Washington, D.C. 20549

Matthew A. Swendiman, Attorney

The Annual report to Shareholders for the period ended August 31, 2016 pursuant to Rule 30e-1 under the Investment Company Act of 1940 (the “1940 Act”), as amended (17 CFR 270.30e-1) is filed herewith.

Letter from the President | 3 |

A Discussion of Fund Performance | 4 |

Supplementary Portfolio Information | 35 |

Financial Statements of the Monteagle Funds | |

Schedules of Investments: | |

Fixed Income Fund | 41 |

Informed Investor Growth Fund | 46 |

Quality Growth Fund | 48 |

Select Value Fund | 52 |

Value Fund | 55 |

The Texas Fund | 58 |

Statements of Assets and Liabilities | 62 |

Statements of Operations | 64 |

Statements of Changes in Net Assets | 66 |

Financial Highlights | 72 |

Notes to Financial Statements | 78 |

Report of Independent Registered Public Accounting Firm | 98 |

Other Information | 99 |

About Your Funds’ Expenses | 100 |

Trustees and Officers of the Trust | 103 |

LETTER FROM THE PRESIDENT (Unaudited) |

Dear Shareholders:

Enclosed is the Annual Report for the Monteagle Funds. I encourage you to carefully review the information presented in this Annual Report as it contains valuable information about your investment.

As you will notice in reviewing the Annual Report, we continue to uncover opportunities in high quality, solid credit and attractive valuation areas.

As we reflect on this past fiscal year, we continue to see several headlines during the period, such as continued slow economic recovery, civil unrest, an uncertain domestic political environment, and arguments over federal monetary policy, that all had a dramatic effect on the markets in which the Monteagle Funds invest. Despite the volatility that these headlines have created in the day-to-day stock markets, we have often said that we view investing as a marathon, not a sprint. As a result, we remain optimistic as we expect that the effect of some of these events will be short-lived although others may take longer to work their way through the system. We believe that remaining disciplined with a longer-term focus will benefit patient investors.

In closing, we would like to thank you for your continued confidence and support of the Monteagle Funds.

Sincerely,

MONTEAGLE FUNDS

Paul B. Ordonio, JD

President

3

MONTEAGLE FIXED INCOME FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) |

How did the Fund Perform?

The Monteagle Fixed Income Fund (the “Fund”) had positive performance during the year. For the year ended August 31, 2016, the Fund had a total return of 3.51%. For the three and six month periods ended August 31, 2016, the Fund had total returns of 1.17% and 1.68% respectively. The returns were primarily influenced by declining longer term interest rates, both in the United States, and abroad. A great deal of influence on U.S. interest rates can be attributed to monetary policy activities particularly tied to the Bank of Japan and the European Central Bank. Both of the aforementioned central banks have been aggressively pursuing asset purchase programs (quantitative easing), in an effort to stimulate economic growth and rekindle inflation. As such, these programs have made U.S. dollar denominated assets more attractive and have increased the demand for U.S. fixed income securities. As demand for these securities has increased, so have prices. Because of the inverse relationship between price and yields (interest rates), increased prices have led to lower interest rates during this fiscal year.

The Fund’s benchmark index, the Barclays Capital Intermediate U.S. Government/Credit Index, had relative returns of 4.07%, 1.46%, and 2.34% for the twelve, three, and six month periods, ended August 31, 2016, respectively.

What Influenced Fund Performance?

This past fiscal year ended August 31, 2016 was one in which we’ve seen aggressive central bank monetary policies adopted in global markets and deflationary pressures abroad. Additionally, we have seen increased uncertainty as a result of the British referendum vote as to whether or not to remain in the European Union. The vote to abandon the union did have a negative impact on global markets, but has yet to be implemented. The significance of the vote goes beyond the economic consequences to the United Kingdom and Europe, but rather calls into question the political viability of a unified Europe comprised of 17 sovereign nations. The potential breakup of the European Union (the contagion effect), and the common currency, did play a role in decreasing growth expectations globally.

While here in the United States, our central bank (the Federal Reserve Bank – i.e. the Fed) modestly tightened monetary policy by increasing the Fed funds overnight lending rate by 0.25% in December 2015, central banks in Europe, Japan, and the United Kingdom have embarked on further easing. The action by the Bank of England (BOE) is in direct response to the market disruption caused by the referendum vote and the increased uncertainty of an economic downturn. On August 4, the BOE reduced its overnight lending rate by 0.25% (to a target rate of 0.25%) and pledged further support to provide liquidity to the banking system through asset purchases of corporate bonds and government bonds.

The Bank of Japan (BOJ) and the European Central Bank (ECB) both deemed it necessary to expand the easing of monetary policy through asset purchase programs and negative overnight lending rates on excess bank reserves. The intent of the ECB and BOJ is to offset deflationary pressures in their respective economies by discouraging saving and increase bank lending, capital investment, and consumer spending.

4

MONTEAGLE FIXED INCOME FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

The movement in interest rates is usually an indication of the market’s expectation for growth, and with growth, we can also expect a certain amount of inflation. Additionally, monetary policy affected by the Federal Reserve Board (through the Fed funds overnight lending rate) does have an impact on the market structure of interest rates. The illusive robust economic growth that has been anticipated since the financial crisis in 2008 and recession end in 2009 has been disappointing given previous post-recession cycles. The growth has been less than expected, not just for us in the United States, but around the world. While we in the United States are doing relatively better than most other economies, there are concerns. The biggest uncertainty we have here in the United States is whether the troubles in other major economies might be a precursor to U.S. weakness, maybe even recessionary conditions at home.

U.S. Treasury Note | August

2015

Rates | November

2015

Rates | February

2016

Rates | May

2016

Rates | August

2016

Rates |

2 Year | 0.74 | 0.93 | 0.78 | 0.88 | 0.81 |

3 Year | 1.05 | 1.22 | 0.90 | 1.03 | 0.93 |

5 Year | 1.55 | 1.65 | 1.21 | 1.37 | 1.20 |

7 Year | 1.95 | 1.99 | 1.52 | 1.67 | 1.46 |

10 Year | 2.22 | 2.21 | 1.74 | 1.85 | 1.58 |

30 Year | 2.96 | 2.97 | 2.62 | 2.65 | 2.23 |

In addition to monetary policy, Fund performance has also been affected by the prospects for economic growth. The above chart illustrates how the bond market has responded to the anemic growth and decreased outlook for inflation in the developed economies, as well as slowing growth in China. The negative interest rates in Europe and Japan have also increased demand for positive yielding U.S. dollar denominated assets. The increased demand for U.S. assets has increased the value (price) of fixed income assets. As a result, interest rates in the United States have remained low. We can see that interest rates for the 2-year Treasury note have barely increased over the year, while rates beyond two years have all decreased. Overall, portfolio performance has benefitted from the movement of interest rates over the last fiscal year.

It has become more apparent that interest rates in the major developed economies are affected by global economic growth prospects and are not limited to just the U.S. economy. As mentioned above, anemic global growth has kept interest rates relatively low and has had a positive influence on Fund performance throughout fiscal 2016. The U.S. economic growth rate as measured by the Real Gross Domestic Product (GDP) over the last year has been steadily declining. Actual 2nd quarter 2015 annualized GDP showed a healthy 3.9% measure of real growth, but has subsequently declined over the following quarters. Readings for the 3rd and 4th quarters of 2015 were 2.0% and 1.4%, respectively. Final GDP for the 1st quarter of 2016 measured 1.1% and preliminary estimates for the latest GDP figures for the 2nd quarter of 2016 are also showing our economy growing at a 1.1% rate. The Eurozone’s last reading showed GDP year-over-year growth as of the 2nd quarter of 2016 at just 1.6%. Eurozone member nations such as Italy, France, Spain, and Germany had year-over-year growth rates of 0.7%, 1.4%, 3.2%, and 3.1% respectively. While

5

MONTEAGLE FIXED INCOME FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

Spain and Germany have shown relatively stronger growth, uncertainties remain regarding the sustainability of this improvement. Emerging market economies such as the so called BRICS (Brazil, Russia, India, China, and South Africa), are also struggling overall. Brazil and Russia are in recession with GDP year-over-year readings (as of 2nd quarter 2016) of -3.8% and -0.6%, respectively. South Africa has also contracted over the past year with the latest reading at -0.2%. India and China are still showing significant growth. Both economies are still expanding at rates of approximately 7%, but at a slowing pace. As the market contemplates whether potential economic growth will accelerate or not, longer-term interest rates will adjust higher or lower depending on what impact growth would have on labor markets, capital investment, consumption, and inflation.

