UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07763

The Masters’ Select Funds Trust

(Exact Name of Registrant as Specified in Charter)

4 Orinda Way, Suite 200-D, Orinda, CA 94563

(Address of Principal Executive Offices)

Kenneth E. Gregory

4 Orinda Way, Suite 200-D

Orinda, CA 94563

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (925) 254-8999

Date of fiscal year end: December 31

Date of reporting period: December 31, 2009

Item 1. Reports to Stockholders.

The Masters’ Select Funds Trust

| Annual Report | |

| The Masters’ Select Equity Fund | |

| The Masters’ Select International Fund | |

| The Masters’ Select Value Fund | |

| The Masters’ Select Smaller Companies Fund | |

| The Masters’ Select Focused Opportunities Fund | |

| December 31, 2009 |

www.mastersfunds.com

In constructing the Masters’ Select Funds, the goal was to design funds that would isolate the stock-picking skills of a group of highly regarded portfolio managers. To meet this objective, we designed the funds with both risk and return in mind, placing particular emphasis on the following factors:

| 1. | Only stock pickers Litman/Gregory believes to be exceptionally skilled are chosen to manage each fund’s sub-portfolios |

| 2. | Of equal importance, each stock picker runs a very concentrated sub-portfolio of not more than 15 of his or her “highest conviction” stocks. In the Focused Opportunities Fund, each stock picker may own no more than seven stocks. |

| 3. | Although each manager’s portfolio is concentrated, Masters’ Select seeks to manage risk partly by building diversification into each Fund. |

| • | With the Equity and International Funds, Litman/Gregory has sought to achieve this by including managers with differing investment styles and market cap orientations. |

| • | With the Smaller Companies Fund, much like Equity and International, Litman/Gregory has brought together managers who use different investment approaches, though each focuses on the securities of smaller companies. |

| • | With the Value Fund, Litman/Gregory has included managers who each take a distinct approach to assessing companies and defining value. Please note that the Value Fund is classified as a “non-diversified” fund; however, its portfolio has historically met the qualifications of a “diversified” fund. |

| • | With the Focused Opportunities Fund, this is done by using multiple managers with diverse investment styles. However, even with this diversification, the Fund is classified as a “non-diversified” fund, as it may hold as few as 15 stocks and no more than 21 stocks. In the future, if more sub-advisors are added, the Fund could become more diversified. |

| 4. | Litman/Gregory believes that excessive asset growth often results in diminished performance. Therefore, each Masters’ Select Fund may close to new investors at a level that Litman/ Gregory believes will preserve each manager’s ability to effectively implement the “select” concept. If more sub-advisors are added to a particular Fund, the Fund’s closing asset level may be increased. |

Portfolio Fit

As with all equity funds, Masters’ Select Funds are appropriate for investors with a long-term time horizon, who are willing to ride out occasional periods when the funds’ net asset values decline. Within that context, we created the Masters’ Select Equity and Masters’ Select International Funds to be used as core equity and international fund holdings. Masters’ Select Smaller Companies Fund has been created to provide a core domestic small cap investment opportunity. We created Masters’ Select Value Fund for investors who seek additional, dedicated value exposure in their portfolios. Masters’ Select Focused Opportunities Fund has been created to provide a core large-cap holding for long-term investors. Although performance in each specific down market will vary, we purposely set the allocations to each manager with the objective of keeping risk about equal to the funds’ overall benchmarks. In the end, the focus on the highest conviction stocks of a group of very distinguished managers with superior track records is what we believe makes the funds ideal portfolio holdings.

| Contents | ||

Our Commitment to Shareholders | 2 | |

Funds’ Performance | 3 | |

Letter to Shareholders | 4 | |

| Masters’ Select Equity Fund | ||

| Equity Fund Review | 7 | |

| Equity Fund Managers | 10 | |

| Equity Fund Value of Hypothetical $10,000 | 10 | |

| Equity Fund Stock Highlights | 11 | |

| Equity Fund Schedule of Investments | 14 | |

| Masters’ Select International Fund | ||

| International Fund Review | 16 | |

| International Fund Managers | 20 | |

| International Fund Value of Hypothetical $10,000 | 20 | |

| International Fund Stock Highlights | 21 | |

International Fund Schedule of Investments | 24 | |

| Masters’ Select Value Fund | ||

| Value Fund Review | 26 | |

| Value Fund Managers | 29 | |

| Value Fund Value of Hypothetical $10,000 | 29 | |

| Value Fund Stock Highlights | 30 | |

| Value Fund Schedule of Investments | 32 | |

| Masters’ Select Smaller Companies Fund | ||

| Smaller Companies Fund Review | 33 | |

| Smaller Companies Fund Managers | 37 | |

| Smaller Companies Fund Value of Hypothetical $10,000 | 37 | |

| Smaller Companies Fund Stock Highlights | 38 | |

| Smaller Companies Fund Schedule of Investments | 40 | |

| Masters’ Select Focused Opportunities Fund | ||

| Focused Opportunities Fund Review | 42 | |

| Focused Opportunities Fund Managers | 44 | |

| Focused Opportunities Fund Value of Hypothetical $10,000 | 44 | |

| Focused Opportunities Fund Stock Highlights | 45 | |

| Focused Opportunities Fund Schedule of Investments | 46 | |

Expense Examples | 47 | |

Statements of Assets and Liabilities | 48 | |

Statements of Operations | 49 | |

| Statements of Changes in Net Assets | ||

| Equity Fund | 50 | |

| International Fund | 50 | |

| Value Fund | 51 | |

| Smaller Companies Fund | 51 | |

| Focused Opportunities Fund | 52 | |

| Financial Highlights | ||

| Equity Fund | 53 | |

| International Fund | 54 | |

| Value Fund | 55 | |

| Smaller Companies Fund | 56 | |

| Focused Opportunities Fund | 57 | |

| Equity and International Investor Class | 58 | |

Notes to Financial Statements | 59 | |

Report of Independent Registered Public Accounting Firm | 71 | |

Other Information | 72 | |

Index Definitions | 76 | |

Industry Terms and Definitions | 78 | |

Tax Information | 79 | |

Trustee and Officer Information | 80 | |

This report is intended for shareholders of the funds and may not be used as sales literature unless preceded or accompanied by a current prospectus for the Masters’ Select Funds. Statements and other information in this report are dated and are subject to change.

Litman/Gregory Fund Advisors, LLC has ultimate responsibility for the funds’ performance due to its responsibility to oversee its investment managers and recommend their hiring, termination and replacement.

Table of Contents 1

Commitment to Shareholders

We are deeply committed to making each Masters’ Select Fund a highly satisfying long-term investment for shareholders. In following through on this commitment we are guided by our core values, which influence four specific areas of service:

First, we are committed to the Masters’ Select concept.

| • | We will only hire managers who we strongly believe will deliver exceptional long-term returns relative to their benchmarks. We base this belief on extremely thorough due diligence research. This not only requires us to assess their stock picking skills, but also to evaluate their ability to add incremental performance by investing in a concentrated portfolio of their highest conviction ideas. |

| • | We will monitor each of the managers so that we can maintain our confidence in their ability to deliver the long-term performance we expect. In addition, our monitoring will seek to assess whether they are staying true to their Masters’ Select mandate. Consistent with this mandate we focus on long-term performance evaluation so that the Masters’ Select stock pickers will not be distracted by short-term performance pressure. |

Second, we will do all we can to ensure that the framework within which our stock pickers do their work further increases the odds of success.

| • | Investments from new shareholders in each Fund are expected to be limited so that each manager’s Masters’ Select asset base remains small enough to retain flexibility to add value through individual stock picking. |

| • | The framework also includes the diversified multi-manager structure that makes it possible for each manager to invest in a concentrated manner knowing that the potential volatility within his or her portfolio will be diluted at the fund level by the performance of the other managers. In this way the multi-manager structure seeks to provide the fund-level diversification necessary to temper the volatility of each manager’s sub-portfolio. |

| • | We will work hard to discourage short-term speculators so that cash flows into the Funds are not volatile. Lower volatility helps prevent our managers from being forced to sell stocks at inopportune times or to hold excessive cash for non-investment purposes. This is why years ago the Funds implemented a 2% redemption fee for the first 180 days of a shareholder’s investment in any Fund, which is paid to each Fund for the benefit of shareholders. |

Third, is our commitment to do all we can from an operational standpoint to maximize shareholder returns.

| • | We will remain attentive to Fund overhead, and whenever we achieve savings we will pass them through to shareholders. For example, we have had several manager changes that resulted in lower sub-advisory fees to our Funds. In every case we have passed through the full savings to shareholders in the form of fee waivers. |

| • | We will provide investors with a low minimum, no-load, no 12b-1 share class for all Masters’ Select Funds, and a low minimum no-load Investor share class for the Masters’ Select Equity Fund and Masters’ Select International Fund. |

| • | We also will work closely with our sub-advisors to make sure they are aware of tax-loss selling opportunities (only to be taken if there are equally attractive stocks to swap into). We account for partial sales on a specific tax lot basis so that shareholders will benefit from the most favorable tax treatment. The goal is not to favor taxable shareholders over tax-exempt shareholders but to make sure that the Masters’ Select stock pickers are taking advantage of tax savings opportunities when doing so is not expected to reduce pre-tax returns. |

Fourth, is our commitment to communicate honestly about all relevant developments and expectations.

| • | We will continue to do this by providing thorough and educational shareholder reports. |

| • | We will continue to provide what we believe are realistic assessments of the investment environment. |

Our commitment to Masters’ Select is also evidenced by our own investment. Our employees have, collectively, substantial investments in the Funds, as does our company retirement plan. In addition, we use the Funds extensively in the client accounts of our investment advisor practice (through our affiliate Litman/Gregory Asset Management, LLC). We have no financial incentive to do so because the fees we receive from Masters’ Select held in client accounts are fully offset against the advisory fees paid by our clients. In fact, we have a disincentive to use the Funds in our client accounts because each Masters’ Select Fund is capacity constrained and by using them in client accounts we are using up capacity for which we may not be paid. But we believe these Funds offer value that we can’t find/obtain elsewhere and this is why we enthusiastically invest in them ourselves and on behalf of our clients.

