking. That is why stocks tend to decline months before a recession has started and often begin to rebound during the depths of recession—as investors look ahead to recovery. As far as longer-term prospects, based on our analysis and at an S&P 500 level of 1380, stock market valuations are attractive based on many metrics and at least reasonable based on others. These valuation metrics tell us nothing about how stocks might do in the short term. But they suggest to us that stocks, as is typically the case, remain likely to outperform their primary competitor, bonds, over reasonably long time frames.

A source of encouragement comes from some of the fund’s sub-advisors who tell us that they are finding more compelling stock picking opportunities now than they have in the last few years. This may be due to the large variance in performance in different sectors. This is unlike the last several years when we were hearing that there were not a lot of valuation discrepancies. So, while the overall market has underlying questions, we are more optimistic about the potential to add value from good stock picking. This is a long-term confidence builder for us, though it does not mean that the fund or the markets will necessarily do well over the short term. In fact, if there is an economic downturn, it is likely that stocks will decline below early January levels before rebounding in anticipation of a recovery.

Whatever the future is for the stock market, over shorter time periods shareholders should be prepared for the fund to track differently than its benchmarks - sometimes positively and sometimes negatively. Recently it has been negatively. But over the longer time horizon based on which the fund is managed, the quality of its stock pickers and the strength of the Masters’ Select concept together give us confidence in our belief that the fund will outperform its benchmarks, as it has since its inception.

Neither the information contained herein nor any opinion expressed shall be construed to constitute an offer to sell or a solicitation to buy any security or any other funds mentioned herein. The views herein are those of Litman/Gregory Fund Advisors, LLC at the time the material is written and may not be reflective of current conditions. Performance quoted represents past performance and does not guarantee future results.

Fund Summary | 11 |

Masters’ Select Equity Fund Leaders and Laggards

For the Six Months Ended December 31, 2007

By Percentage Gain (Loss)

Security | $ Contribution (Loss) | % Change |

| VMware | 20,049 | 76.8% |

| CNinsure, Inc. | 40,898 | 56.8% |

| FMC Technologies, Inc. | 2,721,079 | 52.0% |

| Fairfalx Financial | 5,879,461 | 50.7% |

| Salesforce.com, Inc. | 7,824,801 | 45.6% |

| Amazon.com, Inc. | 12,086,075 | 32.4% |

| Google, Inc. | 8,112,391 | 28.0% |

| Berkshire Hathaway, Inc. Del | 4,103,771 | 28.8% |

| Foxhollow Technologies, Inc. | 974,743 | 24.2% |

| Dril-Quip, Inc. | 1,178,100 | 23.8% |

| 42,941,368 | ||

| Countrywide Financial Corp. | (13,151,849) | (54.3%) |

| Level 3 Communications, Inc. | (8,151,766) | (42.8%) |

| Symmetricom, Inc. | (2,525,824) | (42.5%) |

| Emmis Communications Corp. | (2,464,939) | (40.3%) |

| Capital One Financial Corp. | (4,980,267) | (39.7%) |

| Lennar Corp. | (2,846,768) | (38.7%) |

| Ceradyne, Inc. Calif | (1,744,924) | (38.7%) |

| Sprint Nextel Corp. | (4,653,540) | (36.4%) |

| Conseco, Inc. | (2,270,501) | (34.7%) |

| General Motors Corp. | (4,765,440) | (32.8%) |

| (47,555,818) |

By Dollar Gain (Loss)