Our central bank’s dual mandate of full employment and stable prices (job creation and moderate inflation targeted at 2% on average) are factors to which the market also pays close attention. Improvement in labor statistics has positive implications for economic growth and direct implications for Federal Reserve monetary policy. During the course of this past fiscal year the economy created approximately 200,000 jobs per month. The unemployment rate has declined from 5.1% to 4.9% and the underemployment rate1 from 10.3% to 9.7%. These improvements have led many to believe that our economy is very close to meeting the definition of full employment, and the focus should now shift to inflation.

Undoubtedly, improvement in the unemployment rates has provided some impetus for economic growth. However, there are other measurements that are not necessarily as strong and therefore give an uncertain picture of future growth expectations. We still have a sizeable number of people that are working part-time, but wish to be fully employed. The underemployment rate is still 9.7%. Our economy is also impacted negatively by historically low labor participation rates. As of the end of August we had 62.8% of the available worker population in the labor force.2 Wage growth has also been unimpressive at 2.4% year-over-year. The average number of weekly hours worked is also less than one would expect from an expanding economy at 34.3. So, while the pace of new jobs has been good, they do not appear to be high paying jobs. So, fewer labor market participants, modest wage growth, and fewer hours worked are contributing factors to slower consumer growth and less wage inflation. Both outcomes justify a lower interest rate environment. Overall, labor market conditions have not had a significant impact on Fund performance. To the extent that current unemployment rates are approaching what many consider to be full employment, the outlook for future increases in short-term rates would have a slightly negative impact on the Fund’s performance.

Another important variable that has impacted, and will continue to impact, portfolio performance is expected inflation, not just in the U.S., but globally as well. Inflation measurements for much of the year have been increasing, but are still at or below the Fed’s implicit long-range target for price stability of 2%. The last reading of the CPI (Consumer Price Index) during the fiscal year measured 1.1% year-over-year, while the core CPI (less food and energy) increased 2.3%. Much of

1 | (Total unemployed, plus all persons marginally attached to the labor force, plus total employed part time for economic reasons, as a percent of the civilian labor force plus all persons marginally attached to the labor force). |

2 | (The labor force participation rate is the labor force divided by the total working-age population which is typically defined as those aged 15 (or 16) and older). |

6

MONTEAGLE FIXED INCOME FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

the impact on keeping the CPI fairly low has been the price of oil. As the price of oil has stabilized over the last 12 months, the downward pressure of oil on consumer prices has abated. That is precisely why measurements of CPI that discount the volatile oil prices are clearly very close to target inflation readings of 2% year-over-year. Another measure of price inflation is also tracked by the PCE index (Personal Consumption Expenditure). This has been the preferred measurement gauge of inflation used by the Federal Reserve. The year-over-year change in this index as of the last reading was 1.6%; also below the desired 2% average target for inflation. Furthermore, inflation expectations as measured by the difference in yields between U.S. Treasury notes and U.S. Inflation Protected Treasury Securities (TIPS) are also well below the 2% long-range Fed target. For the 5-year notes, the difference is 1.29%, and for 10-year notes, the difference is 1.47%. Declining inflation expectations over the year would favor bonds with longer maturities. We don’t believe that inflation had a material impact on the Fund’s performance over the year.

Credit conditions in the corporate bond market for the first half of the year were uncertain and did not support the low risk premiums associated with corporate credit conditions. During good economic times, the risk premium over safer U.S. Treasury notes diminishes. During more uncertain economic periods, the market requires more compensation in the form of higher yields (greater risk premiums) in order to hold riskier assets. However, the second half did show improving credit market conditions primarily driven by rising prices for oil. Oil prices had fallen below $30/barrel in January and then again in February of this past year. Considering that just 18 months earlier, oil prices were over $100/barrel, the credit markets did increase the odds of defaults occurring for companies in the energy sector. These uncertainties spread across most sectors of the corporate bond market. However, the reversal of oil prices back to the $45 - $50 range did alleviate some of the concerns associated with the energy sector of the corporate bond market. Additionally, more central bank activity in Europe and Japan was also a contributing factor to credit market outperformance. The table that follows (Table 7) shows that corporate bonds of lower credit quality did outperform during the year, particularly in the final six months.

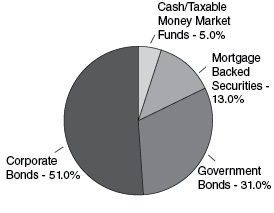

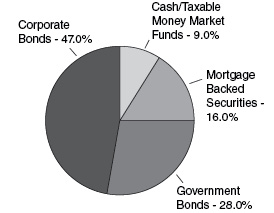

TABLE 2

Comparative Market Sector Weights

Monteagle Fixed Income Fund

August 31, 2015 | August 31, 2016 |

|

|

7

MONTEAGLE FIXED INCOME FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

Our responses to these events have primarily been a disciplined approach to a high quality portfolio profile. We remain committed to the Fund’s strategy of holding a well-diversified portfolio of high quality bonds. We believe that the markets have rewarded our patience and prudence. However, we have made some changes over the last year.

| | ● | During the course of the year we increased the Fund’s market allocation to mortgage-backed securities from 13% to 16% while modestly decreasing the Fund’s allocation to government securities from 31% to 28%. The reallocation from government securities went directly to cash in the last month of the fiscal year. At our discretion, we took some capital gains in August 2016, to offset capital loss credits that were due to expire at the end of the fiscal year. As a result, end of year cash balances were relatively higher than normal. We also decreased the Fund’s allocation to investment grade intermediate corporate bonds to 47% from 51% of the portfolio. As can be seen from the following table, the Fund’s decision to increase the allocation to mortgage-backed securities, while decreasing exposure to corporate bonds, had a less than optimal effect on relative performance. Performance was still positive for the MBS sector, but less than it would have been had the allocation been skewed more toward corporate bonds. |

TABLE 3

Index | Return for Period |

U.S. Treasury: Intermediate | 3.11% |

U.S. Agency Intermediate | 2.03% |

Intermediate Corporate | 6.25% |

Invest. Grade: Industrial — Intermediate | 6.58% |

Invest. Grade: Financial Institutions — Intermediate | 5.70% |

Fixed Rate Mortgage Backed Securities | 3.93% |

| | ● | Portfolio duration decreased slightly over last year. As of August 31, 2016, the Fund’s portfolio duration was 3.6 years (including cash) compared to the portfolio duration of 4.2 years at 2015 fiscal year end. Maturity decreased slightly from 4.8 years at 2015 fiscal year end to 4.3. When compared to the duration and weighted average maturity of 4.1 and 4.4, of the Barclays Intermediate U.S. Government/Credit Index, the Fund’s portfolio is slightly shorter in both measures. We do believe that the maturity structure of the Fund’s portfolio relative to the benchmark index had a slightly negative effect on relative performance. The following chart illustrates the performance of various maturity ranges within the Barclays Intermediate U.S. Government/Credit Index. As we can see, bonds in the 7-10 year maturity range outperformed those having shorter maturities. The portfolio’s securities (not including cash) mature in less than 10 years with the highest percentage maturing in the 3 to 5 year range (30.9%). 26.1% of the Fund’s assets mature in less than 3 years, 55.9%% in 3 to 7 years, and 9.2% in 7 to 10 years. |

8

MONTEAGLE FIXED INCOME FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

TABLE 4

Intermediate U.S. Government/Credit (Returns, Unhedged) Maturity Sectors | 1 yr.

