UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07831

FMI Funds, Inc.

(Exact name of registrant as specified in charter)

100 East Wisconsin Avenue

Suite 2200

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Ted D. Kellner

Fiduciary Management, Inc.

100 East Wisconsin Avenue

Suite 2200

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 226-4555

(Registrant's telephone number, including area code)

Date of fiscal year end: September 30

Date of reporting period: March 31, 2015

Item 1. Reports to Stockholders.

SEMIANNUAL REPORT

March 31, 2015

FMI Large Cap Fund

(FMIHX)

FMI Common Stock Fund

(FMIMX)

FMI International Fund

(FMIJX)

| |  | | |

| | | |

| | FMI Funds | |

| | Advised by Fiduciary Management, Inc. www.fmifunds.com | |

| | | | |

FMI Funds

TABLE OF CONTENTS

| FMI Large Cap Fund | |

| Shareholder Letter | 2 |

| Schedule of Investments | 7 |

| Industry Sectors | 8 |

| | |

| FMI Common Stock Fund | |

| Shareholder Letter | 9 |

| Schedule of Investments | 14 |

| Industry Sectors | 16 |

| | |

| FMI International Fund | |

| Shareholder Letter | 17 |

| Schedule of Investments | 23 |

| Schedule of Forward Currency Contracts | 25 |

| Industry Sectors | 26 |

| | |

| Financial Statements | |

| Statements of Assets and Liabilities | 27 |

| Statements of Operations | 28 |

| Statements of Changes in Net Assets | 29 |

| Financial Highlights | 30 |

| Notes to Financial Statements | 31 |

| | |

| Additional Information | 36 |

| Expense Example | 37 |

| Advisory Agreements | 38 |

| Disclosure Information | 39 |

FMI

Large Cap

Fund

March 31, 2015

Dear Fellow Shareholders:

The FMI Large Cap Fund returned 1.79% in the March quarter compared to the benchmark Standard & Poor’s 500 gain of 0.95%. Sectors that helped this quarter included Distribution Services, Health Services and Consumer Non-Durables, while Health Technology, Technology Services and Process Industries detracted from performance compared to the S&P 500 Index. Stocks that performed well in the period included AmerisourceBergen, UnitedHealth Group and TE Connectivity. These gains were balanced by negative results from American Express, Potash Corp. and PACCAR; we continue to like the long-term outlook for all three of these investments. Cash remained a drag on performance. Other than tactical boosting and trimming, the only across-the-board portfolio move in the quarter was the sale of Cintas, which reached a full valuation.

Aside from a few bumps at the end of the quarter, the six-year bull market remained intact through March. It is difficult to reconcile the trajectory or the level of stock, bond, real estate and most other financial assets over most of the past several years given the fundamentals. It might be tempting to just sit back and enjoy the ride, but having a strong conviction that there is an artificiality to the great success these markets have enjoyed keeps us from joining in the fun. Despite a torrent of fiscal stimulus resulting in a staggering debt load of $18 trillion and enormously accommodative monetary policies, the U.S. economy continues to perform in subpar fashion. U.S. real gross domestic product (GDP) growth over the past five years has averaged 2.3%, less than half the normal rate. Many other developed countries are in the same predicament. International Monetary Fund (IMF) estimates of global GDP growth have recently been cut again, from 3.8% to 3.5%. U.S. industrial production, durable goods spending, and business formations have all recently weakened. Housing starts and existing sales have been up and down, but far below what most predicted for five years after a recession. First quarter retail sales look like they will be down at least 2%. The unemployment rate has improved, but that is modest solace considering the near record-low labor participation rate of 62.8%. While this figure might have some downward influence from baby boomers retiring early with no desire to reenter the workforce, millions have become discouraged and have simply stopped looking for work, and are thus no longer counted as unemployed. Labor’s share of profits is low relative to history and real incomes have been stagnant for over a decade, unless you are in the small slice at the top. Corporate sales and earnings growth rates have declined sharply in recent months (likely to be down in the first quarter), partly due to weak oil prices and the strong dollar, but also affected by a lack of organic fixed business investment, research and development, and people. Corporate executives have become slaves to Wall Street, buying back stock at record-high levels and worshipping at the mergers and acquisitions altar. Government leaders and central bank bureaucrats continue to push the same policies regardless of the outcomes and despite the alarming increase in long-term liabilities and distortions to healthy and sustainable economic activity.

It may be hard to imagine, but since the financial crisis, which was partially due to an excessive credit expansion, the world has added even more debt than it did in the run-up to the peak (2000-2007). Quoting from a McKinsey report:

Seven years after the bursting of a global credit bubble resulted in the worst financial crisis since the Great Depression, debt continues to grow. In fact, rather than reducing indebtedness, or deleveraging, all major economies today have higher levels of borrowing relative to GDP than they did in 2007. Global debt in these years has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points. That poses new risks to financial stability and may undermine global economic growth.1

Most investors continue to put their money and faith with Fed Chairwoman Yellen’s interest rate oracles, but it is clear, at least to us, that she and most of the Fed governors are perplexed by the spotty labor markets and the underlying health of the economy. It comes as no surprise that pumping up asset values in an attempt to induce a wealth effect-driven economic expansion has, and will continue to fail on many levels. While it is logical to expect small wealth effect spending by a few

| 1 | Richard Dobbs, Susan Lund, Jonathan Woetzel, and Mina Mutafchieva. “Debt and (not much) deleveraging.” McKinsey Global Institute Report, February 2015. |

middle and upper-middle income folks who happen to own modest financial asset portfolios that rise substantially, the fact is, the vast majority of financial assets are owned by the top 10% of the population. If we were to double Warren Buffett’s wealth, how much more would he consume? Probably very little, and thus the impact on the economy would be negligible. An unnaturally low interest rate policy favors speculators, deal-makers and financial engineers. Only a vibrant economy with organic growth opportunities will induce true risk-takers to invest in people and capital.

The six-year bull market, combined with tepid fundamentals, has made stocks remarkably expensive from a historical perspective. The median or “typical” stock is higher than we have ever seen, and even more expensive than during the peak of the technology and telecom craze in 1999. Today there are over seventy start-ups with valuations over a billion dollars compared to less than half of that, inflation adjusted, in the 1999-2000 period. Pharmaceutical companies are brawling with each other to pay 5-10 times multi-year-out hoped-for revenue for phase III or recently approved compounds. Unnaturally-low interest rates foster this behavior. Bond valuations have reached epic levels nearly everywhere with ground-hugging rates here in the U.S., and even negative rates in some countries. A number of real estate sectors, particularly those catering to the wealthy, appear highly inflated, reminiscent of ten years ago.2 Real estate investment trusts (REITs) are as pricey as we can ever recall. Strangely, the sheer length of this asset inflation cycle has people feeling emboldened to take more risk rather than trimming their sails. In his book, Inefficient Markets, An Introduction to Behavioral Finance, Andrei Shleifer said, “Investor sentiment reflects the common judgment errors made by a substantial number of investors, rather than uncorrelated random mistakes.”

A tremendous surge of funds moving toward passive index strategies has created an environment where the flows themselves are driving performance. According to Morningstar, in 2014 U.S. active equity funds experienced $98.4 billion of outflows, while passive funds received $166.6 billion of inflows. This self-reinforcing cycle is not uncommon in the latter stages of bull markets. Investors and investment committees continue to capitulate on active management, throwing in the proverbial towel and going passive when they should be de-risking to cash or moving to more conservative active management. Index funds have taken on somewhat of a life of their own, divorced from underlying fundamentals. Last year, just 25 companies, or 5% of the S&P 500 constituents, accounted for approximately 50% of the total return. Eventually, negative developments affect the top-heavy indices, and as long as there is still an active investment community reacting to this, it sets the process in reverse, with the weightiest components falling the hardest as monies flow out, disproportionately hurting index products, which inures to the benefit of the more conservative active managers. The caveat is that these cycles can sometimes be excruciatingly long, as evidenced by the current one. An added feature to the complexion of the market is that unlike in 1999, when performance was also quite concentrated, today’s market, even outside the weightiest names, is still expensive.

Another way to view stock market cycles is to look at the relative performance of growth versus value strategies. Using the Leuthold data, the chart on the following page shows the last forty years of these cycles. Given all that we have said in recent letters about what is happening in the market and the types of companies that are garnering the limelight, it won’t come as a surprise to see that the past seven years have been driven by growth stocks. It has certainly been a headwind for us. Over the entire period, however, value has outperformed growth by a quite substantial 25%. Data stretching back ninety years also shows value outperforming growth. Sharp-eyed observers of this chart will see, however, that there was a brief moment in 1999 where growth had beaten value over a 25-year period. We certainly hope the current seven-year run stops in its tracks, but of course there is no way to predict or assure that.

| 2 | Erin Carlyle. “America’s Most Expensive Home Sales of 2014.” Forbes, December 24, 2014. |

Finally, for those who think prices and markets rarely change quickly, look at oil prices over the second half of 2014. Oil dropped from roughly $100 per barrel in June to approximately $50 in December. A year ago, the overwhelming consensus was that oil was hard to find and prices would grind higher, with many experts calling for $200 oil within a few years. Today the sentiment has completely flipped, with many of the former bulls saying it may be many years before we see $100 again.

