OMB APPROVAL

OMB Number: 3235-0570

Expires: August 31, 2011

Estimated average burden hours per response: 18.9

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8319

ING Partners, Inc.

(Exact name of registrant as specified in charter)

7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

(Address of principal executive offices) | | (Zip code) |

The Corporation Trust Company, 1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: | December 31 |

| |

Date of reporting period: | January 1, 2010 to December 31, 2010 |

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Annual Report

December 31, 2010

Classes ADV, I, S and S2

ING Partners, Inc.

n ING American Century Small-Mid Cap Value Portfolio

n ING Baron Small Cap Growth Portfolio

n ING Columbia Small Cap Value Portfolio

n ING Davis New York Venture Portfolio

n ING JPMorgan Mid Cap Value Portfolio

n ING Legg Mason ClearBridge Aggressive Growth Portfolio

n ING Oppenheimer Global Portfolio

n ING Oppenheimer Global Strategic Income Portfolio

n ING PIMCO Total Return Portfolio

n ING Pioneer High Yield Portfolio

n ING T. Rowe Price Diversified Mid Cap Growth Portfolio

n ING T. Rowe Price Growth Equity Portfolio

n ING Templeton Foreign Equity Portfolio

n ING Thornburg Value Portfolio

n ING UBS U.S. Large Cap Equity Portfolio

n ING Van Kampen Comstock Portfolio

n ING Van Kampen Equity and Income Portfolio

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds' investment objectives, risks, charges, expenses and other information. This information should be read carefully.

MUTUAL FUNDS

TABLE OF CONTENTS

| President's Letter | | | 1 | | |

|

| Market Perspective | | | 3 | | |

|

| Portfolio Managers' Report | | | 6 | | |

|

| Shareholder Expense Examples | | | 40 | | |

|

| Report of Independent Registered Public Accounting Firm | | | 44 | | |

|

| Statements of Assets and Liabilities | | | 45 | | |

|

| Statements of Operations | | | 55 | | |

|

| Statements of Changes in Net Assets | | | 60 | | |

|

| Financial Highlights | | | 69 | | |

|

| Notes to Financial Statements | | | 76 | | |

|

| Summary Portfolios of Investments | | | 102 | | |

|

| Tax Information | | | 208 | | |

|

| Director and Officer Information | | | 210 | | |

|

| Advisory Contract Approval Discussion | | | 214 | | |

|

PROXY VOTING INFORMATION

A description of the policies and procedures that the Portfolios use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the ING Funds' website at www.ingfunds.com; and (3) on the U.S. Securities and Exchange Commission's ("SEC") website at www.sec.gov. Information regarding how the Portfolios voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the ING Funds' website at www.ingfunds.com and on the SEC's website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Portfolios file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. This report contains a summary portfolio of investments for the Portfolios. The Portfolios' Forms N-Q are available on the SEC's website at www.sec.gov. The Portfolios' Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. The Portfolios' Forms N-Q, as well as a complete portfolio of investments, are available without charge upon request from the Portfolios by calling Shareholder Services toll-free at (800) 992-0180.

PRESIDENT'S LETTER

Big Picture vs. Details

Dear Shareholder,

On January 25, 2011, President Obama delivered his second State of the Union address. He called on Americans to put aside partisan differences and harness the nation's creativity to adapt and thrive in a rapidly changing global economy. The president's challenge is timely: the United States is approaching a nexus of intermediate- and long-term concerns, and the choices we make over the next two years could determine the nation's competitiveness in the global economy for decades to come.

There are reasons to be optimistic — the International Monetary Fund ("IMF") predicts the U.S. economy will grow about 3% in 2011. China and India are expected to grow at about 9% and even the euro zone appears to be recovering from crisis; this growth, however, is being accompanied by mounting inflation pressures in certain regions, suggesting that many economies are expanding at unsustainable rates.

As I write this, the World Economic Forum is getting underway in Davos, Switzerland, and there are numerous concerns to deal with. Chief among them are the still-present risk of sovereign debt defaults in the euro zone; high unemployment and banking problems in the advanced economies; and inflationary pressures in emerging markets, especially with regard to food, fuel and commodities.

As we've noted before, uncertainty is a defining characteristic of our age and, in our opinion, is likely to remain so beyond this year. How should you respond within your investment portfolio? Remember that the most important consideration is your long-term goals, not the outlook for 2011. With investment hazards and opportunities everywhere, we believe it makes sense to cast as broad a net as possible around the globe. In our opinion, you want your portfolio to be well diversified so that it is not harmed too much by the trouble spots, and has some exposure to positive trends.

As always, we believe the best approach is a well-diversified portfolio and a well-defined investment plan. As we've noted many times before, it's important to discuss any proposed changes thoroughly with your advisor before taking any action. Thank you for your continued confidence in ING Funds. We look forward to serving your investment needs in the future.

Sincerely,

Shaun Mathews

President and Chief Executive Officer

ING Funds

January 26, 2011

The views expressed in the President's Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaim any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice. Consider the fund's investment objectives, risks, and charges and expenses carefully before investing. The prospectus contains this information and other information about the fund.

International investing poses special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic.

1

(THIS PAGE INTENTIONALLY LEFT BLANK)

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2010

In our semi-annual report we described how, after a 13-month advance through mid-April, a confluence of local and world issues sent global equities, in the form of the MSCI World IndexSM measured in local currencies, including net reinvested dividends ("MSCI" for regions discussed below), reeling to a loss for the first half of the fiscal year. In the second half of the year, the MSCI World IndexSM bounced back and for 2010 returned 10.01%. (The MSCI World IndexSM returned 11.76% for the one year ended December 31, 2010, measured in U.S. dollars.) By year end, investor sentiment had turned distinctly positive, despite the grave concerns that remained.

It was a bumpy ride. Markets from stocks to bonds to currencies were continually buffeted by news and events relating to three main themes: the stuttering U.S. economic recovery, the sovereign debt crisis in the Eurozone and growth dynamics in China.

In the U.S., quarterly gross domestic product ("GDP") growth decelerated from 2.7% (annualized) in the first quarter of 2010 to 1.7% in the second, before recovering to 2.6% in the third. But attention was focused more on employment and housing. The 18-month recession which ended in June of 2009 had cost some 8.7 million jobs. But since then, the unemployment rate had been stuck between 9.4% and 10.1%, barely dented by private sector new jobs averaging 107,000 per month as 2010 ended.

The other weakening link was housing. Sales of new and existing homes collapsed after the expiry in April of a program of tax credits for home buyers and languished thereafter. House prices (based on the S&P/Case-Shiller 20-City Composite Home Price Index), having shown annual increases from February, resumed a downward trend in October with the index still 30% below the peak recorded in April 2006.

To be sure, there were some grounds for optimism as 2010 drew to a close. Consumer spending had risen for five straight months. Investment in equipment and software was growing at double-digit annual percentage rates. On December 30, new unemployment claims were reported below 400,000 for the first time since July 2008. The Federal Reserve in November announced a second round of quantitative easing and would buy $600 billion in Treasury notes and bonds. The mixed mid-term election results forced a "compromise" stimulus package worth an estimated $858 billion for 2011. In combination, these two measures increased the attractiveness of riskier asset classes like equities at the expense of high grade bonds, which sold off.

