| | |

OMB APPROVAL |

OMB Number: | | 3235-0570 |

Expires: | | April 30, 2008 |

Estimated average burden |

hours per response: | | 19.4 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08895

ING Funds Trust

(Exact name of registrant as specified in charter)

| | |

| 7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

| (Address of principal executive offices) | | (Zip code) |

The Corporation Trust Company, 1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: March 31

Date of reporting period: April l, 2007 to September 30, 2007

Funds

Semi-Annual Report

September 30, 2007

Classes A, B, C, I, O, Q and R

Fixed-Income Funds

| n | ING High Yield Bond Fund |

| n | ING Intermediate Bond Fund |

| n | ING National Tax-Exempt Bond Fund |

Money Market Funds

| n | ING Classic Money Market Fund |

| n | ING Institutional Prime Money Market Fund |

| | |

| | E-Delivery Sign-up – details inside |

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully.

| | | | |

| | | |

| | Go Paperless with E-Delivery! | | |

Sign up now for on-line prospectuses, fund reports, and proxy statements. In less than five minutes, you can help reduce paper mail and lower fund costs. Just go to www.ingfunds.com, click on the E-Delivery icon from the home page, follow the directions and complete the quick 5 Steps to Enroll. You will be notified by e-mail when these communications become available on the internet. Documents that are not available on the internet will continue to be sent by mail. |

PROXY VOTING INFORMATION

A description of the policies and procedures that the Funds use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the Funds’ website at www.ingfunds.com; and (3) on the U.S. Securities and Exchange Commission’s (“SEC”) website at www.sec.gov. Information regarding how the Funds voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the Funds’ website at www.ingfunds.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Funds file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the website at www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330; and is available upon request from the Funds by calling Shareholder Services toll-free at (800) 992-0180.

TABLE OF CONTENTS

PRESIDENT’S LETTER

Dear Shareholder,

It is impossible to discuss the current market climate without acknowledging the recent turmoil brought on by problems in the sub-prime mortgage market. Clearly the excesses in this sector of the market and other segments of collateralized debt have created challenges throughout credit markets worldwide.

Amidst the volatility, we at ING Funds remind our shareholders that the creditworthiness and quality of our funds’ holdings is the ultimate priority to us — whether those holdings are part of our money market funds, fixed income funds or equity funds. No one can say for sure how the recent turbulence will impact investment portfolios over the long-term. Market volatility is part of investing and we believe the best way to manage it is to build a well-balanced, fully-diversified portfolio, which aligns with your goals and risk tolerance.

ING Funds remains committed to developing and offering a diverse array of mutual

funds designed to meet the goals of most investors. We urge you to work with your investment professional to make sure you are invested appropriately. Together, you can select the funds that will help you achieve your financial goals. We thank you for choosing ING Funds and look forward to continuing to serve you.

Sincerely,

Shaun P. Mathews

President

ING Funds

October 19, 2007

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaims any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

For more complete information, or to obtain a prospectus for any ING Fund, please call your Investment Professional or ING Funds Distributor, LLC at (800) 992-0180 or log on to www.ingfunds.com. The prospectus should be read carefully before investing. Consider the fund’s investment objectives, risks, and charges and expenses carefully before investing. The prospectus contains this information and other information about the fund. Check with your Investment Professional to determine which funds are available for sale within their firm. Not all funds are available for sale at all firms.

1

MARKET PERSPECTIVE: SIX MONTHS ENDED SEPTEMBER 30, 2007

As our new fiscal year started, economic news had been dominated for months by the deteriorating housing market. In addition to the worries about rising inventories of unsold homes, declining prices, a negative wealth effect on demand and reduced construction activity there had been alarm in the sub-prime mortgage loan sector, where lax lending standards were sending foreclosure rates and default provisions soaring, and some lenders into bankruptcy. Furthermore, the huge volumes of securities backed by such loans were declining in value, if they could find a bid at all. Much of this exposure was held by hedge funds and structured investment vehicles, which financed their purchases with investors’ money and by issuing lower yielding short term commercial paper, a variant of the “carry trade”. If investors of either type lost confidence, the stricken securities would need to be sold at fire sale prices, unless a line of credit had been guaranteed by another financial institution, which would then effectively assume the risk. In June, investment bank Bear Stearns rescued two of its hedge funds in distress over holdings in mortgage bonds.

Yet even into July 2007, few observers believed that sub-prime mortgage problems might lead to recession, as other economic factors appeared robust.

But from mid-July, a series of shocks sent investors scurrying for cover. Federal Open Market Committee (“FOMC”) Chairman Bernanke himself had to acknowledge on July 18, 2007, the day that another set of woeful housing statistics was released, that the sub-prime mortgage situation had “significantly deteriorated.” Within weeks, a large mortgage lender, Countrywide, was reporting that the sub-prime default crisis had spread to other classes of mortgage loans and the securities derived from them. Worse, by month end American Home Mortgage, a lender not of sub-prime mortgages, but the supposedly safer “Alt-A” and adjustable rate loans, revealed that its creditors had initiated margin calls and that bankruptcy was a possibility. A week later it was fact.

Confirmation that the global asset backed commercial paper market was close to atrophy came on August 9, 2007, from an unlikely source when French bank BNP Paribas announced similar problems with its own U.S. mortgage-backed structured investment vehicles. Banks were by now reluctant to lend to each other because no-one could be sure where the exposure to tainted securities ultimately lay. Central banks responded by pouring billions into the inter-bank system. On August 17, 2007, the Federal Reserve Board cut the

discount rate, the rate at which it will lend to banks, by 50 basis points (0.50%), with the accompanying statement silent on inflation risks. This and some of Chairman Bernanke’s other comments signaled a possible cut in the federal funds rate at the FOMC meeting scheduled for September 18, 2007, prompting some to wonder whether he was responding to economic deterioration or the now slumping stock markets.

The matter became academic on September 7, 2007, when a shockingly weak employment report showed the first decline in non-farm payrolls in four years. The federal funds rate reduction duly arrived on September 18, 2007, by an unexpectedly soothing 50 basis points (0.50%), along with another cut in the discount rate by the same amount. Markets in risk assets breathed a collective sigh of relief, although asset-backed commercial paper did not seem that much easier to sell than it did a few weeks earlier.

For the six-month period ended September 30, 2007, U.S. fixed income markets saw a pronounced steepening of the Treasury yield curve. The scene had been set near the end of March when the FOMC removed its tightening bias while still citing inflation as the predominant concern. The yield on the ten-year Treasury Note rose into the summer and reached a five-year high in June 2007, while the yield on three-month Treasury Bill stayed fairly flat. But as confidence unraveled in late July 2007, Treasuries were preferred to other asset classes and, after a brief lag, short Treasuries to longer dated ones, so yields fell across the board, shorter more than longer. For the six-month period ended September 30, 2007, the yield on the ten-year Treasury Note fell 7 basis points (0.07%) to 4.58%, while the yield on the three-month Bill fell 119 basis points (1.19%) to 3.70%. During this time, the broad Lehman Brothers® Aggregate Bond Index(1) (“LBAB Index”) of investment grade bonds returned 2.31%. Not surprisingly given the risk aversion that took hold, the Lehman Brothers® High Yield Bond Index(2), consisting of corporate high yield bonds, returned just 0.56% for the six-month period ended September 30, 2007: in other words, income barely covered capital losses.

In currencies, the perception that European interest rates would rise relative to those in the U.S., along with the actual U.S. rate cut in September 2007, sent the euro to new highs against the dollar and the pound to its best level in over 25 years. The yen was initially dragged down by the “carry trade”, in which speculators borrow in yen at low interest and buy higher yielding securities

2

MARKET PERSPECTIVE: SIX MONTHS ENDED SEPTEMBER 30, 2007

in other currencies. But, these were unwound in the flight from risk. For the six-month period ended September 30, 2007, the dollar fell 5.9% against the euro, 3.4% against the pound and 2.2% on the yen.

