OMB APPROVAL | |

OMB Number: 3235-0288 | |

UNITED STATES | Expires: January 31, 2008 |

SECURITIES AND EXCHANGE COMMISSION | Estimated average burden |

Washington, D.C. 20549 | Hours per response: 2631.00 |

FORM 20-F

Amendment I

(Mark One)

___ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR | |

X__ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended January 31, 2005 |

OR | |

___ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to |

Commission file number 0-28980 | |

ROYAL STANDARD MINERALS INC. (Exact name of Registrant as specified in its charter) | |

(Translation of Registrant's name into English) | |

CANADA (Jurisdiction of incorporation or organization) | |

3258 MOB NECK ROAD HEATHSVILLE, VIRGINIA 22473 (Address of principal executive offices) | |

Securities registered or to be registered pursuant to Section 12(b) of the Act. | |

Title of each class ____________________________________ ____________________________________ | Name of each exchange on which registered ____________________________________ ____________________________________ |

Securities registered or to be registered pursuant to Section 12(g) of the Act. | |

COMMON SHARES | |

(Title of Class) | |

(Title of Class) | |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. | |

(Title of Class) | |

SEC 1852 (6-04) | Persons who respond to the collection of information contained in this form are not required to respond unless the form displays a currently valid OMB control number |

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report. |

43,143,518 Common Shares |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. |

______Yes __X___No |

Indicate by check mark which financial statement item the registrant has elected to follow. |

___X___ Item 17 _____ Item 18 |

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS) |

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. |

______Yes _____No |

PART 1 | ||

ITEM 1 | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 5 |

ITEM 2 | OFFER STATISTICS AND EXPECTED TIMETABLE | 5 |

ITEM 3 | KEY INFORMATION | 5 |

A. | Selected financial data | 5 |

B. | Capitalization and indebtedness | 6 |

C. | Reasons for the offer and use of proceeds | 6 |

D. | Risk factors | 6 |

ITEM 4 | INFORMATION ON THE COMPANY | 9 |

A. | History and development of the company | 9 |

B. | Business overview | 9 |

C. | Organizational structure | 16 |

D. | Property, plants and equipment | 16 |

ITEM 5 | OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 16 |

A. | Operating results | 16 |

B. | Liquidity and capital resources | 19 |

C. | Research and development, patents and licenses, etc. | 21 |

D. | Trend information | 21 |

E. | Off balance sheet arrangements | 21 |

F. | Tabular disclosures of contractual obligations | 21 |

G. | Safe harbor | 21 |

ITEM 6 | DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 21 |

A. | Directors and senior management | 21 |

B. | Compensation | 23 |

C. | Board practices | 25 |

D. | Employees | 30 |

E. | Share ownership | 30 |

ITEM 7 | MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 31 |

A. | Major shareholders | 31 |

B. | Related party transactions | 31 |

C. | Interests of experts and counsel | 31 |

ITEM 8 | FINANCIAL INFORMATION | 31 |

A. | Consolidated statements and other financial information | 31 |

B. | Significant changes | 32 |

ITEM 9 | THE OFFER AND LISTING | 32 |

A. | Offer and listing details | 32 |

B. | Plan of distribution | 34 |

C. | Markets | 34 |

D. | Selling shareholders | 35 |

E. | Dilution | 35 |

F. | Expense of the issue | 35 |

ITEM 10 | ADDITIONAL INFORMATION | 35 |

A. | Share capital | 35 |

B. | Memorandum and articles of association | 35 |

C. | Material contracts | 35 |

D. | Exchange controls | 35 |

E. | Taxation | 37 |

F. | Dividends and paying agents | 38 |

G. | Statements by experts | 38 |

H. | Documents on display | 38 |

I. | Subsidiary information | 38 |

ITEM 11 | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 39 |

ITEM 12 | DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 39 |

PART II | ||

ITEM 13 | DEFAULTS, DIVIDENT ARREARAGES AND DELINQUENCIES | 39 |

ITEM 14 | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 39 |

ITEM 15 | CONTROLS AND PROCEDURES | 39 |

ITEM 16 | [RESERVED] | 40 |

ITEM 16A | AUDIT COMMITTEE FINANCIAL REPORT | 40 |

ITEM 16B | CODE OF ETHICS | 40 |

ITEM 16C | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 40 |

ITEM 16D | EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 40 |

ITEM 16E | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 40 |

PART III | ||

ITEM 17 | FINANCIAL STATEMENTS | 41 |

ITEM 18 | FINANCIAL STATEMENTS | 74 |

ITEM 19 | EXHIBITS | 74 |

SIGNATURES | 74 | |

CERTIFICATIONS | 75 | |

CERTIFICATIONS PURSUANT TO SECTION 906 | 77 |

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not Applicable

Item 2. Offer Statistics and Expected Timetable

Not Applicable

Item 3. Key Information

A. Selected financial data.

The table below presents selected statement of operations and balance sheet data for Royal Standard Minerals Inc. as at and for the fiscal years ended January 31, 2005, 2004, 2003, 2002 and 2001. The selected financial data presented herein is prepared in accordance with accounting principles generally accepted in Canada ("Canadian GAAP") and include the accounts of the Company and its wholly-owned subsidiaries, Southeastern Resources Inc., Pinon Exploration Corporation, Standard Energy Inc., and Manhattan Mining Co., all United States Companies.

A summary of the differences between accounting principles generally accepted in Canada ("Canadian GAAP") and those generally accepted in the United States ("US GAAP") which affect the Company is contained in Note 15 of the Consolidated Financial Statements included with this report.

Royal Standard Minerals Inc.

(An Exploration Stage Enterprise)

Consolidated Financial Statement Data

For the Years Ended January 31

(Expressed in US Currency)

2005 | 2004 | 2003 | 2002 | 2001 | |

Statement of Operations | |||||

Revenue | $0 | $0 | $0 | $10,332 | $8,282 |

Administrative Expenses | $578,632 | $565,907 | $330,598 | $144,690 | $57,158 |

Net loss for the year | ($481,723) | ($554,626) | ($416,803) | $295,648 | ($2,597492) |

Deficit, beginning of year | ($7,377,424) | ($6,822,798) | ($6,405,995) | ($6,701,643) | ($4,104,151) |

Deficit, end of year | ($7,859,147) | ($7,377,424) | ($6,822,798) | ($6,405,995) | ($6,701,643) |

Earnings (loss) per common share | |||||

Basic | ($0.01) | ($0.02) | ($0.02) | $0.02 | ($0.15) |

Diluted | ($0.01) | ($0.02) | ($0.02) | $0.01 | ($0.15) |

Weighted Average Shares Outstanding | 41,090,912 | 31,330,379 | 25,537,033 | 27,031,338 | 23,116,459 |

Balance Sheet | Year Ended January 31 | ||||

2005 | 2004 | 2003 | 2002 | 2001 | |

Current Assets | $541,835 | $273,291 | $377,753 | $619,968 | $251,962 |

Interest in Mineral Properties and Related Deferred Exploration Costs | $2,526,046 | $1,253,444 | $781,039 | $113,078 | $49,380 |

Equipment | $37,735 | $52,656 | $53,688 | $0 | $0 |

Currency Exchange Rates

Except where otherwise indicated, all of the dollar figures in this annual report on Form 20-F, including the financial statements, refer to United States currency. The following table sets forth, for the periods indicated, certain exchange rates based on the exchange rates reported by the Federal Reserve Bank of New York as the noon buying rates in New York City for cable transfers in foreign currencies as certified for customs purposes (the “Noon Buying Rate”). Such rates quoted are the number of U.S. dollars per Cdn $1.00 and are the inverse of rates quoted by the Federal Reserve Bank of New York for the number of Canadian dollars per U.S. $1.00.

Year Ended December 31, | |||||

2000 | 2001 | 2002 | 2003 | 2004 | |

High for the period | .6973 | .6696 | .8532 | .7738 | .8493 |

Low for the period | .6413 | .6266 | .7992 | .6329 | .7196 |

Average rate for the period(1) | .6735 | .6446 | .8308 | .7186 | .7716 |

Rate at end of period | .6666 | .6279 | .8358 | .7738 | .8308 |

_______________

- (1) Based on the average exchange rates on the last day of each month during the applicable period.

