| | |

OMB APPROVAL |

OMB Number: | | 3235-0570 |

Expires: | | August 31, 2011 |

Estimated average burden |

hours per response: | | 18.9 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08895

ING Funds Trust

(Exact name of registrant as specified in charter)

| | |

| 7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

| (Address of principal executive offices) | | (Zip code) |

The Corporation Trust Company, 1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: March 31

Date of reporting period: April l, 2009 to September 30, 2009

Semi-Annual Report

September 30, 2009

Classes A, B, C, I, IS, O, Q, R and W

Fixed-Income Funds

| n | ING High Yield Bond Fund |

| n | ING Intermediate Bond Fund |

Money Market Funds

| n | ING Classic Money Market Fund |

| n | ING Institutional Prime Money Market Fund |

| | |

| | E-Delivery Sign-up – details inside |

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully.

MUTUAL FUNDS |

|

TABLE OF CONTENTS

| | | | |

| | | |

| | Go Paperless with E-Delivery! | | |

Sign up now for on-line prospectuses, fund reports, and proxy statements. In less than five minutes, you can help reduce paper mail and lower fund costs. Just go to www.ingfunds.com, click on the E-Delivery icon from the home page, follow the directions and complete the quick 5 Steps to Enroll. You will be notified by e-mail when these communications become available on the internet. Documents that are not available on the internet will continue to be sent by mail. |

PROXY VOTING INFORMATION

A description of the policies and procedures that the Funds use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the Funds’ website at www.ingfunds.com; and (3) on the U.S. Securities and Exchange Commission’s (“SEC”) website at www.sec.gov. Information regarding how the Funds voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the Funds’ website at www.ingfunds.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Funds file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the website at www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330; and is available upon request from the Funds by calling Shareholder Services toll-free at (800) 992-0180.

Please note that your investment in money market funds: is not a bank deposit, is not insured or guaranteed by the Federal Deposit Insurance Corporation (“FDIC”), the Federal Reserve Board or any other government agency, and is affected by market fluctuations. There is no guarantee that the ING Classic Money Market Fund or the ING Institutional Prime Money Market Fund will achieve its investment objective.

PRESIDENT’S LETTER

Dear Shareholder,

As we move through Autumn, we find ourselves crossing a divide that does not feel like much of a change, yet portends hope for the future. Federal Reserve Chairman Benjamin S. Bernanke recently said that it was “very likely” the recession has ended, though he noted it could take many months for the unemployment rate to drop meaningfully. It may take some time before we notice the recovery in our daily lives.

Yet the equity markets seem to be taking economic events in stride, and have come back impressively since spring. For the 12 months ended September 30, 2009, the Dow Jones Industrial Average and the Standard & Poor’s 500® Composite Stock Price Index have nearly erased their losses; the NASDAQ Composite Index has moved into positive territory for the same period.

At ING Funds, we expect economic growth will accelerate next year and continue in 2011, but with elevated unemployment for the next few years.

How might this affect your investment plans? Despite recent gains in household wealth, many people still face net declines in their portfolios overall and may have pushed their investment goals further into the future. If that is the case for you, it may be prudent to reexamine your portfolio and see if you need to make any adjustments for a longer horizon.

For others, the need to preserve capital or increase income may have become paramount. If these are concerns for you, it may be advisable to review your current investments to determine whether they meet your expected needs.

Only you and your investment advisor can determine the answers to these questions. We urge you to discuss these matters thoroughly with your advisor before making any changes to your investment goals or your portfolio.

Thank you for your continued confidence in ING Funds. We look forward to serving your investment needs in the future.

Sincerely,

Shaun Mathews

President and Chief Executive Officer

ING Funds

November 6, 2009

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and the ING Funds disclaim any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

For more complete information, or to obtain a prospectus for any ING Fund, please call your investment professional or ING Funds Distributor, LLC at (800) 992-0180 or log on to www.ingfunds.com. The prospectus should be read carefully before investing. Consider the fund’s investment objectives, risks, and charges and expenses carefully before investing. The prospectus contains this information and other information about the fund. Check with your investment professional to determine which funds are available for sale within their firm. Not all funds are available for sale at all firms.

1

MARKET PERSPECTIVE: SIX MONTHS ENDED SEPTEMBER 30, 2009

From its earliest days in mid-March, the resurgence of risky asset classes like equities and corporate bonds encountered skeptics. It was based they said, not on good economic news but news that was merely less awful. That banks were making money again relied on extraordinarily low interest rates to depositors and “special” items. The government’s willingness to incur $1.75 trillion in additional debt to bail out banks, insurers, auto companies and people who bought housing beyond their means, while the Federal Reserve printed money to buy the debt and keep interest rates down, would have its day of inflationary reckoning.

But the believers would have none of it. Conditions don’t go from bad to good in one step, they said. The news has to get less bad first. The richest harvest must start with a few green shoots in an empty field. In no time, every commentator seemed to be talking about “green shoots”.

However described, the news on which markets advanced was on balance improving, albeit weakly and erratically.

In housing, the Standard & Poor’s (“S&P”)/Case-Shiller National U.S. Home Price Index(1) of house prices in 20 cities sank a record 19% year-over-year in January. But from there the declines moderated to 13.3% in the most recent report. Sales of existing homes rose for four months, before slipping in September. Still, the proportion of distressed sales was down to less than one third, from nearly half earlier in the year. New home sales, helped by an $8,000 government grant to first-time home buyers, had three straight months of gain through September.

After a fall in first quarter gross domestic product (“GDP”) of 5.5% annualized, the contraction for the second quarter was just 0.7% annualized, and after four straight falls there were high hopes that GDP in the third quarter would rebound. By September, closely watched purchasing managers’ indices were flirting with levels suggesting expansion.

A “Cash-for-Clunkers” program under which the government offered to subsidize the trade-in of old vehicles for newer, more efficient models was vigorously taken up. Retail sales and industrial production were boosted. Auto companies re-opened production lines.

A flimsier green shoot emerged in the employment reports. The September report showed payroll cuts at little more than one third of the January level. But the unemployment rate stood at a 26-year high of 9.7%.

The average work week languished near the lowest since records began in 1964. Wage growth remained insipid. Increasingly commentators asked what kind of real recovery could take place under these conditions and as the various government support programs expired.

In fixed income markets, three-month dollar London Interbank Offered Rate (“LIBOR”), the basis of trillions of dollars of financial agreements, fell below 1% for the first time ever and stayed there. Various measures of spread against LIBOR, indicating willingness to lend, fell to levels well below those seen before the financial crisis emerged.

Bonds at first sight had a solid six months. The Barclays Capital U.S. Aggregate Bond Index(2) of investment grade bonds returned 5.59%. But within this figure there were cross-currents. Improved risk appetite propelled the Barclays Capital Corporate Investment-Grade Bond Index(3) to a 19.41% gain amid surging new issuance. High yield bonds, represented by the Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index(4), did even better, gaining an equity-like 40.24%. At first, the Barclays Capital U.S. Treasury Index(5) lost about 3%, as greater risk appetite was reinforced by concerns about massive government borrowing. The excess yield on 10-year Treasuries over 2-year issues briefly reached a record 275 basis points (“bp”). But ultimately, the fragile economy became uppermost in investors’ minds. They began to feel that inflation would not be an immediate problem and with the Federal Reserve buying Treasuries, seekers of safety could move up the yield curve to get some return rather than receive practically nothing at the very short end. The Barclays Capital U.S. Treasury Index ended the six-month period with just a 0.98% loss. The annual yield on the 90-day Treasury Bills started the fiscal year at 20bp and ended it at 12bp.

In currencies, the dollar relinquished first quarter benefits from its safe haven status, falling 9.5% against the euro, 10.7% against the pound and 7.5% against the yen.

U.S. equities, represented by the S&P 500® Composite Stock Price (“S&P 500®”) Index(6) including dividends, returned 34.0% in the six months through September, led by the Financials component which rose 70.4%. Profits for S&P 500® companies suffered their eighth straight quarter of decline in the second quarter and by the half way point in our fiscal year the price to earnings ratio of the S&P 500® Index,

2

MARKET PERSPECTIVE: SIX MONTHS ENDED SEPTEMBER 30, 2009

based on operating earnings in the trailing four quarters, had not been so high since the first half of 2002.

