UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-08189

J.P. Morgan Fleming Mutual Fund Group, Inc.

(Exact name of registrant as specified in charter)

277 Park Avenue

New York, NY 10172

(Address of principal executive offices) (Zip code)

Gregory S. Samuels

277 Park Avenue

New York, NY 10172

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800)480-4111

Date of fiscal year end: June 30

Date of reporting period: July 1, 2019 through December 31, 2019

FormN-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule30e-1 under the Investment Company Act of 1940 (17 CFR270.30e-1). The Commission may use the information provided on FormN-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by FormN-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in FormN-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule30e-1 under the Investment Company Act of 1940 (17 CFR270.30e-1).

Semi-Annual Report

J.P. Morgan MidCap/Multi-Cap Funds

December 31, 2019 (Unaudited)

JPMorgan Growth Advantage Fund

JPMorgan Mid Cap Equity Fund

JPMorgan Mid Cap Growth Fund

JPMorgan Mid Cap Value Fund

JPMorgan Value Advantage Fund

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ websitewww.jpmorganfunds.comand you will be notified by mail each time a report is posted and provided with a website to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action.

You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary (such as a broker dealer, bank, or retirement plan) or, if you are a direct investor, by going towww.jpmorganfunds.com/edelivery.

You may elect to receive paper copies of all future reports free of charge. Contact your financial intermediary or, if you invest directly with the Funds, email us atfunds.website.support@jpmorganfunds.comor call 1-800-480-4111. Your election to receive paper reports will apply to all funds held within your account(s).

CONTENTS

Investments in a Fund are not deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when a Fund’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on market and other conditions through the end of the reporting period and are subject to change without notice. These views are not intended to predict the future performance of a Fund or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of any Fund.

Prospective investors should refer to the Funds’ prospectuses for a discussion of the Funds’ investment objectives, strategies and risks. Call J.P. Morgan Funds Service Center at1-800-480-4111 for a prospectus containing more complete information about a Fund, including management fees and other expenses. Please read it carefully before investing.

LETTER TO SHAREHOLDERS

February 10, 2020 (Unaudited)

Dear Shareholders,

We’ve entered 2020 with strong momentum at J.P. Morgan Asset Management, propelled by a strong 2019 for financial markets that included a 31.5% total return in the S&P 500 Index.

| | |

| | “Regardless of the market environment, our goal remains to be the most trusted asset manager in the world by using the unique breadth of capabilities to provide our clients and shareholders with the insights and solutions they need to achieve their long-term goals.” — Andrea L. Lisher |

At the end of July 2019, the U.S. Federal Reserve responded to signs of a weakening economy by cutting interest rates for the first time in more than a decade and proceeded to cut rates two more times in 2019. Financial markets responded favorably and the S&P 500 Index reached record highs in late October. Global equity prices were also supported by easing U.S.-China trade tensions, continued growth in corporate profits and accommodative policies of leading global central banks, including a reduction in interest rates and a resumption of monthly asset purchases by the European Central Bank. These tailwinds overshadowed investor concerns about Brexit and weak economic data, allowing for a strong second half of 2019 for financial markets.

While 2019 was largely a rewarding year for investors, 2020 may bring increased market volatility amid geo-political tensions, U.S. elections and a U.S. economy that appears to be in the late stages of a record long expansion. Additionally, the strong equity market returns of the past year may be hard to replicate. On the other hand, we believe leading central banks have clearly signaled they will remain supportive of continued economic expansion, which should benefit financial markets. We believe investors who maintain a well-diversified portfolio and a long-term outlook will be best positioned in the year ahead.

Regardless of the market environment, our goal remains to be the most trusted asset manager in the world by using the unique breadth of capabilities to provide our clients and shareholders with the insights and solutions they need to achieve their long-term goals.

On behalf of J.P. Morgan Asset Management, thank you for entrusting us to manage your assets. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

Andrea L. Lisher

Head of Americas, Client

J.P. Morgan Asset Management

J.P. Morgan MidCap/Multi-Cap Funds

MARKET OVERVIEW

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited)

Equity markets largely provided positive returns for the reporting period on the back of low interest rates, continued corporate profit growth and an easing of U.S.-China trade tensions. Overall, U.S. equity outperformed other equity markets as well as fixed income markets.

In response to slowing economic growth and continued low inflation, the U.S. Federal Reserve in late July 2019 cut interest rates for the first time in more than a decade. The central bank followed with another cut in mid-September and another at the end of October. Equity investors responded to lower interest rates by driving stock prices higher and by the end of October leading equity U.S. indexes had returned to record highs. Within U.S. large cap stocks, growth stocks mostly outperformed value stocks but within mid cap and small cap stocks, value generally outperformed growth.

Bond markets generally provided positive returns for the second half of 2019, led by U.S. high yield bonds (also known as “junk bonds”) and emerging markets debt. Investment grade U.S. corporate debt provided modest returns while yields on U.S. Treasury bonds fell during the period. For the six months ended December 31, 2019, the S&P 500 returned 10.9% and the Russell Midcap Index returned 7.6%.

| | | | | | |

| | | |

| 2 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2019 |

JPMorgan Growth Advantage Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | | | |

| Fund (Class A Shares, without a sales charge)* | | | 10.31% | |

| Russell 3000 Growth Index | | | 11.89% | |

| |

| Net Assets as of 12/31/2019 (In Thousands) | | $ | 9,410,089 | |

INVESTMENT OBJECTIVE**

The JPMorgan Growth Advantage Fund (the “Fund”) seeks to provide long-term capital growth.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class A Shares, without a sales charge, underperformed the Russell 3000 Growth Index (the “Benchmark”) for the six months ended December 31, 2019. The Fund’s security selection in the health care and energy sectors was a leading detractor from performance relative to the Benchmark, while the Fund’s security selection in the producer durables and technology sectors was a leading contributor to relative performance.

Leading individual detractors from relative performance included the Fund’s underweight position in Apple Inc. its overweight position in Exact Sciences Co. and its out-of-Benchmark position in Waste Connections Inc. Shares of Apple, a maker of mobile and desktop devices and computers, rose amid better-than-expected quarterly earnings as well as positive investor response to the company’s newly launched services, products and latest iPhone upgrade cycle. Shares of Exact Sciences, a maker of cancer screening diagnostics, fell amid investor disappointment with its forecast for the third quarter of 2019. Shares of Waste Connections, a solid waste collection and treatment company, fell amid lower demand for recycled materials in China as well as a shift in investor demand toward more cyclical industrial businesses.

Leading individual contributors to relative performance included the Fund’s overweight positions Advanced Micro Devices Inc. and DexCom Inc. and its underweight position in Cisco Systems Inc. Shares of Advanced Micro Devices, a semiconductor maker, rose on growth in revenue and market share during the reporting period. Shares of DexCom, a medical device manufacturer, rose after the company reported better-than-expected earnings and revenue for the third quarter of 2019. Shares of Cisco Systems, a network and information technology provider not held in the Fund, fell following two consecutive quarters of weak revenue growth.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up approach to stock selection, researching individual companies across market capitalizations in an effort to construct portfolios of stocks that have strong fundamentals. The Fund’s portfolio managers sought to invest in high quality companies with durable franchises that, in their view, possessed the ability to generate strong future earnings growth.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Microsoft Corp. | | | 7.5 | % |

| | 2. | | | Apple, Inc. | | | 5.3 | |

| | 3. | | | Alphabet, Inc., Class C | | | 5.2 | |

| | 4. | | | Amazon.com, Inc. | | | 4.3 | |

| | 5. | | | Mastercard, Inc., Class A | | | 2.8 | |

| | 6. | | | UnitedHealth Group, Inc. | | | 2.6 | |

| | 7. | | | Advanced Micro Devices, Inc. | | | 1.9 | |

| | 8. | | | Global Payments, Inc. | | | 1.9 | |

| | 9. | | | Ross Stores, Inc. | | | 1.8 | |

| | 10. | | | PayPal Holdings, Inc. | | | 1.7 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Information Technology | | | 38.3 | % |

| Health Care | | | 14.3 | |

| Consumer Discretionary | | | 13.7 | |

| Industrials | | | 10.8 | |

| Communication Services | | | 9.4 | |

| Financials | | | 6.2 | |

| Materials | | | 2.5 | |

| Others (each less than 1.0%) | | | 1.4 | |

| Short-Term Investments | | | 3.4 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2019. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2019 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 3 | |

