UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08189

J.P. Morgan Fleming Mutual Fund Group, Inc.

(Exact name of registrant as specified in charter)

270 Park Avenue

New York, NY 10017

(Address of principal executive offices) (Zip code)

Frank J. Nasta

270 Park Avenue

New York, NY 10017

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: June 30

Date of reporting period: July 1, 2017 through December 31, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Semi-Annual Report

J.P. Morgan Mid Cap/Multi-Cap Funds

December 31, 2017 (Unaudited)

JPMorgan Growth Advantage Fund

JPMorgan Mid Cap Equity Fund

JPMorgan Mid Cap Growth Fund

JPMorgan Mid Cap Value Fund

JPMorgan Multi-Cap Market Neutral Fund

JPMorgan Value Advantage Fund

CONTENTS

Investments in a Fund are not deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when a Fund’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on market and other conditions through the end of the reporting period and are subject to change without notice. These views are not intended to predict the future performance of a Fund or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of any Fund.

Prospective investors should refer to the Funds’ prospectuses for a discussion of the Funds’ investment objectives, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about a Fund, including management fees and other expenses. Please read it carefully before investing.

CEO’S LETTER

February 1, 2018 (Unaudited)

Dear Shareholder,

The U.S. economy continued to grow in the second half of 2017, supported by a synchronized global economy and central bank policies that also helped lift equity prices in the U.S. and elsewhere.

| | |

| | “Historically high consumer confidence, increased business investment and growth in corporate earnings all indicate that the U.S. economy should continue to expand.” — George C.W. Gatch |

The U.S. economy entered its third longest expansion on record in 2017, and gross domestic product (GDP) rose by 3.2% in the third quarter and an estimated 2.6% in the fourth quarter. During the second half of 2017, unemployment fell to 4.1% in December from 4.3% in June, and U.S. consumer confidence reached a 17-year high in November. Corporate profits rose during the second half of the year amid stable energy prices and a decline in the value of the U.S. dollar.

Notably, the second half of 2017 included three large hurricanes, wildfires and other assorted natural disasters that combined to cause an estimated $306 billion in damage in the U.S. While companies in some specific sectors of the economy reported that Hurricanes Harvey, Irma and Maria affected revenue or earnings, any impact on the larger economy appeared to be limited.

The U.S. Federal Reserve raised interest rates in December 2017 and indicated it would raise rates three more times in the year ahead. However, interest rates overall remained relatively low during the reporting period and provided support for both the domestic economy and financial markets.

Most developed market and emerging market economies also continued to grow in the second half of 2017. Growth in Europe was strong enough that the European Central Bank committed

to reducing its monthly asset purchases by half and the Bank of England raised its benchmark interest rate for the first time in ten years. Japan registered its longest economic expansion in a decade and China’s GDP grew by an estimated 6.8% in the second half of 2017, supported by personal consumption and growth in foreign trade.

Roughly 120 countries, comprising three-fourths of global GDP, had experienced increased economic growth by the end of 2017, according to the International Monetary Fund (IMF).

Meanwhile, global financial markets provided investors with positive returns for the six months ended December 31, 2017. Overall, equity markets outperformed bond markets, with emerging market equities largely outperforming developed market equities.

In the wake of stronger-than-expected growth in the U.S. and other leading economies, the IMF revised its forecast for 2018 U.S. GDP growth to 2.7% from 2.3%. The IMF cited growth from external demand and a reduction in U.S. corporate tax rates from the 2017 Tax Cuts and Jobs Act. Historically high consumer confidence, increased business investment and growth in corporate earnings all indicate that the U.S. economy should continue to expand. We believe investors who maintain a properly diversified portfolio and a long-term outlook will be able to benefit from the current global economic expansion.

We look forward to managing your investment needs for years to come. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

George C.W. Gatch

CEO, Global Funds Management

J.P. Morgan Asset Management

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 1 | |

J.P. Morgan Mid Cap/Multi-Cap Funds

MARKET OVERVIEW

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited)

U.S. equity markets overall provided positive returns throughout the reporting period amid strong growth in corporate profits, stable energy prices and continued low interest rates. During the reporting period, the Standard & Poor’s 500 Index (the “S&P 500”) reached more than two dozen record high closings and had positive returns for each month.

In contrast, the CBOE Volatility Index, which measures S&P 500 options to gauge market expectations of near-term volatility, remained well below its historical average throughout the year and on November 3, 2017 fell to its lowest-ever level.

Overall, growth stocks outperformed value stocks and large cap stocks generally outperformed small cap and mid cap stocks during the reporting period.

| | | | | | |

| | | |

| 2 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2017 |

JPMorgan Growth Advantage Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class A Shares, without a sales charge)* | | | 14.25% | |

| Russell 3000 Growth Index | | | 13.98% | |

| |

| Net Assets as of 12/31/2017 (In Thousands) | | $ | 8,028,738 | |

INVESTMENT OBJECTIVE**

The JPMorgan Growth Advantage Fund (the “Fund”) seeks to provide long-term capital growth.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class A Shares, without a sales charge, outperformed the Russell 3000 Growth Index (the “Benchmark”) for the six months ended December 31, 2017. The Fund’s security selection in the health care sector and its underweight position in the consumer staples sector were leading contributors to performance relative to the Benchmark. The Fund’s security selection and underweight position in the producer durables sector and its security selection in the consumer discretionary sector were leading detractors from relative performance.

Leading individual contributors to relative performance included the Fund’s overweight positions in Kite Pharma Inc. and Arista Networks Inc., and its underweight position in Celgene Corp. Shares of Kite Pharma, a drug maker, rose on news reports that the company had agreed to an acquisition offer from Gilead Sciences Inc. Shares of Arista Networks, a provider of cloud networking technology, rose after the company reported better-than-expected earnings and revenue for the third quarter of 2017. Shares of Celgene, a drug maker not held by the Fund, fell after the company halted development of its drug for Crohn’s disease and reported lower-than-expected revenue for the third quarter of 2017.

Leading individual detractors from relative performance included the Fund’s overweight positions in Acadia Healthcare Corp. and Evolent Health Inc. and its underweight position in Boeing Co. Shares of Acadia Healthcare, a provider of behavioral health care services that was not held in the Benchmark, fell after the company reported lower-than-expected earnings and revenue for the third quarter of 2017. Shares of Evolent Health, a provider of health care consulting, fell after the company reported slower earnings growth and announced plans to raise capital through an issuance of common stock. Shares of Boeing, an aircraft manufacturer, rose amid growth in new orders, an increase in the company’s stock dividend and an $18 billion stock repurchase plan.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up approach to stock selection, researching individual companies across market capitalizations in an effort to construct portfolios of stocks that have strong fundamentals. The Fund’s portfolio managers sought to invest in high quality companies with durable franchises that, in their view, possessed the ability to generate strong future earnings growth.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Alphabet, Inc., Class C | | | 6.3 | % |

| | 2. | | | Apple, Inc. | | | 5.4 | |

| | 3. | | | Amazon.com, Inc. | | | 4.7 | |

| | 4. | | | UnitedHealth Group, Inc. | | | 3.6 | |

| | 5. | | | Facebook, Inc., Class A | | | 3.5 | |

| | 6. | | | Waste Connections, Inc., (Canada) | | | 2.8 | |

| | 7. | | | Charles Schwab Corp. (The) | | | 2.2 | |

| | 8. | | | Mohawk Industries, Inc. | | | 2.2 | |

| | 9. | | | Visa, Inc., Class A | | | 2.0 | |

| | 10. | | | Mastercard, Inc., Class A | | | 1.9 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Information Technology | | | 42.5 | % |

| Consumer Discretionary | | | 14.3 | |

| Industrials | | | 13.3 | |

| Health Care | | | 13.2 | |

| Financials | | | 7.6 | |

| Energy | | | 1.6 | |

| Materials | | | 1.4 | |

| Others (each less than 1.0%) | | | 1.6 | |

| Short-Term Investment | | | 4.5 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2017. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 3 | |