U.S. equities, represented by the Standard & Poor’s 500® Composite Stock Price Index(3) (“S&P 500® Index”) gained 8.4% in the six-month period ended September 30, 2007, almost all of it before May 2007, as corporate earnings stood up well. A near 10% fall between mid-July and mid-August was mostly reclaimed by September 30, 2007.

International markets did not fare as well based on Morgan Stanley Capital International (“MSCI”) local currency indices, as central banks did not reduce local interest rates. During the period, the MSCI Japan® Index(4) lost 1.5% as deflation re-established itself and gross domestic product (“GDP”) contracted. For the six-month period ended September 30, 2007, the MSCI Europe ex UK® Index(5) and the MSCI UK® Index(6) markets rose 4.3% and 7.8%, respectively, as pre-crisis investors were encouraged by improved GDP growth and widespread, large-scale merger and acquisition activity.

(1) The LBAB Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities.

(2) The Lehman Brothers® High Yield Bond Index is an unmanaged index that measures the performance of fixed-income securities generally representative of corporate bonds rated below investment-grade.

(3) The S&P 500® Index is an unmanaged index that measures the performance of securities of approximately 500 of the largest companies in the United States.

(4) The MSCI Japan® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan.

(5) The MSCI Europe ex UK® Index is a free float rising adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK.

(6) The MSCI UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Funds’ performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING’s Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

| | |

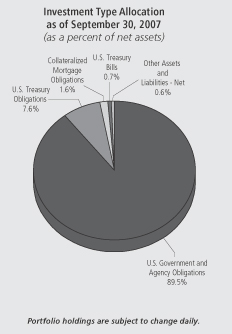

| ING GNMA INCOME FUND | | PORTFOLIO MANAGERS’ REPORT |

ING GNMA Income Fund (the “Fund”) seeks a high level of current income, consistent with liquidity and safety of principal, through investment primarily in Government National Mortgage Association (“GNMA”) mortgage-backed securities (also known as GNMA Certificates) that are guaranteed as to the timely payment of principal and interest by the U.S. government. The Fund is managed by Denis P. Jamison, CFA, Senior Vice President and Senior Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Securities issued by the U.S. Treasury are backed by the full faith and credit of the federal government. Securities issued by individual agencies and organizations may be backed by the full faith and credit of the federal government as to principal or interest but are not direct obligations of the U.S. Treasury. Securities of some agencies and organizations are backed solely by the entity’s own resources or by the ability of the entity to borrow from the U.S. Treasury. Government securities also include certain mortgage-related securities that are sponsored by a U.S. government agency or organization and are not direct obligations of the U.S. government.

Performance: For the six months ended September 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of 1.62% compared to the Lehman Brothers® Mortgage-Backed Securities Index(1) (“Lehman MBS Index”), which returned 2.13% for the same period.

Portfolio Specifics: Rising market volatility was the dominant market theme during the six months ended September 30, 2007. The Merrill Lynch Option Volatility Index — the bond market’s equivalent of the

Chicago Board Options Volatility Index (“VIX”) more than doubled from a low of 0.51% in April to a high of 1.25% in August. This was likely triggered by the combination of rising credit spreads and the prospect of defaults in the sub-prime sector of the private mortgage market. While both Government National Mortgage Association (“GNMA”) and government agency-guaranteed mortgages are not subject to these risks, higher price volatility increases uncertainty regarding prepayments and mortgage cash flow. While Lehman Brothers Intermediate U.S. Treasury index rose 3.5% in the half-year ended September 30, the mortgage-backed securities index gained only 2.1%. Since the Federal Reserve Board’s (the “Fed”) rate cut, the Lehman MBS Index has outpaced Treasury market gains.

GNMA mortgages enjoyed slightly better returns than their agency-guaranteed counterparts during the spring and summer. This was especially true during the market sell-off in May and June. This probably reflects the higher coupon, more defensive bias of the GNMA sector. The Fund’s mortgage portfolio is constructed to mirror the characteristics of the GNMA index. At the close of the September quarter, mortgages represented 91.7% of the Fund portfolio.

In April, with 10-year bond yields at about 4.7%, we increased the Fund’s effective maturity against its peers and its benchmark with the purchase of $80 million of 10- and 30-year U.S. Treasury bonds. Subsequently, yields began to rise, peaking at 5.3% in mid-June. Having lost ground versus our peers and fearing a further increase, we sold half of this position. Yields promptly began to tumble, reaching a low of 4.3% in early September. Our original assumption regarding a slowing of the economy turned out to be correct; however, the May run-up in yields tested that conviction and we blinked. We continue to hold about $45 million worth of 10- and 30-year bonds and, as a result, remain slightly longer than our peers and our benchmark.

GNMA mortgages performed slightly better than agency backed securities during the period. The Fund’s 10-year government bond position (4.4%) also contributed to return over the period. Our purchase and subsequent sale of U.S. Treasury securities detracted from return for the period.

Current Strategy and Outlook: Since the cut in the federal funds rate in September, government bond yields have actually increased. This seemingly illogical outcome is not unusual, although we believe the reaction in the most recent episode has been quicker than normal. In our opinion, if the economy continues to slow, more rate cuts will be forthcoming and a bond rally will likely ensue. If, however, the Fed’s recent actions are merely a palliative to financial market problems and the housing weakness does spill over to the broader economy, then bonds and mortgages likely will post lackluster returns. At this juncture, we believe the former outcome is more probable and will maintain a more aggressive maturity stance than our benchmark and peers.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

(1) | | The Lehman MBS Index is an unmanaged index composed of fixed-income security mortgage pools sponsored by GNMA, FNMA and FHLMC, including GNMA Graduated Payment Mortgages. |

4

| | |

| PORTFOLIO MANAGERS’ REPORT | | ING HIGH YIELD BOND FUND |

ING High Yield Bond Fund (the “Fund”) seeks to provide investors with a high level of current income and total return. The Fund is managed by Randall Parrish, CFA and Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended September 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of 0.89% compared to the Lehman Brothers® High Yield Bond Index(1) and the Lehman Brothers® High Yield Bond — 2% Issuer Constrained Composite Index(2), which returned 0.56% and 1.12%, respectively, for the same period.

Portfolio Specifics: During the second quarter of 2007 — the latter days of which were marked by significant capital markets turmoil — the Fund benefited from its lower credit quality positioning, with an overweight in B-rated bonds, a slight overweight in bonds rated CCCs and a significant underweight in bonds rated BBs. BB-rated bonds were the worst performers, B-rated bonds gained slightly and CCC-rated bonds significantly outper-

Investment Type Allocation

as of September 30, 2007

(as a percent of net assets)

| | |

Corporate Bonds/Notes | | 98.1% |

Mutual Funds | | 2.1% |

Common Stock | | 0.1% |

Repurchase Agreement | | 0.1% |

Other Assets and Liabilities — Net | | (0.4)% |

| | |

Net Assets | | 100.0% |

| | |

Portfolio holdings are subject to change daily.

formed the index. The Fund benefited from an overweight in the wireless sector and underweights in technology and utilities. No industry positions significantly hurt the Fund’s performance in the quarter.

The Fund benefited from gains in a number of bonds, primarily related to actual or announced mergers and acquisitions. Contributors included VWR International, Inc. and Hawaiian Telecom, which added to outperformance when it announced a significant asset sale. The most noteworthy detractor was Advanced Medical Optics, Inc., which announced the recall of an eye-care solution, then made a bid to acquire Bausch & Lomb, Inc.

We entered the third quarter with a cautious short-term view, owing to the continuing volatility in risk assets. As a result, we pared back the risk in the Fund before the worst of the summer sell-off. The Fund remained underweight more Treasury-sensitive BB-rated bonds, which detracted from performance as rates moved sharply lower in July and August. On the other hand, we successfully avoided those market sectors hurt the most in the sell-off. Other than a position in Stanley-Martin Communities, LLC, a small Washington, DC-based homebuilder, the Fund has continued to avoid the homebuilding sector. The only other impactful sector position in the quarter was the avoidance of financial institutions, another sector that fared poorly through the financial market disruptions.