In international markets, referring to MSCI indices in local currencies with net reinvested dividends, the MSCI Japan® Index(7) rose 18.8% for the six months through September, but weakened at the end. A rise in gross domestic product (“GDP”) of 2.3% annualized was due to net exports and government stimulus. Domestic demand was still in the doldrums and deflation had again taken hold. The MSCI Europe ex UK® Index(8) surged 41.0%. After a drop in GDP of 2.5% in the first quarter second quarter GDP barely fell and actually rose in France and Germany. Confidence measures, from investor to business to consumer, continued to advance. The MSCI UK® Index(9) jumped 34.4%. GDP fell for the fifth consecutive quarter and stood 5.5% below the level one year earlier. Yet house prices were by all accounts edging back up again. Purchasing managers’ indices were in or near expansion territory. And in September consumer confidence rose by the most since 1995.

(1) The S&P/Case-Shiller National U.S. Home Price Index tracks the value of single-family housing within the United States. The index is a composite of single family home price indices for the nine U.S. Census divisions and is calculated quarterly.

(2) The Barclays Capital U.S. Aggregate Bond Index is an unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities.

(3) The Barclays Capital Corporate Investment-Grade Bond Index is an unmanaged index that measures the performance USD-denominated, investment-grade, fixed-rate, taxable securities sold by industrial, utility and financial issuers.

(4) The Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index is an unmanaged index that measures the performance of fixed-income securities.

(5) The Barclays Capital U.S. Treasury Index is an unmanaged index that includes public obligations of the U.S. Treasury. Treasury bills, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS and STRIPS, are excluded.

(6) The S&P 500® Index is an unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets.

(7) The MSCI Japan® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan.

(8) The MSCI Europe ex UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK.

(9) The MSCI UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK.

Parentheses denote a negative number when applicable.

All indices are unmanaged and investors cannot invest directly in an index. Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Funds’ performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING’s Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

| | |

| ING GNMA INCOME FUND | | PORTFOLIO MANAGERS’ REPORT |

ING GNMA Income Fund (the “Fund”) seeks to generate a high level of current income, consistent with liquidity and safety of principal, through investment primarily in Government National Mortgage Association (“GNMA”) mortgage-backed securities (also known as GNMA Certificates) that are guaranteed as to the timely payment of principal and interest by the U.S. government. The Fund is managed by Peter Guan, Jeff Dutra and Justin McWhorter, Portfolio Managers* of ING Investment Management Co. — the Sub-Adviser.

Securities issued by the U.S. Treasury are backed by the full faith and credit of the federal government. Securities issued by individual agencies and organizations may be backed by the full faith and credit of the federal government as to principal or interest but are not direct obligations of the U.S. Treasury. Securities of some agencies and organizations are backed solely by the entity’s own resources or by the ability of the entity to borrow from the U.S. Treasury. Government securities also include certain mortgage-related securities that are sponsored by a U.S. government agency or organization and are not direct obligations of the U.S. government.

Performance: For the six-month period ended September 30, 2009, the Fund’s Class A shares, excluding sales charges, provided a total return of 2.57% compared to the Barclays Capital U.S. Mortgage-Backed Securities (“MBS”) Index(1) which returned 3.03%, for the same period.

Portfolio Specifics: Economic pessimism waned as positive surprises dominated economic releases. Emerging economies appear to be outpacing the developed world. Responding to the revival of many economies, investors left the “safe haven” of U.S. Treasury debt and embraced riskier assets. Domestic inflation remained muted. Despite the sell-off in Treasuries, the widely watched Barclays Capital U.S. Aggregate Bond Index reported another strong period with a 5.59% total return. GNMAs posted 2.07% of excess return.(2)

The Federal Reserve (the “Fed”) and the U.S. Treasury Department, combined, have now purchased more than $1 trillion of residential mortgage-backed securities (“RMBS”) and nearly $300 billion of U.S. Treasuries as they engage in quantitative easing. Moreover, the Fed will continue by buying another $300+ billion of RMBS by April of 2010. The big surprise so far this year is the lack of new supply into the market. Origination was expected to increase substantially with the implementation of streamlined refinancing and loan modification programs offered by the government sponsored enterprises (“GSEs”): the Federal Home Loan Mortgage Corporation (“FHLMC”), the Federal National Mortgage Association (“FNMA”) and the Government National Mortgage Association (“GNMA”).

The Fund continued to focus on RMBS with reduced prepayment risk. Security selection became a priority as most areas of the agency RMBS market were priced at fairly rich levels. The Fund’s duration profile was slightly lower and its exposure to higher coupon mortgages was moderately higher than the benchmark.

The Fund’s strategy of investing in higher income specified pools did well with prepayments remaining subdued and prices rising as a result. Specified pools have unique characteristics that we prefer versus the generic, or “TBA” market. While we don’t expect much additional price action from here, the strategy is still attractive compared to current production pools, or freshly minted mortgages, and TBAs. The Fund’s build-up of cash and short-term Treasuries in late August and early September led to a small give-back in performance as interest rates continued to rally and yield spreads narrowed further.

Prepayments remain lower than expected, providing a boost to the premium-coupon mortgages that the Fund owns. As prepayments remain low the carry, or yield, advantage provided by the higher coupon mortgages increases and the amortization of the premium paid decreases. The Fund has maintained an overweight to premium-coupon mortgages throughout 2009. An announcement by the Federal Housing Authority in late September instituting more-rigorous underwriting standards for GNMA borrowers reinforces the barriers to refinancing, which should ultimately benefit premium mortgages. The slight underperformance of the Fund was close to the expense ratio and associated management fees.

Current Strategy & Outlook: The Fed announcement of an official “end-game” to their RMBS purchasing program may provide an impetus for the spreads in sector to widen vs. Treasuries; however, their current purchases will likely continue to be greater than the net supply. We believe this will keep yield spreads tight in the near term. Moreover, while the infusion of liquidity will ultimately lead to higher rates, the Fed will be forced for the near-term to keep rates at historical lows.

Consequently, the Fund will continue to be managed to benefit from slower prepayments combined with the risk of higher interest rates in the future. The predominant focus continues to be on specified GNMA pools and collateralized mortgage obligations (“CMOs”) that we believe provide a superior level of current income while minimizing the risk to prepayments. Special attention is focused on pools with lower loan balances, those with loans in slow prepaying regions, and those that are sufficiently seasoned as to reduce the prepayment sensitivity to interest rate movements. Also, we will continue to seek GNMA CMOs that provide structural prepayment and extension protection in our view.

We believe the downside to the huge government support in the agency mortgage market is that relative value remains sparse and reinvestment of cash flows is at much tighter spreads than one year ago. Therefore, we remain cautious and defensive with regards to reinvesting.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

| * | | Effective May 19, 2009, Peter Guan, Jeff Dutra and Justin McWhorter joined Denis Jamison as portfolio managers to the Fund. Effective September 30, 2009, Mr. Jamison no longer manages the Fund. |

| (1) | | The Barclays Capital U.S. MBS Index is an unmanaged index composed of fixed-income security mortgage pools sponsored by GNMA, FNMA and FHLMC, including GNMA Graduated Payment Mortgages. |

| (2) | | For fixed income asset classes, excess return is defined as the return of an asset class over a U.S. Treasury security of comparable duration. |

4

| | |

| PORTFOLIO MANAGERS’ REPORT | | ING HIGH YIELD BOND FUND |

ING High Yield Bond Fund (the “Fund”) seeks to provide investors with a high level of current income and total return. The Fund is managed by Randall Parrish, CFA and Dan Doyle, Portfolio Managers of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six month period ended September 30, 2009, the Fund’s Class A shares, excluding sales charges, provided a total return of 33.19% compared to the Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index(1) and the Barclays Capital® Corporate High Yield Index(2), which returned 40.17% and 40.57%, respectively, for the same period.

Portfolio Specifics: For the six-month period ended September 30, 2009, the Fund underperformed its benchmark, the Barclays Capital 2% Issuer Constrained High Yield Index.

Economic pessimism waned as positive surprises dominated economic releases. Emerging economies appear to be outpacing the developed world. Responding to the revival of many economies, investors left the “safe haven” of U.S. Treasury debt and embraced riskier assets. Domestic inflation remained muted.