Total

Return | 6 month

Total

Return | 3 month

Total

Return |

All Maturities | 4.07% | 2.34% | 1.46% |

1 - 3 yrs. | 1.49% | 0.94% | 0.51% |

3 - 5 yrs. | 3.60% | 1.99% | 1.25% |

5 - 7 yrs. | 6.01% | 3.28% | 2.14% |

7 - 10 yrs. | 8.80% | 5.06% | 3.16% |

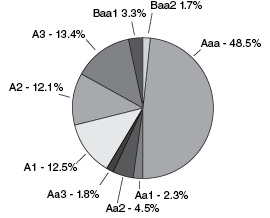

TABLE 5

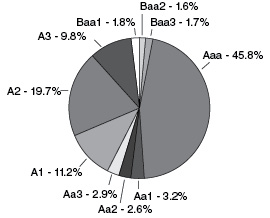

Comparative Credit Quality

Monteagle Fixed Income Fund

Moody’s Ratings August 31, 2015 | Moody’s Ratings August 31, 2016 |

|

|

| | ● | The preceding charts represent the credit quality distribution of the Fund’s securities holdings (not including cash or money market securities) at the beginning and end of this past fiscal year. For consistency of the relative analysis, in our distribution comparison above, we have only included the ratings provided by Moody’s (and not S&P, which rates U.S. government obligations AA+). The Barclays benchmark index still maintains ratings of AAA on U.S. government obligations. |

| | ● | The overall credit quality of the portfolio remained the same over the course of the year. Overall credit quality remains excellent with ratings of AA-/Aa3. |

| | ● | We would also note that at the end of this fiscal year the Fund’s portfolio contained investment grade securities rated below A3/A-. While we are restricted from investing in securities rated below A3/A- at time of purchase, we do have the discretion of holding securities rated Baa/BBB should the rating be the result of a downgrade. It |

9

MONTEAGLE FIXED INCOME FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

| | | is our opinion that the securities in question do not materially affect the overall credit quality of the Fund’s portfolio and do not represent significant credit risk to portfolio value. The following table specifically identifies the securities in question. |

TABLE 6

| MOODY

RTG | S&P

RTG | % of

Portfolio

Market Value |

Halliburton Co, 2%, due 8/1/18 | Baa1 | BBB+ | 1.59% |

AT&T Inc, 5.8%, due 2/15/19 | Baa1 | BBB+ | 1.74% |

Becton Dickinson & Co, 3.125%, due 11/08/21 | Baa2 | BBB+ | 1.68% |

Total | | | 5.01% |

| | ● | The following table provides a summary illustration of how investment grade bonds of varying credit quality have performed over the past year. These are returns of bonds in the Barclay’s Intermediate U.S. Government/Credit Index. The relative performance of credit is indicative of the risk/reward nature of these bonds. We can see that for the full year lower quality bonds had a performance advantage over those of higher quality. As such, the performance of the Monteagle Fixed Income Fund did not fully benefit from the higher returns associated with Baa and A rated bonds. |

TABLE 7

| 1 yr.

Total Return | 6 month

Total Return | 3 month

Total Return |

Aaa | 3.05% | 1.04% | 1.00% |

Aa | 4.13% | 2.27% | 1.30% |

A | 5.86% | 3.63% | 1.87% |

Baa | 6.50% | 6.50% | 2.92% |

Total | 4.07% | 2.34% | 1.46% |

| | ● | For the year, trading was primarily driven by repositioning the Fund’s portfolio to further reduce credit exposure and increase allocations to higher quality mortgage-backed securities. We did realize longer-term gains by selling some of our more seasoned government bonds. In capturing some of the portfolio gains, we did sell bonds having higher coupons. As a result, the overall portfolio’s average coupon was slightly lower at the end of 2016 fiscal year at 2.90% versus 3.03%. |

What is the Fund’s Strategy?

The Fund will continue to invest in high quality intermediate term fixed income securities generally between 2 and 10 years in maturity. The Fund will continue to monitor economic conditions through the use of a proprietary model in an attempt to anticipate interest rate changes and lengthen or shorten the duration of the Fund’s portfolio of securities to maximize total return

10

MONTEAGLE FIXED INCOME FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

with minimal risk. The Fund will also actively manage portfolio holdings across market sectors in order to maximize total return within the scope of permitted investments defined by the Fund’s prospectus. While we have taken prudent steps to diversify the Fund’s assets by limiting exposure to the credit and interest rate risk associated with any one specific issuer, market sector, or maturity range, those risks cannot be completely eliminated without affecting long-term Fund performance. We remain vigilant and will act in your best interest to preserve the Fund’s asset values.

Fund performance shown represents the performance of the Fund’s Class I shares. For complete performance information, please refer to the Average Annual Total Return table in the following performance report. Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end, are available by calling 1-888-263-5593.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please call 1-888-263-5593 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Matrix Capital Group, Inc.

Management’s Discussion of Fund Performance seeks to describe some of the Sub-Adviser’s current opinions and views of the financial markets. Although the Sub-Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed.

11

MONTEAGLE FIXED INCOME FUND

PERFORMANCE — August 31, 2016 (Unaudited) |

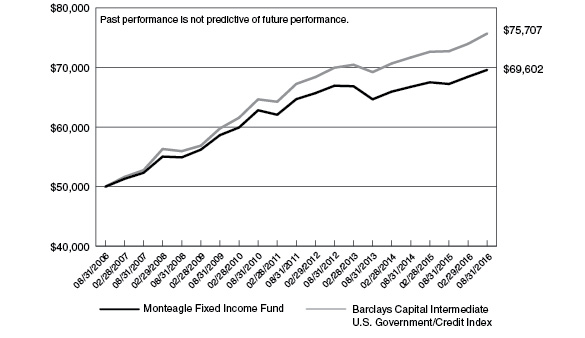

Comparison of the Change in Value of a $50,000 Investment in Monteagle Fixed Income Fund

and the Barclays Capital Intermediate U.S. Government/Credit Index

Average Annual Total Return

(for the periods ended August 31, 2016) |

| | One Year | Five Years | Ten Years | |

Monteagle Fixed Income Fund | 3.51% | 1.47% | 3.39% | |

Barclays Capital Intermediate

U.S. Government/Credit Index | 4.07% | 2.39% | 4.23% | |

The performance information quoted in this annual report assumes the reinvestment of all dividend and capital gain distributions, if any, and represents past performance, which is not a guarantee of future results. The returns shown do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost.

The above graph depicts the performance of the Monteagle Fixed Income Fund versus the Barclays Capital Intermediate U.S. Government/Credit Index (formerly Lehman Brothers U.S. Intermediate Government/Credit Index). The Barclays Capital Intermediate U.S. Government/Credit Index measures the performance of dollar denominated U.S. Treasuries, government-related (i.e. U.S. and foreign agencies, sovereign, supranational and local authority debt), and investment grade credit structures that have a remaining maturity of greater than or equal to one year and less than ten years. Please note that indices do not take into account any fees and expenses of investing in the individual securities that they track, and individuals cannot invest directly in any index.

As with any fund, save an index fund, that commonly compares its performance to the Barclays Capital Intermediate U.S. Government/Credit Bond Index, such a comparison may be said to be inappropriate because of the dissimilarity between the Fund’s investments and the securities comprising the index; so too with the Monteagle Fixed Income Fund, which will not invest in certain securities comprising this index.

12

MONTEAGLE INFORMED INVESTOR GROWTH FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) |

How did the Fund Perform?

The Monteagle Informed Investor Growth Fund (the “Fund”) returned a positive 7.1% for the fiscal year ended August 31, 2016. The S&P 500 Index (“S&P 500”), the Fund’s benchmark, returned a positive 12.6%.

What is the Fund’s Investment Approach?

The Fund invests primarily in medium capitalization stocks (median, generally around $15 billion) of well-managed, financially sound companies, offering under-valued earnings growth rate, earnings yield and earnings surprise momentum, superior return on investment capital and cash flow growth opportunities. These are companies in which management or large and informed investors — individuals and/or funds — are significant common stock owners or buyers, or where the company itself is repurchasing its own shares on the open market. This investment discipline is widely recognized as The Informed Investor Strategy — now marking its 60th year of institutional portfolio management success.

