As filed with the U.S. Securities and Exchange Commission on May 21, 2024

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07831

FMI Funds, Inc.

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

790 North Water Street, Suite 2100

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

John S. Brandser

Fiduciary Management, Inc.

790 North Water Street

Suite 2100

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 226-4545

Registrant's telephone number, including area code

Date of fiscal year end: September 30

Date of reporting period: March 31, 2024

Item 1. Reports to Stockholders.

| (a) |

SEMI-ANNUAL REPORT

March 31, 2024

FMI Common Stock Fund

Investor Class (Ticker Symbol: FMIMX)

Institutional Class (Ticker Symbol: FMIUX)

FMI Large Cap Fund

Investor Class (Ticker Symbol: FMIHX)

Institutional Class (Ticker Symbol: FMIQX)

FMI International Fund

Investor Class (Ticker Symbol: FMIJX)

Institutional Class (Ticker Symbol: FMIYX)

FMI International Fund II – Currency Unhedged

Investor Class (Not Available For Purchase)

Institutional Class (Ticker Symbol: FMIFX)

| FMI Funds, Inc. Advised by Fiduciary Management, Inc. www.fmifunds.com |

FMI Funds, Inc.

TABLE OF CONTENTS

| Shareholder Letter | 1 | |

| FMI Common Stock Fund | ||

| Schedule of Investments | 8 | |

| Industry Sectors | 10 | |

| FMI Large Cap Fund | ||

| Schedule of Investments | 11 | |

| Industry Sectors | 13 | |

| FMI International Fund | ||

| Schedule of Investments | 14 | |

| Schedule of Forward Currency Contracts | 17 | |

| Industry Sectors | 18 | |

| Concentration by Country | 18 | |

| FMI International Fund II – Currency Unhedged | ||

| Schedule of Investments | 19 | |

| Industry Sectors | 22 | |

| Concentration by Country | 22 | |

| Financial Statements | ||

| Statements of Assets and Liabilities | 24 | |

| Statements of Operations | 26 | |

| Statements of Changes in Net Assets | 28 | |

| Financial Highlights | 32 | |

| Notes to Financial Statements | 39 | |

| Expense Example | 51 | |

| Advisory Agreements | 53 | |

| Disclosure Information | 60 | |

| Additional Information | 64 |

FMI Funds, Inc.

Shareholder Letter

(Unaudited)

March 31, 2024

Dear Fellow Shareholders:

Last year’s stock market momentum carried over into the first quarter, with growth stocks leading the charge (once again) across market caps and geographies. Investors seem complacent, as the fundamentals do not appear to justify the current levels of exuberance. Germany, the UK, and Japan are all either in – or teetering on the verge of – a recession. China’s growth is coming under significant pressure, global trade is slowing, geopolitical risks remain elevated, and debt levels continue to march higher. The U.S. economy has been resilient but is expected to decelerate in 2024. The S&P 500 has taken on a life of its own, with an incredible concentration in mega cap technology, leaving most other asset classes in the dust in recent years. Is the S&P 500’s exceptional run of outperformance sustainable? Consider us skeptical.

Before further addressing the question at hand, our first quarter performance commentary is outlined below:

FMI Common Stock Fund: Performance

In the first quarter, the FMI Common Stock Fund (“Common Stock Fund”) increased 8.91%1, compared with 5.18% and 2.90% for the Russell 2000® Index (“Russell 2000”) and Russell 2000® Value Index (“Russell 2000 Value”), respectively. The Common Stock Fund outperformed despite growth eclipsing value by over 4% in the period. Relative to the Russell 2000, FMI’s sector performance was driven by Finance, Producer Manufacturing, and Distribution Services, while Commercial Services, Electronic Technology, and Consumer Non-Durables each lost some ground. Core & Main Inc. Class A, Gates Industrial Corp. PLC, and nVent Electric PLC were among the top performing stocks, as Plexus Corp., Robert Half Inc., and Genpact Ltd. failed to keep pace. With Small/SMID Cap stocks lagging in recent years, the relative valuations have become more appealing.

FMI Large Cap Fund: Performance

In the first quarter, the FMI Large Cap Fund (“Large Cap Fund”) advanced 8.43%2, compared with 10.56% and 8.86% for the S&P 500® Index (S&P 500) and iShares Russell 1000 Value ETF3, respectively. Growth outpaced value by over 2% in the period. Relative to the S&P 500, Finance, Producer Manufacturing, and Consumer Durables were FMI’s top performing sectors, while Health Services, Health Technology, and Electronic Technology underperformed. Top individual contributors included Micron Technology Inc., Progressive Corp., and Eaton Corp. PLC, while UnitedHealth Group Inc., Sony Group Corp. – SP-ADR, and Dollar Tree Inc. weighed. Speculation remains high, as can be seen by the top-performing themes in the U.S. (tracked by Goldman Sachs): Bitcoin Sensitive Equities (+53%), High Beta 12M Winners (+29%), Obesity Drugs (+28%), Artificial Intelligence (+24%), Mega cap Tech (23%), and AI Hardware/Data Centers (+20%). Meanwhile, Quality Compounders (+5%) trailed the market, yet again.

| 1 | The FMI Common Stock Fund Investor Class (FMIMX) and the FMI Common Stock Fund Institutional Class (FMIUX) had a return of 8.91% and 8.92%, respectively, for the first quarter of 2024. |

| 2 | The FMI Large Cap Fund Investor Class (FMIHX) and the FMI Large Cap Fund Institutional Class (FMIQX) had a return of 8.43% and 8.53%, respectively, for the first quarter of 2024. |

| 3 | Source: Bloomberg – returns do not reflect management fees, transaction costs or expenses. Performance is based on market price returns. Beginning 8/10/20, market price returns are calculated using closing price. Prior to 8/10/20, market price returns were calculated using midpoint bid/ask spread at 4:00 PM ET. |

1

FMI International Fund & FMI International Fund II – Currency Unhedged: Performance

In the first quarter, the FMI International Funds (“International Funds”) gained 5.66%4 on a currency hedged basis and 3.47%5 currency unhedged, compared with the MSCI EAFE Index’s increase of 9.96% in local currency (LOC) and 5.78% in U.S. Dollars (USD). The MSCI EAFE Value Index gained 8.54% in LOC and 4.48% in USD. Growth outpaced value by nearly 3% in the period. Relative to the MSCI EAFE Index, the International Funds’ Transportation sector exposure, and the lack of direct exposure in Utilities and Non-Energy Minerals sectors were additive to performance, while Health Technology, Producer Manufacturing, and Commercial Services detracted. Safran S.A., Yokogawa Electric Corp., and Arch Capital Group Ltd. were the top individual performers, while Smiths Group PLC, NOF Corp., and Smith & Nephew PLC lagged. A strong USD was a tailwind for the currency hedged Fund. A key variance in the quarter was FMI’s underweight in Japan, a geography with a portfolio weight of ~7% compared with ~23% for the MSCI EAFE. The Japanese market outperformed significantly to start the year, with the Nikkei 225 up over 20%.

Who Would Have Guessed?

If you had a crystal ball and had known five years ago that the following would happen …

• A once-in-a-century global pandemic, relegating billions of people to shelter in place, bringing entire industries to a screeching halt.

• U.S. inflation goes from 1.9% to over 9%, before settling in at 3.2% (68% higher).

• The U.S. Federal Funds Rate more than doubles, from 2.4% to 5.3%.

• Mortgage rates in the U.S. rise from 4.1% to 6.8%.

• U.S. Federal Debt increases from $22 trillion to $34 trillion, with ballooning deficits.

• U.S. productivity is well below historical averages.

• A regional banking crisis takes place in the U.S. and several banks fail.

• U.S. economy grows real GDP at a below-average rate of only 2.1%.

• Global growth is on pace for the weakest half-decade in 30 years.

• A Cold War with China, Proxy War with Russia (Ukraine), and the Middle East aflame.

• Political dysfunction deepens, creating a massive cultural divide within the U.S.

… where would you have expected the U.S. stock market would be today?

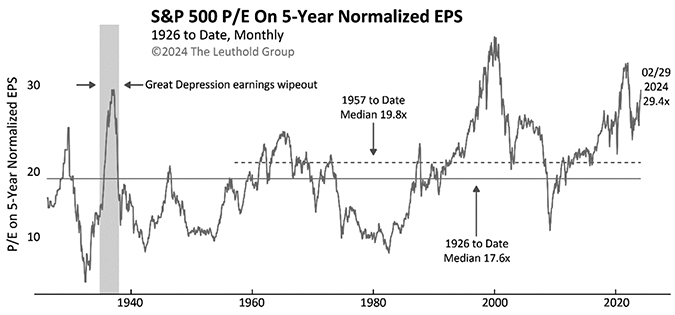

We highly doubt investors would have predicted a rising stock market, much less an S&P 500 up 102% (vs. 48% for the Russell 2000 and 42% for the MSCI EAFE USD). Unprecedented global stimulus surely helped. The S&P 500 grew earnings by ~37% cumulatively, accounting for about a third of the index’s total return (with multiple expansion making up the majority). Earnings growth was boosted by the Magnificent Seven (Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, and Meta Platforms), as the average company grew at a much slower rate. Normalized valuations in the S&P 500 increased considerably, as seen in the graph on the following page:

The market turned a blind eye to numerous negative macro developments, which is not all that uncommon when looking back over a 100-year history. Stocks don’t always follow earnings or macro conditions over 5-year periods. During long periods of time, however, they do eventually track earnings and fundamentals. Periods of excess returns relative to the fundamentals are often followed by periods of subpar returns relative to the fundamentals, and vice versa.

| 4 | The FMI International Fund [currency hedged] Investor Class (FMIJX) and the FMI International Fund [currency hedged] Institutional Class (FMIYX) had a return of 5.66% and 5.70%, respectively, for the first quarter of 2024. |

| 5 | The FMI International Fund [currency unhedged] Institutional Class (FMIFX) had a return of 3.47% for the first quarter of 2024. |

2

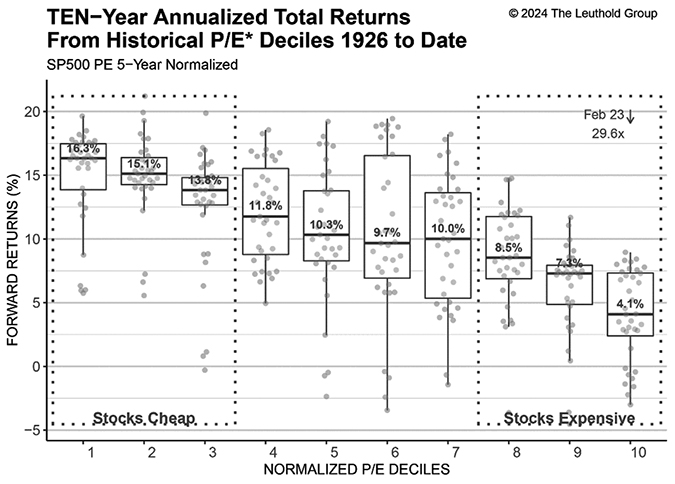

This dynamic is illustrated in the graphic below. The Leuthold Group charts the forward 10-year return from different starting valuation deciles (1st decile = cheapest valuations, 10th decile = most expensive valuations). When valuations are high, the forward-looking returns tend to be below-average. When valuation multiples are low, the forward returns tend to be above-average. Today, the S&P 500 is currently in the 10th decile of historical valuation (on 5-year normalized earnings), one of the most expensive stock markets on record. Since 1926, when starting in the 10th decile of valuation, the forward 10-year returns have averaged only 4.1%. This pales in comparison to the ~15% compound annual return of the last 5 years.