B. Capitalization and indebtedness.

Not Applicable

C. Reasons for the offer and use of proceeds.

Not Applicable

- D. Risk factors.

The operations of Royal Standard involve a number of substantial risks and the securities of Royal Standard are highly speculative in nature. The following risk factors should be considered:

Absence of Public Market

Trading of the Common Shares of Royal Standard on the TSX Venture Exchange and OTC Bulletin Board has been sporadic and very limited and no assurance can be given that an active trading market will develop or be sustained. Investment in Royal Standard is, therefore, not suitable for any investors who may have to liquidate their investments on a timely basis and should only be considered by investors who are able to make a long term investment in Royal Standard.

Risk Inherent to Royal Standard’s Proposed Mining Activities

1. Royal Standard is engaged in the business of acquiring and exploring mineral properties in the hope of locating an economic deposit or deposits of minerals. The property interests of the Company are in the exploration stage only and are without a known body of commercial ore. There can be no assurance that the Company will generate any revenues or be profitable or that the Company will be successful in locating an economic deposit of minerals.

2. There are a number of uncertainties inherent in any exploration and development program, including the location of economic ore bodies, the development of appropriate metallurgical processes, the receipt of necessary governmental permits, and the construction of mining and processing facilities. Substantial expenditures will be required to pursue such exploration and development activities. Assuming discovery of an economic ore body, and depending on the type of mining operation involved, several years may elapse from the initial stages of development until commercial production is commenced. New mining operations frequently experience unexpected problems during the exploration and development stages and during the initial production phase. In addition, preliminary reserve estimates may prove inaccurate. Accordingly, there can be no assurance that the Company’s current exploration and development programs will result in any commercial mining operations.

3. The Company may become subject to liability for cave-ins and other hazards of mineral exploration against which it cannot insure or against which it may elect not to insure because of high premium costs or other reasons. Payment of such liabilities would reduce funds available for acquisition of mineral prospects or exploration and development and would have a material adverse effect on the financial position of the Company.

History of Losses

At January 31, 2005, the Company had an accumulated deficit of U.S. $7,859,147. There can be no assurance that the Company will ever achieve revenues from operations or that its operations will ever be profitable.

Additional Capital

The terms of the Company’s rights to its properties require that the Company expend significant funds on exploratory and other pre-production activities. Should the Company fail to make these expenditures on a timely basis, it would forfeit its rights to the particular projects, including the sums expended through the dates of such forfeitures. The Company’s present capital resources are sufficient to fund these costs. There can be no assurance that the Company will be able to raise additional capital on acceptable terms or at all. In any event, any additional issuance of equity would be dilutive to the Company’s current shareholders.

No History of Operations

The Company is an exploration stage enterprise with no history of prior operations and no earnings. There can be no assurance that the Company’s operations will become profitable in the future. The success of the Company will be dependent on the expertise of its management, the quality of its properties, and its ability to raise the necessary capital to carry out its business plan. If financing is unavailable for any reason, the Company will be unable to acquire and retain its mineral concessions and carry out its business plan.

Regulatory and Economic Factors

Any exploration operations carried on by the Company are subject to government legislation, policies and controls relating to prospecting, development, production, environmental protection, mining taxes and labor standards. In addition, the profitability of any mining prospect is affected by the market for minerals which is influenced by many factors including changing production costs, the supply and demand for minerals, the rate of inflation, the inventory of mineral producers, the political environment and changes in international investment patterns.

Competition

There is significant competition for the acquisition of properties producing or capable of producing gold and precious minerals. The Company may be at a competitive disadvantage in acquiring additional mining properties since it must compete with other individuals and companies, many of which have greater financial resources and larger technical staffs than the Company. As a result of this competition, the Company may be unable to acquire attractive mining properties on terms it considers acceptable.

Title to Properties

The validity of unpatented mining claims on public lands, which constitute most of the property holdings is often uncertain and may be contested and subject to title defects.

Conflict of Interest

Certain directors and officers of the Company are also directors and officers of other natural resource and base metal exploration and development companies. As a result, conflicts may arise between the obligations of these directors to the Company and to such other companies.

Dependence on Key Personnel

The Company’s success will be dependent upon the services of its President and Chief Executive Officer, Mr. Roland Larsen.

Effect of Outstanding Warrants and Options; Negative Effect of Substantial Sales

As of January 31, 2005, the Company had outstanding options and warrants to purchase an aggregate of 9,513,840 Common Shares. All of the foregoing securities represent the right to acquire Common Shares of the Company during various periods of time and at various prices. Holders of these securities are given the opportunity to profit from a rise in the market price of the Common Shares and are likely to exercise its securities at a time when the Company would be able to obtain additional equity capital on more favorable terms. Substantial sales of Common Shares pursuant to the exercise of such options and warrants could have a negative effect on the market price for the Common Shares.

Dividends

The Company does not anticipate paying dividends in the foreseeable future.

Item 4. Information on the Company

- A. History and development of the company.

Royal Standard Minerals Inc. herein referred to as "Royal Standard" or the “Company”, was incorporated pursuant to the laws of Canada by articles of incorporation dated December 10, 1986 under its former name, Ressources Minieres Platinor Inc. (“Ressources”). On April 30, 1996, Royal Standard shareholders approved the acquisition of all the issued and outstanding shares of Southeastern Resources, Inc. (“Southeastern”) in a reverse take-over transaction. Pursuant to this transaction, articles of amendment were filed effective May 14, 1996, pursuant to which the name of Royal Standard was changed to its current form of name and its shares issued and outstanding at that time were consolidated on a 7.5:1 basis. On June 28, 1996, the Common Shares commenced trading on the Montreal Exchange. The Company is continued under the New Brunswick Business Corporations Act and its common shares are listed on the TSX Venture Exchange. The Company also trades in the United States Over-the-Counter Bulletin Board.

The registered office of Royal Standard is located at 56 Temperance Street, Fourth Floor, Toronto, Ontario M5G 2V5 with another office located at 3258 Mob Neck Road, Heathsville, Virginia 22473. The Company also has an office at 1311 N. McCarran Blvd., Unit 102, Sparks, Nevada 89431.