As always, the research team continues working hard to try to find potentially good ideas that we feel have less downside risk than the typical stock. Below we highlight two of these ideas.

TE Connectivity (TEL)

(Analyst: Andy Ramer)

Description

TE Connectivity is the global leader in connectors and sensors, with the broadest portfolio of products in this $165 billion market. Transportation is the company’s largest end market at over 50% of pro forma sales.

Good Business

| | • | Pro forma the sale of Broadband Network Solutions (BNS), approximately 90% of the portfolio provides leading connectivity and sensor solutions. Their focus on providing increasingly complex, application-specific solutions raises the barriers to entry – 80% of sales will be generated from harsh environment applications that require highly-engineered solutions. |

| | • | Connectors and sensors are ubiquitous features in every electronic device. The proliferation of electronics and increasing content penetration is driving demand for TE’s products, which represent a low-single-digit percentage of the bill of materials. |

| | • | Return on invested capital (ROIC) improved to 12.5% in fiscal year 2014, with 3- and 5-year returns on incremental invested capital in the range of 25% to 30%. |

| | • | This business is easy to understand. |

| | • | The balance sheet is strong and the company generates a prodigious amount of free cash flow. |

Valuation

| | • | TE trades for 16.8 times calendar year 2015 earnings per share forecasts, a significant discount to the median and weighted average multiples for the S&P 500 of 18.5 and 21.6, respectively, as well as its closest peer Amphenol, which trades for 23.8 times. |

| | • | Koch Industries announced the acquisition of competitor Molex in September of 2013 for 22 times consensus calendar year 2014 earnings per share estimates. Ascribing a similar multiple to TE would represent upside of around 30%. |

| | • | Free cash flow approximates net income and thus yields 6.0% on calendar year 2015 forecasts. |

Management

| | • | Tom Lynch has served as CEO since January of 2006 and was elected Chairman in January of 2013. Terrence Curtin serves as President and is responsible for all of the Connectivity and Sensors businesses and merger and acquisition activities. Bob Hau joined TE in August of 2012 as CFO. |

| | • | Since being spun off from Tyco International in June of 2007, management has worked to reposition TE as a faster-growing, more profitable enterprise. Most recently, the company announced the sale of its volatile and underperforming BNS division to CommScope in January of 2015 for $3.0 billion, or 10 times EBITDA (earnings before interest, taxes, depreciation and amortization). The majority of the sale proceeds will be used for share repurchases. |

| | • | TE expects to continue to return roughly two-thirds of free cash flow to shareholders over time, with the remaining one-third dedicated to making small- and mid-sized acquisitions. |

Investment Thesis

Increasing electronic content and design wins are expected to result in long-term organic sales growth of 5-7% per year, which in turn should drive approximately 50 basis points of annual operating margin expansion. When combined with stock buybacks, earnings per share is expected to grow at a double-digit compound annual rate. TE is an above-average company that is trading at a well-below-average multiple.

Comcast Corp. (CMCSA)

(Analyst: Dan Sievers)

Description

Comcast Corp. is the largest cable multiple-system operator (MSO) in the U.S., with this business contributing 63% of sales and 76% of EBITDA. In 2014, its networks passed an estimated 54.7 million homes and businesses (+2% year-over-year) with residential subscriber penetration of video at 40.9% (22.2 million subscribers) and internet at 40.2% (22 million subscribers). Comcast’s coaxial networks were rebuilt in the 2000s and now boast high-capacity fiber optic backbones (over 145,000 fiber miles). Business services revenue grew 22% in 2014 to 9% of MSO revenue. Comcast can deliver 105 megabits per second internet speed to all customers on the data over cable service interface specification (DOCSIS) 3.0 standard, with DOCSIS 3.1 promising much higher speeds, even without replacing node-to-home coaxial cables. The remaining 36% of sales and 24% of EBITDA comes from NBC Universal (NBCU), a large media conglomerate acquired from GE (51% in 2009 and 49% in 2012), which owns the NBC and Telemundo broadcast networks, 27 local stations, popular cable networks, major studio assets, and theme parks.

Good Business

| | • | Industry-wide, cable video subscriptions have fallen every year since 2001, and we expect further attrition. Bundled pricing practices distort reported cable video and internet revenue contribution (overstating video). Rising programming costs have rendered video a low-margin business, while residential and business internet services are high-margin businesses (and are growing much faster). |

| | • | Cable MSOs are the low-cost providers of fast broadband internet service, due to the robust nature of existing hybrid fiber/coaxial (HFC) network architectures. Cable internet continues to take residential and business market share from telco DSL, which cannot compete on speed. This is a recurring revenue, high-margin business. |

| | • | The FCC’s recent Open Internet (or Net Neutrality) rule, released March 12, 2015, reclassifies internet access service providers (ISPs) as Title II common carriers under the 1934 Communications Act, but applies forbearance to most of the critical elements surrounding pricing. Reversing forbearance would require solicitation of public comment (over several months) and detailed responses to public criticism and concerns. |

| | | From page 12: “Our forbearance approach results in over 700 codified rules being inapplicable, a “light-touch” approach for the use of Title II. This includes no unbundling of last-mile facilities, no tariffing, no rate regulation…” |

| | | From page 214: “…we do not and cannot envision adopting new ex ante regulation of broadband Internet access service in the future…” |

| | • | NBCU controls an attractive stable of networks (USA, SyFy, E!, Bravo, etc.) and content, including news (NBC, CNBC, MSNBC) and sports (NBC, NBC Sports, Golf), with NBC broadcast contributing significant margin-accretive growth via retransmission consent fees. Overlooked assets include NBCU’s national and local broadcast spectrum and 30 Rockefeller Center. |

Valuation

| | • | If NBCU were valued even at a discount to its peer group average at 10 times 2014 EBITDA (30% of enterprise value), then Comcast Cable is valued at an attractive 7.24 times 2014 EBITDA (70% of enterprise value). |

| | • | Comcast is under-levered with net debt equal to 1.86 times 2014 EBITDA. |

| | • | Comcast trades for 17.3 times estimated 2015 earnings compared to the 10-year P/E average of 23. |

Management

| | • | Brian Roberts (son of founder Ralph Roberts), is President (1990), CEO (2002), and Chairman (2004), and controls one-third voting interest in Comcast through non-traded B share ownership. |

| | • | Comcast has a deep bench of talented executives, several of whom own significant Comcast shares. |

Investment Thesis

Despite the FCC’s recent reclassification, we feel that Comcast is very well positioned for the future. Pundits continue to misunderstand the limited cash flow contribution of cable video, where subscriber reductions produce limited impact. HFC networks capable of providing ever faster internet services should be regarded as appreciating assets. Comcast’s valuation multiples are attractive given its double-digit earnings per share (EPS) outlook, its low debt leverage, the possibility of flat or declining capital intensity, and its ability to utilize its fixed network to offer new and related services (business services, home security, wireless mobile virtual network operator mobile phone services, etc.).

Thank you for your support of the FMI Large Cap Fund.

100 E. Wisconsin Ave., Suite 2200 • Milwaukee, WI 53202 • 414-226-4555

www.fmifunds.com

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS

March 31, 2015 (Unaudited)

| Shares | | | | Cost | | | Value | |

| | | | | | | |

| COMMON STOCKS — 90.7% (a) | | | | | | |

| | | | | | | |

| COMMERCIAL SERVICES SECTOR — 3.7% | | | | | | |

| | | Advertising/Marketing Services — 3.7% | | | | | | |

| | 4,487,800 | | Omnicom Group Inc. | | $ | 316,308,265 | | | $ | 349,958,644 | |

| | | | | | | | | |

| CONSUMER NON-DURABLES SECTOR — 9.3% | | | | | | | | |

| | | | Food: Major Diversified — 7.0% | | | | | | | | |

| | 27,018,000 | | Danone S.A. - SP-ADR | | | 380,798,850 | | | | 365,013,180 | |

| | 4,076,000 | | Nestle’ S.A. - SP-ADR | | | 217,208,806 | | | | 306,598,962 | |

| | | | | | | 598,007,656 | | | | 671,612,142 | |

| | | | Household/Personal Care — 2.3% | | | | | | | | |

| | 5,167,000 | | Unilever PLC - SP-ADR | | | 207,164,661 | | | | 215,515,570 | |

| | | | | | | | | |

| CONSUMER SERVICES SECTOR — 5.9% | | | | | | | | |

| | | | Cable/Satellite TV — 3.2% | | | | | | | | |

| | 5,492,000 | | Comcast Corp. - Cl A | | | 301,243,196 | | | | 310,133,240 | |

| | | | | | | | | | | | |

| | | | Other Consumer Services — 2.7% | | | | | | | | |

| | 4,517,000 | | eBay Inc.* | | | 233,790,000 | | | | 260,540,560 | |

| | | | | | | | | |

| DISTRIBUTION SERVICES SECTOR — 5.0% | | | | | | | | |

| | | | Medical Distributors — 5.0% | | | �� | | | | | |

| | 4,210,000 | | AmerisourceBergen Corp. | | | 123,626,184 | | | | 478,550,700 | |