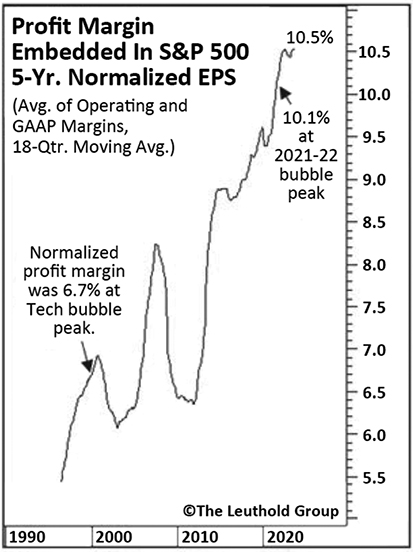

To make matters worse, normalized profit margins in the S&P 500 are currently at a 40-year high, and 56% above where they peaked in the late 1990s tech bubble (see chart on the following page). With both margins and valuations running hot at the same time, we’re left with a potentially unattractive combination.

3

Ultra-low interest rates helped boost valuations (low discount rates) and profit margins (low borrowing costs) in recent years, but the rate environment is much less accommodative today.

Should there be any reversion to the mean in terms of valuations or profit margins (or both), the downside risk could be substantial. Furthermore, it doesn’t help that companies have been facing higher inflation, in both rising input costs and wage growth, which may weigh on profitability over the long-term. The sustainability of the S&P 500’s spectacular run remains an open question, but in our view, improbable.

Not So Active, After All

For many years, the shift from active to passive investing has added fuel to the S&P 500 fire. Active share is a measure of the difference between a portfolio’s holdings and its benchmark index: Active share “always falls between 0% and 100%, with zero indicating a pure passive strategy while a higher reading suggests more active management.” Increasingly, active managers appear to be following the crowd and hugging their benchmarks. As reported by Bloomberg, active core managers have been gravitating toward the S&P 500 Index since 2017, and now have the lowest active share ratio in a decade (see Bank of America chart below). Some active managers have clearly capitulated, as keeping up with the S&P 500 has been elusive.

4

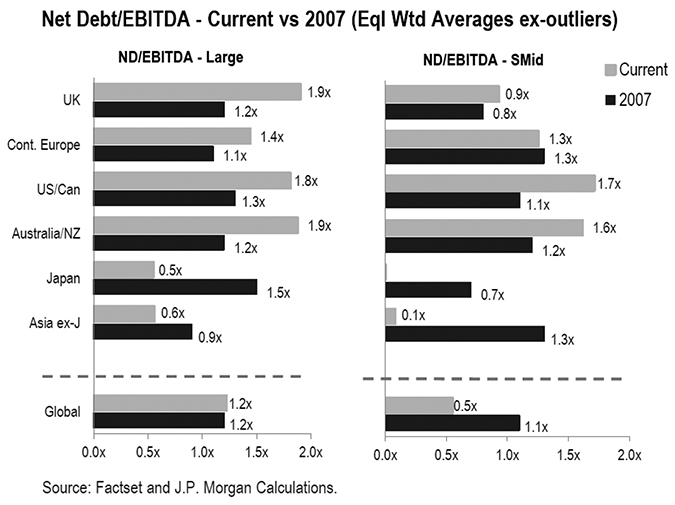

For comparison, FMI’s Common Stock Fund, Large Cap Fund, and International Funds have active shares of 98%, 92%, and 97%, respectively. We look different for a reason. In order to beat the market, you have to do something different. Despite the litany of macro risks, there are always opportunities. We look to invest in advantaged companies that we view as all-weather vehicles through a full cycle. We go where we find the best risk/reward, which can mean zero exposure to some economic sectors when the setup does not fit our eye. We offer our shareholders focused portfolios which trade at a discount to their intrinsic value for temporary reasons. With an investment time horizon of 3-5 years, we let time work on our side, sidestepping the market’s obsession with the here and now. Additionally, we strive to provide downside protection, which may become crucially important given the backdrop. A robust balance sheet is a pre-requisite for our investments. At a time when corporate debt levels in the U.S. and Europe are well above 2007 (which was on the eve of the Great Financial Crisis, as illustrated below), balance sheet strength will likely swing back into focus in the coming years, especially if higher rates are here to stay.

In the Common Stock Fund, we have held the line on business quality, avoiding money-losing businesses, which now comprise roughly 40% of the Russell 2000 constituents. In recent years, we have leaned into high-quality businesses with exposure to housing and construction (Simpson Manufacturing Co. Inc., Fortune Brands Innovations Inc., Beacon Roofing Supply Inc., nVent Electric PLC), which came under pressure due to cyclical concerns and rising interest rates. Our Finance weighting is well below that of the Russell 2000, as it has been more difficult to find financials that meet our quality threshold in the Small Cap arena. We own a number of manufacturers in diversified end-markets (AptarGroup Inc., Donaldson Co. Inc., Fabrinet, Gates Industrial Corp. PLC, ITT Inc.). We do not presently have direct exposure to the Health Technology (which is littered with money-losing biotech companies), Utilities, Transportation, Non-Energy Minerals, and Energy Minerals sectors.

In the Large Cap Fund, we have been finding opportunities outside of the Magnificent Seven, where valuations and expectations are far less lofty (see our December letter for more color). While rising tides have lifted most U.S. Large Cap boats, it’s less extreme apart from mega cap technology. Similar to the Common Stock Fund, we have built positions in companies exposed to housing and

5

construction materials (Carlisle Cos. Inc., Carrier Global Corp., Ferguson PLC, Eaton Corp. PLC, Masco Corp.). We are also overweight in Finance, where we own best-in-class companies in insurance (Progressive Corp., Arch Capital Group Ltd.), discount brokerage (Charles Schwab Corp.), and investment management (BlackRock Inc.). We do not have direct holdings in the Utilities, Transportation, Consumer Durables, Non-Energy Minerals, and Energy Minerals sectors, as we have not found investments that meet our criteria.

In the International Funds, we expanded our travel exposure in recent years (Booking Holdings Inc., Safran S.A., Ryanair Holdings PLC-SP-ADR) when the post-COVID recovery was less certain, added several top-notch UK businesses (B&M European Value Retail S.A., Greggs PLC, Howden Joinery Group PLC) amidst Brexit fears, and built housing and construction materials positions into the aforementioned pressures (Ferguson PLC, Rexel S.A., Ashtead Group PLC, Techtronic Industries Co. Ltd.). We have a significant underweight in the Finance sector, and do not have direct investments in the Utilities, Technology Services, Non-Energy Minerals, and Energy Minerals sectors. We are also underweight Japan, as it has been difficult to find management teams that are shareholder-oriented. While some investors have become enthusiastic about improving corporate governance in Japan, we view most of the company changes as incremental in nature, not needle-moving. We continue to follow the developments on this front, but will remain discerning in our stock selection.

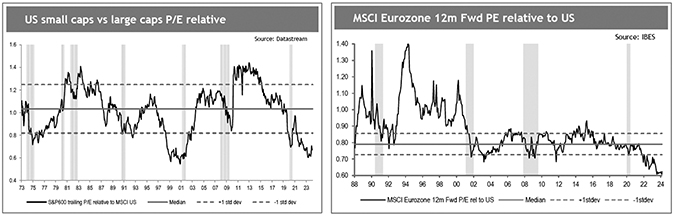

Given the underperformance in recent years, U.S. Small Cap and International stocks continue to trade at a meaningful discount. The following charts illustrate the divergence, with relative valuations around two standard deviations below historical levels. The setup appears favorable.

We remain optimistic as we look forward. All of FMI’s portfolios trade at a sizeable discount to their core benchmarks, while owning well-run, durable businesses. We have great conviction in our research process, which has been finetuned over 40+ years and numerous business cycles. Listed below are holdings from each Fund where the long-term prospects look attractive:

Gates Industrial Corp. PLC (GTES) – FMI Common Stock Fund

Gates manufactures highly engineered power transmission and fluid power solutions. The company is most well-known for its belts, which enable and control motion and are used in a broad range of applications. Blackstone took Gates public in early 2018 and remains the largest shareholder with a 27% ownership interest. Blackstone’s ownership stake is an overhang on the stock as they will inevitably sell their remaining stake. Destocking and a more challenging end market have also weighed on results. These transitory pressures have provided us with an opportunity to own a high-quality, well-run industrial company with solid through-cycle growth prospects and re-rating potential. The company is a leader in its large and fragmented markets with a well-recognized brand known for quality and technological innovation. These markets are largely replacement driven, which helps to reduce cyclicality, and management is targeting a handful of growth opportunities including chain-to-belt conversions, personal mobility, and automotive aftermarket, to name a few, that should drive revenue growth at 2 times underlying industrial

6

production growth. There is also a margin opportunity as management executes on internal initiatives to reduce costs and improve productivity. Finally, with Gates stock trading at around 12 times 2024 P/E, we believe there is an opportunity for Gates to re-rate more in-line with other high-quality industrial peers given its attractive EPS growth outlook and strong return profile.

Charles Schwab Corp. (SCHW) – FMI Large Cap Fund

We last wrote about Charles Schwab a year ago in the midst of the banking crisis. At the time, the worst fears were a bank run and/or balance sheet impairment. Positively, these did not come to pass. As a refresh of our interest in the business, Charles Schwab is a leading discount broker. The business benefits from long run market appreciation and Schwab’s better mousetrap has allowed it to gain share on top of market growth, which has driven long run revenue growth of 10%. The competitive advantage comes from shared economies of scale, whereby Schwab lowers costs to the customer, thereby attracting new assets which then lets them lower costs even more to the customer. The rapid rise in interest rates that precipitated the banking crisis contributed to a challenging last 18 months for Schwab, as clients moved bank cash to higher yielding instruments. This led to a significant, albeit short-term, earnings headwind. As we move into 2024, we believe the worst is behind them. We expect Schwab will experience strong earnings growth for the next few years, driven by accelerating revenue growth and renewed expense discipline. Despite this attractive outlook, Schwab trades for 21 times trough earnings and only 14 times our estimate of normalized earnings.

Weir Group PLC (WEIR LN) – FMI International Funds

Weir is a focused mining technology company. Key products include slurry pumps and ESCO ground engaging tools. The company has undergone a simplification program since Jon Stanton became CEO in 2016. Jon sold Weir’s Flow Control business in 2019 and its Oil & Gas business in 2021 in order to focus on the mining end market. Today, the business employs a razor/razor blade business model, enjoys high barriers to entry, and is highly resilient. The company’s core value proposition to customers is lowest total cost of ownership, which it achieves by manufacturing products that operate more efficiently (using less energy and water) and last longer than alternatives. The cloud hovering over the stock revolves around mining end market concerns, particularly the dearth of large capex projects. We believe these concerns reflect a misunderstanding of Weir’s business model. Weir’s revenue and profitability are driven by the aftermarket, and the aftermarket is largely insensitive to mining capex cycles as evidenced by Weir’s more than 7% aftermarket revenue compound annual growth rate (CAGR) from 2011-2023. Weir targets a mid-to-high single digit organic revenue growth CAGR through the cycle, driven by a favorable ore production backdrop and growing installed base. There is also an opportunity to improve the margin as management executes on its Performance Excellence program and generates operating leverage. All in, we believe double-digit EPS growth through the cycle is an attainable target. The valuation at just over 16 times forward earnings does not reflect the quality of the transformed Weir and through-cycle EPS growth potential.

Thank you for your continued support of Fiduciary Management, Inc.

Please see page 60 for important disclosures.

This shareholder letter is unaudited.