Risk-based fixed income assets posted strong results as positive excess returns(3) broke many records. Investment grade corporate bonds, in general, posted 20.10% of excess return, but financials led the pack with 25.82% of return above comparable duration Treasuries. Generally, lower rated corporate bonds outperformed higher credit quality issuers, as did bonds with longer maturities. High yield, in particular, has been buoyed by about $25.5 billion of inflows into mutual funds so far in 2009, a strong new issues market and a significant decline in default expectations.

During the period the Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index produced 40.17% of total returns bringing year-to-date returns to 49.52%. Returns for the six months continued to favor lower rated issues: CCC-rated bonds returned 70.28% and distressed debt topped 100.00%, while BB- rated bonds notched 27.73% Generally, lower-rated, lower priced bonds outperformed the rest of the high yield universe.

The Fund underperformed the Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index during the period because of its underweights in distressed debt securities specifically, and lower rated issues generally. As the period progressed, however, we added lower-rated bonds, which provided a partial offset. The Fund’s underweights in cyclicals, including technology, consumer cyclicals and chemicals, also hurt results as these areas performed well. Our absence from subordinated bank insurance debt also hurt

performance. Moreover, cash kept on hand for transactions, redemptions or the inflow of subscriptions was a drag during a period of historically high returns for high yield.

Positives from security selection included new purchases of lower priced, lower-rated names such as ServiceMaster, Blockbuster and ArvinMeritor, which we added during the period. Additionally, existing higher risk positions, such as Momentive, Bon-Ton Stores and R.H. Donnelly recovered significantly. The underperformers in the period were primarily higher quality, shorter dated positions that had insufficient upside to keep pace with the strong market — names including Constellation Brands, Inc., DaVita, Inc., EchoStar Communications Corp., Cablevision Systems Corp. and Centennial Communications Corp.

Current Strategy & Outlook: Signs of economic recovery have given investors increased confidence that the worst is past in terms of defaults and wide spreads for the high yield market. We believe that the reopening of both the credit and equity markets may keep the default rate below levels projected just a few months ago, and cash flows into the asset class are likely to continue to support prices despite robust new issuance. Accordingly, we are constructive on the asset class over the near term, though we note that many of the recent vintage leveraged buyouts still have balance sheets that are unsustainable over the longer term. On an historical return/risk basis, the higher quality end of the market is cheap relative to lower quality, but lower quality will likely continue to outperform as long as investors are convinced that economic recovery is on track.

Although the high yield market has posted a record return year-to-date, we believe the returns will remain attractive relative to other investment alternatives going forward. We continue to selectively add cyclical exposure to the portfolio. In recent months, we have added secured or senior

unsecured bonds where we believe there is value through the more senior levels of the capital structure, and we expect to see additional attractive opportunities in the new issue market. We have funded these purchases by selling more defensive positions that have little upside in our view.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

| (1) | | The Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index is an unmanaged index that measures the performance of fixed-income securities. |

| (2) | | The Barclays Capital Corporate High Yield Index is an unmanaged index that measures the performance of fixed-income securities generally representative of corporate bonds rated below investment grade. |

| (3) | | For fixed income asset classes, excess return is defined as the return of an asset class over a U.S. Treasury security of comparable duration. |

Top Ten Holdings*

as of September 30, 2009

(as a percent of net assets)

| | |

General Motors Acceptance Corp.,

6.875%, due 09/15/11 | | 2.4% |

Charter Communications Operating, LLC,

10.375%, due 04/30/14 | | 1.4% |

Chesapeake Energy Corp., 6.625%, due 01/15/16 | | 1.1% |

Ford Motor Credit Co., LLC, 8.700%, due 10/01/14 | | 1.1% |

Nielsen Finance LLC/Nielsen Finance Co.,

0.000%, due 08/01/16 | | 1.1% |

ServiceMaster Co, 10.750%, due 07/15/15 | | 1.0% |

Toys R Us Property Co. I LLC, 10.750%, due 07/15/17 | | 1.0% |

NewPage Corp., 11.375%, due 12/31/14 | | 1.0% |

MetroPCS Wireless, Inc., 9.250%, due 11/01/14 | | 1.0% |

Psychiatric Solutions, Inc., 7.750%, due 07/15/15 | | 1.0% |

| | * | Excludes short-term investments related to ING Institutional Prime Money Market Fund — Class I. |

Portfolio holdings are subject to change daily.

5

| | |

| ING INTERMEDIATE BOND FUND | | PORTFOLIO MANAGERS’ REPORT |

Investment Type Allocation

as of September 30, 2009

(as a percent of net assets)

| | |

Corporate Bonds/Notes | | 39.7% |

U.S. Government Agency Obligations | | 32.8% |

U.S. Treasury Obligations | | 16.4% |

Collateralized Mortgage Obligations | | 13.1% |

Asset-Backed Securities | | 3.6% |

Foreign Government Bonds | | 2.8% |

Preferred Stock | | 0.3% |

Other Assets and Liabilities — Net* | | (8.7)% |

| | |

Net Assets | | 100.0% |

| | |

| | * | Includes short-term investments related to ING Institutional Prime Money Market Fund — Class I and securities lending collateral. |

Portfolio holdings are subject to change daily.

ING Intermediate Bond Fund (the “Fund”) seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity. The Fund is managed by Christine Hurtsellers, Michael Hyman, Peter Guan and Chris Diaz, Portfolio Managers of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six-month period ended September 30, 2009, the Fund’s Class A shares, excluding sales charges, provided a total return of 13.04% compared to the Barclays Capital U.S. Aggregate Bond Index(1), which returned 5.59%, for the same period.

Economic pessimism waned as positive surprises dominated economic releases. Emerging economies appear to be outpacing the developed world. In response, investors left the “safe haven” of U.S. Treasury debt and embraced riskier assets. Domestic inflation remained muted. Despite the sell-off in Treasuries. the Barclays Capital U.S. Aggregate Bond Index returned 5.59% for the period.

Risk-based fixed income assets posted strong, positive excess returns(2) that broke many records. Corporate bonds, in general, posted 20.10% of excess return, but financials led the pack with 25.82% of return above comparable duration Treasuries. Generally, lower rated corporate bonds outperformed higher credit quality issuers, as did bonds with longer maturities. Commercial mortgage-backed securities (“CMBS”) earned 27.00% of excess returns as asset-backed securities (“ABS”) posted 14.22% of excess return. Within ABS, home equity loans outperformed with 36.37%.

High yield bonds continued their strong performance with an excess return of 41.93%, while emerging market debt (“EMD”) came in with 26.22%. High yield has been buoyed by about $25.5 billion of inflows into mutual funds so far in 2009, a strong new-issues market and a significant decline in default expectations.

Portfolio Specifics: The Fund outperformed the benchmark due to significant sector overweights to credit and non-agency residential mortgage-backed securities (“RMBS”), while it dragged from the initial underweight in longer dated CMBS at the beginning of the period. The allocations to non-agency RMBS had a powerful positive impact on both sector allocation and security selection.

Within corporate bonds, our combined overweights to financials and overweights to lower rated bonds also proved beneficial especially in the context of security selection. Eventually, we moved allocations from money center banks, in part, to smaller banks, Real Estate Investment Trusts and insurance companies in a timely fashion as the market began to search out value in these issuers. In general we reduced exposures to “big pharma” — after some early wins — and technology before they stalled slightly in September.

We have underweighted agency debentures and agency RMBS to “fund” our overweights in the riskier sectors; indeed, this call has been intrinsically correct as we were very happy to underweight two modestly winning sectors in order to increase the overweight to an even stronger sector. The Fund benefited modestly from tactical adjustments to our yield curve posture during the period. Foreign security exposures proved beneficial as the dollar fell across most major currencies.

Current Strategy & Outlook: Although concerns about inflation may resurface, we believe that it will not be a problem for the near term. Housing prices have slowed their rate of descent and consumer confidence is turning up. Although our macro outlook is for a modest and drawn-out recovery, we are mindful of the increasing number of upside surprises in the United States and abroad. The brighter news on residential real estate prices remains key to the pace and direction of the economic recovery.

The portfolio maintains a significant overweight to investment grade credit and non-agency RMBS. Additionally, we are overweight CMBS and ABS. We are slightly underweight agency RMBS and may trim further. We will tactically trade duration with a bias to staying neutral in an environment with little interest rate volatility.