| | | | | | | | | |

| ELECTRONIC TECHNOLOGY SECTOR — 3.3% | | | | | | | | |

| | | | Electronic Components — 3.3% | | | | | | | | |

| | 4,475,000 | | TE Connectivity Ltd. | | | 100,434,692 | | | | 320,499,500 | |

| | | | | | | | | |

| ENERGY MINERALS SECTOR — 3.6% | | | | | | | | |

| | | | Oil & Gas Production — 3.6% | | | | | | | | |

| | 5,655,000 | | Devon Energy Corp. | | | 339,561,971 | | | | 341,053,050 | |

| | | | | | | | | |

| FINANCE SECTOR — 14.6% | | | | | | | | |

| | | | Financial Conglomerates — 3.1% | | | | | | | | |

| | 3,804,000 | | American Express Co. | | | 158,739,785 | | | | 297,168,480 | |

| | | | | | | | | | | | |

| | | | Major Banks — 8.0% | | | | | | | | |

| | 11,595,000 | | Bank of New York Mellon Corp. | | | 278,719,587 | | | | 466,582,800 | |

| | 6,715,000 | | Comerica Inc. | | | 205,074,929 | | | | 303,047,950 | |

| | | | | | | 483,794,516 | | | | 769,630,750 | |

| | | | Property/Casualty Insurance — 3.5% | | | | | | | | |

| | 12,450,000 | | Progressive Corp. | | | 312,878,307 | | | | 338,640,000 | |

| | | | | | | | | |

| HEALTH SERVICES SECTOR — 6.5% | | | | | | | | |

| | | | Managed Health Care — 6.5% | | | | | | | | |

| | 5,221,000 | | UnitedHealth Group Inc. | | | 380,557,339 | | | | 617,592,090 | |

| | | | | | | | | |

| INDUSTRIAL SERVICES SECTOR — 3.4% | | | | | | | | |

| | | | Oilfield Services/Equipment — 3.4% | | | | | | | | |

| | 3,845,000 | | Schlumberger Ltd. | | | 252,925,610 | | | | 320,826,800 | |

| | | | | | | | | |

| PROCESS INDUSTRIES SECTOR — 5.1% | | | | | | | | |

| | | | Chemicals: Agricultural — 5.1% | | | | | | | | |

| | 15,240,000 | | Potash Corp. of Saskatchewan Inc. | | | 567,487,693 | | | | 491,490,000 | |

| | | | | | | | | |

| PRODUCER MANUFACTURING SECTOR — 14.7% | | | | | | | | |

| | | | Industrial Conglomerates — 11.1% | | | | | | | | |

| | 1,170,000 | | 3M Co. | | | 70,461,545 | | | | 192,991,500 | |

| | 3,247,000 | | Berkshire Hathaway Inc. - Cl B* | | | 230,453,891 | | | | 468,607,040 | |

| | 3,825,000 | | Honeywell International Inc. | | | 365,316,852 | | | | 398,985,750 | |

| | | | | | | 666,232,288 | | | | 1,060,584,290 | |

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2015 (Unaudited)

| Shares or Principal Amount | | Cost | | | Value | |

| | | | | | | |

| COMMON STOCKS — 90.7% (a) (Continued) | | | | | | |

| | | | | | | |

| PRODUCER MANUFACTURING SECTOR — 14.7% (Continued) | | | | | | |

| | | Trucks/Construction/Farm Machinery — 3.6% | | | | | | |

| | 5,423,000 | | PACCAR Inc. | | $ | 262,138,300 | | | $ | 342,408,220 | |

| | | | | | | | | |

| RETAIL TRADE SECTOR — 3.7% | | | | | | | | |

| | | | Apparel/Footwear Retail — 3.7% | | | | | | | | |

| | 3,325,000 | | Ross Stores Inc. | | | 225,587,760 | | | | 350,322,000 | |

| | | | | | | | | |

| TECHNOLOGY SERVICES SECTOR — 8.9% | | | | | | | | |

| | | | Information Technology Services — 5.8% | | | | | | | | |

| | 5,896,000 | | Accenture PLC | | | 309,670,741 | | | | 552,396,240 | |

| | | | | | | | | | | | |

| | | | Packaged Software — 3.1% | | | | | | | | |

| | 7,225,000 | | Microsoft Corp. | | | 214,465,703 | | | | 293,732,375 | |

| | | | | | | | | |

| TRANSPORTATION SECTOR — 3.0% | | | | | | | | |

| | | | Air Freight/Couriers — 3.0% | | | | | | | | |

| | 5,875,000 | | Expeditors International of Washington Inc. | | | 221,101,865 | | | | 283,057,500 | |

| | | | Total common stocks | | | 6,275,716,532 | | | | 8,665,712,151 | |

| | | | | | | | | | | | |

| SHORT-TERM INVESTMENTS — 8.2% (a) | | | | | | | | |

| | | | Commercial Paper — 8.2% | | | | | | | | |

| $ | 778,800,000 | | U.S. Bank N.A., 0.02%, due 04/01/15 | | | 778,800,000 | | | | 778,800,000 | |

| | | | Total investments — 98.9% | | $ | 7,054,516,532 | | | | 9,444,512,151 | |

| | | | Other assets, less liabilities — 1.1% (a) | | | | | | | 105,016,147 | |

| | | | TOTAL NET ASSETS — 100.0% | | | | | | $ | 9,549,528,298 | |

| * | | Non-income producing security. |

| (a) | | Percentages for the various classifications relate to net assets. |

PLC – Public Limited Company

SP-ADR – Sponsored American Depositary Receipt

The accompanying notes to financial statements are an integral part of this schedule.

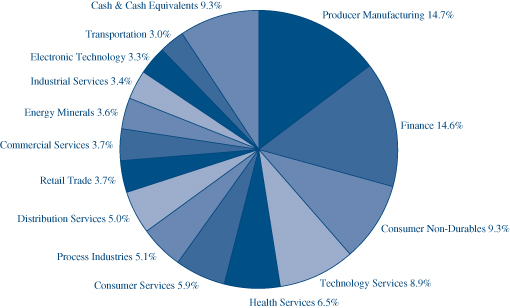

INDUSTRY SECTORS

as of March 31, 2015 (Unaudited)

FMI

Common Stock

Fund

March 31, 2015

Dear Fellow Shareholders:

The FMI Common Stock Fund returned 2.36% in the March quarter compared to the benchmark Russell 2000 Index gain of 4.32%. Sectors that helped this quarter included Commercial Services, Technology Services and Consumer Durables, while Distribution Services, Process Industries and Health Technology detracted from performance compared to the Russell 2000. Stocks that performed well in the period included Genpact, Broadridge Financial and Graham Holdings. These gains were balanced by negative results from Anixter, SQM and Lindsay. Cash was also a significant drag in the quarter. Portfolio activity was relatively subdued in the March quarter. After performing exceptionally well and reaching a full valuation, Cintas was sold. Hanger, a disappointing investment, was also eliminated.

Aside from a few bumps near the end of the quarter, the six-year bull market remained intact through March. It is difficult to reconcile the trajectory or the level of stock, bond, real estate and most other financial assets over most of the past several years given the fundamentals. It might be tempting to just sit back and enjoy the ride, but having a strong conviction that there is an artificiality to the great success these markets have enjoyed keeps us from joining in the fun. Despite a torrent of fiscal stimulus resulting in a staggering debt load of $18 trillion and enormously accommodative monetary policies, the U.S. economy continues to perform in subpar fashion. U.S. real gross domestic product (GDP) growth over the past five years has averaged 2.3%, less than half the normal rate. Many other developed countries are in the same predicament. International Monetary Fund (IMF) estimates of global GDP growth have recently been cut again, from 3.8% to 3.5%. U.S. industrial production, durable goods spending, and business formations have all recently weakened. Housing starts and existing sales have been up and down, but far below what most predicted for five years after a recession. First quarter retail sales look like they will be down at least 2%. The unemployment rate has improved, but that is modest solace considering the near record-low labor participation rate of 62.8%. While this figure might have some downward influence from baby boomers retiring early with no desire to reenter the workforce, millions have become discouraged and have simply stopped looking for work, and are thus no longer counted as unemployed. Labor’s share of profits is low relative to history and real incomes have been stagnant for over a decade, unless you are in the small slice at the top. Corporate sales and earnings growth rates have declined sharply in recent months (likely to be down in the first quarter), partly due to weak oil prices and the strong dollar, but also affected by a lack of organic fixed business investment, research and development, and people. Corporate executives have become slaves to Wall Street, buying back stock at record-high levels and worshipping at the mergers and acquisitions altar. Government leaders and central bank bureaucrats continue to push the same policies regardless of the outcomes and despite the alarming increase in long-term liabilities and distortions to healthy and sustainable economic activity.

