UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-08415

Evergreen Fixed Income Trust

_____________________________________________________________ (Exact name of registrant as specified in charter)

200 Berkeley Street Boston, Massachusetts 02116

_____________________________________________________________ (Address of principal executive offices) (Zip code)

Michael H. Koonce, Esq. 200 Berkeley Street Boston, Massachusetts 02116

____________________________________________________________ (Name and address of agent for service)

Registrant's telephone number, including area code: (617) 210-3200

Date of fiscal year end: Registrant is making an annual filing for one of its series, Evergreen Diversified Bond Fund, for the year ended November 30, 2005. This one series has a November 30 fiscal year end.

Date of reporting period: November 30, 2005

Item 1 - Reports to Stockholders.

Evergreen Diversified Bond Fund

table of contents

1

LETTER TO SHAREHOLDERS

4

FUND AT A GLANCE

5

PORTFOLIO MANAGER COMMENTARY

6

ABOUT YOUR FUND’S EXPENSES

7

FINANCIAL HIGHLIGHTS

11

SCHEDULE OF INVESTMENTS

23

STATEMENT OF ASSETS AND LIABILITIES

24

STATEMENT OF OPERATIONS

25

STATEMENTS OF CHANGES IN NET ASSETS

27

NOTES TO FINANCIAL STATEMENTS

35

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

36

ADDITIONAL INFORMATION

44

TRUSTEES AND OFFICERS

This annual report must be preceded or accompanied by a prospectus of the Evergreen fund contained herein. The prospectus contains more complete information, including fees and expenses, and should be read carefully before investing or sending money.

The fund will file its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The fund’s Form N-Q will be available on the SEC’s Web site at http://www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 800.SEC.0330.

A description of the fund’s proxy voting policies and procedures, as well as information regarding how the fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available by visiting our Web site at EvergreenInvestments.com or by visiting the SEC’s Web site at http://www.sec.gov. The fund’s proxy voting policies and procedures are also available without charge, upon request, by calling 800.343.2898.

Mutual Funds:

NOT FDIC INSURED

MAY LOSE VALUE

NOT BANK GUARANTEED

Evergreen InvestmentsSM is a service mark of Evergreen Investment Management Company, LLC. Copyright 2006, Evergreen Investment Management Company, LLC.

Evergreen Investment Management Company, LLC is a subsidiary of Wachovia Corporation and is an affiliate of Wachovia Corporation's other Broker Dealer subsidiaries.

Evergreen mutual funds are distributed by Evergreen Investment Services, Inc. 200 Berkeley Street, Boston, MA 02116

LETTER TO SHAREHOLDERS January 2006

Dennis H. Ferro President and Chief Executive Officer

Dear Shareholder,

We are pleased to provide the annual report for the Evergreen Diversified Bond Fund, which covers the twelve-month period ended November 30, 2005.

The fixed income markets were faced with a variety of challenges over the past twelve months. U.S. Gross Domestic Product (GDP) growth moderated from the rampant pace associated with recovery to the more normalized pace of economic expansion. Despite this trend, the Federal Reserve (Fed) continued to raise its target for the federal funds rate. Also, higher energy prices and the prospect of increased government spending helped renew inflation fears. And if all that wasn’t enough, hurricanes and credit downgrades in the auto sector combined to further increase the uncertainty in the financial markets. Throughout it all, the portfolio managers of the Fund focused their efforts on protecting principal and maximizing income potential.

The investment period began with a trend for a more moderate pace of growth in the U.S. economy. Yet despite this trend in GDP, the Fed continued its “measured removal of policy accommodation,” raising the target for the federal funds rate by 1/4 point at each monetary policy meeting over the past year. Throughout this paradox of moderating economic growth and tighter monetary policy, Evergreen’s Investment Strategy Committee maintained its belief that the economy had simply experienced a normal transition in the economic cycle, from recovery to expansion. A consequence of this change, though,

1

LETTER TO SHAREHOLDERS continued

was a variety of mixed economic data and as a result, market interest rates fluctuated on seemingly every economic release. Historically, the maturation of the economic cycle had experienced similarly erratic behavior, and since the Fed had been accommodative for such an extended period, we believed that monetary policy was on the path of less stimulation, rather than more restriction, for the U.S. economy.

Despite the surge in energy prices immediately after the hurricanes, long-term bond yields remained low, intensifying debate as to the yield curve’s message. Some felt that long-term inflation was under control, while others believed the flat yield curve signaled the end of the expansion. Considering our forecasts for moderating global growth, mild wage growth and solid domestic productivity, we concluded that long-term pricing pressures were insufficient to halt the economic expansion. In addition, it was our opinion that excess global savings and increased demand from under-funded pensions likely pushed prices higher for the 10-year Treasury, helping to drive market interest rates lower.

This proved to be a challenging development for our fixed income analysts, as market yields for longer-dated maturities began to climb, and spreads widened between high grade and lower-rated bonds. Many companies had also begun shareholder-friendly activities, including share buybacks and dividend increases, pressuring prices for many corporate issues. In addition, growing leveraged buyout activity and the credit downgrades in the auto sector cast a major cloud over the corporate bond market. Yet the portfolio managers of the Fund helped the portfolio with their allocation mix between investment grade and high yield bonds. While income potential increased, credit quality improved, and as the period progressed, the managers became increasingly defensive.

2

LETTER TO SHAREHOLDERS continued

As always, we continue to encourage investors to maintain their fixed income allocations within their long-term portfolios, including exposure to the Fund.

Please visit our Web site, EvergreenInvestments.com, for more information about our funds and other investment products available to you. From the Web site, you may also access a detailed Q & A interview with the portfolio managers for your fund. You can easily reach these interviews by following the link, EvergreenInvestments.com/Annual Updates, from our Web site. Thank you for your continued support of Evergreen Investments.

Sincerely,

Dennis H. Ferro President and Chief Executive Officer Evergreen Investment Company, Inc.

Special Notice to Shareholders:

Please visit our Web site at EvergreenInvestments.com for a statement from President and Chief Executive Officer, Dennis Ferro, addressing NASD actions involving Evergreen Investment Services, Inc. (EIS), Evergreen’s mutual fund distributor or statements from Dennis Ferro and Chairman of the Board of the Evergreen funds, Michael S. Scofield, addressing SEC actions involving the Evergreen funds.

3

FUND AT A GLANCE as of November 30, 2005

MANAGEMENT TEAM

Investment Advisor:

• Evergreen Investment Management Company, LLC

Portfolio Managers:

• Richard M. Cryan

• Douglas Williams, CFA

• David K. Fowley, CFA

• Noel McElreath, CFA

CURRENT INVESTMENT STYLE

Source: Morningstar, Inc.

Morningstar’s style box is based on a portfolio date as of 9/30/2005.

The Fixed income style box placement is based on a fund’s average effective maturity or duration and the average credit rating of the bond portfolio.

PERFORMANCE AND RETURNS

Portfolio inception date: 11/30/1972

Class A

Class B

Class C

Class I

Class inception date

5/20/2005

5/20/2005

5/20/2005

11/30/1972

Nasdaq symbol

EKDLX

EKDMX

EKDCX

EKDYX

Average annual return*

1-year with sales charge

-2.23%

-2.52%

1.31%

N/A

1-year w/o sales charge

2.65%

2.27%

2.27%

2.82%

5-year

6.13%

6.79%

7.09%

7.21%

10-year

5.66%

6.14%

6.14%

6.19%

Maximum sales charge

4.75%

5.00%

1.00%

N/A

Front-end

CDSC

CDSC

* Adjusted for maximum applicable sales charge, unless noted.

Past performance is no guarantee of future results. The performance quoted represents past performance and current performance may be lower or higher. The investment return and principal value of an investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance information current to the most recent month-end for Classes A, B, C or I, please go to EvergreenInvestments.com/fundperformance. The performance of each class may vary based on differences in loads, fees and expenses paid by the shareholders investing in each class. Performance includes the reinvestment of income dividends and capital gain distributions. Performance shown does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Historical performance shown for Class I prior to 5/23/2005 is based on the performance of the fund’s predecessor fund, Vestaur Securities Fund.