The Fund relied primarily on individual security selection to drive performance in a market that began once again to differentiate good credit from bad, and to require higher compensation for higher risk. Most impactful to performance was our avoidance of large negative returns. Of the 81 issuers that posted a negative return of more than 5% in the quarter, the Fund held meaningful positions in only four. We continue to hold positions in two of these — equipment rental firm Neff Corp. and homebuilder Stanley-Martin Communities, LLC, — where we believe prices have been overly beaten up relative to the companies’ underlying fundamentals and business outlooks.

We sold our position in amusement park operator Six Flags due to increasing concern that if consumer spending weakened it would hurt this highly discretionary business. The Fund benefited from the outperformance of a number of holdings, most notably in healthcare, retailers, and non-cable media. In addition, the Fund profited from positions in a number of bonds that traded higher on news of acquisition or take-out.

Current Strategy and Outlook: We expect slower economic growth over the next two to three quarters, but not severe slowing or recession. Corporate profit growth is clearly slowing, but in our opinion, balance sheets are generally in good shape with debt at manageable levels and ample liquidity. The significant spread widening of the third quarter was not accompanied by an increase in defaults or even a meaningful increase in default expectations.

In our opinion, the highly leveraged buyout financings of the past two years will eventually translate into an increase in defaults, but we believe this turn in the credit cycle is still at least a year or two away. The labor market remains an area of concern, as weakness there, we believe, could hurt consumer income and spending. More bad news from the mortgage market or the financial sector could cause another spike in volatility, though we believe current spreads provide compensation for these risks.

Top Ten Industries

as of September 30, 2007

(as a percent of net assets)

| | |

Diversified Financial Services | | 12.5% |

Media | | 11.8% |

Telecommunications | | 8.8% |

Healthcare-Services | | 6.0% |

Chemicals | | 5.5% |

Commercial Services | | 4.8% |

Oil & Gas | | 4.8% |

Retail | | 4.6% |

Forest Products & Paper | | 4.5% |

Electric | | 4.0% |

Portfolio holdings are subject to change daily.

We have selectively added risk over the past month in names we believe represent good value. The Fund remains underweight in BB-rated bonds and overweight in B-rated bonds, reflecting our view that default risk remains low for the foreseeable future. We remain cautious in cyclicals such as homebuilders and auto suppliers. We continue to focus Fund holdings on industries with strong internal cash generation capabilities, such as non-cable media, the largest sector overweight.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

(1) | | The Lehman Brothers® High Yield Bond Index is an unmanaged index that measures the performance of fixed-income securities generally representative of corporate bonds rated below investment grade. |

(2) | | The Lehman Brothers® High Yield Bond — 2% Issuer Constrained Composite Index is an unmanaged index that measures the performance of fixed-income securities. The Composite Index more closely tracks the types of securities in which the Fund invests than the Lehman Brothers® High Yield Bond Index. |

5

| | |

| ING INTERMEDIATE BOND FUND | | PORTFOLIO MANAGERS’ REPORT |

ING Intermediate Bond Fund (the “Fund”) seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity. The Fund is managed by James B. Kauffmann, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended September 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of 1.94% compared to Lehman Brothers® Aggregate Bond Index(1) (“LBAB Index”), which returned 2.31% for the same period.

Portfolio Specifics: The dramatic sell-off in risk-based assets during the summer of 2007 was the primary driver of performance for fixed income portfolio managers and sectors of the bond market. The duration of the portfolio varied over the period from neutral to greater than the index. At various points during the period the Fund’s occasional long duration (higher interest-rate risk) stance made a positive contribution. As markets began to anticipate aggressive Federal Reserve Board (“Fed”) easing and the potential for increasing inflation worries, longer-dated Treasuries lagged shorter-dated maturities in the rally. Since the Fund was overweight the shorter maturities, it benefited from the relative outperformance of those U.S. Treasuries. We also added Treasury Inflation-Protected Securities (“TIPS”) positions as a counterweight to a re-inflationary Fed policy. We implemented our current neutral duration stance shortly before the Fed rate cut when we perceived overbought conditions.

The use of credit default swaps and related derivative indices enabled the Fund to mitigate some of the negative effects of this historic market disruption. The Fund’s underweighting in corporate bonds benefited performance. On the other hand, the Fund’s allocation to floating rate notes and bonds issued by financial entities acted as a drag. Bonds purchased right after the volatility spike in early September — mainly issued by industrial companies — outperformed in September.

Investment Type Allocation

as of September 30, 2007

(as a percent of net assets)

| | |

Collateralized Mortgage Obligations | | 32.4% |

U.S. Treasury Obligations | | 24.4% |

Corporate Bonds/Notes | | 20.8% |

U.S. Government and Agency Obligations | | 20.2% |

Asset-Backed Securities | | 3.9% |

Preferred Stock | | 1.3% |

Mutual Fund | | 1.0% |

Municipal Bonds | | 0.5% |

Other Bonds | | 0.3% |

Purchased Options | | 0.1% |

Repurchase Agreement | | 0.1% |

Other Assets and Liabilities — Net* | | (5.0)% |

| | |

Net Assets | | 100.0% |

| | |

| | * | Includes securities lending collateral. |

Portfolio holdings are subject to change daily.

Mortgage market conditions were terrible; in fact, buyers shunned mortgage-backed securities (“MBS”) categorically for much of the period. While the Fund maintained a nearly neutral position in mortgages, most of its underperformance for the period came from MBS exposure. The vast majority of these mortgage holdings are rated AAA, and none is rated below AA. We continue to monitor and assess any developments in the market with regards to these specific holdings.

Current Outlook and Strategy: In our opinion, for most of the summer fear overcame greed, and now the autumn has witnessed a rebound from oversold conditions. Risk-based markets regained some of their lost ground at quarter-end; however, repercussions from the sub-prime lending crisis may be starting to show up in the real economy.

The Fund is now positioned for a yield curve steepening (that is, greater yield differences between shorter-term and longer-term maturities) as we expect the domestic economy to deteriorate further. Although market consensus suggests that the Fed will stop easing around 4.50%, we worry that the central bank may be compelled to go further. Accordingly, we maintain underweightings in financials, construction and other industries afflicted by the residential real estate market. Our outlook for the U.S. dollar remains negative.

Unease in the credit marketplace persists and we are comfortable with our current credit shorts or underweights. If the macro economy slows as we expect, the recent optimism around credit and new deals will abate. Collateralized debt obligations, collateralized loan obligations, structured investment vehicles and other levered entities were enablers of easy credit, allowing excessive availability of debt at low cost to sometimes feckless borrowers. Now that these vehicles are either liquidated or withering away, an entire base of buyers has been eliminated and this development has long-term implications.

The MBS team has maintained its near neutral posture to the sector as a whole. The team prefers hybrid adjustable-rate mortgages (“ARMs”) to 15-year mortgages. ARMs represent approximately 20% of our MBS allocation compared to an index weighting of nearly 9%. We continue to hold some special situation high-yield bonds despite our negative outlook for the sector. We will wait for more generalized price weakness or more compelling relative value before entering the either market in a large way.

Top Ten Industries

as of September 30, 2007

(as a percent of net assets)

| | |

Collateralized Mortgage Obligations | | 32.4% |

U.S. Treasury Notes | | 18.0% |

Federal Home Loan Mortgage Corporation | | 12.4% |

Federal National Mortgage Corporation | | 7.7% |

Diversified Financial Services | | 6.5% |

Banks | | 5.6% |

Treasury Inflation Indexed Protected Securities | | 3.8% |

U.S. Treasury Bonds | | 2.6% |

Other Asset-Backed Securities | | 1.9% |

Home Equity Asset-Backed Securities | | 1.8% |

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

(1) The | | LBAB Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. |

6

| | |

| PORTFOLIO MANAGERS’ REPORT | | ING NATIONAL TAX-EXEMPT BOND FUND |

ING National Tax-Exempt Bond Fund (the “Fund”) seeks to provide investors with a high level of current income that is exempt from federal income taxes, consistent with the preservation of capital. The Fund is managed by Robert Schonbrunn, Karen Cronk, and Richard Kilbride, Portfolio Managers of ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended September 30, 2007, the Fund’s Class A shares, excluding sales charges, provided a total return of (0.22)% compared to the Lehman Brothers Municipal Bond Index(1) and the Lehman Brothers® Aggregate Bond Index(2) (“LBAB Index”), which returned 1.15% and 2.31%, respectively, for the same period.