Security | $ Contribution (Loss) | % Change |

| Amazon.com, Inc. | 12,086,075 | 32.4% |

| Google, Inc. | 8,112,391 | 28.0% |

| Salesforce.com, Inc. | 7,824,801 | 45.6% |

| Fairfalx Financial | 5,879,461 | 50.7% |

| EOG Resources, Inc. | 5,363,547 | 21.5% |

| Berkshire Hathaway, Inc. Del | 4,103,771 | 28.8% |

| Arcelor Mittal | 3,013,848 | 23.6% |

| Schlumberger Ltd. | 2,838,677 | 18.4% |

| FMC Technologies, Inc. | 2,721,079 | 52.0% |

| AON Corp. | 2,266,340 | 12.5% |

| 54,209,990 | ||

| Countrywide Financial Corp. | (13,151,849) | (54.3%) |

| Level 3 Communications, Inc. | (8,151,766) | (42.8%) |

| Cemex | (6,549,832) | (29.9%) |

| Capital One Financial Corp. | (4,980,267) | (39.7%) |

| General Motors Corp. | (4,765,440) | (32.8%) |

| Sprint Nextel Corp. | (4,653,540) | (36.4%) |

| Tyco International Ltd. | (3,219,329) | (9.1%) |

| Fedex Corp. | (3,196,800) | (19.5%) |

| Eastman Kodak Co. | (3,140,500) | (20.5%) |

| Sealed Air Corp. | (3,055,143) | (24.7%) |

| (54,864,468) |

For the Year Ended December 31, 2007

By Percentage Gain (Loss)

Security | $ Contribution (Loss) | % Change |

| aQuantive, Inc. | 3,894,322 | 107.5% |

| Amazon.com, Inc. | 32,635,085 | 105.7% |

| Taser International Inc. | 4,158,187 | 99.2% |

| Arcelor Mittal | 7,339,710 | 80.9% |

| VMware | 20,049 | 76.8% |

| FMC Technologies, Inc. | 4,112,652 | 75.8% |

| Salesforce.com, Inc. | 10,299,702 | 70.1% |

| U.S. Steel Corp. | 4,949,200 | 58.8% |

| Surmodics, Inc. | 2,272,612 | 58.3% |

| Schlumberger Ltd. | 7,388,838 | 57.5% |

| 77,070,357 | ||

| Countrywide Financial Corp. | (16,193,154) | (55.6%) |

| Pulte Homes, Inc. | (7,676,468) | (51.1%) |

| Symmetricom, Inc. | (2,244,459) | (39.7%) |

| Lennar Corp. | (2,846,768) | (38.7%) |

| Ceradyne, Inc. Calif | (1,744,924) | (38.7%) |

| Network Appliance, Inc. | (3,659,813) | (32.5%) |

| Force Protn, Inc. | (1,284,450) | (32.3%) |

| Capital One Financial Corp. | (4,661,364) | (31.9%) |

| Emmis Communications Corp. | (1,999,968) | (31.8%) |

| Conseco, Inc. | (2,015,222) | (30.5%) |

| (44,326,590) |

By Dollar Gain (Loss)

Security | $ Contribution (Loss) | % Change |

| Amazon.com, Inc. | 32,635,085 | 105.7% |

| Google, Inc. | 11,738,218 | 40.5% |

| Salesforce.com, Inc. | 10,299,702 | 70.1% |

| EOG Resources, Inc. | 9,164,165 | 34.3% |

| Schlumberger Ltd. | 7,388,838 | 57.5% |

| Arcelor Mittal | 7,339,710 | 80.9% |

| Fairfalx Financial | 5,632,621 | 46.9% |

| AON Corp. | 5,499,496 | 32.1% |

| U.S. Steel Corp. | 4,949,200 | 58.8% |

| Taser International Inc. | 4,158,187 | 99.2% |

| 98,805,222 | ||

| Countrywide Financial Corp. | (16,193,154) | (55.6%) |

| Pulte Homes, Inc. | (7,676,468) | (51.1%) |

| Level 3 Communications, Inc. | (5,672,454) | (19.2%) |

| Capital One Financial Corp. | (4,661,364) | (31.9%) |

| Cemex | (4,278,749) | (21.2%) |

| Network Appliance, Inc. | (3,659,813) | (32.5%) |

| Sealed Air Corp. | (3,558,392) | (23.8%) |

| InterActiveCorp | (3,365,948) | (22.4%) |

| Sprint Nextel Corp. | (3,084,351) | (15.9%) |

| American International Group, Inc. | (2,964,196) | (15.8%) |

| (55,114,889) |

12 | The Masters’ Select Funds Trust |

Masters’ Select Equity Fund Managers

INVESTMENT MANAGER | FIRM | TARGET ASSET ALLOCATION | MARKET CAPITALIZATION OF COMPANIES IN PORTFOLIO | STOCK-PICKING STYLE |