Summarizing, these companies qualify for intensive research analysis only if they meet at least one of these five first-screen qualifying selection tests:

| | 1. | The company’s officers and directors are buying its common stock on the open market. |

| | 2. | A major outside investor (minimum 5% shares outstanding owned) has filed a Form 13-D purchase disclosure on the company’s stock. |

| | 3. | The company has announced its intent to repurchase its common stock on the open market. |

| | 4. | A significant percentage of the company’s stock is owned by family/management. |

| | 5. | The current top performing equity mutual funds and/or equity-orientated hedge funds are accumulating the company’s common stock on the open market. |

The buy disciplines are matched by a series of five sell disciplines. They are:

| | 1. | Begin selling if a stock drops a minimum of 8% from an average-cost basis. |

| | 2. | Begin selling when a holding-high loss-limit is triggered. (Stock falls a minimum of 14% from its portfolio holding-high price.) |

| | 3. | Begin selling on preliminary, but confirmed, indications of a breakdown in a company’s financials. |

| | 4. | Possibly selling when informed investors stock transaction signals turn bearish. |

| | 5. | Sell partial positions of a portfolio stock after an unusually day-to-day sharp price run-up. |

13

MONTEAGLE INFORMED INVESTOR GROWTH FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

What Influenced the Fund’s Performance?

The Fund returned a positive 4.5% for the first fiscal quarter ended November 30, 2015 while the S&P 500 posted a return of +6.1%. The Fund’s investment return was influenced during its fiscal quarter, by positive performance in two sectors: Information Technology and Consumer Discretionary.

| | o | The Information Technology sector returned a positive 7.6% for the quarter. Advancing stocks in the sector included: Activsion (AVTI) +21.4%, Verisign (VRSN) +19.8%, Facebook (FB) +16.6%, Manhattan Associates (MANH) +11.4% and Alphabet (GOOGL) +8.0% |

| | o | The Consumer Discretionary sector returned a positive 6.1% for the quarter. Securities in this sector included: Amazon (AMZN) +29.6%, Nike (NKE) +18.4%, Starbucks (SBUX) +12.2%, DR Horton (DHI) +6.4% and O’Reilly Automotive (ORLY) +4.1% |

The Fund returned a -4.8% for the second fiscal quarter ended February 29, 2016 while the S&P 500 posted a return of -6.6%. The Fund’s investment return was influenced during its second fiscal quarter in two sectors: ETFs (Exchange Traded Funds) and Consumer Staples.

| | o | The ETF sector returned a -19.2% for the second quarter. The Powershares QQQ (QQQ) Trust had a -18.7% return and the SPDR S&P 500 Trust (SPY) had a -19.7% return. |

| | o | The Consumer Staples sector returned a flat 0.82% for the quarter. Declining stocks were Clorox (CLX) with a -1.3% return, Constellation Brands (STZ) with a -17.8% return and Hormel Foods (HRL) with a -4.7% return. |

The Fund returned a positive 3.5% for the third fiscal quarter ended May 31, 2016 while the S&P 500 Index posted a return of +9.1%. The Fund’s investment return was influenced during its third fiscal quarter by positive performance in three sectors: Consumer Discretionary, Materials and ETFs (Exchange Traded Funds).

| | o | The Consumer Discretionary sector returned a +10.1% for the quarter. Ulta Salon Cosmetics (ULTA) had a significant return of +28.7%, Dollar General (DG) had a return of -7.8%. |

| | o | The Materials sector returned a +9.2% for the quarter. Agnico Eagle Mines (AEM) had a +23.7% return and Franco Nevada (FNV) had a +11.2% for the period ended May 31, 2016. |

| | o | Finally, the ETFs (Exchanged Traded Funds) sector had a +7.5% return for the period ended May 31, 2016. The Powershares QQQ Trust (QQQ) returned +8.6% and the Spider S&P 500 Trust (SPY) returned +7.9% for the period ended May 31, 2016. |

The Fund returned a +4.1% for the fourth fiscal quarter ended August 31, 2016 while the S&P 500 had the same return of +4.1%. The Fund’s positive investment return was influenced during the fourth quarter by two sectors: Information Technology and Utilities.

| | o | The Information Technology sector had a +12.3% return. NVidia (NVDA) with a +30.2% return, Netease (NTES) returned a +14.6% and EBay (EBAY) with a +10.5% return. |

14

MONTEAGLE INFORMED INVESTOR GROWTH FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

| | o | The Utilities Sector returned a +9.0%. Leading this sector was DTE Energy with a +19.1% return, followed by Pinnacle West (PNW) with a +12.8% return and American Water Works (AWK) with a +9.5% return. |

The five equity holdings that influenced the Fund’s performance positively for the full fiscal-year were Agnico Eaglemines (AEM) +53.6%, Silver Wheaton (SLW) +61.3%, Broadridge Financial (BR) +42.8%, Altria Group (MO) +21.21% and Amazon (AMZN) +60.9%.

The five equity holdings contributing the least to the Fund’s performance for the full fiscal-year were: Abiomed (ABMD) -54.4%, Alliant Energy (LNT) -34.9%, Celgene (CELG) -40.3%, Hormel Foods (HRL) -41.4% and Universal Health Services (UHS) -50.7%.

The total performance return for the portfolio, fiscal year ended August 31, 2016, was aided by the results of IShares 20+ Year Treasury Bond (TLT), up 27.8. Please note that ETFs are used when stock picks are limited due to market variations.

Also, as of the August 31, 2016 fiscal year-end, the Fund held 33.1% in cash. This holding was viewed as a neutral influence on performance during the fiscal year.

Finally, the Fund’s fiscal year ended with the continuation of the Federal Reserve maintaining its low interest rate policy.

What is the Fund’s Strategy?

The current strategy of the Monteagle Informed Investors Growth Fund is bullish in outlook and the intention is to remain virtually fully invested in a select list of uniquely attractive growth stocks that fulfill the rigid Informed Investors growth stock criteria. Positions in cash and ETFs remain a secondary consideration, and are quite subordinate to stock selection priorities.

Fund performance shown represents the performance of the Fund’s Class I shares. For complete performance information, please refer to the Average Annual Total Return table in the following performance report. Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end are available by calling 1-888-263-5593.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please call 1-888-263-5593 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Matrix Capital Group, Inc.

Management’s Discussion of Fund Performance seeks to describe some of the Sub-Adviser’s current opinions and views of the financial markets. Although the Sub-Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed.

15

MONTEAGLE INFORMED INVESTOR GROWTH FUND

PERFORMANCE — August 31, 2016 (Unaudited) |

Comparison of the Change in Value of a $50,000 Investment

in Monteagle Informed Investor Growth Fund and the S&P 500 Index

Average Annual Total Return

(for the periods ended August 31, 2016) |

| | One Year | Five Years | Since

Inception(a) | |

Monteagle Informed Investor Growth Fund | 7.11% | 9.78% | 10.22% | |

S&P 500 Index | 12.55% | 14.67% | 7.96% | |

(a) | Represents the period from the commencement of operations (April 3, 2008) through August 31, 2016. |

The performance information quoted in this annual report assumes the reinvestment of all dividend and capital gain distributions, if any, and represents past performance, which is not a guarantee of future results. The returns shown do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost.

The above graph depicts the performance of the Monteagle Informed Investor Growth Fund versus the S&P 500 Index. The S&P 500 Index by Standard and Poor’s Corp. is a capitalization-weighted index comprising 500 issues listed on various exchanges, representing the performance of the stock market generally. Please note that indices do not take into account any fees and expenses of investing in the individual securities that they track, and individuals cannot invest directly in any index.

As with any fund, save an index fund, that commonly compares its performance to the S&P 500 Index, such a comparison may be said to be inappropriate because of the dissimilarity between the Fund’s investments and the securities comprising the index; so too with the Monteagle Informed Investor Growth Fund, which will not invest in certain securities comprising this index.

16

MONTEAGLE QUALITY GROWTH FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) |

How did the Fund perform?