7

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| COMMON STOCKS — 94.6% | ||||||||

Commercial Services Sector — 10.2% | ||||||||

| Advertising/Marketing Services — 3.1% | ||||||||

| Interpublic Group of Cos. Inc. | 1,930,000 | $ | 62,975,900 | |||||

| Miscellaneous Commercial Services — 3.5% | ||||||||

| Genpact Ltd. | 2,225,000 | 73,313,750 | ||||||

| Personnel Services — 3.6% | ||||||||

| Robert Half Inc. | 940,000 | 74,523,200 | ||||||

| Total Commercial Services | 210,812,850 | |||||||

Consumer Non-Durables Sector — 3.6% | ||||||||

| Apparel/Footwear — 3.6% | ||||||||

Skechers U.S.A. Inc. — Class A(a) | 1,200,000 | 73,512,000 | ||||||

Consumer Services Sector — 3.3% | ||||||||

| Other Consumer Services — 3.3% | ||||||||

Valvoline Inc.(a) | 1,540,000 | 68,637,800 | ||||||

Distribution Services Sector — 17.2% | ||||||||

| Electronics Distributors — 2.7% | ||||||||

Arrow Electronics Inc.(a) | 430,000 | 55,667,800 | ||||||

| Medical Distributors — 4.1% | ||||||||

Henry Schein Inc.(a) | 1,135,000 | 85,715,200 | ||||||

| Wholesale Distributors — 10.4% | ||||||||

| Applied Industrial Technologies Inc. | 270,000 | 53,338,500 | ||||||

Beacon Roofing Supply Inc.(a) | 940,000 | 92,138,800 | ||||||

Core & Main Inc. — Class A(a) | 1,195,000 | 68,413,750 | ||||||

| 213,891,050 | ||||||||

| Total Distribution Services | 355,274,050 | |||||||

Electronic Technology Sector — 8.7% | ||||||||

| Electronic Components — 3.4% | ||||||||

| nVent Electric PLC | 935,000 | 70,499,000 | ||||||

| Electronic Production Equipment — 4.2% | ||||||||

| CTS Corp. | 615,000 | 28,775,850 | ||||||

Plexus Corp.(a) | 610,000 | 57,840,200 | ||||||

| 86,616,050 | ||||||||

| Semiconductors — 1.1% | ||||||||

Fabrinet(a) | 120,000 | 22,682,400 | ||||||

| Total Electronic Technology | 179,797,450 | |||||||

Finance Sector — 13.4% | ||||||||

| Finance/Rental/Leasing — 2.9% | ||||||||

| FirstCash Holdings Inc. | 465,000 | 59,306,100 | ||||||

The accompanying notes to financial statements are an integral part of this schedule.

8

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| COMMON STOCKS — 94.6% (Continued) | ||||||||

Finance Sector — 13.4% (Continued) | ||||||||

| Investment Banks/Brokers — 3.6% | ||||||||

| Houlihan Lokey Inc. — Class A | 580,000 | $ | 74,350,200 | |||||

| Life/Health Insurance — 2.9% | ||||||||

| Primerica Inc. | 240,000 | 60,710,400 | ||||||

| Major Banks — 2.4% | ||||||||

| Zions Bancorporation N.A. | 1,165,000 | 50,561,000 | ||||||

| Multi-Line Insurance — 1.6% | ||||||||

| White Mountains Insurance Group Ltd. | 19,000 | 34,091,700 | ||||||

| Total Finance | 279,019,400 | |||||||

Process Industries Sector — 1.9% | ||||||||

| Containers/Packaging — 1.9% | ||||||||

| AptarGroup Inc. | 275,000 | 39,569,750 | ||||||

Producer Manufacturing Sector — 28.1% | ||||||||

| Auto Parts: OEM — 3.2% | ||||||||

| Donaldson Co. Inc. | 880,000 | 65,718,400 | ||||||

| Building Products — 13.0% | ||||||||

| Carlisle Cos. Inc. | 220,000 | 86,207,000 | ||||||

| Fortune Brands Innovations Inc. | 1,030,000 | 87,210,100 | ||||||

| Simpson Manufacturing Co. Inc. | 470,000 | 96,434,600 | ||||||

| 269,851,700 | ||||||||

| Electrical Products — 1.6% | ||||||||

| Atkore Inc. | 175,000 | 33,313,000 | ||||||

| Industrial Machinery — 8.2% | ||||||||

Gates Industrial Corp. PLC(a) | 3,675,000 | 65,084,250 | ||||||

| ITT Inc. | 385,000 | 52,371,550 | ||||||

| Timken Co. | 585,000 | 51,146,550 | ||||||

| 168,602,350 | ||||||||

| Miscellaneous Manufacturing — 2.1% | ||||||||

| TriMas Corp. | 1,605,000 | 42,901,650 | ||||||

| Total Producer Manufacturing | 580,387,100 | |||||||

Retail Trade Sector — 4.5% | ||||||||

| Specialty Stores — 4.5% | ||||||||

BJ’s Wholesale Club Holdings Inc.(a) | 1,225,000 | 92,671,250 | ||||||

Technology Services Sector — 3.7% | ||||||||

| Information Technology Services — 3.7% | ||||||||

Insight Enterprises Inc.(a) | 415,000 | 76,990,800 | ||||||

TOTAL COMMON STOCKS (Cost $1,293,853,546) | 1,956,672,450 | |||||||

The accompanying notes to financial statements are an integral part of this schedule.

9

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| SHORT-TERM INVESTMENT — 5.2% | ||||||||

| Money Market Fund — 5.2% | ||||||||

First American Treasury Obligations Fund — Class X, 5.22%(b) | 108,379,704 | $ | 108,379,704 | |||||

TOTAL SHORT-TERM INVESTMENT (Cost $108,379,704) | 108,379,704 | |||||||

TOTAL INVESTMENTS — 99.8% (Cost $1,402,233,250) | 2,065,052,154 | |||||||

Other Assets in Excess of Liabilities — 0.2% | 3,103,210 | |||||||

| TOTAL NET ASSETS — 100.0% | $ | 2,068,155,364 | ||||||

Percentages are stated as a percent of net assets.

| PLC | Public Limited Company |

| (a) | Non-income producing security. |

| (b) | The rate shown represents the 7-day effective yield as of March 31, 2024. |

The accompanying notes to financial statements are an integral part of this schedule.

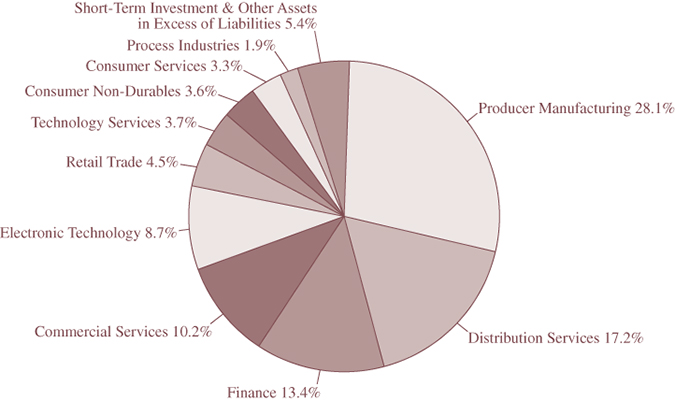

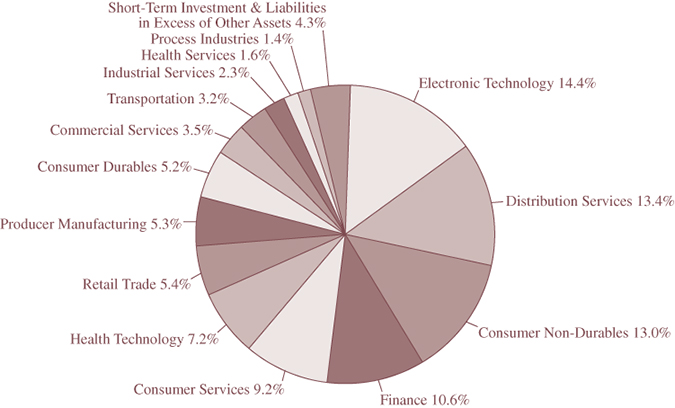

INDUSTRY SECTORS as a percentage of net assets

as of March 31, 2024 (Unaudited)

10

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| COMMON STOCKS — 96.7% | ||||||||

Commercial Services Sector — 2.8% | ||||||||

| Advertising/Marketing Services — 2.8% | ||||||||

| Omnicom Group Inc. | 500,000 | $ | 48,380,000 | |||||

Consumer Non-Durables Sector — 3.2% | ||||||||

| Household/Personal Care — 3.2% | ||||||||

| Unilever PLC — SP-ADR | 1,085,000 | 54,456,150 | ||||||

Consumer Services Sector — 4.2% | ||||||||

| Other Consumer Services — 4.2% | ||||||||

| Booking Holdings Inc. | 20,000 | 72,557,600 | ||||||

Distribution Services Sector — 8.7% | ||||||||

| Food Distributors — 3.1% | ||||||||

| Sysco Corp. | 650,000 | 52,767,000 | ||||||

| Wholesale Distributors — 5.6% | ||||||||

| Ferguson PLC | 445,000 | 97,201,350 | ||||||

| Total Distribution Services | 149,968,350 | |||||||

Electronic Technology Sector — 7.8% | ||||||||

| Computer Processing Hardware — 3.8% | ||||||||

| Sony Group Corp. — SP-ADR | 755,000 | 64,733,700 | ||||||

| Semiconductors — 4.0% | ||||||||

| Micron Technology Inc. | 585,000 | 68,965,650 | ||||||

| Total Electronic Technology | 133,699,350 | |||||||

Finance Sector — 20.5% | ||||||||

| Investment Banks/Brokers — 5.2% | ||||||||

| The Charles Schwab Corp. | 1,230,000 | 88,978,200 | ||||||

| Investment Managers — 4.9% | ||||||||

| BlackRock Inc. | 45,000 | 37,516,500 | ||||||

| Northern Trust Corp. | 520,000 | 46,238,400 | ||||||

| 83,754,900 | ||||||||

| Multi-Line Insurance — 5.4% | ||||||||

Arch Capital Group Ltd.(a) | 425,000 | 39,287,000 | ||||||

| Progressive Corp. | 260,000 | 53,773,200 | ||||||

| 93,060,200 | ||||||||

| Property/Casualty Insurance — 5.0% | ||||||||

Berkshire Hathaway Inc. — Class B(a) | 205,000 | 86,206,600 | ||||||

| Total Finance | 351,999,900 | |||||||

Health Services Sector — 7.6% | ||||||||

| Health Industry Services — 3.0% | ||||||||

| Quest Diagnostics Inc. | 385,000 | 51,247,350 | ||||||

| Managed Health Care — 3.0% | ||||||||

| UnitedHealth Group Inc. | 105,000 | 51,943,500 | ||||||

The accompanying notes to financial statements are an integral part of this schedule.