JPMorgan Growth Advantage Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2017 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | October 29, 1999 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | 8.28 | % | | | 28.09 | % | | | 17.31 | % | | | 9.29 | % |

Without Sales Charge | | | | | 14.25 | | | | 35.19 | | | | 18.58 | | | | 9.88 | |

CLASS C SHARES | | May 1, 2006 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 13.00 | | | | 33.52 | | | | 18.00 | | | | 9.32 | |

Without CDSC | | | | | 14.00 | | | | 34.52 | | | | 18.00 | | | | 9.32 | |

CLASS I SHARES | | May 1, 2006 | | | 14.45 | | | | 35.51 | | | | 18.82 | | | | 10.11 | |

CLASS R2 SHARES | | July 31, 2017 | | | 14.11 | | | | 34.85 | | | | 18.29 | | | | 9.63 | |

CLASS R3 SHARES | | May 31, 2017 | | | 14.31 | | | | 35.25 | | | | 18.60 | | | | 9.91 | |

CLASS R4 SHARES | | May 31, 2017 | | | 14.39 | | | | 35.44 | | | | 18.87 | | | | 10.17 | |

CLASS R5 SHARES | | January 8, 2009 | | | 14.49 | | | | 35.69 | | | | 19.03 | | | | 10.30 | |

CLASS R6 SHARES | | December 23, 2013 | | | 14.54 | | | | 35.83 | | | | 19.13 | | | | 10.34 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (12/31/07 TO 12/31/17)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class R2 and Class R3 Shares prior to their inception date are based on the performance of Class A Shares. The actual returns for Class R2 and Class R3 Shares would have been lower than those shown because Class R2 and Class R3 Shares have higher expenses than Class A Shares.

Returns for Class R4 and Class R5 Shares prior to their inception dates are based on the performance of Class I Shares. The actual returns of Class R4 Shares would have been similar to those shown because Class R4 Shares have similar expenses to Class I Shares. The actual returns of Class R5 Shares would have been different than those shown because Class R5 Shares have different expenses than Class I Shares.

Returns for Class R6 Shares prior to their inception date are based on the performance of Class R5 Shares from January 8, 2009 to December 22, 2013 and Class I Shares prior to January 8, 2009. The actual returns of Class R6 Shares would have been different than those shown because Class R6 Shares have different expenses than Class R5 Shares and Class I Shares.

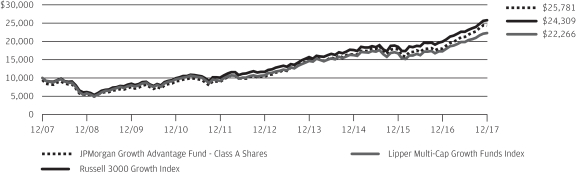

The graph illustrates comparative performance for $10,000 invested in Class A Shares of the JPMorgan Growth Advantage Fund, the Russell 3000 Growth Index and the Lipper Multi-Cap Growth Funds Index from December 31, 2007 to

December 31, 2017. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and includes a sales charge. The performance of the Russell 3000 Growth Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Multi-Cap Growth Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell 3000 Growth Index is an unmanaged index which measures the performance of those Russell 3000 companies (largest 3000 U.S. companies) with higher price-to-book ratios and higher forecasted growth values. The Lipper Multi-Cap Growth Funds Index is an index based on total returns of certain mutual funds within the Fund’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class A Shares have a $1,000 minimum initial investment and carry a 5.25% sales charge.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 4 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2017 |

JPMorgan Mid Cap Equity Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class I Shares)* | | | 9.49% | |

| Russell Midcap Index | | | 9.75% | |

| |

| Net Assets as of 12/31/2017 (In Thousands) | | $ | 3,025,575 | |

INVESTMENT OBJECTIVE**

The JPMorgan Mid Cap Equity Fund (the “Fund”) seeks to provide long-term capital growth.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class I Shares underperformed the Russell Midcap Index (the “Benchmark”) for the six months ended December 31, 2017. The Fund’s security selection in the materials & processing and consumer staples sectors was a leading detractor from performance relative to the Benchmark, while the Fund’s security selection and overweight position in the technology sector and its security selection in the consumer discretionary sector were leading contributors to relative performance.

Leading individual detractors from relative performance included the Fund’s overweight positions in Acadia Healthcare Inc., Intercept Pharmaceuticals Inc. and Newell Brands Inc. Shares of Acadia Healthcare, a provider of behavioral health care services that was not held in the Benchmark, fell after the company reported lower-than-expected earnings and revenue for the third quarter of 2017. Shares of Intercept Pharmaceuticals, a drug maker focused on liver diseases, fell amid investor concerns about the safety of the company’s Ocaliva drug. Shares of Newell Brands, a consumer products maker, fell after the company reported lower-than-expected earnings and sales and reduced its earnings forecast for the full year 2017.

Leading individual contributors to relative performance included the Fund’s overweight positions in Kite Pharma, Hilton Worldwide Holdings Inc. and Arista Networks Inc. Shares of Kite Pharma, a drug maker, rose on news reports that the company had agreed to an acquisition offer from Gilead Sciences Inc. Shares of Hilton Worldwide Holdings, a hotels and property company, rose after the company reported better-than-expected earnings and revenue for the third quarter of 2017 and raised its full year 2017 earnings forecast. Shares of Arista Networks, a provider of cloud networking technology, rose after the company reported better-than-expected earnings and revenue for the third quarter of 2017.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers employed a bottom-up approach to stock selection, constructing a portfolio based on company fundamentals, quantitative screening and proprietary

fundamental analysis. The Fund’s portfolio managers sought to identify dominant franchises with predictable business models they deemed capable of achieving, in their view, sustained growth, as well as undervalued companies with the potential to grow their intrinsic value per share.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Mohawk Industries, Inc. | | | 2.2 | % |

| | 2. | | | Waste Connections, Inc., (Canada) | | | 1.4 | |

| | 3. | | | Hilton Worldwide Holdings, Inc. | | | 1.4 | |

| | 4. | | | Amphenol Corp., Class A | | | 1.3 | |

| | 5. | | | Ameriprise Financial, Inc. | | | 1.1 | |

| | 6. | | | Fortune Brands Home & Security, Inc. | | | 1.1 | |

| | 7. | | | Progressive Corp. (The) | | | 1.0 | |

| | 8. | | | Energen Corp. | | | 1.0 | |

| | 9. | | | Concho Resources, Inc. | | | 1.0 | |

| | 10. | | | S&P Global, Inc. | | | 0.9 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Information Technology | | | 19.4 | % |

| Financials | | | 16.9 | |

| Consumer Discretionary | | | 16.8 | |

| Industrials | | | 13.3 | |

| Health Care | | | 9.0 | |

| Real Estate | | | 5.7 | |

| Energy | | | 4.2 | |

| Utilities | | | 4.1 | |

| Consumer Staples | | | 3.7 | |

| Materials | | | 3.6 | |

| Short-Term Investment | | | 3.3 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2017. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 5 | |

