UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-08879

MFS VARIABLE INSURANCE TRUST III

(Exact name of registrant as specified in charter)

111 Huntington Avenue, Boston, Massachusetts 02199

(Address of principal executive offices) (Zip code)

Christopher R. Bohane

Massachusetts Financial Services Company

111 Huntington Avenue

Boston, Massachusetts 02199

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617)954-5000

Date of fiscal year end: December 31

Date of reporting period: December 31, 2019

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Annual Report

December 31, 2019

MFS® Blended Research® Small Cap Equity Portfolio

MFS® Variable Insurance Trust III

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, the insurance company that offers your contract may determine that it will no longer send you paper copies of the fund’s annual and semiannual shareholder reports unless you specifically request paper copies from the insurance company or from your financial intermediary. Instead, the shareholder reports will be made available on a Web site (insurancefunds.mfs.com or other Web site of which you will be notified), and the insurance company will notify you by mail each time a report is posted and provide you with a Web site link to access the report. Instructions for requesting paper copies will be provided by your insurance company or financial intermediary.

If you already elected to receive shareholder reports by email, you will not be affected by this change and you need not take any action. If your insurance company or financial intermediary offers electronic delivery, you may elect to receive shareholder reports and other communications from the insurance company or financial intermediary by email by following the instructions provided by the insurance company or financial intermediary.

Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge from the insurance company or financial intermediary. You can inform the insurance company or financial intermediary that you wish to continue receiving paper copies of your shareholder reports by contacting your insurance company or financial intermediary. Your election to receive reports in paper will apply to all funds held in your account with your insurance company or financial intermediary.

VSC-ANN

MFS® Blended Research® Small Cap Equity Portfolio

CONTENTS

The report is prepared for the general information of contract owners. It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED• MAY LOSE VALUE• NO BANK OR CREDIT UNION GUARANTEE• NOT A DEPOSIT• NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY OR NCUA/NCUSIF

MFS Blended Research Small Cap Equity Portfolio

LETTER FROM THE EXECUTIVE CHAIR

Dear Contract Owners:

Slowing global growth, low inflation, and trade friction between the United States and China have been hallmarks of the past 12 months. After experiencing an uptick in market volatility in late 2018, markets steadied for most of 2019, thanks in large measure to the adoption of a dovish policy stance on the part of global central banks, focused on supporting economic growth. Negotiations aimed at a “phase one” trade deal between the U.S. and China bore fruit at the end of the period, boosting investor sentiment, while signs of stability emerging from the global manufacturing sector also lifted spirits. Uncertainty over Brexit, along with the ripple effects from the trade conflict, hampered business confidence and investment in the United Kingdom and Europe for much of the period, though investors expect greater clarity regarding Brexit as a result of December’s general election. The pro-Brexit Conservative Party won the election by a comfortable margin and set the stage for the U.K.’s departure from the EU at the end of January.

Markets expect the longest economic expansion in U.S. history will continue, albeit at a slower pace, as trade tensions recede. In an effort to prolong the expansion, the U.S. Federal Reserve lowered interest rates three times between July and October and the European Central Bank loosened policy in September. While the global monetary policy backdrop remains quite accommodative, signs of easing trade tensions and fading global recession fears led to improved market sentiment in late 2019 as investors grew less risk averse. In early 2020, an outbreak of coronavirus emanating from China reintroduced global growth fears, causing an uptick in volatility.

Here at MFS®, we aim to help our clients navigate the growing complexity of the markets and world economies. Our long-term investment philosophy and commitment to the responsible allocation of capital allow us to tune out the noise and uncover what we believe are the best, most durable investment opportunities in the market. Through our powerful global investment platform, we combine collective expertise, thoughtful risk management and long-term discipline to create sustainable value for investors.

Respectfully,

Robert J. Manning

Executive Chair

MFS Investment Management

February 14, 2020

The opinions expressed in this letter are subject to change and may not be relied upon for investment advice. No forecasts can be guaranteed.

1

MFS Blended Research Small Cap Equity Portfolio

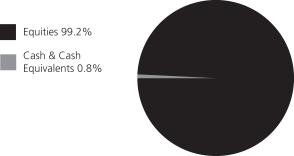

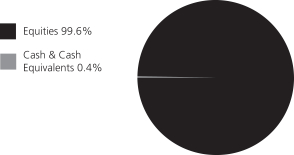

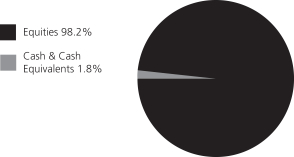

PORTFOLIO COMPOSITION

Portfolio structure

| | | | |

| Top ten holdings | | | | |

| Paylocity Holding Corp. | | | 1.8% | |

| Five9, Inc. | | | 1.6% | |

| Skechers USA, Inc., “A” | | | 1.6% | |

| Cathay General Bancorp, Inc. | | | 1.5% | |

| Prestige Brands Holdings, Inc. | | | 1.4% | |

| Store Capital Corp., REIT | | | 1.4% | |

| Cable One, Inc. | | | 1.4% | |

| KBR, Inc. | | | 1.4% | |

| Tenet Healthcare Corp. | | | 1.4% | |

| Industrial Logistics Properties Trust, REIT | | | 1.4% | |

| | | | |

| Equity sectors (k) | | | | |

| Financial Services | | | 25.2% | |

| Health Care | | | 17.2% | |

| Technology | | | 14.9% | |

| Industrial Goods & Services | | | 6.7% | |

| Autos & Housing | | | 5.7% | |

| Special Products & Services | | | 5.4% | |

| Basic Materials | | | 4.4% | |

| Consumer Staples | | | 3.5% | |

| Energy | | | 3.5% | |

| Leisure | | | 3.4% | |

| Retailing | | | 3.4% | |

| Transportation | | | 2.7% | |

| Utilities | | | 2.4% | |

| Communications | | | 0.8% | |

| (k) | The sectors set forth above and the associated portfolio composition are based on MFS’ own custom sector classification methodology. |

Cash & Cash Equivalents includes any cash, investments in money market funds, short-term securities, and other assets less liabilities. Please see the Statement of Assets and Liabilities for additional information related to the fund’s cash position and other assets and liabilities.

Percentages are based on net assets as of December 31, 2019.

The portfolio is actively managed and current holdings may be different.

2

MFS Blended Research Small Cap Equity Portfolio

MANAGEMENT REVIEW

Summary of Results

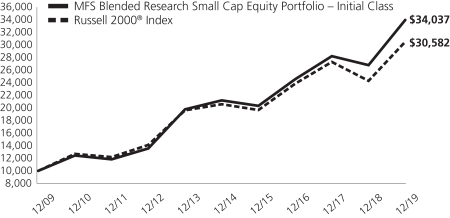

For the twelve months ended December 31, 2019, Initial Class shares of the MFS Blended Research Small Cap Equity Portfolio (fund) provided a total return of 26.78%, while Service Class shares of the fund provided a total return of 26.36%. These compare with a return of 25.52% over the same period for the fund’s benchmark, the Russell 2000® Index.

Market Environment

Fading fears of a near-term global recession, the announcement of a partial trade deal between the United States and China and the decline in uncertainty over Brexit helped bolster market sentiment late in the period. Changes in market sentiment, largely driven by uncertainty over the outcome of trade negotiations between the US and China, had contributed to periodic bouts of volatility during the reporting period. The global economy decelerated, led by weakness in China and Europe, although the pace of the slowdown moderated late in the period amid nascent signs of stabilization in the manufacturing sector.

The deteriorating global growth backdrop, along with declining inflationary pressures, prompted the US Federal Reserve to adopt a more dovish posture beginning in early 2019, resulting in the first interest rate cut in over a decade at the end of July, followed by additional cuts in September and October. The Fed’s actions led to a sharp decline in long-term interest rates during the period’s second half, causing the inversion of portions of the US Treasury yield curve for a time. Amid an improvement in risk sentiment in Q4 2019 and indications of a bottoming in growth and a potential upturn in activity, the Fed indicated in October that further rate cuts were unlikely unless the outlook for the economy materially worsened.

Globally, central banks have tilted more dovish as well, with the European Central Bank unveiling a package of easing measures, which included putting overnight rates deeper into negative territory, restarting its bond-buying program and lengthening the term of cheap loans to banks to three years from two. The central banks of India and Australia are among those that have cut rates several times in recent months, although China has been more cautious in increasing liquidity as it keeps trying to deleverage its economy, cutting rates only marginally.

Emerging markets experienced considerable volatility through the end of 2018, as tighter global financial conditions exposed structural weakness in some countries. Those conditions improved in 2019 as the Fed became more dovish. Notwithstanding the periodic headwinds on market sentiment from significant trade friction between the US and China over much of the year, emerging market hard currency debt and local rates benefited from relatively cheap valuations at the beginning of the period and easier global monetary conditions. These factors, plus the fading of certain global risk factors mentioned above, hastened spread tightening in the latter part of the period. At the same time, idiosyncratic risks spiked in some countries (e.g., Argentina and Lebanon), contributing to increased dispersion in performance among sovereign assets.