JPMorgan Growth Advantage Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNSAS OF DECEMBER 31, 2019 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | October 29, 1999 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | 4.50 | % | | | 28.68 | % | | | 13.43 | % | | | 15.14 | % |

Without Sales Charge | | | | | 10.31 | | | | 35.81 | | | | 14.65 | | | | 15.76 | |

CLASS C SHARES | | May 1, 2006 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 9.04 | | | | 34.12 | | | | 14.09 | | | | 15.18 | |

Without CDSC | | | | | 10.04 | | | | 35.12 | | | | 14.09 | | | | 15.18 | |

CLASS I SHARES | | May 1, 2006 | | | 10.45 | | | | 36.13 | | | | 14.91 | | | | 16.00 | |

CLASS R2 SHARES | | July 31, 2017 | | | 10.13 | | | | 35.44 | | | | 14.36 | | | | 15.47 | |

CLASS R3 SHARES | | May 31, 2017 | | | 10.30 | | | | 35.79 | | | | 14.66 | | | | 15.77 | |

CLASS R4 SHARES | | May 31, 2017 | | | 10.46 | | | | 36.14 | | | | 14.94 | | | | 16.05 | |

CLASS R5 SHARES | | January 8, 2009 | | | 10.55 | | | | 36.33 | | | | 15.11 | | | | 16.22 | |

CLASS R6 SHARES | | December 23, 2013 | | | 10.61 | | | | 36.49 | | | | 15.24 | | | | 16.29 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

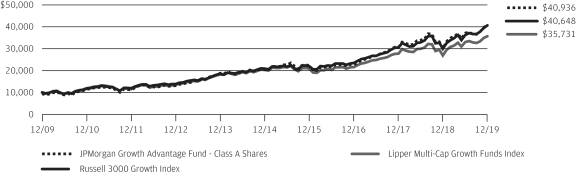

TEN YEAR PERFORMANCE(12/31/09 TO 12/31/19)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. Forup-to-datemonth-end performance information pleasecall 1-800-480-4111.

Returns for Class R2 and Class R3 Shares prior to their inception dates are based on the performance of Class A Shares. The actual returns for Class R2 Shares would have been lower than those shown because Class R2 Shares have higher expenses than Class A Shares. The actual returns for Class R3 Shares would have been similar to those shown because Class R3 Shares have similar expenses to Class A Shares.

Returns for Class R4 Shares prior to their inception dates are based on the performance of Class I Shares. The actual returns of Class R4 Shares would have been different to those shown because Class R4 Shares have different expenses to Class I Shares.

Returns for Class R6 Shares prior to their inception date are based on the performance of Class R5 Shares from January 8, 2009 to December 22, 2013 and Class I Shares prior to January 8, 2009. The actual returns of Class R6 Shares would have been different than those shown because Class R6 Shares have different expenses than Class R5 and Class I Shares.

The graph illustrates comparative performance for $10,000 invested in Class A Shares of the JPMorgan Growth Advantage Fund, the Russell 3000 Growth Index and the LipperMulti-Cap Growth Funds Index from December 31, 2009 to December 31, 2019. The performance of the Fund assumes reinvestment of all

dividends and capital gain distributions, if any, and includes a sales charge. The performance of the Russell 3000 Growth Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the LipperMulti-Cap Growth Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell 3000 Growth Index is an unmanaged index which measures the performance of those Russell 3000 companies (largest 3000 U.S. companies) with higherprice-to-book ratios and higher forecasted growth values. The LipperMulti-Cap Growth Funds Index is an index based on total returns of certain mutual funds within the Fund’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class A Shares have a $1,000 minimum initial investment and carry a 5.25% sales charge.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 4 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2019 |

JPMorgan Mid Cap Equity Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class I Shares)* | | | 7.46% | |

| Russell Midcap Index | | | 7.58% | |

| |

| Net Assets as of 12/31/2019 (In Thousands) | | $ | 1,723,019 | |

INVESTMENT OBJECTIVE**

The JPMorgan Mid Cap Equity Fund (the “Fund”) seeks long-term capital growth.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class I Shares underperformed the Russell Midcap Index (the “Benchmark”) for the six months ended December 31, 2019. The Fund’s security selection in the energy and industrials sectors was a leading detractor from performance relative to the Benchmark, while the Fund’s security selection in the health care and information technologies sectors was a leading contributor to relative performance.

Leading individual detractors from relative performance included the Fund’s overweight position in Sage Therapeutics Inc. and its out-of-Benchmark positions in Progressive Corp. and Waste Connections Inc. Shares of Sage Therapeutics, a drug development company, fell after the company’s anti-depression drug candidate failed in a late-stage clinical trial. Shares of Progressive, a provider of property and casualty insurance, fell after the company reported a higher-than-expected core loss ratio for the second quarter of 2019. Shares of Waste Connections, a solid waste collection and treatment company, fell amid lower demand for recycled materials in China as well as a shift in investor demand toward more cyclical industrial businesses.

Leading individual contributors to relative performance included the Fund’s overweight positions in Advanced Micro Devices Inc., DexCom Inc. and Lam Research Corp. Shares of Advanced Micro Devices, a semiconductor maker, rose on growth in revenue and market share during the reporting period. Shares of DexCom, a medical device manufacturer, rose after the company reported better-than-expected earnings and revenue for the third quarter of 2019. Shares of Lam Research, a maker of semiconductor manufacturing equipment, rose after the company reported better-than-expected earnings for its fiscal first quarter and amid a broader rebound in shares of semiconductor equipment makers.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers employed a bottom-up approach to stock selection, constructing a portfolio based on company fundamentals, quantitative screening and proprietary

fundamental analysis. The Fund’s portfolio managers sought to identify dominant franchises with predictable business models they deemed capable of achieving, in their view, sustained growth, as well as undervalued companies with the potential to grow their intrinsic value per share.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Advanced Micro Devices, Inc. | | | 1.6 | % |

| | 2. | | | Global Payments, Inc. | | | 1.5 | |

| | 3. | | | O’Reilly Automotive, Inc. | | | 1.4 | |

| | 4. | | | Fiserv, Inc. | | | 1.3 | |

| | 5. | | | Synopsys, Inc. | | | 1.3 | |

| | 6. | | | Amphenol Corp., Class A | | | 1.2 | |

| | 7. | | | AMETEK, Inc. | | | 1.2 | |

| | 8. | | | CBRE Group, Inc., Class A | | | 1.2 | |

| | 9. | | | Hilton Worldwide Holdings, Inc. | | | 1.1 | |

| | 10. | | | Xcel Energy, Inc. | | | 1.1 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Information Technology | | | 20.9 | % |

| Consumer Discretionary | | | 14.3 | |

| Financials | | | 13.8 | |

| Industrials | | | 12.7 | |

| Health Care | | | 10.3 | |

| Real Estate | | | 7.4 | |

| Utilities | | | 5.3 | |

| Materials | | | 4.3 | |

| Communication Services | | | 3.0 | |

| Energy | | | 3.0 | |

| Consumer Staples | | | 1.9 | |

| Short-Term Investments | | | 3.1 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2019. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2019 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 5 | |

JPMorgan Mid Cap Equity Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited) (continued)

| | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNSAS OFDECEMBER 31, 2019 | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | November 2, 2009 | | | | | | | | | | | | | | |