It may be hard to imagine, but since the financial crisis, which was partially due to an excessive credit expansion, the world has added even more debt than it did in the run-up to the peak (2000-2007). Quoting from a McKinsey report:

Seven years after the bursting of a global credit bubble resulted in the worst financial crisis since the Great Depression, debt continues to grow. In fact, rather than reducing indebtedness, or deleveraging, all major economies today have higher levels of borrowing relative to GDP than they did in 2007. Global debt in these years has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points. That poses new risks to financial stability and may undermine global economic growth.1

Most investors continue to put their money and faith with Fed Chairwoman Yellen’s interest rate oracles, but it is clear, at least to us, that she and most of the Fed governors are perplexed by the spotty labor markets and the underlying health of the economy. It comes as no surprise that pumping up asset values in an attempt to induce a wealth effect-driven economic expansion has, and will continue to fail on many levels. While it is logical to expect small wealth effect spending by a few

| 1 | Richard Dobbs, Susan Lund, Jonathan Woetzel, and Mina Mutafchieva. “Debt and (not much) deleveraging.” McKinsey Global Institute Report, February 2015. |

middle and upper-middle income folks who happen to own modest financial asset portfolios that rise substantially, the fact is, the vast majority of financial assets are owned by the top 10% of the population. If we were to double Warren Buffett’s wealth, how much more would he consume? Probably very little, and thus the impact on the economy would be negligible. An unnaturally low interest rate policy favors speculators, deal-makers and financial engineers. Only a vibrant economy with organic growth opportunities will induce true risk-takers to invest in people and capital.

The six-year bull market, combined with tepid fundamentals, has made stocks remarkably expensive from a historical perspective. The median or “typical” stock is higher than we have ever seen, and even more expensive than during the peak of the technology and telecom craze in 1999. Today there are over seventy start-ups with valuations over a billion dollars compared to less than half of that, inflation adjusted, in the 1999-2000 period. Pharmaceutical companies are brawling with each other to pay 5-10 times multi-year-out hoped-for revenue for phase III or recently approved compounds. Unnaturally-low interest rates foster this behavior. Bond valuations have reached epic levels nearly everywhere with ground-hugging rates here in the U.S., and even negative rates in some countries. A number of real estate sectors, particularly those catering to the wealthy, appear highly inflated, reminiscent of ten years ago.2 Real estate investment trusts (REITs) are as pricey as we can ever recall. Strangely, the sheer length of this asset inflation cycle has people feeling emboldened to take more risk rather than trimming their sails. In his book, Inefficient Markets, An Introduction to Behavioral Finance, Andrei Shleifer said, “Investor sentiment reflects the common judgment errors made by a substantial number of investors, rather than uncorrelated random mistakes.”

A tremendous surge of funds moving toward passive index strategies has created an environment where the flows themselves are driving performance. According to Morningstar, in 2014 U.S. active equity funds experienced $98.4 billion of outflows, while passive funds received $166.6 billion of inflows. This self-reinforcing cycle is not uncommon in the latter stages of bull markets. Investors and investment committees continue to capitulate on active management, throwing in the proverbial towel and going passive when they should be de-risking to cash or moving to more conservative active management. Index funds have taken on somewhat of a life of their own, divorced from underlying fundamentals. Last year, just 25 companies, or 1.25% of the Russell 2000 constituents, accounted for approximately 75% of the total return. Eventually, negative developments affect the top-heavy indices, and as long as there is still an active investment community reacting to this, it sets the process in reverse, with the weightiest components falling the hardest as monies flow out, disproportionately hurting index products, which inures to the benefit of the more conservative active managers. The caveat is that these cycles can sometimes be excruciatingly long, as evidenced by the current one. An added feature to the complexion of the market is that unlike in 1999, when performance was also quite concentrated, today’s market, even outside the weightiest names, is still expensive.

In the small- and mid-cap area of the market, the top-heavy sectors include REITs (investors chasing yield) and healthcare (strong biotech and mergers & acquisitions influence). Using just healthcare to illustrate, the chart on the following page shows performance of the small- and mid-cap S&P indices, the Russell 2000 and the small- and mid-cap S&P healthcare subsector results since the bottom of the 2009 market. The small- and mid-cap healthcare indices were up 436% and 425%, respectively, over this period, vastly outperforming the general benchmarks, which were also astounding. In the wake of this blitzkrieg, valuations are approaching levels we don’t even know how to describe. Eventually, logic and a sense for history suggests this movie is likely to play in reverse, which should be a big boost to our relative performance.

| 2 | Erin Carlyle. “America’s Most Expensive Home Sales of 2014.” Forbes, December 24, 2014. |

Finally, for those who think prices and markets rarely change quickly, look at oil prices over the second half of 2014. Oil dropped from roughly $100 per barrel in June to approximately $50 in December. A year ago, the overwhelming consensus was that oil was hard to find and prices would grind higher, with many experts calling for $200 oil within a few years. Today the sentiment has completely flipped, with many of the former bulls saying it may be many years before we see $100 again.

As always, the research team continues working hard to try to find potentially good ideas that we feel have less downside risk than the typical stock. Below we highlight two of these ideas.

ManpowerGroup Inc. (MAN)

(Analyst: Rob Helf)

Description

ManpowerGroup (Manpower) is the world’s third largest provider of workforce solutions and temporary staffing services. The company places over 3 million workers in temporary, contract, and permanent positions at more than 400,000 employers annually. It is also the largest provider of career transition services (Right Management) and provides valuable employee training.

Good Business

| | • | Manpower is one of the leading staffing companies in the world and can deliver its workforce solutions in over 80 countries. |

| | • | The company benefits from the secular trend of temporary staffing. Demand for temp staffing is growing as companies face a shortage of talent, but also require flexibility to manage costs. |

| | • | The company’s margins should increase due to its greater mix of higher-value services. |

| | • | The industry is relatively fragmented, which should allow Manpower to take share from competitors that cannot compete with its scale, technology and recruiting resources. |

| | • | The company has generated a return on invested capital (ROIC) of 11% over the past decade, comfortably exceeding its cost of capital. |

| | • | If the company were to achieve margins closer to its largest international competitors, earnings per share (EPS) could be $8.00-9.00, or 60% higher than the current EPS run rate. |

| | • | The company’s balance sheet is in excellent shape with cash in excess of debt. The business model generates a good deal of free cash, and management has been a good steward of capital. |

Valuation

| | • | Manpower trades at approximately 16.5 times forward EPS, 9.0 times earnings before interest and taxes (EBIT) and 0.30 times enterprise value-to-sales (EV/Sales). |

| | • | The company’s price-to-earnings (P/E) multiple is about in line with the company’s 5- and 10-year historical averages. On a 10-year basis, Manpower has traded in a range of 0.20-0.35 times EV/Sales. With most stocks trading at least one standard deviation above their long-term historical mean, the company is a relative value. |

| | • | The company’s earnings before interest, taxes and amortization (EBITA) goal equates to EPS power of $6.50-7.00, implying an 11 times multiple. If the company were to achieve margins in line with European competitors, EPS power would be over $8.00. |

Management

| | • | Jonas Prising was named Manpower’s fourth CEO last May. Previously, he was President and head of the Americas and Southern Europe Region. He has been with the company since 1999 and strikes us as a very capable hands-on leader. |

| | • | Darryl Green is COO. He previously held the role of President and EVP of the Asia region. |

| | • | Mike Van Handel is CFO. He joined the company in 1989 and has been a solid financial leader for over two decades. |

| | • | Management compensation is based on economic profit, EPS and operating margin. |

Investment Thesis

We initiated a position in Manpower late last fall as macro worries about the European economy and cautious company comments resulted in significant share underperformance. Europe is a significant contributor to the company’s revenues and income, and this aspect will always be closely monitored. The initial position proved timely as the shares rebounded smartly. While Europe is still a mess, it’s clear that on the margin, employers are favoring temporary workers over permanent employees. Longer-term, a global economic recovery and positive secular prospects for staffing, combined with a reasonable valuation, make Manpower an attractive position.

MSC Industrial Direct Co. Inc. (MSM)

(Analyst: Matt Sullivan)

Description

MSC Industrial Direct is one of the largest direct marketers and distributors of metalworking and maintenance, repair and operations (MRO) supplies to customers throughout North America. MSC operates through a network of twelve customer fulfillment centers and 103 branch offices. The company employs one of the industry’s largest sales forces and distributes approximately 850,000 industrial products from approximately 3,000 suppliers to around 364,000 customers across every U.S. state, Puerto Rico, and Canada.

Good Business

| | • | Almost every industrial, manufacturing and service business has an ongoing need for MRO supplies. |

| | • | Over the past five and ten years, MSC has earned an average ROIC of 20%, which exceeds the company’s cost of capital. |

| | • | MSC earns above-average margins for a distributor by providing an integrated, low-cost solution to the purchasing, management and administration of customers’ MRO needs. The company has scale advantages over smaller competitors, which allows them to provide superior services. |

| | • | The company has a diverse set of customers and suppliers. No customer or supplier accounted for more than 6% of sales in 2014. |

| | • | MSC is modestly levered with a debt-to-capital ratio of approximately 28%. |

| | • | MSC is a high free cash flow business, as it doesn’t require a large amount of capital expenditures. |

Valuation

| | • | MSC’s 2015 estimated P/E ratio is 18.1 times, which is approximately one standard deviation below the company’s 5-year average of 20 times. |

| | • | MSC is trading at an EV/Sales ratio of 1.75 times, which compares favorably to its 5- and 10-year average EV/Sales ratios of 2.1 times and 2.0 times, respectively. |

| | • | MSC has underperformed broader market indices such as the S&P 500 and the Russell 2000 by a significant amount over the past one and two years. The company trades at a discount to the Russell 2000 despite having superior growth and return characteristics. |

Management

| | • | MSC has an impressive ROIC track record, indicating that management has allocated capital efficiently over time. |

| | • | Sid Jacobson founded the company in 1941, and his family owns just under 30% of the company. The Jacobson family controls voting power via dual class shares. |

| | • | Erik Gershwind, grandson of Sid Jacobson, assumed the CEO position starting in 2013. He has been on the board since 2010. Gershwind has been with the company since 1996. Prior to being named CEO, Gershwind was the Chief Operating Officer from 2009-2013. |

| | • | Mitchell Jacobson has been Chairman of the Board since 1998. He was also CEO from 1995-2005. At the beginning of 2013, his position was changed from Executive Chairman to non-executive Chairman. |

Investment Thesis

MSC is a durable, high-quality franchise that is trading at a reasonable valuation. While growth has slowed recently across the industrial distribution industry, we believe that the longer-term sales growth opportunity for MSC remains attractive. The company also has the ability to expand its operating margin as it continues to grow sales, and leverage recent fixed capital investments. This combination should lead to above-average long-term earnings growth. With the prospect for modest multiple expansion, the stock appears to be an attractive investment opportunity.