In the Eurozone, after default was narrowly averted on Greece's maturing bonds, the creation in May of a European Financial Stabilization "mechanism", funded with up to €750 billion seemed to calm nerves for a while. But in October, attention turned to Ireland, where the Irish government had injected huge sums into local banks, rendering its own fiscal position untenable. The November 29, 2010 European Union/International Monetary Fund bail-out worth €67.5 billion left markets unimpressed. Suddenly it was May again with downgrades, soaring yields on peripheral Eurozone bonds, fears of contagion, falling stock markets and doubts about the viability of the euro itself. The European Central Bank aggressively bought sovereign bonds and the mood settled. But with Spain's banks needing to refinance €85 billion of debt in 2011, the issue remains unresolved.

Investors watched nervously as China, the source of much of the world's growth, wrestled with inflation, which reached 5.1% in November, and a housing bubble. The authorities tightened mortgage requirements, raised banks' reserve ratio requirements six times in 2010 and interest rates twice in the last quarter. More interest rate increases seem inevitable.

In U.S. fixed income markets, the Barclays Capital U.S. Aggregate Bond Index of investment grade bonds returned 6.54% in 2010. A slight balance towards risk aversion in the first half gave way to improved risk appetite in the second. For the whole year, the Barclays Capital U.S. Treasury index returned 5.87%, underperforming the Barclays Capital Corporate Investment Grade Bond Index with a return of 9.00%, but both fell well short of the Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index which gained 14.94% for the one year period.

U.S. equities, represented by the S&P 500® Index including dividends, rose 15.06% in 2010, including its best September, a return of 8.92%, since 1939 and best December, a return of 6.68%, since 1991. Prices were supported by strong earnings reports, with operating earnings per share for S&P 500® companies recording four straight quarters of annual growth. Equities also benefited from improved risk appetite through the quantitative easing initiative and stimulus package referred to above.

In currencies, the worst of the gloom about the Eurozone in early June was replaced by renewed pessimism about the dollar in a stalling economy, before markets were seized by another bout of Eurozone angst. For the year, the dollar gained 8.15% against the euro and 2.95% against the pound, but lost 11.59% to the yen, which was sold in the market by the Bank of Japan after breaching 15-year high levels.

In international markets, the MSCI Japan® Index returned just 0.57% for the year after a strong last quarter, as quarterly GDP growth bounced back to 1.1% and the yen retreated from multi-year peaks. The tone of the market was generally poor with household spending fragile and consumer prices down for 21 months. The MSCI Europe ex UK® Index returned 4.84%, with Germany up 15.97% and Portugal, Italy, Ireland, Greece and Spain all falling. This broadly reflected the two-tier economy that has developed, with economic statistics favoring more soundly based countries at the expense of the peripherals. The MSCI UK® Index advanced 12.18%, despite the prospect of severe public spending cuts intended to eliminate an 11% budget deficit. Supporting sentiment was resilient, if perhaps temporary, quarterly GDP growth averaging 0.9% in the second half of the year.

Parentheses denote a negative number.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Portfolios' performance is subject to change since the period's end and may be lower or higher than the performance data shown. Please call (800) 262-3862 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING's Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

BENCHMARK DESCRIPTIONS

| Index | | Description | |

| MSCI World IndexSM | | An unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. | |

|

| S&P/Case-Shiller 20-City Composite Home Price Index | | A composite index of the home price index for the top 20 Metropolitan Statistical Areas in the United States. The index is published monthly by Standard & Poor's. | |

|

| Barclays Capital U.S. Aggregate Bond Index | | An unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. | |

|

| Barclays Capital U.S. Treasury Index | | An unmanaged index that includes public obligations of the U.S. Treasury. Treasury bills, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS and STRIPS, are excluded. | |

|

| Barclays Capital Corporate Investment Grade Bond Index | | The corporate component of the Barclays Capital U.S. Credit Index. The U.S. Credit Index includes publicly-issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. The index includes both corporate and non-corporate sectors. The corporate sectors are industrial, utility and finance, which includes both U.S. and non-U.S. corporations. | |

|

| Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index | | An unmanaged index that includes all fixed income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million, and at least one year to maturity. | |

|

| S&P 500® Index | | An unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets. | |

|

| MSCI Japan® Index | | A free float-adjusted market capitalization index that is designed to measure developed market market equity performance in Japan. | |

|

| MSCI Europe ex UK® Index | | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK. | |

|

| MSCI UK® Index | | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK. | |

|

| Russell 2500TM Value Index | | Measures the performance of those Russell 2500 companies with lower price-to-book ratios and lower forecasted growth values. | |

|

| S&P Small Cap 600/Citigroup Value Index | | Measures the performance of those S&P 600 Index companies with lower price-to-book ratios. | |

|

| Russell 2000® Growth Index | | An unmanaged index that measures the performance of securities of smaller U.S. companies with greater than average growth orientation. | |

|

| Russell 2000® Index | | An unmanaged index that measures the performance of securities of small U.S. companies. | |

|

| Russell 2000® Value Index | | An unmanaged index that measures the performance of those Russell 2000® companies with lower price-to-book ratios and lower than forecasted growth values. | |

|

| Russell Midcap® Value Index | | Measures the performance of those Russell Midcap companies with lower price-to-book ratios and lower forecasted growth values. | |

|

| Russell 3000® Growth Index | | An unmanaged index that measures performance of broad growth segment of the U.S. Equity universe. It includes those Russell 3000® companies with higher price-to-book ratios and higher forecasted growth values. | |

|

| MSCI All Country World IndexSM | | A broad-based unmanaged index comprised of equity securities in countries around the world, including the United States, other developed countries and emerging markets. | |

|

| S&P/Citigroup World Government Bond Index | | S&P/Citigroup World Government Bond Index is an unmanaged index of bonds from 14 world government bond markets with maturities of at least one year. | |

|

| Bank of America/Merrill Lynch High Yield Master II Index | | A broad-based index consisting of all U.S. dollar-denominated high-yield bonds with a minimum outstanding amount of $100 million and with a maturity of greater than one year period. The quality rating is less than BBB by Standard & Poor's. | |

|

| Bank of America/Merrill Lynch All U.S. Convertibles (Speculative Grade) Index | | An unmanaged index that includes about 270 convertible securities and represents the non-investment-grade convertible market. | |

|

| S&P MidCap 400 Index | | A broad-based unmanaged capitalization weighted index of mid-capitalization companies. | |

|

4

BENCHMARK DESCRIPTIONS (CONTINUED)

| Index | | Description | |

| Russell Midcap® Growth Index | | An unmanaged index that measures the performance of those companies included in the Russell Midcap® Index with relatively higher price-to-book ratios and higher forecasted growth values. | |

|

| MSCI All Country World ex U.S. IndexSM | | A free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets, excluding the U.S. It includes the reinvestment of dividends and distributions net of withholding taxes, but does not reflect fees, brokerage commissions or other expenses of investing. | |

|

| Russell 1000® Index | | An unmanaged, comprehensive large-cap index measuring the performance of the largest 1,000 U.S. incorporated companies. | |

|

| Russell 1000 Value® Index | | An unmanaged index that measures the performance of those Russell 1000® securities with lower price-to-book ratios and lower forecasted growth values. | |

|

| Barclays Capital U.S. Government/Credit Bond Index | | An index made up of the Barclays Capital Government and Credit indices, including securities issued by the U.S. government and its agencies and publicly issued U.S. corporate and foreign debentures and secured notes that meet specified maturity, liquidity and quality requirements. | |

|

5

ING AMERICAN CENTURY SMALL-MID CAP VALUE PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING American Century Small-Mid Cap Value Portfolio (the "Portfolio") seeks long-term capital growth. Income is a secondary objective. The Portfolio is managed by a team of portfolio managers comprised of Benjamin Z. Giele and James Pitman (responsible for the management of the Small Cap Value portion of the Portfolio) and Kevin Toney, Phillip N. Davidson, and Michael Liss (responsible for the Mid Cap Value portion of the Portfolio), Portfolio Managers of American Century Investment Management, Inc. — the Sub-Adviser.

