UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08361

Goldman Sachs Variable Insurance Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606-6303

(Address of principal executive offices) (Zip code)

Robert Griffith, Esq.

Goldman Sachs & Co. LLC

200 West Street

New York, NY 10282

Copies to:

Stephen H. Bier, Esq.

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: December 31

Date of reporting period: December 31, 2023

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Annual Report to Shareholders is filed herewith. |

Goldman Sachs Variable Insurance Trust

| | |

| ∎ | | GOLDMAN SACHS MULTI-STRATEGY ALTERNATIVES PORTFOLIO |

| | |

| ∎ | | GOLDMAN SACHS TREND DRIVEN ALLOCATION FUND |

TABLE OF CONTENTS

|

| |

Effective January 24, 2023, open-end mutual funds and exchange traded funds will be required to provide shareholders with streamlined annual and semi-annual shareholder reports (“Tailored Shareholder Reports”). Funds will be required to prepare a separate Tailored Shareholder Report for each share class of a fund that highlights key information to investors. Other information, including financial statements, will no longer appear in a fund’s shareholder report, but will be available online, delivered free of charge upon request, and filed with the SEC on a semi-annual basis on Form N-CSR. The new requirements have a compliance date of July 24, 2024. |

| | | | | | |

| | | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee | | |

MARKET REVIEW

Goldman Sachs Variable Insurance Trust Funds — Goldman Sachs VIT Multi Asset Strategies Funds

Market Review

Ongoing inflation trends and macroeconomic data, central bank monetary policy, interest rate volatility, geopolitical events, and U.S. and European banking stress had the greatest influence on the capital markets during the 12-month period ended December 31, 2023 (the “Reporting Period”).

During the first quarter of 2023, when the Reporting Period began, investors focused on the evolution of the European energy crisis, the speed of China’s economic reopening and the pace of U.S. disinflation. In the U.S., inflation was not moderating as quickly as U.S. Federal Reserve (“Fed”) policymakers had hoped, and they maintained a hawkish stance, raising the target federal funds (“fed funds”) rate twice during the quarter—by 25 basis points each time. (Hawkish tends to suggest higher interest rates; opposite of dovish. A basis point is 1/100th of a percentage point.) In March 2023, investor sentiment was dominated by worries about the U.S. and European banking sectors. Swift response from U.S. and European policymakers rather quickly calmed nerves, but the turmoil made the Fed’s decisions on interest rates more complex given its objective of mitigating downside risks to economic growth while combating persistent inflation amid a tight labor market. Investor concerns about a potential European energy crisis eased, while China’s economy continued to reopen after the Chinese government had finally lifted its stringent zero-COVID policy in January 2023. For the first quarter overall, global equities generated solidly positive returns, with developed markets equities outperforming emerging markets equities. There was substantial dispersion of returns across broad equity indices, with growth equities materially outperforming value equities. Within developed equity markets, non-U.S. equities outpaced U.S. equities. In the U.S. equity market, information technology equities broadly outperformed financials and energy equities. As for global fixed income, yields broadly declined during the first quarter, leading to positive bond returns.

During the second quarter of 2023, as economic growth remained resilient, many market participants reconsidered their previous expectations of a global economic slowdown. Central banks focused on combating inflation, which decreased but remained elevated. In May, the Fed raised the fed funds rate by 25 basis points to a range between 5.00% and 5.25%. The European Central Bank and Bank of England also raised their policy rates 50 basis points and 75 basis points, respectively. In June, the Fed left the fed funds rate unchanged, but according to the Fed’s median dot plot projection, policymakers increased their estimate for the peak rate to 5.6%, up from 5.1% in March. (The dot plot shows interest rate projections of the members of the Federal Open Market Committee.) For the second quarter overall, global equities recorded positive returns, with developed markets equities outperforming emerging markets equities on the back of better than consensus expected first quarter corporate earnings in the developed markets. European equities, while posting positive returns, underperformed other developed equity markets, such as Japan and the U.S. In the U.S., equity gains were fueled by rallies in the information technology and consumer discretionary sectors. The advance in the information technology sector was driven in part by market expectations of artificial intelligence (“AI”) potential and the growing demand for AI processors. Regarding global fixed income, performance was broadly negative during the second quarter as bond yields increased. Duration-sensitive assets sold off as higher interest rates and expectations for further monetary policy tightening weighed on market sentiment.

During the third quarter of 2023, most asset classes posted losses despite a relatively benign macroeconomic backdrop. Inflation data continued to improve across major developed markets, leading central banks to signal that they were at, or close to, their peak policy rates. In the U.S., economic growth remained resilient, while upward momentum in inflation and the labor market began to weaken—a welcome development for the Fed as it sought to reach its inflation target on a sustainable basis. Policymakers, having raised the fed funds rate by 25 basis points at their July meeting, remained on hold at their September meeting. Elsewhere, Europe and U.K. inflation surprised to the downside; China continued its efforts in support of its economy; and the Bank of Japan began to gradually normalize its monetary policy. In addition, investors had to grapple with some unexpected events during the third quarter. In August, for example, Fitch Ratings downgraded its U.S. credit rating from AAA to AA+, and the markets confronted the possibility of a U.S. government shutdown, which was then narrowly avoided in September. For the third quarter overall, global equities produced negative returns, with developed markets equities performing the worst. U.S. equities and emerging markets equities also declined. In global fixed income, bond yields rose amid significant interest rate volatility. Investors remained wary of inflation, as data indicated it might be stickier, or more persistent, than consensus expected, and markets seemed to expect the Fed and other developed markets central banks to keep interest rates higher for longer.

Most asset classes generated gains during the fourth quarter of 2023, benefiting from a positive backdrop that included strong economic growth, resilient labor markets, subdued inflationary pressures across developed economies, and signals from major central banks regarding the end of their rate hiking cycles. Broadly, the performance of the capital markets was driven by investors’ reactions to lower inflation and a dovish Fed. As a result of a significant slowdown in inflation, the potential of an economic “soft

MARKET REVIEW

landing” increased, leading to a sharp drop in interest rates and a broad-based rally across the capital markets. (A soft landing, in economics, is a cyclical downturn that avoids recession. It typically describes attempts by central banks to raise interest rates just enough to stop an economy from overheating and experiencing high inflation, without causing a significant increase in unemployment, or a hard landing.) At both their November and December meetings, Fed policymakers left the fed funds rate unchanged in a range between 5.25% and 5.50%. The Fed also signaled in December that it may have reached the peak of its monetary policy tightening cycle, with its median dot plot projection indicating there could be 75 basis points of rate cuts in 2024. For the fourth quarter overall, global equities posted significantly positive returns, with U.S. equities outperforming developed markets equities and emerging markets equities. In the U.S. equity market, gains were led by information technology, financials and consumer discretionary stocks, while energy stocks performed the worst due to a drop in oil prices. In global fixed income, yields rose during October and then fell significantly in November and December, leading to positive bond returns for the fourth quarter overall.

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

INVESTMENT OBJECTIVE

The Portfolio seeks long-term growth of capital.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Multi-Asset Solutions (“MAS”) Group discusses the Goldman Sachs Variable Insurance Trust – Goldman Sachs Multi-Strategy Alternatives Portfolio’s (the “Portfolio”) performance and positioning for the 12-month period ended December 31, 2023 (the “Reporting Period”).

How did the Portfolio perform during the Reporting Period?

During the Reporting Period, the Portfolio’s Institutional, Service and Advisor Shares generated average annual total returns of 7.90%, 7.77% and 7.53%, respectively. These returns compare to the 5.01% average annual total return of the Portfolio’s benchmark, the ICE BofA 3-Month U.S. Treasury Bill Index during the same period.

Please note that the Portfolio’s benchmark being the ICE BofA 3-Month U.S. Treasury Bill Index is a means of emphasizing that the Portfolio has an unconstrained strategy. That said, this Portfolio employs a benchmark agnostic strategy and thus comparisons to a benchmark index are not particularly relevant.

What key factors were responsible for the Portfolio’s performance during the Reporting Period?

The Portfolio’s performance is driven by three sources of return: long-term strategic asset allocation to market exposures, medium-term and short-term dynamic allocations, and excess returns from investments in Underlying Funds. Long-term strategic asset allocation is the process by which the Portfolio’s assets are allocated across underlying asset classes and strategies in a way that considers the risks of each underlying asset class and strategy. Medium-term dynamic allocation is the process by which we adjust the portfolio for changes in the business or economic cycle, while short-term dynamic allocation is the implementation of tactical market views with the goal of improving the Portfolio’s risk-adjusted return. The risk-adjusted return on an investment takes into account the risk associated with that investment relative to other potential investments. Excess returns from investments in Underlying Funds is by how much the Underlying Funds outperform or underperform their respective benchmark indices.

During the Reporting Period, the Portfolio generated positive absolute returns, largely because of long-term strategic asset allocation. Short-term dynamic allocation and selection within the Underlying Funds also bolstered performance. Medium-term dynamic allocation detracted slightly from the Portfolio’s returns.