Portfolio Specifics: The six months ended September 30, 2007 were a period of volatility and change in the municipal bond market. The sub-prime mortgage problem, which came to a head in the summer, was caused by an over-leveraged financial system chasing higher yields and had broad impact across the entire financial world, including municipal bonds. When interest rates were very low in 2003, some aggressive investors used leveraged vehicles to produce higher returns. As the yield curve flattened (short term rates were as high as long term rates), these arbitrageurs substituted municipals, which had a steeper yield curve, for taxable issues.

In a variation of what is known as the “carry trade,” arbitrageurs bought mostly longer-term municipals and borrowed at short-term taxable rates. This trade worked well and arbitrageurs became significant buyers of municipal bonds. The carry trade was a factor in the strong performance of longer term municipals for the two-year period prior to March 2007. At the same time, investors reaching for higher yields also bought lower quality issues, which compressed the “spread” or difference in yield between the highest-quality, AAA-rated issues and lower-quality issues. The sub-prime problem directly affected both of these trends.

As longer term interest rates rose in the second quarter and then fell in July and August, arbitrageurs were squeezed and their carry trades didn’t work. They stopped buying and tried to unwind their positions, selling into a weak bid, which caused an imbalance in long-term municipals. At the same time, investors became worried about potential credit problems, and sold lower-quality issues of all financial assets including municipal bonds.

Both of these developments hurt the Fund. Although rated AA/AA2 overall, the Fund held almost 12% in BBB-rated bonds, which were marked down significantly. In the expectation that interest rates would be declining, the Fund held approximately 30% in longer term issues and had a higher sensitivity to interest rate change than the benchmark. Interest rates declined in the third quarter, but longer term municipals did not benefit as much as comparable taxable issues because of the arbitrage selling pressure. The Fund’s three worst-performing holdings suffered both these conditions — the BBB markdown and the sell-off of long-duration bonds — and incurred losses as a result.

Top Ten Holdings

as of September 30, 2007

(as a percent of net assets)

| | |

Pleasant Valley School District, CA,

5.850%, due 08/01/31 | | 4.3% |

Harris County Health Facilities Development Corp., TX, 5.750%, due 07/01/27 | | 4.2% |

Port Authority of New York & New Jersey,

6.250%, due 12/01/11 | | 3.9% |

Payne County Economic Development Authority, OK, 6.375%, due 06/01/30 | | 3.9% |

New York State Dormitory Authority,

5.500%, due 07/01/15 | | 3.8% |

Oklahoma Industries Authority,

6.000%, due 08/15/19 | | 3.8% |

De Kalb-Ogle Etc. Counties Community College, IL District No. 523, 5.750%, due 02/01/11 | | 3.8% |

Interlocken Metropolitan District, CO,

5.750%, due 12/15/19 | | 3.8% |

Clovis Public Financing Authority, CA,

5.000%, due 08/01/26 | | 3.8% |

Lebanon County Health Facilities Authority, PA,

6.000%, due 11/15/35 | | 3.7% |

Portfolio holdings are subject to change daily.

The roughly 40% of the portfolio invested in issues due within five years performed well during the period. The Fund maintains a favorable yield and coupon advantage to the benchmark, with a yield to maturity of 4.70% versus 4.12% and a coupon of 5.38% compared to 5.00%.

Current Strategy and Outlook: We believe the residential housing market continues to be a drag on the economy and should eventually slow consumer spending. In our opinion, the negative repercussions from the sub-prime crisis should lessen as over-leveraged and serious credit problems are distinguished from areas such as municipals, where the fundamentals are sound. We believe that the wide spreads currently separating BBB credits from AAAs will narrow, allowing us to reevaluate their positions in the portfolio. The portfolio has a higher sensitivity to interest rate movement than the benchmark with the expectation that municipals will perform relatively better than taxable bonds in coming periods.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

(1) | The Lehman Brothers Municipal Bond Index is an unmanaged index of approximately 1,100 investment grade tax-exempt bonds classified into four sectors: general obligation, revenue, insured and pre-refunded. |

(2) | The LBAB Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. |

7

| | |

| ING CLASSIC MONEY MARKET FUND | | PORTFOLIO MANAGERS’ REPORT |

ING Classic Money Market Fund (the “Fund”) seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity and the maintenance of a stable $1.00 net asset value per share. The Fund is managed by David S. Yealy, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Portfolio Specifics: The markets for short-term money market securities remained virtually unchanged during April and May. Longer-term money market rates increased in June, despite inflation data that should have given the markets and the Federal Open Market Committee (“FOMC”) some comfort. The latter half of the six-month period was challenging for money market and short-term investors. What started as a sub-prime, hedge fund and collateralized debt obligation (“CDO”) problem widened to affect most mortgage markets, money market securities and even interbank overnight lending. Commercial paper rates and LIBOR skyrocketed as there was a flight to quality as money market investors discounted the worst case scenario for their counterparties. Eventually the liquidity crisis verged on becoming a banking crisis.

In August, the Federal Reserve Board (the “Fed”) sought to calm overnight lending markets by flooding the banking system with cash and lowering the nearly forgotten discount rate 0.50%. The Fed made additional moves in August and early September to increase liquidity and improve investor confidence. When that failed to fully return the markets to normal, the FOMC practiced a little “shock and awe” by surprising most market observers with a 0.50% cut in the fed funds rate and the discount rate. Short-term liquidity and market confidence has improved steadily, albeit slowly, since the Fed took these steps.

During the first half of the period, the Fund took advantage of the swings in yields, buying securities in the six-month to thirteen-month maturity range when yields moved higher. The Fund was well positioned going into the liquidity crisis and we were able to

take advantage of the market dislocation. The Fund had over 40% of its assets in floating-rate securities tied to LIBOR. These securities saw their rates increase as the coupons reset based on the high level of LIBOR rates during this market disruption.

The Fund also maintained a weighted average maturity (“WAM”) in the 40-51 day range during the quarter, ending the quarter at 51 days. This was above the average WAM of our competitors, as measured by iMoneyNet, who were shortening during this period.

Current Strategy and Outlook: We expect liquidity and the overall market for money market securities to improve slowly over the next few weeks and months. Additional moves by the Fed will be determined by the continued market stress on certain assets classes, interbank market liquidity; as well as by economic growth, the job market and inflation. The market is expecting the Fed to ease another 0.25% or more by year-end. We see a risk that the effect from the deteriorating housing market and, to a lesser extent, a slowing in the job market could spill over into the economy and we believe push us toward a recession. This, we believe, is not now fully priced into the market.

Our current strategy is to continue to take advantage of the high LIBOR rates by buying additional floating-rate securities of highly rated issuers and selectively adding duration by buying longer-term fixed rate securities.

While the Fund’s yield will fluctuate with changes in general market rates for the types of assets it holds, we do not expect the recent events with sub-prime and other synthetic structures like CDOs to directly affect the performance of our money market funds.

Principal Risk Factor(s): An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

8

| | |

| PORTFOLIO MANAGERS’ REPORT | | ING INSTITUTIONAL PRIME MONEY MARKET FUND |

ING Institutional Prime Money Market Fund (the “Fund”) seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity and the maintenance of a stable $1.00 net asset value per share. The Fund is managed by David S. Yealy, Portfolio Manager of ING Investment Management Co. — the Sub-Adviser.

Portfolio Specifics: The markets for short-term money market securities remained virtually unchanged during April and May. Longer-term money market rates increased in June, despite inflation data that should have given the markets and the Federal Open Market Committee (“FOMC”) some comfort. The latter half of the six-month period was challenging for money market and short-term investors. What started as a sub-prime, hedge fund and collateralized debt obligation (“CDO”) problem widened to affect most mortgage markets, money market securities and even interbank overnight lending. Commercial paper rates and LIBOR skyrocketed as there was a flight to quality as money market investors discounted the worst case scenario for their counterparties. Eventually the liquidity crisis verged on becoming a banking crisis.