While we believe highly in the ability of the Funds’ sub-advisors, our commitments are not intended as guarantees of future results.

While the Funds are no-load, there are management fees and operating expenses that do apply, as well as a 12b-1 fee that applies to Investor class shares.

Please refer to the prospectus for further details.

2 The Masters’ Select Funds Trust

| Average Annual Total Returns | ||||||||||||||||||||

| Three- | Since | |||||||||||||||||||

| Institutional Class Performance as of 12/31/2009 | One Year | Year | Five-Year | Ten-Year | Inception | |||||||||||||||

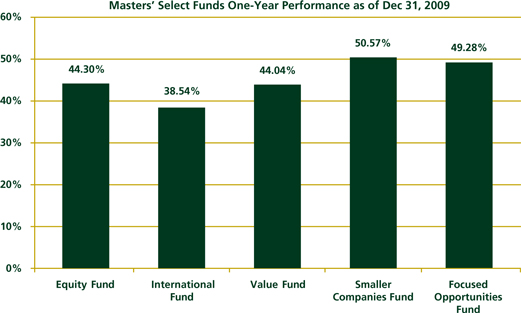

| Masters’ Select Equity Fund (12/31/1996) | 44.30 | % | -7.04 | % | -1.61 | % | 1.17 | % | 5.90 | % | ||||||||||

| Russell 3000 Index | 28.34 | % | -5.42 | % | 0.76 | % | -0.20 | % | 5.22 | % | ||||||||||

| Custom Equity Index | 27.35 | % | -5.61 | % | 0.89 | % | 0.34 | % | 5.29 | % | ||||||||||

| Lipper Multi Cap Core Fund Index | 35.34 | % | -4.59 | % | 1.42 | % | 0.67 | % | 5.21 | % | ||||||||||

| Gross Expense Ratio: 1.25% Net Expense Ratio as of 4/30/09: 1.24% | ||||||||||||||||||||

| Masters’ Select International Fund (12/1/1997) | 38.54 | % | -3.02 | % | 6.89 | % | 3.99 | % | 9.08 | % | ||||||||||

| S&P Global (ex U.S.) LargeMid Cap Index | 42.55 | % | -2.45 | % | 6.65 | % | 3.20 | % | 6.43 | % | ||||||||||

| Lipper International Fund Index | 35.33 | % | -4.48 | % | 4.88 | % | 1.95 | % | 5.45 | % | ||||||||||

| Gross Expense Ratio: 1.22% Net Expense Ratio as of 4/30/09: 1.07% | ||||||||||||||||||||

| Masters’ Select Value Fund (6/30/2000) | 44.04 | % | -9.52 | % | -2.07 | % | n/a | 3.17 | % | |||||||||||

| Russell 3000 Value Index | 19.76 | % | -8.91 | % | -0.24 | % | n/a | 3.43 | % | |||||||||||

| Lipper Multi-Cap Value Index | 26.58 | % | -7.90 | % | -0.56 | % | n/a | 3.35 | % | |||||||||||

| Gross Expense Ratio: 1.29% Net Expense Ratio as of 4/30/09: 1.27% | ||||||||||||||||||||

| Masters’ Select Smaller Companies Fund (6/30/2003) | 50.57 | % | -5.47 | % | -0.50 | % | n/a | 5.39 | % | |||||||||||

| Russell 2000 Index | 27.17 | % | -6.07 | % | 0.51 | % | n/a | 6.61 | % | |||||||||||

| Lipper Small Cap Core Index | 34.50 | % | -4.07 | % | 1.54 | % | n/a | 7.24 | % | |||||||||||

| Gross Expense Ratio: 1.40% Net Expense Ratio as of 4/30/09: 1.39% | ||||||||||||||||||||

| Masters’ Select Focused Opportunities Fund (6/30/2006) | 49.28 | % | -6.60 | % | n/a | n/a | -3.03 | % | ||||||||||||

| S&P 500 Index | 26.45 | % | -5.63 | % | n/a | n/a | -1.53 | % | ||||||||||||

Gross Expense Ratio: 1.36% Net Expense Ratio as of 4/30/09: 1.28% | ||||||||||||||||||||

Performance quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the funds may be lower or higher than the performance quoted. To obtain the performance of the funds as of the most recently completed calendar month, please visit www.mastersfunds.com. The funds impose a 2.00% redemption fee on shares held less than 180 days. Performance does not reflect the redemption fee. If reflected, performance would be lower.

The performance quoted does not include a deduction for taxes that a shareholder would pay on distributions or the redemption of fund shares. Indexes are unmanaged, do not incur expenses, taxes or fees and cannot be invested in directly. See pages 76-77 for the index definitions.

Each of the funds may invest in foreign securities. Investing in foreign securities exposes investors to economic, political and market risks and fluctuations in foreign currencies. The Master’s Select International Fund will invest in emerging market countries, which involve additional risks such as government dependence on a few industries or resources, government-imposed taxes on foreign investment or limits on the removal of capital from a country, unstable government, and volatile markets. Each of the funds may invest in the securities of small companies. Small-company investing subjects investors to additional risks, including security price volatility and less liquidity than investing in larger companies. Masters’ Select Value and Masters’ Select Focused Opportunities are non-diversified funds, which means that each respective fund may concentrate more of its assets in fewer individual holdings than a diversified fund. Though primarily equity funds, the Value and Focused Opportunities funds may invest portions of assets in securities of distressed companies. Debt obligations of distressed companies typically are unrated, lower rated, in default or close to default and may become worthless.

Gross and net expense ratios are for the institutional share class and are per the Prospectus dated April 30, 2009. Through April 30, 2010, Litman/Gregory has contractually agreed to waive a portion of its advisory fees effectively reducing total advisory fees to approximately 0.95% of the average daily net assets of the International Fund, 1.08% of the average daily net assets of the Value Fund and 1.02% of the Focused Opportunities Fund. Litman/Gregory may voluntarily waive a portion of its advisory fee in addition to those fees that are contractually waived. Litman/Gregory has agreed not to seek recoupment of advisory fees waived. Through April 30, 2010, Litman/Gregory has voluntarily agreed to waive a portion of its management fee to pass through any costs benefits resulting from sub-advisor breakpoints, changes in the sub-advisory fee schedules or allocations within the Equity Fund, the International Fund, the Value Fund, the Smaller Companies Fund, and the Focused Opportunities Fund.

Funds’ Performance 3

A year ago the first line of our shareholder report stated that 2008 had been the worst year for the stock market since 1931. A year later we’ve experienced, collectively, the best year ever for the Masters’ Select funds. Each domestic fund returned over 40% on the year, ranging from 44.0% for Masters’ Select Value to 50.6% for Masters’ Select Smaller Companies. The returns were strong on an absolute basis and also relative to each fund’s benchmark, ranging from Masters’ Select Equity’s 16.0 percentage point advantage over the Russell 3000 Index to Masters’ Select Smaller Companies 23.4 percentage point margin over the Russell 2000 Index. Masters’ Select International did not do as well though it posted a very solid 38.5% return.

Though we did not anticipate the magnitude of Masters’ Select 2009 outperformance, we did believe that the markets had become dysfunctional in the third and fourth quarter of 2008 and that many stocks were extremely mis-priced. We wrote about this in our reports beginning with our third quarter 2008 report. We believe last year’s performance can be explained in large part by our sub-advisors’ discipline in sticking to their fundamental approaches and believing in their research. In many cases, they stayed with stocks that had hurt them in 2008 and subsequently benefited from powerful rebounds as markets began again to price stocks based on underlying company fundamentals. In short, they avoided the whipsaw that can critically damage the returns of many investors.