With Sales Charge** | | | | 1.68% | | | 25.59 | % | | | 8.21 | % | | | 12.46 | % |

Without Sales Charge | | | | 7.31 | | | 32.56 | | | | 9.38 | | | | 13.07 | |

CLASS C SHARES | | November 2, 2009 | | | | | | | | | | | | | | |

With CDSC*** | | | | 6.05 | | | 30.89 | | | | 8.84 | | | | 12.51 | |

Without CDSC | | | | 7.05 | | | 31.89 | | | | 8.84 | | | | 12.51 | |

CLASS I SHARES | | January 1, 1997 | | 7.46 | | | 32.91 | | | | 9.73 | | | | 13.44 | |

CLASS R2 SHARES | | March 14, 2014 | | 7.18 | | | 32.22 | | | | 9.11 | | | | 12.91 | |

CLASS R5 SHARES | | March 14, 2014 | | 7.54 | | | 33.09 | | | | 9.86 | | | | 13.52 | |

CLASS R6 SHARES | | March 14, 2014 | | 7.58 | | | 33.21 | | | | 9.94 | | | | 13.57 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE(12/31/09 TO 12/31/19)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. Forup-to-datemonth-end performance information pleasecall 1-800-480-4111.

Returns for Class R2 Shares prior to their inception date are based on the performance of Class A Shares from December 31, 2009 to March 13, 2014. The actual returns of Class R2 Shares would have been lower than those shown because Class R2 Shares have higher expenses than Class A Shares.

Returns for Class R5 and Class R6 Shares prior to their inception dates are based on the performance of Class I Shares. The actual returns of Class R5 and Class R6 Shares would have been different because Class R5 and Class R6 Shares have different expenses than Class I Shares.

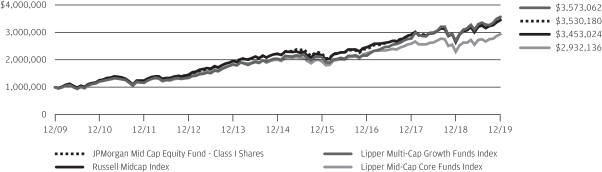

The graph illustrates comparative performance for $1,000,000 invested in the Class I Shares of JPMorgan Mid Cap Equity Fund, the Russell Midcap Index, the Lipper Multi-Cap Core Funds Index and the Lipper Multi-Cap Growth Funds Index from December 31, 2009 to December 31, 2019. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the Russell

Midcap Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the bench mark, if applicable. The performance of the Lipper Mid-Cap Core Funds Index and the Lipper Multi-Cap Growth Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell Midcap Index is an unmanaged index which measures the performance of the 800 smallest companies in the Russell 1000 Index. The Lipper Mid-Cap Core Funds Index and the Lipper Multi-Cap Growth Funds Index are indices based on total returns of certain mutual funds within designated categories as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class I Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 6 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2019 |

JPMorgan Mid Cap Growth Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class I Shares)* | | | 7.96% | |

| Russell Midcap Growth Index | | | 7.45% | |

| |

| Net Assets as of 12/31/2019 (In Thousands) | | | $4,842,246 | |

INVESTMENT OBJECTIVE**

The JPMorgan Mid Cap Growth Fund (the “Fund”) seeks growth of capital.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class I Shares outperformed the Russell Midcap Growth Index (the “Benchmark”) for the six months ended December 31, 2019. The Fund’s security selection in the consumer discretionary and financial services sectors was a leading contributor to performance relative to the Benchmark, while the Fund’s security selection in the materials & processing sector was the sole significant detractor from relative performance.

Leading individual contributors to relative performance included the Fund’s overweight positions in Advanced Micro Devices Inc. and Insulet Corp. and its out-of-Benchmark position in Generac Holdings Inc. Shares of Advanced Micro Devices, a semiconductor maker, rose on growth in revenue and market share during the reporting period. Shares of Insulet, a maker of insulin infusion devices, rose after the company reported better-than-expected earnings and growth in product revenue for the third quarter of 2019. Shares of Generac Holdings, a maker of electrical generators and related products, rose amid scheduled electricity blackouts in California and natural disasters elsewhere during the reporting period.

Leading individual detractors from relative performance included the Fund’s overweight positions in Sage Therapeutics and Exact Sciences Corp. and its out-of-Benchmark position in Waste Connections Inc. Shares of Sage Therapeutics, a drug development company, fell after the company’s anti-depression drug candidate failed in a late-stage clinical trial. Shares of Exact Sciences, a maker of cancer screening diagnostics, fell amid investor disappointment with its forecast for the third quarter of 2019. Shares of Waste Connections, a solid waste collection and treatment company, fell amid lower demand for recycled materials in China as well as a shift in investor preferences toward more cyclical industrial businesses.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up approach to stock selection, researching individual companies in an effort to construct a portfolio of stocks that have strong funda-

mentals. The Fund’s portfolio managers sought to invest in high quality companies with durable franchises that, in their view, possessed the ability to generate strong future earnings growth.

| | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** |

| | | | | | | | |

| | 1. | | | Advanced Micro Devices, Inc. | | | 3.0 | % |

| | 2. | | | Global Payments, Inc. | | | 2.9 | |

| | 3. | | | O’Reilly Automotive, Inc. | | | 2.7 | |

| | 4. | | | Fiserv, Inc. | | | 2.6 | |

| | 5. | | | Synopsys, Inc. | | | 1.7 | |

| | 6. | | | Lam Research Corp. | | | 1.6 | |

| | 7. | | | Ingersoll-Rand plc | | | 1.6 | |

| | 8. | | | Waste Connections, Inc. | | | 1.5 | |

| | 9. | | | Lululemon Athletica, Inc. | | | 1.5 | |

| | 10. | | | Zebra Technologies Corp., Class A | | | 1.5 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Information Technology | | | 34.4 | % |

| Consumer Discretionary | | | 16.4 | |

| Industrials | | | 16.4 | |

| Health Care | | | 14.0 | |

| Financials | | | 5.9 | |

| Materials | | | 3.8 | |

| Communication Services | | | 3.2 | |

| Real Estate | | | 1.1 | |

| Energy | | | 0.7 | |

| Short-Term Investments | | | 4.1 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2019. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2019 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 7 | |

JPMorgan Mid Cap Growth Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNSAS OF DECEMBER 31, 2019 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | February 18, 1992 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | 2.11 | % | | | 31.94 | % | | | 10.52 | % | | | 13.39 | % |

Without Sales Charge | | | | | 7.78 | | | | 39.23 | | | | 11.71 | | | | 14.00 | |

CLASS C SHARES | | November 4, 1997 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 6.55 | | | | 37.55 | | | | 11.16 | | | | 13.44 | |

Without CDSC | | | | | 7.55 | | | | 38.55 | | | | 11.16 | | | | 13.44 | |

CLASS I SHARES | | March 2, 1989 | | | 7.96 | | | | 39.66 | | | | 12.06 | | | | 14.36 | |

CLASS R2 SHARES | | June 19, 2009 | | | 7.64 | | | | 38.89 | | | | 11.48 | | | | 13.80 | |

CLASS R3 SHARES | | September 9, 2016 | | | 7.80 | | | | 39.23 | | | | 11.71 | | | | 14.01 | |

CLASS R4 SHARES | | September 9, 2016 | | | 7.92 | | | | 39.55 | | | | 11.99 | | | | 14.29 | |

CLASS R5 SHARES | | November 1, 2011 | | | 8.03 | | | | 39.85 | | | | 12.21 | | | | 14.49 | |

CLASS R6 SHARES | | November 1, 2011 | | | 8.07 | | | | 39.96 | | | | 12.27 | | | | 14.55 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE(12/31/09 TO 12/31/19)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. Forup-to-datemonth-end performance information please call1-800-480-4111.