Historical performance shown for Classes A, B and C prior to their inception is based on the performance of Class I. The historical returns for Classes A, B and C have not been adjusted to reflect the effect of each class’ 12b-1 fee. These fees are 0.30% for Class A and 1.00% for Classes B and C. Class I does not, and Vestaur Securities Fund did not pay a 12b-1 fee. If these fees had been reflected, returns for Classes A, B and C would have been lower.

The advisor is waiving a portion of its advisory fee and reimbursing a portion of the 12b-1 fee for Class A. Had the fees not been waived or reimbursed, returns would have been lower.

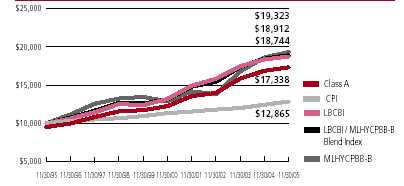

LONG-TERM GROWTH

Comparison of a $10,000 investment in the Evergreen Diversified Bond Fund Class A shares, versus a similar investment in the Lehman Brothers Corporate Bond Index (LBCBI), the Merrill Lynch High Yield, Cash Pay, BB-B Index† (MLHYCPBB-B), the LBCBI/MLHYCPBB-B Blend Index and the Consumer Price Index (CPI).

The LBCBI, MLHYCPBB-B and the LBCBI/MLHYCPBB-B Blend Index are unmanaged market indexes and do not include transaction costs associated with buying and selling securities, any mutual fund expenses or any taxes. The CPI is a commonly used measure of inflation and does not represent an investment return. It is not possible to invest directly in an index.

† Copyright 2006. Merrill Lynch, Pierce, Fenner & Smith Incorporated. All rights reserved.

4

PORTFOLIO MANAGER COMMENTARY

The fund’s Class A shares returned 2.65%* for the twelve-month period ended November 30, 2005, excluding any applicable sales charges. During the same period, the Lehman Brothers Corporate Bond Index returned 2.04%, the Merrill Lynch High Yield, Cash Pay, BB-B Index† returned 3.68% and the LBCBI/MLHYCPBB-B Blend Index returned 2.38% .

The fund seeks maximum income without undue risk of principal.

The fund performed well during a challenging period for bond investing, as interest rates on longer maturity securities began moving up and the yield differences between higher-rated and lower-rated bonds began to widen. In May 2005, following a fund merger, we raised our target allocation to higher-yielding, lower-rated bonds from approximately 7% of fund assets to approximately 20% of assets. The remaining 80% of assets stayed in high-grade securities, predominately corporate bonds. This generally helped performance, as the high-yield bond market maintained a performance edge over investment-grade bonds. However, the fund followed a conservative approach to high-yield investing and avoided the more volatile areas in the high-yield market, including longer-maturity, high-yield bonds and emerging market debt.

Within the fund’s high-grade portfolio allocation, we saw more opportunities in the lower-rated areas of our investment universe, emphasizing BBB-rated corporate bonds for much of the period. We did, however, become more defensive and raised the overall credit quality of the portfolio as the period progressed. We maintained a relatively defensive posture to guard against the negative price impacts of rising interest rates. Portfolio duration for most of the period was in the range of 4.9 to 5 years. In addition, as pressure on interest rates began building, we reduced our exposure to interest-rate sensitive industries. We favored bonds of higher quality, large-cap companies with more diversified businesses. We also reduced our exposure to the troubled automotive industry. Within the high-yield, or below-investment-grade portion of the portfolio, we focused on the upper credit quality tiers, BB- and B-rated bonds, avoiding any bonds rated CCC or lower. No bonds in the fund’s portfolio defaulted on their payments. We tended to take advantage of opportunities among higher-coupon bonds and tried to retain investments in bonds with good income flows for as long as possible.

Strong results from several tactical moves, including our investments in the insurance industry and in the subordinated debt of several higher-quality corporate issuers helped the high-grade portfolio perform well. In general, our defensive positioning to guard against the threat of rising interest rates helped performance. Among those positions that added to results were the fund’s positions in two non-U.S dollar, investment-grade credits, Mexican peso bonds and South African rand bonds. Holding back results, however, was the fund’s position in bonds of food and drug retailer Albertson’s and of check printing company Deluxe. We sold Albertson’s, but maintained a position in Deluxe bonds, which recovered some of their value later in the period.

Within our high-yield portfolio, the best performer was the fund’s position in bonds of Stratus Technologies, which rose in value as the company introduced new fault-tolerant computer services. We took profits and sold the holding. The fund’s positions in bonds of several energy-related companies performed well, led by the excellent results from bonds of Hanover Compressor, which produces compressors used in natural gas pipelines. Disappointments included securities issued by Millar Western, a forest products company hurt by rising commodity prices, and drug retailer Jean Coutu, which experienced difficulties integrating its acquisitions of stores in the Eckerd’s and Brooks chains. We sold both these positions.

Class I shares are only offered in the following manner: (1) to investment advisory clients of Evergreen Investment Management Company, LLC (or its advisory affiliates) when purchased by such advisor(s) on behalf of its clients, (2) through arrangements entered into on behalf of the Evergreen funds with certain financial services firms, (3) to certain institutional investors and (4) to persons who owned Class Y shares in registered name in an Evergreen fund on or before December 31, 1994 or who owned shares of any SouthTrust fund in registered name as of March 18, 2005 or shares of Vestaur Securities Fund as of May 20, 2005.

Class I shares are only available to institutional shareholders with a minimum of $1 million investment, which may be waived in certain situations.

The fund’s investment objective is nonfundamental and may be changed without a vote of the fund’s shareholders. High yield, lower-rated bonds may contain more risk due to the increased possibility of default.

The return of principal is not guaranteed due to fluctuation in the NAV of the fund caused by changes in the price of the individual bonds held by the fund and the buying and selling of bonds by the fund. Bond funds have the same inflation, interest rate and credit risks that are associated with the individual bonds held by the fund. Generally, the value of bond funds rise when prevailing interest rates fall and fall when interest rates rise.

Foreign investments may contain more risk due to the inherent risks associated with changing political climates, foreign market instability and foreign currency fluctuations.

U.S. government guarantees apply only to certain securities held in the fund’s portfolio and not to the fund’s shares.

* Performance prior to the inception of Class A on 5/20/2005 is based on the performance of the fund’s predecessor fund, Vestaur Securities Fund.

† Copyright 2006. Merrill Lynch, Pierce, Fenner & Smith Incorporated. All rights reserved.

All data is as of November 30, 2005, and subject to change.

5

ABOUT YOUR FUND’S EXPENSES

The Example below is intended to describe the fees and expenses borne by shareholders and the impact of those costs on your investment.

Example

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads), redemption fees and exchange fees; and (2) ongoing costs, including management fees, distribution (12b-1) fees and other fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from June 1, 2005 to November 30, 2005.

The example illustrates your fund’s costs in two ways:

• Actual expenses

The section in the table under the heading “Actual” provides information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the appropriate column for your share class, in the column entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

• Hypothetical example for comparison purposes

The section in the table under the heading “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees or exchange fees. Therefore, the section in the table under the heading “Hypothetical (5% return before expenses)” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning

Ending

Account

Account

Expenses

Value

Value

Paid During

6/1/2005

11/30/2005

Period*

Actual

Class A

$ 1,000.00

$

998.13

$ 4.86

Class B

$ 1,000.00

$

994.64

$ 8.35

Class C

$ 1,000.00

$

994.64

$ 8.35

Class I

$ 1,000.00

$

999.63

$ 3.36

Hypothetical

(5% return

before expenses)

Class A

$ 1,000.00

$ 1,020.21

$ 4.91

Class B

$ 1,000.00

$ 1,016.70

$ 8.44

Class C

$ 1,000.00

$ 1,016.70

$ 8.44

Class I

$ 1,000.00

$ 1,021.71

$ 3.40

* For each class of the Fund, expenses are equal to the annualized expense ratio of each class (0.97% for Class A, 1.67% for Class B, 1.67% for Class C and 0.67% for Class I), multiplied by the average account value over the period, multiplied by 183 / 365 days.

