UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07831

FMI Funds, Inc.

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

100 East Wisconsin Avenue

Suite 2200

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

John S. Brandser

Fiduciary Management, Inc.

100 East Wisconsin Avenue

Suite 2200

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 226-4545

Registrant's telephone number, including area code

Date of fiscal year end: September 30

Date of reporting period: March 31, 2022

Item 1. Reports to Stockholders.

| (a) |

SEMI-ANNUAL REPORT

March 31, 2022

FMI Large Cap Fund

Investor Class (Ticker Symbol: FMIHX)

Institutional Class (Ticker Symbol: FMIQX)

FMI Common Stock Fund

Investor Class (Ticker Symbol: FMIMX)

Institutional Class (Ticker Symbol: FMIUX)

FMI International Fund

Investor Class (Ticker Symbol: FMIJX)

Institutional Class (Ticker Symbol: FMIYX)

FMI International Fund II – Currency Unhedged

Investor Class (Not Available For Sale)

Institutional Class (Ticker Symbol: FMIFX)

| |

FMI Funds, Inc. | |

| Advised by Fiduciary Management, Inc. | |

| www.fmifunds.com | |

FMI Funds, Inc.

TABLE OF CONTENTS

| FMI Large Cap Fund | |||

| Shareholder Letter | 1 | ||

| Schedule of Investments | 9 | ||

| Industry Sectors | 11 | ||

| FMI Common Stock Fund | |||

| Shareholder Letter | 12 | ||

| Schedule of Investments | 19 | ||

| Industry Sectors | 21 | ||

| FMI International Fund and FMI International Fund II – Currency Unhedged | |||

| Shareholder Letter | 22 | ||

| FMI International Fund | |||

| Schedule of Investments | 30 | ||

| Schedule of Forward Currency Contracts | 34 | ||

| Industry Sectors | 35 | ||

| Concentration by Country | 35 | ||

| FMI International Fund II – Currency Unhedged | |||

| Schedule of Investments | 36 | ||

| Industry Sectors | 40 | ||

| Concentration by Country | 40 | ||

| Financial Statements | |||

| Statements of Assets and Liabilities | 42 | ||

| Statements of Operations | 44 | ||

| Statements of Changes in Net Assets | 46 | ||

| Financial Highlights | 50 | ||

| Notes to Financial Statements | 57 | ||

| Expense Example | 69 | ||

| Advisory Agreements | 71 | ||

| Disclosure Information | 78 | ||

| Additional Information | 81 | ||

FMI

Large Cap

Fund

(unaudited)

| March 31, 2022 |

Dear Fellow Shareholders:

The FMI Large Cap Fund (“Fund”) declined 6.16%1 in the March quarter compared to a 4.60% drop in the Standard & Poor’s 500 Index, and 0.74% loss in the Russell 1000 Value Index. Areas where the Fund had little exposure such as Energy & Non-Energy Minerals, and our overweighting in Producer Manufacturing, explain the lion’s share of the difference between the Fund and the Russell 1000 Value. Compared to the S&P 500, sectors that helped performance included Finance, Technology Services, and Commercial Services. Sectors that detracted included Producer Manufacturing, Health Technology, and Energy Minerals. Berkshire Hathaway Inc. — Cl B, Omnicom Group Inc., and Dollar Tree Inc. added to performance in the quarter while Masco Corp., Quest Diagnostics Inc., and PPG Industries Inc. detracted. Since the Russian invasion of Ukraine on February 24, the market has moved in somewhat of a barbell fashion, with Energy/Non-Energy Minerals and Industrial Service companies tied to these segments driving the value trade, while many speculative growth names also moved up sharply.

Quarterly investment letters across the land will be focused on the Russian invasion and what it means for geopolitical stability, supply chains, energy, inflation, globalization, economic growth, and interest rates. All of these elements were in play long before the invasion. Although markets have largely ignored it, China and Russia substantially increased their belligerence toward the U.S. (and the “West”) in recent years. A new two-pronged cold war with China and Russia has been underway for some time. Historically, sanctions have not been terribly effective, as authoritarian leaders (Mussolini, Castro, Kim Jung Un/IL, Chavez, Maduro, Khomeini) survived by controlling the narrative and crushing popular dissent. Maybe the coordinated effort of a surprisingly large number of Russian trading partners and central banks will prove to be the exception. We don’t expect Putin to change course because of sanctions or exposure of war atrocities, but perhaps Xi Jinping has taken notice and pauses any moves on Taiwan. On a gross basis, China exported $577 billion to the U.S. and $701 billion to the European Union in 2021. China can ill afford a trade war with the West, although the reverse is also true. The war has already had impacts on commodities, intermediate products, and the supply chain. Energy and mineral prices have blown out. Inflation, which started rising rapidly twelve months ago, remains at a 40-year high. For at least three decades, the world’s inflation picture has benefitted from a giant Chinese labor arbitrage that is now in the rearview mirror, as the Chinese working-age population is no longer growing, and wages there have risen markedly. Additionally, both politically and strategically, the West will need to secure more production domestically or with friendly regimes – whether it be in energy, materials, or manufactured goods – adding to inflation pressure in the short-to-intermediate term. While the end of the pandemic and possible slowing of the economy may bring inflation down somewhat, we cannot avoid the ramifications tied to years of quantitative easing, rapid money supply growth, and unprecedented fiscal expansion. The market hasn’t figured this out yet, in fact,

_______________

1 | The FMI Large Cap Fund Investor Class (FMIHX) and the FMI Large Cap Fund Institutional Class (FMIQX) had a return of -6.16% and -6.12%, respectively, for the first quarter of 2022. |

1

speculative activity has reemerged in recent weeks. Despite this, if higher interest rates and inflation characterize the landscape for the next several years, it likely spells the end of the era of unbridled speculation and high multiples. We believe the Fund is well-positioned to thrive in the tougher world that may be upon us.

Interest Rates and Inflation

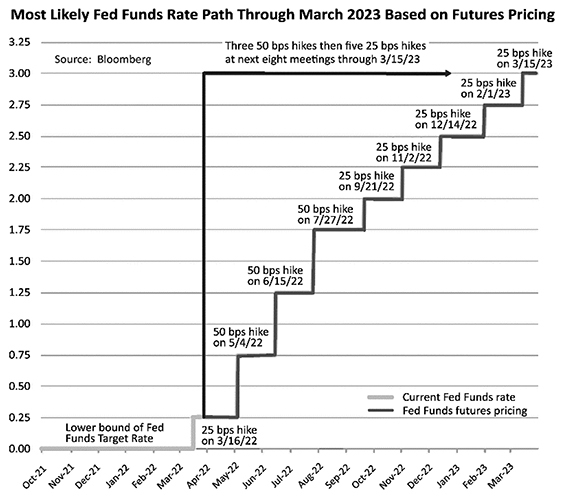

Below is the latest illustration of the expected Fed Funds Rate to March 2023. If these moves come to pass, the recent 0% Fed Funds Rate would be 3%.

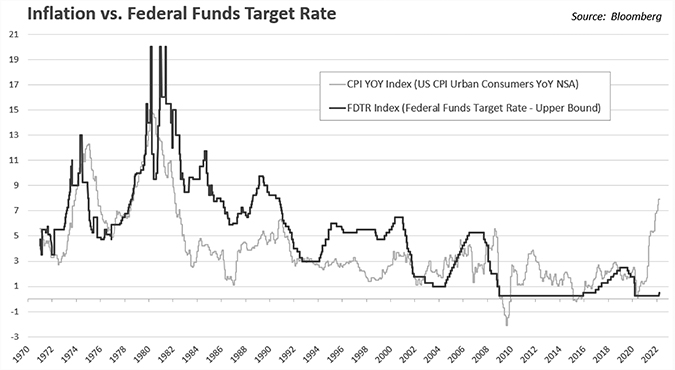

Now observe the below chart showing the Fed Funds Rate and the inflation rate over fifty years. Tracking the Federal Funds Target Rate back to 1971, the average inflation rate as measured by CPI from 1971 until today is 3.9%.

2

Inflation Episode 1

The CPI went from 2.7% to 12.3% from the 3rd quarter of 1972 to the 4th quarter of 1974. The Fed Funds rate went from 5% to 13% from the 3rd quarter of 1972 to the 2nd quarter of 1974. From the 4th quarter of 1974 to the 4th quarter of 1976, CPI went from 12.3% to 4.9%.

Inflation Episode 2

CPI went from 4.9% to 14.8% from the 4th quarter of 1976 to the 1st quarter of 1980. Fed Funds went from 6% to 20% from the 4th quarter of 1976 to the 1st quarter of 1980. Inflation finally got to a more normal level by the 4th quarter of 1982. From the 1st quarter of 1980 to the 4th quarter of 1982, CPI averaged 9.7% while the Fed Funds target rate averaged 13.6%.

Inflation Episode 3

CPI went from 1.1% to 6.2% from the 4th quarter of 1986 to the 3rd quarter of 1990. Fed Funds went from 6% to 9.75% from the 4th quarter of 1986 to the 1st quarter of 1989. CPI from the 3rd quarter of 1990 to the 4th quarter of 1991 went from 6.2% to 3.1%. CPI was under control from 1991 until the financial crisis in 2008, averaging 2.7% while the Fed Funds target rate averaged 3.95%.

Virtually every time inflation spiked over the past fifty years, the Fed Funds Rate went higher than the inflation rate to tame it. How many investors today believe the Fed Funds Rate is on a path toward 8%? Inflation is taking longer to stabilize than expected and Chairman Powell is pointing toward short-term supply chain problems, or transient war impacts. The stock and bond markets seem to agree it’s a temporary challenge. As of 3/31/22 the S&P 500 is only 5.2% off its high, and the bond market (using inflation-adjusted Treasury securities) expects five-year inflation to drop dramatically. A recent study from AllianceBernstein concluded that only 1.5 percentage points of the 7.9% inflation rate is likely due to one-time supply chain effects. More traditional monetary factors appear to be the culprit. In a recent piece from The Wall Street Journal by Hanke and Hanlon,2 titled, “Jerome Powell is Wrong. Printing Money Causes Inflation,” the authors point out that in two separate communications with Congress over the past year, Powell said the connection between money supply growth and inflation ended 40 years ago. The below chart throws cold water on these assertions.