JPMorgan Mid Cap Equity Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2017 | |

| |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | November 2, 2009 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | 3.58 | % | | | 14.61 | % | | | 13.40 | % | | | 8.21 | % |

Without Sales Charge | | | | | 9.32 | | | | 20.96 | | | | 14.63 | | | | 8.79 | |

CLASS C SHARES | | November 2, 2009 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 8.03 | | | | 19.34 | | | | 14.06 | | | | 8.35 | |

Without CDSC | | | | | 9.03 | | | | 20.34 | | | | 14.06 | | | | 8.35 | |

CLASS I SHARES | | January 1, 1997 | | | 9.49 | | | | 21.35 | | | | 15.03 | | | | 9.10 | |

CLASS R2 SHARES | | March 14, 2014 | | | 9.17 | | | | 20.63 | | | | 14.41 | | | | 8.69 | |

CLASS R5 SHARES | | March 14, 2014 | | | 9.55 | | | | 21.46 | | | | 15.12 | | | | 9.14 | |

CLASS R6 SHARES | | March 14, 2014 | | | 9.57 | | | | 21.54 | | | | 15.16 | | | | 9.16 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (12/31/07 TO 12/31/17)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class A and Class C Shares prior to their inception date are based on the performance of Class I Shares. The actual returns of Class A and Class C Shares would have been lower than those shown because Class A and Class C Shares have higher expenses than Class I Shares.

Returns for Class R2 Shares prior to their inception date are based on the performance of Class A Shares from November 2, 2009 to March 13, 2014 and Class I Shares prior to November 2, 2009. The actual returns of Class R2 Shares would have been lower than those shown because Class R2 Shares have higher expenses than Class A and Class I Shares.

Returns for Class R5 and Class R6 Shares prior to their inception date are based on the performance of Class I Shares. The actual returns of Class R5 and Class R6 Shares would have been different because Class R5 and Class R6 Shares have different expenses than Class I Shares.

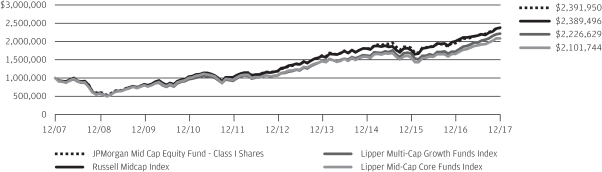

The graph illustrates comparative performance for $1,000,000 invested in the Class I Shares of JPMorgan Mid Cap Equity Fund, the Russell Midcap Index, the Lipper Multi-Cap Core Funds Index and the Lipper Multi-Cap Growth Funds Index from December 31, 2007 to December 31, 2017. The performance of the

Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the Russell Midcap Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Mid-Cap Core Funds Index and the Lipper Multi-Cap Growth Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell Midcap Index is an unmanaged index which measures the performance of the 800 smallest companies in the Russell 1000 Index. The Lipper Mid-Cap Core Funds Index and the Lipper Multi-Cap Growth Funds Index are indices based on total returns of certain mutual funds within designated categories as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class I Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 6 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2017 |

JPMorgan Mid Cap Growth Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class I Shares)* | | | 12.02% | |

| Russell Midcap Growth Index | | | 12.45% | |

| |

| Net Assets as of 12/31/2017 (In Thousands) | | $ | 3,501,658 | |

INVESTMENT OBJECTIVE**

The JPMorgan Mid Cap Growth Fund (the “Fund”) seeks growth of capital.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class I Shares underperformed the Russell Midcap Growth Index (the “Benchmark”) for the six months ended December 31, 2017. The Fund’s security selection in the financial services and health care sectors was a leading detractor from performance relative to the Benchmark, while the Fund’s security selection in the technology and consumer discretionary sectors was a leading contributor to relative performance.

Leading individual detractors from relative performance included the Fund’s overweight positions in Acadia Healthcare Inc., Intercept Pharma Inc. and Premier Inc. Shares of Acadia Healthcare, a provider of behavioral health care services that was not held in the Benchmark, fell after the company reported lower-than-expected earnings and revenue for the third quarter of 2017. Shares of Intercept Pharmaceuticals, a drug maker focused on liver diseases, fell amid investor concerns about the safety of the company’s Ocaliva drug. Shares of Premier, a health care supply chain services company, fell after the company reported lower-than-expected earnings for its fiscal fourth quarter of 2017.

Leading individual contributors to relative performance included the Fund’s overweight positions in Kite Pharma Inc., Arista Networks Inc. and Splunk Inc. Shares of Kite Pharma, a drug maker not held in the Benchmark, rose on news reports that the company had agreed to an acquisition offer from Gilead Sciences Inc. Shares of Arista Networks, a provider of cloud networking technology, rose after the company reported better-than-expected earnings and revenue for the third quarter of 2017. Shares of Splunk, a software provider, rose after the company reported better-than-expected earnings and sales for the third quarter of 2017.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up approach to stock selection, researching individual companies in an effort to construct a portfolio of stocks that have strong fundamentals. The Fund’s portfolio managers sought to invest in high

quality companies with durable franchises that, in their view, possessed the ability to generate strong future earnings growth.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Waste Connections, Inc., (Canada) | | | 2.8 | % |

| | 2. | | | Mohawk Industries, Inc. | | | 2.3 | |

| | 3. | | | Concho Resources, Inc. | | | 2.0 | |

| | 4. | | | S&P Global, Inc. | | | 1.8 | |

| | 5. | | | Global Payments, Inc. | | | 1.8 | |

| | 6. | | | Ross Stores, Inc. | | | 1.7 | |

| | 7. | | | Illumina, Inc. | | | 1.7 | |

| | 8. | | | Hilton Worldwide Holdings, Inc. | | | 1.5 | |

| | 9. | | | Lennox International, Inc. | | | 1.5 | |

| | 10. | | | Eagle Materials, Inc. | | | 1.5 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Information Technology | | | 29.7 | % |

| Industrials | | | 18.2 | |

| Consumer Discretionary | | | 17.3 | |

| Health Care | | | 11.8 | |

| Financials | | | 11.2 | |

| Materials | | | 2.8 | |

| Energy | | | 2.3 | |

| Consumer Staples | | | 1.1 | |

| Real Estate | | | 1.1 | |

| Short-Term Investment | | | 4.5 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31 2017. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 7 | |

JPMorgan Mid Cap Growth Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2017 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | February 18, 1992 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | 5.95 | % | | | 22.31 | % | | | 14.48 | % | | | 7.90 | % |

Without Sales Charge | | | | | 11.82 | | | | 29.07 | | | | 15.72 | | | | 8.48 | |

CLASS C SHARES | | November 4, 1997 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 10.57 | | | | 27.43 | | | | 15.15 | | | | 7.92 | |

Without CDSC | | | | | 11.57 | | | | 28.43 | | | | 15.15 | | | | 7.92 | |

CLASS I SHARES | | March 2, 1989 | | | 12.02 | | | | 29.50 | | | | 16.08 | | | | 8.81 | |

CLASS R2 SHARES | | June 19, 2009 | | | 11.71 | | | | 28.80 | | | | 15.52 | | | | 8.31 | |

CLASS R3 SHARES | | September 9, 2016 | | | 11.83 | | | | 29.05 | | | | 15.72 | | | | 8.48 | |

CLASS R4 SHARES | | September 9, 2016 | | | 11.96 | | | | 29.39 | | | | 16.01 | | | | 8.76 | |

CLASS R5 SHARES | | November 1, 2011 | | | 12.06 | | | | 29.68 | | | | 16.23 | | | | 8.91 | |

CLASS R6 SHARES | | November 1, 2011 | | | 12.08 | | | | 29.72 | | | | 16.30 | | | | 8.94 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (12/31/07 TO 12/31/17)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for the Class R2, Class R3, Class R4, Class R5 and Class R6 Shares prior to their inception dates are based on the performance of Class I Shares. Prior performance for Class R2, Class R3 and Class R4 Shares has been adjusted to reflect the differences in expenses between classes. The actual returns of Class R5 and Class R6 Shares would have been different than those shown because Class R5 and Class R6 Shares have different expenses than Class I Shares.