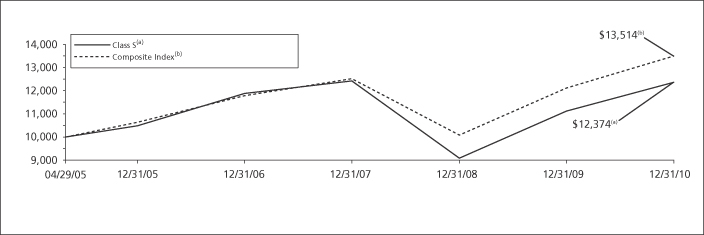

Performance: For the year ended December 31, 2010, the Portfolio's Class S shares provided a total return of 22.02% compared to the Russell 2500TM Value Index and the S&P Small Cap 600/Citigroup Value Index, which returned 24.82% and 24.72%, respectively, for the same period.

Portfolio Specifics: The stock market posted double-digit gains for the one-year reporting period, its second-straight annual increase. Although the economy expanded in response to government stimulus spending, growth slowed during the spring, raising concern about the sustainability of the recovery. Although unemployment remained high, consumers modestly increased their spending. As fears of a double-dip recession eased, investors generally favored higher-risk stocks. They sought out higher-yielding securities because of very low interest rates. Growth stocks beat value stocks across the capitalization spectrum.

Small Cap Value* — In this environment, the portfolio provided a positive total return and outperformed on a relative basis. Contributing the most to relative results were positions in the information technology and energy sectors. In information technology, the software industry was a significant source of strength. Key holdings were Quest Software, Inc., a developer of enterprise management solutions; Sybase, Inc., a maker of mobile and database software; and Motricity, Inc., a provider of wireless data services. In energy, the portfolio benefited from security selection among oil and gas companies. A notable contributor was exploration company Mariner Energy, Inc. The industrials and consumer discretionary sectors detracted. In industrials, investments in the construction and engineering industry dampened relative results. A notable detractor was Granite Construction, Inc., a well-capitalized builder of highways, dams, airport infrastructure, and mass transit facilities. In consumer discretionary, the portfolio's mix of diversified consumer services companies hampered relative performance. Key detractors were Corinthian Colleges, Inc. and Lincoln Educational Services Corp., both of which are post-secondary career-oriented education companies.

Mid Cap Value* — Although the portfolio provided a positive total return in this environment, it underperformed in relative terms. Detracting the most from relative results were positions in the financials, energy, and consumer discretionary sectors. In financials, the portfolio was hampered by an underweight in commercial banks. Its mix of capital markets names also dampened relative performance. Two notable detractors were Northern Trust Corp. and State Street Corp. In energy, investments among oil and gas companies slowed progress versus the benchmark. Key detractors were Imperial Oil Ltd., a Canadian energy company and EQT Corp., a low-cost producer of unconventional tight-shale natural gas. In consumer discretionary, security selection among hotel, leisure, restaurant, and specialty retailing stocks dampened relative results. Home improvement retailer Lowe's Cos., Inc. was a notable detractor. Specialty retailing also provided the portfolio's top contributor PetSmart, Inc. Also adding to relative performance were the utilities and information technology sectors. In utilities, security selection among high-quality regulated utilities boosted results. In information technology, an underweight position was advantageous. A key contributor was Teradyne, Inc., a semiconductor test equipment maker.

Current Strategy and Outlook: The portfolio management team takes a fundamental, bottom-up approach, evaluating each company individually on its own merits and building the portfolio from the ground up, one stock at a time.

Small Cap Value* — As of December 31, 2010, the portfolio was broadly diversified, with overweight positions relative to the benchmark in consumer discretionary, industrials, and information technology and underweights in financials and utilities.

Mid Cap Value* — As of December 31, 2010, the portfolio was broadly diversified, with overweight positions relative to the benchmark in industrials, consumer staples, and healthcare, and underweights in financials and utilities.

Industry Allocation

as of December 31, 2010

(as a percent of net assets)

| Financials | | | 27.2 | % | |

| Industrials | | | 15.0 | % | |

| Consumer Discretionary | | | 11.1 | % | |

| Energy | | | 8.3 | % | |

| Health Care | | | 7.5 | % | |

| Information Technology | | | 7.4 | % | |

| Consumer Staples | | | 6.9 | % | |

| Utilities | | | 6.8 | % | |

| Materials | | | 4.4 | % | |

| Exchange-Traded Funds | | | 2.7 | % | |

| Telecommunication Services | | | 1.4 | % | |

| Other Assets and Liabilities — Net* | | | 1.3 | % | |

| Net Assets | | | 100.0 | % | |

* Includes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I and securities lending collateral.

Portfolio holdings are subject to change daily.

Top Ten Holdings*

as of December 31, 2010

(as a percent of net assets)

| Republic Services, Inc. | | | 1.8 | % | |

| Imperial Oil Ltd. | | | 1.6 | % | |

| iShares Russell Midcap Value Index Fund | | | 1.6 | % | |

| Northern Trust Corp. | | | 1.4 | % | |

| HCC Insurance Holdings, Inc. | | | 1.3 | % | |

| Lowe's Cos., Inc. | | | 1.3 | % | |

| Kimberly-Clark Corp. | | | 1.2 | % | |

| ConAgra Foods, Inc. | | | 1.1 | % | |

| Beckman Coulter, Inc. | | | 1.1 | % | |

| Zimmer Holdings, Inc. | | | 1.0 | % | |

* Excludes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I and securities lending collateral.

Portfolio holdings are subject to change daily.

* For purposes of these discussions, "the portfolio" refers to each respectively managed portion of ING American Century Small-Mid Cap Value Portfolio.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

6

PORTFOLIO MANAGERS' REPORT

ING AMERICAN CENTURY SMALL-MID CAP VALUE PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2010 | |

| | | 1 Year | | 5 Year | | Since Inception

of Classes ADV, I and S

May 1, 2002 | | Since Inception

of Class S2

February 27, 2009 | |

| Class ADV | | | 21.80 | % | | | 6.12 | % | | | 7.86 | % | | | — | | |

| Class I | | | 22.36 | % | | | 6.65 | % | | | 8.40 | % | | | — | | |

| Class S | | | 22.02 | % | | | 6.38 | % | | | 8.13 | % | | | — | | |

| Class S2 | | | 21.87 | % | | | — | | | | — | | | | 47.39 | % | |

| Russell 2500TM Value Index | | | 24.82 | % | | | 3.85 | % | | | 7.51 | % | | | 48.74 | %(1) | |

| S&P SmallCap 600/Citigroup Value Index | | | 24.72 | % | | | 4.06 | % | | | 6.45 | % | | | 47.66 | %(1) | |

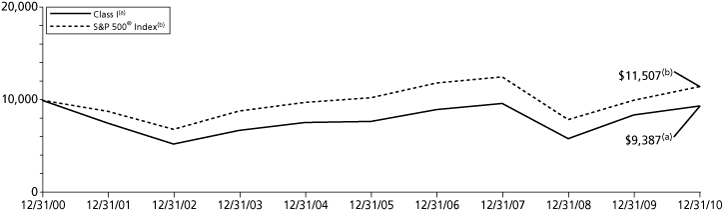

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING American Century Small-Mid Cap Value Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 262-3862 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on marked and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance of the indices is shown from March 1, 2009.