_______________

2 | Steve Hanke, professor, and Nicholas Hanlon, chief of staff, at the Johns Hopkins Institute of Applied Economics. |

3

Why is the market not yet buying the high inflation, higher rate thesis? One possible explanation gaining traction is the notion that we are headed for a recession, complete with demand destruction and falling prices, or at least a much slower growth rate in the CPI. Given the downward action in many stocks recently (aside from energy and commodities), this seems plausible. Yield curves have flattened in recent weeks. Inverted yield curves (short-term rates exceeding long-term rates) have a better-than-average track record of predicting recessions. Talking to our companies, however, and observing demand across many industries, it does not feel like a downturn is imminent. Perhaps stagflation is on the horizon. Whether underlying economic growth remains solid or weakens enough to cause a recession, we do not see inflation returning to 2% anytime soon. Moreover, with quantitative easing ending, Fed Funds rising, and bond investors wanting more compensation for the risk of inflation, longer maturity interest rates may continue to normalize. As we indicated in our letter of December 31, 2021, the 10-Year Treasury’s median yield since 1957 is 5.38% compared to 2.34% today (up from 1.51% as of 12/31/21). It is hard to imagine P/E multiples remaining near all-time highs with the discount rate escalating.

Market Behavior

The value move in the market this year is mostly related to hydrocarbon exploration and production stocks, as well as other commodity-oriented equities. The Fund has little-to-no exposure to these sectors, as over long periods of time, most of the companies in these sectors have proven unable to earn their cost of capital and are highly volatile. These stocks periodically race higher, but elevated commodity prices almost always spur a supply response that typically ends the rally. Higher raw material prices have temporarily affected a few of our stocks, but these companies have good market power and are already raising prices aggressively. We expect within a few quarters that margins will recover.

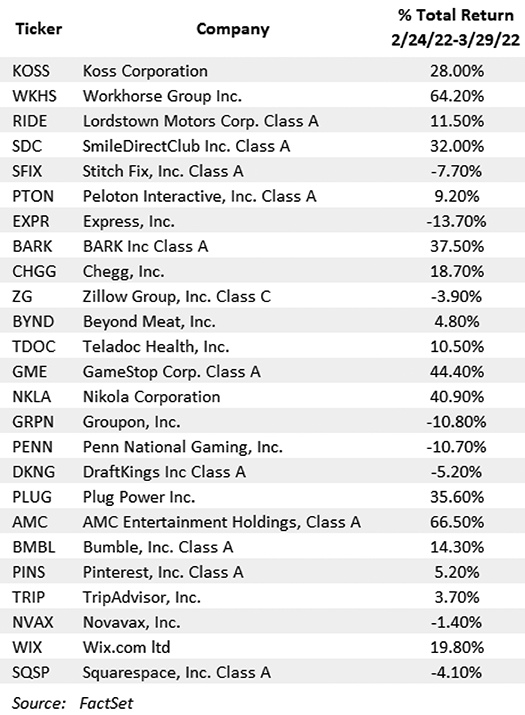

In the latter parts of last year and into the beginning of this year, the market was correcting a significant amount of excess, and it looked like the growth fever had broken. In our letter of December 31, 2021, we presented a table with a number of notable names down between 50-90% from their highs. Strangely, considering war, inflation, and rapidly rising rates, many meme stocks and other speculative issues have once again rallied. The same names are depicted below, with their performance since the Russian invasion through 3/29/22. Based on EBIT, only four of these companies have earnings.

4

Remarkably, the Nasdaq-100 and S&P 500 indices are up 6.25% and 5.80% through 3/31/22, respectively, since the war started. Tesla, Inc. went up 57% from its low on February 24 ($700) to the close on March 29th ($1099), which equates to an advance of $413 billion. To put that in perspective, the 24 trading day gain in Tesla was greater than the entire market value of Walmart, Inc.! Tesla trades for 120 times estimated 2022 GAAP3 earnings, compared to Walmart’s 21.8 multiple (1/2023 fiscal year). Robinhood Markets, Inc. gained 47% from February 24th to March 29th, which gives another indication of how the speculative candle has reignited. Additionally, the high yield market has outperformed investment grade credits and treasuries, both year-to-date and, inexplicably, post the Russian invasion. It is difficult to understand this; our only explanation is that after years of aggressive behavior being rewarded, investors’ muscle memory remains strong, kicking in whenever trouble surfaces, knowing the Fed has a long history of coming to the rescue (or losing its nerve when it comes to interest rate hikes). Of course, the difference this time around is that market interest rates are rising sharply, and inflation is proving to be sticky. It could also be that the market is anticipating the end of the war and are thus bidding up the most aggressive growth stocks; it is hard to know for sure. What does seem apparent is that investor psychology has not been significantly tempered by rates, inflation, or a war.

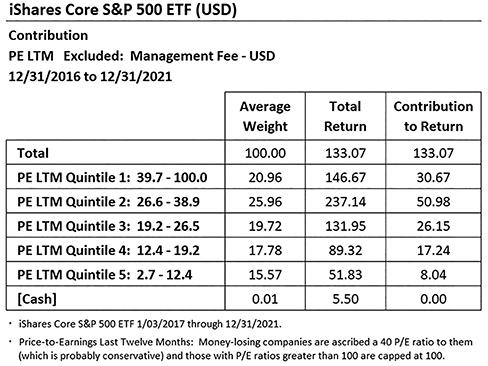

Though the S&P 500 has outperformed the FMI Large Cap Fund over the past five years, it hasn’t meaningfully outperformed on a fundamental basis. As in any multi-year time-frame, we’ve had some companies that have come up short, but even with these, we estimate that the Large Cap Fund, on a median basis, grew sales and earnings at 5.5% and 12.4%, respectively, in the five years ending 12/31/21. Similarly measured, we estimate the S&P 500 (using the iShares S&P 500 as a proxy) over that time frame grew sales and earnings at 5.9% and 12.7%, respectively.4 Throughout this period, our portfolio valuation was considerably cheaper than the S&P 500 and our balance sheets were better (and these conditions remain today). In hindsight, one could say we cared too much about risk. We certainly did not expect interest rates to remain low for so long and valuations to expand and remain high. Contrary to decades of history, over the last 5 years, for all but one quintile, the higher the trailing price-to-earnings ratio, the better the stock performance, as illustrated by the below table.

In hindsight, almost every stock sold for valuation reasons looks like a mistake. Perhaps we underestimated the power of some of the big technology companies to continue growing. Moreover, many of the heaviest-weighted companies in the S&P 500 outperformed significantly, which was a major factor, as most of these companies were in the technology arena where we were underweight

_______________

3 | Generally accepted accounting principles. |

4 | Because of COVID, 2020 had many negative growth rates and thus, comparison to 2021 was impossible to calculate. Therefore, we took 2021 earnings and compared them to 2019, chain linking this growth rate to the other years. |

5

due to very high valuations. We had a few problem stocks that, in retrospect, may have been too complicated, a couple where we misjudged the quality of the management, and a handful that were really hit by COVID. We’ve made some adjustments, are optimistic about the COVID-affected names, and are confident in the lineup we have today. We make no apologies about having a deep concern about downside risk and sticking with high-quality businesses and relatively low valuations. The portfolio trades at roughly a 30-50% discount to the iShares S&P 500 based on an array of valuation metrics. These attributes should be rewarded in time, although no one knows when the music will stop and aggressive behavior penalized.

As per usual in the March letter, we include below a brief commentary on two portfolio holdings.

Carlisle Cos. Inc. (CSL)

(Analyst: Ben Karek)

Description

Carlisle is a diversified manufacturer of a broad range of products selling into industries such as commercial construction, aerospace, transports, and general industrial. The company is headquartered in Scottsdale, AZ and operates in three segments: Carlisle Construction Materials (CCM), Carlisle Interconnect Technologies (CIT), and Carlisle Fluid Technologies (CFT). CCM accounts for 80% of sales and 99% of EBIT, with marginal earnings contribution from CIT and CFT. Carlisle’s geographic exposure is U.S. (84%), Europe (7%), Asia (4%), and Other (5%). Its operating companies are given significant autonomy and responsibility for the performance of their businesses.

Good Business

| • | The majority of Carlisle’s sales are in markets where it enjoys #1 or #2 positions. | |

| • | The company’s largest segment, CCM, derives 70% of its sales from aftermarket. Commercial roofs are replaced roughly every 25 years, and we are approaching a long runway of replacement demand through 2030. | |

| • | Carlisle’s products are specialized, highly engineered, and recurring in nature. | |

| • | The company’s businesses are necessary and easy to understand. | |

| • | It is conservatively financed at 2.2 times forward net debt/EBITDA. | |

| • | They are cash generative, with free cash flow averaging >100% of net income. | |

| • | Return on total capital has averaged 12% over the last five years. |

Valuation

| • | The stock trades at a reasonable 17.0 times 2022 P/E ratio, which approximates its 10-year average. We believe a mix shift toward buildings products will structurally expand its fair multiple. |

Management

| • | Carlisle has a strong track record of value creation; its returns on invested capital are above its cost of capital, despite completing numerous small and mid-size acquisitions. Its shares have meaningfully outperformed the S&P 500 and the Russell 2000 indices over the last 5, 10, and 15 years, while still trading at a reasonable multiple. | |

| • | CEO Chris Koch, who owns $45 million in the stock, took over in 2016 and has demonstrated a continuity with the Carlisle model and a willingness to shrink the portfolio of businesses if it creates value. We believe we are entering a period where this could accelerate, with Carlisle becoming a pureplay building products company. | |

| • | Carlisle’s variable compensation includes metrics on sales, EBIT margin, and working capital. We believe these roughly approximate business value creation over time. |

6

Investment Thesis

Over the last six years, Carlisle has been on a simplification journey by selling two of its smaller, lower-quality businesses. We expect that the company will continue down this path by selling CIT and CFT over the next couple years. What will remain is a pureplay building products company with a good long-term demand profile and pricing power. Carlisle, like many others, is currently dealing with unprecedented cost inflation. The company has historically shown the ability to pass through raw material inflation, albeit with a lag, as evidenced by the decade-long margin expansion that this segment has experienced through multiple cycles. Carlisle was one of the rare industrials who was price/cost neutral in 2021, and it is also set to benefit from a decade-long reroofing cycle that should allow for +3-4% volume growth before considering any benefit from new construction. Despite strong and improving fundamentals, the shares have recently traded sideways and reached a level that we believe makes it a compelling addition to the Fund.