For the fiscal year ended August 31, 2016, domestic equity markets posted attractive returns despite a number of headwinds: decelerating economic growth, declining earnings, and political turmoil in many parts of the world. Global central banks continued to provide additional liquidity to financial markets, hoping to stimulate economic activity. The incremental liquidity boosted asset prices more than real economic activity, resulting in rising equity valuations and, for many countries, negative nominal interest rates.

The fund’s strategy, to invest in high-quality companies capable of generating sustainable earnings growth and positive earnings surprises, would be expected to lag during periods when investors seek higher-risk stocks with little regard to valuation. Such has been the case in the seven-plus years subsequent to the financial crisis of 2008-2009, including the most recent fiscal year. Investors have been trained to react to central bank actions and commentary, counting on continued liquidity injections to push markets higher.

For the fiscal year, the Monteagle Quality Growth Fund (the “Fund”) increased 7.5% compared with a gain of 12.6% for the S&P 500 Index (“S&P 500”). Cash holdings reduced performance by 101 basis points as it became increasingly difficult through the year to identify stocks meeting the Fund’s investment discipline in an environment of declining earnings and rising valuations. Most of the remaining underperformance came from long-term portfolio holdings that posted disappointing earnings. Many of these, including CVS Health, Express Scripts, Walt Disney and Celgene were top 10 performers in the prior year and remain portfolio holdings. Sector allocation had a negligible impact for the year.

Relative to the Russell 1000 Growth Index (“Russell 1000”) benchmark, the Fund underperformed by 302 basis points for the fiscal year. Cash holdings reduced performance by 84 basis points. Underweight positions in Microsoft and Facebook accounted for a sizable portion of the disappointing performance. Sector allocation had a negligible impact for the year.

During the fiscal year, individual holdings contributing most positively to relative returns were Johnson & Johnson (pharmaceuticals, up 30.6%), Albemarle (specialty chemicals, up 80.1%), J.M. Smucker (foods, up 31.0%), Edwards Lifesciences (medical devices, up 48.1%), and Trimble Navigation (technology devices, up 45.0%). Individual stocks reducing performance the most were CF Industries (agricultural chemicals, down 52.8%), Polaris Industries (leisure products, down 37.8%), and Goldman Sachs (investment banking, down 8.7%).

Viewing each quarter of 2016 individually provides evidence of the portfolio’s strategy: providing protection during market downturns while capturing much of the gains during market rallies. Specifically, the portfolio meaningfully outperformed in the down quarter (second quarter of fiscal 2016) while lagging in the quarters posting positive returns. Capital preservation in downturns is an important element in the portfolio’s conservative strategy.

For the first quarter ending November 30, 2015, the portfolio returned 3.8% compared with 6.1% for the S&P 500 and 6.2% for the Russell 1000. Stock selection was particularly challenged during the period, with many long-time, high-quality holdings reporting disappointing results including Qualcomm, CF Industries, Polaris Industries, CVS Health, and W.W. Grainger.

17

MONTEAGLE QUALITY GROWTH FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

For the second quarter ending February 29, 2016, the portfolio declined just 5.9% compared with a 6.6% decline for the S&P 500 and a 7.0% decline for the Russell 1000. Investors reacted negatively to the U.S. Federal Reserve’s decision to hike interest rates for the first time since 2006, assuming a continual series of interest rate increases was forthcoming and an end to the Federal Reserve’s support of financial markets. Most of the Fund’s outperformance resulted from its quality bias, emphasizing companies with strong balance sheets and cash flows. From a sector perspective, this was most evident in an overweight in Consumer Staples and positive stock selection in Healthcare.

For the third quarter ending May 31, 2016, the portfolio gained 6.7% compared with a 9.1% gain for the S&P 500 and a 7.8% gain for the Russell 1000. Investors shifted to an aggressive ‘risk-on’ strategy once Federal Reserve reversed its intention to normalize interest rates. Much of the Fund’s underperformance resulted from its modest cash holdings as positive stock selection offset the negative impacts of the Fund’s high quality stance.

For the fourth quarter ending August 31, 2016, the portfolio returned 3.1% compared with a 4.1% gain for the S&P 500 and a 3.8% gain for the Russell 1000. Again, the Fund’s underperformance can be attributed to modest cash holdings and a high-quality stance, particularly in Consumer Staples. An underweight in the outperforming Information Technology sector was more than offset by positive selection in the sector.

Changes to the portfolio during the year reflect an effort to eliminate holdings reaching the upper end of our valuation expectations while retaining an emphasis on quality in newly added holdings. All stock selection results from a bottom-up process, yet the aerospace industry is one area expected to experience organic growth and is well-represented in new purchases. A common theme among positions sold is reduced exposure to the consumer.

New holdings added over the past year include Allergan (pharmaceuticals), Alexion (biotechnology), Altria (tobacco), Cigna (managed care), Community Health (hospitals), Dollar General (general merchandise), Dish Networks (cable & satellite), Edwards Lifesciences (medical devices), Generac (industrial machinery), Hanesbrands (apparel), Honeywell (aerospace), Ralph Lauren (apparel), Eli Lilly (pharmaceuticals), Lockheed Martin (aerospace), McDonalds (restaurants), Northrop Grumman (aerospace), Orbital ATK (aerospace), Synchrony Financial (consumer finance), TJX (retail), and Welltower (healthcare REIT).

Purchases were funded by the elimination of positions in Allergan (pharmaceuticals), Blackrock (asset management), Chevron (integrated energy), Cinemark (entertainment), Cisco Systems (communications equipment), Community Health (hospitals), Deckers (footwear), Dunkin Brands (restaurants), W.W. Grainger (industrial distribution), Hershey Foods (foods), Honeywell (aerospace), Pfizer (pharmaceuticals), Polaris Industries (leisure products), J.M. Smucker (food), and Walmart (general merchandise).

What is the Fund’s Strategy?

The Fund will continue to focus on maintaining a diversified portfolio of high-quality companies delivering sustainable above-average growth and positive earnings surprises relative to expectations. Investors are currently fixated on global central banker statements and potential actions. High frequency trading organizations have essentially developed investment strategies

18

MONTEAGLE QUALITY GROWTH FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

to merely front-run central banker activity. At some point, markets will normalize and underlying fundamentals will determine stock prices. The Fund’s advisor believes the companies with strong balance sheets and cash flows will weather the normalization process well and provide rewarding investments in the aftermath.

Fund performance shown represents the performance of the Fund’s Class I shares. For complete performance information, please refer to the Average Annual Total Return table in the following performance report. Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end, are available by calling 1-888-263-5593.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please call 1-888-263-5593 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Matrix Capital Group, Inc.

Management’s Discussion of Fund Performance seeks to describe some of the Sub-Adviser’s current opinions and views of the financial markets. Although the Sub-Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed.

19

MONTEAGLE QUALITY GROWTH FUND

PERFORMANCE — August 31, 2016 (Unaudited) |

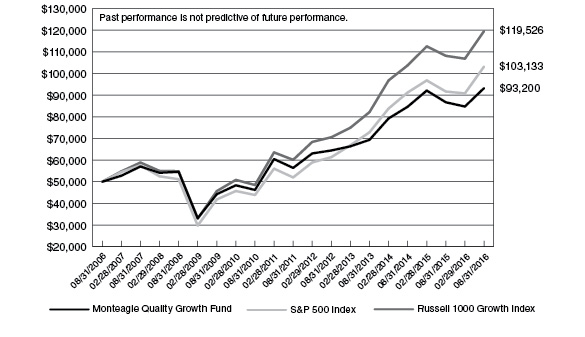

Comparison of the Change in Value of a $50,000 Investment in Monteagle Quality Growth Fund,

the S&P 500 Index and the Russell 1000 Growth Index

Average Annual Total Return

(for the periods ended August 31, 2016) |

| | One Year | Five Years | Ten Years | |

Monteagle Quality Growth Fund | 7.52% | 10.57% | 6.43% | |

S&P 500 Index | 12.55% | 14.67% | 7.50% | |

Russell 1000 Growth Index | 10.54% | 14.72% | 9.10% | |

The performance information quoted in this annual report assumes the reinvestment of all dividend and capital gain distributions, if any, and represents past performance, which is not a guarantee of future results. The returns shown do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost.