How Whipsaw Can Destroy Returns

Whipsaw is a potential problem for all investors—professionals and individuals. In the case of individuals the phenomena is best exemplified by performance chasing. Funds that have had a good run of performance tend to get plenty of flattering media attention that spotlights the fund’s management team and their good decisions. The media exposure and performance record ultimately convince investors that they should invest in the fund. None of this is surprising and there are certainly funds that have performed well that are run by truly skilled stock pickers. The challenge is figuring out which fund managers are truly skilled and which are lucky. It’s our perception that through no fault of their own, most fund investors simply don’t have the practical tools—the knowledge, experience, data, time, and access to managers—to do this well or, in some cases the temperament to stick with deserving managers when they hit an inevitable slump. As a result their decision to invest in a fund frequently follows a lengthy run of great performance, which unfortunately is often close to the point at which it may begin to experience a performance slump. After suffering through a period of poor performance, the fund investor eventually loses patience and jumps to another hot fund, potentially repeating the process.

A great example of whipsaw was discussed in a December 31, 2009 article in the Wall Street Journal. The article reported that the best fund of the decade was CGM Focus, which delivered a 10-year average annualized return of 18.2%. However, according to data from the fund research firm Morningstar, the average return earned by investors in this fund was, incredibly, a loss of -10.8%—almost 30 percentage points less per year than the fund actually earned! How was that possible? Morningstar calculates their investor returns by dollar-weighting them so that the return earned for each period is weighted based on the dollars invested in the fund. This means that a fund’s investor return can be less than the actual return earned by the fund, if investors tended to have more dollars invested when the fund performed poorly than when it performed well. CGM Focus, though it has a great long-term record, also is a highly volatile fund which has tended to experience periods of extreme out- and underperformance. This type of very hot or very cold performance makes it a strong candidate for investor whipsaw. After its hot streaks investors read or heard about it and invested. But cold streaks often followed and after a year or two of poor performance investors would dump their shares—missing out on the rebound that often followed.

4 The Masters’ Select Funds Trust

When we created the first Masters’ Select Fund in 1996, we hoped that the combination of a compelling line-up of managers, a long-term mandate to own only their highest-conviction stocks, and Litman/Gregory’s expertise in setting the manager lineup would give shareholders the confidence to view the funds as long-term core holdings—potentially avoiding whipsaw. We want to reiterate that message as we consider the funds’ performance path over the past several years. After a strong multi-year run of performance in the first half of the 1990s, we attracted a lot of assets to the funds. Subsequently, we had a stretch of poor performance for several of our funds that led some shareholders to sell, and in turn miss the sharp subsequent rebound that began roughly a year ago. Masters’ Select Equity had a similar experience after a poor relative performance year in 1998 led to redemptions. The fund went on to outperform its benchmark for six straight years, eventually attractive strong inflows that led us to temporarily close the fund. As discussed, this pattern of buying and selling is common throughout the fund industry. But we’ve always sought through our communications to help our shareholders understand what they should expect from the funds and what Litman/Gregory’s role is, and thereby retain the confidence required to benefit from both the rebounds that often follow the difficult stretches, and ultimately the long-term performance we are seeking to deliver.

In short, shareholders should recognize that there will likely be periods of shorter-term underperformance because active managers invest differently from a benchmark. However, without this “benchmark risk” there can be no long-term outperformance – if you invest the same as the benchmark, your performance will match the benchmark (and trail after expenses). We are comfortable with higher levels of benchmark risk for four reasons: 1) we believe our lineup of managers is skilled and their willingness to invest differently will generate long-term outperformance; 2) our managers have a mandate to own only their highest-conviction stocks and to ignore the short-term when they believe it has no bearing on their long term return expectations; 3) Litman/Gregory has put together a lineup of managers with complementary skills and approaches, which brings an element of diversification, and 4) we closely monitor the managers to ensure that they continue to deserve our confidence.

When one of our managers has a difficult stretch of performance, we go back to our original investment thesis, and ask “what did we like about this manager and are the reasons for our high level of confidence still in place?” The same approach can (and we believe should) be applied by a Masters’ Select shareholder to the Funds. The four reasons noted above comprise this simple thesis for Masters’ Select, and Litman/Gregory’s mission as the fund’s advisor is to apply all of our considerable due diligence knowledge and experience to safeguard that it is being followed. This means frequent discussions with our managers to assess the quality of their thinking on an ongoing basis and to make sure they remain mindful of their mandate to give us only their best ideas. Ultimately it means keeping underperforming managers when our research tells us it is right to do so, and to firing managers when our research tells us that is the right thing to do—but not simply because a manager has slumped for a year or two. Taken together, we believe all of this constitutes the Masters’ Select edge, and this is critical for our shareholders to understand when they make the decision to invest with us— hopefully a decision that will lead to many years as a shareholder as part of a lifetime of investing.

Challenges Ahead

The recovery of the stock market that began last March was no doubt a relief to most investors. However, challenges remain. While we may have emerged from recession, the economy remains fragile with too much debt on household balance sheets and piles of debt rapidly building on our government’s balance sheet. More than ever we believe skilled stock picking will be an important factor in investor returns in the coming years. While we would prefer a more inviting macro outlook we believe that the environment in the years ahead will likely be to the relative advantage of skilled stock pickers with the ability to focus only on their most compelling opportunities. We believe our Masters’ Select managers fall into this category.

While many of our managers are well known in the investment world and mutual fund circles, one recently received a particularly impressive honor. David Herro, one of the sub-advisors to Masters’ Select International and also a manager of Oakmark International, was recently named as the International Manager of the Decade by Morningstar, an independent fund research firm and data provider. Masters’ Select shareholders have benefited from Herro’s considerable skills for the entire decade and more—he has been running a portion of Masters’ Select International since the fund’s inception in 1997.

As we look ahead it is worth noting that each of the Masters’ Select funds has sizable tax loss carryforwards that make it highly unlikely that they will make a capital gains distribution in 2010 and possibly beyond.

We continue to invest alongside you. Litman/Gregory principals, employees and the Masters’ Select independent trustees collectively owned $11.1 million in Masters’ Select fund shares as of 12/31/09.

As always we thank you for your trust and confidence and will continue to do all that we can to earn it.

Sincerely,

Ken Gregory and Jeremy DeGroot

Litman/Gregory Fund Advisors, LLC

Advisor to the Masters’ Select Funds

Shareholder Letter 5

Performance discussions for the Equity Fund and the International Fund are specifically related to the Institutional share class.

Some of the comments are based on current management expectation and are considered “forward-looking statements”. Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statement by words such as “estimate”, “may”, “expect”, “should”, “could”, “believe”, “plan”, and similar terms. We cannot promise future returns and our opinions are a reflection of our best judgment at the time this report is compiled.

Opinions expressed are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security.

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

References to other mutual funds should not be interpreted as an offer of these securities.

Diversification does not assure a profit or protect against a loss in a declining market.

Any tax or legal information provided is merely a summary of our understanding and interpretation of some of the current income tax regulations and is not exhaustive. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation. Neither the Fund nor any of its representatives may give legal or tax advice.

Please see pages 76-77 for index definitions. You cannot invest directly in an index.

Please see page 78 for industry definitions.

6 The Masters’ Select Funds Trust

Masters’ Select Equity Fund returned 24.5% for the six months ended December 31st. That return compared favorably to the Russell 3000 Index 23.2% return. For all of 2009 Masters’ Select Equity delivered a very strong 44.3% return, significantly better than the 28.3% return for the benchmark. (These returns pertain to the fund’s original share class. A no-transaction fee share class was launched in the middle of 2009.)

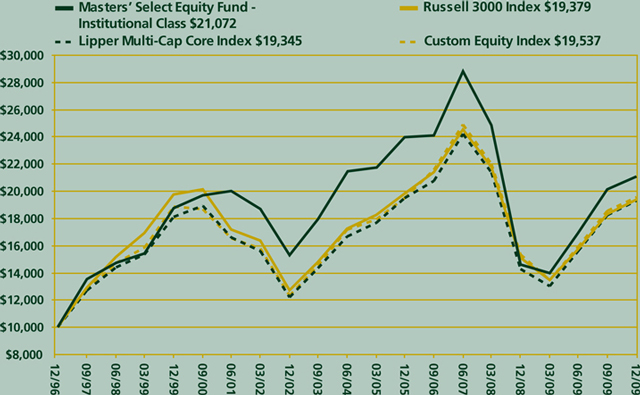

We are obviously very pleased with these returns. And with the first decade of the century now complete we look back on what has been a very tough 10 years for the stock market. We take some satisfaction in the fact that over the last 10 years Masters’ Select Equity out-returned its Russell 3000 Index benchmark by 1.37 percentage points per year. On a hypothetical $10,000 investment this would have amounted to an additional $1,436 at the end of the decade. Masters’ Select Equity also out-returned its benchmark since the fund’s inception. And it has beaten the S&P 500 Index since its inception and over ten years.