Long-term strategic asset allocation added to the Portfolio’s performance during the Reporting Period, with most strategic allocations contributing positively. Among the exceptions were a strategic allocation to U.S. Treasury futures and the Portfolio’s U.S. interest rate options strategy, which seeks to profit if interest rates fall, remain constant or rise less than anticipated. Both of these strategic allocations detracted from the Portfolio’s performance, as U.S. Treasury yields rose during the Reporting Period. (Our long U.S. interest rate options strategy is a macroeconomic hedge that buys options on short-term interest rates, including call options. A call option is an option that gives the holder the right to buy a certain quantity of an underlying security at an agreed-upon price at any time up to an agreed-upon date.) Among liquid alternatives strategies, the Portfolio was hampered by its strategic allocation to managed futures.

Medium-term dynamic allocation detracted modestly from the Portfolio’s performance during the Reporting Period. Specifically, the Portfolio was hindered by our medium-term dynamic views that it has decreased exposure to corporate credit and an increased duration position. (Duration is a measure of a portfolio’s sensitivity to changes in interest rates.)

Short-term dynamic allocations, which are primarily implemented through the use of derivatives and exchange-traded funds (“ETFs”), had a positive impact on the Portfolio’s performance during the Reporting Period. Within equities, the Portfolio benefited most from its short-term dynamic allocations to the energy sector and to the Eurozone banking sector. In fixed income, the Portfolio was helped by its short-term dynamic allocation to emerging markets debt, though this was offset somewhat by its short-term dynamic allocation to two-year and 10-year U.S. Treasury futures, which hurt.

Overall, security selection within the Underlying Funds added to the Portfolio’s returns, with many fixed income and equity Underlying Funds outperforming their benchmark indices during the Reporting Period. The Goldman Sachs Strategic Income Fund and Goldman Sachs Emerging Markets Equity Insights Fund outperformed their respective benchmark indices the most during the Reporting Period. In addition, the Goldman Sachs Core Fixed Income Fund outperformed its benchmark index between May 2023, when it was added as an Underlying Fund, and the end of the Reporting Period. The Goldman Sachs High Yield Fund and Goldman Sachs Global Infrastructure Fund underperformed their respective benchmark indices most during the Reporting Period. The performance of liquid alternative Underlying Funds was positive overall, with the Goldman Sachs Long Short Credit Strategies Fund significantly outperforming its cash benchmark. On the other hand, the Goldman Sachs Managed Futures Strategy Fund underperformed its cash benchmark during the Reporting Period.

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

How was the Portfolio positioned at the beginning of the Reporting Period?

At the beginning of the Reporting Period, the Portfolio was positioned, in terms of its total net assets, with 35.7% in liquid alternative strategies, 29.5% in real assets/satellite asset classes, 16.19% in directional views and the balance in cash. Liquid alternatives strategies generally include, but are not limited to, momentum or trend trading strategies (investment decisions based on trends in asset prices over time), hedge fund beta (long term total returns consistent with investment results that approximate the return and risk patterns of a diversified universe of hedge funds), managed risk investment strategies (which seek to manage extreme risk scenarios by implementing daily and monthly risk targets across a diversified mix of asset classes) and unconstrained fixed income strategies (which have the ability to move across various fixed income sectors). Real assets/satellite asset classes generally include, but are not limited to, commodities, global real estate securities, global infrastructure securities, master limited partnerships, emerging markets equities and emerging markets debt. Directional views include more traditional beta investments, such as U.S. equities and non-U.S. developed markets equities. This above sector breakout is inclusive of derivative exposure across all asset classes.

How did you manage the Portfolio’s allocations during the Reporting Period?

During the Reporting Period, we made adjustments to the Portfolio’s long-term strategic asset allocation. Specifically, during May 2023, we increased the Portfolio’s strategic allocations to core fixed income, high yield corporate bonds, high yield loans and emerging markets debt.

Within medium-term dynamic allocations, in January 2023, we increased the Portfolio’s exposures to U.S. large-cap equities, emerging markets equities and emerging markets debt. In February, we further increased the Portfolio’s exposure to emerging markets debt, while reducing its exposure to U.S. large-cap equities. During April, we added to the Portfolio’s emerging markets debt exposure. In May, we increased the Portfolio’s exposure to managed futures and reduced its exposure to corporate credit. We also decreased exposure to emerging markets equities overall. Additionally, we increased the Portfolio’s exposure to global infrastructure securities. During August, we reduced the Portfolio’s investments in two-year U.S. Treasury futures. In October, we increased exposures to high yield corporate bonds and global infrastructure securities. We decreased the Portfolio’s investments in 10-year U.S. Treasury futures and non-U.S. developed markets equities. During November, we further increased the Portfolio’s exposure to high yield corporate bonds and increased its exposure to high yield loans. We increased both of these exposures again during December, while reducing the Portfolio’s exposure to non-U.S. developed markets equities and its investments in two-year U.S. Treasury futures.

During the Reporting Period, we continued to express our short-term dynamic views mainly through the use of ETFs and derivatives. Using these instruments, we maintained tactical exposures to U.S. equities, non-U.S. developed markets equities, fixed income and currencies. Among notable short-term tactical allocations were investments in Eurozone bank futures, U.S. dollar/Japanese yen currency forwards, U.S. dollar/Brazilian real currency forwards and energy master limited partnerships. In October 2023, we increased the Portfolio’s overall equity risk by increasing its exposure to non-U.S. developed markets equities.

Regarding Underlying Funds, as mentioned previously, we added the Goldman Sachs Core Fixed Income Fund as an Underlying Fund in May 2023.

How was the Portfolio positioned at the end of the Reporting Period?

At the end of the Reporting Period, the Portfolio was positioned, in terms of its total net assets, with 41.00% in liquid alternative strategies, 50.19% in real assets/satellite asset classes, 7.10% in directional views and the balance in cash. This above sector breakout is inclusive of derivative exposure across all asset classes.

How did the Portfolio use derivatives and similar instruments during the Reporting Period?

During the Reporting Period, the Portfolio employed equity index futures to effect long exposures in European large-cap equities (neutral impact on performance) and emerging markets equities (negative impact).

Within fixed income during the Reporting Period, the Portfolio used interest rate futures to express views on the U.S. Treasury yield curve (negative impact) and on the German government bond yield curve (positive impact). The Portfolio also used interest rate options in a macroeconomic hedge that seeks to profit if interest rates fall, remain constant or rise less than anticipated (negative impact). Finally, within short-term tactical views on currencies, the Portfolio employed forward foreign currency exchange contracts (neutral impact).

Additionally, some of the Underlying Funds used derivatives during the Reporting Period to apply their active investment views with greater versatility and potentially to afford greater risk management precision. As market conditions warranted during the Reporting Period, some of these Underlying Funds engaged in forward foreign currency exchange contracts, financial futures contracts, options, swap contracts and structured securities to attempt to enhance portfolio return and for hedging purposes.

What is the Portfolio’s tactical view and strategy for the months ahead?

At the end of the Reporting Period, we believed the U.S. was still in the late stages of the economic cycle. Although our base case was for a “soft landing” in 2024, we thought the risks of a recession remained above average as long as the Fed maintained its restrictive posture. (A soft landing, in economics, is a cyclical downturn that avoids recession. It typically describes attempts by central banks to raise interest rates just enough to stop an economy from overheating and experiencing high inflation, without

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

causing a significant increase in unemployment, or a hard landing.) Because of the Fed’s progress on inflation during the Reporting Period, we expected policymakers to shift their focus to economic growth in the near term, which could lead to a rate cutting cycle. While U.S. wage growth was near levels consistent with the Fed’s long-term targets, the job market remained tight and unemployment was still below 4%.

In our view, bonds continued to look attractive at the end of the Reporting Period, even though their yields had fallen from recent highs. We also believed bonds could provide portfolio diversification benefits in the event of an economic downturn. Overall, we thought the resilience of the U.S. economy and declining inflation would be supportive for U.S. equities, although their high valuations relative to history could remain a headwind. At the end of the Reporting Period, the Portfolio’s equity and fixed income allocations were near our long-term neutral positions. Going forward, we continued to believe a dynamic investment approach and careful risk management should help us identify attractive opportunities, both regionally and across asset classes.