Returns for the Class R3, Class R4, Class R5 and Class R6 Shares prior to their inception dates are based on the performance of Class I Shares. Prior performance for Class R3 and Class R4 Shares has been adjusted to reflect the differences in expenses between classes. The actual returns of Class R5 and Class R6 Shares would have been different than those shown because Class R5 and Class R6 Shares have different expenses than Class I Shares.

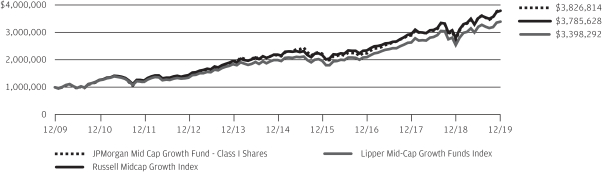

The graph illustrates comparative performance for $1,000,000 invested in Class I Shares of the JPMorgan Mid Cap Growth Fund, the Russell Midcap Growth Index and the Lipper Mid-Cap Growth Funds Index from December 31, 2009 to December 31, 2019. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the Russell Midcap Growth Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital

gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Mid-Cap Growth Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell Midcap Growth Index is an unmanaged index which measures the performance of those Russell Midcap companies with higherprice-to-book ratios and higher forecasted growth values. The Lipper Mid-Cap Growth Funds Index is an index based on total returns of certain mutual funds within designated categories as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class I Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 8 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2019 |

JPMorgan Mid Cap Value Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class L Shares)* | | | 7.11% | |

| Russell Midcap Value Index | | | 7.66% | |

| |

| Net Assets as of 12/31/2019 (In Thousands) | | $ | 17,143,311 | |

INVESTMENT OBJECTIVE**

The JPMorgan Mid Cap Value Fund (the “Fund”) seeks growth from capital appreciation.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class L Shares underperformed the Russell Midcap Value Index (the “Benchmark”) for the six months ended December 31, 2019. The Fund’s security selection in the energy and financials sectors was a leading detractor from performance relative to the Benchmark, while the Fund’s security selection in the health care and materials sectors was a leading contributor to relative performance.

Leading individual detractors from relative performance included the Fund’s overweight positions in Expedia Group Inc. and Middleby Corp. and its underweight position in State Street Corp. Shares of Expedia, a provider of online travel booking, fell amid increased competition and lower-than-expected earnings and revenue for the third quarter of 2019. Shares of Middleby, a food service equipment manufacturer, fell after the company reported lower-than-expected sales for the third quarter of 2019 and weak results for the second quarter of 2019. Shares of State Street, a banking and financial services company not held in the Fund, rose after the company reported better-than-expected earnings for the third quarter of 2019.

Leading individual contributors to relative performance included the Fund’s out-of-Benchmark positions in CDW Corp. and Sherwin-Williams Co. and its overweight position in Tiffany & Co. Shares of CDW, a provider of information technology and services, rose following the company’s initial public offering in June and its inclusion in the S&P 500 Index. Shares of Sherwin-Williams, a paints and coatings manufacturer, rose amid quarterly earnings growth and after the settlement of decades-long lead paint litigation with the state of California. Shares of Tiffany, a luxury retailer, rose after the company agreed to a $16.2 billion acquisition by LVMH Moet Hennessey Louis Vuitton SE.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up approach to stock selection and sought to identify durable franchises possessing the ability to generate, in their view, sustainable levels of free cash flow.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Xcel Energy, Inc. | | | 2.2 | % |

| | 2. | | | WEC Energy Group, Inc. | | | 2.1 | |

| | 3. | | | CMS Energy Corp. | | | 2.1 | |

| | 4. | | | Loews Corp. | | | 1.9 | |

| | 5. | | | M&T Bank Corp. | | | 1.9 | |

| | 6. | | | Diamondback Energy, Inc. | | | 1.7 | |

| | 7. | | | Williams Cos., Inc. (The) | | | 1.6 | |

| | 8. | | | Sempra Energy | | | 1.6 | |

| | 9. | | | T. Rowe Price Group, Inc. | | | 1.6 | |

| | 10. | | | AutoZone, Inc. | | | 1.5 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Financials | | | 22.1 | % |

| Real Estate | | | 13.5 | |

| Consumer Discretionary | | | 11.9 | |

| Utilities | | | 10.9 | |

| Industrials | | | 8.8 | |

| Information Technology | | | 6.7 | |

| Health Care | | | 6.6 | |

| Energy | | | 5.4 | |

| Materials | | | 4.8 | |

| Consumer Staples | | | 3.9 | |

| Communication Services | | | 2.8 | |

| Short-Term Investments | | | 2.6 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2019. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2019 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 9 | |

JPMorgan Mid Cap Value Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNSAS OF DECEMBER 31, 2019 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | April 30, 2001 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | 1.23 | % | | | 19.37 | % | | | 5.65 | % | | | 11.51 | % |

Without Sales Charge | | | | | 6.84 | | | | 26.00 | | | | 6.79 | | | | 12.11 | |

CLASS C SHARES | | April 30, 2001 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 5.57 | | | | 24.35 | | | | 6.25 | | | | 11.54 | |

Without CDSC | | | | | 6.57 | | | | 25.35 | | | | 6.25 | | | | 11.54 | |

CLASS I SHARES | | October 31, 2001 | | | 7.00 | | | | 26.34 | | | | 7.07 | | | | 12.39 | |

CLASS L SHARES | | November 13, 1997 | | | 7.11 | | | | 26.63 | | | | 7.32 | | | | 12.65 | |

CLASS R2 SHARES | | November 3, 2008 | | | 6.71 | | | | 25.70 | | | | 6.52 | | | | 11.82 | |

CLASS R3 SHARES | | September 9, 2016 | | | 6.85 | | | | 26.00 | | | | 6.79 | | | | 12.11 | |

CLASS R4 SHARES | | September 9, 2016 | | | 6.99 | | | | 26.32 | | | | 7.06 | | | | 12.39 | |

CLASS R5 SHARES | | September 9, 2016 | | | 7.07 | | | | 26.51 | | | | 7.25 | | | | 12.62 | |

CLASS R6 SHARES | | September 9, 2016 | | | 7.14 | | | | 26.67 | | | | 7.32 | | | | 12.66 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE(12/31/09 TO 12/31/19)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. Forup-to-datemonth-end performance information please call1-800-480-4111.

Returns for Class R3 Shares prior to their inception dates are based on the performance of Class A Shares. The actual returns of Class R3 Shares would have been lower than those shown because Class R3 Shares have higher expenses than Class A Shares.

Returns for the Class R4 Shares prior to their inception date are based on the performance of Class I Shares. The actual returns of Class R4 Shares would have been lower because Class R4 Shares have higher expenses than Class I Shares.

Returns for the Class R5 and R6 Shares prior to their inception dates are based on the performance of Class L Shares. The actual returns of Class R5 Shares would have been lower than those shown because Class R5 Shares have higher expenses than Class L Shares. The actual returns for Class R6 Shares would have been similar to those shown because Class R6 Shares have similar expenses to Class L Shares.

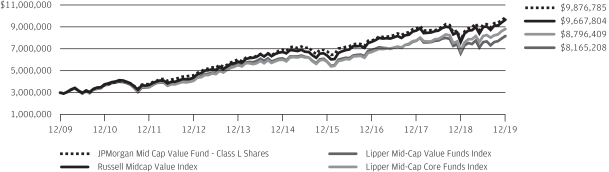

The graph illustrates comparative performance for $3,000,000 invested in Class L Shares of the JPMorgan Mid Cap Value Fund, the Russell Midcap Value Index, the LipperMid-Cap Value Funds Index and the LipperMid-Cap Core Funds Index from December 31, 2009 to December 31, 2019. The performance of the Fund assumes reinvestment of all dividends and capital gain

distributions, if any, and does not include a sales charge. The performance of the Russell Midcap Value Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the LipperMid-Cap Value Funds Index and the LipperMid-Cap Core Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell Midcap Value Index is an unmanaged index which measures the performance of those Russell Midcap companies with lowerprice-to-book ratios and lower forecasted growth values. The LipperMid-Cap Value Funds Index and the LipperMid-Cap Core Funds Index are indices based on total returns of certain mutual funds within designated categories as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class L Shares have a $3,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 10 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2019 |

JPMorgan Value Advantage Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class L Shares)* | | | 8.88% | |

| Russell 3000 Value Index | | | 8.80% | |

| |

| Net Assets as of 12/31/2019 (In Thousands) | | | $11,947,202 | |

INVESTMENT OBJECTIVE**

The JPMorgan Value Advantage Fund (the “Fund”) seeks to provide long-term total return from a combination of income and capital gains.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class L Shares outperformed the Russell 3000 Value Index (the “Benchmark”) for the six months ended December 31, 2019. The Fund’s security selection in the materials and consumer discretionary sectors was a leading contributor to performance relative to the Benchmark, while the Fund’s security selection in the information technology and communication services sector was a leading detractor from relative performance.