CarMax Inc. (KMX)

(Analyst: Jordan Teschendorf)

Business Description

CarMax, headquartered in Richmond, VA, is the largest and most profitable used car retailer in the U.S., selling a combined 1.596 million used vehicles annually through retail and wholesale channels across its 226 stores and omni-channel platform. The company has just 4% of a huge $750 billion market. It operates across two segments, CarMax Sales Operation and CarMax Auto Finance (CAF), together covering all aspects of auto merchandising, service, and financing. By segment, the profit is also split into CarMax Sales Operations (80%) and CAF (20%).5 CarMax Sales Operation has three primary sources of revenue: Used (78% of sales and 63% of segment gross profit), Wholesale (19% of sales and 21% of segment gross profit), and Other (3% of sales and 16% of segment gross profit).

Good Business

| • | The CarMax brand stands for providing a large selection of high-quality used vehicles at fair prices, and it has earned the trust of customers since beginning operations nearly 30 years ago. | |

| • | The company has demonstrated consistent growth and leading profitability in one of the largest retail markets in the world ($750 billion). Sales and earnings per share (EPS) have grown at +8% and +11% annually over the last decade, with return on equity averaging approximately 20%. | |

| • | Competitive advantages include brand strength, sourcing, fulfillment, and technology capability. We see opportunity for an acceleration in share gains with omni-channel consumer adoption. | |

| • | Excluding non-recourse notes payable, the company’s balance sheet is well-capitalized with 1.8 times net debt/EBITDA. | |

Valuation | ||

| • | The stock trades at 13.4 times forward EPS, approximately one standard deviation below its 5, 10, and 15-year averages. | |

| • | In a poor environment, with slower volume growth, disappointing operating leverage, and more challenging credit results, we model earnings power could decrease to $6 per share. The stock trades at 16.1 times this depressed figure. | |

_______________

5 | CAF income as a percentage of CAF income plus CarMax Sales gross profit. Note CarMax does not separately assign SG&A to CAF for accounting purposes. |

7

| • | Assuming a reasonably supportive used vehicle market and strong execution, earnings could exceed $9 per share over the next four to five years. The stock trades at 10.7 times this figure. |

Management

| • | Bill Nash has been President and CEO since September 2016 and has been with the company since its founding, previously holding executive roles within the company’s merchandising, auction, and human resources areas. | |

| • | Enrique Mayor-Mora has been CFO since October 2019. He’s been with CarMax since 2011, previously serving as VP of Finance and VP of Treasury. | |

| • | Management is well-regarded by industry experts, peers, and employees. | |

| • | The company has a strong corporate culture. |

Investment Thesis

CarMax is a profitable, well-managed, and growing franchise serving one of the largest retail markets in the world. Its stock price has fallen over 33% from its 52-week high as investors have grown concerned on normalizing demand trends, rising interest rates, and used vehicle affordability. We acknowledge these concerns, although we expect the company to continue growing over the long term in a highly fragmented marketplace, and are encouraged by investments being made to reinforce its already strong customer proposition. We are pleased to buy this leading franchise at a steep discount to the market and its historical average.

Thank you for your confidence in the FMI Large Cap Fund.

Please see page 78 for important disclosures.

This shareholder letter is unaudited.

8

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS

March 31, 2022 (Unaudited)

| Shares | Cost | Value | |||||||||

| COMMON STOCKS — 97.6% (a) | |||||||||||

COMMERCIAL SERVICES SECTOR — 3.0% | |||||||||||

| Advertising/Marketing Services — 3.0% | |||||||||||

| 1,030,000 | Omnicom Group Inc. | $ | 68,504,464 | $ | 87,426,400 | ||||||

CONSUMER DURABLES SECTOR — 3.9% | |||||||||||

| Electronics/Appliances — 3.9% | |||||||||||

| 1,100,000 | Sony Group Corp. — SP-ADR* | 69,013,676 | 112,981,000 | ||||||||

CONSUMER NON-DURABLES SECTOR — 3.1% | |||||||||||

| Household/Personal Care — 3.1% | |||||||||||

| 1,960,000 | Unilever PLC — SP-ADR | 77,967,671 | 89,317,200 | ||||||||

CONSUMER SERVICES SECTOR — 6.8% | |||||||||||

| Cable/Satellite TV — 3.1% | |||||||||||

| 1,915,000 | Comcast Corp. — Cl A | 83,291,504 | 89,660,300 | ||||||||

| Other Consumer Services — 3.7% | |||||||||||

| 46,000 | Booking Holdings Inc.* | 79,545,826 | 108,028,700 | ||||||||

ELECTRONIC TECHNOLOGY SECTOR — 3.7% | |||||||||||

| Semiconductors — 3.7% | |||||||||||

| 1,390,000 | Micron Technology Inc. | 74,786,313 | 108,267,100 | ||||||||

FINANCE SECTOR — 23.0% | |||||||||||

| Investment Banks/Brokers — 3.8% | |||||||||||

| 1,330,000 | The Charles Schwab Corp. | 48,094,571 | 112,132,300 | ||||||||

| Major Banks — 2.9% | |||||||||||

| 615,000 | JPMorgan Chase & Co. | 39,147,333 | 83,836,800 | ||||||||

| Multi-Line Insurance — 8.4% | |||||||||||

| 1,375,000 | Arch Capital Group Ltd.* | 51,382,441 | 66,577,500 | ||||||||

| 502,000 | Berkshire Hathaway Inc. — Cl B* | 25,434,039 | 177,160,820 | ||||||||

| 76,816,480 | 243,738,320 | ||||||||||

| Property/Casualty Insurance — 4.9% | |||||||||||

| 270,000 | Chubb Ltd. | 35,441,992 | 57,753,000 | ||||||||

| 760,000 | Progressive Corp. | 57,274,070 | 86,632,400 | ||||||||

| 92,716,062 | 144,385,400 | ||||||||||

| Regional Banks — 3.0% | |||||||||||

| 755,000 | Northern Trust Corp. | 64,469,113 | 87,919,750 | ||||||||

HEALTH SERVICES SECTOR — 8.5% | |||||||||||

| Health Industry Services — 2.6% | |||||||||||

| 561,510 | Quest Diagnostics Inc. | 54,535,451 | 76,848,258 | ||||||||

| Managed Health Care — 3.5% | |||||||||||

| 200,000 | UnitedHealth Group Inc. | 14,281,660 | 101,994,000 | ||||||||

| Medical/Nursing Services — 2.4% | |||||||||||

| 2,110,000 | Fresenius Medical Care AG & Co. KGaA | 85,121,631 | 71,064,800 | ||||||||

The accompanying notes to financial statements are an integral part of this schedule.

9

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2022 (Unaudited)

| Shares | Cost | Value | |||||||||

| COMMON STOCKS — 97.6% (a) (Continued) | |||||||||||

HEALTH TECHNOLOGY SECTOR — 5.2% | |||||||||||

| Medical Specialties — 5.2% | |||||||||||

| 2,400,000 | Koninklijke Philips N.V. — SP-ADR | $ | 108,433,816 | $ | 73,272,000 | ||||||

| 2,450,000 | Smith & Nephew PLC — SP-ADR | 88,708,491 | 78,155,000 | ||||||||

| 197,142,307 | 151,427,000 | ||||||||||

INDUSTRIAL SERVICES SECTOR — 2.3% | |||||||||||

| Oilfield Services/Equipment — 2.3% | |||||||||||

| 1,655,000 | Schlumberger Ltd. | 31,847,576 | 68,368,050 | ||||||||

PROCESS INDUSTRIES SECTOR — 3.0% | |||||||||||

| Containers/Packaging — 0.6% | |||||||||||

| 93,430 | Avery Dennison Corp. | 16,608,728 | 16,254,017 | ||||||||

| Industrial Specialties — 2.4% | |||||||||||

| 530,000 | PPG Industries Inc. | 51,926,045 | 69,467,100 | ||||||||

PRODUCER MANUFACTURING SECTOR — 13.6% | |||||||||||

| Building Products — 4.4% | |||||||||||

| 2,490,000 | Masco Corp. | 84,285,829 | 126,990,000 | ||||||||

| Electrical Products — 1.9% | |||||||||||

| 360,000 | Eaton Corp. PLC | 32,796,682 | 54,633,600 | ||||||||

| Industrial Machinery — 2.5% | |||||||||||

| 460,000 | Dover Corp. | 62,435,851 | 72,174,000 | ||||||||

| Miscellaneous Manufacturing — 1.7% | |||||||||||

| 206,438 | Carlisle Cos. Inc. | 49,796,897 | 50,767,233 | ||||||||

| Trucks/Construction/Farm Machinery — 3.1% | |||||||||||

| 1,035,000 | PACCAR Inc. | 52,230,730 | 91,152,450 | ||||||||

RETAIL TRADE SECTOR — 12.5% | |||||||||||

| Apparel/Footwear Retail — 1.9% | |||||||||||

| 925,000 | The TJX Companies Inc. | 38,825,953 | 56,036,500 | ||||||||

| Discount Stores — 8.7% | |||||||||||

| 625,000 | Dollar General Corp. | 44,736,530 | 139,143,750 | ||||||||

| 725,000 | Dollar Tree Inc.* | 63,136,566 | 116,108,750 | ||||||||

| 107,873,096 | 255,252,500 | ||||||||||

| Specialty Stores — 1.9% | |||||||||||

| 565,000 | CarMax Inc.* | 61,080,505 | 54,511,200 | ||||||||

TECHNOLOGY SERVICES SECTOR — 9.0% | |||||||||||

| Information Technology Services — 0.9% | |||||||||||

| 140,758 | CDW Corp. | 25,328,678 | 25,180,199 | ||||||||

| Internet Software/Services — 6.1% | |||||||||||

| 45,000 | Alphabet Inc. — Cl A* | 106,405,145 | 125,160,750 | ||||||||

| 240,000 | Meta Platforms Inc. Cl A | ||||||||||

| (formerly Facebook Inc.)* | 76,040,052 | 53,366,400 | |||||||||

| 182,445,197 | 178,527,150 | ||||||||||

The accompanying notes to financial statements are an integral part of this schedule.