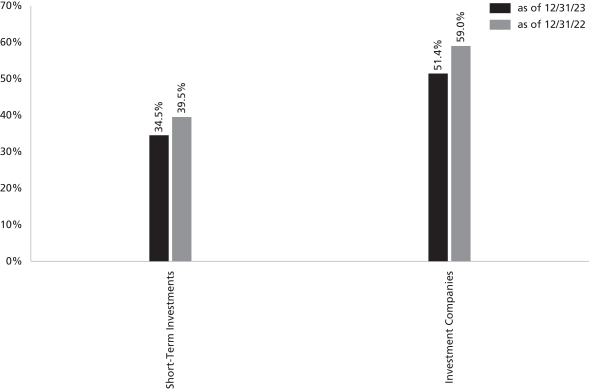

FUND BASICS

Multi-Strategy Alternatives Portfolio

as of December 31, 2023

|

|

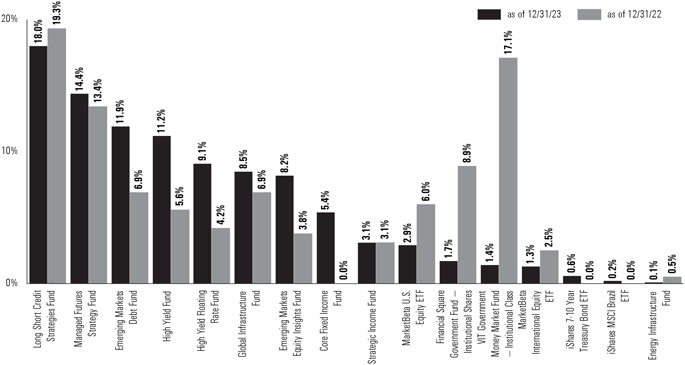

OVERALL UNDERLYING FUND AND ETF WEIGHTINGS1 |

| | 1 | The Portfolio is actively managed and, as such, its composition may differ over time. The percentage shown for each Underlying Fund and ETF reflects the value of that Underlying Fund or ETF as a percentage of net assets of the Portfolio. Figures in the graph above may not sum to 100% due to rounding and/or exclusion of other assets and liabilities. Underlying sector allocations of exchange traded funds and investment companies held by the Portfolio are not reflected in the graph above. The graph depicts the Portfolio’s investments but may not represent the Portfolio’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

| | | For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

Performance Summary

December 31, 2023

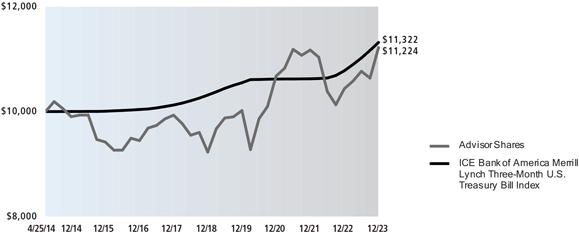

The following graph shows the value, as of December 31, 2023, of a $10,000 investment made on April 25, 2014 (commencement of the Fund’s operations) in Advisor Shares at NAV. For comparative purposes, the performance of the Portfolio’s benchmark, the ICE Bank of America Merrill Lynch Three-Month U.S. Treasury Bill Index, is shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and, in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

|

|

Multi-Strategy Alternatives Portfolio’s Lifetime Performance |

|

Performance of a $10,000 investment, with distributions reinvested, from April 25, 2014 through December 31, 2023. |

| | | | | | |

| | | |

Average Annual Total Returns through December 31, 2023* | | One Year | | Five Years | | Since Inception |

| | | |

Institutional (Commenced on April 25, 2014) | | 7.90% | | 4.41% | | 1.59% |

| | | | | | | |

| | | |

Service (Commenced on April 25, 2014) | | 7.77% | | 4.16% | | 1.35% |

| | | | | | | |

| | | |

Advisor (Commenced on April 25, 2014) | | 7.53% | | 4.00% | | 1.20% |

| | | | | | | |

| * | These returns assume reinvestment of all distributions at NAV. Because Institutional, Service and Advisor Shares do not involve sales charge, such a charge is not applied to their Average Annual Total Returns. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST TREND DRIVEN ALLOCATION FUND

INVESTMENT OBJECTIVE

The Fund seeks total return while seeking to provide volatility management.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Quantitative Investment Strategies (“QIS”) Team discusses the Variable Insurance Trust – Goldman Sachs Trend Driven Allocation Fund’s (the “Fund”) performance and positioning for the 12-month period ended December 31, 2023 (the “Reporting Period”).

How did the Fund perform during the Reporting Period?

During the Reporting Period, the Fund’s Institutional and Service Shares generated average annual total returns of 15.85% and 15.57%, respectively. These returns compare to the 15.90% average annual total return of the Fund’s blended benchmark during the same time period. The components of the Fund’s blended benchmark, which is comprised 60% of the MSCI World Index (Net, USD, Hedged) and 40% of the Bloomberg U.S. Treasury Index (Total Return, Unhedged, USD), generated average annual total returns of 24.30% and 4.05%, respectively, during the same time period.

During the Reporting Period, the Fund’s overall annualized volatility was 11.13%, more than the Fund’s blended benchmark’s annualized volatility of 10.54% during the same time period. By way of comparison, the S&P 500® Index’s annualized volatility was 15.15% during the Reporting Period.

What key factors were responsible for the Fund’s performance during the Reporting Period?

The Fund primarily seeks to achieve its investment objective by investing in a portfolio of equity and fixed income asset classes, with the expectation of investing at least 50% of its assets in equities and a minimum of 30% of its assets in fixed income, assuming normal market conditions. The Investment Adviser makes investment decisions based upon its analysis of macro factors, most notably “trends” from around the world. The trends analyzed by the Investment Adviser are based on, but are not limited to, relative considerations around the prices and volatility of the underlying markets. If recent prices are higher than measures of historical prices for an asset, the Investment Adviser generally considers there to be a positive (strong) trend for these assets, whereas recent prices below such measures generally indicate negative (poor) trends. If the current measure of volatility is elevated relative to historic realizations of this volatility measure for an asset, the Investment Adviser generally considers there to be a negative (poor) trend for this asset, whereas volatility that is less elevated indicates positive (strong) trends. As a result of the trends analysis, the Investment Adviser may allocate more of the Fund’s assets to investments with relatively strong recent trends and allocate assets away from investments with relatively poor recent trends.

In addition, as a continuing part of the Fund’s investment strategy, the Investment Adviser seeks to manage volatility and limit losses by allocating the Fund’s assets away from risky investments in distressed or volatile market environments. In this context, volatility is a statistical measurement of the magnitude of up and/or down fluctuations in the value of a financial instrument or index. While the Investment Adviser attempts to manage the Fund’s volatility, there can be no guarantee that the Fund will be successful.

During the Reporting Period, the Fund performed in line with its blended benchmark. Because of heightened equity market volatility driven by geopolitical tensions in the Middle East, the Fund’s drawdown control and volatility management mechanisms were activated in October, actively de-risking the Fund into cash. (A drawdown is a peak-to-trough decline during a specific time period and is a measure of downside volatility.) The increase in the Fund’s cash allocation detracted slightly from its relative performance for the Reporting Period overall. On the positive side, the Fund benefited from its underweight versus the blended benchmark in fixed income, which added to relative returns.

From an absolute return perspective, the Fund was helped by its allocations to U.S. large-cap equities, which posted gains amid a rally in the information technology sector. Exposure to European and Japanese equities added further to absolute performance. The Fund also benefited from its participation in the fed funds market. Conversely, allocations to U.S. Treasury securities detracted from the Fund’s absolute returns.

What was the Fund’s volatility during the Reporting Period?

As part of our investment approach, we seek to mitigate the Fund’s volatility. As mentioned earlier, for the Reporting Period overall, the Fund’s overall annualized volatility was 11.13%, more than its blended benchmark’s annualized volatility of 10.54%. By way of comparison, the S&P 500® Index’s annualized volatility was 15.15% during the Reporting Period.

How was the Fund positioned during the Reporting Period?

During the Reporting Period, we managed the Fund’s allocations across equity and fixed income markets based upon an analysis of market factors and trends from around the world. At the beginning of the Reporting Period, the Fund’s total assets were allocated 69.5% to equities, 30.5% to fixed income and 0% to cash. (Many of these positions were implemented through the use of

GOLDMAN SACHS VARIABLE INSURANCE TRUST TREND DRIVEN ALLOCATION FUND

exchanged-traded index future contracts.) Within the equity allocation, the Fund had significant exposure to U.S. large-cap equities and, to a lesser extent, to European, Japanese and U.K. equities. Within the fixed income allocation, the Fund had substantial exposure to U.S. Treasury securities at the beginning of the Reporting Period.

Between January and September 2023, we made no significant changes to the Fund’s allocations. In October, as equity market volatility increased, we reduced the Fund’s allocations to U.S. large-cap equities, Japanese equities, European equities and U.K. equities. We also decreased its allocation to U.S. Treasury securities and increased its cash position. In November, we unwound these changes, and at the end of the Reporting Period, the Fund’s allocations were near where they were at the beginning of the Reporting Period.

How did the Fund use derivatives and similar instruments during the Reporting Period?

During the Reporting Period, the Fund employed exchange-traded equity index futures to gain exposure to U.S. large-cap stocks and to European, Japanese and U.K. equities. The use of these instruments had a positive impact overall on absolute returns. In addition, the Fund used bond futures to gain exposure to U.S. Treasury securities, which had a negative impact on the Fund’s performance during the Reporting Period.

What is the Fund’s tactical asset allocation view and strategy for the months ahead?