B. Business overview.

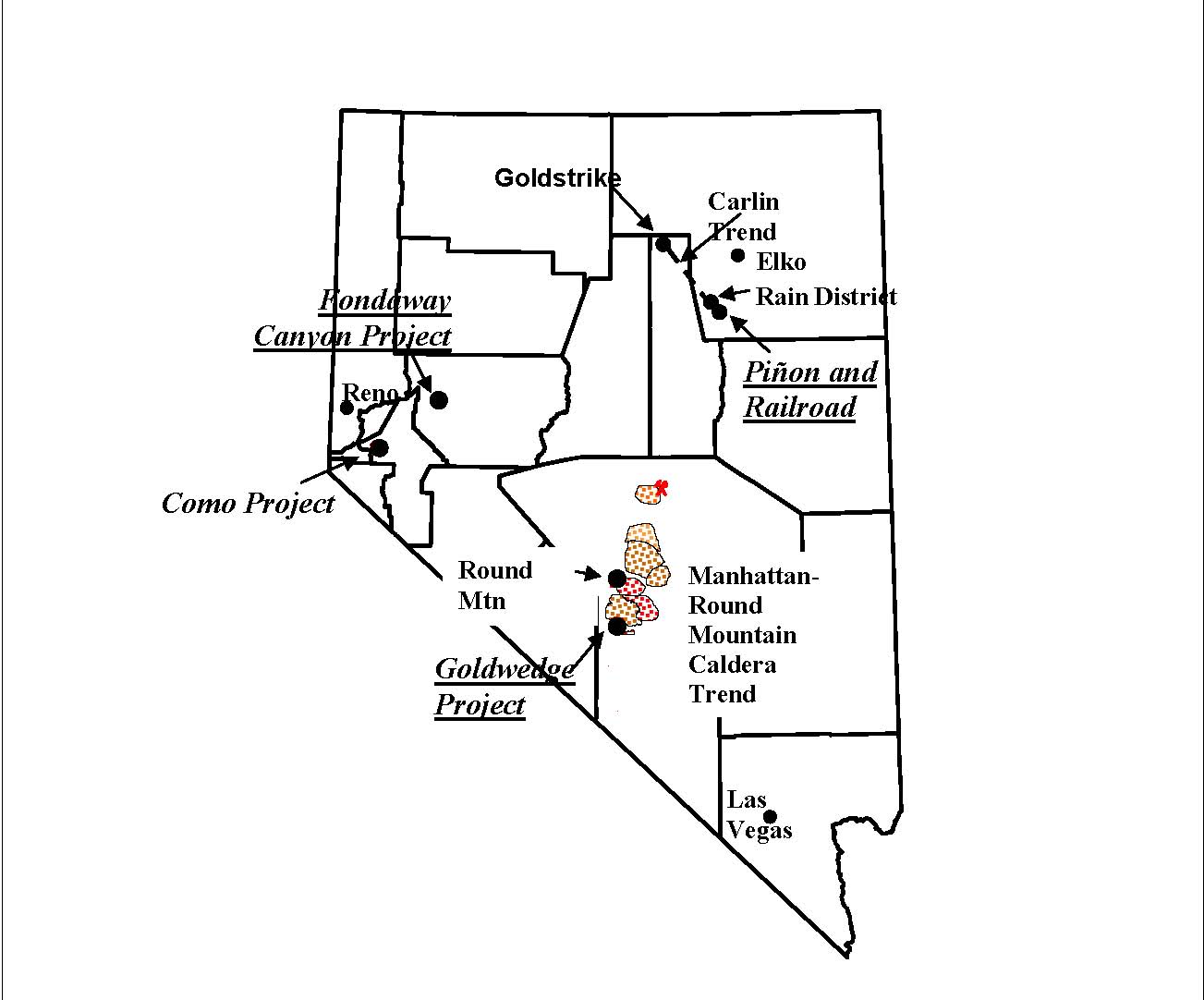

Royal Standard is a mineral exploration company engaged in locating, acquiring exploring and the development of gold and precious metal deposits in the state of Nevada. Royal Standard currently has five advanced and exploration-stage projects, the Manhattan and Gold Wedge programs in Nye County, the Pinon and Railroad projects in Elko County, the Fondaway project in Churchill County, Nevada and the Como project in Lyon County.

At the present time, the Company’s activities are limited to exploratory searches for ore and energy minerals. The Company has not generated any revenues from operations at this time. The Company is evaluating the potential for economic extraction of known deposits of ore grade material on the Company’s mineral exploration properties. See Item # 3.D. - Risk Factors.

Manhattan/Round Mountain Caldera Program

The project area is located southeast of the town of Round Mountain, Nevada east of State route 376. The town of Manhattan is located approximately 15 miles south of Round Mountain. The Manhattan project is located approximately 7 miles east of route 376 on route 377 and 1.5 miles west of the town of Manhattan.

The Manhattan/Round Mountain Caldera program is the Company’s most advanced district play. The land position in the Manhattan Mining District is comprised of 70 patented and unpatented lode-mining claims. Drill testing the extensions of the Goldwedge deposit in addition to the evaluation of several additional lode and placer properties that the Company controls in the district could significantly increase the gold resource estimates.

Freeport Gold, Tenneco (Echo Bay) recognized the potential of the district (to include the Goldwedge deposit that is currently under control by RSM) however, these deposits were not suited for open pit mining. At that time the large mining companies did not consider the underground development projects feasible. Although Sunshine Mining Co. considered an underground mine development in 1988 on the Goldwedge deposit, continued exploration by Crown Resources and others on MMC claims indicated sections (5+’-30’) of potentially mineable grades greater than 0.5 opt gold. The continued downturn in the gold market, tightened corporate budgets and high holding costs for the properties forced many companies to turn back the land positions to the claim owners. Currently, MMC controls approximately 4,000 feet of strike length. Approximately 1,000-1,200 feet of this strike length has been drill tested indicating positive results.

Goldstrike

Fondaway

Canyon Project

Manhattan-Round Mountain Caldera Trend

Pinon and

Railroad

Round Mtn

Como Project

Goldwedge Project

Carlin Trend

Elko

Reno

Las Vegas

RainDistrict

Goldwedge Project

The Goldwedge, one of several deposits in the Manhattan area, is currently under evaluation to include an underground bulk sample. The bulk sample will be processed on site. The Goldwedge contains excellent exploration potential for future growth. Based upon the results of 70 drill holes primarily within the central zone over a strike length of 1,000+ feet and 100’-500’ of vertical extent reveal continuous gold oxide mineralization of potential mineable thickness and quality. RSM has analyzed all of the drill data as part of a detailed geologic inventory of the project.

The project ownership includes staked BLM lands; options of BLM claims owned by others and patented mining claims owned by the Company. All payments, maintenance fees, option payments and taxes to state and federal authorities are current under state and federal guidelines.

The Goldwedge deposit occurs at the intersection of north and northwest trending faults. In the deposit area, the north trending Reliance fault is mineralized within the Ordovician Zanzibar limestone and siltstone. The target mineralization occurs within multiple high angle structures over a width of between 100-200 feet primarily within the Zanzibar limestone. RSM has evaluated all of the pertinent drill data as part of a detailed inventory of the deposit geometry, size and overall grade. The current exploration model suggests that the Goldwedge deposit and the extensions may contain large gold resources at depth near the contact with the Manhattan Caldera margin.

The Goldwedge deposit is located approximately 8 miles south of the large Round Mountain gold mine. All mine and mill (plant) and water use permits were achieved in early, 2003. In 2004 the Company constructed a 700 foot (underground) decline and cross cut to test one of the gold mineralized structures within a 100+ wide structural zone. Additionally, RSM completed the surface facilities necessary to process the material to be mined onsite to include silt ponds, ore pad and the onsite gold processing plant. The Company acquired a full production scale gold recovery (gravity) plant that will be utilized to process the mined material as part of the test mining program.

Expenses during fiscal 2004 on the Goldwedge and Manhattan Projects were $1,077,277 bringing total RSM expenses on these projects to $1,513,427. Future expenditures are expected to be an additional $2 million over the next two years.

Currently Sierra Power, a commercial electric supplier, services this site. The Company has all of the necessary water rights secured from the State of Nevada.

This project is an advanced exploration project without known reserves and the proposed program is exploratory in nature.

The underground bulk sampling and decline development program will be expanded in 2005. This effort will include drifting on one of the mineralized zones and processing this material through an onsite (gravity) plant. The surface facilities and the gold recovery plant will be completed during the fourth quarter 2005.

The underground program has several objectives including a test mining program and the establishment of the appropriate mining methods that will be applied to the future development of the property.

The underground development as well as surface and underground drilling will be directed toward expanding the resources on this property as well as the completion and testing of the recovery plant design.

Pinon and Railroad Projects-Carlin Trend South

This project is located south of the town of Carlin, Nevada in Elko County, Nevada. The project land position is located east of Nevada state route 276 and extends for 10+ miles in a north-south direction south of the town of Carlin. The best access to the project is via I-80 to Carlin and south on route 276 to the property position.

The land position includes unpatented BLM lands, patented lands and fee lands. All payments, maintenance fees to federal and state authorities are current. Landowner option payments are also current and in good standing for this more than 16,000 acre land position.

The Pinon properties are located on the southern portion of the Carlin gold belt about 10 miles south of Newmont’s Rain mine Since its inception, various joint-venture partners have spent more than $10 MM on the project.

The Pinon and Railroad projects are located on the southern portion of the Carlin Trend immediately south of Newmont’s Rain gold district. The Carlin Trend is one of the most prolific gold trends in the world and has produced more than 50 million ounces of gold. The properties are located within a well-mineralized region, which only adds to the potential for expanding the known gold deposits and making new discoveries. Much of the district wide exploration was undertaken prior to the start of the 1980’s and 1990’s. Since the mid-1990’s the cumulative knowledge of “Carlin-type” gold deposits has expanded tremendously. This expanded knowledge can be used to re-interpret all of the available data, which will likely identify new exploration targets on the ground controlled by RSM. Also, during the past 10+ years numerous high-grade gold deposits have been discovered along the Carlin Trend that can be mined using underground techniques. Many of these deeper deposits are associated with surface oxidized gold deposits. Essentially no deeper exploration has been conducted under the Pinon and Railroad deposits, or at other places on the property. The exploration opportunity offers the possibility for discovery of additional gold deposits at Pinon-Railroad.