Performance as of December 31, 2009

| Average Annual Total Returns | ||||||||||||||||||||

| One- | Three- | Five- | Ten- | Since | ||||||||||||||||

| year | Year | Year | Year | Inception | ||||||||||||||||

| Masters’ Select Equity Fund - Institutional Class (12/31/96) | 44.30 | % | -7.04 | % | -1.61 | % | 1.17 | % | 5.90 | % | ||||||||||

| Russell 3000 Index | 28.34 | % | -5.42 | % | 0.76 | % | -0.20 | % | 5.22 | % | ||||||||||

| S&P 500 Index | 26.45 | % | -5.63 | % | 0.41 | % | -0.95 | % | 5.01 | % | ||||||||||

Performance data quoted represents past performance; past performance is no guarantee of future results. See page 3 for a detailed discussion of the risks and costs associated with investing in the Masters’ Select Equity Fund.

Given our primary focus of delivering better returns than the broad stock market index over the long run, we place the greatest importance on long-term performance. In that regard we are pleased that Masters’ Select Equity has bested its Russell 3000 benchmark in each of the 37 rolling 10-year periods since its inception. (The first rolling 10-year period is measured 10 years after the fund’s inception. Each month-end thereafter a new 10-year period is added.) This long-term performance was achieved with ups and downs along the way. Highlights included a strong 2009 and six consecutive calendar years outperforming the Russell 3000 Index—a stretch that ran from 1999 through 2004. The lowlight was, without a doubt, 2008.

Four of the fund’s sub-advisors have been part of Masters’ Select since it was launched—Mason Hawkins, Dick Weiss, the Friess Associates team headed by Bill D’Alonzo, and the Chris Davis/ Ken Feinberg team (originally Chris Davis’ father, Shelby Davis was the lead manager on their portion of the portfolio). All four have delivered returns that have bested their benchmarks and they have been committed partners on the fund. In recent years, growth teams from Sands Capital and Turner Investment Partners were added, as was value manager Clyde McGregor of Harris Associates.1 We continue our commitment to maintaining a mix of highly skilled stock pickers who give the fund exposure to a breadth of styles and market caps and who, in several cases, also invest globally.

Portfolio Commentary

A number of factors contributed to the fund’s performance during 2009. The highlights follow.

Performance of managers: In 2009, six of the seven Masters’ Select Equity stock pickers outperformed their respective benchmarks while one manager significantly underperformed his respective benchmark. Of the six outperforming managers, the margin of outperformance ranged from 2.2 percentage points to 50.8 percentage points, with four managers beating their benchmark by a margin of 20 percentage points or more.

As we have written in the past, we do not expect short-term outperformance from every manager in every time period, however long term outperformance relative to benchmarks is our goal for all of our investment managers. Through December 31, 2009, all four of the sub-advisors who have been on the fund since its inception 13 years ago have achieved that goal. The other three sub-advisors have yet to build a long-term record on Masters’ Select Equity. We believe, but obviously cannot guarantee, that they will ultimately outperform as well. (So far, two of the three have done so over their tenure to date.)

Sector and stock-picking impact: Though all Masters’ Select portfolios are driven by bottom-up stock picking, the sector exposure that results may provide some insight into the funds’ relative performance. Based on our attribution analysis for the year, which looks at the relative contribution to performance from sectors and stocks, Masters’ Select Equity’s overall sector exposure added some value relative to the Russell 3000 benchmark, but stock selection was the primary contributor to the fund’s strong performance relative to its benchmark. This is consistent with what we expect over the long run. The fund’s overweighting to the strong-performing consumer-discretionary sector was a positive, as was its underweighting to the weaker consumer staples and utilities sectors. The fund’s average cash weighting of over 4% during the year was a drag on performance given strong stock returns in 2009. In terms of stock selection, four of the fund’s 10 largest contributors were technology names, including holdings Sun Microsystems, Google, and Apple, which were each up more than 100%. Energy names Chesapeake Energy, EOG Resources, and Canadian Natural Resources were also among the fund’s top 10 contributors for the year. The two biggest detractors from performance were Tyco Electronics and ConocoPhillips, which each cost the fund less than a percentage point of return. See page 11 for commentary written by the fund’s sub-advisors on some of the fund’s holdings.

Fund Summary 7

Masters’ Select Equity Fund Contribution by Holding

For the Year Ended December 31, 2009

Top 10 Contributors

| Portfolio | ||||

| Security | Contribution | |||

| Sun Microsystems, Inc. | 3.04 | % | ||

| Liberty Media Holding Corp. – Entertainment | 2.72 | % | ||

| American Express Co. | 2.14 | % | ||

| Google, Inc. – Class A | 2.04 | % | ||

| Chesapeake Energy Corp. | 1.93 | % | ||

| EOG Resources, Inc. | 1.55 | % | ||

| Canadian Natural Resources Ltd. | 1.40 | % | ||

| Dell, Inc. | 1.28 | % | ||

| Level 3 Communications, Inc. | 1.25 | % | ||

| Apple, Inc. | 1.18 | % | ||

Bottom 10 Contributors

| Portfolio | ||||

| Security | Contribution | |||

| Tyco Electronics Ltd. | (0.68 | )% | ||

| Conoco Phillips | (0.65 | )% | ||

| J.P. Morgan Chase & Co. | (0.55 | )% | ||

| A123 Systems, Inc. | (0.27 | )% | ||

| Cephalon, Inc. | (0.22 | )% | ||

| Synaptics, Inc. | (0.21 | )% | ||

| First Solar, Inc. | (0.21 | )% | ||

| General Mills, Inc. | (0.20 | )% | ||

| HUB Group, Inc. | (0.20 | )% | ||

| CapitalSource, Inc. | (0.20 | )% | ||

Portfolio mix: There were two notable shifts in the portfolio’s sector allocations during the year. One was an increase in the fund’s allocation to health care, from 9.7% to 16.6%. Among new health care holdings, the largest portfolio weightings include Kinetic Concepts, Omnicare, Merck, and Johnson & Johnson. The other change was a reduction in consumer-related holdings in the consumer-discretionary and consumer staples sectors. Nevertheless, the fund remains overweighed to the consumer-discretionary sector. Among the largest consumer-related holdings that remain in portfolio are Disney, Costco, and Mohawk. Consumer holdings that were sold from the portfolio include Advance Auto Parts, CVS Caremark, and BJs Wholesale.

The fund’s portfolio has always looked quite different than its Russell 3000 benchmark. The differences are apparent not only in the sector exposure but also the fund’s sizable exposure to foreign domiciled companies such as Cemex SA, Cheung Kong Holdings, Ltd and New Oriental Education and Technology.

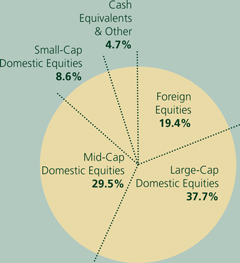

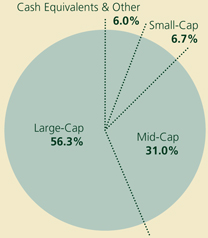

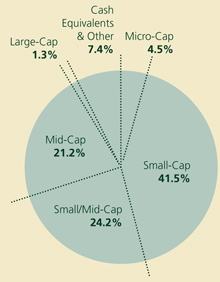

By Asset Class

Market Capitalization:

Small-Cap Domestic < $1.7 billion

Mid-Cap Domestic

Large-Cap Domestic > $12.2 billion

* Totals may not add up to 100% due to rounding.

By Sector

| Sector Allocation | |||||||||||||

| Russell 3000 | |||||||||||||

| Fund as of | Fund as of | Index as of | |||||||||||

12/31/08 | 12/31/09 | 12/31/09 | |||||||||||

| Consumer Discretionary | 17.4 | % | 12.0 | % | 10.5 | % | |||||||

| Consumer Staples | 7.0 | % | 2.6 | % | 10.1 | % | |||||||

| Energy | 15.6 | % | 13.3 | % | 10.8 | % | |||||||

| Finance | 17.8 | % | 18.8 | % | 14.9 | % | |||||||

| Health Care & Pharmaceuticals | 9.7 | % | 16.6 | % | 12.7 | % | |||||||

| Industrials | 7.4 | % | 9.6 | % | 10.8 | % | |||||||

| Technology | 17.2 | % | 17.1 | % | 19.3 | % | |||||||

| Telecom | 1.0 | % | 1.7 | % | 3.0 | % | |||||||

| Utilities | 0.0 | % | 0.0 | % | 3.9 | % | |||||||

| Materials | 3.6 | % | 3.6 | % | 4.1 | % | |||||||

| Cash Equivalents & Other | 3.2 | % | 4.7 | % | 0.0 | % | |||||||

| 100.0 | % | 100.0 | % | 100.0 | % | ||||||||

8 The Masters’ Select Funds Trust

It is important that investors understand what we are seeking to accomplish with Masters’ Select. By virtue of the quality of our stock pickers, their focus on only their highest conviction holdings, the fund’s overall diversification in terms of the number of stocks and managers, and the oversight of Litman/Gregory, we seek to offer a core equity fund holding that investors can have confidence in over the long run. It is our hope that investors with a clear understanding of what we believe constitutes the long-term edge for Masters’ will be in a better position to accept the inevitable shorter-term swings in performance and thereby earn satisfying long-term returns. We believe our long-term record relative to broad stock market benchmarks such as the Russell 3000 Index and S&P 500 validates this confidence.