6

FINANCIAL HIGHLIGHTS

(For a share outstanding throughout the period)

Year Ended

November 30,

CLASS A

20051,2

Net asset value, beginning of period

$

14.83

Income from investment operations

Net investment income (loss)

0.413

Net realized and unrealized gains or losses on investments

(0.28)

Total from investment operations

0.13

Distributions to shareholders from

Net investment income

(0.43)

Net asset value, end of period

$

14.53

Total return4

0.89%

Ratios and supplemental data

Net assets, end of period (thousands)

$226,450

Ratios to average net assets

Expenses including waivers/reimbursements but excluding expense reductions

0.97%5

Expenses excluding waivers/reimbursements and expense reductions

1.15%5

Net investment income (loss)

5.28%5

Portfolio turnover rate

55%

1 Effective at the close of business on May 20, 2005, the Fund acquired the net assets of Vestaur Securities Fund. Vestaur Securities Fund became the accounting and performance survivor in this transaction . Class A shares of Vestaur Securities Fund did not exist prior to the transaction . As a result, accounting and performance information for Class A shares commenced on May 20, 2005.

2 For the period from May 20, 2005 (commencement of class operations), to November 30, 2005.

3 Net investment income (loss) per share is based on average shares outstanding during the period.

4 Excluding applicable sales charges

5 Annualized

See Notes to Financial Statements

7

FINANCIAL HIGHLIGHTS

(For a share outstanding throughout the period)

Year Ended

November 30,

CLASS B

20051,2

Net asset value, beginning of period

$

14.83

Income from investment operations

Net investment income (loss)

0.363

Net realized and unrealized gains or losses on investments

(0.28)

Total from investment operations

0.08

Distributions to shareholders from

Net investment income

(0.38)

Net asset value, end of period

$

14.53

Total return4

0.52%

Ratios and supplemental data

Net assets, end of period (thousands)

$20,439

Ratios to average net assets

Expenses including waivers/reimbursements but excluding expense reductions

1.67%5

Expenses excluding waivers/reimbursements and expense reductions

1.85%5

Net investment income (loss)

4.58%5

Portfolio turnover rate

55%

1 Effective at the close of business on May 20, 2005, the Fund acquired the net assets of Vestaur Securities Fund. Vestaur Securities Fund became the accounting and performance survivor in this transaction . Class B shares of Vestaur Securities Fund did not exist prior to the transaction . As a result, accounting and performance information for Class B shares commenced on May 20, 2005.

2 For the period from May 20, 2005 (commencement of class operations), to November 30, 2005.

3 Net investment income (loss) per share is based on average shares outstanding during the period.

4 Excluding applicable sales charges

5 Annualized

See Notes to Financial Statements

8

FINANCIAL HIGHLIGHTS

(For a share outstanding throughout the period)

Year Ended

November 30,

CLASS C

20051,2

Net asset value, beginning of period

$

14.83

Income from investment operations

Net investment income (loss)

0.363

Net realized and unrealized gains or losses on investments

(0.28)

Total from investment operations

0.08

Distributions to shareholders from

Net investment income

(0.38)

Net asset value, end of period

$

14.53

Total return4

0.52%

Ratios and supplemental data

Net assets, end of period (thousands)

$27,764

Ratios to average net assets

Expenses including waivers/reimbursements but excluding expense reductions

1.67%5

Expenses excluding waivers/reimbursements and expense reductions

1.85%5

Net investment income (loss)

4.58%5

Portfolio turnover rate

55%

1 Effective at the close of business on May 20, 2005, the Fund acquired the net assets of Vestaur Securities Fund. Vestaur Securities Fund became the accounting and performance survivor in this transaction . Class C shares of Vestaur Securities Fund did not exist prior to the transaction. As a result, accounting and performance information for Class C shares commenced on May 20, 2005.

2 For the period from May 20, 2005 (commencement of class operations), to November 30, 2005.

3 Net investment income (loss) per share is based on average shares outstanding during the period.

4 Excluding applicable sales charges

5 Annualized

See Notes to Financial Statements

9

FINANCIAL HIGHLIGHTS

(For a share outstanding throughout each period)

Year Ended November 30,

CLASS I

20051

20041

20031

20021,2

20011

Net asset value, beginning of period

$ 15.14

$ 15.14

$

14.27

$ 14.88

$ 14.50

Income from investment operations

Net investment income (loss)

0.793

0.93

0.95

1.00

1.10

Net realized and unrealized gains or losses on investments

(0.41)

0.02

0.91

(0.56)

0.39

Total from investment operations

0.38

0.95

1.86

0.44

1.49

Distributions to shareholders from

Net investment income

(0.86)

(0.95)

(0.99)

(1.05)

(1.11)

Tax basis return of capital

(0.13)4

0

0

0

0

Total distributions to shareholders

(0.99)

(0.95)

(0.99)

(1.05)

(1.11)

Net asset value, end of period

$ 14.53

$ 15.14

$

15.14

$ 14.27

$ 14.88

Total return

2.82%

6.47%

13.43%

3.06%

10.67%

Ratios and supplemental data

Net assets, end of period (thousands)

$65,893

$97,235

$97,277

$91,666

$94,577

Ratios to average net assets

Expenses including waivers/reimbursements but excluding expense reductions

0.79%

0.94%

0.91%

1.01%

0.98%

Expenses excluding waivers/reimbursements and expense reductions

0.88%

0.97%

0.94%

1.01%

0.98%

Net investment income (loss)

5.50%

6.10%

6.43%

6.96%

7.43%

Portfolio turnover rate

55%

23%

45%

40%

63%

1 Effective at the close of business on May 20, 2005, the Fund acquired the net assets of Vestaur Securities Fund. Vestaur Securities Fund became the accounting and performance survivor in this transaction . The financial highlights for the periods prior to May 23, 2005 are those of Vestaur Securities Fund. The per share information has been restated to give effect to this transaction. Total return performance reflects the total return of Vestaur Securities Fund based on its net asset value.

2 As required, effective December 1, 2001, the Fund has adopted the provisions of the AICPA Audit and, Companies Accounting Guide, Audits of Investment and began amortizing premium and accreting discount on its fixed-income securities. The effects of this change for the year ended November 30, 2002 were a decrease in net investment income per share of $0.03; an increase in net realized gains or losses per share of $0.03; and a decrease in the ratio of net investment income to average net assets of 0.25%. The above per sha re information, ratios and supplemental data for the period prior to December 1, 2001 have not been restated to reflect this change in presentation.

3 Net investment income (loss) per share is based on average shares outstanding during the period.

4 Return of capital relates to former Vestaur Securities Fund shareholders and is based on average shares outstanding from December 1, 2004 through May 20, 2005.