Our credit team believes that financials may be the new cyclicals and should be overweighted as the economy confirms a recovery phase. We are positive on issues that benefit from commodities including dollar-denominated issues of foreign entities. Nevertheless, we are tactically concerned about a temporary widening in credit spreads as 2009 closes and will take steps to mitigate that risk synthetically.

We are also maintaining our active risk to Brazil (currency and debt) with emphasis on the high yields available in short-dated bonds. Allocations to the currencies of India and Indonesia follow our positive theme for emerging economies.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

| (1) | | The Barclays Capital U.S. Aggregate Bond Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. |

| (2) | | For fixed income asset classes, excess return is defined as the return of an asset class over a U.S. Treasury security of comparable duration. |

Top Ten Holdings*

as of September 30, 2009

(as a percent of net assets)

| | |

U.S. Treasury Note, 3.625%, due 08/15/19 | | 5.7% |

U.S. Treasury Note, 4.250%, due 05/15/39 | | 5.2% |

Federal National Mortgage Association,

6.000%, due 10/14/39 | | 4.3% |

Federal National Mortgage Association,

5.500%, due 10/15/35 | | 4.0% |

U.S. Treasury Note, 1.750%, due 08/15/12 | | 2.0% |

Federal National Mortgage Association,

6.500%, due 10/01/31 | | 1.4% |

Federal Home Loan Mortgage Corporation,

5.000%, due 11/15/34 | | 1.3% |

U.S. Treasury Note, 2.375%, due 08/31/14 | | 1.3% |

Federal Home Loan Mortgage Corporation,

5.500%, due 08/15/20 | | 1.2% |

Brazil Notas do Tesouro Nacional Series F,

10.000%, due 01/01/17 | | 1.2% |

| | * | Excludes short-term investments related to ING Institutional Prime Money Market Fund — Class I. |

Portfolio holdings are subject to change daily.

6

| | |

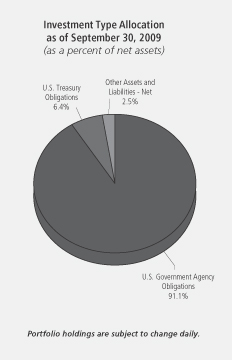

| PORTFOLIO MANAGERS’ REPORT | | ING CLASSIC MONEY MARKET FUND |

Investment Type Allocation

as of September 30, 2009

(as a percent of net assets)

| | |

Commercial Paper | | 62.1% |

U.S. Government Agency Obligations | | 17.9% |

Repurchase Agreement | | 12.5% |

Corporate Bonds/Notes | | 4.3% |

Certificates of Deposit | | 3.8% |

Other Assets and Liabilities — Net | | (0.6)% |

| | |

Net Assets | | 100.0% |

| | |

Portfolio holdings are subject to change daily.

ING Classic Money Market Fund (the “Fund”) seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity and the maintenance of a stable $1.00 net asset value per share. The Fund is managed by David S. Yealy, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Portfolio Specifics: The six-months ended September 30, 2009 were a period of historically low yields and returns for money market mutual funds and short-term money market securities, with numerous funds having to waive fees in order to provide a zero or slight positive return.

The Federal Open Market Committee (“FOMC”) maintained the targeted federal funds rate in a range of 0.00-0.25% and continued

the quantitative easing program in place. Economic releases during the quarter were much more upbeat and positive compared to the previous few quarters. However, rising foreclosures and unemployment remain significant headwinds to any recovery in housing and consumer spending.

Money market yields declined over the period as the various programs put into place by the Federal Reserve (the “Fed”), U.S. Department of the Treasury (“U.S. Treasury”) and other central banks across the globe helped to stabilize the markets and the global economies. The improved market conditions for short-term investors were reflected in the large drop in London Interbank Offered Rate (“LIBOR”). The three-month U.S. LIBOR declined from 1.19% at the end of March to 0.29% at the end of September.

Our focus during this period has not been on maximizing yield and returns but rather on preservation of capital, reducing risk and increasing liquidity due to extreme risks in the market. The Fund did take on interest rate risk, maintaining a longer than average weighted average maturity (“WAM”) for most of the period by buying longer term U.S. Treasury and agency securities.

Current Strategy & Outlook: It is our opinion that the economy is finding a bottom and is poised to turn positive entering the final quarter of 2009. We are not expecting a sharp recovery but see it as more of a long and slow recovery, as unemployment and housing continue to be a drag on consumer spending and confidence. We expect the FOMC will be forced to keep the federal funds rate in the 0.00-0.25% range for the foreseeable future, until economic and market conditions improve significantly. In our view, an increase in short-term rates will depend on how soon and how quickly the Fed can remove its quantitative easing.

As we become more comfortable that the economic recovery is taking hold and the risks of a relapse of the credit crisis are diminished, we are no longer relying primarily on U.S. Treasuries and agencies for the Fund’s longer-term exposures. We have started to modestly increase exposure to selective top-tier corporate and bank issuers and to extend maturities in those issuers further out the yield curve. We plan to maintain an extended WAM with the view that the Fed will not be in a position to raise short-term rates until mid-2010 at the earliest.

Principal Risk Factors: Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

Please see Note 16 in the “Notes to Financial Statements” section for information regarding the Fund’s participation during the reporting period in the U.S. Treasury Department’s Temporary Money Market Guarantee Program, which expired on September 19, 2009.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

7

| | |

| ING INSTITUTIONAL PRIME MONEY MARKET FUND | | PORTFOLIO MANAGERS’ REPORT |

ING Institutional Prime Money Market Fund (the “Fund”) seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity and the maintenance of a stable $1.00 net asset value per share. The Fund is managed by David S. Yealy, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Portfolio Specifics: The six-months ended September 30, 2009 were a period of historically low yields and returns for money market mutual funds and short-term money market securities, with numerous funds having to waive fees in order to provide a zero or slight positive return.

The Federal Open Market Committee (“FOMC”) maintained the targeted federal funds rate in a range of 0.00-0.25% and continued the quantitative easing program in place. Economic releases during the quarter were much more upbeat and positive compared to the previous few quarters. However, rising foreclosures and unemployment remain significant headwinds to any recovery in housing and consumer spending.

Money market yields declined over the period as the various programs put into place by the Federal Reserve (the “Fed”), U.S. Department of the Treasury (“U.S. Treasury”) and other central banks across the globe helped to stabilize the markets and the global economies. The improved market conditions for short-term investors are reflected in the large drop in the London Interbank Offered Rate (“LIBOR”). The three-month U.S. LIBOR declined from 1.19% at the end of March to 0.29% at the end of September.

Our focus during this period has not been on maximizing yield and returns but rather on preservation of capital, reducing risk and increasing liquidity due to extreme risks in the market. The Fund did take on interest rate risk, maintaining a longer than average weighted average maturity (“WAM”) for most of the period by buying longer term U.S. Treasury and agency securities.

Current Strategy & Outlook: It is our opinion that the economy is finding a bottom and is poised to turn positive entering the final quarter of 2009. We are not expecting a sharp recovery but see it as more of a long and slow recovery, as unemployment and housing continue to be a drag on consumer spending and confidence. We expect the FOMC will be forced to keep the federal funds rate in the 0.00-0.25% range for the foreseeable future, until economic and market conditions improve significantly. In our view, an increase in short-term rates will depend on how soon and how quickly the Fed can remove its quantitative easing.

As we become more comfortable that the economic recovery is taking hold and the risks of a relapse of the credit crisis are diminished, we are no longer relying primarily on U.S. Treasuries and agencies for the Fund’s longer-term exposures. We have started to modestly increase exposure to selective top-tier corporate and bank issuers and to extend maturities in those issuers further out the yield curve. We plan to maintain an extended WAM with the view that the Fed will not be in a position to raise short-term rates until mid-2010 at the earliest.

Principal Risk Factors: Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

Please see Note 16 in the “Notes to Financial Statements” section for information regarding the Fund’s participation during the reporting period in the U.S. Treasury Department’s Temporary Money Market Guarantee Program, which expired on September 19, 2009.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

8

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED)

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees, and exchange fees, and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2009 to September 30, 2009. The Funds’ expenses are shown without the imposition of any sales charges or fees. Expenses would have been higher if such charges were included.