11

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| COMMON STOCKS — 96.7% (Continued) | ||||||||

Health Services Sector — 7.6% (Continued) | ||||||||

| Medical/Nursing Services — 1.6% | ||||||||

| Fresenius Medical Care AG & Co. KGaA — SP-ADR | 1,440,000 | $ | 27,763,200 | |||||

| Total Health Services | 130,954,050 | |||||||

Health Technology Sector — 3.8% | ||||||||

| Medical Specialties — 3.8% | ||||||||

Koninklijke Philips N.V. — SP-ADR(a) | 1,775,000 | 35,500,000 | ||||||

| Smith & Nephew PLC — SP-ADR | 1,210,000 | 30,685,600 | ||||||

| 66,185,600 | ||||||||

| Total Health Technology | 66,185,600 | |||||||

Industrial Services Sector — 1.7% | ||||||||

| Contract Drilling — 1.7% | ||||||||

| Schlumberger Ltd. | 525,000 | 28,775,250 | ||||||

Process Industries Sector — 4.4% | ||||||||

| Containers/Packaging — 4.4% | ||||||||

| Avery Dennison Corp. | 340,000 | 75,905,000 | ||||||

Producer Manufacturing Sector — 13.5% | ||||||||

| Building Products — 8.6% | ||||||||

| Carlisle Cos. Inc. | 180,000 | 70,533,000 | ||||||

| Masco Corp. | 975,000 | 76,908,000 | ||||||

| 147,441,000 | ||||||||

| Electrical Products — 1.7% | ||||||||

| Eaton Corp. PLC | 95,000 | 29,704,600 | ||||||

| Industrial Machinery — 3.2% | ||||||||

| Carrier Global Corp. | 955,000 | 55,514,150 | ||||||

| Total Producer Manufacturing | 232,659,750 | |||||||

Retail Trade Sector — 11.0% | ||||||||

| Apparel/Footwear Retail — 1.2% | ||||||||

| The TJX Cos. Inc. | 210,000 | 21,298,200 | ||||||

| Discount Stores — 5.6% | ||||||||

| Dollar General Corp. | 345,000 | 53,840,700 | ||||||

Dollar Tree Inc.(a) | 325,000 | 43,273,750 | ||||||

| 97,114,450 | ||||||||

| Specialty Stores — 4.2% | ||||||||

CarMax Inc.(a) | 830,000 | 72,301,300 | ||||||

| Total Retail Trade | 190,713,950 | |||||||

Technology Services Sector — 7.5% | ||||||||

| Information Technology Services — 2.4% | ||||||||

| CDW Corp. | 165,000 | 42,203,700 | ||||||

The accompanying notes to financial statements are an integral part of this schedule.

12

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| COMMON STOCKS — 96.7% (Continued) | ||||||||

Technology Services Sector — 7.5% (Continued) | ||||||||

| Internet Software/Services — 5.1% | ||||||||

Alphabet Inc. — Class A(a) | 580,000 | $ | 87,539,400 | |||||

| Total Technology Services | 129,743,100 | |||||||

TOTAL COMMON STOCKS (Cost $1,071,722,258) | 1,665,998,050 | |||||||

| SHORT-TERM INVESTMENT — 2.5% | ||||||||

| Money Market Fund — 2.5% | ||||||||

First American Treasury Obligations Fund — Class X, 5.22%(b) | 42,480,463 | 42,480,463 | ||||||

TOTAL SHORT-TERM INVESTMENT (Cost $42,480,463) | 42,480,463 | |||||||

TOTAL INVESTMENTS — 99.2% (Cost $1,114,202,721) | 1,708,478,513 | |||||||

Other Assets in Excess of Liabilities — 0.8% | 14,534,041 | |||||||

| TOTAL NET ASSETS — 100.0% | $ | 1,723,012,554 | ||||||

Percentages are stated as a percent of net assets.

| PLC | Public Limited Company |

| SP-ADR | Sponsored American Depositary Receipt |

| (a) | Non-income producing security. |

| (b) | The rate shown represents the 7-day effective yield as of March 31, 2024. |

The accompanying notes to financial statements are an integral part of this schedule.

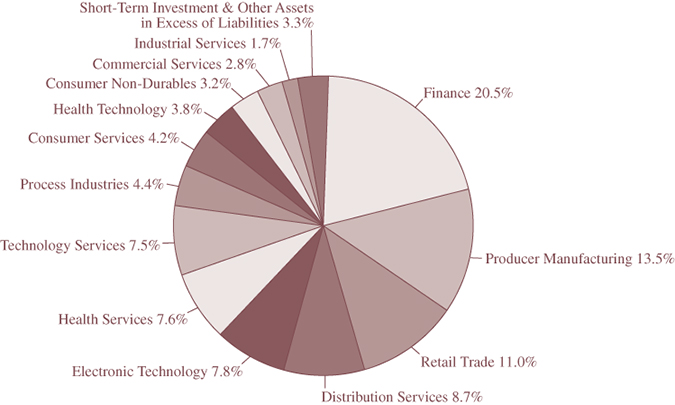

INDUSTRY SECTORS as a percentage of net assets

as of March 31, 2024 (Unaudited)

13

FMI International Fund

SCHEDULE OF INVESTMENTS

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| LONG-TERM INVESTMENTS — 94.4% | ||||||||

| COMMON STOCKS — 89.8% | ||||||||

Bermuda — 4.7% | ||||||||

| Miscellaneous Commercial Services — 2.4% | ||||||||

| Genpact Ltd. | 3,465,000 | $ | 114,171,750 | |||||

| Multi-Line Insurance — 2.3% | ||||||||

Arch Capital Group Ltd.(a) | 1,220,000 | 112,776,800 | ||||||

| Total Bermuda | 226,948,550 | |||||||

Britain — 26.7%(b) | ||||||||

| Beverages: Alcoholic — 2.9% | ||||||||

| Diageo PLC | 3,765,000 | 139,313,154 | ||||||

| Beverages: Non-Alcoholic — 2.5% | ||||||||

| Coca-Cola Europacific Partners PLC | 1,770,000 | 123,811,500 | ||||||

| Electrical Products — 2.1% | ||||||||

| Smiths Group PLC | 4,950,000 | 102,605,984 | ||||||

| Electronics/Appliances — 2.6% | ||||||||

| Howden Joinery Group PLC | 10,840,000 | 124,087,285 | ||||||

| Finance/Rental/Leasing — 2.0% | ||||||||

| Ashtead Group PLC | 1,345,000 | 95,803,158 | ||||||

| Food: Specialty/Candy — 3.6% | ||||||||

| Greggs PLC | 4,825,000 | 175,018,048 | ||||||

| Household/Personal Care — 3.8% | ||||||||

| Unilever PLC | 3,670,000 | 184,240,495 | ||||||

| Major Banks — 2.1% | ||||||||

| Lloyds Banking Group PLC | 158,900,000 | 103,919,959 | ||||||

| Medical Specialties — 2.0% | ||||||||

| Smith & Nephew PLC | 7,615,000 | 95,331,957 | ||||||

| Trucks/Construction/Farm Machinery — 3.1% | ||||||||

| Weir Group PLC | 5,950,000 | 151,988,015 | ||||||

| Total Britain | 1,296,119,555 | |||||||

Curacao — 2.2% | ||||||||

| Contract Drilling — 2.2% | ||||||||

| Schlumberger Ltd. | 1,975,000 | 108,249,750 | ||||||

France — 14.0% | ||||||||

| Aerospace & Defense — 3.6% | ||||||||

| Safran S.A. | 780,000 | 176,648,494 | ||||||

| Regional Banks — 1.8% | ||||||||

| Edenred SE | 1,629,966 | 87,031,900 | ||||||

The accompanying notes to financial statements are an integral part of this schedule.

14

FMI International Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| LONG-TERM INVESTMENTS — 94.4% (Continued) | ||||||||

| COMMON STOCKS — 89.8% (Continued) | ||||||||

France — 14.0% (Continued) | ||||||||

| Restaurants — 4.9% | ||||||||

| Sodexo S.A. | 2,750,000 | $ | 235,739,882 | |||||

| Wholesale Distributors — 3.7% | ||||||||

| Rexel S.A. | 6,665,000 | 180,041,143 | ||||||

| Total France | 679,461,419 | |||||||

Germany — 1.6% | ||||||||

| Medical/Nursing Services — 1.6% | ||||||||

| Fresenius Medical Care AG & Co. KGaA | 2,035,000 | 78,194,478 | ||||||

Hong Kong — 2.5% | ||||||||

| Tools & Hardware — 2.5% | ||||||||

| Techtronic Industries Co. Ltd. | 9,100,000 | 123,649,574 | ||||||

Ireland — 3.2% | ||||||||

| Airlines — 3.2% | ||||||||

| Ryanair Holdings PLC — SP-ADR | 1,065,000 | 155,053,350 | ||||||

Japan — 7.3% | ||||||||

| Chemicals: Specialty — 1.3% | ||||||||

| NOF Corp. | 4,770,000 | 65,326,035 | ||||||

| Computer Processing Hardware — 4.3% | ||||||||

| Sony Group Corp. | 2,425,000 | 207,945,520 | ||||||

| Electronic Equipment/Instruments — 1.7% | ||||||||

| Yokogawa Electric Corp. | 3,630,000 | 83,596,619 | ||||||

| Total Japan | 356,868,174 | |||||||

Jersey — 7.5% | ||||||||

| Wholesale Distributors — 7.5% | ||||||||

| Ferguson PLC | 1,670,000 | 365,386,342 | ||||||

Luxembourg — 5.3% | ||||||||

| Discount Stores — 5.3% | ||||||||

| B&M European Value Retail S.A. | 37,400,000 | 257,829,218 | ||||||

Netherlands — 3.2% | ||||||||

| Medical Specialties — 2.1% | ||||||||

Koninklijke Philips N.V.(a) | 5,085,000 | 101,771,284 | ||||||

| Miscellaneous Commercial Services — 1.1% | ||||||||

Pluxee N.V.(a) | 1,777,190 | 52,534,773 | ||||||

| Total Netherlands | 154,306,057 | |||||||

Singapore — 2.2% | ||||||||

| Major Banks — 2.2% | ||||||||

| DBS Group Holdings Ltd. | 4,040,000 | 107,818,790 | ||||||

The accompanying notes to financial statements are an integral part of this schedule.

15

FMI International Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| LONG-TERM INVESTMENTS — 94.4% (Continued) | ||||||||

| COMMON STOCKS — 89.8% (Continued) | ||||||||

Switzerland — 5.1% | ||||||||

| Medical Distributors — 2.0% | ||||||||

| DKSH Holding AG | 1,435,000 | $ | 97,695,459 | |||||

| Pharmaceuticals: Major — 3.1% | ||||||||

| Roche Holding AG | 585,000 | 149,361,641 | ||||||

| Total Switzerland | 247,057,100 | |||||||

United States — 4.3% | ||||||||

| Other Consumer Services — 4.3% | ||||||||

| Booking Holdings Inc. | 57,000 | 206,789,160 | ||||||

TOTAL COMMON STOCKS (Cost $3,481,645,294) | 4,363,731,517 | |||||||

| PREFERRED STOCK — 4.6% | ||||||||

South Korea — 4.6% | ||||||||

| Telecommunications Equipment — 4.6% | ||||||||

| Samsung Electronics Co. Ltd. | 4,515,000 | 225,353,590 | ||||||

TOTAL PREFERRED STOCK (Cost $121,528,178) | 225,353,590 | |||||||

TOTAL LONG-TERM INVESTMENTS (Cost $3,603,173,472) | 4,589,085,107 | |||||||

| SHORT-TERM INVESTMENT — 5.0% | ||||||||

| Money Market Fund — 5.0% | ||||||||

First American Treasury Obligations Fund — Class X, 5.22(b) | 244,867,068 | 244,867,068 | ||||||

TOTAL SHORT-TERM INVESTMENT (Cost $244,867,068) | 244,867,068 | |||||||

TOTAL INVESTMENTS — 99.4% (Cost $3,848,040,540) | 4,833,952,175 | |||||||

Money Market Deposit Account — 0.0%(c) | 223,781 | |||||||

Other Assets in Excess of Liabilities — 0.6% | 30,099,314 | |||||||

| TOTAL NET ASSETS — 100.0% | $ | 4,864,275,270 | ||||||

Percentages are stated as a percent of net assets.

| PLC | Public Limited Company |

| SP-ADR | Sponsored American Depositary Receipt |

| (a) | Non-income producing security. |

| (b) | The rate shown represents the 7-day effective yield as of March 31, 2024. |

| (c) | The U.S. Bank Money Market Deposit Account (the “MMDA”) is a short-term vehicle in which the Fund holds cash balances. The MMDA will bear interest at a variable rate that is determined based on market conditions and is subject to change daily. The rate as of March 31, 2024 was 5.17%. This MMDA is held as collateral for certain forward currency contracts. |

The accompanying notes to financial statements are an integral part of this schedule.