7

ING BARON SMALL CAP GROWTH PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Baron Small Cap Growth Portfolio (the "Portfolio") seeks capital appreciation. The Portfolio is managed by Ronald Baron, Founder, Chief Executive Officer, Chief Investment Officer, Chairman, and Portfolio Manager of BAMCO, Inc. ("BAMCO") — the Sub-Adviser.

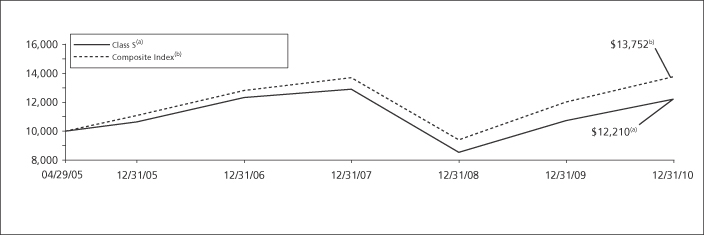

Performance: For the year ended December 31, 2010, the Portfolio's Class S shares provided a total return of 26.50% compared to the Russell 2000® Growth Index and the Russell 2000® Index, which returned 29.09% and 26.85%, respectively, for the same period.

Portfolio Specifics: The Portfolio provided positive returns in 2010 in a year of market volatility. The U.S. economy delivered positive quarterly GDP growth since the third quarter of 2009, avoiding double-dip recession. The equity markets were volatile, spurred in part by the sovereign debt crisis in Europe and investor sentiment favoring fixed income securities and cash. For most of the year there were outflows from the U.S. equity markets and many businesses continued to keep significant cash on the sidelines. With this as a backdrop, the U.S. Federal Reserve provided additional stimulus in the form of quantitative easing which buoyed the stock market in September and through the fourth quarter, achieving its 52-week high in December.

The sector weightings of this Portfolio typically differ significantly from those of the Russell 2000® Growth Index. There are important trends occurring in several industries that we believe offer growth opportunities over the next few years independent of normal business cycles. In our search for new companies, we seek businesses with visionary leaders that are separating themselves from competitors through efficient operations, strong balance sheets, unique assets or properties and, in many cases, innovative and game changing technology.

The sectors that contributed the most to absolute performance were consumer discretionary, energy, and healthcare. Given the strength of the market during the fourth quarter, there were no detractors at the sector level for the year. Specific stocks that contributed the most to absolute performance were Under Armour, Inc. ("Under Armour"), Edwards Lifesciences Corp. ("Edwards") and Molycorp, Inc. ("Molycorp"). In addition to improved consumer sentiment and spending, Under Armour performed well due to its successful sneaker launch, improved merchandizing, and online sales growth. In addition to solid operating results, Edwards, a leading manufacturer of tissue heart valves, reported that its recent trial exceeded expectations and its upcoming trial will include two of its products. In our view, Edwards has a significant advantage over its competitors. Molycorp, producer of rare earths, is a company with a unique asset and barriers to entry, and we believe it is poised to grow due to favorable supply-demand trends in the rare earths market.

The individual stocks that detracted from absolute performance in a meaningful way were few; the three that hurt performance the most were Equinix, Inc. ("Equinix"), DeVry, Inc. ("DeVry") and Strayer Education, Inc. ("Strayer"). Equinix declined for the year due primarily to its earnings preannouncement in early October in which management lowered revenue guidance. U.S. education stocks, including DeVry and Strayer, languished all year. Most recently, post-secondary stocks came under pressure due to uncertainty around proposed tough new regulations. We continue to own these stocks because we are bullish on the long-term fundamentals of the industries and markets in which they operate and believe the companies are addressing their short-term issues and have solid multi-year growth prospects.

Relative to the Russell 2000® Growth Index, the Portfolio's investments in healthcare, energy and materials had a positive impact on relative performance. In addition to Edwards and Molycorp discussed above, Concho Resources, Inc., whose shares rose this year, contributed the most to relative performance within the energy sector. In addition to higher oil prices, the company benefitted from improving operational performance and a well timed and large acquisition.

The Portfolio's sectors that lagged relative to those of the Russell 2000® Growth Index were information technology, consumer discretionary and industrials. In addition to Equinix, DeVry and Strayer discussed above, Tetra Tech, Inc. ("Teta Tech"), a leading environmental engineering and consulting firm, was a detractor from relative performance in 2010. The company's shares came under pressure on fears of slowing infrastructure spending. After a rare earnings miss during the company's first quarter, Tetra Tech recovered strongly during the balance of the year.

Current Strategy and Outlook: The Portfolio invests in small-sized U.S. growth companies that we believe have the potential for producing outsized returns within four or five years. The Portfolio may retain companies whose market capitalizations rise beyond their original purchase price range. We think the stock market continues to undervalue many publicly traded companies relative to their prospects and relative to competitive fixed income instruments. Based upon our daily conversations with business executives, we believe the economy is now providing support for those businesses rather than serving as a headwind. We believe confidence is building and should translate into differentiated valuations and higher earnings multiples. Ultimately we believe investors make the most money when earnings multiples increase, not just when earnings increase. In our opinion, with current historically low interest rates, attractive stock price valuations and economic growth increasing, this could occur.

We believe that stock markets, commodity prices and interest rates, among other things, are unpredictable. We also believe that businesses' values over the long term are determined by their growth opportunities, financial strength and earnings, sustainable competitive advantages, and management talent. These analyses, valuations and comparisons are how we decide whether our fast growing, publicly owned businesses are attractively priced, not by guessing whether stock markets will rise or fall in the near term. We believe the growth prospects for the businesses in which we have invested are favorable. Our research remains focused on the long-term potential of the businesses in which we invest, and the Portfolio will remain focused on a select number of growth companies.

Industry Allocation

as of December 31, 2010

(as a percent of net assets)

| Consumer Discretionary | | | 26.9 | % | |

| Health Care | | | 13.3 | % | |

| Information Technology | | | 11.4 | % | |

| Financials | | | 11.3 | % | |

| Energy | | | 11.2 | % | |

| Industrials | | | 11.1 | % | |

| Consumer Staples | | | 6.0 | % | |

| Materials | | | 2.7 | % | |

| Utilities | | | 1.2 | % | |

| Telecommunication Services | | | 0.8 | % | |

| Other Assets and Liabilities — Net* | | | 4.1 | % | |

| Net Assets | | | 100.0 | % | |

* Includes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I.

Portfolio holdings are subject to change daily.