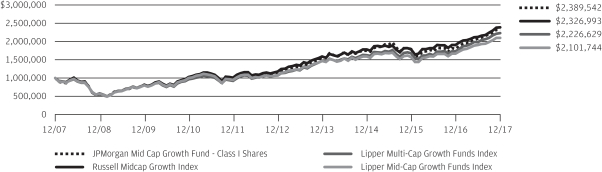

The graph illustrates comparative performance for $1,000,000 invested in Class I Shares of the JPMorgan Mid Cap Growth Fund, the Russell Midcap Growth Index, the Lipper Mid-Cap Growth Funds Index and the Lipper Multi-Cap Growth Funds Index from December 31, 2007 to December 31, 2017. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the Russell Midcap Growth Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all

dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Mid-Cap Growth Funds Index and the Lipper Multi-Cap Growth Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell Midcap Growth Index is an unmanaged index which measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values. The Lipper Mid-Cap Growth Funds Index and the Lipper Multi-Cap Growth Funds Index are indices based on total returns of certain mutual funds within designated categories as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class I Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 8 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2017 |

JPMorgan Mid Cap Value Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class L Shares)* | | | 6.92% | |

| Russell Midcap Value Index | | | 7.76% | |

| |

| Net Assets as of 12/31/2017 (In Thousands) | | $ | 19,142,055 | |

INVESTMENT OBJECTIVE**

The JPMorgan Mid Cap Value Fund (the “Fund”) seeks growth from capital appreciation.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class L Shares underperformed the Russell Midcap Value Index (the “Benchmark”) for the six months ended December 31, 2017. The Fund’s security selection in the materials and consumer staples sectors was a leading detractor from performance relative to the Benchmark, while the Fund’s underweight position and security selection in the real estate sector and its security selection in the information technology sector were leading contributors to relative performance.

Leading individual detractors from relative performance included the Fund’s overweight positions in Newell Brands Inc., Expedia Inc. and Ball Corp. Shares of Newell Brands, a consumer products maker, fell after the company reported lower-than-expected earnings and sales and reduced its earnings forecast for the full year 2017. Shares of Expedia, an online travel booking company not held in the Benchmark, fell after the company reported lower-than-expected earnings and revenue for the third quarter of 2017. Shares of Ball, a packaging manufacturer, fell after the company reported lower-than-expected earnings and sales for the third quarter of 2017.

Leading individual contributors to relative performance included the Fund’s overweight positions in Gap Inc., Kohl’s Corp. and PBF Energy Inc. Shares of Gap, a brand apparel retailer, rose on better-than-expected earnings for the third quarter of 2017 and amid investor expectations the company would benefit from the Tax Cut and Jobs Act of 2017. Shares of Kohl’s, a department store chain, rose amid improvements in the company’s store traffic trends and expense controls. Shares of PBF Energy, a petroleum refiner, rose amid a rise in U.S. fuel prices in the wake of Hurricanes Harvey and Irma.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up approach to stock selection and sought to identify durable franchises possessing the ability to generate, in their view, sustainable levels of free cash flow.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Energen Corp. | | | 2.0 | % |

| | 2. | | | Mohawk Industries, Inc. | | | 2.0 | |

| | 3. | | | EQT Corp. | | | 1.8 | |

| | 4. | | | Loews Corp. | | | 1.8 | |

| | 5. | | | M&T Bank Corp. | | | 1.7 | |

| | 6. | | | Xcel Energy, Inc. | | | 1.6 | |

| | 7. | | | Williams Cos., Inc. (The) | | | 1.6 | |

| | 8. | | | CMS Energy Corp. | | | 1.5 | |

| | 9. | | | WEC Energy Group, Inc. | | | 1.5 | |

| | 10. | | | T Rowe Price Group, Inc. | | | 1.5 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Financials | | | 22.8 | % |

| Consumer Discretionary | | | 15.9 | |

| Real Estate | | | 9.9 | |

| Information Technology | | | 8.7 | |

| Utilities | | | 8.2 | |

| Industrials | | | 8.1 | |

| Consumer Staples | | | 6.1 | |

| Energy | | | 6.1 | |

| Health Care | | | 5.9 | |

| Materials | | | 4.4 | |

| Short-Term Investment | | | 3.9 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2017. The Fund’s portfolio composition is subject to change. |

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 9 | |

JPMorgan Mid Cap Value Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2017 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | April 30, 2001 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | 1.08 | % | | | 7.20 | % | | | 12.33 | % | | | 8.48 | % |

Without Sales Charge | | | | | 6.66 | | | | 13.13 | | | | 13.55 | | | | 9.07 | |

CLASS C SHARES | | April 30, 2001 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 5.38 | | | | 11.54 | | | | 12.96 | | | | 8.52 | |

Without CDSC | | | | | 6.38 | | | | 12.54 | | | | 12.96 | | | | 8.52 | |

CLASS I SHARES | | October 31, 2001 | | | 6.79 | | | | 13.41 | | | | 13.82 | | | | 9.34 | |

CLASS L SHARES | | November 13, 1997 | | | 6.92 | | | | 13.67 | | | | 14.10 | | | | 9.61 | |

CLASS R2 SHARES | | November 3, 2008 | | | 6.52 | | | | 12.86 | | | | 13.25 | | | | 8.81 | |

CLASS R3 SHARES | | September 9, 2016 | | | 6.66 | | | | 13.15 | | | | 13.55 | | | | 9.07 | |

CLASS R4 SHARES | | September 9, 2016 | | | 6.78 | | | | 13.37 | | | | 13.81 | | | | 9.34 | |

CLASS R5 SHARES | | September 9, 2016 | | | 6.85 | | | | 13.58 | | | | 14.07 | | | | 9.60 | |

CLASS R6 SHARES | | September 9, 2016 | | | 6.90 | | | | 13.68 | | | | 14.10 | | | | 9.61 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (12/31/07 TO 12/31/17)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class R2 and Class R3 Shares prior to their inception dates are based on the performance of Class A Shares. The actual returns of Class R2 and Class R3 Shares would have been lower than those shown because Class R2 and Class R3 Shares have higher expenses than Class A Shares.

Returns for the Class R4 Shares prior to their inception date are based on the performance of Class I Shares. The actual returns of Class R4 Shares would have been lower because Class R4 Shares have higher expenses than Class I Shares.

Returns for the Class R5 and R6 Shares prior to their inception dates are based on the performance of Class L Shares. The actual returns of Class R5 Shares would have been lower than those shown because Class R5 Shares have higher expenses than Class L Shares. The actual returns for Class R6 Shares would have been similar to those shown because Class R6 Shares have similar expenses to Class L Shares.