16

FMI International Fund

SCHEDULE OF FORWARD CURRENCY CONTRACTS

March 31, 2024 (Unaudited)

| U.S. $Value on | U.S. $Value on | |||||||||||||||||||

| March 31, 2024 | March 31, 2024 | Unrealized | ||||||||||||||||||

| Settlement | Currency to | of Currency to | Currency to | of Currency to | Appreciation | |||||||||||||||

| Date | Counterparty | be Delivered | be Delivered | be Received | be Received | (Depreciation) | ||||||||||||||

| 4/19/24 | State Street Bank | 1,250,000,000 | $ | 1,577,874,847 | 1,582,985,500 | $ | 1,582,985,500 | $ | 5,110,653 | |||||||||||

| and Trust Co. | British Pound | U.S. Dollar | ||||||||||||||||||

| 4/19/24 | The Bank of | 800,000,000 | 863,836,788 | 872,020,000 | 872,020,000 | 8,183,212 | ||||||||||||||

| New York Mellon | Euro | U.S. Dollar | ||||||||||||||||||

| 4/19/24 | JPMorgan Chase | 825,000,000 | 105,482,919 | 105,621,819 | 105,621,819 | 138,900 | ||||||||||||||

| Bank, N.A. | Hong Kong Dollar | U.S. Dollar | ||||||||||||||||||

| 4/19/24 | The Bank of | 48,000,000,000 | 318,148,358 | 328,250,017 | 328,250,017 | 10,101,659 | ||||||||||||||

| New York Mellon | Japanese Yen | U.S. Dollar | ||||||||||||||||||

| 4/19/24 | JPMorgan Chase | 125,000,000 | 92,670,051 | 93,183,575 | 93,183,575 | 513,524 | ||||||||||||||

| Bank, N.A. | Singapore Dollar | U.S. Dollar | ||||||||||||||||||

| 4/19/24 | State Street Bank | 230,000,000,000 | 171,053,925 | 171,003,717 | 171,003,717 | (50,208 | ) | |||||||||||||

| and Trust Co. | South Korea Won | U.S. Dollar | ||||||||||||||||||

| 4/19/24 | State Street Bank | 20,000,000,000 | 14,874,254 | 14,985,764 | 14,985,764 | 111,510 | ||||||||||||||

| and Trust Co. | South Korea Won | U.S. Dollar | ||||||||||||||||||

| 4/19/24 | The Bank of | 200,000,000 | 222,307,268 | 233,045,910 | 233,045,910 | 10,738,642 | ||||||||||||||

| New York Mellon | Swiss Franc | U.S. Dollar | ||||||||||||||||||

| $ | 3,366,248,410 | $ | 3,401,096,302 | $ | 34,847,892 | |||||||||||||||

The accompanying notes to financial statements are an integral part of this schedule.

17

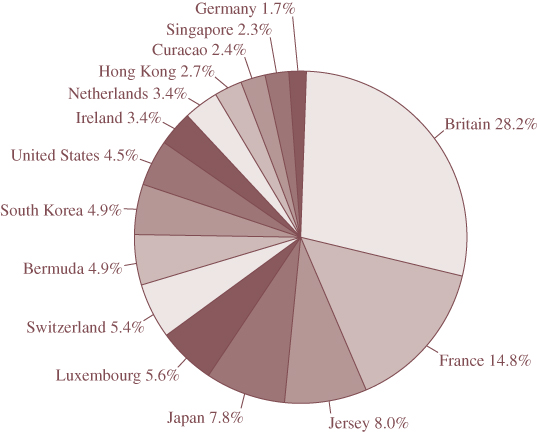

FMI International Fund

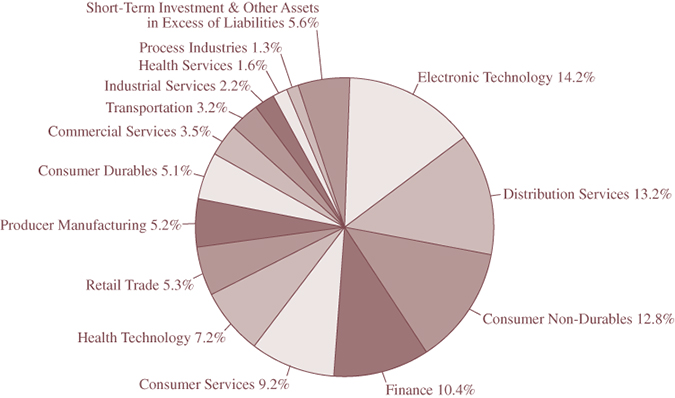

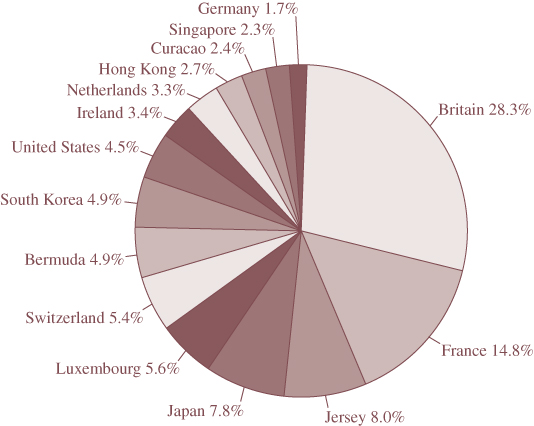

INDUSTRY SECTORS as a percentage of net assets

as of March 31, 2024 (Unaudited)

CONCENTRATION BY COUNTRY based on domicile of issuer as

a percentage of long-term investments only

as of March 31, 2024 (Unaudited)

18

FMI International Fund II – Currency Unhedged

SCHEDULE OF INVESTMENTS

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| LONG-TERM INVESTMENTS — 95.7% | ||||||||

| COMMON STOCKS — 91.0% | ||||||||

Bermuda — 4.7% | ||||||||

| Miscellaneous Commercial Services — 2.4% | ||||||||

| Genpact Ltd. | 58,850 | $ | 1,939,108 | |||||

| Multi-Line Insurance — 2.3% | ||||||||

Arch Capital Group Ltd.(a) | 20,725 | 1,915,819 | ||||||

| Total Bermuda | 3,854,927 | |||||||

Britain — 27.1% | ||||||||

| Beverages: Alcoholic — 2.9% | ||||||||

| Diageo PLC | 63,900 | 2,364,438 | ||||||

| Beverages: Non-Alcoholic — 2.6% | ||||||||

| Coca-Cola Europacific Partners PLC | 30,000 | 2,098,500 | ||||||

| Electrical Products — 2.1% | ||||||||

| Smiths Group PLC | 84,000 | 1,741,192 | ||||||

| Electronics/Appliances — 2.6% | ||||||||

| Howden Joinery Group PLC | 184,400 | 2,110,858 | ||||||

| Finance/Rental/Leasing — 2.0% | ||||||||

| Ashtead Group PLC | 22,850 | 1,627,585 | ||||||

| Food: Specialty/Candy — 3.7% | ||||||||

| Greggs PLC | 82,000 | 2,974,400 | ||||||

| Household/Personal Care — 3.8% | ||||||||

| Unilever PLC | 62,350 | 3,130,080 | ||||||

| Major Banks — 2.2% | ||||||||

| Lloyds Banking Group PLC | 2,705,800 | 1,769,583 | ||||||

| Medical Specialties — 2.0% | ||||||||

| Smith & Nephew PLC | 129,850 | 1,625,588 | ||||||

| Trucks/Construction/Farm Machinery — 3.2% | ||||||||

| Weir Group PLC | 101,000 | 2,579,965 | ||||||

| Total Britain | 22,022,189 | |||||||

Curacao — 2.3% | ||||||||

| Contract Drilling — 2.3% | ||||||||

| Schlumberger Ltd. | 33,500 | 1,836,135 | ||||||

France — 14.1% | ||||||||

| Aerospace & Defense — 3.7% | ||||||||

| Safran S.A. | 13,200 | 2,989,436 | ||||||

| Regional Banks — 1.8% | ||||||||

| Edenred SE | 27,527 | 1,469,802 | ||||||

The accompanying notes to financial statements are an integral part of this schedule.

19

FMI International Fund II – Currency Unhedged

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| LONG-TERM INVESTMENTS — 95.7% (Continued) | ||||||||

| COMMON STOCKS — 91.0% (Continued) | ||||||||

France — 14.1% (Continued) | ||||||||

| Restaurants — 4.9% | ||||||||

| Sodexo S.A. | 46,600 | $ | 3,994,720 | |||||

| Wholesale Distributors — 3.7% | ||||||||

| Rexel S.A. | 113,150 | 3,056,512 | ||||||

| Total France | 11,510,470 | |||||||

Germany — 1.6% | ||||||||

| Medical/Nursing Services — 1.6% | ||||||||

| Fresenius Medical Care AG & Co. KGaA | 34,875 | 1,340,065 | ||||||

Hong Kong — 2.6% | ||||||||

| Tools & Hardware — 2.6% | ||||||||

| Techtronic Industries Co. Ltd. | 154,500 | 2,099,325 | ||||||

Ireland — 3.2% | ||||||||

| Airlines — 3.2% | ||||||||

| Ryanair Holdings PLC — SP-ADR | 18,000 | 2,620,620 | ||||||

Japan — 7.4% | ||||||||

| Chemicals: Specialty — 1.4% | ||||||||

| NOF Corp. | 81,000 | 1,109,310 | ||||||

| Computer Processing Hardware — 4.3% | ||||||||

| Sony Group Corp. | 41,200 | 3,532,930 | ||||||

| Electronic Equipment/Instruments — 1.7% | ||||||||

| Yokogawa Electric Corp. | 61,600 | 1,418,609 | ||||||

| Total Japan | 6,060,849 | |||||||

Jersey — 7.6% | ||||||||

| Wholesale Distributors — 7.6% | ||||||||

| Ferguson PLC | 28,375 | 6,208,286 | ||||||

Luxembourg — 5.4% | ||||||||

| Discount Stores — 5.4% | ||||||||

| B&M European Value Retail S.A. | 635,200 | 4,378,960 | ||||||

Netherlands — 3.2% | ||||||||

| Medical Specialties — 2.1% | ||||||||

Koninklijke Philips N.V.(a) | 86,500 | 1,731,213 | ||||||

| Miscellaneous Commercial Services — 1.1% | ||||||||

Pluxee N.V.(a) | 29,810 | 881,201 | ||||||

| Total Netherlands | 2,612,414 | |||||||

The accompanying notes to financial statements are an integral part of this schedule.