As we look ahead to what may be another challenging decade, we believe that the range of returns delivered by equity funds could be quite wide, with differences partly driven by stock picking skill. Whatever the environment, we look ahead with a great deal of confidence in our group of sub-advisors. Each of the original four have proven themselves to us with 13 years of benchmark-beating performance. These four have averaged 3.90 percentage points of average annual outperformance relative to their benchmarks over that time (this is an equal-weighted average of each sub-advisors performance over his benchmark). It is also true that some, though not all, of the managers who we did not retain had less successful performance, and we have learned important lessons from that experience. In that regard, we believe that the new sub-advisors we hired (Clyde McGregor and the Sands and Turner teams) are particularly well suited to running concentrated portfolios. With their addition we believe the Masters’ Select Equity team is stronger than it has ever been.

As we move into 2010 we do so with at tax loss carry forward equal to 26.5% of the fund’s end of year assets. It is unlikely that the fund will make a capital gain distribution in 2010 and possibly beyond.

As always we value your confidence and look forward to investing with you for years to come.

| 1 | The managers and their respective benchmarks are: Bill D’Alonzo: Russell 2500 Growth Index; Christopher Davis and Ken Feinberg: S&P 500 Index; Mason Hawkins: Russell 3000 Value Index; Clyde McGregor: Russell 3000 Value Index; Frank Sands Jr, and Michael Sramek: Russell 1000 Growth Index; Bob Turner: Russell 1000 Growth Index; Dick Weiss: Russell 2000 Index. |

Neither the information contained herein nor any opinion expressed shall be construed to constitute an offer to sell or a solicitation to buy any security or any other funds mentioned herein. The views herein are those of Litman/Gregory Fund Advisors, LLC at the time the material is written and may not be reflective of current conditions.

Diversification does not assure a profit or protect against a loss in a declining market.

Fund Summary 9

Masters’ Select Equity Fund Managers

| MARKET | |||||

| TARGET | CAPITALIZATION | ||||

| INVESTMENT | MANAGER | OF COMPANIES | STOCK-PICKING | ||

| MANAGER | FIRM | ALLOCATION | IN PORTFOLIO | STYLE | |

| Christopher Davis/ | Davis Selected Advisers, L.P. | 20% | Mostly large companies | Growth at a | |

| Kenneth Feinberg | reasonable price | ||||

| Bill D’Alonzo and Team | Friess Associates, LLC | 10% | All sizes, emphasis is | Growth | |

| on small and mid-sized | |||||

| companies | |||||

| Mason Hawkins | Southeastern Asset | 20% | All sizes and global, may | Value | |

| Management, Inc. | have up to 50% foreign | ||||

| stocks | |||||

| Clyde McGregor | Harris Associates L.P. | 20% | Mostly mid- and large- | Value | |

| sized companies | |||||

| Frank Sands, Jr./ | Sands Capital | 10% | All sizes, but mostly large | Growth | |

| Michael Sramek | Management, LLC | and mid-size companies | |||

| Robert Turner/ | Turner Investment | 10% | All sizes, but mostly large | Growth | |

| Christopher McHugh/ | Partners, Inc. | and mid-size companies | |||

| William McVail | |||||

| Richard Weiss | Wells Capital | 10% | All sizes, emphasis is | Growth at a | |

| Management, Inc. | on small and mid-sized | reasonable price | |||

| companies |

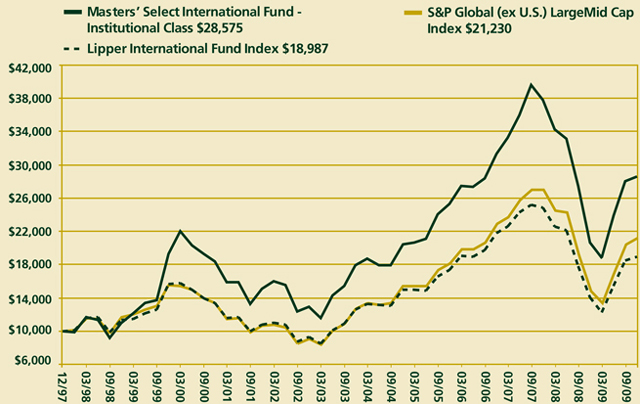

Equity Fund Value of Hypothetical $10,000

The value of a hypothetical $10,000 investment in the Masters’ Select Equity Fund from inception (12/31/96) to present compared with the Russell 3000 Index and the Lipper Multi-Cap Core Index.

The hypothetical $10,000 investment at fund inception includes changes due to share price and reinvestment of dividends and capital gains. The chart does not imply future performance. Indices are unmanaged, do not incur fees, expenses or taxes and cannot be invested in directly.

10 The Masters’ Select Funds Trust

Masters’ Select Equity Fund Stock Highlights

Inverness Medical Innovations, Inc. – Bill D’Alonzo

When medical conditions are caught early and treated continuously, it typically results in good outcomes and cost savings. By combining rapid diagnostic tools with health management services, Inverness helps on both sides of the equation.

NYSE-listed Inverness Medical Innovations, Inc. (IMA) is the world’s largest manufacturer of rapid point-of-care and at-home diagnostic tests. Following a series of recent acquisitions, it’s also the second largest domestic provider of health management services through its Alere subsidiary. With programs designed to cover the entire lifespan, from maternity to end-of-life care, Inverness focuses in the areas of cardiology, women’s health, infectious disease, oncology and drug abuse. Revenues grew 27 percent in the 12 months through September to $1.9 billion.

September-quarter earnings grew 61 percent, beating estimates by 21 percent. Quarterly sales increased 22 percent, driven by a 32 percent jump in diagnostic product revenue. Demand for flu tests as a result of the H1N1 pandemic and cardiology tests that diagnose congestive heart failure drove results.

The Friess Associates team spoke to Vice President of Finance Jon Russell regarding growth opportunities for the company’s rapid HIV tests. Due to the benefits of early detection, the Center for Disease Control now recommends routine rather than risk-based HIV testing. The company’s new HIV viral load test for earlier HIV diagnosis was rolled out in Africa earlier this year.

An alliance between CVS and Alere highlights the scalability of Inverness’ business model as it attempts to lower costs and give consumers greater control of health care decisions. Participants will have access to services ranging from in-home monitoring devices for at-risk patients to face-to-face counseling at approximately 500 MinuteClinics and nearly 7,000 CVS locations.

The Friess Associates team purchased Inverness at 12 times 2010 earnings estimates. Wall Street expects the company to grow earnings 15 percent in that period.

Merck & Co., Inc. – Christopher Davis/Kenneth Feinberg

Merck is one of the world’s largest pharmaceutical companies, is very profitable with 30% operating margins, is highly cash generative, and has a strong balance sheet with net debt equal to only about one year’s net income. It will benefit from both the aging of the population in the developed world and the growing disposable incomes in the developing world. Seniors over the age of 65 have three times as many prescriptions as the rest of the population and American baby boomers are just starting to turn 65. Also, health care as a % of GDP is 18% in the U.S. and 10-11% in many Western European countries but only 6-8% in emerging markets such as China and Brazil. Over the next couple of decades, health care spending should grow faster than GDP in these emerging markets.

Following the November 2009 closing of the Schering-Plough acquisition, Merck has the enviable combination of one of the best patent expiration profiles in the industry and the best pipeline amongst its peers. With 18 late-stage compounds, several of which are potential blockbusters, Merck is poised to overcome the 20% of sales facing patent expirations over the next five years. Merck is also well exposed to faster growing international markets with over half of sales from foreign countries. Earnings growth is expected to be in the mid to high single digits a year over the next five year period.

The management team led by CEO Dick Clark is experienced and disciplined. Capital discipline has been particularly good. Before the Schering-Plough deal, Merck had only spent 7% of its free cash flow generated over the past decade on acquisitions. Head of Research Peter Kim leads one of the most respected R&D teams in the industry.

One question we always ask ourselves is “Where could we be wrong?” Although health care reform has generated a great deal of headlines we estimate the proposed initiatives will reduce Merck’s earnings by a manageable 5% - in part because over half the sales are outside the U.S. Another potential concern is that in September 2010, Merck is scheduled to go to arbitration regarding the status of its rheumatoid arthritis joint venture with Johnson & Johnson. We believe Merck has a strong position but in any case the risk again remains manageable as the JV accounts for approximately 7% of earnings.

A longer term risk is the potential impact of the IMPROVE-IT trial which should produce results in 2013. The cholesterol-lowering drugs Zetia and Vytorin account for 9% of sales and the trial is designed to assess whether their ability to lower LDL cholesterol results in positive clinical outcomes. We are optimistic about the potential for a positive trial result given the large body of evidence supporting lowering LDL cholesterol, but should the results be negative we feel the current low valuation of 11x our estimate of 2010 owner earnings with a 4% dividend yield provides an adequate margin of safety.