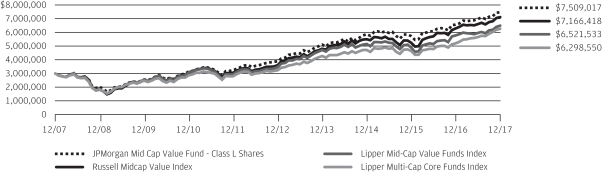

The graph illustrates comparative performance for $3,000,000 invested in Class L Shares of the JPMorgan Mid Cap Value Fund, the Russell Midcap Value Index, the Lipper Mid-Cap Value Funds Index and the Lipper Multi-Cap Core Funds Index from December 31, 2007 to December 31, 2017. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the

Russell Midcap Value Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Mid-Cap Value Funds Index and the Lipper Multi-Cap Core Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell Midcap Value Index is an unmanaged index which measures the performance of those Russell Midcap companies with lower price-to-book ratios and lower forecasted growth values. The Lipper Mid-Cap Value Funds Index and the Lipper Multi-Cap Core Funds Index are indices based on total returns of certain mutual funds within designated categories as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class L Shares have a $3,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | |

| | | |

| 10 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2017 |

JPMorgan Multi-Cap Market Neutral Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class I Shares)* | | | 4.01% | |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index | | | 0.55% | |

| |

| Net Assets as of 12/31/17 (In Thousands) | | $ | 124,055 | |

INVESTMENT OBJECTIVE**

The JPMorgan Multi-Cap Market Neutral Fund (the “Fund”) seeks long-term capital preservation and growth by using strategies designed to produce returns which have no correlation with general domestic market performance.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class I Shares outperformed the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (the “Benchmark”) for the six months ended December 31, 2017. U.S. equity securities, which were not included in the Benchmark, generally outperformed U.S. Treasury bonds during the reporting period. The Fund’s overall security selection in the consumer discretionary and health care sectors helped the Fund’s performance relative to the Benchmark, while the Fund’s overall security selection in the real estate and financials sectors detracted from relative performance.

Leading individual contributors to Fund returns included its long positions in NRG Energy Inc. and United Rentals Inc. and its short position in Envision Healthcare Corp. Shares of NRG Energy, an electricity utility, rose after the company unveiled a plan to sell assets and cut operation costs. Shares of United Rentals, an equipment rental company, rose after reporting several consecutive quarters of better-than-expected earnings. Shares of Envision Healthcare, an owner/operator of surgical centers and hospitals, fell amid lower-than-expected earnings for the third quarter of 2017 and investor concerns about billing practices as a company subsidiary.

Leading individual detractors from Fund returns included its short positions in Interactive Brokers Group Inc., Cavium Inc. and Wex Inc. Shares of Interactive Brokers Group, an investment broker/dealer and securities trading company, rose after the company reported better-than-expected earnings and revenue for the third quarter of 2017. Shares of Cavium, a semiconductor manufacturer, rose after the company agreed to be acquired for about $6 billion by Marvell Technology Group Ltd. Shares of Wex, a provider of payment processing and information management services, rose after the company reported better-than-expected earnings for the third quarter of 2017.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers employed a bottom-up approach to stock selection, constructing a portfolio based on company fundamentals, quantitative screening and proprietary fundamental analysis. The Fund’s portfolio managers sought to identify dominant franchises with predictable business models deemed capable of achieving, in their view, sustained growth, as well as undervalued companies with the potential to grow their intrinsic value per share. Companies that ranked lowest based on these factors were selected by the Fund’s portfolio managers for possible short sales.

| | | | | | | | |

| TOP TEN LONG POSITIONS OF THE PORTFOLIO*** | |

| | 1. | | | Best Buy Co., Inc. | | | 1.1 | % |

| | 2. | | | Huntsman Corp. | | | 1.1 | |

| | 3. | | | Owens Corning | | | 1.0 | |

| | 4. | | | Boeing Co. (The) | | | 1.0 | |

| | 5. | | | United Rentals, Inc. | | | 1.0 | |

| | 6. | | | Caterpillar, Inc. | | | 1.0 | |

| | 7. | | | Centene Corp. | | | 1.0 | |

| | 8. | | | Total System Services, Inc. | | | 1.0 | |

| | 9. | | | Synovus Financial Corp. | | | 1.0 | |

| | 10. | | | AbbVie, Inc. | | | 1.0 | |

| | | | | | | | |

| TOP TEN SHORT POSITIONS OF THE PORTFOLIO**** | |

| | 1. | | | WEX, Inc. | | | 1.2 | % |

| | 2. | | | Compass Minerals International, Inc. | | | 1.2 | |

| | 3. | | | Trinity Industries, Inc. | | | 1.2 | |

| | 4. | | | Casey’s General Stores, Inc. | | | 1.2 | |

| | 5. | | | Hexcel Corp. | | | 1.2 | |

| | 6. | | | ViaSat, Inc. | | | 1.2 | |

| | 7. | | | Watsco, Inc. | | | 1.2 | |

| | 8. | | | Vulcan Materials Co. | | | 1.1 | |

| | 9. | | | Akamai Technologies, Inc. | | | 1.1 | |

| | 10. | | | Snap-on, Inc. | | | 1.1 | |

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 11 | |

JPMorgan Multi-Cap Market Neutral Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited) (continued)

| | | | |

LONG POSITION PORTFOLIO COMPOSITION BY SECTOR*** | |

| Information Technology | | | 22.5 | % |

| Industrials | | | 16.2 | |

| Consumer Discretionary | | | 15.1 | |

| Health Care | | | 11.0 | |

| Financials | | | 6.6 | |

| Consumer Staples | | | 5.7 | |

| Materials | | | 4.2 | |

| Utilities | | | 3.8 | |

| Energy | | | 3.0 | |

| Real Estate | | | 1.2 | |

| Short-Term Investment | | | 10.7 | |

| | | | |

SHORT POSITION PORTFOLIO COMPOSITION BY SECTOR**** | |

| Information Technology | | | 25.4 | % |

| Industrials | | | 20.3 | |

| Consumer Discretionary | | | 15.3 | |

| Health Care | | | 12.5 | |

| Financials | | | 6.7 | |

| Consumer Staples | | | 6.1 | |

| Materials | | | 4.8 | |

| Utilities | | | 4.1 | |

| Energy | | | 2.7 | |

| Real Estate | | | 1.1 | |

| Others (each less than 1.0%) | | | 1.0 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total long investments as of December 31, 2017. The Fund’s portfolio composition is subject to change. |

| **** | | Percentages indicated are based on total short investments as of December 31, 2017. The Fund’s portfolio composition is subject to change. |

| | | | | | |

| | | |

| 12 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2017 |

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2017 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | May 23, 2003 | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | (1.52 | )% | | | (2.36 | )% | | | 0.57 | % | | | (0.28 | )% |

Without Sales Charge | | | | | 3.91 | | | | 3.08 | | | | 1.66 | | | | 0.25 | |

CLASS C SHARES | | May 23, 2003 | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | 2.65 | | | | 1.55 | | | | 1.14 | | | | (0.39 | ) |

Without CDSC | | | | | 3.65 | | | | 2.55 | | | | 1.14 | | | | (0.39 | ) |

CLASS I SHARES | | May 23, 2003 | | | 4.01 | | | | 3.30 | | | | 1.91 | | | | 0.49 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (12/31/07 TO 12/31/17)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