20

FMI International Fund II – Currency Unhedged

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2024 (Unaudited)

| Shares | Value | |||||||

| LONG-TERM INVESTMENTS — 95.7% (Continued) | ||||||||

| COMMON STOCKS — 91.0% (Continued) | ||||||||

Singapore — 2.3% | ||||||||

| Major Banks — 2.3% | ||||||||

| DBS Group Holdings Ltd. | 68,700 | $ | 1,833,453 | |||||

Switzerland — 5.2% | ||||||||

| Medical Distributors — 2.1% | ||||||||

| DKSH Holding AG | 24,375 | 1,659,461 | ||||||

| Pharmaceuticals: Major — 3.1% | ||||||||

| Roche Holding AG | 9,950 | 2,540,425 | ||||||

| Total Switzerland | 4,199,886 | |||||||

United States — 4.3% | ||||||||

| Other Consumer Services — 4.3% | ||||||||

| Booking Holdings Inc. | 970 | 3,519,044 | ||||||

TOTAL COMMON STOCKS (Cost $61,279,720) | 74,096,623 | |||||||

| PREFERRED STOCK — 4.7% | ||||||||

South Korea — 4.7% | ||||||||

| Telecommunications Equipment — 4.7% | ||||||||

| Samsung Electronics Co. Ltd. | 76,700 | 3,828,266 | ||||||

TOTAL PREFERRED STOCK (Cost $3,327,870) | 3,828,266 | |||||||

TOTAL LONG-TERM INVESTMENTS (Cost $64,607,590) | 77,924,889 | |||||||

| SHORT-TERM INVESTMENT — 4.4% | ||||||||

| Money Market Fund — 4.4% | ||||||||

First American Treasury Obligations Fund — Class X, 5.22%(b) | 3,542,930 | 3,542,930 | ||||||

TOTAL SHORT-TERM INVESTMENT (Cost $3,542,930) | 3,542,930 | |||||||

TOTAL INVESTMENTS — 100.1% (Cost $68,150,520) | 81,467,819 | |||||||

Liabilities in Excess of Other Assets — (0.1)% | (79,725 | ) | ||||||

| TOTAL NET ASSETS — 100.0% | $ | 81,388,094 | ||||||

Percentages are stated as a percent of net assets.

| PLC | Public Limited Company |

| SP-ADR | Sponsored American Depositary Receipt |

| (a) | Non-income producing security. |

| (b) | The rate shown represents the 7-day effective yield as of March 31, 2024. |

The accompanying notes to financial statements are an integral part of this schedule.

21

FMI International Fund II – Currency Unhedged

INDUSTRY SECTORS as a percentage of net assets

as of March 31, 2024 (Unaudited)

CONCENTRATION BY COUNTRY based on domicile of issuer as

a percentage of long-term investments only

as of March 31, 2024 (Unaudited)

22

(This Page Intentionally Left Blank.)

23

FMI Funds, Inc.

STATEMENTS OF ASSETS AND LIABILITIES

March 31, 2024 (Unaudited)

| FMI | |||||||||||||||||

| FMI | FMI | FMI | International | ||||||||||||||

| Common Stock | Large Cap | International | Fund II – Currency | ||||||||||||||

| Fund | Fund | Fund | Unhedged | ||||||||||||||

| ASSETS: | |||||||||||||||||

| Investments in securities, | |||||||||||||||||

at value(1) | $ | 2,065,052,154 | $ | 1,708,478,513 | $ | 4,833,952,175 | $ | 81,467,819 | |||||||||

| Cash | — | 89,300 | 223,767 | — | |||||||||||||

| Restricted cash | — | — | 640,000 | — | |||||||||||||

| Receivable from shareholders | |||||||||||||||||

| for purchases | 4,802,392 | 13,217,269 | 7,994,205 | 14,675 | |||||||||||||

| Dividends, interest and | |||||||||||||||||

| other receivables | 644,699 | 3,204,093 | 19,012,062 | 345,007 | |||||||||||||

| Receivable for | |||||||||||||||||

| investments sold | — | — | 826,899 | 32,146 | |||||||||||||

| Unrealized appreciation on | |||||||||||||||||

| forward currency contracts | — | — | 34,898,100 | — | |||||||||||||

| Prepaid directors’ retainer | 586 | 586 | 586 | 586 | |||||||||||||

| Prepaid expenses | 118,588 | 47,958 | 128,483 | 20,117 | |||||||||||||

| Total assets | $ | 2,070,618,419 | $ | 1,725,037,719 | $ | 4,897,676,277 | $ | 81,880,350 | |||||||||

| LIABILITIES: | |||||||||||||||||

| Payable to brokers | |||||||||||||||||

| for collateral received | $ | — | $ | — | $ | 640,000 | $ | — | |||||||||

| Payable to brokers | |||||||||||||||||

| for investments purchased | — | — | 25,919,841 | 437,758 | |||||||||||||

| Payable to shareholders | |||||||||||||||||

| for redemptions | 1,211,878 | 1,140,589 | 3,806,604 | — | |||||||||||||

| Payable for foreign | |||||||||||||||||

| currency transactions | — | — | 74,117 | 1,198 | |||||||||||||

| Payable to adviser | |||||||||||||||||

| for management fees | 1,182,191 | 723,843 | 2,645,211 | 31,790 | |||||||||||||

| Payable to custodian | 6,016 | 13,085 | 84,989 | 3,734 | |||||||||||||

| Unrealized depreciation on | |||||||||||||||||

| forward currency contracts | — | — | 50,208 | — | |||||||||||||

| Other liabilities | 62,970 | 147,648 | 180,037 | 17,776 | |||||||||||||

| Total liabilities | 2,463,055 | 2,025,165 | 33,401,007 | 492,256 | |||||||||||||

| Net assets | $ | 2,068,155,364 | $ | 1,723,012,554 | $ | 4,864,275,270 | $ | 81,388,094 | |||||||||

| NET ASSETS: | |||||||||||||||||

| Capital stock | $ | 1,400,210,192 | $ | 1,067,068,171 | $ | 4,296,893,725 | $ | 72,051,552 | |||||||||

| Total distributable | |||||||||||||||||

| earnings/(accumulated | |||||||||||||||||

| deficit) | 667,945,172 | 655,944,383 | 567,381,545 | 9,336,542 | |||||||||||||

| Net assets | $ | 2,068,155,364 | $ | 1,723,012,554 | $ | 4,864,275,270 | $ | 81,388,094 | |||||||||

The accompanying notes to financial statements are an integral part of these financial statements.

24

FMI Funds, Inc.

STATEMENTS OF ASSETS AND LIABILITIES (Continued)

March 31, 2024 (Unaudited)

| FMI | |||||||||||||||||

| FMI | FMI | FMI | International | ||||||||||||||

| Common Stock | Large Cap | International | Fund II – Currency | ||||||||||||||

| Fund | Fund | Fund | Unhedged | ||||||||||||||

| CALCULATION OF NET | |||||||||||||||||

| ASSET VALUE PER SHARE: | |||||||||||||||||

| Investor Class Shares: | |||||||||||||||||

| Net assets | $ | 772,213,580 | $ | 1,012,240,191 | $ | 1,215,940,656 | $ | — | |||||||||

| Shares outstanding | 20,775,354 | 62,466,107 | 33,944,634 | — | |||||||||||||

| Shares authorized | |||||||||||||||||

| ($0.0001 par value) | 300,000,000 | 300,000,000 | 300,000,000 | — | |||||||||||||

| Net asset value, offering and | |||||||||||||||||

| redemption price per share | $ | 37.17 | $ | 16.20 | $ | 35.82 | $ | — | |||||||||

| Institutional Class Shares: | |||||||||||||||||

| Net assets | $ | 1,295,941,784 | $ | 710,772,363 | $ | 3,648,334,614 | $ | 81,388,094 | |||||||||

| Shares outstanding | 34,808,558 | 43,988,665 | 101,401,628 | 3,740,145 | |||||||||||||

| Shares authorized | |||||||||||||||||

| ($0.0001 par value) | 300,000,000 | 300,000,000 | 300,000,000 | 300,000,000 | |||||||||||||

| Net asset value, offering and | |||||||||||||||||

| redemption price per share | $ | 37.23 | $ | 16.16 | $ | 35.98 | $ | 21.76 | |||||||||

(1) | Identified cost of investments | $ | 1,402,233,250 | $ | 1,114,202,721 | $ | 3,848,040,540 | $ | 68,150,520 | ||||||||

The accompanying notes to financial statements are an integral part of these financial statements.

25

FMI Funds, Inc.

STATEMENTS OF OPERATIONS

For the Six Month Period Ending March 31, 2024 (Unaudited)

| FMI | |||||||||||||||||

| FMI | FMI | FMI | International | ||||||||||||||

| Common Stock | Large Cap | International | Fund II – Currency | ||||||||||||||

| Fund | Fund | Fund | Unhedged | ||||||||||||||

| INCOME: | |||||||||||||||||

Dividends(1) | $ | 7,037,604 | $ | 10,410,704 | $ | 48,305,210 | $ | 839,990 | |||||||||

| Interest | 2,679,107 | 880,069 | 6,867,645 | 95,526 | |||||||||||||

| Total income | 9,716,711 | 11,290,773 | 55,172,855 | 935,516 | |||||||||||||

| EXPENSES: | |||||||||||||||||

| Management fees | 6,847,556 | 5,250,844 | 16,000,936 | 282,431 | |||||||||||||

| Shareholder servicing fees | |||||||||||||||||

| (Investor Class) | 318,141 | 583,097 | 614,983 | — | |||||||||||||

| Administration and | |||||||||||||||||

| accounting services | 185,402 | 175,209 | 438,135 | 16,290 | |||||||||||||

| Printing and postage expense | 39,178 | 66,008 | 363,867 | 3,104 | |||||||||||||

| Transfer agent fees | 39,794 | 39,617 | 55,100 | 9,161 | |||||||||||||

| Custodian fees | 27,175 | 32,067 | 246,241 | 14,455 | |||||||||||||

| Registration fees | 56,060 | 36,344 | 75,182 | 15,141 | |||||||||||||

| Board of Directors fees | 41,914 | 41,914 | 41,914 | 41,914 | |||||||||||||

| Professional fees | 19,469 | 20,292 | 22,392 | 19,182 | |||||||||||||

| Other expenses | 44,730 | 52,224 | 153,256 | 17,794 | |||||||||||||

| Total expenses | |||||||||||||||||

| before reimbursement | 7,619,419 | 6,297,616 | 18,012,006 | 419,472 | |||||||||||||

| Less expenses | |||||||||||||||||

| reimbursed by adviser | — | — | — | (80,555 | ) | ||||||||||||

| Net expenses | 7,619,419 | 6,297,616 | 18,012,006 | 338,917 | |||||||||||||

| NET INVESTMENT INCOME | 2,097,292 | 4,993,157 | 37,160,849 | 596,599 | |||||||||||||

The accompanying notes to financial statements are an integral part of these financial statements.

26

FMI Funds, Inc.

STATEMENTS OF OPERATIONS (Continued)

For the Six Month Period Ending March 31, 2024 (Unaudited)

| FMI | ||||||||||||||||

| FMI | FMI | FMI | International | |||||||||||||

| Common Stock | Large Cap | International | Fund II – Currency | |||||||||||||

| Fund | Fund | Fund | Unhedged | |||||||||||||

| NET REALIZED GAIN (LOSS) | ||||||||||||||||

| ON INVESTMENTS: | ||||||||||||||||

| Securities | $ | 8,354,859 | $ | 80,537,717 | $ | 50,875,717 | $ | 794,989 | ||||||||

| Forward currency contracts | — | — | 116,170,067 | — | ||||||||||||

| Foreign currency transactions | — | — | 6,973,858 | (4,012 | ) | |||||||||||

| NET REALIZED GAIN (LOSS) | ||||||||||||||||

| ON INVESTMENTS | 8,354,859 | 80,537,717 | 174,019,642 | 790,977 | ||||||||||||

| NET CHANGE IN UNREALIZED | ||||||||||||||||

| APPRECIATION/DEPRECIATION | ||||||||||||||||

| ON INVESTMENTS: | ||||||||||||||||

| Securities | 345,620,144 | 247,082,099 | 468,228,821 | 8,074,177 | ||||||||||||

| Forward currency contracts | — | — | (154,437,854 | ) | — | |||||||||||

| Foreign currency transactions | — | — | 104,951 | 4,834 | ||||||||||||

| NET CHANGE IN UNREALIZED | ||||||||||||||||

| APPRECIATION/DEPRECIATION | ||||||||||||||||

| ON INVESTMENTS | 345,620,144 | 247,082,099 | 313,895,918 | 8,079,011 | ||||||||||||

| NET GAIN (LOSS) | ||||||||||||||||

| ON INVESTMENTS | 353,975,003 | 327,619,816 | 487,915,560 | 8,869,988 | ||||||||||||

| NET INCREASE (DECREASE) IN | ||||||||||||||||

| NET ASSETS RESULTING | ||||||||||||||||

| FROM OPERATIONS | $ | 356,072,295 | $ | 332,612,973 | $ | 525,076,409 | $ | 9,466,587 | ||||||||

(1) Net withholding taxes | $ | — | $ | (24,301 | ) | $ | (5,049,855 | ) | $ | (88,991 | ) | |||||

The accompanying notes to financial statements are an integral part of these financial statements.