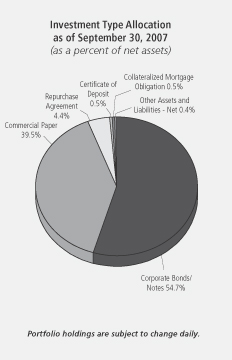

Investment Type Allocation

as of September 30, 2007

(as a percent of net assets)

| | |

Corporate Bonds/Notes | | 60.6% |

Commercial Paper | | 34.6% |

Repurchase Agreement | | 5.6% |

Certificates of Deposit | | 1.4% |

Collateralized Mortgage Obligation | | 0.3% |

Other Assets and Liabilities — Net | | (2.5)% |

| | |

Net Assets | | 100.0% |

| | |

Portfolio holdings are subject to change daily.

In August, the Federal Reserve Board (the “Fed”) sought to calm overnight lending markets by flooding the banking system with cash and lowering the nearly forgotten discount rate 0.50%. The Fed made additional moves in August and early September to increase liquidity and improve investor confidence. When that failed to fully return the markets to normal, the FOMC practiced a little “shock and awe” by surprising most market observers with a 0.50% cut in the fed funds rate and the discount rate. Short-term liquidity and market confidence has improved steadily, albeit slowly, since the Fed took these steps.

During the first half of the period, the Fund took advantage of the swings in yields, buying securities in the six-month to thirteen-month maturity range when yields moved higher. The Fund was well positioned going into the liquidity crisis and we were able to take advantage of the market dislocation. The Fund had over 40% of its assets in floating-rate securities tied to LIBOR. These securities saw their rates increase as the coupons reset based on the high level of LIBOR rates during this market disruption.

The Fund also maintained a weighted average maturity (“WAM”) in the 36-52 day range during the quarter, ending the quarter at 49 days. This was above the average WAM of our competitors, as measured by iMoneyNet, who were shortening during this period.

Current Strategy and Outlook: We expect liquidity and the overall market for money market securities to improve slowly over the next few weeks and months. Additional moves by the Fed will be determined by the continued market stress on certain assets classes, interbank market liquidity; as well as by economic growth, the job market and inflation. The market is expecting the Fed to ease another 0.25% or more by year-end. We see a risk that the effect from the deteriorating housing market and, to a lesser extent, a slowing in the job market could spill over into the economy and we believe push us toward a recession. This, we believe, is not now fully priced into the market.

Our current strategy is to continue to take advantage of the high LIBOR rates by buying additional floating-rate securities of highly rated issuers and selectively adding duration by buying longer-term fixed rate securities.

While the Fund’s yield will fluctuate with changes in general market rates for the types of assets it holds, we do not expect the recent events with sub-prime and other synthetic structures like CDOs to directly affect the performance of our money market funds.

Principal Risk Factor(s): An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Fund may differ from that presented for other ING Funds.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

9

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED)

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees, and exchange fees; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2007 to September 30, 2007. The Funds’ expenses are shown without the imposition of any sales charges or fees. Expenses would have been higher if such charges were included.

Actual Expenses

The first section of the table shown, “Actual Fund Return,” provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of the table shown, “Hypothetical 5% Return,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | ING GNMA Income Fund | | Beginning

Account

Value

April 1, 2007 | | Ending

Account

Value

September 30, 2007 | | Annualized

Expense

Ratio | | | Expenses Paid

During the

Period Ended

September 30, 2007* |

| | Actual Fund Return | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,016.20 | | 0.95 | % | | $ | 4.79 |

| | Class B | | | 1,000.00 | | | 1,013.60 | | 1.70 | | | | 8.56 |

| | Class C | | | 1,000.00 | | | 1,013.60 | | 1.70 | | | | 8.56 |

| | Class I | | | 1,000.00 | | | 1,018.70 | | 0.65 | | | | 3.28 |

| | Class Q | | | 1,000.00 | | | 1,016.70 | | 0.90 | | | | 4.54 |

| | Hypothetical (5% return before expenses) | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,020.25 | | 0.95 | % | | $ | 4.80 |

| | Class B | | | 1,000.00 | | | 1,016.50 | | 1.70 | | | | 8.57 |

| | Class C | | | 1,000.00 | | | 1,016.50 | | 1.70 | | | | 8.57 |

| | Class I | | | 1,000.00 | | | 1,021.75 | | 0.65 | | | | 3.29 |

| | Class Q | | | 1,000.00 | | | 1,020.50 | | 0.90 | | | | 4.55 |

| | | | | | | | | | | | | | |

| * | | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/366 to reflect the most recent fiscal half-year. |

10

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED) (CONTINUED)

| | | | | | | | | | | | | | |

| | | ING High Yield Bond Fund | | Beginning

Account

Value

April 1, 2007 | | Ending

Account

Value

September 30, 2007 | | Annualized

Expense

Ratio | | | Expenses Paid

During the

Period Ended

September 30, 2007* |

| | Actual Fund Return | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,008.90 | | 1.10 | % | | $ | 5.52 |

| | Class B | | | 1,000.00 | | | 1,005.00 | | 1.85 | | | | 9.27 |

| | Class C | | | 1,000.00 | | | 1,005.00 | | 1.85 | | | | 9.27 |

| | Hypothetical (5% return before expenses) | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,019.50 | | 1.10 | % | | $ | 5.55 |

| | Class B | | | 1,000.00 | | | 1,015.75 | | 1.85 | | | | 9.32 |

| | Class C | | | 1,000.00 | | | 1,015.75 | | 1.85 | | | | 9.32 |

| | ING Intermediate Bond Fund | | | | | | | | | | | | |

| | Actual Fund Return | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,019.40 | | 0.69 | % | | $ | 3.48 |

| | Class B | | | 1,000.00 | | | 1,015.50 | | 1.44 | | | | 7.26 |

| | Class C | | | 1,000.00 | | | 1,015.50 | | 1.44 | | | | 7.26 |

| | Class I | | | 1,000.00 | | | 1,021.10 | | 0.35 | | | | 1.77 |

| | Class O | | | 1,000.00 | | | 1,019.40 | | 0.69 | | | | 3.48 |

| | Class R | | | 1,000.00 | | | 1,018.10 | | 0.94 | | | | 4.74 |

| | Hypothetical (5% return before expenses) | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,021.55 | | 0.69 | % | | $ | 3.49 |

| | Class B | | | 1,000.00 | | | 1,017.80 | | 1.44 | | | | 7.26 |

| | Class C | | | 1,000.00 | | | 1,017.80 | | 1.44 | | | | 7.26 |

| | Class I | | | 1,000.00 | | | 1,023.25 | | 0.35 | | | | 1.77 |

| | Class O | | | 1,000.00 | | | 1,021.55 | | 0.69 | | | | 3.49 |

| | Class R | | | 1,000.00 | | | 1,020.30 | | 0.94 | | | | 4.75 |

| | ING National Tax-Exempt Bond Fund | | | | | | | | | | | | |

| | Actual Fund Return | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 997.80 | | 0.87 | % | | $ | 4.35 |

| | Class B | | | 1,000.00 | | | 994.00 | | 1.62 | | | | 8.08 |

| | Class C | | | 1,000.00 | | | 994.10 | | 1.62 | | | | 8.08 |

| | Hypothetical (5% return before expenses) | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,020.65 | | 0.87 | % | | $ | 4.39 |

| | Class B | | | 1,000.00 | | | 1,016.90 | | 1.62 | | | | 8.17 |

| | Class C | | | 1,000.00 | | | 1,016.90 | | 1.62 | | | | 8.17 |

| | ING Classic Money Market Fund | | | | | | | | | | | | |

| | Actual Fund Return | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,023.60 | | 0.77 | % | | $ | 3.90 |

| | Class B | | | 1,000.00 | | | 1,020.40 | | 1.37 | | | | 6.92 |

| | Class C | | | 1,000.00 | | | 1,020.40 | | 1.37 | | | | 6.92 |

| | Hypothetical (5% return before expenses) | | | | | | | | | | | | |

| | Class A | | $ | 1,000.00 | | $ | 1,021.15 | | 0.77 | % | | $ | 3.89 |

| | Class B | | | 1,000.00 | | | 1,018.15 | | 1.37 | | | | 6.91 |

| | Class C | | | 1,000.00 | | | 1,018.15 | | 1.37 | | | | 6.91 |

| | ING Institutional Prime Money Market Fund | | | | | | | | | | | | |

| | Actual Fund Return | | $ | 1,000.00 | | $ | 1,026.90 | | 0.10 | % | | $ | 0.51 |

| | Hypothetical (5% return before expenses) | | $ | 1,000.00 | | $ | 1,024.50 | | 0.10 | % | | $ | 0.51 |

| | | | | | | | | | | | | | |

| * | Expenses are equal to each Fund’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/366 to reflect the most recent fiscal half-year. |