At the end of the Reporting Period, the Fund’s total assets were allocated 69.0% to equities, 31% to fixed income and 0% to cash. (Many of these positions were implemented through the use of exchanged-traded index future contracts.) Within the equity allocation, the Fund had significant exposure to U.S. large-cap equities and, to a lesser extent, to European, Japanese and U.K. equities. Within the fixed income allocation, the Fund had substantial exposure to U.S. Treasury securities at the end of the Reporting Period.

Going forward, we intend to position the Fund based on analyses of trends from around the world, while dynamically managing the volatility, or risk, of the overall portfolio. In general, the Fund will seek to invest at least 50% of its assets in equity investments and at least 30% of its assets in fixed income investments. The Fund may deviate from these strategic allocations in order to allocate more of the Fund’s assets to investments with relatively strong recent trends and allocate assets away from investments with relatively poor recent trends. When volatility increases, our goal is to preserve capital by proportionally increasing the Fund’s cash exposure and reducing its exposure to riskier asset classes. There is no guarantee the Fund’s dynamic management strategy will cause it to achieve its investment objective.

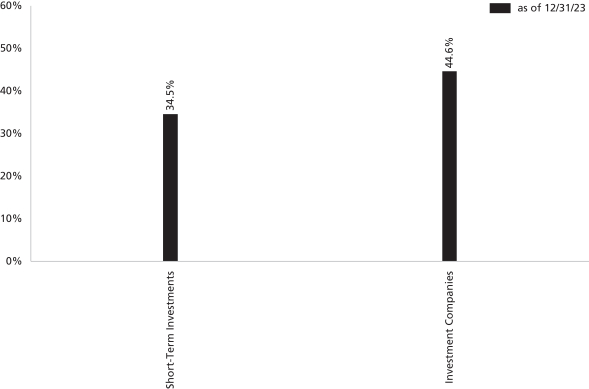

FUND BASICS

Trend Driven Allocation Fund

as of December 31, 2023

| | 1 | The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. Figures in the above graph may not sum to 100% due to the exclusion of other assets and liabilities. The underlying composition of exchange traded funds and investment companies held by the Fund are not reflected in the graph above. Consequently, the Fund’s overall composition may differ from the percentages contained in the graph above. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

| | | For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST TREND DRIVEN ALLOCATION FUND FUND

Performance Summary

December 31, 2023

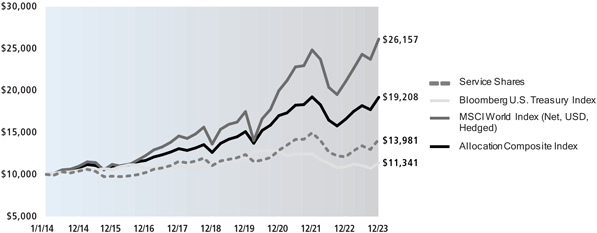

The following graph shows the value, as of December 31, 2023, of a $10,000 investment made on January 1, 2014 in Service Shares at NAV. For comparative purposes, the performance of the Fund’s blended benchmark, the Allocation Composite Index, (comprised of the Morgan Stanley Capital International (MSCI) World Index (Net, USD, Hedged) (60%) and the Bloomberg U.S. Treasury Index (Total Return, USD, Unhedged) (40%)) is shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and, in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

|

|

Trend Driven Allocation Fund’s 10 Year Performance |

|

Performance of a $10,000 investment, with distributions reinvested, from January 1, 2014 through December 31, 2023.

|

| | | | | | |

| | | |

Average Annual Total Returns through December 31, 2023* | | One Year | | Five Years | | Ten Years |

| | | |

Institutional | | 15.85% | | 5.07% | | 3.66% |

| | | | | | | |

| | | |

Service | | 15.57% | | 4.81% | | 3.41% |

| | | | | | | |

| * | These returns assume reinvestment of all distributions at NAV. Because Institutional and Service Shares do not involve sales charge, such a charge is not applied to their Average Annual Total Return. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-ASSET STRATEGIES FUNDS

Index Definitions

ICE BofAML Three-Month T-Bill Index measures total return on cash, including price and interest income, based on short-term government Treasury Bills of about 90-day maturity, as reported by Bank of America Merrill Lynch.

MSCI ACWI Investable Market Index captures large, mid and small cap representation across 23 developed markets and 27 emerging markets countries.

MSCI Emerging Markets Index captures large-cap and mid-cap representation across 26 emerging markets countries. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

Bloomberg U.S. Treasury Index measures U.S. dollar-denominated, fixed-rate, nominal debt issued by the U.S. Treasury. Treasury bills are excluded by the maturity constraint.

MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across 23 developed markets countries. It covers approximately 85% of the free float-adjusted market capitalization in each country.

S&P 500® Index is a U.S. stock market index based on the market capitalizations of 500 large companies having common stock listed on the New York Stock Exchange or NASDAQ. The S&P 500® Index components and their weightings are determined by S&P Dow Jones Indices.

It is not possible to invest directly in an unmanaged index.

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

|

Schedule of Investments December 31, 2023 |

| | | | | | | | |

| | | Shares | | Description | | Value | |

| |

| | Underlying Funds (Class R6 Shares)(a) – 90.0% | |

| |

| | Equity – 16.8% | |

| | 258,348 | | Goldman Sachs Global Infrastructure Fund | | $ | 3,219,022 | |

| | 386,922 | | Goldman Sachs Emerging Markets Equity Insights Fund | | | 3,134,071 | |

| | 4,466 | | Goldman Sachs Energy Infrastructure Fund | | | 49,255 | |

| | | | | | | | |

| | | | | | | 6,402,348 | |

| | | |

| |

| | Fixed Income – 73.2% | |

| | 866,585 | | Goldman Sachs Long Short Credit Strategies Fund | | | 6,863,356 | |

| | 558,562 | | Goldman Sachs Managed Futures Strategy Fund | | | 5,490,662 | |

| | 478,172 | | Goldman Sachs Emerging Markets Debt Fund | | | 4,542,639 | |

| | 757,078 | | Goldman Sachs High Yield Fund | | | 4,254,780 | |

| | 388,593 | | Goldman Sachs High Yield Floating Rate Fund | | | 3,458,481 | |

| | 221,396 | | Goldman Sachs Core Fixed Income Fund | | | 2,061,193 | |

| | 124,143 | | Goldman Sachs Strategic Income Fund | | | 1,165,702 | |

| | | | | | | | |

| | | | | | | 27,836,813 | |

| | | |

| | TOTAL UNDERLYING FUNDS (CLASS R6 SHARES)

(Cost $33,612,750) | | | 34,239,161 | |

| | | |

| | | | | | | | |

| |

| | Exchange Traded Funds – 4.9% | |

| | | |

| | 16,873 | | Goldman Sachs MarketBeta U.S. Equity ETF(a)(b) | | | 1,102,650 | |

| | 8,847 | | Goldman Sachs MarketBeta International Equity ETF(a) | | | 475,349 | |

| | 2,255 | | iShares 7-10 Year Treasury Bond ETF | | | 217,360 | |

| | 2,343 | | iShares MSCI Brazil ETF | | | 81,911 | |

| | | |

| | |

| | TOTAL EXCHANGE TRADED FUNDS

(Cost $1,579,562) | | | 1,877,270 | |

| | | |

| | | |

| | | Shares | | Dividend Rate | | Value | |

| |

| | Investment Companies (Institutional Shares) – 3.1%(a) | |

| |

| | Goldman Sachs Financial Square Government Fund | |

| | 635,024 | | 5.248% | | | 635,024 | |

| |

| | Goldman Sachs VIT Government Money Market Fund | |

| | 536,056 | | 5.270 | | | 536,056 | |

| | | |

| | |

| | Total Investment Companies (Cost $1,171,080) | | | 1,171,080 | |

| | | |

| |

| | TOTAL INVESTMENTS BEFORE SECURITIES LENDING | |

| | REINVESTMENT VEHICLE (Cost $36,363,392) | | | 37,287,511 | |

| | | |

| | | | | | | | |

| | | Shares | | Dividend Rate | | Value | |

| |

| | Securities Lending Reinvestment Vehicle – 0.0%(a) | |

| |

| | Goldman Sachs Financial Square Government Fund – Institutional Shares | |

| | 6,700 | | 5.248% | | $ | 6,700 | |

| | (Cost $6,700) | |

| | | |

| | TOTAL INVESTMENTS – 98.0% | | | | |

| | (Cost $36,370,092) | | $ | 37,294,211 | |

| | | |

| | OTHER ASSETS IN EXCESS OF LIABILITIES – 2.0% | | | 750,279 | |

| | | |

| | NET ASSETS – 100.0% | | $ | 38,044,490 | |

| | | |

| | |

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. |

| |

| (a) | | Represents an affiliated issuer. |

| (b) | | All or a portion of security is on loan. |

| | |

| |

| Currency Abbreviations: |

| BRL | | Brazilian Real |

| CHF | | Swiss Franc |

| EUR | | Euro |

| USD | | United States Dollar |

| | |

| The accompanying notes are an integral part of these financial statements. | | 13 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

|

Schedule of Investments (continued) December 31, 2023 |

|

|

ADDITIONAL INVESTMENT INFORMATION |

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS — At December 31, 2023, the Portfolio had the following forward foreign currency exchange contracts:

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS WITH UNREALIZED GAIN

| | | | | | | | | | | | | | | | | | | | | | | | |

| Counterparty | | Currency Purchased | | | | Currency Sold | | | | | | Settlement Date | | | | Unrealized Gain | |

| |

Morgan Stanley Co., Inc. | | | | | | | | | | | | | | | | | | | | | | | | |

| | USD | | 78,378 | | | | BRL | | | 380,000 | | | | | | | 2/2/2024 | | | | $ | 286 | |

| | EUR | | 50,000 | | | | USD | | | 54,185 | | | | | | | 3/20/2024 | | | | | 1,184 | |

|

| |

| | | | | | | | | |

TOTAL | | | | | | | | | | | | | | | | | | | | | | $ | 1,470 | |

|

| |

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS WITH UNREALIZED LOSS

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Counterparty | | Currency Purchased | | | | Currency Sold | | | | | Settlement Date | | | | | | Unrealized Loss |

| |

Morgan Stanley Co., Inc. | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | BRL | | 380,000 | | | | | USD | | | 78,701 | | | | | | | 1/3/2024 | | | | | | | | (473) | |

| | USD | | 77,265 | | | | | BRL | | | 380,000 | | | | | | | 1/3/2024 | | | | | | | | (962) | |

| | USD | | 57,660 | | | | | CHF | | | 50,000 | | | | | | | 3/20/2024 | | | | | | | | (2,267) | |

|

| |

| | | | | | | | | |

TOTAL | | | | | | | | | | | | | | | | | | | | | | | | | | $ | (3,702) | |

|

| |

FUTURES CONTRACTS — At December 31, 2023, the Portfolio had the following futures contracts:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | Unrealized |

| | | Number of | | | | Expiration | | | | | | Notional | | | | | | Appreciation/ |

| Description | | Contracts | | | | Date | | | | | | Amount | | | | | | (Depreciation) |

| |

Long position contracts: | | | | | | | | | | | | | | | | | | | | | | | | |

EURO STOXX 50 Index | | 2 | | | | | 03/15/24 | | | | | | | $ | 100,305 | | | | | | | $ | (312) | |

EURO-BUND Week Op Mar24 | | 1 | | | | | 03/07/24 | | | | | | | | 151,429 | | | | | | | | 4,818 | |

U.S. Treasury 10 Year Note | | 9 | | | | | 03/19/24 | | | | | | | | 1,014,609 | | | | | | | | 30,652 | |

|

| |

| | | | | | | |

Total | | | | | | | | | | | | | | | | | | | | | | | 35,158 | |

|

| |

| | | | | | | |

Short position contracts: | | | | | | | | | | | | | | | | | | | | | | | | |

Euro Bund Future | | (1) | | | | | 03/07/24 | | | | | | | | (151,429 | ) | | | | | | | 766 | |

|

| |

| | | | | | | |

Total Futures Contracts | | | | | | | | | | | | | | | | | | | | | | $ | 35,924 | |

|

| |

| | |

| 14 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

|

|

ADDITIONAL INVESTMENT INFORMATION (continued) |

PURCHASED OPTIONS CONTRACTS — At December 31, 2023, the Fund had the following purchased option contracts:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | Premiums Paid | | Unrealized | |

| | | Exercise | | | Expiration | | | Number of | | | | | Market | | | (Received) by | | Appreciation/ | |

| Description | | Rate | | | Date | | | Contracts | | | Notional Amount | | Value | | | the Fund | | (Depreciation) | |

Purchased Option Contracts: Calls | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | $96.75 | | | | 06/12/2026 | | | | 6 | | | $ | 1,453,650 | | | $ | 11,850 | | | $ | 9,314 | | | $ | 2,536 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.50 | | | | 12/12/2025 | | | | 26 | | | | 6,300,775 | | | | 27,463 | | | | 31,260 | | | | (3,798) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.50 | | | | 12/12/2025 | | | | 5 | | | | 1,211,688 | | | | 11,281 | | | | 9,024 | | | | 2,257 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.50 | | | | 09/12/2025 | | | | 28 | | | | 6,783,000 | | | | 28,000 | | | | 31,565 | | | | (3,565) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.63 | | | | 09/12/2025 | | | | 1 | | | | 242,250 | | | | 1,969 | | | | 1,860 | | | | 109 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.50 | | | | 09/12/2025 | | | | 5 | | | | 1,211,250 | | | | 10,719 | | | | 8,512 | | | | 2,207 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.25 | | | | 06/13/2025 | | | | 24 | | | | 5,807,400 | | | | 25,950 | | | | 29,712 | | | | (3,762) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.75 | | | | 06/13/2025 | | | | 6 | | | | 1,451,850 | | | | 11,663 | | | | 9,764 | | | | 1,899 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.63 | | | | 06/13/2025 | | | | 1 | | | | 241,975 | | | | 1,750 | | | | 1,723 | | | | 27 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.25 | | | | 06/13/2025 | | | | 5 | | | | 1,209,875 | | | | 11,375 | | | | 9,199 | | | | 2,176 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 98.00 | | | | 03/14/2025 | | | | 13 | | | | 3,138,850 | | | | 5,363 | | | | 4,093 | | | | 1,270 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.25 | | | | 03/14/2025 | | | | 18 | | | | 4,346,100 | | | | 14,737 | | | | 32,665 | | | | (17,927) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.00 | | | | 03/14/2025 | | | | 18 | | | | 4,346,100 | | | | 18,450 | | | | 23,892 | | | | (5,442) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.50 | | | | 03/14/2025 | | | | 1 | | | | 241,450 | | | | 1,537 | | | | 1,693 | | | | (156) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 98.00 | | | | 12/13/2024 | | | | 20 | | | | 4,813,500 | | | | 5,500 | | | | 4,047 | | | | 1,454 | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.25 | | | | 12/13/2024 | | | | 21 | | | | 5,054,175 | | | | 11,550 | | | | 33,518 | | | | (21,969) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.25 | | | | 12/13/2024 | | | | 1 | | | | 240,675 | | | | 1,337 | | | | 1,574 | | | | (237) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.25 | | | | 09/13/2024 | | | | 12 | | | | 2,877,150 | | | | 3,300 | | | | 15,979 | | | | (12,679) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 96.00 | | | | 09/13/2024 | | | | 1 | | | | 239,763 | | | | 975 | | | | 1,421 | | | | (446) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 95.38 | | | | 09/13/2024 | | | | 5 | | | | 1,198,813 | | | | 8,781 | | | | 20,390 | | | | (11,609) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 95.25 | | | | 09/13/2024 | | | | 4 | | | | 959,050 | | | | 7,850 | | | | 15,996 | | | | (8,146) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 98.50 | | | | 06/14/2024 | | | | 47 | | | | 11,219,487 | | | | 2,056 | | | | 7,034 | | | | (4,978) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.75 | | | | 06/14/2024 | | | | 40 | | | | 9,548,500 | | | | 2,750 | | | | 53,460 | | | | (50,710) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.25 | | | | 06/14/2024 | | | | 8 | | | | 1,909,700 | | | | 800 | | | | 7,667 | | | | (6,867) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 95.38 | | | | 06/14/2024 | | | | 5 | | | | 1,193,562 | | | | 4,094 | | | | 18,375 | | | | (14,282) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 95.13 | | | | 06/14/2024 | | | | 4 | | | | 954,850 | | | | 4,725 | | | | 14,119 | | | | (9,394) | |

| 3 Month Secured Overnight | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Financing Rate | | | 97.75 | | | | 03/15/2024 | | | | 46 | | | | 10,926,725 | | | | 862 | | | | 54,441 | | | | (53,578) | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 15 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI - STRATEGY ALTERNATIVES PORTFOLIO

|

Schedule of Investments (continued) December 31, 2023 |

|

|

ADDITIONAL INVESTMENT INFORMATION (continued) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | Premiums Paid | | | Unrealized | |

| | | Exercise | | | Expiration | | | Number of | | | | | | Market | | | (Received) by | | | Appreciation/ | |

| Description | | Rate | | | Date | | | Contracts | | | Notional Amount | | | Value | | | the Fund | | | (Depreciation) | |

3 Month Secured Overnight Financing Rate | | $ | 95.38 | | | | 03/15/2024 | | | | 5 | | | $ | 1,187,687 | | | $ | 719 | | | $ | 15,921 | | | $ | (15,202) | |

3 Month Secured Overnight Financing Rate | | | 95.00 | | | | 03/15/2024 | | | | 8 | | | | 1,900,300 | | | | 2,650 | | | | 23,424 | | | | (20,774) | |