Schlumberger Ltd. – Frank Sands Jr./Michael Sramek

Schlumberger Ltd. (SLB) was added to the Select Equity and Focused Opportunities funds by Sands Capital Management in September, 2009. Schlumberger is the world’s largest oilfield services company and the clear industry leader in most of the high-margin, high-value-added, exploration-related oilfield service lines such as wireline, logging while drilling, directional drilling, well testing, drilling fluids, coiled tubing, and seismic. These technology-focused services are essential for discovering and producing more oil and natural gas so that increasingly constrained global supply can meet structurally higher global demand over the long term. While there are no doubt cyclical influences in Schlumberger’s business (as we are experiencing currently), over the long-term we expect the structural supply/ demand forces to overwhelm the cyclicality, drive increased adoption of Schlumberger’s services, and help to generate average-annual EPS growth of nearly 20% for the business.

The Great Recession of 2008-2009 clearly interrupted the secular trend of growing global energy demand. Global demand for oil and natural gas fell approximately 3% and 5%, respectively, causing a sharp decline in prices and a severe slowdown in drilling activity, especially in North America. This sequence of events adversely impacted the entire energy complex including Schlumberger, whose third quarter revenues and earnings declined 25% and 48% y/y, respectively. While these results were very weak in an absolute sense, they were slightly better than consensus expectations, and much better than those of its competitors (evidencing share gains and product differentiation for Schlumberger).

Fund Summary 11

Yet this period during which the short-term cyclical forces are dominating the long-term secular forces and causing an acute slowdown in the industry is likely to be relatively short-lived. We believe a rebound in hydrocarbon demand is inevitable, followed by a return to trend-line growth. Further, we think this rebound is likely soon, and that Schlumberger will be an outsized beneficiary of it. Already, economic indicators around the globe are improving, especially in emerging markets where most of the incremental demand for hydrocarbons is derived. The active rig fleet has stabilized and is actually growing again (especially the deepwater rig fleet, where service intensity can be five-to-ten times higher than land activity), services pricing appears to have reached a floor, and early signals are pointing to higher global upstream spending in 2010 over 2009 (in some cases substantial increases). And of course oil prices have risen from under $35/ barrel at the beginning of 2009 to over $80, while natural gas prices have risen from $3 to almost $6.

More importantly, none of the structural supply constraints for oil and natural gas have improved, and in fact the pullback in drilling activity has exacerbated the already fragile long-term supply situation for incremental oil and natural gas. Thus the core driver of Schlumberger’s growth (i.e., providing solutions that help to alleviate these supply constraints) remains intact. Additionally, the need to bring additional hydrocarbon production on-line has been spring-loaded, which is likely to lead to a sharp rebound in Schlumberger’s business as soon as demand does in fact normalize.

Finally, with a one-year-forward P/E of 24X’s on temporarily depressed earnings (below its historical average of 26X’s normalized earnings), Schlumberger’s stock does not currently appear to us to reflect the potential for a material recovery, let alone such a sharp rebound and sustained above-average growth thereafter. As this occurs, substantial appreciation in the shares is likely to follow, and hence we believe this is an opportune time to add the business to the portfolios.

American Superconductor Corp. – Robert Turner

The principal activities of American Superconductor Corporation (AMSC) are to design, develop, manufacture and market high temperature superconductor (HTS) wires and power electronic converters. The company operates through two segments namely: AMSC Superconductors and AMSC Power Systems. The AMSC Wire division develops and markets HTS wires. The superconductors division develops and markets electric motors and generators based on HTS wires. The Power electronic systems division designs, develops and markets power electronic converters and integrated systems. The product offerings are sold to electrical equipment manufacturers, industrial power users, builders of ships that utilize electric drives and businesses that produce and deliver electric power. American Superconductor offers an array of proprietary technologies and solutions spanning the electric power infrastructure, from generation to delivery to end use. The company is also a leader in alternative energy, providing proven, megawatt-scale wind turbine designs and electrical control systems. The company also offers a host of Smart Grid technologies for power grid operators that enhance the reliability, efficiency and capacity of the grid, and seamlessly integrate renewable energy sources into the power infrastructure. These include superconductor power cable systems, grid-level surge protectors and power electronics-based voltage stabilization systems. The company’s technologies are protected by a broad and deep intellectual property portfolio consisting of hundreds of patents and licenses worldwide. The company has operations in the United States and Germany.

Growth Opportunities: The majority of American Superconductor’s business is in power systems where the company facilitates increased electrical grid capacity and also supplies electrical systems used in wind turbines. The wind energy industry is the fastest growing source of energy according to the Global Wind Energy Council (GWEC). With 120 of Giga Watts installed throughout the world at the end of 2008, the GWEC predicts that by 2020 worldwide demand could exceed 1,000 Giga Watts. There is no greater example of this expected growth than in China. American Superconductor is heavily exposed to wind power expansion in China through its customer Sinovel Wind Co. Ltd., which represents 75% of American Superconductor’s revenues. Sinovel is a subsidiary of a state-run Chinese utility which provides good visibility into the ability for projects to receive funding and we believe Sinovel will be the main driver of future earnings for American Superconductor. China expects to expand its wind capacity with a target of 120 to 150 GW of wind capacity by 2020, which would be a significant increase from the 20 GW capacity China currently uses. With this expansion, we expect to see substantial business awarded to Sinovel, considering that Sinovel controls 40% market share of the Chinese wind market. In addition to the Sinovel relationship, other turbines customers that American Superconductor can utilize include China’s Dongfang Turbine Co. and China’s CSR Zhuzhou Electric Locomotive Research Institute Co. In addition to China, the company has also recently won relatively large contracts in Australia, the UK, and the U.S. and should also benefit from the planned expansion of Sinovel in the UK and U.S. Hyundai Heavy Industries is an example of a new client that is not based in China which illustrates the company’s diversification. On the horizon, American Superconductor’s D-VAR system will provide the company with solid exposure to new smart grid contracts, which are set to roll out over the next two years in various regions throughout the world. Additionally, American Superconductor should also profit from the Tres Amigas project, which will enable the three U.S. power grids to buy and sell electricity amongst each other. American Superconductor should be a key supplier to the Tres Amigas project based in New Mexico and slated for completion by 2012. With that said, we believe that the booming Chinese wind industry and American Superconductor’s relationship with Sinovel should be the key drivers to future growth and strong earnings for the company in 2010 and beyond.

12 The Masters’ Select Funds Trust

Valuation of Company: The security is trading at 36 times its fiscal year 2011 earnings and 30 times fiscal year 2012 earnings based on Street consensus EPS estimates. While the multiple may seem high for an industrial stock, we believe it is more than justified given the company’s growth prospects. American Superconductor is projected to grow revenues over 36% in fiscal year 2011 and another 24% in fiscal year 2012. Earnings over the same period are expected to appreciate 92% and 24% respectively. Based on global initiatives to upgrade power grids and new interconnect standards that require more efficient output, we believe American Superconductor has an attractive opportunity in front of them, given the $600,000 average selling price for their D-VAR system (Dynamic Volt-Amp-Reactive) and their industry leading market share. We believe these estimates will move higher over the next 12 months as we see a 20% upside to current consensus.

Time Warner Cable, Inc. – Dick Weiss

Time Warner Cable, Inc. (TWC) provides video, data, and voice service to residential and commercial customers in the United States. The company serves approximately 14.6 million customers across 28 states primarily in New York, the Carolinas, Ohio, California, and Texas. TWC had been an integral part of Time-Warner for many decades. In early 2007, approximately 20% was spun out to Time-Warner shareholders to establish a market value. The remaining stock was distributed in 2008 so that virtually all of the stock is owned by the public. This is a key difference TWC has with its peers Comcast and Cablevision, where majority voting control is held by insiders.

The cable business has been positively impacted over the last several years from its dominant high speed data network (HSD), which has allowed them to benefit disproportionately from the growth in the internet; cable has a bandwidth advantage over the telephone copper wired network. By bundling video, HSD and telephone, the cable companies have been able to sharply increase their revenue per subscriber as well as control churn to some degree. This bundled product has engineered a response by AT&T and Verizon to enter the video business to lessen the loss of phone lines and DSL. The entrance of the telco’s has been a key negative overhang for the stock.

Looking forward, this competitive dynamic should begin to shift positively back towards the cable business, including TWC, as video penetration slows for the large telecom providers due to their builds becoming more costly and operationally complex. For Cable TV, a new source of growth has emerged in the form of the small/medium company commercial telephone business. While currently only 5% of TWC’s revenue, commercial telco is expected to grow faster and be more profitable than its existing mix of business. In addition to growing commercial telco, TWC and other cable operators have begun to launch a mobile broadband product on the Clearwire network that will allow them to satisfy the growing desire of consumers to access the web outside of the home. This product will not materially generate earnings in the near term, but successful early penetration will give investors confidence about another long term revenue stream and increase the multiple on current earnings.

A near-term earnings tailwind is the improvement in the advertising markets as the economy moves past the advertising depression of the last few years. While advertising revenue is a relatively small revenue contributor for TWC at approximately 5%, the incremental profits are extremely high and will drop to the bottom line. Longer term, advertising revenue may grow materially as TWC, working with other cable operators, plans to build a national interactive advertising platform. This would provide advertisers with the feedback they desire from the internet with the viewing experience they desire from television.