Contributors to Performance

Security selection and, to a lesser extent, an overweight position in both thetechnology and consumer staplessectors contributed to performance relative to the Russell 2000® Index. Within thetechnology sector, the fund’s overweight positions in cloud-based software solutions provider Paylocity Holding and security risk intelligence solutions provider Rapid7 (h), and holding shares of software engineering solutions and technology services provider EPAM Systems (b)(h), aided relative results. The stock price of Rapid7 appreciated during the period as the company reported strong financial results, driven by strength in average recurring revenues. Within theconsumer staplessector, holding shares of plant-based meats producer Beyond Meat (b)(h) and multi-national food company Pilgrim’s Pride (b) helped relative returns.

Security selection within theenergysector also bolstered relative performance, led by the timing of the fund’s ownership in shares of oilfield services company ProPetro Holding (h).

Elsewhere, the fund’s overweight positions in engineering, procurement and construction company KBR and hospital operator Tenet Healthcare supported relative results. The share price of KBR advanced, as the company reported solid financial results, due to strong performance in both of its energy solutions and government solutions segments. In addition, holding shares of lifestyle footwear developer Skechers USA (b) and internet and cable service provider Cable One (b) further benefited relative returns.

Detractors from Performance

During the reporting period, security selection within thehealth caresector detracted from relative performance. Within this sector, the fund’s overweight positions in biopharmaceutical company Acorda Therapeutics, global specialty pharmaceutical company Mallinckrodt (h) (United Kingdom), pharmaceutical company AMAG Pharmaceuticals (h) and medical technology company Avanos Medical weakened relative results. The stock price of Acorda Therapeutics declined after the company reported that revenues from its recently launched Parkinson’s drug Inbrija were slightly lower than expectations, which limited visibility about the future trajectory of its sales. Additionally, not holding shares of targeted small molecule pharmaceuticals developer Array Biopharma further weighed on relative returns.

3

MFS Blended Research Small Cap Equity Portfolio

Management Review – continued

Security selection in both thebasic materialsandspecial products & servicessectors also held back relative returns. Within thebasic materialssector, the timing of the fund’s ownership in shares of paper products manufacturer Verso (h) and renewable fuels provider Renewable Energy Group (h) detracted from relative returns. Within thespecial products & servicessector, an overweight position in research, data and advisory services provider Forrester Research dampened relative returns. The stock price of Forrester Research declined during the period, as management lowered its full-year 2019 guidance due to a lower-than-expected contribution from its SiriusDecisions business.

Stocks in other sectors that further hindered relative results included the timing of the fund’s overweight ownership in shares of firearms manufacturer American Outdoor Brands (h) and telecommunications company Shenandoah Telecommunications (h).

Respectfully,

Portfolio Manager(s)

Jim Fallon, Matt Krummell, Jonathan Sage, and Jed Stocks

| (b) | Security is not a benchmark constituent. |

| (h) | Security was not held in the portfolio at period end. |

The views expressed in this report are those of the portfolio manager(s) only through the end of the period of the report as stated on the cover and do not necessarily reflect the views of MFS or any other person in the MFS organization. These views are subject to change at any time based on market or other conditions, and MFS disclaims any responsibility to update such views. These views may not be relied upon as investment advice or an indication of trading intent on behalf of any MFS portfolio. References to specific securities are not recommendations of such securities, and may not be representative of any MFS portfolio’s current or future investments.

4

MFS Blended Research Small Cap Equity Portfolio

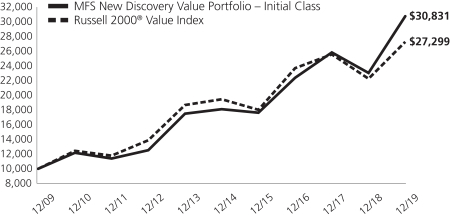

PERFORMANCE SUMMARY THROUGH 12/31/19

The following chart illustrates the historical performance of the fund in comparison to its benchmark(s). Benchmarks are unmanaged and may not be invested in directly. Benchmark returns do not reflect any fees or expenses. The performance of other share classes will be greater than or less than that of the class depicted below. (See Notes to Performance Summary.)

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your units, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. The performance shown does not reflect the deduction of taxes, if any, that a contract holder would pay on fund distributions or the redemption of contract units. The returns for the fund shown also do not reflect the deduction of expenses associated with variable products, such as mortality and expense risk charges, separate account charges, and sales charges imposed by the insurance company separate accounts. Such expenses would reduce the overall returns shown.

Growth of a Hypothetical $10,000 Investment

Total Returns through 12/31/19

Average annual total returns

| | | | | | | | | | | | |

| | | Share Class | | Class Inception Date | | 1-yr | | 5-yr | | 10-yr | | |

| | | Initial Class | | 7/17/00 | | 26.78% | | 9.89% | | 13.03% | | |

| | | Service Class | | 5/01/06 | | 26.36% | | 9.60% | | 12.73% | | |

| | | | |

| Comparative benchmark(s) | | | | | | | | |

| | | Russell 2000® Index (f) | | 25.52% | | 8.23% | | 11.83% | | |

| (f) | Source: FactSet Research Systems Inc. |

Benchmark Definition(s)

Russell 2000® Index – constructed to provide a comprehensive barometer for securities in the small-cap segment of the U.S. equity universe. The index includes 2,000 of the smallest U.S. companies based on total market capitalization, representing approximately 10% of the investable U.S. equity market. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this document. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor, or endorse the content of this document.

It is not possible to invest directly in an index.

Notes to Performance Summary

Average annual total return represents the average annual change in value for each share class for the periods presented.

Performance results reflect any applicable expense subsidies and waivers in effect during the periods shown. Without such subsidies and waivers the fund’s performance results would be less favorable. Please see the prospectus and financial statements for complete details. All results are historical and assume the reinvestment of any dividends and capital gains distributions.

5

MFS Blended Research Small Cap Equity Portfolio

Performance Summary – continued

Performance prior to close of business December 7, 2012, reflects time periods when another adviser or subadviser was responsible for selecting investments for the fund under a different investment objective and different investment strategies.

Performance results do not include adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles and may differ from amounts reported in the financial highlights.

From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower.

6

MFS Blended Research Small Cap Equity Portfolio

EXPENSE TABLE

Fund Expenses Borne by the Contract Holders during the Period,

July 1, 2019 through December 31, 2019

As a contract holder of the fund, you incur ongoing costs, including management fees; distribution and/or service(12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period July 1, 2019 through December 31, 2019.

Actual Expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight the fund’s ongoing costs only and do not take into account the fees and expenses imposed under the variable contracts through which your investment in the fund is made. Therefore, the second line for each share class in the table is useful in comparing ongoing costs associated with an investment in vehicles (such as the fund) which fund benefits under variable annuity and variable life insurance contracts and to qualified pension and retirement plans only, and will not help you determine the relative total costs of investing in the fund through variable annuity and variable life insurance contracts. If the fees and expenses imposed under the variable contracts were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | |

| Share Class | | | | Annualized

Expense Ratio | | | Beginning

Account Value

7/01/19 | | | Ending

Account Value

12/31/19 | | | Expenses Paid

During Period (p)

7/01/19-12/31/19 | |

| Initial Class | | Actual | | | 0.52% | | | | $1,000.00 | | | | $1,069.14 | | | | $2.71 | |

| | Hypothetical (h) | | | 0.52% | | | | $1,000.00 | | | | $1,022.58 | | | | $2.65 | |

| Service Class | | Actual | | | 0.77% | | | | $1,000.00 | | | | $1,066.31 | | | | $4.01 | |

| | Hypothetical (h) | | | 0.77% | | | | $1,000.00 | | | | $1,021.32 | | | | $3.92 | |

| (h) | 5% class return per year before expenses. |

| (p) | “Expenses Paid During Period” are equal to each class’s annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by 184/365 (to reflect theone-half year period). |