11

STATEMENTS OF ASSETS AND LIABILITIESASOF SEPTEMBER 30, 2007 (UNAUDITED)

| | | | | | | | | | | | |

| | | ING

GNMA

Income

Fund | | | ING

High Yield

Bond

Fund | | | ING

Intermediate

Bond

Fund | |

ASSETS: | | | | | | | | | | | | |

Investments in securities at value+* | | $ | 589,537,161 | | | $ | 139,444,789 | | | $ | 1,276,630,039 | |

Investments in affiliates** | | | — | | | | 725,145 | | | | — | |

Short-term investments*** | | | 3,960,552 | | | | — | | | | — | |

Short-term investments at amortized cost | | | — | | | | 150,000 | | | | 312,583,909 | |

Short-term investments in affiliates at amortized cost | | | — | | | | 2,300,000 | | | | 11,600,000 | |

Cash | | | 1,618,253 | | | | — | | | | 10,834,352 | |

Cash collateral for futures | | | — | | | | — | | | | 1,876,229 | |

Foreign currencies at value**** | | | — | | | | — | | | | 185,314 | |

Receivables: | | | | | | | | | | | | |

Investment securities sold | | | 204 | | | | 1,103,383 | | | | 107,769,607 | |

Fund shares sold | | | 766,176 | | | | 136,883 | | | | 3,418,864 | |

Dividends and interest | | | 2,895,531 | | | | 3,304,920 | | | | 9,350,088 | |

Variation margin receivable | | | — | | | | — | | | | 283,048 | |

Unrealized appreciation on forward foreign currency contracts | | | — | | | | — | | | | 184,407 | |

Upfront payments made on swap agreements | | | — | | | | 165,130 | | | | 3,917,919 | |

Unrealized appreciation on swap agreements | | | — | | | | 532,017 | | | | 4,889,254 | |

Prepaid expenses | | | 38,556 | | | | 22,505 | | | | 52,182 | |

Reimbursement due from manager | | | — | | | | 3,307 | | | | 30,198 | |

| | | | | | | | | | | | |

Total assets | | | 598,816,433 | | | | 147,888,079 | | | | 1,743,605,410 | |

| | | | | | | | | | | | |

LIABILITIES: | | | | | | | | | | | | |

Payable for investment securities purchased | | | — | | | | 1,805,626 | | | | 193,643,840 | |

Payable for fund shares redeemed | | | 1,239,458 | | | | 443,513 | | | | 2,481,098 | |

Payable for futures variation margin | | | — | | | | — | | | | 149,881 | |

Payable upon receipt of securities loaned | | | — | | | | — | | | | 311,352,909 | |

Unrealized depreciation on forward currency contracts | | | — | | | | — | | | | 207,847 | |

Upfront payments received on swap agreements | | | — | | | | 180,100 | | | | 1,490,078 | |

Unrealized depreciation on swap agreements | | | — | | | | 72,824 | | | | 3,257,297 | |

Income distribution payable | | | — | | | | 411,381 | | | | 814,265 | |

Payable to affiliates | | | 454,191 | | | | 126,619 | | | | 532,666 | |

Payable to custodian due to bank overdraft | | | — | | | | 2,690,757 | | | | — | |

Payable for trustee fees | | | 558 | | | | 5,694 | | | | 8,852 | |

Other accrued expenses and liabilities | | | 200,683 | | | | 85,172 | | | | 277,459 | |

Options written ***** | | | — | | | | — | | | | 571,425 | |

| | | | | | | | | | | | |

Total liabilities | | | 1,894,890 | | | | 5,821,686 | | | | 514,787,617 | |

| | | | | | | | | | | | |

NET ASSETS | | $ | 596,921,543 | | | $ | 142,066,393 | | | $ | 1,228,817,793 | |

| | | | | | | | | | | | |

NET ASSETS WERE COMPRISED OF: | | | | | | | | | | | | |

Paid-in capital | | $ | 617,635,234 | | | $ | 507,655,014 | | | $ | 1,248,726,525 | |

Undistributed net investment income (distributions in excess of net investment income) | | | 1,198,527 | | | | (49,988 | ) | | | 113,046 | |

Accumulated net realized loss on investments, foreign currency related transactions, futures, swaps, and written options | | | (16,938,173 | ) | | | (365,061,029 | ) | | | (9,439,388 | ) |

Net unrealized depreciation on investments, foreign currency related transactions, futures, swaps, and written options | | | (4,974,045 | ) | | | (477,604 | ) | | | (10,582,390 | ) |

| | | | | | | | | | | | |

NET ASSETS | | $ | 596,921,543 | | | $ | 142,066,393 | | | $ | 1,228,817,793 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

+ Including securities loaned at value | | $ | — | | | $ | — | | | $ | 304,166,324 | |

* Cost of investments in securities | | $ | 594,510,402 | | | $ | 140,387,506 | | | $ | 1,289,192,962 | |

** Cost of investments in affiliates | | $ | — | | | $ | 719,225 | | | $ | — | |

*** Cost of short-term investments | | $ | 3,961,356 | | | $ | — | | | $ | — | |

****Cost of foreign currencies | | $ | — | | | $ | — | | | $ | 186,454 | |

*****Premiums received for options written | | $ | — | | | $ | — | | | $ | 316,790 | |

See Accompanying Notes to Financial Statements

12

STATEMENTS OF ASSETS AND LIABILITIESASOF SEPTEMBER 30, 2007 (UNAUDITED) (CONTINUED)

| | | | | | | | | |

| | | ING GNMA

Income Fund | | ING High Yield

Bond Fund | | ING

Intermediate

Bond Fund |

Class A: | | | | | | | | | |

Net assets | | $ | 497,444,649 | | $ | 97,202,321 | | $ | 739,452,339 |

Shares authorized | | | unlimited | | | unlimited | | | unlimited |

Par value | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 |

Shares outstanding | | | 59,930,244 | | | 11,136,658 | | | 72,710,178 |

Net asset value and redemption price per share | | $ | 8.30 | | $ | 8.73 | | $ | 10.17 |

Maximum offering price per share (2.50%)(1) | | $ | 8.51 | | $ | 8.95 | | $ | 10.42 |

Class B: | | | | | | | | | |

Net assets | | $ | 49,478,033 | | $ | 33,159,578 | | $ | 44,411,280 |

Shares authorized | | | unlimited | | | unlimited | | | unlimited |

Par value | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 |

Shares outstanding | | | 5,992,684 | | | 3,802,363 | | | 4,375,072 |

Net asset value and redemption price per share(2) | | $ | 8.26 | | $ | 8.72 | | $ | 10.15 |

Maximum offering price per share | | $ | 8.26 | | $ | 8.72 | | $ | 10.15 |

Class C: | | | | | | | | | |

Net assets | | $ | 34,919,021 | | $ | 11,704,494 | | $ | 76,975,593 |

Shares authorized | | | unlimited | | | unlimited | | | unlimited |

Par value | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 |

Shares outstanding | | | 4,223,646 | | | 1,341,162 | | | 7,578,155 |

Net asset value and redemption price per share(2) | | $ | 8.27 | | $ | 8.73 | | $ | 10.16 |