The Railroad project increased the property position within the district to approximately 16,000 acres of leases, unpatented and patented mining claims. This effort included the acquisition of nearly 500 unpatented and 19 patented mining claims that lie immediately south of Newmont’s Minings Rain district in Elko County, Nevada.

The Web formation is mineralized above the Devils Gate limestone at the Pinon and Railroad deposits. At Pinon, the known mineralization has not been connected to a strongly mineralized fault. However, higher-grade economic mineralization has been encountered at very shallow depths, mineralized oxide zones occur along a 1,300 feet strike length and occur less than 90 feet below the surface. These deposits occur as primarily stratabound deposits within the Web formation and locally into the underlying Devils Gate formation.

The Pinon and Railroad projects include approximately 16,000 acres comprising unpatented BLM lode mining claims, patents and leased fee lands. The focus of RSM’s current effort is to evaluate the potential for future development of near surface oxide gold-silver deposits. Approximately 600 shallow drill holes have been completed on 6 near surface deposits. The depth extensions of these deposits are not well understood, as deeper drilling has not been sufficient to develop an acceptable understanding of this mineralization.

The Company has developed the necessary construction plans for the Pinon-Railroad project to include surface, heap leach facilities design and open pit modeling of the deposits. The 2004 program involved work on the BLM permit application. All of this work has been completed in preparation for the filing of a mining permit application with the US Bureau of Mines (BLM) by year-end 2005. A second objective is to complete feasibility studies for the Pinon and Railroad near surface oxide deposits.

Plans for 2005 include completing the necessary drilling and field evaluations to build the necessary data base to complete the process of filing for a mining permit application with the state and federal authorities in late 2005-early 2006 for this advanced exploration stage property.

Currently there is no infrastructure in terms of buildings and other facilities. There is unpaved road access to the property. Power will have to be brought in from the Rain operations located about 10 miles to the north or from highway 276 located about 5 miles to the west. Water will be sourced on the property.

Total exploration expenditures on this project have exceeded $10 million and an additional $15 million will be required to develop a 5,000 ton per day heap leach operation on this project. As of January 31, 2005, RSM and its partners have spent approximately $2.7 million on the Pinon and Railroad projects. Plans include the achievement of a mining permit by mid-2006 followed project financing.

The property is without known reserves and the proposed program is exploratory in nature.

Fondaway Canyon Project

The 100% controlled Fondaway Canyon gold project is located in Churchill County, Nevada in the Stillwater range. The project is accessible east from Fallon, Nevada via State of Nevada route 116 an unpaved road. The Fondaway deposit is located on the west flank of the Stillwater Range at Fondaway Canyon.

The Fondaway Canyon gold property consists of 148 unpatented BLM lode mining claims (approximately 3,000 acres) located on the western slope of the Stillwater Range. All of the maintenance filing fees are current and in good standing. Nearly-vertical, east-west trending mineralized shear zones host the Half Moon, Paperweight, Hamburger Hill and South Pit gold resources that is hosted within a Mesozoic sedimentary package. The Mesozoic sedimentary package has been intruded by a Mesozoic-Tertiary aged intrusive.

The vertical extent tested by recent drilling of the higher grade gold mineralized shear zones is greater than 1,000 feet. Horizontal continuation of gold mineralization as at the Paperweight and Hamburger Hill mineralized shear zone is 3,700 feet with widths commonly between 5’-20+ feet. Drilling and assay records indicate that 568 holes have been drilled for a total estimated footage of 200,000 feet of RC drilling and 22,000 feet of core drilling to include 455 reverse circulation, 49 core holes and 64 air track holes. Tenneco Minerals Inc., the most active company, drilled approximately 350 holes (130,000 feet) and drove a 500’ adit for sulfide metallurgical sampling during the period 1987-1996. Tenneco also operated a small oxide gold open pit mine for a short time during this period. Nevada Contact Inc. (NCI) acquired the property in 2001 and drilled 11 reverse circulation holes. RSM acquired the property from NCI in early 2003 as part of a property swap with NCI retaining a 1% NSR overriding royalty in the Fondaway Canyon property and $25,000 advance minimum royalty payments to the claim holder until 2006 at which time the payments increase to $35,000 per year that includes a 3% NSR royalty until buyout. There is a buyout option of $600,000 for the owners’ interest.

RSM plans to further drill test the sulfide resource as part of a program to upgrade the indicated and inferred resources on the property. This effort will involve drilling underground within the Tenneco adit along with a surface drilling program. A bulk sampling program for metallurgical analysis of the sulfide resource will also be included as part of an effort to develop a gold recovery process that will achieve the desired results.

No field work was completed on this project in 2004 and no field work is planned in 2005. The only effort has been the renewal of the Company’s water rights and related permits. Plans are to commence an exploration effort in 2006 that will include surface drilling within the vicinity of the Tenneco adit.

Sierra Pacific Power Co exists on the property. RSM has the current water rights to the property.

Estimates of prior expenditures on this property are approximately $5-6 million. The largest portion of these expenditures was contributed by Tenneco Minerals and Tundra Mines LTD. This work included extensive drilling, development of a small open pit production project and an advanced exploration adit on the property. As of January 31, 2005, RSM has spent $96,028 on this project.

The property is without known reserves and the proposed program is exploratory in nature

Como District

The property is located approximately 8 miles southeast of the famous Comstock Lode and 2-3 miles southeast of the town of Dayton, Nevada, and includes 47 unpatented lode claims and 5 patented claims.

The Como district consists of at least eight gold-silver bearing structures that occur within a Tertiary age andesitic volcanic sequence that hosts the mineralization. Prospectors looking for mineralization similar to the Comstock Lode discovered Como in 1860. The property has had some historical gold and silver underground production with the Como vein producing about 20,000 ounces of gold and 500,000 ounces of silver at a gold equivalent grade of nearly 0.3 opt. The higher-grade underground vein extensions are largely undrilled and will be tested by RSM. Over the past 20 years modern exploration methods have continued to advance the understanding of the geologic framework and have identified two bulk mineable gold-silver deposits that will require further work to ascertain the economic potential. Since the 1960’s several large companies have explored the property to include St. Joe American, Amoco, Meridian Gold and Amax Gold Inc. (who identified a low-grade open pit resource, based on 46 holes.) for a large tonnage bulk mineable gold target.. More recently (2000) Anglo Gold Corp. explored the property for a potential multi-million ounce target.. Anglo released the property in 2001 after drilling 8 holes and completing considerable surface geologic mapping, rock chip and geochemical sampling. RSM acquired its option on the Como gold-silver project based upon the previous exploration results.

It is difficult to estimate prior expenditures on this property due to the large number of mining companies that have explored this property over the last 30 years.

No exploration work was completed on the property in 2004 and will not be completed in 2005. In 2006 RSM plans to complete surface geophysical, magnetics, and surface geochemical sampling in 2006.

- C. Organizational structure.

The Company has four wholly owned subsidiaries, Southeastern Resources Inc., Pinon Exploration Corporation, Standard Energy Inc., and Manhattan Mining Co., all United States Companies.

- D. Property, plants and equipment.

The registered office of Royal Standard is located at 56 Temperance Street, Fourth Floor, Toronto, Ontario M5G 2V5 with another office located at 3258 Mob Neck Road, Heathsville, Virginia 22473. The Company also has an office at 1311 N. McCarran Blvd., Unit 102, Sparks, Nevada 89431.

Item 5. Operating and Financial Review and Prospects

- A. Operating results.

Royal Standard is an exploration stage enterprise and is in the process of exploring its resource properties and has not determined whether the properties contain economically recoverable reserves. The recovery of the amounts shown for the resource properties and the related deferred expenditures is dependent upon the existence of economically recoverable reserves, confirmation of the Company's interest in the underlying mineral claims, the ability of the Company to obtain necessary financing to complete the exploration, and upon future profitable production.

Royal Standard is an exploration- stage enterprise and, as such, currently has no producing properties and no operating income or cash flow, other than interest earned on funds invested in short-term deposits (see Item 3.D. – Key Information - Risk Factors).

The net loss for the year ended January 31, 2005 was $481,723 as compared to $554,626 for the year ended January 31, 2004. General and Administrative expenses and Consulting fees decreased by a total of $103,832. However, Stock Option Compensation increased by $110,266 resulting in little change in total Expenses. Expenses were $578,632 for the year ended January 31, 2005 as compared to $565,907 for the year ended January 31 2004. The increase in Stock Option Compensation is attributed to the granting of 775,000 stock options to employees and directors of the Company on May 4, 2004.