7

MFS Blended Research Small Cap Equity Portfolio

PORTFOLIO OF INVESTMENTS – 12/31/19

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| COMMON STOCKS – 99.2% | | | | | | | | |

| Aerospace – 1.3% | | | | | | | | |

| CACI International, Inc., “A” (a) | | | 5,200 | | | $ | 1,299,948 | |

| | | | | | | | |

| Apparel Manufacturers – 2.0% | | | | | | | | |

| Levi Strauss & Co., “A” | | | 19,638 | | | $ | 378,817 | |

| Skechers USA, Inc., “A” (a) | | | 35,426 | | | | 1,530,049 | |

| | | | | | | | |

| | | | | | $ | 1,908,866 | |

| | | | | | | | |

| Automotive – 2.0% | |

| IAA, Inc. (a) | | | 18,913 | | | $ | 890,046 | |

| Stoneridge, Inc. (a) | | | 34,573 | | | | 1,013,680 | |

| | | | | | | | |

| | | | | | $ | 1,903,726 | |

| | | | | | | | |

| Biotechnology – 6.1% | |

| Acorda Therapeutics, Inc. (a) | | | 60,139 | | | $ | 122,684 | |

| Adaptive Biotechnologies Corp. (a) | | | 5,232 | | | | 156,541 | |

| Akebia Therapeutics, Inc. (a) | | | 79,474 | | | | 502,276 | |

| Arena Pharmaceuticals, Inc. (a) | | | 10,165 | | | | 461,694 | |

| Bio-Techne Corp. | | | 5,108 | | | | 1,121,257 | |

| Bruker BioSciences Corp. | | | 10,493 | | | | 534,828 | |

| Coherus BioSciences, Inc. (a) | | | 28,916 | | | | 520,633 | |

| CytomX Therapeutics, Inc. (a) | | | 45,397 | | | | 377,249 | |

| Esperion Therapeutics, Inc. (a) | | | 12,400 | | | | 739,412 | |

| Exelixis, Inc. (a) | | | 8,418 | | | | 148,325 | |

| Macrogenics, Inc. (a) | | | 33,461 | | | | 364,056 | |

| Pieris Pharmaceuticals, Inc. (a) | | | 22,334 | | | | 80,849 | |

| Retrophin, Inc. (a) | | | 19,225 | | | | 272,995 | |

| Varex Imaging Corp. (a) | | | 17,336 | | | | 516,786 | |

| | | | | | | | |

| | | | | | $ | 5,919,585 | |

| | | | | | | | |

| Broadcasting – 0.4% | |

| Sinclair Broadcast Group, Inc. | | | 11,101 | | | $ | 370,107 | |

| | | | | | | | |

| Brokerage & Asset Managers – 0.1% | |

| LPL Financial Holdings, Inc. | | | 1,381 | | | $ | 127,397 | |

| | | | | | | | |

| Business Services – 1.0% | |

| Forrester Research, Inc. (a) | | | 21,230 | | | $ | 885,291 | |

| World Fuel Services Corp. | | | 2,930 | | | | 127,221 | |

| | | | | | | | |

| | | | | | $ | 1,012,512 | |

| | | | | | | | |

| Cable TV – 1.4% | |

| Cable One, Inc. | | | 915 | | | $ | 1,361,950 | |

| | | | | | | | |

| Chemicals – 0.4% | |

| Ingevity Corp. (a) | | | 3,912 | | | $ | 341,831 | |

| | | | | | | | |

| Computer Software – 4.3% | |

| Cornerstone OnDemand, Inc. (a) | | | 21,726 | | | $ | 1,272,057 | |

| Everbridge, Inc. (a) | | | 1,585 | | | | 123,757 | |

| Paylocity Holding Corp. (a) | | | 14,591 | | | | 1,762,885 | |

| RingCentral, Inc. (a) | | | 3,473 | | | | 585,791 | |

| SecureWorks Corp. (a)(l) | | | 22,111 | | | | 368,369 | |

| | | | | | | | |

| | | | | | $ | 4,112,859 | |

| | | | | | | | |

| Computer Software – Systems – 3.2% | | | | | | | | |

| Box, Inc., “A” (a) | | | 12,383 | | | $ | 207,787 | |

| Five9, Inc. (a) | | | 23,707 | | | | 1,554,705 | |

| | | | | | | | |

| | |

| Issuer | | Shares/Par | | | Value ($) | |

| COMMON STOCKS – continued | | | | | | | | |

| Computer Software – Systems – continued | | | | | |

| Insight Enterprises, Inc. (a) | | | 3,761 | | | $ | 264,360 | |

| Verint Systems, Inc. (a) | | | 18,425 | | | | 1,020,008 | |

| | | | | | | | |

| | | | | | $ | 3,046,860 | |

| | | | | | | | |

| Construction – 1.1% | |

| Eagle Materials, Inc. | | | 5,809 | | | $ | 526,644 | |

| Toll Brothers, Inc. | | | 14,425 | | | | 569,932 | |

| | | | | | | | |

| | | | | | $ | 1,096,576 | |

| | | | | | | | |

| Consumer Products – 1.6% | |

| Prestige Brands Holdings, Inc. (a) | | | 34,199 | | | $ | 1,385,060 | |

| USANA Health Sciences, Inc. (a) | | | 1,584 | | | | 124,423 | |

| | | | | | | | |

| | | | | | $ | 1,509,483 | |

| | | | | | | | |

| Consumer Services – 1.0% | |

| Grand Canyon Education, Inc. (a) | | | 9,760 | | | $ | 934,910 | |

| | | | | | | | |

| Electrical Equipment – 2.6% | |

| TriMas Corp. (a) | | | 39,666 | | | $ | 1,245,909 | |

| WESCO International, Inc. (a) | | | 20,686 | | | | 1,228,542 | |

| | | | | | | | |

| | | | | | $ | 2,474,451 | |

| | | | | | | | |

| Electronics – 3.6% | |

| Amkor Technology, Inc. (a) | | | 63,420 | | | $ | 824,460 | |

| Jabil Circuit, Inc. | | | 20,139 | | | | 832,345 | |

| Plexus Corp. (a) | | | 13,374 | | | | 1,028,996 | |

| Sanmina Corp. (a) | | | 13,754 | | | | 470,937 | |

| Silicon Laboratories, Inc. (a) | | | 2,626 | | | | 304,563 | |

| | | | | | | | |

| | | | | | $ | 3,461,301 | |

| | | | | | | | |

| Energy – Independent – 1.6% | |

| Arch Coal, Inc. | | | 5,880 | | | $ | 421,831 | |

| Delek U.S. Holdings, Inc. | | | 10,423 | | | | 349,483 | |

| Par Pacific Holdings, Inc. (a) | | | 9,215 | | | | 214,157 | |

| Warrior Met Coal, Inc. | | | 14,289 | | | | 301,926 | |

| WPX Energy, Inc. (a) | | | 20,105 | | | | 276,243 | |

| | | | | | | | |

| | | | | | $ | 1,563,640 | |

| | | | | | | | |

| Engineering – Construction – 3.9% | |

| Great Lakes Dredge & Dock Corp. (a) | | | 40,074 | | | $ | 454,038 | |

| KBR, Inc. | | | 44,432 | | | | 1,355,176 | |

| Matrix Service Co. (a) | | | 18,919 | | | | 432,867 | |

| Quanta Services, Inc. | | | 27,439 | | | | 1,117,042 | |

| Tutor Perini Corp. (a) | | | 32,528 | | | | 418,310 | |

| | | | | | | | |

| | | | | | $ | 3,777,433 | |

| | | | | | | | |

| Food & Beverages – 3.3% | |

| Hostess Brands, Inc. (a) | | | 88,794 | | | $ | 1,291,065 | |

| Ingredion, Inc. | | | 10,930 | | | | 1,015,944 | |

| Pilgrim’s Pride Corp. (a) | | | 27,325 | | | | 893,937 | |

| | | | | | | | |

| | | | | | $ | 3,200,946 | |

| | | | | | | | |

| Forest & Paper Products – 0.4% | |

| Boise Cascade Corp. | | | 11,466 | | | $ | 418,853 | |

| | | | | | | | |

8

MFS Blended Research Small Cap Equity Portfolio

Portfolio of Investments – continued

| | | | | | | | |

| | |

| Issuer | | Shares/Par | | | Value ($) | |

| COMMON STOCKS – continued | | | | | |

| Gaming & Lodging – 1.2% | | | | | | | | |

| Everi Holdings, Inc. (a) | | | 12,430 | | | $ | 166,935 | |

| Wyndham Hotels & Resorts, Inc. | | | 16,499 | | | | 1,036,302 | |

| | | | | | | | |

| | | | | | $ | 1,203,237 | |

| | | | | | | | |

| Health Maintenance Organizations – 1.0% | |

| Magellan Health Services, Inc. (a) | | | 3,091 | | | $ | 241,871 | |

| Molina Healthcare, Inc. (a) | | | 5,575 | | | | 756,471 | |

| | | | | | | | |

| | | | | | $ | 998,342 | |

| | | | | | | | |

| Insurance – 4.5% | | | | | | | | |

| American Equity Investment Life Holding Co. | | | 32,264 | | | $ | 965,661 | |

| Brighthouse Financial, Inc. (a) | | | 1,127 | | | | 44,212 | |

| CNO Financial Group, Inc. | | | 32,999 | | | | 598,272 | |

| Essent Group Ltd. | | | 15,580 | | | | 810,004 | |

| MGIC Investment Corp. | | | 53,727 | | | | 761,312 | |

| Radian Group, Inc. | | | 33,645 | | | | 846,508 | |

| Universal Insurance Holdings, Inc. | | | 12,406 | | | | 347,244 | |

| | | | | | | | |

| | | | | | $ | 4,373,213 | |

| | | | | | | | |