Our private market value is substantially above the current stock price. While CATV will never again sell at OIBD1 P/E levels of 8-10x, the stocks should sell for more than the telcos given their faster growth and competitive advantages. In TWC’s case, the downside is limited by its large free cash flow which will essentially transfer the enterprise value from the bondholders to the shareholders over a period of time. At a P/E of 5.5x OIBD, the stock appears attractive.

Kinetic Concepts, Inc. – Clyde McGregor

Kinetic Concepts, Inc. is held in both the Value Fund and the Equity Fund. Please refer to the discussion on page 30.

1 Operating income before depreciation

In keeping with Southeastern Asset Management’s disclosure policies, Mason Hawkins has not contributed commentary on his holdings for this report.

See page 78 for Industry Terms and Definitions

Neither the information contained herein nor any opinion expressed shall be construed to constitute an offer to sell or a solicitation to buy any securities mentioned herein. The views herein are those of the portfolio managers at the time the commentaries are written and may not be reflective of current conditions.

Fund Summary 13

Masters’ Select Equity Fund

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2009

| Shares | Value | ||||

| COMMON STOCKS: 95.3% | |||||

| Consumer Discretionary: 12.0% | |||||

| 15,500 | Amazon.com, Inc.* | $ | 2,085,060 | ||

| 252,042 | DIRECTV – Class A* | 8,405,601 | |||

| 244,000 | Disney (Walt) Co. | 7,869,000 | |||

| 278,000 | Interpublic Group of Companies, Inc.* | 2,051,640 | |||

| 38,600 | Kohl’s Corp.* | 2,081,698 | |||

| 103,000 | Las Vegas Sands Corp.* | 1,538,820 | |||

| 116,000 | Mohawk Industries, Inc.* | 5,521,600 | |||

| 20,800 | New Oriental Education & | ||||

| Technology Group – ADR* | 1,572,688 | ||||

| 78,500 | Petsmart, Inc. | 2,095,165 | |||

| 278,620 | Pulte Homes, Inc.* | 2,786,200 | |||

| 49,500 | Time Warner Cable, Inc. | 2,048,805 | |||

| 38,056,277 | |||||

| Consumer Staples: 2.6% | |||||

| 18,400 | Coca–Cola Co. | 1,048,800 | |||

| 74,330 | Costco Wholesale Corp. | 4,398,106 | |||

| 46,650 | Procter & Gamble Co. | 2,828,389 | |||

| 8,275,295 | |||||

| Energy: 13.3% | |||||

| 88,200 | Canadian Natural Resources Ltd. | 6,345,990 | |||

| 159,100 | Cenovus Energy Inc. | 4,009,320 | |||

| 356,000 | Chesapeake Energy Corp. | 9,213,280 | |||

| 80,100 | EnCana Corp. | 2,594,439 | |||

| 56,590 | EOG Resources, Inc. | 5,506,207 | |||

| 29,500 | FMC Technologies, Inc.* | 1,706,280 | |||

| 60,000 | National Oilwell Varco, Inc. | 2,645,400 | |||

| 21,000 | Range Resources Corp. | 1,046,850 | |||

| 39,500 | Schlumberger Ltd. | 2,571,055 | |||

| 61,000 | Smith International, Inc. | 1,657,370 | |||

| 17,000 | Transocean, Inc.* | 1,407,600 | |||

| 72,700 | XTO Energy, Inc. | 3,382,731 | |||

| 42,086,522 | |||||

| Finance: 18.8% | |||||

| 200,600 | American Express Co. | 8,128,312 | |||

| 368,500 | Bank of New York Mellon Corp. | 10,306,945 | |||

| 56 | Berkshire Hathaway, Inc. – Class A* | 5,555,200 | |||

| 120,000 | CapitalSource, Inc. | 476,400 | |||

| 107,500 | Charles Schwab Corp. | 2,023,150 | |||

| 527,000 | Cheung Kong Holdings Ltd. – ADR | 6,756,140 | |||

| 26,000 | Fairfax Financial Holdings Ltd. | 10,138,960 | |||

| 167,490 | Genworth Financial, Inc.* | 1,901,011 | |||

| 109,700 | Glacier Bancorp, Inc. | 1,505,084 | |||

| 70,000 | HCC Insurance Holdings, Inc. | 1,957,900 | |||

| 128,000 | Loews Corp. | 4,652,800 | |||

| 223,294 | Ocwen Financial Corp.* | 2,136,924 | |||

| 75,300 | Transatlantic Holdings, Inc. | 3,923,883 | |||

| 59,462,709 | |||||

| Health Care, Pharmaceuticals & Biotechnology: 16.6% | |||||

| 39,990 | Alexion Pharmaceuticals, Inc.* | 1,952,312 | |||

| 37,900 | Celgene Corp.* | 2,110,272 | |||

| 107,500 | Covidien Ltd. | 5,148,175 | |||

| 49,600 | Genzyme Corp.* | 2,430,896 | |||

| 81,000 | Health Management Association, Inc.* | 588,870 | |||

| 38,000 | Illumina, Inc.* | 1,164,700 | |||

| 7,500 | Intuitive Surgical, Inc.* | 2,274,900 | |||

| 48,700 | Inverness Medical Innovations, Inc.* | 2,021,537 | |||

| 46,100 | Johnson & Johnson | 2,969,301 | |||

| 142,600 | Kinetic Concepts, Inc.* | 5,368,890 | |||

| 62,000 | Laboratory Corporation of | ||||

| America Holdings* | 4,640,080 | ||||

| 42,300 | Life Technologies Corp.* | 2,209,329 | |||

| 332,400 | MDS, Inc.* | 2,542,860 | |||

| 85,300 | Merck & Co., Inc | 3,116,862 | |||

| 58,000 | Mindray Medical International Ltd. – | ||||

| ADR | 1,967,360 | ||||

| 178,000 | Omnicare, Inc. | 4,304,040 | |||

| 72,000 | Patterson Companies, Inc.* | 2,014,560 | |||

| 84,149 | Psychiatric Solutions, Inc.* | 1,778,910 | |||

| 62,920 | Vermillion, Inc.* | 1,727,154 | |||

| 78,000 | Warner Chilcott PLC – Class A* | 2,220,660 | |||

| 52,551,668 | |||||

| Industrials: 9.6% | |||||

| 48,100 | American Superconductor Corp.* | 1,967,290 | |||

| 33,300 | Clean Harbors, Inc.* | 1,985,013 | |||

| 137,290 | Continental Airlines, Inc.* | 2,460,237 | |||

| 25,500 | FedEx Corp. | 2,127,975 | |||

| 64,610 | Genco Shipping & Trading Ltd.* | 1,445,972 | |||

| 129,500 | Kirby Corp.* | 4,510,485 | |||

| 87,800 | McDermott International, Inc.* | 2,108,078 | |||

| 99,100 | Rockwell Collins, Inc. | 5,486,176 | |||

| 150,300 | Snap-on, Inc. | 6,351,678 | |||

| 420,000 | Taser International, Inc.* | 1,839,600 | |||

| 30,282,504 | |||||

| Materials: 3.6% | |||||

| 82,840 | AK Steel Holding Corp. | 1,768,634 | |||

| 27,500 | Barrick Gold Corp. | 1,082,950 | |||

| 525,000 | Cemex S.A.B. de C.V. – ADR | 6,205,500 | |||

| 26,600 | Monsanto Co. | 2,174,550 | |||

| 11,231,634 | |||||

| Technology: 17.1% | |||||

| 65,530 | ASML Holding N.V . | 2,233,918 | |||

| 62,640 | Aixtron AG – ADR | 2,098,440 | |||

| 457,390 | Alcatel-Lucent – ADR | 1,518,535 | |||

| 12,300 | Apple, Inc.* | 2,593,578 | |||

| 174,000 | Ariba, Inc.* | 2,178,480 | |||

| 107,600 | Aruba Networks Inc.* | 1,147,016 | |||

| 85,000 | Avago Technologies Ltd.* | 1,554,650 | |||

| 233,200 | Broadridge Financial Solutions, Inc. | 5,260,992 | |||

| 98,560 | CyberSource Corp.* | 1,982,041 | |||

| 115,000 | Cypress Semiconductor Corp.* | 1,214,400 | |||

| 513,000 | Dell, Inc.* | 7,366,680 | |||

| 216,355 | Finisar Corp.* | 1,929,887 | |||

| 8,650 | Google, Inc. – Class A* | 5,362,827 | |||

| 78,900 | JDA Software Group, Inc.* | 2,009,583 | |||

| 244,120 | Micron Technology, Inc.* | 2,577,907 | |||

| 46,800 | Netlogic Microsystems Inc.* | 2,164,968 | |||

| 145,000 | NVIDIA Corp.* | 2,708,600 | |||

| 54,800 | QUALCOMM, Inc. | 2,535,048 | |||

| 330,087 | Symmetricom, Inc.* | 1,716,452 | |||

| 54,000 | Telvent GIT, S.A. | 2,104,920 | |||

| 94,875 | Western Union Co. | 1,788,394 | |||

| 54,047,316 | |||||

14 The Masters’ Select Funds Trust

SCHEDULE OF INVESTMENTS IN SECURITIES at December 31, 2009

| Shares/ | ||||||

| Principal | ||||||

| Amount | Value | |||||

| Telecommunication Services: 1.7% | ||||||

| 3,587,480 | Level 3 Communications, Inc.* | $ | 5,488,844 | |||

| TOTAL COMMON STOCKS | ||||||

| (cost $262,500,154) | 301,482,769 | |||||

| SHORT-TERM INVESTMENTS: 5.0% | ||||||

| 15,920,000 | State Street Bank & Trust., 0.005%, | |||||

| 12/31/09, due 01/04/10 [collateral: | ||||||

| par value $15,210,000, | ||||||

| Fannie Mae, 5.625%, due 07/15/2037, | ||||||

| value $16,255,688] (proceeds | ||||||

| $15,920,009) | 15,920,000 | |||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||