Leading individual contributors to performance relative to the Benchmark included the Fund’s overweight positions in Bank of America Corp., PNC Financial Services Group Inc. and Martin Marietta Materials Inc. Shares of Bank of America and PNC Financial Services Group, both diversified financial services companies, rose amid broader gains in shares of large banks during the reporting period. Shares of Martin Marietta, a provider of crushed stone, sand and gravel, rose after the company reported revenue growth for the second quarter of 2019 and raised its forecast for the full year 2019.

Leading individual detractors from relative performance included the Fund’s underweight positions in JPMorgan Chase & Co., Intel Corp. and AT&T Corp., none of which were held in the Fund. Shares of JPMorgan Chase, which the Fund is prohibited from holding, rose amid broader gains in stocks of large banks during the reporting period. Shares of Intel, a manufacturer of computer products and technologies, rose amid strong demand for semiconductors during the reporting period. Shares of AT&T, a telecommunications provider, rose after the company announced plans to cut $1.5 billion in costs, increase in its dividend and repurchase of 100 million shares.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up approach to stock selection and sought to identify durable franchises possessing the ability to generate, in the portfolio managers’ view, significant levels of free cash flow.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Bank of America Corp. | | | 3.7 | % |

| | 2. | | | Capital One Financial Corp. | | | 2.2 | |

| | 3. | | | PNC Financial Services Group, Inc. (The) | | | 2.1 | |

| | 4. | | | Wells Fargo & Co. | | | 1.9 | |

| | 5. | | | Loews Corp. | | | 1.8 | |

| | 6. | | | Chevron Corp. | | | 1.8 | |

| | 7. | | | Pfizer, Inc. | | | 1.6 | |

| | 8. | | | Delta Air Lines, Inc. | | | 1.5 | |

| | 9. | | | ConocoPhillips | | | 1.5 | |

| | 10. | | | Verizon Communications, Inc. | | | 1.5 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Financials | |

| 31.4

| %

|

| Health Care | | | 10.3 | |

| Energy | | | 8.7 | |

| Consumer Discretionary | | | 7.1 | |

| Industrials | | | 7.0 | |

| Real Estate | | | 6.9 | |

| Utilities | | | 5.6 | |

| Communication Services | | | 5.0 | |

| Information Technology | | | 4.8 | |

| Consumer Staples | | | 4.7 | |

| Materials | | | 4.3 | |

| Short-Term Investments | | | 4.2 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2019. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2019 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 11 | |

JPMorgan Value Advantage Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2019 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNSAS OF DECEMBER 31, 2019 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | February 28, 2005 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | 2.98 | % | | | 20.08 | % | | | 6.53 | % | | | 11.39 | % |

Without Sales Charge | | | | | 8.67 | | | | 26.72 | | | | 7.68 | | | | 12.00 | |

CLASS C SHARES | | February 28, 2005 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 7.40 | | | | 25.09 | | | | 7.15 | | | | 11.44 | |

Without CDSC | | | | | 8.40 | | | | 26.09 | | | | 7.15 | | | | 11.44 | |

CLASS I SHARES | | February 28, 2005 | | | 8.80 | | | | 27.03 | | | | 7.95 | | | | 12.27 | |

CLASS L SHARES | | February 28, 2005 | | | 8.88 | | | | 27.20 | | | | 8.17 | | | | 12.52 | |

CLASS R2 SHARES | | July 31, 2017 | | | 8.53 | | | | 26.39 | | | | 7.41 | | | | 11.72 | |

CLASS R3 SHARES | | September 9, 2016 | | | 8.65 | | | | 26.70 | | | | 7.67 | | | | 11.99 | |

CLASS R4 SHARES | | September 9, 2016 | | | 8.81 | | | | 27.05 | | | | 7.95 | | | | 12.27 | |

CLASS R5 SHARES | | September 9, 2016 | | | 8.91 | | | | 27.23 | | | | 8.15 | | | | 12.52 | |

CLASS R6 SHARES | | September 9, 2016 | | | 8.94 | | | | 27.36 | | | | 8.22 | | | | 12.55 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE(12/31/09 TO 12/31/19)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. Forup-to-datemonth-end performance information please call1-800-480-4111.

Returns for Class R2 and Class R3 Shares prior to their inception date are based on the performance of Class A Shares. The actual returns of Class R2 Shares would have been lower than those shown because Class R2 Shares have higher expenses than Class A Shares. Returns for Class R3 Shares would have been similar to those shown because Class R3 Shares have similar expenses to Class A Shares.

Returns for the Class R4 Shares prior to their inception date are based on the performance of Class I Shares. The actual returns of Class R4 Shares would have been similar to those shown because Class R4 Shares have similar expenses to Class I Shares.

Returns for the Class R5 and Class R6 Shares prior to their inception dates are based on the performance of Class L Shares. The actual returns for Class R5 and Class R6 Shares would have been different to those shown because Class R5 and Class R6 Shares have different expenses to Class L Shares.

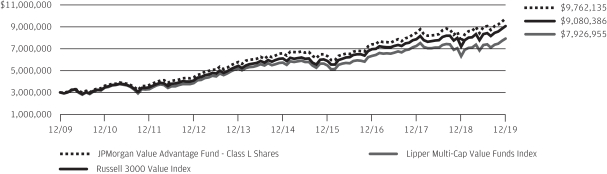

The graph illustrates comparative performance for $3,000,000 invested in Class L Shares of the JPMorgan Value Advantage Fund, the Russell 3000 Value Index and the LipperMulti-Cap Value Funds Index from December 31, 2009 to

December 31, 2019. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the Russell 3000 Value Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the LipperMulti-Cap Value Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell 3000 Value Index is an unmanaged index which measures the performance of those Russell 3000 companies (largest 3000 U.S. companies) with lowerprice-to-book ratios and lower forecasted growth values. The LipperMulti-Cap Value Funds Index is an index based on total returns of certain mutual funds within the Fund’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class L Shares have a $3,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 12 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2019 |

JPMorgan Growth Advantage Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2019 (Unaudited)