The above graph depicts the performance of the Monteagle Quality Growth Fund versus the S&P 500 Index and the Russell 1000 Growth Index. The S&P 500 Index by Standard and Poor’s Corp. is a capitalization-weighted index comprising 500 issues listed on various exchanges, representing the performance of the stock market generally. The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. Please note that indices do not take into account any fees and expenses of investing in the individual securities that they track, and individuals cannot invest directly in any index.

As with any fund, save an index fund, that commonly compares its performance to the S&P 500 Index and the Russell 1000 Growth Index, such a comparison may be said to be inappropriate because of the dissimilarity between the Fund’s investments and the securities comprising the indices; so too with the Monteagle Quality Growth Fund, which will not invest in certain securities comprising these indices.

20

MONTEAGLE SELECT VALUE FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) |

How did the Fund perform?

For the year ended August 31, 2016, the Monteagle Select Value Fund (the “Fund”) had a return of 4.75%. The S&P 500 Index (“S&P 500” or “Index”) had a return of 12.55% for the same period. Despite the underperformance of this rolling one year, the Fund has outperformed the Index year-to-date. The Fund’s net asset value per share as of August 31, 2016 was $11.83 versus $15.86 on August 31, 2015. Despite the negative return, another capital gain distribution will be occurring as a result of continued realized gains over the last year.

What is the Fund’s investment approach?

The Fund’s investment goal is long-term capital appreciation. The Fund uses a “value investing” style by investing under normal circumstances at least 80 percent of its assets in common stock of domestic companies believed to be under-priced relative to comparable securities determined by price-to-earnings ratios, cash flows or other measures. The Fund’s adviser predominately utilizes a reversion-to-the-mean strategy on stock selection in order to achieve its results rather than trying to time market fluctuations. The adviser limits the pool of stocks to consider for purchase to only those equities in the S&P 500. In selecting stocks, the Fund’s adviser establishes valuation parameters by using relative ratios or target prices to evaluate companies on several levels. Additionally, the adviser will generally have the Fund hold between 40 and 60 equities and diversify its holdings across numerous industries. The Fund seeks to maintain a minimum average weighted market capitalization of $5 billion.

Value stocks are broadly defined as equities which have a price-to-earnings ratio and a price-to-book ratio less than the relative market average with dividends tending to be higher than the relative market average. Also, value stocks tend to have a beta (a measure of the stocks price volatility relative to the overall market, i.e. the S&P 500) less than 1.0.

What influenced the Fund’s performance?

During the twelve months ended August 31, 2016, the Fund’s performance was affected by continued volatility in the U.S. equity market. This included “Brexit” (Britain leaving the European Union) as well as the general concern of rising interest rates and its effect on the markets. Calendar year 2016 began with a fall of over 10% in the first 45 days (total fall from most recent high was approximately 13.3%). The day Brexit occurred the domestic equity market fell 3% on the open and volatility swelled. The overall movement as a result of Brexit was over 5%. Over the last twelve months, there have been several equity market corrections of 5% or greater. Janet Yellen and the Federal Reserve continue to keep the market guessing regarding the timing of rising interest rates. This time last year about 90% of major economists believed rates would be higher by September 2016. However, the Fed has been reluctant to further raise rates after its first move in December. At the time of this writing, traders in the futures market are putting about 18% odds on an October increase and 43% on December with the vast majority of the remainder being further into 2017. The Fed has indicated a rate hike in 2016 should be coming but have given enough doubt for investors to be divergent on the timing. With the Index ending approximately twenty-five points off all-time highs, this calendar year has delivered decent returns thus far. The Fund’s

21

MONTEAGLE SELECT VALUE FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

focus on a “value style, reversion-to-the-mean” strategy has led to lagging performance with the high levels of volatility in the general market over the last year. However, longer term the Fund has performed attractively overall compared to the S&P 500 Index.

For the first quarter ended November 30, 2015, the portfolio holdings of the Fund underperformed the Index. The investments of the Fund experienced a -1.56% return versus a return for the Index of 6.07%. The cash balance of the portfolio at the end of the first was 15.02%, invested in cash and money funds while the equities represent 84.98% of the assets. The cash balance remained high in order to hold cash for the large capital gains distribution that occurred at the end of the calendar year.

The broad sectors of the Index that improved the most on average during the first quarter were the Information Technology (11.82%), Consumer Discretionary (10.01%), and Industrials (8.91%) sectors while the Utilities (0.28%), Health Care (0.55%), and the Telecommunication Services (1.20%) sectors were the lowest performing within the Index. After the Index experienced one of the largest all-time intra-day declines on record in late August, the Index returned to near highs for the year in early November. As of the end of November, the Index finished higher than it began the year by approximately 1.04%.

As of the end of the first quarter, the portfolio holdings continued to be diversified across many sectors of the Index with less exposure to the Utilities, Consumer Staple and Materials sectors. The largest sector allocations are Energy, Consumer Discretionary and Financial. The Fund’s positive portfolio performance was primarily attributed to its top performing stock picks of Tesoro Petroleum (25.83%), General Electric Co. (21.66%), and Discovery Communications (17.07%). The Fund’s portfolio performance was most negatively affected by Fossil Group, Inc. (-37.53%), Joy Global (-36.68%) and Allegheny Technology Inc. (-30.47%). During the first quarter, eleven disposals were made. Some of these were sold in order to remove securities that achieved their target price and make room for securities with more appreciation potential. Others were sold in order to realize losses to offset a portion of the large capital gains distribution for the Fund. These securities were sold under the procedural “out process” as determined by the holding period for the strategy. Subsequent to these disposals, no purchases were made in order to hold cash for the large capital gains distribution that will occur in December. As of the end of the first quarter, cash represented 15.02% of the assets.

For the second quarter ended February 29, 2016, the portfolio holdings of the Fund outperformed the Index. The investments of the Fund experienced a -5.76% return versus a return for the Index of -6.59%. The cash balance of the portfolio at second quarter-end was 6.86%, invested in cash and money funds while the equities represent 93.14% of the assets.

The broad sectors of the Index that improved the most on average during the second quarter were the Telecommunication Services (13.01%), Utilities (9.68%), and Consumer Staples (4.56%) sectors while the Financials (-10.98%), Energy (-10.97%), and the Consumer Discretionary (-7.40%) sectors were the lowest performing within the Index. The Index fell (to the lowest level since April 2014) after falling approximately 13.3% from its recent high. The subsequent bounce in the Index was almost 7%, while the Index closed the quarter slightly off that “bounce” level.

22

MONTEAGLE SELECT VALUE FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

As of the end of the second quarter, the portfolio holdings continued to be diversified across many sectors of the Index with less exposure to the Consumer Staple, Utilities and Communications sectors. The largest sector allocations are Consumer Discretionary, Industrial and Energy. The Fund’s positive portfolio performance was primarily attributed to its top performing stock picks of Mattel, Inc. (32.74%), Michael Kors Holdings (31.68%), and Fossil Group, Inc. (21.94%). The Fund’s portfolio performance was most negatively affected by Transocean LTD. (-39.76%), Conoco Philips (-36.48%) and United Rentals, Inc. (-34.45%). During the second quarter, five disposals were made. Some of these were sold in order to remove securities that achieved their target price and make room for securities with more appreciation potential. Others were sold in order to remove securities with large losses and little appreciation potential to achieve their target price. Moreover, these securities were sold under the procedural “out process” as determined by the holding period for the strategy. Subsequent to these disposals, three securities were purchased in securities with good appreciation potential according to the overriding investment strategy for the Fund. As of the end of the second quarter, cash represented 6.86% of the assets.

For the third quarter ended May 31, 2016, the portfolio holdings of the Fund underperformed the Index. The investments of the Fund experienced an 8.94% return versus a return for the Index of 9.12%. The cash balance of the portfolio at the third quarter-end was 0.59%, invested in cash and money funds while the equities represent 99.41% of the assets.