Thank you for your support of the FMI Common Stock Fund.

100 E. Wisconsin Ave., Suite 2200 • Milwaukee, WI 53202 • 414-226-4555

www.fmifunds.com

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS

March 31, 2015 (Unaudited)

| Shares | | | | Cost | | | Value | |

| | | | | | | |

| COMMON STOCKS — 86.7% (a) | | | | | | |

| | | | | | | |

| COMMERCIAL SERVICES SECTOR — 17.8% | | | | | | |

| | | Advertising/Marketing Services — 3.6% | | | | | | |

| | 2,290,000 | | Interpublic Group of Cos. Inc. | | $ | 40,919,310 | | | $ | 50,654,800 | |

| | | | | | | | | | | | |

| | | | Financial Publishing/Services — 1.4% | | | | | | | | |

| | 159,000 | | Dun & Bradstreet Corp. | | | 10,558,429 | | | | 20,409,240 | |

| | | | | | | | | | | | |

| | | | Miscellaneous Commercial Services — 8.9% | | | | | | | | |

| | 2,952,000 | | Genpact Ltd.* | | | 50,388,712 | | | | 68,634,000 | |

| | 28,000 | | Graham Holdings Co. | | | 19,941,991 | | | | 29,389,640 | |

| | 1,970,000 | | RPX Corp.* | | | 32,092,859 | | | | 28,348,300 | |

| | | | | | | 102,423,562 | | | | 126,371,940 | |

| | | | Personnel Services — 3.9% | | | | | | | | |

| | 375,000 | | ManpowerGroup Inc. | | | 25,857,829 | | | | 32,306,250 | |

| | 375,000 | | Robert Half International Inc. | | | 9,805,701 | | | | 22,695,000 | |

| | | | | | | 35,663,530 | | | | 55,001,250 | |

| | | | | | | | | |

| CONSUMER DURABLES SECTOR — 3.2% | | | | | | | | |

| | | | Homebuilding — 2.2% | | | | | | | | |

| | 23,000 | | NVR Inc.* | | | 23,099,075 | | | | 30,559,180 | |

| | | | | | | | | | | | |

| | | | Recreational Products — 1.0% | | | | | | | | |

| | 295,000 | | Sturm, Ruger & Co. Inc. | | | 14,748,562 | | | | 14,640,850 | |

| | | | | | | | | |

| CONSUMER SERVICES SECTOR — 1.6% | | | | | | | | |

| | | | Other Consumer Services — 1.6% | | | | | | | | |

| | 195,000 | | UniFirst Corp. | | | 20,554,264 | | | | 22,949,550 | |

| | | | | | | | | |

| DISTRIBUTION SERVICES SECTOR — 13.0% | | | | | | | | |

| | | | Electronics Distributors — 7.5% | | | | | | | | |

| | 522,000 | | Anixter International Inc.* | | | 34,784,281 | | | | 39,739,860 | |

| | 611,000 | | Arrow Electronics Inc.* | | | 8,448,216 | | | | 37,362,650 | |

| | 742,000 | | ScanSource Inc.* | | | 18,446,489 | | | | 30,162,300 | |

| | | | | | | 61,678,986 | | | | 107,264,810 | |

| | | | Medical Distributors — 3.4% | | | | | | | | |

| | 999,000 | | Patterson Cos. Inc. | | | 21,489,097 | | | | 48,741,210 | |

| | | | | | | | | | | | |

| | | | Wholesale Distributors — 2.1% | | | | | | | | |

| | 422,000 | | MSC Industrial Direct Co. Inc. | | | 33,825,314 | | | | 30,468,400 | |

| | | | | | | | | |

| ELECTRONIC TECHNOLOGY SECTOR — 3.7% | | | | | | | | |

| | | | Aerospace & Defense — 1.8% | | | | | | | | |

| | 836,400 | | FLIR Systems Inc. | | | 25,359,714 | | | | 26,162,592 | |

| | | | | | | | | | | | |

| | | | Electronic Production Equipment — 1.9% | | | | | | | | |

| | 778,000 | | MKS Instruments Inc. | | | 20,990,133 | | | | 26,304,180 | |

| | | | | | | | | |

| ENERGY MINERALS SECTOR — 1.7% | | | | | | | | |

| | | | Oil & Gas Production — 1.7% | | | | | | | | |

| | 209,000 | | Cimarex Energy Co. | | | 11,099,281 | | | | 24,053,810 | |

| | | | | | | | | |

| FINANCE SECTOR — 10.4% | | | | | | | | |

| | | | Finance/Rental/Leasing — 2.1% | | | | | | | | |

| | 312,000 | | Ryder System Inc. | | | 12,982,106 | | | | 29,605,680 | |

| | | | | | | | | | | | |

| | | | Property/Casualty Insurance — 4.3% | | | | | | | | |

| | 719,000 | | Greenlight Capital Re Ltd.* | | | 17,658,369 | | | | 22,864,200 | |

| | 765,000 | | W.R. Berkley Corp. | | | 18,953,509 | | | | 38,640,150 | |

| | | | | | | 36,611,878 | | | | 61,504,350 | |

| | | | Regional Banks — 4.0% | | | | | | | | |

| | 551,000 | | Cullen/Frost Bankers Inc. | | | 31,916,228 | | | | 38,063,080 | |

| | 695,000 | | Zions Bancorporation | | | 16,588,315 | | | | 18,765,000 | |

| | | | | | | 48,504,543 | | | | 56,828,080 | |

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2015 (Unaudited)

| Shares or Principal Amount | | Cost | | | Value | |

| | | | | | | |

| COMMON STOCKS — 86.7% (a) (Continued) | | | | | | |

| | | | | | | |

| HEALTH SERVICES SECTOR — 1.0% | | | | | | |

| | | Health Industry Services — 1.0% | | | | | | |

| | 1,140,000 | | Allscripts Healthcare Solutions Inc.* | | $ | 14,008,183 | | | $ | 13,634,400 | |

| | | | | | | | | |

| HEALTH TECHNOLOGY SECTOR — 3.4% | | | | | | | | |

| | | | Medical Specialties — 3.4% | | | | | | | | |

| | 507,000 | | Varian Medical Systems Inc.* | | | 37,672,040 | | | | 47,703,630 | |

| | | | | | | | | |

| PROCESS INDUSTRIES SECTOR — 12.5% | | | | | | | | |

| | | | Chemicals: Agricultural — 2.0% | | | | | | | | |

| | 1,551,000 | | Sociedad Quimica y Minera de Chile S.A. - SP-ADR | | | 45,414,934 | | | | 28,305,750 | |

| | | | | | | | | | | | |

| | | | Chemicals: Specialty — 2.3% | | | | | | | | |

| | 350,000 | | Compass Minerals International Inc. | | | 25,351,902 | | | | 32,623,500 | |

| | | | | | | | | | | | |

| | | | Containers/Packaging — 3.1% | | | | | | | | |

| | 838,000 | | Avery Dennison Corp. | | | 25,612,339 | | | | 44,338,580 | |

| | | | | | | | | | | | |

| | | | Industrial Specialties — 5.1% | | | | | | | | |

| | 594,000 | | Donaldson Co. Inc. | | | 22,315,683 | | | | 22,399,740 | |

| | 1,169,000 | | H.B. Fuller Co. | | | 43,714,899 | | | | 50,115,030 | |

| | | | | | | 66,030,582 | | | | 72,514,770 | |

| | | | | | | | | |

| PRODUCER MANUFACTURING SECTOR — 11.1% | | | | | | | | |

| | | | Building Products — 2.3% | | | | | | | | |

| | 565,000 | | Armstrong World Industries Inc.* | | | 29,890,997 | | | | 32,470,550 | |