Actual Expenses

The first section of the table shown below, “Actual Fund Return,” provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of the table shown below, “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Actual Fund Return | | Hypothetical (5% return before expenses) |

| | | Beginning

Account

Value

April 1, 2009 | | Ending

Account Value

September 30, 2009 | | Annualized Expense Ratio | | | Expenses Paid

During the

Period Ended

September 30, 2009* | | Beginning

Account

Value

April 1, 2009 | | Ending

Account Value

September 30, 2009 | | Annualized Expense Ratio | | | Expenses Paid

During the

Period Ended

September 30, 2009* |

ING GNMA Income Fund | | | | | | | | | | | | | | | | |

Class A | | $ | 1,000.00 | | $ | 1,025.70 | | 0.94 | % | | $ | 4.77 | | $ | 1,000.00 | | $ | 1,020.36 | | 0.94 | % | | $ | 4.76 |

Class B | | | 1,000.00 | | | 1,023.10 | | 1.69 | | | | 8.57 | | | 1,000.00 | | | 1,016.60 | | 1.69 | | | | 8.54 |

Class C | | | 1,000.00 | | | 1,022.10 | | 1.69 | | | | 8.57 | | | 1,000.00 | | | 1,016.60 | | 1.69 | | | | 8.54 |

Class I | | | 1,000.00 | | | 1,027.20 | | 0.63 | | | | 3.20 | | | 1,000.00 | | | 1,021.91 | | 0.63 | | | | 3.19 |

Class Q | | | 1,000.00 | | | 1,027.10 | | 0.88 | | | | 4.47 | | | 1,000.00 | | | 1,020.66 | | 0.88 | | | | 4.46 |

Class W | | | 1,000.00 | | | 1,027.20 | | 0.63 | | | | 3.20 | | | 1,000.00 | | | 1,021.91 | | 0.63 | | | | 3.19 |

ING High Yield Bond Fund | | | | | | | | | | | | | | | | |

Class A | | $ | 1,000.00 | | $ | 1,331.90 | | 1.10 | % | | $ | 6.43 | | $ | 1,000.00 | | $ | 1,019.55 | | 1.10 | % | | $ | 5.57 |

Class B | | | 1,000.00 | | | 1,325.00 | | 1.85 | | | | 10.78 | | | 1,000.00 | | | 1,015.79 | | 1.85 | | | | 9.35 |

Class C | | | 1,000.00 | | | 1,327.10 | | 1.85 | | | | 10.79 | | | 1,000.00 | | | 1,015.79 | | 1.85 | | | | 9.35 |

Class I | | | 1,000.00 | | | 1,335.50 | | 0.77 | | | | 4.51 | | | 1,000.00 | | | 1,021.21 | | 0.77 | | | | 3.90 |

| * | | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/365 to reflect the most recent fiscal half-year. |

9

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED) (CONTINUED)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Actual Fund Return | | Hypothetical (5% return before expenses) |

| | | Beginning

Account

Value

April 1, 2009 | | Ending

Account Value

September 30, 2009 | | Annualized Expense Ratio | | | Expenses Paid

During the

Period Ended

September 30, 2009* | | Beginning

Account

Value

April 1, 2009 | | Ending

Account Value

September 30, 2009 | | Annualized Expense Ratio | | | Expenses Paid

During the

Period Ended

September 30, 2009* |

ING Intermediate Bond Fund | | | | | | | | | | | | | | | | |

Class A | | $ | 1,000.00 | | $ | 1,130.40 | | 0.68 | % | | $ | 3.63 | | $ | 1,000.00 | | $ | 1,021.66 | | 0.68 | % | | $ | 3.45 |

Class B | | | 1,000.00 | | | 1,126.30 | | 1.43 | | | | 7.62 | | | 1,000.00 | | | 1,017.90 | | 1.43 | | | | 7.23 |

Class C | | | 1,000.00 | | | 1,126.30 | | 1.43 | | | | 7.62 | | | 1,000.00 | | | 1,017.90 | | 1.43 | | | | 7.23 |

Class I | | | 1,000.00 | | | 1,132.20 | | 0.36 | | | | 1.92 | | | 1,000.00 | | | 1,023.26 | | 0.36 | | | | 1.83 |

Class O | | | 1,000.00 | | | 1,130.20 | | 0.68 | | | | 3.63 | | | 1,000.00 | | | 1,021.66 | | 0.68 | | | | 3.45 |

Class R | | | 1,000.00 | | | 1,130.00 | | 0.93 | | | | 4.97 | | | 1,000.00 | | | 1,020.41 | | 0.93 | | | | 4.71 |

Class W | | | 1,000.00 | | | 1,132.10 | | 0.36 | | | | 1.92 | | | 1,000.00 | | | 1,023.26 | | 0.36 | | | | 1.83 |

ING Classic Money Market Fund | | | | | | | | | | | | | | | | |

Class A | | $ | 1,000.00 | | $ | 1,001.50 | | 0.59 | %•• | | $ | 2.95 | | $ | 1,000.00 | | $ | 1,022.11 | | 0.59 | %•• | | $ | 2.96 |

Class B | | | 1,000.00 | | | 1,001.50 | | 0.59 | •• | | | 2.95 | | | 1,000.00 | | | 1,022.11 | | 0.59 | •• | | | 2.96 |

Class C | | | 1,000.00 | | | 1,001.50 | | 0.59 | •• | | | 2.95 | | | 1,000.00 | | | 1,022.11 | | 0.59 | •• | | | 2.96 |

ING Institutional Prime Money Market Fund | | | | | | | | | | | | | | | | |

Class I | | $ | 1,000.00 | | $ | 1,002.60 | | 0.22 | % | | $ | 1.10 | | $ | 1,000.00 | | $ | 1,023.97 | | 0.22 | % | | $ | 1.12 |

Class IS | | | 1,000.00 | | | 1,003.90 | | 0.25 | | | | 1.26 | | | 1,000.00 | | | 1,023.82 | | 0.25 | | | | 1.27 |

| * | | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/365 to reflect the most recent fiscal half-year. |

| •• | | Expense ratios reflect waivers of 0.18%, 0.81% and 0.81% of distribution and shareholder servicing fees for Classes A, B and C, respectively, in order to maintain a yield of not less than zero. |

10

STATEMENTS OF ASSETS AND LIABILITIESASOF SEPTEMBER 30, 2009 (UNAUDITED)

| | | | | | | | | | | | |

| | | ING GNMA Income Fund | | | ING High Yield Bond Fund | | | ING Intermediate Bond Fund | |

ASSETS: | | | | | | | | | | | | |

Investments in securities at value+* | | $ | 773,741,474 | | | $ | 98,649,046 | | | $ | 985,308,141 | |

Short-term investments** | | | — | | | | — | | | | 4,989,886 | |

Short-term investments in affiliates*** | | | — | | | | 2,002,000 | | | | 12,331,000 | |

Cash | | | 20,927,867 | | | | 606 | | | | 5,250 | |

Cash collateral for futures | | | — | | | | — | | | | 12,383,065 | |

Foreign currencies at value**** | | | — | | | | — | | | | 119,351 | |

Receivables: | | | | | | | | | | | | |

Investment securities sold | | | 248 | | | | 243,298 | | | | 54,150,421 | |

Investments securities sold on a delayed-delivery or when-issued basis | | | — | | | | — | | | | 50,589,917 | |

Fund shares sold | | | 2,527,171 | | | | 360,536 | | | | 970,060 | |

Dividends and interest | | | 3,278,926 | | | | 2,394,129 | | | | 9,282,479 | |

Variation margin | | | — | | | | — | | | | 170,250 | |

Receivable for collateral held at broker (Note 2) | | | — | | | | — | | | | 330,000 | |

Unrealized appreciation on forward foreign currency contracts | | | — | | | | — | | | | 31,832 | |

Upfront payments made on swap agreements | | | — | | | | — | | | | 2,617,753 | |

Unrealized appreciation on swap agreements | | | — | | | | — | | | | 1,246,668 | |

Prepaid expenses | | | 57,572 | | | | 41,067 | | | | 51,234 | |

Reimbursement due from manager | | | — | | | | 19,938 | | | | — | |

| | | | | | | | | | | | |

Total assets | | | 800,533,258 | | | | 103,710,620 | | | | 1,134,577,307 | |

| | | | | | | | | | | | |

LIABILITIES: | | | | | | | | | | | | |

Payable for investment securities purchased | | | 4,592,360 | | | | 1,993,116 | | | | 28,296,281 | |