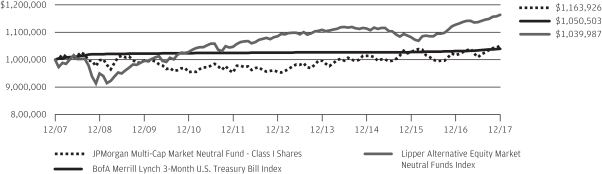

The graph illustrates comparative performance for $1,000,000 invested in Class I Shares of the JPMorgan Multi-Cap Market Neutral Fund, the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index and the Lipper Alternative Equity Market Neutral Funds Index from December 31, 2007 to December 31, 2017. The performance of the Fund assumes reinvestment of all dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Alternative Equity Market Neutral Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the

Fund. The BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. Each month the index is rebalanced and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, 3 months from the rebalancing date. The Lipper Alternative Equity Market Neutral Funds Index is an index based on total returns of certain mutual funds within the Fund’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class I Shares have a $1,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 13 | |

JPMorgan Value Advantage Fund

FUND COMMENTARY

SIX MONTHS ENDED DECEMBER 31, 2017 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Fund (Class L Shares)* | | | 9.47% | |

| Russell 3000 Value Index | | | 8.51% | |

| |

| Net Assets as of 12/31/2017 (In Thousands) | | $ | 12,266,834 | |

INVESTMENT OBJECTIVE**

The JPMorgan Value Advantage Fund (the “Fund”) seeks to provide long-term total return from a combination of income and capital gains.

WHAT WERE THE MAIN DRIVERS OF THE FUND’S PERFORMANCE?

The Fund’s Class L Shares outperformed the Russell 3000 Value Index (the “Benchmark”) for the six months ended December 31, 2017. The Fund’s security selection in the industrials sector and its overweight position in the financials sector were leading contributors to performance relative to the Benchmark, while the Fund’s security section in the materials and consumer discretionary sectors was a leading detractor from relative performance.

Leading individual contributors to performance relative to the Benchmark included the Fund’s underweight position in General Electric Co. and its overweight positions in T. Rowe Price Group Inc. and Kohl’s Corp. Shares of General Electric, an industrial conglomerate not held by the Fund, fell amid the company’s efforts to implement a restructuring plan. Shares of T. Rowe Price Group, a provider of mutual funds and financial advisory services, rose amid growth in the company’s assets under management and the overall strength of the financials sector. Shares of Kohl’s, a department store chain, rose amid improvements in the company’s store traffic trends and expense controls.

Leading individual detractors from relative performance included the Fund’s overweight positions in Dish Network Corp. and Ball Corp. and its underweight position in Intel Corp. Shares of Dish Network, a subscription TV provider, fell after the company reported lower-than-expected earnings for the third quarter of 2017. Shares of Ball, a packaging manufacturer, fell after the company reported lower-than-expected earnings and sales for the third quarter of 2017. Shares of Intel, a semiconductor maker not held by the Fund, rose amid gains in the broader semiconductor sector.

HOW WAS THE FUND POSITIONED?

The Fund’s portfolio managers utilized a bottom-up approach to stock selection and sought to identify durable franchises possessing the ability to generate, in the portfolio managers’

view, significant levels of free cash flow. During the reporting period, the Fund’s largest average overweight positions were in the consumer discretionary sector, where the Fund’s portfolio managers found what they believed to be compelling investment opportunities. The Fund’s largest average underweight position was in the health care sector.

| | | | | | | | |

| TOP TEN EQUITY HOLDINGS OF THE PORTFOLIO*** | |

| | 1. | | | Wells Fargo & Co. | | | 3.2 | % |

| | 2. | | | Bank of America Corp. | | | 3.1 | |

| | 3. | | | Capital One Financial Corp. | | | 2.4 | |

| | 4. | | | Pfizer, Inc. | | | 2.3 | |

| | 5. | | | Delta Air Lines, Inc. | | | 1.9 | |

| | 6. | | | Exxon Mobil Corp. | | | 1.8 | |

| | 7. | | | Loews Corp. | | | 1.7 | |

| | 8. | | | Johnson & Johnson | | | 1.6 | |

| | 9. | | | M&T Bank Corp. | | | 1.6 | |

| | 10. | | | PNC Financial Services Group, Inc. (The) | | | 1.6 | |

| | | | |

PORTFOLIO COMPOSITION BY SECTOR*** | |

| Financials | | | 31.2 | % |

| Consumer Discretionary | | | 13.8 | |

| Health Care | | | 8.5 | |

| Energy | | | 7.5 | |

| Industrials | | | 7.1 | |

| Information Technology | | | 6.9 | |

| Consumer Staples | | | 6.2 | |

| Real Estate | | | 6.0 | |

| Utilities | | | 4.6 | |

| Materials | | | 4.0 | |

| Telecommunication Services | | | 0.8 | |

| Short-Term Investment | | | 3.4 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Fund’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of December 31, 2017. The Fund’s portfolio composition is subject to change. |

| | | | | | |

| | | |

| 14 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2017 |

| | | | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF DECEMBER 31, 2017 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | | 6 MONTH* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS A SHARES | | | February 28, 2005 | | | | | | | | | | | | | | | | | |

With Sales Charge** | | | | | | | 3.48 | % | | | 7.69 | % | | | 12.24 | % | | | 8.32 | % |

Without Sales Charge | | | | | | | 9.21 | | | | 13.67 | | | | 13.46 | | | | 8.90 | |

CLASS C SHARES | | | February 28, 2005 | | | | | | | | | | | | | | | | | |

With CDSC*** | | | | | | | 7.95 | | | | 12.11 | | | | 12.90 | | | | 8.36 | |

Without CDSC | | | | | | | 8.95 | | | | 13.11 | | | | 12.90 | | | | 8.36 | |

CLASS I SHARES | | | February 28, 2005 | | | | 9.35 | | | | 13.96 | | | | 13.75 | | | | 9.18 | |

CLASS L SHARES | | | February 28, 2005 | | | | 9.47 | | | | 14.23 | | | | 14.03 | | | | 9.46 | |

CLASS R2 SHARES | | | July 31, 2017 | | | | 9.07 | | | | 13.37 | | | | 13.18 | | | | 8.63 | |

CLASS R3 SHARES | | | September 9, 2016 | | | | 9.20 | | | | 13.65 | | | | 13.46 | | | | 8.90 | |

CLASS R4 SHARES | | | September 9, 2016 | | | | 9.32 | | | | 13.94 | | | | 13.75 | | | | 9.18 | |

CLASS R5 SHARES | | | September 9, 2016 | | | | 9.43 | | | | 14.12 | | | | 14.01 | | | | 9.45 | |

CLASS R6 SHARES | | | September 9, 2016 | | | | 9.50 | | | | 14.23 | | | | 14.04 | | | | 9.46 | |

| ** | | Sales Charge for Class A Shares is 5.25%. |

| *** | | Assumes a 1% CDSC (contingent deferred sales charge) for the 6 month and one year periods and 0% CDSC thereafter. |

TEN YEAR PERFORMANCE (12/31/07 TO 12/31/17)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class R2 and Class R3 Shares prior to their inception date are based on the performance of Class A Shares. The actual returns of Class R2 would have been lower than those shown because Class R2 Shares have higher expenses than Class A Shares. Returns for Class R3 Shares would have been similar to those shown because Class R3 Shares have similar expenses to Class A Shares.

Returns for the Class R4 Shares prior to their inception date are based on the performance of Class I Shares. The actual returns of Class R4 Shares would have been similar to those shown because Class R4 Shares have similar expenses to Class I Shares.