See Notes to Financial Statements

10

SCHEDULE OF INVESTMENTS

November 30, 2005

Principal

Amount

Value

AGENCY COMMERCIAL MORTGAGE-BACKED SECURITIES 1.5%

FIXED-RATE 1.5%

FHLMC, Ser. M009, Class A, 5.40%, 10/15/2021 (h) (cost $5,250,245)

$ 5,245,000

$

5,250,245

AGENCY MORTGAGE-BACKED COLLATERALIZED MORTGAGE

OBLIGATIONS 0.3%

FIXED-RATE 0.3%

FNMA:

Ser. 2002-T12, Class A3, 7.50%, 05/25/2042

31,369

32,667

Ser. 2002-T19, Class A3, 7.50%, 07/25/2042

486,705

510,859

Ser. 2003-W4, Class 4A, 7.50%, 10/25/2042

333,371

349,186

Total Agency Mortgage-Backed Collateralized Mortgage Obligations

(cost $917,163)

892,712

AGENCY MORTGAGE-BACKED PASS THROUGH SECURITIES 0.5%

FIXED-RATE 0.5%

FHLMC:

6.00%, 01/01/2032

9,781

9,865

6.50%, 09/25/2043

208,450

213,075

7.50%, 09/01/2013 - 08/25/2042

311,089

322,863

9.00%, 12/01/2016

242,243

261,042

9.50%, 12/01/2022

34,517

37,823

FNMA:

9.00%, 02/01/2025 - 09/01/2030

281,653

307,947

10.00%, 09/01/2010 - 04/01/2021

198,222

219,434

GNMA:

8.00%, 03/15/2022 - 08/15/2024

119,971

128,338

8.25%, 05/15/2020

90,745

97,871

8.50%, 09/15/2024 - 01/15/2027

89,004

96,849

9.00%, 12/15/2019

64,309

70,112

9.50%, 09/15/2019

30,798

34,069

10.00%, 01/15/2019 - 03/15/2020

58,907

65,819

Total Agency Mortgage-Backed Pass Through Securities

(cost $1,819,774)

1,865,107

AGENCY REPERFORMING MORTGAGE-BACKED PASS THROUGH

SECURITIES 0.2%

FNMA:

Ser. 2003-W1, Class 2A, 7.50%, 12/25/2042

509,034

536,333

Ser. 2003-W2, Class 1A3, 7.50%, 07/25/2042

174,500

180,221

Total Agency Reperforming Mortgage-Backed Pass Through Securities

(cost $733,336)

716,554

ASSET-BACKED SECURITIES 2.7%

Credit Suisse First Boston Mtge. Securities Corp., Ser. 1996-2, Class A-6, 7.18%,

02/25/2018

162,635

162,194

GE Capital Mtge. Svcs., Inc., Ser. 1999-H, Class A-7, 6.27%, 04/25/2029

Dominion Resources Capital Trust I, 7.83%, 12/01/2027

500,000

537,614

Dominion Resources Capital Trust III, 8.40%, 01/15/2031

3,000,000

3,595,758

MidAmerican Energy Holdings Co., 8.48%, 09/15/2028

3,000,000

3,752,055

7,885,427

Total Corporate Bonds (cost $237,961,417)

238,204,388

FOREIGN BONDS - CORPORATE (PRINCIPAL AMOUNT

DENOMINATED IN CURRENCY INDICATED) 0.6%

FINANCIALS 0.6%

Commercial Banks 0.6%

European Investment Bank, 8.00%, 10/21/2013 ZAR (cost $2,080,000)

13,000,000

2,059,271

FOREIGN BONDS - GOVERNMENT (PRINCIPAL AMOUNT

DENOMINATED IN CURRENCY INDICATED) 1.5%

Mexico, 8.00%, 12/28/2006 MXN (cost $4,967,549)

53,591,500

5,066,436

MUNICIPAL OBLIGATIONS 0.2%

HOUSING 0.2%

Virginia HDA RB, Ser. J, 6.75%, 12/01/2021 (cost $538,377)

$

500,000

530,280

U.S. TREASURY OBLIGATIONS1.2%

U.S. Treasury Notes:

4.50%, 11/15/2010

1,000,000

1,003,555

4.50%, 11/15/2015

3,000,000

3,001,407

Total U.S. Treasury Obligations (cost $4,020,351)

4,004,962

WHOLE LOAN SUBORDINATE COLLATERALIZED MORTGAGE

OBLIGATIONS 0.2%

Financial Asset Securitization, Inc., Ser. 1997-NAM2, Class B-2, 7.88%,

07/25/2027 (cost $654,655)

637,279

636,006

YANKEE OBLIGATIONS - CORPORATE 10.5%

CONSUMER DISCRETIONARY0.4%

Hotels, Restaurants & Leisure0.2%

Intrawest Corp., 7.50%, 10/15/2013

635,000

642,143

See Notes to Financial Statements 19

SCHEDULE OF INVESTMENTS continued

November 30, 2005

Principal

Amount

Value

YANKEE OBLIGATIONS - CORPORATE continued

CONSUMER DISCRETIONARY continued

Media 0.2%

Rogers Cable, Inc., 5.50%, 03/15/2014

$

750,000

$

698,438

CONSUMER STAPLES 1.3%

Beverages 1.3%

Companhia Brasileira De Bebidas, 10.50%, 12/15/2011

3,500,000

4,357,500

FINANCIALS 5.1%

Commercial Banks 4.5%

Banco Bradesco SA, 8.75%, 10/24/2013

750,000

830,625

Barclays Bank plc, 8.55%, 09/29/2049 144A

4,000,000

4,623,868

Royal Bank of Scotland Group plc, 9.12%, 03/31/2049

5,000,000

5,742,100

Standard Chartered plc, FRN, 4.50%, 07/29/2049

5,000,000

4,006,250

15,202,843

Diversified Financial Services 0.6%

Preferred Term Securities, Ltd., FRN, 5.46%, 06/24/2034 144A

2,000,000

2,044,160

INDUSTRIALS 0.3%

Industrial Conglomerates 0.3%

Tyco International Group SA:

6.375%, 10/15/2011

500,000

518,997

7.00%, 06/15/2028

500,000

540,224

1,059,221

INFORMATION TECHNOLOGY 0.2%

Electronic Equipment & Instruments 0.2%

Celestica, Inc., 7.875%, 07/01/2011

710,000

715,325

MATERIALS 0.6%

Chemicals 0.2%

Nova Chemicals Corp., 6.50%, 01/15/2012

650,000

638,625

Containers & Packaging 0.2%

Norampac, Inc., 6.75%, 06/01/2013

650,000

630,500

Metals & Mining 0.2%

Novelis, Inc., 7.25%, 02/15/2015 144A

865,000

813,100

TELECOMMUNICATION SERVICES 2.6%

Diversified Telecommunication Services 2.3%

British Telecommunications plc, 8.875%, 12/15/2030

750,000

993,130

France Telecom SA, 8.50%, 03/01/2031

1,000,000

1,323,279

Telecom Italia Capital Corp.:

Ser. B, 5.25%, 11/15/2013

500,000

490,670

Ser. C, 6.375%, 11/15/2033

2,100,000

2,102,077

Telefonos De Mexico SA, 5.50%, 01/27/2015

3,000,000

2,941,203

7,850,359

See Notes to Financial Statements 20

SCHEDULE OF INVESTMENTS continued

November 30, 2005

Principal

Amount

Value

YANKEE OBLIGATIONS - CORPORATE continued

TELECOMMUNICATION SERVICES continued

Wireless Telecommunication Services 0.3%

Rogers Wireless, Inc., 6.375%, 03/01/2014

$ 175,000

$

174,781

Vodafone Group plc, 7.75%, 02/15/2010

700,000

768,597

943,378

Total Yankee Obligations-Corporate(cost $35,864,208)

35,595,592

Shares

Value

PREFERRED STOCKS 4.0%

FINANCIALS 2.3%

Capital Markets 1.4%

Lehman Brothers, Inc.

200,000

4,912,500

Thrifts & Mortgage Finance0.9%

Fannie Mae

55,000

3,050,784

TELECOMMUNICATION SERVICES 1.1%

Diversified Telecommunication Services1.1%

Centaur Funding Corp. 144A

2,880

3,681,000

UTILITIES 0.6%

Electric Utilities 0.6%

Southern California Edison

20,000

2,035,000

Total Preferred Stocks (cost $13,848,911)

13,679,284

Principal

Amount

Value

SHORT-TERM INVESTMENTS0.3%

U.S. TREASURY OBLIGATIONS0.1%

U.S. Treasury Bills, 4.13%, 05/11/2006 + ƒ

$ 500,000

490,765

Shares

Value

MUTUAL FUND SHARES 0.2%

Evergreen Institutional Money Market Fund ø

673,940

673,940

Total Short-Term Investments (cost $1,164,705)

1,164,705

Total Investments (cost $335,148,770)98.4%

334,464,213

Other Assets and Liabilities1.6%

6,081,498

Net Assets 100.0%

$

340,545,711

See Notes to Financial Statements 21

SCHEDULE OF INVESTMENTS continued

November 30, 2005

(h) Security is valued at fair value as determined by the investment advisor in good faith, according to procedures approved by the Board of Trustees.