The broad sectors of the Index that improved the most on average during the third quarter were the Energy, Financials and the Materials sectors while the Telecommunication Services, Consumer Staples and Utilities sectors were the lowest performing within the Index. After the huge fall in the first two months of the year, the Index generally rose from the end of February through the end of May, ending the third quarter just off highs.

As of the end of the third quarter, the portfolio holdings continued to be diversified across many sectors of the Index with less exposure to the Utilities, Consumer Staple and Communications sectors. The largest sector allocations are Financial, Industrial and Consumer Discretionary. The Fund’s positive portfolio performance was primarily attributed to its top performing stock picks of Jacobs Engineering Group, Diamond Offshore Drilling and Freeport-McMoRan, Inc. The Fund’s portfolio performance was most negatively affected by Michael Kors Holdings, Fossil Group, Inc. and The Mosaic Co. During the third quarter, four disposals were made in order to remove securities that achieved their target price and make room for securities with more appreciation potential. These securities were sold under the procedural “out process” as determined by the holding period for the strategy. Subsequent to these disposals, twelve purchases were made during the remainder of the quarter. Some of these were “averaging into” existing securities while the majority were new securities. All of these exhibited good appreciation potential according to the overriding investment strategy for the Fund. As of the end of the third quarter, the Fund was fully invested with cash less than one percent of the assets.

For the fourth quarter ended August 31, 2016, the portfolio holdings of the Fund underperformed the Index. The investments of the Fund experienced a 3.65% return versus a return for the Index of 4.10%. For the year-to-date period ended August 31, 2016, the portfolio holdings of the Fund outperformed the Index with the investments of the Fund experiencing a 9.99% annualized return

23

MONTEAGLE SELECT VALUE FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

versus a 7.82% return for the Index. The rolling one-year return resulted in underperformance by the Fund, with a return of 4.75% versus 12.55% for the Index. The cash balance of the portfolio at quarter-end was 8.5%, invested in cash and money funds while the equities represent 91.5% of the assets.

The broad sectors of the Index that improved the most on average during the fourth quarter were the Information Technology, Real Estate (which is now separated from financials) and the Industrials sectors while the Utilities, Consumer Staples and Financials sectors were the lowest performing within the Index. The Index experienced another small correction of over 5% in June subsequent to the “Brexit” announcement but then fairly quickly returned back to “pre-Brexit” levels. The S&P 500 ended August near all-time highs.

As of the end of the fourth quarter and Fund year, the portfolio holdings continued to be diversified across many sectors of the Index with less exposure to the Real Estate (again, now separated from financials), Consumer Staples and Communications sectors. The largest sector allocations are Financial, Consumer Discretionary and Industrial. The Fund’s positive portfolio performance was primarily attributed to its top performing stock picks of Morgan Stanley, Michael Kors Holdings and The Mosaic Co. The Fund’s portfolio performance was most negatively affected by Darden Restaurants, Inc., Discovery Communications and Freeport-McMoRan, Inc. During the fourth quarter, three disposals were transacted in order to make room for securities with more appreciation potential. One of which, C.H. Robinson Worldwide, was sold after it achieved its target price. The other two disposals, Diamond Offshore Drilling and Xerox Corp., were sold after being non-performing securities that reached a maximum holding period. While sold to realize a loss, this will reduce the overall capital gains distribution that will occur later this year. All of these securities were sold under the procedural “out process” as determined by the holding period for the strategy. Subsequent to these disposals, no purchases were made in order to hold a slightly elevated level of cash with the market remaining near all-time highs. Moreover, as of the end of the fourth quarter and Fund year-end the cash balance was higher than typical.

What is the Fund’s strategy?

The Fund will continue to concentrate on equities contained in the S&P 500 which generally consists of large name brand corporations with good fundamentals and broad product diversification. The Fund’s adviser will continue to be disciplined in the use of its predominate strategy of reversion-to-the-mean by applying its “value investing” approach valuation model; thereby, allowing the market’s volatility to identify those securities that become under-valued and are poised to be the next performers in the market. Sector allocation in the Fund’s portfolio will primarily be determined by which companies are available for purchase pursuant to the Fund’s strategy. It is anticipated that the Fund may hold higher levels of cash during extended periods of market uncertainty and will selectively invest the cash into equities identified by the primary investment strategy as opportunities present themselves or for dollar-cost-averaging into currently held positions. This strategy is executed with a long-term outlook and will have periods of under-performance and out-performance versus its Index. Therefore, the Fund’s daily performance can and will vary dependant upon current market conditions.

24

MONTEAGLE SELECT VALUE FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

Fund performance shown represents the performance of the Fund’s Class I shares. For complete performance information, please refer to the Average Annual Total Return table in the following performance report. Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end, are available by calling 1-888-263-5593.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please call 1-888-263-5593 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Matrix Capital Group, Inc.

Management’s Discussion of Fund Performance seeks to describe some of the Sub-Adviser’s current opinions and views of the financial markets. Although the Sub-Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed.

25

MONTEAGLE SELECT VALUE FUND

PERFORMANCE — August 31, 2016 (Unaudited) |

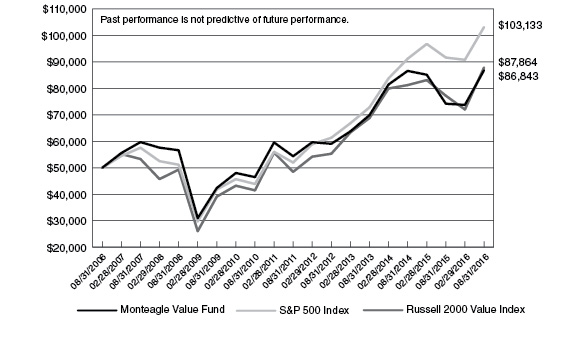

Comparison of the Change in Value of a $50,000 Investment

in Monteagle Select Value Fund and the S&P 500 Index

Average Annual Total Return

(for the periods ended August 31, 2016) |

| | One Year | Five Years | Ten Years | |

Monteagle Select Value Fund | 4.75% | 14.18% | 5.50% | |

S&P 500 Index | 12.55% | 14.67% | 7.50% | |

The performance information quoted in this annual report assumes the reinvestment of all dividend and capital gain distributions, if any, and represents past performance, which is not a guarantee of future results. The returns shown do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost.

The above graph depicts the performance of the Monteagle Select Value Fund versus the S&P 500 Index. The S&P 500 Index by Standard and Poor’s Corp. is a capitalization-weighted index comprising 500 issues listed on various exchanges, representing the performance of the stock market generally. Please note that indices do not take into account any fees and expenses of investing in the individual securities that they track, and individuals cannot invest directly in any index.

As with any fund, save an index fund, that commonly compares its performance to the S&P 500 Index, such a comparison may be said to be inappropriate because of the dissimilarity between the Fund’s investments and the securities comprising the index; so too with the Monteagle Select Value Fund, which will not invest in certain securities comprising this index.

26

MONTEAGLE VALUE FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) |

How did the Fund Perform?

For the year ended August 31, 2016, the Monteagle Value Fund (the “Fund”) reported a total return of positive 17.05%. The S&P 500 Index (“S&P 500”) had total returns of 12.55% for the same time period. The Fund’s net asset value per share as of August 31, 2016 was $14.41 versus $13.36 at August 31, 2015. The Fund paid a capital gains distribution of $0.85 per share in December, 2015.

What is the Fund’s investment approach?

The Fund’s investment goal is to achieve maximum returns through investing in undervalued companies. The Fund determines value usually based on price-to-earnings ratios, but also reviews historical price to book value ratios, dividend yield and balance sheet quality in determining whether prospective investments are truly undervalued. The adviser will hold 40 to 50 equities. The Fund seeks to maintain a minimum average market capitalization of $5 billion. The current average market capitalization exceeds $67 billion. The current price earnings ratio is 13.7 times 2017 earnings and currently yields 3.2 percent. The S&P 500 currently trades at 16.9 times 2017 earnings and yields 2.1 percent.