Maximum offering price per share | | $ | 8.27 | | $ | 8.73 | | $ | 10.16 |

Class I: | | | | | | | | | |

Net assets | | $ | 15,031,644 | | | n/a | | $ | 304,307,008 |

Shares authorized | | | unlimited | | | n/a | | | unlimited |

Par value | | $ | 0.001 | | | n/a | | $ | 0.001 |

Shares outstanding | | | 1,809,187 | | | n/a | | | 29,915,652 |

Net asset value and redemption price per share | | $ | 8.31 | | | n/a | | $ | 10.17 |

Maximum offering price per share | | $ | 8.31 | | | n/a | | $ | 10.17 |

Class O: | | | | | | | | | |

Net assets | | | n/a | | | n/a | | $ | 52,415,771 |

Shares authorized | | | n/a | | | n/a | | | unlimited |

Par value | | | n/a | | | n/a | | $ | 0.001 |

Shares outstanding | | | n/a | | | n/a | | | 5,151,427 |

Net asset value and redemption price per share | | | n/a | | | n/a | | $ | 10.18 |

Maximum offering price per share | | | n/a | | | n/a | | $ | 10.18 |

Class Q: | | | | | | | | | |

Net assets | | $ | 48,196 | | | n/a | | | n/a |

Shares authorized | | | unlimited | | | n/a | | | n/a |

Par value | | $ | 0.001 | | | n/a | | | n/a |

Shares outstanding | | | 5,794 | | | n/a | | | n/a |

Net asset value and redemption price per share | | $ | 8.32 | | | n/a | | | n/a |

Maximum offering price per share | | $ | 8.32 | | | n/a | | | n/a |

Class R: | | | | | | | | | |

Net assets | | | n/a | | | n/a | | $ | 11,255,802 |

Shares authorized | | | n/a | | | n/a | | | unlimited |

Par value | | | n/a | | | n/a | | $ | 0.001 |

Shares outstanding | | | n/a | | | n/a | | | 1,105,045 |

Net asset value and redemption price per share | | | n/a | | | n/a | | $ | 10.19 |

Maximum offering price per share | | | n/a | | | n/a | | $ | 10.19 |

(1) | | Maximum offering price is computed at 100/97.50 of net asset value. On purchases of $100,000 or more, the offering price is reduced. |

(2) | | Redemption price per share may be reduced for any applicable contingent deferred sales charges. |

See Accompanying Notes to Financial Statements

13

STATEMENTS OF ASSETS AND LIABILITIESASOF SEPTEMBER 30, 2007 (UNAUDITED)

| | | | | | | | |

| | | ING

National Tax-

Exempt Bond

Fund | | | ING Classic

Money Market

Fund | |

ASSETS: | | | | | | | | |

Investments in securities at value* | | $ | 27,059,488 | | | $ | — | |

Short-term investments at amortized cost | | | — | | | | 1,096,911,518 | |

Cash | | | 422,719 | | | | 139,255 | |

Receivables: | | | | | | | | |

Fund shares sold | | | 2,755 | | | | 3,080,803 | |

Dividends and interest | | | 370,160 | | | | 4,019,804 | |

Prepaid expenses | | | 16,640 | | | | 252,470 | |

| | | | | | | | |

Total assets | | | 27,871,762 | | | | 1,104,403,850 | |

| | | | | | | | |

LIABILITIES: | | | | | | | | |

Payable for investment securities purchased | | | — | | | | 1,795,382 | |

Payable for fund shares redeemed | | | 186 | | | | 571,116 | |

Income distribution payable | | | 74,790 | | | | 23,160 | |

Payable to affiliates | | | 24,530 | | | | 598,457 | |

Payable for trustee fees | | | 1,546 | | | | 4,455 | |

Other accrued expenses and liabilities | | | 22,118 | | | | 114,558 | |

| | | | | | | | |

Total liabilities | | | 123,170 | | | | 3,107,128 | |

| | | | | | | | |

NET ASSETS | | $ | 27,748,592 | | | $ | 1,101,296,722 | |

| | | | | | | | |

NET ASSETS WERE COMPRISED OF: | | | | | | | | |

Paid-in capital | | $ | 27,784,779 | | | $ | 1,101,425,545 | |

Distributions in excess of net investment income | | | (1,192 | ) | | | (888 | ) |

Accumulated net realized loss on investments | | | (26,980 | ) | | | (127,935 | ) |

Net unrealized depreciation on investments | | | (8,015 | ) | | | — | |

| | | | | | | | |

NET ASSETS | | $ | 27,748,592 | | | $ | 1,101,296,722 | |

| | | | | | | | |

| | | | | | | | |

* Cost of investments in securities | | $ | 27,067,503 | | | $ | — | |

| | |

Class A: | | | | | | | | |

Net assets | | $ | 22,805,512 | | | $ | 1,066,350,429 | |

Shares authorized | | | unlimited | | | | unlimited | |

Par value | | $ | 0.001 | | | $ | 0.001 | |

Shares outstanding | | | 2,263,433 | | | | 1,066,451,318 | |

Net asset value and redemption price per share | | $ | 10.08 | | | $ | 1.00 | |

Maximum offering price per share (2.50%)(1) | | $ | 10.33 | | | $ | 1.00 | |

Class B: | | | | | | | | |

Net assets | | $ | 2,624,962 | | | $ | 22,344,177 | |

Shares authorized | | | unlimited | | | | unlimited | |

Par value | | $ | 0.001 | | | $ | 0.001 | |

Shares outstanding | | | 260,725 | | | | 22,365,719 | |

Net asset value and redemption price per share(2) | | $ | 10.07 | | | $ | 1.00 | |

Maximum offering price per share | | $ | 10.07 | | | $ | 1.00 | |

Class C: | | | | | | | | |

Net assets | | $ | 2,318,118 | | | $ | 12,602,116 | |

Shares authorized | | | unlimited | | | | unlimited | |

Par value | | $ | 0.001 | | | $ | 0.001 | |

Shares outstanding | | | 230,050 | | | | 12,609,110 | |

Net asset value and redemption price per share(2) | | $ | 10.08 | | | $ | 1.00 | |

Maximum offering price per share | | $ | 10.08 | | | $ | 1.00 | |

(1) | | Maximum offering price is computed at 100/97.50 of net asset value. On purchases of $100,000 or more, the offering price is reduced. |

(2) | | Redemption price per share may be reduced for any applicable contingent deferred sales charges. |

See Accompanying Notes to Financial Statements

14

STATEMENT OF ASSETS AND LIABILITIESASOF SEPTEMBER 30, 2007 (UNAUDITED)

| | | |

| | | ING

Institutional Prime

Money Market

Fund |

ASSETS: | | | |

Short-term investments at amortized cost | | $ | 856,010,976 |

Cash | | | 22,998 |

Receivables: | | | |

Fund shares sold | | | 35,495,000 |

Dividends and interest | | | 4,235,761 |

Prepaid expenses | | | 48,311 |

| | | |

Total assets | | | 895,813,046 |

| | | |

LIABILITIES: | | | |

Payable for fund shares redeemed | | | 56,449,000 |

Income distribution payable | | | 3,884,664 |

Payable to affiliates | | | 65,353 |

Other accrued expenses and liabilities | | | 6,336 |

| | | |

Total liabilities | | | 60,405,353 |

| | | |

NET ASSETS | | $ | 835,407,693 |

| | | |

NET ASSETS WERE COMPRISED OF: | | | |

Paid-in capital | | $ | 835,363,400 |

Undistributed net investment income | | | 31,120 |

Accumulated net realized gain on investments | | | 13,173 |

| | | |

NET ASSETS | | $ | 835,407,693 |

| | | |

| |

Net assets | | $ | 835,407,693 |

Shares authorized | | | unlimited |

Par value | | $ | 0.001 |

Shares outstanding | | | 835,392,436 |

Net asset value and redemption price per share | | $ | 1.00 |

See Accompanying Notes to Financial Statements

15

STATEMENTS OF OPERATIONSFORTHE SIX MONTHS ENDED SEPTEMBER 30, 2007 (UNAUDITED)

| | | | | | | | | | | | |

| | | ING GNMA

Income

Fund | | | ING

High Yield

Bond Fund | | | ING

Intermediate

Bond Fund | |

INVESTMENT INCOME: | | | | | | | | | | | | |

Dividends, net of foreign taxes withheld*(1) | | $ | — | | | $ | 53,858 | | | $ | 446,403 | |