144A Security that may be sold to qualified institutional buyers under Rule 144A of the Securities Act of 1933, as amended. This security has been determined to be liquid under guidelines established by the Board of Trustees, unless otherwise noted.

+ Rate shown represents the yield to maturity at date of purchase.

ƒ All or a portion of this security was pledged to cover initial margin requirements for open futures contracts.

ø Evergreen Investment Management Company, LLC is the investment advisor to both the Fund and the money market fund.

Summary of Abbreviations

CDO

Collateralized Debt Obligation

FHLMC

Federal Home Loan Mortgage Corp.

FNMA

Federal National Mortgage Association

FRN

Floating Rate Note

GNMA

Government National Mortgage Association

HDA

Housing Development Authority

MXN

Mexican Peso

RB

Revenue Bond

REIT

Real Estate Investment Trust

ZAR

South African Rand

The following table shows the percent of total investments (excluding equity positions) by credit quality based on Moody’s and Standard & Poor’s ratings as of November 30, 2005 (unaudited):

AAA

11.1%

AA

2.2%

A

30.1%

BBB

34.4%

BB

9.1%

B

10.0%

NR

3.1%

100.0%

The following table shows the percent of total investments (excluding equity positions) by maturity as of November 30, 2005 (unaudited):

Less than 1 year

2.1%

1 to 3 year(s)

3.8%

3 to 5 years

14.6%

5 to 10 years

44.5%

10 to 20 years

11.5%

20 to 30 years

23.5%

100.0%

See Notes to Financial Statements 22

STATEMENT OF ASSETS AND LIABILITIES

November 30, 2005

Assets

Investments in securities, at value (cost $334,474,830)

$

333,790,273

Investments in affiliated money market fund, at value (cost $673,940)

673,940

Total investments

334,464,213

Receivable for securities sold

4,227,422

Principal paydown receivable

1,208

Receivable for Fund shares sold

31,537

Interest receivable

5,917,754

Receivable for daily variation margin on open futures contracts

22,656

Prepaid expenses and other assets

241,687

Total assets

344,906,477

Liabilities

Dividends payable

616,445

Payable for securities purchased

3,096,440

Payable for Fund shares redeemed

561,041

Advisory fee payable

1,503

Distribution Plan expenses payable

1,317

Due to other related parties

1,277

Accrued expenses and other liabilities

82,743

Total liabilities

4,360,766

Net assets

$

340,545,711

Net assets represented by

Paid-in capital

$

397,572,979

Overdistributed net investment income

(189,584)

Accumulated net realized losses on investments

(56,628,029)

Net unrealized losses on investments

(209,655)

Total net assets

$

340,545,711

Net assets consists of

Class A

$

226,450,022

Class B

20,438,768

Class C

27,764,129

Class I

65,892,792

Total net assets

$

340,545,711

Shares outstanding (unlimited number of shares authorized)

Class A

15,588,577

Class B

1,406,997

Class C

1,911,260

Class I

4,535,955

Net asset value per share

Class A

$

14.53

Class A — Offering price (based on sales charge of 4.75%)

$

15.25

Class B

$

14.53

Class C

$

14.53

Class I

$

14.53

See Notes to Financial Statements 23

STATEMENT OF OPERATIONS

Year Ended November 30, 2005

Investment income

Interest (net of foreign withholding taxes of $158)

$

14,260,579

Dividends

496,164

Income from affiliate

32,425

Total investment income

14,789,168

Expenses

Advisory fee

1,150,818

Distribution Plan expenses

Class A

374,446

Class B

111,522

Class C

155,543

Administrative services fee

188,736

Transfer agent fees

401,837

Trustees’ fees and expenses

38,735

Printing and postage expenses

95,869

Custodian and accounting fees

74,278

Registration and filing fees

17,382

Professional fees

42,581

Interest expense

38

Other

15,262

Total expenses

2,667,047

Less: Expense reductions

(4,253)

Fee waivers and expense reimbursements

(345,862)

Net expenses

2,316,932

Net investment income

12,472,236

Net realized and unrealized gains or losses on investments

Net realized gains and losses on:

Securities

198,569

Foreign currency related transactions

(2,163)

Futures contracts

(38,354)

Net realized gains on investments

158,052

Net change in unrealized gains or losses on investments

(7,406,911)

Net realized and unrealized gains or losses on investments

(7,248,859)

Net increase in net assets resulting from operations

$

5,223,377

See Notes to Financial Statements 24

STATEMENTS OF CHANGES IN NET ASSETS

Year Ended November 30,

2005 (a) (b)

2004 (b)

Operations

Net investment income

$

12,472,236

$

5,927,000

Net realized gains on investments

158,052

650,032

Net change in unrealized gains or losses

on investments

(7,406,911)

(519,723)

Net increase in net assets resulting from

operations

5,223,377

6,057,309

Distributions to shareholders from

Net investment income

Class A

(6,953,533)

0

Class B

(543,738)

0

Class C

(757,969)

0

Class I

(5,026,549)

(6,100,208)

Tax basis return of capital

Class I

(881,232)

0

Total distributions to shareholders

(14,163,021)

(6,100,208)

Shares

Shares

Capital share transactions

Proceeds from shares sold

Class A

113,587

1,676,634

0

0

Class B

115,193

1,706,735

0

0

Class C

55,353

827,909

0

0

Class I

27,527

416,249

0

0

4,627,527

0

Net asset value of shares issued in

reinvestment of distributions

Class A

339,379

5,028,431

0

0

Class B

24,321

360,292

0

0

Class C

37,763

559,591

0

0

Class I

72,438

1,072,180

0

0

7,020,494

0

Automatic conversion of Class B shares to

Class A shares

Class A

49,845

737,264

0

0

Class B

(49,845)

(737,264)

0

0

0

0

Payment for shares redeemed

Class A

(1,351,925)

(20,009,362)

0

0

Class B

(123,613)

(1,824,435)

0

0

Class C

(267,045)

(3,957,574)

0

0

Class I

(2,177,521)

(32,439,871)

0

0

(58,231,242)

0

Net asset value of shares issued in

acquisition

Class A

16,437,691

243,734,394

0

0

Class B

1,440,941

21,365,593

0

0

Class C

2,085,189

30,912,915

0

0

Class I

190,270

2,821,118

0

0

298,834,020

0

(a) For Class A, B and C shares, for the period from May 20, 2005 (commencement of class operations), to November 30, 2005.

(b) Effective at the close of business on May 20, 2005, the Fund acquired the net assets of Vestaur Securities Fund. Vestaur Securities Fund became the accounting and performance survivor in this transaction. The information above for the period prior to May 23, 2005 is that of Vestaur Securities Fund. The capital share activity for Class I has been restated to give effect to this transaction.

See Notes to Financial Statements 25

STATEMENTS OF CHANGES IN NET ASSETS continued

Year Ended November 30,

2005 (a) (b)

2004 (b)

Capital share transactions

(continued)

Net increase in net assets resulting from

capital share transactions

$

252,250,799

$

0

Total increase (decrease) in net assets

243,311,155

(42,899)

Net assets

Beginning of period

97,234,556

97,277,455

End of period

$

340,545,711

$

97,234,556

Overdistributed net investment income

$

(189,584)

$

0

(a) For Class A, B and C shares, for the period from May 20, 2005 (commencement of class operations), to November 30, 2005.