Fund’s adviser also makes industry determinations based upon interest rate cycles. Historical relationships between short-term and long-term U.S. Treasury securities impact industry weightings as easier money promotes growth in inflation while tight money favors disinflation.

As a general rule, new investments are made based on historical quantitative valuation measures that the Fund deems as undervalued. Conversely, the positions which are sold usually reach quantitative valuation measures that the Fund deems fully or overvalued. Decisions to reduce or sell partial holdings are based on industry overweightings.

The Fund also makes investments for the long-term holding the positions for three to five years unless extraordinary events such as mergers, acquisitions or deterioration of the industry or company.

What influenced the Fund’s performance?

During the year ended August 31, 2016, the Fund outperformed the S&P 500 as economically sensitive companies exhibited market strength in response to modest economic activity since February 2016. Many of the Fund’s holdings pay higher dividends than the S&P 500. The major market indices have more recently added growth companies into the respective index which pay lower or no dividend. Record low interest rates has market participants scrambling for yield.

The market responded to improving corporate earnings in 2016 with modest gains. The Federal Reserve has not raised interest rates since December 2015 primarily because corporate revenues have not grown in a meaningful way over the past twelve months. Targeted inflation rates of 2% have not been achieved. In fact, the fear is growing that the real prices in wages and finished goods are dropping, not rising. The unemployment rate has dropped below 4.9% in the past twelve months although an estimated 10 million workers have given up on looking for work. The very fact that three levels of aggressive monetary policy by the Federal Reserve has not produced the

27

MONTEAGLE VALUE FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

desired 2% inflation rate means that interest rate policy will not be changed in a meaningful way anytime soon. The Great Inflation has certainly been put on hold as disinflationary forces have quelled any hopes of a robust economy anytime soon.

During the first quarter ended November 30, 2015 the Fund underperformed the S&P 500 returning 4.22% versus 6.07% for the S&P 500. Generally speaking, most stocks reached intermediate lows at the very end of September. Commodity prices dropped to fifteen year lows during the quarter. Subsequently, energy stocks, mining stocks and their related industrials all declined during the period.

During the quarter the Fund made no changes in its holdings.

During the second quarter ended February 29, 2016 the Fund outperformed the S&P 500. During the quarter ended February 29, 2016 the Fund returned -4.61% versus -6.59% for the S&P 500. The Federal Reserve raised interest rates 0.25% during December 2015. Any future interest rate increases would be data dependent going forward.

During the quarter, the U.S. dollar continued to strengthen based on the increase in interest rates. Consequently, any commodity based industries saw prices capitulate at the end of 2015.

During the quarter the Fund sold Dupont, Chemours Company, D.R. Horton, NRG Energy, Holly Frontier, Barrick Gold, Freeport McMoran, Yamana Gold, and Medtronics PLC. Additionally, the Fund added positions in IBM, Archer Daniels-Midland, Ryder Systems, Qualcomm, International Paper, Eastman Chemical, Seagate Technology and Olin Corporation. The Fund increased its positions in Triumph Group and Greif Inc.

During the third quarter ended May 31, 2016 the Fund slightly outperformed the S&P 500 returning 9.79% versus 9.12%. The overall market appears to reach a bottom during early February as significant price appreciation in all industrial sectors occurred during the quarter. Money supply growth rose to 8% during the quarter supporting rising stock prices.

The Fund outperformed the S&P 500 during the quarter as prospects improved for the industrial companies the Fund has in its holdings. During the quarter, the Fund sold its positions in Ford Motor Co., Rogers Communications, Boston Scientific, Nomura Securities, and Tidewater, Inc. The Fund made new investments in Astra Zeneca, Pfizer, Inc., Cal-Maine Foods, Inc., and MDC Holdings.

During the August 31, 2016 quarter, the Fund outperformed the S&P 500 returning 7.24% versus 4.10%. Over the past twelve months, the Fund outperformed the S&P 500 returning 17.05% versus 12.55%. The overall stock market continues to be volatile yet exhibiting positive returns since February 2016. Since December 2015, interest rates set by the Federal Reserve have not changed as the overall economic data suggests that the economy is anemic at best.

We still believe the reasons for positive stock market returns for the next five years include historical low interest rates, improving housing market, and rising employment.

The Fund outperformed the S&P 500 because of the strength in the industrial sectors that the Fund holds. During the quarter, the Fund sold its positions in Republic Service Group, Worthington Industries, Sonoco, Abercrombie and Fitch, Triumph Group, Mosaic Co., and Transocean LTD.

28

MONTEAGLE VALUE FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) (Continued) |

The Fund made new investments into Trinity Industries, Cooper Tire and Rubber, Pilgrim’s Pride, Schlumberger LTD, Macy’s, Inc., and American Railcar. The Fund increased its positions in Rayonier, Inc., and General Electric Co.

What is the Fund’s current strategy?

The Fund continues to focus on consistency in earnings in its holdings. The Fund remains committed to economically sensitive issues including telecommunications, pharmaceuticals, materials, and industrials. The Fund has a modest overweight in materials, telecommunications, and industrials as the economic recovery continues to sputter and recent Fed policy statements indicated they were concerned that it would be willing to accept higher inflation as it fends off deflationary forces. The Fund is underweight financials, health, technology, consumer discretion, and consumer staples. The Fund has increased its holdings into international ADR’s believing the worldwide recovery has begun.

Fund performance shown represents the performance of the Fund’s Class I shares. For complete performance information, please refer to the Average Annual Total Return table in the following performance report. Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end are available by calling 1-888-263-5593.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please call 1-888-263-5593 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Matrix Capital Group, Inc.

Management’s Discussion of Fund Performance seeks to describe some of the Sub-Adviser’s current opinions and views of the financial markets. Although the Sub-Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed.

29

MONTEAGLE VALUE FUND

PERFORMANCE — August 31, 2016 (Unaudited) |

Comparison of the Change in Value of a $50,000 Investment

in Monteagle Value Fund, the S&P 500 Index and the Russell 2000 Value Index

Average Annual Total Return

(for the periods ended August 31, 2016) |

| | One Year | Five Years | Ten Years | |

Monteagle Value Fund | 17.05% | 9.82% | 5.68% | |

S&P 500 Index | 12.55% | 14.67% | 7.50% | |

Russell 2000 Value Index | 13.80% | 12.62% | 5.80% | |

The performance information quoted in this annual report assumes the reinvestment of all dividend and capital gain distributions, if any, and represents past performance, which is not a guarantee of future results. The returns shown do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The investment return and principal value of an investment will fluctuate and, therefore, an investor’s shares, when redeemed, may be worth more or less than their original cost.

The above graph depicts the performance of the Monteagle Value Fund versus the S&P 500 Index and the Russell 2000 Value Index. The S&P 500 Index by Standard and Poor’s Corp. is a capitalization-weighted index comprising 500 issues listed on various exchanges, representing the performance of the stock market generally. The Russell 2000 Value Index measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values. Please note that indices do not take into account any fees and expenses of investing in the individual securities that they track, and individuals cannot invest directly in any index.

As with any fund, save an index fund, that commonly compares its performance to the S&P 500 Index and the Russell 2000 Value Index, such a comparison may be said to be inappropriate because of the dissimilarity between the Fund’s investments and the securities comprising the indices; so too with the Monteagle Value Fund, which will not invest in certain securities comprising these indices.

30

THE TEXAS FUND

A DISCUSSION OF FUND PERFORMANCE (Unaudited) |

How did the Fund perform?

For the year ended August 31, 2016 The Texas Fund (the “Fund”) was down -0.45% for the one year trailing period while the S&P 500 Index (“S&P 500”) was up 12.55%. This period saw a continuation of lower energy prices as well as a more volatile market in the S&P 500. The worst period over the course of the past year was from November 5, 2015 to February 11, 2016 in both the Texas Fund (-17.80%) and the S&P 500 (-12.35%). From February 11, 2016 through August 31, 2016 the Texas Fund matched the S&P 500’s performance as it was up 20.16% with the S&P 500 also up 20.16%. The Fund’s net asset value per share as of August 31, 2016 was $8.88 versus $8.92 as of August 31, 2015.