| Craig Blum/Stephen | TCW Investment Management | 20% | Mostly mid- and | Growth |

| Burlingame | Company | large-sized companies | ||

| Christopher Davis/ | Davis Selected Advisers, L.P. | 20% | Mostly large companies | Growth at a |

| Kenneth Feinberg | reasonable price | |||

| Bill D’Alonzo and Team | Friess Associates, LLC | 10% | Small and mid-sized | Growth |

companies | ||||

| Mason Hawkins | Southeastern Asset Management, Inc. | 20% | All sizes and global, | Value |

may have up to 50% | ||||

foreign stocks | ||||

| Bill Miller | Legg Mason Capital Management, Inc. | 20% | All sizes, but mostly | Eclectic, may invest |

large and mid-sized | in traditional value | |||

companies | stocks or growth | |||

stocks | ||||

| Dick Weiss | Wells Capital Management, Inc. | 10% | Small and mid-sized | Growth at a |

companies | reasonable price |

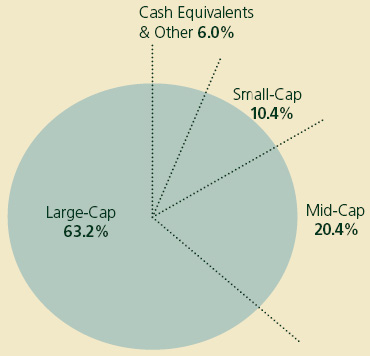

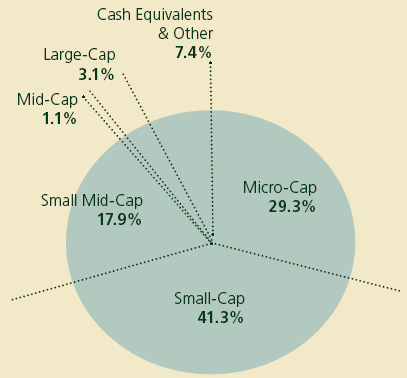

Portfolio Composition*

As reflected in this chart, your fund is well diversified in terms of market capitalization. The fund holds 79 securities, exclusive of cash equivalents.

By Asset Class

Market Capitalization:

Small-Cap Domestic < $2.5 billion

Mid-Cap Domestic

Large-Cap Domestic > $18.3 billion

| * | Totals may not add up to 100% due to rounding. |

By Sector

Sector Allocation | |||||||

| Fund | Russell 3000 Index | ||||||

| Consumer Discretionary | 18.0 | % | 9.6 | % | |||

| Consumer Staples | 2.1 | % | 9.0 | % | |||

| Energy | 12.6 | % | 12.0 | % | |||

| Finance | 22.6 | % | 17.6 | % | |||

| Health Care & Pharmaceuticals | 2.8 | % | 12.0 | % | |||

| Industrials | 6.3 | % | 12.1 | % | |||

| Technology | 20.7 | % | 16.6 | % | |||

| Telecom | 2.7 | % | 3.3 | % | |||

| Utilities | 0.0 | % | 3.9 | % | |||

| Materials | 9.5 | % | 3.9 | % | |||

| Cash Equivalents & Other | 2.7 | % | 0.0 | % | |||

| 100.0 | % | 100.0 | % | ||||

Fund Summary | 13 |

Masters’ Select Equity Fund Stock Highlights

Salesforce.com, Inc. - Craig Blum and Steve Burlingame

Salesforce.com is the leading provider of Software as a Service (SaaS), with over 1,000,000 paying subscribers at more than 38,000 customers. The company has less than 10% market share in customer relationship management (CRM) software, their first targeted market. With a lower cost of ownership and a superior product offering, Salesforce.com is aggressively growing its subscriber base in CRM software and leveraging its technology platform to attack additional software markets. Over the long run, we believe the company’s strategy is likely to significantly expand their addressable market, increase revenue per customer, and widen profit margins.