(b) Effective at the close of business on May 20, 2005, the Fund acquired the net assets of Vestaur Securities Fund. Vestaur Securities Fund became the accounting and performance survivor in this transaction. The information above for the period prior to May 23, 2005 is that of Vestaur Securities Fund. The capital share activity for Class I has been restated to give effect to this transaction.

See Notes to Financial Statements 26

NOTES TO FINANCIAL STATEMENTS

1. ORGANIZATION

Evergreen Diversified Bond Fund (the “Fund”) is a diversified series of Evergreen Fixed Income Trust (the “Trust”), a Delaware statutory trust organized on September 18, 1997. The Trust is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”).

The Fund offers Class A, Class B, Class C and Institutional (“Class I”) shares. Class A shares are sold with a front-end sales charge. However, Class A share investments of $1 million or more are not subject to a front-end sales charge but will be subject to a contingent deferred sales charge of 1.00% upon redemption within one year. Class B shares are sold without a front-end sales charge but are subject to a contingent deferred sales charge that is payable upon redemption and decreases depending on how long the shares have been held. Class C shares are sold without a front-end sales charge but are subject to a contingent deferred sales charge that is payable upon redemption within one year. Class I shares are sold without a front-end sales charge or contingent deferred sales charge. Each class of shares, except Class I shares, pays an ongoing distribution fee.

Effective at the close of business on May 20, 2005, the Fund acquired the net assets of Vestaur Securities Fund, a diversified closed-end management investment company, in a tax-free exchange for Class I shares of the Fund. Vestaur Securities Fund became the accounting and performance survivor in this transaction. As a result, the accounting and performance history of Vestaur Securities Fund has been carried forward in the financial statements herein. In addition, since Class A, Class B and Class C shares of Vestaur Securities Fund did not exist prior to the reorganization, the accounting and performance information of these respective classes of shares of the Fund reflects the commencement of operations on May 20, 2005.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. The policies are in conformity with generally accepted accounting principles in the United States of America, which require management to make estimates and assumptions that affect amounts reported herein. Actual results could differ from these estimates.

a. Valuation of investments

Portfolio debt securities acquired with more than 60 days to maturity are fair valued using matrix pricing methods determined by an independent pricing service which takes into consideration such factors as similar security prices, yields, maturities, liquidity and ratings. Securities for which valuations are not readily available from an independent pricing service may be valued by brokers which use prices provided by market makers or estimates of market value obtained from yield data relating to investments or securities with similar characteristics.

Listed equity securities are usually valued at the last sales price or official closing price on the national securities exchange where the securities are principally traded.

27

NOTES TO FINANCIAL STATEMENTS continued

Short-term securities with remaining maturities of 60 days or less at the time of purchase are valued at amortized cost, which approximates market value.

Investments in other mutual funds are valued at net asset value. Securities for which market quotations are not readily available or not reflective of current market value are valued at fair value as determined by the investment advisor in good faith, according to procedures approved by the Board of Trustees.

b. Repurchase agreements

Securities pledged as collateral for repurchase agreements are held by the custodian bank or in a segregated account in the Fund’s name until the agreements mature. Collateral for certain tri-party repurchase agreements is held at the counterparty’s custodian in a segregated account for the benefit of the Fund and the counterparty. Each agreement requires that the market value of the collateral be sufficient to cover payments of interest and principal. However, in the event of default or bankruptcy by the other party to the agreement, retention of the collateral may be subject to legal proceedings. The Fund will only enter into repurchase agreements with banks and other financial institutions, which are deemed by the investment advisor to be creditworthy pursuant to guidelines established by the Board of Trustees.

c. Foreign currency translation

All assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts at the date of valuation. Purchases and sales of portfolio securities and income items denominated in foreign currencies are translated into U.S. dollar amounts on the respective dates of such transactions. The Fund does not separately account for that portion of the results of operations resulting from changes in foreign exchange rates on investments and the fluctuations arising from changes in market prices of securities held. Such fluctuations are included with the net realized and unrealized gains or losses on investments.

d. Futures contracts

In order to gain exposure to or protect against changes in security values, the Fund may buy and sell futures contracts. The primary risks associated with the use of futures contracts are the imperfect correlation between changes in market values of securities held by the Fund and the prices of futures contracts, and the possibility of an illiquid market.

Futures contracts are valued based upon their quoted daily settlement prices. The aggregate principal amounts of the contracts are not recorded in the financial statements. Fluctuations in the value of the contracts are recorded in the Statement of Assets and Liabilities as an asset or liability and in the Statement of Operations as unrealized gains or losses until the contracts are closed, at which point they are recorded as net realized gains or losses on futures contracts.

e. When-issued and delayed delivery transactions

The Fund records when-issued or delayed delivery securities as of trade date and maintains security positions such that sufficient liquid assets will be available to make payment for the securities purchased. Securities purchased on a when-issued or delayed delivery basis are marked-to-market

28

NOTES TO FINANCIAL STATEMENTS continued

daily and begin earning interest on the settlement date. Losses may occur on these transactions due to changes in market conditions or the failure of counterparties to perform under the contract.

f. Securities lending

The Fund may lend its securities to certain qualified brokers in order to earn additional income. The Fund receives compensation in the form of fees or interest earned on the investment of any cash collateral received. The Fund also continues to receive interest and dividends on the securities loaned. The Fund receives collateral in the form of cash or securities with a market value at least equal to the market value of the securities on loan, including accrued interest. In the event of default or bankruptcy by the borrower, the Fund could experience delays and costs in recovering the loaned securities or in gaining access to the collateral. The Fund has the right under the lending agreement to recover the securities from the borrower on demand.

g. Security transactions and investment income

Security transactions are recorded on trade date. Realized gains and losses are computed using the specific cost of the security sold. Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums. Dividend income is recorded on the ex-dividend date. Foreign income and capital gains realized on some securities may be subject to foreign taxes, which are accrued as applicable.

h. Federal taxes

The Fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income, including any net capital gains (which have already been offset by available capital loss carryovers). Accordingly, no provision for federal taxes is required.

i. Distributions

Distributions to shareholders from net investment income are accrued daily and paid monthly. Distributions from net realized gains, if any, are recorded on the ex-dividend date. Such distributions are determined in conformity with income tax regulations, which may differ from generally accepted accounting principles.

Reclassifications have been made to the Fund’s components of net assets to reflect income and gains available for distribution (or available capital loss carryovers, as applicable) under income tax regulations. The primary permanent differences causing such reclassifications are due to net realized foreign currency gains or losses, certain capital loss carryovers assumed as a result of acquisitions, mortgage paydown gains and losses, consent fees on tendered bonds and premium amortization. During the year ended November 30, 2005, the following amounts were reclassified:

Paid-in capital

$ 46,129,668

Overdistributed net investment income

2,370,763

Accumulated net realized losses on investments

(48,500,431)

29

NOTES TO FINANCIAL STATEMENTS continued

j. Class allocations

Income, common expenses and realized and unrealized gains and losses are allocated to the classes based on the relative net assets of each class. Distribution fees, if any, are calculated daily at the class level based on the appropriate net assets of each class and the specific expense rates applicable to each class.

3. ADVISORY FEE AND OTHER TRANSACTIONS WITH AFFILIATES

Evergreen Investment Management Company, LLC (“EIMC”), an indirect, wholly-owned subsidiary of Wachovia Corporation (“Wachovia”), is the investment advisor to the Fund and is paid a fee at an annual rate of 2% of the Fund’s gross investment income plus an amount determined by applying percentage rates to the average daily net assets of the Fund, starting at 0.31% and declining to 0.16% as average daily net assets increase. Prior to May 23, 2005, Vestaur Securities Fund, the accounting and performance survivor, paid EIMC an annual fee of 0.50% of its average monthly net assets plus 2.50% of its investment income.