The Corporation owns 100% interest in five (5) projects in four (4) gold-silver districts in Nevada. These projects include the Gold Wedge, Nye County, Pinon and Railroad Projects, Elko County, Fondaway Canyon, Churchill County and Como, Lyon County, Nevada.

The Gold Wedge project represents the most advanced project located in the Manhattan district about eight (8) miles south of the Round Mountain mine and has been issued a mine and mill permit by the Nevada Department of Environmental Protection (NDEP). In March, 2004 the Company completed a $2.2 CDN million private placement. These funds were directed toward the construction of a 700 foot (underground) decline and cross cut to test one of the gold mineralized structures within a 100+ wide structural zone. Additionally, RSM completed the surface facilities necessary to process the material to be mined onsite to include silt ponds, ore pad and the onsite gold processing plant. The Company acquired a full production scale gold recovery (gravity) plant that will be utilized to process the mined material as part of the test mining program.

In 2004, work on the BLM permit application for the Pinon-Railroad project continued. The Company developed the necessary construction plans for the Pinon-Railroad project including surface, heap leach facilities design and open pit modeling of the deposits. All of this work was completed in preparation for the filing of a mining permit application with the US Bureau of Mines (BLM) by year-end 2005. A second objective is to complete feasibility studies for the Pinon/Railroad near surface oxide deposits.

The net loss for the year ended January 31, 2004 was $516,869 as compared to $416,803 for the year ended January 31, 2003. The increase of $100,066 in net loss for the year is primarily attributable to an increase in expenses of the Corporation for the year ended January 31, 2004. Expenses were $565,907 for the year ended January 31, 2004 as compared to $330,598 for the year ended January 31 2003. The increase of $235,309 in the expenses of the Corporation for the year ended January 31, 2004 is attributable to, among other things, increased operating expenses on the Corporation’s properties. In order to maintain the ongoing activities on the highest priority projects in Nevada the Corporation will contribute a minimum of $1,800,000 to maintain progress toward the Gold Wedge development program in 2004.

The Corporation focused its efforts in 2003 on the Pinon and Railroad projects located on the southern portion of the Carlin Trend in Elko County, Nevada. The current land position includes more than 16,000 acres of unpatented, patented and fee leases. The effort in 2003 focused on the four (4) drilled out (600 drill holes) near surface measured oxide gold-silver resources. This work included drilling, trenching, pit modeling, plant and heap leach facility design and metallurgical (column) leach testing of the deposits. All of this work was to establish the economic potential of an open pit heap leach project and to develop the data necessary to complete a mine permit application to the US Bureau of Land Management (BLM) by mid-year 2004. Expenditures on this project in 2003 were about $1 million.

The Corporation carried out a detailed evaluation of all of the available data for the Fondaway gold and Como gold-silver projects and NI-43-101 reports were prepared for each project in 2003. These reports are filed on SEDAR along with the Goldwedge and Pinon-Railroad project reports.

Nevada Projects

In fiscal 2003 and 2002, the Company entered into certain option agreements to purchase up to 100% interest in patented and unpatented lode-mining claims in Nye, Elko and Lyon Counties, Nevada. Details of the option agreements are as follows:

Project | Required Cash Payments to Optionors | Royalty(1) | Exercise of Option |

Gold Wedge Nye County | Commencing in fiscal 2002. $5,000 each in first two years; $10,000 in third year; $15,000 in fourth year and $20,000 in fifth and sixth years | 3% NSR | July 2006 $200,000 |

Manhattan Nye County | Commencing in fiscal 2002. $1,000 per month from August 2001 to August 2002; $2,000 per month from September 2002 to July, 2006 | 5% NSR | August 2006 $500,000 |

Fondaway Canyon Churchill County | Commencing in fiscal 2003. $25,000 in year one, $30,000 in years two and three and $35,000 each of the next seven years | 3% NSR | July 2013 $600,000 |

Como Lyon County | Commencing in fiscal 2003. $25,000in years one and two covering years three and four, $20,000 in year five, $25,000 in year six | 4% NSR | May 2008 $1,000,000 |

Railroad Elko County | Commencing in fiscal 2003. $15,000 in the first year and increases by $5,000 each of the next six years | 5% NSR | August 2008 $2,000,000 |

1. NSR – Net Smelter Royalty

A reclamation bon has been posted by the Company to secure clean-up expenses if the concerned properties are abandoned or closed.

Gold Wedge Project

During 2004, the Company posted a bond regarding the Gold Wedge property as required by the State of Nevada. The bond remains attached to the Gold Wedge property.

ComoProject

On September 15, 2004, the Company granted an option (the “Option”) to Sharpe Resources Corporation (“Sharpe”) to acquire a 60% interest in the Company’s gold project located in Lyon County, Nevada (the “Project”), in consideration for which Sharpe has issued 2,000,000 common shares to the Company at a deemed value of $78,125 ($100,000 CDN). To exercise the option, Sharpe must maintain the unpatented and patented mining claims on the Project, must pay all required option, annual advanced minimum royalty payments and deliver a completed positive feasibility study in compliance with National Instrument 43-101 in respect of the Project.

Pinon Project – Cord Lease

In August 2002, the Company entered into a mining lease agreement to lease certain properties located in Elko County, Nevada for a period of five years. The lessors will retain a 5% net smelter royalty with no option to purchase.

Pinon Project – Tomera Lease

In August 2002, the Company entered into a mining lease agreement to lease certain properties located in Elko County, Nevada for a period of seven years. The lessor will retain a 5% net smelter royalty.

In addition, the Company entered into an irrevocable lease agreement with the surface and minerals rights owners of the Pinon Project properties.

- B. Liquidity and capital resources.

The Corporation’s cash balance as of January 31, 2005 was $392,697 compared to $189,732 at January 31, 2004. The increase in the cash balance is attributable to the private placement offerings completed during the fiscal year 2004. On February 3, 2004, the Company closed a private placement offering of 1,075,000 units at a price of $0.25 CDN per unit for gross proceeds of $268,750 CDN. Each unit consisted of one common share and one-half common share purchase warrant. Each whole purchase warrant entitled the holder to subscribe for one additional common share at a price of $0.30 CDN until February 2, 2005.

On April 16, 2004, the Company closed a private placement offering o 6,320,000 units at a price of $0.35 CDN per unit for gross proceeds of $2,212,000 CDN. Each unit consisted of one common share and one-half common share purchase warrant. Each whole purchase warrant entitles the holder to subscribe for one additional common share at a price of $0.50 CDN until April 15, 2006.

Current assets as at January 31, 2005 were $541,835. Total assets as at January 31, 2005 were $3,237,383 as compared to $1,579,391 at January 31, 2004. This represents an increase of $1,657,992 from 2004 due to the increased activity on the Company’s projects, particularly at the Gold Wedge Project where the Company completed construction of a 700 foot (underground) decline and cross cut. Additionally, RSM completed the surface facilities necessary to process the material to be mined onsite including silt ponds, ore pad and the onsite gold processing plant. Additionally, the Company acquired a full production scale gold recovery (gravity) plant that will be utilized to process the mined material as part of the test mining program.

Current liabilities as at January 31, 2005 were $104,087 compared to $106,178 in 2004, and represent current trade payables.

On a forward going basis equity and debt financings will remain the single major source of cash flow for the Corporation. The primary reason is that current production cash flow is insufficient to allow the Corporation to grow at a rate to increase the necessary production capacity to achieve profitability in the near term. As revenue from operations improve the capital requirement of the Corporation will also improve. However, debt and equity financings will continue to be a source of capital to expand the Corporation’s activities in the future.

The Corporation is authorized to issue an unlimited number of Common Shares of which 43,143,518 are outstanding as at January 31, 2005. As at January 31, 2005 the Corporation had outstanding options to purchase 4,185,000 common shares with exercise prices from $0.17-0.40 per share and expiration dates ranging from May 2005 to May 2009.