Traditional enterprise software from the likes of Microsoft, Oracle, Peoplesoft, etc. requires substantial up-front expense for customers, with mixed long-term returns on investment. Additionally, customers using traditional software are often forced to upgrade to a new version of the software every 3-5 years. Salesforce.com allows their products to be trialed for free and then charges customers a flat monthly subscription fee per user. Salesforce.com hosts the application on their servers and stores the client’s data in their databases, which often enables lower cost of ownership for the customer. Since Salesforce.com controls the applications itself, it is able to provide constant updates to the software based on the usage patterns and feedback of subscribers. The company has a superior model for innovation that provides constant improvements on a monthly, not yearly basis.

Salesforce.com’s strategy of delivering Software as a Service over the Internet, charging customers on a monthly basis per user, and constantly upgrading the product offering presents a significant threat to the business models of traditional software vendors. To date, the strategic responses from Oracle and Peoplesoft have failed to forestall Salesforce.com’s momentum and market share gains. Microsoft’s Live / Dynamics strategy, representing a hydra of products and technologies, will purportedly offer a Software as a Service product line to compete with Salesforce.com in 2008. Traditional software vendors are constrained by cultures and incentives optimized for selling big up-front software licenses for products that get upgraded every 3-5 years. These businesses aren’t organized to offer product innovations every few months and pay sales reps and channel partners based on a subscription revenue model. We think it will be a cultural challenge for traditional software vendors to successfully execute a Software as a Service strategy while simultaneously supporting a huge legacy product line of traditional enterprise software products. The virtues of Software as a Service contradict many of the selling points of traditional software, which creates a confusing and inconsistent value proposition for companies seeking to navigate both paradigms simultaneously.

Our analysis suggests that Salesforce.com has reached critical mass and that the market is underestimating their long-term ability to attack additional software markets with their innovative product offerings.

Bank of New York Mellon Corp. - Christopher Davis and Kenneth Feinberg

Bank of New York and Mellon Financial merged in mid-2007 and today is the largest custody bank in the world. Bank of New York Mellon (BK) is a big bank with a market capitalization of $54 billion however over 80% of its revenues come from fees rather than lending activities. We believe that despite being a “financial stock” at a time when most financial stocks are suffering from weakening balance sheets and declining earnings due to missteps in subprime mortgage lending, CDO exposure, SIV exposure, highly leveraged lending exposure and deteriorating credit trends to name just a few items, BK has only negligible exposure to any of these problem areas. We believe that not only should BK provide attractive returns for shareholders over the long term but also could provide a relative advantage should the macroeconomic environment deteriorate meaningfully.

BK is a leader in almost all of its business lines. 25% of earnings come from the asset servicing businesses in which the largest business line is the custody business. Every time a security is purchased by an institutional investor the certificate must be safely housed in a bank. BK is the #1 player globally in the custody business with $21 trillion in assets under custody or a 15% worldwide share of a $140 trillion market. Importantly, BK provides outstanding customer service and has been gaining profitable market share as smaller banks have exited the business over the years because they did not have the scale to make the necessary technology investments to remain competitive with the leaders including BK, State Street, JP Morgan Chase and Northern Trust.

25% of profits come from the issuer services business whose largest business line is the corporate trust business. All those bond coupons that get paid annually must find their way to the rightful owner of the security with almost no errors and that is what BK does.

25% of earnings comes from the asset and wealth management business where BK is one of the largest players in the world with $1.1 trillion in assets under management. They have a broad array of capabilities including equities, fixed income, money markets as well as several hedge funds and their long term performance has been quite good.