Payable for investment securities purchased on a delayed-delivery or when-issued basis | | | — | | | | — | | | | 183,932,506 | |

Payable for variation margin | | | — | | | | — | | | | 80,647 | |

Payable for fund shares redeemed | | | 1,168,792 | | | | 212,994 | | | | 4,183,008 | |

Payable upon receipt of securities loaned | | | — | | | | — | | | | 5,655,857 | |

Payable for terminated investment contracts (Note 11) | | | — | | | | 461,580 | | | | 1,368,703 | |

Upfront payments received on swap agreements | | | — | | | | — | | | | 1,369,759 | |

Unrealized depreciation on swap agreements | | | — | | | | — | | | | 1,993,743 | |

Income distribution payable | | | — | | | | 283,134 | | | | 679,013 | |

Payable to affiliates | | | 599,438 | | | | 83,801 | | | | 362,792 | |

Payable for trustee fees | | | 14,039 | | | | 6,562 | | | | 14,515 | |

Other accrued expenses and liabilities | | | 214,757 | | | | 114,206 | | | | 470,903 | |

| | | | | | | | | | | | |

Total liabilities | | | 6,589,386 | | | | 3,155,393 | | | | 228,407,727 | |

| | | | | | | | | | | | |

NET ASSETS | | $ | 793,943,872 | | | $ | 100,555,227 | | | $ | 906,169,580 | |

| | | | | | | | | | | | |

NET ASSETS WERE COMPRISED OF: | | | | | | | | | | | | |

Paid-in capital | | $ | 776,453,172 | | | $ | 297,741,775 | | | $ | 1,079,989,191 | |

Undistributed net investment income (distributions in excess of net investment income) | | | 1,482,889 | | | | (212,027 | ) | | | 33,659,010 | |

Accumulated net realized loss on investments, foreign currency related transactions, futures, swaps, and written options | | | (12,841,285 | ) | | | (198,647,004 | ) | | | (218,498,305 | ) |

Net unrealized appreciation on investments, foreign currency related transactions, futures, and swaps | | | 28,849,096 | | | | 1,672,483 | | | | 11,019,684 | |

| | | | | | | | | | | | |

NET ASSETS | | $ | 793,943,872 | | | $ | 100,555,227 | | | $ | 906,169,580 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

+ Including securities loaned at value | | $ | — | | | $ | — | | | $ | 5,542,113 | |

* Cost of investments in securities | | $ | 744,892,378 | | | $ | 96,976,563 | | | $ | 971,381,898 | |

** Cost of short-term investments | | $ | — | | | $ | — | | | $ | 5,655,857 | |

*** Cost of short-term investments in affiliates | | $ | — | | | $ | 2,002,000 | | | $ | 12,331,000 | |

****Cost of foreign currencies | | $ | — | | | $ | — | | | $ | 124,821 | |

See Accompanying Notes to Financial Statements

11

STATEMENTS OF ASSETS AND LIABILITIESASOF SEPTEMBER 30, 2009 (UNAUDITED) (CONTINUED)

| | | | | | | | | |

| | | ING GNMA Income Fund | | ING High Yield Bond Fund | | ING Intermediate Bond Fund |

Class A: | | | | | | | | | |

Net assets | | $ | 614,081,767 | | $ | 76,966,910 | | $ | 418,820,944 |

Shares authorized | | | unlimited | | | unlimited | | | unlimited |

Par value | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 |

Shares outstanding | | | 70,141,827 | | | 10,994,657 | | | 45,653,718 |

Net asset value and redemption price per share | | $ | 8.75 | | $ | 7.00 | | $ | 9.17 |

Maximum offering price per share (2.50%)(1) | | $ | 8.97 | | $ | 7.18 | | $ | 9.41 |

Class B: | | | | | | | | | |

Net assets | | $ | 32,325,058 | | $ | 13,167,332 | | $ | 22,759,189 |

Shares authorized | | | unlimited | | | unlimited | | | unlimited |

Par value | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 |

Shares outstanding | | | 3,713,320 | | | 1,882,821 | | | 2,485,713 |

Net asset value and redemption price per share(2) | | $ | 8.71 | | $ | 6.99 | | $ | 9.16 |

Maximum offering price per share | | $ | 8.71 | | $ | 6.99 | | $ | 9.16 |

Class C: | | | | | | | | | |

Net assets | | $ | 98,085,697 | | $ | 10,418,240 | | $ | 49,638,372 |

Shares authorized | | | unlimited | | | unlimited | | | unlimited |

Par value | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 |

Shares outstanding | | | 11,257,207 | | | 1,488,644 | | | 5,418,294 |

Net asset value and redemption price per share(2) | | $ | 8.71 | | $ | 7.00 | | $ | 9.16 |

Maximum offering price per share | | $ | 8.71 | | $ | 7.00 | | $ | 9.16 |

Class I: | | | | | | | | | |

Net assets | | $ | 42,443,997 | | $ | 2,745 | | $ | 354,674,455 |

Shares authorized | | | unlimited | | | unlimited | | | unlimited |

Par value | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 |

Shares outstanding | | | 4,842,583 | | | 393 | | | 38,660,697 |

Net asset value and redemption price per share | | $ | 8.76 | | $ | 6.99 | | $ | 9.17 |

Maximum offering price per share | | $ | 8.76 | | $ | 6.99 | | $ | 9.17 |

Class O: | | | | | | | | | |

Net assets | | | n/a | | | n/a | | $ | 42,155,601 |

Shares authorized | | | n/a | | | n/a | | | unlimited |

Par value | | | n/a | | | n/a | | $ | 0.001 |

Shares outstanding | | | n/a | | | n/a | | | 4,593,640 |

Net asset value and redemption price per share | | | n/a | | | n/a | | $ | 9.18 |

Maximum offering price per share | | | n/a | | | n/a | | $ | 9.18 |

Class Q: | | | | | | | | | |

Net assets | | $ | 74,798 | | | n/a | | | n/a |

Shares authorized | | | unlimited | | | n/a | | | n/a |

Par value | | $ | 0.001 | | | n/a | | | n/a |

Shares outstanding | | | 8,521 | | | n/a | | | n/a |

Net asset value and redemption price per share | | $ | 8.78 | | | n/a | | | n/a |

Maximum offering price per share | | $ | 8.78 | | | n/a | | | n/a |

Class R: | | | | | | | | | |

Net assets | | | n/a | | | n/a | | $ | 15,971,929 |

Shares authorized | | | n/a | | | n/a | | | unlimited |

Par value | | | n/a | | | n/a | | $ | 0.001 |

Shares outstanding | | | n/a | | | n/a | | | 1,738,758 |

Net asset value and redemption price per share | | | n/a | | | n/a | | $ | 9.19 |

Maximum offering price per share | | | n/a | | | n/a | | $ | 9.19 |

Class W: | | | | | | | | | |

Net assets | | $ | 6,932,555 | | | n/a | | $ | 2,149,090 |

Shares authorized | | | unlimited | | | n/a | | | unlimited |

Par value | | $ | 0.001 | | | n/a | | $ | 0.001 |

Shares outstanding | | | 790,378 | | | n/a | | | 234,480 |

Net asset value and redemption price per share | | $ | 8.77 | | | n/a | | $ | 9.17 |

Maximum offering price per share | | $ | 8.77 | | | n/a | | $ | 9.17 |

| (1) | | Maximum offering price is computed at 100/97.50 of net asset value. On purchases of $100,000 or more, the offering price is reduced. |

| (2) | | Redemption price per share may be reduced for any applicable contingent deferred sales charges. |

See Accompanying Notes to Financial Statements

12

STATEMENTS OF ASSETS AND LIABILITIESASOF SEPTEMBER 30, 2009 (UNAUDITED)

| | | | | | | | |

| | | ING Classic Money Market Fund | | | ING Institutional Prime

Money Market Fund | |

ASSETS: | | | | | | | | |

Short-term investments at amortized cost | | $ | 884,777,157 | | | $ | 1,124,911,589 | |

Repurchase agreements | | | 125,893,000 | | | | 422,431,000 | |

Cash | | | 9,999,965 | | | | 182 | |

Receivables: | | | | | | | | |

Fund shares sold | | | 1,372,479 | | | | 86,387,122 | |

Dividends and interest | | | 484,715 | | | | 472,102 | |

Prepaid expenses | | | 149,135 | | | | 44,397 | |

| | | | | | | | |

Total assets | | | 1,022,676,451 | | | | 1,634,246,392 | |

| | | | | | | | |

LIABILITIES: | | | | | | | | |

Payable for investment securities purchased | | | 16,999,306 | | | | 10,249,715 | |