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Common Stocks — 98.6% | | | | | | | | |

| | |

Automobiles — 1.6% | | | | | | | | |

| | |

Tesla, Inc. * (a) | | | 354 | | | | 148,172 | |

| | | | | | | | |

| | |

Banks — 1.5% | | | | | | | | |

| | |

East West Bancorp, Inc. | | | 1,248 | | | | 60,753 | |

| | |

First Republic Bank | | | 705 | | | | 82,838 | |

| | | | | | | | |

| | |

| | | | | | | 143,591 | |

| | | | | | | | |

| | |

Biotechnology — 3.7% | | | | | | | | |

| | |

Amgen, Inc. | | | 509 | | | | 122,584 | |

| | |

Exact Sciences Corp. * | | | 782 | | | | 72,338 | |

| | |

Exelixis, Inc. * (a) | | | 2,317 | | | | 40,817 | |

| | |

Intercept Pharmaceuticals, Inc. * (a) | | | 336 | | | | 41,674 | |

| | |

Regeneron Pharmaceuticals, Inc. * | | | 123 | | | | 45,996 | |

| | |

Sage Therapeutics, Inc. * (a) | | | 297 | | | | 21,448 | |

| | | | | | | | |

| | |

| | | | | | | 344,857 | |

| | | | | | | | |

| | |

Building Products — 0.9% | | | | | | | | |

| | |

Fortune Brands Home & Security, Inc. | | | 1,240 | | | | 81,028 | |

| | | | | | | | |

| | |

Capital Markets — 3.9% | | | | | | | | |

| | |

BlackRock, Inc. | | | 136 | | | | 68,266 | |

| | |

Charles Schwab Corp. (The) | | | 1,476 | | | | 70,208 | |

| | |

Nasdaq, Inc. | | | 666 | | | | 71,313 | |

| | |

S&P Global, Inc. | | | 475 | | | | 129,699 | |

| | |

TD Ameritrade Holding Corp. | | | 519 | | | | 25,809 | |

| | | | | | | | |

| | |

| | | | | | | 365,295 | |

| | | | | | | | |

| | |

Commercial Services & Supplies — 2.6% | | | | | | | | |

| | |

Copart, Inc. * | | | 1,047 | | | | 95,242 | |

| | |

Waste Connections, Inc. | | | 1,597 | | | | 145,005 | |

| | | | | | | | |

| | |

| | | | | | | 240,247 | |

| | | | | | | | |

| | |

Communications Equipment — 0.4% | | | | | | | | |

| | |

Arista Networks, Inc. * (a) | | | 204 | | | | 41,443 | |

| | | | | | | | |

| | |

Construction Materials — 0.8% | | | | | | | | |

| | |

Vulcan Materials Co. (a) | | | 552 | | | | 79,439 | |

| | | | | | | | |

| | |

Containers & Packaging — 1.7% | | | | | | | | |

| | |

Avery Dennison Corp. | | | 631 | | | | 82,560 | |

| | |

Ball Corp. | | | 1,164 | | | | 75,244 | |

| | | | | | | | |

| | |

| | | | | | | 157,804 | |

| | | | | | | | |

| | |

Electrical Equipment — 2.0% | | | | | | | | |

| | |

AMETEK, Inc. | | | 811 | | | | 80,929 | |

| | |

Generac Holdings, Inc. * | | | 1,047 | | | | 105,348 | |

| | | | | | | | |

| | |

| | | | | | | 186,277 | |

| | | | | | | | |

|

Electronic Equipment, Instruments & Components — 2.8% | |

| | |

Amphenol Corp., Class A | | | 646 | | | | 69,949 | |

| | |

Keysight Technologies, Inc. * | | | 843 | | | | 86,517 | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| | | | | | | | |

|

Electronic Equipment, Instruments & Components — continued | |

| | |

Zebra Technologies Corp., Class A * | | | 424 | | | | 108,230 | |

| | | | | | | | |

| | |

| | | | | | | 264,696 | |

| | | | | | | | |

| | |

Entertainment — 3.1% | | | | | | | | |

| | |

Netflix, Inc. * | | | 300 | | | | 96,909 | |

| | |

Spotify Technology SA * | | | 520 | | | | 77,736 | |

| | |

Take-Two Interactive Software, Inc. * | | | 954 | | | | 116,768 | |

| | | | | | | | |

| | |

| | | | | | | 291,413 | |

| | | | | | | | |

| | |

Health Care Equipment & Supplies — 1.8% | | | | | | | | |

| | |

DexCom, Inc. * | | | 387 | | | | 84,630 | |

| | |

Intuitive Surgical, Inc. * | | | 149 | | | | 88,318 | |

| | | | | | | | |

| | |

| | | | | | | 172,948 | |

| | | | | | | | |

| | |

Health Care Providers & Services — 3.9% | | | | | | | | |

| | |

Acadia Healthcare Co., Inc. * (a) | | | 1,167 | | | | 38,774 | |

| | |

Anthem, Inc. | | | 253 | | | | 76,384 | |

| | |

UnitedHealth Group, Inc. | | | 852 | | | | 250,324 | |

| | | | | | | | |

| | |

| | | | | | | 365,482 | |

| | | | | | | | |

| | |

Health Care Technology — 1.5% | | | | | | | | |

| | |

Teladoc Health, Inc. * | | | 1,161 | | | | 97,191 | |

| | |

Veeva Systems, Inc., Class A * | | | 303 | | | | 42,634 | |

| | | | | | | | |

| | |

| | | | | | | 139,825 | |

| | | | | | | | |

| | |

Hotels, Restaurants & Leisure — 0.6% | | | | | | | | |

| | |

Hilton Worldwide Holdings, Inc. | | | 511 | | | | 56,712 | |

| | | | | | | | |

| | |

Household Durables — 0.7% | | | | | | | | |

| | |

Garmin Ltd. | | | 717 | | | | 69,956 | |

| | | | | | | | |

| | |

Insurance — 0.9% | | | | | | | | |

| | |

Progressive Corp. (The) | | | 1,163 | | | | 84,219 | |

| | | | | | | | |

| | |

Interactive Media & Services — 6.1% | | | | | | | | |

| | |

Alphabet, Inc., Class C * | | | 374 | | | | 500,187 | |

| | |

Facebook, Inc., Class A * | | | 348 | | | | 71,488 | |

| | | | | | | | |

| | |

| | | | | | | 571,675 | |

| | | | | | | | |

| | |

Internet & Direct Marketing Retail — 4.4% | | | | | | | | |

| | |

Amazon.com, Inc. * | | | 225 | | | | 416,318 | |

| | | | | | | | |

| | |

IT Services — 10.5% | | | | | | | | |

| | |

Booz Allen Hamilton Holding Corp. | | | 1,202 | | | | 85,490 | |

| | |

Fiserv, Inc. * | | | 937 | | | | 108,299 | |

| | |

Global Payments, Inc. | | | 991 | | | | 180,862 | |

| | |

Mastercard, Inc., Class A | | | 908 | | | | 270,971 | |

| | |

PayPal Holdings, Inc. * | | | 1,485 | | | | 160,589 | |

| | |

Shopify, Inc., Class A (Canada) * | | | 134 | | | | 53,435 | |

| | |

Visa, Inc., Class A | | | 689 | | | | 129,407 | |

| | | | | | | | |

| | |

| | | | | | | 989,053 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2019 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 13 | |

JPMorgan Growth Advantage Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2019 (Unaudited) (continued)

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Common Stocks — continued | | | | | | | | |