Top Ten Holdings*

as of December 31, 2010

(as a percent of net assets)

| Vail Resorts, Inc. | | | 2.9 | % | |

| MSCI, Inc. — Class A | | | 2.9 | % | |

| Dick's Sporting Goods, Inc. | | | 2.6 | % | |

| Choice Hotels International, Inc. | | | 2.5 | % | |

| Mettler Toledo International, Inc. | | | 2.4 | % | |

| Molycorp, Inc. | | | 2.3 | % | |

| Genesee & Wyoming, Inc. | | | 2.2 | % | |

| Core Laboratories NV | | | 2.1 | % | |

| AMERIGROUP Corp. | | | 2.1 | % | |

| Edwards Lifesciences Corp. | | | 1.9 | % | |

* Excludes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I.

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

8

PORTFOLIO MANAGERS' REPORT

ING BARON SMALL CAP GROWTH PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2010 | |

| | | 1 Year | | 5 Year | | Since Inception

of Classes ADV, I and S

May 1, 2002 | | Since Inception

of Class S2

February 27, 2009 | |

| Class ADV | | | 26.24 | % | | | 3.95 | % | | | 7.87 | % | | | — | | |

| Class I | | | 26.85 | % | | | 4.45 | % | | | 8.42 | % | | | — | | |

| Class S | | | 26.50 | % | | | 4.20 | % | | | 8.15 | % | | | — | | |

| Class S2 | | | 26.28 | % | | | — | | | | — | | | | 45.42 | % | |

| Russell 2000® Growth Index | | | 29.09 | % | | | 5.30 | % | | | 6.05 | % | | | 49.72 | %(1) | |

| Russell 2000® Index | | | 26.85 | % | | | 4.47 | % | | | 6.44 | % | | | 48.56 | %(1) | |

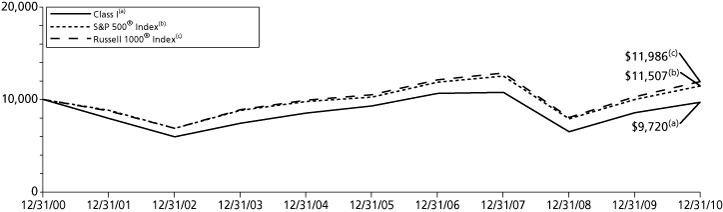

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Baron Small Cap Growth Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 262-3862 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on marked and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance of the index is shown from March 1, 2009.

9

ING COLUMBIA SMALL CAP VALUE PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Columbia Small Cap Value Portfolio (the "Portfolio") seeks long-term growth of capital. The Portfolio is managed by Christian Stadlinger and Jarl Ginsberg, Portfolio Managers, of Columbia Management Investment Advisers, LLC — the Sub-Adviser.*

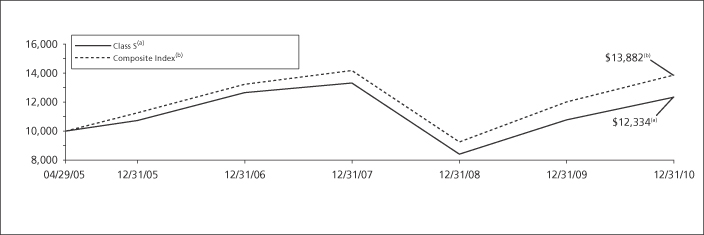

Performance: For the year ended December 31, 2010, the Portfolio's Class I shares provided a total return of 25.48% compared to the Russell 2000® Value Index, which returned 24.50% for the same period.

Portfolio Specifics: The "risk on vs. risk off" trade characterized much of 2010, as investors either believed that global growth prospects were good and European risks were contained, or they believed that growth prospects were deteriorating and risk was high. In November, the Federal Reserve launched round two of quantitative easing through purchases of government bonds. Equity markets responded positively to this announced monetary stimulus. The economy also received a fiscal policy boost for 2011, as tax cuts of previous years were extended for another two years. Meanwhile, companies continued to report strong earnings and economic data towards the end of the year also came in slightly better than expected.

The small cap market provided strong absolute returns in 2010 as measured by the Russell 2000® Value Index. The Portfolio also outperformed its benchmark, the Russell 2000® Value Index. On an absolute basis, most sectors in the Portfolio saw positive double digit performance. The Portfolio benefited from both the choices in sector allocation as well as stock selection. Overall, the largest contributions came from information technology, consumer staples and consumer discretionary sectors. The Portfolio's largest detractors were due to stock selection in the financials and materials sectors.

Stock selection in the information technology sector drove contributions. The most meaningful contributions came from semiconductor companies Cirrus Logic and Atmel Corporation. Cirrus Logic, Inc. which provides audio chips for products such as the iPhone and iPad, saw its shares more than double. Atmel rose on exposure to a stronger emergence of smart phones and touch screen applications. Stock selection in food products contributed to performance in the consumer staples sector with contributions by pasta maker American Italian Pasta Co. Our investments in specialty retail were positives, such as retail footwear companies and Pier 1 Imports, Inc. Auto supply companies and parts suppliers to the trucking industry were strong contributors in the consumer discretionary sector.

While the Portfolio did benefit from an underweight position to the financials sector for the third year in a row, this was offset by stock selection as the Portfolio had focused on conservatively managed banking and real estate investment trust companies while the market focused on credit recovery stories.

Current Strategy and Outlook: Our investment process is to focus our research on those companies which we believe are attractively valued and where we believe the valuation gap is likely to shrink in the near term. We accomplish this by focusing on what we call an "upward inflection point," which essentially means we want stocks that are both inexpensive and are showing improving operating performance metrics. In thinking about the types of situations that are attractive to us, our opportunities typically encompass one or more of the following: 1) "Out-of-the-limelight" companies missed by the Wall Street research community; 2) cyclically-driven opportunities in industries that have been out of favor and show signs of resurgence; and 3) companies with compressed operating margins that we believe are poised to expand within a reasonable timeframe.

That said, moving into 2011 the Portfolio begins the year with a cyclical tilt — overweight the industrials and information technology sectors. The interest rate sensitive sectors of financials and utilities sectors are underweighted.

Industry Allocation

as of December 31, 2010

(as a percent of net assets)

| Financials | | | 28.9 | % | |

| Industrials | | | 19.9 | % | |

| Information Technology | | | 14.6 | % | |

| Consumer Discretionary | | | 10.6 | % | |

| Energy | | | 7.3 | % | |

| Materials | | | 6.4 | % | |

| Health Care | | | 5.4 | % | |

| Utilities | | | 3.6 | % | |

| Consumer Staples | | | 2.9 | % | |

| Telecommunication Services | | | 0.5 | % | |

| Other Assets and Liabilities — Net* | | | (0.1 | )% | |

| Net Assets | | | 100.0 | % | |

* Includes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I.

Portfolio holdings are subject to change daily.

Top Ten Holdings*

as of December 31, 2010

(as a percent of net assets)

| United Rentals, Inc. | | | 1.2 | % | |

| New Jersey Resources Corp. | | | 1.2 | % | |

| Kindred Healthcare, Inc. | | | 1.1 | % | |

| U-Store-It Trust | | | 1.1 | % | |

| Swift Energy Co. | | | 1.1 | % | |

| IBERIABANK Corp. | | | 1.1 | % | |

| Textainer Group Holdings Ltd. | | | 1.1 | % | |

| Boise, Inc. | | | 1.0 | % | |

| LaSalle Hotel Properties | | | 1.0 | % | |

| Wabash National Corp. | | | 1.0 | % | |

* Excludes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I.