Returns for the Class R5 and R6 Shares prior to their inception dates are based on the performance of Class L Shares. The actual returns of Class R5 Shares would have been lower than those shown because Class R5 Shares have higher expenses than Class L Shares. The actual returns for Class R6 Shares would have been similar to those shown because Class R6 Shares have similar expenses to Class L Shares.

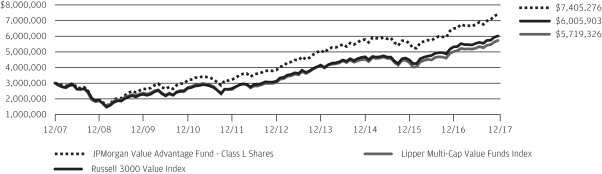

The graph illustrates comparative performance for $3,000,000 invested in Class L Shares of the JPMorgan Value Advantage Fund, the Russell 3000 Value Index and the Lipper Multi-Cap Value Funds Index from December 31, 2007 to December 31, 2017. The performance of the Fund assumes reinvestment of all

dividends and capital gain distributions, if any, and does not include a sales charge. The performance of the Russell 3000 Value Index does not reflect the deduction of expenses or a sales charge associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper Multi-Cap Value Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Fund. The Russell 3000 Value Index is an unmanaged index which measures the performance of those Russell 3000 companies (largest 3000 U.S. companies) with lower price-to-book ratios and lower forecasted growth values. The Lipper Multi-Cap Value Funds Index is an index based on total returns of certain mutual funds within the Fund’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

Class L Shares have a $3,000,000 minimum initial investment.

Fund performance may reflect the waiver of the Fund’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. Also, performance shown in this section does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 15 | |

JPMorgan Growth Advantage Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2017 (Unaudited)

(Amounts in thousands)

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | Common Stocks — 95.5% | |

| | | | Consumer Discretionary — 14.3% | |

| | | | Automobiles — 0.5% | |

| | 143 | | | Tesla, Inc. (a) | | | 44,430 | |

| | | | | | | | |

| | | | Distributors — 1.1% | |

| | 2,107 | | | LKQ Corp. (a) | | | 85,679 | |

| | | | | | | | |

| | | | Hotels, Restaurants & Leisure — 2.4% | |

| | 1,153 | | | Hilton Grand Vacations, Inc. (a) | | | 48,370 | |

| | 1,170 | | | Hilton Worldwide Holdings, Inc. | | | 93,471 | |

| | 975 | | | Norwegian Cruise Line Holdings Ltd. (a) | | | 51,935 | |

| | | | | | | | |

| | | | | | | 193,776 | |

| | | | | | | | |

| | | | Household Durables — 2.2% | |

| | 649 | | | Mohawk Industries, Inc. (a) | | | 178,976 | |

| | | | | | | | |

| | | | Internet & Direct Marketing Retail — 7.5% | | | | |

| | 321 | | | Amazon.com, Inc. (a) | | | 374,932 | |

| | 439 | | | Netflix, Inc. (a) | | | 84,232 | |

| | 52 | | | Priceline Group, Inc. (The) (a) | | | 90,710 | |

| | 620 | | | Wayfair, Inc., Class A (a) | | | 49,800 | |

| | | | | | | | |

| | | | | | | 599,674 | |

| | | | | | | | |

| | | | Textiles, Apparel & Luxury Goods — 0.6% | |

| | 1,466 | | | Gildan Activewear, Inc., (Canada) | | | 47,355 | |

| | | | | | | | |

| | | | Total Consumer Discretionary | | | 1,149,890 | |

| | | | | | | | |

| | | | Consumer Staples — 0.7% | |

| | | | Beverages — 0.7% | |

| | 851 | | | Monster Beverage Corp. (a) | | | 53,860 | |

| | | | | | | | |

| | | | Energy — 1.6% | |

| | | | Oil, Gas & Consumable Fuels — 1.6% | |

| | 512 | | | Concho Resources, Inc. (a) | | | 76,867 | |

| | 493 | | | EOG Resources, Inc. | | | 53,146 | |

| | | | | | | | |

| | | | Total Energy | | | 130,013 | |

| | | | | | | | |

| | | | Financials — 7.6% | |

| | | | Banks — 2.4% | |

| | 807 | | | Comerica, Inc. | | | 70,056 | |

| | 1,345 | | | East West Bancorp, Inc. | | | 81,816 | |

| | 480 | | | First Republic Bank | | | 41,604 | |

| | | | | | | | |

| | | | | | | 193,476 | |

| | | | | | | | |

| | | | Capital Markets — 5.2% | |

| | 132 | | | BlackRock, Inc. | | | 67,861 | |

| | 3,488 | | | Charles Schwab Corp. (The) | | | 179,184 | |

| | 646 | | | Nasdaq, Inc. | | | 49,594 | |

| | 721 | | | S&P Global, Inc. | | | 122,171 | |

| | | | | | | | |

| | | | | | | 418,810 | |

| | | | | | | | |

| | | | Total Financials | | | 612,286 | |

| | | | | | | | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Health Care — 13.2% | |

| | | | Biotechnology — 2.7% | |

| | 878 | | | Exact Sciences Corp. (a) | | | 46,114 | |

| | 513 | | | Intercept Pharmaceuticals, Inc. (a) | | | 29,987 | |

| | 199 | | | Sage Therapeutics, Inc. (a) | | | 32,843 | |

| | 546 | | | Spark Therapeutics, Inc. (a) | | | 28,086 | |

| | 519 | | | Vertex Pharmaceuticals, Inc. (a) | | | 77,792 | |

| | | | | | | | |

| | | | | | | 214,822 | |

| | | | | | | | |

| | | | Health Care Equipment & Supplies — 1.6% | |

| | 974 | | | DENTSPLY SIRONA, Inc. | | | 64,092 | |

| | 168 | | | Intuitive Surgical, Inc. (a) | | | 61,383 | |

| | | | | | | | |

| | | | | | | 125,475 | |

| | | | | | | | |

| | | | Health Care Providers & Services — 5.4% | |

| | 1,883 | | | Acadia Healthcare Co., Inc. (a) | | | 61,455 | |

| | 235 | | | Humana, Inc. | | | 58,371 | |

| | 809 | | | Teladoc, Inc. (a) | | | 28,180 | |

| | 1,297 | | | UnitedHealth Group, Inc. | | | 285,915 | |

| | | | | | | | |

| | | | | | | 433,921 | |

| | | | | | | | |

| | | | Health Care Technology — 0.8% | |

| | 2,202 | | | Evolent Health, Inc., Class A (a) | | | 27,084 | |

| | 724 | | | Veeva Systems, Inc., Class A (a) | | | 40,012 | |

| | | | | | | | |

| | | | | | | 67,096 | |

| | | | | | | | |

| | | | Life Sciences Tools & Services — 0.9% | |

| | 346 | | | Illumina, Inc. (a) | | | 75,488 | |

| | | | | | | | |

| | | | Pharmaceuticals — 1.8% | |

| | 437 | | | Jazz Pharmaceuticals plc (a) | | | 58,856 | |

| | 1,221 | | | Revance Therapeutics, Inc. (a) | | | 43,658 | |

| | 6,300 | | | TherapeuticsMD, Inc. (a) | | | 38,053 | |

| | | | | | | | |

| | | | | | | 140,567 | |

| | | | | | | | |

| | | | Total Health Care | | | 1,057,369 | |

| | | | | | | | |

| | | | Industrials — 13.3% | |

| | | | Airlines — 1.5% | |

| | 1,001 | | | Delta Air Lines, Inc. | | | 56,067 | |

| | 953 | | | Southwest Airlines Co. | | | 62,400 | |

| | | | | | | | |

| | | | | | | 118,467 | |

| | | | | | | | |

| | | | Building Products — 2.2% | |

| | 1,024 | | | Fortune Brands Home & Security, Inc. | | | 70,110 | |

| | 511 | | | Lennox International, Inc. | | | 106,317 | |

| | | | | | | | |

| | | | | | | 176,427 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 16 | | | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | DECEMBER 31, 2017 |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | Common Stocks — continued | |