| | |

Life Sciences Tools & Services — 1.8% | | | | | | | | |

| | |

Illumina, Inc. * | | | 223 | | | | 74,078 | |

| | |

Thermo Fisher Scientific, Inc. | | | 301 | | | | 97,818 | |

| | | | | | | | |

| | |

| | | | | | | 171,896 | |

| | | | | | | | |

| | |

Machinery — 3.2% | | | | | | | | |

| | |

Gardner Denver Holdings, Inc. * (a) | | | 950 | | | | 34,850 | |

| | |

Ingersoll-Rand plc (a) | | | 507 | | | | 67,430 | |

| | |

Nordson Corp. (a) | | | 308 | | | | 50,089 | |

| | |

Parker-Hannifin Corp. | | | 258 | | | | 52,999 | |

| | |

Stanley Black & Decker, Inc. | | | 597 | | | | 98,980 | |

| | | | | | | | |

| | |

| | | | | | | 304,348 | |

| | | | | | | | |

| | |

Media — 0.4% | | | | | | | | |

| | |

New York Times Co. (The), Class A (a) | | | 1,212 | | | | 38,987 | |

| | | | | | | | |

| | |

Oil, Gas & Consumable Fuels — 0.5% | | | | | | | | |

| | |

EOG Resources, Inc. | | | 607 | | | | 50,800 | |

| | | | | | | | |

| | |

Pharmaceuticals — 2.0% | | | | | | | | |

| | |

Catalent, Inc. * | | | 904 | | | | 50,867 | |

| | |

Elanco Animal Health, Inc. * | | | 1,511 | | | | 44,508 | |

| | |

Jazz Pharmaceuticals plc * (a) | | | 507 | | | | 75,670 | |

| | |

TherapeuticsMD, Inc. * | | | 4,983 | | | | 12,058 | |

| | | | | | | | |

| | |

| | | | | | | 183,103 | |

| | | | | | | | |

| | |

Professional Services — 1.2% | | | | | | | | |

| | |

FTI Consulting, Inc. * | | | 303 | | | | 33,552 | |

| | |

IHS Markit Ltd. * | | | 1,011 | | | | 76,156 | |

| | | | | | | | |

| | |

| | | | | | | 109,708 | |

| | | | | | | | |

|

Real Estate Management & Development — 0.9% | |

| | |

CBRE Group, Inc., Class A * | | | 1,434 | | | | 87,865 | |

| | | | | | | | |

| | |

Road & Rail — 1.2% | | | | | | | | |

| | |

Lyft, Inc., Class A * | | | 852 | | | | 36,645 | |

| | |

Old Dominion Freight Line, Inc. | | | 401 | | | | 76,168 | |

| | | | | | | | |

| | |

| | | | | | | 112,813 | |

| | | | | | | | |

|

Semiconductors & Semiconductor Equipment — 6.3% | |

| | |

Advanced Micro Devices, Inc. * | | | 3,979 | | | | 182,468 | |

| | |

KLA Corp. | | | 450 | | | | 80,212 | |

| | |

Microchip Technology, Inc. (a) | | | 370 | | | | 38,757 | |

| | |

NVIDIA Corp. | | | 508 | | | | 119,438 | |

| | |

QUALCOMM, Inc. | | | 1,401 | | | | 123,593 | |

| | |

Xilinx, Inc. | | | 488 | | | | 47,741 | |

| | | | | | | | |

| | |

| | | | | | | 592,209 | |

| | | | | | | | |

| | |

Software — 13.6% | | | | | | | | |

| | |

Fair Isaac Corp. * | | | 102 | | | | 38,105 | |

| | |

Intuit, Inc. | | | 456 | | | | 119,335 | |

| | |

Microsoft Corp. | | | 4,534 | | | | 714,980 | |

| | |

salesforce.com, Inc. * | | | 738 | | | | 119,963 | |

| | |

ServiceNow, Inc. * | | | 321 | | | | 90,512 | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| | | | | | | | |

| | |

Software — continued | | | | | | | | |

| | |

Slack Technologies, Inc., Class A * (a) | | | 701 | | | | 15,763 | |

| | |

Synopsys, Inc. * | | | 494 | | | | 68,780 | |

| | |

Trade Desk, Inc. (The), Class A * (a) | | | 318 | | | | 82,532 | |

| | |

Zscaler, Inc. * (a) | | | 631 | | | | 29,351 | |

| | | | | | | | |

| | |

| | | | | | | 1,279,321 | |

| | | | | | | | |

| | |

Specialty Retail — 5.8% | | | | | | | | |

| | |

Home Depot, Inc. (The) | | | 726 | | | | 158,435 | |

| | |

National Vision Holdings, Inc. * | | | 1,201 | | | | 38,954 | |

| | |

O’Reilly Automotive, Inc. * | | | 239 | | | | 104,788 | |

| | |

Ross Stores, Inc. | | | 1,512 | | | | 176,004 | |

| | |

Tractor Supply Co. (a) | | | 715 | | | | 66,847 | |

| | | | | | | | |

| | |

| | | | | | | 545,028 | |

| | | | | | | | |

|

Technology Hardware, Storage & Peripherals — 5.4% | |

| | |

Apple, Inc. | | | 1,734 | | | | 509,086 | |

| | | | | | | | |

| | |

Textiles, Apparel & Luxury Goods — 0.9% | | | | | | | | |

| | |

Lululemon Athletica, Inc. * | | | 356 | | | | 82,382 | |

| | | | | | | | |

| |

Total Common Stocks

(Cost $5,268,713) | | | | 9,277,996 | |

| | | | | |

Short-Term Investments — 3.4% | | | | | | | | |

| | |

Investment Companies — 1.5% | | | | | | | | |

| | |

JPMorgan Prime Money Market Fund Class IM Shares, 1.77% (b) (c)

(Cost $139,991) | | | 139,949 | | | | 139,991 | |

| | | | | | | | |

Investment of Cash Collateral from Securities Loaned — 1.9% | |

| | |

JPMorgan Securities Lending Money Market Fund Agency SL Class Shares, 1.82% (b) (c) | | | 164,015 | | | | 164,031 | |

| | |

JPMorgan U.S. Government Money Market Fund Class IM Shares, 1.53% (b) (c) | | | 18,429 | | | | 18,429 | |

| | | | | | | | |

Total Investment of Cash Collateral from Securities Loaned

(Cost $182,459) | | | | | | | 182,460 | |

| | | | | |

Total Short-Term Investments

(Cost $322,450) | | | | 322,451 | |

| | | | | | | | |

Total Investments — 102.0%

(Cost $5,591,163) | | | | 9,600,447 | |

Liabilities in Excess of

Other Assets — (2.0)% | | | | (190,358 | ) |

| | | | | |

NET ASSETS — 100.0% | | | | | | | 9,410,089 | |

| | | | | |

Percentages indicated are based on net assets.

| | |

| (a) | | The security or a portion of this security is on loan at December 31, 2019. The total value of securities on loan at December 31, 2019 is approximately $179,510,000. |

| (b) | | Investment in an affiliated fund, which is registered under the Investment Company Act of 1940, as amended, and is advised by J.P. Morgan Investment Management Inc. |

| (c) | | The rate shown is the current yield as of December 31, 2019. |

| * | | Non-income producing security. |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 14 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2019 |

JPMorgan Mid Cap Equity Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2019 (Unaudited)