Portfolio holdings are subject to change daily.

* Prior to April 30, 2010, the Portfolio was managed by investment sleeves. Effective April 30, 2010, the investment sleeve managed by Stephen Barbaro and Jeremy Javidi was eliminated and the assets of that sleeve were redeployed into the sleeve managed by Mr. Stadlinger and Mr. Ginsberg.

The Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

10

PORTFOLIO MANAGERS' REPORT

ING COLUMBIA SMALL CAP VALUE PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2010 | |

| | | 1 Year | | Since Inception

of Class ADV

December 29, 2006 | | Since Inception

of Class I

April 28, 2006 | | Since Inception

of Class S

May 1, 2006 | | Since Inception

of Class S2

February 27, 2009 | |

| Class ADV | | | 24.98 | % | | | 1.21 | % | | | — | | | | — | | | | — | | |

| Class I | | | 25.48 | % | | | — | | | | 1.85 | % | | | — | | | | — | | |

| Class S | | | 25.28 | % | | | — | | | | — | | | | 1.70 | % | | | — | | |

| Class S2 | | | 25.04 | % | | | — | | | | — | | | | — | | | | 46.93 | % | |

| Russell 2000® Value Index | | | 24.50 | % | | | (0.95 | )%(1) | | | 0.94 | %(2) | | | 0.94 | % | | | 47.29 | %(3) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Columbia Small Cap Value Portfolio against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 262-3862 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on marked and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance of the index is shown from January 1, 2007.

(2) Since inception performance of the index is shown from May 1, 2006.

(3) Since inception performance of the index is shown from March 1, 2009.

11

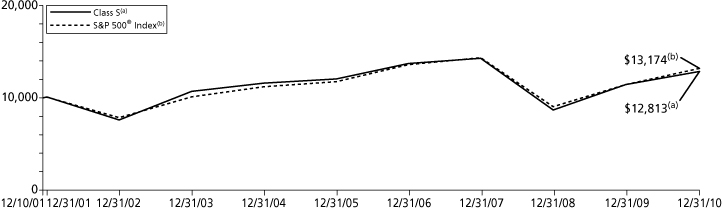

ING DAVIS NEW YORK VENTURE PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Davis New York Venture Portfolio (the "Portfolio") seeks long-term growth of capital. The Portfolio is managed by Christopher C. Davis and Kenneth C. Feinberg, Portfolio Managers, with Davis Selected Advisers, L.P. ("Davis Advisers") — the Sub-Adviser.

Performance: For the year ended December 31, 2010, the Portfolio's Class S shares provided a total return of 11.99% compared to the S&P 500® Index, which returned 15.06% for the same period.

Portfolio Specifics: The Portfolio had more invested in financials than any other sector and they were the most important contributor to the Portfolio's absolute performance. The Portfolio's financial companies outperformed the corresponding sector within the S&P 500® Index ("Index") and had a higher relative average weighting. Berkshire Hathaway, Inc., Wells Fargo & Co., and Progressive Corp. were among the most important contributors to performance while JPMorgan Chase Bank was among the most important detractors from performance.

Consumer staple companies were the second most important contributor to absolute performance. The Portfolio's consumer staple companies outperformed the corresponding sector within the Index and had a higher relative average weighting. Costco Wholesale Corp. and Coca-Cola Co. were among the most important contributors to performance.

While energy companies made positive contributions to absolute performance, they were the most important reason that the Portfolio lagged the Index. The Portfolio's energy companies under-performed the corresponding sector within the Index but had a higher relative average weighting in this stronger performing sector. Occidental Petroleum Corp. and Canadian Natural Resources Ltd. were among the most important contributors to performance while EOG Resources, Inc., Transocean, Inc., and China Coal Energy Co. were among the most important detractors from performance.

Industrial companies also made positive contributions to absolute performance but were the second most important detractor from relative performance versus the Index. The Portfolio's industrial companies underperformed the corresponding sector within the Index and had a lower relative average weighting in this stronger performing sector.

Other companies detracting from performance included Hewlett-Packard Co., Visa, Inc., and H&R Block, Inc. The Fund no longer owns H&R Block, Inc.

The Portfolio held approximately 19% of its assets in foreign companies (including american depositary receipts) at December 31, 2010. As a whole, these companies outperformed the domestic companies held by the Portfolio during 2010.

Current Strategy and Outlook: Our long-term focus usually results in low portfolio turnover. We try not to overreact to past short-term performance from individual holdings on either the upside or the downside. The Portfolio's investment strategy is to perform extensive research to buy durable companies at what we believe is a discount to their intrinsic values and to hold them for the long term. We focus deliberately on the future, considering each company's long-term business fundamentals.

As of December 31, 2010, only two companies had dropped out of the Portfolio's top 10 holdings from the end of 2009. This is consistent with our low-turnover strategy. The Portfolio continues to own both companies that dropped out, Berkshire Hathaway, Inc. and JPMorgan Chase Bank, but in reduced amounts. The two new additions to the Portfolio's top 10 holdings, CVS Caremark Corp. and Loews Corp., were both among the Portfolio's top 20 holdings as of the end of 2009.

Industry Allocation

as of December 31, 2010

(as a percent of net assets)

| Financials | | | 27.2 | % | |

| Consumer Staples | | | 16.7 | % | |

| Energy | | | 15.3 | % | |

| Health Care | | | 13.7 | % | |

| Materials | | | 8.4 | % | |

| Information Technology | | | 5.8 | % | |

| Consumer Discretionary | | | 5.7 | % | |

| Industrials | | | 5.0 | % | |

| Telecommunication Services | | | 0.4 | % | |

| Other Assets and Liabilities — Net* | | | 1.8 | % | |

| Net Assets | | | 100.0 | % | |

* Includes short-term investments related to commercial paper.

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2010

(as a percent of net assets)

| Costco Wholesale Corp. | | | 4.3 | % | |

| Wells Fargo & Co. | | | 4.3 | % | |

| American Express Co. | | | 4.1 | % | |

| Bank of New York Mellon Corp. | | | 3.9 | % | |

| Occidental Petroleum Corp. | | | 3.8 | % | |

| CVS Caremark Corp. | | | 3.5 | % | |

| Devon Energy Corp. | | | 3.2 | % | |

| Canadian Natural Resources Ltd. | | | 3.1 | % | |

| EOG Resources, Inc. | | | 3.0 | % | |

| Loews Corp. | | | 3.0 | % | |

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

12

PORTFOLIO MANAGERS' REPORT

ING DAVIS NEW YORK VENTURE PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2010 | |

| | | 1 Year | | 5 Year | | Since Inception

of Classes ADV, I and S

December 10, 2001 | |

| Class ADV | | | 11.79 | % | | | 0.98 | % | | | 2.53 | % | |

| Class I | | | 12.33 | % | | | 1.50 | % | | | 3.04 | % | |

| Class S | | | 11.99 | % | | | 1.22 | % | | | 2.77 | % | |

| S&P 500® Index | | | 15.06 | % | | | 2.29 | % | | | 3.08 | %(1) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Davis New York Venture Portfolio against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 262-3862 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on marked and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance of the index is shown as of December 1, 2001.