Total purchased option contracts | | | | | | | | | | | 384 | | | $ | 92,210,150 | | | $ | 240,056 | | | $ | 491,642 | | | $ | (251,586) | |

| | |

| 16 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST TREND DRIVEN ALLOCATION FUND

|

Schedule of Investments December 31, 2023 |

| | | | | | | | |

| | | Shares | | Dividend Rate | | Value | |

| |

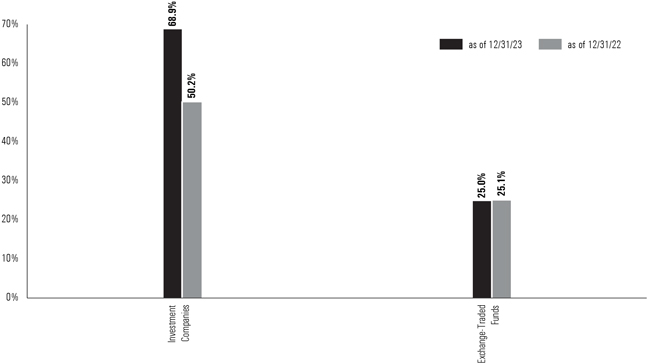

| | Investment Companies (Institutional Shares) – 68.9%(a) | |

| | Goldman Sachs Financial Square Government Fund | |

| | 40,408,374 | | 5.248% | | $ | 40,408,374 | |

| | Goldman Sachs Financial Square Treasury Instruments Fund | |

| | 38,864,945 | | 5.206 | | | 38,864,945 | |

| | Goldman Sachs Financial Square Treasury Obligations Fund | |

| | 38,870,537 | | 5.241 | | | 38,870,537 | |

| | Goldman Sachs Financial Square Treasury Solutions Fund | |

| | 38,392,063 | | 5.231 | | | 38,392,063 | |

| | Goldman Sachs VIT Government Money Market Fund | |

| | 35,050,510 | | 5.270 | | | 35,050,510 | |

| | | |

| |

| | Total Investment Companies | |

| | (Cost $191,586,429) | | | 191,586,429 | |

| | | |

| | | |

| | | | Description | | | | |

| |

| | Exchange-Traded Funds – 25.0% | |

| | | |

| | 75,565 | | iShares Core S&P 500 ETF | | | 36,092,111 | |

| | 76,300 | | Vanguard S&P 500 ETF | | | 33,327,840 | |

| | | |

| | TOTAL EXCHANGE-TRADED FUNDS | |

| | (Cost $41,770,457) | | | 69,419,951 | |

| | | |

| | TOTAL INVESTMENTS – 93.9% | |

| | (Cost $233,356,886) | | $ | 261,006,380 | |

| | | |

| | OTHER ASSETS IN EXCESS OF LIABILITIES – 6.1% | | | 17,006,589 | |

| | | |

| | NET ASSETS – 100.0% | | $ | 278,012,969 | |

| | | |

The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets.

| (a) | Represents an affiliated issuer. |

| | |

| |

| | | ADDITIONAL INVESTMENT INFORMATION |

FUTURES CONTRACTS — At December 31, 2023, the Fund had the following futures contracts:

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | Unrealized | |

| | | Number of | | | Expiration | | | Notional | | | Appreciation/ | |

| Description | | Contracts | | | Date | | | Amount | | | (Depreciation) | |

Long position contracts: | | | | | | | | | | | | | | | | |

EURO STOXX 50 Index | | | 372 | | | | 03/15/24 | | | $ | 18,656,714 | | | $ | (113,834 | ) |

FTSE 100 Index | | | 84 | | | | 03/15/24 | | | | 8,304,937 | | | | 189,035 | |

S&P 500 E-Mini Index | | | 348 | | | | 03/15/24 | | | | 83,868,000 | | | | 2,119,971 | |

TOPIX Index | | | 76 | | | | 03/07/24 | | | | 12,752,908 | | | | 144,576 | |

U.S. Treasury 10 Year Note | | | 752 | | | | 03/19/24 | | | | 84,776,250 | | | | 2,966,400 | |

| Total Futures Contracts | | | | | | | | | | | | | | $ | 5,306,148 | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 17 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-ASSET STRATEGIES FUNDS

|

Statements of Assets and Liabilities December 31, 2023 |

| | | | | | | | | | | | |

| | | | | Multi-Strategy

Alternatives Portfolio | | | Trend Driven Allocation

Fund |

| | | | |

| | Assets: | | | | | | | | | | |

| | | | |

| | Investments in affiliated issuers, at value (cost $36,081,010 and $191,586,429, respectively)(a) | | $ | 36,988,240 | | | $ | 191,586,429 | | | |

| | Investments in unaffiliated issuers, at value (cost $282,382 and $41,770,457, respectively) | | | 299,271 | | | | 69,419,951 | | | |

| | Investments in affiliated securities lending reinvestment vehicle, at value which equals cost | | | 6,700 | | | | — | | | |

| | Purchased Options, at value (premiums paid $491,642 and $–, respectively) | | | 240,056 | | | | — | | | |

| | Cash | | | 609,445 | | | | 8,113,476 | | | |

| | Foreign Currency, at value (cost $– and $210,979, respectively) | | | — | | | | 218,392 | | | |

| | Receivables: | | | | | | | | | | |

| | Reimbursement from investment adviser | | | 8,975 | | | | 3,928 | | | |

| | Due from broker | | | 6,242 | | | | — | | | |

| | Dividends | | | 6,012 | | | | 507,445 | | | |

| | Fund shares sold | | | 4,289 | | | | 129,201 | | | |

| | Collateral for futures contracts | | | — | | | | 8,513,209 | | | |

| | Unrealized gain on forward foreign currency exchange contracts | | | 1,470 | | | | — | | | |

| | Variation margin on futures contracts | | | 150 | | | | — | | | |

| | Other assets | | | 5,609 | | | | — | | | |

| | |

| | Total assets | | | 38,176,459 | | | | 278,492,031 | | | |

| | |

| | | | | | | | | | | | |

| | | | |

| | Liabilities: | | | | | | | | | | |

| | | | |

| | Variation margin on futures contracts | | | — | | | | 119,610 | | | |

| | Unrealized loss on forward foreign currency exchange contracts | | | 3,702 | | | | — | | | |

| | Payables: | | | | | | | | | | |

| | Distribution and Service fees and Transfer Agency fees | | | 59,233 | | | | 63,082 | | | |

| | Fund shares redeemed | | | 13,064 | | | | 80,609 | | | |

| | Payable upon return of securities loaned | | | 6,700 | | | | — | | | |

| | Management fees | | | — | | | | 149,871 | | | |

| | Accrued expenses | | | 49,270 | | | | 65,890 | | | |

| | |

| | Total liabilities | | | 131,969 | | | | 479,062 | | | |

| | |

| | | | |

| | Net Assets: | | | | | | | | | | |

| | | | |

| | Paid-in Capital | | | 41,984,156 | | | | 275,331,784 | | | |

| | Total distributable earnings (loss) | | | (3,939,666 | ) | | | 2,681,185 | | | |

| | |

| | NET ASSETS | | $ | 38,044,490 | | | $ | 278,012,969 | | | |

| | | Net Assets: | | | | | | | | | | |

| | | Institutional | | $ | 1,979,415 | | | $ | 441,961 | | | |

| | | Service | | | 12,055,069 | | | | 277,571,008 | | | |

| | | Advisor | | | 24,010,006 | | | | — | | | |

| | | Total Net Assets | | $ | 38,044,490 | | | $ | 278,012,969 | | | |

| | | Shares Outstanding $0.001 par value (unlimited number of shares authorized): | | | | | | | | | | |

| | | Institutional | | | 222,735 | | | | 38,651 | | | |

| | | Service | | | 1,355,623 | | | | 24,455,403 | | | |

| | | Advisor | | | 2,716,108 | | | | — | | | |

| | | Net asset value, offering and redemption price per share: | | | | | | | | | | |

| | | Institutional | | $ | 8.89 | | | $ | 11.43 | | | |

| | | Service | | | 8.89 | | | | 11.35 | | | |

| | | Advisor | | | 8.84 | | | | — | | | |

| | (a) | Includes loaned securities having a market value of $6,535 and $–, respectively. |

| | |

| 18 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-ASSET STRATEGIES FUNDS

|

Statements of Operations For the Fiscal Year Ended December 31, 2023 |

| | | | | | | | | | | | | | |

| | | | | Multi-Strategy

Alternatives

Portfolio | | | Trend Driven

Allocation Fund | |

| | | | |

| | Investment income: | | | | | | | | | | | | |

| | | | |

| | Dividends — affiliated Underlying Funds | | $ | 1,517,736 | | | $ | 7,021,522 | | | | | |

| | | | |

| | Securities lending income, net of rebates received or paid to borrowers – affiliated issuer | | | 7,432 | | | | — | | | | | |