10

FMI Large Cap Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2022 (Unaudited)

| Shares | Cost | Value | |||||||||

| COMMON STOCKS — 97.6% (a) (Continued) | |||||||||||

TECHNOLOGY SERVICES SECTOR — 9.0% (Continued) | |||||||||||

| Packaged Software — 2.0% | |||||||||||

| 520,000 | SAP SE — SP-ADR | $ | 67,611,380 | $ | 57,699,200 | ||||||

| Total common stocks | 1,990,527,209 | 2,846,040,527 | |||||||||

| Principal Amount | |||||||||||

| SHORT-TERM INVESTMENTS — 3.2% (a) | |||||||||||

| Bank Deposit Account — 3.2% | |||||||||||

| $ | 94,072,606 | U.S. Bank N.A., 0.096%^ | 94,072,606 | 94,072,606 | |||||||

| Total short-term investments | 94,072,606 | 94,072,606 | |||||||||

| Total investments — 100.8% | $ | 2,084,599,815 | 2,940,113,133 | ||||||||

Other liabilities, less assets — (0.8%) (a) | (23,861,271 | ) | |||||||||

| TOTAL NET ASSETS — 100.0% | $ | 2,916,251,862 | |||||||||

| * | Non-income producing security. |

| ^ | The rate shown is as of March 31, 2022. |

| (a) | Percentages for the various classifications relate to total net assets. |

| PLC | Public Limited Company |

| SP-ADR | Sponsored American Depositary Receipt |

The accompanying notes to financial statements are an integral part of this schedule.

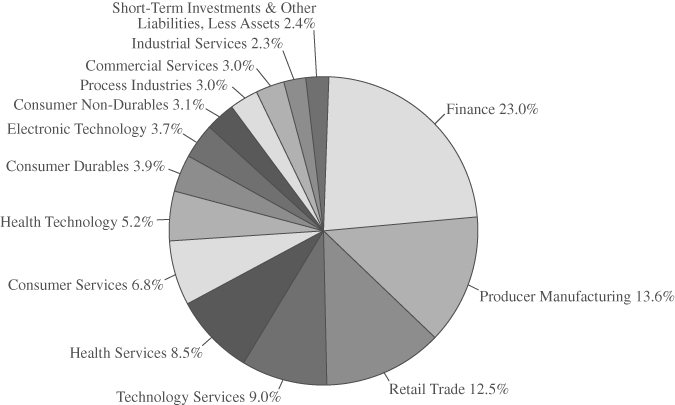

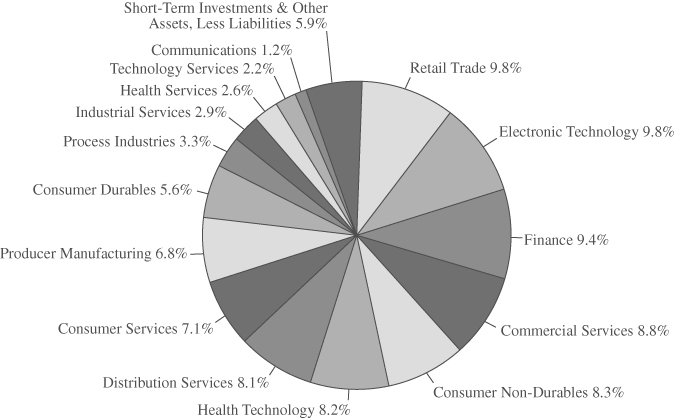

INDUSTRY SECTORS as a percentage of net assets

as of March 31, 2022 (Unaudited)

11

FMI

Common Stock

Fund

(unaudited)

| March 31, 2022 |

Dear Fellow Shareholders:

The FMI Common Stock Fund (“Fund”) declined 4.58%1 in the March quarter compared to a 7.53% drop in the Russell 2000 Index, and 2.40% loss in the Russell 2000 Value Index. Areas where the Fund had little exposure, such as Energy Minerals & Utilities, accounted for the performance difference between the Fund and the Russell 2000 Value. Compared to the Russell 2000, sectors that helped performance included Commercial Services, Health Technology, and Technology Services. Sectors that detracted included Energy Minerals, Industrial Services, and Utilities. Henry Schein Inc., Zions Bancorporation N.A., and Robert Half International Inc. added to performance in the quarter while LCI Industries, Genpact Ltd., and LGI Homes Inc. detracted. Since the Russian invasion of Ukraine on February 24, the market has moved in somewhat of a barbell fashion, with Energy/Non-Energy Minerals and Industrial Service companies tied to these segments driving the value trade, while many speculative growth names also moved up sharply.

Quarterly investment letters across the land will be focused on the Russian invasion and what it means for geopolitical stability, supply chains, energy, inflation, globalization, economic growth, and interest rates. All of these elements were in play long before the invasion. Although markets have largely ignored it, China and Russia substantially increased their belligerence toward the U.S. (and the “West”) in recent years. A new two-pronged cold war with China and Russia has been underway for some time. Historically, sanctions have not been terribly effective, as authoritarian leaders (Mussolini, Castro, Kim Jung Un/IL, Chavez, Maduro, Khomeini) survived by controlling the narrative and crushing popular dissent. Maybe the coordinated effort of a surprisingly large number of Russian trading partners and central banks will prove to be the exception. We don’t expect Putin to change course because of sanctions or exposure of war atrocities, but perhaps Xi Jinping has taken notice and pauses any moves on Taiwan. On a gross basis, China exported $577 billion to the U.S. and $701 billion to the European Union in 2021. China can ill afford a trade war with the West, although the reverse is also true. The war has already had impacts on commodities, intermediate products, and the supply chain. Energy and mineral prices have blown out. Inflation, which started rising rapidly twelve months ago, remains at a 40-year high. For at least three decades, the world’s inflation picture has benefitted from a giant Chinese labor arbitrage that is now in the rearview mirror, as the Chinese working-age population is no longer growing, and wages there have risen markedly. Additionally, both politically and strategically, the West will need to secure more production domestically or with friendly regimes – whether it be in energy, materials, or manufactured goods – adding to inflation pressure in the short-to-intermediate term. While the end of the pandemic and possible slowing of the economy may bring inflation down somewhat, we cannot avoid the ramifications tied to years of quantitative easing, rapid money supply growth, and unprecedented fiscal expansion. The market hasn’t figured this out yet, in fact, speculative activity has reemerged in recent weeks. Despite this, if higher interest rates and inflation characterize the landscape for the next several years, it likely spells the end of the era of unbridled speculation and high multiples. We believe the Fund is well-positioned to thrive in the tougher world that may be upon us.

_______________

1 | The FMI Common Stock Fund Investor Class (FMIMX) and the FMI Common Stock Fund Institutional Class (FMIUX) had a return of -4.58% and -4.55%, respectively, for the first quarter of 2022. |

12

Interest Rates and Inflation

Below is the latest illustration of the expected Fed Funds Rate to March 2023. If these moves come to pass, the recent 0% Fed Funds Rate would be 3%.

Now observe the below chart showing the Fed Funds Rate and the inflation rate over fifty years. Tracking the Federal Funds Target Rate back to 1971, the average inflation rate as measured by CPI from 1971 until today is 3.9%.

Inflation Episode 1

The CPI went from 2.7% to 12.3% from the 3rd quarter of 1972 to the 4th quarter of 1974. The Fed Funds rate went from 5% to 13% from the 3rd quarter of 1972 to the 2nd quarter of 1974. From the 4th quarter of 1974 to the 4th quarter of 1976, CPI went from 12.3% to 4.9%.

13

Inflation Episode 2

CPI went from 4.9% to 14.8% from the 4th quarter of 1976 to the 1st quarter of 1980. Fed Funds went from 6% to 20% from the 4th quarter of 1976 to the 1st quarter of 1980. Inflation finally got to a more normal level by the 4th quarter of 1982. From the 1st quarter of 1980 to the 4th quarter of 1982, CPI averaged 9.7% while the Fed Funds target rate averaged 13.6%.

Inflation Episode 3

CPI went from 1.1% to 6.2% from the 4th quarter of 1986 to the 3rd quarter of 1990. Fed Funds went from 6% to 9.75% from the 4th quarter of 1986 to the 1st quarter of 1989. CPI from the 3rd quarter of 1990 to the 4th quarter of 1991 went from 6.2% to 3.1%. CPI was under control from 1991 until the financial crisis in 2008, averaging 2.7% while the Fed Funds target rate averaged 3.95%.

Virtually every time inflation spiked over the past fifty years, the Fed Funds Rate went higher than the inflation rate to tame it. How many investors today believe the Fed Funds Rate is on a path toward 8%? Inflation is taking longer to stabilize than expected and Chairman Powell is pointing toward short-term supply chain problems, or transient war impacts. The stock and bond markets seem to agree it’s a temporary challenge. As of 3/31/22 the S&P 500 is only 5.2% off its high, and the bond market (using inflation-adjusted Treasury securities) expects five-year inflation to drop dramatically. A recent study from AllianceBernstein concluded that only 1.5 percentage points of the 7.9% inflation rate is likely due to one-time supply chain effects. More traditional monetary factors appear to be the culprit. In a recent piece from The Wall Street Journal by Hanke and Hanlon,2 titled, “Jerome Powell is Wrong. Printing Money Causes Inflation,” the authors point out that in two separate communications with Congress over the past year, Powell said the connection between money supply growth and inflation ended 40 years ago. The below chart throws cold water on these assertions.