From time to time, EIMC may voluntarily or contractually waive its fee and/or reimburse expenses in order to limit operating expenses. During the year ended November 30, 2005, EIMC waived its advisory fee in the amount of $343,119 and reimbursed Distribution Plan expenses (see Note 4) relating to Class A shares in the amount of $2,743.

Evergreen Investment Services, Inc. (“EIS”), an indirect, wholly-owned subsidiary of Wachovia, is the administrator to the Fund. As administrator, EIS provides the Fund with facilities, equipment and personnel and is paid an annual rate determined by applying percentage rates to the aggregate average daily net assets of the Evergreen funds (excluding money market funds), starting at 0.10% and declining to 0.05% as the aggregate average daily net assets of the Evergreen funds (excluding money market funds) increase.

Evergreen Service Company, LLC (“ESC”), an indirect, wholly-owned subsidiary of Wachovia, is the transfer and dividend disbursing agent for the Fund. ESC receives account fees that vary based on the type of account held by the shareholders in the Fund. For the year ended November 30, 2005, the transfer agent fees were equivalent to an annual rate of 0.17% of the Fund’s average daily net assets.

4. DISTRIBUTION PLANS

EIS also serves as distributor of the Fund’s shares. The Fund has adopted Distribution Plans, as allowed by Rule 12b-1 of the 1940 Act, for each class of shares, except Class I. Under the Distribution Plans, distribution fees are paid at an annual rate of 0.30% of the average daily net assets for Class A shares and 1.00% of the average daily net assets for each of Class B and Class C shares.

For the period ended November 30, 2005, EIS received $3,178 from the sale of Class A shares and $28,009 and $236 in contingent deferred sales charges from redemptions of Class B and Class C shares, respectively.

30

NOTES TO FINANCIAL STATEMENTS continued

5. ACQUISITION

Effective at the close of business on May 20, 2005, the Fund acquired the net assets of Vestaur Securities Fund in a tax-free exchange for Class I shares of the Fund at an exchange ratio of 0.93. The acquired net assets consisted primarily of portfolio securities with unrealized appreciation of $49,458. The aggregate net assets of the Fund and Vestaur Securities Fund immediately prior to the acquisition were $298,834,020 and $95,236,951, respectively. The aggregate net assets of the Fund immediately after the acquisition were $394,070,971. Vestaur Securities Fund was the accounting and performance survivor in this transaction.

6. SECURITIES TRANSACTIONS

Cost of purchases and proceeds from sales of investment securities (excluding short-term securities) were as follows for the year ended November 30, 2005:

Cost of Purchases

Proceeds from Sales

U.S.

Non-U.S.

U.S.

Non-U.S.

Government

Government

Government

Government

$13,673,138

$115,351,644

$8,925,223

$150,046,922

At November 30, 2005, the Fund had open short futures contracts outstanding as follows:

Initial

Value at

Contract

November 30,

Unrealized

Expiration

Contracts

Amount

2005

Gain

December

100 U.S. Treasury

2005

Notes Futures

$11,125,281

$10,873,437

$ 251,844

December

45 U.S. Treasury

2005

Bonds Futures

5,272,509

5,052,656

219,853

On November 30, 2005, the estimated aggregate cost of securities for federal income tax purposes was $336,883,073. The gross unrealized appreciation and depreciation on securities based on tax cost was $5,550,633 and $7,969,493, respectively, with a net unrealized depreciation of $2,418,860.

As of April 30, 2005, the Fund had $46,930,085 in capital loss carryovers for federal income tax purposes expiring on April 30 of the following years:

Expiration

2007

2008

2009

2010

2013

$7,055,922

$19,652,642

$11,338,929

$4,586,980

$4,295,612

In addition, on May 20, 2005, the Fund acquired $8,190,723 of capital loss carryovers from its merger with Vestaur Securities Fund, expiring on April 30 of the following years:

Expiration

2007

2008

2009

2010

$258,682

$1,451,536

$3,049,670

$3,430,835

31

NOTES TO FINANCIAL STATEMENTS continued

Certain portions of the capital loss carryovers of the Fund were assumed as a result of acquisitions. These losses are subject to certain limitations prescribed by the Internal Revenue Code.

7. INTERFUND LENDING

Pursuant to an Exemptive Order issued by the SEC, the Fund may participate in an interfund lending program with certain funds in the Evergreen fund family. This program allows the Fund to borrow from, or lend money to, other participating funds. During the year ended November 30, 2005, the Fund did not participate in the interfund lending program.

8. DISTRIBUTIONS TO SHAREHOLDERS

As of November 30, 2005, the components of distributable earnings on a tax basis were as follows:

Overdistributed

Unrealized

Capital Loss

Ordinary Income

Depreciation

Carryovers

$189,584

$1,716,876

$55,120,808

The differences between the components of distributable earnings on a tax basis and the amounts reflected in the Statement of Assets and Liabilities are primarily due to wash sales, premium amortization and marked-to-market income on futures contracts.

The tax character of distributions paid were $14,163,021 and $6,100,208 of ordinary income for the years ended November 30, 2005 and November 30, 2004, respectively.

The components of distributable earnings and the tax character of distributions paid are estimated at November 30, 2005. The actual amounts to be distributed will not be determined until April 30, 2006 when the Fund completes its tax year end.

9. EXPENSE REDUCTIONS

Through expense offset arrangements with ESC and the Fund’s custodian, a portion of fund expenses has been reduced.

10. DEFERRED TRUSTEES’ FEES

Each Trustee of the Fund may defer any or all compensation related to performance of their duties as Trustees. The Trustees’ deferred balances are allocated to deferral accounts, which are included in the accrued expenses for the Fund. The investment performance of the deferral accounts is based on the investment performance of certain Evergreen funds. Any gains earned or losses incurred in the deferral accounts are reported in the Fund’s Trustees’ fees and expenses. At the election of the Trustees, the deferral account will be paid either in one lump sum or in quarterly installments for up to ten years.

11. FINANCING AGREEMENT

The Fund and certain other Evergreen funds share in a $150 million unsecured revolving credit commitment for temporary and emergency purposes, including the funding of redemptions, as permitted by each participating fund’s borrowing restrictions. Borrowings under this facility bear

32

NOTES TO FINANCIAL STATEMENTS continued

interest at 0.50% per annum above the Federal Funds rate. All of the participating funds are charged an annual commitment fee of 0.09% of the unused balance, which is allocated pro rata.

During the year ended November 30, 2005, the Fund had average borrowings outstanding of $1,002 at a rate of 3.80% and paid interest of $38.

12. CONCENTRATION OF RISK

The Fund may invest a substantial portion of its assets in an industry or sector and, therefore, may be more affected by changes in that industry or sector than would be a comparable mutual fund that is not heavily weighted in any industry or sector.

13. REGULATORY MATTERS AND LEGAL PROCEEDINGS

Since September 2003, governmental and self-regulatory authorities have instituted numerous ongoing investigations of various practices in the mutual fund industry, including investigations relating to revenue sharing, market-timing, late trading and record retention, among other things. The investigations cover investment advisors, distributors and transfer agents to mutual funds, as well as other firms. EIMC, EIS and ESC (collectively, “Evergreen”) have received subpoenas and other requests for documents and testimony relating to these investigations, are endeavoring to comply with those requests, and are cooperating with the investigations. Evergreen is continuing its own internal review of policies, practices, procedures and personnel, and is taking remedial action where appropriate.