The Corporation’s cash balance as of January 31, 2004 was $189,732 compared to $283,030 at January 31, 2003. The fact that there is little change in the cash balance is attributable to the completion of a C$1.5 million equity financing in July, 2003 coupled with large expenditures before yearend. Current assets as at January 31, 2004 were $273,291 Total assets as at January 31, 2004 were $1,617,148 representing an increase of $404,668 from 2002 due to the addition of the Fondaway Canyon project and additional expenditures on the Corporation’s Pinon-Railroad project. Current liabilities as at January 31, 2004 were $106,178 compared to $82,300 and represent current trade payables as at January 31, 2003.

On April 17, 2002, the Company entered into an agreement with an unrelated party (the "Lender") to obtain a $5,000,000 financing facility. The agreement stipulated that the Company deposit with the Lender an interest earning refundable contingency fee of 1.5% of the facility ($75,000) which will be held in trust until the loan is advanced.

The agreement's closing date originally set to June 31, 2002, was later extended to June 17, 2003. If this agreement had closed on or before May 1, 2003, the Lender would have disbursed the funds to the Company, net of closure fees of 3.5% of the facility ($175,000). In addition, the Company was to issue 1,000,000 share purchase warrants to the Lender. Each warrant would have entitled the Lender to acquire one common share of the Company. The price of the warrants would have been set, based upon the 10 day moving average of the stock price prior to the closing date and would have had a two year term from the date of closing.

The agreement expired without the closing of the $5,000,000 financing facility. The Company pursued legal action against the Lender in an attempt to recover the funds advanced. On August 31, 2004, the Company recovered $54,050. The unrecoverable amount was charged to the current years operations.

On May 2, 2002, the Company completed a private placement of 7 million shares of the Company at Canadian $0.15 per share for proceeds of Canadian $1,050,000 (approximately US $650,000).

Due to the nature of the Company’s mining business, the acquisition, exploration, and, if warranted, the development of mining properties requires significant expenditures prior to achieving commercial production. Royal Standard will seek to finance such expenditures through the sale of equity, joint venture arrangements with other mining companies or the sale of interests in its properties. There can be no assurance, however, that the Company will be successful in raising capital on acceptable terms or in amounts sufficient to finance exploration expenditures and/or satisfy its commitments under its agreements with third parties. In the event that the Company does not raise capital as planned, it will forfeit its rights to the properties, including the sums expended through the dates of such forfeitures. See Item 3.D. – Key Information - Risk Factors.

C. Research and development, patents and licenses, etc.

See Items 4.B. and 5. A. above.

D. Trend information.

See Items 4.B. and 5. A. above.

- E. Off balance sheet arrangements.

There are none.

- F. Tabular disclosures of contractual obligations.

Not applicable.

- G. Safe harbor.

Not applicable.

Item 6. Directors, Senior Management and Employees

- A. Directors and senior management.

The following table sets out the names of and related information concerning each of the officers and directors of Royal Standard.

NAME | OFFICE HELD | SINCE |

Roland M. Larsen Heathsville, VA | President, Chief Executive Officer and Director | May, 1996 |

Kimberly L. Koerner Brambleton, VA | Director & Treasurer | May, 2001 |

MacKenzie I. Watson Monteral, Quebec | Director | May, 1996 |

James C. Dunlop Toronto, Ontario | Director | May, 1996 |

The following discussion provides information on the principal occupations of the above-named directors and executive officers of the Company within the preceding five years.

Roland M. Larsen

Mr. Larsen has 30 years of experience in the natural resource industry, both in exploration and management roles. From November 1993 to the present, he has been serving as the President of Sharpe Resources Corporation, a junior natural resource issuer. From 1981 to 1991, Mr. Larsen served District/Regional Exploration Manager with Inc. and BHP Minerals, Inc., both of which are junior natural resource issuers. Earlier in his career, he worked with BHP Minerals International Inc. for a period of ten years, where he was the Exploration Manager of the Eastern United States and the North Atlantic Region. Prior to that he was the Senior Geologist for NL Industries, Inc. In addition, he has several years of experience working with consulting engineering firms including Derry, Michner and Booth, and Watts Griffis & McOuat Limited. He is a member of the Society of Economic Geologists, the American Association of Professional Geologists and the Society of American Institute of Mining, Metallurgy, and Exploration Inc. Mr. Larsen holds a B.Sc. and M.Sc. degrees in geology.

Kimberly L. Koerner

Ms. Koerner is a Financial Analyst and Consultant. She has been serving as the Treasurer of the Company from May 1996 to the present. Ms. Koerner has also been serving as the Secretary and Treasurer of Sharpe Energy Company, a U.S. subsidiary of Sharpe Resources Corporation, from November, 1995 to the present. From April 1992 to February 1994, she served as the Assistant Director of the National Association of Printing and Publishing Technology, a trade association. Mrs. Koerner has B.Sc. degree in Finance from the University of South Carolina.

MacKenzie I. Watson

From October 1986 to the present, Mr. Watson has been the Chief Executive Officer and a director of Freewest Resources Inc., a junior natural resource issuer. A geological consultant, he also serves as a director of Sharpe and as President and a director of Consolidated Gold Hawk Resources Inc., a junior natural resource issuer. He was involved in the discovery of the Holloway Gold deposit in the Province of Ontario with Hemlo Gold Mines. Earlier in his career, he was President and Exploration Manager of Lynx-Canada Exploration Ltd., which, under his leadership, discovered numerous precious, base metals and coal deposits. Prior thereto, he was a project geologist for the Icon Syndicate, where he participated in the discovery of the Sullivan Mines in Chibougamau, Quebec. He is currently a director of the Prospectors and Developers Association of Canada. Mr. Watson holds a B.Sc. from the University of New Brunswick.

James C. Dunlop

From October 1994 to the present, Mr. Dunlop has been serving as the Managing Director of Canada Trust Investment Group Inc., a subsidiary of Canada Trust. He also serves as a director of Sharpe. From October 1986 to October 1994, he served as the Senior Vice President of CIBC-Investment Management Corp. Since graduating with a B.A. from University of Western Ontario in 1972, Mr. Dunlop has worked at increasingly senior positions within the Canadian investment community. Royal Standard benefits from Mr. Dunlop’s counsel on economic and commodity matters and from his contacts in the investment community.

- B. Compensation.

Compensation of Officers

The following table summarizes, for the three most recently completed financial years of the Corporation, information concerning the compensation earned by the Chief Executive Officer of the Corporation, the Chief Financial Officer of the Corporation, each the Corporation’s three most highly compensated executive officers of the Corporation who was serving as an executive officer as at the end of the most recently completed financial year or who was not serving as an officer of the Corporation at the end of the most recently completed financial year-end, and whose aggregate compensation exceeded $150,000 (the “Named Executive Officer”).

Summary Compensation Table

Name and Principal Position | Year | Annual Compensation | Long Term Compensation | All Other Compen-sation (US$) | ||

Other Annual Salary Bonus Compensation (US$) (US$) (US$) | Securities Under Options Granted (#) | Restricted Shares or Restricted Share Units (US$) | LTIP Payouts (US$) | |||

Roland M Larsen, President and CEO | 2005(1) 2004(3) 2003(5) | Nil Nil 60,000 Nil Nil 60,000 Nil Nil Nil | 675,000 (2) 220,000 (4) 480,000 (6) | Nil Nil Nil | Nil Nil Nil | 36,000 36,000 Nil |

Notes:

(1) For the twelve months ended January 31, 2005.

(2) Options issued on May 4, 2004, having an exercise price of $0.36 and an expiry date on May 4, 2009.

(3) For the twelve months ended January 31, 2004.

(4) Options issued on December 12, 2003, having an exercise price of $0.265 and an expiry date on December 12, 2008.

(5) For the twelve months ended January 31, 2003.

(6) Options issued on April 25, 2002, having an exercise price of $0.26 and an expiry date on April 25, 2007

(7) The Corporation does not have and did not have a Chief Financial Officer.