Prior to October 31, 2005, the Portfolio was sub-advised by Salomon Brothers Asset Management Inc. Effective October 31, 2005, the Portfolio's principal investment strategies and name changed.

13

ING JPMORGAN MID CAP VALUE PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING JPMorgan Mid Cap Value Portfolio (the "Portfolio") seeks growth from capital appreciation. The Portfolio is managed by Jonathan K.L. Simon, Lawrence Playford and Gloria Fu, Portfolio Managers of J.P. Morgan Investment Management Inc. — the Sub-Adviser.

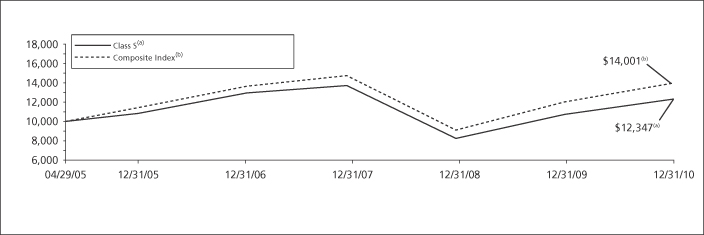

Performance: For the year ended December 31, 2010, the Portfolio's Class S shares provided a total return of 22.97% compared to the Russell Midcap® Value Index, which returned 24.75% for the same period.

Portfolio Specifics: Despite a year marred by various economic and political concerns, not to mention considerable market volatility, U.S. stocks manage to post healthy gains in 2010. While the Portfolio participated in much of the market's advance, the Portfolio underperformed its benchmark due mostly to stock selection in the energy, healthcare and consumer discretionary sectors. Alternatively, stock selection in the information technology, materials and utilities sectors contributed to results.

A top contributor to performance was the diversified insurance company, Old Republic International Corp. The stock was a strong performer on improving trends in its mortgage guaranty segment while its title insurance business has benefited from brisk refinancing activity.

Another contributor was Tyco Electronics Ltd., a global provider of engineered electronic components, network solutions, specialty products and undersea telecommunication systems. The company delivered solid results throughout the year. Tyco aggressively cut costs during the downturn and appears to be benefiting from the broad-based economic recovery.

H&R Block, Inc., a provider of tax, banking, and business and consulting services, was a top detractor from performance. The stock came under pressure as higher levels of unemployment led to a decline in tax returns and investor concerns over the continuing trend of individuals shifting to do-it-yourself tax preparation products. Given these headwinds, as well as significant turnover of senior management, we sold the stock and redeployed proceeds to what we believe are more attractive investment opportunities.

Another detractor from performance was Wilmington Trust Corp., a mid-Atlantic financial services and banking firm. Shares of the stock declined significantly as severe credit losses began to accelerate across a greater portion of its loan portfolio. This resulted in the company announcing that it would merge with Buffalo-based M&T Bank Corp. To eliminate the risk of the merger not materializing, the stock was removed from the Portfolio.

Current Strategy and Outlook: Our strategy employs a bottom-up approach to stock selection, constructing the Portfolio based on company fundamentals, quantitative screening and proprietary fundamental analysis. Our aim is to identify what we believe are undervalued companies that have the potential to increase their intrinsic values per share and to purchase these companies at a discount.

Industry Allocation

as of December 31, 2010

(as a percent of net assets)

| Financials | | | 24.0 | % | |

| Consumer Discretionary | | | 18.4 | % | |

| Utilities | | | 10.4 | % | |

| Industrials | | | 8.8 | % | |

| Energy | | | 8.6 | % | |

| Materials | | | 6.6 | % | |

| Health Care | | | 6.0 | % | |

| Consumer Staples | | | 5.6 | % | |

| Information Technology | | | 5.4 | % | |

| Telecommunication Services | | | 2.3 | % | |

| Other Assets and Liabilities — Net* | | | 3.9 | % | |

| Net Assets | | | 100.0 | % | |

* Includes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I and securities lending collateral.

Portfolio holdings are subject to change daily.

Top Ten Holdings*

as of December 31, 2010

(as a percent of net assets)

| Gap, Inc. | | | 2.0 | % | |

| Loews Corp. | | | 1.9 | % | |

| Republic Services, Inc. | | | 1.8 | % | |

| Tyco Electronics Ltd. | | | 1.7 | % | |

| Energen Corp. | | | 1.6 | % | |

| Becton Dickinson & Co. | | | 1.6 | % | |

| Williams Cos., Inc. | | | 1.6 | % | |

| CMS Energy Corp. | | | 1.6 | % | |

| Devon Energy Corp. | | | 1.6 | % | |

| Ball Corp. | | | 1.5 | % | |

* Excludes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I and securities lending collateral.

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

14

PORTFOLIO MANAGERS' REPORT

ING JPMORGAN MID CAP VALUE PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2010 | |

| | | 1 Year | | 5 Year | | Since Inception

of Classes ADV, I and S

May 1, 2002 | | Since Inception

of Class S2

February 27, 2009 | |

| Class ADV | | | 22.63 | % | | | 4.03 | % | | | 7.67 | % | | | — | | |

| Class I | | | 23.30 | % | | | 4.55 | % | | | 8.22 | % | | | — | | |

| Class S | | | 22.97 | % | | | 4.29 | % | | | 7.95 | % | | | — | | |

| Class S2 | | | 22.75 | % | | | — | | | | — | | | | 41.20 | % | |

| Russell Midcap® Value Index | | | 24.75 | % | | | 4.08 | % | | | 8.13 | % | | | 51.18 | %(1) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING JPMorgan Mid Cap Value Portfolio against the index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 262-3862 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on marked and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance of the index is shown from March 1, 2009.

15

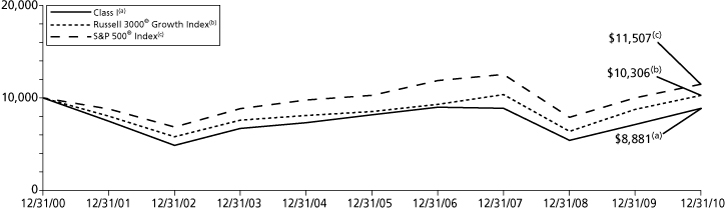

ING LEGG MASON CLEARBRIDGE AGGRESSIVE GROWTH PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Legg Mason ClearBridge Aggressive Growth Portfolio (the "Portfolio") seeks long-term growth of capital. The Portfolio is managed by Richard Freeman, Managing Director, Senior Portfolio Manager and Evan Bauman, Managing Director, Portfolio Manager, of ClearBridge Advisors, LLC — the Sub-Adviser.

Performance: For the year ended December 31, 2010, the Portfolio's Class I shares provided a total return of 24.47% compared to the Russell 3000® Growth Index and the S&P 500® Index, which returned 17.64% and 15.06%, respectively, for the same period.

Portfolio Specifics: The year began well for the stock market, continuing the previous year's rally into January, but it soon stumbled over fears about the potential impact of the European sovereign debt crisis and fell to new lows in February. The market managed to recover over the remainder of the first quarter and rose into the start of the second, but was shaken badly by the dramatic May 6th intraday point drop known as the "Flash Crash" and driven to new lows for the year in July by weaker-than-expected employment data. Those lows were tested over the summer as investors continued to forgo stocks for the relative safety of U.S. Treasuries, which fell to record low yields after weak housing sales data fueled fears that the fragile economy would collapse into a "double-dip" recession.