Why is the market not yet buying the high inflation, higher rate thesis? One possible explanation gaining traction is the notion that we are headed for a recession, complete with demand destruction and falling prices, or at least a much slower growth rate in the CPI. Given the downward action in many stocks recently (aside from energy and commodities), this seems plausible. Yield

_______________

2 | Steve Hanke, professor, and Nicholas Hanlon, chief of staff, at the Johns Hopkins Institute of Applied Economics. |

14

curves have flattened in recent weeks. Inverted yield curves (short-term rates exceeding long-term rates) have a better-than-average track record of predicting recessions. Talking to our companies, however, and observing demand across many industries, it does not feel like a downturn is imminent. Perhaps stagflation is on the horizon. Whether underlying economic growth remains solid or weakens enough to cause a recession, we do not see inflation returning to 2% anytime soon. Moreover, with quantitative easing ending, Fed Funds rising, and bond investors wanting more compensation for the risk of inflation, longer maturity interest rates may continue to normalize. As we indicated in our letter of December 31, 2021, the 10-Year Treasury’s median yield since 1957 is 5.38% compared to 2.34% today (up from 1.51% as of 12/31/21). It is hard to imagine P/E multiples remaining near all-time highs with the discount rate escalating.

Market Behavior

The value move in the market this year is mostly related to hydrocarbon exploration and production stocks, as well as other commodity-oriented equities. The Fund has little-to-no exposure to these sectors, as over long periods of time, most of the companies in these sectors have proven unable to earn their cost of capital and are highly volatile. These stocks periodically race higher, but elevated commodity prices almost always spur a supply response that typically ends the rally. Higher raw material prices have temporarily affected a few of our stocks, but these companies have good market power and are already raising prices aggressively. We expect within a few quarters that margins will recover.

In the latter parts of last year and into the beginning of this year, the market was correcting a significant amount of excess, and it looked like the growth fever had broken. In our letter of December 31, 2021, we presented a table with a number of notable names down between 50-90% from their highs. Strangely, considering war, inflation, and rapidly rising rates, many meme stocks and other speculative issues have once again rallied. The same names are depicted below, with their performance since the Russian invasion through 3/29/22. Based on EBIT, only four of these companies have earnings.

Remarkably, the Nasdaq-100 and Russell 2000 indices are up 6.25% and 3.90% through 3/31/22, respectively, since the war started. Tesla, Inc. went up 57% from its low on February 24 ($700) to the close on March 29th ($1099), which equates to an advance of $413 billion. To put

15

that in perspective, the 24 trading day gain in Tesla was greater than the entire market value of Walmart, Inc.! Tesla trades for 120 times estimated 2022 GAAP3 earnings, compared to Walmart’s 21.8 multiple (1/2023 fiscal year). Robinhood Markets, Inc. gained 47% from February 24th to March 29th, which gives another indication of how the speculative candle has reignited. Additionally, the high yield market has outperformed investment grade credits and treasuries, both year-to-date and, inexplicably, post the Russian invasion. It is difficult to understand this; our only explanation is that after years of aggressive behavior being rewarded, investors’ muscle memory remains strong, kicking in whenever trouble surfaces, knowing the Fed has a long history of coming to the rescue (or losing its nerve when it comes to interest rate hikes). Of course, the difference this time around is that market interest rates are rising sharply, and inflation is proving to be sticky. It could also be that the market is anticipating the end of the war and are thus bidding up the most aggressive growth stocks; it is hard to know for sure. What does seem apparent is that investor psychology has not been significantly tempered by rates, inflation, or a war.

Looking back over the years, we have been surprised by how long interest rates have stayed low. It has created many problems, which we have discussed at length in previous letters and will not address here. One byproduct is high valuations that have rewarded speculative behavior. Throughout these years, our portfolio valuations have been considerably cheaper than the benchmark, and our balance sheets were better (and these conditions remain today). In hindsight, one could say we cared too much about risk. Data on price-to-earnings (P/E) ratios for the Russell 2000 is very difficult to develop, owing to the fact that roughly 40% (as of 2/28/22) of the companies do not have earnings. But in the S&P 500, contrary to decades of history, over the last 5 years, for all but one quintile, the higher the trailing price-to-earnings ratio, the better the stock performance, as illustrated by the below table.

In hindsight, almost every stock sold for valuation reasons looks like a mistake. We had a few problem stocks that, in retrospect, may have been too complicated, a couple where we misjudged the quality of the management, and a handful that were really hit by COVID. We’ve made some adjustments, are optimistic about the COVID-affected names, and are confident in the lineup we have today. We make no apologies about having a deep concern about downside risk and sticking with high-quality businesses and relatively low valuations. The Fund trades at a 15-50% discount to the iShares Russell 2000 based on an array of valuation metrics. These attributes should be rewarded in time.

As per usual in the March letter, we include a brief commentary on two portfolio holdings.

_______________

3 | Generally accepted accounting principles. |

16

Skechers U.S.A. Inc. — Cl A (SKX)

(Analyst: Matt Sullivan)

Description

Skechers is the third largest footwear brand in the world. The company designs, manufactures, and distributes footwear for men, women, and children in U.S. and international markets. Its products cover a wide range of footwear categories including casuals, dress casuals, sandals, boots, work boots, performance footwear, and kids footwear. The company operates in three business segments: Domestic Wholesale (23% of sales), International Wholesale (48% of sales), and Direct-to-Consumer (29% of sales). In total, international sales account for approximately 60% of revenue.

Good Business

| • | Excluding net cash on the balance sheet, return on invested capital (ROIC) is in the mid-teens, which easily exceeds the company’s cost of capital. | |

| • | Skechers has established a brand over the past 30 years that customers associate with comfortable, quality shoes at low prices, which we believe is an attractive niche. | |

| • | This is a scaled player in the industry that can efficiently design, manufacture, market, and distribute shoes all over the world. | |

| • | The company has exposure to a wide range of domestic and international distribution channels, including both third party and owned e-commerce websites. Consumers can find the company’s products however they’d like to shop. | |

| • | Sketchers sells a broad assortment of shoes and uses a fast follower model, which we believe reduces fashion risk. | |

| • | The company is in a net cash position and the business is easy to understand. |

Valuation

| • | Excluding net cash on the balance sheet, Skechers trades for 12.3 times our next 12-months earnings per share (EPS) estimate, which is below the company’s 5-year average and is a significant discount to the Russell 2000, as well as other comparable companies serving similar end markets. | |

| • | The EV/sales multiple is 1.0 times, which is below the company’s 5-year average of 1.2 times. |

Management

| • | Management and the board own ~41 million shares of stock, which equates to ~26% of the company. | |

| • | The company’s founder, Robert Greenberg, is Chairman and CEO. | |

| • | Michael Greenberg, son of the founder, is President, and has been at Skechers for 29 years. |

Investment Thesis

Skechers has built an impressive global business over many years. The growth and ROIC track record of the company has been terrific. We believe the company can continue to grow nicely and with rising margins over the next number of years, as it keeps expanding internationally and further develops its direct-to-consumer business, which includes fully owned stores and the Skechers.com website. These segments sport accretive margins, meaning outsized growth in these channels will boost consolidated company margins. Near-term supply chain challenges are weighing on the stock’s multiple and distracting from Skechers’ attractive longer-term outlook. The company has a fortress balance sheet, reports GAAP earnings, and doesn’t engage in mergers and acquisitions activity. All in, this appears to be a rare value in a very expensive market.

17

nVent Electric PLC (NVT)

(Analyst: Dain Tofson)

Description

nVent is a global provider of electrical connection and protection solutions. It was spun out of Pentair in 2018. The company is headquartered in Minneapolis, MN, although it’s incorporated in Ireland, and reports three segments: Enclosures (51% of sales and 40% of EBITA), Electrical & Fastening Solutions (27% of sales and 36% of EBITA), and Thermal Management (22% of sales and 24% of EBITA). By geography, sales are split 63% U.S. and Canada, 23% Developed Europe, 11% Developing, and 3% Other Developed. By vertical, sales are split 43% Industrial, 28% Commercial & Residential, 21% Infrastructure, and 8% Energy.

Good Business

| • | The company has industry-leading positions and strong brands across its segments. Key brands include Hoffman and Schroff in Enclosures, Raychem and Tracer in Thermal Management, and Erico and Caddy in Electrical & Fastening Solutions. | |

| • | The cost of the products typically represents a small proportion of the total cost of a customer’s end systems. | |

| • | nVent operates in an attractive industry structure with relatively high barriers to entry. | |

| • | EBITA margin was 17.7% in 2021, which is better than the average industrial company. | |

| • | nVent generates consistent free cash flow throughout an economic cycle, and has attractive ROIC prospects. |

Valuation

| • | The stock trades at 16.0 times 2022 consensus EPS versus industrial peers at >20.0 times. |

Management

| • | The management team led by Beth Wozniak has executed well since the spinout and has invested in new product launches, a digital transformation, and structural cost reductions. | |

| • | Management has laid out sensible capital allocation priorities including (1) reinvesting in the company to drive organic growth, (2) maintaining a competitive dividend, and (3) pursuing bolt-on acquisitions and/or share repurchases with an objective to allocate capital to the highest return, while appropriately managing liquidity and leverage. | |

| • | Randy Hogan, non-executive Chairman of the Board, was the CEO of Pentair from 2001 until the spinout. Pentair significantly outperformed the S&P 500 during his tenure as CEO. |

Investment Thesis

nVent has industry-leading positions, strong brands across its segments, leverage to mega-trends such as electrification, and consistent free cash flow generation throughout an economic cycle. It’s a better-than-average industrial business, in our opinion; however, the stock trades at a discount to industrial peers. The opportunity to own an above-average industrial business at a below-average price is an attractive proposition. Additionally, management’s investments since the spinout should increase the earnings power of the business, and subsequently, magnify the earnings gains in an upcycle. Finally, there is takeout optionality given nVent’s size and business quality.

Thank you for your confidence in the FMI Common Stock Fund.

Please see page 78 for important disclosures.

This shareholder letter is unaudited.