Payable for fund shares redeemed | | | 94,041 | | | | 37,850,567 | |

Income distribution payable | | | — | | | | 215,918 | |

Payable to affiliates | | | 243,607 | | | | 99,606 | |

Payable for trustee fees | | | 24,038 | | | | 6,787 | |

Other accrued expenses and liabilities | | | 265,234 | | | | 246,743 | |

| | | | | | | | |

Total liabilities | | | 17,626,226 | | | | 48,669,336 | |

| | | | | | | | |

NET ASSETS | | $ | 1,005,050,225 | | | $ | 1,585,577,056 | |

| | | | | | | | |

NET ASSETS WERE COMPRISED OF: | | | | | | | | |

Paid-in capital | | $ | 1,005,010,399 | | | $ | 1,585,386,023 | |

Distributions in excess of net investment income | | | (3,182 | ) | | | (21,216 | ) |

Accumulated net realized gain on investments | | | 43,008 | | | | 212,249 | |

| | | | | | | | |

NET ASSETS | | $ | 1,005,050,225 | | | $ | 1,585,577,056 | |

| | | | | | | | |

See Accompanying Notes to Financial Statements

13

STATEMENTS OF ASSETS AND LIABILITIESASOF SEPTEMBER 30, 2009 (UNAUDITED) (CONTINUED)

| | | | | | |

| | | ING Classic Money Market Fund | | ING Institutional Prime Money Market Fund |

Class A: | | | | | | |

Net assets | | $ | 985,128,460 | | | n/a |

Shares authorized | | | unlimited | | | n/a |

Par value | | $ | 0.001 | | | n/a |

Shares outstanding | | | 985,067,853 | | | n/a |

Net asset value and redemption price per share | | $ | 1.00 | | | n/a |

Maximum offering price per share | | $ | 1.00 | | | |

Class B: | | | | | | |

Net assets | | $ | 11,702,201 | | | n/a |

Shares authorized | | | unlimited | | | n/a |

Par value | | $ | 0.001 | | | n/a |

Shares outstanding | | | 11,720,681 | | | n/a |

Net asset value and redemption price per share(1) | | $ | 1.00 | | | n/a |

Maximum offering price per share | | $ | 1.00 | | | n/a |

Class C: | | | | | | |

Net assets | | $ | 8,219,564 | | | n/a |

Shares authorized | | | unlimited | | | n/a |

Par value | | $ | 0.001 | | | n/a |

Shares outstanding | | | 8,222,514 | | | n/a |

Net asset value and redemption price per share(1) | | $ | 1.00 | | | n/a |

Maximum offering price per share | | $ | 1.00 | | | n/a |

Class I: | | | | | | |

Net assets | | | n/a | | $ | 1,585,576,056 |

Shares authorized | | | n/a | | | unlimited |

Par value | | | n/a | | $ | 0.001 |

Shares outstanding | | | n/a | | | 1,585,414,058 |

Net asset value and redemption price per share | | | n/a | | $ | 1.00 |

Maximum offering price per share | | | n/a | | $ | 1.00 |

Class IS: | | | | | | |

Net assets | | | n/a | | $ | 1,000 |

Shares authorized | | | n/a | | | unlimited |

Par value | | | n/a | | $ | 0.001 |

Shares outstanding | | | n/a | | | 1,000 |

Net asset value and redemption price per share | | | n/a | | $ | 1.00 |

Maximum offering price per share | | | n/a | | $ | 1.00 |

| (1) | | Redemption price per share may be reduced for any applicable contingent deferred sales charges. |

See Accompanying Notes to Financial Statements

14

STATEMENTS OF OPERATIONSFORTHE SIX MONTHS ENDED SEPTEMBER 30, 2009 (UNAUDITED)

| | | | | | | | | | | |

| | | ING GNMA Income Fund | | ING High Yield Bond Fund | | | ING Intermediate Bond Fund | |

INVESTMENT INCOME: | | | | | | | | | | | |

Dividends(1) | | $ | — | | $ | 3,263 | | | $ | 85,123 | |

Interest | | | 18,823,263 | | | 5,015,263 | | | | 24,423,115 | |

Securities lending income, net | | | — | | | — | | | | 192,108 | |

| | | | | | | | | | | |

Total investment income | | | 18,823,263 | | | 5,018,526 | | | | 24,700,346 | |

| | | | | | | | | | | |

EXPENSES: | | | | | | | | | | | |

Investment management fees | | | 1,838,465 | | | 238,307 | | | | 788,872 | |

Distribution and service fees: | | | | | | | | | | | |

Class A | | | 765,964 | | | 89,067 | | | | 547,227 | |

Class B | | | 177,373 | | | 65,355 | | | | 115,644 | |

Class C | | | 431,313 | | | 45,632 | | | | 257,941 | |

Class O | | | — | | | — | | | | 50,307 | |

Class Q | | | 86 | | | — | | | | — | |

Class R | | | — | | | — | | | | 40,750 | |

Transfer agent fees: | | | | | | | | | | | |

Class A | | | 203,081 | | | 56,386 | | | | 274,729 | |

Class B | | | 11,763 | | | 10,334 | | | | 14,449 | |

Class C | | | 28,565 | | | 7,243 | | | | 32,337 | |

Class I | | | 2,509 | | | — | | | | 95,711 | |

Class O | | | — | | | — | | | | 24,988 | |

Class Q | | | 3 | | | — | | | | 5 | |

Class R | | | — | | | — | | | | 10,122 | |

Class W | | | 408 | | | — | | | | 600 | |

Administrative service fees | | | 391,159 | | | 46,727 | | | | 464,041 | |

Shareholder reporting expense | | | 47,785 | | | 26,927 | | | | 97,545 | |

Registration fees | | | 57,568 | | | 49,791 | | | | 58,647 | |

Professional fees | | | 28,030 | | | 22,029 | | | | 40,459 | |

Custody and accounting expense | | | 42,505 | | | 15,018 | | | | 77,850 | |

Trustee fees | | | 9,236 | | | 2,535 | | | | 17,175 | |

Miscellaneous expense | | | 11,646 | | | 6,973 | | | | 25,528 | |

Interest expense | | | — | | | 168 | | | | 1,431 | |

| | | | | | | | | | | |

Total expenses | | | 4,047,459 | | | 682,492 | | | | 3,036,358 | |

Net waived and reimbursed fees | | | — | | | (84,726 | ) | | | (146,206 | ) |

| | | | | | | | | | | |

Net expenses | | | 4,047,459 | | | 597,766 | | | | 2,890,152 | |

| | | | | | | | | | | |

Net investment income | | | 14,775,804 | | | 4,420,760 | | | | 21,810,194 | |

| | | | | | | | | | | |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS, FOREIGN CURRENCY RELATED TRANSACTIONS, FUTURES, SWAPS, AND WRITTEN OPTIONS | | | | | | | | | | | |

Net realized gain (loss) on: | | | | | | | | | | | |

Investments | | | 1,933,698 | | | (4,191,102 | ) | | | (45,361,087 | ) |

Foreign currency related transactions | | | — | | | — | | | | 1,242,025 | |

Futures | | | — | | | — | | | | 3,052,084 | |

Swaps | | | — | | | (68,304 | ) | | | 80,208 | |

Written Options | | | — | | | — | | | | (44,800 | ) |

| | | | | | | | | | | |

Net realized gain (loss) on investments, foreign currency related transactions, futures, swaps, and written options | | | 1,933,698 | | | (4,259,406 | ) | | | (41,031,570 | ) |

| | | | | | | | | | | |

Net change in unrealized appreciation or depreciation on: | | | | | | | | | | | |