27

FMI Common Stock Fund

STATEMENTS OF CHANGES IN NET ASSETS

For the Six Month Period Ending March 31, 2024 (Unaudited) and For the Year Ended September 30, 2023

| 2024 | 2023 | ||||||||

| OPERATIONS: | |||||||||

| Net investment income | $ | 2,097,292 | $ | 5,338,663 | |||||

| Net realized gain (loss) on investments | 8,354,859 | 49,844,575 | |||||||

| Net change in unrealized appreciation/depreciation | |||||||||

| on investments | 345,620,144 | 186,175,485 | |||||||

| Net increase (decrease) in net assets from operations | 356,072,295 | 241,358,723 | |||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM: | |||||||||

| Investor Class | (17,421,723 | ) | (24,761,425 | ) | |||||

| Institutional Class | (31,829,415 | ) | (43,252,225 | ) | |||||

| Total distributions (Note 8) | (49,251,138 | ) | (68,013,650 | ) | |||||

| FUND SHARE ACTIVITIES: | |||||||||

| Net increase (decrease) in net assets | |||||||||

| derived from Fund share activities (Note 9) | 304,953,175 | 336,093,353 | |||||||

| TOTAL INCREASE (DECREASE) | 611,774,332 | 509,438,426 | |||||||

| NET ASSETS AT THE BEGINNING OF THE PERIOD | 1,456,381,032 | 946,942,606 | |||||||

| NET ASSETS AT THE END OF THE PERIOD | $ | 2,068,155,364 | $ | 1,456,381,032 | |||||

| FUND SHARE TRANSACTIONS: | |||||||||

| Net increase (decrease) in shares outstanding (Note 9) | 9,126,859 | 11,064,838 | |||||||

The accompanying notes to financial statements are an integral part of these financial statements.

28

FMI Large Cap Fund

STATEMENTS OF CHANGES IN NET ASSETS

For the Six Month Period Ending March 31, 2024 (Unaudited) and For the Year Ended September 30, 2023

| 2024 | 2023 | ||||||||

| OPERATIONS: | |||||||||

| Net investment income | $ | 4,993,157 | $ | 12,424,663 | |||||

| Net realized gain (loss) on investments | 80,537,717 | 224,712,914 | |||||||

| Net change in unrealized appreciation/depreciation | |||||||||

| on investments | 247,082,099 | 123,293,235 | |||||||

| Net increase (decrease) in net assets from operations | 332,612,973 | 360,430,812 | |||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM: | |||||||||

| Investor Class | (94,753,313 | ) | (195,562,163 | ) | |||||

| Institutional Class | (67,059,664 | ) | (141,809,940 | ) | |||||

| Total distributions (Note 8) | (161,812,977 | ) | (337,372,103 | ) | |||||

| FUND SHARE ACTIVITIES: | |||||||||

| Net increase (decrease) in net assets | |||||||||

| derived from Fund share activities (Note 9) | (66,192,598 | ) | (476,826,899 | ) | |||||

| TOTAL INCREASE (DECREASE) | 104,607,398 | (453,768,190 | ) | ||||||

| NET ASSETS AT THE BEGINNING OF THE PERIOD | 1,618,405,156 | 2,072,173,346 | |||||||

| NET ASSETS AT THE END OF THE PERIOD | $ | 1,723,012,554 | $ | 1,618,405,156 | |||||

| FUND SHARE TRANSACTIONS: | |||||||||

| Net increase (decrease) in shares outstanding (Note 9) | (4,355,574 | ) | (27,616,579 | ) | |||||

The accompanying notes to financial statements are an integral part of these financial statements.

29

FMI International Fund

STATEMENTS OF CHANGES IN NET ASSETS

For the Six Month Period Ending March 31, 2024 (Unaudited) and For the Year Ended September 30, 2023

| 2024 | 2023 | ||||||||

| OPERATIONS: | |||||||||

| Net investment income | $ | 37,160,849 | $ | 68,966,866 | |||||

| Net realized gain (loss) on investments | 174,019,642 | (216,154,731 | ) | ||||||

| Net change in unrealized appreciation/depreciation | |||||||||

| on investments | 313,895,918 | 1,044,743,127 | |||||||

| Net increase (decrease) in net assets from operations | 525,076,409 | 897,555,262 | |||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM: | |||||||||

| Investor Class | — | (116,170,330 | ) | ||||||

| Institutional Class | — | (331,682,134 | ) | ||||||

| Total distributions (Note 8) | — | (447,852,464 | ) | ||||||

| FUND SHARE ACTIVITIES: | |||||||||

| Net increase (decrease) in net assets | |||||||||

| derived from Fund share activities (Note 9) | 253,629,401 | 665,106,078 | |||||||

| TOTAL INCREASE (DECREASE) | 778,705,810 | 1,114,808,876 | |||||||

| NET ASSETS AT THE BEGINNING OF THE PERIOD | 4,085,569,460 | 2,970,760,584 | |||||||

| NET ASSETS AT THE END OF THE PERIOD | $ | 4,864,275,270 | $ | 4,085,569,460 | |||||

| FUND SHARE TRANSACTIONS: | |||||||||

| Net increase (decrease) in shares outstanding (Note 9) | 7,661,539 | 22,790,348 | |||||||

The accompanying notes to financial statements are an integral part of these financial statements.

30

FMI International Fund II – Currency Unhedged

STATEMENTS OF CHANGES IN NET ASSETS

For the Six Month Period Ending March 31, 2024 (Unaudited) and For the Year Ended September 30, 2023

| 2024 | 2023 | ||||||||

| OPERATIONS: | |||||||||

| Net investment income | $ | 596,599 | $ | 1,166,440 | |||||

| Net realized gain (loss) on investments | 790,977 | (3,305,489 | ) | ||||||

| Net change in unrealized appreciation/depreciation | |||||||||

| on investments | 8,079,011 | 18,801,887 | |||||||

| Net increase (decrease) in net assets from operations | 9,466,587 | 16,662,838 | |||||||

| DISTRIBUTIONS TO SHAREHOLDERS FROM: | |||||||||

| Institutional Class | (1,165,735 | ) | (830,255 | ) | |||||

| Total distributions (Note 8) | (1,165,735 | ) | (830,255 | ) | |||||

| FUND SHARE ACTIVITIES: | |||||||||

| Net increase (decrease) in net assets | |||||||||

| derived from Fund share activities (Note 9) | 1,898,831 | 6,370,101 | |||||||

| TOTAL INCREASE (DECREASE) | 10,199,683 | 22,202,684 | |||||||

| NET ASSETS AT THE BEGINNING OF THE PERIOD | 71,188,411 | 48,985,727 | |||||||

| NET ASSETS AT THE END OF THE PERIOD | $ | 81,388,094 | $ | 71,188,411 | |||||

| FUND SHARE TRANSACTIONS: | |||||||||

| Net increase (decrease) in shares outstanding (Note 9) | 92,049 | 336,674 | |||||||

The accompanying notes to financial statements are an integral part of these financial statements.

31

FMI Common Stock Fund

FINANCIAL HIGHLIGHTS

(Selected data for each share of the Fund outstanding throughout each period)

Investor Class

| (Unaudited) | ||||||||||||||||||||||||

| For the | ||||||||||||||||||||||||

| Six Month | ||||||||||||||||||||||||

| Period Ending | ||||||||||||||||||||||||

| March 31, | Years Ended September 30, | |||||||||||||||||||||||

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | |||||||||||||||||||

| PER SHARE OPERATING | ||||||||||||||||||||||||

| PERFORMANCE: | ||||||||||||||||||||||||

| Net asset value, | ||||||||||||||||||||||||

| beginning of period | $ | 31.31 | $ | 26.72 | $ | 33.23 | $ | 22.25 | $ | 26.39 | $ | 27.55 | ||||||||||||

| Income from | ||||||||||||||||||||||||

| investment operations: | ||||||||||||||||||||||||

| Net investment | ||||||||||||||||||||||||

income (loss)(1) | 0.03 | 0.11 | 0.03 | 0.08 | 0.17 | 0.15 | ||||||||||||||||||

| Net realized and unrealized | ||||||||||||||||||||||||

| gain (loss) on investments | 6.80 | 6.35 | (2.57 | ) | 11.11 | (3.02 | ) | 0.94 | ||||||||||||||||

| Total from | ||||||||||||||||||||||||

| investment operations | 6.83 | 6.46 | (2.54 | ) | 11.19 | (2.85 | ) | 1.09 | ||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

| Distributions from | ||||||||||||||||||||||||

| net investment income | (0.09 | ) | (0.04 | ) | (0.11 | ) | (0.21 | ) | (0.11 | ) | (0.10 | ) | ||||||||||||

| Distributions from | ||||||||||||||||||||||||

| net realized gains | (0.88 | ) | (1.83 | ) | (3.86 | ) | — | (1.18 | ) | (2.15 | ) | |||||||||||||

| Total from distributions | (0.97 | ) | (1.87 | ) | (3.97 | ) | (0.21 | ) | (1.29 | ) | (2.25 | ) | ||||||||||||

| Net asset value, end of period | $ | 37.17 | $ | 31.31 | $ | 26.72 | $ | 33.23 | $ | 22.25 | $ | 26.39 | ||||||||||||

| TOTAL RETURN | 22.02 | %(2) | 25.08 | % | (9.10 | %) | 50.49 | % | (11.51 | %) | 5.28 | % | ||||||||||||

| RATIOS/SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of | ||||||||||||||||||||||||

| period (in 000’s $) | 772,214 | 531,535 | 357,946 | 423,286 | 345,428 | 529,234 | ||||||||||||||||||

| Ratio of expenses to | ||||||||||||||||||||||||

| average net assets | 0.95 | %(3) | 0.99 | % | 1.00 | % | 1.01 | % | 1.02 | % | 1.02 | % | ||||||||||||

| Ratio of net investment | ||||||||||||||||||||||||

| income (loss) to | ||||||||||||||||||||||||

| average net assets | 0.18 | %(3) | 0.35 | % | 0.09 | % | 0.28 | % | 0.71 | % | 0.59 | % | ||||||||||||

Portfolio turnover rate(4) | 8 | %(2) | 23 | % | 36 | % | 29 | % | 32 | % | 28 | % | ||||||||||||

| (1) | Net investment income (loss) per share was calculated using average shares outstanding. |

| (2) | Not annualized. |

| (3) | Annualized. |

| (4) | Portfolio turnover rate is disclosed for the Fund as a whole. |

The accompanying notes to financial statements are an integral part of these financial statements.