18

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS

March 31, 2022 (Unaudited)

| Shares | Cost | Value | |||||||||

| COMMON STOCKS — 96.3% (a) | |||||||||||

COMMERCIAL SERVICES SECTOR — 21.3% | |||||||||||

| Advertising/Marketing Services — 4.4% | |||||||||||

| 1,279,000 | Interpublic Group of Cos. Inc. | $ | 23,665,275 | $ | 45,340,550 | ||||||

| Miscellaneous Commercial Services — 11.8% | |||||||||||

| 455,000 | CDK Global Inc. | 22,288,066 | 22,149,400 | ||||||||

| 131,000 | Concentrix Corp. | 21,183,829 | 21,819,360 | ||||||||

| 200,000 | FTI Consulting Inc.* | 23,470,798 | 31,444,000 | ||||||||

| 1,043,000 | Genpact Ltd. | 21,872,178 | 45,380,930 | ||||||||

| 88,814,871 | 120,793,690 | ||||||||||

| Personnel Services — 5.1% | |||||||||||

| 155,000 | ManpowerGroup Inc. | 10,113,108 | 14,557,600 | ||||||||

| 326,000 | Robert Half International Inc. | 13,750,987 | 37,222,680 | ||||||||

| 23,864,095 | 51,780,280 | ||||||||||

CONSUMER DURABLES SECTOR — 1.5% | |||||||||||

| Homebuilding — 1.5% | |||||||||||

| 158,000 | LGI Homes Inc.* | 21,447,789 | 15,433,440 | ||||||||

CONSUMER NON-DURABLES SECTOR — 3.1% | |||||||||||

| Apparel/Footwear — 3.1% | |||||||||||

| 770,000 | Skechers U.S.A. Inc. — Cl A* | 34,921,452 | 31,385,200 | ||||||||

DISTRIBUTION SERVICES SECTOR — 13.2% | |||||||||||

| Electronics Distributors — 2.5% | |||||||||||

| 215,000 | Arrow Electronics Inc.* | 4,060,851 | 25,505,450 | ||||||||

| Medical Distributors — 5.3% | |||||||||||

| 482,000 | Henry Schein Inc.* | 28,716,693 | 42,025,580 | ||||||||

| 393,000 | Herbalife Nutrition Ltd.* | 20,597,164 | 11,931,480 | ||||||||

| 49,313,857 | 53,957,060 | ||||||||||

| Wholesale Distributors — 5.4% | |||||||||||

| 235,000 | Applied Industrial Technologies Inc. | 15,033,348 | 24,125,100 | ||||||||

| 528,000 | Beacon Roofing Supply Inc.* | 28,401,724 | 31,299,840 | ||||||||

| 43,435,072 | 55,424,940 | ||||||||||

ELECTRONIC TECHNOLOGY SECTOR — 6.6% | |||||||||||

| Electronic Components — 6.6% | |||||||||||

| 1,004,000 | nVent Electric PLC | 22,230,604 | 34,919,120 | ||||||||

| 405,000 | Plexus Corp.* | 30,903,780 | 33,133,050 | ||||||||

| 53,134,384 | 68,052,170 | ||||||||||

FINANCE SECTOR — 19.9% | |||||||||||

| Finance/Rental/Leasing — 4.8% | |||||||||||

| 510,000 | FirstCash Holdings Inc. | 23,121,515 | 35,873,400 | ||||||||

| 184,000 | Triton International Ltd. | 11,496,005 | 12,913,120 | ||||||||

| 34,617,520 | 48,786,520 | ||||||||||

The accompanying notes to financial statements are an integral part of this schedule.

19

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2022 (Unaudited)

| Shares | Cost | Value | |||||||||

| COMMON STOCKS — 96.3% (a) (Continued) | |||||||||||

FINANCE SECTOR — 19.9% (Continued) | |||||||||||

| Investment Banks/Brokers — 2.9% | |||||||||||

333,000 | Houlihan Lokey Inc. — Cl A | $ | 16,329,299 | $ | 29,237,400 | ||||||

| Life/Health Insurance — 2.3% | |||||||||||

| 171,000 | Primerica Inc. | 23,078,014 | 23,396,220 | ||||||||

| Multi-Line Insurance — 1.3% | |||||||||||

| 12,000 | White Mountains Insurance Group Ltd. | 10,542,912 | 13,634,880 | ||||||||

| Real Estate Development — 5.0% | |||||||||||

| 230,000 | The Howard Hughes Corp.* | 22,299,619 | 23,830,300 | ||||||||

| 1,133,000 | Kennedy-Wilson Holdings Inc. | 19,953,832 | 27,633,870 | ||||||||

| 42,253,451 | 51,464,170 | ||||||||||

| Regional Banks — 3.6% | |||||||||||

| 560,000 | Zions Bancorporation N.A. | 16,009,613 | 36,713,600 | ||||||||

HEALTH TECHNOLOGY SECTOR — 2.8% | |||||||||||

| Medical Specialties — 2.0% | |||||||||||

| 422,000 | Dentsply Sirona Inc. | 15,794,081 | 20,770,840 | ||||||||

| Pharmaceuticals: Major — 0.8% | |||||||||||

| 433,817 | Phibro Animal Health Corp. | 11,185,315 | 8,654,649 | ||||||||

PROCESS INDUSTRIES SECTOR — 2.3% | |||||||||||

| Industrial Specialties — 2.3% | |||||||||||

| 450,000 | Donaldson Co. Inc. | 20,302,487 | 23,368,500 | ||||||||

PRODUCER MANUFACTURING SECTOR — 17.1% | |||||||||||

| Building Products — 1.7% | |||||||||||

| 164,000 | Simpson Manufacturing Co. Inc. | 18,845,085 | 17,882,560 | ||||||||

| Industrial Machinery — 4.4% | |||||||||||

| 534,000 | Flowserve Corp. | 13,201,252 | 19,170,600 | ||||||||

| 847,000 | Gates Industrial Corp. PLC* | 13,584,417 | 12,755,820 | ||||||||

| 106,000 | Woodward Inc. | 4,291,548 | 13,240,460 | ||||||||

| 31,077,217 | 45,166,880 | ||||||||||

| Miscellaneous Manufacturing — 11.0% | |||||||||||

| 180,000 | Brady Corp. — Cl A | 8,964,075 | 8,328,600 | ||||||||

| 222,000 | Carlisle Cos. Inc. | 16,155,706 | 54,594,240 | ||||||||

| 148,000 | LCI Industries | 21,035,310 | 15,363,880 | ||||||||

| 1,071,000 | TriMas Corp. | 24,577,630 | 34,368,390 | ||||||||

| 70,732,721 | 112,655,110 | ||||||||||

RETAIL TRADE SECTOR — 2.2% | |||||||||||

| Specialty Stores — 2.2% | |||||||||||

| 339,000 | BJ’s Wholesale Club Holdings Inc.* | 18,298,643 | 22,919,790 | ||||||||

The accompanying notes to financial statements are an integral part of this schedule.

20

FMI Common Stock Fund

SCHEDULE OF INVESTMENTS (Continued)

March 31, 2022 (Unaudited)

| Shares | Cost | Value | |||||||||

| COMMON STOCKS — 96.3% (a) (Continued) | |||||||||||

TECHNOLOGY SERVICES SECTOR — 6.3% | |||||||||||

| Information Technology Services — 6.3% | |||||||||||

| 345,000 | Insight Enterprises Inc.* | $ | 22,543,701 | $ | 37,025,400 | ||||||

| 502,000 | KBR Inc. | 19,641,037 | 27,474,460 | ||||||||

| 42,184,738 | 64,499,860 | ||||||||||

| Total common stocks | 713,908,742 | 986,823,759 | |||||||||

Principal Amount | |||||||||||

| SHORT-TERM INVESTMENTS — 3.7% (a) | |||||||||||

| Bank Deposit Account — 3.7% | |||||||||||

| $ | 37,638,101 | U.S. Bank N.A., 0.096%^ | 37,638,101 | 37,638,101 | |||||||

| Total short-term investments | 37,638,101 | 37,638,101 | |||||||||

| Total investments — 100.0% | $ | 751,546,843 | 1,024,461,860 | ||||||||

Other assets, less liabilities — 0.0% (a) | 83,587 | ||||||||||

| TOTAL NET ASSETS — 100.0% | $ | 1,024,545,447 | |||||||||

| * | Non-income producing security. |

| ^ | The rate shown is as of March 31, 2022. |

| (a) | Percentages for the various classifications relate to total net assets. |

| PLC | Public Limited Company |

The accompanying notes to financial statements are an integral part of this schedule.

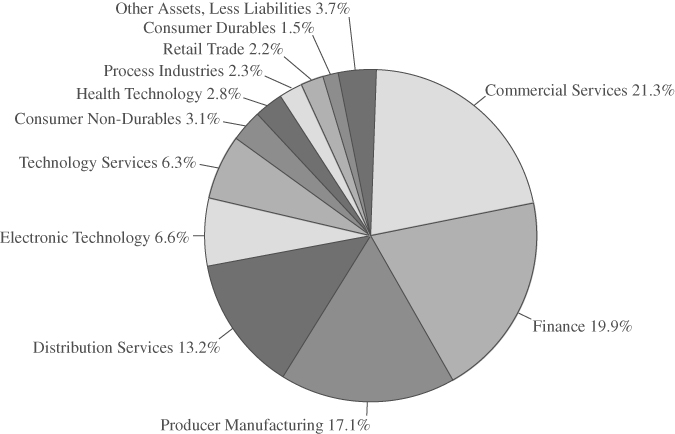

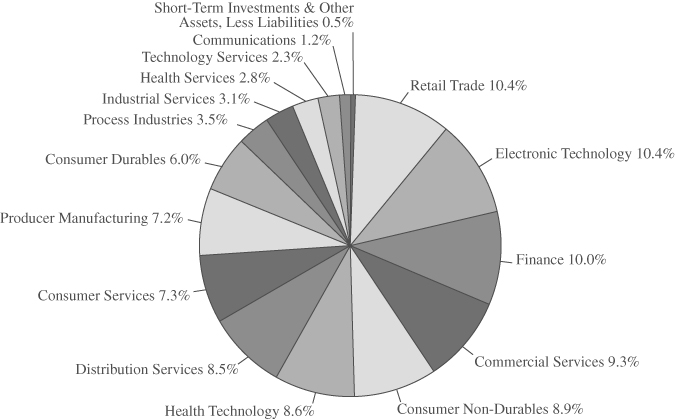

INDUSTRY SECTORS as a percentage of net assets

as of March 31, 2022 (Unaudited)

21

FMI International Fund

and

FMI International Fund II – Currency Unhedged

(unaudited)

| March 31, 2022 |

Dear Fellow Shareholders:

Global equities declined during the March quarter as Russia’s invasion of Ukraine left a dark cloud of uncertainty over financial markets. The FMI International portfolios were outperforming handily up until the eve of the war (February 24, 2022), ahead of the comparable MSCI EAFE indices by around 3%. Unfortunately, the tide turned after the onset of the invasion, as energy, commodity, and defense-related stocks — sectors where FMI has minimal exposure given our focus on business quality — soared. Growth stocks also rebounded strongly in the latter part of the period, amounting to an even tougher comparison.