| | | | Commercial Services & Supplies — 3.6% | |

| | 1,536 | | | Copart, Inc. (a) | | | 66,340 | |

| | 3,122 | | | Waste Connections, Inc., (Canada) | | | 221,457 | |

| | | | | | | | |

| | | | | | | 287,797 | |

| | | | | | | | |

| | | | Machinery — 4.9% | |

| | 383 | | | John Bean Technologies Corp. | | | 42,470 | |

| | 300 | | | Middleby Corp. (The) (a) | | | 40,498 | |

| | 858 | | | Oshkosh Corp. | | | 78,002 | |

| | 211 | | | Parker-Hannifin Corp. | | | 42,052 | |

| | 625 | | | Stanley Black & Decker, Inc. | | | 106,039 | |

| | 599 | | | WABCO Holdings, Inc. (a) | | | 85,913 | |

| | | | | | | | |

| | | | | | | 394,974 | |

| | | | | | | | |

| | | | Road & Rail — 1.1% | |

| | 692 | | | Old Dominion Freight Line, Inc. | | | 91,039 | |

| | | | | | | | |

| | | | Total Industrials | | | 1,068,704 | |

| | | | | | | | |

| | | | Information Technology — 42.5% | |

| | | | Communications Equipment — 1.3% | |

| | 266 | | | Arista Networks, Inc. (a) | | | 62,771 | |

| | 297 | | | Palo Alto Networks, Inc. (a) | | | 43,076 | |

| | | | | | | | |

| | | | | | | 105,847 | |

| | | | | | | | |

| | | | Electronic Equipment, Instruments & Components — 1.8% | |

| | 803 | | | Amphenol Corp., Class A | | | 70,486 | |

| | 2,254 | | | Corning, Inc. | | | 72,093 | |

| | | | | | | | |

| | | | | | | 142,579 | |

| | | | | | | | |

| | | | Internet Software & Services — 10.8% | |

| | 483 | | | Alphabet, Inc., Class C (a) | | | 505,730 | |

| | 1,585 | | | Facebook, Inc., Class A (a) | | | 279,672 | |

| | 1,583 | | | GoDaddy, Inc., Class A (a) | | | 79,613 | |

| | | | | | | | |

| | | | | | | 865,015 | |

| | | | | | | | |

| | | | IT Services — 8.0% | |

| | 1,091 | | | Global Payments, Inc. | | | 109,382 | |

| | 1,020 | | | Mastercard, Inc., Class A | | | 154,372 | |

| | 1,298 | | | PayPal Holdings, Inc. (a) | | | 95,581 | |

| | 878 | | | Square, Inc., Class A (a) | | | 30,447 | |

| | 1,223 | | | Vantiv, Inc., Class A (a) | | | 89,974 | |

| | 1,400 | | | Visa, Inc., Class A | | | 159,582 | |

| | | | | | | | |

| | | | | | | 639,338 | |

| | | | | | | | |

| | | | Semiconductors & Semiconductor Equipment — 5.7% | |

| | 1,444 | | | Applied Materials, Inc. | | | 73,802 | |

| | 508 | | | Broadcom Ltd. | | | 130,377 | |

| | 996 | | | Cavium, Inc. (a) | | | 83,520 | |

| | 310 | | | Lam Research Corp. | | | 57,080 | |

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Semiconductors & Semiconductor Equipment — continued | |

| | 599 | | | NVIDIA Corp. | | | 115,906 | |

| | | | | | | | |

| | | | | | | 460,685 | |

| | | | | | | | |

| | | | Software — 9.5% | |

| | 528 | | | Adobe Systems, Inc. (a) | | | 92,579 | |

| | 1,096 | | | Electronic Arts, Inc. (a) | | | 115,135 | |

| | 589 | | | Guidewire Software, Inc. (a) | | | 43,717 | |

| | 1,680 | | | Microsoft Corp. | | | 143,733 | |

| | 428 | | | Red Hat, Inc. (a) | | | 51,343 | |

| | 978 | | | salesforce.com, Inc. (a) | | | 99,971 | |

| | 589 | | | ServiceNow, Inc. (a) | | | 76,787 | |

| | 1,055 | | | Splunk, Inc. (a) | | | 87,388 | |

| | 514 | | | Take-Two Interactive Software, Inc. (a) | | | 56,399 | |

| | | | | | | | |

| | | | | | | 767,052 | |

| | | | | | | | |

| | | | Technology Hardware, Storage & Peripherals — 5.4% | |

| | 2,560 | | | Apple, Inc. | | | 433,203 | |

| | | | | | | | |

| | | | Total Information Technology | | | 3,413,719 | |

| | | | | | | | |

| | | | Materials — 1.4% | |

| | | | Construction Materials — 1.4% | |

| | 982 | | | Eagle Materials, Inc. | | | 111,204 | |

| | | | | | | | |

| | | | Real Estate — 0.9% | |

| | | | Real Estate Management & Development — 0.9% | |

| | 1,709 | | | CBRE Group, Inc., Class A (a) | | | 74,017 | |

| | | | | | | | |

| | | | Total Common Stocks

(Cost $4,517,978) | | | 7,671,062 | |

| | | | | | | | |

| | Short-Term Investment — 4.6% | |

| | | | Investment Company — 4.6% | |

| | 365,445 | | | JPMorgan U.S. Government Money Market Fund, Institutional Class Shares,

1.14% (b) (l)

(Cost $365,445) | | | 365,445 | |

| | | | | | | | |

| | | | Total Investments — 100.1%

(Cost $4,883,423) | | | 8,036,507 | |

| | | | Liabilities in Excess of

Other Assets — (0.1)% | | | (7,769 | ) |

| | | | | | | | |

| | | | NET ASSETS — 100.0% | | $ | 8,028,738 | |

| | | | | | | | |

Percentages indicated are based on net assets.

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| DECEMBER 31, 2017 | | J.P. MORGAN MID CAP/MULTI-CAP FUNDS | | | | | 17 | |

JPMorgan Mid Cap Equity Fund

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF DECEMBER 31, 2017 (Unaudited)

(Amounts in thousands)

| | | | | | | | |

| SHARES | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | Common Stocks — 96.4% | |

| | | | Consumer Discretionary — 16.8% | |

| | | | Auto Components — 0.4% | |

| | 253 | | | BorgWarner, Inc. | | | 12,925 | |

| | | | | | | | |

| | | | Automobiles — 0.7% | |

| | 19 | | | Tesla, Inc. (a) | | | 5,916 | |

| | 101 | | | Thor Industries, Inc. | | | 15,207 | |

| | | | | | | | |

| | | | | | | 21,123 | |

| | | | | | | | |

| | | | Distributors — 1.2% | |

| | 129 | | | Genuine Parts Co. | | | 12,230 | |

| | 545 | | | LKQ Corp. (a) | | | 22,145 | |

| | | | | | | | |

| | | | | | | 34,375 | |

| | | | | | | | |

| | | | Diversified Consumer Services — 0.4% | |