In connection with one of these investigations, on July 28, 2004, the staff of the Securities and Exchange Commission (“SEC”) informed Evergreen that the staff intends to recommend to the SEC that it institute an enforcement action against Evergreen. The SEC staff’s proposed allegations relate to (i) an arrangement pursuant to which a broker at one of EIMC’s affiliated broker-dealers had been authorized, apparently by an EIMC officer (no longer with EIMC), to engage in short-term trading, on behalf of a client, in Evergreen Mid Cap Growth Fund (formerly Evergreen Emerging Growth Fund and prior to that, known as Evergreen Small Company Growth Fund) during the period from December 2000 through April 2003, in excess of the limitations set forth in the fund’s prospectus, (ii) short-term trading from September 2001 through January 2003, by a former Evergreen portfolio manager, of Evergreen Precious Metals Fund, a fund he managed at the time, (iii) the sufficiency of systems for monitoring exchanges and enforcing exchange limitations as stated in the fund’s prospectuses, and (iv) the adequacy of e-mail retention practices. In connection with the activity in Evergreen Mid Cap Growth Fund, EIMC reimbursed the fund $378,905, plus an additional $25,242, representing what EIMC calculated at that time to be the client’s net gain and the fees earned by EIMC and the expenses incurred by this fund on the client’s account. In connection with the activity in Evergreen Precious Metals Fund, EIMC reimbursed the fund $70,878, plus an additional $3,075, representing what EIMC calculated at that time to be the portfolio manager’s net gain and the fees earned by EIMC and expenses incurred by the fund on the portfolio manager’s account. Evergreen is currently engaged in discussions with the staff of the SEC concerning its recommendation.

33

NOTES TO FINANCIAL STATEMENTS continued

The staff of the National Association of Securities Dealers (“NASD”) had notified EIS that it has made a preliminary determination to recommend that disciplinary action be brought against EIS for certain violations of the NASD’s rules. The recommendation relates principally to allegations that EIS (i) arranged for fund portfolio trades to be directed to broker-dealers (including Wachovia Securities, LLC, an affiliate of EIS) that sold Evergreen fund shares during the period of January 2001 to December 2003 and (ii) provided non-cash compensation by sponsoring offsite meetings attended by Wachovia Securities, LLC brokers during that period. EIS is cooperating with the NASD staff in its review of these matters.

Any resolution of these matters with regulatory authorities may include, but not be limited to, sanctions, penalties or injunctions regarding Evergreen, restitution to mutual fund shareholders and/or other financial penalties and structural changes in the governance or management of Evergreen’s mutual fund business. Any penalties or restitution will be paid by Evergreen and not by the Evergreen funds.

In addition, the Evergreen funds and EIMC and certain of its affiliates are involved in various legal actions, including private litigation and class action lawsuits. EIMC does not expect that any of such legal actions currently pending or threatened will have a material adverse impact on the financial position or operations of any of the Evergreen funds or on EIMC’s ability to provide services to the Evergreen funds.

Although Evergreen believes that neither the foregoing investigations nor any pending or threatened legal actions will have a material adverse impact on the Evergreen funds, there can be no assurance that these matters and any publicity surrounding or resulting from them will not result in reduced sales or increased redemptions of Evergreen fund shares, which could increase Evergreen fund transaction costs or operating expenses, or have other adverse consequences on the Evergreen funds.

34

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Trustees and Shareholders Evergreen Fixed Income Trust

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of the Evergreen Diversified Bond Fund, a series of Evergreen Fixed Income Trust, as of November 30, 2005, and the related statement of operations for the year then ended, statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of November 30, 2005 by correspondence with the custodian and brokers, or by other appropriate auditing procedures where replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Evergreen Diversified Bond Fund, as of November 30, 2005, the results of its operations, changes in its net assets and financial highlights for each of the years or periods described above in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts January 27, 2006

35

ADDITIONAL INFORMATION (unaudited)

On May 20, 2005, Vestaur Securities Fund merged with the Fund. Vestaur Securities Fund became the accounting and performance survivor in this transaction. Prior to the merger, Vestaur Securities Fund paid a distribution of $0.21 per share to its shareholders of record on March 31, 2005, of which $0.188 was from net income and $0.022 was from paid-in capital. In addition, Vestaur Securities Fund paid a distribution of $0.11 per share to its shareholders of record on May 6, 2005, all of which was from paid-in capital. If you were a shareholder of Vestaur Securities Fund at the time of either of these distributions, you will receive in early 2006 a Form 1099-DIV from Vestaur Securities Fund that will inform you of the tax character of these distributions.

36

ADDITIONAL INFORMATION (unaudited) continued

INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE FUND’S INVESTMENT

ADVISORY AGREEMENT

Each year, the Fund’s Board of Trustees is required to consider whether to continue in place the Fund’s investment advisory agreement. In September 2005, the Trustees, including a majority of the Trustees who are not interested persons (as that term is defined in the 1940 Act) of the Fund or of EIMC, approved the continuation of the Fund’s investment advisory agreement.

At the same time, the Trustees considered the continuation of the investment advisory agreements for all of the Evergreen funds, and the description below refers in many cases to the Trustees’ process and conclusions in connection with their consideration of this matter for all of the Evergreen funds. In all of its deliberations, the Board of Trustees and the disinterested Trustees were advised by independent counsel to the disinterested Trustees and counsel to the Evergreen funds.

The review process. The 1940 Act requires that the Board of Trustees request and evaluate, and that EIMC furnish, such information as may reasonably be necessary to evaluate the terms of the Fund’s advisory agreement. The review process began formally in spring 2005, when a committee of the Board (the “Committee”), working with EIMC management, determined generally the types of information the Board would review and set a timeline for the review process. In late spring, counsel to the disinterested Trustees sent to EIMC a formal request for information to be furnished to the Trustees. In addition, the independent data provider Lipper Inc. (“Lipper”) was engaged to provide fund-specific and industry-wide data to the Board containing information of a nature and in a format generally prescribed by the Committee.

The Trustees reviewed EIMC’s responses to the request for information, with the assistance of counsel for the disinterested Trustees and for the Evergreen funds and an independent industry consultant retained by the disinterested Trustees, and requested and received additional information following that review. The Committee met in person with the representatives of EIMC in early September. At a meeting of the full Board of Trustees later in September, the Committee reported the results of its discussions with EIMC, and the full Board met with representatives of EIMC, engaged in further review of the materials provided to them, and approved the continuation of each of the advisory and sub-advisory agreements.

The disinterested Trustees discussed the continuation of the Fund’s advisory agreement with representatives of EIMC and in multiple private sessions with legal counsel at which no personnel of EIMC were present. In considering the continuation of the agreement, the Trustees did not identify any particular information or consideration that was all-important or controlling, and each Trustee attributed different weights to various factors. The Trustees evaluated information provided to them both in terms of the Evergreen mutual funds generally and with respect to the Fund specifically as they considered appropriate; although the Trustees considered the continuation of the agreement as part of the larger process of considering the continuation of the advisory contracts for all of the Evergreen funds, their determination to continue the advisory agreement for each of the Evergreen funds was ultimately made on a fund-by-fund basis.

37

ADDITIONAL INFORMATION (unaudited) continued

This summary describes the most important, but not necessarily all, of the factors considered by the Board and the disinterested Trustees.

Information reviewed. The Board of Trustees and committees of the Board of Trustees meet periodically during the course of the year. At those meetings, the Board receives a wide variety of information regarding the services performed by EIMC, the investment performance of the Fund and the other Evergreen funds, and other aspects of the business and operations of the funds. At those meetings, and in the process of considering the continuation of the agreements, the Trustees considered information regarding, for example, the Fund’s investment results; the portfolio management team for the Fund and the experience of the members of that team, and any recent changes in the membership of the team; portfolio trading practices; compliance by the Fund and EIMC with applicable laws and regulations and with the Fund’s and EIMC’s compliance policies and procedures; services provided by affiliates of EIMC to the Fund and shareholders of the Fund; and other information relating to the nature, extent, and quality of services provided by EIMC. The Trustees considered the rates at which the Fund pays investment advisory fees, the total expense ratio of the Fund, and the efforts generally by EIMC and its affiliates as sponsors of the Fund. The data provided by Lipper showed the fees paid by the Fund and the Fund’s total expense ratio in comparison to other similar mutual funds, in addition to data regarding the investment performance by the Fund in comparison to other similar mutual funds. The Trustees were assisted by the independent industry consultant in reviewing the information presented to them.