For the quarter, the FMI International portfolios fell by 5.96% (currency hedged)1 and 8.32% (currency unhedged),2 respectively, compared with an MSCI EAFE Index down 3.73% in local currency (LOC) and 5.91% in U.S. Dollars (USD). The MSCI EAFE Value Index gained 2.68% in LOC and 0.33% in USD. Industrial Services, Producer Manufacturing, and Finance contributed to the FMI International portfolios performance, while Distribution Services, Energy, and Non-Energy Minerals all hurt on a relative basis. Schlumberger Ltd., CK Hutchison Holdings Ltd., and Chubb Ltd. were the strongest individual performers, while Ferguson PLC, Samsung Electronics Co. Inc., and Akzo Nobel N.V. each lagged. A strong USD boosted FMI’s currency-hedged performance.

State of War

Russia’s large-scale invasion of Ukraine has quickly proven to be a humanitarian catastrophe. Thousands of innocent lives have been lost, over 4 million refugees have fled the country,3 homes have been destroyed, and infrastructure obliterated. Our hearts go out to those who are suffering through this needless tragedy. From where we stand today, the path of the war remains unknown, as Russian President Vladimir Putin is far from predictable or rational. Much has been written about the conflict, potential outcomes, and global ramifications; our discussion will center on the economic impact and what it could mean for our portfolios.

The FMI International portfolios’ exposure to Russia and Ukraine is quite limited, with no direct investments in either country, and around 1% of our aggregate revenue there. Both economies are expected to contract by over 30% this year.4 Unfortunately, the economic impact of the war is also far broader, spanning the globe. Energy and commodity prices have skyrocketed as Western nations have imposed the most sweeping economic sanctions against a major country in decades,

_______________

1 | The FMI International Fund [currency hedged] Investor Class (FMIJX) and the FMI International Fund [currency hedged] Institutional Class (FMIYX) had a return of -5.96% and -5.89%, respectively, for the first quarter of 2022. |

2 | The FMI International Fund [unhedged] Institutional Class (FMIFX) had a return of -8.32% for the first quarter of 2022. |

3 | Jon Henley. “More than 4 million have fled Russia’s ’senseless’ war on Ukraine, says UN.” The Guardian, March 30, 2022. |

4 | Mohamed A. El-Erian. “The Ukraine War’s Multifaceted Economic Fallout.” March 7, 2022. https://www.project-syndicate.org/ |

22

with the United States banning the import of Russian oil, gas, and coal. We witnessed the largest one-week price increase in commodities ever,5 with heavy Russia/Ukraine exports including Wheat (80%+ from January average price), Fertilizer (70%+), Nickel (60%+), Maize (40%+), and Palladium (30%+) on the move, in addition to the aforementioned fossil fuels. Russia supplies around 19% of the world’s natural gas and 11% of its oil, with Europe being highly dependent on Russian energy imports. The European Union gets around 40% of its gas from Russia and 27% of its oil.6 Shockingly, gas spot prices in Europe are ten times higher than they were a year ago, while the price for oil has nearly doubled7. If elevated prices hold, we’d expect to see a supply response. As they say in commodity markets: “The cure for high prices is high prices.” Long-term, we also expect to see Europe diversify away from Russian fossil fuels. Unfortunately, the near-term pain appears unavoidable.

Rising energy and food prices are coming at a time when Europe and the U.S. (prior to the war) had already been facing the highest level of inflation in decades. After $30 trillion of global fiscal and monetary stimulus since 2020,8 and years of aggressive money printing and quantitative easing, the European Central Bank (ECB) and the Fed were well behind the curve in terms of raising interest rates (neither had even started). The commodity spike, in addition to another round of supply chain disruptions and increasing transportation costs, will add more fuel to the inflation fire. In Germany, for example, consumer prices rose 7.6% in March,9 the highest level in more than 40 years, after producer prices had risen by 25.9% in February.10 Europe’s economy, given its proximity to the war and reliance on Russian energy, is likely to be the hardest hit. The OECD11

_______________

5 | Bloomberg Commodity Index (BCOM). |

6 | Rowena Mason, Heather Stewart, Julia Kollewe. “UK to phase out Russian oil imports by 2023 and explore ending gas imports.” The Guardian, March 8, 2022. |

7 | “Economic and Social Impacts and Policy Implications of the War in Ukraine.” OECD Economic Outlook, March 17, 2022. https://www.oecd.org/economic-outlook/ |

8 | Michael Hartnett, David Jones, Shirley Wu, and Myung-Jee Jung. “The Flow Show: Buy Signal.” BofA Global Research. March 24, 2022. |

9 | Zuzanna Szymanska and Miranda Murray. “’Welcome back to the 1970s’: Oil, gas prices push German inflation above 7%.” Reuters, March 30, 2022. |

10 | “German producer prices jump by record 25.9%.” Reuters, March 21, 2022. |

11 | Organisation for Economic Co-operation and Development. |

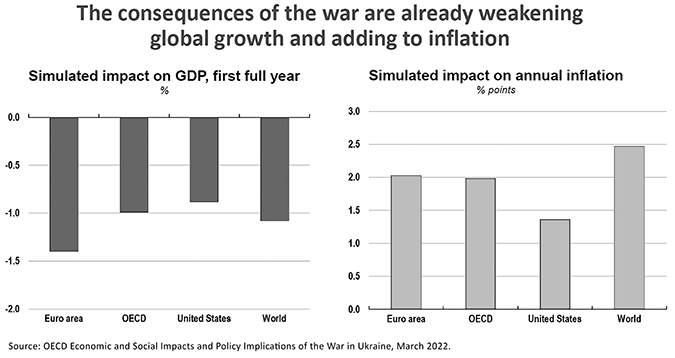

23

estimated the potential impact to economic growth and inflation from the war in the chart below. Tough times may lie ahead for the global consumer, as companies look to maintain profits by continuing to raise prices to offset rising input costs. Unfortunately, given the composition of their income, assets, and consumption baskets, high inflation tends to have an outsized impact on low-income households, as they tend to spend disproportionately more on food and energy.12

Compared with the MSCI EAFE Index, the FMI International portfolios’ revenue exposure is over-indexed to the UK (13.6% vs. 6.1%), and under-indexed to the rest of Europe (20.2% vs. 25.8%). We believe we are well-positioned from a relative standpoint. The UK is much less dependent on Russian energy than the rest of the continent, importing only 4% of its gas and 8% of its oil from Russia.13 Furthermore, we have long argued that Brexit was the right move for the UK, as they have distanced themselves from the dysfunction of the EU, which has demonstrated an inability to reform, a lack of desire to address their own structural problems, and a propensity for high government debt levels that could once again become a problem.

Our domestic UK businesses are durable. B&M European Value Retail S.A. is a leading discount retailer that performs well in most economic environments, offering low prices on consumables and necessities. Greggs PLC is the UK’s top convenience food-to-go store operator, selling baked goods, food, and coffee at value prices, resulting in repeat consumption. Lloyds Banking Group PLC, the UK’s largest bank, is predominantly a mortgage and credit card lender; it is well-capitalized, has a low-cost position, and de minimis exposure to Russia. The risk profile of the Eurozone banks (which we do not own) is far greater, as their Russian (and other counterparty) exposure is much less clear, and sovereign debt is being carried on their balance sheets with little-to-no capital requirements. Howden Joinery Group PLC is the UK’s largest supplier of fitted kitchens. Although we could certainly see an air pocket if discretionary spending falls, effectively all of their business is replacement, the company runs with no debt, and they have a history of taking market share during periods of dislocation.

_______________

12 | Indermit Gill and Peter Nagle. “Inflation could wreak vengeance on the world’s poor.” Brookings Institute, March 18, 2022. |

13 | Rowena Mason, Heather Stewart, Julia Kollewe. “UK to phase out Russian oil imports by 2023 and explore ending gas imports.” The Guardian, March 8, 2022. |

24

The balance of our European exposure is well-diversified, though there are certainly some risk points we are monitoring. Leisure travel in Europe is a near-term concern for Booking Holdings Inc. and Safran S.A., but demand should recover as time passes. Oil derivatives are a significant percentage of the raw material costs at Akzo Nobel N.V., with a pricing lag weighing on current profitability. However, price increases are coming and tend to be sticky, as paints and coatings companies often see margin expansion after significant inflationary periods. Rexel S.A. (electrical distribution) faces the prospect of a slowdown in commercial construction, but 50-60% of their European commercial business is retrofit, which should prove more resilient. We are constantly monitoring the downside risks of our holdings. Collectively, given their business quality and balance sheet strength, we’d expect our companies to hold up well during challenging times.

The portfolios have very little exposure to Exploration & Production and commodity-related stocks, which were a big driver of returns in the quarter. Over long periods of time, most of the companies in these sectors have failed to earn their cost of capital, and are highly volatile. Commodities, by definition, lack differentiation. Poor discipline and bad actors can ruin the business economics. While these can be great trading stocks, like we are seeing today, they do not fit our eye in terms of business quality and long-term value creation.

Back to the Disco Era?