| | | | | | | | | | | | |

| | | | Industrial Machinery — 4.3% | | | | | | | | |

| | 610,000 | | Kennametal Inc. | | | 23,404,699 | | | | 20,550,900 | |

| | 788,400 | | Woodward Inc. | | | 33,703,657 | | | | 40,216,284 | |

| | | | | | | 57,108,356 | | | | 60,767,184 | |

| | | | Miscellaneous Manufacturing — 2.7% | | | | | | | | |

| | 155,000 | | Carlisle Cos. Inc. | | | 3,201,500 | | | | 14,357,650 | |

| | 200,000 | | Valmont Industries Inc. | | | 29,746,404 | | | | 24,576,000 | |

| | | | | | | 32,947,904 | | | | 38,933,650 | |

| | | | Trucks/Construction/Farm Machinery — 1.8% | | | | | | | | |

| | 327,000 | | Lindsay Corp. | | | 26,159,321 | | | | 24,933,750 | |

| | | | | | | | |

| TECHNOLOGY SERVICES SECTOR — 6.5% | | | | | | | |

| | | | Data Processing Services — 4.8% | | | | | | | | |

| | 1,240,000 | | Broadridge Financial Solutions Inc. | | | 26,543,472 | | | | 68,212,400 | |

| | | | | | | | | | | | |

| | | | Internet Software/Services — 1.7% | | | | | | | | |

| | 890,000 | | Progress Software Corp.* | | | 19,784,358 | | | | 24,181,300 | |

| | | | | | | | |

| TRANSPORTATION SECTOR — 0.8% | | | | | | | |

| | | | Marine Shipping — 0.8% | | | | | | | | |

| | 156,000 | | Kirby Corp.* | | | 4,789,332 | | | | 11,707,800 | |

| | | | Total common stocks | | | 931,821,504 | | | | 1,231,847,186 | |

| | | | | | | | | | | | |

| SHORT-TERM INVESTMENTS — 13.3% (a) | | | | | | | |

| | | | Commercial Paper — 13.3% | | | | | | | | |

| $ | 189,600,000 | | U.S. Bank N.A., 0.02%, due 04/01/15 | | | 189,600,000 | | | | 189,600,000 | |

| | | | Total investments — 100.0% | | $ | 1,121,421,504 | | | | 1,421,447,186 | |

| | | | Liabilities, less other assets — (0.0%) (a) | | | | | | | (556,386 | ) |

| | | | TOTAL NET ASSETS — 100.0% | | | | | | $ | 1,420,890,800 | |

| * | | Non-income producing security. |

| (a) | | Percentages for the various classifications relate to net assets. |

SP-ADR – Sponsored American Depositary Receipt

The accompanying notes to financial statements are an integral part of this schedule.

FMI Common Stock Fund

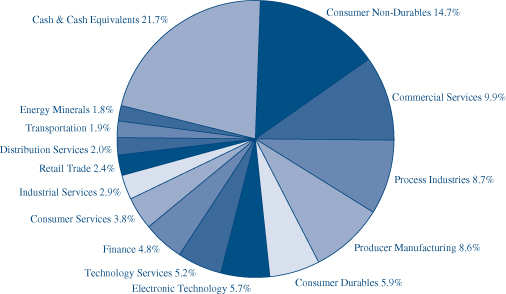

INDUSTRY SECTORS

as of March 31, 2015 (Unaudited)

FMI

International

Fund

March 31, 2015

Dear Fellow Shareholders:

Global equity markets roared out of the gates in the first quarter of 2015, led by big gains in Germany (+22.03%), France (+18.04%), the UK (+4.77%) and Japan (+10.41%).1 Unprecedented money printing efforts by global central banks pushed asset prices to new heights, with stock and bond valuations becoming more bloated by the day. The growing disconnect between asset valuations and fundamentals continues to widen at an alarming pace, as economic reality is being masked by free money and market manipulation. These circumstances are less than ideal for contrarian value investors such as ourselves who focus on bottom-up security analysis and downside protection — that is, at least until some fear returns. In this context, the FMI International Fund (FMIJX) rose by 7.94% in the quarter, when compared with an MSCI EAFE Index gain of 10.85% in local currency and 4.88% in U.S. Dollars (USD). The Consumer Non-Durables, Consumer Durables, and Commercial Services sectors aided the Fund’s relative performance, while Process Industries, Producer Manufacturing and Industrial Services all detracted. Top performing stocks included Amorepacific Corp., Pirelli, and LG Household & Health Care, while Sociedad Quimica y Minera de Chile, Potash Corp. and Schlumberger lagged the market. A higher-than-normal cash position weighed on relative performance, while currency hedging provided a boost.

In looking back over the last six years, we are simply amazed at the growing level of complacency among market participants. If someone had told us in March of 2009 that over the next six years the U.S. would have the worst economic “recovery” on record, Europe would go nowhere and fail to address the root causes of a sovereign debt crisis, Japan would have four separate recessions, China’s growth would slow dramatically and a potential real estate and/or credit bubble would form, Russia would seize Crimea from Ukraine and its economy would slow dramatically, Brazil’s growth would contract (in 2015), unrest in the Middle East would be on the rise, and printing money (which has never worked) would be the only game in town, we would have been shocked to learn that stock markets would go on a historic bull run. U.S. and German stock markets have nearly tripled (greater than 19% compound annual growth rate, or CAGR), while the UK, France and Japan are all up more than 2.25 times (greater than 14% CAGR).1 For those who might think we are cherry-picking the bottom in 2009, the three-year stock market performance is equally stunning while facing a similar macro backdrop, with Japan’s stock market +91.61% (approximately 24% CAGR), Germany +72.25% (about 20%), France +63.99% (around 18%), the U.S. +56.46% (approximately 16%), and the UK +36.72% (about 11%).1 It’s a remarkable run when you consider how weak both the economic and business fundamentals have been. While many of our contemporaries are “drinking the Kool-Aid,” we remain highly skeptical and will continue to proceed with heightened caution.

Europe: Greater Fool

Europe has officially joined the quantitative easing (QE) party, with the European Central Bank (ECB) announcing a €1 trillion bond-buying program (€60 million per month) through September of 2016.2 Thanks to the proliferation of the ECB [money] printing presses, the euro fell to a 12-year low versus the U.S. dollar, while some government (i.e. Germany, Holland, France, etc.) and corporate (i.e. Nestlé) bond yields turned negative, a feat that we never thought we’d see in our investing career. A negative bond yield guarantees investors a loss on their money if they hold the bond to maturity. The Financial Times reports that “More than a quarter of the entire market of European government bonds now has yields below zero – a total of $2 trillion, according to J.P. Morgan.” Include Japan, and the global total eclipsed $3.6 trillion during the quarter.3,4 While we have heard all the “justifications” for buying government bonds with negative yields — including deflation (positive real yields), currency speculation, and central bank easing (i.e. interest rate cuts or QE) — ultimately, investors are banking on a “greater fool theory,” or the “notion that any price, no matter how unrealistic, can be justified if a

| 1 | The following market indices are being referred to above: Japan TOPIX, UK FTSE All-Share, France CAC, Germany DAX, and U.S. Standard & Poor’s 500. |

| 2 | Brian Blackstone. “Europe’s Central Bank Bets Big On Stimulus.” The Wall Street Journal, March 10, 2015. |

| 3 | Elaine Moore. “QE hopes draw investors to negative yields.” Financial Times, February 26, 2015. |

| 4 | Nikolaos Panigirtzoglou, et al. “F&L Library: Negative Yields.” J.P. Morgan Markets, February 3, 2015. |

buyer believes that there is another buyer [fool] who will pay an even-higher price for the same item.”5 This inevitably leads to significant asset booms and busts. Investors are now depending on central banks, indexed/passive funds, commercial banks (negative deposit rates) or some other “greater fool” to bail them out. The last one standing will surely get burned, and our guess is that the taxpayer will be the one on the hook, one way or another.

| |

| © Unkreatives - Dreamstime.com – Euro EC | |

Meanwhile, ECB President Mario Draghi is already declaring victory, announcing an improvement in the economic outlook and inflation picture, and calling an end to the eurozone crisis. “Our monetary policy decisions have worked,” Draghi proclaimed. “It’s with some certain degree of satisfaction that the governing council has acknowledged this.” He also noted that “Until a month ago, nobody had any doubts that public debt – sovereign debt – in the euro area was actually very, very big. Now some people worry we won’t have enough bonds [for the QE bond-buying program].”6 Draghi appears to have a pretty warped sense of reality. If the current economic environment in the eurozone of anemic growth, high unemployment, fat budget deficits, and ballooning debt levels is the result of policies that have “worked,” we would be worried to see what failure looks like. Perhaps Draghi is really just trying to find a way to justify his shiny new €1.25 billion ECB headquarters in Frankfurt, Germany, which was more than €400 million over budget and reeks of waste. As the ECB has taken on new areas of “competence” and now has its hands in just about everything, the staff has expanded to nearly 2,600. The ECB spent over €430,000 per workspace (2,900), a cost equivalent to buying each employee a brand new home. Nearly 7,000 protestors showed up at the inaugural opening, with one cynical banner reading, “Free caviar for everyone.”7,8 Touché. If the ECB can’t stay within budget, how are they going to get eurozone countries to do so?

| |

| Source: Bloomberg | |

The short answer is they are not. The currency union’s “rules” for budget deficits are laughable, as they are constantly disregarded by member countries with minimal repercussions. France, for example, which is the eurozone’s second largest economy, has broken the rules in 11 out of the last 16 years and is expected to continue to do so for the next three years. In addition, exceptionally low financing conditions may exacerbate the problem, lessening the motivation for countries like France to enact necessary reforms to make their economies more competitive.9 The Wall Street Journal writes that, “Since 1978, French [quarter over quarter] economic growth has clocked in at an average rate of 0.45%” and, “unemployment hasn’t fallen below 7% in over 30 years.”10 Clearly the challenges France faces are deep and structural in nature. No matter how big the money printing campaign, or negative the interest rates, there is no quick fix to make these underlying problems just go away.