Management is outstanding, led by CEO Bob Kelly. Bob was formerly the CFO at First Union and led the superior integration of the merger between First Union and Wachovia. Bob is a no-nonsense fellow who thinks about creating superior long term shareholder value. Bob holds his people accountable with margin goals that are benchmarked against the appropriate peers and openly displayed to chart progress. Bob is also a super-numerate fellow who hates corporate waste and understands the importance of allocating capital in driving long term value. BK generates enormous free cash flow and we expect aggressive share repurchases to begin in early 2008.

14 | The Masters’ Select Funds Trust |

To date the merger between these two big banks has gone almost flawlessly as over 99% of customer relationships have been retained. BK also expects to generate $700 million in expense savings by the end of 2009 and between $250-400 million of revenue synergies by 2011. We hope they can exceed these goals. 30% of revenues now come from overseas but this figure could approach 50% of total revenues in five years as emerging markets and cross border investing continue to boom.

At only 14x what we expect BK can earn in 2008, the price one must pay to own these high ROE, recurring revenue global businesses with a very talented and shareholder oriented management team seems extremely compelling. We expect BK to be able to increase earnings per share for many years to come.

Hornbeck Offshore Services, Inc. - Bill D’Alonzo

With more energy industry activity taking place in deep ocean waters, getting crews and critical equipment to these locations has become more complex. Hornbeck steers the best supply ships to the places they are most needed.

NYSE-listed Hornbeck Offshore Services provides marine transportation services with a fleet of 45 technically-advanced offshore supply vessels (OSVs), primarily in the Gulf of Mexico. With the youngest fleet of any public company, Hornbeck commands roughly 21 percent of the new generation OSV market in the Gulf. It also operates 17 oceangoing tugs and 21 tank barges that transport petroleum and petroleum products.

September-quarter earnings grew 27 percent, exceeding expectations by 31 percent. Revenues increased 22 percent from a year ago. The age and capabilities of Hornbeck’s fleet enable a 93 percent utilization rate compared to a peer average of 65 percent while also earning two times the average per-day rate for its services.

The Friess team spoke with Hornbeck Chief Financial Officer Jim Harp regarding favorable industry dynamics. The offshore oil and gas market is expected to add 153 new rigs over the next four years, with 68 deepwater rigs currently under construction. All of these will require attendant supply vessels with the age, size and design specifications that Hornbeck’s fleet possesses.

Hornbeck also increasingly profits from high-margin projects not related to direct drilling activity, including platform and subsea installations, floating production platforms, decommissioning work and well testing. Hornbeck’s acquisition of Nabors Industries’ Sea Mar fleet earlier this year nearly doubled its size by adding 20 supply vessels. Hornbeck also has a strong pipeline of new generation ships under construction.

The Friess team bought Hornbeck at just 9 times 2008 earnings estimates. Wall Street expects the company to complete 2007 with 27 percent earnings growth.

Freddie Mac - Bill Miller

Freddie Mac is held in both the Equity Fund and the Value Fund. Please refer to the discussion appearing on page 34.

W-H Energy Service Inc. - Dick Weiss

W-H Energy Services, Inc. (W-H Energy) is an oil services company that provides products and services used in connection with the drilling and completion of oil and natural gas wells and the production of oil and gas. Since W-H Energy was established in 1989, the company has completed over 20 acquisitions. The company currently employs approximately 3,000 people and is headquartered in Houston, Texas.

W-H Energy’s business focuses on products and services that provide alternatives to the integrated services typically marketed by the major oilfield service companies. The company operates within two business segments, Drilling Products & Services and Completion & Workover Products and Services. The Drilling Products & Services division provides a variety of drilling services: logging-while-drilling (LWD), measurement-while-drilling (MWD), directional drilling, and down-hole drilling motors; drilling fluids; and rental tools. LWD & MWD are high tech services with limited competition. In the Completion & Workover division the company provides cased-hole wireline logging, perforating, tubing conveyed perforating services; coiled tubing services; completion fluids; and rental tools. While approximately 90% of W-H Energy’s revenue is derived in the US, the Company has expanded its international operations into areas such as Brazil, the North Sea, Italy and the Middle East.