But following indications from the Fed in late August of a second round of monetary stimulus, known as Quantitative Easing Part II ("QE2"), the market reversed course and began to rally at the start of September. The advance continued into the fourth quarter as stocks reacted positively to the midterm election results and the start of QE2 in November, the extension of the Bush-era tax package in December and improving economic and corporate earnings data.

The Portfolio's overall stock selection helped its performance relative to the benchmark index, while overall sector allocation detracted from relative performance. In particular, stock selection in the healthcare, information technology ("IT"), consumer discretionary, energy and materials sectors helped the Portfolio's relative performance, while stock selection in the industrials sector detracted from performance. The Portfolio's overweight positions in the healthcare and energy sectors and its underweight positions in the industrials and materials sectors detracted from relative performance, while underweight positions in the IT and consumer staples sectors and an overweight in the consumer discretionary sector helped relative performance. The leading individual contributors to Portfolio performance included Genzyme Corp., Biogen Idec, Inc. and UnitedHealth Group, Inc. in the healthcare sector, Cablevision Systems Corp. in the consumer discretionary sector and Weatherford International Ltd. in the energy sector. The leading detractors from relative performance included L-3 Communications Holdings, Inc. in the industrials sector, Seagate Technology, Inc. in the IT sector and Vertex Pharmaceuticals Inc., Amgen, Inc. and Covidien PLC in the healthcare sector.

Current Strategy and Outlook: Stock market valuations and corporate balance sheet strength is driving merger and acquisition activity, which is very positive in terms of big cash deals. We continue to view earnings health for companies as fairly good, while stocks on a price-to-earnings basis are still not expensive in comparison to other asset classes. That said, the market is up a lot off the bottom in March 2009 — that's where the yin-and-yang of our outlook lies — and we simply can't be as bullish as we were two years ago, but again we think the preconditions are just not present for any type of significant bear market to start anytime soon. Our focus is on what we believe are high quality growth equities with strong balance sheets, and in this type of slow growth domestic environment we have clearly seen this past year that those companies can out-execute the average company. Looking ahead, we still want to own companies we believe can grow in a challenging economy, with strong balance sheets and significant free cash flows.

Industry Allocation

as of December 31, 2010

(as a percent of net assets)

| Health Care | | | 35.9 | % | |

| Consumer Discretionary | | | 20.1 | % | |

| Energy | | | 18.8 | % | |

| Information Technology | | | 15.9 | % | |

| Industrials | | | 7.5 | % | |

| Materials | | | 1.8 | % | |

| Financials | | | 0.8 | % | |

| Other Assets and Liabilities — Net* | | | (0.8 | )% | |

| Net Assets | | | 100.0 | % | |

* Includes short-term investments related to Blackrock Liquidity Funds TempFund Portfolio — Class I and securities lending collateral.

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2010

(as a percent of net assets)

| Anadarko Petroleum Corp. | | | 8.4 | % | |

| Weatherford International Ltd. | | | 7.8 | % | |

| Biogen Idec, Inc. | | | 7.5 | % | |

| Genzyme Corp. | | | 6.2 | % | |

| UnitedHealth Group, Inc. | | | 6.1 | % | |

| Cablevision Systems Corp. | | | 5.5 | % | |

| Amgen, Inc. | | | 5.3 | % | |

| Comcast Corp. — Special Class A | | | 4.5 | % | |

| Forest Laboratories, Inc. | | | 4.3 | % | |

| Sandisk Corp. | | | 3.3 | % | |

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

16

PORTFOLIO MANAGERS' REPORT

ING LEGG MASON CLEARBRIDGE AGGRESSIVE GROWTH PORTFOLIO

| Average Annual Total Returns for the Periods Ended December 31, 2010 | |

| | | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Classes ADV and S

December 10, 2001 | | Since Inception

of Class S2

March 8, 2010 | |

| Class ADV | | | 23.84 | % | | | 1.16 | % | | | — | | | | 1.31 | % | | | — | | |

| Class I | | | 24.47 | % | | | 1.67 | % | | | (1.18 | )% | | | — | | | | — | | |

| Class S | | | 24.15 | % | | | 1.42 | % | | | — | | | | 1.56 | % | | | — | | |

| Class S2 | | | — | | | | — | | | | — | | | | — | | | | 16.01 | % | |

| Russell 3000® Growth Index | | | 17.64 | % | | | 3.88 | % | | | 0.30 | % | | | 2.80 | %(1) | | | 18.85 | %(2) | |

| S&P 500® Index | | | 15.06 | % | | | 2.29 | % | | | 1.41 | % | | | 3.08 | %(1) | | | 15.77 | %(2) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Legg Mason ClearBridge Aggressive Growth Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 262-3862 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on marked and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance for the indices is shown from December 1, 2001.

(2) Since inception performance for the indices is shown from March 1, 2010.

Prior to December 16, 2002, the Portfolio was managed by Massachusetts Financial Services Company. Effective December 16, 2002, the Portfolio's name changed.

17

ING OPPENHEIMER GLOBAL PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Oppenheimer Global Portfolio (the "Portfolio") seeks capital appreciation. The Portfolio is managed by Rajeev Bhaman, Senior Vice President of OppenheimerFunds, Inc. — the Sub-Adviser.

Performance: For the year ended December 31, 2010, the Portfolio's Class S shares provided a total return of 15.80% compared to the MSCI World IndexSM and the MSCI All Country World IndexSM, which returned 11.76% and 12.67%, respectively, for the same period.

Portfolio Specifics: Over the reporting period, events on the global economic scale unfolded much as we expected. We have seen a two-speed recovery, with slow, sub-par growth in the developed world and continued rapid growth in the emerging economies. We believe this is likely to persist for some time. Consumer debt in the U.S. generally continued to fall. Unemployment figures remained stubbornly high and housing markets in many economies, most significantly in the United States, continued to struggle. Understandably, consumer confidence remained low. To add to the tumult, the Eurozone's debt crisis sent markets sharply lower over the spring and summer.

In contrast, emerging markets continued to witness very strong growth during the period. Indeed, growth was so strong that we saw a tightening of monetary policy in order to rein in growth to sustainable levels and to keep a lid on inflation. High inflation, particularly in food prices, can put great pressure on economic, political and market stability in developing nations.

Our bottom-up approach of investing led us to overweight positions in the information technology and consumer discretionary sectors, where we have, in the past, consistently found the most companies that have the potential to grow faster over the long term compared to the overall market. These two sectors were the top two positive contributors to performance this reporting period. Within information technology, the largest contributors were U.S.-based companies Intuit, Inc., Altera Corp., and Juniper Networks, Inc., the Indian business software and outsourcing giant Infosys Technologies Ltd., and Swedish telecommunications giant Telefonaktiebolaget LM Ericsson. In consumer discretionary, the greatest contributors to performance included French luxury goods group LVMH Moet Hennessy Louis Vuitton SA, cruise and vacation company Carnival Corp., German automobile manufacturer BMW AG, Spanish company Industria de Diseno Textil SA, which is known worldwide for its Zara brand, and Tod's SpA, the Italian footwear manufacturer.