| Internet – 0.6% | |

| LogMeIn, Inc. | | | 6,786 | | | $ | 581,832 | |

| | | | | | | | |

| Leisure & Toys – 1.4% | | | | | | | | |

| Brunswick Corp. | | | 19,825 | | | $ | 1,189,103 | |

| Funko, Inc., “A” (a) | | | 10,879 | | | | 186,684 | |

| | | | | | | | |

| | | | | | $ | 1,375,787 | |

| | | | | | | | |

| Machinery & Tools – 4.3% | | | | | | | | |

| ACCO Brands Corp. | | | 24,011 | | | $ | 224,743 | |

| AGCO Corp. | | | 15,420 | | | | 1,191,195 | |

| Allison Transmission Holdings, Inc. | | | 6,705 | | | | 323,985 | |

| ITT, Inc. | | | 6,639 | | | | 490,688 | |

| Park-Ohio Holdings Corp. | | | 12,661 | | | | 426,043 | |

| Regal Beloit Corp. | | | 12,354 | | | | 1,057,626 | |

| Titan Machinery, Inc. (a) | | | 30,610 | | | | 452,416 | |

| | | | | | | | |

| | | | | | $ | 4,166,696 | |

| | | | | | | | |

| Medical & Health Technology & Services – 3.7% | |

| Allscripts Healthcare Solutions, Inc. (a) | | | 8,259 | | | $ | 81,062 | |

| HealthEquity, Inc. (a) | | | 8,642 | | | | 640,113 | |

| Medpace Holdings, Inc. (a) | | | 3,761 | | | | 316,150 | |

| Premier, Inc., “A” (a) | | | 32,396 | | | | 1,227,160 | |

| Tenet Healthcare Corp. (a) | | | 35,429 | | | | 1,347,365 | |

| | | | | | | | |

| | | | | | $ | 3,611,850 | |

| | | | | | | | |

| Medical Equipment – 3.8% | | | | | | | | |

| AngioDynamics, Inc. (a) | | | 24,658 | | | $ | 394,775 | |

| Avanos Medical, Inc. (a) | | | 13,423 | | | | 452,355 | |

| CONMED Corp. | | | 8,314 | | | | 929,755 | |

| CUTERA, Inc. (a) | | | 2,284 | | | | 81,790 | |

| Envista Holdings Corp. (a) | | | 16,540 | | | | 490,246 | |

| Integer Holdings Corp. (a) | | | 9,964 | | | | 801,404 | |

| IntriCon Corp. (a) | | | 5,849 | | | | 105,282 | |

| LivaNova PLC (a) | | | 1,587 | | | | 119,707 | |

| Orthofix Medical, Inc. (a) | | | 5,389 | | | | 248,864 | |

| | | | | | | | |

| | | | | | $ | 3,624,178 | |

| | | | | | | | |

| | | | | | | | |

| | |

| Issuer | | Shares/Par | | | Value ($) | |

| COMMON STOCKS – continued | | | | | |

| Metals & Mining – 0.3% | | | | | | | | |

| Olympic Steel, Inc. | | | 4,432 | | | $ | 79,421 | |

| Ryerson Holding Corp. (a) | | | 17,176 | | | | 203,192 | |

| Schnitzer Steel Industries, Inc., “A” | | | 2,216 | | | | 48,043 | |

| | | | | | | | |

| | | | | | $ | 330,656 | |

| | | | | | | | |

| Natural Gas – Distribution – 0.4% | | | | | | | | |

| MDU Resources Group, Inc. | | | 7,895 | | | $ | 234,561 | |

| Southwest Gas Holdings, Inc. | | | 1,395 | | | | 105,978 | |

| | | | | | | | |

| | | | | | $ | 340,539 | |

| | | | | | | | |

| Natural Gas – Pipeline – 0.3% | | | | | | | | |

| Equitrans Midstream Corp. | | | 23,026 | | | $ | 307,627 | |

| | | | | | | | |

| Oil Services – 2.8% | | | | | | | | |

| Cactus, Inc., “A” | | | 32,900 | | | $ | 1,129,128 | |

| Liberty Oilfield Services, Inc. | | | 65,720 | | | | 730,807 | |

| MRC Global, Inc. (a) | | | 58,663 | | | | 800,163 | |

| | | | | | | | |

| | | | | | $ | 2,660,098 | |

| | | | | | | | |

| Other Banks & Diversified Financials – 12.7% | | | | | |

| Bank OZK | | | 39,076 | | | $ | 1,192,013 | |

| Cathay General Bancorp, Inc. | | | 36,864 | | | | 1,402,675 | |

| Curo Group Holdings Corp. (a) | | | 40,562 | | | | 494,045 | |

| East West Bancorp, Inc. | | | 13,961 | | | | 679,901 | |

| Enova International, Inc. (a) | | | 21,425 | | | | 515,486 | |

| First Hawaiian, Inc. | | | 43,592 | | | | 1,257,629 | |

| Hanmi Financial Corp. | | | 55,896 | | | | 1,117,641 | |

| Herc Holdings, Inc. (a) | | | 15,174 | | | | 742,616 | |

| Navient Corp. | | | 10,634 | | | | 145,473 | |

| OFG Bancorp | | | 6,510 | | | | 153,701 | |

| OneMain Holdings, Inc. | | | 11,489 | | | | 484,261 | |

| Popular, Inc. | | | 10,775 | | | | 633,031 | |

| Regional Management Corp. (a) | | | 20,399 | | | | 612,582 | |

| Triton International Ltd. of Bermuda | | | 16,636 | | | | 668,767 | |

| UMB Financial Corp. | | | 4,657 | | | | 319,657 | |

| Umpqua Holdings Corp. | | | 46,259 | | | | 818,784 | |

| Wintrust Financial Corp. | | | 14,841 | | | | 1,052,227 | |

| | | | | | | | |

| | | | | | $ | 12,290,489 | |

| | | | | | | | |

| Pharmaceuticals – 2.7% | | | | | | | | |

| Assertio Therapeutics, Inc. (a) | | | 84,104 | | | $ | 105,130 | |

| Catalent, Inc. (a) | | | 5,192 | | | | 292,310 | |

| Horizon Therapeutics PLC (a) | | | 26,562 | | | | 961,544 | |

| Lannett Co., Inc. (a) | | | 38,574 | | | | 340,223 | |

| Phibro Animal Health Corp., “A” | | | 16,050 | | | | 398,521 | |

| United Therapeutics Corp. (a) | | | 5,245 | | | | 461,980 | |

| | | | | | | | |

| | | | | | $ | 2,559,708 | |

| | | | | | | | |

| Railroad & Shipping – 1.7% | | | | | | | | |

| DHT Holdings, Inc. | | | 59,997 | | | $ | 496,775 | |

| Dorian LPG Ltd. (a) | | | 43,760 | | | | 677,405 | |

| Teekay Tankers LTD., “A” (a) | | | 19,419 | | | | 465,473 | |

| | | | | | | | |

| | | | | | $ | 1,639,653 | |

| | | | | | | | |

| Real Estate – 9.3% | | | | | | | | |

| CoreCivic, Inc., REIT | | | 39,145 | | | $ | 680,340 | |

| Easterly Government Properties, REIT | | | 54,210 | | | | 1,286,403 | |

9

MFS Blended Research Small Cap Equity Portfolio

Portfolio of Investments – continued

| | | | | | | | |

| | |

| Issuer | | Shares/Par | | | Value ($) | |

| COMMON STOCKS – continued | | | | | |

| Real Estate – continued | | | | | | | | |

| Essential Properties Realty Trust, REIT | | | 21,976 | | | $ | 545,225 | |

| Industrial Logistics Properties Trust, REIT | | | 59,401 | | | | 1,331,770 | |

| Life Storage, Inc., REIT | | | 11,004 | | | | 1,191,513 | |

| Service Properties Trust, REIT | | | 19,869 | | | | 483,413 | |

| Spirit Realty Capital, Inc., REIT | | | 23,453 | | | | 1,153,419 | |

| STAG Industrial, Inc., REIT | | | 30,158 | | | | 952,088 | |

| STORE Capital Corp., REIT | | | 36,591 | | | | 1,362,649 | |

| | | | | | | | |

| | | | | | $ | 8,986,820 | |

| | | | | | | | |

| Restaurants – 0.7% | | | | | | | | |

| Wendy’s Co. | | | 31,036 | | | $ | 689,310 | |

| | | | | | | | |

| Specialty Chemicals – 1.6% | | | | | | | | |

| Element Solutions, Inc. (a) | | | 57,434 | | | $ | 670,829 | |

| Univar Solutions, Inc. (a) | | | 34,800 | | | | 843,552 | |

| | | | | | | | |

| | | | | | $ | 1,514,381 | |

| | | | | | | | |

| Specialty Stores – 0.3% | | | | | | | | |

| Hudson Ltd., “A” (a) | | | 18,538 | | | $ | 284,373 | |

| | | | | | | | |

| Telecommunications – Wireless – 0.4% | | | | | |

| Telephone and Data Systems, Inc. | | | 15,476 | | | $ | 393,555 | |

| | | | | | | | |

| Telephone Services – 0.5% | | | | | | | | |

| ATN International, Inc. | | | 8,915 | | | $ | 493,802 | |

| | | | | | | | |

| Trucking – 1.0% | | | | | | | | |

| Forward Air Corp. | | | 14,063 | | | $ | 983,707 | |

| | | | | | | | |

| Utilities – Electric Power – 2.7% | | | | | | | | |

| Clearway Energy, Inc., “A” | | | 50,384 | | | $ | 963,342 | |

| NRG Energy, Inc. | | | 18,759 | | | | 745,670 | |

| Portland General Electric Co. | | | 8,650 | | | | 482,584 | |