Lastly, lost in Draghi’s victory dance is that nagging little Greece “issue.” In late January, radical left-wing Syriza party leader Alexis Tsipras was elected as Greece’s Prime Minister, on an anti-austerity platform calling for a restructuring of the country’s debt. After much wrangling with what was formerly known as the Troika (ECB, European Commission, International Monetary Fund), in February Eurozone finance ministers agreed to kick the can down the road and extend

| 5 | http://www.businessdictionary.com/definition/greater-fool-theory.html |

| 6 | Jack Ewing. “Mario Draghi of E.C.B. Predicts an Improved Economy When Stimulus Program Begins Monday.” The New York Times, March 5, 2015. |

| 7 | John O’Donnell and Frank Siebelt. “Protesters, police clash near new European bank HQ in Frankfurt.” Reuters, March 18, 2015. |

| 8 | A.B. Sanderson. “ECB Overspends By €400 Million On Luxury Offices As It Preaches Austerity.” Breitbart, February 25, 2015. |

| 9 | Stefan Wagstyl and Duncan Robinson. “Eurozone hawks voice fears over dangers of QE.” Financial Times, March 13, 2015. |

| 10 | Bret Stephens. “Packing Time for France’s Jews.” The Wall Street Journal, January 19, 2015. |

Greece’s €240 billion bailout until the end of June, with contentious negotiations ongoing as Greece is forced to come up with a credible reform agenda. In the meantime, the Greek economy is slowing, tax revenues are falling short of expectations, and cash is being pulled out of the banking system. While many investors seem to have already erased the European debt crisis from recent memory, we caution our readers that history has a habit of repeating itself. Near-term pain in Greece appears inevitable and once again may be difficult to contain (i.e. contagion), with an outright default, debt restructuring, or exit of the eurozone (“Grexit”) appearing to be an increasingly likely outcome.

Japan: The Abe Put?

In a world of experimental money printing, ultra-low interest rates, and inflated asset prices, Japan may be the worst of all offenders. The “Abenomics” QE program, which is nearly three times the size (as a percentage of gross domestic product, or GDP) of the United States’ unprecedented bond-buying program of 2013, is meant to drive economic growth and boost inflation. In the process, the yen has fallen off a cliff while bond prices have reached extreme levels (including negative yields). Passing under the radar, however, has been the Bank of Japan’s (BOJ) increased efforts to also directly pump up domestic equity prices, mainly in the form of buying exchange-traded funds (ETFs). The Wall Street Journal reports that the BOJ is targeting an annual goal of ¥3 trillion ($25 billion) in ETF purchases, three times the size of previous levels. The report explains that in the last two years the BOJ has been entering the stock market, on average, every three days, and mostly when sentiment has been weak (76% of the days the market opened down). The BOJ estimates that it will have a book value of ¥6.8 trillion by year-end, or approximately 1.2% of the total market cap of the Tokyo Stock Exchange, which is valued at about ¥550 trillion.11 Furthermore, the Government Pension Investment Fund, which manages ¥127.3 trillion, is more than doubling their domestic equity exposure from 12% to 25%, which equates to ¥31.8 trillion, or 5.8% of the total market.12 With the government implicitly backing approximately 7% of all domestic equity assets, it’s not hard to see (at least in part) why Japan’s stock market performance has been so remarkably robust.

When looking at the fundamentals in Japan, it’s hard to get excited. Economic growth is subpar, with the Organisation for Economic Co-operation and Development (OECD) forecasting just 0.75% GDP growth in 2015, and 1% in 2016. While a weakening yen may optically imply some improvement, it’s more of an illusion than a reality. For example, The Wall Street Journal writes that “Japanese households earn 7.5% less in inflation-adjusted terms now than before the 2008 financial panic, and about half of that decline has come during Tokyo’s ‘quantitative easing’ program.”13 Not surprisingly, household spending remains weak, having fallen on a real basis for ten straight months, and eleven out of the last twelve. Additionally, while headline export numbers in yen terms might suggest a strong rebound off the bottom, after adjusting for the exchange rate, volumes remain more than 30% below the peak levels of late 2007 and early 2008. Ultimately exporters are not benefiting as much as expected with the move in the yen, as they are padding their profits in lieu of lowering prices to take market share. With valuations elevated due to the run-up of the stock market, investment opportunities in Japan remain limited.

China: Near-Term Risks Remain

China’s growth continues to slow rapidly. At 7.4% in 2014, it was China’s slowest GDP growth in 24 years, down from 7.7% in 2012 and 2013, and an average of more than 10% from 1980-2010.14 Premier Li Keqiang announced a 2015 growth target of “around 7%,” but acknowledged that “with downward pressure on China’s economy building and deep-seated problems in development surfacing, the difficulties we will encounter in the year ahead may be even more formidable than those of last year.”15 The International Monetary Fund (IMF) downgraded China’s GDP growth forecast to 6.8% in 2015 (and 6.3% in 2016), largely a result of the slowdown in property and investment.14 As expressed in prior letters, we believe the true underlying growth is materially lower than the official government figures, and would not be surprised to see China’s near-term growth rate slow significantly from here.

China is in the midst of an extraordinary debt binge, with total debt virtually quadrupling in the last seven years, from approximately $7 trillion in 2007 to about $28 trillion in 2014, or a CAGR of around 22%.16 However, approximately $21 trillion of newly-minted debt has only generated about $6 trillion in GDP growth. Subsequently, total debt as a percentage of

| 11 | Takashi Nakamichi and Tatsuo Ito. “Tokyo Stocks’ Rally Worries Central Bankers.” The Wall Street Journal, March 12, 2015. |

| 12 | Anna Kitanaka, Shigeki Nozawa, and Yoshiaki Nohara. “Japan’s Pension Fund Cutting Local Bonds to Buy Equities.” Bloomberg, October 31, 2014. |

| 13 | “Japan Devaluation Warning For Europe.” The Wall Street Journal, March 17, 2015. |

| 14 | Jamil Anderlini. “China expands at weakest rate in 24 years.” Financial Times, January 20, 2015. |

| 15 | Jamil Anderlini, Tom Mitchell and Gabriel Wildau. “Premier admits to flaws in Chinese Model.” Financial Times, March 5, 2015. |

| 16 | Jamil Anderlini and Tom Mitchell. “Beijing pledges readiness to bolster sagging growth as slowdown continues.” Financial Times, March 15, 2015. |

GDP has risen from 167% in 2008 to 247% in 2014, according to Morgan Stanley; each incremental dollar of debt is driving less and less GDP growth.17 To illustrate the challenge at hand, The Wall Street Journal reports that “As much as 50% of China’s local government borrowing services existing debt, requiring more borrowing to produce growth.” In 2005 it required less than 1.5 units of debt to produce one unit of economic growth, and by 2013 more than 4 units of debt were required for the same result.18 Unfortunately, China’s debt-fueled growth, which is reliant on fixed investment, is not sustainable. Despite China’s recent interest rate cuts and additional actions to spur increased bank lending, the underlying flaws in the economic model continue to muddy the near-term outlook. While China’s long-term prospects are promising, the near-term risks warrant added prudence.

Listed below are descriptions of two current FMIJX holdings. Makita (6586 JT) was a recent addition to the portfolio, and provides the Fund with exposure to a rebounding global construction market through a high-quality power tools business at a discount valuation. We have owned Rolls-Royce (RR/ LN) in the Fund since inception, and while the investment has not gone as we had hoped in recent times, with a clean sheet of paper we believe the long-term thesis remains intact. While we still anticipate a bumpy ride in the near-term as margins and cash compress with the launch of new civil aerospace programs, end-markets (defense, marine and energy), remain pressured and the cost base is reset, the long-term margin and secular growth opportunity is an attractive one. Rolls-Royce is an above-average business with significant barriers to entry, trading at a below-average valuation — a favorable value proposition.

Makita Corp. (6586 JT)

(Analyst: Matthew Goetzinger)

Description

Makita is the second largest global manufacturer of power tools. The Power Tools group is the company’s dominant business at 70% of revenues. Garden Equipment, Household and Other Products accounts for 15% of total revenues, and includes chain saws, petrol brush cutters, hedge trimmers, industrial vacuum cleaners, and handheld vacuum cleaners for home use. Recurring Parts, Repair and Accessories revenues account for the residual 15% of company revenues.