| | | | |

| | Dividends — unaffiliated issuers | | | 5,767 | | | | 1,386,276 | | | | | |

| | | |

| | | | |

| | Total Investment Income | | | 1,530,935 | | | | 8,407,798 | | | | | |

| | | |

| | | | | | | | | | | | | | |

| | | | |

| | Expenses: | | | | | | | | | | | | |

| | | | |

| | Distribution and/or Service (12b-1) fees(a) | | | 106,960 | | | | 687,361 | | | | | |

| | | | |

| | Professional fees | | | 70,760 | | | | 62,837 | | | | | |

| | | | |

| | Custody, accounting and administrative services | | | 64,041 | | | | 54,037 | | | | | |

| | | | |

| | Management fees | | | 54,701 | | | | 2,175,600 | | | | | |

| | | | |

| | Printing and mailing costs | | | 50,240 | | | | 40,667 | | | | | |

| | | | |

| | Trustee fees | | | 21,513 | | | | 20,329 | | | | | |

| | | | |

| | Shareholder Administration fees — Service Shares | | | 14,214 | | | | — | | | | | |

| | | | |

| | Transfer Agency fees(a) | | | 7,293 | | | | 55,079 | | | | | |

| | | | |

| | Shareholder meeting expense | | | 1,480 | | | | 10,982 | | | | | |

| | | | |

| | Other | | | 10,677 | | | | 28,167 | | | | | |

| | | |

| | | | |

| | Total expenses | | | 401,879 | | | | 3,135,059 | | | | | |

| | | |

| | | | |

| | Less — expense reductions | | | (201,504 | ) | | | (613,589 | ) | | | | |

| | | |

| | | | |

| | Net expenses | | | 200,375 | | | | 2,521,470 | | | | | |

| | | |

| | | | |

| | NET INVESTMENT INCOME | | | 1,330,560 | | | | 5,886,328 | | | | | |

| | | |

| | | | | | | | | | | | | | |

| | | | |

| | Realized and Unrealized gain (loss): | | | | | | | | | | | | |

| | | | |

| | Net realized gain (loss) from: | | | | | | | | | | | | |

| | | | |

| | Investments — unaffiliated issuers | | | 16,667 | | | | 3,613,645 | | | | | |

| | | | |

| | Investment — affiliated Underlying Funds | | | (121,496 | ) | | | — | | | | | |

| | | | |

| | Futures contracts | | | (47,283 | ) | | | 8,151,940 | | | | | |

| | | | |

| | Foreign currency transactions | | | 41 | | | | 93,649 | | | | | |

| | | | |

| | Purchased Options | | | (133,344 | ) | | | — | | | | | |

| | | | |

| | Forward foreign currency exchange contracts | | | (1,682 | ) | | | — | | | | | |

| | | | |

| | Capital gain distributions from affiliated Underlying Funds | | | 2,817 | | | | — | | | | | |

| | | | |

| | Net change in unrealized gain (loss) on: | | | | | | | | | | | | |

| | | | |

| | Investments — unaffiliated issuers | | | 16,889 | | | | 11,313,902 | | | | | |

| | | | |

| | Investment — affiliated Underlying Funds | | | 1,676,504 | | | | — | | | | | |

| | | | |

| | Futures contracts | | | 42,145 | | | | 10,549,348 | | | | | |

| | | | |

| | Foreign currency translations | | | (1,617 | ) | | | 140,370 | | | | | |

| | | | |

| | Purchased Options | | | (27,138 | ) | | | — | | | | | |

| | | | |

| | Forward foreign currency exchange contracts | | | (2,082 | ) | | | — | | | | | |

| | | |

| | Net realized and unrealized gain | | | 1,420,421 | | | | 33,862,854 | | | | | |

| | | |

| | NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 2,750,981 | | | $ | 39,749,182 | | | | | |

| | | |

| | (a) | Class specific Distribution and/or Service and Transfer Agency fees were as follows: |

| | | | | | | | | | | | | | | | | | | | | | |

| | | Distribution and/or

Service (12b-1) fees | | | Transfer Agency Fees | | | |

| Fund | | Service | | | Advisor | | | Institutional | | | Service | | | Advisor | |

Multi-Strategy Alternatives Portfolio | | $ | 14,214 | | | $ | 92,746 | | | $ | 382 | | | $ | 2,274 | | | $ | 4,637 | |

Trend Driven Allocation Fund | | | 687,361 | | | | – | | | | 90 | | | | 54,989 | | | | – | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 19 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-ASSET STRATEGIES FUNDS

|

Statements of Changes in Net Assets December 31, 2023 |

| | | | | | | | | | | | | | | | | | |

| | | | | Multi-Strategy Alternatives Portfolio | | | Trend Driven Allocation Fund | |

| | | | | |

| | | | | For the Fiscal Year Ended

December 31, 2023 | | | For the Fiscal Year Ended

December 31, 2022 | | | For the Fiscal Year Ended

December 31, 2023 | | | For the Fiscal Year Ended

December 31, 2022 | |

| | | | | |

| | From operations: | | | | | | | | | | | | | | | | |

| | | | | |

| | Net investment income | | $ | 1,330,560 | | | $ | 1,559,129 | | | $ | 5,886,328 | | | $ | 404,319 | |

| | | | | |

| | Net realized gain (loss) | | | (284,280 | ) | | | (3,743,647 | ) | | | 11,859,234 | | | | (33,971,393) | |

| | | | | |

| | Net change in unrealized gain (loss) | | | 1,704,701 | | | | (1,315,124 | ) | | | 22,003,620 | | | | (32,715,194) | |

| | | |

| | | | | |

| | Net increase (decrease) in net assets resulting from operations | | | 2,750,981 | | | | (3,499,642 | ) | | | 39,749,182 | | | | (66,282,268) | |

| | | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | Distributions to shareholders: | | | | | | | | | | | | | | | | |

| | | | | |

| | From distributable earnings: | | | | | | | | | | | | | | | | |

| | | | | |

| | Institutional Shares | | | (130,485 | ) | | | (84,430 | ) | | | (8,240 | ) | | | (20,604) | |

| | | | | |

| | Service Shares | | | (765,139 | ) | | | (388,859 | ) | | | (4,606,548 | ) | | | (10,871,371) | |

| | | | | |

| | Advisor Shares | | | (1,504,491 | ) | | | (806,855 | ) | | | – | | | | – | |

| | | |

| | | | | |

| | Total distributions to shareholders | | | (2,400,115 | ) | | | (1,280,144 | ) | | | (4,614,788 | ) | | | (10,891,975) | |

| | | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | From share transactions: | | | | | | | | | | | | | | | | |

| | | | | |

| | Proceeds from sales of shares | | | 7,733,501 | | | | 76,038,713 | | | | 12,946,328 | | | | 25,924,207 | |

| | | | | |

| | Reinvestment of distributions | | | 2,400,115 | | | | 1,280,144 | | | | 4,614,788 | | | | 10,891,975 | |

| | | | | |

| | Cost of shares redeemed | | | (9,199,182 | ) | | | (65,417,529 | ) | | | (42,122,016 | ) | | | (49,855,165) | |

| | | |

| | | | | |

| | Net increase (decrease) in net assets resulting from share transactions | | | 934,434 | | | | 11,901,328 | | | | (24,560,900 | ) | | | (13,038,983) | |

| | | |

| | | | | |

| | TOTAL INCREASE (DECREASE) | | | 1,285,300 | | | | 7,121,542 | | | | 10,573,494 | | | | (90,213,226) | |

| | | |

| | | | | | | | | | | | | | | | | | |

| | | | | |

| | Net Assets: | | | | | | | | | | | | | | | | |

| | | | | |

| | Beginning of year | | | 36,759,190 | | | | 29,637,648 | | | | 267,439,475 | | | | 357,652,701 | |

| | | |

| | | | | |

| | End of year | | $ | 38,044,490 | | | $ | 36,759,190 | | | $ | 278,012,969 | | | $ | 267,439,475 | |

| | | |

| | |

| 20 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

|

Financial Highlights Selected Data for a Share Outstanding Throughout Each Year |