| Spark Energy, Inc., “A” | | | 40,119 | | | | 370,298 | |

| | | | | | | | |

| | | | | | $ | 2,561,894 | |

| | | | | | | | |

Total Common Stocks

(Identified Cost, $80,880,618) | | | | | | $ | 95,814,981 | |

| | | | | | | | |

| | | | | | | | |

| | |

| Issuer | | Shares/Par | | | Value ($) | |

| INVESTMENT COMPANIES (h) – 0.8% | | | | | |

| Money Market Funds – 0.8% | | | | | | | | |

| MFS Institutional Money Market Portfolio, 1.7% (v) (Identified Cost, $757,875) | | | 757,875 | | | $ | 757,875 | |

| | | | | | | | |

|

| COLLATERAL FOR SECURITIES LOANED – 0.1% | |

| State Street Navigator Securities Lending Government Money Market Portfolio, 1.58% (j) (Identified Cost, $96,250) | | | 96,250 | | | $ | 96,250 | |

| | | | | | | | |

OTHER ASSETS, LESS

LIABILITIES – (0.1)% | | | | | | | (129,797 | ) |

| | | | | | | | |

| NET ASSETS – 100.0% | | | | | | $ | 96,539,309 | |

| | | | | | | | |

| (a) | | Non-income producing security. |

| (h) | | An affiliated issuer, which may be considered one in which the fund owns 5% or more of the outstanding voting securities, or a company which is under common control. At period end, the aggregate values of the fund’s investments in affiliated issuers and in unaffiliated issuers were $757,875 and $95,911,231, respectively. |

| (j) | | The rate quoted is the annualizedseven-day yield of the fund at period end. |

| (l) | | A portion of this security is on loan. See Note 2 for additional information. |

| (v) | | Affiliated issuer that is available only to investment companies managed by MFS. The rate quoted for the MFS Institutional Money Market Portfolio is the annualizedseven-day yield of the fund at period end. |

The following abbreviations are used in this report and are defined:

| REIT | | Real Estate Investment Trust |

See Notes to Financial Statements

10

MFS Blended Research Small Cap Equity Portfolio

FINANCIAL STATEMENTS | STATEMENT OF ASSETS AND LIABILITIES

This statement represents your fund’s balance sheet, which details the assets and liabilities comprising the total value of the fund.

| | | | |

At 12/31/19 | | | | |

| |

Assets | | | | |

Investments in unaffiliated issuers, at value, including $164,318 of securities on loan (identified cost, $80,976,868) | | | $95,911,231 | |

Investments in affiliated issuers, at value (identified cost, $757,875) | | | 757,875 | |

Receivables for | | | | |

Fund shares sold | | | 11,854 | |

Interest and dividends | | | 90,699 | |

Other assets | | | 817 | |

Total assets | | | $96,772,476 | |

| |

Liabilities | | | | |

Payables for | | | | |

Fund shares reacquired | | | $80,433 | |

Collateral for securities loaned, at value (c) | | | 96,250 | |

Payable to affiliates | | | | |

Investment adviser | | | 2,059 | |

Administrative services fee | | | 127 | |

Shareholder servicing costs | | | 18 | |

Distribution and/or service fees | | | 836 | |

| Payable for independent Trustees’ compensation | | | 11 | |

Accrued expenses and other liabilities | | | 53,433 | |

Total liabilities | | | $233,167 | |

Net assets | | | $96,539,309 | |

| |

Net assets consist of | | | | |

Paid-in capital | | | $74,886,118 | |

Total distributable earnings (loss) | | | 21,653,191 | |

Net assets | | | $96,539,309 | |

Shares of beneficial interest outstanding | | | 8,474,411 | |

| | | | | | | | | | | | |

| | | |

| | | Net assets | | | Shares

outstanding | | | Net asset value

per share | |

Initial Class | | | $35,440,620 | | | | 3,040,726 | | | | $11.66 | |

Service Class | | | 61,098,689 | | | | 5,433,685 | | | | 11.24 | |

| (c) | Non-cash collateral is not included. |

See Notes to Financial Statements

11

MFS Blended Research Small Cap Equity Portfolio

FINANCIAL STATEMENTS | STATEMENT OF OPERATIONS

This statement describes how much your fund earned in investment income and accrued in expenses. It also describes any gains and/or losses generated by fund operations.

| | | | |

Year ended 12/31/19 | | | | |

| |

Net investment income (loss) | | | | |

Income | | | | |

Dividends | | | $1,184,560 | |

Income on securities loaned | | | 34,990 | |

Dividends from affiliated issuers | | | 18,901 | |

Other | | | 16,446 | |

Foreign taxes withheld | | | (1,542 | ) |

Total investment income | | | $1,253,355 | |

Expenses | | | | |

Management fee | | | $373,749 | |

Distribution and/or service fees | | | 149,917 | |

Shareholder servicing costs | | | 5,100 | |

Administrative services fee | | | 23,340 | |

Independent Trustees’ compensation | | | 3,100 | |

Custodian fee | | | 5,237 | |

Shareholder communications | | | 13,986 | |

Audit and tax fees | | | 54,887 | |

Legal fees | | | 807 | |

Miscellaneous | | | 26,137 | |

Total expenses | | | $656,260 | |

Reduction of expenses by investment adviser | | | (9,119 | ) |

Net expenses | | | $647,141 | |

Net investment income (loss) | | | $606,214 | |

| |

Realized and unrealized gain (loss) | | | | |

Realized gain (loss) (identified cost basis) | | | | |

Unaffiliated issuers | | | $6,772,411 | |

Affiliated issuers | | | 295 | |

Net realized gain (loss) | | | $6,772,706 | |

Change in unrealized appreciation or depreciation | | | | |

Unaffiliated issuers | | | $14,566,646 | |

Net realized and unrealized gain (loss) | | | $21,339,352 | |

Change in net assets from operations | | | $21,945,566 | |

See Notes to Financial Statements

12

MFS Blended Research Small Cap Equity Portfolio

FINANCIAL STATEMENTS | STATEMENTS OF CHANGES IN NET ASSETS

These statements describe the increases and/or decreases in net assets resulting from operations, any distributions, and any shareholder transactions.

| | | | | | | | |

| | | Year ended | |

| | | 12/31/19 | | | 12/31/18 | |

Change in net assets | | | | | | | | |

| | |

From operations | | | | | | | | |

Net investment income (loss) | | | $606,214 | | | | $531,740 | |

Net realized gain (loss) | | | 6,772,706 | | | | 15,299,479 | |

Net unrealized gain (loss) | | | 14,566,646 | | | | (18,798,977 | ) |

Change in net assets from operations | | | $21,945,566 | | | | $(2,967,758 | ) |

Total distributions to shareholders | | | $(15,999,143 | ) | | | $(12,885,061 | ) |

Change in net assets from fund share transactions | | | $5,008,803 | | | | $(6,124,153 | ) |

Total change in net assets | | | $10,955,226 | | | | $(21,976,972 | ) |

| | |

Net assets | | | | | | | | |

At beginning of period | | | 85,584,083 | | | | 107,561,055 | |

At end of period | | | $96,539,309 | | | | $85,584,083 | |

See Notes to Financial Statements

13

MFS Blended Research Small Cap Equity Portfolio

FINANCIAL STATEMENTS | FINANCIAL HIGHLIGHTS

The financial highlights table is intended to help you understand the fund’s financial performance for the past 5 years. Certain information reflects financial results for a single fund share. The total returns in the table represent the rate that an investor would have earned (or lost) on an investment in the fund share class (assuming reinvestment of all distributions) held for the entire period.