W-H Energy has exhibited a commitment to technological advancement, most notably in measurement-while-drilling (MWD) and logging-while-drilling (LWD). Recent successes include the PathMaker™ 3-D, which allows accurate real-time steering and feedback operators desire, and PZIG™, which moves critical drill-bit location measurement equipment from 35’ behind the drill bit to 11” behind, the equivalent of steering an automobile (drill bit) from the rearview mirror versus the windshield. W-H Energy remains focused on technology. We expect the company will continue to grow via new technologies and will make technology-based acquisitions a priority. The company is continuing to add MWD and LWD equipment as capacity remains tight. The continued shift toward higher technology revenue could prove beneficial to margins.

W-H Energy is one of the few small-cap oil service companies that have a strong technology component to its business. This technology component is leveraged to the secular growth trend in directional drilling. The company is also expanding its presence in the Rockies and has deepwater growth opportunities. Accelerating decline rates and growth in unconventional drilling provide a strong backdrop for W-H Energy’s services.

Fund Summary | 15 |

While the international markets represent only 10%-11% of W-H Energy’s revenue, we expect double-digit growth of international revenues in 2008. We expect a meaningful increase in revenue contribution to come from Saudi Arabia during 2008 as a 10 rig deal ramps up in the 1H. All international revenue is derived from the companies M/LWD and directional drilling services.

Valuation is compelling. W-H Energy is trading at 5.2x TEV/EBITDA, 1.5x sales, and 11.5x EPS our 2008 forecast. Additionally, the company is currently trading near the low end of its historical forward-12- month earnings valuation ranges. We believe investor preoccupation with international oil plays at the expense of domestic focused service companies has given us the opportunity to purchase a stock comprised of unique assets and hard to duplicate technology.

In keeping with Southeastern Asset Management’s disclosure policies, Mason Hawkins has not contributed commentary on his holdings for this report.

See page 77 for Industry Terms and Definitions

Neither the information contained herein nor any opinion expressed shall be construed to constitute an offer to sell or a solicitation to buy any securities mentioned herein. The views herein are those of the portfolio managers at the time the commentaries are written and may not be reflective of current conditions.

16 | The Masters’ Select Funds Trust |

Masters’ Select Equity Fund

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2007

Shares | Value | ||

COMMON STOCKS: 97.3% | |||

Consumer Discretionary: 17.5% | |||

| 374,920 | Amazon.com, Inc.* | $ | 34,732,589 |

| 210,000 | Conn’s, Inc.* | 3,593,100 | |

| 434,000 | DIRECTV Group, Inc. (The)* | 10,034,080 | |

| 438,000 | Disney (Walt) Co. | 14,138,640 | |

| 550,000 | Eastman Kodak Co. | 12,028,500 | |

| 520,000 | Emmis Communications Corp. - Class A* | 2,002,000 | |

| 384,000 | General Motors Corp. | 9,557,760 | |

| 335,000 | IAC/InterActiveCorp* | 9,018,200 | |

| 39,300 | Las Vegas Sands Corp.* | 4,049,865 | |

| 250,000 | Lennar Corp. | 4,472,500 | |

| 68,000 | Liberty Media Holding Corp. - Capital* | 7,921,320 | |

| 449,250 | Liberty Media Holding Corp. - Interactive* | 8,571,690 | |

| 136,000 | News Corp. | 2,786,640 | |

| 75,000 | Ruby Tuesday, Inc. | 731,250 | |

| 123,638,134 | |||

Consumer Staples: 2.1% | |||

| 18,300 | Altria Group, Inc. | 1,383,114 | |

| 192,300 | Costco Wholesale Corp. | 13,414,848 | |

| 14,797,962 | |||

Energy: 12.6% | |||

| 93,600 | Canadian Natural Resources Ltd. | 6,845,904 | |

| 200,900 | ConocoPhillips | 17,739,470 | |