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Multi-Strategy Alternatives Portfolio |

| | |

| | | | | Institutional Shares |

| | |

| | | | | Year Ended December 31, |

| | | | | | |

| | | | | 2023 | | 2022 | | 2021 | | 2020 | | 2019 |

| | | | | | |

| | Per Share Data | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | Net asset value, beginning of year | | | $ | 8.81 | | | | $ | 9.77 | | | | $ | 9.46 | | | | $ | 9.02 | | | | $ | 8.51 | |

| | | |

| | | | | | |

| | Net investment income(a)(b) | | | | 0.36 | | | | | 0.38 | | | | | 0.23 | | | | | 0.25 | | | | | 0.30 | |

| | | | | | |

| | Net realized and unrealized gain (loss) | | | | 0.35 | | | | | (0.99 | ) | | | | 0.25 | | | | | 0.39 | | | | | 0.48 | |

| | | |

| | | | | | |

| | Total from investment operations | | | | 0.71 | | | | | (0.61 | ) | | | | 0.48 | | | | | 0.64 | | | | | 0.78 | |

| | | |

| | | | | | |

| | Distributions to shareholders from net investment income | | | | (0.63 | ) | | | | (0.35 | ) | | | | (0.17 | ) | | | | (0.20 | ) | | | | (0.27) | |

| | | |

| | | | | | |

| | Net asset value, end of year | | | $ | 8.89 | | | | $ | 8.81 | | | | $ | 9.77 | | | | $ | 9.46 | | | | $ | 9.02 | |

| | | |

| | | | | | |

| | Total Return(c) | | | | 7.90 | % | | | | (6.24 | )% | | | | 5.03 | % | | | | 7.05 | % | | | | 9.11% | |

| | | |

| | | | | | |

| | Net assets, end of year (in 000’s) | | | $ | 1,979 | | | | $ | 2,203 | | | | $ | 2,515 | | | | $ | 1,520 | | | | $ | 1,309 | |

| | | | | | |

| | Ratio of net expenses to average net assets(d) | | | | 0.22 | % | | | | 0.20 | % | | | | 0.22 | % | | | | 0.21 | % | | | | 0.25% | |

| | | | | | |

| | Ratio of total expenses to average net assets(d) | | | | 0.77 | % | | | | 0.69 | % | | | | 1.02 | % | | | | 1.39 | % | | | | 1.60% | |

| | | | | | |

| | Ratio of net investment income to average net assets | | | | 3.98 | % | | | | 4.08 | % | | | | 2.29 | % | | | | 2.73 | % | | | | 3.30% | |

| | | | | | |

| | Portfolio turnover rate(e) | | | | 23 | % | | | | 199 | % | | | | 25 | % | | | | 5 | % | | | | 26% | |

| | | |

| | (a) | Calculated based on the average shares outstanding methodology. |

| | (b) | Recognition of net investment income by the Fund is affected by the timing of declaration of dividends by the Underlying Funds in which the Fund invests. |

| | (c) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. |

| | (d) | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (e) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 21 |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

|

Financial Highlights (continued) Selected Data for a Share Outstanding Throughout Each Year |

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Multi-Strategy Alternatives Portfolio |

| | |

| | | | | Service Shares |

| | |

| | | | | Year Ended December 31, |

| | | | | | |

| | | | | 2023 | | 2022 | | 2021 | | 2020 | | 2019 |

| | | | | | |

| | Per Share Data | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | Net asset value, beginning of year | | | $ | 8.81 | | | | $ | 9.76 | | | | $ | 9.45 | | | | $ | 9.02 | | | | $ | 8.52 | |

| | | |

| | | | | | |

| | Net investment income(a)(b) | | | | 0.34 | | | | | 0.31 | | | | | 0.20 | | | | | 0.23 | | | | | 0.32 | |

| | | | | | |

| | Net realized and unrealized gain (loss) | | | | 0.34 | | | | | (0.95 | ) | | | | 0.26 | | | | | 0.38 | | | | | 0.43 | |

| | | |

| | | | | | |

| | Total from investment operations | | | | 0.68 | | | | | (0.64 | ) | | | | 0.46 | | | | | 0.61 | | | | | 0.75 | |

| | | |

| | | | | | |

| | Distributions to shareholders from net investment income | | | | (0.60 | ) | | | | (0.31 | ) | | | | (0.15 | ) | | | | (0.18 | ) | | | | (0.25) | |

| | | |

| | | | | | |

| | Net asset value, end of year | | | $ | 8.89 | | | | $ | 8.81 | | | | $ | 9.76 | | | | $ | 9.45 | | | | $ | 9.02 | |

| | | |

| | | | | | |

| | Total Return(c) | | | | 7.77 | % | | | | (6.54 | )% | | | | 4.84 | % | | | | 6.70 | % | | | | 8.82% | |

| | | |

| | | | | | |

| | Net assets, end of year (in 000’s) | | | $ | 12,055 | | | | $ | 11,356 | | | | $ | 6,538 | | | | $ | 3,472 | | | | $ | 2,857 | |

| | | | | | |

| | Ratio of net expenses to average net assets(d) | | | | 0.47 | % | | | | 0.45 | % | | | | 0.47 | % | | | | 0.46 | % | | | | 0.51% | |

| | | | | | |

| | Ratio of total expenses to average net assets(d) | | | | 1.02 | % | | | | 0.88 | % | | | | 1.28 | % | | | | 1.65 | % | | | | 1.86% | |

| | | | | | |

| | Ratio of net investment income to average net assets | | | | 3.74 | % | | | | 3.34 | % | | | | 2.04 | % | | | | 2.51 | % | | | | 3.54% | |

| | | | | | |

| | Portfolio turnover rate(e) | | | | 23 | % | | | | 199 | % | | | | 25 | % | | | | 5 | % | | | | 26% | |

| | | |

| | (a) | Calculated based on the average shares outstanding methodology. |

| | (b) | Recognition of net investment income by the Fund is affected by the timing of declaration of dividends by the Underlying Funds in which the Fund invests. |

| | (c) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. |

| | (d) | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (e) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| 22 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS VARIABLE INSURANCE TRUST MULTI-STRATEGY ALTERNATIVES PORTFOLIO

|

Financial Highlights (continued) Selected Data for a Share Outstanding Throughout Each Year |

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Goldman Sachs Multi-Strategy Alternatives Portfolio |

| | |

| | | | | Advisor Shares |

| | |

| | | | | Year Ended December 31, |

| | | | | | |

| | | | | 2023 | | 2022 | | 2021 | | 2020 | | 2019 |

| | | | | | |

| | | Per Share Data | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | Net asset value, beginning of year | | | $ | 8.77 | | | | $ | 9.73 | | | | $ | 9.42 | | | | $ | 8.99 | | | | $ | 8.49 | |

| | | |

| | | | | | |

| | Net investment income(a)(b) | | | | 0.32 | | | | | 0.37 | | | | | 0.18 | | | | | 0.20 | | | | | 0.24 | |

| | | | | | |

| | Net realized and unrealized gain (loss) | | | | 0.34 | | | | | (1.01 | ) | | | | 0.26 | | | | | 0.39 | | | | | 0.49 | |

| | | |

| | | | | | |

| | Total from investment operations | | | | 0.66 | | | | | (0.64 | ) | | | | 0.44 | | | | | 0.59 | | | | | 0.73 | |

| | | |

| | | | | | |

| | Distributions to shareholders from net investment income | | | | (0.59 | ) | | | | (0.32 | ) | | | | (0.13 | ) | | | | (0.16 | ) | | | | (0.23) | |

| | | |

| | | | | | |

| | Net asset value, end of year | | | $ | 8.84 | | | | $ | 8.77 | | | | $ | 9.73 | | | | $ | 9.42 | | | | $ | 8.99 | |

| | | |

| | | | | | |

| | Total Return(c) | | | | 7.53 | % | | | | (6.61 | )% | | | | 4.66 | % | | | | 6.56 | % | | | | 8.60% | |

| | | |

| | | | | | |

| | Net assets, end of year (in 000’s) | | | $ | 24,010 | | | | $ | 23,200 | | | | $ | 20,585 | | | | $ | 17,698 | | | | $ | 15,410 | |

| | | | | | |

| | Ratio of net expenses to average net assets(d) | | | | 0.62 | % | | | | 0.60 | % | | | | 0.62 | % | | | | 0.61 | % | | | | 0.64% | |

| | | | | | |

| | Ratio of total expenses to average net assets(d) | | | | 1.17 | % | | | | 1.09 | % | | | | 1.44 | % | | | | 1.79 | % | | | | 2.01% | |

| | | | | | |

| | Ratio of net investment income to average net assets | | | | 3.58 | % | | | | 3.99 | % | | | | 1.89 | % | | | | 2.28 | % | | | | 2.61% | |

| | | | | | |

| | Portfolio turnover rate(e) | | | | 23 | % | | | | 199 | % | | | | 25 | % | | | | 5 | % | | | | 26% | |

| | | |

| | (a) | Calculated based on the average shares outstanding methodology. |

| | (b) | Recognition of net investment income by the Fund is affected by the timing of declaration of dividends by the Underlying Funds in which the Fund invests. |

| | (c) | Assumes investment at the NAV at the beginning of the year, reinvestment of all dividends and distributions, a complete redemption of the investment at the NAV at the end of the year and no sales or redemption charges (if any). Total returns would be reduced if a sales or redemption charge was taken into account. Returns do not reflect the impact of taxes to shareholders relating to Fund distributions or the redemption of Fund shares. |

| | (d) | Expense ratios exclude the expenses of the Underlying Funds in which the Fund invests. |

| | (e) | The Fund’s portfolio turnover rate is calculated in accordance with regulatory requirements, without regard to transactions involving short term investments and certain derivatives. If such transactions were included, the Fund’s portfolio turnover rate may be higher. |

| | |

| The accompanying notes are an integral part of these financial statements. | | 23 |

GOLDMAN SACHS TREND DRIVEN ALLOCATION FUND

|