| | | | | | | | | | | | | | | | | | | | |

| Initial Class | | Year ended | |

| | | | | |

| | | 12/31/19 | | | 12/31/18 | | | 12/31/17 | | | 12/31/16 | | | 12/31/15 | |

| | | | | |

Net asset value, beginning of period | | | $11.25 | | | | $13.47 | | | | $13.23 | | | | $12.29 | | | | $16.04 | |

| | | | | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) (d) | | | $0.10 | | | | $0.09 | | | | $0.11 | | | | $0.11 | (c) | | | $0.15 | |

Net realized and unrealized gain (loss) | | | 2.56 | | | | (0.40 | ) | | | 1.70 | | | | 2.35 | | | | (0.94 | ) |

Total from investment operations | | | $2.66 | | | | $(0.31 | ) | | | $1.81 | | | | $2.46 | | | | $(0.79 | ) |

| | | | | |

| Less distributions declared to shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.10 | ) | | | $(0.13 | ) | | | $(0.12 | ) | | | $(0.16 | ) | | | $(0.10 | ) |

From net realized gain | | | (2.15 | ) | | | (1.78 | ) | | | (1.45 | ) | | | (1.36 | ) | | | (2.86 | ) |

Total distributions declared to shareholders | | | $(2.25 | ) | | | $(1.91 | ) | | | $(1.57 | ) | | | $(1.52 | ) | | | $(2.96 | ) |

Net asset value, end of period (x) | | | $11.66 | | | | $11.25 | | | | $13.47 | | | | $13.23 | | | | $12.29 | |

Total return (%) (k)(r)(s)(x) | | | 26.78 | | | | (5.11 | ) | | | 14.97 | | | | 20.90 | (c) | | | (4.15 | ) |

| | | | | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 0.54 | | | | 0.54 | | | | 0.53 | | | | 0.42 | (c) | | | 0.54 | |

Expenses after expense reductions (f) | | | 0.53 | | | | 0.53 | | | | 0.52 | | | | 0.41 | (c) | | | 0.53 | |

Net investment income (loss) | | | 0.81 | | | | 0.69 | | | | 0.82 | | | | 0.92 | (c) | | | 1.03 | |

Portfolio turnover | | | 59 | | | | 72 | | | | 81 | | | | 72 | | | | 78 | |

Net assets at end of period (000 omitted) | | | $35,441 | | | | $29,936 | | | | $36,195 | | | | $28,715 | | | | $27,795 | |

| |

| Service Class | | Year ended | |

| | | | | |

| | | 12/31/19 | | | 12/31/18 | | | 12/31/17 | | | 12/31/16 | | | 12/31/15 | |

| | | | | |

Net asset value, beginning of period | | | $10.92 | | | | $13.12 | | | | $12.92 | | | | $12.03 | | | | $15.75 | |

| | | | | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) (d) | | | $0.07 | | | | $0.06 | | | | $0.07 | | | | $0.08 | (c) | | | $0.12 | |

Net realized and unrealized gain (loss) | | | 2.46 | | | | (0.39 | ) | | | 1.67 | | | | 2.29 | | | | (0.93 | ) |

Total from investment operations | | | $2.53 | | | | $(0.33 | ) | | | $1.74 | | | | $2.37 | | | | $(0.81 | ) |

| | | | | |

| Less distributions declared to shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.06 | ) | | | $(0.09 | ) | | | $(0.09 | ) | | | $(0.12 | ) | | | $(0.05 | ) |

From net realized gain | | | (2.15 | ) | | | (1.78 | ) | | | (1.45 | ) | | | (1.36 | ) | | | (2.86 | ) |

Total distributions declared to shareholders | | | $(2.21 | ) | | | $(1.87 | ) | | | $(1.54 | ) | | | $(1.48 | ) | | | $(2.91 | ) |

Net asset value, end of period (x) | | | $11.24 | | | | $10.92 | | | | $13.12 | | | | $12.92 | | | | $12.03 | |

Total return (%) (k)(r)(s)(x) | | | 26.36 | | | | (5.35 | ) | | | 14.70 | | | | 20.58 | (c) | | | (4.38 | ) |

| | | | | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 0.79 | | | | 0.79 | | | | 0.78 | | | | 0.67 | (c) | | | 0.79 | |

Expenses after expense reductions (f) | | | 0.78 | | | | 0.78 | | | | 0.77 | | | | 0.66 | (c) | | | 0.78 | |

Net investment income (loss) | | | 0.56 | | | | 0.43 | | | | 0.55 | | | | 0.66 | (c) | | | 0.79 | |

Portfolio turnover | | | 59 | | | | 72 | | | | 81 | | | | 72 | | | | 78 | |

Net assets at end of period (000 omitted) | | | $61,099 | | | | $55,648 | | | | $71,366 | | | | $74,453 | | | | $82,794 | |

See Notes to Financial Statements

14

MFS Blended Research Small Cap Equity Portfolio

Financial Highlights – continued

| (c) | Amount reflects aone-time reimbursement of expenses by the custodian (or former custodian) without which net investment income and performance would be lower and expenses would be higher. |

| (d) | Per share data is based on average shares outstanding. |

| (f) | Ratios do not reflect reductions from fees paid indirectly, if applicable. |

| (k) | The total return does not reflect expenses that apply to separate accounts. Inclusion of these charges would reduce the total return figures for all periods shown. |

| (r) | Certain expenses have been reduced without which performance would have been lower. |

| (s) | From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower. |

| (x) | The net asset values and total returns have been calculated on net assets which include adjustments made in accordance with U.S. generally accepted accounting principles required at period end for financial reporting purposes. |

See Notes to Financial Statements

15

MFS Blended Research Small Cap Equity Portfolio

NOTES TO FINANCIAL STATEMENTS

| (1) | | Business and Organization |

MFS Blended Research Small Cap Equity Portfolio (the fund) is a diversified series of MFS Variable Insurance Trust III (the trust). The trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as anopen-end management investment company. The shareholders of each series of the trust are separate accounts of insurance companies, which offer variable annuity and/or life insurance products, and qualified retirement and pension plans.

The fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services – Investment Companies.

| (2) | | Significant Accounting Policies |

General– The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. In the preparation of these financial statements, management has evaluated subsequent events occurring after the date of the fund’s Statement of Assets and Liabilities through the date that the financial statements were issued. The fund will generally focus on securities of small size companies which may be more volatile than those of larger companies.

Balance Sheet Offsetting– The fund’s accounting policy with respect to balance sheet offsetting is that, absent an event of default by the counterparty or a termination of the agreement, the International Swaps and Derivatives Association (ISDA) Master Agreement, or similar agreement, does not result in an offset of reported amounts of financial assets and financial liabilities in the Statement of Assets and Liabilities across transactions between the fund and the applicable counterparty. The fund’s right to setoff may be restricted or prohibited by the bankruptcy or insolvency laws of the particular jurisdiction to which a specific master netting agreement counterparty is subject. Balance sheet offsetting disclosures, to the extent applicable to the fund, have been included in the fund’s Significant Accounting Policies note under the captions for each of the fund’sin-scope financial instruments and transactions.

Investment Valuations– Equity securities, including restricted equity securities, are generally valued at the last sale or official closing price on their primary market or exchange as provided by a third-party pricing service. Equity securities, for which there were no sales reported that day, are generally valued at the last quoted daily bid quotation on their primary market or exchange as provided by a third-party pricing service. Short-term instruments with a maturity at issuance of 60 days or less may be valued at amortized cost, which approximates market value.Open-end investment companies are generally valued at net asset value per share. Securities and other assets generally valued on the basis of information from a third-party pricing service may also be valued at a broker/dealer bid quotation. In determining values, third-party pricing services can utilize both transaction data and market information such as yield, quality, coupon rate, maturity, type of issue, trading characteristics, and other market data. The values of foreign securities and other assets and liabilities expressed in foreign currencies are converted to U.S. dollars using the mean of bid and asked prices for rates provided by a third-party pricing service.

The Board of Trustees has delegated primary responsibility for determining or causing to be determined the value of the fund’s investments (including any fair valuation) to the adviser pursuant to valuation policies and procedures approved by the Board. If the adviser determines that reliable market quotations are not readily available, investments are valued at fair value as determined in good faith by the adviser in accordance with such procedures under the oversight of the Board of Trustees. Under the fund’s valuation policies and procedures, market quotations are not considered to be readily available for most types of debt instruments and floating rate loans and many types of derivatives. These investments are generally valued at fair value based on information from third-party pricing services. In addition, investments may be valued at fair value if the adviser determines that an investment’s value has been materially affected by events occurring after the close of the exchange or market on which the investment is principally traded (such as foreign exchange or market) and prior to the determination of the fund’s net asset value, or after the halt of trading of a specific security where trading does not resume prior to the close of the exchange or market on which the security is principally traded. Events that occur after foreign markets close (such as developments in foreign markets and significant movements in the U.S. markets) and prior to the determination of the fund’s net asset value may be deemed to have a material effect on the value of securities traded in foreign markets. Accordingly, the fund’s foreign equity securities may often be valued at fair value. The adviser generally relies on third-party pricing services or other information (such as the correlation with price movements of similar securities in the same or other markets; the type, cost and investment characteristics of the security; the business and financial condition of the issuer; and trading and other market data) to assist in determining whether to fair value and at what value to fair value an investment. The value of an investment for purposes of calculating the fund’s net asset value can differ depending on the source and method used to determine value. When fair valuation is used, the value of an investment used to determine the fund’s net asset value may differ from quoted or published prices for the same investment. There can be no assurance that the fund could obtain the fair value assigned to an investment if it were to sell the investment at the same time at which the fund determines its net asset value per share.