32

FMI Common Stock Fund

FINANCIAL HIGHLIGHTS

(Selected data for each share of the Fund outstanding throughout each period)

Institutional Class

| (Unaudited) | ||||||||||||||||||||||||

| For the | ||||||||||||||||||||||||

| Six Month | ||||||||||||||||||||||||

| Period Ending | ||||||||||||||||||||||||

| March 31, | Years Ended September 30, | |||||||||||||||||||||||

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | |||||||||||||||||||

| PER SHARE OPERATING | ||||||||||||||||||||||||

| PERFORMANCE: | ||||||||||||||||||||||||

| Net asset value, | ||||||||||||||||||||||||

| beginning of period | $ | 31.37 | $ | 26.77 | $ | 33.29 | $ | 22.28 | $ | 26.42 | $ | 27.59 | ||||||||||||

| Income from | ||||||||||||||||||||||||

| investment operations: | ||||||||||||||||||||||||

| Net investment | ||||||||||||||||||||||||

income (loss)(1) | 0.05 | 0.15 | 0.07 | 0.12 | 0.20 | 0.18 | ||||||||||||||||||

| Net realized and unrealized | ||||||||||||||||||||||||

| gain (loss) on investments | 6.81 | 6.35 | (2.58 | ) | 11.12 | (3.02 | ) | 0.93 | ||||||||||||||||

| Total from | ||||||||||||||||||||||||

| investment operations | 6.86 | 6.50 | (2.51 | ) | 11.24 | (2.82 | ) | 1.11 | ||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

| Distributions from | ||||||||||||||||||||||||

| net investment income | (0.12 | ) | (0.07 | ) | (0.15 | ) | (0.23 | ) | (0.14 | ) | (0.13 | ) | ||||||||||||

| Distributions from | ||||||||||||||||||||||||

| net realized gains | (0.88 | ) | (1.83 | ) | (3.86 | ) | — | (1.18 | ) | (2.15 | ) | |||||||||||||

| Total from distributions | (1.00 | ) | (1.90 | ) | (4.01 | ) | (0.23 | ) | (1.32 | ) | (2.28 | ) | ||||||||||||

| Net asset value, end of period | $ | 37.23 | $ | 31.37 | $ | 26.77 | $ | 33.29 | $ | 22.28 | $ | 26.42 | ||||||||||||

| TOTAL RETURN | 22.08 | %(2) | 25.22 | % | (8.99 | %) | 50.68 | % | (11.41 | %) | 5.40 | % | ||||||||||||

| RATIOS/SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of | ||||||||||||||||||||||||

| period (in 000’s $) | 1,295,942 | 924,846 | 588,996 | 516,985 | 344,811 | 448,262 | ||||||||||||||||||

| Ratio of expenses to | ||||||||||||||||||||||||

| average net assets | 0.84 | %(3) | 0.87 | % | 0.89 | % | 0.90 | % | 0.90 | % | 0.91 | % | ||||||||||||

| Ratio of net investment | ||||||||||||||||||||||||

| income (loss) to | ||||||||||||||||||||||||

| average net assets | 0.28 | %(3) | 0.48 | % | 0.22 | % | 0.39 | % | 0.84 | % | 0.71 | % | ||||||||||||

Portfolio turnover rate(4) | 8 | %(2) | 23 | % | 36 | % | 29 | % | 32 | % | 28 | % | ||||||||||||

| (1) | Net investment income (loss) per share was calculated using average shares outstanding. |

| (2) | Not annualized. |

| (3) | Annualized. |

| (4) | Portfolio turnover rate is disclosed for the Fund as a whole. |

The accompanying notes to financial statements are an integral part of these financial statements.

33

FMI Large Cap Fund

FINANCIAL HIGHLIGHTS

(Selected data for each share of the Fund outstanding throughout each period)

Investor Class

| (Unaudited) | ||||||||||||||||||||||||

| For the | ||||||||||||||||||||||||

| Six Month | ||||||||||||||||||||||||

| Period Ending | ||||||||||||||||||||||||

| March 31, | Years Ended September 30, | |||||||||||||||||||||||

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | |||||||||||||||||||

| PER SHARE OPERATING | ||||||||||||||||||||||||

| PERFORMANCE: | ||||||||||||||||||||||||

| Net asset value, | ||||||||||||||||||||||||

| beginning of period | $ | 14.62 | $ | 14.98 | $ | 20.96 | $ | 18.81 | $ | 20.14 | $ | 22.85 | ||||||||||||

| Income from | ||||||||||||||||||||||||

| investment operations: | ||||||||||||||||||||||||

| Net investment | ||||||||||||||||||||||||

income (loss)(1) | 0.04 | 0.09 | 0.11 | 0.15 | 0.18 | 0.25 | ||||||||||||||||||

| Net realized and unrealized | ||||||||||||||||||||||||

| gain (loss) on investments | 3.11 | 2.64 | (2.73 | ) | 4.25 | 0.03 | (5) | 0.55 | ||||||||||||||||

| Total from | ||||||||||||||||||||||||

| investment operations | 3.15 | 2.73 | (2.62 | ) | 4.40 | 0.21 | 0.80 | |||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

| Distributions from | ||||||||||||||||||||||||

| net investment income | (0.14 | ) | (0.11 | ) | (0.16 | ) | (0.30 | ) | (0.17 | ) | (0.28 | ) | ||||||||||||

| Distributions from | ||||||||||||||||||||||||

| net realized gains | (1.43 | ) | (2.98 | ) | (3.20 | ) | (1.95 | ) | (1.37 | ) | (3.23 | ) | ||||||||||||

| Total from distributions | (1.57 | ) | (3.09 | ) | (3.36 | ) | (2.25 | ) | (1.54 | ) | (3.51 | ) | ||||||||||||

| Net asset value, end of period | $ | 16.20 | $ | 14.62 | $ | 14.98 | $ | 20.96 | $ | 18.81 | $ | 20.14 | ||||||||||||

| TOTAL RETURN | 22.67 | %(2) | 19.95 | % | (15.86 | %) | 24.48 | % | 0.71 | % | 5.72 | % | ||||||||||||

| RATIOS/SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of | ||||||||||||||||||||||||

| period (in 000’s $) | 1,012,240 | 919,253 | 1,001,682 | 1,422,451 | 1,475,504 | 2,337,118 | ||||||||||||||||||

| Ratio of expenses to | ||||||||||||||||||||||||

| average net assets | 0.83 | %(3) | 0.84 | % | 0.83 | % | 0.82 | % | 0.81 | % | 0.82 | % | ||||||||||||

| Ratio of net investment | ||||||||||||||||||||||||

| income (loss) to | ||||||||||||||||||||||||

| average net assets | 0.57 | %(3) | 0.63 | % | 0.60 | % | 0.72 | % | 0.99 | % | 1.25 | % | ||||||||||||

Portfolio turnover rate(4) | 7 | %(2) | 14 | % | 25 | % | 17 | % | 28 | % | 20 | % | ||||||||||||

| (1) | Net investment income (loss) per share was calculated using average shares outstanding. |

| (2) | Not annualized. |

| (3) | Annualized. |

| (4) | Portfolio turnover rate is disclosed for the Fund as a whole. |

| (5) | Realized and unrealized gain (loss) per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the year, and may not reconcile with the aggregate gains on the Statement of Operations due to share transactions for the year. |

The accompanying notes to financial statements are an integral part of these financial statements.

34

FMI Large Cap Fund

FINANCIAL HIGHLIGHTS

(Selected data for each share of the Fund outstanding throughout each period)

Institutional Class

| (Unaudited) | ||||||||||||||||||||||||

| For the | ||||||||||||||||||||||||

| Six Month | ||||||||||||||||||||||||

| Period Ending | ||||||||||||||||||||||||

| March 31, | Years Ended September 30, | |||||||||||||||||||||||

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | |||||||||||||||||||

| PER SHARE OPERATING | ||||||||||||||||||||||||

| PERFORMANCE: | ||||||||||||||||||||||||

| Net asset value, | ||||||||||||||||||||||||

| beginning of period | $ | 14.59 | $ | 14.96 | $ | 20.94 | $ | 18.80 | $ | 20.13 | $ | 22.85 | ||||||||||||

| Income from | ||||||||||||||||||||||||

| investment operations: | ||||||||||||||||||||||||

| Net investment | ||||||||||||||||||||||||

income (loss)(1) | 0.05 | 0.11 | 0.14 | 0.18 | 0.21 | 0.25 | ||||||||||||||||||

| Net realized and unrealized | ||||||||||||||||||||||||

| gain (loss) on investments | 3.11 | 2.63 | (2.73 | ) | 4.24 | 0.02 | (5) | 0.58 | ||||||||||||||||

| Total from | ||||||||||||||||||||||||

| investment operations | 3.16 | 2.74 | (2.59 | ) | 4.42 | 0.23 | 0.83 | |||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

| Distributions from | ||||||||||||||||||||||||

| net investment income | (0.16 | ) | (0.13 | ) | (0.19 | ) | (0.33 | ) | (0.19 | ) | (0.32 | ) | ||||||||||||

| Distributions from | ||||||||||||||||||||||||

| net realized gains | (1.43 | ) | (2.98 | ) | (3.20 | ) | (1.95 | ) | (1.37 | ) | (3.23 | ) | ||||||||||||

| Total from distributions | (1.59 | ) | (3.11 | ) | (3.39 | ) | (2.28 | ) | (1.56 | ) | (3.55 | ) | ||||||||||||

| Net asset value, end of period | $ | 16.16 | $ | 14.59 | $ | 14.96 | $ | 20.94 | $ | 18.80 | $ | 20.13 | ||||||||||||

| TOTAL RETURN | 22.82 | %(2) | 20.07 | % | (15.73 | %) | 24.63 | % | 0.84 | % | 5.89 | % | ||||||||||||

| RATIOS/SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of | ||||||||||||||||||||||||

| period (in 000’s $) | 710,772 | 699,152 | 1,070,491 | 1,788,717 | 1,924,284 | 2,652,783 | ||||||||||||||||||

| Ratio of expenses to | ||||||||||||||||||||||||

| average net assets | 0.71 | %(3) | 0.71 | % | 0.69 | % | 0.68 | % | 0.67 | % | 0.68 | % | ||||||||||||

| Ratio of net investment | ||||||||||||||||||||||||

| income (loss) to | ||||||||||||||||||||||||

| average net assets | 0.69 | %(3) | 0.77 | % | 0.73 | % | 0.85 | % | 1.13 | % | 1.26 | % | ||||||||||||

Portfolio turnover rate(4) | 7 | %(2) | 14 | % | 25 | % | 17 | % | 28 | % | 20 | % | ||||||||||||

| (1) | Net investment income (loss) per share was calculated using average shares outstanding. |

| (2) | Not annualized. |

| (3) | Annualized. |

| (4) | Portfolio turnover rate is disclosed for the Fund as a whole. |

| (5) | Realized and unrealized gain (loss) per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the year, and may not reconcile with the aggregate gains on the Statement of Operations due to share transactions for the year. |

The accompanying notes to financial statements are an integral part of these financial statements.

35

FMI International Fund

FINANCIAL HIGHLIGHTS

(Selected data for each share of the Fund outstanding throughout each period)

Investor Class

| (Unaudited) | ||||||||||||||||||||||||

| For the | ||||||||||||||||||||||||

| Six Month | ||||||||||||||||||||||||

| Period Ending | ||||||||||||||||||||||||

| March 31, | Years Ended September 30, | |||||||||||||||||||||||

| 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | |||||||||||||||||||

| PER SHARE OPERATING | ||||||||||||||||||||||||

| PERFORMANCE: | ||||||||||||||||||||||||

| Net asset value, | ||||||||||||||||||||||||

| beginning of period | $ | 31.90 | $ | 28.25 | $ | 35.36 | $ | 27.69 | $ | 31.89 | $ | 33.80 | ||||||||||||

| Income from | ||||||||||||||||||||||||

| investment operations: | ||||||||||||||||||||||||

| Net investment | ||||||||||||||||||||||||