| (cost $15,920,000) | 15,920,000 | |||||

| TOTAL INVESTMENTS IN SECURITIES | ||||||

| (cost $278,420,154): 100.3% | 317,402,769 | |||||

| Liabilities in Excess of Other Assets: (0.3)% | (1,151,983 | ) | ||||

Net Assets: 100% | $ | 316,250,786 | ||||

| Percentages are stated as a percent of net assets. | ||||||

| ADR | American Depository Receipt |

| * | Non-Income Producing Security |

The accompanying notes are an integral part of these financial statements.

Schedule of Investments 15

During an outstanding year for stocks around the globe, Masters’ Select International lagged its benchmark but generated strong absolute returns that ranked in the top 17% by Morningstar in the Foreign Large Blend Category (see below for more details). For the six months ended December 31, the fund returned 19.7% versus 24.4% for its benchmark, the S&P Global ex-US Large Mid Index. For the full year the fund gained 38.5%, while its benchmark was up 42.6%.

At Masters’ Select our primary focus is on long-term performance. In that regard Masters’ Select International has a strong record relative to its benchmark. Since its inception over 12 years ago, the fund’s average annual return of 9.1% is well ahead of its benchmark’s 6.4% return. It has also out-returned its benchmark over 10 years and over every one of the 26 rolling 10-year periods since its inception. (The first rolling 10-year period is measured 10 years after the fund’s inception. Each month thereafter a new 10-year period is added.) Relative to its peers it has also performed extremely well with better than top quintile performance in trailing time periods—as of December 31 2009, Morningstar, Inc. ranked Masters’ Select International Fund in the top 17th, 16th, 11th and 10th percentiles among 823, 635, 462, and 249 Foreign large Blend Funds over the trailing one-, three-, five- and ten-year periods, respectively, based on total return.1

Performance as of December 31, 2009

| Average Annual Total Returns | ||||||||||||||||||||

| Three- | Since | |||||||||||||||||||

| One-Year | Year | Five-Year | Ten-Year | Inception | ||||||||||||||||

| Masters’ Select | ||||||||||||||||||||

| International Fund | ||||||||||||||||||||

| - Institutional Class | ||||||||||||||||||||

| (12/1/97) | 38.54 | % | -3.02 | % | 6.89 | % | 3.99 | % | 9.08 | % | ||||||||||

| S&P Global (ex U.S.) | ||||||||||||||||||||

| LargeMid Cap Index | 42.55 | % | -2.45 | % | 6.65 | % | 3.20 | % | 6.43 | % | ||||||||||

Performance data quoted represents past performance; past performance is no guarantee of future results. See page 3 for a detailed discussion of the risks and costs associated with investing in the Masters’ Select International Fund.

As we consider the fund’s performance it is useful to consider not just the fund’s benchmark (the S&P Global ex-U.S. Large Mid Index), but also real-world investable alternatives to those benchmarks. Low-cost index funds are the obvious alternative. In that regard it is interesting to observe the performance of some index funds in the international equity space relative to the underlying indexes. To assess this we looked at the Morningstar Fund Analyst Picks in the Foreign Large Blend category. There are nine funds that Morningstar recommends, and as of the end of 2009, Masters’ Select International continues to be one of them.2 Of the nine, two are index funds. The best performing of the two is the Vanguard Total International Stock Index, with expenses of 0.27%. The Vanguard fund tracks a broad MSCI benchmark that includes emerging markets and so its investment universe is comparable to the Masters’ Select International benchmark.

The following table matches up the return of the Vanguard fund with the broad international index that Masters’ Select uses as its benchmark.

| Average Annual Total Return | ||||||||||||||||

| as of 12/31/09 | ||||||||||||||||

| Three- | ||||||||||||||||

| One-Year | Year | Five-Year | Ten-Year | |||||||||||||

| Vanguard Total | ||||||||||||||||

| International Index Fund | 36.73 | % | -4.07 | % | 5.26 | % | 2.29 | % | ||||||||

| S&P Global (ex U.S.) | ||||||||||||||||

| LargeMid Cap Index | 42.55 | % | -2.45 | % | 6.65 | % | 3.20 | % | ||||||||

Interestingly, the performance of the Vanguard Total International Index Fund versus our S&P Global ex-U.S. Large Mid Index benchmark was quite different in 2009, with the fund not doing nearly as well as the benchmark. The index fund also underperformed over longer trailing time periods when compared to the S&P Global ex-U.S. benchmark, though much of the longer-term underperformance is explained by 2009. The Vanguard fund underperformed its own benchmark index by 3.69 percentage points in 2009, and it underperformed ours by a larger 5.82 percentage points. We think this is an interesting observation as we compare real world investing for an index fund, which involves expenses and potential transaction-related complications, to the somewhat hypothetical world of a benchmark. The bottom line is that the Vanguard Total International Index Fund, a highly regarded index fund which offer a real world investable alternative for passive investors, returned meaningfully less than our S&P Global ex-U.S. Large Mid Index benchmark over all trailing time periods over the last ten years (1, 3, 5, 10 year time periods).

Portfolio Commentary

A number of factors contributed to the fund’s performance during 2009. The highlights follow.

Performance of managers: In 2009, three of the fund’s six managers outperformed their respective benchmarks. For the year, the performance of individual managers ranged from 22.1% to 51.0%. There are five managers who have been with the fund for at least three years. Three out of these five have beaten their benchmarks over their full tenure with Masters’ Select International, while one has roughly matched the index.3 We expect that over shorter periods we will have a mix of underperforming and outperforming managers. Longer term, we expect all of our managers to beat their respective benchmarks. Time will tell if we are right.

Sector/country and stock-picking impact: Though all the Masters’ Select funds are driven by bottom-up stock picking, the sector and regional exposures that result from this process may provide some insight into the fund’s relative performance. Based on our attribution analysis versus the S&P Global ex-U.S. Large Mid Index, the fund’s cash position and overall sector exposures detracted from relative performance. With the broad international market up nearly 43% for the year, the fund’s average cash weighting of over 5% was a drag on performance. (Most of the cash was held at the sub-advisor level though we held a small portion at the fund level for part of the year to cover redemptions—the fund’s redemptions stopped in mid-2009 and it had steady net inflows over the remainder of the year). In terms of sectors, an underweighting to materials, the strongest-performing sector in 2009, hurt the fund’s relative performance. However, the fund benefited from its underweighting to utilities, the weakest-performing sector. The fund on average had an overweighted position to health care during the year. This also detracted from relative performance.

16 The Masters’ Select Funds Trust

At the country and regional level, the Masters’ Select country allocations aided performance in 2009. The fund’s underweighting to Japan helped relative performance as that country significantly underperformed the rest of the international markets. An overweighting to Latin America was also positive as it rose almost 100% during the year.

Stock selection overall contributed positively to the fund’s relative performance. It was strong in the consumer discretionary and telecommunications sectors. In the consumer sector, Carpetright, a British retailer focused on floor coverings, was up over 200%. In telecoms, Netia, a Polish telecom company, and Millicom International Cellular, a Luxembourg-based company that provides wireless services to many emerging-market countries, were up over 110% and 60%, respectively. All three stocks had a material impact on the fund’s absolute and relative performance. On the negative side, stock selection within financials was poor. Swiss Re, a Swiss reinsurer, was down over 50% before it was sold by one of the fund’s managers (it was purchased several months later by a different manager in the fund). See page 21 for commentary written by the fund’s sub-advisors on some of the fund’s holdings.

Leaders and laggards: The table below lists the biggest contributors and detractors to the fund’s performance over the past 12 months. It is important to understand that whether a stock has lost (or made) money for Masters’ Select International for the past 12 months tells us nothing about how successful the holding has been during the entire period it was held, or how successful it may become. The fund will hold many stocks for significantly longer periods of time and the success of these holdings won’t be known until they are ultimately sold. So in that respect, while it is interesting to know how specific stocks performed during the period, this information may be of limited value in assessing the ultimate success of these stock holdings.