16

MFS Blended Research Small Cap Equity Portfolio

Notes to Financial Statements – continued

Various inputs are used in determining the value of the fund’s assets or liabilities. These inputs are categorized into three broad levels. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, an investment’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. The fund’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and considers factors specific to the investment. Level 1 includes unadjusted quoted prices in active markets for identical assets or liabilities. Level 2 includes other significant observable market-based inputs (including quoted prices for similar securities, interest rates, prepayment speed, and credit risk). Level 3 includes unobservable inputs, which may include the adviser’s own assumptions in determining the fair value of investments. The following is a summary of the levels used as of December 31, 2019 in valuing the fund’s assets or liabilities:

| | | | | | | | | | | | | | | | |

| Financial Instruments | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Equity Securities | | | $95,814,981 | | | | $— | | | | $— | | | | $95,814,981 | |

| Mutual Funds | | | 854,125 | | | | — | | | | — | | | | 854,125 | |

| Total | | | $96,669,106 | | | | $— | | | | $— | | | | $96,669,106 | |

For further information regarding security characteristics, see the Portfolio of Investments. The fund held one worthless level 3 security at the beginning of the period which was disposed of during the period for $0 and no realized gain or loss.

Security Loans– Under its Securities Lending Agency Agreement with the fund, State Street Bank and Trust Company, as lending agent, loans the securities of the fund to certain qualified institutions (the “Borrowers”) approved by the fund. Security loans can be terminated at the discretion of either the lending agent or the fund and the related securities must be returned within the earlier of the standard trade settlement period for such securities or within three business days. The loans are collateralized by cash and/or U.S. Treasury and federal agency obligations in an amount typically at least equal to the market value of the securities loaned. On loans collateralized by cash, the cash collateral is invested in a money market fund. The market value of the loaned securities is determined at the close of business of the fund and any additional required collateral is delivered to the fund on the next business day. The lending agent provides the fund with indemnification against Borrower default. In the event of Borrower default, the lending agent will, for the benefit of the fund, either purchase securities identical to those loaned or, when such purchase is commercially impracticable, pay the fund the market value of the loaned securities. In return, the lending agent assumes the fund’s rights to the related collateral. If the collateral value is less than the cost to purchase identical securities, the lending agent is responsible for the shortfall, but only to the extent that such shortfall is not due to a decline in collateral value resulting from collateral reinvestment for which the fund bears the risk of loss. At period end, the fund had investment securities on loan, all of which were classified as equity securities in the fund’s Portfolio of Investments, with a fair value of $164,318. The fair value of the fund’s investment securities on loan and a related liability of $96,250 for cash collateral received on securities loaned are both presented gross in the Statement of Assets and Liabilities. Additionally, these loans were collateralized by U.S. Treasury Obligations of $75,959 held by the lending agent. The collateral on securities loaned exceeded the value of securities on loan at period end. The liability for cash collateral for securities loaned is carried at fair value, which is categorized as level 2 within the fair value hierarchy. A portion of the income generated upon investment of the collateral is remitted to the Borrowers, and the remainder is allocated between the fund and the lending agent. On loans collateralized by U.S. Treasury and/or federal agency obligations, a fee is received from the Borrower, and is allocated between the fund and the lending agent. Income from securities lending is separately reported in the Statement of Operations. The dividend and interest income earned on the securities loaned is accounted for in the same manner as other dividend and interest income.

Indemnifications– Under the fund’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the fund. Additionally, in the normal course of business, the fund enters into agreements with service providers that may contain indemnification clauses. The fund’s maximum exposure under these agreements is unknown as this would involve future claims that may be made against the fund that have not yet occurred.

Investment Transactions and Income– Investment transactions are recorded on the trade date. Interest income is recorded on the accrual basis. Dividends received in cash are recorded on theex-dividend date. Certain dividends from foreign securities will be recorded when the fund is informed of the dividend if such information is obtained subsequent to theex-dividend date. Dividend payments received in additional securities are recorded on theex-dividend date in an amount equal to the value of the security on such date.

The fund may receive proceeds from litigation settlements. Any proceeds received from litigation involving portfolio holdings are reflected in the Statement of Operations in realized gain/loss if the security has been disposed of by the fund or in unrealized gain/loss if the security is still held by the fund. Any other proceeds from litigation not related to portfolio holdings are reflected as other income in the Statement of Operations.

Tax Matters and Distributions– The fund intends to qualify as a regulated investment company, as defined under Subchapter M of the Internal Revenue Code, and to distribute all of its taxable income, including realized capital gains. As a result, no provision for federal income tax is required. The fund’s federal tax returns, when filed, will remain subject to examination by the Internal Revenue Service for a three year period. Management has analyzed the fund’s tax positions taken on federal and state tax returns for all open

17

MFS Blended Research Small Cap Equity Portfolio

Notes to Financial Statements – continued

tax years and does not believe that there are any uncertain tax positions that require recognition of a tax liability. Foreign taxes, if any, have been accrued by the fund in the accompanying financial statements in accordance with the applicable foreign tax law. Foreign income taxes may be withheld by certain countries in which the fund invests. Additionally, capital gains realized by the fund on securities issued in or by certain foreign countries may be subject to capital gains tax imposed by those countries.

Distributions to shareholders are recorded on theex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles. Certain capital accounts in the financial statements are periodically adjusted for permanent differences in order to reflect their tax character. These adjustments have no impact on net assets or net asset value per share. Temporary differences which arise from recognizing certain items of income, expense, gain or loss in different periods for financial statement and tax purposes will reverse at some time in the future.

Book/tax differences primarily relate to wash sale loss deferrals.

The tax character of distributions declared to shareholders for the last two fiscal years is as follows:

| | | | | | | | |

| | | Year ended

12/31/19 | | | Year ended

12/31/18 | |

| Ordinary income (including any short-term capital gains) | | | $4,407,046 | | | | $2,614,042 | |

| Long-term capital gains | | | 11,592,097 | | | | 10,271,019 | |

| Total distributions | | | $15,999,143 | | | | $12,885,061 | |

The federal tax cost and the tax basis components of distributable earnings were as follows:

| | | | |

| As of 12/31/19 | | | | |

| |

| Cost of investments | | | $82,529,700 | |

| Gross appreciation | | | 18,350,955 | |

| Gross depreciation | | | (4,211,549 | ) |

| Net unrealized appreciation (depreciation) | | | $14,139,406 | |

| |

| Undistributed ordinary income | | | 1,856,313 | |

| Undistributed long-term capital gain | | | 5,657,472 | |

Multiple Classes of Shares of Beneficial Interest– The fund offers multiple classes of shares, which differ in their respective distribution and/or service fees. The fund’s income, realized and unrealized gain (loss), and common expenses are allocated to shareholders based on the daily net assets of each class. Dividends are declared separately for each class. Differences in per share dividend rates are generally due to differences in separate class expenses. The fund’s distributions declared to shareholders as reported in the Statements of Changes in Net Assets are presented by class as follows:

| | | | | | | | |

| | |

| | | Year ended

12/31/19 | | | Year ended

12/31/18 | |

| Initial Class | | | $5,626,679 | | | | $4,510,678 | |

| Service Class | | | 10,372,464 | | | | 8,374,383 | |

| Total | | | $15,999,143 | | | | $12,885,061 | |

| (3) | | Transactions with Affiliates |

Investment Adviser– The fund has an investment advisory agreement with MFS to provide overall investment management and related administrative services and facilities to the fund. The management fee is computed daily and paid monthly at an annual rate of 0.40% of the fund’s average daily net assets. MFS has agreed in writing to reduce its management fee by a specified amount if certain MFS mutual fund assets exceed thresholds agreed to by MFS and the fund’s Board of Trustees. For the year ended December 31, 2019, this management fee reduction amounted to $9,119, which is included in the reduction of total expenses in the Statement of Operations. The management fee incurred for the year ended December 31, 2019 was equivalent to an annual effective rate of 0.39% of the fund’s average daily net assets.