The risk of a global recession has undoubtedly increased due to the war. As penned by The Wall Street Journal, “Economists are increasingly warning of a possible bout of stagflation, particularly in Europe, a situation of high inflation and low growth that afflicted major economies during the 1970s. Back then, central banks responded to a surge in oil prices with easy-money policies that caused a wage-price spiral. Now, some central banks might give up on their plans to increase interest rates after keeping them down during the pandemic.”14 Herein lies the conundrum. If central banks stay accommodative and keep rates too low for too long, they could lose control of inflation (we think they already have). If they raise interest rates too aggressively, they risk choking off the growth of the economy. Years of profligate government spending and money printing have left central banks no choice but to try to “thread the needle.” We do not envy their position, but in many ways it has been self-made. The Fed and Bank of England are finally moving down the path of rate hikes (albeit slowly), while the ECB and Bank of Japan continue to drag their feet. Time is of the essence.

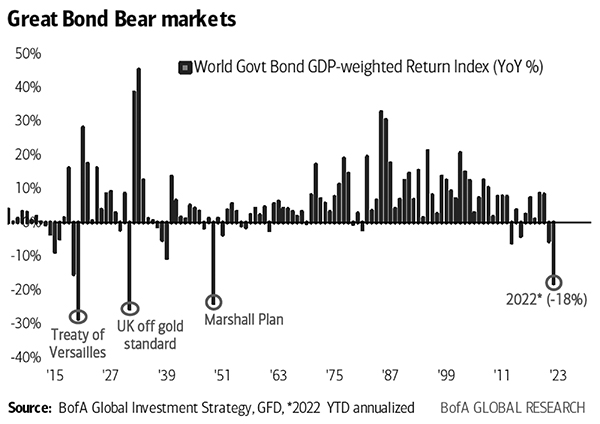

Fortunately, despite the disappointing reluctance of central banks to raise rates more decisively, market forces are starting to move interest rates higher on their own accord. Higher rates mean lower bond prices, so it appears that a global bond bear market is finally upon us, per the chart below. To approach something that starts to resemble normalcy, we still have a very long way for rates to go. At the very least, it is encouraging to see negative yielding debt falling precipitously, from $18.3 trillion in late 2020 to under $3 trillion today.15 As we’ve said many times, money is not supposed to be free (or even worse, negative yielding). We welcome a day when price discovery determines the cost of capital, not manipulation by central banks.

_______________

14 | Tom Fairless. “Global Economy Braces for Impact of Russia’s War on Ukraine.” The Wall Street Journal, March 7, 2022. |

15 | Bloomberg. |

25

If indeed the next economic cycle features higher interest rates and inflation, as it appears it will, we should be operating from a position of strength. Our quality businesses have pricing power given their advantaged competitive positions. Our companies’ solid balance sheets should allow for investment and market share gains during tough times, while their levered competitors are compromised. High valuation multiples may get knocked down off their perch, allowing for our valuation discipline and discount to the market to shine through. We remain optimistic, but discerningly cautious.

Taking Taiwan

At the outset of the Ukraine war, observers wondered whether Russia’s invasion would embolden China to attempt to annex Taiwan. This would be another extremely negative development with significant global economic implications. Taiwan is home to the world’s leading semiconductor company (Taiwan Semiconductor Mfg. Co. Ltd.) and the most advanced semiconductor technology. China is significantly behind in this area, with little chance of quickly catching up through organic investment. In recent years, China has muscled its way into second place in the global economy and will remain a powerful force. However, China President Xi Jinping has been clear in his intentions to make China number one in economic, military, and geopolitical leadership over the next two decades. We hope Xi Jinping will learn some valuable lessons from the war, giving him some pause. Russia clearly miscalculated the military resolve of Ukraine, as their advancement has been much slower than originally anticipated. Furthermore, the swift and unprecedented sanctions from the West were bolder than many expected. Taiwan is of great strategic importance to the West and its invasion could elicit an even fiercer economic response, if not a military one as well. China’s reliance on approximately $1.3 trillion of exports to the U.S. and Europe16 may be an additional deterrent to a 21st Century Cold War. We hope that these factors will keep China from going too far, but recognize that anything is possible. With the U.S. and Europe keenly aware of Taiwan’s global significance, we hope there will be enough diplomatic pressure to forestall another war.

[As a reminder, FMI does not have any direct investments in China. China’s authoritarian government, rule of law, lack of disclosure, accounting practices, management distrust, and poor corporate governance have been roadblocks. When we cannot do our customary level of due diligence, we simply pass.]

_______________

16 | Bloomberg. |

26

While there is tremendous uncertainty in the world, with it comes new opportunities. Though some of our investments have been recently out-of-step with the market (the nature of contrarian investing), in the fullness of time we expect their positive attributes to prevail. As Ben Graham wisely said: “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” We remain focused on finding strong businesses that can weather the storm, are soundly financed, and trade below their intrinsic value.

Described below are two holdings where we see an attractive risk/reward:

Sodexo S.A. (SW FP)

(Analyst: Dain Tofson)

Description

Sodexo is a leading global caterer, facilities manager, and benefits and rewards services provider. The company is headquartered in Paris, France, and controlled by the Bellon family. Sodexo reports two segments: On-site Services and Benefits & Rewards Services. On-site Services represented 96% of revenue and 79% of EBITA in fiscal year (FY) 2019. By service type, On-site Services revenue was split 66% food services and 34% facilities management services. By geography, On-Site Services revenue was split 45% North America, 39% Europe, and 16% rest of the world. Benefits & Rewards Services represented 4% of revenue and 21% of EBITA in FY 2019. By activity, Benefits & Rewards Services revenue was split 77% Employee Benefits and 23% Services Diversification, which includes fuel passes and public benefits programs. By geography, Benefits & Rewards Services revenue was split 67% Europe, USA, and Asia and 33% Latin America.

Good Business

| • | Sodexo is one of the largest players in On-site Services and Benefits & Rewards Services. In On-site Services, the company’s scale gives them procurement advantages over smaller competitors. In Benefits & Rewards Services, Sodexo’s large, two-sided network constitutes a defensible moat. | |

| • | The On-Site Services industry is large and fragmented. The large players such as Sodexo have a long runway to take market share from smaller operators. | |

| • | The business is relatively stable and defensive in non-pandemic downturns, with client retention rates around 93-94%, new sales development around 7%, and consistent same site sales growth. | |

| • | Returns on capital employed have generally been mid-teens or higher. | |

| • | The company has a strong balance sheet with net debt-to-EBITDA of 1.7 times. | |

| • | This is an easily understandable business. |

Valuation

| • | The stock trades at around 14 times FY 2023 earnings per share (EPS) versus 17-18 times historically, which is at a discount to the MSCI EAFE Index, despite being a much better-than-average business. | |

| • | The stock is trading at a discount to the company’s sum-of-the-parts value. | |

| • | We believe Sodexo can improve its EBITA margin more than consensus expectations. If the company can earn 6.25% EBITA margin on FY 2023 consensus revenue, then that implies €1.4 billion of EBITA and inexpensive valuation multiples of 8.4 times EV/EBITA and 11.9 times EV/NOPAT. |

Management

| • | Sophie Bellon is Chairwoman and CEO. The Bellon family is turning into a “self-activist,” having embarked on a plan to improve performance and unlock value in the business. |

27

| • | Sodexo is a member of several Sustainability Indices and ranks amongst leaders in its sector for the sixteenth consecutive year. | |

| • | Long-term incentive compensation is based on revenue, margin, total shareholder return versus peers, and corporate responsibility. |

Investment Thesis

Sodexo is a very FMI-like business – it has solid growth prospects in structurally attractive industries, relatively defensive performance, mid-teens or higher return on capital employed, a solid balance sheet, and is easy to understand. However, despite the company’s attractive intrinsic qualities, the business and stock have been through a multiyear period of underperformance. The underperformance began in 2018 due to management issues in On-site Services North America Healthcare and On-site Services Education sectors, and was followed by pandemic-induced lockdowns in 2020 and 2021 that significantly impacted the overall business. However, there are signs that the future looks brighter than the past. Trends are improving in these two sectors, and the acute phase of the pandemic looks to be coming to an end. In our opinion, Sodexo is posed for a strong recovery, but the market hasn’t recognized this yet.

Greggs PLC (GRG LN)

(Analyst: Jordan Teschendorf)

Description

Greggs is the UK’s leading convenience food-to-go store operator, offering fresh prepared baked items, food, coffee, other drinks, and snacks from convenient locations at value prices. It operates a unique vertically integrated model, manufacturing and distributing the majority of the products it sells. Greggs serves over 6.5 million customers each week from its shop network (2,181 at year-end 2021) and estimates it has around 5% market share in the UK “food-on-the-go” sector (sized at £24 billion in 2019; growing mid-single digits). As of 12/31/21, approximately 17% of Greggs shops were franchised.

Good Business

| • | Greggs has historically grown strongly in good economic periods, and has been resilient in recessions. Prior to COVID the company grew sales for >35 consecutive years, including +7%/+5% in 2008-2009. | |

| • | Greggs sells products that are low-ticket (£3 estimated average transaction value), consumed immediately, and often need to be replenished during the day. The company’s vertically integrated model, large scale, and network density enable it to deliver fresh-baked foods and ingredients for on-site preparation multiple times daily to each shop in its network, control and assure food quality, flex its range to meet changing tastes/preferences, and drive economies of scale across the value chain. | |

| • | Consistent operational delivery in the industry creates habitual purchasing behavior. Greggs operational model within stores is built on speed-of-service, with efficient layouts, teams, and the latest technologies. As Greggs expands its network, its convenience and value to the customer improves while fixed cost and overhead per store declines, justifying further expansion. | |

| • | The industry has proven to be rational, with pricing offsetting inflation over time. | |

| • | Return on invested capital is 21%, fully burdened for leases. Greggs recently outlined a significant investment program over the next several years, supporting an acceleration in its growth rate. With strong execution, the business is capable of growing its shop base around 7% annually with strong unit economics. |

28

| • | The company is conservatively financed, with net financial cash on the balance sheet. Net cash has averaged around 15% of the invested capital base over the last two decades. | |

| • | Since the 1980s, Greggs has shared 10% of annual profits with employees. |

Valuation

| • | The stock trades at 10.6 times trailing EV/EBITDA, a discount to its long-term historical average, despite improved growth prospects. | |