Stock Option Plan

The Corporation maintains a stock option plan (the "Plan") for directors, officers, consultants who provide ongoing services, and employees of the Corporation and its affiliates. The purpose of the Plan is to develop the interest of bona fide Officers, Directors, Employees, Management Corporation Employees, and Consultants of Royal Standard Minerals Inc. and it subsidiaries in the growth and development of the Corporation by providing them with the opportunity through stock options to acquire an increased proprietary interest in the Corporation. The Plan is administered by the Board of Directors of the Corporation. The Board may from time to time designate those to whom options to purchase common shares of the Corporation may be granted, and the number of Common Shares to be optioned to each, provided that:

- (a) the total number of Common Shares issuable pursuant to the Plan shall not exceed 10% of the issued and outstanding Common Shares, subject to adjustment as set forth in section 10 of the Plan and further subject to the applicable rues and regulations of all regulatory authorities to which the Corporation is subject;

- (b) the number of Common Shares reserved for issuance, within a one-year period, to any one Optionee shall not exceed 5% of the Outstanding Common Shares;

- (c) the number of Common Shares reserved for issuance, within a one-year period, to any one Consultant of the Corporation may not exceed 2% of the Outstanding Common Shares;

- (d) the aggregate number of Common Shares reserved for issuance, within a one-year period, to Employees or Consultants conducting Investor Relations Activities may not exceed 2% of the Outstanding Common Shares.

Compensation of Directors

Directors who are not officers of the corporation are not currently paid any fees for their services as directors; however, such directors are entitled to receive compensation from the corporation to the extent that they provide services to the corporation. Any such compensation is based on rates that would be charged by such a director for such services to an arm's length party. During the twelve months ended January 31, 2005, no such services were rendered and, accordingly, no compensation was paid.

All directors are reimbursed for their expenses and travel incurred in connection with attending directors meetings. Special remuneration, at per diem rates, may be paid to any director (other than executive officers of the Corporation) undertaking special services, at the request of the directors, any committee of the directors or the President of the Corporation, beyond those services ordinarily required of a director of the Corporation.

Directors who are not officers are also entitled to participate in the Corporation's Stock Option Plan and, at the time of joining the board, directors may be granted options to purchase Common Shares. During the twelve months ended January 31, 2005, options were granted to acquire 775,000 common shares of the Corporation to directors of the Corporation under the Corporation's Stock Option Plan.

Other Compensation Matters

There were no long-term incentive awards made to the executive officers of the Corporation during the twelve months ended January 31, 2005. There are no pension plan benefits in place for the Named Executive Officer and none of the Named Executive Officer, officers or directors of the Corporation are indebted to the Corporation. In addition, there are no plans in place with respect to the Named Executive Officer for termination of employment or change in responsibilities.

Compensation Policy

The executive compensation policy of the Corporation is determined with a view to securing the best possible talent to run the Corporation. Executives expect to reap additional income from the appreciation in the value of the Common Shares they hold in the Corporation, including stock options.

Salaries are commensurate with those in the industry with additional options awarded to executive officers in lieu of higher salaries. Bonuses may be paid in the future for significant and specific achievements, which have a strategic impact on the fortunes of the Corporation. Salaries and bonuses are determined on a judgmental basis after review by the board of directors of the contribution of each individual, including the executive officers of the Corporation. Although they may be members of the board of directors, the executive officers do not individually make any decisions with respect to their respective salary or bonus. In certain cases, bonuses of certain individuals, other than the executive officers, may be tied to specific criteria put in place at the time of engagement.

The grant of stock options under the Corporation’s Stock Option Plan is designed to give each option holder an interest in preserving and maximizing shareholder value in the longer term and to reward employees for both past and future performance. Individual grants are determined by an assessment of an individual's current and expected future performance, level of responsibilities and the importance of his/her position with and contribution to the Corporation.

- C. Board practices.

In April 2003 the Company implemented new corporate governance policies pursuant to which the Company has begun to implement new, improved corporate governance practices.

Responsibilities of the Board of Directors

The Board recognizes it is responsible for the stewardship of the business and affairs of the Company and has adopted a set of principles and practices setting out its stewardship responsibilities. Under its mandate, the Board seeks to discharge such responsibility by reviewing, discussing and approving the Company’s strategic planning and organizational structure, and supervising management to ensure that the foregoing enhance and preserve the underlying value of the Company for the benefit of all shareholders. As part of the strategic planning process, the Board contributes to the development of a strategic direction for the Company by reviewing, on an annual basis, the Company’s principal opportunities, the processes that are in place to identify such opportunities and the full range of business risks facing the Company, including strategic, financial, operational, leadership, partnership and reputation risks. On an ongoing basis, the Board also reviews with management how the strategic environment is changing, what key business risks and opportunities are appearing and how they are managed, including the implementation of appropriate systems to manage these risks and opportunities. The performance of management, including the Company’s Chief Executive Officer, is also supervised to ensure that the affairs of the Company are conducted in an ethical manner. The Board, directly and through its committees, ensures that the Company puts in place, and reviews at least on an annual basis, comprehensive communication policies to address how the Company (i) interacts with analysts, investors, other key stakeholders and the public, and (ii) complies with its continuous and timely disclosure obligations and avoids selective. Finally, the Board monitors the integrity of corporate internal control procedures and management information systems to manage such risks and ensure that the value of the underlying asset base is not eroded.

The Board from time to time delegates to senior executives the authority to enter into certain types of transactions, including financial transactions, subject to specified limits. According to the Company’s policy, investments and other similar expenditures above the specified limits, including major capital projects as well as material transactions outside the ordinary course of business, whether on or off balance sheet, are reviewed by, and subject to, the prior approval of the Board.

Following are the principles of the Company’s corporate governance arrangements:

- • Subject to the relatively small size of the Company and to business needs, the size of the Board must be kept to a sufficiently low number to facilitate open and effective dialogue and full participation and contribution of each Director.

- • The Board must function as a cohesive team, with shared responsibilities and accountabilities that are clearly defined, understood and respected.

- • The Board must have the ability to exercise all its supervisory responsibilities independent of any influence by management.

- • The Board must have access to all the information needed to carry out its full responsibilities. Information must be available in a timely manner and in a format conducive to effective decision making.

- • The Board must develop, implement, and measure effective corporate governance practices, processes and procedures.

Committees of the Board

There are currently two committees of the board of directors. The board does not have, nor does it currently intend to form, a nominating committee. It is the view of the board of directors that its current size (four) is small enough to make such additional committees counter productive. In addition to regularly scheduled meetings of the board, its members are in continuous contact with one another and with the members of senior management. If the size of the board were to be enlarged or if the Company were to undergo a substantial change in its business and operations, consideration would at that point be given to the formation of additional committees, including a nominating committee. The mandate and activities of each of the Company’s committees are as follows:

Audit Committee

The Audit Committee shall be composed of three members or such greater number as the board of directors may from time to time determine. A majority of the members of the Audit Committee shall be resident Canadians and unrelated to the Corporation and all members of the Audit Committee shall be non-management directors. Members shall be appointed annually from among the members of the board of directors. The Chair of the Audit Committee shall be appointed by the board of directors. All members of the Audit Committee shall be financially literate. An Audit Committee member who is not financially literate may be appointed to the Audit Committee provided that the member becomes financially literate within a reasonable period of time. The following persons have been initially appointed to the Audit Committee, with the Chair to be as designated:

James C. Dunlop (Chair)

Roland M. Larsen

Mackenzie I. Watson

The Audit Committee’s primary duties and responsibilities are to:

a) Identify and monitor the management of the principal risks that could impact the financial reporting of the Corporation;

b) Monitor the integrity of the Corporation’s financial reporting process and system of internal controls regarding financial reporting and accounting compliance;

c) Monitor the independence and performance of the Corporation’s external auditors;

d) Provide an avenue of communication among the external auditors, management and the Board of Directors.

The Audit Committee has the authority to conduct any investigation appropriate to fulfilling its responsibilities, and it has direct access to the external auditors as well as anyone in the organization. The Audit Committee has the ability to retain, at the Corporation’s expense, special legal, accounting, or other consultants or experts it deems necessary in the performance of its duties.