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Common Stocks — 97.3% | |

|

Aerospace & Defense — 0.4% | |

| | |

HEICO Corp., Class A | | | 85 | | | | 7,568 | |

| | | | | | | | |

|

Auto Components — 0.7% | |

| | |

Aptiv plc | | | 54 | | | | 5,092 | |

| | |

BorgWarner, Inc. | | | 153 | | | | 6,639 | |

| | | | | | | | |

| | |

| | | | | | | 11,731 | |

| | | | | | | | |

|

Automobiles — 0.8% | |

| | |

Tesla, Inc. * | | | 20 | | | | 8,367 | |

| | |

Thor Industries, Inc. (a) | | | 63 | | | | 4,695 | |

| | | | | | | | |

| | |

| | | | | | | 13,062 | |

| | | | | | | | |

|

Banks — 5.3% | |

| | |

Citizens Financial Group, Inc. | | | 234 | | | | 9,490 | |

| | |

Comerica, Inc. | | | 61 | | | | 4,379 | |

| | |

East West Bancorp, Inc. | | | 109 | | | | 5,331 | |

| | |

Fifth Third Bancorp | | | 410 | | | | 12,590 | |

| | |

First Republic Bank | | | 150 | | | | 17,644 | |

| | |

Huntington Bancshares, Inc. | | | 458 | | | | 6,911 | |

| | |

M&T Bank Corp. | | | 91 | | | | 15,375 | |

| | |

TCF Financial Corp. | | | 64 | | | | 2,984 | |

| | |

Truist Financial Corp. | | | 226 | | | | 12,744 | |

| | |

Zions Bancorp NA | | | 68 | | | | 3,536 | |

| | | | | | | | |

| | |

| | | | | | | 90,984 | |

| | | | | | | | |

|

Beverages — 0.6% | |

| | |

Constellation Brands, Inc., Class A | | | 37 | | | | 7,044 | |

| | |

Keurig Dr Pepper, Inc. | | | 128 | | | | 3,695 | |

| | | | | | | | |

| | |

| | | | | | | 10,739 | |

| | | | | | | | |

|

Biotechnology — 1.7% | |

| | |

Agios Pharmaceuticals, Inc. * | | | 48 | | | | 2,275 | |

| | |

Alnylam Pharmaceuticals, Inc. * | | | 37 | | | | 4,299 | |

| | |

BioMarin Pharmaceutical, Inc. * | | | 29 | | | | 2,482 | |

| | |

Exact Sciences Corp. * | | | 96 | | | | 8,895 | |

| | |

Exelixis, Inc. * | | | 236 | | | | 4,162 | |

| | |

Intercept Pharmaceuticals, Inc. * | | | 32 | | | | 3,947 | |

| | |

Sage Therapeutics, Inc. * | | | 42 | | | | 3,051 | |

| | | | | | | | |

| | |

| | | | | | | 29,111 | |

| | | | | | | | |

|

Building Products — 1.0% | |

| | |

Fortune Brands Home & Security, Inc. | | | 249 | | | | 16,287 | |

| | | | | | | | |

|

Capital Markets — 4.4% | |

| | |

Ameriprise Financial, Inc. | | | 64 | | | | 10,625 | |

| | |

MarketAxess Holdings, Inc. | | | 14 | | | | 5,383 | |

| | |

MSCI, Inc. | | | 30 | | | | 7,787 | |

| | |

Nasdaq, Inc. | | | 68 | | | | 7,299 | |

| | |

Northern Trust Corp. | | | 92 | | | | 9,793 | |

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

| | | | | | | | |

| | |

Capital Markets — continued | | | | | | | | |

| | |

Raymond James Financial, Inc. | | | 103 | | | | 9,228 | |

| | |

S&P Global, Inc. | | | 32 | | | | 8,856 | |

| | |

T. Rowe Price Group, Inc. | | | 111 | | | | 13,575 | |

| | |

TD Ameritrade Holding Corp. | | | 58 | | | | 2,872 | |

| | | | | | | | |

| | |

| | | | | | | 75,418 | |

| | | | | | | | |

|

Chemicals — 0.6% | |

| | |

Sherwin-Williams Co. (The) | | | 17 | | | | 9,968 | |

| | | | | | | | |

|

Commercial Services & Supplies — 1.5% | |

| | |

Copart, Inc. * | | | 141 | | | | 12,849 | |

| | |

Waste Connections, Inc. | | | 148 | | | | 13,447 | |

| | | | | | | | |

| | |

| | | | | | | 26,296 | |

| | | | | | | | |

| | |

Communications Equipment — 0.5% | | | | | | | | |

| | |

Arista Networks, Inc. * | | | 33 | | | | 6,743 | |

| | |

CommScope Holding Co., Inc. * | | | 151 | | | | 2,145 | |

| | | | | | | | |

| | |

| | | | | | | 8,888 | |

| | | | | | | | |

| | |

Construction Materials — 1.2% | | | | | | | | |

| | |

Martin Marietta Materials, Inc. | | | 31 | | | | 8,576 | |

| | |

Vulcan Materials Co. | | | 87 | | | | 12,559 | |

| | | | | | | | |

| | |

| | | | | | | 21,135 | |

| | | | | | | | |

| | |

Consumer Finance — 0.1% | | | | | | | | |

| | |

Ally Financial, Inc. | | | 39 | | | | 1,198 | |

| | | | | | | | |

| | |

Containers & Packaging — 2.5% | | | | | | | | |

| | |

Avery Dennison Corp. | | | 77 | | | | 10,092 | |

| | |

Ball Corp. | | | 273 | | | | 17,639 | |

| | |

Silgan Holdings, Inc. | | | 278 | | | | 8,649 | |

| | |

Westrock Co. | | | 158 | | | | 6,790 | |

| | | | | | | | |

| | |

| | | | | | | 43,170 | |

| | | | | | | | |

| | |

Distributors — 0.3% | | | | | | | | |

| | |

Genuine Parts Co. | | | 52 | | | | 5,532 | |

| | | | | | | | |

|

Diversified Consumer Services — 0.4% | |

| | |

Bright Horizons Family Solutions, Inc. * | | | 50 | | | | 7,554 | |

| | | | | | | | |

| | |

Electric Utilities — 2.1% | | | | | | | | |

| | |

Edison International | | | 132 | | | | 9,931 | |

| | |

Entergy Corp. | | | 72 | | | | 8,647 | |

| | |

Xcel Energy, Inc. | | | 289 | | | | 18,342 | |

| | | | | | | | |

| | |

| | | | | | | 36,920 | |

| | | | | | | | |

| | |

Electrical Equipment — 2.6% | | | | | | | | |

| | |

Acuity Brands, Inc. | | | 58 | | | | 7,957 | |

| | |

AMETEK, Inc. | | | 214 | | | | 21,356 | |

| | |

Generac Holdings, Inc. * | | | 91 | | | | 9,162 | |

| | |

Hubbell, Inc. | | | 37 | | | | 5,459 | |

| | | | | | | | |

| | |

| | | | | | | 43,934 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2019 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 15 | |

JPMorgan Mid Cap Equity Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2019 (Unaudited) (continued)

| | | | | | | | |

| INVESTMENTS | | SHARES

(000) | | | VALUE

($000) | |

Common Stocks — continued | | | | | | | | |

|

Electronic Equipment, Instruments & Components — 4.7% | |

| | |

Amphenol Corp., Class A | | | 198 | | | | 21,408 | |

| | |

Arrow Electronics, Inc. * | | | 82 | | | | 6,922 | |

| | |

CDW Corp. | | | 69 | | | | 9,904 | |

| | |

FLIR Systems, Inc. | | | 95 | | | | 4,949 | |

| | |

Keysight Technologies, Inc. * | | | 178 | | | | 18,263 | |

| | |

SYNNEX Corp. | | | 46 | | | | 5,944 | |

| | |

Zebra Technologies Corp., Class A * | | | 51 | | | | 13,062 | |

| | | | | | | | |

| | |

| | | | | | | 80,452 | |

| | | | | | | | |

| | |

Entertainment — 1.3% | | | | | | | | |

| | |

Spotify Technology SA * | | | 71 | | | | 10,683 | |

| | |

Take-Two Interactive Software, Inc. * | | | 100 | | | | 12,241 | |

| | | | | | | | |

| | |

| | | | | | | 22,924 | |

| | | | | | | | |

|

Equity Real Estate Investment Trusts (REITs) — 6.0% | |

| | |

American Campus Communities, Inc. | | | 99 | | | | 4,672 | |

| | |

American Homes 4 Rent, Class A | | | 206 | | | | 5,394 | |

| | |

AvalonBay Communities, Inc. | | | 54 | | | | 11,411 | |

| | |

Boston Properties, Inc. | | | 81 | | | | 11,120 | |

| | |

Brixmor Property Group, Inc. | | | 333 | | | | 7,188 | |

| | |

Essex Property Trust, Inc. | | | 23 | | | | 6,790 | |

| | |

Federal Realty Investment Trust | | | 67 | | | | 8,568 | |

| | |

JBG SMITH Properties | | | 88 | | | | 3,508 | |

| | |

Kimco Realty Corp. | | | 295 | | | | 6,103 | |

| | |

Outfront Media, Inc. | | | 213 | | | | 5,716 | |

| | |

Rayonier, Inc. | | | 206 | | | | 6,733 | |

| | |

Regency Centers Corp. | | | 75 | | | | 4,754 | |

| | |

Ventas, Inc. | | | 64 | | | | 3,690 | |

| | |

Vornado Realty Trust | | | 125 | | | | 8,328 | |

| | |

Weyerhaeuser Co. | | | 184 | | | | 5,556 | |

| | |