The investment adviser has agreed in writing to pay a portion of the fund’s total annual operating expenses, excluding interest, taxes, extraordinary expenses, brokerage and transaction costs, and investment-related expenses, such that total annual operating expenses do not exceed 0.60% of average daily net assets for the Initial Class shares and 0.85% of average daily net assets for the Service Class shares. This written agreement will continue until modified by the fund’s Board of Trustees, but such agreement will continue at least until April 30, 2021. For the year ended December 31, 2019, the fund’s actual operating expenses did not exceed the limit and therefore, the investment adviser did not pay any portion of the fund’s expenses related to this agreement.

Distributor– MFS Fund Distributors, Inc. (MFD), a wholly-owned subsidiary of MFS, is the distributor of shares of the fund. The Trustees have adopted a distribution plan for the Service Class shares pursuant to Rule12b-1 under the Investment Company Act of 1940.

18

MFS Blended Research Small Cap Equity Portfolio

Notes to Financial Statements – continued

The fund’s distribution plan provides that the fund will pay MFD distribution and/or service fees equal to 0.25% per annum of its average daily net assets attributable to Service Class shares as partial consideration for services performed and expenses incurred by MFD and financial intermediaries (including participating insurance companies that invest in the fund to fund variable annuity and variable life insurance contracts, sponsors of qualified retirement and pension plans that invest in the fund, and affiliates of these participating insurance companies and plan sponsors) in connection with the sale and distribution of the Service Class shares. MFD may subsequently pay all, or a portion, of the distribution and/or service fees to financial intermediaries.

Shareholder Servicing Agent– MFS Service Center, Inc. (MFSC), a wholly-owned subsidiary of MFS, receives a fee from the fund for its services as shareholder servicing agent. For the year ended December 31, 2019, the fee was $4,618, which equated to 0.0049% annually of the fund’s average daily net assets. MFSC also receives payment from the fund forout-of-pocket expenses paid by MFSC on behalf of the fund. For the year ended December 31, 2019, these costs amounted to $482.

Administrator– MFS provides certain financial, legal, shareholder communications, compliance, and other administrative services to the fund. Under an administrative services agreement, the fund reimburses MFS the costs incurred to provide these services. The fund is charged an annual fixed amount of $17,500 plus a fee based on average daily net assets. The administrative services fee incurred for the year ended December 31, 2019 was equivalent to an annual effective rate of 0.0250% of the fund’s average daily net assets.

Trustees’ and Officers’ Compensation– The fund pays compensation to independent Trustees in the form of a retainer, attendance fees, and additional compensation to Board and Committee chairpersons. The fund does not pay compensation directly to Trustees or officers of the fund who are also officers of the investment adviser, all of whom receive remuneration from MFS for their services to the fund. Certain officers and Trustees of the fund are officers or directors of MFS, MFD, and MFSC.

Other– This fund and certain other funds managed by MFS (the funds) had entered into a service agreement (the ISO Agreement) which provided for payment of fees solely by the funds to Tarantino LLC in return for the provision of services of an Independent Senior Officer (ISO) for the funds. Frank L. Tarantino served as the ISO and was an officer of the funds and the sole member of Tarantino LLC. Effective June 30, 2019, Mr. Tarantino retired from his position as ISO for the funds, and the ISO Agreement was terminated. For the year ended December 31, 2019, the fee paid by the fund under this agreement was $110 and is included in “Miscellaneous” expense in the Statement of Operations. MFS had agreed to bear all expenses associated with office space, other administrative support, and supplies provided to the ISO.

The fund invests in the MFS Institutional Money Market Portfolio which is managed by MFS and seeks current income consistent with preservation of capital and liquidity. This money market fund does not pay a management fee to MFS.

The fund is permitted to engage in purchase and sale transactions with funds and accounts for which MFS serves as investment adviser orsub-adviser (“cross-trades”) pursuant to a policy adopted by the Board of Trustees. This policy has been designed to ensure that cross-trades conducted by the fund comply with Rule17a-7 under the Investment Company Act of 1940. During the year ended December 31, 2019, the fund engaged in purchase transactions pursuant to this policy, which amounted to $1,273,878.

The adviser has voluntarily undertaken to reimburse the fund from its own resources on a quarterly basis for the cost of investment research embedded in the cost of the fund’s securities trades. This agreement may be rescinded at any time. For the year ended December 31, 2019, this reimbursement amounted to $14,851, which is included in “Other” income in the Statement of Operations.

For the year ended December 31, 2019, purchases and sales of investments, other than short-term obligations, aggregated $54,550,467 and $64,370,715, respectively.

19

MFS Blended Research Small Cap Equity Portfolio

Notes to Financial Statements – continued

| (5) | | Shares of Beneficial Interest |

The fund’s Declaration of Trust permits the Trustees to issue an unlimited number of full and fractional shares of beneficial interest. Transactions in fund shares were as follows:

| | | | | | | | | | | | | | | | |

| | | Year ended 12/31/19 | | | Year ended 12/31/18 | |

| | | | |

| | | Shares | | | Amount | | | Shares | | | Amount | |

| Shares sold | | | | | | | | | | | | | | | | |

Initial Class | | | 340,890 | | | | $4,063,323 | | | | 261,230 | | | | $3,403,663 | |

Service Class | | | 563,636 | | | | 6,702,429 | | | | 558,043 | | | | 6,746,807 | |

| | | 904,526 | | | | $10,765,752 | | | | 819,273 | | | | $10,150,470 | |

| | | | |

| Shares issued to shareholders in reinvestment of distributions | | | | | | | | | | | | | | | | |

Initial Class | | | 558,757 | | | | $5,626,679 | | | | 321,961 | | | | $4,510,678 | |

Service Class | | | 1,067,126 | | | | 10,372,463 | | | | 615,311 | | | | 8,374,383 | |

| | | 1,625,883 | | | | $15,999,142 | | | | 937,272 | | | | $12,885,061 | |

| | | | |

| Shares reacquired | | | | | | | | | | | | | | | | |

Initial Class | | | (520,733 | ) | | | $(6,389,300 | ) | | | (608,313 | ) | | | $(8,423,623 | ) |

Service Class | | | (1,294,674 | ) | | | (15,366,791 | ) | | | (1,515,630 | ) | | | (20,736,061 | ) |

| | | (1,815,407 | ) | | | $(21,756,091 | ) | | | (2,123,943 | ) | | | $(29,159,684 | ) |

| | | | |

| Net change | | | | | | | | | | | | | | | | |

Initial Class | | | 378,914 | | | | $3,300,702 | | | | (25,122 | ) | | | $(509,282 | ) |

Service Class | | | 336,088 | | | | 1,708,101 | | | | (342,276 | ) | | | (5,614,871 | ) |

| | | 715,002 | | | | $5,008,803 | | | | (367,398 | ) | | | $(6,124,153 | ) |

The fund and certain other funds managed by MFS participate in a $1.25 billion unsecured committed line of credit, subject to a $1 billion sublimit, provided by a syndicate of banks under a credit agreement. Borrowings may be made for temporary financing needs. Interest is charged to each fund, based on its borrowings, generally at a rate equal to the highest of one month LIBOR, the Federal Funds Effective Rate and the Overnight Bank Funding Rate, plus an agreed upon spread. A commitment fee, based on the average daily, unused portion of the committed line of credit, is allocated among the participating funds. In addition, the fund and other funds managed by MFS have established unsecured uncommitted borrowing arrangements with certain banks for temporary financing needs. Interest is charged to each fund, based on its borrowings, at rates equal to customary reference rates plus an agreed upon spread. For the year ended December 31, 2019, the fund’s commitment fee and interest expense were $508 and $0, respectively, and are included in “Miscellaneous” expense in the Statement of Operations.

| (7) | | Investments in Affiliated Issuers |

An affiliated issuer may be considered one in which the fund owns 5% or more of the outstanding voting securities, or a company which is under common control. For the purposes of this report, the following were affiliated issuers:

| | | | | | | | | | | | | | | | | | | | | | | | |

| Affiliated Issuers | | Beginning

Value | | | Purchases | | | Sales

Proceeds | | | Realized

Gain

(Loss) | | | Change in

Unrealized

Appreciation or

Depreciation | | | Ending

Value | |

| MFS Institutional Money Market Portfolio | | | $1,018,574 | | | | $19,459,105 | | | �� | $19,720,099 | | | | $295 | | | | $— | | | | $757,875 | |

| | | | | | |

| Affiliated Issuers | | | | | | | | | | | | | | Dividend

Income | | | Capital Gain

Distributions | |

| MFS Institutional Money Market Portfolio | | | | | | | | | | | | | | | | | | | $18,901 | | | | $— | |

20

MFS Blended Research Small Cap Equity Portfolio

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of MFS Variable Insurance Trust III and the Shareholders of MFS Blended Research Small Cap Equity Portfolio:

Opinion on the Financial Statements and Financial Highlights