Good Business

| | • | The global power tool market is highly concentrated, with the top four major companies controlling approximately two-thirds of the market. Positively, the market functions as a rationally competitive oligopoly. |

| | • | Makita is the industry’s low-cost producer. Tool manufacturing is an assembly business. |

| | • | Approximately 55% of company sales are made into the replacement market. Tool price points are modest. |

| | • | The company’s 5-year average cash adjusted return on invested capital (ROIC) exceeds 12%. |

| | • | Makita’s balance sheet is pristine, with net cash of ¥169 billion (¥1,244 per share). |

| | • | The company controls its own destiny. |

Valuation

| | • | Relative to forecasted Fiscal Year 2015 estimated revenues, Makita trades at an enterprise value-to-sales (EV/S) multiple of 1.4 times. This compares to the company’s 10-year average EV/S multiple of 1.46 times. Given the company’s mid-teens EBIT margins (earnings before interest and taxes), Makita should trade closer to 2 times revenues. |

| | • | Over the past five years, Makita has held a fairly pedestrian median forward price-to-earnings ratio (P/E) of 16.1 times. On a cash-adjusted basis, the company’s current multiple is 12 times. Peers trade at an average of 18 times earnings. |

| | • | In early 2013, Bain acquired Apex Tools for $1.6 billion — or 8.6 times earnings before interest, taxes, depreciation and amortization, or EBITDA (12.5% EBITDA margin). At 7.3 times EBITDA, Makita trades at a discount to the private market value ascribed to a smaller and less profitable tools company. |

| | • | Down-side margin of safety is provided by a cash rich balance sheet, as well as the company’s historical ability to preserve profitability in tough environments. Note that Fiscal Year 2010 margins troughed at 12.4%. |

| 17 | “China Deleveraging – The Long, Bumpy Ride Continues.” Morgan Stanley, March 10, 2015. |

| 18 | Lingling Wei and Bob Davis. “Debt that once boosted its cities now burdens China.” The Wall Street Journal, January 28, 2015. |

Management

| | • | Makita has a long-tenured management team that has seen little turnover. |

| | • | The company is led by Chairman Masahiko Goto. Goto has led the company since May 1989, and owns 1.9 million shares, or 1.4% of the shares outstanding. |

| | • | In addition to a fair and transparent governance structure, Makita’s capital allocation practices are aligned with shareholders. The company targets a 30% payout ratio, opportunistically buys back stock, and targets organic growth. |

Investment Thesis

As the industry’s low cost producer, Makita maintains a market leadership position within the consolidated global power tools market. A strong track record of innovation, and the resulting brand equity established with the company’s core professional user, has resulted in a durable and highly profitable business model. Current macroeconomic and foreign exchange concerns have unduly pressured Makita’s valuation relative to the long-term prospects of the business. Supported by a strong cash-rich balance sheet and a shareholder-friendly management team, Makita shares represent an attractive means to gain exposure to a rebounding global construction market.

Rolls-Royce Holdings PLC (RR/ LN)

(Analyst: Jonathan Bloom)

Description

Rolls-Royce Holdings PLC develops, manufacturers and services complex, integrated power systems for use on land and sea, and by air. The company operates in the following segments (as a percentage of total 2015 estimated revenue and profits): Civil Aerospace (53% revenue and 55% profits), Defense Aerospace (14% and 21%), Power Systems (18% and 15%), Marine (11% and 7%), and Energy (4% and 2%). The largest geographic segments include the U.S. (27%), UK (12%), Rest of Europe (22%), and Asia (30%). The Civil and Defense Aerospace (A&D) segments focus primarily on commercial and military aero engines; Power Systems includes diesel engines and power systems for marine, industrial, oil & gas, defense and power generation end markets; the Marine segment focuses on power, propulsion and motion control for ships and submarines; and the Energy segment includes nuclear systems for civil power generation and naval propulsion.

Good Business

| | • | Wide body commercial aero engines have a duopoly market structure with Rolls-Royce and GE dominating the space. A high level of technological expertise, advanced engineering, and government regulation creates significant barriers to entry. |

| | • | Nearly 50% of group revenues come from aftermarket services, as aero engines are often sold near break-even, but come with profitable long-term service contracts. This is a razor/razorblade business model, creating an annuity-like aftermarket revenue stream. An aero engine’s life cycle is around 20-30 years, with major overhauls every 5-6 years. |

| | • | Most commercial airlines opt to purchase replacement parts from the original equipment manufacturer. |

| | • | The company has an order book of £73.7 billion. Long-term drivers include emerging market demand, population growth, fuel efficiency, demand for energy, urbanization, increasing affluence, etc. |

| | • | ROIC (return on invested capital) has averaged approximately 12% over the past 5 years. With 250-350 basis points of margin opportunity in the medium term, ROIC should improve further. |

| | • | The company has a solid balance sheet, with debt-to-total capital of 26% and net debt of only £38 million. |

Valuation

| | • | Rolls-Royce trades at an enterprise value-to-revenue multiple of approximately 1.2 times, compared with an operating margin of about 11% and a mid-term target of 13.5-14.5% — a significant discount to intrinsic value. |

| | • | The stock trades at a forward P/E of 16.0 times, a discount to the weighted average multiple of the MSCI EAFE Index at 19.5 times, despite being a better-than-average business with above-average growth prospects over a long-term investment horizon. |

| | • | Current dividend yield is 2.3%. This is issued via “C shares” which are redeemable for cash. |

Management

| | • | Mr. John Rishton took over as CEO in 2011, and has had his share of ups and downs. We are pleased with his focus on cost reduction and cash generation, but have been disappointed with execution, communication, and certain capital allocation decisions (mergers and acquisitions). Overall, the jury is still out. |

| | • | Mr. Rishton’s 2014 compensation fell by more than 50% when compared with 2013, after a disappointing year. We were pleased to see that management was held accountable for performance. |

Investment Thesis

Rolls-Royce is a quality business with dominant market positions, significant barriers to entry, and an annuity-like recurring revenue stream from its service businesses. The company has attractive top-line growth prospects as illustrated by its £73.7 billion order book, a significant opportunity to expand operating margins that are well below peers, and a renewed operational focus on cost reduction and cash generation. While the stock has underperformed recently due to near-term headwinds on earnings and cash, end-market pressures (defense, marine and energy), and the rebasing of its cost structure, the long-term investment opportunity remains an attractive one. At the current valuation, we have an opportunity to own a world-class business at a reasonable valuation. While it still may be a bumpy ride in the near-term, long-term investors should be rewarded for their patience.

Thank you for your support of the FMI International Fund.

100 E. Wisconsin Ave., Suite 2200 • Milwaukee, WI 53202 • 414-226-4555

www.fmifunds.com

FMI International Fund

SCHEDULE OF INVESTMENTS

March 31, 2015 (Unaudited)

| Shares | | | | Cost | | | Value | |

| | | | | | | |

| LONG-TERM INVESTMENTS — 78.3% (a) | | | | | | |

| COMMON STOCKS — 73.6% (a) | | | | | | |

| | | | | | | |

| COMMERCIAL SERVICES SECTOR — 9.9% | | | | | | |

| | | Advertising/Marketing Services — 3.3% | | | | | | |

| | 2,420,000 | | WPP PLC (Jersey) (b) | | $ | 50,572,426 | | | $ | 54,959,463 | |

| | | | | | | | | | | | |

| | | | Miscellaneous Commercial Services — 3.0% | | | | | | | | |

| | 580,000 | | Secom Co. Ltd. (Japan) (b) | | | 34,519,987 | | | | 38,686,193 | |

| | 4,549,740 | | Taiwan Secom (Taiwan) (b) | | | 11,601,042 | | | | 12,286,863 | |

| | | | | | | 46,121,029 | | | | 50,973,056 | |

| | | | Personnel Services — 3.6% | | | | | | | | |

| | 733,000 | | Adecco S.A. (Switzerland) (b) | | | 52,542,789 | | | | 60,929,522 | |

| | | | | | | | | |

| CONSUMER DURABLES SECTOR — 5.3% | | | | | | | | |

| | | | Automotive Aftermarket — 3.3% | | | | | | | | |

| | 3,398,000 | | Pirelli & C. SpA (Italy) (b) | | | 48,378,295 | | | | 56,245,925 | |

| | | | | | | | | | | | |

| | | | Tools & Hardware — 2.0% | | | | | | | | |

| | 645,000 | | Makita Corp. (Japan) (b) | | | 30,552,121 | | | | 33,424,106 | |

| | | | | | | | | |

| CONSUMER NON-DURABLES SECTOR — 10.6% | | | | | | | | |

| | | | Food: Major Diversified — 5.4% | | | | | | | | |

| | 825,000 | | Danone S.A. (France) (b) | | | 56,104,543 | | | | 55,611,248 | |

| | 473,000 | | Nestle’ S.A. (Switzerland) (b) | | | 34,992,611 | | | | 35,618,055 | |

| | | | | | | 91,097,154 | | | | 91,229,303 | |

| | | | Household/Personal Care — 5.2% | | | | | | | | |

| | 397,000 | | Henkel AG & Co. KGaA (Germany) (b) | | | 36,937,550 | | | | 40,967,397 | |

| | 1,121,000 | | Unilever PLC (Britain) (b) | | | 47,049,718 | | | | 46,771,791 | |

| | | | | | | 83,987,268 | | | | 87,739,188 | |

| CONSUMER SERVICES SECTOR — 3.8% | | | | | | | | |

| | | | Hotels/Resorts/Cruiselines — 2.0% | | | | | | | | |

| | 29,145,000 | | Genting Malaysia Berhad (Malaysia) (b) | | | 34,505,762 | | | | 33,253,969 | |

| | | | | | | | | | | | |

| | | | Restaurants — 1.8% | | | | | | | | |

| | 1,783,000 | | Compass Group PLC (Britain) (b) | | | 28,730,385 | | | | 30,951,418 | |

| | | | | | | | | |