Interest(2) | | | 16,983,303 | | | | 6,611,895 | | | | 34,266,953 | |

Securities lending income | | | — | | | | — | | | | 338,024 | |

| | | | | | | | | | | | |

Total investment income | | | 16,983,303 | | | | 6,665,753 | | | | 35,051,380 | |

| | | | | | | | | | | | |

EXPENSES: | | | | | | | | | | | | |

Investment management fees | | | 1,429,658 | | | | 387,686 | | | | 1,012,985 | |

Distribution and service fees: | | | | | | | | | | | | |

Class A | | | 631,175 | | | | 124,900 | | | | 892,228 | |

Class B | | | 267,877 | | | | 189,934 | | | | 232,105 | |

Class C | | | 177,123 | | | | 70,636 | | | | 381,665 | |

Class O | | | — | | | | — | | | | 66,015 | |

Class Q | | | 61 | | | | — | | | | — | |

Class R | | | — | | | | — | | | | 21,268 | |

Transfer agent fees: | | | | | | | | | | | | |

Class A | | | 159,330 | | | | 71,812 | | | | 476,445 | |

Class B | | | 16,905 | | | | 27,420 | | | | 30,986 | |

Class C | | | 11,178 | | | | 10,196 | | | | 50,952 | |

Class I | | | 1,582 | | | | — | | | | 60,243 | |

Class O | | | — | | | | — | | | | 35,252 | |

Class Q | | | 6 | | | | — | | | | — | |

Class R | | | — | | | | — | | | | 5,678 | |

Administrative service fees | | | 304,180 | | | | 76,016 | | | | 595,867 | |

Shareholder reporting expense | | | 58,257 | | | | 25,803 | | | | 118,004 | |

Registration fees | | | 42,565 | | | | 29,069 | | | | 58,700 | |

Professional fees | | | 24,705 | | | | 10,614 | | | | 51,554 | |

Custody and accounting expense | | | 41,025 | | | | 15,063 | | | | 112,728 | |

Trustee fees | | | 10,065 | | | | 915 | | | | 19,808 | |

Miscellaneous expense | | | 14,154 | | | | 8,294 | | | | 37,027 | |

Interest expense | | | — | | | | 1,792 | | | | 344 | |

| | | | | | | | | | | | |

Total expenses | | | 3,189,846 | | | | 1,050,150 | | | | 4,259,854 | |

Net waived and reimbursed fees | | | — | | | | (12,880 | ) | | | (164,136 | ) |

| | | | | | | | | | | | |

Net expenses | | | 3,189,846 | | | | 1,037,270 | | | | 4,095,718 | |

| | | | | | | | | | | | |

Net investment income | | | 13,793,457 | | | | 5,628,483 | | | | 30,955,662 | |

| | | | | | | | | | | | |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS, | | | | | | | | | | | | |

FOREIGN CURRENCY RELATED TRANSACTIONS, FUTURES, WRITTEN OPTIONS, AND SWAPS: | | | | | | | | | | | | |

Net realized gain (loss) on: | | | | | | | | | | | | |

Investments | | | (2,215,766 | ) | | | 871,728 | | | | 1,568,291 | |

Foreign currency related transactions | | | — | | | | — | | | | (184,728 | ) |

Futures, swaps, and written options | | | — | | | | (210,212 | ) | | | 1,389,974 | |

| | | | | | | | | | | | |

Net realized gain (loss) on investments, foreign currency related transactions, futures, swaps, and written options | | | (2,215,766 | ) | | | 661,516 | | | | 2,773,537 | |

| | | | | | | | | | | | |

Net change in unrealized appreciation or depreciation on: | | | | | | | | | | | | |

Investments | | | (2,083,418 | ) | | | (5,712,621 | ) | | | (12,373,309 | ) |

Foreign currency related transactions | | | — | | | | — | | | | 17,881 | |

Futures, swaps, and written options | | | — | | | | 391,705 | | | | 1,634,985 | |

| | | | | | | | | | | | |

Net change in unrealized appreciation or depreciation on investments, foreign currency related transactions, futures, swaps, and written options | | | (2,083,418 | ) | | | (5,320,916 | ) | | | (10,720,443 | ) |

| | | | | | | | | | | | |

Net realized and unrealized loss on investments, foreign currency related transactions, futures, swaps, and written options | | | (4,299,184 | ) | | | (4,659,400 | ) | | | (7,946,906 | ) |

| | | | | | | | | | | | |

Increase in net assets resulting from operations | | $ | 9,494,273 | | | $ | 969,083 | | | $ | 23,008,756 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

* Foreign taxes withheld | | $ | — | | | $ | — | | | $ | 761 | |

(1) Dividends at September 30, 2007 include dividends from affiliates of $50,268 for ING High Yield Bond Fund | | | | | | | | | | | | |

(2) Affiliated income | | $ | — | | | $ | 14,542 | | | $ | 1,392,767 | |

See Accompanying Notes to Financial Statements

16

STATEMENTS OF OPERATIONSFORTHE SIX MONTHS ENDED SEPTEMBER 30, 2007 (UNAUDITED)

| | | | | | | | | | | |

| | | ING

National Tax-

Exempt Bond

Fund | | | ING

Classic Money

Market Fund | | | ING

Institutional Prime

Money Market

Fund |

INVESTMENT INCOME: | | | | | | | | | | | |

Interest | | $ | 643,051 | | | $ | 26,887,333 | | | $ | 26,320,020 |

| | | | | | | | | | | |

Total investment income | | | 643,051 | | | | 26,887,333 | | | | 26,320,020 |

| | | | | | | | | | | |

EXPENSES: | | | | | | | | | | | |

Investment management fees | | | 40,653 | | | | 1,233,904 | | | | 387,502 |

Distribution and service fees: | | | | | | | | | | | |

Class A | | | 28,166 | | | | 3,594,493 | | | | — |

Class B | | | 13,101 | | | | 111,507 | | | | — |

Class C | | | 9,745 | | | | 35,293 | | | | — |

Transfer agent fees | | | — | | | | — | | | | 1,098 |

Class A | | | 2,028 | | | | 106,981 | | | | — |

Class B | | | 236 | | | | 2,494 | | | | — |

Class C | | | 175 | | | | 786 | | | | — |

Administrative service fees | | | 13,551 | | | | — | | | | — |

Shareholder reporting expense | | | 1,977 | | | | 94,062 | | | | 6,078 |

Registration fees | | | 24,668 | | | | 282,163 | | | | 29,699 |

Professional fees | | | 2,135 | | | | 33,966 | | | | 13,911 |

Custody and accounting expense | | | 615 | | | | 51,240 | | | | 22,065 |

Trustee fees | | | 549 | | | | 11,895 | | | | 4,773 |

Miscellaneous expense | | | 1,541 | | | | 24,465 | | | | 14,880 |

| | | | | | | | | | | |

Total expenses | | | 139,140 | | | | 5,583,249 | | | | 480,006 |

Net waived and reimbursed fees | | | (4,183 | ) | | | (1,688,775 | ) | | | — |

| | | | | | | | | | | |

Net expenses | | | 134,957 | | | | 3,894,474 | | | | 480,006 |

| | | | | | | | | | | |

Net investment income | | | 508,094 | | | | 22,992,859 | | | | 25,840,014 |

| | | | | | | | | | | |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | | | | | | | | | | | |

Net realized gain (loss) on investments | | | (20,164 | ) | | | 3,411 | | | | 11,953 |

Net change in unrealized appreciation or depreciation on investments | | | (548,321 | ) | | | — | | | | — |

| | | | | | | | | | | |

Net realized and unrealized gain (loss) on investments | | | (568,485 | ) | | | 3,411 | | | | 11,953 |

| | | | | | | | | | | |