The Audit Committee shall, in addition to any other duties and responsibilities specifically assigned or delegated to it from time to time by the board of directors:

a) Meet with the independent external auditors (the “auditors”) and the senior management of the Corporation to review the year-end audited financial statements of the Corporation which require approval by the board of directors, prior to the issuance of any press release in respect thereof;

b) Review with senior management and, if necessary, the auditors, the interim financial statements of the Corporation prior to the issuance of any press release in respect thereof;

c) Review the MD&A and press releases containing financial results of the Corporation;

d) Review all prospectuses, material change reports and annual information forms;

e) Review the audit plans and the independence of the auditors;

f) Meet with the auditors independently of management;

g) In consultation with senior management, review annually and recommend for approval by the board of directors:

(i) the appointment of auditors at the annual general meeting of shareholders of the Corporation;

(ii) the remuneration of the auditors; and

(iii) pre-approve all non audit services to be provided to the Corporation by the external auditor;

h) review with the auditors:

(i) the scope of the audit;

(ii) significant changes in the Corporation's accounting principles, practices or policies; and

(iii) new developments in accounting principles, reporting matters or industry practices which may materially affect the financial statements of the Corporation;

i) review with the auditors and senior management the results of the annual audit, and make appropriate recommendations to the board of directors, having regard to, among other things:

(i) the financial statements;

(ii) management's discussion and analysis and related financial disclosure contained in continuous disclosure documents;

(iii) significant changes, if any, to the initial audit plan;

(iv) accounting and reporting decisions relating to significant current year events and transactions;

(v) the audit findings report and management letter, if any, outlining the auditors' findings and recommendations, together with management's response, with respect to internal controls and accounting procedures; and

(vi) any other matters relating to the conduct of the audit, including the review and opportunity to provide comments in respect of any press releases announcing year end financial results prior to issue and such other matters which should be communicated to the Audit Committee under generally accepted auditing standards;

j) Review with the auditors the adequacy of management's internal control procedures and management information systems and inquiring of management and the auditors about significant risks and exposures to the Corporation that may have a material adverse impact on the Corporation's financial statements, and inquiring of the auditors as to the efforts of management to mitigate such risks and exposures;

k) Monitor policies and procedures for reviewing directors' and officers' expenses and perquisites, and inquire about the results of such reviews;

l) Review and approve written risk management policies and guidelines including the effectiveness of the overall process for identifying the principal risks affecting financial reporting;

m) Review issues relating to legal, ethical and regulatory responsibilities to monitor management's efforts to ensure compliance Including any legal matters that could have a significant impact on the Corporation’s financial statements, the Corporation’s compliance with applicable laws and regulations and inquiries received from regulators of governmental agencies; and,

n) Establish procedures for:

a. the receipt, retention and treatment of complaints received by the issuer regarding accounting, internal accounting controls, or auditing matters; and

b. the confidential, anonymous submission by employees of the issuer of concerns regarding questionable accounting or auditing matters.

Corporate Governance Committee

The Corporate Governance Committee is responsible for the development, maintenance, and disclosure of the Company’s corporate governance practices. The mandate of the committee includes:

- • developing criteria governing the size and overall composition of the Board;

- • conducting an annual review of the structure of the Board and its committees, as well as of the mandates of such committees;

- • recommending new nominees for the Board (in consultation with the Chairman and the Chief Executive Officer); and

- • recommending the compensation of directors ensuring that the Company’s policy on disclosure and insider trading, including communication to the different stakeholders about the Company and its subsidiaries, documents filed with securities regulators, written statements made in documents pertaining to the Company’s continuous disclosure obligations, information contained on the Company’s Web site and other electronic communications, relationships with investors, the media and analysts is timely, factual and accurate, and broadly disseminated in accordance with all applicable legal and regulatory requirements.

The committee also coordinates the annual evaluation of the Board, the committees of the Board and individual directors. All issues identified through this evaluation process are then discussed by the Corporate Governance Committee and are reported to the Board. Finally, it also has the responsibility for annually initiating a discussion at the Board level on the performance evaluation and remuneration of the President and Chief Executive Officer.

Conflicts of Interest

Some of the directors and officers of Royal Standard also serve as directors and officers of other companies involved in the resource exploration sector. Consequently, there exists a possibility for any such officer or director to be placed in a position of conflict. Each such director or officer is subject to fiduciary duties and obligations to act honestly and in good faith with a view to the best interests of the Company. Similar duties and obligations will apply to such other companies. Thus any future transaction between the Company and such other companies will be for bona fide business purposes and approved by a majority of disinterested directors of the Company.

D. Employees.

In addition to the officers and directors, the company has one full time employee, Timothy D. Master, Exploration Manager and one part-time secretary. Mr. Master has more than 25 years of experience in exploration and development of gold-silver, base metals and uranium deposits in the US. He has spent the last 13 years in Nevada gold exploration and reserve delineation. He has worked as a staff geologist for Chevron Resources, Gencor, Western States Minerals, Atlas Minerals, Callahan Mining and Western Mine Development. Consulting-contract positions were held with Weyerhaeuser, Kennecott, Glamis and Echo Bay. His experience includes generative prospect identification, acquisitions and reserve definition, both surface and underground. His current position has focused on the acquisition and delineation of shallow underground mineable reserves at Manhattan and other promising projects in Nevada. He is a member of SEG and has a M.S. degree in geology from the University of Wyoming.

E. Share ownership.

Name | Office Held | Number of Common Shares Beneficially Owned or Over Which Control is Exercised1 |

Roland M. Larsen | President, CEO & Director | 661,487 |

Mackenzie I. Watson | Director | 373,000 |

James C. Dunlop | Director | Nil |

Kimberly L. Koerner | Director | 163,000 |

1. The information as to shares beneficially owned or over which control or direction is exercised not being within the knowledge of the corporation has been furnished by the respective individuals.

Item 7. Major Shareholders and Related Party Transactions

- A. Major Shareholders

The following table shows as at April 27, 2005, each person who is known to the Corporation, or its directors and officers to beneficially own, directly or indirectly, or to exercise control or direction over shares carrying more than 10% of the voting rights attached to all outstanding shares of the Corporation entitled to be voted.

Name of Shareholder | Number of Common Shares Owned | Percentage of Common Shares Outstanding (1) |

CDS & Co. (2) Toronto, Ontario | 32,996,942 | 61.5% |

- (1) Based on 53,683,018 Common Shares issued and outstanding as at April 27, 2005.

- (2) This is a nominee account. To the knowledge of the Corporation, there is no beneficial ownership of these shares by this nominee. The shares are held by a number of securities dealers and other intermediaries holding shares on behalf of their clients who are the beneficial owners.

B. Related party transactions.

No director, senior officer, principal holder of securities or any associate or affiliate thereof of Royal Standard or the Company has any material interest, direct or indirect, in any transaction since the commencement of the Corporation’s last completed financial year or in any proposed transaction which, in either case, has or will materially affect the Corporation, except as disclosed in the financial statements included herein.

C. Interests of experts and counsel.

Not Applicable.

Item 8. Financial Information

- A. Consolidated Statements and Other Financial Information

Following is a list of financial statements filed as part of the annual report under Item #17

- − Auditor's Report for Royal Standard Minerals Inc. for the year ended January 31, 2005, 2004 and 2003

- − Consolidated Balance Sheets of Royal Standard Minerals Inc. as at January 31, 2005 and 2004

- − Consolidated Statements of Operations and Deficit of Royal Standard Minerals Inc. for the years ended January 31, 2005, 2004, 2003

- − Consolidated Statements of Cash Flows of Royal Standard Minerals Inc. for the years ended January 31, 2005, 2004, 2003

- − Notes to the Consolidated Financial Statements of Royal Standard Minerals Inc.

The consolidated financial statements of Royal Standard Minerals Inc. were prepared in accordance with generally accepted accounting principles in Canada and are expressed in United States dollars. For a discussion of the reconciliation of such financial statements to United States generally accepted accounting principles, see note #15 of the notes to the consolidated financial statements of Royal Standard Minerals Inc.

B. Significant Changes.

On March 31, 2005 the Company announced a private placement of 8,750,000 units at a price of $0.35 CDN for gross proceeds of $2,531,829. Each unit consists of one common share and one-half common share purchase warrant ("warrant"). Each whole warrant will entitle the holder to subscribe for one additional share at a price of $0.50 CDN per share until March 31, 2007.

The warrants have been estimated at $575,087 using the Black-Scholes option pricing model using the following assumptions: dividend yield 0%; expected volatility 100%; risk-free interest rate 4.5%; and expected life of 2 years.

In addition, Canaccord, the agent acting for the offering, as partial compensation for their services, received 82,000 common shares and 1,353,500 warrants, each warrant entitling Canaccord to acquire one additional common share of the Company at an exercise price of $0.50 CDN until March 31, 2007. The fair value of these warrants has been estimated as $177,915 using the Black-Scholes option pricing model with the same assumptions as noted above.

Item 9. The Offer and Listing

- A. Offer and listing details.