Investments | | | 2,861,574 | | | 25,659,959 | | | | 130,817,752 | |

Foreign currency related transactions | | | — | | | — | | | | 1,264,968 | |

Futures | | | — | | | — | | | | 488,367 | |

Swaps | | | — | | | 287,074 | | | | 237,125 | |

| | | | | | | | | | | |

Net change in unrealized appreciation on investments, foreign currency related transactions, futures, and swaps | | | 2,861,574 | | | 25,947,033 | | | | 132,808,212 | |

| | | | | | | | | | | |

Net realized and unrealized gain on investments, foreign currency related transactions, futures, swaps, and written options | | | 4,795,272 | | | 21,687,627 | | | | 91,776,642 | |

| | | | | | | | | | | |

Increase in net assets resulting from operations | | $ | 19,571,076 | | $ | 26,108,387 | | | $ | 113,586,836 | |

| | | | | | | | | | | |

| | | | | | | | | | | |

(1) Dividends from affiliates | | $ | — | | $ | 3,203 | | | $ | 53,107 | |

See Accompanying Notes to Financial Statements

15

STATEMENTS OF OPERATIONSFORTHE SIX MONTHS ENDED SEPTEMBER 30, 2009 (UNAUDITED)

| | | | | | | |

| | | ING Classic Money Market Fund | | | ING Institutional Prime Money Market Fund |

INVESTMENT INCOME: | | | | | | | |

Interest | | $ | 3,441,726 | | | $ | 2,898,361 |

| | | | | | | |

Total investment income | | | 3,441,726 | | | | 2,898,361 |

| | | | | | | |

EXPENSES: | | | | | | | |

Investment management fees | | | 1,458,776 | | | | 522,239 |

Distribution and service fees: | | | | | | | |

Class A | | | 4,290,412 | | | | — |

Class B | | | 69,375 | | | | — |

Class C | | | 45,200 | | | | — |

Transfer agent fees: | | | | | | | |

Class A | | | 64,019 | | | | |

Class B | | | 753 | | | | — |

Class C | | | 495 | | | | — |

Class I | | | — | | | | 201,231 |

Shareholder reporting expense | | | 156,762 | | | | 40,973 |

Registration fees | | | 230,838 | | | | 32,588 |

Professional fees | | | 67,891 | | | | 97,094 |

Custody and accounting expense | | | 75,994 | | | | 94,666 |

Trustee fees | | | 24,450 | | | | 21,555 |

Guarantee fees (Note 16) | | | 253,789 | | | | 363,496 |

Miscellaneous expense | | | 33,604 | | | | 48,573 |

| | | | | | | |

Total expenses | | | 6,772,358 | | | | 1,422,417 |

Net waived and reimbursed fees | | | (3,327,706 | ) | | | — |

| | | | | | | |

Net expenses | | | 3,444,652 | | | | 1,422,417 |

| | | | | | | |

Net investment income (loss) | | | (2,926 | ) | | | 1,475,944 |

| | | | | | | |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | | | | | | | |

Net realized gain on investments | | | 295,224 | | | | 188,562 |

| | | | | | | |

Increase in net assets resulting from operations | | $ | 292,298 | | | $ | 1,664,506 |

| | | | | | | |

See Accompanying Notes to Financial Statements

16

STATEMENTS OF CHANGES IN NET ASSETS (UNAUDITED)

| | | | | | | | | | | | | | | | |

| | | ING GNMA Income Fund | | | ING High Yield Bond Fund | |

| | | Six Months Ended September 30, 2009 | | | Year Ended March 31, 2009 | | | Six Months Ended September 30, 2009 | | | Year Ended March 31, 2009 | |

FROM OPERATIONS: | | | | | | | | | | | | | | | | |

Net investment income | | $ | 14,775,804 | | | $ | 26,880,070 | | | $ | 4,420,760 | | | $ | 8,791,288 | |

Net realized gain (loss) on investments and swaps | | | 1,933,698 | | | | 395,796 | | | | (4,259,406 | ) | | | (19,275,591 | ) |

Net change in unrealized appreciation or depreciation on investments and swaps | | | 2,861,574 | | | | 14,446,282 | | | | 25,947,033 | | | | (14,806,857 | ) |

| | | | | | | | | | | | | | | | |

Increase (decrease) in net assets resulting from operations | | | 19,571,076 | | | | 41,722,148 | | | | 26,108,387 | | | | (25,291,160 | ) |

| | | | | | | | | | | | | | | | |

FROM DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | | | | | | | | | |

Net investment income: | | | | | | | | | | | | | | | | |

Class A | | | (12,641,780 | ) | | | (22,932,802 | ) | | | (3,565,027 | ) | | | (5,651,666 | ) |

Class B | | | (613,211 | ) | | | (1,526,184 | ) | | | (605,596 | ) | | | (1,292,734 | ) |

Class C | | | (1,446,463 | ) | | | (1,624,129 | ) | | | (420,644 | ) | | | (647,080 | ) |

Class I | | | (900,585 | ) | | | (1,151,718 | ) | | | (133 | ) | | | (12,515 | ) |

Class Q | | | (1,387 | ) | | | (1,935 | ) | | | — | | | | — | |

Class W | | | (145,020 | ) | | | (55,336 | ) | | | — | | | | — | |

Return of capital: | | | | | | | | | | | | | | | | |

Class A | | | — | | | | — | | | | — | | | | (1,363,089 | ) |

Class B | | | — | | | | — | | | | — | | | | (346,757 | ) |

Class C | | | — | | | | — | | | | — | | | | (174,874 | ) |

Class I | | | — | | | | — | | | | — | | | | (2,081 | ) |

| | | | | | | | | | | | | | | | |

Total distributions | | | (15,748,446 | ) | | | (27,292,104 | ) | | | (4,591,400 | ) | | | (9,490,796 | ) |

| | | | | | | | | | | | | | | | |

FROM CAPITAL SHARE TRANSACTIONS: | | | | | | | | | | | | | | | | |

Net proceeds from sale of shares | | | 144,073,015 | | | | 295,311,177 | | | | 15,859,346 | | | | 34,528,518 | |

Reinvestment of distributions | | | 13,036,302 | | | | 22,747,989 | | | | 2,589,745 | | | | 4,988,124 | |

| | | | | | | | | | | | | | | | |

| | | 157,109,317 | | | | 318,059,166 | | | | 18,449,091 | | | | 39,516,642 | |

Cost of shares redeemed | | | (128,905,334 | ) | | | (189,713,958 | ) | | | (18,110,315 | ) | | | (44,343,192 | ) |

| | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets resulting from capital share transactions | | | 28,203,983 | | | | 128,345,208 | | | | 338,776 | | | | (4,826,550 | ) |

| | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets | | | 32,026,613 | | | | 142,775,252 | | | | 21,855,763 | | | | (39,608,506 | ) |

| | | | | | | | | | | | | | | | |

NET ASSETS: | | | | | | | | | | | | | | | | |

Beginning of period | | | 761,917,259 | | | | 619,142,007 | | | | 78,699,464 | | | | 118,307,970 | |

| | | | | | | | | | | | | | | | |

End of period | | $ | 793,943,872 | | | $ | 761,917,259 | | | $ | 100,555,227 | | | $ | 78,699,464 | |

| | | | | | | | | | | | | | | | |

Undistributed net investment income (distributions in excess of net investment income) at end of period | | $ | 1,482,889 | | | $ | 2,455,531 | | | $ | (212,027 | ) | | $ | (41,387 | ) |

| | | | | | | | | | | | | | | | |

See Accompanying Notes to Financial Statements

17

STATEMENTS OF CHANGES IN NET ASSETS (UNAUDITED)

| | | | | | | | | | | | | | | | |

| | | ING Intermediate Bond Fund | | | ING Classic Money Market Fund | |

| | | Six Months Ended September 30, 2009 | | | Year Ended March 31, 2009 | | | Six Months Ended September 30, 2009 | | | Year Ended March 31, 2009 | |

FROM OPERATIONS: | | | | | | | | | | | | | | | | |

Net investment income (loss) | | $ | 21,810,194 | | | $ | 59,477,948 | | | $ | (2,926 | ) | | $ | 20,023,863 | |

Net realized gain (loss) on investments, foreign currency related transactions, futures, swaps, and written options | | | (41,031,570 | ) | | | (139,525,797 | ) | | | 295,224 | | | | 1,949,010 | |

Net change in unrealized appreciation or depreciation on investments, foreign currency related transactions, futures, and swaps | | | 132,808,212 | | | | (70,451,358 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

Increase (decrease) in net assets resulting from operations | | | 113,586,836 | | | | (150,499,207 | ) | | | 292,298 | | | | 21,972,873 | |

| | | | | | | | | | | | | | | | |